Embed Size (px)

Citation preview

Valuing an Insurance Enterprise Valuing an Insurance Enterprise and Reserve Estimates Using and Reserve Estimates Using Bootstrapped Statutory Loss Bootstrapped Statutory Loss

InformationInformationWilliam C. ScheelWilliam C. Scheel

DFA Technologies, LLCDFA Technologies, [email protected]@mindspring.com

CAS 2001 DFA SeminarCAS 2001 DFA Seminar

22

ConceptsConcepts

Target sufficiency levelTarget sufficiency level Minimum sufficiency levelMinimum sufficiency level Capital releaseCapital release

33

TechniquesTechniques

Bootstrapping loss trianglesBootstrapping loss triangles Simulation of ultimate loss links, payment Simulation of ultimate loss links, payment

patterns and asset returnspatterns and asset returns Non-Linear optimization using proxy assets Non-Linear optimization using proxy assets

and target sufficiency levelsand target sufficiency levels Programming with COM in Visual Basic for Programming with COM in Visual Basic for

Applications (Excel VBA)Applications (Excel VBA)

44

Target Sufficiency LevelTarget Sufficiency Level

Fair value of future cash flowsFair value of future cash flows Present value of deferred annuity valued at Present value of deferred annuity valued at

riskless rate of returnriskless rate of return Net amount necessary to transfer future Net amount necessary to transfer future

claims paymentsclaims payments

55

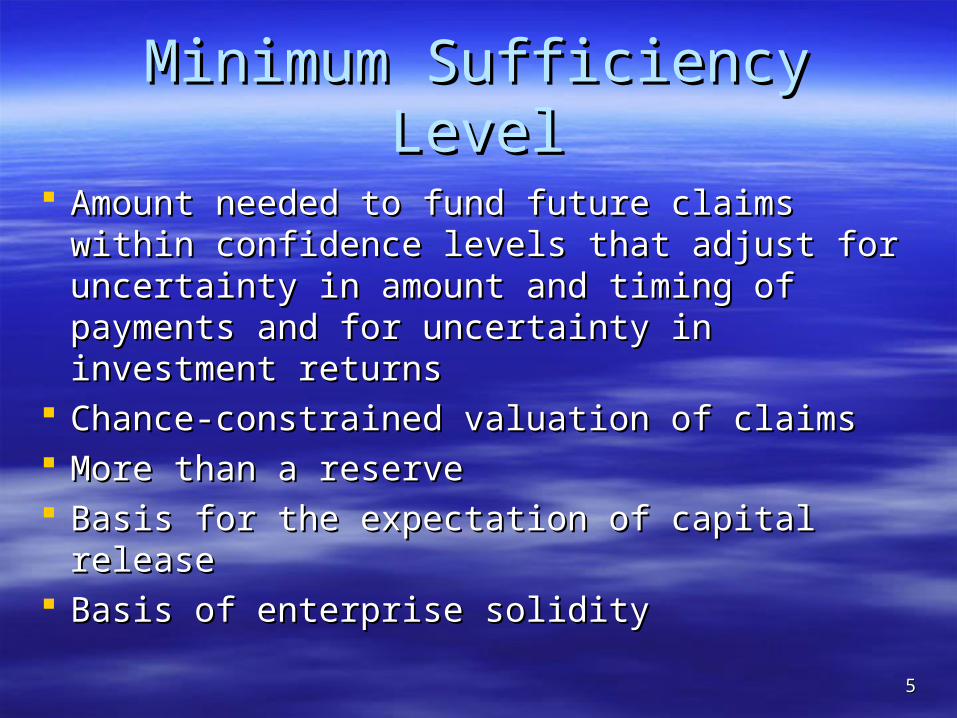

Minimum Sufficiency LevelMinimum Sufficiency Level

Amount needed to fund future claims within Amount needed to fund future claims within confidence levels that adjust for uncertainty confidence levels that adjust for uncertainty in amount and timing of payments and for in amount and timing of payments and for uncertainty in investment returnsuncertainty in investment returns

Chance-constrained valuation of claimsChance-constrained valuation of claims More than a reserveMore than a reserve Basis for the expectation of capital releaseBasis for the expectation of capital release Basis of enterprise solidityBasis of enterprise solidity

66

Capital ReleaseCapital Release

Initial excess sufficiency plus present value of Initial excess sufficiency plus present value of expected capital release is the value of the expected capital release is the value of the enterpriseenterprise

Amount of capital held in excess of expected Amount of capital held in excess of expected sufficiency. It is sufficiency. It is expectedexpected to be released to to be released to shareholders rather than to be used to pay shareholders rather than to be used to pay obligations.obligations.

Capital release occurs when minimum sufficiency Capital release occurs when minimum sufficiency levels decrease over timelevels decrease over time

Like reserves, capital release can only be Like reserves, capital release can only be measured probabilisticallymeasured probabilistically

77

Sources of Expected Capital Sources of Expected Capital ReleaseRelease

Target sufficiency level is higher than Target sufficiency level is higher than expected present value of claimsexpected present value of claims

Value of assets is higher than expected Value of assets is higher than expected value needed to achieve this deferred target value needed to achieve this deferred target sufficiency levelsufficiency level

88

Sources of Insurance Enterprise Sources of Insurance Enterprise ValueValue

Assets exceeding minimum sufficiency levelAssets exceeding minimum sufficiency level Expectation of capital release in the futureExpectation of capital release in the future

99

Relationship Among Sufficiency Relationship Among Sufficiency Levels and Capital ReleaseLevels and Capital Release

EOP Target sufficiency level

BOP Minimum sufficiency level

Time

Investment return and claims experience expected to produce operating result in this area

High probably area and source of capital release expectation

1010

Capital ReleaseCapital Release

1(1 ) ( )t t t t tSR MSL p C MSL where:

tSR = Capital released at the end of period t,

tMSL = Minimum sufficiency level at the beginning of period t,

tp = Portfolio return during period t,

tC = Claims payments during period t.

1111

Current Excess ValueCurrent Excess Value

Source of Value Amount

Current market value 5,534,719

Less:

Current min sufficiency level 1,591,549

Current ultimate loss for lines not analyzed 2,565

Net Current excess value 3,940,605

PV E(capital release) (@.05) 297,109

1212

Distribution of Capital ReleaseDistribution of Capital Release

Period 1 Period 2 Period 3 Period 4 Period 5 Period 6 Period 7 Period 8 Period 9

Mean 133,441 59,222 51,999 39,575 17,900 15,222 8,490 6,766 4,395

Standard Deviation 113,283 45,983 48,344 36,444 13,694 12,471 7,220 5,709 2,895

Median 127,131 58,012 50,623 37,486 17,596 14,711 8,308 6,558 4,360

5 percentile -42,909 -15,214 -23,636 -16,731 -4,230 -4,442 -3,078 -1,956 -347

10 percentile -6,434 1,953 -8,050 -4,987 402 -195 -905 -535 678

25 percentile 54,018 27,826 18,292 13,848 8,234 6,438 3,511 2,681 2,431

75 percentile 208,578 89,464 83,842 63,171 27,064 23,719 13,385 10,634 6,361

90 percentile 280,925 118,269 114,969 88,253 35,390 31,348 17,719 14,450 8,200

95 percentile 325,144 135,291 134,078 101,404 41,021 35,717 20,375 16,522 9,103

1313

Bootstrapping Loss TrianglesBootstrapping Loss Triangles

Would rather use individual claims Would rather use individual claims informationinformation

Multivariate sampling of lines of business Multivariate sampling of lines of business yields covariance matrixyields covariance matrix

Ultimate link ratiosUltimate link ratios Paid/Ultimate ratiosPaid/Ultimate ratios

1414

Feasible Region for Bootstrap Sampling of a Link Ratio

12 24 36 48 60 72 84 96 108 120

1990 92,906 123,086 121,828 121,312 120,960 120,786 120,667 120,986 120,907 120,685

1991 126,731 130,026 127,583 126,730 125,640 127,269 126,636 126,266 125,893

1992 157,558 159,071 158,104 159,525 157,525 157,873 157,124 156,249

1993 163,692 163,139 161,354 161,677 160,495 160,421 159,270

1994 167,469 164,228 163,903 163,628 161,827 159,595

1995 230,837 229,624 227,953 226,813 226,454

1996 202,686 201,266 202,338 200,922

1997 259,065 260,110 256,783

1998 222,746 221,905

1999 268,705

1515

Portions of a Bootstrap Sample in Shaded Regions

12 24 36 48 60 72 84 96 108 120

1990 92,906 123,086 121,828 121,312 120,960 160,421 159,270 120,986 120,907 120,685

1991 126,731 130,026 121,828 121,312 125,640 127,269 126,636 126,266 125,893

1992 157,558 159,071 158,104 159,525 157,525 127,269 126,636 156,249

1993 163,692 163,139 163,903 163,628 160,495 120,786 120,667

1994 167,469 164,228 202,338 200,922 161,827 159,595

1995 230,837 229,624 161,354 161,677 226,454

1996 202,686 201,266 161,354 161,677

1997 259,065 260,110 256,783

1998 222,746 221,905

1999 268,705

1616

Statistics for Link1 Statistics for Link1 Line of Business Correlation Matrix

Home PPA CAL WC CMP Spcl_Liab OL_OCC Reins_A Reins_B Reins_C PPA 0.0089 CAL -0.0031 -0.0028 WC -0.0075 -0.0067 0.0016 CMP 0.0119 0.0104 -0.0026 -0.0103 Spcl_Liab -0.0157 -0.0147 0.0108 0.0072 -0.0146 OL_OCC -0.0212 -0.0187 0.0049 0.0179 -0.0269 0.0244 Reins_A -0.0539 -0.0454 0.0172 0.0369 -0.0583 0.0684 0.1030 Reins_B -0.0047 -0.0132 0.0103 0.0059 -0.0043 -0.0670 0.0354 0.0052 Reins_C 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 Property_ShortTail 0.0026 0.0023 -0.0006 -0.0020 0.0031 -0.0027 -0.0050 -0.0146 -0.0042 0.0000

Line of Business Ultimate Link1 Paid/Ultimate Ratio1

Expected

Value Standard Deviation

Expected Value

Standard Deviation

Home 1.0353 0.0795 0.8822 0.0159 PPA 0.9935 0.0713 0.5829 0.0431 CAL 0.9715 0.0475 0.4263 0.0370 WC 0.9585 0.0784 0.4345 0.0337 CMP 1.0177 0.1014 0.5408 0.0233 Spcl_Liab 1.1854 0.3476 0.7765 0.0877 OL_OCC 0.8596 0.1921 0.2174 0.0584 Reins_A 0.9823 0.3608 0.5491 0.1999 Reins_B 1.4092 0.5176 0.7865 0.0474 Reins_C 1.2188 0.0000 0.5461 0.2491

Property_ShortTail 1.0040 0.0270 0.9861 0.0075

Steps in Valuation of Target SufficiencySteps in Valuation of Target Sufficiency

1.1. Perform a bootstrap of link ratios for ultimate loss. Perform a bootstrap of link ratios for ultimate loss.

2.2. Use bootstrapped ultimate link ratios to derive correlation Use bootstrapped ultimate link ratios to derive correlation matrix and other statistics. matrix and other statistics.

3.3. Using the correlation matrices and statistics, simulate Using the correlation matrices and statistics, simulate ultimate links for each line of business using multinormal ultimate links for each line of business using multinormal methods.methods.

4.4. Apply the simulated ultimate link ratios to the latest Apply the simulated ultimate link ratios to the latest ultimate loss triangle diagonal. ultimate loss triangle diagonal.

5.5. Perform a second-stage simulation using the probability Perform a second-stage simulation using the probability distribution of paid-to-ultimate ratios (payment patterns).distribution of paid-to-ultimate ratios (payment patterns).

6.6. Use the cash flows to calculate annuity-equivalent values Use the cash flows to calculate annuity-equivalent values for future loss cash flow. Do this at each forward for future loss cash flow. Do this at each forward calendar period. calendar period.

1818

Target Sufficiency StatisticsTarget Sufficiency Statistics

All Lines Period 1 Period 2 Period 3 Period 4 Period 5 Period 6 Period 7 Period 8 Period 9 Period 10

Mean 1,798,921 1,282,873 896,766 650,352 484,940 369,549 278,479 199,570 124,023 47,013

Standard Deviation 91,557 55,185 37,405 21,528 12,388 8,818 6,451 4,571 2,833 845

Median 1,798,343 1,281,362 895,937 649,768 484,449 369,120 278,192 199,447 123,920 46,980

5 percentile 1,649,169 1,195,019 837,174 615,604 465,394 355,541 268,231 192,349 119,508 45,660

10 percentile 1,682,185 1,214,548 850,383 623,497 469,507 358,660 270,411 193,797 120,432 45,956

25 percentile 1,737,040 1,244,796 870,057 634,645 476,207 363,456 274,039 196,427 122,083 46,435

75 percentile 1,860,955 1,319,754 920,838 664,331 492,981 375,434 282,777 202,531 125,786 47,557

90 percentile 1,913,878 1,352,208 944,923 678,150 500,876 380,722 286,849 205,513 127,761 48,135

95 percentile 1,948,887 1,374,690 960,082 686,303 506,422 384,138 289,258 207,396 128,899 48,491

1919

Moving from Targets to Minimum Moving from Targets to Minimum Sufficiency LevelsSufficiency Levels

Targets risk-adjust only for uncertainty in Targets risk-adjust only for uncertainty in amount of payments and timing of paymentsamount of payments and timing of payments

What asset levels are required to meet What asset levels are required to meet sufficiency targets?sufficiency targets?

What portfolio allocation?What portfolio allocation? Technique: use non-linear optimizationTechnique: use non-linear optimization

2020

Optimization TechniquesOptimization Techniques

Objective: Minimize level of assets Objective: Minimize level of assets necessary to meet sufficiency targetsnecessary to meet sufficiency targets

Subject to: Portfolio constraints for proxy Subject to: Portfolio constraints for proxy assets and minimum sufficiency probability assets and minimum sufficiency probability constraintconstraint

What BOP assets should be held to met EOP sufficiency levels within acceptable levels of risk?

2121

Techniques Using Microsoft Excel Techniques Using Microsoft Excel and Frontline Premium Solverand Frontline Premium Solver

Workbook A: Non-linear version of Solver posits trial Workbook A: Non-linear version of Solver posits trial solution (portfolio allocation) solution (portfolio allocation)

Workbook B Workbook B (COM object instantiated by A)(COM object instantiated by A): Has 2,500 : Has 2,500 simulated asset returns, target sufficiency level and simulated asset returns, target sufficiency level and chance-constrained probability (all provided by A). Gets chance-constrained probability (all provided by A). Gets trial portfolio allocation from A.trial portfolio allocation from A.

B determines BOP value of target for each asset simulation B determines BOP value of target for each asset simulation using trail solution weights.using trail solution weights.

Using this BOP distribution, B returns chance-constrained Using this BOP distribution, B returns chance-constrained minimum sufficiency level to A as objective value.minimum sufficiency level to A as objective value.

Workbook A repeats trial solution tests until it finds the Workbook A repeats trial solution tests until it finds the minimum value returned by workbook Bminimum value returned by workbook B

2222

Minimum Sufficiency Levels and Optimal Investment PortfoliosMinimum Sufficiency Levels and Optimal Investment Portfolios Period 1 Period 2 Period 3 … Period 8 Period 9 Period 10

Min Sufficiency Level 1,591,549 1,064,347 680,513…

78,977 37,711 0

Required EOP target assets 1,683,785 1,128,672 722,708…

83,439 39,879 0

EAFEU .067 .073 .146…

.063 .015

INTLUHD .189 .039 .126…

.226 .036

S&P5 .163 .023 .0…

.082 .039

USTB .067 .465 .063…

.058 .559

R_MID .050 .0 .097…

.119 .023

HIYLD .122 .148 .002…

.098 .159

CONV .036 .055 .131…

.041 .003

LBCORP .032 .068 .023…

.105 .0

LBGVT .123 .011 .325…

.046 .148

LBMBS .151 .117 .088…

.164 .017

Expected Return 1,770,939 1,162,538 759,151…

87,867 40,883

Standard Deviation 105,186 40,051 44,333…

5,284 1,176

0.1 Percentile 1,635,357 1,112,691 704,420…

81,043 39,420

0.2 Percentile 1,683,802 1,128,682 722,719…

83,447 39,880

0.9 Percentile 1,908,091 1,215,841 816,402…

94,726 42,410

Sharpe ratio .712 .697 .759…

.697 .580

2323

Capital Release Measurement Capital Release Measurement TechniqueTechnique

1.1. Randomly generate investment scenario. Randomly generate investment scenario. Using portfolio allocation, determine Using portfolio allocation, determine period’s return and apply to minimum period’s return and apply to minimum sufficiency value for period 1 (MSLsufficiency value for period 1 (MSL11).).

2.2. Generate liabilities and subtract from (1)Generate liabilities and subtract from (1)

3.3. Compare (2) with MSLCompare (2) with MSL22 to get observation to get observation on capital release distributionon capital release distribution

4.4. Repeat steps (1) to (3) many times to Repeat steps (1) to (3) many times to obtain distribution for capital releaseobtain distribution for capital release

2424

Expected Capital ReleaseExpected Capital Release

2525

SummarySummary

Target sufficiency measured from bootstrapped Target sufficiency measured from bootstrapped ultimate links and paid/ultimate ratios. Risk ultimate links and paid/ultimate ratios. Risk adjustment for amount and timing of losses.adjustment for amount and timing of losses.

Minimum sufficiency levels derived from (1) using Minimum sufficiency levels derived from (1) using non-linear optimization applied to simulated asset non-linear optimization applied to simulated asset returns and required targets. Risk adjustment for returns and required targets. Risk adjustment for uncertainty in investment returns.uncertainty in investment returns.

Release of capital measured from simulations of Release of capital measured from simulations of assets and liabilities using minimum sufficiency assets and liabilities using minimum sufficiency levels.levels.

2626

Questions?Questions?

William C. Scheel, Ph.D.DFA Technologies, LLC93 Silkey RoadNorth Granby, CT 06060-1419(860) [email protected]