Embed Size (px)

Citation preview

1

SASOL SOUTH AFRICA (PTY) LTDUnaudited Financial Information

30 June 2017

2

Sasol South Africa (Pty) Ltd

Registration number 1968/013914/07

Unaudited Financial Information for the year ended 30 June 2017

Contents

Page

Income statement 3

Statement of comprehensive income 3

Statement of financial position 4

Statement of changes in equity 5

Statement of cash flows 6

Notes to the financial information 7

This financial information has not been audited or approved by the directors.

3

Income Statementfor the year ended 30 June

2017 2016Note Rm Rm

Turnover 1 80 083 77 948Materials, energy and consumables used 2 (35 641) (31 564)Selling and distribution costs (2 624) (2 977)Maintenance expenditure (4 749) (5 017)Employee-related expenditure 3 (12 584) (11 043)Exploration expenditure and feasibility costs (591) (672)Depreciation and amortisation (8 447) (8 067)Other expenses and income (4 649) (4 934)

Translation (losses)/gains 4 (619) 1 020Other operating expenses and income 5 (4 030) (5 954)

Remeasurement items 7 (6 165) (16 317)Equity accounted profits net of tax 18 10 6Operating profit/(loss) 4 643 (2 637)Finance income 6 1 253 739Finance costs 6 (2 578) (1 744)Profit/(loss) before tax 3 318 (3 642)Taxation 9 47 981

Profit/(loss) for the year 3 365 (2 661)

Statement of comprehensive incomefor the year ended 30 June

2017 2016Rm Rm

Profit/(loss) for the year 3 365 (2 661)Other comprehensive income, net of taxItems that can be subsequently reclassified to the income statement 3 4 Effect of cash flow hedges 4 5 Tax on items that can be subsequently reclassified to the income statement (1) (1)Items that cannot be subsequently reclassified to the income statement (5) 245 Remeasurement on post-retirement benefit obligation (7) 341 Tax on items that cannot be subsequently reclassified to the income statement 2 (96)

Total comprehensive income/(loss) for the year 3 363 (2 412)

4

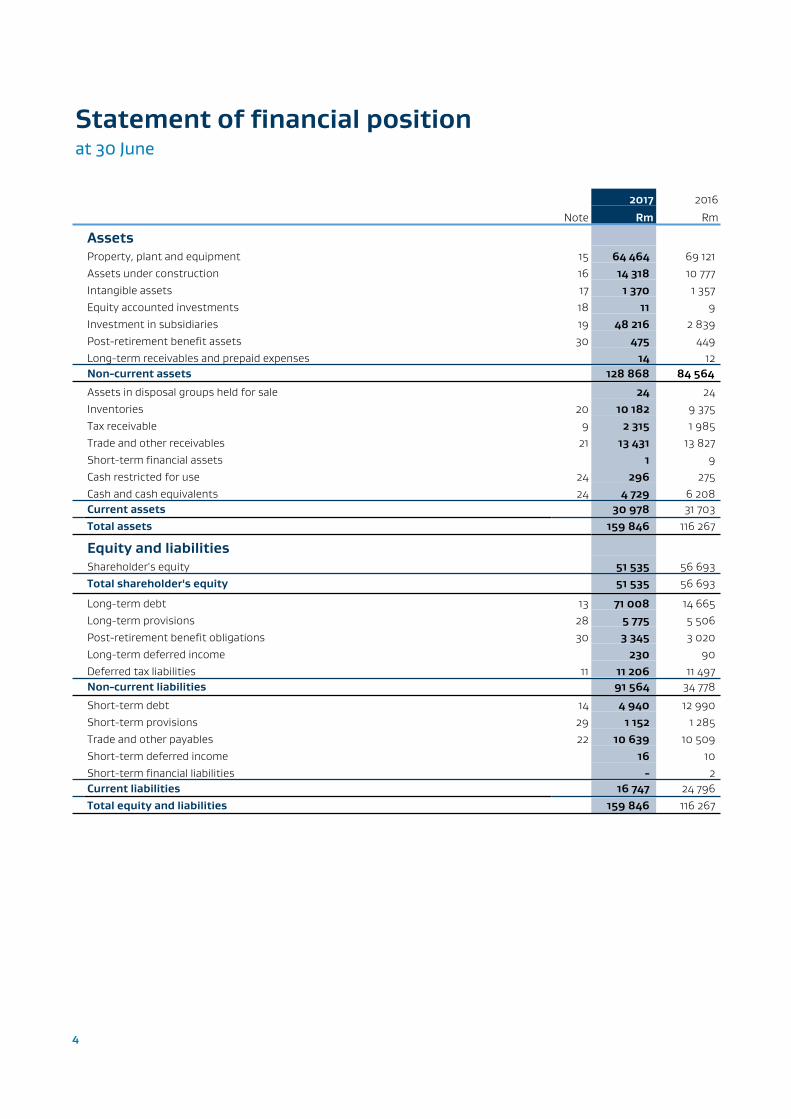

Statement of financial positionat 30 June

2017 2016

Note Rm Rm

AssetsProperty, plant and equipment 15 64 464 69 121Assets under construction 16 14 318 10 777Intangible assets 17 1 370 1 357Equity accounted investments 18 11 9Investment in subsidiaries 19 48 216 2 839Post-retirement benefit assets 30 475 449Long-term receivables and prepaid expenses 14 12Non-current assets 128 868 84 564

Assets in disposal groups held for sale 24 24Inventories 20 10 182 9 375Tax receivable 9 2 315 1 985Trade and other receivables 21 13 431 13 827Short-term financial assets 1 9Cash restricted for use 24 296 275Cash and cash equivalents 24 4 729 6 208Current assets 30 978 31 703Total assets 159 846 116 267

Equity and liabilitiesShareholder's equity 51 535 56 693Total shareholder's equity 51 535 56 693

Long-term debt 13 71 008 14 665Long-term provisions 28 5 775 5 506Post-retirement benefit obligations 30 3 345 3 020Long-term deferred income 230 90Deferred tax liabilities 11 11 206 11 497Non-current liabilities 91 564 34 778

Short-term debt 14 4 940 12 990Short-term provisions 29 1 152 1 285Trade and other payables 22 10 639 10 509Short-term deferred income 16 10Short-term financial liabilities - 2Current liabilities 16 747 24 796Total equity and liabilities 159 846 116 267

5

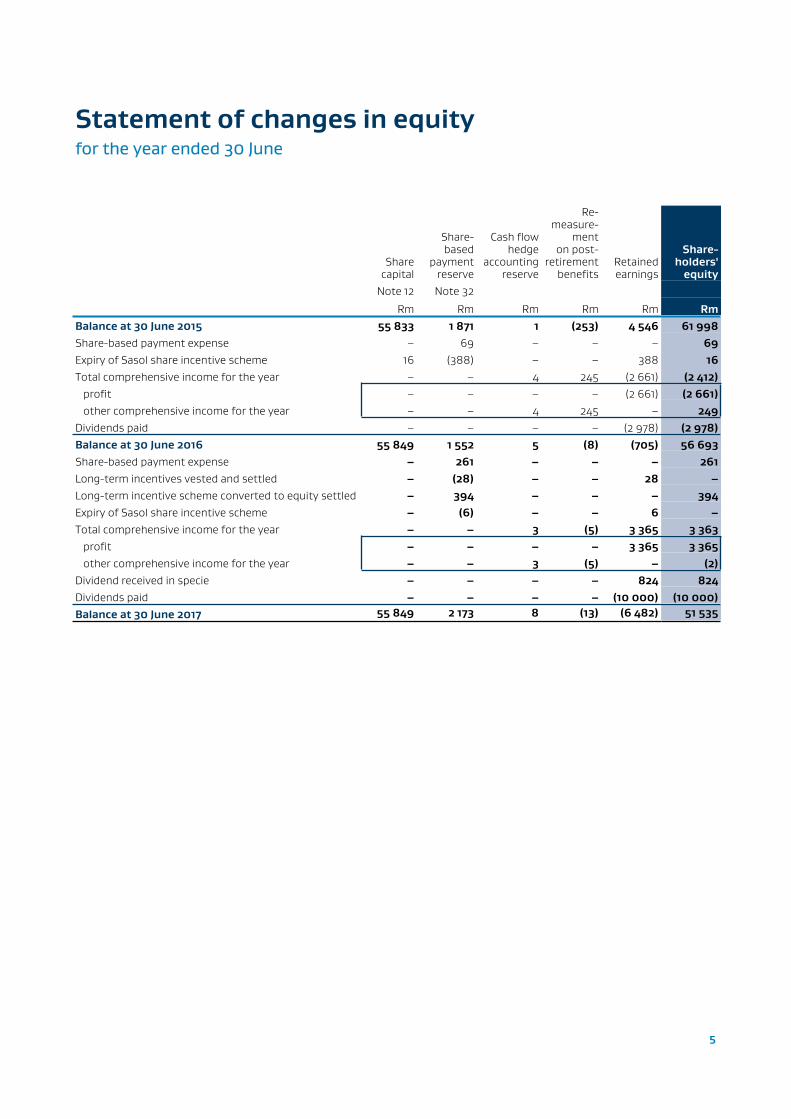

Statement of changes in equityfor the year ended 30 June

Share capital

Share-based

payment reserve

Cash flow hedge

accountingreserve

Re-measure-

menton post-

retirementbenefits

Retainedearnings

Share-holders'

equityNote 12 Note 32

Rm Rm Rm Rm Rm RmBalance at 30 June 2015 55 833 1 871 1 (253) 4 546 61 998Share-based payment expense – 69 – – – 69Expiry of Sasol share incentive scheme 16 (388) – – 388 16Total comprehensive income for the year – – 4 245 (2 661) (2 412) profit – – – – (2 661) (2 661) other comprehensive income for the year – – 4 245 – 249Dividends paid – – – – (2 978) (2 978)Balance at 30 June 2016 55 849 1 552 5 (8) (705) 56 693Share-based payment expense – 261 – – – 261Long-term incentives vested and settled – (28) – – 28 –Long-term incentive scheme converted to equity settled – 394 – – – 394Expiry of Sasol share incentive scheme – (6) – – 6 –Total comprehensive income for the year – – 3 (5) 3 365 3 363 profit – – – – 3 365 3 365 other comprehensive income for the year – – 3 (5) – (2)Dividend received in specie – – – – 824 824Dividends paid – – – – (10 000) (10 000)Balance at 30 June 2017 55 849 2 173 8 (13) (6 482) 51 535

6

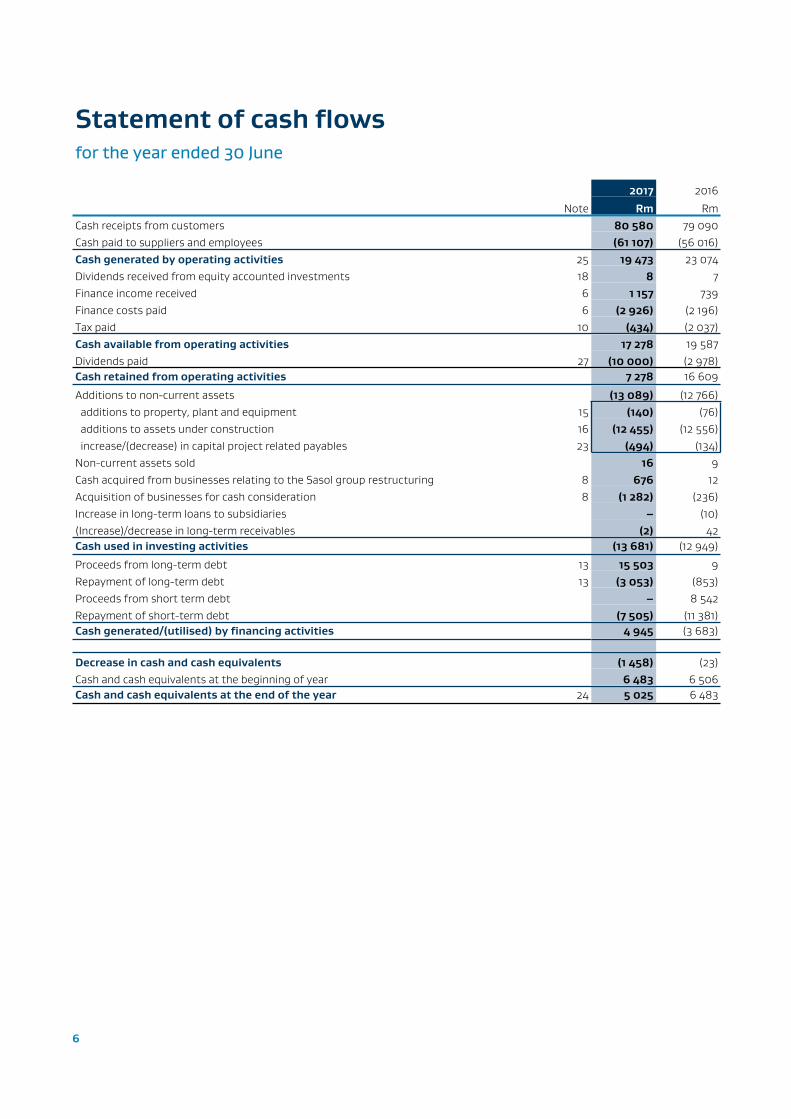

Statement of cash flowsfor the year ended 30 June

2017 2016

Note Rm RmCash receipts from customers 80 580 79 090Cash paid to suppliers and employees (61 107) (56 016)Cash generated by operating activities 25 19 473 23 074Dividends received from equity accounted investments 18 8 7Finance income received 6 1 157 739Finance costs paid 6 (2 926) (2 196)Tax paid 10 (434) (2 037)Cash available from operating activities 17 278 19 587Dividends paid 27 (10 000) (2 978)Cash retained from operating activities 7 278 16 609

Additions to non-current assets (13 089) (12 766) additions to property, plant and equipment 15 (140) (76) additions to assets under construction 16 (12 455) (12 556) increase/(decrease) in capital project related payables 23 (494) (134)Non-current assets sold 16 9Cash acquired from businesses relating to the Sasol group restructuring 8 676 12Acquisition of businesses for cash consideration 8 (1 282) (236)Increase in long-term loans to subsidiaries – (10)(Increase)/decrease in long-term receivables (2) 42Cash used in investing activities (13 681) (12 949)

Proceeds from long-term debt 13 15 503 9Repayment of long-term debt 13 (3 053) (853)Proceeds from short term debt – 8 542Repayment of short-term debt (7 505) (11 381)Cash generated/(utilised) by financing activities 4 945 (3 683)

Decrease in cash and cash equivalents (1 458) (23)Cash and cash equivalents at the beginning of year 6 483 6 506Cash and cash equivalents at the end of the year 24 5 025 6 483

7

Notes to the financial information

2017 2016

for the year ended 30 June Rm Rm

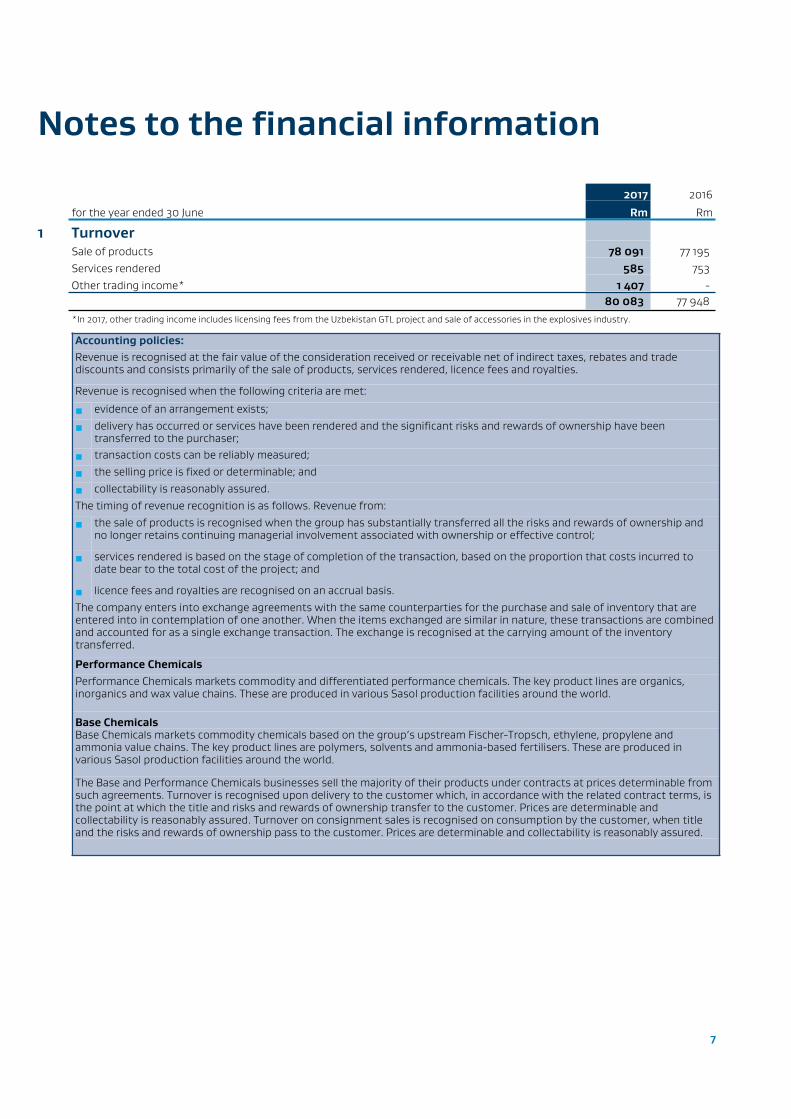

1 TurnoverSale of products 78 091 77 195Services rendered 585 753Other trading income* 1 407 -

80 083 77 948

*In 2017, other trading income includes licensing fees from the Uzbekistan GTL project and sale of accessories in the explosives industry.

Accounting policies:Revenue is recognised at the fair value of the consideration received or receivable net of indirect taxes, rebates and trade discounts and consists primarily of the sale of products, services rendered, licence fees and royalties.

Revenue is recognised when the following criteria are met:

■ evidence of an arrangement exists;

■ delivery has occurred or services have been rendered and the significant risks and rewards of ownership have been transferred to the purchaser;

■ transaction costs can be reliably measured;

■ the selling price is fixed or determinable; and

■ collectability is reasonably assured.The timing of revenue recognition is as follows. Revenue from:

■ the sale of products is recognised when the group has substantially transferred all the risks and rewards of ownership and no longer retains continuing managerial involvement associated with ownership or effective control;

■ services rendered is based on the stage of completion of the transaction, based on the proportion that costs incurred to date bear to the total cost of the project; and

■ licence fees and royalties are recognised on an accrual basis.The company enters into exchange agreements with the same counterparties for the purchase and sale of inventory that are entered into in contemplation of one another. When the items exchanged are similar in nature, these transactions are combined and accounted for as a single exchange transaction. The exchange is recognised at the carrying amount of the inventory transferred.

Performance ChemicalsPerformance Chemicals markets commodity and differentiated performance chemicals. The key product lines are organics, inorganics and wax value chains. These are produced in various Sasol production facilities around the world.

Base ChemicalsBase Chemicals markets commodity chemicals based on the group’s upstream Fischer-Tropsch, ethylene, propylene and ammonia value chains. The key product lines are polymers, solvents and ammonia-based fertilisers. These are produced in various Sasol production facilities around the world.

The Base and Performance Chemicals businesses sell the majority of their products under contracts at prices determinable from such agreements. Turnover is recognised upon delivery to the customer which, in accordance with the related contract terms, is the point at which the title and risks and rewards of ownership transfer to the customer. Prices are determinable and collectability is reasonably assured. Turnover on consignment sales is recognised on consumption by the customer, when title and the risks and rewards of ownership pass to the customer. Prices are determinable and collectability is reasonably assured.

8

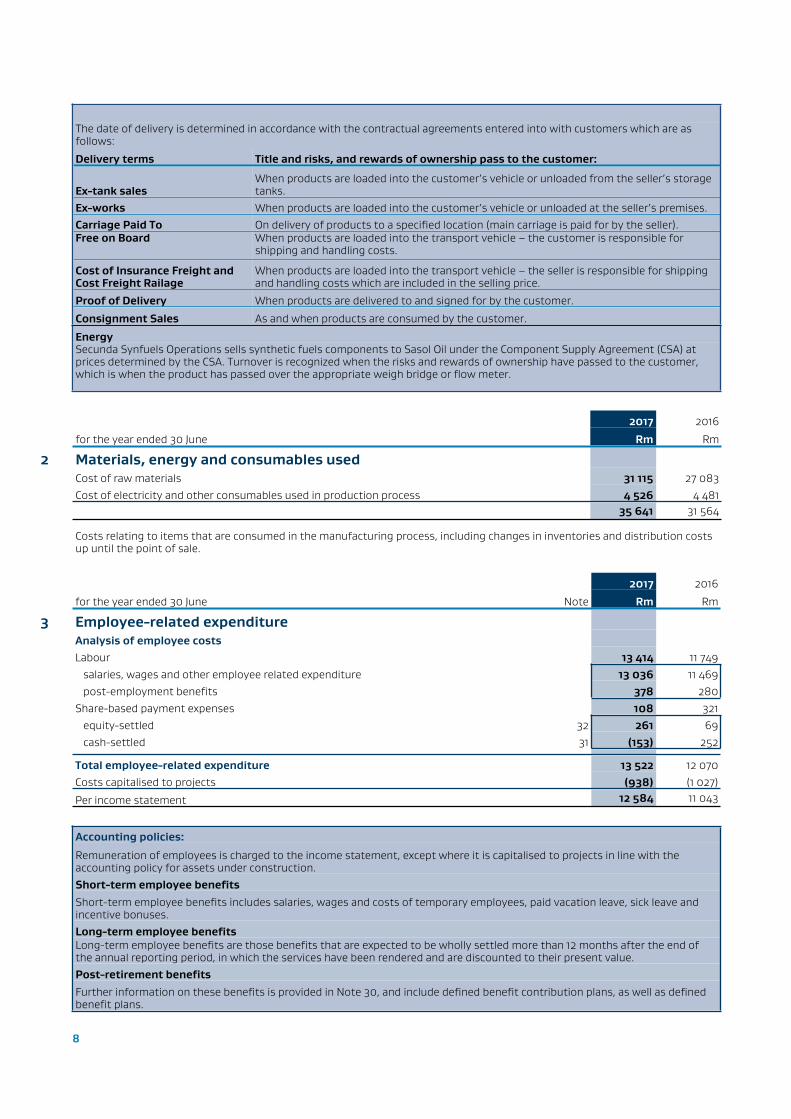

The date of delivery is determined in accordance with the contractual agreements entered into with customers which are as follows:

Delivery terms Title and risks, and rewards of ownership pass to the customer:

Ex-tank salesWhen products are loaded into the customer’s vehicle or unloaded from the seller’s storage tanks.

Ex-works When products are loaded into the customer’s vehicle or unloaded at the seller’s premises.Carriage Paid To On delivery of products to a specified location (main carriage is paid for by the seller).Free on Board When products are loaded into the transport vehicle – the customer is responsible for

shipping and handling costs.

Cost of Insurance Freight and Cost Freight Railage

When products are loaded into the transport vehicle – the seller is responsible for shipping and handling costs which are included in the selling price.

Proof of Delivery When products are delivered to and signed for by the customer.

Consignment Sales As and when products are consumed by the customer.

EnergySecunda Synfuels Operations sells synthetic fuels components to Sasol Oil under the Component Supply Agreement (CSA) at prices determined by the CSA. Turnover is recognized when the risks and rewards of ownership have passed to the customer, which is when the product has passed over the appropriate weigh bridge or flow meter.

2017 2016

for the year ended 30 June Rm Rm

2 Materials, energy and consumables usedCost of raw materials 31 115 27 083Cost of electricity and other consumables used in production process 4 526 4 481

35 641 31 564

Costs relating to items that are consumed in the manufacturing process, including changes in inventories and distribution costs up until the point of sale.

2017 2016

for the year ended 30 June Note Rm Rm

3 Employee-related expenditureAnalysis of employee costsLabour 13 414 11 749 salaries, wages and other employee related expenditure 13 036 11 469 post-employment benefits 378 280Share-based payment expenses 108 321 equity-settled 32 261 69 cash-settled 31 (153) 252

Total employee-related expenditure 13 522 12 070Costs capitalised to projects (938) (1 027)

Per income statement 12 584 11 043

Accounting policies:

Remuneration of employees is charged to the income statement, except where it is capitalised to projects in line with the accounting policy for assets under construction. Short-term employee benefitsShort-term employee benefits includes salaries, wages and costs of temporary employees, paid vacation leave, sick leave and incentive bonuses. Long-term employee benefits Long-term employee benefits are those benefits that are expected to be wholly settled more than 12 months after the end of the annual reporting period, in which the services have been rendered and are discounted to their present value.Post-retirement benefitsFurther information on these benefits is provided in Note 30, and include defined benefit contribution plans, as well as defined benefit plans.

9

2017 2016

for the year ended 30 June Rm Rm

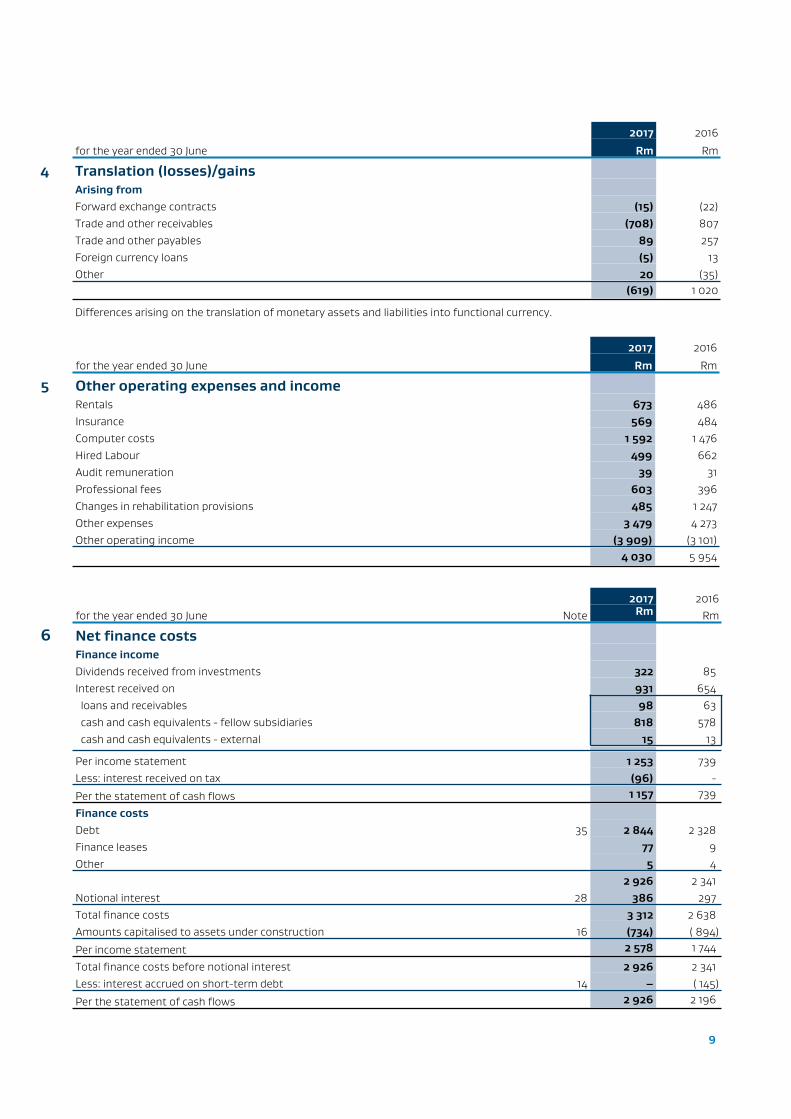

4 Translation (losses)/gainsArising fromForward exchange contracts (15) (22)Trade and other receivables (708) 807Trade and other payables 89 257Foreign currency loans (5) 13Other 20 (35)

(619) 1 020

Differences arising on the translation of monetary assets and liabilities into functional currency.

2017 2016

for the year ended 30 June Rm Rm

5 Other operating expenses and incomeRentals 673 486Insurance 569 484Computer costs 1 592 1 476Hired Labour 499 662Audit remuneration 39 31Professional fees 603 396Changes in rehabilitation provisions 485 1 247Other expenses 3 479 4 273Other operating income (3 909) (3 101)

4 030 5 954

2017 2016for the year ended 30 June Note Rm Rm

6 Net finance costsFinance incomeDividends received from investments 322 85Interest received on 931 654 loans and receivables 98 63 cash and cash equivalents - fellow subsidiaries 818 578 cash and cash equivalents - external 15 13

Per income statement 1 253 739Less: interest received on tax (96) -

Per the statement of cash flows 1 157 739

Finance costsDebt 35 2 844 2 328Finance leases 77 9Other 5 4

2 926 2 341Notional interest 28 386 297Total finance costs 3 312 2 638Amounts capitalised to assets under construction 16 (734) ( 894)

Per income statement 2 578 1 744

Total finance costs before notional interest 2 926 2 341Less: interest accrued on short-term debt 14 – ( 145)

Per the statement of cash flows 2 926 2 196

10

2017 2016

for the year ended 30 June Note Rm Rm

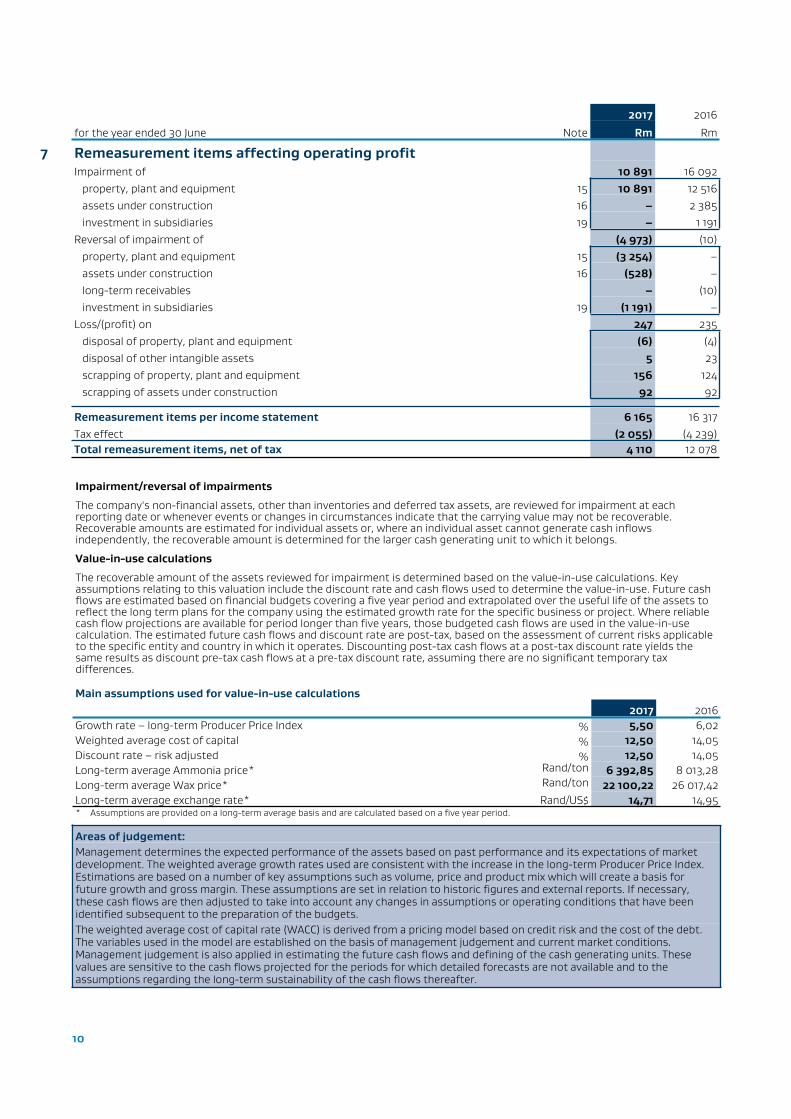

7 Remeasurement items affecting operating profitImpairment of 10 891 16 092 property, plant and equipment 15 10 891 12 516 assets under construction 16 – 2 385 investment in subsidiaries 19 – 1 191Reversal of impairment of (4 973) (10) property, plant and equipment 15 (3 254) – assets under construction 16 (528) – long-term receivables – (10) investment in subsidiaries 19 (1 191) –Loss/(profit) on 247 235 disposal of property, plant and equipment (6) (4) disposal of other intangible assets 5 23 scrapping of property, plant and equipment 156 124 scrapping of assets under construction 92 92

Remeasurement items per income statement 6 165 16 317Tax effect (2 055) (4 239)Total remeasurement items, net of tax 4 110 12 078

Impairment/reversal of impairments

The company's non-financial assets, other than inventories and deferred tax assets, are reviewed for impairment at each reporting date or whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Recoverable amounts are estimated for individual assets or, where an individual asset cannot generate cash inflows independently, the recoverable amount is determined for the larger cash generating unit to which it belongs.

Value-in-use calculations

The recoverable amount of the assets reviewed for impairment is determined based on the value-in-use calculations. Key assumptions relating to this valuation include the discount rate and cash flows used to determine the value-in-use. Future cash flows are estimated based on financial budgets covering a five year period and extrapolated over the useful life of the assets to reflect the long term plans for the company using the estimated growth rate for the specific business or project. Where reliable cash flow projections are available for period longer than five years, those budgeted cash flows are used in the value-in-use calculation. The estimated future cash flows and discount rate are post-tax, based on the assessment of current risks applicable to the specific entity and country in which it operates. Discounting post-tax cash flows at a post-tax discount rate yields the same results as discount pre-tax cash flows at a pre-tax discount rate, assuming there are no significant temporary tax differences.

Main assumptions used for value-in-use calculations2017 2016

Growth rate – long-term Producer Price Index % 5,50 6,02Weighted average cost of capital % 12,50 14,05Discount rate – risk adjusted % 12,50 14,05Long-term average Ammonia price* Rand/ton 6 392,85 8 013,28Long-term average Wax price* Rand/ton 22 100,22 26 017,42Long-term average exchange rate* Rand/US$ 14,71 14,95* Assumptions are provided on a long-term average basis and are calculated based on a five year period.

Areas of judgement:Management determines the expected performance of the assets based on past performance and its expectations of market development. The weighted average growth rates used are consistent with the increase in the long-term Producer Price Index. Estimations are based on a number of key assumptions such as volume, price and product mix which will create a basis for future growth and gross margin. These assumptions are set in relation to historic figures and external reports. If necessary, these cash flows are then adjusted to take into account any changes in assumptions or operating conditions that have been identified subsequent to the preparation of the budgets.The weighted average cost of capital rate (WACC) is derived from a pricing model based on credit risk and the cost of the debt. The variables used in the model are established on the basis of management judgement and current market conditions. Management judgement is also applied in estimating the future cash flows and defining of the cash generating units. These values are sensitive to the cash flows projected for the periods for which detailed forecasts are not available and to the assumptions regarding the long-term sustainability of the cash flows thereafter.

11

7 Remeasurement items affecting operating profit continuedSignificant impairments of assets in 2017

Base Chemicals cash generating units (CGUs)

At 30 June 2017 the prior period impairment in the Polythene and the Mining Reagents and Chlor Vinyls CGU’s were reversed by R2 036 million and R1 211 million, respectively. At 30 June 2017 the recoverable amounts of the Polythene and the Mining Reagents and Chlor Vinyls CGU’s are R10 176 million and R3 083 million, respectively.

The impairment reversals were largely due to stronger product prices driven by a revised outlook in respect of new on-stream global ethylene capacity.

The Blends and Mining Chemicals and the Methanol CGU’s were further impaired by R15 million and R207 million, respectively. At 30 June 2017 the recoverable amounts of the Blends and Mining Chemicals and the Methanol CGUs are negative R707 million and negative R226 million, respectively.

The performance of the Polythene and Mining Reagents and Chlor Vinyls CGUs is highly sensitive to Rand / US$ exchange rate and WACC movements. A 5% change in the exchange rate assumption could change the recoverable amount by approximately R5 353 million for the Polythene CGU and R3 352 million for the Mining Reagents and Chlor Vinyls CGU. A 1% change in the WACC could change the recoverable amount by approximately R661 million for the Polythene CGU and R237 million for the Mining Reagents and Chlor Vinyls CGU. The macro-economic factors are outside of the control of management. We continue to monitor these asset CGUs for further impairments or signs of recovery indicating a reversal of impairment.

Performance Chemicals CGUs

The Performance Chemicals CGUs were further impaired by R10 669 million at 30 June 2017 due to the R6 154 million and R4 155 million impairments in the Wax and the Ammonia CGUs, respectively. At 30 June 2017 the recoverable amounts of the Wax and Ammonia CGUs are R4 052 million and R109 million, respectively.

The performance of the Wax CGU is highly sensitive to the prevailing market prices of Wax, the Rand/US$ and Rand/EUR exchange rate movements. The impairment was largely driven by lower margins resulting from lower sales prices & volumes as well as the strengthening of the Rand against the US Dollar and EURO, when compared to financial year 2016. A 5% change in the Wax sales prices would result in R 2 800 million change in the recoverable amount, whereas a 5% change in the Rand/US$ and Rand/EUR would result in a change of R2 016 million in the recoverable amount. A 1% change in WACC would change the recoverable amount by approximately R370 million.

The impairment in the Ammonia value chain CGU is as a result of the downturn in the commodity and agricultural industries impacting negatively on the performance of the Fertiliser and Explosive businesses within the Ammonia value chain CGU. A further drop in the Ammonia sales prices, due to a global over supply, also contributed to further lowering product margins in 2017.

The recoverable amount of the Ammonia CGU is largely impacted by global Ammonia prices and the Rand/US$ exchange rate. A 5% change in the global Ammonia price or Rand/US$ exchange rate assumptions, could change the recoverable amount by approximately R1 961 million. A 1% change in WACC could change the recoverable amount by approximately R220 million.

The global market prices and macro-economic factors are outside the control of management. We continue to monitor these CGUs for further impairments and signs of recovery indicating a reversal of impairment.

Sasol Acrylates Group

The impairment in the investment in the Sasol Acrylates Group was fully reversed by R1 191 million at 30 June 2017. Sasol Acrylates South Africa (Pty) Ltd fully reversed the impairment of its own assets at 30 June 2017, based on an update in the distributorship agreement between Sasol Acrylates (South Africa) (Pty) Ltd and Sasol Base Chemicals, a division of Sasol South Africa (Pty) Ltd, confirming that the value of the investment in the Sasol Acrylates Group is recoverable.

Significant impairments of assets in prior periods

Base Chemicals cash generating units (CGUs)

The Base Chemicals CGUs were impaired by R7 063 million at 30 June 2016 mainly due to a R3 130 million impairment in the Polythene CGU, a R3 115 million impairment in the Mining Reagents and Chlor Vinyls CGU and a R581 million impairment in the Methyl Isobutl Ketone (MIBK) CGU. At 30 June 2016 the recoverable amounts of the Polythene, Mining Reagents and Chlor Vinyls and MIBK CGUs are R6 515 million, R1 831 million and zero, respectively.

These impairments were largely driven the strengthening of the Rand against the US Dollar and an increase in the WACC. The performance of the Polythene and Mining Reagents and Chlor Vinyls CGUs is highly sensitive to Rand / US$ exchange rate and WACC movements. A 5% change in the exchange rate assumption could change the recoverable amount by approximately R2 123 million for the Polythene CGU and R1 653 million for the Mining Reagents and Chlor Vinyls CGU. A 1% change in the WACC could change the recoverable amount by approximately R340 million for the Polythene CGU and R200 million for the Mining Reagents and Chlor Vinyls CGU. The macro-economic factors are outside of the control of management. We continue to monitor these asset CGUs for further impairments or signs of recovery indicating a reversal of impairment.

Performance Chemicals CGUs

The Performance Chemicals CGUs were impaired by R7 220 million at 30 June 2016 due to the R5 231 million and R1 989 million impairments in the Wax and the Ammonia CGUs, respectively. At 30 June 2016 the recoverable amounts of the Wax and Ammonia CGUs are R10 062 million and R4 833 million, respectively.

The performance of the Wax CGU is highly sensitive to prevailing market prices of Wax and Rand/US$ exchange rate movements. The interdependency of these factors on the sales volumes also has a significant impact on the value in use. The impairment was largely driven by lower margins due to lower sales prices as well as the strengthening of the Rand against the US Dollar. A 5% overall change in the Wax market price and Rand/US$ exchange rate assumptions could change the recoverable amount by approximately R1,3 billion. A 1% change in the WACC could change the recoverable amount by approximately R630 million.

12

The impairment in the Ammonia value chain CGU is as a result of the downturn in the commodity and agricultural industries impacting negatively on the performance of the Fertiliser and Explosive businesses within the Ammonia value chain CGU. A significant drop in Ammonia sales prices, due to a global over supply, also contributed to lower product margins.

The value in use of the Ammonia CGU is heavily impacted by global ammonia prices, the Rand/US$ exchange rate and WACC movements. A 5% change in the global ammonia price and Rand/US$ exchange rate assumptions, considering the related impact on volumes, could change the recoverable amount by approximately R750 million. A 1% change in the WACC could change the recoverable amount by approximately R300 million.

The global market prices and macro-economic factors are outside of the control of management. We continue to monitor these CGUs for further impairments or signs of recovery indicating a reversal of impairment.

Sasol Acrylates Group

The net investment value in the Sasol Acrylates Group was fully impaired by R1 191 million at 30 June 2016. The investment value is not considered to be recoverable, due to the current and expected future product selling prices in the Acrylates market being depressed because of the low global oil price outlook. Sasol Acrylates SA (Pty) Ltd fully impaired its own assets at 30 June 2016 confirming that the value of Sasol South Africa (Pty) Ltd’s (SSA) investment is not recoverable.

Sensitivity to changes in assumptions

Management has considered the sensitivity of the value-in-use calculations to various key assumptions such as commodity prices, exchange rates and the WACC rate. These sensitivities have been taken into consideration in determining the required impairments and reversals of impairments.

Accounting policies:

Remeasurement items are items of income and expense recognised in the income statement that are less closely aligned to the operating or trading activities of the reporting entity and includes, inter alia, the impairment of non-current assets, profit or loss on disposal of non-current assets and scrapping of assets. The company’s non-financial assets, other than inventories and deferred tax assets, are reviewed at each reporting date or whenever events or changes in circumstances indicate that the carrying amount may not be recoverable, to determine whether there is any indication of impairment. An impairment test is performed on all goodwill, intangible assets not yet in use and intangible assets with indefinite useful lives at each reporting date.

The recoverable amount of an asset is defined as the amount that reflects the greater of the fair value less costs of disposal and value in use that can be attributed to an asset as a result of its ongoing use by the entity. Value in use is estimated using a discounted cash flow model. The future cash flows are adjusted for risks specific to the asset and are discounted using a discount rate derived from the group's weighted average cost of capital. The recoverable amount may be adjusted to take into account recent market transactions for a similar asset.

Some assets are an integral part of the value chain but are not capable of generating independent cash flows because there is no active market for the product streams produced from these assets, or the market does not have the ability to absorb the product streams produced from these assets or it is not practically possible to access the market due to infrastructure constraints that would be costly to construct. Product streams produced by these assets form an input into another process and accordingly do not have an active market. These assets are classified as corporate assets in terms of IAS 36 when their output supports the production of multiple product streams that are ultimately sold into an active market.

The company’s corporate assets are allocated to the relevant cash generating unit based on a cost or volume contribution metric. Costs incurred by the corporate asset are allocated to the appropriate cash generating unit at cost. If there is an indication that a corporate asset may be impaired, then the recoverable amount is determined for the cash-generating unit to which the corporate asset belongs.

In Southern Africa, the coal value chain originates with feedstock mined in Secunda and Sasolburg and continues along the integrated processes of the operating business units, ultimately resulting in fuels and chemicals-based product lines. Similarly, the gas value chain starts with the feedstock obtained in Mozambique and continues along the refinement processes in Secunda and Sasolburg, ultimately resulting in fuels and chemicals-based product lines. The groups of assets which support the different product lines, including corporate asset allocations, are considered to be separate cash generating units.

Certain products are sometimes produced incidentally from the main conversion processes and can be sold into active markets. When this is the case, the assets that are directly attributable to the production of these products, are classified as separate cash generating units. The cost of conversion of these products is compared against the revenue when assessing the asset for impairment.

13

2017 2016

for the year ended 30 June Rm Rm

8 Acquisition of businessProperty, plant and equipment 1 152 292Assets under construction 58 2Intangible assets 100 –Post-retirement benefit assets 34 –Deferred tax asset/(liability) 43 (58)Inventory 53 –Trade and other receivables 1 095 –Long-term provisions (449) –Retirement benefit obligations (132) –Trade and other payables (1 339) –Other short-term provisions (9) –Other – –Net book value (excluding cash) 606 236Cash acquired per cash flow statement 676 –Net book value acquired 1 282 236

On 1 July 2016 Sasol South Africa (Pty) Ltd acquired the net book value of Sasol Technology (Pty) Ltd, excluding current registered intellectual property, for a cash consideration of R1,3 billion.

Accounting policies:Common control transactions are business combinations between entities which are ultimately controlled by Sasol Limited. The company applies the predecessor accounting method when accounting for common control transactions, whereby the assets and liabilities of the combining entities are not adjusted to fair value but are rather transferred at their carrying amounts at the date of the transaction. Any difference between the consideration paid/transferred and the net asset value ‘acquired’ is recognised in retained earnings. No new goodwill will be recognised as a result of the common control transaction. The statement of financial position and income statement will be adjusted from the date of the transaction.

2017 2016

for the year ended 30 June Note Rm Rm

9 TaxationSouth African normal tax 200 1 623 current year 360 1 730 prior years (160) (107)Foreign tax – current year – 6

Income tax 200 1 629Deferred tax – South Africa 11 (249) (2 610) current year (260) (2 699) prior years 11 89

Deferred tax – foreign – prior year 11 2 –(47) (981)

14

2017 2016

for the year ended 30 June % %

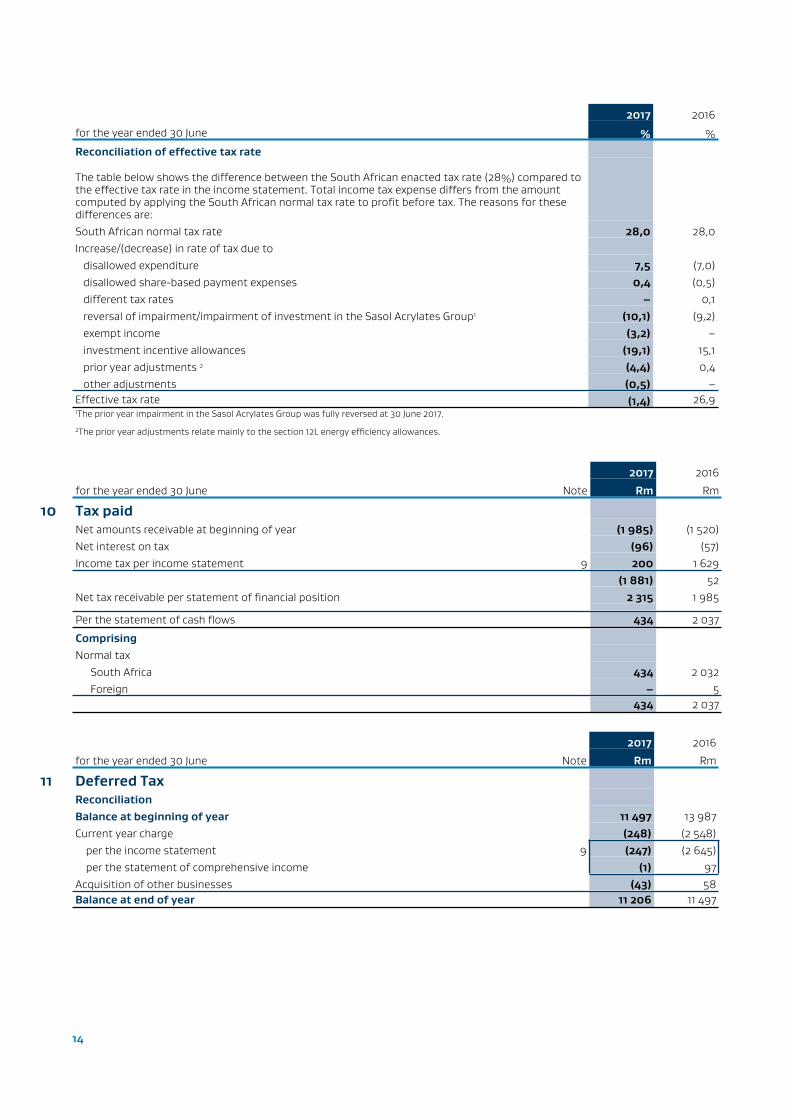

Reconciliation of effective tax rate

The table below shows the difference between the South African enacted tax rate (28%) compared to the effective tax rate in the income statement. Total income tax expense differs from the amount computed by applying the South African normal tax rate to profit before tax. The reasons for these differences are:South African normal tax rate 28,0 28,0Increase/(decrease) in rate of tax due to disallowed expenditure 7,5 (7,0) disallowed share-based payment expenses 0,4 (0,5) different tax rates – 0,1 reversal of impairment/impairment of investment in the Sasol Acrylates Group1 (10,1) (9,2) exempt income (3,2) – investment incentive allowances (19,1) 15,1 prior year adjustments 2 (4,4) 0,4 other adjustments (0,5) –Effective tax rate (1,4) 26,91The prior year impairment in the Sasol Acrylates Group was fully reversed at 30 June 2017.

2The prior year adjustments relate mainly to the section 12L energy efficiency allowances.

2017 2016

for the year ended 30 June Note Rm Rm

10 Tax paidNet amounts receivable at beginning of year (1 985) (1 520)Net interest on tax (96) (57)Income tax per income statement 9 200 1 629

(1 881) 52Net tax receivable per statement of financial position 2 315 1 985

Per the statement of cash flows 434 2 037

ComprisingNormal tax

South Africa 434 2 032Foreign – 5

434 2 037

2017 2016

for the year ended 30 June Note Rm Rm

11 Deferred TaxReconciliationBalance at beginning of year 11 497 13 987Current year charge (248) (2 548) per the income statement 9 (247) (2 645) per the statement of comprehensive income (1) 97Acquisition of other businesses (43) 58Balance at end of year 11 206 11 497

15

2017 2016

for the year ended 30 June Rm Rm

11 Deferred Tax continuedDeferred tax is attributable to temporary differences on the followingNet deferred tax liabilities:Property, plant and equipment 14 675 15 080Current assets (24) 7Current liabilities (193) (195)Short- and long-term provisions (3 090) (2 894)Financial liabilities 2 –Other (161) (501)

11 206 11 497

Accounting policies:The income tax charge is determined based on net income before tax for the year and includes deferred tax.

The current tax charge is the tax payable on the taxable income for the financial year applying enacted or substantively enacted tax rates and includes any adjustments to tax payable in respect of prior years.

Deferred tax is provided for using the liability method, on all temporary differences between the carrying amount of assets and liabilities for accounting purposes and the amounts used for tax purposes and on any tax losses. No deferred tax is provided on temporary differences relating to:■ the initial recognition of goodwill;

■ the initial recognition (other than in a business combination) of an asset or liability to the extent that neither accounting nor taxable profit is affected on acquisition; and

■ investments in subsidiaries, associates and interests in joint arrangements to the extent that the temporary difference will probably not reverse in the foreseeable future and the control of the reversal of the temporary difference lies with the parent, investor, joint venturer or joint operator.

The provision for deferred tax is calculated using enacted or substantively enacted tax rates at the reporting date that are expected to apply when the asset is realised or liability settled.Deferred tax assets and liabilities are offset when the related income taxes are levied by the same taxation authority, there is a legally enforceable right to offset and there is an intention to settle the balances on a net basis.

Areas of judgement:A deferred tax asset is recognised to the extent that it is probable that future taxable profits will be available against which the deferred tax asset can be utilised. The provision of deferred tax assets and liabilities reflects the tax consequences that would follow from the expected recovery or settlement of the carrying amount of its assets and liabilities.

16

2017 2016

for the year ended 30 June Rm Rm

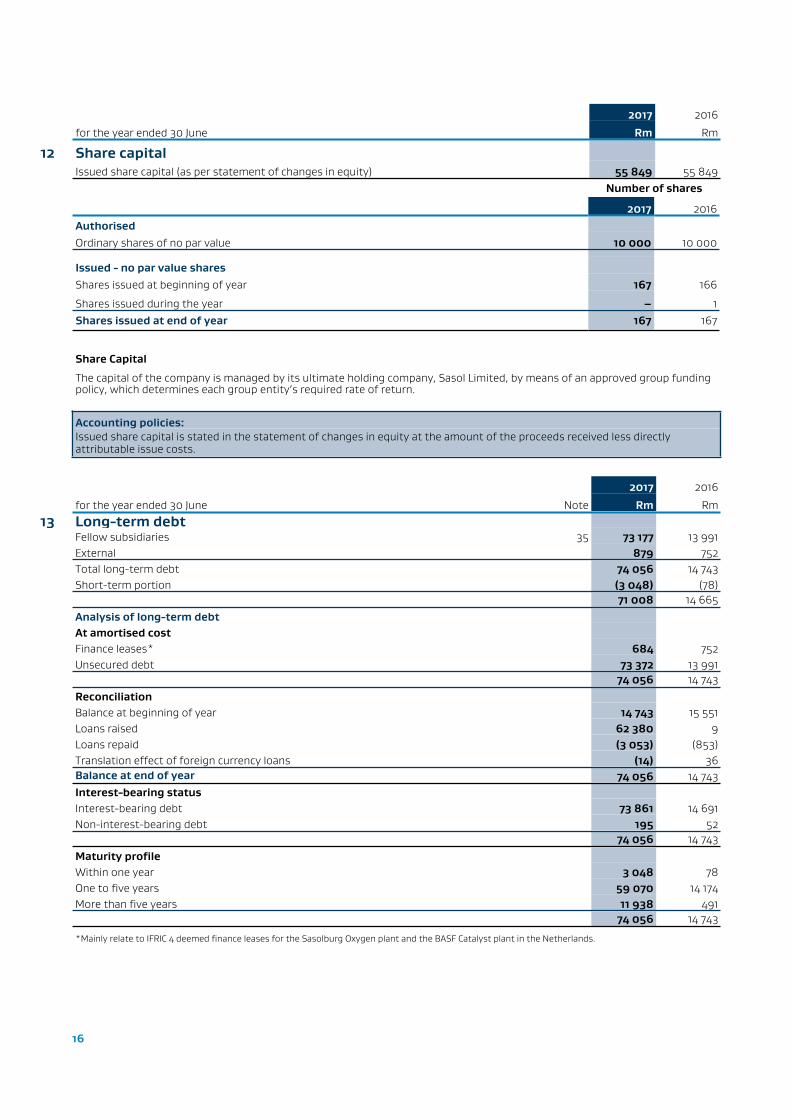

12 Share capitalIssued share capital (as per statement of changes in equity) 55 849 55 849

Number of shares

2017 2016AuthorisedOrdinary shares of no par value 10 000 10 000

Issued - no par value sharesShares issued at beginning of year 167 166

Shares issued during the year – 1Shares issued at end of year 167 167

Share Capital

The capital of the company is managed by its ultimate holding company, Sasol Limited, by means of an approved group funding policy, which determines each group entity’s required rate of return.

Accounting policies:Issued share capital is stated in the statement of changes in equity at the amount of the proceeds received less directly attributable issue costs.

2017 2016

for the year ended 30 June Note Rm Rm

13 Long-term debtFellow subsidiaries 35 73 177 13 991External 879 752Total long-term debt 74 056 14 743Short-term portion (3 048) (78)

71 008 14 665Analysis of long-term debtAt amortised costFinance leases* 684 752Unsecured debt 73 372 13 991

74 056 14 743ReconciliationBalance at beginning of year 14 743 15 551Loans raised 62 380 9Loans repaid (3 053) (853)Translation effect of foreign currency loans (14) 36Balance at end of year 74 056 14 743Interest-bearing statusInterest-bearing debt 73 861 14 691Non-interest-bearing debt 195 52

74 056 14 743Maturity profileWithin one year 3 048 78One to five years 59 070 14 174More than five years 11 938 491

74 056 14 743

*Mainly relate to IFRIC 4 deemed finance leases for the Sasolburg Oxygen plant and the BASF Catalyst plant in the Netherlands.

17

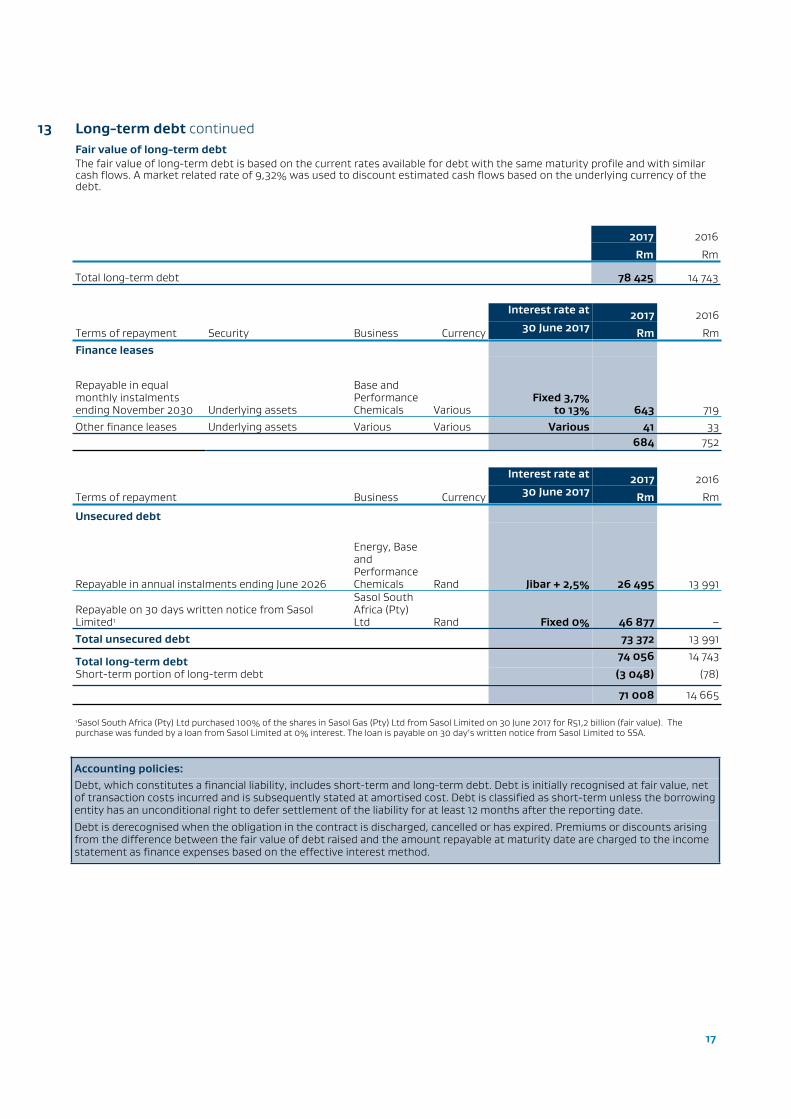

13 Long-term debt continuedFair value of long-term debt The fair value of long-term debt is based on the current rates available for debt with the same maturity profile and with similar cash flows. A market related rate of 9,32% was used to discount estimated cash flows based on the underlying currency of the debt.

2017 2016

Rm Rm

Total long-term debt 78 425 14 743

Interest rate at 2017 2016

Terms of repayment Security Business Currency 30 June 2017 Rm RmFinance leases

Repayable in equal monthly instalments ending November 2030 Underlying assets

Base and Performance Chemicals Various

Fixed 3,7%to 13% 643 719

Other finance leases Underlying assets Various Various Various 41 33684 752

Interest rate at 2017 2016

Terms of repayment Business Currency 30 June 2017 Rm Rm

Unsecured debt

Repayable in annual instalments ending June 2026

Energy, Base and Performance Chemicals Rand Jibar + 2,5% 26 495 13 991

Repayable on 30 days written notice from Sasol Limited1

Sasol South Africa (Pty) Ltd Rand Fixed 0% 46 877 –

Total unsecured debt 73 372 13 991

Total long-term debt 74 056 14 743

Short-term portion of long-term debt (3 048) (78)

71 008 14 665

1Sasol South Africa (Pty) Ltd purchased 100% of the shares in Sasol Gas (Pty) Ltd from Sasol Limited on 30 June 2017 for R51,2 billion (fair value). The purchase was funded by a loan from Sasol Limited at 0% interest. The loan is payable on 30 day’s written notice from Sasol Limited to SSA.

Accounting policies:Debt, which constitutes a financial liability, includes short-term and long-term debt. Debt is initially recognised at fair value, net of transaction costs incurred and is subsequently stated at amortised cost. Debt is classified as short-term unless the borrowing entity has an unconditional right to defer settlement of the liability for at least 12 months after the reporting date.Debt is derecognised when the obligation in the contract is discharged, cancelled or has expired. Premiums or discounts arising from the difference between the fair value of debt raised and the amount repayable at maturity date are charged to the income statement as finance expenses based on the effective interest method.

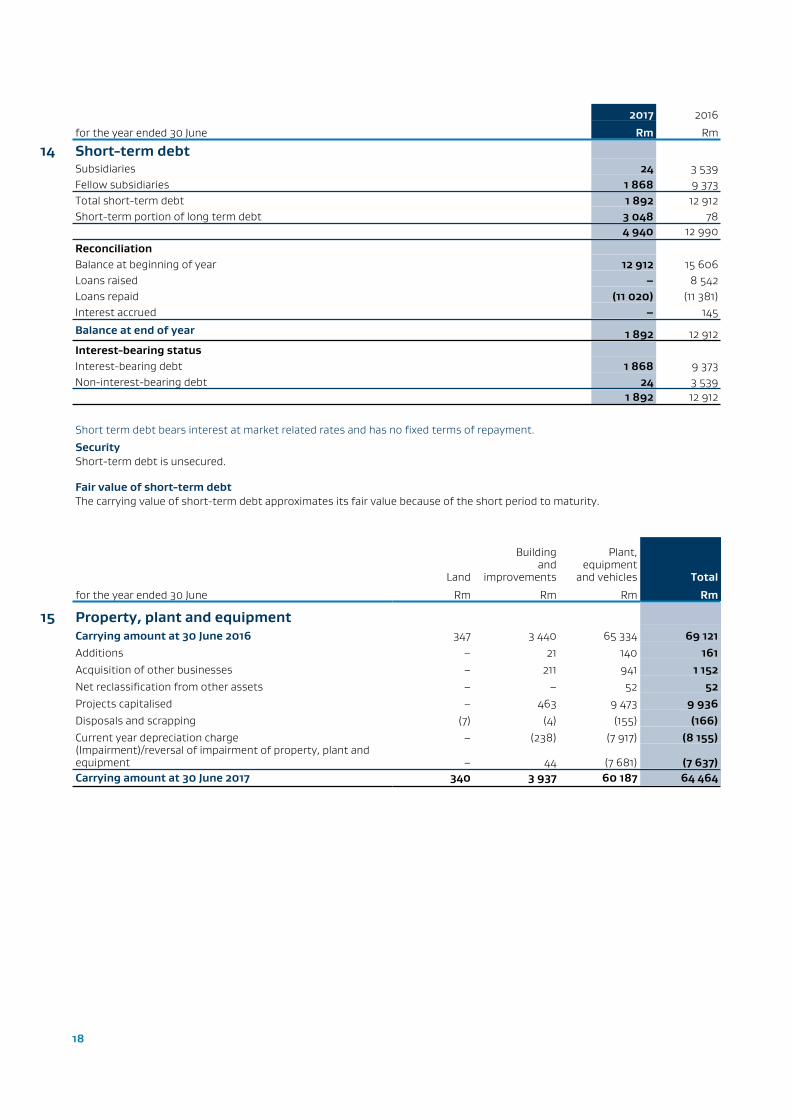

18

2017 2016

for the year ended 30 June Rm Rm

14 Short-term debtSubsidiaries 24 3 539Fellow subsidiaries 1 868 9 373Total short-term debt 1 892 12 912Short-term portion of long term debt 3 048 78

4 940 12 990ReconciliationBalance at beginning of year 12 912 15 606Loans raised – 8 542Loans repaid (11 020) (11 381)Interest accrued – 145

Balance at end of year 1 892 12 912Interest-bearing statusInterest-bearing debt 1 868 9 373Non-interest-bearing debt 24 3 539

1 892 12 912

Short term debt bears interest at market related rates and has no fixed terms of repayment.

SecurityShort-term debt is unsecured.

Fair value of short-term debt The carrying value of short-term debt approximates its fair value because of the short period to maturity.

Land

Buildingand

improvements

Plant,equipment

and vehicles Total

for the year ended 30 June Rm Rm Rm Rm

15 Property, plant and equipmentCarrying amount at 30 June 2016 347 3 440 65 334 69 121Additions – 21 140 161Acquisition of other businesses – 211 941 1 152Net reclassification from other assets – – 52 52Projects capitalised – 463 9 473 9 936Disposals and scrapping (7) (4) (155) (166)Current year depreciation charge – (238) (7 917) (8 155)(Impairment)/reversal of impairment of property, plant and equipment – 44 (7 681) (7 637)Carrying amount at 30 June 2017 340 3 937 60 187 64 464

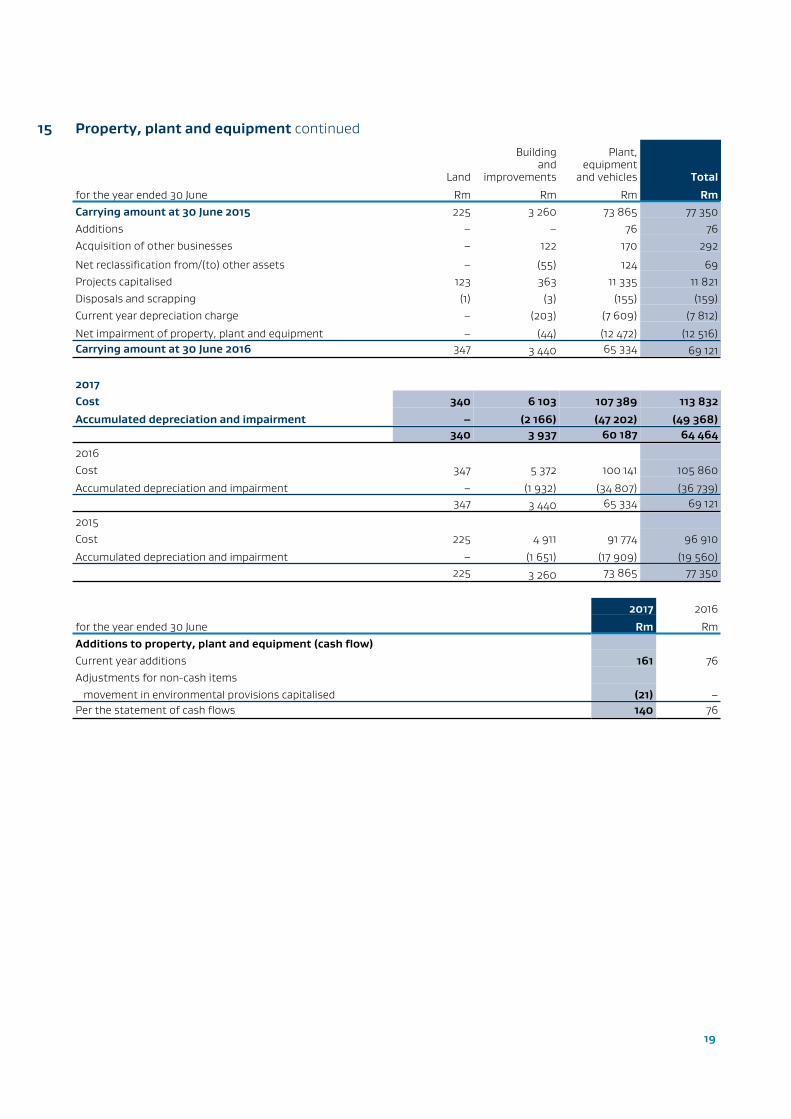

19

15 Property, plant and equipment continued

Land

Buildingand

improvements

Plant,equipment

and vehicles Total

for the year ended 30 June Rm Rm Rm RmCarrying amount at 30 June 2015 225 3 260 73 865 77 350Additions – – 76 76Acquisition of other businesses – 122 170 292

Net reclassification from/(to) other assets – (55) 124 69Projects capitalised 123 363 11 335 11 821Disposals and scrapping (1) (3) (155) (159)Current year depreciation charge – (203) (7 609) (7 812)

Net impairment of property, plant and equipment – (44) (12 472) (12 516)Carrying amount at 30 June 2016 347 3 440 65 334 69 121

2017Cost 340 6 103 107 389 113 832

Accumulated depreciation and impairment – (2 166) (47 202) (49 368)340 3 937 60 187 64 464

2016Cost 347 5 372 100 141 105 860

Accumulated depreciation and impairment – (1 932) (34 807) (36 739)347 3 440 65 334 69 121

2015Cost 225 4 911 91 774 96 910

Accumulated depreciation and impairment – (1 651) (17 909) (19 560)225 3 260 73 865 77 350

2017 2016

for the year ended 30 June Rm RmAdditions to property, plant and equipment (cash flow)Current year additions 161 76Adjustments for non-cash items movement in environmental provisions capitalised (21) –Per the statement of cash flows 140 76

20

2017 2016

for the year ended 30 June Rm RmLeased assetsCarrying value of capitalised leased assets (included in plant, equipment and vehicles) 923 916 cost 1 307 1 250 accumulated depreciation (384) (334)

Capital commitments (excluding equity accounted investments)

Capital commitments, excluding capitalised interest, include all projects for which specific board approval has been obtained. Projects still under investigation for which specific board approvals have not yet been obtained are excluded from the following:Authorised and contracted for 16 038 15 744Authorised but not yet contracted for 13 608 11 365

Less expenditure to the end of year (11 473) (12 907)18 173 14 202

Estimated expenditureWithin one year 12 077 12 913

One to five years 6 096 1 28918 173 14 202

FundingCapital expenditure will be financed from funds generated out of normal business operations, exisitng borrowing facilities, specific project financing and additional capital contributions from Sasol Limited.

Accounting policies:Property, plant and equipment is stated at cost less accumulated depreciation and accumulated impairment losses. Land is not depreciated.When plant and equipment comprises major components with different useful lives, these components are accounted for as separate items.

Property, plant and equipment is depreciated to its estimated residual value on a straight- line basis over its expected useful life.

Areas of judgement:

The depreciation methods, estimated remaining useful lives and residual values are reviewed at least annually. The estimation of the useful lives of property, plant and equipment is based on historic performance as well as expectations about future use and therefore requires a significant degree of judgement to be applied by management.The following depreciation rates apply in the company:Buildings and improvements 2 – 5 %

Plant 4 – 5 %Equipment 10 – 33 %

Vehicles 20 – 33 %

21

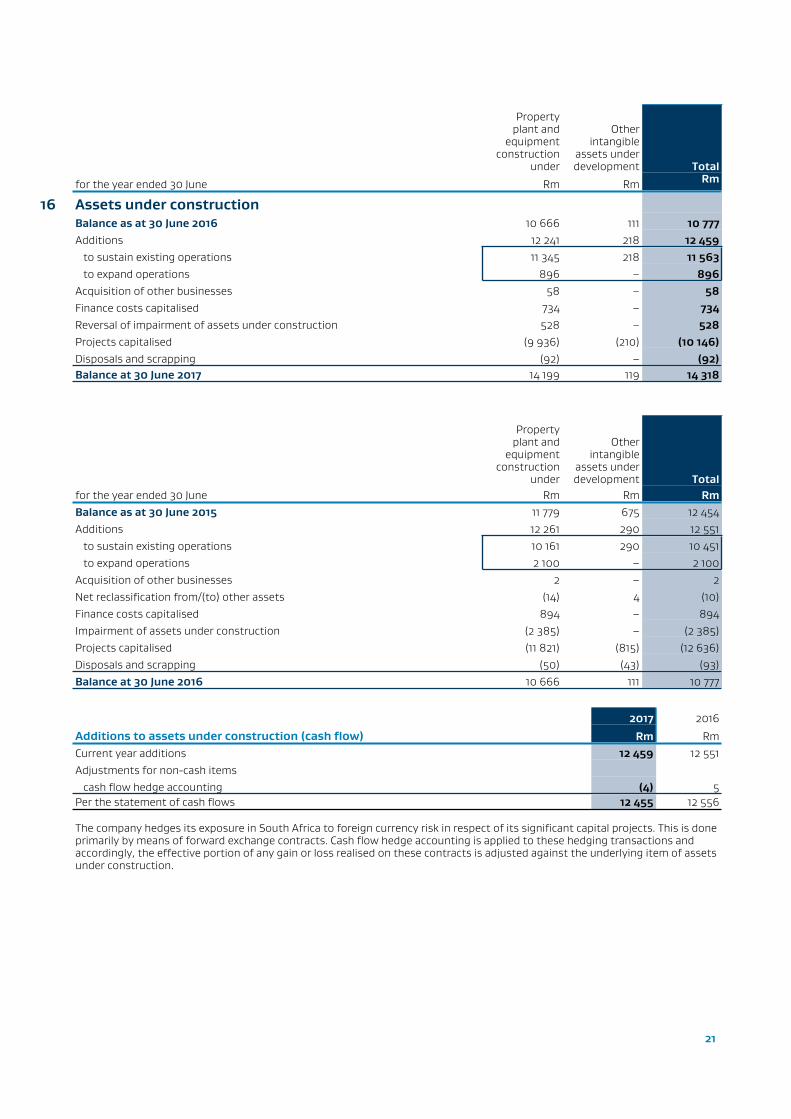

Propertyplant and

equipmentconstruction

under

Otherintangible

assets underdevelopment Total

for the year ended 30 June Rm Rm Rm

16 Assets under constructionBalance as at 30 June 2016 10 666 111 10 777Additions 12 241 218 12 459 to sustain existing operations 11 345 218 11 563 to expand operations 896 – 896Acquisition of other businesses 58 – 58Finance costs capitalised 734 – 734Reversal of impairment of assets under construction 528 – 528Projects capitalised (9 936) (210) (10 146)Disposals and scrapping (92) – (92)Balance at 30 June 2017 14 199 119 14 318

Propertyplant and

equipmentconstruction

under

Otherintangible

assets underdevelopment Total

for the year ended 30 June Rm Rm RmBalance as at 30 June 2015 11 779 675 12 454Additions 12 261 290 12 551 to sustain existing operations 10 161 290 10 451 to expand operations 2 100 – 2 100Acquisition of other businesses 2 – 2Net reclassification from/(to) other assets (14) 4 (10)Finance costs capitalised 894 – 894Impairment of assets under construction (2 385) – (2 385)Projects capitalised (11 821) (815) (12 636)Disposals and scrapping (50) (43) (93)Balance at 30 June 2016 10 666 111 10 777

2017 2016

Additions to assets under construction (cash flow) Rm RmCurrent year additions 12 459 12 551Adjustments for non-cash items cash flow hedge accounting (4) 5Per the statement of cash flows 12 455 12 556

The company hedges its exposure in South Africa to foreign currency risk in respect of its significant capital projects. This is done primarily by means of forward exchange contracts. Cash flow hedge accounting is applied to these hedging transactions and accordingly, the effective portion of any gain or loss realised on these contracts is adjusted against the underlying item of assets under construction.

22

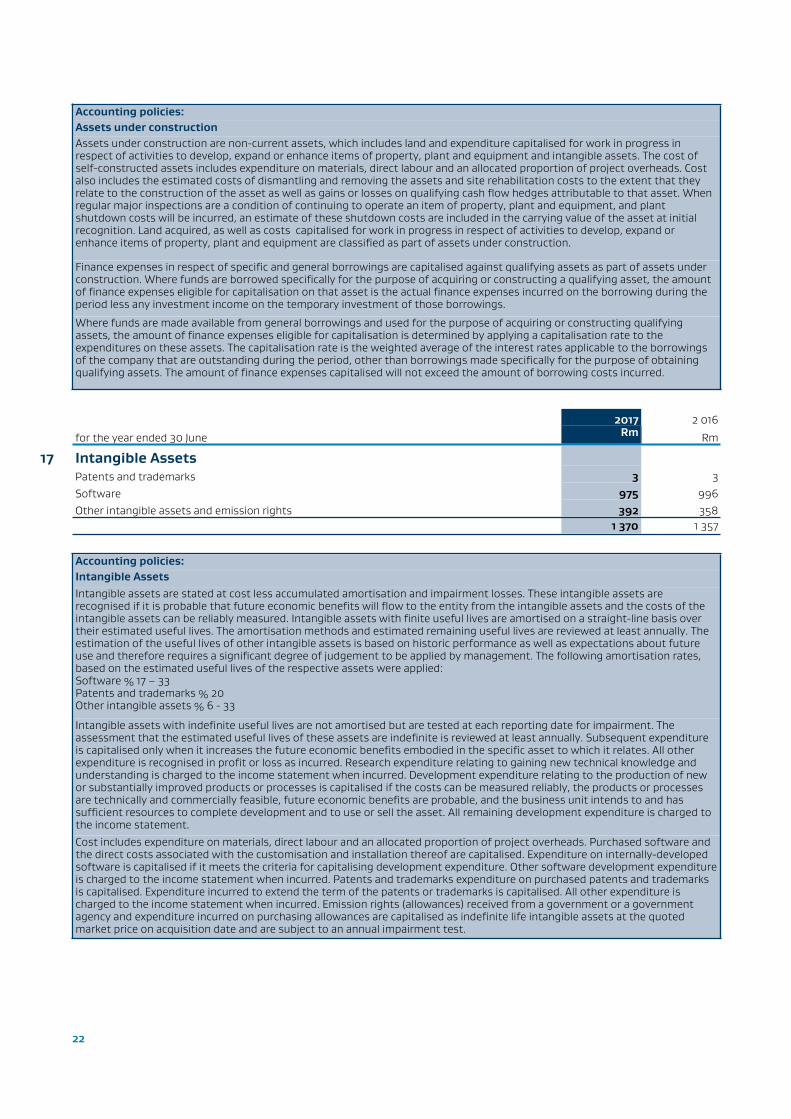

Accounting policies:Assets under constructionAssets under construction are non-current assets, which includes land and expenditure capitalised for work in progress in respect of activities to develop, expand or enhance items of property, plant and equipment and intangible assets. The cost of self-constructed assets includes expenditure on materials, direct labour and an allocated proportion of project overheads. Cost also includes the estimated costs of dismantling and removing the assets and site rehabilitation costs to the extent that they relate to the construction of the asset as well as gains or losses on qualifying cash flow hedges attributable to that asset. When regular major inspections are a condition of continuing to operate an item of property, plant and equipment, and plant shutdown costs will be incurred, an estimate of these shutdown costs are included in the carrying value of the asset at initial recognition. Land acquired, as well as costs capitalised for work in progress in respect of activities to develop, expand or enhance items of property, plant and equipment are classified as part of assets under construction.

Finance expenses in respect of specific and general borrowings are capitalised against qualifying assets as part of assets under construction. Where funds are borrowed specifically for the purpose of acquiring or constructing a qualifying asset, the amount of finance expenses eligible for capitalisation on that asset is the actual finance expenses incurred on the borrowing during the period less any investment income on the temporary investment of those borrowings.

Where funds are made available from general borrowings and used for the purpose of acquiring or constructing qualifying assets, the amount of finance expenses eligible for capitalisation is determined by applying a capitalisation rate to the expenditures on these assets. The capitalisation rate is the weighted average of the interest rates applicable to the borrowings of the company that are outstanding during the period, other than borrowings made specifically for the purpose of obtaining qualifying assets. The amount of finance expenses capitalised will not exceed the amount of borrowing costs incurred.

2017 2 016

for the year ended 30 June Rm Rm

17 Intangible AssetsPatents and trademarks 3 3Software 975 996Other intangible assets and emission rights 392 358

1 370 1 357

Accounting policies:Intangible AssetsIntangible assets are stated at cost less accumulated amortisation and impairment losses. These intangible assets are recognised if it is probable that future economic benefits will flow to the entity from the intangible assets and the costs of the intangible assets can be reliably measured. Intangible assets with finite useful lives are amortised on a straight-line basis over their estimated useful lives. The amortisation methods and estimated remaining useful lives are reviewed at least annually. The estimation of the useful lives of other intangible assets is based on historic performance as well as expectations about future use and therefore requires a significant degree of judgement to be applied by management. The following amortisation rates, based on the estimated useful lives of the respective assets were applied:Software % 17 – 33Patents and trademarks % 20Other intangible assets % 6 - 33

Intangible assets with indefinite useful lives are not amortised but are tested at each reporting date for impairment. The assessment that the estimated useful lives of these assets are indefinite is reviewed at least annually. Subsequent expenditure is capitalised only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is recognised in profit or loss as incurred. Research expenditure relating to gaining new technical knowledge and understanding is charged to the income statement when incurred. Development expenditure relating to the production of new or substantially improved products or processes is capitalised if the costs can be measured reliably, the products or processes are technically and commercially feasible, future economic benefits are probable, and the business unit intends to and has sufficient resources to complete development and to use or sell the asset. All remaining development expenditure is charged to the income statement.

Cost includes expenditure on materials, direct labour and an allocated proportion of project overheads. Purchased software and the direct costs associated with the customisation and installation thereof are capitalised. Expenditure on internally-developed software is capitalised if it meets the criteria for capitalising development expenditure. Other software development expenditure is charged to the income statement when incurred. Patents and trademarks expenditure on purchased patents and trademarks is capitalised. Expenditure incurred to extend the term of the patents or trademarks is capitalised. All other expenditure is charged to the income statement when incurred. Emission rights (allowances) received from a government or a government agency and expenditure incurred on purchasing allowances are capitalised as indefinite life intangible assets at the quoted market price on acquisition date and are subject to an annual impairment test.

23

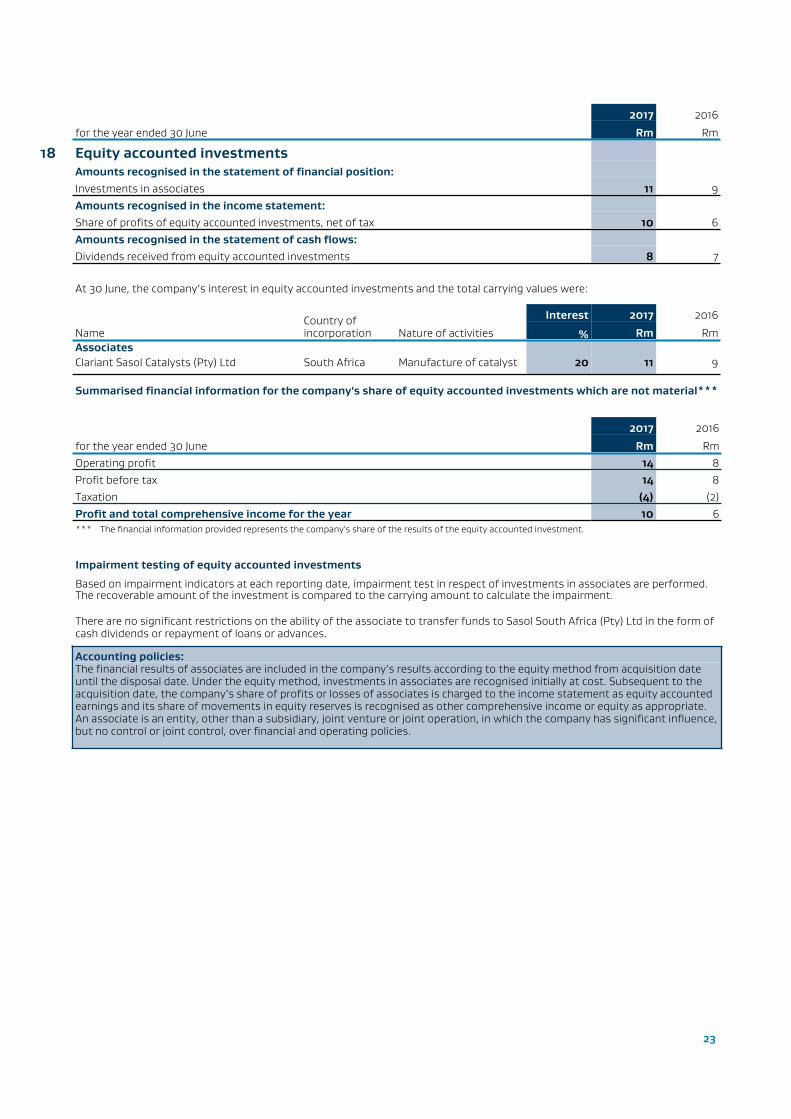

2017 2016

for the year ended 30 June Rm Rm

18 Equity accounted investmentsAmounts recognised in the statement of financial position:Investments in associates 11 9Amounts recognised in the income statement:Share of profits of equity accounted investments, net of tax 10 6Amounts recognised in the statement of cash flows:Dividends received from equity accounted investments 8 7

At 30 June, the company’s interest in equity accounted investments and the total carrying values were:

Interest 2017 2016

NameCountry of incorporation Nature of activities % Rm Rm

AssociatesClariant Sasol Catalysts (Pty) Ltd South Africa Manufacture of catalyst 20 11 9

Summarised financial information for the company's share of equity accounted investments which are not material***

2017 2016

for the year ended 30 June Rm RmOperating profit 14 8Profit before tax 14 8Taxation (4) (2)Profit and total comprehensive income for the year 10 6*** The financial information provided represents the company's share of the results of the equity accounted investment.

Impairment testing of equity accounted investments

Based on impairment indicators at each reporting date, impairment test in respect of investments in associates are performed. The recoverable amount of the investment is compared to the carrying amount to calculate the impairment.

There are no significant restrictions on the ability of the associate to transfer funds to Sasol South Africa (Pty) Ltd in the form of cash dividends or repayment of loans or advances.

Accounting policies:The financial results of associates are included in the company’s results according to the equity method from acquisition date until the disposal date. Under the equity method, investments in associates are recognised initially at cost. Subsequent to the acquisition date, the company’s share of profits or losses of associates is charged to the income statement as equity accounted earnings and its share of movements in equity reserves is recognised as other comprehensive income or equity as appropriate. An associate is an entity, other than a subsidiary, joint venture or joint operation, in which the company has significant influence, but no control or joint control, over financial and operating policies.

24

2017 2016

for the year ended 30 June Rm Rm

19 Investment in subsidiariesReflected as non-current assetsInvestments at costBalance at the beginning of the year 2 820 4 006Reversal of impairment/(impairment) of investment in subsidiary 1 191 (1 191)Acquisition of investment in subsidiary 46 877 5Repayment of capital (2 691) –Balance at end of year 48 197 2 820Shareholder loans to subsidiaries 19 19

48 216 2 839Reflected as non-current liabilitiesShort-term loans from subsidiariesBalance at the beginning of the year 3 539 3 539Loans repaid (3 515) –

24 3 539

Interest in significant operating subsidiaries

The following table presents each of the company’s significant subsidiaries (including direct and indirect holdings), the nature of activities, the percentage of shares of each subsidiary owned and the country of incorporation at 30 June.

There are no significant restrictions on the ability of the company’s subsidiaries to transfer funds to Sasol South Africa (Pty) Ltd in the form of cash dividends or repayment of loans or advances.

% of equity owned Investment at cost

NameCountry of incorporation Nature of activities 2017 2016 2017 2016

% % Rm RmSignificant operating subsidiariesDirectSasol Dyno Nobel (Pty) Ltd Republic of

South AfricaProduction and marketing of commercial explosive accessories and detonating cord

50 50 114 114

Sasol Acrylates (South Africa) (Pty) Ltd

Republic of South Africa

Production of acrylic acid and acrylates

50 50 819 –

Sasol Acrylates (Pty) Ltd Republic of South Africa

Marketing of acrylic acid and acrylates

100 100 372 –

Sasol General Holdings (Pty) Ltd

Republic of South Africa

Dormant 100 100 – 2 691

The Republic of Mozambique Pipeline Investment Company (Pty) Ltd (ROMPCO (Pty) Ltd)

Republic of South Africa

Operation of natural gas transmission pipeline between Temane and Secunda

50 50 5 5

Sasol Gas (Pty) Ltd 1 Republic of South Africa

Marketing, distribution and transportation of pipeline gas and the maintenance of pipelines used to transport gas

100 – 46 877 –

Our other interest in subsidiaries are not considered significant

1As from 30 June 2017 the Sasol Gas (Pty) Ltd investment is held by Sasol South Africa (Pty) Ltd. Refer to note 13 for more details.

25

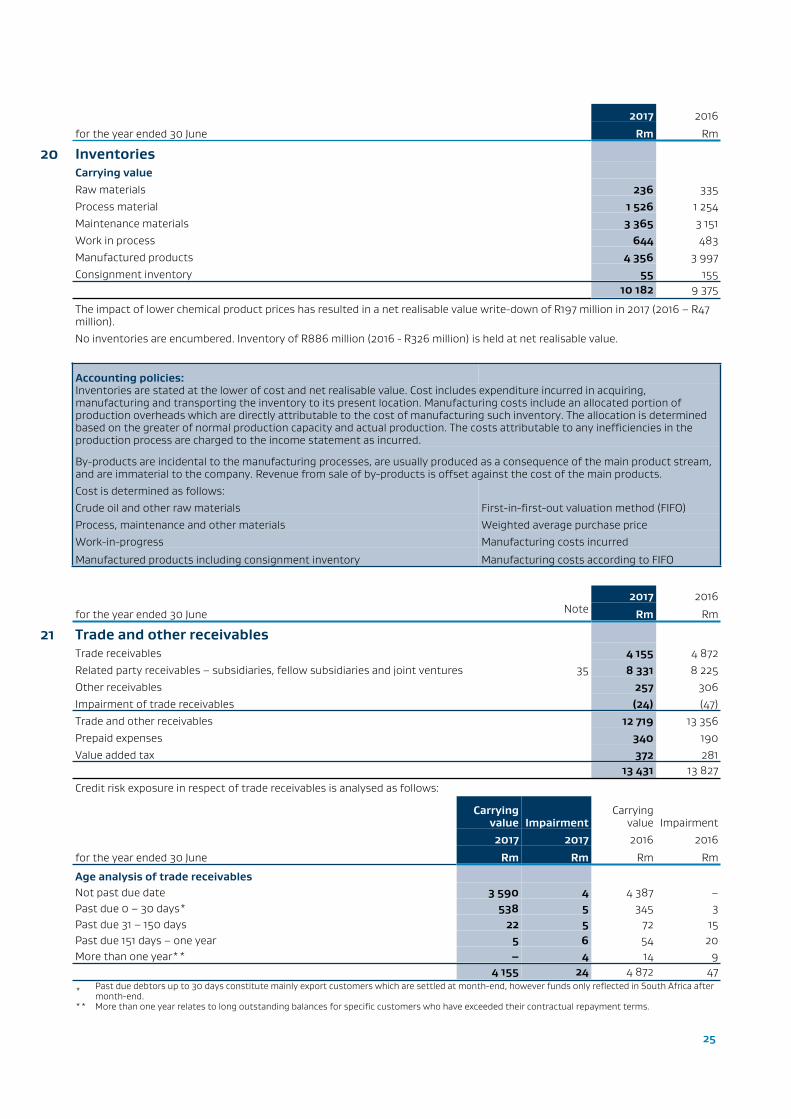

2017 2016

for the year ended 30 June Rm Rm

20 InventoriesCarrying valueRaw materials 236 335Process material 1 526 1 254Maintenance materials 3 365 3 151Work in process 644 483Manufactured products 4 356 3 997Consignment inventory 55 155

10 182 9 375

The impact of lower chemical product prices has resulted in a net realisable value write-down of R197 million in 2017 (2016 – R47 million).No inventories are encumbered. Inventory of R886 million (2016 - R326 million) is held at net realisable value.

Accounting policies:Inventories are stated at the lower of cost and net realisable value. Cost includes expenditure incurred in acquiring, manufacturing and transporting the inventory to its present location. Manufacturing costs include an allocated portion of production overheads which are directly attributable to the cost of manufacturing such inventory. The allocation is determined based on the greater of normal production capacity and actual production. The costs attributable to any inefficiencies in the production process are charged to the income statement as incurred.

By-products are incidental to the manufacturing processes, are usually produced as a consequence of the main product stream, and are immaterial to the company. Revenue from sale of by-products is offset against the cost of the main products.Cost is determined as follows:Crude oil and other raw materials First-in-first-out valuation method (FIFO)Process, maintenance and other materials Weighted average purchase priceWork-in-progress Manufacturing costs incurred

Manufactured products including consignment inventory Manufacturing costs according to FIFO

2017 2016

for the year ended 30 June Note Rm Rm

21 Trade and other receivablesTrade receivables 4 155 4 872Related party receivables – subsidiaries, fellow subsidiaries and joint ventures 35 8 331 8 225Other receivables 257 306Impairment of trade receivables (24) (47)Trade and other receivables 12 719 13 356Prepaid expenses 340 190Value added tax 372 281

13 431 13 827

Credit risk exposure in respect of trade receivables is analysed as follows:

Carrying value Impairment

Carryingvalue Impairment

2017 2017 2016 2016

for the year ended 30 June Rm Rm Rm Rm

Age analysis of trade receivablesNot past due date 3 590 4 4 387 –Past due 0 – 30 days* 538 5 345 3Past due 31 – 150 days 22 5 72 15Past due 151 days – one year 5 6 54 20More than one year** – 4 14 9

4 155 24 4 872 47

* Past due debtors up to 30 days constitute mainly export customers which are settled at month-end, however funds only reflected in South Africa after month-end.

** More than one year relates to long outstanding balances for specific customers who have exceeded their contractual repayment terms.

26

Impairment of trade receivables

Trade receivables that are not past their due date are not considered to be impaired, except where they are part of individually impaired trade receivables. The individually impaired trade receivables mainly relate to certain customers who are trading in difficult economic circumstances.

The following customers represent more than 10% of the company’s trade and other receivables:

Sasol Oil (Pty) Ltd – R2 644 million (2016 – R2 969 million)

Sasol Chemicals North America LLC – R1 714 million (2016 – R1 628 million)

Fair value of trade receivables

The carrying value approximates fair value because of the short period to maturity of these instruments.

Collateral

The company holds no collateral over the trade receivables which can be sold or pledged to a third party.

Accounting policies:

Trade and other receivables are recognised initially at fair value and subsequently stated at amortised cost using the effective interest method, less impairment losses.

2017 2016

for the year ended 30 June Note Rm Rm

22 Trade and other payablesTrade payables external 3 595 3 775Related party payables - subsidiaries, fellow subsidiaries and joint ventures 35 2 840 3 385Accrued expenses 1 074 947Related party payables - third parties 18 51Trade payables 7 527 8 158Other payables* 3 108 2 351Value added tax 4 –

10 639 10 509* Other payables includes inter alia employee-related payables and capital project related payables.

The following entities represents more than 10% of the company's trade payables:

Sasol Mining (Pty) Ltd (2017 – R1 519 million; 2016 - R1 343 million)

Eskom (2016 – R488 million)

Fair value of trade and other payables

The carrying value approximates fair value because of the short period to settlement of these obligations.

Accounting policies:Trade and other payables are initially recognised at fair value and subsequently stated at amortised cost. Capital project related payables are excluded from working capital, as the nature and risks of these payables are not considered to be aligned to operational trade payables.

27

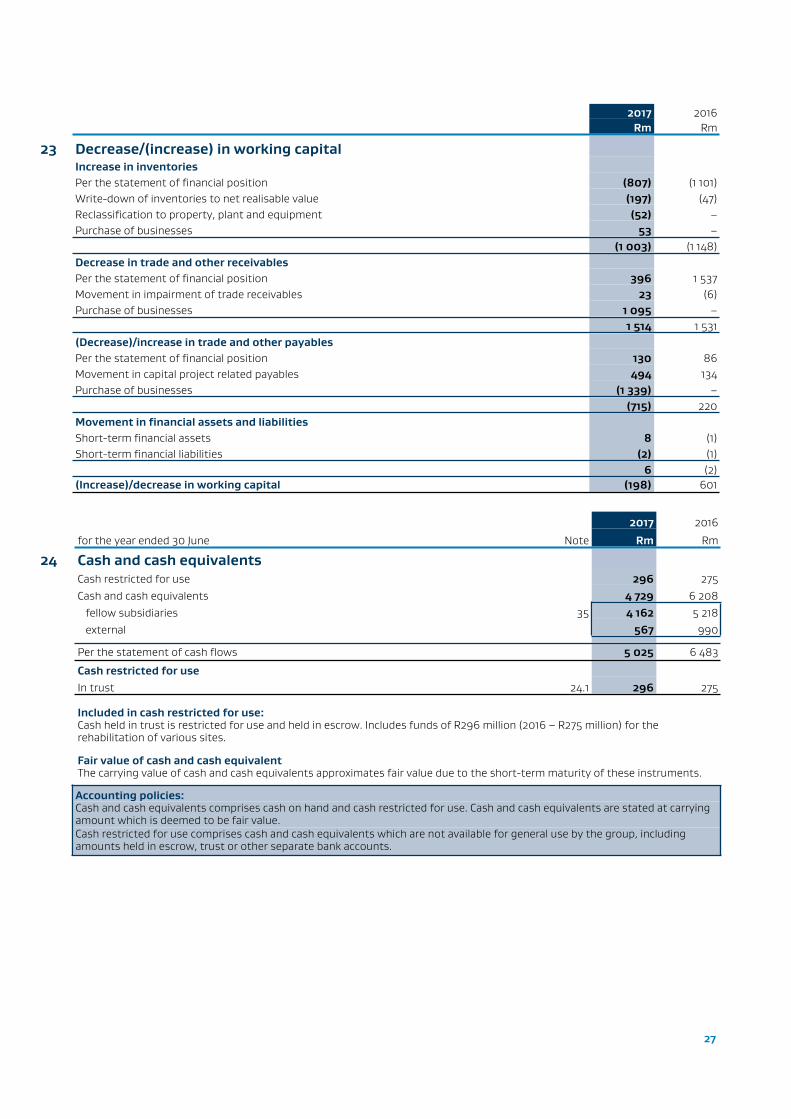

2017 2016Rm Rm

23 Decrease/(increase) in working capitalIncrease in inventoriesPer the statement of financial position (807) (1 101)Write-down of inventories to net realisable value (197) (47)Reclassification to property, plant and equipment (52) –Purchase of businesses 53 –

(1 003) (1 148)Decrease in trade and other receivablesPer the statement of financial position 396 1 537Movement in impairment of trade receivables 23 (6)Purchase of businesses 1 095 –

1 514 1 531(Decrease)/increase in trade and other payablesPer the statement of financial position 130 86Movement in capital project related payables 494 134Purchase of businesses (1 339) –

(715) 220Movement in financial assets and liabilitiesShort-term financial assets 8 (1)Short-term financial liabilities (2) (1)

6 (2)(Increase)/decrease in working capital (198) 601

2017 2016

for the year ended 30 June Note Rm Rm

24 Cash and cash equivalentsCash restricted for use 296 275Cash and cash equivalents 4 729 6 208 fellow subsidiaries 35 4 162 5 218 external 567 990

Per the statement of cash flows 5 025 6 483

Cash restricted for useIn trust 24.1 296 275

Included in cash restricted for use:Cash held in trust is restricted for use and held in escrow. Includes funds of R296 million (2016 – R275 million) for the rehabilitation of various sites.

Fair value of cash and cash equivalentThe carrying value of cash and cash equivalents approximates fair value due to the short-term maturity of these instruments.

Accounting policies:Cash and cash equivalents comprises cash on hand and cash restricted for use. Cash and cash equivalents are stated at carrying amount which is deemed to be fair value. Cash restricted for use comprises cash and cash equivalents which are not available for general use by the group, including amounts held in escrow, trust or other separate bank accounts.

28

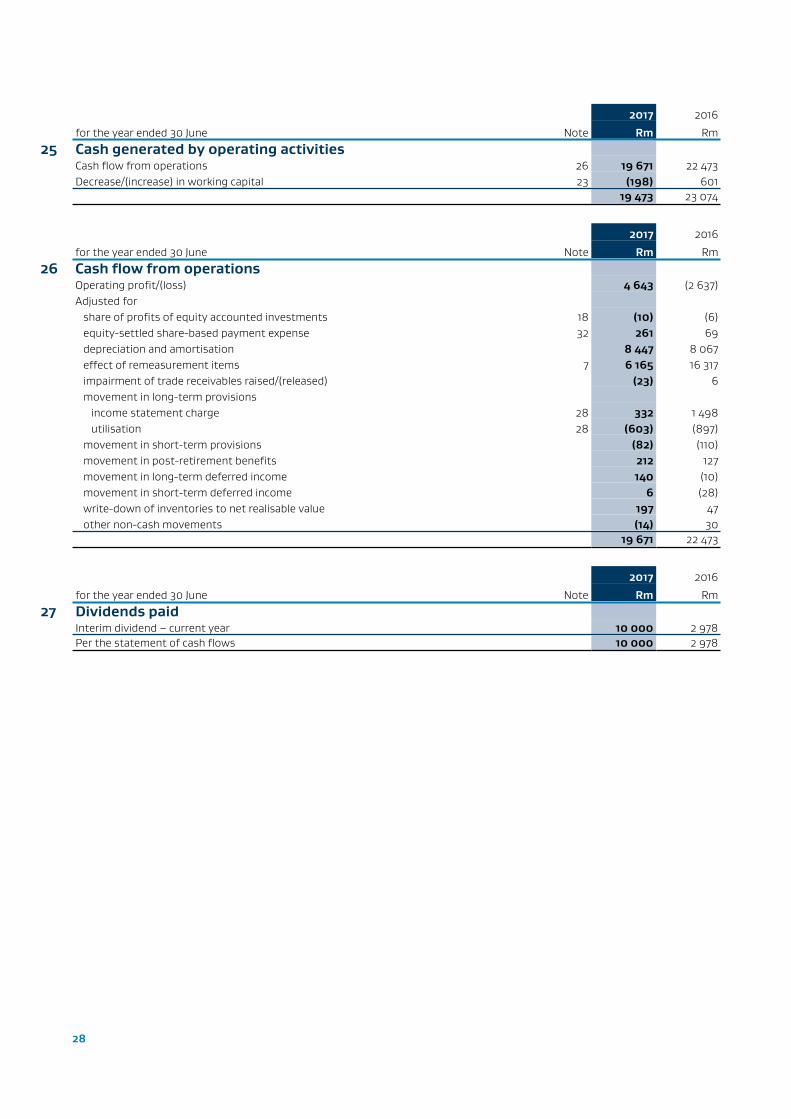

2017 2016

for the year ended 30 June Note Rm Rm

25 Cash generated by operating activitiesCash flow from operations 26 19 671 22 473Decrease/(increase) in working capital 23 (198) 601

19 473 23 074

2017 2016

for the year ended 30 June Note Rm Rm

26 Cash flow from operationsOperating profit/(loss) 4 643 (2 637)Adjusted for share of profits of equity accounted investments 18 (10) (6) equity-settled share-based payment expense 32 261 69 depreciation and amortisation 8 447 8 067 effect of remeasurement items 7 6 165 16 317 impairment of trade receivables raised/(released) (23) 6 movement in long-term provisions income statement charge 28 332 1 498 utilisation 28 (603) (897) movement in short-term provisions (82) (110) movement in post-retirement benefits 212 127 movement in long-term deferred income 140 (10) movement in short-term deferred income 6 (28) write-down of inventories to net realisable value 197 47 other non-cash movements (14) 30

19 671 22 473

2017 2016

for the year ended 30 June Note Rm Rm

27 Dividends paidInterim dividend – current year 10 000 2 978Per the statement of cash flows 10 000 2 978

29

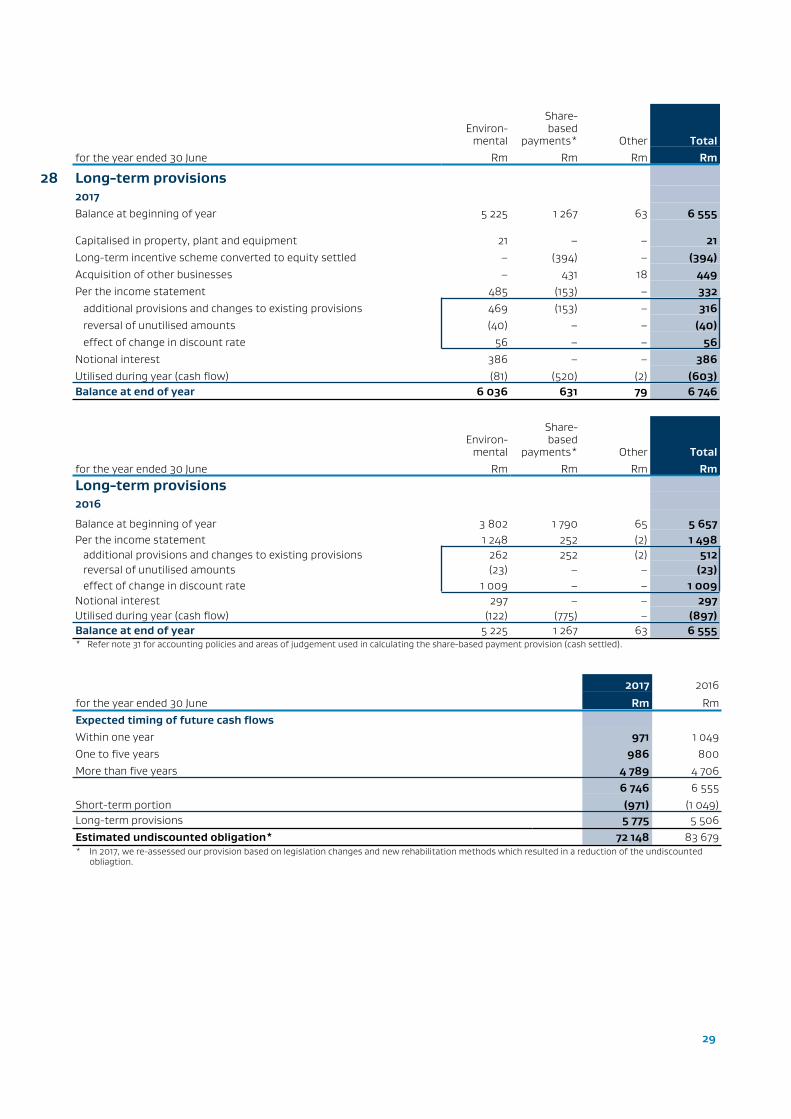

Environ-mental

Share-based

payments* Other Totalfor the year ended 30 June Rm Rm Rm Rm

28 Long-term provisions2017Balance at beginning of year 5 225 1 267 63 6 555

Capitalised in property, plant and equipment 21 – – 21Long-term incentive scheme converted to equity settled – (394) – (394)Acquisition of other businesses – 431 18 449Per the income statement 485 (153) – 332 additional provisions and changes to existing provisions 469 (153) – 316 reversal of unutilised amounts (40) – – (40) effect of change in discount rate 56 – – 56Notional interest 386 – – 386Utilised during year (cash flow) (81) (520) (2) (603)Balance at end of year 6 036 631 79 6 746

Environ-mental

Share-based

payments* Other Totalfor the year ended 30 June Rm Rm Rm RmLong-term provisions2016

Balance at beginning of year 3 802 1 790 65 5 657Per the income statement 1 248 252 (2) 1 498 additional provisions and changes to existing provisions 262 252 (2) 512 reversal of unutilised amounts (23) – – (23) effect of change in discount rate 1 009 – – 1 009Notional interest 297 – – 297Utilised during year (cash flow) (122) (775) – (897)Balance at end of year 5 225 1 267 63 6 555* Refer note 31 for accounting policies and areas of judgement used in calculating the share-based payment provision (cash settled).

2017 2016

for the year ended 30 June Rm RmExpected timing of future cash flowsWithin one year 971 1 049One to five years 986 800More than five years 4 789 4 706

6 746 6 555Short-term portion (971) (1 049)Long-term provisions 5 775 5 506Estimated undiscounted obligation* 72 148 83 679* In 2017, we re-assessed our provision based on legislation changes and new rehabilitation methods which resulted in a reduction of the undiscounted

obliagtion.

30

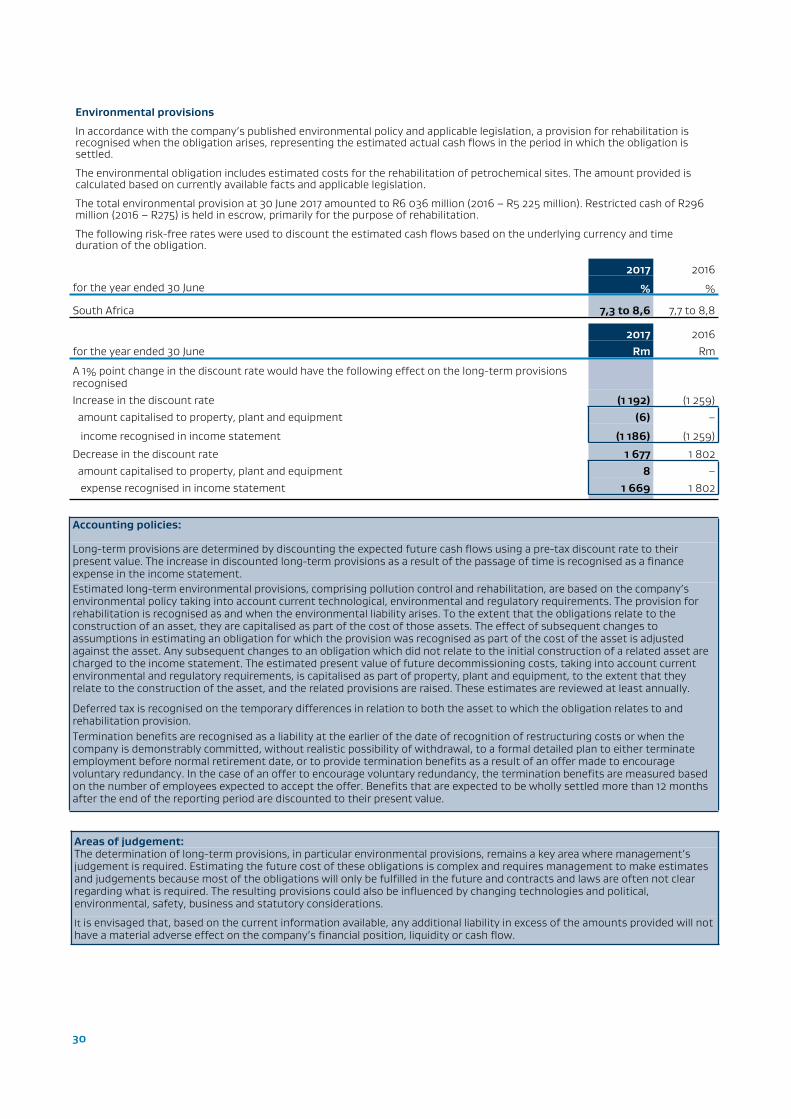

Environmental provisions

In accordance with the company’s published environmental policy and applicable legislation, a provision for rehabilitation is recognised when the obligation arises, representing the estimated actual cash flows in the period in which the obligation is settled.

The environmental obligation includes estimated costs for the rehabilitation of petrochemical sites. The amount provided is calculated based on currently available facts and applicable legislation.

The total environmental provision at 30 June 2017 amounted to R6 036 million (2016 – R5 225 million). Restricted cash of R296 million (2016 – R275) is held in escrow, primarily for the purpose of rehabilitation.

The following risk-free rates were used to discount the estimated cash flows based on the underlying currency and time duration of the obligation.

2017 2016

for the year ended 30 June % %

South Africa 7,3 to 8,6 7,7 to 8,8

2017 2016for the year ended 30 June Rm Rm

A 1% point change in the discount rate would have the following effect on the long-term provisions recognisedIncrease in the discount rate (1 192) (1 259) amount capitalised to property, plant and equipment (6) –

income recognised in income statement (1 186) (1 259)

Decrease in the discount rate 1 677 1 802 amount capitalised to property, plant and equipment 8 – expense recognised in income statement 1 669 1 802

Accounting policies:

Long-term provisions are determined by discounting the expected future cash flows using a pre-tax discount rate to their present value. The increase in discounted long-term provisions as a result of the passage of time is recognised as a finance expense in the income statement.Estimated long-term environmental provisions, comprising pollution control and rehabilitation, are based on the company’s environmental policy taking into account current technological, environmental and regulatory requirements. The provision for rehabilitation is recognised as and when the environmental liability arises. To the extent that the obligations relate to the construction of an asset, they are capitalised as part of the cost of those assets. The effect of subsequent changes to assumptions in estimating an obligation for which the provision was recognised as part of the cost of the asset is adjusted against the asset. Any subsequent changes to an obligation which did not relate to the initial construction of a related asset are charged to the income statement. The estimated present value of future decommissioning costs, taking into account current environmental and regulatory requirements, is capitalised as part of property, plant and equipment, to the extent that they relate to the construction of the asset, and the related provisions are raised. These estimates are reviewed at least annually.

Deferred tax is recognised on the temporary differences in relation to both the asset to which the obligation relates to and rehabilitation provision.Termination benefits are recognised as a liability at the earlier of the date of recognition of restructuring costs or when the company is demonstrably committed, without realistic possibility of withdrawal, to a formal detailed plan to either terminate employment before normal retirement date, or to provide termination benefits as a result of an offer made to encourage voluntary redundancy. In the case of an offer to encourage voluntary redundancy, the termination benefits are measured based on the number of employees expected to accept the offer. Benefits that are expected to be wholly settled more than 12 months after the end of the reporting period are discounted to their present value.

Areas of judgement:The determination of long-term provisions, in particular environmental provisions, remains a key area where management’s judgement is required. Estimating the future cost of these obligations is complex and requires management to make estimates and judgements because most of the obligations will only be fulfilled in the future and contracts and laws are often not clear regarding what is required. The resulting provisions could also be influenced by changing technologies and political, environmental, safety, business and statutory considerations.

It is envisaged that, based on the current information available, any additional liability in excess of the amounts provided will not have a material adverse effect on the company’s financial position, liquidity or cash flow.

31

2017 2016

for the year ended 30 June Note Rm Rm

29 Short-term provisionsOther provisions 40 113Short-term portion of long-term provisions 28 971 1 049 post-retirement benefit obligations 30 141 123

1 152 1 285

2017 2016

for the year ended 30 June Rm Rm

30 Post-retirement benefit obligationsPost-retirement benefit asset 475 449

The post-retirement benefit assets form part of the asset recognised in terms of the Sasol Pension Fund's defined benefit plan. Full disclosure is provided in the consolidated annual financial statements of Sasol Limited.

2017 2016

for the year ended 30 June Rm RmPost-retirement benefit obligations 3 486 3 143Less short-term portion post-retirement healthcare benefits (141) (123)Total long-term post retirement benefit obligations 3 345 3 020

Post-retirement healthcare benefits

The company provides post-retirement healthcare benefits to certain of its retirees employed prior to 1 January 1998, who retire and satisfy the necessary requirements of the medical fund. The post-retirement healthcare liability forms part of the Sasol Limited group's post-retirement benefit obligation. Full disclosure is provided in the Sasol Limited consolidated annual financial statements.Accounting policies:The company operates or contributes to defined contribution pension plans and defined benefit pension plans for its employees. These plans are generally funded through payments to trustee-administered funds as determined by annual actuarial calculations.

Defined contribution pension plans are plans under which the group pays fixed contributions into a separate legal entity and has no legal or constructive obligation to pay further amounts. Contributions to defined contribution pension plans are charged to the income statement as an employee expense in the period in which related services are rendered by the employee.The company’s net obligation in respect of defined benefit pension plans is actuarially calculated separately for each plan by deducting the fair value of plan assets from the gross obligation for post-retirement benefits. The gross obligation is determined by estimating the future benefit attributable to employees in return for services rendered to date.This future benefit is discounted to determine its present value, using discount rates based on government bonds that have maturity dates approximating the terms of the company’s obligations and which are denominated in the currency in which the benefits are expected to be paid. Independent actuaries perform this calculation annually using the projected unit credit method.

Defined contribution members employed before 2009 have an option to purchase a defined benefit pension with their member share. This option gives rise to actuarial risk, and as such, these members are accounted for as part of the defined benefit fund and are disclosed as such.Past service costs are charged to the income statement at the earlier of the following dates:■ when the plan amendment or curtailment occurs; and■ when the group recognises related restructuring costs or termination benefits.

Actuarial gains and losses arising from experience adjustments and changes to actuarial assumptions, the return on plan assets (excluding amounts included in net interest on the defined benefit liability/(asset)) and any changes in the effect of the asset ceiling (excluding amounts included in net interest on the defined benefit liability/(asset)) are remeasurements that are recognised in other comprehensive income in the period in which they arise.

Where the plan assets exceed the gross obligation, the asset recognised is limited to the lower of the surplus in the defined benefit plan and the asset ceiling determined using a discount rate based on government bonds.Surpluses and deficits in the various plans are not offset.

The entitlement to healthcare benefits is usually based on the employee remaining in service up to retirement age and the completion of a minimum service period. The expected costs of these benefits are accrued on a systematic basis over the expected remaining period of employment, using the accounting methodology described in respect of defined benefit pension plans above. Independent actuaries perform the calculation of this obligation annually.

32

Healthcare benefits Pension benefits

Last actuarial valuation – South Africa 31 March 2017 31 March 2017Full/interim valuation Full FullValuation method adopted Projected unit credit Projected unit creditThe plans have been assessed by the actuaries and have been found to be in sound financial positions.

Principal actuarial assumptions

Weighted average assumptions used in performing actuarial valuations determined in consultation with independent actuaries.

South Africa2017 2016

at valuation date % %Healthcare cost inflation initial 7,5 7,5 ultimate 7,5 7,5

Discount rate – post-retirement medical benefits 9,8 9,9Discount rate – pension benefits 10,1 9,8Pension increase assumption 5,2 4,9Average salary increases 5,5 * 5,5 *

Weighted average duration of the obligation – post-retirement medical obligation 15 years 17 years

Weighted average duration of the obligation – pension obligation 13 years 14 years Assumptions regarding future mortality are based on published statistics and mortality tables.* In line with our low oil price Response Plan, we are forecasting salary increases linked to inflation.

2017 2016

for the year ended 30 June Rm Rm

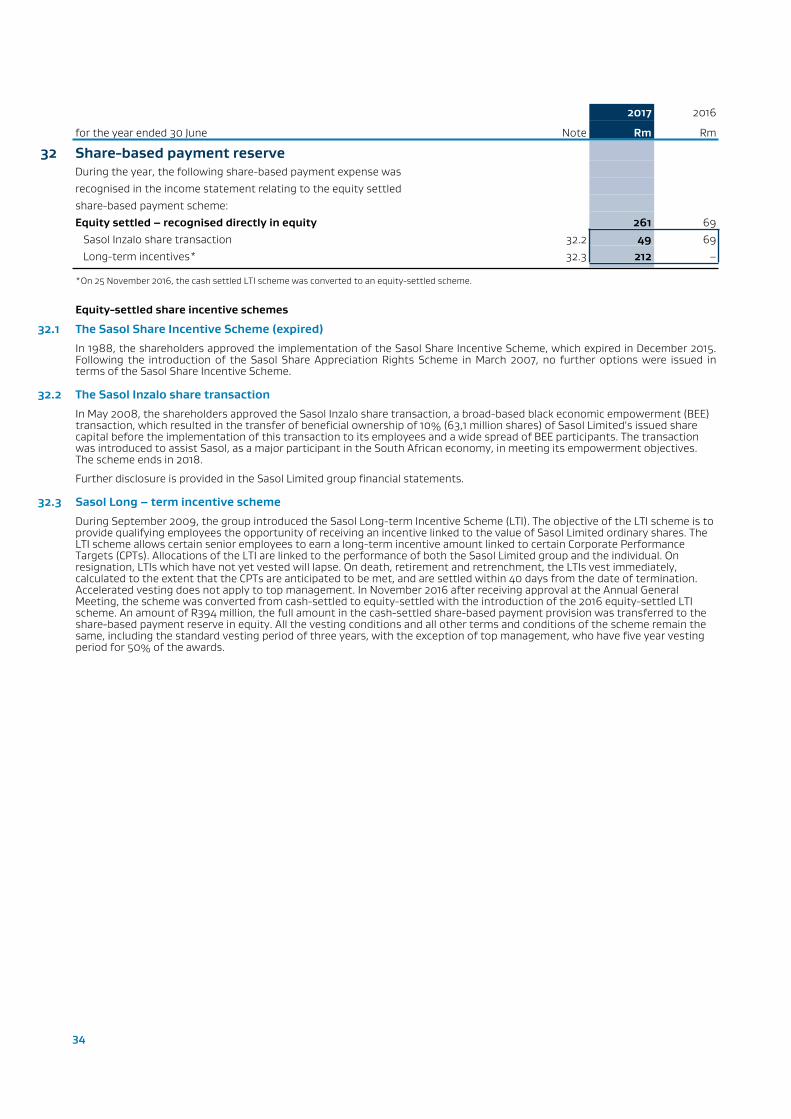

31 Cash-settled share-based payment provision

During the year, the following share-based payment expenses were recognised in the income statement relating to cash-settled arrangements (refer to note 32 for the equity settled share-based payment disclosure):Share-based payment expense – movement in long-term provisionsSasol Share Appreciation Rights Scheme (74) (36)Sasol Long-term Incentive Scheme* 227 288

153 252*On 25 November 2016, the cash-settled LTI scheme was converted to an equity-settled share-based payment scheme.

Sasol's share price decreased by 8% over the financial year to a closing price on 30 June 2017 of R366,50. This has resulted in a R153 million credit being recognised in the current year.

The Sasol Share Appreciation Rights Scheme (closed since 2013)

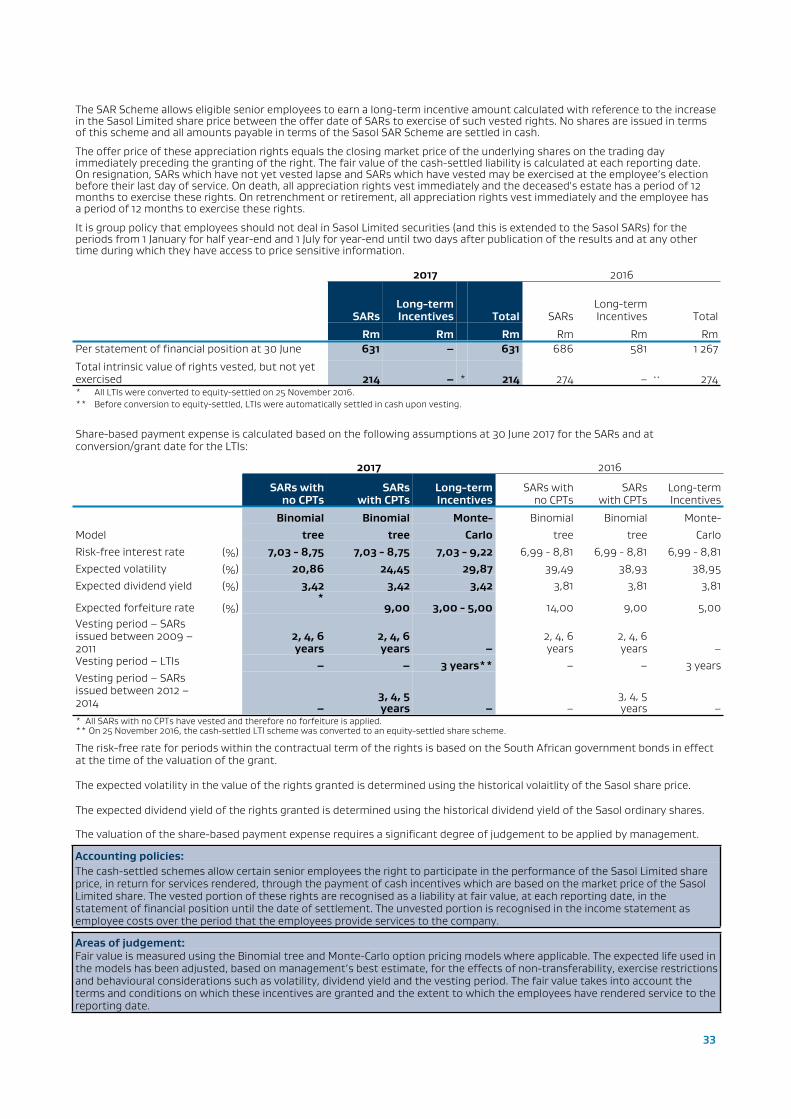

The maximum number of rights to be issued under the cash-settled Sasol Share Appreciation Rights Scheme (SARs) and the cash-settled Sasol Long-term Incentive Scheme (LTIs) shall not at any time exceed 69 million shares/rights. The maximum number of shares issued under the equity-settled LTI scheme (2016) may not exceed 32,5 million representing 5% of Sasol Limited’s issued share capital at the time of approval.

2017 2016

Total rights/units granted Number NumberShare Appreciation Rights 8 062 023 6 932 010Long-term Incentive Units1

– 2 913 3258 062 023 9 845 335

1 On 25 November 2016, the cash settled LTI scheme was converted to an equity settled share based payment scheme.

33

The SAR Scheme allows eligible senior employees to earn a long-term incentive amount calculated with reference to the increase in the Sasol Limited share price between the offer date of SARs to exercise of such vested rights. No shares are issued in terms of this scheme and all amounts payable in terms of the Sasol SAR Scheme are settled in cash.

The offer price of these appreciation rights equals the closing market price of the underlying shares on the trading day immediately preceding the granting of the right. The fair value of the cash-settled liability is calculated at each reporting date. On resignation, SARs which have not yet vested lapse and SARs which have vested may be exercised at the employee’s election before their last day of service. On death, all appreciation rights vest immediately and the deceased's estate has a period of 12 months to exercise these rights. On retrenchment or retirement, all appreciation rights vest immediately and the employee has a period of 12 months to exercise these rights.

It is group policy that employees should not deal in Sasol Limited securities (and this is extended to the Sasol SARs) for the periods from 1 January for half year-end and 1 July for year-end until two days after publication of the results and at any other time during which they have access to price sensitive information.

2017 2016

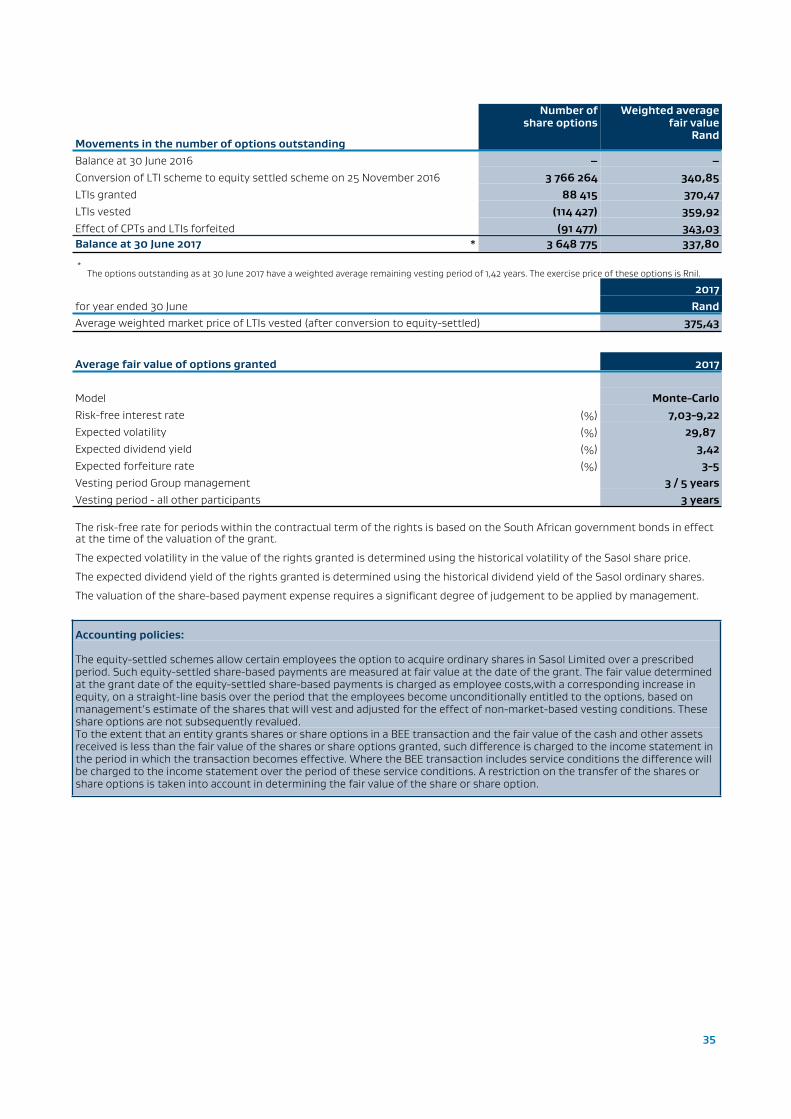

SARs Long-term Incentives Total SARs

Long-termIncentives Total