Embed Size (px)

Citation preview

Turkish Natural Gas Market

Koray Kalaycioglu

Network Regulations Group

Natural Gas Market Department EMRA - Turkey December 2017

2

TO ESTABLISH A FINANCIALLY VIABLE, STABLE, TRANSPARENT COMPETITIVE ENERGY MARKET

TO ENSURE ADEQUATE EFFICIENT, CONTINUOUS HIGH QUALITY, LOW COST ENVIRONMENT FRIENDLY SUPPLY

SUBJECT TO

INDEPENDENT REGULATION

AND SUPERVISION

ELECTRICITY MARKET LAW No.6446 NATURAL GAS MARKET LAW No.4646 PETROLEUM MARKET LAW No. 5015

LPG MARKET LAW No. 5307

Energy Market Regulatory Authority

• An independent, administratively and financially autonomous public institution.

• EMRA Board is the representative and decision making body of the Authority.

• EMRA is responsible mainly for Preparation of secondary legislation Issuing licenses Setting out the annual eligibility limits Monitoring market performance and ensuring the conformity with the market rules Drafting, amending, enforcing and auditing performance standards, distribution and customer service codes Approving the regulated tariffs Setting out the pricing principles for tariffs

Energy Market Regulatory Authority

0

10

20

30

40

50

60

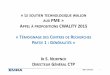

22,2

27,3 30,9

35,3 36,8 35,2 37,4

43,6 45,2 45,9 48,7 48 46,4

[DEĞER]?

BCM/YEAR

Annual Natural Gas Consumption in Turkey

Year Consumptions (million sm3) Change from the Previous Year

(%)

2007 35.395 14,24

2008 36.865 4,15

2009 35.219 -4,47

2010 37.411 6,22

2011 43.697 16,80

2012 45.242 3,53

2013 45.918 1,50

2014 48.717 6,10

2015 47.999 -1,47

2016 46.395 -3,34

2017 ~54.000 +12,08

Annual Natural Gas Consumption in Turkey

Main Characteristics of the Gas Market • Entry to the market is free through licensing.

• Regulated third party access (rTPA) is granted, and the EMRA Board is authorized to conclude all disputes on TPA.

• Pro-rata is applied for capacity allocations for the network, storage facilities, LNG terminals and FSRUs on a yearly basis.

• Tariffs of the TSO, storage facilities, LNG terminals, FSRUs and DSOs are regulated.

• Legal & account unbundling is applied.

• Imports is liberalized through gas release and new contracts.

• Existing DSOs are privatized and new DSOs are licensed by tender process.

• Static precautions are taken in terms of limiting market share.

• Non-discriminatory conduct between domestic and foreign investors is adopted.

Source: EMRA

Main Characteristics of the Gas Market (2016)

Consumption

46,4 bcm Conversion: 36.1%

Industry: 30.4%

Household: 25.0%

Services: 6.7%

Others: 1.8%

Import

46,35 bcm Pipeline: 83.5%

LNG: 16.5%

Production

367 mcm 2 production areas

9 active firms

Export

675 mcm Kipi, Greece

End-users 13,5 million 13 million subscribers

500 thousand eligible customers

Licenses are required in order to engage in any natural gas market activity,

Separate licenses are required for each market activity and

each facility,

Types of Licenses • Import License • Import License (Spot LNG) • Transmission License • Storage License • Distribution License • Wholesale License • CNG License • Export License

Licensing & Market Entry

LICENSE TYPES COUNT

STORAGE 8

EXPORT 8

TRANSMISSION 17 (1 + 16)

IMPORT (Spot LNG) 43

IMPORT (Long Term) 17 (10 + 7)

CNG SALES 77

CNG TRANSPORT & DISRTBUTION 38

WHOLESALE 49

DISTRIBUTION 72

TOTAL 251

Natural Gas Market Players

Gas Market Model

Producers

Importers (10+7+43)

Wholesalers (49)

Transmission (2+15)

Distribution (72)

Eligible Customers (500K)

Captive Customers (13M)

Export (8)

SUPPLY WHOLESALE NETWORK CONSUMPTION

Storage (8)

NGML

Network Code and

Tranmission Tariffs

Based on Entry/Exit

System

Contract

Release

Tender

LNG &

Spot LNG

Import

Set Free

LNG Termial

Codes Published

Storage

Facility

Code

Published

First Private

Importer Using

the Network

After the

Contract Release

Model

Transport

Agreements

in

Distribution

Zones

2014 2008 2009 2010 2011 2012 2013 2005 2006 2007 2001 2002 2003 2004

New

Contracts

by Private

Importers

from

Terminated

BOTAŞ

Contracts

National

Balancing

Point and

Transfer

Points

Determined

Trade in

National

Balancing

Point

First Private

Import

License From

a Country

BOTAŞ didn’t

have

an agreement

Beginnig of

Licensing of

the Market

Players

All non-

household

customers are

eligible

Wholesale

Tariffs

Set Free

Milestones in Market Liberalization

2018 2016 2017

The First

FSRU (Etki)

licensed

The Etki FRSU

Terminal Code was

approved

EMRA issued the

By-law on

Organized Natural

Gas Wholesale

Market

EMRA approved the

Market Operation

Rules for the

Organized Natural

Gas Wholesale

Market

Salt Lake

Underground

Storage Code

Dörtyol FSRU

Terminal

Licensing

and Approval

of the

Terminal

Code

Start of

Operation of the

Natural Gas

Continious Trade

Platform

Milestones in Market Liberalization

Natural Gas Infrastructure & Entry Points

2 ~13.000 km pipeline length m 4 entry points

/ 9 compressor stations j 1 exit point

Natural Gas Infrastructure & Entry Points

Name of the

facility

Operating

Year

Connected

country

Sort of capacity

(Entry/exit/bilateral)*

Capacity

(bcm/year)

Access

Conditions:

rTPA or

nTPA

Transmission

pipeline (km)

Malkoclar

(Western

Line)

1986 Russia Entry 14

bcm/year

rTPA 842 km

Gurbulak

2001 Iran Entry 9,6

bcm/year

rTPA 1491 km

Durusu

(Blue

Stream)

2003 Russia Entry 16

bcm/year

rTPA 1261 km

Turkgozu

2006 Azerbaijan Entry 6,6

bcm/year

rTPA 113 km

Kipi

2007 Greece Exit 0,7

bcm/year

rTPA 296 km

Underground Storage & LNG

TPAO Silivri Underground Storage

25 mcm/day

2.841 bcm/year

BOTAŞ Tuz Golu Underground Storage

13 (40) mcm/day

0.25 (5.4) bcm/year

Etki Liman FSRU

LNG Terminal 14 mcm/day

5 bcm/year

Egegaz Aliağa

LNG Terminal 40 mcm/day

6 bcm/year

BOTAŞ FSRU

LNG Terminal (Planned)

20 mcm/day

BOTAŞ M. Eregli LNG Terminal 22.5 mcm/day 8.2 bcm/year

Underground Storage Facilities

Name of the

facility

Operating

Year

Capacity Access

Conditions:

rTPA or nTPA

Transmi

ssion

pipeline

(km)

Send-out/

Withdrawal

(mm3/day)

Injection

(mm3/day)

Tank/Reservoir

(bcm)

BOTAS Silivri

Underground

Storage

2007 25 mm3/day

(40 mm3/day)

16 mm3/day 2,8 bcm

(4,3 bcm)

rTPA

BOTAS Tuz

Golu

Underground

Storage

2016 13 mm3/day

(40 mm3/day)

mm3/day 0.25 bcm

(5.4 bcm)

rTPA

LNG Facilities

Name of the

facility

Operating

Year

Regasificatio

n Capacity

Injection

Capacity

(mcm/day)

Tank Capacity

(mcm)

Access

Conditions:

rTPA or nTPA

BOTAŞ Marmara

LNG Terminal

1994 22,5

mcm/day

8,2 bcm/year

151 mcm/day 153 mcm

(255.000 LNG m3)

rTPA

EGEGAZ Aliaga

LNG Terminal

2006 40 mcm/day

6 bcm/year

81 mcm/day 168 mcm

(280.000 LNG m3)

rTPA

Etki Liman FSRU

Terminal

2016 14,1

mcm/day

5 bcm/year

86 mcm/day 84 mcm

(143.000 LNG m3)

rTPA

FSRU Practice

• In March 2016 EMRA Board issued decision on the licensing regime of the floating LNG terminals: Acknowledgement

• License granted in May 2016.

• Basic Operating Procedures and Guidelines of the first FSRU terminal approved in November 2016.

• The terminal operation initiated in early December 2016.

EXPORT

TOTAL TANK CAPACITY

SENDOUT TO

THE NETWORK

SENDOUT TO LAND

VEHICLES

22.5 mm3/day - 8,2 bcm/year

40 mm3/day - 6 bcm/year

14 mm3/day - 5 bcm/year

=56 mm3/day - 19.2 bcm/year

255,000 (3 x 85.000)

280,000 (2 x 140.000)

143,000

=678,000 m3 LNG

5,2 bcm long term

2,5 bcm spot

=7.7 bcm (2015)

75 vehicles/day

100 vehicles/day

=175 vehicles/day

LNG Facilities in Turkey (2016)

BOTAS LNG EGEGAZ LNG ETKI FSRU

Natural Gas Imports by Country

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Russia Iran Azerbaijan Algeria Nigeria Others*

Spot LNG Imports by Country (2016)

US 11,4%

Belgium 4,0% France

4,2%

Netherlands [YÜZDE]

Qatar 43,3%

Egypt 4,7%

Nigeria 8,4%

Norway [YÜZDE]

Trinidad and Tobago 15,6%

Natural Gas Consumption by Sector (2016)

Electricity Generation

36,1%

Industry 30,4%

Households 25,0%

Government Offices and

Business 6,1%

Others 2,4%

Natural Gas Distribution in 2017

Monthly Seasonality of Consumption in 2016

1,4 1,3 1,2 1,3 1,2 1,4 1,5 1,8 1,3 1,5 1,6

1,2

2,5 1,8

1,4 0,8

0,4 0,3 0,2 0,2

0,2 0,5

1,1 2,2

1,3

1,2

1,3

1,2

1,2 1,1 1,0 1,1

1,0

1,3

1,4

1,4

0,5

0,4 0,3

0,2

0,1 0,1 0,1 0,1

0,1

0,2

0,3

0,5

0

1

2

3

4

5

6

7

bcm

Power Residential Industrial Service

Key Performance Indicators 2014 2015 2016 2017

Number of TSOs 1 1 1 1

Pipeline length (km) 12.561 12.963 13.000 13.000

Pipeline pressure (barg) 50-75 50-75 50-75 50-75

Annual consumption (bcm) 48.717 47.999 46.500 54.000

Seasonal demand swing (%) 0,14 0,2 0,19 0,21

Daily peak demand (mcm) 195 224 220 243

Length of pipeline/consumption (km/bcm)

258 270 280 280

Storage capacity/consumption (%) 5,5% 5,9% 6,1% 5,7%

LNG terminal capacity/consumption (%) 29% 30% 41% 47%

LNG + storage daily send out / peak demand (%)

29% 27% 41% 212%

Number of entry zones 9 9 9 9

Number of exit zones 1 1 1 1

Number of compressor stations 9 9 9 9

Pipeline length / # of compressor stations

1396 1440 1444 1444

Virtual Trade Amounts by Month (2016)

0,00

500,00

1 000,00

1 500,00

2 000,00

2 500,00

Transfer Points UDN Total

Organized Natural Gas Wholesale Market

• In line with the Turkey’s objective of becoming natural gas trade center, organized natural gas market will be established for the purchase and sale of natural gas and will be operated by Energy Exchange (EPİAŞ).

• In November 2016, first draft of the By-Law on Organized Natural Gas Wholesale Market was published by EMRA.

• Organized Natural Gas Wholesale Market Usage Procedures and Principles was published in September 2017.

• The regulation aims to let the market players trade natural gas anonymously in an organized liberal market operating by continuous trade principles, besides letting the transmission system operator balance the system by entering the continuous trade platform when needed.

• The Organized Natural Gas Wholesale Market is expected to give the players much needed price signals about the market.

• The market simulations on the Continuous Trade Platform is will start on 1 April 2018.

Aims of the Organized Natural Gas Market

The Organized Natural Gas Wholesale Market will provide

• A tool for the TSO to maintain the physical balance of the system,

• A platform where the market players can trade gas day-ahead and intraday,

• The means for the market players to balance themselves,

• Market based reference prices.

Characteristics of the Market • Participating in the market is completely voluntary.

• All market players willing to enter the market shall have a Standard Transportation Contract signed with the TSO, BOTAŞ.

• A contract must also be signed with EPİAŞ in order to participate in Continuous Trade Platform.

• The TSO may enter the system as a Residual Balancer when needed.

• Non-market based methods may be used when the TSO can’t balance the system by trading in the market.

• Net matchings will be entered to Electronic Bulletin Board of BOTAŞ as nominations for the EPİAŞ virtual entry/exit points.

• Residual Balancer Price, Balancing Gas Buy Price and Balancing Gas Sell Price will be calculated based on the market-based balancing operations.

• Daily Reference Price will be weighted aggregate of the day-ahead and intraday contracts.

Contracts

TAKAS

BANK

EPİAŞ

TRADERS

BOTAŞ

CTP

C

CHPC

MDC: Market Delivery Contract CHC: Clearing House Contract STC: Standard Transportation Contract CHPC: Clearing House-Participant Contract CTPC: Continuous Trade Participant Contract

NETWORK CODE/TRADING RULES

Transmission Operation Rules Market Operation Rules

TRADING POINT PRINCIPLES

PHYSICAL NATIONAL BALANCING POINT

SYSTEM OPERATOR/MARKET OPERATOR

BOTAŞ EPİAŞ

ORGANIZED NATURAL GAS WHOLESALE MARKET

Continuous Trade

Continuous Trade Platform

Issues of Debate

• Pay-as-bid or Marginal Price?

• Bids limited or not by the Bank Guarantee?

• Bids and offers on the market limited or unlimited?

• Residual Balancer enters the market freely & anonymously or on a fixed time?

• Limit for the bids-offers for Residual Balancing?

• Imbalance fees based on Daily Reference Price or Residual Balancer Price?

• When and how non-market based methods shall be used for balancing the system?

• Cost of the non-market based methods included in the balancing fees or not?

Aliağa LNG

Etki FSRU

FSRU

Marmara LNG

Pemi

Malkoçlar 8 Contracts

Silivri Underground

Akçakoca

Blue Stream 2 Contracts

Azerbaycan 1 Contract

TANAP

Mersin Underground

Tuz Gölü Underground

Iraq

Eastern Mediterranean

7 Entry Points 2 Production Areas 5 LNG Terminals 3 Underground Storages

Turkish Trade Center

Turkmenistan 1 Contract

Tools of the Trade

Iran 1 Contract

Dortyol FSRU

Well-developed Natural Gas Trade Center

Establishing a Gas Trade Center that will provide a reference price for the region

New Infrastructure Investments

Making new investments such as LNG terminals, storage facilities, transmission lines and compressors, in order to meet the demand and improve the trade

Demand Side Market

Reshaping the purchase contracts with regards to the regional and seasonal price signals about the market

Price Signals

Giving the much needed regional and seasonal price signals about the market that will lead to new contracts and investments

Day Ahead and Intra-day Markets

Letting the market players trade natural gas anonymously in an organized liberal market operating by continuous trade principles

Balancing Platform

Allowing the market players to balance their portfolios and the transmission system operator balance the system

Turkish Gas Market Targets

• Entry-exit zones & entry-exit tariff system

• Model Transport Agreements for distribution zones - Basis for Interoperability Regulation

• Amendments in the network code for TANAP entry point

• Balancing regime fully compliant with EU regulations

• Amendments in the Network Code and regulations in the Market Usage Procedures & Principles aiming better transparency

• National TYNDP introduced by organized market directive

• Daily forecasts in Electronic Bulletin Board of BOTAŞ

Steps Taken for Better Harmonization

• Redefining Gas Day & Gas Year compliant with EU regulations

• Reviewing and redesigning the Capacity Allocation Mechanism (Daily capacity, auctions & secondary markets)

• Adopting measurement units based on energy rather than volume

• A unified and comprehensive transparency regulation

Improvements to Make

Countries Compared (2014)

Turkey Italy France Germany Netherland

s

UK

Number of TSO 1 2 2 15 1 3

Pipeline Entry/Exit

Points

4/1 6/2 6/4 22/16 6/12 5/3

NG Pipeline Length (km) 12.561 33.339 15.322 26.985 8.531 7.660

Number of Compressors 9 11 30 25 15 28

Consumption (bcm) 48,7 56,8 35,9 70,9 32,1 66,7

Residential &

Commercial

24,9% 47% 58,6% 46,2% 50,4% 52,9%

Power 48,1% 28,6% 6% 15,5% 15,3% 26,5%

Industrial 25,4% 21,6% 31,3% 36,9% 32,4% 17,4%

Other 1,5% 2,8% 4,1% 1,4% 1,9% 3,2%

Countries Compared (2014)

Turkey Italy France Germany Netherlands UK

LNG 15% 8% 20% 0% 1,5% 14%

Pipeline 84% 81% 78% 92% 31% 41%

Production 1% 11% 2% 8% 67% 45%

First RUS/27 RUS/21,3 NOR/15.5 RUS/38.5 NOR/9.4 NOR/10.4

Second IRN/8,9 NLD/8.3 QAT/7.1 NOR/27.7 RUS/3.5 QAT/10.4

Third AZE/6.1 DZA/6.2 NLD/4.9 NLD/18.1 GBR/1.7 NLD/6.6

Other 7,3 15,6 7,1 0,7 8,7 1,3

Countries Compared (2014)

Turkey Italy France Germany Netherlands UK

Length of

pipeline/consumption

(km/bcm) 258 587 427 381 266 115

Seasonal demand swing

(%) 0,14 0,47 0,33 0,34 0,25

# of Underground Gas

Storage/ Capacity (bcm) 1/2,8 13/16,6 17/12,0 58/24,6 5/12,9 8/5,0

Storage

Capacity/Consumption 5,5% 29% 33% 35% 40% 8%

# of LNG Terminals /

Annual Capacity (bcm) 2/12,2 3/14,8 3/22 0/0 1/12 4/52

LNG terminal

capacity/consumption

(%)

29% 26% 61% 0% 37% 78%

Pipeline length / #

compressor stations 1.396 3.030 510 1.079 568 274