Embed Size (px)

Citation preview

High transport costs are a barrier to trade—The costs of international transport servicesare a crucial determinant of a developing coun-try’s export competitiveness. Shipping costsoften represent a more binding constraint togreater participation in international trade thantariffs and other trade barriers. Across econ-omies, a doubling of shipping costs is associ-ated with slower annual growth of more thanone-half of a percentage point. Transport costsdetermine the potential access to foreign mar-kets, which, in turn, explains up to 70 percentof variations in countries’ gross domestic prod-uct (GDP) per capita.

—reflecting geography and income—Transport costs depend on a mixture of geo-graphic and economic circumstances. Adversegeographic locations and low-income levels—the latter being associated with poor infra-structure and low traffic volumes—pose an in-herent challenge for many countries’ trade anddevelopment prospects—at least in the shortto medium term.

—but also competitive forces in service marketsPublic trade barriers and private commercialpractices hamper the provision of internationalmaritime and air transport services. Policies to-ward maritime transport, such as cargo reser-vation and limitations on the provision of portservices, often protect inefficient service pro-viders and unduly restrain competition. At the

same time, competition restraining practicesamong shipping lines and port terminal opera-tors around the world pose the risk that thebenefits of government reforms will be cap-tured by private firms. International air trans-port is one of the services sectors most pro-tected from international competition. Thecurrent regime of bilateral air service agree-ments largely denies access to efficient outsidecarriers. International airline alliances, whileenhancing network efficiency, can also be detri-mental if they impede effective competition.

Policy reform can lower costs—In most countries, policy can make better useof existing transport resources and signifi-cantly improve the efficiency of services. At thedomestic level, targeted infrastructure invest-ments, regional cooperation on transportation,and trade facilitation initiatives can play animportant role in improving the transportcompetitiveness of exporters. As discussed inchapter 3, liberalizing services policy can pro-duce substantial cost reductions and widen theavailability and choice of services. The prepon-derance of anticompetitive practices by trans-port service providers also demands the de-velopment of efficiency-oriented competitionpolicies.

—and multilateral policies can besupportive of domestic reformsMultilateral negotiations on transport servicesunder the General Agreement on Trade in Ser-vices (GATS) Agreement have, so far, not un-

97

Transport Services:Reducing Barriers to Trade

4

leashed substantial liberalization, nor havecountries bound existing policies to gain cred-ibility in their domestic reforms. Indeed, thenegotiations on maritime transport were theonly post–Uruguay Round services negotia-tions that completely failed. International airtransport services are largely outside the scopeof the GATS. The new round of services ne-gotiations offers the possibility of creating arules-based services regime for maritime trans-port, as well as an opportunity to develop aframework under which a multilateral regimefor air transport services could be phased in.Moreover, the multilateral trading system canplay a useful role in developing procompeti-tive regulatory principles for the transport sec-tor, and in fostering international cooperationon competition policy matters more generally.

High transport costs penalize exports

High transport costs push down profitsand wagesThe efficiency of transport services greatly de-termines the ability of firms to compete in for-eign markets. For a small economy—for whichworld prices of traded goods are largelygiven—higher costs of transportation feed intoimport and export prices. To remain competi-tive, exporting firms that face higher shippingcosts must pay lower wages to workers, acceptlower returns on capital, or be more produc-tive. The pressure on factor prices and produc-tivity is even higher for industries with a highshare of imported inputs. In these cases, smalldifferences in transport costs can easily deter-mine whether or not export ventures are at allprofitable. In developing countries, for labor-intensive manufacturing industries such as tex-tiles, high transport costs most likely translateinto lower wages, directly affecting the stan-dard of living of workers and their dependents.

The cost structures of firms are equally af-fected by the quality of transport services. If ser-vices are unreliable and infrequent, or if a coun-try lacks third party logistics providers who

efficiently handle small shipments, firms arelikely to maintain higher inventory holdings atevery stage of the production chain. The costsof financing large inventories can be significant,especially in countries with high real interestrates. Gausch and Kogan (2001) find that in-ventory holdings in the manufacturing sector in developing countries are two to five timeshigher than in the United States, and estimatethat cutting inventory levels in half could reduceunit costs of production by over 20 percent. Atthe wholesale and retail levels, firms dependgreatly on high quality transport services in dis-tributing products to geographically dispersedmarkets. For example, seamless transport ser-vices were critical to Kodak’s decision to inte-grate once-separate national warehousing oper-ations in the Mercosur countries into one tradebloc–wide operation located in Brazil, thus reap-ing economies of scale in distribution.1

Long journeys have a similar effect. Theydelay payments if goods are exported on acost, insurance, and freight (c.i.f.) basis or im-porters may demand a time discount if goodsare delivered free on board (f.o.b.). If productsare perishable (such as food) or subject to fre-quent changes in consumer preferences (suchas high-fashion textiles), longer journeys leadto additional losses in terms of a product’sshortened lifetime in the export market. Box4.1 illustrates the complex logistical arrange-ments that ensure the timely delivery ofKenyan cut flowers to European consumers.One recent estimate, based on comparisons be-tween air and ocean freight rates for U.S. im-ports, puts the per day cost for shipping de-lays at 0.8 percent of the value of trade formanufactured products. Only a small fractionof these costs can be attributed to the capitalcosts for the goods during the time they are onboard the ship.2 Delivery time is found to havea more pronounced effect for imports of inter-mediate products (Hummels 2000), suggestingthat the fast delivery of goods is crucial for themaintenance of multinational vertical productchains. Quality aspects of transportation arethus likely to be an important factor in the lo-cation decisions of multinational companies.

G L O B A L E C O N O M I C P R O S P E C T S

98

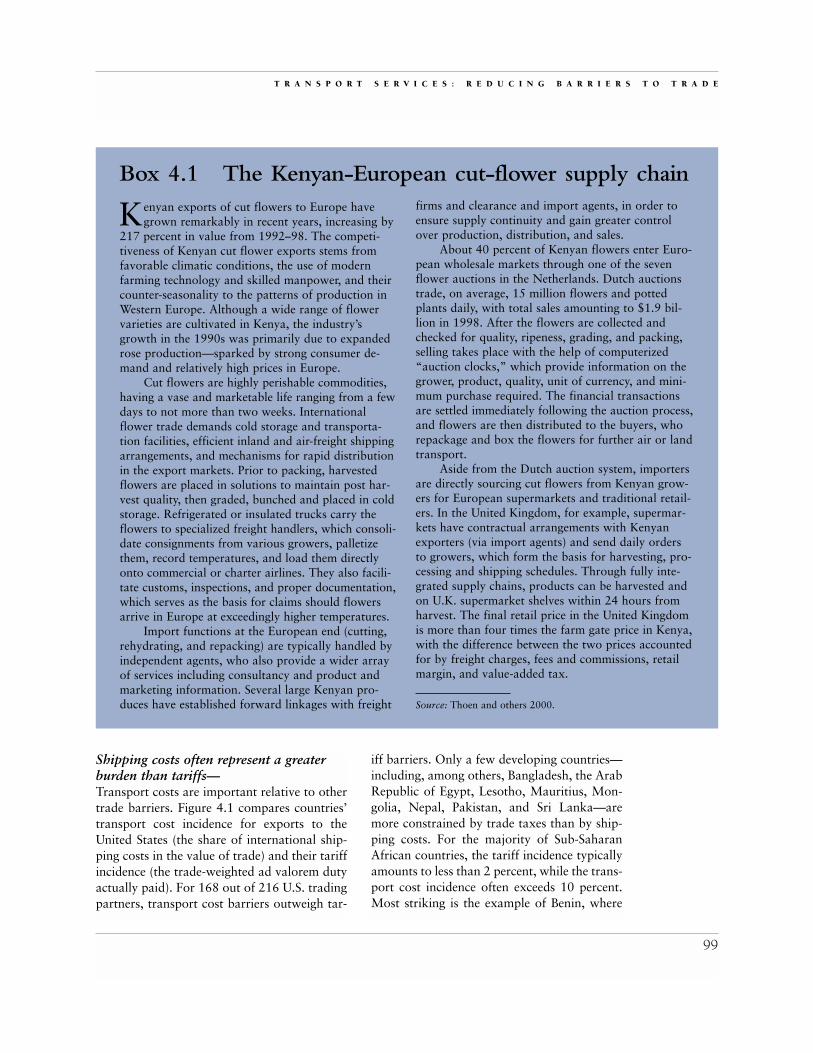

Shipping costs often represent a greaterburden than tariffs—Transport costs are important relative to othertrade barriers. Figure 4.1 compares countries’transport cost incidence for exports to theUnited States (the share of international ship-ping costs in the value of trade) and their tariffincidence (the trade-weighted ad valorem dutyactually paid). For 168 out of 216 U.S. tradingpartners, transport cost barriers outweigh tar-

iff barriers. Only a few developing countries—including, among others, Bangladesh, the ArabRepublic of Egypt, Lesotho, Mauritius, Mon-golia, Nepal, Pakistan, and Sri Lanka—aremore constrained by trade taxes than by ship-ping costs. For the majority of Sub-SaharanAfrican countries, the tariff incidence typicallyamounts to less than 2 percent, while the trans-port cost incidence often exceeds 10 percent.Most striking is the example of Benin, where

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

99

Kenyan exports of cut flowers to Europe havegrown remarkably in recent years, increasing by

217 percent in value from 1992–98. The competi-tiveness of Kenyan cut flower exports stems fromfavorable climatic conditions, the use of modernfarming technology and skilled manpower, and theircounter-seasonality to the patterns of production inWestern Europe. Although a wide range of flowervarieties are cultivated in Kenya, the industry’sgrowth in the 1990s was primarily due to expandedrose production—sparked by strong consumer de-mand and relatively high prices in Europe.

Cut flowers are highly perishable commodities,having a vase and marketable life ranging from a fewdays to not more than two weeks. Internationalflower trade demands cold storage and transporta-tion facilities, efficient inland and air-freight shippingarrangements, and mechanisms for rapid distributionin the export markets. Prior to packing, harvestedflowers are placed in solutions to maintain post har-vest quality, then graded, bunched and placed in coldstorage. Refrigerated or insulated trucks carry theflowers to specialized freight handlers, which consoli-date consignments from various growers, palletizethem, record temperatures, and load them directlyonto commercial or charter airlines. They also facili-tate customs, inspections, and proper documentation,which serves as the basis for claims should flowersarrive in Europe at exceedingly higher temperatures.

Import functions at the European end (cutting,rehydrating, and repacking) are typically handled byindependent agents, who also provide a wider arrayof services including consultancy and product andmarketing information. Several large Kenyan pro-duces have established forward linkages with freight

Box 4.1 The Kenyan-European cut-flower supply chainfirms and clearance and import agents, in order toensure supply continuity and gain greater controlover production, distribution, and sales.

About 40 percent of Kenyan flowers enter Euro-pean wholesale markets through one of the sevenflower auctions in the Netherlands. Dutch auctionstrade, on average, 15 million flowers and pottedplants daily, with total sales amounting to $1.9 bil-lion in 1998. After the flowers are collected andchecked for quality, ripeness, grading, and packing,selling takes place with the help of computerized“auction clocks,” which provide information on thegrower, product, quality, unit of currency, and mini-mum purchase required. The financial transactionsare settled immediately following the auction process,and flowers are then distributed to the buyers, whorepackage and box the flowers for further air or landtransport.

Aside from the Dutch auction system, importersare directly sourcing cut flowers from Kenyan grow-ers for European supermarkets and traditional retail-ers. In the United Kingdom, for example, supermar-kets have contractual arrangements with Kenyanexporters (via import agents) and send daily ordersto growers, which form the basis for harvesting, pro-cessing and shipping schedules. Through fully inte-grated supply chains, products can be harvested andon U.K. supermarket shelves within 24 hours fromharvest. The final retail price in the United Kingdomis more than four times the farm gate price in Kenya,with the difference between the two prices accountedfor by freight charges, fees and commissions, retailmargin, and value-added tax.

Source: Thoen and others 2000.

exports faced duties equivalent to 0.6 percentof total exports, but shipping costs represented22.7 percent of trade. Amjadi and Yeats (1995)confirm that freight rates for African exportsto the United States are considerably higherthan on similar goods originating in othercountries—contributing to the region’s lacklus-ter trade performance over the last two orthree decades.3

In interpreting the relative importance oftransport costs and tariffs, several pointsshould be kept in mind. First, the freight ratecalculations, based on c.i.f/f.o.b. comparisons,understates the true door-to-door shippingcost, because only the international leg of thetransport journey is considered. The impor-tance of port and inland transportation costsvary substantially by country and exporter lo-cation, but can take up as much as two-thirdsof the total door-to-door costs (see below). Sec-ond, the U.S. tariff schedule is lower comparedto other countries, and exporters face otherpolicy-induced barriers to trade besides tariffs.4

Indeed, for some product groups, restrictionsimplied by standards or domestic regulationsrepresent a bigger obstacle to trade than importtaxes. Third, it is somewhat arbitrary to lookonly at transport services and ignore the costsof other producer services critical to the supplyof foreign markets. High costs of communica-tions, legal assistance, or export finance, forexample, represent other sources of inefficien-cies that may erode exporters’ competitive-ness.5 Finally, transport costs—as distinct fromtariffs—cannot be brought down to zero.

One recent estimate finds that a doublingof the ad valorem freight rate leads, on aver-age, to a fall in aggregate import values be-tween five- and six-fold.6 These are rough cal-culations, however, and the effect is likely tovary substantially across countries and indus-tries. Much depends on the degree to whichhigher shipping costs are directly passed on toconsumer prices. Another factor is the pricesensitivity of final demand and the degree towhich imports from one location can be sub-stituted with imports from another location,or from domestic sources. If final demand ishighly price sensitive, and goods from differ-ent locations are good substitutes, small changesin shipping costs can have a substantial effecton bilateral imports.7

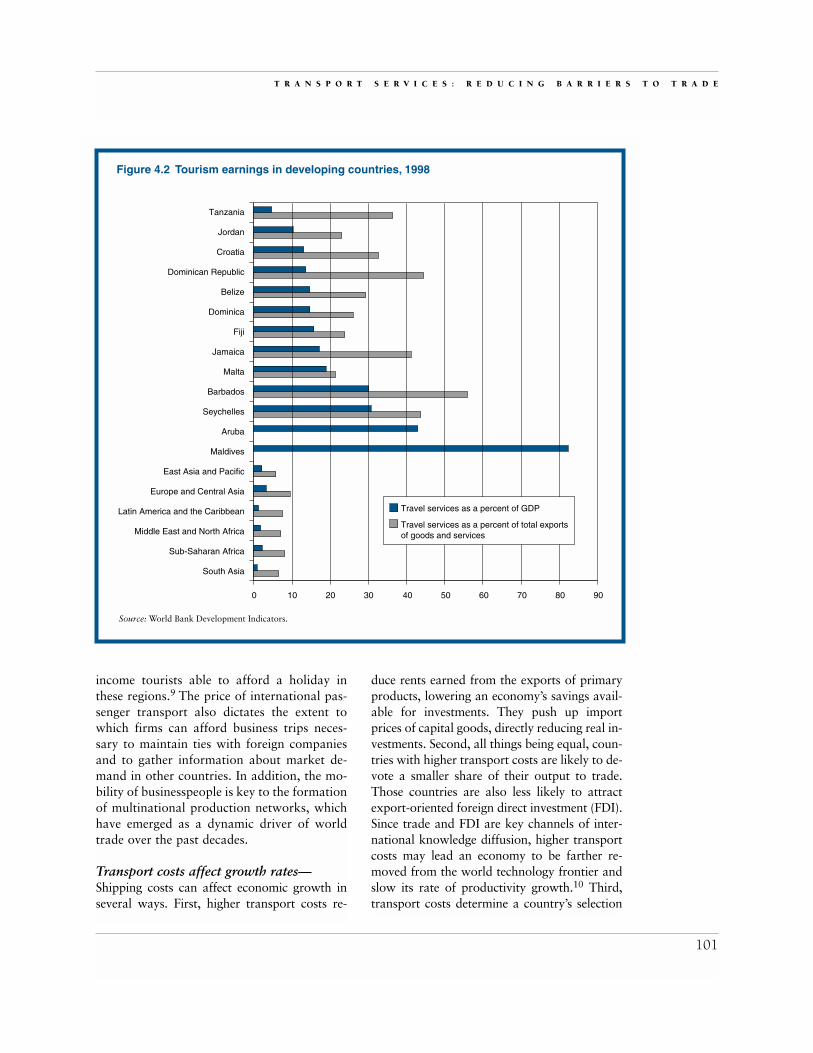

—and restrain trade in services—Transport costs also represent a barrier totrade in services. Though difficult to quantify,this is important for developing countries thatrely heavily on tourism services as a source offoreign exchange (figure 4.2). Tourists are sen-sitive to travel costs, especially where closesubstitute destinations exist. Estimates varysubstantially across locations, but a doublingin travel costs may reduce tourism demand asmuch as eight-fold.8 More than 90 percent oftourists arrive in developing countries by air,underscoring the importance of efficient airtransport services for this export industry. For example, air transport costs in East andSouthern Africa are reported to be up to tentimes higher than for Florida, in the UnitedStates, limiting the pool of lower- and middle-

G L O B A L E C O N O M I C P R O S P E C T S

100

Figure 4.1 Transport costs are oftenhigher than tariffsNominal tariff

Note: Data refer to 1998. Five countries (Benin, Guinea,Solomon Island, Togo, and Western Samoa) exhibit atransport cost incidence greater than 20 percent and arenot shown.

Source: U.S. Bureau of Census.

00 2 4 6 8 10 12 14 16 19 20

45°

2

4

6

8

10

12

14

16

18

20

Transport cost

income tourists able to afford a holiday inthese regions.9 The price of international pas-senger transport also dictates the extent towhich firms can afford business trips neces-sary to maintain ties with foreign companiesand to gather information about market de-mand in other countries. In addition, the mo-bility of businesspeople is key to the formationof multinational production networks, whichhave emerged as a dynamic driver of worldtrade over the past decades.

Transport costs affect growth rates—Shipping costs can affect economic growth inseveral ways. First, higher transport costs re-

duce rents earned from the exports of primaryproducts, lowering an economy’s savings avail-able for investments. They push up importprices of capital goods, directly reducing real in-vestments. Second, all things being equal, coun-tries with higher transport costs are likely to de-vote a smaller share of their output to trade.Those countries are also less likely to attractexport-oriented foreign direct investment (FDI).Since trade and FDI are key channels of inter-national knowledge diffusion, higher transportcosts may lead an economy to be farther re-moved from the world technology frontier andslow its rate of productivity growth.10 Third,transport costs determine a country’s selection

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

101

Figure 4.2 Tourism earnings in developing countries, 1998

Source: World Bank Development Indicators.

Tanzania

Jordan

Croatia

Dominican Republic

Belize

Dominica

Fiji

Jamaica

Malta

Barbados

Seychelles

Aruba

Maldives

East Asia and Pacific

Europe and Central Asia

Latin America and the Caribbean

Middle East and North Africa

Sub-Saharan Africa

South Asia

0 10 20 30 40 50 60 70 80 90

Travel services as a percent of GDP

Travel services as a percent of total exportsof goods and services

of trading partners. If export markets largelyconsist of poor, slow-growing markets andthere are significant costs (including transporta-tion) of switching to new, richer, and faster-growing markets, countries may be constrainedin their growth potential. This dilemma may beespecially severe for small landlocked countriesfar away from major economic centers.11

Controlling for a large number of socioeco-nomic, geographic, and institutional factors,Radelet and Sachs (1998) find that developingcountries with lower shipping costs experi-enced more rapid growth of manufacturingexports relative to GDP in the period from1965 to 1990. In addition, when exploring therelationship between shipping costs and over-all economic growth across economies, thestudy concludes that a doubling of the cost oftransportation is associated with slower an-nual growth of slightly more than one-half ofa percentage point.

—and help to explain regional variationsin incomeTransport costs—as opposed to tariffs facedby exporters—vary widely across trading na-tions. The availability, price, and quality oftransportation services therefore have strongimplications for what countries produce andwith whom they trade.

In a theoretical analysis, Venables andLimão (1999) find that transport costs maycause the world to be divided into “zones ofspecialization.” The more transport-intensive agood is, the more likely it is that it is exportedby countries that exhibit lower shipping coststo the economic center. By contrast, exceedinglyhigh shipping costs to a major economic centercan lead a country to be self-sufficient in a par-ticular good—despite the fact that it may nothold a comparative advantage in its productionsolely based on its factor endowments. Coun-tries with higher transport costs but identicalfactor endowments also exhibit lower real in-comes, as more resources are devoted to trans-portation and the gains from trade are smaller.

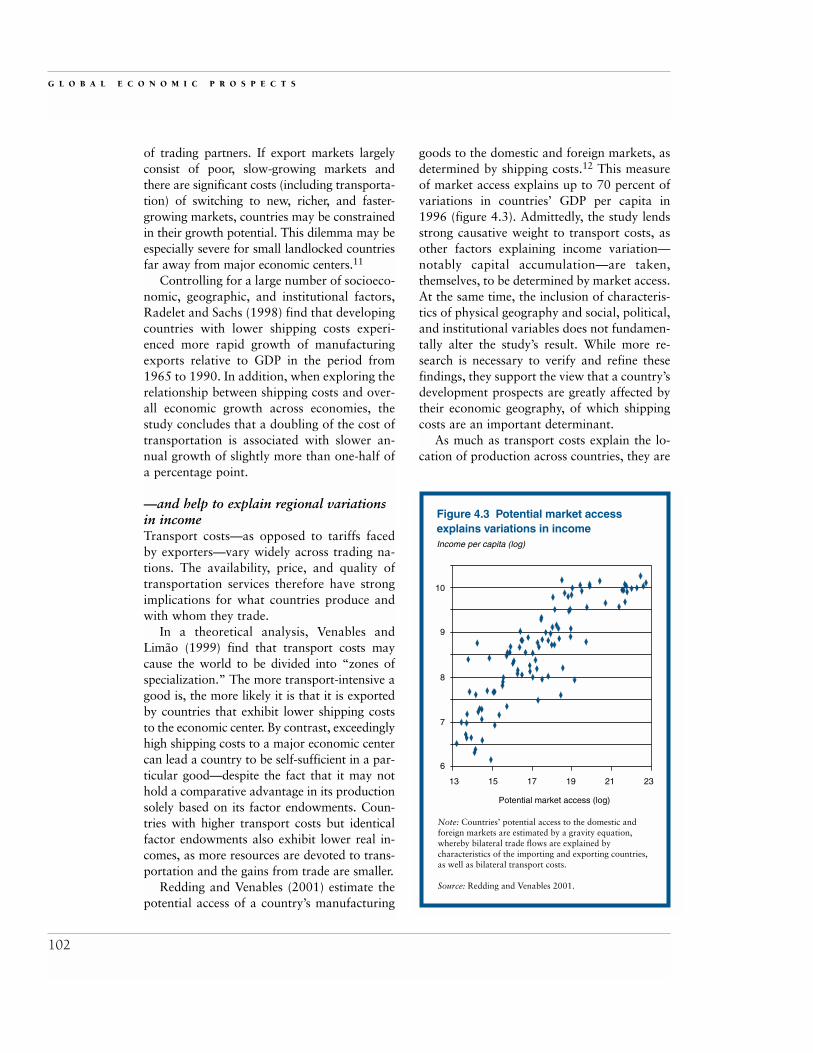

Redding and Venables (2001) estimate thepotential access of a country’s manufacturing

goods to the domestic and foreign markets, asdetermined by shipping costs.12 This measureof market access explains up to 70 percent ofvariations in countries’ GDP per capita in1996 (figure 4.3). Admittedly, the study lendsstrong causative weight to transport costs, asother factors explaining income variation—notably capital accumulation—are taken,themselves, to be determined by market access.At the same time, the inclusion of characteris-tics of physical geography and social, political,and institutional variables does not fundamen-tally alter the study’s result. While more re-search is necessary to verify and refine thesefindings, they support the view that a country’sdevelopment prospects are greatly affected bytheir economic geography, of which shippingcosts are an important determinant.

As much as transport costs explain the lo-cation of production across countries, they are

G L O B A L E C O N O M I C P R O S P E C T S

102

Figure 4.3 Potential market accessexplains variations in incomeIncome per capita (log)

Note: Countries’ potential access to the domestic andforeign markets are estimated by a gravity equation,whereby bilateral trade flows are explained bycharacteristics of the importing and exporting countries,as well as bilateral transport costs.

Source: Redding and Venables 2001.

13

10

9

8

7

6

15 17

Potential market access (log)

19 21 23

equally important in affecting the location ofexporting firms within countries. As foreigntrade barriers are removed, firms have an in-centive to move to regions with good access toforeign markets, such as border areas or portcities—especially if exports account for a largefraction of total sales. For example, closer tiesbetween the United States and Mexico causeda rapid expansion of manufacturing employ-ment in northern Mexico at the expense of theMexico City manufacturing belt.13 Agglomer-ation forces may create a self-reinforcing pro-cess, whereby entire industries move towardexporting centers, causing sharp regional in-equalities in production and income. The sever-ity of this process depends on the efficiency ofinternal transport systems—as illustrated in box4.2 on China.14

Transport services thus matter for tradecompetitiveness. Even if tariff and nontariffbarriers to trade were removed, cross-countryevidence suggests that the penalty of high ship-ping costs will continue to hold down growthrates and income of countries with poor inter-national transport links. Furthermore, ineffi-cient internal transport systems can sharpeneconomic inequalities within countries, withhinterland regions being disconnected from in-ternational commerce. Two questions that im-mediately arise in this context are why somecountries pay more for transport services thanothers, and what governments can do to im-prove the transport competitiveness of tradingfirms.

Why some countries pay more for transport services: geography and income

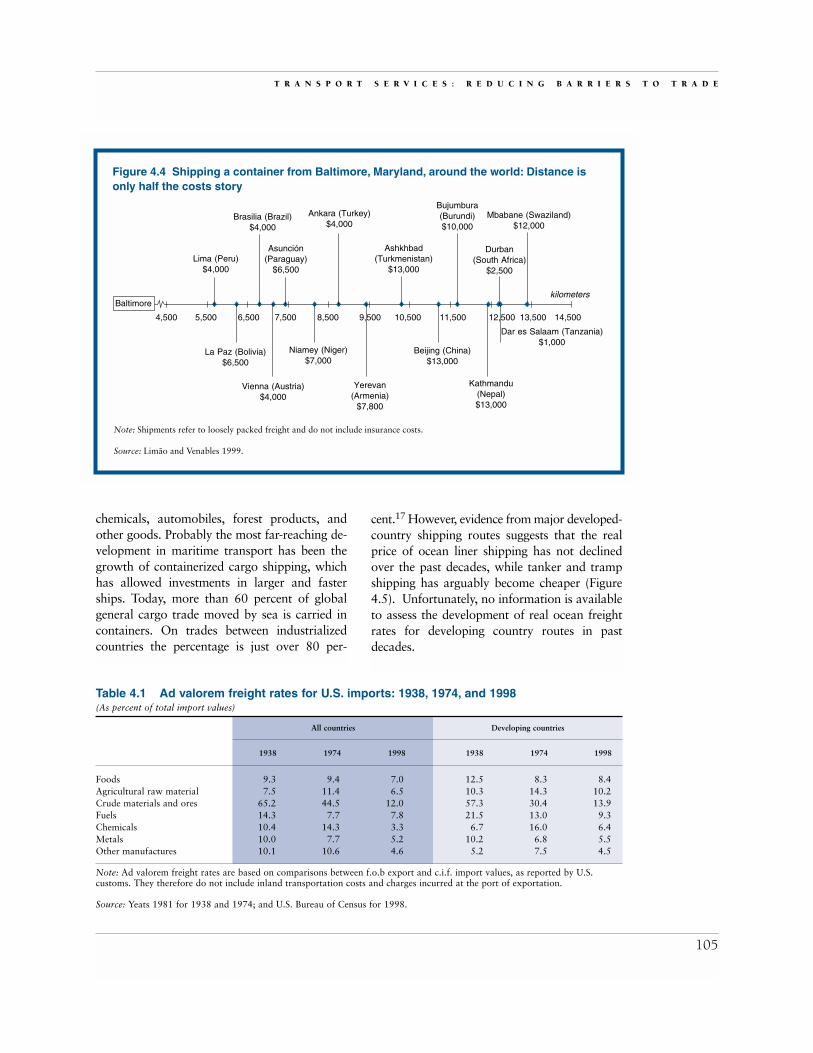

International transport costs vary dramaticallyTransport costs vary widely across countries.According to the price quotes of one U.S. freightforwarder, it costs $1,000 to ship a 40-footcontainer from Baltimore to Dar es Salaam, thelargest port city in Tanzania (figure 4.4). Yet theprice of shipping the same container to Durban

(South Africa) is $2,500 and goes up to $4,000for Vienna (Austria), $6,500 for Asunción(Paraguay), $7,800 for Yerevan (Armenia),$10,000 for Bujumbura (Burundi), and $13,000for Kathmandu (Nepal). The geographic dis-tance from Baltimore alone cannot explain thesedramatic price differences. Transport costs aredetermined by factors that can be changed in theshort run by policy, and those that cannot. Thissection concentrates on the second set of de-terminants. Despite advances in transport tech-nology, a large number of developing coun-tries continue to be challenged by geography interms of being landlocked or far away from the world’s economic centers. In addition, poorphysical infrastructure and thin traffic densities,typically associated with low-income econ-omies, represent additional impediments totransport competitiveness (although policy canalter these constraints in the longer term). Thus,high shipping costs undeniably represent a con-straining factor in the trade and developmentprospects of many developing countries.

Advances in transport technology—Innovations in transportation have been an im-portant factor in the globalization of goodsmarkets observed in the late twentieth century.An examination of ad valorem freight rates forU.S. imports, for which detailed data are avail-able, suggests that the share of shipping costsin the value of trade in 1998 was smaller for allmajor commodity groups compared to 1938,and for all but two goods classes compared to1974 (see table 4.1).15 However, declining advalorem freight rates may also be due to changesin the composition of trade or in unit values oftraded commodities, due, for example, to im-provements in the quality of goods.

Ocean, air, road, and railway shipping haveeach seen a different mix of technological andinstitutional innovations, with profound impli-cations on how traded goods are shipped fromone location to another.16 Ocean shipping is arelatively mature industry, yet there have beenimportant advances in maritime transport tech-nology over the past decades. Specialized shipshave emerged for dry bulk commodities, oil,

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

103

G L O B A L E C O N O M I C P R O S P E C T S

104

Aremarkable feature of China’s dramatic expan-sion in international trade over the past two

decades has been the concentration of export-orientedindustries in coastal regions. The four main coastalprovinces (Guangdong, Jiangsu, Fujian, and Shangkai)have been the main recipients of outward-oriented for-eign investment, with the remaining portion going toeither other coastal provinces or regions adjoiningcoastal areas. The provinces in the central core—usu-ally referred to as lagging provinces—barely benefitedfrom the incoming investment. While dispersion ofexport-oriented units have narrowed coastal incomedisparities—with the south coast regions catching upwith the hitherto affluent east coast—the export boomhas exacerbated the coastal-inland gap. Thus, whileChina’s economic reforms have been successful in rais-ing living standards for a considerable share of thepopulation, a large number of Chinese people ininland provinces still live below the poverty line.

Another contributing factor to coastal agglomera-tion has been various inefficiencies in China’s internaltransport systems. Transport infrastructure disparitiesbetween the coastal and inland provinces narrowedconsiderably following policies aimed at promotingmore regionally balanced economic development since 1990. However, indications of increasing inter-provincial trade between inland regions, and betweeninland and coastal regions, suggests that it is not theavailability of transport infrastructure per se that haveprecluded inland provinces from actively participatingin foreign trade. Rather the inadequacies associatedwith transport services are the more binding constraintto better integrating China’s hinterland economy.

The compositional shift of exports from low-value raw materials to high-value manufactured goodshas made transport increasingly suitable for container-ization. Though there has been significant increase inthe volume of container traffic in China since 1990,the increase is largely confined to coastal regions, andassociated with the oceangoing leg of travel. Containertraffic in inland areas is much less, with no significantchange in the percentage of sea-borne containers trav-eling beyond port cities and coastal provinces. Truckrates for moving a container 500 kilometers inland areestimated to be about three times more, and the trip

Box 4.2 Inefficient internal transport systemscontribute to the concentration of China’s exportindustries in coastal regions

time five times longer, than they would be in Europeor the United States. China’s railways still charge what is, in effect, a penalty rate for moving containers.Priority on the congested rail network is still given tolow-value bulk freight (mostly coal), rather than tohigh-value freight, such as containers.

Surveys based on major foreign shippers, shippinglines, and freight forwarders based in the United States,Japan, and Hong Kong (China) indicate that China’stransport systems, particularly inland transport, arewell below international standards. First, respondentspointed to the lack of container freight stations, yards,and trucks in inland regions. Second, border proce-dures were perceived to be cumbersome and time-consuming, due to the many certification requirementsand duplication of documents—in part, a consequenceof the lack of coordination between the different gov-ernment agencies involved in the various modes oftransport. Third, container-tracking capability wasparticularly poor, with shippers often unaware of theircontainers’ whereabouts. Shippers attributed this topoorly trained staff, the lack of a reliable recovery sys-tem, and the poor accountability system in governmentagencies. Fourth, the intermodal transport system wasfound to be poorly integrated, with no streamlinedprocedures to support the continuous movement ofcontainers between the coast and inland.

Another source of inefficiencies is the dominanceof state-owned enterprises and the lack of competitionin transport service markets. Since pricing in many ofthe intermediate transport service activities is con-trolled, the companies have little incentive for aggres-sively pursuing cost-cutting methods. Due to a lack ofcompetition, intermediate service providers representthe interests of transport operators. Hence value-addedservice and reliability, hallmarks of winning businessconfidence in a modern economy, are not practiced bymost participants. Investment by foreign enterprises orjoint ventures between foreign and domestic enterprisesin intermediate transport services is limited in inland re-gions. Though foreign investment is not prohibited,there are restrictions on investors’ activities.

Source: Atinc 1997; Graham and Wada 2001; Naughton 2001;and World Bank 1996.

chemicals, automobiles, forest products, andother goods. Probably the most far-reaching de-velopment in maritime transport has been thegrowth of containerized cargo shipping, whichhas allowed investments in larger and fasterships. Today, more than 60 percent of globalgeneral cargo trade moved by sea is carried incontainers. On trades between industrializedcountries the percentage is just over 80 per-

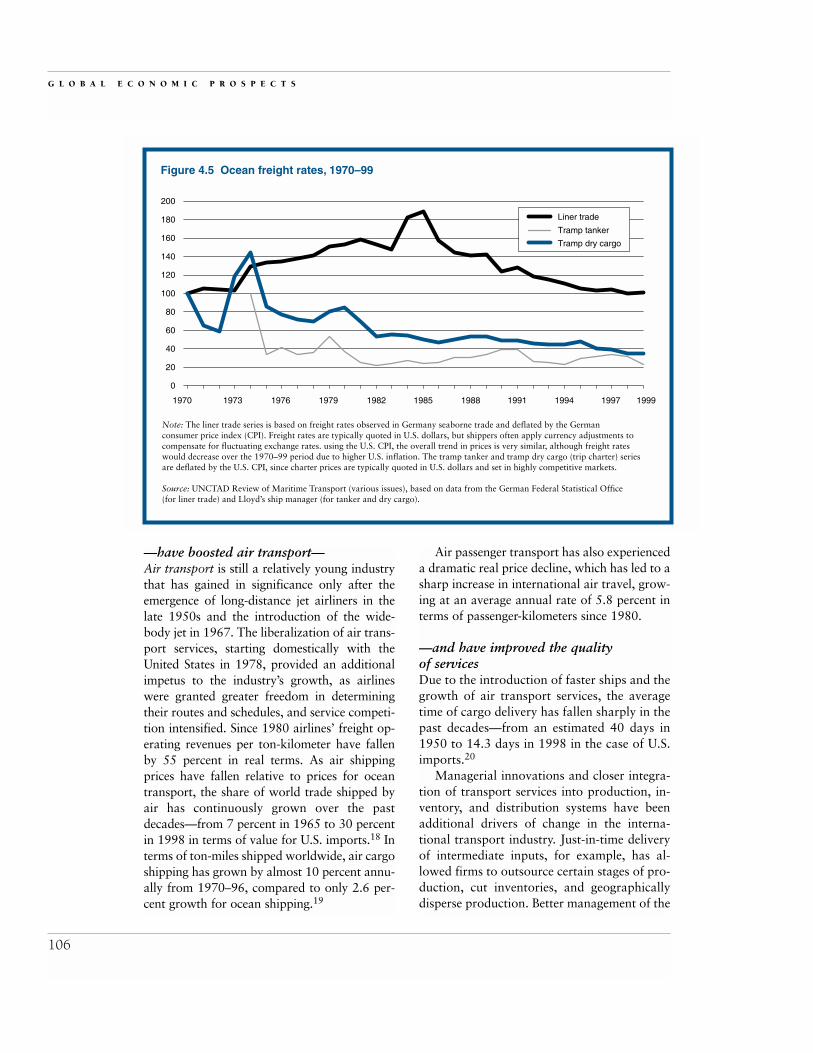

cent.17 However, evidence from major developed-country shipping routes suggests that the realprice of ocean liner shipping has not declinedover the past decades, while tanker and trampshipping has arguably become cheaper (Figure4.5). Unfortunately, no information is availableto assess the development of real ocean freightrates for developing country routes in pastdecades.

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

105

Figure 4.4 Shipping a container from Baltimore, Maryland, around the world: Distance isonly half the costs story

Note: Shipments refer to loosely packed freight and do not include insurance costs.

Source: Limão and Venables 1999.

Brasilia (Brazil)$4,000

Vienna (Austria)$4,000

Lima (Peru)$4,000

La Paz (Bolivia)$6,500

4,500 5,500 6,500 7,500 14,500

kilometers

Mbabane (Swaziland)$12,000

Dar es Salaam (Tanzania)$1,000

Kathmandu(Nepal)$13,000

Niamey (Niger)$7,000

Asunción(Paraguay)

$6,500

Ankara (Turkey)$4,000

Yerevan(Armenia)

$7,800

Ashkhbad(Turkmenistan)

$13,000

Beijing (China)$13,000

Bujumbura(Burundi)$10,000

Durban(South Africa)

$2,500

13,50012,50011,50010,5009,5008,500

Baltimore

Table 4.1 Ad valorem freight rates for U.S. imports: 1938, 1974, and 1998(As percent of total import values)

All countries Developing countries

1938 1974 1998 1938 1974 1998

Foods 9.3 9.4 7.0 12.5 8.3 8.4Agricultural raw material 7.5 11.4 6.5 10.3 14.3 10.2Crude materials and ores 65.2 44.5 12.0 57.3 30.4 13.9Fuels 14.3 7.7 7.8 21.5 13.0 9.3Chemicals 10.4 14.3 3.3 6.7 16.0 6.4Metals 10.0 7.7 5.2 10.2 6.8 5.5Other manufactures 10.1 10.6 4.6 5.2 7.5 4.5

Note: Ad valorem freight rates are based on comparisons between f.o.b export and c.i.f. import values, as reported by U.S.customs. They therefore do not include inland transportation costs and charges incurred at the port of exportation.

Source: Yeats 1981 for 1938 and 1974; and U.S. Bureau of Census for 1998.

—have boosted air transport—Air transport is still a relatively young industrythat has gained in significance only after theemergence of long-distance jet airliners in thelate 1950s and the introduction of the wide-body jet in 1967. The liberalization of air trans-port services, starting domestically with theUnited States in 1978, provided an additionalimpetus to the industry’s growth, as airlineswere granted greater freedom in determiningtheir routes and schedules, and service competi-tion intensified. Since 1980 airlines’ freight op-erating revenues per ton-kilometer have fallenby 55 percent in real terms. As air shippingprices have fallen relative to prices for oceantransport, the share of world trade shipped byair has continuously grown over the pastdecades—from 7 percent in 1965 to 30 percentin 1998 in terms of value for U.S. imports.18 Interms of ton-miles shipped worldwide, air cargoshipping has grown by almost 10 percent annu-ally from 1970–96, compared to only 2.6 per-cent growth for ocean shipping.19

Air passenger transport has also experienceda dramatic real price decline, which has led to asharp increase in international air travel, grow-ing at an average annual rate of 5.8 percent interms of passenger-kilometers since 1980.

—and have improved the quality of servicesDue to the introduction of faster ships and thegrowth of air transport services, the averagetime of cargo delivery has fallen sharply in thepast decades—from an estimated 40 days in1950 to 14.3 days in 1998 in the case of U.S.imports.20

Managerial innovations and closer integra-tion of transport services into production, in-ventory, and distribution systems have beenadditional drivers of change in the interna-tional transport industry. Just-in-time deliveryof intermediate inputs, for example, has al-lowed firms to outsource certain stages of pro-duction, cut inventories, and geographicallydisperse production. Better management of the

G L O B A L E C O N O M I C P R O S P E C T S

106

Figure 4.5 Ocean freight rates, 1970–99

Note: The liner trade series is based on freight rates observed in Germany seaborne trade and deflated by the German consumer price index (CPI). Freight rates are typically quoted in U.S. dollars, but shippers often apply currency adjustments to compensate for fluctuating exchange rates. using the U.S. CPI, the overall trend in prices is very similar, although freight rates would decrease over the 1970–99 period due to higher U.S. inflation. The tramp tanker and tramp dry cargo (trip charter) seriesare deflated by the U.S. CPI, since charter prices are typically quoted in U.S. dollars and set in highly competitive markets.

Source: UNCTAD Review of Maritime Transport (various issues), based on data from the German Federal Statistical Office (for liner trade) and Lloyd’s ship manager (for tanker and dry cargo).

0

20

40

60

80

100

120

140

160

180

200

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 1999

Liner trade

Tramp tanker

Tramp dry cargo

supply chain has enabled producers of perish-able commodities to compete in distant con-sumer markets. These managerial changeshave, in turn, led many transport operators tobecome multidimensional providers of logis-tics services—including packing and labeling,freight forwarding, insurance and banking, theprocessing of border formalities, tracking ofshipments, and other services. The growth ofthese services has, in part, been propelled bythe falling cost and increasing power of com-munications and computing, as logistics pri-marily involves the processing of information.

Geography continues to exert its own tyranny—Despite technological advances, however, geog-raphy continues to be an important determi-nant of international variations in transportcosts. The distance between the origin anddestination points of a transport journey di-rectly affects the variable cost of shipping inthe form of fuel, wear and tear of vehicles, andthe amount of time that goods are traveling.

Due to the existence of fixed costs of trans-portation, however, the effect of distance ontransport costs is less than proportionate, sug-gesting that distance matters more where thecosts of packaging, documentation, port ser-vices, and other distant-invariant activities aresmall.21 Typically, a 1 percent increase in dis-tance causes trade volumes to fall by slightlymore than 1 percent—although this large ef-fect is also due to factors other than transportcosts.22 Countries that share a common bor-der are found, on average, to trade signifi-cantly more than countries without a commonborder, which can in many instances be attrib-uted to more integrated transport networksand the existence of bilateral customs agree-ments that reduce transit times.

—especially for landlocked countriesThe effect of distance depends greatly, how-ever, on the mode of transport. By one esti-mate, an additional kilometer of overlandtransport adds seven times more to transportcosts than an additional kilometer by sea.23 It

is thus not surprising that landlocked countriespay, on average, more for shipping exports andimports than coastal economies. Multiple stud-ies have documented the “penalty” of beinglandlocked, and estimates usually put the addi-tional cost of transportation at more than 50percent of that paid by countries with maritimeports.24 For many shipments to landlockedcountries this “penalty” is likely to be higher.For example, the price quotes for containershipments from Baltimore reveal that the costof shipment to Durban (South Africa) is$2,500, whereas the cost to Mbabane (Swazi-land) via Durban comes to $12,000—a land-locked “penalty” of 380 percent (figure 4.4).Aside from longer overland distances, traffic toand from landlocked economies often suffersfrom higher transaction costs due to the com-plexities of coordinating multimodal transportjourneys and the crossing of multiple borders.

It is thus not surprising to find that land-locked countries have only 30 percent of thetrade volume of average coastal economies;that none of the 15 developing countries withthe fastest export growth is landlocked; andthat all 15 of those economies are located ei-ther directly on major shipping routes or closeto a major developed-country market.25 Thestudy by Redding and Venables (2001) pro-vides additional proof of the burden of geog-raphy: access to the coast raises per capita in-come by 64 percent, while halving the distanceto all trading partners increases per capitaincome by 74 percent. While these figures pro-vide a pessimistic view on the trade and devel-opment prospects of geographically disadvan-taged countries, in the long run new economiccenters emerge. High-income landlocked econ-omies such as Switzerland, or the state of Col-orado in the United States demonstrate thatsuch disadvantages need not be permanent.

Infrastructure links the hinterland to the world—Transport infrastructure, encompassing road,railway, and internal waterway networks, sea-ports and airports, warehousing facilities, andsupporting communications systems, is a key

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

107

prerequisite to efficient transport services. Whengoods originate or terminate in remote regions,inland shipping accounts for a substantial shareof the total door-to-door transport charge (fig-ure 4.6). If internal transportation networksare dense, remote regions are in a better posi-tion to supply foreign markets. In countrieswith well-developed infrastructures, exporterscan typically choose among alternative modesof transport (truck, railroad, or internal water-way) and alternative seaports and airports toship their goods abroad. Aside from greaterflexibility, increased modal and port choicedirectly promotes competition and limits thepotential abuse of market power by transportoperators serving chokepoints. Based on anindex that captures the densities of coun-tries’ road, railway, and telecommunicationsnetworks, Limão and Venables (1999) confirmthat better infrastructure translates into signif-icantly lower transport costs.26 Moreover, ahigher infrastructure density in transit coun-tries reduces transport costs to landlocked econ-omies. Both own and transit country infra-

structures are found to be important determi-nants of bilateral trade flows.27

—and poor countries are at adisadvantagePoor infrastructure conditions are often the di-rect result of low income levels, as the resourcesavailable for infrastructure investments are lim-ited. Nonetheless, governments play an impor-tant role in expanding the reach and improvingthe quality of existing infrastructure. Invest-ments in transport infrastructure often take asignificant share of developing countries’ GDP.28

Governments in many countries—in part dri-ven by the need to cut public expenditures—have increasingly turned to the private sectorfor financing such large investments. Successfulinvolvement of private investors necessitates anattractive investment climate, transparent andcarefully designed concession contracts, and a credible overall policy regime.29 Yet wherecommercial risks are too high, public sector in-vestments are still required—especially in thepoorest countries that are typically not able toattract private investment. Governments alsoplay a crucial role in infrastructure planning.Road, railway, and port capacities need to ac-commodate projected growth in trade. The de-sign and construction of transport networksneed to be coordinated with neighboring coun-tries, which is especially important for smalland landlocked economies.

Economies of scale and scopeThere are large economies of scale in the provi-sion of shipping services. Greater transporta-tion flows allow service providers to operatelarger vehicles and to spread fixed route costsover a larger number of shipments. The capac-ity of containerships operating on the majorEast-West trading routes is several times that ofthose operating on North-South routes, wheretraffic density is substantially smaller. Control-ling for other determinants of liner freightprices, shipments from the port of Lagos, Nige-ria, to southern California would be 24 percentcheaper, if traffic on this route would be thesame as from the port of Hong Kong (China)

G L O B A L E C O N O M I C P R O S P E C T S

108

Figure 4.6 Decomposing the costs ofdoor-to-door shipmentsU.S. dollars

Note: Costs refer to the cheapest route of shipment.Insurance and bank processing charges are excluded.Source: Subramanian and Arnold 2001.

0Containerized carpet

shipment fromKathmandu (Nepal)

to Munich (Germany)

Tea shipment(8.4 tons) from

Karimganj (India)to Liverpool (UK)

500

1,000

1,500

2,000

2,500

3,000

Ocean freightCustoms inspectionCargo handling and transferDocumentation & forwardingInland transport

to the same region.30 Furthermore, due to rela-tively low trading volumes, developing coun-tries often face longer travel times and less fre-quent services, as ocean carriers require a largernumber of stops to fill vessels.31

At sufficiently large traffic volumes, trans-port operators can reap economies of scope byoffering services on connected routes. Throughhub-and-spokes systems, maritime and oceantransport operators have been able to cut costs,while at the same time offering transport linksbetween a larger number of locations at higherfrequencies. The overwhelming share of inter-continental ocean trade is today delivered byhub-and-spoke systems, through major portssuch as Hong Kong (China), Los Angeles, Rot-terdam, or Singapore. By contrast, most oceancarriers serving the routes to and from WestAfrica still operate under so-called multipleports of call systems. However, given currenttraffic levels, commodity mix, port infrastruc-tures, and inland transportation systems, Páls-son (1997) finds that the adoption of a hub-and-spoke system would not systematicallyyield substantial cost savings. Future growth intrade as well as infrastructure improvementsmay change this calculus. Yet the implementa-tion of a hub-and-spoke system would still re-quire the willingness of the spoke countries toaccept lower traffic volumes to the benefit ofthe hub port.

Why some countries pay more:policy-driven factors

Government policy can inadvertently in-flate transport costs. Most developing

countries enact rules that detract from usingexisting transport resources efficiently. Theserules drive up transport-related transactioncosts and often preserve monopolies in servicemarkets.

Reducing high transaction costs in-country—High costs of transport-related transactions—such as frequent reloading of goods, customsclearance, fulfillment of documentation require-

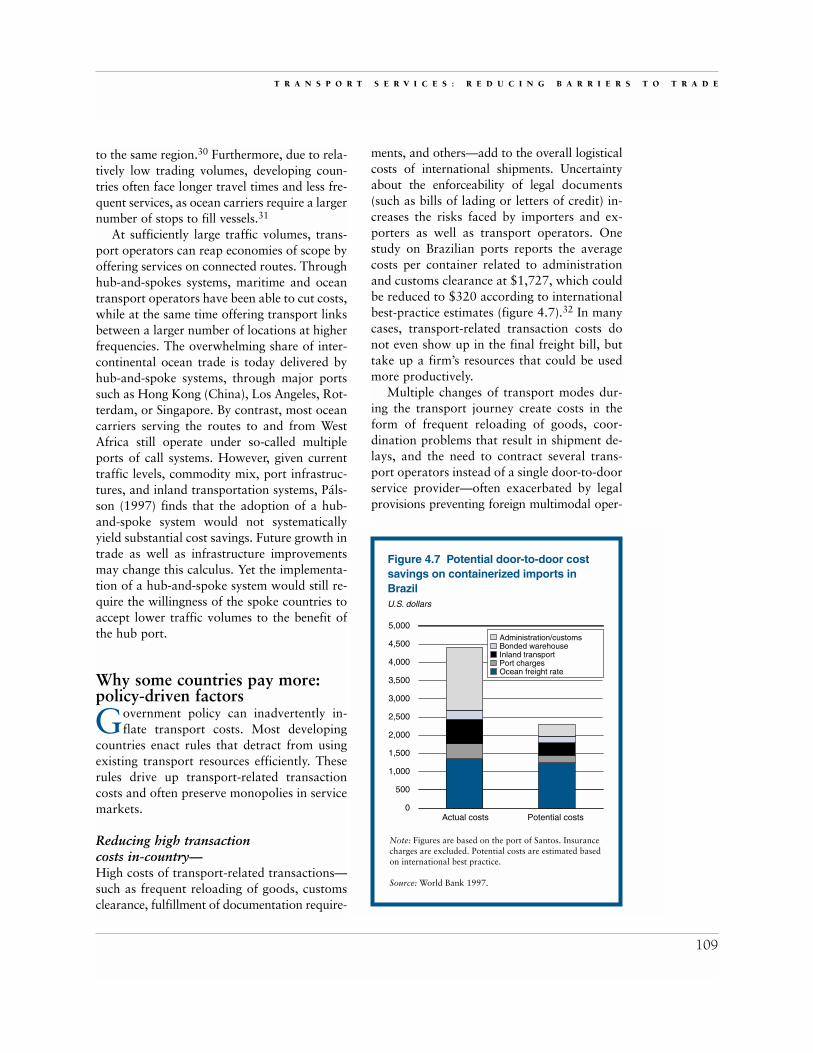

ments, and others—add to the overall logisticalcosts of international shipments. Uncertaintyabout the enforceability of legal documents(such as bills of lading or letters of credit) in-creases the risks faced by importers and ex-porters as well as transport operators. Onestudy on Brazilian ports reports the averagecosts per container related to administrationand customs clearance at $1,727, which couldbe reduced to $320 according to internationalbest-practice estimates (figure 4.7).32 In manycases, transport-related transaction costs donot even show up in the final freight bill, buttake up a firm’s resources that could be usedmore productively.

Multiple changes of transport modes dur-ing the transport journey create costs in theform of frequent reloading of goods, coor-dination problems that result in shipment de-lays, and the need to contract several trans-port operators instead of a single door-to-doorservice provider—often exacerbated by legalprovisions preventing foreign multimodal oper-

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

109

Figure 4.7 Potential door-to-door costsavings on containerized imports inBrazilU.S. dollars

Note: Figures are based on the port of Santos. Insurancecharges are excluded. Potential costs are estimated basedon international best practice.

Source: World Bank 1997.

0Actual costs Potential costs

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000Administration/customsBonded warehouseInland transportPort chargesOcean freight rate

ators from undertaking door-to-door contracts.Containerization has substantially reduced thereloading costs of multimodal journeys, as goodsare packed once at the factory’s door and un-packed at the importer’s site. Indeed, con-tainerization has fostered the integration oftransport service providers toward multi-modal operations, which internalizes transac-tion costs resulting from modal switches. Eventhough containerization of general cargo hastaken hold in many developing country–ports,containers are less frequently used for inlandtransport (especially in Africa)—obviating oneof the main cost-saving characteristics of con-tainer shipping.33 The main reasons for thisare long inland turnaround times for contain-ers, risks of loss or damage to containers, andinadequate road infrastructure unsuited to con-tainer loads. Limitations on the cross-borderprovision of trucking services create bottle-necks at the border, because goods have to bereloaded onto different carriers. Different na-tional standards regarding safety requirements,vehicle sizes, railway gauges, or coupling andbraking systems similarly constrain the smoothcross-border movements of goods.

Although official customs fees are typicallyonly a small portion of overall transportationcosts, inefficiency in customs procedures can re-sult in congestion and long queues at the bor-der. For example, at the key border crossing-point between India and Bangladesh as many as1,500 trucks queue up on both sides of the bor-der, and waiting times vary between one andfive days.34 Inefficiencies often are the resultof understaffing, burdensome documentationrequirements, poorly defined procedures, andthe need to obtain approval from many offi-cials. High trade protection typically results inmore complex customs requirements—for ex-ample, through the need to obtain import li-censes before goods are shipped. Corruption isendemic in many developing country portsand is more widespread the more opaque arethe customs procedures, and the greater thediscretion of customs officials.

Advances in information technologies havecreated a large scope for reducing transport-

related transaction costs. The development ofthe electronic data interchange (EDI) system,for example, has substituted the traditionalpaper documentation routines for customsclearance. Through the global positioning sys-tem, firms can monitor the location of vehiclesand better time loading and reloading. TheInternet has opened new ways of organizingtransport movements, creating more flexibleand efficient transport markets with reduceduncertainty regarding the quality of shipments.Yet use of these technologies is still primarilyconfined to developed countries and largeports. Lack of communications infrastructureand the necessary skills, as well as an inade-quate legal framework for electronic signatures,often present obstacles to the dissemination oftransport-related information technology in thedeveloping world.

—requires coordinated government actionThere is much that governments can do to re-duce transport-related transaction costs, usu-ally under the umbrella of so-called trade facil-itation initiatives. Such programs can result insignificant reductions in direct and indirectshipping costs in relatively short time periods.They are most effective if implemented in part-nership with the private sector (box 4.3). An-other role for governments is to create an ap-propriate legal and regulatory framework formultimodal transport, which often representsone of the most pressing constraints to the pro-vision of efficient door-to-door services. Coop-eration on standard-setting and the conclusionof mutual-recognition agreements with neigh-boring countries can facilitate the cross-bordermovement of goods by trucks. While countriesshould remain free to adopt their preferred reg-ulatory standards, it is important to ensurethat such standards do not unnecessarily dis-criminate against foreign–service providers (seechapter 3).

From public monopoly to private competitionFor a long time the provision of many trans-port services was the domain of public monop-

G L O B A L E C O N O M I C P R O S P E C T S

110

olies, and indeed state-owned enterprisescontinue to be a dominant force in many coun-tries’ transport sectors. Public monopolies wereoften justified by natural monopoly argu-ments, such as in the case of port operations,which require large infrastructure investments.Prestige arguments (for example, the desire tooperate a national flag airline) and securityconcerns (self-sufficiency in times of war) af-forded a justification for limiting the participa-tion of foreign service providers in domestictransport operations. Such arguments are be-coming increasingly harder to defend. Privateentry and competitive market structures haveproved to be feasible for virtually all transportservices and, to a large extent, have led to effi-ciency gains and lower prices for consumers.Moreover, the principle of comparative advan-

tage fully applies to the provision of transportservices, as it does to other traded commodi-ties. By opening up domestic markets to for-eign competition, shippers can choose among abroader spectrum of services and opt for ser-vice operators with superior technologies orlower operating costs.

Maritime transport—Due to differences in commodity type as wellas to technological improvements in the ship-ping industry—most importantly, container-ization—international maritime freight trans-port has developed specialized branches. Linershipping, meaning maritime transport of com-modities by regular lines, which publish in ad-vance their calls in different harbors, is dis-tinct from tramp shipping, which refers to

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

111

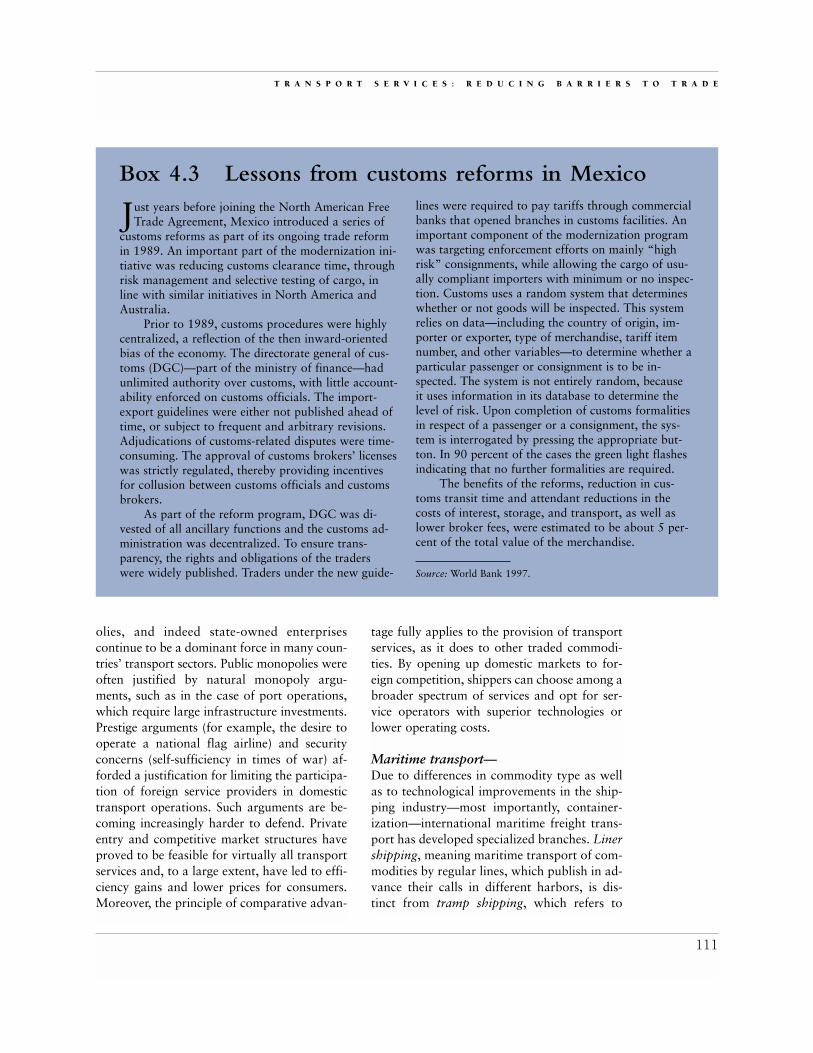

Just years before joining the North American FreeTrade Agreement, Mexico introduced a series of

customs reforms as part of its ongoing trade reformin 1989. An important part of the modernization ini-tiative was reducing customs clearance time, throughrisk management and selective testing of cargo, inline with similar initiatives in North America andAustralia.

Prior to 1989, customs procedures were highlycentralized, a reflection of the then inward-orientedbias of the economy. The directorate general of cus-toms (DGC)—part of the ministry of finance—hadunlimited authority over customs, with little account-ability enforced on customs officials. The import-export guidelines were either not published ahead oftime, or subject to frequent and arbitrary revisions.Adjudications of customs-related disputes were time-consuming. The approval of customs brokers’ licenseswas strictly regulated, thereby providing incentivesfor collusion between customs officials and customsbrokers.

As part of the reform program, DGC was di-vested of all ancillary functions and the customs ad-ministration was decentralized. To ensure trans-parency, the rights and obligations of the traderswere widely published. Traders under the new guide-

Box 4.3 Lessons from customs reforms in Mexicolines were required to pay tariffs through commercialbanks that opened branches in customs facilities. Animportant component of the modernization programwas targeting enforcement efforts on mainly “highrisk” consignments, while allowing the cargo of usu-ally compliant importers with minimum or no inspec-tion. Customs uses a random system that determineswhether or not goods will be inspected. This systemrelies on data—including the country of origin, im-porter or exporter, type of merchandise, tariff itemnumber, and other variables—to determine whether aparticular passenger or consignment is to be in-spected. The system is not entirely random, becauseit uses information in its database to determine thelevel of risk. Upon completion of customs formalitiesin respect of a passenger or a consignment, the sys-tem is interrogated by pressing the appropriate but-ton. In 90 percent of the cases the green light flashesindicating that no further formalities are required.

The benefits of the reforms, reduction in cus-toms transit time and attendant reductions in thecosts of interest, storage, and transport, as well aslower broker fees, were estimated to be about 5 per-cent of the total value of the merchandise.

Source: World Bank 1997.

transport performed irregularly, depending onmomentary demand. Typically, liner carrierstransport commodities with a higher degree ofindustrial processing using containers, whilenoncontainerized raw materials (such as crudeand refined oil, iron ore, grain, coal, or baux-ite) tend to be carried in tramp carriers.

—is affected by government policies—Tramp shipping is generally believed to be ahighly competitive market that is, as a rule,free from restrictions.35 Prices are set in spotmarkets based on either time charter or voyagecharter contracts. In contrast, liner shippinghas traditionally been subject both to trade re-strictions and private cooperation. The mostimportant policy-imposed barriers applied tointernational maritime transport have beenvarious cargo reservation schemes. These re-quire that part of the cargo carried in tradewith other states must be transported only byflagships (ships carrying a national flag) orships interpreted as national by other criteria.

Cargo reservation takes various forms. Itcan be imposed unilaterally if ships flying na-tional flags are given the exclusive right totransport a specified share of the cargo passingthrough the country’s ports. An alternativeform involves cargo sharing with trading part-ners on the basis of bilateral or internationalagreements. A specific form of multilateralcargo reservation scheme is the United NationsConference on Trade and Development (UNC-TAD) Liner Code of Conduct, which was con-ceived to encourage the development of theshipping industry of developing countries byguaranteeing domestic lines a minimum (40percent) share of traffic, and ensuring their par-ticipation in international liner conferences.36

Cargo reservation schemes have probablydeclined in significance, as more and morecountries have phased them out. In addition,the increased transfer of ships to open reg-istries to enable the ship owners to benefitfrom more efficient cost conditions has furtherdiluted the importance of cargo sharing. TheUNCTAD Liner Code, which was never ap-plied on a large scale, is even less visible today,

being applied mostly to routes between WestAfrica and Europe (box 4.4). Nevertheless,countries ranging from Benin to India stillhave in place reservation policies that at leastnominally restrict the scope for trade.

—and the practices of ocean carriersCompetition-restraining practices in linertransport take the form of cooperative agree-ments among maritime carriers on technical or commercial matters. Carriers’ cooperativehabits are deeply rooted in the history of mar-itime transportation. The first shipping cartels,covering the routes between the United King-dom and Calcutta, India, date back to 1875.By joining carrier agreements, shipping compa-nies retain their juridical independence, butconsent to common practices with the othermembers regarding pricing, traffic distribution,or vessel capacity utilization. One of the mostcommon types of agreement are liner confer-ence agreements, which typically provide forthe fixing of and adherence to uniform freighttariff rates and conditions of service. Liner con-ferences also employ exclusive contracts andother loyalty-inducing instruments to deterentry of outside shipping lines.37 Another typeof carrier agreement includes cooperative work-ing and discussion agreements, which establishexclusive or preferential working relationshipsbetween shipping lines, and provide a forumfor information sharing but do not necessarilyengage in unique price setting. A more recentform of private cooperation is strategic alliances,which aim at closely integrating vessel opera-tion activities and service networks.

It has been frequently pointed out that inrecent years the power of liner conferences and other cooperative arrangements has beeneroded. In the 1990s efficient outside shippinglines were able to gain a significant share of themarket on many routes. Moreover, more liberalregulations affecting international shippinghave weakened the command of rate-fixingagreements. For example, the Ocean ShippingReform Act of 1998 in the United States intro-duced the confidentiality of key service contractterms, allowing greater scope for price com-

G L O B A L E C O N O M I C P R O S P E C T S

112

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

113

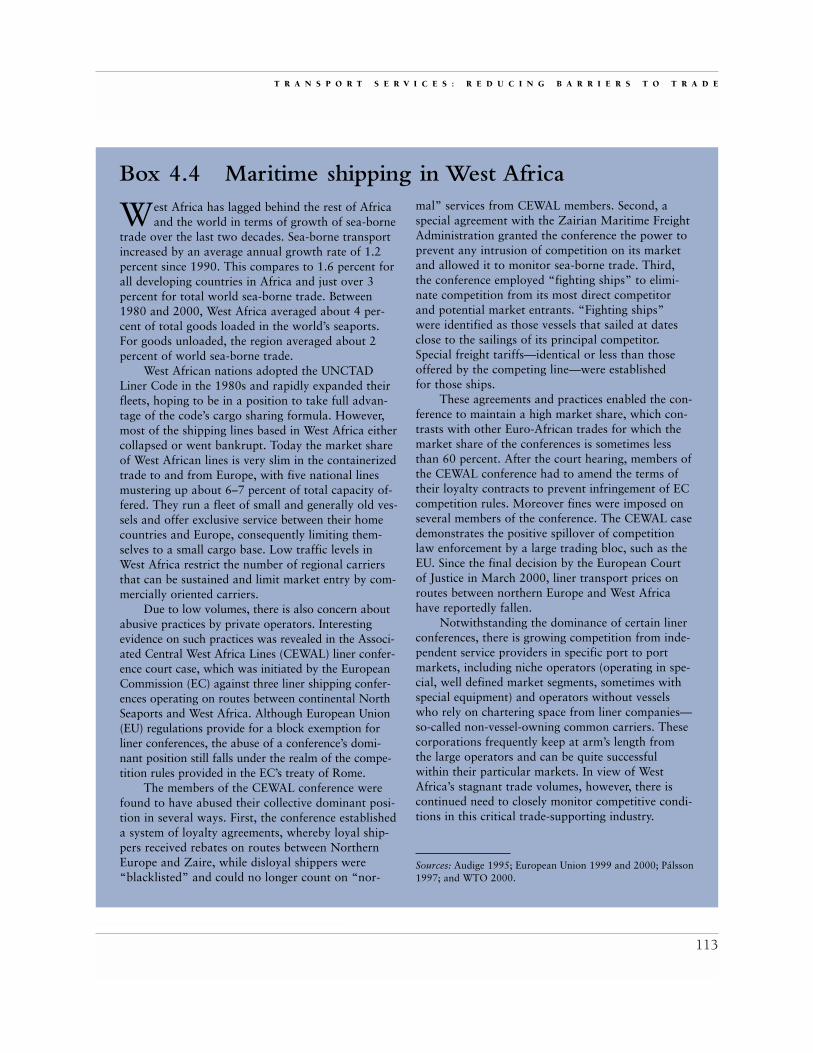

West Africa has lagged behind the rest of Africaand the world in terms of growth of sea-borne

trade over the last two decades. Sea-borne transportincreased by an average annual growth rate of 1.2percent since 1990. This compares to 1.6 percent forall developing countries in Africa and just over 3percent for total world sea-borne trade. Between1980 and 2000, West Africa averaged about 4 per-cent of total goods loaded in the world’s seaports.For goods unloaded, the region averaged about 2percent of world sea-borne trade.

West African nations adopted the UNCTADLiner Code in the 1980s and rapidly expanded theirfleets, hoping to be in a position to take full advan-tage of the code’s cargo sharing formula. However,most of the shipping lines based in West Africa eithercollapsed or went bankrupt. Today the market shareof West African lines is very slim in the containerizedtrade to and from Europe, with five national linesmustering up about 6–7 percent of total capacity of-fered. They run a fleet of small and generally old ves-sels and offer exclusive service between their homecountries and Europe, consequently limiting them-selves to a small cargo base. Low traffic levels inWest Africa restrict the number of regional carriersthat can be sustained and limit market entry by com-mercially oriented carriers.

Due to low volumes, there is also concern aboutabusive practices by private operators. Interestingevidence on such practices was revealed in the Associ-ated Central West Africa Lines (CEWAL) liner confer-ence court case, which was initiated by the EuropeanCommission (EC) against three liner shipping confer-ences operating on routes between continental NorthSeaports and West Africa. Although European Union(EU) regulations provide for a block exemption forliner conferences, the abuse of a conference’s domi-nant position still falls under the realm of the compe-tition rules provided in the EC’s treaty of Rome.

The members of the CEWAL conference werefound to have abused their collective dominant posi-tion in several ways. First, the conference establisheda system of loyalty agreements, whereby loyal ship-pers received rebates on routes between NorthernEurope and Zaire, while disloyal shippers were“blacklisted” and could no longer count on “nor-

Box 4.4 Maritime shipping in West Africamal” services from CEWAL members. Second, aspecial agreement with the Zairian Maritime FreightAdministration granted the conference the power toprevent any intrusion of competition on its marketand allowed it to monitor sea-borne trade. Third,the conference employed “fighting ships” to elimi-nate competition from its most direct competitorand potential market entrants. “Fighting ships” were identified as those vessels that sailed at datesclose to the sailings of its principal competitor.Special freight tariffs—identical or less than thoseoffered by the competing line—were established for those ships.

These agreements and practices enabled the con-ference to maintain a high market share, which con-trasts with other Euro-African trades for which themarket share of the conferences is sometimes lessthan 60 percent. After the court hearing, members ofthe CEWAL conference had to amend the terms oftheir loyalty contracts to prevent infringement of ECcompetition rules. Moreover fines were imposed onseveral members of the conference. The CEWAL casedemonstrates the positive spillover of competitionlaw enforcement by a large trading bloc, such as theEU. Since the final decision by the European Courtof Justice in March 2000, liner transport prices onroutes between northern Europe and West Africahave reportedly fallen.

Notwithstanding the dominance of certain linerconferences, there is growing competition from inde-pendent service providers in specific port to portmarkets, including niche operators (operating in spe-cial, well defined market segments, sometimes withspecial equipment) and operators without vesselswho rely on chartering space from liner companies—so-called non-vessel-owning common carriers. Thesecorporations frequently keep at arm’s length fromthe large operators and can be quite successfulwithin their particular markets. In view of WestAfrica’s stagnant trade volumes, however, there iscontinued need to closely monitor competitive condi-tions in this critical trade-supporting industry.

Sources: Audige 1995; European Union 1999 and 2000; Pálsson1997; and WTO 2000.

petition. It is also important to recognize thatprivate cooperation can bring benefits to con-sumers of shipping services—notably due toimproved network coordination, which cangenerate economies of scope and a wider choiceof services available to shippers.

Yet one recent study, which examines theimpact of price-fixing and cooperative work-ing agreements on liner freight rates for U.S.imports, concludes that private practices con-tinue to exercise a significant influence onliner freight rates, and that the hypotheticalbreakup of carrier agreements could lead tocost savings of as much as 20 percent (see box4.5). In practice, the extent to which linerfreight rates are pushed up by private anti-competitive practices is likely to differ acrossroutes. Developing country routes are arguablymore prone to such practices, since low overalltraffic volumes limit the number of competi-tors that can be commercially sustained (seebox 4.4).

Seaport services are increasingly driven byprivate capital and competition—In performing their function as the interfacebetween various modes of transport, seaportsprovide multiple services. The management ofships in ports requires a mixture of services re-lated to berthing, including pilotage, towing,and tug assistance. Cargo handling is the mostimportant service in moving goods throughseaports, accounting for 70 to 90 percent oftotal port charges. Other services related tocargo manipulation include customs clearance,storage, and warehousing. Specialized agentsor consignees take on the paperwork and allmatters related to the use of port facilities bya ship. Finally, there is a series of ancillary ser-vices to crew members and ships, includingprovisioning, fueling and watering, garbagecollecting, and repair facilities.38

The last decades have seen profoundchanges in the organization of seaports—thegeneral trend being toward increased privatesector participation and greater competitionwithin and between ports. A variety of owner-ship and operational structures have emerged

with regard to port management and coor-dination, the provision of infrastructure, andthe supply of services. For example, under theLandlord Port concept—which is becomingwidespread worldwide—the public Port Au-thority owns the basic infrastructure—land,access, and protection assets—and leases itout to private operators on a long-term con-cession basis. Under the Tool Port concept thePort Authority owns the infrastructure, the su-perstructure, and heavy equipment, and rentsit to private operators, which carry out com-mercial operations under licenses. The PortAuthority usually retains all regulatory func-tions in the case of landlord and tool ports. Inonly a few ports in the world has port landbeen sold to private operators, and all publicmanagement and regulatory functions beentransferred to the private sector.39

—but smaller ports are at a disadvantage—The feasibility of competitive provision of portservices, especially cargo handling, depends onseveral factors. The availability of port spaceposes a constraint to the number and the de-gree of specialization of port terminals. Sec-ond, traffic levels have to be sufficiently large,such that it is feasible to operate several termi-nals at full capacity. Experience has shown thatthe operation of more than one container ter-minal only becomes viable if port traffic ex-ceeds 150,000 twenty-foot equivalent units(TEUs) per year. Third, competition betweenports depends on geographic factors, the den-sity and quality of inland transport networks,and overall traffic volumes in the greater portregion. In practice, competitive forces arelikely to lead to a cost-efficient provision ofservices only in large seaports and regionalhubs. For smaller ports, ex ante competition,in the form of auctions where private firms bidfor the right to operate a terminal, can extractpotential monopoly or oligopoly rents thatservice providers expect to generate. Further-more, it is necessary to accompany private portparticipation with appropriate regulation overtariffs charged by service providers. Indeed, the

G L O B A L E C O N O M I C P R O S P E C T S

114

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

115

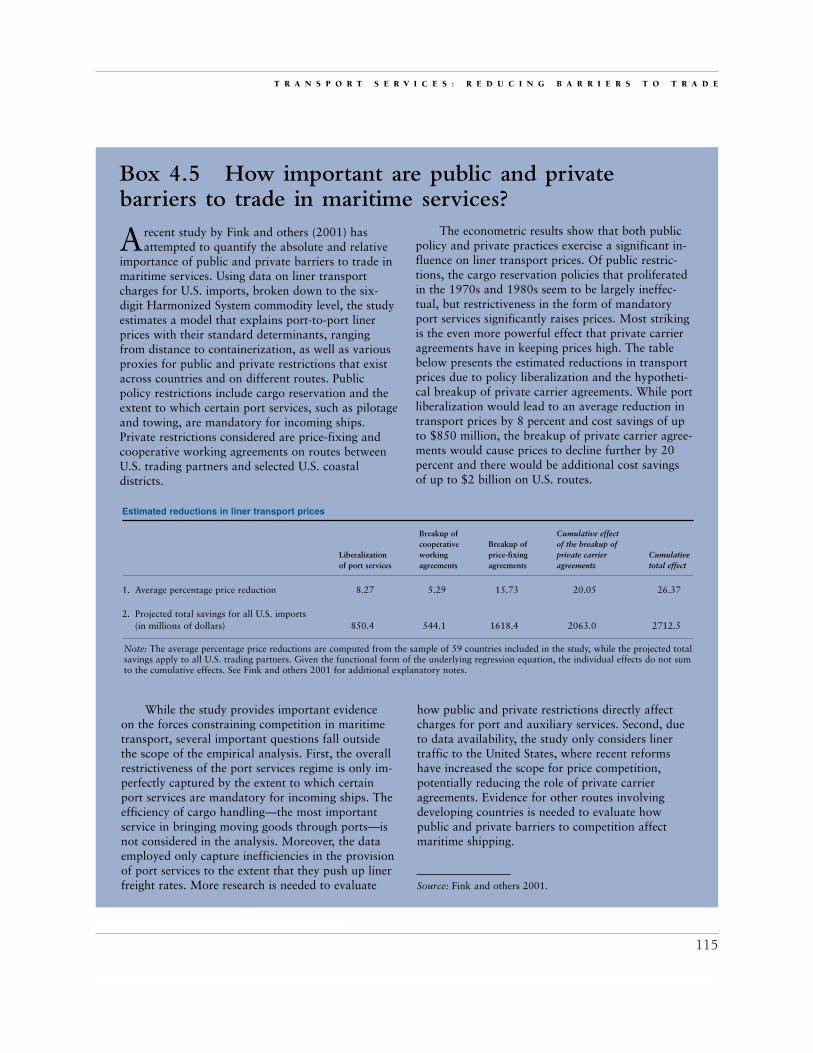

Arecent study by Fink and others (2001) hasattempted to quantify the absolute and relative

importance of public and private barriers to trade inmaritime services. Using data on liner transportcharges for U.S. imports, broken down to the six-digit Harmonized System commodity level, the studyestimates a model that explains port-to-port linerprices with their standard determinants, rangingfrom distance to containerization, as well as variousproxies for public and private restrictions that existacross countries and on different routes. Publicpolicy restrictions include cargo reservation and theextent to which certain port services, such as pilotageand towing, are mandatory for incoming ships.Private restrictions considered are price-fixing andcooperative working agreements on routes betweenU.S. trading partners and selected U.S. coastaldistricts.

Box 4.5 How important are public and privatebarriers to trade in maritime services?

The econometric results show that both publicpolicy and private practices exercise a significant in-fluence on liner transport prices. Of public restric-tions, the cargo reservation policies that proliferatedin the 1970s and 1980s seem to be largely ineffec-tual, but restrictiveness in the form of mandatoryport services significantly raises prices. Most strikingis the even more powerful effect that private carrieragreements have in keeping prices high. The tablebelow presents the estimated reductions in transportprices due to policy liberalization and the hypotheti-cal breakup of private carrier agreements. While portliberalization would lead to an average reduction intransport prices by 8 percent and cost savings of upto $850 million, the breakup of private carrier agree-ments would cause prices to decline further by 20percent and there would be additional cost savings of up to $2 billion on U.S. routes.

Estimated reductions in liner transport prices

1. Average percentage price reduction 8.27 5.29 15.73 20.05 26.37

2. Projected total savings for all U.S. imports(in millions of dollars) 850.4 544.1 1618.4 2063.0 2712.5

Liberalizationof port services

Breakup ofcooperativeworkingagreements

Breakup ofprice-fixingagreements

Cumulative effectof the breakup ofprivate carrieragreements

Cumulativetotal effect

Note: The average percentage price reductions are computed from the sample of 59 countries included in the study, while the projected totalsavings apply to all U.S. trading partners. Given the functional form of the underlying regression equation, the individual effects do not sumto the cumulative effects. See Fink and others 2001 for additional explanatory notes.

While the study provides important evidence on the forces constraining competition in maritimetransport, several important questions fall outsidethe scope of the empirical analysis. First, the overallrestrictiveness of the port services regime is only im-perfectly captured by the extent to which certainport services are mandatory for incoming ships. Theefficiency of cargo handling—the most importantservice in bringing moving goods through ports—isnot considered in the analysis. Moreover, the dataemployed only capture inefficiencies in the provisionof port services to the extent that they push up linerfreight rates. More research is needed to evaluate

how public and private restrictions directly affectcharges for port and auxiliary services. Second, dueto data availability, the study only considers linertraffic to the United States, where recent reformshave increased the scope for price competition,potentially reducing the role of private carrieragreements. Evidence for other routes involvingdeveloping countries is needed to evaluate howpublic and private barriers to competition affectmaritime shipping.

Source: Fink and others 2001.

creation of regulatory capacity is an importantelement in every port reform package—notonly to monitor and set tariffs, but also to en-sure the safety and quality of services supplied.

With few exceptions, such as Singapore,public port monopolies are typically associatedwith inefficient and expensive services; experi-ence has shown that liberalization programscan, in principle, greatly improve performance(see box 4.6). Yet achieving successful liberal-ization is a complex task—even in developedcountries. To attract long-term private inves-tors, the overall policy regime has to be credi-ble and consistent over time. At the same time,governments need to ensure that efficiencygains are passed on to port users, which re-quires carefully designed concession contractsex ante and appropriate regulatory mechanismsex post. Thus a country with weak institutions,high overall economic uncertainty, a reputationfor policy reversal, and limited regulatory ca-pacity arguably faces a significantly more diffi-cult task in managing the liberalization process.Another frequently encountered obstacle in re-forms is the adjustment to the labor force inport. Due to technological progress, port oper-ations have, over the past decades, becomemore capital-intensive, such that moderniza-tion typically requires the reduction of excesslabor. Forming consensus with workers on thedesign of reforms, retraining programs, andmeasures to soften the social impact of labor re-ductions can overcome some of the resistanceof often-powerful port unions.40

—and powerful operators are emerging atthe global levelOpening port services to the participation offoreign operators can bring special benefits, asmultinational companies often bring technol-ogy, experience, and managerial know-how.Large global port operators can also offer aloyal customer base, networking possibilities,and access to finance. Yet a number of ob-servers have voiced concerns about the risingglobal concentration of the industry. A rela-tively small group of port operators has estab-lished a regional or worldwide presence; by one

estimate this small group now accounts forabout 40 percent of the world’s annual con-tainer liftings.41 While consolidation may bringbenefits to port users, there is the danger thatdominant operators may abuse their marketpower—for example, by offering exclusive con-tracts to shipping lines if they use their world-wide facilities. Such practices may pose the riskthat the benefits from port liberalization are tosome extent captured by foreign firms.

International air transport services areheavily restricted—International air transport is divided into sched-uled passenger, freight, and mail services, andchartered services that depend on momentarydemand. In 1998, scheduled services repre-sented 87 percent of revenues, of which theoverwhelming share (88 percent) came fromthe movement of passengers.42 Internationalairfreight transport can be further divided intopassenger belly-hold freight and dedicatedfreight services. Passenger belly-hold freight istypically cheaper, because freight rates are setat marginal cost, whereas dedicated freightservices need to recover the full costs of oper-ating the aircraft.

Trade in international air transport servicesis heavily restricted by governments around the world—more so than international mari-time transport. Market access of foreign pas-senger and cargo carriers is largely determinedthrough a complex system of bilateral air ser-vice agreement (ASAs), which typically desig-nate the airlines allowed to operate on bilateralroutes, the number and frequency of flightsthey operate, what types of aircraft they use,and how much they charge.43 ASAs also deter-mine the traffic rights of airlines operating onbilateral routes, which are defined by so-calledfreedoms of the air. Under third and fourthfreedom rights, airlines are allowed to carrytraffic between their home countries and for-eign countries. Fifth freedom rights permit anairline of one country to carry traffic betweentwo other countries, provided the flight origi-nates or terminates in its own country. Themost liberal—yet rarely granted—traffic rights

G L O B A L E C O N O M I C P R O S P E C T S

116

T R A N S P O R T S E R V I C E S : R E D U C I N G B A R R I E R S T O T R A D E

117

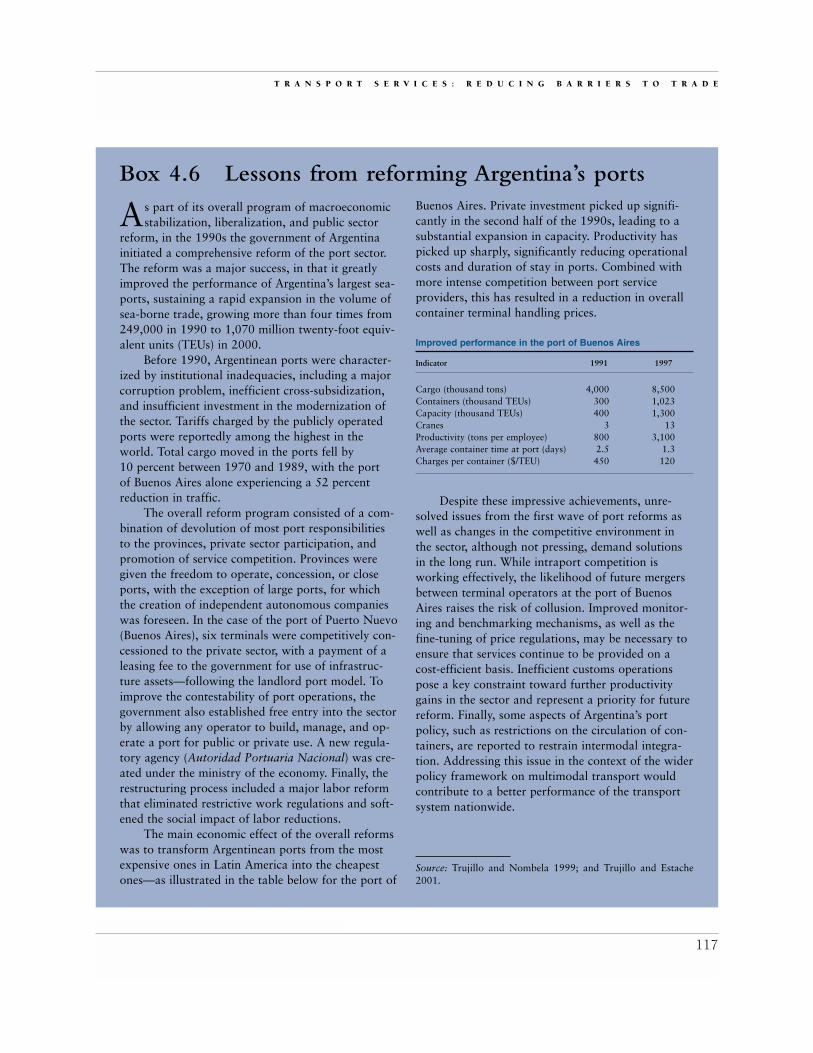

As part of its overall program of macroeconomicstabilization, liberalization, and public sector

reform, in the 1990s the government of Argentinainitiated a comprehensive reform of the port sector.The reform was a major success, in that it greatlyimproved the performance of Argentina’s largest sea-ports, sustaining a rapid expansion in the volume ofsea-borne trade, growing more than four times from249,000 in 1990 to 1,070 million twenty-foot equiv-alent units (TEUs) in 2000.

Before 1990, Argentinean ports were character-ized by institutional inadequacies, including a majorcorruption problem, inefficient cross-subsidization,and insufficient investment in the modernization ofthe sector. Tariffs charged by the publicly operatedports were reportedly among the highest in theworld. Total cargo moved in the ports fell by 10 percent between 1970 and 1989, with the port of Buenos Aires alone experiencing a 52 percentreduction in traffic.

The overall reform program consisted of a com-bination of devolution of most port responsibilitiesto the provinces, private sector participation, andpromotion of service competition. Provinces weregiven the freedom to operate, concession, or closeports, with the exception of large ports, for whichthe creation of independent autonomous companieswas foreseen. In the case of the port of Puerto Nuevo(Buenos Aires), six terminals were competitively con-cessioned to the private sector, with a payment of aleasing fee to the government for use of infrastruc-ture assets—following the landlord port model. Toimprove the contestability of port operations, thegovernment also established free entry into the sectorby allowing any operator to build, manage, and op-erate a port for public or private use. A new regula-tory agency (Autoridad Portuaria Nacional) was cre-ated under the ministry of the economy. Finally, therestructuring process included a major labor reformthat eliminated restrictive work regulations and soft-ened the social impact of labor reductions.

The main economic effect of the overall reformswas to transform Argentinean ports from the mostexpensive ones in Latin America into the cheapestones—as illustrated in the table below for the port of

Box 4.6 Lessons from reforming Argentina’s portsBuenos Aires. Private investment picked up signifi-cantly in the second half of the 1990s, leading to asubstantial expansion in capacity. Productivity haspicked up sharply, significantly reducing operationalcosts and duration of stay in ports. Combined withmore intense competition between port serviceproviders, this has resulted in a reduction in overallcontainer terminal handling prices.

Improved performance in the port of Buenos Aires

Indicator 1991 1997

Cargo (thousand tons) 4,000 8,500Containers (thousand TEUs) 300 1,023Capacity (thousand TEUs) 400 1,300Cranes 3 13Productivity (tons per employee) 800 3,100Average container time at port (days) 2.5 1.3Charges per container ($/TEU) 450 120