Embed Size (px)

Citation preview

Report No. 8588yVE

VenezuelaA Review of the 1990-1993 Public SectorInvestment Program(In Two Volumes) Volume IIDecember 20, 1990Latin American and Caribbean RegionCountry Oepartment IIICountry Operations Division I

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a resticted distribution and may be used by recipientsonly in the perforinance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

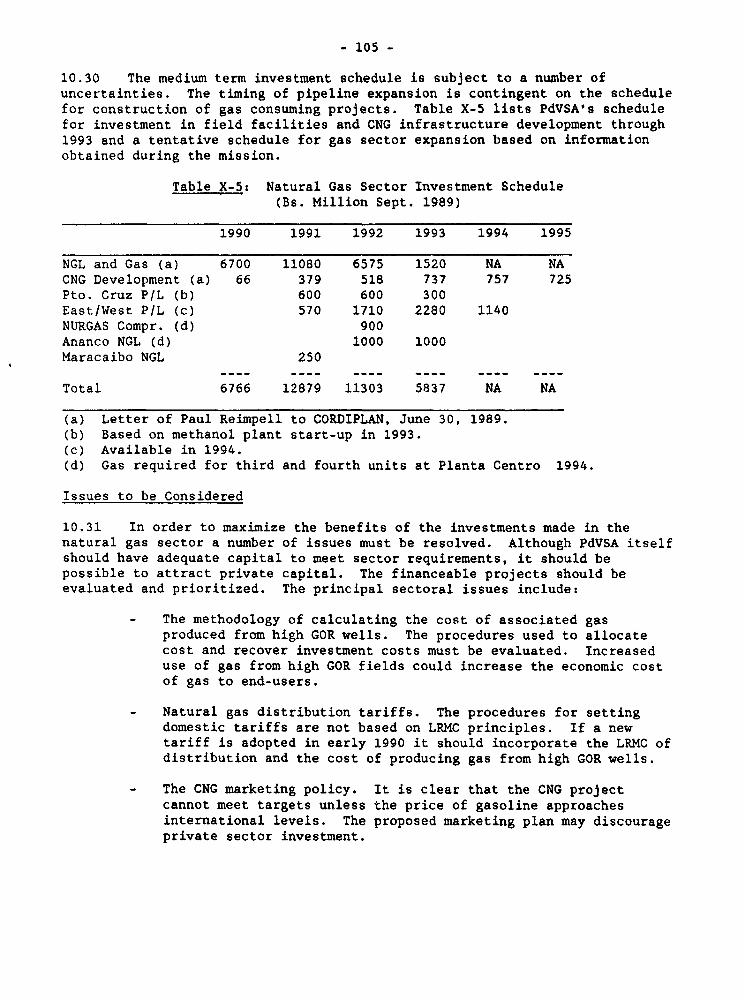

iscl

osur

e A

utho

rized

CURRENCY NOUIVALENTS

currency Unit - Bolivar

fxchange Rate as of December 31, 1989

US$l - Bs.43

Weiahts and Measures

Metric System

GOVERNMENT OF VENEZUELA FISCAL YEAR

January 1 - December 31

This report is based on the findings of a World Bank public Rectorinvestment review mission that visited Venezuela in December 198... Themission comprised Kazuko Uchimura (LA3C1, Mission Leader), Eduardo Wallentin(LA3C1, macro-framework, planning), Jaime Porras (consultant, budget), RubenSuarez (consultant, educati','i and health), Julio Linares (LA3IE, housing),Christian Gomez (IDS, roads.; Jose Baigorria (LATIE, railways), Axel Peuker(YP, railways), Carlos Hurtado (consultant, railways), Eduardo Bitran(consultant, railways), Chris Ousey (consultant, urban transport), AlanHarding (LATIN, ports), Hernan Garcia (LATIE, power), Tom Joyce (consultant,natural gas) and Mayra Zermeno (LA3C1, aluminum and steel). Ricardo Hausmannand Gustavo Marquez (consultants) prepared background papers on planning andsocial sector expenditures, respectively. Vicente Ferrer, who led a separateagriculture sector mission in October 1989 contributed the chapter onagriculture. Laura Santalla typed and compiled the successive drafts.

FOR OFFICIAL USE ONLY

PRINCIPAL AC S AM) TEM USED IN THE REPORT

ALCASA Caroni Alnlnulm(Aluminlo del Caroni)

AMTC Metropolitan Pubilc Transportation Authorities(Autorldades Metropolltanas del Transporte Publico)

ASRH Autonomous Service for Rural How ing(Serviclo Autonomo de Vlvnda Rural)

BANDAWRO Agricultural Development Bank(anco de Desarrollo Agricola)

BANAP Natlonal Savings and Loans Bank(Banco Naclonal de Ahorros y Prestamos)

INTERALLMINA Interamerican Alzninum Company(Interamericana de Alumina)

BAUXIVEN Bauxite of Venezuela(Bauxita Venezolana)

CADAFE Development and Cooperation for Electrical Power Company(Companla Anonima de Desarrollo y Fomento Electrico)

CAMETRO Caracas Metro Company(Companla del Metro de Caracas)

CENDES Center for Development Studies(Centro de Estudios para el Desarrollo)

COMEXAGRO Agricultural Commodities Marketing and Export Company(Compania Agricola de Mercado y Exortacion)

CONARE Natlonal Reforestation Company(Compania Nacional de Reforestaclon)

CORDIPLAN Ministry of Coordination and Plaming(Ministerlo de Planificaclon y Coordinacion)

COVENIN Venezuelan Industrlal Standards Commission(Comislon Venezolana de Regulaclones ndustriales)

CLUA Metropolitan Urban Commission(Comision Metropolltana Urbana)

CVG QGayana Regional Corporation(Corporaclon Venezolana de Guayana)

CSB Simon Bolivar Centre(Centro Simon Bolivar)

DINCA National Department of Administrative Accounting(DePartamento Naclonal de Contadurla Administrativa)

nGSVT Road Transportation Bureau(Oficina de Transporte por Carretera)

EDELCA Caronl Electric Company(Electrificacion del Caronl)

FCA Agricultural Credit Fund(Fondo de Credito Agricola)

FEDE Foundation for Educational Buildings and Infrastructure(Fundacion de Edificaciones y Dotaciones Educativas)

FGMA Gran Mariscal do Ayacucho Foundation(Fundacion Gran Mariscal de Ayacucho)

FEDESP Foundation for Special Education(Fundaclon paraEducaclon Especial)

FESILVEN Venezuela Ferrosillcon Company(Venezolana de Ferrosiliclo)

FERROMINERA Orlnoco Iron Ore Company(Ferrominera Orlnoco)

FIMA Founoatlon for the Maintenance of Public HealthInfrastructure

(Fundaclon para el Mantenlmlento de la Infraestructurade Salud Publica)

FONDEFRU Fruit Development Fund(Fondo para el Desarrollo Fruticola)

FONAIAP National Fund for Agricultural Research(Fondo Naclonal para Investigaclon Agricola)

FONCAFE Natlonal Coffee Fund(Fondo Naclonal del Cafe)

FONCACAO National Cacao Fund(Fondo Nacional del Cacao)

FIV Venezuela Investment Fund(Fondo do Inversiones de Venezuela)

FONOUR Foundation for Urban Developmient(Fundaclon para el Desarrollo Urbano)

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

2

IAN tlonal Agrarian kistitute(Instituto Naclonal Agricoh)

INAVI NatWna Ho¢ tste(ntltuto Nacklnai de Vlvlenda)

INAUC Autbotus fstituti of the Universlty Hospitalof Caracas

(instituto AutonQo del Hospital de la Universidadde Caracas)

INAGER National ititute of Geriatrics and Gerontology(hntituto Naclonai de Gerlatria y Gerontotogla)

ICAP Agricultural and LtAestock CredIt ttute(Instituto de Credlto Agricola y Gantadero)

INH tIonal institute of Hygene(Instltuto Naclonal de NIglene)

INN National nstitute of lutritlon(Instituto Naclonal de Nutr!clon)

INCE NatIonal institute of Educational Assstancs(instltuto Natlonal de Cooperaclon Edulativa)

PSAME kistitute for the Provision of Health Careand Social Assistance for the EWloyees ofthe Ministry of Education

(instituto para la Provislon del Culdado de laSalud y Asistencla Soclal para Empleados delMInisteric de Ekcaclon)

MARNR Ministry of Enviroment and Natural Resources(MInisterlo del Amblente y Reousos Naturales)

-uTC Ministry of Trarsportation and Cownications(Ministerio de Transporte y Coaunlcaclones)

MINDUR Ministry of Urban Develoment(MInisterlo de Desarrollo Urbano)

MSAS MInistry of Health(Ministerlo de SaIt)

OCEPRE Central Budget Offlce(Oficina Central de Presipuesto)

OCEI Central Statistical Office(Oficina Central de Estadistica)

OCG Office of the Controller General(Oflcina del Contralor General)

D PI Office of Coordination of lntergoverrmental Programs(Oflcina de Coordinacion de Programas

Intergbenamnmtaies)OM>U kni~lh~clpal OffIce of Urban Piainhg

(Oflcina tiiclpal de Pianificaclon Urbana)OPSIS Operational Off Ice for the Intercomected System

(Oficina de Operaces de Sistemas Interconectados)PO;SA Venezuela Petroleum Company

(Petroleos de Venezla)SAFORVEN Venelan Automous Forestry Service

(Serviclo Venzolano Autonoo Forestal)soR Sldenry of Orinoco

(Siderutrgla del Orlnoco)StAp Savhns and Loan System

(Sistema d Ahorro y Prestamo)VENAA Aluwih of Venezuela

(Venezolana de Alumtnilo)

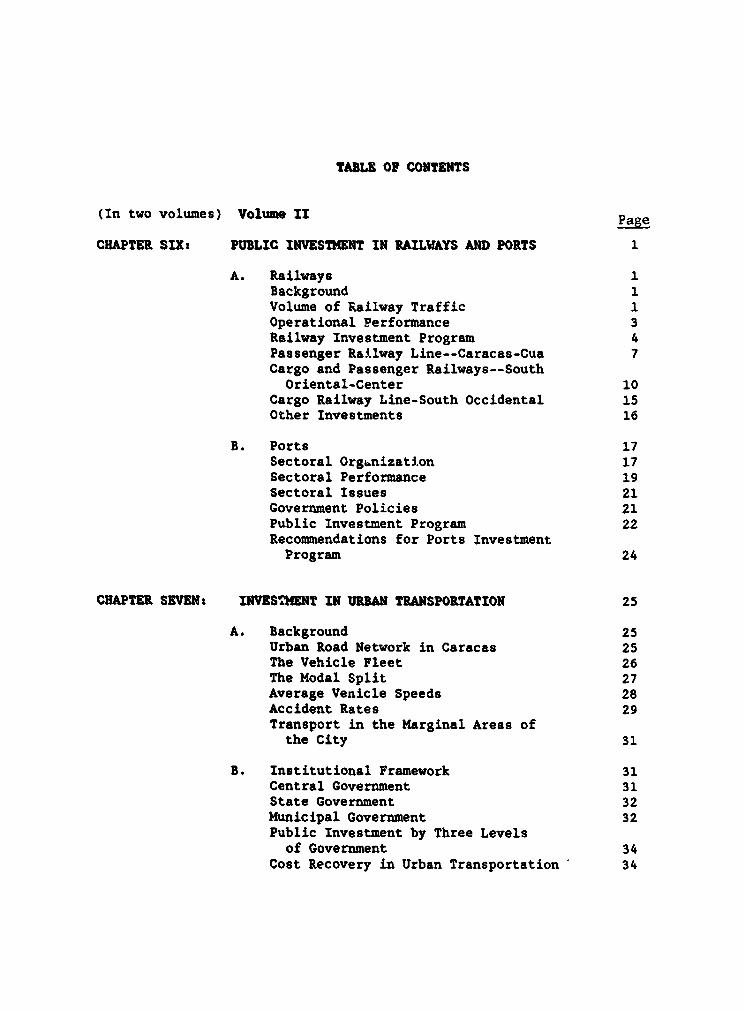

TABLE OF CONTENTS

(In two volumes) Volume II Page

CHAPTER SIX: PUBLIC INVESTMENT IN RAILWAYS AND PORTS 1

A. Railways 1Background 1Volume of Railway Traffic 1Operational Performance 3Railway Investment Program 4Passenger Railway Line--Caracas-Cua 7Cargo and Passenger Railways--South

Oriental-Center 10Cargo Railway Line-South Occidental 15Other Investments 16

B. Ports 17Sectoral Org4nization 17Sectoral Performance 19Sectoral Issues 21Government Policies 21Public Investment Program 22Recommendations for Ports Investment

Program 24

CHAPTER SVENt INVESTMENT IN URBAN TRANSPORTATION 25

A. Background 25Urban Road Network in Caracas 25The Vehicle Fleet 26The Modal Split 27Average Venicle Speeds 28Accident Rates 29Transport in the Marginal Areas ofthe City 31

B. Institutional Framework 31Central Government 31State Government 32Municipal Government 32Public Investment by Three Levels

of Government 34Cost Recovery in Urban Transportation 34

2

C. Organization of Public Transportationin Caracas 35

Por Puesto 35Regular Buses 37Metro 40Metrobus 42

D. Traffic Systems Management 42Bus Regulation and Coordination 42Taxi Regulation 43Traffic Enforcement 43

E. Public Sector Investment 43Public Sector Planning of UrbanTransport Investment 43

1990-1993 Investment Program inUrban Roads 44

Proposed CAMETRO Investment 1990-1993 44General Assessment of CAMETRO's Proposals 46

CHAPTER EIGHT: AGRICULTURE SECTOR PUBLIC INVESTMENT PROGRAM 50

A. Background 50Structure of Agriculture in Venezuela 50Institutional Framework 50

B. Sector Policies and Performance 51

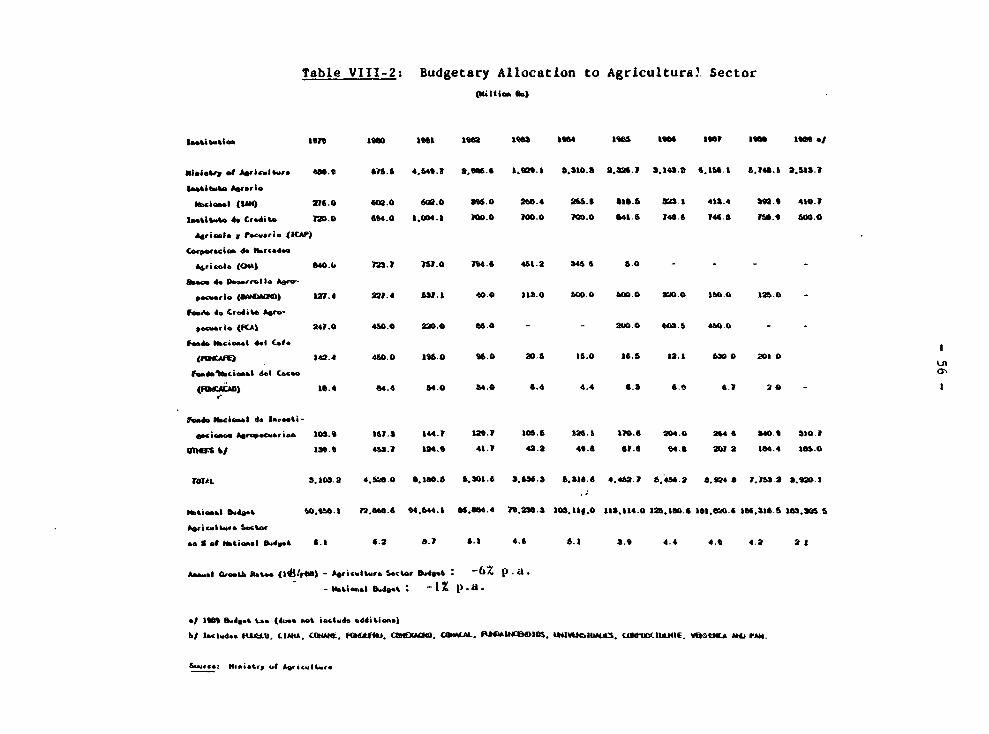

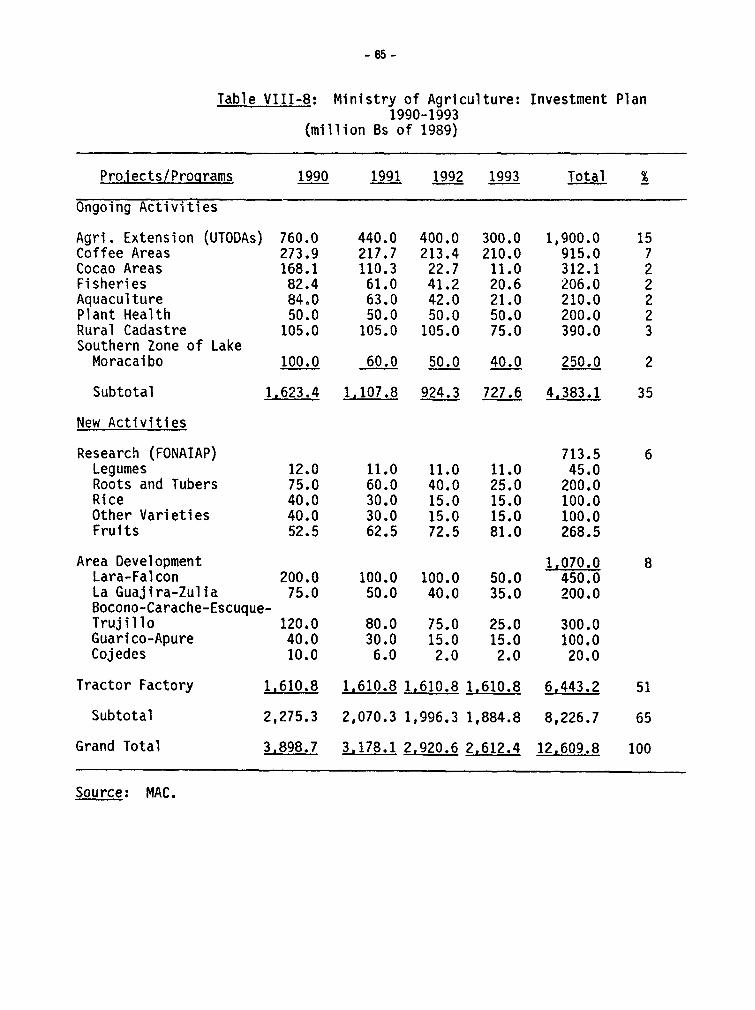

C. Public Investment Program 53Level and Trends in Public SectorAgricultural Expenditure, 1979-1989 53

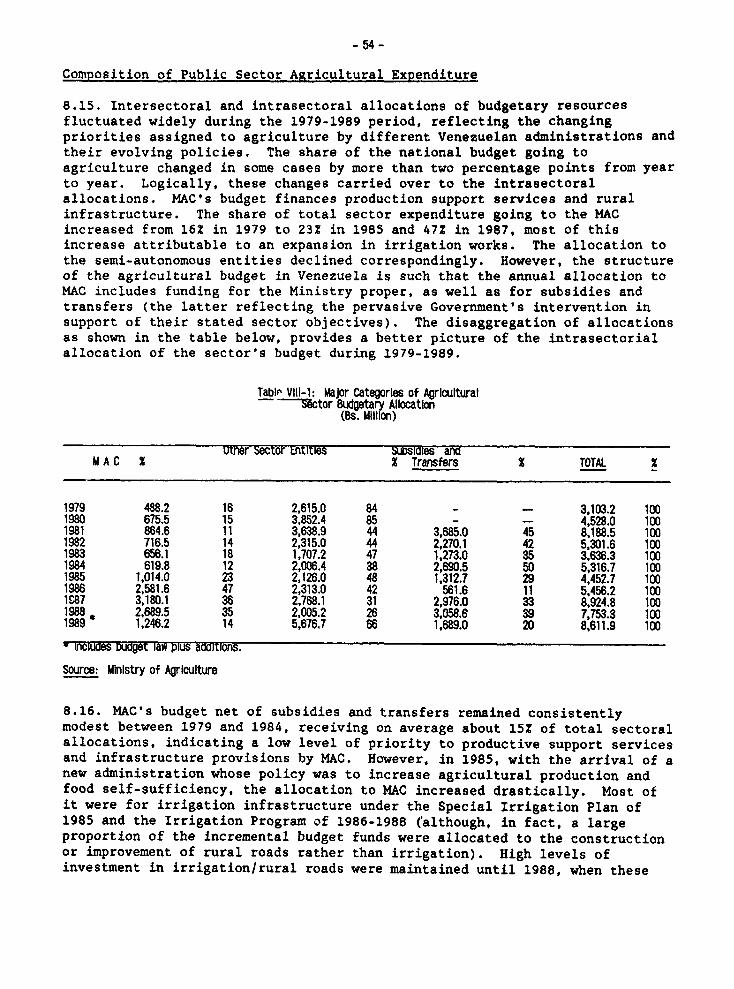

Composition of Public Sector AgriculturalExpenditure 54

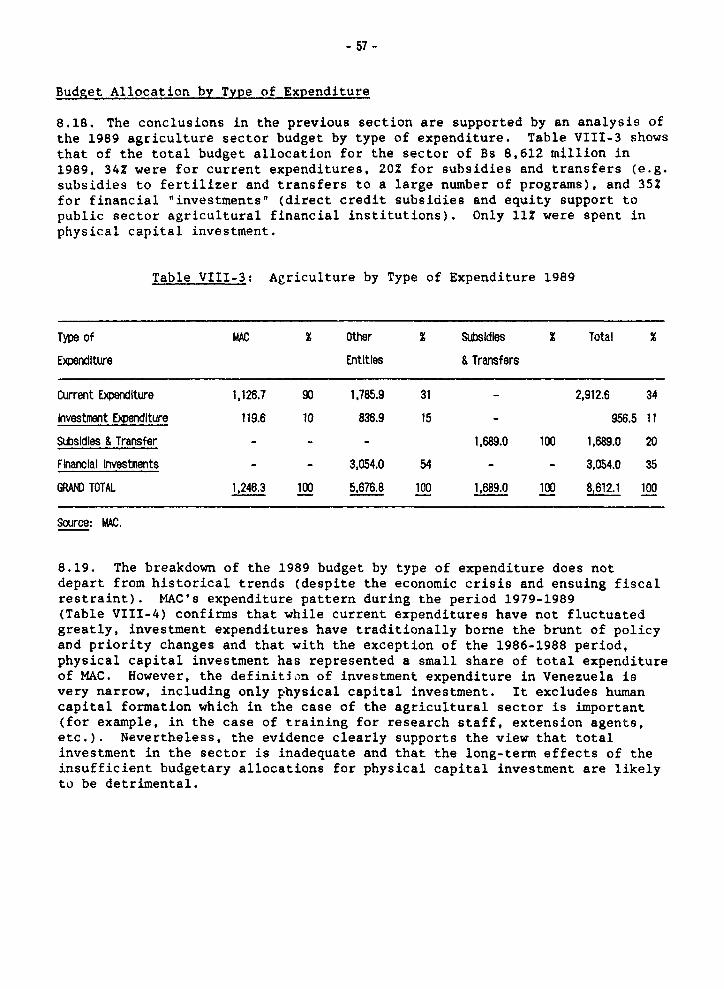

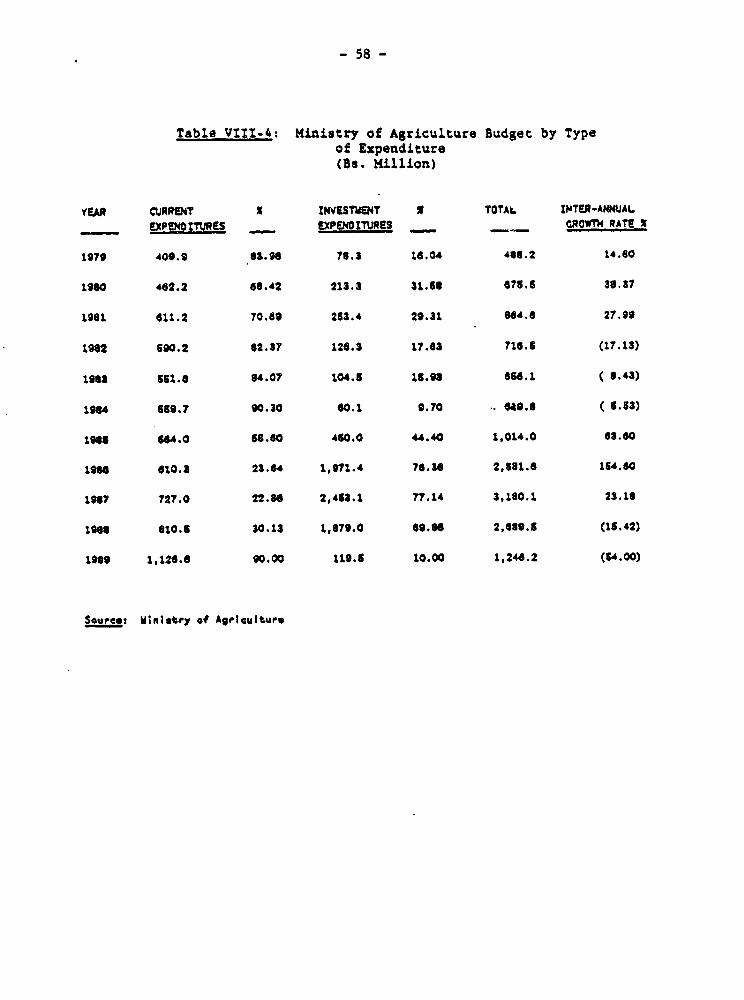

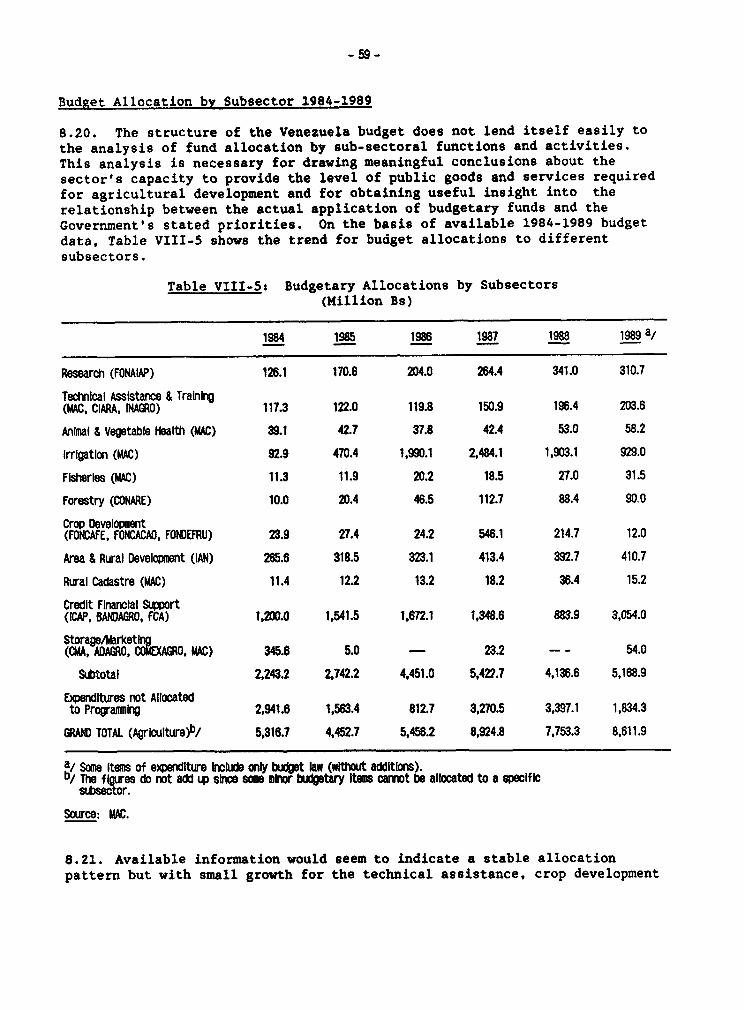

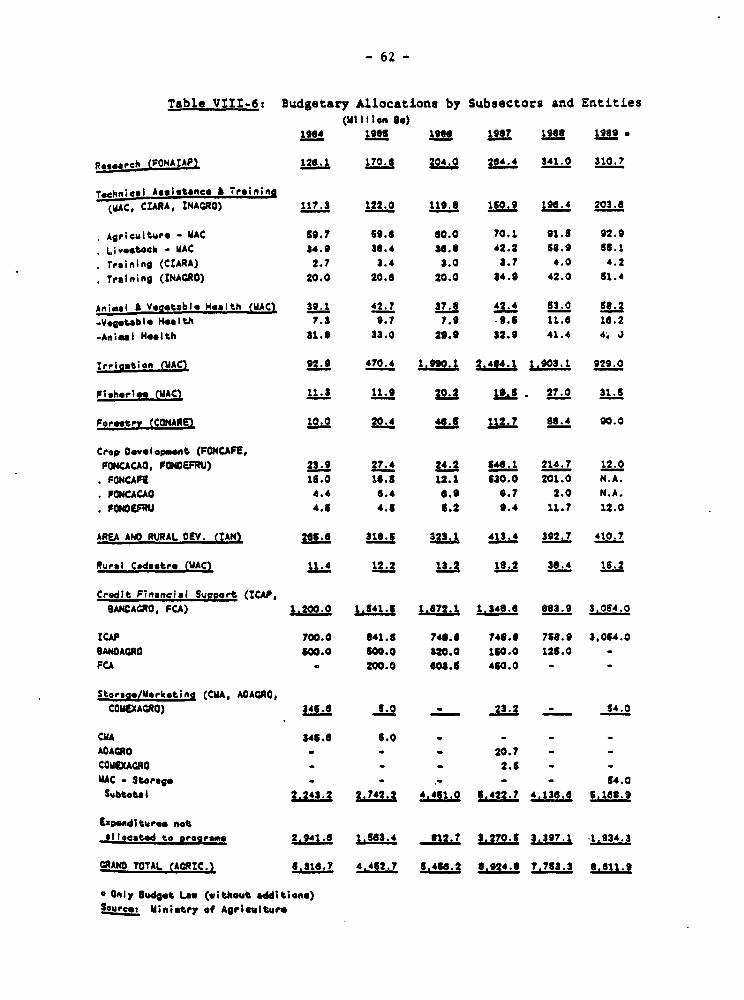

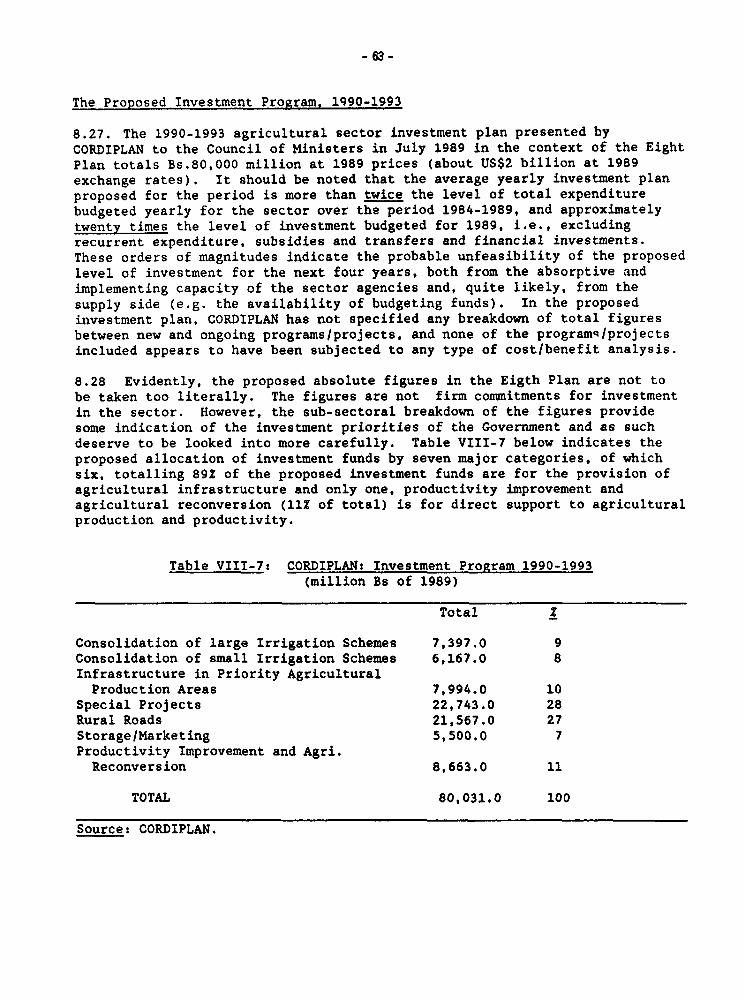

Budget Allocation by Type of Expenditure 57Budget Allocation by Subsector 1984-1989 59Sufficiency of Budgetary Allocations 60Level of Self-Financing 61The Proposed Investment Program, 1990-1993 63Mission's Comments 66

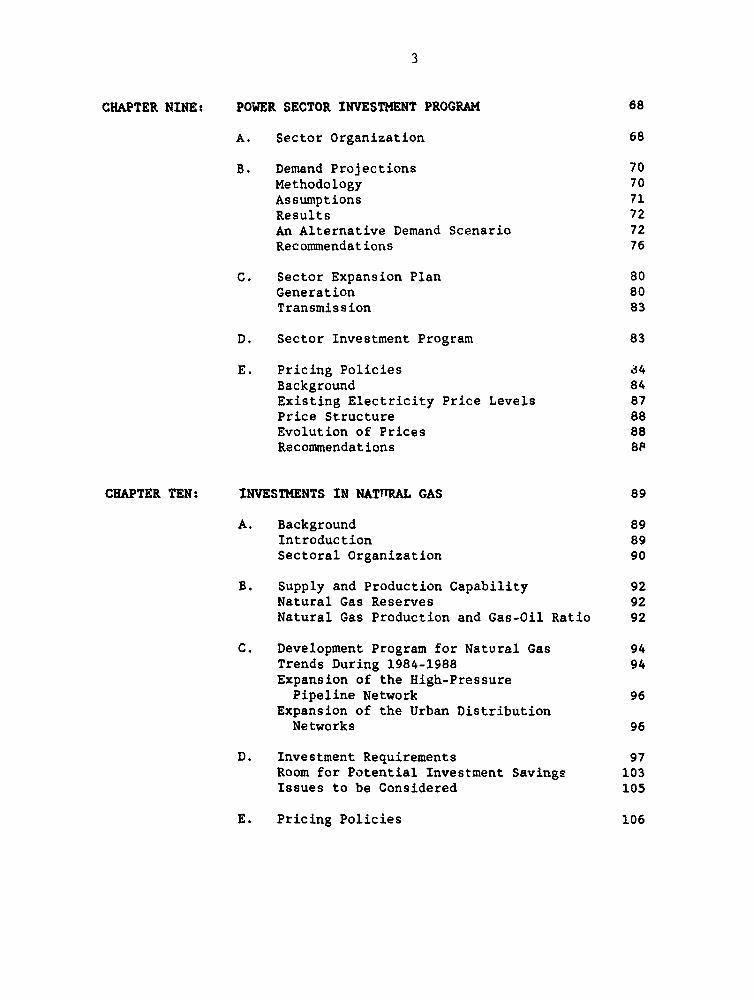

3

CHAPTER NINE: POWER SECTOR INVESTMENT PROGRAM 68

A. Sector Organization 68

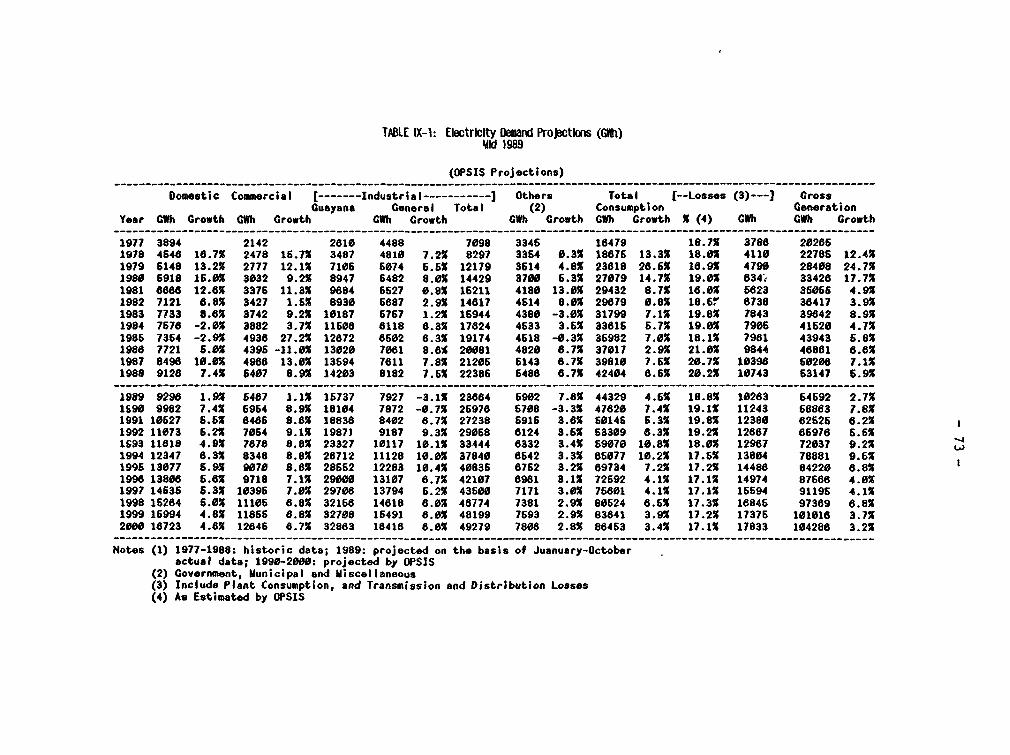

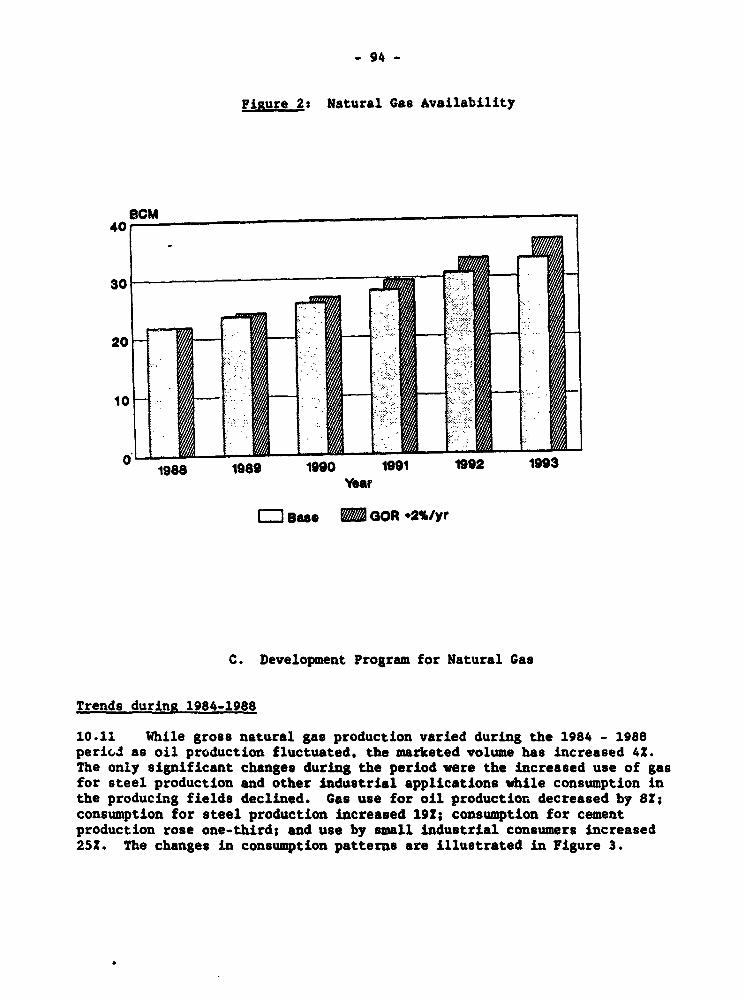

B. Demand Projections 70Methodology 70Assumptions 71Results 72An Alternative Demand Scenario 72Recommendations 76

C. Sector Expansion Plan 80Generation 80Transmission 83

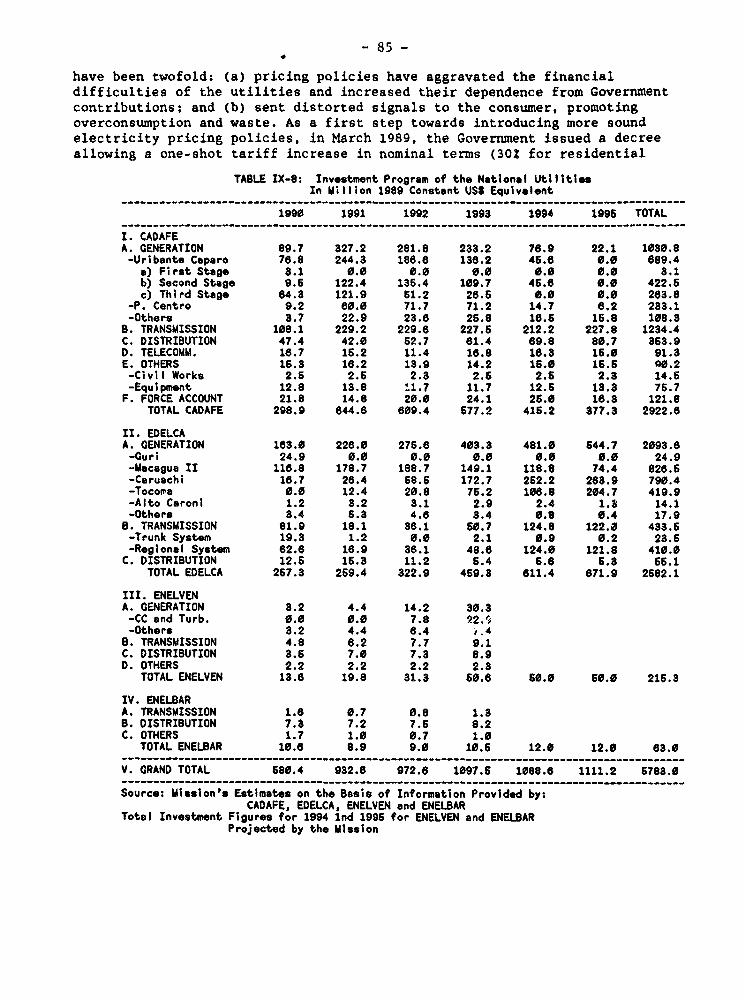

D. Sector Investment Program 83

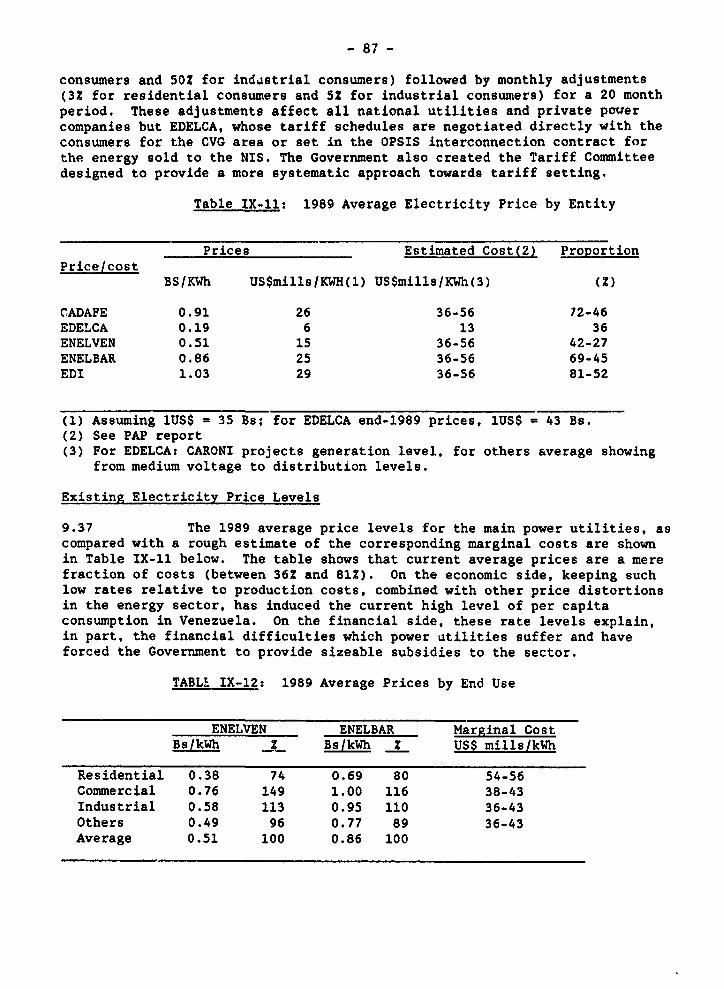

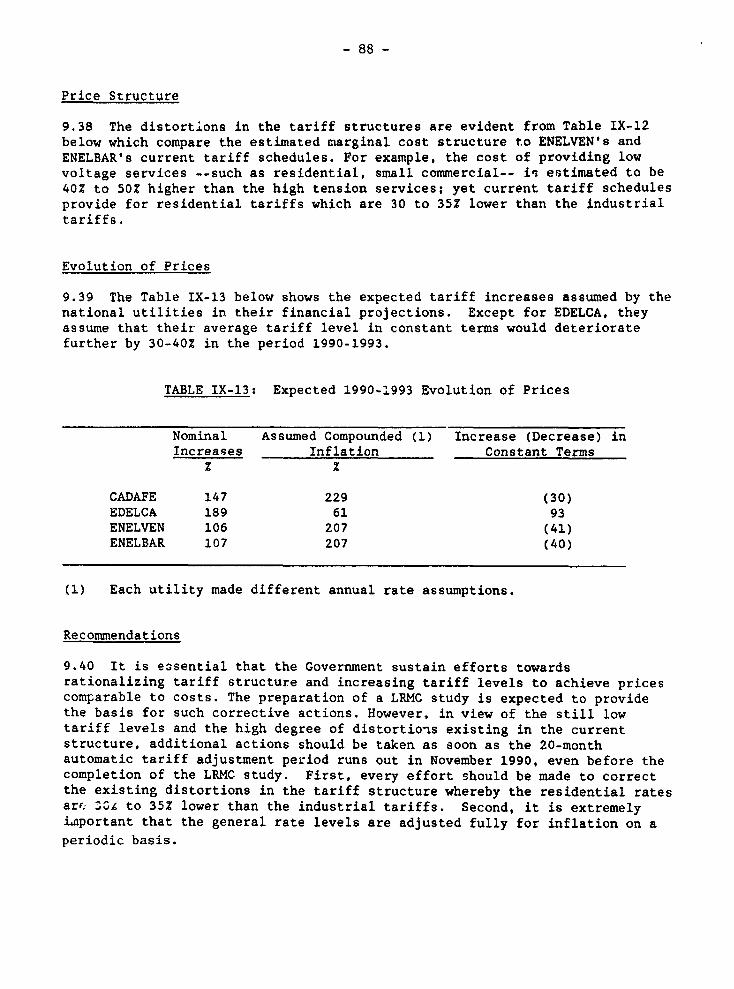

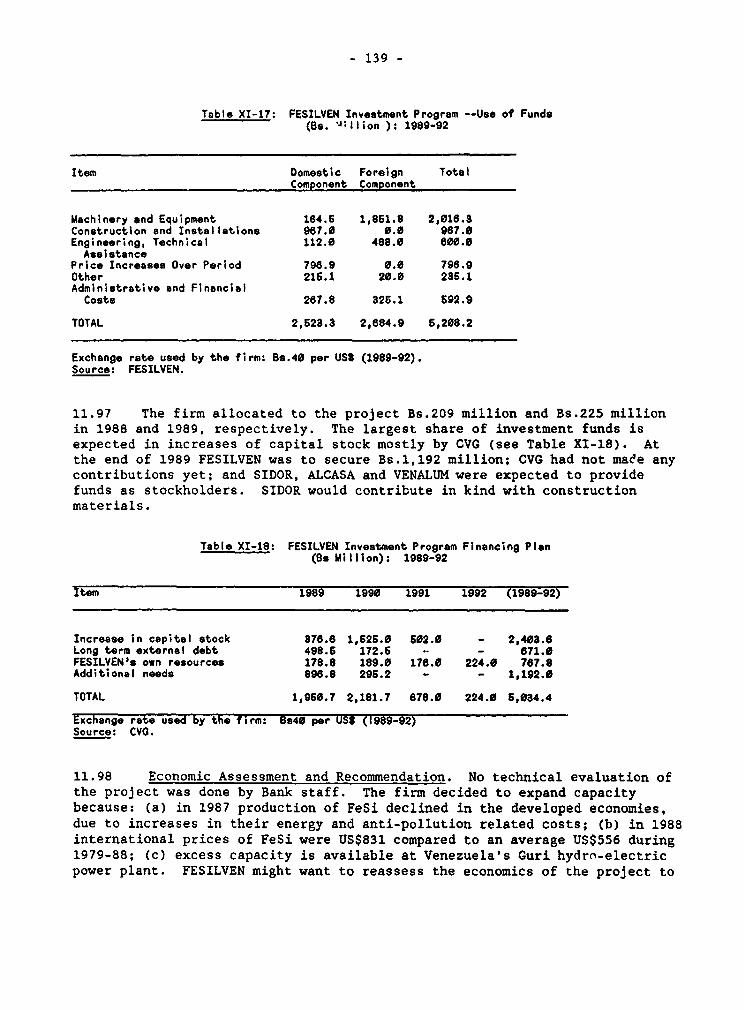

E. Pricing Policies (44Background 84Existing Electricity Price Levels 87Price Structure 88Evolution of Prices 88Recommendations 8P

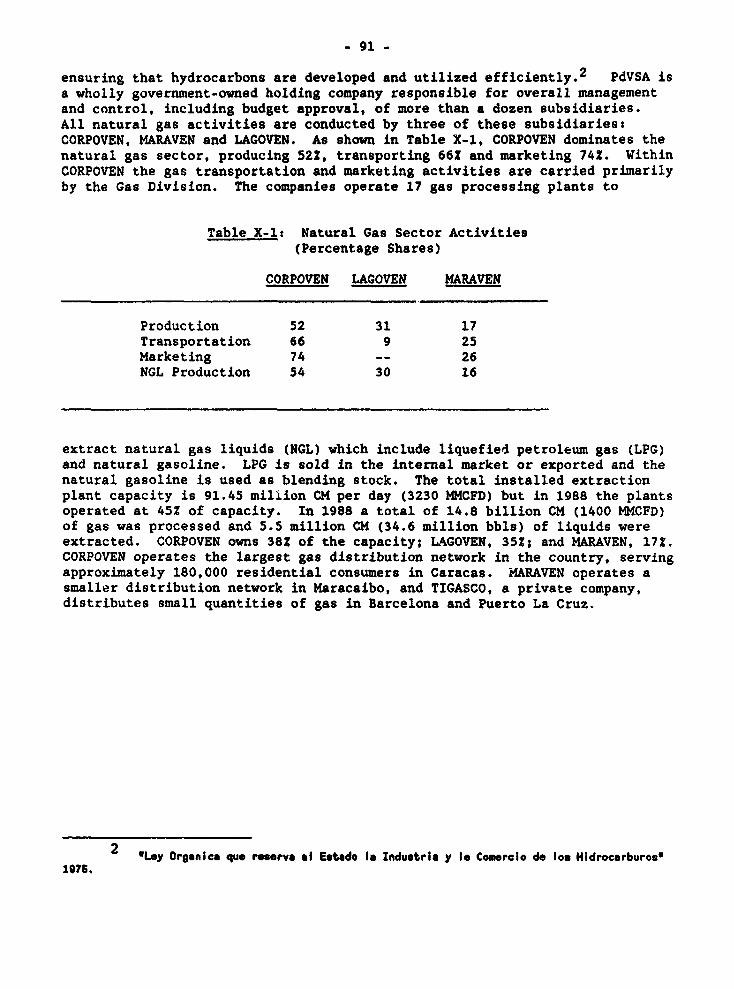

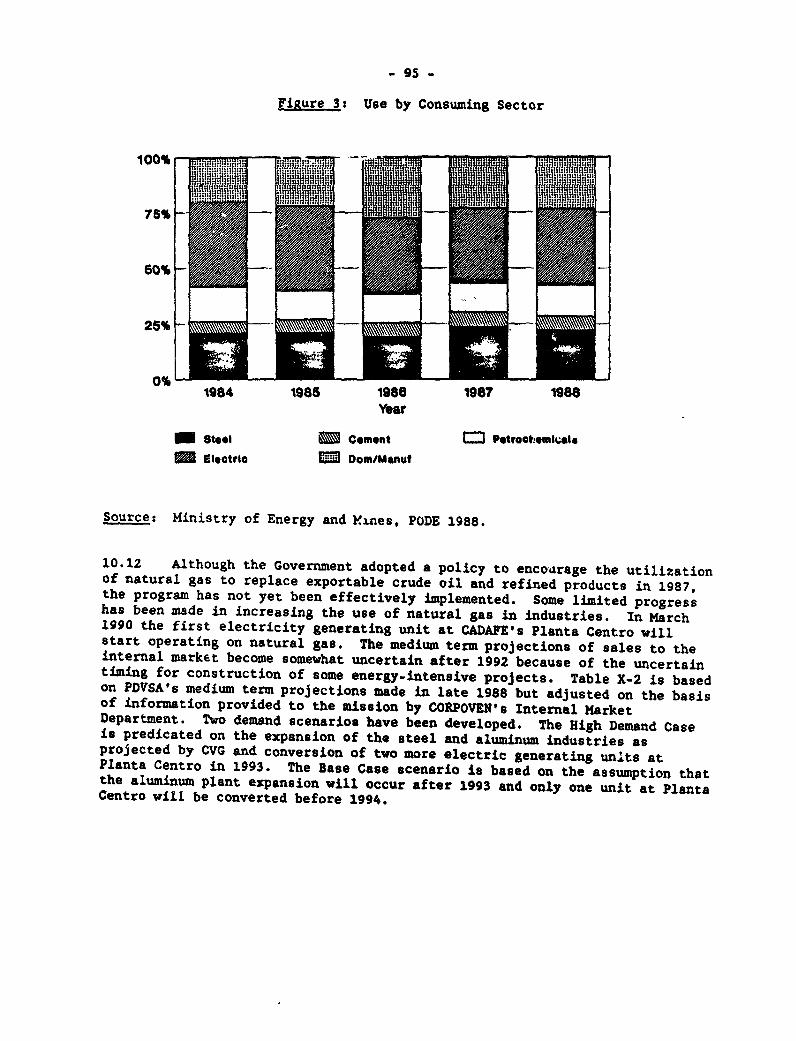

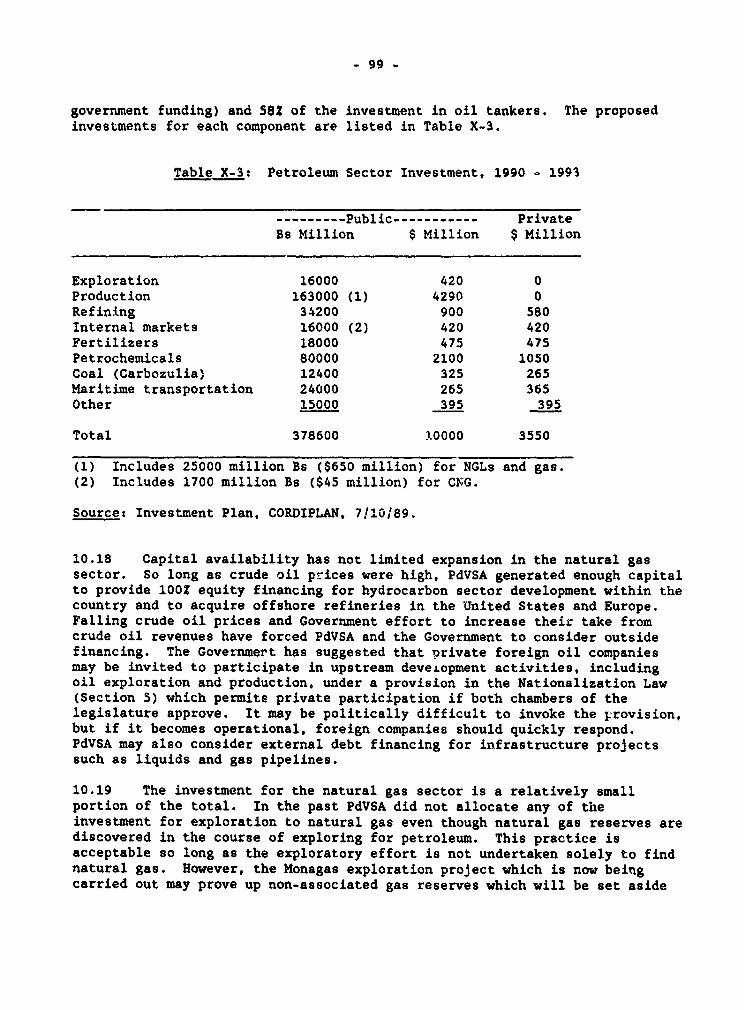

CHAPTER TEN: INVESTMENTS IN NATTTAL GAS 89

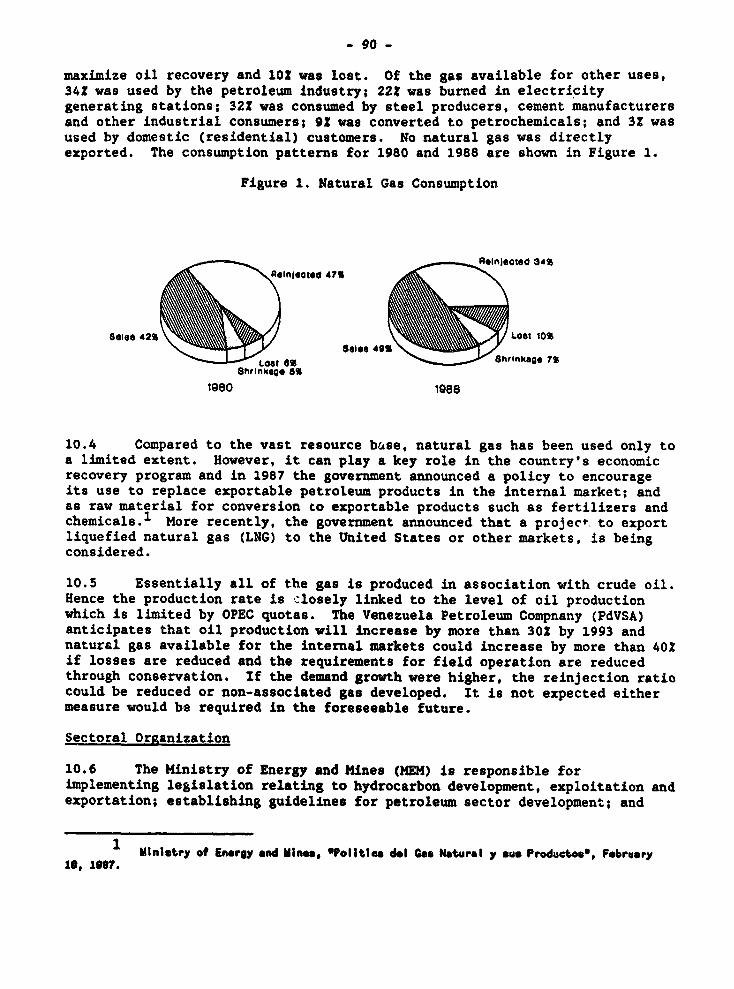

A. Background 89Introduction 89Sectoral Organization 90

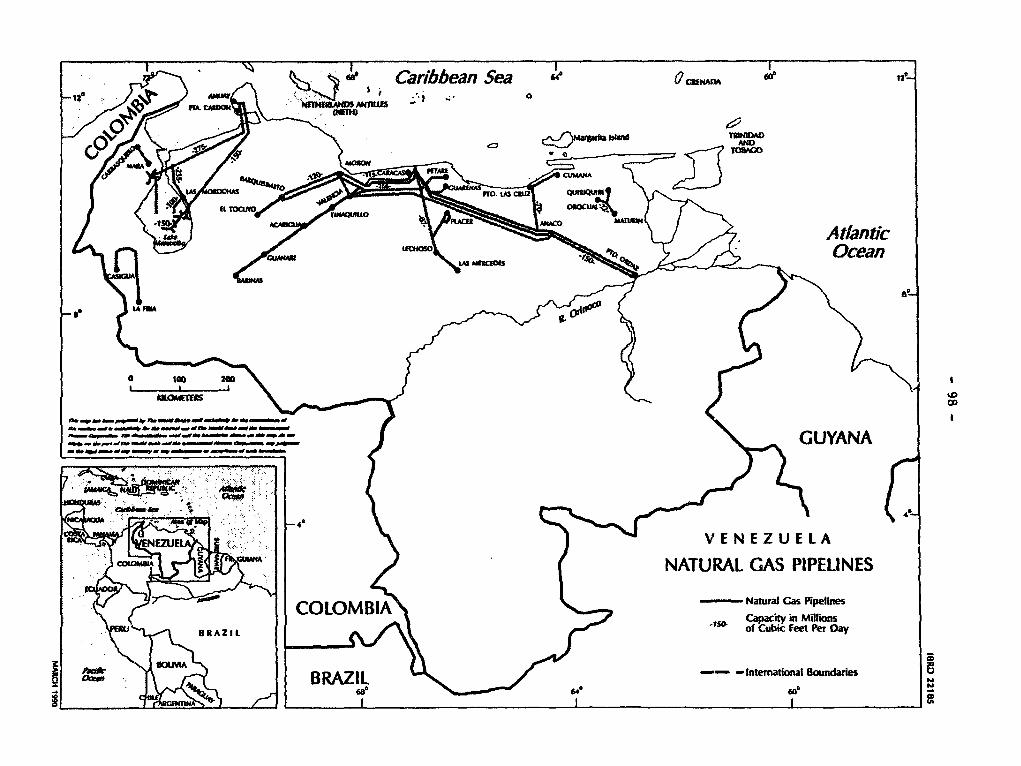

B. Supply and Production Capability 92Natural Gas Reserves 92Natural Gas Production and Gas-Oil Ratio 92

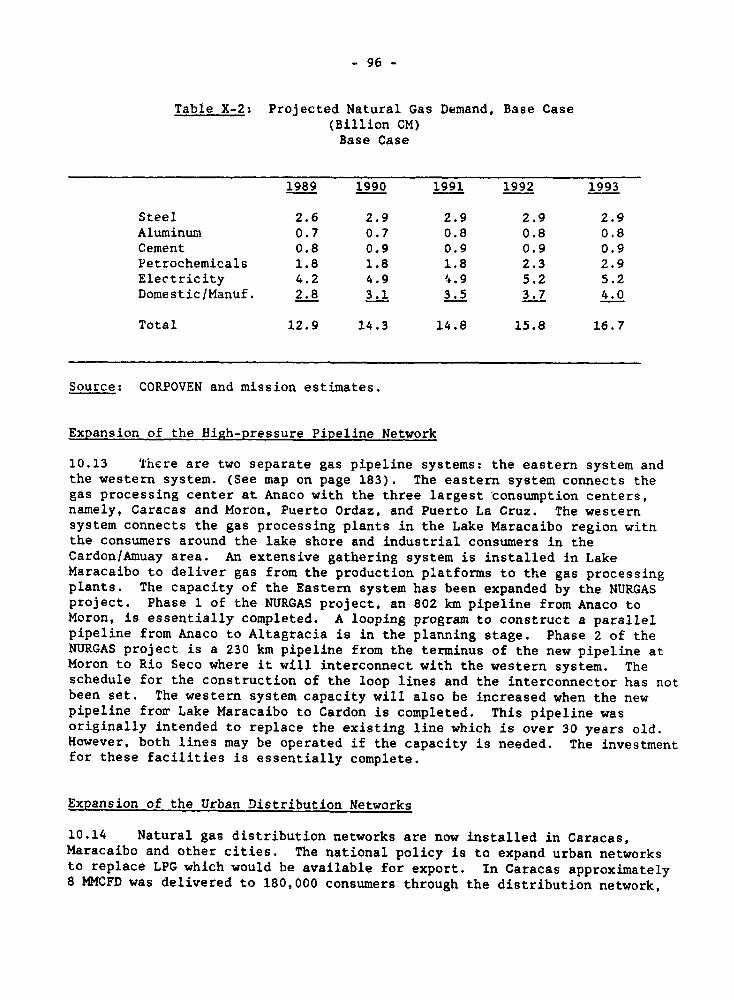

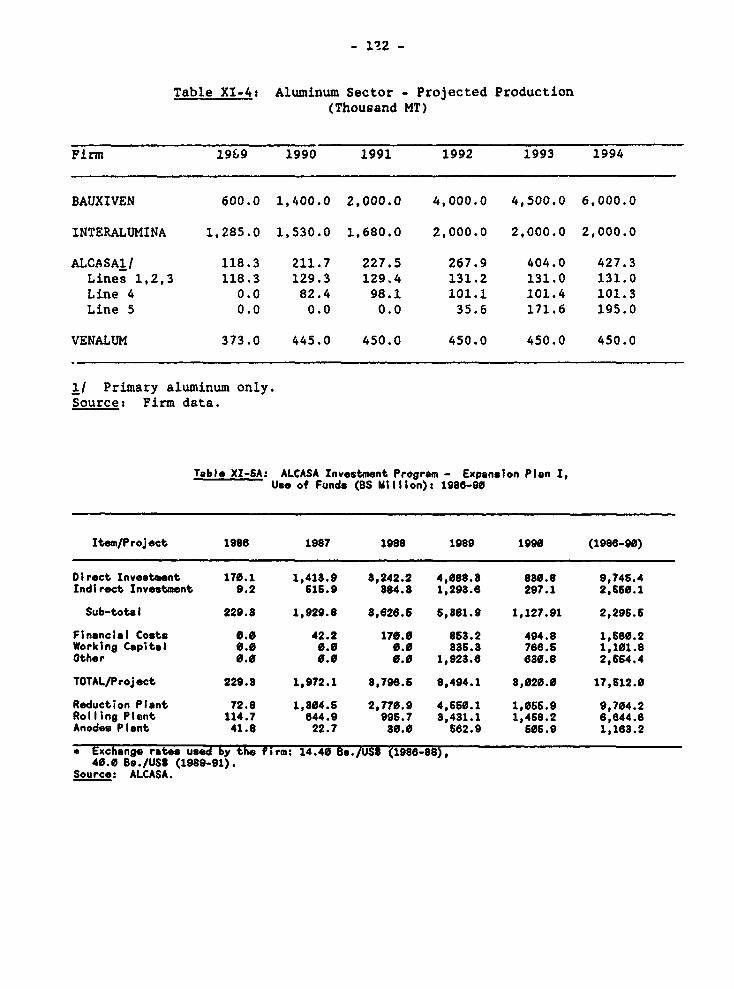

C. Development Program for Natural Gas 94Trends During 1984-1988 94Expansion of the High-PressurePipeline Network 96

Expansion of the Urban DistributionNetworks 96

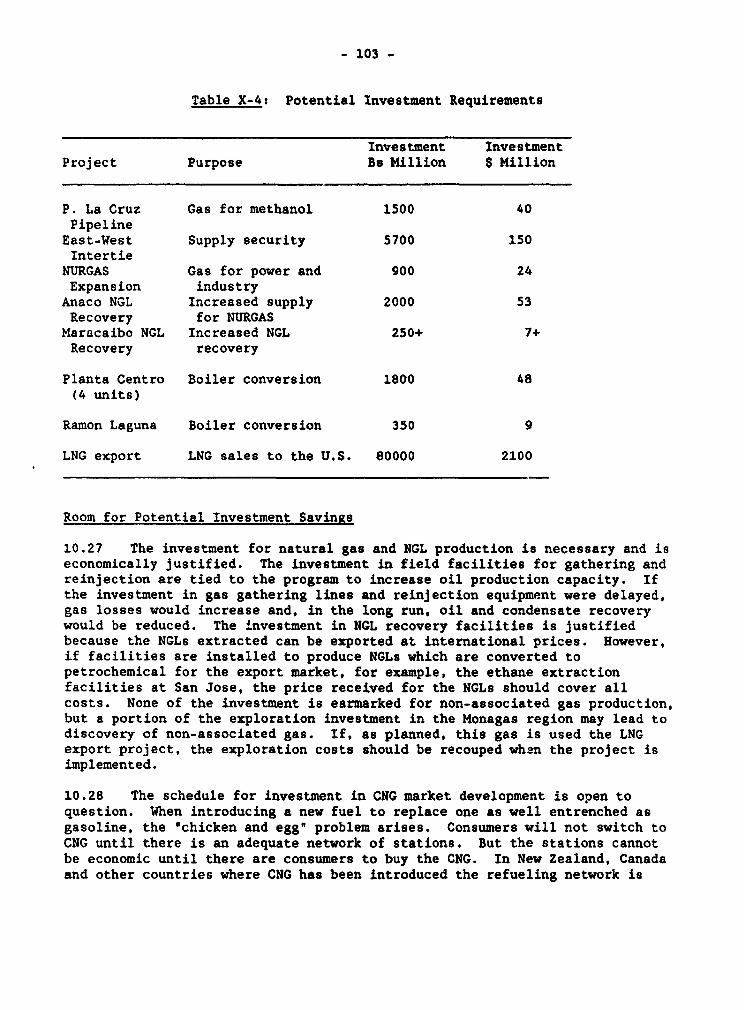

D. Investment Requirements 97Room for Potential Investment Savings 103Issues to be Considered 105

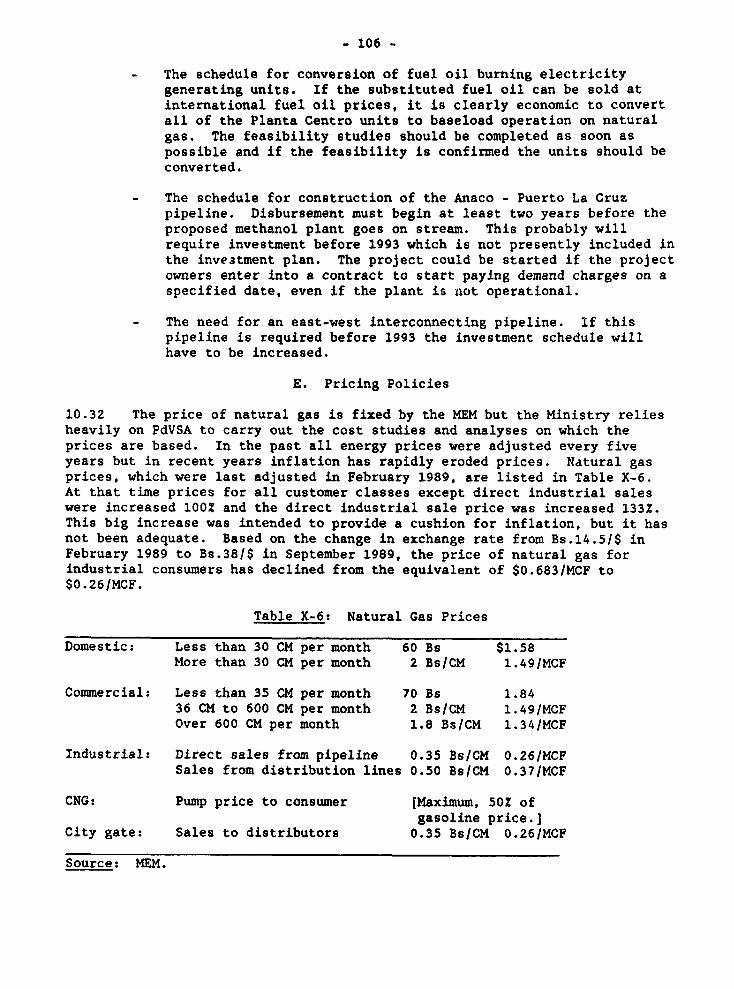

E. Pricing Policies 106

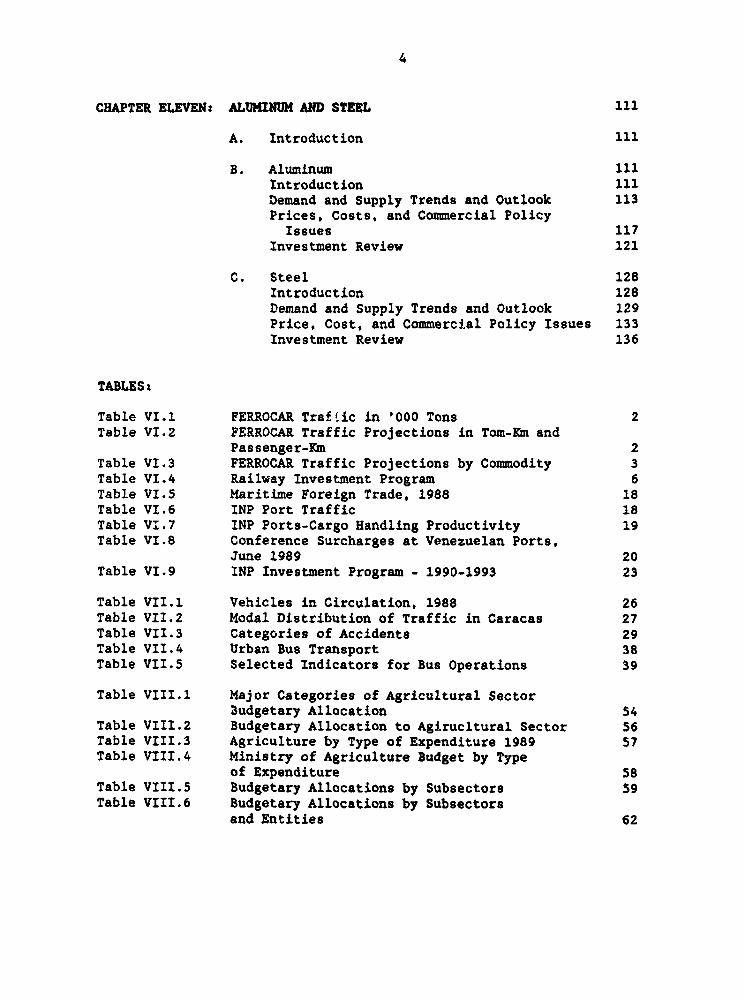

4

CHAPTER ELEVENs ALUMINUM AND STEEL 111

A. Introduction 111

B. Aluminum 111Introduction 111Demand and Supply Trends and Outlook 113Prices, Costs, and Commercial PolicyIssues 117

Investment Review 121

C. Steel 128Introduction 128Demand and Supply Trends and Outlook 129Price, Cost, and Commercial Policy Issues 133Investment Review 136

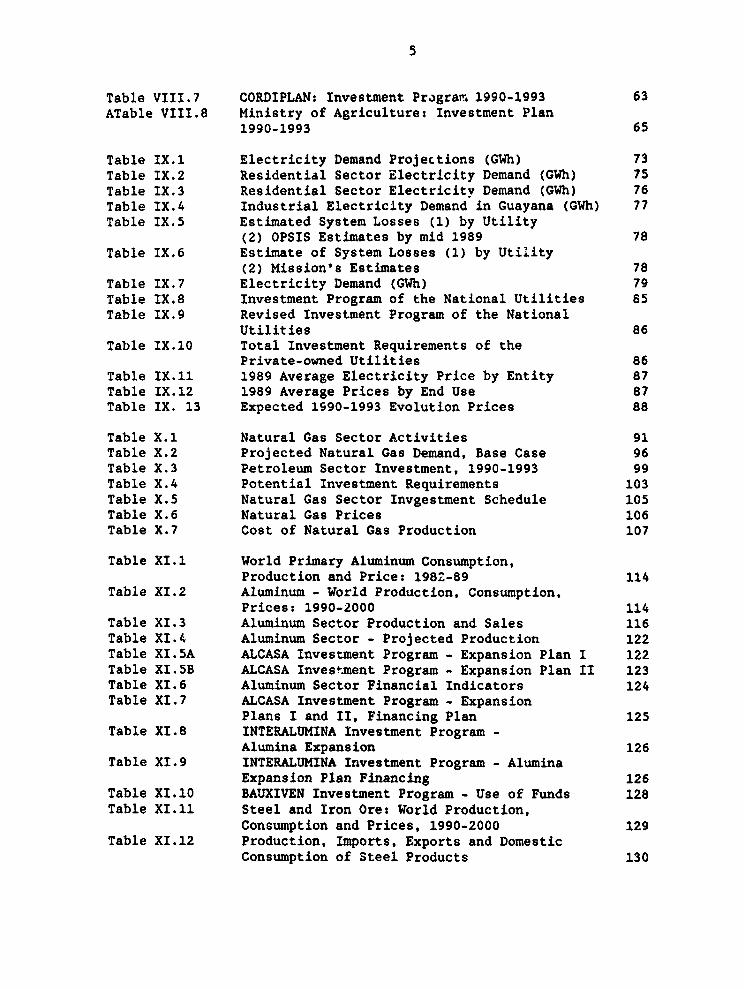

TABLES:

Table VI.1 FERROCAR Traf tic in '000 Tons 2Table VI.2 FERROCAR Traffic Projections in Tom-Km and

Passenger-Km 2Table VI.3 FERROCAR Traffic Projections by Commodity 3Table VI.4 Railway Investment Program 6Table VI.5 Maritime Foreign Trade, 1988 18Table VI.6 INP Port Traffic 18Table VI.7 INP Ports-Cargo Handling Productivity 19Table VI.8 Conference Surcharges at Venezuelan Ports,

June 1989 20Table VI.9 INP Investment Program - 1990-1993 23

Table VII.1 Vehicles in Circulation, 1988 26Table VII.2 Modal Distribution of Traffic in Caracas 27Table VII.3 Categories of Accidents 29Table VII.4 Urban Bus Transport 38Table VII.5 Selected Indicators for Bus Operations 39

Table VIII.1 Major Categories of Agricultural SectorBudgetary Allocation 54

Table VIII.2 Budgetary Allocation to Agirucltural Sector 56Table VIII.3 Agriculture by Type of Expenditure 1989 57Table VIII.4 Ministry of Agriculture Budget by Type

of Expenditure 58Table VIII.5 Budgetary Allocations by Subsectors 59Table VIII.6 Budgetary Allocations by Subsectors

and Entities 62

5

Table VIII.7 CORDIPLAN: Investment PragraTr, 1990-1993 63ATable VIII.8 Ministry of Agriculture: Investment Plan

1990-1993 65

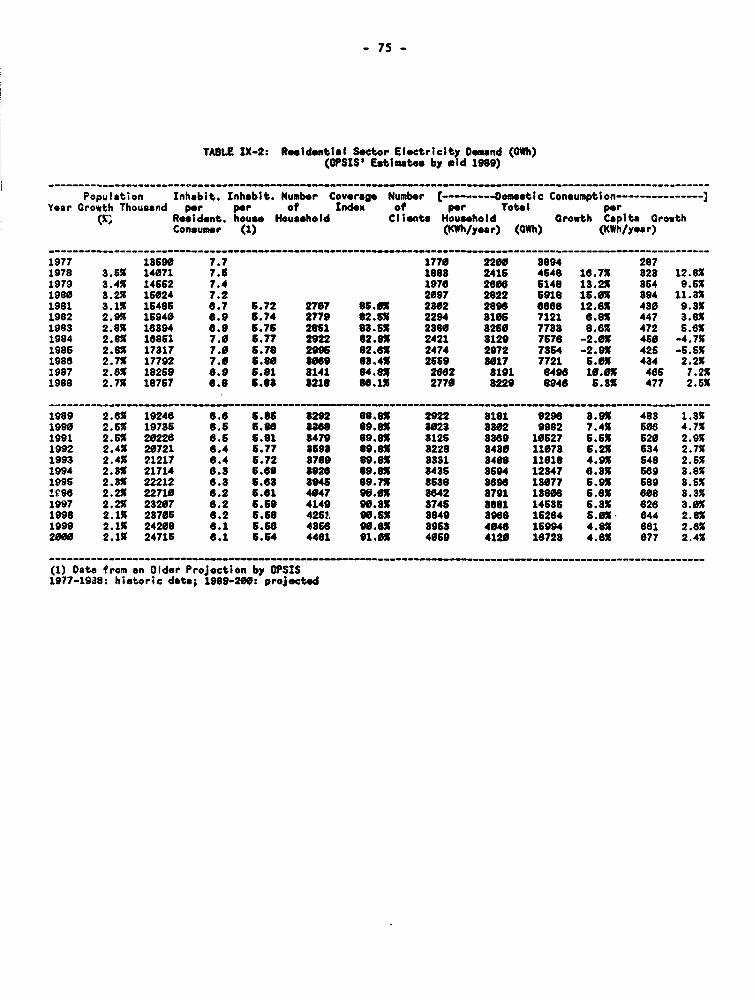

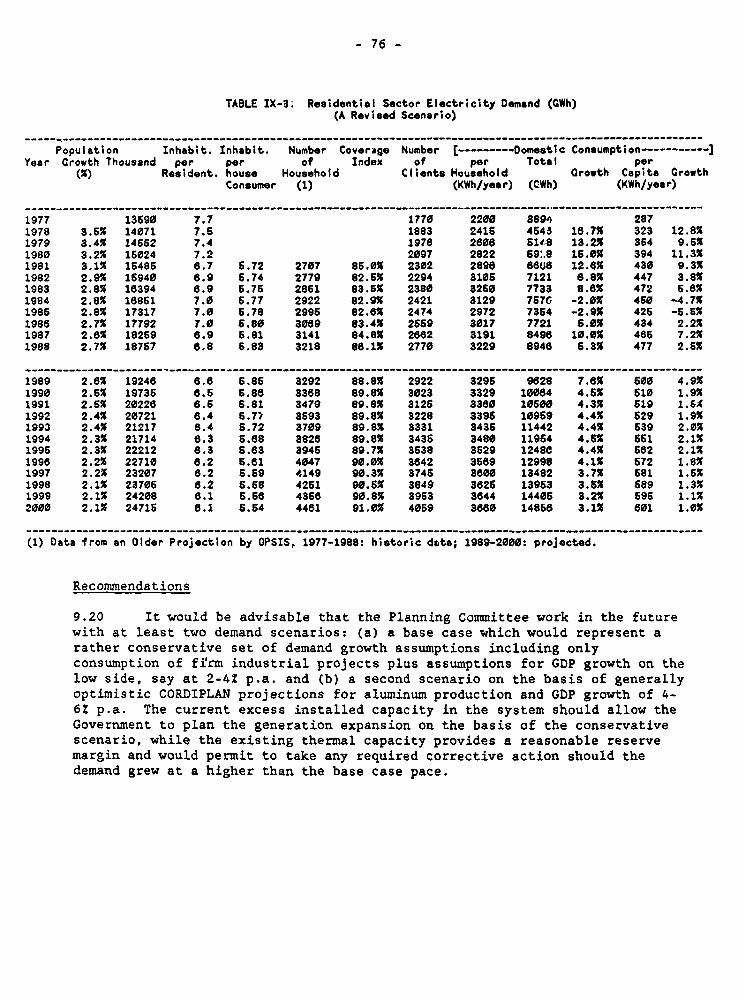

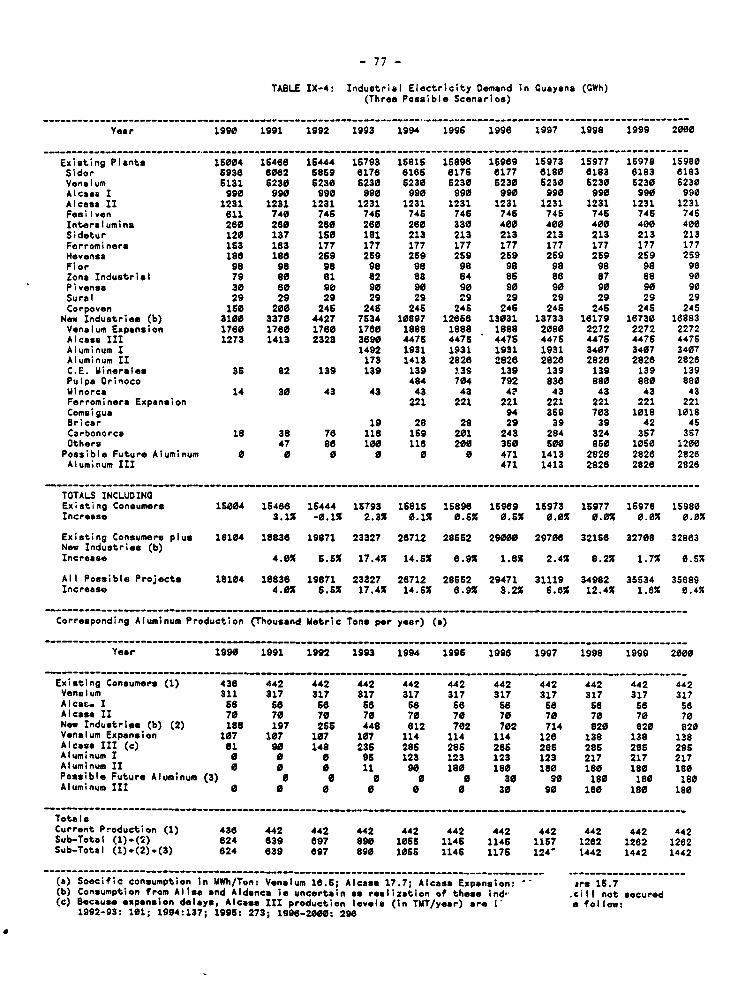

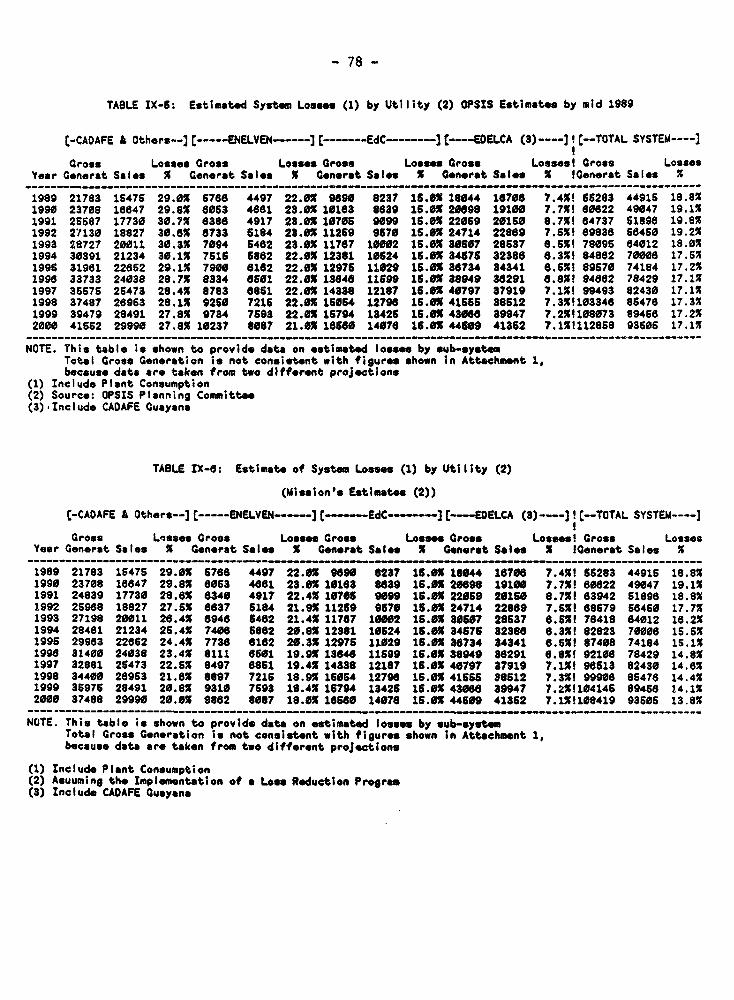

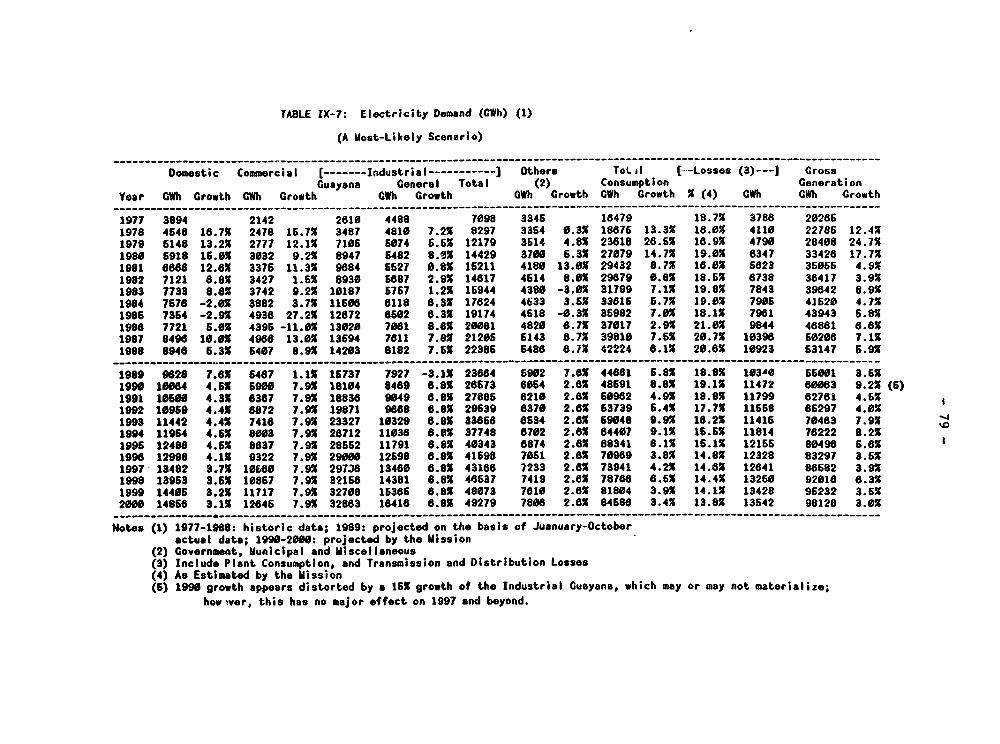

Table IX.1 Electricity Demand Projections (GWh) 73Table IX.2 Residential Sector Electricity Demand (GWh) 75Table IX.3 Residential Sector Electricitv Demand (GWh) 76Table IX.4 Industrial Electricity Demand in Guayana (GWM) 77Table IX.5 Estimated System Losses (1) by Utility

(2) OPSIS Estimates by mid 1989 78Table IX.6 Estimate of System Losses (1) by Utility

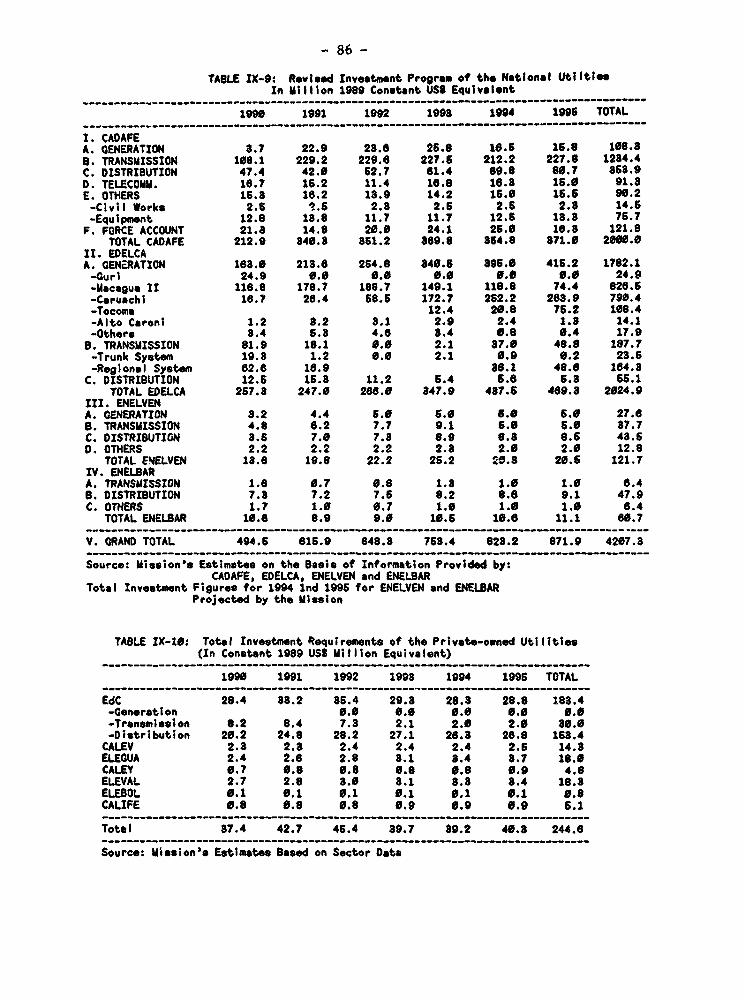

(2) Mission's Estimates 78Table IX.7 Electricity Demand (GWh) 79Table IX.8 Investment Program of the National Utilities 85Table IX.9 Revised Investment Program of the National

Utilities 86Table IX.10 Total Investment Requirements of the

Private-owned Utilities 86Table IX.11 1989 Average Electricity Price by Entity 87Table IX.12 1989 Average Prices by End Use 87Table IX. 13 Expected 1590-1993 Evolution Prices 88

Table X.1 Natural Gas Sector Activities 91Table X.2 Projected Natural Gas Demand, Base Case 96Table X.3 Petroleum Sector Investment, 1990-1993 99Table X.4 Potential Investment Requirements 103Table X.5 Natural Gas Sector Invgestment Schedule 105Table X.6 Natural Gas Prices 106Table X.7 Cost of Natural Gas Production 107

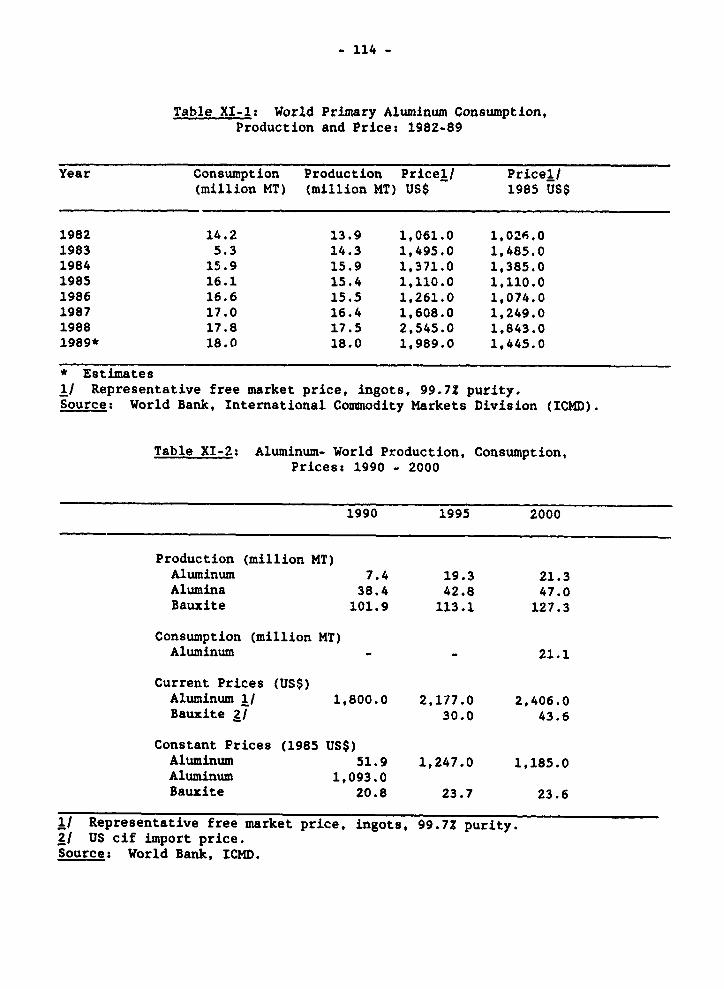

Table XI.1 World Primary Aluminum Consumption,Production and Price: 1982-89 114

Table XI.2 Aluminum - World Production, Consumption,Prices: 1990-2000 114

Table XI.3 Aluminum Sector Production and Sales 116Table XI.4 Aluminum Sector - Projected Production 122Table XI.5A ALCASA Investment Program - Expansion Plan I 122Table XI.5B ALCASA Invest.ment Program - Expansion Plan II 123Table XI.6 Aluminum Sector Financial Indicators 124Table XI.7 ALCASA Investment Program - Expansion

Plans I and II, Financing Plan 125Table XI.8 INTERALUMINA Investment Program -

Alumina Expansion 126Table XI.9 INTERALUMINA Investment Program - Alumina

Expansion Plan Financing 126Table XI.10 BAUXIVEN Investment Program - Use of Funds 128Table XI.11 Steel and Iron Ore: World Production,

Consumption and Prices, 1990-2000 129Table XI.12 Production, Imports, Exports and Domestic

Consumption of Steel Products 130

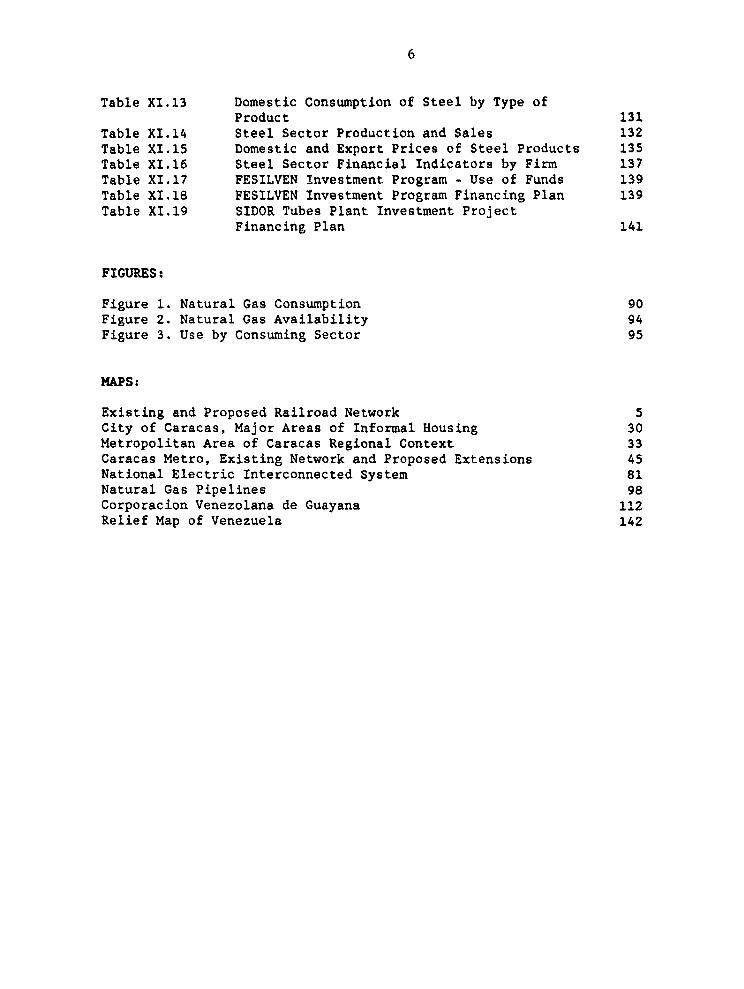

6

Table XI.13 Domestic Consumption of Steel by Type ofProduct 131

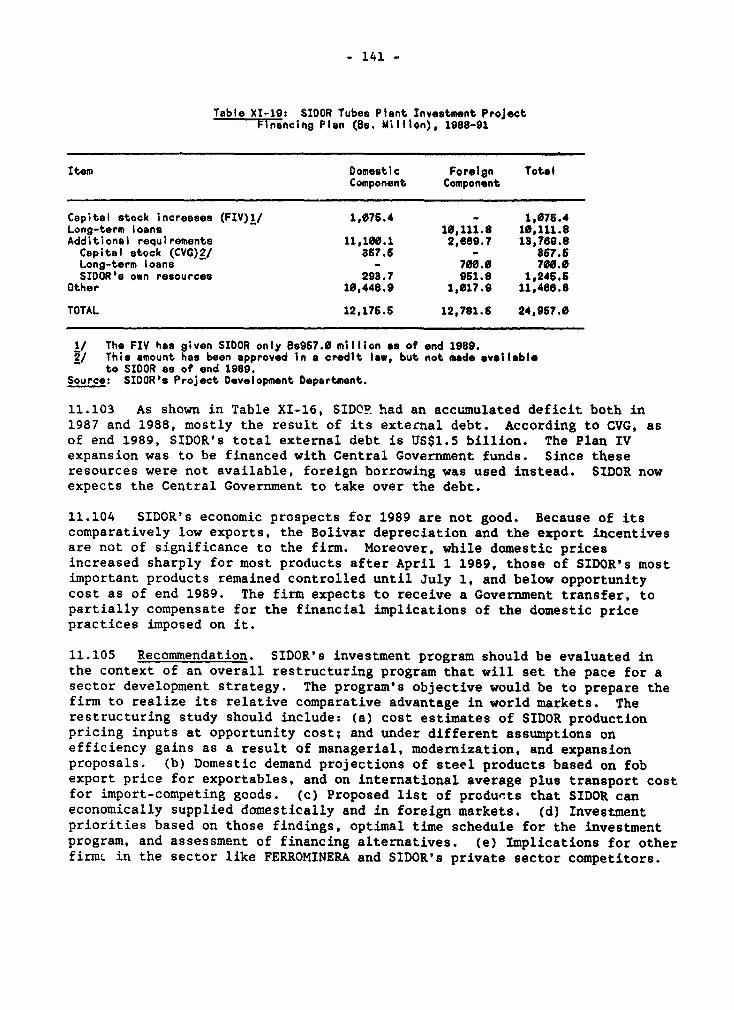

Table XI.14 Steel Sector Production and Sales 132Table XI.15 Domestic and Export Prices of Steel Products 135Table XI.16 Steel Sector Financial Indicators by Firm 137Table XI.17 FESILVEN investment Program - Use of Funds 139Table XI.18 FESILVEN Investment Program Financing Plan 139Table XI.19 SIDOR Tubes Plant Investment Project

Financing Plan 141

FIGURES:

Figure 1. Natural Gas Consumption 90Figure 2. Natural Gas Availability 94Figure 3. Use by Consuming Sector 95

MAPS:

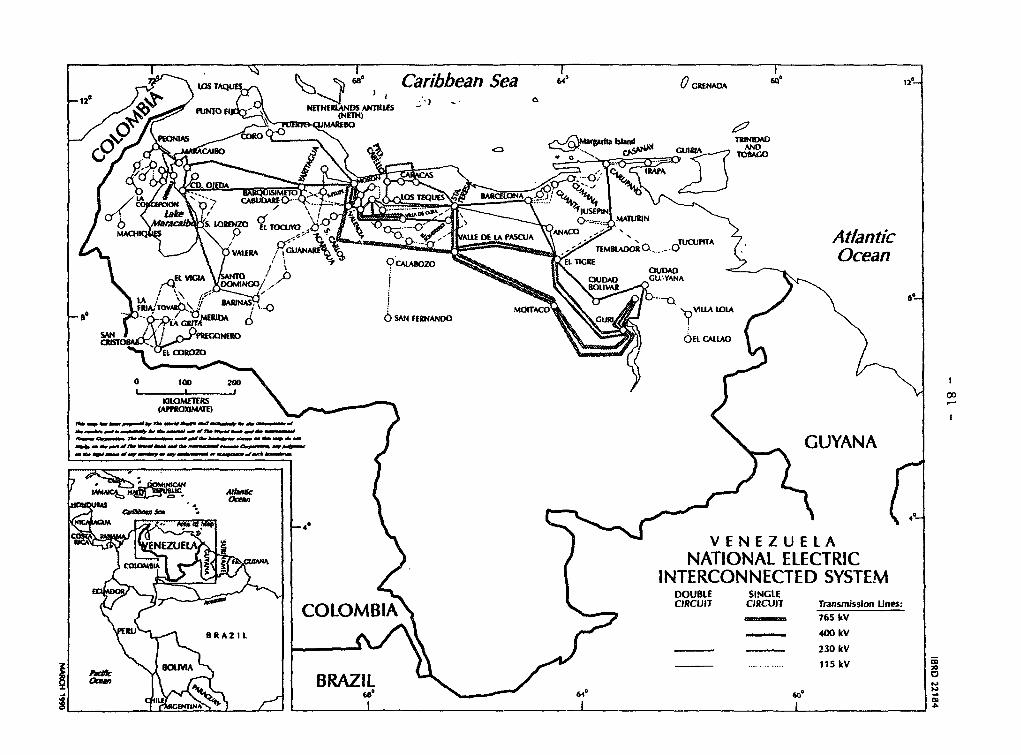

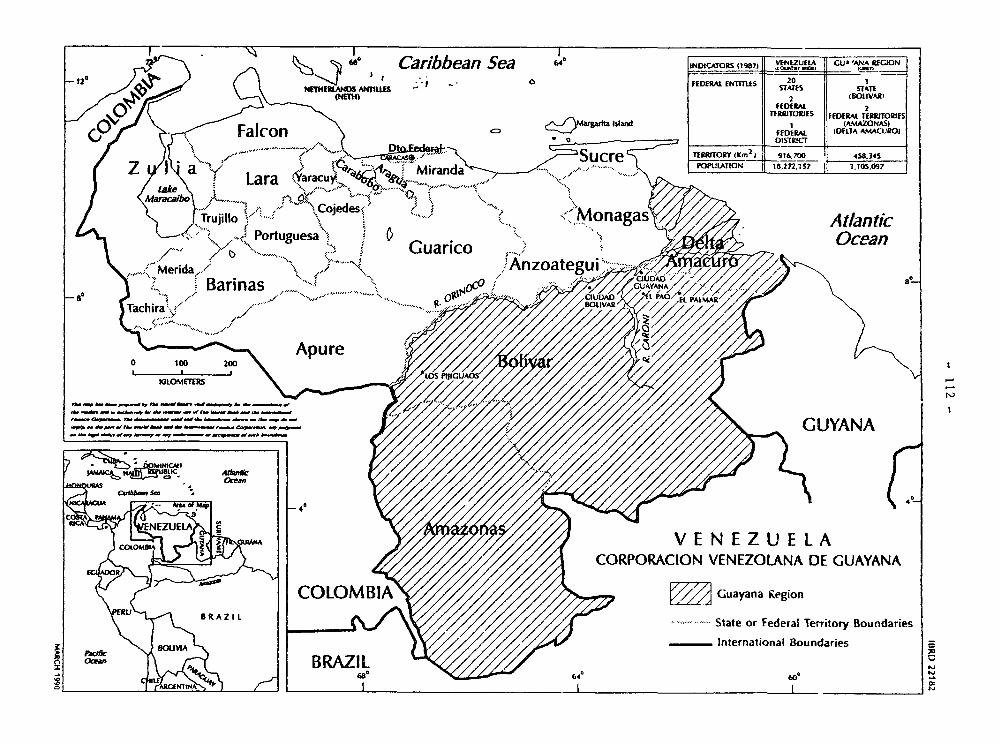

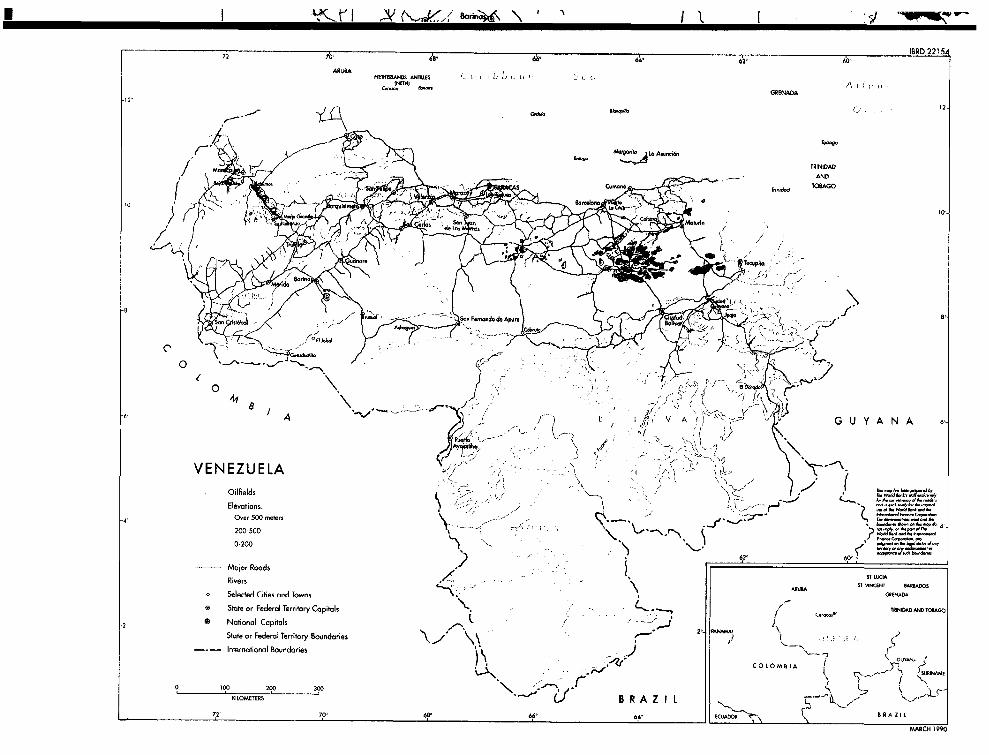

Existing and Proposed Railroad Network 5City of Caracas, Major Areas of Informal Housing 30Metropolitan Area of Caracas Regional Context 33Caracas Metro, Existing Network and Proposed Extensions 45National Electric Interconnected System 81Natural Gas Pipelines 98Corporacion Venezolana de Guayana 112Relief Map of Venezuela 142

Chapter 6

Public Investment in Railways and Ports

A. Railways

Background

6.1 The Autonotous Institute for the Administration of the State Railways(FERROCAR), a decentralized public entity affiliated with the Ministry ofTransport and Communication (MTC), was created in 1946 to develop, maintainand manage the national railways. Prior to 1946, the railways in Venezuelahad consisted of a number of private lines, geographically-dispersed andtotally non-integrated. These lines together with their rolling stock andfacilities were abandoned and d'smantled in the early 1950s as the Governmentlaunched its first National Railway Plan. This plan callea for the creationof an integrated national railway network linking the major cities of thecountry. As part of this strategy, a 173 km line between Puerto Cabello andBarquisimeto was built; its operation commenced in 1957. In 1983, the 66 kmYaritagua-Acarigua section was added to the original line. These railwaylines linking Puerto Cabello, Barquisimeto and Acarigua together with specialpurpose regional lines serving the mining areas it, the sourtb-east and center(see para. 6.2 below) constitute the sum total of VeLaezuela's national railwaynetwork.

6.2 The existing special-purpose lines were built essentially to serve thecountry's mining industry. The railway lines Puerto Ordaz-Cerro Bolivar (141km) and San Felix-El Pao (55 km) were constructed by the Orinoco MiningCompany and the Iron Mines Company, respectively, to haul iron ore. When theiron ore industry was nationalized, the railways were placed under themanagement of the company FERROMINERA del Orinoco, a branch of the GuayanaRegional Corporation (CVG). The 27km Guanta-Naricual line was built totransport coal from the El Naricual Mine in the state of Anzoategui. Today,this line is operated by the Compaflia Anonima Minas de Naricual (CARMINA).

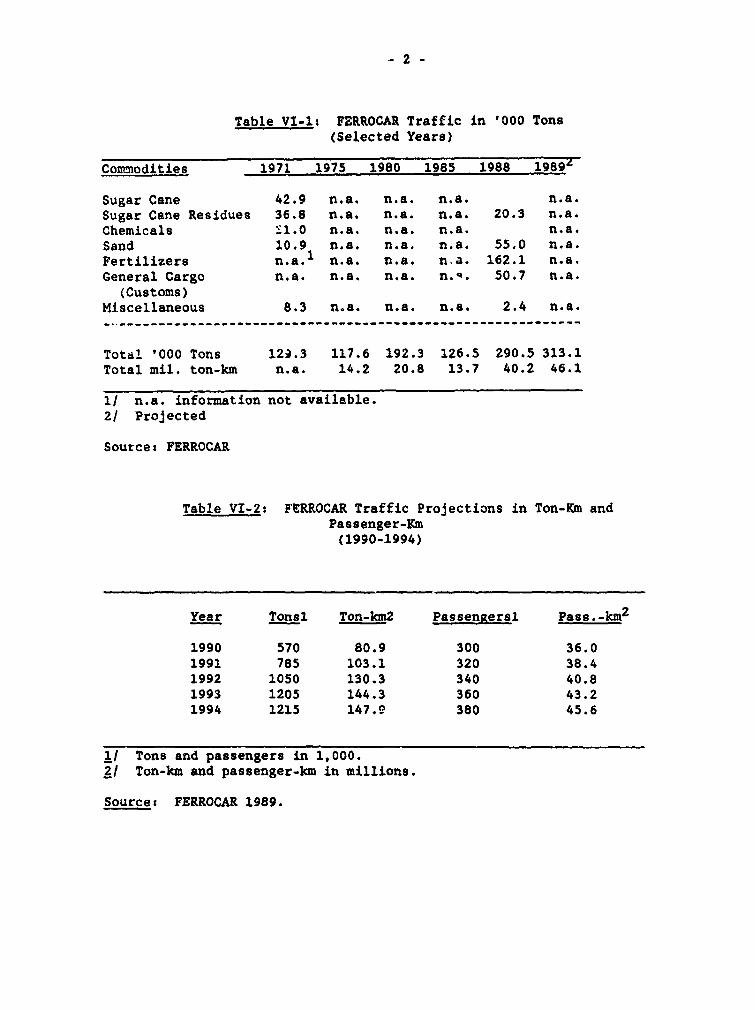

Volume of Railway Traffic

6.3 FERROCAR's freight traffic totalled 0.3 million tons or 40.2 millionton-km during 1988 - an increase of almost 2002 over the traffic levels of theearly 1970s. The volume of traffic during 1989 is estimated to have reachedthe same level as in the previous year. The main commodities transported werefertilizer (55Z of total traffic), sand (19Z), and sugar cane residues (7X);the general cargo amounted to 182 of total traffic. The number of passengerstransported annually during the period 1970-1989 has remained fairly constantat about 300,000 passengers or 37.0 million pass-km.

Table VI-I: FERROCAR Traffic in '000 Tons(Selected Years)

Commodities 1971 1975 1980 1985 1988 1989

Sugar Cane 42.9 n.a. n.a. n.a. n.a.Sugar Cane Residues 36.8 n.a. n.a. n.a. 20.3 n.a.Chemicals S1.0 n.a. n.a. n.a. n.a.Sand 10.9 n.a. n.a. n.a. 55.0 n.a.Fertilizers n.a.1 n.a. n.a. n.a. 162.1 n.a.General Cargo n.a. n.a. n.a. n.e. 50.7 n.a.

(Customs)Miscellaneous 8.3 n.a. n.a. n.a. 2.4 n.a.

Total '000 Tons 129.3 117.6 192.3 126.5 290.5 313.1Total mil. ton-km n.a. 14.2 20.8 13.7 40.2 46.1

1/ n.a. information not available.2/ Projected

Source: FERROCAR

Table VI-2: PERROCAR Traffic Projections in Ton-Km andPassenger-Km(1990-1994)

Year Tonsl Ton-km2 Passen_ersl Pass.-km2

1990 570 80.9 300 36.01991 785 103.1 320 38.41992 1050 130.3 340 40.81993 1205 144.3 360 43.21994 1215 147.9 380 45.6

1/ Tons and passengers in 1,000.2/ Ton-km and passenger-km in millions.

Source: FERROCAR 1989.

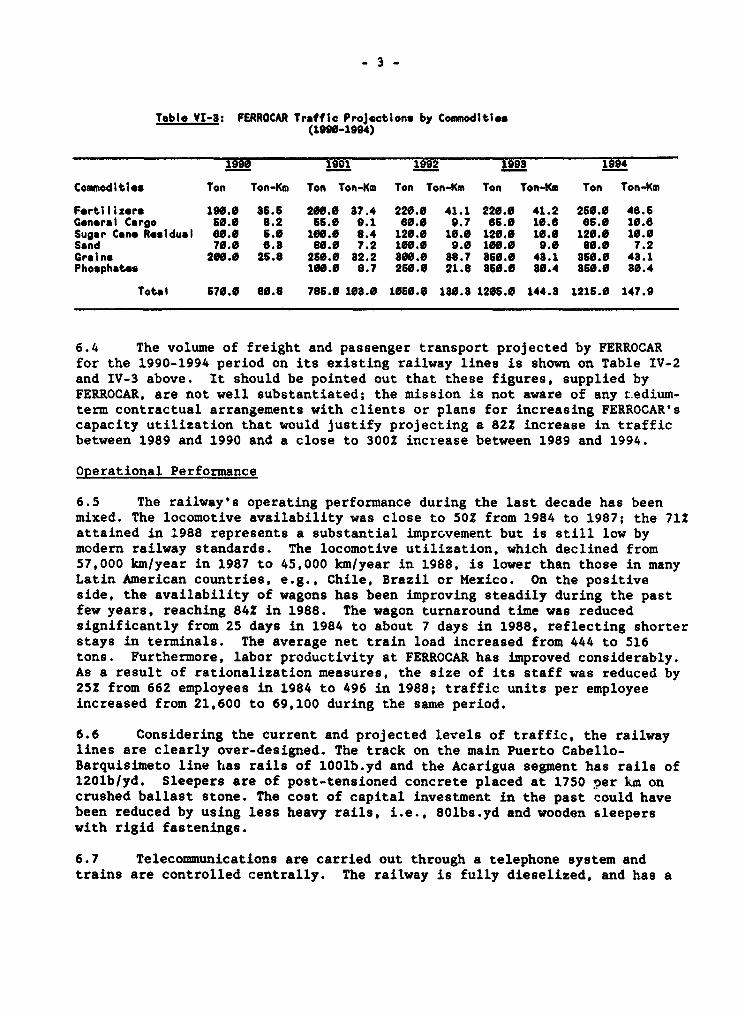

Table VI-3: FERROCAR Traffic Projections by Commodities(100-1994)

1990 1901 1992 1993 1994

Commodities Ton Ton-Km Ton Ton-Km Ton Ton-Km Ton Ton-Km Ton Ton-Km

Fertilizers 190.0 85.6 200.0 37.4 220.0 41.1 220.0 41.2 260.0 46.6General Cargo 560.0 8.2 65.0 9.1 6o.o 9.7 65.0 10.6 66.0 10.6Sugar Can. Residual 69.0 6.0 100.0 8.4 120.0 10.0 120.0 10.0 120.0 10.0Sand 70.0 0.8 80.0 7.2 100.0 9.0 166.0 9.0 60.0 7.2Groins 200.0 26.8 250.0 82.2 800.0 88.7 850.0 48.1 856.6 48.1Phosphates 100.0 8.7 260.0 21.8 380.0 80.4 860.0 86.4

Total 670.0 80.8 786.0 103.0 1060.0 186.3 1206.0 144.8 1216.0 147.9

6.4 The volume of freight and passenger transport projected by FERROCARfor the 1990-1994 period on its existing railway lines is shown on Table IV-2and IV-3 above. It should be pointed out that these figures, supplied byFERROCAR, are not well substantiated; the mission is not aware of any t.edium-term contractual arrangements with clients or plans for increasing FERROCAR'scapacity utilization that would justify projecting a 82Z increase in trafficbetween 1989 and 1990 and a close to 3002 increase between 1989 and 1994.

Operational Performance

6.5 The railway's operating performance during the last decade has beenmixed. The locomotive availability was close to 50Z from 1984 to 1987; the 712attained in 1988 represents a substantial imprGvement but is still low bymodern railway standards. The locomotive utilization, which declined from57,000 km/year in 1987 to 45,000 km/year in 1988, is lower than those in manyLatin American countries, e.g., Chile, Brazil or Mexico. On the positiveside, the availability of wagons has been improving steadily during the pastfew years, reaching 842 in 1988. The wagon turnaround time was reducedsignificantly from 25 days in 1984 to about 7 days in 1988, reflecting shorterstays in terminals. The average net train load increased from 444 to 516tons. Furthermore, labor productivity at FERROCAR has improved considerably.As a result of rationalization measures, the size of its staff was reduced by252 from 662 employees in 1984 to 496 in 1988; traffic units per employeeincreased from 21,600 to 69,100 during the same period.

6.6 Considering the current and projected levels of traffic, the railwaylines are clearly over-designed. The track on the main Puerto Cabello-Barquisimeto line has rails of lOOlb.yd and the Acarigua segment has rails of1201b/yd. Sleepers are of post-tensioned concrete placed at 1750 Der km oncrushed ballast stone. The cost of capital investment in the past could havebeen reduced by using less heavy rails, i.e., 80lbs.yd and wooden sleeperswith rigid fastenings.

6.7 Telecommunications are carried out through a telephone system andtrains are controlled centrally. The railway is fully dieselized, and has a

total fleet of 17 locomotiver of which 65Z or 11 units are 32-33 years old.The main line locomotives (7uZ) are of 1,500/1,700/2,000 HP, and the rest areshunters of 150/415 HP. The rolling sto-k fleet is composed of 264 wagonsprocured in 1957 when operations started and 12 passenger coaches which are 7years old. The availability of both fleets has averaged a low 60% during thelast few years, indicating less than efficient maintenance practices and aneed for rationalization of the workshops.

6.8 There are some basic measures that FERROCAR must take to improve usoperations. The availability of the railway fleet which averaged 60% in theprevious years needs to be increased. This would entail the rationalizationof the two workshops at Puerto Cabello and Bucaramanga. FERROCAR must takeaction to increase the train capacity, further reduce the wagon turnaroundtime, and improve inventory practices for spare parts. Finally, operationalplanning must be strengthened. This would requires keeping good trafficrecords, arranging medium term contracts with prospective clients, andintegrating planning.

Railway Investment Program

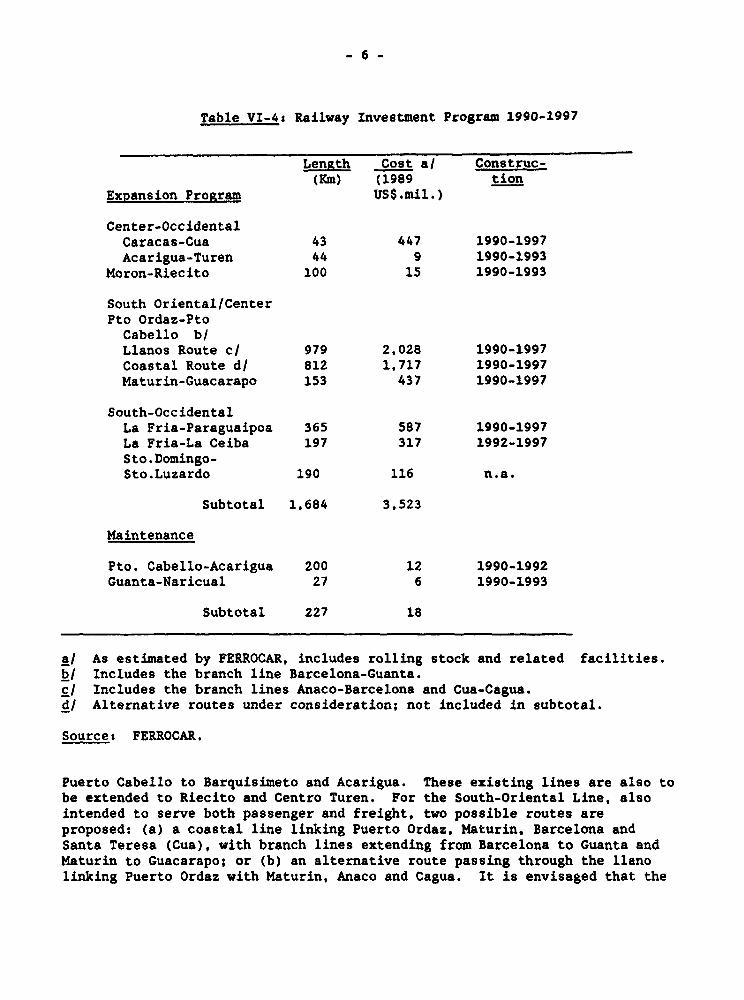

6.9 The Government is now considering an ambitious railway investmentprogram for the 1990-1997 period estimated to cost US$ 3.5 billion (1989dollars). The railway investment proposals covering the Eighth Plan period(1990-1993) amount to US$1.5 billion. (See Table VI-4 below).

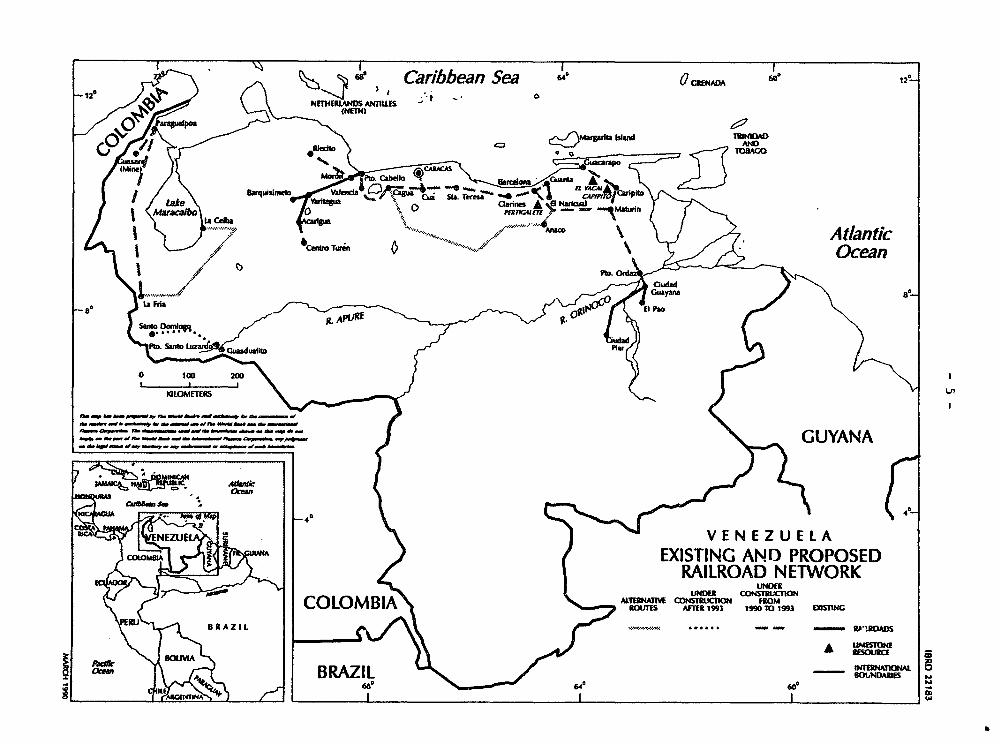

6.10 The stated objective underlying this ambitious expansion of thenational railway network is regional development. By means of new railwaylinks, it 4.s hoped to integrate the different regions of Venezuela into asingle economy and direct economic activities anc migration into lessdeveloped parts of the country. In the first phase of the expansion program,it is proposed to connect the Guayana region in the southeast to the country'scenter-west. There are also plans to construct new railway lines in Tachiraand Zulia in the southwest. In the second phase, sometime early in the nextcentury, it is hoped to link the Center-Occidental and South-Oriental segmentsto the South-Occidental lines, thus completing the national railway network.(See map on page 5).

6.11 All in all, the investment program for 1990-1997 consists of theconstruction of 1,684 km of new railway lines. Looking at the individualcomponents under the expansion program, the Caracas-Cua (Sta. Teresa) and Cua-Puerto Cabello sections of the Center-Occidental Line are conceived of ascargo and passenger lines designed to link up with existing railway lines from

Caribbean Sea 6aR ot2°

I . -tL - - I

43 ~ ~ XITIGAND POOE

'IT 199 90 T 'O 19 Ocean

a U Fft fti UMB

}~~~~~~~~~~~~~~ I

_e*___wn.__*____ _ w[ \ GUYANA

AM rg 40

. -4 S a_-ff ~~VENEZUELA

2 / ~~~~~~~~~~~EXISTING AND PROPOSED

~~~~~~~~~~~~~~~~~~~~~~~~~LEtO3) CONSIIN FOMBB>^SE,,\~~~~~~~C LM ROTE AM 199 199 M 1993 t S1NG

+W HK~~BAZIlt ...... -- _ _ b%(m

'< 1 > N\ v ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~A uxerw8 . ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~RS o AZIL 64 6°'

W

- 6 -

Table VI-4s Railway Investment Program 1990-1997

LenRth Cost a/ Construc-(Km) (1989 tion

Expansion Program USS.mil.)

Center-OccidentalCaracas-Cua 43 447 1990-1997Acarigua-Turen 44 9 1990-1993

Moron-Riecito 100 15 1990-1993

South Oriental/CenterPto Ordaz-PtoCabello b/Llanos Route c/ 979 2,028 1990-1997Coastal Route d/ 812 1,717 1990-1997Maturin-Guacarapo 153 437 1990-1997

South-OccidentalLa Fria-Paraguaipoa 365 587 1990-1997La Fria-La Ceiba 197 317 1992-1997Sto.Domingo-Sto.Luzardo 190 116 n.a.

Subtotal 1,684 3,523

Maintenance

Pto. Cabello-Acarigua 200 12 1990-1992Guanta-Naricual 27 6 1990-1993

Subtotal 227 18

a/ As estimated by FERROCAR, includes rolling stock and related facilities.bI Includes the branch line Barcelona-Guanta.c/ Includes the branch lines Anaco-Barcelona and Cua-Cagua.d/ Alternative routes under consideration; not included in subtotal.

Source: FERROCAR.

Puerto Cabello to Barquisimeto and Acarigua. These existing lines are also tobe extended to Riecito and Centro Turen. For the South-Oriental Line, alsointended to serve both passenger and freight, two possible routes areproposed: (a) a coastal line linking Puerto Ordaz, Maturin, Barcelona andSanta Teresa (Cua), with branch lines extending from Barcelona to Guanta andMaturin to Guacarapo; or (b) an alternative route passing through the llanolinking Puerto Ordaz with Maturin, Anaco and Cagua. It is envisaged that the

- 7 -

South-Occidental Line would be dedicated to cargo; routes considered are (a)the two segments Domingo-Puerto Santo Luzardo and F,ia-Paraguaipoa, oralternatively, (b) La Fria-La Ceiba.

6.12 The public agencies involved (FERROCAR, FERROMINERA and CORPOSUR-OESTEhave undertaken only very rudimentary economic and financial analyses of theindividual components of the railway expansion program. To complete athorough economic analysis of these projects, these agencies will need tocompile detailed and reliable data on the anticipated volume of traffic, andto undertake comparisons of costs and benefits with the competing modes oftransport (e.g., river and road transport) for each segment of the plannedrailway network. Moreover, final engineering studies have not been completedfor projects which are scheduled to start in 1990.

6.13 On the basis of available information and the best estimates thatcould be made, the Bank mission has carried out simple profile analyses ofthe individual components of the proposed railway expansion program. Theresults are summarized in the remainder of the chapter. Generally speaking,the internal rates of returu appear too low to justify these projects in theforeseeable future, at least before the turn of the century. Until additionalanalyses prove otherwise, it would be prudent to postpone all general cargoand passenger railway projects. It would appear preferable to expand inter-urban bus services, improve shipping operations and invest in highwaymaintenance. The profile analyses also indicate that there appears to belittle incremental benefit in completing an intergrated railway system. Withrespect to the segments of the railway network dedicated to specific cargo,the investment would need to be studied carefully in the context of thevarious mining and industrial activities that these lines are intended toserve. The Government might consider having these mining companies andindustrial enterprises participate in financing these railway investments.

Passenger Railway Line--Caracas-Cua

6.14 FERROCAR has proposed a passenger 43 km railway line linking Caracaswith Cua, a town in the Tuy valley. Two additional passenger stations arebeing planned in the city of Charallave. Total capital cost spread over the1990-1997 period is estimated at US$ 227 million (1989 prices). The operatingcosts vary between US$0.025 and US$O.015 per passenger-km. A possibility ofadding freight traffic under this project is under consideration, but, so far,no feasibility studies have been done for this alternative. The biddingprocess was initiated in November 1989 before the final engineering studieswere completed.

6.15 This project essentially an urban passenger line intended to linkCaracas, which has run out of space for further development, to Cua, arelatively underdeveloped and sparsely populated town in the Tuy Valley,considered to be one of the most promising candidates for future growth withinthe expanding Caracas Metropolitan Area. It is also assumed that the Caracas-Cua line would capture important passexAger flows from other cities in theCenter-West region if and when the proposed railway line between PuertoCabello and Puerto Ordaz is completed to provide the linkage. By 2001, it is

estimated that the Caracas-Cua line would have a rush hour traffic of 3,400passengers per hour in one direction. By 2010, this number is projected todouble. A critical assumption here is that this passenger traffic will bebetter served by a railway line than by an expansion of the existing highwaysystem.

6.16 These projections of passenger traffic are extremely optimistic. Animportant factor that determines how much urban passenger traffic this linemight attract is its integration with the Caracas inner-city urban transport.CAMETRO, a public agency operating the Caracas Metro, is planning to build by1993 its third line linking inner-Caracas to El Valle in the South-East ofCaracas at total cost of around US$ 1 billion. FERROCAR wants to build atransfer station to the metro line at Mercado, approximately 2 km South-Eastof El Valle. The low population density in this area probably would notjustify an extension of the proposed metro line to Mercado, a necessarycondition if the Caracas-Cua line is to compete with the alternative mode ofurban transport, i.e., roads.

6.17 Even if the rail and metro lines were to be linked at Mercado, it isdoubtful that the Caracas-Cua railway line would be competitive. The railwaystation in Caracas is planned at an unfavorable location at the extreme south-east end of the city, and only a limited number of railway stations areplanned in the Tuy Valley. It appears likely that an important proportion ofcommuters, from scattered origins in the Tuy Valley and with scattereddestinations in Caracas, would prefer to use buses or cars. This is even morelikely to be the case for commuters along the railway line Cua-Pto. Cabello orSta.Teresa-Cua.

6.18 Assessment. The project costs comprise capital expenditures andrailway operating costs. The project benefits consist of (a) savings invehicle operating costs for bus and car passengers who transfer to trains;(b) passenger flows generated by the project; (c) savings in terms of traveltime and congestion costs; (d) savings in highway maintenance; and (e) savingsin location costs. A preliminary evaluation of the project has been done byTRANSPLAN, a local consultancy firm.

6.19 The Bank mission's profile analysis of the Caracas-Cua line is be.sedon the following assumptions:

(a) capital cost, as estimated by FERROCAR, is US$447 million over the1990-1997 period;

(b) train operating costs are a function of the size of the passengertraffic and vary between US$0.015 and US$0.025 per passenger-km;

- 9 -

(c)vehicle operating cost estimates, based on the calculations oftransport specialists familiar with Venezuela, amount to US$ 0.015per passenger/km for buses US$0.04 per passenger km. for cars;l/

(d)passenger traffic is estimated at 22,000 per day in 1997,increasing to 79,000 per day by 2010 (based on FERROCARestimates);21

(e) time savings are evaluated at US$0.28 per bus passenger, based onan average monthly wage of US$200 and 15 minutes per trip;

(f) for sake of simplicity, congestion externalities are not takeninto account here, and savings in highway maintenance expenditureare considered too insignificant for inclusion;

(g) location costs consist of savings in housing and relatedinfrastructure costs for families with jobs in Caracas that decideto settle in the Tuy Valley because of the new railway line. Itis assumed that 31,000 families would be induced to settle in theTuy Valley between 1997 and 2010, and based on informationprovided by the Urban Development Center of the UniversityCentral, the savings in location costs are estimated at US$2,000per family.

Based on these assumptions, the internal rate of return (IRR) of the Caracas-Cua line is -0.4Z excluding the location costs savings. IRR including thelocation costs savings is 0.4Z. In either case, these extremely unfavorablerates of return clearly demonstrate that the project cannot be justified oneconomic grounds. This conclusion holds true regardless of whether the lineis viewed as an independent project or as part of a greater railway network.

6.20 As mentioned above, FERROCAR is considering the possibility of addingfreight traffic to the project. However, the operational and economicimplications of this alternative have not been seriously studied. From atechnical point of view, the acquisition of land within Caracas to build afreight terminal and related cargo handling facilities is li'kely to presentproblems. Clearly, the addition of freight traffic would not enhance theprofitability of the project or change the basic conclusion that this projectcannot be justified on economic grounds.

-/ To derive these costs, it is assumed that buses have a maximum capacity of 56 passengers anda rate of capacity utilization 67X with six trips a day, and adopting the assumption of theTRANSPLAN study, 330 operating days a year. It is also assumed that 20% of all railway passengerswould have been previously using cars which on the average would have two passengers and operate260 days a year.

- FERROCAR's estimate of future traffic does not distinguish between those passengers thatswitch to railway from other modes of transport and the passenger traffic that is generated bythe project.

- 10 -

6.21 The extension of the inter-city bus service, which has proven to be anefficient mode of transportation in other Latin American countries, appears tobe a more favorable alternative. Assuming a capacity of 56 passengers perbus, the rush hour demand predicted for 2001 would be fewer than 70 buses perhour. In 2010, demand would increase to 130 buses per hour. This flow couldbe fully accommodated by a bus service if an exclusive lane for buses werecreated.

CarRo and Passenger Railways--South Oriental-Center

6.22 A cargo and passenger railway line South Oriental proposed by FERROCARis intended to link Guayana with the coastal and central regions. There aretwo alternative routes proposed. CVG favors the coastal route from PuertoOrdaz through Maturin and Barcelona to Cua, whereas FERROCAR prefers the routepassing through the llanos, the interior of the country, linking a railwayline from Puerto Ordaz through Maturin and Anaco to Cagua with another linethat connects Puerto Cabello with Cua. The llanos proposal also includes abranch line Anaco-Barcelona, and both proposals include a branch line fromBarcelona to Guanta. intended to connect the Guayana-Center line to the coalrailway Guanta-Naricual. The proposed coastal and the llanos routes measure812 km and 979 km, respectively. The Guayana-Center line is intended totransport steel, aluminum, paper, beverages and general cargo from south tonorth, and recycled steel, beverages, other minerals, general cargo and, ifthe coastal route is adopted, limestone from north to south.

6.23 Another section of the South Oriental railway line, which can also bestudied as an independent project, is the Puerto Ordaz-Maturin-Guacarapo line.This proposed line is intended for transporting export iron ore to a deep seawater port (to be constructed at some future date) in the north, and if thecoastal route were to be rejected, for carrying limestone to the south. Boththe Maturin-Guacarapo branch and the segment Puerto Ordaz-Cagua or,alternatively, Puerto Ordaz-Cua, would fall under the jurisdiction of CVG,while the segment Cua-Puerto Cabello would be managed by FERROCAR.

6.24 Pto. Ordaz-Maturin-Guacarapo. The principal beneficiaries of thisline are the CVG companies, in particular FERROMINERA. Currently, FERROMINERAexports around 13 million tons of iron ore. FERROMINERA's current expansionplan would allow the company to increase its iron ore exports to at least 19million tons. Since 1989, when FERROMINERA obtained a 10 year lease for theuse of a transfer station with a capacity of 15 million tons per year,FERROMINERA has been able to use larger ships to export iron ore. (Out oftotal iron ore exports, around 8 million tons can be transported in ships witha capacity of over 60 thousand tons). If the Pto.Ordaz-Guacarapo railway linewere to be built, it would capture the iron ore traffic passing through thetransfer station--a potential flow of 8.5 million tons of iron in 1998.According to very ambitious projections by FERROMINERA, this traffic wouldcontinue to grow at a rate of 7.3Z per year after 1997.

6.25 Limestone is an important input in the operations of CVG companies inGuayana. By 1998, annual limestone flows to Guayana are projected to reach1.3 million by 1998, growing at a rate of 3Z per year. Large limestone fields

- 11 -

are located around Barcelonia, Caripito and Guacarapo. Currently, limestone istransported by trucks from mines close to Barcelona. However, the choice ofthe field to be exploited depends crucially on the costs of transportation.Should the Puerto Ordaz-Guacarapo railway line materialize, the mostprofitable option would be to exploit the limestone fields close to Caripitoand to transport the limestone by rail. An alternative option, according toSIDOR, is to develop the fields close to Guacarapo, El Yacal and El Yaque.The limestone extracted from these fields would need to be transported firstby cable or a special train over a distance of 15 km to a specialized port,and then shipped to Guayana. For this. the corresponding facilities woulaneed to be constructed.

6.26 Assessment. In this section, the segment Puerto Ordaz-Maturin-Guacarapo is evaluated both as an individual project and part of the networkGuayana-Center. As an independent project, the capital expenditures for thePto. Ordaz-Maturin-Guacarapo segment amount to US$798 million. As part of theline Pto. Ordaz-Pto. Cabello, capital expenditures for the branch Maturin-Guacarapo are estimated at US$ 437 million. The operating costs are assumedto be US$0.015 per ton-km.

6.27 As indicated earlier, this railway section is assumed to capture thetraffic in iron ore exports amounting to around 8.5 million in 1998. Thebenefits generated by the project are the savings in the marginal transferoperating costs incurred by shipping these iron ore exports to the sea.According to CVG officials, these marginal costs do not exceed US$7 per ton ofiron ore transported. This estimate has also been confirmed by a World Banktransport specialist. The annual limestone flows to Guayana are projected toincrease to 1.3 million by 1998, growing at 3? annually. With this railwayline completed, CVG is likely to exploit the limestone fields close toCaripito and to transport the limestone by train. Assuming an increase ingasoline and diesel prices to international levels, the cost of shippinglimestone extracts from fields close to Guacarapo would be the relevantmeasure of project benefit. Port investments necessary for this operationwould be in the neighborhood of US$50 million, and total transport costs wouldamount to around US$9 per ton.

6.28 Given these alternatives and the flows of limestone and iron ore asdescribed above, a profile analysis of the railway line Pto.Ordaz-Maturin-Guacarapo yields an internal rate of return of 2.57Z. As part of Guayana-Center railway network, the segment Maturin-Guacarapo yields an internal rateof return of 3.46Z. In either case, investment in Pto.Ordaz-Maturin-Guacarapocannot be justified on economic ground at this time. Instead, it would appearpreferable to explore the shipping alternative. If the demand projections byFERROMINERA prove accurate, a railway project might be warranted around theturn of the century.

6.29 Pto. Ordaz-Maturin-Pto. Cabello. In this section, the profileanalysis focuses on the coastal route which links Guayana to the Center, Pto.Ordaz-Maturin-Barcelona-Cua-Pto. Cabello. The capital expenditures for thisproject, if designed exclusively as a cargo railway line, amount to US$ 1.72billion. Operating costs vary between US$0.015 and US$0.035 per ton-km.

- 12 -

Preliminary studies by TRANSPLAN demonstrate that the coastal route is farmore cost-effective than the llanos route Pto. Ordaz-Maturin-Anaco-Cagua witha branch line from Anaco to Barcelona. Whereas both railway lines havesimilar expected operating costs, capital expenditures for the Ilanos routeexceeds those for the coastal route by US$ 300 million, or 202. In addition,the llanos route would not allow the railway to -apture of the important cargotraffic between Caracas and Barcelona.

6.30 To quantify cargo flows on the line Pto.Ordaz-Maturin-Pto.Cabello, itis useful to define three nodes -Guayana, Barcelona, and the Center- and toproject the volume of freight traffic between these nodes. Apart from generalcargo and various minerals, the most important items of freight traffic onthis route are steel and aluminum that move between Guayana and the Center,and limestone and soda that move between Guayana and Barcelona. Other itemsinclude beverages, recycled steel, paper and petrochemicals. Venezuela's mainproducer of steel products, SIDOR, is located in Guayana. Its domestic salesin 1988 amounted to 2.1 million tons in 1988 out of total sales of 2.8 milliontons. According to CVG officials and World Bank analysts, the restructuringof SIDOR will reduce significantly the nwuber of product lines and the volumeof output, and increase sharply the share of exports in total SIDORproduction. Thus, we project SIDOR's total production at approximately twomillion tons in 1998, growing at 3Z per annum thereafter, with a share ofdomestic sales maintained at 45Z.

6.31 The modal distribution of this flow depends on the cost diff.,entialsand risk considerations: SIDOR is not willing to rely on only one mode toavoid becoming vulnerable to labor disputes. In 1988, 25% of its domesticallysold products were transported by ship, even though the cost of this modeexceeded trucking costs by 15-30Z. With the increase of diesel prices tointernational levels, this relative cost pattern will be reversed: trulckingcost will increase to US$0.045 per ton-km, exceeding shipping costs by 50-80%.In view of this cost differential and the transport diversification policiesadopted by SIDOR described above, it is assumed that 60? of the domesticallysold steel would be shipped at a cost of US$ 16 to Barcelona and US$20 to theCenter by 1998. If this railway line were to be built, the railway mode wouldhave a US$20 cost advantage over shipping. Accordingly, it is assumed thatrailway would capture 60X of SIDOR's domestic steel flows. This scenarioassumes that SIDOR continues its diversification policies and that PDVSAstarts production of tubes in Zulia, which will not be served by railway.

6.32 The country's main aluminum producing companies, ALCASA and VENALUM,are also located in Guayana. In 1987, these firms sold 185,000 tins in thedomestic market, of which 98,000 tons were consumed within Guayana, 71,000tons transported to the Center and 16,000 tons sent to the Barcelona area.Under ALCASA's and VENALUM's current expansion plans, their domestic salesoutside Guayana will increase to around 200,000 tons by 1998. The Bank staffregard this estimate as overly optimistic, if not unrealistic. Nonetheless,for the purpose of analysis here, these domestic sales figures were used. Forlack of better information, we simply assumed a 3X annual growth in the seleof aluminum products after 1998. Currently, aluminum for domestic consumptionis transported principally by trucks. With diesel prices increasing to

- 13 -

international le% , ALCASA would have a strong incentive to coordinate itstransportation poli.y with SIDOR to make use of SIDOR's shipping capacity. Itis therefore assumed tha-, by 1997, 502 of domestically sold aluminum thatleaves Guayana would be transportei by ships. Should thi3 railway segment bebuilt, it can be expected to capture 70% of the flows for domestic consumptionleaving Guayana.

6.33 Currently, around 800,000 tons of limestone are transported by trucksfrom the Barcelona area to Guayana. By 1998, over 1.3 million tons will beconsumed in Guayana. With this railway segment completed, it is assumed thatthis entire flow would be transported by train. The relevant factor toconsider in estimating the benefits of the railway project is the cost ofshipping limestone from fields close to Guacarapo to Guayana as describedabove. Another traffic component of great importance is the general cargo.In 1987, 1.2 million tons of general cargo were transported by truck betweenPuerto Ordaz, Barcelona and the Center. We assume that this flow will increaseto over 5 million tons by 1998, and grow at a rate of 32 thereafter. If thisrailway line were to be built, it can be expected to capture 302 of this flow.

6.34 Finally, there are several investment projects that need to beconsidered in evaluating the Puerto Ordaz-Puerto Cabello railway line. First,it is planned to establish a pulp and paper plant in Guayana with a capacityof 400,000 tons, of which 150,000 tons will be transported to the Center. Inthe absence of railways, we assume that 60% of this flow will be transportedby truck and 40% by ships. It is assumed that railway could capture 80% ofthis flow. Second, a petrochemical project is under review for the Barcelonaarea. For the purpose of our analysis here, it is assumed that by 1997, thisnew petrochemical complex would generate flows of 130,000 tons of caustic sodato the aluminum plants in Guayana and 100,000 tons of other petrochemicalproducts to the Center. It is also expected that these flows would betransported by trucks. It is assumed here that the railway line, if built,could capture 100X of the soda flows and 8O0 of the other petrochemicals.

6.35 The Guayana-Center railway is supposed to transport both cargo andpassengers. However, the investment figures provided by FERROCAR -- US$ 1.7billion for the coastal route, and US$ 2 billion for the lianos route-- do notinclude the cost of infrastructure or equipment required to accommodatepassenger traffic. The information of the potential passenger traffic is alsosketchy. TRANSPLAN has provided FERROCAR three origin-destination matrices,estimating railway passenger flows for Venezuela for the years 1995, 2005 and2010. According to these estimates, in the year 2005, 136,000 passengers willtravel daily between Guayana and the regions South-West of Puerto Cabello; by2010, the traffic will increase to 437,000 passengers. These estimates--whichdo not include the flows within the Center region between Puerto Cabello,Caracas, and Sta. Teresa-- would imply passenger traffic would be growing at26% per year, an unlikely scenario. The flows within the Center region areassumed to increase to 250,000 passengers per day in 2005, jumping to 473,000passengers per day in 2010. This highly optimistic demand estimate contrastssharply with the experience of passenger railway services in other LatinAmerican countries.

- 14 -

6.36 Assessment. A profile analysis of the Puerto Ordaz-Maturin-Barcelona-Puerto Cabello railway line dedicated to cargo traffic yields an internal rateof return of 1.62Z. Thus, this investment cannot be justified on economicbrounds. An inclusion of passenger traffic in the analysis raises theinternal rate of return of the joint railway lines Puerto Ordaz-Puerto Cabelloand Caracas-Cua to 5.92. However, it should be noted that this IRR representsthe upper limit because, as seen above, it incorporates the most optimisticassumptions regarding the potential benefits of this project. The capitalcost of US$2.16 billion for this project does not even include any investmentsin infrastructure or equipment needed to operate the Puerto Ordaz-PuertoCabello segment as a passenger line. Hence, our analysis includes only theoperating costs for the passenger traffic. In addition, the passenger flowestimates are clearly too optimistic not only by international comparison butalso taking into account the poor performance of the existing passengerrailway line Puerto Cabello-Barquisimeto/Acarigua.

6.37 The experience of other countries with railways demonstrates that itis not advisable to base the justifications of a long-distance railway line onthe prospect of transferring sufficient numbers of passengers from othermodes. This is unlikely to happen. At the very minimum, one should provide amore rigorous analysis of the potential benefits of a passenger railway line.At this point in time, expansion of inter-urban bus services appear to be ofhigher priority than construction of a passenger railway line. With respectto cargo traffic, it would appear preferable to expand shipping operations andinvest in highway maintenance.

6.38 Railway Network South Oriental. The complete network South Oriental -Center links the line Puerto Ordaz-Maturin-Barcelona-Puerto Cabello with thebranch line Maturin-Guacarapo as well as the line Caracas-Cua segment ifpassenger transport is considered. Generally-speaking, the traffic flows tobe handled by this network correspond to the sum total of all the flowsconsidered under the individual projects described above. However, thelimestone traffic would originate in the area of Barcelona only if thisnetwork were to be built. Alternatively, the limestone traffic couldoriginate in the area of Guacarapo and be transported by ship. As a cargorailway line, total investment cost of the joint railway lines Puerto Ordaz-Puerto Cabello and Maturin-Guacarapo adds up to US$ 2.15 billion. Theinternal rate of return of this project is 2.06Z. Disregarding infrastructureinvestment requirements for the line Puerto Ordaz-Puerto Cabello dedicated topassenger transport, capital expenditures for the combined cargo and passengerrailway lines Puerto Ordaz-Puerto Cabello/Haturin-Guacarapo/Caracas-Cur add upto US$ 2.6 billion. As explained in the previous section, the analysis of thepotential benefits of the inclusion of passenger traffic is still at apreliminary phase. A profile analysis indicates that the internal rate ofreturn for this project is 5.62 and represents an upper limit. To conclude,the analysis of the network South Oriental-Center in its entirety does notchange the recommendations given with respect to its individual segments.Prom an economic point of view, advancing the construction of a railwaynetwork for Venezuela cannot be justified at this point in time. Instead, anexpansion of bus services for passengers and shipping operations for cargo,and better maintenance of highways appear to be preferable options.

- 15 -

Cargo Railway Line-South Occider.tal

6.39 The regional development corporation for the southwest region,CORPuSUROESTE, has proposed two major railway projects in the state ofTachira. One is intended to link the phosphate and coal mines of Monte Frescowith one of the ports in the north via La Fria. The other project is intendedto link Monte Fresco with PL-. Stos. Luzardo north of Guasdalito, at the Apureriver. The second project is premised upon the Government undertaking theOrinoco-Apure river navigation project. To judge the prospects of theseprojects, it is important to realize that currently less than 100,000 tons ofcargo are being transported between Tachira and Zulia, and less than 200,000tons via the Orinoco between Tachira and Guayana. The railway projects thuscan only be justified in the context of the future exploitation of phosphateand coal mines in the Monte Fresco area. The analysis below assumes that allmining projects would be realized as planned by CORPOSUROESTE. It should benoted, however, that most of these projects are still at a very preliminarystage of evaluation and may not be implemented in the foreseeable future.Horeover, there are competing projects in the states of Zulia (for coal) andFalcon (phosphate).

6.40 Monte Fresco-La Fria to Para-uaipoa or La Ceiba. CORPOSUROESTE hasproposed three alternative routes for connecting Monte Fresco-La Fria to aport in the North. The first proposal is to connect Monte Fresco-Le. Fria toParaguaipoa (365 km), north of Maracaibo. Capital expenditures for thisproject add up to US$ 587 million. The second proposal is to connect MonteFresco-La Fria to La Ceiba (197 km), a port on Lake Maracaibo in the state ofTrujillo. Capital expenditures for this project amount to US$ 317 million.Both routes are proposed for construction between 1992 and 1997. The thirdproposal is to connect Monte Fresco-La Fria to a line proposed by FERROCAR,Turen-Barquisimeto. Given that no information is available on this thirdoption, our evaluation focuses on the first two routes. In our evaluation, weassume that the following projects are implemented:

(a) Phosphate Mines in havay and Monte Fresco. By 1997, the MonteFresco phosphate mine is projected to produce 300,000 tons ofmicronized phosphoric rock to be sold in the domestic market. TheNavay mine is expected to produce 250,000 tons phosphoric acid and1.2 million tons of phosphoric rock for the export market. It isassumed that the railway would capture 502 of the domesticallysold phosphoric rocks from '.onte Fresco (the remainder beingtransported by road to the Orinoco river), 1002 of the rock fromNavay and 702 of the phosphoric acid.

(b) Coke Production in North-West Tachira. There are three importantcoal mines in the northwest of Tachira: Lobater, Las Adjuntas andHato de la Virgen. Currently, production is around 100,000 tons,but there are plans to increase production to 2.5 million tons by1996. In parallel to this expansion, a conversion plant toproduce 1 million tons of coke is planned. The main consumer ofthis coke will be CVG. For this analysis, it is assumed that the

- 16 -

railway Monte Fresco-Sto. Domingo-Pto. Stos. Luzaido would not bebuilt and that 1002 of the coke flow is transported by the MonteFresco-La Fria railway line.

(c) Sto.Domingo Coal Mine. CORPOSUROESTE plans to extract 1.5 milliontons of coal from a mine close to Sto. Domingo. For the purposeof our analysis, it is assumed that 50% of this coal will beexported, and that 602 of total coal extracted will be to a portin the Nortk by railway.

If all of the above projects were implemented, the Monte Fresco-La Friarailway line would transport a total f1ow of 3.5 million tons of cargo by1998. If there were no railway transport, this flow would have to betransported by trucks. If the route Monte Fresco-La Fria-La Ceiba were to bechosen, additional capital expenditures would be necessary for exporting coal.La Ceiba can only handle ships with a capacity of less than 30 thousand tons,and it would be necessary to construct a transfer station. The marginal costof the transfer operation is estimated at US$ 7 per ton.

6.41 Assessment. A profile analysis of the railway line Monte Fresco-LaFria-Paraguaipoa yields an internal rate of return of 4.532. The internalrate of return of the competing proposal Monte Fresco-La Fria-La Ceiba is9.55Z. Thus, this latter project warrants another good look provided that thevarious mining projects that this line is intended to serve actuallymaterialize. In evaluating this proposal, it might be advisable to considerthe possibility of a diesel operated railway system instead of the electricoperated system proposed by CORPOSUROESTE.

6.42 Monte Fresco-Sto.Domingo-Pto.Stos.Luzardo. In tandem with the railwayline Monte Fresco-La Fria, CORPOSUROESTE proDoses to build a railway lineMonte Fresco-Sto. Domingo-Puerto Stos. Luzardo, linking Tachira to the Apureriver. A preliminary analysis of the cargo flows between both regions wouldappear to cast doubt on the economic viability of this project, even if theMonte Fresco-La Fria did not materialize. If the latter were to be built,there would be even less justification for a railway to the Apure river. Thefreight traffic between Tachira and Guayana could easily be transported byrailway to a northern port and from there by ship to Pto. Ordaz. Moreover,the Monte Fresco-Sto. Domingo railway project is premised upon the Governmentundertaking the very ambitious Orinoco-Apure river navigation project. Wetherefore strongly recommend extreme caution; a thorough evaluation of thisproject must be undertaken before any decision is made on the project.

Other Investments

6.43 Acarigua-Turen. Capital expenditures for the railway line Acarigua-Turen (44 km) are estimated at US$ 9 million. The construction is to becompleted by 1993. US$5 million have already been allocated for 1990. Thisproject is an extension of the existing line Pto.Cabello-Acarigua. It willtransport between 500,000 and 800,000 tons of agro-industrial commoditiesannually. No economic study justifying this project has been provided, and theavailable information does not permit one to make any judgment on its economic

- 17 -

viability. It is recommended to postpone this project until completion of aneconomic evaluation.

6.44 Moron-Riecito and Guanta-Naricual. Capital expenditures for therailway Moron-Riecito (100 km) add up to US$ 15 million. The construction isscheduled for completion by 1993. US$5 million have already been allocatedfor 1990. This project is designed to serve exclusively a carbon mine inRiecito. The expenditures for maintenance and acquisition of equipment forthe railway Guanta-Naricual (27 km) amount to USS 6 million. US$1.5 millionhave already been allocated for 1990. This line is dedicated to the coal mineEl Naricual. Th"re appears to be little justification for the Government toundertake this mnd of projects form an integral part of the miningoperations. If the mining operations are profitable with the inclusion of thespecial transport investments required to haul the ores, these line should bebuilt and financed by these mining enterprises.

6.45 Pto. Cabello-Acarigua. The expenditures for the rehabilitation andmaintenance of the railway line Pto.Cabello-Acarigua (200 km) are estimated toadd up during 1990-1992 to US$12 million. US$4 million have already beenallocated for 1990. This rehabilitation/maintenance program includesreplacement of sleepers, replacement and cleaning of ballast, welding ofrails, improvements in communications, and rehabilitation of yards, stationsand structures. While there appears to be a general need for maintenancewhich had been neglected in previous years, there is not enough information topass judgement on the specifics of this program.

B. Ports

Sectoral Organization

6.46 The maritime foreign trade of Venezuela amounts to approximately 35million tons per year, excluding petroleum. The ports that handle this trademay be divided into four institutional groups:

(a)National Port Institute (INP) ports: these handle general cargo,containerized cargo and some bulks, and are located on the northcoast and in Lake Maracaibo;

(b) Guayana Regional Corporation (CVG) ports: these handle bulkmaterials and the general cargo inputs and outputs of the CVGindustries. They are located on the River Orinoco, with afloating terminal for iron-ore transference at the mouth of theri ea r;

(c)Oth'.r industrial terminals: these are "single industry" terminals,located mostly on the North coast and in Lake Maracaibo; and

(d) Petroleum ports of Lake Maracaibo, which are not considered inthis review.

- 18 -

6.47 The tonnage handled by each group of ports is shown in Table VI-5.The CVG ports handle the greatest tonnage, with 21.5 million in 1988,including iron ore. Next come the public ports of INP with 9.7 million tons,then the private terminals with 4.3 million tons. The INP ports handle over902 of the general cargo nnd practically all the containerized traffic ofVenezuela. The annual port traffic of the eight INP ports that handle cargois shown in Table VI-6, including 0.4 million tons of coastal traffic. PuertoCabello handles about 50X of all INP traffic, followed by La Guaira with 20Z.Containerized traffic now exceeds one million tons per annum and has grown ata rate of 212 per annum. since 1986. In addition to the above ports, there arevarious river ports, fishing ports and tourism ports, not engaged in foreigntrade.

Table V1-S: Maritime Foroiln Trade, 1988 1/

Croup Volume (Million ton)

'NP 9.7CVG ports 21 6Other ports 4.8

1/ Excluding petroleum export.Source: Mission etimates based on figures trom INP, CVG

and Customs.

Table VI-6: INP Port Traffic (1984-1988)Ctons 1000)

Containerized RD I ROi984 1985 198B- 1987 1988

Pto. Cobello 4,650.2 4,788.2 8,967.1 4,929.6 5,760.9La Qualre 1,588.6 1,768.0 1,517.2 1,816.42,1109?Maraceibo 8638. 804.0 618.6 772.21,117.1Quanta 182.1 306.3 884.0 829.8 830.8Pto. Sucr 81.7 888 60.9 68.8 111.7Guaranao 169.8 168.4 64.0 86.8 116.9El Cuamache 8.8 19.7 21.1 14.9 25.7Carupano 18.8 -- 0.1 -- 22.4

7,414.8 7,911.9 6,568.0 7,807.5 10,101.2

Source: Foreign trsd, and coastal.

6.48 Responsibility for the nation's ports is with the Ministry of Transportand Communications (MTC), though the CVG ports operate with a high degree ofautonomy. MTC is responsible also for the port captains, lights and buoys andother marine activities. The Ministry of the Environment (MARNR) isresponsible for related aspects, especially of the river and lake ports.

- 19 -

Dredging and river control works are the responsibility of the NationalInstitute for Canals (INC), which depends on the MTC.

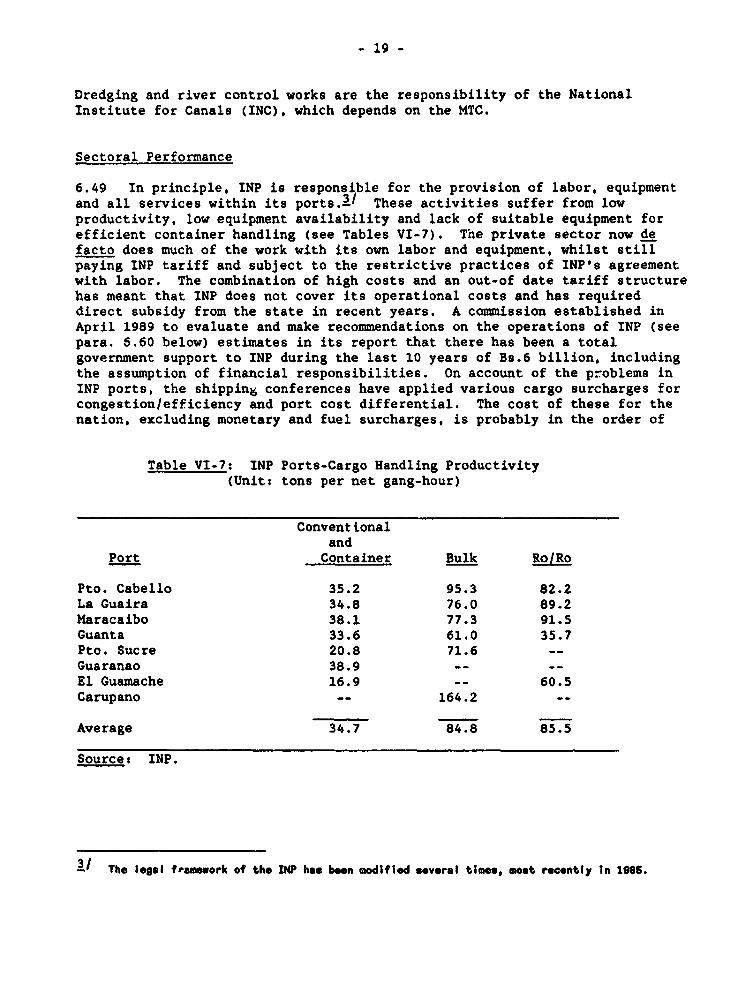

Sectoral Performance

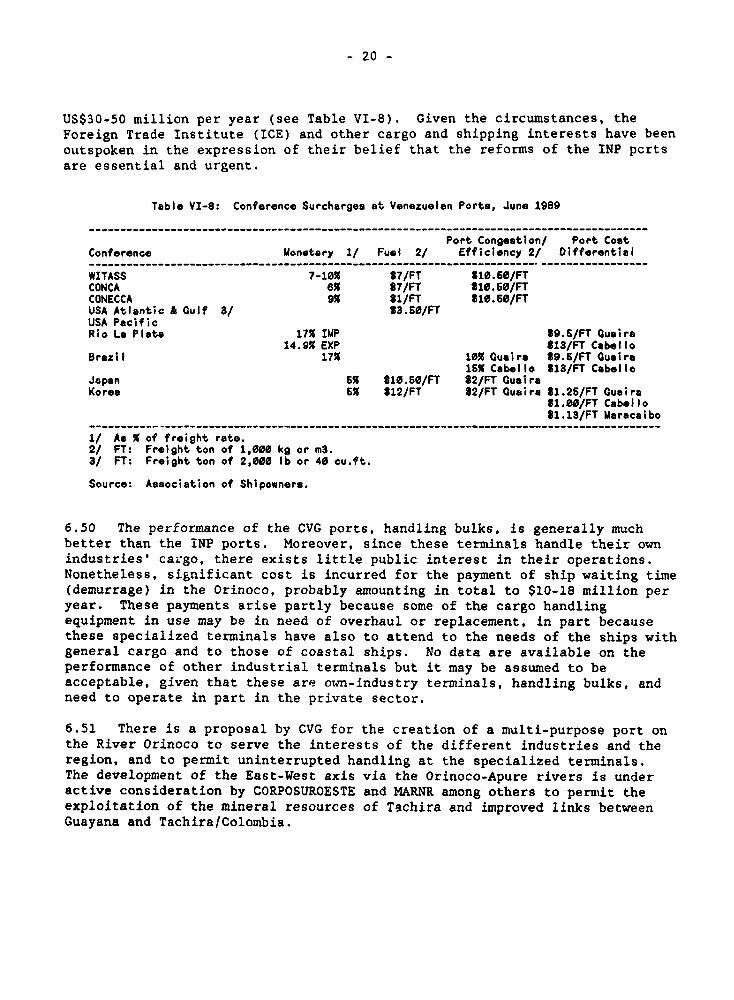

6.49 In principle, INP is responsible for the provision of labor, equipmentand all services within its ports.3/ These activities suffer from lowproductivity, low equipment availability and lack of suitable equipment forefficient container handling (see Tables VI-7). The private sector now defacto does much of the work with its own labor and equipment, whilst stillpaying INP tariff and subject to the restrictive practices of INP's agreementwith labor. The combination of high costs and an out-of date tariff structurehas meant that INP does not cover its operational costs and has requireddirect subsidy from the state in recent years. A commission established inApril 1989 to evaluate and make recommendations on the operations of INP (seepara. 6.60 below) estimates in its report that there has been a totalgovernment support to INP during the last 10 years of Bs.6 billion, includingthe assumption of financial responsibilities. On account of the problems inINP ports, the shipping conferences have applied various cargo surcharges forcongestion/efficiency and port cost differential. The cost of these for thenation, excluding monetary and fuel surcharges, is probably in the order of

Table VI-7: INP Ports-Cargo Handling Productivity(Unit: tons per net gang-hour)

Conventionaland

Port Container Bulk Ro/Ro

Pto. Cabello 35.2 95.3 82.2La Guaira 34.8 76.0 89.2Maracaibo 38.1 77.3 91.5Guanta 33.6 61.0 35.7Pto. Sucre 20.8 71.6 --

Guaranao 38.9 El Guamache 16.9 - 60.5Carupano -- 164.2 --

Average 34.7 84.8 85.5

Source: INP.

31 The legal framework of the INP has been modifiod several time, most recently In 1986.

- 20 -

US$30-50 million per year (see Table VI-8). Given the circumstances, theForeign Trade Institute (ICE) and other cargo and shipping interests have beenoutspoken in the expression of their belief that the reforms of the INP pcrtsare essential and urgent.

Table VI-8: Conference Surcharges at Venezuelan Ports, June 1989

------------------------------------------------------------------- __--------__----------

Port Congestion/ Port CostConference Monetary 1/ Fuel 2/ Efficiency 2/ Differential------------------------------------------------------------- __--------_.-_---------------

WITASS 7-10% 87/FT 810.60/FTCONCA e% 87/FT 810.60/FTCONECCA 9% 81/FT 810.60/FTUSA Atlantic A Gulf 3/ 83.60/FTUSA PacificRio La Plata 17% IMP 89.6/FT Gusira

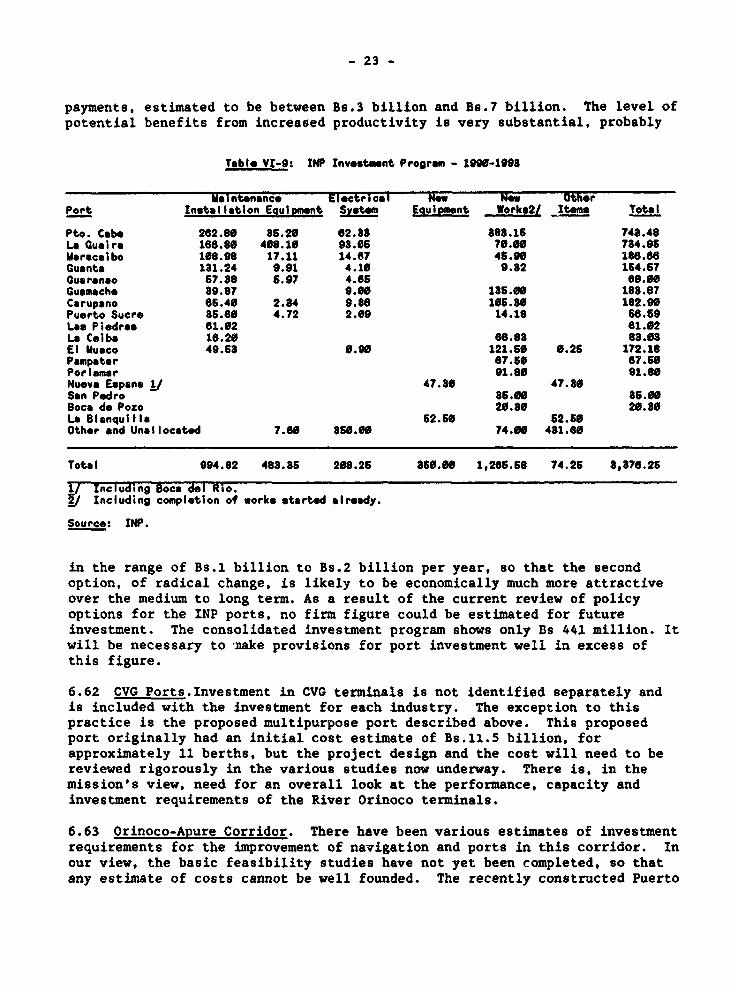

14.9% EXP 813/FT CabelloBrazil 17% 10% Cuaire 89.6/FT Oucire

16% Cabel lo 813/FT CabelloJapan 6% 810.60/FT 82/FT GuairaKorea 6% 812/FT 82/FT Guaira 81.26/FT Guaira

81.00/FT Cabello81.13/FT Maracaibo

1/ As X of freight rate.2/ FT: Freight ton of 1,000 kg or m3.3/ FT: Freight ton of 2,000 lb or 40 cu.ft.

Source: Association of Shipowners.

6.50 The performance of the CVG ports, handling bulks, is generally muchbetter than the iNP ports. Moreover, since these terminals handle their ownindustries' cargo, there exists little public interest in their operations.Nonetheless, significant cost is incurred for the payment of ship waiting time(demurrage) in the Orinoco, probably amounting in total to $10-18 million peryear. These payments arise partly because some of the cargo handlingequipment in use may be in need of overhaul or replacement, in part becausethese specialized terminals have also to attend to the needs of the ships withgeneral cargo and to those of coastal ships. No data are available on theperformance of other industrial terminals but it may be assumed to beacceptable, given that these are own-industry terminals, handling bulks, andneed to operate in part in the private sector.

6.51 There is a proposal by CVG for the creation of a multi-purpose port onthe River Orinoco to serve the interests of the different industries and theregion, and to permit uninterrupted handling at the specialized terminals.The development of the East-West axis via the Orinoco-Apure rivers is underactive consideration by CORPOSUROESTE and MARNR among others to permit theexploitation of the mineral resources of Tachira and improved links betweenGuayana and Tachira/Colombia.

- 21 -

Sectoral Issues

6.52 The principal issues of concern in the port sector at this time are:

(a) the improvement of the performance of the public port sector. Thisincludes three main elements: (i) the role of INP at national and atport level; (ii) the role of the private sector in port operations;and (iii) related to both of these, the future of the laboragreemen.s; and

(b) the reduction of ship waiting time in the River Orinoco.

6.53 Other issues concern the role of coastal shipping as an alternative toinvestment in railway development (see Section A above), and the role of rivertransport in the Orinoco-Apure (see paras. 6.43 and 6.63). Another importantissue relates to port development in Lake Maracaibo where the deepening of theentrance channel has had very serious environmental effects in the penetrationof salt water. The Bank's recent Venezuela Environmental Issues Paper makessome reference to this problem which the Government is presently studyingthrough the INC with technical support from the Netherlands.

Government Policies

6.54 The Government through MTC is actively addressing the issue of publicports. A mixed private/public sector commission was set up in April 1989,basically to propose alternative schemes for increased private sectorparticipation in the ports and the compensation of surplus INP labor.Following on from the work of this commission, the Government established inOctober 1989 a committee of four minister and the president of INP to define asolution to INP's problems. This committee in December 1989 received a paperprepared by the president of INP setting out the implications of two basicoptions: a continuation of present policies with gradual improvements or, thetotal restructuring of INP including a radical reduction of its work forcewith a compensation package, and the re-engagement of the minimum necessarylabor in the context of increased private sector participation. This paperhas now been considered by the Government and the second option, of radicalreform, has been adopted with the concurrence of labor unions.

6.55 There has been no clear tariff policy for the public ports. The presenttariff level is low, contributing to the financial problems of INP. Portusers currently pay less for INP tariff than they incur in the cost ofsupplementing deficiencies with their own labor and equipment. A revisedtariff schedule is now before the economic cabinet for approval.

6.56 The Government's interest in the Orinoco ports remains relativelysecondary although the creation in 1986 of a commission for River Orinoco isindicative of an increasing concern. The commission is essentially a harborauthority, concerned chiefly with shipping movement. CVG, through its generalmanager for industrial and mining activities has commissioned studies for the

- 22 -

proposed port. The results of these studies are expected this year.Transport planning within CVG has up to now been at industry level, resultingin the loss of opportunities to take advantage of economies of scale,particularly for coastal shipping. It is understood that the revisedadministrative structure for CVG will include a corporate transport planningactivity.

6.57 The concern with Orinoco-Apure development has up to now beenconcentrated mainly in MARNR and CVG. The issue is one of regional and miningdevelopment more than transport, though transport costs will play a vital rolein determining the feasibility of these developments. Some greater degree ofcoordination of the river transport aspects will be provided by a commissionestablished in November 1989 under the leadership of MTC and INC, though thecommission has not yet addressed the central problem of project feasibility.

6.58 In fact, the issues of the role of coastal shipping, particularly as analternative to railway transport, and the development of Orinoco-Apure rivertransport are key issues in the transportation sector. These questions,however, cannot be addressed fully in the present report because the necessaryeconomic technical analyses have not been completed by the relevantauthorities in Venezuela.

Public Investment Program

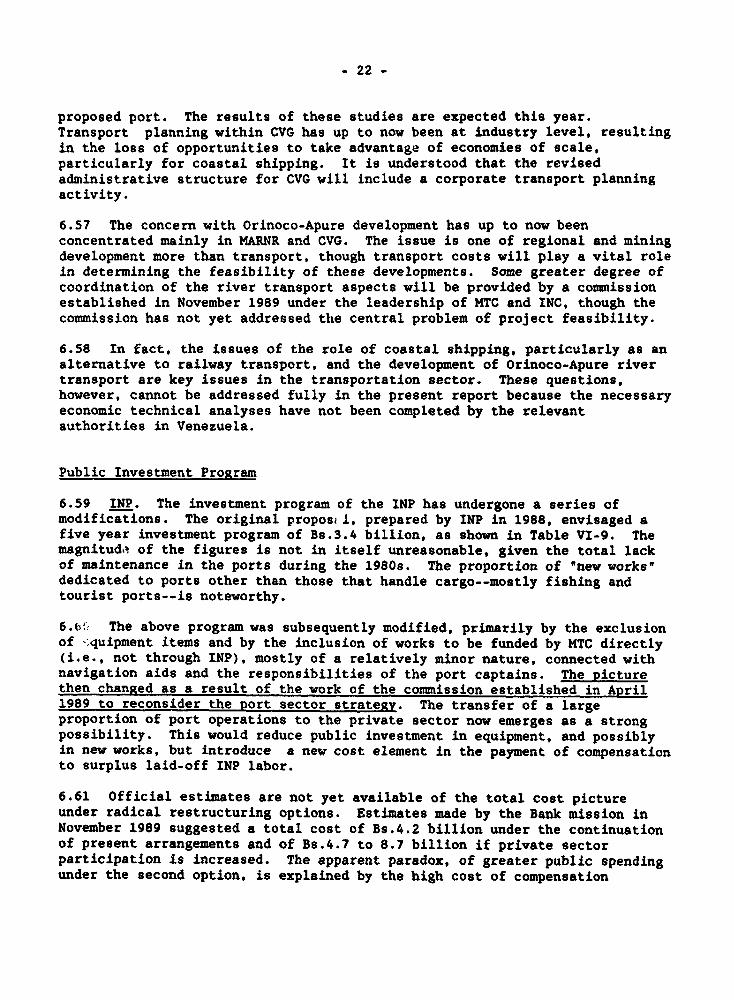

6.59 INP. The investment program of the INP has undergone a series ofmodifications. The original proposil, prepared by INP in 1988, envisaged afive year investment program of Bs.3.4 billion, as shown in Table VI-9. Themagnitud,' of the figures is not in itself unreasonable, given the total lackof maintenance in the ports during the 1980s. The proportion of "new works,dedicated to ports other than those that handle cargo--mostly fishing andtourist ports--is noteworthy.

6.6': The above program was subsequently modified, primarily by the exclusionof -;quipment items and by the inclusion of works to be funded by HTC directly(i.e., not through INP), mostly of a relatively minor nature, connected withnavigation aids and the responsibilities of the port captains. The picturethen chanRed as a result of the work of the commission established in April1989 to reconsider the Rort sector strateRy. The transfer of a largeproportion of port operations to the private sector now emerges as a strongpossibility. This would reduce public investment in equipment, and possiblyin new works, but introduce a new cost element in the payment of compensationto surplus laid-off INP labor.

6.61 Official estimates are not yet available of the total cost pictureunder radical restructuring options. Estimates made by the Bank mission inNovember 1989 suggested a total cost of Bs.4.2 billion under the continuationof present arrangements and of Bs.4.7 to 8.7 billion if private sectorparticipation is increased. The apparent paradox, of greater public spendingunder the second option, is explained by the high cost of compensation

- 23 -

payments, estimated to be between Bs.3 billion and Bs.7 billion. The level ofpotential benefits from increased productivity is very substantial, probably

Table VI-9: INP Investment Program - 1990-1993

Malntenance Electrical Now NOw OtherPort Installotion Equipment System Equipment Work*2/ Items Totel

Pto. Cabe 282.80 36.20 82.88 888.16 748.48La Cuasir 168.80 408.10 08.06 ?0.00 784.95MsracsIbo 168.98 17.11 14.67 4S.90 188.88Guants 131.24 9.91 4.10 9.82 164.67Guarenao 57.88 8.97 4.85 68.0MGuamache 89.87 9.00 136.00 188.87Carupano 65.40 2.84 9.88 106.86 182.90Puerto Sucre 8.860 4.72 2.09 14.18 66.59Los Piedras 61.62 61.02La Celba 18.20 88.68 88.08El Muaco 49.68 0.90 121.50 0.26 172.18Pampatar 87.60 67.60Porlamar 91.80 91.80Nueva Eapana y 47.80 47.80San Padro 85.00 85.00Boca de Poxo 20.80 20.30La Blanquilll 52.60 52.t0Other and Unallocated 7.60 860.00 74.00 481.60

Total 994.82 483.36 208.25 860.00 1,265.68 74.26 8,876.26

1/ Including Boca del Rio./ Including completion of works started already.

Source: INP.

in the range of Bs.l billion to Bs.2 billion per year, so that the secondoption, of radical change, is likely to be economically much more attractiveover the medium to long term. As a result of the current review of policyoptions for the INP ports, no firm figure could be estimated for futureinvestment. The consolidated investment program shows only Bs 441 million. Itwill be necessary to nake provisions for port investment well in excess ofthis figure.

6.62 CVG Ports.Investment in CVG terminals is not identified separately andis included with the investment for each industry. The exception to thispractice is the proposed multipurpose port described above. This proposedport originally had an initial cost estimate of Bs.11.5 billion, forapproximately 11 berths, but the project design and the cost will need to bereviewed rigorously in the various studies now underway. There is, in themission's view, need for an overall look at the performance, capacity andinvestment requirements of the River Orinoco terminals.

6.63 Orinoco-Apure Corridor. There have been various estimates of investmentrequirements for the improvement of navigation and ports in this corridor. Inour view, the basic feasibility studies have not yet been completed, so thatany estimate of costs cannot be well founded. The recently constructed Puerto

- 24 -

Santos Lisardo is estimated to have cost about Bs.15 million, though futureinvestment will necessarily cost much more. There are various associatedinvestments, such as the dams for river control. The whole complex ofprojects require much more serious studies before reliable cost estimates canbe made.

Recommendations for Ports Investment Program

6.64 INP Ports. On the assumption that the policy for increasedparticipation of the private sector will be adopted, the following policiesfor investment in the public ports are suggested for the next five years:

US$ Million

maintenance of installations 30-40maintenance of equipment __new works (to be reviewed) 50compensation payments 100-150

Maintenance of equipment should be self-financing through sale or leasingarrangements.

6.65 Other MTC Port Investments. This is likely to require US$10-20 millionover the five year period.

6.66 CVG Ports. For the reasons given above (para. 6.50), no reliableestimate is available but investment in the order of US$50-100 million islikely to be required for maintaining the various terminals and for the start-up of the multipurpose terminal during the five year period.

6.67 Orinoco-Apure. It would be prudent to allow a sum of around US$20million for minor improvement works over the five-year period.

Chapter 7

Investments in Urban Transportation

A. Background

7.1 In this chapter, we attempt to evaluate the public sector investmentprogram for Caracas' urban transportation in the context of some key issuesthat have emerged in the sector in recent years. Ideally, this report wouldhave covered urban transportation throughout Venezuela. In practice, thecomplexity of the situation in Caracas is such that there was littleopportunity to extend the scope of work to include other urban centers. It ishoped that some of the main conclusions would nevertheless be relevant to thesituation outside Caracas.

Urban Road Network in Caracas

7.2 In 1983 it was estimated that the urban road network of Caracas had atotal extent of 1.300kms, made up as follows:1

- 65kms of urban motorway/expressways;- llSkms of other principal roads;- 230kms of secondary roads; and- 890kms of local roads.

It seems likely that this estimate relates principally to the city's pavedroads and excludes most of the unpaved roads in the marginal areas of Caracas.

7.3 The total length of paved roads outside the marginal areas will nothave increased greatly since 1983. Thus, for example, a document produced bythe Caracas Metro Company (CAMETRO) in 1988 estimates the total length of thenetwork to be only lOOkms more than in 1983 (i.e., 1,400kms).2 The length ofspeedways under the jurisdiction of the Ministry of Transportation andCommunications (MTC) has increased from 65kms to 73kms. Other roads are theresponsibility of the States (i.e., Federal District and Miranda) or themunicipalities.

7.4 The general level of maintenance of the principal road network isgood. Some parts of the secondary network suffer from localized problems butthese are not generally serious. The major problem of road maintenance isfound in the marginal areas of the city (see para. 7.13).

1 Quoted in 'Los Vehiculos Por Puesto on el Transporte Urbano de Caracas' by Ing. Ian Thomson,Naciones Unidas-CEPAL, 1986.

2 Cited in *Proyecto de Ley Programa para la Contratecion y Financlamlento del Metro doCaraces', 1988.

- 26 -

The Vehicle Fleet

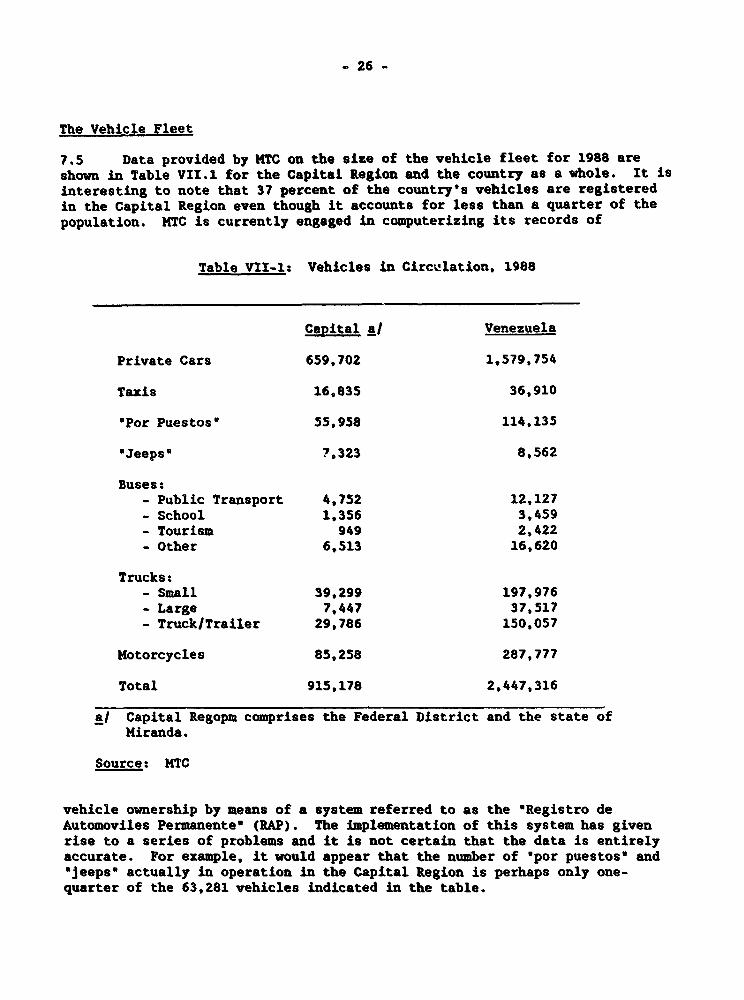

7.5 Data provided by KTC on the size of the vehicle fleet for 1988 areshown in Table VII.1 for the Capital Region and the country as a whole. It isinteresting to note that 37 percent of the country's vehicles are registeredin the Capital Region even though it accounts for less than a quarter of thepopulation. MTC is currently engaged in computerizing its records of

Table VII-Is Vehicles in Circu.-lation, 1988

Capital a/ Venezuela

Private Cars 659,702 1,579,754

Taxis 16,835 36,910

'Por Puestos' 55,958 114,135

'Jeeps' 7,323 8,562

Buses:- Public Transport 4,752 12,127- School 1,356 3,459- Tourism 949 2,422- Other 6,513 16,620

Trucks:- Small 39,299 197,976- Large 7,447 37,517- Truck/Trailer 29,786 150,057

Motorcycles 85,258 287,777

Total 915,178 2,447,316

a/ Capital Regopm comprises the Federal District and the state ofMiranda.

Source: MTC

vehicle ownership by means of a system referred to as the 'Registro deAutomoviles Permanente (RAP). The implementation of this system has givenrise to a series of problems and it is not certain that the data is entirelyaccurate. For example, it would appear that the number of 'por puestos' and"jeeps actually in operation in the Capital Region is perhaps only one-quarter of the 63,281 vehicles indicated in the table.

- 27 -

The Modal Split