Embed Size (px)

Citation preview

Using Technology to transformChallenges to Opportunities

…the case of Thenhipalam Co-operative Rural Bank

Sreejith MullasseriAsst Secretary,Thenhipalam Co-operative Rural Bank Ltd, Malappuram Dist.Kerala State

Manikumar SDeputy General Manager & Member of FacultyBankers Institute of Rural Development, Lucknow

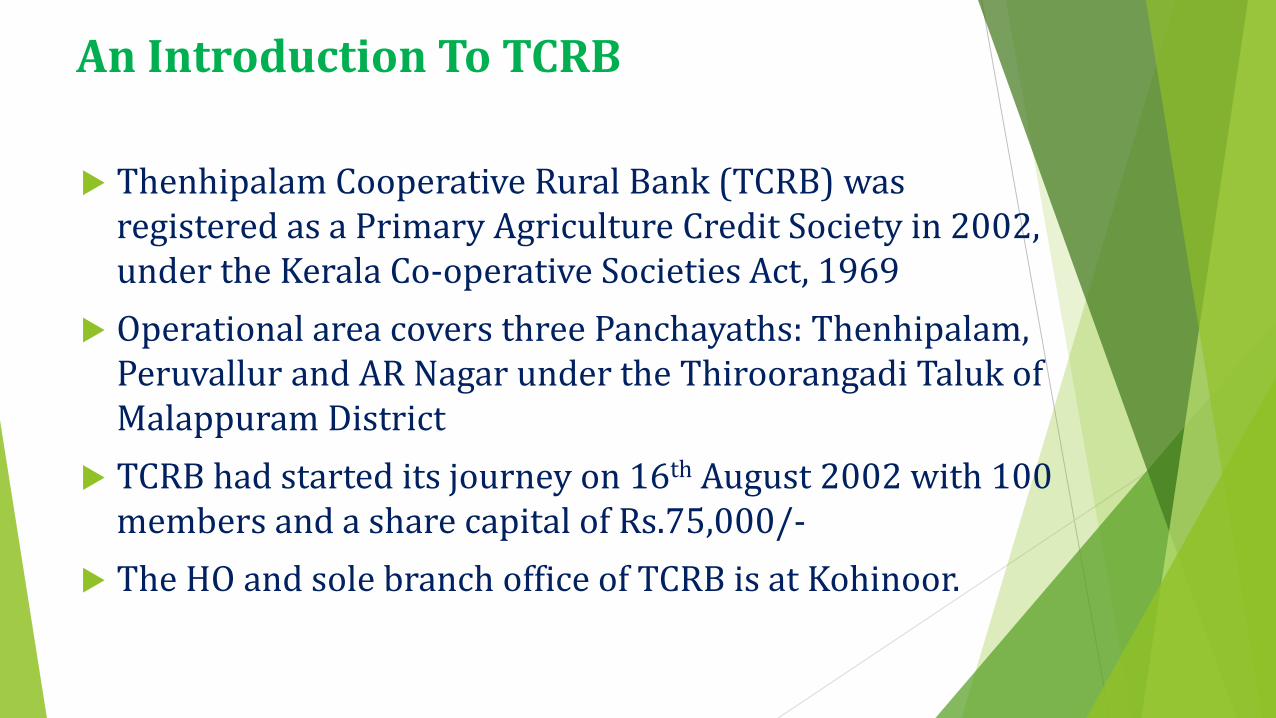

An Introduction To TCRB

Thenhipalam Cooperative Rural Bank (TCRB) was registered as a Primary Agriculture Credit Society in 2002, under the Kerala Co-operative Societies Act, 1969

Operational area covers three Panchayaths: Thenhipalam, Peruvallur and AR Nagar under the Thiroorangadi Taluk of Malappuram District

TCRB had started its journey on 16th August 2002 with 100 members and a share capital of Rs.75,000/-

The HO and sole branch office of TCRB is at Kohinoor.

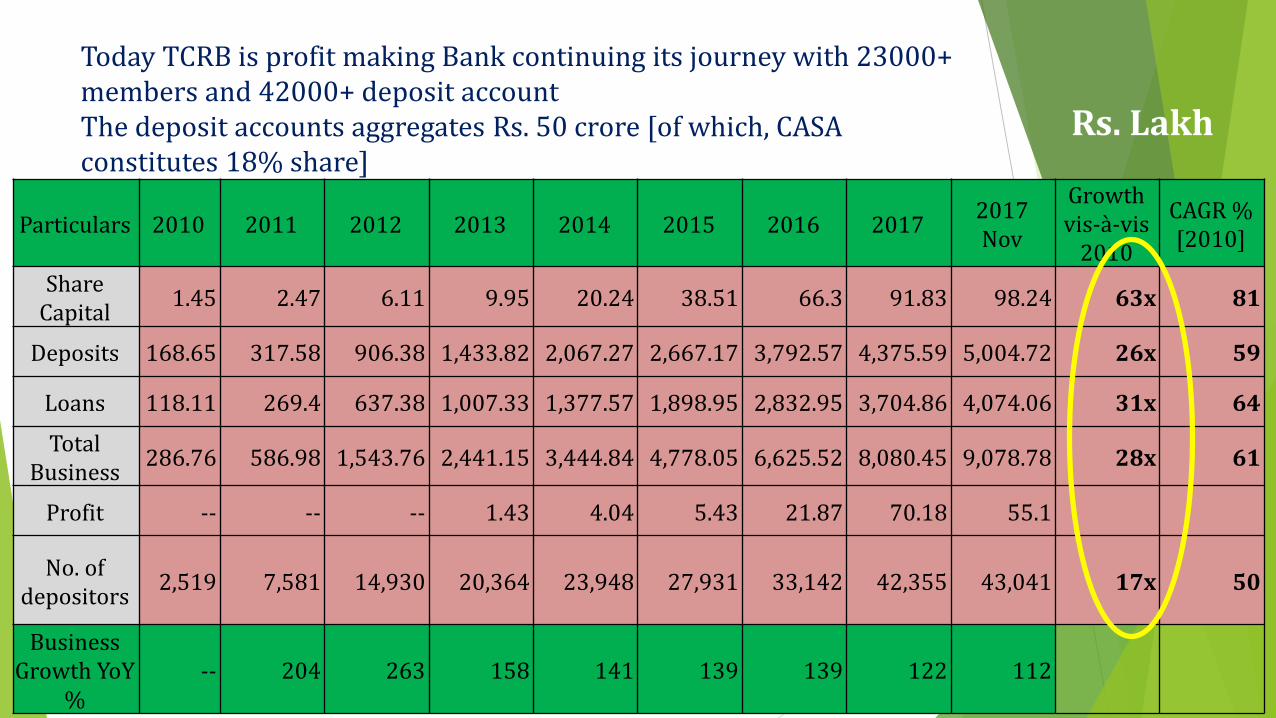

Today TCRB is profit making Bank continuing its journey with 23000+ members and 42000+ deposit account The deposit accounts aggregates Rs. 50 crore [of which, CASA constitutes 18% share]

Particulars 2010 2011 2012 2013 2014 2015 2016 20172017 Nov

Growth vis-à-vis

2010

CAGR % [2010]

Share Capital

1.45 2.47 6.11 9.95 20.24 38.51 66.3 91.83 98.24 63x 81

Deposits 168.65 317.58 906.38 1,433.82 2,067.27 2,667.17 3,792.57 4,375.59 5,004.72 26x 59

Loans 118.11 269.4 637.38 1,007.33 1,377.57 1,898.95 2,832.95 3,704.86 4,074.06 31x 64

Total Business

286.76 586.98 1,543.76 2,441.15 3,444.84 4,778.05 6,625.52 8,080.45 9,078.78 28x 61

Profit -- -- -- 1.43 4.04 5.43 21.87 70.18 55.1

No. of depositors

2,519 7,581 14,930 20,364 23,948 27,931 33,142 42,355 43,041 17x 50

Business Growth YoY

%-- 204 263 158 141 139 139 122 112

Rs. Lakh

The journey of TCRB from then to now was not a cake walk

But they have the courage to fight, have the willpower, teamwork and the motto to win and prove themselves

Through this willpower, teamwork and hard work they came out successful.

Background

TCRB had never reported profit, since its inception, till 2009.

In 2010, the new Management Committee took charge.

The Bank, then had only 3 permanent employees and a need was felt to bring in more professionalism in the functioning of the Bank.

Since TCRB faced liquidity crunch, the Bank approached Malappuram District Cooperative Bank for financial support, without success

The new management then met the then District Development Manager (DDM) of NABARD, Shri. KP Padmakumar, to seek a financial assistance of Rs.10 lakhs for the Bank.

But the DDM of NABARD did not give them any funds, nor did he promise any. He gave them an idea instead: Why not set up a Farmers Club??

Why not set up a Farmer’s Club????

The DDM convinced the Bank team that their priority should be to find ways to increase the business volumes by widening and deepening the Bank’s presence, and forming a FC could be the first step.

The DDM also offered to sponsor the setting up of the new FC under the Farmers’ Club Programme [FCP] of NABARD.

Thus the BC concept got its birth and the history begins there..

Financial Inclusion through Farmers’ Club… a novel initiative

In Dec 2010, the “Green Earth Farmers’ Club [GEFC] was set up by the TCRB, with 15 progressive farmers as members

DDM of NABARD played a vital role

GEFC conducted various programs like farmers’ camps, awareness classes, lectures by agricultural experts, etc.

Gained much publicity and acceptance through social media, enhanced the reach and visibility of both TCRB and GEFC

In April 2011, GEFC was made a BC of TCRB

Today, GEFC boasts of a membership of 123, of which 90 members are also working as BC Agents of GEFC.

Green Earth Farmers Club at a glance!!

• GEFC is running GSETI (self employment training Institute)

• GEFC is having Four divisions

Business correspondent

Agriculture Division

Non Farm Division

GSETI

Direct income for 130+ rural, poor families

• GEFC won 2nd Best Farmers Club award in Kerala for 2012-13 from NABARD

• Best Farmer’s Club state award for 2013-14

• Professionally Managed FC

• Five Offices at various places of Thiroorangadi Taluk

Technology adoption… the key to transformation

2010 TBA Installed

2012 CBS Implemented for a Single Branch Bank

IT Support at Bank

ATM, Micro ATM introduced

BC software

Agent Banking KIT

App For Employees: Orbit Lite

Hand shake with digital world….Feel the changes…

Make history….

The process of providing financial products and services needed by vulnerable groups such as weaker sections and low-income groups at an affordable cost in a fair and

transparent manner by co-operative sector.

Co-operative Financial Inclusion- Re-christened FI approach

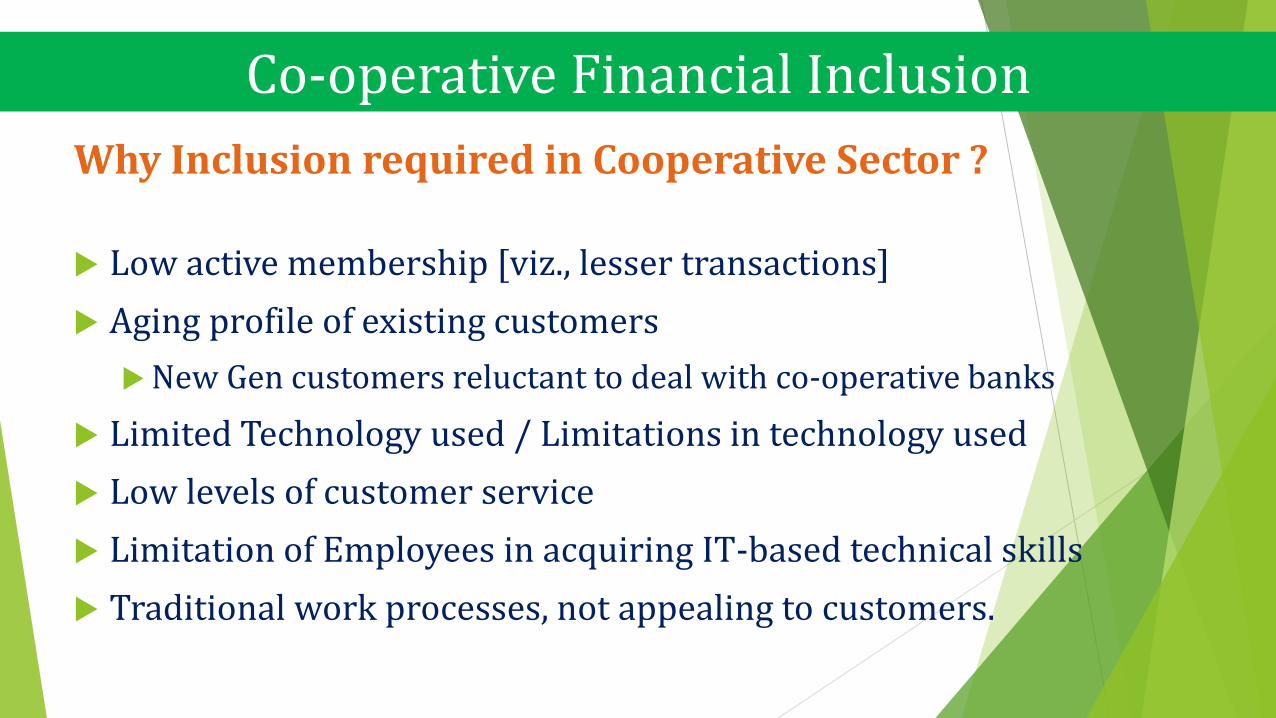

Why Inclusion required in Cooperative Sector ?

Low active membership [viz., lesser transactions]

Aging profile of existing customers

New Gen customers reluctant to deal with co-operative banks

Limited Technology used / Limitations in technology used

Low levels of customer service

Limitation of Employees in acquiring IT-based technical skills

Traditional work processes, not appealing to customers.

Co-operative Financial Inclusion

Challenges facing by Cooperative Banks

• Commercial banks are starting more rural branches/USBs

• NBFC’s opening new branches even in small areas

• Cannot compete with commercial/new generation banks

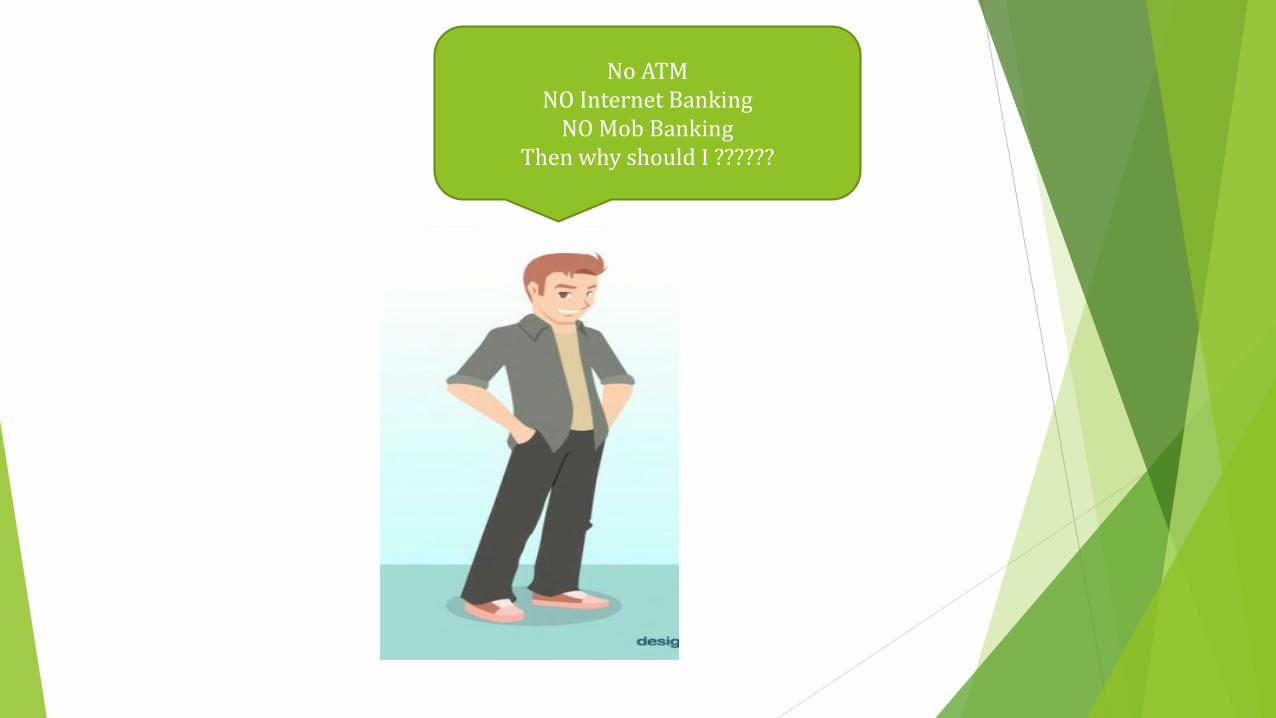

• Non availability of Internet banking, SMS Banking, ATM services

• Political considerations affecting functioning of Co-operative Banks

• NBFCs are acting as Business correspondent of Commercial Banks

• Citizen Service Centres started to act as the BCs of Federal Bank.

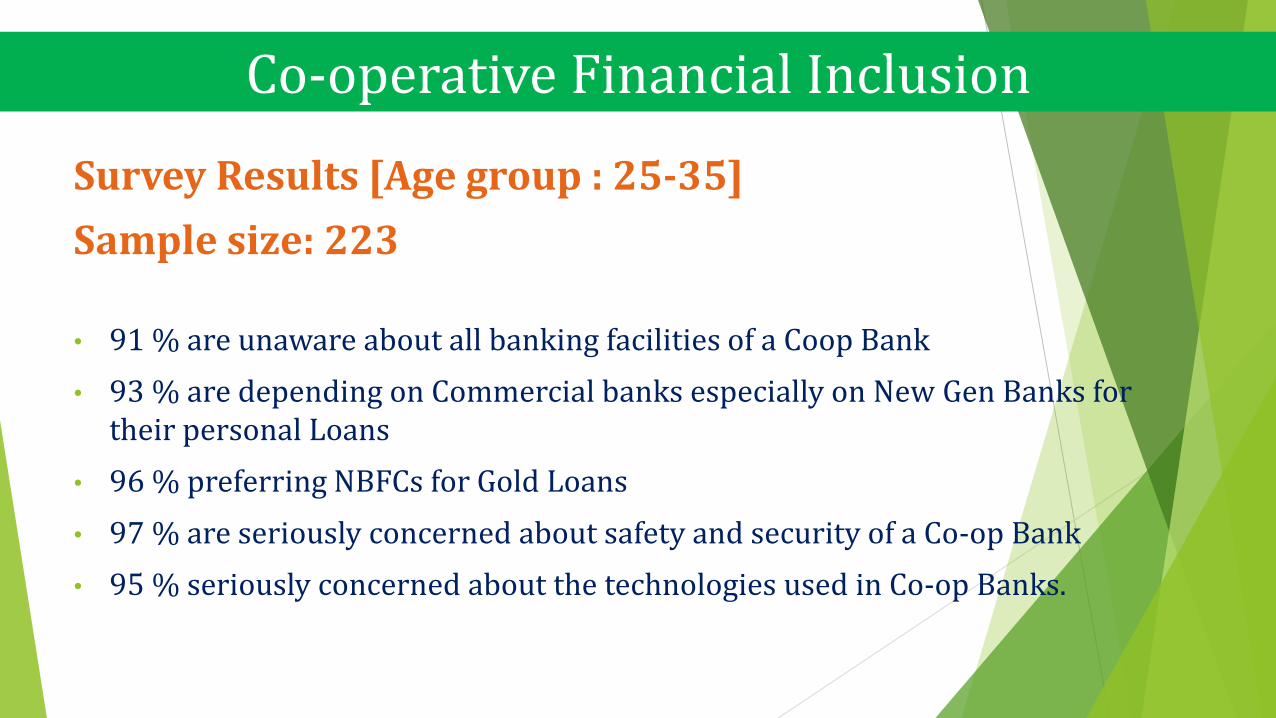

Survey Results [Age group : 25-35]

Sample size: 223

• 91 % are unaware about all banking facilities of a Coop Bank

• 93 % are depending on Commercial banks especially on New Gen Banks for their personal Loans

• 96 % preferring NBFCs for Gold Loans

• 97 % are seriously concerned about safety and security of a Co-op Bank

• 95 % seriously concerned about the technologies used in Co-op Banks.

Co-operative Financial Inclusion

No ATMNO Internet Banking

NO Mob Banking Then why should I ??????

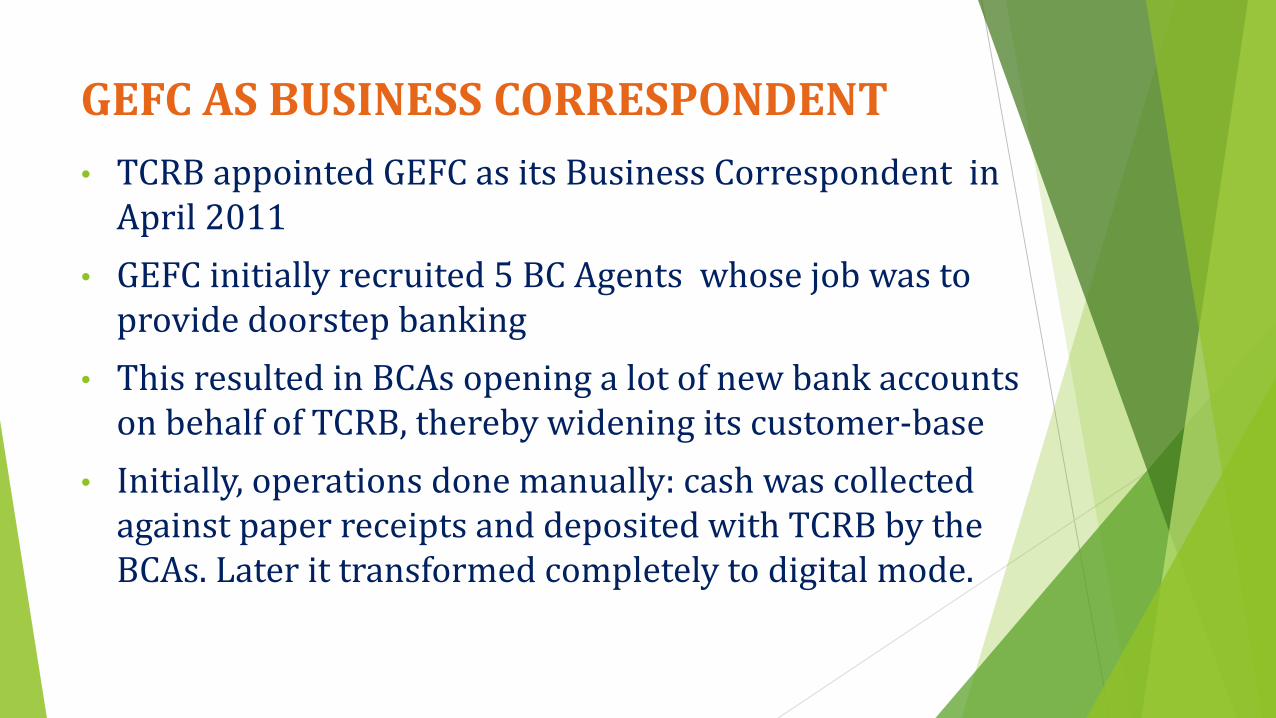

GEFC AS BUSINESS CORRESPONDENT

• TCRB appointed GEFC as its Business Correspondent in April 2011

• GEFC initially recruited 5 BC Agents whose job was to provide doorstep banking

• This resulted in BCAs opening a lot of new bank accounts on behalf of TCRB, thereby widening its customer-base

• Initially, operations done manually: cash was collected against paper receipts and deposited with TCRB by the BCAs. Later it transformed completely to digital mode.

BCAs at field

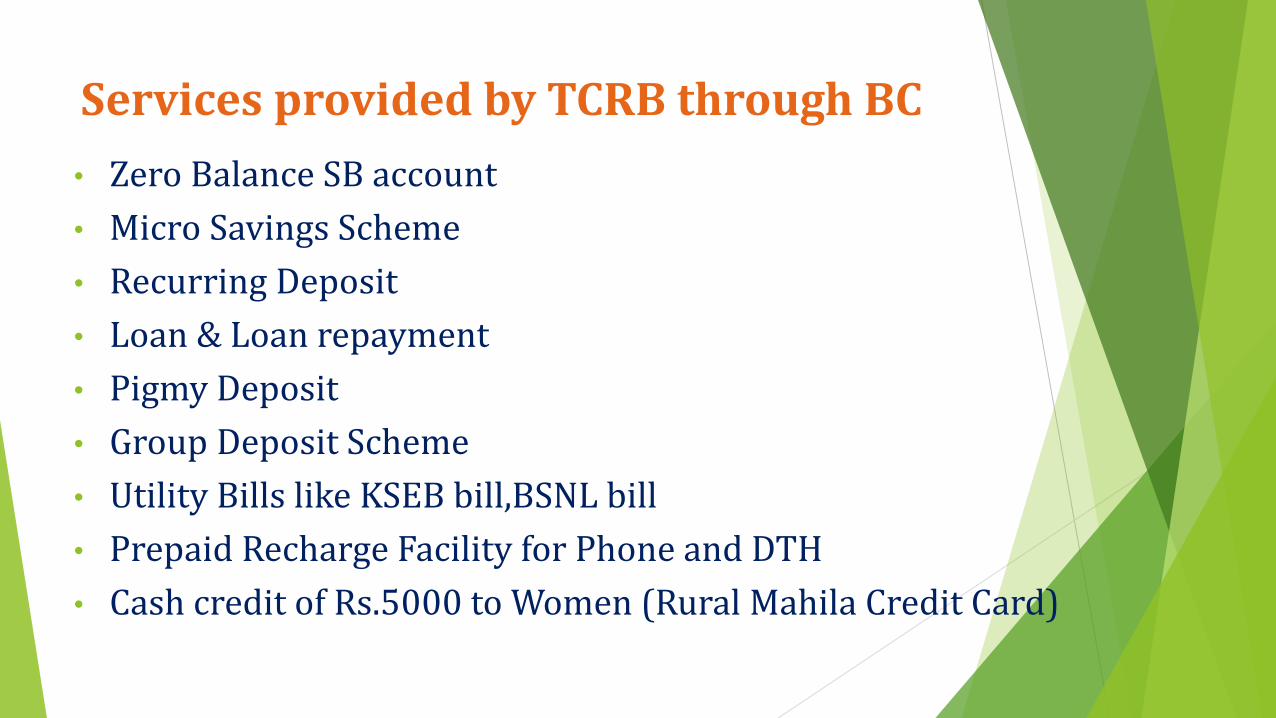

Services provided by TCRB through BC

• Zero Balance SB account

• Micro Savings Scheme

• Recurring Deposit

• Loan & Loan repayment

• Pigmy Deposit

• Group Deposit Scheme

• Utility Bills like KSEB bill,BSNL bill

• Prepaid Recharge Facility for Phone and DTH

• Cash credit of Rs.5000 to Women (Rural Mahila Credit Card)

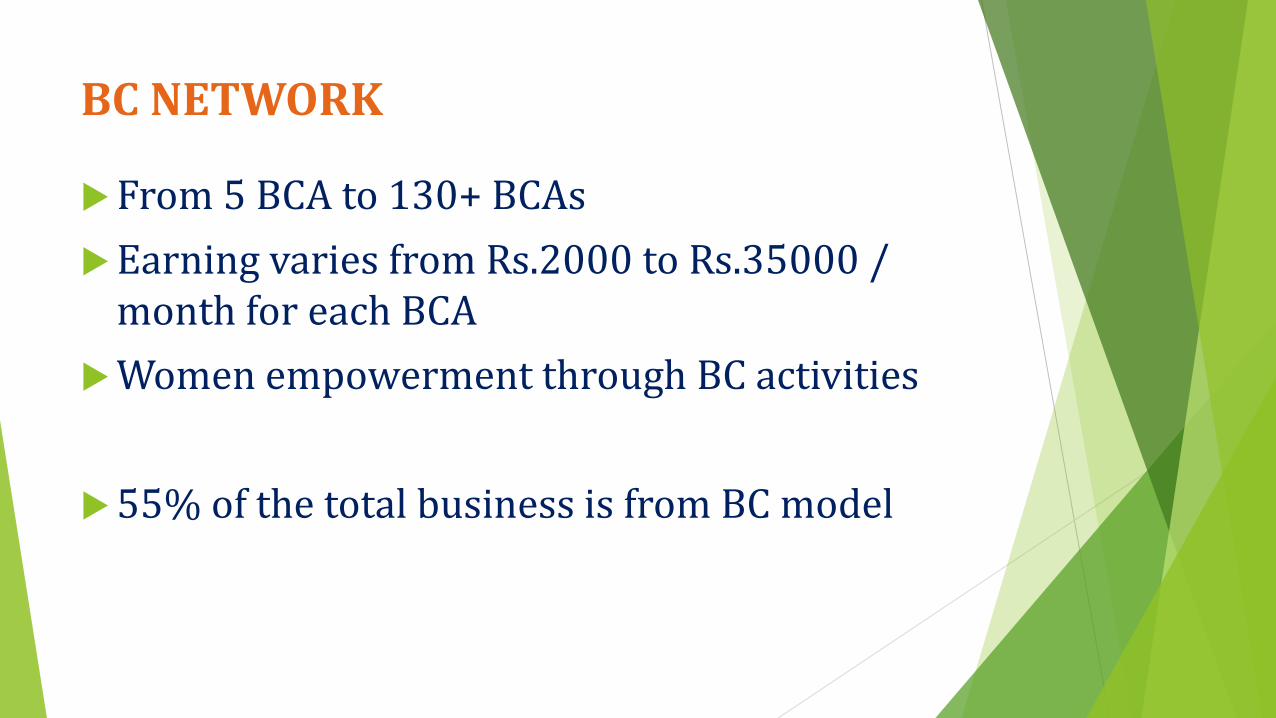

BC NETWORK

From 5 BCA to 130+ BCAs

Earning varies from Rs.2000 to Rs.35000 / month for each BCA

Women empowerment through BC activities

55% of the total business is from BC model

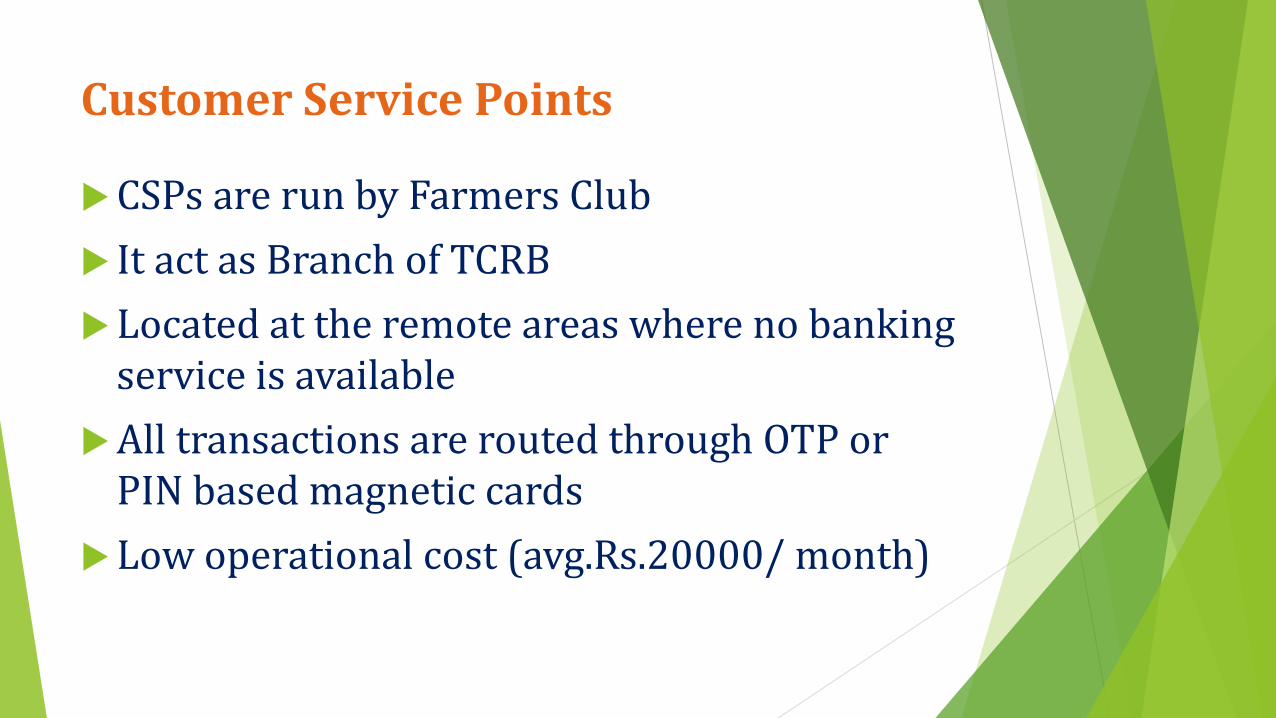

Customer Service Points

CSPs are run by Farmers Club

It act as Branch of TCRB

Located at the remote areas where no banking service is available

All transactions are routed through OTP or PIN based magnetic cards

Low operational cost (avg.Rs.20000/ month)

CSP

Then… Now…

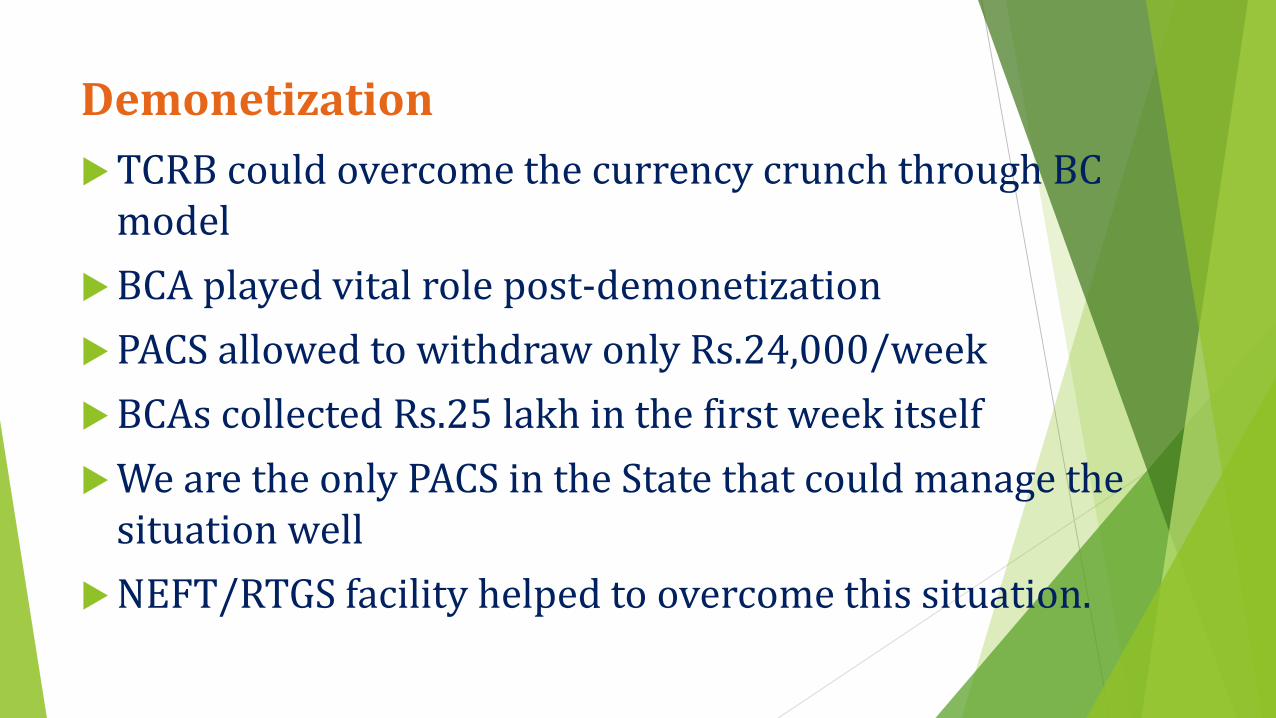

Demonetization

TCRB could overcome the currency crunch through BC model

BCA played vital role post-demonetization

PACS allowed to withdraw only Rs.24,000/week

BCAs collected Rs.25 lakh in the first week itself

We are the only PACS in the State that could manage the situation well

NEFT/RTGS facility helped to overcome this situation.

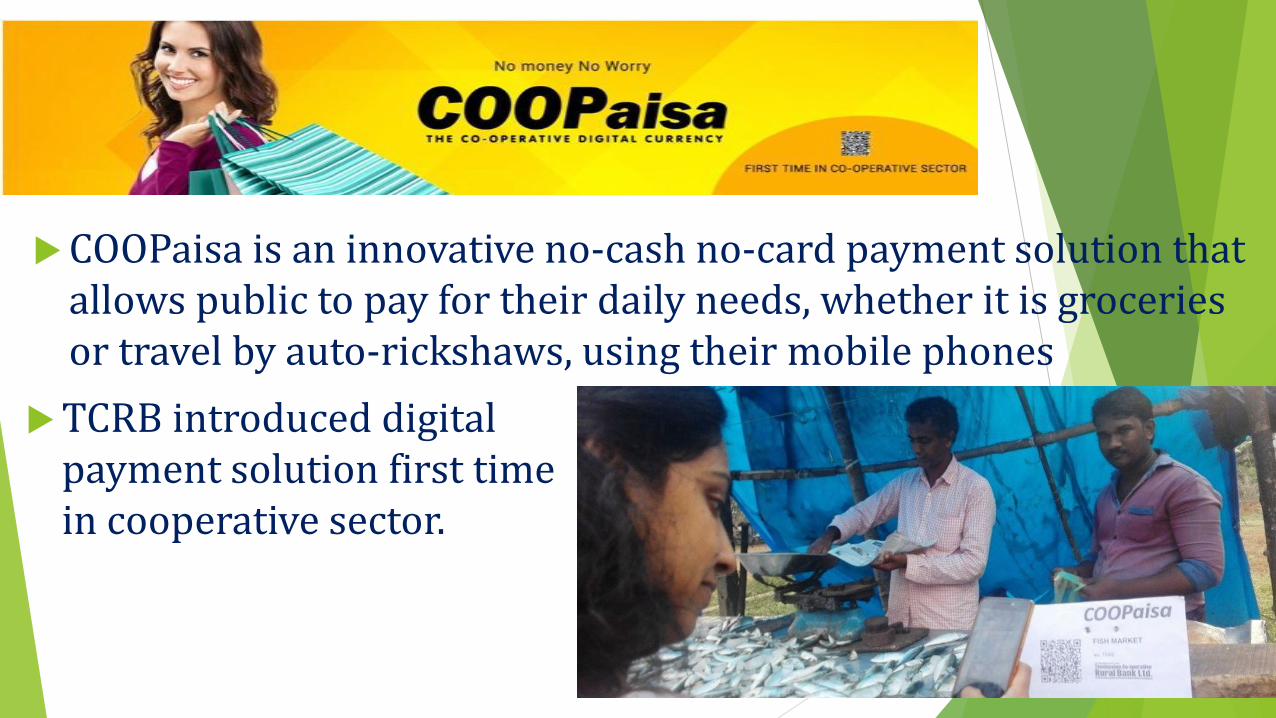

COOPaisa

COOPaisa is an innovative no-cash no-card payment solution that allows public to pay for their daily needs, whether it is groceries or travel by auto-rickshaws, using their mobile phones

TCRB introduced digital payment solution first time in cooperative sector.

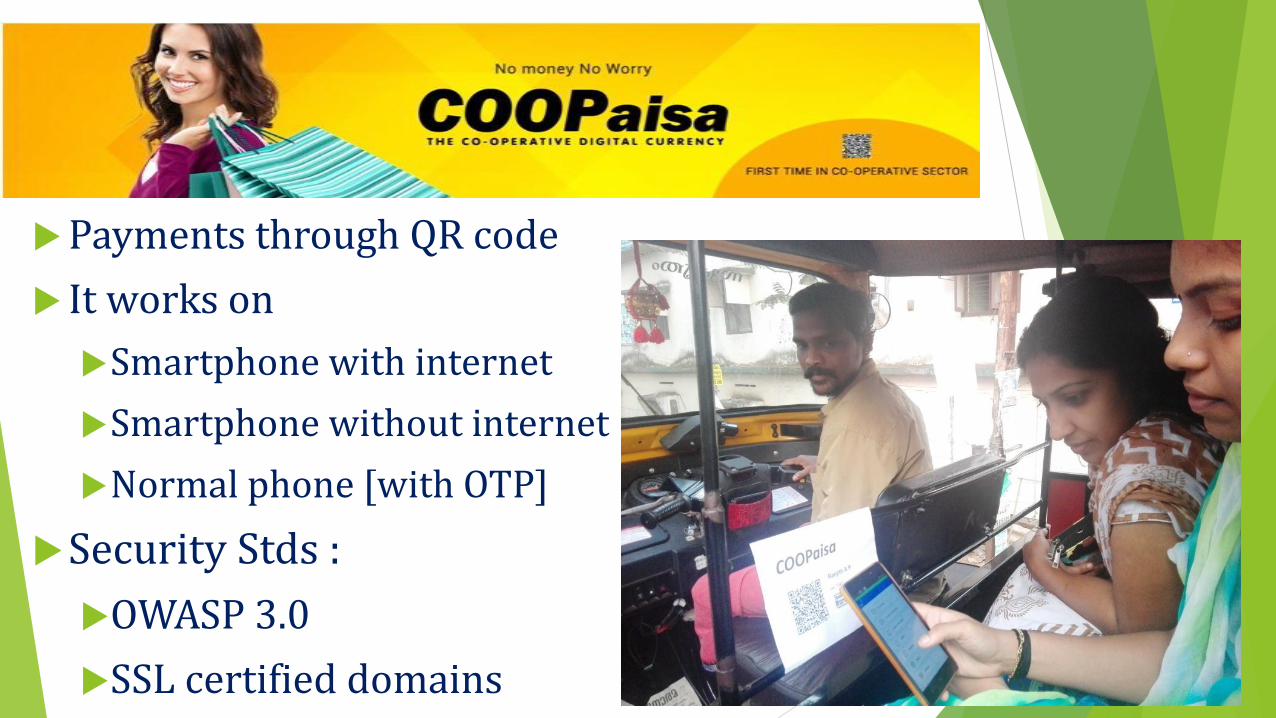

Payments through QR code

It works on

Smartphone with internet

Smartphone without internet

Normal phone [with OTP]

Security Stds :

OWASP 3.0

SSL certified domains

Platinum Credit Card

Virtual credit card for mobile app customers

Credit limit of Rs.5000/ month

Targeting to digitalize the traditional Dept Book with kirana shop.

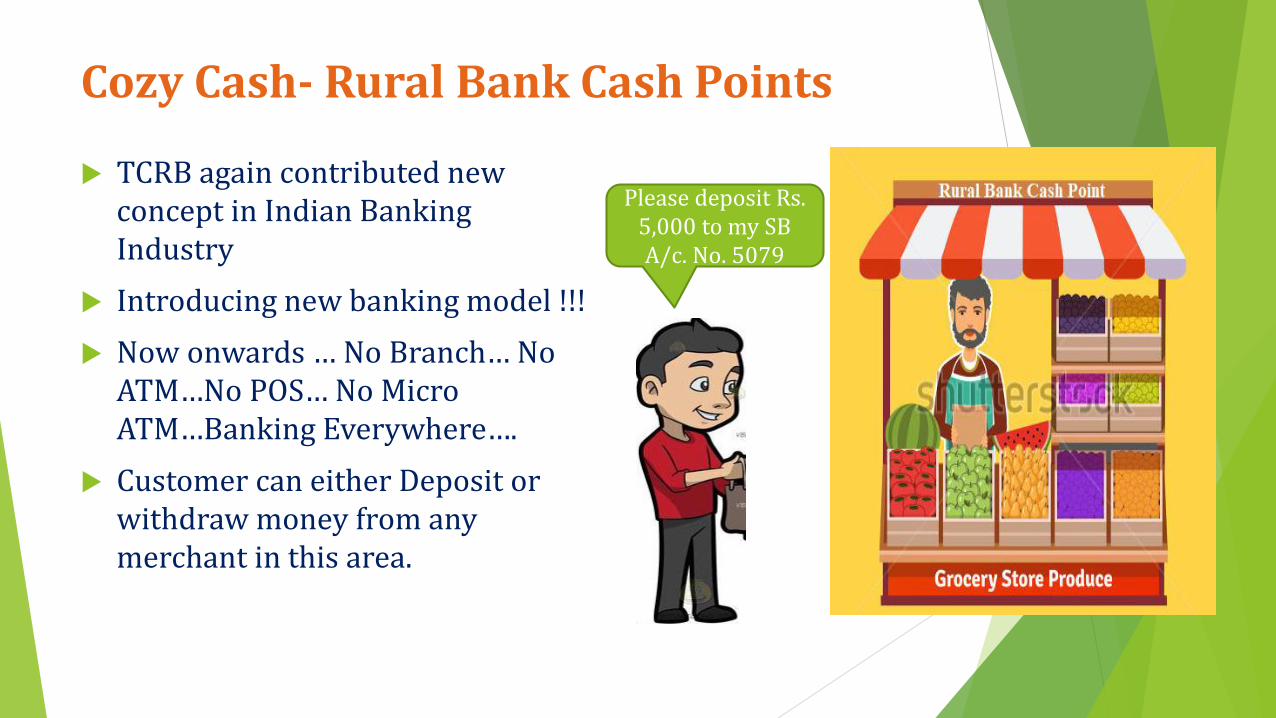

Cozy Cash- Rural Bank Cash Points

TCRB again contributed new concept in Indian Banking Industry

Introducing new banking model !!!

Now onwards … No Branch… No ATM…No POS… No Micro ATM…Banking Everywhere….

Customer can either Deposit or withdraw money from any merchant in this area.

Please deposit Rs. 5,000 to my SB A/c. No. 5079

IT Products

BEACONPRO

BEACON ORBIT

MyBank

COOPaisa

Orbitlite

Online banking – www.onlinetcrb.com

Agent Collection KIT

Shoppe_ Merchant’s App

ATM

Micro ATM

H2H service

GL mitra Software

SMS Alert

Misscall alert

eSSl

Cash Points

Platinum Credit Account

DDFS

Accolades FCBA 2017

Best BC Performance

FCBI Awards [Banking Frontiers] 2016

Best in IT

Best Youth Customer Engagement

Best Green Initiative

FCBI Awards [Banking Frontiers] 2015

Best CEO

Best Bank for Payment Solutions

Best Bank in Deposit Growth

NABARD Awards

Best Performing PACS in SHG-BLP in Kerala State: 2016-17

Karshaka Mitram Awards 2012-13.

Conclusion

TCRB recorded 1435% growth in business within 6 years

On an average, 55% of the business of TCRB is routed through BC

We have proved that Technology can transform challenges to opportunities…