Embed Size (px)

Citation preview

1

Welcome

Grants Management Manual Overview

Introductions

• Sponsored Programs– Lori Burchard, Director – Becky Hayes, Assistant Director (Pre-award)– Beverly Robertson, Assistant Director (Post-award)

• Grants Accounting– Debra Leonard, Manager– Mike Login, Sr. Accountant

What is a Sponsored Project?

• Any externally funded research or scholarly activity that has a defined scope of work or set of objectives, which provides a basis for sponsor expectations.

• This more specifically involves research, demonstration, professional development, instruction, training, curriculum development, community and public service, or other scholarly activity involving funds, materials, other forms of compensation, or exchanges of in-kind efforts under awards or agreements.

Sponsored Project Conditions• Submitted in response to an RFP (request for proposal) or similar

solicitation. • Specific line of scholarly or scientific inquiry typically documented in a

statement of work.• Includes a set of objectives which provides a basis for sponsor expectations.• Commits University resources, such as personnel effort or use of equipment,

facilities, etc.• Includes a detailed budget.• Involves the use of human subjects, laboratory animals, radioactive or

hazardous materials, recombinant DNA, carcinogens, pathogens, or proprietary materials.

• Agreement between sponsor and university.• Specified period of performance.

Sponsored Project Conditions, cont.• Expected deliverables, such as reports, financial accounting, or

intellectual property ownership.• Includes conditions for specific formal fiscal reports and/or invoicing.• Restricts or monitors publications or use of results or requires

protection of confidential info.• Includes disposition of property resulting from the project such as

equipment, records, activity reports, theses and dissertations, rights in data, software, copyrights, inventions or research-related materials.

• Specifies fiduciary responsibilities such as adherence to a budget, project audit, payment contingencies, return of any unexpended funds at the end of the project.

• Sponsor is involved in making decisions regarding project or stands to benefit from the work.

Review Questions – Sponsored Project Definition

• Dr. Q. Tee receives a check from the Very Large Medical Device Corporation. She insists it be deposited into a designated fund for her access. What’s the best way to proceed?

• A subaward is considered a sponsored project. True or False

Roles and Responsibilities of Sponsored Programs

• Assists PI with implementation and management of the sponsored program and has the following specific responsibilities:

• Reviews, approves, and submits proposals on behalf of the institution

• Negotiates contracts and financial arrangements and serves as a liaison with sponsors throughout the life of the project

• Guides PIs in interpretation or clarification of federal regulations, funding agency requirements, award terms, and University policies

• Initiates paperwork to establish a sponsored project fund/ index account for the project

• Develops the project spending plan that allocates the approved budget to University expenditure accounts and serves as the budget for the sponsored project fund/index

Roles and Responsibilities of Sponsored Programs – cont.

• Provides guidance with administrative issues that may arise including change in level of effort of key personnel, change in budget or change in scope of work that may require sponsor approval

• Administers the Organizational Prior Approval System as delegated by Federal Expanded Authorities to the University including grantee-approved no cost extensions and budget revisions

• Reviews and approves appointment forms for employees supported by sponsored projects

• Reviews and approves cost transfers and salary distribution revision forms submitted more than 90 days after the original charge

Roles and Responsibilities of Sponsored Programs – cont.

• Provides information on copyright and patent procedures, export control, reporting requirements and closeout procedures

• Completes intellectual property and fixed asset reporting

• Prepares and administers subcontracts and subawards

• Works with Institutional Advancement and the University Foundation to determine Sponsored Project/Gift decisions.

Roles and Responsibilities of Grants Accounting

● Establishes, maintains (includes budget input), and terminates sponsored project funds/indexes in the financial accounting system (Banner)

● Notifies PI and appropriate parties of sponsored project funds/indexes creation

● Shares responsibility with Sponsored Programs for the formulation, implementation and interpretation of policies and procedures regarding sponsored projects

● Prepares and submits billings to sponsor on a timely basis

● Manages the collection of grant funds, Letter-of-Credit (LOC) draw down of funds and sponsored project accounts receivable

Roles and Responsibilities of Grants Accounting – cont.

● Informs PI and department of payment problems with sponsors

● Coordinates the preparation and submission of financial reports to the sponsoring agency

● Monitors grant expenditures, for allowability and allocability

● Reviews purchase orders, check requisitions and salary forms

● Processes cost transfer requests and journal entries

● Reviews and processes payment of approved subrecipient invoices

● Monitors the fulfillment of cost share obligations

● Monitors program income

● Oversees the administration of the effort reporting function

● Monitors overdrafts of sponsored project funds/indexes and coordinates with department to ensure timely resolution

● Prepares the indirect cost allocation entry at year-end based upon University indirect distribution agreement

● Monitors subrecipient A-133 audit reports

● Assists with the development and negotiation of the Facilities and Administrative rate agreement with the University’s cognizant federal agency, the Department of Health and Human Services

● Assists with the government, private sponsor and public accounting firm audits

● Prepares various institutional reports and surveys, principal contact for sponsor fiscal officers

Roles and Responsibilities of Grants Accounting – cont.

Roles and Responsibilities of Departments

• Ensures the PI follows University policies and assumes project administrative responsibilities

• Reviews and authorizes appropriate forms initiated by PI for payroll authorizations, new hires, purchases, cost transfers, and other related grant expenditures

• Maintains accurate departmental records that document and verify expenditures charged to the sponsored project fund/index made on purchasing cards, travel reimbursements and other electronic transactions

• Assures the appropriate indirect cost rates are being requested in sponsored projects budgets

• Assists the principal investigator in utilizing the Flashline reports

Roles and Responsibilities of Departments – cont.

• Monitors any cost sharing commitments, along with the source of the cost share.

• Assures necessary commitments will be in place prior to the award and appropriately documented in the cost share fund/index

• Monitors project expenditures and use of funds through Banner and associated FlashLine reports

• Ensures costs are within sponsor and University guidelines

Roles and Responsibilities of Departments – cont.

• Assigns correct expenditure accounts to check requests, p-card reconciliations, cost transfers, etc.

• Notifies the PI of any changes in Kent State University policies and procedures

• Provides oversight on all aspects of program income

• Obtains a thorough understanding of direct, unallowable, and indirect costs

Roles and Responsibilities of PIs

• Manages and conducts the project as funded while adhering to federal regulations, funding agency guidelines, and University policies and procedures

• Understands the terms and conditions of the award/agreement, including any special or unusual conditions

• Manages the financial aspects of the project

Roles and Responsibilities of PIs – cont.

• Review and approves payments of subrecipient invoices in a timely fashion

• Regularly monitors expenditures• Conducts the project using the highest ethical

standards and declares any potential conflicts of interest

• Cooperates with Sponsored Programs to develop the project spending plan

• Ensures that any cost sharing commitments are met and appropriately documented.

Roles and Responsibilities of PIs – cont.

• Recruits and hires personnel on the project• Oversees the work of all personnel, including students,

utilized on the project.• Consults with Sponsored Programs for necessary

approvals on budgetary & programmatic changes: NCEs, revisions, etc.

• Prepares and submits technical reports and any other required deliverables on a timely basis

• Ensures that all project members are familiar with and abide by the federal and University compliance policies

Roles and Responsibilities of PIs – cont.

• Submits grant proposals to Sponsored Programs and other review bodies in a timely manner

• Participates in training regarding University policies, compliance issues, proposal improvement, and agency specific issues.

• Keeps organized records of paperwork for audit purposes or in case of questions.

• Obtains a thorough understanding of direct, unallowable, and indirect costs.

Review Questions – Roles and Responsibilities

• Who signs an award agreement?• Who’s responsible for financial reporting to

the funder for a sponsored project?• Who can access financial status reports in

Flashline?• Who is responsible for timely charges to a

sponsored project? • Who maintains receipts for expense?

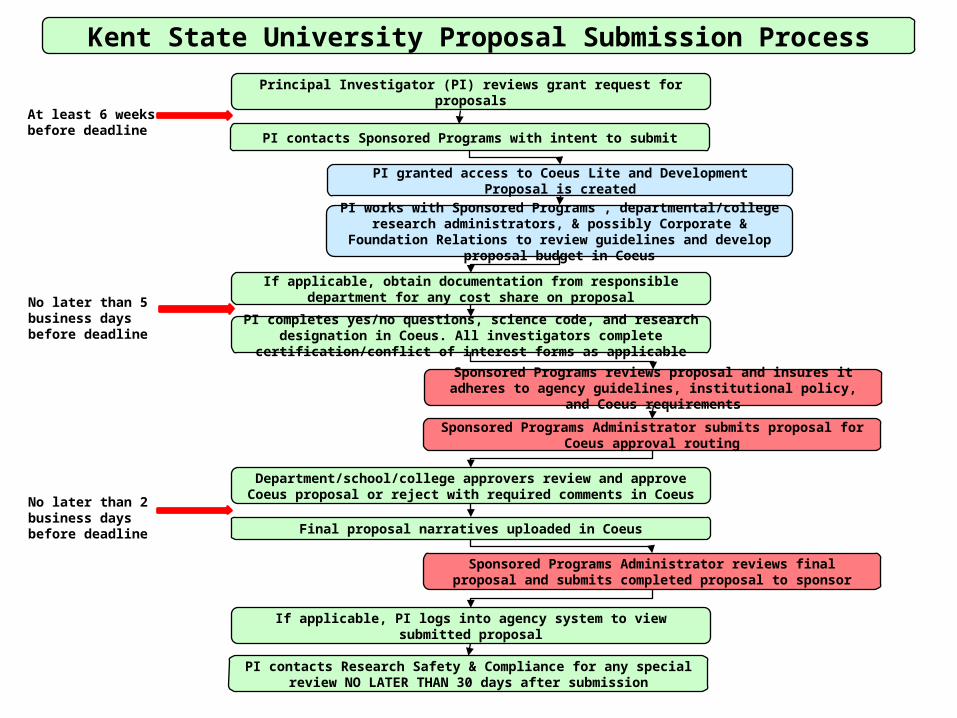

Kent State University Proposal Submission Process

Principal Investigator (PI) reviews grant request for proposals

PI contacts Sponsored Programs with intent to submit

PI granted access to Coeus Lite and Development Proposal is created

PI works with Sponsored Programs , departmental/college research administrators, & possibly Corporate & Foundation Relations to review

guidelines and develop proposal budget in Coeus

If applicable, obtain documentation from responsible department for any cost share on proposal

PI completes yes/no questions, science code, and research designation in Coeus. All investigators complete certification/conflict of interest forms as applicable

Sponsored Programs reviews proposal and insures it adheres to agency guidelines, institutional policy, and Coeus requirements

Sponsored Programs Administrator submits proposal for Coeus approval routing

Department/school/college approvers review and approve Coeus proposal or reject with required comments in Coeus

Final proposal narratives uploaded in Coeus

Sponsored Programs Administrator reviews final proposal and submits completed proposal to sponsor

If applicable, PI logs into agency system to view submitted proposal

PI contacts Research Safety & Compliance for any special review NO LATER THAN 30 days after submission

At least 6 weeks before deadline

No later than 5 business days before deadline

No later than 2 business days before deadline

Award set-up and administration

• Frequently terms of an award need to be negotiated with a funder to prevent acceptance of terms that are either not permitted (ex. indemnification) or not possible to execute (ex. financial reporting requirements that are less than 45 days).

• Another instance may be where less is awarded than what was requested.

• Awards are made to the University or the University Foundation on behalf of the PI, who is primarily responsible for carrying out the requirements of the award.

Award set-up and administration

• After accepting the award Sponsored Programs verifies that other requirements have been met, such as IRB approval/exemption when human subjects are involved; FCOI compliance requirements have been met for PHS awards.

• A spending plan is created that details the budget for the initial grant period along with other details about the project – PI(s), funder, grant period, project period, etc.

• A fund request is prepared and sent to Grants Accounting along with the spending plan so a restricted index will be established.

• The PI(s) and departmental personnel receive an email from the Controller’s office with the assigned index number along with important information about managing and monitoring an award.

Award set-up and administration

Text from email accompanying completed fund request:• Attached is the completed "Request for a New Restricted Fund." The

sponsored project index number, cost share index number (if applicable), and fund, org, and program codes, and responsible accountant are listed at the bottom of this form. The index numbers can be used to charge budgeted items for your project.

• As PI you are responsible for execution and fiscal oversight of the project. Please review the award document, proposal, program announcement, and any other pertinent documents for this project to understand key fiscal and programmatic requirements.

• Grants management manual sections will assist in understanding requirements and procedures that apply to sponsored projects. Please refer to the section on Staffing the Project for information on processing personnel appointments/charges, including Salary Distribution Revision forms for current employees who will be working on the project.

Award set-up and administration

Text from email accompanying completed fund request (cont.) :• Financial reports and invoices are prepared by your Grants

Accountant. Please contact him/her for assistance if you are preparing a report that requires financial information. Financial information should be prepared or approved by Grants Accounting before submission to the sponsor so they are in agreement with Banner financial system records.

• We look forward to working with you on this project. Questions about requirements of the project including the terms and conditions, budget changes, extensions, or general compliance issues can be directed to Sponsored Programs. Questions about invoicing, and financial issues can be directed to Grants Accounting.

Award set-up and administration

• When an undocumented check arrives in your department , the following steps can help determine if it’s related to a sponsored project:

1) if not readily evident what the check is for, check in Coeus first. If no information there, contact your faculty to determine who may have submitted a proposal / worked with an outside entity to secure funding for a project.

2) Secure details from the faculty member, such as rfp/announcement or other details provided by the funder about the project.

3) Determine if this is a sponsored project based on definition. If it meets any of the criteria contact Sponsored Programs for assistance.

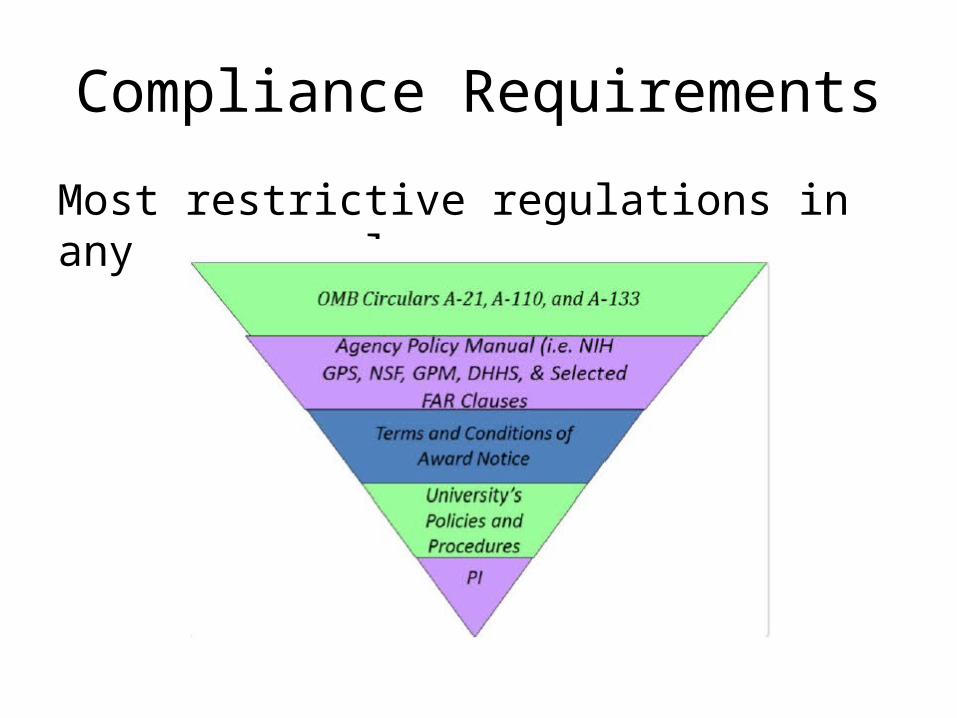

Compliance Requirements

Most restrictive regulations in any case apply:

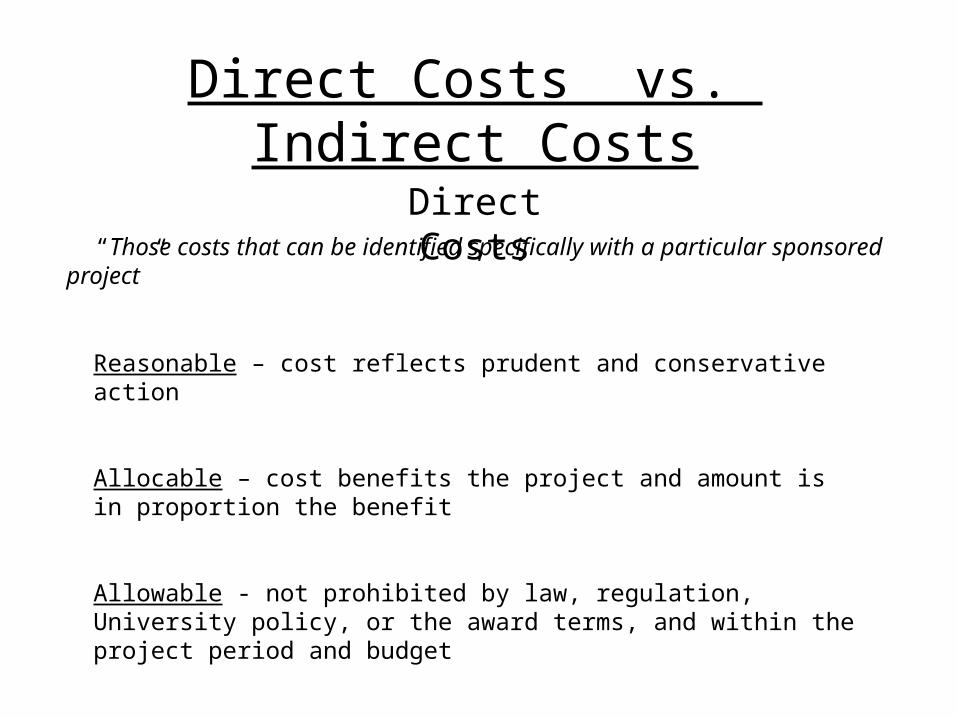

Direct Costs vs. Indirect Costs

“Those costs that can be identified specifically with a particular sponsored project”

Direct Costs

Reasonable – cost reflects prudent and conservative action

Allocable – cost benefits the project and amount is in proportion the benefit

Allowable - not prohibited by law, regulation, University policy, or the award terms, and within the project period and budget

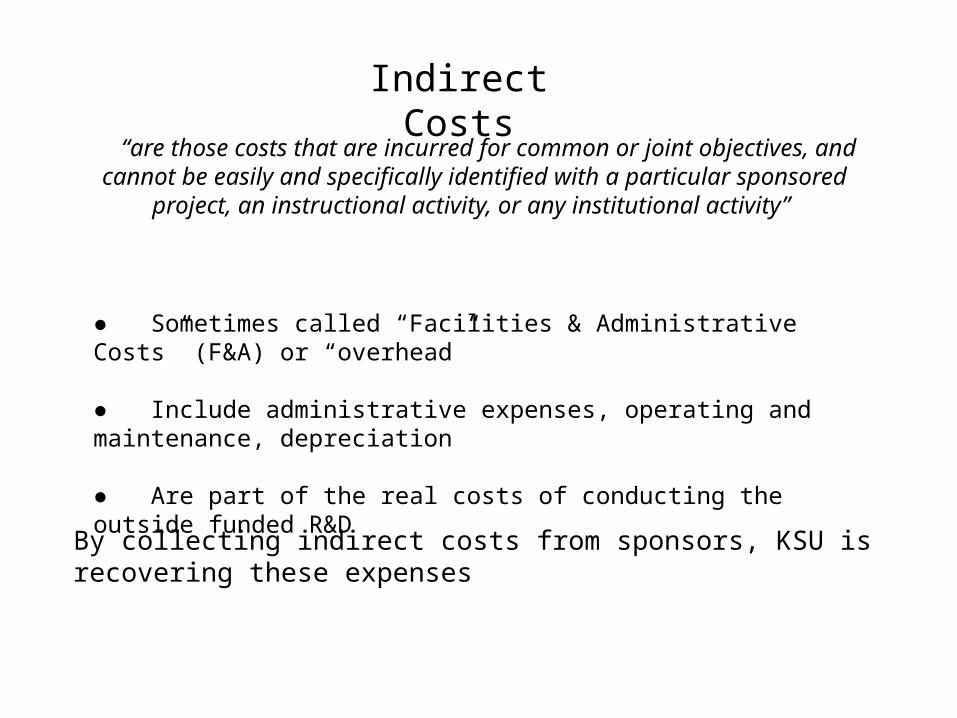

“are those costs that are incurred for common or joint objectives, and cannot be easily and specifically identified with a particular sponsored project, an instructional

activity, or any institutional activity”

Indirect Costs

● Sometimes called “Facilities & Administrative Costs” (F&A) or “overhead”

● Include administrative expenses, operating and maintenance, depreciation

● Are part of the real costs of conducting the outside funded R&D

By collecting indirect costs from sponsors, KSU is recovering these expenses

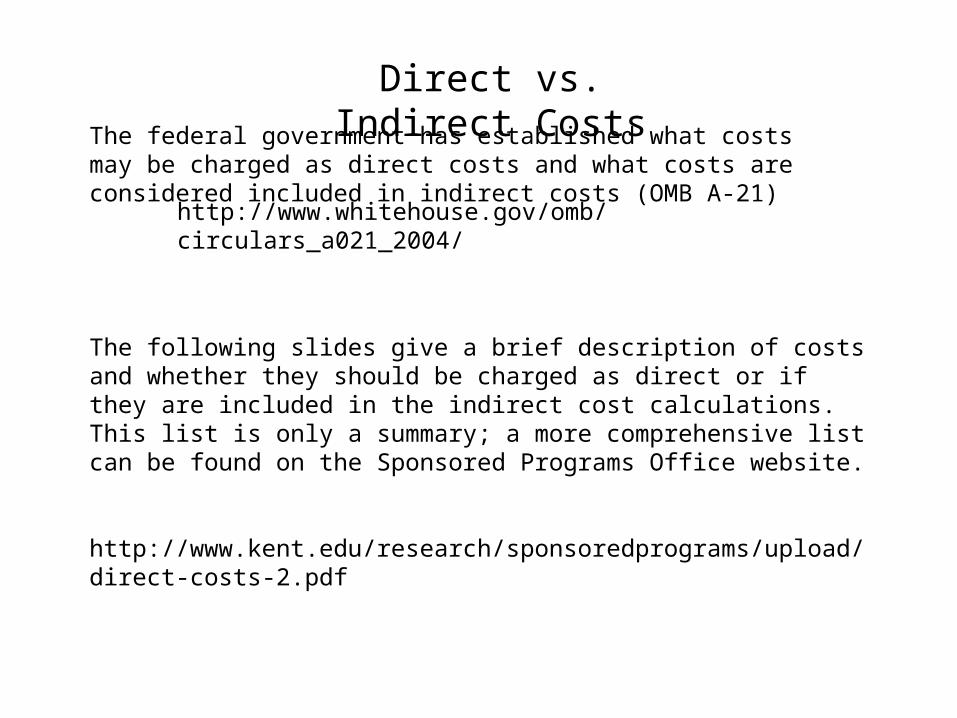

The federal government has established what costs may be charged as direct costs and what costs are considered included in indirect costs (OMB A-21)

http://www.whitehouse.gov/omb/circulars_a021_2004/

The following slides give a brief description of costs and whether they should be charged as direct or if they are included in the indirect cost calculations. This list is only a summary; a more comprehensive list can be found on the Sponsored Programs Office website.

http://www.kent.edu/research/sponsoredprograms/upload/direct-costs-2.pdf

Direct vs. Indirect Costs

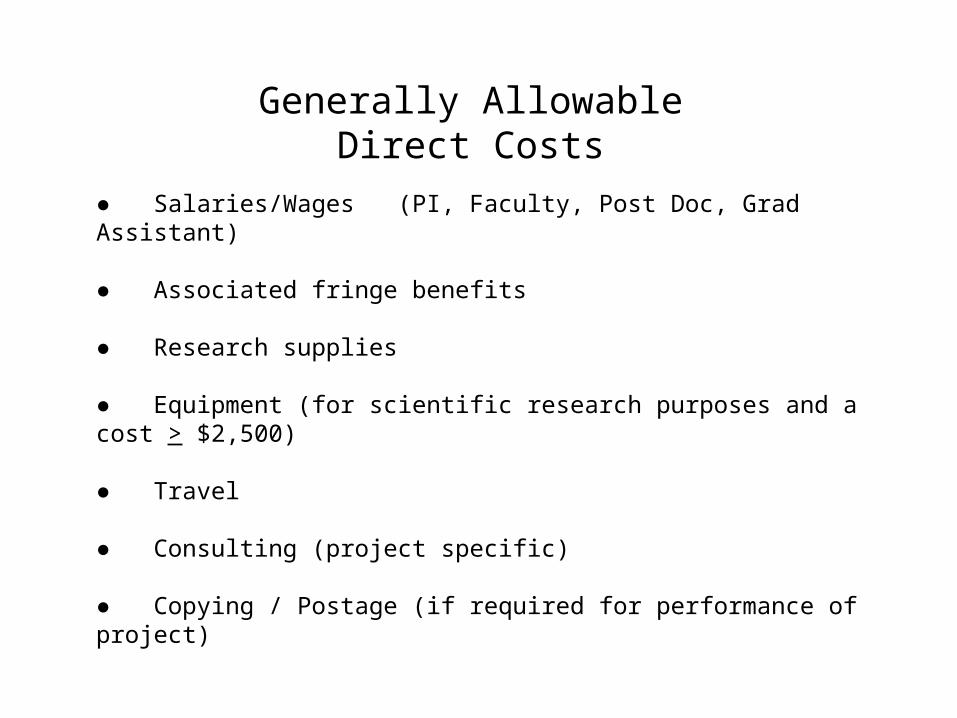

Generally Allowable Direct Costs

● Salaries/Wages (PI, Faculty, Post Doc, Grad Assistant)

● Associated fringe benefits

● Research supplies

● Equipment (for scientific research purposes and a cost > $2,500)

● Travel

● Consulting (project specific)

● Copying / Postage (if required for performance of project)

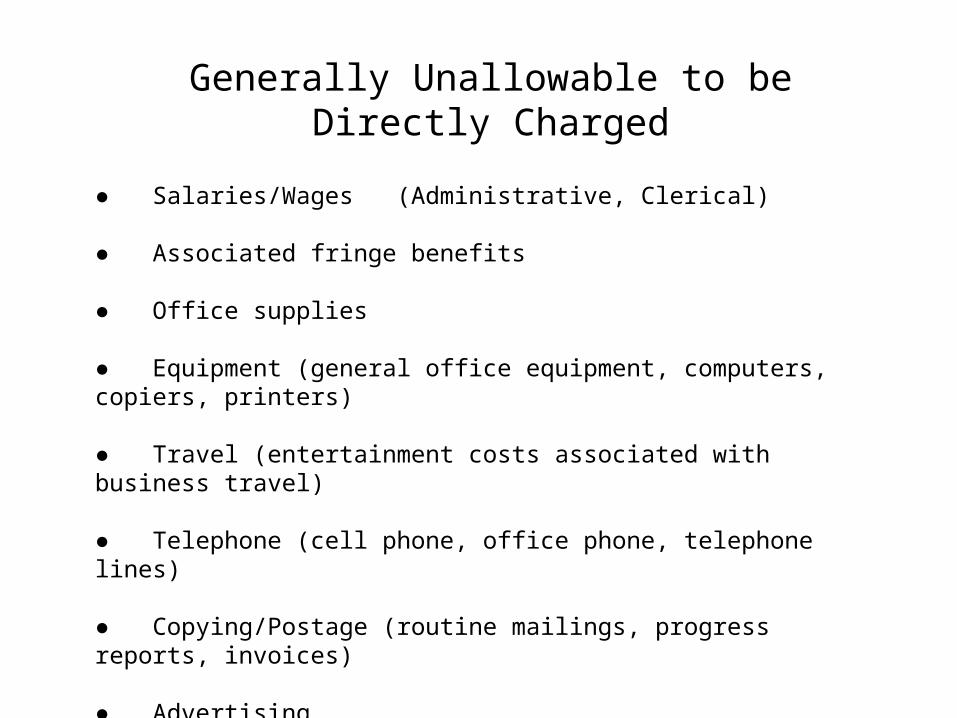

Generally Unallowable to be Directly Charged

● Salaries/Wages (Administrative, Clerical)

● Associated fringe benefits

● Office supplies

● Equipment (general office equipment, computers, copiers, printers)

● Travel (entertainment costs associated with business travel)

● Telephone (cell phone, office phone, telephone lines)

● Copying/Postage (routine mailings, progress reports, invoices)

● Advertising

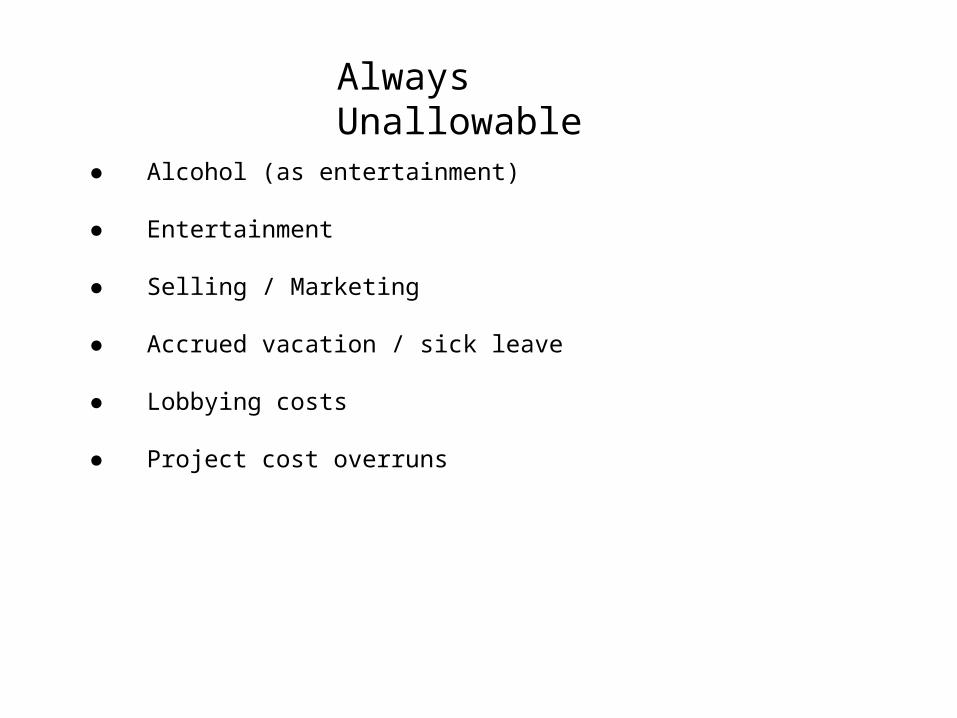

Always Unallowable

● Alcohol (as entertainment)

● Entertainment

● Selling / Marketing

● Accrued vacation / sick leave

● Lobbying costs

● Project cost overruns

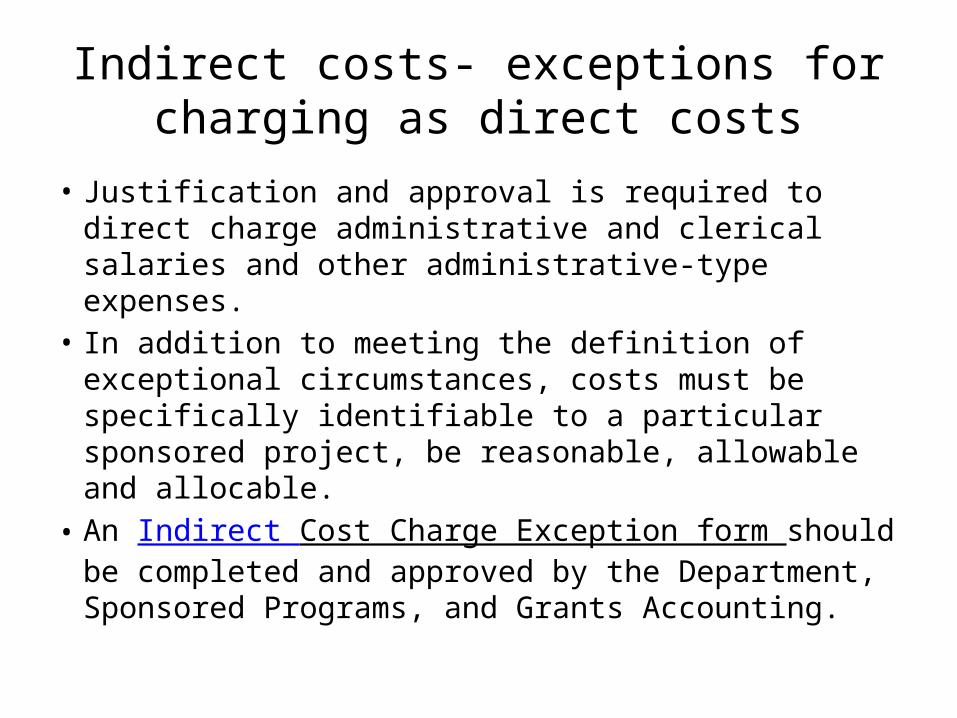

Indirect costs- exceptions for charging as direct costs

• Justification and approval is required to direct charge administrative and clerical salaries and other administrative-type expenses.

• In addition to meeting the definition of exceptional circumstances, costs must be specifically identifiable to a particular sponsored project, be reasonable, allowable and allocable.

• An Indirect Cost Charge Exception form should be completed and approved by the Department, Sponsored Programs, and Grants Accounting.

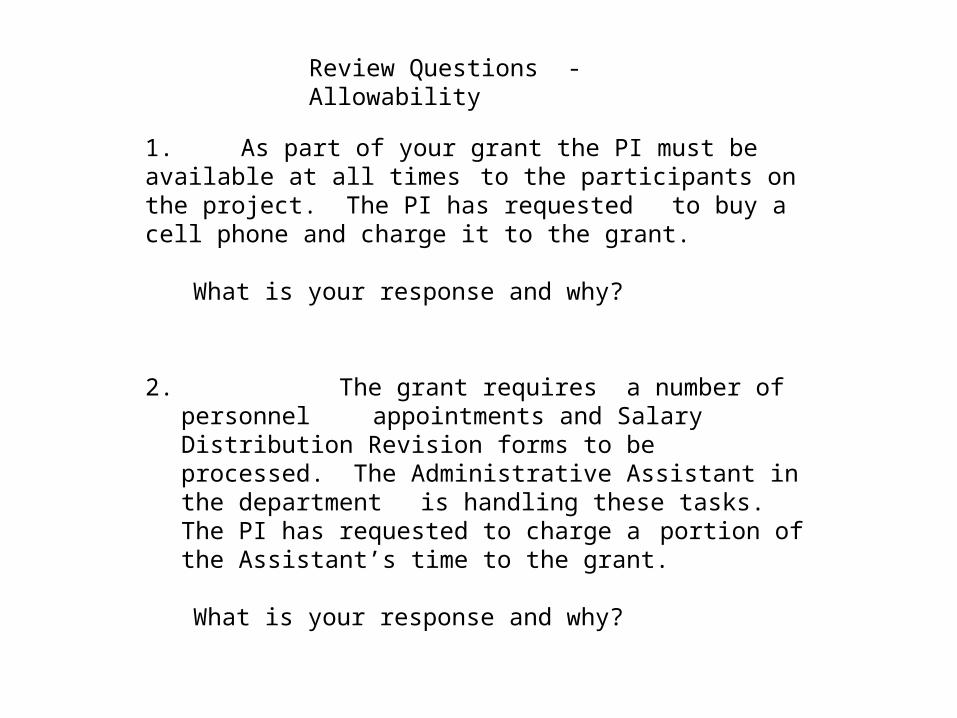

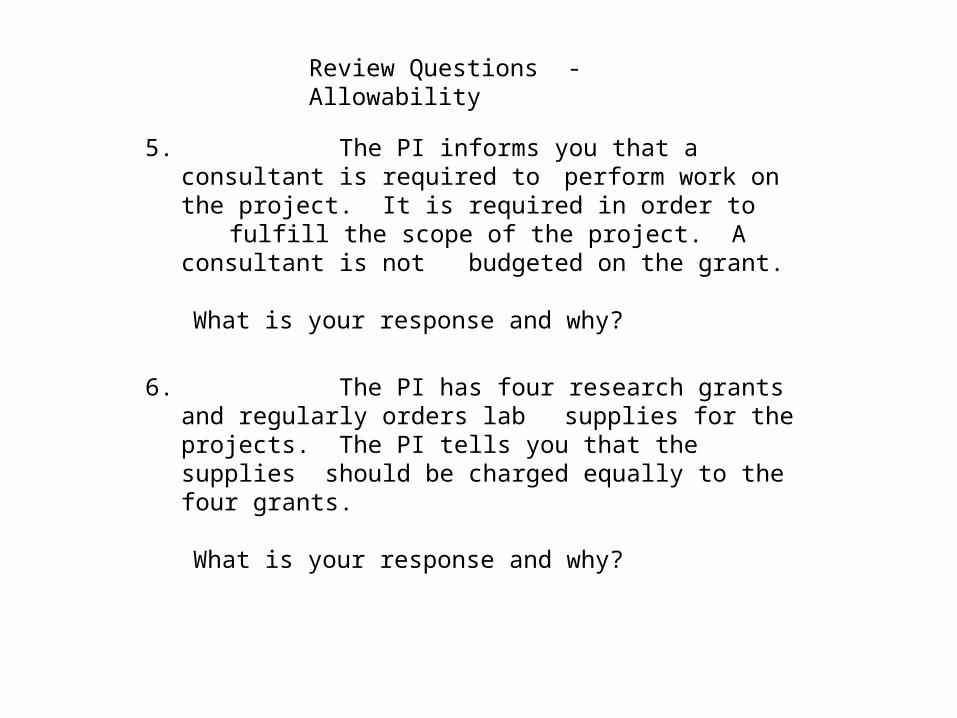

Review Questions - Allowability

1. As part of your grant the PI must be available at all times to the participants on the project. The PI has requested to buy a cell phone and charge it to the grant.

What is your response and why?

2. The grant requires a number of personnel appointments and Salary Distribution Revision forms to be processed. The Administrative Assistant in the department is handling these tasks. The PI has requested to charge a portion of the Assistant’s time to the grant.

What is your response and why?

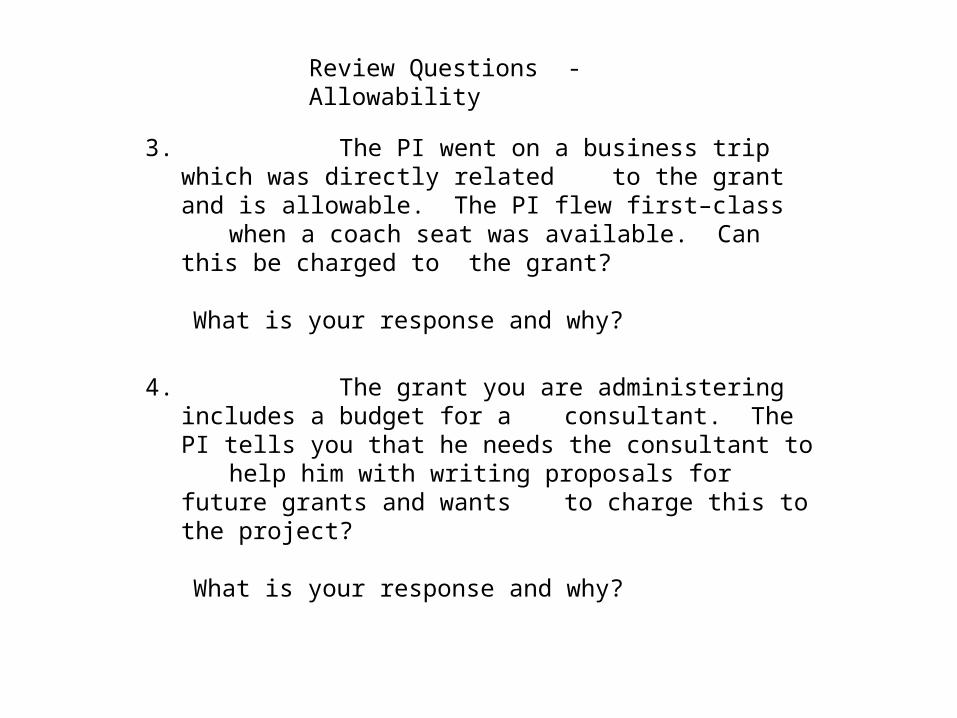

Review Questions - Allowability

3. The PI went on a business trip which was directly related to the grant and is allowable. The PI flew first–class when a coach seat was available. Can this be

charged to the grant?

What is your response and why?

4. The grant you are administering includes a budget for a consultant. The PI tells you that he needs the

consultant to help him with writing proposals for future grants and wants to charge this to the project?

What is your response and why?

Review Questions - Allowability

5. The PI informs you that a consultant is required to perform work on the project. It is required in order to fulfill the scope of the project. A consultant is not budgeted on the grant.

What is your response and why?

6. The PI has four research grants and regularly orders lab supplies for the projects. The PI tells you that the

supplies should be charged equally to the four grants.

What is your response and why?

Review Questions - Allowability

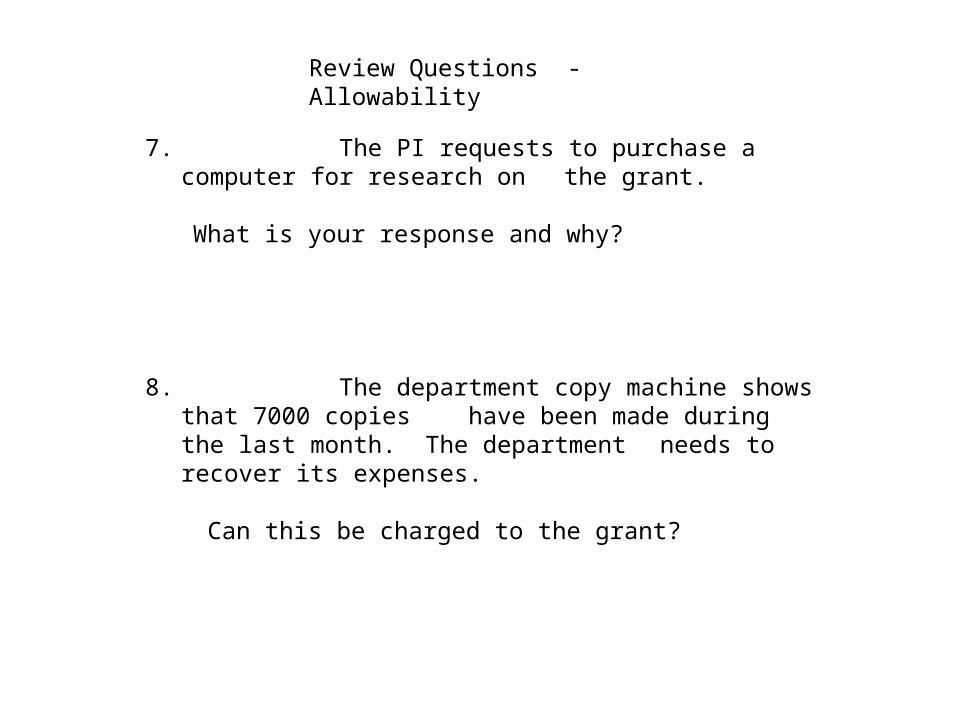

7. The PI requests to purchase a computer for research on the grant.

What is your response and why?

8. The department copy machine shows that 7000 copies have been made during the last month. The

department needs to recover its expenses.

Can this be charged to the grant?

Review Questions - Allowability

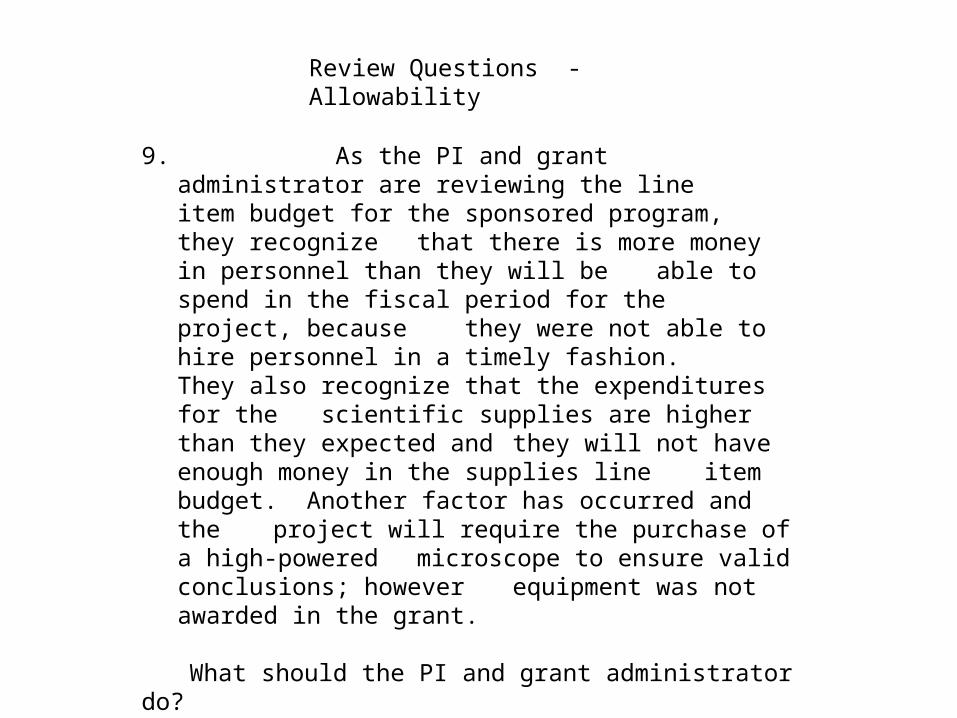

9. As the PI and grant administrator are reviewing the line item budget for the sponsored program, they

recognize that there is more money in personnel than they will be able to spend in the fiscal period for the project, because they were not able to hire personnel in a timely fashion. They also recognize that the expenditures for the scientific supplies are higher than they expected and

they will not have enough money in the supplies line item budget. Another factor has occurred and the project will require the purchase of a high-powered microscope to ensure valid conclusions; however equipment was not awarded in the grant.

What should the PI and grant administrator do?

Review Questions - Allowability

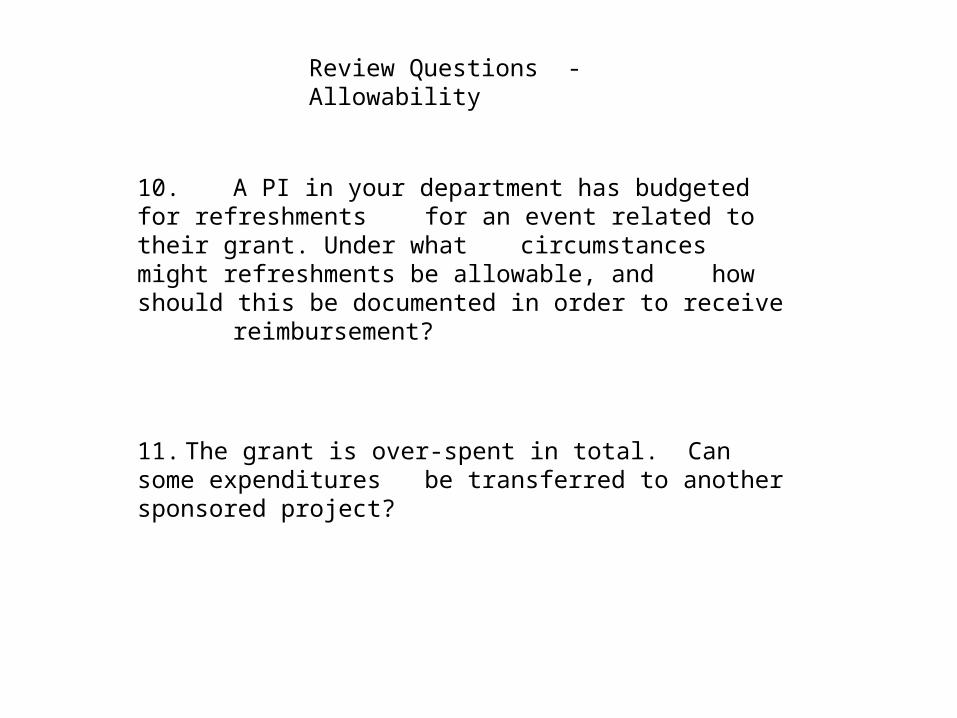

10. A PI in your department has budgeted for refreshments for an event related to their grant. Under what

circumstances might refreshments be allowable, and how should this be documented in order to receive reimbursement?

11. The grant is over-spent in total. Can some expenditures be transferred to another sponsored project?

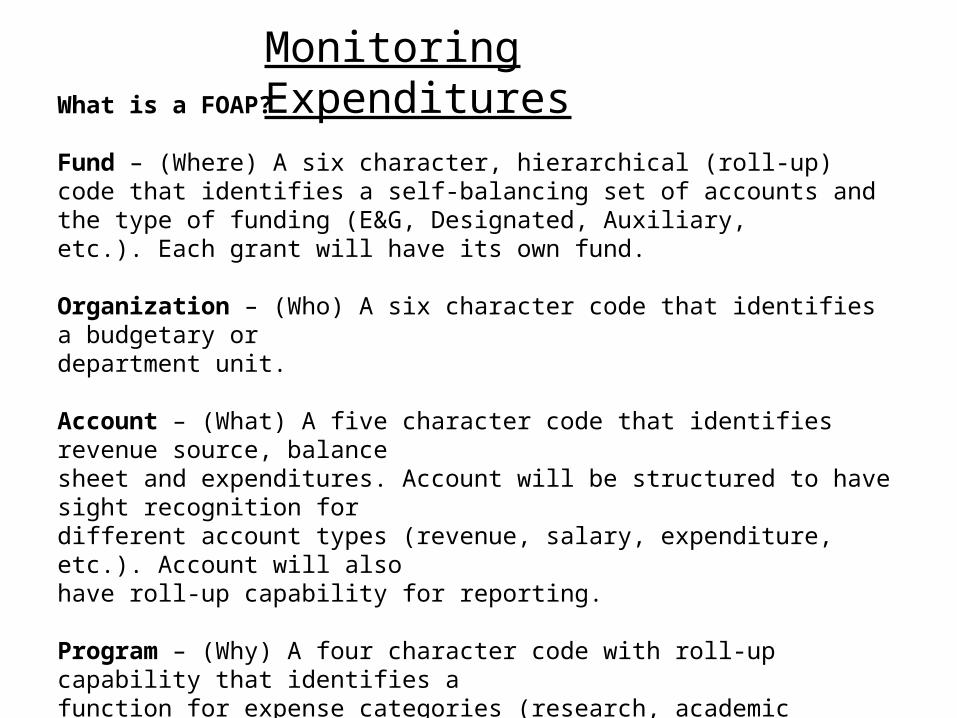

Monitoring ExpendituresWhat is a FOAP?

Fund – (Where) A six character, hierarchical (roll-up) code that identifies a self-balancing set of accounts and the type of funding (E&G, Designated, Auxiliary,etc.). Each grant will have its own fund.

Organization – (Who) A six character code that identifies a budgetary ordepartment unit.

Account – (What) A five character code that identifies revenue source, balancesheet and expenditures. Account will be structured to have sight recognition fordifferent account types (revenue, salary, expenditure, etc.). Account will alsohave roll-up capability for reporting.

Program – (Why) A four character code with roll-up capability that identifies afunction for expense categories (research, academic support, instruction, etc.). The Index, although not part of the FOAP, plays a large role in data entry. Consider an index as a convenience tool, replacing the need to enter the entire FOAP string, generally, with the exception of account.

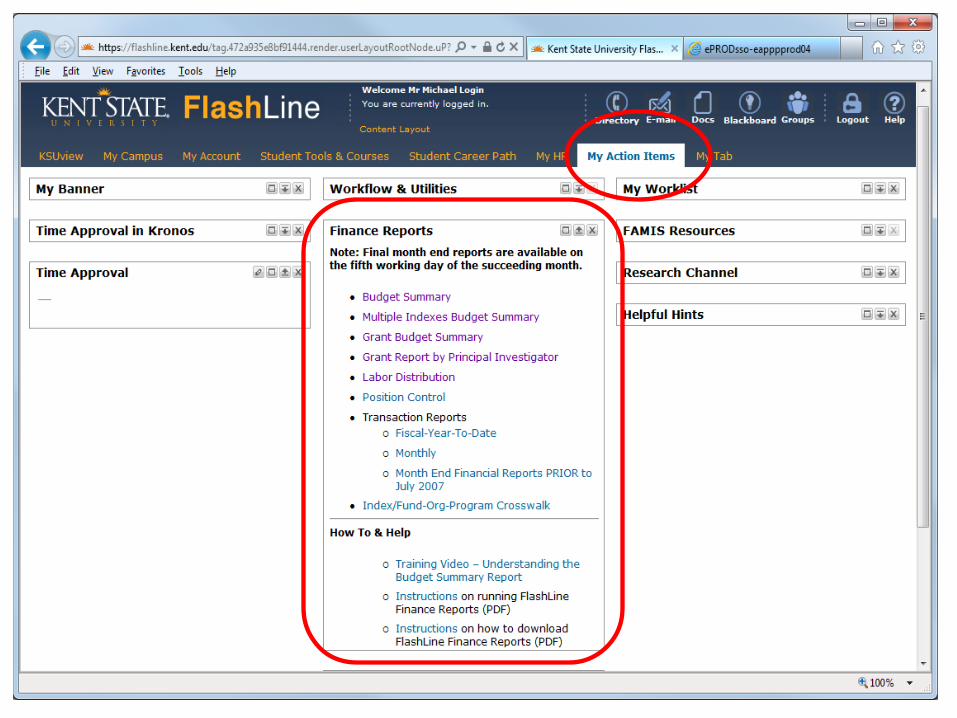

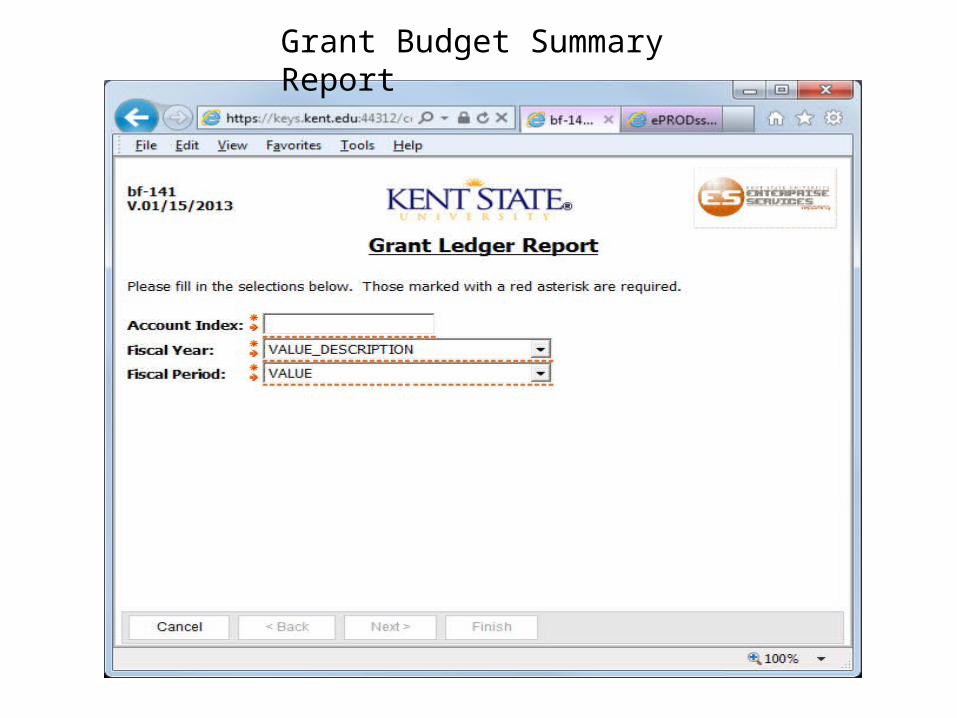

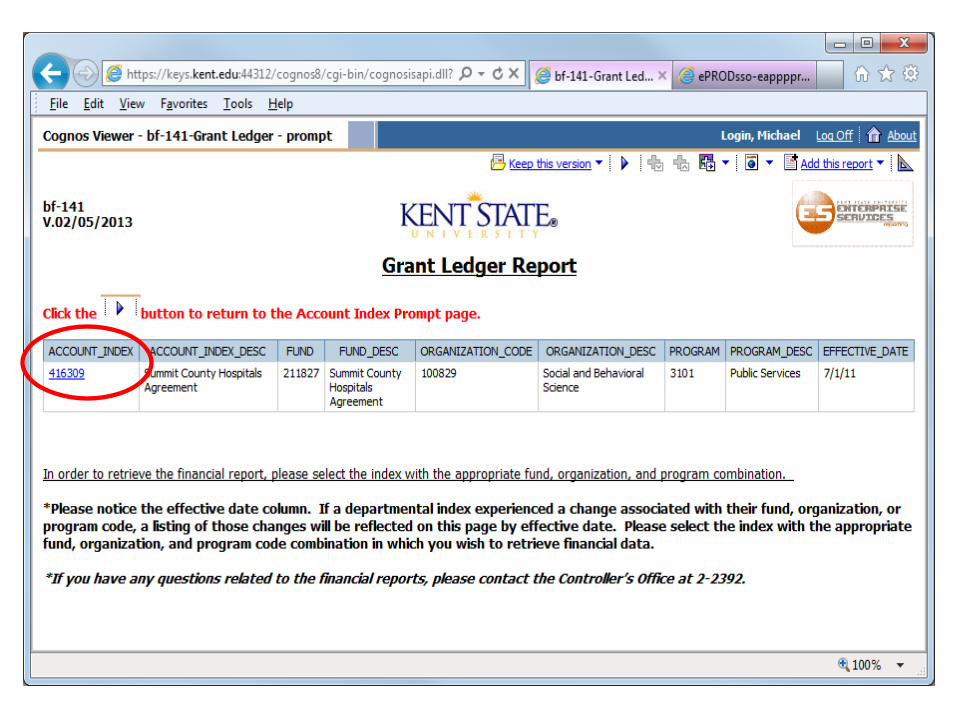

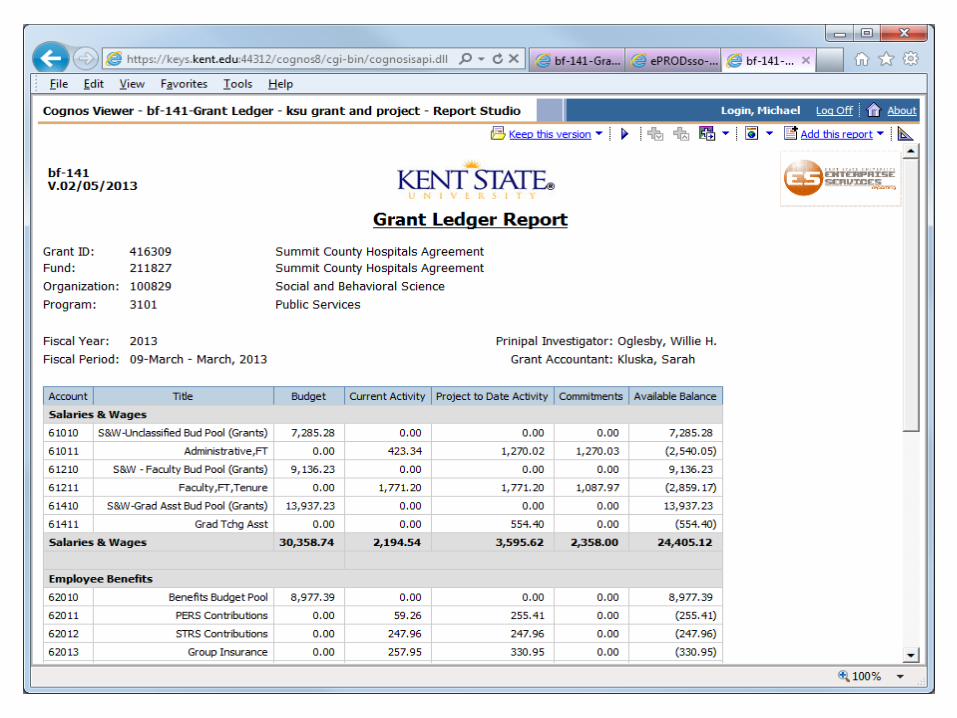

Grant Budget Summary Report

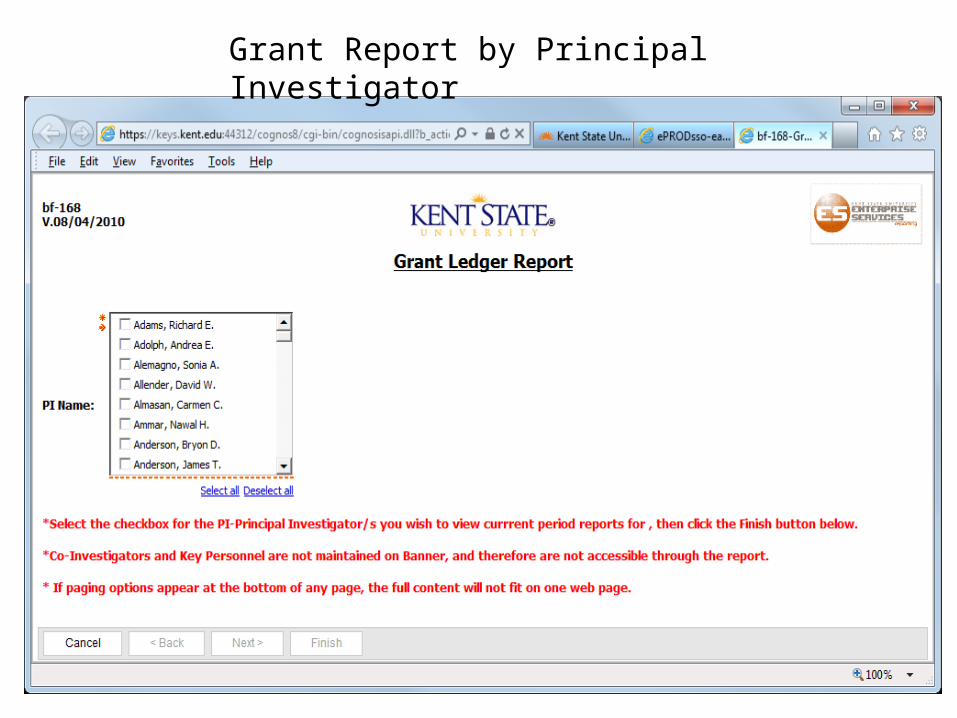

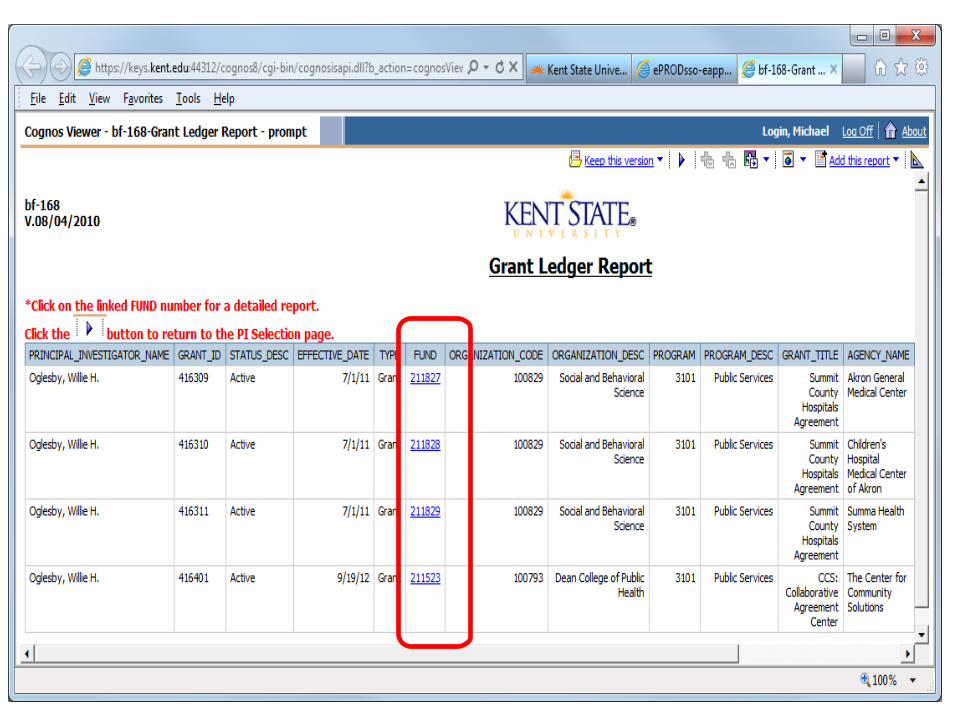

Grant Report by Principal Investigator

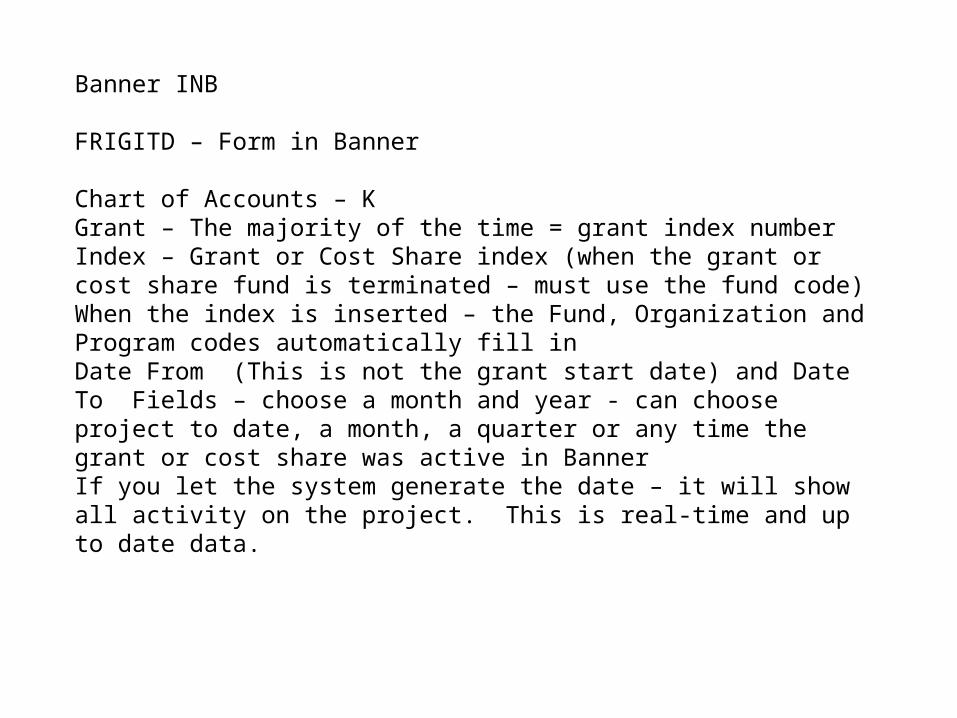

Banner INB FRIGITD – Form in Banner

Chart of Accounts – KGrant – The majority of the time = grant index numberIndex – Grant or Cost Share index (when the grant or cost share fund is terminated – must use the fund code)When the index is inserted – the Fund, Organization and Program codes automatically fill inDate From (This is not the grant start date) and Date To Fields – choose a month and year - can choose project to date, a month, a quarter or any time the grant or cost share was active in BannerIf you let the system generate the date – it will show all activity on the project. This is real-time and up to date data.

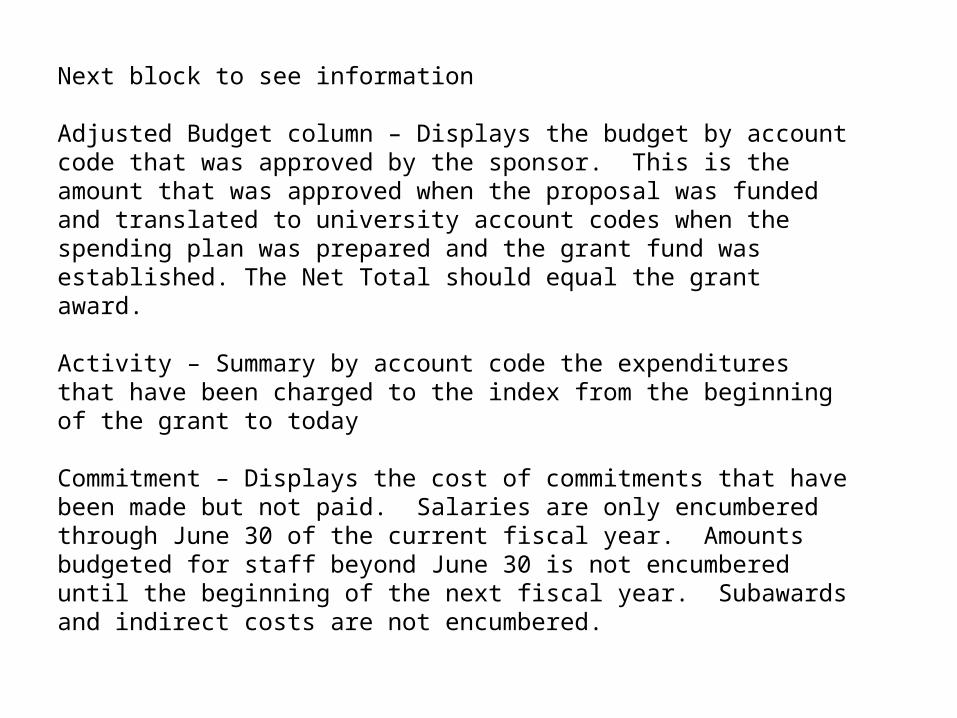

Next block to see information

Adjusted Budget column – Displays the budget by account code that was approved by the sponsor. This is the amount that was approved when the proposal was funded and translated to university account codes when the spending plan was prepared and the grant fund was established. The Net Total should equal the grant award.

Activity – Summary by account code the expenditures that have been charged to the index from the beginning of the grant to today

Commitment – Displays the cost of commitments that have been made but not paid. Salaries are only encumbered through June 30 of the current fiscal year. Amounts budgeted for staff beyond June 30 is not encumbered until the beginning of the next fiscal year. Subawards and indirect costs are not encumbered.

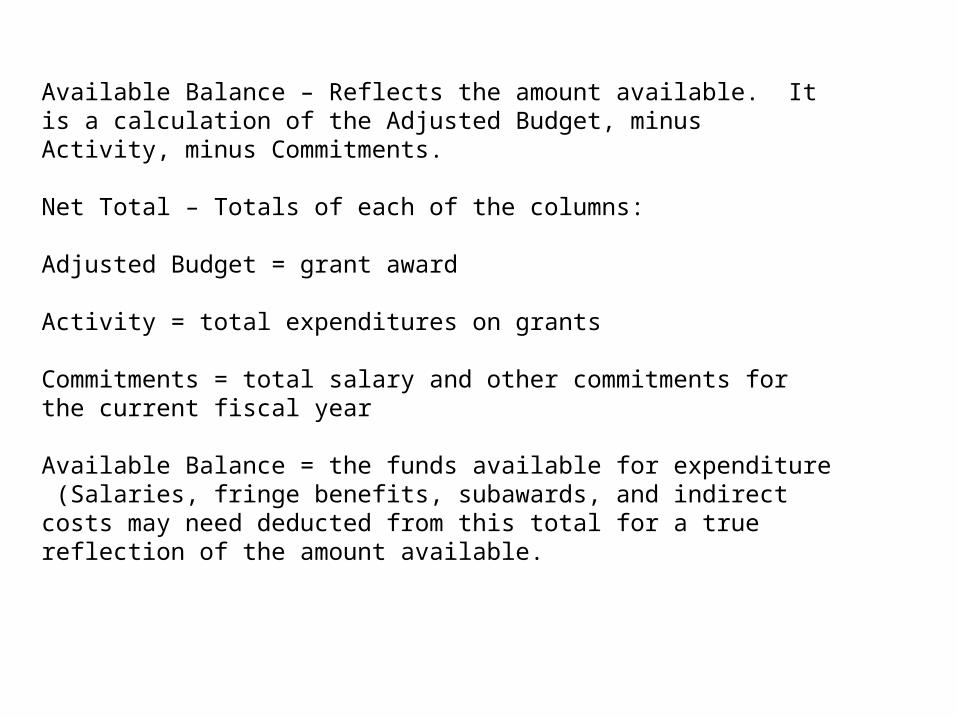

Available Balance – Reflects the amount available. It is a calculation of the Adjusted Budget, minus Activity, minus Commitments.

Net Total – Totals of each of the columns:

Adjusted Budget = grant award

Activity = total expenditures on grants

Commitments = total salary and other commitments for the current fiscal year

Available Balance = the funds available for expenditure (Salaries, fringe benefits, subawards, and indirect costs may need deducted from this total for a true reflection of the amount available.

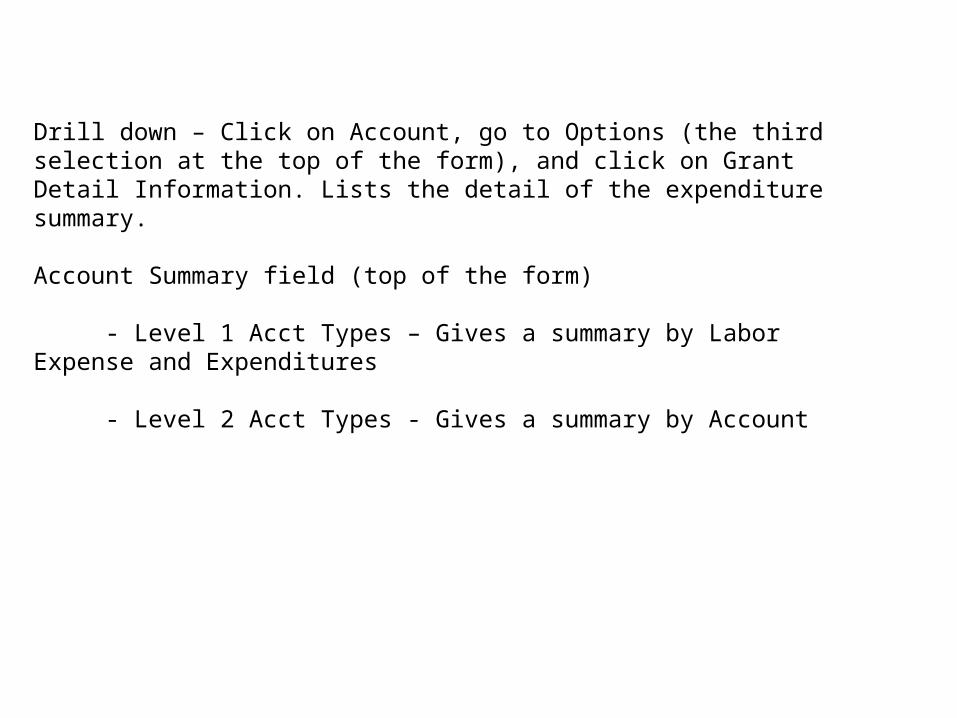

Drill down – Click on Account, go to Options (the third selection at the top of the form), and click on Grant Detail Information. Lists the detail of the expenditure summary.

Account Summary field (top of the form)

- Level 1 Acct Types – Gives a summary by Labor Expense and Expenditures

- Level 2 Acct Types - Gives a summary by Account

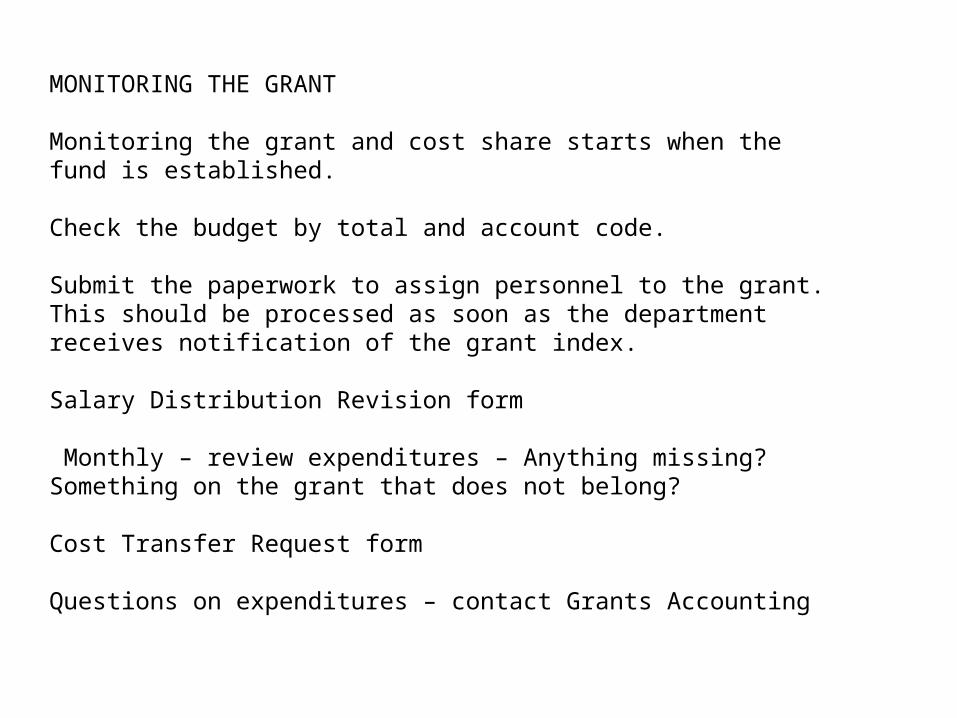

MONITORING THE GRANT

Monitoring the grant and cost share starts when the fund is established.

Check the budget by total and account code.

Submit the paperwork to assign personnel to the grant. This should be processed as soon as the department receives notification of the grant index.

Salary Distribution Revision form

Monthly – review expenditures – Anything missing? Something on the grant that does not belong?

Cost Transfer Request form

Questions on expenditures – contact Grants Accounting

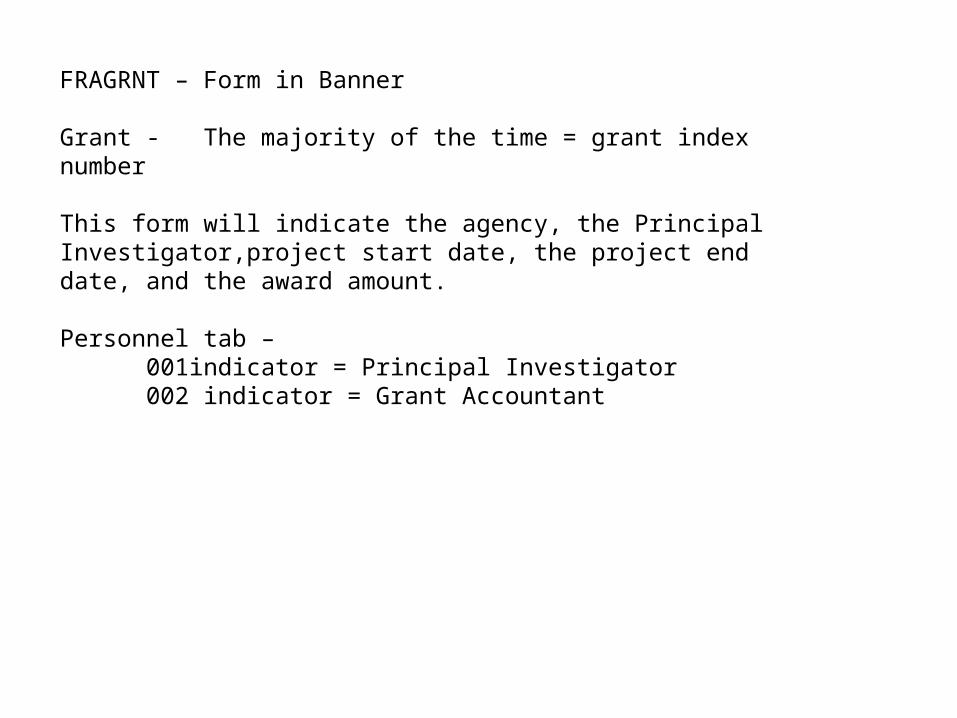

FRAGRNT – Form in Banner

Grant - The majority of the time = grant index number

This form will indicate the agency, the Principal Investigator,project start date, the project end date, and the award amount.

Personnel tab – 001indicator = Principal Investigator 002 indicator = Grant Accountant

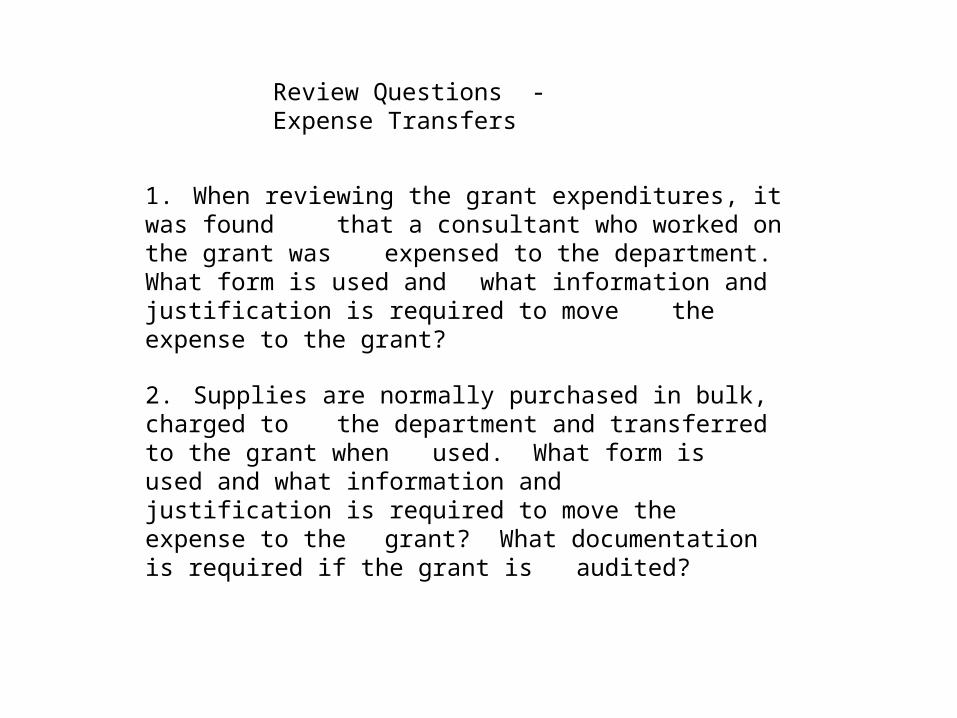

Review Questions - Expense Transfers

1. When reviewing the grant expenditures, it was found that a consultant who worked on the grant was

expensed to the department. What form is used and what information and justification is required to move the expense to the grant?

2. Supplies are normally purchased in bulk, charged to the department and transferred to the grant when used. What form is used and what information and justification is required to move the expense to the grant? What documentation is required if the grant is audited?

Review Questions - Expense Transfers

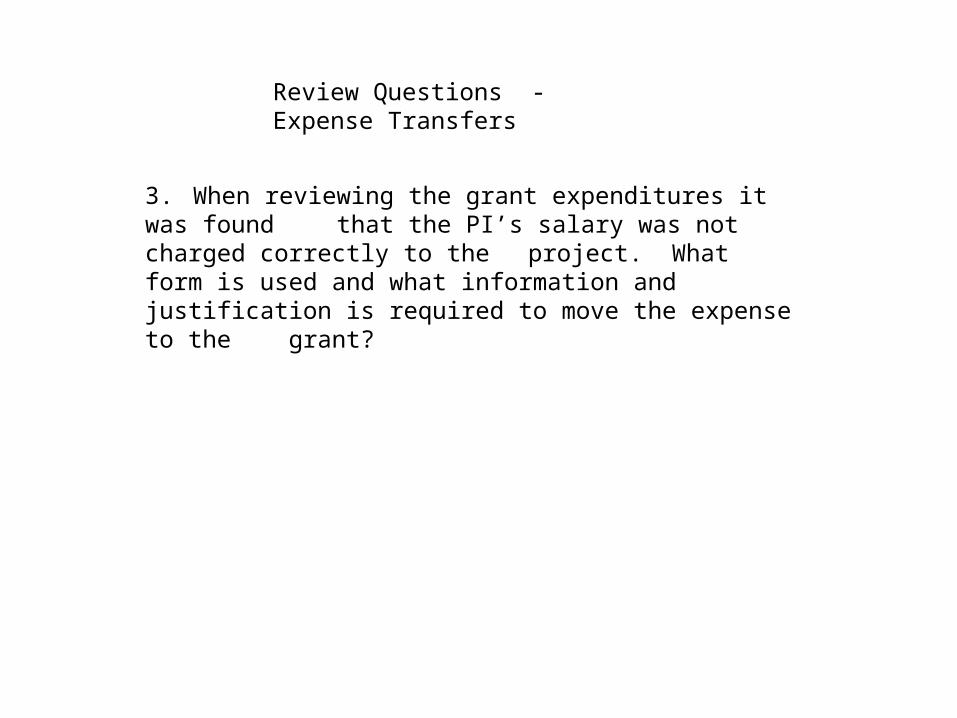

3. When reviewing the grant expenditures it was found that the PI’s salary was not charged correctly to the project. What form is used and what information and justification is required to move the expense to the grant?

Prior Approvals

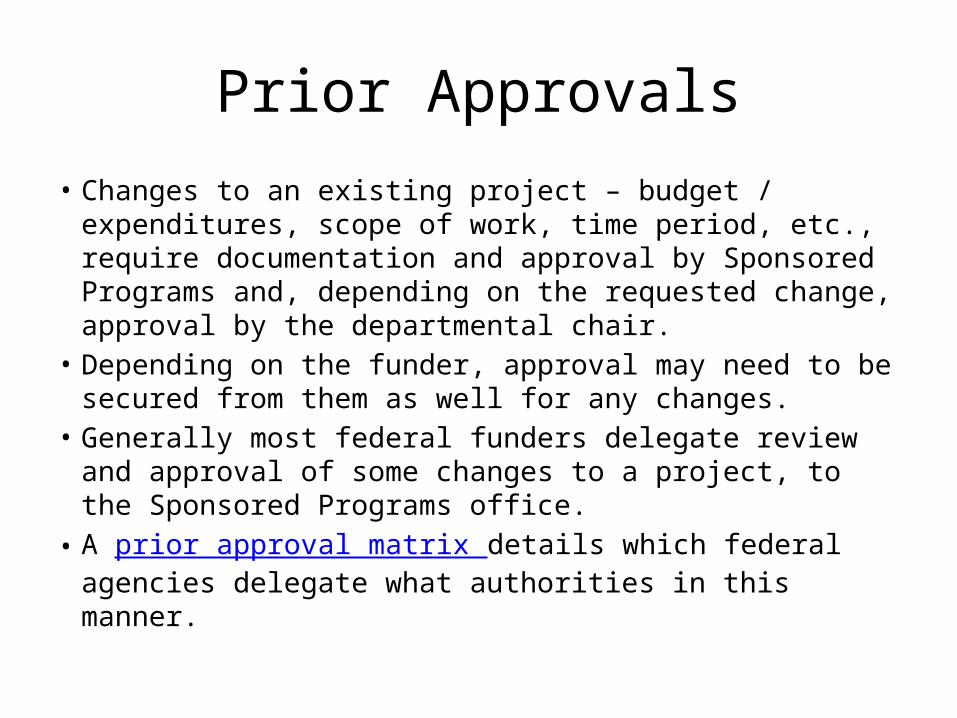

• Changes to an existing project – budget / expenditures, scope of work, time period, etc., require documentation and approval by Sponsored Programs and, depending on the requested change, approval by the departmental chair.

• Depending on the funder, approval may need to be secured from them as well for any changes.

• Generally most federal funders delegate review and approval of some changes to a project, to the Sponsored Programs office.

• A prior approval matrix details which federal agencies delegate what authorities in this manner.

Prior Approvals

• Most requests to change an aspect of a project are initiated by the PI using the Institutional Prior Approval form for Sponsored Projects.

• NSF requests for first extensions must be submitted through Fastlane, rather than documented on the Prior Approval form.

• Requests are occasionally initiated by Grants Accounting or Sponsored Programs if, for example, a budget category is overspent by more than 10% or $500, whichever is less. For audit purposes this also requires the Institutional Prior Approval form.

Project Reporting

• Technical Reports– Annual Progress Report– Final Technical – Prepared by PI– Submitted by PI or Sponsored Programs depending on award

requirements– Sponsored Programs maintains copy for auditable records

• Financial Reports– Prepared by Grants Accounting based on expenditures recorded in the

index– PIs have the opportunity to review prior to submission to they agency– Timing and format vary by agency and award requirements

Project Closeout• Final technical and financial reports typically required ninety days

after the project end• No additional expenditures may be incurred after the project end

date• Permits sufficient time for expenditures incurred before the end of

the project to be liquidated and gives the principal investigator time to prepare the technical report

• Patent disclosure, equipment disposition, and other required reports may be required after the termination date or with the final report

• Grant/contract records are subject to annual audit; they must be retained for a minimum of three years from the date the final reports are filed or approved

References

• Grants Management Manual http://www.kent.edu/research/sponsoredprograms/awardadmin.cfm (compliance section has many helpful links)

• Grants Financial Administration Forms http://www.kent.edu/research/sponsoredprograms/forms-and-instructions.cfm

• University Forms Library http://www.kent.edu/bas/forms/index.cfm

![BURCHARD FÜHRER - fuehrergruppe.de · Ein Magazin der Burchard Führer GmbH 22. Jahrgang Ausgabe 1/18 BURCHARD FÜHRER SINDEN SIE IN DIESER AUSGABE Ausbildung 2018;u ]ov _;Wo1_ bl](https://img.pdfslide.net/doc/110x75/5e05802bad6b4d332001c75f/burchard-foehrer-ein-magazin-der-burchard-fhrer-gmbh-22-jahrgang-ausgabe-118.jpg)