Embed Size (px)

Citation preview

UNITED STATES OF AMERICA Before the

RECEIVED

JUL 13 2016 oFFlcE oi= rRE8fcR'frARv

SECURITIES AND EXCHANGE COMMISSION

In the Matter of

BIOELECTRONICS CORPORATION, IBEX,LLC, ST. JOHN'S, LLC, ANDREW J. WHELAN, KELLY A. WHELAN, AND ROBERT P. BEDWELL,

Respondents.

File No. 3-17104

SECOND SUPPLEMENT AL DECLARATION OF ANDREW WHELAN IN SUPPORT OF RESPONDENTS' MOTION FOR SUMMARY DISPOSITION

Stanley C. Morris, Esq. Brian T. Corrigan, Esq. CORRIGAN & MORRIS LLP 201 Santa Monica Boulevard, Suite 475 Santa Monica, California 90401-2212 Telephone: 310-394-2828 Facsimile: 310-394-2825 [email protected] bcorrigan@cormorl lp. com

Counsel for Respondents, Bioelectronics Corporation; IBEX, LLC; St. John's, LLC; Andrew J. Whelan; and Kelly A. Whelan

I, Andrew Whelan, declare as follows:

1. I have personal knowledge of the facts stated herein and if called on would and

could testify competently thereto.

2. This declaration supports the motion of BioElectronics Corporation ("BIEL"),

IBEX, LLC ("IBEX"), St. John's, LLC ("St. John's"), Andrew J. Whelan and Kelly A. Whelan

(collectively, "Respondents") for summary disposition on the Division's claims against

Respondents.

3. BIEL hired Drew Walker based on his representation to me that he was a lawyer

and CPA who could assist BIEL in its efforts to comply with applicable securities laws. At all

times during Drew Walker's engagement with BIEL, he held himself out to be a lawyer and I

believed that he was. On a daily basis, during his engagement, I regularly sought legal advice

from Mr. Walker and reasonably relied on such advice.

4. Attached hereto at Exhibit 1 is a true and correct copy of excerpts of the

investigative transcript of Robert Bedwell obtained from the Securities and Exchange

Commission in this action.

5. Attached as Exhibit 2 is a true and correct copy of the Curriculum Vitae of Esther

Ko, emails between Esther Ko and Joseph Noel, and Esther Ko and Mary Whelan, and a

document titled "Bill and Hold Memo" prepared by Esther Ko for purposes of advising BIEL

and its auditors regarding the revenue recognition issues related to the eMarkets and Y esDTC

2009 transactions. My understanding is that such document was a draft memo. Esther Ko is an

outside accountant engaged to assist the Company and its auditors in their efforts to complete the

2009 financial statements and audit for BIEL. The language in the footnote at the end of the

document contains loose language not prepared by me or for purposes relating to this dispute.

2

6. The product sold to Y esDTC in connection with the initial purchase, as defined in

the December 30, 2009 Distributorship Agreement between YesDTC and BIEL, was delivered to

Y esDTC by BIEL on that date. Such product was maintained at BIEL' s warehouse for

YesDTC's benefit. It is true that the product sold to YesDTC never shipped. That is because

YesDTC never obtained approval from Japan, its sole licensed territory, to sell the product in

Japan, and abandoned the product at BIEL.

7. I testified at my investigative testimony that I thought that YesDTC's rights in the

product had been forfeited. As a non-lawyer, I found myself caught in an SEC investigation

deposition, without knowledge of the charges the SEC was contemplating or an ability to prepare

with my counsel adequately for such deposition, offered a layperson's unprepared answer. Since

that time, I have reviewed the Distributorship Agreement and, based thereon, understand that

YesDTC retained ownership rights in the product purchased with the initial purchase, but had no

license to sell it having failed to obtain approval from Japan to do so in Japan, YesDTC's one

and only exclusive territory. If YesDTC had a lawful use for such product, it had every right to

ship it from BIEL to wherever such lawful use would occur. For example, had YesDTC

purchased a license from BIEL for a different distribution area, it could have sold the product in

such distribution area without having to purchase it a second time. My testimony was intended

to convey that simple truth. Under the circumstances, it would be unlawful for YesDTC to

attempt to sell the purchased product in Japan. As a result, I testified that if Y esDTC had sought

shipment of the product in order to make illegal sales of the product in Japan or elsewhere, BIEL

could not and would not participate in such unlawful activity.

8. YesDTC chose not to do that, and instead to abandon the product to BIEL.

Accordingly, YesDTC never caused BIEL to ship that product.

3

9. Nevertheless, delivery did occur on December 31, 2009, because the transfer of

title and risk from BIEL to Y esDTC occurred on December 30, 2009 and Y esDTC had paid

$100,000, and promised to pay the remaining $50,000 within 90 days under the terms of the

Distributorship Agreement. The revenue recognized was actually received, as reported, and is

retained to this day by BIEL. Recognition of such sale in the 2009 Form 1 OK filed by BIEL was

appropriate.

10. The goods sold to YesDTC were finished.

11. Delivery of product from BIEL to eMarkets was made to eMarkets throughout

2009, and all such deliveries were completed on or before December 31, 2009. Delivery

occurred when title and risk of loss passed, and the finished product was segregated in BIEL' s

inventory subject to eMarkets' instructions for shipment.

12. As Mary Whelan attested, and told Esther Ko at the time, eMarkets expected to

have BIEL ship its product to customers before the end of 2010. See Exhibit 2.

13. Attached hereto as Exhibit 3 is a true and correct copy of the Distribution

Agreement between eMarkets and BIEL.

14. While the Distribution Agreement does not require that eMarkets purchase the

specific units that were the subject of the bill and hold disclosures in BIEL's 2009 Form lOK, the

general terms of the parties' Distribution Agreement applied and gave written structure to the

parties' agreement pertaining to that specific bill and hold purchase.

15. All of the product related to the eMarkets bill and hold transaction referenced in

the 2009 Form lOK was delivered in 2009. As to shipments, BIEL made 89 shipments in 2009

alone to eMarkets' customers. Although eMarkets has not yet completed its sales of all inventory

purchased in 2009, more than 10,000 have shipped.

4

15. eMarkets' product was warehoused in a separate section of BIEL's warehouse

does not render the contract invalid or the delivery ineffective. Indeed, such facts were fully

disclosed to BIEL's auditor, Robert Bedwell, of Berenfeld, Spritzer, Shechter & Sheer, and later,

Cherry Bekaert, and BIEL' s attorneys, and BIEL relied on such professionals in making such

disclosures.

16. The Division at pages 5, 7 and 26 of its Opposition, misrepresents that the

products purchased by eMarkets were not finished, relying on excerpts of deposition transcript

testimony of Mary Whelan and me, quoted out of context. The products sold by BIEL and

purchased by eMarkets in 2009 as reflected in the 2009 Form lOK were in finished form. To the

extent additional product components, shipping services and shipping costs were added to such

finished products in connection with shipping them to particular eMarkets customers, per each

customer's specifications, BIEL separately charged eMarkets and eMarkets separately

compensated BIEL on case by case basis. These additional sales and charges are not included in

the revenues recorded in the 2009 financial statements. In approximately 7 5% of the cases, no

additional products or components were added to shipments made to eMarkets' customers

because, in those cases, no additional components were requested by the customer. Although my

testimony indicated that adhesive components were added, such comment would not apply to

eMarkets' veterinary products. Because eMarkets' customers intended to use such products on

animals with fur or hair, adhesives were not regularly, if ever, a component that was added to the

eMarkets product that had been purchased from BIEL and was segregated in BIEL' s warehouse.

17. Kelly Whelan was a consultant, at times, for BIEL, but never an employee. Kelly

Whelan never received a salary or a W2 from BioElectronics.

5

18. The Division contends that "as further incentive, a lump sum of free trading BIEL

shares" were paid to IBEX in exchange for making a loan. Opposition at 2. No such lump sum

of free trading BIEL shares was made to IBEX as part of IBEX making a loan to BIEL.

19. The Division contends that IBEX' s convertible loan agreements "grant[ ed] IBEX

twice the number of free trading shares it had sold for BIEL's benefit." Opposition, at 3. IBEX

never sold shares for BIEL' s benefit. IBEX sold stock for IBEX' s benefit; and later sold

convertible notes for IBEX' s benefit. The convertible notes did not grant IBEX any shares - and

certainly not "twice the number of free trading shares" sold. IBEX received only a convertible

note for its loan. That convertible note allowed IBEX to convert debt into stock at a fixed

conversion price of 50% discount to the market on date of investment. The convertible note did

not state that such shares would be free trading. Instead, the shares would only become free

trading after the convertible note and stock to be issued thereunder had been held for at least the

statutory period required under Rule 144. At no time did BIEL grant IBEX twice the number of

free trading shares that IBEX had sold in order to fund the loan. That simply never happened.

20. The Division contends that "IBEX was not the only entity used for these

transactions. Starting in mid-2010, St. John's entered into similar transactions." Opposition, p.

3. The false implication is that only IBEX and St. John's financed BIEL. BIEL borrowed

substantial funds from several other lenders, including those not related in any way to me, on

substantially similar terms.

21. I did not and had no authority to order the transfer agent to issue shares without

restriction. I requested that it do so, as appropriate. But, it is my understanding that transfer

agents have independent duties that require them to conduct due diligence regarding issuing

shares without restriction. In each case, BIEL's transfer agent required, among other things, a

formal written legal opinion letter opining that issuance of the shares without restriction was

6

lawful. St. John's never sold shares to any so-called "Liquidating Entities" or in any manner

described as a "private placement." IBEX sold its convertible debt to private third parties. St.

John's sold its stock through a registered broker.

22. I did not prepare the statements contained in the "Bill and Hold Memo". That

"Bill and Hold Memo" appears to be a draft. The Division falsely implies that the "Bill and

Hold Memo" constituted the only statements made to the auditors by BIEL and me, such that if

something was not stated in this draft memo, then it was never disclosed. That is not the case.

The Bill and Hold memo was the result of many discussions and emails among Mary Whelan,

Richard Staelin, Joseph Noel, Esther Ko, Robert Bedwell and others, the end result of which was

the representations contained in BIEL's 2009 Form lOK, together with the certification by

BIEL's independent auditor of the transactions being stated in compliance with Generally

Accepted Accounting Principles.

23. Of course, BIEL would not have delivered the product purchased if Y esDTC had

intended to sell the product illegally, as BIEL would not knowingly participate in the

commission of a violation of applicable law. The auditors presumably know that, and should

presume that BIEL would not violate applicable law. Not telling the auditor that BIEL would

not violate the law is not a material omission. Finally, there was no fact to disclose in terms of

whether and when Y esDTC could be shipped its purchased product, as the circumstances under

which such products would be delivered are simply when doing so would be lawful. Had

YesDTC sought possession of its products for legal and permissible use, such as Mr. Noel's own

personal use, or, upon acquisition by YesDTC of another territory, use at a trade show or for sale

of such products in that territory, BIEL would, of course, have delivered such product.

24. IBEX loaned money under the terms of convertible notes, held those notes often

for three years or more, then sold some of that debt off to third parties in private sales. IBEX

7

still holds a great deal of BIEL debt. IBEX used the proceeds of such sales as IBEX saw fit. In

some cases, IBEX loaned money to BIEL in exchange for new convertible debt, most of which

IBEX still holds. IBEX never funneled any money to BIEL. IBEX did not receive "a new grant

of unrestricted shares" when such loan was made. IBEX received convertible debt only. It

would have the right to shares only upon conversion and, if IBEX chose not to convert, it would

have the right to cash on redemption. The new convertible note did not "replace[] the shares

IBEX sold." IBEX sold its long-held convertible note. And, any new convertible note was not a

replacement of the note sold, but a new convertible debt instrument issued in exchange and in the

amount of any new loan made.

25. BIEL, IBEX and St. John's went to great lengths to document their financing

transactions, secure legal opinion letters, disclose in public filings and otherwise comply with the

federal securities laws applicable to such transactions. The large number of transactions, coupled

with IBEX' s dutiful compliance with the federal securities laws and timely reporting of such

transactions, reflects my daughter's, my wife's and my sincere efforts to provide ful disclosure

and comply with the securities laws, not evade them. It is also noteworthy, again, that IBEX did

not sell stock into the public market, as misrepresented, but sold convertible notes to private

investors at a discount.

26. eMarkets had been purchasing and selling BIEL products throughout 2009, had

existing customers at the time of the 2009 purchases from BIEL, and was actively negotiating to

sell to large retail pet stores. In 2012, the Division was provided with over 400 emails in Mary

Whelan's documents with the details of shipments and copies of customer orders and invoices.

89 sales and shipments were made in 2009 from BIEL's warehouse of eMarkets' inventory to

eMarkets' customers.

8

27. The Division falsely implies that Respondents have fabricated evidence of

delivery, shipment, possession, passing of title, transfer of risk of loans and a final binding

agreement among the parties. Opposition, p. 18. That is simply not true.

28. BIEL does not have a class of securities registered pursuant to section 12 of the

Act and is not required to file reports pursuant to section 15( d) of the Act, Section l 3(b )(2) does

not apply.

29. Footnote 1 of page 1 of the Opposition, and footnote 2 of page 2 of the Order

instituting this proceeding, argues: "BioElectronics' Section 12 reporting obligation arose as a

result of its filing a Form 8A-12g on February 12, 2006 in conjunction with a registration

statement on Form SB-2. The Form 8A-12g went effective by operation of law under Section

12(g) 60 days after filing, even though the Form SB-2 was subsequently withdrawn." Notably,

the Division cites no law and offers no evidence to support its assertion. That registration was

withdrawn formally on March 18, 2007, well before any of the alleged transactions and

disclosures made in this case. It is my understanding that when BIEL withdrew its registration

statement, it was no longer effective for any purpose, including to impose reporting requirements

arising from Section l 3(b )(2).

30. BIEL' s countermeasures to ensure proper accounting, despite the financial

inability to engage additional personnel, was to hire John Glass, CPA and Esther Ko, CPA as

well as purported lawyer, Drew Walker, to assist me to compile the financial statements in

accordance with GAAP. BIEL used outside competent accountants to compile the financial

statements which were then reviewed by Robert Bedwell and other capable auditors through

2010 and the OTCMarkets examiners thereafter to assure compliance with applicable reporting

guidelines. The Financial Statements are accompanied by either a completed audit certification

or with an Opinion Letter attesting to the disclosures from the Company's Securities Attorney.

9

31. Independent director, Richard Staelin, a highly qualified member ofBIEL's

Board, and a fonner Deputy Dean of the Fuqua School of Business at Duke University, provided

meaningful oversight to me as BIEL's sole executive for much of this period as well as BIEL's

accountants and auditor. BIEL's internal controls were adequate under the circumstances of a

company with sparse resources and few transactions and resulted in accurate :financial

statements.

32. As is evident from Mr. Bedwell's testimony, pages 140-147, Mr. Bedwell was

provided full and fair disclosure of all relevant facts pertaining to the so-called Bill and Hold

transactions, including full access to the applicable contracts, the email exchanges with Esther

Ko, an outside accountant engaged by BIEL to timely prepare the 2009 :financial statements, and

the cooperation of everyone involved, in order to ensure fair and accurate financial disclosures.

Mr. Bedwell confirmed that where the customer says that he or she expects to ship the product

before a date certain, that is sufficient, under some circumstances, such as this one, to constitute

a fixed delivery schedule. I relied on Mr. Bedwell's advice in certifying BIEL's 2009 :financial

statements.

I declare under penalty of perjury under the laws of the United States that the foregoing is

true and correct and that this declaration was executed this 10th. day of July 2016.

10

~

'-

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

In the Matter of:

File No. H0-11713-A

BIOELECTRONICS CORP.

WITNESS: Robert Bedwell

PAGES: 118 through 163

Place: Securities and Exchange Commission

801 Brickell Avenue

Suite 1800

Miami, Florida 33131

DATE: Wednesday, August 27, 2014

The above-entitled matter came on for hearing,

pursuant to notice, at 9:44 a.m.

Diversified Reporting Services, Inc.

(202) 467-9200

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000011

118

1 APPEARANCES:

2

3 On behalf of the Securities and Exchange Commission:

4 THOMAS ROGERS, ESQ.

5 JEFFREY ANDERSON, Office of the Chief Accountant

6 BRAD MROSKI, Assistant Chief Accountant

7 Securities and Exchange Commission

8 Division of Enforcement

9 100 F St. NE

10 Room 7531

11 Washington, DC 20549

12 202.551.4776

13

14 On behalf of the Witness:

15 ROBERT BEDWELL, PRO SE

16

17

18

19

20

21

22

23

24

25

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000012

119

~

"'-

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

C 0 N T E N T S

WITNESS: EXAMINATION

Robert Bedwell 123

EXHIBITS

87

88

DESCRIPTION IDENTIFIED

Subpoena 124

Audit Program Document 156

(8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000013

120

121

1 P R 0 C E E D I N G S

2 MR. ROGERS: We are on the record at 9:44 a.m., on

3 August 27, 2014 at the Securities and Exchange Commission in

4 Miami, Florida. The office is located at 801 Brickell Avenue,

s Miami, Florida 33131. The Commission has issued a formal order

6 of investigation in this matter, which you were shown prior to

7 the opening of the record. The formal order empowers me to

8 administer the following oath.

9 Please raise your right hand.

10 Whereupon,

11 ROBERT BEDWELL,

12 having first been duly sworn to tell the truth, the whole truth,

13 and nothing but the truth, was examined and testified as follows:

14 THE WITNESS: I do.

15 MR. ROGERS: Please state and spell your full name for the

16 record, and give me your date of birth and Social Security

17 Number as well.

18 THE WITNESS: Robert, R-0-B-E-R-T; Phillip, P-H-I-L-L-I-P;

19 Bedwell, B-E-D-W-E-L-L; ;

20 MR. ROGERS: My name is Tom Rogers; I am an attorney in the

21 Enforcement Division of the U.S. Securities and Exchange

22 Commission. With me are Brad Mroski and Jeffrey Anderson,

23 accountants also in the SEC's enforcement division.

24 This is an investigation by the United States Securities

25 Exchange Commission entitled: In the matter of BioElectronics,

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000014

122

1 File Number H011713.

2 We are investigating whether there have been violations of

3 certain provisions of federal securities law. However, the

4 facts developed in this investigation might constitute

s violations of other federal, state, civil or criminal laws.

6 Prior to opening the record, you were provided with a copy of

7 the formal order of investigation in this matter.

8 The formal order will be available to you during the

9 proceeding. If you -- have you had an opportunity to review the

10 formal order?

11 THE WITNESS: Yes.

12 MR. ROGERS: Do you have any questions about the formal

13 order.

14 THE WITNESS: No.

15 MR. ROGERS: Also, prior to the opening of the record, you

16 were provided with a copy of the commission's supplemental

17 information form, Form 1662, which has been pre-marked as

18 Exhibit Number 1.

19 Have you had an opportunity to read Exhibit Number 1?

20 THE WITNESS: Yes.

21 MR. ROGERS: Do you have any questions about Exhibit Number

22 1.

23 THE WITNESS: No.

24 MR. ROGERS: As I said before, you can leave those in front

25 of you. At the end of your testimony, I am going to ask for

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000015

123

1 them back. You can look at them at any time. You will have

2 them.

3 THE WITNESS: Uh-huh.

4 MR. ROGERS: Mr. Bedwell, are you represented by counsel

5 here today?

6 THE WITNESS: No.

7 MR. ROGERS: Okay. I want you to be aware that you have

8 the right to be represented by counsel. If at any time during

9 the proceedings you wish to consult counsel, I will halt the

10 testimony until have had enough time to consult with an

11 attorney; is that clear.

12 THE WITNESS: Yes.

13 MR. ROGERS: Do you have any questions about this?

14 THE WITNESS: No.

15 MR. ROGERS: Okay. Have you taken any medications that

16 might affect your ability to understand and respond to my

17 questions today?

18 THE WITNESS: No.

19 MR. ROGERS: Is there any reason you cannot give full and

20 complete testimony?

21 THE WITNESS: No.

22 EXAMINATION

23 BY MR. ROGERS:

24 Q I'm going to show you what has been pre-marked as

25 Exhibit 87.

(8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000016

124

1 (SEC Exhibit No. 87 was marked

2 for identification.)

3 Exhibit 87 is an August 8, 2014 subpoena issued to you

4 in this investigation requesting testimony. Exhibit 87 requires

5 you to appear for testimony. Is Exhibit 87 a copy of the

6 subpoena pursuant to which you appeared here today?

7 A Yes.

8 Q Okay. Prior to our meeting today, I provided you with

9 a disc containing the audit documents supplied by the accounting

10 firm Cherry, Bekaert and Holland.

11 Did you bring the disc with you today?

12 A Yes.

13 Q Can I have it, please?

14 A Yes.

15 Q All right. For the record, you have handed that over

16 to me.

17 Did you make any copies, electronic or otherwise of

18 these documents?

19 A No.

20 Q Do you want to hold onto any of these documents during

21 testimony? Did you print any out that you want to reference?

22 A No.

23 Q I think you did that during our first time together

24 and didn't know if you wanted to do that again.

25 A Just made some notes, very brief notes.

(8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000017

1 Q So there's nothing for you to give back to me at the

2 end of testimony; there are no other documents or no other

3 discs, this is the entirety?

4 A There is nothing to give back to you, other than that.

5 Q Okay. Mr. Bedwell, have you discussed with anyone,

6 other than your attorney -- have you discussed with anyone what

7 your testimony here today will be?

8 A No. No. I did -- well, I did call BioElectronics

9 just to find out what was going on with them. That's it, I

10 called them.

11 Q Okay. Who did you talk to?

12 A To Andrew Whelan.

13 Q And when was that?

14 A About a week or two ago.

15 Q And what did you discuss?

16 A I told him I was subpoenaed for testimony for this.

17 Q What was his response?

18 A That he was surprised that an investigation was still

19 ongoing. I told him, are you aware that an investigation is

20 going? And he said, yes, that a number of other people within

21 the company had been called for testimony.

22 Q Anything else?

23 A That's basically it. I said to him that -- you know,

24 that I was subpoenaed, that this wasn't a voluntary testimony,

25 and that was the extent of the conversation.

(8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000018

125

126

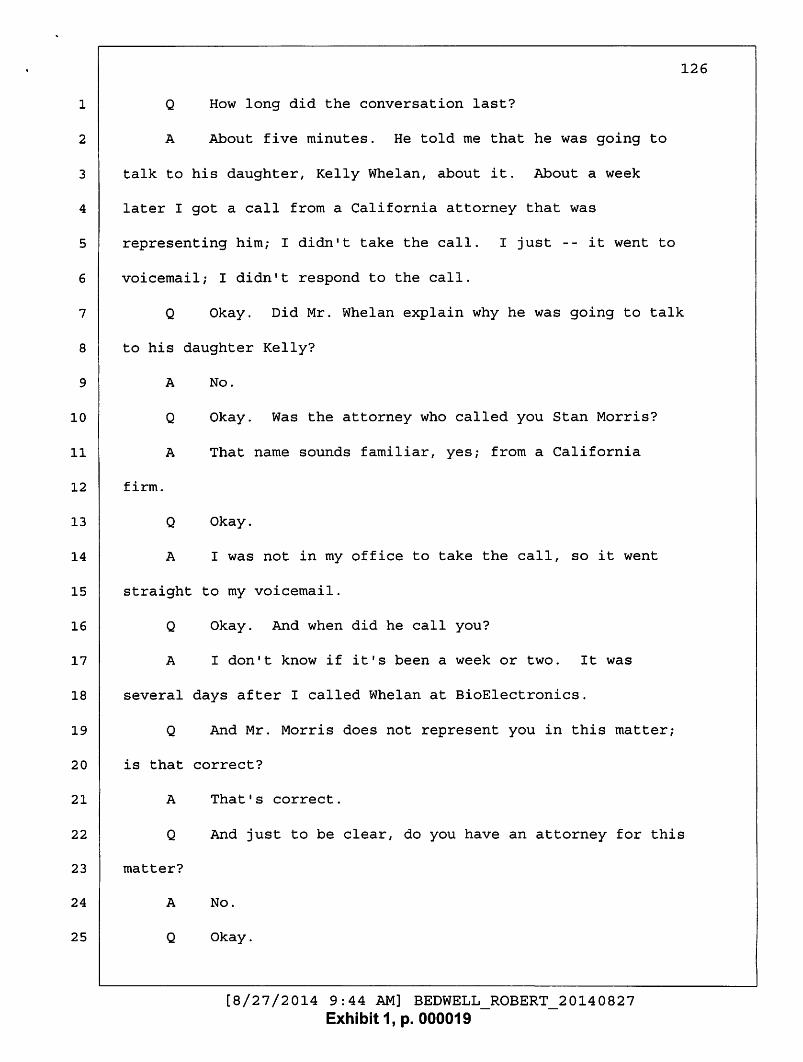

1 Q How long did the conversation last?

2 A About five minutes. He told me that he was going to

3 talk to his daughter, Kelly Whelan, about it. About a week

4 later I got a call from a California attorney that was

5 representing him; I didn't take the call. I just -- it went to

6 voicemail; I didn't respond to the call.

7 Q Okay. Did Mr. Whelan explain why he was going to talk

8 to his daughter Kelly?

9 A No.

10 Q Okay. Was the attorney who called you Stan Morris?

11 A That name sounds familiar, yes; from a California

12 firm.

13 Q Okay.

14 A I was not in my office to take the call, so it went

15 straight to my voicemail.

16 Q Okay. And when did he call you?

17 A I don't know if it's been a week or two. It was

18 several days after I called Whelan at BioElectronics.

19 Q And Mr. Morris does not represent you in this matter;

20 is that correct?

21 A

22 Q

23 matter?

24 A

25 Q

That's correct.

And just to be clear, do you have an attorney for this

No.

Okay.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000019

127

1 MR. MROSKI: Is this that the first time you had spoken

2 with Mr. Whelan regarding this investigation?

3 THE WITNESS: Yes.

4 MR. MROSKI: Was he aware that you had previously given

5 testimony in this matter?

6 THE WITNESS: No. I didn't tell him that.

7 MR. MROSKI: Okay.

8 BY MR. ROGERS:

9 Q Before we begin the substantive questioning, I would

10 like to review with you additional procedures that are to be

11 followed during testimony. This is something we went over last

12 time, but I think we should do it again.

13 The proceeding is being conducted on the record. If

14 you would like to go off the record, let us know and if it's

15 appropriate, we'll go off the record. Please understand that

16 the court reporter will only go off the record at the SEC

17 staff's direction.

18 You are under oath, so you must answer truthfully and

19 accurately. Do you understand that providing false testimony

20 can subject you to criminal sanctions?

21 A Yes.

22 Q The court reporter is taking down everything that's

23 said today; it's important that you speak clearly and that I

24 speak clearly and we all speak clearly. Because the proceedings

25 are being sound-recorded, please keep up your voice and respond

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000020

128

1 to all questions verbally, rather than through gestures.

2 Is that clear?

3 A Yes.

4 Q We both cannot speak at the same time. Please wait

5 for me to finish my questions before you start to answer, and I

6 will give you the same courtesy. If you do not understand any

7 of my questions, please ask me to clarify or rephrase in some

8 fashion so that you can understand.

9 Is that clear?

10 A Yes.

11 Q Okay. And I will remind you that you have the right

12 to have counsel with you today. If at any time you wish to

13 consult counsel, we'll pause the testimony and give you a chance

14 to do so.

15 Is that clear?

16 A Yes.

17 Q Okay. And I think I went through all of these

18 instructions as if I was going to ask all of the questions;

19 actually, all of us are going to ask questions, so they pertain

20 to all of us. I think that's obvious, but I'm going state it

21 for the record.

22 Do you understand these procedures?

23 A

24 Q

25 A

Yes.

Do you have any questions about any of them?

No.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000021

1 Q Okay. Prior to our last meeting, October 30, 2013,

2 you were asked to complete a background questionnaire. At the

3 time, that questionnaire was entered into the record as Exhibit

4 65. I'm going to hand you 65 now.

5 Just take a minute and look at that. I am going to

6 ask you a few questions to see if we need to update any of it.

7 Let me know when you are ready.

8 A Okay.

9 Q Do you recognize the document?

10 A Yes.

11 Q I think there have been a couple -- at least there's

12 one update that I am aware of. I think you have a different

13 address now.

14 A Yes.

15 Q Is that correct?

16 A Yes.

17 Q So your current address is the address that's on the

18 subpoena; why don't you go ahead and give it to us for the

19 record.

20 A

21 .

22 Q

23 updated?

24 A

25 Q

, Coral Springs, Florida

Okay. Is there anything else that needs to be

No.

Telephone number?

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000022

129

130

1 A Telephone number, cell number is the same. The home

2 number is changed. I no longer have a home telephone number; I

3 just have a cell phone number.

4 Q The bank accounts, brokerage accounts?

5 A Securities account, I have a 40l(k} now with my

6 present employer.

7 Q We are going to go into that, I think, in a minute

8 separately.

9 Why don't you state for the record who is your current

10 employer.

11 A Mallah Furman; M-A-L-L-A-H, F-U-R-M-A-N.

12 Q On Page 5, there's Question 18, have you ever

13 testified in proceedings conducted by the staff Securities

14 Exchange Commission; you checked no. I don't think that's

15 accurate.

16 A Yeah. I didn't remember whether we discussed at that

17 meeting that I remembered being here in this office before. The

18 testimony that I gave was related to a company called Banyan

19 Investments, I think it was B-A-N-Y-A-N. So I -- and then, of

20 course, the previous testimony that I gave --

21 Q Do you remember what year that was?

22 A with BioElectronics.

23 No.

24 Q Let me update -- have you ever been deposed in

25 connection with any court proceedings? You said yes, and it was

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000023

131

1 Rucks v. Cherry, Bekaert, and Holland.

2 Anything else to add to that?

3 A Not that I recall.

4 Q And you've never been named as a defendant by the SEC

5 or any other federal agency; is that correct?

6 A No.

7 Q Are your account licenses up to date?

8 A Yes.

9 Q And that's with what state?

10 A Florida.

11 Q Okay. That's all I have on 65.

12 I'm going to ask you to pass that just so we can keep

13 our documents straight.

14 MR. MROSKI: Just with your regards to your current

15 employer, what's your current position?

16 THE WITNESS: I'm an audit principal.

17 MR. MROSKI: Okay. And the firm itself, what's the nature

18 of their clients? Public clients? Non-public clients?

19 THE WITNESS: Both.

20 MR. MROSKI: Do you serve as principal on any public

21 clients?

22 THE WITNESS: Yes.

23 MR. ROGERS: I'm going to turn over the questioning to Mr.

24 Mroski at this point.

25 EXAMINATION

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000024

132

1 BY MR. MROSKI:

2 Q Mr. Bedwell, for my benefit and for Mr. Anderson's

3 benefit, since we were not here last time, I know that you went

4 through your background and previous employment. It's going to

5 be helpful for us just to get an understanding, and I will -- if

6 it's okay with you, I will refer to Berenfeld, Spritzer,

7 Shechter & Sheer as just Berenfeld.

8 A Okay. Yes.

9 Q And the same for Cherry, Bekaert and Holland, I'll

10 just Cherry Bekaert or CBH, if that's okay.

11 It's our understanding that you were with Berenfeld,

12 and Berenfeld got acquired by Cherry Bekaert; is that correct?

13 A Berenfeld dissolved. In December of 2005, the

14 partnership dissolved. The partners joined Cherry Bekaert

15 almost simultaneously. It was not considered a merger or an

16 acquisition. So that, technically, is not correct that

17 Berenfeld was acquired by CBH.

18 Q Okay. And you said December 2005?

19 A I think -- I'm trying to remember the dates. It's

20 December 2010, I think it was.

21 Q December 2010?

22 A Yeah. I joined Berenfeld in 2005.

23 Q Okay. So you joined Berenfeld in 2005; for all

24 intents and purposes, in 2010 Berenfeld just dissolved?

25 A Correct.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000025

133

1 Q And then Cherry Bekaert just picked up a lot of the

2 A Partners and employees.

3 Q The previous employees of Berenfeld?

4 A Yes.

5 Q Okay. Who were you with prior to Berenfeld?

6 A With Bloom, Gettis, Habib, Silver and Terrone, located

7 in Miami.

8 Q Located in Miami.

9 And did that firm do any work with BioElectronics?

10 A No.

11 Q Okay. When did BioElectronics become a Berenfeld

12 client?

13 A I don't know if it was 2006 or 2007. I don't

14 remember.

15 Q Okay. And were you on the account from day one?

16 A Yes.

17 Q And how did they come to be a client of Berenfeld?

18 A My partner, Tracey Winetraub, had a prior business

19 relationship with the president of BioElectronics, Andrew

20 Whelan.

21 Q

22 A

23 Q

24 A

25 Q

Okay. What was the nature of that relationship?

I don't recall.

Was Tracey a partner

Yes.

-- of the firm?

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000026

134

1 Was he an audit partner?

2 A Yes.

3 Q Any particular reason he didn't serve as the lead

4 partner on the engagement?

5 A I don't really know, other than ...

6 Q Let me phrase it a different way: How did you come to

7 serve as lead partner on the engagement?

8 A Tracey assigned the account to me. Tracey was the

9 lead audit partner. He was head of the department, and he

10 assigned the account to me.

11 Q Okay. And that was approximately 2007?

12 A Six or seven, yes. I don't remember exactly.

13 Q And then in 2010 when Berenfeld dissolved and Cherry

14 Bekaert took over the BioElectronics audit -- that's -- that's

15 my understanding, correct me if I am wrong.

16 A Correct.

17 Q Did you remain as the main audit partner for Cherry

18 Bekaert?

19 A I was actually the copartner. There was another

20 partner out of our Roanoke office. His name was Randall Burton,

21 B-U-R-T-0-N. Randall actually ran the account; given the

22 proximity between the two offices, it was assigned to his

23 off ice

24 Q

25 A

Okay.

-- and his staff.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000027

135

1 Q And when you say 11 copartner, 11 what is a copartner?

2 A We agreed to -- that I would serve as the engagement

3 quality control partner on the engagement and review the

4 engagement once it was completed. I was also involved in the

5 planning at the onset of the engagement.

6 Q Okay. So in PCOB standards language, Mr. Burton was

7 the lead client service partner and you were the quality control

8 partner?

9 A Yes.

10 Q Okay. And in 2009, when Berenfeld still had the audit

11 and the firm was still in existence, Berenfeld signed the audit

12 opinion for the 2009-lOK?

13 A Yes.

14 Q Did Cherry Bekaert ever issue an opinion on

15 BioElectronics financials?

16 A No.

17 Q Okay. And for the 2009 audit opinion, you were the

18 lead client service partner and the signing partner on that?

19 A Yes.

20 Q I'd would like to go to -- you mentioned that -- I'm

21 sorry -- Tracey, I forgot his last name.

22 A Winetraub.

23 Q Had the relationship with Mr. Whelan; did you have any

24 relationship with Mr. Stalin or anybody else at the company --

25 A No.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000028

136

1 Q prior to the engagement?

2 A No.

3 MR. ANDERSON: Where did Berenfeld have offices?

4 THE WITNESS: Our offices were in Coral Gables, Florida,

5 and Fort Lauderdale area.

6 MR. ANDERSON: And for Cherry Bekaert?

7 THE WITNESS: Same two offices, Coral Gables and Fort

8 Lauderdale.

9 BY MR. MROSKI:

10 Q Why when Cherry Bekaert picked you up and other

11 Berenfeld employees, why was the decision made not to have you

12 continue as the lead client service partner?

13 A As I noted before, the proximity to the offices

14 between Florida, South Florida and the Roanoke office.

15 Mr. Burton also had public company experience that was assigned

16 to his office.

17 Q How does that differ from the proximity issue prior to

18 Cherry Bekaert? I mean, you've always been in Miami, right?

19 A Correct.

20 Q Okay. So was there anything else that lead to him

21 taking over as the partner? Was it a time on account issue,

22 or ...

23 A No. No. I have no knowledge of what the decision

24 making was other than the reason that was given to me, which was

25 the proximity.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000029

137

1 Q Okay. And who told you that? Who gave you that

2 reason?

3 A Ray Quentin, who was the technical service partner in

4 the firm, Cherry Bekaert.

5 Q Okay. So it was his decision to make that change?

6 A Yes. It was a new client for Cherry Bekaert, so they

7 made that decision internally.

8 Q Okay. And did Mr. Burton have any prior relationship

9 with Mr. Whelan or BioElectronics or anybody at the company?

10 A No. Not that I am aware of.

11 Q And what was BioElectronics' response to the change in

12 the lead client service partner?

13 A They were fine. I mean, they still could contact me

14 if they had questions or, you know, if they had concerns about

15 the service that was being provided to them.

16 Q They weren't unhappy, to your knowledge

17 A No.

18 Q -- with the change?

19 Okay. I would like to talk a little bit about a

20 couple of the bill and hold transactions that you guys discussed

21 at your previous testimony. I am happy that you had a chance to

22 review the work papers Mr. Rogers sent to you.

23 Thinking back to 2009, the first question I want to

24 just get an understanding of is: How did you become aware of

25 the existence of these transactions?

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000030

138

1 I am referring specifically to YesDTC and E-markets.

2 A How did I become aware of them?

3 Q Yes.

4 A Through, you know, the examination of the county

5 records, as part of the planning for the engagement, they

6 provided us copies of contracts or agreements that they had with

7 the two companies that you noted.

8 Q Do you recall, in that particular year, did the

9 planning for the engagement occur prior to the end of the fiscal

10 year, or did it occur subsequent to the end of the fiscal year?

11 A I don't remember when -- I don't remember the dates,

12 the exact dates.

13 Q Okay. So this is something, though, that you

14 identified or Berenfeld identified, as opposed to BioElectronics

15 coming to you and saying, we've entered into bill and hold

16 transactions?

17 A That's correct. I don't recall them specifically

18 characterizing them as bill and hold transactions. I remember

19 discussions in the planning meetings where we looked at the

20 characteristics of the agreements. And after inquiries with

21 management, we determined that they met the criteria or the

22 characteristics of that type of transaction.

23 MR. ANDERSON: How did management characterize those

24 transactions?

25 THE WITNESS: I don't recall those specific discussions.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000031

139

1 You know, they were significant transactions, so we concentrated

2 on them during the client -- in terms of -- since they

3 constituted a significant portion of the revenues for that

4 particular year.

5 MR. ANDERSON: Did you get the impression that management

6 felt those two contracts for YesDTC and E-markets were not any

7 different than any of their other revenue contracts and styles?

8 THE WITNESS: Looking back at it, you know, through the

9 benefit of hindsight, I believe that they didn't think they were

10 out of character, out of any of their other transactions.

11 We, you know, had issued management letters talking

12 previous to that and obviously subsequent to, you know, the

13 completion of the engagement -- about the quality of their

14 accounting staff; specifically their understanding of U.S. GAAP.

15 And so I think that initially they didn't think that they

16 were out of character. I think that's a correct

17 characterization.

18 BY MR. MROSKI:

19 Q I'm going to show you what's been previously marked as

20 Exhibit 19. This looks like a memo from Andy Whelan. It's

21 titled, Bill and Hold Memo, Audit of 2013.

22 Take a second to familiarize yourself with that.

23 A

24 Q

25 A

Okay.

Why did Mr. Whelan write this memo?

This is in response to our questions concerning the

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000032

140

1 character of these two transactions E-Markets and YesDTC.

2 Q Okay.

3 MR. ROGERS: Before we go any further, I would like to ask

4 a question.

5 Is it your belief that Andrew Whelan wrote this memo?

6 THE WITNESS: No.

7 MR. ROGERS: Who do you think wrote it?

8 THE WITNESS: They had hired an accounting consultant, I

9 believe her name was Esther Ko, K-0, to assist them in some of

10 the reporting issues that they were trying to catch up, in terms

11 of, you know, past filings and so forth; get their financial

12 statements and accounting records up to date.

13 They hired Ms. Ko and she -- I believe she produced this

14 memo on behalf of Andy Whelan. I don't have any

15 firsthand-knowledge of that, but that's my belief both at the

16 time and looking back at it in hindsight.

17 MR. ROGERS: Why do you think it was Ms. Ko and not

18 Mr. Whelan?

19 THE WITNESS: It's my understanding of Mr. Whelan was that

20 he didn't have the -- either the knowledge or resources to put

21 together a technical memo of this, you know, in reference to

22 the -- you know, the codification, for example; in references to

23 the codification.

24 MR. ROGERS: There is no date on this memo; do you remember

25 when you first saw it?

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000033

141

1 THE WITNESS: I don't remember the exact date, no.

2 MR. ROGERS: Can you give me an proximate date?

3 THE WITNESS: It would have been some time during the

4 you know, the course of the audit in response to our questions.

5 So it would have been some time after planning and before

6 conclusion.

7 MR. ROGERS: Okay. So you think you got this memo prior to

8 the conclusion of the audit?

9 THE WITNESS: Yes.

10 MR. ROGERS: Okay. And can you give me a date for the

11 conclusion of the audit?

12 THE WITNESS: No. Unfortunately, I didn't concentrate on

13 dates, you know, in terms of when I was reviewing the work

14 papers; so I can only give you approximations. I think the 2009

15 audit was conducted some time during 2010; I don't remember the

16 exact dates.

17 MR. ROGERS: Do you think the audit was completed before

18 the company filed its 2009-10-K?

19 THE WITNESS: Yes. So it would have been prior to

20 March 2010.

21 MR. ROGERS: Okay. A general issue: I think you said the

22 company was trying to catch up with its accounting records; is

23 that what you said?

24 THE WITNESS: Yes.

25 MR. ROGERS: Was it your impression that the company's

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000034

142

1 accounting procedures and controls were less than tidy?

2 THE WITNESS: I think our management letter for that year

3 speaks for itself. I mean, we cited a number of weaknesses,

4 some of which had to do with, you know, the quality of the

5 accounting staff, their knowledge, the timeliness of -- I don't

6 recall whether or not, looking back at it in hindsight, in terms

7 of timeliness of closings and so forth.

8 MR. ROGERS: Thank you. I'm going to let Mr. Mroski take

9 the lead.

10 BY MR. MROSKI:

11 Q Going back to this memo, beginning on the bottom of

12 the first page and then onto the second page, it lists out

13 general revenue recognition criteria, and then Subsection B is

14 bill and hold revenue criteria?

15 A Uh-huh. Yes.

16 Q Take a minute to look at those and let me know if that

17 is consistent with your understanding of the criteria, to

18 recognize revenue on a bill and hold agreement or transaction.

19 A Yes. Generally speaking, yes, it is.

20 Q Okay.

21 A In accordance with my understanding of the accounting

22 standards.

23 Q Okay. So just to kind of summarize it: It's fair to

24 say you know, just to really summarize it: It's fair to say

25 that through the course of the audit, you guys got the YesDTC

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000035

143

1 and E-Market agreements, per your firm file, you identified it

2 as a potential bill and hold transaction, you discussed it with

3 management and asked them to write a memo supporting the

4 accounting treatment for bill and hold; is that correct?

5 A Correct. We questioned the revenue recognition,

6 related to the fact, initially, that the delivery of goods

7 hadn't occurred. And so we initially characterized this as a

8 sales cutoff issue, in terms of, you know, all the criteria of

9 revenue recognition. And they came back to us and indicated

10 they believed that it met the criteria. We asked them to give

11 us a memo to support that -- their assertion.

12 Q Okay. These handwritten notes on Page 2, are those

13 yours?

14 A No.

15 Q Do you know who made those notations?

16 A No.

17 Q Let's talk about some of the bill and hold criteria,

18 and specifically what Berenfeld did to test management's

19 assertion with respect to these items.

20 I guess looking at Number 3, the buyer, not the

21 seller, must request that the transaction be on a bill and hold

22 basis.

23 What did you guys do, from an audit standpoint, to

24 test that assertion?

25 A My recollection is we looked at correspondence between

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000036

144

1 the buyer and seller to see whether or not that that fact could

2 be corroborated.

3 Q Okay.

4 A Management was asserting that the buyer had

5 requested -- both buyers had requested that the transaction be

6 on this basis.

7 Q Okay. So you looked at communication between

8 BioElectronics management and these customers, like e-mails

9 or ...

10 A Yeah. Whatever I -- I don't recall the specific media

11 or the form of the correspondence, but ...

12 Q Okay. There must be a fixed -- and back to the

13 handwritten notes: Do you recall those notation being on there

14 when you originally received this memo from the company?

15 A No.

16 Q Okay. Number 4, it stipulates that there must be a

17 fixed schedule for the delivery of the goods.

18 Was that something that was present in the agreements?

19 A My recollection is there was a stated date, in terms

20 of delivery.

21 Q Okay. Was it a stated date in terms of delivery, or

22 was it more certain amount of product must be taken by this

23 date?

24 A I don't remember what our specific decision making was

25 on it. I do recall that there was a date provided, a schedule

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000037

145

1 provided for the taking -- taking possession of the goods.

2 Q Okay. Actually, if you flip over to the third page,

3 it's down in the bill and hold criteria section, Item Number 4;

4 is this the work of Berenfeld?

5 A No.

6 Q Who put this spreadsheet schedule together?

7 A This was part of the document that was provided to us

8 by the company.

9 Q Okay. If you look at the column titled E-Markets,

10 under Item Number 4 under Bill and Hold Criteria, it says that

11 the goods will be shipped by December 31st 2010.

12 Do you see that?

13 A Yes.

14 Q In your opinion, is that a fixed delivery schedule?

15 A You know, I can't comment on that. I don't recall the

16 nature of our conversations to follow up on that -- on that

17 final comment there.

18 Q Where would we be able to see evidence of your

19 followup on that comment from an audit work paper standpoint?

20 A I don't remember. I think we had our own memo, or we,

21 you know, discussion in there about these comments. I don't

22 remember whether it was attached to this memo, but there was

23 you know, our consideration of all of the criteria and our

24 efforts that we took to corroborate those assertions.

25 Q Maybe even just pulling it back a little, just on it's

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000038

146

1 face, without regards to what Berenfeld may or may not have

2 done, just on the representation here: The goods will be

3 shipped by December 31, 2010. In your opinion, would that

4 constitute a fixed delivery schedule, without any other

5 information?

6 A I can't make a comment on that, because I would not

7 have gone with this just from the face of the representation.

8 This is a client memo; this is not our this is not our

9 document. So, as I said, we must have done some followup. I

10 don't remember exactly what it was, but we did follow up to

11 ensure that what the client telling us has been represented to

12 them by the customer, it was, in fact, what the customer

13 represented to them.

14 Q I understand. I am just trying to be more general.

15 And just generally speaking, would more -- would it be necessary

16 to be more specific, in your opinion, in terms of a delivery

17 date, to meet that fixed delivery schedule criteria; without

18 regards to this transaction, just generally speaking?

19 A Again, I would want to see a specific schedule that

20 says we're going to take delivery or such-and-such number of

21 units by such-and-such date.

22 Q Okay. And so, in your opinion, that would constitute

23 a fixed delivery schedule?

24 A

25 Q

I'm not sure what you are asking me there.

Well, let me put it to you -- it's not a trick

(8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000039

147

1 question. Let me put it to you like this: If I say I'm going

2 to take 100 units within the next three months, would that

3 constitute a fixed delivery schedule in your opinion?

4 A No. It has to be taken in the context of a

5 transaction, as it's been explained to us. So if, for whatever

6 reason, the customer, for example, has their own customers that

7 say, okay, we'll take X number of units by such-and-such a date,

8 and the customer doesn't have the warehouse to store the goods,

9 you know, my client's customer, then I may be willing to accept

10 an explanation that I am taking delivery of X number of units by

11 this date, because the resale customer won't take delivery until

12 a certain point in time.

13 So if you're talking in a theoretical standpoint, then

14 that would be, I believe, an acceptable explanation --

15 Q Okay.

16 A for why the customer would request a bill and hold

17 transaction.

18 Q And in your opinion that would -- the scenario that

19 you outlined, that would meet bill and hold transaction

20 criteria?

21 A Again, it's a fixed schedule for delivery of the

22 goods, it must be reasonable. The reasonableness, from that

23 standpoint, would be in the context of the transaction; the

24 resale customer doesn't want to take possession of the goods

25 until a certain date. I think it's very common.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000040

148

1 I have -- you know, not necessarily bill and hold

2 transactions, but situations where a supplier will make an order

3 based on the timing of the sales. If it's a product that is

4 sold during a holiday season, I don't expect the customers to

5 take orders throughout the year. So I think the explanations

6 provided there are reasonable.

7 Q Okay.

8 MR. ANDERSON: Did you ever receive a more specific

9 delivery schedule from BioElectronics?

10 THE WITNESS: I don't recall.

11 BY MR. MROSKI:

12 Q Going back to the second page of the memo, Item

13 Number 5 states: The seller must not have retained any specific

14 performance obligations.

15 I am actually on Page 2. You can look at that one

16 too, because it lays it out in both places. Were you aware of

17 any additional performance obligations that BioElectronics had

18 with respect to these two agreements?

19 A No.

20 Q It was your understanding that the goods were

21 finished, all of the fixtures were on them, nothing else needed

22 to be done?

23 A No. The management had represented that they had

24 segregated the goods; the goods were complete, they were in

25 their storage area and were set aside and segregated for the

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000041

149

1 customer. So there was no other performance obligations. The

2 goods were sold in the condition that they left in the storage

3 area of the warehouse.

4 Q What did you said management had represented

5 what did Berenfeld do to test management's representation that

6 the goods were complete?

7 A Again, just going on recollection, we asked where the

8 goods were stored and segregated in the warehouse, and the

9 client showed us where they were. I mean, we are looking at

10 boxed units of patches. So there is really not much, in a way,

11 that has to be done other than to package them.

12 Q Are there any finishing activities that you're aware

13 of that have to be done, like fixing Velcro or labeling packages

14 or anything of that nature?

15 A Again, if we saw the packages were boxed and in a

16 condition represented to us as being ready to be shipped, I

17 don't think there is any reason to go beyond that, in terms of

18 an explanation. It would be similar to any other warehousing

19 situation where I am observing boxes of finished goods that are

20 ready to be shipped to customers. And my recollection of the

21 staff that observed that for us told us that they were boxed and

22 ready to be shipped.

23 Q Okay.

24 MR. ANDERSON: Who was that staff member?

25 THE WITNESS: Two staff members, Brian Lifestein and Angie

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000042

150

1 Slaney, S-L-A-N-E-Y.

2 MR. ANDERSON: And they physically went to the warehouse

3 and examined the --

4 THE WITNESS: Yes, the storage area was adjacent to the

5 offices where they were working.

6 BY MR. MROSKI:

7 Q Oh, so it wasn't in the same building, the storage?

8 A It's a storage room that's adjacent to the offices; I

9 mean, you could literally walk from the offices into the storage

10 area.

11 Q Okay. One room connected to the next?

12 A Yeah.

13 Q Okay. And you had mentioned in your previous

14 testimony, if memory serves, that it was a relatively small

15 area; is that correct?

16 A Yes.

17 Q Okay. So you have actually, kind of, started into

18 next question which is the six criteria listed here, which is

19 MR. ROGERS: Before we go there, I want to go back to five.

20 I want to direct your attention to the third page of

21 Exhibit 19. And under Performance Obligations, there is a

22 column for each E-markets and Yes, which is YesDTC, that's my

23 understanding; is that your understanding as well?

24 THE WITNESS: Yes.

25 MR. ROGERS: Okay. The fifth row there, under performance

(8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000043

151

1 obligations, it's filled in with yes, there is no additional

2 performance obligation, and then there is an asterisk under the

3 Yes column. And the asterisk down on the bottom refers to a

4 contingency clause, that the rights granted by company to

5 distributor are made under the assumption that regulatory

6 clearance to sell the company's product in Japan would be

7 relatively easily obtained. Should distributor be unable to

8 gain regulatory clearance within six months of contract

9 execution, this agreement is voidable at the option of the

10 distributor. That's end of the quote.

11 Were you aware of the contingency that's being discussed

12 there?

13 THE WITNESS: I don't recall this specific discussion, but

14 we reviewed this document.

15 MR. ROGERS: And I am the only one on this side of the

16 table who is not an accountant, so I may not use the right

17 words, and if these other two would like to jump in, please do.

18 But that indicates to me that the distributor, YesDTC,

19 could walk away from this contract at any time within six months

20 of signing it.

21 So how is that -- how does that qualify as clear revenue

22 from an auditor's point of view?

23 THE WITNESS: Again, I don't recall our specific

24 discussions about this.

25 MR. ROGERS: What would you have done to follow up on this

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000044

152

1 clause?

2 THE WITNESS: We would have looked at the contingency and

3 had a discussion about the contingency and whether, in fact, it

4 had been overcome in order for the criteria to pass.

5 MR. ROGERS: I need more specifics on that. What would

6 that look like?

7 THE WITNESS: I can't tell you. I don't know what the -- I

8 don't remember what the specific regulatory issue that they're

9 bringing up here; I don't recall what that was.

10 BY MR. MROSKI:

11 Q Well, it says on the second line: Obtaining

12 regulatory clearance to sell the company's products in Japan.

13 A I'm not sure what you want me to answer there. What

14 your response -- what my response should be there.

15 Q Is it your understanding that the company, YesDTC, did

16 not have regulatory clearance to sell BioElectronics' products

17 in Japan when this memo was written?

18 A No. That's not my understanding.

19 Q You said you reviewed this document; do you interpret

20 that language a different way?

21 A Again, I don't recall the nature of the discussions or

22 our followup on this.

23 MR. ROGERS: Where would we look in the auditing records to

24 find something indicating that questions were raised about

25 whether YesDTC had obtained regulatory approval -- Japanese

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000045

153

1 regulatory approval?

2 THE WITNESS: Within the work papers associated with this

3 memo.

4 MR. ROGERS: I guess what I need is something a little more

5 specific. I am not an accountant. I

6 THE WITNESS: I can't provide that to you. I don't -- I

7 looked at as many of the work papers and documents as I could

8 within the disc. There was numerous repetitions of documents

9 and so forth in there, so it became mind-numbing to try to

10 review every single document in there. So I don't recall where

11 it's listed there.

12 MR. ROGERS: I understand that. And, I guess, my question

13 is a little bit more general. I don't understand the filing

14 system for work papers. And it's my understanding, maybe that's

15 wrong, that it's a fairly standard system, that the software

16 used is one that's used from one accounting firm to another. So

17 all I am looking for is some sort of heading, some sort of

18 general file where I can go and look for it.

19 THE WITNESS: There are work papers specific to this

20 transaction titled Bill and Hold Sales, where our followup

21 inquiries, what we did corroborate any explanations that were

22 provided to us by management, any documents that we examined,

23 those are all specifically referenced on the work paper.

24 I can't offer you anything other than that, because I

25 didn't retain anything beyond what's -- what was in the work

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000046

154

1 papers. So whatever Cherry, Bekaert and Holland has provided

2 you is in the work papers.

3 MR. ROGERS: And is it -- do you believe that you were the

4 one who followed up with management on this type of question, or

5 do you think it was someone else?

6 THE WITNESS: I don't remember.

7 MR. ROGERS: If it wasn't you, who would it be?

8 THE WITNESS: It would have been the manager on the

9 engagement, Brain Lifestein, or a senior or some conjunction.

10 MR. ROGERS: You need to give me those

11 THE WITNESS: Angela Slaney and Brian Lifestein.

12 BY MR. MROSKI:

13 Q With suspect to YesDTC, did they ever obtain clearance

14 to sell the product in Japan?

15 A I don't recall.

16 Q You don't recall.

17 And you're referencing the revenue work papers and the bill

18 and hold work papers, and I will tell you that I've been through

19 those. So if the followup of these items does not exist in

20 those work papers, is it fair to say that they weren't --

21 everything that was done was represented in the work papers? Is

22 that fair to say?

23 A I don't know.

24 Q Okay. Going down to Item Number 6, goods are

25 segregated; what's your understanding of what that means?

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000047

155

1 A That they are held in an area that's easily

2 identified -- identifiable to the viewer.

3 Q Okay. Separate and apart from any other inventory in

4 the warehouse?

5 A We asked, specifically, that question; I do remember

6 that.

7 Q Who did you ask that question to?

8 A To -- I don't remember who the person was that was in

9 charge of the warehouse at that time. It was an operations

10 person that worked with us during our inventory work.

11 Q Okay. Did you guys independently verify the goods

12 were segregated?

13 A I don't know how you want me to respond to that.

14 Q Did anybody from the audit firm go and look and see if

15 the goods were physically -- did they just ask somebody --

16 A I previously testified that both Brian Lifestein and

17 Angela Slaney were at the location. They responded back to me

18 that they were pointed to specific goods that were identified as

19 part of this transaction.

20 Q Okay. Just bear with me, because I wasn't here for

21 your previous testimony.

22 A Okay. That's fine. I had mentioned that just a few

23 moments ago.

24 Q My question was very specific, though. I understand

25 that they were onsite, but this is a specific audit procedure

(8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000048

156

1 that I am asking if it was performed, which is going and

2 physically verifying and saying, yes, as an auditor, I see these

3 goods are segregated. My question was: Did that occur, or was

4 it a representation from the person at the warehouse that says,

5 yeah, those goods are segregated?

6 A As part of my review of the work papers and the work

7 that my team performed in the field, I asked them specifically

8 whether or not they observed these items as being physically

9 separated; they indicated yes.

10 Q Okay. Did you personally, physically view the

11 segregated items?

12 A No.

13 MR. MROSKI: I am going to have this marked. I believe

14 we're on 88.

15 (Exhibit Number 88 was marked for

16 identification.)

17 BY MR. MROSKI:

18 Q I am going to show you a copy of the Audit Program For

19 Inventory Observation for the 2009 fiscal audit.

20 You can go ahead and take a second to review that.

21 A

22 Q

23 A

24 Q

25 said?

Okay.

Who is A.S.?

Angel Slaney.

Okay. And she was the senior on the account, you

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000049

157

1 MR. ROGERS: Just for the record, where are you reading

2 A.S.?

3 MR. MROSKI: There is a column where specific procedures

4 are listed in the main column, and there is a column, performed

5 by, and date. And throughout the document you see A.S., and

6 then the date, January 25th, 2010.

7 BY MR. MROSKI:

8 Q If you flip over to the third page, I am looking down

9 at the very bottom, at Item Number 7.

10 Does that appear to you that Angela Slaney is

11 representing there is no bill and hold transactions?

12 A Yes.

13 Q Okay. Why would that be?

14 A Because I think at the time, we weren't aware that

15 these were -- these transactions were either characterized as

16 bill and hold, or we were still waiting for the technical

17 support for what they purported them to be. So when we

18 initially did the inventory observation, I don't think that we

19 were specifically attuned to looking for inventory that was

20 segregated.

21 Q How did you go back and make sure it was segregated at

22 that point?

23 A We were in the field, and once we knew that this

24 transaction was being characterized as such, we asked them to

25 show us where the inventory was and how it was segregated.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000050

158

1 Q But at that point, you couldn't have been aware that

2 it was segregated as of the year end?

3 A We performed our inventory procedures after year end,

4 so ...

5 Q As of January 25, 2010, almost a month after year end,

6 you guys haven't determined that there were bill and hold

7 transactions?

8 A I don't remember the dates that we did the inventory

9 observation. The dates of the signoff may not necessarily be

10 the dates that we did the inventory observation. So I don't

11 know if this January 25th date is, in fact, the date that we

12 performed the inventory observation.

13 Q Did you review this work paper?

14 A Yes.

15 Q How can we tell?

16 A There would have been a signoff in the -- the work

17 papers are electronic; there would have been a signoff in the

18 electrical binder.

19 Q Do we have a copy of its -- I know what you are

20 talking about. It's almost a homepage.

21 A There were screenshots of the various audit work paper

22 indexes that were provide by Cherry Bekaert on that disc.

23 Q

24 A

25

Okay. How long

Could we go off the record for just a moment?

MR. ROGERS: Are you in the middle of something?

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000051

159

1 MR. MROSKI: No. That's fine. We can take a couple of

2 minutes.

3 MR. ROGERS: All right. Let's go off the record at 10:40.

4 {Whereupon, a discussion was held off the record.)

5 MR. ROGERS: We are back on the record at 10:52.

6 Mr. Bedwell, while we were off the record, we had a discussion

7 about how to proceed; is that correct?

8 THE WITNESS: Yes.

9 MR. ROGERS: And I am going to attempt to sum it up here,

10 and please correct me if you think that's wrong.

11 You have requested that we give you some sort of comfort as

12 to where we are going with the questioning and what your role is

13 here today; is that correct?

14 THE WITNESS: Yes.

15 MR. ROGERS: Okay. We cannot give you that comfort. Given

16 that we're at that point, you have said that you would feel

17 comfortable if you had an attorney present; is that correct?

18 THE WITNESS: Yes.

19 MR. ROGERS: Okay. So what we'll do is we'll convene --

20 end testimony for today, and I will give you a chance to find an

21 attorney, and have that attorney contact me and then we'll

22 reconvene. I'll most likely issue a new subpoena, and then

23 we'll reconvene at some time in the near future.

24 Is that acceptable to you?

25 THE WITNESS: Yes.

[8/27/2014 9:44 AM] BEDWELL_ROBERT_20140827 Exhibit 1, p. 000052

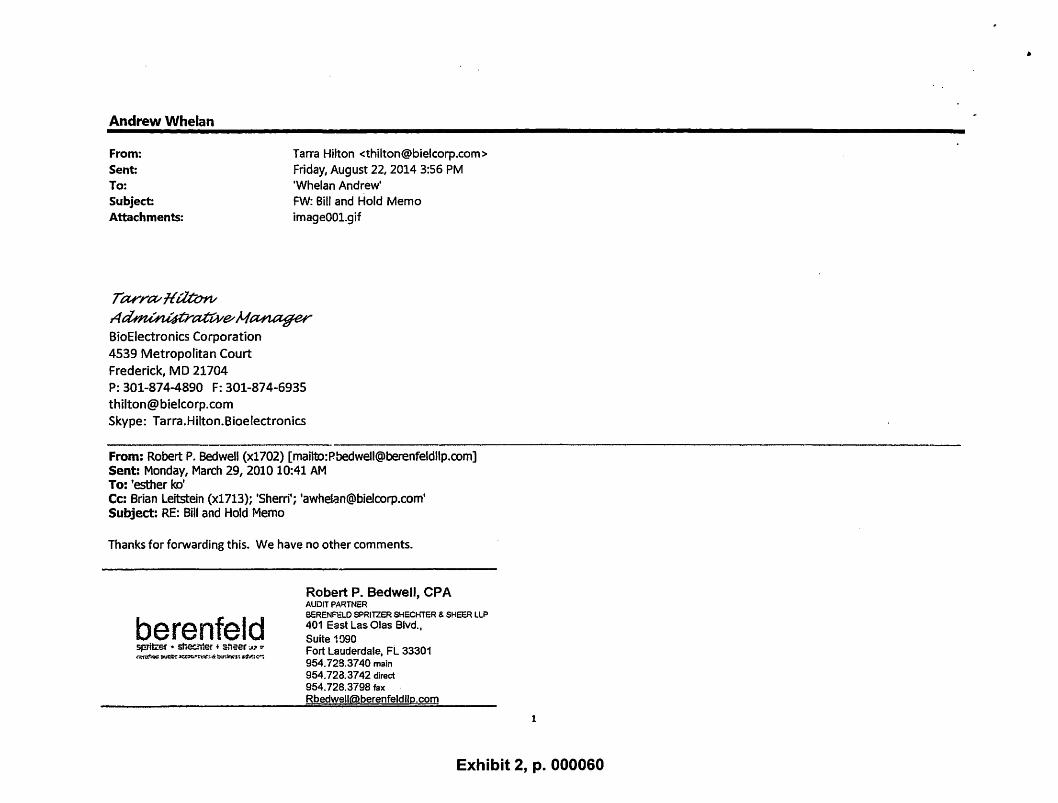

Please make these changes and then issue the memo as final (i.e., without the draft watermark).

Thanks,

Bob

berenfeld spritzer .. sheci"rte: • sheer .J.• = '4rtit.f~ Nit:& ~ti.?'&f\Lt~:. ~I.vs~\ 4dv_,s<i;"

Robert P. Bedwell, CPA AUDIT PARWER BERENFELO SPRITZER SHECHTER & SHEER LLP 401 East Las Olas Blvd., Suite 1090 Fort Lauderdale, FL 33301 954.728.;3740 main 954.728.3742 direct 954. 728.3798 fax [email protected] berenfeldllp.com

From: esther ko [mailto: l Sent: Tuesday, March 23, 2010 12:10 PM To: Robert P. Bedwell {x1702) Cc: Brian Leitstein {x1713); Sherri Subject: Bill and Hold Memo

Hi Bob,

Attached is the Company's drafted memo on the bill and hold transactions. Please review and let me know if you have any comments.

Thanks, Esther

******************************** NOTICE: To ensure compliance with Treasury Regulations (31 CFR Part 10, § 10,3 5), we inform you that any tax advice contained in this correspondence was not intended or written by us to be used, and cannot be used by you or anyone else, for the purpose of avoiding penalties imposed by the Internal Revenue Code.

2

Exhibit 2, p. 000053

From: Andy Whelan, President To: Work paper

PURPOSE

BloElectronics Bill and Hold Memo

Audit of 2009

To identify the amount of bill and hold revenue for the year ended of December 31, 2009 and analyze if such amount is qualified to recognize as revenue according to GAAP.

BACKGROUND During 2009, the Company recognized bill and hold revenue related to two customers, eMarkets Group, LLC1 ("eMarkets") and YesDTC, lnc.2 ("YES"). The following summarizes the related finandal information:

Bill and Hold revenue for the year ended December 31, 2009:

eMarkets YES TOTAL Sales a 215,853 150,000 365,853 COGS SB,679 27,900 86,579

Gross Margin 157,174 122,100 279,274

Collection as at 12.31.09 b 105,018 100,000 205,018

Collection yet to receive a-b 110,835 50,000 160,835

ACCOUNTING PRONOUNCEMENT According to ASC 605-10-S99 SEC Materials, SEC summarizes the revenue recognition criteria (as previously discussed in SAB 101), and sets forth criteria under FN17 to be met in order to recognize revenue when delivery has not occurred.

A) General revenue recognition criteria:

1. Persuasive evidence of an arrangement exists, FN3

l eMarkets Group, LLC (eMarkets) Is a company owned and controlled by a member of the board of directors and sister of the company's president. The agreement provides for eMarkets to be the exclusive distributor of the Company's line of products to customers In certain countries outside of the United States for a period of 3 years. The distribution agreement lists the prices to be paid for the company's products by eMarkets and provides for the Company to provide training and customer support at Its own cost to support the distributor's sales function. The terms and conditions of the agreement are comparable to any Independent distributors of the Company.

2 VesDTC, Inc. (YES) Is BloElectronlcs' distributor In Japan.

Exhibit 2, p. 000054

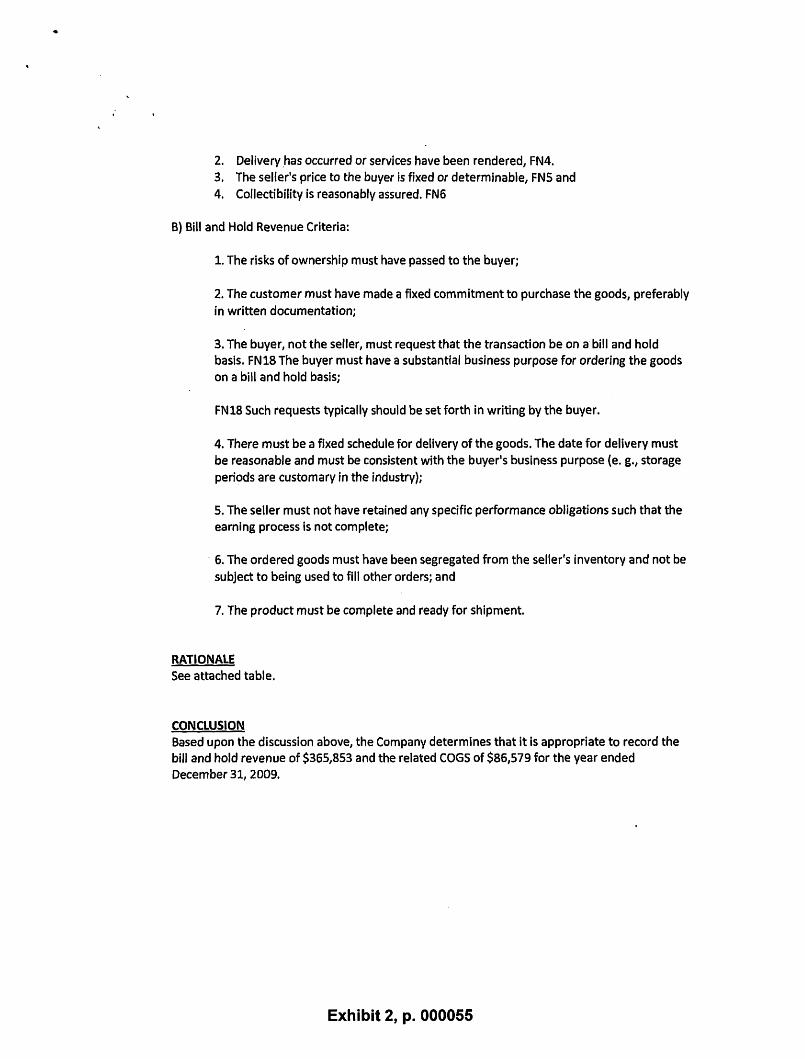

2. Delivery .has occurred or services have been rendered, FN4. 3. The seller's price to the buyer is fixed or determinable, FNS and 4. Collectibility is reasonably assured. FN6

B) Bill and Hold Revenue Criteria:

1. The risks of ownership must have passed to the buyer;

2. The customer must have made a fixed commitment to purchase the goods, preferably

in written documentation;

3. The buyer, not the seller, must request that the transaction be on a bill and hold basis. FN18 The buyer must have a substantial business purpose for ordering the goods on a bill and hold basis;

FN18 Such requests typically should be set forth in writing by the buyer.

4. There must be a fixed schedule for delivery of the goods. The date for delivery must be reasonable and must be consistent with the buyer's business purpose (e. g., storage

periods are customary in the industry);

5. The seller must not have retained any specific performance obligations such that the earning process is not complete;

· 6. The ordered goods must have been segregated from the seller's inventory and not be

subject to being used to fill other orders; and

7. The product must be complete and ready for shipment.

RATIONALE See attached table.