Embed Size (px)

Citation preview

University of Nigeria Research Publications

NWAKOBY, Obiora Christopher

Aut

hor

PG/MBA/90/10751

Title

Multinationals in Nigeria: Hedging Against Foreign Exchange and Interest Rate Risk

Facu

lty

Business Administration

Dep

artm

ent

Banking and Finance

Dat

e

October, 1991

Sign

atur

e

.WULTINATIONALS IN NIGERIA : Ilcvlging against foreign cxclmnge and

in tcrcst rate risk.

Subraitted in partial fulfilment of the I ~ I S 1 1 MI1 t DC~PCC in thv

Depur tn~cnt of' Banking and Finance

Ibpartmcnt of Banking and Financv University of Nigeria

Enugu Campus

Nvakoby Obiora Chris topher , a post-graduate student

i n the Departanent of Banking and Finance, University

of Nigeria, with the r e g i s t r a t i o n number PG/MBA/~O/I 0751

has s a t i s f a c t o r i l y completed t he requirements lor t h e

award of Master of Business Administration Degree i n

Banking & Finance.

The work embodied i n t h i s D i s se r t a t i on i s o r i g i n a l and

has no t been submitted before i n p a r t o r full f o r any

diploma o r degree i n t h i s o r any o t h e r un ive rs i ty .

D E D I C A T I O N

This dissertat ion is dedicated to my loving 4

parents

LATE MR. C .A. NWAKOBY

AND

MRS. C. NWAKOBY

ACKNOWLEDGEMENT ----I----------

I am indebted t o my supervisor DR. B.E. Chikeleze f o r h i s

inumerable con t r ibu t ions towards t he success of t h i s research

work. I cannot thank you enough.

My g r a t i t u d e a l s o goes t o a l l the f i nanc i a l executives of I

some of the major Mul t ina t ional Companies f o r the mater ia l s

and information they gave me f o r t h i s work. I r e g r e t not

mentioning t h e i r names ( a t t h e i r r eques t ) .

Many thanks t o my boss, Mr W.N. Ekemezie f o r h i s co-operation T4

3 and understanding and Mrs. ~da - Ibeka who typed t he manu-

s c r i p t f o r a good Job wel l done.

I apprecia te the many he lp fu l comments and suggest ions of

Ogwueleka PeN. Miss and some of my col leagues , M r . 0. Okafor

0suJ i ~ l p h o n s u s , Mojekwu I., ~ w a ~ a C., OsuJi C.S. Miss,

Onuegbu S. Miss, Esiaba M. Miss, Iroh D.N., Obidike A. Miss,

Anieke E., Amadi wokocha and Madueke G. Miss.

I a l s o owe my family, the Nwakobys', a considerable debt

f o r con t r ibu t ing a t d i f f e r e n t l e v e l s of my education. My

spac i a l thanks t o my loving mother, Mrs. Chr i s ty Nwakoby,

meka, Nkiruka, Ifeyinwa, a l l Nwakoby and Mrs. Chinwe

Chukwunenye f o r t h e i r support.

F ina l ly , I thank the Almighty Cod, without whose b less ing

and guidance, t h i s p r o j e c t wouldn't have been a success.

NWAKOBY O.C.

ABSTRACT

N u l t i n a t i o n e l C o m p s n i e s i n . N i g e r i a a r e t h o s e w h o s e

P a r ~ n t b o d i e s a r e a b r o a d . T h e y a r e S u b s i d i a r i e s o f t h e i r

.I C ~ n t r a l O f f i c u s w h i c h a c t a s t h e i r a d m i n i s t r a t i w c . U n i t . They

C o n t r o l m o s t o f t h e V i a b l e L e c t o r s o f t l ~ c E : ig r - r i ?n cconorily.

Tt lc is G r i q i r l d a t e : ; i - ~ c C t o t i i s L o r y .

T ~ I E N i g e r i a n ~ c o n o m y , i n r e c e n t t i m e s , W i t n e s s e d a l o t o f

p e s n t i v e f l u c t u a t i o n s i n i t s f o r e i g n u x c h a n g o r ~ t e t h o u g h t h ~

i n t t ; r e s t r a t u i s p e g g e d a t 2 1 % .

b

The r i s k a s s o c i a t e d w i t h such f l u c t u a t i o n s i n c l u d e

a c c o u ~ t i n g a n d a c o n o m i c r i s k s . when t h e c a s h f l o w e f f e c t o f

a n r j xchanyo l o s s i s a n i rnpodimc!nt t o t h e 0 p r ; r a t i o n s o f thci

f'irfll, s c o n o r r ~ i c r i s k i s o x p a r i e n c e d w t . ~ i l c a c c o u n t i n g r i s k

affect^ c a c h f l o w p r o f e c t j o n s , p r o f i t e ~ d l o s s a c c o u n t a n d

I o rdc . , r t o c:nsuri, t l r a t t h e y d o n o t o n l y b r e a k e v e n o r i a r e p r o f l t a l l e , r r ~ u l t i n a t i o ~ a l C o m p a n i e s e rnploy v a r i o u s

h e d g i n g p o l i c i e s wl~icll i n c l u d e Lxol i i~nyr? p l a n : ~ i n y , f o r w a r d

c ,xc t ranye O u n t r a c t s , s o u r c i n g o f w o r k i r q C a p i t a l f roru

l o w i n t c r c ? s t r a t o Cot . rn t r ic . s , s o u r c i n g o f w o r k i n g C a p i t a l

f r o m t h e C a p i t s 1 m a r k e t , a d j u s t m o n t o f , p r i c a s o f t h e i r

p r o d u c t s t o r e f l e c t t h e p r e s e n t r c ! a l i t i c , , i n t ~ i r n z l c o r ~ t r o l

a n d t e c h n i q u c 2 , p r r , p ~ y r n c ? n t s l e a d i n g & L a g g i n g a n d t h e n a c c e l e v -

a t i o n o f r e m i s s i o n o u t s i d e t h e C o u n t r y whnn t h e y s n n s o t , h a t t h e

m o n e t a r y a u t h o r i t i e s a p p e a r l i k e l y t o i n s t i t u t e e x c h a n g e

r o s t r i c t i o n s .

As f o l s i y n e x c h a n g o r a t e a n d i n t e r e s t r a t e i s d i r e c t l y

a f f a c t c d b y e a c h o t h e r , a l l h e d g i n g p o l i c i a s #jncompal;s a

c o ~ , s i r j c . r a t i o n o f b o t h .

T h e p ~ o j e c t i s d i v i d e d i n t o 5 c h a p t e r s .

C h a p t e r 1 i n t r o d u c u s t h e p r o j e c t . I t s t a t e s wily tile r k s e a r c h

w o r k wos considered i m p o r t a n t t o b e c a r r i e d O I J t , 3 1 1 t l n l o o

Ctlaptc r 2 , reviews a v a i l a b l e l i t c r z t u r c s o n t l i o t o p i c .

I C h a p t e r 3 o x p l a i n s t h e r u s e a r c h m e t h o d o l o g y a d o p t e d .

C l ~ a p t n r 4 t r e a t s r i s k a n a l y s i s . Undr . r t h i s C t i ; ~ ( , t ~ r , t h e

b e h e v i o u r o f f o r e i y n o x c l ~ a n c , e r n t o s a n d i n t n r o s t r ~ t e s was

analysc+d ( T r o n d a n a l y s i s ) .

1 Thb a n a l y s i s C o m p r i s e d of p e r c ~ n t a y e a n a l y s i s a n d 1.; I

m e t h o d o f p r o j e c t i n g a v e r a g e k j U ~ D o l l a r e x c h a n g e r a t e u s i n g

i P a s t r e c o r d s .

# J l ~ u m a i n t h e m of' t h e p r o j e c t w l ~ i c t l i a h e d y i n g a g a i n s t

r i s k was d u e l y s x p l a i n e d .

C h a p t e r 5 c o n c l u d ~ s t h e p r o j e c t a n d Ul f f ea s s u g g e s t i o n s

a n d r e c o m m u n d a t i o n s .

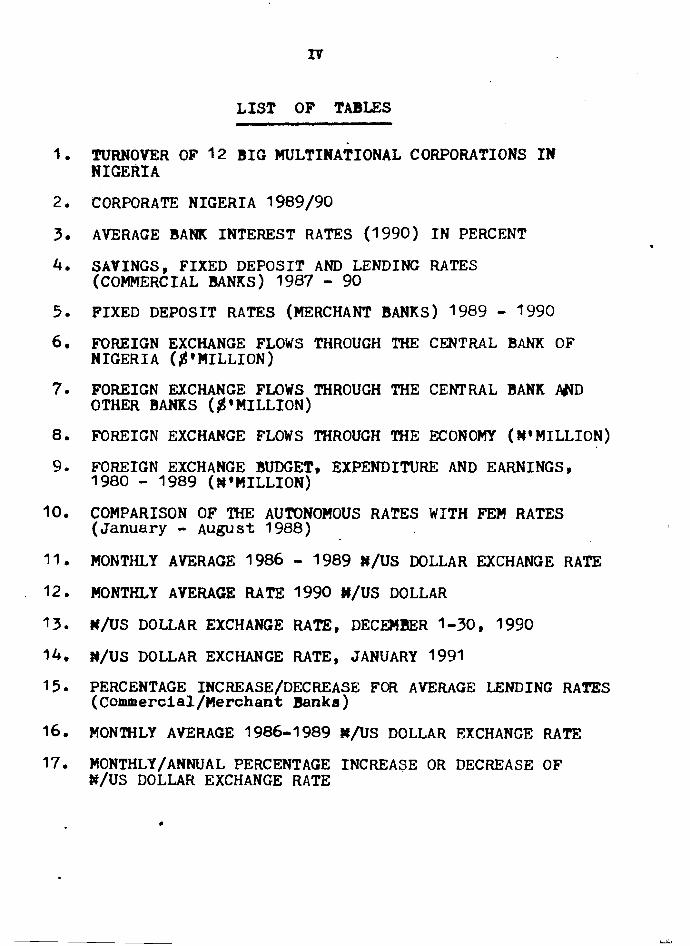

LIST O F TABIBS

TURNOVER OF 12 N I G E R I A

CORPORATE N I G E R I A 1989/90

AVERAGE BANK I N T E R E S T RATES (1990) I N PERCENT

SAVINGS, F I X E D D E P O S I T AND LENDING RATES (COMMERCIAL BANKS) 1987 - 90

F I X E D D E P O S I T RA'FES (MERCHANT BANKS) 1989 - 1990

FOREIGN EXCHANGE FLOWS THROUGH THE CENTRAL BANK O F N I G E R I A (#'WILLION)

FOREIGN EXCHANGE FWWS THROUGH THE CENTRAL BANK W D OTHER BANKS ($'MILLION)

FOREIGN EXCHANGE BUDGET, EXPENDITURE AND EARNINGS, 1980 - 1989 (# 'MILLION)

COMPARISON O F THE AUTONOWOUS RATES WITH FEW RATES (January - ~ u g u s t 1988)

MONTHLY AYERAGE 1986 - 1989 #/US DOLLAR EXCHANGE RATE

MONTHLY AVERAGE RATE 1990 #/US DOLLAR

#/US DOLLAR EXCHANGE RATE, D E C M B E R 1-30, 1990

#/US DOLLAR EXCHANGE RATE, JANUARY 1 991

PERCENTAGE INCREASE/DECREASE FOR AVERAGE LENDING RATES ( ~ o m m e r c i a l / ~ e r c h a n t ~ a n k a )

MQNTHLY AVERAGE 1986-1989 #/US DOLLAR EXCHANGE RATE

MONTHLY/ANNUAL PERCENTAGE INCREASE OR DECREASE O F #/US DOLLAR EXCHANGE RATE

L I S T OF FIGURES -----------------

10 COMMERCIAL BANKS' DISTRIBUTION OF

LOANS AND ADVANCES (w'M)

2 0 DEMAND - SUPPLY OF FOREIGN EXCHANGE B

( J A ~ A R Y - MARCH 1990)

3. 7 990 F'OREICN EXCHAWE BUDGET ALLOCATION

C E R T I F I C A T I O N

DEDICATION

ACKNOWLEWEMENT

L I S T O F TABLES

L I S T O F

CHAPTER 1

INTRODUCTION ... . . . STATEMENT O F THE PROBLEM ... ... O B J E C T I V E O F THE STUDY ... ... S I G N I F I C A N C E AND IMPORTANCE OF THE: STUDY * * * SCOPE O F THE STUDY ... ... CHAPTER 2

LITERATURE REVIEW

THE N I G E R I A N E C O N O ~ I An Appraisal from 1960 to date ... ...

CORPORATE PERFORMANCE ANALYSIS .*. ... I N T E R E S T RATE P O L I C Y AND BE?iAVIOUR BEFORE

AND AFTER DEREGULATION FOREIGN EXCHANGE P O L I C Y AND MONITORING . * . 0 - 0

FOREIGN EXCHANGE CONTROL TOOLS . . . . . . FOREIGN EXCHANGE POLICY AND CONTROL UNDER THE STRUCTURAL ADJUSTMENT PROGRAMME (SAP ) . . . FOREIGN EXCHANGE CONSERVATION I N N I G E R I A ...

RESEARCH METHODOLOCIY

RESEARCH APPROACH SOURCES O F DATE 3.2.1 P r i m a r y source8 3.2.2 secondary aources DATA ANALYSIS METHOD

CHAPTER 4 RISK ANALYSIS

R I S K STRUCTURE ... . . . 4.1.1 mreign mchange and In teres t

4.1.2 C a u s e s of Exposurea ... ... 65

4.2 TREND ANALYSIS ... ... 67 4.2.1 DfB-Znc percantage ~nalysis . . . . . . 4.2.2 ProJected Average ##/US

Dollar Exchange Rate For 1991 . . . 73 4.3 HEWING POLICIES AGAINST RISK . a . . a . 77

4.3.1 Calculating c o s t of Hedging . ... 83

CHAPTER 5

5.1 C O N C L U S I O N e e e ..a 86 5.2 SUGOESTIONS AND RECOMMENDATIONS e e * a*. 92

NOTES . . . . . . 97 BIBLIGRAPHY ... . . . 99

CHAPTER I

1 ' I N T R O D U C T I O N

~ l t h o u g h t h e r e i s no g e n e r a l l y a c c e p t a b l e d e f i n i t i o n

of m u l t i n a t i o n a l companies, it i s however d l s t i n g u i -

s h a b l e from o t h e r companies i n terms of d i r e c t i n v e s t -

ment abroad and d i r e c t i n t e r e s t i n t h e bus iness envi-

ronment i n which it has such inves tments , i L,y-

Eehrman (1969) m i d t h u t the hal lmark of a m u l t i n a t i o n a l ,?' , '! c o r p o r a t i o n a r e c o n t r o l and i n t e g r a t i o n o f a f f i l i a t e s . j

M u l t i n a t i o n a l s has i t s r o o t s f a r back i n h i s t o r y . b

M u l t i n a t i o n a l s d i d n o t grow i n a vacuum. They f l o u -

r i s h e d becvuse alter world wur 11, the m&Jur' d a v a l u y a d . I /

/

countries l e d by U,g, s a t a b l i s h e d a framework f o r t h e

world economy t h a t encouraged t h e free flow of goods

and p r i v a t e c a p i t a l between c o u n t r i e s on market 2 p r i n c ' l p l e s ,

The f a c t o r s t h v t were in s t rumen ta l i n spark ing t h e

r a p i d e v o l u t i o n o f m u l t i n a t i o n a l c o r p o r a t i o n s a r e i n

3 p a r t environmental and i n p a r t "managerialn . The rBT"ctor8 t h a t induced firms t o s e t up f a c i l i t i e s

f o r manufacturing and marketing abroad a r e t h e

a t t r a c t i o n o f a growl% market, t h e s t imu lus of

government restrictions on d i r e c t t r a d e , encouragement

by t h e go$crment of t h e h o s t n a t i o n and managerial

a s p e c t s o f t h e f i r m and t h e i n d u s t r y group which i t

i s a member. Whether l a r g e o r sma l l , m u l t i n a t i o n a l

c o r p o r a t i o n s a r e open t o a s s o r t e d c r i t i c i s m a from a

v a r i e t y of q u a r t e r a . Notably amongst them a r e t h e

e x p l o i t a t i o n of people and r e s o u r c e s and t h e e x e r c i s e

of enormous p o l i t i c a l i n f l u e n c e t h a t p l a c e s t h e

m u l t i n a t i o n a l s beyond t h e c o n t r o l of n a t i o n - s t a t e s .

There i s a g e n e r a l f e e l i n g now t h a t a s e t of i n t e r - J

,4 n a t i o n a l g u i d e l i n e s endorsed by t h e United Nat ions , I I

I n a t i o n a l governments and t h e m u l t i n a t i o n a l s themselves !?

b ;: i s a b s o l u t e l y e s s e n t i a l t o l a y a founda t ion f o r $

4 llgoodn world c o r p o r a t e c i t i z e n s h i p . I n t h e i n t e r n a t i o n a l a r ena , where cur rency e x c h a n ~ e

occu r s between c o u n t r i e s , as a r e s u l t of o p e r a t i o n s of

m u l t i n a t i o n a l s , a n a t i o n a l monetary u n i t h a s no l e ~ a l

t ende r . T ransac t ions by m u l t i n a t i o n a l s can only be

auhieved through t h e convers ion o f one cur rency i n t o

a n o t h e r , and t h i s p r o c e s s is c a l l e d f o r e i g n exchange,

The market i n which c l a ims t o f o r e i g n c u r r e n c i e s a r e

bought and s o l d i n terms of domestic money i s known

as t h e f o r e i g n exchange market.

The b a s i c f u n c t i o n o f t h e f o r e i g n exchange market i s

t o t r a n e r a r purchas ina power from one n a t i o n t o another .

This i s dona through v a r i o u s f o r e i g n exchange bankers

and t h e fo'reign exchange depar tments of commercial p

banks who buy and s e l l f o r e i g n exchange.

Foreign exchange ea rn ings from i n t e r n a t i o n a l t r a d e

t r a n s a c t i o n s and e x t e r n a l a i d a r e v i t a l f o r t h e

economic t r ans fo rma t ion of less-developed c o u n t r i e s

of which Niger ia i s one.

According t o 030 (1990). between 1960 and 1985,

Niger ia went through varying development experience

which r equ i red prudent management of a v a i l a b l e f o r e i g n i

exchange resources . Inadequate f o r e i g n exchange was I

i' a na3or c o n s t r a i n t i n t h e execut ion of t h e f i rs t

8

National development p lan , 1962 - 1968, a s i t u a t i o n

t h a t wa6 accentua ted by t h e prosecut ion of t h e c i v i l

war between J u l y 1967 and January 1970. The per iod

1970 - 1980 witnessed a dramatic improvement i n

~ i g e r i a ' s f o r e i g n exchange p b s i t i o n fol lowing t h e

. s u b s t a n t i a l i n c r e a s e s i n crude o i l p r i c e s i n 1973-74

and 1979.

Following the c o l l a p s e of t h e world o i l market i n

the e a r l y 1980as , N i ~ e r i a once more en tered a very , f \ , i!

t i g h t f o r e i g n exchanae p o s i t i o n e s p e c i a l l y i n t h e \ P,,

i!: c o n t e x t of prev ious commitaents. Despi te t h e f a c t

t h a t f o r e i g n exchange management s i n c e 1986 has I,\

'1% I

responded adequately t o the needs of t h e economy, it \ ,

has r a i s e d s e v e r a l i s s u e s which t h e des ign of f u t u r e I 1 \

n a t i o n a l development s t r a t e g i e s must t a k e i n t o account.

Forolgn exuhange may t h e r e f o r e be d e f i n e d aa t h e

monetary a s s e t used f o r t h e s e t t l e m e n t o f c u r r e n t

i n t e r n a t i o n a l t r a n s a c t i o n s and f o r f i n a n c i n g

i n b a l a n c e s i n a c o u n t r y ' s e x t e r n a l payments p o s i t i o n

vis-a-via o t h e r c o u n t r i e s . The main sou rces of

f o r e i g n exchange t o a count ry i n c l u d e f o r e i g n cur rency

r e c e i p t s from t h e e x p o r t s of goods and s e r v i c e s , in f low

of f o r e i g n c a p i t a l such as l o a n s and investments, a s

. w e l l a a g r a n t s o r g i f t s which r e p r e s e n t u n i l a t e r a l b

t r a n s f e r s . Foreign exchange, based on t h e above, can

be de f ined as a component o f a c o u n t r y ' s o f f i c i a l

e x t e r n a l r e s e r v e s which may be de f ined a s t h e t o t a l

s t o c k of e x t e r n a l assets which are a v a i l a b l e t o t h e

monetqry a u t h o r i t i e s of a count ry f o r t h e s e t t l e m e n t

of i n t e r n a t i o n a l economic t r a n s a c t i o n s .

M u l t i n a t i o n a l s can r a i s e money i n t e r n a l l y ( i e w i t h i n

t h e coun t ry ) f o r t h e i r o p e r a t i o n s . This i s done wi th

a good a n a l y s i s o f i n t e r e s t r a t e s .

I n t e r e s t r a t s the world over i s t h e p r i c e of c a p i t a l

and c o n s t i t u t e e a r e t u r n on c a p i t a l f o r t h e l e n d e r o r

i n c l u d i n g t h e r e d u c t i o n of i n f l a t i o n , promotion of

o a p i t a l f lows and discouragement o f c a p i t a l f l i g h t .

- 5 -

With the d e r e g u l a t i o n of i n t e r e s t r a t e s and t h e

a t t e n d a n t compet i t ion on r a t e a pa id f o r d e p o s i t s , banks

can now o f f e r any r a t e s t o t h e i r customers wi th in t h e

range p resc r ibed by t h e Cen t ra l Bank of Niger ia . This

freedom could l ead t o i n c r e a s e i n t h e c o s t g f funds i n

t h e economy.

Thie r e sea rch t h e r e f o r e i s conducted with t h e view t o

o u t l i n i n g some of t h e b a s i c r i s k s a s s o c i a t e d with

f o r e i g n exchange and i n t e r e s t r a t e s and a l s o determining b

how they a re conta ined by t h e m u l t i n a t i o n a l s with

bus iness i n t e r e s t s i n Nigeria.

STATEMENT OF THE PROBLEM

M u l t i n a t i o n a l s i n N ige r i a as' a l r e a d y de f ined can be

simply p u t as a l l bus ines s concerns o p e r a t i n g i n

Niger ia whose o p e r a t i o n s c u t s a c c r o s s o t h e r n a t i o n s .

Whether t h e i r headqua r t e r s a r e s i t u a t e d i n Ni$er la o r

n o t , does n o t debare them from f a c i n g t h e r e a l i t i e s of

t h e i r cognate environment which i s Niger ia .

For e f f i c i e n t o p e r a t i o n , they must procure f o r e i g n

exchange ( t h a t is exchanging n a i r a wi th i t s equ iva len t 4

of o t h e r f o r e i g n c u r r e n c i e s ) . This f o r e i g n cur rency ,

s o procured, i s normally used i n impor t a t ion o r expor-

t a t i o n a c t i v i t i e s . There a r e i n h e r e n t problems i n

procur ing f o r e i g n exchange i n Niger ia . Most s i g n i f i -

Gent amongst others arc

( a ) t h e l i m i t e d amount made a v a i l a b l e t o

banks through FEM ( f o r e i g n exchange

marke t ) ,

( b ) cumbersome procedures towards procure

ment and

( c ) f l u c t u a t i o n s ( t h a t i s i n c r e a s e o r

dec rease i n va lue ) which is normally

caused by market f o r c e s o f demand and

supply, i n f l u e n c e of i n t e r n a t i o n a l

c r e d i t o r g a n i s a t i o n s l i k e P a r i s c l u b ,

World Bank, IMF e t c and t h e deva lua t ion

of the l o c a l currency ( n a i r a ) through

t h e i n t r o d u c t i o n o f .FEM.

Another f a c t o r t h a t a f f e c t s t h e o p e r ~ t i o n of mult ina-

t i o n a l s i n Niger ia i s i n t e r e s t r a t e . Thia f a encoun-

t e r e d when they seek f o r c r e d i t s from banks. I n t e r e s t

r a t e which i s t h e r a t e of i n t e r e s t charged by bunks on

va r ioua money market i n s t rumen t s and f o r g iv ing o u t

l o a n s t o i t s customers , of which m u l t i n a t i o n a l s a r e

a major p a r t , i s normally in f luenced by r e g u l a r govern-

ment monetary and f i s c a l p o l i c i e s and market forces of

demand and supply.

To g rapp le wi th a l l t h e s e problems i s no mean f e a t .

The q u e s t i o n s t h a t r e a d i l y come t o mind a r e t h e

followin&:-

i ) how do m u l t i n o t i o n ~ l s o p e r a t i n g

i n Niger ia hedge o r gu ide a g a i n s t

t h e s e problems o u t l i n e d ?

i i ) how does t h e i r s o l u t i o n package o r

p o l i c i e s look l i k e ?

i i i ) what a r e the coun te r s from t h e

c o u n t r i e e apex f i n a n c i a l l n o t l t u t i o n

t o ensure that t h e economy o f t h e

country i s n o t adverse ly a f f e c t e d ? #

i v ) why must t h e government a l low t h e s e

r a t e s t o be determined by t h e f o r c e s

of demand and supply knowing q u i t e

w e l l t h a t the countries f inanc ia l

markets are not f u l l y matured and

developed?

The d e c i s i o n t o embark on a study o f t h i s nature,

therefore, was borne out o f the need t o f i n d out how

mult inationals i n Nigeria operate prof i tably under t h e

environment of these problems outlined above.

- 9 -

1.3 pBJF,CTIVE OF THE STUDY

The a c t i v i t i e s o f m u l t i n a t i o n a l s a f f e c t t h e s t a t e of

t h e Niger ian economy,

For t h e economy t o be on a sound f o o t i n g , t h e a c t i v i t i e s

of t h e s e m u l t i n a t i o n a l s should be c a r e f u l l y monitored

and t h e government propound and en fo rce p o l i c i e s t o com-

plement t h e aforementioned.

The o b j s c t i v t ~ of t h i s s tudy i s t o probe and f i n d o u t

t h e d i f f e r e n t convent iona l and Mnconventional p o l i c i e s

employed by m u l t i n a t i o n a l e o p e r a t i n g i n Niger ia i nb

checking f o r e i g n exchange and i n t e r e s t r a t e r i s k s . I t

i s meant t o a c t as a gu ide t o t h e enab l ing f i n a n c i a l /

economic a u t h o r i t i e s i n Nigekia i n de te rmin ing t h e

R ~ ~ U C ~ U I - ~ untl cor;tr*ntn of the Bronc? t . t~ry b i r r ( ! t ' i n c e l

p o l i c i e s .

The c o n t e n t s of t h i s p r o j e c t w i l l , no doubt , h e l p any

member o f t h e Nigeria s o c i e t y who i s i n t e r e s t e d i n t h e

economic w e l l being of t h e count ry .

- 10 - 1.4 SICNLFICANCE AND IMPORTANCE OF THE STUDY

The m u l t i n a t i o n a l s ope ra t ing i n Niger ia , t h e C e n t r a l

Bank of Niger ia and o t h e r i n d i v i d u a l s who a r e i n t e r e s t e d

i n t h e we l f a re of t h e Niger ian economy need t o have a

good knowledge of t h e behaviour o r f l u c t u a t i o n s of

t h e v a l u e of n a i r a i n r e l a t i o n t o f o r e i g n c u r r e n c i e s

and i n t e r e s t r a t e s . The r i s k of such f l u c t u a t i o n s being

The knowledge w i l l h e l p them determine t h e s t r u c t u r e

of t h e bus ines s environment a v a i l a b l e t o them and de

a b l e t o f o r e c a s t f u t u r e cond i t ions . Good bus iness i s

t h e a b i l i t y t o make p r o f i t and s u s t a i n t h e l i f e of t h e

company. One can only ach ieve t h i s through a proper

knowledge of interest r a t e and fopeign exchange

behaviours.

This s tudy , t h e r e f o r e , w i l l p rov ide t h e r equ i r ed

knowledge of p a s t t r e n d s , and f u t u r e f o r e c a s t of

f o r e i g n exchange and i n t e r e s t r a t e va lues v i s -a -v is

m u l t i n a t i o n a l s ope ra t ing i n Niger ia . I t i s meant t o

i d e n t i f y obvious gaps i n the knowledge of f o r e i g n

exchange and i n t e r e s t r a t e a n a l y s i s .

The c o n t e n t of t h e s tudy i s meant t o g i v e a n up-to-date

knowledge i n t r end a n a l y s i s and f o r e c a s t i n g f u t u r e

op t ions . me methodology employed i s s c i e n t i f i c and

g i v e s a q u a n t i t a t i v e a n a l y s i s of the s u b j e c t m a t t e r

t o t h e b e n e f i t of t h e reader .

This s tudy is t h e r e f o r e of immense importance o r

va lue t o multinationals ope ra t ing i n Niber ia , t he

C e n t r a l Bank of Niger ia , Researchers i n t h e f i e l d of

f i n a n c i a l a n a l y s i s , p r a c t i t i o n e r s and p r o f e s s i o n a l s

and persons o r e n t i t i e s who a r e i n t e r e s t e d i n t h e f i e l d

of f inance .

It w i l l a s s i s t t h e m u l t i n a t i o n a l s i n r e g u l a t i n g t h e i r

bus iness , t h a t is knowing when t o ope ra t e i n a c e r t a i n

way o r t a k e c e r t a i n dec i s ions , be i t s t r a t e g i c o r

otherwise. The func t ions namely, planning, organiging,

d i r e c t i n g and c o n t r o l l i n g by t h e o rgan i sa t iona w i l l be

made more e a s i e r and meaningful.

The Cen t ra l Bank of Niger ia , as a banker t o banks

(commercial banks, merchant banks and f inance houses) ,

wi th t h e h e l p of t h i s r e sea rch work w i l l know how, when

and which types of r e g u l a t o r y laws t o i s s u e t o banks

and f inance houses, a l though it is widely bel ieved t h a t

f inance houses a r e n o t f u l l y r egu la t ed comparatively

with t h e i r c o u n t e r p a r t s i n t h e banking business . With

this s tudy , t h e CBN w i l l a l s o determine how t o r e g u l a t e

t h e f i n a n c i a l involvements of a l l m u l t i n a t i o n a l s i n

Niger ia with a view t o '!Short C i r c u i t i n g " t h e i r ou t l ined

hrd6in6 p o l i c i e s . R ~ s e a r c h e r s w i l l f i n d t h i s a s a base

f o r continued assessment and f u r t h e r r e sea rch on t h e

The value of the inves t iga t ion t o profess ionals ,

prac t i t ioners and persons or corporate bodies cannot

be over-emphasised.

A knowledge o f the f a c t that indiv iduals , profess ionals

or prac t i t ioners are involved i n the operation of these

mult inationals , CBN and banka throws more l i g h t in to

the envisaged importance o f t h i s study.

- 13 - 1 .5 SCOPE OF THE STUDY

I n under-going t h i s s tudy , s p e c i a l e f f o r t wae made t o

cove r t h e a c t i v i t i e s o f m u l t i n a t i o n a l s o p e r a t i n g i n the

fo l lowing s e c t o r s of the Niger ian economy. The companys I I

were n o t quoted d i r e c t l y i n the s tudy because t h a t was ,

t h e bases f o r a l lowing one have a n i n s i g h t i n t o t h e i r ,/

b) Pharmaceut ica l s b

,

c ) Petroleum

These a r e a s were chosen because of t h e i n h e r e n t u se of

f o r e i g n c u r r e n c i e s i n t h e conduct o f t h e i r bus iness .

They e i t h e r manufacture, impopt o r e x p o r t p roduc ts from

NiBeria.

Emphasise waa made i n i n v e s t i ~ a t i n g i n t o t h e produc ts

t hey d e a l on, p r i c e of such p roduc t s , p l a n t s i t e and

c a p a c i t y u t i l i s a t i o n , and t h e promotional mix they employ.

A n a n a l y s i s of t h e r i s k which they a r e exposed t o i n

t e r n s of f o r e i g n exchange procurement and i n t e r e s t r a t e

was made. I n a n a l y s i n g f o r e i g n exchange r i s k s , t h e

scope was reduced t o n a i r a i n r e l a t i o n t o US d o l l a r s

which i s the maJor i n t e r n a t i o n a l l y accepted and u n i v e r s a l

cur rency i n c i r c u l a t i o n , a l s o i t w i l l be remembered t h a t

most m u l t i n a t i o n a l s o p e r a t i n g i n Niger ia a r e Americans.

f n t e r e a t ra t s a n a l y s i s c o n s i s t e d of a l l r e l e v a n t

money m a r k e t rates.

The branches of t hose companies covered a re s i t u a t e d

i n Lagos ( L Q ~ o s s t a t e ) , Aba ( ~ b i a s t a t e ) and P o r t

Harcourt (R ive r s s t a t e ) . I n v e s t i g a t i o n was concentra&d

i n Lr8oa b e l n g tilo u r e u where ttle Heud Of f 1 ( cr l -

Corporate headqua r t e r s of most o f them a r e s i t u a t e d .

During i n v e s t i g a t i o n s , persona l i n t e r v i e w s and

p h y s i c a l i n s p e c t i o n of documents were done through h e l p b

of f i n a n c e and marketing managers and accountan ts .

In format ions g o t d u r i n g i n v e a t i g a t i o n s i n c l u d e

o p e r a t i o n a l b r i e f s and d i f f e r e n t hedging p o l i c i e s they

employ i n running t h e i r o r g a n i s a t i o n s ,

Although t h e r e s e a r c h was conducted s u c c e s s f u l l y , it

was however, w i th some weaknesses and s h o r t comings,

One found it hard t o g a i n a c c e s s t o some of t h e o f f i c i a l s

of t h e companies and i n most c a s e s was met wi th out-

r i g h t re lusml from them t o dicrclooe coriyurly y v l l c i a t r

which they be l ieved w a s only f o r i n t e r n a l consumption.

Never the less , some success was recorded.

To be a b l e t o cover a l l t h e a r e a s mentioned above, a

l o t of money was s p e n t on t r a n s p o r t a t i o n ( e s p e c i a l l y

i n Lagos), f eed ing and accommodation.

F i n a l l y , a major c o n s t r a i n t t o t h e i n v e s t i g a t i o n was

' t h e s h o r t t ime @ven f o r t h e conduct and r e p o r t i n g of

such an e l a b o r a t e i n v e s t i g a t i o n .

- 15 - I t i s believed that subsequent researchers w i l l

continue from where I stopped.

CHAPTER 2

LITER-

2.1 THE NIGERIAN ECONOMY: 'N-60 TO DATE

The s t r u c t u r e of t h e Nigerian econony, i n t h e p a s t

t h r e e decades, has gradual ly changed from predominantly

o~ricultusal economy i n the 196Q's t o a n economy mainly

sus ta ined with t h e s a l e of o i l from the mid I970ts .

The growth i n o i l earn ings i n t h e mid 19701s was not I

I

f u l l y i n t c r n a l i s e d i n t o the economic system, a s a r e s u l t , ' b

t h e consumption p a t t e r n became import o r i en ted . Unfor- I

t u n a t e l y , when the o i l g l u t came, t h e economy was I i

adverse ly a f f e c t e d t o t h e e x t e n t t h a t i t l e d t o the I

emergency of t r a d e a r r e a r s . A growing deb t burden a l s o ,

surfaced i n t h e e a r l y 1980's as a r e s u l t of jumbo loans

cont rac ted from t h e i n t e r n a t i o n a l c a p i t a l market.

D r . (Mrs) Toyin P h i l i p s i n one of h e r a r t i c l e s s t a t e d

t h a t the e x t e r n a l deb t outs tanding s h o t up d r a s t i c a l l y

f rom $593.6 million i n 1976 t o $18.6 b i l l i o n i n 1986

and t o vbout $30 b i l l i o n i n 1990. The p u r s u i t of an

overvalued exchange r a t e po l i cy , the subsequent r e l e -

g a t i o n of t h e a g r i c u l t u r a l s e c t o r t o the background,

heavy publ ic s e c t o r spending and t h e huge debt over-hang,

a l l combined t o c r e a t e d i s t o r t i o n s i n t h e production,

consumption and payments p a t t e r n s , The p r e c i p i t o u s

d e c l i n e i n o i l earn ings i n the 1980's necess i t a t ed

a pol icy re -d i rec t ion aimed a t re -a l igning the domeatic

5 product ion p a t t e r n wi th the l o c a l r e source base.

To address t h e s e problems, t h e government i n agreement

w i t h the Cent ra l Bank of Niger ia in t roduced c e r t a i n

po l i cy reforms.

This was named t h e s t r u c t u r a l Adjustment Programme

(SAP) geared towards re-el l ignment of t h e n a i r a exchange

r a t e t o r e f l e c t market f o r c e s , t r a d e l i b e r a l i s a t i o n ,

p r i v a t i s a t i a n and commercial isat ion of government

owned e n t e r p r i s e s and t h e promotion of loca l ly-sourced

raw m a t e r i a l s and de- regula t ion of t h e economy. 6

me economic c r i s i s which t h e economy found h e r s e l f i n ,

before t h e SAP, inc luded t h e r educ t ion i n the a b i l i t y

of t h e country t o feed h e r s e l f due t a a d e c l i n e i n the

average growth r a t e of aggrega te output and p e r c a p i t a l

income, i n t h e f a c t of r ap id expansion i n populat ion.

The s i t u a t i o n was accentuated by t h e high l e v e l s of

unemployment and domestic i n f l a t i o n and a n a c c e l e r a t i w

environmental degrada t ion . This was compounded by t h e

h igh r i s e i n f o r e i g n d e b t burden.

AlhaJi A. A b e d (1991) b e l i e v e s t h a t wrong macro-

economic po l i cy p u r s u i t s p r i o r t o t h e reforms i n i t i a t e d

i n 1986, f o s t e r e d the d e t e r i o r a t i o n w i t h i n the Nigerian

economy. Among t h e po l i cy l a p s e s which he h igh l igh ted

were l a rge ' f i s c a l d e f i c i t s , r a p i d monetary expansion,

p r i c i n g and t r a d e r e s t r i c t i o n s , f o r e i g n exchange con t ro l8

and currency over-valuat ion. Other causes of t h e

- 18 - economic downturn included low p r o d u c t i v i t y i n

a g r i c u l t u r e and i n d u s t r y , environmental degrada t ion

a r i s i n g from unfavourable c l i m a t i c cond i t ions , weak

i n t e r n a l markets, low and u n s t a b l e work market p r i c e s

f o r expor t s and l a c k of v i a b l e i n n o v a t i ~ n s and c a p i t a l

f o r inves tmint .

The p o l i c y reforms which were suggested by Ahmed

inc luded r a t i o n a l i s a t i o n of p u b l i c spending through

cut-back i n the s i z e of t h e p u b l i c s e r v i c e , commercia- b

l i s a t i o n and/or p r i v a t i s a t i o n of many p u b l i c e n t e r p r i s e 8

i n a d d i t i o n t o r educ t ion i n spending on s u b s i d i e s and

a b o l i t i o n and/or reform of i n e f f i c i e n t p a r a s t a t a l s ,

adopt ion of more r e a l i s t i c t r a d e and p r i c i n g p o l i c i e s ,

i n t r o d u c t i o n of l i b e r a l t r a d e and f o r e i g n exchange

p r a c t i c e s and a gene ra l s h i f t t o market f o r c e s i n t h e

a l l o c a t i o n o f r e sources , r educ t ion i n cumbersome

s e c t o r a l c r e d i t c o n t r o l s and a l l o c a t i v e p o l i c i e s , eape-

c i a l l y i n i n t e r e s t r a t e de regu la t ion . Ahmed concluded

by s t a t i n g t h a t the main e f f e c t of t h e po l i cy r e f o m s

s o f a r i s t h e obvious c o r r e c t i o n of d i s t o r t i o n s i n

r e l a t i v e p r i c e s i n t h e product , money and f o r e i g n

exchange markets.

Authur Nwankwo (1981 ) be l i eves t h a t rnul t i n a t i o n a l s

ope ra t ing i n t h e country con t r ibu ted immensely t o the

economic c r i s i s . H e s t a t e d t h a t t h e proclaimed c o n t r i -

bu t ions of mul t ina t iona l - co rpora t ions t o t h e development

- 19 - of t h e economics of t h e developing c o u n t r i e s i n

g e n e r a l and Niger ia i n p a r t i c u l a r a r e l a r g e l y i l l u s o r y .

They b r i n g i n some investment funds i n this r ega rd ,

b u t they g e n e r a t e a huge amount of p r o f i t s a s a r e s u l t

o f t h e p r i v i l e d g e s which a r e g ran ted t o them and t h e b monopol i s t i c p o s i t i o n which they en joy .

H e concluded by proc la iming , ".... the government

which l e g i t i m a t e l y a s p i r e s t o l e a d black Afr ica , must

c u t o f f t h e p e r v a s s i v e t e n t a c l e s of t h e m u l t i n a t i o n a l s . ' 7

N i g e r i a t s very s u r v i v a l depends on t h i a . b

A . R . p r i n d l (1976) i n h i s own a s s e r t i o n t h i n k s

d i f f e r e n t l y from Nwankwots view. H i s view is t h a t

"The M u l t i n a t i o n a l Companies, which a r e now at t h e

h e a r t of a hea ted deba te as t o t h e i r motives and e f f e c t

on l o c a l economics have n o t drown i n t o l a r g e homogenous

u n i t s as t h e c a s u a l obse rve r mil:ht b e l i e v e . Rather ,

t h e i r growth h a s l e d t o fragmentation of t h e s e i n t e r -

n a t i o n a l l y d i s p e r s e d companies, which t ends t o i n c r e a s e

d i r e c t l y a s a f u n c t i o n of t h e i r s i z e . This fiagmenta-

t i o n comes from a number of s t r u c t u r a l and environmental

f a c t o r s , and a c c e n t u a t e s the problem of managing t h o

f i n a n c i a l f u n o t i o n of t h e f i r m . Impediments such a s

d i s t a n c e , u n r e l i a b l e aommunications and d i f f e r e n t t ime

8 zones are well-known1'.

The i s s u e of the bad e f f e c t s o f m u l t i n a t i o n a l s t o t h e

economy of t h e h o s t country can be reviewed based on

P r i n d l t a argument. !they contend with a l o t of p r o b l e m

that a l l i s n o t w e l l with them a s a g a i n s t what

Nwankwo th inks . The a n t i c i p a t e d c o n t r o l and a l l e g i a n c e

t o t h e pa ren t body abroad i s minimised with time, i f

P r i n d l t s i d e a i s r e a l i s t i c .

2.2 CORPORATE PERFORMANCE ANALYSIS

Most of the co rpora te bodies i n Niaer ia a r e multina-

t i o n a l s . Because of t h e remarkable i n c r e a s e i n t h e i r

number and -the a f f e c t 8 on the Nigerian economy vis-a-vis

r e a l i s t i c fo re ign exchange and i n t e r e s t r a t e s , a

review of t h e i r performance becomes d e s i r a b l e .

The Nigerian governaent has a l s o continued t o encourage

f o r e i g n investment even though i n the l a s t few yea r s

it has, under the i n d e g i n i s a t i o n decree , i n s i s t e d on

equ i ty p a r t i c i p a t i o n i n some' businesses by Nigerian

c i t i z e n s . Nwankwo (1981) ind ica ted t h a t t h e s e mul t ina t iona l s

corpora t ions a r e inves t ing i n developing c o u n t r i e s ,

n o t f o r any a l t r u i s t i c motives, as they accep t , but f o r

the s e l f i s h i n t e r e s t of making p r o f i t s under the f r e e

e n t e r p r i s e system of capi ta l i sm. H i s a s s e r t i o n i s

J u s t i f i e d by t h e f a c t t h a t Nigeria i s a developing

country and runs a f r e e e n t e r p r i s e c a p i t a l i s t system.

The degreeeof presence of mul t ina t iona l corpora t ions i n

Nigeria was est imated by Nwankwo who s a i d t n a t p r i v a t e

cap1 t u l 1rlveutnt:tlt htts been eetirnate~f t o t ~ e ~rc*atc?r

t h a n p u b l i c inves tment du r ing the first n a t i o n a l deve-

lopment p l a n p e r i o d , 1962-68. The a c t u a l investment

was abou t #1,60Omillion a s a g a i n e t t h e planned p u b l i c

inves tment o f #1,500 m i l l i o n . I n t h e second Nat iona l

development p l a n , 1970-74, t h e planned Net p u b l i c

inves tment programme was W1,380 m i l l i o n . Only i n t h e

t h i r d Nat ional development p l a n was p u b l i c investment

e s t ima ted t o be much greater t han t h e t a r g e t p r i v a t e

i n v e a t a e n t and this was t h e r e s u l t o f i nc reased govern-

ment revenue from petroleum ( o i l ) . While t h e planned

nominal p u b l i c c a p i t a l programme was Pf20rnillion, t h e

i n d i c a t i v e nominal inves tment programme f o r t h e p r i v a t e

s e c t o r vaa approximately W1 million? Nwenkwo however

expla ined t h a t no t a l l p r i v a t e inves tments i n Niger ia

i s under taken by fo re igne r s . . ~ l t h o u g h t h i s i s t r u e ,

t h e p o i n t s t i l l remains t h a t t h e p r i v a t e inves tments i n

N ige r i a i s dominated by m u l t i n a t i o n a l co rpo ra t ions .

The tu rnove r of t h e twelve (12) b i g m u l t i n a t i o n a l

c o r p o r a t i o n s i n Ni8er ia as a t 1991 i s expla ined by t h e

fo l lowing t a b l e .

S/NO N A M E TURNOVER (M' b i l l i o n )

U . A . C .

BEREC UNION BANK

P . z, N I G E R I A N BOTTLING CO

F I R S T BANK

U . B . A . 3. C . 0. A .

NATIONAL O I L

LEVER BROTHERS

TOTAL 1 2 . G U I N N E S S 1 . 0 0 1 \I,

, r;. I ,

TABLE 1 /"

I

SOURCE: T h e Financiol Post

The outlook of Corporate Nig@ria i s f u l l of g a i n s and

pains .

J u s t when you th ink they have been submerged by the

W i s s i l e s n of Nige r i a ' s addust ing economy, t h e i r hands

pop o u t of the rubb les t o f l a s h impressive t r a d i n g

r e s u l t s .

The f i g u r e s a r e l a r g e f o r p r o f i t s and even run i n t o

b i l l i o n s of n a i r a f o r turnover a s explained by t a b l e 1

above.

~ n a l y s i n g * t h e i r performance f o r the per iod of 1 9 9 1 , t h e chairman of Levent is Motors, Chief S . ~ d e John s a i d

t h a t m o s t of t h e problems which m i l i t a t e d a g a i n s t the

procurement of components f o r t h e manufacture of buses

have been l a r g e l y over-come,. Consequently, buses have

now begun t o r o l l o u t from t h e moniya f a c t o r y and

s u b s t a n t i a l s a l e s have a l r e a d y been achieved i n t h e

c u r r e n t y e a r v . i*

Their prob,lama as he p u t r e r e t h e c u r r e n t lack of

adequate l i q u i d i t y i n the domestic economy a s wel l a s

t h e r e l a t i v e sho r t age of f o r e i g n exchange f o r f i nanc ing

imports .

The Chairman of Guinness PLC, M r . P.M. Mbanefo i n Bn

addres s t o the s h a r e h o l d e r s s t a t e d "1 am pleased t o

r e p o r t t h a t your company achieved product ion r a t e s , i n

excese of 80 p e r c e n t o f i n s t a l l e d c a p a c i t y and we a r e

a b l e t o s e l l a l l t h a t we could produce. During t h e

p e r i o d , new brew houses were'commissioned i n a l l our

brewer ies a t a c o s t approaching #I90 m i l l i o n n a i r a t o

enab le t h e company t o use l o c a l g in" .

M.T. Chellaram i n h i s own speech enumerated a l l the

p r o b l e m which h i s company exper ienced. This included

s e v e r e domestic i n f l a t i o n a r y p r e s s u r e f u e l l e d mainly

by con t inu ing d e p r e c i a t i o n of t h e n a i r a , i n c r e a s e i n

- h a d a g e t a r i f f s , unequil ibrum i n f o r e i g n exchange

earnings/expendi t u r e , i n d u s t r i a l c a p a c i t y , under -u t i l i -

sa t i o n and* h igh r a t o of unemployment . Chief M. Okoya Thomas i n r e s p e c t of C.F.A.O. s a i d

" i n t h e e a r l y p a r t of the y e a r , t h e governments economic

p o l i c y r e s u l t e d i n c o n d i t i o n s which were very f avourab le

t o oompanies suoh se ours; Coneumer demund was s t r o n g

and r e a l i n t e r e s t rates were nega t ive when viewed i n

conJunct ion wi th the r a t e of i n f l a t i o n , However, by

mid-year, government had in t roduced a s e r i e s of measures

which had the e f f e c t of reducing l i q u i d i t y i n the

banking system: this r e s u l t e d i n a sharp r i s e i n

i n t e r e a t rutes and o weakening o f consumer demand which

i n t u r n adve r se ly a f f e c t e d ou r r e s u l t s . "

AlhuJ2 G. J, Abdulkadir , chairman o f a ~ongl .omerate ,b

was o f t h e view t h a t "dur ing the e a r l i e r p a r t o f t h e

y e a r , the economy was subJec ted t o s eve re i n f l a t i o n a r y

p r e s s u r e s and measures were in t roduced by government t o

mop up excess l i q u i d i t y i n t h e banking system, These

measures helped t o bring down tho r a t e of i n f l a t i o n and

e t u b l l i s e the f o r e i g n exchange value of the n a i r a . The

e f f e c t of the governments t i g h t monetary p o l i c y however,

w t l s that i n t e r e s t r a t e s e s c a l a t e d .

AlhaJ i Abdulkadir , as opposed t o o t h e r a n a l y s t s , w a s

of the view tha t the rate of i n f l a t i o n has come down

and the f o r e i g n exchange va lue h a s s t a b i l i s e d . Ti?is i s

f a r from t h e p r e s e n t s i t u a t i o n where t h e i n t e r e s t r a t e

and f o r e i g n exchange r a t e have cont inued t o f l u c t u a t e .

The o i l i n d u s t r y was n o t l e f t ou t i n t h e p r o f i t s p r e e

d e s p i t e t h e unfavourable economic cond i t i ons . I n h i s

'own words, t h e Chairman of Nat iona l O i l , Major General

- 25 - Hasaan Usman Ka t s ina ( r t d ) s a i d " i n s p i t e o f t h e

adverse ~3 i tuaL ion i n the money m a r k e t i n 1989, the

baldnce sheet of your company remained s t rong . Most

of t h e c a y i t d l p r o j e c t s under-taken i n 1909 were

geared towards main ta in ing the s t r o n g compet i t ive pos i -

t i o n of your company w i t h amyhasise on key areas of t h e

manufactur ing d i d lnilrketing a c tlfi t i e s . "

I n h i s own a n d l y ~ i s , Otunba Ojora of Agiy a t t r i b u t e d

the i~nprovement recorded i n t h e i r p r o f i t t o pa-urleri-1;

ndnugement of t h e i r r e s o u r c e s and We stability i n t h e

demand fd r t h e i r l u b r i c a n t s i n the market.

An a n a l y s i s of a l l the problems which most cf t h e

m u l t i n a t i o n a l s r e p o r t e d inc luded i n f l a t i o n which h a s

marg ina l i s ed consumers incouie, h igh c o s t prof ire,

t i g h t monetary and f i s c a l p o l i c y , harsh economic

cl lmhta, Cerltrul B m k o f Niger ia mop-up of excess

l i q u i d i t y , p r o f i t d e c l i n e due t o p r o v i s i o n Sorb bud

work, d e c l i n e I n market demand, l o c a l sou rc ing of raw

n m t e r i a l s , h igh i n t e r e s t r a t e s , r i s i n g c o s t o f p roduc t ion ,

d e y r e c l u t l ~ va lue of t h e n a i r a , h i g h c o s t o f importa ,

h i g h t a r i f f s , i nc reased competion and scarce f o r e i 8 n

exchange.

It w a s obslerved t h a t the problem of h igh and f l u c t u a t i n g

i n t e r e s t r a t e s and s c a r c e and f l u c t u a t i n g f o r e i g n

e x c h a n ~ e r a t e s was t h e two problems t h a t i s common t o

- 26 - a l l of t h e mul t ina t iona l s opera t in8 i n N i ~ e r i a .

Despite all these problems, the mult inat lonsl ls s t i l l

made huge p r o f i t s and maintained a sound balance shee t .

~ l t h o u g h they a r e supposed t o c o n t r i b u t e t o the deve-

lopment o f Nigeria , an a n a l y s i s o f t h e : performance

i n terms of t h e i r con t r ibu t ions i n technology revealed

a b a s i c cause of f u r t h e r unemployment and a f u r t h e r

concen t ra t ion of a l ready extremely unequal income

d i s t r i b u t i o n , while not ing t h e excessive p r i c e s they

charge i n t r a n s f e r r i n d t h i s technoloey . b

Upon examination, t h e f i n a n c i a l con t r ibu t ion t u r n s o u t

t o be a f i n a n c i a l d r a i n , decreasing both c u r r e n t con-

sumption and a v a i l a b l e l o c a l s a v i w s end thus f u t u r e

consumption f o r the vast maJori ty of N i ~ e r i a n s .

The balance of payments c o n t r i b u t i o n a l s o l ed t o

~ i m i l a r conclusions. While p o t e n t i a l inf lows were

minimised, balance of payments outflows were accpntuated

through import over p r i c i n g and i n f l a t e d roya l ty

payments.

These i s s u e s were n o t addressed by these companies who

were more i n t e r e s t e d i n t h e i r f i n a n c i a l p o s i t i o n as

a g a i n s t the i n t e r e s t of t h e i r h o s t coun t r i e s .

For them t o achieve t h e i r o b j e c t i v e s , they cons tan t ly

monitor thp economic environment of the country and

based on t h e i r f ind ings , they employ p o l i c i e s t h a t he lp

'them through. This was confirmed by Chief Joseph

Adebola OgundeJi of Barec PLC, who said "it has remained

- 27 - d i f f i c u l t t o f ind f o r e i e n exchange f o r our opera t ionsM.

Add1 tionally, the economy remains l e ~ a than bouyant.

I n s p i t e of one l i m i t e d opera t ion , your Board has pu t

i n p lace necessary measuree t o eneure t h a t your company

remaine p r o f i t a b l e . We a r e approaching, a l b e i t con-

t i n o u s l y , t r a d i n g i n o t h e r l i n e s of ~ e n e r a l ~ o o d s

buein@ss apart from our t r a d i t i o n a l l i n e 8 of battery

systems, t o r c h e s and hand-lampsn.

Ahmsd Joda of SCOA explained t h a t they have continued

t o maintain a s teady t r a i n i n g programme both i n s i d e

and outaide the country, to ensure t h a t t h e i r s t a f f @

a r e f a m i l i a r with changing cond i t ions brought ,,,Ut

by changing technology and t h e very d i f f i c u l t economic.

cond i t ions i n which they have t o opera te .

I t i s bel ieved t h a t a l o t of o t h e r p o l i c i e s has been

employed t o hedge a g a i n s t fo re ign exchange and i n t e r e s t

r a t e r i s k s . A eood example i s poly products whose

Chairman Chief J. l kin-George s a i d t h a t they have

r e s o r t e d t o high borrowing a s a r e s u l t of i n c r e a s e i n

lending r a t e s , d e c l i n e i n exchange of t h e na i ra and

high i n f l a t i o n r a t e s .

The t a b l e below shows the average turnover of t h e

d i f f e r e n t s e c t o r s of the Nigerian economy with other

d e t a i l s . These s e c t o r s a r e highly dominated by t h e #

mul t ina t iona l s .

From the t a b l e , one can see t h a t d e s p i t e a l l odds,

many companies a r e pos t ing h igher r e tu rns .

CORPORj

SECTOR

AUTOMOBILE

BANKING BREWERIES

B U I L D I N G S

CHEMICALS

COMMERCIAL

COMPUTER/OFFICE EQUIPMENT

CONCLOMERATES

CONSTRUCTION

SOAP & T O I L E T E R I E S

FO~D/BEVERAGES & TOBACCO FOOTWEAR

INDUSTRIAL/DOMESTIC PRODUCTS

INSURANCE

MACNINERY/MARK PACKAGING

PETROLEUM

P U B L I S H I N C

TEXTILES

TABLE 2

- 28 - 'E NICER11

AVERAGE TURNOVER (#?m)

1989/90 AVERAGE P R O F I T W m )

P R O F I T 1 AVERADE AS 96 OF DIVIDEND TURNOVER, (k)

SOURCE: The financial p o s t (calcu1atAc;ns baaed on

annual r e p o r t s ) .

2.3 INTEREST RATE POLICY AND BEHAVIOUR BEFORE AND AFTER DEREG~~TXITON I n t e r e s t r a t e s were c o n t r o l l e d and r egu la t ed u p t i l l

I986 when t h e S t r u c t u r a l AdJus tment Programme was

in t roduced . The r a t e s were g r a d u a l l y de regu la t ed from

1986 and l a t e r decon t ro l l ed from August 1987, Since

then , a l l d i r e c t c o n t r o l s were removed and t h e r a t e s

l e f t a lmos t e n t i r e l y t o market f o r c e s ,

I n t e r e s t r a t e s were f i rs t used a s ins t rument of monetary

p o l i c y i n Niger ia between 1959 and 1962 a s a means of

r e p a r t r i a t i n g shor t - term funds from abroad t o Niger ia . B

I n 1963 t h e minimum r e d i s c o u n t r a t e was reduced by

0.5% t o 4.0%. i n December 1964 it was r a i s e d by 1.0%

t o 5.0% and i n May 1968 i t was reduced by 0.5% t o 4.05%.

It remained a t t h i s l e v e l u n t i l Apr i l 1975 when it waa

reduced f u r t h e r by 1.0% t o 3.05%.

I n t h e 1976-77 budget, t h e f e d e r a l government accepted

t h e recommendation of t h e a n t i - i n f l a t i o n t a s k f o r c e

which decided t h a t t h e i n t e r e s t r a t e s f o r commercial

bank8 and Merchant banks loans t o t h e p roduc t ive s e c t o r

s h a l l range between 6,096 and 8.096 and t h a t l oans t o the

non-productive s e c t o r s w i l l a t t r a c t i n t e r e s t of up t o 10 a l i m i t o f 10.0% however computed.

I n t h e 1978-90 budget t h e r a t e s were g radua l ly r a i s e d

by 1.0 p e r c e n t i n o r d e r t o promote sav ings , check

i n f l a t i o n , improve resource a l l o c a t i o n , encourage domestic

non-bunk f i n a n c i a l i n a t i t u t l o n s t o buy government bonds

- 30 - t o f inance development prodec ts and a t t r a c t f o r e i g n

investment. The minimum lending r a t e was r a i s e d from

6.0 - 7.0 p e r c e n t and maximm from 10.0 t o 11.0 percent .

The r a t e s f o r t h e p re fe r red s e c t o r s a r e inc reased from

t h e prev ious maximum of 8.0 p e r c e n t t o 9.0 p e r cen t .

The i n t e r e s t r a t e f o r the favoured s e c t o r - t h e

A(gricultura1 C r e d i t Scheme a t t r a c t s a r a t e of i n t e r e s t

ranging from 4.0 p e r c e n t t o 6.0 p e r c e n t .

I n 1980, t h e r e was a s l i g h t upward r e v i s i o n of most

i n t e r e s t r a t e s . The l ending r a t e s of commercial banks b

i nc reased on the average by 0.5 p e r c e n t whi le r a t e s

ohtiro~se on lvv r l e to U I ~ favoured sector-ti ui Ute-! acurwmy

remained unchanged. This r a t e was r e t a i n e d i n 1981

f i s c a l year .

The i n t e r e s t r a t e s were r ev i sed i n January, Apri l and

December 1982. The f irst two were i n t h e upward d i r ec -

t i o n , whi le the t h i r d downward. By Apri l a l l r a t e s

were r ev i sed upwards by 2.0 p e r c e n t above t h e i r

r e s p e c t i v e l e v e l s a s a t January 1982. However i n

November t h e r e was a downward r e v i s i o n of 1.0 p e r c e n t

a c r o s s t h e board.

I n 1983 t h e r a t e s were r e t a i n e d while i t was ad jus t ed

upward i n 1984 by 1.5 - 2.0 p e r c e n t with the except ion

of lending r a t e s f o r a g r i c u l t u r e . #

I n 1985, tho s t r u c t u r e of i n t e r e s t r a t e was untouched.

It 18, t h e r e f o r e , c l e a r t h a t before 1985, t h e r a t e s

were f u l l y c o n t r o l l e d through t h e governments monetary

and f i s c a l p o l i c i e s .

With t h i s c o n t r o l , t h e r a t e s were moved around wi th

the sole aim of r e a l l s i n g a r ~ a l i e t l c i n t e r e s t r a t e .

The achievements were n o t encouraging o r s a t i s f a c t o r y

s o t h e system of c o n t r o l was r e l axed . This l e d t o t h e

b i r t h of t h e S t r u c t u r a l Adjustment Programme.

The S t r u c t u r a l AdJustment Programme (SAP) was in t roduced

i n 1986. A s t h e r a t e s were l e f t e n t i r e l y t o market

f o r c e s , which was pu re ly t h e main package i n SAP, t he

minimum r e d i s c o u n t r a t e was r e v i s e d downwards from b

15.0 p e r c e n t t o 12.75 p e r c e n t on 29 th December 1987.

It remained unchanged a t 12.75 p e r c e n t throughout 1988

and was l a t e r r a i s e d t o 13.25 p e r c e n t which took e f f e c t

from 3 ls t January 1989. I n reaponse t o h igh i n f l a t i o n

rats i n 1989, the minimum r e d i s c o u n t r a t e (MRR) was

r e v i s e d upwards t o 18.50. From January 1991 the MRR

was r e v i s e d downwards t o 15.5 p e r c e n t and the banks

were expected t o relate i n t e r e s t rates charged by them

t o t h e i r l o s t o f funds . Banks l end ing r a t e s a r e

c u r r e n t l y pegged t o a maximum of 21.0 p e r c e n t p e r annum.

The u s e r s o f fund are no t happy with t h i s development.

The i r c o n t e n t i o n being t h a t t h e 21.0 p e r c e n t c e i l i n g

i s s t i l l t o o h igh . m n k s on t h e o t h e r hand t h i n k t h a t

t h e r a t e should be r e v i s e d upwards. The government i s

l e f t wi th h e problem of s t r e i n g i' balance between t h e

two views a l though the 21.0 p e r c e n t i s h igh ly favoured

by most i n d i v i d u a l s ,

The s t a n c e of t h e CBN a s r ega rds i ts i n t e r e s t r a t e

p o l i c y i s t o ensure p o s i t i v e - r e t u r n s on Savings, promote

i n d u s t r i a l expansion and encourage hea l thy compet i t ion

among t h e banks,

Because of this compet i t ion, i n t e r e s t on co rpora t e

d e p o s i t s took a d i f f e r e n t t w i s t . There u r e now i n t e r e s t

r a t e v a r i a t i o n s between banks and t h e i r co rpora t e

d e p o s i t o r s .

According t o t h e Managing D i r e c t o r of Lion Bank,

M r , Paul Y. LuguJa, n t h e c r a s h i n i n t e r e s t r a t e s ha%

induced banks t o in t roduce p r e f e r e n t i a l i n t e r e s t r a t e s

because they want t o r e t a i n t h e i r c o r p o r a t e customersft,

With a prime lending r a t e (PLR) of 29.0 p e r c e n t and

h i g h e s t sav ings d e p o s i t i n t e r e s t r a t e of 22.0 p e r c e n t ,

LuguJa sees t h e c u r r e n t i n t e r bank ra tes of between

16.0 p e r c e n t and 18.0 p e r c e n t a s Ma temporary balance

because t h e r e a r e no economic a c t i v i t i e s t h a t w i l l

i n J e c t more money i n t o t h e economy, except t h e l i f t i n 8

of ban on politic sf^.

According t o t h e Cen t ra l Bank of Niger ia monetary

po l i cy f o r 1990, t h e inter-bank i n t e r e s t r a t e should

be a% l e a s t 1 , O p e r c e n t p o i n t below the prime r a t e f o r

each lending bank.

The import'ance of de regu la t ion of i n t e r e s t r a t e s t o u who o u t l i n e d

banks was made c l e a r e r by F.0, Orcsot sthe bas ic func t ions of i n t e r e s t r a t e s i n an economy

- 33 - and summarised them under t h r e e broad aspec t s . F i r s t ,

i n t e r e s t r a t e s , a s r e t u r n on f i n a n c i a l a s s e t s serve as

i n c e n t i v e t o save r s , making them d e f e r p r e s e n t consumption

t o a f u t u r e da te . The r e l e v a n t i n t e r e s t r a t e s i n t h i s

case a r e t h e depos i t r a t e s co r rec ted f o r p r i c e i n f l a t i o n

( o r more p r e c i s e l y expected i n f l a t i o n r a t e ) . In t h i s

connection, i n t e r e s t r a t e s a f f e c t the a v a i l a b i l i t y of

saving, and t o the e x t e n t t h a t depos i t r a t e s vary

depending on the matur i ty of the f i n a n c i a l a s s e t s , they

a l s o inf luence t h e a l l o c a t i o n of c u r r e n t saving among

the a s s e t s . Second, i n t e r e s t r a t e s , being a componGnt

of c o s t of c a p i t a l , a f f e c t the demand for ,and a l l o c a t i o n

of loanable funds.

The a p p l i c a b l e r a t e of i n t e r e s t i n t h i s case i s t h e

bank lending r a t e , t h e changes i n which a f f e c t the c o s t

of c a p i t a l which in f luences i n v e s t o r ' s wi l l ingness t o

i n v e s t i n machine and equipment ( r e a l investment). I n

t h i s way, t h e l e v e l of i n t e r e s t ( lending) r a t e could

in f luence growth i n f i n a n c i a l instrument , output and

employment. Third, t h e domestic i n t e r e s t r a t e s i n

conjuc t ion with the r a t e of r e t u r n on f o r e i g n f i n a n c i a l

&sue t u , exyec tell exchange r a t e and expec t d lrii'lcltiun

r a t e , determine the a l l o c a t i o n of accummulated savings

among domestic f i n a n c i a l a s s e t s , fo re ign a s s e t s , and

goods t h a t J a r e hedged a g a i n s t i n f l a t i o n , t h e specu la t ive

movements of funds in to /ou t of domestic/foreign a s s e t s

depends on t h e r e l a t i v e l e v e l of i n t e r e s t r a t e s and

whichever i s appropriate among exchange r a t e , i n f l a t i o n 11 r a t e and fore ign i n t e r e s t r a t e s .

Since deregulat ion under SAP; the r a t e s of i n t e r e s t on

loanable funds and deposi ts have been f luc tua t ing

( s ee t ab l e 3 ) .

TABLE 3

Average bank. i n t e r e s t r a t e s (1990) i n per cent .

PRIME CURRENT

SAVINGS '7 DAYS

30 DAYS

3 MONTHS

6 MONTHS

12 MONTHS

MAY 9 20.86

5.01 14.42 14.44 14.89 16.79 16.32 47.32

MAY 17 20.24

5.00 14.30 14.47 15.96 1'7.50 16.36 15.60

SOURCE: Various banks (ca lcu la t ions based on simple average).

- 35 - One of t he causes of t h e s e f l u c t u a t i o n s i s explained by t h e f a c t t h a t t h e i r might be a n autonomous i n c r e a s e

i n t h e demand f o r money, which causee t h e l end ing r a t e s

t o r i s e on a s u s t a i n e d b a s i s ,

According t o Oresotu, " t h e upsurge i n t h e i n t e r e s t r a t e s

wi tnessed s i n c e d e r e g u l a t i o n of t h e r a t e s may be p a r t l y

due t o t h e combined e f f e c t s of the de regu la to ry p o l i c i e s

ln t roduced i n d i f f e r e n t s e c t o r s of t h e economy on t h e

money and c v p i t v l murkata together w i t h the r o v t r i c t l v e

monetary p o l i c y s t a n c e dur ing the periodll.

The on going p r i v a t i s a t i o n programme has l e d t o the b

f l o a t a t i o n of new s h a r e s i n a d d i t i o n t o debentures and

t h e r i g h t s i s s u e s of s t o c k s which has had t h e e f f e c t of

i n c r e a s i n g the demand f o r money.

As a r e s u l t o f this i n c r e a s e , t h e ernergiw excess

demand f o r money balances h a s t r a n s l a t e d i n t o h ighe r

bank l end ing r a t e s a s t h e banks need t o r a t i o n only t h e

p e r m i s s i b l e c r e d i t dur ing t h e per iod .

This c h a r a c t e r i s t i c of t h e money market means t h a t t h e

i n t e r e s t r a t e s o f f e r e d d e p o s i t o r s and charged t o borrowers

by t%c commercial and merchant banks a r e l a r g e l y d e t e r -

mined by institutional i n s t e a d of market f o r c e s , This

p u t s a ques t ion

being e f f e c t e d .

Cadbury Niger ia *

market t o r a i s e

having r a i s e d u

on t h e e x t e n t and n a t u r e of d e r e g u l a t i o n

Limited r e c e n t l y went t o the c a p i t a l

money f o r i t s working c a p ' t a l a f t e r

#5O m i l l i o n loan t o bu i ld i t s c e r e a l

conversion p l a n t (CCP) and a l s o Onwuka Hi-Tek which

i n 1987 sourced a mul t ip le loan f a c i l i t y of #22 milliom,

this yea r does n o t th ink t h a t opt ion i s s t i l l v iab le ,

It i s looking f o r o t h e r avenues t o r a i s e a working

c a p i t a l of M25 mil l ion .

A l l these goea t o prove t h a t with improved performance

of the n a i r a and i t s r e l a t i v e s c a r c i t y i n the market,

funds may s t i l l have t o 80 up i f t h e apex authority i n -

a i s t s that r a t e s be determined by m a r k e t f o r c e s r t l ther

than regu la to ry measures, b

FIGURE 1: COMMERCIAL BANKS' DISTRIBUTION OF ZOANS AND A D V ~ S (#'MI

. ~ g r i c u l t u r e ~ . ~ e n u f a c t u r i ~

SOURCE: CBN

TABLE 4 :

FIXED DEPOSITS AND LENDING RATES AL BANXS) 1~m .I

MONTH/ YEAR

1 987

January

February March

April

May June

July Augut3t

September

October November December

AVERAGE ( 1 987 )

I 988 - January

February March

April

May June July

A W J s t September

b

October November

December

AVERAGE (1 988)

SAVINGS AVERAGE AVERAGE DEPOSIT FIXED LENDING RATE DEP . RATE RATE

MONTH/ YEAR

S A V I N G S AVERAGE DEPOSIT FIXED RATE DEP. RATE

1989 - January 12.0 13.5 February 12.0 13.5 March 12.0 13.8

~ p r i l 12.0 13.8

May 12.0 13.7 June 12.0 13.6

July 12.0 14.6

~ u g u s t 12.7 15.6 September 12.0 16.7

October 13.6 17.2

November 15.8 18.3

December 16.4 - 19.5 - AVERAGE ( 1 989) 12.9 15.3 - - 1990 - January 17.5 20.5

February 17.5 * 20.0

March 17.5 20.7

April

May June July Auguet September 18.7 21 .0

October 18.8 21.4

November 18.8 21 ,3 December 18,8 - 20.8 - AVERAGE ( 1 990) 18.4 22.9

_I_ .11.I(.-

AVERAGE LENDING R.ATE

SOURCE: CENTRAL BANI[ OF N I G E R I A XJLLION (VARIOUS ISSUES)

- 39 - TABLE 5

FIXED DEPOSITS RATES (MERCHANT BANKS) 1989,1990

1989 - January

February March

A p r i 1

May June July Au~rua t September

October November decernber

AVERAGE (1989)

1 990 - January February March

I & 1-1 1

May June

July Augur; t Sep ternher

October Noveni ber Gecember

4VFRbAGE ( 1990)

AVERAGE DEPOSIT *

RATE

A VEHACE LENDING RATE

- 17.5 18,ti

.17 * '9

17.8 18*7 24.7

25.7 2 5 . 3 27.0 28.0

29.9 - 22 08 -

29.2

30.5 29.2

28.5

28.8

23.5 27 07 28.1

717.8

28.2 28.2

27.4 - 78.6 -

'SOURCE: CENTRAL BANK OF IJICERIA: BULLION (VARIOUS ISSUES)

- 4 0 -

2.4 FOREIGN EXCHANGE POLICY AND MONITORING

The y r i r x i p l e s of f o r e i g n exchange t r a n s a c t i o n s come d i n t o y l a y when two coun t r i e s . engage i n f i n a n c i a l t r a n s -

a c t i o n s i n r e s p e c t of t h e s a l e and purchase of goods and

sel*vi ctss o r c a p i t a l t r a n s a c t i o n s .

Theee t r a n s & c t i o n s are guided by t h e r a t e s a v a i l a b l e .

Foreign exchange r a t e between t h e currency u n r t s o f two

c o u n t r i e s means the n m b e r of t h e u n i t s o f une n a t i o n a l

currency t ha t a r e needed t o buy one u n i t 01 the o t h e r

n a t i o n a l currency. By l i n k i n g t o g e t h e r t h e c u r r e n c i e s

o r mor~ey u n i t s o f d i f f e r e n t c o u n t r i e s , f o r e i g n exchgnge

rates makef comparison of i n t e r n a t i o n a l c o s t s and p r i c e s

of good8 vr~d s e r v i c e s p o s e i b le . Consequently , they y l a y

P dominant r o l e i n de te rmin ing t h e volume and d i r e c t i o n

of i n t e r n a t i o n a l t r a d e . ~;?"@JL I n w e ' t~ keep f o r e i g n exchange r a t e a t a meaningful

va lue , i t has t o be shaped by a f o r e i g n exchange po l i cy .

The need f o r t h i s p o l i c y a r i s e s a s a r e s u l t of' economic

tkleory of comparative c o s t as w e l l a s i n t e r n a t i o n a l

r e s o u r c e endowment d i f f e r e n t i a l s and inba lance . No

count ry can l a y a b s o l u t e c la im on s e l f s u f f i c i e n c y i n

i t s r e s o u r c e requirements o r l a y a b s o l u t e c la im on a

p e r f e c t l y balanced supply of resources '? With t h i s ,

the need f o r p o l i c y formula t ion and management of t h e

r e s o u r c e s becomes inevitable.

According .to R . A . Olukole (1991 ), f o r e i g n cur rency ,

o therwise known a s f o r e i g n exchange, i s one of t h e

sca rce resources p a r t i c u l a r l y i n a developing economy.

Unless t h e po l i cy frame work and management of this

s c a r c e resources i e p r o p e r l y . a r t i c u l a t e d i n terms of

i t s revenue genera t ion and expenditure , o r inf low and

outflow, a country runs the r i s k of balance of t r a d e o r

balance of payment problems.

During the pre-SFEM per iod , a l l r e c e i p t s and remit tances

of f o r e i g n exchange were made by the Cent ra l Bank of of

Nigskia on behalfLauthoriaed d e a l e r s who c a r r i e d ou t

the i n s t r u c t i o n s of t h e i r customers i n r e s p e c t of

f o r e i g n exchange t r ansac t ions . b

The exchange c o n t r o l a c t 1962 ves ted i n the monetary

a u t h o r i t i e x the power t o approve a11 a p p l i c a t i o n s f o r

f o r e i g n exchange i n r e s p e c t of a l l import t r ansac t ione

and i n v i s i b l e t r a d e t r ansac t ions .

The exchange r a t e was c o n t r o l l e d and regula ted s o l e l y

by Cent ra l Bank of Nigekia dur ing the pre-SFEM period.

I t was then determined i n r e l a t i o n t o the performance

of the U.S. d o l l a r and pound s t e r l i n g i n t h e world

f o r e i g n exchange market.

Olukole maintained t h a t the count ry ' s exchange r a t e

maintained p a r i t y with the pound s t e r l i n g u n t i l the

devalua t ion of t h e pound i n 1 . He s a i d t h a t the T7 country before 1971 adopted t h e Gold Content approach

under which the va lue of the Nigeria currency was

derived vis-a-vis the Gold Contents of the pound

s t e r l i n g and the U.S Dollar. From h i s analysis, the

- 42 - value of n a i r a was pegged aga in s t a basket of cu r renc ies

from January 1972 and an import weighted basket approach

i n 1978. I n 1984 and 1985 the exchange r a t e waa de te r -

mined through the va lue of the pound s t e r l i n g and U.S,

Dollar which wan then used a s a s o l e currency of i n t e r -

vent ion. Olukole concluding, remarked t h a t the exchange

r a t e po l i cy was p r ec i s e ly t h a t of a crawling peg between

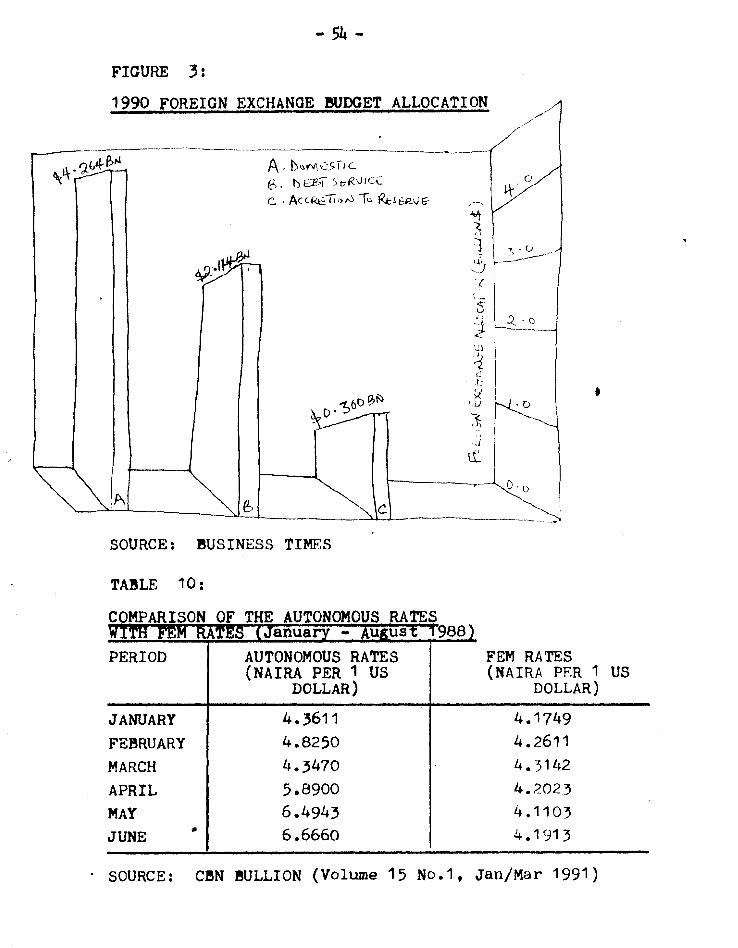

+ One o f the p o l i c i e s which# aimed a t f ind ing a r e a l i s t i c

exchange rate of n a i r a was the in t roduc t ion o f the

second-t ier fo re fan exchange market (SFEM) as a cop

component of t h e S t ruc tu r a l AdJustment Programme i n

1986 - 1988.

The Second-tier f o r e ign exchange market (SFEM)

s t a r t e d with the first bidding sess ion (auc t ion) on

29th September 1986 i n the c e n t r a l Bank of Nigeria. On

t h a t da te , t he exchange r a t e i n the f i r s t - t i e r ' fo re ign

exchange market which was being admin i s t ra t ive ly de te r -

mined was #7,5697 t o 1 U S d o l l a r while t he r a t e i n SFEM

was ~4 .6174 , thus showing a deprec ia t ion of 66 per cen t

when the l a t t e r was compared with the former. The

first-tier fo r e ign exchange market was terminated and

a un i f i ed fo r e ign exchange market ( ~ m ) was evolved on

2nd July 1987 under a f l o a t i n g exchange r i d e system

13 with an edchange r a t e of N3.7375 t o 1 US d o l l a r . The SFEM was made up of the auct ion and the interbank

market, On 14th January 1987, the interbank market r a t e

was deregula ted . I n a cont inous sea rch f o r a r e a l i s t i c

exchange r a t e , va r ious p r i c i n g methods have been used

s i n c e the i ncep t ion of SFEM. During the 1 s t and 2nd

bidding s e s s i o n s on 26th September and 20th October both

i n 1986, t h e c e n t r a l Bank of Nigeria used the simple

average of t h e success fu l bid r a t e s i n s e l l i n g fo rex t o

the authoriaed d e a l e r s . Marginal r a t e w a s however used

as a cut-off p o i n t t o determine success fu l bidders. The

use of the marginal r a t e continued u n t i l 19th March

1987 when the exchange r a t e had deprec ia ted from ~ 3 , 9 1 9 5

t o ~ 4 . 0 2 0 3 per 1 US d o l l a r . AS a r e s u l t , the Dutch B

a u c t i o n system was introduced on 2nd Apri l 1987. The

Dutch auc t ion system (DAS) remained i n f o r c e till the

end of 1988 when t h e r e wqs an observed wide d i f f e r e n t i a l

of about 55 per c e n t between the FEM r a t e s and t h e

autonomous market r a t e , a s i t u a t i o n which caused enough

concern t o n e c e s s i t a t e a review.

On January 9, 1989, a modified f o r e i g n exchange market

(FEM) was introduced and t h e r e was a f u s i o n of the

a u c t i o n r a t e and the autonomous r a t e . A s from t h a t d a t e

a un i f i ed exchange r a t e became app l i cab le i n t h e banking

system and the f o r t h n i g h t l y bidding sess ion under t h e

Dutch auc t ion system waa replaced by a d a i l y bidding

seaeion. The exchange r a t e i n the f i r s t d a i l y auc t ion ,

was 6 . 8 7 0 t o 1 US d o l l a r from t h e c l o s i n g r a t e of

As a r e s u l t o f a n o t t oo i a p r e s s i v e performance of the

d a i l y a u c t i o n system, the Dutch auc t ion system was re -

in t roduced w i t h t h e use of me marginal r a t e under which

t h e a u t h o r i S N d e a l e r a were obl iged t o b id f o r t h e i r

customers and n& l o n g e r f o r themselves. AS a r e s u l t of

t h e m policies, a review of the n a t u r e of f o r e i g n exchange

flowe between t h i s per iod becomes p e r t i n e n t .

Data on the foreign exchange f lowa through t h e Central

Bank o f Niger ia i n February 1990 showed a n e t in f low of

$220.5million, i n c o n t r a s t t o the n e t outflow of $98.4 14 m i l l i o n i n the preceding month . b

I n September 1990, fo re ign exchange flows showed a n e t

in f low of $74.3million, compared wi th t h e n e t in f low of

$21 3 . h n i l l i o n i n t h e praceeding month?

October 1990 showed a n e t outf low of $4242.lmillion i n

contrast to the net inflow o'f $312.3 m i l l i o n i n t h e 16 greceeding month.

The fo l lowing yea r i n January 1491, it ind ica ted a n e t

inf low of $250.4million, i n c o n t r a s t t o t h e n e t outflow

of $1 39. J m i l l i o n i n t h e preoeeding month??

TABLE 6

SOURCE : Economf c and F i n a n c i ~ l Review 1.1

IF Volume 28, No.2 June 1990

- TABLE 7

CN EXCHANGE FLOWS THROUGH THE A L BANK AND OTHER BANKS ( S ' ~ L L I O _ N ~

C A W 8lBXSD I QUARTER

Amdm

I provisibnal

SECOND 1 QUARTER APR- JUNE

1990 3

2033.0 1557.6 +475.4

A

PERCENTAGE CHANGE BETWEEN 7&3=

mow 1 933. 3 . On 1431.1

#O#..oft 502.2

(1) cm (I 68.1 ) (11) Othar Bank# (32.1)

RIRST QUARTER JAN-MAR

1990 2

2674.6 1978 a 8

+65)5.8

5.' .. . CATEOORY

d

INFLOW oUTFT .OW

NETFLOW

+27.8

OmaLOW

' (1) Virfbla

(2) Inviribla

I Debt 8errioo

t) LC& Repaymen*

U) Int. poyment

3. Otherr

(3) Artenomoum

L.. Outflaw

M h v L o w b

SECOND QUARTER APR- JUNE

1989 1

1591.2 1550.0

+41.2

-24.0

+Oe5-21.3

APRIL 1 990

(3)

t1053.9 -31 a?

/ - 4 6-

9W"' 2 5 FOREIGN EXCHANGE CONTROL TOOLS

For e f f e c t i v e moni tor ing and management of f o r e i g n

exchanae r a t e s and v a l u e s , the C e n t r a l Benk of Niger ia

employs d i f f e r e n t t o o l s amongst which i s the exchange

r a t e p o l i c y e a r l i e r d i scussed .

The main i n a t r m e n t s employed i n t h e management of

f o r e i g n exchange r e sources a r e exchange c o n t r o l , po r t -

f o l i o d i v e r s i f i c a t i o n and a d m i n i s t r a t i v e measures.

Olukole (1991) de f ined exchange c o n t r o l as a mechanism

by which a count ry seeks t o conserve, mob i l i s e , cen t r a -

l i s a and r a t i o n a l i s e i t s f o r e i g n exchange r e ~ o u r c e s ~ f o r

the s e t t l e m e n t of i n t e r n a t i o n a l t r a n s a c t i o n s i n

accordance wi th t h e p r i o r i t y of t h e country . Transac-

t i o n s i d e n t i f i e d as being of high p r i o r i t y a r e favoured

f o r the purpose of disbursements whi le t hose of low

p r i o r i t y a r e e i t h e r discouraged o r denied f o r e i g n

exchange f a c i l i t i e s .

Exchange c o n t r o l i s r e s t r i c t i v e , s e l e c t i v e and might

be s t r i n g e n t . The main source of a u t h o r i t y f o r the

a d m i n i s t r a t i o n of f o r e i g n exchange t r a n s a c t i o n s i n 'a

Niger ia i s t h e erchange c o n t r o l a c t 1962. Under t h e

p r o v i s i o n s of t h e a c t , a u t h o r i t y f o r t h e g r a n t o f ,

approva ls i n r e s p e c t of f o r e i g n exchange t r a n s a c t i o n s \k

i s ves t ed i n t h e M i n i s t e r of f i nance . However, most

of the f u n c t i o n s of the p r i v a t e s e c t o r t r a n s a c t i o n s

were de l ega ted t o the Cent ra l Bank of Niger ia which i n

t u r n de l eka ted approving a u t h o r i t y f o r most t r a n s a c t i o n s

t o t h e au tho r i sed d e a l e r s .

The exchange c o n t r o l i n Niger ia was a regime of a b s o l u t e

c o n t r o l , c o n t r o l of i n t e r e s t r a t e s , c o n t r o l o f exchange

rates and c o n t r o l of wages.

The a d m i n i s t r a t i v e c o n t r o l wae e f f e c t e d i n 1902 and

1983 when the Cent ra l Bank used the requirement of

Form "MW r e g i s t r a t i o n a s a supplementary ins t rument o f

import c o n t r o l . The Cen t r a l Bank under t h i s , monitored

t h e u t i l i s a t i o n of import l i c e n s e s . This was t o ensure

t h a t the presc r ibed va lues on t h e l i c e n c e s were not

exceeded and t h a t the i t e m imported were i n keepink

wi th the under ly ing import l i c e n c e s . ?he Comprehensive

Import duperv is ion acheme (CISS) was a l s o a form o f

a d m i n i s t r a t i v e c o n t r o l . I ts o b j e c t i v e was t o ensure

t h a t the count ry rece ived va lue f o r h e r expendi ture .