Embed Size (px)

Citation preview

Small SatellitesChanging the Economics of Space

Professor Sir Martin Sweeting OBE FRS FREngExecutive Chairman, SSTL

Chairman, Surrey Space CentreUnited Kingdom

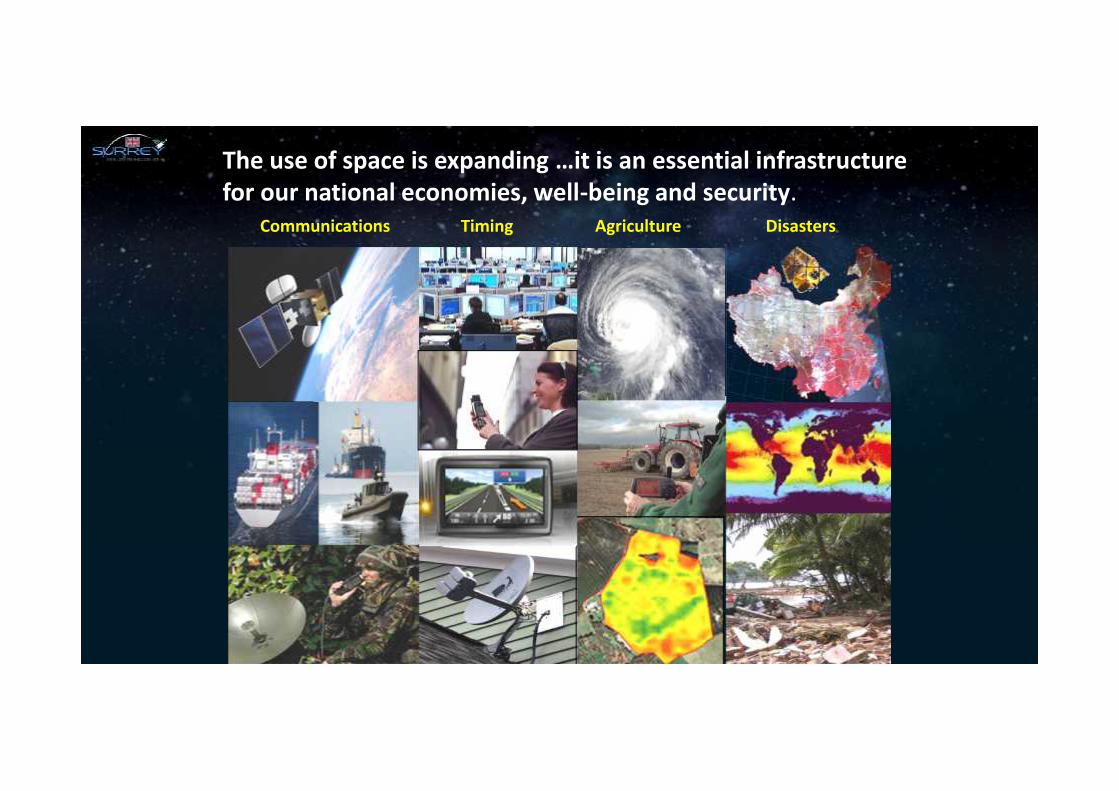

Communications Timing Agriculture Disasters

The use of space is expanding …it is an essential infrastructurefor our national economies, well-being and security.

Everyone has access to spaceSpace is no longer the preserve of super-powers or the mosttechnically-advanced or wealthy of nations …

The emergence of small, highly capable but inexpensive satelliteshas put sophisticated space assets with reach of almost every nation

1960’s

1980’s

2000’s

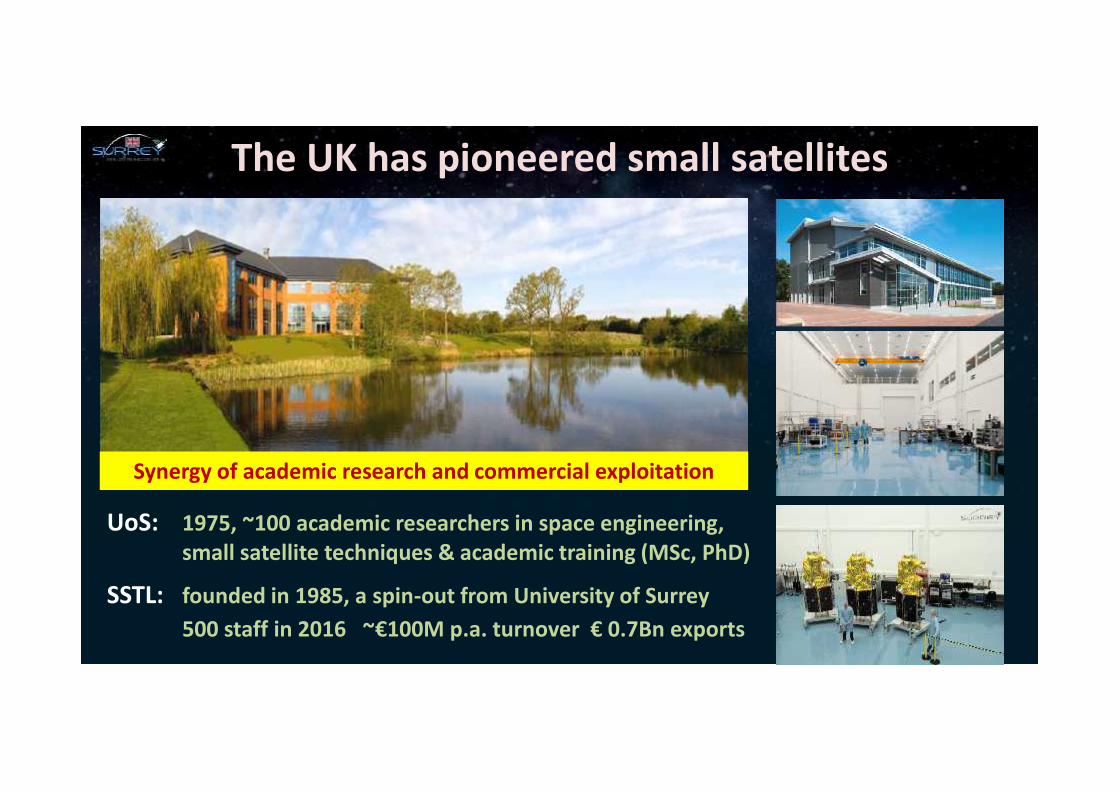

UoS: 1975, ~100 academic researchers in space engineering,small satellite techniques & academic training (MSc, PhD)

SSTL: founded in 1985, a spin-out from University of Surrey500 staff in 2016 ~€100M p.a. turnover € 0.7Bn exports

Synergy of academic research and commercial exploitation

The UK has pioneered small satellites

Innovation in Space and for SpaceThe challenges of space often drive innovation on Earth

But…

Advances in terrestrial consumer electronics andmanufacturing processes have revolutionised the approach to

space through COTS – small satellites

Changing the Economics of Space

SSTL GEOQUANTUM

SSTL NovaSAR

SSTL 300 S1

SSTL 300

SSTL 150

SSTL 100

SSTL-X50

Nanosats

SSTL small satellites

4000kg 400kg 150kg 50kg 5kgMini Micro NanoSmall

Different capabilities for different applications

Surrey has launched 50 satellites in 35 years1979 1992

1998 2015

DELTA ARIANE TSYKLON ZENIT SS18/Dnepr COSMOS ATHENA SOYUZ PSLVATLAS

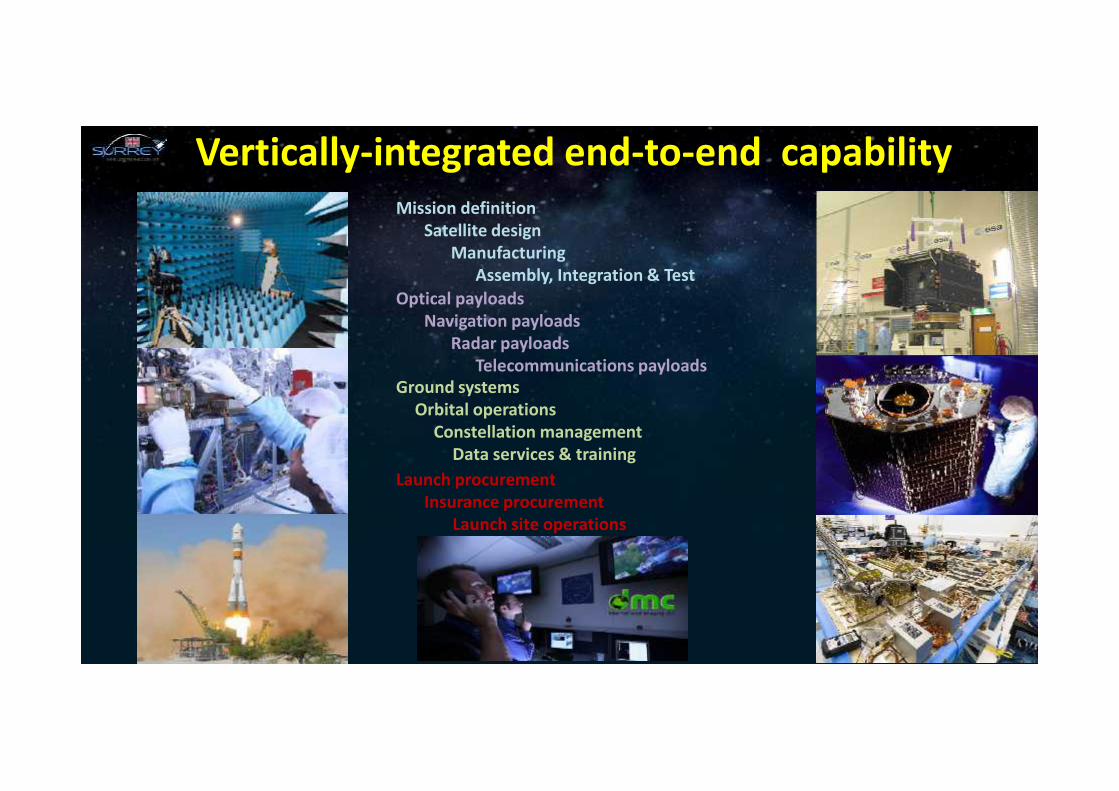

Vertically-integrated end-to-end capabilityMission definition

Satellite designManufacturing

Assembly, Integration & TestOptical payloads

Navigation payloadsRadar payloads

Telecommunications payloadsGround systems

Orbital operationsConstellation management

Data services & trainingLaunch procurement

Insurance procurementLaunch site operations

Major contracts : platforms, payloads or complete missions 95% export

7

4

3

2

1

2

8

2

61

17

25

2

1

1

114

International business

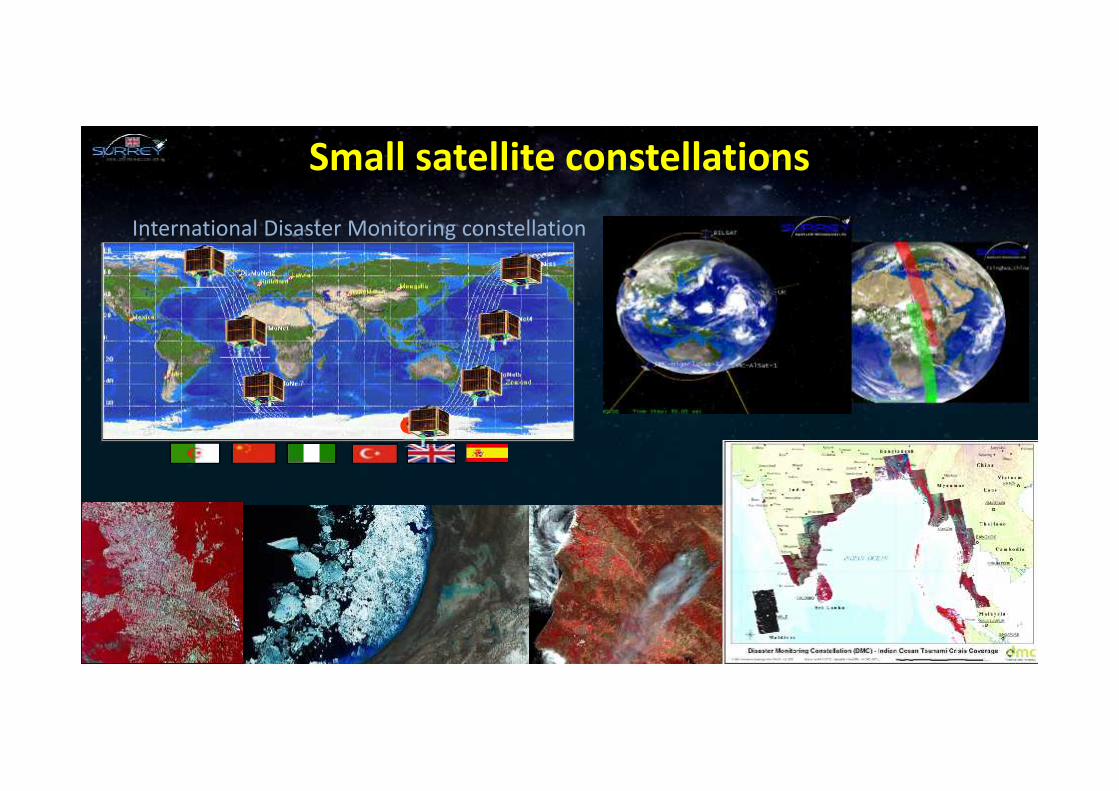

Small satellite constellationsInternational Disaster Monitoring constellation

11

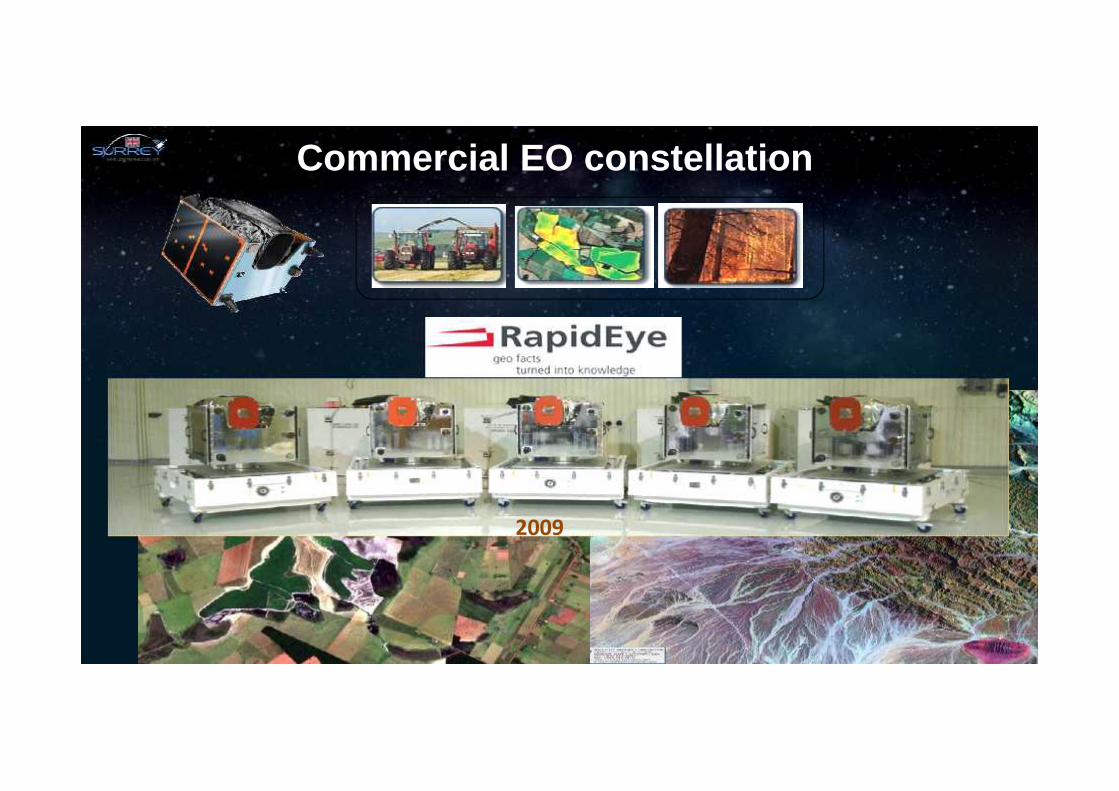

Commercial EO constellation

2009

New EO Business ModelEO ‘capacity leasing’ model (similar to GEO comms)

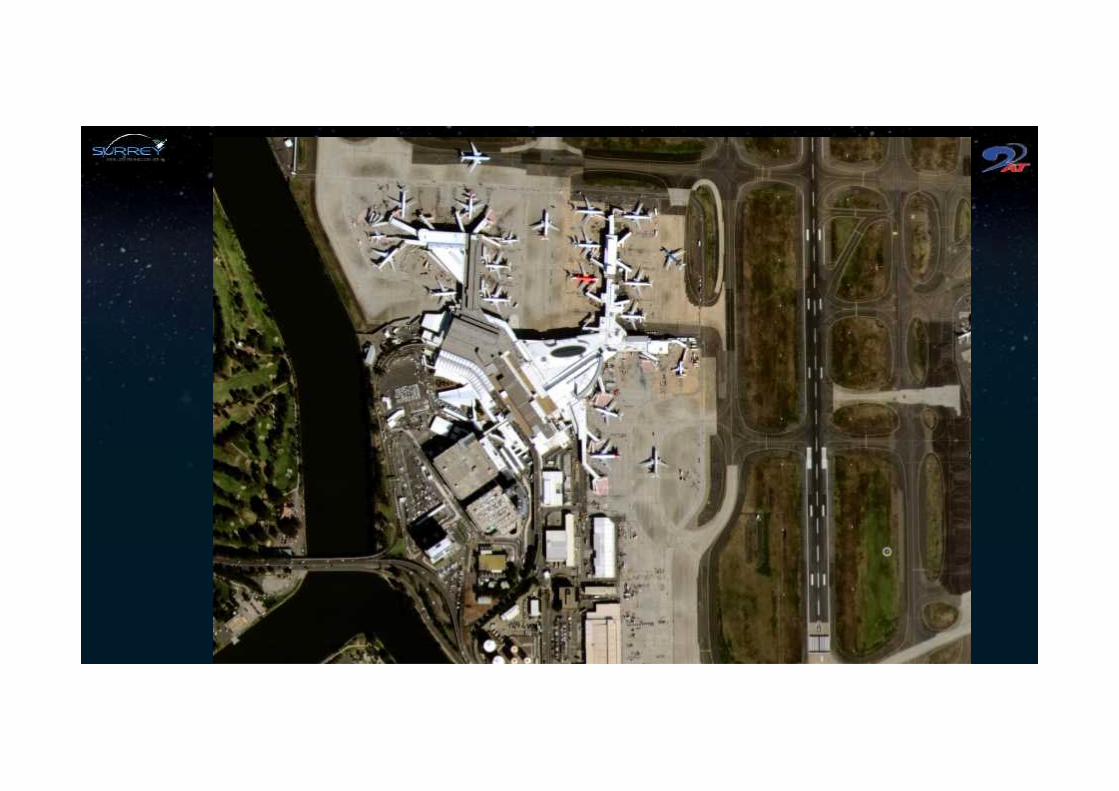

Dedicated constellation (“DMC3/TripleSat”)

High resolution (1m GSD) optical EO

Low cost minisatellites• Launched July 2015• 3 spacecraft• Leased for 7 years• Operational commercial service• Worldwide reach• Daily revisit worldwide

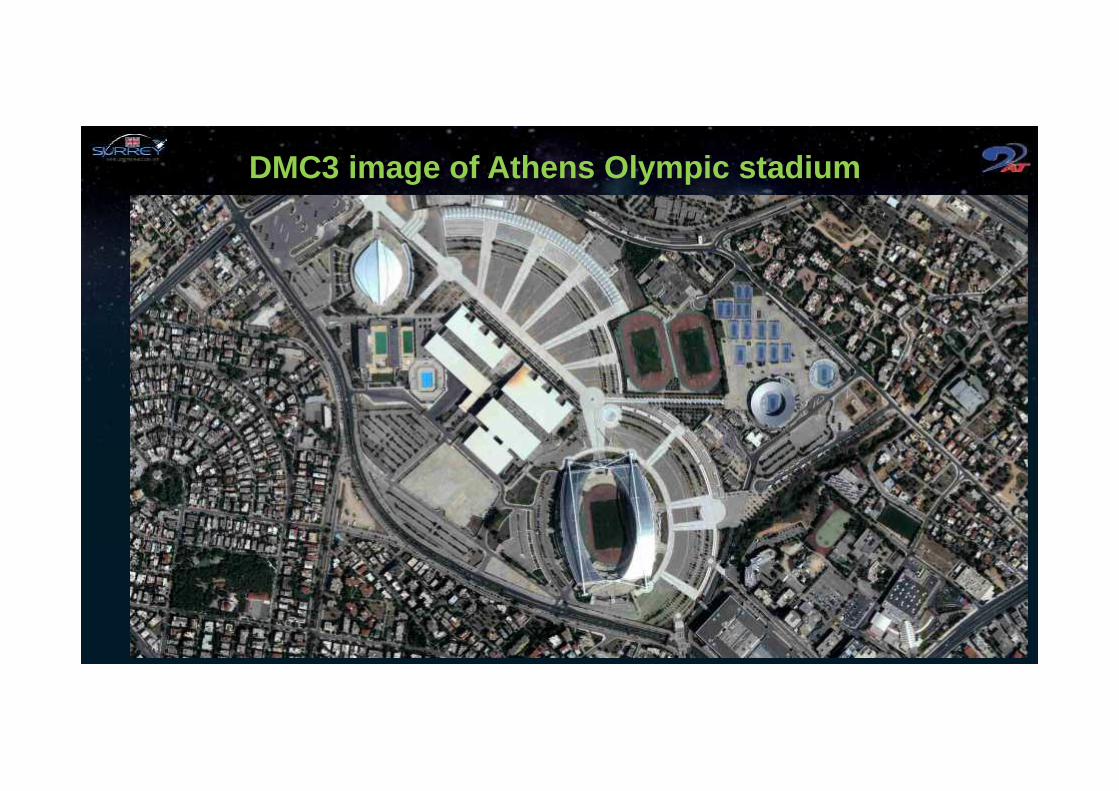

DMC3 image of Athens Olympic stadium

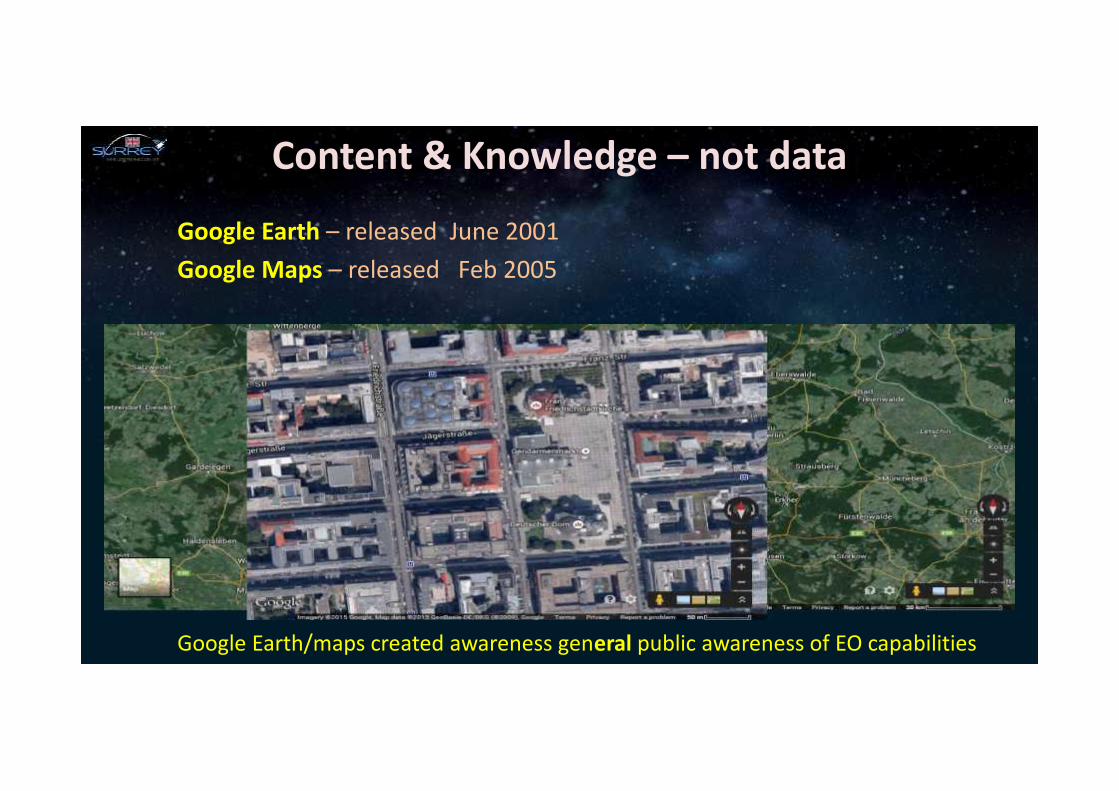

Content & Knowledge – not data

Google Earth – released June 2001Google Maps – released Feb 2005

Google Earth/maps created awareness general public awareness of EO capabilities

From Skybox, Robinson, JACIE presentation

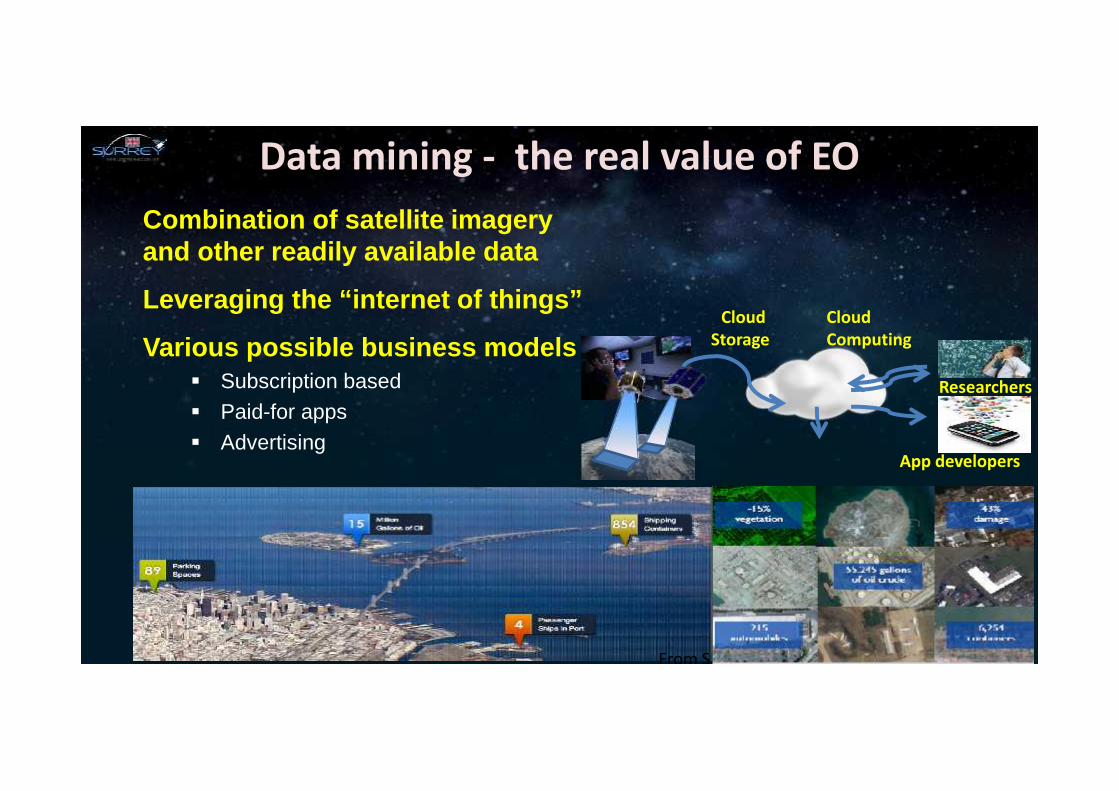

Combination of satellite imageryand other readily available data

Leveraging the “internet of things”

Various possible business models Subscription based Paid-for apps Advertising

Data mining - the real value of EO

App developers

CloudStorage

Researchers

CloudComputing

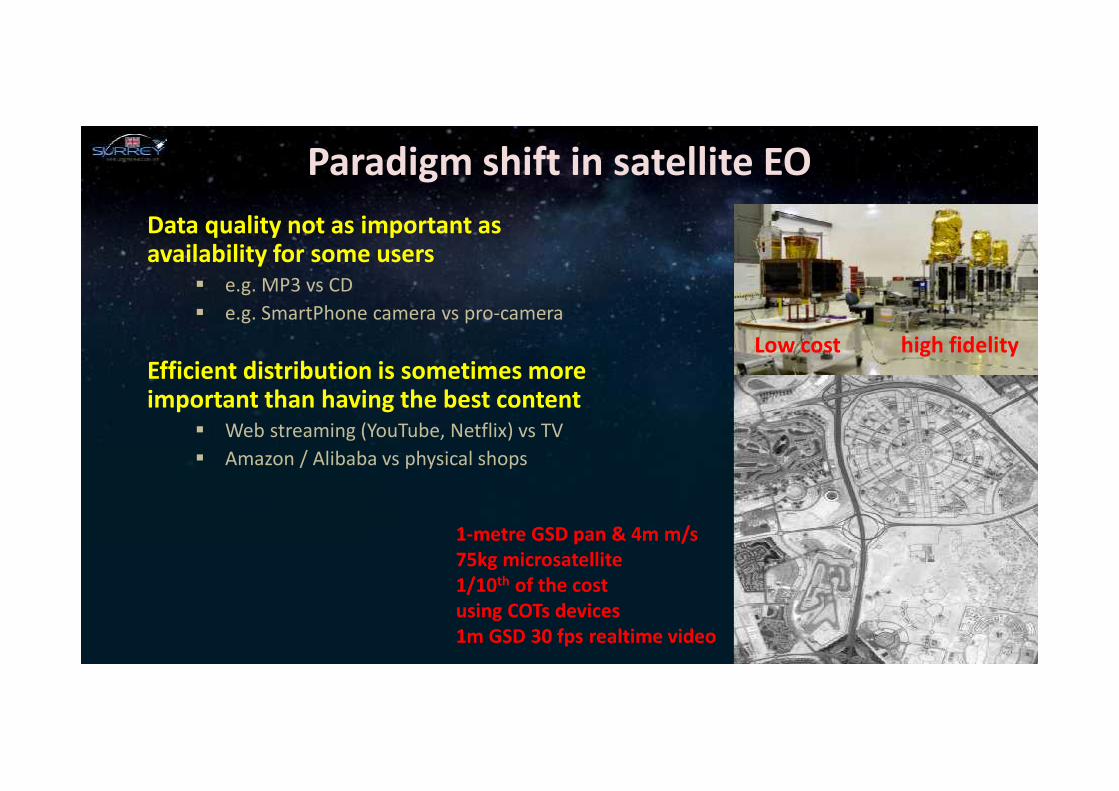

Paradigm shift in satellite EOData quality not as important asavailability for some users

e.g. MP3 vs CD e.g. SmartPhone camera vs pro-camera

Efficient distribution is sometimes moreimportant than having the best content

Web streaming (YouTube, Netflix) vs TV Amazon / Alibaba vs physical shops

Low cost high fidelity

1-metre GSD pan & 4m m/s75kg microsatellite1/10th of the costusing COTs devices1m GSD 30 fps realtime video

A split in the data provision market?

19

• High quality, ultra-high resolution (DigitalGlobe, Airbus CIS, eGEOS, etc.)• Global coverage, multiple bands, free (LandSat, Sentinel)• A few expensive assets

• Best distribution and availability - Immediate access• Acceptable quality, IT business model• Large constellations of cheap assets, high temporal resolution• Addressing largely new markets for EO data

EO data market

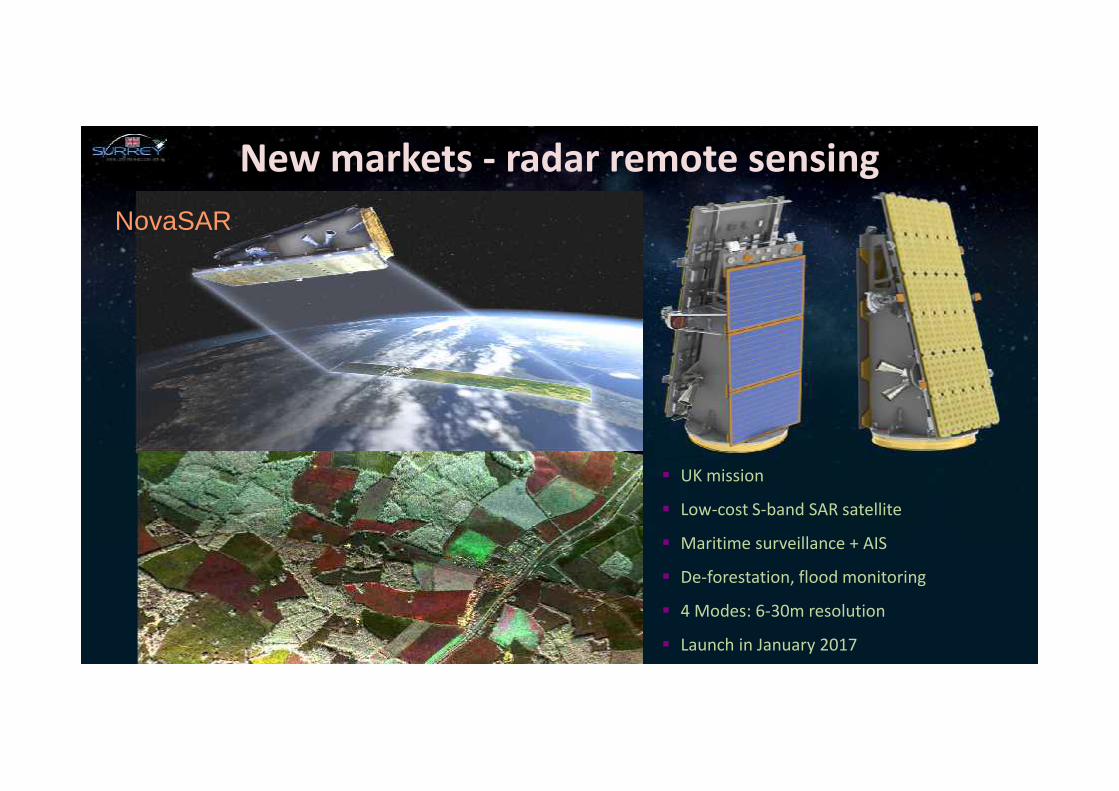

UK mission

Low-cost S-band SAR satellite

Maritime surveillance + AIS

De-forestation, flood monitoring

4 Modes: 6-30m resolution

Launch in January 2017

New markets - radar remote sensingNovaSAR

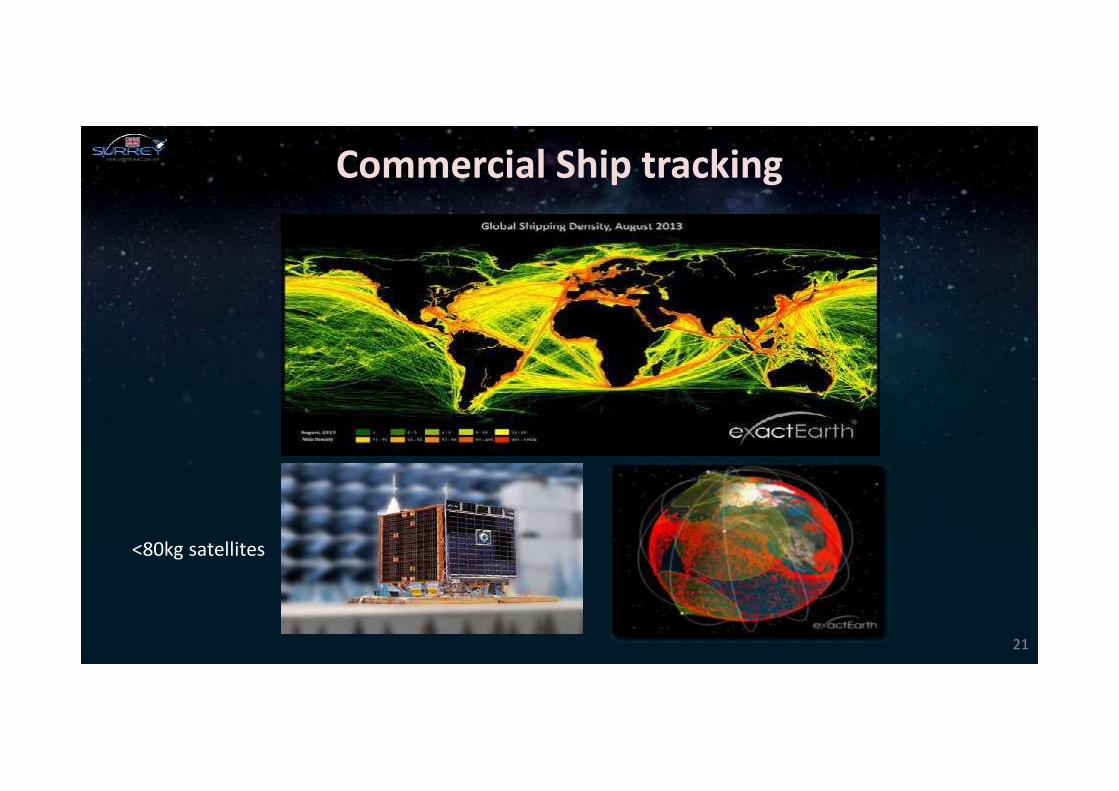

Commercial Ship tracking

21

<80kg satellites

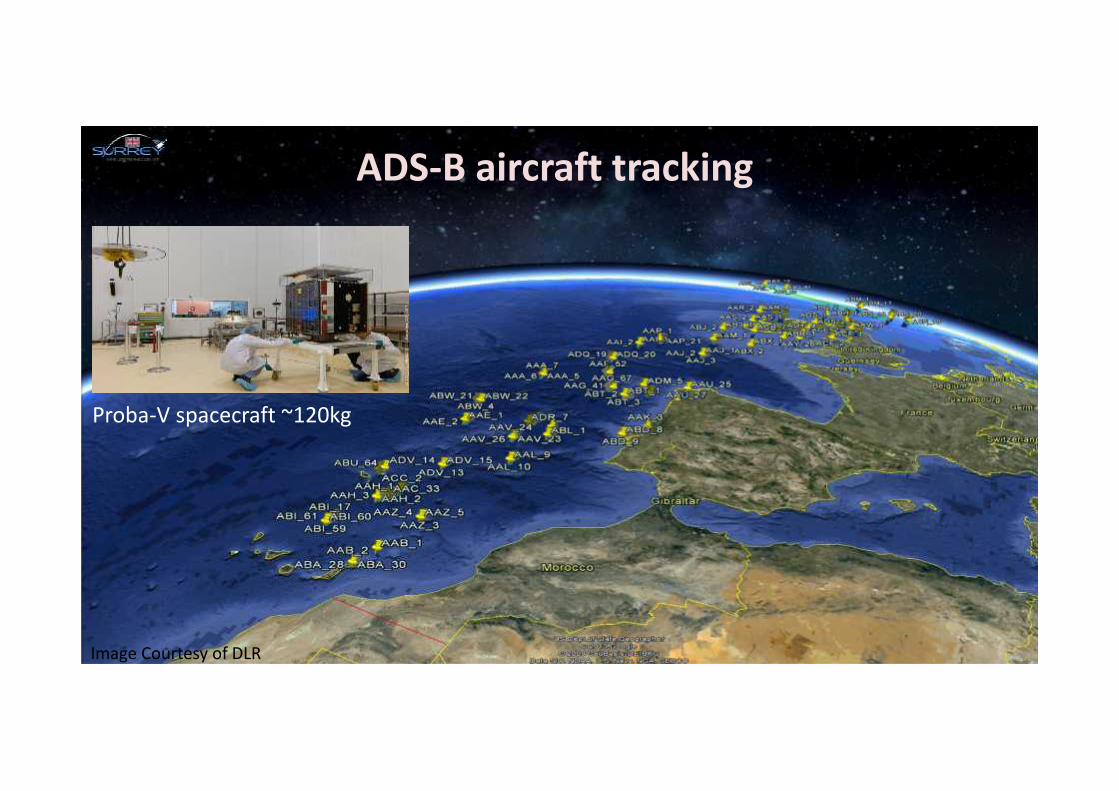

ADS-B aircraft tracking

Proba-V spacecraft ~120kg

Image Courtesy of DLR

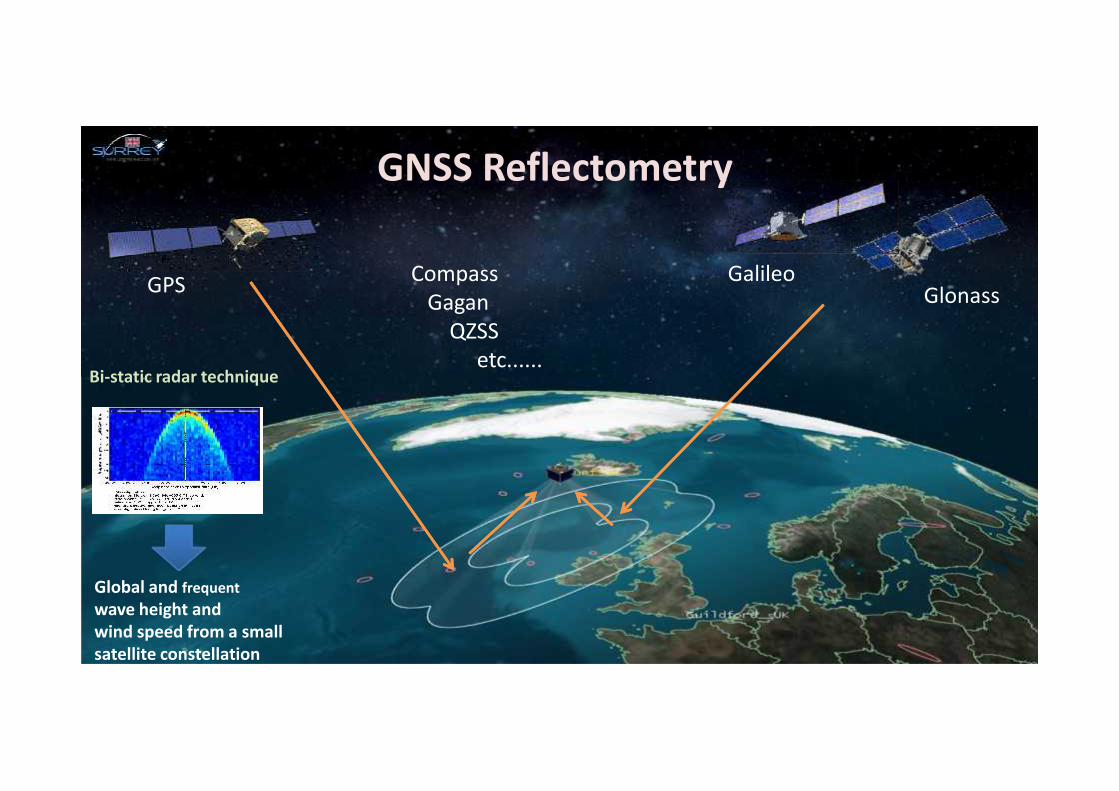

GNSS Reflectometry

23

GPS GlonassGalileoCompass

GaganQZSS

etc......

Global and frequentwave height andwind speed from a smallsatellite constellation

Bi-static radar technique

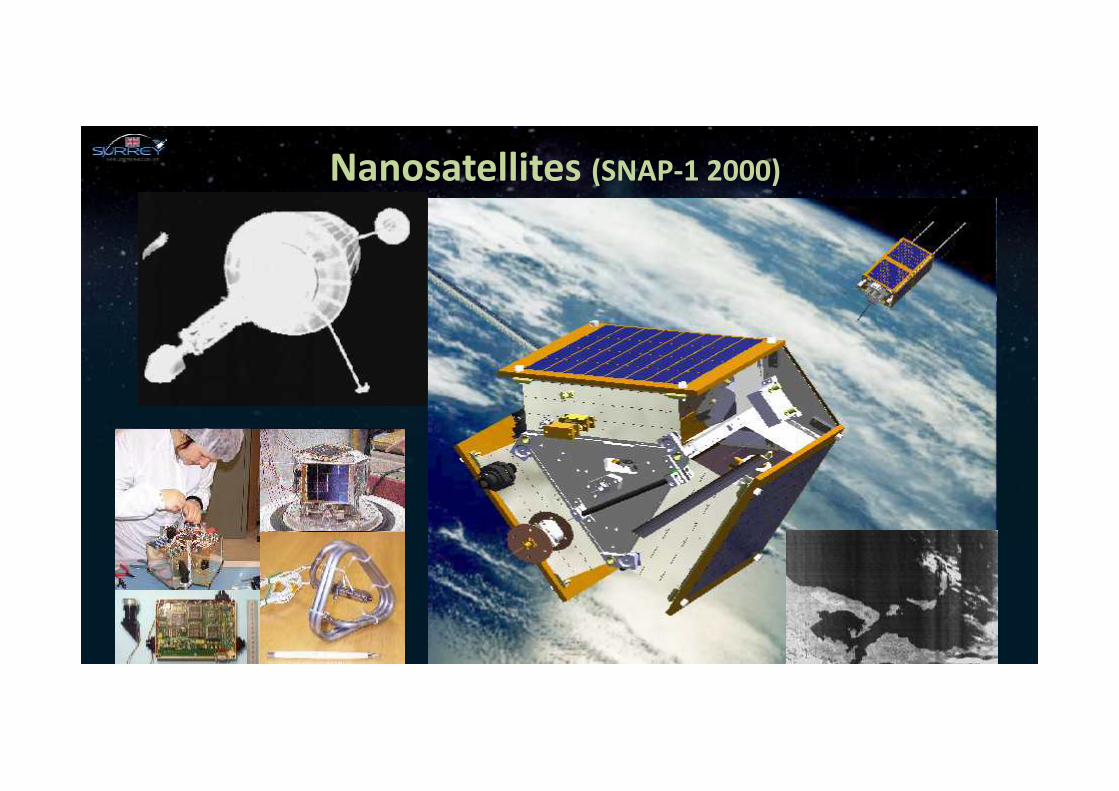

SNAP-1 nanosatelliteNanosatellites (SNAP-1 2000)

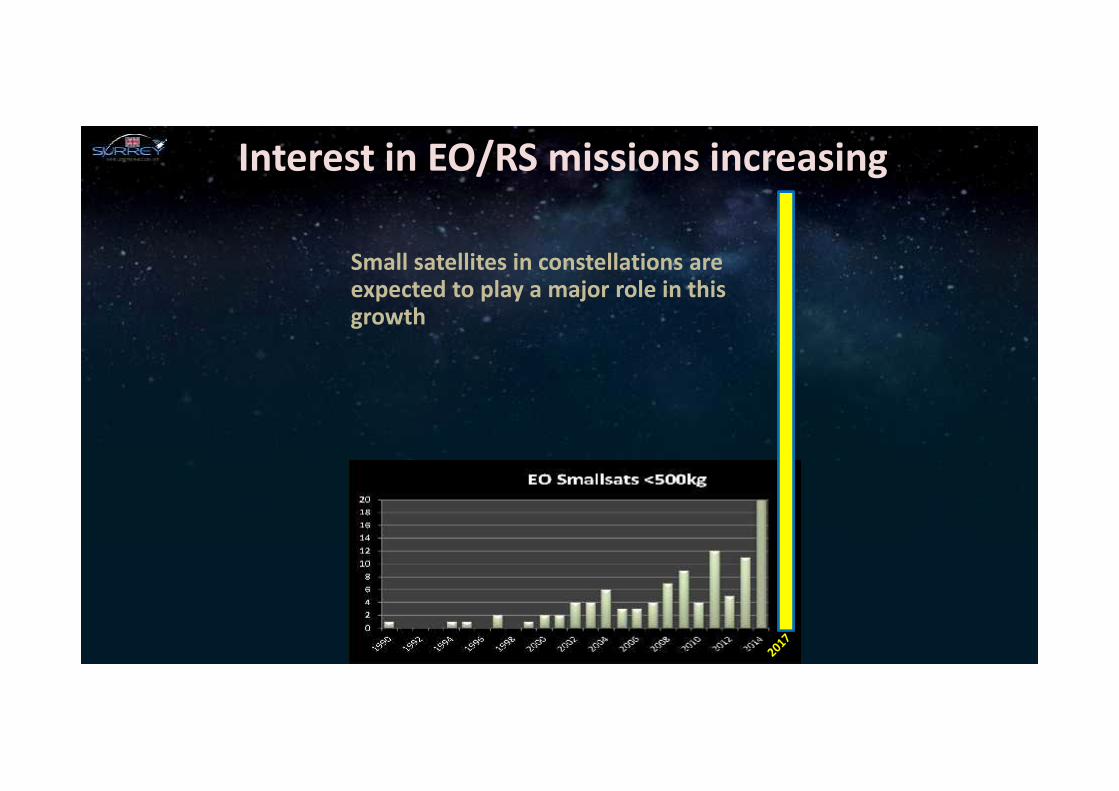

Interest in EO/RS missions increasing

Small satellites in constellations areexpected to play a major role in thisgrowth

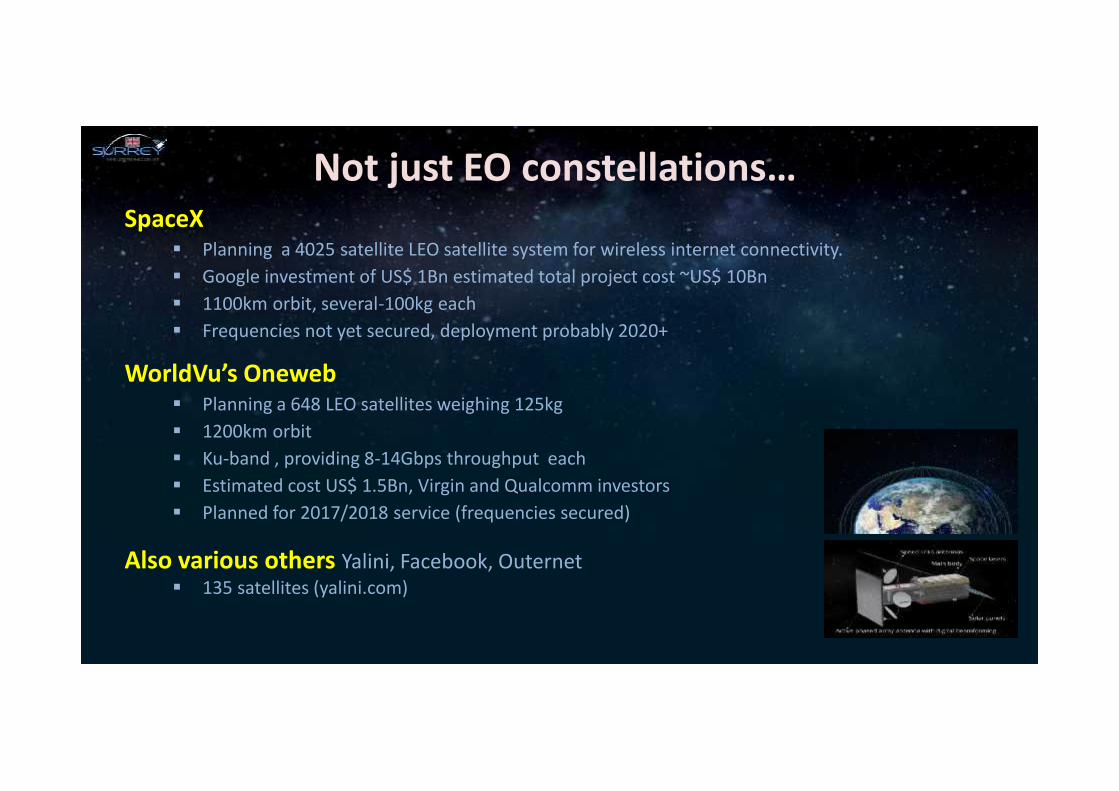

Not just EO constellations…SpaceX

Planning a 4025 satellite LEO satellite system for wireless internet connectivity. Google investment of US$ 1Bn estimated total project cost ~US$ 10Bn 1100km orbit, several-100kg each Frequencies not yet secured, deployment probably 2020+

WorldVu’s Oneweb Planning a 648 LEO satellites weighing 125kg 1200km orbit Ku-band , providing 8-14Gbps throughput each Estimated cost US$ 1.5Bn, Virgin and Qualcomm investors Planned for 2017/2018 service (frequencies secured)

Also various others Yalini, Facebook, Outernet 135 satellites (yalini.com)

GALILEO: Navigation for Europe

GIOVE-A: to secure Europe’s Galileo navigation systemBuilt by SSTL in 30 months, €30M, launched on timeStill operational after 11 years in orbit!

SSTL has designed & delivered the 22 Galileo navigationpayloads for the full operational constellation

0

20

40

60

80

100

120

140

160

180

1970 1975 1980 1985 1990 1995 2000 2005 2010

Nano

Micro

Mini

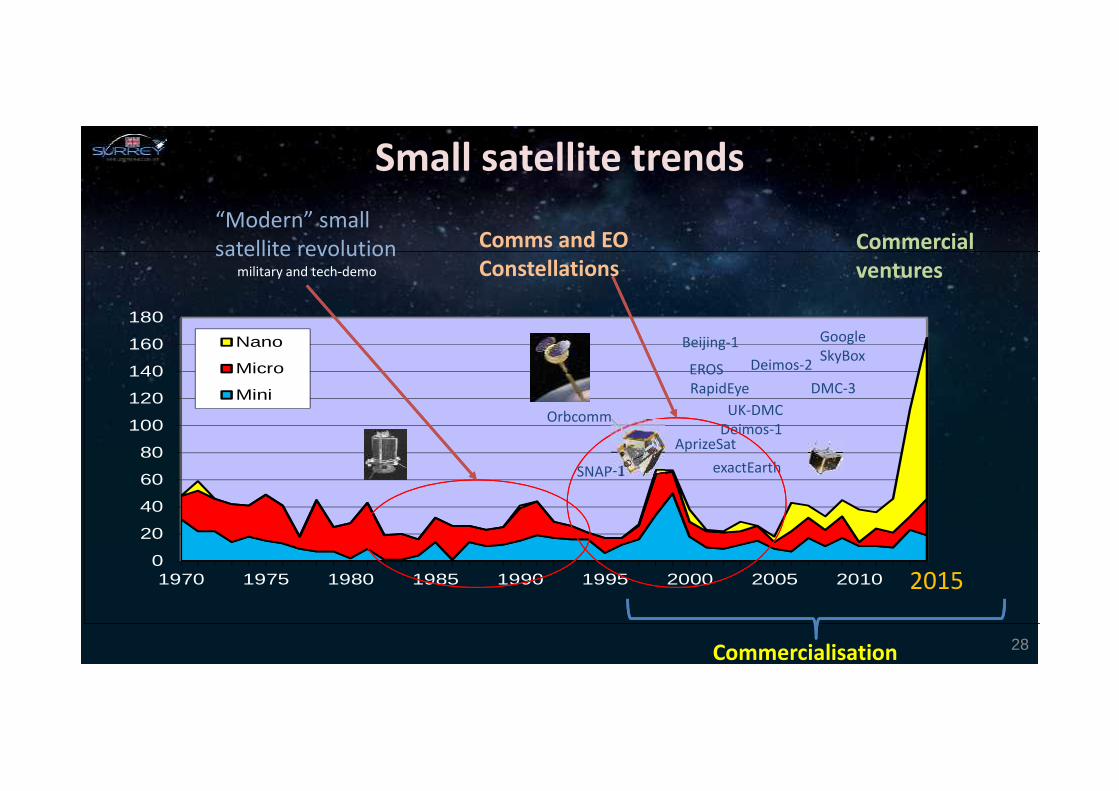

Small satellite trends

28

Commercialventures

Commercialisation

RapidEyeUK-DMC

Deimos-1

Beijing-1

EROS

GoogleSkyBox

exactEarth

DMC-3Deimos-2

Comms and EOConstellations

Orbcomm

AprizeSat

SNAP-1

“Modern” smallsatellite revolution

military and tech-demo

2015

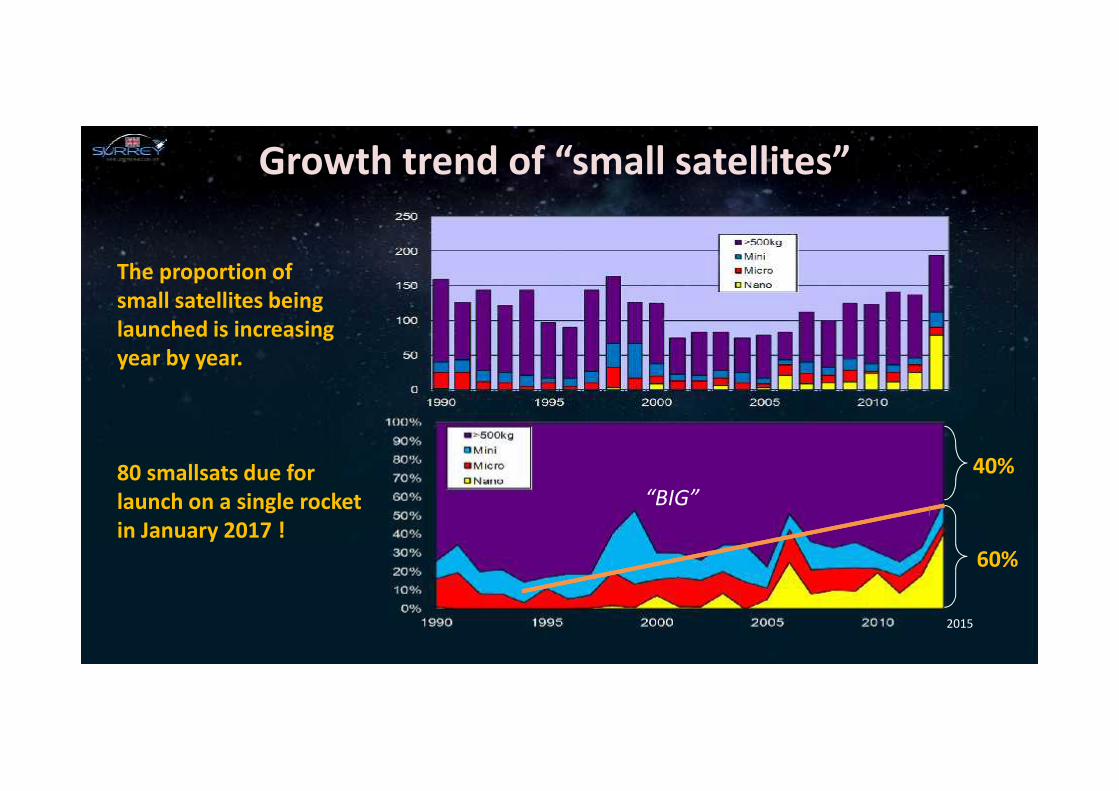

Growth trend of “small satellites”

The proportion ofsmall satellites beinglaunched is increasingyear by year.

80 smallsats due forlaunch on a single rocketin January 2017 !

“BIG”40%

60%

2015

• Gowth in civil government use

• Surge in academic ownership

• Surge in commercial use ofsmallsats

• Decline in security sectorowned smallsats (althoughrecent recovery)

Smallsat customers

0

20

40

60

80

100

120

140

160

180

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Smallsat customer evolution<500kg

University / Academic

Commercial

Government

Security

Amateur / private

Over the last decade

Small satellites stimulating new business

Small satellites are increasingly being used in commercial ventures– Communications (OneWeb, SpaceX, Samsung, Yalini, etc…)– Earth Observation, including meteorology and video– AIS (ships) and soon ADS-B (aircraft)

Many new initiatives leverage– Nanosatellite/CubeSat and Microsatellite technologies– Constellations

Non-traditional (space) business models– Venture capital– IT business models

• High development tempo• Focus on applications and end-users

– Crowd-funding• Ardusat / Nanosatisfy and Skycube satellites launched

A glimpse of the Future ….

In-orbit robotic assemblyof multiple ‘mirror-craft toform large adaptableobservation platforms

… leading to in-orbitmanufacture

SPACE CENTRE

CalTech-JPL

Impending explosion …Numerous constellation proposalsLEO communications & remote sensing1000’s of satellites : nano-, micro- and mini-satellites

New ‘mega-constellations’ would dramatically increase temporal resolutionpersistent observation – continuous communications – IP ad hoc networksLand and maritime monitoring – civil and defence

Key technologies: sat-ground optical links, adaptive antennas‘Big Data’ challenges to extract knowledge from both space & non-space sourcesEconomic launch capacity – critical for success of smallsat business‘free data’ to stimulate applications – but who pays for the satellites?Content will be king

Questions…Safe constellation maintenance (propulsion)

Space traffic control?

Debris mitigation policies? Debris removal – dual use?

What EO data policies are needed in this new era?(e.g. ‘shutter control’ & privacy)

Economic launch capacity – critical for success of smallsat business especially forconstellation replenishment (national launch/space-ports?)

RoI?? Danger of a ‘constellation bubble’ (remember Iridium & GlobalStar)

Space may become dominated by non-state players (e.g. Google et al)

Small satellites: changing the economics of space