Embed Size (px)

Citation preview

Copyright Castalia Limited. All rights reserved. Castalia is not liable for any loss caused by reliance on this document. Castalia is a part of the worldwide Castalia Advisory Group.

Urban Infrastructure for Southern Mongolia-Background Study

Final Report

Report to the World Bank

December 2008

Table of Contents Executive Summary i

1 Introduction 1

1.1 What Is the Purpose of This Paper? 1

1.2 What Is the Structure of This Paper? 3

2 Existing Projections of Population and Plans for Infrastructure Development in South Gobi 4

2.1 What are Government Projections and Plans? 4

2.2 What are Mining Companies’ Projections and Plans? 14

3 Lessons from International Mining Experience 19

3.1 What Problems does Influx Cause? 24

3.2 How to Predict Influx? 29

3.3 How to Avoid the Problems Caused by Influx? 38

3.4 What are the Social Advantages and Disadvantages of Each Recruitment and Settlement Model? 43

3.5 How can Governments Maximize the Economic Benefits from Mining Activities? 46

4 Influx Scenarios and Infrastructure Needs in South Gobi 52

4.1 What Range of Influx Scenarios is Likely? 52

4.2 How Much Infrastructure Is Needed and What Will It Cost? 58

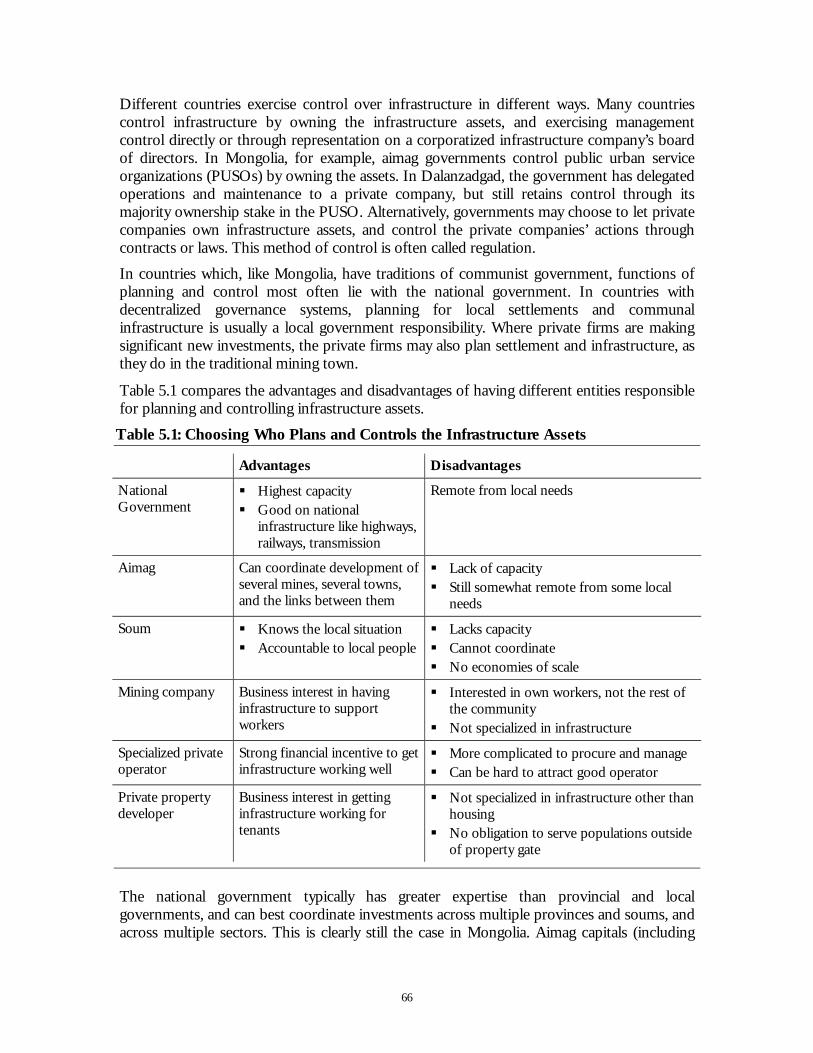

5 Options for Meeting Infrastructure Needs in South Gobi 63

5.1 Who Can Plan and Control the Infrastructure Assets? 64

5.2 Who Can Fund and Finance the Infrastructure? 66

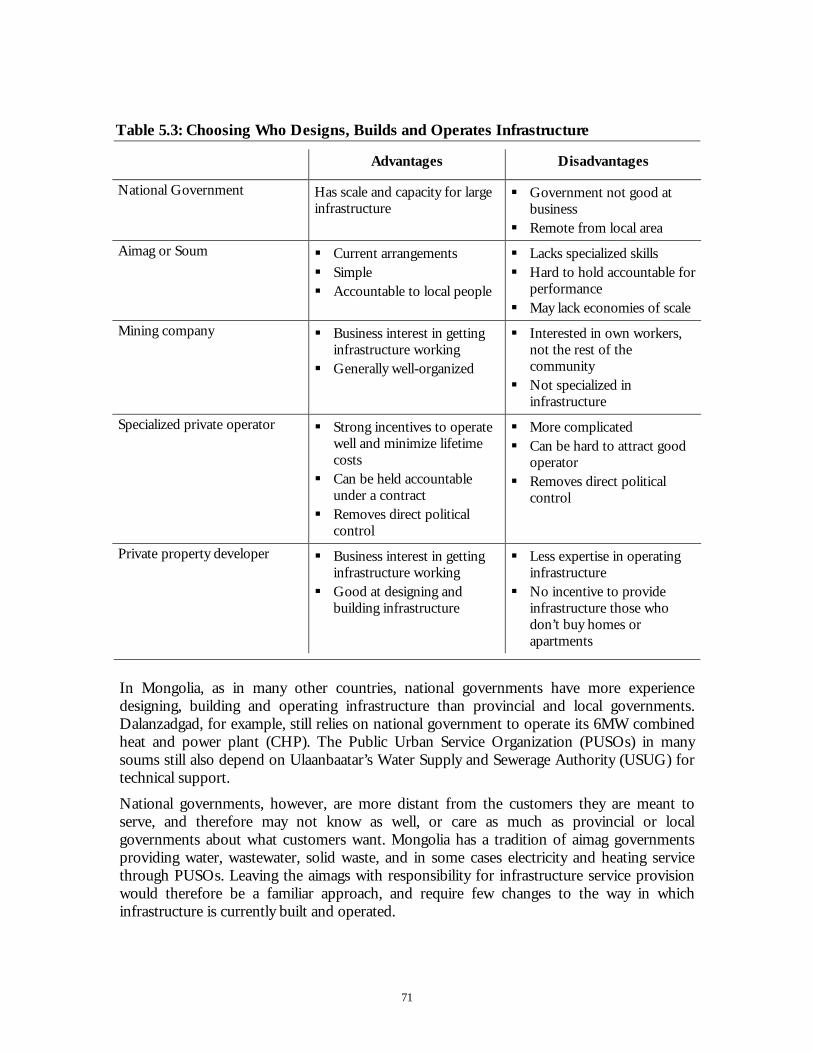

5.3 Who Can Design, Build and Operate the Infrastructure? 69

6 Choosing the Right Option for Infrastructure Provision 72

6.1 What Are the Tradeoffs between Options for Providing Infrastructure Services? 72

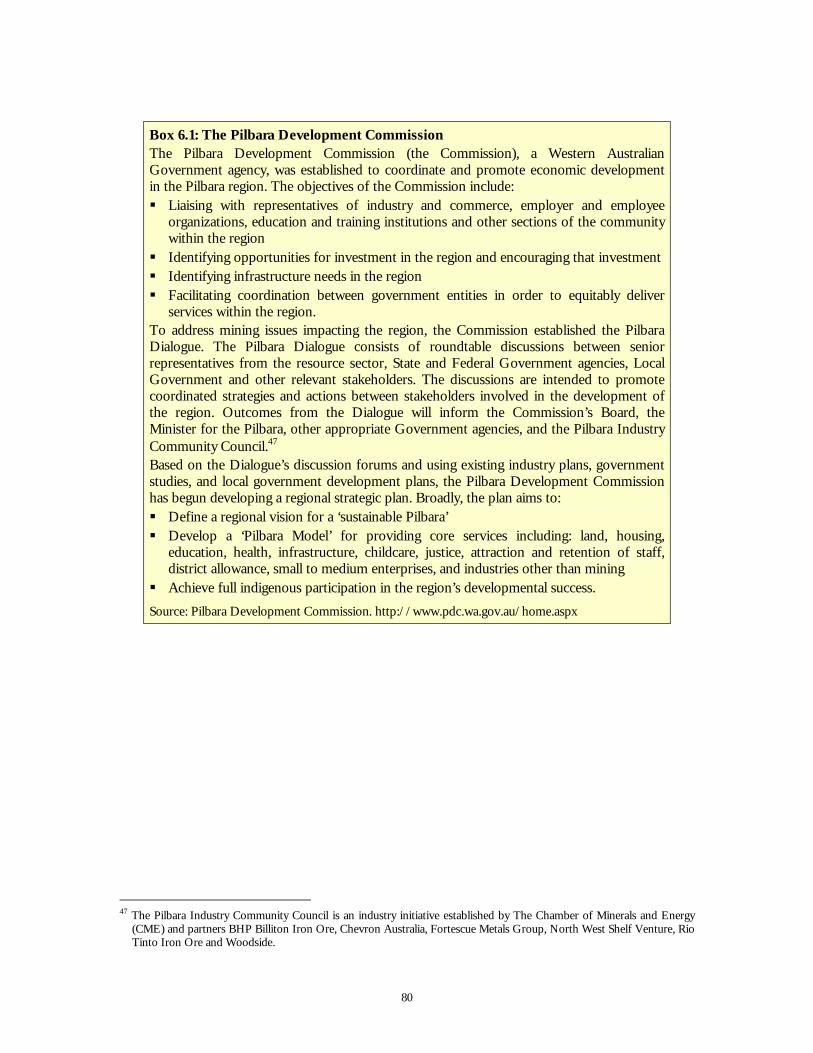

6.2 How Can Mongolia Minimize the Tradeoffs? One Possible Approach 78

6.3 What Are the Next Steps? 82

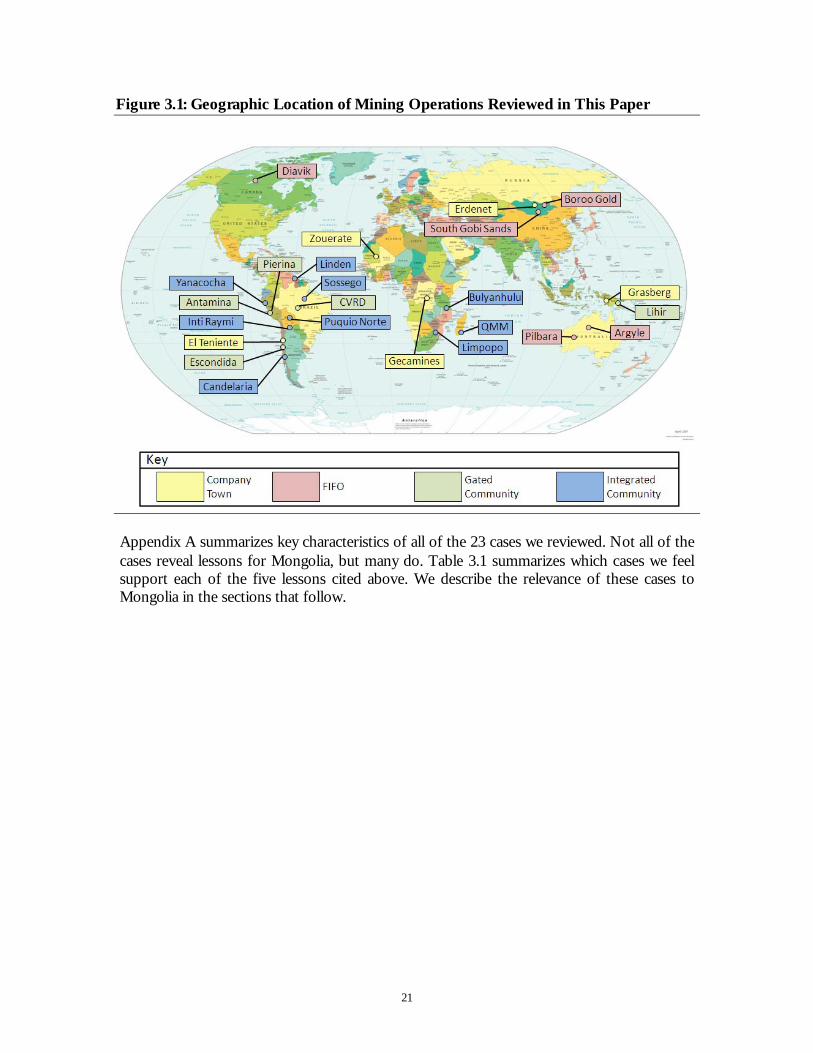

Appendices Appendix A : International Cases 83

Appendix B : Zouerate In-Depth Case Study 97

Appendix C : User’s Guide for Castalia Infrastructure Costing Model 112

Tables Table 1.1: Categories of Populations Used in This Paper 2

Table 2.1: Local Infrastructure Capacity Requirements—Engineering Geodesy Study 9

Table 2.2: Local Infrastructure Capacity Requirements—New Town Co. Ltd. Study 10

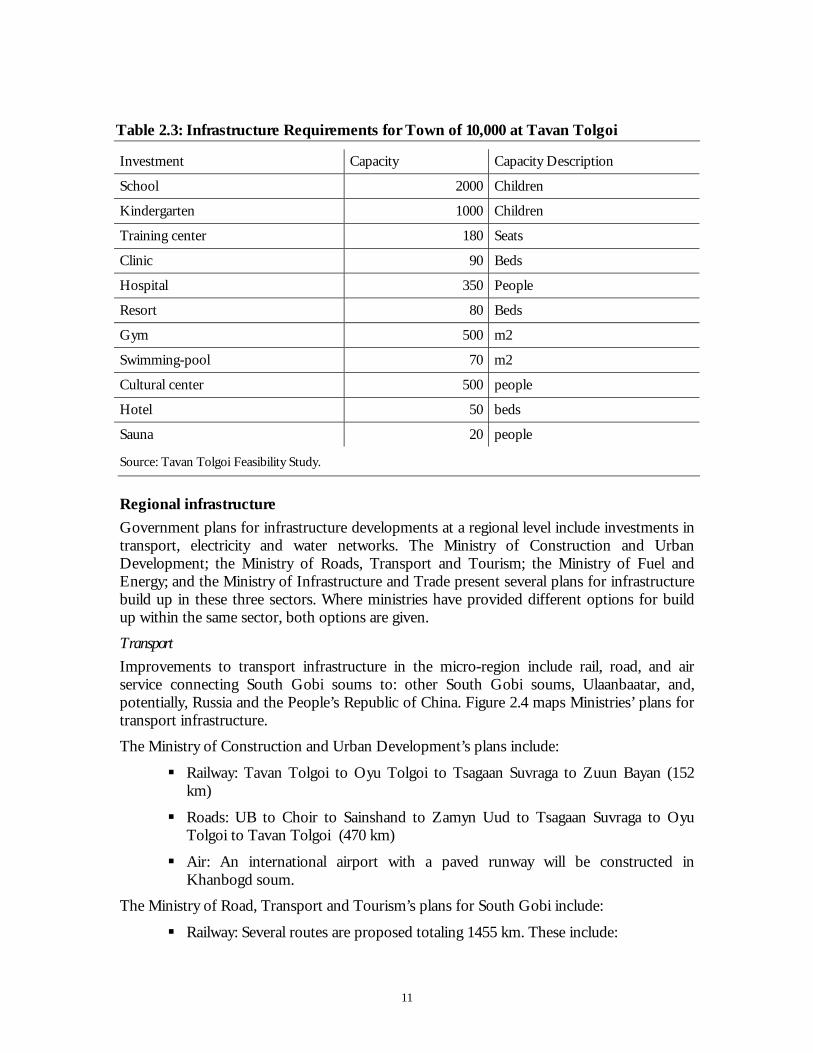

Table 2.3: Infrastructure Requirements for Town of 10,000 at Tavan Tolgoi 11

Table 2.4: Infrastructure Needs in Khanbogd by 2020 16

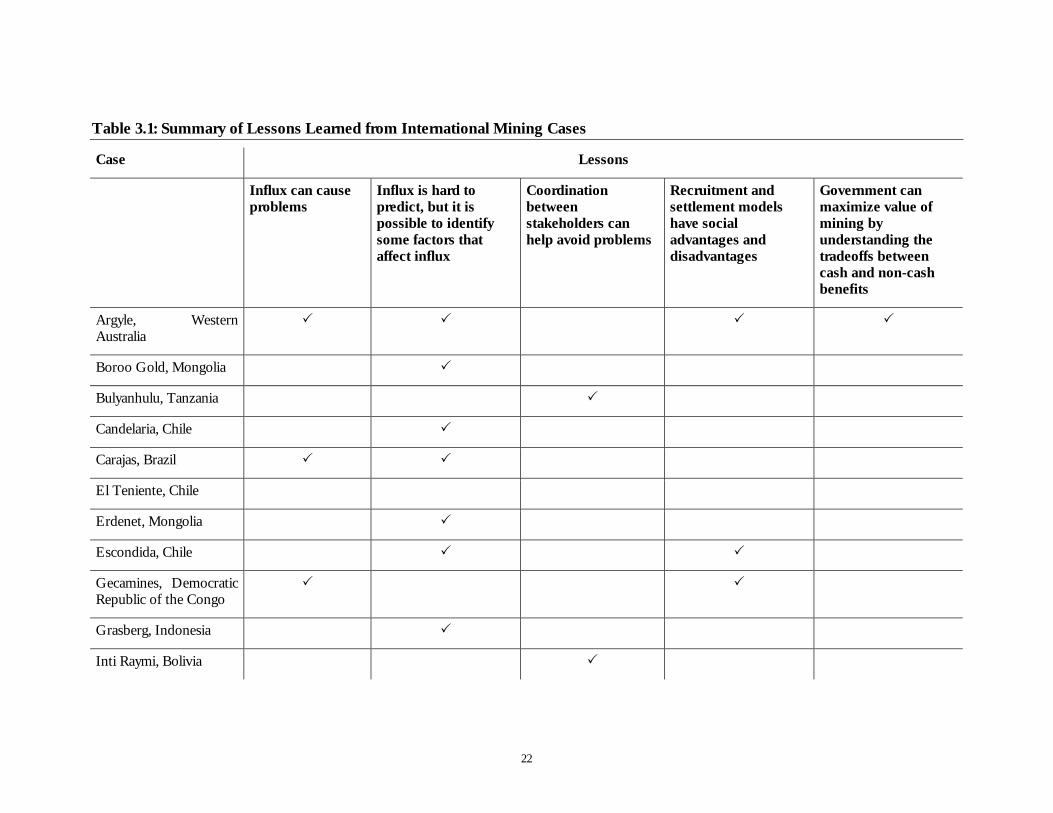

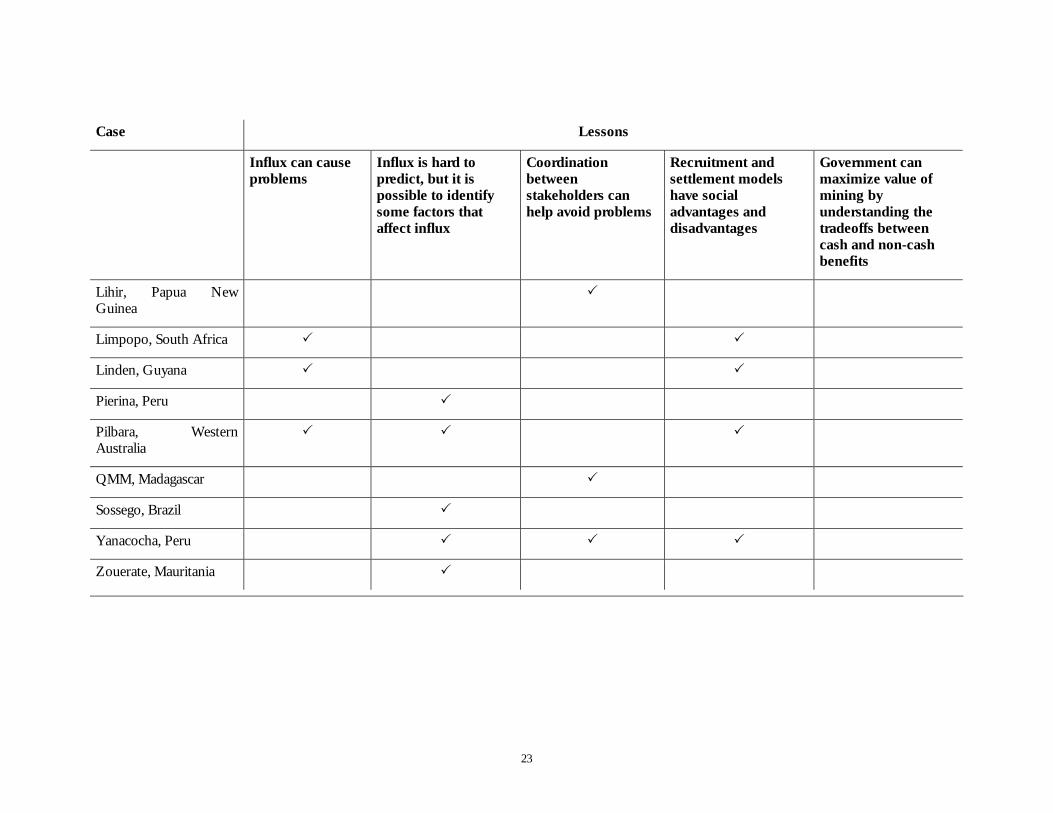

Table 3.1: Summary of Lessons Learned from International Mining Cases22

Table 3.2: Influx in the Mining Cases Studied 31

Table 3.3: Comparison of Typical Models for Mining Recruitment and Settlement 32

Table 3.4: Influx and Remoteness in the Mining Cases Studied 37

Table 3.5: Influx and GDP per Capita in the Mining Cases Studied 37

Table 4.1: Physical Infrastructure Needs and Costs of Buildings 59

Table 4.2: Physical Infrastructure Needs and Costs of Water Supply 59

Table 4.3: Physical Infrastructure Needs and Costs of Sanitation 60

Table 4.4: Physical Infrastructure Needs and Costs of Electricity 60

Table 4.5: Physical Infrastructure Needs and Costs of Heating 60

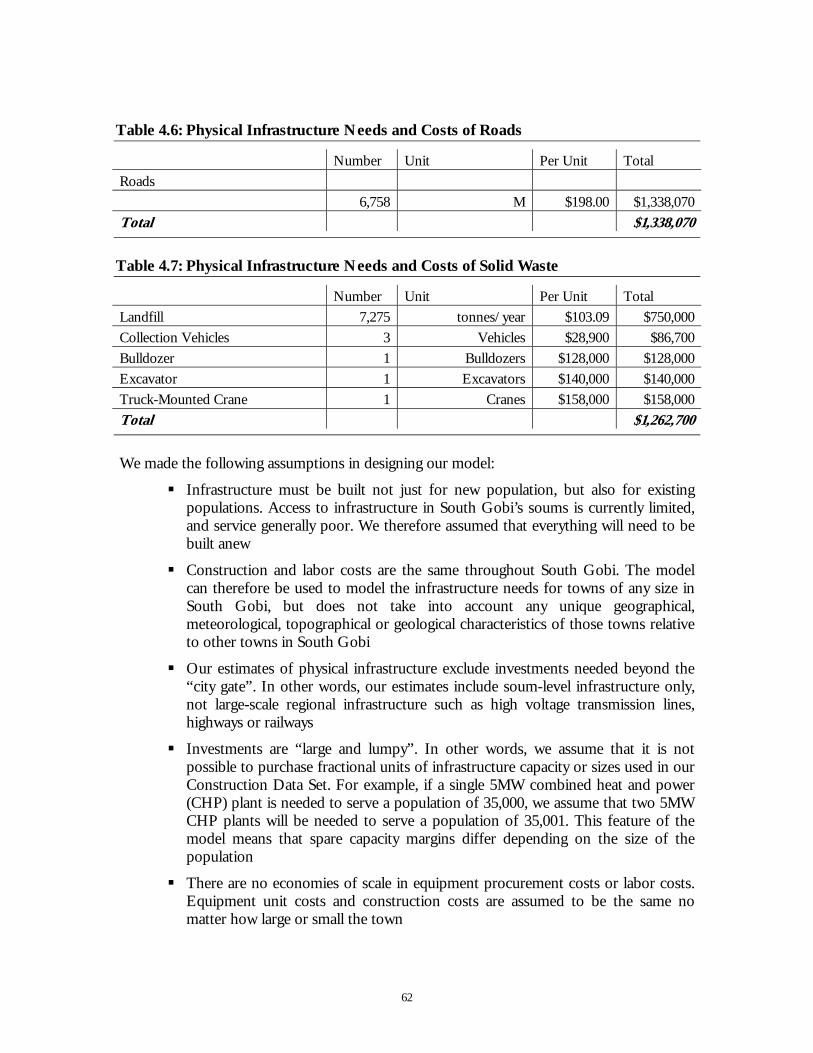

Table 4.6: Physical Infrastructure Needs and Costs of Roads 61

Table 4.7: Physical Infrastructure Needs and Costs of Solid Waste 61

Table 5.1: Choosing Who Plans and Controls the Infrastructure Assets 65

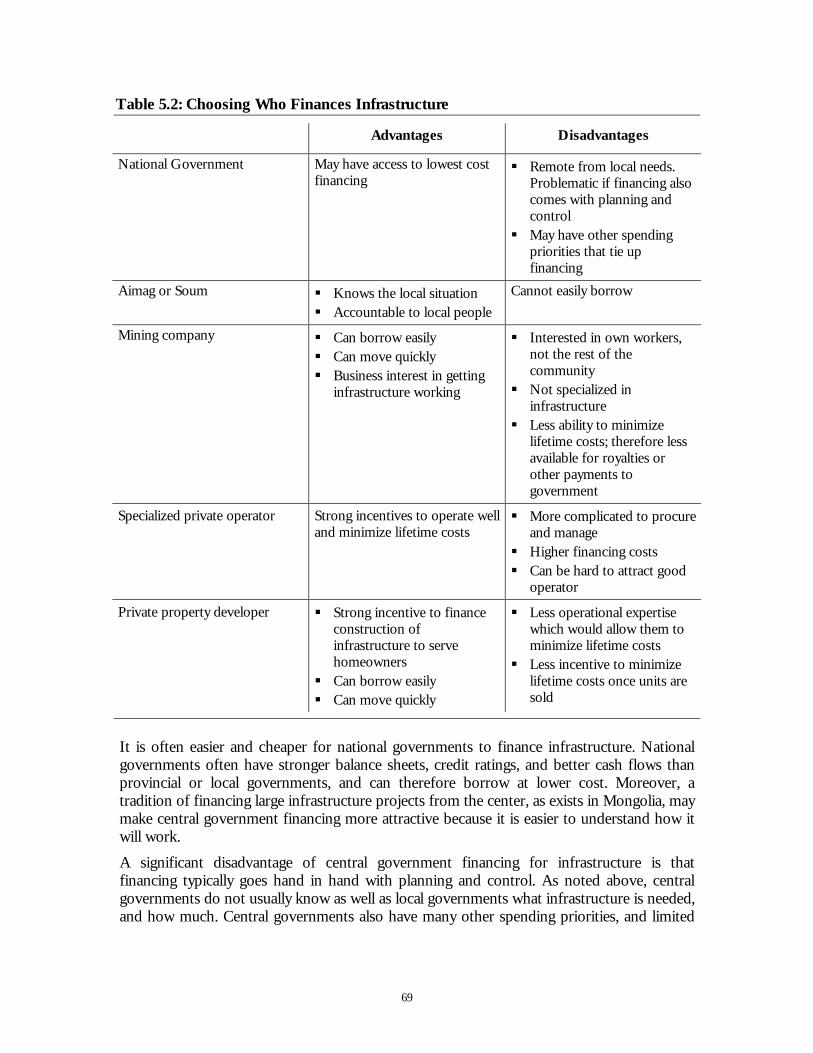

Table 5.2: Choosing Who Finances Infrastructure 68

Table 5.3: Choosing Who Designs, Builds and Operates Infrastructure 70

Table 6.1: Who Should Provide Infrastructure Services in South Gobi? 73

Table 6.2: Which Organizations Are Best at Which Functions? 76

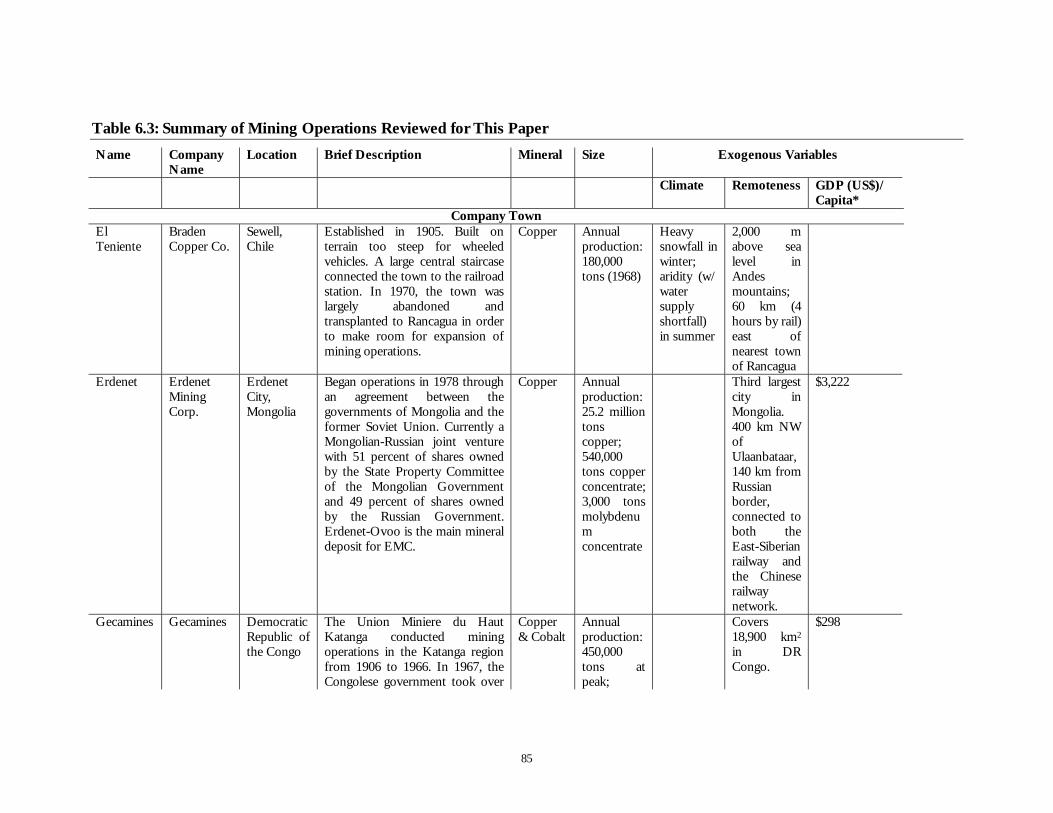

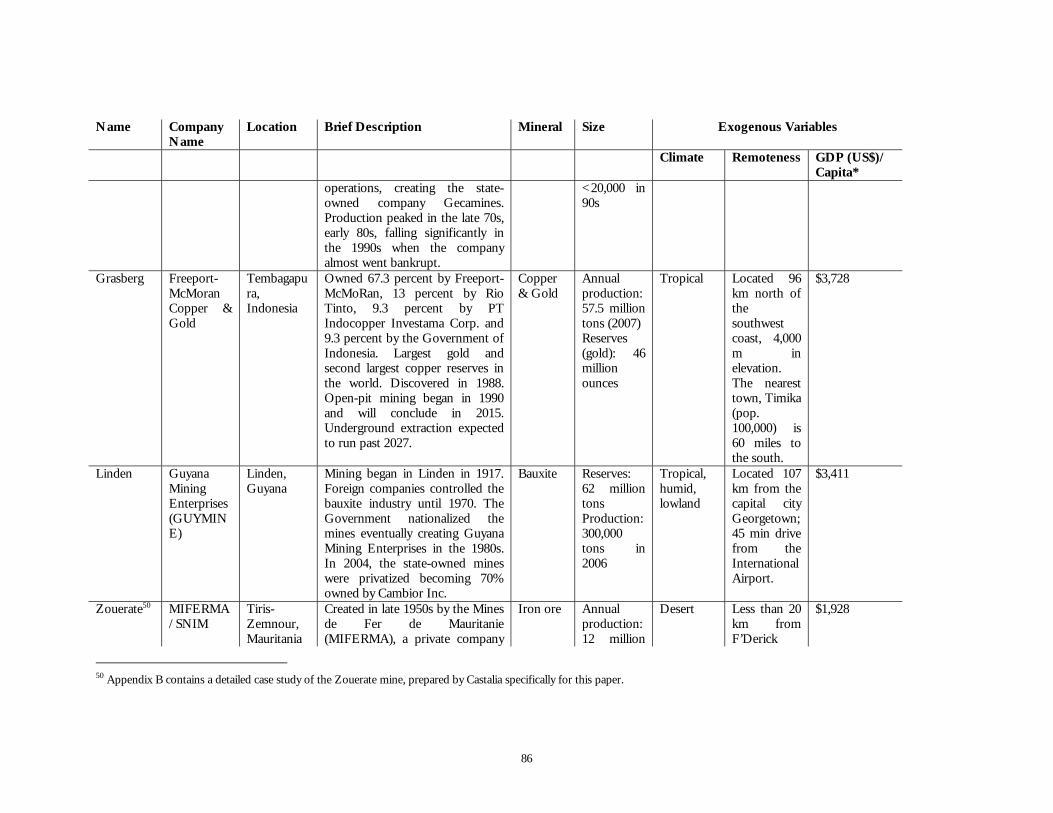

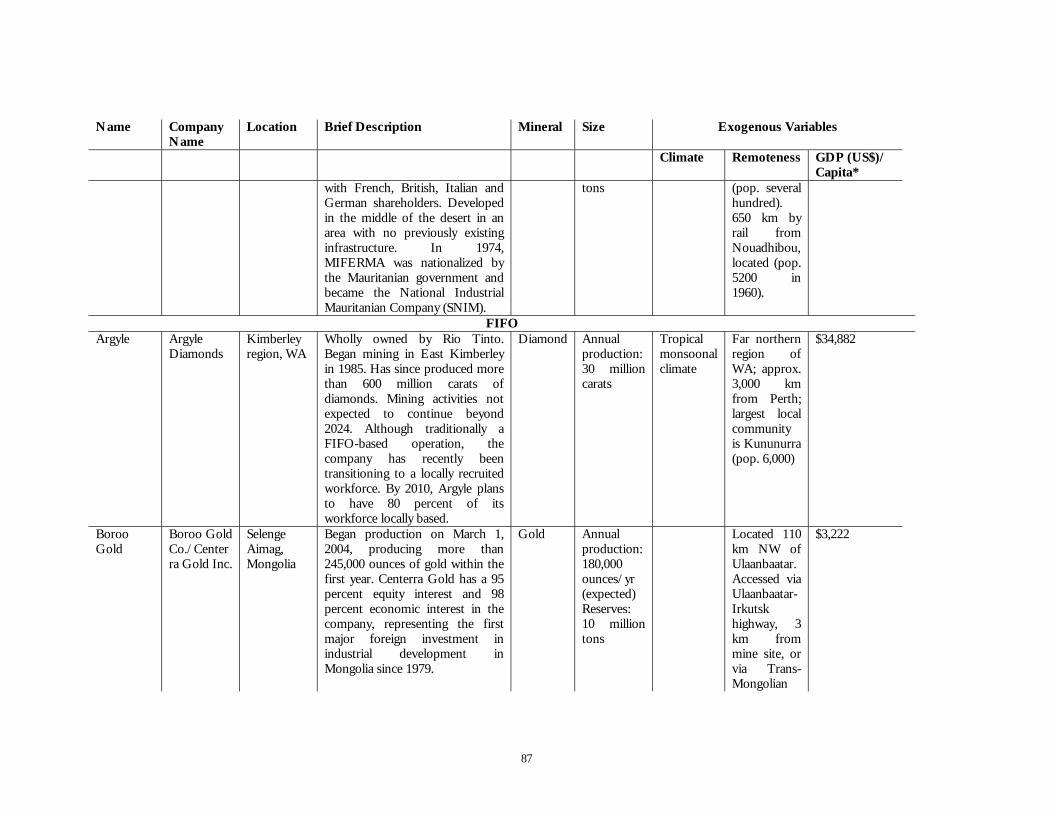

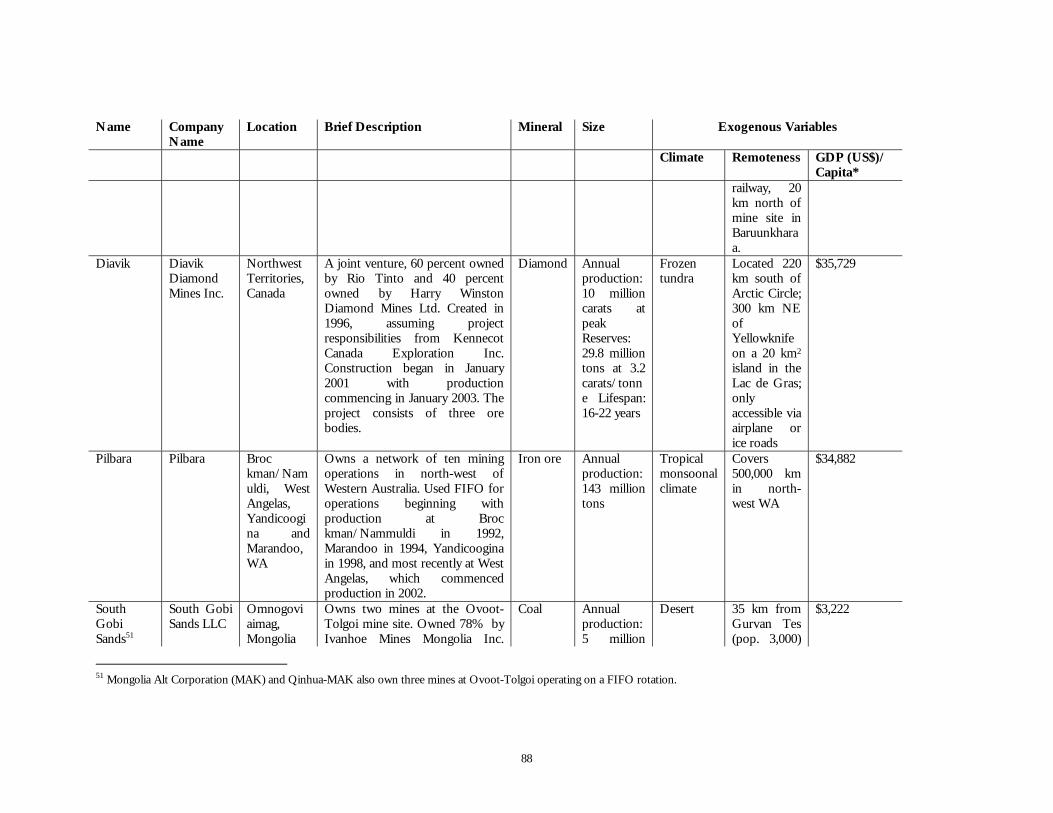

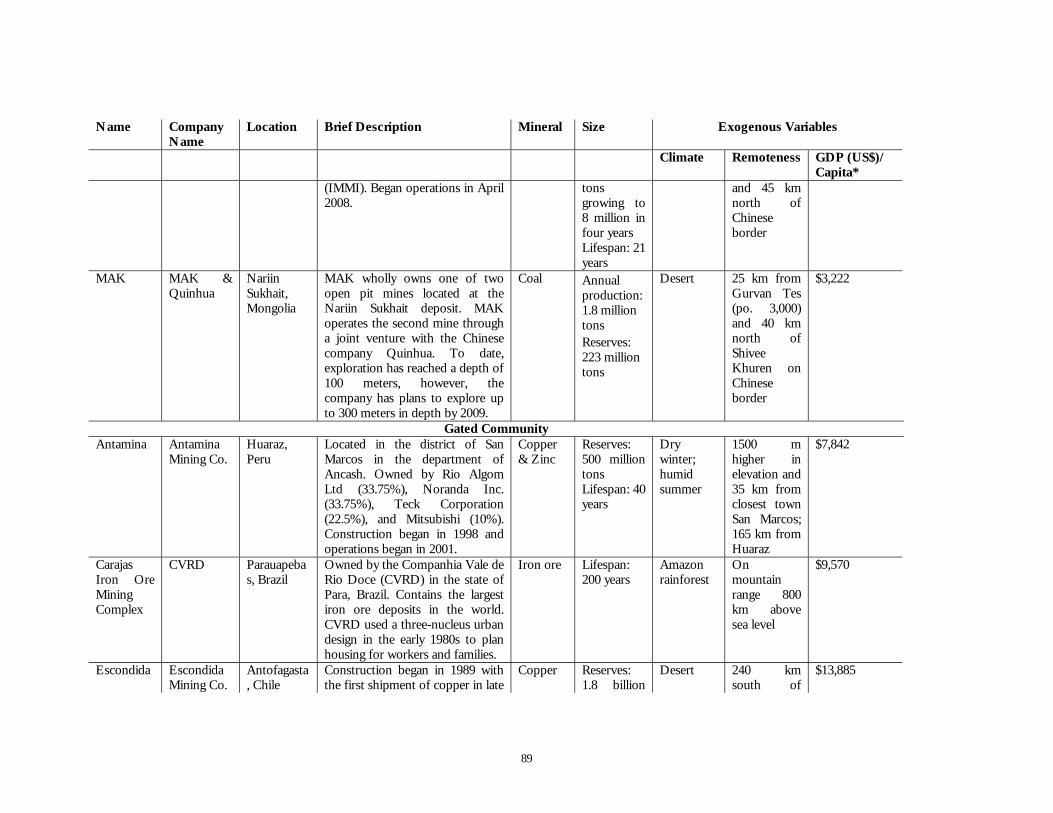

Table 6.3: Summary of Mining Operations Reviewed for This Paper 84

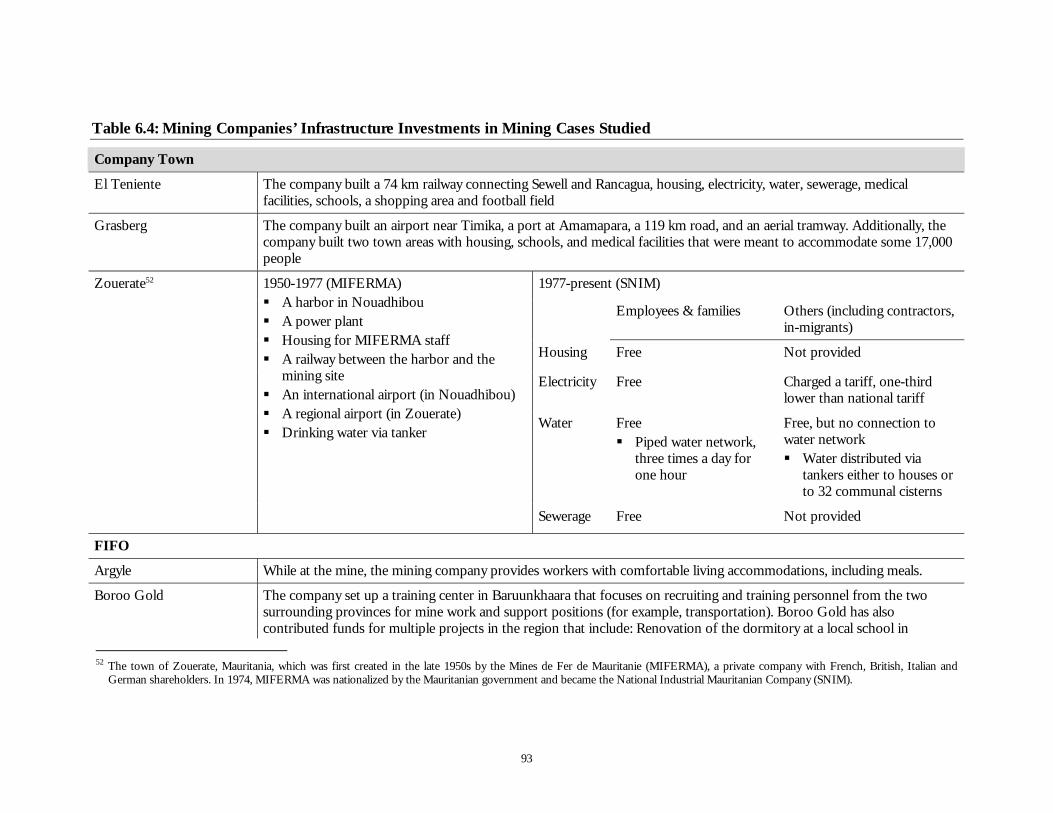

Table 6.4: Mining Companies’ Infrastructure Investments in Mining Cases Studied 92

Table 6.5: Recruitment Percentage Breakdown in Mining Cases Studied 95

Table 6.6: Iron Ore Production and Export 1963 to 1973 98

Table 6.7: Ethnic Background of MIFERMA Employees in 1970 99

Table 6.8: Population Growth in Zouerate Compared to National and Regional Growth 102

Figures Figure 2.1: Map of South Gobi, Mine Sites and Soum Locations 5

Figure 2.2: MoCUD Consultants’ Population Forecast for South Gobi – Scenario 1 7

Figure 2.3: MoCUD Consultants’ Population Forecast for South Gobi – Scenario 2 7

Figure 2.4: Government Ministries’ Infrastructure Plans for the Transport Sector 12

Figure 2.5: Government Ministries’ Infrastructure Plans for the Power Sector 13

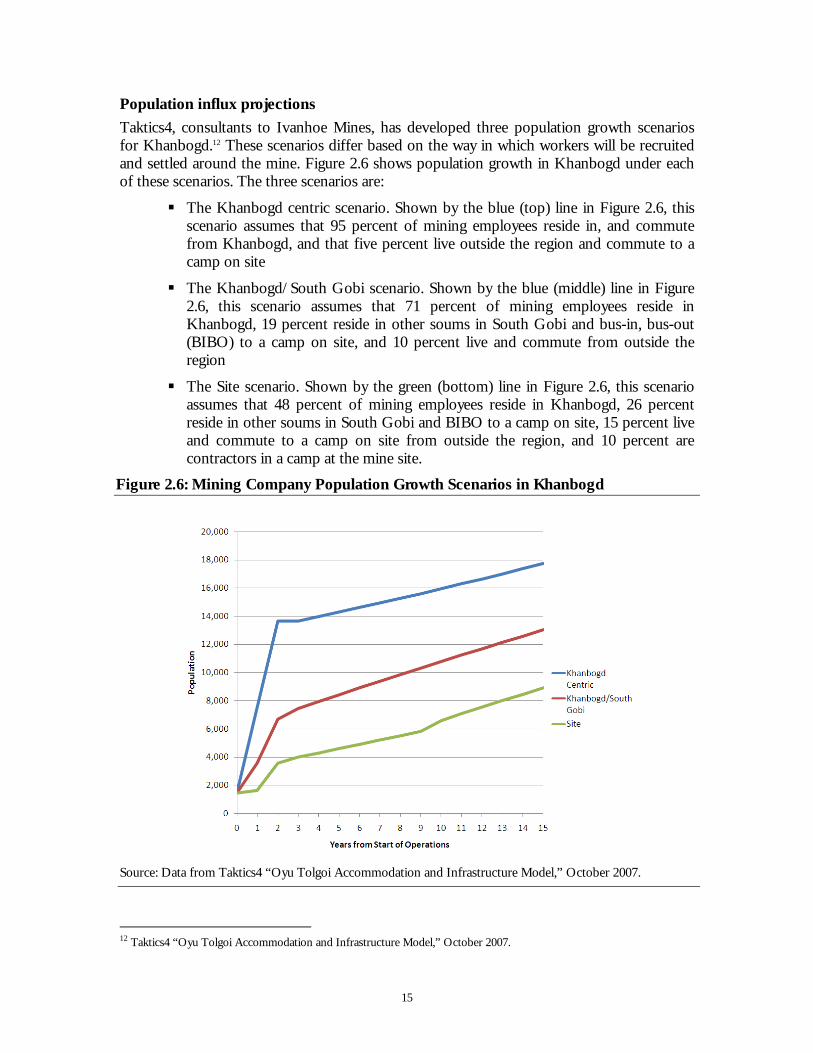

Figure 2.6: Mining Company Population Growth Scenarios in Khanbogd 15

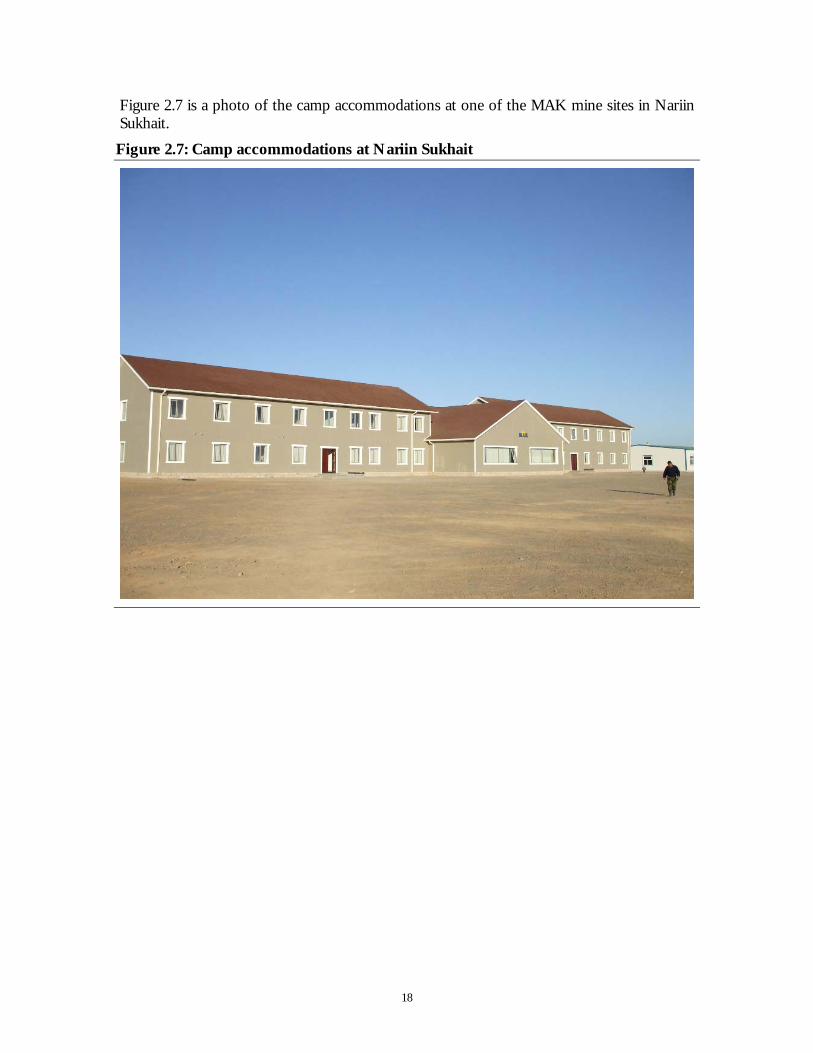

Figure 2.7: Camp accommodations at Nariin Sukhait 18

Figure 3.1: Geographic Location of Mining Operations Reviewed in This Paper 21

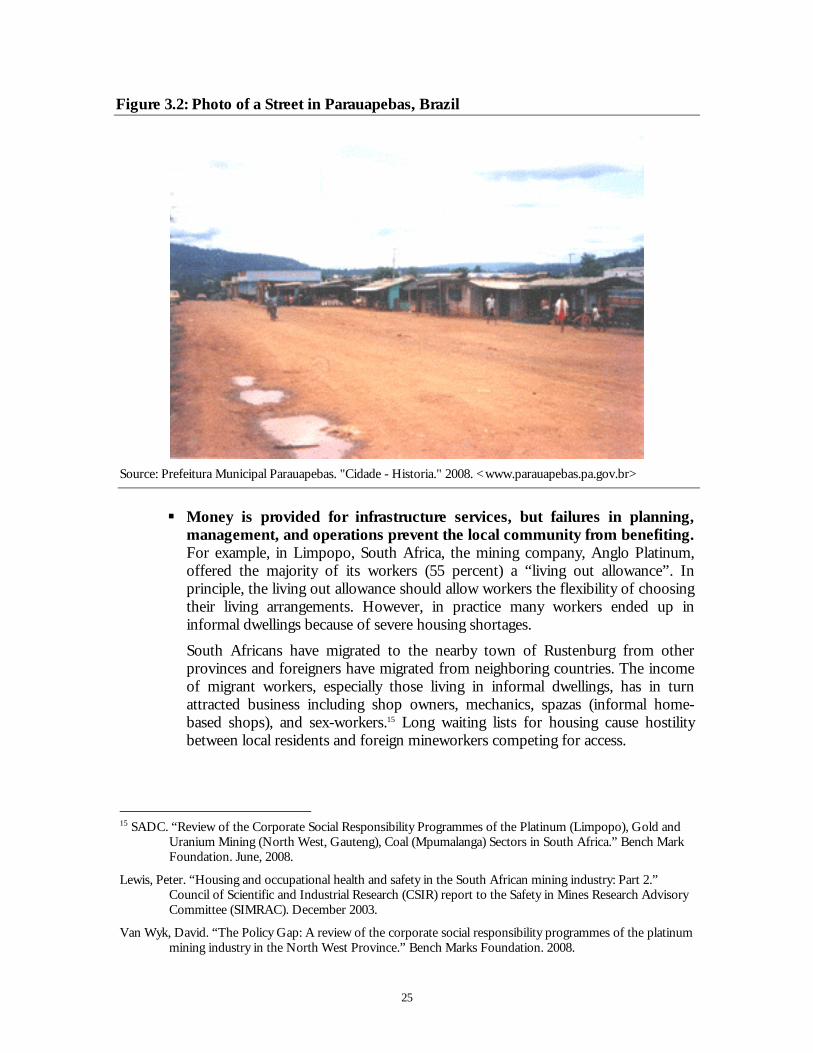

Figure 3.2: Photo of a Street in Parauapebas, Brazil 25

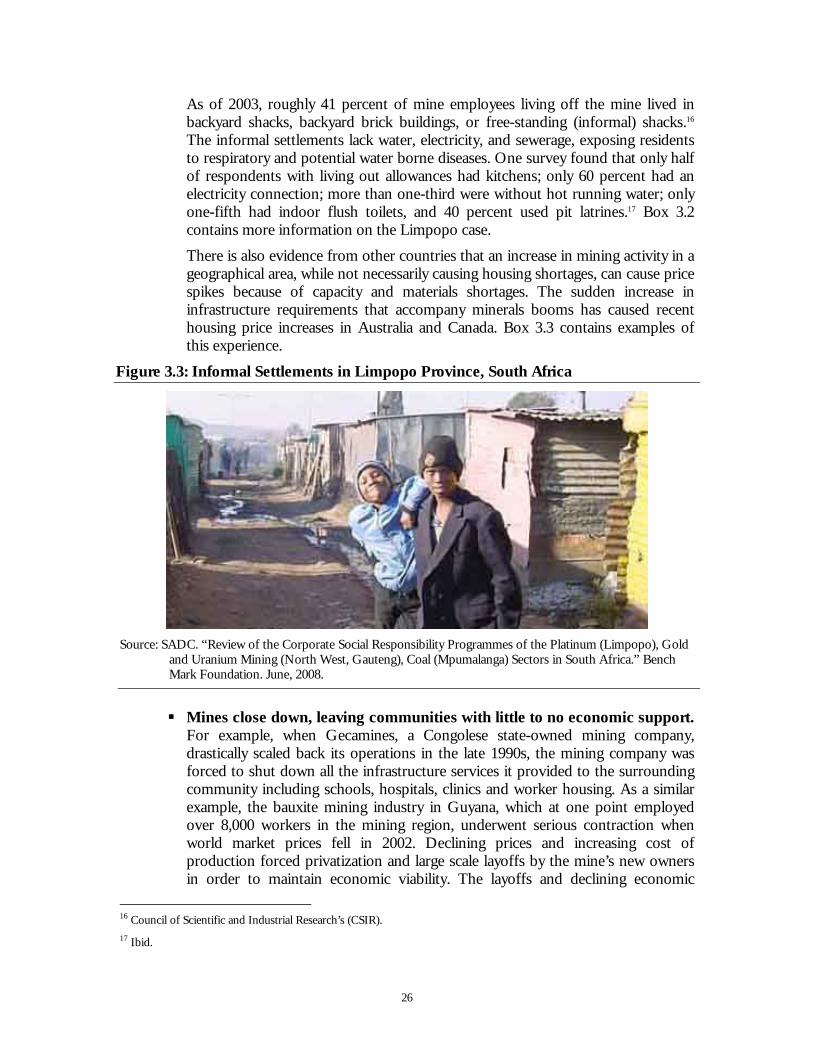

Figure 3.3: Informal Settlements in Limpopo Province, South Africa 26

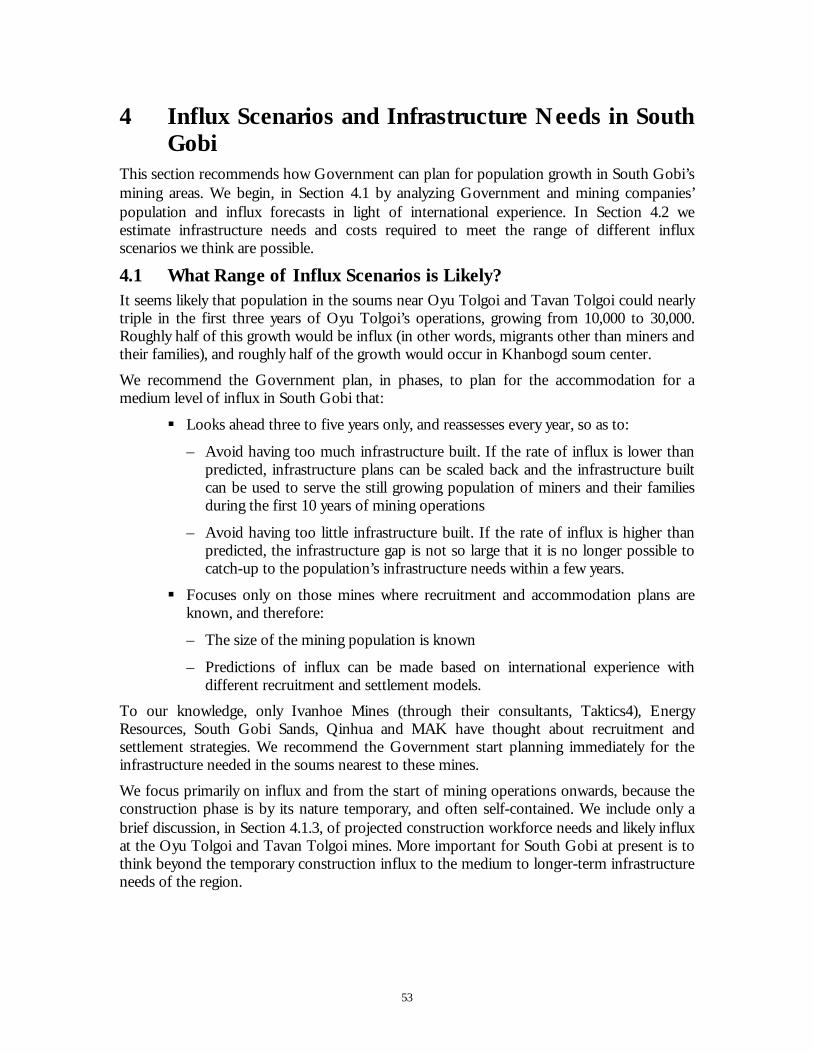

Figure 4.1: Taktics4 Predictions for Population Growth in Khanbogd 53

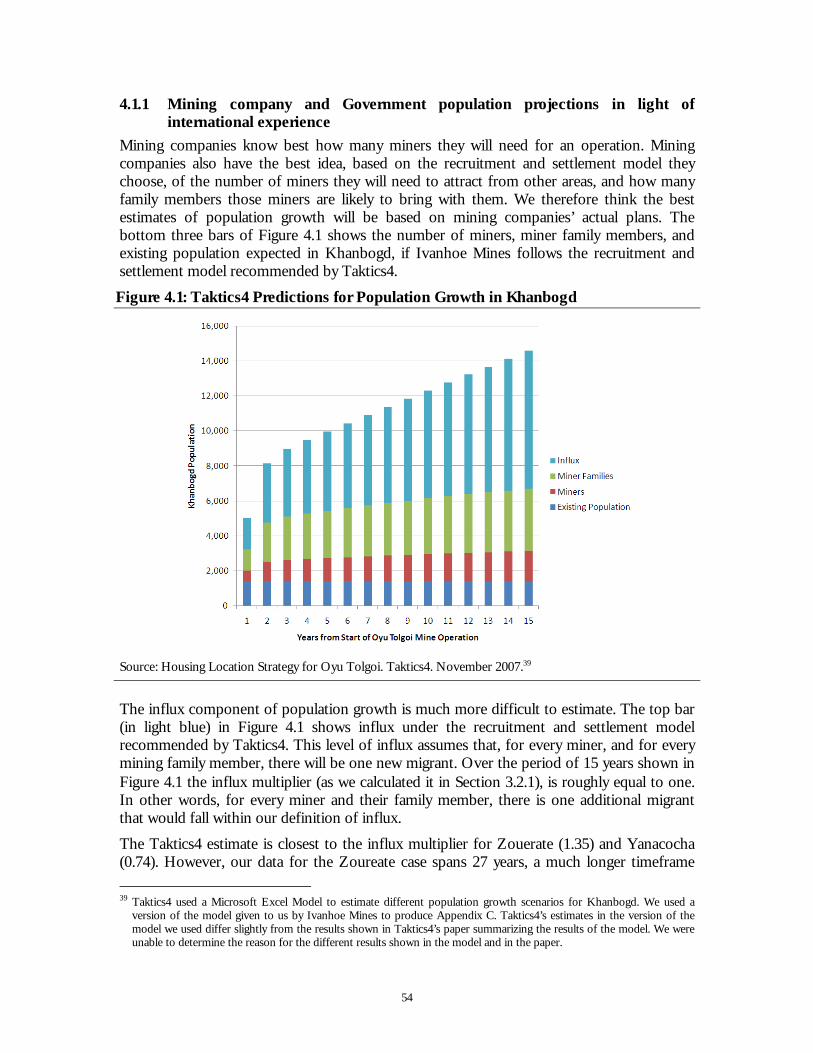

Figure 4.2: Khanbogd Influx with MoCUD Population Growth Assumptions 54

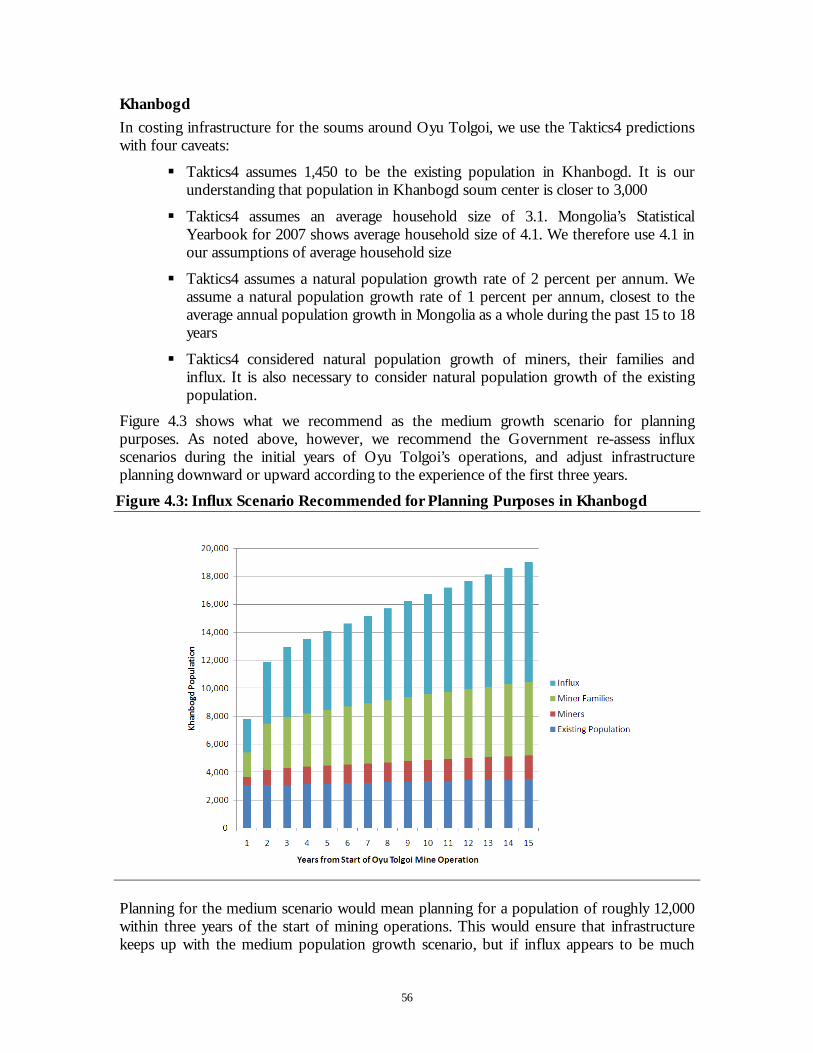

Figure 4.3: Influx Scenario Recommended for Planning Purposes in Khanbogd 55

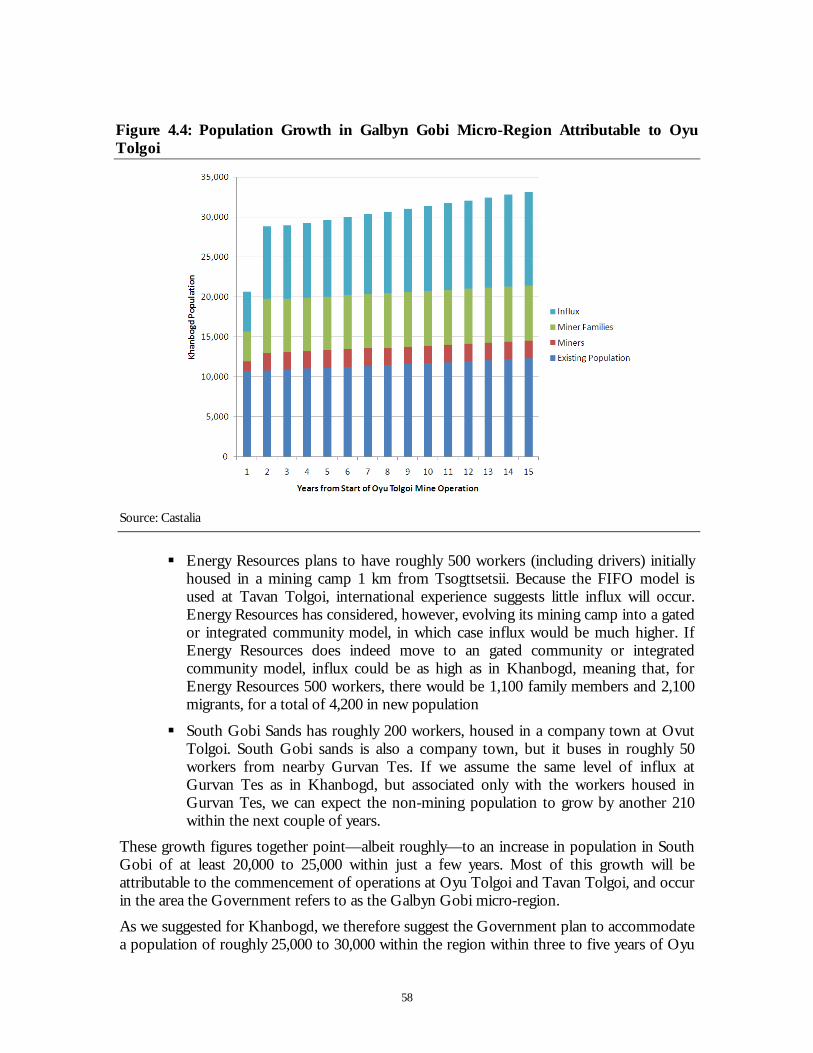

Figure 4.4: Population Growth in Galbyn Gobi Micro-Region Attributable to Oyu Tolgoi 57

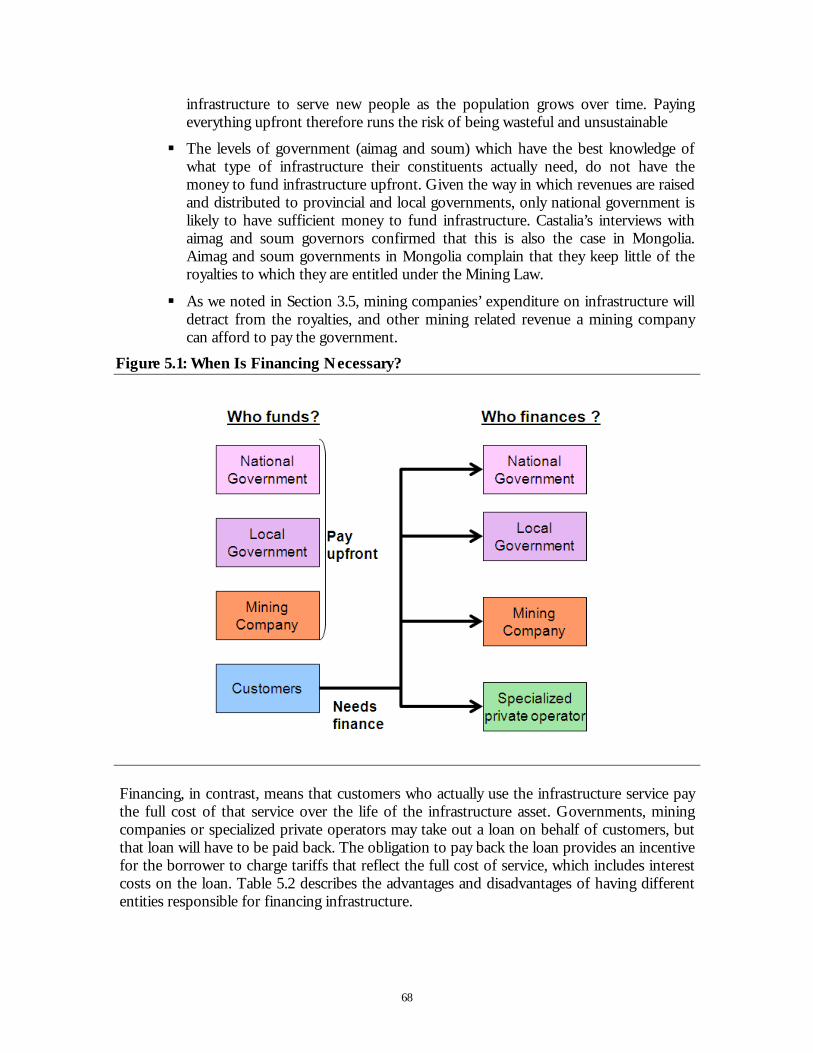

Figure 5.1: When Is Financing Necessary? 67

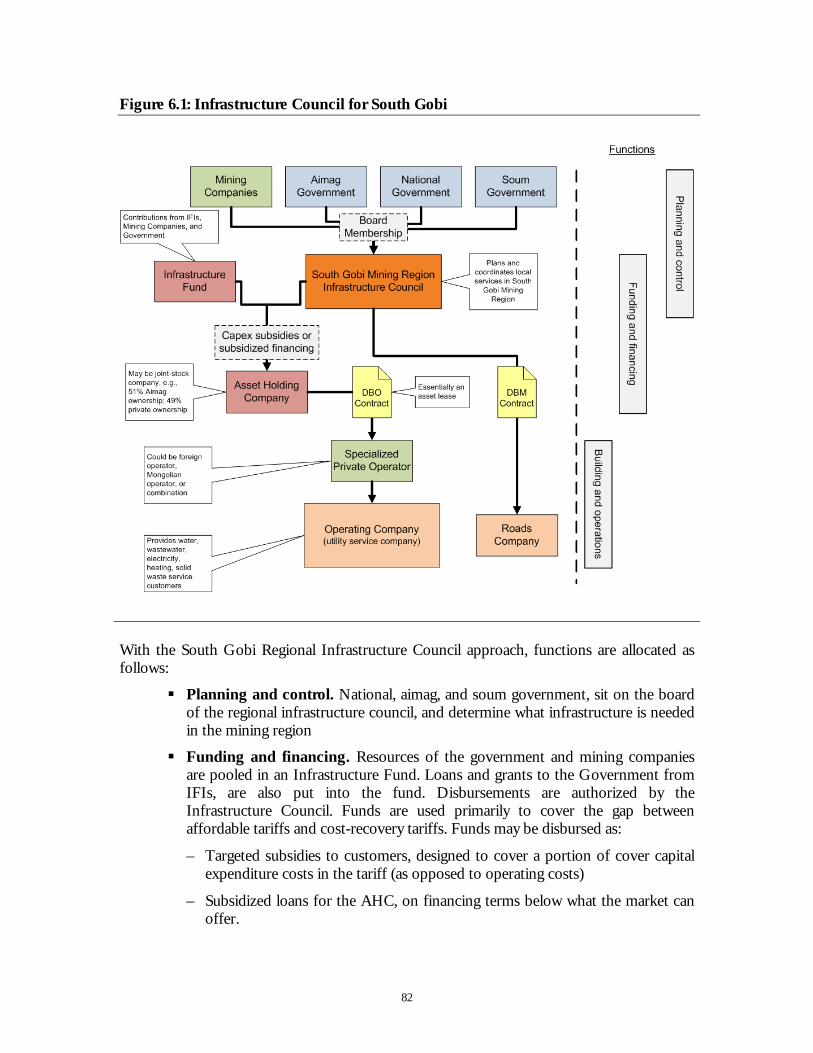

Figure 6.1: Infrastructure Council for South Gobi 81

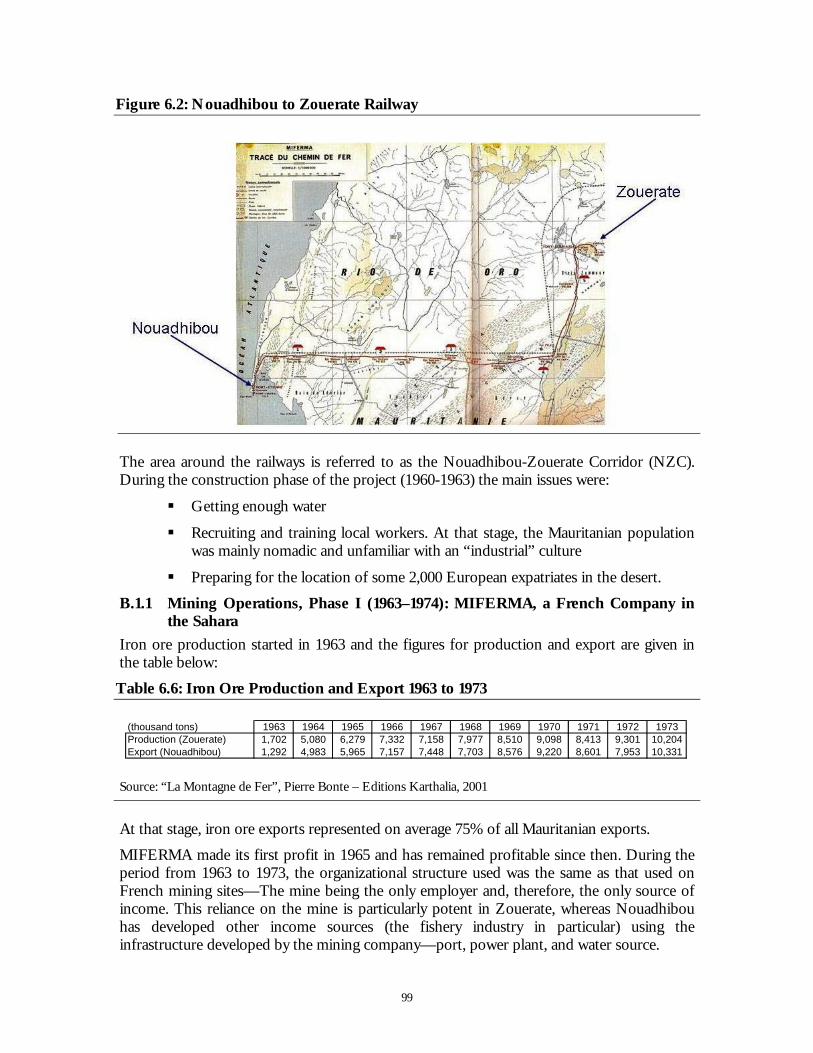

Figure 6.2: Nouadhibou to Zouerate Railway 98

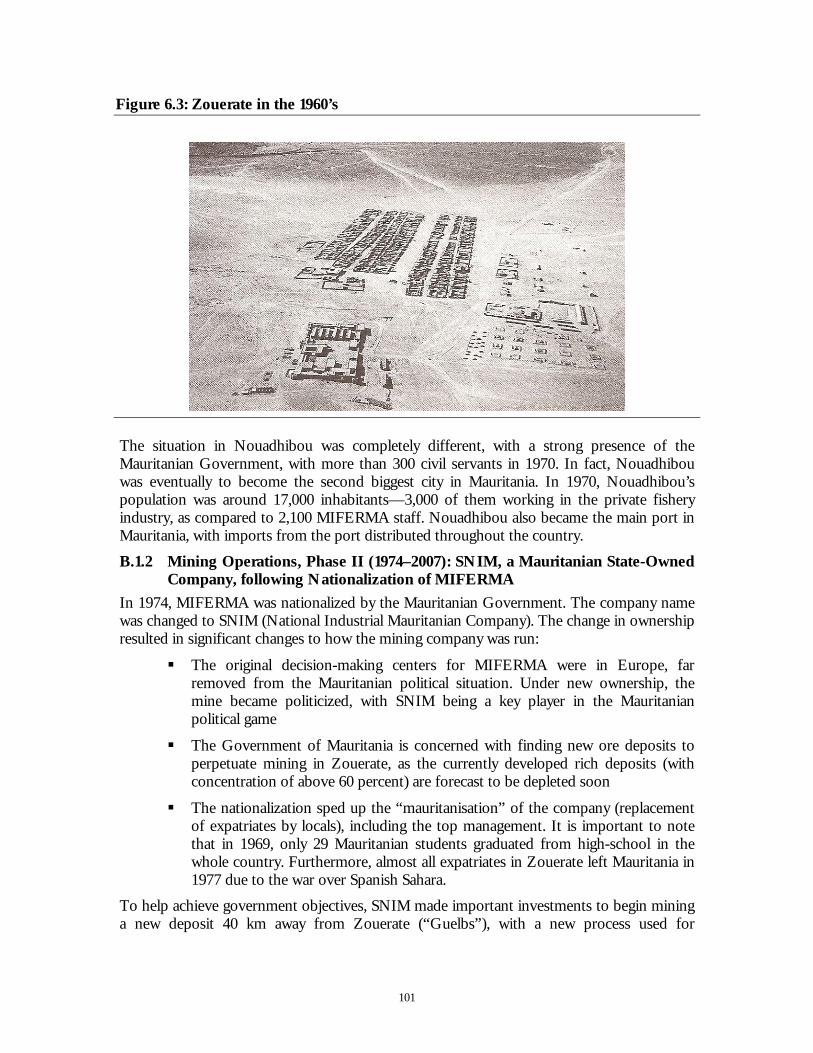

Figure 6.3: Zouerate in the 1960’s 100

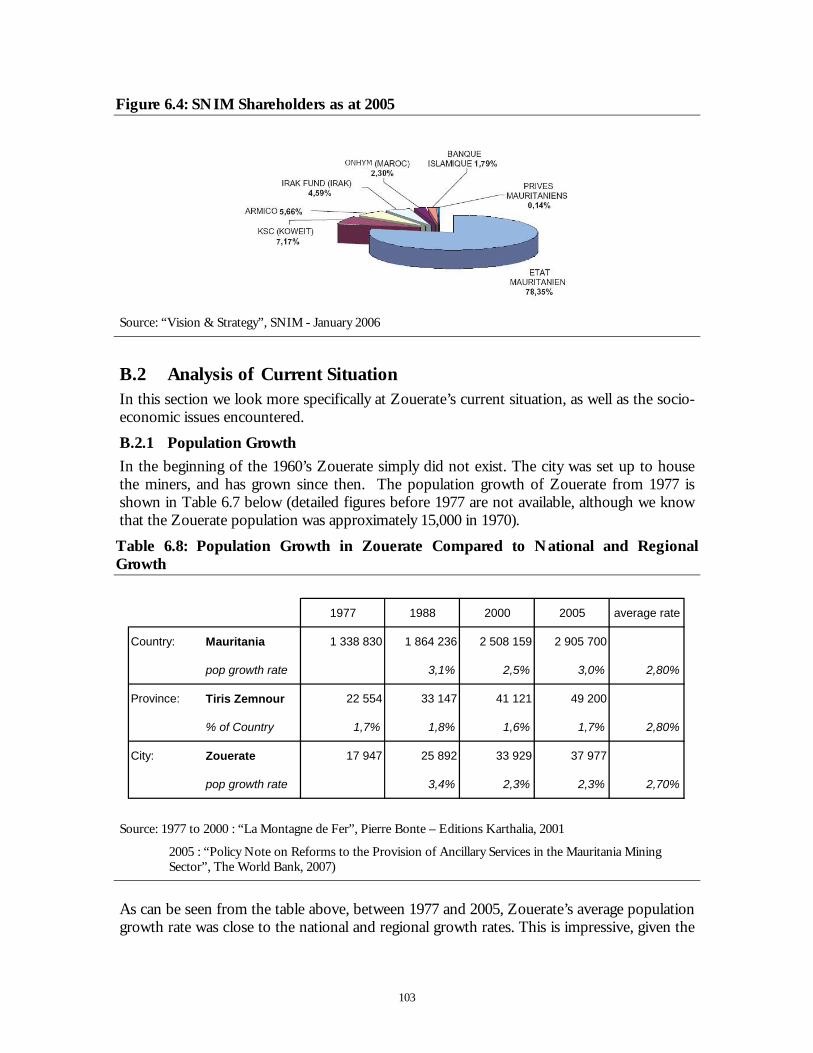

Figure 6.4: SNIM Shareholders as at 2005 102

Figure 6.5: Zouerate in 2006 103

Figure 6.6: Anchors Ready to Be Shipped from Zouerate to Nouadhibou 106

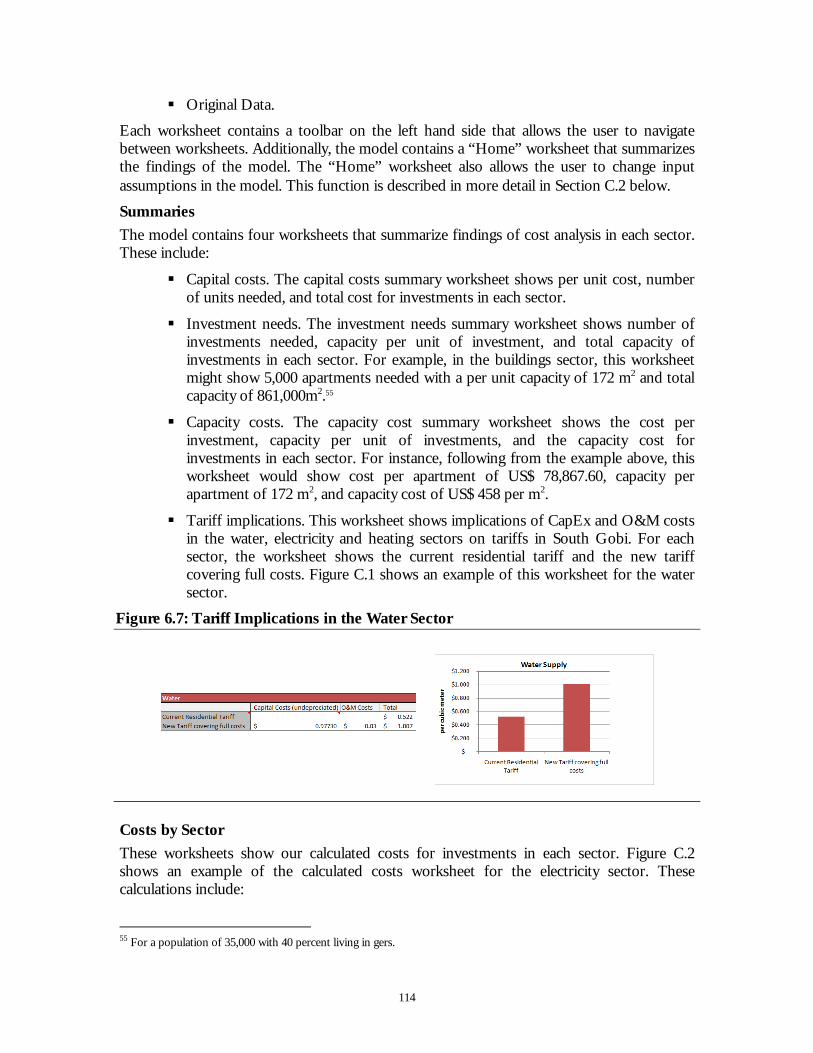

Figure 6.7: Tariff Implications in the Water Sector 113

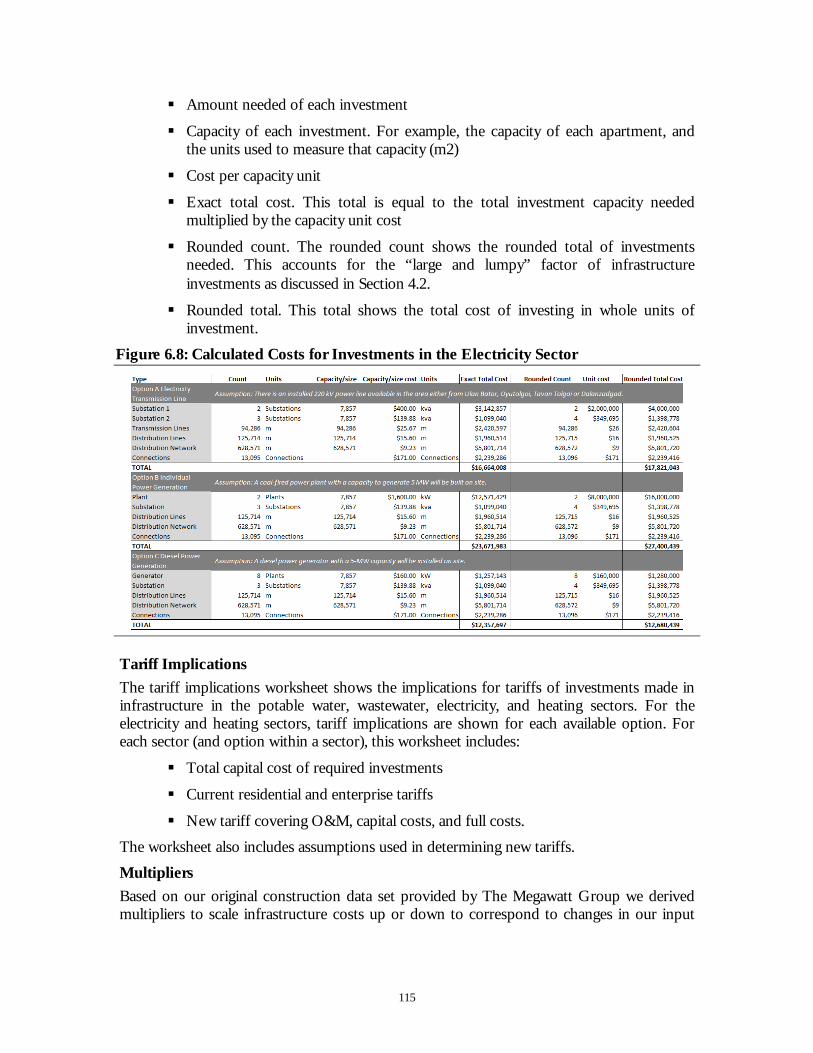

Figure 6.8: Calculated Costs for Investments in the Electricity Sector 114

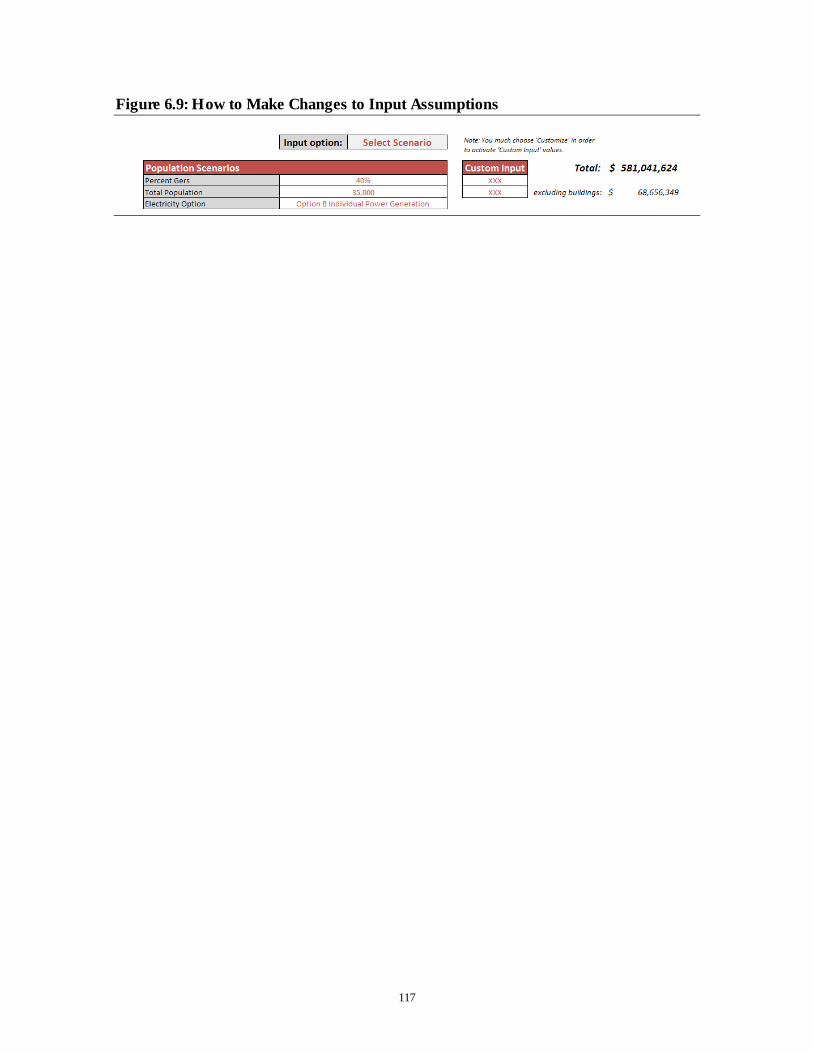

Figure 6.9: How to Make Changes to Input Assumptions 116

Boxes Box 3.1: Gated Community: The Núcleo Urbano de Carajás and

Parauapebas, Brazil 27

Box 3.3: Housing Shortages in Limpopo Province, South Africa 28

Box 3.3: Mineral Industry Booms and Housing Prices 29

Box 3.4: The Inti Raymi Foundation 39

Box 3.5: Yanacocha Association and Yanacocha Women’s Association 40

Box 3.5: Lihir Islands’ Village Development Scheme, Papua New Guinea 41

Box 3.6: QMM’s Community Relations Program 42

Box 3.7: KMCL’s Social Development Program 42

Box 6.1: The Pilbara Development Commission 79

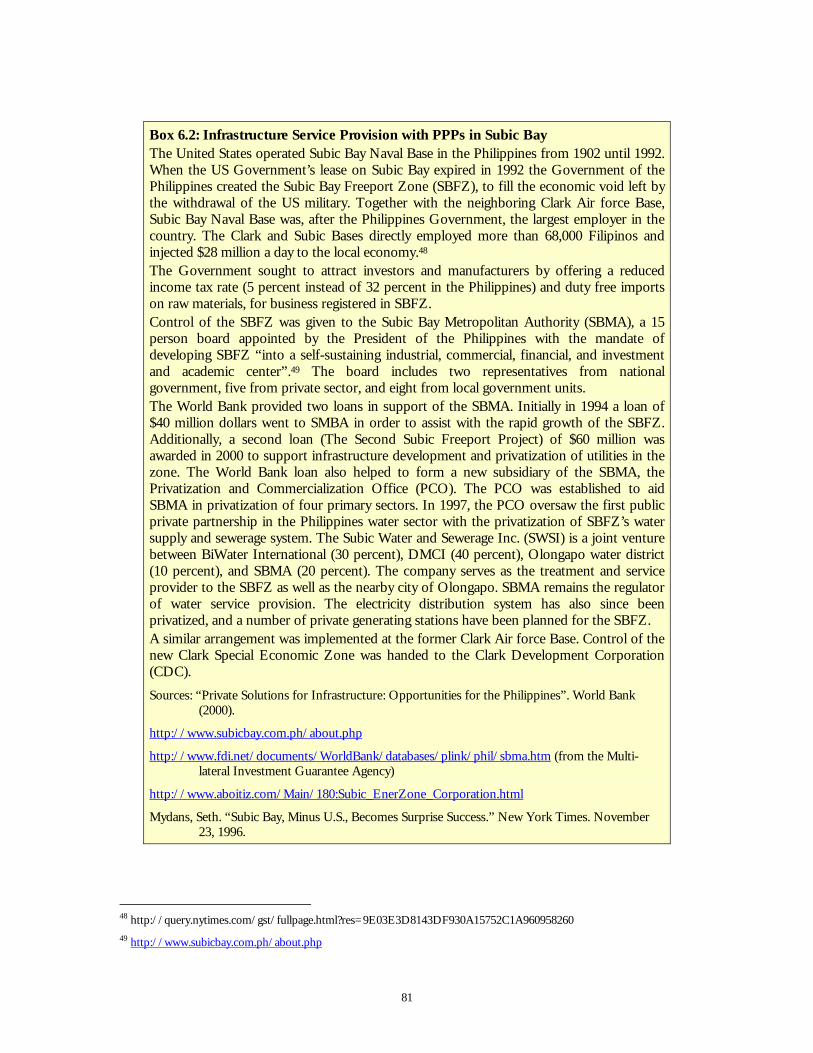

Box 6.1: Infrastructure Service Provision with PPPs in Subic Bay 80

i

Executive Summary What is the context for this work?

The economic opportunities created by large new mines in Mongolia’s South Gobi region are likely to attract migrants. These migrants will need infrastructure services currently in short supply in South Gobi and the surrounding aimags.

An increase in the demand for infrastructure in South Gobi presents, on the one hand, opportunities for economic growth, and on the other hand, the potential for economic, social and political problems.

What is the purpose of this paper?

The purpose of this paper is to inform the Government’s thinking about the development of population centers around the mines in South Gobi; helping it to make the most of the opportunities for economic growth, while minimizing the potential for economic, social and political problems. More specifically, the World Bank has asked Castalia to:

Review international experience with population influx to mining regions. Throughout this paper, we define “influx” as migrants, other than miners and their families, who come to an area in search of economic opportunities or infrastructure created directly or indirectly by a mining operation

Determine which infrastructure services will be needed to support population influx near the mines in South Gobi aimag, and how much capacity will need to be built

Estimate the cost of the infrastructure needed Identify options for providing the infrastructure the new populations will need, and

help the Government of Mongolia (“the Government”) identify the advantages and disadvantages of each of these options.

Why does influx matter?

Mining offers governments opportunities for improvement in national, regional and local economic welfare and living conditions. However, international experience has shown that towns or settlements near mines are often ill prepared to deal with dramatic population influx. High levels of influx can lead to degradation of living conditions, tensions between locals and migrants, and hardship for migrants whose expectations of economic opportunity fall short. Squalor, degradation and hardship result.

What plans are there to accommodate influx?

The Government of Mongolia has put considerable thought into population growth in South Gobi’s mining areas, and the infrastructure needed to accommodate that growth. Some of the mining companies operating in South Gobi have also developed their own population projections and their own plans for recruiting and housing workers. Unfortunately, the government and mining company plans for soum-level development differ considerably from one another, as do the various ministries’ plans for regional development.

What are Government’s plans to accommodate influx?

A Regional Development Concept (RDC), approved by the Mongolian Parliament in 2001, defines the policy for urban and rural development in Mongolia through 2020.1 The Ministry of Construction and Urban Development (MoCUD) has projected population growth over the next one to two decades, and developed plans for both regional and soum-level communal infrastructure in South Gobi based on the RDC. Several other Government ministries, including MoCUD; the Ministries of Road, Transport and Tourism; Fuel and Energy; and Infrastructure and Trade, have also developed plans for regional infrastructure in South Gobi. Because of the burgeoning mining industry in South Gobi, the Government also

1 Parliament Resolution No. 57.

ii

developed a more specific plan for what it calls the Galbyn Gobi micro-region. The Galbyn Gobi micro-region is defined as the area to be directly affected by mines at Tsagaansuvraga, Oyu Tolgoi and Tavan Tolgoi. MoCUD’s consultants have predicted that the population of micro-region, which is now 10,500, will grow to roughly 120,000 by 2020. Consultants to MoCUD have outlined two possible plans for developing infrastructure in the micro-region. One plan, envisions development dispersed throughout five soums in the micro-region. A second plan would create two new towns, one located between the Tavan Tolgoi and Oyu Tolgoi mine sites, and another located near the Tsaagansuvraga mining area. In addition to these soum-level plans, a number of ministries have developed plans for large-scale regional infrastructure investments in roads, rail, electricity, and water supply to serve the mines and the soums in the micro-region.

What are mining companies plans to accommodate influx?

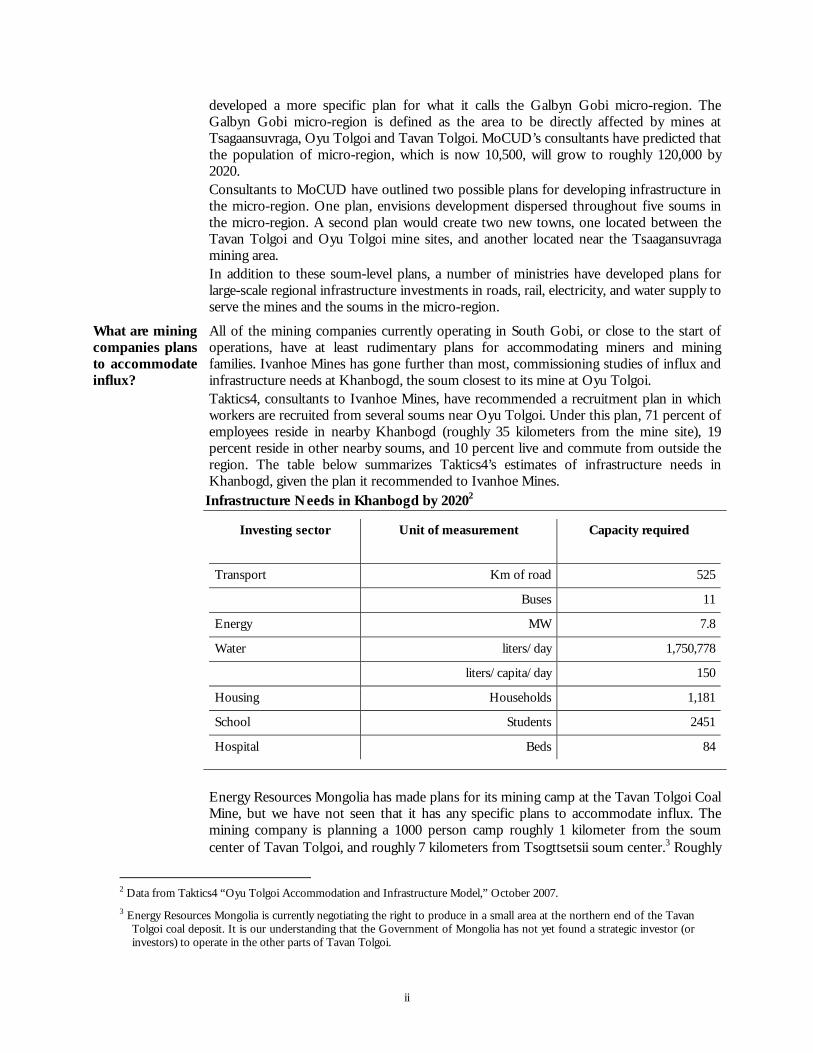

All of the mining companies currently operating in South Gobi, or close to the start of operations, have at least rudimentary plans for accommodating miners and mining families. Ivanhoe Mines has gone further than most, commissioning studies of influx and infrastructure needs at Khanbogd, the soum closest to its mine at Oyu Tolgoi. Taktics4, consultants to Ivanhoe Mines, have recommended a recruitment plan in which workers are recruited from several soums near Oyu Tolgoi. Under this plan, 71 percent of employees reside in nearby Khanbogd (roughly 35 kilometers from the mine site), 19 percent reside in other nearby soums, and 10 percent live and commute from outside the region. The table below summarizes Taktics4’s estimates of infrastructure needs in Khanbogd, given the plan it recommended to Ivanhoe Mines.

Infrastructure Needs in Khanbogd by 20202

Investing sector Unit of measurement Capacity required

Transport Km of road 525

Buses 11

Energy MW 7.8

Water liters/day 1,750,778

liters/capita/day 150

Housing Households 1,181

School Students 2451

Hospital Beds 84

Energy Resources Mongolia has made plans for its mining camp at the Tavan Tolgoi Coal Mine, but we have not seen that it has any specific plans to accommodate influx. The mining company is planning a 1000 person camp roughly 1 kilometer from the soum center of Tavan Tolgoi, and roughly 7 kilometers from Tsogttsetsii soum center.3 Roughly

2 Data from Taktics4 “Oyu Tolgoi Accommodation and Infrastructure Model,” October 2007. 3 Energy Resources Mongolia is currently negotiating the right to produce in a small area at the northern end of the Tavan

Tolgoi coal deposit. It is our understanding that the Government of Mongolia has not yet found a strategic investor (or investors) to operate in the other parts of Tavan Tolgoi.

iii

500 to 600 workers will fly-in, fly out from the camp, and be housed in pre-fabricated, dormitory style housing. The prefabricated housing will have 24-hour electricity and water supply, heating, air conditioning, and indoor sewerage. Another 500 workers (predominantly drivers) will live permanently in gers next to the prefabricated housing, but within the camp gates.

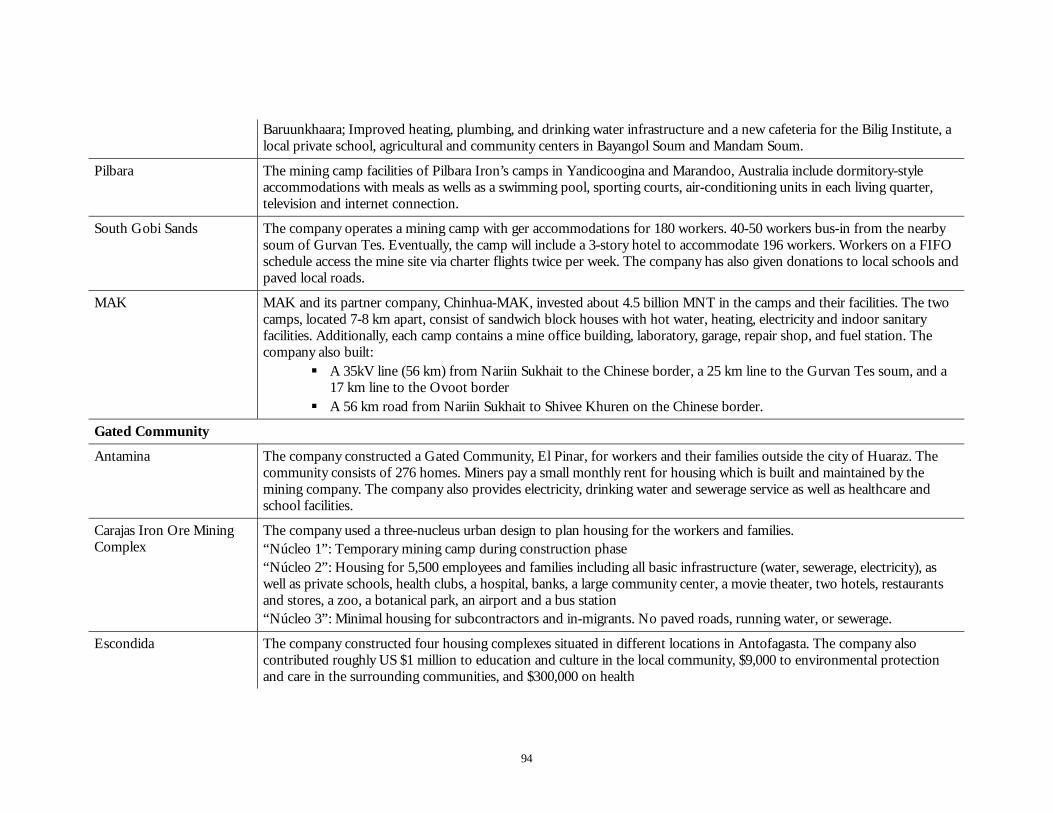

South Gobi Sands owns two coal mines at the Ovoot-Tolgoi mine site in South Gobi Aimag. The company began operations in April 2008. South Gobi Sands currently has a mining camp with ger accommodations for 180 workers. Roughly 40 to 50 workers are bused in and out from the nearby soum of Gurvan Tes every two weeks. All other workers are flown in and out from Ulaanbaatar. South Gobi sands is planning a 3-story hotel to replace the gers in 2009. The hotel will accommodate 196 workers.

Mongolian Alt Corporation (MAK) owns and operates two mining operations at the Nariin Sukhait coal deposit, near Ovoot-Tolgoi. Currently, all workers are accommodated in camps at the mine sites. The two camps, located 7-8 km apart, consist of sandwich block houses with hot water, heating, electricity and indoor sanitary facilities. Each camp also contains a mine office building, laboratory, garage, repair shop, and fuel station.

International experience offers five lessons …

International mining experience indicates five lessons for development of mining areas in Southern Mongolia. The lessons come from a review of more than 20 examples of mining experience in North and South America, Africa, and Australasia.

1. Influx can cause problems

Influx can cause degradation of living conditions, tensions between locals and migrants, and hardship for migrants whose expectations of economic opportunity fall short. Problems result, in particular, when: People move to areas near mines in hope of work, but find none. These migrants

then often live in harsh climates with no work and no services. This was the case for many migrants who moved to the Vila de Parauapebas near Brazil’s Carajas Iron Ore Complex. Parauapebas was planned primarily to accommodate suppliers to the mine and to the mine workers and their families living in a nearby gated town. The mining company spent US$3 million in infrastructure in Parauapebas, but the investment was not enough to keep up with massive number of migrants that came in search of jobs

Money is provided for infrastructure services, but failures in planning, management, and operations prevent the local community from benefiting. For example, in Limpopo, South Africa, the mining company, Anglo Platinum, offered the majority of its workers a “living out allowance”. Because of a severe housing shortage, many workers ended up in informal dwellings without water, electricity, or sewerage service

Mines close down, leaving communities with little to no economic support. For example, when Gecamines, a Congolese state-owned mining company, drastically scaled back its operations in the late 1990s, the mining company was forced to shut down all the infrastructure services it provided to the surrounding community including schools, hospitals, clinics and worker housing.

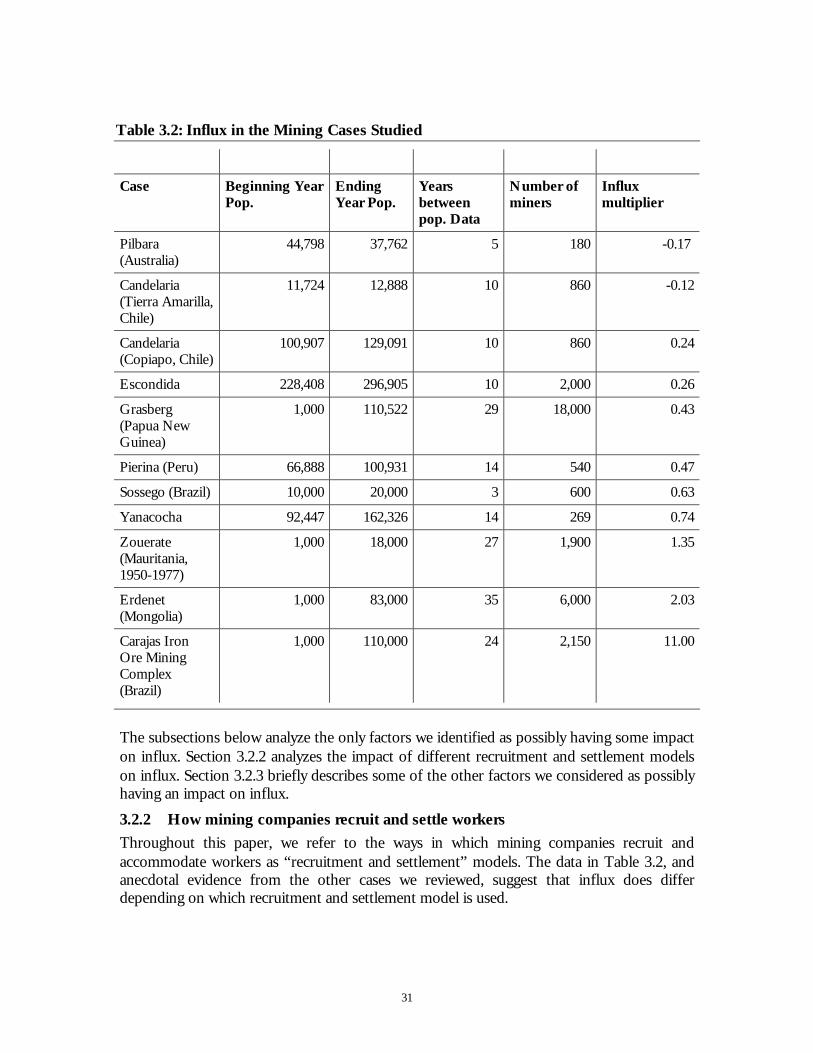

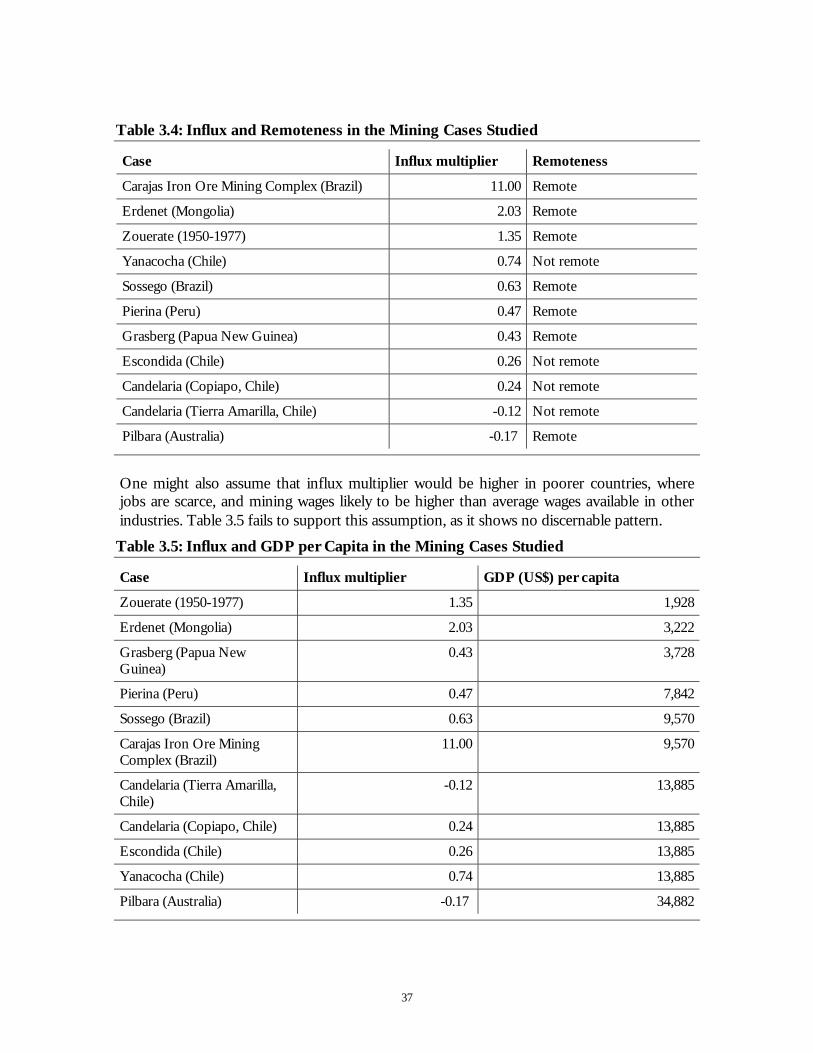

2. Influx is hard to predict, but recruitment and settlement strategies matter

The mining cases we reviewed show a wide range of influx, and offer little explanation of what causes it. We considered a range of factors as possible causes of influx, but only recruitment and settlement models—the way in which workers are recruited and accommodated by the mining companies—appear to have an impact on influx. Influx is generally lower when the Fly-in, fly-out (FIFO) or Bus-in, bus-out (BIBO) recruitment and settlement models are used rather than other models. The four main models for recruitment and settlement are:

iv

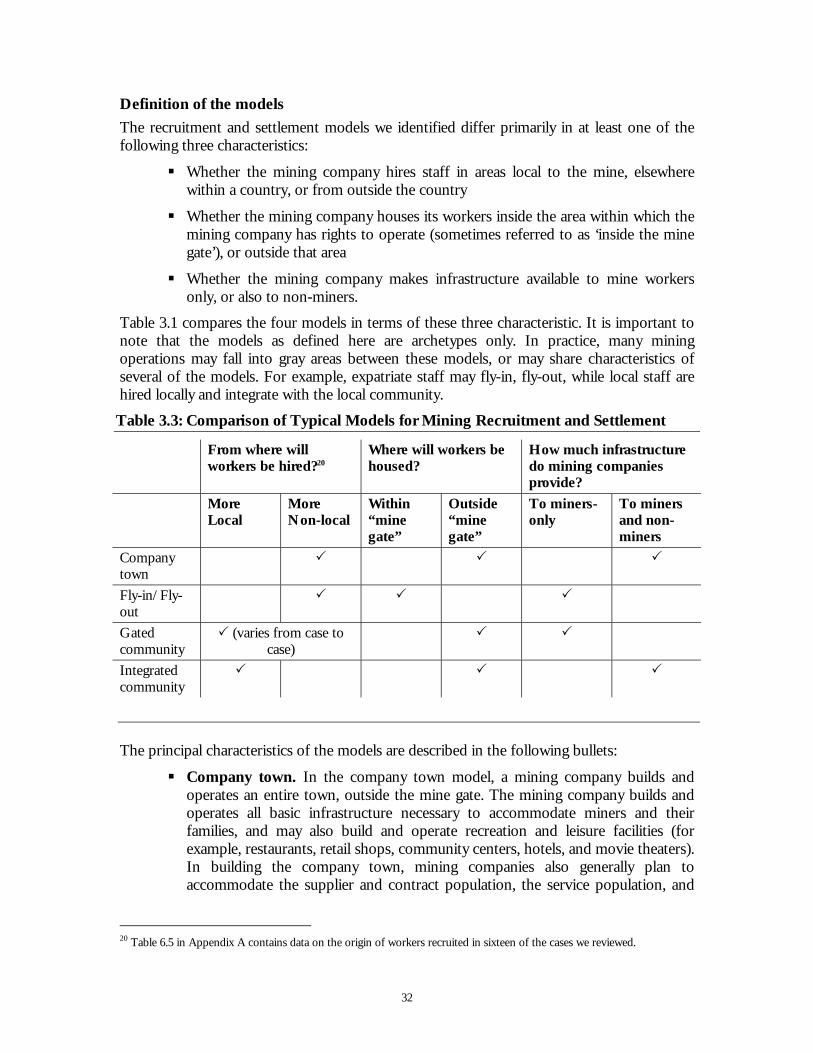

Company town. In the company town model, a mining company builds and operates an entire town, outside the mine gate. The mining company builds and operates all basic infrastructure necessary to accommodate miners and their families, and may also build and operate recreation and leisure facilities (for example, restaurants, retail shops, community centers, hotels, and movie theaters). In building the company town, mining companies also generally plan to accommodate the supplier and contract population, the service population, and possibly some of the existing population. Recruitment strategies in the company town model vary considerably from case to case. The recruitment of miners may be from local areas or may be from distant areas

Fly-in, fly-out (FIFO). In the fly-in, fly out model, workers and their families live in regions, often metropolitan areas, located far away from the site of mining operations. Typically, workers commute to the mining site on a “14-days on/7-days off” rotation or “9 days on/5 days off” rotation. In this model, there is no recruitment from, and no infrastructure development in local communities. The mining company builds a mining camp, inside the mine gate, with enough infrastructure for mine employees only. A variation on the FIFO model is the bus-in, bus-out (BIBO) model used where commuting distances allow for it, or airstrips are not available

Integrated community. In the integrated community model workers and their families live within existing communities located near the mine. The mining company contributes to infrastructure development in these communities in varying degrees. If the mining company does provide some infrastructure, non-miners are typically not excluded from that infrastructure. Workers are often recruited locally under this model, but may also be recruited from elsewhere, and required to relocate to the existing towns around the mine

Gated community. In the gated community model, workers and their families are housed in a new neighborhood bordering on, or within an existing local community. The gated community is outside the mine gate, and has most infrastructure necessary to support miners their families. The mining company may make use of some existing infrastructure, such as roads or electricity connections, to provide service to the gated community, and may expect that, for leisure and entertainment, workers will leave the gated community. Workers may be hired locally, from elsewhere within the country, or from abroad.

3. Coordination between governments, local communities, and mining companies can avoid problems caused by influx

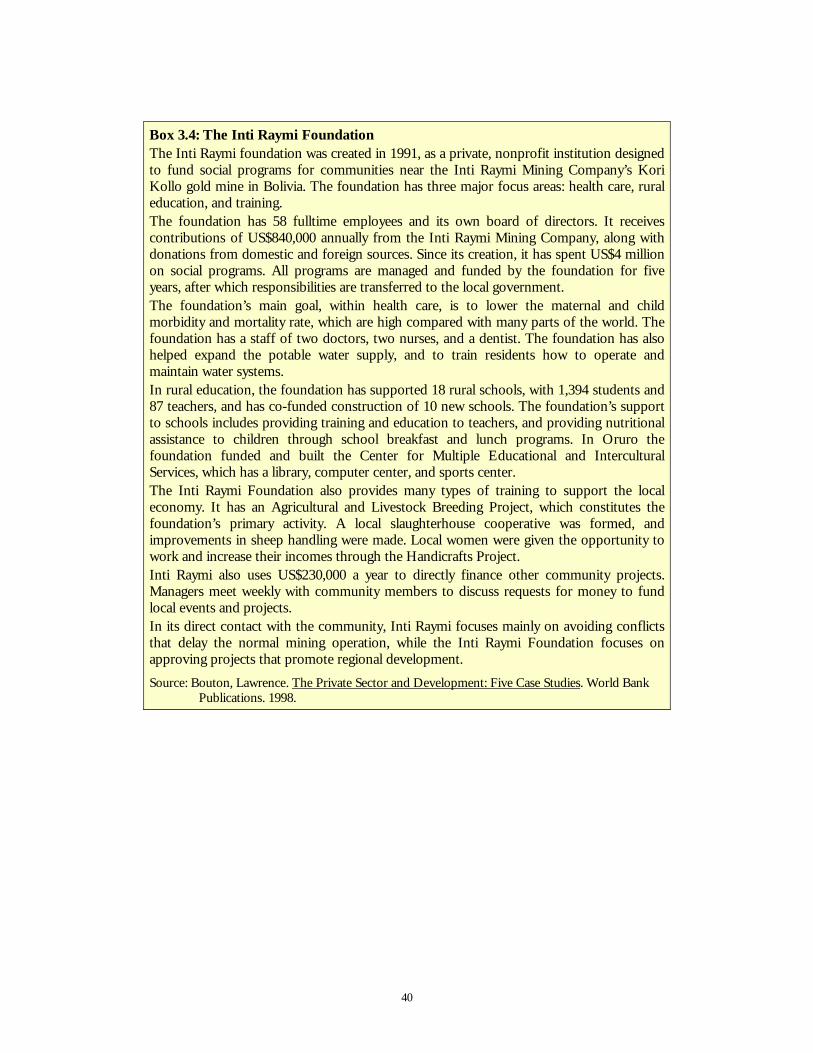

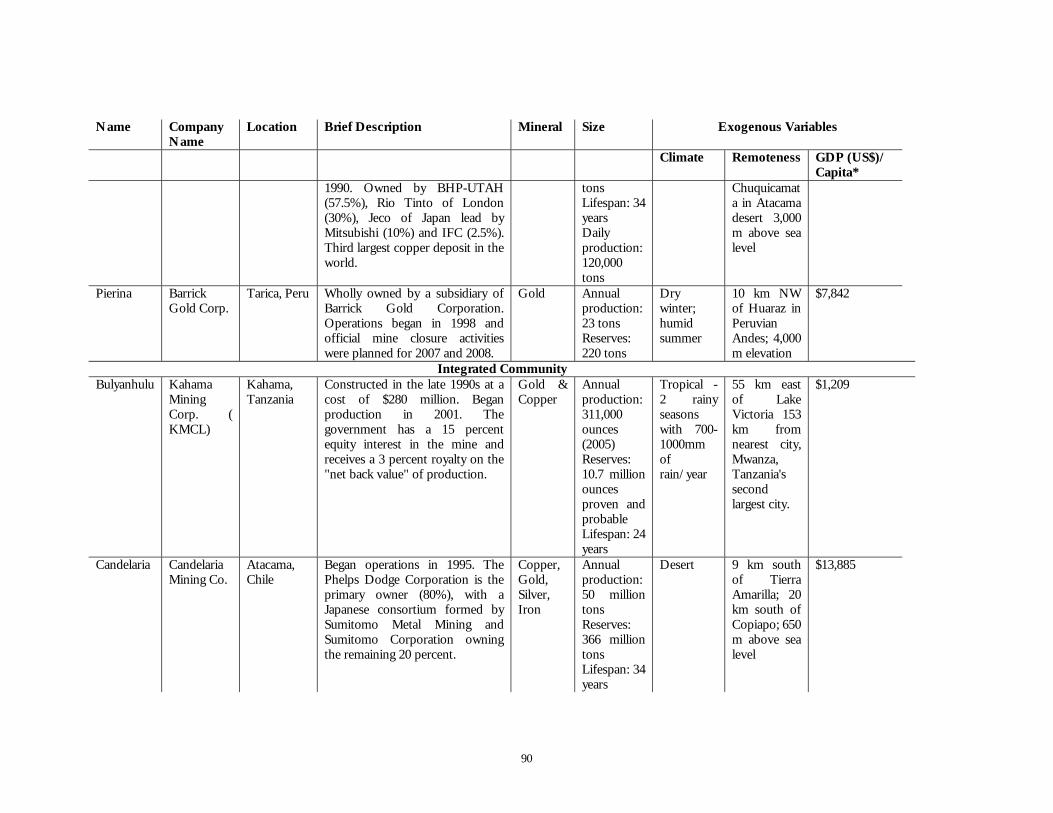

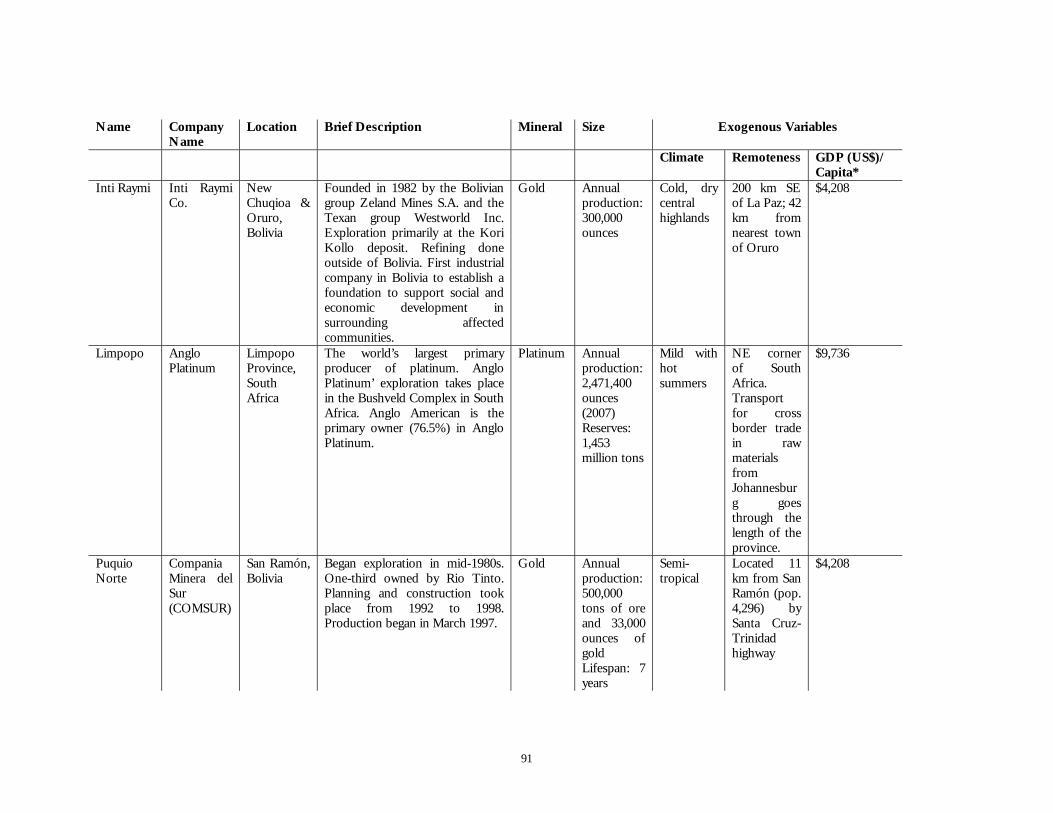

Governments and mining companies can reduce the problems caused by influx through coordination and planning. Mining experience in Paraupebas and Limpopo (described above) stand out as examples of how governments and mining companies failed to accommodate the infrastructure needs of local populations. In Parauapebas, infrastructure was planned to accommodate miners, but not influx. In Limpopo, cash was made available to accommodate workers, but without regard to the capacity of the market to deliver affordable housing. Miners and non-miners were therefore left without proper infrastructure. Experiences at several mining areas throughout the world offer better examples of how the needs of local populations can be accommodated. Mining areas in Peru, Bolivia, Papua New Guinea, Madagascar, and Tanzania offer examples of how local development programs or foundations were established to let mining companies, local governments, and donors to pool funds and jointly manage the expenditure of funds for infrastructure. For example: The Inti Raymi foundation was created in 1991, as a private, nonprofit institution

designed to fund social programs for communities near the Inti Raymi Mining Company’s Kori Kollo gold mine in Bolivia. The foundation has three major focus areas: health care, rural education, and training. The foundation has 58 fulltime

v

employees and its own board of directors. It receives contributions of US$840,000 annually from the Inti Raymi Mining Company, and donations from other domestic and foreign sources

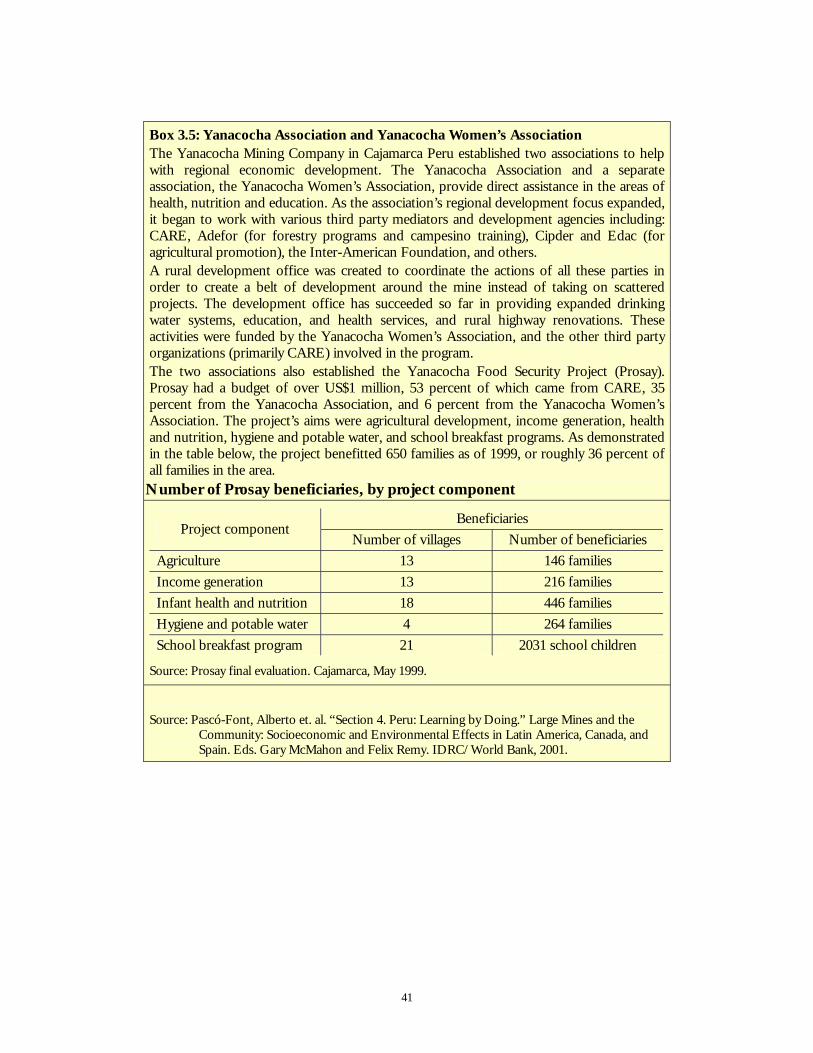

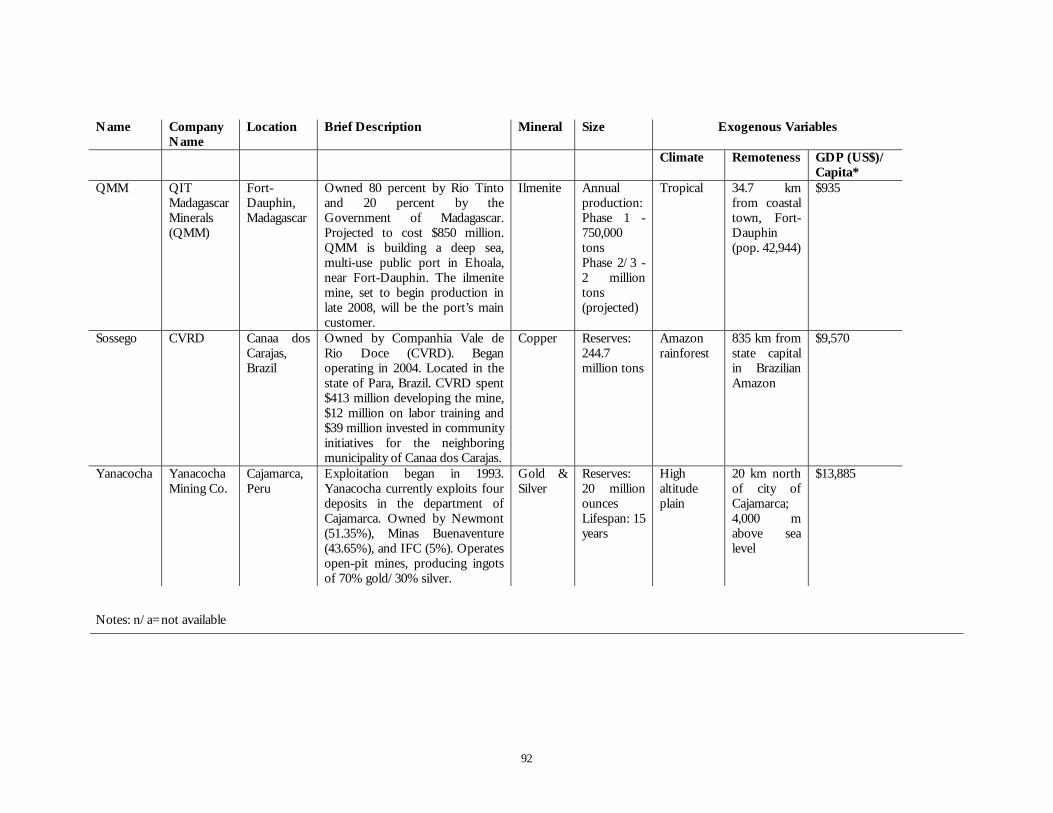

The Yanacocha Mining Company established two associations to help with regional economic development near its gold and silver mine in Cajamarca, Peru. The Yanacocha Association and a separate association, the Yanacocha Women’s Association, provide assistance in the areas of health, nutrition and education. In infrastructure, the associations have provided expanded drinking water systems, education, and health services, and rural highway renovations

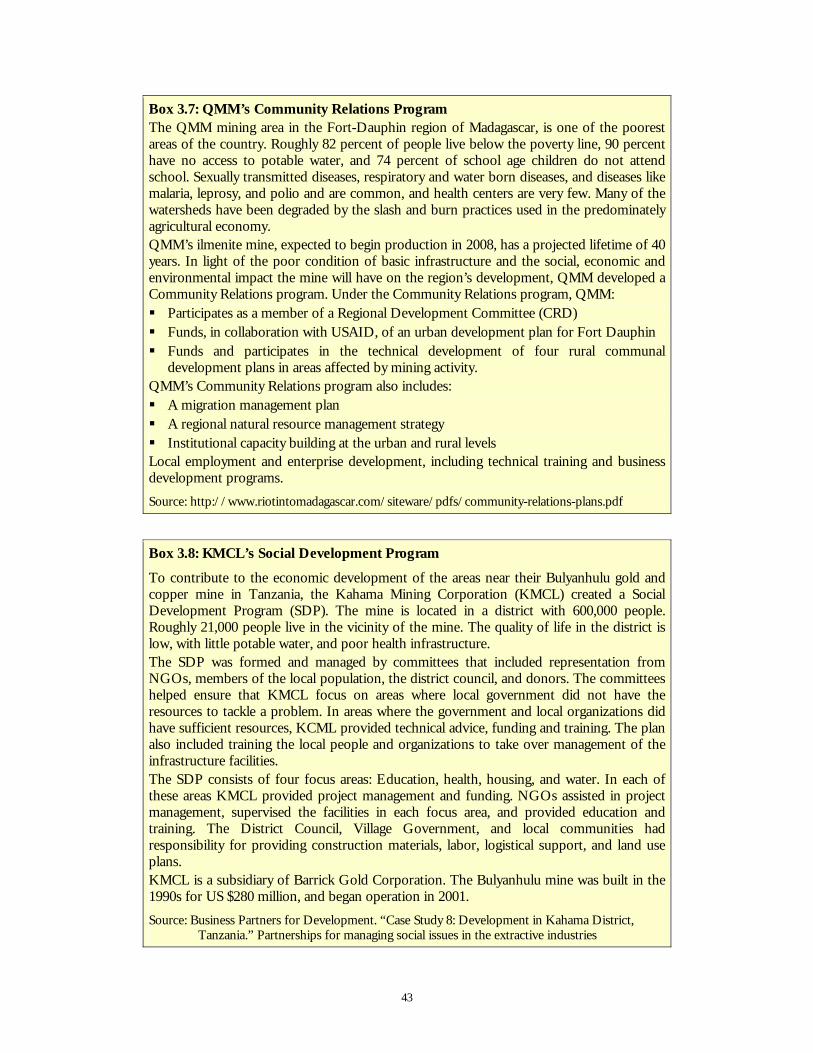

To contribute to the economic development of the areas near their Bulyanhulu gold and copper mine in Tanzania, the Kahama Mining Corporation (KMCL) created a Social Development Program (SDP). The SDP consists of four focus areas: Education, health, housing, and water. The SDP was formed and managed by committees that included representation from NGOs, members of the local population, the district council, and donors. The committees helped ensure that KMCL focus on areas where local government did not have the resources to tackle a problem. In areas where the government and local organizations did have sufficient resources, KCML provided technical advice, funding and training. NGOs assisted in project management, supervised the facilities in each focus area, and provided education and training. The District Council, Village Government, and local communities had responsibility for providing construction materials, labor, logistical support, and land use plans.

4. Each recruitment and settlement model has advantages and disadvantages

Mining operations have both positive and negative social impacts. We found that social impacts differ depending on how workers are recruited and accommodated, and we therefore group the advantages and disadvantages by the recruitment and settlement models introduced earlier. The positive and negative social impacts of each recruitment and settlement model are as follows: Company Towns. Company towns show positive and negative social impacts.

Positive social impacts of the company town are the health benefits of the family-centered style of accommodations. Negative social impacts come from the town’s dependence on the mining company for employment and economic activity. When mines close, families must often move in order to find employment opportunities elsewhere. Few alternative employment opportunities typically exist due to the remoteness of many mining operations, and where such opportunities do exist, mine workers may not have transferable skills

FIFO. FIFO has a positive social impact in that it allows workers some flexibility to choose where they live. Miners’ families also therefore have more flexibility in choosing which jobs to take, and what social infrastructure to live near (for example, schools and hospitals). The only requirement is that they be able to reach the airport from which they are flown to the mine site. FIFO also has a limited cultural, environmental, or economic impact on local areas, because the increase in the mining population is limited to mine workers, and is kept within the mine gate. FIFO’s negative social impacts may include an increase in family dysfunction and parenting problems as a result of workers’ prolonged separation from their families. FIFO also provides no direct jobs or infrastructure near the mine site. This may cause tensions with local populations who feel they should benefit from the mine’s presence

Gated Community. The positive social impacts of the gated community model include the health benefits of workers living with their families, and the more limited cultural, environmental, and economic impact on local areas than under the company town model. Negative social impacts stem from possible social tensions between the mining population and existing population

vi

Integrated Community. Positive social impacts of the integrated community model include the fact that workers can live with their families, and the fact that existing populations around the mine stand to benefit from infrastructure and jobs created by the mine. Negative impacts include the risk of social tensions because of cultural differences or income disparities between the mine workers and existing population.

5. Governments can maximize value from mining by…

A government’s objectives are, generally speaking, to maximize economic welfare for the country. A government can maximize the benefits from mining activity by: Recognizing what motivates mining companies, and how this motivation affects the

decisions mining companies make Having its own clear vision of the tradeoffs between the fiscal benefits (government

revenue from mining activity), and external social benefits (improved welfare for the country as a whole) of mining activity.

…recognizing what motivates mining companies, and…

Private mining companies will generally choose the recruitment and settlement model that promises to earn the most revenue at lowest cost, thereby maximizing profits. Revenues, in a commodity business like mining, where mining companies are generally price takers, depend primarily on volumes extracted. Maximizing profits in the mining business is therefore focused on minimizing costs for any volume extracted. The financial impact on a mining company of each of the recruitment and settlement models are as follows: Company Town. The cost to the mining company of building a company town is

usually higher than the cost to the mining company of other recruitment and settlement models, because of the high levels of capital expenditure required

FIFO. Mining companies see the FIFO model as a better alternative to the company town model because upfront capital expenditures on physical infrastructure are lower. FIFO also allows the mining companies to draw from a larger labor pool.

Gated Community. The gated community model requires more upfront infrastructure investment than FIFO, because the gated community must support workers and their families living near the mine on a permanent basis. The upfront capital costs of the gated community model are therefore likely to be higher than in the FIFO model, but lower than in the company town model

Integrated Community. The integrated community model generally requires less capital expenditure than the company town and gated communities’ models. The financial implications for the mining companies vary depending on how much the companies spend on infrastructure or social services in the communities near the mine. This in turn depends on what infrastructure already exists to support workers, and what additional infrastructure the mining company feels it needs to build in order to comply with its social license to operate.

…understanding the tradeoffs between cash and non-cash benefits.

A government’s primary goal in granting a mining concession should be to maximize the value to the country as a result of mining. Generally, governments receive this value from a mining operation as: Cash, through taxes on the mining companies’ operations or royalties from the mine Other external benefits (net of external costs) that add to national welfare, but are

difficult to measure and accrue to the population. For example, training provided by mine companies may lift the skill level of the community as a whole over time, or employment provided in service industries may offer attractive jobs in areas that currently have little formal employment

Governments can increase the cash they receive through negotiations with mining companies, or by holding open competitions for mineral resources and awarding concessions to the highest bidders. However, mines can only yield as much value as their product can be sold for. Because of this, there will be tradeoffs between governments’

vii

goal to maximize cash income from mining, and its desire to have mining companies spend money on other things like infrastructure or training. The recruitment and settlement model chosen therefore affects how much cash mining companies are able to pay. To the extent that mining companies are forced to spend money building infrastructure, they will have less available to pay in taxes and royalties. An example of the tradeoffs between cash payments and infrastructure provision can be seen in Bolivia, where the country’s Mining Code permits companies to invest in community infrastructure and to offset this against tax liabilities.

What range of influx scenarios is most likely in Southern Mongolia?

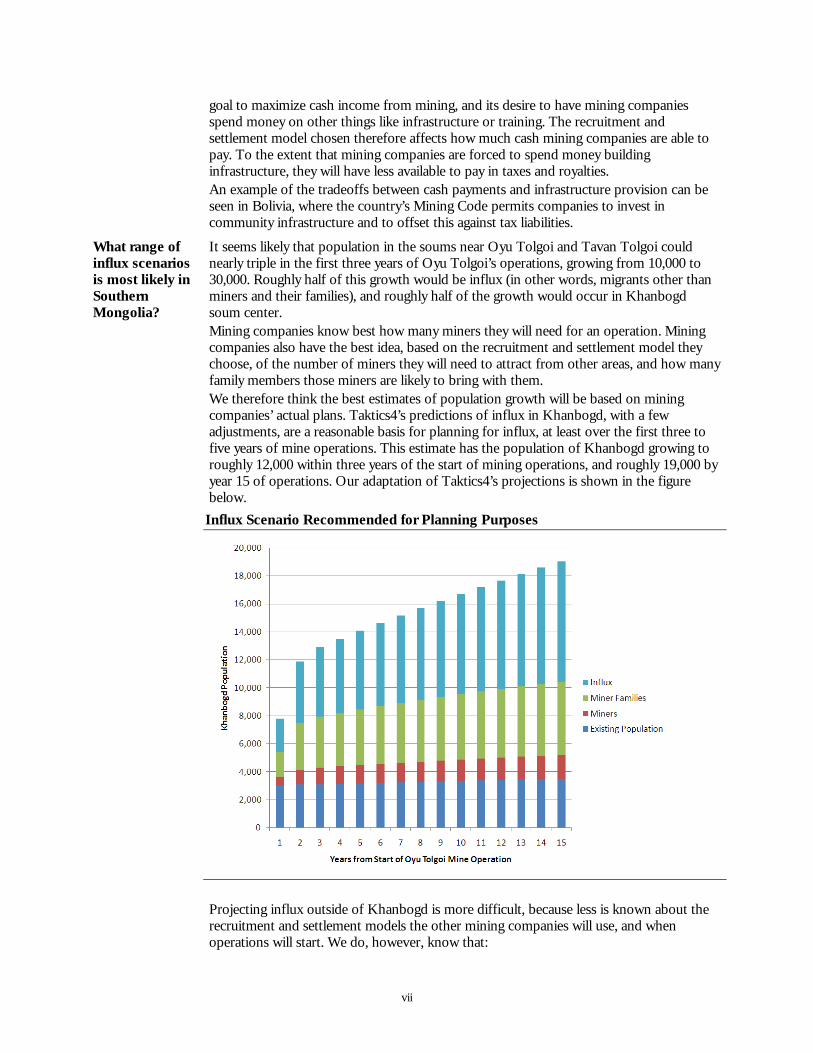

It seems likely that population in the soums near Oyu Tolgoi and Tavan Tolgoi could nearly triple in the first three years of Oyu Tolgoi’s operations, growing from 10,000 to 30,000. Roughly half of this growth would be influx (in other words, migrants other than miners and their families), and roughly half of the growth would occur in Khanbogd soum center. Mining companies know best how many miners they will need for an operation. Mining companies also have the best idea, based on the recruitment and settlement model they choose, of the number of miners they will need to attract from other areas, and how many family members those miners are likely to bring with them. We therefore think the best estimates of population growth will be based on mining companies’ actual plans. Taktics4’s predictions of influx in Khanbogd, with a few adjustments, are a reasonable basis for planning for influx, at least over the first three to five years of mine operations. This estimate has the population of Khanbogd growing to roughly 12,000 within three years of the start of mining operations, and roughly 19,000 by year 15 of operations. Our adaptation of Taktics4’s projections is shown in the figure below.

Influx Scenario Recommended for Planning Purposes

Projecting influx outside of Khanbogd is more difficult, because less is known about the recruitment and settlement models the other mining companies will use, and when operations will start. We do, however, know that:

viii

Under the recruitment and settlement model recommended by Taktics4, there will be roughly 1,500 to 2,000 more miners and their families settled in soums outside of Khanbogd. If we assume the same level of influx in the other soums where Oyu Tolgoi’s miners will live, South Gobi’s population will grow by nearly 50 percent within the first five years of operations, from 45,000 to 65,000-70,000

Energy Resources plans to have roughly 500 workers (including drivers) initially housed in a mining camp 1 kilometer from Tsogttsetsii. Because the FIFO model is used at Tavan Tolgoi, international experience suggests little influx will occur. Energy Resources has considered, however, evolving its mining camp into a gated or integrated community model, in which case influx would be much higher. If Energy Resources does indeed move to an gated community or integrated community model, influx could be as high as in Khanbogd. This means that for Energy Resources’ 500 workers, there would be 1,100 family members and 2,100 migrants, for a total of 4,200 in new population

South Gobi Sands has roughly 200 workers, housed in a mining camp at Ovut Tolgoi. South Gobi Sands also uses BIBO to a limited extent, bussing in roughly 50 workers from nearby Gurvan Tes. If we assume the same level of influx at Gurvan Tes as in Khanbogd, but associated only with the workers housed in Gurvan Tes, we can expect the non-mining population to grow by another 210 within the next couple of years.

These growth figures together point—albeit roughly—to an increase in population in South Gobi of at least 20,000 to 25,000 within just a few years.

How to plan for the influx?

We recommend the Government plan to accommodate influx in South Gobi in phases. We recommend the government plan for a medium influx growth scenario in South Gobi that: Looks ahead 3 to 5 years only, and reassesses every year, so as to:

Avoid having too much infrastructure built. If the rate of influx is lower than predicted, infrastructure plans can be scaled back and the infrastructure built can be used to serve the still growing population of miners and their families during the first 10 years of mining operations

Avoid having too little infrastructure built. If the rate of influx is higher than predicted, the infrastructure gap is not so large that it is no longer possible to catch-up to the population’s infrastructure needs within a few years.

Focuses only on those mines where recruitment and accommodation plans are known, and therefore: The size of the mining population is known Predictions of influx can be made based on international experience with different

recruitment and settlement models. In Khanbogd, this means planning for a population of roughly 12,000 within three years of the start of mining operations. This would ensure that infrastructure keeps up with the medium population growth scenario, but if influx appears to be much lower during three years of mining operations, building plans can be slowed or halted without creating too much spare capacity. If influx continues to be low, the infrastructure built in years one to three will still be needed to serve the existing population, the miners and their families. Even with no influx, the existing population and the mining population will reach roughly 8,000 by year three, and nearly 10,000 by year 10. Most infrastructure assets built in years one to three should continue to be useful through year 10. The infrastructure built in year 3 could therefore be used to serve the growing population of miners and their families through year 10. For South Gobi as a whole, this means planning to accommodate a population of roughly 25,000 to 30,000 in the Galbyn Gobi micro-region within the first three to five years of

ix

Oyu Tolgoi’s operations. If influx is slower than predicted, the Government can readjust its plans after year three, without stranding too much capacity. The mining and existing populations in the micro-region will exceed 20,000 by year 15 of operations, without any influx, and without the start of operations at the Tavan Tolgoi sites still lacking a strategic investor.

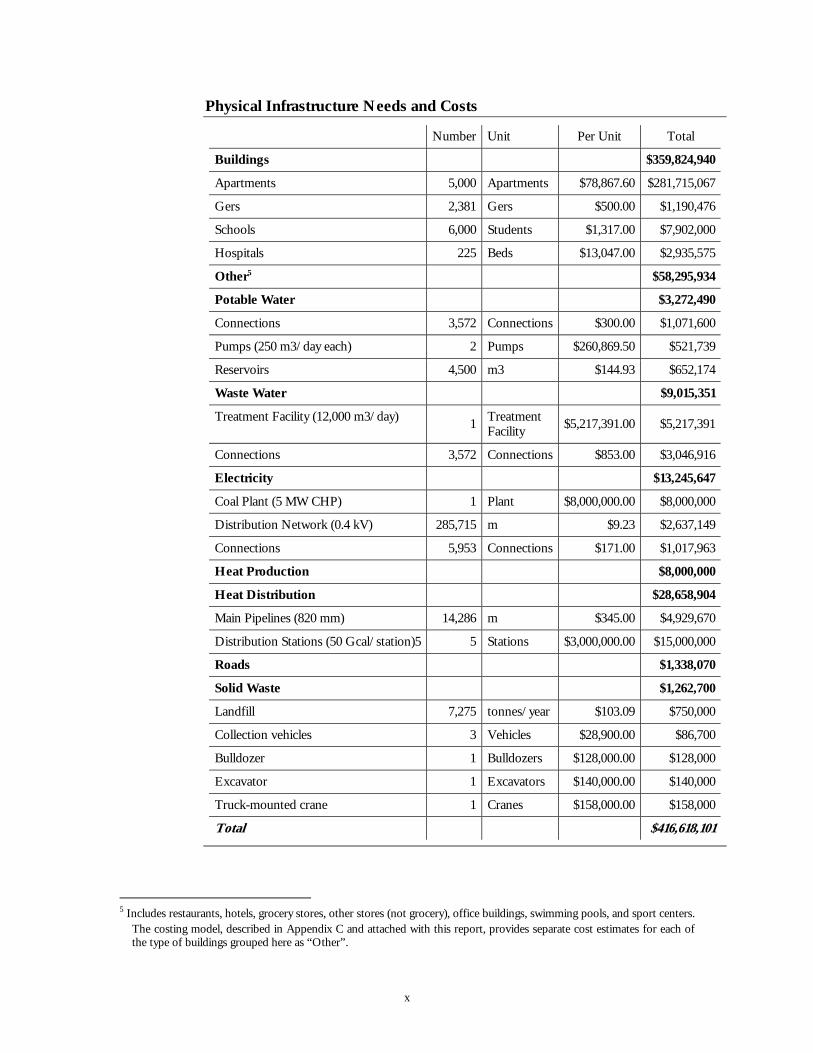

How much infrastructure is needed and what will it cost?

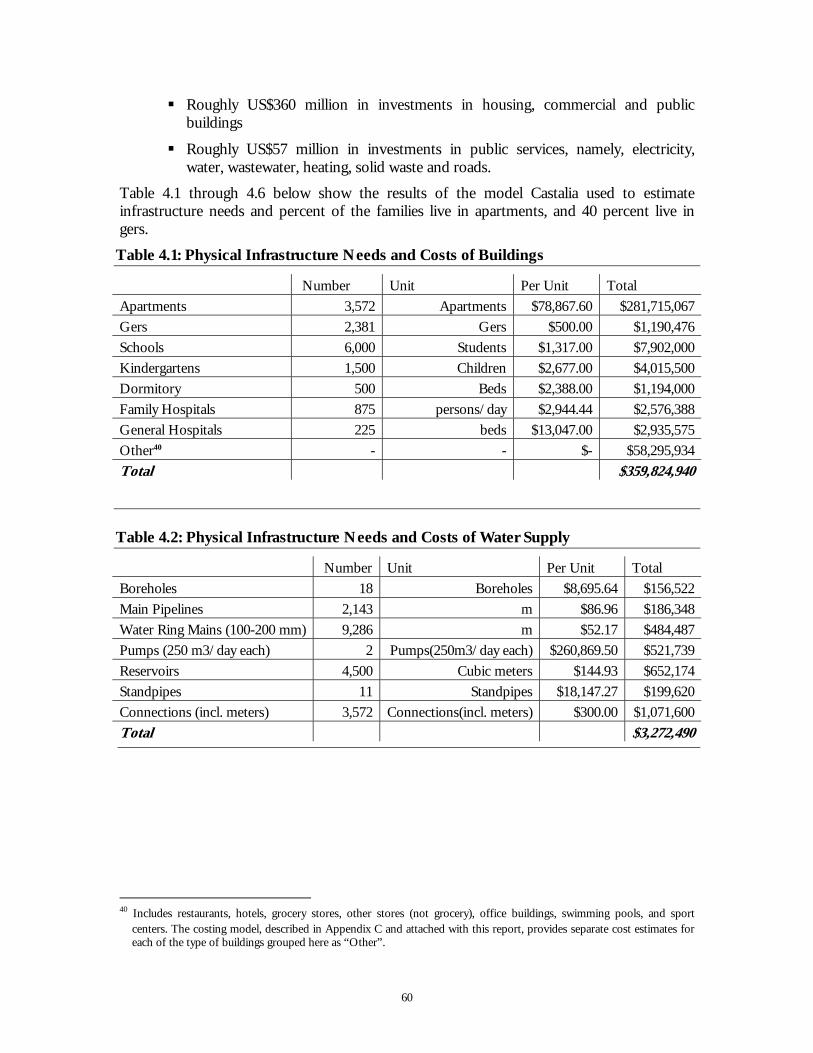

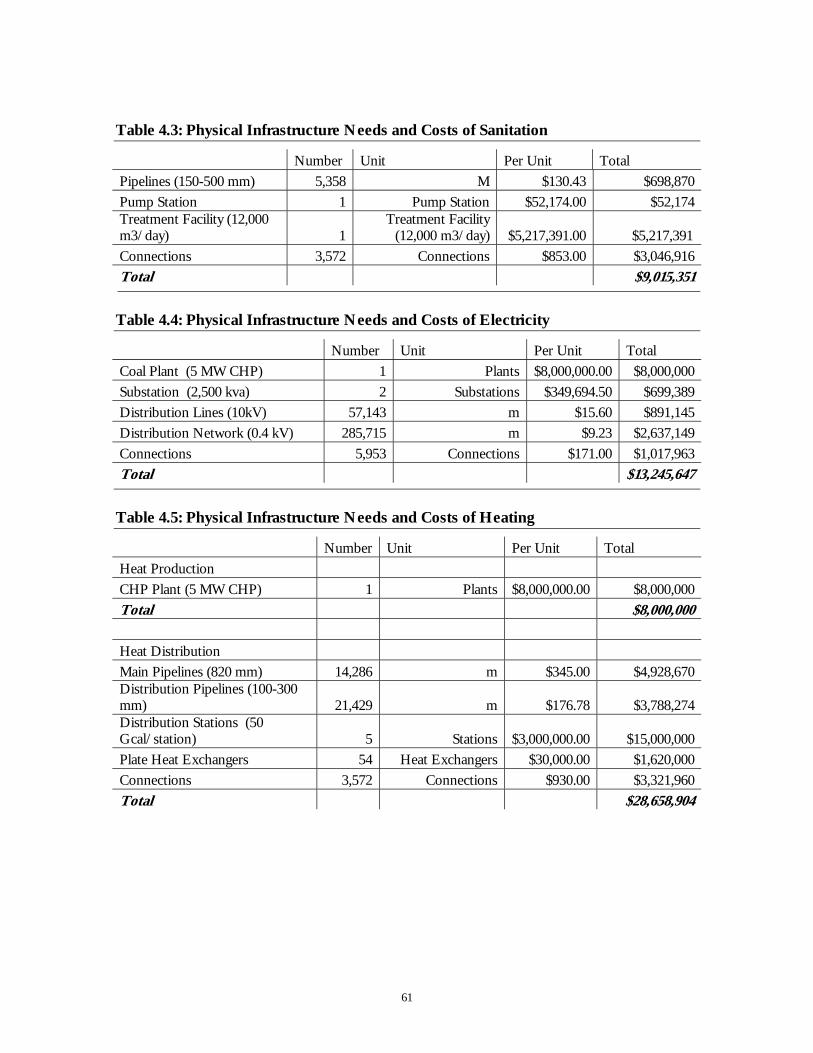

If, as we have suggested could happen, the population of the Galbyn Gobi micro-region grows to 25,000 by year three of mining operations, we expect the soums in the micro-region to need roughly US$417 million in building and infrastructure investment.4 Of this total, we expect the soums in the micro-region will need: Roughly US$360 million in investments in housing, commercial and public buildings Roughly US$57 million in investments in public services, namely, electricity, water,

wastewater, heating, roads, and solid waste. The table below shows the results of the model Castalia used to estimate infrastructure needs and infrastructure costs, assuming a population of 25,000 in which 60 percent of the families live in apartments, and 40 percent live in gers.

4 Throughout this paper, we use the term infrastructure broadly to include: utility services (water, wastewater, heating, and

electricity), solid waste, housing, public administration buildings, and social infrastructure (hospitals and schools).

x

Physical Infrastructure Needs and Costs

Number Unit Per Unit Total

Buildings $359,824,940

Apartments 5,000 Apartments $78,867.60 $281,715,067

Gers 2,381 Gers $500.00 $1,190,476

Schools 6,000 Students $1,317.00 $7,902,000

Hospitals 225 Beds $13,047.00 $2,935,575

Other5 $58,295,934

Potable Water $3,272,490

Connections 3,572 Connections $300.00 $1,071,600

Pumps (250 m3/day each) 2 Pumps $260,869.50 $521,739

Reservoirs 4,500 m3 $144.93 $652,174

Waste Water $9,015,351

Treatment Facility (12,000 m3/day) 1 Treatment Facility $5,217,391.00 $5,217,391

Connections 3,572 Connections $853.00 $3,046,916

Electricity $13,245,647

Coal Plant (5 MW CHP) 1 Plant $8,000,000.00 $8,000,000

Distribution Network (0.4 kV) 285,715 m $9.23 $2,637,149

Connections 5,953 Connections $171.00 $1,017,963

Heat Production $8,000,000

Heat Distribution $28,658,904

Main Pipelines (820 mm) 14,286 m $345.00 $4,929,670

Distribution Stations (50 Gcal/station)5 5 Stations $3,000,000.00 $15,000,000

Roads $1,338,070

Solid Waste $1,262,700

Landfill 7,275 tonnes/year $103.09 $750,000

Collection vehicles 3 Vehicles $28,900.00 $86,700

Bulldozer 1 Bulldozers $128,000.00 $128,000

Excavator 1 Excavators $140,000.00 $140,000

Truck-mounted crane 1 Cranes $158,000.00 $158,000

Total $416,618,101

5 Includes restaurants, hotels, grocery stores, other stores (not grocery), office buildings, swimming pools, and sport centers.

The costing model, described in Appendix C and attached with this report, provides separate cost estimates for each of the type of buildings grouped here as “Other”.

xi

How to meet South Gobi’s infrastructure needs

Providing infrastructure services requires that at least three major functions be fulfilled, namely: Planning and control: Some organization must decide what physical infrastructure is

needed, where it should go, how much capacity is needed, and when that capacity needs to be expanded

Designing, building, operating and maintaining: Some organization must design, build, operate and maintain the physical infrastructure needed to produce and deliver infrastructure services. Once the infrastructure is planned, some organization’s engineers must do a detailed design, some organization must build the infrastructure according to the design

Funding and financing: Someone must pay to have the infrastructure built, and someone must pay for its ongoing operation. Organizations that cannot pay for all of the equipment upfront will have to look for another entity to lend or finance the payments over time.

A single organization may fulfill all of these functions, as happens in the company town model discussed above. Alternatively, the functions may be allocated to multiple organizations. For example, a government may plan and control its roads, but may hire a private sector engineering procurement and construction (EPC) contractor to design and maintain its roads. In Mongolia, the principal organizations that might possibly take responsibility for these different functions include: Government, which may mean

National government Aimag government Soum government

Mining companies A private company, other than the mining company, which may include:

A “specialized private operators”, specialized in delivering infrastructure services A property developer. Mongolia has some recent experience in Ulaanbaatar in which

private property developers build and operate communal services in private housing or apartment complexes.

What are the pros and cons of each institutional option for planning and control?

National governments typically have greater expertise than provincial and local governments, and can best coordinate investments across multiple provinces and soums, and across multiple sectors. This is clearly still the case in Mongolia. Aimag capitals (including Dalanzadgad) rely on national government to run their power plants. The PUSOs, which provide water services in many soums often look to Ulaanbaatar’s Water Supply and Sewerage Authority (USUG) for technical support. On the other hand, national governments are not likely to understand or appreciate the needs of provincial and local populations as well as provincial and local government officials do. National governments are often better at planning and controlling large-scale infrastructure investments than smaller-scale infrastructure investments within provinces, towns and cities. We see evidence of this in Mongolia, where the national government has a lot of plans for transmission lines, roads, and rail lines, but fewer detailed plans for infrastructure within towns near South Gobi’s mines. As shown by our description of the company town recruitment and settlement model, mining companies historically have also played a role in planning and controlling infrastructure. Mining companies, however, may lack the inclination or skills to plan and control infrastructure for towns that include miners as well as non-miners. A government

xii

entity, whether national, provincial, or national, has incentives for planning infrastructure that are better aligned with those of the non-mining populations, and typically has more experience planning infrastructure for towns, and controlling those infrastructure assets. Private property developers have expertise in planning housing complexes, and the infrastructure required to serve those complexes. Private property developers also have a strong business interest in getting infrastructure up and running for their future tenants. Private property developers are not, however, necessarily experts in planning large-scale network infrastructure such as water and wastewater treatment facilities, or heating and electricity production, nor are they required to serve populations that cannot afford, or do not want to live in their apartments or homes.

What are the pros and cons of each institutional option for funding?

We use the term “fund” to mean the same thing as “pay for”. We use the term “fund” as distinct from “finance”. By “finance”, we mean “lend” or “invest in”, with the expectation of receiving ones initial capital expenditure plus a return equal to the time value of money plus some risk premium. If the government or a mining company ‘funds’ all of the infrastructure upfront, there is no need for ‘financing’. The biggest advantage of paying for the entire infrastructure upfront is its simplicity. The biggest disadvantage is that, if the government or the mining company pays upfront, it may not be able or may not be inclined to recover the full costs of service. Governments often have political inclinations to keep tariffs low. Mining companies may similarly feel political or social pressure to keep tariffs low. As a consequence, there may not be enough money coming in to pay to replace the assets when they wear out, or to pay to expand infrastructure to serve new people as the population grows over time.

What are the pros and cons of each institutional option for financing?

Financing, in contrast to funding, means that customers who actually use the infrastructure service pay the full cost of that service over the life of the infrastructure asset. Governments, mining companies or specialized private operators may take out a loan on behalf of customers, but that loan will have to be paid back. The obligation to pay back the loan provides an incentive for the borrower to charge tariffs that reflect the full cost of service, which includes interest costs on the loan. It is often easier and cheaper for national governments to finance infrastructure. National governments often have stronger balance sheets, credit ratings, and better cash flows than provincial or local governments, and can therefore borrow at lower cost. Moreover, a tradition of financing large infrastructure projects from the center, as exists in Mongolia, may make central government financing more attractive because it is easier to understand how it will work. A significant disadvantage of central government financing for infrastructure is that financing typically goes hand in hand with planning and control. As noted above, central governments do not usually know as well as local governments what infrastructure is needed, and how much. Central governments also have many other spending priorities, and limited funds. Mining companies may also finance infrastructure, as in the company town or gated community recruitment and settlement models. Mining companies have strong commercial incentives to finance infrastructure to support their mining operations, and may have easier access to capital. However, mining companies will have less of an incentive to finance infrastructure that is not essential to their operations. The other disadvantages of having a mining companies finance infrastructure is that mining companies are not experts in infrastructure financing, nor will they necessarily have the incentives to minimize a project’s lifetime costs. The higher a project’s lifetime costs, the higher the cost-recovery tariff customers will face, or the higher the subsidy governments will have to pay to help customers afford the tariff.

xiii

Like mining companies and specialized private operators, private property developers will likely have good access to capital, and will be able to move quickly. Private property developers also have a strong incentive to finance the construction of infrastructure so that new owners want to move in. However, private property developers may not have the operational expertise to minimize the lifetime costs of network infrastructure, nor may they have an incentive to minimize those lifetime costs once all of the units are sold.

What are the pros and cons of each institutional option for designing, building, and operating?

In Mongolia, as in many other countries, national governments have more experience designing, building and operating infrastructure than provincial and local governments. National governments, however, are more distant from the customers they are meant to serve, and therefore may not know as well, or care as much as provincial or local governments about what customers want. Mongolia has a tradition of aimag governments providing water, wastewater, solid waste, and in some cases electricity and heating service through PUSOs. Leaving the aimags with responsibility for infrastructure service provision would therefore be a familiar approach, and require few changes to the way in which infrastructure is currently built and operated. The principal disadvantage of having any government entity provide infrastructure services is that governments—whether national, local, or provincial—tend not to be particularly good at running businesses efficiently. Evidence of this in South Gobi can again be seen in the Dalanzadgad’s CHP. Power and heating outages at the plant are common. Only one of the two units at the plant are operational, with operating costs upwards of USD 0.30/kWh, despite the fact that the plant has access to very cheap coal.6 Private companies, unlike most governments, respond well to commercial incentives, and therefore can be given incentives to build and operate infrastructure efficiently. Private mining companies respond well to commercial incentives but designing, building and operating infrastructure for people other than those working in the mine is not part of a mining company’s core business. This means that they are neither particularly motivated nor good at designing, building and operating infrastructure. Mining companies may agree to provide some infrastructure to non-miners, but they will typically seek to limit their responsibility to designing and building, not operating the infrastructure. Private property developers may be good at designing and building infrastructure, but are less likely to specialize in building and operating infrastructure other than housing. Moreover, their interest in providing infrastructure services does not extend to those who cannot afford to be homeowners within their development, or do not want to be. Hiring a specialized private contractor to design, build, and operate infrastructure requires a contract which specifies the infrastructure the private firm must deliver, and the cost of that infrastructure. This contract gives the private firm strong incentives to deliver the infrastructure the government wants, at an agreed price, without offsetting the royalties or taxes the mining company has available to pay. Moreover, a specialized infrastructure operator is just that—a private firm that has made infrastructure service provision the focus of its business activity. The principal disadvantages of hiring a specialized private operator are that procurement is often more time consuming and complicated than traditional government procurement, and there is always a risk that private operators may not be interested, given the terms the government is prepared to offer. In procuring a specialized private operator, government must also be willing to sacrifice some degree of political control of infrastructure, which it may not always be willing to do.

How can the government

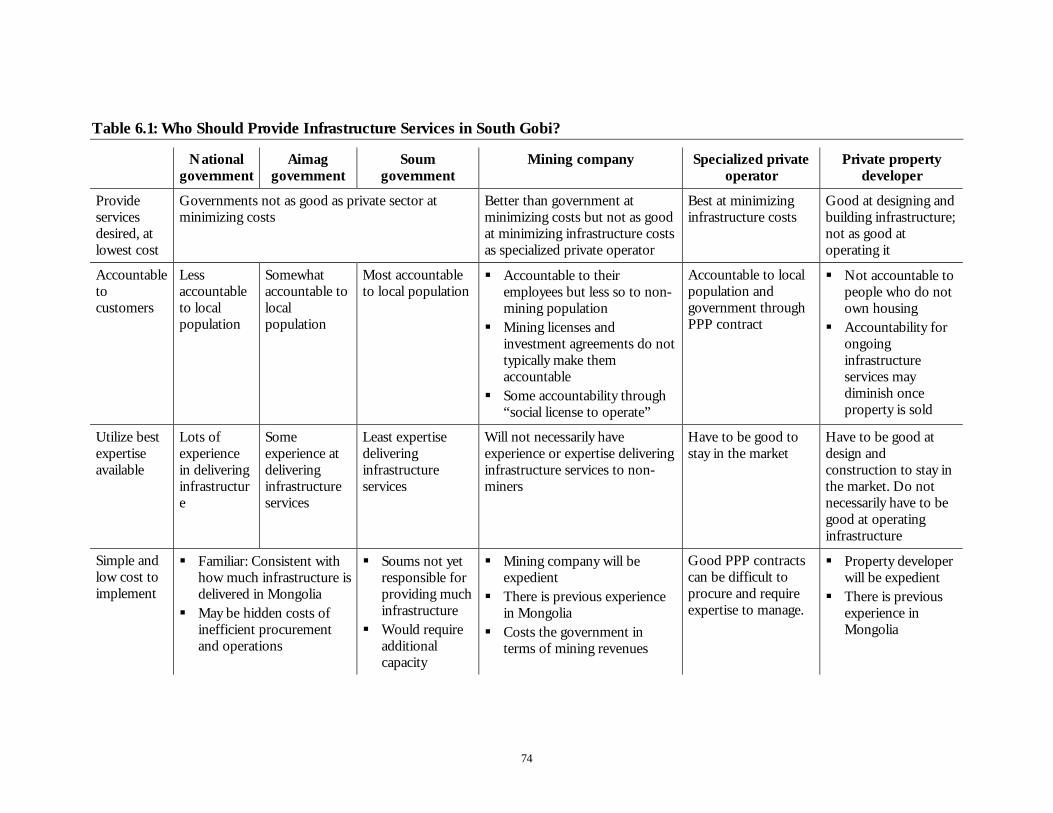

We recommend the government use five criteria to determine the best option for providing communal infrastructure in South Gobi’s towns. The best option for providing

6 On a tour of the CHP plan in Dalanzadgad, Castalia was told that coal costs roughly US$20 per metric ton.

xiv

choose the right option?

infrastructure services in any sector will: Provide the infrastructure services people need, at lowest cost Be accountable to the people who use the infrastructure Utilize the best available expertise in building and operating the infrastructure Be simple and low cost to implement Have proven to work well elsewhere in Mongolia and elsewhere in the world.

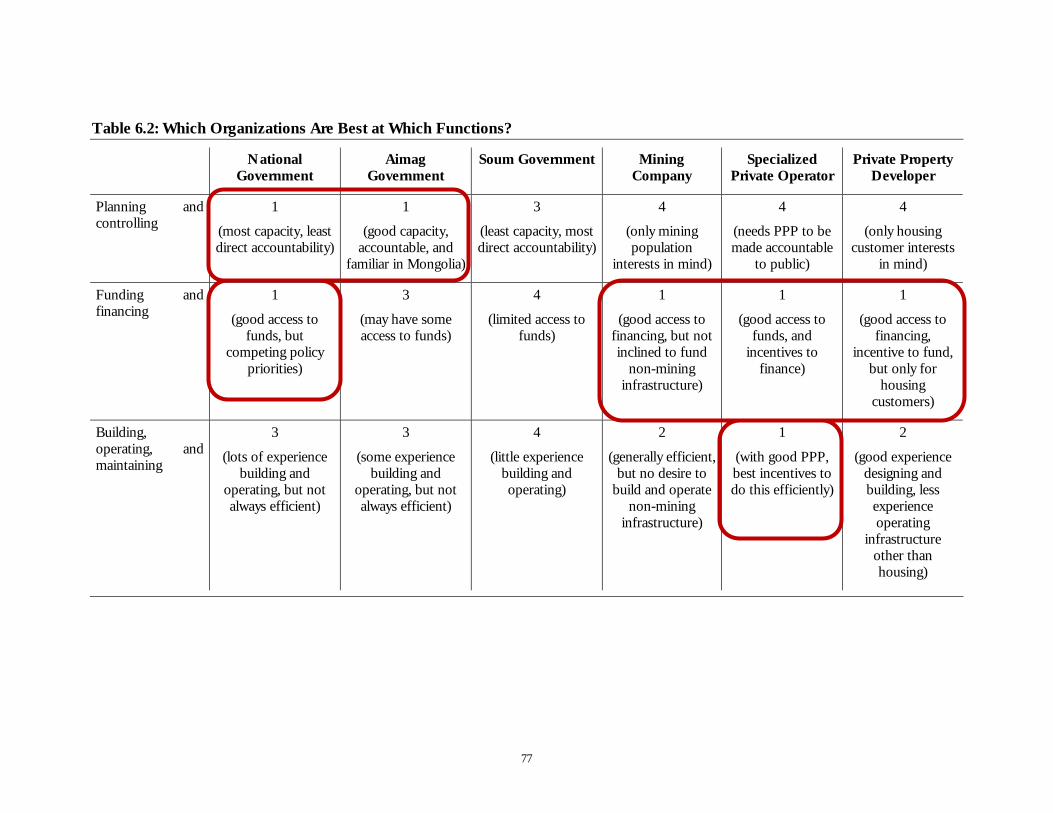

What are the principal tradeoffs between options?

Each of the institutional options for infrastructure services delivery has tradeoffs. The most important tradeoffs are: The private sector can deliver infrastructure services more efficiently than government

(lower cost for a given level of service quality), and has more expertise in infrastructure service delivery, but procurement of specialized private operators may be more difficult and take longer than traditional government procurement

Mining companies and private property developers often have the capital and expertise to build infrastructure but typically have less expertise than specialized infrastructure operators, fewer incentives to extend infrastructure to non-mining populations, and fewer incentives to operate and maintain that infrastructure

Government is more accountable to its population than private operators, but the private sector can be made accountable to government and customers through PPP contracts

National government has more expertise in infrastructure service provision than provincial (aimag) and soum (local) governments, but is less directly accountable to local populations

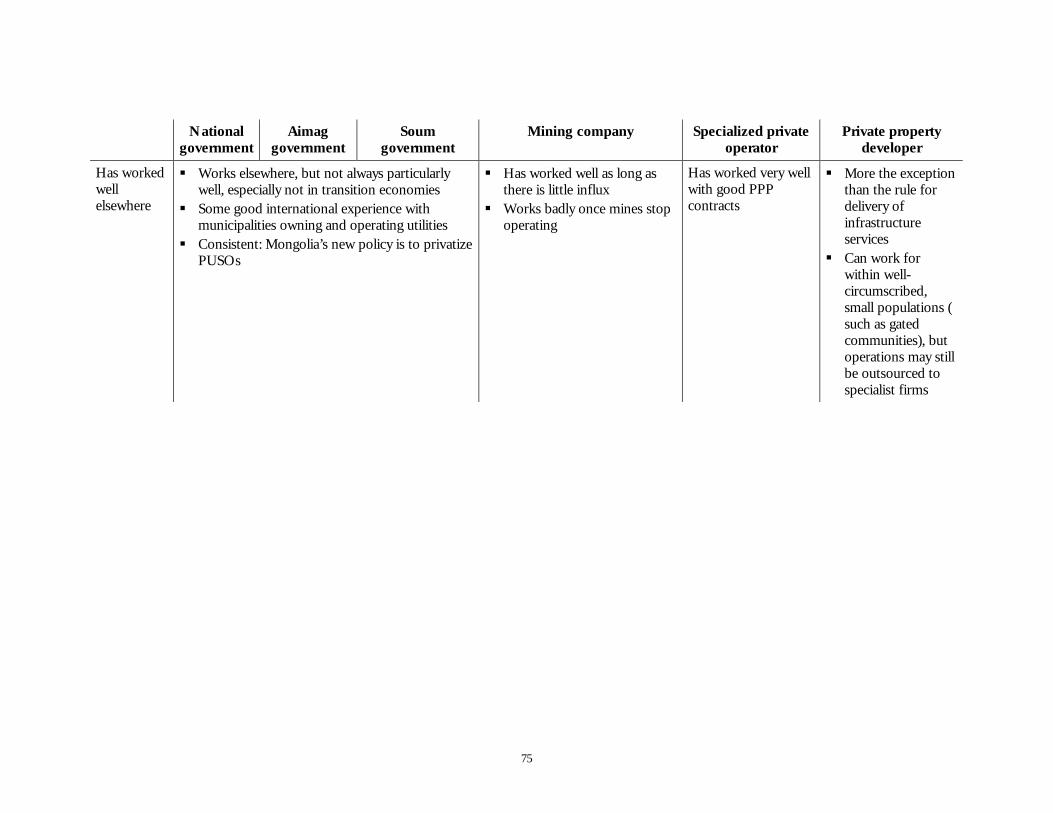

There is a tradition of aimags providing infrastructure services to soums in Mongolia through PUSOs, but there is also a new policy to increasingly privatize the PUSOs as a way of improving performance.7

The tradeoffs highlight that different organizations are strongest in different functions. The private sector is best at operating efficiently, while governments are best at ensuring an acceptable level of service is delivered to the right customers at an affordable price. Provincial and local governments know best what infrastructure is needed, and are under the most direct pressure to deliver that infrastructure. The private sector and national government can more easily finance infrastructure than provincial and local governments.

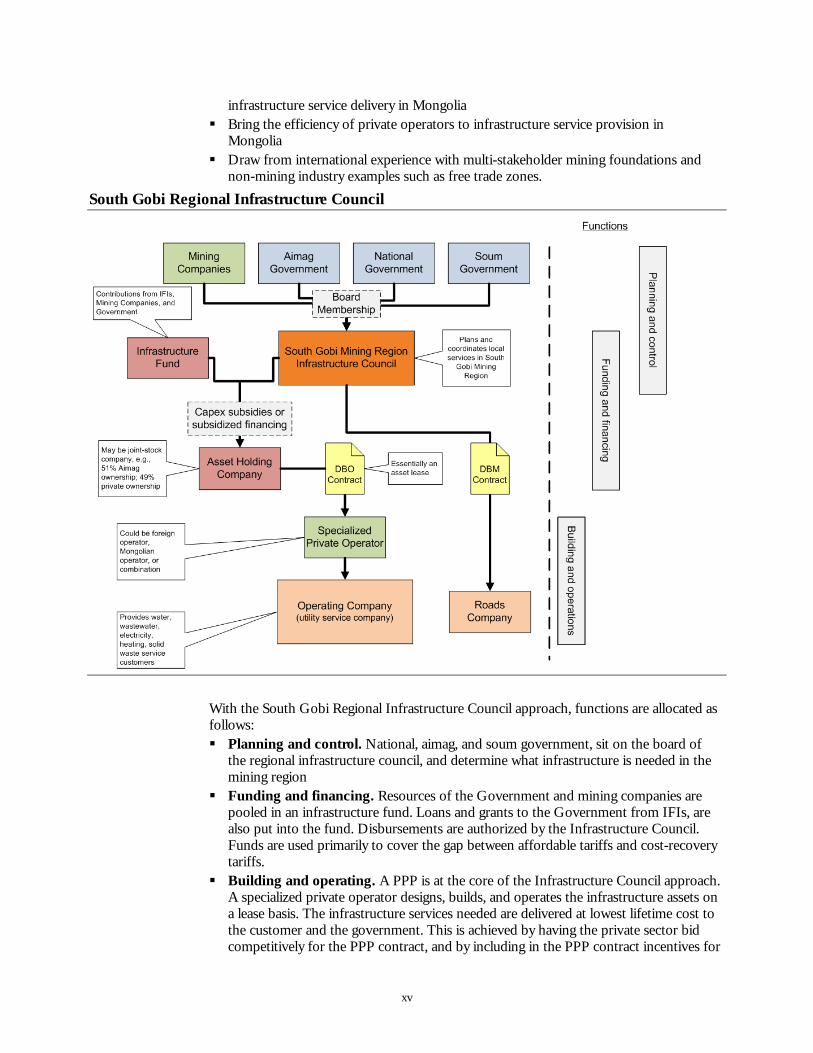

How can Mongolia minimize the tradeoffs?

There are approaches for infrastructure service delivery that harness the strengths of the different organizations who might be involved. The figure below shows an example of an arrangement that could work well in Mongolia. We call this the “infrastructure council” approach. The approach is designed to: Coordinate planning between government and the mining companies, and coordinate

planning between national, aimag, and soum governments Ensure that local, non-mining infrastructure needs are well represented, by including

representation from the soums Be consistent with the geographical realities of mining in South Gobi, and what we

understand to be South Gobi’s Governors’ vision for the economic development of his province

Pool funds available from the IFIs, government, and mining companies for infrastructure investment

Remain consistent with what we understand to be the legal framework for

7 Many of the PUSOs have now signed management contracts with local private operators. Decree 182, passed in 2007,

allows for the privatization of as much as 49 percent of PUSO ownership.

xv

infrastructure service delivery in Mongolia Bring the efficiency of private operators to infrastructure service provision in

Mongolia Draw from international experience with multi-stakeholder mining foundations and

non-mining industry examples such as free trade zones. South Gobi Regional Infrastructure Council

With the South Gobi Regional Infrastructure Council approach, functions are allocated as

follows: Planning and control. National, aimag, and soum government, sit on the board of

the regional infrastructure council, and determine what infrastructure is needed in the mining region

Funding and financing. Resources of the Government and mining companies are pooled in an infrastructure fund. Loans and grants to the Government from IFIs, are also put into the fund. Disbursements are authorized by the Infrastructure Council. Funds are used primarily to cover the gap between affordable tariffs and cost-recovery tariffs.

Building and operating. A PPP is at the core of the Infrastructure Council approach. A specialized private operator designs, builds, and operates the infrastructure assets on a lease basis. The infrastructure services needed are delivered at lowest lifetime cost to the customer and the government. This is achieved by having the private sector bid competitively for the PPP contract, and by including in the PPP contract incentives for

xvi

building and operating the infrastructure as efficiently as possible. The operator collects tariffs, delivers service, and pays the government a fee to cover the capital costs of the asset holding company. Service quality and coverage targets for electricity, water and sanitation, heating, and solid waste, are set in the PPP contract between the government and a private operator.

What are the next steps for Mongolia?

The ability of the government and mining companies to cooperate will make or break the Integrated Community recruitment and settlement model planned for Oyu Tolgoi. Because Oyu Tolgoi appears poised to define much of the development in the region (until strategic investors are identified for the other reserves at Tavan Tolgoi) we recommend the government and mining companies begin immediately to coordinate infrastructure planning. A multi-lateral infrastructure council, like the one we have described above, is a good platform for that coordination. The membership of the council should include representation from as many government agencies as will have a hand in, or be affected by development in South Gobi, and as many mining companies as currently have mining licenses and concrete plans recruiting and settling workers. The mining companies and the government need to agree as soon as possible on: Population projections, for the short-, medium- and long-terms, and how much

infrastructure will be needed to serve the expected population increase Where infrastructure should be built to accommodate influx, including whether the

infrastructure should go into new or existing soums near the mines What, roughly, will the infrastructure cost, and who will fund and finance it Who will plan, design, build, and operate the infrastructure.

We have provided projections, estimates, and recommendations above, but what is most important is that the Government and mining companies reach consensus, and work with the same assumptions about population growth, infrastructure needs, and how best to meet those needs.

1

1 Introduction Mongolia’s South Gobi Region is poised to experience a major economic boom. Several international companies, attracted by the discovery of copper, gold and coal deposits, are establishing world-class mining facilities. Other large mining investments are proposed in the near future. The mines will need people to work in them, and the direct and indirect economic opportunities created by the new mines are likely to attract migrants. These migrants will need infrastructure services currently in short supply, or entirely absent from many parts of South Gobi and the surrounding aimags.

An increase in population in South Gobi presents, on the one hand, opportunities for economic growth, and on the other hand, the potential for economic, social and political problems. Internationally, rapid population influx to mining regions has often led to such problems because of the strain it puts on a region’s resources, and the inability of governments and mine operators to provide the necessary infrastructure.

1.1 What Is the Purpose of This Paper? The World Bank has asked Castalia to:

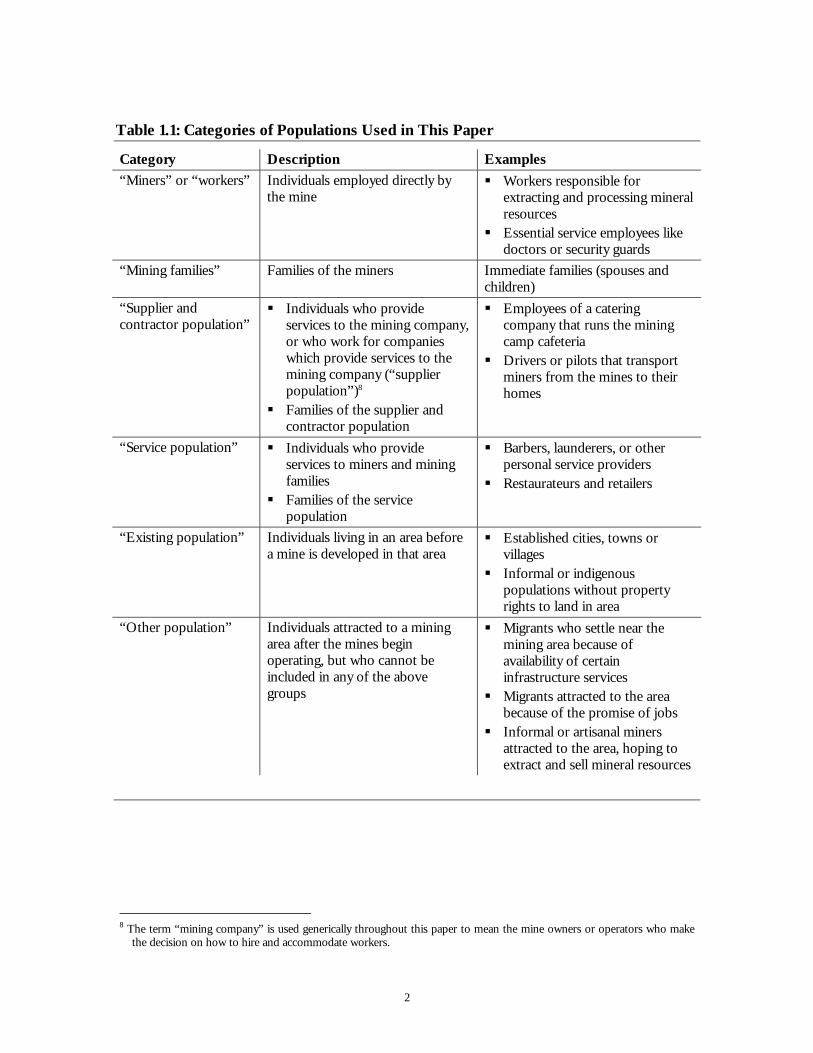

Review international experience with population influx to mining regions. Throughout this paper, we define “influx” as migrants, other than miners and their families, who come to an area in search of economic opportunities or infrastructure created directly or indirectly by a mining operation. We call “non-influx” the sum of miners, their families, and population existing in an area before mining operations start. We will refer to miners and mining families as part of the “mining population”. We will refer to the other categories of populations collectively as the “non-miners” or “non-mining population”. Table 1.1 shows the categories of populations we consider in this paper

Determine the infrastructure services and investments that will be needed by the increased population near the mines in South Gobi aimag, how much capacity will need to be built, and how much it will cost. Throughout this paper, we use the term infrastructure broadly to include: utility services (water, wastewater, heating, and electricity), solid waste, housing, public administration buildings, hospitals and schools

Identify institutional options for providing the infrastructure, and help the Government of Mongolia (“the Government”) identify the advantages and disadvantages of each of these options.

The purpose of this paper is therefore to inform the Government’s thinking about the development of population centers around the mines in South Gobi; helping the Government to make the most of the opportunities for economic growth, while minimizing the potential for economic, social and political problems.

2

Table 1.1: Categories of Populations Used in This Paper

Category Description Examples

“Miners” or “workers” Individuals employed directly by the mine

Workers responsible for extracting and processing mineral resources

Essential service employees like doctors or security guards

“Mining families” Families of the miners Immediate families (spouses and children)

“Supplier and contractor population”

Individuals who provide services to the mining company, or who work for companies which provide services to the mining company (“supplier population”)8

Families of the supplier and contractor population

Employees of a catering company that runs the mining camp cafeteria

Drivers or pilots that transport miners from the mines to their homes

“Service population” Individuals who provide services to miners and mining families

Families of the service population

Barbers, launderers, or other personal service providers

Restaurateurs and retailers

“Existing population” Individuals living in an area before a mine is developed in that area

Established cities, towns or villages

Informal or indigenous populations without property rights to land in area

“Other population” Individuals attracted to a mining area after the mines begin operating, but who cannot be included in any of the above groups

Migrants who settle near the mining area because of availability of certain infrastructure services

Migrants attracted to the area because of the promise of jobs

Informal or artisanal miners attracted to the area, hoping to extract and sell mineral resources

8 The term “mining company” is used generically throughout this paper to mean the mine owners or operators who make

the decision on how to hire and accommodate workers.

3

1.2 What Is the Structure of This Paper? We review, in Section 2, existing predictions of population influx in South Gobi, and the infrastructure planned to accommodate that influx. We describe the Government’s and mining companies’ predictions of influx, and their plans to provide infrastructure.

In Section 3, we describe international experience with population influx and infrastructure service delivery in towns near mines, and draw lessons for the new mining areas in South Gobi.

In Section 4 we estimate how much infrastructure South Gobi’s towns will need, and what that infrastructure will cost, under several different assumptions of population influx. As part of this analysis, we compare the Government’s predictions of influx, and the mining companies’ predictions of influx to international experience with influx in mining areas.

In Section 5, we identify the options available for providing infrastructure services in South Gobi, and analyze the advantages and disadvantages of each option. As part of this section, we will describe the different functions necessary to provide infrastructure services.

We conclude, in Section 6, by recommending how the Government can decide between the options described in Section 5.

4

2 Existing Projections of Population and Plans for Infrastructure Development in South Gobi

The Government of Mongolia has put considerable thought into population growth in South Gobi’s mining areas, and the infrastructure needed to accommodate that growth. Some of the mining companies operating in South Gobi have also developed their own population projections and their own plans for recruiting and housing workers. This report aims to help the parties reach consensus on the development of South Gobi’s mining areas by analyzing both Government and mining company plans and projections in light of international experience.

We summarize in Section 2.1 our understanding of the Government’s plans for South Gobi’s mining areas, and the population forecasts driving those plans. In Section 2.1.3 we summarize our understanding of the mining companies’ plans for infrastructure in the soums around the mines in South Gobi, and their projections of growth for the mining and non-mining populations.

2.1 What are Government Projections and Plans? A Regional Development Concept (RDC), approved by the Mongolian Parliament in 2001, defines the policy for urban and rural development in Mongolia through 2020.9 The Ministry of Construction and Urban Development (MoCUD) has projected population growth over the next one to two decades, and developed plans for both regional and soum-level communal infrastructure in South Gobi based on the RDC. Several other Government ministries, including MoCUD; the Ministries of Road, Transport and Tourism; Fuel and Energy; and Infrastructure and Trade, have also developed plans for regional infrastructure in South Gobi.

2.1.1 Regional Development Plan

Mongolia’s Regional Development Concept develops separate plans for five economic zones: Western, Khangai, Central, Eastern, and Ulaanbaatar City. South Gobi (Umnugobi) falls within the Central economic zone, as do six other aimags: Darkhan-Uul, Selenge, Tuv, Gobisumber, Dornogobi, and Dundgobi.

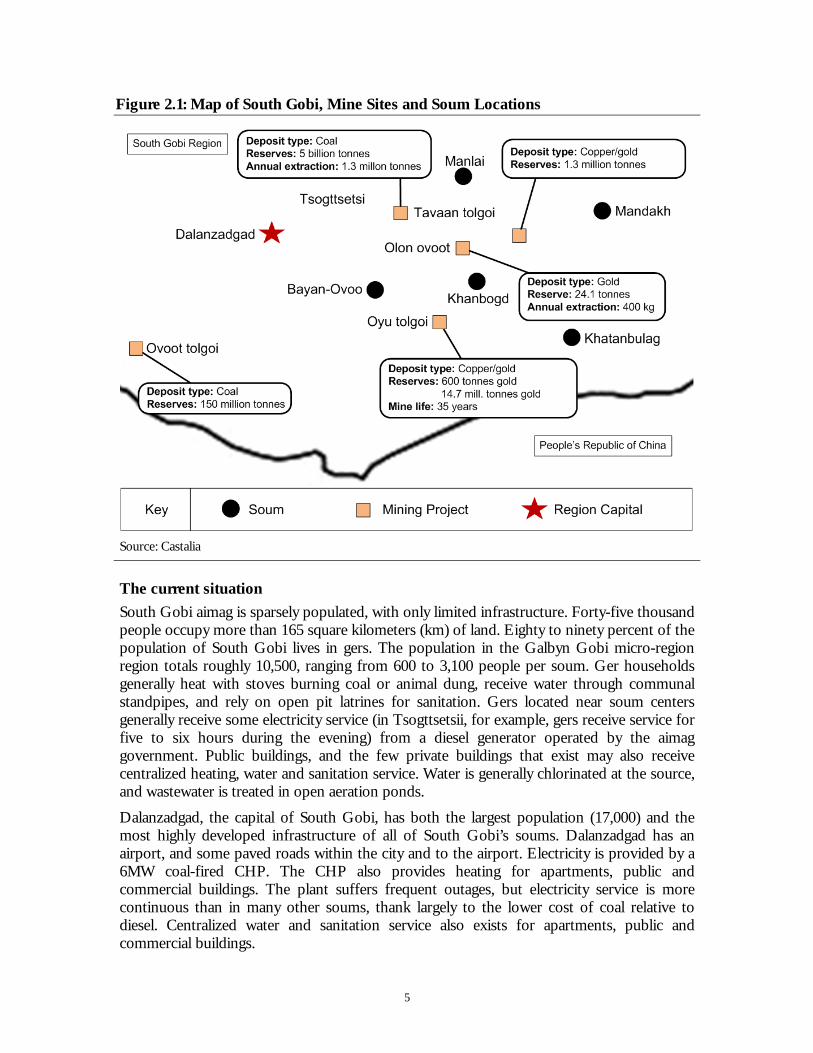

Because of the burgeoning mining industry in South Gobi, the Government also developed a more specific plan for what it calls the Galbyn Gobi micro-region. The Galbyn Gobi micro-region is defined as the area to be directly affected by mines at Tsagaansuvraga, Oyu Tolgoi and Tavan Tolgoi. The micro-region includes Tsogttsetsii, Manlai, Khanbogd, and Bayan-Ovoo soums in the Umnugobi aimag, and Khatanbulag and Mandah soum in the Dornogobi aimag. Figure 2.1 shows a map of the Galbyn Gobi micro-region, its mines and soums.

9 Parliament Resolution No. 57.

5

Figure 2.1: Map of South Gobi, Mine Sites and Soum Locations

Source: Castalia

The current situation

South Gobi aimag is sparsely populated, with only limited infrastructure. Forty-five thousand people occupy more than 165 square kilometers (km) of land. Eighty to ninety percent of the population of South Gobi lives in gers. The population in the Galbyn Gobi micro-region region totals roughly 10,500, ranging from 600 to 3,100 people per soum. Ger households generally heat with stoves burning coal or animal dung, receive water through communal standpipes, and rely on open pit latrines for sanitation. Gers located near soum centers generally receive some electricity service (in Tsogttsetsii, for example, gers receive service for five to six hours during the evening) from a diesel generator operated by the aimag government. Public buildings, and the few private buildings that exist may also receive centralized heating, water and sanitation service. Water is generally chlorinated at the source, and wastewater is treated in open aeration ponds.

Dalanzadgad, the capital of South Gobi, has both the largest population (17,000) and the most highly developed infrastructure of all of South Gobi’s soums. Dalanzadgad has an airport, and some paved roads within the city and to the airport. Electricity is provided by a 6MW coal-fired CHP. The CHP also provides heating for apartments, public and commercial buildings. The plant suffers frequent outages, but electricity service is more continuous than in many other soums, thank largely to the lower cost of coal relative to diesel. Centralized water and sanitation service also exists for apartments, public and commercial buildings.

6

The plans

Consultants to the Ministry of Construction and Urban Development outlined two possible plans for developing infrastructure in the Galbyn Gobi micro-region.10 One plan, developed by consultants Engineering Geodesy, envisions development dispersed throughout five soums in the micro-region. In this plan, non-mining industries would be developed throughout the five soums to accompany the growth in the mining industry. These industries are:

In Tsogttsetsii, a coking and chemical industry, poultry and pig farming, a construction materials industry, and other small and medium enterprises

In Bayan-Ovoo, barter trade and service facilities, duty free, frontier guard, emergency authorities; public epidemic and law and order institutions, livestock farming, and fruit and berry farms

In Khanbogd, transport services (air, rail, and road); warehousing and packaging, printing, irrigated farming, livestock farming, meat and meat processing, ecological research and monitoring, tree nurseries, and an air navigation authority

In Manlai, livestock farming, and vegetable growing

In Mandah, mining enrichment industries, transportation services, tourist camps; fruit and vegetable farming, sewing, and wool knitting factories.

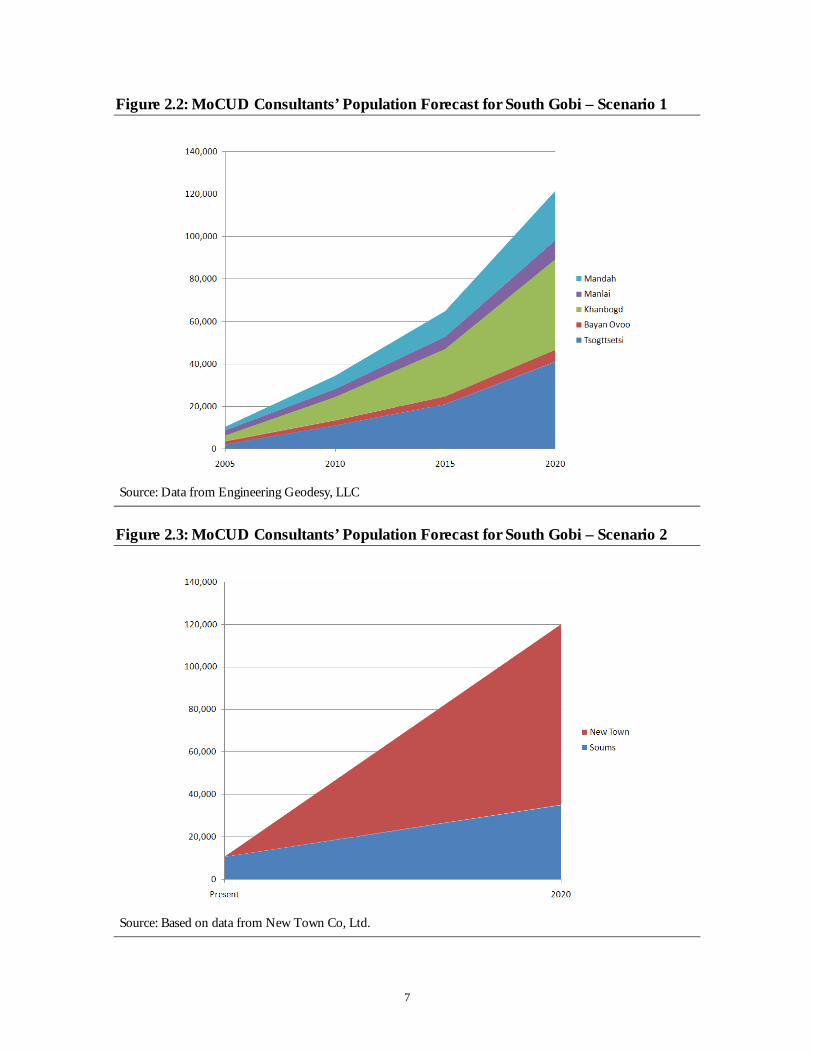

A second plan, developed by New Town Co. Ltd., would create two new towns, one located between the Tavan Tolgoi and Oyu Tolgoi mine sites, and another located near the Tsaagan Suvraga mining area. Under this plan, the new towns would be the center for economic activity in the micro-region. Other soums in the micro-region would be mostly involved in agricultural production.

2.1.2 MoCUD Population Projections

Engineering Geodesy and New Town Co. Ltd. have each developed scenarios for population growth in the soums near South Gobi’s mines. The MoCUD projections we have seen project overall population growth only, not influx.

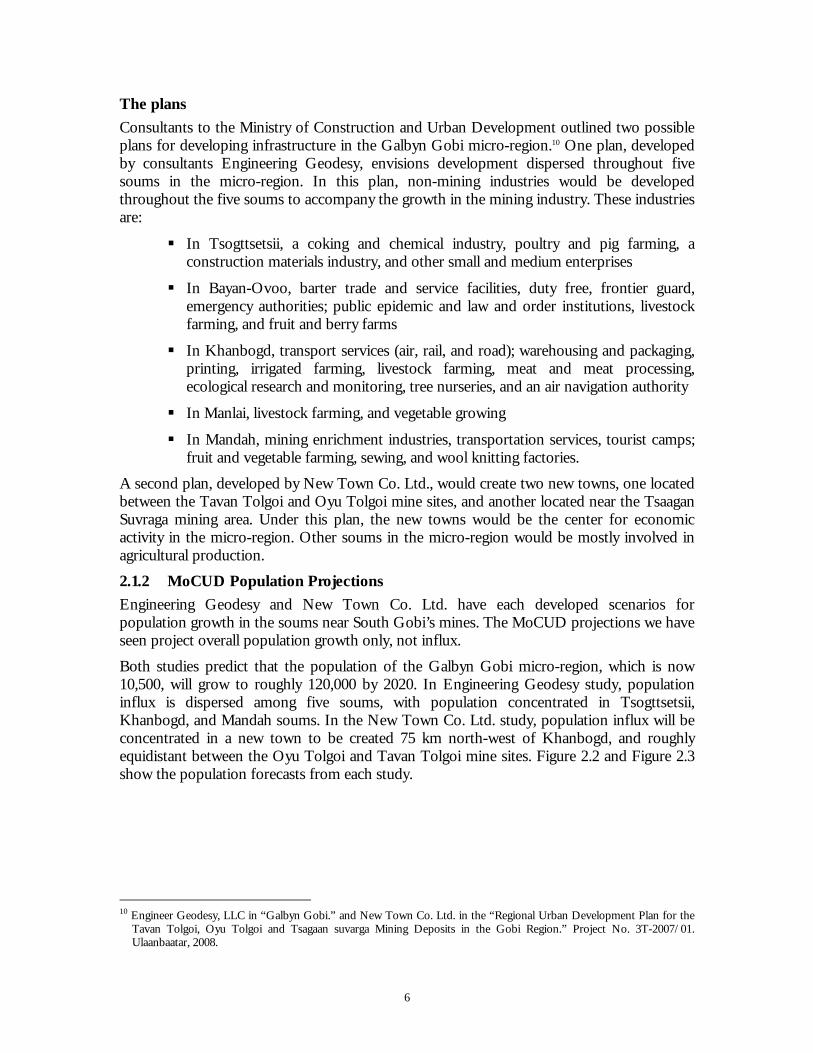

Both studies predict that the population of the Galbyn Gobi micro-region, which is now 10,500, will grow to roughly 120,000 by 2020. In Engineering Geodesy study, population influx is dispersed among five soums, with population concentrated in Tsogttsetsii, Khanbogd, and Mandah soums. In the New Town Co. Ltd. study, population influx will be concentrated in a new town to be created 75 km north-west of Khanbogd, and roughly equidistant between the Oyu Tolgoi and Tavan Tolgoi mine sites. Figure 2.2 and Figure 2.3 show the population forecasts from each study.

10 Engineer Geodesy, LLC in “Galbyn Gobi.” and New Town Co. Ltd. in the “Regional Urban Development Plan for the

Tavan Tolgoi, Oyu Tolgoi and Tsagaan suvarga Mining Deposits in the Gobi Region.” Project No. 3T-2007/01. Ulaanbaatar, 2008.

7

Figure 2.2: MoCUD Consultants’ Population Forecast for South Gobi – Scenario 1

Source: Data from Engineering Geodesy, LLC

Figure 2.3: MoCUD Consultants’ Population Forecast for South Gobi – Scenario 2

Source: Based on data from New Town Co, Ltd.

8

2.1.3 Government Plans for Infrastructure

The Engineering Geodesy and New Town Co. Ltd. Studies described above also include plans for communal infrastructure for the soums near the Oyu Tolgoi and Tavan Tolgoi mines. A number of other ministries, have also developed plans for regional infrastructure throughout South Gobi. MoCUD, and the Ministries of Road, Transport and Tourism; Fuel and Energy; and Infrastructure and Trade, have all presented plans for infrastructure buildup in the region. The Government has also commissioned a feasibility study assessing infrastructure needs at Tavan Tolgoi. The subsections below summarize these plans.

Government plans for communal infrastructure in the soums

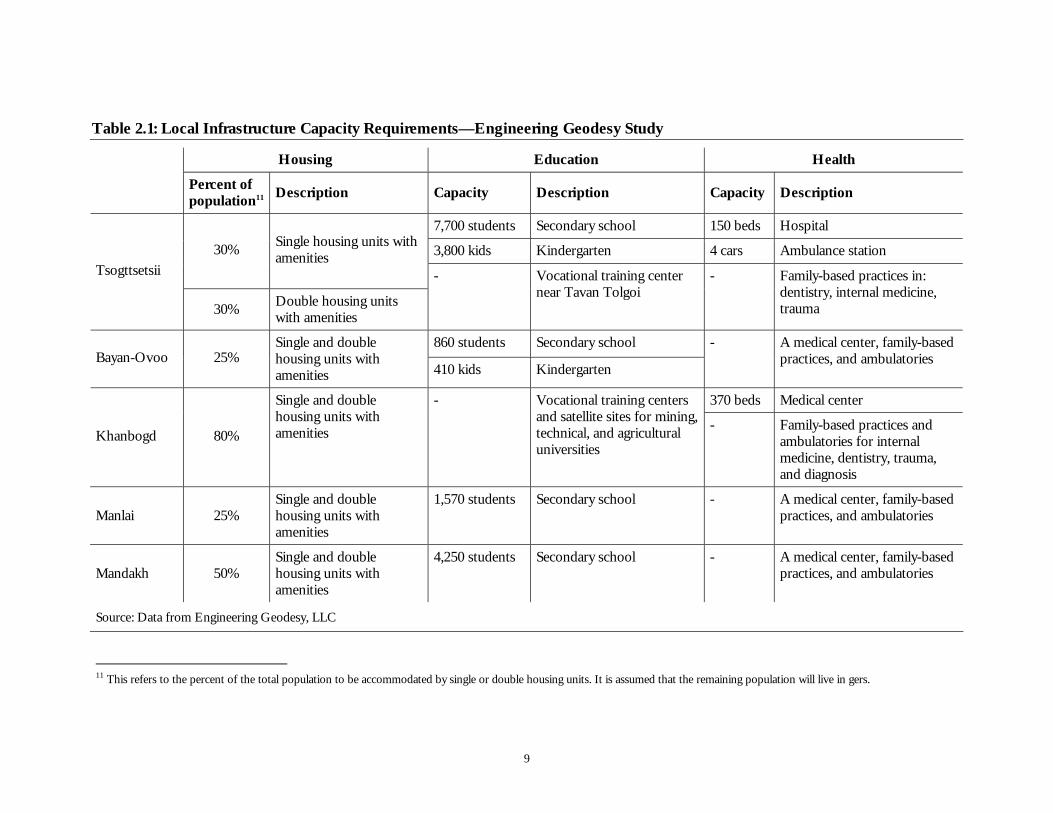

One of the studies commissioned by MoCUD (by Engineering Geodesy) estimates infrastructure needs for populations dispersed throughout five soums in the Galbyn Gobi micro-region: Tsogttsetsii, Bayan-Ovoo, Khanbogd, Manlai, and Mandakh. The other study commissioned by MoCUD (by New Town Co. Ltd.) estimates infrastructure needs for population concentrated in a new town located between the Tavan Tolgoi and Oyu Tolgoi mine sites, with remaining local infrastructure development dispersed throughout the five soums discussed in the first study. Table 2.1 and Table 2.2 show the local infrastructure capacity requirements of each scenario.

9

Table 2.1: Local Infrastructure Capacity Requirements—Engineering Geodesy Study

Housing Education Health Percent of

population11 Description Capacity Description Capacity Description

7,700 students Secondary school 150 beds Hospital

3,800 kids Kindergarten 4 cars Ambulance station 30% Single housing units with amenities

Tsogttsetsii

30% Double housing units with amenities

- Vocational training center near Tavan Tolgoi

- Family-based practices in: dentistry, internal medicine, trauma

860 students Secondary school Bayan-Ovoo 25%

Single and double housing units with amenities 410 kids Kindergarten

- A medical center, family-based practices, and ambulatories

370 beds Medical center

Khanbogd 80%

Single and double housing units with amenities

- Vocational training centers and satellite sites for mining, technical, and agricultural universities

- Family-based practices and ambulatories for internal medicine, dentistry, trauma, and diagnosis

Manlai 25% Single and double housing units with amenities

1,570 students Secondary school - A medical center, family-based practices, and ambulatories

Mandakh 50% Single and double housing units with amenities

4,250 students Secondary school - A medical center, family-based practices, and ambulatories

Source: Data from Engineering Geodesy, LLC

11 This refers to the percent of the total population to be accommodated by single or double housing units. It is assumed that the remaining population will live in gers.

10

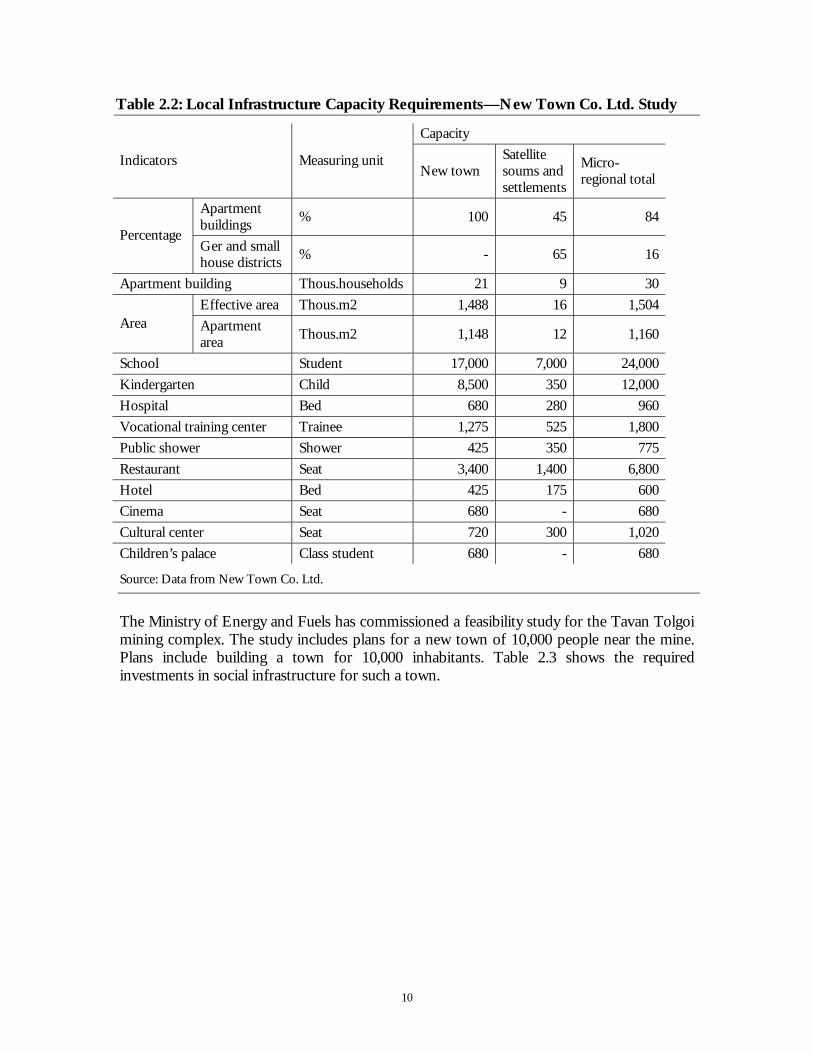

Table 2.2: Local Infrastructure Capacity Requirements—New Town Co. Ltd. Study

Capacity

Indicators Measuring unit New town

Satellite soums and settlements

Micro-regional total

Apartment buildings % 100 45 84

Percentage Ger and small house districts % - 65 16

Apartment building Thous.households 21 9 30Effective area Thous.m2 1,488 16 1,504

Area Apartment area Thous.m2 1,148 12 1,160

School Student 17,000 7,000 24,000Kindergarten Child 8,500 350 12,000Hospital Bed 680 280 960Vocational training center Trainee 1,275 525 1,800Public shower Shower 425 350 775Restaurant Seat 3,400 1,400 6,800Hotel Bed 425 175 600Cinema Seat 680 - 680Cultural center Seat 720 300 1,020Children’s palace Class student 680 - 680

Source: Data from New Town Co. Ltd.

The Ministry of Energy and Fuels has commissioned a feasibility study for the Tavan Tolgoi mining complex. The study includes plans for a new town of 10,000 people near the mine. Plans include building a town for 10,000 inhabitants. Table 2.3 shows the required investments in social infrastructure for such a town.

11

Table 2.3: Infrastructure Requirements for Town of 10,000 at Tavan Tolgoi

Investment Capacity Capacity Description

School 2000 Children

Kindergarten 1000 Children

Training center 180 Seats

Clinic 90 Beds

Hospital 350 People

Resort 80 Beds

Gym 500 m2

Swimming-pool 70 m2

Cultural center 500 people

Hotel 50 beds

Sauna 20 people

Source: Tavan Tolgoi Feasibility Study.

Regional infrastructure

Government plans for infrastructure developments at a regional level include investments in transport, electricity and water networks. The Ministry of Construction and Urban Development; the Ministry of Roads, Transport and Tourism; the Ministry of Fuel and Energy; and the Ministry of Infrastructure and Trade present several plans for infrastructure build up in these three sectors. Where ministries have provided different options for build up within the same sector, both options are given.

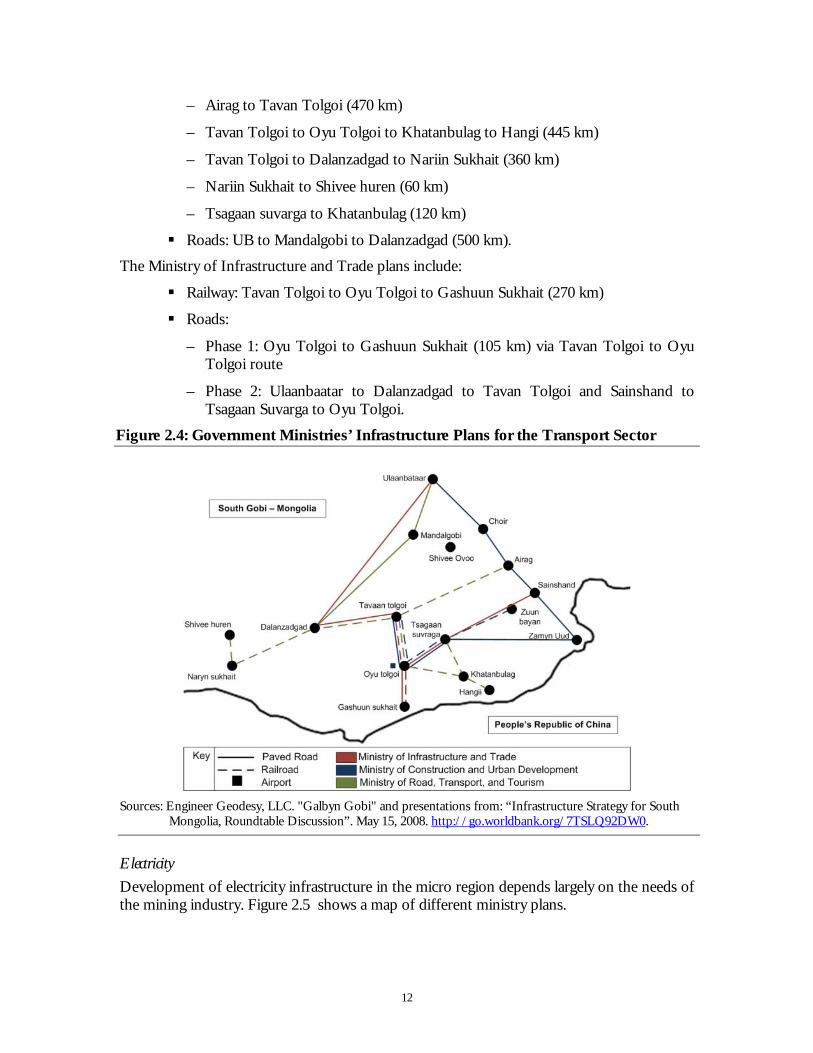

Transport Improvements to transport infrastructure in the micro-region include rail, road, and air service connecting South Gobi soums to: other South Gobi soums, Ulaanbaatar, and, potentially, Russia and the People’s Republic of China. Figure 2.4 maps Ministries’ plans for transport infrastructure.

The Ministry of Construction and Urban Development’s plans include:

Railway: Tavan Tolgoi to Oyu Tolgoi to Tsagaan Suvraga to Zuun Bayan (152 km)

Roads: UB to Choir to Sainshand to Zamyn Uud to Tsagaan Suvraga to Oyu Tolgoi to Tavan Tolgoi (470 km)

Air: An international airport with a paved runway will be constructed in Khanbogd soum.

The Ministry of Road, Transport and Tourism’s plans for South Gobi include:

Railway: Several routes are proposed totaling 1455 km. These include:

12

– Airag to Tavan Tolgoi (470 km)

– Tavan Tolgoi to Oyu Tolgoi to Khatanbulag to Hangi (445 km)

– Tavan Tolgoi to Dalanzadgad to Nariin Sukhait (360 km)

– Nariin Sukhait to Shivee huren (60 km)

– Tsagaan suvarga to Khatanbulag (120 km)

Roads: UB to Mandalgobi to Dalanzadgad (500 km).

The Ministry of Infrastructure and Trade plans include:

Railway: Tavan Tolgoi to Oyu Tolgoi to Gashuun Sukhait (270 km)

Roads:

– Phase 1: Oyu Tolgoi to Gashuun Sukhait (105 km) via Tavan Tolgoi to Oyu Tolgoi route

– Phase 2: Ulaanbaatar to Dalanzadgad to Tavan Tolgoi and Sainshand to Tsagaan Suvarga to Oyu Tolgoi.

Figure 2.4: Government Ministries’ Infrastructure Plans for the Transport Sector

Sources: Engineer Geodesy, LLC. "Galbyn Gobi" and presentations from: “Infrastructure Strategy for South

Mongolia, Roundtable Discussion”. May 15, 2008. http://go.worldbank.org/7TSLQ92DW0.

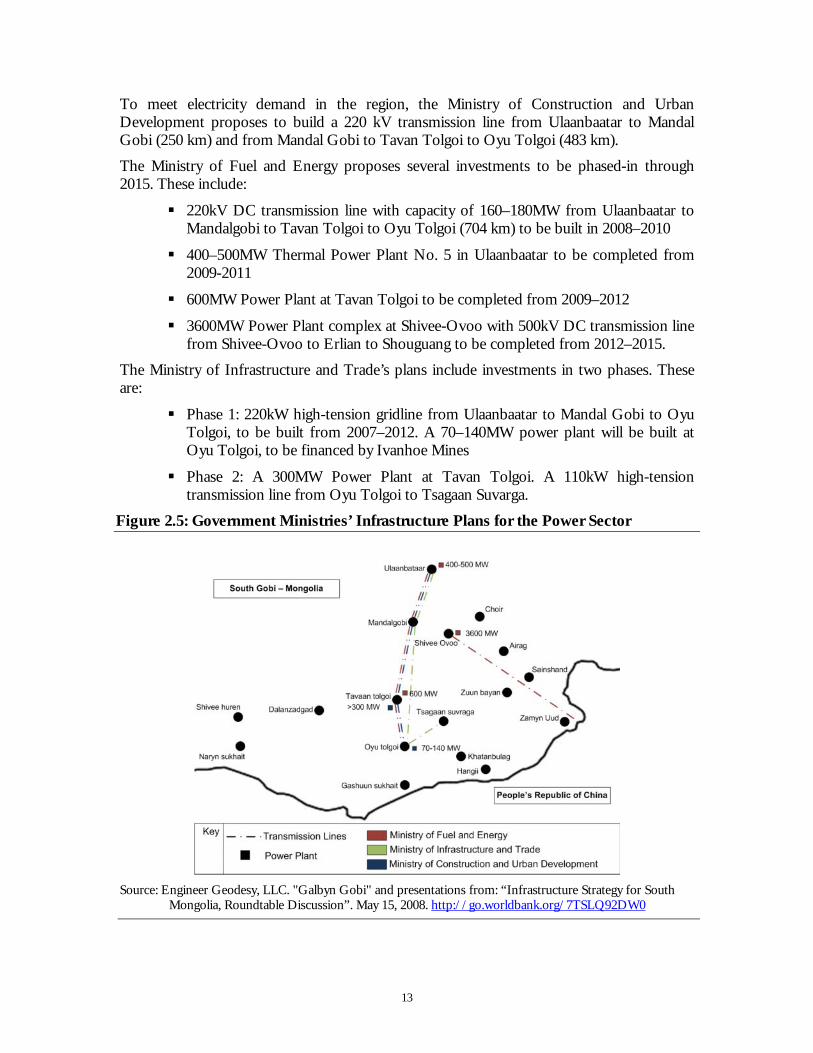

Electricity Development of electricity infrastructure in the micro region depends largely on the needs of the mining industry. Figure 2.5 shows a map of different ministry plans.

13

To meet electricity demand in the region, the Ministry of Construction and Urban Development proposes to build a 220 kV transmission line from Ulaanbaatar to Mandal Gobi (250 km) and from Mandal Gobi to Tavan Tolgoi to Oyu Tolgoi (483 km).

The Ministry of Fuel and Energy proposes several investments to be phased-in through 2015. These include:

220kV DC transmission line with capacity of 160–180MW from Ulaanbaatar to Mandalgobi to Tavan Tolgoi to Oyu Tolgoi (704 km) to be built in 2008–2010

400–500MW Thermal Power Plant No. 5 in Ulaanbaatar to be completed from 2009-2011

600MW Power Plant at Tavan Tolgoi to be completed from 2009–2012

3600MW Power Plant complex at Shivee-Ovoo with 500kV DC transmission line from Shivee-Ovoo to Erlian to Shouguang to be completed from 2012–2015.

The Ministry of Infrastructure and Trade’s plans include investments in two phases. These are:

Phase 1: 220kW high-tension gridline from Ulaanbaatar to Mandal Gobi to Oyu Tolgoi, to be built from 2007–2012. A 70–140MW power plant will be built at Oyu Tolgoi, to be financed by Ivanhoe Mines

Phase 2: A 300MW Power Plant at Tavan Tolgoi. A 110kW high-tension transmission line from Oyu Tolgoi to Tsagaan Suvarga.

Figure 2.5: Government Ministries’ Infrastructure Plans for the Power Sector

Source: Engineer Geodesy, LLC. "Galbyn Gobi" and presentations from: “Infrastructure Strategy for South

Mongolia, Roundtable Discussion”. May 15, 2008. http://go.worldbank.org/7TSLQ92DW0

14

Water The Ministry of Construction and Urban Development has developed options for meeting increased water demand in the region due to population influx and water needs of the mining industry. Population growth is expected to increase demand for water six to 14 times its current levels. Options for meeting the water needs include:

Selenge river. The Selenge river has been identified as a possible source for water needs in the region from 2010–2020. Water would be provided via the Selenge, Bulgan, Central, Dundgobi, Umnigobi, and Dornobogi route

Kherlen river. A large water tank could be constructed with a main canal pipeline to divert some of the Kherlen river flow towards Baruun Urt, Tsagaan suvraga and Oyu Tolgoi. Smaller pipelines would connect soums and dwellings with the main canal transmission line. Pipeline routes might include:

– Mainline: Kherlen river to Choir to Undershil to Mandah, 242 km