Embed Size (px)

Citation preview

UCB Inspired by patients.Driven by science.

9 month interim report

Brussels, 20 October 2017

9M 2017 reportDisclaimer and safe harbor 2

Forward-looking statementsThis presentation contains forward-looking statements, including, without limitation, statements containing the words “believes”, “anticipates”,“expects”, “intends”, “plans”, “seeks”, “estimates”, “may”, “will”, and “continue” and similar expressions. These forward-looking statements are basedon current plans, estimates and beliefs of management. By their nature, such forward-looking statements are not guarantees of future performanceand are subject to known and unknown risks, uncertainties, and assumptions which might cause the actual results, financial condition, performance orachievements of UCB, or industry results, to be materially different from any future results, performance, or achievements expressed or implied bysuch forward-looking statements contained in this presentation.

Important factors that could result in such differences include but are not limited to: changes in general economic, business and competitiveconditions, the inability to obtain necessary regulatory approvals or to obtain them on acceptable terms, costs associated with research anddevelopment, changes in the prospects for products in the pipeline or under development by UCB, effects of future judicial decisions or governmentalinvestigations, product liability claims, challenges to patent protection for products or product candidates, changes in laws or regulations, exchangerate fluctuations, changes or uncertainties in tax laws or the administration of such laws and hiring and retention of its employees. There is noguarantee that new product candidates in the pipeline will progress to product approval or that new indications for existing products will be developedand approved. Products or potential products which are the subject of partnerships, joint ventures or licensing collaborations may be subject todifferences between the partners. Also, UCB or others could discover safety, side effects or manufacturing problems with its products after they aremarketed. Moreover, sales may be impacted by international and domestic trends toward managed care and health care cost containment and thereimbursement policies imposed by third-party payers as well as legislation affecting biopharmaceutical pricing and reimbursement.

Given these uncertainties, the public is cautioned not to place any undue reliance on such forward-looking statements. These forward-lookingstatements are made only as of the date of this presentation. UCB expressly disclaims any obligation to update any such forward-looking statementsin this presentation to reflect any change in its expectations with regard thereto or any change in events, conditions, for circumstances on which anysuch statement is based, unless such statement is required pursuant to applicable laws and regulations.

In the event of any differences between this Presentation and the Annual or Half Year Report, the information included in the Report shall prevail.

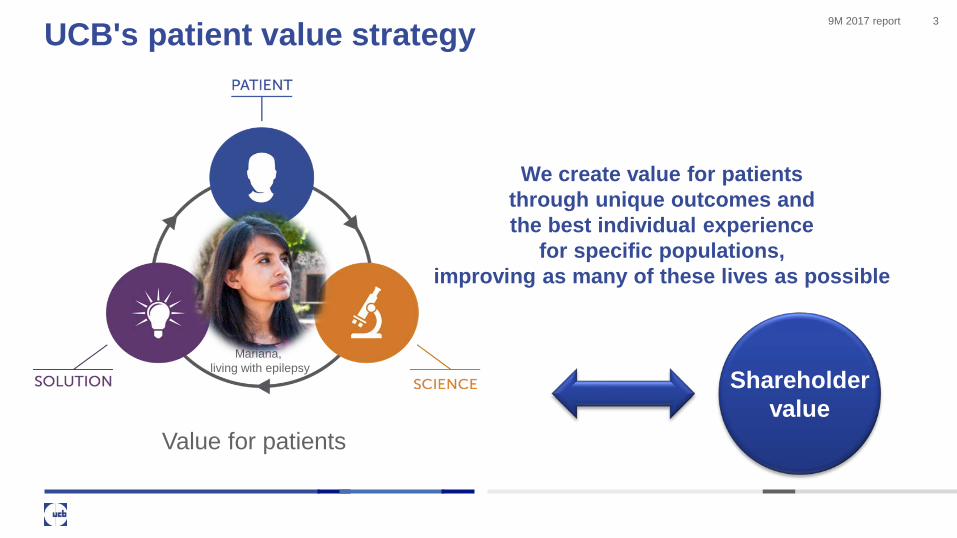

9M 2017 reportUCB's patient value strategy 3

We create value for patients through unique outcomes and the best individual experience

for specific populations, improving as many of these lives as possible

Shareholder value

Value for patients

Mariana, living with epilepsy

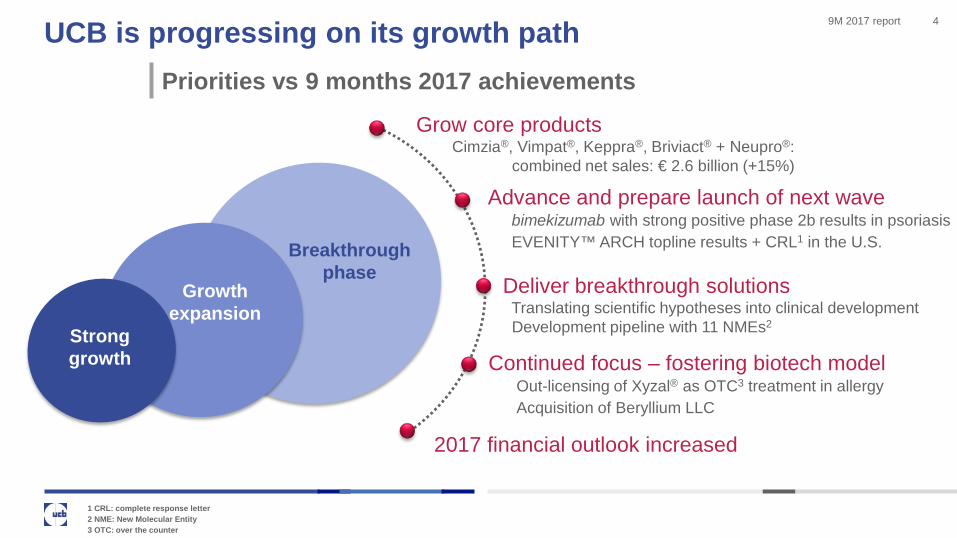

9M 2017 reportUCB is progressing on its growth path 4

1 CRL: complete response letter2 NME: New Molecular Entity3 OTC: over the counter

Grow core productsCimzia®, Vimpat®, Keppra®, Briviact® + Neupro®:

combined net sales: € 2.6 billion (+15%)

Advance and prepare launch of next wavebimekizumab with strong positive phase 2b results in psoriasisEVENITY™ ARCH topline results + CRL1 in the U.S.

Deliver breakthrough solutionsTranslating scientific hypotheses into clinical developmentDevelopment pipeline with 11 NMEs2

Continued focus – fostering biotech modelOut-licensing of Xyzal® as OTC3 treatment in allergyAcquisition of Beryllium LLC

Stronggrowth

Growth expansion

Breakthrough phase

2017 financial outlook increased

Priorities vs 9 months 2017 achievements

9M 2017 report9 months 2017 key financial highlights 5

On track to deliver FY 2017 guidance

* 2016 figures have been restated reflecting IFRS 15 implementation in 2017Numbers may not add due to roundingCER: constant exchange rate

€ million 9M 2017 9M 2016* Actual CER

Revenue 3 331 3 042 9% 9%

Immunology / Cimzia® 1 022 927 10% 10%

Neurology 1 601 1352 18% 19%

Vimpat® 707 586 20% 20%

Keppra® 607 538 13% 14%

Briviact® 57 11 > 100% > 100%

Neupro® 230 217 6% 6%

9M 2017 report

Translating scientific hypotheses into clinical development6

1 APDS - Activated PI3K Delta Syndrome2 MG – myasthenia gravis

bimekizumab (IL17A/F)

psoriasis

psoriatic arthritis

ankylosing spondylitis

Phase 3 start: end 2017

Phase 2b results: Q1 2018

Phase 2b results: Q1 2018

dapirolizumab pegol (CD40L antibody)systemic lupus erythematosus Phase 2b results: H2 2018 (Partner: Biogen)

padsevonil (PPSI)highly drug resistant epilepsy Phase 2b start: Q1 2018

seletalisib (PI3K δ inhibitor)Sjögren’s syndrome + APDS1 (Phase 1b) Phase 2a results: end 2017

rozanolixizumab (FcRn)immune thrombocytopenia + MG2 Phase 2a results: Q1 2018 / H2 2018

UCB4144 / VR942 - asthma Phase 2a start: 2018 (Partner: Vectura)

UCB6673 ; UCB7858 ; UCB0159

UCB3491 ; UCB0599neurology

immunology

FilingPhase 3Phase 2Phase 1

9M 2017 report

2017 financial targets

2017 financial outlook 7

…increased cross all key performance indicators…

rEBITDA: recurring Earnings Before Interest, Taxes, Depreciation and Amortization charges* Based on ~188 million weighted average shares outstanding

Revenue € 4.4 - 4.5 billion

rEBITDA € 1.25 – 1.35 billion

Core EPS* € 4.10 – 4.50

Guidance beyond 2017unchanged

rEBITDA / revenue ratio 30% in 2018

'CVN' net sales ≥ € 3.1 billion by 2020

Briviact® net sales ≥ € 450 million by 2026

9M 2017 reportUCB's patient value strategy 8

We create value for patients through unique outcomes and the best individual experience

for specific populations, improving as many of these lives as possible

Shareholder value

Value for patients

Mariana, living with epilepsy

Further factsand figures

9

9M 2017 report 10Strong Cimzia® performance across all regions

Net sales1

R&D milestones

1 2016 figures have been restated reflecting IFRS 15 implementation in 2017 2 nr axSpA: non-radiographic axial spondyloarthritisNumbers may not add due to rounding CER: constant exchange rates

• Crohn’s disease• rheumatoid arthritis• psoriatic arthritis• axial spondyloarthritis /

ankylosing spondylitis

2024 patent expiry (U.S. & EU) 2026 (Japan)

• Astellas (Japan - 2012)• Dermira (psoriasis - 2014)

1 307 million 2016 net sales≥ 1.5 billion peak sales by 2020

Cimzia®

psoriasisPhase 3 results

(Jan 2017)

nr axSpA²Phase 3 results

(U.S. - mid 2018)

CRIBPhase 4 results

(Jan 2017)

psoriasis + psoriatic arthritis

Phase 3 start(Japan - Feb 2017)

psoriasis + psoriatic arthritis

Phase 3 results(Japan - Q4 2018)

€ million 9M 2017 9M 2016 Act CER

U.S. 656 590 11% 11%

Europe 271 250 8% 9%

Japan 25 25 2% 5%

International markets 70 62 13% 13%

Total Cimzia® 1 022 927 10% 10%

CRIB & CRADLEFiling

(EU - May 2017)

JIAComplete

Response Letter (U.S. - Mar 2017)

CRIB & CRADLEFiling

(U.S. - June 2017)

psoriasisFiling

(EU - Aug 2017)

psoriasisFiling

(U.S. - Oct 2017)

9M 2017 report

4.1%

3.0%

3.5%

4.0%

4.5%

5.0%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Cimzia® RA R3M Patient Share

8.9% 9.8%

17.7%

0%

5%

10%

15%

20%

Anti TNF Biologics Cimzia®

Cimzia® vs. RA Market Growth

10.2%12.9%

6.3%

0%

5%

10%

15%

20%

Anti TNF Biologics Cimzia®

Cimzia® vs. Rheumatology1

Market Growth

5.9%

4.5%

5.0%

5.5%

6.0%

6.5%

Jul-16 Sep-16 Nov-16 Jan-17 Mar-17 May-17 Jul-17

Cimzia® RheumatologyR3M Patient Share

-4.3%

-2.1%

0.7%

-6%

-4%

-2%

0%

2%Anti TNF Biologics Cimzia®

Cimzia® vs. Rheumatology1

Market Growth

Cimzia® in-market performance 11

1 Rheumatology market = rheumatoid arthritis (RA) + psoriatic arthritis (PsA) + ankylosing arthritis (AS) in the U.S. or axial spondylitis (AxSPA) in EU.For the U.S., the Cimzia® and market growth are based on MAT 2017 vs MAT 2016For Europe & Japan, the Cimzia® and market growth are calculated for Aug ’17 versus Aug ’16, the patient share trend is based on R3M

U.S.

+5.0%

+0.4%

Europe Japan

Source: U.S: IMS Source of Business Report May 2017

8.4%

7.5%

8.0%

8.5%

9.0%

9.5%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Cimzia® Rheumatology1

R3M Patient Share

-0.1%

Source: IMS MIDAS - In-Market KPI’s are based on Exit Patients (Aug 2017)

+8.8%

+0.3%

Source: IMS MIDAS; Cimzia® patients are considered 100% in RA - In-Market KPI’s are based on Exit Patients (Aug 2017)

-3.9%

9M 2017 reportVimpat® performance 12

Robust growth in all markets, launch in Japan

1 2016 figures have been restated reflecting IFRS 15 implementation in 2017 2 POS: Partial-onset seizures, also known as focal seizuresNumbers may not add due to rounding 3 CHMP: Committee for Medicinal Products for Human UseCER: constant exchange rate 4 PGTCS: Primary Generalized Tonic-Clonic Seizures

epilepsy POS2

2022 patent expiry (U.S. & EU) 2024 (Japan)

Daiichi Sankyo (Japan -2014)

814 million 2016 net sales> 1.2 billion peak sales by 2020

Vimpat® Net sales1

R&D milestonesepilepsy POS2

pediatricFiling

(U.S. – Mar 2017)

epilepsy POS2

ped. adj. therapyPhase 3 results

(Mar 2017)

epilepsy PGTCS3

adj. therapyPhase 3 results

(2019)

€ million 9M 2017 9M 2016 Act CER

U.S. 540 446 21% 20%

Europe 128 111 15% 16%

Japan 8 3 > 100% > 100%

International markets 31 26 18% 15%

Total Vimpat® 707 586 20% 20%

epilepsy POS –pediatric Approval

(EU - Sep 2017)

epilepsy POS –monotherapy

Approval(Japan - Aug 2017)

9M 2017 report

3.3%

2.5%

2.7%

2.9%

3.1%

3.3%

3.5%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Vimpat® – R3M TDx Share

4.1%

3.5%

3.7%

3.9%

4.1%

4.3%

4.5%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Vimpat® – R3M TRx Share

1.5%

10.1%

0%

5%

10%

15%

20%

AED Market Vimpat®

Vimpat® vs. AED Market Growth (TRx)

7.4%

0%

5%

10%

15%

20%

AED Market Vimpat®

Vimpat® vs. AED Market Growth (TDx)

0.6%

15.1%

0%

5%

10%

15%

20%

AED Market Vimpat®

Vimpat® vs. AED Market Growth (TDx)

Vimpat® in-market performance 13

AED market: All molecules in ATC3= N3A + Phenobarbital in N5B. In Europe and Japan, the TDx of all these molecules are factored for epilepsy usage. In the U.S., the TRx of 26 of these molecules are factored for epilepsy usage.

U.S.

+8.6%

+0.3%

Europe Japan

Source data U.S.: U.S. IMS NPA - In-Market KPIs are based on TRx

+14.5%

+0.4%

Source data EU: IMS MIDAS - In-Market KPI’s are based on TDx

Numbers to be populated when sufficient data is

available

0.57%

0.0%0.1%0.2%0.3%0.4%0.5%0.6%

Aug-16 Oct-16 Dec-16 Feb-17 Apr-17 Jun-17 Aug-17

Vimpat® – R3M TDx Share

Source data JP: IMS MIDAS - In-market KPI’s are based on TDx

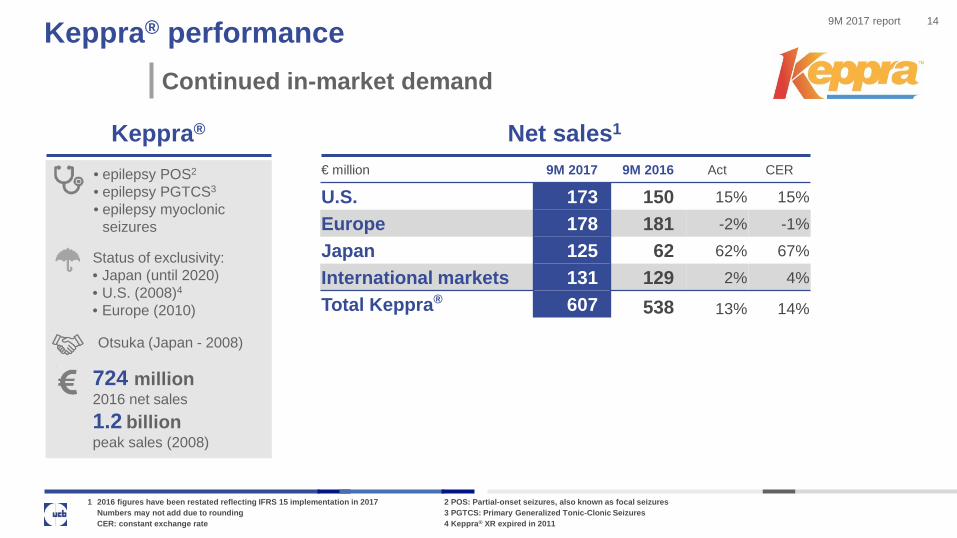

9M 2017 report 14

Continued in-market demand

1 2016 figures have been restated reflecting IFRS 15 implementation in 2017 2 POS: Partial-onset seizures, also known as focal seizuresNumbers may not add due to rounding 3 PGTCS: Primary Generalized Tonic-Clonic SeizuresCER: constant exchange rate 4 Keppra® XR expired in 2011

Keppra® performance

Keppra® Net sales1

• epilepsy POS2

• epilepsy PGTCS3

• epilepsy myoclonic seizures

Status of exclusivity:• Japan (until 2020)• U.S. (2008)4

• Europe (2010)

Otsuka (Japan - 2008)

724 million 2016 net sales1.2 billion peak sales (2008)

€ million 9M 2017 9M 2016 Act CER

U.S. 173 150 15% 15%

Europe 178 181 -2% -1%

Japan 125 62 62% 67%

International markets 131 129 2% 4%

Total Keppra® 607 538 13% 14%

9M 2017 report

12.6%

10.0%

12.0%

14.0%

16.0%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Keppra® – R3M TDx Share

7.4%

39.4%

0%

10%

20%

30%

40%

50%

AED Market Keppra®

Keppra® vs. AED Market Growth (TDx)

0.6%

3.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

AED Market Keppra®

Keppra® vs. AED Market Growth (TDx)

0.8%0.0%

0.5%

1.0%

1.5%

2.0%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Keppra® – R3M TRx Share

1.5%

-12.5%-15.0%

-10.0%

-5.0%

0.0%

5.0%

AED Market Keppra®

Keppra® vs. AED Market Growth (TRx)

15.0%

10.0%

12.0%

14.0%

16.0%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Keppra® – R3M TDx Share

Keppra® in-market performance 15

AED market: All molecules in ATC3= N3A + Phenobarbital in N5B. In Europe, the TDx of all these molecules are factored for epilepsy usage. In the U.S., the TRx of 26 of these molecules are factored for epilepsy usage. For U.S., Keppra® includes Keppra® XR. For EU, Keppra® does not include UCB levetiracetam.

U.S.

-14.0%

-0.1%

Europe Japan

Source data U.S.: U.S. IMS NPA - In-market KPI’s are based on TRx

+2.6%

+0.1%

Source data EU: IMS MIDAS - In-market KPI’s are based on TDx

+32.0%

Source data JP: IMS MIDAS - In-market KPI’s are based on TDx

+2.9%

9M 2017 report 16

New treatment option for patients living with epilepsy

Briviact® launch

Net sales1

R&D milestones

Briviact®

1 2016 figures have been restated reflecting IFRS 15 implementation in 2017 2 POS: Partial-onset seizures, also known as focal seizuresNumbers may not add due to rounding CER: constant exchange rate

epilepsy POS2 –monotherapy

Filing(U.S. – Jan 2017)

epilepsy POS2

2026 patent expiry (U.S. & EU)

18 million 2016 net sales> 450 million peak sales by 2026

Available to patients in:• Some EU countries• North America

€ million 9M 2017 9M 2016 Act CER

U.S. 40 5 > 100% > 100%

Europe 16 6 > 100% > 100%

International markets 1 0 > 100% > 100%

Total Briviact® 57 11 > 100% > 100%

epilepsy POS2 –ped. adj. therapy

Filing(EU – Jul 2017)

epilepsy POS2 –pediatricFiling

(U.S. – Jul 2017)

epilepsy POS2 –adj. therapy

Phase 3 start(Japan – Aug 2017)

epilepsy POS2 –monotherapy

Approval(U.S. – Sep 2017)

9M 2017 reportBriviact® in-market performance 17

A new therapeutic option in the AED market

AED market: All molecules in ATC3= N3A + Phenobarbital in N5B. In EU, the TDx of all these molecules are factored for epilepsy usage. In the US, the TRx of 26 of these molecules are factored for epilepsy usage.

U.S. Europe

Source data U.S.: U.S. IMS NPAIn-Market KPIs are based on TRx

Source data EU: IMS MIDASIn-Market KPI’s are based on TDx

0.20%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

May-16 Aug-16 Nov-16 Feb-17 May-17 Aug-17

Briviact® – R3M TRx Share 0.46%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

May-16 Aug-16 Nov-16 Feb-17 May-17 Aug-17

Briviact® – R3M TDx Share

9M 2017 reportNeupro® performance 18

1 2016 figures have been restated reflecting IFRS 15 implementation in 2017 Numbers may not add due to rounding CER: constant exchange rate

• Parkinson’s disease• restless legs syndrome

2021 patent expiry (U.S. & EU) 2024 (Japan)

Otsuka (Japan - 2002)

302 million 2016 net sales≥ 400 million peak sales by 2020

Neupro® Net sales1

€ million 9M 2017 9M 2016 Act CER

U.S. 72 58 24% 23%

Europe 122 118 3% 4%

Japan 26 30 -15% -15%

International markets 10 10 -1% -4%

Total Neupro® 230 217 6% 6%

9M 2017 report

28.8%

25%

26%

27%

28%

29%

30%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Neupro® PD – R3M TDx Share

6.7%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Neupro® PD – R3M TRx Share

1.1% 0.6%

6.5%

-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

PD Market PD KeyCompetitors

Neupro®

Neupro® PD vs. PD (KC) Market Growth (TDx)

17.7%

16.0%

16.5%

17.0%

17.5%

18.0%

18.5%

Aug-16 Nov-16 Feb-17 May-17 Aug-17

Neupro® PD – R3M TDx Share

0.0% -1.2%

12.7%

-2%0%2%4%6%8%

10%12%14%

PD Market PD KeyCompetitors

Neupro®

Neupro® PD vs. PD (KC) Market Growth (TDx)

0.1% 0.1%

-2.0%-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

PD Market PD KeyCompetitors

Neupro®

Neupro® PD vs. PD (KC) Market Growth (TRx)

Neupro® in-market performance 19

PD market: All molecules in ATC3= N4A. In the Europe and Japan, the TDx of all these molecules are factored for PD usage. In the U.S., only the TRx of Rotigotine, Pramipexole and Ropinirole are factored for PD usagePD Key Competitors (KC) market: The 8 DA’s (Dopamine Antagonists): Bromocriptine, Cabergoline, Lisuride, Pergolide, Rotigotine, Pramipexole, Piribedil, Ropinirole. In the US, only Rotigotine, Pramipexole and Ropinirole are factored for PD usage, hence the PD market and PD KC market are the same.

U.S.

-2.1%

+0.1%

Europe Japan

Source data U.S.: U.S. IMS NPA - In-market KPI’s are based on TRx

+5.9%

+0.8%

Source data EU: IMS MIDAS - In-market KPI’s are based on TDx

+13.9%

+3.0%

Source data JP: IMS MIDAS - In-market KPI’s are based on TDx

9M 2017 reportEVENITY™ (romosozumab) 20

An innovative investigational bone-building therapy

STRUCTURE, FRAME, BRIDGE and ARCHPhase 3 studies completed

Opportunity to build bone in high-risk osteoporosis patients, especially post-fracture

Uniquely increase bone formation and decrease bone resorption

Under regulatory review in the U.S., Canada and JapanComplete Response Letter in the U.S. (July 2017)

™

Manorama,living with osteoporosis

EVENITY™ is the trade name of romosozumab which has been provisionally approved by the U.S. Food & Drug Administration (FDA) and the European Medicines Agency (EMA). EVENITY™ (romosozumab) is developed in partnership with Amgen globally.

9M 2017 reportTranslating scientific hypothesis into clinical differentiation 21

Bimekizumab

Specific targeting both IL-17A and IL-17F

will improve therapeutic efficacy versus targeting IL-17A alone

IL-17F

IL-17RAIL-17RC

IL-17A

Skin and joint inflammation

Partial blockade anti-IL-17A therapeutics

Bimekizumab complete and specific blockade IL-17A & IL-17F

Innovative breakthrough molecules

9M 2017 reportBimekizumab: Strong positive results from BE ABLE 22

Demonstrates skin clearance in phase 2b psoriasis study

* Affected body surface area of at least 10% and PASI of at least 12

250 patientsModerate to severe chronic

plaque psoriasis*

placebo12 weeks

bimekizumab12 weeks

Up to 79% of patients achieved at least 90%

skin clearance (PASI90)

Up to 60% of patients achieved complete skin

clearance (PASI100)

9M 2017 report

• 159 patients with moderate to severe rheumatoid arthritis

• 44 weeks

• placebo

• safety and tolerability + efficacy of bimekizumab as an add-on therapy to Cimzia®

Add on to Cimzia®

(NCT02430909)

Phase 2a results June 2017

Bimekizumab current development program 23

First monoclonal antibody neutralizing both IL-17A and IL-17F

* Defined as a patient who achieves 90% reduction from baseline in the PASI scoreSource: www.clinicaltrial.gov

• 200 patients with active psoriatic arthritis

• 48 weeks

• placebo

• ACR50 response @ week 12

Psoriatic arthritis(NCT02969525)

Phase 2b results Q1 2018

• 250 patients moderate to severe chronic plaque psoriasis

• 48 weeks

• placebo

• PASI90* response@ week 12

Psoriasis(NCT02905006)

Phase 2b results July 2017

Duration

Comparator

Endpoint

Results

• 285 patients with active ankylosing spondylitis

• 48 weeks

• placebo

• ASAS40 response @ week 12

Ankylosing spondylitis(NCT02963506)

Phase 2b results Q1 2018

Phase 3 to start end 2017

9M 2017 reportBimekizumab Ambition: Complete skin clearance together with profound effects on articular and non-articular symptoms

24

Patient unmet need emerges at the interface between psoriatic skin disease and the debilitating impact of inflammation in joints and other tissues, warranting an integrated resolution of the diverse disease manifestations

Therapeutic hypothesis: Specific targeting of both IL-17A and IL-17F will improve therapeutic efficacy versus targeting IL-17A alone

Bimekizumab: the first humanized monoclonal IgG1 antibody that potently and selectively neutralizes both IL-17A & IL-17F

Clinical experience to date: Psoriasis Ph2b study and early clinical studies in Psoriatic Arthritis and mild Psoriasis support that IL-17F neutralization is differentiating:• Speed of clinical response• Depth of clinical response • Maintenance of clinical response1,2

IL-17F

IL-17RAIL-17RC

IL-17A

Skin and Joint inflammation

Partial blockade anti- IL-17A therapeutics

Bimekizumab complete and specific blockade IL-17A & IL-17F

1. Glatt et al. Br J Clin Pharmacol. 201705;83(5):991-1001.2. Glatt et al. Ann Rheum Dis. 2016;75(Suppl 2):95-95.

9M 2017 report

UCB0159immunologyPhase 1 start

rozanolixizumabmyasthenia gravis

Phase 2a start

Vimpat®

epilepsy POS –ped. adj. therapy

Filing (U.S.)

bimekizumab add on to Cimzia®

rheumatoid arthritisPhase 2a results

R&D milestones in 2017

POS: Partial-Onset Seizures, also known as focal seizures CRL: complete response letterCHMP: Committee for Medicinal Products for Human Use ITP: immune thrombocytopenia

25

neurologyimmunologybone

romosozumabosteoporosis in

post-menopausal women (ARCH)Phase 3 results

padsevonilhighly drug

resistant epilepsyPhase 2a results

Vimpat®

epilepsy POS –ped. adj. therapy Phase 3 results

Cimzia®

psoriasisPhase 3 results

bimekizumab psoriasis

Phase 2b results

seletalisibSjögren’s syndrome

Phase 2a results

Cimzia®

psoriasis / psoriatic arthritis - Phase 3

start (Japan)

Briviact®

epilepsy POS –monotherapyFiling (U.S.)

Briviact®

epilepsy POS –ped. adj. therapy

Filing (EU & U.S.)

Vimpat®

epilepsy POS –pediatric

CHMP opinion (EU)

radiprodil / UCB3491

infantile epilepsyPhase 1b start

Cimzia®

juvenile idiopathic arthritis

CRL (U.S.)

romosozumabosteoporosis in

post-menopausal women

CRL (U.S.)

Cimzia®

psoriasisFiling (EU)

Vimpat®

epilepsy POS –monotherapy

Approval (Japan)

Briviact®

epilepsy POS –adj. therapy

Phase 3 start(Japan)

Vimpat®

epilepsy POS –pediatric

Approval (EU)

Briviact®

epilepsy POS –monotherapy

Approval (U.S.)

Cimzia®

psoriasisFiling (U.S.)

bimekizumab psoriasis

Phase 3 start

9M 2017 report

2018 2019

R&D milestones

nr axSpA: non-radiographic axial spondyloarthritisSLE: Systemic Lupus ErythematosusPGTCS: Primary generalized tonic-clonic seizures

26

neurologyimmunologybone

Cimzia®

nr axSpA (U.S.)Phase 3 results

dapirolizumab pegolSLE

Phase 2b results

Vimpat®

epilepsy PGTCS –adj. therapy

Phase 3 results

bimekizumab psoriatic arthritisPhase 2b results

bimekizumab ankylosing spondylitis

Phase 2b results

Cimzia®

psoriasis / psoriatic arthritis - Phase 3

results (Japan)

rozanolixizumab / UCB7665

myasthenia gravisPhase 2a results

radiprodil / UCB3491

infantile epilepsyPhase 1b results

rozanolixizumab / UCB7665

ITPPhase 2a results

UCB4144 / VR942asthma

Phase 2a start

Briviact®

epilepsy POS –adj. therapy

Phase 3 results(Japan)

9M 2017 report"Biotech model" - partnering examples 27

INN Indication Partner Status today

vedolizumab moderate to severe: • ulcerative colitis (UC)• Crohn’s disease (CD)

Takeda available to patients since 2014

reslizumab eosinophilic asthma Teva available to patients since 2016

inotuzumab ozogamicin(CMC544)

acute lymphoblastic leukemia (ALL)

Pfizer Approved in EU (June 2017)Approved in the U.S. (August 2017)

olokizumab rheumatoid arthritis (RA) R Pharm Phase 3 ongoing

9M 2017 reportUCB HY 2017 financial highlights 28

Core product growth drive top and bottom line

CER: constant exchange rate*one-time other revenue of € 56 million for out-licensing the OTC-allergy drug Xyzal® (levoceterizine)

CER

+10%

+32%+35%

Actual

Revenue• Revenue adjusted for divestitures and one-time revenue*• Net sales up by 10% (+9% CER) to € 2 billion• Net sales adjusted for divestitures +14% (+13% CER)

€ 2.2 billion

Total operating expenses • Overall operating expense ratio improved to 47%• R&D expense phasing

€ 1.05 billion

Recurring EBITDA • Higher gross profit • Improved operating expenses ratio

€ 742 million

Profit of the Group• € 431 million attributable to UCB shareholders (+44%)

€ 451 million

Core earnings per share Based on 188 million weighted average shares outstanding (2016: 188 million)

€ 2.53

+12%

+43%

+47% +42%

+6% +5%

+13%

adjusted

+38%

9M 2017 reportContinuously improved product mix 29

Cimzia®, Vimpat®, Keppra®, Briviact® + Neupro® = 85% of net sales

CER = constant currency exchange rates* Excluding € 8 million hedging

Cimzia® +11% (+9% CER)• Sustainable growth in a competitive

environmentVimpat® +25% (+22% CER)

• Robust growth in all markets

Keppra® +17% (+16% CER)• Driven by Japan, international

markets and stocking effects

Briviact® € 36 million• Solid launch curve

Neupro® +9% (+8% CER)• Continued growth

HY 2017 net sales*€ 2 043 million

(+10%; CER: +9%)

9M 2017 report 302017 HY - Top line growth leads to improved ratios*Sustainable growth and margin improvement

69% 69% 70% 71%75%

FY 2013 FY 2014 FY 2015 FY 2016 HY 2017

60% 57% 55% 52%47%

FY 2013FY 2014FY 2015FY 2016 HY2017

* versus revenue

Gross margin ratio* Operating expense ratio*

rEBITDA ratio tracking towards 30% target

FY 2013 FY 2014 FY2015 FY2016 2018e

30%

21%

18%17%

25%

9M 2017 reportUCB - A global networked player 31

Recent investments and partnerships in technology platforms

The RNA-Medicines Company

Research collaboration for stratified-medicine approach to the development of novel therapeutics for epilepsy

Research collaboration generating unprecedented understanding of the cellular composition of complex tissues, and to assess responses to therapies

Acquisition of leadingcapabilities for proteinexpression and structuralbiology

Acquisition of discovery platform targeting RNA with small molecules

Research collaboration to advance the development of multi-specific therapeutic antibodies in I-O

And "UCB Ventures Fund" to capture external innovation

9M 2017 report2017 HY recurring EBITDA 32

Solid growth - Improved operating expenses ratio

CER: constant exchange rate * 2016 figures have been adjusted reflecting IFRS 15 implementation in 2017EBIT: Earnings before interest and taxesEBITDA: Earning before interests, taxes, depreciation and amortization charges

For the six months ended 30 June Actual Variance € million 2017 2016 Actual rates CER

Revenue 2 230 1 996 10% 9% Net sales 2 036 1 853 10% 9% Royalty income and fees 58 51 14% 15% Other revenue 136 92 48% 45%

Gross profit 1 666 1 424 17% 15% Marketing and selling expenses -464 -448 3% 2% Research and development expenses -474 -458 4% 4% General and administrative expenses -93 -87 6% 6% Other operating income / expenses (-) -16 1 n/a n/a

Total operating expenses -1 047 -992 6% 5%

Recurring EBIT (REBIT) 619 432 43% 39% Amortization of intangible assets -78 -82 -5% -5% Depreciation charges -45 -36 28% 28%

Recurring EBITDA (REBITDA) 742 549 35% 32%

9M 2017 report2017 HY profit 33

CER: constant exchange rateEBIT: Earnings before interest and taxes

For the six months ended 30 June Actual Variance

€ million 2017 2016 Actual rates CER

Recurring EBIT 619 432 43% 39% Impairment charges 4 -11 n/a n/a Restructuring expenses -7 -9 -24% -23% Gain on disposals 0 77 n/a n/a Other non-recurring income / expenses (-) 3 -7 7% 6%

Total non-recurring income / expenses (-) 1 50 -99% -98%

EBIT (operating profit) 619 482 28% 24% Net financial expenses (-) -55 -65 -15% -15% Result from associates 0 0 n/a n/a

Profit before income taxes 564 417 35% 31% Income tax expense (-) / credit -114 -91 25% 21%

Profit from continuing operations 450 325 38% 34% Profit / loss (-) from discontinued operations 1 -9 n/a n/a

Profit 451 316 43% 38% Attributable to UCB shareholders 431 300 44% 39% Attributable to non-controlling interests 20 16 47% 42%

9M 2017 report2017 HY core earnings per share 34

Strong growth of core net profit

For the six months ended 30 June Actual Variance

€ million 2017 2016 Actual rates CER

Profit 451 316 43% 38% Attributable to UCB shareholders 431 300 44% 39% Attributable to non-controlling interests 20 16 47% 42%

Profit attributable to UCB shareholders 431 300 44% 39% Total non-recurring income (-) / expenses -1 -50 n/a n/a Income tax on non-recurring expenses (-) / credit -1 -9 n/a n/a Financial one-off income (-) / expenses 0 28 n/a n/a Income tax on financial one-off income / expenses (-) 0 0 n/a n/a Profit (-) / loss from discontinued operations -1 9 n/a n/a Amortization of intangibles linked to sales 61 62 n/a n/a Income tax on amortization of intangibles linked to sales -12 -16 n/a n/a

Core profit attributable to UCB shareholders 477 325 47% 42% Weighted average number of shares (million) 188 188 0% n/a

Core EPS attributable to UCB shareholders 2.53 1.72 47% 42%

9M 2017 report

590

- -

250 176

75

350 350168

118

29 18

243

368 368 350

176

Liquidassets

2017 2018 2019 2020 2021 2022 2023 2024 beyond

EIB loanInstitutional eurobondBelgian retail bondOther loans

Debt maturity schedule (@ 30 June 2017)35

EIB: European Investment Bank

€ m

illion

9M 2017 reportOne UCB today: A global player 36

Presence in 38 countries complemented by a robust network of partners

As at December 2016

7 527employees

globally

9M 2017 reportOne UCB today: A global player 37

Presence in 38 countries complemented by a robust network of partners

• Atlanta, GA• Raleigh, NC

• 1 143 employees• 15% of global workforce

• € 983 million • 48% of global sales*

U.S.

• Tokyo• Saitama

• 405 employees• 5% of global workforce

• € 177 million• 9% of global sales*

Japan

• Braine-l’Alleud & Brussels, Belgium

• Monheim, Germany• Bulle, Switzerland• Slough, U.K.

• 4 352 employees• 58% of global workforce

• € 629 million• 31% of global sales*

Europe

Net sales

Major sites • Shangai & Zuhai, China

• 1 627 employees• 22% of global workforce

• € 255 million• 12% of global sales*

International markets

Employees

* Net sales before hedging

9M 2017 report 38Stable shareholder base with free-float of 60%Weighted average shares outstanding in 2017: 188 million

“Free float” investors by region

Source: Notifications and UCB underlying ownership analysis

9M 2017 report 39

ן Antje Witte, Vice President Investor Relations• Phone: +32 2 559 9414• E-mail: [email protected]

ן Isabelle Ghellynck, Director Investor Relations• Phone: +32 2 559 9588• E-mail: [email protected]

ן Nathalie Deldime, Investor Relations Manager• Phone: +32 2 559 9291• E-mail: [email protected]

ן Check out our new IR App – stay tuned wherever you go

Your UCB Investor Relations team