Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

VAT Fundamentals for U.S. Companies Buying or Selling in the European UnionBuying or Selling in the European UnionEnsuring VAT and U.S. Use Tax Compliance on Goods and Services Transactions

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, JUNE 28, 2012

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Britta Eriksson, President and CEO, Euro VAT Refund Inc., Culver City, Calif., , , y,

Mark Houtzager, Principal, US VAT Inc., New York

Chris Walsh, Chief Tax Officer, International, Vertex Inc., Berwyn, Pa.

Bobby Bui, Senior Manager, State and Local Tax, KPMG, Houston

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Attendees must stay on the line for at least 100 minutes in order to qualify for a full 2 credits of CPE. Attendance is monitored as required by NASBA.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

VAT Fundamentals for U.S. Companies B i S lli i th E Buying or Selling in the European Union Seminar

June 28, 2012

Mark Houtzager, US VAT [email protected]

Britta Eriksson, Euro VAT Refund [email protected]

Bobby Bui, [email protected]

Chris Walsh, Vertex Inc. [email protected]

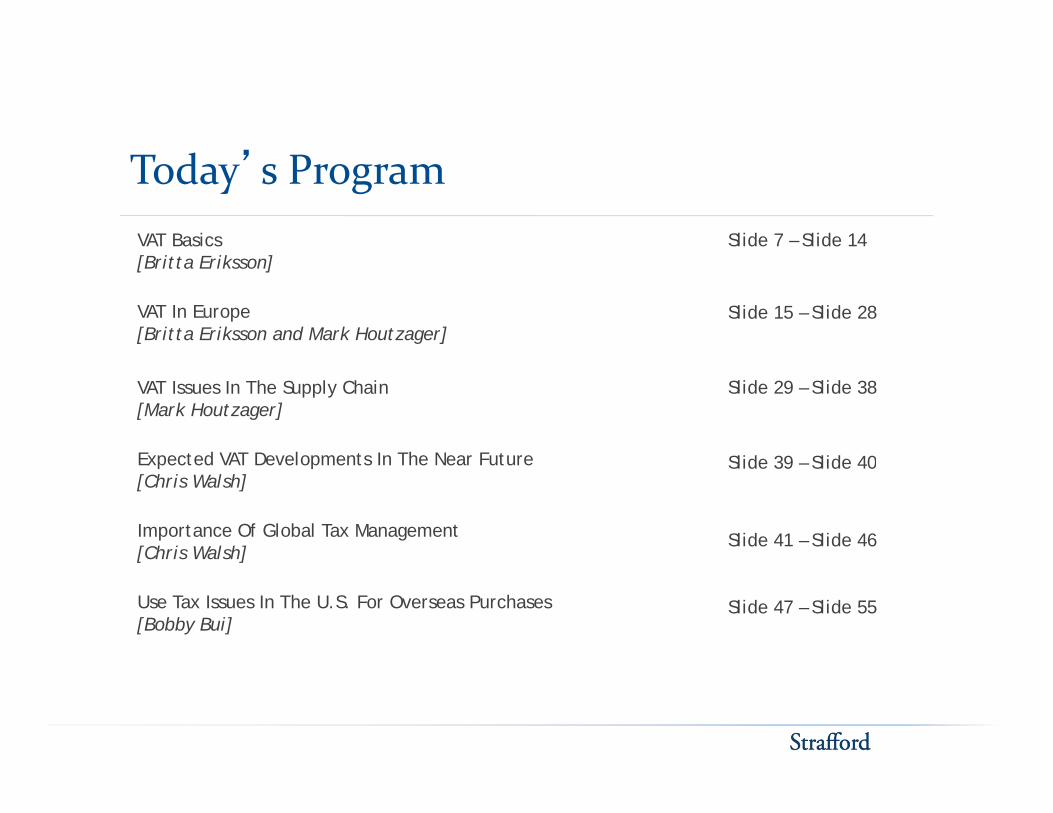

’Today’s ProgramVAT Basics Slide 7 – Slide 14[Britta Eriksson]

VAT In Europe[Britta Eriksson and Mark Houtzager]

Slide 15 – Slide 28

VAT Issues In The Supply Chain[Mark Houtzager]

Expected VAT Developments In The Near Future

Slide 29 – Slide 38

Slid 39 Slid 40Expected VAT Developments In The Near Future[Chris Walsh]

Importance Of Global Tax Management[Chris Walsh]

Slide 39 – Slide 40

Slide 41 – Slide 46[ ]

Use Tax Issues In The U.S. For Overseas Purchases[Bobby Bui]

Slide 47 – Slide 55

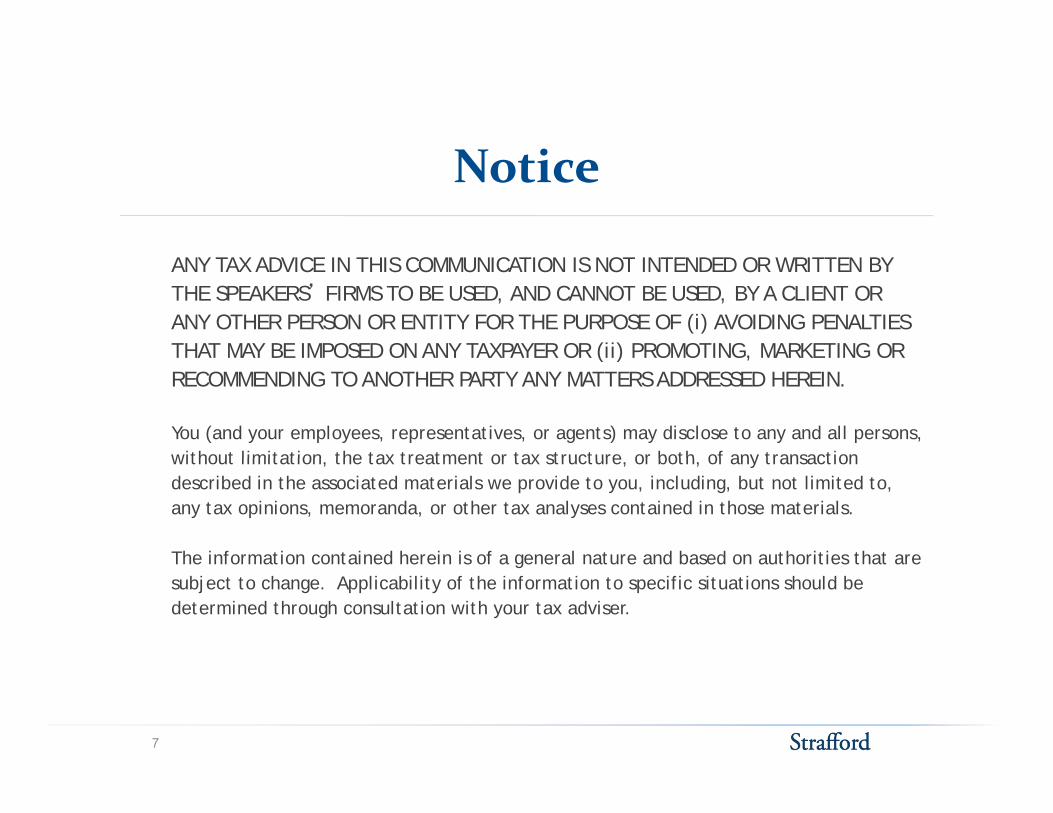

N iNotice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation the tax treatment or tax structure or both of any transaction without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

7

VAT BASICSBritta Eriksson, Euro VAT Refund Inc.

VAT BASICS

U.S. Sales Tax

Assessed only on goods, not to services generally

Only paid by the end user (business or private person)

Is a cost to the business when it has to be paid

U.S. is almost the only country in the world that has sales tax instead of VATinstead of VAT.

9

Value-Added Tax

Consumption tax is added to most goods and services in all levels of the production and distribution chain.

Implemented tax in most countries in the world except the U.S.

Is almost never a cost to the business

Is a cost to the private personIs a cost to the private person

10

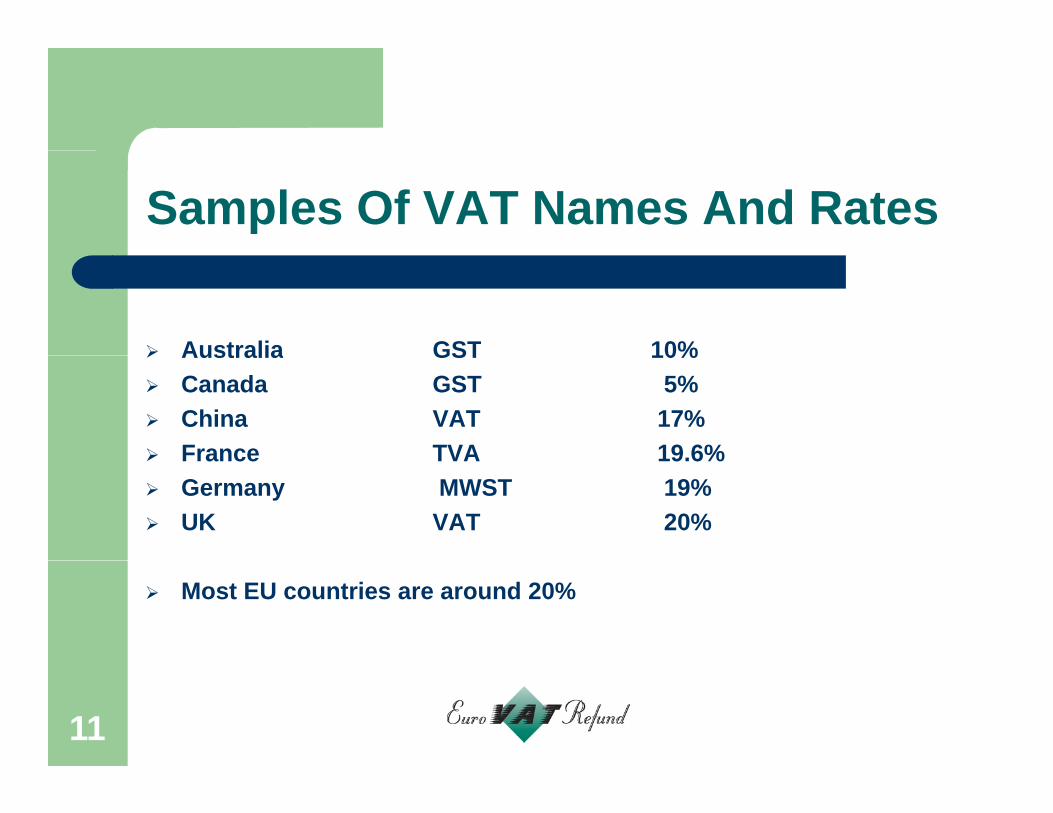

Samples Of VAT Names And Rates

Australia GST 10% Australia GST 10% Canada GST 5% China VAT 17% France TVA 19.6% France TVA 19.6% Germany MWST 19% UK VAT 20%

Most EU countries are around 20%

11

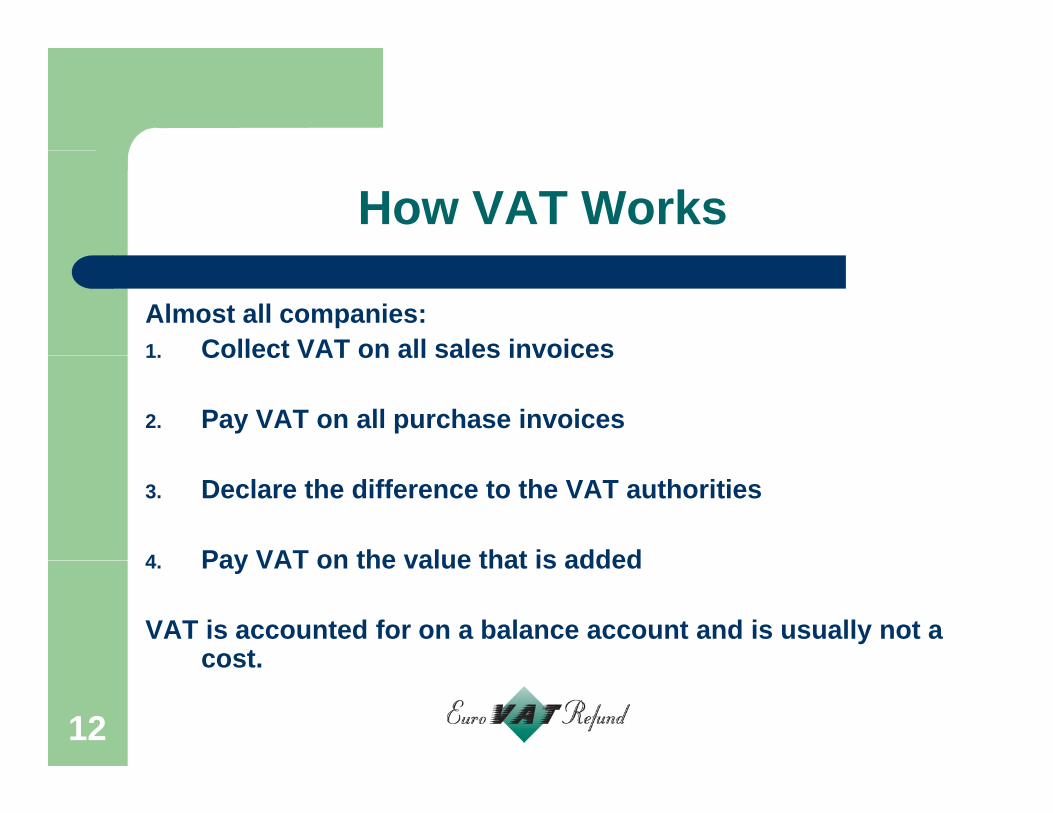

How VAT Works

Almost all companies:1. Collect VAT on all sales invoices1. Collect VAT on all sales invoices

2. Pay VAT on all purchase invoices

3. Declare the difference to the VAT authorities

4 Pay VAT on the value that is added4. Pay VAT on the value that is added

VAT is accounted for on a balance account and is usually not a costcost.

12

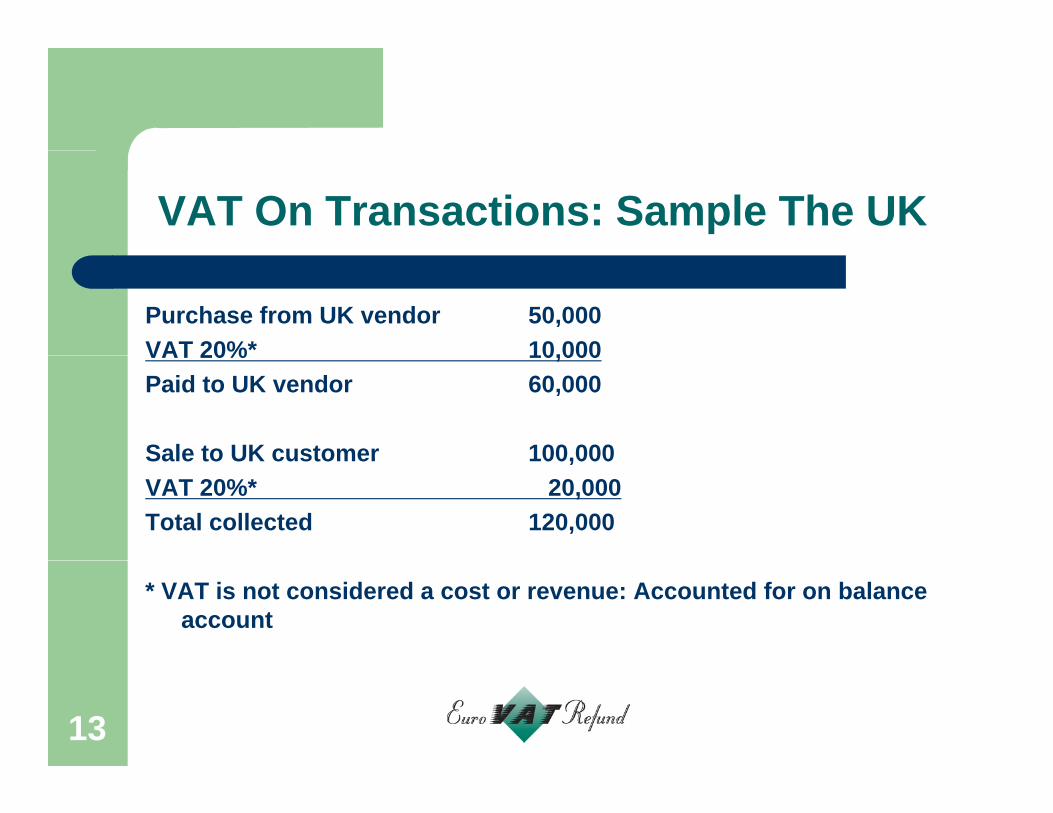

VAT On Transactions: Sample The UK

Purchase from UK vendor 50,000VAT 20%* 10,000VAT 20% 10,000Paid to UK vendor 60,000

Sale to UK customer 100,000Sale to UK customer 100,000VAT 20%* 20,000 Total collected 120,000

* VAT is not considered a cost or revenue: Accounted for on balance account

13

VAT Declaration To The TaxVAT Declaration To The Tax Authorities And Margin

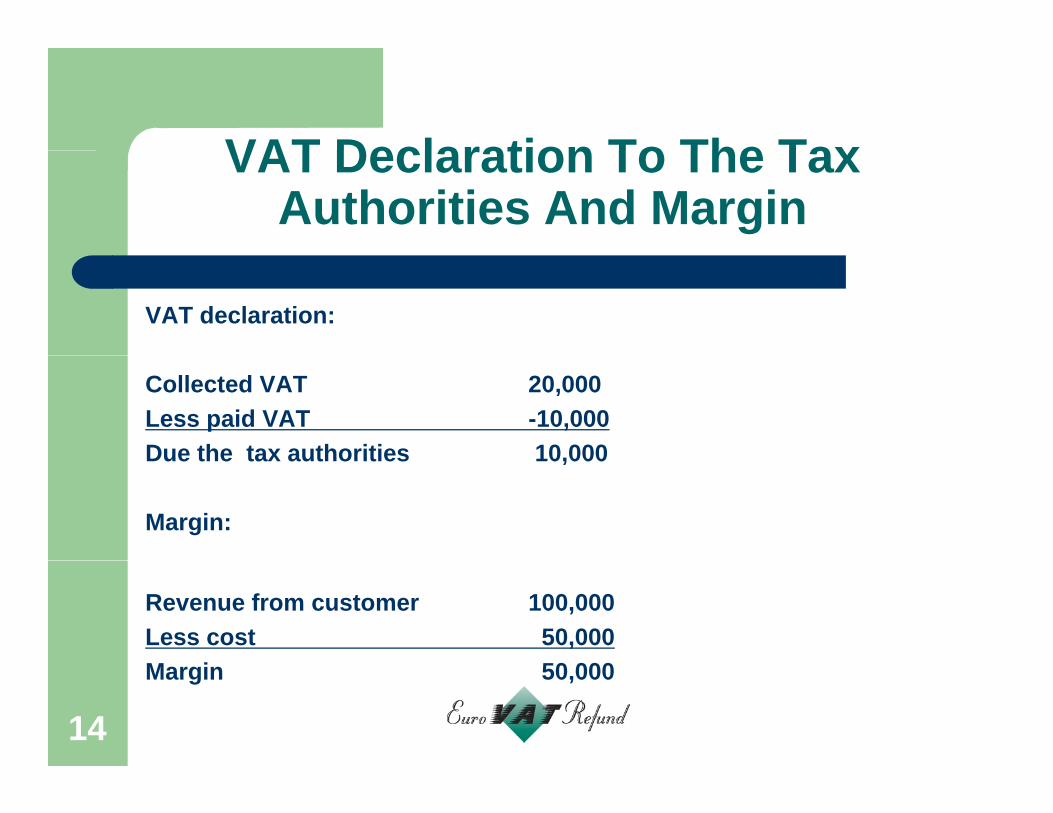

VAT declaration:

Collected VAT 20,000Less paid VAT -10,000Due the tax authorities 10,000Due the tax authorities 10,000

Margin:

Revenue from customer 100,000Less cost 50,000M i 50 000Margin 50,000

14

B i E ik E VAT R f d I

VAT IN EUROPE

Britta Eriksson, Euro VAT Refund Inc.Mark Houtzager, US VAT Inc.

VAT IN EUROPE

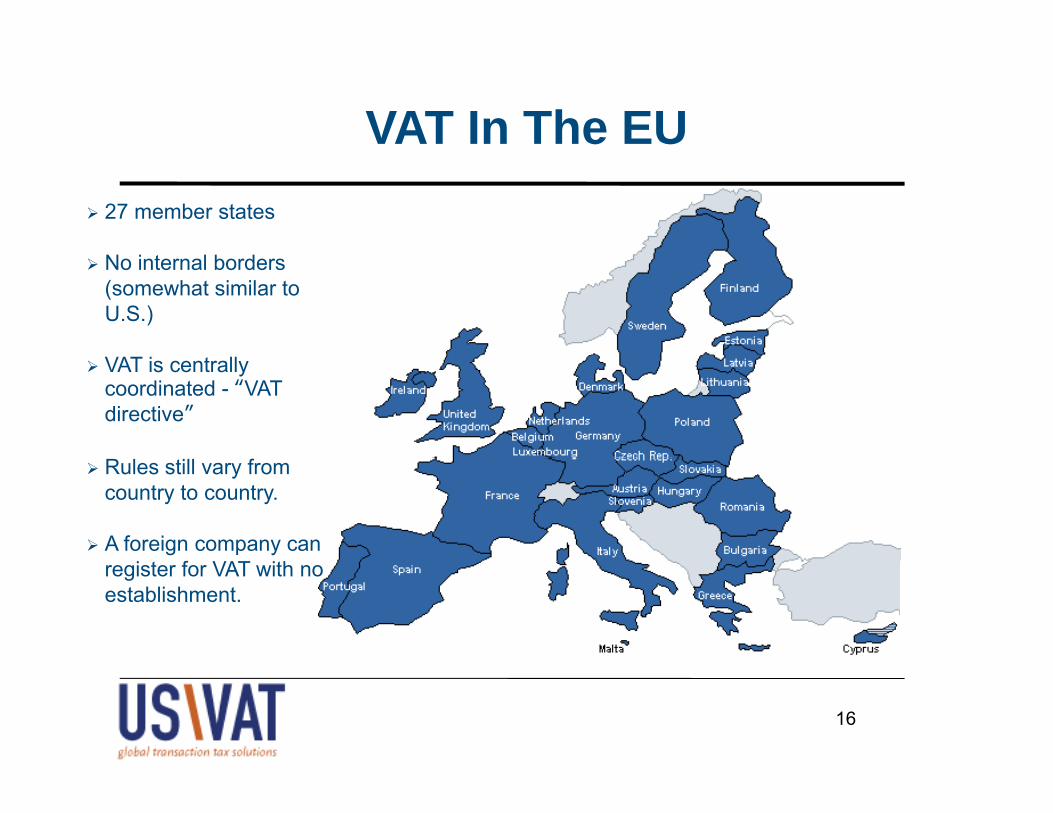

VAT In The EU 27 member states

No internal borders (somewhat similar to U.S.)

VAT is centrally coordinated - “VAT directive”

Rules still vary from country to country.

A foreign company can register for VAT with no establishment.

16

VAT In The EU (Cont.)( )

VAT rates

VAT comes in different rates. Typically, VAT jurisdictions have a standard rate, a lower rate and a zero rate.

The average VAT rate in the European Union is about 20%. Rates of up to 25% (Denmark, Sweden) and 27% (Hungary) are

common. Lower rates are for basic necessities (food, clothing). The zero rate often applies when goods or services leave the

country. There are exceptions.country. There are exceptions.

1717

VAT In The EU (Cont.)( )

When is VAT charged?

VAT is charged on most goods and services sold to any customer within the seller’s own EU country. Example: UK companies charges 20% UK VAT on most goods and services to all UK customers.

VAT is not charged on certain sales:- VAT exempt or zero-rate products, i.e. financial services

Sales to companies located in other EU countries or outside- Sales to companies located in other EU countries or outsidethe EU (reverse charge). There are exceptions.

1818

VAT In The EU (Cont.)( )VAT reverse charges

Supply is taxable for VATVAT is not levied from supplier but rather from buyer (business)B lf VATBuyer self-assesses VATBuyer reports on VAT return, claims the reverse-charged VAT as input tax on the same VAT return - no cash outlay in most countries

Typical supplies covered:• International services• Intra-EU supplies of goods• Certain domestic supplies (varies by country)

1919

VAT In The EU (Cont.)( )

VAT reverse charges (Cont.)

Example 1: Cross-border supply of goods in the EUGerman company sells and ships goods to a French company.p y p g p yGerman company does not charge German VAT.French buyer must self-assess French VAT.

Example 2: Consulting services in the EUUK company provides consulting services to an Irish company.UK company does not charge UK VAT.Irish buyer must self-assess VAT.

2020

VAT In The EU (Cont.)( )

VAT reverse charges (Cont.)

Example 3: International services to EU companiesUK business downloads software from a U.S. software provider.pU.S. company does not have to charge UK VAT.UK business is to self-assess UK VAT and deduct it at the same time. The VAT will not be a cost to the company.time. The VAT will not be a cost to the company.

2121

VAT In The EU (Cont.)( )

VAT where reverse charge does not apply

Example 4: International services to EU private personsUK private person downloads software from a U.S. software p pprovider.U.S. company must register for VAT in one of the EU countriesU.S. company must charge VAT of the customer’s country to theU.S. company must charge VAT of the customer s country to the private person.Private person cannot deduct the VAT. The final price will include VAT (UK VAT is 20%) and will be a cost to private person.VAT (UK VAT is 20%) and will be a cost to private person.

2222

VAT In The EU (Cont.)( )

U.S. company sometimes must register for VAT in the EU

Examples of reasons for the VAT registration:

Acts as the importer of goods and sells to EU customers Ships to fulfillment warehouses and sells to EU customers Purchases goods from EU vendors and ships and sell to EU Purchases goods from EU vendors, and ships and sell to EU customer Sells software to private persons in the EUO i f t d h i th EUOrganizes a conference or tradeshow in the EU

2323

VAT In The EU (Cont.)( )

VAT registration for US company means:

Sample Germany:

1. Register for VAT in Germany2. Pay 19% VAT on goods imported or purchased from Germany3 Charge 19% VAT to the customers in Germany3. Charge 19% VAT to the customers in Germany.4. File VAT returns to the German tax authorities

Benefits: In the end, the VAT will not be a cost to the U.S. company or to the EU customers.

2424

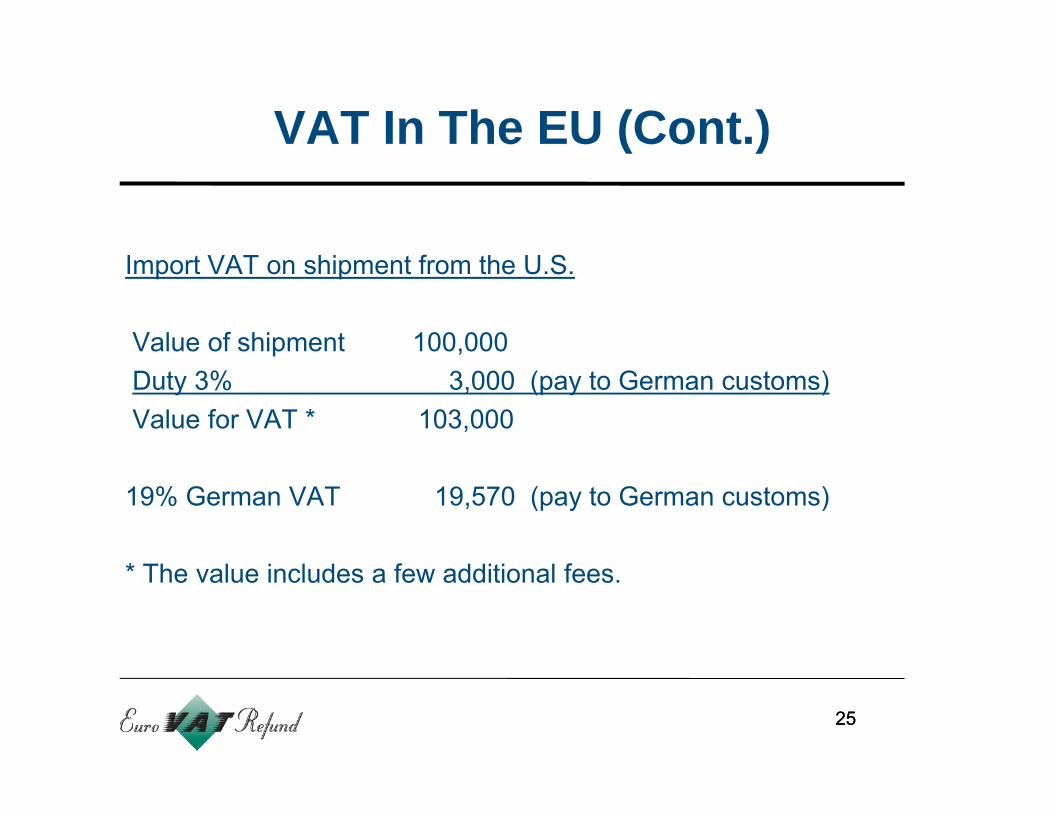

VAT In The EU (Cont.)( )

Import VAT on shipment from the U.S.

Value of shipment 100,000pDuty 3% 3,000 (pay to German customs)Value for VAT * 103,000

19% German VAT 19,570 (pay to German customs)

* The value includes a few additional fees.

2525

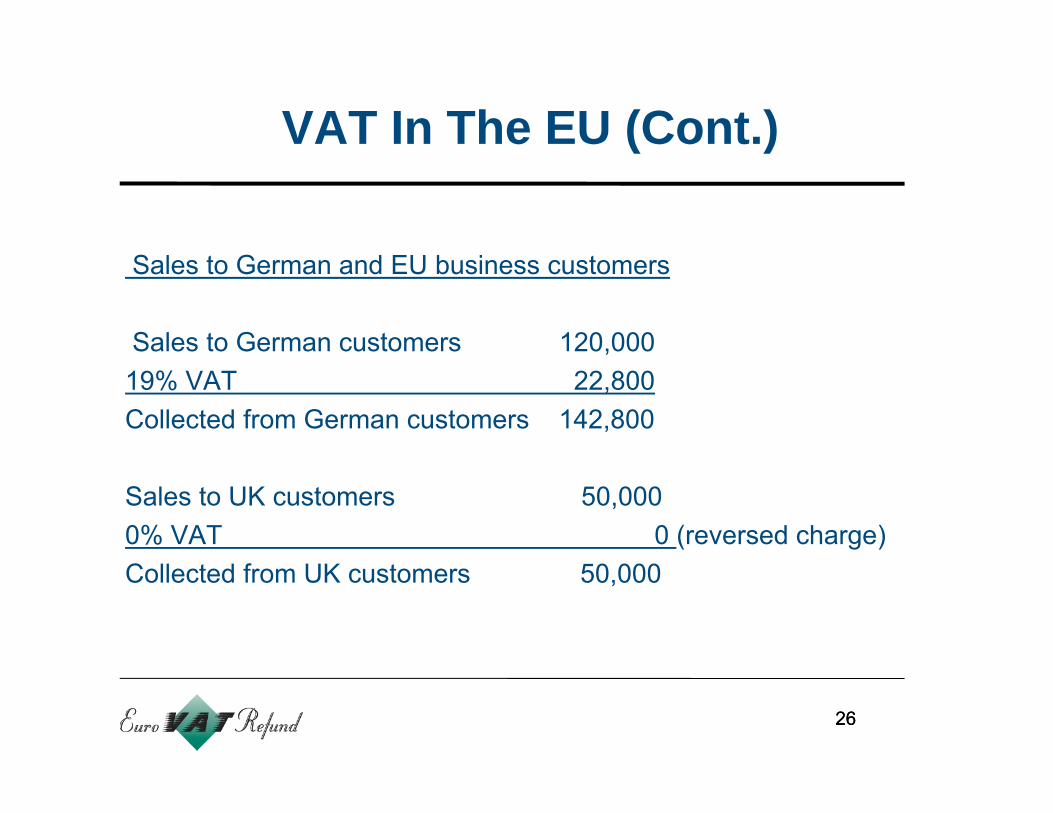

VAT In The EU (Cont.)( )

Sales to German and EU business customers

Sales to German customers 120,00019% VAT 22,800Collected from German customers 142,800

Sales to UK customers 50,0000% VAT 0 (reversed charge)Collected from UK customers 50,000

2626

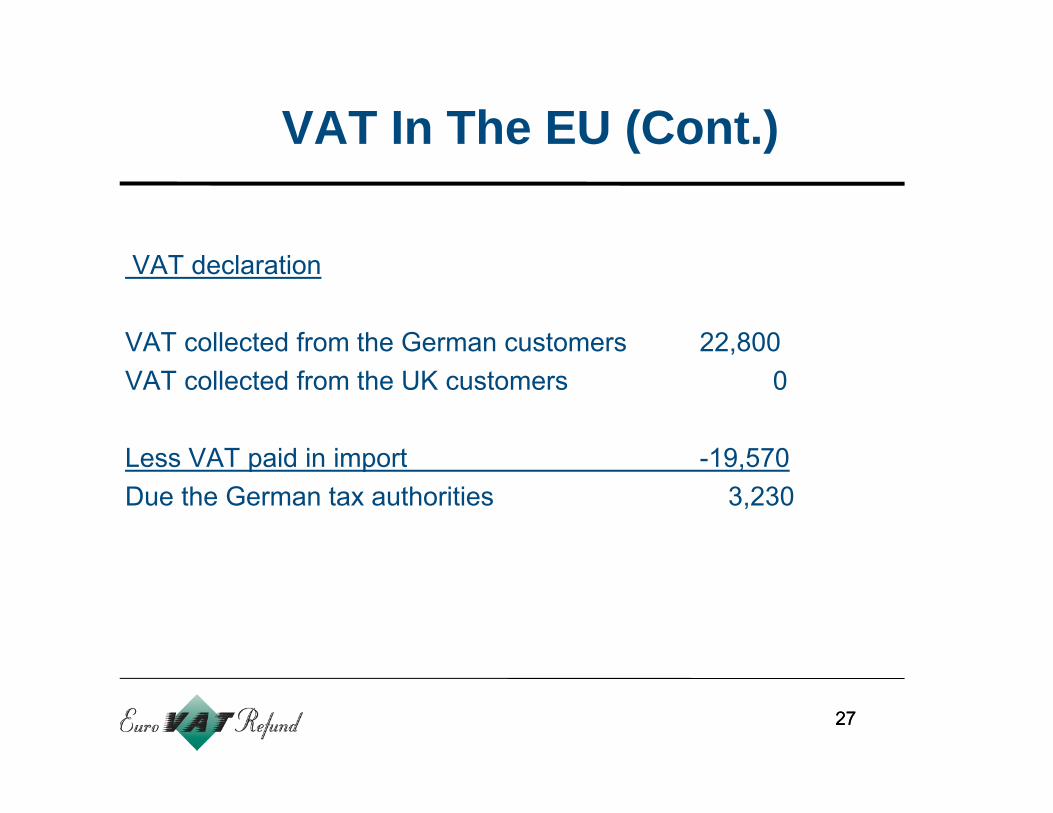

VAT In The EU (Cont.)( )

VAT declaration

VAT collected from the German customers 22,800VAT collected from the UK customers 0

Less VAT paid in import 19 570Less VAT paid in import -19,570Due the German tax authorities 3,230

2727

VAT In The EU (Cont.)( )

Try to register in a “VAT-friendly” EU country

Western EU and Scandinavia are easiest to work with.

Southern and Eastern EU countries are more costly and difficultSouthern and Eastern EU countries are more costly and difficult.

2828

VAT ISSUES IN THE SUPPLY Mark Houtzager, US VAT Inc.

CHAIN

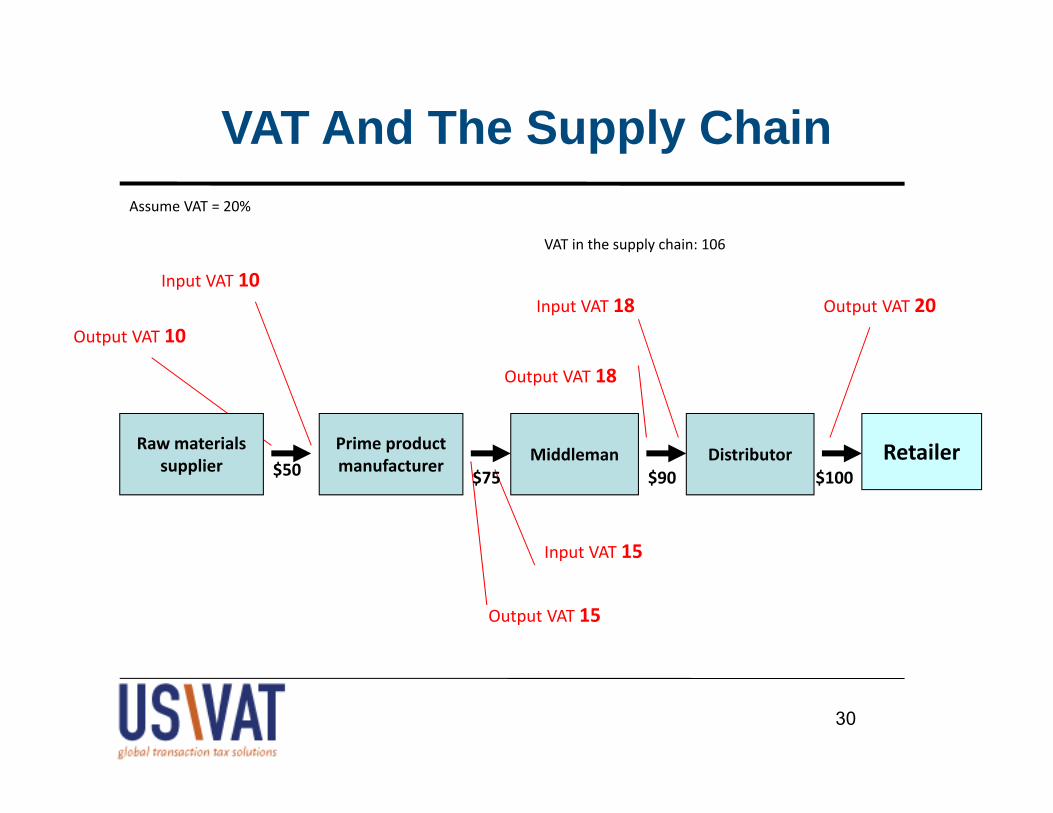

VAT And The Supply Chain

VAT in the supply chain: 106

pp yAssume VAT = 20%

Output VAT 20Output VAT 10

Input VAT 10Input VAT 18

Output VAT 18

RetailerMiddleman DistributorPrime product Raw materials

Input VAT 15

RetailerMiddleman Distributormanufacturer$100$90$75

supplier $50

Output VAT 15

p

30

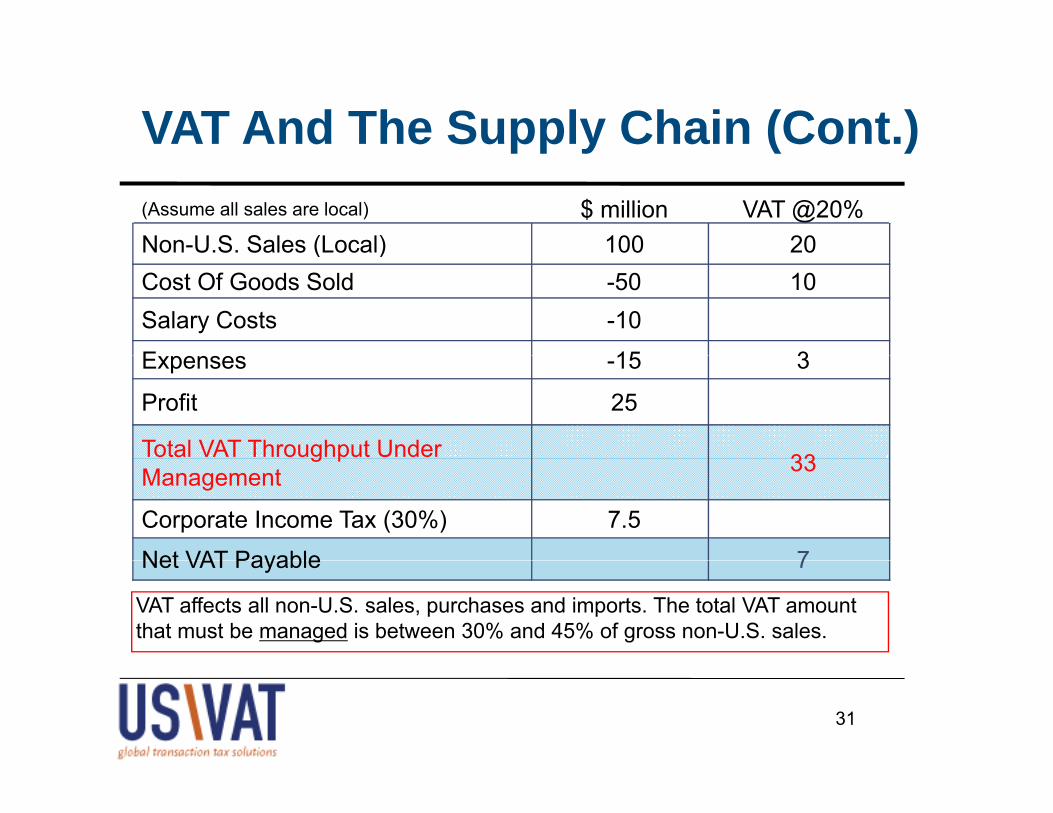

VAT And The Supply Chain (Cont.)pp y ( )(Assume all sales are local) $ million VAT @20%Non-U.S. Sales (Local) 100 20( )Cost Of Goods Sold -50 10Salary Costs -10

E 15 3Expenses -15 3

Profit 25

Total VAT Throughput Under 33g pManagement 33

Corporate Income Tax (30%) 7.5

Net VAT Payable 7Net VAT Payable 7

VAT affects all non-U.S. sales, purchases and imports. The total VAT amount that must be managed is between 30% and 45% of gross non-U.S. sales.

31

VAT And The Supply Chain (Cont.)pp y ( )

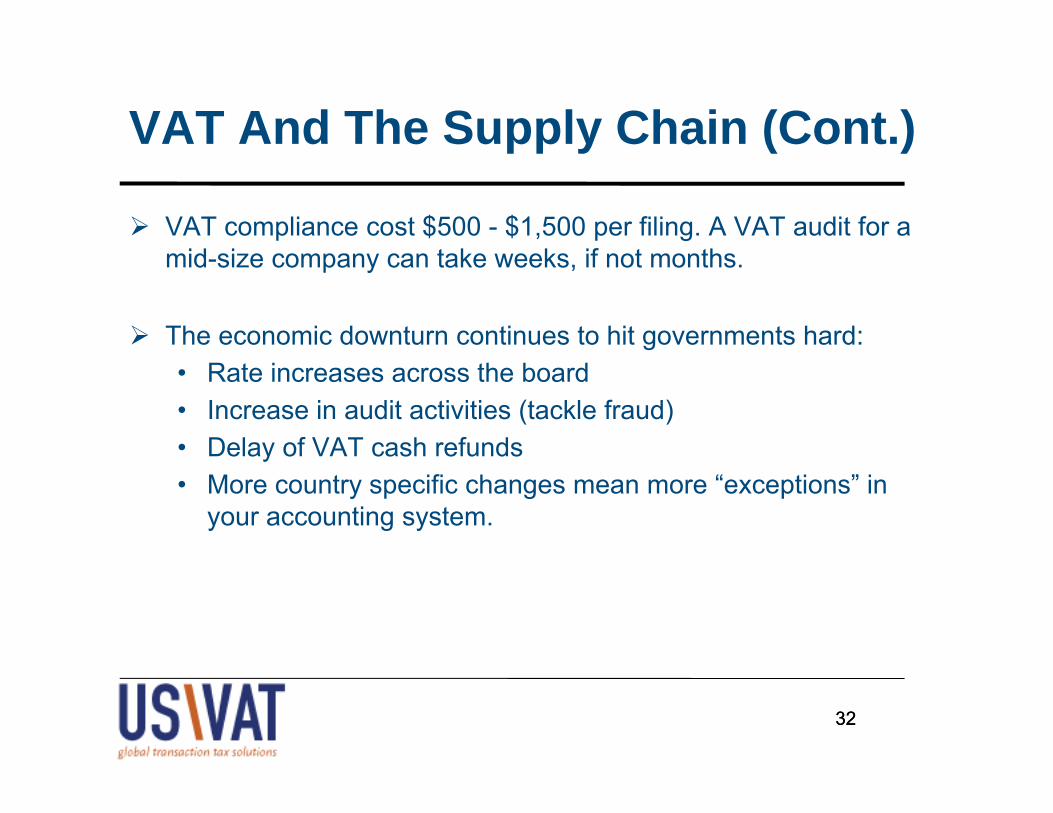

VAT compliance cost $500 - $1,500 per filing. A VAT audit for a id i t k k if t thmid-size company can take weeks, if not months.

The economic downturn continues to hit governments hard:• Rate increases across the board• Increase in audit activities (tackle fraud)• Delay of VAT cash refundsy• More country specific changes mean more “exceptions” in

your accounting system.

3232

Optimize Your VAT Positionp

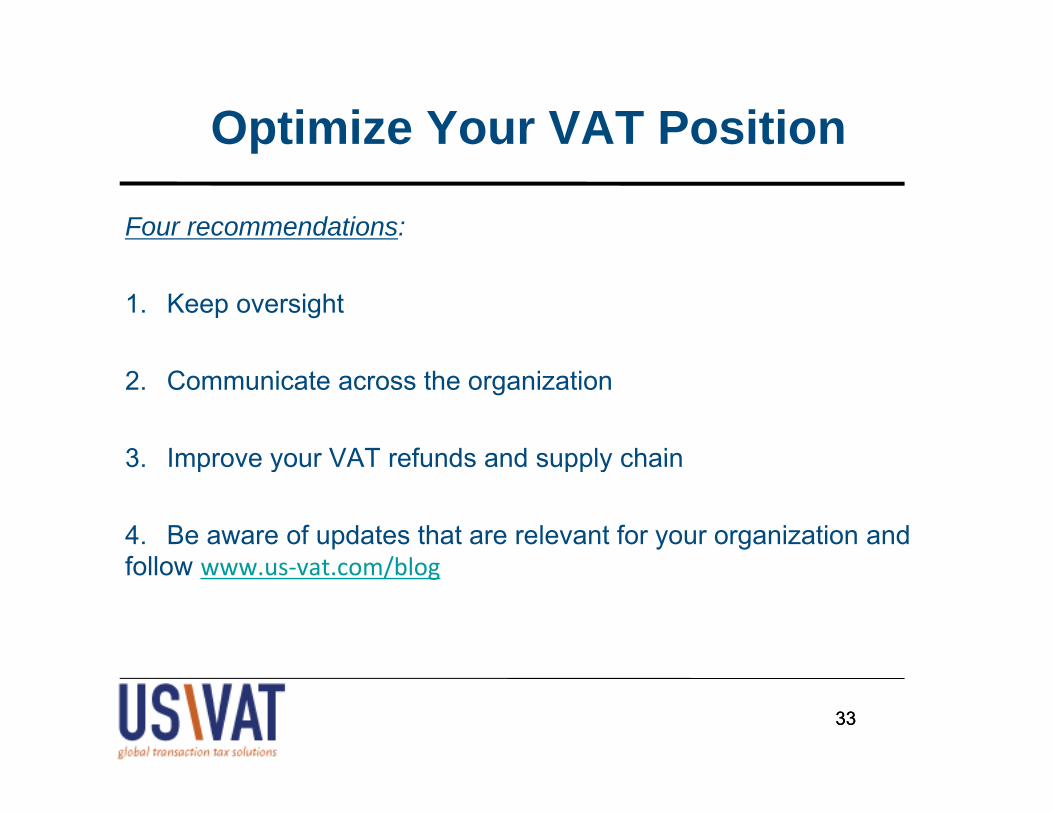

Four recommendations:

1. Keep oversight

2. Communicate across the organization

3 Improve your VAT refunds and supply chain3. Improve your VAT refunds and supply chain

4. Be aware of updates that are relevant for your organization and f ll t /blfollow www.us‐vat.com/blog

3333

Optimize Your VAT Position (Cont.)p ( )Keep oversightUse “dashboard” functionality in ERP systems to review filingUse dashboard functionality in ERP systems to review filing position

• VAT returns• Various other filings such as sales listings statisticalVarious other filings, such as sales listings, statistical

returns(“intrastat”)• Consider VAT “bolt-ons” (Vertex, ADP Taxware, Sabrix)

Consider long term VAT strategyConsider long-term VAT strategy• Current VAT issues in Country A may become issues in

Country B, if distribution arrangements are similar.ERP implementations acquisitions business restructuring• ERP implementations, acquisitions, business restructuring, etc. are excellent opportunities to start thinking about a comprehensive VAT strategy.

3434

Optimize Your VAT Position (Cont.)p ( )

Communicate

Maintain ongoing communication with various stakeholders:• Sales• Business development• Tax• LogisticsLogistics• Finance

Decide who has global responsibility for VAT; recruit VAT managerDecide who has global responsibility for VAT; recruit VAT manager

3535

Optimize Your VAT Position (Cont.)p ( )

Make money - optimize VAT refunds

Opportunity for U.S. multi-nationals to reclaim VAT on foreign expenses (hotel, travel, inter-company changes, import VAT)

Available in a number of EU countries and a few non-EU countries

Refunds in Spain, Greece, Italy and some other EU countries are difficult or impossible.

3636

Optimize Your VAT Position (Cont.)p ( )

Make money - optimize VAT refunds (Cont.)

Deadlines (generally June 30 after the calendar year in which the VAT has been incurred, but not for the UK)

Original hard-copy invoices required

Sophisticated data-analysis tools are useful. No VAT cost should remain unconsidered.

Let me know if you want to optimize your VAT refunds

3737

Optimize Your VAT Position (Cont.)p ( )

Make money - optimize the supply chain

Optimize use of reverse charges and other simplifications• Cash flow and compliance cost savings for companies that

operate across regions

Bad debt relief• If a customer doesn’t pay, the output VAT paid to the

government can be reclaimed.• Very simple and straightforward opportunity, but oftenVery simple and straightforward opportunity, but often

overlooked; does not require a credit invoice

3838

EXPECTED VAT Chris Walsh, Vertex Inc.

DEVELOPMENTS IN THE NEAR FUTUREFUTURE

WhatIsHappeningInTheWorldOfVAT?

China is piloting the expansion of its VAT system and phasing out its business tax.

India is redesigning its direct and indirect tax systems. A new dual GST system is on its way.

Europe is seeking VAT simplification.p g p• Green paper outputs, EU invoicing directive

Japan is doubling its consumption tax rate. Gulf Cooperation Council member countries are introducing Gulf Cooperation Council member countries are introducing

GSTs. Malaysia is introducing a GST.

40

IMPORTANCE OF GLOBAL TAX Chris Walsh, Vertex Inc.

MANAGEMENT

WhyManageVAT?

Indirect taxes have assumed a higher profile.• Rates have risen and globalization has continued, increasing g , g

the tax throughput in MNCs.• Increased percentage of government revenue coming from

indirect taxes such as VAT, so greater focus and more audits , gin this area

• Introduction of VAT/GST or major reforms in many countries adds uncertainty and complexity.y p y

• Promotion by OECD, IMF, World Bank, etc.

Global shift away from direct taxes to indirect taxes resource Global shift away from direct taxes to indirect taxes – resource shift may be required?

42

CorporateGovernance:RiskManagement

Sarbanes‐Oxley applies to VAT in the same way as it applies to other taxes.• Best practices• 404 attestations (U.S.)• Senior accounting officer attestations (UK)Senior accounting officer attestations (UK)

Interest and penalties for non‐compliance

Risk can arise due to internal or external factors.

Operational, compliance, supply chain, financial accounting, reputational risks

43

CorporateGovernance:Transparency

Demands for greater transparency and disclosure• Tax authorities• Regulators• Legislators• Investors• Investors• Tax justice campaigners• Media

Each has a different agenda/viewpoint.

44

Compliance

Need for global, internal networks and effective communications

VAT awareness and appropriate registration are key to avoiding major problems.j p

Automation and outsourcing should be considered when there is no internal resourceis no internal resource.

45

VATManagementChallenges Doing more with less

Availability of tax data for reporting

Financial systems require constant updating with accurate, timely tax data.• More than 13,000 taxing jurisdictions globally for

transaction taxes

Uncertainty due to legislative and policy changes (GAAR, SAAR), case law, etc.case law, etc.

Connecting VAT with corporate changes in supply chain management M&A activity transfer pricing etcmanagement, M&A activity, transfer pricing, etc.

46

USE TAX ISSUES IN THE U.S. Bobby Bui, KPMG

FOR OVERSEAS PURCHASES

Agenda For This Section

Use tax issues in the U.S. for overseas imports

– Importation of new vs used equipment– Importation of new vs. used equipment

– Sales tax credits for use tax paid

– Use tax base– Use tax base

– Audit considerations

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 48

Importation Of Equipment Into The U.S. 45 states and the District of Columbia impose a sales tax. All states imposing a sales tax also

impose a corresponding use tax.

All jurisdictions imposing a use tax give the taxpayer credit for sales tax paid to another state.All jurisdictions imposing a use tax give the taxpayer credit for sales tax paid to another state.

Importing NEW Equipment into the U.S.

– Assumption foreign seller will not be charging U.S. taxes, creating a use tax obligation for th hthe purchaser

– Issues:

Does this transaction get processed in the same manner as other purchase g p ptransactions (i.e., reviewed by AP and accrue use tax where no sales tax was charged)?

– Is there an applicable exemption (e.g., manufacturing)?

Is the jurisdiction where the equipment is received the same as where it will be used?

Which party bears the cost of freight/delivery?

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 49

Importation Of Equipment Into The U.S. (Cont.)

Importing USED equipment into the U.S.

– Assumption foreign VAT was paid, if applicable, and equipment was previously used by either taxpayer or an affiliate prior to importation into the U Sused by either taxpayer or an affiliate prior to importation into the U.S.

Issues:

– How is the transaction booked (e.g., inter-company charge, journal entry) ( g p y g j y)to move the assets from overseas to the U.S.?

– How long was the equipment used outside the U.S. prior to bringing it into the country?y

■ A number of states (e.g., Florida, Texas) provide for a use tax exemption on equipment used for a period of time prior to importation into the state.

Was there a change in ownership (i e transfer of equipment from E U– Was there a change in ownership (i.e., transfer of equipment from E.U. affiliate to U.S. affiliate)?

– Was VAT previously paid on the equipment?

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 50

Sales Tax Credits Against Use TaxSt t t t t d t id l t dit f VAT idStates statutes do not provide a sales tax credit for VAT paid.

States generally allow for credits for sales tax paid against use tax incurred.

– 45 states and the District of Columbia allow for credit

Credit: Texas will allow as a credit against Texas use tax due, any combined amounts of legally imposed sales or use taxes paid on the same property to another state or any subdivision of another state. Tex. Admin. Code 3.338

– Statutes generally require reciprocity (other state grants a corresponding credit) and specifically identify “sales tax” paid to offset use taxspecifically identify sales tax paid, to offset use tax.

Reciprocity: No credit will be allowed for taxes paid on tangible personal property in any state which does not give credit for taxes paid on similar property in Alabama. The Commissioner of Revenue shall require such proof of payment of tax to another state as he deems to be necessary and proper Alabama § 40 23 65he deems to be necessary and proper. Alabama § 40-23-65

– Statute is specific to taxes paid to another “state” and finds that foreign countries are not “states,” per the requirements

– Foreign jurisdictions also do not have any type of reciprocal agreement for sales taxes paidForeign jurisdictions also do not have any type of reciprocal agreement for sales taxes paid in the U.S.

– Therefore, absent an exemption, importation of previously used equipment may incur additional U.S. state sales tax in addition to VAT already paid.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 51

Sales Tax Credits Against Use Tax (Cont.)State guidance on lack of VAT credits against use tax liability

Virginia Public Document Ruling No. 00-81 (May 11, 2000)

– Credit may only be allowed for a “similar tax” paid to another state.y y

Illinois Dept. of Rev. General Information Letter ST 07-0167-GIL (Dec. 31, 2007)

– Illinois does not provide any credit for foreign taxes that may be incurred to a customer in another country.

Maryland Revenews, Spring 2000 (March 1, 2000)

– Maryland allows a use tax credit for sales taxes paid to another state, but foreign value-added taxes (VATs) do not qualify for the credit.

New York Advisory Opinion TSB-A-99(2)S (Jan. 19, 1999)

– A sales or use tax was not legally due or paid to any other state or jurisdiction within any other state, within the meaning and intent of the exemption provided in Sect. 1118(7)( ) h th t i d b f i t1118(7)(a) , where the tax was imposed by a foreign country.

North Carolina FAQs About Use Tax (March 7, 2007)

– May not claim a credit for sales tax or value-added tax paid to another country

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 52

Use Tax Base What is tax base?

– Tax base is the amount subject to tax, including certain separately stated chargescharges.

– States vary on their definition of tax base for both use tax purposes (e.g., original purchase price, FMV, value of in-state use).

I T “ l i ” “ i t ” th t t l t f hi h– In Texas, “sales price” or “receipts” mean the total amount for which a taxable item is sold, leased, or rented; or valued in money; without a deduction for the cost of:

The taxable item sold leased or rented The taxable item sold, leased or rented

The materials used, labor or service employed, interest, losses or other expenses

The transportation or installation of tangible personal property

Transportation incident to the performance of a taxable service. Tex. Tax Code Ann. §151.007(a)(1)-(4)

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 53

Use Tax Base (Cont.)

For imported property, determination of whether the follow charges are subject to use tax as part of the tax base

– Shipping/freight charges/handling charges

– Installation

– Foreign taxes paid on acquisition of property

– Import duties

For new equipment purchased from a vendor, must consider whether any of these charges may be excluded from the amounts subject to use tax

For used equipment must consider whether tax is based on the original For used equipment, must consider whether tax is based on the original purchase price, current FMV or some other value

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 54

Audit ConsiderationsImport transactions under audit

Similar to use tax imposed on purchases from remote vendors that lack nexus with the customer’s state foreign vendors are not likely to chargenexus with the customer’s state, foreign vendors are not likely to charge sales tax on the invoice.

Generally, use tax audits would encompass all purchases, including those from overseas vendors.

Area of exposure can include importation of used equipment.

Does the company have sufficient controls in place to review imported Does the company have sufficient controls in place to review imported purchases for use tax accruals?

What about documentation on inter-company transfers of assets/redeployment of used assets?

For purchases, is the company able to identify if VAT was paid on the purchase as well, and whether that was a proper tax charge from the

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 55

p , p p gvendor?