Embed Size (px)

Citation preview

Ukraine World Bank Rural Finance Project (P076553)

Initial Feasibility Study of Developing Weather Index Insurance

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences

Report prepared by

Jerry R. Skees, Ulrich Hess, and Hector Ibarra1

December, 2002

1. Skees is president of GlobalAgRisk; Hess is with the International Finance Corporation of the World Bank Group; Ibarra is director of reinsurance with Argoasemex in Mexico. This report was conducted as an initial feasibility study for using index-based agricultural insurance in Ukraine as part of a World Bank Rural Finance Project (P076553). The objectives of this study were: 1) to perform an initial assessment of developing and introducing weather index and other index-based insurance in Ukraine; and 2) to educate and familiarize key stakeholders in the Ukraine with the concepts of index-based insurance and to inform the rural finance and agricultural insurance policy making process of the potential consequences on their current legislation. A number of professionals contributed to the overall effort. The authors wish to thank the Deputy Prime Minister Kazachenko and the head of the Agrarian Policy secretariat, Dr. Shevzov, for hosting and helping with meetings and guidance for the mission. World Bank professionals in Kiev were also instrumental in helping organize meetings inside Ukraine. A complete list of those we met while in Ukraine appears in Appendix A. Our sincere gratitude is extended to all who spent time helping us understand more about Ukraine and this issue in particular. As with any undertaking of this nature, our translations and assessments of information we gathered is subject to error. We apologize for any misinterpretations of the information and welcome comments and feedback to correct any errors. The corresponding author can be reached at [email protected]. Anne Goes contributed to Section 4 of this report. Finally, a personal thank you is extended to Celeste Sullivan for her diligence in editing and formatting this report.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Table of Contents

ii

Skees, Hess, Ibarra

Table of Contents

Table of Contents.....................................................................................................................ii

Illustrations...............................................................................................................................v

Figures ..................................................................................................................................................v Tables ...................................................................................................................................................v

Executive Summary ................................................................................................................vi

Why Weather Index Insurance?.......................................................................................................... vii Main Findings of the Initial Assessment............................................................................................. viii

Agriculture in Ukraine ......................................................................................................................................viii Risk Profile for Ukrainian Farmers ................................................................................................................... ix Link: Rural Finance Crop Insurance ............................................................................................................ ix Risk Profile of Ukraine Agriculture.................................................................................................................... ix The Likely Cost of Farm-Level Crop Insurance in Ukraine ............................................................................... x Insurance Sector in General.............................................................................................................................. x Crop Insurance in Ukraine................................................................................................................................ xi Reinsurance ....................................................................................................................................................xiii Proposed Compulsory Crop Insurance ...........................................................................................................xiii Prototype Weather Index Insurance Contract .................................................................................................xiv Regulatory Framework .................................................................................................................................... xv Infrastructure: Weather Data and Weather Stations ....................................................................................... xv Weather Index Development...........................................................................................................................xvi Backstop Facility for Weather Risk Insurance Retention in the Ukraine.........................................................xvi Education and Familiarization Work During the Mission................................................................................xvii

Comments on the Feasibility of Weather Index Insurance in the Ukraine ........................................ xvii Future Assessments for Evaluating the Potential of Index-Based Insurance ...................................xviii

A. Conduct a full feasibility study................................................................................................................... xviii B. Pilot project .................................................................................................................................................xix C. Phase I: Investment phase .........................................................................................................................xix D. Phase II: Sustainable private sector-led weather index insurance.............................................................xix E. Expenditure items .......................................................................................................................................xix F. Technical assistance (regulatory, feasibility, dissemination, education).....................................................xix G. Goods .........................................................................................................................................................xix H. Backstop facility ..........................................................................................................................................xix

Section 1: Experience with Multiple-Peril Crop Insurance ...................................................1

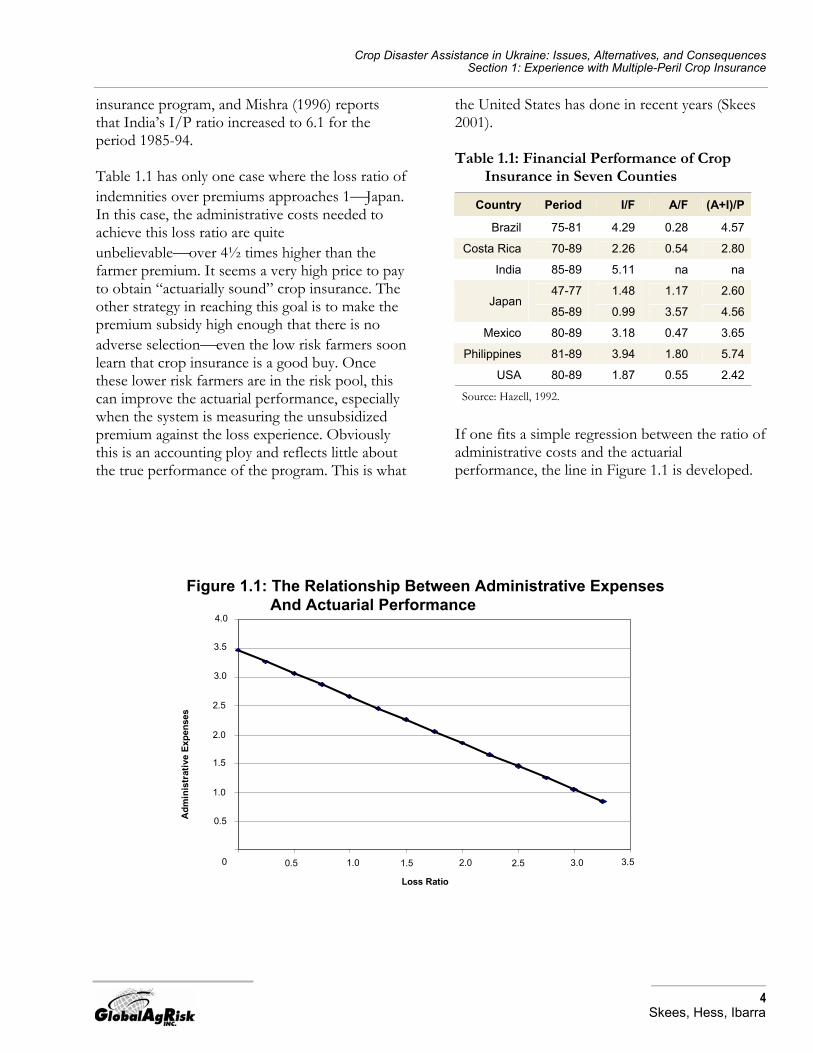

Requirements for Multiple-Peril Crop Insurance ...................................................................................2 The U.S. Federal Crop Insurance Program ..........................................................................................2 Actuarial Performance of the Crop Insurance Programs ......................................................................3 Compulsory Crop Insurance in Ukraine ................................................................................................6

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Table of Contents

iii

Skees, Hess, Ibarra

Section 2: Reinsurance............................................................................................................7

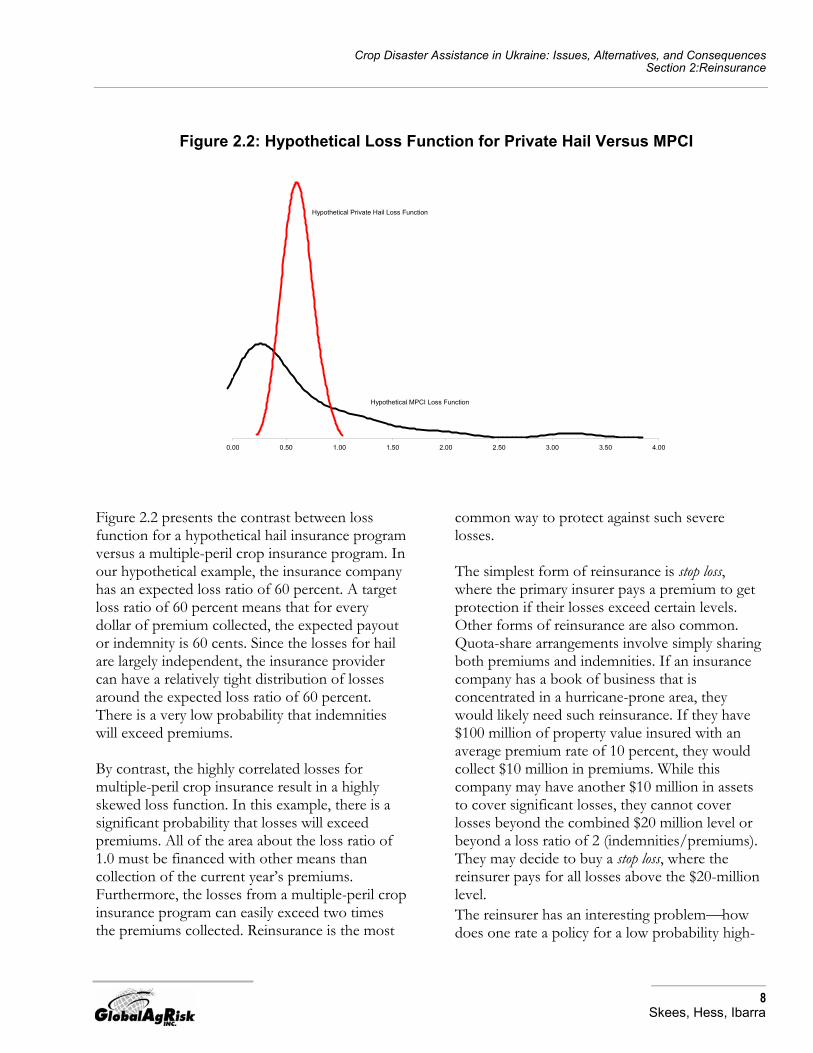

Problems with Traditional Markets ......................................................................................................10 New Market Instruments for Sharing Catastrophe Risk ......................................................................10

Exchange-Traded Indexes .............................................................................................................................. 11 Risk-Linked Securities..................................................................................................................................... 12

Markets for Weather-Based Securities ...............................................................................................12 Reinsurance and Weather Markets.....................................................................................................13 Conclusion ..........................................................................................................................................13

Section 3: Finding a Better Approach to Crop Insurance: Index Insurance Alternatives 15

Prototype Weather Index Insurance Contract for Ukraine ..................................................................16 Experience with Index Insurance ........................................................................................................17 Basis Risk ...........................................................................................................................................18 Summary of the Relative Advantages and Disadvantages of Index Insurance ..................................20

Section 4: Assessing the Market for Agricultural Insurance in Ukraine ...........................23

The Status and Structure of the Agricultural Sector in Ukraine...........................................................24 Farm Size and Ownership Patterns ....................................................................................................24 Access to credit and financial services ...............................................................................................25 Risk Profile for Ukrainian Farmers ......................................................................................................25 Demand for Agricultural Insurance: Links to Rural Finance................................................................26

Section 5: Modeling Risk for Major Crops in Ukraine .........................................................29

Methodology for Developing Loss Cost Estimates..............................................................................30 Aggregation of Indemnities and Liabilities...........................................................................................32 Mapping Crop Risk in Ukraine ............................................................................................................33

Section 6: The Ukrainian Risk Profile...................................................................................35

Likely Cost of Farm-Level Insurance...................................................................................................37

Section 7:Development of the Insurance Market of Ukraine During the 1990s ................38

Insurance Market for the Period 1995-2001: Major Performance Indicators ......................................39 Analysis of the Actual Insurance Market .............................................................................................40

Market Structure .............................................................................................................................................. 42 Market Distribution by Line of Business .......................................................................................................... 42 Underwriting Results ....................................................................................................................................... 43

Supply of Agricultural Insurance .........................................................................................................44

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Table of Contents

iv

Skees, Hess, Ibarra

Profitability Analysis of the Industry ....................................................................................................46 Investment Risk ..................................................................................................................................47 Reinsurance........................................................................................................................................48 Other Possibilities for Supplying Index Insurance Contracts ..............................................................50

Section 8: Considering the Regulatory Framework for Index-Based Insurance Products .............................................................................................52

Regulatory History...............................................................................................................................52 Weather Index Insurance in the Ukrainian Regulatory Framework.....................................................53 Weather Derivative Versus Weather Index Insurance ........................................................................53 The Relevance of Compulsory Crop Insurance in Ukraine .................................................................55 Regulatory Capacity............................................................................................................................55 The Current Regulatory Set-up in Ukraine..........................................................................................56 Weather-Risk Reinsurance and Moral Hazard....................................................................................56 Other Issues for the Ukraine Regulatory Regime ...............................................................................56

Section 9: Designing a Risk Management Component of the Rural Finance Project ......58

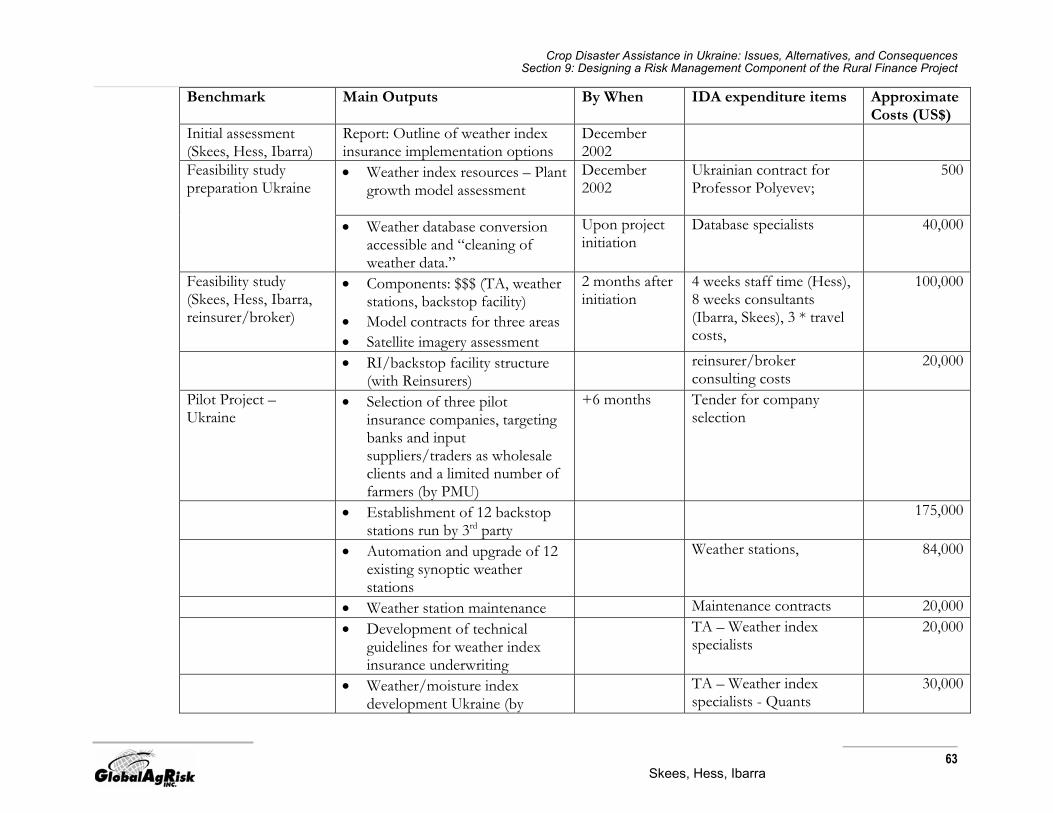

Description of Sub-Component: Weather Index Insurance Products..................................................58 Weather-Risk Transfer Mechanism: International Reinsurance and the Ukraine Government (GoU) Backstop Facility .................................................................................................................................59 Summary of Benchmarks....................................................................................................................60

A. Full feasibility study..................................................................................................................................... 60 B. Pilot project ................................................................................................................................................. 60 C. Phase I: Investment phase ......................................................................................................................... 61 D. Phase II: Sustainable private sector-led weather index insurance............................................................. 61 E. Expenditure items ....................................................................................................................................... 61 F. Technical assistance (regulatory, feasibility, dissemination, education)..................................................... 61 G. Goods ......................................................................................................................................................... 61 H. Backstop facility .......................................................................................................................................... 61

Backstop Facility for Weather-Risk Insurance Retention in Ukraine...................................................61

Appendix A: List of Meetings................................................................................................65

Appendix B: Soils in Ukraine ................................................................................................67

Major Topographical Features ............................................................................................................67 Major Soil Types .................................................................................................................................67

Appendix C: FAS Assessment of Ukraine, June 2002 ........................................................68

References..............................................................................................................................71

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Lists of Illustrations

v

Skees, Hess, Ibarra

Illustrations

Figures 1.1: The Relationship Between Administrative Expenses and Actuarial Performance ........................................ 4 2.1: Independent Versus Correlated Risk.................................................................................................................... 7 2.2: Hypothetical Loss Function for Private Hail Versus MPCI ............................................................................. 8 3.1:The Relationships Between Estimating Farm Yields, the Number of Observations, and the Standard

Deviation of Farm Yields ..................................................................................................................................... 19 5.1: Actual and Detrended Yields for Wheat in Zaporizhia ................................................................................... 30 5.2: Map of Value of Five Crops by Oblast .............................................................................................................. 32 5.3: Map of Relative Risk in Ukraine Using a 95 Percent Area-Yield Insurance Program ................................ 33 6.1: Regional Map for Relatively Homogenous Regions in Ukraine..................................................................... 35 6.2: Comparison of Country-Loss Function to Regional-Loss Function............................................................. 36 7.1: Total Insurance Premiums and Indemnities ..................................................................................................... 39 7.2: Historical Loss Ratio............................................................................................................................................. 39 7.3: Evolution of Total Number of Insurance Companies .................................................................................... 40 7.4: Total Insurance Market by Line of Business..................................................................................................... 42 7.5: Profits as Percentage of Total Capital ................................................................................................................ 46 7.6: Reinsurance to Residents and Non-Residents .................................................................................................. 48 7.7: Relative Importance of the Reinsurance Market .............................................................................................. 48 7.8: Total Reinsurance by Type of Business ............................................................................................................. 49 9.1: Sample Structure for Risk Layering .................................................................................................................... 59 9.2: Possible Structure for Risk Sharing .................................................................................................................... 62

Tables 1.1: Financial Performance of Crop Insurance in Seven Counties.......................................................................... 4 4.1: Ukraine Land Use Estimates 2000...................................................................................................................... 23 4.2: Grain Area, Yield, and Production: All Farms, 1987-1998, (10-year Average) ............................................ 23 4.3: Agricultural Production in Ukraine in 2000 ...................................................................................................... 24 4.4: The Number and Size of Private Farms in Ukraine on January 1, 2001....................................................... 25 4.5: Number of Agricultural Entities in Ukraine as of April 2001 ........................................................................ 28 5.1: Estimates of Value at Risk in 2001 (in UAH 1,000,000) ................................................................................. 31 5.2: Relative Pure Premium Risk for Different Crops by Oblast Using a 95 Percent Area-Yield Insurance

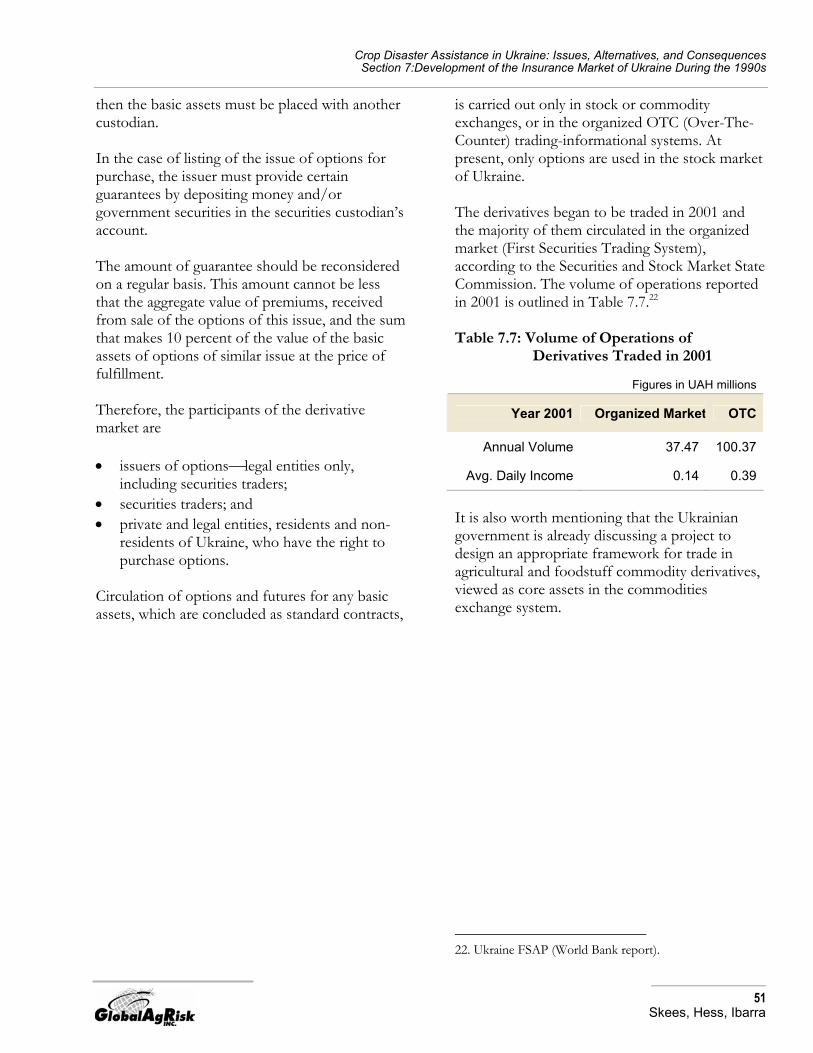

Program. .................................................................................................................................................................. 34 6.1: Correlation of Crop Insurance Loss Ratios Among the Five Regions.......................................................... 36 7.1: Comparison of Market Density of Insurance Among Select Developing Countries.................................. 40 7.2: Top 30 Non-Life Companies .............................................................................................................................. 41 7.3: Profile of Various Insurance Offerings in Ukraine .......................................................................................... 43 7.4: Data for 12 Categories of Voluntary Property Insurance ............................................................................... 44 7.5: Composite Share of Ukraine Companies........................................................................................................... 47 7.6: Foreign Reinsurers in 2000/2001 By Country of Origin ................................................................................ 49 7.7: Volume of Operations of Derivatives Traded in 2001 .................................................................................... 51

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

vi

Skees, Hess, Ibarra

Executive SummaryThe transition to markets has been difficult for Ukraine. A country with significant agricultural potential, Ukraine has nearly one-third of the world’s “black soils.” Yet many tillable hectares remain idle and yields are well below their potential. Agricultural development progress has slipped since the beginning of the new Ukrainian Republic. While many components are needed to strengthen the agricultural sector, efforts to build the financial sector are among the most important. Risk sharing markets such as agricultural insurance and exchange markets can contribute to the financial sector development. To that end, this report is focused on the public policy issues involved in considering the role of government and markets in developing sustainable agricultural insurance markets. Making choices among competing public policy alternatives is never easy, especially when considering the allocation of limited government funds. The primary data collection for this report occurred in the summer of 2002, in the midst of a major policy initiative on agricultural insurance. Regulations on compulsory crop insurance were released in July 2002. Crop insurance is included as a compulsory insurance for all activities of state-owned agricultural businesses, as well as for sugar beet and grain crops for all private businesses. Further, the designs of the proposed crop insurance program include many features that are similar to the United States (U.S.) crop insurance program, including premium subsidies. Given the move toward such crop insurance programs, it was determined that some assessment of the world experience with multiple-peril crop insurance was needed within this report. Section 1 provides this assessment. Given the classic problems with providing multiple-peril crop insurance, there are essentially no real private market efforts. In nearly every case, heavy government financing through subsidies has been a necessary component.

Therefore, most multiple-peril crop insurance programs that are available today are limited to countries with developed economies. The U.S. program has been particularly expensive, with farmers paying only 25 percent of the total cost for the insurance. Further, there are few multiple-peril programs that have not had tremendous actuarial problems in the beginning years. The conclusion presented in this study is that the current course for crop insurance in Ukraine could also be quite expensive to the government. Thus, the challenge is to leverage the limited fiscal resources of Ukraine to the largest extent possible to make agricultural insurance as widely available as possible across Ukraine. This is no small task, especially given the nature of crop risk. Crop yield disasters are generally correlated across large geographic areas when one person has a wreck, many others have a wreck at the same time. This creates a tremendous financial challenge. Financing frequent and severe crop losses requires special considerations. Thus, section 2 of this report focuses on reinsurance for these types of risk. Given the desire to create sustainable crop insurance in Ukraine, the major focus of this report is on the opportunity to introduce index-based insurance, in particular, weather-based indexes. Section 3 examines why this alternative is promising given the limitations of traditional approaches to crop insurance. Section 4 provides a cursory review of agriculture in Ukraine as a means of raising the right questions about the potential market for agricultural insurance. Given the risk and the wide range of crops across Ukraine, one would think that agricultural insurance has a significant potential in Ukraine. Nonetheless, farmers in Ukraine are not familiar with such insurance and the educational challenge will be significant. Further, since many farmers are not familiar with making purchase decisions regarding other inputs, this adds to the challenge.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

vii

Skees, Hess, Ibarra

The report also examines the risk profile for major crops in Ukraine in Sections 5 and 6. This analysis is encouraging as it demonstrates that there are some potential offsets if a countrywide portfolio of crop insurance were provided. Some regions of Ukraine have low correlations in crop yields, suggesting that a carefully crafted risk-pooling arrangement within the country could provide savings before going to international reinsurance markets. Section 7 examines the insurance and financial markets in Ukraine in some detail. There is very limited experience with agricultural insurance in Ukraine. Further, the insurance companies have limited experience in providing insurance for risks that are correlated. Use of international reinsurance has been limited. These factors combine to raise even more questions regarding the requirement for compulsory crop insurance. One must ask what insurance companies in Ukraine are prepared to deliver the type of crop insurance program that is being proposed. It is not likely that any insurance provider in Ukraine is in the position to do this. A number of regulatory issues are reviewed in Section 8 of the report. Clearly, offering index-based insurance would require regulators in Ukraine to think differently about insurance. This section develops some of the challenges to the regulatory environment. Finally, the report concludes by developing the detailed requirements for pursuing the alternative approaches that are presented for agricultural insurance in Ukraine.

Why Weather Index Insurance? One of the factors contributing to the scarcity of credit in rural areas is the inability to secure loans with collateral. While land tenure constraints have been a major constraint in this regard, the lack of insurance opportunities available to potential borrowers has also limited access to credit by agricultural borrowers. If crops fail, the repayment capacity of borrowers may be uncertain. This makes lenders reluctant to extend

credit to farmers. When insurance markets are working, borrowers can use private insurance as a risk mitigation alternative. For agricultural borrowers this insurance normally takes the form of “business interruption insurance” and primarily involves crop or weather insurance. While agricultural insurance may be an important innovation in Ukraine, there are many reasons to proceed with caution. Traditional multiple-peril crop insurance that indemnifies the individual farm loss is likely not a workable solution in the short term. As is more fully developed in Section 1, such insurance is subject to high administrative cost if it is to be free of adverse selection and moral hazard. And if investments are not made in monitoring and information on farm yields, the insurance will likely experience higher losses than the initial rating. This will result in serious actuarial problems. Further, since there are large correlated risk involved in multiple-peril crop insurance (i.e., drought, excess rain, and freeze), there is an extra cost of providing reinsurance. In short, there are two major added costs to traditional crop insurance: 1) administrative costs and 2) reinsurance costs. These extra costs can be quite high in an emerging economy with little or no experience in providing multiple-peril crop insurance. One form of agricultural insurance that mitigates these costs is weather insurance. The monitoring costs of weather insurance should be less as there is no need to perform farm-level loss adjustments and the balance of information about the weather is equally shared by the insured and the insurer (unlike with traditional farm-level insurance where the farmer will always know more about the yield than the insurer). Further, the reinsurer is more likely to provide better terms when the insurance is based upon weather events and not farm-level losses. Thus, weather insurance could be a preferred alternative to crop insurance, as it avoids moral hazard problems. Payout is determined by an objective parameter the combination of a series of weather-related metrics (e.g., mm of rain, soil moisture, etc).

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

viii

Skees, Hess, Ibarra

Weather index insurance may be well suited to the agricultural production in regions in Ukraine where there are wide spread crop losses. Among the causes of loss, drought was mentioned as the most important in many of the discussions. To the extent that drought covers a vast region, weather index insurance could serve as a foundation for agricultural insurance in Ukraine. Such insurance would cover the major correlated risk while avoiding many of the problems associated with farm-level crop insurance (Skees, Hazel, and Miranda, 1999). While weather index insurance is simpler than offering multiple-peril insurance, there are a number of preconditions for offering such insurance: 1) the historic weather data must be easily obtainable and reliable; 2) a sound infrastructure for providing secure and reliable weather data in a timely fashion must be in place; 3) local providers of such insurance must have ready access to international capital markets; and 4) there should be a strong relationship between economic loss and well-defined weather events (limited basis risk2).

Main Findings of the Initial Assessment

Agriculture in Ukraine Privatization of farms has been very slow to emerge as most policies and agricultural supports have excluded privately owned farms. The majority of state-run farms had been restructured into joint stock companies known as Collective Agricultural Enterprises (CAE) during the 1990s. These enterprises were reformed in 2000 to establish more secure property rights, though most remain in pseudo-collective ownership in

2. Basis risk occurs when the farmer has a loss and does not receive a payment from the weather insurance or when the farmer does not have a loss and receives a payment. While the problem of not receiving a payment is the most serious, insurance companies should be able to address this problem over time with add-on products. The issue of overpayment should not be viewed as a problem as long as the farmer has insurable interest. Such a possibility gives the farmer the proper incentives to continue to try to make a crop even though the neighbors are having losses.

the form of agricultural enterprises or joint stock and limited liability companies. Small household plots still remain the most productive sector, however, producing the majority of the country’s food supply. Movement towards market liberalization has removed some of the price distortions created under central planning. This has resulted in declines in commodity prices, while prices for agricultural inputs have increased. There is adequate supply of domestic and foreign input suppliers of chemical inputs. Demand for chemical inputs is limited, however, because producers do not have easy access to finance and credit (cyclical problem). Access to credit is extremely limited, especially for small private farms that were excluded from earlier government supported credit programs, such as credit barters and interest subsidies. Seasonal credit for the purchase of essential inputs, such as fuel and lubricants can be obtained through commercial lenders, input suppliers, or the state. However, foreign suppliers are growing more reluctant to extend credit because of problems with repayment. In a survey of chief executives of agricultural enterprises in the Ukraine, 28 percent reported failure or delay in credit repayment (Taylor Nelson Sofres (TNS) Ukraine, 2002). Borrowers need to be creditworthy (profitable) to obtain loans, but lack of access to credit poses a constraint on production improvements. Obstacles to credit reported in the survey include high interest rates (30 percent) and no mortgage (lack of collateral). Profitable farmers have access to credit because they can repay their debts. Less profitable farmers have difficulty obtaining credit and, therefore, inputs. For this category of farmers, their low productivity is exacerbated by an inability to increase productivity without access to capital. The result on output is low yields, depleted soils, and other problems. All of these issues make any movement toward using historic farm yields as the benchmark for establishing crop insurance coverage problematic.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

ix

Skees, Hess, Ibarra

Risk Profile for Ukrainian Farmers The major risk facing farmers in Ukraine appears to be market risk. A lack of market infrastructure to support the sale and movement of agricultural products has hindered the development of a market economy. Producers cannot guarantee an outlet or price for their product because of the instability of the transition economy. Declining commodity prices and high input prices compound these problems. The TNS development survey of agricultural enterprises in the Ukraine revealed that farmers’ failure to repay credit was most often attributable to problems related to the sale of produce (71 percent of respondents) primarily resulting from low product prices, limited demand, lack of market information, and high interest rates (53 percent of respondents). Only 12 percent cited bad harvests as the reason for their inability to repay their debts. (TNS Ukraine, 2002). This suggests that in recent years, market and price declines pose more of a risk to farmers’ profitability than yield risks. However, one must be careful with such an interpretation since price declines are a general market condition rather than price risk. The survey also revealed that the most commonly cited production-related problems concerned inefficiencies in crop management such as use of chemical inputs and machinery, as well as problems with new seed varieties. While regional differences were very evident, few farmers reported production related problems resulting from lack of financing or natural disasters. Link: Rural Finance Crop Insurance Generally, rural credit requires fixed assets as well as equipment and personal guarantees as collateral. Equipment in Ukraine is old and of limited value. Increasingly, rural finance institutions are considering using future harvest gains as collateral. To hedge against crop losses, these lenders are also interested in insuring the harvest. Currently, the major banks active in agricultural lending, such as Aval with a total of 4600 loans and 30 percent market share, simply do not lend on the basis of uninsured collateral. The farmer has to produce a proper insurance policy written by a pre-approved insurer to obtain

credit. At the current time, interest rates do not vary according to insurance coverage. Most banks set up their own insurance companies to provide for their own lending insurance needs. Nonetheless, frequently the insurance polices cover only very limited risks as a means of keeping premiums low. These policies are often somehow artificial and destined only to comply with government regulations imposing the insurance of collateral. Several banks demonstrated lack of awareness of real crop risks. Therefore, the real coverage of their collateral is restricted to some risks, with no inclusion of major severe risks, in particular, drought risk. Still, the banks demonstrated a keen interest in more appropriate crop insurance covers that would allow them to extend loans to the riskier groups such as smaller farmers with limited traditional collateral. Risk Profile of Ukraine Agriculture Crop-yield data were obtained from the Government Agrarian Policy Coordination Council. These data were for all 25 oblasts from 1970-2001. The crops include: maize, sunflowers, sugar beets, wheat, and barley. These data allow for a rudimentary assessment of risk for Ukraine. After making the appropriate adjustment for yield trends and the current value at risk, the procedures presented in Section 5 and 6 of this report allow for a risk assessment of the major crops in Ukraine. The map on the following page provides a geographic view of the estimates of value at risk for the five crops in Ukraine by oblast. While the major values are concentrated in the center of Ukraine, there is a good geographic spread of the value represented by these five crops across Ukraine. Ultimately the work performed in Section 6 provides an indication that the risk spread is also good for Ukraine. For example, the correlation of crop yields between the eastern section of Ukraine and the southern region around Odessa is nearly zero. This type of risk offset presents unique opportunities for structuring risk-swapping arrangements within Ukraine for crop insurance providers who may

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

x

Skees, Hess, Ibarra

find that they are geographically concentrated in sales of crop insurance in the future. The Likely Cost of Farm-Level Crop Insurance in Ukraine The risk assessment performed in Section 6 also provides an opportunity to make an initial cost estimate of the Ukrainian government’s proposed mandatory crop insurance program. This program would pay for yields that are below 70 percent of the simple five-year average of farm-level yields. This is similar to the U.S. Actual Production History (APH) program for multiple-peril crop insurance. Based on that experience and some assumptions about the needed loads for premium rates in this setting, the likely premiums needed to support such a program will exceed 10 percent. Further, the program will have excess losses because of poor insurance infrastructure and lack of experience at making loss adjustments. To make a crude estimate of cost, we assume that the premium base would be driven by insuring $1 billion of crop value (well less than 30 percent of the total crop value in Ukraine). At this level of participation and with a 10 percent premium rate, the premium base would be roughly $100 million.

The analyses above suggest that loss ratios in the 300 percent range are possible with such a program. Thus, with even modest crop insurance program participation, the cost could exceed $300 million in the worst crop years. There is no consideration about how to finance this large exposure. International reinsurers will be very hesitant to enter given the current design. If the government were to supply a 25 percent subsidy, the government annual average cost would easily exceed $25 million for only the premium subsidy. Again, this value is based on only 30 percent participation; the subsidy alone for a fully subscribed program would likely exceed $100 million. More cost would be added to the program given the need for the government to support the reinsurance at some level. Insurance Sector in General The insurance sector is divided into three types of activities. The first involves the protection of property and obligations of major international corporations. Often local companies “front” this business for international insurers. The second activity is carried out by domestic companies for domestic clients. For this segment the regulator receives high number of complaints (more than

Map of Value of Five Crops by Oblast

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xi

Skees, Hess, Ibarra

320 last year). Only a fraction of this business is reinsured. The third type of activity is carried out by captive insurers. These are companies established as subsidiaries or affiliates of other corporations or associated groups. Insurance policies are produced for the parent organization. The supervisory authority estimates that 20 percent of the top 50 companies are captive companies. Among these captives are companies that do not insure any risk, but act as tax optimization schemes. Overall insurance penetration is low with 1.5 percent of GDP (2001) or US$12 per capita, total gross non-life premium income was around US$500 million in 2001, total reserves amounted to US$180 million. These figures comprise a substantial amount of tax avoidance schemes, possibly up to 25 percent of total premiums.3 Due to unclear nature and business purpose of the market participants, traditional underwriting performance measurement such as expense ratios and claims ratios are less meaningful. Collateral and agricultural banking are linked in very significant ways. Banks in Ukraine report a relatively high share of their credit going into agricultural activities (e.g., Aval reports about 30 percent). Since land tenure is not well established, banks are generally unable to use land as a collateral item. Acceptable agricultural collateral includes the following: • Fixed assets (like agricultural equipment).

These kinds of assets have to be notarized and insured.

• Future harvest. • Personal guarantees of managers of

agricultural enterprises. In general, banks require that all types of collateral have insurance. As a result, banks have become a major driver of the agricultural insurance market. Some banks, like Aval, report having insurance

3. Source:Ukraine FSAP Insurance report, page 8. World Bank.

representatives from their own insurance companies, as well as others at their branch offices. They also reported providing their credit executives with guidelines to choose the proper type of insurance to cover the future harvest pledged as collateral. Nevertheless, several reports, like the FSAP, have outlined the inability of the credit officers in the banks to select the appropriate coverage. Crop Insurance in Ukraine Crop insurance is underdeveloped; only three or four companies offer limited coverage. The former state monopolist, Oranta, now owned up to 49 percent by privates, notably Ukrsotzbank, has a large network of agents in the country and a crop insurance portfolio of UAH 9 million. Donetsk-based Aska has a portfolio of around US $10 million, of which up to 10 percent is crop insurance. ERC Frankona reinsures part of the Aska portfolio. This is significant as it indicates some willingness by a major agricultural insurer to participate in the Ukrainian agricultural insurance market. Ostra-Kiev, also has a relationship with an international reinsurer for one contract with a major food processor (premium is UAH 2 million). The market currently offers harvest insurance and input cost insurance policies. Input cost insurance is mostly linked to agricultural credit collateral requirements and is generally limited to very low insured sums. Harvest insurance covers hail, hurricanes, excessive precipitation, freeze, and fire risk. Drought is not covered; however, there are plans to include this risk as well. The government compulsory insurance is a multiple-peril crop insurance that would pay using a five-year average of farm yields with current prices minus a deductible of 20-40 percent. The equation for liability is Liability = Yield x (1-deductible) x Price x

Hectares

where yield is the five-year simple average of farm yields

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xii

Skees, Hess, Ibarra

Premium rates are to range from 2-7 percent . The scientific basis for establishing premium rates could not be determined. Data on expense ratios are not available, but are expected to be very high due to the lack of professional loss adjustment systems and scarcity of qualified loss-adjustors. The low loss ratios of the insurers in the crop insurance market suggest potential problems as it appears that insurance covers minimum risk exposures and rarely incurs claims. Lack of farmer trust of these systems was a common theme among those who were interviewed. Data are available at an aggregate level, the largest non-life loss ratios are on the order of 30-45 percent, whilst expense ratios are in the same range. In developed economies, loss ratios for private hail insurance are on the order of 60-70 percent, with expense and profits accounting for the residual 30-40 percent. The preliminary assessment of the mission is that the market is exposed to high reputation risk as a large portion of companies do not pay claims because of their nature, some companies seem to be paying claims only to a limited extent and many companies seem to be rather inefficient, as evidenced by the high expense ratios.4 Insurance for total loss of harvest was reported as the main source of business for new entrants to this market, like Garant Auto and Skide-West. They recognized that the demand for insurance appearing two to three years ago attached to agricultural credit from banks. As a result of formal requests from banks to do so, the companies reported having designed their insurance products to serve the needs of the banks. Since the cost of total loss insurance was reported below 1 percent, banks frequently issue these policies. Nonetheless even in the total loss products, drought coverage is usually excluded. Insurance companies are also concerned about the lack of appropriate statistics to value risk in agriculture.

4. The FSAP insurance report arrives at similar findings.

Partial loss coverage is mainly offered by Oranta. They reported total insurance premiums of UAH 9 million in agricultural insurance. This company evolved into a joint stock company after being a state-owned company in Soviet times when they held a complete monopoly of the market. They inherited a big infrastructure and today they still have the biggest network of branches with 550. Oranta reported that they insure all types of risk except drought, which seems to be the most catastrophic risk in Ukraine. They offer some version of the multiple-peril crop insurance program envisioned by the government. Main crops to be insured were winter wheat, sugar beet, potatoes and specialty crops, but grains seems to have a far greater relative importance than the other mentioned crops. Drought is also excluded from this type of coverage. Oranta reported a loss ratio in agricultural insurance (indemnities/premiums) of 70-80 percent. They also reported an extensive workforce to administer this type of insurance in their branches (loss adjusters, administrative personnel, etc.). Even though the information available is limited, the results suggest that partial loss agricultural insurance schemes in Ukraine generate a negative result (indemnities plus administrative expenses seem to be greater than the premiums received), which is in line with the international experience. It is important to highlight the fact that the net result seems to be negative even excluding drought, which appears to be the most correlated risk in Ukraine that affects agriculture. In Ukraine, insurance providers have to be licensed insurance institutions, constituted as joint stock companies, and approved by the Ministry of Finance. Insurers licensed for life insurance activity shall not have the right to conduct other types of insurance activity. Therefore, any other market participants, like input suppliers, can’t underwrite insurance policies. Nevertheless, market players, like input suppliers, have a very important direct relationship and contact with the farmers, giving them more information about the technology and production practices used.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xiii

Skees, Hess, Ibarra

Therefore, they could become important sources for better insurance design or marketing channels. Reinsurance The total capital of the insurance industry in Ukraine is only US$358 million for all lines of business, therefore retention capacity is very limited inside Ukraine. Non-life companies reinsure around 50 percent of gross premiums. Any type of crop insurance, traditional or index-based, requires reinsurance capacity. In particular, the systemic or correlated risk portion of crop insurance, the weather risk part, needs to be reinsured to limit the exposure of the single insurer. Total risk exposure for grains and sugar beets in the Ukraine is around US $3.1 billion, if only 30 percent of this sum were to be insured against crop losses, the sum insured would be US $1 billion. At a 10 percent premium rate, premiums collected may be US $100 million. There would be a tremendous need for reinsurance given this level of activity. Insurance companies expressed a limited appetite for crop insurance risk retention beyond 10 percent, which is typical for this line of business. Thus, a comprehensive insurance/reinsurance system for crop yields in Ukraine is in the very early stages of development. Reinsurance activity in the Ukraine is limited, particularly for correlated risk. Due to the lack of ownership of property and other long-term assets in Ukraine and the restrictive investment regulation of foreign assets, companies use foreign reinsurance to minimize the foreign exchange and maturity mismatch between assets and liabilities. Oranta is only ceding 4 percent of the premiums to the reinsurance industry, either national or internationally. This is a very important fact because it means the agricultural risk is almost certainly being retained inside Ukraine. As the names of the reinsurance companies were not available, it was not possible to value the solvency of the foreign reinsurers providing limited capacity to the Ukrainian market.

Skide-West and Garant Auto report developing contacts with specialized reinsurance professionals in Europe, mainly through Partner Re (Erich Kasten). They mentioned, with some degree of confidence, the ability to seed their total loss insurance policies abroad. Further, they indicated their ideal retention in this type of risk has been established by their executive board at approximately 5 percent, meaning they are not willing to retain an important share of these kinds of risk. Thus, a significant reinsurance capacity for agricultural risks would be extremely important. Given past experience, it is questionable if international reinsurers are actually willing to provide such capacity. Two considerations were noted: 1. Reinsurance capacity for drought in the short

term is considered almost impossible to find. 2. The international reinsurance community is

very reluctant to offer capacity for the agricultural sector in Ukraine due to the perceived underdevelopment of the sector. Nevertheless, Marsh (the reinsurance broker) has placed the first multi-peril agricultural risk for irrigated potatoes (500 hectares). The risks covered were drought, frost, hail, and secondary diseases (usually associated with excess humidity). As it is an irrigated land, drought is defined as coverage for lack of irrigation. This is quite different from the drought risk discussed throughout this report. This drought risk is defined as a lack of rain for rain-fed production areas

Proposed Compulsory Crop Insurance The new law on insurance promulgated in November 2001 made 34 types of insurance compulsory for certain categories; one of them is crop insurance. Crop insurance thereby was supposed to be compulsory for all activities of state-owned agricultural businesses, as well as for sugar beet and grain crop insurance for all private businesses. A regulation passed by the cabinet of ministers in July 2002 specifies the coverage and premiums as well as policy wordings of this insurance. Premiums are supposed to range between 8.5 and 9.5 percent. Premium subsidies

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xiv

Skees, Hess, Ibarra

are foreseen in another law, the law on “Stimulation of Agriculture Development, 2001-2004”5. A number of concerns regarding the introduction of compulsory crop insurance in the Ukraine are presented: • Forcing farmers to purchase insurance will

ultimately lead to a failed system. The economic literature suggests that moral hazard problems will be compounded as even the better farm managers are more prone to change their behavior in ways that increase risk when they are forced to purchase insurance.

• Since it will be impossible to classify risk and distinguish between the better farm managers versus the poorer farm managers, compulsory insurance will tax the better farm managers and transfer the tax to the poorer farm managers. Such a tax would lead to more inefficiency in the farming economy in Ukraine.

• Ultimately the system would result in an overall tax on farming, as insurance companies do not have the proper financial or technical resources to properly deliver on the collected premiums.

• Finally, there is no real experience with compulsory crop insurance in the world the U.S. tried a form of compulsory crop insurance in 1995 and abandoned it after one season.

Many of the concerns regarding compulsory crop insurance also extend to weather index insurance. Such insurance will work best only if it is voluntary. In particular, since weather insurance has a basis risk, the consequences of compulsory weather index insurance contracts that do not 5. Law of Ukraine, Stimulation of Agricultural Development for the Period 2001-2004, June 2001. Article 15: Obligatory insurance of agricultural crops harvest and perennial plants is partially compensated from the state budget of Ukraine in the amount of not less than 50 percent of losses incurred by agricultural enterprises.

compensate the expected yield shortfalls would be devastating for the crop insurance sector in the Ukraine and the concept of weather index insurance as a whole. Prototype Weather Index Insurance Contract To provide an illustration of the concept of weather index insurance, a prototype insurance contract was developed using a yield and weather dataset for the one county (Artemisvsk) in the Donetsk oblast. The prototype contract would pay based on shortfalls in precipitation during the critical growing period and freezing temperatures shortly after planting. Again, the purpose of this prototype is to illustrate the concept of weather index insurance to the Ukrainian industry participants. • •Crop: Winter wheat • •Weather station: Artemivsk (Donetsk oblast) • •Weather index: A) cumulative rainfall April

10 – June 20 (10day capped at 45mm); B) minimum temperature

• •Insured sum per hectare (max. payout): US$100

• •RAIN: Payout Trigger: 94mm (80 percent of average); Payout per mm of rain deficit: US$0.9

• •FREEZE: Payout for first day with temperature below –1Co: US$12, Second day US$5, Third day US$2

• •Premium rates with loads in the 6-7 percent range.

This contract provided promising results in terms of the relationship between revenue losses and weather events simulated in the past. Between 1984 and 2001 the contract would have paid for losses in major disaster years (other than 1987). The construction of accurate indexes is complicated by the trend breaks in the yield data after 1990 and the insufficient available price data. Nevertheless this prototype weather index contract suggests that the correlation between precipitation during the latter months of winter wheat cycle, as well as freeze events is promising for developing weather insurance in this particular locale.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xv

Skees, Hess, Ibarra

Regulatory Framework The insurance laws and regulations slightly disadvantage international reinsurance compared to national reinsurance and application of the rules results in administrative burdens for insurance companies. 1. Insurance and reinsurance are not

differentiated in the Law of Insurance, so institutions that obtain the approval for conducting insurance activity in Ukraine can provide both services to the domestic market. The law specifies that insurance shall be carried out in Ukraine only by Ukrainian resident insurers.

2. Reinsurance involving a non resident is not restricted in terms of the amount (percentage) of premium ceded outside of Ukraine, but should comply with the procedures specified in the special norms for that purpose, particularly when fees or premiums ceded to non residents exceed 50 percent of their total amount received from the start of the calendar year.

3. Even though the total amount to be ceded to non-residents is not capped, the amounts of required insurance reserves of the unearned premiums do not decrease for premiums ceded to foreign reinsurance institutions. Ninety percent of these reserves have to be invested inside Ukraine, therefore, institutions that cede more than 10 percent of their premium incur the additional financial cost of keeping additional reserves.

4. Reinsurance regulations do not distinguish yet between low and high rated reinsurers for the purpose of determination of reserve requirements, as well as the administrative approval of reinsurance treaties.

5. Administrative and tax procedures seem to be inadequate and cumbersome and therefore penalize international reinsurance transactions. All interviewed companies with

significant reinsurance activity reported problems with the relevant authorities.

6. Supervisory capacity seems to be very limited

as to reinsurance activity in the country. Reporting standards, on-site supervision, and sanction powers are still inadequate.

Infrastructure: Weather Data and Weather Stations The Hydro meteorological service in the country runs a total of 187 active meteorological stations with traditional equipment. Placement of these stations is roughly 50 kilometers apart. Observations are made for temperature and precipitation. Of these, 147 stations perform special observations as well, such as the measurement of deposits of humidity in the soil and soil temperature. These observations are relevant for the monitoring of crop conditions and phases of plant development. Since the stations are not automatic, the information is manually aggregated at oblast level and then transmitted electronically to the central weather service. On the basis of these observations and very advanced crop growth simulation models, the weather service performs crop yield forecasting for the major crops. Proper seeding and planting depend on these forecasts. These models appear relatively useful as they also provide an index of the crop yield relative to the average (i.e., percent above or below the average). According to the deputy head of the weather service, historical data begin in 1891 for most of the stations and are reliable and reasonably complete (i.e., few missing observations). However, the historical data sets are stored on an old computer system, making it inaccessible in electronic format at this time. This should be an easy problem to address and may be an appropriate use of support loans.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xvi

Skees, Hess, Ibarra

Weather Index Development Agronomist and Agro-meteorological professionals in the Ukraine such as Anatoliy Polevoy from Odessa Ecological University (former HydroMet Institute) or Vitaliy Dmitrenko from the Agrometeorology institute in Kiev have a long history of modeling crop yields using structured plant growth simulation models (some of this work dates to 1961). These models allow for plant growth using given soils, input packages, management, and weather events. It is appropriate to keep the soils, input packages, and management fixed. Thus, once every other input variable is locked down to a representative case in a region, weather becomes the most important random variable that determines crop yields. Thus, these models can be used to determine the expected (or average) yield per hectare given an average weather. The models are used now by professionals in the meteorological agency during the season to track the crop yield. These models basically report the percent above or below the average yield for different regions and different

crops. Even satellite data generating vegetative indexes are used for this work. This work provides obviously an excellent basis for the development of weather indexes. The main shortcoming of the weather-monitoring infrastructure is the lack of automated stations and the existent but unavailable historical data. In addition, the operating budget for these stations has been low since 1990, raising the concern about the existing infrastructure. Backstop Facility for Weather Risk Insurance Retention in the Ukraine One of the reasons for the lack of demand for agricultural insurance is supply driven. Insurance companies do not underwrite systemic risks such as drought, floods, and frost, which are some of the major risks faced by farmers involved in crop production. Ukrainian insurance companies would need international reinsurance should they decide to write these types of agricultural insurance. A goal for the Ukrainian agricultural insurance program should be to create an

Farmers/agribusinesses

Insurance Company- A

Insurance Company- B

Insurance Company- C

Risk pool for drought, floods and frost risk (swaps for weather indexes from one region to another)

Basic Risk Layer

Intermediate Risk Layer

Catastrophic Risk Layer

Competitive risk transfer

Government Risk Fund

GoU/World Bank Facility/ Intl RI

International Reinsurance(RI)

Possible Structure for Risk Sharing

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xvii

Skees, Hess, Ibarra

institutional structure that allows the underwriting of agricultural insurance in the Ukraine to retain as much risk inside the country as possible, before going to international reinsurance markets. One option for effective risk transfer is the aggregation of risk according to pre-established underwriting guidelines and templates using a Ukrainian risk pool. The risk would then be reinsured through a government-backed fund and national and international reinsurance based on transparent and competitive premium ratemaking principles. Through the aggregation and layering of the risk, reinsurers would first of all be interested in reinsuring Ukrainian risk and then would be forced to price the risk competitively. For a country like Ukraine there is a strong risk of a reinsurance market failure. Individual insurance companies face sometimes insurmountable difficulties to even access international reinsurance markets, let alone obtain competitive prices. International reinsurers simply do not have the capacity to work with fragmented and non-transparent risk portfolios in the Ukraine. Opportunity costs for reinsurers are too high compared to the benefits and expected profits. Therefore the combination of introducing a transparent index insurance product and an efficient and well-regulated risk pool can overcome this market failure. Education and Familiarization Work During the Mission

The team used presentations6 and individual discussions to educate and familiarize the main players in the crop insurance world of Ukraine. The mission carried out two major presentations of the weather index insurance concept and related policy issues for insurance professionals, as well as a policy discussion with industry participants and government officials. The first presentation at the beginning of the mission addressed a group of around 20 industry professionals and generated much interest. A final

6. The two PowerPoint presentations that were made in the closing workshop are reproduced at the very end of this document.

presentation to an even larger number of professionals, including the deputy prime minister, also addressed agricultural insurance policy issues, such as compulsory insurance. Between the two presentations the agrarian policy secretariat organized a policy debate that mainly discussed the issue of compulsory insurance. The individual familiarization work with industry participants can be considered successful insofar as at least two companies expressed strong interest of developing weather index insurance in the near future. Notably, the company ASKA has put together the first weather index insurance policy for a client following the mission seminar and visit to ASKA headquarters in Donetsk.

Comments on the Feasibility of Weather Index Insurance in the Ukraine The mission had access to very limited yield and weather data. Evidence from the analyzed data, as well as qualitative assessments in the field and interviews with market participants, lead to the following preliminary conclusions on desirability and feasibility of weather index insurance in the Ukraine: Demand. Very preliminary indications from the market suggest that rural credit will drive the demand for crop insurance. The goal of rural lending that will eventually reach smaller farmers who do not have sufficient traditional collateral can be facilitated with proper crop insurance. Farmers tend to understand weather risk very well and at least the slightly larger and more sophisticated farmers should understand the particular nature of weather index insurance. The Ukraine has a large number of previously state-owned large agricultural industry complexes that have studied weather and yield relationships for a long time and therefore can provide demonstrative effects for surrounding farmers. Supply the insurance market. The market is very thin and fragmented. Very few banks are ready to lend to agriculture and very few insurance companies are in a position to insure crops.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xviii

Skees, Hess, Ibarra

Nevertheless, a few insurers made the first steps with training people, as well as selling crop insurance and are willing to venture into new insurance formulas as they realize the high expense ratios of traditional crop insurance. Weather risk and weather risk transfer. The volatility of yields and crop revenues is very high in Ukraine. Particularly the major grain producing oblasts in the south are exposed to systematic drought risk. Any type of crop insurance requires the efficient weather risk transfer at the insurance or reinsurance level. Only weather index insurance can provide an efficient risk transfer mechanism that renders these risks insurable in the Ukraine. Countrywide loss ratio simulations for a pure premium based agricultural insurance suggest that losses in excess of 200 percent would occur one out of five years. Thus, even if the premium rate were doubled to account for the catastrophic risk in crop yields, the insurance industry would lose money 1 out of 5 years. This is very high frequency, making the prospective for private reinsurance more problematic. Weather risk (and price risk) hampers development of rural credit. The uncertainties related to lending to farmers are compounded by the absence of weather and price hedging mechanisms in the Ukraine. Weather service infrastructure can be developed. The issue of weather station placement and automation must be addressed. Historical data of sufficient quality seem to exist, although the mission could not analyze more than one dataset so far. Moral hazard (tampering with weather data) could be addressed by the automation of weather stations, set up of fallback stations by reinsurers, and satellite data use for verification purposes. Weather index development resources. Ukraine has important resources that allow for the quick development of efficient weather indexes for many regions in the country. Policy framework. Currently, reinsurance is allowed for and used, but international reinsurance is

penalized in terms of insurance reserve costs. Crop insurance has been made compulsory for two major crops, which does not allow for the introduction of weather index insurance as a new compulsory crop insurance policy, but rather as voluntary insurance. Preliminary conclusion: Weather index insurance seems to be desirable and feasible at this stage and warrants further work to test these hypotheses.

Future Assessments for Evaluating the Potential of Index-Based Insurance Ukraine has good resources in the area of plant growth simulation models and crop forecasting in general. The purpose of any future assessment would be to better understand these resources and gain first insights in the potential use of the models and crop forecasting history for the development of weather indexes. What follows are recommended next steps: A. Conduct a full feasibility study The objectives of the feasibility study are to • Deepen the issues developed in this report. • Test the hypotheses formulated by the initial

assessments. • Develop viable methodologies and indexes

that insurance companies can use as prototypes and for test cases.

• Model weather indexes and develop and test statistical and agronomical models to calculate the relationship between yield and weather variables jointly with the Ukrainian researchers.

• Design complementary risk management models for insurance companies.

• Analyze countrywide risk pooling to determine the correlated exposure and the potential to hedge risks inside Ukraine.

• Perform local spatial correlation analysis to determine the appropriate number of weather stations.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Executive Summary

xix

Skees, Hess, Ibarra

B. Pilot project The objectives of pilot projects are to test the feasibility and market viability of the concept. Main activities of the project are to • Select proper pilot counties where strong

relationships between crop yields and weather are present and those counties that have already automated weather stations or that can easily establish automated stations.

• Perform focus groups within the selected counties to determine the weather events that are of most concern to farmers in the selected regions.

• Establish properly formatted historical databases for crop yields per county, weather variables per county, including agro-meteorological variables like soil moisture and temperature, as well as farm-level data.

• Set up weather databases, mainly temperature and precipitation data that have to be made available in a proper format.

• Automate weather stations in the pilot areas. • Formulate technical underwriting guidelines. • Establish ground rules for backstop facility. • Transfer the technological platform to

insurance companies (pricing models, operational skills, portfolio management).

• Educate farmers, brokers, agents, banks, and agro-processing and other stakeholders.

• Organize study tour to weather index insurance schemes (Alberta and Ontario, Canada).

• Assist insurance companies in the development of insurance policies and pilot cases in selected counties.

• Design an effective and efficient subsidization mechanism that is largely incentive-neutral in a study.

• Study of the pilot project results: incentives, demand, communication between farmers, appropriate client level (banks, input suppliers or farmers).

C. Phase I: Investment phase Following the full analysis and assessment of the feasibility study and pilot projects, GoU and World Bank would explore the following investment options: Acquisition and installation of automated stations

a. Test analysis of the density of the network according to the weather exposure of Ukraine. b. Design adequate maintenance program to ensure the quality of observations across time.

Backstop facility for weather risk (the actual level of the stop loss will be determined analytically given the budget constraints). D. Phase II: Sustainable private sector-led weather index insurance Following the successful implementation of a pilot and a full program for two to three years, the private sector shall be in a position to operate without government provided backstop facilities. E. Expenditure items

F. Technical assistance (regulatory, feasibility, dissemination, education) Consultants G. Goods Weather stations Pilot phase: Twelve automated weather stations in three pilot oblasts H. Backstop facility Disbursement mechanisms Project management

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Section 1: Experience with Multiple-Peril Crop Insurance

1

Skees, Hess, Ibarra

Section 1: Experience with Multiple-Peril Crop Insurance Multiple-peril insurance would seem to address the issue of handling major crop failures, especially since most farmers would prefer to have farm-level insurance, assuming it can be priced appropriately. However, significant problems have plagued multiple-peril crop insurance programs. It is important to understand these problems as this establishes the base for helping the Ukrainian government in their search for solutions. Two types of crop insurance programs dominate world experience: named peril insurance (such as hail), and multiple-peril insurance, which covers losses from many perils (e.g., drought, flooding, wind, insects, and freeze). Hail coverage can also include losses from fire and wind damage. Hail insurance is generally successful around the world for a variety of reasons: the losses are more nearly independent; there is less adverse selection and moral hazard, and good data and methods exist to both underwrite and assess losses. Crop-hail insurance is not discussed since it does not handle major crop failures such as droughts. Further, with assistance from the international reinsurance industry, private companies in Ukraine should be able to offer private hail insurance. While many look to the U.S. experience as a model for what might be considered, there are some important limitations for countries trying to replicate the U.S. program. Today, North American farmers pay only a fraction of the total cost of the crop insurance offered by the government (about 25 percent). There are few countries around the world that can afford such heavy subsidies. Further, looking back and understanding the growing pains of the U.S. crop insurance program gives any country reason to pause. For over 15 years the U.S. program suffered from serious actuarial problems. Crop insurance losses exceeded unsubsidized premiums in every year but one, from 1981 to 1993. By the early 1990s, the U.S. aggregate loss ratio was about 1.5, meaning that the program was paying

out $1.50 for every dollar of accounting-based total premium.7 While the national number today is closer to $1.08 in many regions, serious actuarial problems still plague the program. In the early years, private companies were reimbursed over 38 percent for every dollar of unsubsidized premium. While that number is below 25 percent today, the companies also expect to make about 15 percentage points for each dollar of total premium that they retain for risk sharing. Higher reimbursement expenses in the early years helped build the elaborate infrastructure that is in place today allowing companies to deliver the crop insurance program for less than in the past. The major lessons to be gleaned from the United States and other developed countries’ experience are • delivering farm-level, multiple-peril crop

insurance is complex and expensive; • actuarial problems are to be expected when

developing farm-level, multiple-peril crop insurance; and

• allowing private companies to sell government crop insurance products creates a new political force that creates still more demand for subsidies.

Experience to date indicates that it is extremely difficult, without massive government subsidies, to insure farm-level crop yields from losses caused by any number of natural perils. Those who seek effective, agricultural risk management tools, offered with little or no government subsidy, need to understand the underlying problems with farm-level, multiple-peril crop insurance. These problems are discussed below. This discussion sets the stage for considering an alternative form of insurance that makes 7. Loss ratios for the U.S. program are not calculated using the farmer paid premiums. Rather they are calculated using the premium as if it were not subsidized. This is referred to as the total premium. If farmer paid premiums are used, the loss ratios are much higher.

Crop Disaster Assistance in Ukraine: Issues, Alternatives, and Consequences Section 1: Experience with Multiple-Peril Crop Insurance

2

Skees, Hess, Ibarra