Embed Size (px)

Citation preview

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 1/71

1

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 2/71

Message:

The signing of the Joint Memorandum Circular (JMC) No. 1 Series of 2007 proved to bethe landmark policy in the synchronization and harmonization of the core LGUoperations. As a result, the JMC triggered the issuance of several updated manualsfrom the four signatory agencies, Department of the Interior and Local Government(DILG), National Economic and Development Authority (NEDA), Department of Finance(DOF) and Department of Budget and Management (DBM). Furthermore the four agencies have strengthened the coordination with the Housing and Land UseRegulatory Board (HLURB) completing the membership of the JMC composite team.

As advocates of decentralization and devolution, the GTZ-Decentralization Program(DP) respects the autonomy of the LGUs. With the JMC in place, the oversight agencies

themselves can only prescribe what tools can be used in implementing the core LGUoperations. Hence, the DP looked into each of the tools to help and make it easilyavailable for the LGUs as well as decentralization practitioners. This Compendiumoutlines the basic elements in each of the core LGU operations. These are the:

Activities, Required Outputs, Suggested Approaches/Tools and the Reference Manuals.With this publication, the LGUs can choose what tool best suites them.

The Compendium is a five (5) volume document cross-referencing to the various tools

on the core LGU operations. Volume 1: Integrated Guide summarizes the general stepsof the core LGU operations. On the other hand the detailed explanations anddescriptions can be found on the succeeding volumes: Volume 2: Planning Tools and

Approaches, Volume 3: Investment Programming Tools and Approaches, Volume 4:

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 3/71

TABLE OF CONTENTS

I. Local Planning 7

A.Required Planning Documents 7B.Suggested Planning Structure and Organizational Activities 8C.Basic Planning Steps 12D.Plan Formats 23E.Planning Calendar per JMC 25

II. Investment Programming 26

A. Required Documents for Local Investment Programming 26B. Suggested Institutional Structure for the Preparation

of the Investment Program and Organizational Activities 26

C. Basic Steps in Investment Programming 28D. Suggested Format of Local Investment Plans 33E. Calendar of Activities on Investment Programming 34

III. Revenue Administration and Resource Mobilization 34

A. Required Outputs and Documents 34B. Suggested Institutional Structure for the Preparation of

the Required Outputs and Documents on Revenue Administration 35C. Basic Processes in the Preparation of the

Required Outputs and Documents 36D Formats 42

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 4/71

List of Tables, Figures and Annexes

List of Tables

1 Required Planning Outputs and Guides2 Suggested Approaches and Tools in Organizing Planning Teams3 Suggested Approaches and Tools in Assessing the Planning Environment4 Suggested Approaches and Tools in Setting Goals, Targets and Objectives

5 Suggested Approaches and Tools in the Formulation of Strategies and Policies6 Suggested Approaches and Tools in the Identification of Programs, Projects and

Activities 7 Suggested Approaches and Tools in Setting the Legislative Agenda8 Suggested Approaches and Tools in Public Consultations Prior to Plan Approval9 Suggested Approaches and Tools in Plan Implementation 10 Suggested Approaches and Tools in Monitoring and Evaluating Plan

Implementation11 Proposed Schedule of Planning Activities per JMC12 Required Outputs in Investment Programming and Guides

13 Suggested Approaches and Tools in Establishing Investment Programming Policies 14 Suggested Approaches and Tools in the Initial Identification and Screening of Projects15 Suggested Approaches and Tools in Ranking Programs, Projects and Activities16 Suggested Approaches and Tools in Conducting the Financial Analysis of Projects 17 Required Outputs in Investment Programming and Guides18 Proposed Schedule of Activities Related to Investment Programming per JMC19 Major Outputs Related to Revenue Administration and Resource Mobilization

20 Suggested Approaches and Tools in Financial Planning and Resource Mobilization21 Suggested Approaches and Tools in Preparing the Statement of Receipt and

Expenditures22 Suggested Approaches and Tools in Revenue Forecasting23 Key Players in the Budget Process24 Suggested Approaches and Tools in Budget Preparation

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 5/71

ACRONYMS

AMPS Assessment Matrix of Project Sustainability ADB Asian Development Bank AIP Annual Investment Program ARO Allotment Release Order BLGF Bureau of Local Government FinanceCBMS Community-Based Monitoring SystemCDP Comprehensive Development PlanCDS City Development StrategyCFA Cash Flow AnalysisCLUP Comprehensive Land Use PlanDBM RO Department of Budget and Management – Regional OfficeDILG Department of the Interior and Local GovernmentDFPPT Detailed Financial and Physical Performance TargetsDOF Department of FinanceELA Executive and Legislative Agenda

EO Executive Order GFI Government Financial InstitutionHLURB Housing and Land Use Regulatory BoardJMC Joint Memorandum Circular No. 001 on Local Planning, Investment

Programming, Revenue Administration, Budgeting and Expenditure ManagementLBA Local Budget AuthorizationLBAc Local Budget AccountabilityLBE Local Budget ExecutionLBM Local Budget MatrixLBP Local Budget PreparationLBPE Local Budget Performance EvaluationLBR Local Budget ReviewLCE Local Chief Executive

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 6/71

NGAS New Government Accounting SystemOPIF Organizational Performance Indicator Framework

PDC Provincial Development CouncilPDIP Provincial Development Investment Plan/ProgramPDPFP Provincial Development and Physical Framework PlanPEM Public Expenditure ManagementPLPEM Provincial/Local Planning and Expenditure ManagementPLUC Provincial Land Use CommitteePOPDEV Population and DevelopmentPPAs Program/ Project/ ActivityPPDC Provincial Planning Development Coordinator PPMP Project Procurement Management PlanPPFP Provincial Physical Framework PlanPRR Performance Review ReportRAAO Registry of Appropriations, Allotments and ObligationsRAAOCO Registry of Appropriations, Allotments and Obligations Capital OutlaysRAAOFE Registry of Appropriations, Allotment and Obligations Financial ExpensesRAAOMO Registry of Appropriations, Allotments and Obligations Maintenance & Other

Operating Expenses

RAAOPS Registry of Appropriations, Allotments and Obligations Personal ServicesRBOM Revised Budget Operations ManualRPS Rationalized Planning System/Rationalized Local Planning

System of the PhilippinesRRMC Revised Revenue Mobilization CoursebookSCFF Statement of Cash Flow ForecastSFPPT Summary of Financial and Physical Performance TargetsSRE Statement of Receipts and ExpendituresSWOT Strengths-Weaknesses-Opportunities-ThreatsTOWS Total Overall Weighted ScoreUNDP United Nations Development ProgramZO Zoning Ordinance

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 7/71

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 8/71

I. LOCAL PLANNING

The preparation of medium and long-term development strategies provides localgovernment units (LGUs) with an objective basis for making decisions that enable them toprioritize their immediate needs more rationally and accurately in the face of challenges of emerging urban development.

A. Required Planning Documents

Plan documents take on many forms at the local level. The Local GovernmentCode mandates LGUs to prepare two (2) major plans – a land use plan and acomprehensive plan. In addition, the Department of the Interior and Local Government(DILG) has promoted the preparation of term-based plans – the Executive–Legislative

Agenda (ELA). Several manuals have been prepared to guide the LGUs in thepreparation of these plan documents. Table 1 summarizes the different planningdocuments required at the local level and the guides that have been prepared to assistthe LGUs.

1. Land Use or Physical Plans

1.1 Physical Framework Plan

In the case of provinces, the land use plan may take on two forms: (1) theProvincial Physical Framework Plan (PPFP) required by the Housing and LandUse Regulatory Board (HLURB); and/or (2) the Provincial Development andPhysical Framework Plan (PDPFP), which is a recent document being endorsed

by the National Economic and Development Authority. The latter is a merger of the traditionally separate Provincial Development Plan and the PPFP. Themerger is aimed at eliminating overlaps in the separate planning outputs andaddresses the spatial-sectoral, and medium-term and long-term disconnect that

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 9/71

been advocating the preparation of the Comprehensive Development Plan (CDP) at thecity and municipal levels.1 To date, some cities have been preparing a City Development

Strategy (CDS) Report which may be considered a comprehensive plan.2

Another comprehensive development plan is the Executive-Legislative Agenda (ELA) which isclassified more as a “term-based” plan but whose coverage may be liken to the usualcomprehensive plan except that the time period is shorter (i.e. three years) compared tothe usual six-year comprehensive plan.

B. Suggested Planning Structure and Organizational Activities

In all of the planning guidelines, the planning process always starts with theorganization of the planning team. In the preparation of any plan, the suggestedcomposition of the planning team, the initial organizational activities and the legaldocuments needed to start the planning process are almost the same (refer to Table 4).The common features are described below:

1.The Composition of the Planning Team:

The planning structure is usually composed of the following:

1.1The Local Chief Executiv e

Plans to be effective should get the support of the Local Chief Executive(LCE) which provides the overall direction and motivation for the preparation of any plan in the locality, be it in the province, city or municipalities. The LCE actsas Chair of the Local Development Council.

1.2The Local Development Councils

The Provincial, City and Municipal Development Councils are tasked withoverseeing the overall planning process, providing policy direction together withth L l Chi f E ti d i ti th S i i tti th di ti f

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 10/71

Table 1. Required Planning Outputs and Guides

Type of Plan/ Local GovernmentUnits

Major Output:Development Plans

Time Period Covered Planning Guide

A. Land Use or Physical Plans

1. ProvincesProvincial PhysicalFramework Plan (PPFP)

10 years Guidelines for theFormulation of theProvincial PhysicalFramework Plan (PLPEM) (HLURB;

1991)Provincial Development& Physical FrameworkPlan (PDPFP)

Six years (or two 3-year political terms of theGovernor); physicalframework may extendbeyond the 6-year medium term plan

Guidelines onProvincial /LocalPlanning &ExpenditureManagement (ADB/NEDA;2007)

2. Cities/ Municipalities Comprehensive LandUse Plan (CLUP)-turned

Zoning Ordinance

10 years to be reviewedevery 3 years; 30

years3

, with updatingevery 9-10 years, or ideally during censusyears

CLUP Guidebook:Guide to CDP

Preparation (HLURB; 2006)

B. Comprehensive Plans

1. Provinces Provincial Development& Physical FrameworkPlan (PDPFP)

Six years (or two 3-year political terms of theGovernor)

Guidelines onProvincial /LocalPlanning &ExpenditureManagement

(ADB/NEDA;2007)

2. Cities/ Municipalities ComprehensiveDevelopment Plan (CDP)

3-6 years Enhanced Guideto CDPP ti

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 11/71

Figure 1. Typical Planning Structure4

1.4Local Planning and Development Coordinators/Offices

The provincial, city and municipal offices usually act as the technicalsecretariat to any planning activity in the respective LGUs. As such, theyorganize the meetings of the Local Development Councils, prepare the technicalinputs to the meetings, undertake the necessary researches and studies which

id i t t th l i d th i l t ti f th

LocalSanggunian

Local Chief Executive

Local DevelopmentCouncil

Local PlanningDevelopment

Office

Other LGUDepartments

Sectoral, Functional

Committees and TechnicalWorking Groups

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 12/71

Based on past experiences, successful planning usually would have thefollowing ingredients: (1) the participation of the local chief executive; (2) the buy-

in of the different sectors and stakeholders because of the highly consultative andparticipatory process adopted in the preparation of the plan; and (3) the technicalsupport provided by the planning and development office.

Once the planning team has been named, the LGU needs to: (1) preparethe work plan including the timing of the activities; (2) assess the resourcesneeded to prepare the plan and the sourcing of the funds; (3) organize theplanning teams and all the technical working groups and/or sector committees;(4) preparing the legal documents (e.g. Executive Order, resolution of theSanngunian) on the conduct of the plan; (5) public dissemination of the planningactivities.

The different manuals have been quite useful in providing the tools for assisting the LGUs prepare for the plan activities. Some of these tools aresummarized in Table 2.

Table 2. Suggested Approaches and Tools in Organizing Planning Teams

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Analysis of Existingplans

•Decision on the form

and content of plan to beprepared/updated

•Status of Plan Charts •CDP (pp. 25 - 26)

2. Planning Committeecomposition

•Members of the

Planning Team

•Suggested members

of the Team

•CDP Guide (p.19);

CDS Toolkit (p.2-3);PPFP Guide (pp.8-10);CLUP Guide (p.17-18)

3. Identification of St k h ld

•Stakeholders to be •Tools in Identifying •CLUP (p. 25); CDP

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 13/71

C. Basic Planning Steps

All of the guides for local planning include the processes for preparing localplans. The processes for preparing land use plans and comprehensive plans are listeddown in Tables 3 and 4, respectively. At a glance, it is obvious that there are common or basic planning steps which are followed as part of the planning process.7 Theseprocesses can be divided into three major parts: (1) the preparation of the plandocument; (2) the approval of the plan; and (3) plan implementation and monitoring.

1. Preparation of the Plan Document

1.1 Information Base Generation and Situation Analysis/Assessment of Planning Environment 8

This stage basically answers the question, 'Where are we right now?' It isboth analytical and diagnostic, geared towards identifying issues, potentials and

future development needs and spatial requirements of the community.

The situation analysis has to start with the generation of the data or information for assessing the planning environment. Some of the manualsidentify detailed data sets which the LGU may gather to start the analysis. Dataand information gathered at this stage goes into a profile or characterization of the planning area which could provide a diagnosis of the state of the LGU.However, the analysis would depend primarily on the availability of localstatistics. The suggested data sets in some of the manuals are listed in Appendix1.1.

There are two methods for assessing the planning environment, thetechnical and participatory methods Technical assessment is based on factual

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 14/71

Table 3. Suggested Approaches and Tools in Assessing the PlanningEnvironment

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Data Generation ●Data or statisticalcompendium and maps

●Sources of data andindicators:oCommunity-Based

Monitoring System(CBMS);oLocal Development

Indicator System (LDIS);oMinimum Basic Needs

(MBN) SurveyoCross-sectoral and

special concerns●Financial Profile

●

List of DataRequirements

●Preparation of BaseMaps●Density Categories for Density Maps●Slope Categories

●Slope Criteria for Land

Suitability Maps

● CDP (pp. C-E)

●CDP (pp.65-67), RPS(pp.75-80)

●

CDS (p.2-7)

●CDP (pp. H - N)

●CDS (pp.2-8 to 2-10)

●CLUP (pp.41-42),PLPEM Vol 2 (p.26),CDP (pp. 45-59; A-C;)●PPFP Guidelines

(pp.13; 124-133)

●CLUP (p.40)

● PLPEM Vol 2(p. 47)

●PLPEM Vol 2(p. 55)

●PLPEM Vol 2

(p. 60)

2. Analysis of thePlanning Environment

•Technical Analysis of

the Environment

2.0 General Tools●Problem Analysis ●CDP (p.67)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 15/71

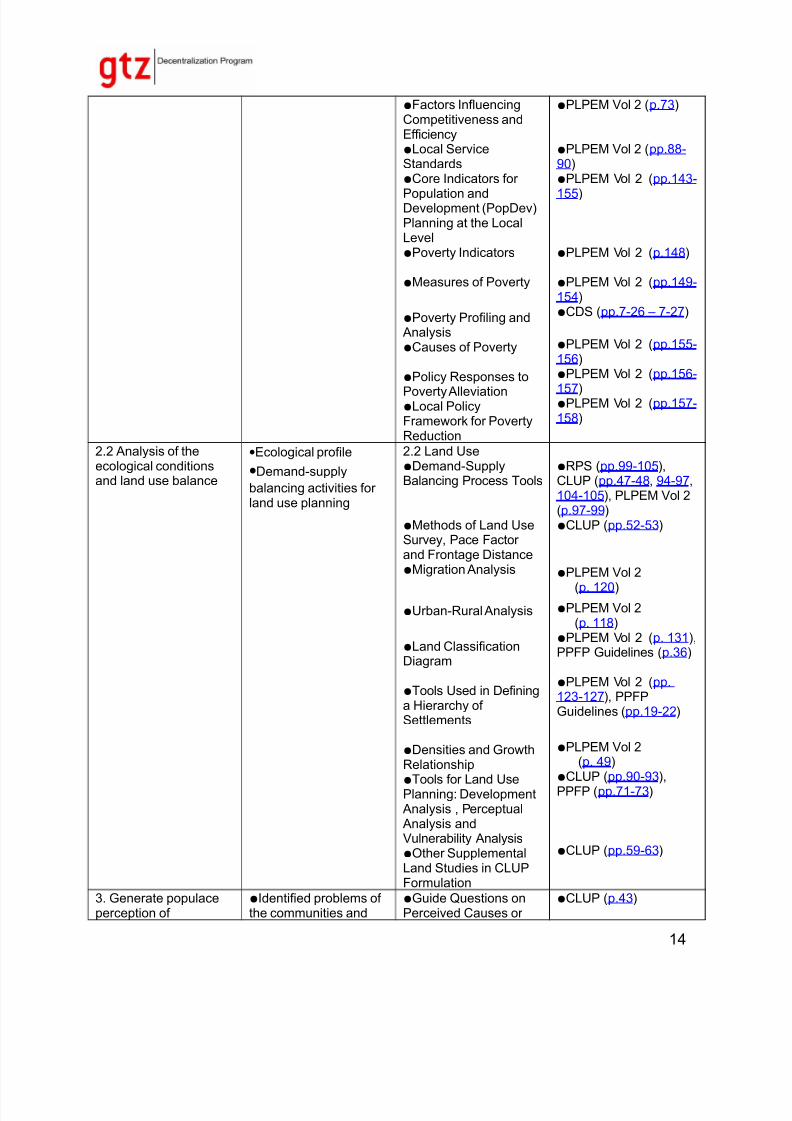

●Factors InfluencingCompetitiveness and

Efficiency●Local ServiceStandards●Core Indicators for Population andDevelopment (PopDev)Planning at the LocalLevel●Poverty Indicators

●Measures of Poverty

●Poverty Profiling and Analysis●Causes of Poverty

●Policy Responses toPoverty Alleviation●Local PolicyFramework for PovertyReduction

●PLPEM Vol 2 (p.73)

●PLPEM Vol 2 (pp.88-90)●PLPEM Vol 2 (pp.143-155)

●PLPEM Vol 2 (p.148)

●PLPEM Vol 2 (pp.149-154)●CDS (pp.7-26 – 7-27)

●PLPEM Vol 2 (pp.155-156)●PLPEM Vol 2 (pp.156-157)●PLPEM Vol 2 (pp.157-

158)

2.2 Analysis of theecological conditionsand land use balance

•Ecological profile

•Demand-supply

balancing activities for land use planning

2.2 Land Use●Demand-SupplyBalancing Process Tools

●Methods of Land UseSurvey, Pace Factor

and Frontage Distance●Migration Analysis

Urban Rural Analysis

●RPS (pp.99-105),CLUP (pp.47-48, 94-97, 104-105), PLPEM Vol 2(p.97-99)●CLUP (pp.52-53)

●PLPEM Vol 2(p. 120)

●PLPEM Vol 2

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 16/71

development issues sectors within the LGU Sources of Degradation●Development Issues

●Participatory IssueIdentification●Public Consultations

●PLPEM Vol 2 (pp.

104-105)●CDS (p.7-25)

●CDS (p.2-11)

Suggested approaches and tools are described in detail in Chapter 2 of Volume II

(pp. 19 - 79 )

1.2 Formulation/Revisiting of Vision and Setting of Goals, Objectives and

Targets

Upon assessment of the local planning environment, the communityforms a collective long-term vision for the locality through a consensus by allstakeholders, derived from an analysis of the community's competitiveadvantages.

A vision is a desired state of the LGU and its people. It is thestakeholders’ shared image of the LGU’s future. It describes what the LGU wantsto become or where it wants to go and answers the question, “How do you seeyour LGU in the future?”

Because a vision covers a fairly long time horizon, it is appropriatelyformed alongside preparations for land use plans. The vision provided by landuse plans must be adopted by the CDP and other short-term plans to contributeto its eventual realization. Moreover, the local vision should not deviate from,but rather, be a local variation of the very aspiration of the national government

so that LGUs, as political and territorial subdivisions, will be able to attain their fullest development as self-reliant communities and become effective partners inthe attainment of national goals (Sec. 2, a. RA 7160).

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 17/71

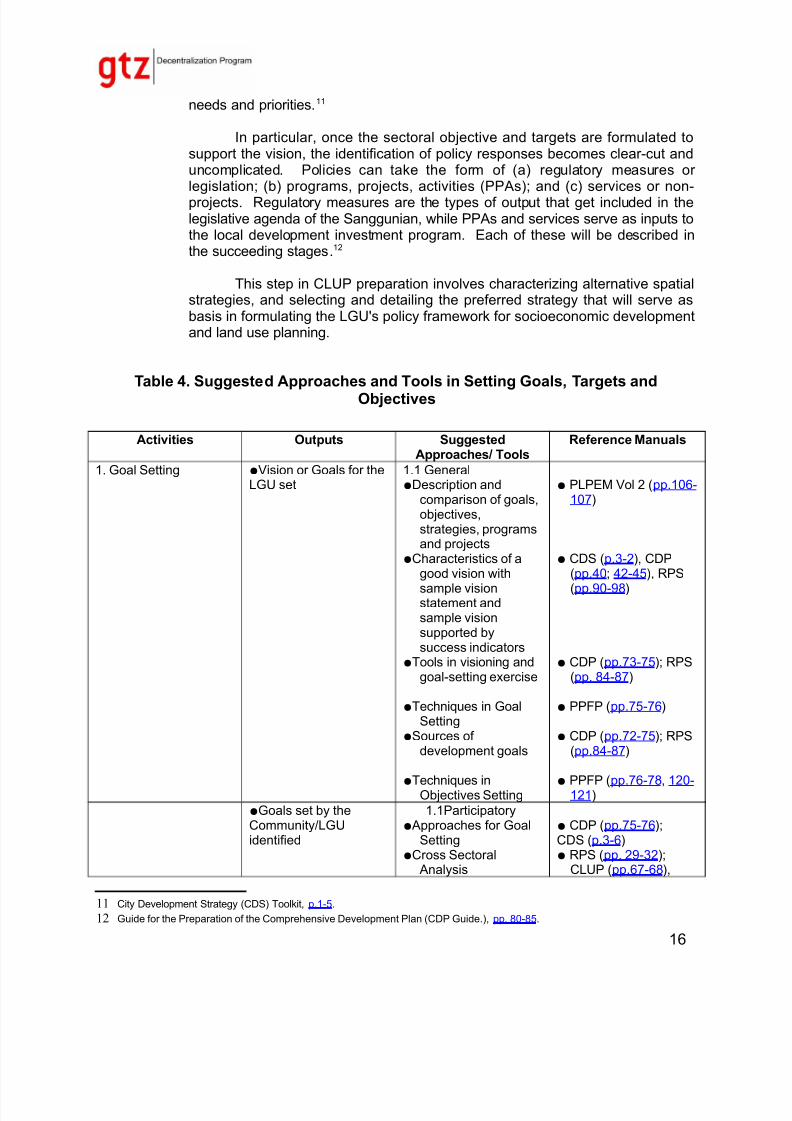

needs and priorities.11

In particular, once the sectoral objective and targets are formulated tosupport the vision, the identification of policy responses becomes clear-cut anduncomplicated. Policies can take the form of (a) regulatory measures or legislation; (b) programs, projects, activities (PPAs); and (c) services or non-projects. Regulatory measures are the types of output that get included in thelegislative agenda of the Sanggunian, while PPAs and services serve as inputs tothe local development investment program. Each of these will be described inthe succeeding stages.12

This step in CLUP preparation involves characterizing alternative spatialstrategies, and selecting and detailing the preferred strategy that will serve asbasis in formulating the LGU's policy framework for socioeconomic developmentand land use planning.

Table 4. Suggested Approaches and Tools in Setting Goals, Targets andObjectives

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Goal Setting ●Vision or Goals for theLGU set

1.1 General●Description and

comparison of goals,objectives,strategies, programsand projects

●Characteristics of agood vision withsample visionstatement and

● PLPEM Vol 2 (pp.106-107)

● CDS (p.3-2), CDP(pp.40; 42-45), RPS(pp.90-98)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 18/71

Approaches and tools are described in detail in Chapter 3 of Volume II ( pp. 80-

88)

1.4 Determining Programs, Projects and Activities (PPAs)

The LGU identifies specific programs, projects and activities that need tobe implemented under each strategy identified in the previous phase. This list willserve as inputs to the investment programming process that will produce theLocal Development Investment Plan (LDIP) for cities/municipalities and theProvincial Development Investment Program (PDIP) for provinces, which are thebases for determining the level of public investments needed to be appropriatedfor in the LGU’s annual budget.13

Programs are sets of projects that translate strategies to specific actionplans. Some strategies may involve only one project in which case a programmay be unnecessary. Each strategy may require more than one program.Programs may involve several sectors although the sectoral focus should beclear. Sometimes synonymous with project, it may cover a period of three (3) to

six (6) years.14

Table 5. Suggested Approaches and Tools in the Formulation of Strategies andPolicies

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Identification of

strategies

Strategies for sectors

identified

1.1 Technical

Approaches•Fishbone analysis

•Flowchart

●CDP (p.59); CDS (p.7-16)

●CDS (p.7-17)CDS ( 7 17 7 18)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 19/71

Strategies

•Structure Maps

•Matrix of Proposed

Land and Water Uses

(pp.106-108, 111-113), CLUP (pp.98-

100)●CLUP (pp.77-78)●CLUP (p.106)

2. Evaluation, Selectionand Ranking of Strategies

Prioritized set of strategies

2.1 Evaluation andSelection of PreferredStrategy

•Cost-Benefit Analysis

(CBA) and Social CBA

•

Planning BalanceSheet

•Goal-Achievement

Matrix

•Checklist of Criteria

2.2 Ranking of Strategies

•Simple ranking

•Pairwise ranking

●RPS (pp.113-114),CLUP (pp.83-86)

●

RPS (pp.114-115)

●RPS (pp.115-116)

●PPFP (pp.83-84s)

●CDS (pp.4-3,4-4)●CDS (p.7-24)

3. Identification of Programs and Projectsfor each strategy

PPAs, services andlegislations for eachstrategy identified

Suggested PresentationFormats

•Sample Table linking

programs and projects,services and legislationsto strategies

•Summary Matrix of

Strategies and PPAs

•Executive SummaryMatrix Template

•CDP (p.84); RPS

(p.154)

•PLPEM Vol. 2 (p.113)

•CDS (p.4-4)

Approaches and tools are described in detail in Chapter 4 of Volume II (pp.88-107)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 20/71

or “non – project” may be upgraded into a project.

Table 6. Suggested Approaches and Tools in the Identification of Programs,Projects and Activities

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Identification of PPAs PPAs corresponding toeach strategiesidentified

• Action planning

flowcharts

• Activity Network

Diagram

• Affinity Diagram

•Project identification

sources●Gantt Charts●Types of investments

●CDS (pp.5-1, 5-2)

●CDS (p.7-11)

●CDS (p.7-11)●JMC (pp.71-72)

●CDS (p.7-19)●RPS (pp.32-33)

2. Conduct of Consultations in theIdentification of Projects

●City ConsultationMethod●Mini-Consultation

●CDS (p.7-12)

●CDS (p.6-6)

Approaches and tools are described in detail in Chapter 5 of Volume II (pp. 106-108)

1.5. Drawing up of Legislative Requirements and Preparing the Legislative AgendaRPS Chapter 6, p.151; CDP Chapter III, Part 4 , pp.121-128

The legislative requirements of the development plan are the priority

legislations that need to be enacted by the Sanggunian to support development prioritiesof the LGU in the medium- and long-term. These may include new legislation as well asamendments and updates to existing legislation that have been identified as part of thestrategic regulatory measures to address issues and concerns determined in the

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 21/71

●Sample table of legislative requirements

●CDP (p.118)

Executive-Legislative Agenda

●Sample matrix formatof the ELA

●RPS (p.151); RevisedRevenue MoblizationCoursebook, Module VII(p.30)

Approaches and tools are described in detail in Chapter 6 of Volume II (pp. 110-111)

2. Consolidation, Presentation and Approval of Plans

This stage involves consolidating all the outputs generated from the previousstages, updating the LCE, LDC and other key stakeholders with respect to proposedstrategies and PPAs, updating Plan drafts, and conducting public consultations/hearingson the draft development and land use plans. Inputs from public consultations shall beconsidered for incorporation into the final draft of these plans. The format of the plan willbe discussed later.

The next step involves submission of the draft plans to the local Sanggunian for approval. In the case of CLUPs, the Land Use Plan and draft Zoning Ordinance withappropriate revisions according to the public hearings conducted, are submitted to theSanggunian. The draft CLUP is further subjected to mandatory review and subsequentapproval by authorized bodies. The appropriate review bodies for corresponding CLUPsare the following: (a) Sangguniang Panlalawigan and the Provincial Land UseCommittee (PLUC) for component cities and municipalities; (b) Housing and Land UseRegulatory Board (HLURB) and PLUC for highly-urbanized cities and independent

component cities; and (c) the Metro Manila Development Authority (MMDA) and HLURBfor Metro Manila Cities and Municipalities.

An issue that has been raised and which has been clarified by the concerned

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 22/71

SemistructuredInterviews●

Flow Chart of PublicHearings for CLUP andZO

●

CLUP (p.130)

Presentation of the Planto Sanggunian

Approved CDP, CDSand PDPFP and a duly-enacted ZoningOrdinance withprescribed maps,Sanggunian resolutions

•CLUP Step 8 on

Drafting theZoning Ordinance

●CLUP (pp.114-123)

The tools are described in detail in Chapter 7 of Volume II (pp. 1121-113)

3. Plan Implementation and Monitoring

3.1 Plan Implementation

This stage requires the establishment of detailed operational plans andinstitutional mechanisms for the implementation of the mandated plans. For this

purpose, the Local Government Code (LGC) allows great flexibility for LGUs todesign and implement its own organizational structure and staffing pattern takinginto consideration the vision, mission, goals and objectives contained in their landuse and development plans. LGU “creativity” in governance or in making use of LGU authority levers as employed by successful cities and municipalities is keyto successful plan implementation. An effective way to harness resources at thisstage is to establish partnerships and cooperation arrangements with LGUstakeholders.

3.2 Plan Monitoring and Evaluation (M & E)

Monitoring and evaluation is an essential management tool instituted tomeasure progress as plan implementation proceeds providing a flow of

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 23/71

35)

Suggested tools are described in detail in Chapter 8 of Volume II (pp.114-118)

As part of a continuous and cyclical planning process, monitoring andevaluation (M&E) serves as a link between two planning cycles. 16 Its principal aimis to build the planning database for the successor plans as it produces newinformation from the assessment of impacts of plans, programs and projects asimplemented, the effects of regulatory measures as enforced, and the outcomesof developments in the area that had not come under the control or influence of the local planning system. This means M&E also determines changes attributed

not just to planned, but to unplanned developments as well. These changes aremanifested in the following: (a) social and economic well-being of inhabitants; (b)quantity and quality of the physical environment; and (c) institutional capabilitiesfor local governance. 17 In this manner, plan M&E functions as a measure of LGUperformance providing indications on how future efforts might be improved

Specifically, monitoring is a continuous process of data collection andanalysis to check whether a project is running according to plan and to make

adjustments if required. It is an evaluative study directed to the short term. Onthe other hand, evaluation is a systematic process of collecting and analyzinginformation about the activities and results of a project in order to determine theproject’s relevance and/or to make decisions to improve its efficiency andeffectiveness.18 For this purpose, monitoring can provide quantitative andqualitative data that can serve as inputs to evaluation.19

The frequency of Plan M&E should be synchronized with various planningcycles: annually, for purposes of the AIP and the budget cycle; once every three

years for the revision of the short-term CDP and ELA; and longer cycles for thesix-year medium-term CDP and long term CDP and CLUP revisions. Ideally,every census year, which happens after a lapse of nine to ten years, should bemarked out for conducting comprehensive data collection to update the

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 24/71

development plan (statistical compendiumand thematic maps)

performance monitoringsystem (LGPMS)●Core indicators for gender-responsivepopulation anddevelopment (POPDEV)planning at the locallevel●M & E strategytemplate● Annual or End-of-Term

Accomplishment Report

template●Community-basedmonitoring system

●CLUP (p.188)

●CDP (p.137, 140)

●CDP (pp.138-139)

●CDP (pp.136-137)

2. Monitoring of ProjectImplementation

Status report of projectimplementation

●ProjectImplementationMonitoringSystem/Scheme

●CLUP (pp.183-184)

3. Monitoring of landuse plans

Updated ecologicalprofile

●Quality of Life Assessment

●Land Use Changes

●CLUP (pp.31-35), CDP(pp. 69-70), RPS (p.

145)●CLUP (p.183)

4. Conduct of consultations for monitoring andevaluation of planimplementation

Schedule of consultations andpeople feedback onplan implementation

●Schedule of conducting plan M&Es●Participatory decision-making process●Regular feedbackmechanisms (e.g.suggestion box)

●RPS (pp. 200-202)

●CDS (pp.5-12 to 5-14)

●CDP (pp.134-135);

Suggested tools are described in detail in Chapter 9 of Volume II (pp. 118-132).

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 25/71

formulation (e.g. resolutions) ;(b) preface or foreword; and (c) table of contents.

2.Background information on the LGU22

This section provides basic information on the LGU which may consist of (1) brief history; (2) location; (3) land area and political subdivisions; (4) demographic profile; (5)physical resources; (6) economy of the LGU; (7) infrastructure; (8) environment; (9) landuse and physical framework.

3.Vision/statement Statement

This section articulates the aspiration of the LGU as formulated by the localgovernment in consultation with its constituents. The presentation of the vision issometimes complemented with the general strategies to attain the vision, which isseparate from the more detailed sector strategies.

4.Development Issues/problems23

This section is the outcome of the analysis of the present planning environment

which compares the present situation, the “where we are” and the vision or “where wewant to go. Some manuals reserve a separate chapter on a discussion of these issues,together with the emerging general goals and objectives of the LGUs. The discussionusually covers cross-sector or special issues/problems.

5.Sector chapters

All of the plans have sector chapters which usually contains the following: (a)goals, (b) objectives; (c) targets; (d) strategies; (e) plans, programs and activities; and (f)proposed legislative measures. Some manuals recommend that project profiles beincluded as an annex to the development plan.

The manuals also recommend common broad sector classifications as follows:

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 26/71

settlements plan; (b) an infrastructure plan; and (c) land use plan.

E. Planning Calendar per JMC

In general, comprehensive development plans are medium-term plans, whichmay cover three to six years, though in general CDPs are known to cover six years tocoincide with the term of the President. However, there are comprehensive plans, whichhave longer time periods (e.g. those prepared using the CDS for cities). The LGUs may

opt to adopt their own time frame, though for consistency, it is best that the time framesof development plans (except for the physical plans) at the national, regional and locallevels should be the same to facilitate vertical integration. There is an opportunity for synchronizing the coverage of plans in 2010, if the government will require the updatingand/or new plans to start in 2010.

In relation to the process of plan preparation, the JMC was precisely formulatedand signed to synchronize the planning budgeting calendars. Specifically for the

preparation of comprehensive plans, the activities should conform to the followingschedule:

Table 11. Proposed Schedule of Planning Activities per JMC

Activity Period Covered Outputs

A. Normal Year

1. Setting guidelines for datagathering by the ProvincialPlanning DevelopmentCommittee (PPDC)

1st week of January Guidelines for data gathering

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 27/71

2. Formulation of developmentvision, goals, strategies,objectives/targets andidentification of PPAs

Whole month of July Vision, goals, strategies,objectives/targets andidentification of PPAs

3. Harmonization andcomplementation of vision, goalsand strategic directions betweenand among provinces andcomponent cities andmunicipalities

July Harmonized vision, goals andstrategic directions

4. Approval of the PPFP andCDP

July Approved PPFP and CDP

II. INVESTMENT PROGRAMMING

Investment programming in the context of the LGU’s planning and development function

involves generating the programs and projects derived from the detailed elaboration of the localland use and development plans. This is expected to modify, guide, direct, control or otherwiseelicit the desired private sector response in order to accelerate local economic development,raise the level of socio-cultural well-being, improve the standard of public services, utilities andinfrastructures, and, on the whole, attain the desired urban form as reflected in the LGU's landuse plan and the general welfare goals in its local development plan.24

A.Required Documents for Local Investment Programming

The main outputs of investment programming are the Local DevelopmentInvestment Program (LDIP) for cities and municipalities and the Provincial DevelopmentInvestment Program (PDIP) for provinces which are the principal instruments for

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 28/71

1.1.PDIP Committee

This committee will be responsible in laying out policies, directions, andthe action plan that will guide the preparation of the PDIP. Working with atechnical secretariat, the PDIP Committee will be responsible for the actualpreparation of the PDIP. This committee may be composed of the followingmembers:

a.Executive Committee of the Provincial Development Council (PDC);

b.Provincial Finance Committee, which can be expanded by constituting a PDIP Finance

Subcommittee. The PDIP Finance Subcommittee should be composed of the PFC plus theChairman of the Committee on Appropriations of the Sangguniang Panlalawigan, the Provincial

Assessor, the Provincial Accountant, and the representative from the banking sector. As part of the PDIP Committee, the group will be responsible for coming up with multi-year revenue andexpenditure forecasts, assessing the development investment financing capacity of theprovince, and developing appropriate financing strategies for consideration by the PDIPCommittee; andc.Other local officials and other members of the PDC who can provide substantive inputs to

PDIP formulation

1.2. PDIP Technical Secretariat

The secretariat shall provide technical and administrative support to theCommittee. It is recommended that the Provincial Planning and DevelopmentOffice staff take on this role.

1.1. PDIP Coordinator

Responsible for coordinating and monitoring the PDIP process on behalf of the committee

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 29/71

(League of Cities)

B. Annual Investment Program

Provinces/Cities/Municipalities

Annual InvestmentProgram One year (annualslice of theLDIP/PDIP

Guidelines onProvincial /LocalPlanning &ExpenditureManagement (ADB/NEDA; 2007)

Enhanced Guide toCDP Preparation (DILG; 2008)

The City

DevelopmentStrategy Toolkit (League of Cities)

C. Basic Steps in Investment Programming

2.Pre- LDIP Activities

1.1 Establish Investment Programming Policies

Investment policies that will guide the whole PDIP process will beestablished by the local investment programming committee. Key issues toresolve include the methods of financing and criteria for prioritization. Thesepolicies must be developed within the overall planning, financial, institutional andlegal framework governing the operations of LGUs.25

. 1. 2 Develop and Define the Prioritization Approach

The LGU's investment programming committee sets out the evaluationprocess and prioritization criteria which in general should be consistent with the

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 30/71

For Land DevelopmentProjects

2. Establishinginvestmentprogramming policies

Investmentprogramming policies

1.Types of Investments2.Types of FiscalRegulatory Devices

●RPS (pp.32-33)●PLPEM Vol3 or CDP

2. Developing theprioritization approach

Tools to be used inprioritization of projects

1.Checklist of PossibleCriteria2.Criteria for Determining Level of Urgency3.Must or Want Criteria

4.Guide Questions for Screnning PPAs &MFOs

●CDS (p.5-5)

●PS (p.176); CDP(p.95)

●CDS (pp.5-6, 5-7)●

PLPEM Vol 4 (p.49)

Suggested approaches and tools are described in detail in Chapter 1 of Volume III.

2. Preparation of the LDIP

2.1 Identification of PPAs (from local development plans)27

This stage consolidates and conducts an initial screening of the list of programs and projects found in the local development plans. This requiressoliciting and compiling project ideas or proposals from plans, sectoralcommittees and other sources, consolidating these by sector, initially screeningfor repetitive or redundant proposals and removing these from the list, as well asfor conflict, compatibility or complementarity of projects, prioritizing programs and

projects according to level of urgency and preparing project briefs.28

Projectstaken from other sources should at least be consistent with plan objectives. 29

2.2 Produce a Ranked List of Programs and Projects30

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 31/71

2.4 Iteratively Develop the LDIP/PDIP Financing Plan and Finalize theInvestment Schedule32

The annual investment requirement estimated in Stage 2.4 is matchedwith the initial annual investment capacity (funding capability) estimated in Stage2.5. The matching process is an iterative or repetitive process. Each iterationinvolves adjustments in the investment requirement side or in the fundingcapability side or in both. If the initial funding capability estimated in Step 2.5fails to match the total investment requirements generated in Step 4, theLDIP/PDIP Committee will have to (a) re-examine the project list generated inStep 4 to consider scaling down, phasing, or deferring projects, with the objective

of reducing project cost for the appropriate year(s) in which the deficit(s) occur;and/or (b) relax the investment budget constraint by raising additional localrevenues, borrowing capital funds and/or re-allocating funds from the operatingbudget to the investment budget.33 A second round of matching then takes place,and the iterative process goes on until total annual funding requirements matchtotal annual funding capacity. On reaching such a balance, the LDIP/PDIPfinancing plan and investment schedule is finalized and inputted to the draftLDIP/PDIP.34

In financial planning for the LDIP/PDIP, the local invesstmentprogramming committee will investigate the financing options and the fiscalfeasibility of funding the various project requests considering the following: (a)alternative funding sources, (b) revenue mobilization, (c) the process of formulating the financing plan, (d) resource mobilization tools, and (e) creditfinancing.

Table 14. Suggested Approaches and Tools in the Initial Identificationand Screening of Projects

Activities Outputs Suggested Approaches/ Reference Manuals

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 32/71

2. Screening of Projects First level evaluation of projects found in thedevelopment plan andadditional or newprojects

1. Assessment Matrix of Project Sustainability(AMPS).2. Conflict-Compatibility-Complementarity

Assessment3. Checklist of ProjectJustification Information4. Initial Project Screening

●CLUP (pp.178-179)

●RPS (pp.175, 188);CDP (pp.93-94)

●PLPEM Vol 3(pp.38, 42)●RPS (pp.174-175);CDP (p.93)

3. Initial prioritization of projects

Prioritized list of projectsfrom step 2 above

presented in appropriateforms (e.g. project briefs)

Formalization Process

•Documentation of ProjectProposals (LDIP/PDIPProject Proposal Form,Equipment Request Form,Project Brief, Random List of projects

●PLPEM Vol 3(pp.37-38)

●PLPEM Vol 3(pp.37-41), RPS(pp.143, 174, 187);CDP (pp. 95-96);CLUP (p.180)

4. Review of ProjectProposals

Preliminary list of projects screened on thebasis of technical and

socio-political criteria

•Checklist of Project

Justification Information

•Review Checklist for

Project Proposals

●PLPEM Vol 3,pp.38, 42)●PLPEM Vol 3.

p. 42

Suggested approaches and tools are described in detail in Chapter 2 of VolumeIII.

Table 15. Suggested Approaches and Tools in Ranking Programs, Projects and Activities

Activities Outputs Suggested

Approaches/ Tools

Reference Manuals

Ranking of Projects Ranked PPAs with costestimates

• Analytic Hierarchy

Process

•Decision Analysis

●PLPEM Vol 3 (pp.34-35)

●CDS (pp 5 5 to 5 7)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 33/71

draft LDIP/PDIP for review and endorsement to the local Sanggunian; the Sangguniandeliberates and then legally adopts the LDIP/PDIP. The current-year slice of the

LDIP/PDIP or the Annual Investment Program (AIP) is then submitted for considerationin the annual Executive Budget/Provincial Budget. The local investment programmingcommittee shall endorse the AIP to the local budget officer for the budget preparationand for determining the annual budgetary allocations for PPAs vis-à-vis allocations for other purposes.

The adoption of the LDIP/PDIP by the local Sanggunian is not a bindingcommitment to fund programs beyond the first year, hence, the succeeding years’ slices

will be subjected to review and updating during the annual pre-budget period.

Table 16. Suggested Approaches and Tools in Conducting the FinancialAnalysis of Projects

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Undertake Financial Analysis

•Revenue and

expenditure projections,

•Financial analyses of

projects,

•Financial and

economic studies of projects (optional)

•Project proposals

1. Financial Capacity Analysis2. Financial PlanningModel3. Revenue MobilizationConsiderations3.1. BenchmarkingIndicators3.2 RevenueMobilization Tools3.3 Conditions for

Subsidy Provision4. Scoring Method for Determining Subsidy

●CDS and RPS35

●PLPEM Vol 3 (pp.92-94)

●PLPEM Vol 3 (p.96)

●PLPEM Vol 3 (pp.108-114)

●PLPEM Vol 3 (p.98)

●PLPEM Vol 3 (p.99)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 34/71

Selecting the FinancingInstrument

2. Preparation of theLDIP documents

- Final list of PPAs-LDIP/PDIP FinancingPlan-Investment Schedule

1. Summary Tables (w/formats)

A. Investment ProgramProject SummaryB. Investment BudgetSummaryC. Revenue SummaryD. AIP Summary.2. PED Guidelines

●PLPEM Vol 3 (pp.60-62)

●PLPEM Vol 5 on

Project Evaluation andDevelopment (PED)

Suggested approaches and tools are described in detail in Chapter 5 of VolumeIII.

4. LDIP Implementation

4.1 Identification of Areas for Complementation of PPAs and Updating theInvestment Plan

After legally adopting the PDIP and in accordance with investmentprogramming guidelines, areas for complementation of PPAs between theprovince and its component cities and municipalities should be identified to comeup with PPAs that can be jointly implemented by the province and its componentLGUs.

The LDIP/PDIP is updated annually to reflect changing field and financingconditions, and to include new project requests arising fromchanges/adjustments in the local development plans. Each year the LGU shouldreview revise and extend the LDIP/PDIP for another year so that it always

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 35/71

D. Suggested Format of Local Investment Plans

The information requirements for programs, projects and activities to bepresented in the AIP shall be placed in the prescribed AIP Summary Form withthe following categories37: AIP Reference Code, Program/Project/ActivityDescription, Implementing Agency/Office, Schedule of Implementation, ExpectedOutput, Source of Fund and Estimated Cost.

E. Calendar of Activities on Investment Programming

Table 18: Proposed Schedule of Activities Related to InvestmentProgramming per JMC

Activity Period Covered Outputs

A. Election Year: LDIPPreparation

1. Identification of areas for complementation of PPAsbetween and among provincesand their component cities andmunicipalities

June to July 1-31 Joint programs and projects

2. Prioritization of PPAs June to July 1-31 Prioritized PPAs

3. Matching of PPAs withavailable financing resources

and determination of additionalrevenue sources to finance thePPAs

LDIP, revenue generationmeasures

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 36/71

knowledge of the LGU's fiscal health, present and prospective financial profile and capacity tomobilize resources would provide policy-makers with information on level of the LGUs’ resource

envelope and the extent of intervention it needs to undertake to expand the resource pie andthereby fund its prioritized PPAs.

A. Required Outputs and Documents

The Local Finance Committee (LFC) is charged under the 1991 LGC with thesetting of the “level of the annual expenditures and the ceilings of spending for economic, social, and general services based on the approved local development plans”(Section. 316, c). As such, they should undertake the required financial plan

development in close coordination with the Local Development Council (LDC) for consideration and approval of the Sanggunian. But financial planning starts withresource mobilization, which is a basic information for budgeting. Hence, the overisgtagencies have taken the initiative to update/prepare manuals to assist the LGUs in beingto tap its authority under the LGC to raise revenues.

Table 19 summarizes the basic outputs which the LGUs are required to prepareas part of its financial planning and management responsibilities.

Table 19. Major Outputs Related to Revenue Administration and Resource Mobilization

Major Outputs for all LGULevels

Time Period Covered Guide

Resource MobilizationStrategies

Multi-year Revised Revenue MobilizationCoursebook (RRMC) Draft Manual,Volume 1 (Modules I-IV) and Volume2 (Modules V-XI)

Revenue Forecast At least one fiscal year; canbe multi-year

RRMC Draft Manual, Volume 1(Modules I-IV) and Volume 2(Modules V-XI), PLPEM Volume 4:Tools and Techniques on Budgeting

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 37/71

private sector representative (preferably an investment banker), and a representative fromcivil society. 38

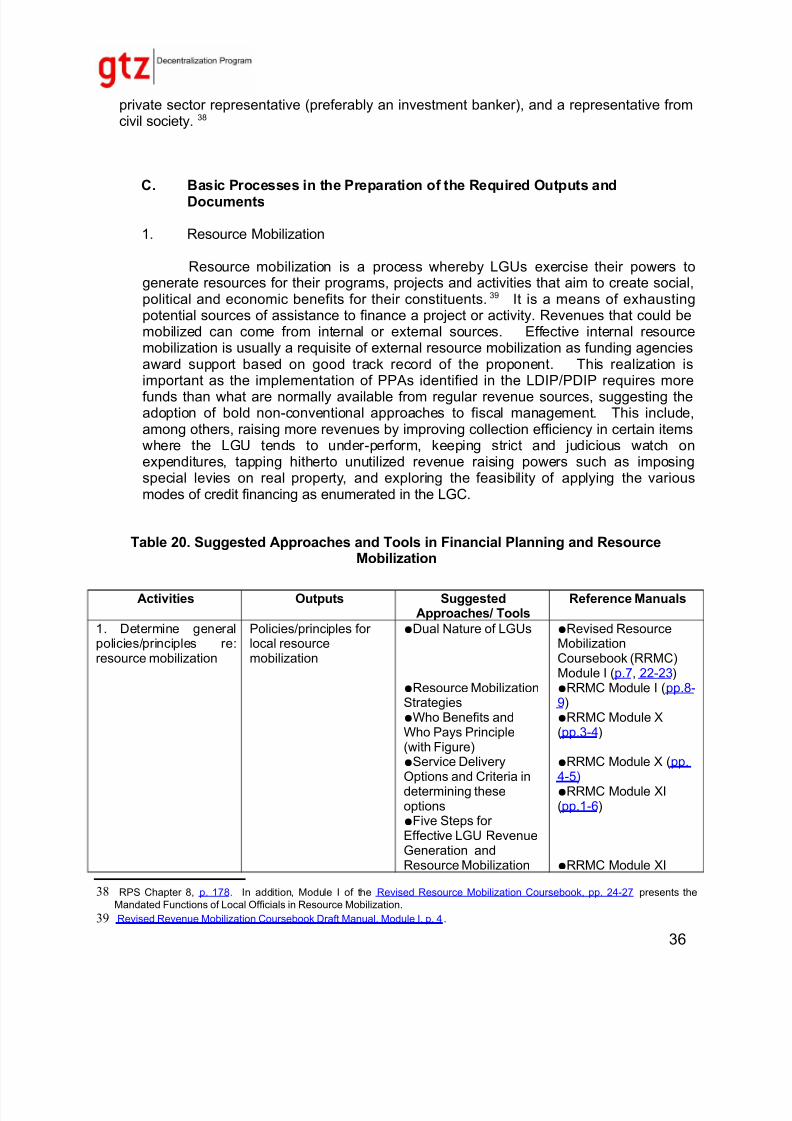

C. Basic Processes in the Preparation of the Required Outputs andDocuments

1. Resource Mobilization

Resource mobilization is a process whereby LGUs exercise their powers to

generate resources for their programs, projects and activities that aim to create social,political and economic benefits for their constituents.39 It is a means of exhaustingpotential sources of assistance to finance a project or activity. Revenues that could bemobilized can come from internal or external sources. Effective internal resourcemobilization is usually a requisite of external resource mobilization as funding agenciesaward support based on good track record of the proponent. This realization isimportant as the implementation of PPAs identified in the LDIP/PDIP requires morefunds than what are normally available from regular revenue sources, suggesting the

adoption of bold non-conventional approaches to fiscal management. This include,among others, raising more revenues by improving collection efficiency in certain itemswhere the LGU tends to under-perform, keeping strict and judicious watch onexpenditures, tapping hitherto unutilized revenue raising powers such as imposingspecial levies on real property, and exploring the feasibility of applying the variousmodes of credit financing as enumerated in the LGC.

Table 20. Suggested Approaches and Tools in Financial Planning and Resource

Mobilization

Activities Outputs SuggestedA h / T l

Reference Manuals

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 38/71

Strategy

●Strategic Plan toManage the Fiscal Gap●Distinct Classes of Potential RevenueSources●LGU ResourceStructure●Key Features of theLocal Tax Structure●Criteria of a Good

Revenue Structure●FundamentalPrinciples in LocalTaxation●Central Grants

●LGU Impositions

(pp.6-7)●JMC (p.83)40

●RRMC Module I (p.28)

●RRMC Module II(pp.17-19)●RRMC Module II(pp.5-7)●RRMC Module II(pp.8-9)●RRMC Module I(pp.13-20)

●RRMC Module II(pp.2-3)

2. Raising revenues by

type of taxReal Property Tax Real property taxadministration tools,assessment andcollection strategies, taxmaps

•Classification of Real

Property•Stages in Real

Property Tax Administration

• Approaches to

Determine PropertyValues

•Types of Real Property

Impositions

•Exemptions fromPaying of RPT/Land-Based Taxes

•Other Features of RPT

●RRMC Mod III (p.5)

●RRMC Mod III (p.7)

●RRMC Mod III (pp.32-33)

●RRMC Mod III (pp.8-9)

●RRMC Mod III (pp.19-

20)

●RRMC Mod III (pp.19-21)

RRMC M d III ( 21)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 39/71

and Other relatedTaxes

measures for businessand other related taxes

Impositions:Business-RelatedTaxes

•Revenue

Enhancement Measuresfor Business-RelatedTaxes2. Other Local Taxes inProvinces and Cities

•Revenue

Enhancement Measuresfor Professional Taxes

3. Business Taxes: Cityand MunicipalImpositions

•Business Tax

Computation

•Surcharge and

Penalties4. Rate Structure

5. Rate Structure for New Business

•Revenue

Enhancement Measuresfor Business Taxes6. Other Local Taxes for Cities and Municipalities●RevenueEnhancement Measures

for Community Taxes7. Other Local Tax AllLGUs May Impose8. Computation of Sales

●RRMC Mod IV (pp.2-6)

●RRMC Mod IV (pp.24-26)●RRMC Mod IV (p.26)

●RRMC Mod IV (pp.7-8)

●RRMC Mod IV (p.9)

●RRMC Mod IV (p.9)

●RRMC Mod IV (pp.12-15)

●RRMC Mod IV (p.15)

●RRMC Mod IV (pp.20-24)

●RRMC Mod IV (pp.26-28)●RRMC Mod IV (pp.28-29)

●RRMC Mod IV (p.29)

●RRMC Mod IV (pp.29-)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 40/71

Charges●Setting Rates for Charges3.Charges/Receiptsfrom Local EconomicEnterprises (LEEs)●RevenueEnhancement Measuresfor Fees and Chargesfrom LEEs

12)●RRMC Mod V (pp.11-12)●RRMC Mod VI (pp.1-3)

●RRMC Mod VI (pp. 9-12, 14-15)

3. Other Financing

OptionsCredit Financing

Credit finance program;

financing options andpayment schemes

1.Financing Schemes

•Factors to

Consider inWeighing Short-Term Over Term-Financing

•Payment Schemes

•Limitations on LGU

Debt Servicing

2.LGU Credit FinancingOptions

•Ensuring

Contractor Compliance

3.Credit FinanceProgram4.Role of GovernmentFinancial Institutions

(GFIs)5.Role of the MunicipalDevelopment Fund(MDF)

●RRMC Mod VIII (pp.4-

5)●RRMC Mod VIII (pp.5-6)

●RRMC Mod VIII (p.6)●RRMC Mod VIII (pp.6-7)●

RRMC Mod VIII (pp.7-32)●RRMC Mod VIII (p.32)

●RRMC Mod VIII(pp.35-36)●RRMC Mod VIII (p.37)

●RRMC Mod VIII (p.37)

●RRMC Mod VIII

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 41/71

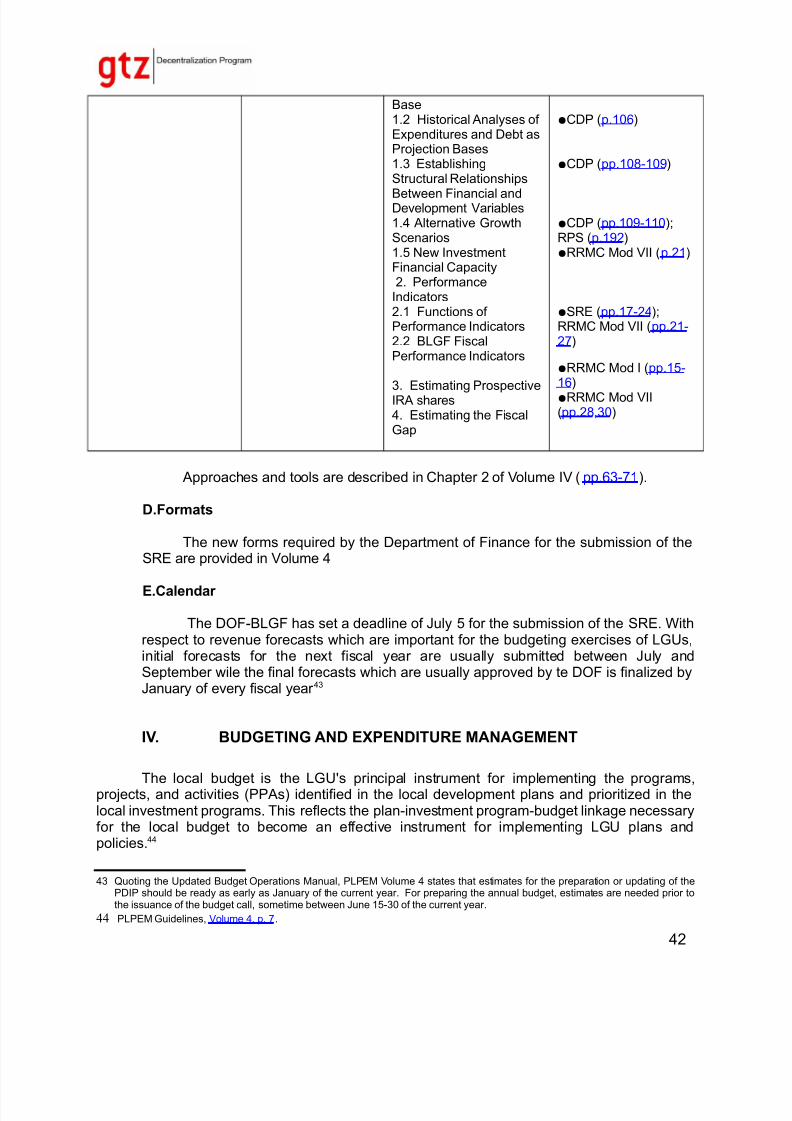

Suggested approaches and tools are described in Chapter 1 of Volume IV.

2. Preparation of the Statement of Receipt and Expenditure (SRE)

Aside from resource mobilization and revenue generation efforts, the LGUsshould have realistic and real-time revenue/income data to ensure delivery of qualityservice. This can be achieved through the use of the Statement of Receipt andExpenditures (SRE) System that can generate real-time accurate data and analysis thatLGUs can use in planning, budgeting and decision-making.41

The SRE presents the income and expenditures for the General Fund, the

Special Education Fund and the sum of both funds. The data presented in the SRE aresub-totals of the major caption of various account classifications from its main sourcedocuments, namely: (a) Statement of Receipt Sources; and the (b) Statement of Expenditures. The SRE is divided into three major segments: (a) current operatingsegment; (b) non-operating receipts and expenditures and (c) fund balance segments.

Table 21. Suggested Approaches and Tools in Preparing the Statement of Receipt andExpenditures

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

Build a revenue /incomedatabase or theStatement of Receiptand Expenditure (SRE)System

Statement of Receiptand ExpendituresSystem, SRE Reports

●SRE System and SREReports● Accounting policiesused in SREpreparation

●SRE Framework●Deadline for Submission of Reportsand Copy Distribution

●SRE (pp.6, 8, 10-15)

●SRE (p.4)

●SRE(pp. 10-11, 38)●SRE (pp.6-7)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 42/71

tools, the LGUs can perform forecasting exercises and evaluate their ownrevenue targets. Adjustments can be made by the Local Treasurer based on his

expert opinion considering the LGU's performance record, and appreciation of extraordinary circumstances. These forecasts at the LGU level will again besubjected to further 'negotiations' with the Regional Offices of the DOF-BLGF.The regional 'negotiated' annual revenue forecast will then be reconciled with therevenue targets by the BLGF Central Office using the BLGF Model. This processaims to reconcile the central office's “top-to-bottom”, with the local Treasurer's“bottom-up”, forecasting perspective.42

3.2 Estimating the Fiscal Gap

Local Governments constantly have to face the dilemma of never havingenough to finance the financial requirements for delivering basic services andfacilities and pursuing their developmental goals. One step towards the solutionof this dilemma is to be able to estimate the fiscal gap as an aid in identifying theappropriate financing option available to the LGUs.

Table 22. Suggested Approaches and Tools in Revenue Forecasting

Activities Outputs Suggested Approaches/Tools

Reference Manuals

1. Forecast Revenues Revenue forecasts 1. General Tools1.1 Average AnnualGrowth Rate Method1.2 Linear RegressionTechnique (in general andby hand)

1.3 Use of current andconstant values

1.4 Standardizing data

●RRMC Mod VII (p.13)

●RRMC Mod VII (pp.13-14, 17-19)

●RRMC Mod VII (p.3)

●RRMC Mod VII (pp.4,

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 43/71

Base1.2 Historical Analyses of Expenditures and Debt as

Projection Bases1.3 EstablishingStructural RelationshipsBetween Financial andDevelopment Variables1.4 Alternative GrowthScenarios1.5 New InvestmentFinancial Capacity

2. PerformanceIndicators2.1 Functions of Performance Indicators2.2 BLGF FiscalPerformance Indicators

3. Estimating ProspectiveIRA shares

4. Estimating the FiscalGap

●CDP (p.106)

●CDP (pp.108-109)

●CDP (pp.109-110);RPS (p.192)●RRMC Mod VII (p.21)

●SRE (pp.17-24);RRMC Mod VII (pp.21-27)

●RRMC Mod I (pp.15-16)●RRMC Mod VII(pp.28,30)

Approaches and tools are described in Chapter 2 of Volume IV (pp.63-71).

D.Formats

The new forms required by the Department of Finance for the submission of the

SRE are provided in Volume 4

E.Calendar

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 44/71

The budget process in LGUs consists of five phases that form part of a continuingprocess or cycle: budget preparation, authorization, review, execution and accountability. Thisprocess is reinforced by the adoption of the principles of Public Expenditure Management(PEM) Framework of fiscal discipline, allocative efficiency and operational efficiency. The PEMfosters the plan-budget connection in three ways: installing a multi-year perspective inbudgeting, adopting a top-down approach, and promoting a greater performance-orientation inthe budget process.45

A. Required Outputs and Guides

Major Outputs for all LGU Levels Time Period Covered Guide

Annual or Supplemental Budget, BudgetMessage, Local Expenditure Program(LEP), Budget of Expenditures &Sources of Financing (BESF), LocalBudget Matrix (LBM), Local BudgetPreparation Forms, Local Budget

Authorization Forms, Local BudgetReview Forms, Local Budget ExecutionForms, LGU Performance ReviewReport (LPRR)

One fiscal year Revised Budget OperationsManual, PLPEM Volume 4

B. Suggested Institutional Structure for the Preparation of the RequiredOutputs and Documents in Budgeting and Expenditure Management

1. Key Players in the Budget Process

R.A. No. 7160 or the Local Government Code of 1991 outlines themandates of the responsible officials and committees in each of the five phases

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 45/71

(b) Local BudgetOfficer

Local BudgetOfficer

Local BudgetOfficer

(c) Local

Accountant

Local Accountant Local Accountant

(d) LocalPlanning andDevelopmentCoordinator

Local FinanceCommittee

Provincial FinanceCommittee

Local Planningand DevelopmentCoordinator

Local Planning andDevelopmentCoordinator

Heads of Department or Offices

Heads of Department or Offices

Department of Budget andManagementRegional Offices

Department Head Heads of Department or Offices

2. Organizational Activities

The Revised Budget Operations Manual introduces the user to thegeneral guidelines and concepts of good governance as advocated by the UnitedNations Development Program (UNDP). LGUs shall allow and practice genuineparticipation of people in the planning and budgeting processes to promote and

establish transparency and accountability in all their fiscal transactions. LGUsare encouraged to enhance participative planning and budgeting in differentvenues: through formal institutions, digital governance and workshops. LGUsshall establish priorities and allocate resources during investment programmingof PPAs as major links to budgeting. The ranked PPAs and their correspondingresource requirements become the basis for preparing budget proposals on anannual basis. A key consideration at the start of the budget process should thenbe the integration of projects and activities embodied in the AIP into the ExecutiveBudget.46

C. Process

Phase 1: Budget Preparation

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 46/71

Table 24. Suggested Approaches and Tools in Budget Preparation

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Issue the budget call Budget Call ●Budget Forum ●RBOM (p.55)

2. Prepare and submitbudget proposals.

Budget proposalsshowing target outputsand estimated costs for the budget year, Project

ProcurementManagement Plan

● Analyzing LGUIncome Trend andComposition● Analyzing LGU

Expenditure Trend andComposition●Formulating Multi-Year Revenue Estimates●Setting ExpenditureCeilings● Approaches for Costing Regular

Activities●Defining PerformanceIndicators Using theOPIF●Guide Questions for Evaluating Targets for the Budget Year

●PLPEM Vol 4 (pp.25-27)

●PLPEM Vol 4 (pp.32-

37)

●PLPEM Vol 4 (pp.38-46)●PLPEM Vol 4 (pp.56-60)●RBOM (pp.105-109)

●PLPEM Vol 4 (pp.47 -55)

●RBOM (pp.104-105)

3 Conduct of technicalbudget and evaluationof budget proposals

Technical budgethearings, evaluatedbudget proposals

●Guide Questions for Evaluating Targets for the Budget Year

●RBOM (pp.104-105)

4. Prepare the

Executive Budget

Executive Budget

consisting of the budgetmessage, the LEP andthe BESF49, LocalBudget Preparation

●Guidelines on

Preparing the LocalExpenditure Program●Guidelines onPreparing the Budget

●RBOM (pp.57-60)

●RBOM (pp.61-63)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 47/71

pertain to the expenditure ceiling by office/sector, allocation scheme by major final output(MFO) and PPA, budget calendar and budget preparation forms, and other administrative guidelines.

1.2 Prepare and submit budget proposals to the LBO

The heads of departments and offices in the LGU submit to the LBO their proposals for inclusion in the executive budget. In making their proposals, they will needto consider two factors: (a) the specific objectives or target outputs for the budget year which should consider the MFOs and performance indicators for all PPAs of a particular

department/office; and (b) estimates of current operating and capital outlay costs whichshould be within budgetary ceilings.

Guided by the expected results and cost estimates in the approved AIP, a ProjectProcurement Management Plan (PPMP) is also prepared simultaneously with the budgetproposal. The PPMP provides details on the mode and schedule of procurement,technical description and specifications of the goods, equipment and civil works to beprocured and their proposed budgets.

1.3 Conduct budget hearings and evaluate budget proposals

The purpose of technical budget hearings is to rationalize the existence of theoffice/department and to validate the target output and cost estimates for the budgetyear. This should be conducted for at least 10 working days (August 15 to 25). Inaddition, members of the LFC shall evaluate all budget proposals to check whether outputs can be attained or accomplished with the funds allocated for the purpose.

1.4 Prepare the Executive Budget

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 48/71

sources of financing the expenditure program for the budget year are also disclosed toshow how the past, current, and proposed budget are financed by the LGU.

1.5 Submit Executive Budget to the Sanggunian

On or before October 16 of the current year, the LCE must submit the executivebudget to the Local Sanggunian (as failure would subject him to sanctions).

To expedite the approval of the budget, the LCE may certify that the proposedmeasure is urgent. In response, the Sanggunian shall consider the budget as a prioritymeasure.

Three budget documents are prepared for the annual budget. However, whenthe LCE submits a supplemental budget to the Sanggunian for legislative approval, theLEP and BESF may not be required; instead the funding source must be identified –additional realized income, or new revenue measure, or, in times of calamity,realignment of appropriation.

Phase 2: Budget Authorization50

Budget authorization starts from the time the LCE presents the proposedexecutive budget to the local Sanggunian for its review and ends with the enactment of the Appropriation Ordinance and approval thereof by the LCE. The legislative debateand deliberation on the proposed executive budget essentially focus on: (1) itsconsistency with the LGU's goals and objectives as articulated in its development plan;and (2) its conformity with the budgetary provisions of the Local Government Code.

Table 25. Suggested Approaches and Tools in Budget Authorization

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 49/71

(LBAF) No.1A andNo.1B (Forms)

2. Deliberate on the

budget

Budget hearings,

budget deliberations,budget review matricesfor budgetaryrequirements andlimitations

●Guide Questions for

Deliberations

●RBOM (pp.119-120)

3. Authorize the annualbudget

AppropriationOrdinance,Supplemental

Appropriations51 or Re-

enacted budget if LocalSanggunian fails toauthorize the proposedbudget

- -

4. Approve the Appropriation Ordinance

Approved AppropriationOrdinance52 for CurrentOperating Expendituresand Capital Outlays

- -

Suggested approaches and tools are described in detail in Chapter 2 of VolumeV (pp.40-47)

2.1 Check and evaluate the budget documents submitted

As one of the standing committees created within the local Sanggunian, theCommittee of Appropriations is responsible for the preliminary review and evaluation of the executive budget and for the conduct of its own budget hearings. The Committeethen renders its report and recommendation to the Sanggunian proper.53 TheSanggunian, with the assistance of the LFC, may refer to the BESF to facilitate theevaluation of, and deliberation on the executive budget in terms of compliance with thebudgetary requirements and general limitations. Both the Revenue and Expenditure

54

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 50/71

2.3 Authorize the Annual Budget

On or before the end of the current year, that is, before the beginning of the fiscalyear and after the budget deliberation, the Sanggunian authorizes the annual budgetthrough an Appropriation Ordinance.

If the Sanggunian fails to enact the Appropriation Ordinance after 90 days fromthe beginning of the fiscal year, the Appropriation Ordinance of the preceding year shallbe deemed reenacted and shall remain in force until a new ordinance is passed. Noordinance authorizing supplemental appropriations can be passed in place of annual

appropriations.56

2.4 Approve the Appropriation Ordinance

The Appropriation Ordinance enacted by the Sanggunian shall be presented tothe LCE who must sign if he approves of it. Otherwise, he will veto the ordinance (totallyor partially) and, with his objections in writing, return it to the Sanggunian within 15 daysin the case of a province and 10 days in the case of a city/municipality. The Sanggunianmay override the veto by a two-thirds vote. The Ordinance revoked by the Sanggunian,shall no longer be presented to the LCE for reconsideration and hence becomeseffective without any need for approval of the LCE.

An approved Appropriation Ordinance takes effect on January 1, the beginning of the ensuing fiscal year. Changes in the annual budget may be authorized by way of supplemental budgets through an enactment of the Sanggunian.57

Phase 3: Budget Review

The budget review phase is unique for the budgets of LGUs. 58 Its primarypurpose is to determine whether the ordinance has complied with the budgetary

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 51/71

Table 26. Suggested Approaches and Tools in Budget Review

Activities Outputs SuggestedApproaches/ Tools

Reference Manuals

1. Check the Appropriation Ordinanceand supportingdocuments

Checked budgetdocuments(AppropriationOrdinance andsupporting documents)

●Checklists onDocumentary andSignature Requirements

●RBOM (p.149)

2. Review the Appropriation Ordinance

Reviewed AppropriationOrdinance

●Checklist of Compliance with

BudgetaryRequirements●Checklist of Compliance withGeneral Limitations

●PLPEM Vol 4 (pp.66-67)

●PLPEM Vol 4 (pp.67-68)

3. Issue the reviewaction

Review action in theform of a letter from theDBM RO or aSanggunian resolution59, stamp of review

•Table Recapitulatingthe Findings andPossible Action (LocalBudget Review FormNo. 2)

•RBOM (p.160)

Suggested approaches and tools are described in detail in Chapter 3 of VolumeV (pp. 44-47)

3.1 Check the Appropriation Ordinance and the Supporting Documents

Using LBR Forms No. 1A and No. 1B, the DBM RO or SangguniangPanlalawigan shall check if the required budget documents with the required signatures

have been submitted together with the Appropriation Ordinance. If found lacking, said Appropriation Ordinance shall not be reviewed and shall be officially returned by thesereviewing authorities to the LGU concerned through the Secretary to the Sanggunian inwriting requiring the resubmission of the same with the necessary supporting

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 52/71

passes the Appropriation Ordinance. Failure of the reviewing agency or body to takeaction within the reglementary period of review shall have same effect as if the

Appropriation Ordinance has been reviewed.

Phase 4: Budget Execution

This involves the release and actual disbursement of funds appropriated andalloted for specific functions and activities in the Appropriations Ordinance. A critical

aspect of this phase is the collection of funds, such that disbursements do not exceedappropriations. While seemingly a separate activity, the collection and/or receipt of revenues are considered an integral part of budget execution.

Table 27. Suggested Approaches and Tools in Budget Execution

Activities Outputs Suggested

Approaches/ Tools

Reference Manuals

1. Release allotments Authorization to incur obligations using LocalBudget Execution (LBE)Form No. 1-LocalBudget Matrix (LBM);and LBE Form No. 2-

Allotment ReleaseOrder (ARO)

•Local Budget Matrix(LBM) (Form)

• Allotment ReleaseOrder (ARO) (Form)

•PLPEM Vol 4 (71-72,106); RBOM (pp.177-179, 187)•RBOM (p.188)

2. Prepare the cashprogram andfinancial/physicalperformance targets

Cash Program,Statement of Cash FlowForecast (SCFF), LBEForm 3-Summary of Fi i l d Ph i l

•Cash Flow Forecasting(CFF)

•Statement of CashFl F t (SCFF)

•PLPEM Vol 4 (pp.72-73); RBOM (p.180)

•RBOM (p.180)

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 53/71

expenditures per responsibility center: Registry of Appropriations, Allotments andObligations Capital Outlays (RAAOCO); Registry of Appropriations, Allotments andObligations Maintenance & Other Operating Expenses (RAAOMO); Registry of

Appropriations, Allotments and Obligations Personal Services (RAAOPS); and Registryof Appropriations, Allotment and Obligations Financial Expenses (RAAOFE).

The system of recording in the registries shall follow the New Government Accounting System (NGAS) prescribed by the Commission on Audit.

4.2 Release the allotments

The LCE issues the authorization to incur obligations through the allotmentsystem using the Local Budget Matrix (LBM) and the Allotment Release Order (ARO) asrelease documents. Under this system, obligations may be incurred as long as they arewithin the allotment ceiling and need not be supported by cash in the meantime.

The LBM is the yearly overall financial plan of the LGU. It is equivalent to theapproved Appropriations Ordinance disaggregated into components or categories. Thisis issued to each department/office to serve as a comprehensive authority to disburse.The LBM also provides a device for the imposition of reserves, non-release of unprogrammed items, earmarking of funds for later release, some of which needclearance.

4.3 Pr epare the Cash Program and Financial/Physical Performance Targets

In addition to the LBM and ARO, the allotment system uses Cash Programs and

Cash Flow and the Financial and Physical Performance Targets as control tools in theobligation and disbursement of funds.

Cash flow planning and programming entail forecasting and tabulating the cash

7/28/2019 Vo1 Integrated Compedium

http://slidepdf.com/reader/full/vo1-integrated-compedium 54/71

The Summary Financial and Physical Performance Targets (SFPPT) reflects thebudget allocation for the budget year and the targeted performance indicators under each major final output (MFO) and PPA. These targets are based on historical data of actual output of regular activities considering their average growth and the peculiar requirements of certain PPAs. The targets are prepared for the entire calendar year for each department to serve as basis in comparing actual level of accomplishment for thepreceding year and knowing the available resources for the budget year. This shall besupported with a Detailed Financial and Physical Performance Targets (DFPPT) whichpresents the quarterly breakdown of the Financial Allocation that would be needed toaccomplish a specific level of target for each PPA for a particular quarter. Inaccomplishing the SFPPT and DFPPT, Department/Office Heads with the assistance of

their staff, should focus on the core functions of their department/office and on thedelivery of high impact activities at reasonable costs and qualities.

4.4 Obligate and disburse funds for the implementation of Programs/Project/Activities