Embed Size (px)

Citation preview

Use of Glass in Solar Energy Applications:Now & in the Future:

Corona Solar Group, LLCCanton GA. 30114www.coronasolargroup.com

Discussion Point’s:Market Now

Energy/Markets/Manufacturing/Policy/Trade

Products Nowc-Si/Thin Film/CSP/CPV/BIPV

Industry FutureValue ChainMovements

Future Markets

Future Products c-Si/a-Si/CIGS/Thermal/CSP/BIPV/Hydrogen

Conclusion’s

Current Issues & Topics:

o Is the solar industry going to survive?o Why do you need subsidies?o If Solar is so good why can’t it compete on a level playing

field with current utility power?o What to do about the module dumping issue?o When will we reach grid parity?o Will glass play a major roll in the future of solar?o Is there a cheaper solution other than glass in modules?o What is the best way to keep manufacturing in the United

States?o What new product’s or technologies are in the pipeline?

Market Now

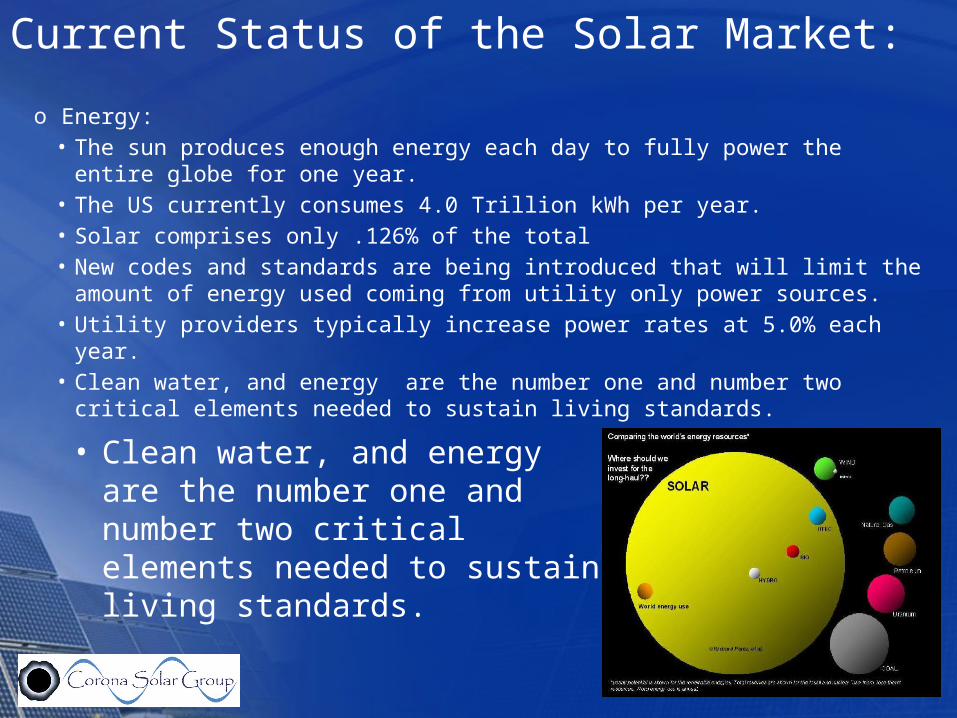

Current Status of the Solar Market:

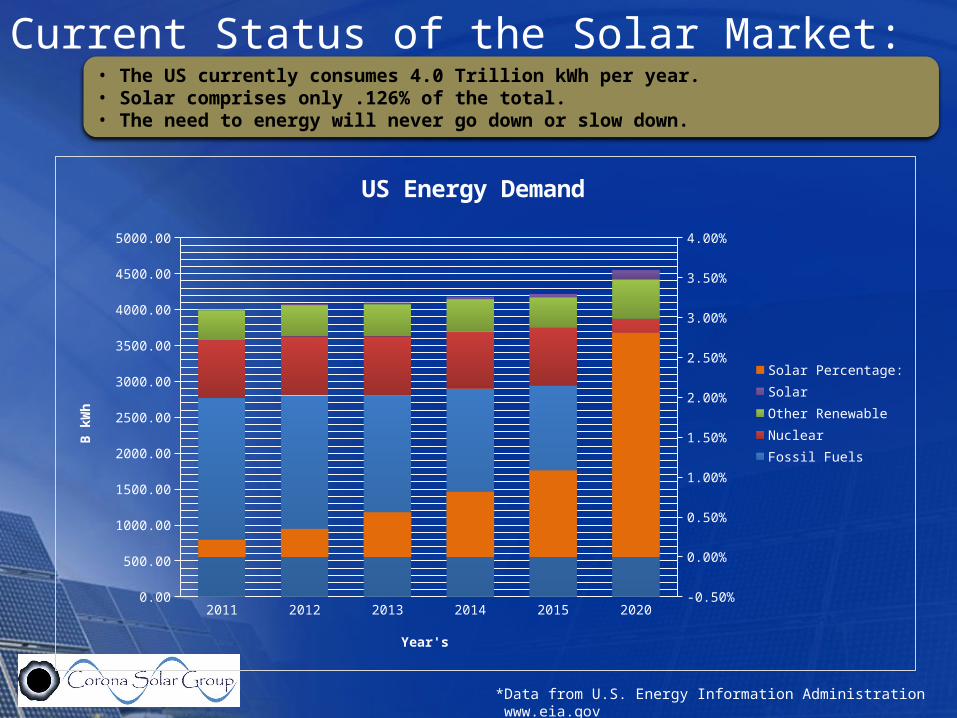

o Energy:• The sun produces enough energy each day to fully power the entire globe

for one year.• The US currently consumes 4.0 Trillion kWh per year.• Solar comprises only .126% of the total• New codes and standards are being introduced that will limit the amount of

energy used coming from utility only power sources.• Utility providers typically increase power rates at 5.0% each year. • Clean water, and energy are the number one and number two critical

elements needed to sustain living standards.• Clean water, and energy are the number one and number two critical elements needed to sustain living standards.

2011 2012 2013 2014 2015 20200.00

500.00

1000.00

1500.00

2000.00

2500.00

3000.00

3500.00

4000.00

4500.00

5000.00

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

US Energy Demand

Solar Percentage:

Solar

Other Renewable

Nuclear

Fossil Fuels

Year's

B k

Wh

• The US currently consumes 4.0 Trillion kWh per year.• Solar comprises only .126% of the total.• The need to energy will never go down or slow down.

Current Status of the Solar Market:

*Data from U.S. Energy Information Administration www.eia.gov

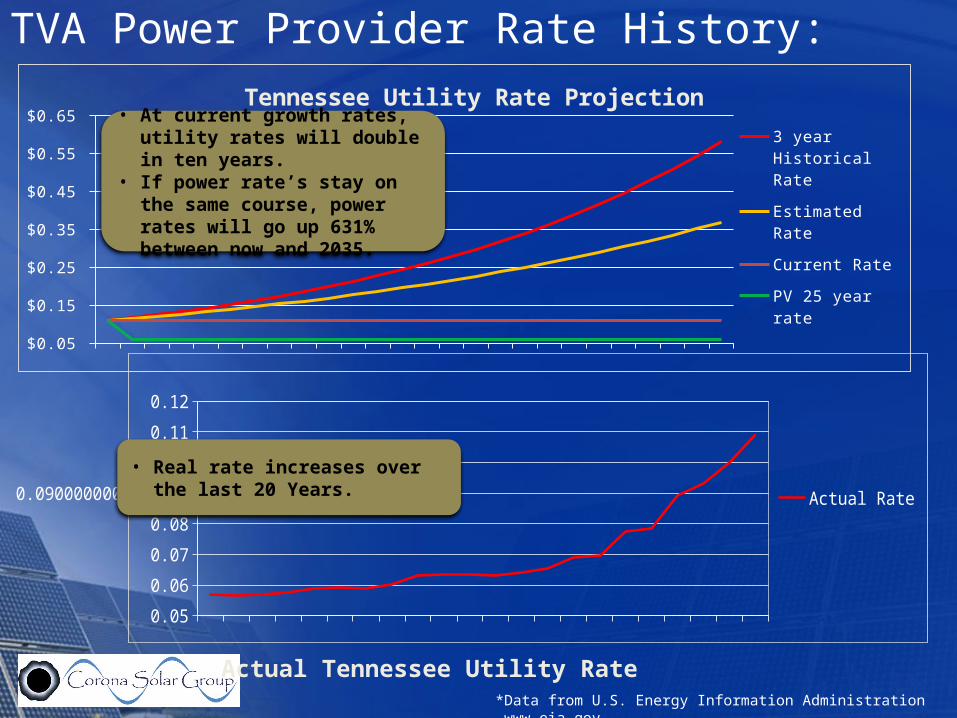

$0.05

$0.15

$0.25

$0.35

$0.45

$0.55

$0.65

3 year Historical Rate

Estimated Rate

Current Rate

PV 25 year rate

Tennessee Utility Rate Projection

*Data from U.S. Energy Information Administration www.eia.gov

TVA Power Provider Rate History:

0.05

0.06

0.07

0.08

0.0900000000000001

0.1

0.11

0.12

Actual Rate

• At current growth rates, utility rates will double in ten years.

• If power rate’s stay on the same course, power rates will go up 631% between now and 2035.

Actual Tennessee Utility Rate

• Real rate increases over the last 20 Years.

Current Status of the Solar Market:

o Markets:o North American Grid Parity is getting much closer:

o Hawaii, West Coast, North East, Florida, Caribbean…o North America is viewed as the next big solar demand

market by most expert analyst.o South America is relatively untouched, and is poised to be

a great potential solar market.o Current Products are “Engineering Sound”, but not

marketing sound. (Apple II to IPAD theorem). The product need to be made more pleasing to the eye.

o Financial markets are getting better, but financing is still not easy. New models will be coming on the scene.

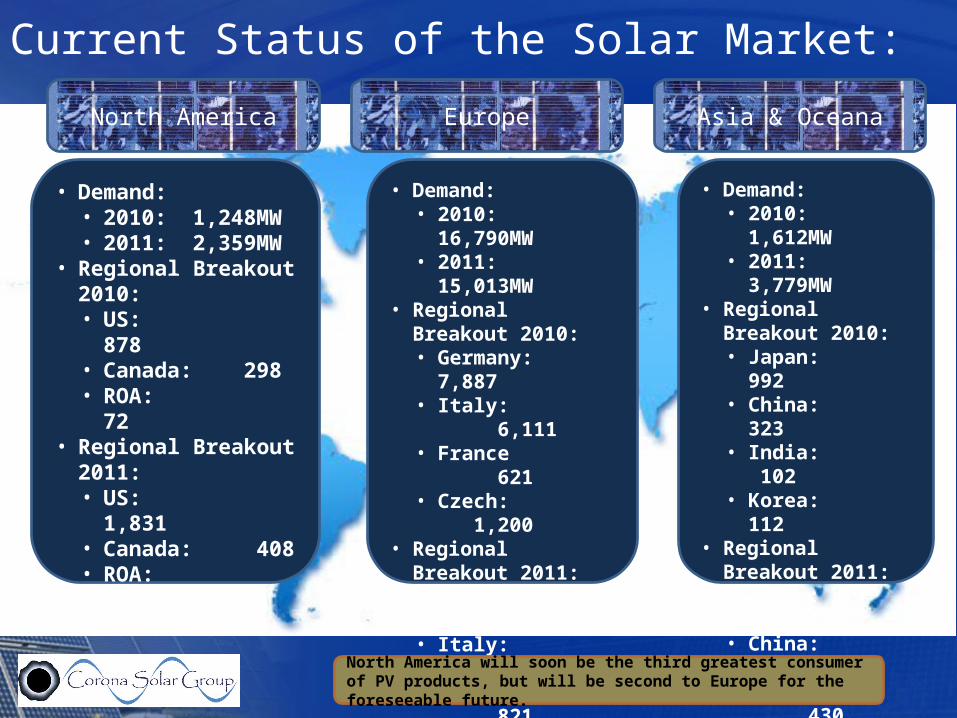

North America Europe Asia & Oceana

• Demand:• 2010: 1,248MW• 2011: 2,359MW

• Regional Breakout 2010:• US: 878• Canada: 298• ROA: 72

• Regional Breakout 2011:• US: 1,831• Canada: 408• ROA: 120

• Demand:• 2010: 16,790MW• 2011: 15,013MW

• Regional Breakout 2010:• Germany: 7,887• Italy: 6,111• France 621 • Czech: 1,200

• Regional Breakout 2011:• Germany: 7,507• Italy: 4,740 • France: 821• Czech: 310

• Demand:• 2010: 1,612MW• 2011: 3,779MW

• Regional Breakout 2010:• Japan: 992• China: 323• India: 102 • Korea: 112

• Regional Breakout 2011:• Japan: 1,488• China: 1,372• India: 430 • Korea: 134

North America will soon be the third greatest consumer of PV products, but will be second to Europe for the foreseeable future.

Current Status of the Solar Market:

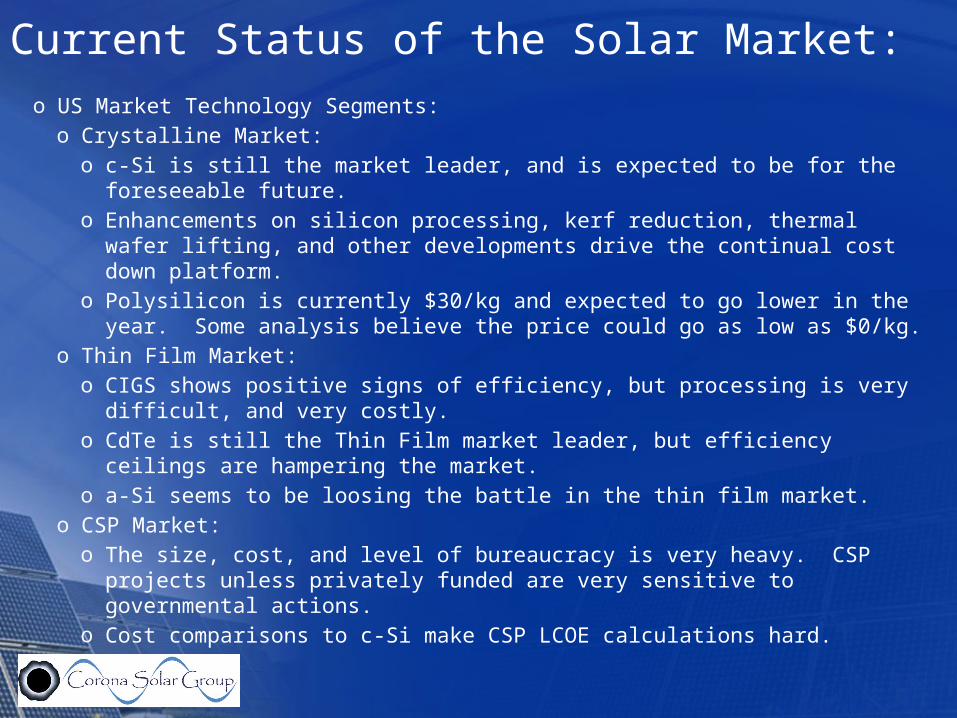

Current Status of the Solar Market:o US Market Technology Segments:

o Crystalline Market:o c-Si is still the market leader, and is expected to be for the foreseeable

future.o Enhancements on silicon processing, kerf reduction, thermal wafer lifting,

and other developments drive the continual cost down platform.o Polysilicon is currently $30/kg and expected to go lower in the year. Some

analysis believe the price could go as low as $0/kg.o Thin Film Market:

o CIGS shows positive signs of efficiency, but processing is very difficult, and very costly.

o CdTe is still the Thin Film market leader, but efficiency ceilings are hampering the market.

o a-Si seems to be loosing the battle in the thin film market.o CSP Market:

o The size, cost, and level of bureaucracy is very heavy. CSP projects unless privately funded are very sensitive to governmental actions.

o Cost comparisons to c-Si make CSP LCOE calculations hard.

Current Status of the Solar Market:

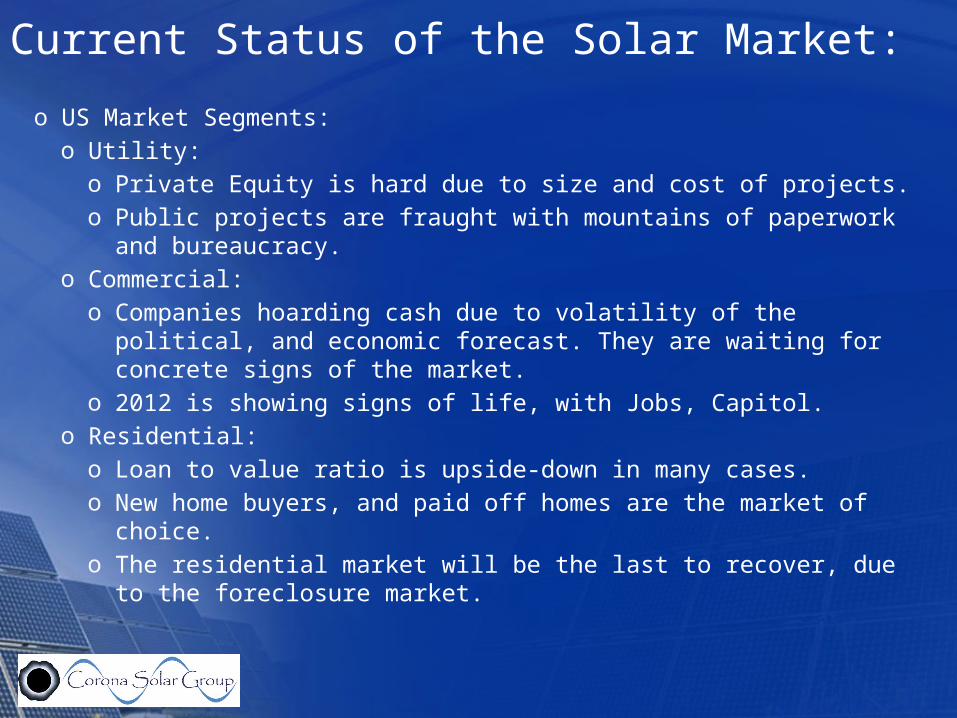

o US Market Segments:o Utility:

o Private Equity is hard due to size and cost of projects.o Public projects are fraught with mountains of paperwork and

bureaucracy.o Commercial:

o Companies hoarding cash due to volatility of the political, and economic forecast. They are waiting for concrete signs of the market.

o 2012 is showing signs of life, with Jobs, Capitol.o Residential:

o Loan to value ratio is upside-down in many cases.o New home buyers, and paid off homes are the market of choice.o The residential market will be the last to recover, due to the

foreclosure market.

Current Status of the Solar Market:

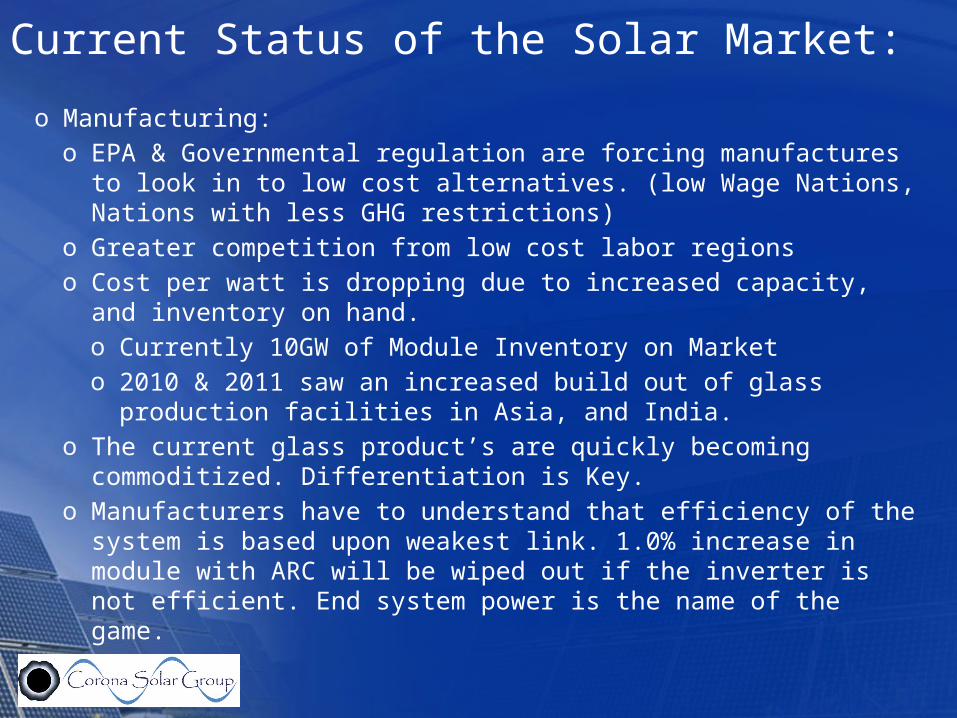

o Manufacturing:o EPA & Governmental regulation are forcing manufactures to look in to

low cost alternatives. (low Wage Nations, Nations with less GHG restrictions)

o Greater competition from low cost labor regionso Cost per watt is dropping due to increased capacity, and inventory on

hand.o Currently 10GW of Module Inventory on Marketo 2010 & 2011 saw an increased build out of glass production facilities

in Asia, and India.o The current glass product’s are quickly becoming commoditized.

Differentiation is Key. o Manufacturers have to understand that efficiency of the system is based

upon weakest link. 1.0% increase in module with ARC will be wiped out if the inverter is not efficient. End system power is the name of the game.

Current Status of the Solar Market:

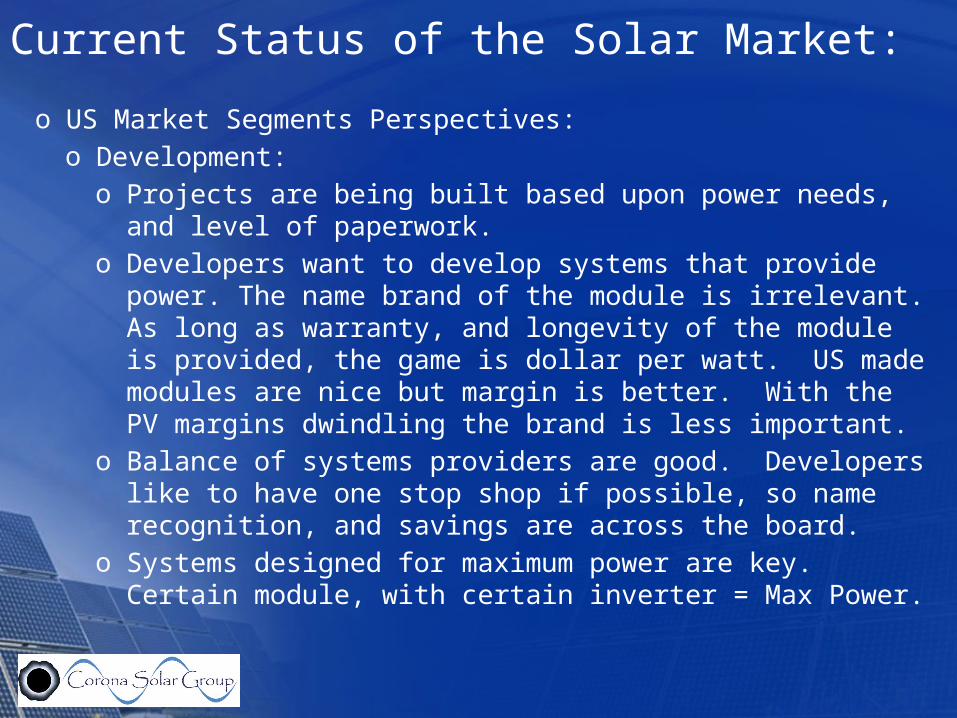

o US Market Segments Perspectives:o Development:

o Projects are being built based upon power needs, and level of paperwork.

o Developers want to develop systems that provide power. The name brand of the module is irrelevant. As long as warranty, and longevity of the module is provided, the game is dollar per watt. US made modules are nice but margin is better. With the PV margins dwindling the brand is less important.

o Balance of systems providers are good. Developers like to have one stop shop if possible, so name recognition, and savings are across the board.

o Systems designed for maximum power are key. Certain module, with certain inverter = Max Power.

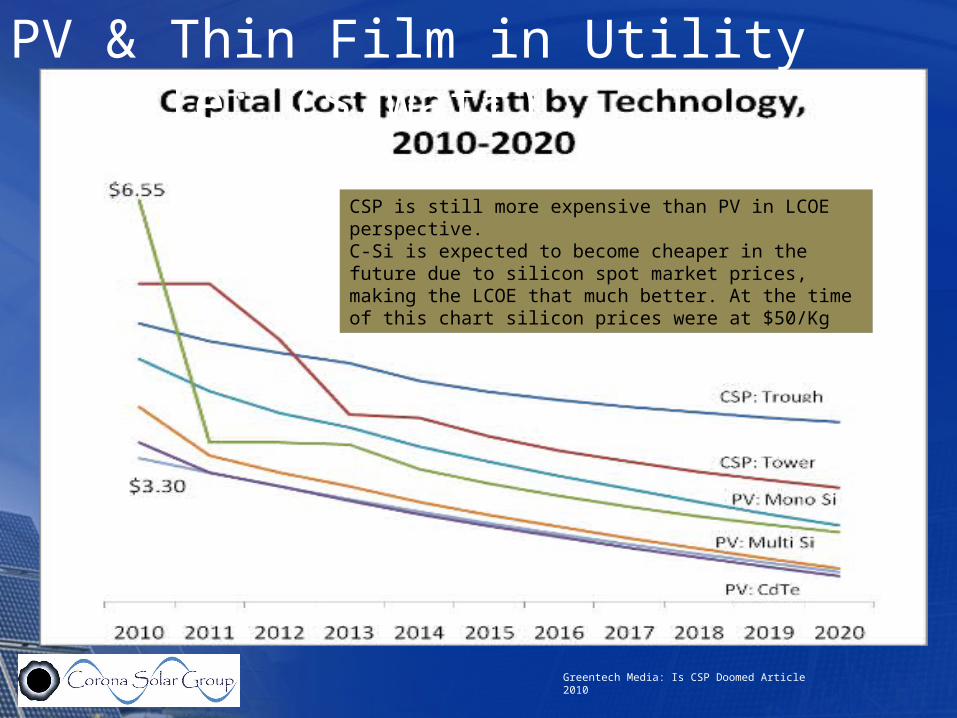

PV & Thin Film in Utility Scale: ($/Watt)

CSP: Dish

Greentech Media: Is CSP Doomed Article 2010

CSP is still more expensive than PV in LCOE perspective.C-Si is expected to become cheaper in the future due to silicon spot market prices, making the LCOE that much better. At the time of this chart silicon prices were at $50/Kg

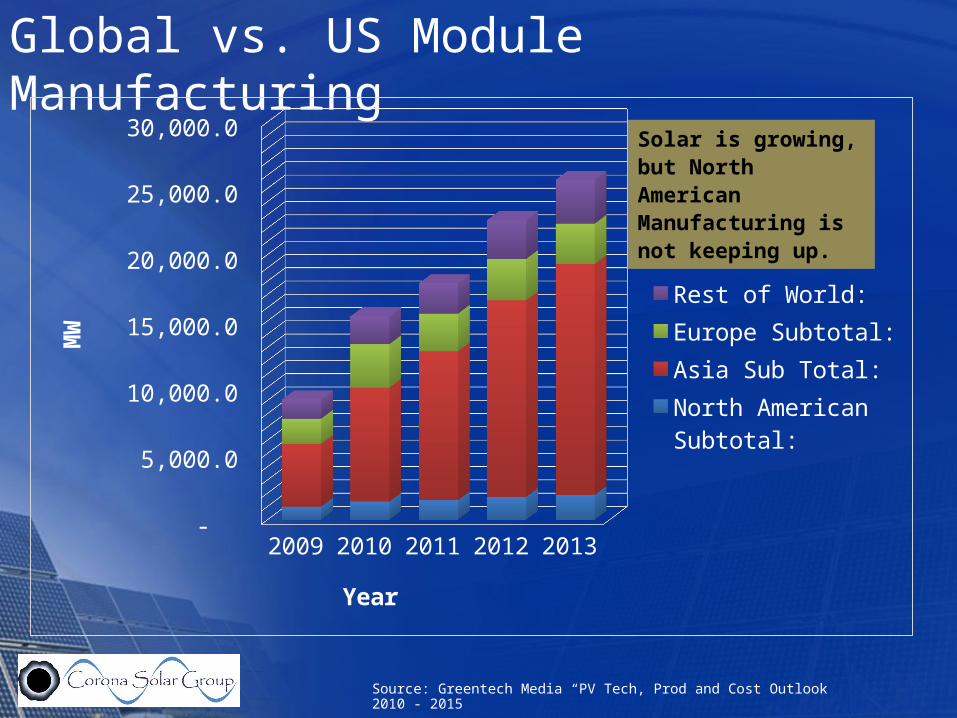

Global vs. US Module Manufacturing

2009 2010 2011 2012 2013 -

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

Rest of World:Europe Subtotal:Asia Sub Total:North American Subto-tal:

Year

MW

Solar is growing, but North American Manufac-turing is not keeping up.

Source: Greentech Media “PV Tech, Prod and Cost Outlook 2010 - 2015

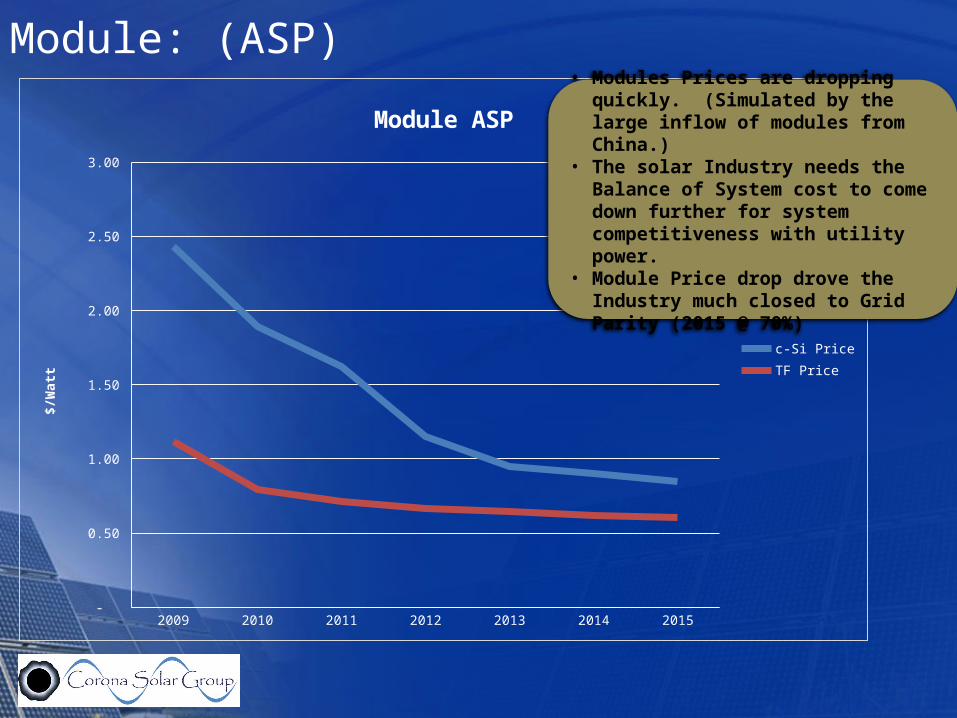

Module: (ASP)

2009 2010 2011 2012 2013 2014 2015 -

0.50

1.00

1.50

2.00

2.50

3.00

Module ASP

c-Si Price

TF Price

$/W

att

• Modules Prices are dropping quickly. (Simulated by the large inflow of modules from China.)

• The solar Industry needs the Balance of System cost to come down further for system competitiveness with utility power.

• Module Price drop drove the Industry much closed to Grid Parity (2015 @ 70%)

Current Status of the Solar Market:

o Policy:o Europe has aggressive governmental policy, but has (Boom,

and Bust issues).o Canada has adopted a FiT strategy, and is currently

modifying it based upon installed numbers.o The United States has no real Energy Policy.o Typically it is up to the states to mandate State Energy Policy.o EPA is aggressively cutting GHG emission's. This is a double

sided sword. o Possible Trade restriction with regard to China.o Each city in each state has differing methodologies for

permitting, and building.

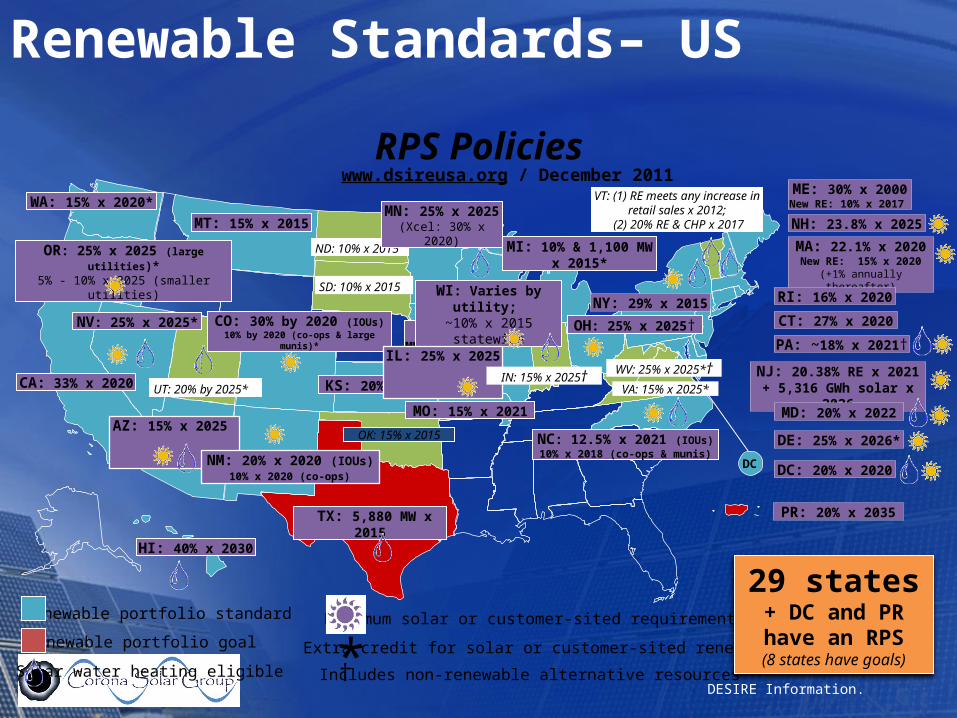

RPS Policies

Renewable portfolio standard

Renewable portfolio goal

www.dsireusa.org / December 2011

Solar water heating eligible *† Extra credit for solar or customer-sited renewables

Includes non-renewable alternative resources

WA: 15% x 2020*

CA: 33% x 2020

NV: 25% x 2025*

AZ: 15% x 2025

NM: 20% x 2020 (IOUs) 10% x 2020 (co-ops)

HI: 40% x 2030

Minimum solar or customer-sited requirement

TX: 5,880 MW x 2015

UT: 20% by 2025*

CO: 30% by 2020 (IOUs)10% by 2020 (co-ops & large

munis)*

MT: 15% x 2015 ND: 10% x

2015

SD: 10% x 2015

IA: 105 MW

MN: 25% x 2025

(Xcel: 30% x 2020)

MO: 15% x 2021

WI: Varies by utility;

~10% x 2015 statewide

MI: 10% & 1,100 MW x 2015*

OH: 25% x 2025†

ME: 30% x 2000New RE: 10% x 2017

NH: 23.8% x 2025

MA: 22.1% x 2020 New RE: 15% x 2020

(+1% annually thereafter)

RI: 16% x 2020

CT: 27% x 2020NY: 29% x 2015

NJ: 20.38% RE x 2021+ 5,316 GWh solar x

2026

PA: ~18% x 2021†

MD: 20% x 2022

DE: 25% x 2026*

DC: 20% x 2020

NC: 12.5% x 2021 (IOUs)10% x 2018 (co-ops & munis)

VT: (1) RE meets any increase in retail sales x

2012; (2) 20% RE & CHP x 2017

KS: 20% x 2020

OR: 25% x 2025 (large utilities)*

5% - 10% x 2025 (smaller utilities)

IL: 25% x 2025

29 states + DC and PR have an RPS(8 states have

goals)

OK: 15% x 2015

PR: 20% x 2035

WV: 25% x 2025*†VA: 15% x 2025*

DC

IN: 15% x 2025†

Renewable Standards– US

DESIRE Information.

Why do you need Subsidy?

o Subsidy:o Tax Credit’s, Grants, Loans, others…o The Oil Industry has been around since 1870 beginning with the

standard oil company.o Oil companies have been receiving governmental subsides since

1916 when federal government instituted income tax incentives to encourage individuals and corporations to drill for oil.

o From the 1950s onward, the federal government financed research into nuclear power.

o More recently, the federal government has provided research funding and other financing to expand the availability of renewable energy sources.

o ALL U.S. Energy Sources receive subsidy’s.

Why do you need subsidy?

o The Oil industry has had 142 years to develop, install, and define their models albeit cost, infrastructure, and development.

o It is naive to think that a new power source will not need help to become a real source of power in the US.

o The renewable industry in its short time period has come down 673% ASP Module.

o The efficiency of modules has risen from 11% in 2004 to 16.0% in 2012 in c-Si average module efficiency.

o Grid Parity where the cost of utility power, and the cost of solar power is equal, is not far away. Some experts believe the 70% on the country will be at grid parity by 2015.

o Do we need Subsidy’s? Yes, at this point it does help out with cost reductions.

o If Solar and all other fuels were to loose the subsidy so that the entire field is flat, solar would not need them.

Current Status of the Solar Market:

o Trade Restrictions:o Pros: (Manufacturing)(Downstream)

o Longer time for cost down planso Less market volatilityo Job Security (Short term downstream)

o Con’s: (Development)(Upstream)o Grid Parity & Competitiveness of Industry taking longer.o Global manufacturing retaliation (Tariffs)o Market shrinkageo Job Layoff’s (Upstream)o Product will divert around (Through Taiwan, or Mexico) No real

effect to price reduction.o The Question is what is best for the Industry? In the end the whole is

greater than the some of the parts!

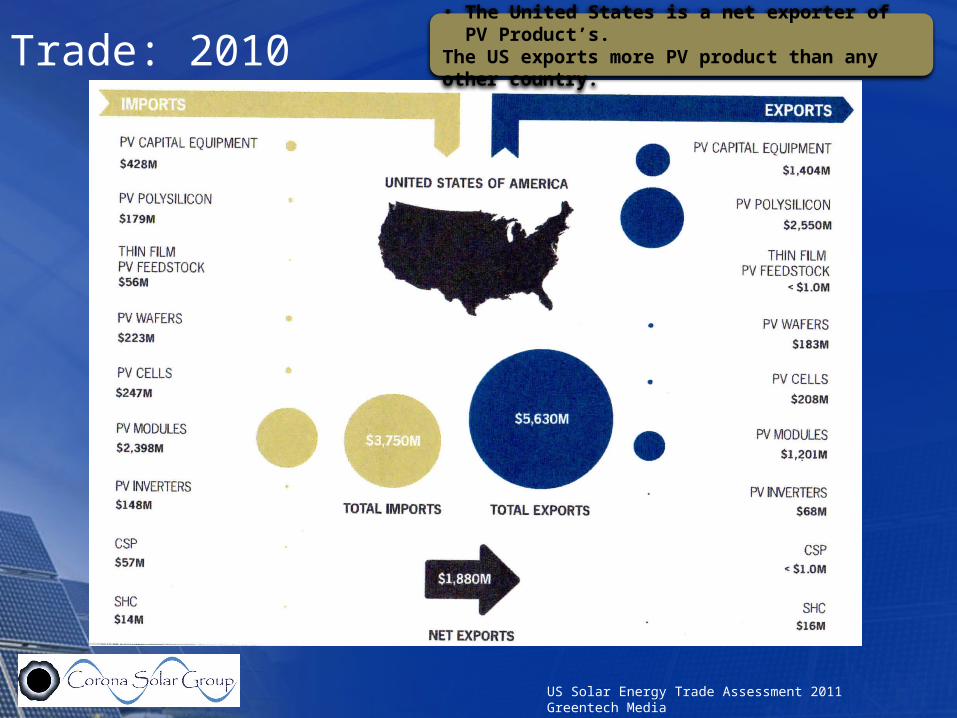

Trade: 2010• The United States is a net exporter of PV

Product’s.The US exports more PV product than any other country.

US Solar Energy Trade Assessment 2011 Greentech Media

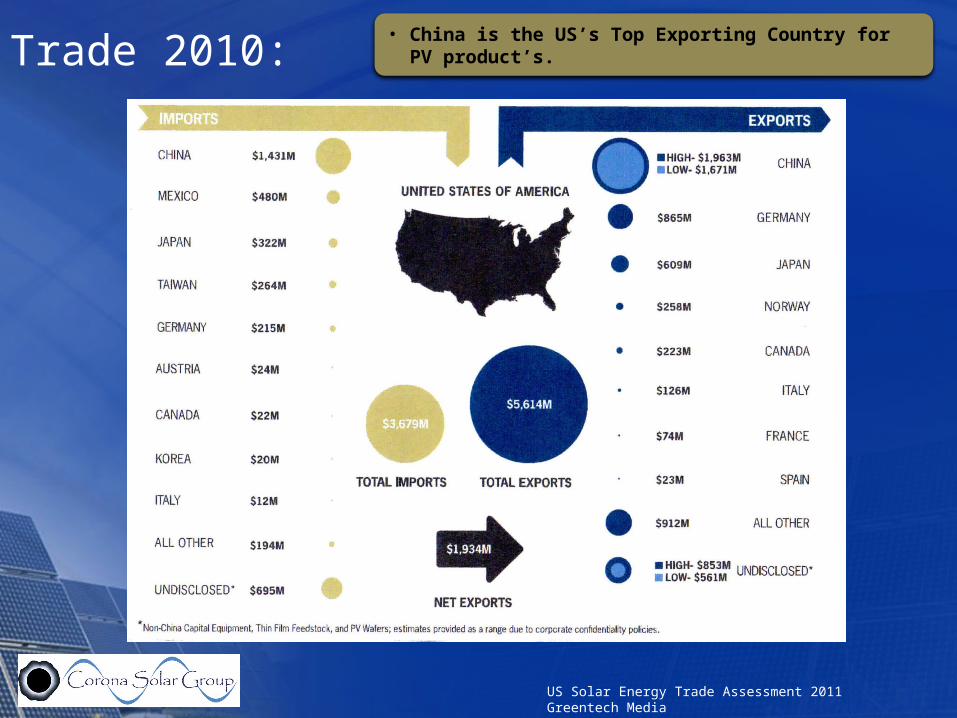

Trade 2010: • China is the US’s Top Exporting Country for PV product’s.

US Solar Energy Trade Assessment 2011 Greentech Media

Products Now

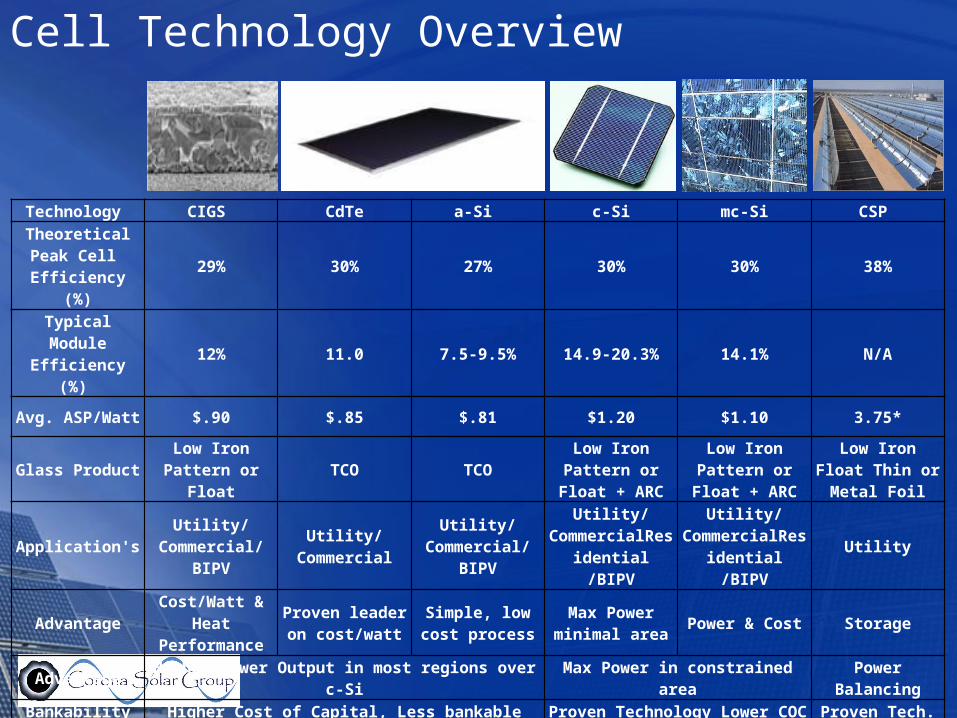

Cell Technology Overview

Technology CIGS CdTe a-Si c-Si mc-Si CSP Theoretical Peak

Cell Efficiency (%) 29% 30% 27% 30% 30% 38%

Typical Module Efficiency (%) 12% 11.0 7.5-9.5% 14.9-20.3% 14.1% N/A

Avg. ASP/Watt $.90 $.85 $.81 $1.20 $1.10 3.75*

Glass Product Low Iron Pattern or Float TCO TCO Low Iron Pattern or

Float + ARCLow Iron Pattern or

Float + ARCLow Iron Float Thin

or Metal Foil

Application's Utility/Commercial/BIPV Utility/Commercial Utility/

Commercial/BIPVUtility/

CommercialResidential /BIPV

Utility/CommercialResiden

tial /BIPVUtility

Advantage Cost/Watt & Heat Performance

Proven leader on cost/watt

Simple, low cost process

Max Power minimal area Power & Cost Storage

Advantage Higher Power Output in most regions over c-Si Max Power in constrained area Power BalancingBankability Higher Cost of Capital, Less bankable Proven Technology Lower COC Proven Tech.

2011 MW Prod NA 24 321 0 1059 5Projected Market

Share 2013 NA 4.00% 14.00% 54.00% 28%

Sustainable Position: Long Term Mid Term Mid Term Long Term Long Term

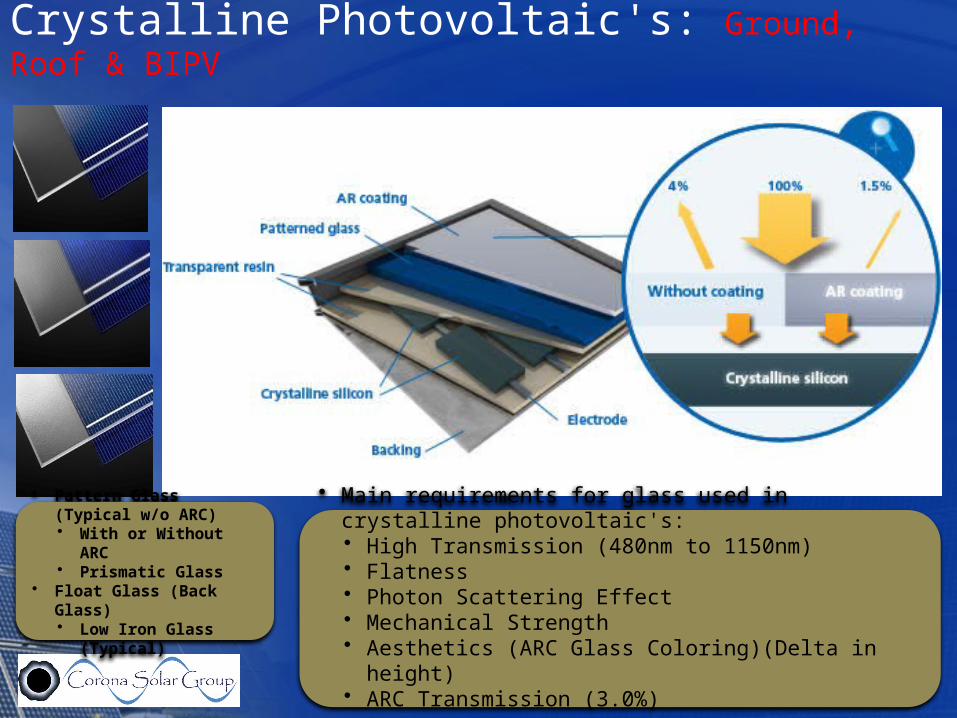

Crystalline Photovoltaic's: Ground, Roof & BIPV

• Main requirements for glass used in crystalline photovoltaic's:• High Transmission (480nm to 1150nm)• Flatness• Photon Scattering Effect• Mechanical Strength• Aesthetics (ARC Glass Coloring)(Delta in height)• ARC Transmission (3.0%)

• Pattern Glass (Typical w/o ARC)• With or Without ARC• Prismatic Glass

• Float Glass (Back Glass)• Low Iron Glass (Typical)

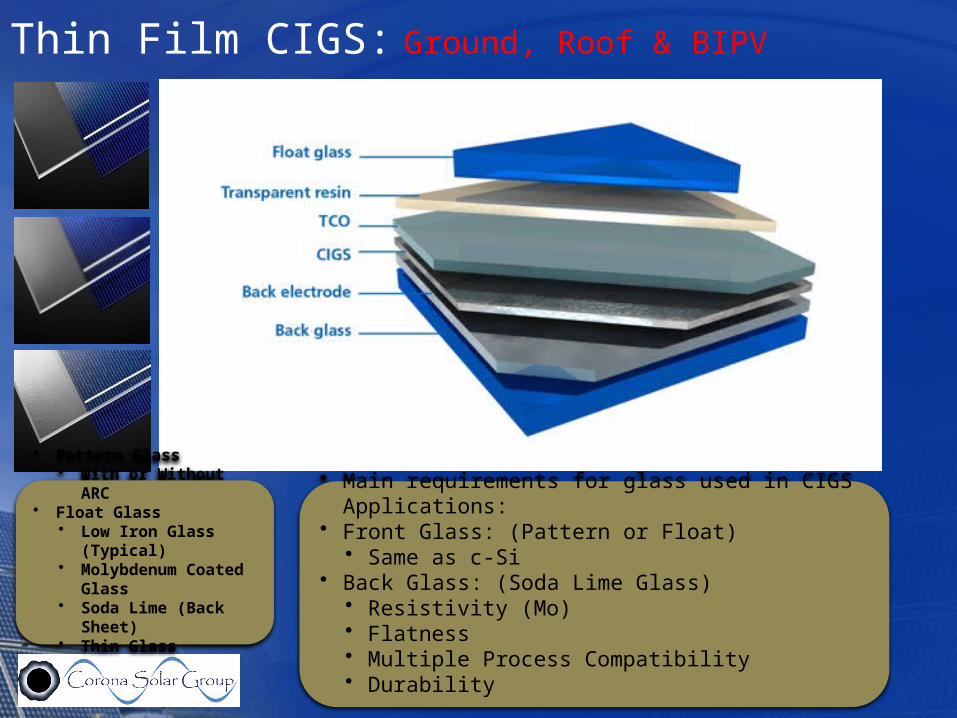

Thin Film CIGS: Ground, Roof & BIPV

• Main requirements for glass used in CIGS Applications:• Front Glass: (Pattern or Float)

• Same as c-Si• Back Glass: (Soda Lime Glass)

• Resistivity (Mo)• Flatness• Multiple Process Compatibility• Durability

• Pattern Glass• With or Without ARC

• Float Glass• Low Iron Glass (Typical)• Molybdenum Coated

Glass• Soda Lime (Back Sheet)• Thin Glass

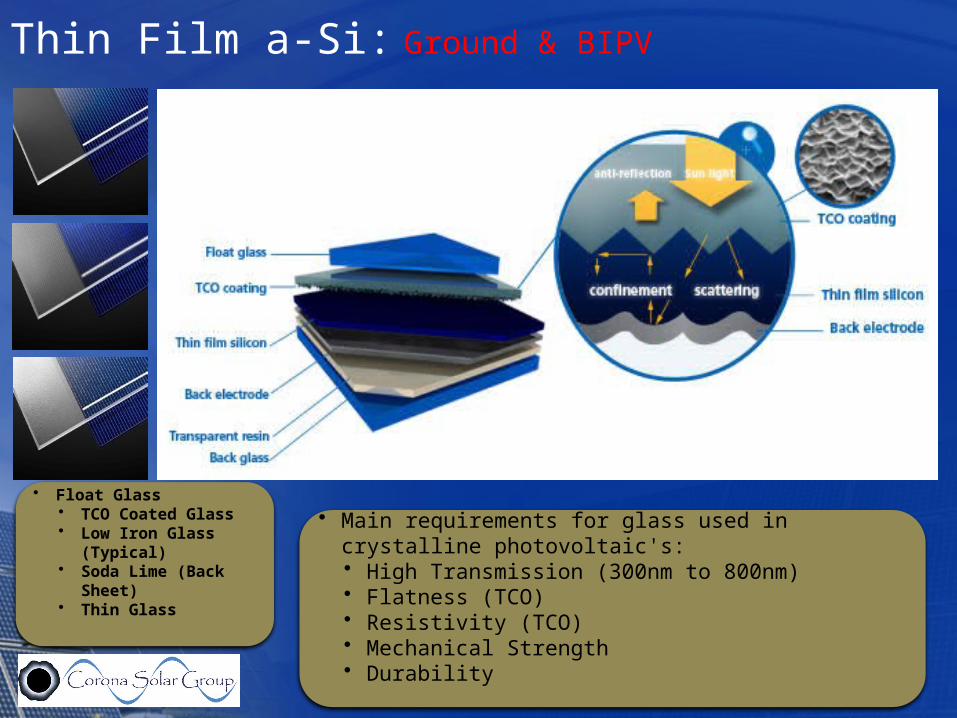

Thin Film a-Si: Ground & BIPV

• Main requirements for glass used in crystalline photovoltaic's:• High Transmission (300nm to 800nm)• Flatness (TCO)• Resistivity (TCO)• Mechanical Strength• Durability

• Float Glass• TCO Coated Glass• Low Iron Glass (Typical)• Soda Lime (Back Sheet)• Thin Glass

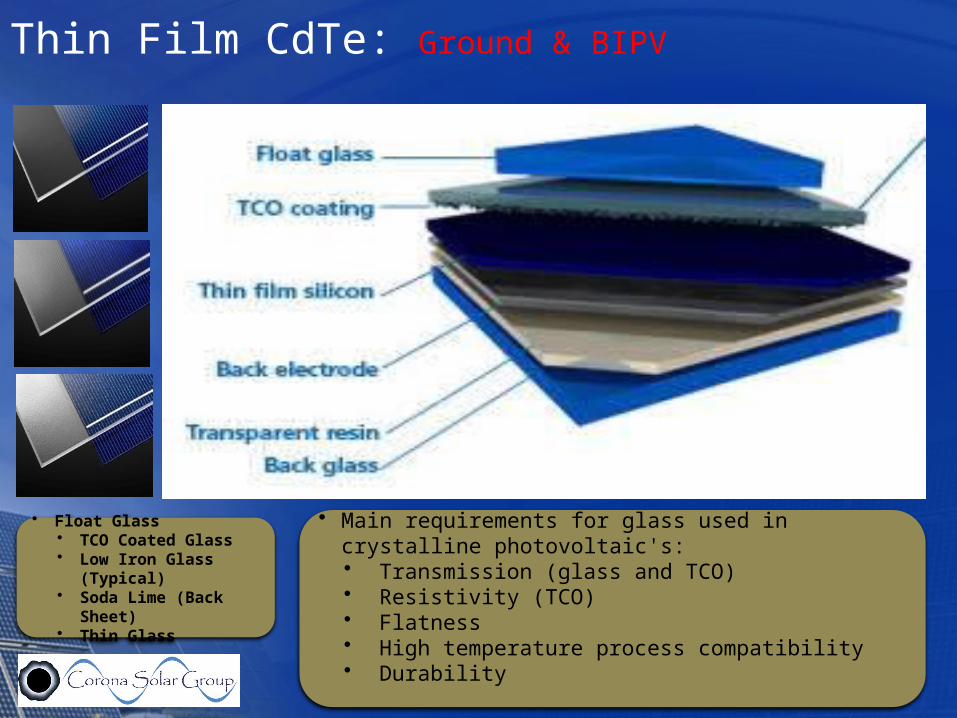

Thin Film CdTe: Ground & BIPV

• Main requirements for glass used in crystalline photovoltaic's:• Transmission (glass and TCO)• Resistivity (TCO)• Flatness• High temperature process compatibility• Durability

• Float Glass• TCO Coated Glass• Low Iron Glass (Typical)• Soda Lime (Back Sheet)• Thin Glass

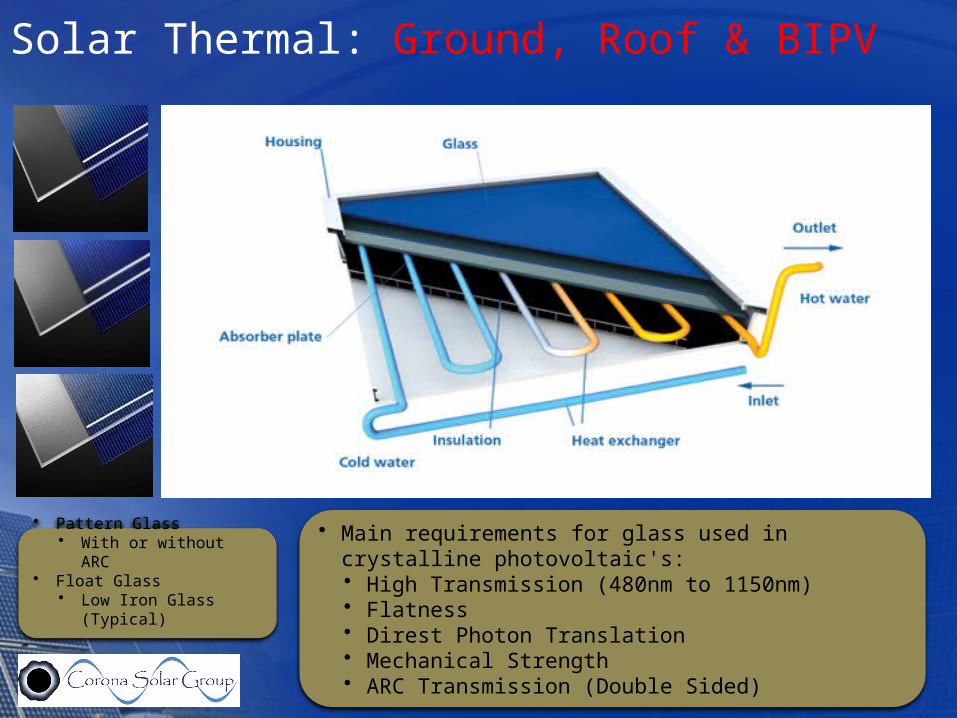

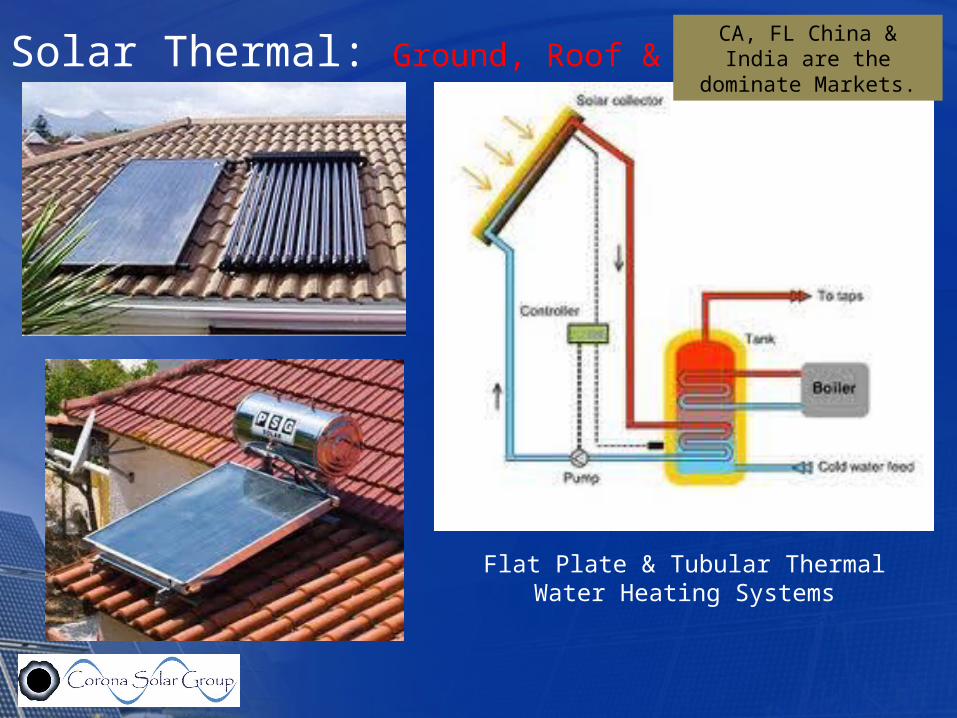

Solar Thermal: Ground, Roof & BIPV

• Main requirements for glass used in crystalline photovoltaic's:• High Transmission (480nm to 1150nm)• Flatness• Direst Photon Translation• Mechanical Strength• ARC Transmission (Double Sided)

• Pattern Glass• With or without ARC

• Float Glass• Low Iron Glass (Typical)

Solar Thermal: Ground, Roof & BIPV

Solatex Solite

Flat Plate & Tubular Thermal Water Heating Systems

CA, FL China & India are the dominate Markets.

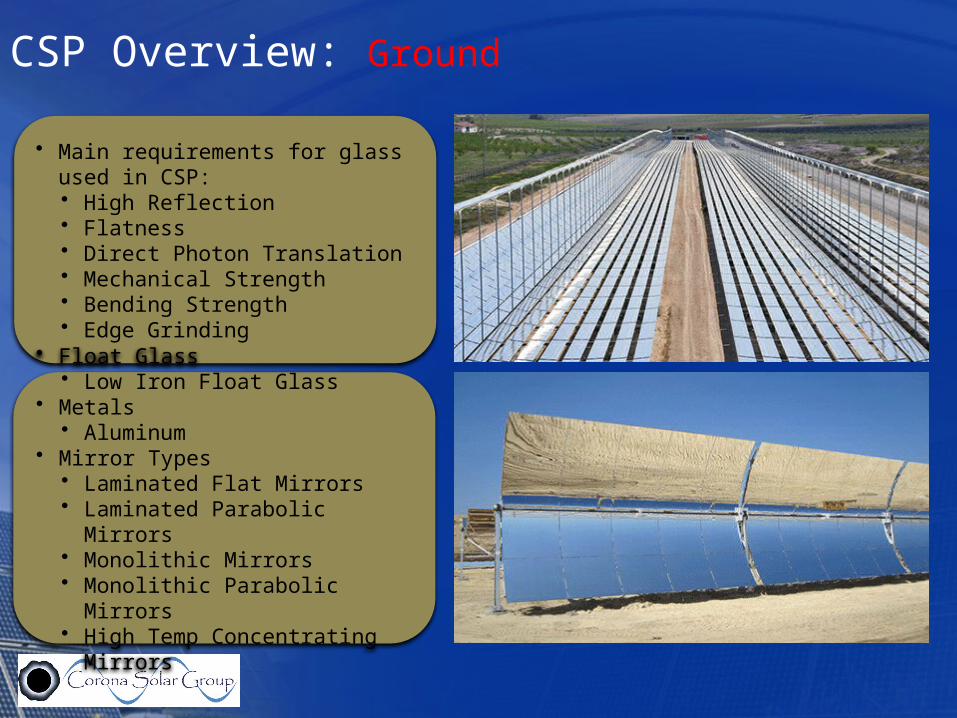

• Main requirements for glass used in CSP:• High Reflection• Flatness• Direct Photon Translation• Mechanical Strength• Bending Strength• Edge Grinding

• Float Glass• Low Iron Float Glass

• Metals• Aluminum

• Mirror Types• Laminated Flat Mirrors• Laminated Parabolic Mirrors• Monolithic Mirrors• Monolithic Parabolic Mirrors• High Temp Concentrating Mirrors

CSP Overview: Ground

BIPV Overview: Roof & BIPV

o BIPV is relatively New to North America.o It is not the first the first thought to the

Architecto Europe is much farther ahead on North

America with regard to design, and development.

o North America is growing in BIPV. BIPV is mainly being viewed as a new build concept.

o The current products are Engineer minded design, and application.

o Energy generation is second to aesthetics.o Principal technology is c-Si (Due to

Efficiency)

Industry Future

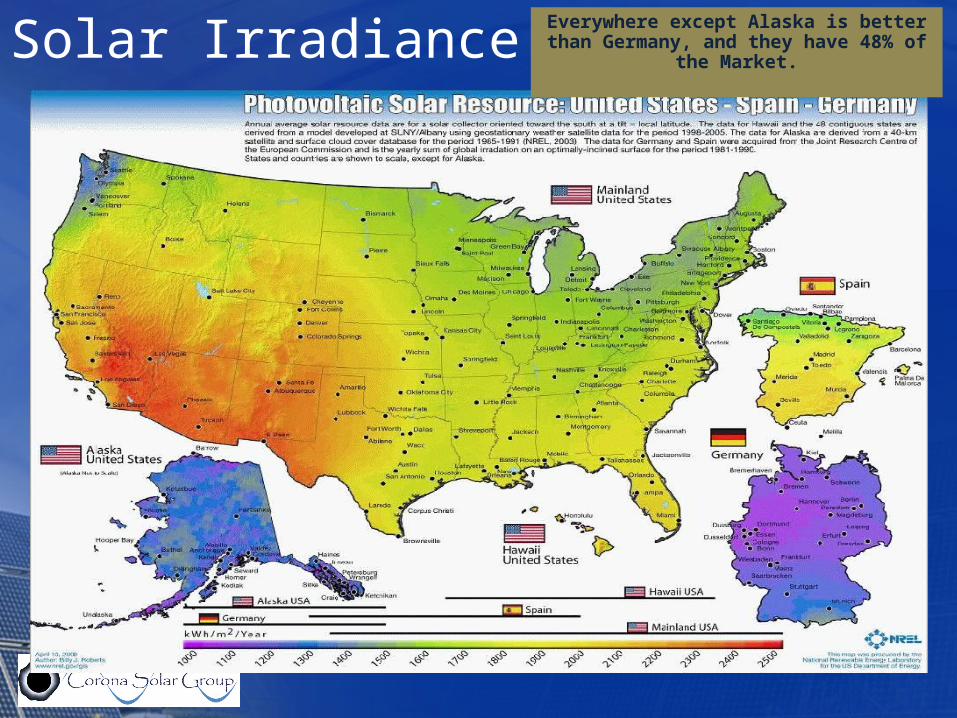

Solar Irradiance Levels: Everywhere except Alaska is better than Germany, and they have 48% of the Market.

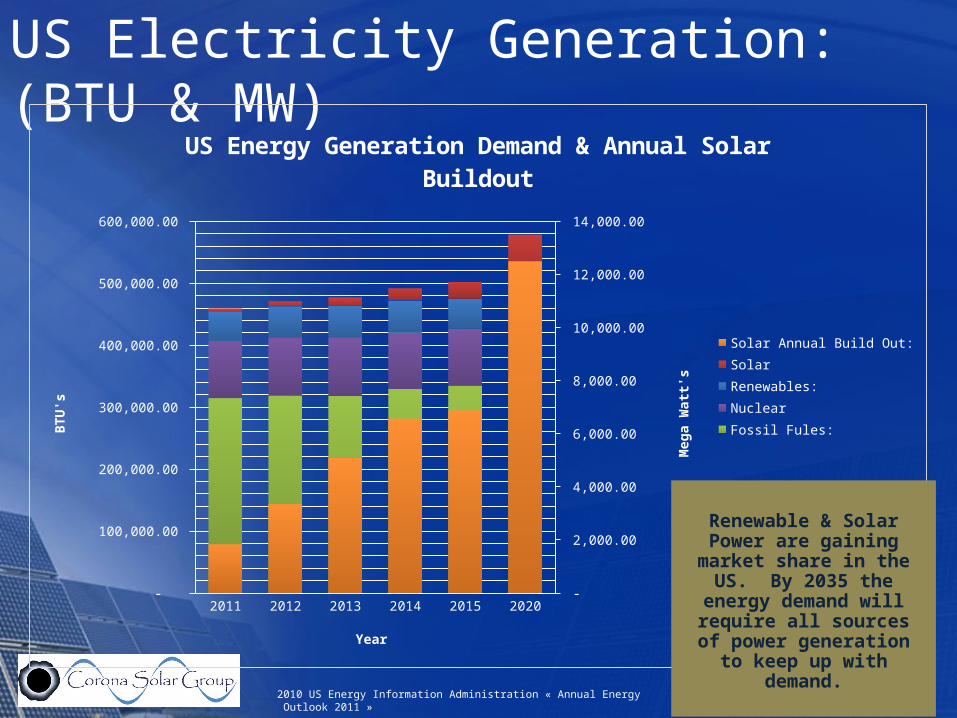

US Electricity Generation: (BTU & MW)

2010 US Energy Information Administration « Annual Energy Outlook 2011 »

2011 2012 2013 2014 2015 2020 -

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

600,000.00

-

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

US Energy Generation Demand & Annual Solar Buildout

Solar Annual Build Out:

Solar

Renewables:

Nuclear

Fossil Fules:

Year

BT

U's

Meg

a W

att's

Renewable & Solar Power are gaining market share in the US.

By 2035 the energy demand will require all sources of

power generation to keep up with demand.

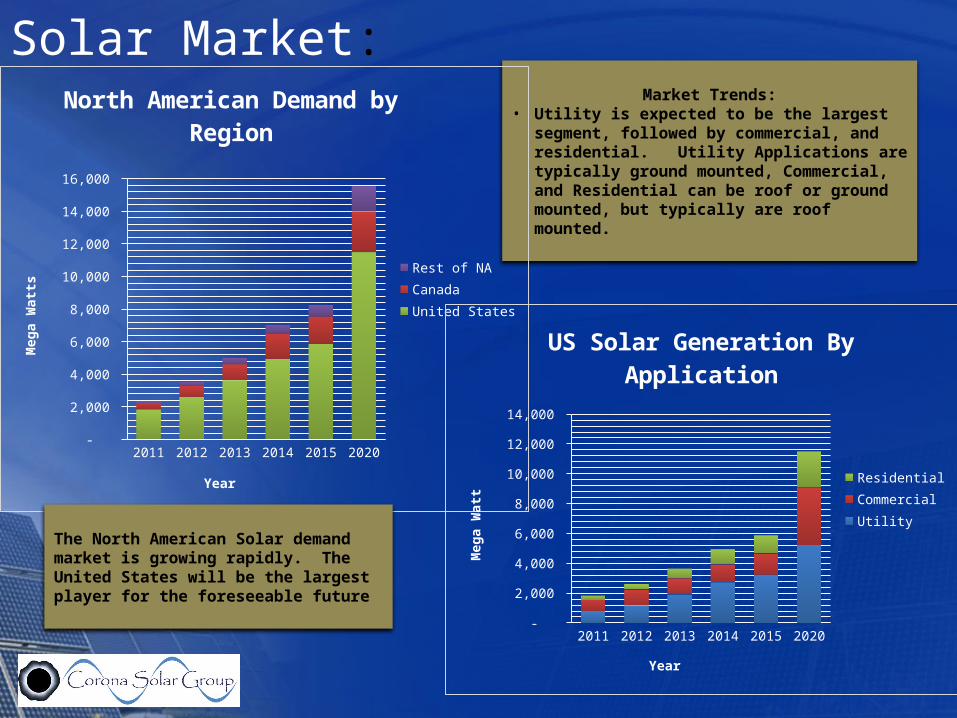

Solar Market:Market Trends:

• Utility is expected to be the largest segment, followed by commercial, and residential. Utility Applications are typically ground mounted, Commercial, and Residential can be roof or ground mounted, but typically are roof mounted.

2011 2012 2013 2014 2015 2020 -

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

North American Demand by Region

Rest of NA

Canada

United States

Year

Meg

a W

atts

2011 2012 2013 2014 2015 2020 -

2,000

4,000

6,000

8,000

10,000

12,000

14,000

US Solar Generation By Applica-tion

Residential

Commercial

Utility

Year

Meg

a W

att

The North American Solar demand market is growing rapidly. The United States will be the largest player for the foreseeable future

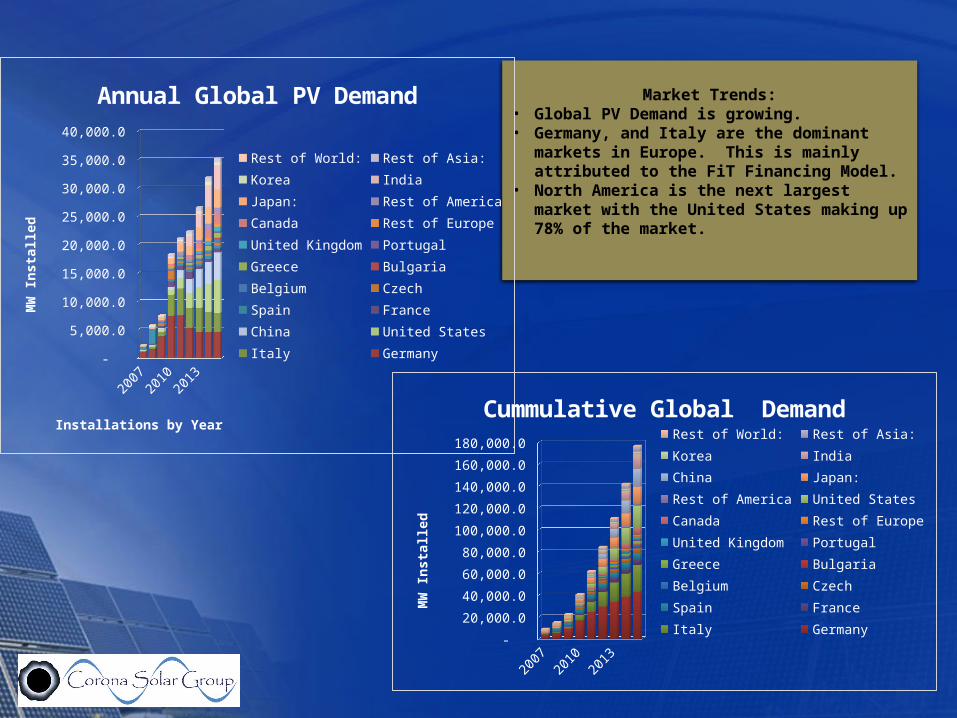

Market Trends:• Global PV Demand is growing. • Germany, and Italy are the dominant markets in

Europe. This is mainly attributed to the FiT Financing Model.

• North America is the next largest market with the United States making up 78% of the market.

2007

2009

2011

2013

2015

-

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

35,000.0

40,000.0

Annual Global PV Demand

Rest of World: Rest of Asia:

Korea India

Japan: Rest of America

Canada Rest of Europe

United Kingdom Portugal

Greece Bulgaria

Belgium Czech

Spain France

China United States

Italy Germany

Installations by Year

MW

In

stal

led

2007

2009

2011

2013

2015

-

20,000.0

40,000.0

60,000.0

80,000.0

100,000.0

120,000.0

140,000.0

160,000.0

180,000.0

Cummulative Global Demand

Rest of World: Rest of Asia:

Korea India

China Japan:

Rest of America United States

Canada Rest of Europe

United Kingdom Portugal

Greece Bulgaria

Belgium Czech

Spain France

Italy Germany

MW

In

stal

led

Value Chain Movements

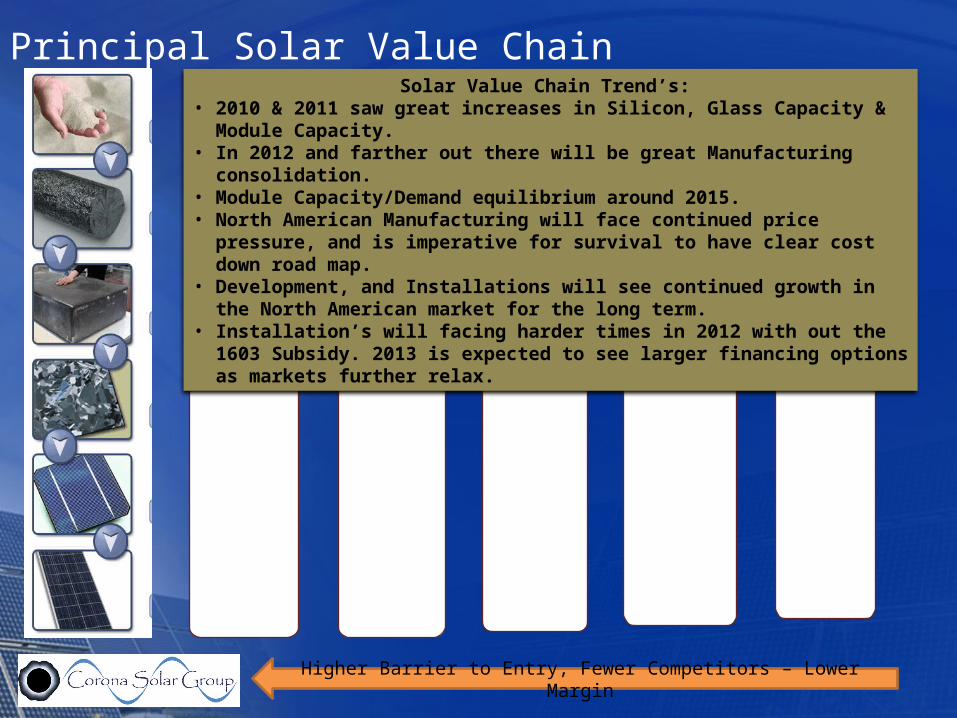

Principal Solar Value Chain

Polysilicon Production & Processing:• Wacker• GCL Silicon• Hemlock• MEMC• REC• M. Setek• Tokuyama• DC Chemical• Deutsche Solar• ErSol• LDK• MEMC• PV Crystalox• Yingli• Others…

Cell & Module Manufacturing • SMA

• PV Powered• Frontious• Blue

• DPW• Cant Sink• Hilti• Raxx• Shoals Tech

• Many Others

Inverter & Framing

• Suniva (Georgia)• Sharp (Tennessee)• ECD (Unisolar)• JA Solar• Kyocera• Motech• Q-Cells• REC• Sanyo• Schott• Sharp• SunPower• Suntech• AGC• PPG• Guardian• Centro Solar• Zero Cote• Honeywell• 3M• DuPont

Design & Development

• PG&E• NV Energy• Cal Edison• Arizona Public• FP&L• Excell• Georgia Power• Duke Energy

• Fortune 50• Farmers• Small Business• Manufacturing• Home Owners• Governments• Islands• Co-Operatives• hundreds more

Utilities & Owners

• Corona Solar• Outpost Solar• Solar City• Conergy• Dependable Solar• Deutsche Solar• Donauer

Solartechnik• GroSolar• Ibersolar Energia• Isofoton• MHH Solartechnik• Phaesun• Phonix Sonnenstrom• REC• SunPower• SunTechnics• Wirsol• Yingli Green Energy

Higher Barrier to Entry, Fewer Competitors – Lower Margin

Solar Value Chain Trend’s: • 2010 & 2011 saw great increases in Silicon, Glass Capacity & Module Capacity. • In 2012 and farther out there will be great Manufacturing consolidation.• Module Capacity/Demand equilibrium around 2015.• North American Manufacturing will face continued price pressure, and is imperative for

survival to have clear cost down road map. • Development, and Installations will see continued growth in the North American market

for the long term. • Installation’s will facing harder times in 2012 with out the 1603 Subsidy. 2013 is expected

to see larger financing options as markets further relax.

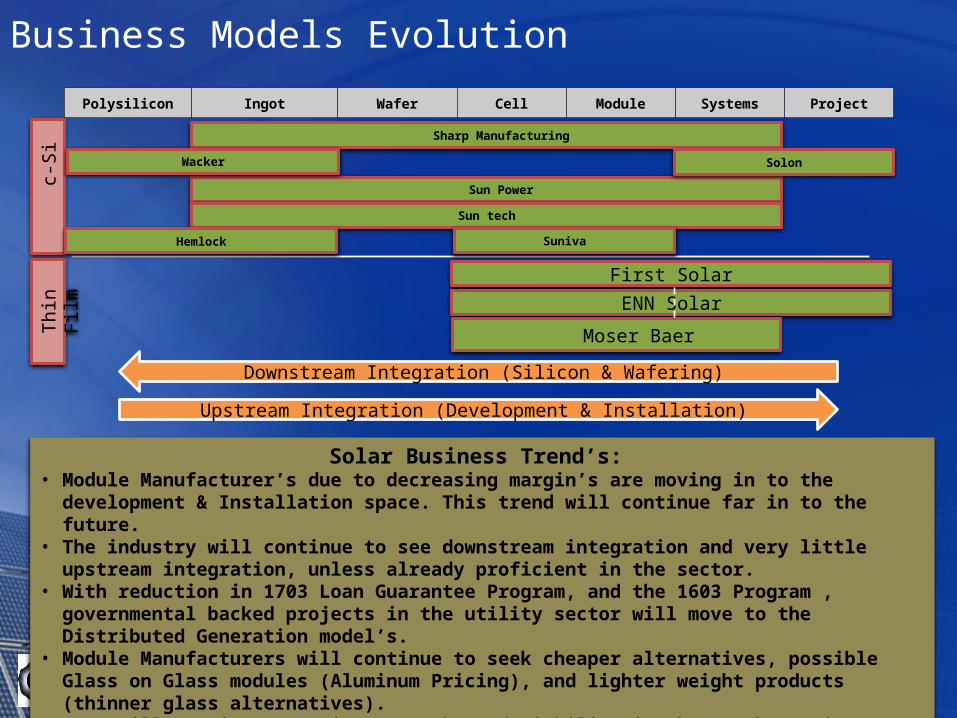

Business Models Evolution

Polysilicon Ingot Wafer Cell Module Systems Project

c

-Si

T

hin

Film

First Solar

ENN Solar

Moser Baer

Sun Power

Sun tech

Sharp Manufacturing

Solon

Solar Business Trend’s: • Module Manufacturer’s due to decreasing margin’s are moving in to the development & Installation space. This

trend will continue far in to the future.• The industry will continue to see downstream integration and very little upstream integration, unless already

proficient in the sector.• With reduction in 1703 Loan Guarantee Program, and the 1603 Program , governmental backed projects in the

utility sector will move to the Distributed Generation model’s.• Module Manufacturers will continue to seek cheaper alternatives, possible Glass on Glass modules (Aluminum

Pricing), and lighter weight products (thinner glass alternatives).• BIPV will continue to gain strength, and viability in the North American market.

Downstream Integration (Silicon & Wafering)

Upstream Integration (Development & Installation)

Wacker

SunivaHemlock

Future Markets

Solar Markets of the Future:

o Caribbean:o With the cost of power at upwards of $.65/kWh with

tariff fees, and trash removal at $120/ton. Solar and Hydrogen projects are right for this market.

o Current energy production is predominantly made with diesel generators. This drive expensive fossil to be shipped in to islands with very shallow water lanes.

o The Caribbean market while dominated by monopoly style utilities with deep political connection are realizing the benefits of Solar and Hydrogen energy production.

Solar Markets of the Future:

o South America:o This market is perfectly fixed in the best sun area in

the world. o The cities are growing, and even with an abundance

of fossil fuels, the region is understanding that this will not last, and now is the time to look at alternative energy production methods.

o Solar Power (All forms) will play a part in this market.o Bio Mass (Hydrogen), will also get a good foothold

here.

Solar Products of the Future:

o Residential:o c-Si will still be the dominate leader in the market. c-Si will have

to adapt to sleaker designs for aesthetics.o CIGS is also become a market force with adaptation such as the

solar shingle, especially as efficiency increases.o Commercial (Energy):

o c-Si will still be the market leader, as energy production, and ROI is main driver.

o Commercial (Aesthetics'):o a-Si, CdTe, CIGS, and c-Si will all be players in the BIPV industry.

New design parameters will have to be met to afford the architect the flexibility needed for avant-garde design. Product must follow design idea. The product cannot lead the artistic idea.

Solar Products of the Future:

o Utility:o Hydrogen products will become a force to recon with in the utility market.

Hydrogen Hybrid Solar Projects will become more mainstream.o Energy production, and maintenance are the only thing that matters.

Efficiency, water needs, and reclamation are the utility driving forces. ENERGY PRODUCTION IS THE ONLY FACTOR OVERALL ELSE.

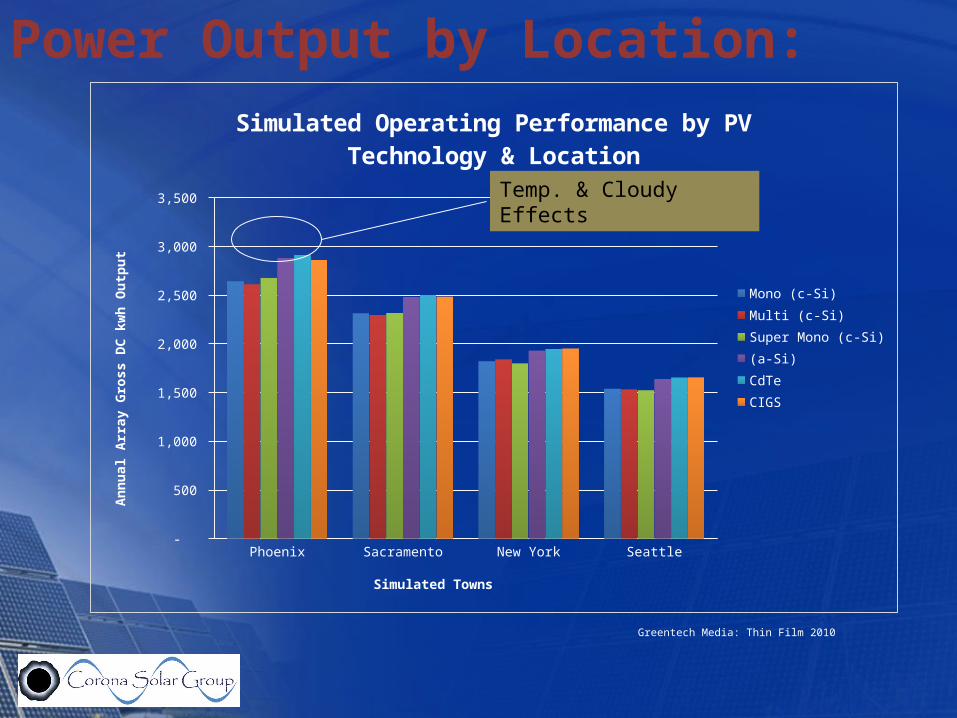

o Thin films with their excellent use of the solar spectrum, enabling more power manufacturing capability than c-Si will make them a viable option. See Chart Following.

o Distributed Generation (DG) will be the mantra going forward. Time to market, bureaucracy, financing, and availability of private land will drive this.

o Storage will always be a primary concern.o New storage techniques will be developed:

o Gravity Storage (PV)o Molten Salts (CSP)

Phoenix Sacramento New York Seattle -

500

1,000

1,500

2,000

2,500

3,000

3,500

Simulated Operating Performance by PV Technology & Location

Mono (c-Si)

Multi (c-Si)

Super Mono (c-Si)

(a-Si)

CdTe

CIGS

Simulated Towns

An

nu

al A

rray

Gro

ss D

C k

wh

Ou

tpu

t

Greentech Media: Thin Film 2010

Temp. & Cloudy Effects

Power Output by Location:

Future Product’s

Solar Products of the Future:

o Crystalline Silica c-Si:o Crystalline will be the dominate technology in the foreseeable future.o Continued development will continue on material loss, efficiency, and

production. Efficiency will become the lesser of the three.o c-Si will still dominate the residential, and commercial markets.

Utility will be mixed with TF & CSP.o $/Watt by 2015 will be around $.85/watto Improved module design to move to less obtrusive, and sleek design.

(Dow Solar Shingle)o BIPV color developed product for Architectural enhancement.

(Thickness of AR Coating)o Incorporated in to the design of the home from beginning for better

design case, and wiring design.o Photon translating Glass for maximum photon translation to solar cell.

Solar Products of the Future:

o a-Si: Thin Film:o a-Si is hampered not by the theoretical, but practical

limits of efficiency.o The special inherent qualities of amorphous align it to

special application in the BIPV arena. (Awnings, Shadow enhancements, Etc…)

o a-Si will be coupled more with c-Si for Hybrid cell’s with larger spectrum coverage.

o BIPV should be a large focus for a-Si. This product has great potential in this market.

o New adaptive designs for architectural markets will be needed.

Solar Products of the Future:

o CIGS:o CIGS will be the dominate player with regard to

efficiency, and heat tolerance.o Due to sensitivity and difficulty in taking product to

production level, few manufacturers will stay with product, so manufacturing base will be limited.

o CIGS should always be cost conscience, so Glass/Glass products will be the dominate product.

Solar Products of the Future:

o BIPV:o North America will be come a large market for BIPV.

There is extensive work being done on the standards side, with percentages of building energy derived from renewable resources. DOE is driving for 5% of building energy to come from renewable sources.

o From the Lease and Sell perspective, BIPV building due to the lower cost of energy, and new building techniques with renewable products. The building will have better resale value for a longer period of time.

Solar Products of the Future:

o Thermal:o Thermal will always be a good market. South

America is next large thermal, and Solar Market.o Thermal with adaptive design can greatly benefit the

BIPV market. o CSP:o CSP will play a large role in the future of solar. Some

experts say that as much as 25% will come from CSP. I believe that number to be to high, but CSP will play a large role in Utility level power production. What the number will be is anyone's guess.

Solar Products of the Future:

o New Technologies:o Hydrogen Power:

o Energy derived from hydrogen gas itself, or mixed with a fuel cell.o Hydrogen generation plants that intake biomass, and or garbage, and

output hydrogen gas, and water will be come very predominate in the future.

o The cost of energy production is 1/3 the cost of Solar, and has no storage problems.

o This is an excellent choice for large commercial, and Utility level energy generation.

o This technology will enable Coal fired plant reuse options saving utilities millions of dollars with plant shut downs, and or expensive scrubbing methods.

o Leveraging existing asset base with existing power infrastructure will make old, and obsolete plants back online with minimal investment.

o The energy needs of the future will not cannibalize any product, but will need each one to be able to power the future.

• Global Solar demand is growing from 7.5GW in 2009 to 31.8GW in 2015 (494% Increase)

• Global Solar Power has a great potential to be a significant part of the energy, and environmental solution of the future.

• North American demand has grown from .6GW in 2009 to 2.3GW in 2011 ( 438% Increase)

• North America is expected to grow to 8.7GW by 2015• North America is not keeping up pace with the forecasted

demand.• Low Cost Countries see the value in the market, and are driving

their economies to be the dominate solar supplier.

Conclusions

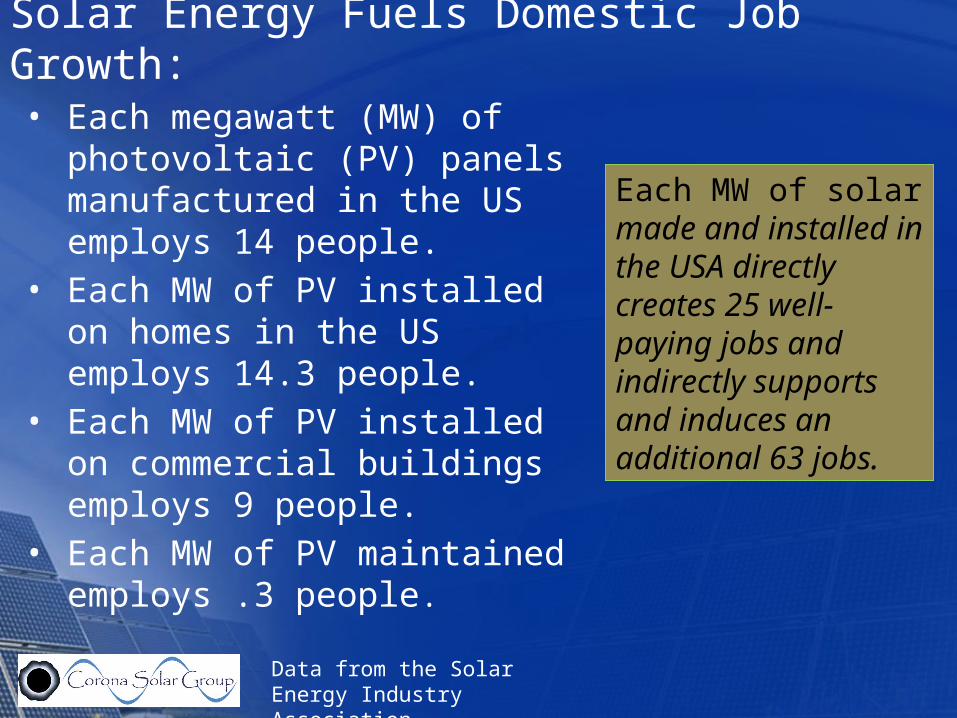

Solar Energy Fuels Domestic Job Growth:• Each megawatt (MW) of

photovoltaic (PV) panels manufactured in the US employs 14 people.

• Each MW of PV installed on homes in the US employs 14.3 people.

• Each MW of PV installed on commercial buildings employs 9 people.

• Each MW of PV maintained employs .3 people.

Each MW of solar made and installed in the USA directly creates 25 well‐paying jobs and indirectly supports and induces an additional 63 jobs.

Data from the Solar Energy Industry Association

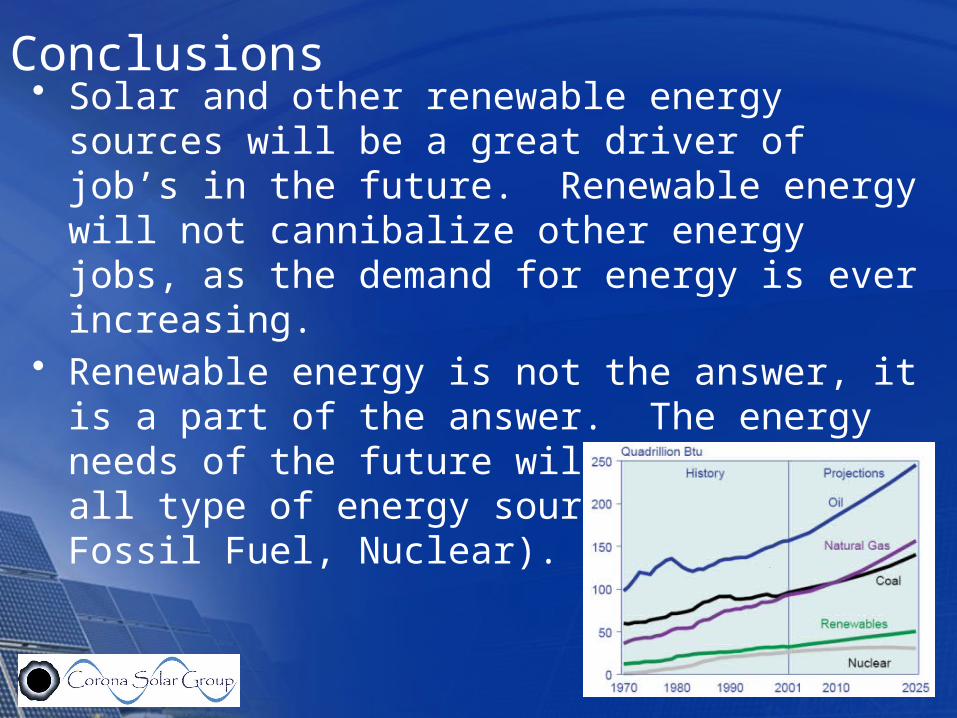

• Solar and other renewable energy sources will be a great driver of job’s in the future. Renewable energy will not cannibalize other energy jobs, as the demand for energy is ever increasing.

• Renewable energy is not the answer, it is a part of the answer. The energy needs of the future will be driven by all type of energy sources (Renewable, Fossil Fuel, Nuclear).

Conclusions

Thank You!

Corona Solar Group, LLCOffice: 770-74-7559Cell: 678-234-8302

![The Canton advocate (Canton, D.T. [S.D.]). (Canton, D.T](https://img.pdfslide.net/doc/110x75/627da8d50d94944094392a89/the-canton-advocate-canton-dt-sd-canton-dt-.jpg)