Embed Size (px)

Citation preview

Valuing ASCs and Recent Trends in ASC Transactions

Presented By

Todd J. Mello, ASA, CVA, MBA, Founding Partner

Presentation Outline

• Valuation 101: Approaches and Methods and other 411

• Do’s and Don’ts

• Value Enhancers and Value Detractors

• Minority vs. Majority/Control

• History, Purpose and Limitations of the Survey

• What are Valuation Multiples?

• Reported Earnings Multiples

• Other Survey Observations (time permitting)

2 Valuing ASCs and Recent Trends in ASC Transactions

Valuation 101

• Valuation is forward looking

• Why get a valuation?

• Standard of value in most healthcare transactions is Fair Market Value. The definition of fair market value in healthcare is slightly different than

the standard valuation definition.

• the price at which property would change hands between a hypothetical willing and able buyer and a hypothetical willing and able seller, acting at arm’s length in an open and unrestricted market, when neither is under compulsion to buy or sell … between well informed parties who are not otherwise in a position to generate business for the other party…

• Implications of “hypothetical”

3 Valuing ASCs and Recent Trends in ASC Transactions

Valuation 101

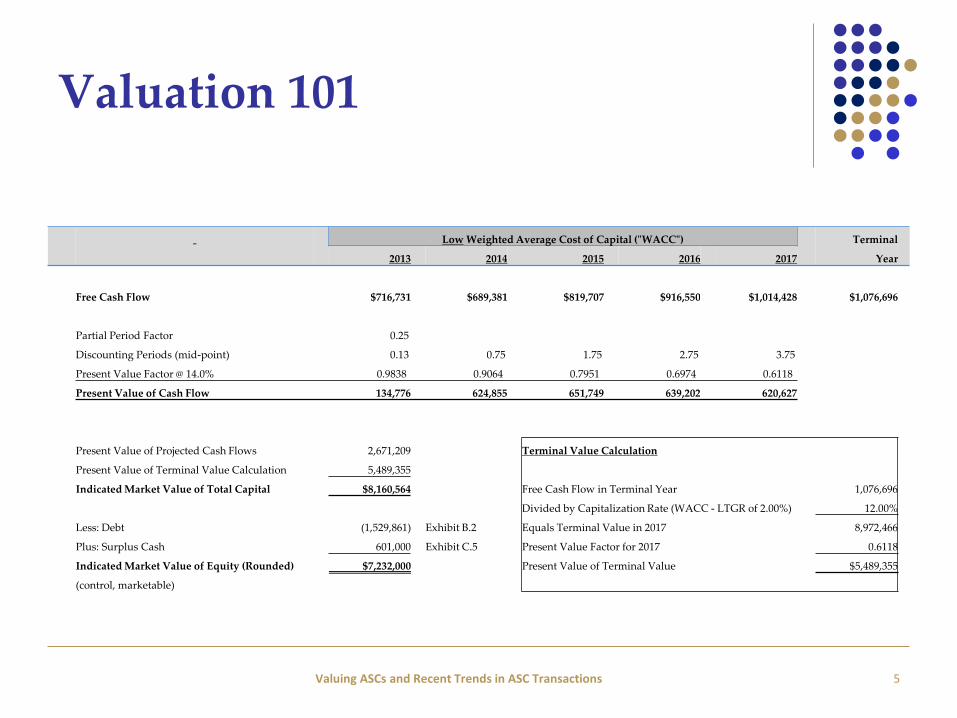

• Income Approach – A general way of determining a value indication of a business, business ownership interest, security, or intangible asset using one or more methods that convert anticipated future economic benefits into a single present amount.

• Most common methods: Discounted Cash Flow Method and Capitalization of Earnings Method

• When and why?

• Example: next slide

4 Valuing ASCs and Recent Trends in ASC Transactions

Valuation 101

5 Valuing ASCs and Recent Trends in ASC Transactions

Low Weighted Average Cost of Capital ("WACC") Terminal

2013 2014 2015 2016 2017 Year

Free Cash Flow $716,731 $689,381 $819,707 $916,550 $1,014,428 $1,076,696

Partial Period Factor 0.25

Discounting Periods (mid-point) 0.13 0.75 1.75 2.75 3.75

Present Value Factor @ 14.0% 0.9838 0.9064 0.7951 0.6974 0.6118

Present Value of Cash Flow 134,776 624,855 651,749 639,202 620,627

Present Value of Projected Cash Flows 2,671,209 Terminal Value Calculation

Present Value of Terminal Value Calculation 5,489,355

Indicated Market Value of Total Capital $8,160,564 Free Cash Flow in Terminal Year 1,076,696

Divided by Capitalization Rate (WACC - LTGR of 2.00%) 12.00%

Less: Debt (1,529,861) Exhibit B.2 Equals Terminal Value in 2017 8,972,466

Plus: Surplus Cash 601,000 Exhibit C.5 Present Value Factor for 2017 0.6118

Indicated Market Value of Equity (Rounded) $7,232,000 Present Value of Terminal Value $5,489,355

(control, marketable)

Valuation 101

• Market Approach – A general way of determining a value indication of a business, business ownership interest, security, or intangible asset using one or more methods that compare the subject to similar businesses, business ownership interests, securities, or intangible assets that have been sold.

• Most common methods: Guideline Publicly Traded Method and Comparative Transactions Method

• When and why?

6 Valuing ASCs and Recent Trends in ASC Transactions

What are Valuation Multiples?

The Meaning Behind the Numbers

The Finance Definition (a.k.a. Appraiser speak)

“A mathematical expression of risk and growth, which when applied to a perpetually recurring earnings stream results in an indication of value”

A multiple is mathematically expressed as follows:

• Where, (K) represents the rate of return (risk), and

• (G) represents the growth rate of the earnings stream

7

)(

1

gK

Valuing ASCs and Recent Trends in ASC Transactions

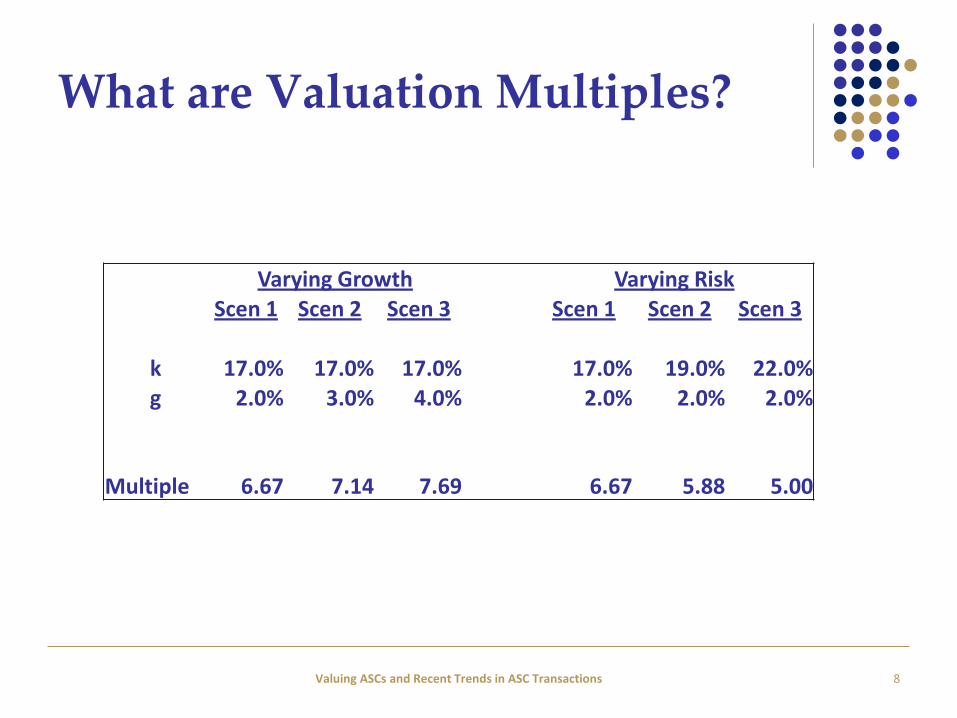

What are Valuation Multiples?

Varying Growth Varying Risk Scen 1 Scen 2 Scen 3 Scen 1 Scen 2 Scen 3

k 17.0% 17.0% 17.0% 17.0% 19.0% 22.0% g 2.0% 3.0% 4.0% 2.0% 2.0% 2.0%

Multiple

6.67

7.14

7.69

6.67

5.88

5.00

8 Valuing ASCs and Recent Trends in ASC Transactions

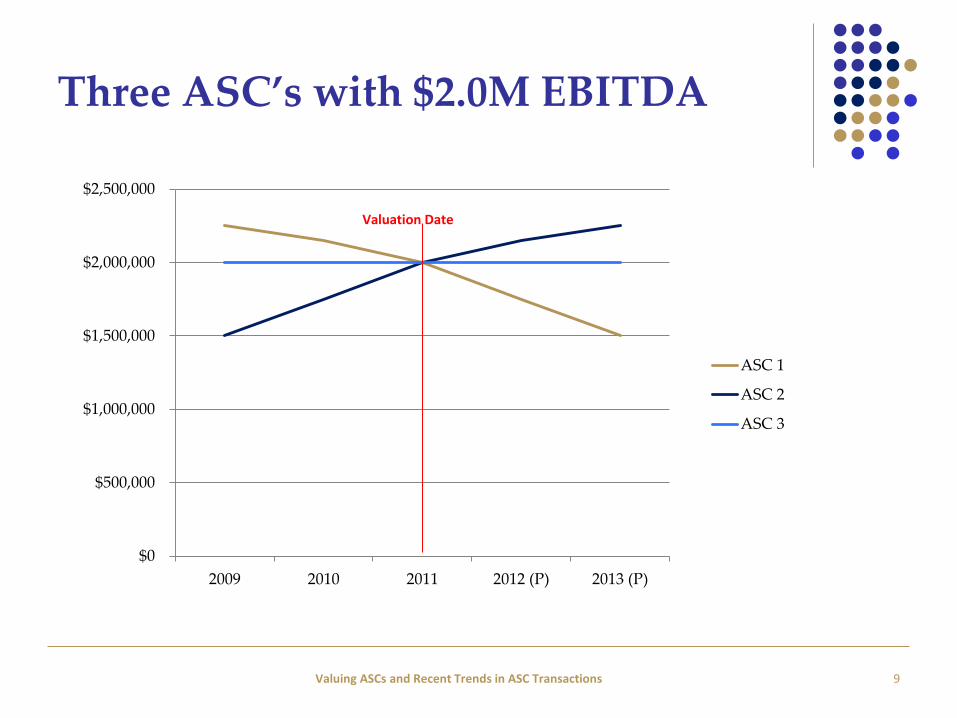

Three ASC’s with $2.0M EBITDA

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

2009 2010 2011 2012 (P) 2013 (P)

ASC 1

ASC 2

ASC 3

Valuation Date

9 Valuing ASCs and Recent Trends in ASC Transactions

Valuation 101

• Asset or Cost Approach – A general way of determining a value indication of a business, business ownership interest, or security using one or more methods based on the value of the assets net of liabilities.

• When and why?

10 Valuing ASCs and Recent Trends in ASC Transactions

Minority vs. Majority Control

• Interests providing absolute control (e.g., greater than a 50% interest) are worth more than interests which do not have the same control rights.

• Control granted by the governing documents. Examples include:

• Major equipment purchases and investments

• Debt signing authority

• Admitting new owners

• Granting physician privileges

11 Valuing ASCs and Recent Trends in ASC Transactions

Do’s and Don’ts

• In connection with a hospital’s 100% acquisition of an ASC, can we consider overlaying hospital’s fee structure onto valuation?

• If a new surgeon who has not done any (or a material amount) of cases is looking to buy in, should you include his/her cases in connection with valuing the interest?

• An ASC has done a poor job on collecting from Medicare; can we factor billing improvements into our valuation?

• An ASC experienced a one-time material adverse event in the most recently completed year. Can we ignore for purposes of valuation?

• An ASC is looking to but out one investor at $X and sell an interest to a new investor at 75% of $X.

• Assume a hospital want to buy an ASC for purposes of shutting it down. Impact to value?

• Others?

12 Valuing ASCs and Recent Trends in ASC Transactions

Value Enhancers/Detractors

• Enhancers • Multispecialty (diversification of case types)

• Diversification of surgeons – majority of cases not done by a single surgeon

• High % of cases performed by owners who are “motivated” to continue working

• An established history of continually seeking new owners

• History and expectation of continued distributions

• Growth in cases and earnings; reimbursement growth less certain

• Little debt over time

• Barriers to entry (e.g. CON)

• Predominantly in network with Commercial payors

• Others?

13 Valuing ASCs and Recent Trends in ASC Transactions

Value Enhancers/Detractors

• Detractors (opposite of previous slide) • Reliance on single specialty (not always)

• Lack of diversification of surgeons – majority of cases done by a single surgeon

• High % of cases performed by non-owners

• Little vision on extending center life cycle

• Lack of distributions or lack of consistency in distributing cash flow

• No growth or loss in volume, revenue

• Excessive debt

• Predominantly out-of-network with Commercial payors

• Others?

14 Valuing ASCs and Recent Trends in ASC Transactions

History, Purpose & Limitations of the Survey

• Since 2003, HAI has published ten annual ASC surveys

• Why? To provide a centralized source of market intelligence on valuation trends within the ASC industry.

• 2014 was largest to date with 25 companies respondents

• Disclaimer: Survey should not be used in lieu of a formal valuation.

15 Valuing ASCs and Recent Trends in ASC Transactions

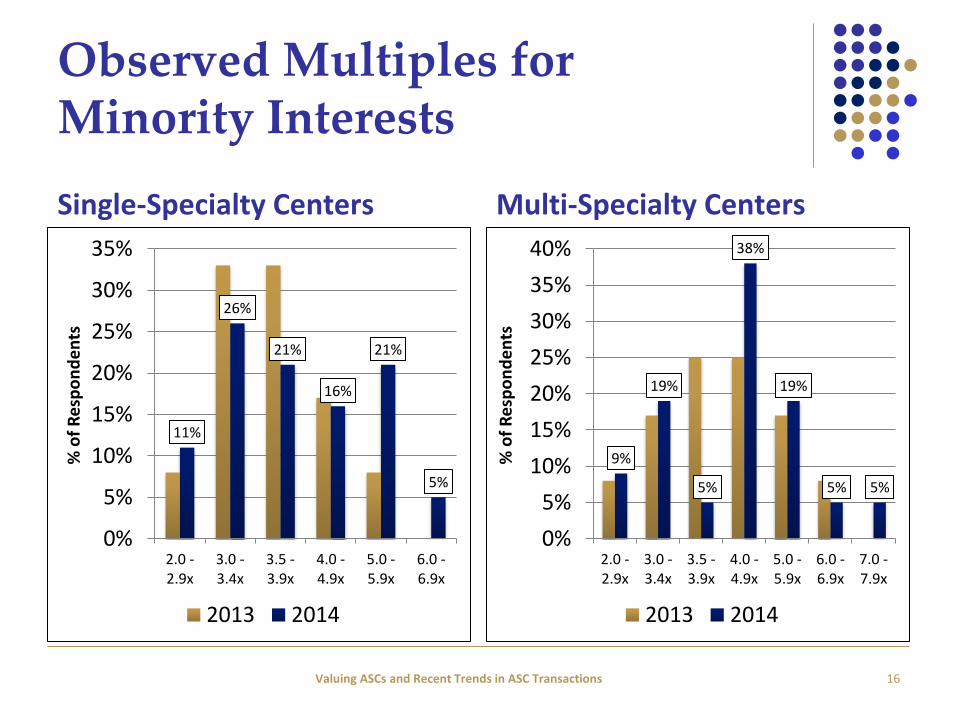

Observed Multiples for Minority Interests

Single-Specialty Centers Multi-Specialty Centers

16

11%

26%

21%

16%

21%

5%

0%

5%

10%

15%

20%

25%

30%

35%

2.0 -2.9x

3.0 -3.4x

3.5 -3.9x

4.0 -4.9x

5.0 -5.9x

6.0 -6.9x

% o

f R

esp

on

de

nts

2013 2014

9%

19%

5%

38%

19%

5% 5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2.0 -2.9x

3.0 -3.4x

3.5 -3.9x

4.0 -4.9x

5.0 -5.9x

6.0 -6.9x

7.0 -7.9x

% o

f R

esp

on

de

nts

2013 2014

Valuing ASCs and Recent Trends in ASC Transactions

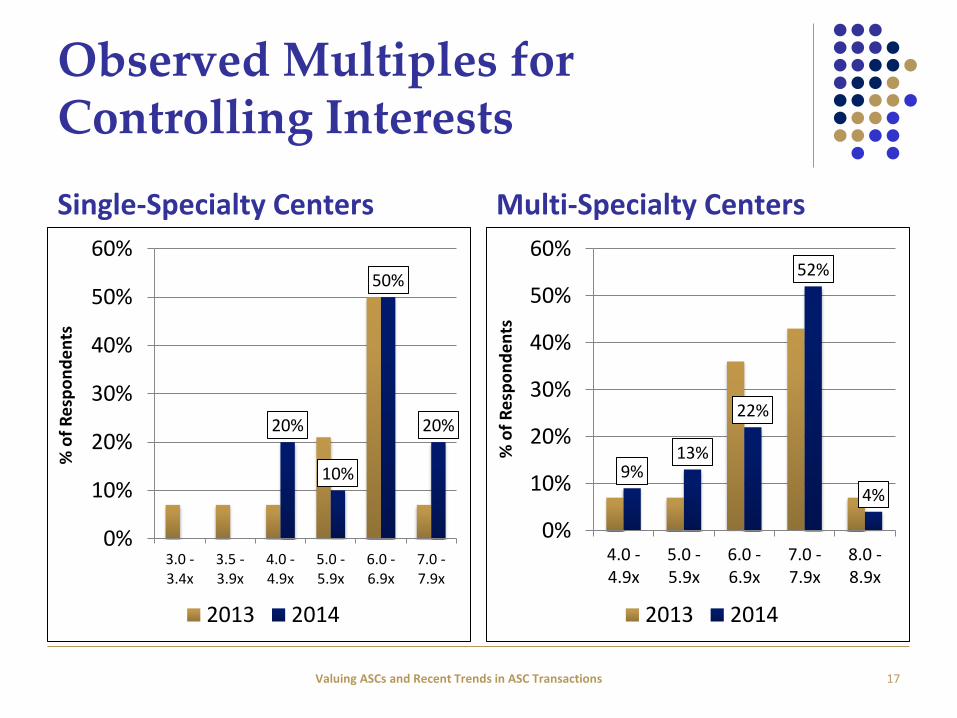

Observed Multiples for Controlling Interests

Single-Specialty Centers Multi-Specialty Centers

17

20%

10%

50%

20%

0%

10%

20%

30%

40%

50%

60%

3.0 -3.4x

3.5 -3.9x

4.0 -4.9x

5.0 -5.9x

6.0 -6.9x

7.0 -7.9x

% o

f R

esp

on

de

nts

2013 2014

9% 13%

22%

52%

4%

0%

10%

20%

30%

40%

50%

60%

4.0 -4.9x

5.0 -5.9x

6.0 -6.9x

7.0 -7.9x

8.0 -8.9x

% o

f R

esp

on

de

nts

2013 2014

Valuing ASCs and Recent Trends in ASC Transactions

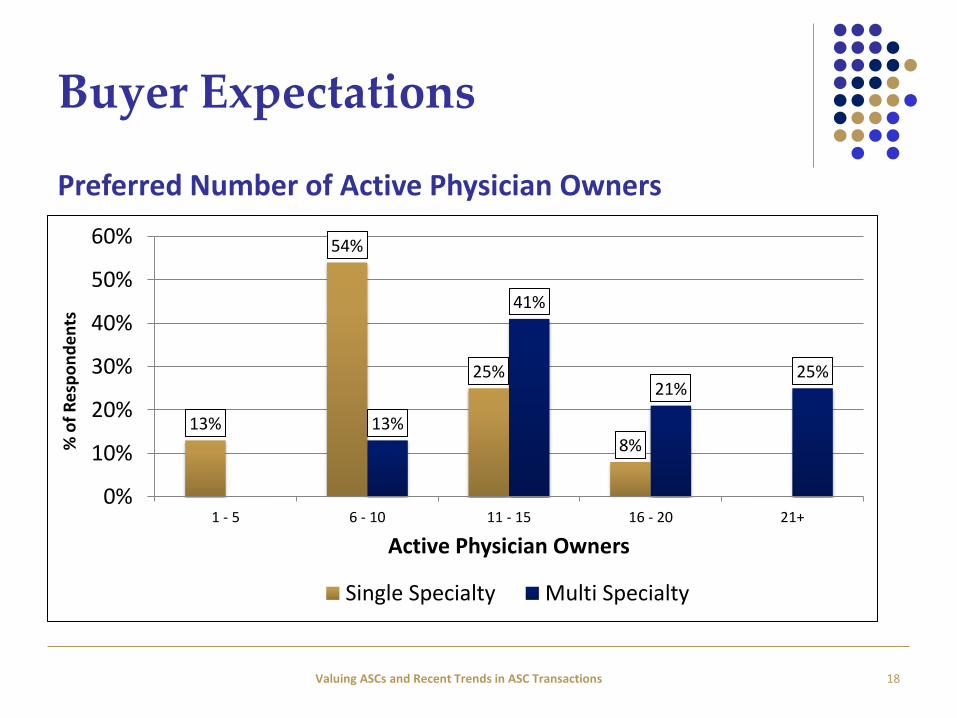

Buyer Expectations

18

Preferred Number of Active Physician Owners

13%

54%

25%

8% 13%

41%

21% 25%

0%

10%

20%

30%

40%

50%

60%

1 - 5 6 - 10 11 - 15 16 - 20 21+

% o

f R

esp

on

de

nts

Active Physician Owners

Single Specialty Multi Specialty

Valuing ASCs and Recent Trends in ASC Transactions

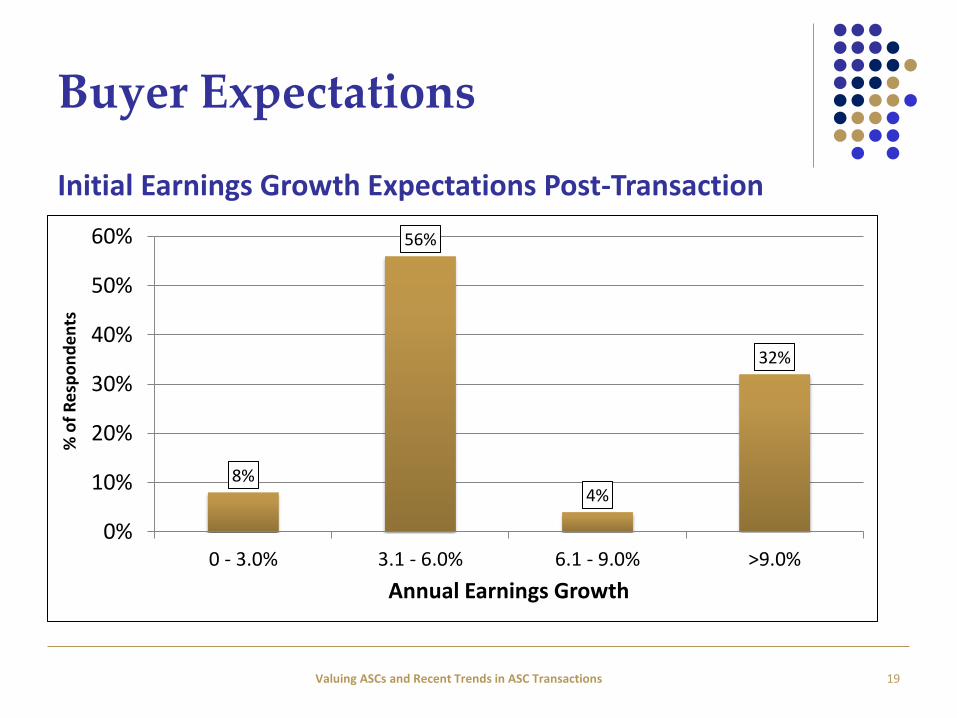

Buyer Expectations

19

Initial Earnings Growth Expectations Post-Transaction

8%

56%

4%

32%

0%

10%

20%

30%

40%

50%

60%

0 - 3.0% 3.1 - 6.0% 6.1 - 9.0% >9.0%

% o

f R

esp

on

de

nts

Annual Earnings Growth

Valuing ASCs and Recent Trends in ASC Transactions

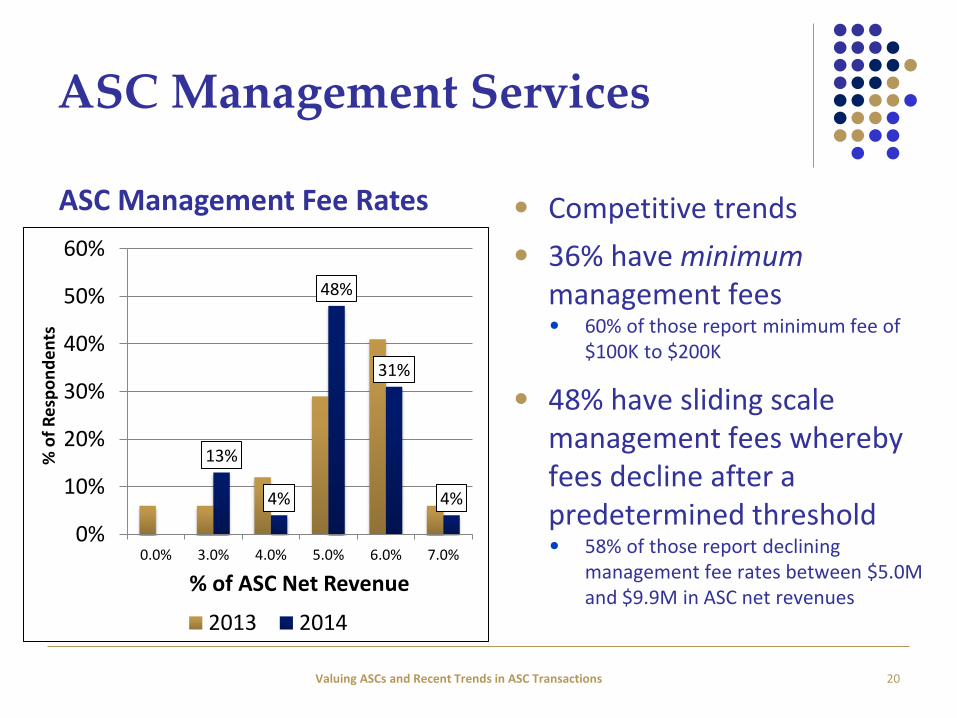

ASC Management Services

• Competitive trends

• 36% have minimum management fees • 60% of those report minimum fee of

$100K to $200K

• 48% have sliding scale management fees whereby fees decline after a predetermined threshold • 58% of those report declining

management fee rates between $5.0M and $9.9M in ASC net revenues

20

13%

4%

48%

31%

4%

0%

10%

20%

30%

40%

50%

60%

0.0% 3.0% 4.0% 5.0% 6.0% 7.0%

% o

f R

esp

on

de

nts

% of ASC Net Revenue

2013 2014

ASC Management Fee Rates

Valuing ASCs and Recent Trends in ASC Transactions

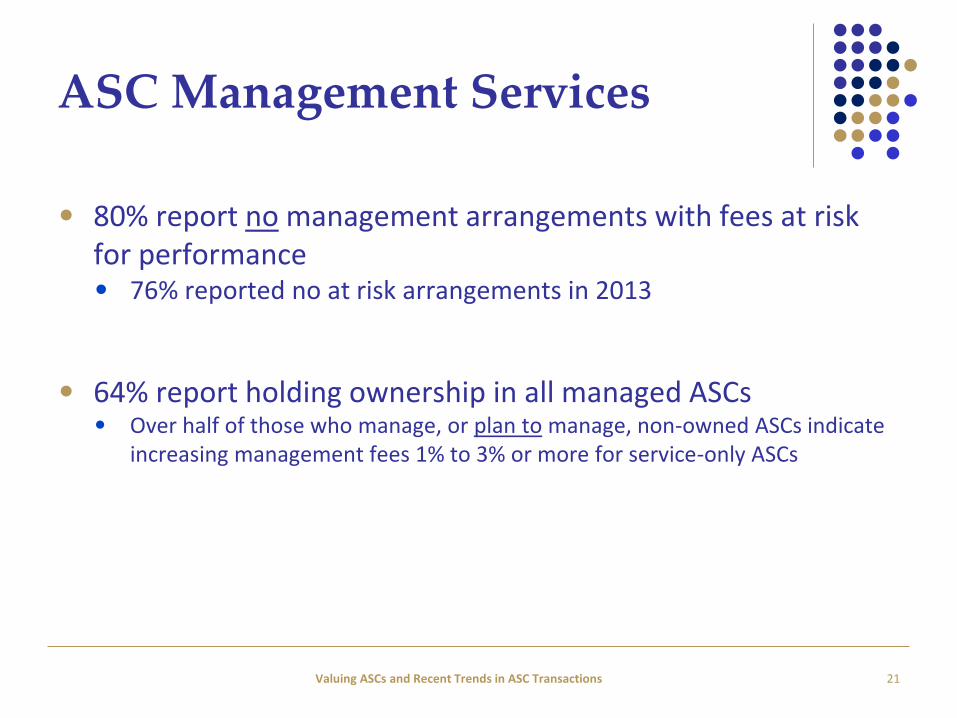

ASC Management Services

• 80% report no management arrangements with fees at risk for performance • 76% reported no at risk arrangements in 2013

• 64% report holding ownership in all managed ASCs • Over half of those who manage, or plan to manage, non-owned ASCs indicate

increasing management fees 1% to 3% or more for service-only ASCs

21 Valuing ASCs and Recent Trends in ASC Transactions

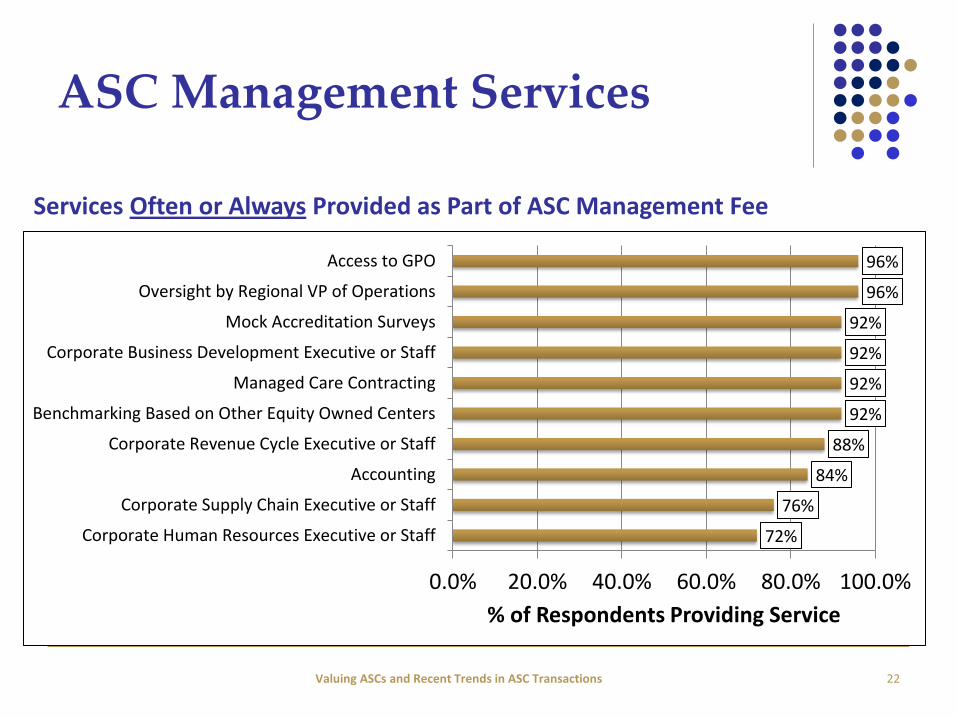

ASC Management Services

22

72%

76%

84%

88%

92%

92%

92%

92%

96%

96%

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

Corporate Human Resources Executive or Staff

Corporate Supply Chain Executive or Staff

Accounting

Corporate Revenue Cycle Executive or Staff

Benchmarking Based on Other Equity Owned Centers

Managed Care Contracting

Corporate Business Development Executive or Staff

Mock Accreditation Surveys

Oversight by Regional VP of Operations

Access to GPO

% of Respondents Providing Service

Services Often or Always Provided as Part of ASC Management Fee

Valuing ASCs and Recent Trends in ASC Transactions

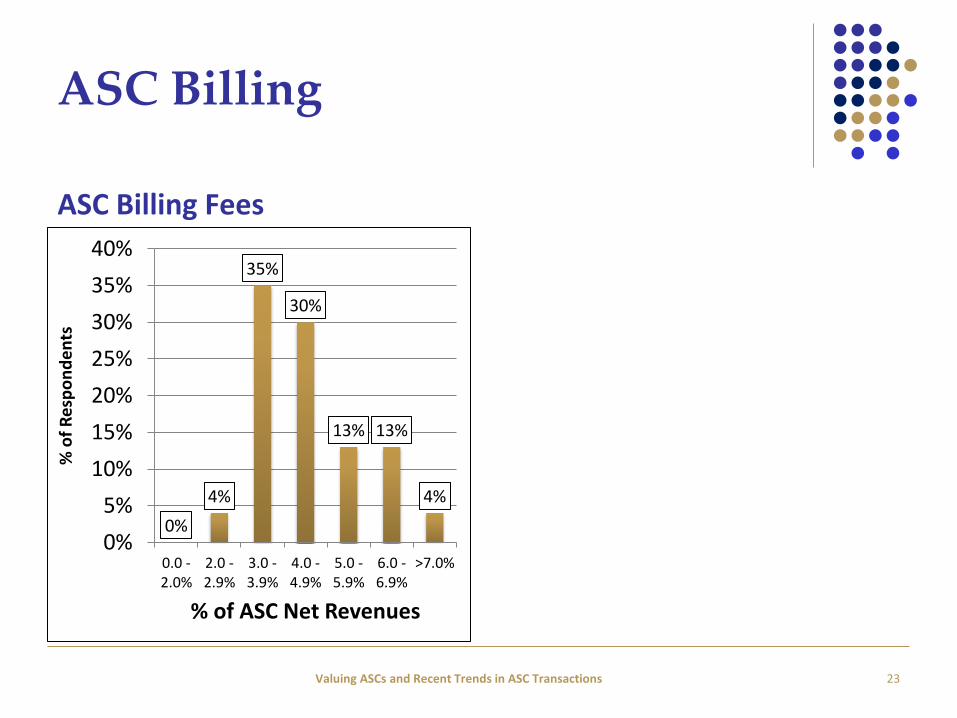

ASC Billing

ASC Billing Fees

23

0%

4%

35%

30%

13% 13%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0.0 -2.0%

2.0 -2.9%

3.0 -3.9%

4.0 -4.9%

5.0 -5.9%

6.0 -6.9%

>7.0%

% o

f R

esp

on

de

nts

% of ASC Net Revenues

Valuing ASCs and Recent Trends in ASC Transactions

QUESTIONS?

24 Valuing ASCs and Recent Trends in ASC Transactions

Valuing ASCs and Recent Trends in ASC Transactions

Todd J. Mello • [email protected]

HealthCare Appraisers, Inc. – Denver Office

(303) 688-0700