Embed Size (px)

Citation preview

U.S. Retail IndustryHome Depot | Costco | Walmart

Presented By:

Caitlin LloydHans TantioJacob KlimowiczJoe ZhouPascal Setiadi

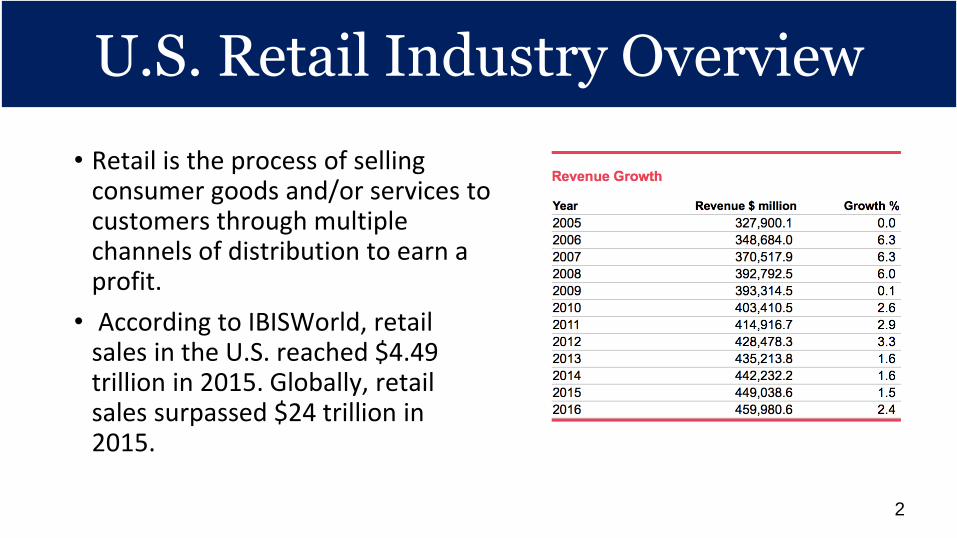

• Retail is the process of selling consumer goods and/or services to customers through multiple channels of distribution to earn a profit.

• According to IBISWorld, retail sales in the U.S. reached $4.49 trillion in 2015. Globally, retail sales surpassed $24 trillion in 2015.

U.S. Retail Industry Overview

2

U.S. Retail Industry OverviewU.S. Retail Industry Overview

3

Leading 100 American retailers in 2015, based on U.S. retail sales (in billion U.S. dollars)

Leading 100 American retailers in 2015, based on U.S. retail sales (in billion U.S. dollars)

4

Leading supermarkets in the United States in 2015, based on retail sales (in billion U.S. dollars)

Leading supermarkets in the United States in 2015, based on retail sales (in billion U.S. dollars)

5

103.58

56.54

43.82

33.8

21.08

15.29

14.7

14.62

10.13

8.25

8.09

6.99

6.64

4.79

4.74

0 20 40 60 80 100 120

The Kroger Co.

Albertsons

Ahold USA/Royal Ahold

Publix Super Markets

H-E-B Grocery

Whole Foods Markets

Wal-Mart Stores (Neighborhood Market)

Wakefern/ShopRite

Southeastern Grocers (Bi-Lo)

Wegmans

Hy-Vee

Giant Eagle

WinCo

Supervalu

Save Mart

Sales in billion U.S. dollars

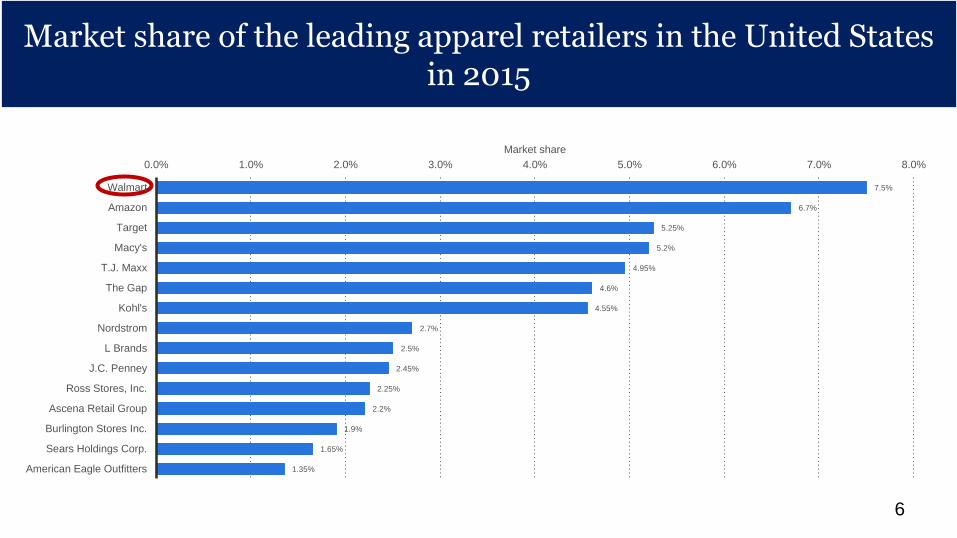

Market share of the leading apparel retailers in the United States in 2015

Market share of the leading apparel retailers in the United States in 2015

6

7.5%

6.7%

5.25%

5.2%

4.95%

4.6%

4.55%

2.7%

2.5%

2.45%

2.25%

2.2%

1.9%

1.65%

1.35%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0%

Walmart

Amazon

Target

Macy's

T.J. Maxx

The Gap

Kohl's

Nordstrom

L Brands

J.C. Penney

Ross Stores, Inc.

Ascena Retail Group

Burlington Stores Inc.

Sears Holdings Corp.

American Eagle Outfitters

Market share

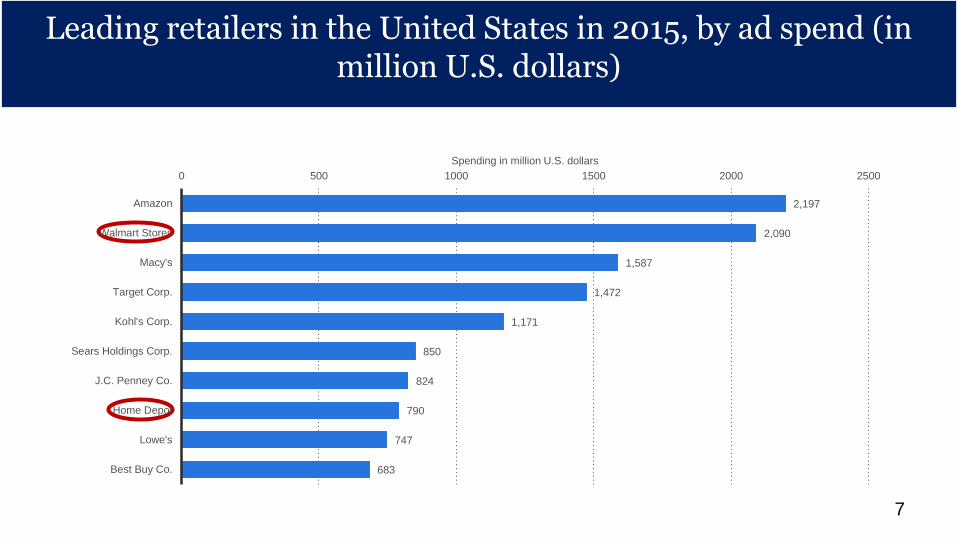

Leading retailers in the United States in 2015, by ad spend (in million U.S. dollars)

Leading retailers in the United States in 2015, by ad spend (in million U.S. dollars)

7

2,197

2,090

1,587

1,472

1,171

850

824

790

747

683

0 500 1000 1500 2000 2500

Amazon

Walmart Stores

Macy's

Target Corp.

Kohl's Corp.

Sears Holdings Corp.

J.C. Penney Co.

Home Depot

Lowe's

Best Buy Co.

Spending in million U.S. dollars

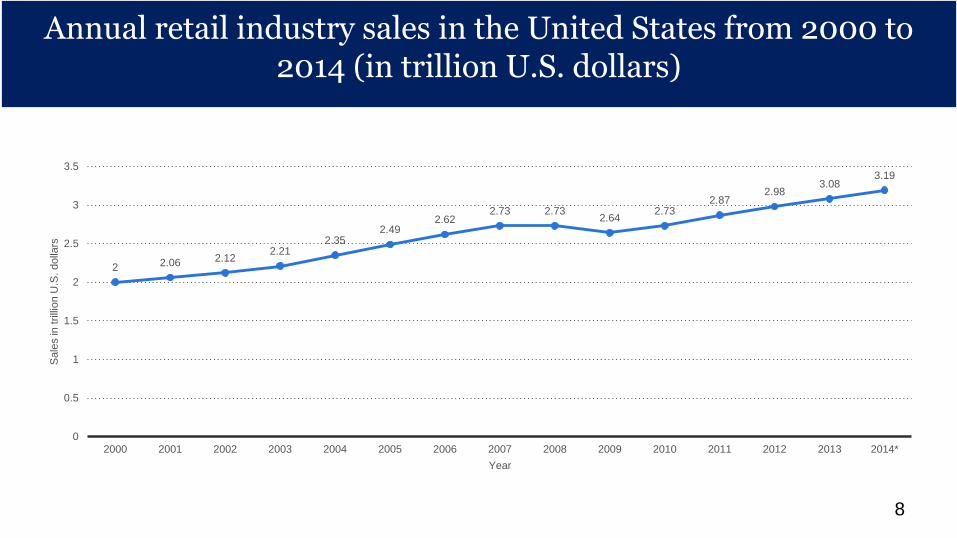

Annual retail industry sales in the United States from 2000 to 2014 (in trillion U.S. dollars)

Annual retail industry sales in the United States from 2000 to 2014 (in trillion U.S. dollars)

8

2 2.06 2.122.21

2.352.49

2.622.73 2.73

2.642.73

2.872.98

3.083.19

0

0.5

1

1.5

2

2.5

3

3.5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Sale

s in

trilli

on U

.S. dolla

rs

Year

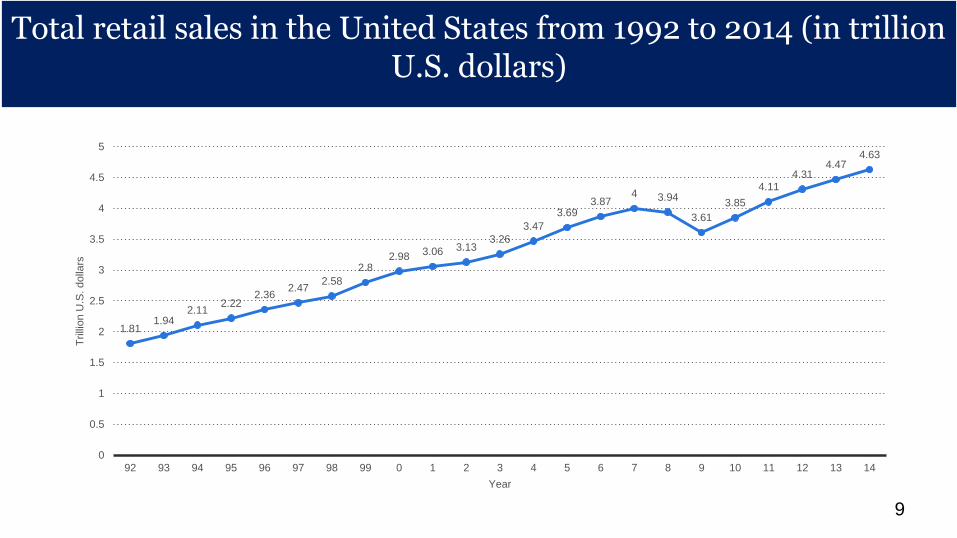

Total retail sales in the United States from 1992 to 2014 (in trillion U.S. dollars)

Total retail sales in the United States from 1992 to 2014 (in trillion U.S. dollars)

9

1.811.94

2.112.22

2.362.47

2.58

2.82.98 3.06 3.13

3.26

3.47

3.693.87

4 3.94

3.61

3.85

4.114.31

4.474.63

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14

Trilli

on U

.S. dolla

rs

Year

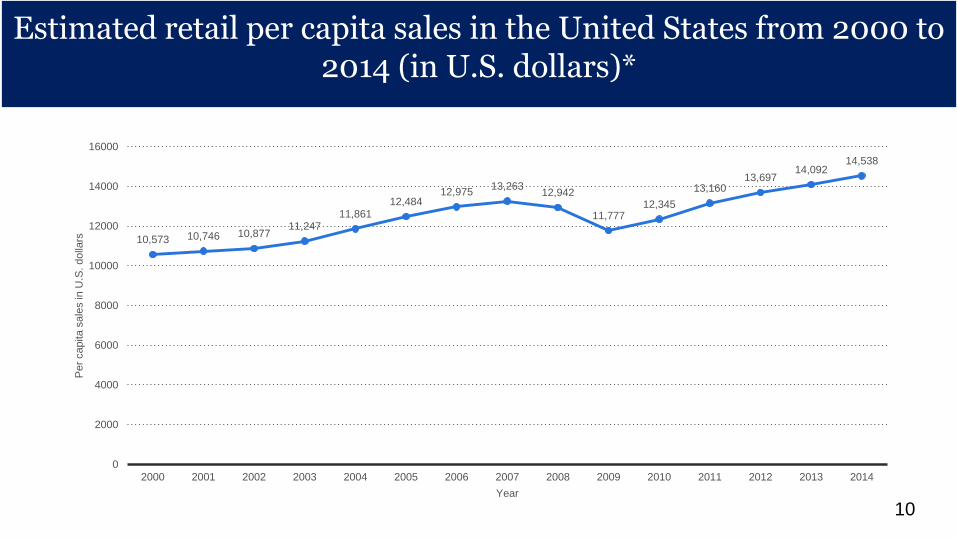

Estimated retail per capita sales in the United States from 2000 to 2014 (in U.S. dollars)*

Estimated retail per capita sales in the United States from 2000 to 2014 (in U.S. dollars)*

10

10,573 10,746 10,87711,247

11,86112,484

12,97513,263

12,942

11,77712,345

13,16013,697

14,09214,538

0

2000

4000

6000

8000

10000

12000

14000

16000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Per

capita s

ale

s in

U.S

. dolla

rs

Year

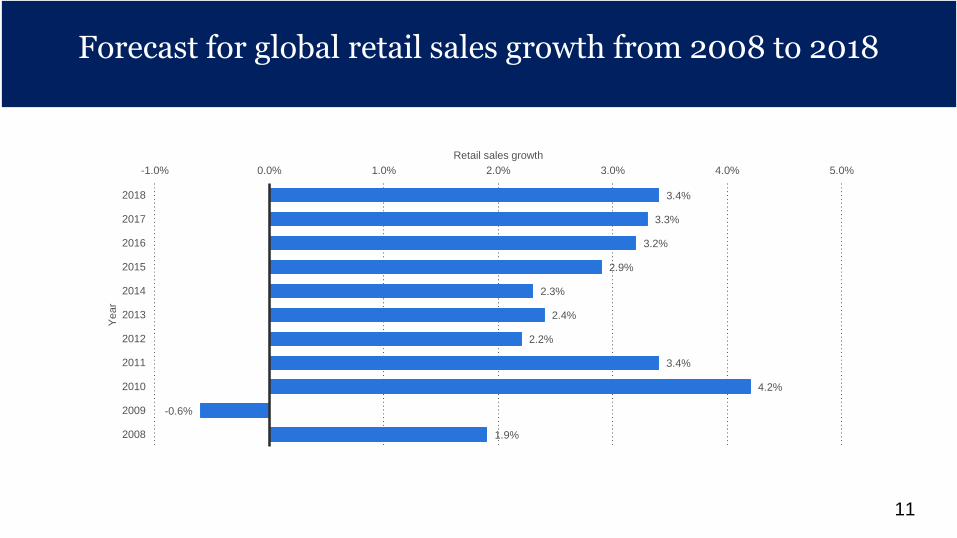

Forecast for global retail sales growth from 2008 to 2018Forecast for global retail sales growth from 2008 to 2018

11

3.4%

3.3%

3.2%

2.9%

2.3%

2.4%

2.2%

3.4%

4.2%

-0.6%

1.9%

-1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

2018

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

Retail sales growth

Year

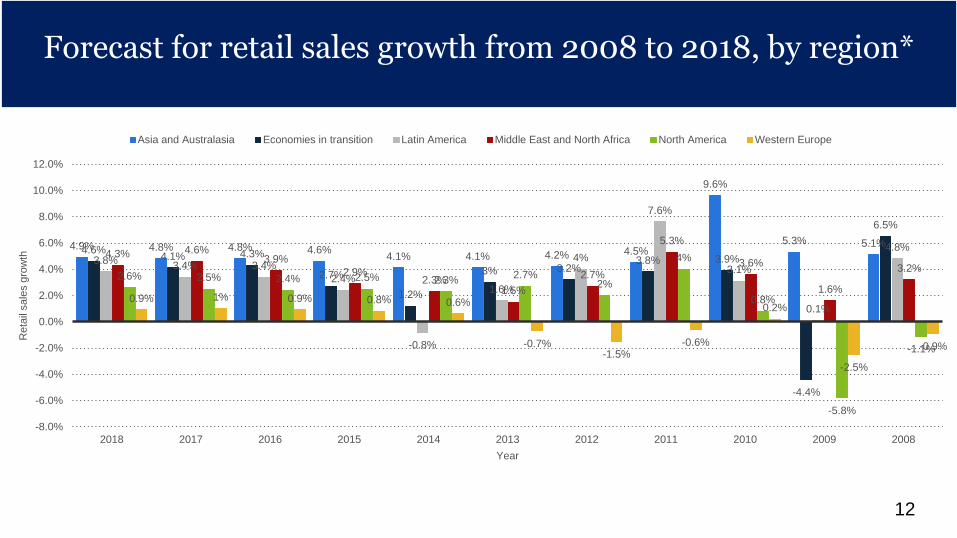

Forecast for retail sales growth from 2008 to 2018, by region*

Forecast for retail sales growth from 2008 to 2018, by region*

12

4.9% 4.8% 4.8% 4.6%4.1% 4.1% 4.2% 4.5%

9.6%

5.3% 5.1%4.6%

4.1% 4.3%

2.7%

1.2%

3% 3.2%3.8% 3.9%

-4.4%

6.5%

3.8%3.4% 3.4%

2.4%

-0.8%

1.6%

4%

7.6%

3.1%

0.1%

4.8%4.3% 4.6%

3.9%

2.9%2.3%

1.5%

2.7%

5.3%

3.6%

1.6%

3.2%2.6% 2.5% 2.4% 2.5% 2.3%

2.7%2%

4%

0.8%

-5.8%

-1.1%

0.9% 1% 0.9% 0.8% 0.6%

-0.7%-1.5%

-0.6%

0.2%

-2.5%

-0.9%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008

Reta

il sale

s g

row

th

Year

Asia and Australasia Economies in transition Latin America Middle East and North Africa North America Western Europe

Change in the number of stores worldwide of the leading 50 U.S.-based retailers* from 2009 to 2010

Change in the number of stores worldwide of the leading 50 U.S.-based retailers* from 2009 to 2010

13

58.6%

11.3%10.9%8.1%7.4%7.4%7%6.2%5.8%5.5%5.3%5.3%5.3%5%4.7%4.6%3.4%3.2%3.1%2.5%

2.4%2.3%2% 2%1.7%1.7%

1.3%

1.3%1.2%1.1%0.9%0.6%0.6%0.5%0.3%0.3%0.1%0%

0%

0%

-0.2%-0.4%-0.9%-1.1%-1.2%-1.4%-2%-2.3%-4.2%-11%-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Change f

rom

2009 t

o 2

010

Retailer

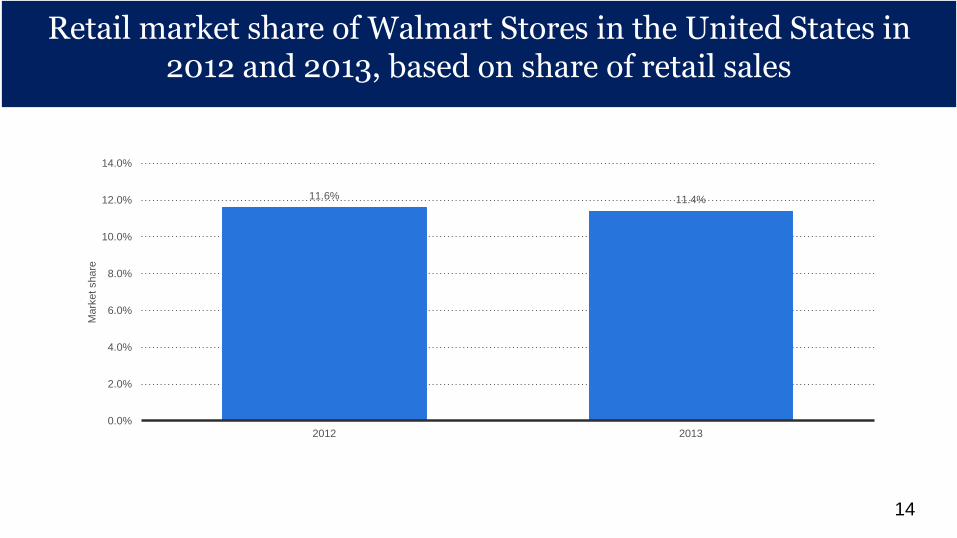

Retail market share of Walmart Stores in the United States in 2012 and 2013, based on share of retail sales

Retail market share of Walmart Stores in the United States in 2012 and 2013, based on share of retail sales

14

11.6% 11.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2012 2013

Mark

et share

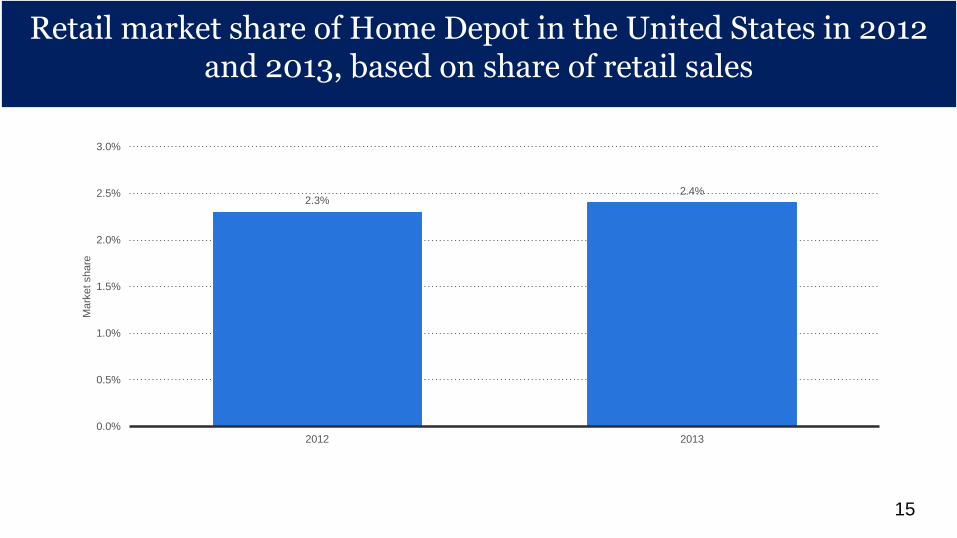

Retail market share of Home Depot in the United States in 2012 and 2013, based on share of retail sales

Retail market share of Home Depot in the United States in 2012 and 2013, based on share of retail sales

15

2.3%2.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2012 2013

Mark

et share

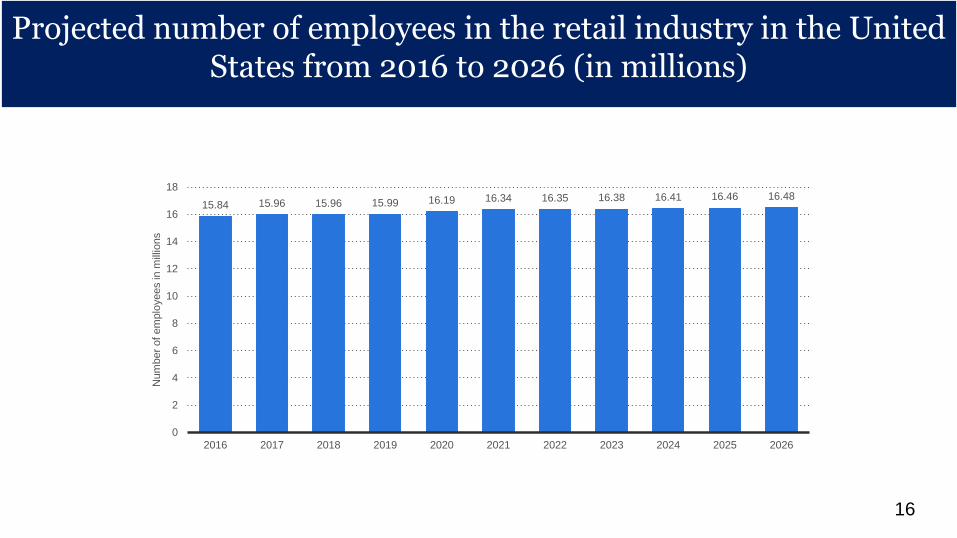

Projected number of employees in the retail industry in the United States from 2016 to 2026 (in millions)

Projected number of employees in the retail industry in the United States from 2016 to 2026 (in millions)

16

15.84 15.96 15.96 15.99 16.19 16.34 16.35 16.38 16.41 16.46 16.48

0

2

4

6

8

10

12

14

16

18

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Num

ber

of em

plo

yees in

mill

ions

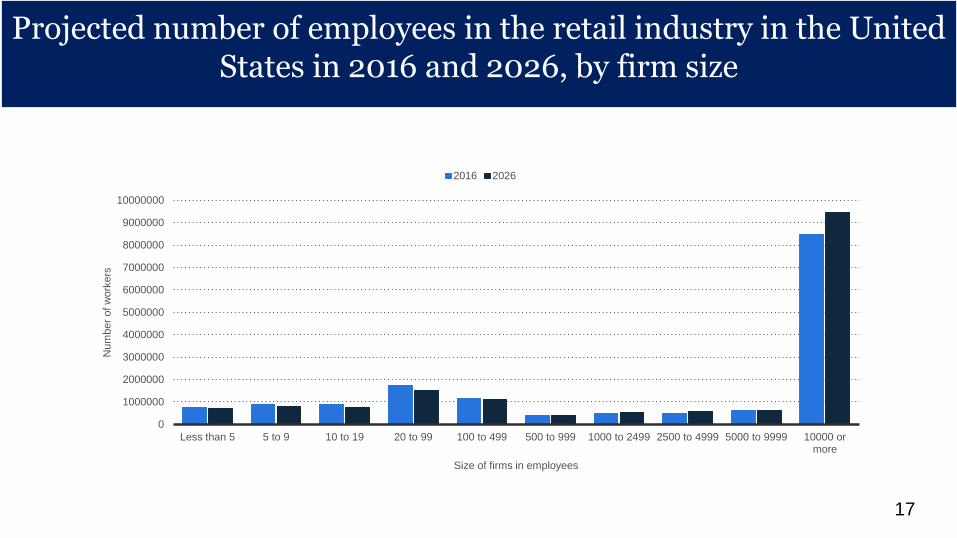

Projected number of employees in the retail industry in the United States in 2016 and 2026, by firm size

Projected number of employees in the retail industry in the United States in 2016 and 2026, by firm size

17

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

9000000

10000000

Less than 5 5 to 9 10 to 19 20 to 99 100 to 499 500 to 999 1000 to 2499 2500 to 4999 5000 to 9999 10000 ormore

Num

ber

of w

ork

ers

Size of firms in employees

2016 2026

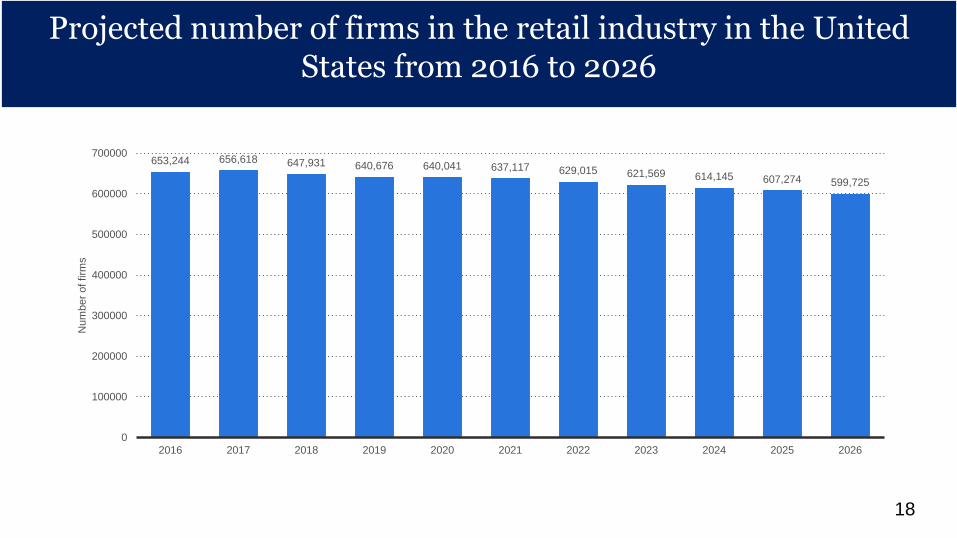

Projected number of firms in the retail industry in the United States from 2016 to 2026

Projected number of firms in the retail industry in the United States from 2016 to 2026

18

653,244 656,618 647,931 640,676 640,041 637,117 629,015 621,569 614,145 607,274 599,725

0

100000

200000

300000

400000

500000

600000

700000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Num

ber

of firm

s

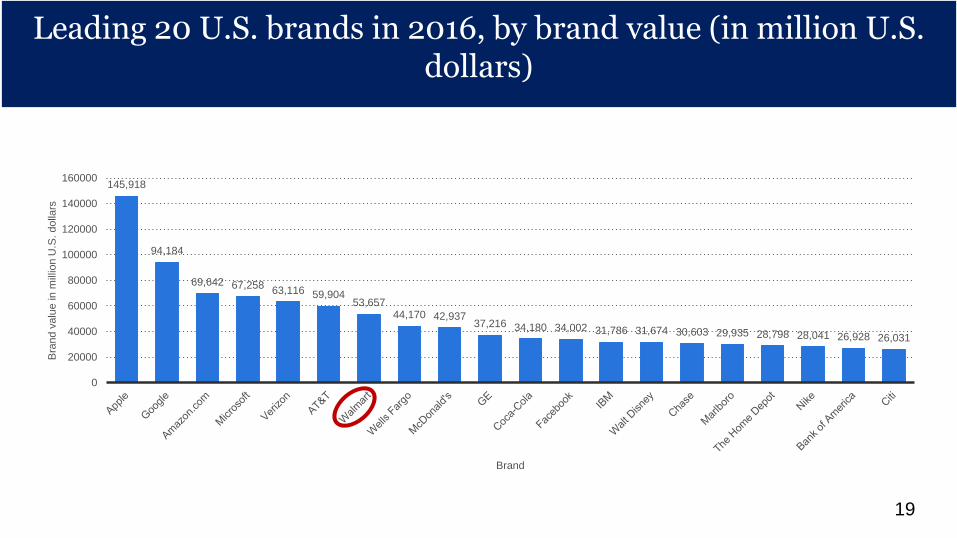

Leading 20 U.S. brands in 2016, by brand value (in million U.S. dollars)

Leading 20 U.S. brands in 2016, by brand value (in million U.S. dollars)

19

145,918

94,184

69,642 67,25863,116 59,904

53,65744,170 42,937

37,216 34,180 34,002 31,786 31,674 30,603 29,935 28,798 28,041 26,928 26,031

0

20000

40000

60000

80000

100000

120000

140000

160000

Bra

nd v

alu

e in

mill

ion U

.S. dolla

rs

Brand

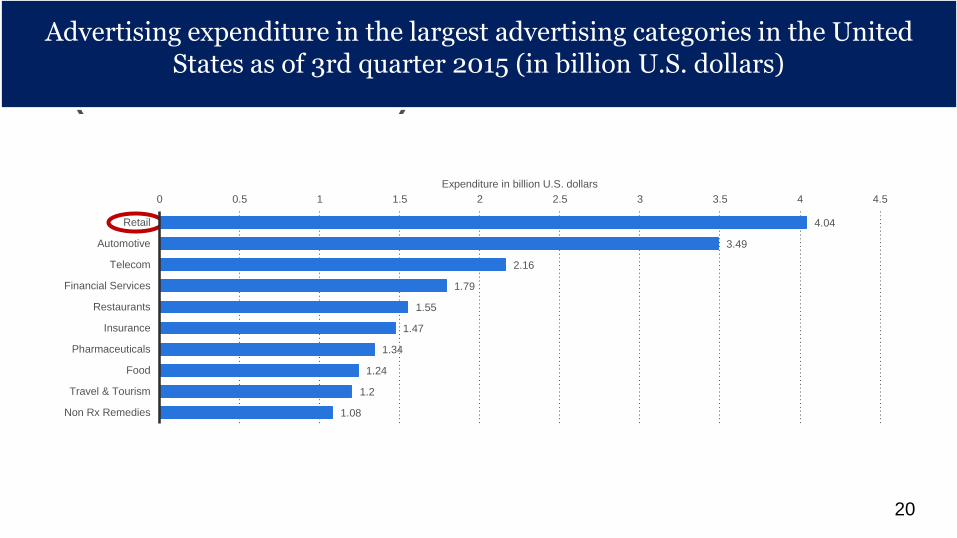

Advertising expenditure in the largest advertising categories in the United States as of 3rd quarter 2015 (in billion U.S. dollars)

Advertising expenditure in the largest advertising categories in the United States as of 3rd quarter 2015 (in billion U.S. dollars)

20

4.04

3.49

2.16

1.79

1.55

1.47

1.34

1.24

1.2

1.08

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

Retail

Automotive

Telecom

Financial Services

Restaurants

Insurance

Pharmaceuticals

Food

Travel & Tourism

Non Rx Remedies

Expenditure in billion U.S. dollars

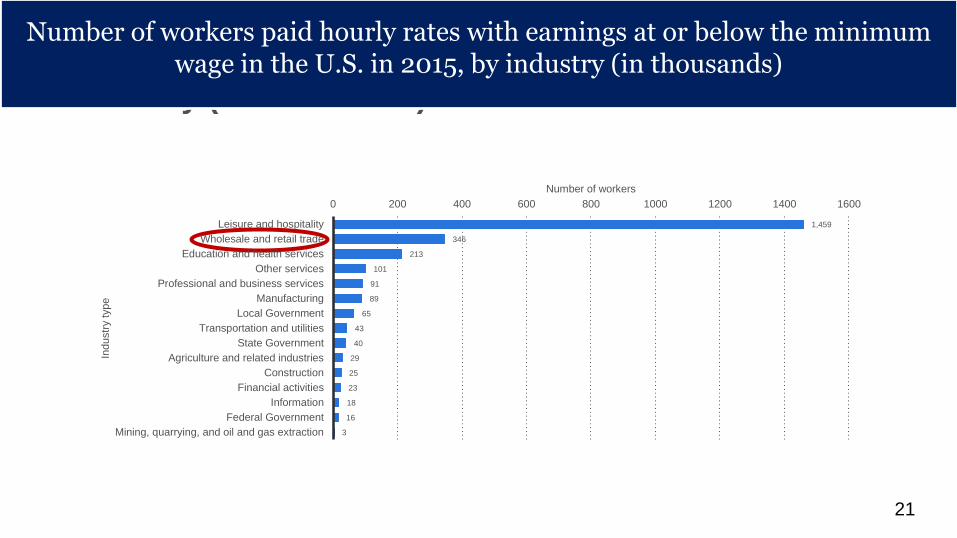

Number of workers paid hourly rates with earnings at or below the minimum wage in the U.S. in 2015, by industry (in thousands)

Number of workers paid hourly rates with earnings at or below the minimum wage in the U.S. in 2015, by industry (in thousands)

21

1,459

346

213

101

91

89

65

43

40

29

25

23

18

16

3

0 200 400 600 800 1000 1200 1400 1600

Leisure and hospitality

Wholesale and retail trade

Education and health services

Other services

Professional and business services

Manufacturing

Local Government

Transportation and utilities

State Government

Agriculture and related industries

Construction

Financial activities

Information

Federal Government

Mining, quarrying, and oil and gas extraction

Number of workers

Industr

y type

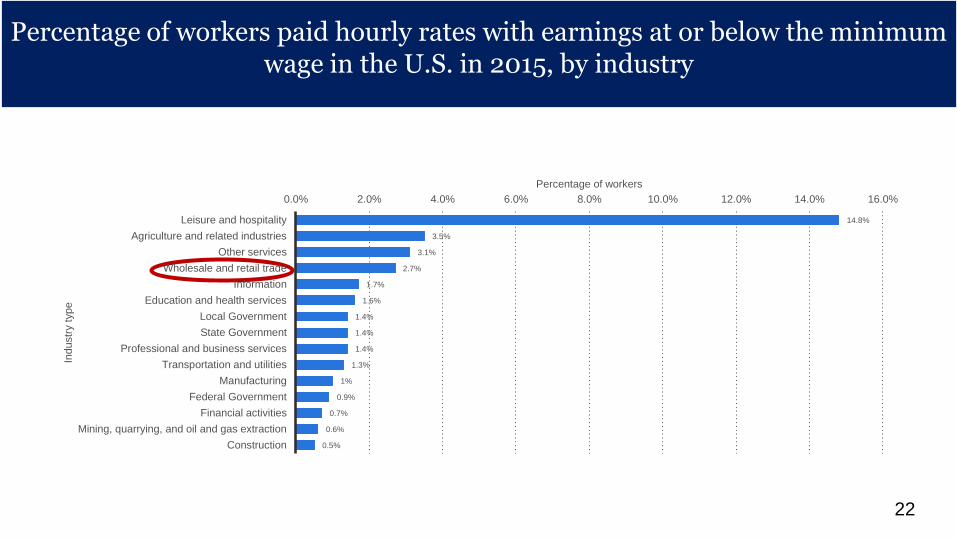

Percentage of workers paid hourly rates with earnings at or below the minimum wage in the U.S. in 2015, by industry

22

14.8%

3.5%

3.1%

2.7%

1.7%

1.6%

1.4%

1.4%

1.4%

1.3%

1%

0.9%

0.7%

0.6%

0.5%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%

Leisure and hospitality

Agriculture and related industries

Other services

Wholesale and retail trade

Information

Education and health services

Local Government

State Government

Professional and business services

Transportation and utilities

Manufacturing

Federal Government

Financial activities

Mining, quarrying, and oil and gas extraction

Construction

Percentage of workers

Industr

y type

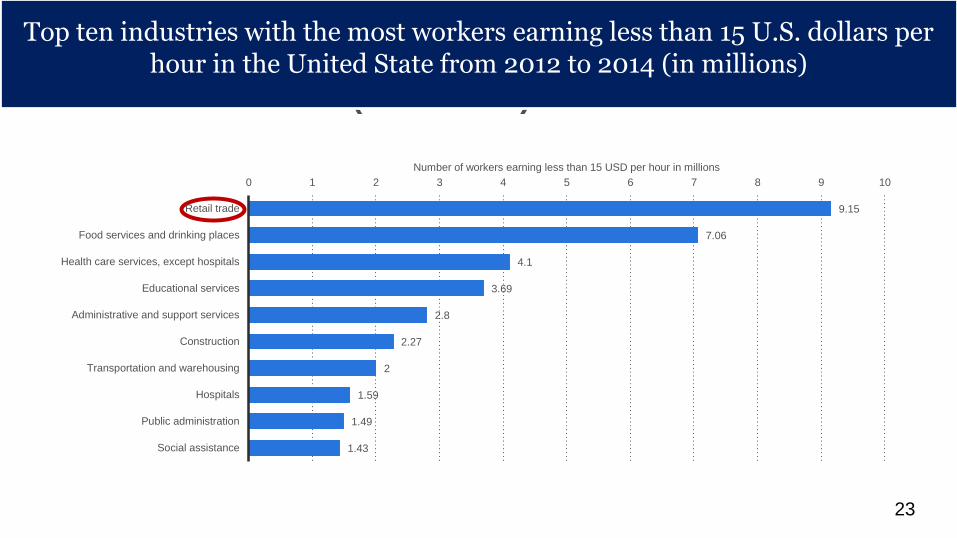

Top ten industries with the most workers earning less than 15 U.S. dollars per hour in the United State from 2012 to 2014 (in millions)

Top ten industries with the most workers earning less than 15 U.S. dollars per hour in the United State from 2012 to 2014 (in millions)

23

9.15

7.06

4.1

3.69

2.8

2.27

2

1.59

1.49

1.43

0 1 2 3 4 5 6 7 8 9 10

Retail trade

Food services and drinking places

Health care services, except hospitals

Educational services

Administrative and support services

Construction

Transportation and warehousing

Hospitals

Public administration

Social assistance

Number of workers earning less than 15 USD per hour in millions

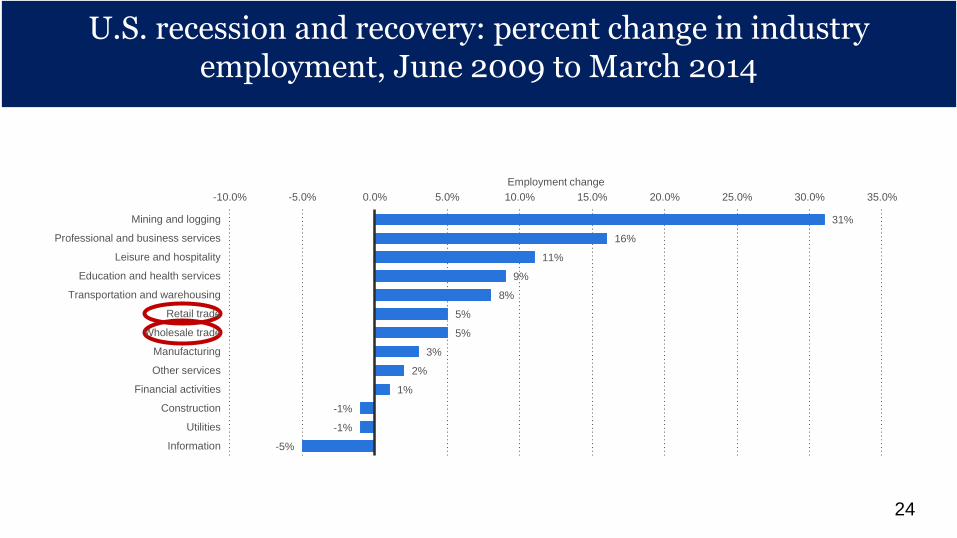

U.S. recession and recovery: percent change in industry employment, June 2009 to March 2014

U.S. recession and recovery: percent change in industry employment, June 2009 to March 2014

24

31%

16%

11%

9%

8%

5%

5%

3%

2%

1%

-1%

-1%

-5%

-10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0%

Mining and logging

Professional and business services

Leisure and hospitality

Education and health services

Transportation and warehousing

Retail trade

Wholesale trade

Manufacturing

Other services

Financial activities

Construction

Utilities

Information

Employment change

U.S. Retail Industry OverviewU.S. Retail Industry Overview

25

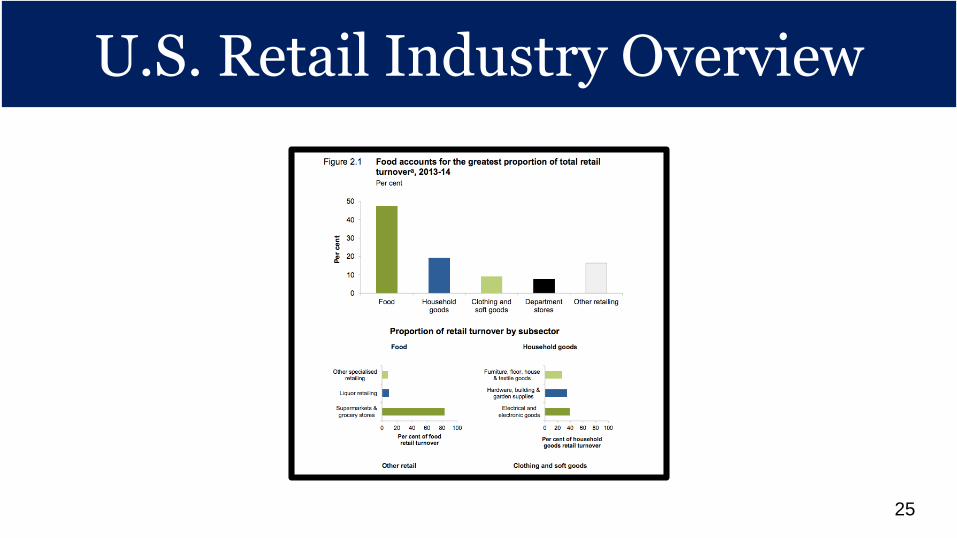

U.S. retail industry overview

• Sales per square foot is a popular sales metric used in the retailing industry. Sales per square foot is simply the average revenue a retail business creates for every square foot of sales space.

• Retail sales per square foot is a popular way for retailers to determine how successful store sales have been.

• The average regional mall sales per square foot is $341 and most big box retailers average between $250 to $350.

U.S. Retail Industry Overview

26

Retail sales per footRetail Sales Per Foot

27

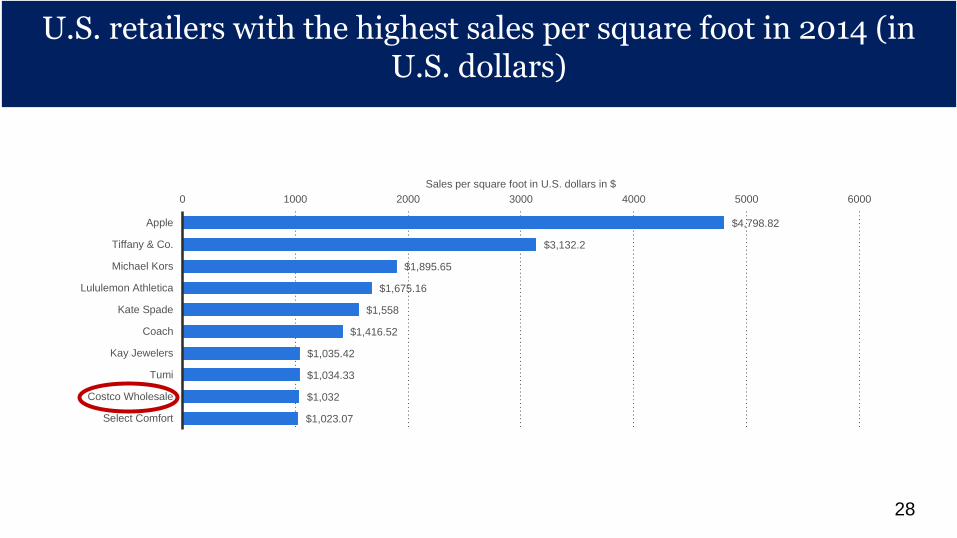

U.S. retailers with the highest sales per square foot in 2014 (in U.S. dollars)

U.S. retailers with the highest sales per square foot in 2014 (in U.S. dollars)

28

$4,798.82

$3,132.2

$1,895.65

$1,675.16

$1,558

$1,416.52

$1,035.42

$1,034.33

$1,032

$1,023.07

0 1000 2000 3000 4000 5000 6000

Apple

Tiffany & Co.

Michael Kors

Lululemon Athletica

Kate Spade

Coach

Kay Jewelers

Tumi

Costco Wholesale

Select Comfort

Sales per square foot in U.S. dollars in $

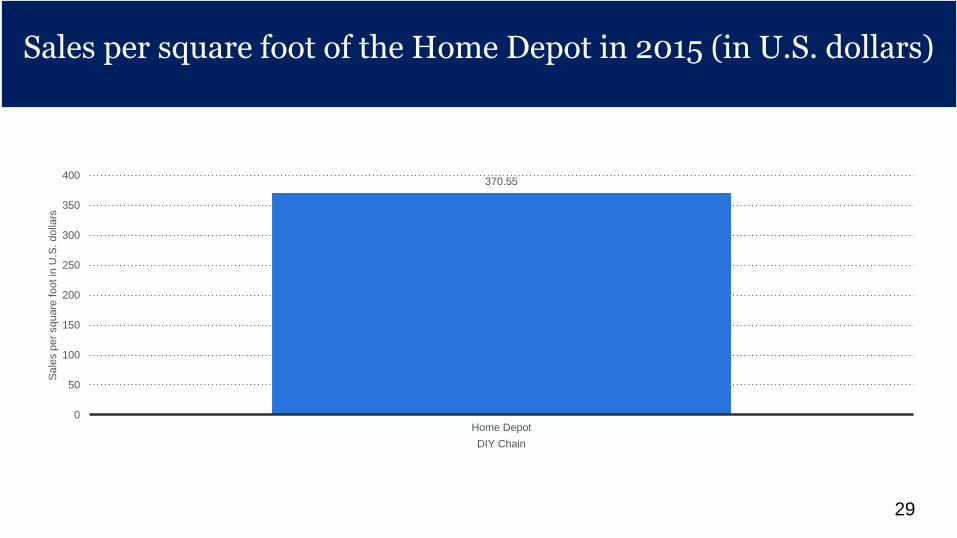

Sales per square foot of the Home Depot in 2015 (in U.S. dollars)

Sales per square foot of the Home Depot in 2015 (in U.S. dollars)

29

370.55

0

50

100

150

200

250

300

350

400

Home Depot

Sale

s p

er

square

foot in

U.S

. dolla

rs

DIY Chain

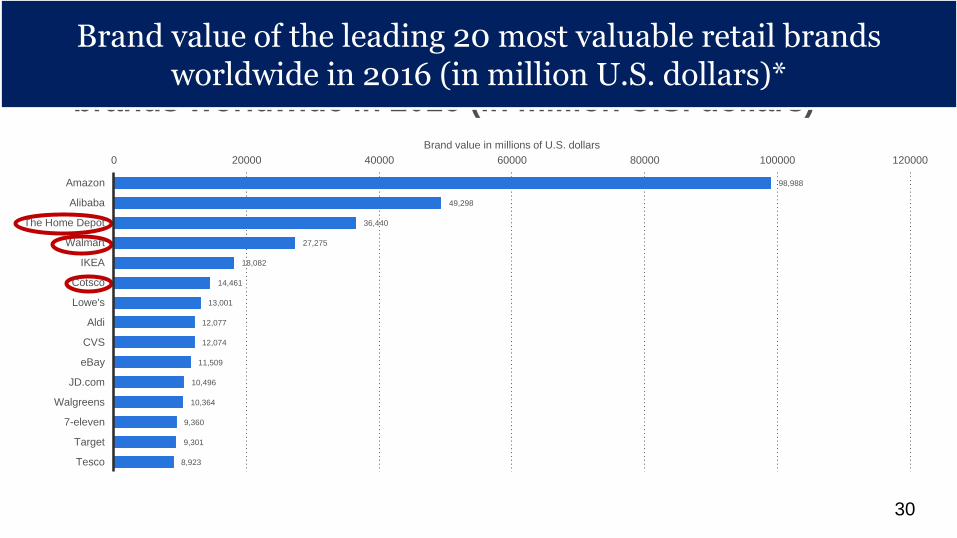

Brand value of the leading 20 most valuable retail

brands worldwide in 2016 (in million U.S. dollars)*

Brand value of the leading 20 most valuable retail brands worldwide in 2016 (in million U.S. dollars)*

30

98,988

49,298

36,440

27,275

18,082

14,461

13,001

12,077

12,074

11,509

10,496

10,364

9,360

9,301

8,923

0 20000 40000 60000 80000 100000 120000

Amazon

Alibaba

The Home Depot

Walmart

IKEA

Cotsco

Lowe's

Aldi

CVS

eBay

JD.com

Walgreens

7-eleven

Target

Tesco

Brand value in millions of U.S. dollars

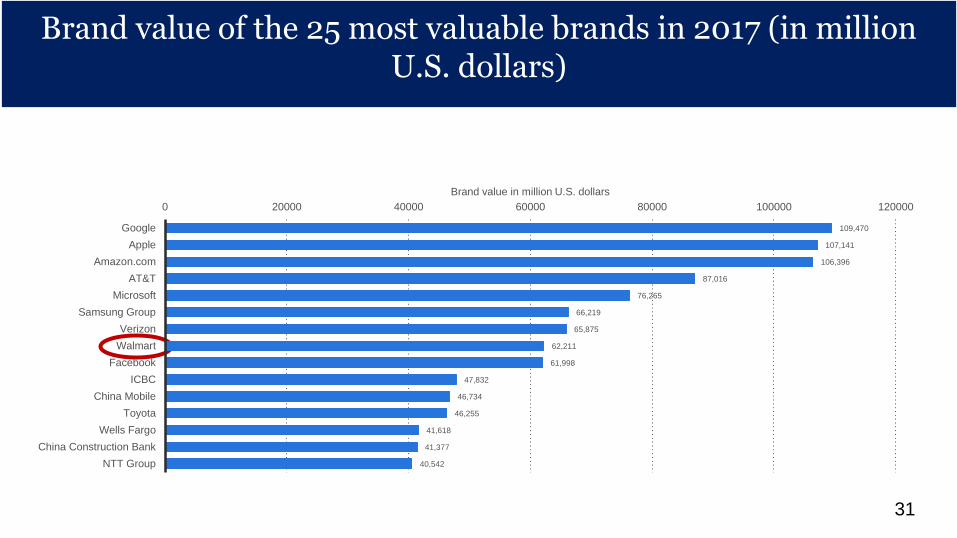

Brand value of the 25 most valuable brands in 2017 (in million U.S. dollars)

Brand value of the 25 most valuable brands in 2017 (in million U.S. dollars)

31

109,470

107,141

106,396

87,016

76,265

66,219

65,875

62,211

61,998

47,832

46,734

46,255

41,618

41,377

40,542

0 20000 40000 60000 80000 100000 120000

Apple

Amazon.com

AT&T

Microsoft

Samsung Group

Verizon

Walmart

ICBC

China Mobile

Toyota

Wells Fargo

China Construction Bank

NTT Group

Brand value in million U.S. dollars

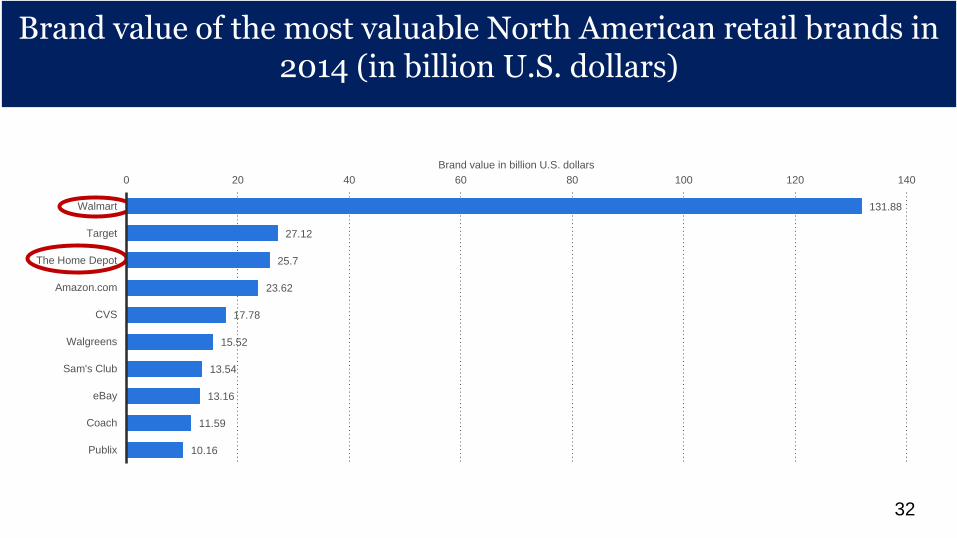

Brand value of the most valuable North American retail brands in 2014 (in billion U.S. dollars)

Brand value of the most valuable North American retail brands in 2014 (in billion U.S. dollars)

32

131.88

27.12

25.7

23.62

17.78

15.52

13.54

13.16

11.59

10.16

0 20 40 60 80 100 120 140

Walmart

Target

The Home Depot

Amazon.com

CVS

Walgreens

Sam's Club

eBay

Coach

Publix

Brand value in billion U.S. dollars

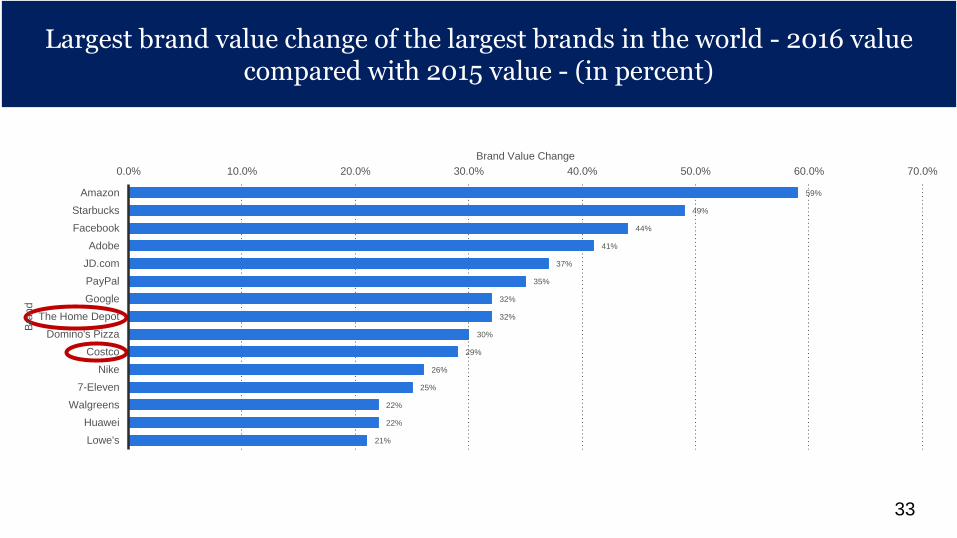

Largest brand value change of the largest brands in the world - 2016 value compared with 2015 value - (in percent)

33

59%

49%

44%

41%

37%

35%

32%

32%

30%

29%

26%

25%

22%

22%

21%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Amazon

Starbucks

Adobe

JD.com

PayPal

The Home Depot

Domino's Pizza

Costco

Nike

7-Eleven

Walgreens

Huawei

Lowe's

Brand Value Change

Bra

nd

Brand value of the leading 20 most valuable retail brands worldwide in 2016 (in million U.S. dollars)*

Brand value of the leading 20 most valuable retail brands worldwide in 2016 (in million U.S. dollars)*

34

98,988

49,298

36,440

27,275

18,082

14,461

13,001

12,077

12,074

11,509

10,496

10,364

9,360

9,301

8,923

0 20000 40000 60000 80000 100000 120000

Amazon

Alibaba

The Home Depot

Walmart

IKEA

Cotsco

Lowe's

Aldi

CVS

eBay

JD.com

Walgreens

7-eleven

Target

Tesco

Brand value in millions of U.S. dollars

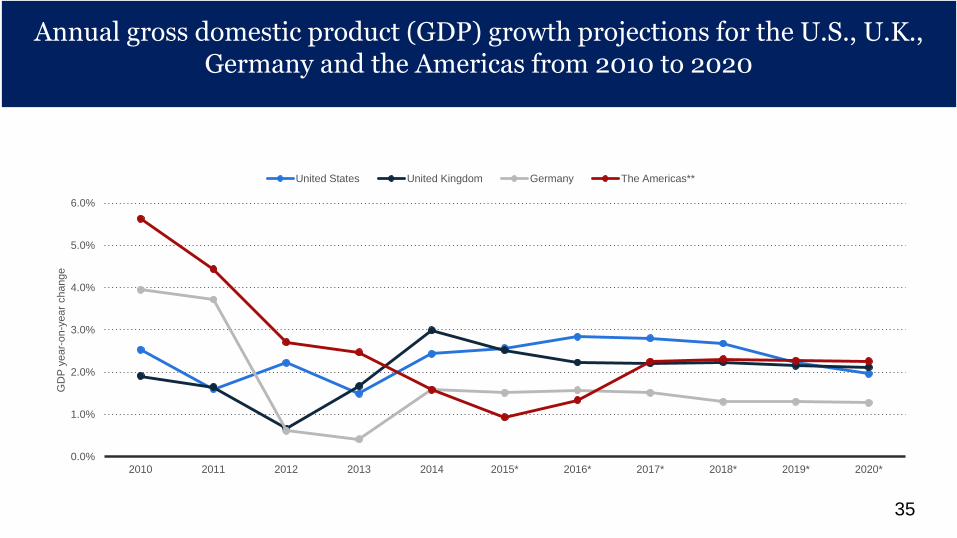

Annual gross domestic product (GDP) growth projections for the U.S., U.K., Germany and the Americas from 2010 to 2020

Annual gross domestic product (GDP) growth projections for the U.S., U.K., Germany and the Americas from 2010 to 2020

35

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2010 2011 2012 2013 2014 2015* 2016* 2017* 2018* 2019* 2020*

GD

P y

ear-

on-y

ear

change

United States United Kingdom Germany The Americas**

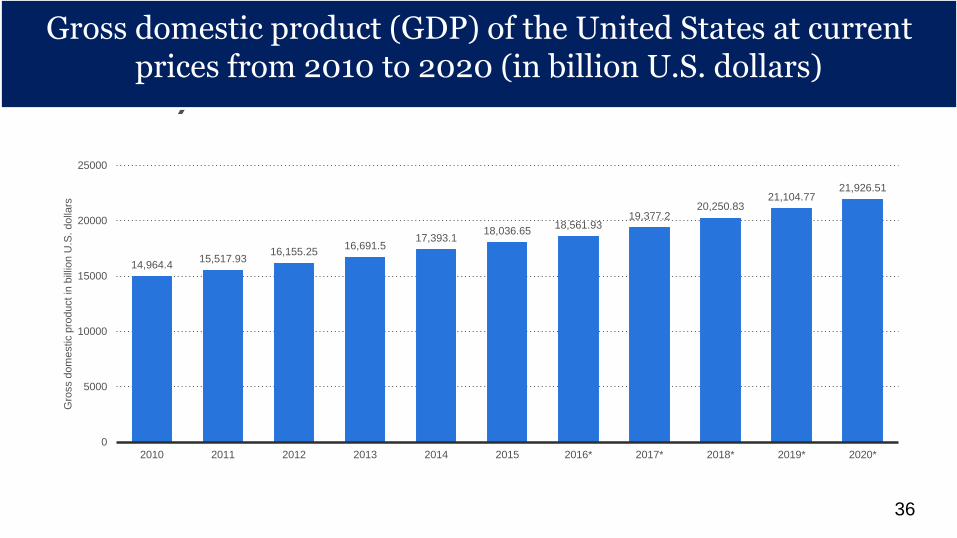

Gross domestic product (GDP) of the United States at current prices from 2010 to 2020 (in billion U.S. dollars)

Gross domestic product (GDP) of the United States at current prices from 2010 to 2020 (in billion U.S. dollars)

36

14,964.415,517.93

16,155.2516,691.5

17,393.118,036.65

18,561.9319,377.2

20,250.8321,104.77

21,926.51

0

5000

10000

15000

20000

25000

2010 2011 2012 2013 2014 2015 2016* 2017* 2018* 2019* 2020*

Gro

ss d

om

estic p

roduct in

bill

ion U

.S. dolla

rs

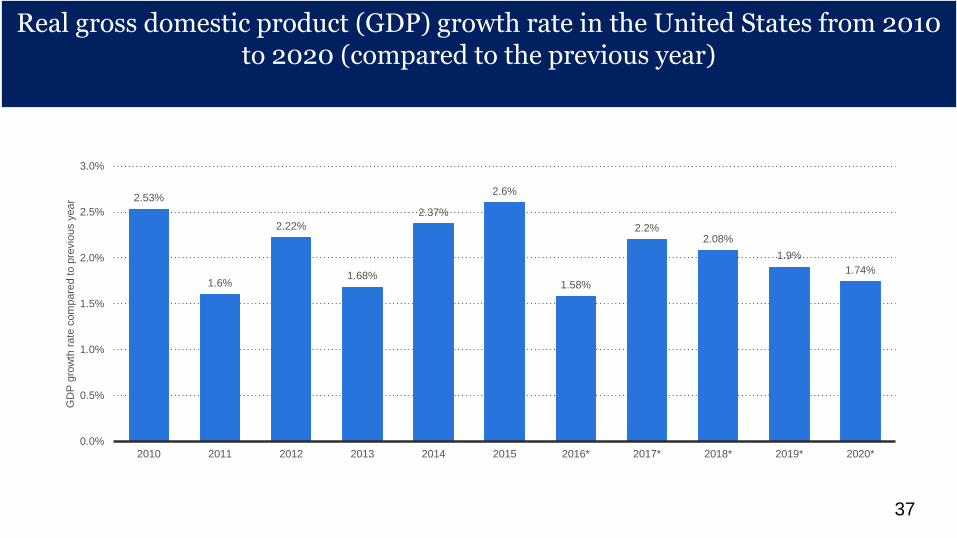

Real gross domestic product (GDP) growth rate in the United States from 2010 to 2020 (compared to the previous year)

Real gross domestic product (GDP) growth rate in the United States from 2010 to 2020 (compared to the previous year)

37

2.53%

1.6%

2.22%

1.68%

2.37%

2.6%

1.58%

2.2%2.08%

1.9%

1.74%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2010 2011 2012 2013 2014 2015 2016* 2017* 2018* 2019* 2020*

GD

P g

row

th r

ate

com

pare

d to p

revio

us y

ear

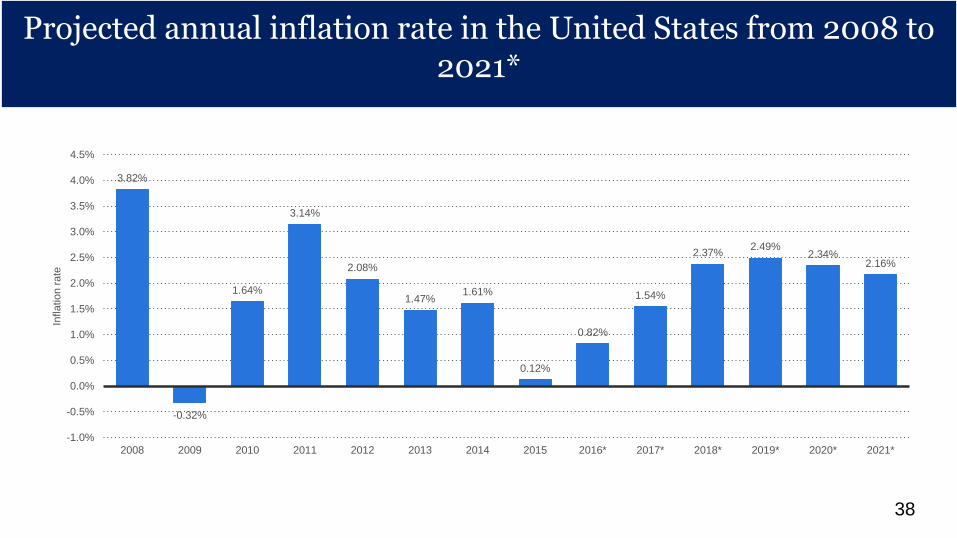

Projected annual inflation rate in the United States from 2008 to 2021*

Projected annual inflation rate in the United States from 2008 to 2021*

38

3.82%

-0.32%

1.64%

3.14%

2.08%

1.47%1.61%

0.12%

0.82%

1.54%

2.37%2.49%

2.34%2.16%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2008 2009 2010 2011 2012 2013 2014 2015 2016* 2017* 2018* 2019* 2020* 2021*

Infla

tio

n r

ate

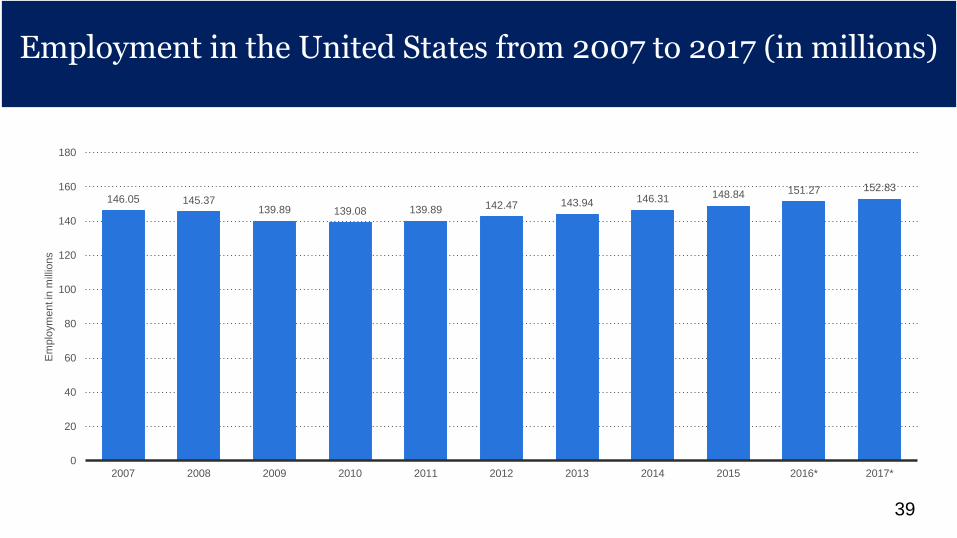

Employment in the United States from 2007 to 2017 (in millions)

Employment in the United States from 2007 to 2017 (in millions)

39

146.05 145.37139.89 139.08 139.89 142.47 143.94 146.31 148.84 151.27 152.83

0

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016* 2017*

Em

plo

ym

ent in

mill

ions

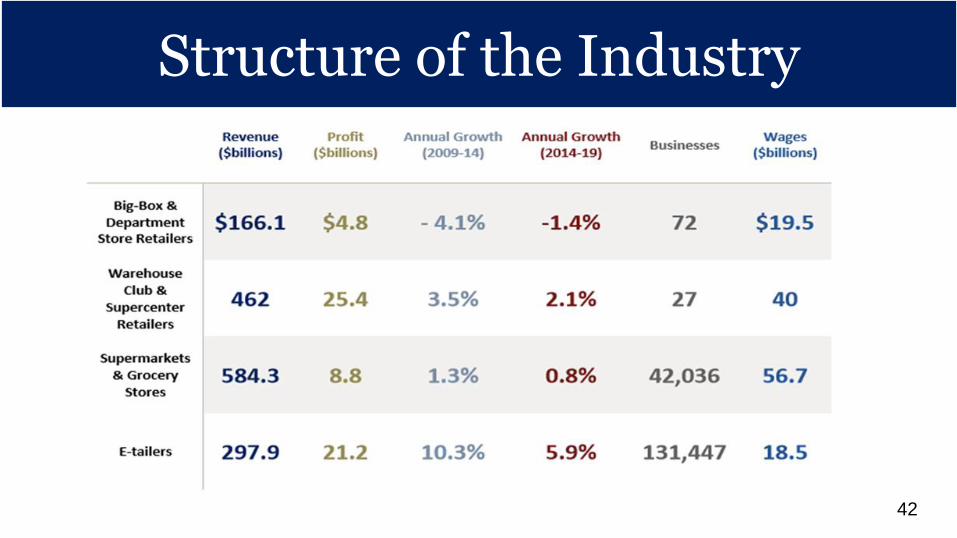

Big-Box & Department Store Retailers:

•Broad range of general merchandise, such as apparel, jewelry, cosmetics, home furnishings, general household products, toys, appliances and sporting goods

•Discount department stores are also included

•Walmart, Best Buy, The Home Depot and Ikea

Warehouse Club & Supercenter Retailers:

•General line of grocery products, along with merchandise items.

•Warehouse clubs offer customers a wide selection of goods (often in bulk) at discounted prices, in exchange for a membership fee paid by each customer.

•Costco and BJ’s Wholesale Club

Structure of the Industry: competition and market dynamics

40

Supermarkets & Grocery Stores:

•General lines of food products, including fresh and prepared meats, poultry and seafood, canned and frozen foods, fresh fruits and vegetables and various dairy products

•Safeway, Whole Foods Market and The Kroger Company

E-tailers:

•Selling retail goods on the Internet

•Including e-commerce and online auction websites whose primary activity is selling goods online

Dell and Amazon.com

Structure of the Industry: competition and market dynamics

41

Structure of the IndustryStructure of the Industry

42

Key Factors for Success

Ability to Control Stock on Hand

Seasonal goods and products

Most of annual sales occurring between October and December

Require tight stock control measures to ensure reordering and to maximize sales.

Customer Centric Workforce

Retail stores require sales staff that are friendly, helpful and provide excellent customer service

Ability to Expand and Curtail

Expand operations during peak periods to meet increased demand (i.e., Christmas trading)

Curtail operations during weaker trading conditions (i.e., economic slowdown)

Attractive Product Presentation

Effective layout and design, good shelf management, friendly and helpful service and a clean environment

Strong Logistics and Distribution Backbone

Control margins and costs through efficient and effective logistics and distribution systems between its manufacturers and among its stores to properly manage inventory

Key Factors for Success

43

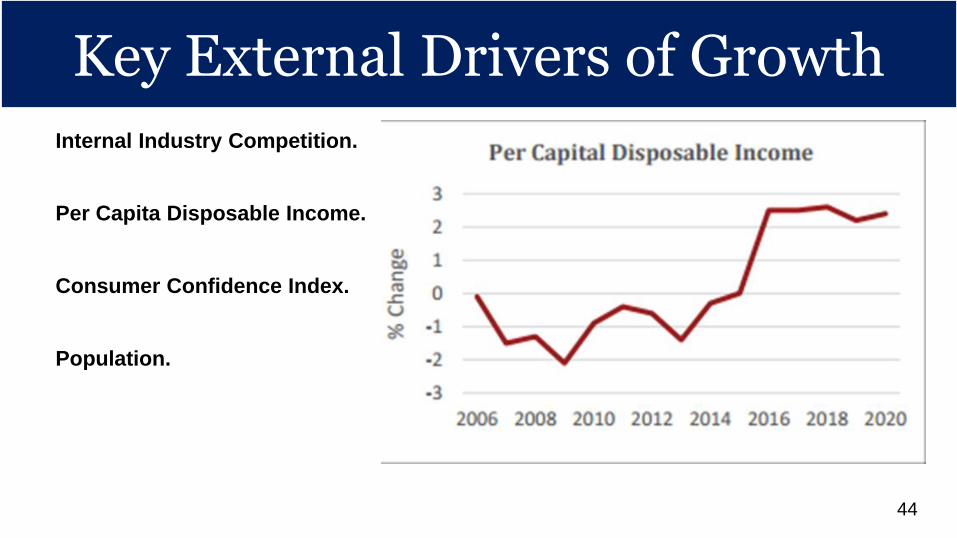

Key External Drivers of Growth

Internal Industry Competition.

Per Capita Disposable Income.

Consumer Confidence Index.

Population.

Key External Drivers of Growth

44

Retail Industry Mature Life Cycle

Industry value added (IVA): a measure of an industry or industry segment’s contribution to the U.S. economy

Decline phase: IVA falls below GDP

Growth phase: IVA outpaces GDP

Mature phase: IVA mirrors GDP

U.S. GDP is anticipated to rise an at annualized rate of 2.5% in the 10 years to 2020.

Retail Industry Mature Life Cycle

4545

Retail Industry Mature Life Cycle

The Big-Box & Department Store Retailer:

Decline phase

In the 10 years to 2020, IVA is expected to decline at an annualized rate of about 4.6%

The Warehouse Club & Supercenter Retailer:

Mature phase

In the 10 years to 2020, IVA is forecast to increase at a rate of 2.5% per year on average, mirroring U.S. GDP

Retail Industry Mature Life Cycle

46

Retail Industry Mature Life Cycle The Supermarkets and Grocery Stores:

Mature phase

The Supermarkets and Grocery Stores industry is in the mature stage of its life cycle. However, in the 10 years to 2020, IVA is expected to increase at a relatively slow rate of 0.6% per year on average.

The E-tailer:

Growth phase

In the 10 years to 2020, IVA is expected to increase at an average annual rate of 12.8%. High IVA growth relative to the economy as a whole is highly indicative of a growing life cycle stage.

Retail Industry Mature Life Cycle

47

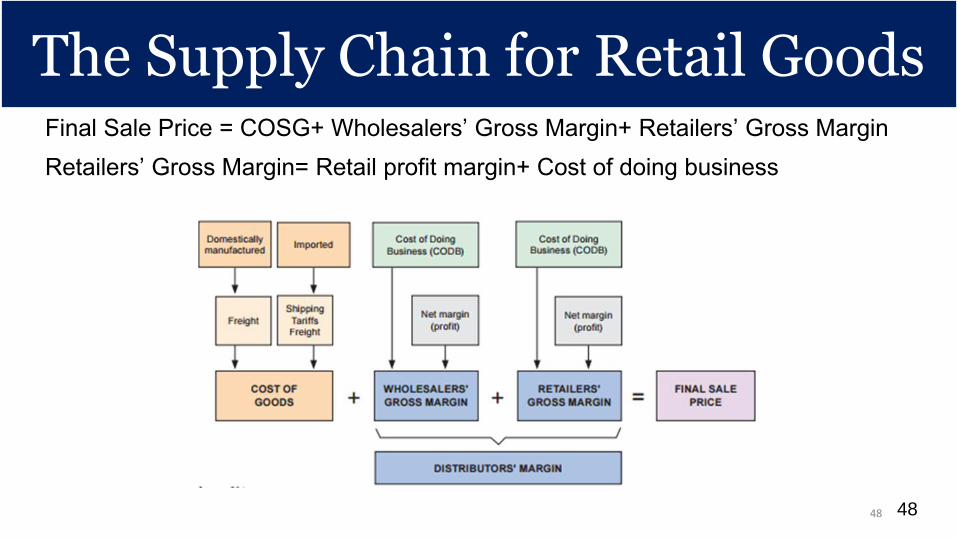

The Supply Chain for Retail GoodsFinal Sale Price = COSG+ Wholesalers’ Gross Margin+ Retailers’ Gross Margin

Retailers’ Gross Margin= Retail profit margin+ Cost of doing business

The Supply Chain for Retail Goods

4848

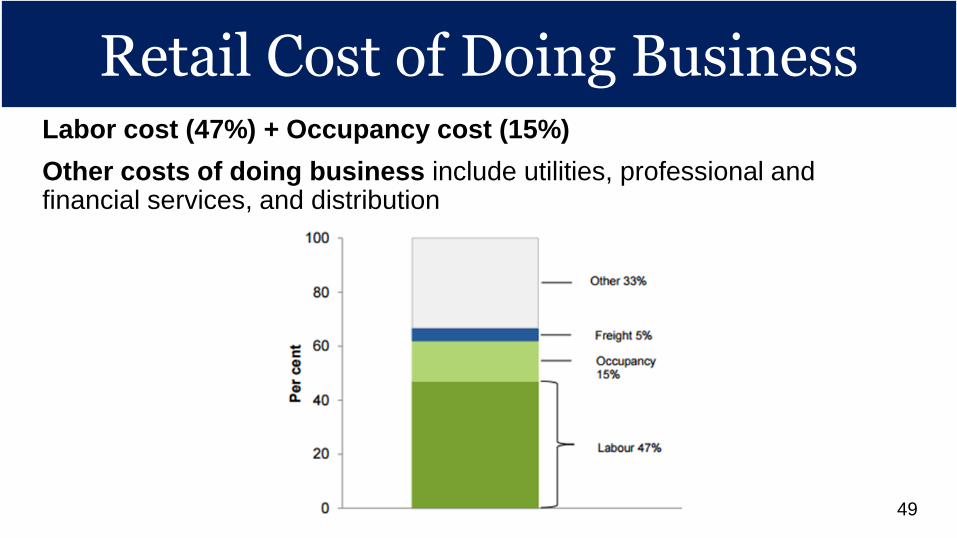

Retail Cost of Doing Business Labor cost (47%) + Occupancy cost (15%)

Other costs of doing business include utilities, professional and financial services, and distribution

Retail Cost of Doing Business

49

Retail Cost of Doing Business

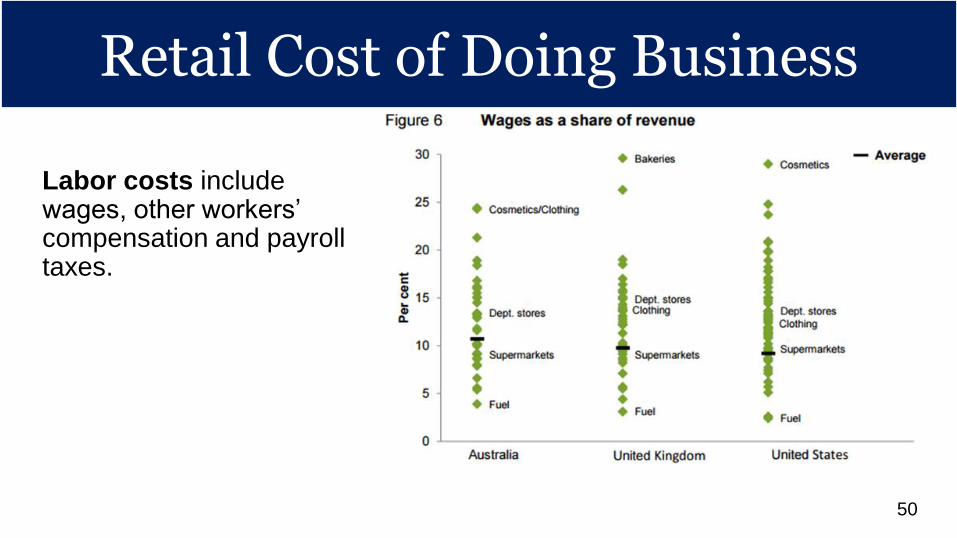

Labor costs include wages, other workers’ compensation and payroll taxes.

Retail Cost of Doing Business

50

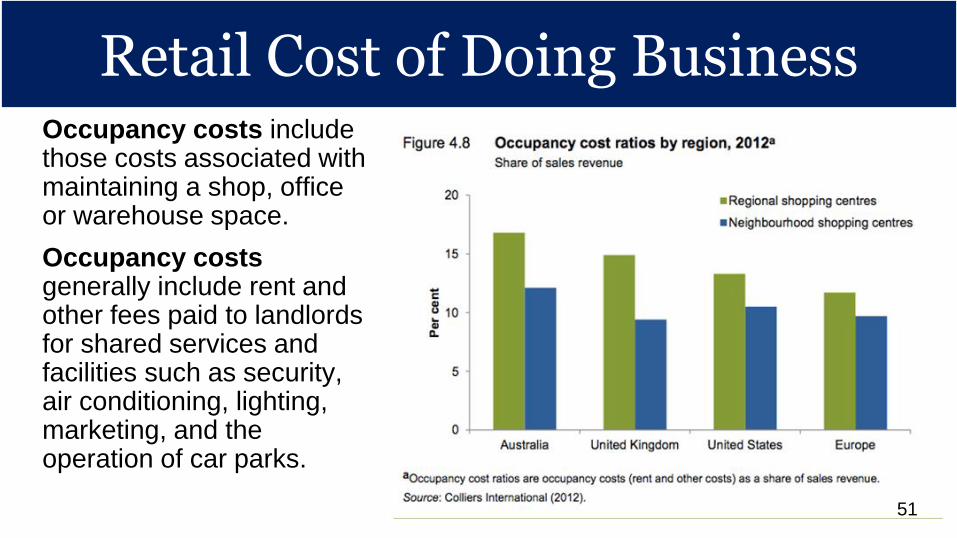

Retail Cost of Doing Business Occupancy costs include those costs associated with maintaining a shop, office or warehouse space.

Occupancy costs generally include rent and other fees paid to landlords for shared services and facilities such as security, air conditioning, lighting, marketing, and the operation of car parks.

Retail Cost of Doing Business

51

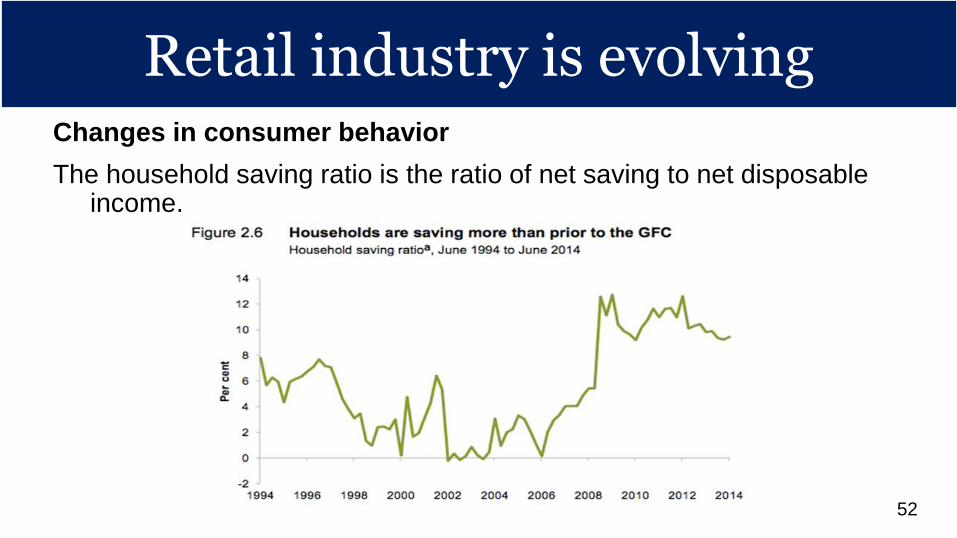

Retail industry is evolvingChanges in consumer behavior

The household saving ratio is the ratio of net saving to net disposable income.

Retail industry is evolving

52

Retail industry is evolvingTechnological change

Retail industry is evolving

53

54

55

Stock Overview

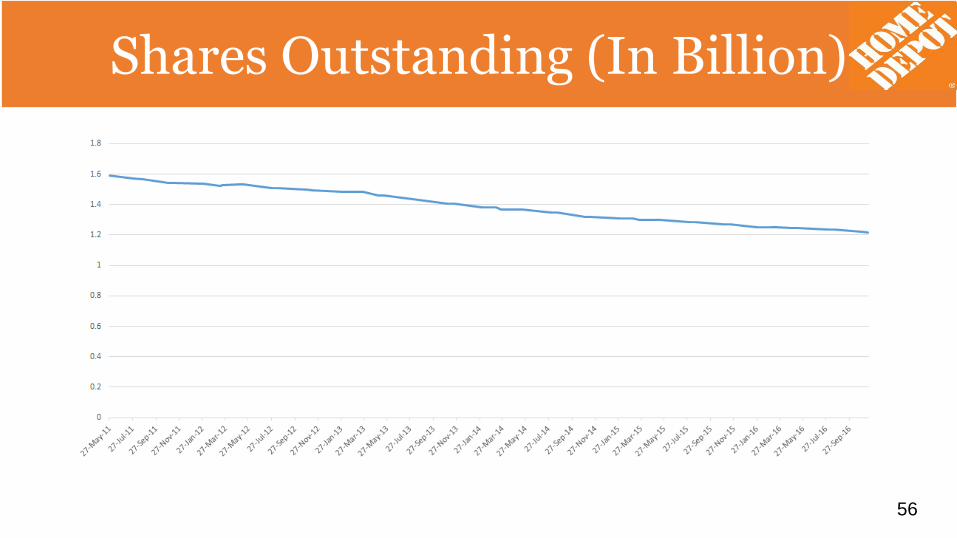

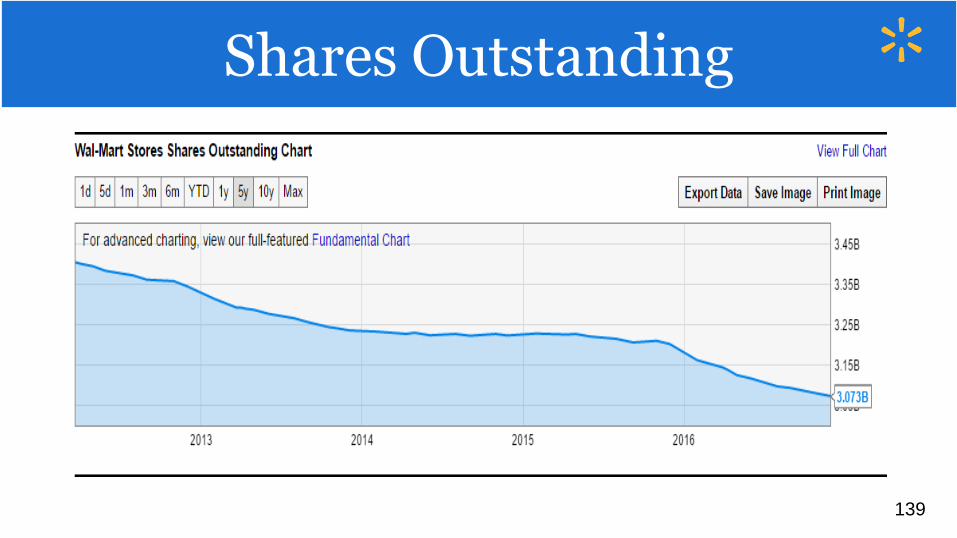

Shares Outstanding (In Billion)

56

Shares Outstanding (In Billion)

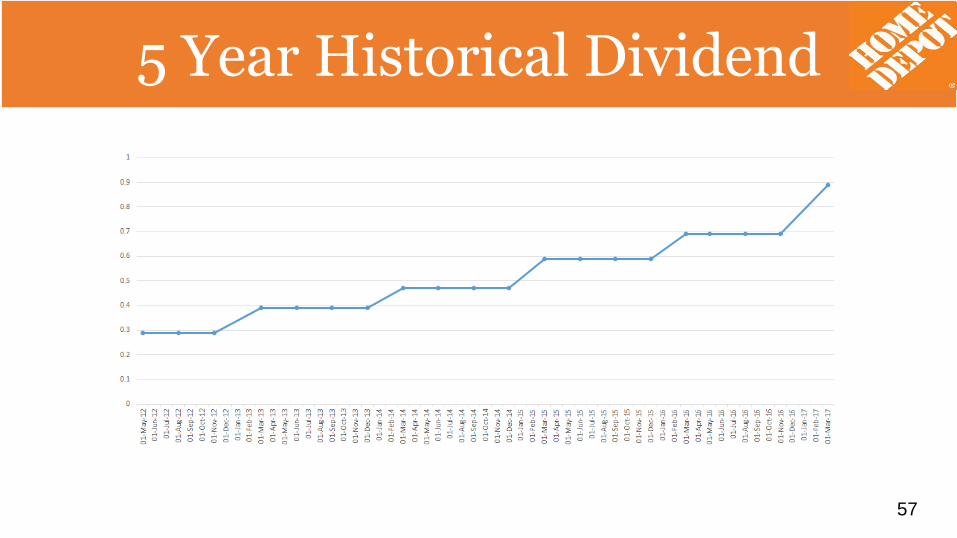

5-Year Historical Dividend

57

5 Year Historical Dividend

5 Day Performance

58

5 Day Performance

1 Year Performance

59

1 Year Performance

1 Year Trading Volume

60

1 Year Trading Volume

5 Year Performance

61

5 Year Performance

5 Year Trading Volume

62

5 Year Trading Volume

Max Trading Performance

63

Max Trading Performance

Max Trading Volume

64

Max Trading Volume

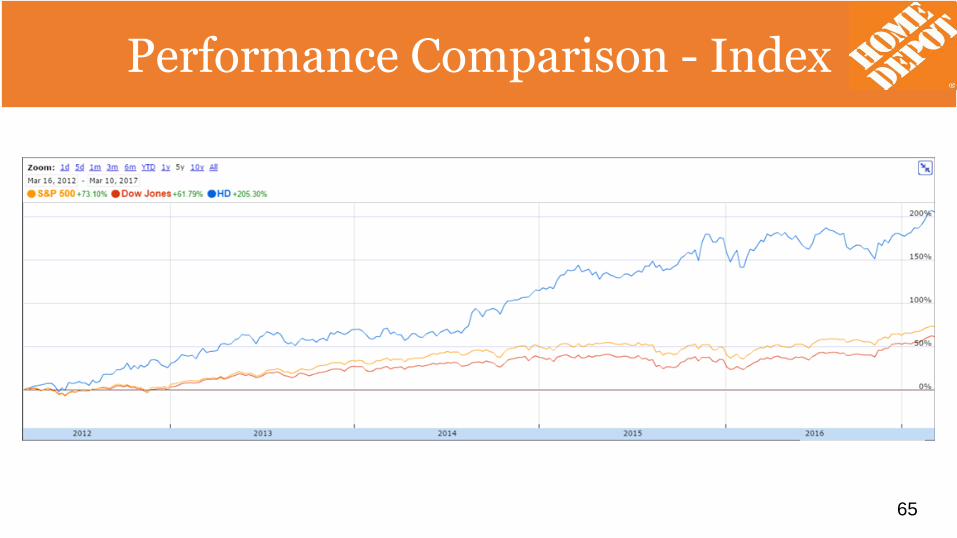

Performance Comparison - Index

65

Performance Comparison - Index

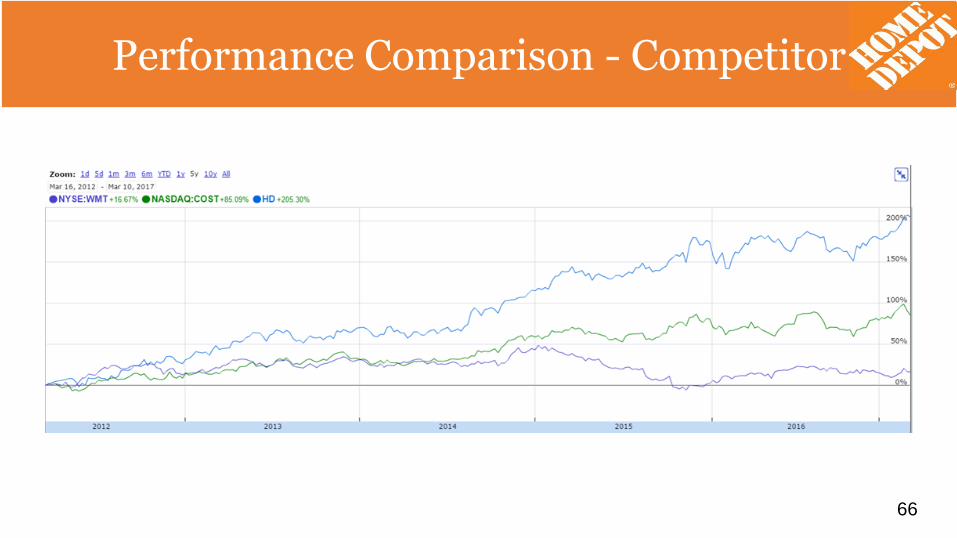

Performance Comparison - Competitors

66

Performance Comparison - Competitor

Home Depot Major Institutional Holders

67

Major Institutional Holders

Home Depot History

•1979- In Atlanta, Georgia, founded by Bernie Marcus and Arthur Blank when they opened their first two one-stop do-it-yourself warehouse-style stores•1981- The Home Depot went public on NASDAQ•1984- They moved to the New York Stock Exchange •1994- The company arrived in Canada with the acquisition of Aikenhead's home improvement centers•2001- They opened in Mexico through the acquisition of Total HOME•2003- The Home Depot had grown from three stores employing 200 people to more than 1,700 stores employing 300,000 people2005 - Acquired National Waterworks Holding for $1.35 billion in cash•2006- The company extended its reach to China by acquiring The Home Way, a 12 store chain2015 - Acquired Interline Brands Inc for $1.63 billion in cashToday - More than 2,200 stores in the U.S., Canada, and Mexico with an average of 105,000 square feet of indoor retail space, interconnected with an e-commerce business.

68

Home Depot History

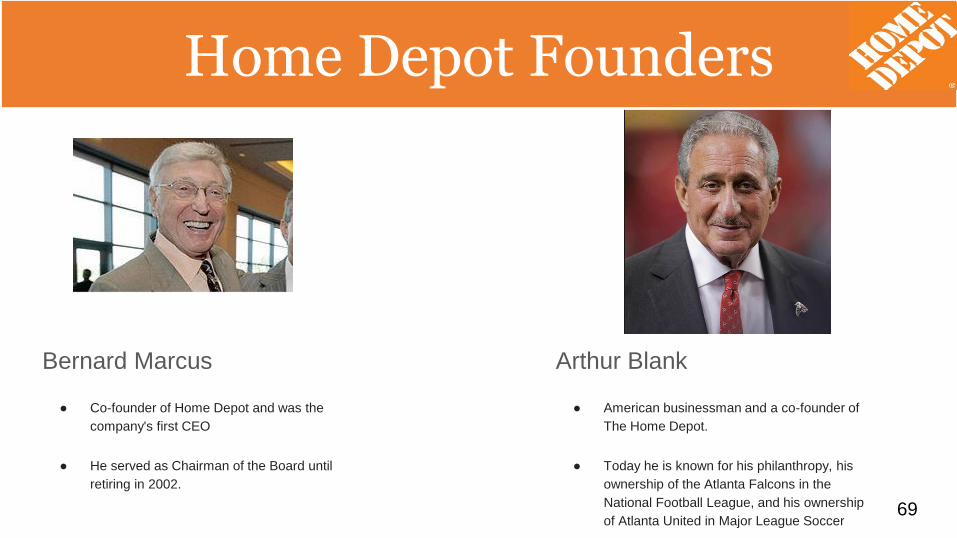

Home Depot Founders

Bernard Marcus

● Co-founder of Home Depot and was the

company's first CEO

● He served as Chairman of the Board until

retiring in 2002.

Arthur Blank

● American businessman and a co-founder of

The Home Depot.

● Today he is known for his philanthropy, his

ownership of the Atlanta Falcons in the

National Football League, and his ownership

of Atlanta United in Major League Soccer69

Home Depot Founders

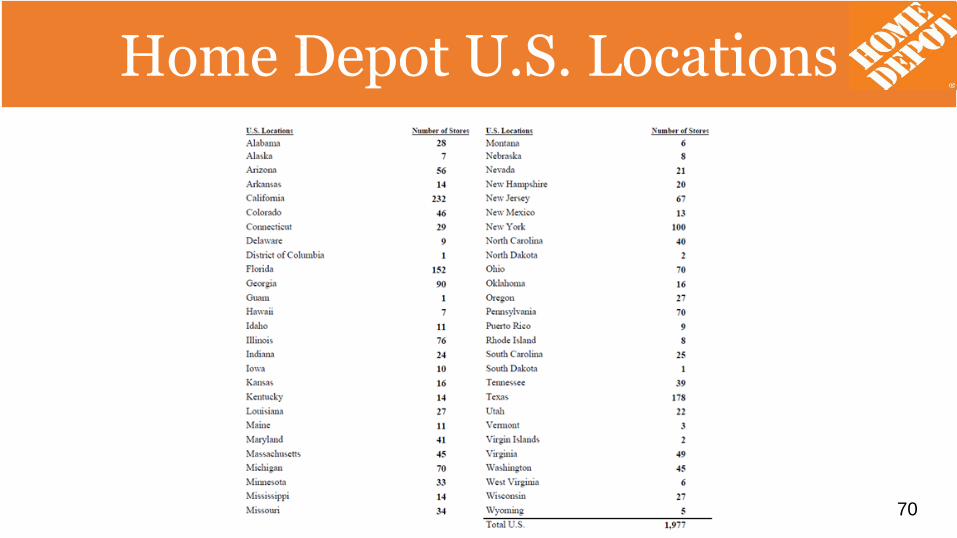

Home Depot U.S. Locations

70

Home Depot U.S. Locations

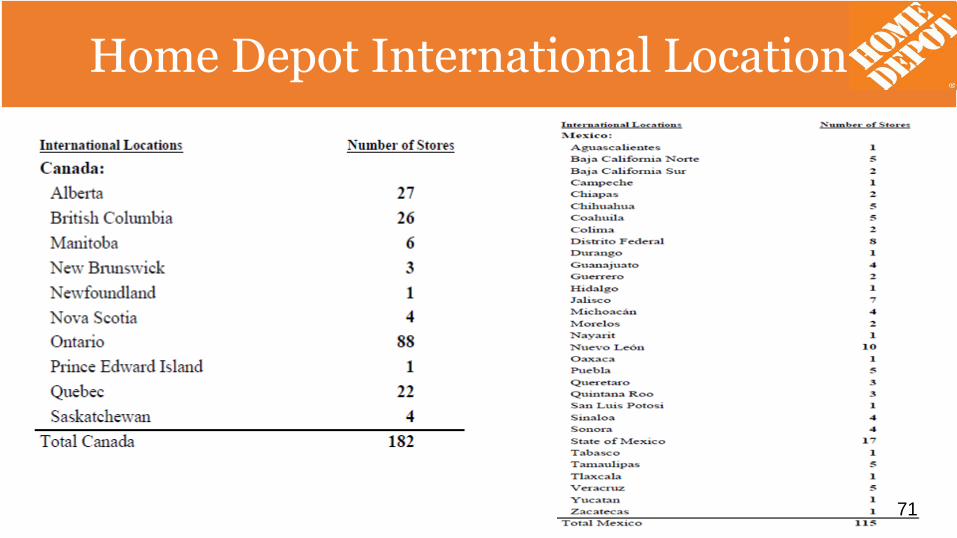

Home Depot International Locations

71

Home Depot International Locations

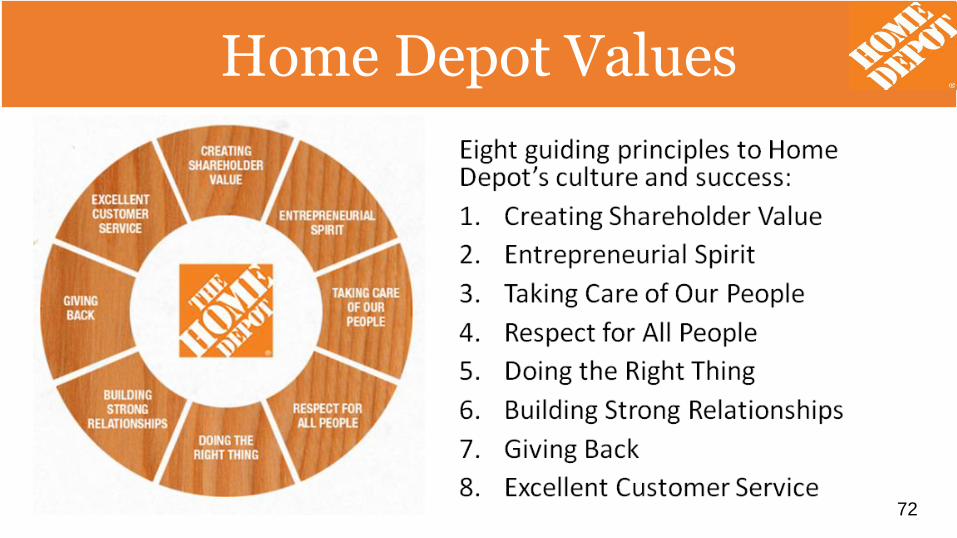

Home Depot Values

72

Home Depot Values

Home Depot Inverted Pyramid

73

Home Depot Inverted Pyramid

Three-Legged Stool Strategic Framework

74

Three-Legged Stool Strategic Framework

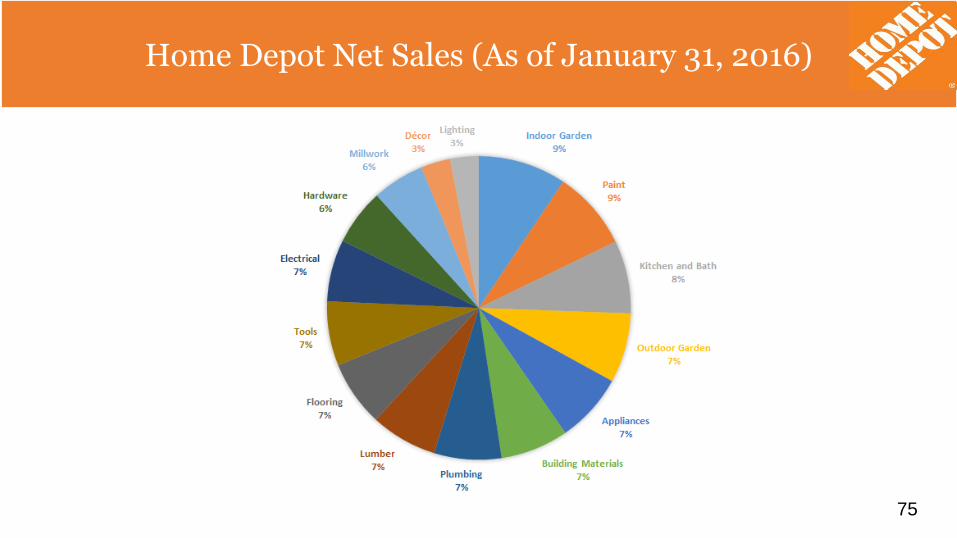

Home Depot Net Sales (As of January 31, 2016)

75

Home Depot Net Sales (As of January 31, 2016)

Home Depot Net Sales (As of January 31, 2016)

•The Company operates within a single reportable segment primarily within North America.

•Net Sales for the Company outside the U.S. were $8.0 billion, $8.5 billion and $8.5 billion for fiscal 2015, 2014 and 2013, respectively.

•Long-lived assets outside the U.S. totaled $2.3 billion and $2.5 billion as of January 31, 2016 and February 1, 2015, respectively.

76

Home Depot Net Sales (As of January 31, 2016)

Looking Ahead

Home Depot set forth their new long-term financial targets. By the end of fiscal 2018, they expect to grow sales to $101 billion while achieving a 14.5 percent operating margin and a 35 percent return on invested capital.

77

Looking Ahead

Home Depot E-Commerce

78

Home Depot E-Commerce

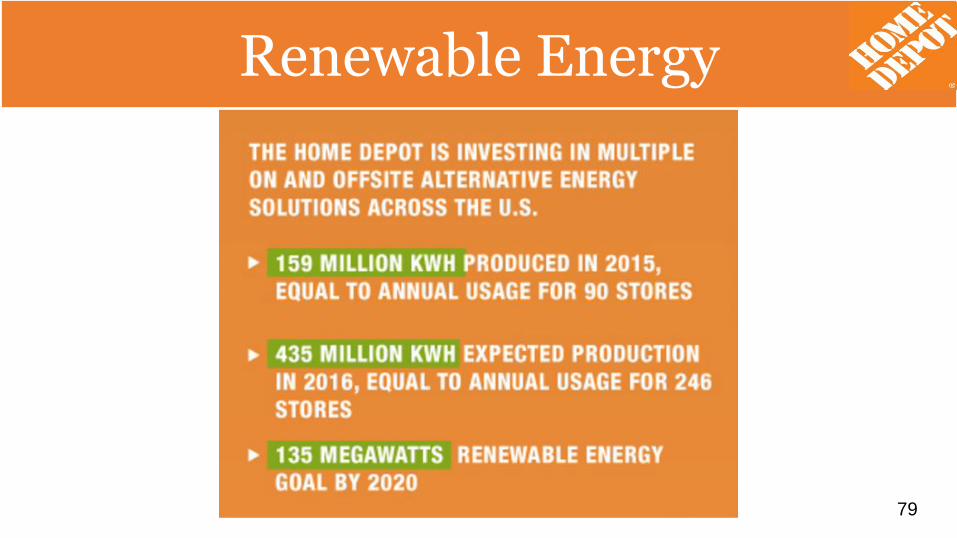

Home Depot and Renewable Energy

79

Renewable Energy

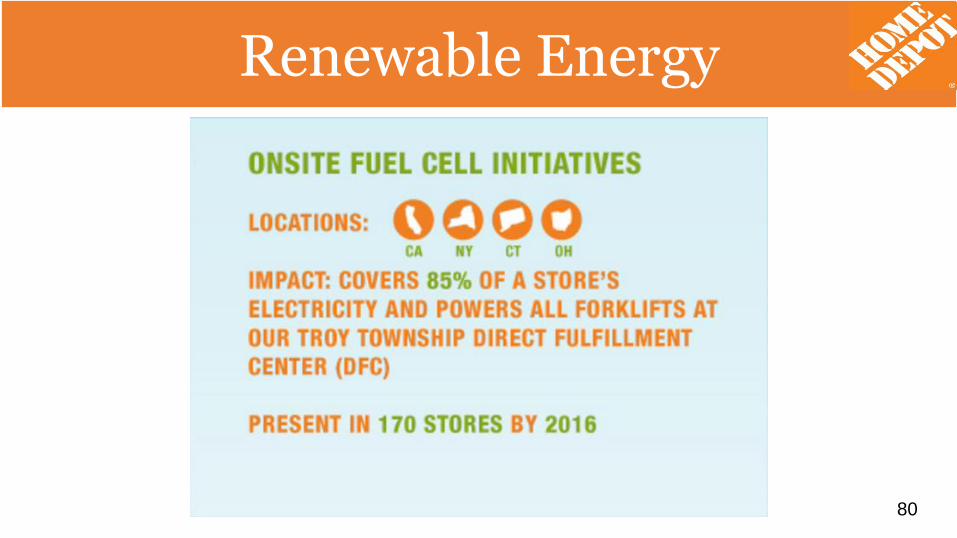

Home Depot and Renewable Energy

80

Renewable Energy

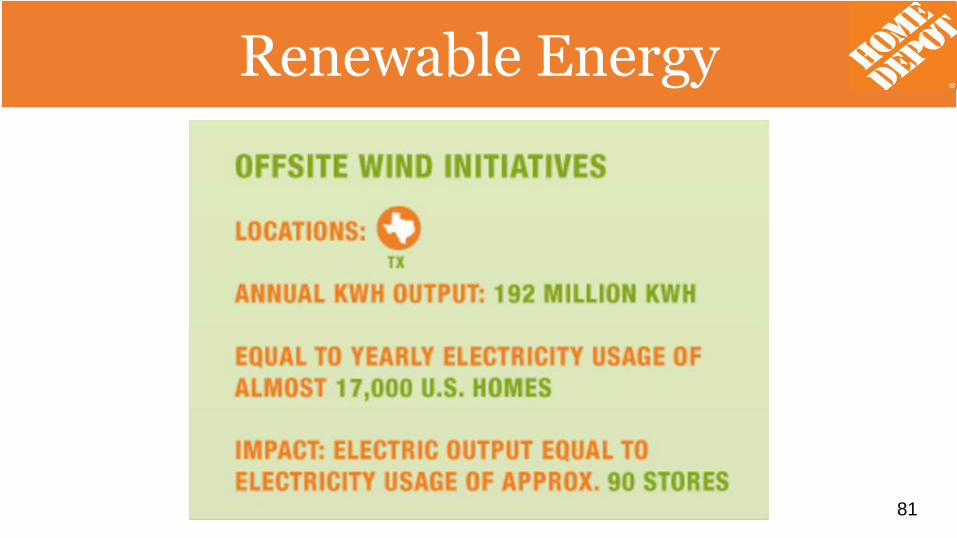

Home Depot and Renewable Energy

81

Renewable Energy

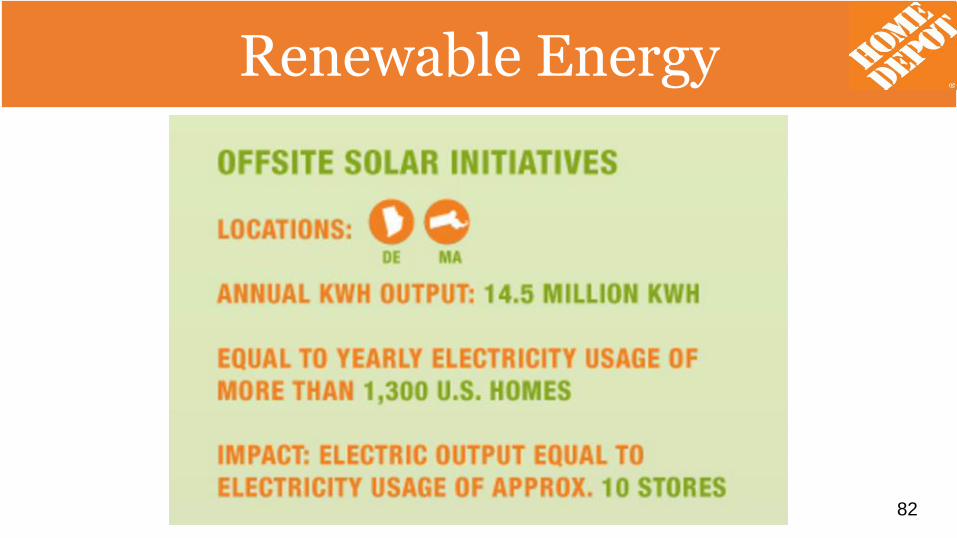

Home Depot and Renewable Energy

82

Renewable Energy

Home Depot Management

83

Management

CRAIG MENEAR

Chairman, CEO and President

Craig Menear is chairman, CEO and president of The Home Depot.

Joined The Home Depot in 1997,

Served in various roles with retailers such as IKEA, Builders Emporium, Grace Home Centers and Montgomery Ward in addition to also previously operating his own independent retail business.

He currently serves on the board of the Atlanta Committee for Progress.

Earned a bachelor of arts degree from Michigan State University’s Eli Broad College of Business.

Home Depot Management

84

ManagementANN-MARIE CAMPBELL

Executive Vice President - U.S. Stores

Joined The Home Depot in 1985 as a cashier in South Florida

During her career at the company, she has served in a variety of positions, including store manager, district manager and regional vice president. She has also served as vice president of operations, vice president of merchandising and special orders, vice president of retail marketing and sales for Home Depot Direct, vice president of vendor services and, most recently, president of the Southern Division of The Home Depot.

In 2014, Fortune Magazine listed her among the top 50 most powerful women in business.

Graduated from Georgia State University, where she earned a bachelor’s degree in philosophy and a master’s degree in business administration.

Home Depot Management

85

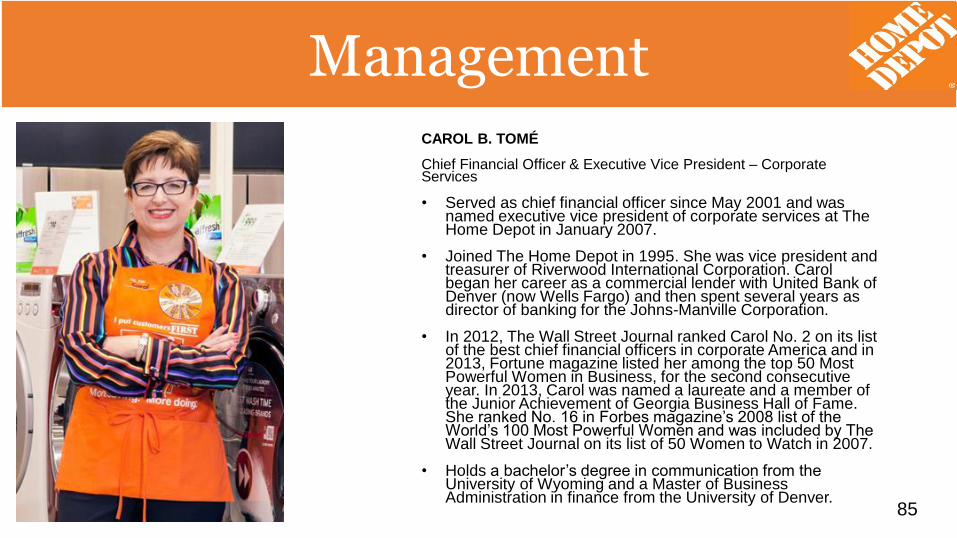

ManagementCAROL B. TOMÉ

Chief Financial Officer & Executive Vice President – Corporate Services

• Served as chief financial officer since May 2001 and was named executive vice president of corporate services at The Home Depot in January 2007.

• Joined The Home Depot in 1995. She was vice president and treasurer of Riverwood International Corporation. Carol began her career as a commercial lender with United Bank of Denver (now Wells Fargo) and then spent several years as director of banking for the Johns-Manville Corporation.

• In 2012, The Wall Street Journal ranked Carol No. 2 on its list of the best chief financial officers in corporate America and in 2013, Fortune magazine listed her among the top 50 Most Powerful Women in Business, for the second consecutive year. In 2013, Carol was named a laureate and a member of the Junior Achievement of Georgia Business Hall of Fame. She ranked No. 16 in Forbes magazine’s 2008 list of the World’s 100 Most Powerful Women and was included by The Wall Street Journal on its list of 50 Women to Watch in 2007.

• Holds a bachelor’s degree in communication from the University of Wyoming and a Master of Business Administration in finance from the University of Denver.

Home Depot Management

86

ManagementMATT CAREY

Executive Vice President & Chief Information Officer

Joined The Home Depot in 2008

Matt’s team designed and launched an industry-first proprietary mobile device we call the

“First Phone,” which functions as a phone and walkie-talkie with the added functionality of

mobile checkout, inventory management, product search and business analytics.

Before joining The Home Depot in 2008, Matt served as senior vice president and chief

technology officer at eBay.

Matt spent more than 20 years with Wal-Mart, where he was senior vice president and chief

technology officer. During his tenure at Wal-Mart, he managed the rollout of the wireless RF

infrastructure, had responsibility for the company’s Mainframe Large Systems and Data

Warehouse, and led the implementation and integration of Walmart.com, Samsclub.com

and the grocery home delivery business in the U.K. He also was responsible for

implementing Goodlinks, which provided wireless real-time email and calendaring functions.

Matt earned an associate’s degree in information systems from Oklahoma State University

– Okmulgee.

Home Depot Management

87

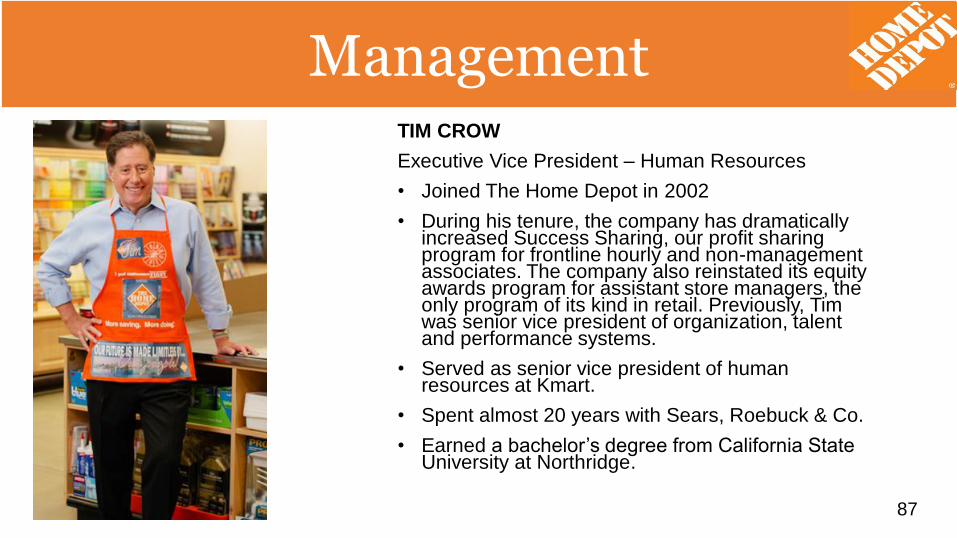

ManagementTIM CROW

Executive Vice President – Human Resources

• Joined The Home Depot in 2002

• During his tenure, the company has dramatically increased Success Sharing, our profit sharing program for frontline hourly and non-management associates. The company also reinstated its equity awards program for assistant store managers, the only program of its kind in retail. Previously, Tim was senior vice president of organization, talent and performance systems.

• Served as senior vice president of human resources at Kmart.

• Spent almost 20 years with Sears, Roebuck & Co.

• Earned a bachelor’s degree from California State University at Northridge.

Home Depot Management

88

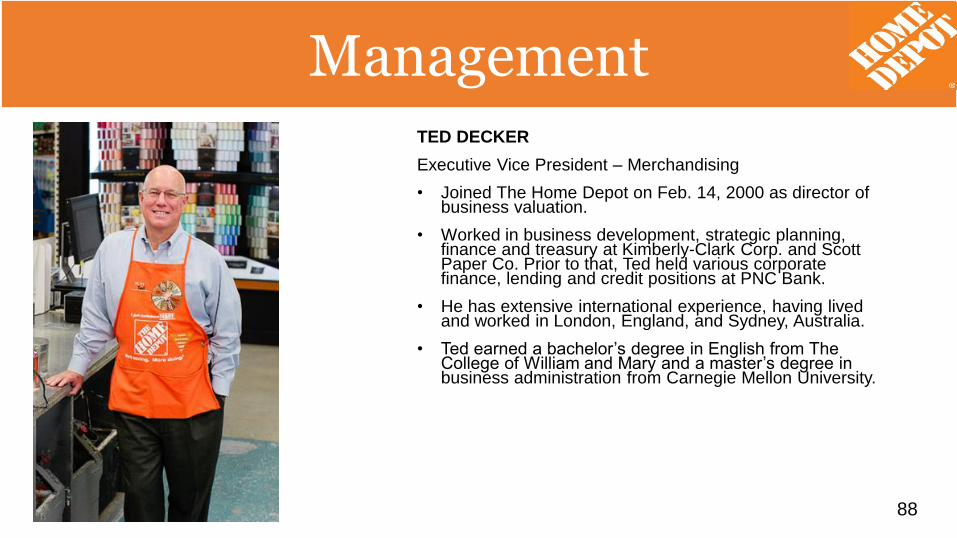

ManagementTED DECKER

Executive Vice President – Merchandising

• Joined The Home Depot on Feb. 14, 2000 as director of business valuation.

• Worked in business development, strategic planning, finance and treasury at Kimberly-Clark Corp. and Scott Paper Co. Prior to that, Ted held various corporate finance, lending and credit positions at PNC Bank.

• He has extensive international experience, having lived and worked in London, England, and Sydney, Australia.

• Ted earned a bachelor’s degree in English from The College of William and Mary and a master’s degree in business administration from Carnegie Mellon University.

Home Depot Management

89

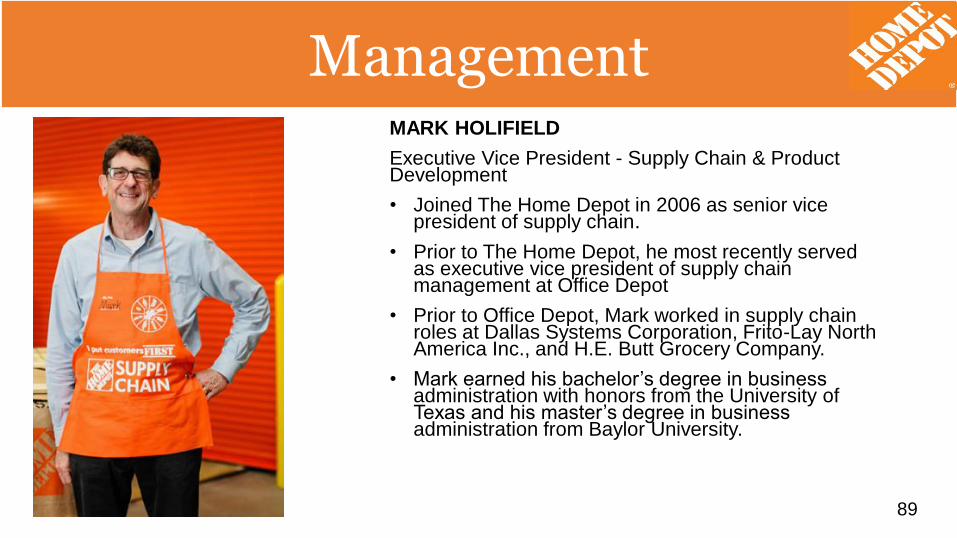

ManagementMARK HOLIFIELD

Executive Vice President - Supply Chain & Product Development

• Joined The Home Depot in 2006 as senior vice president of supply chain.

• Prior to The Home Depot, he most recently served as executive vice president of supply chain management at Office Depot

• Prior to Office Depot, Mark worked in supply chain roles at Dallas Systems Corporation, Frito-Lay North America Inc., and H.E. Butt Grocery Company.

• Mark earned his bachelor’s degree in business administration with honors from the University of Texas and his master’s degree in business administration from Baylor University.

Home Depot Management

90

ManagementBILL LENNIE

Executive Vice President – Outside Sales & Service

• Previously, Bill served as president of The Home Depot Canada where he was responsible for the sales, merchandising, ecommerce, supply chain, human resources, IT development and operations of 182 stores in Canada.

• Bill returned to The Home Depot in 2009 from Dick’s Sporting Goods where he was senior vice president of merchandising, hardlines. His career at The Home Depot began in 1992, when he joined as a merchant for Millwork and Building Materials. In 2001, Bill focused his leadership on the Company’s Kitchen, Bath and Appliance departments and was promoted to senior vice president of décor in 2002.

• Before joining The Home Depot, Bill was a divisional merchandise manager for Lowe’s. Prior to that, he spent eight years with Menards in Eau Claire, Wis., as the millwork plant manager for its manufacturing division.

Home Depot Management

91

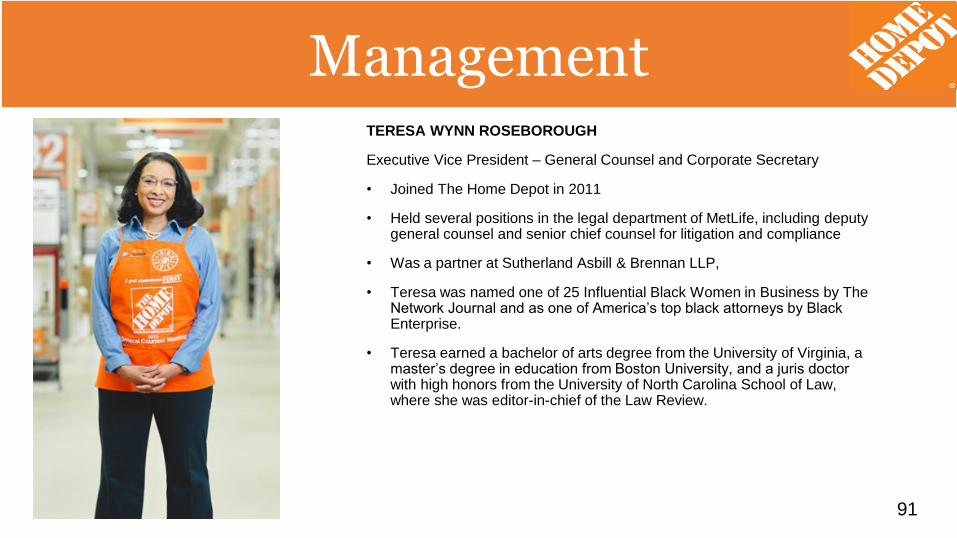

ManagementTERESA WYNN ROSEBOROUGH

Executive Vice President – General Counsel and Corporate Secretary

• Joined The Home Depot in 2011

• Held several positions in the legal department of MetLife, including deputy general counsel and senior chief counsel for litigation and compliance

• Was a partner at Sutherland Asbill & Brennan LLP,

• Teresa was named one of 25 Influential Black Women in Business by The Network Journal and as one of America’s top black attorneys by Black Enterprise.

• Teresa earned a bachelor of arts degree from the University of Virginia, a master’s degree in education from Boston University, and a juris doctor with high honors from the University of North Carolina School of Law, where she was editor-in-chief of the Law Review.

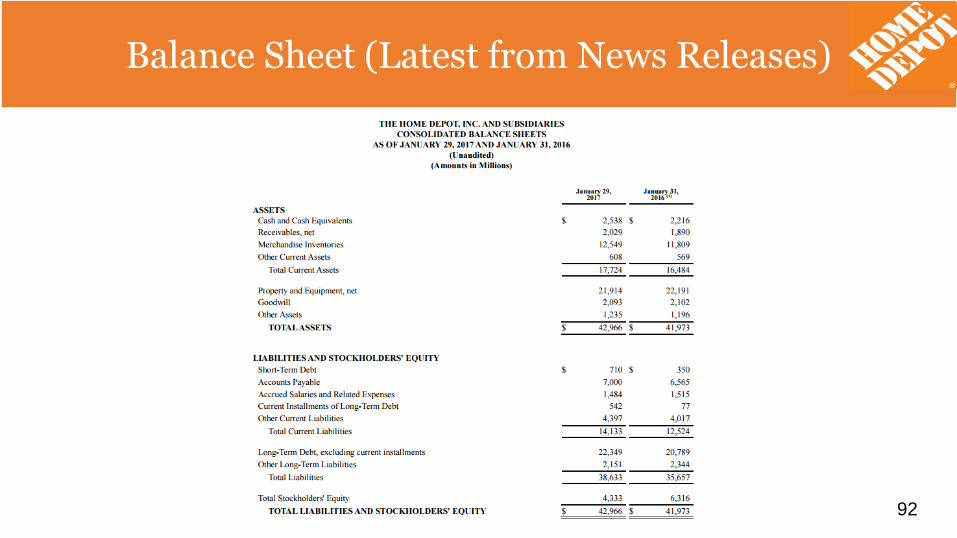

Balance Sheet (Latest from News Releases)

92

Balance Sheet (Latest from News Releases)

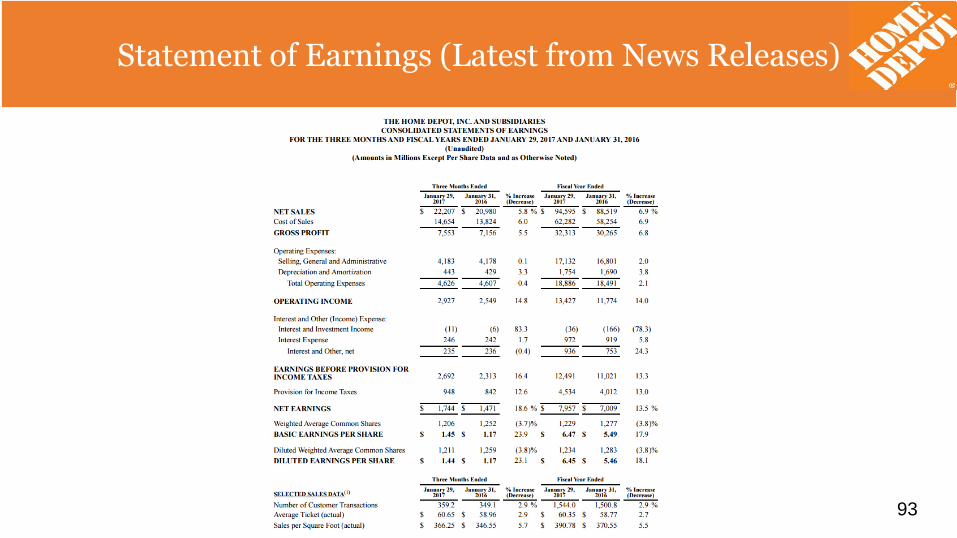

Statement of Earnings (Latest from News Releases)

93

Statement of Earnings (Latest from News Releases)

Statement of Cashflows (Latest from News Releases)

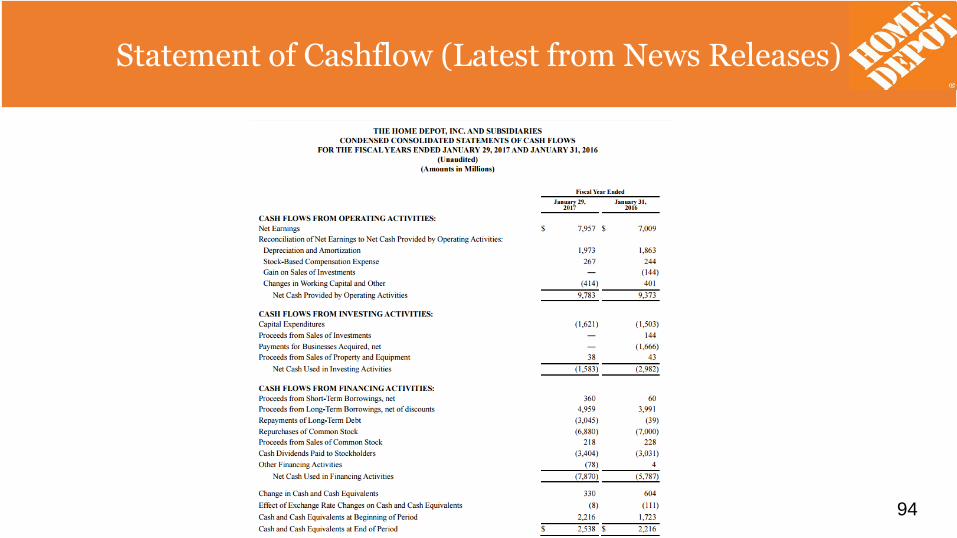

94

Statement of Cashflow (Latest from News Releases)

Recommendation

95

Recommendation

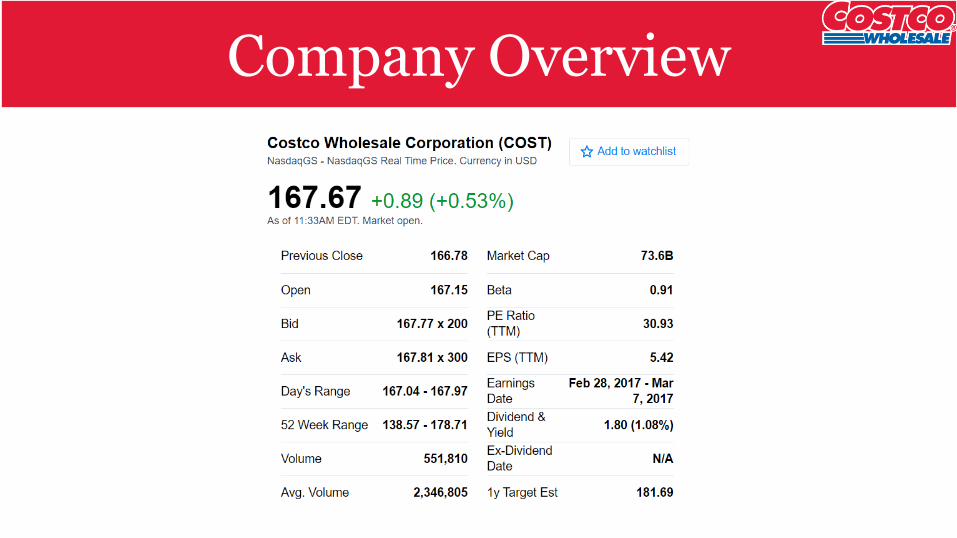

Company Overview

Company History

• First store opened in San Diego, CA in 1976 under the name Price Club

• Costco was founded in 1983 in Seattle, WA

• Costco was the first company to ever grow from $0 to $3B in sales in less than 6 years

• In 1993, the companies merged under the Costco name

• "keep costs down and pass on the savings to our members"

Company History

97

Company History

• 1948: Sol Price opened Fed Mart

• 1976: Opened first store as Price Club in San Diego

• 1983: Founders James Sinegal and Jeffrey Brotman opened first warehouse in Seattle

• 1993: Costco and Price Club merged to PriceCostco

• 1994: Founders of Price Club left Costco

• 1997: Company name was changed to Costco Wholesaler

Company History

98

Costco’s Code of Ethics

1. Obey the law

2. Take care of our members

3. Take care of our employees

4. Respect our suppliers

if we do these four things throughout our organization, then we will achieve our ultimate goal, which is to:

5. Reward our shareholders

Costco’s Code of Ethics

99

Company Overview

• Listed on Nasdaq

• Included in S&P 500, Russell 1000

• Ticker symbol: COST

• Industry: Discount variety store

• 2nd largest retail company in the United States (Wal-Mart is 1st)

Company Overview

100

Company Overview

As of March 11, 2017:

• Stock price: $165.37

• Day's range: $164.99 - $166.50

• 52 week range: $138.57 - $178.71

• Market capitalization: $72.64B

• Earnings per share: $5.48

• P/E: $30.18

• Dividend yield: 1.09%

• Shares outstanding: 438.94M

Company Overview

101

Major Institutional HoldersMajor Institutional Holders

102

5 DayPerformance

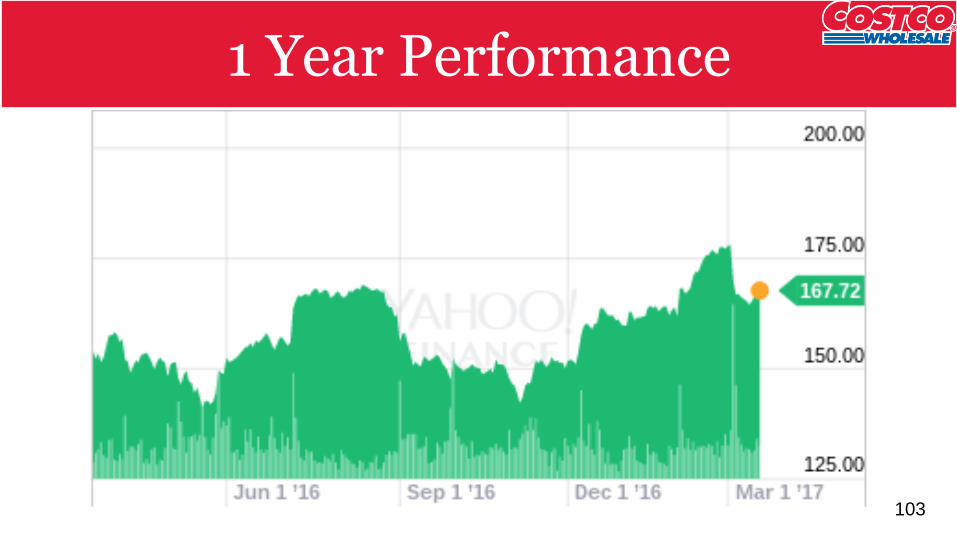

1 Year 1 Year Performance

103

5 Year 5 Year Performance

104

Max Max Performance

105

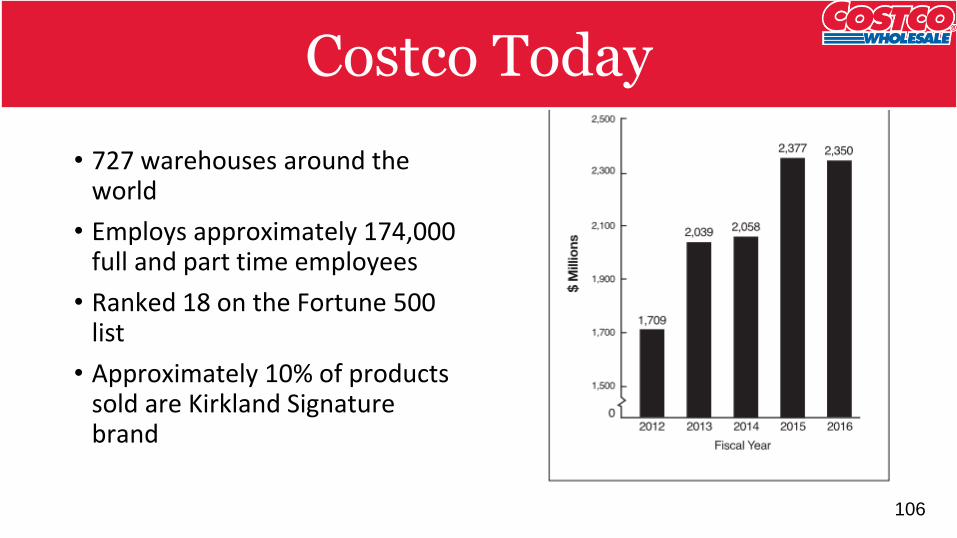

Costco Today

• 727 warehouses around the world

• Employs approximately 174,000 full and part time employees

• Ranked 18 on the Fortune 500 list

• Approximately 10% of products sold are Kirkland Signature brand

Costco Today

106

ManagementJames Sinegal, Former President and CEO (1994 - 2012)

• Co-founder and first CEO• Earned $583,000 annually in salary

and bonuses• Business Administration graduate

from San Diego State University• One of Time’s 100 Most Influential

People of 2006

Management

107

Management

W. Craig Jelinek, President and CEO since 2012.

• Salary: $700,000 plus a bonus of up to $81,600

• Studied at San Diego State University

• Cares about employees, paying higher than industry average salaries and allowing them to take holidays off

Management

108

Management

Jeffrey Brotman, Co-founder and chairman of the board since 1994.

• Salary: $650,000 plus a bonus of up to $81,000

• Studied law at the University of Washington

• 2rd generation of his family as a retail entrepreneur

• Former director at Starbucks and Sweet Factory

Management

109

Competition

Low cost, high volume retail competitors:

• Wal-Mart

• Sam's Club (a Wal-Mart subsidiary)

• Target

Competing on:

• Price

• Convenience

Competition

110

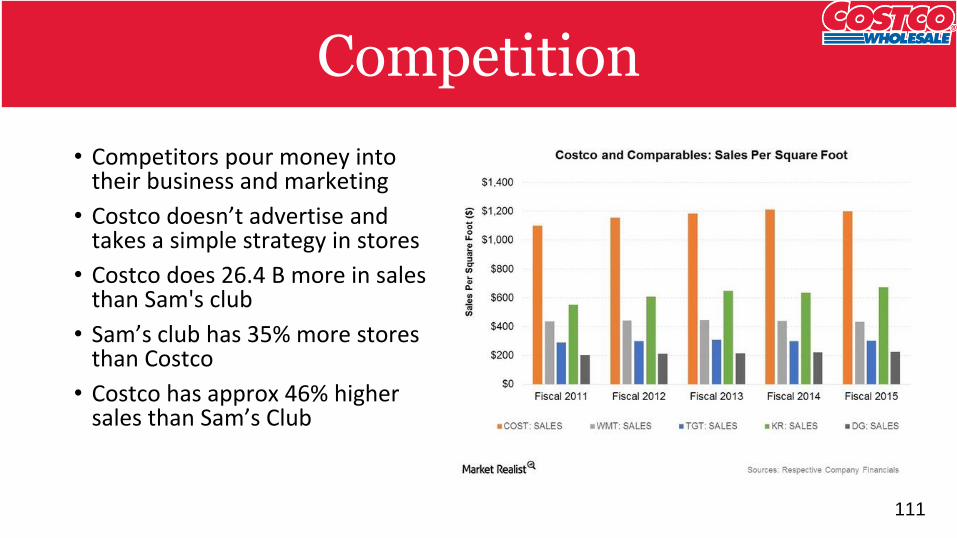

Competition

• Competitors pour money into their business and marketing

• Costco doesn’t advertise and takes a simple strategy in stores

• Costco does 26.4 B more in sales than Sam's club

• Sam’s club has 35% more stores than Costco

• Costco has approx 46% higher sales than Sam’s Club

Competition

111

Cost Structure and Revenue Composition

• Goods sold in stores just cover costs, don’t act as a source of revenue

• Revenue is generated through membership sales

Cost Structure and Revenue Composition

112

Cost Structure and Revenue Composition

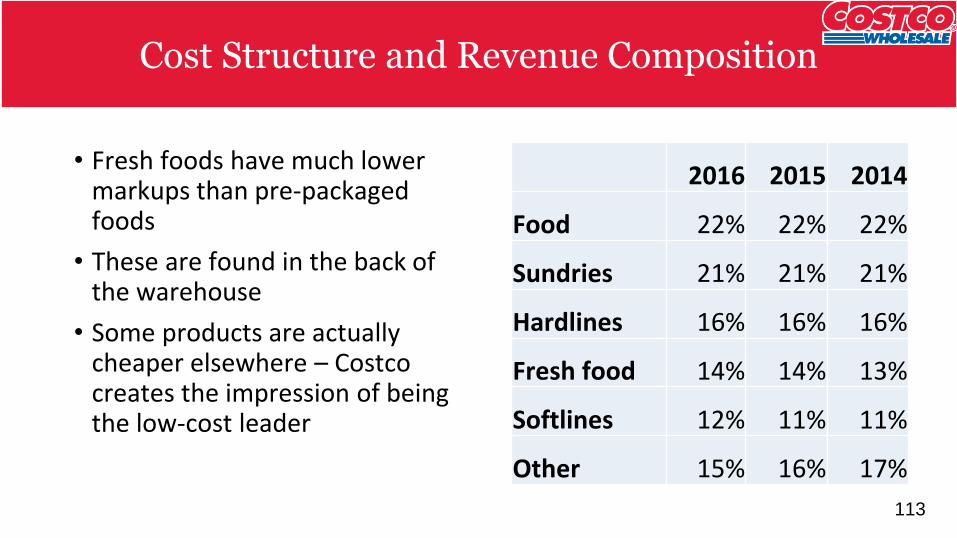

• Fresh foods have much lower markups than pre-packaged foods

• These are found in the back of the warehouse

• Some products are actually cheaper elsewhere – Costco creates the impression of being the low-cost leader

2016 2015 2014

Food 22% 22% 22%

Sundries 21% 21% 21%

Hardlines 16% 16% 16%

Fresh food 14% 14% 13%

Softlines 12% 11% 11%

Other 15% 16% 17%

Cost Structure and Revenue Composition

113

Strategy: Revenue Production

• Membership costs $55-$110

• Average markup is approximately 10%, slightly higher with the Kirkland Signature house brand

• Slim markups just cover costs, profit is generated by annual membership costs

• Store layout to entice buyers to purchase items with higher markups

• Rapid inventory turnover

Strategy: Revenue Production

114

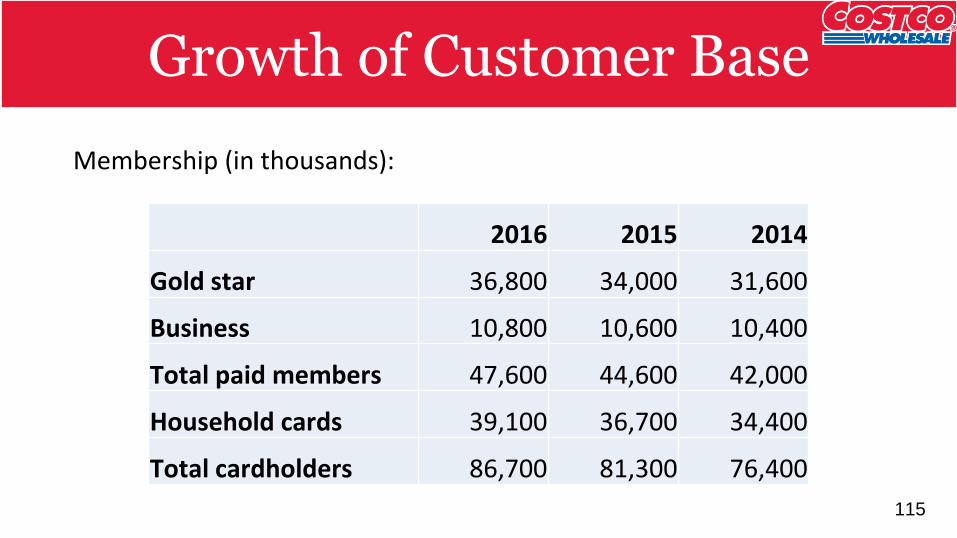

Growth of Customer Base

Membership (in thousands):

2016 2015 2014

Gold star 36,800 34,000 31,600

Business 10,800 10,600 10,400

Total paid members 47,600 44,600 42,000

Household cards 39,100 36,700 34,400

Total cardholders 86,700 81,300 76,400

Growth of Customer Base

115

Strategy: Cost Control

• SG&A: 10.4% of sales

• No advertising

• Lowest shrinkage in the industry

• Entrances and exits are controlled

• Membership format limits theft

• Good relations among employees limits internal theft

Strategy: Cost Control

116

Strategy: Cost Control

• Volume purchasing

• Purchasing directly from manufacturers

• Pre-paying vendors to receive payment discounts

• Minimizing stocking fees

• Utilizing warehouse space

• No elaborate facilities and rent is lower since it is not in a prime location

• No lights on most days to save electricity

Strategy: Cost Control

117

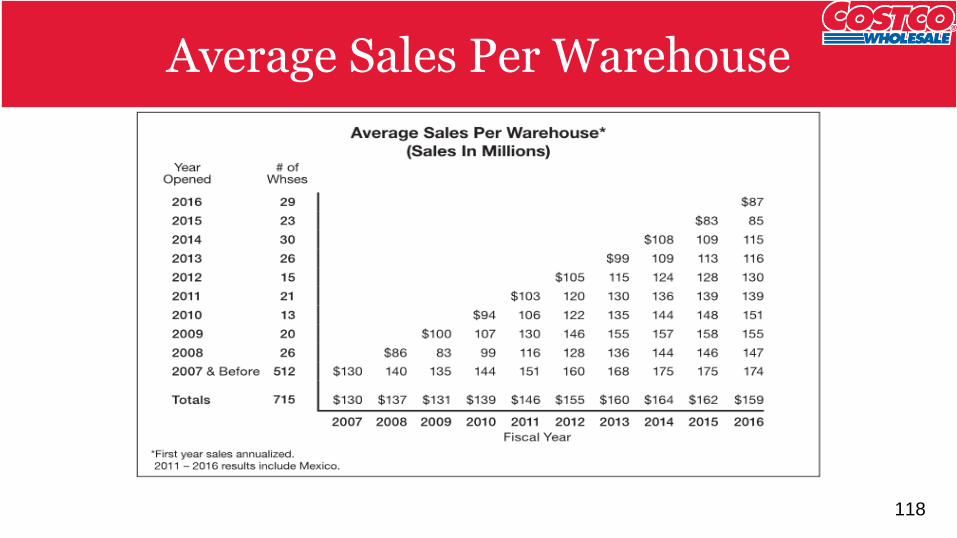

Average Sales Per Warehouse

118

Product Line

• Limiting products to fast selling models, sizes and colors (~4000 items)

• Rapid inventory turnover

• No-name products can be marked by more than 14%; private items 15%

• Volume purchasing

• Purchasing directly from manufacturers

• Pre-paying vendors to receive payment discounts

• Minimizing stocking fees

• Utilizing warehouse space

Product Line

119

Regulatory Environment

• Costco is present in many different countries, all with different regulations and standards

• Proper and accurate accounting information must be filed

• Changes in tax rates in some countries could be an advantage or disadvantage

Regulatory Environment

120

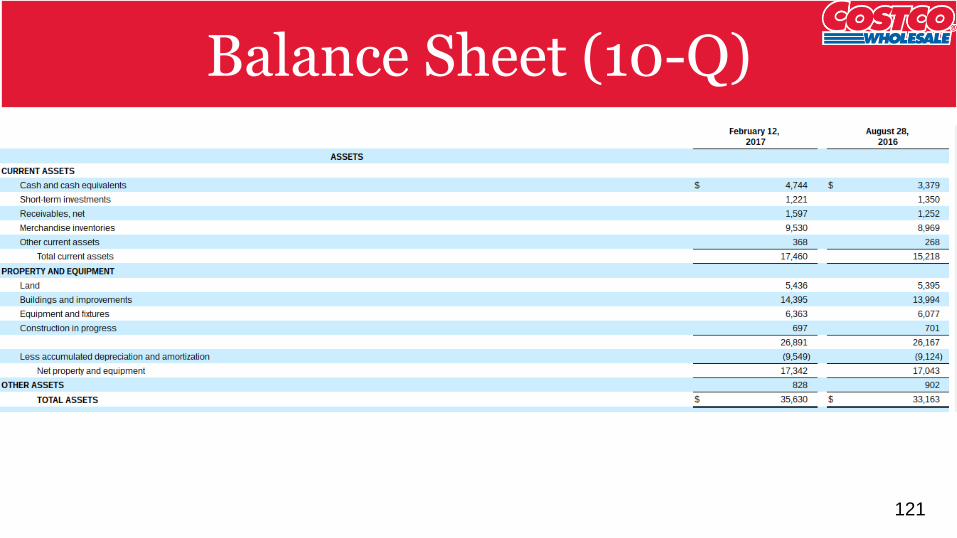

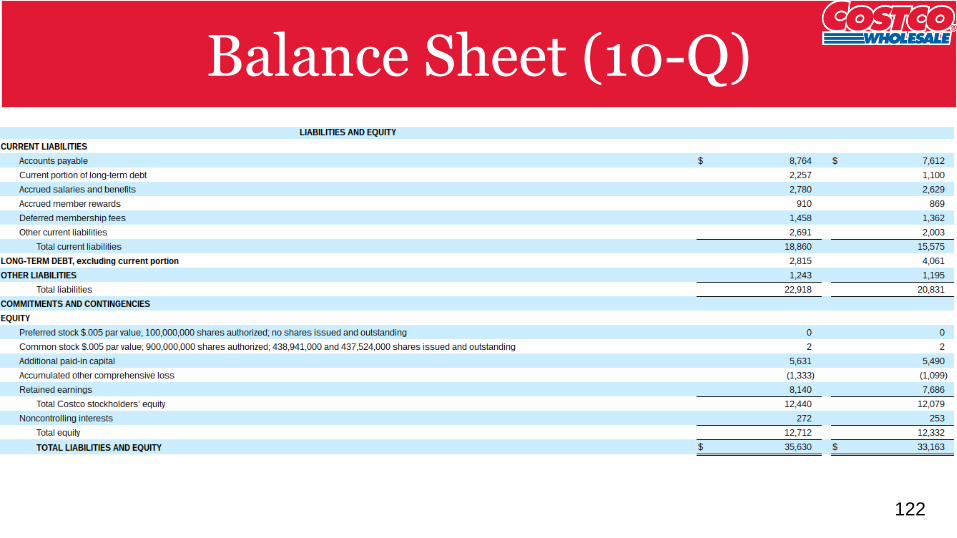

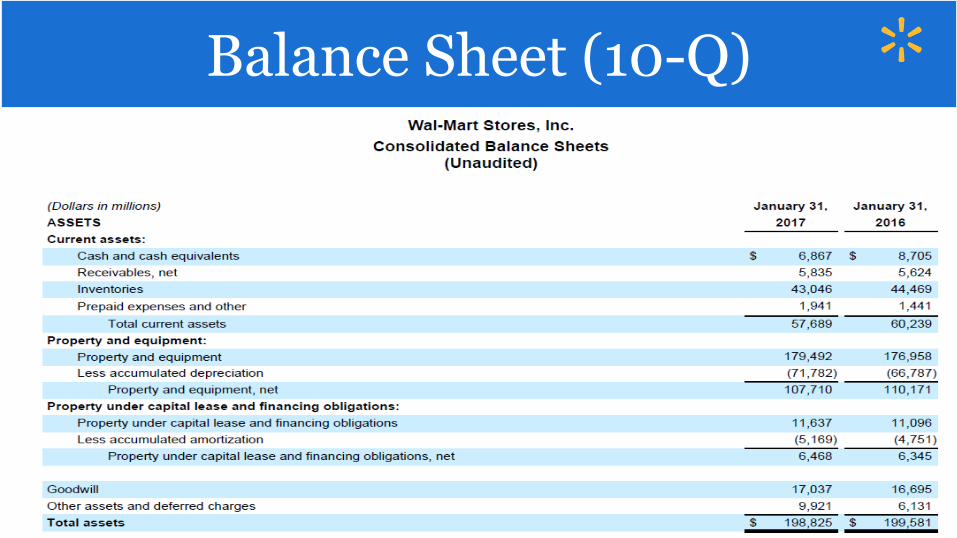

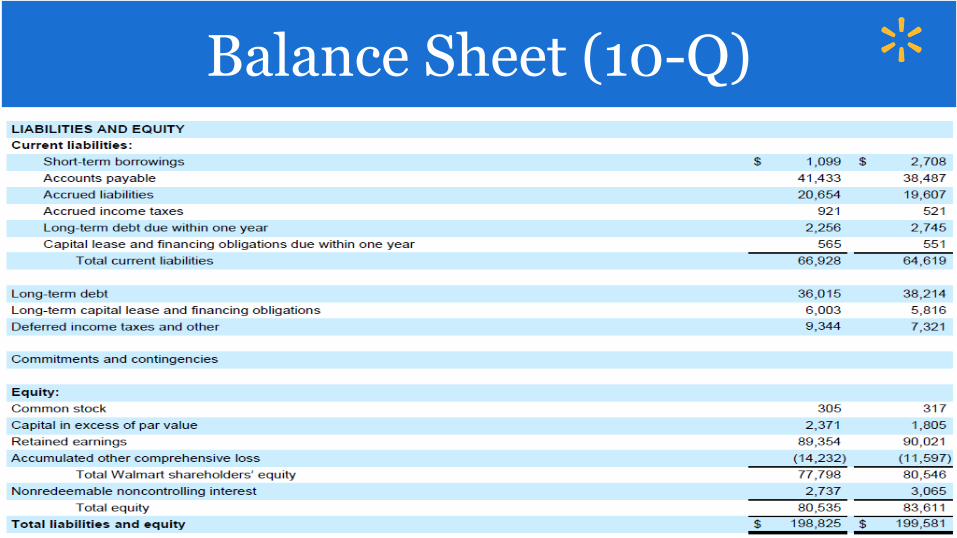

Balance Sheet (10-Q)Balance Sheet (10-Q)

121

Balance Sheet (10-Q)Balance Sheet (10-Q)

122

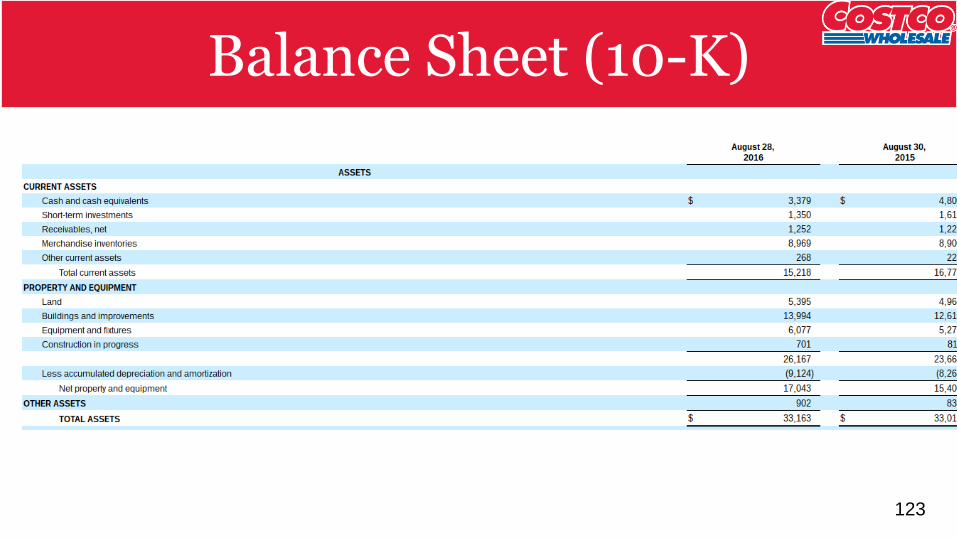

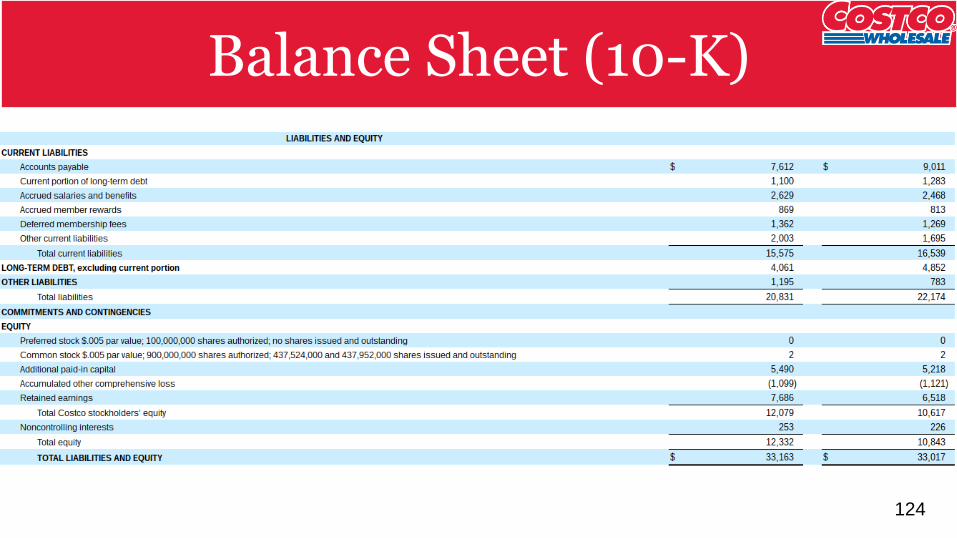

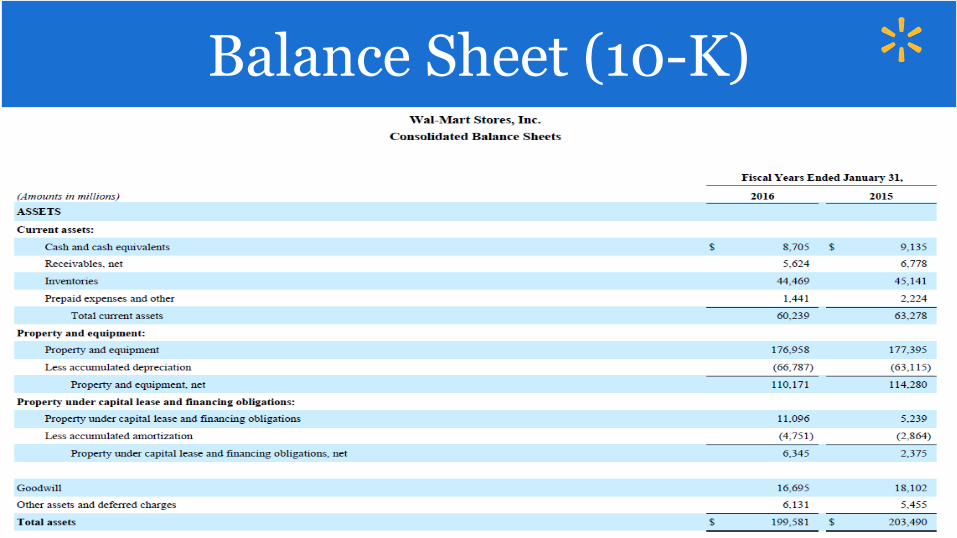

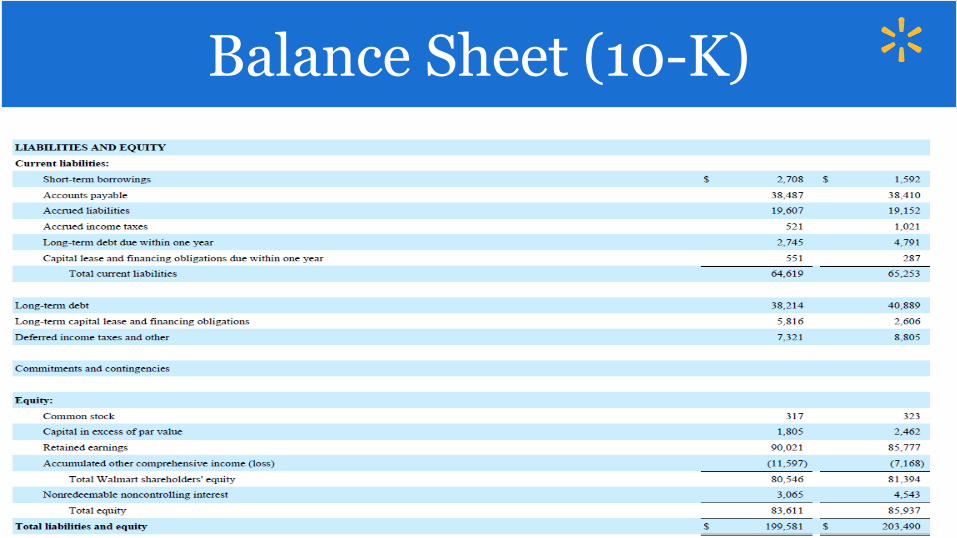

Balance Sheet (10-K)Balance Sheet (10-K)

123

Balance Sheet (10-K)Balance Sheet (10-K)

124

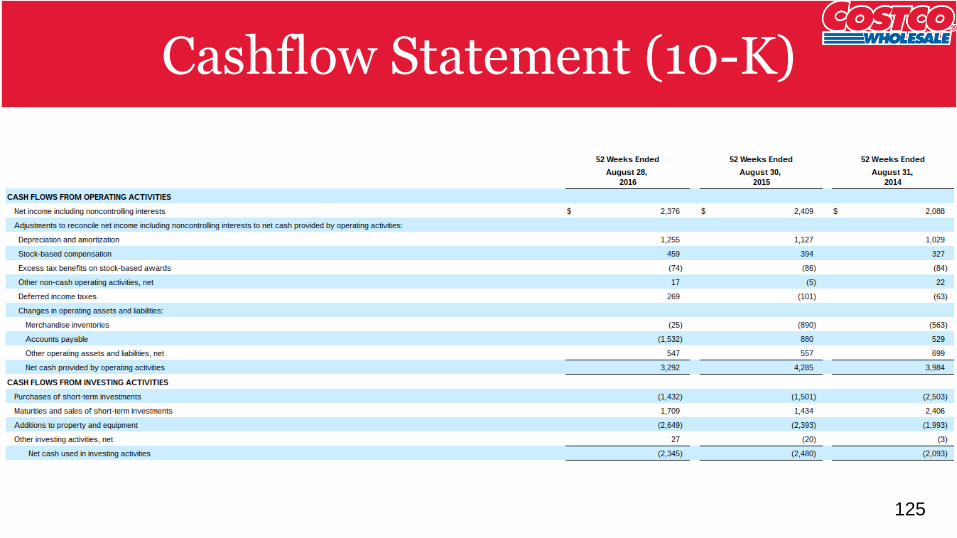

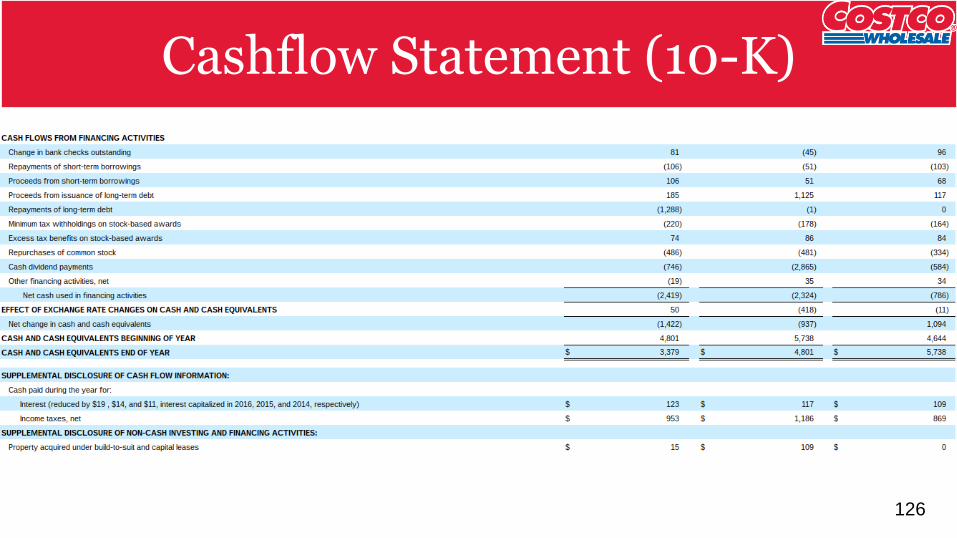

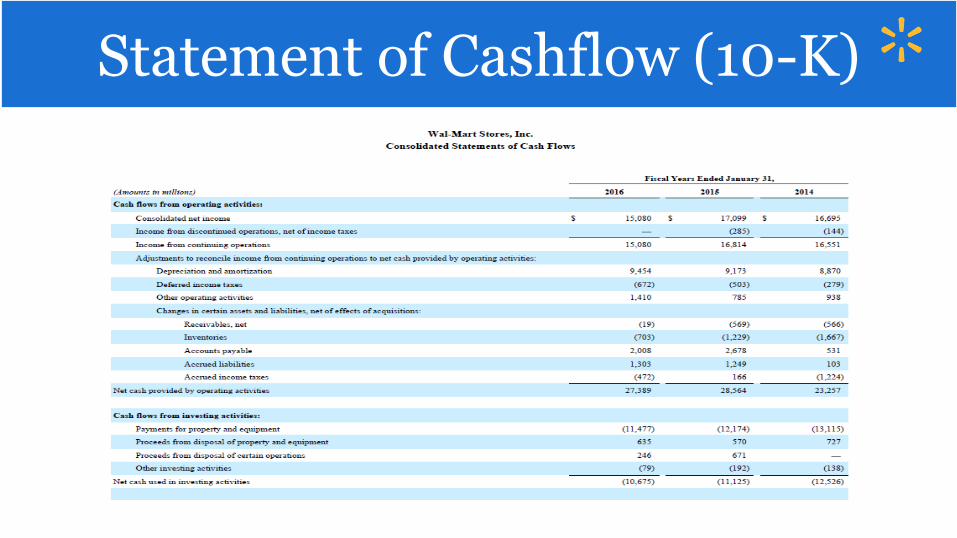

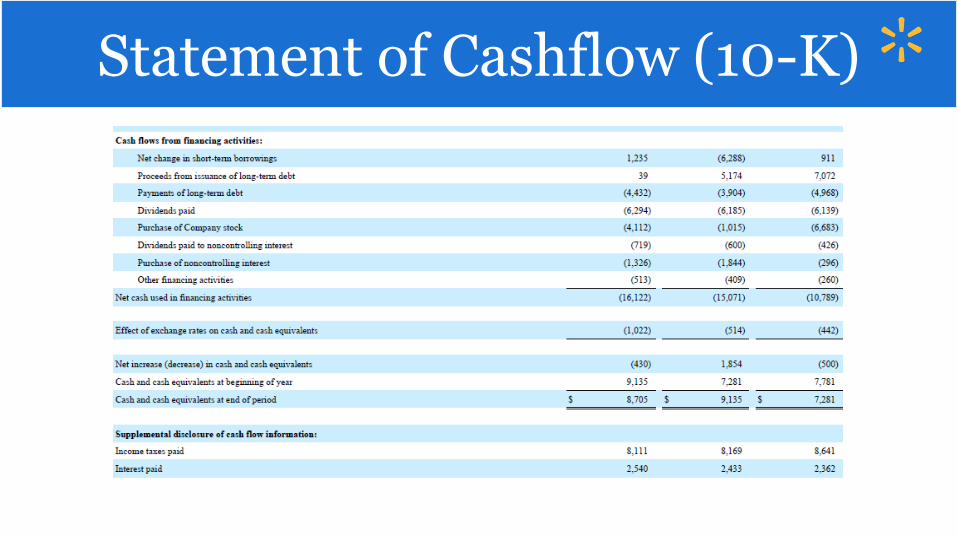

Cash Flow Statement (10-K)Cashflow Statement (10-K)

125

Cash Flow Statement (10-K)Cashflow Statement (10-K)

126

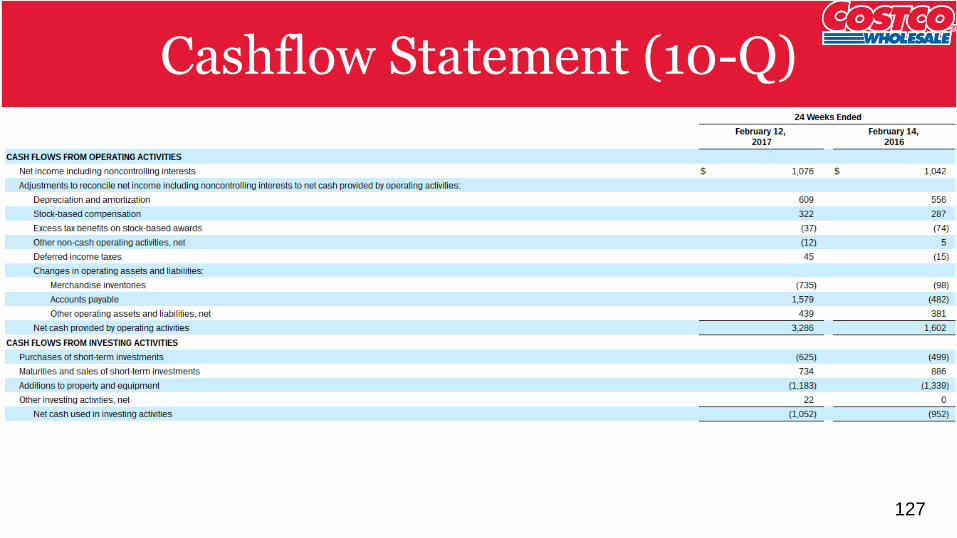

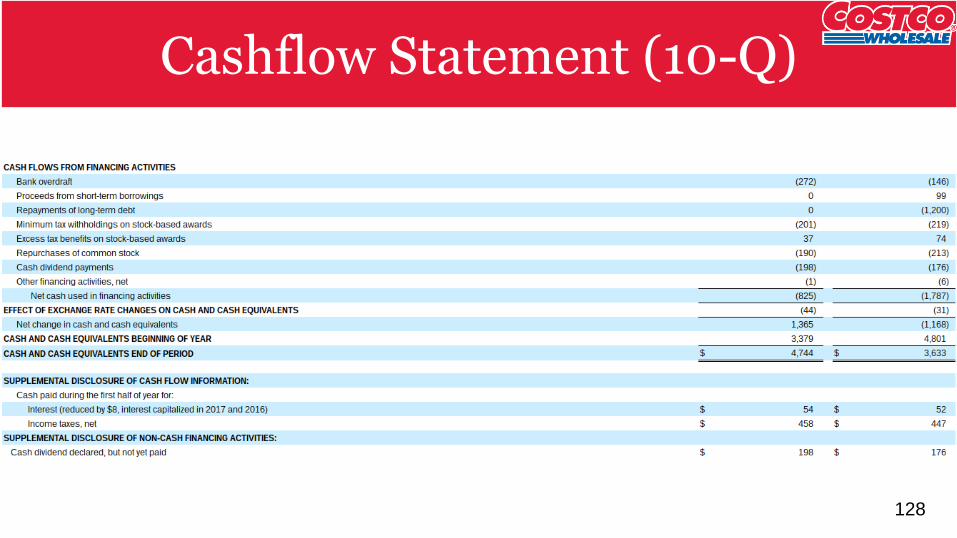

Cash Flow Statement (10-Q) Cashflow Statement (10-Q)

127

Cash Flow Statement (10-Q)Cashflow Statement (10-Q)

128

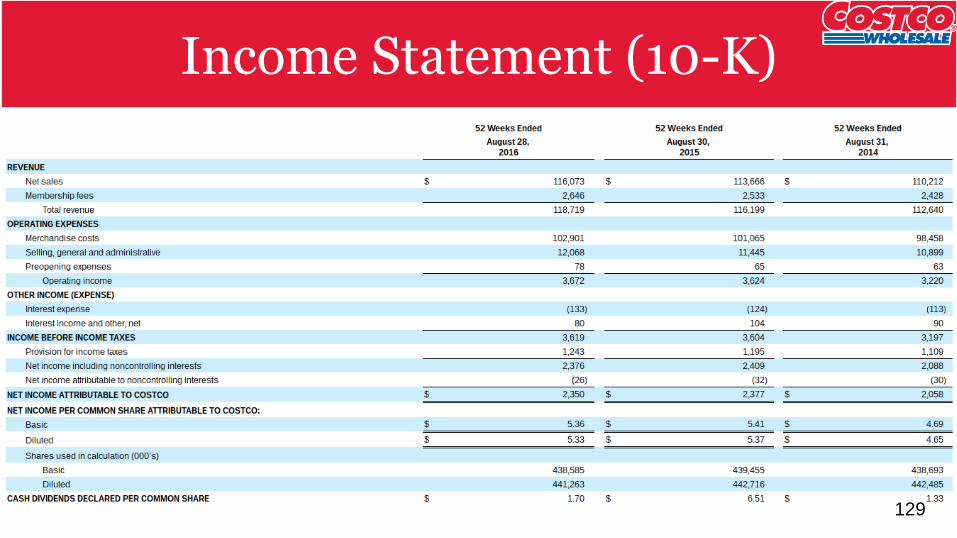

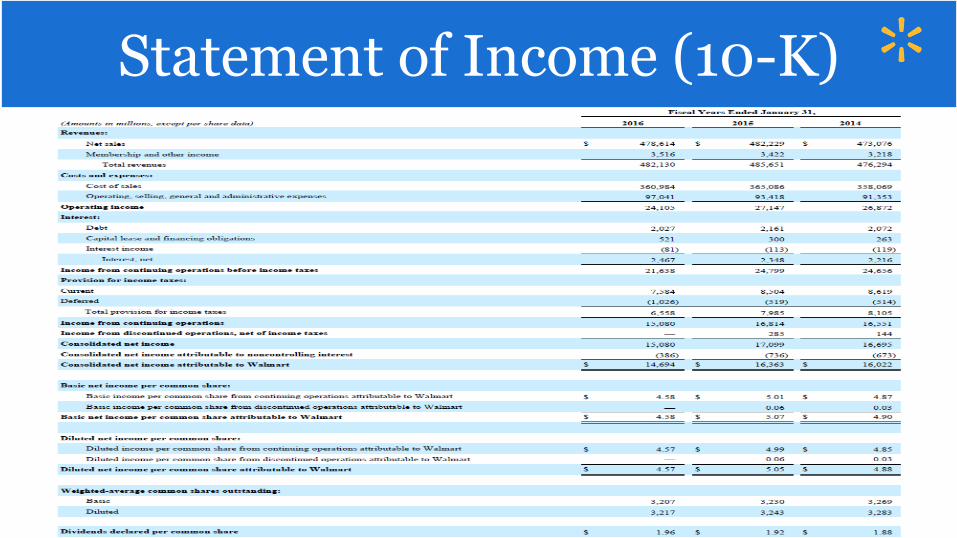

Income Statement (10-K)Income Statement (10-K)

129

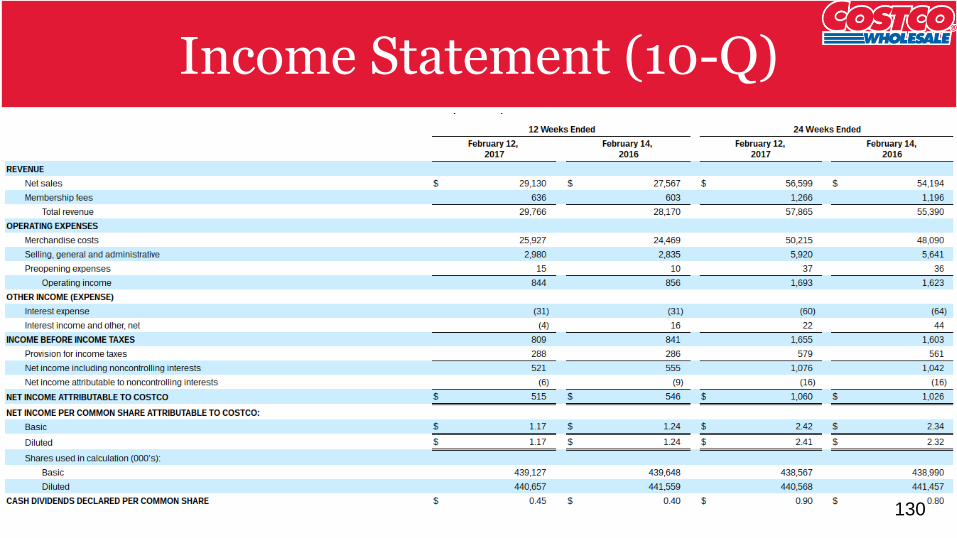

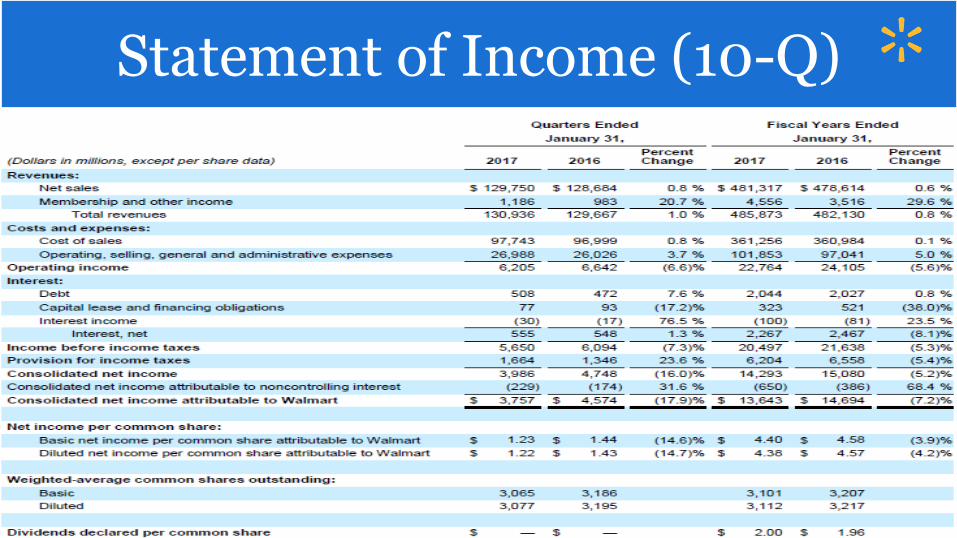

Income Statement (10-Q)Income Statement (10-Q)

130

Value Drivers

• Low cost of goods achieved through distribution and supply chain

• Image of low cost – some products are actually cheaper elsewhere

• Location

• Variety in product line

• Sales per square foot advantage

Value Drivers

131

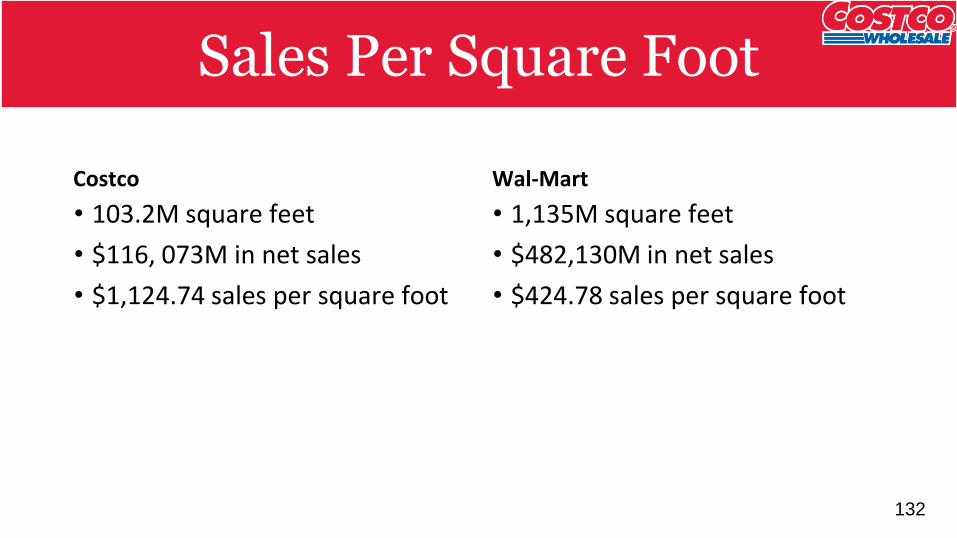

Sales Per Square Foot

Costco

• 103.2M square feet

• $116, 073M in net sales

• $1,124.74 sales per square foot

Wal-Mart

• 1,135M square feet

• $482,130M in net sales

• $424.78 sales per square foot

Sales Per Square Foot

132

Costco’s Industry

As stated in the 2016 annual report:

• The industry is highly competitive and saturated

• The online retail market has enhanced competition

• Competitors may have more funds, better access to merchandise and greater market penetration than Costco does

• The inability to respond to these pressures could negatively impact financial results

Costco’s Industry

133

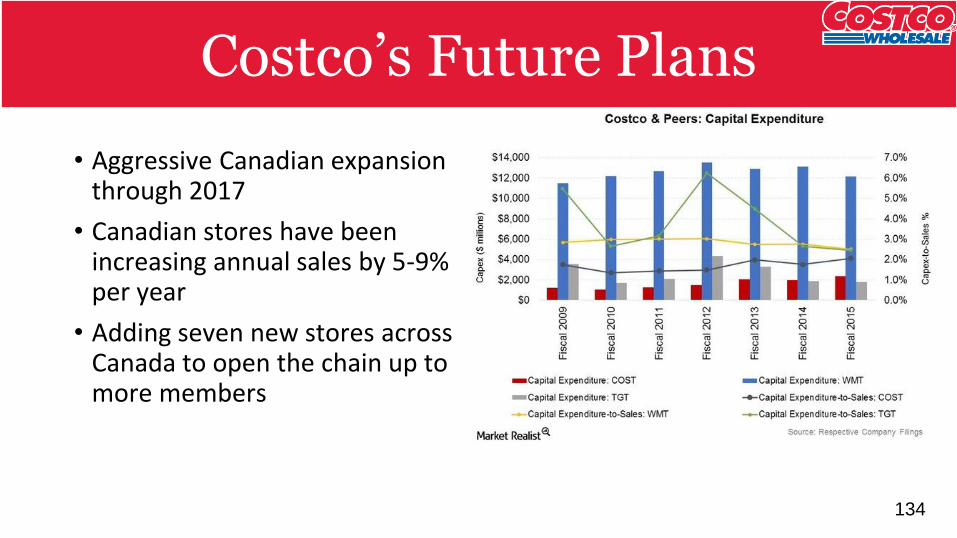

Costco’s Future Plans

• Aggressive Canadian expansion through 2017

• Canadian stores have been increasing annual sales by 5-9% per year

• Adding seven new stores across Canada to open the chain up to more members

Costco’s Future Plans

134

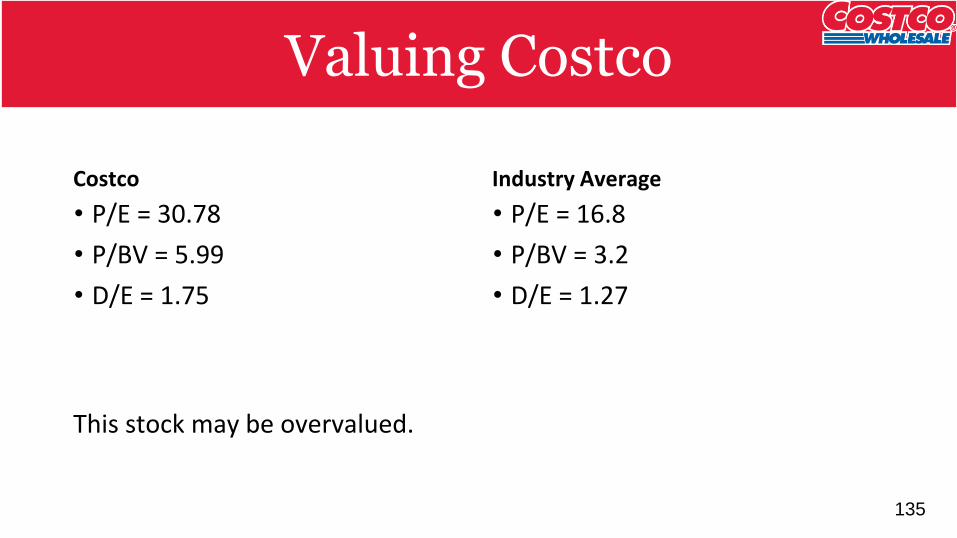

Valuing Costco

Costco

• P/E = 30.78

• P/BV = 5.99

• D/E = 1.75

Industry Average

• P/E = 16.8

• P/BV = 3.2

• D/E = 1.27

This stock may be overvalued.

Valuing Costco

135

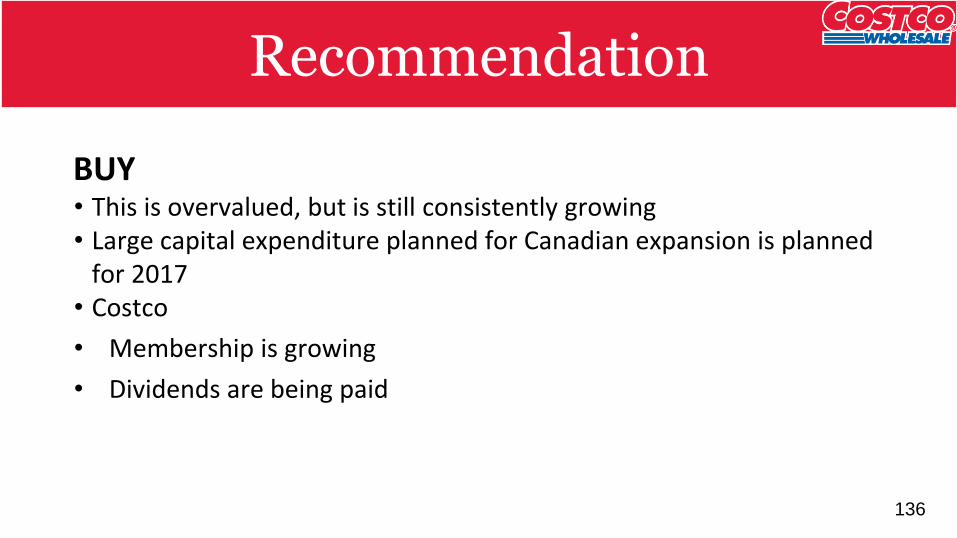

Recommendation

BUY• This is overvalued, but is still consistently growing• Large capital expenditure planned for Canadian expansion is planned

for 2017• Costco

• Membership is growing

• Dividends are being paid

Recommendation

136

Company Overview

138

Shares Outstanding

139

5 Day Performance

140

1 Year Performance

141

1 Year Trading Range

142

5 Year Performance

143

5 Year Trading Range

144

5 Year Exponential Moving Average (50 and 100 Days)

145

10 Year Performance

146

10 Year Trading Range

147

5 year Exponential moving average(50 and 100 days)

10 Year Exponential Moving Average (50 and 100 Days)

148

Max Performance

149

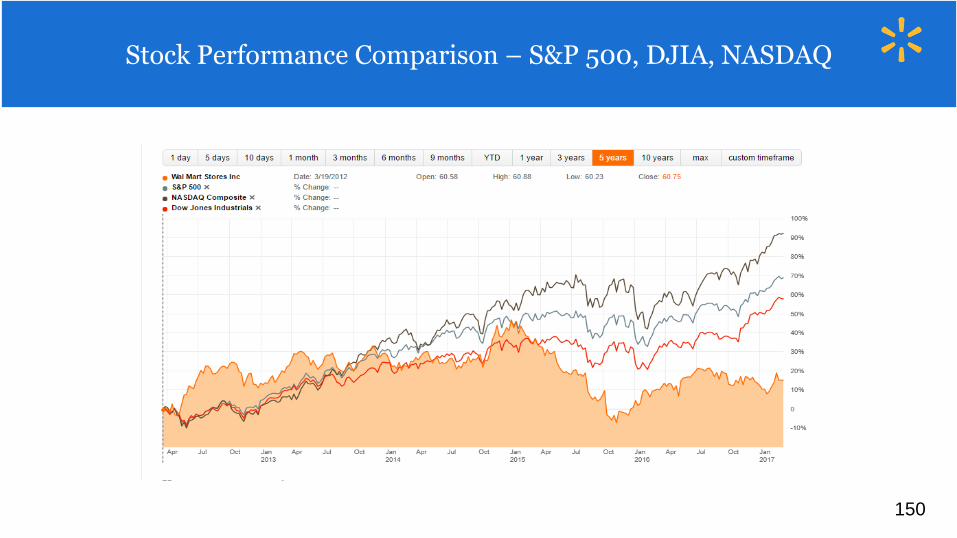

Stock Performance Comparison – S&P 500, DJIA, NASDAQ

150

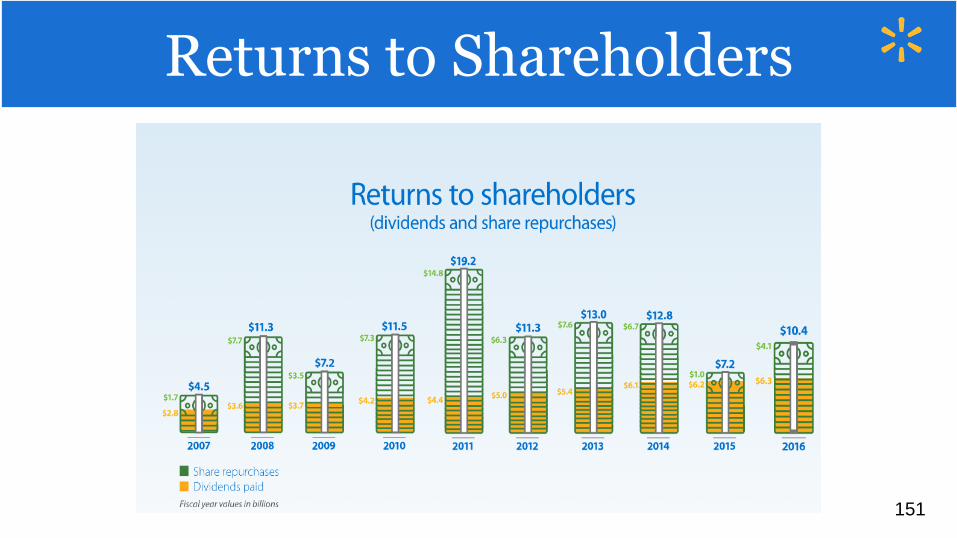

Returns to Shareholders

151

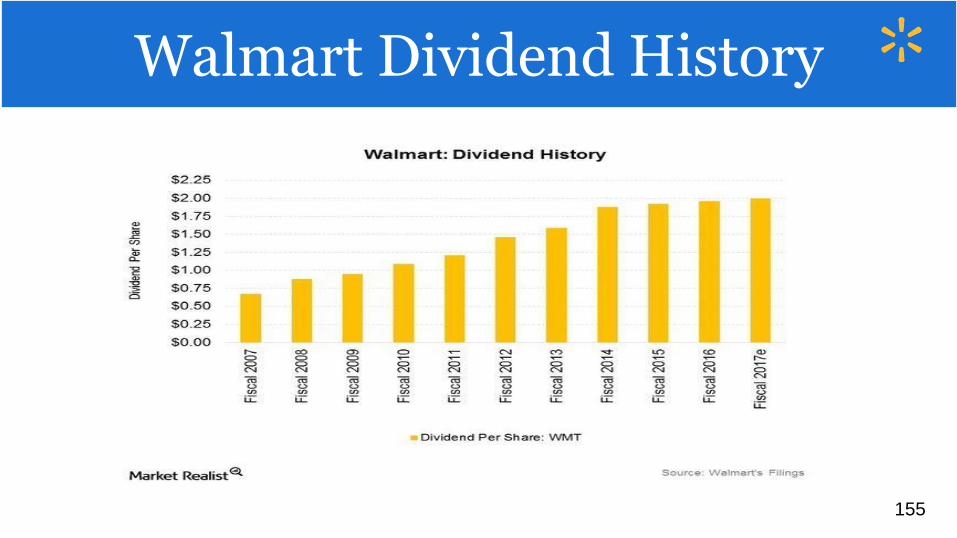

• This year, Walmart announced a dividend increase to $2.00 per share, marking the 43rd consecutive year of dividend increases for Walmart.per

• Walmart total dividend payments were 6.3 billion, $6.2 billion , $6.1 billion and $5.4 billion for fiscal 2016, 2015 , 2014 and 2013 , respectively.

• share.

Dividends Dividends

152

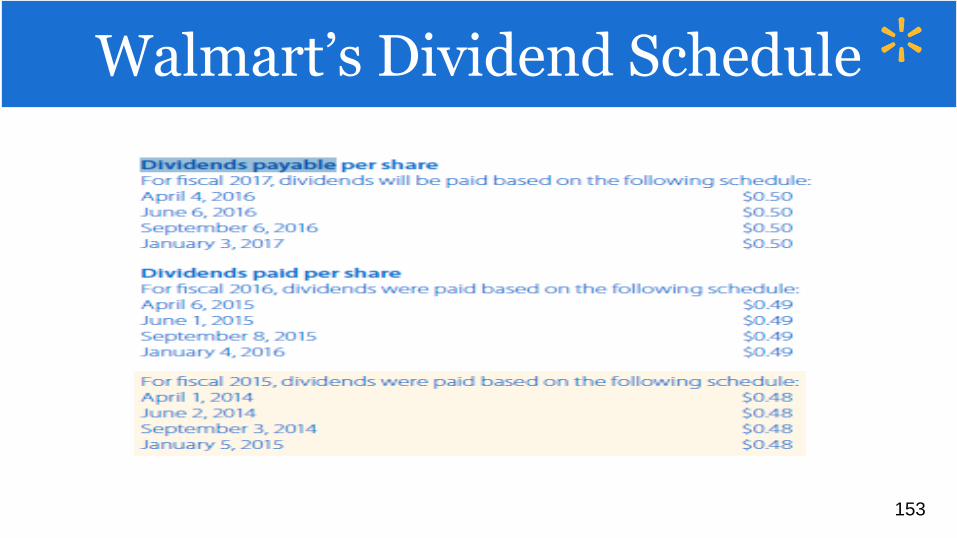

Walmart’s Dividend Schedule

153

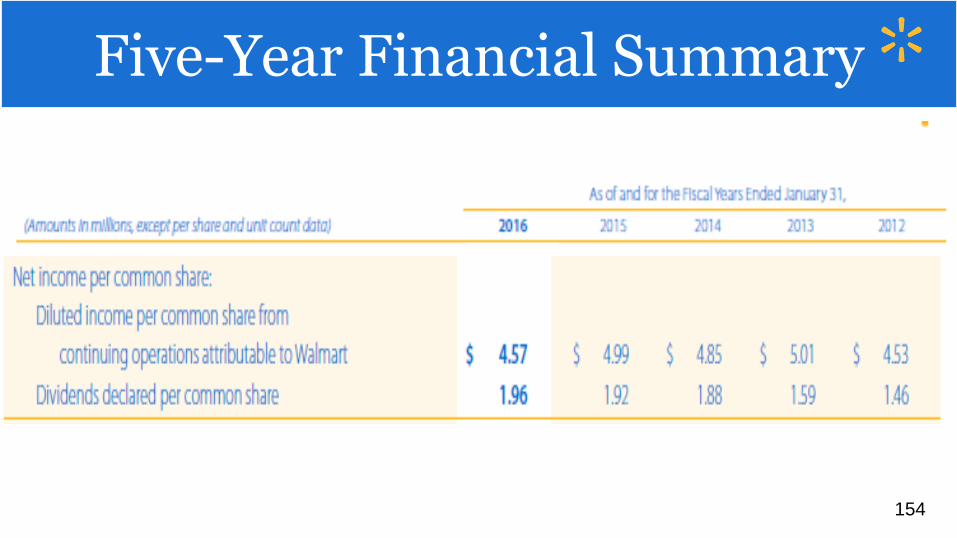

Five-Year Financial Summary

154

Walmart: Dividend HistoryWalmart Dividend History

155

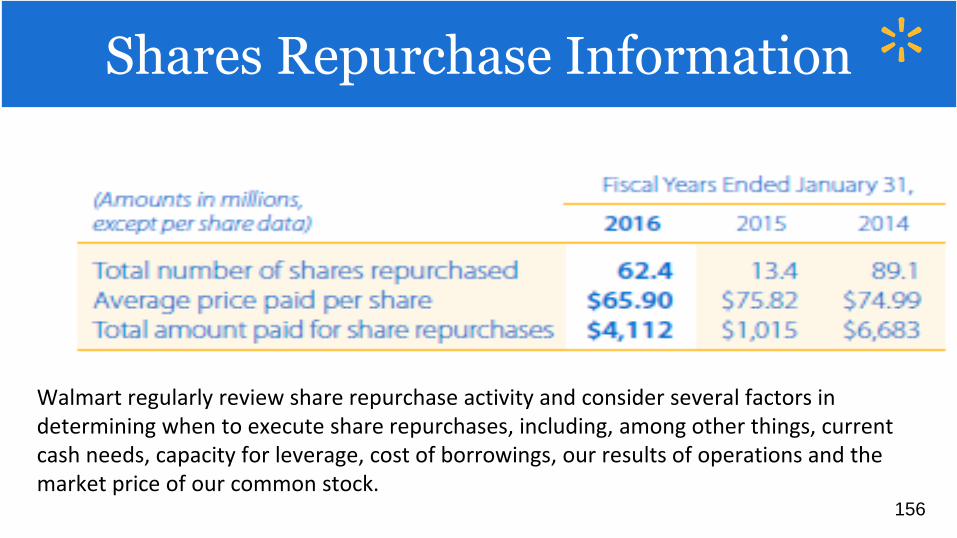

Walmart regularly review share repurchase activity and consider several factors in determining when to execute share repurchases, including, among other things, current cash needs, capacity for leverage, cost of borrowings, our results of operations and the market price of our common stock.

Shares Repurchase Information

156

Major Institutional HoldersMajor Institutional Holders

157

A Snapshot of Walmart

158

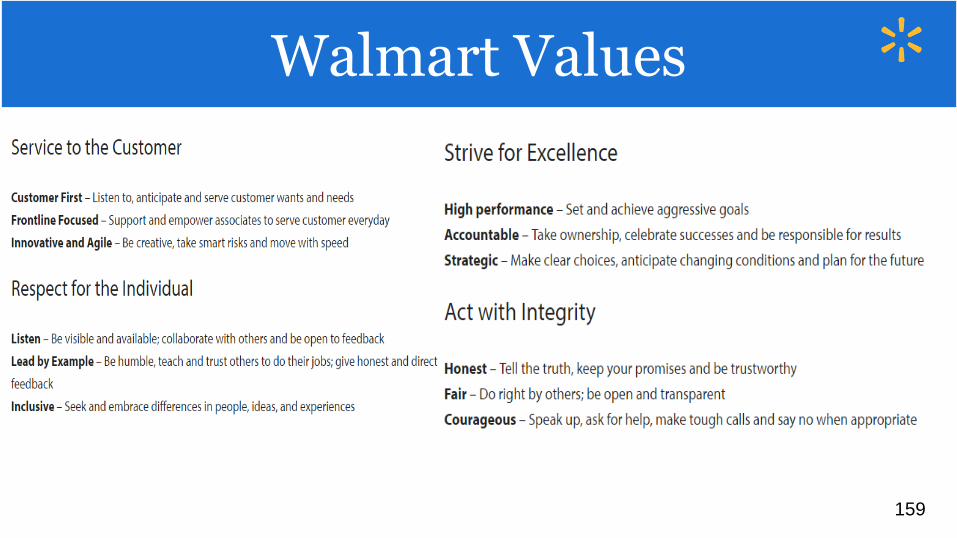

Walmart Values

159

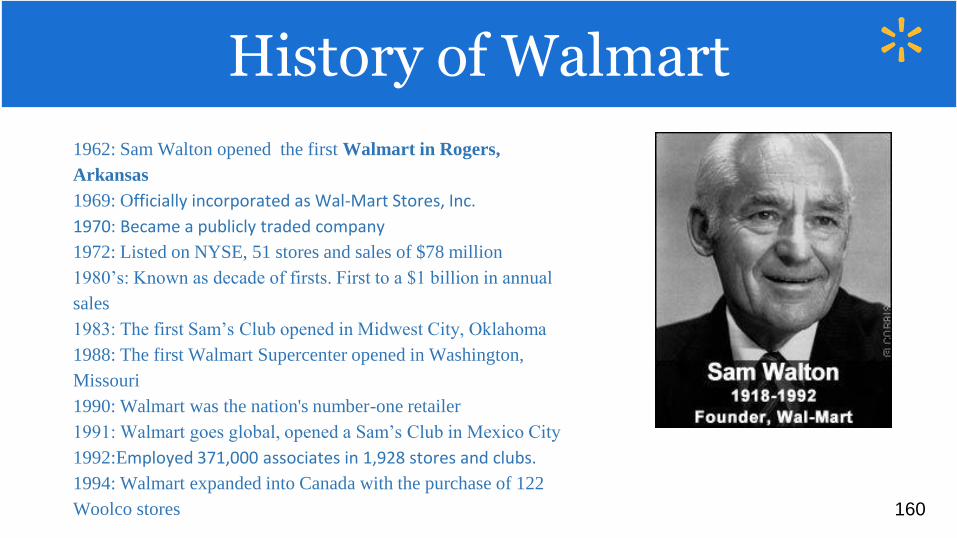

1962: Sam Walton opened the first Walmart in Rogers,

Arkansas

1969: Officially incorporated as Wal-Mart Stores, Inc.

1970: Became a publicly traded company

1972: Listed on NYSE, 51 stores and sales of $78 million

1980’s: Known as decade of firsts. First to a $1 billion in annual

sales

1983: The first Sam’s Club opened in Midwest City, Oklahoma

1988: The first Walmart Supercenter opened in Washington,

Missouri

1990: Walmart was the nation's number-one retailer

1991: Walmart goes global, opened a Sam’s Club in Mexico City

1992:Employed 371,000 associates in 1,928 stores and clubs.

1994: Walmart expanded into Canada with the purchase of 122

Woolco stores

History of Walmart

160

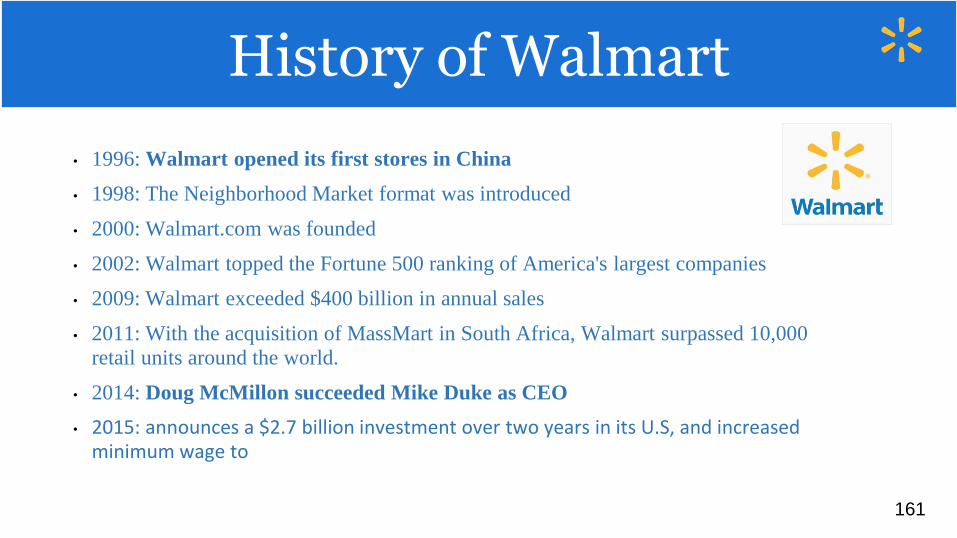

• 1996: Walmart opened its first stores in China

• 1998: The Neighborhood Market format was introduced

• 2000: Walmart.com was founded

• 2002: Walmart topped the Fortune 500 ranking of America's largest companies

• 2009: Walmart exceeded $400 billion in annual sales

• 2011: With the acquisition of MassMart in South Africa, Walmart surpassed 10,000

retail units around the world.

• 2014: Doug McMillon succeeded Mike Duke as CEO

• 2015: announces a $2.7 billion investment over two years in its U.S, and increased minimum wage to

History of Walmart ContinuedHistory of Walmart

161

World Map of Walmart storesWorld Map of Walmart Stores

162

Total number of Walmart stores worldwide from 2008 to 2016

Total Number of Walmart Stores Worldwide (2008 – 2016)

163

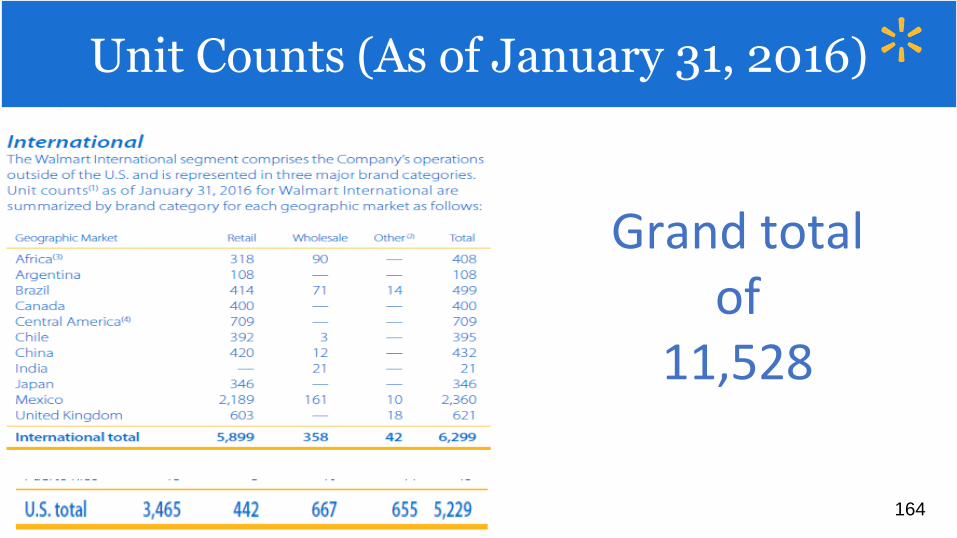

Unit Counts as of January 31, 2016

Grand total of

11,528

Unit Counts (As of January 31, 2016)

164

Net Sales Breakdown

165

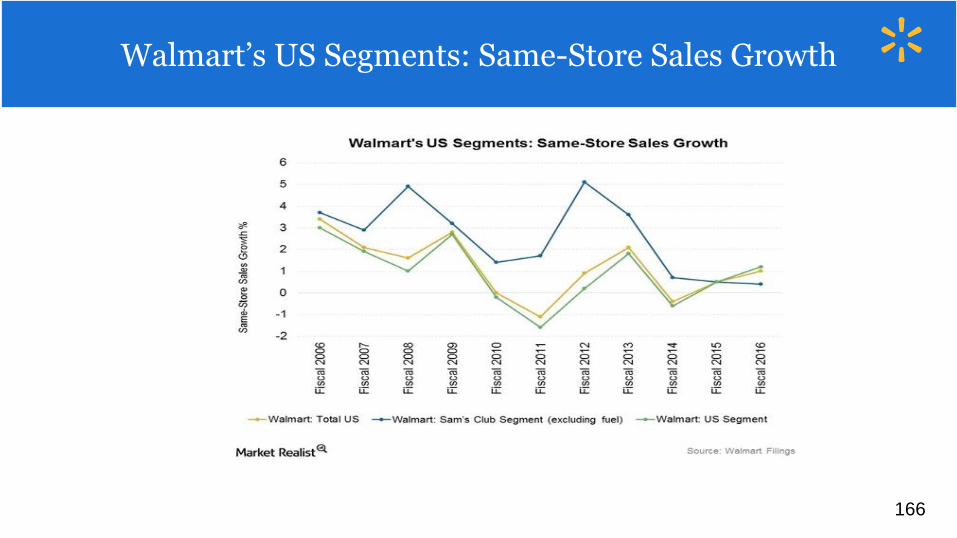

Walmart’s US Segments: Same-Store Sales Growth

166

E-commerce Sales Performance vs Competitorse-Commerce Sales Performance

167

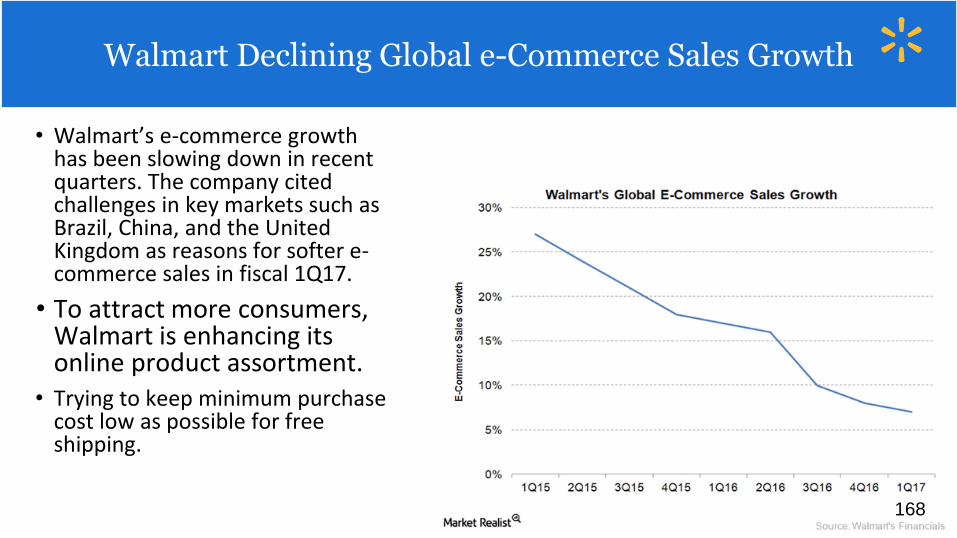

• Walmart’s e-commerce growth has been slowing down in recent quarters. The company cited challenges in key markets such as Brazil, China, and the United Kingdom as reasons for softer e-commerce sales in fiscal 1Q17.

• To attract more consumers, Walmart is enhancing its online product assortment.

• Trying to keep minimum purchase cost low as possible for free shipping.

Walmart’s declining global E-commerce Sales GrowthWalmart Declining Global e-Commerce Sales Growth

168

Acquisition of Jet.com

It’s the largest acquisition in E-commerce history: $3 billion in cash plus up to $300 million in shares. And all for a two-year-old company that’s just getting off the ground.

By purchasing Jet, Walmart’s biggest attempt to stick it to Amazon and take a share of the E-commerce pie, the offline retail giant has cunningly opened up an opportunity to slide in as one of the biggest go-to online retailers for customers and sellers alike.

The promise Jet brings is grounded in its technology specifically, the powerful AI software which Jet’s online platform is built on.

Unique to Jet, the proprietary algorithm pulls data from their vast marketplace of third party sellers, serving their customers with the best products, at the best price, by the best possible means of delivery.

Recent Events

169

Acquisition of Shoebuy.com

And future plans

Wal-Mart is kicking off the

year with the acquisition of

ShoeBuy.com, an online shoe

retailer that competes

with Amazon's Zappos.

The acquisition

reportedly cost $70

million.

Apparel is the largest online

sales category in the United

States. It shouldn't be a huge

surprise that Amazon is the

largest online seller of clothing

in the country.

The ShoeBuy acquisition

is a perfect fit to launch

sales of the "long-tail,

high-margin" categories

Wal-Mart is lacking.

A big budget for improvements and acquisitionsWal-Mart plans on spending $1.1 billion on

its e-commerce operations in fiscal 2018,

up from $900 million this year. But Wal-

Mart developed that plan before it acquired

Jet.com and put Marc Lore in charge of

growing its e-commerce business.

Recent Events

170

Walton FamilyWalton Family

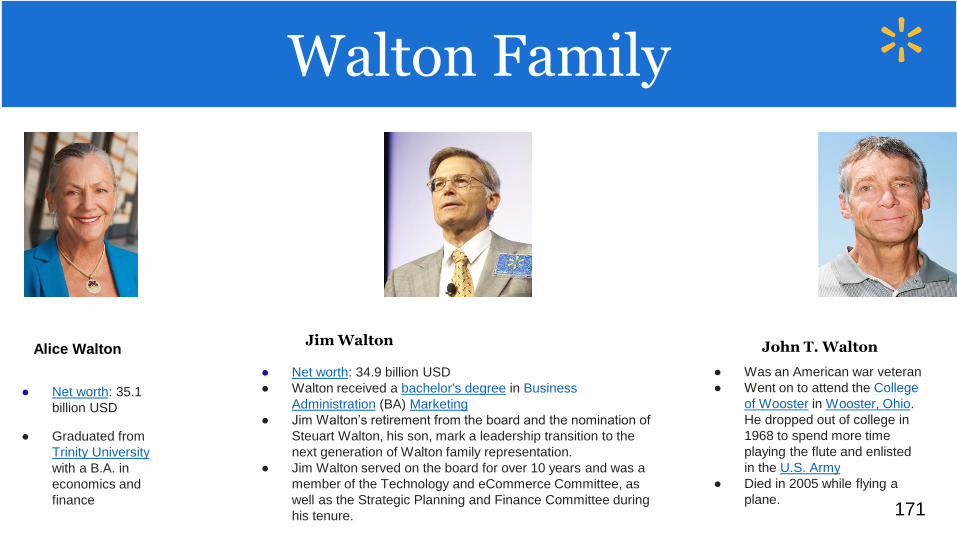

Alice Walton

● Net worth: 35.1

billion USD

● Graduated from

Trinity University

with a B.A. in

economics and

finance

Jim Walton

● Net worth: 34.9 billion USD

● Walton received a bachelor's degree in Business

Administration (BA) Marketing

● Jim Walton’s retirement from the board and the nomination of

Steuart Walton, his son, mark a leadership transition to the

next generation of Walton family representation.

● Jim Walton served on the board for over 10 years and was a

member of the Technology and eCommerce Committee, as

well as the Strategic Planning and Finance Committee during

his tenure.

John T. Walton

● Was an American war veteran

● Went on to attend the College

of Wooster in Wooster, Ohio.

He dropped out of college in

1968 to spend more time

playing the flute and enlisted

in the U.S. Army

● Died in 2005 while flying a

plane. 171

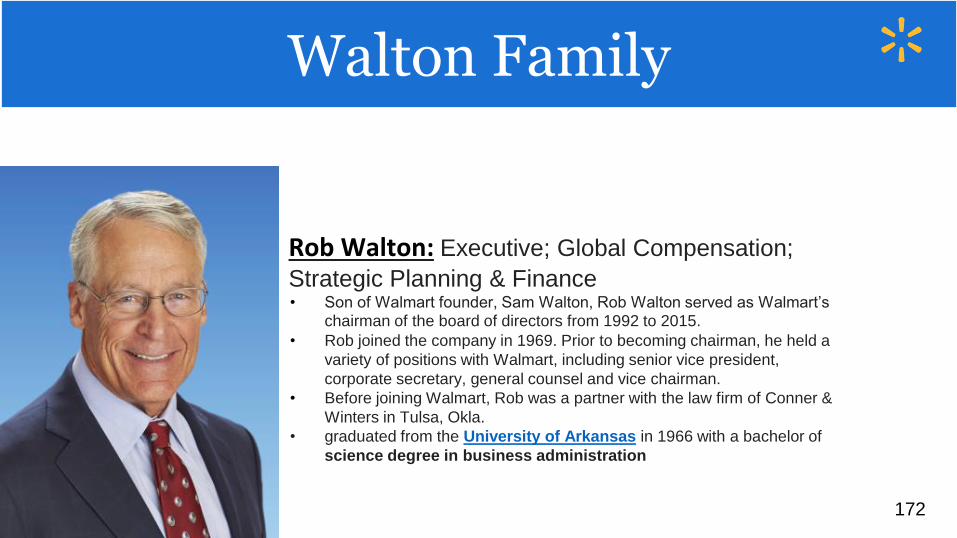

Rob Walton: Executive; Global Compensation;

Strategic Planning & Finance• Son of Walmart founder, Sam Walton, Rob Walton served as Walmart’s

chairman of the board of directors from 1992 to 2015.

• Rob joined the company in 1969. Prior to becoming chairman, he held a

variety of positions with Walmart, including senior vice president,

corporate secretary, general counsel and vice chairman.

• Before joining Walmart, Rob was a partner with the law firm of Conner &

Winters in Tulsa, Okla.

• graduated from the University of Arkansas in 1966 with a bachelor of

science degree in business administration

Walton Family

172

Steuart Walton: CEO, Game Composites Ltd.• Is the chief executive officer of Game Composites, Ltd., a company he

founded in 2013 that designs and builds small composite aircraft.

• Elected to the Walmart Board of Directors in 2016, he is the grandson of

Walmart founder Sam Walton.

• He previously worked for the London office of Allen & Overy, LLP handling

matters related to debt equity offerings by non-U.S. entities.

• Steuart also worked for Walmart’s international division focusing on mergers

and acquisitions.

• Steuart holds a bachelor’s degree in business administration from the

University of Colorado at Boulder and a law degree from Georgetown

University Law Center.

Walton Family

173

Walmart Management

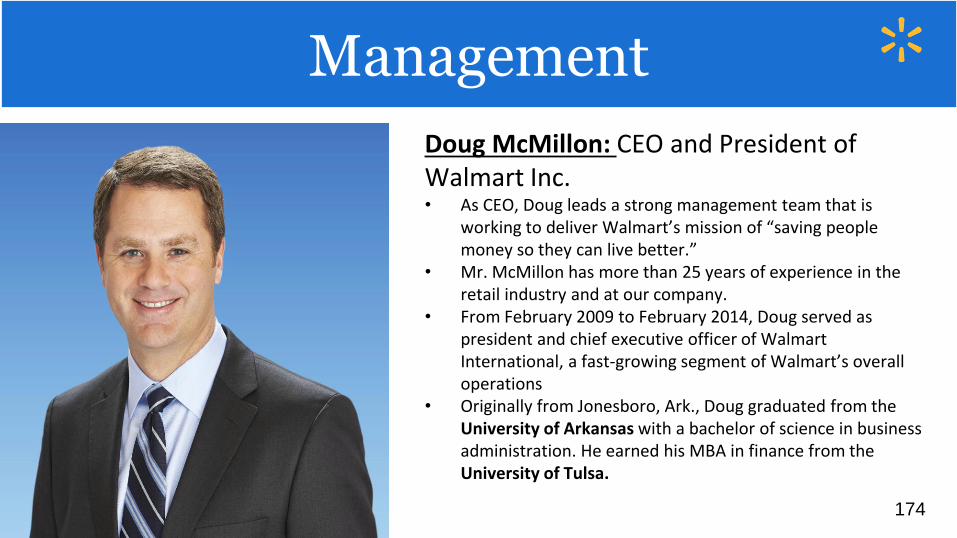

Doug McMillon: CEO and President of Walmart Inc.• As CEO, Doug leads a strong management team that is

working to deliver Walmart’s mission of “saving people money so they can live better.”

• Mr. McMillon has more than 25 years of experience in the retail industry and at our company.

• From February 2009 to February 2014, Doug served as president and chief executive officer of Walmart International, a fast-growing segment of Walmart’s overall operations

• Originally from Jonesboro, Ark., Doug graduated from the University of Arkansas with a bachelor of science in business administration. He earned his MBA in finance from the University of Tulsa.

Management

174

Greg Foran: CEO and president of Walmart U.S.• Greg is responsible for the strategic direction and performance of

more than 4,500 Walmart stores and 1.3 million associates'. • Greg is a 35-year retail veteran with extensive experience in

marketing, operational and executive roles. He most recently served as president and CEO of Walmart Asia and was responsible for the company’s operations in China, Japan and India, as well as business development throughout the continent.

• Prior to Walmart, Greg held a number of roles with Woolworths, the leading retailer in Australia and New Zealand. He served as the managing director of supermarkets, liquor and petrol with responsibility for more than $40 billion in sales at that time.

• Greg attended two advanced management programs at both Harvard University and the University of Virginia. Greg also has a diploma in management from the New Zealand Institute of Management in Auckland, New Zealand.

Management

175

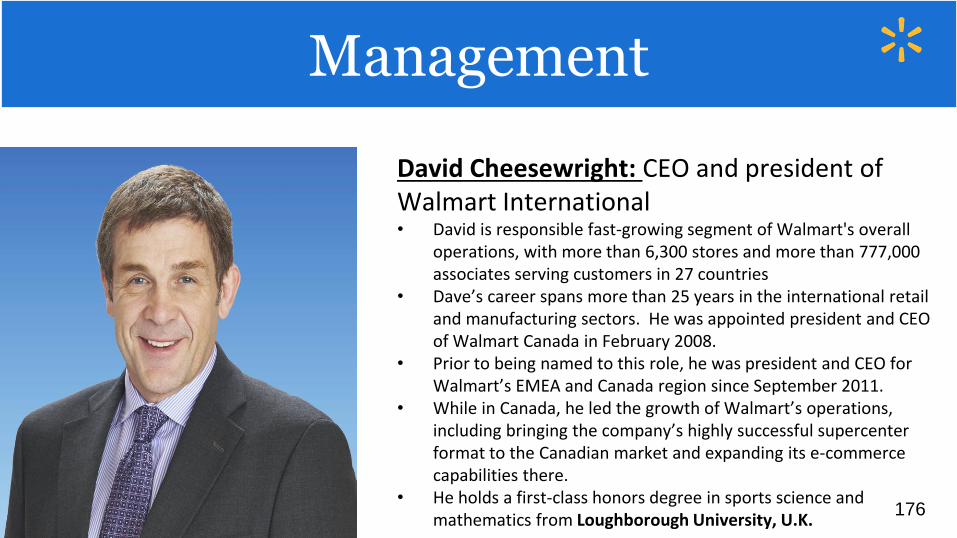

David Cheesewright: CEO and president of Walmart International• David is responsible fast-growing segment of Walmart's overall

operations, with more than 6,300 stores and more than 777,000 associates serving customers in 27 countries

• Dave’s career spans more than 25 years in the international retail and manufacturing sectors. He was appointed president and CEO of Walmart Canada in February 2008.

• Prior to being named to this role, he was president and CEO for Walmart’s EMEA and Canada region since September 2011.

• While in Canada, he led the growth of Walmart’s operations, including bringing the company’s highly successful supercenter format to the Canadian market and expanding its e-commerce capabilities there.

• He holds a first-class honors degree in sports science and mathematics from Loughborough University, U.K.

Management

176

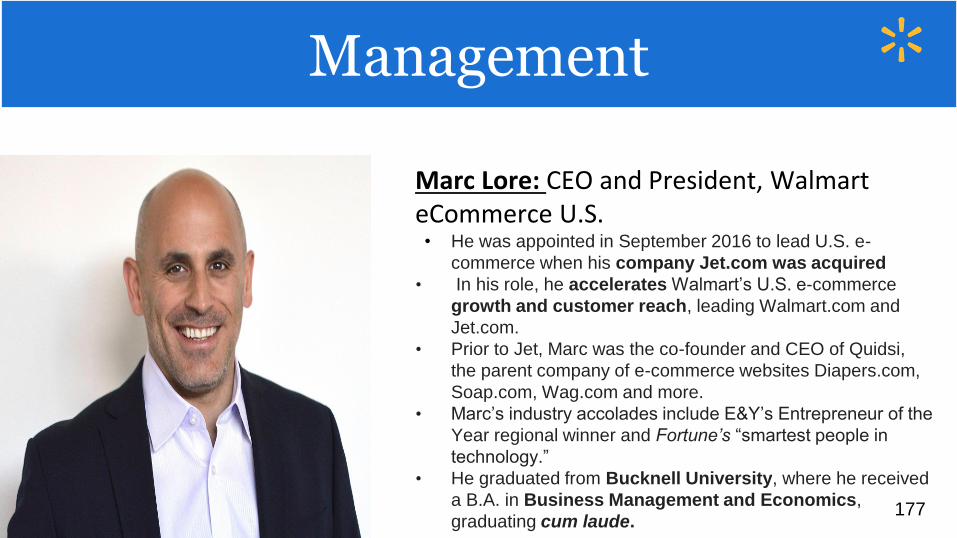

Marc Lore: CEO and President, Walmart eCommerce U.S.• He was appointed in September 2016 to lead U.S. e-

commerce when his company Jet.com was acquired

• In his role, he accelerates Walmart’s U.S. e-commerce

growth and customer reach, leading Walmart.com and

Jet.com.

• Prior to Jet, Marc was the co-founder and CEO of Quidsi,

the parent company of e-commerce websites Diapers.com,

Soap.com, Wag.com and more.

• Marc’s industry accolades include E&Y’s Entrepreneur of the

Year regional winner and Fortune’s “smartest people in

technology.”

• He graduated from Bucknell University, where he received

a B.A. in Business Management and Economics,

graduating cum laude.

Management

177

Claire Babineaux-Fontenot: Executive Vice President and Treasurer for Wal-mart Stores, Inc.• Claire joined the company in 2004 as vice president of audits and

tax policy. In 2007, she was promoted to senior vice president and chief tax officer.

• Prior to Walmart, Claire was partner at the law firm of Adams & Reese, where she was leader of the firm’s tax practice and partner-in-charge of the Baton Rouge office.

• Claire has been recognized throughout her career for her strong commitment to diversity. Won the Dave Jackson Trailblazer Award

• Claire is a graduate of the University of Louisiana at Lafayette and earned her law degree from Southern University Law Center in Baton Rouge. She also holds a master of laws degree in taxation from Southern Methodist University’s Dedman School of Law in Dallas.

Management

178

Brett Biggs: Executive vice president and Chief Financial officer for Walmart• Brett is responsible for accounting and control, corporate strategy

and development, business planning and analysis, internal auditing, treasury, tax, global shared services and several other key areas of the company.

• Before being appointed to his current role, he was executive vice president and chief financial officer for Walmart International, where he was responsible for all global finance activities.

• Prior to joining Walmart in 2000, Brett held various M&A and corporate finance positions with Leggett & Platt, Phillips Petroleum Co. and Price Waterhouse.

• Brett graduated Summa Cum Laude from Harding University with a bachelor’s degree in accounting and later received a MBA with Honors from Oklahoma State University. He serves in various advisory roles at Harding University.

Management

179

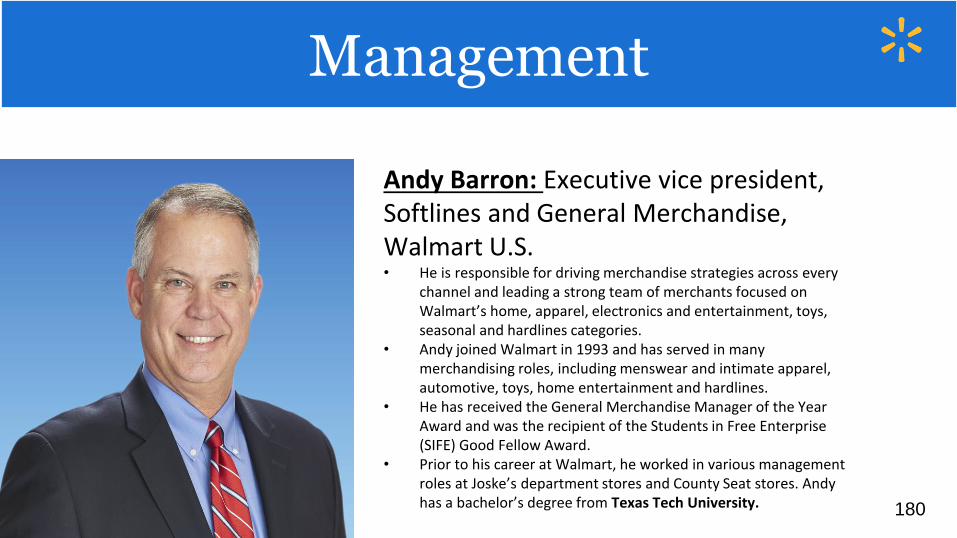

Andy Barron: Executive vice president, Softlines and General Merchandise, Walmart U.S.• He is responsible for driving merchandise strategies across every

channel and leading a strong team of merchants focused on Walmart’s home, apparel, electronics and entertainment, toys, seasonal and hardlines categories.

• Andy joined Walmart in 1993 and has served in many merchandising roles, including menswear and intimate apparel, automotive, toys, home entertainment and hardlines.

• He has received the General Merchandise Manager of the Year Award and was the recipient of the Students in Free Enterprise (SIFE) Good Fellow Award.

• Prior to his career at Walmart, he worked in various management roles at Joske’s department stores and County Seat stores. Andy has a bachelor’s degree from Texas Tech University.

Management

180

Walmart

Dan Bartlett: Executive vice president, Corporate Affairs for Walmart • He is responsible for government relations and public policy,

corporate communications, philanthropy, and the company’s social responsibility and sustainability initiatives.

• Before joining Walmart, Dan was president and CEO of the U.S. division of Hill+Knowlton Strategies, where he served as a strategic advisor to business leaders representing key sectors of the American and global economy.

• He served in several high-ranking positions at the White House, completing his service as counselor to President George W. Bush in July 2007.

• Dan is a graduate of the University of Texas at Austin and serves on the advisory board of UT Austin’s College of Communication.

Management

181

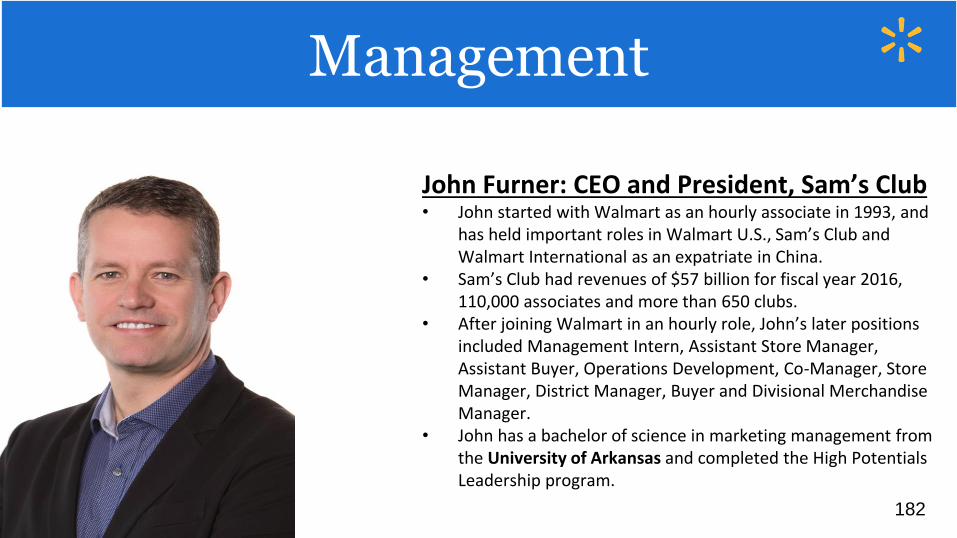

John Furner: CEO and President, Sam’s Club• John started with Walmart as an hourly associate in 1993, and

has held important roles in Walmart U.S., Sam’s Club and Walmart International as an expatriate in China.

• Sam’s Club had revenues of $57 billion for fiscal year 2016, 110,000 associates and more than 650 clubs.

• After joining Walmart in an hourly role, John’s later positions included Management Intern, Assistant Store Manager, Assistant Buyer, Operations Development, Co-Manager, Store Manager, District Manager, Buyer and Divisional Merchandise Manager.

• John has a bachelor of science in marketing management from the University of Arkansas and completed the High Potentials Leadership program.

Management

182

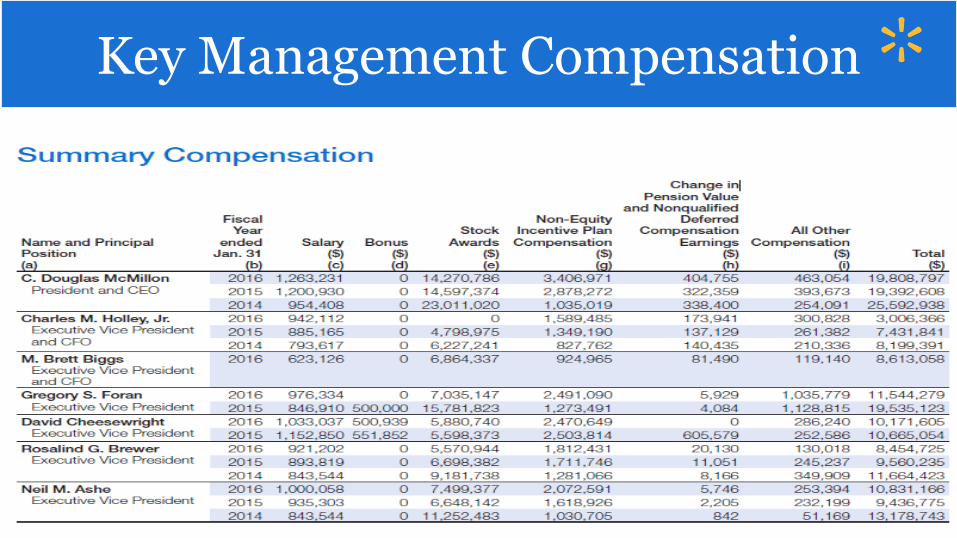

Key Management Compensation

Consolidated Balance sheets 2017 10-Q(Assets)Balance Sheet (10-Q)

Consolidated Balance sheets 2017 10-Q(Liabilities+Equity)Balance Sheet (10-Q)

188

Balance Sheet (10-K)

189

Balance Sheet (10-K)

Statement of Income (10-K)

Consolidated Statements of Income 2017 Q4

Statement of Income (10-Q)

Statement of Cashflow (10-K)

Statement of Cashflow (10-K)

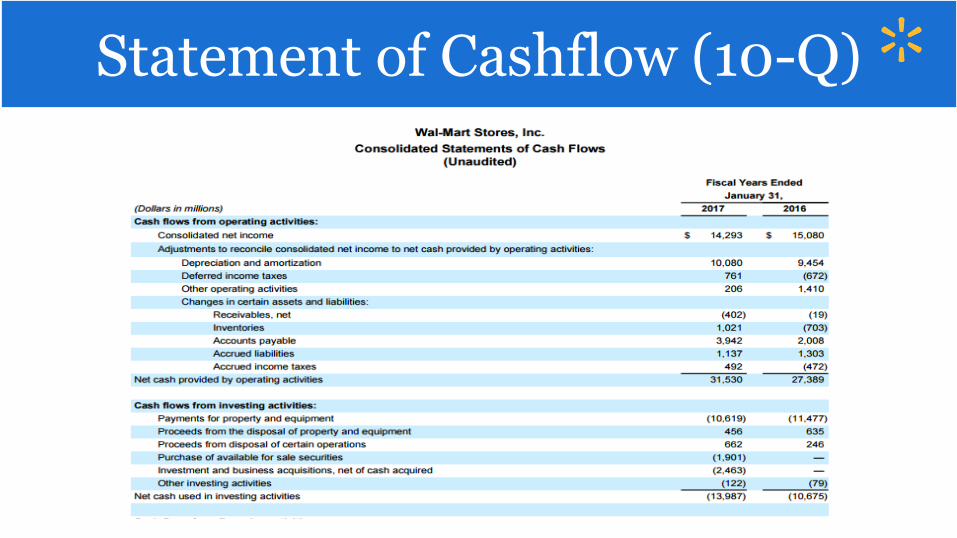

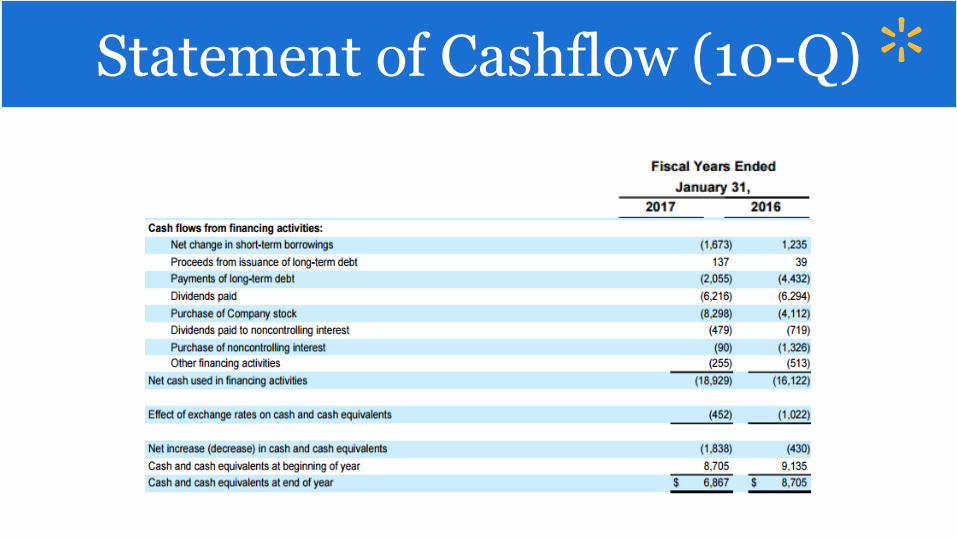

Consolidated statements of Cash flows 2017 10-QStatement of Cashflow (10-Q)

Consolidated statements of Cash flows 2017 10-QStatement of Cashflow (10-Q)

Recommendation!Recommendation

Consolidated Balance sheets 10-Q (Assets)

197

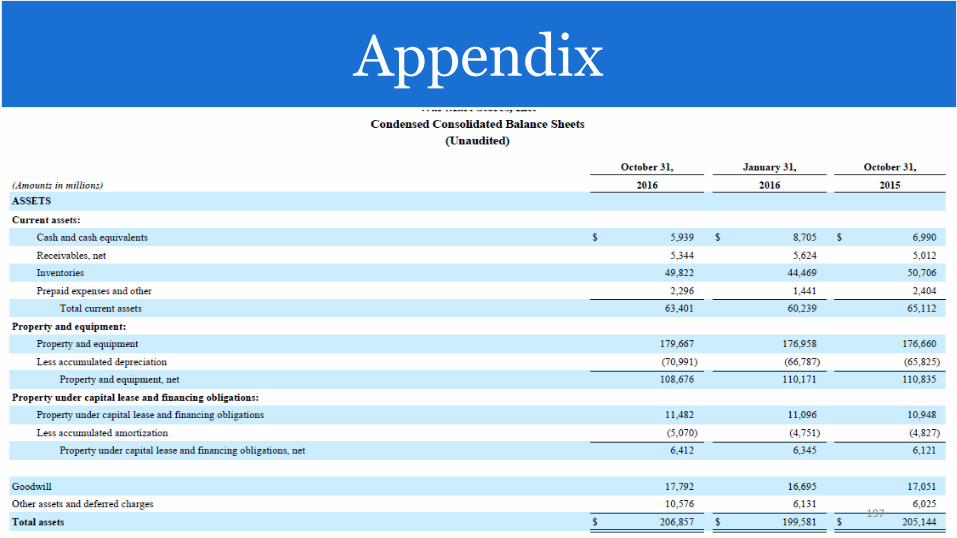

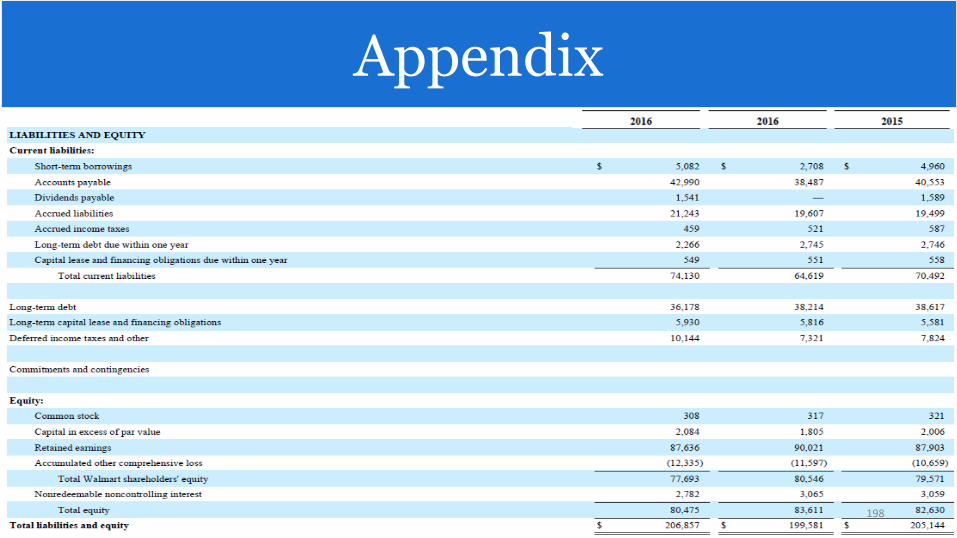

Appendix

Consolidated Balance sheets 10-Q (Liabilities)

198

Appendix

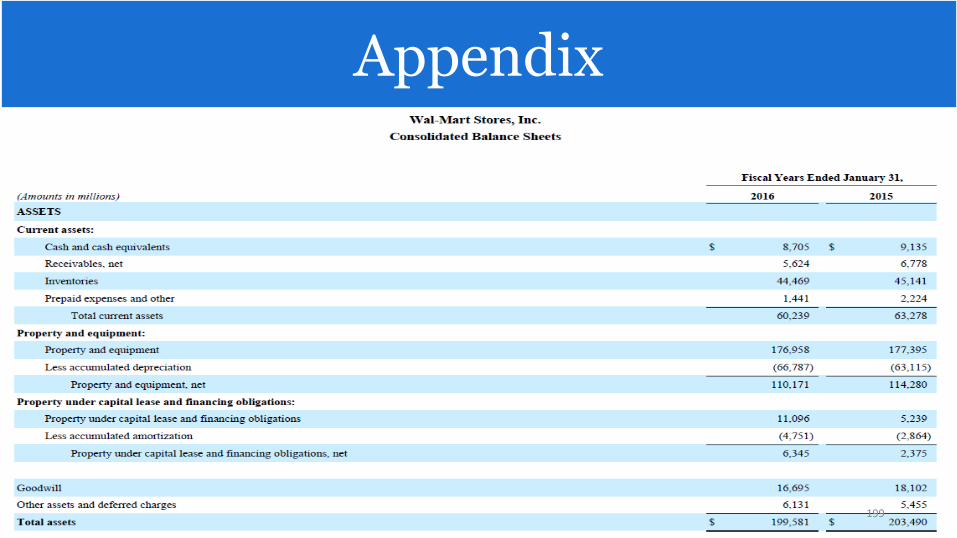

Consolidated Balance sheets 10-K (Assets)

199

Appendix

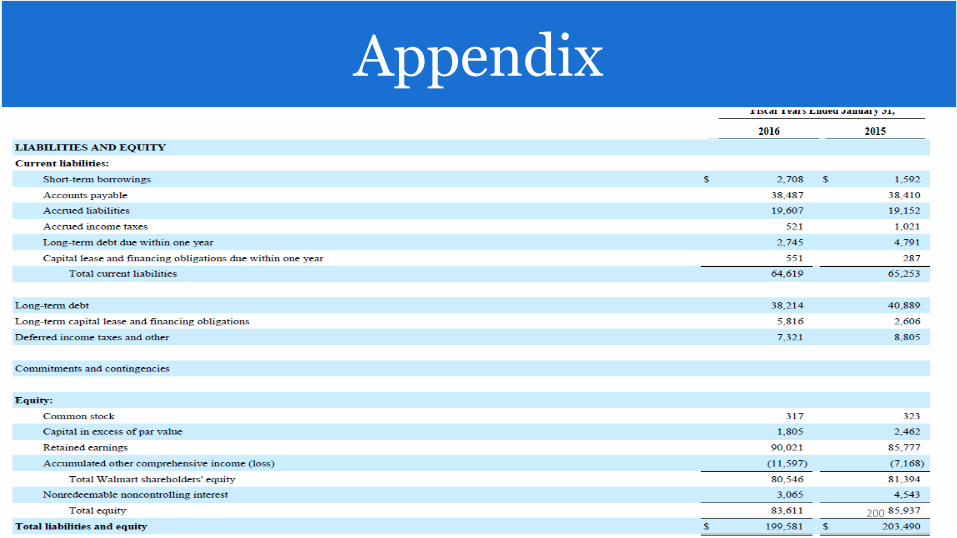

Consolidated Balance sheets 10-K (Liabilities)

200

Appendix

Consolidated Statements of Income 10-K

201

Appendix

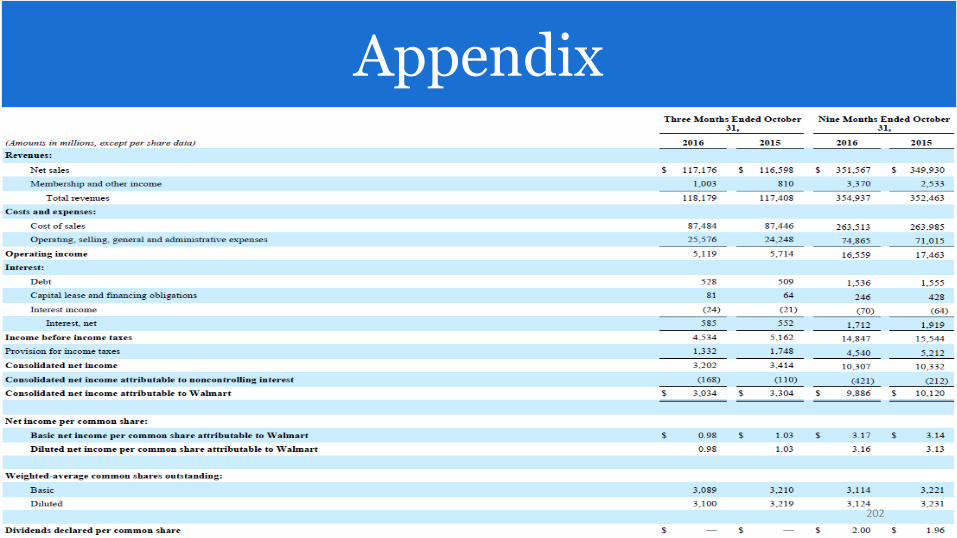

Consolidated Statements of Income 10-Q

202

Appendix

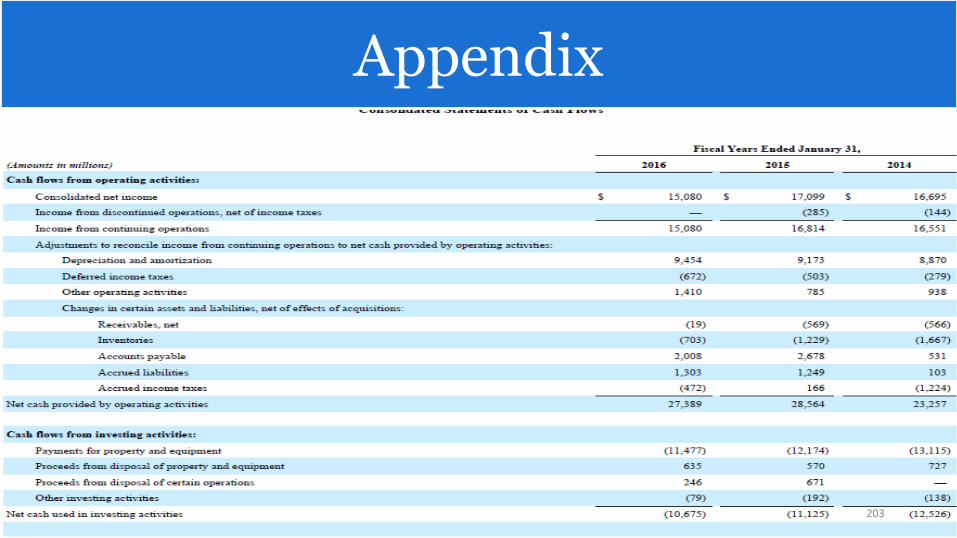

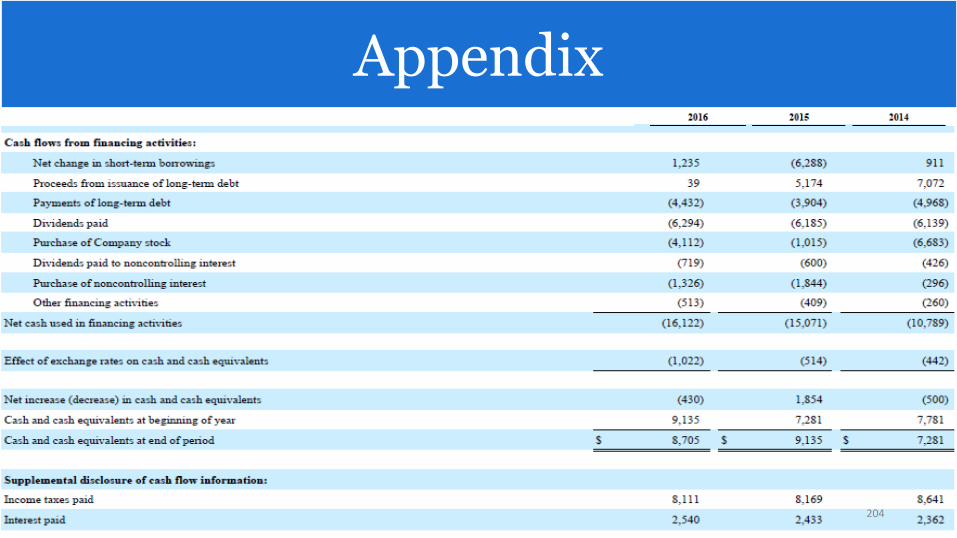

Consolidated statements of Cash flows 10-K

203

Appendix

Consolidated statements of Cash flows 10-K

204

Appendix

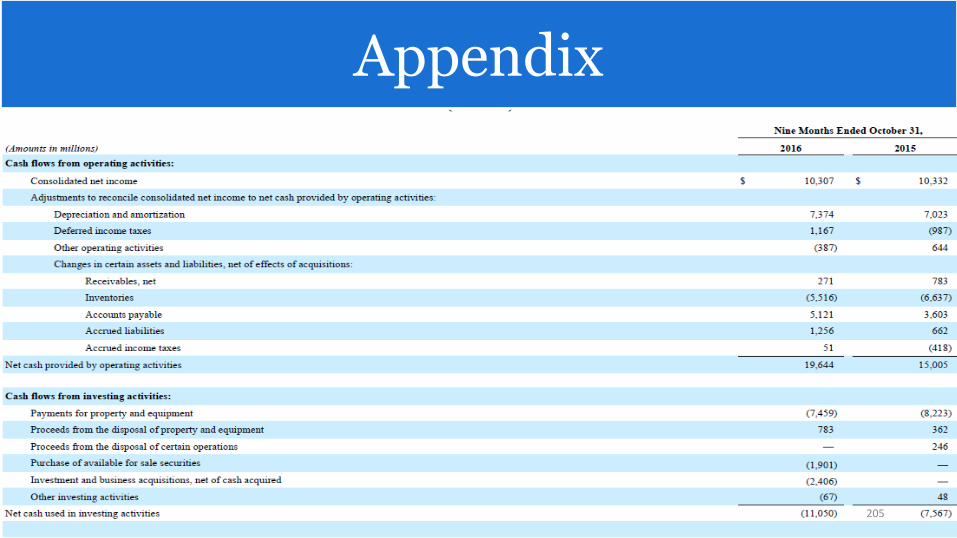

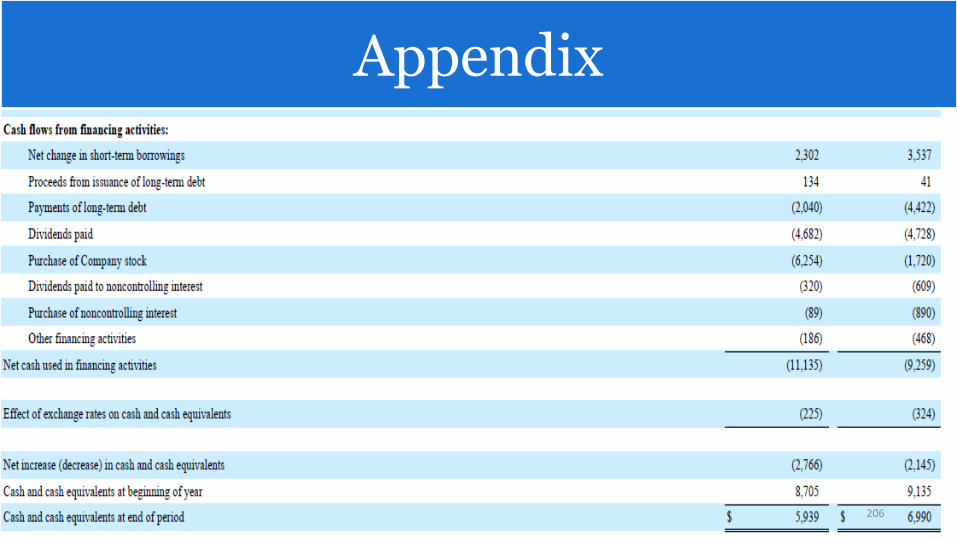

Consolidated statements of Cash flows 10-Q

205

Appendix

Consolidated statements of Cash flows 10-Q

206

Appendix

Consolidated Balance sheets 2016-2015 10k (Assets)

207

Appendix

Consolidated Balance sheets 2016-2015 10k (Liabilities+Equity)

208

Appendix

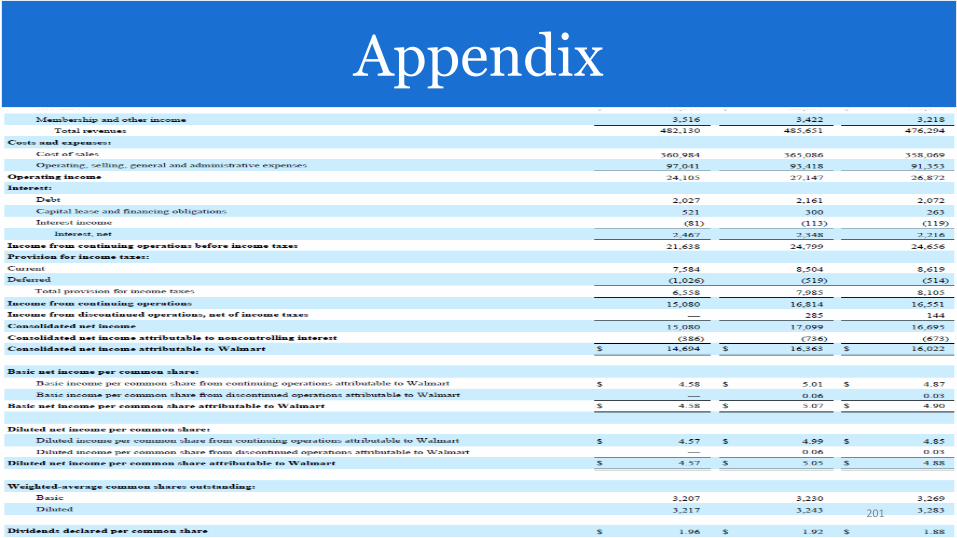

Consolidated Statements of Income 2016-2014 10K

209

Appendix

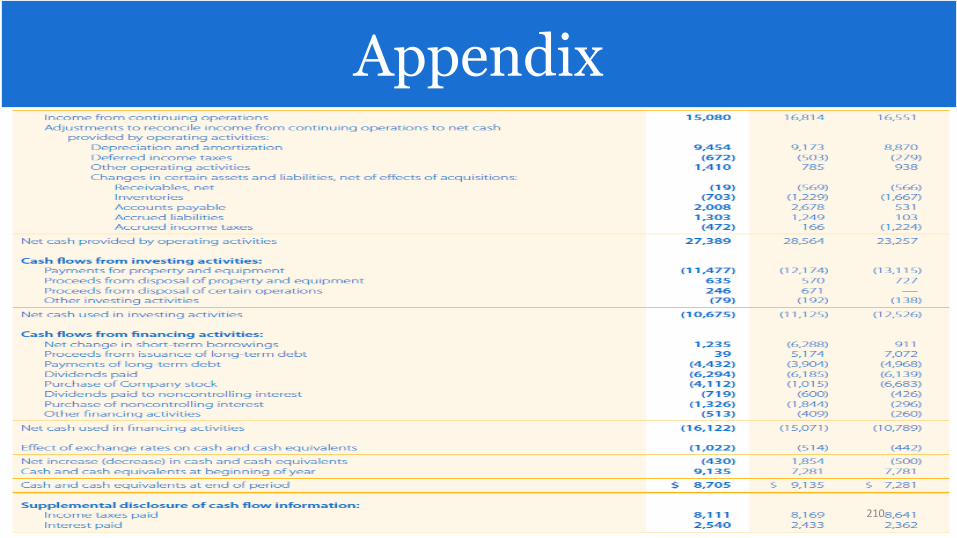

Consolidated statements of Cash flows 2016-2014 10k

210

Appendix

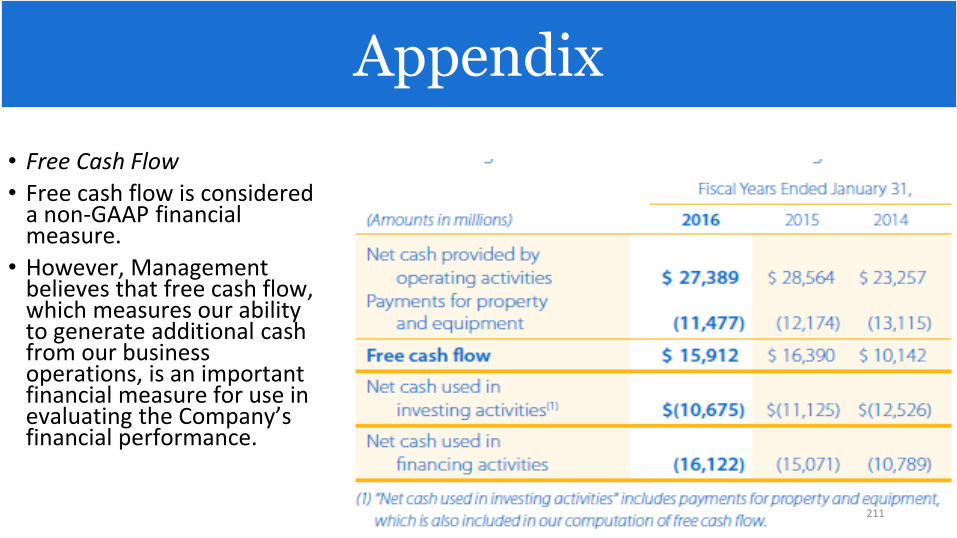

• Free Cash Flow

• Free cash flow is considered a non-GAAP financial measure.

• However, Management believes that free cash flow, which measures our ability to generate additional cash from our business operations, is an important financial measure for use in evaluating the Company’s financial performance.

211

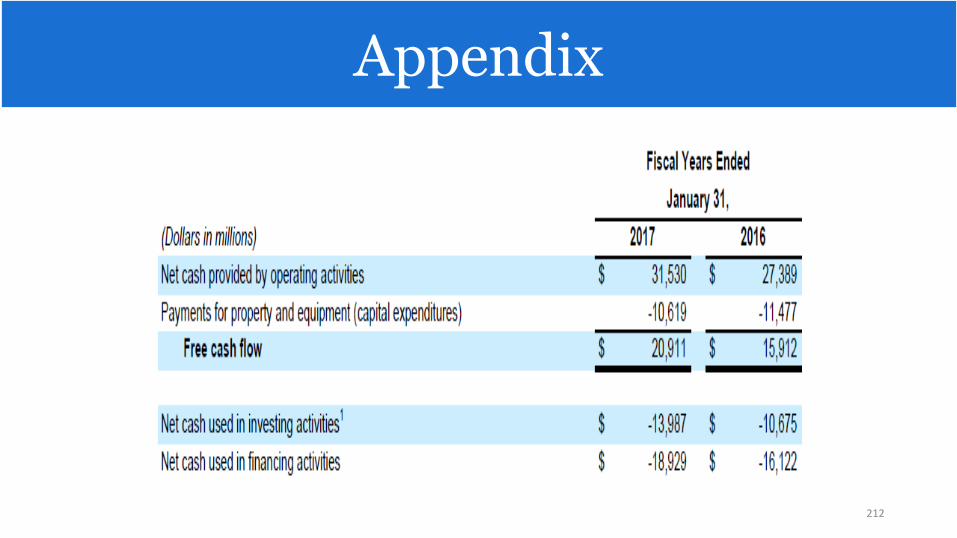

Appendix

212

Appendix

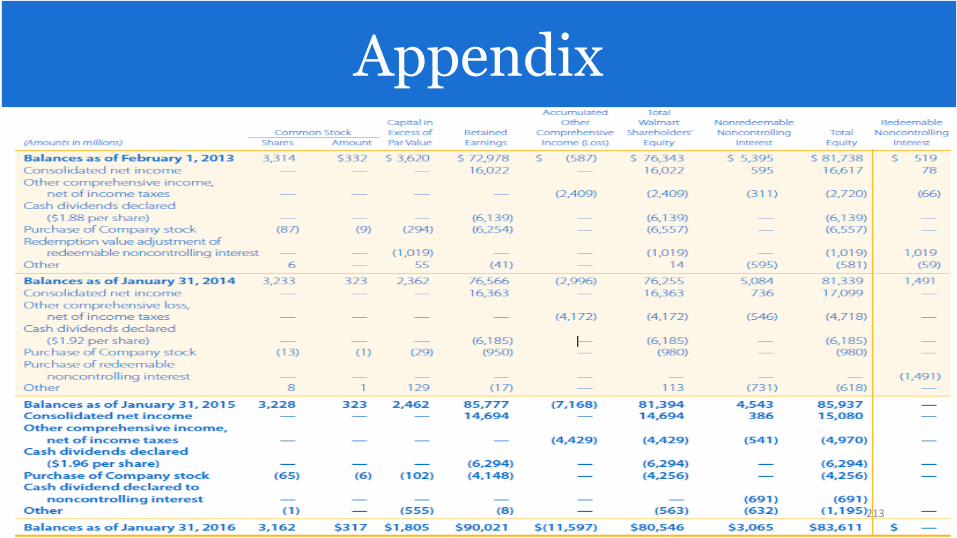

Consolidated statement of Shareholders Equity and redeemable

non-controlling interest 2016(10k)

213

Appendix

![Harmonics Study of Common Low Wattage LED …anale-ing.uem.ro/2017/8.pdfMarket Size, Share, Development, Growth and Demand Forecast to 2020. [4] BIS Research, Global Smart Light Fixture](https://img.pdfslide.net/doc/110x75/5f0a46847e708231d42adcec/harmonics-study-of-common-low-wattage-led-anale-inguemro20178pdf-market-size.jpg)