Embed Size (px)

Citation preview

Non-parametric estimation of intraday spot volatility: disentangling

instantaneous trend and seasonality

Thibault Vattera,∗, Hau-Tieng Wub, Valerie Chavez-Demoulina, Bin Yuc

aFaculty of Business and Economics (HEC), University of Lausanne, Switzerland.bDepartment of Mathematics, University of Toronto, Canada.

cDepartment of Statistics, University of California, Berkeley, USA.

Abstract

We provide a new framework to model trends and periodic patterns in high-frequency financial

data. Seeking adaptivity to ever changing market conditions, we enlarge the Fourier Flexible

Form into a richer functional class: both our smooth trend and the seasonality are non-

parametrically time-varying and evolve in real time. We provide the associated estimators

and show with simulations that they behave adequately in the presence of heteroskedastic and

heavy tailed noise and jumps. A study of echange rates returns sampled from 2010 to 2013

suggest that failing to factor in the seasonality’s dynamic properties may lead to misestimation

of the intraday spot volatility.

Keywords: Intraday spot volatility, Seasonality, Foreign exchange returns, Time-frequency

analysis, Synchrosqueezing

JEL: C14, C22, C51, C52, C58, G17

∗Corresponding author: Thibault Vatter. Phone: +41 21 693 61 04. Postal Address: Office 3016, AnthropoleBuilding, University of Lausanne, 1015 Lausanne, Switzerland.

Email addresses: [email protected] (Thibault Vatter), [email protected] (Hau-TiengWu), [email protected] (Valerie Chavez-Demoulin), [email protected] (Bin Yu)

Preprint submitted to Elsevier December 6, 2014

1. Introduction

Over the last two decades, increasingly easier access to high frequency data has offered a

magnifying glass to study financial markets. Analysis of these data poses unprecedented chal-

lenges to econometric modeling and statistical analysis. As for traditional financial time series

(e.g. daily closing prices), the most critical variable at higher frequencies is arguably the asset

return: from the pricing of derivatives to portfolio allocation and risk-management, it is a

cornerstone both for academic research and practical applications. Because its properties are

of such utmost importance, a vast literature sparked to find high-frequency models consistent

with the new observed features of the data.

Among all characteristics of the return, its second moment structure is empirically found

as preponderant, partly because of its power to asses market risk. Therefore, its time-varying

nature has received a lot of attention in the literature (see e.g. Andersen et al. 2003). While

most low frequency stylized features find themselves at higher frequencies, an empirical reg-

ularity is left unaddressed by most models designed to capture heteroskedasticity in financial

time series. It is now well documented that seasonality, namely intraday patterns due to the

cyclical nature of market activity, represents one of the main sources of misspecification for

usual volatility models (see e.g. Guillaume et al. 1994; Andersen and Bollerslev 1997, 1998).

More specifically, some periodicity in the volatility is inevitable, due, for instance, to mar-

ket openings and closings around the world, but is unaccounted for in the vast majority of

econometrics models. To avoid misspecification bias, one possibility is to explicitly incorporate

the seasonality in traditional models, for instance with the periodic-GARCH of Bollerslev and

Ghysels (1996). Alternatively, a pre-filtering step combined with a non-periodic model can

be used as in Andersen and Bollerslev (1997, 1998); Boudt et al. (2011); Muller et al. (2011);

Engle and Sokalska (2012). Even though an explicit inclusion of seasonality is advocated as

more efficient (see Bollerslev and Ghysels 1996), the resulting models are at the same time less

flexible and computationally more expensive. While they may potentially propagate errors,

two-step procedures are more convenient and often consistent whenever each step is consistent

2

(see Newey and McFadden 1994).

As a result, seasonality pre-filtering has received a considerable amount of attention in

the literature dedicated to high-frequency financial time series. In this context, an attractive

approach is to generalize the removal of weekends and holidays from daily data and use the

“business clock” (see Dacorogna et al. (1993)); a new time scale where time goes faster when the

market is inactive and conversely during “power hours”, at the cost of synchronicity between

assets. The other approach, which allows researchers to work in physical time (removing only

closed market periods), is to model the periodic patterns directly, either non-parametrically

with estimators of scale (e.g. in Martens et al. (2002); Boudt et al. (2011); Engle and Sokalska

(2012)) or using smoothing methods (e.g. splines in Giot (2005)) or parametrically with the

Fourier Flexible Form (FFF) (see Gallant (1981)), introduced by Andersen and Bollerslev

(1997, 1998) in the context of intraday volatility in financial markets.

Until now, the standard assumption in the literature is to consider a constant seasonality

over the sample period. However, it is seldom verified empirically and few studies acknowledge

this issue. Notably, Deo et al. (2006) uses frequency leakage as evidence in favor of a slowly

varying seasonality. Furthermore, Laakkonen (2007) observes that smaller sample periods yield

improved seasonality estimators. In this paper, we argue that the constant assumption can

only hold for arbitrary small sample periods, because the entire shape of the market (and

its periodic patterns) evolves over time. Contrasting with seasonal adjustments considered in

the literature, we relax the assumption of constant seasonality and suggest a non-parametric

framework to obtain “instantaneous” estimates of trend and seasonality.

From a time-frequency decomposition of the data, the proposed method extracts an instan-

taneous trend and seasonality, estimated respectively from the lowest and highest frequencies.

In fact, it is comparable to a “dynamic” combination of realized-volatility or bipower vari-

ation (RV/BV) and Fourier Flexible Form (FFF). In this case, the instantaneous trend and

seasonality can be estimated respectively using rolling moving averages (for the RV/BV part)

or rolling regressions (for the FFF part). Nonetheless, our model differs in several aspects.

First, it disentangles in a single step the trend from the seasonality. Second, it yields natu-

3

rally smooth pointwise estimates. Third, it is data-adaptive in the sense that there are less

parameters to fine tune. Fourth, the trend estimate is more robust to jumps in the log-price

than traditional realized measures such as the realized volatility of bipower variation.

There is a major reason why dynamic seasonality models are important when modeling

intraday returns, concerning practitioners and academics alike: non-dynamic models may lead

to severe underestimation/overestimation of intraday spot volatility. Hence there are pos-

sible implications whenever seasonality pre-filtering is used as an intermediate step. From

a risk management viewpoint, intraday measures such as intraday Value-at-Risk (VaR) and

Expected-shortfall (ES) under the assumption of constant seasonality may suffer from inappro-

priate high quantile estimation. In other words, the assumption may lead to alternate periods

of underestimated (respectively overestimated) VaR and ES when the seasonality is higher

(respectively lower) than suggested by a constant model. In the context of jump detection,

the assumption may induce an underestimation (respectively overestimation) of the number

and size of jumps when the seasonality is higher (respectively lower).

The rest of the paper is organized as follows. In Section 2, we describe our model for the

intraday return, from a continuous-time point of view to the discretized process. To relax the

constant seasonality assumption, we define a class of seasonality models which includes the

Fourier Flexible Form (FFF) as a special case. In Section 3, we provide a detailed exposition

of a method aimed at studying the class of models defined in Section 2. We start by recalling

the link between the FFF and the Fourier transform. We then sketch the theoretical basics

of time-frequency analysis, that was introduced to overcome this limitation (see Daubechies

(1992); Flandrin (1999)). Finally, we introduce the Synchrosqueezing transform, which is

specially aimed at studying the class of models defined in Section 2, and we provide associated

estimators of instantaneous trend and seasonality. In Section 4, we estimate the model using

four years of high-frequency data on the CHF/USD, EUR/USD, GBP/USD and JPY/USD

exchange rates. To obtain confidence intervals for the estimated trend and seasonality, we

develop tailor-made resampling procedures. In Section 5, we conduct simulations to study

the properties of the estimators from Section 3. We show that they are robust to various

4

heteroskedasticity and jumps specifications. We conclude in Section 6.

2. Intraday seasonality

On a generic filtered probability space, suppose that the log-price of the asset, denoted as p(t),

is determined by the continuous-time jump diffusion process

dp(t) = µ(t)dt+ σ(t)dW (t) + q(t)dI(t), (1)

where µ(t) is a continuous and locally bounded variation process, σ(t) > 0 is the stochastic

volatility with cadlag sample paths, W (t) is a standard Brownian motion and I(t) is a finite

activity counting process with jump size q(t) = p(t)− p(t−) independent from W (t).

An example of stochastic volatility popularized in Heston (1993) is the square-root process

from Cox et al. (1985), where σ2(t) = h2(t) and

dh2(t) = κ{θ − h2(t)

}dt+ ξh(t)dZ(t), (2)

with Z(t) another Brownian motion such that cov {dW (t), dZ(t)} = ρdt and 2κθ > ξ2 ensuring

that σ2(t) > 0 almost surely (Feller’s condition). When I(t) is a compound Poisson process

with intensity λ and q ∼ N(µJ , σ2J) (conditional on a jump occurring), then (1) along with (2)

boil down to the model from Bates (1996).

While usual continuous-time models may display realistic features of asset prices behavior

at a daily frequency, seasonality is invariably missing. Contrasting with this observation, the

econometric literature on high-frequency data often decomposes the spot volatility into three

separate components: the first being slowly time-varying, the second periodic and the third

purely stochastic (see e.g. Andersen and Bollerslev 1997; Engle and Sokalska 2012). As such,

5

we may consider a continuous-time model where the volatility satisfies

σ(t) = eT (t)+s(t)h(t), (3)

with T (t) slowly varying, s(t) quickly time-varying and periodic and h(t) the intraday stochas-

tic volatility (e.g. a square-root process (2)). In other words, we decompose the volatility into

three component: T (t) is the trend, s(t) the seasonality, and h(t) is the intraday stochastic

component.

Although trading happens in continuous time, the price process is only collected at discrete

points in time. Ignoring the drift term, equations (1) and (3) suggest a natural discrete-time

model for the return process as

rn = eTn+snhnwn + qnIn, (4)

where n = t/τ with τ the sampling interval, as well as

• Tn and sn representing the trend and seasonality in the volatility,

• hn the intraday volatility component,

• wn the white noise,

• and qnIn the discretized finite activity counting process.

In Sections 2.1 and 2.2, we describe flexible continuous-time versions of the seasonality s(t)

and trend T (t). In Section 2.3, we put all the pieces back together in an adaptive volatility

model, where seasonality and trend are discretely sampled from the continuous-time versions.

2.1. The adaptive seasonality model

The seasonal behavior inside a time series can be described by repeating oscillation as time

evolves. Due to complicated underlying dynamics, the oscillatory behavior might change from

6

time to time. Intuitively, to capture this effect, we consider the adaptive seasonality model

s(t) =K∑k=1

ak(t) cos {2πkφ(t) + ξk} , (5)

where K ∈ N, ak(t) > 0, φ′(t) > 0, φ(0) = 0 and ξk ∈ R. The function ak(t) is called

the amplitude modulation (AM), φ(t) the phase function, ξk the phase shift, and φ′(t) the

instantaneous frequency (IF).

When the phase function is linear (ωt with ω > 0) and amplitude modulations are constant

(ak > 0 ∀k), then the model reduces to the Fourier Flexible Form (FFF) (see Gallant (1981)).

When the phase function is non-linear, the IF generalizes the concept of frequency, capturing

the number of oscillations one observes during an infinitesimal time period. As for the AM, it

represents the “instantaneous” magnitude of the oscillation.

While those time-varying quantities allow to capture momentary behavior, there is in gen-

eral no unique representation for an arbitrary s satisfying (5), even if K = 1. Indeed, there ex-

ists an infinity of smooth pairs of functions α(t) and β(t) so that cos(t) = {1 + α(t)} cos {t+ β(t)},

1 + α(t) > 0 and 1 + β′(t) > 0. This is known as the identifiability problem studied in Chen

et al. (2014). To resolve this issue, it is necessary to restrict the functional class and we borrow

the following definition from Chen et al. (2014):

Definition 1 (Intrinsic Mode Function Class Ac1,c2ε ). For fixed choices of 0 < ε � 1 and

ε � c1 < c2 < ∞, the space Ac1,c2ε of Intrinsic Mode Functions (IMFs) consists of functions

f : R→ R, f ∈ C1(R) ∩ L∞(R) having the form

f(t) = a(t) cos {2πφ(t)} , (6)

7

where a : R→ R and φ : R→ R satisfy the following conditions for all t ∈ R:

a ∈ C1(R) ∩ L∞(R), inft∈R

a(t) > c1, supt∈R

a(t) < c2, (7)

φ ∈ C2(R), inft∈R

φ′(t) > c1, supt∈R

φ′(t) < c2, (8)

|a′(t)| ≤ ε |φ′(t)|, |φ′′(t)| ≤ ε |φ′(t)|. (9)

This definition describes functions, referred to as IMF, mainly satisfying two requirements.

First, the AM and IF are both continuously differentiable and bounded from above and below.

Second, the rate of variation of both the AM and IF are small compared to the IF itself.

With the extra conditions on the IMF, the identifiability issue can be resolved in the following

way (Chen et al., 2014, Theorem 2.1). Suppose f(t) = a1(t) cos {2πφ1(t)} ∈ Ac1,c2ε can be

represented in a different form, for instance f(t) = a2(t) cos {2πφ2(t)}, which also satisfies the

conditions of Ac1,c2ε . Define α(t) = φ1(t) − φ2(t) and β(t) = a1(t) − a2(t), then α ∈ C2(R),

β ∈ C1(R) and |α′(t)| ≤ Cε, |α(t)| ≤ Cε and |β(t)| < Cε for all t ∈ R for a constant C

depending only on c1. In a nutshell, if a member of Ac1,c2ε can be represented in two different

forms, then the differences in phase function, AM and IF between the two forms are controllable

by the small model constant ε. In this sense, we are able to define AM and IF rigorously.

Because these conditions exclude jumps in AM and IF, in this paper, we make the working

assumption that the seasonality component of the market evolves slowly over time. As such,

we do not try to model abrupt changes. Note that the usual tests for structural breaks are

aimed at detecting if and where a break occurs, and they are not the modeling target of the

class Ac1,c2ε . To asses its validity when modeling financial data, we assume that the seasonality

belongs to the Ac1,c2ε class and resort to confidence interval estimation.

Note that the model from equation (5) comprises more than one oscillatory components.

To resolve the identifiability problem in this case, further conditions are necessary.

Definition 2 (Adaptive seasonality model Cc1,c2ε ). The space Cc1,c2ε of superpositions of IMFs

8

consists of functions f having the form

f(t) =K∑k=1

fk(t) and fk(t) = ak(t) cos {2πkφ(t) + ξk} (10)

for some finite K > 0 such that for each k = 1, . . . , K,

ξk ∈ R, ak(t) cos {2πkφ(t) + ξk} ∈ Ac1,c2ε and φ(0) = 0. (11)

Functions in the class Cc1,c2ε are composed of more than one IMF satisfying the condition

(11). In this case, an identifiability theorem similar to the one for Ac1,c2ε can be proved similarly

as that in (Chen et al., 2014, Theorem 2.2): if a member of Cc1,c2ε can be represented in two

different forms, then the two forms have the same number of IMFs, and the differences in their

phase function, AM and FM for each IMF are small. To summarize, with the Cc1,c2ε model and

its identifiability theorem, the IF and AM are well defined up to an uncertainty of order ε.

A popular member of Cc1,c2ε is the Fourier Flexible Form (FFF) (see Gallant (1981)), intro-

duced by Andersen and Bollerslev (1997, 1998) in the context of intraday seasonality. Using

Fourier series to decompose any periodic function into simple oscillating building blocks, a

simplified1 version of the FFF reads

s(t) =K∑k=1

[ak cos (2πkt) + bk sin (2πkt)] , (12)

where the sum of sines and cosines with integer frequencies captures the intraday patterns in the

volatility. Thus, we can view s(t) in (12) as a member of Cc1,c2ε with φ(t) = t, ξk = arctan(ak/bk)

and ak(t) =√a2k + b2

k for k = 1, . . . , K, that is with a fixed daily oscillation.

1Andersen and Bollerslev (1997, 1998) also consider the addition of dummy variables to capture weekdayeffects or particular events such as holidays in particular markets, but also unemployment reports, retail salesfigures, etc. While the periodic model captures most of the seasonal patterns, their dummy variables allow toquantify the relative importance of calendar effects and announcement events.

9

2.2. The adaptive trend model

For the remainder of this paper, we use Fy(ω) =∫∞−∞ y(t)e−i2πωtdt and Py(ω) = |Fy(ω)|2 for

the Fourier transform and power spectrum of a weakly stationary process y.

Fix a Schwartz function ψ so that suppFψ ⊂ [1 − ∆, 1 + ∆], where 0 < ∆ < 1 and Fψ

denotes its Fourier transform.

Definition 3 (Adaptive trend model T c1ε ). For fixed choices of 0 < ε � 1 and ε � c1 < ∞,

the space T c1ε consists of functions T : R→ R, T ∈ C1(R) so that FT exists in the distribution

sense, and

∣∣∣∣∫ T (t)1√aψ

(t− ba

)dt

∣∣∣∣ ≤ CT ε and

∣∣∣∣∫ T ′(t)1√aψ

(t− ba

)dt

∣∣∣∣ ≤ CT ε (13)

for all b ∈ R and a ∈(

0, 1+∆c1

], for some CT ≥ 0.

As we ideally want a trend to be slowly time-varying, the intuition behind (13) is as a bound

on how fast a function oscillates locally. A special case satisfying (13) is a continuous function

T for which its Fourier transform FT exists and is compactly supported in(− 1−∆

1+∆c1,

1−∆1+∆

c1

).

There are two well-known examples of such trend functions; the first is the polynomial

function T (t) =∑L

l=1 αltl, where αl ∈ R, which is commonly applied to model trends. By a

direct calculation, its Fourier transform is supported at 0. The second is a harmonic function

T (t) = cos(2πωt) with “very low” frequency (i.e., with |ω| < 1−∆1+∆

c1), as its Fourier transform

is supported at ±ω.

More generally, using Plancheral theorem, one can verify that suppFT ⊂(− 1−∆

1+∆c1,

1−∆1+∆

c1

)implies

∫T (t) 1√

aψ( t−b

a)(t)dt = 0 for all a ∈ (0, 1+∆

c1] and all b ∈ R. In our case however,

the trend is non-parametric by assumption and its Fourier transform might in all generality

be supported everywhere in the Fourier domain. If this is so, then(13) describes a trend that

essentially captures the slowly varying features of those models (i.e., its local behavior is similar

to that of a polynomial or a very low frequency periodic function) but is more general.

10

2.3. The adaptive volatility model

Let the return process be as in (4). We define the log-volatility process as

yn = log |rn| .

Furthermore, we assume that the log-volatility process follows an adaptive volatility model,

that is

yn = Tn + sn + zn, (14)

where

• sn, discretely sampled from s(t) ∈ Cc1,c2ε , is the volatility seasonality,

• Tn, discretely sampled from T (t) ∈ T c1ε , is the volatility trend,

• and zn = log∣∣hnwn + qnIne

−(Tn+sn)∣∣ is an additive noise process that satisfies E(zn) <∞

and var(zn) <∞.

It should be noted that boundedness of the mean and variance for the noise is a mild condition

for reasonable econometric models (see the two remarks below).

Remark. Assume first there are neither jumps (In = 0) nor intraday heteroskedasticity (hn = 1)

and that wn follows a standardized generalized error distribution (GED), wn ∼ GED(ν), with

density given by

fν(w) =ν

21+1/νΓ(1/ν)λνe−|w/λν |ν

2 ,

where λν ={

2−2/νΓ(1/ν)/Γ(3/ν)}1/2

and Γ is the gamma function. As noted in Hafner

and Linton (2014), the GED nests the normal distribution when ν = 2, has fatter (thinner)

tails when ν < 2 (ν > 2) and is log-concave for ν > 1. Furthermore, because E (logw2n) =

{2ψ(1/ν)/ν + log Γ(1/ν)− log Γ(3ν)} and var (logw2n) = (2/ν)2Ψ(1/ν) (see Hafner and Linton

11

2014) with ψ and Ψ the digamma and trigamma functions (i.e., the first and second derivatives

of log Γ), then E(zn) < E (logw2n) <∞ and var(zn) < var (logw2

n) <∞ when ν > 0.

Remark. To introduce intraday heteroskedasticity (still without jumps), it is convenient to use

the EGARCH(1,1) of Nelson (1991). Defining vn = log |hn|, the model is obtained by writting

vn = γ + βvn−1 + θwn−1 + α (|wn−1| − E |wn−1|) ,

where γ, β, θ, α ∈ R and |β| < 1. For this model, it is straightforward that

var(log h2

nw2n

)=θ2 + α2var (|wn|)

1− β2+ var

(logw2

n

).

Because var |wn| <∞ for the GED (see Hafner and Linton (2014)), then var(zn) <∞ follows.

For other heteroskedasticity models, note that

E{

(log |hnwn|)2} ≤ [√E{

(log |wn|)2}+√

E{

(log |hn|)2}]2

by Cauchy-Schwartz inequality. Hence, if both E{

(log |wn|)2} and E{

(log |hn|)2} are bounded,

then var(zn) < ∞ follows. When jumps are added to the model, it is in general not possible

to obtain a closed formula for E(zn) and var(zn). However, boundedness of the mean and

variance is strongly supported by our simulations for cases of practical interest.

Within this framework, every specific choice of trend T , seasonality s and noise z yields

a different model. Due to their non-parametric nature, estimating T , s or the AM and IF

inside s is non-trivial. In practice, the problem would get much easier in the FFF case,

that is in the case of a “constant” seasonal pattern. However, this assumption is challenged

by empirical evidence. In Laakkonen (2007), the author observes that an FFF estimated

yearly, then quarterly and finally weekly performs better and better at capturing periodicities

in the data. Whereas this sub-sampling is interpretable as a varying seasonality, it is still

piecewise constant. As a piecewise constant function implies that the system under study

12

undergoes structural changes (i.e., shocks) at every break point, it is an unlikely candidate for

the market’s seasonality. We take the point of view of Deo et al. (2006), where the authors use

frequency leakage in the power spectrum of the absolute return to argue that the seasonality

is not (piecewise) constant but slowly varying. While they allow non-integer frequencies, their

“generalized FFF” parameters are still constant for the whole sample. In other words, they

correct for frequency leakage, but do not allow for potential slowly varying frequencies and

amplitude modulations (i.e., time-varying FFF parameters). Dynamic alternatives include

either arbitrarily small intervals or a rolling version of their “generalized FFF”. In the first

case, an arbitrarily increase in the estimator’s variance (as in the issue of testing for a general

smooth member of Ac1,c2ε ) is expected. In the second case, which we compare to our method

in section 4, it is not clear a priori how one would choose the optimal window size.

In Section 3, we propose an alternative framework to study the time-frequency properties

of the log-volatility process. Allowing the trend and seasonality to evolve dynamically over

time, we are able to obtain T and s in the adaptive volatility model in a single-step. In fact,

if the log-volatility process yn is stationary or close to stationary in some sense, a transform

called the Synchrosqueezing transform (SST) theoretically helps to obtain accurate pointwise

estimates of T ∈ T c1ε and s ∈ Ac1,c2ε (Daubechies et al. (2011); Chen et al. (2014)).

3. From Fourier to Synchrosqueezing

In this Section, we start by recalling the relationship between the harmonic model and the

Fourier transform. We then sketch the theoretical basics of the time-frequency analysis. Fi-

nally, we present the Synchrosqueezing transform (SST), which is specifically aimed at studying

the adaptive volatility model. Its theoretical properties are discussed at the end of the Section.

3.1. Fourier transform and the harmonic model

Oscillatory signals are ubiquitous in many fields. Seasonality is a synonym of oscillation broadly

used in finance, econometrics, public health, biomedicine, etc. There are several “character-

13

istics” one can use to describe an oscillatory signal (see Flandrin (1999)): for example, how

often an oscillation repeats itself “on average”, how large an oscillation is “on average”, etc.

To capture these features, the following harmonic model is widely used:

y(t) =K∑k=1

ak cos(2πωkt+ ξk), (15)

where∑a2k < ∞, ak > 0, ωk > 0 and ξk ∈ R. The quantities ak, ωk and ξk are respectively

called the amplitude, the frequency and the initial phase of the k-th component of y. As we

stated in Section 2, both the FFF and its generalized version from Deo et al. (2006) are based

on this model.

When a given signal satisfies model (15), the Fourier transform is helpful in determining the

oscillatory features ak and ωk. For y(t) defined in (15), we recall (see (Folland, 1999, Chapter

9)) that its Fourier transform is

Fy(ω) =1

2

K∑k=1

akeiξkδ(ω − ωk) +

1

2

K∑k=1

ake−iξkδ(ω + ωk),

where δ is the Dirac measure. Thus, if a signal satisfies the harmonic model, the frequency ωk

and the amplitude ak can be read directly from its Fourier transform. For more details on the

property of the Fourier transform Fy(ω) of a function y(t) with t, ω ∈ R, we refer the reader

to (Folland, 1999, Chapter 9).

As useful as the harmonic model can be, it does not fit well many real signals. Indeed,

due to their underlying nature, the oscillatory pattern might change over time. For instance,

the signal may oscillate more often in the beginning but less in the end, or oscillate stronger

in the beginning but weaker in the end. We call these time-varying patterns the dynamics of

the seasonality, and it is well known that capturing the dynamics is beyond the scope of the

harmonic model. Unfortunately, when departing from static models such as (15) to consider

dynamic models such as the whole class Cc1,c2ε , the usefulness of the Fourier transform is also

limited due to the loss of time localization of events. In other words, because of its incapacity

14

to capture momentary behavior, we cannot use the Fourier transform to analyze the dynamics

of seasonality.

3.2. Time-frequency analysis

To overcome the limitation of the Fourier transform, time-frequency analysis was introduced

(see Daubechies (1992); Flandrin (1999) and the references inside for the historical discussion).

Heuristically, to capture the dynamics of the oscillatory signal, we take a small subset of

the given signal y(t) around a given time t0, and analyze its power spectrum. Ideally, this

provides information about the local behavior of y(t) around t0. We repeat the analysis at

all times, and the result is referred to as the time-frequency (TF) representation of the signal.

Mathematically, this idea is implemented by the short-time Fourier transform (STFT) and

continuous wavelet transform (CWT).

The STFT is defined by

Gy(t, ω) =

∫y(s) g(s− t) e−i2πωsds , (16)

where ω > 0 is frequency, and g is the window function associated with the STFT which

extracts the local signal for analysis. g has to be smooth enough and such that∫g(t)dt = 1.

The CWT is defined by

Wy(t, a) =

∫y(s) a−1/2 ψ

(s− ta

)ds , (17)

where a > 0. We call a the wavelet’s scale and ψ the mother wavelet which is smooth enough

and such that∫ψ(t)dt = 0.

In a nutshell, we select a subset of the whole signal by the window function or the mother

wavelet, and study how the signal oscillates locally. From the viewpoint of frame analysis, the

STFT and CWT are defined as the inner products between the signal to be analyzed and a

pre-assigned family of “templates”, or atoms – which are {g(· − t)e−i2πω·}ω∈R+,t∈R in STFT

15

and {a−1/2 ψ( ·−ta

)}a∈R+,t∈R in CWT. Furthermore, this inner product provides a way to resolve

events simultaneously in time (by translation) and frequency (by modulation and dilatation

respectively), but the properties of their respective templates yield different trade-offs between

temporal and frequency resolution due to the Heisenberg uncertainty principle. Take the high

frequency region for example. The STFT offers a better frequency resolution in frequency

events but an inferior resolution in time. In contrast, the CWT provides an inferior resolution

in frequency but a better resolution in time.

To further understand the time-frequency (TF) analysis, we consider the continuous wavelet

transform (CWT) of a purely harmonic signal y(t) = A cos(2πωt), and the same reasoning

follows for the short-time Fourier transform (STFT). From the Plancheral theorem, the CWT

of y becomes

Wy(t, a) = Aa1/2Fψ(ωa)ei2πωt. (18)

We observe that if Fψ(ω) is concentrated around ω = 1, then Wy(t, a) is concentrated around

a = 1/ω.

In the remainder of this section, we focus on the CWT, and assume a continuous time

version of the adaptive volatility model (14). We consider

y(t) = T (t) + s(t) + z(t), (19)

where T ∈ T c1ε , s ∈ Ac1,c2ε and z a generalized random process with power spectrum Pz

satisfying∫

(1 + |ω|)−2ldPz(ω) < ∞ for some l > 0. We denote the discretely sampled time-

series by y = {yn}n∈Z, where yn = y(nτ) and τ > 0 is the sampling interval.

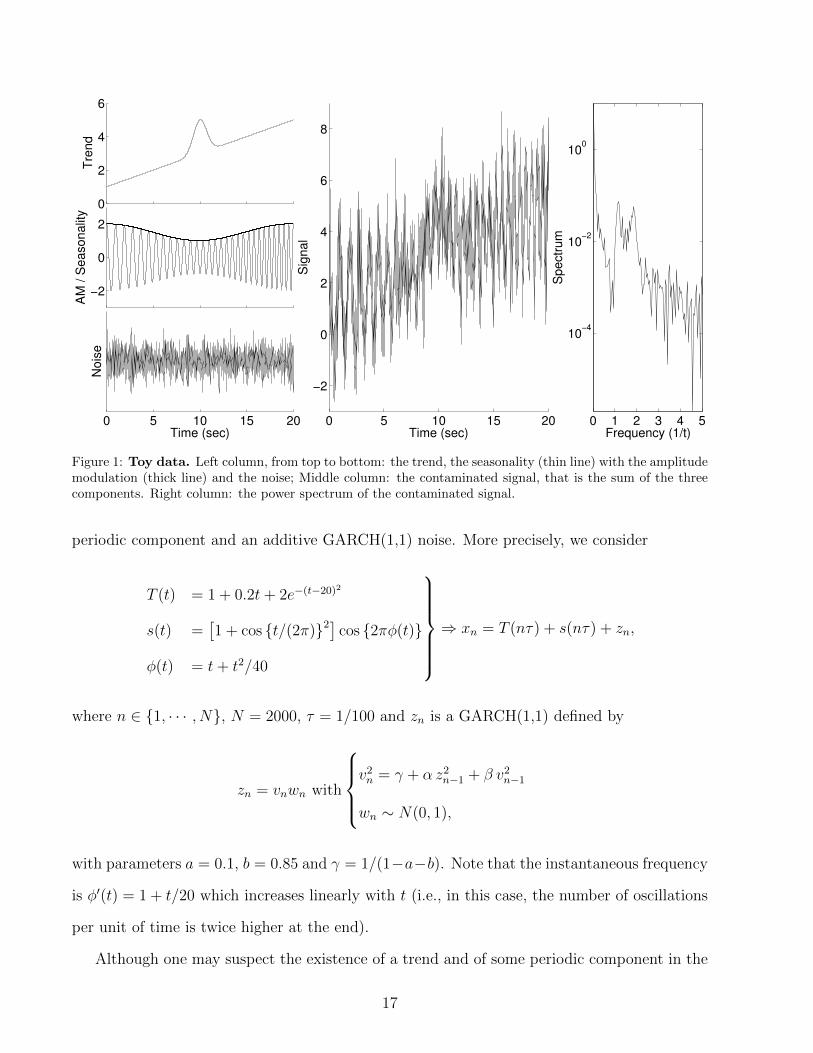

In Figure 1, we show a simulated toy dataset to be used in the remainder of this section.

The contaminated signal is the sum of a trend, an amplitude modulated-frequency modulated-

16

0 5 10 15 20

−2

0

2

4

6

8

Time (sec)

Sig

nal

0 1 2 3 4 5

10−4

10−2

100

Frequency (1/t)

Spectr

um

0

2

4

6

Tre

nd

−2

0

2

AM

/ S

easonalit

y

0 5 10 15 20Time (sec)

Nois

e

Figure 1: Toy data. Left column, from top to bottom: the trend, the seasonality (thin line) with the amplitudemodulation (thick line) and the noise; Middle column: the contaminated signal, that is the sum of the threecomponents. Right column: the power spectrum of the contaminated signal.

periodic component and an additive GARCH(1,1) noise. More precisely, we consider

T (t) = 1 + 0.2t+ 2e−(t−20)2

s(t) =[1 + cos {t/(2π)}2] cos {2πφ(t)}

φ(t) = t+ t2/40

⇒ xn = T (nτ) + s(nτ) + zn,

where n ∈ {1, · · · , N}, N = 2000, τ = 1/100 and zn is a GARCH(1,1) defined by

zn = vnwn with

v2n = γ + α z2

n−1 + β v2n−1

wn ∼ N(0, 1),

with parameters a = 0.1, b = 0.85 and γ = 1/(1−a−b). Note that the instantaneous frequency

is φ′(t) = 1 + t/20 which increases linearly with t (i.e., in this case, the number of oscillations

per unit of time is twice higher at the end).

Although one may suspect the existence of a trend and of some periodic component in the

17

right column of Figure 1, both the amplitude modulations and the increasing frequency are

rather difficult (if not impossible) to see. Furthermore, although the power spectrum of the

contaminated signal that we display in the right column of Figure 1 suggests events localized

both at very low frequencies and in the [1, 2] interval, the information displayed is insufficient

to understand the dynamics of the system.

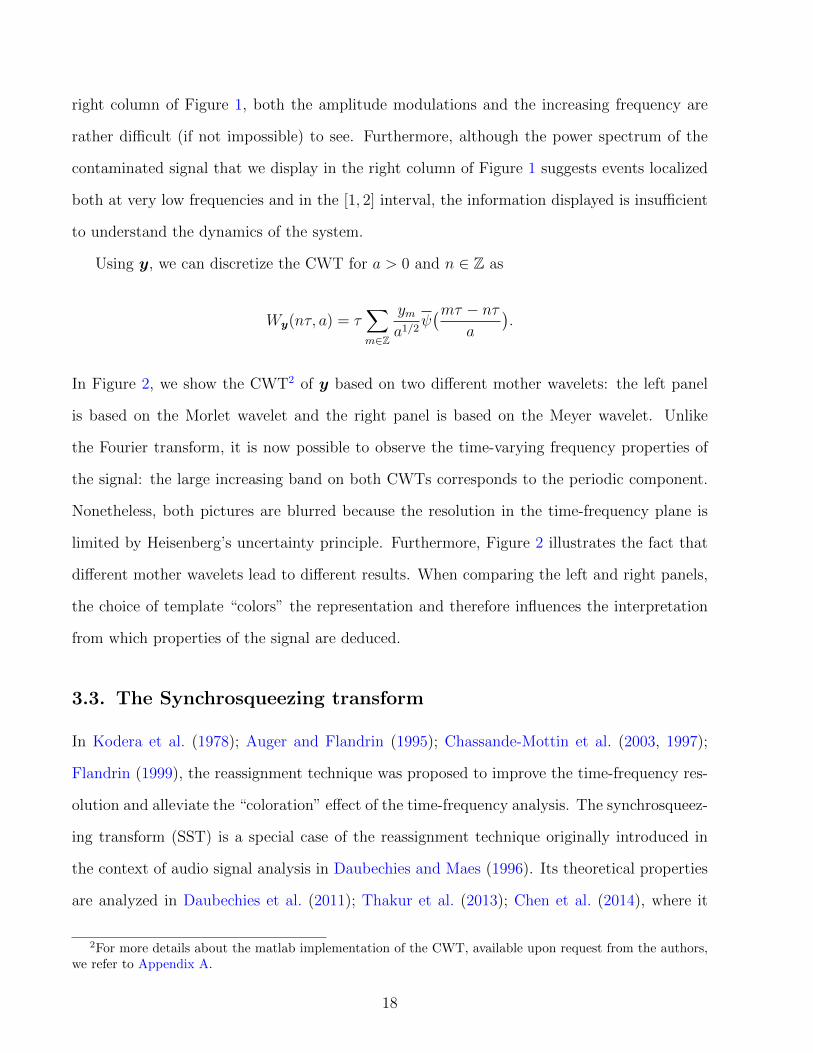

Using y, we can discretize the CWT for a > 0 and n ∈ Z as

Wy(nτ, a) = τ∑m∈Z

yma1/2

ψ(mτ − nτ

a

).

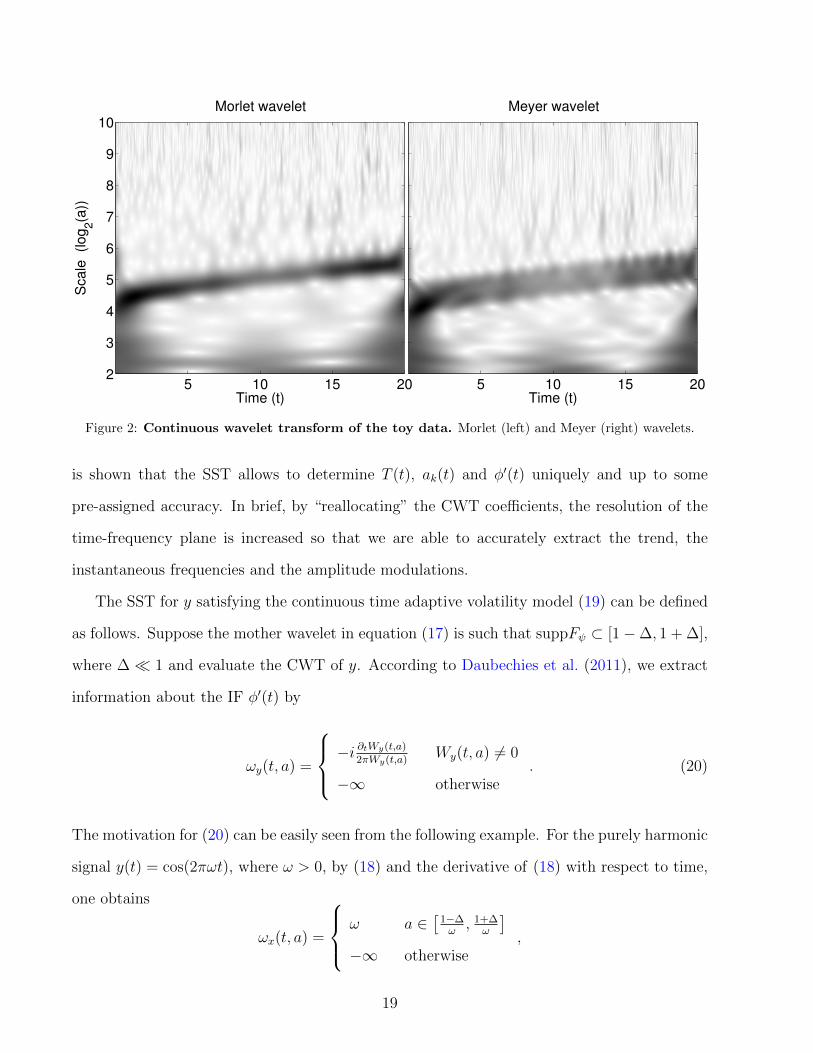

In Figure 2, we show the CWT2 of y based on two different mother wavelets: the left panel

is based on the Morlet wavelet and the right panel is based on the Meyer wavelet. Unlike

the Fourier transform, it is now possible to observe the time-varying frequency properties of

the signal: the large increasing band on both CWTs corresponds to the periodic component.

Nonetheless, both pictures are blurred because the resolution in the time-frequency plane is

limited by Heisenberg’s uncertainty principle. Furthermore, Figure 2 illustrates the fact that

different mother wavelets lead to different results. When comparing the left and right panels,

the choice of template “colors” the representation and therefore influences the interpretation

from which properties of the signal are deduced.

3.3. The Synchrosqueezing transform

In Kodera et al. (1978); Auger and Flandrin (1995); Chassande-Mottin et al. (2003, 1997);

Flandrin (1999), the reassignment technique was proposed to improve the time-frequency res-

olution and alleviate the “coloration” effect of the time-frequency analysis. The synchrosqueez-

ing transform (SST) is a special case of the reassignment technique originally introduced in

the context of audio signal analysis in Daubechies and Maes (1996). Its theoretical properties

are analyzed in Daubechies et al. (2011); Thakur et al. (2013); Chen et al. (2014), where it

2For more details about the matlab implementation of the CWT, available upon request from the authors,we refer to Appendix A.

18

Scale

(log

2(a

))

Morlet wavelet

Time (t)5 10 15 20

2

3

4

5

6

7

8

9

10Meyer wavelet

Time (t)5 10 15 20

Figure 2: Continuous wavelet transform of the toy data. Morlet (left) and Meyer (right) wavelets.

is shown that the SST allows to determine T (t), ak(t) and φ′(t) uniquely and up to some

pre-assigned accuracy. In brief, by “reallocating” the CWT coefficients, the resolution of the

time-frequency plane is increased so that we are able to accurately extract the trend, the

instantaneous frequencies and the amplitude modulations.

The SST for y satisfying the continuous time adaptive volatility model (19) can be defined

as follows. Suppose the mother wavelet in equation (17) is such that suppFψ ⊂ [1−∆, 1 + ∆],

where ∆� 1 and evaluate the CWT of y. According to Daubechies et al. (2011), we extract

information about the IF φ′(t) by

ωy(t, a) =

−i∂tWy(t,a)

2πWy(t,a)Wy(t, a) 6= 0

−∞ otherwise. (20)

The motivation for (20) can be easily seen from the following example. For the purely harmonic

signal y(t) = cos(2πωt), where ω > 0, by (18) and the derivative of (18) with respect to time,

one obtains

ωx(t, a) =

ω a ∈[

1−∆ω, 1+∆

ω

]−∞ otherwise

,

19

which is the desired information about its IF. Then the SST is defined by

Sy(t, ω) =

∫a : |Wy(t,a)|>Γ

Wy(t, a) a−3/2 δ {ωy(t, a)− ω } da, (21)

where Γ > 0 is the threshold chosen by the user, ω > 0 is the frequency and ωy(t, a) is defined

in (20). Keeping in mind that the frequency is reciprocally related to the scale, then (21) can

be understood as follows: based on the IF information ωy, at each time t, we collect the CWT

coefficients at scale a where a seasonal component with frequency close to ω is detected. This

additional step allows to mitigate the coloration due to the choice of template.

To discretize the SST, ωy is first obtained as

ωy(nτ, a) =

−i∂tWy(nτ, a)

2πWy(nτ, a)when |Wy(nτ, a)| 6= 0;

−∞ when |Wy(nτ, a)| = 0,

where ∂tWy(nτ, a) is defined as

∂tWy(nτ, a) = τ∑m∈Z

yma3/2

ψ′(mτ − nτ

a

).

Similarly, Sy(t, ω) is discretized as

Sy(nτ, ω) =

∫a: |Wy(nτ,a)|≥Γ

δ {|ωy(nτ, a)− ω|}Wy(nτ, a)a−3/2da.

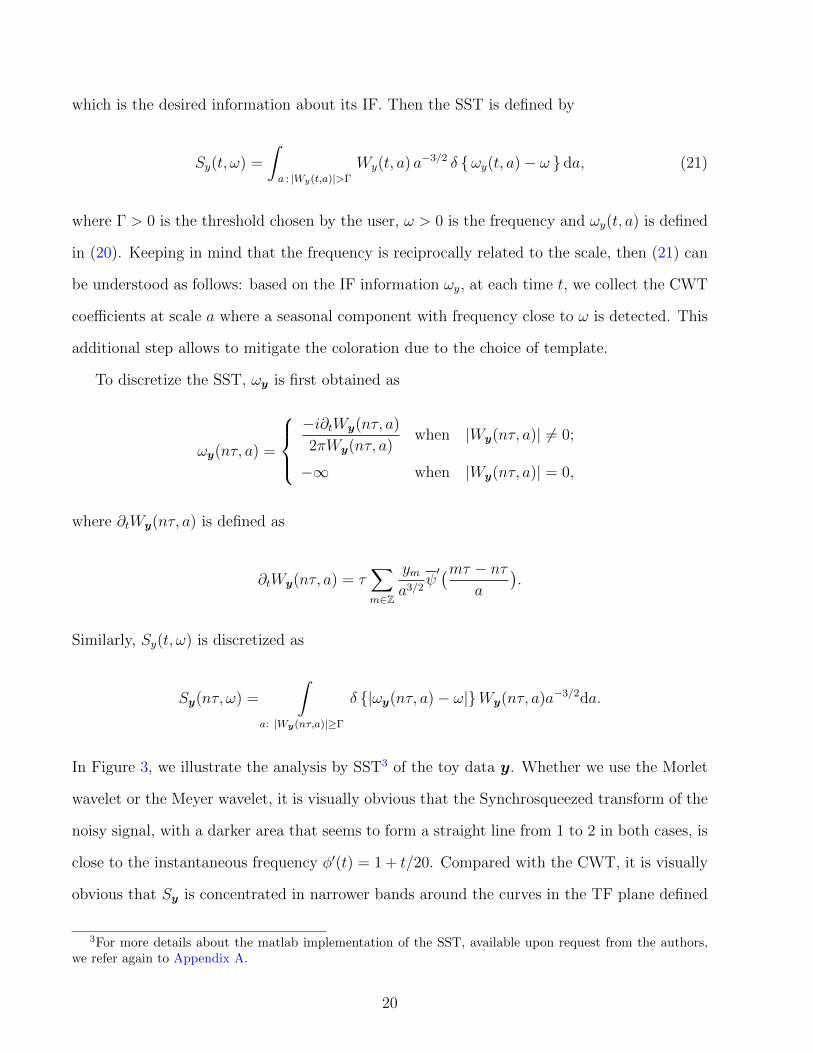

In Figure 3, we illustrate the analysis by SST3 of the toy data y. Whether we use the Morlet

wavelet or the Meyer wavelet, it is visually obvious that the Synchrosqueezed transform of the

noisy signal, with a darker area that seems to form a straight line from 1 to 2 in both cases, is

close to the instantaneous frequency φ′(t) = 1 + t/20. Compared with the CWT, it is visually

obvious that Sy is concentrated in narrower bands around the curves in the TF plane defined

3For more details about the matlab implementation of the SST, available upon request from the authors,we refer again to Appendix A.

20

Fre

quency (ω

)

Morlet wavelet

Time (t)5 10 15 20

5

4

3

2

1

Meyer wavelet

Time (t)5 10 15 20

Figure 3: Synchrosqueezed transform of the toy data. On the left: Morlet wavelet. On the right: Meyerwavelet.

by (t, kφ′(t)) (here with k = 1).

Using any curve extraction technique, it is possible to estimate the IF with high accuracy

and we denote this quantity as φ′. Furthermore, the restriction of Sy to the k-th narrow band

suffices to obtain an estimator of the k-th (complex) component of y as

fCk (nτ) =

1

Rψ

∫|kφ′(nτ)−ω|≤∆

Sy(nτ, ω)dω, (22)

where Rψ =∫ Fψ(ω)

ωdω. Then the corresponding estimator of the k-th (real) component fk and

amplitude modulations at time nτ are defined as

fk(nτ) = <{fCk (nτ)

}and ak(nτ) =

∣∣∣fCk (nτ)

∣∣∣ , (23)

where <(z) denotes the real part of z ∈ C. Finally, the restriction of Sy under a low-frequency

21

0 2 4 6 8 10 12 14 16 18 20−1

0

1

2

3

4

5

6

7

Time (sec)

Tru

e f

un

ctio

n v

s r

eco

nstr

ucte

d0

2

4

6

Tre

nd

1.1

1.3

1.5

1.7

1.9

IF

0 5 10 15 20

−2

0

2

Time (sec)

AM

/ S

ea

so

na

lity

Figure 4: Reconstruction of the components. Left column, from top to bottom: the trend, the instan-taneous frequency and the seasonality (thin line) with the amplitude modulation (thick line) with the trueunderlying function (black) and reconstructed result (red); Right column: the true signal, that is the sum ofthe trend and the seasonality, (black) and the reconstructed function (red).

threshold ωl suffices to obtain an estimator of the trend of y as

T (nτ) = <{

1

Rψ

∫ ωl

0

Sy(nτ, ω)dω

}(24)

= yn −<{

1

Rψ

∫ ∞ωl

Sy(nτ, ω)dω

}.

The theoretical properties of the above estimators have been shown in (Chen et al., 2014,

Theorem 3.2). Suppose y satisfies additional technical conditions on the second derivatives of

the amplitude modulations and trend4 in order to handle the discretization. If the sampling

interval τ satisfies 0 < τ ≤ 1−∆(1+∆)c2

, then with high probability fk, φ′k and ak (respectively T )

are accurate up to Cτε (respectively Cτ,T ε) where Cτ (respectively Cτ,T ) is a constant decreasing

with τ . We refer the reader to Chen et al. (2014) for the precise statement of the theorem and

more discussions.

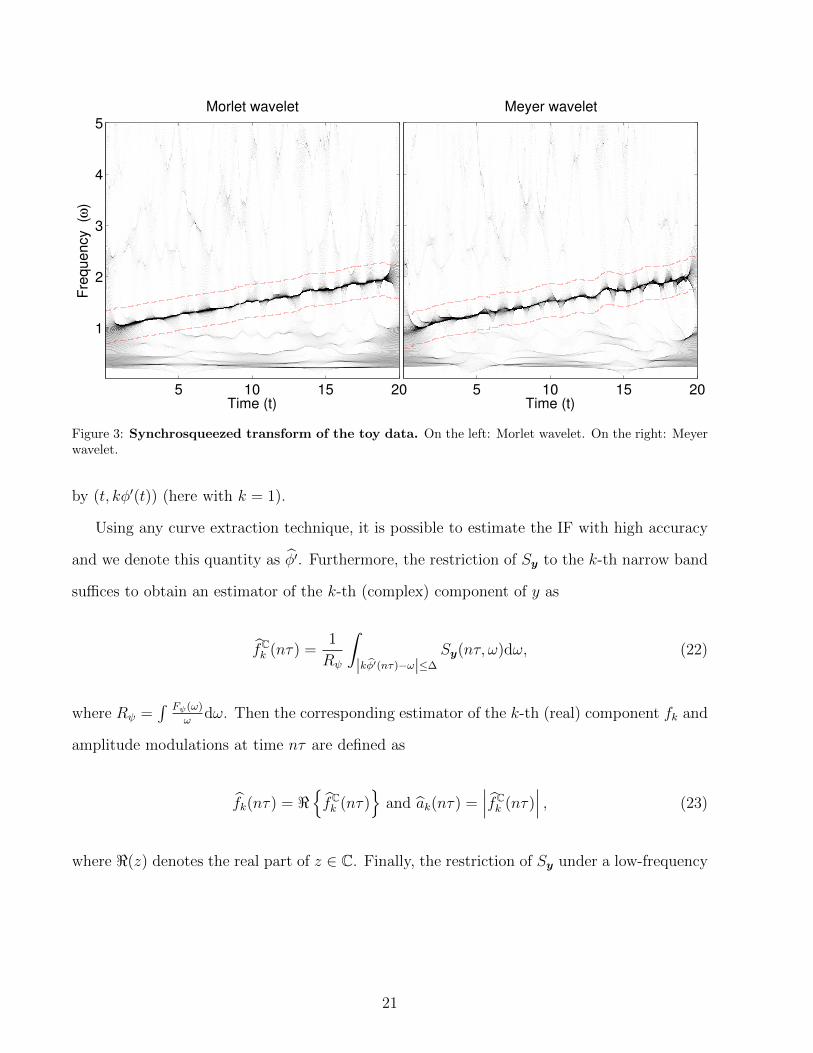

In Figure 4, we show the reconstructed component for the toy data using a Morlet mother

wavelet, where integration bands in (22) are the dashed red lines from Figure 3. Because the

4ak(t) ∈ C2(R) and supt∈R |a′′k(t)| ≤ εc2 for all k = 1, . . . ,K, and T ∈ C2(R) so that∣∣∣∫ T ′′(t) 1√

aψ(t−ba

)dt∣∣∣ ≤

CT ε for all b ∈ R and a ∈ (0, 1+∆c1

]

22

reconstruction is not dependent on the chosen mother wavelets5, it is not shown here for the

Meyer wavelet. Usually, while the instantaneous frequency is recovered precisely, the estimated

amplitude modulations are less ideal. Although this is important when the goal is forecasting,

it can be dampened by further smoothing the amplitude (here with a simple moving average

filter of length 1/τ).

In summary, for the harmonic model (15), the Fourier transform allows us to extract the

features of interest of the oscillation. When it comes to the adaptive volatility model (14), we

count on the synchrosqueezing transform to extract the oscillatory features of a given signal.

4. Application to foreign exchange data

As an empirical application, we study the EUR/USD, EUR/GBP, JPY/USD and USD/CHF

exchange rates from the beginning of 2010 to the end of 2013. We avoid the data preprocessing

by using pre-filtered 5-minute bid-ask pairs obtained from Dukascopy Bank SA6. The log-price

pn is computed as the average between the log bid and log ask prices and the return rn is

defined as the change between two consecutive log prices.

Because trading activity unquestionably drops during weekends and certain holidays (see

e.g. Dacorogna et al. 1993; Andersen and Bollerslev 1998), we exclude a number of days from

the sample, always from 21:05 GMT the night before until 21:00 GMT that evening. For

instance, weekends start on Friday at 21:05 GMT and last until Sunday at 21:00 GMT. Using

this definition of the trading day, we remove the fixed holidays of Christmas (December 24 -

December 26) and New Year’s (December 31 - January 2), as well as the moving holidays of

Martin Luther King’s Day, President’s Day, Good Friday, Memorial Day, July Fourth (also

when it is observed on July 3 or 5), Labor Day and Thanksgiving. After the cuts, we obtain

a sample of 998 days of data, containing 288 · 998 = 287424 intraday returns.

5This statement is correct up to the moments of the chosen mother wavelet ψ. The reconstruction errordepends on the first three moments of the chosen mother wavelet and its derivative but not on the profile of ψ(Daubechies et al. (2011); Chen et al. (2014))

6http://www.dukascopy.com/

23

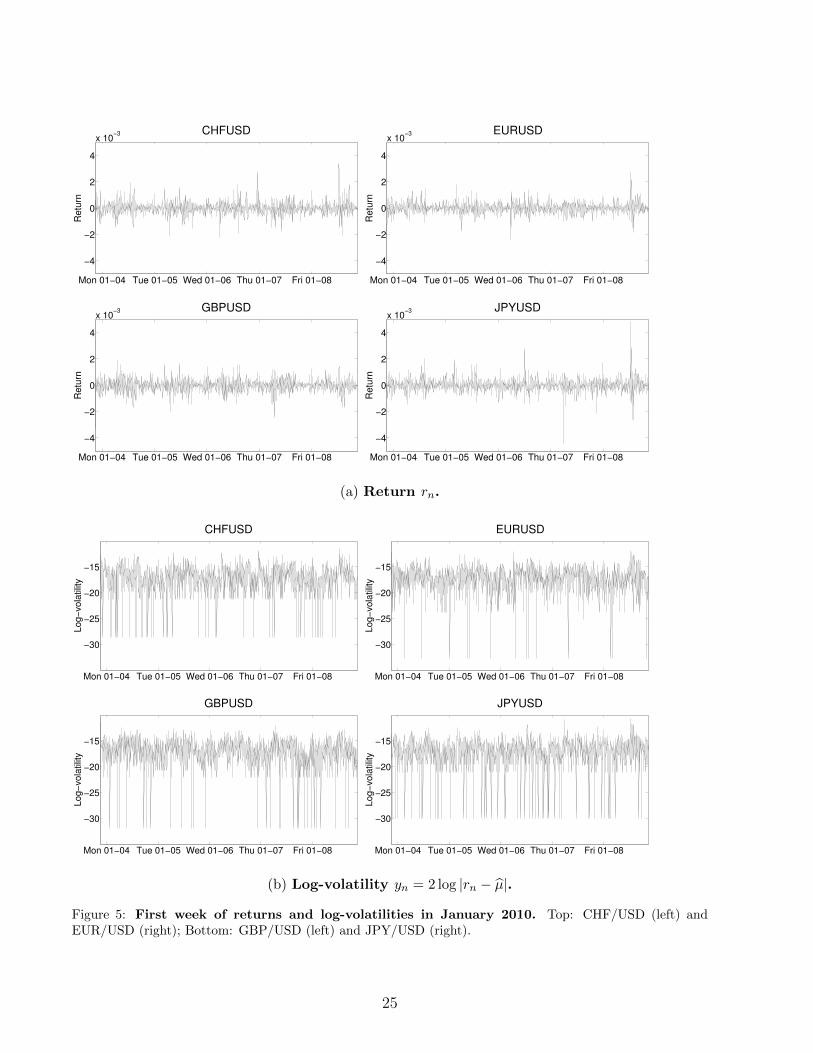

In panel 5a of Figure 5, we show the return rn for the four considered exchange rates

for the first week of trading, that is from January 3, 2010 (Sunday) at 21:05 pm GMT to

January 8, 2010 (Friday) at 21:00 pm GMT (1440 observations). While heteroskedasticity is

obviously present, it is arguably easier to discern its periodicity by looking at the log-volatility

yn = log |rn − µ| in panel 5b. Note that the smallest observations correspond to the case where

the price does not move during the 5 minutes interval (i.e., rn = 0 and yn = log |µ|).

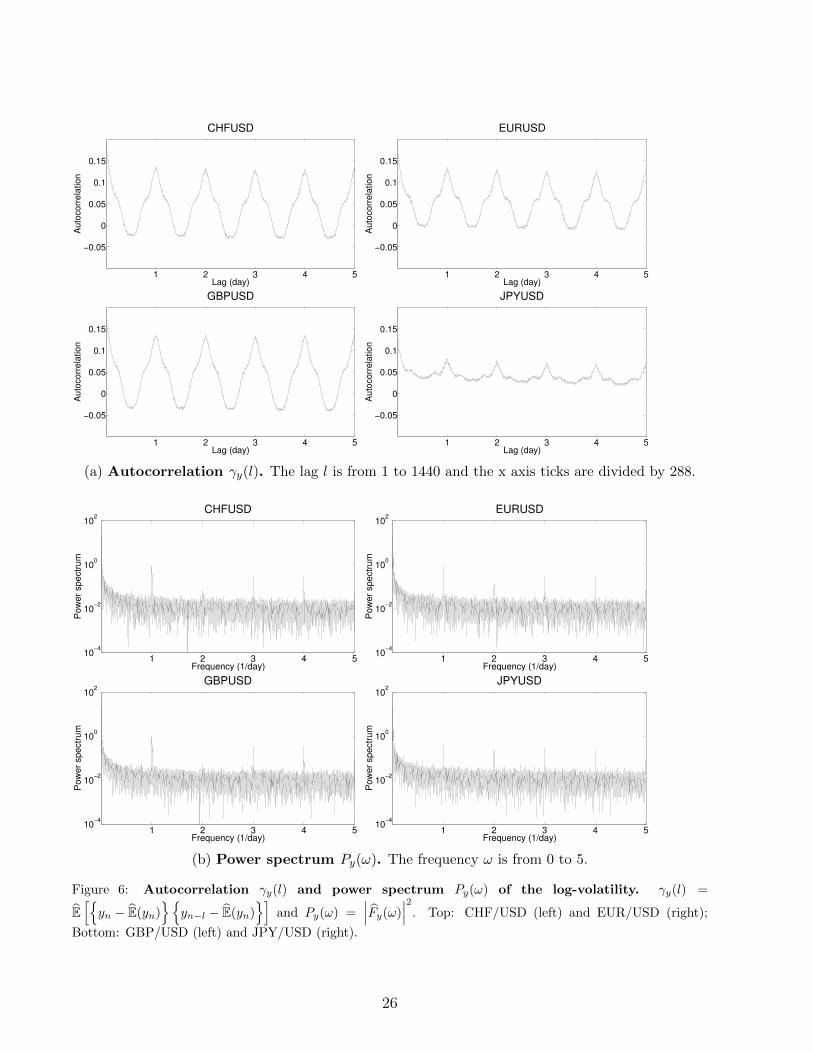

In Figure 6, the autocorrelation (Panel 6a) and the power spectrum (Panel 6b) of the log-

volatility indicate strong (daily) periodicities in the log-volatility. Although the shapes are

different for the various exchange rates, they all essentially display the same information: on

average, the seasonality is composed of periodic components of integer frequency. Note that

“on average” emphasizes the fact that both representations are only part of the picture. As

illustrated in Section 3, this representation misses the dynamics of the signal: for example, some

of the underlying periodic components may strengthen, weaken or even completely disappear

at some point. Another observation is that the JPY/USD curves are fairly different from the

others. First, according to the autocorrelation, the overall magnitude of oscillations (i.e., the

importance of the daily periodicity) is smaller. Second, according to the height of the power

spectrum’s second peak, the amplitude of the second component is much larger.

In Figure 7, we display |Sy(t, ω)|, the absolute value of the Synchrosqueezed transform,

in shades of gray for frequencies 0.5 ≤ ω ≤ 4.5. For all exchange rates, we observe much

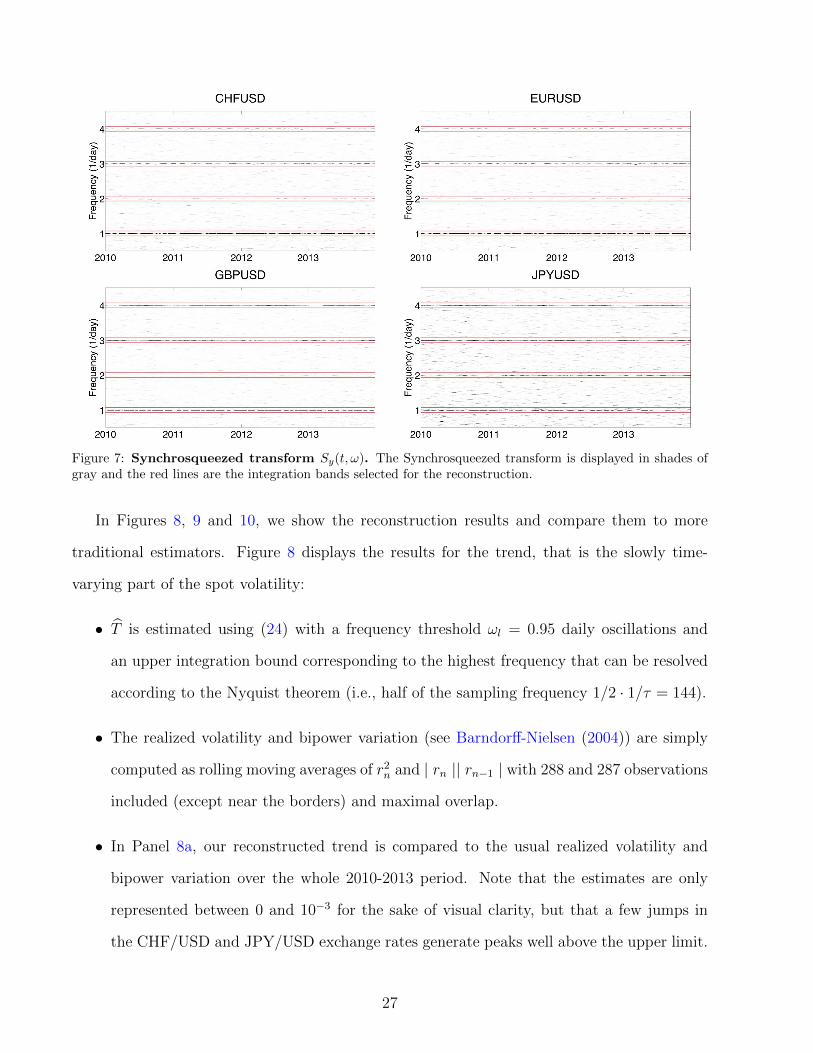

darker curves (indicating higher values of |Sx(t, ω)|) at integer frequencies. As expected from

the power spectrums in Figure 6, the curves at 2 daily oscillations for all exchange rates

are very thin and sometimes fading, except for the JPY/USD. This apparent linearity of the

instantaneous frequency at integer values lends support for an amplitude-modulated version

of the FFF or, in other words, a member of Ac1,c2ε such that |φ(t)| = t. Although this kind

of constant frequency/amplitude modulated model can be estimated in different ways, we

carry the analysis within the SST framework. The red lines are the integration bands for the

reconstruction of the k-th periodic component using (22) and (23), that is at ω = k ±∆ with

k ∈ {1, 2, 3, 4} and ∆ = 0.02.

24

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−4

−2

0

2

4

x 10−3 CHFUSD

Retu

rn

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−4

−2

0

2

4

x 10−3 EURUSD

Retu

rn

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−4

−2

0

2

4

x 10−3 GBPUSD

Retu

rn

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−4

−2

0

2

4

x 10−3 JPYUSD

Retu

rn

(a) Return rn.

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−30

−25

−20

−15

CHFUSD

Log−

vola

tilit

y

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−30

−25

−20

−15

EURUSD

Log−

vola

tilit

y

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−30

−25

−20

−15

GBPUSD

Log−

vola

tilit

y

Mon 01−04 Tue 01−05 Wed 01−06 Thu 01−07 Fri 01−08

−30

−25

−20

−15

JPYUSD

Log−

vola

tilit

y

(b) Log-volatility yn = 2 log |rn − µ|.

Figure 5: First week of returns and log-volatilities in January 2010. Top: CHF/USD (left) andEUR/USD (right); Bottom: GBP/USD (left) and JPY/USD (right).

25

1 2 3 4 5

−0.05

0

0.05

0.1

0.15

CHFUSD

Lag (day)

Au

toco

rre

latio

n

1 2 3 4 5

−0.05

0

0.05

0.1

0.15

EURUSD

Lag (day)

Au

toco

rre

latio

n

1 2 3 4 5

−0.05

0

0.05

0.1

0.15

GBPUSD

Lag (day)

Au

toco

rre

latio

n

1 2 3 4 5

−0.05

0

0.05

0.1

0.15

JPYUSD

Lag (day)

Au

toco

rre

latio

n

(a) Autocorrelation γy(l). The lag l is from 1 to 1440 and the x axis ticks are divided by 288.

1 2 3 4 510

−4

10−2

100

102

CHFUSD

Frequency (1/day)

Po

we

r sp

ectr

um

1 2 3 4 510

−4

10−2

100

102

EURUSD

Frequency (1/day)

Po

we

r sp

ectr

um

1 2 3 4 510

−4

10−2

100

102

GBPUSD

Frequency (1/day)

Po

we

r sp

ectr

um

1 2 3 4 510

−4

10−2

100

102

JPYUSD

Frequency (1/day)

Po

we

r sp

ectr

um

(b) Power spectrum Py(ω). The frequency ω is from 0 to 5.

Figure 6: Autocorrelation γy(l) and power spectrum Py(ω) of the log-volatility. γy(l) =

E[{yn − E(yn)

}{yn−l − E(yn)

}]and Py(ω) =

∣∣∣Fy(ω)∣∣∣2. Top: CHF/USD (left) and EUR/USD (right);

Bottom: GBP/USD (left) and JPY/USD (right).

26

Figure 7: Synchrosqueezed transform Sy(t, ω). The Synchrosqueezed transform is displayed in shades ofgray and the red lines are the integration bands selected for the reconstruction.

In Figures 8, 9 and 10, we show the reconstruction results and compare them to more

traditional estimators. Figure 8 displays the results for the trend, that is the slowly time-

varying part of the spot volatility:

• T is estimated using (24) with a frequency threshold ωl = 0.95 daily oscillations and

an upper integration bound corresponding to the highest frequency that can be resolved

according to the Nyquist theorem (i.e., half of the sampling frequency 1/2 · 1/τ = 144).

• The realized volatility and bipower variation (see Barndorff-Nielsen (2004)) are simply

computed as rolling moving averages of r2n and | rn || rn−1 | with 288 and 287 observations

included (except near the borders) and maximal overlap.

• In Panel 8a, our reconstructed trend is compared to the usual realized volatility and

bipower variation over the whole 2010-2013 period. Note that the estimates are only

represented between 0 and 10−3 for the sake of visual clarity, but that a few jumps in

the CHF/USD and JPY/USD exchange rates generate peaks well above the upper limit.

27

• In Panel 8b, the three trend estimates are compared over a shorter time period in the

summer of 2011, that is in the middle of United States debt-ceiling crisis/European

sovereign debt crisis of 2011. Our reconstructed trend visibly constitutes a smoothed

version of the usual volatility measures, which usually fall inside the 95% confidence

interval except for upward spikes due to jumps. Notice the steep volatility increase

in all exchange rates as stock markets around the worlds started to fall following the

downgrading of America’s credit rating on 6 August 2011 by Standard & Poor’s. This

is especially true for the Swiss Franc, facing increasing pressure from currency markets

because considered a safe investment in times of economic uncertainty.

Figures 9 and 10 display the results for the amplitude modulations and seasonality:

• s is estimated using (22) and (23), as well as s(nτ) =∑K

k=1 fk(nτ).

• The Fourier Flexible Form/rolling Fourier Flexible Form (FFF/rFFF) are estimated us-

ing the ordinary least-square estimator on the whole sample/a four-weeks rolling window.

• In Figure 9, we show the amplitude modulations of the first periodic component. It is

noteworthy that when a unique FFF is estimated for the whole sample, the correspond-

ing amplitude is very close to the mean amplitude obtained with the SST. Furthermore,

we observe that the rFFF closely tracks the SST but is far wigglier. This was expected

because the SST estimator is essentially an instantaneous (and smooth by construction)

version of the FFF. Finally, notice that, as expected from Figure 6, the amplitude mod-

ulations of the first component in the JPY/USD are much smaller than the three other

exchange rates.

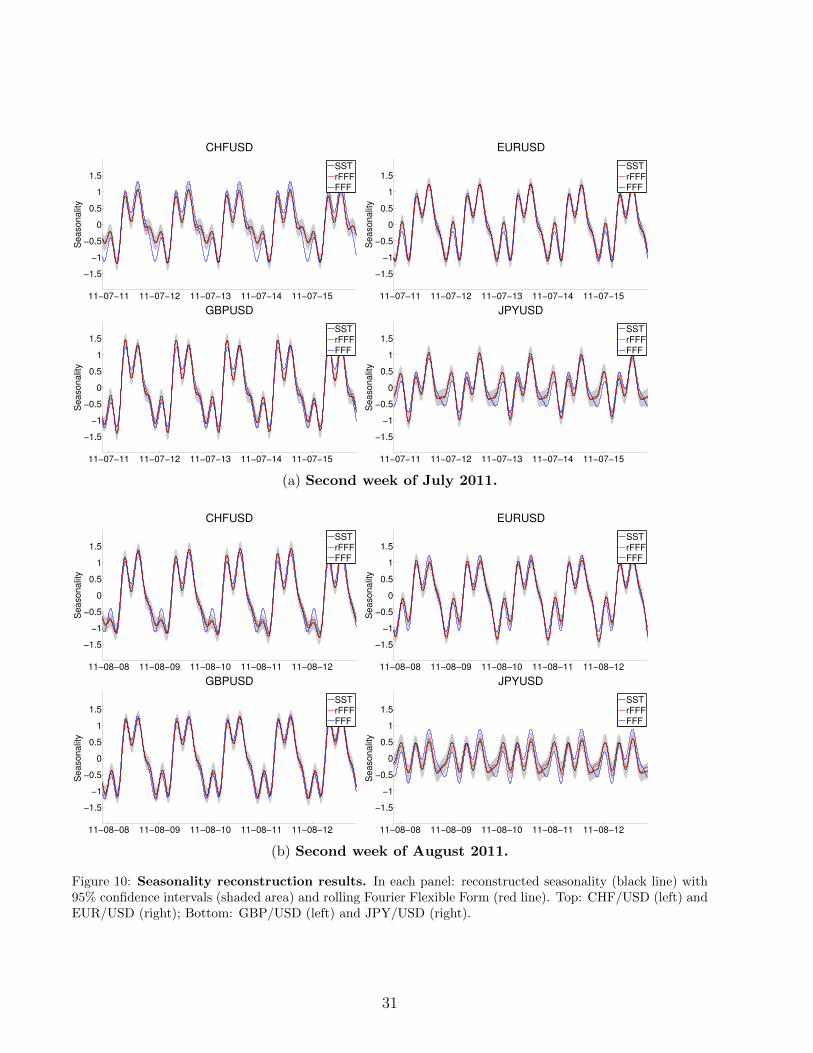

• In Panels 10a and 10b of Figure 10, we show the seasonality estimated as a sum of the

four periodic components: the FFF represents the average daily oscillation, the rFFF

is a wiggly estimate of the dynamics and the SST extracts a smooth instantaneous

seasonality. As in Figure 9, we observe that the overall magnitude of oscillation is much

smaller in the JPY/USD exchange rate.

28

2010 2011 2012 2013

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

CHFUSD

exp(T)RVBV

2010 2011 2012 2013

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

EURUSD

exp(T)RVBV

2010 2011 2012 2013

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

GBPUSD

exp(T)RVBV

2010 2011 2012 2013

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

JPYUSD

exp(T)RVBV

(a) Trend reconstruction for 2010-2013.

Jul 2011 Aug 2011 Sep 2011

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

CHFUSD

exp(T)RVBV

Jul 2011 Aug 2011 Sep 2011

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

EURUSD

exp(T)RVBV

Jul 2011 Aug 2011 Sep 2011

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

GBPUSD

exp(T)RVBV

Jul 2011 Aug 2011 Sep 2011

0.2

0.4

0.6

0.8

x 10−3

Tre

nd

JPYUSD

exp(T)RVBV

(b) Zoom during the summer of 2011.

Figure 8: Trend reconstruction results. In each panel: reconstructed trend (black line), realized volatility(red line) and bipower variation (blue line). In Panel 8b: 95% confidence intervals for the reconstructed trend(shaded area). Top: CHF/USD (left) and EUR/USD (right); Bottom: GBP/USD (left) and JPY/USD (right).

29

2010 2011 2012 2013

0.2

0.6

1

1.4

Am

plit

ud

e 1

CHFUSD

SSTrFFFFFF

2010 2011 2012 2013

0.2

0.6

1

1.4

Am

plit

ud

e 1

EURUSD

SSTrFFFFFF

2010 2011 2012 2013

0.2

0.6

1

1.4

Am

plit

ud

e 1

GBPUSD

SSTrFFFFFF

2010 2011 2012 2013

0.2

0.6

1

1.4

Am

plit

ud

e 1

JPYUSD

SSTrFFFFFF

Figure 9: Amplitude modulations reconstruction results. In each panel: reconstructed amplitude mod-ulations of the first component (black line) with 95% confidence intervals (shaded area), Fourier Flexible Form(dashed line) and rolling Fourier Flexible Form (red line). Top: CHF/USD (left) and EUR/USD (right);Bottom: GBP/USD (left) and JPY/USD (right).

Remark. In Chen et al. (2014), the authors give theoretical bounds on the error committed

when reconstructing the trend and seasonality with the SST. However, those bounds have

two disadvantages: they are both very rough and impractical to implement. To obtain the

confidence intervals displayed in Figures 8, 9 and 10, we used the following procedure:

1. Use T (nτ) and fk(nτ) to recover the residuals

zn = yn − T (nτ)−K∑k=1

fk(nτ)

for n ∈ {1, · · · , N}.

2. Bootstrap B samples zbn for b ∈ {1, · · · , B} and n ∈ {1, · · · , N}.

3. Add back T (nτ) and fk(nτ) to zbn in order to obtain

ybn = zbn + T (nτ) +K∑k=1

fk(nτ)

30

11−07−11 11−07−12 11−07−13 11−07−14 11−07−15

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

CHFUSD

SSTrFFFFFF

11−07−11 11−07−12 11−07−13 11−07−14 11−07−15

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

EURUSD

SSTrFFFFFF

11−07−11 11−07−12 11−07−13 11−07−14 11−07−15

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

GBPUSD

SSTrFFFFFF

11−07−11 11−07−12 11−07−13 11−07−14 11−07−15

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

JPYUSD

SSTrFFFFFF

(a) Second week of July 2011.

11−08−08 11−08−09 11−08−10 11−08−11 11−08−12

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

CHFUSD

SSTrFFFFFF

11−08−08 11−08−09 11−08−10 11−08−11 11−08−12

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

EURUSD

SSTrFFFFFF

11−08−08 11−08−09 11−08−10 11−08−11 11−08−12

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

GBPUSD

SSTrFFFFFF

11−08−08 11−08−09 11−08−10 11−08−11 11−08−12

−1.5

−1

−0.5

0

0.5

1

1.5

Se

aso

na

lity

JPYUSD

SSTrFFFFFF

(b) Second week of August 2011.

Figure 10: Seasonality reconstruction results. In each panel: reconstructed seasonality (black line) with95% confidence intervals (shaded area) and rolling Fourier Flexible Form (red line). Top: CHF/USD (left) andEUR/USD (right); Bottom: GBP/USD (left) and JPY/USD (right).

31

for b ∈ {1, · · · , B} and n ∈ {1, · · · , N}.

4. Estimate T b(nτ) and f bk(nτ) for b ∈ {1, · · · , B} and n ∈ {1, · · · , N} to compute pointwise

confidence intervals.

As zn are found to be autocorrelated, a naive bootstrapping scheme is not appropriate. To

deal with this dependence issue, we use the automatic block-length selection procedure from

Politis and White (2004) along with circular block-bootstrap. In our case, the pointwise boot-

strapped distribution of the estimates is found to be approximately normal. However, a bias

correction proves to be necessary, which is achieved for instance for the trend by substracting

the bootstrapped bias∑B

b=1 Tb(nτ)/B − T (nτ) from the estimate T (nτ).

In summary, an impressing feature of our estimated trend is its robustness to jumps, which

affect both the realized volatility and, albeit to a lesser extent, the bipower variation. Regarding

the seasonality, Figures 9 and 10 strongly suggest that it evolves dynamically over time. Finally,

although similar estimates of trend and seasonality can be obtained with moving averages and

rolling regressions respectively, the SST provides smooth estimates and does not require an

arbitrary choice of the length of the window or the rolling overlap. One could argue that the

choice of mother wavelet is also arbitrary, but as illustrated in Section 2, the influence of this

choice on the SST estimators is negligible. In any case, the main message is that dynamic

methods are necessary to properly understand the seasonality, as static models can lead to

severe underestimation/overestimation of the intraday spot volatility.

5. Simulation study

In this section, we present simulations that use a realistic setting. To study the properties of the

estimators from Section 3, we directly sample 1000 times 150 days of data (i.e., 288·150 = 43200

observations) from the adaptive volatility model from equation (14), that is

yn = Tn + sn + zn,

32

where Tn and sn are deterministic functions and

zn = log∣∣hnwn + qnIne

−(Tn+sn)∣∣

with hn, wn and qnIn as described in Section 2. Using the EUR/USD sample (cf. Section 4, for

more details), we collect the first 150 days of extracted trend and seasonality, the latter either

with constant amplitude (estimated with the FFF) or with amplitude modulations (estimated

with the SST). Furthermore, we use the exponential of the estimated residuals (see Section

4) to obtain realistic parameters to simulate hnwn from either a GED(ν) (with hn = 1), an

EGARCH(1,1) or a GARCH(1,1). Finally, for the sake of simplicity, we assume that the two

components of the jump process are

• qn = eTn+snjn, where jn ∼ N(0, σj) with σj ∈ {4σw, 10σw} with σw the standard deviation

of the estimated i.i.d. GED(ν),

• and In ∼ B(1, λ) data) with λ ∈ {1/288, 1/1440}, that is one jump per day or week on

average.

Note that the assumption of proportionality to eTn+sn does not affect the following results.

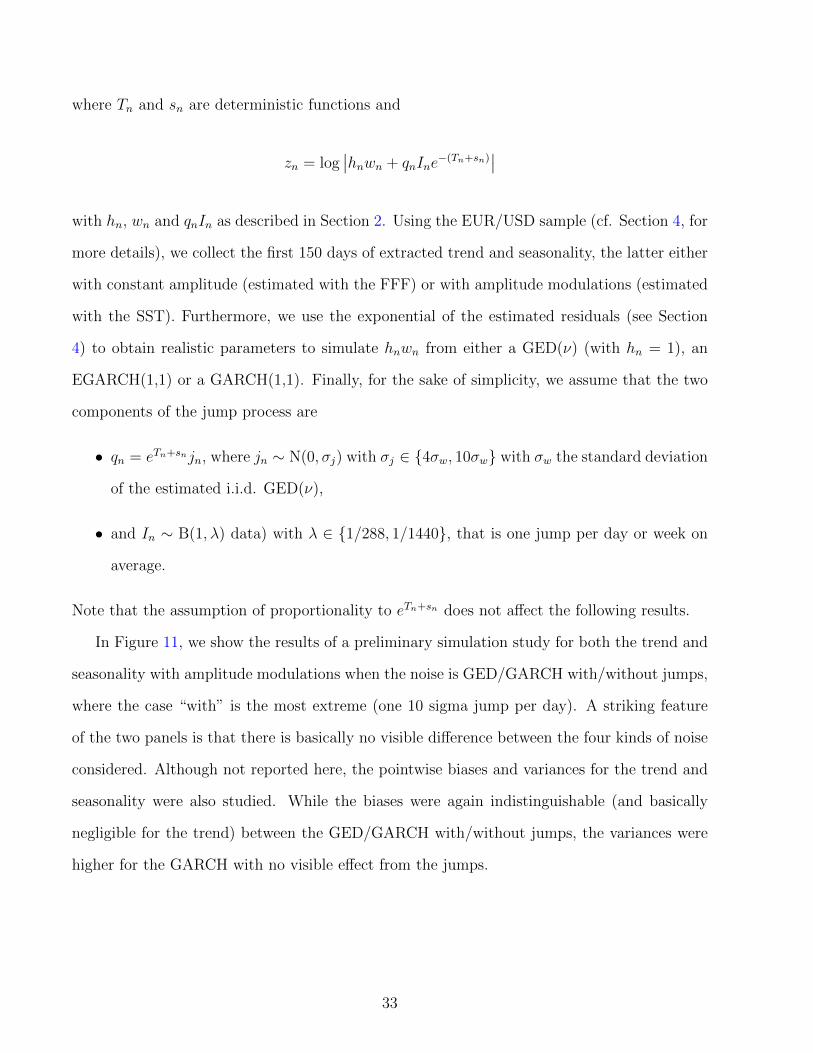

In Figure 11, we show the results of a preliminary simulation study for both the trend and

seasonality with amplitude modulations when the noise is GED/GARCH with/without jumps,

where the case “with” is the most extreme (one 10 sigma jump per day). A striking feature

of the two panels is that there is basically no visible difference between the four kinds of noise

considered. Although not reported here, the pointwise biases and variances for the trend and

seasonality were also studied. While the biases were again indistinguishable (and basically

negligible for the trend) between the GED/GARCH with/without jumps, the variances were

higher for the GARCH with no visible effect from the jumps.

33

30 60 90 120

1

2

3

4

x 10−4

Days

Tre

nd

w ∼ GED, no jumps

estimated exp(trend)true exp(trend)

30 60 90 120

1

2

3

4

x 10−4

Days

Tre

nd

w ∼ GED, λj = 1/288, σj = 10σw

estimated exp(trend)true exp(trend)

30 60 90 120

1

2

3

4

x 10−4

Days

Tre

nd

w ∼ GARCH, no jumps

estimated exp(trend)true exp(trend)

30 60 90 120

1

2

3

4

x 10−4

Days

Tre

nd

w ∼ GARCH, λj = 1/288, σj = 10σw

estimated exp(trend)true exp(trend)

(a) Trend for the whole (simulated) data.

1 2 3 4

−1

0

1

Days

Se

aso

na

lity

w ∼ GED, no jumps

estimated seasonalitytrue seasonality

1 2 3 4

−1

0

1

Days

Se

aso

na

lity

w ∼ GED, λj = 1/288, σj = 10σw

estimated seasonalitytrue seasonality

1 2 3 4

−1

0

1

Days

Se

aso

na

lity

w ∼ GARCH, no jumps

estimated seasonalitytrue seasonality

1 2 3 4

−1

0

1

Days

Se

aso

na

lity

w ∼ GARCH, λj = 1/288, σj = 10σw

estimated seasonalitytrue seasonality

(b) Seasonality for the first week of the (simulated) data.

Figure 11: Trend and seasonality preliminary simulation results. In each panel: mean estimate (blackline), true quantity (red line) and estimated 95% confidence intervals (shaded area).

34

To compare the results quantitatively, we use two criteria, namely the average integrated

squared error/absolute error (AISE/AIAE), defined as

AISE = E[∫ 150

0

{x(t)− x(t)}2 dt

]and AIAE = E

{∫ 150

0

| x(t)− x(t) | dt},

where the expectation is taken over all simulations for each component x ∈ {T, s}. The results

presented in Table 1 can be summarized as follows:

• As observed in Figure 11, the jumps do not affect the results, but the choice of process

for hnwn does. Furthermore, the effect of this choice is comparatively more pronounced

on the AISE, which is a measure of the total estimator’s variance.

• There is no relation between the seasonality dynamics and the trend’s estimate; whether

the former is with constant amplitude or with amplitude modulations, the AISE/AIAE

are similar. However, for the seasonality, the AISE/AIAE are higher in the latter case.

Constant Amplitude GED EGARCH(1,1) GARCH(1,1)

No jumpsAISE 1.50/0.30 1.97/0.49 1.83/0.44AIAE 11.36/5.38 13.25/6.80 12.71/6.47

λ = 1/288, σj = 4σwAISE 1.48/0.30 1.95/0.49 1.81/0.44AIAE 11.27/5.39 13.16/6.80 12.64/6.47

λ = 1/1440, σj = 4σwAISE 1.49/0.30 1.97/0.49 1.82/0.44AIAE 11.34/5.38 13.23/6.80 12.69/6.47

λ = 1/288, σj = 10σwAISE 1.47/0.31 1.94/0.49 1.81/0.44AIAE 11.24/5.41 13.14/6.82 12.63/6.49

λ = 1/1440, σj = 10σwAISE 1.49/0.30 1.96/0.49 1.82/0.44AIAE 11.33/5.38 13.22/6.80 12.69/6.47

Amplitude modulations GED EGARCH(1,1) GARCH(1,1)

No jumpsAISE 1.45/0.48 1.93/0.68 1.79/0.63AIAE 11.20/6.66 13.14/7.95 12.60/7.64

λ = 1/288, σj = 4σwAISE 1.43/0.48 1.91/0.68 1.77/0.63AIAE 11.11/6.67 13.06/7.96 12.53/7.65

λ = 1/1440, σj = 4σwAISE 1.45/0.48 1.93/0.68 1.78/0.63AIAE 11.18/6.66 13.12/7.95 12.58/7.65

λ = 1/288, σj = 10σwAISE 1.42/0.49 1.90/0.68 1.77/0.63AIAE 11.09/6.68 13.04/7.97 12.52/7.66

λ = 1/1440, σj = 10σwAISE 1.44/0.48 1.92/0.68 1.78/0.63AIAE 11.17/6.66 13.12/7.96 12.58/7.65

Table 1: Trend and seasonality complete simulation results. In each cell: trend (left) and seasonality(right).

35

6. Discussion

Our disentangling of instantaneous trend and seasonality of the intraday spot volatility is an

extension of classical econometric models that provides adaptivity to ever changing markets.

The proposed method suggests a realistic framework for the high frequency time series behav-

ior. First, it lets the realized volatility be modeled as an instantaneous trend which evolves in

real time within the day. Second, it allows the seasonality to be non-constant over the sample.

In a simulation study using a realistic setting, numerical results confirm that the proposed

estimators for the trend and seasonality components have an appropriate behavior. We show

that this result holds even in presence of heteroskedastic and heavy tailed noise and is also

robust to jumps.

Using the CHF/USD, EUR/USD, GBP/USD and USD/JPY exchange rates sampled every

5 minutes between 2010 and 2013, we confirm empirically that the oscillation frequency is

constant, as suggested originally in the Fourier Flexible Form from Andersen and Bollerslev

(1997, 1998). In the four exchange rates, we show that the amplitude modulations of the

periodic components and hence the overall magnitude of oscillation evolve dynamically over

time. As such, neglecting those modulations in the periodic part of the volatility would imply

either an overestimation (when the periodic components are lower than their mean value)

or an underestimation (when the periodic components are higher than their mean value).

Furthermore, we show that the SST estimator gives results comparable to a smooth version of

a rolling Fourier Flexible Form. However, the adaptivity of SST should still be emphasized,

as it does not require ad-hoc choices neither of the rolling overlapping ratio nor of the length

of each window as for a parametric regression.

While we illustrate our model by simultaneously disentangling the low and high frequency

components of the intraday spot volatility in the FX market, it is possible to embed the new

methodology into a forecasting exercise. Although this is beyond the scope of the present paper,

which is rather aimed at presenting the modeling framework, the exercise may be useful in

the context of an investor’s optimal portfolio choice or for risk-management purposes. Further

36

research directions include the extension of the framework to both the non-homogeneously

sampled (“tick-by-tick”) as well as multivariate data. We will return to these questions and

related issues in future works.

Acknowledgements

Most of this research was conducted while the corresponding author was visiting the Berkeley

Statistics Department. He is grateful for its support and helpful discussions with the members

both in Bin Yu’s research group and the Coleman Fung Risk Management Research Center.

This research is also supported in part by the Center for Science of Information (CSoI), a US

NSF Science and Technology Center, under grant agreement CCF-0939370, and by NSF grants

DMS-1160319 and CDS&E-MSS 1228246.

References

Andersen, T. G. and Bollerslev, T. (1997), “Intraday periodicity and volatility persistence in

financial markets,” Journal of Empirical Finance, 4, 115–158.

— (1998), “Deutsche Mark - Dollar Volatility : Intraday Activity Patterns , Macroeconomic

Announcements,” The Journal of Finance, 53, 219–265.

Andersen, T. G., Bollerslev, T., Diebold, F. X., and Labys, P. (2003), “Modeling and Fore-

casting Realized Volatility,” Econometrica, 71, 579–625.

Auger, F. and Flandrin, P. (1995), “Improving the readability of time-frequency and time-scale

representations by the reassignment method,” IEEE Trans. Signal Process., 43, 1068–1089.

Barndorff-Nielsen, O. E. (2004), “Power and Bipower Variation with Stochastic Volatility and

Jumps,” Journal of Financial Econometrics, 2, 1–37.

37

Bates, D. S. (1996), “Jumps and stochastic volatility: exchange rate processes implicit in

deutsche mark options,” Review of Financial Studies, 9, 69–107.

Bollerslev, T. and Ghysels, E. (1996), “Periodic autoregressive conditional heteroscedasticity,”

Journal of Business & Economic Statistics, 14, 139–151.

Boudt, K., Croux, C., and Laurent, S. (2011), “Robust estimation of intraweek periodicity in

volatility and jump detection,” Journal of Empirical Finance, 18, 353–367.

Chassande-Mottin, E., Auger, F., and Flandrin, P. (2003), “Time-frequency/time-scale reas-

signment,” in Wavelets and signal processing, Boston, MA: Birkhauser Boston, Appl. Numer.

Harmon. Anal., pp. 233–267.

Chassande-Mottin, E., Daubechies, I., Auger, F., and Flandrin, P. (1997), “Differential reas-

signment,” Signal Processing Letters, IEEE, 4, 293–294.

Chen, Y.-C., Cheng, M.-Y., and Wu, H.-T. (2014), “Non-parametric and adaptive modelling

of dynamic periodicity and trend with heteroscedastic and dependent errors,” Journal of the

Royal Statistical Society: Series B (Statistical Methodology), 76, 651–682.

Cox, J. C., Ingersoll Jonathan E., J., and Ross, S. A. (1985), “A Theory of the Term Structure

of Interest Rates,” Econometrica, 53, 385–407.

Dacorogna, M. M., Muller, U. A., Nagler, R. J., Olsen, R. B., and Pictet, O. V. (1993),

“A geographical model for the daily and weekly seasonal volatility in the foreign exchange

market,” Journal of International Money and Finance, 12, 413–438.

Daubechies, I. (1992), Ten Lectures on Wavelets, Philadelphia: Society for Industrial and

Applied Mathematics.

Daubechies, I., Lu, J., and Wu, H.-T. (2011), “Synchrosqueezed wavelet transforms: An em-

pirical mode decomposition-like tool,” Applied and Computational Harmonic Analysis, 30,

243–261.

38

Daubechies, I. and Maes, S. (1996), “A nonlinear squeezing of the continuous wavelet transform

based on auditory nerve models,” in Wavelets in Medicine and Biology, CRC-Press, pp. 527–

546.

Deo, R., Hurvich, C., and Lu, Y. (2006), “Forecasting realized volatility using a long-memory

stochastic volatility model: estimation, prediction and seasonal adjustment,” Journal of

Econometrics, 131, 29–58.

Engle, R. F. and Sokalska, M. E. (2012), “Forecasting intraday volatility in the US equity

market. Multiplicative component GARCH,” Journal of Financial Econometrics, 10, 54–83.

Flandrin, P. (1999), Time-frequency/time-scale Analysis, Wavelet Analysis and Its Applica-

tions, Academic Press Inc.

Folland, G. B. (1999), Real Analysis: Modern Techniques and Their Applications, Wiley-

Interscience.

Gallant, R. (1981), “On the bias in flexible functional forms and an essentially unbiased form:

The fourier flexible form,” Journal of Econometrics, 15, 211–245.

Giot, P. (2005), “Market risk models for intraday data,” The European Journal of Finance,

11, 309–324.

Guillaume, D. M., Pictet, O. V., and Dacorogna, M. M. (1994), “On the intra-daily perfor-

mance of GARCH processes,” Working papers, Olsen and Associates.

Hafner, C. M. and Linton, O. (2014), “An almost closed form estimator for the EGARCH

model,” SSRN Electronic Journal.

Heston, S. L. (1993), “A closed-form solution for options with stochastic volatility with appli-

cations to bond and currency options,” Review of Financial Studies, 6, 327–343.

Kodera, K., Gendrin, R., and Villedary, C. (1978), “Analysis of time-varying signals with small

BT values,” Acoustics, Speech and Signal Processing, IEEE Transactions on, 26, 64–76.

39

Laakkonen, H. (2007), “Exchange rate volatility, macro announcements and the choice of in-

traday seasonality filtering method,” Research Discussion Papers 23/2007, Bank of Finland.

Martens, M., Chang, Y.-C., and Taylor, S. J. (2002), “A comparison of seasonal adjustment

methods when forecasting intraday volatility,” The Journal of Financial Research, 25, 283–

299.

Muller, H.-G., Sen, R., and Stadtmuller, U. (2011), “Functional data analysis for volatility,”

Journal of Econometrics, 165, 233–245.

Nelson, D. B. (1991), “Conditional heteroskedasticity in asset returns a new approach,” Econo-

metrica, 29, 347–370.

Newey, W. K. and McFadden, D. (1994), “Large sample estimation and hypothesis testing,” in

Handbook of Econometrics, eds. Engle, R. F. and McFadden, D. L., Elsevier North Holland,

vol. 4, pp. 2111–2245.

Politis, D. N. and White, H. (2004), “Automatic Block-Length Selection for the Dependent

Bootstrap,” Econometric Reviews, 23, 53–70.

Thakur, G., Brevdo, E., Fuckar, N. S., and Wu, H.-T. (2013), “The Synchrosqueezing algorithm

for time-varying spectral analysis: robustness properties and new paleoclimate applications,”

Signal Processing, 93, 1079–1094.

Appendix A. Implementations details

In this section we provide the numerical SST implementation detail. The Matlab code is

available from the authors upon request and we refer the readers to Thakur et al. (2013) for

more implementation details.

We fix a discretely sampled time series y = {yn}Nn=1, where xn = x(nτ) with τ the sampling

40

interval and N = 2L for L ∈ N+. Note that we use the bold notation to indicate the numerical

implementation (or the discrete sampling) of an otherwise continuous quantity.

Step 1: numerically implement Wy(t, a). We discretize the scale axis a by aj = 2j/nvτ ,

j = 1, . . . , Lnv, where nv is the “voice number” chosen by the user. In practice we choose

nv = 32. We denote the numerical CWT as a N × na matrix Wy. This is a well studied step

and our CWT implementation is modified from that of wavelab7.

Step 2: numerically implement ωy(a, t).

The next step is to calculate the IF information function ωy(a, t) (20). The ∂tWy(a, t) term

is implemented directly by finite difference at t axis and we denote the result as a N × na

matrix ∂tWy. The ωy(a, t) is implemented as a N × na matrix wy by the following entry-wise

calculation:

wx(i, j) =

−i∂tWy(i,j)

2πWy(i,j)when Wy(i, j) 6= 0

NaN when Wy(i, j) = 0.,

where NaN is the IEEE arithmetic representation for Not-a-Number.

Step 3: numerically implement Sy(t, ω).

We now compute the Synchrosqueezing transform Sy (21). We discretize the frequency

domain [ 1Nτ, 1

2τ] by equally spaced intervals of length ∆ω = 1

Nτ. Here 1

Nτand 1

2τare the minimal

and maximal frequencies detectable by the Fourier transform theorem. Denote nω = b12τ− 1Nτ

∆ωc,

which is the number of the discretization of the frequency axis. Fix γ > 0, Sy is discretized as

a N × nω matrix Sy by the following evaluation

Sy(i, j) =∑

k:|wy(i,k)−j∆ω |≤∆ω/2, |Wy(i,j)|≥γ

log(2)√aj

∆ωnvWy(i, k),

where i = 1, . . . , N and j = 1, . . . , nω. Notice that the number γ is a hard thresholding

parameter, which is chosen to reduce the influence of noise and numerical error. In practice we

simply choose γ as the 0.1 quantile of |Wy |. If the error is Gaussian white noise, the choice

7http://www-stat.stanford.edu/~wavelab/

41

of γ is suggested in Thakur et al. (2013). In general, determining how to adaptively choose γ

is an open problem.

Step 4: Estimate IF, AM and trend from Sy.

We fit a discretized curve c∗ ∈ ZNnω , where Znω = {1, . . . , nω} is the index set of the

discretized frequency axis, to the dominant area of Sy by maximizing the following functional

over c ∈ ZNnω :

[ N∑m=1

log

(|Sy(m, cm)|∑nω

i=1

∑Nj=1 |Sy(j, i)|

)− λ

N∑m=2

|cm − cm−1|2],

where λ > 0. The first term is used to capture the maximal value of Sy at each time and

the second term is used to impose regularity of the extracted curve. In other words, the user-

defined parameter λ determines the “smoothness” of the resulting curve estimate. In practice

we simply choose λ = 10. Denote the maximizer of the functional as c∗ ∈ RN . In that case,

the estimator of the IF of the k-th component at time t = nτ is defined as

φ′k(n) := c∗(n)∆ω,

where φ′k ∈ RN . With c∗, the k-th component ak(t) cos(2πφk(t)) and its AM, ak(t) at time

t = nτ are estimated by:

fk(n) := < 2

Rψ∆ω