Embed Size (px)

Citation preview

MessageMessage

` 20/- COPY

MANAGING COMMITTEE

VOLUME - V JULY 2015l

Baroda Branch of Western India Regional Council ofThe Institute of Chartered Accountants of India

The Institute of Chartered Accountants of India(Setup by an Act of Parliament)

INDEX

CA. Yash N Bhatt 99243 88339

CA. Viral K Shah 98243 62211

CA. Arpan Dodia 98983 83530

CA. Dhiren Parikh 93762 11099

CA. Abhishek Nagori 94260 75397

CA. Nayan Kothari 98244 33445

CA. Kejal Pandya 98259 77220

CA. Utpal Shah 98250 28960

CA. Hitesh Agrawal 99980 28737

Chairman

Vice-Chairman

Secretary

Treasurer

Ex-officio

Immediate Past Chairman

Committee Member &Study Circle Convener

Committee Member

Committee Member

EDITORIAL TEAM

CA. Yash Bhatt

CA. Hitesh Agrawal

CA. Jay Shah

CA. Sanjay Joshi

Forthcoming Events ... 02

Direct Tax Updates ... 02

Judicial Decisions on Excise andService Tax ... 03

3D ... 04

Indirect Tax Updates ... 06

FAQs on IFRS transactions ... 06

ICAI CORNER ... 07

Recent Changes in Withholding Taxes ... 09

Due Date Planner ... 10

PhotoFlash ... 11

THE INSTITUTE OF CHARTEREDACCOUNTANTS OF INDIA

Tel. :E-mail :

Web :

ICAI Bhawan, Post Box No. 7100,Indraprastha Marg, New Delhi - 110002.

+91 (11) [email protected]

www.icai.org

“ICAI Bhawan”, Kalali-Tandalja Road, Atladra,Vadodara - 390 012. +91 8511077115

+91 8511125959+91 (265) 2681115 / 2680593

BARODA BRANCH OF WIRC OF ICAI

M.:Chairman Mobile:

Telefax :E-mail:

Web :

WESTERN INDIA REGIONAL COUNCIL

Tel. :Email :

Web :

ICAI Tower, Plot no C-40, G BlockOpp MCA Ground, Bandra Kurla Complex,

Bandra (E), Mumbai - 400 051+022-33671400/33671500

The monsoons have just brought relief from the scorching summer this year. However,

our members have just started warming up to the tax and audit season and by the time

this newsletter will be circulated; members will be immersed in filling of returns for

income of non-audit cases.

The month of June 2015 saw some very well appreciated programs including the

Conference for members in industry, which had luminaries such as CA. Sujal Shah, CA.

Sanjeev Shah, CA. N. P. Sarda, CA.Nikhil Gupta, CA. Vijay Maniar, CS. Keyoor Bakshi to

name a few.... addressing the audience on very important topics. The program also saw a

very unique session of panel discussion on compliances – changes & challenges, which

was greatly appreciated by the members for its fresh and unique format. In June 2015

Baroda Branch had organized Felicitation of Team WIRC & Half day seminar on ICDS.

On July 1, we will be celebrating the 67th CA day. It is indeed a very proud moment for all

members. For the first time we are arranging free medical check up for CAs above 50 years

along with spouse at ICAI Bhawan headed by renowned Hospitals of the city followed by

cultural evening.

The month of July 2015 will see Baroda Branch of WIRC of ICAI with long awaited National

Convention for CA students. The preparation for the same is on in full swing with an army

of members and students working day and night to ensure its success. I urge all the

members to encourage their articles to volunteer in the preparations of the National

Convention and attend the same and I am sure that students will benefit from the same.

Chairman

CA. Yash N. Bhatt

Baroda Branch of WIRC of ICAI

2The best way out is always through

Forthcoming EventsBRANCH EVENTS

CPE 3RELOOK AT AUDIT UNDER AMENDED COMPANIES ACT, 2013

FORTHCOMING COURSES

Day & Date :

Topic :

Faculty :

Organised by :

FEES :

Thursday, July 30, 2015

Timings :

Venue :

3:00 pm to 6:00 pm

Relook at audit under amended Companies Act,2013

CA. Himanshu Kishnadwala, Mumbai

Auditorium, ICAI Bhawan

Baroda Branch of WIRC of ICAI and Baroda CPEStudy Circle

Nil for Study Circle members300/- upto 25th July 2015 / 400/-

thereafter for other members

`

` `

ISA Professional Training batch

Starting :

Fees :

Certificate Course on Indirect Taxes

Starting :

Fees :

Tentatively from 1st August, 2015

(14 days, weekend basis, Saturday-Sunday)

17500/-

Tentatively from 25th July, 2015

(12 days, weekend basis, Saturday-Sunday)

15000/-

`

`

Direct Tax UpdatesWritten by CA. Narendra Hindocha

1. Income Tax Returns

ITR 1

SimilarITR 4S

new Form

ITR 2A

only Passport Number,

(expatriate),

2. Repair of an asset before putting it to use

3. Credit under section 115JAA

In view of representations, it was announced that theIncome-tax return forms earlier notified would be reviewed.The changes after the review are briefly as under:

- Earlier, simplified Form was not available toIndividuals having

- benefit also available to individuals and HUFsavailing simplified Form applicable to businessincome assessable on presumptive basis.

- To make available a simple form for assessees having

but not capital gains,can be used if they do not have income from

business/profession or foreign asset/foreign income orcontrol upon them and do not claim double taxationavoidance regulations.

- areintroduced in Form ITR 2 and the New Form ITR 2A so as toreduce the size of the form.

- In lieu of foreign travel details, ifavailable, required to be given in Forms ITR-2 and ITR-2A.

- Only the IFS code and

Details accountsdormant for three years are not required.

- An individual who is not an Indian citizen and is in India ona business, employment or student visawould not mandatorily be required to report the foreignassets acquired by him during the previous years in whichhe was non-resident if no income is derived from suchassets during the relevant previous year.

In view of the delay in notification, the due date for filing thesereturns to be 31st August, 2015.

If a person buys a used asset and repairs it before putting it touse, we would consider the expenditure on repairs to be akinto expenditure on acquisition of asset. However, it was held incase of CIT v. Machado Sons (Mad) 363 ITR(Online) 385 thatexpenditure on replacements and renovation of a boat whichwas not put to use in year of purchase before repairs weremade to it, was

According to the decision in case of 3F Industries Ltd vs JointCommissioner of Income-tax (2014) TaxCorp(LJ) 3233(ITAT-VISAKHAPATNAM), `tax’ includes surcharge and cessand consequently credit under section 115JAA is required to

exempt income exceeding Rs.5000/-.

This ceiling is now removed except in case of

agricultural income.

more than one house as also agricultural income

exceeding Rs.5000/-

Schedules which are required only if applicable,

account number of

current/savings bank account and not the balance in

these accounts will be required.

allowable as revenue expenditure.

CPE 2

Day & Date :

Time :

Topics :

Faculty :

Mentor :

Venue :

Fees :

Tuesday, July 14, 2015

06.00 pm to 08.00 pm

Conference Room, ICAI Bhawan

Rs. 200/- (for Non-Members)

How to handle Service Tax Departmental Audit

CA. Dipak Mavani

CA. Anirudh Sonpal

WICASA EVENT

01.07.2015 Celebration of CA Foundation Day and WICASA Barodabirthday

04.07.2015 Elocution Competition

0.07.2015 Quiz Competition

08.07.2015 Educational Tour

11.07.2015 Full day seminar on Project Finance

12.07.2015 4th Students Study Circle on FEMA by Purvang Musale

15.07.2015 Career Councelling programe at New Era School

18.07.2015 Half day seminar on Foreign Remittance Compliance underIncome Tax Act by CA. Abhishek Nagori,RCM ,Baroda

23-24.07.2015 National Convention at Baroda

STUDY CIRCLE EVENT

Baroda Branch of WIRC of ICAI

I love those who yearn for the impossible3

be given after adding surcharge andcess to the tax. It also held that it isimmaterial that the prescribed form ofreturn indicates otherwise.

However, there will be proceduralissues relating to the implementationof the correct view considering thatdif ferent sof twares including,software of Income-tax Department,have taken different stands from timeto time regarding the inclusion orexclusion of surcharge and cess forcomputing the amount of credit andthe stage at which credit is required tobe given.

In case of [2014] 45 taxmann.com283 (AAR - New Delhi) Authority ForAdvance Rulings (Income-Tax), NewDelhi, Royal Bank of Scotland, In re, itwas held that

at sourcefrom contribution to SuperannuationFund which was made on the basis ofan actuarial report

showing amount relating toeach employee. It was held thatEmployer's contribution to thesuperannuation fund

at the timeof making contribution to the fund.Thus, such contribution could not betreated as taxable perquisite in thehands employee until he was entitledto receive it, in spite of the provisionsof Section 17(2)(vii).

Section 269SS prohibits acceptanceof deposits in cash. Violation attractspenalty at the rate of 100%. Thisprovision is often sought to bebypassed by describing deposit asamount received towards sale ofgoods or fixed assets or share capital.This ploy did not work well in case of[2014] 44 taxmann.com 418 (Delhi -Trib.) IN THE ITAT DELHI BENCH 'E'M.G. Estate (P.) Ltd. v. AdditionalCommissioner of Income-tax, Range -

4. Contribution to Superannuation fund

5. Bypassing section 269SS bydescribing amount as shareapplication

Income-tax was not

required to be deducted

without there

being any details to give breakup of

thereof

assures only

future benefit to employees and they

didn't get any vested right

6, New Delhi. It was held that the

comparedto the amount claimed to be receivedas share application money.

In case of K A Chaudhary, reported at356 ITR 618, the Supreme Courtapproved the decision of Andhra HighCourt to the effect that developmentofficer of Life Insurance Corporation ofIndia was

claim

that the amount was on account of

share application money was

incorrect considering that the

amount of authorized capital as

well as amount of actual allotment

of shares was very small

liable to tax on incentive

bonus under the Head 'Salaries'

without deduction of any expenses.

6. Deduc t ion o f expenses fo rdevelopment officers of LIC

Judicial Decisions on

Excise and Service TaxReviewed By CA. Anirudh Sonpal

I. REFUND AND INTEREST

II. CENVAT CREDIT

The petitioner had deposited ServiceTax of Rs.15 lacs during the course ofinvestigation by revenue authorities.Upon appeal to the Cestat, the demandwas not sustainable, as a result ofwhich the revenue authoritiespreferred an appeal against the orderof the Tribunal. The petitioner filed awrit application before the HonourableP&H High Court. While disposing thewrit, the Honourable High Courtobserved that mere pendency ofappeal preferred by the revenueauthorities against the Tribunal’s orderwas no ground to delay refund due asper the order of the Tribunal. TheHonourable High Court further orderedto pay interest @15% on the refunddue from the date it became due afterexcluding three months from the dateof the order of the Tribunal.[LSE Secur i t ies Ltd vs AsstCommissioner, Chandigarh- P&HH.C.]

2.1 The appellant was manufacturer oftractors which were exempted from

excise duty wef 9-7-2004. Theappellant had claimed cenvat credit ofexcise duty on inputs and used thesame against payment of excise dutypayable on tractors. On the date whenthe tractors became exempt, theappellant had already taken credit ofduty paid on inputs lying in stock orcontained in finished tractors lying instock and had utilized the credit forpayment of excise duty on tractorsbefore they were exempted from duty.The Honourable Gogh Court held thatthe cenvat credit was legally taken andutilized at the relevant time and hencewas not liable to be reversed.[ Tractor & Farm Equipment Ltd vsCCE, Madurai-II – Madras H.C.]

2.2 The basic principle of Cenvat creditbeing to avoid cascading effect,genuine credit earned by one unit isnot disallowed for set off againstliability of other in absence of anyprohibition thereto by law - Ratio ofKarnataka High Court ruling in ECOFIndustries applicable, subject tocaveat that the manner of distributionof credit should not be contrary to Rule7 of the Cenvat Credit Rules, 2004.[Aurobindo Pharma Ltd vs CCE –Chennai Cestat]

2.3 By- product Acid Oil emerges duringthe manufacture of refined vegetableoil and by-product Hydrol emergesduring the manufacture of DextroseMonohydrate/Dextrose Anhydrous.The main products are dutiablewhereas the by-products are exemptfrom excise duty. Since themanufacturer had claimed cenvatcredit of inputs used in themanufacture of dutiable final productsand resultant by-products, the revenueauthorities demanded 8% of duty onthe sale value of by-products underRule 6 of the Cenvat Credit Rules,2004.

While dismissing the revenue appeal,the Hon Cestat held that it wasimpossible for the respondents tomaintain separate account andinventory of the inputs/input services

Baroda Branch of WIRC of ICAI

There is nothing stronger in the world than gentleness 4

meant for dutiable final products andexempted final products as this can bedone only if two different finalproducts, one dutiable and the otherexempted are being manufacturedconsciously; when compliance of aprovision is impossible, an assesseecannot be penalized for his failure tocomply with the same-Lex non cogitad impossibilia is a well settled legalprinciple; provisions of Rule 6(2) readwith Rule 6(3)(b) of Cenvat CreditRules, 2002/2004 would not beapplicable in such cases when incourse of manufacture of dutiable finalproducts, some exempted finalproducts also emerge as inevitable by-product.[CCE vs Goyal Proteins Ltd – DelhiCestat]

2.4 CENVAT credit availed on InputSer vices used in relat ion tomanufacturing activity at Pune has nonexus with renting of immovableproperty as output service at Mumbai;Credit cannot be utilized for payingservice tax liability on the renting ofimmovable property service providedin Mumbai.[Dai Ichi Karkaria Ltd vs CCE –Mumbai Cestat]

Appeal before the Commissioner(Appeals) was to be filed within 60days from the date of communicationof the impugned order. TheCommissioner(Appeals) has power tocondone delay for a further period of30 days and beyond this grace period,the Commissioner(Appeal) had nopower to condone and delay andhence the appeal was rightly rejected.Section 35 of the CEA,1944 is aspecial law provision of Limitation Actis expressly ruled out.[Parsi Dairy Farm vs Asst Commr ofCE – Bombay H.C.]

Where brand name of another personis used, SSI exemption is not available;using the brand name of anotherperson with his permission does not

III. APPEALS

IV. EXEMPTIONS

make the assessee owner of the brandname and hence SSI exemption is notavailable.[CCE vs Vetcare Organic Pvt Ltd – SC]

The issue was whether assembly,installation and commissioning ofswitching system along with powerplant and inverter would amount tomanufacture. The assessee had epurchased switching systems, whichwas the main component of atelephone exchange, which is anelectrical apparatus for line telephony;the power plant and inverter are onlyauxiliary equipments since the powerplant supplies 48V DC current forfunctioning the switching system andinverter is required for standby periodin case of power break down.Therefore, Switching Systems whichhave been purchased remainedswitching systems only even afterinstallation and no new commoditywith distinct commercial identity orcharacter or use had emerged.[BSNL vs CCE – Delhi Cestat]

Whereas coaching provided for IIT andother entrance examinations alongwith intermediate (+2) Course wastaxable under ‘Commercial Training orCoaching services’, substantialdemand of crores of rupees was notsustained on grounds of limitations.The Honourable Cestat had observedthat delay in furnishing informationsought for by Revenue from theappellant cannot be a ground forinvocation of extended period since allthe powers of a Court with regard toattendance of witness, discovery ofinformation/ documents, etc. arevested in the adjudicating authority.Only for failure on the part of theadjudicating authority to exercisejurisdiction vested in him, extendedperiod was not invokable; demandwas upheld only for the normal periodand penalties were set aside.[Sri Chaitanya Educational Committeevs CCE&ST – Bangalore Cestat]

V. MANUFACTURE

VI. EXTENDED PERIOD

3-DWritten by CA. Abhay Desai

ANALYSIS OF AN IMPORTANT JUDGMENTON WORKS CONTRACT

insights

Recently Punjab and Haryana HighCourt in the case of CHD Developers Ltd. v.State of Haryana [2015] 57 taxmann.com315 (Punjab & Haryana) delivered animportant judgment with respect to VATliability in the hands of builders anddevelopers. Key of the judgmentare as under:

1) There are three essential conditionswhich are to be fulfilled for levy of VATon works contract. This are:

a) There must be a works contract,

b) The goods should have beeninvolved in the execution of a workscontract, and

c) The property in those goods mustbe transferred to a third party eitheras goods or in some other form.

It has been held that agreementbetween the promoter / builder /developer and the flat purchaser toconstruct a flat and thereafter sell theflat with some portion of land doesinvolve activity of construction whichwould be covered under the term'works contract'.

2) The act iv i ty o f const r uc t ionundertaken by the developer, etc.would be works contract only from thestage he enters into a contract with theflat purchaser. Thus the value additionmade to the goods transferred after theagreement is entered into with the flatpurchaser can only be madechargeable to tax by the StateGovernment.

Lao Tzu said “The key to growth is the

introduction of higher dimensions of

consciousness into our awareness”.

Thinking about an issue only from one-

dimension may result in faulty action. This is

also true for indirect taxes. One has to think

from all points of view to get the best

answer. This column attempts to discuss

various issues pertaining to indirect taxes

from all the three dimensions i.e. Central

Excise, Service Tax & VAT.

Baroda Branch of WIRC of ICAI

When you have a dream, you've got to grab it and never let go5

3) The value of the goods which canconstitute the measures for the levy ofthe tax has to be the value of the goodsat the time of incorporation of thegoods in the works.

4) There are two methods permissible forpayment of tax. One is deductivemethod and other is compositionmethod. Under the deductive method(normal method), a dealer can eitherclaim deduction of actual labour,services and other like chargesincluding the profit element thereon ifthe dealer is maintaining proper books.Otherwise i.e. when proper recordsare not available a dealer can claimstandard deduction prescribed in lawtowards labour charges. Rule 25 ofHaryana Value Added Tax Rules, 2003prov ides fo r above re fe r reddeductions in case of normal method.However it does not explicitly providefor deduction of value of land. HenceState Government is directed to bringnecessary changes in law to providefor deduction towards value of land aslevy is only on the property in goodstransferred.

5) As the composition method as it isoptional in nature, once a dealer optsfor composition scheme which isoptional, he gets various advantagesand privileges which otherwise are notavailable to ordinary VAT dealers. Asthe composition provisions are notcharging provisions, composition taxis to be paid on the total considerationand this could not be challenged.Hence value of land cannot beexcluded under the compositionmethod.

6) No tax can be charged from thedeveloper/bui lder/promoter orcontractor in respect of the value ofgoods incorporated in the workscontract after the agreement with thef lat purchaser on which thesubcontractor has already paid the taxand that his assessment has becomefinal.

1) View of the Hon. High Court that underdeductive method, value of land

OUR COMMENTS

should be explicitly granted as adeduction is welcome. Even underGujarat Value Added Tax (GVAT) Act,2003 as per definition of sale price u/s2(24), only value representing labourcharges are granted as deduction.Value of land is not explicitlymentioned. Relying on the abovedecision, value of land is also allowedas deduction and the referredjudgment will now avoid litigation onthis issue.

2) We beg to differ with the view of Hon.High Court that under compositionmethod, as it is optional and not acharging provision, no deductiontoward value of land can be granted.Reasoning for the same is as follows:

a) Value on which tax is to be paidunder the composition scheme is“total considerat ion”. Hon.Supreme Court in case of Ku.Sonia Bhatia v. State of UP andothers – (AIR 1981 SC 1274) heldthat consideration means areasonable equivalent for othervaluable benefit passed on by thepromisor to the promisee. In caseof developer model whereproceeds from sale of flats are tobe shared between developer andland owner in a pre-definedproportion, value of land receivedby the developer is not theconsideration in his hands. In suchcircumstances, value of land willnot form par t of the totalconsideration under compositionscheme.

b) Without prejudice to above,composition method is prescribedb e c a u s e i n p r a c t i c a lcircumstances a dealer is not in aposition to determine separatevalue of goods and separate valueof services in case of indivisibleworks contract. It no whereenvisages inclusion of value ofimmovable property.

c) Composition scheme is in lieu oftax leviable under the chargingsection. For instance, as per Sec.14A of GVAT Act , 2003,composition tax is payable in lieu

of tax payable under Sec. 7 of theAct. As VAT cannot be levied onvalue of immovable property,inclusion of same for compositiontax results into levy of VAT onimmovable property which isoutside the scope of VAT Act.

d) Purchase and sale of immovableproper ty is covered underrespective State Stamp Duty laws.Thus stamp duty is payable on thevalue of land. Subjecting the sameagain to VAT will result into doubletaxation. Hon. SC in case of L & T(65 VST 1) has held that stampduty and VAT are mutuallyexclusive and hence both cannotbe levied on same value.

In view of above, it would be highlyappreciated if the State Government’scome out with the clarification aboutexclusion of value of land also undercomposition scheme. This will go along way in smooth and easycompliance.

3) In the above decision, Hon. High Courthas also taken a view that deduction ofsub-contractor’s portion can only begranted if the respective sub-contractor has paid the tax andassessment is final. Said view must beread keeping in mind the provisions ofHVAT Act. Sec. 42(2) of the HVAT Actis reproduced below for readyreference:

It is because of express provisions oflaw, Hon. High Court took the view thatdeduction can be granted only after taxhas been paid and assessment is finalof the sub-contractor.

“(2) If the contractor proves to the

satisfaction of the assessing authority

that the tax has been paid by the

subcontractor on the sale of the goods

involved in the execution of the works

contract by the subcontractor and the

assessment of such tax has become

final, the contractor shall not be liable

to pay tax on the sale of such goods

but he shall be entitled to claim input

tax, if any, in respect of them if the

same has not been availed of by the

subcontractor.”

Baroda Branch of WIRC of ICAI

It is by acts and not by ideas that people live 6

In contrast, as per Rule 18AA(1) ofGVAT Rules, deduction is to be grantedof any amount paid by way of price forsub-contract made with a registereddealer. Thus only condition forclaiming deduction is that sub-contractor should be a registereddealer. Hence there is no requirementthat the sub-contractor should havepaid the tax before claiming thededuction.

We have tried to analyze the decisionof Hon. High Court in depth. Yourviews on the same are most welcome.

CONCLUSION

Indirect Tax UpdatesWritten by CA. Manilal Parsiya

Finance minister approves formation of 2c o m m i t t e e s f o r f a c i l i t a t i n gimplementation of Goods and ServicesTax from 1-4-2016 – press release, dated17-6-2015

A Steering Committee been formed underthe Co-Chairmanship of AdditionalSecretary, Department of Revenue andMember Secretary, Empowered Committeeof State Finance Ministers. This Committeehas Members from Department of Revenue,Central Board of Excise & Customs, Goodsand Services Tax Network (GSTN) andrepresentatives of State Governments. ThisCommittee shall monitor the progress of ITpreparedness of GSTN/CBEC/Taxauthorities, finalisation of reports of all theSub-Committees constituted on differentaspects relating to the mechanics of GSTand drafting of CGST, IGST and SGSTlaws/rules. The Committee shall alsomonitor the progress on consultations withvarious stakeholders like trade and industryand training of officers.

Another Committee has been formed underthe Chairmanship of the Chief EconomicAdvisor; Ministry of Finance to recommendpossible tax rates under GST that would beconsistent with the present level of revenuecollection of Centre and States. Whilemaking recommendations, this Committeewould take into account expected levels ofgrowth of economy, different levels ofcompliance and broadening of tax baseunder GST. The Committee would also

analyse the Sector-wise and State-wiseimpact of GST on the economy. TheCommittee is expected to give its reportwithin two months.

Meanwhile, progress is underway to finalisevarious aspects of GST design like businessprocesses, payment systems, mattersrelating to dual control, threshold,exemptions, place of supply rules and alsomaking of model GST, SGST and IGST lawsand rules. This task is being undertakenthrough various Sub-Committees formedby the Empowered Committee which hasofficers from Government of India as well asState Governments as Members.

Goods and Services Tax Network (GSTN) istaking steps for preparing the ITinfrastructure for roll out of GST. The ITinfrastr ucture shal l enable onl ineregistration, filing of returns and gettingrefunds. Various State Governments arealso preparing the necessary back end ITinfrastructure for implementation of GSTwhich shall relate to aspects likeassessments and audit.

Periodic reviews are being held in theDepartment of Revenue to monitor theprogress of all the above activities.

With the introduction of partial reversecharge mechanism (partial RCM) concept,various service providers are facing thesituations of accumulated CENVAT Credit.In order to grant refund of such accumulatedCENVAT Credit to such service providers,Rule 5B of CENVAT Credit Rules, 2004 readwith Notification No. 12/2014-CE (NT)dated 3rd March, 2014, are introduced inthe Statute. The said notification prescribesprocedures, safeguards, conditions andlimitations for refund of such unutilisedCENVAT Credit to following 3 output serviceproviders; namely: Renting of a motorvehicle designed to carry passengers onnon-abated value, to any person who is notengaged in a similar business; Supply ofmanpower for any purpose or securityservices; or Service portion in the executionof a works contract.

Withdrawal of refund of unutilisedCENVAT Credit in respect of supply ofmanpower or security service providersfalling under partial RCM - Notification No.15/2015-CE (NT) dated 19/5/2015

Vide Union Budget 2015-2016, with effectfrom 1st April, 2015, supply of manpowerservices and security services are coveredunder full Reverse Charge Mechanism.Consequently, with effect from 1st April,2015, refund of accumulated CENVATCredit is not allowed to supply of manpowerservice providers as well as security serviceproviders.

An AMNESTY Scheme was announced lastyear vide G.R. No. GST-1014-884-VATCELL dated 14/10/2014. The operativeperiod of the scheme was from 14/10/2014to 11/4/2015. Vide G.R. No.GST-1014-884-VAT CELL Dt. 26/5/2015, the AMNESTYScheme has been further extended foradditional 4 months i.e. for period from12/4/2015 to 11/8/2015. General Terms &Conditions and benefits under the schemeare the same as per the old scheme with theexception of interest @ 18% p.a. on amountof Tax payable for the period from14/10/2014 to the date of payment shallhave to be paid in addition to the Taxpayable.

Amnesty Scheme under Gujarat VAT

FAQs on IFRS: IAS 21:Ind AS 27: Separate

Financial Statements:Written by CA. Prashant Upadhyay

1) Which type of entities are requiredto comply with the standard?

2) What are the requirements forseparate financial statements tocomply with the standard?

3) How investments in subsidiaries,joint ventures and associates aredisclosed in case of separatefinancial statements?

This standard shall be applied inaccounting for investments insubsidiaries, joint ventures andassociates when an entity elects, or isrequired by law, to present separatefinancial statements.

Separate financial statements shall beprepared in accordance with allapplicable Ind AS, except as providedin Para 10.

In separate f inancia l statements,

Baroda Branch of WIRC of ICAI

In a gentle way, you can shake the world7

investments are presented by parent(ie. An investor with control of asubsidiary) or an investor with jointcontrol of, or significant influenceover, an investee, in which theinvestments are accounted for at costor in accordance with Ind AS 109,Financial Instruments.

The entity shall apply the sameaccounting for each category ofinvestments. Investments accountedfor at cost shall be accounted for inaccordance with Ind AS 105, Non-current Assets Held for Sale andDiscontinued Operations, when theyare classified as held for sale (orincluded in a disposal group that isclassified as held for sale).

In terms with para 11, if an entityelects, in accordance with para 18 ofInd AS 28, to measure its investmentsin associates or joint ventures at fairvalue through profit or loss inaccordance with Ind AS 109, it shallalso account for those investments inthe same way in its separate financialstatements.

In terms of para 13, where a parentreorganizes the structure of its groupby establishing a new entity as itsparent in a manner that satisfiesfollowing criteria:

a) New parent obtains control byissuing equity instruments inexchange

b) Assets and liabilities of new groupand original group are sameimmediately before and afterreorganization &

c) Owners of original group hassame absolute and relativeinterests in net assets of originalgroup and new group immediatelybefore and after reorganization.

Then if new parent accountsinvestments in accordance with para10(a) new parent shall measureinvestments at cost in separate

4) Due to reorganization, structure ofgroup entity establishes a new entityas its parent, how investments aredisclosed for a new entity?

financial statements. Also in terms ofpara 14, an entity that is not a parentmight establish a new entity as itsparent in a manner that satisfies thecriteria in para 13.

In terms of Para 15, entity shall applyall relevant standards to separatefinancial statements.

Where parent in terms of para 4(a) ofInd AS 110, elects not to prepareconsolidated financial statements, itshall disclose:

a) The fact that the financialstatements are separate financialstatements, that exemption fromconsolidation has been used, thename and principal place ofbusiness (and countr y ofincorporation, if different) of theent i ty whose consol idatedfinancial statements that complywith Ind AS have been producedfor public use; and the addresswhere those consol idatedf i n a n c i a l s t a t e m e n t s a r eobtainable.

b) List of significant investments insubsidiaries, joint ventures andassociates, including:

i) The name of those investees

ii) The principal place of business(and country of incorporation, ifdifferent) of those investees.

iii) Its proportion of the ownershipinterest (and its proportion ofvoting rights, if different) held inthose investees.

c) A description of the method usedto account for the investmentslisted under (b).

When an investment entity preparesseparate financial statements as itsonly financial statements, it shalldisclose fact. The investment entityshall also present the disclosuresrelating to investment entities requiredby Ind AS 112, Disclosure of Interestin Other Entities (Para 16A).

When a parent (other than a parentcovered by paragraphs 16-16A) or an

5) What are disclosure requirementsunder standard?

investor with joint control off, orsignificant influence over, an investeep r epa r es sepa ra t e f i n anc i a lstatements, the parent or investorshall identify the financial statementsprepared in accordance with Ind AS110, Ind AS 111 or Ind AS 28 to whichthey relate. The parent or investor shallalso disclose in its separate financialstatements:

a) The fact that the statements areseparate financial statements

b) A list of significant investments insubsidiaries, joint ventures andassociates, including :

i) The name of those investees.

ii) The principal place of business(and country of incorporation, ifdifferent) of those investees.

iii) Its proportion of the ownershipinterest (and its proportion ofthe voting rights, if different)held in those investees.

c) A description of the method usedto account for the investmentslisted under (b). (Para 17)

ICAI CORNERComplied by : CA Pradeep K Agrawal &

CA Rahul H Parikh, BarodaSource: www.icai.org

A-BRIEF OF FEW ANNOUNCEMENTS BYICAI FROM 24-APR-15 TO 23-MAY-15:

1 Scholarship from S.Vaidyanath AiyarMemorial Fund (SVAMF), ICAI for2014-2015. - (28-04-2015) :

The Managing Committee of theS.Vaidyanath Aiyar Memorial Fundhave decided to award scholarships to100 students (who are currentlyundergoing ar ticled training inaccordance with The Char teredAccountants Regulations, 1988 whoare poor, needy but meritorious)requiring scholarship to pursue theChartered Accountancy course @ Rs.1000/- p.m. for one year with effectfrom 1st April, 2014 to 31st March,2015 to be paid in lump sum, subjectto filing of application for the same.(Ford e t a i l s h t t p : / / w w w. i c a i . o r g /new_post.html?post_id=11554&c_id=219)

Baroda Branch of WIRC of ICAI

Thinking: the talking of the soul with itself 8

2 Auditor’s Report on Consolidated

Financial Statements under the

Companies Act, 2013 - (01-: 05-

2015) :

3 The Companies Act, 2013 - Section

132 - Constitution of National

Financial Reporting Authority. - (08-

05-2015):

The Auditing and Assurance StandardsBoard, under the authority of theCouncil, has already issued theillustrative formats of the auditor’srepor t on standalone financialstatements of a company under theCompanies Act 2013 in December2014. While reporting in respect of theprovisions of, inter alia, section 143(3)and section 143(11) of the CompaniesAct, 2013 in their report on CFS, theauditors may draw guidance from theaforementioned formats and suitablyreword the same, as required, to meetthe circumstances of audit of CFS.(For details: http://www.icai.org/new_post.html?post_id=11569&c_id=219 )

The Standing Committee on Finance(2014-15), Sixteenth Lok Sabha in itsthir teenth report on Demands ofGrants (2015-16) of Ministry ofCorporate Affairs has inter alia madef o l l o w i n g o b s e r v a t i o n /recommendation in the para 81:

“The Committee note that NationalFinancing Regulatory Authority (NFRA)has been set up as an oversight bodyhaving quasi-judicial authorityincluding suo moto investigationpowers in cases of professionalm i sconduc t by a Cha r t e r edAccountant/ f i rm of Char teredAccountants, imposition of penaltythereof, debarring members of theInstitute of Chartered Accountant ofIndia (ICAI), if proved guilty, etc. TheCommittee fur ther note that theconstitution of NFRA is a result of therecommendation of the StandingCommittee on Finance whichexamined the Companies Bill, 2009and recommended that the scope ofthe National Advisory Committee onAccounting Standards (NACAS) as

included in the Companies Act, 1956should be expanded not only to set andoversee auditing and accountingstandards, but also to monitor thequality of audit undertaken across thecorporate sector. The Committeefurther observe that similar oversightbodies also exist in other countries, forexample, Financial Services Authority(FSA) in United Kingdom and PublicCompany Accounting Oversight Board(PCAOB) in United States of America.However, as issues relating to conflictof mandate with regard to disciplinarymatters between the NFRA and the Actgoverning the Institute of ChartedAccountants of India has been raised,the Committee desire that the Ministrymay ensure that in the process ofconstituting NFRA, it does not createtwo parallel jurisdictions, governingthe same issue. The Committee wouldlike the NFRA to function as anove rs i gh t body w i t hou t anyjurisdictional conflict or overlap. Thisaspect may be addressed, when therules governing NFRA are finalised byt h e M i n i s t r y. ” ( Fo r d e t a i l s :h t t p : / / w w w . i c a i . o r g /new_post.html?post_id=11583&c_id=219 )

(For details: http://220.227.161.86/37597research27174.pdf )

( For details: http://220.227.161.86/37627gn-csr150515.pdf )

Comments Comments/suggestionsmay kindly be sent to the e-mail: c l c g c @ i c a i . i n(For details: http://220.227.161.86/37652clcgc27251.pdf)

4 Issue of Guidance Note on

Accounting for Derivative Contracts-

(12-05-2015) :

5 Issue of Guidance Note on

Accounting for Expenditure on

Corporate Social Responsibility

Activities (15-05-2015):

6 Exposure Draft on the Managerial

Remuneration under the Companies

Act 2013. - (18-05-2015) :

7 Circular with regard to malicious

mails. - (23-05-2015) :

In light of the case of Shreya Singhal vsUnion of India, judgment of the Hon’bleSupreme Court and the facts ofcirculation of malicious emails, theCouncil in its 342nd meeting held on5th and 6th May, 2015 meetingdecided as under:

• That the Circular No. 1-CA(7)/165/2014 dated 17th April,2014 published in May 2014 issueof the Char tered AccountantJournal and hosted on the websiteof the Institute containing theprovisions of section 66 A of theInformation Technology Act, 2000stands withdrawn.

• That while the members of theInstitute are free to express theirviews in respect of the affairs of theInstitute by any means but whiledoing so members are advised toexercise reasonable restraint so asto avoid defamation of any personor the Institute in order to maintaindecency and morality in the interestof the profession or the Institute.

• That the members are accordinglyhereby advised to desist inengaging themselves from sendingmalicious emails against theInstitute or its members, which maybring disrepute to the profession orthe Institute.

• That in case any member is foundengaged in sending maliciousemails against the Institute, itsmembers or otherwise spreadingfalse, misleading or defamatorystatements, may invite action underthe applicable provisions of theChartered Accountants Act, 1949and the rules framed there under.

• That besides above, in case anymember is found engaged insending such malicious emails, theaction may also be initiated underany other law of the land asapplicable.

All the members of the ICAI are herebyadvised to take note of the aboved e c i s i o n o f t h e C o u n c i l .(For details http://www.icai.org/

Baroda Branch of WIRC of ICAI

9 Prayer is man's greatest power!

new_post.html?post_id=11612&c_id=219 )

The Committee on Public Finance &Government Accounting, is a non-standing technical Committee ofInstitute of Chartered Accountants ofIndia formed under the regulatoryp rov is ions o f the Char te redAccountant Act. The Committeecollaborates with various ministriesand professional bodies to drawsynergies in enhancing accountabilityand transparency including publicservice delivery mechanism anduploading the public interest. Itendeavours towards increasing therole of ICAI and its members in thevarious financial inclusion initiatives ofthe Government. The Committee isa l s o i n v o l v e d i n v a r i o u sstudies/research proposals in the fieldof Public Finance and GovernmentAccounting.

The Committee on Public Finance &Government Accounting invitesResearch Proposals on the followingtopics:

1) Study of “Government AccountingSys tem in Deve loped andD e v e l o p i n g C o u n t r i e s - AComparative Analysis”

2) Study of “Public Finance Structure:N a t i o n a l & I n t e r n a t i o n a lPerspective”

(For details: http://www.icai.org/new_post.html?post_id=11578&c_id=219)

http://www.icai.org/new_post.html?post_id=11597&c_id=219

B-OPPORTUNITIES FOR MEMBERS TO

CONTRIBUTE TO OUR OWN ICAI :

1 Call for Research Proposal on the

Topics of Public Finance &

Government Accounting. - (06-05-

2015) :

2 Allotment of assignment of Checkers

in respect of CA exams held in May

2015 - on Checkers Portal. - (19-05-

2015) :

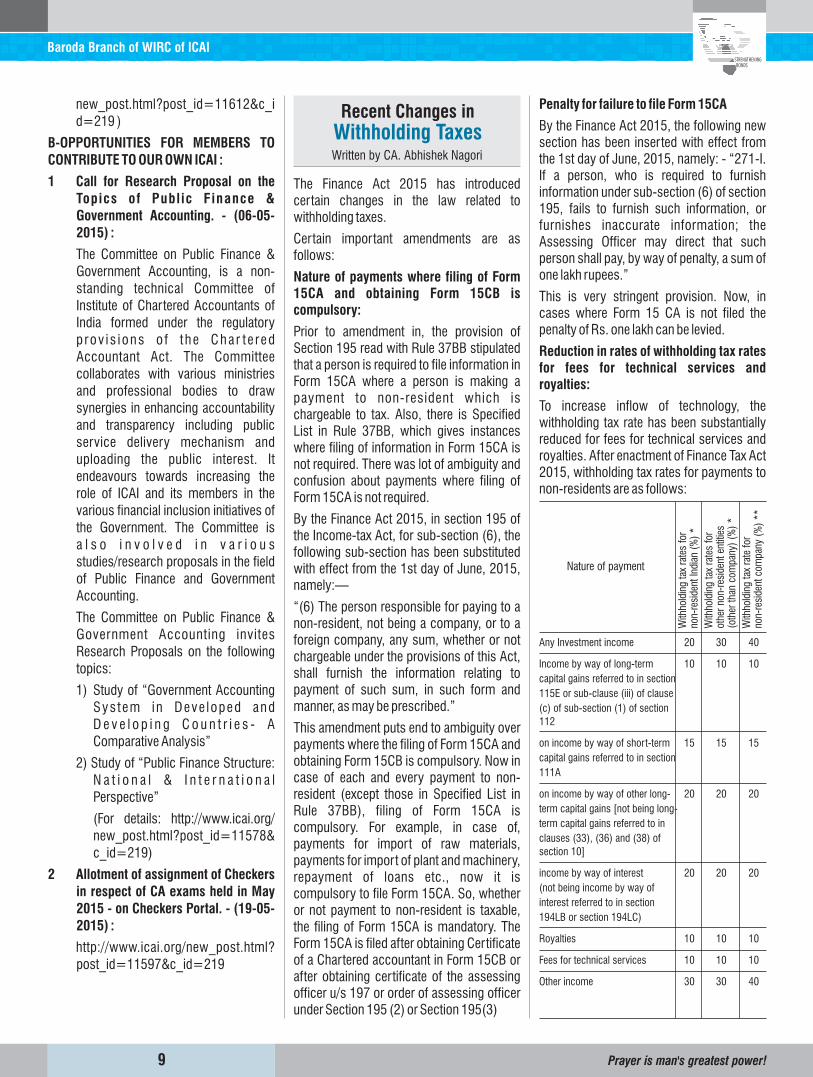

Recent Changes inWithholding TaxesWritten by CA. Abhishek Nagori

The Finance Act 2015 has introducedcertain changes in the law related towithholding taxes.

Certain important amendments are asfollows:

Prior to amendment in, the provision ofSection 195 read with Rule 37BB stipulatedthat a person is required to file information inForm 15CA where a person is making apayment to non-resident which ischargeable to tax. Also, there is SpecifiedList in Rule 37BB, which gives instanceswhere filing of information in Form 15CA isnot required. There was lot of ambiguity andconfusion about payments where filing ofForm 15CA is not required.

By the Finance Act 2015, in section 195 ofthe Income-tax Act, for sub-section (6), thefollowing sub-section has been substitutedwith effect from the 1st day of June, 2015,namely:—

“(6) The person responsible for paying to anon-resident, not being a company, or to aforeign company, any sum, whether or notchargeable under the provisions of this Act,shall furnish the information relating topayment of such sum, in such form andmanner, as may be prescribed.”

This amendment puts end to ambiguity overpayments where the filing of Form 15CA andobtaining Form 15CB is compulsory. Now incase of each and every payment to non-resident (except those in Specified List inRule 37BB), filing of Form 15CA iscompulsory. For example, in case of,payments for import of raw materials,payments for import of plant and machinery,repayment of loans etc., now it iscompulsory to file Form 15CA. So, whetheror not payment to non-resident is taxable,the filing of Form 15CA is mandatory. TheForm 15CA is filed after obtaining Certificateof a Chartered accountant in Form 15CB orafter obtaining certificate of the assessingofficer u/s 197 or order of assessing officerunder Section 195 (2) or Section 195(3)

Nature of payments where filing of Form15CA and obtaining Form 15CB iscompulsory:

Penalty for failure to file Form 15CA

Reduction in rates of withholding tax ratesfor fees for technical services androyalties:

By the Finance Act 2015, the following newsection has been inserted with effect fromthe 1st day of June, 2015, namely: - “271-I.If a person, who is required to furnishinformation under sub-section (6) of section195, fails to furnish such information, orfurnishes inaccurate information; theAssessing Officer may direct that suchperson shall pay, by way of penalty, a sum ofone lakh rupees.”

This is very stringent provision. Now, incases where Form 15 CA is not filed thepenalty of Rs. one lakh can be levied.

To increase inflow of technology, thewithholding tax rate has been substantiallyreduced for fees for technical services androyalties. After enactment of Finance Tax Act2015, withholding tax rates for payments tonon-residents are as follows:

Nature of payment

With

hold

ing

tax

rate

s fo

rno

n-re

side

nt In

dian

(%

) *

With

hold

ing

tax

rate

s fo

rot

her

non-

resi

dent

ent

ities

(oth

er th

an c

ompa

ny)

(%)

*

With

hold

ing

tax

rate

for

non-

resi

dent

com

pany

(%

) **

Any Investment income 20 30 40

Income by way of long-term 10 10 10

capital gains referred to in section

115E or sub-clause (iii) of clause

(c) of sub-section (1) of section

112

on income by way of short-term 15 15 15

capital gains referred to in section

111A

on income by way of other long- 20 20 20

term capital gains [not being long-

term capital gains referred to in

clauses (33), (36) and (38) of

section 10]

income by way of interest 20 20 20

(not being income by way of

interest referred to in section

194LB or section 194LC)

Royalties 10 10 10

Fees for technical services 10 10 10

Other income 30 30 40

Baroda Branch of WIRC of ICAI

Nothing is worth more than this day 10

Important Due Dates for July, 2015 Written by CA. Abhijit J. Kotecha

Above rates shall be increased by a surcharge, calculated in the following manner:

Payee

where the income or the aggregate

of such incomes paid or likely to be paid

and subject to the deduction

withholding tax rate

shall be increased

by a surcharge

calculated at the

rate of (%)

*individual or Hindu undivided family or association of persons or body

of individuals, whether incorporated or not, or every artificial juridical

person referred to in sub-clause (vii) of clause (31) of section 2 of the

Income-tax Act or co-operative society or firm or local authority

** every company other than a domestic company

**every company other than a domestic company

exceeds one crore rupees

exceeds one crore rupees but does not

exceed ten crore rupees

exceeds ten crore rupees

12

2

5

DATES COMPLIANCE PERIOD

05-Jul-15 Service Tax Payment - Monthly Cases / Quarterly Cases June'15, April'15 - June'15

Excise Duty Payment (for NON SSI) June'15

06-Jul-15 Excise Duty E-Payment (for NON SSI) June'15

Service Tax E-payment - Monthly Cases / Quarterly Cases June'15, April'15 - June'15

07-Jul-15 Submission to the Commissioner of Income Tax of Forms - 15G / H (two copies),received in the month of June '2015 June'15

TDS payment / TCS E-payment June'15

09-Jul-15 VAT / CST E-Return - Monthly (For VAT or CST > Rs. 5,000/-) April'15

10-Jul-15 Excise Returns - ( Monthly Return by Large Units / Return by EOU / Monthly return of receipt & consumption ofeach of Principal Inputs, assessees required to submit ER-5 return) June'15

Excise Returns - ( Quarterly Return by SSI/ assessees availing SSI concession) April'15 - June'15

15-Jul-15 TDS / TCS Return - Quarterly April'15 - June'15

Excise Returns - (Quarterly return by first and second stage Registered dealers) April'15 - June'15

Excise Duty Payment (for SSI) June'15, April'15 - June'15

PF Payment June' 15

Payment of Professional Tax June' 15

Corporate Governence Report - filing with Stock Exchange April'15 - June'15

Return of employees joining & leaving service under PF Act June' 15

Excise Duty E-Payment (for SSI) June'15

16-Jul-15 Excise Duty E-Payment (for SSI) June'15

20-Jul-15 Excise Return -Quarterly cases (for SSI) April'15 - June'15

21-Jul-15 Security Reconcilation Audit for Listed Companies (Filing with Stock Exchange) April'15 - June'15

ESIC Payment June' 15

22-Jul-15 VAT / CST payment / E - payment - Monthly & Quarterly Cases June'15, April'15 - June'15

25-Jul-15 PF Return (Monthly) June' 15

30-Jul-15 VAT / CST E-Return - Monthly - (For VAT or CST <= Rs. 5,000/-) May'15

VAT Return - Hard copy - Lumpsum or other than Lumpsum April'15 - June'15

Shareholding pattern - filing with Stock Exchange April'15 - June'15

TDS Certificate issuance - Form 16A (for other than Salary cases) April'15 - June'15

PHOTOFLASH

Baroda Branch of WIRC of ICAI

11 How glorious a greeting the sun gives the mountains!

Career Counselling & Classroom Training For CPT on 10 6 2015

Conference for Members in Industries on 13 6 2015

Direct Tax Refresher Course (DTRC) ON 20 6 2015

Half day seminar on Income Computation & Disclosure Standard (ICDS) on 12 6 2015

Study Circle Meeting on“Industry Specific Internal control 1 6 2015

Study Circle Meeting onDCF Valuation of Equity or Enterprise 16 6 2015

CA. Nayan Kothari Mr. Divyesh Dholakia

CA. N. C. Hegde CA. Nihar Jambusaria

CA. N P Sarda CA. Sanjeev S Shah

CA. Vardhan Dharkar CA. Vijay Maniar

CA. Nikhil Gupta

MR. Keyoor Bakshi CA. Sujal Shah

CA. Dhinal Shah

CA. Vinay sehgal CA. Bharat Gajjar CA. Tejal Parikh

Baroda Branch of WIRC of ICAI

DISCLAIMER : The ICAI and the Baroda Branch of WIRC of ICAI is not in any way responsible for the result of any action taken on the basis of the advertisement published in the Newsletter. The members,however, may bear in mind the provisions of the Code of Ethics while responding to the advertisements. The views and opinion expressed or implied in the Newsletter are those of the authors / contributors and donot necessarily reflect those of Baroda Branch. Unsolicited matters are sent at the owner's risk and the publisher accepts no liability for loss or damage. Material in this publication may not be reproduced, whetherin part or in whole, without the consent of Baroda Branch. Members are requested to kindly send material of professional interest to The same may bepublished in the newsletter subject to availability of space & editorial editing.

[email protected]/[email protected]

If undelivered, please return to :

Baroda Branch of WIRC ofThe Institute of Chartered Accountants of India

www.baroda-icai.org WIRC : www.wirc-icai.org ICAI: www.icai.orgl l

Back Cover (4 color) 15,000 Inside Front/Back Cover (4 color) Full Page (1 Color) Half Page (1 Color) 5,000

ADVERTISEMENT TARIFF : * Discount - 3 to 6 issue of 10%, 7 to 12 issue 15% * Circulated to more than 1800 Chartered Accountants

ADVERTISEMENTS :

SUBSCRIPTION RATES :

PRINTED AND PUBLISHED BY : Published at

Printed at

The tariff for advertising given below are duly approved by the Managing Committee of the Baroda Branch. Advertisements are received directly by the Branch and no advertising agency hasbeen appointed for this purpose.

This Newsletter is circulated without any charges to its members and other important categories of recipients as per ICAI Advisory on Newsletters. Subscription rate is Rs. 20/- per issuefor others.

CA. Yash N Bhatt on behalf of Baroda Branch of WIRC of ICAI. “ICAI Bhawan”, Kalali-Tandalja Road, Atladra, Vadodara - 390 012

Multiprints, 30/B, Gandhi Oil Mill Compound, Near BIDC, Gorwa, Vadodara - 390016. Ph.: 0265-2285592

“ICAI Bhawan”, Kalali-Tandalja Road,

Atladra, Vadodara - 390 012.

+91 265 2681115 / 2680593 8511077115Telefax : M:

7,50010,000

12From what we get, we can make a living; what we give, however, makes a life

Falicitation of Team WIRC & Newly Qualified CA 12 06 2015

CA. Dilip Apte CA. Subodh Kedia CA. Sunil Patodia CA. Sushrut Chitale

![[XLS] micr.xlsx · Web viewAJMER MAIN JLN.HOSPI.RD BRANCH AKLUJ AKOTA-BARODA KANDIVLI-EST BRANCH BANSMANDI, ALLAHABAD ALIPURA ALIPORE ALIGARH BRANCH ALKAPURI BRANCH ALLABAD MAIN BRANCH](https://img.pdfslide.net/doc/110x75/5ab79b957f8b9ac10d8beef0/xls-micrxlsxweb-viewajmer-main-jlnhospird-branch-akluj-akota-baroda-kandivli-est.jpg)