Embed Size (px)

Citation preview

1 | P a g e

Transforminglives:CanSavingsandCreditGroupmembershipworkforpeople

affectedbyHIV/AIDS?ASouthAfricanCaseStudy

Photograph1‐SaveActSCGsmembers,EasternCape(Photo:CarolynCornilsScherer)

ResearchconductedbyAnnieBarber

August,2011

CommissionedbyUniversitasForumwithpartialfundingfromFinMarkTrust.SupportfromVesperSocietyandHanefBhamjeeisgratefullyacknowledged.

2 | P a g e

Photograph 2 ‐ Research participant, Xaxazana

Abstract

ThisstudyinvestigatestheroleofSavingsandCreditGroups(SCGs)inimprovingthecoping

strategiesofpoor,ruralhouseholdsaffectedbyHIV/AIDS.Today,morethan5.6millionSouth

AfricansareHIVpositive1.Everydayaround1000ofthesepeopledie,whileatthesametime,

morethan1200becomenewlyinfected(Gow,2010).Withmoststakeholderslookingtothe

healthsectorforsolutionsthereisalackofpracticallivelihoodstrategiesforpeopletoweather

thedebilitatingshockscausedbythedisease.Theseshocksforcevulnerablehouseholdsto

employirreversiblecopingstrategiesandthreatentotraptheminpoverty.

Thisstudypresentsimportantevidenceofconsumptionsmoothingandimprovedcoping

mechanismsamongpeopleaffectedbyHIV/AIDS(PABHA)whoaremembersofSCGs.Stable

levelsofconsumptionamongparticipantssuggestthattheyaremoreprotectedfrominsecure

andvolatileflowsofincomeandaremoreabletomeetbasichouseholdneeds.Resultsindicate

thatcopingstrategieshavebeenstrengthened,andoverallvulnerabilitytotheimpactof

adverseshockshasbeencushioned.Withthistargetgroupbeinglargelytypicalofrural

populationsaffectedbyHIV/AIDSinSouthAfrica,itislikelythatthesameimpactcanbe

achievedonamuchlargerscaleandthereisthusgreatscopeforprojectreplicationinother

areas.

Keywords: Microsavings, HIV/AIDS, consumption smoothing, poor rural households

1 UNAIDS South Africa: http://www.unaids.org/en/Regionscountries/Countries/SouthAfrica/

3 | P a g e

Acknowledgement

Forconstantsupport,motivationanddiscussions,IthanktheExecutiveDirectorofSaveAct,AntonKrone.HisdedicationtothecauseofimprovingthelivesofpoorpeopleinSouthAfricaisinspiringandcommendable.Throughhisworkhehasmadeenormousimpact.

Forassistance,company,guidanceanddedicationIthanktheSaveActstaffoftheEasternCapeOffice.SimbongileDubaandNolufefeNonjeke‐Dlanjwa,youaretrulyaninspiration,thankyouforyourunwaveringenthusiasmforthisstudyevenwhenyouwerestretchedtocapacity.SamellaandGladys,thisreportcouldnothavebeencompletedwithoutyou.IamalsogratefultoSaveActKZNstaff.Yourworkinspiresmeeveryday.Thankyoutoalltheprojectparticipantswhoacceptedandtrustedmeandgavetheirtimetothisstudy.Youareachievingsomethingwonderful,pleasekeepstrivingforimprovement.

Lastly,Iwouldliketothankmyparents,IanandVickyBarber,fortheirloveandsupport.Youhavesupportedmypassionfordevelopmentfromtheverybeginning,evenwhenittakesmefarfromhome.Thankyouforlisteningtomyexcitementandsupportingmeduringthedifficultandstressfultimes.Tomyfather,yourconstantproofreadingandconstructivecriticismwasinvaluable.Tomymother,thankyouforsupportingmeinmytimesofneed.

ThiswouldnothavebeenpossiblewithoutthegeneroussupportofUniversitasandFinMarkTrust.

Acronyms

AIDS AcquiredImmune‐deficiencySyndromeARVs AntiretroviralmedicationCBOs Community‐basedOrganisationsCHBC CommunityHome‐basedCareESF EmergencySocialFundFHH Female‐headedHouseholdGBV Gender‐basedViolenceHIV HumanImmune‐deficiencyvirusIGA IncomegeneratingActivityJHH Jointly‐headedHouseholdPABHA PeopleAffectedbyHIV/AIDSPLWHA PeopleLivingWithHIV/AIDSR SouthAfricanRand(R1.00=0.15USD)SSI Semi‐structuredIndividualInterviewsSCG SavingsandCreditGroupSG (HIV/AIDS)SupportGroup

4 | P a g e

Definitions

Consumptionsmoothing:

Theabilityofahouseholdtoinsulatespendinglevelsfromdipsindisposableincomeby

borrowingandsavingsothatbasicneeds,forexamplefoodandeducation,donotsufferasa

resultofafinancialshock(MurdochinZeller,1999)andlevelsofexpendituredonotclosely

trackincomepatterns.

Stokvel:

AsavingsorinvestmentsocietythatistraditionaltoruralSouthAfrica.Membersregularly

contributeanagreedamounttoagroupfundfromwhichtheyreceivealumpsumpayment2.

Mashonisas:

LocalXhosatermfor‘loansharks’chargingoftenusuriousinterestratesofupto60%.

TableofContents1PurposeofResearch....................................................................................................................................................61.1TheModel....................................................................................................................................................................61.2TheModelandHIV/AIDS.....................................................................................................................................82LocalContext................................................................................................................................................................103Methodology..................................................................................................................................................................143.1Theparticipants.......................................................................................................................................................153.2Limitations..................................................................................................................................................................174ResultsandAnalysis……………….............................................................................................................................184.1SeasonalityAnalysis...............................................................................................................................................184.2TrendAnalysis..........................................................................................................................................................234.3LoanUsage...................................................................................................................................................................274.4HomeImprovements..............................................................................................................................................284.5Health............................................................................................................................................................................284.6ProductiveActivities...............................................................................................................................................294.7GenderDynamics.....................................................................................................................................................295Conclusion......................................................................................................................................................................316References......................................................................................................................................................................327Appendices.....................................................................................................................................................................34Appendix1..............................................................................................................................................34Appendix2..............................................................................................................................................35Appendix3..............................................................................................................................................36Appendix4..............................................................................................................................................37Appendix5..............................................................................................................................................39Appendix6..............................................................................................................................................43

2 Oxford Dictionaries: http://oxforddictionaries.com/definition/stokvel

5 | P a g e

TablesandFigures

Table Page#

Table1:SaveActImplementingPartners 9

Table2:UnemploymentRates 12

Table3:SocialGrantsReceived 12

Table4:HIVInfectionRates 13

Table5:GenderProportionsinEducation 14

Table6:ParticipantCharacteristics 16

Table7:HIV/AIDSGroupMembership 16

Table8:MostCitedHomeImprovements 28

Figure Page#

Figure1:HIV/AIDSLinkages 17

Figure2:SeasonalityAnalysisofIncome 18

Figure3:SeasonalityAnalysisofExpenditure 19

Figure4:SeasonalityofSavings 20

Figure5:SeasonalityAnalysisofCredit 21

Figure6:SeasonalityAnalysis 22

Figure7:CrisisTrendAnalysis,5YearsAgo 23

Figure8:CrisisTrendAnalysis,LastYear 24

Figure9:CrisisTrendAnalysis,ThisYear 25

Figure10:LoanUsageRatings 27

6 | P a g e

1. PurposeofResearch

ThisresearchisbasedfirmlyinthecontextoftheHIV/AIDSepidemicinSouthAfrica.The

purposeistoinvestigatetheroleofSavingsandCreditGroups(SCGs)inhelpingpoor,rural

householdsaffectedbyHIV/AIDStoachieveconsumptionsmoothingandthusimprovecoping

strategies.

Untilrecently,theAIDSepidemicinSouthAfricafacedpoliticalneglectanddenial.TheSouth

Africangovernmentrefusedtomakeantiretroviralmedication(ARVs)publiclyavailableuntil

2008‐theendofformer‐PresidentMbeki’srule.Thisneglectfedanepidemicthathasreached

disastrousproportions:todaymorethan5.6millionSouthAfricansareHIVpositive3.Thisis

morethananyothercountryintheworld.Everydayaround1000ofHIV/AIDSaffectedpeople

die,whileatthesametime,morethan1200peoplebecomenewlyinfected(Gow,2010).

TheresultofthisisnotonlyepicproportionsofpeoplelivinganddyingwithHIV/AIDS.Ithas

alsoshapedanddistortedthecountry’sresponsetotheepidemic.Withtheabsenceofmedical

treatmentavailabletothepublic,thefocusofallSouthAfricanAIDSactivismoverthelast

decadehasbeenARVrollout(ibid).Withmoststakeholderslookingtothehealthsectorfor

solutions,thereissignificantneglectofotherHIV/AIDSstrategies.Despitecommonconsensus

aroundthelinksbetweenpovertyandHIV(Donahue,2000),thereisalackofpractical

livelihoodandcopingstrategiesforpeopletoweatherthelingeringanddebilitatingshocks

causedbythedisease.

TheprincipalpolicyimplicationofthispaperisthattheroleofSCGmembershipforthecoping

mechanismsofPABHAisnotwellrecognised,andisunderutilisedinthepolicyarena.Itaimsto

demonstratehowSCGsofferanimportantstrategytomitigatetheeffectsofHIV/AIDSon

heavilyaffectedcommunitiesandhouseholds.Thiscasestudydocumentstheexperiencesofa

successfulprogramme,demonstratingthatPABHAarejustassuccessfulsaversandSCG

membersasothers.

1.1TheModel

Foundedin2005inSouthAfrica,SaveActprovidessupportfortheformationofSCGstoalmost

10,000membersacrosstwoprovinces(KwaZulu‐NatalandtheEasternCape).EachSCG

3 UNAIDS South Africa: http://www.unaids.org/en/Regionscountries/Countries/SouthAfrica/

7 | P a g e

consistsofuptotwenty‐fivememberswitheverymemberreceivingbasicfinancialeducation

beforebeginningtheirfirstsavingscycle.SaveActalsoofferstheIsiqaloenterprisecoursefor

membersaimingtodevelopanincome‐generatingactivity(IGA).

ThemodelemployedbySaveActissavings‐ledandinvolvesnoexternalcredit.Embeddedin

localknowledge,itbuildsontheoldtraditionalStokvelpracticeinruralareasbutinvolvesstrict

adherencetorulesandprocedureswithtightmonitoringandmentorshipfromSaveActField

Officers.EachSCGelectsitsownManagementCommittee,includingachairperson,bookkeeper

andkey‐holders.EverySCGformalisesitsownindividualGroupConstitutionoutliningthebasic

rulesofpractice.Tosave,memberspurchasesharesinthegroup‐thepriceofashare(normally

R50–R100)isagreedintheConstitution.Byprovidingaformalsavingsmechanismforpoor

peoplethismodelchallengesthemyththat‘poorpeoplecan’tsave’.Infact,poorpeoplesave

morefrequentlythananyothergroup,preciselybecausetheymust(Collinsetal,2009).

Memberscanpurchasebetweenoneandfivesharespermeetingbutarenotobligedto

purchaseshareseverymonth.Arecordofshare‐purchasesiskeptbyboththebookkeeper,Field

Officerandisrecordedineachmember’sindividual‘ShareBook’.Eachsavingscyclelastsfor

twelvemonthswithmembersmeetingonmonthly.Thecapitalaccumulatedthroughthe

purchasingofsharesisdistributedbetweenmembersthroughsmallloansonrequestand

approvalofthegroupthroughouttheyear.ArateofinterestdecidedintheGroupConstitution

(normally10%permonth)ischargedforeachloan.Loanscanbepaidbackoverathree‐four

monthperiod.Thetotalaccumulatedcapital,includingtheprofitsmadeonloaninterestis

sharedbetweenmembersinanannuallump‐sumaccordingtotheamountofsharesheldby

eachmember.AverageannualprofitsmadeonsavingsinSaveActgroupsare40%butcanbeas

highas80%.

8 | P a g e

Photograph3:ASaveActsharebook

EachSCGalsobuildsanEmergencySocialFund(ESF)bycontributingasmallmonthlyamount

agreedintheConstitution(usuallyR10.00).TheESFisusedtoassistgroupmembersintimesof

crisisorhardship,theexacttermsofwhicharespecifiedintheGroupConstitution.TheESFis

givenasagrantandrequiresnorepayment.Attheendofasavingscycle,anyremainingmoney

fromtheESFmaybesharedoutorkeptforthenextcycledependingonthewishesofSCG

members.

1.2ThemodelandHIV/AIDS

Inrecognitionthatthelivesoftheirclientsunfoldinacomplexandmultifacetedcontextand

thatAIDSisapartofthiscontext,SaveActmadethedecisiontopartnerwithlocalHIV/AIDS‐

orientedCommunityBasedOrganisations(CBOs)tospecificallytargetPABHA.AllofSaveAct’s

EasternCapeimplementingpartnershaveHIV/AIDSexpertise,howeverallHIV/AIDS‐linked

SCGsaretreatedlikeanyotherandaregivennoHIV/AIDS‐specificsupportfromSaveAct4.

SaveAct’simplementingpartnersareoutlinedbelow:

4 Comment made by Nolufefe Nonjeke‐Dlanjwa – Programme Co‐ordinator, Eastern Cape during an interview with the researcher, June, 2011.

9 | P a g e

Table1:SaveActImplementingPartners

Implementing Partner Activities

Masangane Treatment

Programme (MTP)

Mobilising PLWHA, SCG Promotion, Support to

PLWHA, GBV

Matatiele Advice Centre

(MAC)

SCG Promotion, Life‐skills training, Para‐legal

Support, GBV

Bathehi Ba Kgotso Youth

Organisation (BBKYO)

Mobilising Youth, SCG Promotion, Life‐skills

training, Support to PLWHA, GBV

Mt Fletcher Advice Centre

(MFAC)

SCG Promotion, Life‐skills training, Para‐legal

Support, PLWHA, GBV

Siyanakekela Community

Development (SCD)

SCG Promotion, Life‐skills training, Para‐legal

Support, PLWHA, GBV

HIV/AIDS‐affectedhouseholdsaremorelikelytofacerecurringanddebilitatingfinancialshocks

thatcanpushhouseholdsdeeperintoapovertytrap.Recurringboutsofillnessanddeatherode

thefinancialresourcesofimmediateandextendedfamiliesastheypayformultiplehospital

trips,medicalexpenses,andfuneralcosts(Donahue,2000).Thedeathorsicknessofaprincipal

breadwinneraffectsthewellbeingofthewholehouseholdaswellasanyconnectedsupporting

households.

Intheeventofanadverseshocksuchasdeathorsickness,householdswithnoeffectivesafety‐

netarelikelytoemployoneormoreofthefollowingstrategies:

Reducefoodconsumption(e.g.byskippingmealsandreducingqualityoffood);

Cutbackonnon‐emergencyhealthcosts;

Removechildrenfromschoolordelaypaymentofschoolfeesorrelatedcosts;

Sellvaluableassets;

Burdenkinship,extendedfamilyandcommunitymemberswithrequestsforassistance;

BorrowfromMashonisasatusuriouslyhighinterestrates

SCGmembershipcanhelpHIV/AIDS‐affectedhouseholdstoachieveconsumptionsmoothing

andthusavoidemployinganyofthenegativeandpotentiallyirreversiblecopingstrategies

outlinedabove.Thegoalisthathouseholdsbuilduptheirassetandsavingsbasesothat

10 | P a g e

transitoryincomeshocksdonotaffectconsumptionpatterns(MurdochinZeller,1999).SCG

membershavecheapandimmediateaccesstocreditsothattheyavoidresortingtothesaleof

assetsandborrowingatexorbitantrates,astrategywhichcoulddestroyfutureproductive

capacity(Donahue,2000).

2. LocalContext

ScopeandScale

ThisstudyisbasedonSaveAct’sEasternCapeactivitiestargetingPABHA.Basedintheremote

ruraltownofMatatiele,theEasternCapeofficeservesatotalofover3,500SCGmemberswith

oneProgrammeCoordinator,twoFieldOfficersandfivesmall‐scaleimplementingpartners,

monitoredandsupportedbySaveActstaff.

SaveActtargetedPABHAthroughstrategicpartnershipwithlocalHIV/AIDSCBOs.SCGswere

formedontopofexistingHome‐basedCarer(HBC)andSupportGroups(SG).TheseSCGsthen

greworganically,allowingsomenewmemberstojoin.SaveActsupportsfourSGsandsixHBCs,

servingtengroupswithatotalof158members5.Threegroupswereformedin2008,five

formedin2009twoin20106.Averagegroupmembershipisfifteenpeople,withagenderratio

of88%female:12%male.SCGsareinsixlocalsub‐villagelevelareasintheAlfredNzoand

UkhahlambaDistrictsoftheEasternCapeincluding,Matatiele,Xaxazana,Khoapa,Mpharane,

KhubetsoanaandDikamoreng.TheseareasfallundertheMatatieleandElundiniLocal

Municipalities.

5 While these nine groups are openly affected by HIV/AIDS, SaveAct staff members are aware of large numbers of other SCG members in non‐HIV/AIDS‐specific groups who are affected by the disease5. This study however, focuses on the nine HIV/AIDS‐specific SCGs. 6 A full list of groups can be found in the annex.

11 | P a g e

PovertyLevels

With74%ofitspopulationlivingbelowthepovertyline,theEasternCapehasthehighestrate

ofextremepovertyinSouthAfrica7.IntheAlfredNzodistrict,82.3%8ofthepopulationlivein

poverty.ThisismuchhigherthaneventheProvincialnorm.Povertylevelsarefoundtoberising

intheEasternCape,fromaprovincialaverageof71%in2004(HumanSciencesResearch

Council)to74%in20119.

TherootcausesofhighpovertyratesintheEasternCape,aformerdesignated‘Homeland’10,are

linkedtothepoliciesandpracticesoftheapartheidregime.Eveninthepost‐liberationera,rural

areasintheEasternCapeshowtheeffectsofapartheidplanningandarecharacterisedby

economicmarginalisationandadistinctlackofservicesandinfrastructure.Thisisalsoinlarge

partduetothesheerisolationandgenerallylowereconomicpotentialofthearea.

7 Alfred Nzo District Municipality Annual Report, 2011 8 Ibid 9 Ibid 10The Eastern Cape wasone of ten tribally basedself‐governinghomelands called bantustans, provided with massively inferior services and resources compared to those of ‘White South Africa’.

12 | P a g e

Unemployment

Table2:UnemploymentRates

South Africa %

General unemployment rate 24

Alfred Nzo and Ukhahlamba

Unemployment 75

Not generating any income 69.8

Earn more than R1600/mth 6.7

Depend on govt. social grants 33.5

Source:AlfredNzoDistrictMunicipalityAnnualReport,2011,StatisticsS.Africa,LatestKeyIndicators,2010

Entrepreneuriallevelsarelowandmosthouseholdsrelyonseasonalmigrantworkand

remittances11.

WithSouthAfrica’shighgeneralunemploymentrate,theonlyviablelivelihoodoptionforthe

poorinAlfredNzoandUkhahlambaisself‐employment.Thisincludesmainlyseasonalpetty

IGAsandsmall‐scaleagriculture.InSouthAfrica’sdominantformaleconomywithmarkets

monopolisedbylargewholesaleandretailfoodandcommoditysectors,eventhemost

successfulsmall‐scaleproducersexperiencesignificantobstaclestoparticipatinginthese

markets.ManyhouseholdsinAlfredNzoandUkhahlambaexperiencesevereeconomic

instability,withperiodicshocksthatleadtodebilitatingspiralsofdebtandhunger.Financial

literacylevelsarelowandmanyfallpreytotheeconomicallycripplinginterestratesofloan

sharks.

SocialConditions

Table3:SocialGrantsReceived

Social Grants Received

Child Support Grant (including foster grant)

Old Age Pension

People with HIV/Aids with low CD4 counts. Source:AlfredNzoDistrictMunicipalityAnnualReport,2011

11Alfred Nzo District Municipality Annual Report, 2011

13 | P a g e

Table4:HIVInfectionRates

HIV infection Rates

% of total population

Alfred Nzo 26

Ukhahlamba 19 Source:Ibid

TheareaexperienceshighlevelsofHIV/AIDSandassociatedopportunisticinfectionssuchas

Tuberculosis,resultinginlowlifeexpectancylevels.Accesstoqualityhealthcareisscarceandis

madedifficultbythevastnessofterrain,pooraccessroadsandlackofpublictransport.

HIV/AIDSsupporthasbeenparticularlypoor.Therearenowstepsinplacetotrytoredressthe

situation,howeveralargeportionofthosewhoshouldbeonARVsarenotcurrentlyon

treatment.

GenderRelations

The2011WorldHealthSurveyrevealedfallinglifeexpectancyforSouthAfricanwomento55

yearsfrom59in2000and68in199012.Whereaslifeexpectancyisconsistentlyrising

throughouttherestoftheworld,ithasbeenfallingforSouthAfricanwomenfortwodecades.

ThisislargelyattributedtohighHIVinfectionrates.

TheHIV/AIDSinfectionriskisexacerbatedforwomenbyhighlevelsofgenderinequalityand

gender‐basedviolence(GBV).ArecentsurveyconductedbytheDepartmentofSocial

DevelopmentforAlfredNzorevealeddisturbinglyhighlevelsofacceptanceofGBVasthenorm

incomparisonwithattitudesinotherareas13.ThissuggeststhatGBVisaseriousproblem.GBV

andgenderinequalitymakeswomenlargelypowerlesstoensuresafesexandcondomusage,

potentiallyacceleratingthespreadofHIV.Therearealsohighlevelsoffemale‐headed

households(FHHs)(58%14),withwomenandchildrencarryingasignificantburdenofthe

effectsoftheepidemicandothersocialills.

GenderinequalityisfurtherhighlightedinAlfredNzoandUkhahlambabyslightbut

consistentlyhigherratesofmalesineducationthanfemales.Thesignificanceofthisbecomes

apparentwhenitishighlightedthatfemalesconstituteahigherproportionofthelocal

population.Seebelow:

12WHO, World Health Survey, 201113Alfred Nzo Department of Social Development Nodal Baseline Survey, 200814Ibid

14 | P a g e

Table5:GenderProportionsinEducation

District Proportion of the population %

Alfred Nzo Male 45 Female 55

Ukhahlamba Male 45 Female 55 Proportion in Secondary Education

Alfred Nzo Male 52 Female 48

Proportion in Tertiary Education Alfred Nzo Male 53

Female 47 Source:AlfredNzoDepartmentofSocialDevelopmentNodalBaselineSurvey,2008

ServiceDelivery

The2007AlfredNzoSocialDevelopmentbaselinerevealedthat:97%ofhousingisinformal;

93%ofhouseholdsdonothavestandardsanitation;93%ofhouseholdshavenorefuse

collection;90%donotreceivestandardwaterservices;35%donothaveelectricityforlighting;

and,housesare9%morelikelythaninanyotherareatobeheadedbyafemale.

3. Methodology

Ofthe158membersserved,aone‐thirdsamplesizeoffifty‐threeSCGmemberswasselected.

Whileresearchisconductedwithindividuals,theeffectsofHIV/AIDSspanwholehouseholds

andfamilynetworksandthereforequestionsareconcernedwithhouseholdaswellas

individuallevelanalysis.ResearchwasconductedinthefieldfromMarch–June,2011insix

initialsessions,twoofwhichconsistedofmorethanoneSCG,followedupbyrepeatedsitevisits

andSemi‐structuredIndividualInterview(SSI)sessions.

Researchtechniquesfollowamainlyqualitativeapproach.Thelivesofthetargetpopulationare

embeddedinthecomplex,messyandunpredictablerealitiesoftheeveryday.Theresearcher

recognisesthatthetargetgroupof‘PABHA’isnotasinglehomogenoussectorofsocietywitha

prefabricatedsetofcommonneeds.Whileasagroup,PABHAmayfacesomecommon

challengesandshocks,memberswillmeetadiverserangeofchallengeswithadiverserangeof

responses.Theaimofthisstudyisthereforetoaskboth‘what?’and‘why?’Thus,while

15 | P a g e

quantitativestudyhasspecificadvantages,inthiscaseitwouldfailtocapturethediversityof

experiencesandthecomplexunderlyingreasonsbehindthedata.

Fourprincipalresearchtoolswereemployedwithallfifty‐threeparticipants:seasonality

analysis,crisistrendanalysis,loanusagerankingandgeneralquestionnaires.Afurthertwenty‐

oneoftheseparticipantswererandomlyselectedforsemi‐structuredindividualinterviews

(SSIs).EachtoolusesParticipatoryRuralAppraisal(PRA)methodstouncoverthecomplexity

andmessinessbehindthecopingstrategiesofPABHA.Thetwocomplementarytools,

seasonalityanalysisandcrisistrendanalysis,wereusedbasedonastudyofconsumption

smoothingbyHögman(2009)15andformedthebasisaroundwhichtheothermethodswere

chosen.Thesetoolswerecombinedwithfieldobservationsbytheresearcherandin‐depth

discussionsandinterviewswithkeystaffmembersandFieldOfficers.

Whileseasonalityanalysisisusefulfortrackingmonthlyflowsofincome,expenditure,credit

andsavings(ibid)(SeeAppendix1),crisistrendanalysisprovidesatimereference,allowingthe

researchertotrackchangesintheuse/availabilityofcertainfinancialinstrumentsoverfive‐

years(Appendix2).Theseexercisesarebasedonthepremisethatifexpenditurepatterns(used

hereasaproxyforconsumption)nolongercloselyfollowincomelevelsandSCGservicesare

becomingmoreandmoredominantinrelationtootheroptions,itcanbeconcludedthatSCG

membershiphascontributedtoconsumptionsmoothing(Högman,2009).Theloanusage

exerciseoffersanindicationofthedifferentneedsandprioritiesofparticipants(Appendix3)

andthegeneralquestionnaireextractsmoredetailfrommembersregardingtheeffectsofSCG

membership(Appendix4).SSIswereopen‐endedtoallowparticipantstospeakfreelyofthe

aspectsofSCGmembershipmostimportanttothem(Appendix5).

Allresearchactivitieswereconductedinlocallanguages,mainlyXhosaandSotho,withtheaid

ofalocaltranslator.SessionswerecarriedoutincommunitymeetingplacesandSSIswere

carriedoutonacasebycasebasisinlocationsconvenientforparticipants.

3.1TheParticipants

CompleteSample:

ResearchtookplaceinfourofthesixprojectareaswithsevenofthetenrelevantSCGs.Selection

reliedontimingofgroupmeetings,attendanceandpracticalityissues.Oftheparticipants,88%

15 This analysis is based on the model of consumption smoothing developed by Aghion and Murdoch (2005).

16 | P a g e

werefemaleand12%weremale,reflectingtheoverallgenderdimensionsofallrelevant

groups.Allhouseholdsinthisstudyarepoororverypoorandarereliantonacombinationof

socialgrants,remittances,sporadicpiecejobsandsmallIGAs.AllareaffectedbyHIV/AIDSand

arevulnerabletoshocksrelatedbutnotlimitedtotheepidemic.

Semi‐structuredIndividualInterviews(SSIs):

Effortwasmadetoincludeparticipantsfromasmanyprojectareasaspracticallypossibleand

consistedofmembersfromthreeofthesixareas.Participantcharacteristicscanbeoutlinedas

follows:

Table6:ParticipantCharacteristics

Participant Characteristics Total %

Female 86%

Male 14%

In 2nd savings cycle 52%

In 3rd savings cycle 48%

From FHH 48%

From JHH 52%

Averagehouseholdsizeis6members,thelowestbeingonememberandthehighestbeing

eleven.

Table7:HIV/AIDSGroupMembership

HIV/AIDS Group Membership Total

Home‐based Carer 48% Support Group Member 4%

Ex‐support Group Member 34%

No HIV‐related Group 14%

17 | P a g e

HIV/AIDSLinkages:

33%wereopenlyHIV‐positive16themselves.14%weresupportingsomebodywithHIV

internally,and52%weresupportingoneormultiplepeopleinexternalhouseholds.47%of

householdswereeitherfullyorpartiallysupportingchildrenorphanedbyAIDS.Thespecific

breakdownofHIV/AIDSlinkagesisoutlinedbelow:

Figure1–HIV/AIDSLinkages

Source:Author’sowndata–valuesrepresentnumbersofpeopleaffected.

3.2Limitations

Amajorobstaclewasthatoflanguageandwhileatranslatorwasused,theauthormustbe

sensitivetoissuesofmisinterpretation.Anadditionalchallengewastheisolationandpractical

conditionsinthearea.Withlimitedresourcesandtime,thisresearchwascarriedoutoverthe

harshwintermonthsturningsimpleissuessuchastraveltoremoteareasandattendance

levels17intosignificantobstacles.Whilemakingresearchconditionsdifficult,thistimingoffered

valuableinsightintothelivesofPABHAattheirmostdifficulttimeoftheyear–atimethatis

rarelydocumentedfirst‐handbyoutsiders.Anadditionalconcernwasthatgroupmembers

wouldbereluctanttodiscusssensitiveissuesofHIV/AIDS,moneyanddeath.Thisissuewas

overcomebyattemptstogainthetrustofparticipantsthroughaseriesofmeetingsand

16 The actual number could be higher as two participants declined to state their HIV‐status and three declined

to identify exactly who was affected. 17 Considering the target group of PABHA, the winter months proved difficult as some participants were suffering from illness and unable to attend meetings. To overcome this, a small series of home visits were made.

79

7 64 3 2

12

0

5

10

15

20

Self Sister Brother Cousin / Aunt

Child Other / Extended Family

Unknown HHs Fully / Partially

Supporting Orphan

18 | P a g e

introductionsfromtrustedSaveActFieldOfficers.Contrarytoexpectations,theresearcher

foundthatthemajorityofparticipantswereopenandwillingtodiscusssensitiveissuesand

wereeagertoshareexperiences,bothpositiveandnegative.

Eachoftheselimitationshasinevitablyimpactedthisstudy,howevereveryeffortwasmadeto

minimisethisimpact.

4Results

ResultsfromthegeneralquestionnairesandSSIswillbereferredtoforbackgroundand

additionaldetailthroughoutallfollowingresultssections.

4.1SeasonalityAnalysis‐ConsumptionSmoothing

Figure2‐SeasonalityAnalysisofIncome

Source:Author’sowndata–includesallgroupincometotals.ForfulltableofallresultsseeAppendix1.

Incomeflowsvaryquitesubstantiallythroughouttheyear.ThroughSSIsanddiscussions,most

participantsidentifiedmonthlysocialgrantpaymentsasincomesources,toppedupbyirregular

moneyfromremittances,localpiecejobsand(seasonalandsporadic)IGAs.Somemembers

reliedonasmallsalaryfromworkasahome‐basedcarer,whichispaidirregularlyand

erraticallybytheDepartmentofSocialDevelopment.IncomeishighestinMarch,June,

September/OctoberandDecember.BetweenMarchandMaysomevegetableandhome‐grown

0

20

40

60

80

100

120

140

160

Jan Feb March April May June July Aug Sept Oct Nov Dec

Month of the Year

19 | P a g e

cropharvestsoccurcontributingtoaslightriseinincome.Manyinformalstokvelgroupshave

anannualpay‐outbetweenOctoberandDecember.ManySCGshare‐outsalsooccuraroundthis

time.

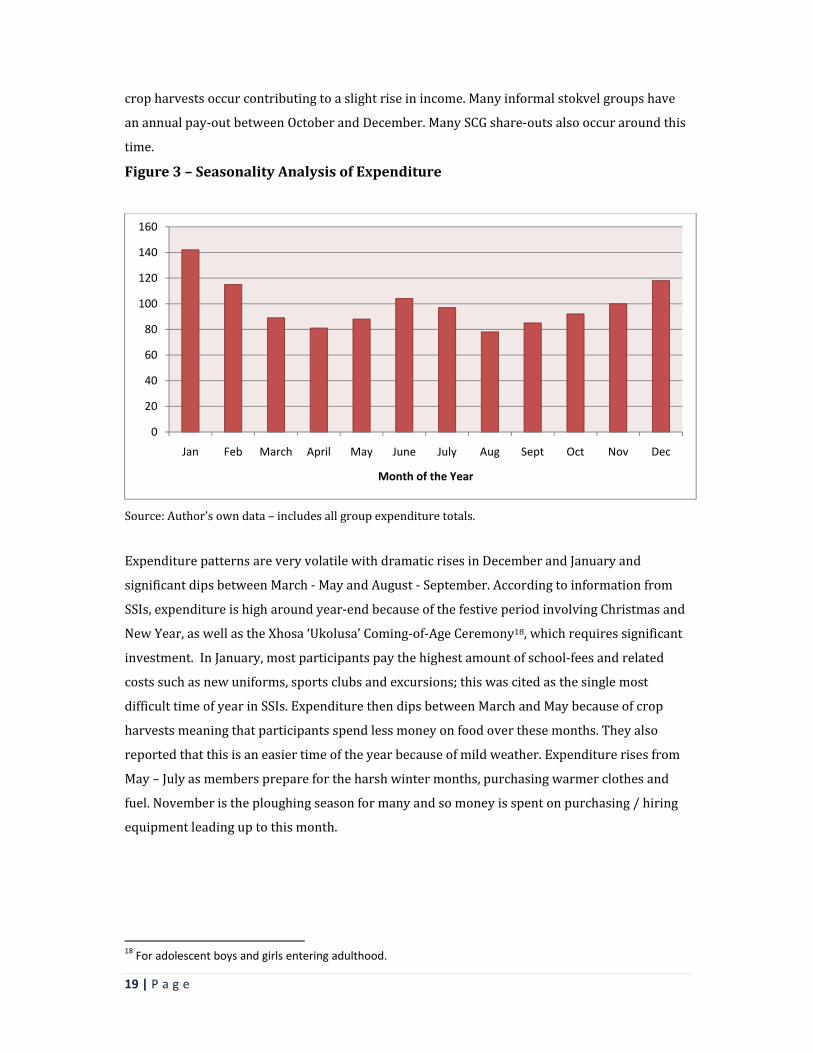

Figure3–SeasonalityAnalysisofExpenditure

Source:Author’sowndata–includesallgroupexpendituretotals.

ExpenditurepatternsareveryvolatilewithdramaticrisesinDecemberandJanuaryand

significantdipsbetweenMarch‐MayandAugust‐September.Accordingtoinformationfrom

SSIs,expenditureishigharoundyear‐endbecauseofthefestiveperiodinvolvingChristmasand

NewYear,aswellastheXhosa‘Ukolusa’Coming‐of‐AgeCeremony18,whichrequiressignificant

investment.InJanuary,mostparticipantspaythehighestamountofschool‐feesandrelated

costssuchasnewuniforms,sportsclubsandexcursions;thiswascitedasthesinglemost

difficulttimeofyearinSSIs.ExpenditurethendipsbetweenMarchandMaybecauseofcrop

harvestsmeaningthatparticipantsspendlessmoneyonfoodoverthesemonths.Theyalso

reportedthatthisisaneasiertimeoftheyearbecauseofmildweather.Expenditurerisesfrom

May–Julyasmemberspreparefortheharshwintermonths,purchasingwarmerclothesand

fuel.Novemberistheploughingseasonformanyandsomoneyisspentonpurchasing/hiring

equipmentleadinguptothismonth.

18 For adolescent boys and girls entering adulthood.

0

20

40

60

80

100

120

140

160

Jan Feb March April May June July Aug Sept Oct Nov Dec

Month of the Year

20 | P a g e

Figure4–SeasonalityAnalysisofSavings

Source:Author’sowndataincludingallgroupsavingstotals.

Itisinterestingtonotethatwhilesavingslevelscouldbeexpectedtocloselytrackincome,the

datalineistheleastvolatileofall,followingarelativelystablepatternthroughouttheyear.This

givesanindicationofthecommitmentofthetargetgrouptotheirsavingsactivities.Itisnot

clearfromthisresearchwhetherthisisinanywayconnectedtoHIV/AIDSlinkagesandthusthe

potentiallyincreasedneedtodevelopaneffectivesafety‐net.Savingslevelscanbeseentorise

graduallytowardstheyear‐end.Manyparticipantsexplainedthattheybeginsavingatthistime

inanticipationofhighexpenditureinJanuaryandasexpected,thisisthemonthwiththelowest

levelsofsavings.

Photograph 4 ‐ Research participant, Mpharane

0

20

40

60

80

100

120

140

Jan Feb March April May June July Aug Sept Oct Nov Dec

Month of the Year

21 | P a g e

Figure5–SeasonalityAnalysisofCredit

Source:Author’sowndataincludingallgroupcredittotals.

Creditlevelsarehighlyvolatile,risingsubstantiallyinJanuaryandthendippingtorelatively

lowerlevelsthroughoutmostofthefollowingmonths.Creditlevelscouldbeanticipatedtobe

higharoundyear‐endhoweverthisisnotthecase.Levelsactuallydroparoundthistime.In

SSIs,manymembersexplainedadesirenottotakeloansduringthefestiveperiodin

anticipationofhighlevelsofexpenditureinJanuary.Manypredictdifficultyinrepaymentatthis

timeandsorefrainfromtakinglargeloansaroundDecember,savingmoneyfromshare‐outs

andloansearlierintheyearinstead.ThisisadvicethatisreiteratedinSaveAct’sfinancial

educationtohelpmembersavoidrepaymentdifficulties.Asexpected,creditlevelsrise

dramaticallyinJanuarytocoverschoolfeesandrelatedcosts.Theyalsoriseslightlyjustbefore

andduringthewintermonthswhenSSIrespondentsreportspendingextraonmedicalcosts,

warmclothes,fuelandfood.

0

20

40

60

80

100

120

140

160

Jan Feb March April May June July Aug Sept Oct Nov Dec

Month of the Year

22 | P a g e

Figure6–SeasonalityAnalysisofIncome,Expenditure,Savings,andCredit

Source:Author’sowndataincludingalltotals.

Flowsofeconomicactivityvarygreatlyovertheyear.Creditis,perhapssurprisingly,themost

volatileofalldatalines.Thisvolatilitycouldbeattributedtothefactthatmanyparticipantstake

credittodealwithafinancialcrisis,thenatureofwhicharead‐hocandunpredictable.Asnoted

above,themoststabledatalineisthatofsavings,thisissurprisinglyunrelatedtoincomelevels.

Anexplanationforthisisthepossibilitythat,asreportedinsomeSSIs,memberssaveasmall

proportionofloansincaseofanemergencyordifficultyinrepayingthustoppingupsavings

levelsevenwhenincomelevelsarelow.Asignificantresultisthatexpenditurelevelsdonot

closelyfollowincomeflows.Infactduringlowincomeperiods,expenditureisatitshighest

(January)andspendinglevelsdipwhenincomelevelsarerelativelyhighfromMarch–May.

Thisishighlyindicativeofconsumptionsmoothing,suggestingthatparticipantsareinsome

wayprotectedfromthevolatilityofincomelevelsandstrongfinancialpressures.

ThisevidenceissupplementedbytherecurringthemeinSSIsof‘control’.Theabilitytoplanand

savewascitedasoneofthethreemostimportantbenefitsofSCGmembershipby29%of

participants.AsNomsaDidi(SCGmember,Xaxazana)states;“Icannowplanandbudgetforthe

futuresohavemorecontrolovermylife”.Whiletheutilityofcreditwasfrequentlyunderlined,

theadvantagesofsavingappearedtobeequallyappreciated.Membersdescribedthecoping

strategiestheyareabletoemploytoprepareforroutinelydifficulttimes.AsZandileMalgas

0

20

40

60

80

100

120

140

160

Seasonality Analysis

Sum of Income

Sum of Expenditure

Sum of Savings

Sum of Credit

23 | P a g e

commented,“thereisnomoreuncertaintyattheendofeachmonthbecauseIknowIwillhave

enoughmoney”.Whenaskedaboutfrequencyofloanuse,anaveragefigureof5.2loansper

memberwasgiven.14%ofparticipantsreportedhavingdifficultyrepayingcredit.Thesefigures

suggestthatloansarebeingtakenonaregular,butnotoverwhelmingbasis.

4.2TrendAnalysisofCreditUse–CrisisMitigation

Figure7–Crisistrendanalysis:FiveYearsAgo

Source:Author’sowndata,totalofallgroupsforfiveyearsago.Seeappendix2forfullresultstable.

Fiveyearsagofamilywasthemostfrequentlyusedsourceoffundsintimesofcrisis.Thisis

followedbyuseofinformalgroupssuchasstokvelsandburialsocieties.Whenaskedabout

interestratesonmoneyborrowedfromstokvels,responsesrangedfrom30%–40%‐afigure

ashighassomeloansharksor‘Mashonisas’.Mashonisaswerethethirdmostfrequentlyused

financialinstrumentindealingwithadverseshocks,withinterestratescitedasaround50%‐

60%permonth.Fourthmostfrequentlyusedwasownsavings,thisbacksupthetheorythat

poorpeoplecananddofrequentlysave.Formalbankloanservicesarefifthat13%.When

discussed,itbecameclearthatparticipantsincludedlocal‘microcredit’companiesinthissector,

manyofwhichchargeinterestratesofupto40%.SaveActserviceswerenotusedasthisis

beforeitsexistenceinthearea.

Family39%

Loan Shark17%

SAVEACT Loan0%

SAVEACT Social Fund0%

Formal Bank Loan

11%

Informal Savings Group (high interest)21%

Sale of Assets0%Own Savings

12%

24 | P a g e

Figure8–CrisisTrendAnalysis:LastYear

Source:Author’sowndata–totalofallgroupsforlastyear

Inresultsregardinglastyear,themostfrequentlyusedfinancialserviceintimesofcrisisis

SaveActCredit.Thisisfollowed

bytheSaveActEmergency

SocialFundat17%,thenfamily

at16%.Usageofinformal

savingsgroupssuchasstokvels

remainsrelativelyhigh,falling

from21%to12%betweenthis

yearandfiveyearsago.Theuse

ofMashonisashasdropped

dramaticallytojust1%,ashas

useofformalbankloans(2%).

Uselevelsofownsavings

Family16%

Loan Shark1%

SAVEACT Loan39%

SAVEACT Social Fund17%

Formal Bank Loan2%

Informal Savings Group12%

Sale of Assets2%

Own Savings11%

Last Year

Photograph 5 ‐ Research Participant, Xaxazana

25 | P a g e

remainsimilarandsaleofassetshascreptupfrom0%to2%.

Figure9–CrisisTrendAnalysis:ThisYear

Source:Author’sowndata–totalofallgroupsforthisyear.

Resultsfrom‘thisyear’and‘lastyear’areverysimilar.At38%,SaveActloansarethemost

frequentlyusedfinancialinstrumentintimesoffinancialcrisis,thistimetheyare,however,

followedbyfamilyat15%.TheSaveActSocialFundusageappearstodropto13%.When

discussedinSSIsitbecameclearthatthisisbecausetheFundisonlypaidoutforcertaincrises

stipulatedintheGroupConstitutionandwithinterviewstakingplaceinthemiddleofasavings

cycle,circumstancesqualifyingmembersasfundrecipientsmaynothaveoccurred.Useof

Mashonisasremainslowat1%,asdoesthatofformalbankloans‐2%.Usageofotherinformal

savingsgroupsandownsavingsremainsstable.

Theaboveresultsindicatethatcrisiscopingstrategieshavechangedsignificantlyamong

participantsoverfiveyears,withSaveActSCGservicesbecomingthemostdominant.A

significantresultisthesubstantialdecreaseinuseofMashonisasfrom17%tojust1%.Another

significanttrendisthedecreaseoffrequencyatwhichSCGmembersborrowfromfamily,which

Family15%

Loan Shark1%

SAVEACT Loan38%

SAVEACT Social Fund

13%

Formal Bank Loan2%

Informal Savings Group

15%

Sale of Assets4%

Own Savings12%

This Year

26 | P a g e

fellfrom39%to15%.Nowat38%,usagelevelsofSaveActcreditseemtohavedirectlyreplaced

thoseofborrowingfromthefamily.Itisnoteworthythatuselevelsofownsavingshave

remainedrelativelyconstant,suggestingthatthesehouseholdsmaysavebothwithinand

outsideoftheirSCGs.

SSIsrevealedthevalueandsomeofthereasonsbehindthesechanges.Arecurrentthemewas

thediminishingneedforMashonisas.Whenaskedtoidentifythethreemostbeneficialeffectsof

SCGmembership,theoverallmostfrequentlycitedbenefitwas‘freedomfromdebts’.Thiswas

identifiedby43%ofparticipants,with24%citing‘lowinterestrates’,19%‘self‐reliance’and

14%‘accesstomoneyinacrisis’.52%claimedthattheynolongeruseMashonisasand33%

reportednolongerhavingtoborrowfromfamilyorneighbours.28%reportnowbeingableto

assistfamilyandcommunitymembersfinanciallywhereasbeforetheywerestronglydependent

onthem.83%oftheseparticipantswereopenlyHIV‐positiveandattributedthischangedirectly

toSCGmembership.Anadditional52%explicitlycommentedthattheyfeelself‐sufficientand

contributemoretotheirhousehold,againdirectlyattributingthistoSCGactivities.

AnothersignificanttrendwasamoreintelligentuseofMashonisas.MembersuseMashonisas

orotherhigh‐interestmoneylendersintheeventofacrisisoccurringinbetweenSCGmeetings.

TheythenimmediatelyrepaywithaSaveActloanfromtheirnextmeeting.Inthiswaytheyare

takingadvantageofloansharkconveniencebutavoidingpaymentofusuriousinterestrates.

ThisdatasuggeststhatSCGmembershipisallowingPLWHAtoemploystrongercoping

mechanismsintimesofcrisisandavoidstrongrelianceonfamily,neighboursorhigh‐interest

debts.SSIdiscussionsrevealthatitisalsoeasingtheburdenonhouseholdssupportingoneor

morepeoplelivingwithHIV/AIDS,ordealingwiththedeathofarelativefromanAIDS‐related

illness.AsSaveActserviceshavebecomedominantandrepresenttheonlyapparentmajor

changeinthetargetgroup’saccesstofinancialservices,itcanbedeductedthatthesechangesin

behaviourcanbelargelyattributedtoSCGmembership.

27 | P a g e

4.3LoanUsage19

Figure10–LoanUsageRatings

Source:Author’sowndata–totalofallloanusageratings

Themostfrequentuseofcreditisforinvestmentsinhomeimprovements.Thisfindingis

supportedbyquestionnaireresultsshowingthat94.2%ofallparticipantshavespentmorethan

R1000onhomeimprovementsinthepasttwelvemonths.Thenextmostfrequentpurposeisto

coverschool‐feesandrelatedcosts.Thisisfollowedcloselybyexpenditureonhealth‐related

costsandisespeciallysignificantforPLWHAwhoarelikelytohavehighoutgoingsrelatedto

health.Alsoimportanttonoteisthatrepaymentofpreviousdebtsconstitutesthefourthmost

frequentuseofcredit.Transportalsoconstitutesasignificantproportionofcreditusage.When

discussedinSSIs,participantsexplainedthatthislargelycoveredtransporttohospitalsinan

emergency,monthlytransporttocollectARVmedicationandtransporttoschools.Thetotalof

creditspentonIGAs,bothnewandexisting,isjointfifth.Livestockandfoodaretheleast

frequentcategoriesofcreditusage.

19 This tool was changed after the first research session took place meaning that this tool represents a sample size of 44 rather than the full 53.

Food9%

Repayment of Previous Debts

12%

Livestock3%

New IGA3%

Existing IGA7%

School Fees14%

Home Improvements

19%

Medicines / Doctor /

Hospital fees13%

Transport10%

Other e.g Blankets, Fuel, Airtime,

10%

28 | P a g e

Thisdatashowsthatcreditisusedtocoverbasicneedssuchasfood,transport,schoolingand

healthcosts.Theneedforcredittomeetthesebasicneedsindicatesthehighvulnerabilitylevels

ofclients.Italsoindicatesthattheconsumptionsmoothingevidentintheaboveseasonality

analysisresultsissignificantlyrelatedtotheaccesstocheapandimmediateSCGcredit.Results

doshowsignsofmoreproductiveactivitiestakingplace,suchasinvestmentsinhome

improvements,newandexistingIGAs,livestockandrepaymentofpreviousdebts.Thissuggests

increasesineconomicstability.

4.4HomeImprovements

AccordingtoKHANA(2011),homeimprovementwillnotnormallytakepriorityforapoor

householdunlesstherearebothincreasedfundsflowingintothehouseandconfidencethat

theywillbemaintained.Thislevelofinvestmentindicatesasubstantialincreaseinhousehold

economicstability.InSSIs,participantsnotedthathomeimprovementsleadtoanincreased

feelingofwellbeing.ThosewhoareHIV‐positivethemselvesorsupportingPLWHAcommented

thatabetter,saferandwarmerhomeenvironmentwasaffectingtheirhealthinapositiveway.

Table8:MostCitedHomeImprovements

Plastering work to protect against cold

Purchase of water tanks

Repairing leaks and ceilings

Purchase of appliances e.g. cooking stove and fridge

Purchase of household furniture e.g. beds, wardrobes, cupboards

4.5Health

WhenaskedabouttheextracostsassociatedwithHIV/AIDS,SSIparticipantscitedfoodas

primary.Extraexpenditureonheatingandwarmclothesduringwintertopreventexposureto

coldwasalsomentioned,aswellasincreaseddoctor/medicalfees.Thesecostsareallrelatedto

adviceon‘livingpositively’withHIV/AIDS20.Resultsfromthegeneralquestionnaireshowthat

88%ofparticipantsfeelmoreableto‘livepositively’withHIVorsupportHIV‐positive

20 SG and HBC group members receive advice from an HIV/AIDS CBO on how to ‘live positively’ with HIV – this

centres mainly around diet, home environment, avoiding exposure to cold and being open about status.

29 | P a g e

dependentstodoso.38%ofSSIparticipantscited‘improvedhealth’asthemostimportant

benefitofSCGmembership,with90%reportingimproveddietandnutritionsincejoiningthe

SCGandtwoparticipantsdirectlynotingthattheyhadexperiencedariseinCD4‐cellcount

levels.

4.6ProductiveActivity

Thisstudyconsidersrepaymentofpreviousdebts‘productiveactivity’asitallowsparticipants

toescapepotentialpovertytraps.Throughdebtrepayment,householdscanregainfinancial

controlandbegintoemploymoreproductivecopingstrategies.With10%ofallcreditbeing

usedtoinvestinIGAs,itisclearthatthistargetgroupareusingSCGmembershipforproductive

activity.GeneralquestionnaireresultsrevealedthathalfofallparticipantshaveusedSCG

membershiptoeitherinitiateorexpandanIGA.Thisevidenceissupportedbyinformationfrom

SSIs,with52.3%ofparticipantsreportinginvolvementinanIGAandmanyrelyingdirectlyon

theirmicro‐businessactivitiesforsurvival.AsZodwaDodo,singleHIV‐positivemotheroffour,

states;“mybusinessismyfamilybecausewithoutitwewouldnotsurvive”.91%ofSSI

participantsclaimedtohavesignificantlyexpandedexistingIGAssincejoiningtheirSCG,

although9%reportednochangeandonewomanvoicedconcernsregardingmarketsaturation.

With3%ofallloansbeingusedtostartanewIGA,itappearsthatSCGmembershiphasbrought

aboutsomepositivechangesinlevelsofproductiveactivity,althoughthisislimited.

4.7GenderDynamics

Questionsfiveandeightofthegeneralquestionnaireregardingself‐confidenceandhousehold

statusweredesignedtocaptureasenseofthegenderdynamicsamongparticipants,aswellas

potentiallyreflectingonissuesofHIV/AIDSstigma(seeappendix4).100%ofparticipants

respondedpositivelytobothquestions.Theseweretheonlytwoquestionstoreceivesuch

overwhelminglypositiveresponsessuggestinglargeimpactinthesedomains.Recurrentthemes

inSSIswithbothmenandwomencentredonincreasesinself‐confidenceandself‐esteem,with

manyattributingthesechangestoincreasingself‐sufficiency.

Inter‐householdRelationships

Themajorityofparticipantsreportedincreasedlevelsofrespect.Justunderhalfofthewomen

intheSSIsamplewereunmarriedandreportedbeingprincipalhouseholddecision‐makers.All

marriedwomenreportedeithersharingthisrolewithhusbandsorplayingalimitedpartinthe

30 | P a g e

process.Somefemaleparticipantsrelayedstoriesofincreasedparticipationinhousehold

decisionmaking.Theyattributedthischangetothefactthathusbandsnoticedconcretechanges

inhouseholdlivingstandardsstemmingfromSCGactivities.Othersreportedhavingalways

sharedthisresponsibilityequallywiththeirhusbands,whileasmallpercentagereportedno

significantchanges.Overall,theexperiencesofdifferentparticipants,bothmaleandfemale,are

diverseandhighlydynamic.OnecommonimpactofSCGmembershiponallparticipants

however,isasenseofincreasedself‐worthandself‐confidence.Forsomeparticipantsthishas

thepotentialtotranslateintoconcretechangesinrelationshipswhileforothersthisisamore

difficultprocess.

Extra‐householdRelationships

DuringSSIs,participantswereaskedaboutstatusinthecommunity.95%ofparticipants

reportedanimprovedstatusasaresultofSCGactivities.Formanyparticipants,thiscentred

aroundnolongerbeingdependentonothersandbeingabletomakevisibleimprovementsto

housingwithoutincurringlargedebts.

Photograph 6 ‐ Noamen Nongenzi with her 6 children and sister in their new kitchen, Khoapa

31 | P a g e

5. Conclusions:

ThesituationsofpoorruralhouseholdsaffectedbyHIV/AIDSareextremelycomplexand

difficulttograspatasinglepointintime.Inspiteofthis,thisstudypresentsimportantevidence

ofconsumptionsmoothingandimprovedcopingmechanismsamongPABHA.Withresultsfrom

thetrendanalysiscoupledwiththeseasonalityanalysisandotherdata,itisreasonableto

assumethatthechangesweredueinasignificantmeasuretoSCGactivities.

Resultsclearlyshowthatlevelsofexpendituredonotcloselytrackincomeflows.Thereisalsoa

stabledemandforsavingandcheapcreditamongstparticipants.Usageofloanssharksand

otherhighinterest‐chargingmoneylendershasdecreaseddramatically,ashastheincidenceof

borrowingfromfamilymembers.Inturn,useofSCGloansintimesofcrisishasincreased

substantially,becomingthedominantfinancialinstrumentforparticipants.Theseresults

suggestthatriskreductionactivitiesamongPABHAhavebeenstrengthened.Thetargetgroup

areavoidingirreversiblecopingstrategiesandaregraduallyengaginginmoreproductive

activities.Stablelevelsofconsumptionsuggestthattheyaremoreprotectedfrominsecureand

volatileflowsofincomeandarethusmoreabletomeetbasicneeds.Resultsindicatethatthe

impactofadverseshockshasbeencushionedandcopingstrategiesstrengthened,thusoverall

vulnerabilitytopovertyhasdecreasedamongparticipants.

Consumptionsmoothingandstrengthenedriskreductionactivitieshaveresultedinpositive

effectsonthehealthofparticipantsaswellastangibleimprovementsinlivingconditions.In

addition,improvementsinwellbeingareevident,withqualitativeevidencethatPABHAofboth

gendershavebeenempoweredthroughthisexperience.Thereisalsofurtherqualitative

evidencethatgenderrelationsareshiftingslightlyasaresultofSCGmembership,withwomen

experiencingmorerespectandmorefrequentlytakingpartinhouseholddecision‐making

processes.

Asignificantindicationofprojectsuccessisthelargeandconstantlyincreasingdemandfor

SaveActservicesamongparticipantsandthefactthat98%ofallPABHAhaverecommendedthe

programmetoarelative,friendorneighbour.Demandinthetargetareaiscurrentlytoohighfor

SaveActtomeetandplanstoexpandandspreadtheprojecttonewareasareunderway.With

thistargetgroupbeinglargelytypicalofruralpopulationsaffectedbyHIV/AIDSinSouthAfrica,

itislikelythatthesameimpactcanbeachievedonamuchlargerscaleandthereisthusgreat

scopeforprojectreplicationinotherareas.

32 | P a g e

6. References

AlfredNzoDepartmentofSocialDevelopmentNodalBaselineSurvey,StrategyandTactics(2008)http://www.sarpn.org.za/documents/d0003004/Alfred_Nzo_DSD_nodal_baseline.pps[Accessed18/05/2011]

AlfredNzoDistrictMunicipalityAnnualReport,2011,derivedfromStatisticsSouthAfrica:CommunitySurvey2007:http://www.andm.gov.za/site/index.php/2011/05/annual‐report/[Accessed18/05/2011]

Cameron,Edwin,(2005)WitnesstoAIDS,Tafelberg.ISBN:0624041999

Collins,DandLeibbrand,M,(2007)TheFinancialImpactofHIV/AIDSonPoorHouseholdsinSouthAfrica,AIDS2007,21(suppl7):S75–S81Availableonlineat:http://www.financialdiaries.com/files/CollinsLeibbrandtAIDS217.pdf[Accessed:24/05/2011]

Collins,Morduch,RutherfordandRuthven,(2009)PortfoliosofthePoor:HowtheWorld'sPoor

Liveon$2aDay,PrincetonUniversityPress

deAghion,ArmendárizandMorduch,Jonathan,(2005),TheEconomicsofMicrofinance,

Cambridge,TheMITPress,pp.1‐346

Donahue(Thompson),Jill,(2000)MicrofinanceandHIV/AIDS:…It’sTimetoTalk,USAIDhttp://www.microfinancegateway.org/gm/document‐1.9.29149/2740_file_02740.pdf

Fourie,PercheandSchoeman,(2010),DonorAssistanceforAIDSinSouthAfrica:ManyActors,MultipleAgendas,StrategicreviewforSouthernAfrica,vol.32,no.2,pp.93‐120

Gow,Jeff,(2010)TheHIV/AIDSEpidemicinAfrica:ImplicationsforU.SPolicy,HealthAffairs,http://content.healthaffairs.org/content/21/3/57.full

33 | P a g e

Högman,Alve,(2009)MicrosavingsEffectsonConsumptionSmoothing:ACaseStudyofSouthAfrica,ThesisWorkD,UppsalaUniversity,DepartmentofEconomics,Sweden

Hosegoodetal,(2007),Revealingthefullextentofhouseholds’experiencesofHIVandAIDSinruralSouthAfrica,SocSciMed,Vol65(6):1249–1259

Eriksen,Kayse,(2009)AnAssessmentoftheRoleofSocialInsuranceFundsinMicro‐Savings:TheCaseofSAVEAct,UniversityofKwaZuluNatal,Durban,SouthAfrica

KHANA,(2011)EvaluationofMicrofinancePilotProjectforHIV‐affectedFamilies,USAID,http://www.aidsalliance.org/includes/Publication/Microfinance_Pilot_Project.pdf[Accessed03/06/2011]

MCNEILL,(2009),‘CONDOMSCAUSEAIDS’:POISON,PREVENTIONANDDENIALINVENDA,SOUTHAFRICA,AfricanAffairs,108/432,353–370

StatisticsSouthAfrica,LatestKeyIndicators,2010http://www.statssa.gov.za/keyindicators/keyindicators.asp[Accessed18/05/2011]

WHO,WorldHealthSurvey,(2011),http://www.who.int/gho/mortality_burden_disease/life_tables/life_tables/en/index.html[Accessed18/05/2011]

Zeller,Manfred,(1999)TheRoleofMicro‐FinanceforIncomeandConsumptionSmoothing,InternationalFoodPolicyResearchInstitute,Availableonlineat:http://www.microfinancegateway.org/gm/document‐1.9.25376/20683_20683.pdf[Accessed:12/07/2011]

34 | P a g e

7. Appendices:

Appendix1:

Seasonality

Analysis

Thistoolgrounds

thecasestudyina

seasonal

understandingof

someofthe

patterns,risksand

financialpressures

facedbyPABHA

andhowmembers

usetheirSCGsand

otherservicestorespondtothese.Itallowstheresearchertomonitortherelationshipbetween

income,expenditure,savingsandcreditandtotrackthestabilityofconsumption(expenditure)

levelsovertheperiodofayear.Itisasimplediagrammingexercisecompletedbyparticipants

themselves.Astraightforwardchartisdrawnonalargepieceofpapershowingallthemonths

oftheyearandthefoursections:income,expenditure,savingsandcredit.Theparticipantsare

thenaskedtoindicatescoresforeachmonthforthefourfactorswithaminimumofzeroanda

maximumofthree.Thisprovidesasimplerankingofeachsectionforeachmonthoftheyear.

Appendix1 SeasonalityAnalysisandresults

Appendix4 GeneralQuestionnaireandresults

Appendix2 CrisisTrendAnalysisandresults

Appendix5 Semi‐structuredIndividualInterviews

Appendix3 LoanUsageExerciseandresults

Appendix6 IndicatorTree

Photograph 6 Example of a seasonality analysis chart (in Xhosa) before use.

35 | P a g e

SeasonalityAnalysisresults,allgrouptotals:

Month SumofIncome SumofExpenditure SumofSavings SumofCredit

Jan 84 142 97 121

Feb 82 115 103 77

March 105 89 105 70

April 99 81 108 88

May 98 88 106 81

June 103 104 104 83

July 96 97 104 60

Aug 100 78 108 66

Sept 112 85 110 73

Oct 111 92 115 76

Nov 107 100 121 65

Dec 133 118 120 65

Appendix2:

CrisisTrendAnalysis

Thecrisistrendanalysisprovidesadetailedinsightintotheoptionsandservicesavailableto

PABHAintimesoffinancialcrisis.Italsoprovidesatimereference,allowingtheresearcherto

trackchangesintheuse/availabilityofcertainfinancialinstrumentsoverafive‐yearperiod.

Togetherwithapilotgroup,theresearcherdevelopedalistofthefinancialservicesavailable

andusedbythetargetgroup.Participantsareaskedtoscoretheoptionsusingthesamesimple

rankingsystememployedintheseasonalityanalysistoindicatetheusagelevelsofdifferent

services.Thematrixincludesatimeaxisdividedintothreesections:thisyear,lastyear,andfive

yearsago.Thisexerciseisbasedonthepremisethatif:a)SCGservicesarebecomingmoreand

moredominantinrelationtootheroptions,and:b)Expenditurelevelsdonotcloselytrack

incomepatterns,itcanbeconcludedthatSCGmembershiphascontributedtowards

consumptionsmoothing(Högman,2009).

36 | P a g e

CrisisTrendAnalysisresults,allgrouptotals:

SourceofMoney GroupOne GroupTwo

Timeline BeforeSaveAct

LastYear

ThisYear

BeforeSaveAct

LastYear

ThisYear

Family 14 3 3 15 7 6

LoanShark 0 0 0 3 0 0

SAVEACTLoan 0 18 6 0 21 23

SAVEACTSocialFund 0 6 0 0 7 4

FormalBankLoan 3 0 0 2 0 0

InformalSavingsGroup(highinterest)

15 0 0 0 2 1

SaleofAssets 0 0 0 0 1 1

OwnSavings 0 0 0 9 6 8

SourceofMoney GroupThree GroupFourTimeline Before

SaveActLastYear

ThisYear

BeforeSaveAct

LastYear

ThisYear

Family 13 6 6 6 6 3

LoanShark 3 0 3 10 0 0

SAVEACTLoan 0 11 14 0 20 18

SAVEACTSocialFund 0 6 7 0 8 0

FormalBankLoan 3 0 0 5 4 5

InformalSavingsGroup(highinterest)

0 7 2 6 6 16

SaleofAssets 0 3 8 0 0 3

OwnSavings 0 9 0 0 0 1

SourceofMoney GroupFive GroupSixTimeline Before

SaveActLastYear

ThisYear

BeforeSaveAct

LastYear

ThisYear

Family 0 3 0 37 25 26

LoanShark 9 0 0 11 3 0

SAVEACTLoan 0 12 9 0 42 42

SAVEACTSocialFund 0 9 9 0 18 18

FormalBankLoan 3 3 0 8 0 0

InformalSavingsGroup(highinterest)

3 9 6 22 15 18

SaleofAssets 0 3 0 0 0 0

OwnSavings 0 0 0 16 22 25

Appendix3:

LoanUsageExercise

Thisdiagrammingexerciseagainfollowsthesamerankingsystemoutlinedabove.Together

withthepilotgroup,theresearcheroutlinedalistofpossibleloanusages,forexample,food,

homeimprovements,schoolfees.Participantswerethenaskedtorankeachoptiontoindicate

37 | P a g e

howtheyspendloanstakenfromtheirSCG.Basedonthepremisethatloansaretakento

supplementexistingdisposableincome,thisexercisegivesaninsightintothedifferentneeds

andprioritiesofparticipantsandhowSCGmembershipisaffectingtheirabilitiestomeet

certainneeds.

LoanUsageRankingresults,allgrouptotals:

LoanUse Food RepaymentofPreviousDebts

Livestock NewIGA ExistingIGA

GroupOne

n/a n/a n/a n/a n/a

GroupTwo

5 7 3 0 15

GroupThree

6 13 3 8 6

GroupFour

17 16 9 4 9

GroupFive

7 11 0 2 2

GroupSix

7 11 0 2 2

LoanUse SchoolFees

HomeImprovements

Medicines/Doctor/Hospitalfees

Transport Other

GroupOne

n/a n/a n/a n/a n/a

GroupTwo

16 21 14 18 6

GroupThree

17 19 6 8 10

GroupFour

14 18 16 13 6

GroupFive

10 15 12 5 12

GroupSix

10 15 12 5 12

Appendix4:GeneralquestionnairesAsimplequestionnairewasadministeredtoallparticipantsinordertoextractmoredetailfrom

membersregardingtheeffectsofSCGmembership.Forthis,indicatorswereselectedto

measurekeyeffectsofSCGmembershipforPABHA,questionsdirectlyrelatingtothese

indicatorswerethendeveloped.Pleaseseebelowforacopyofthequestionnairesusedandsee

Appendix6foracopyoftheindicatortree.

38 | P a g e

39 | P a g e

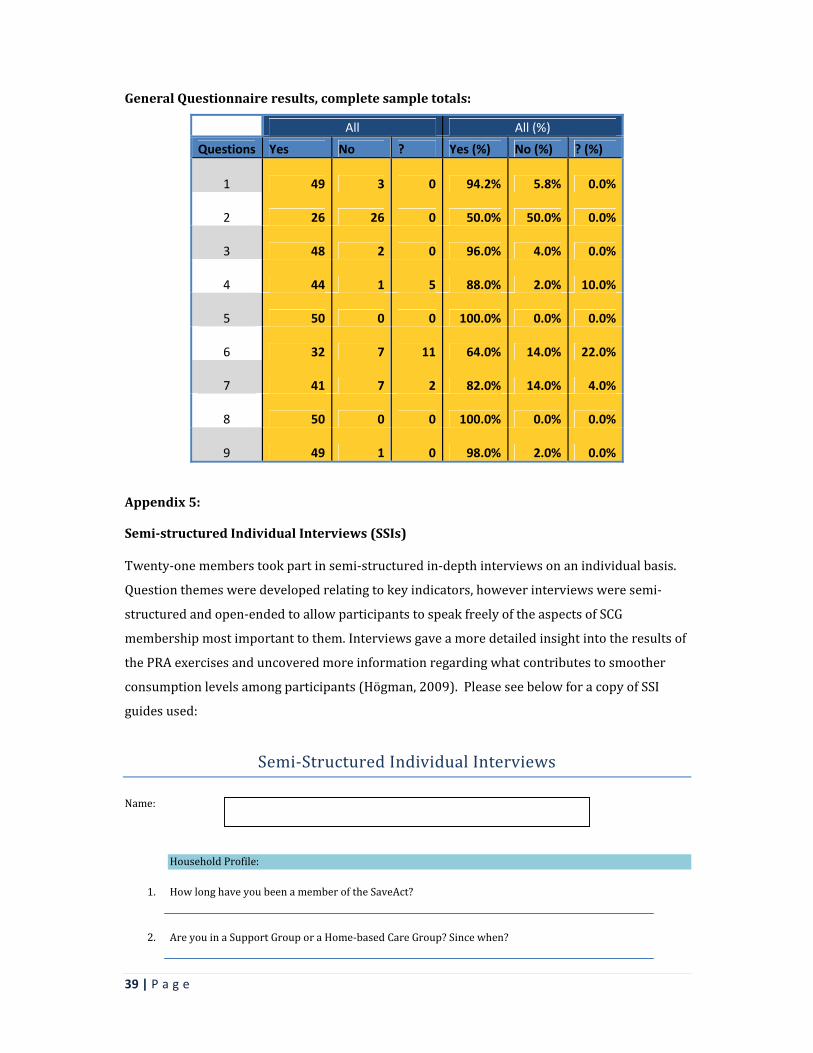

GeneralQuestionnaireresults,completesampletotals:

All All (%)

Questions Yes No ? Yes (%) No (%) ? (%)

1 49 3 0 94.2% 5.8% 0.0%

2 26 26 0 50.0% 50.0% 0.0%

3 48 2 0 96.0% 4.0% 0.0%

4 44 1 5 88.0% 2.0% 10.0%

5 50 0 0 100.0% 0.0% 0.0%

6 32 7 11 64.0% 14.0% 22.0%

7 41 7 2 82.0% 14.0% 4.0%

8 50 0 0 100.0% 0.0% 0.0%

9 49 1 0 98.0% 2.0% 0.0%

Appendix5:

Semi‐structuredIndividualInterviews(SSIs)Twenty‐onememberstookpartinsemi‐structuredin‐depthinterviewsonanindividualbasis.

Questionthemesweredevelopedrelatingtokeyindicators,howeverinterviewsweresemi‐

structuredandopen‐endedtoallowparticipantstospeakfreelyoftheaspectsofSCG

membershipmostimportanttothem.Interviewsgaveamoredetailedinsightintotheresultsof

thePRAexercisesanduncoveredmoreinformationregardingwhatcontributestosmoother

consumptionlevelsamongparticipants(Högman,2009).PleaseseebelowforacopyofSSI

guidesused:

Semi‐StructuredIndividualInterviews

Name:

HouseholdProfile:

1. HowlonghaveyoubeenamemberoftheSaveAct?

2. AreyouinaSupportGrouporaHome‐basedCareGroup?Sincewhen?

40 | P a g e

3. Whatactivitiesdoyoudointhegroup?

4. Howmanypeopleareinyourhousehold?

5. Howmanychildrendoyouhave?Whatages?Doyoucareforanychildrenthatarenotyourown?

6. IfSINGLE,butwithchildren,isthefatheralive?Doesheprovideanyfinancialsupport?

7. Isanyoneelseinthehousehold?Example,sister/mother/mother‐in‐law/grandchildren/cousins/aunts?

8. Doyoufinanciallysupportanyotherfamilymembersorfamilymember’schildren?

9. Dothechildrengotoschool?

10. DoyoufeelmoreabletopayschoolexpensessincejoiningSaveAct?

11. Whoistheheadofthehousehold?

12. Whoisthemainearnerinthehousehold?Whatdotheydotoearnmoney?HIV/AIDSProfile:

13. Areyouyourself,oranyoneinyourextendedfamilyaffectedbyHIV/AIDS?Thisinformationwillbekeptconfidential

14. Areyou/personaffectedbyHIVtakingARVmedication?((Whynot?))

15. HowdoyougettothehospitaltocollectARVs?Whopaysforthetransport?Howmuchdoesitcost?

16. CanyouthinkofanyextraexpensesthataredirectlyrelatedtoHIV/AIDS?

17. DoesHIV/AIDSstopyou/yourfamilymemberwithHIVfromworking/takingpartinsmallincome‐generatingactivities?

18. HaveyouoranyoneinyourfamilyhadanAIDS‐relatedillnessinthelast12months?

19. Haveyoulostafamilymember(includingextendedfamilymembers)toAIDSoranothersickness?

20. Haveyoureceivedanyemotionalsupportinthelast12months?Fromwho?

21. Haveyouhadanynegativeexperienceswhenpeoplefindoutthatyou/someoneinyourfamilyhave/hasHIV/AIDS?Examples?

41 | P a g e

22. Doyouspendalotofmoneyeachmonthonmedicalexpenses?LoanUsageprofile:

23. Howmanytimesdoyouborrowmoney(onaverage)fromyourgroupin1year?

24. Whendidyoulasttakealoanfromthegroup?

Did you use that loan to? Please tick

Invest in an income generating activity?

Lend to a family member / friend?

Make home improvements?

Buy furniture?

Pay school costs?

Save for an emergency?

Pay funeral costs?

Buy medication / doctor fees?

Pay for transport?

To repay another loan / debt?

OTHER? Please state

25. Haveyoueverhadanydifficultyrepayingyourlastloan?Whatwasthereasonforthis?

26. Doesbeingsick/badhealtheverpreventyoufromparticipatinginthesavingsgroup?EconomicProductivityProfile:

27. Overthelast12monthshaveyouusedaloantoinvestinanincome‐generatingactivity?Ifyes,whatdidyoudo?Ifno,whatstopsyoufromstartingasmallbusiness/whatarethemainobstacles?

28. Doyouevergetsickandhavetotakeabreakfromanincomegeneratingactivity?

29. Wasthereeveratimewhenyoudidn’thaveenoughmoneytocarryoutthesmallbusinessactivity?

30. Ifyes,howlongdidthislastfor?Whatcausedthis?

31. HasyourbusinessgotbiggersincejoiningtheSCG?Wellbeing/EmpowermentProfile

32. DoyoufeelthatbeingamemberofSaveActhelpsyou/personaffectedbyHIVtofollowadvicefromMasanganeto‘livepositivelywithHIV/AIDS’? Ifyes,inwhatway?Pleasegiveexamples?

42 | P a g e

33. Duringthepast12months,hasyourhousehold’sdietworsened,gotbetterorstayedthesame?

34. Whatisthemostdifficulttimeoftheyear?Whyisitthemostdifficult?

35. Howdoyoucopeduringthedifficulttimeoftheyear?

36. Howmanymealsdoyoueatperday?

37. Isthismorethanbeforeyoustartedparticipatinginthesavingsgroup?

38. Doyoufeelthatyourhouseholdstatushasimprovedsinceyoujoinedthesavingsgroup?Canyougiveanexample?

39. Ifmarried,howhastherelationshipwiththehusbandchangedsincejoiningtheSCG?How?

40. Doyoumakemoredecisionsinthehousenow?

41. Doyoufeelmorerespectedinthecommunity–byyourneighbours,friendsandextendedfamily?

42. DoyouhavemorehopeforthefuturesincejoiningtheSCG?

43. DoyoufeelthatyoursupportnetworkhasgrownstrongersinceyoujoinedtheSCG?Doyoufeelclosertothepeopleinthegroupforexample?

44. Whatdoyouplantodowiththeshare‐outmoneyfromthisyear?

45. DoyouplantojoinanSCGagainnextyear?Crisisprofile

46. Haveyouhadafinancialcrisisinthepast12months?Examples:funeral,sickness…

47. Didyoueatlesswell/lessregularlyasaresultofthiscrisis?

48. Didyouhaveanoutstandingloanatthetimethatyouexperiencedthelastcrisis?

49. Ifyes,wereyouabletokeepupwithrepaymentsordidyouhavetodefault?Whathappened?

43 | P a g e

50. Haveyouorsomeoneelseinyourgroupeverusedthesocialfund?Howdidithelp/whatwasitusedfor?

51. Whatarethebest3thingsaboutSaveAct?

52. Isthereanythingwecanchangetomakethingsbetter?

Appendix6:

Indicators

AnamountofmorethanR1000spentonhome‐improvementswasselectedasonekeyindicator

ofincreasedfinancialwellbeing.Thisisasignificantindicatorbecausethislevelofinvestmentis

notusuallypossibleunlessthereisasubstantialincreaseinhouseholdeconomicstability.

AccordingtoKHANA(2011),homeimprovementwillnotnormallytakepriorityforapoor

householdunlesstherearebothincreasedfundsflowingintothehouseandconfidencethat

theywillbemaintained.

PleaseseebelowforacopyoftheIndicatorTreedevelopedforthisstudy:

Didyouuse….? PleaseTickMashonisa?

SaveActLoan

SaveActSocialFund

OtherhighinterestloanfromStokvel?

BurialSociety?

Sellproperty/householdpossessions?

Usesavingsinthehome?

Leavetheareatofindemployment?

Sendchildrentostaywithrelatives?

Usemoneythatwasmeantforthesmallbusinessactivity?

ReducespendingonFood?

Reducespendingonschoolfees?

Reducespendingonotherthings?OTHER?Pleaseexplain

44 | P a g e