Embed Size (px)

Citation preview

Treasury Lessons Learned from the Credit Crunch

November 2010

Glen [email protected] : 0207 158 1677

1

A quick evolution of the crisis

Sub Prime Defaults: Excess liquidity in the system, “search for yield”, relaxed credit policies

Structured Product Valuations: Investors question the credit rating of SIP’s, too much disintermediation

Bank Liquidity Crisis: Wholesale funding dries up as trust evaporates, leading to bank failures

Financial System Bailout: Unprecedented Central Bank (liquidity) and Government (capital) bailouts to secure the

financial system

Real Economic Crisis: Significant reduction in credit and loss of confidence causes the “Great Recession”

Sovereign Debt Crisis: Government response to bank failures, slower economy and an existing debt burden

leads to significant austerity measures being taken

What is next? Stagnant inflation QE Major currency devaluations Economic reverberations in emerging markets

Credit

Liquidity

Funding

Interest Rates

FX

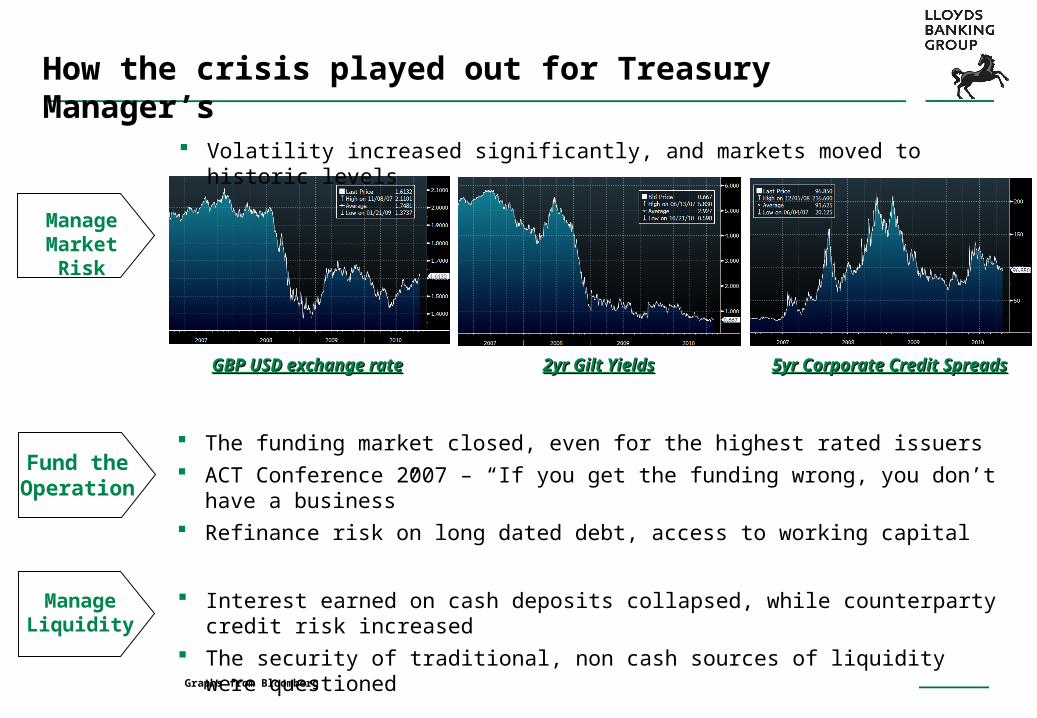

How the crisis played out for Treasury Manager’s

The funding market closed, even for the highest rated issuers ACT Conference 2007 – “If you get the funding wrong, you don’t have a business” Refinance risk on long dated debt, access to working capital

Manage Market Risk

Fund the Operation

Manage Liquidity

Interest earned on cash deposits collapsed, while counterparty credit risk increased The security of traditional, non cash sources of liquidity were questioned

GBP USD exchange rateGBP USD exchange rate 2yr Gilt Yields2yr Gilt Yields 5yr Corporate Credit Spreads5yr Corporate Credit Spreads

Volatility increased significantly, and markets moved to historic levels

Graphs from Bloomberg

Liquidity and Funding Risk

Many “givens” before the crisis have had to be fundamentally revised Treasury Managers have had to radically rethink the way they fund their organisations, and manage their cash

liquidity

In the past, the funding model relied on banks offering cheap short and medium term money (and in many instances long dated money, especially in the public sector – PFI, infrastructure, local authorities)

Over reliance on securitisation / SIV’s to use short dated wholesale money to fund long dated assets

The model became discredited Capital mobility created the need for disintermediation of banks Investors relied too heavily on the historic, model driven, credit rating approach, and less on fundamental credit

analysis of the underlying assets

Investor

Capital Mkt

Rated Notes

AAA ~ Mezz

SIV

SecuritisationBanks Borrower

Liquidity and Funding Risk – what have Treasurer’s learned

1.1. Treasurers have realised the need to diversify funding sourcesTreasurers have realised the need to diversify funding sources Avoid reliance on a single source of funding

UK Housing Association reliance on bank funding (because it was cheap) Mitigate refinancing risk

spread maturities (across the curve), markets (EUR, GBP, USD), counterparties (banks, capital market, securitisation, private placements)

However, we still face challenges:However, we still face challenges: The capital markets are efficient for large, single name, rated issuers - what about the small guy !!

2.2. Treasurers have realised the need to reconsider the priority and management of cashTreasurers have realised the need to reconsider the priority and management of cash Cash is king, but it is expensive to hold

run lean with bank liquidity lines in reserve, or be over borrowed with long term cash Cash flow forecasting and cash centralisation

Significant priority on accurately forecasting cash available within the organisation (adopt a warehouse approach to cash flow management)

Important for multinationals (different currencies, bank accounts, political risks) and large national entities (UK charity with numerous local bank accounts)

Active management of cash resources Method of investing (bank deposit, money market fund) Investment policy (security, liquidity, yield) and the over reaction to risk (lose sight of risk ~ return

relationship)

Liquidity and Funding Risk – what have Treasurer’s learned

3.3. Treasurers are reassessing the relationship they have with their banking counterpartiesTreasurers are reassessing the relationship they have with their banking counterparties Supportive relationship approach vs seeing banking as a commodity provider

Lending became commoditised – margin were thin, relationships become stressed when it matters The quality of your lender matters

“you should only borrow from someone you would lend to” Availability of undrawn facilities when conditions are tough Derivative counterparty lines – what happens when a bank fails and you owe the bank

4.4. Treasurers need to think the ‘unthinkable’ when borrowing money with lender optionalityTreasurers need to think the ‘unthinkable’ when borrowing money with lender optionality Downgrade triggers in derivative contracts

Who expected a AAA note to be downgraded to junk – post cash collateral Banks provided liquidity facilities against high quality collateralised SIV’s (collateral such as government

obligations, local authority loans, PFI loans) When the wholesale markets stopped funding SIV’s, these assets were brought back onto balance sheet

UK local authorities borrowed using LOBO loans, with investor triggers included to reduce the coupon Trigger would only be exercised if rates moved significantly higher, and that the LA could then refinance

itself at the PWLB at Gilt yields Refinance also driven by the lenders cost of funds, and LA’s now borrow from the PWLB at Gilts + 1%

Market Risk

The crisis continues to be felt in the market on a daily basiscrisis continues to be felt in the market on a daily basis Significant increase in implied volatility

VIX : (10% in Jan 2007, 60% in Sept 2008, 20% today)

1yr vol on 2yr GBP swap rates : (60bps in Jan 2007, 137bps in Sept 2008, 81bps today)

GBP USD currency vol : (7% in Jan 2007, 25% in Sept 2008, 11% today)

We have tested and remained at many “all time lows” 2yr Gilts at 0.64%, 5yr Gilt at 1.57%, 10yr Gilts at 2.98%

We have seen the unthinkable happen Long dated forward starting real yields in the UK were negative in 2010

It is crucial that individual policies on market risk are aligned on a consolidated basisIt is crucial that individual policies on market risk are aligned on a consolidated basis Far greater interest in Corporate Wide ALM

Combine all market risks facing the organisation (interest rate, foreign exchange, credit, commodity, inflation) and its pension fund (equity, interest rate, inflation, longevity)

The objective is to identify how the risks impact each other, and how to manage the complex portfolio Integrated Financial Risk Management

Market Risk – what have Treasurer’s learned

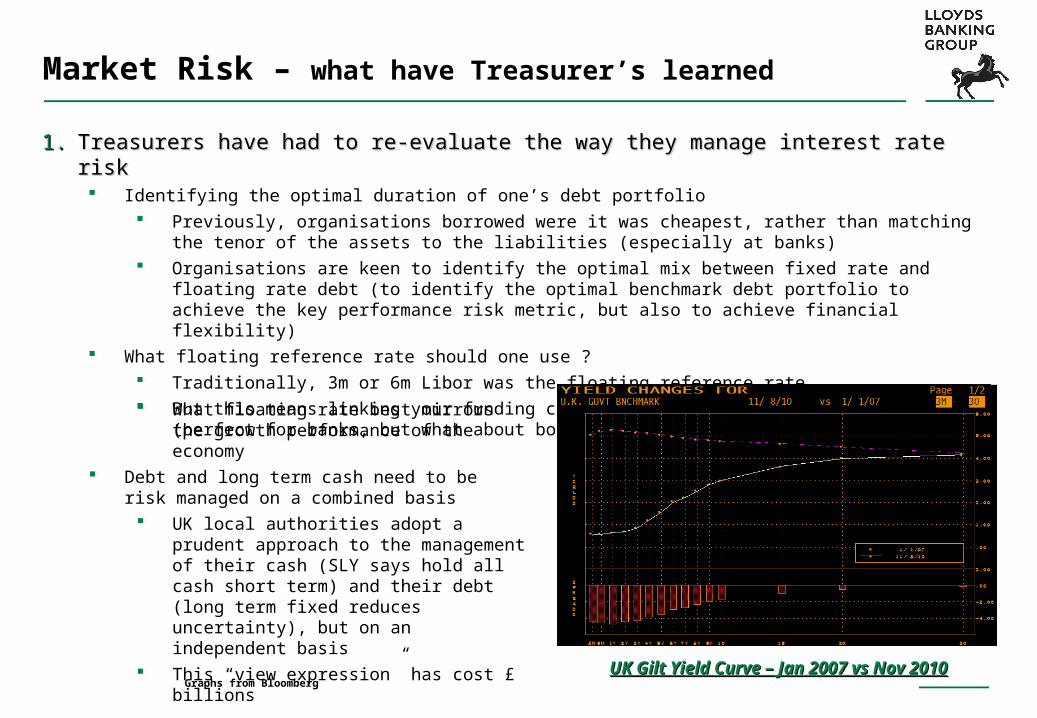

1.1. Treasurers have had to re-evaluate the way they manage interest rate riskTreasurers have had to re-evaluate the way they manage interest rate risk Identifying the optimal duration of one’s debt portfolio

Previously, organisations borrowed were it was cheapest, rather than matching the tenor of the assets to the liabilities (especially at banks)

Organisations are keen to identify the optimal mix between fixed rate and floating rate debt (to identify the optimal benchmark debt portfolio to achieve the key performance risk metric, but also to achieve financial flexibility)

What floating reference rate should one use ? Traditionally, 3m or 6m Libor was the floating reference rate But this means linking your funding cost to the cost of bank borrowing (perfect for banks, but what about

borrowers ?) What floating rate best mirrors the growth

performance of the economy Debt and long term cash need to be risk managed

on a combined basis UK local authorities adopt a prudent approach

to the management of their cash (SLY says hold all cash short term) and their debt (long term fixed reduces uncertainty), but on an independent basis

This “view expression” has cost £ billions

UK Gilt Yield Curve – Jan 2007 vs Nov 2010UK Gilt Yield Curve – Jan 2007 vs Nov 2010Graphs from Bloomberg

Market Risk – what have Treasurer’s learned

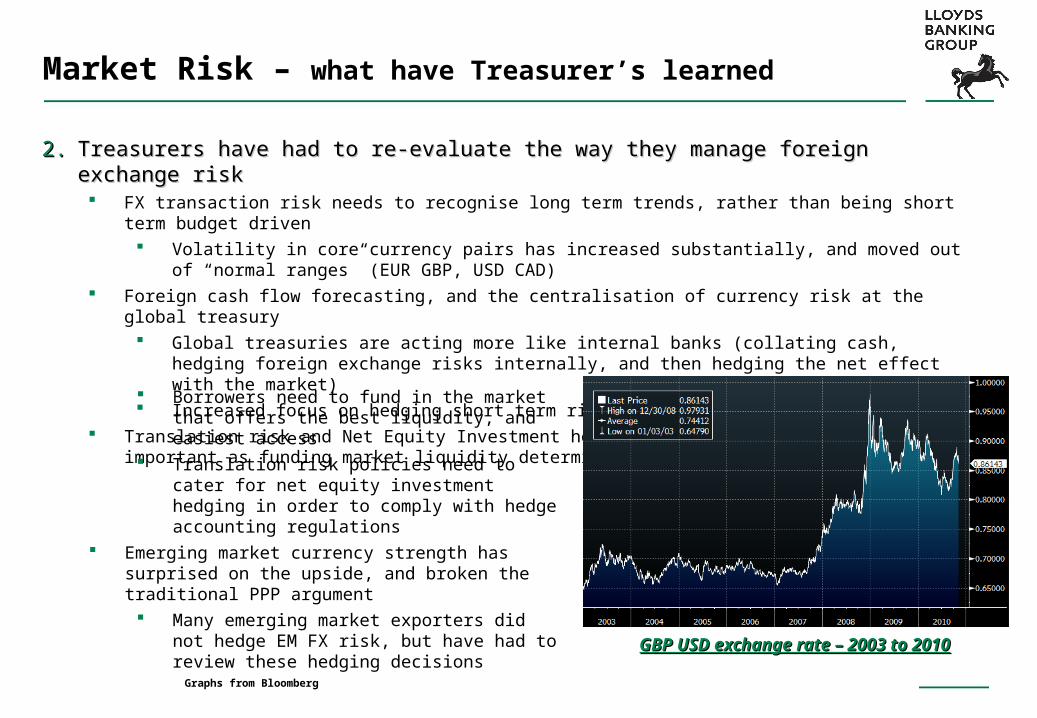

2.2. Treasurers have had to re-evaluate the way they manage foreign exchange riskTreasurers have had to re-evaluate the way they manage foreign exchange risk FX transaction risk needs to recognise long term trends, rather than being short term budget driven

Volatility in core currency pairs has increased substantially, and moved out of “normal ranges” (EUR GBP, USD CAD)

Foreign cash flow forecasting, and the centralisation of currency risk at the global treasury Global treasuries are acting more like internal banks (collating cash, hedging foreign exchange risks

internally, and then hedging the net effect with the market) Increased focus on hedging short term risks to improve cash flow certainty

Translation risk and Net Equity Investment hedging is becoming increasingly important as funding market liquidity determines where you borrow

GBP USD exchange rate – 2003 to 2010GBP USD exchange rate – 2003 to 2010

Borrowers need to fund in the market that offers the best liquidity, and easiest access

Translation risk policies need to cater for net equity investment hedging in order to comply with hedge accounting regulations

Emerging market currency strength has surprised on the upside, and broken the traditional PPP argument Many emerging market exporters did not hedge

EM FX risk, but have had to review these hedging decisions

Graphs from Bloomberg

Credit Risk

The credit crisis fundamentally changed the landscape on how credit was evaluated and risk The credit crisis fundamentally changed the landscape on how credit was evaluated and risk managedmanaged For many treasurers, credit analysis was based on the credit rating of the instrument (the rating agencies did

the job of rating credit, so why do I need to do this myself) Investment policies were written from a credit rating perspective (if it’s rated, I can buy it) Credit information was derived from the actions of rating agencies (downgrades, credit watch, etc) rather than

following the market price of the credit risk (through CDS, z-spreads) Treasurers were behind the curve in terms of information flow

Counterparty exposures were also assumed to be one wayCounterparty exposures were also assumed to be one way Credit was assumed to be something that a lender had to its borrower (but what happened if your lender was to

fail) This had significant implications on the OTC uncollateralised derivative market between banks and their clients

Credit Risk – what have Treasurer’s learned

1.1. Treasurers have had to re-evaluate the way they manage credit risk in their cash investment Treasurers have had to re-evaluate the way they manage credit risk in their cash investment portfoliosportfolios Credit ratings have been supplemented with market based information, and fundamental credit analysis Counterparty limits have been tightened up significantly, requiring greater diversification. But is diversification

achievable in a vanilla format ? Invest in foreign currency assets to get diversification, means hedging currency risk

Credit risk is also being managed by limiting the tenor of the investment But this has distorted the market significantly, as an over reaction has lead to greater conservatism UK local authorities fundamentally reviewed their investment policies following the Icelandic Bank failures.

But are they missing simple opportunities that offer significant reward for the level of risk ?

2.2. Treasurers have had to enhance their counterparty risk management policiesTreasurers have had to enhance their counterparty risk management policies Hedging reduces risk, but the risk of the hedge counterparty needs to be managed carefully

Collateral agreements reduce risk but increase cash flow uncertainty Exchange traded products have low counterparty risk, but don’t offer the hedge flexibility of the OTC

market Supplier credit risk needs to be managed carefully, especially when long dated contracts are agreed

Consider long dated energy supply agreements, and the potential m-t-m risk if the supplier defaults Organisations are questioning whether they are best placed to manage credit risk on short dated accounts

receivable, and whether they have allocated the appropriate level of capital against potential future loss Does the policy address hedging, securitisation, factoring, insurance

Operational Risk – what have Treasurer’s learned

1.1. Treasurers have had to become a lot more proactive and flexible in the way they establish Treasurers have had to become a lot more proactive and flexible in the way they establish policies, and communicate these within the organisationpolicies, and communicate these within the organisation It is recognised that we live in uncertain times, and treasury management policies need to be designed to be

adaptive to the changing markets, but within a tight control framework Treasury management committees need to act quickly and decisively, requiring the necessary delegated

authority and trust. Improved reporting techniques to explain risk

There is a greater focus on getting the right treasury management systems and software in place Global cash flow forecasting and management Real time management of market risks Integration of back office control and reporting into front office management systems

Conclusions

1.1. The credit crisis fundamentally changed the way Treasuries are measuring, monitoring and The credit crisis fundamentally changed the way Treasuries are measuring, monitoring and managing riskmanaging risk

2.2. Liquidity and funding risk remains the key priority of the treasury managerLiquidity and funding risk remains the key priority of the treasury manager1.1. Diversify fundingDiversify funding

2.2. Prioritise cash managementPrioritise cash management

3.3. Reassess your bank relationshipReassess your bank relationship

4.4. Think the ‘unthinkable’ about your lending relationshipThink the ‘unthinkable’ about your lending relationship

3.3. Market risk remains a daily risk facing the organisation, and treasurers are re-evaluating Market risk remains a daily risk facing the organisation, and treasurers are re-evaluating the way they manage interest rate and foreign exchange riskthe way they manage interest rate and foreign exchange risk

4.4. The management of credit risk around cash surpluses and counterparty exposures reflects The management of credit risk around cash surpluses and counterparty exposures reflects a market based approach, rather than being ratings drivena market based approach, rather than being ratings driven

5.5. Operationally, treasury departments are more flexible and have greater autonomy to react Operationally, treasury departments are more flexible and have greater autonomy to react to future market shocksto future market shocks