Embed Size (px)

Citation preview

THE SEARS TOWER

A CASE STUDY OF THE DEVELOPMENT, RE-FINANCINGS AND SALE OF NORTH AMERICA’S TALLEST BUILDING

Students: Ben Bove, Aristithis Loukas, Rich McPhillips, Eddie Meder, Kevin Merchant, Agustin Rizo, Greg Trimmer, Susan Weaver, Neal White, and John Wilbeck. Faculty Member: Joseph L. Pagliari, Jr.

January 1, 2007

This case study has been prepared solely for purposes of class discussion. It should not be construed as a judgment about or endorsement of any particular business matter. Moreover, the information contained herein has been obtained from sources we believe to be reliable; however, we make no representation or warranty as to their accuracy.

The Sears Tower January 1, 2007

I. Executive Summary ............................................................................................................. 1 II. Overview of The Sears Tower ............................................................................................ 3

Background of Sears & Roebuck Co........................................................................................ 3Sears Consolidates Chicago Operations ................................................................................. 3 Tower Construction & Architectural Significance ................................................................ 4Retail Industry Background in the 1970s - 1980s.................................................................. 9Sears Encounters Hard Times and Decides to Leave the Tower ............................................ 9Sears Relocates its Headquarters .......................................................................................... 13

III. A Series of Tower Refinancings (1990-2003) .................................................................. 15The MetLife / AEW Years .................................................................................................... 16The MetLife / Trizec Years ................................................................................................... 21September 11, 2001............................................................................................................... 23Trizec Decides to Exit the Sears Tower ................................................................................ 27The MetLife Years................................................................................................................. 29MetLife’s Decision to Purchase the Sears Tower ................................................................. 30 MetLife’s Decision to Sell the Sears Tower .......................................................................... 30

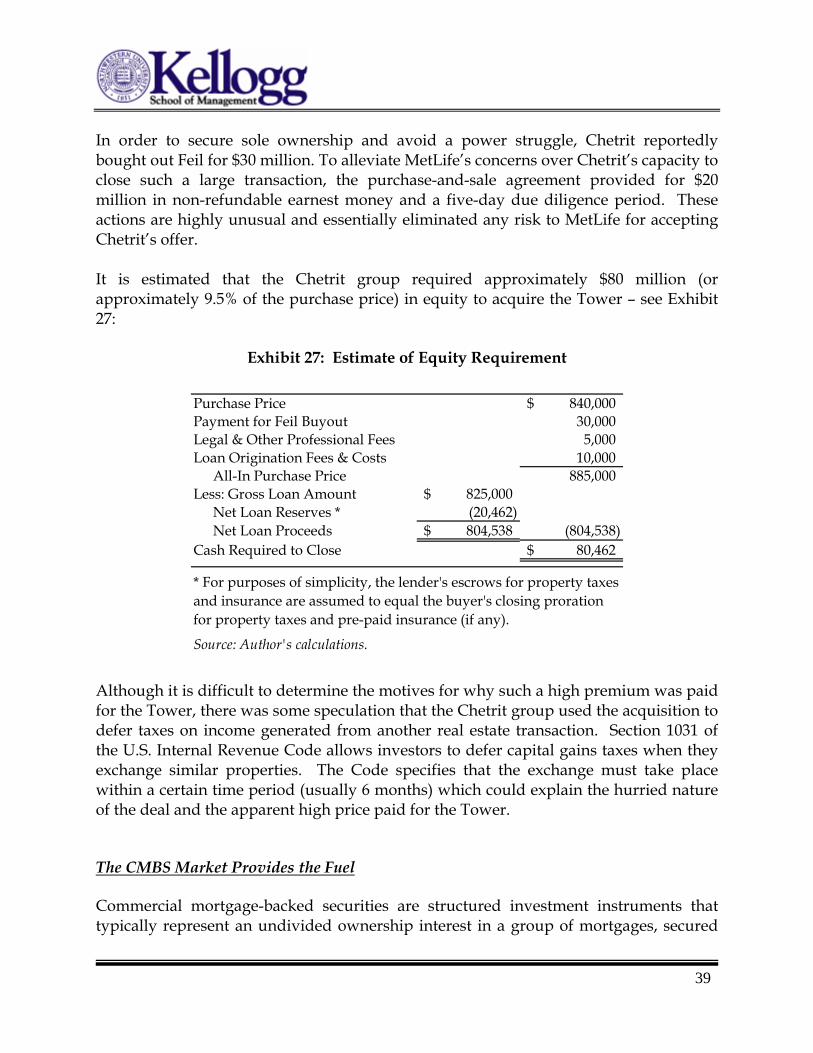

IV. Joseph Chetrit and Company Acquire the Sears Tower .............................................. 32 Valuation of the Tower in 2004 ............................................................................................ 32 Aggressive Financing Leads to Sky High Prices & Emergence of Private Buyers ............. 36 Chetrit Group Wins the Deal ............................................................................................... 37 The CMBS Market Provides the Fuel................................................................................... 39The Sears Tower Today (2006) ............................................................................................. 50 The State of the Office Market .............................................................................................. 53Repositioning Possibilities for the Sears Tower.................................................................... 57

V. Conclusion .......................................................................................................................... 61VI. Case Questions ................................................................................................................... 62 VII. Acknowledgments ............................................................................................................. 66 VIII. Appendices ......................................................................................................................... 68

1

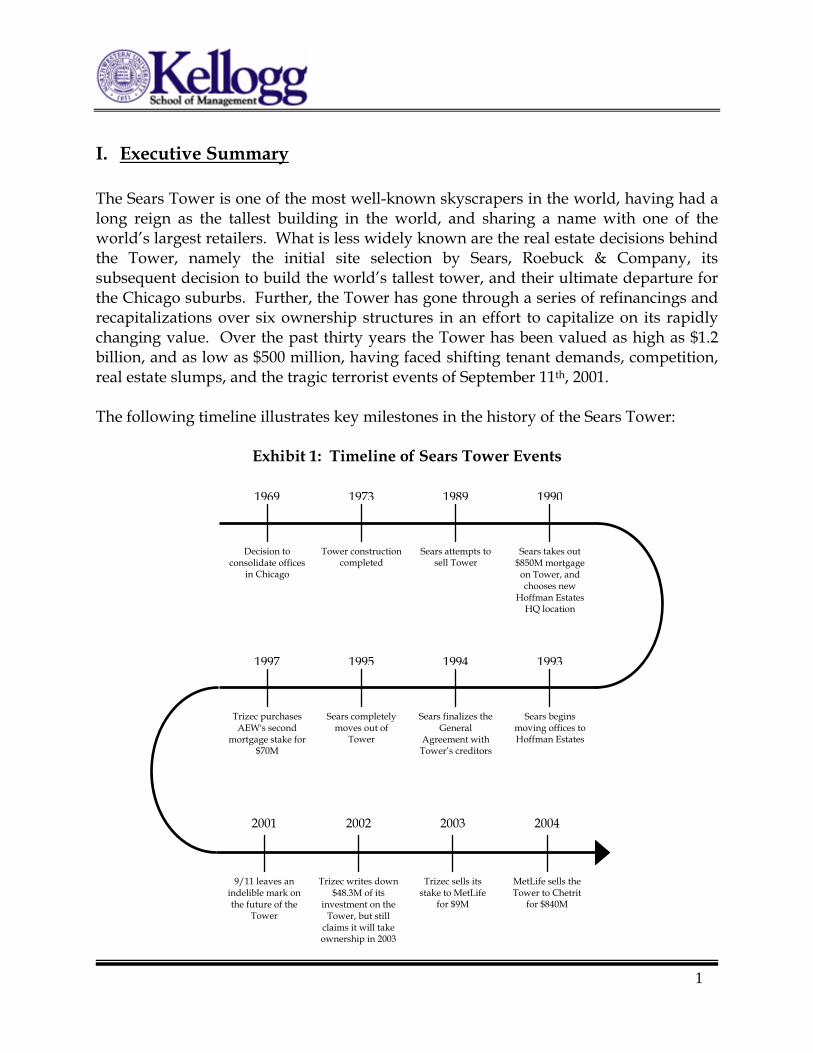

I. Executive Summary The Sears Tower is one of the most well-known skyscrapers in the world, having had a long reign as the tallest building in the world, and sharing a name with one of the world’s largest retailers. What is less widely known are the real estate decisions behind the Tower, namely the initial site selection by Sears, Roebuck & Company, its subsequent decision to build the world’s tallest tower, and their ultimate departure for the Chicago suburbs. Further, the Tower has gone through a series of refinancings and recapitalizations over six ownership structures in an effort to capitalize on its rapidly changing value. Over the past thirty years the Tower has been valued as high as $1.2 billion, and as low as $500 million, having faced shifting tenant demands, competition, real estate slumps, and the tragic terrorist events of September 11th, 2001. The following timeline illustrates key milestones in the history of the Sears Tower:

Exhibit 1: Timeline of Sears Tower Events

Sears takes out $850M mortgage

on Tower, and chooses new

Hoffman Estates HQ location

Sears attempts to sell Tower

Tower construction completed

Decision to consolidate offices

in Chicago

1990 1989 1973 1969

Sears begins moving offices to Hoffman Estates

Sears finalizes the General

Agreement with Tower’s creditors

Sears completely moves out of

Tower

Trizec purchases AEW's second

mortgage stake for $70M

1993 1994 1995 1997

MetLife sells the Tower to Chetrit

for $840M

Trizec sells its stake to MetLife

for $9M

Trizec writes down $48.3M of its

investment on the Tower, but still

claims it will take ownership in 2003

9/11 leaves an indelible mark on the future of the

Tower

2004 2003 2002 2001

The Sears Tower January 1, 2007

As one of fastest-growing retailers of the 20th century, Sears, Roebuck and Company had an impressive need for space and a desire to consolidate its vast operations under one roof. Several sites in Illinois were considered and Sears quickly settled on 233 South Wacker Drive for its convenience to major transportation nodes and widespread city support. Skidmore, Owings & Merrill were retained as architects and created a flexible, yet open design based on a “megamodule” system of structural tubes. Sears presence at the Tower, however, was short lived; in 1990, Sears moved to a new headquarters complex in Hoffman Estates, a suburb outside of Chicago. Unable to find a buyer to purchase the Tower during the late 1980s, Sears instead leveraged the value of the Tower and borrowed $850 million in 1990, thereby injecting cash into its balance sheet. In 1994, Sears entered into a complex financial arrangement transferring effective control of the Tower to its creditors MetLife ($600 million first mortgage loan) and AEW ($250 million second mortgage loan). Between 1997 and 2003, TrizecHahn – which had acquired AEW’s interest – attempted to buy a controlling stake in the Tower but reversed course due to the economic downturn after September 11, 2001. Subsequently, Trizec sold its position to MetLife. After serving as the primary loan note holder for the past 13 years, MetLife now had full control of the Tower. In 2004, MetLife sold the Tower to a small investor group led by Joseph Chetrit for $840 million. In a great twist of irony, Chetrit’s financing package ($600 million in first-mortgage financing and $225 million in mezzanine financing) looks eerily similar to the financing package supplied by MetLife and AEW nearly 15 years earlier. Fueling the purchase was a combination of historically low interest rates and an aggressive lending environment. Chetrit was able to secure an interest-only loan covering 93% of the purchase price of the Tower. As of the date of this writing, Chetrit is reportedly looking to refinance the Tower, using a combination of outside equity and a fixed-rate loan. Despite the Tower’s turbulent history, an impressive rent roll, a desirable Chicago CBD location, a design well ahead of its time and a perceived premier status have made the Tower an attractive acquisition for investors since it was built. What does the future hold for the Tower? There are several key questions that must be considered in the context of the Chicago office market and national investment trends. They include: Will the Chetrit acquisition of the Tower prove financially viable? Will lenders remain as aggressive? Will the Tower be repositioned for another purpose or kept as primarily office space?

2

3

II. Overview of The Sears Tower

Background of Sears & Roebuck Co. 1

Sears, Roebuck & Company (“Sears”) was formed in 1893 as a mail-order watch company in Chicago, Illinois, and was the innovative idea of Richard Sears, a railway station agent from Minneapolis, Minnesota. Early on, Sears and his partner, Alvah C. Roebuck, recognized that there was a lucrative market to sell general merchandise using a mail-order business model. At this time, the United States was largely an agricultural economy. Rural farmers primarily bought their goods at the local general store and, since little competition existed in these locations, were often faced with intolerably high markups on the items they purchased. By purchasing goods in bulk to take advantage of volume discounts, Sears utilized the rail and postal systems to deliver goods to rural customers at prices well below those of the local general stores. Sears’ mail order business took off. Sales reached $400,000 by 1893, and surpassed $750,000 by 1895. The company began producing a general merchandise catalog with over 500 pages offering items ranging from shoes, women's garments and china to firearms, furniture and buggies. As Sears expanded, they leased various buildings throughout Chicago. By 1906, they constructed a 40-acre, $5 million2, 3 million square foot mail-order plant and office building on Chicago's West Side. At that time, it was the largest commercial building in the world.

Sears Consolidates Chicago Operations

Sears’ continued success led to the expansion of its offices and retail stores nationwide as well as internationally. In December 1967, Sears, Roebuck & Co reached $1 billion of sales in a single month, a new record for Sears. By 1969, Sears earned $8.9 billion in annual sales up from $8.2 billion the year prior, thus breaking its own sales record for 15 consecutive years. That same year, the company’s management, under the direction of Chairman Gordon Metcalf and President Arthur Wood, decided to consolidate its Chicago office locations into one building. The company had an immediate need for approximately 3 million square feet of space and wanted to ensure it would have room to expand in the future. Rumors circulated about where the new headquarters would be. Sears had previously moved its Allstate Insurance division to Northbrook, Illinois, a northern suburb of Chicago. Speculation came to an end in April 1969, when Sears named Cushman and

1 Sears Archives. Sears, Roebuck & Co. 23 May 2006 <www.searsarchives.com/history/history1887.htm>. 2 Adjusted for inflation, this expenditure would have roughly equaled $100 million in today’s dollars.

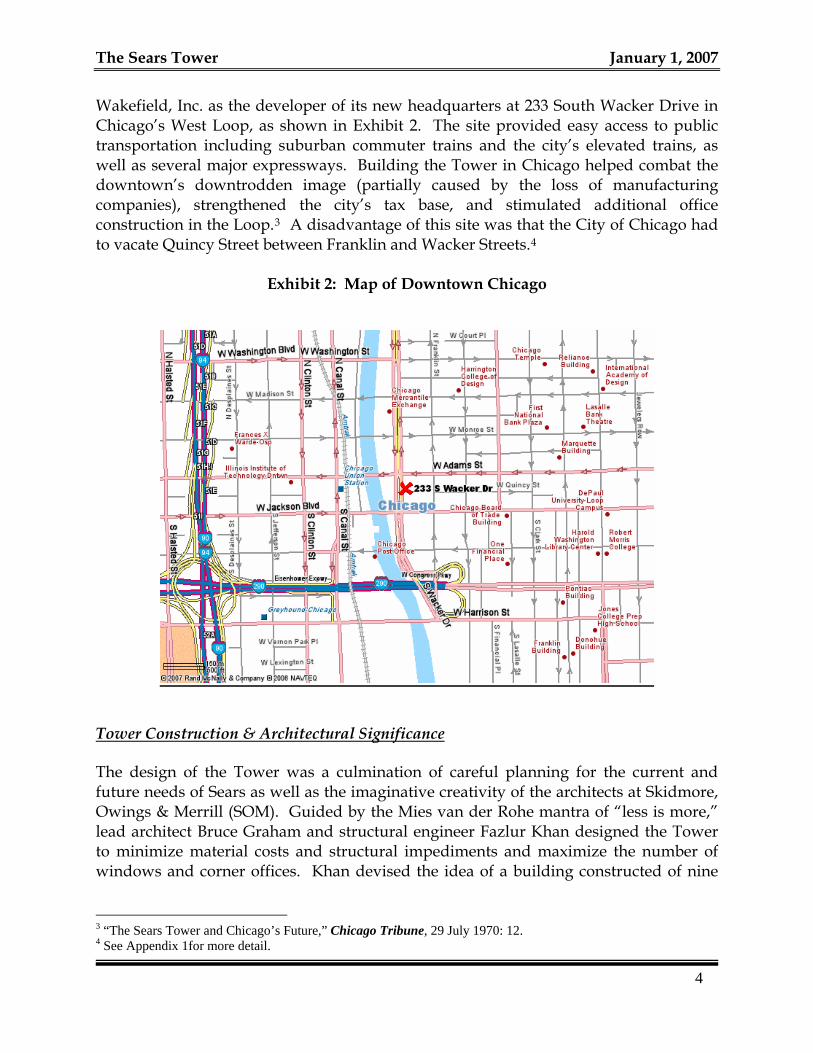

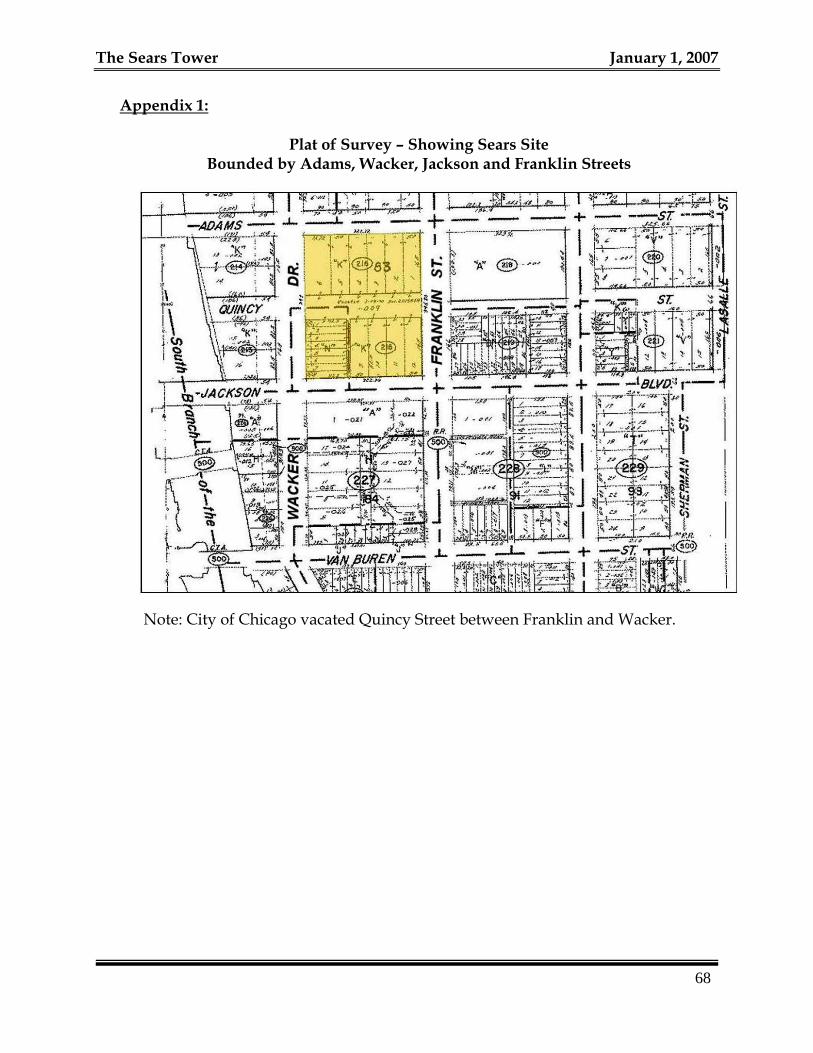

The Sears Tower January 1, 2007 Wakefield, Inc. as the developer of its new headquarters at 233 South Wacker Drive in Chicago’s West Loop, as shown in Exhibit 2. The site provided easy access to public transportation including suburban commuter trains and the city’s elevated trains, as well as several major expressways. Building the Tower in Chicago helped combat the downtown’s downtrodden image (partially caused by the loss of manufacturing companies), strengthened the city’s tax base, and stimulated additional office construction in the Loop.3 A disadvantage of this site was that the City of Chicago had to vacate Quincy Street between Franklin and Wacker Streets.4

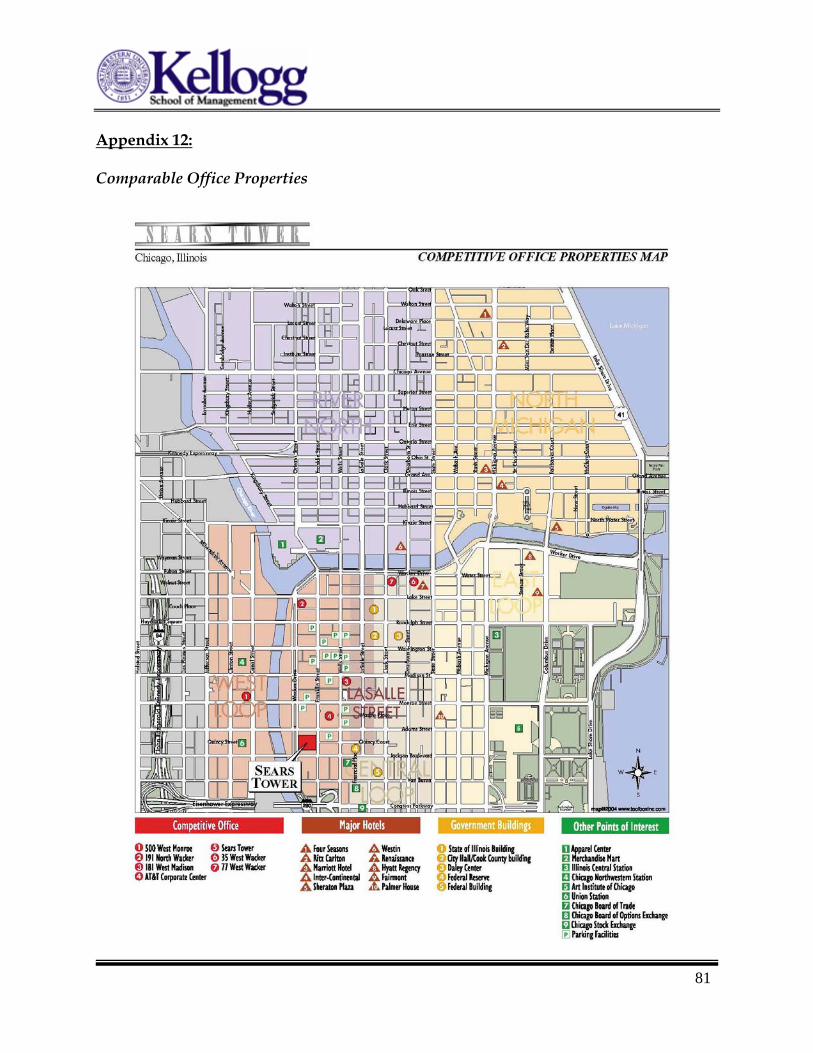

Exhibit 2: Map of Downtown Chicago

Tower Construction & Architectural Significance

The design of the Tower was a culmination of careful planning for the current and future needs of Sears as well as the imaginative creativity of the architects at Skidmore, Owings & Merrill (SOM). Guided by the Mies van der Rohe mantra of “less is more,” lead architect Bruce Graham and structural engineer Fazlur Khan designed the Tower to minimize material costs and structural impediments and maximize the number of windows and corner offices. Khan devised the idea of a building constructed of nine

3 “The Sears Tower and Chicago’s Future,” Chicago Tribune, 29 July 1970: 12.

4

4 See Appendix 1for more detail.

5

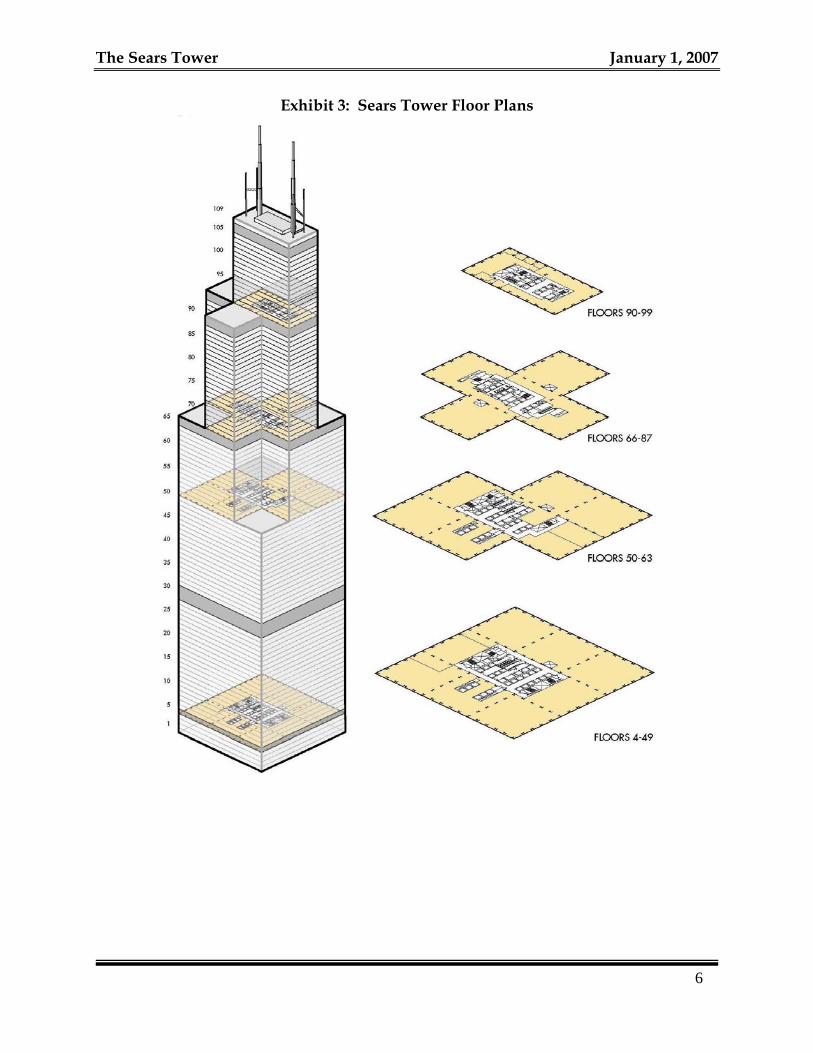

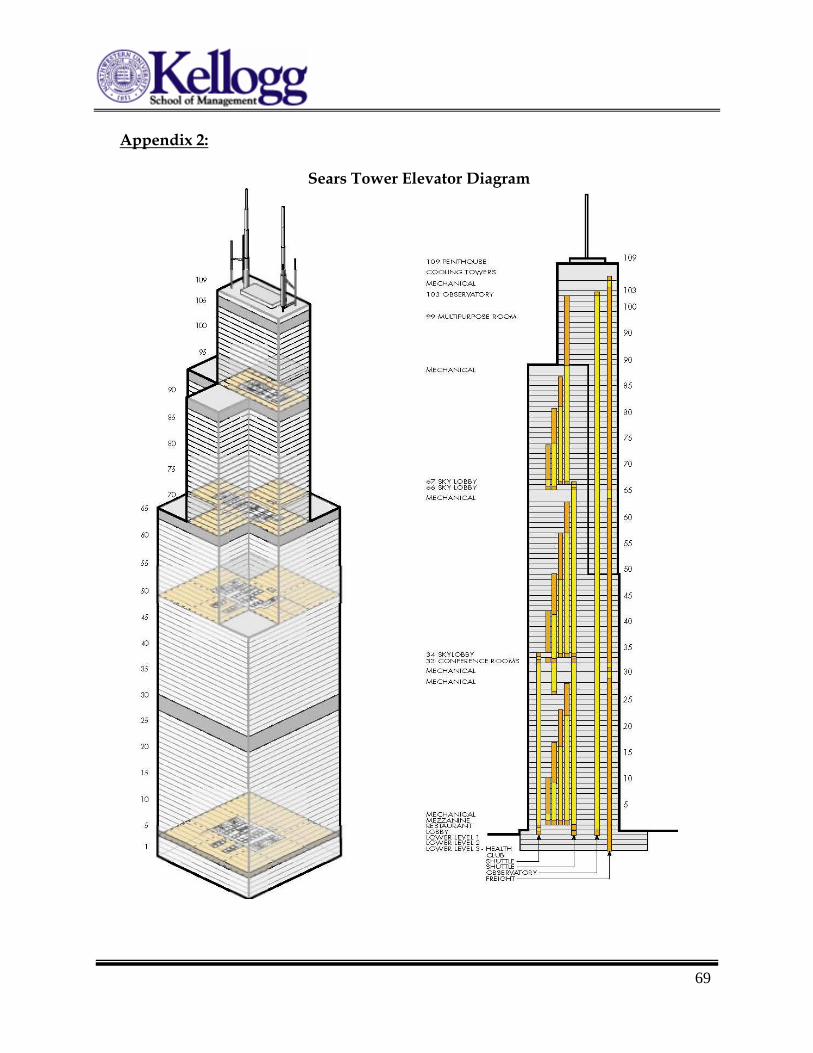

tubes that varied in height to help support the weight of the structure on itself.5 All nine tubes would rise to the 49th floor. Two of the corner modules would end at the 50th floor. Two more tubes would end at the 66th floor. Then three tubes would end at the 89th floor, leaving only two tubes reaching to the 110th floor. See Exhibit 3. This “megamodule” system with its setbacks fashioned the distinctive, husky-shouldered look of the building and created four distinct floor plans to appeal to differing types of prospective tenants. The “megamodule” system created larger floor plans at the lower levels where Sears would house its merchandise and catalog operations in the 3 million square feet it required. The upper floors would consist of smaller floor plates to appeal to smaller firms. Exhibit 4 summarizes the square footage. With the upper floors having a higher ratio of window space to floor space, Sears could charge premium rental rates for these spaces until it needed to reclaim the space. The Tower was initially designed to be the largest high-rise in the city of Chicago. However, after some discussion, the height of the Tower was increased so that it would surpass the then-current record for world’s tallest building.

5 As shown in Appendix 2, the Tower’s height and design created interesting elevator banks.

The Sears Tower January 1, 2007

Exhibit 3: Sears Tower Floor Plans

6

7

Exhibit 4: Overview of the Sears Tower Rentable Square Footage (RSF)

Building Use Gross Area Rentable AreaOffice 3,973,870 3,550,304Retail (LL - 2nd Floor) 464,156 199,398Skydeck & Broadcast 126,608 60,769

Total 4,564,634 3,810,471

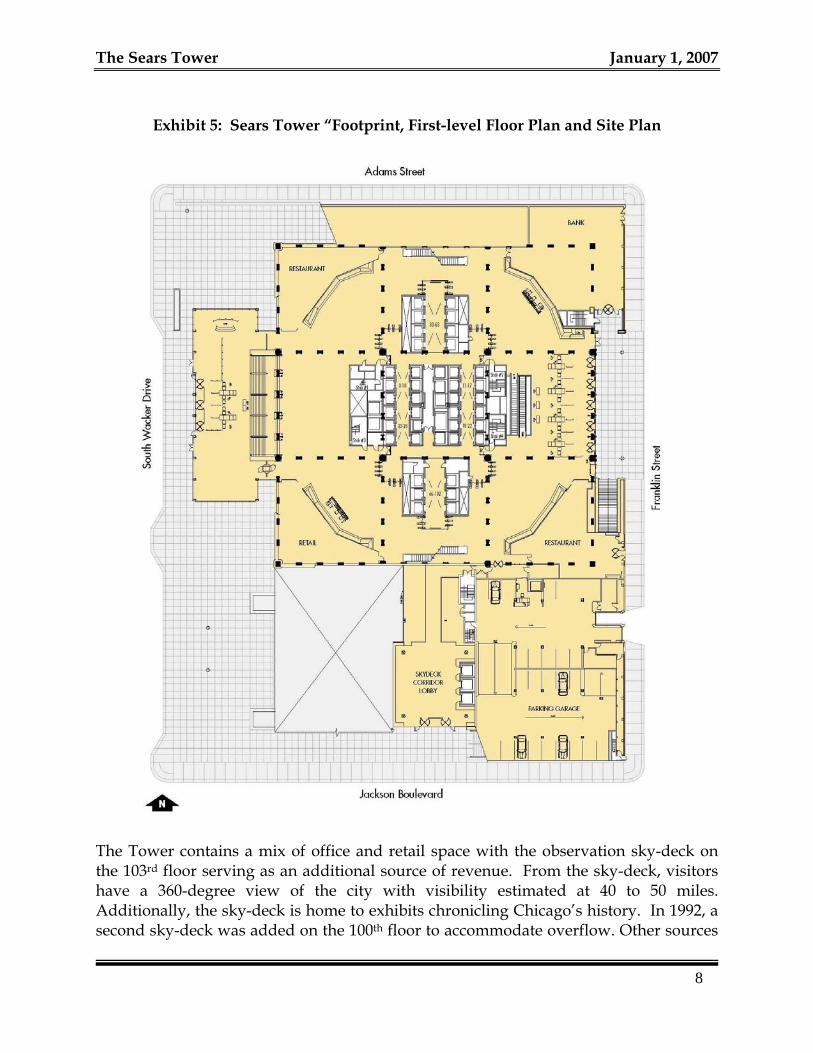

Source: Eastdil Secured, February 2004. Construction on the Tower began in April 1971 and was completed in May 1973. The total acquisition costs including land and construction costs totaled approximately $199 million, which Sears internally financed. (On an inflation-adjusted basis,6 the $199 million in total acquisition costs in 1971 is equivalent to approximately $986 million in 2006 dollars). The distinctive steel and bronze-tinted glass façade of the Tower’s 110 stories ascend 1,450 feet and 7 inches, the maximum height permitted by the Federal Aviation Administration in 1970.7 At the time the Tower was completed, it replaced the twin towers of the World Trade Center in New York City as the world’s tallest building. Twenty-five years later, the Tower lost that title to the Petronas Towers in Kuala Lumpur, Malaysia. The Sears Tower encompasses 4.56 million gross square feet, with approximately 3.8 million rentable square feet including approximately 199,308 rentable square feet of retail space. The footprint of the building covers approximately 50,625 square feet, as shown in Exhibit 5. An excerpt from the Sears Tower marketing materials (www.thesearstower.com) describes the interior of the building as:

“Each floor of the building is divided into 75-foot, column-free squares, or “megamodules,” which provide maximum planning, flexibility and efficiency. Building columns are uniformly spaced fifteen feet on center and exterior window mullions are spaced five feet on center for ease of office layout. The floor dimensions provide extremely flexible space, ideal for any office use including trading floor, open or perimeter office layouts or multi-tenant designs. Twelve feet, 10 ½ inch slab heights allow for high finished ceilings or raised floor or special ceiling configurations.”

6 ftp://ftp.bls.gov/pub/special.requests/cpi/cpiai.txt 7 Nagelberg, Alvan, “Sears to Construct Tallest Building in the World, 110 Stories,” Chicago Tribune, 28 July 1970: 1.

The Sears Tower January 1, 2007

Exhibit 5: Sears Tower “Footprint, First-level Floor Plan and Site Plan

The Tower contains a mix of office and retail space with the observation sky-deck on the 103rd floor serving as an additional source of revenue. From the sky-deck, visitors have a 360-degree view of the city with visibility estimated at 40 to 50 miles. Additionally, the sky-deck is home to exhibits chronicling Chicago’s history. In 1992, a second sky-deck was added on the 100th floor to accommodate overflow. Other sources

8

9

of revenue include a 160-car underground parking garage below the building as well as easement rights to 810 parking spaces (out of 950 total) in the Franklin Street Garage located across from the east side of the building.

Retail Industry Background in the 1970s - 1980s

In the early to mid 1970s, the U.S. experienced slowing retail sales due to increasing joblessness. The country entered an economic recession in 1973, its first since the end of World War II. At this time, retailers were receiving mixed signals. Reports of increasing retail sales bolstered executive’s confidence to build inventories in one month; then, slowing sales would cause retail management to invoke aggressive price-reduction strategies to trim inventory levels in the next month. Inflation grew to 12% between 1974 and 1975 while retail sales only increased by 7%.8 The US economy recovered from the recession in 1976, but by 1979, consumer spending decreased as energy costs increased. Consumers again felt the effects of price inflation, which brought on another recession in the early 1980s. The 1980s also brought with it a new retail culture. Specialty retailers led the economic recovery for the retail sector, posting higher sales and earnings increases than the general merchandise department stores. Additionally, discount stores such as K-Mart and Wal-Mart and junior department stores such as Kohl’s challenged the traditional department stores model.

Sears Encounters Hard Times and Decides to Leave the Tower

Sears was losing market share in both its retail stores and its catalog business. Sears’ merchandise group struggled against the big-box discount retail stores. Losing market share to Wal-Mart and others, Sears’ management decided to create its own low-price strategy. However, in sharp contrast to Sears’ original model of integrating low-cost procurement in order to offer low prices, this time around Sears dropped prices before it could secure lower costs from its suppliers. The costs of operating its 82-year-old distribution system were much higher than those, for example, of the leaner Wal-Mart. To help offset deteriorating retail profits, Sears had expanded into the financial services industry to diversify its operations. It added Allstate Insurance, Dean Witter, and Coldwell Banker over the years. The Sears catalog business also lost share to specialty retail catalogs. In 1987, Sears began planning cost-cutting measures, which included trimming marketing budgets

8 Slom, Stanley H. and Rothmyer, Karen, “Reeling Retailers,” The Wall Street Journal. 6 Feb 1975: 1.

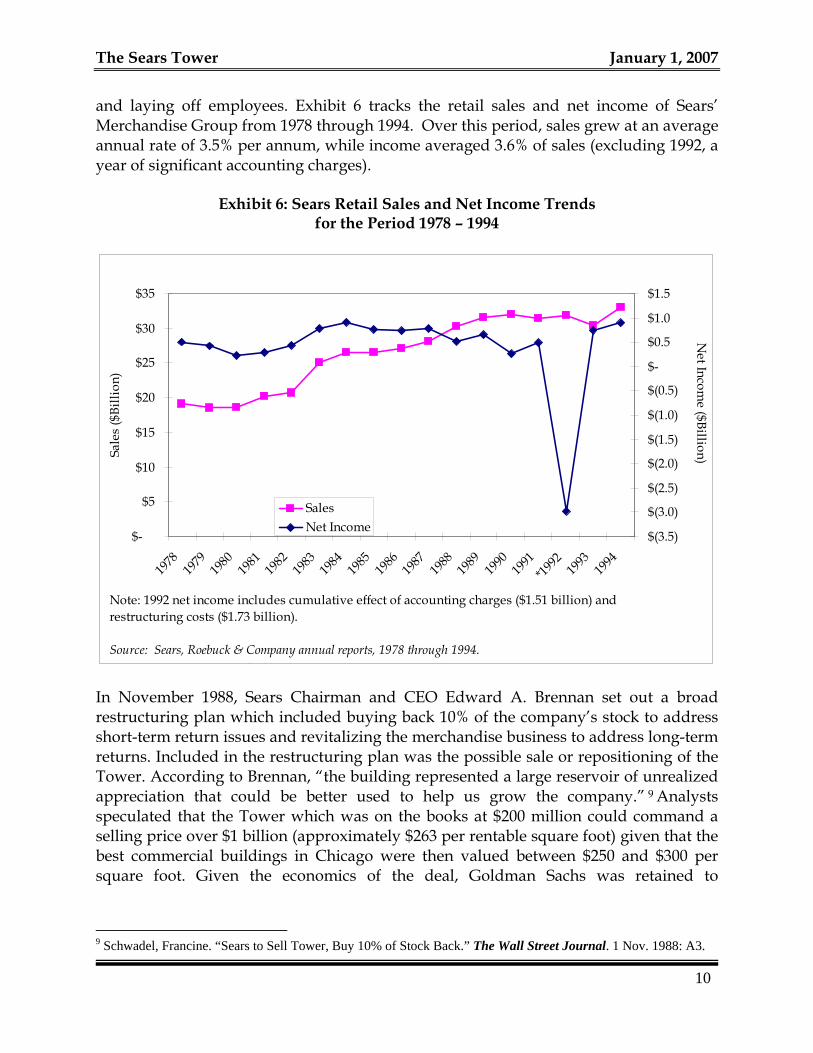

The Sears Tower January 1, 2007 and laying off employees. Exhibit 6 tracks the retail sales and net income of Sears’ Merchandise Group from 1978 through 1994. Over this period, sales grew at an average annual rate of 3.5% per annum, while income averaged 3.6% of sales (excluding 1992, a year of significant accounting charges).

Exhibit 6: Sears Retail Sales and Net Income Trends

for the Period 1978 – 1994

$-

$5

$10

$15

$20

$25

$30

$35

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

*1992 19

9319

94

Sale

s ($

Billi

on)

$(3.5)

$(3.0)

$(2.5)

$(2.0)

$(1.5)

$(1.0)

$(0.5)

$-

$0.5

$1.0

$1.5

Net Incom

e ($Billion)

SalesNet Income

N

Note: 1992 net income includes cumulative effect of accounting charges ($1.51 billion) and restructuring costs ($1.73 billion).

Source: Sears, Roebuck & Company annual reports, 1978 through 1994.

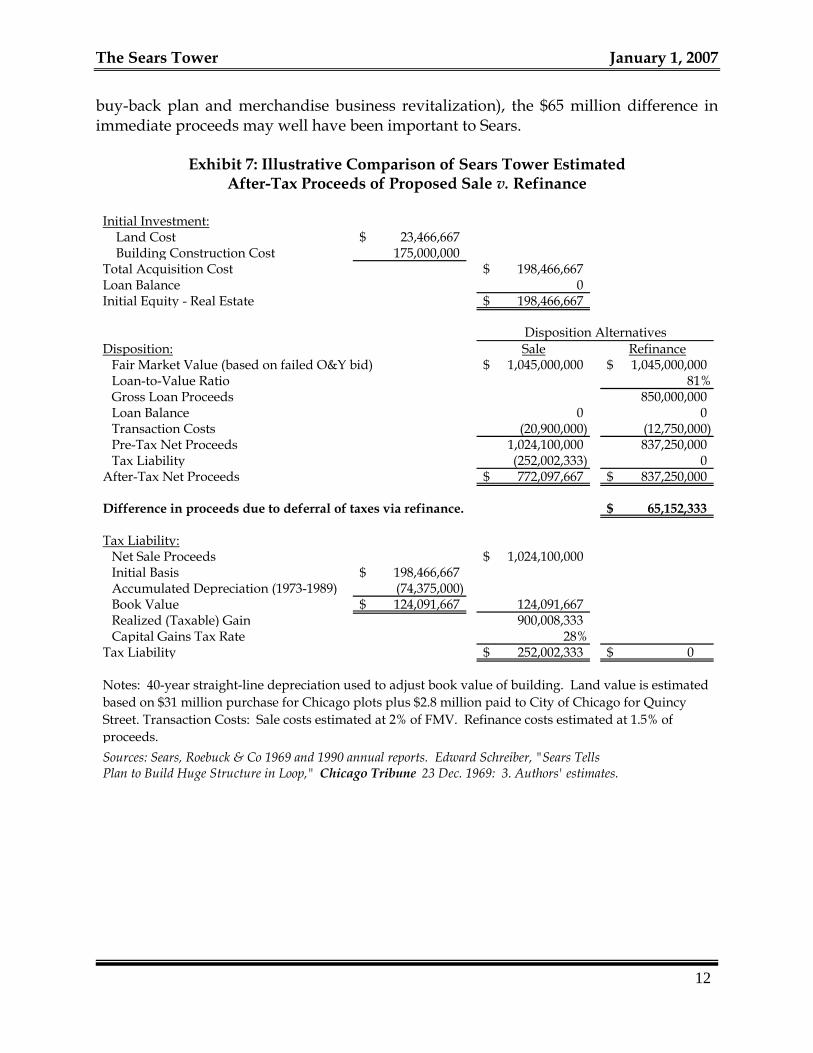

In November 1988, Sears Chairman and CEO Edward A. Brennan set out a broad restructuring plan which included buying back 10% of the company’s stock to address short-term return issues and revitalizing the merchandise business to address long-term returns. Included in the restructuring plan was the possible sale or repositioning of the Tower. According to Brennan, “the building represented a large reservoir of unrealized appreciation that could be better used to help us grow the company.” 9 Analysts speculated that the Tower which was on the books at $200 million could command a selling price over $1 billion (approximately $263 per rentable square foot) given that the best commercial buildings in Chicago were then valued between $250 and $300 per square foot. Given the economics of the deal, Goldman Sachs was retained to

10

9 Schwadel, Francine. “Sears to Sell Tower, Buy 10% of Stock Back.” The Wall Street Journal. 1 Nov. 1988: A3.

11

orchastrate the sale of the Sears Tower and, shortly thereafter, Toronto-based Olympia & York Developments Ltd. emerged as the primary bidder with a $1.045 billion offer. However, the potential sale of the Tower was tainted by two looming factors. First, as part of its restructuring, Sears planned to relocate all but 600 of its 8,700 employees to a separate (but undetermined) location. This would leave the Tower almost two-thirds vacant and the new owner would be faced with the formidable task of leasing the space soon after its purchase. This task was further hindered by the construction of 1.2 million square feet of office space next door at 311 S. Wacker where developers of this building were reportedly offering concessions of 5 years worth of free rent to lock in tenants for 15 years or more.10 Second, the building had appreciated significantly over the past decade and a half. The sale of the building was sure to trigger a reassessment of the property value, thus significantly increasing the new owner’s real estate taxes. The Wall Street Journal reported that as part of the sales negotiations, Sears was willing to pay Olympia & York rent for six years on the space it would vacate in the Tower.11 However, due to failed negotiations over the Tower’s property-tax burden, Olympia & York withdrew its bid for the Tower in September, 1989. Thereafter, Sears decided instead to refinance the Tower for approximately $850 million in order to procure the money needed for its stock buy-back, which had been initially funded by working capital. The details of the refinancing are discussed in a subsequent section. Exhibit 7 provides a pro forma comparison of selling the building for Olympia & York’s bid at $1.045 billion dollars12 to refinancing the building at $850 million. Our internal estimates suggest that the sale of the building would have resulted in a taxable gain of approximately $900 million, which at the 1989 capital gains tax rate of 28% would have resulted in a $252 million tax liability. With a mortgage amount of $850 million on the Tower, the refinancing would have generated $65 million more in after-tax proceeds for Sears’ immediate redeployment. Refinancing, however, is a tax-deferred solution. The capital gains tax associated with the refinancing would ultimately be due at the point in the future when the Tower is eventually sold. In theory, the tax liability associated with the refinancing could be deferred indefinitely, while preserving the option to sell the Tower at a later date.13 Given Sears’ broad restructuring plan (including a 10% stock

10 Elstrom, Peter J. “Office Glut Sparks Boon for Tenants; Developers Compete in Discount Frenzy.” Crain’s Chicago Business. 20 Aug. 1990: 1. 11 Barsky, Neil. “Edifice Rex: Toronto’s Reichmann Scales the Heights of Real Estate.” The Wall Street Journal. 5 Sept. 1989: A1.12 The break-even sale price (i.e., gross sale price at which the net after-tax proceeds would have equaled the net refinancing proceeds) would have equaled $1.137 billion. 13 The tax liability could be further deferred through the use of §1031 like-kind exchange. Given Sears’ extensive real estate holdings and the nature of its core business, such an exchange would seem quite plausible.

The Sears Tower January 1, 2007 buy-back plan and merchandise business revitalization), the $65 million difference in immediate proceeds may well have been important to Sears.

Exhibit 7: Illustrative Comparison of Sears Tower Estimated

After-Tax Proceeds of Proposed Sale v. Refinance

Initial Investment: Land Cost 23,466,667$ Building Construction Cost 175,000,000 Total Acquisition Cost 198,466,667$ Loan Balance 0Initial Equity - Real Estate 198,466,667$

Disposition: Sale RefinanceFair Market Value (based on failed O&Y bid) 1,045,000,000$ 1,045,000,000$ Loan-to-Value Ratio 81%Gross Loan Proceeds 850,000,000 Loan Balance 0 0Transaction Costs (20,900,000) (12,750,000) Pre-Tax Net Proceeds 1,024,100,000 837,250,000 Tax Liability (252,002,333) 0

After-Tax Net Proceeds 772,097,667$ 837,250,000$

Difference in proceeds due to deferral of taxes via refinance. 65,152,333$

Tax Liability:Net Sale Proceeds 1,024,100,000$ Initial Basis 198,466,667$ Accumulated Depreciation (1973-1989) (74,375,000) Book Value 124,091,667$ 124,091,667 Realized (Taxable) Gain 900,008,333 Capital Gains Tax Rate 28%

Tax Liability 252,002,333$ 0$

Sources: Sears, Roebuck & Co 1969 and 1990 annual reports. Edward Schreiber, "Sears TellsPlan to Build Huge Structure in Loop," Chicago Tribune 23 Dec. 1969: 3. Authors' estimates.

Disposition Alternatives

Notes: 40-year straight-line depreciation used to adjust book value of building. Land value is estimated based on $31 million purchase for Chicago plots plus $2.8 million paid to City of Chicago for Quincy Street. Transaction Costs: Sale costs estimated at 2% of FMV. Refinance costs estimated at 1.5% of proceeds.

12

13

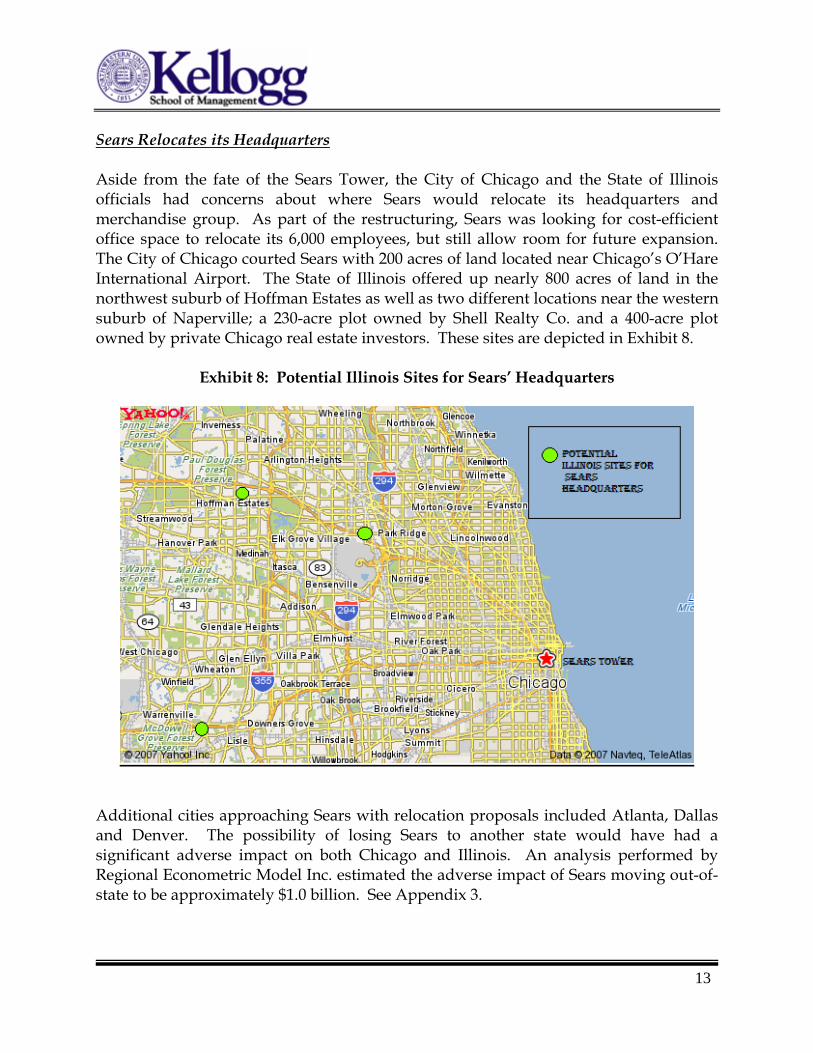

Sears Relocates its Headquarters Aside from the fate of the Sears Tower, the City of Chicago and the State of Illinois officials had concerns about where Sears would relocate its headquarters and merchandise group. As part of the restructuring, Sears was looking for cost-efficient office space to relocate its 6,000 employees, but still allow room for future expansion. The City of Chicago courted Sears with 200 acres of land located near Chicago’s O’Hare International Airport. The State of Illinois offered up nearly 800 acres of land in the northwest suburb of Hoffman Estates as well as two different locations near the western suburb of Naperville; a 230-acre plot owned by Shell Realty Co. and a 400-acre plot owned by private Chicago real estate investors. These sites are depicted in Exhibit 8.

Exhibit 8: Potential Illinois Sites for Sears’ Headquarters

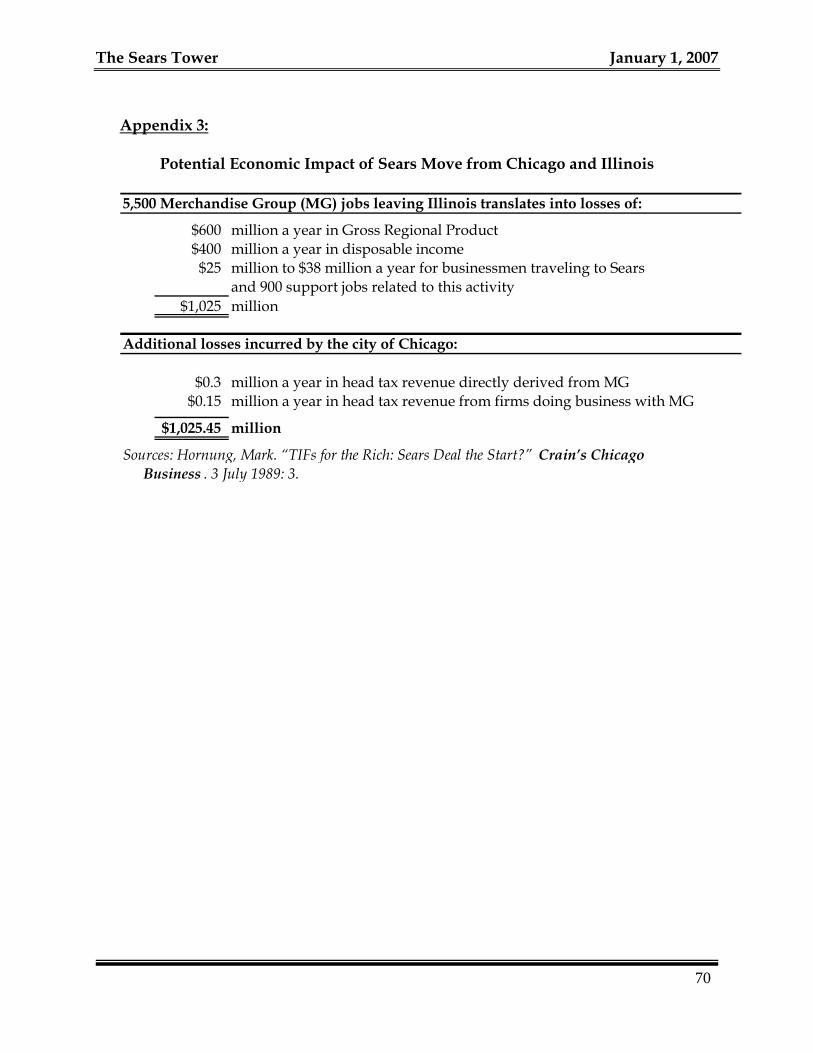

Additional cities approaching Sears with relocation proposals included Atlanta, Dallas and Denver. The possibility of losing Sears to another state would have had a significant adverse impact on both Chicago and Illinois. An analysis performed by Regional Econometric Model Inc. estimated the adverse impact of Sears moving out-of-state to be approximately $1.0 billion. See Appendix 3.

The Sears Tower January 1, 2007 Clearly, the city and state were deeply concerned and highly motivated to accommodate Sears. The Chicago/O’Hare and Hoffman Estates locations were among the frontrunners in the competition for Sears, as the company had its roots in Chicago. The cost of relocating 3,000 salaried employees was estimated around $100 million. The State of Illinois was offering to deem the proposed locations as State Enterprise Zones so that Sears would be exempt of the 5% sales tax on construction materials for its development of the land. Additionally, the State of Illinois pledged $49 million in direct subsidies for land infrastructure and road improvements. (See Appendix 4 for a summary of the Chicago/O’Hare and Hoffman Estates relocation packages).

The City of Chicago offered to purchase an 80-acre plot of land located near O’Hare airport. The City would have leased the land to Sears for a negligible amount ($10 per year) for 99 years. Adjacent to the 80-acre tract of land was a 140-acre plot of land which Sears would have the option to purchase at market prices. Not to be outdone, Illinois state legislature drafted a provision whereby a tax increment financing (TIF) district would be created for the prosperous Hoffman Estates suburb, legislation which at that time was typically reserved for blighted communities. The TIF district designation would allow Hoffman Estates to purchase the land for the potential Sears site by floating tax-exempt long-term bonds. The debt service on the bonds would then be paid by Sears via the incremental property tax increases generated from the real estate development. By January 1990, Sears made its decision to move out of Chicago and relocate its headquarters and Merchandise Group to Hoffman Estates. The two-year move out of the Tower began in 1993, the same year in which Sears discontinued publishing its general merchandise catalog.

14

15

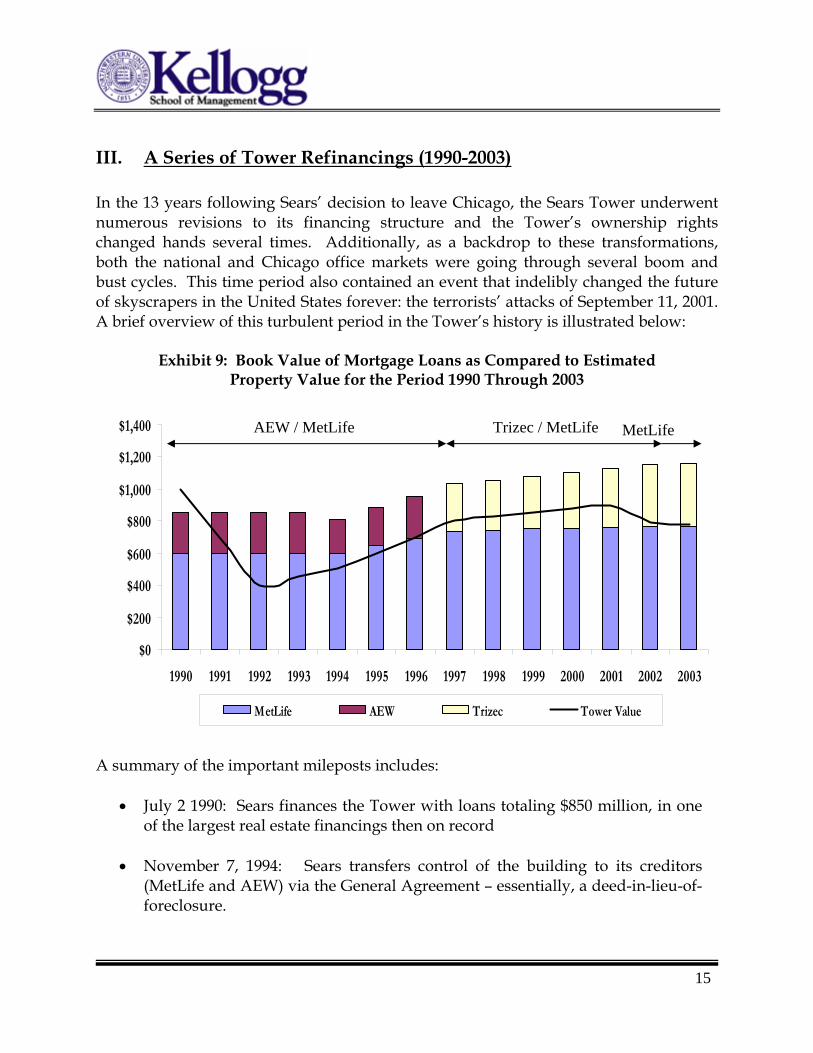

III. A Series of Tower Refinancings (1990-2003) In the 13 years following Sears’ decision to leave Chicago, the Sears Tower underwent numerous revisions to its financing structure and the Tower’s ownership rights changed hands several times. Additionally, as a backdrop to these transformations, both the national and Chicago office markets were going through several boom and bust cycles. This time period also contained an event that indelibly changed the future of skyscrapers in the United States forever: the terrorists’ attacks of September 11, 2001. A brief overview of this turbulent period in the Tower’s history is illustrated below:

Exhibit 9: Book Value of Mortgage Loans as Compared to Estimated

Property Value for the Period 1990 Through 2003

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

MetLife AEW Trizec Tower Value

AEW / MetLife Trizec / MetLife MetLife

A summary of the important mileposts includes:

• July 2 1990: Sears finances the Tower with loans totaling $850 million, in one of the largest real estate financings then on record

• November 7, 1994: Sears transfers control of the building to its creditors (MetLife and AEW) via the General Agreement – essentially, a deed-in-lieu-of-foreclosure.

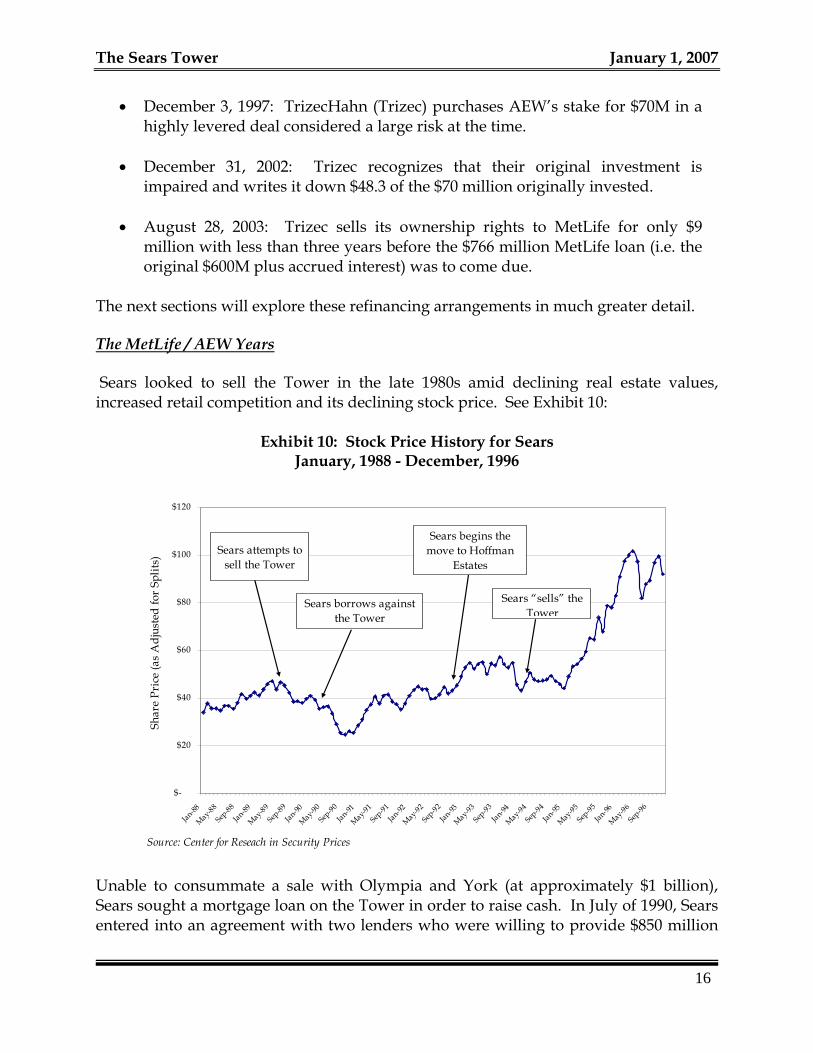

The Sears Tower January 1, 2007

• December 3, 1997: TrizecHahn (Trizec) purchases AEW’s stake for $70M in a highly levered deal considered a large risk at the time.

• December 31, 2002: Trizec recognizes that their original investment is

impaired and writes it down $48.3 of the $70 million originally invested.

• August 28, 2003: Trizec sells its ownership rights to MetLife for only $9 million with less than three years before the $766 million MetLife loan (i.e. the original $600M plus accrued interest) was to come due.

The next sections will explore these refinancing arrangements in much greater detail.

The MetLife / AEW Years

Sears looked to sell the Tower in the late 1980s amid declining real estate values, increased retail competition and its declining stock price. See Exhibit 10:

Exhibit 10: Stock Price History for Sears January, 1988 - December, 1996

$-

$20

$40

$60

$80

$100

$120

Jan-88

May-88

Sep-88

Jan-89

May-89

Sep-89

Jan-90

May-90

Sep-90

Jan-91

May-91

Sep-91

Jan-92

May-92

Sep-92

Jan-93

May-93

Sep-93

Jan-94

May-94

Sep-94

Jan-95

May-95

Sep-95

Jan-96

May-96

Sep-96

Source: Center for Reseach in Security Prices

Shar

e Pr

ice

(as

Adj

uste

d fo

r Sp

lits)

Sears borrows against the Tower

Sears “sells” the Tower

Sears attempts to sell the Tower

Sears begins the move to Hoffman

Estates

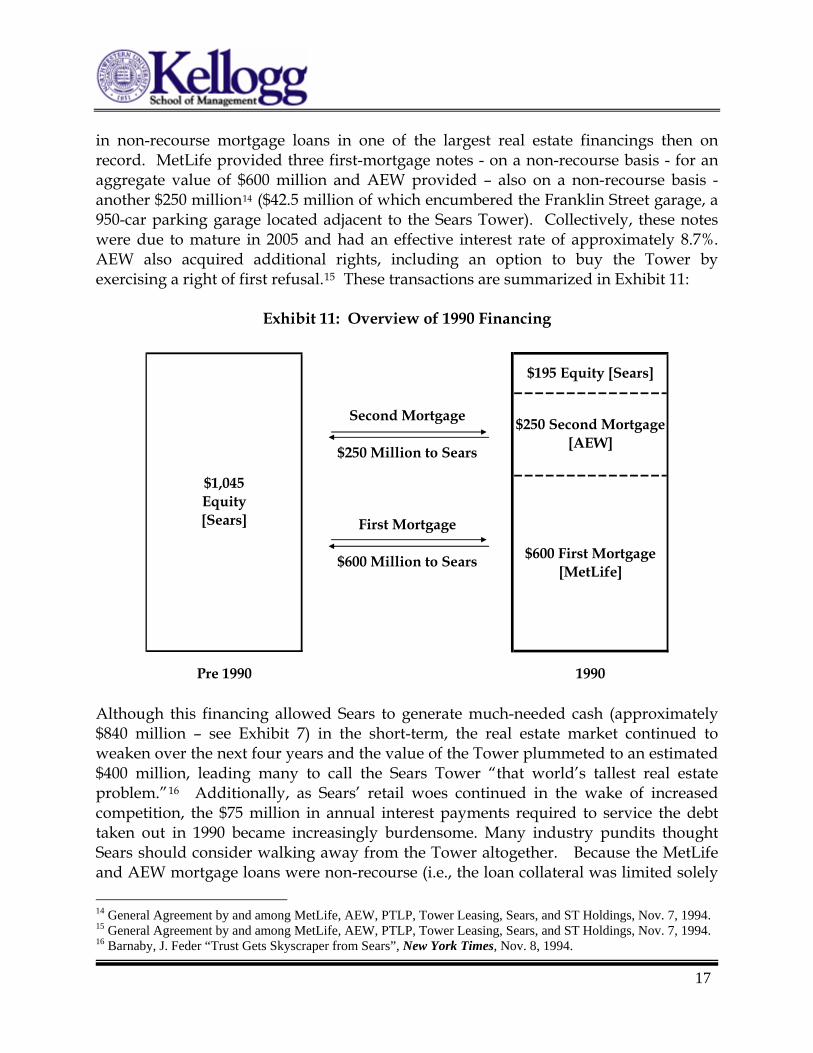

Unable to consummate a sale with Olympia and York (at approximately $1 billion), Sears sought a mortgage loan on the Tower in order to raise cash. In July of 1990, Sears entered into an agreement with two lenders who were willing to provide $850 million

16

17

in non-recourse mortgage loans in one of the largest real estate financings then on record. MetLife provided three first-mortgage notes - on a non-recourse basis - for an aggregate value of $600 million and AEW provided – also on a non-recourse basis - another $250 million14 ($42.5 million of which encumbered the Franklin Street garage, a 950-car parking garage located adjacent to the Sears Tower). Collectively, these notes were due to mature in 2005 and had an effective interest rate of approximately 8.7%. AEW also acquired additional rights, including an option to buy the Tower by exercising a right of first refusal.15 These transactions are summarized in Exhibit 11:

Exhibit 11: Overview of 1990 Financing

Pre 1990 1990

$1,045 Equity [Sears]

Second Mortgage

$250 Million to Sears

First Mortgage

$600 Million to Sears $600 First Mortgage [MetLife]

$195 Equity [Sears]

$250 Second Mortgage [AEW]

Although this financing allowed Sears to generate much-needed cash (approximately $840 million – see Exhibit 7) in the short-term, the real estate market continued to weaken over the next four years and the value of the Tower plummeted to an estimated $400 million, leading many to call the Sears Tower “that world’s tallest real estate problem.”16 Additionally, as Sears’ retail woes continued in the wake of increased competition, the $75 million in annual interest payments required to service the debt taken out in 1990 became increasingly burdensome. Many industry pundits thought Sears should consider walking away from the Tower altogether. Because the MetLife and AEW mortgage loans were non-recourse (i.e., the loan collateral was limited solely 14 General Agreement by and among MetLife, AEW, PTLP, Tower Leasing, Sears, and ST Holdings, Nov. 7, 1994. 15 General Agreement by and among MetLife, AEW, PTLP, Tower Leasing, Sears, and ST Holdings, Nov. 7, 1994. 16 Barnaby, J. Feder “Trust Gets Skyscraper from Sears”, New York Times, Nov. 8, 1994.

The Sears Tower January 1, 2007

18

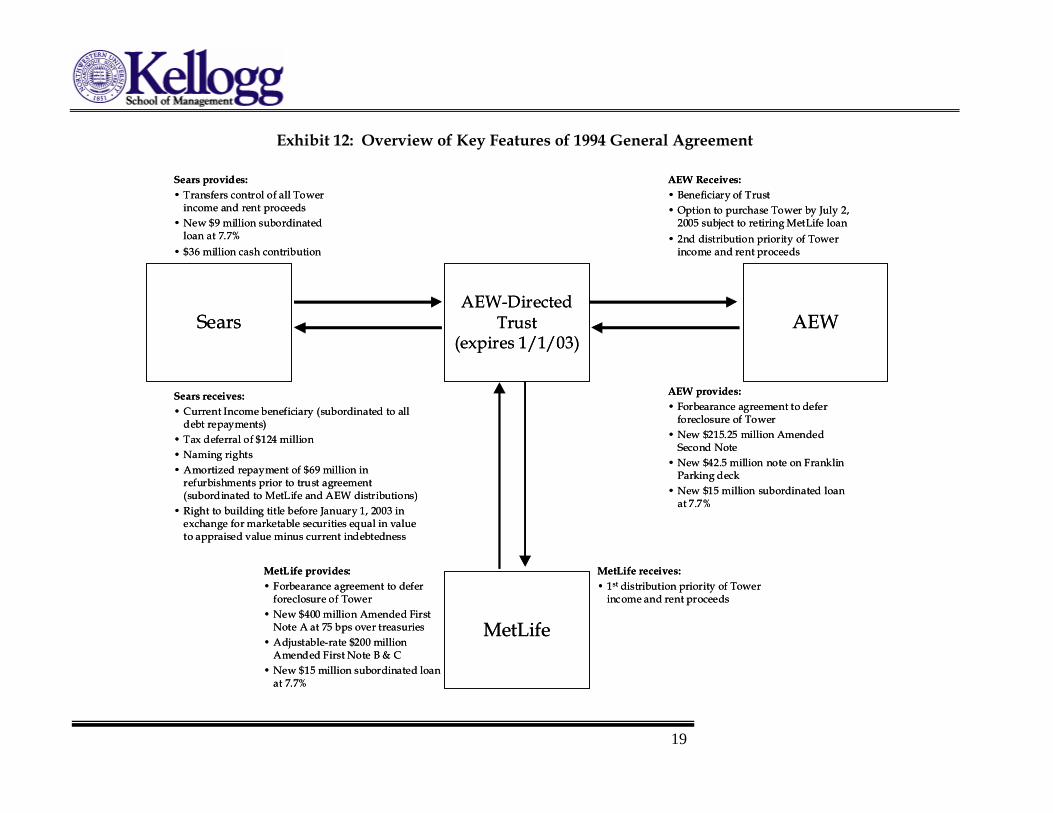

to the real estate assets) none of Sears’ corporate assets were exposed to satisfying any loan shortfall. In 1993, Sears entered into negotiations with MetLife and AEW to restructure the Tower’s finances. After more than a year of negotiating, they finalized a deal. Under the terms of the complex arrangement (the “1994 General Agreement”), Sears essentially transferred all control, but technically not ownership, of the building to an AEW-directed trust which would hold the Tower until 2003. AEW would then have the option to take title of the building from the trust in 2003 provided AEW could retire the remaining MetLife loan balance (if AEW could not retire the MetLife loan balance, then MetLife would have the option to take title to the Tower). As a demonstration of its continued ownership interests, the trust also received a cash contribution of $36 million and a subordinated loan of $9 million from Sears. According to Sears Vice-chairman James Denny, the rationale for such as decision was as follows:

“Sears believes the move helps it retain enough of an economic interest in the Tower to legally defer taxes on the ownership transfer, despite escaping liability for the building's debt.”

This transaction also allowed Sears to remove $845 million in long-term debt from its balance sheet and, when combined with the $501 million asset book value, to record a before-tax profit of $344 million. However, because ownership was not set to transfer until 2003, Sears was able to defer its tax liability of $149 million for approximately 10 years.17 For all intents and purposes, Sears had – after 20 years – finally fully divested itself of control of the Sears Tower. However, as part of the agreement, the Sears name would remain on the Tower. Exhibit 12 overviews the flow of potential benefits and liabilities for each party included in the 1994 General Agreement:

17 Sears 1994 10-K.

19

Sears

Sears provides:• Transfers control of all Tower

income and rent proceeds• New $9 million subordinated

loan at 7.7%• $36 million cash contribution

MetLife

AEW-Directed Trust

(expires 1/1/03)AEW

AEW Receives: • Beneficiary of Trust • Option to purchase Tower by July 2,

2005 subject to retiring MetLife loan• 2nd distribution priority of Tower

income and rent proceeds

AEW provides:• Forbearance agreement to defer

foreclosure of Tower• New $215.25 million Amended

Second Note• New $42.5 million note on Franklin

Parking deck• New $15 million subordinated loan

at 7.7%

Sears receives:• Current Income beneficiary (subordinated to all

debt repayments)• Tax deferral of $124 million• Naming rights• Amortized repayment of $69 million in

refurbishments prior to trust agreement (subordinated to MetLife and AEW distributions)

• Right to building title before January 1, 2003 in exchange for marketable securities equal in value to appraised value minus current indebtedness

MetLife provides:• Forbearance agreement to defer

foreclosure of Tower• New $400 million Amended First

Note A at 75 bps over treasuries• Adjustable-rate $200 million

Amended First Note B & C • New $15 million subordinated loan

at 7.7%

MetLife receives:• 1st distribution priority of Tower

income and rent proceeds

Sears

Sears provides:• Transfers control of all Tower

income and rent proceeds• New $9 million subordinated

loan at 7.7%• $36 million cash contribution

MetLife

AEW-Directed Trust

(expires 1/1/03)AEW

AEW Receives: • Beneficiary of Trust • Option to purchase Tower by July 2,

2005 subject to retiring MetLife loan• 2nd distribution priority of Tower

income and rent proceeds

AEW provides:• Forbearance agreement to defer

foreclosure of Tower• New $215.25 million Amended

Second Note• New $42.5 million note on Franklin

Parking deck• New $15 million subordinated loan

at 7.7%

Sears receives:• Current Income beneficiary (subordinated to all

debt repayments)• Tax deferral of $124 million• Naming rights• Amortized repayment of $69 million in

refurbishments prior to trust agreement (subordinated to MetLife and AEW distributions)

• Right to building title before January 1, 2003 in exchange for marketable securities equal in value to appraised value minus current indebtedness

MetLife provides:• Forbearance agreement to defer

foreclosure of Tower• New $400 million Amended First

Note A at 75 bps over treasuries• Adjustable-rate $200 million

Amended First Note B & C • New $15 million subordinated loan

at 7.7%

MetLife receives:• 1st distribution priority of Tower

income and rent proceeds

Exhibit 12: Overview of Key Features of 1994 General Agreement

The Sears Tower January 1, 2007 Note that Sears advanced $43 million (a $9 million loan and $36 million in equity) in new funds, while MetLife capitalized $15 million in previously unpaid interest expense and AEW capitalized approximately $24 million in unpaid interest expense as part of the General Agreement. From a legal perspective, a lender is frequently better served by recapitalizing previously unpaid interest and converting it to principal. Bankruptcy courts tend to view unpaid principal more sacrosanctly than unpaid interest. Exhibit 13 outlines the distribution priorities received by each participant to the 1994 General Agreement under various estimates of the residual value of the Tower after 15 years.

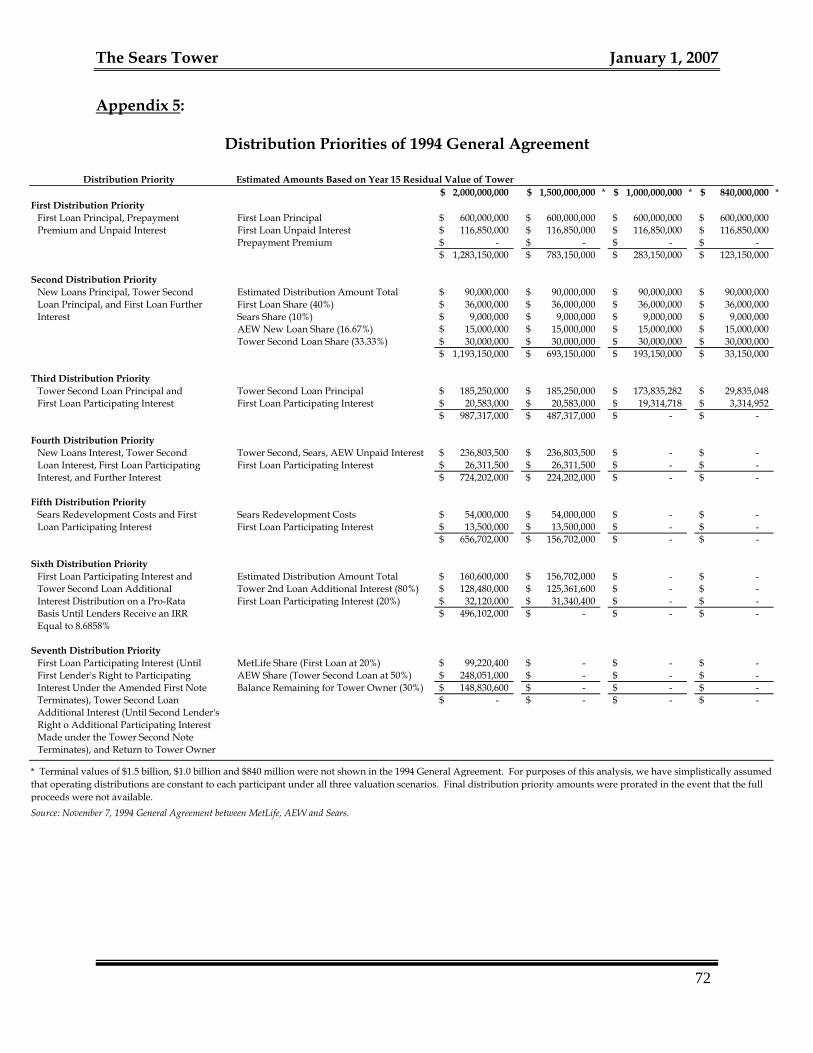

Exhibit 13: Distribution Priorities of 1994 General Agreement Summary by Key Participants

Participant Estimated Amounts Based on Year 15 Residual Value of Tower ($000s) *$2 Billion $1.5 Billion $1.0 Billion $840 Million

___$___ __%__ ___$___ __%__ ___$___ __%__ ___$___ __%__

MetLife $944,585 47% $844,585 56% $772,165 77% $756,165 90%AEW 992,415 50% 592,415 39% 218,835 22% 74,835 9%Sears 63,000 3% 63,000 4% 9,000 1% 9,000 1%

Total $2,000,000 100% $1,500,000 100% $1,000,000 100% $840,000 100%

Source: November 7, 1994 General Agreement between MetLife, AEW and Sears. Authors' estimates.

* Terminal values of $1.5, $1.0 billion and $840 million were not shown in the 1994 General Agreement. For purposes of this analysis, we have simplistically assumed that operating distributions are constant to each participant under all three valuation scenarios.

As indicated above, MetLife, as the holder of the first-mortgage note, is clearly in the best position to recoup the principal and loan interest provided to the Sears Tower. As stated in the 1994 General Agreement, cash flows and residual Tower value were allocated to the participants based on a schedule of seven distribution priorities. Generally, MetLife Notes A, B, and C held the highest priority positions followed by the Tower Second Note by AEW and finally any distributions made to Sears. Appendix 5 provides greater detail of the distribution priorities and allocations for each participant under various residual value scenarios for the Tower. Please note that the $840 million price shown above represents the eventual sales price in 2004. Effectively, the 1994 General Agreement and resulting transaction served as a deed-in-lieu-of-foreclosure. By transferring all control of the building into the trust, Sears was released from its mortgage debt obligations; however, Sears essentially no longer had an interest in the underlying real estate. Sears was an owner in name only. The deed-in-lieu-of-foreclosure agreement between Sears, AEW and MetLife allowed all three

20

21

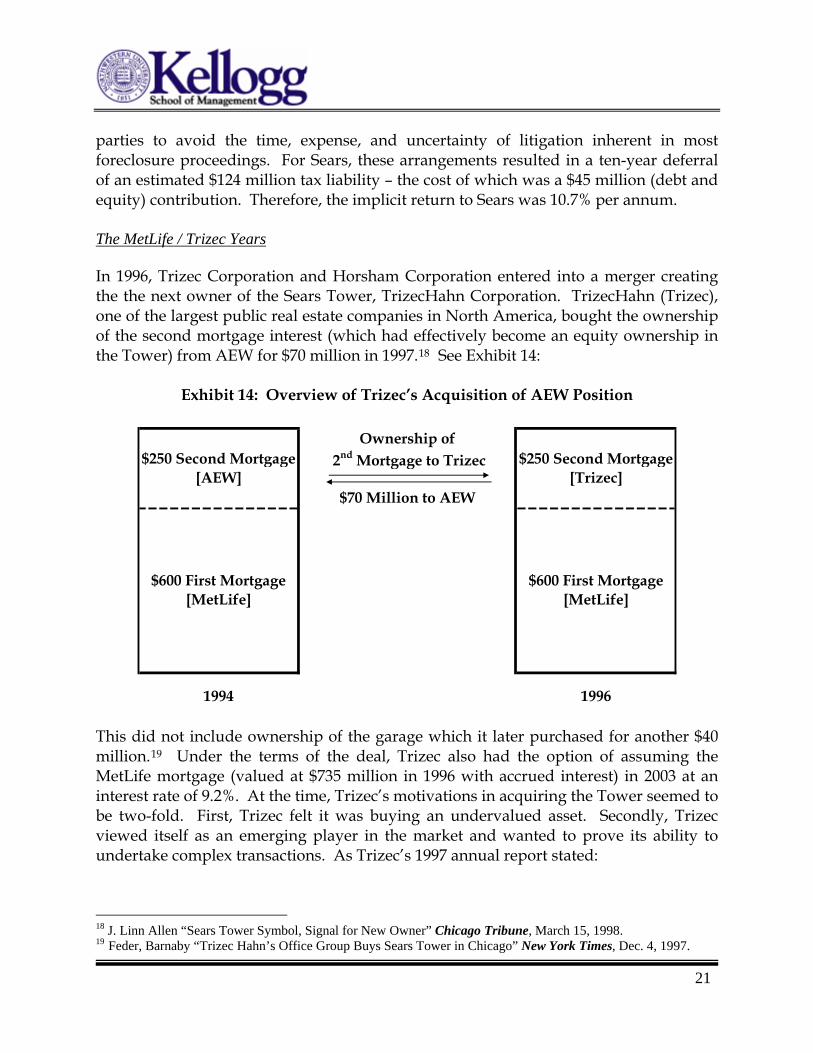

parties to avoid the time, expense, and uncertainty of litigation inherent in most foreclosure proceedings. For Sears, these arrangements resulted in a ten-year deferral of an estimated $124 million tax liability – the cost of which was a $45 million (debt and equity) contribution. Therefore, the implicit return to Sears was 10.7% per annum. The MetLife / Trizec Years In 1996, Trizec Corporation and Horsham Corporation entered into a merger creating the the next owner of the Sears Tower, TrizecHahn Corporation. TrizecHahn (Trizec), one of the largest public real estate companies in North America, bought the ownership of the second mortgage interest (which had effectively become an equity ownership in the Tower) from AEW for $70 million in 1997.18 See Exhibit 14:

Exhibit 14: Overview of Trizec’s Acquisition of AEW Position

Ownership of 2nd Mortgage to Trizec

1994 1996

$600 First Mortgage [MetLife]

$600 First Mortgage [MetLife]

$250 Second Mortgage [AEW]

$250 Second Mortgage [Trizec]

$70 Million to AEW

This did not include ownership of the garage which it later purchased for another $40 million.19 Under the terms of the deal, Trizec also had the option of assuming the MetLife mortgage (valued at $735 million in 1996 with accrued interest) in 2003 at an interest rate of 9.2%. At the time, Trizec’s motivations in acquiring the Tower seemed to be two-fold. First, Trizec felt it was buying an undervalued asset. Secondly, Trizec viewed itself as an emerging player in the market and wanted to prove its ability to undertake complex transactions. As Trizec’s 1997 annual report stated:

18 J. Linn Allen “Sears Tower Symbol, Signal for New Owner” Chicago Tribune, March 15, 1998. 19 Feder, Barnaby “Trizec Hahn’s Office Group Buys Sears Tower in Chicago” New York Times, Dec. 4, 1997.

The Sears Tower January 1, 2007

“…our ability to understand and manage complex transactions, involving multiple affected parties, results from the depth of our management team and our relationships with industry participants. One such example was [our] purchase of an interest in the Sears Tower in December 1997. The seller held a set of complicated rights, including a second mortgage and effective control of the Tower, but received no current cash payments on its investment. However, this position did have substantial appreciation potential given the property’s strong market position in Chicago, which has been experiencing rapid rental rate growth. By understanding and ultimately acquiring this complex position, TrizecHahn was able to acquire effective control of the Sears Tower, a world-class, quality office building, on favorable terms.”

Trizec projected that the Sears Tower would quickly reach a value of $1 billion and looked for this property to be the prize of its portfolio. Trizec felt the Chicago office market was improving. Given that the Tower had a large number of leases about to expire, Trizec felt it could renegotiate higher rents. Many industry pundits however felt the Trizec move was extremely risky. As one insider put it:

“In 1997, just about everyone felt the only way to ‘own’ the Tower was to get the first mortgage. Even though Trizec technically bought the ownership rights to the building, it was a huge gamble because conventional wisdom was that the only way to really control the building was to get the first mortgage, but Met was not about to let go. However, as a result, Trizec was able to purchase the second mortgage for an extremely reduced rate.”

Nevertheless, some of Trizec’s optimism can be attributed to the strength of the firm during this time period. In 1998 Green Street Advisors indicated that Trizec’s strengths included the breadth of the firm’s global investment opportunities and a visionary management team. During this period, Green Street20 suggested that Trizec warranted a share price of about $23.00. At the time of their report, Trizec’s share price was $19.88. For the first few years, Trizec’s projection seemed on the mark as the Sears Tower experienced occupancy rates of up to 97.0% – see Exhibit 15 for vacancy rates from 1997-2006 – and its value has been estimated to have increased to over $900 million.

22

20 “Green Street Advisors Research – TrizecHahn Corp,” Green Street Advisors 1998.

23

Exhibit 15: Direct and Indirect Vacancy Rates for the Sears Tower For the period 1997 through 2005

0%

5%

10%

15%

20%

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Vac

ancy

Rat

e Direct Vacancy

Total Vacancy

Sublet Vacancy

Source: CoStar.

However, as the new millennium dawned, Trizec was dealt successive blows from two of the most dramatic events in modern American history. These events had indirect and direct consequences for Trizec. First was September 11, 2001, one of the largest tragedies in American history, which caused “permanent impairment” to the Sears Tower according to a PriceWaterhouseCoopers study. Shortly thereafter, the sudden collapse of Enron sent shockwaves through the world and financial markets and left Trizec without its fourth-largest tenant, one that represented 2% of the company’s total rentable space.21

September 11, 2001

The 9/11 attacks and the resulting economic downturn were devastating for major, urban real estate markets, and Chicago was no different. Both market or (“spot”) rents and market vacancy were adversely affected despite the sound fundamentals in even the strongest CBD markets. Moreover, due to its global prominence as the largest building in the United States and one of the largest in the world, the rents and occupancy levels specific to the Sears Tower suffered more than most other office buildings. Two of the Tower’s largest tenants, Goldman Sachs and Merrill Lynch, representing over 300,000 square feet, immediately announced plans to vacate the

21 “Trizec’s Triple Double,” Canadian Business Magazine, December 9, 2002.

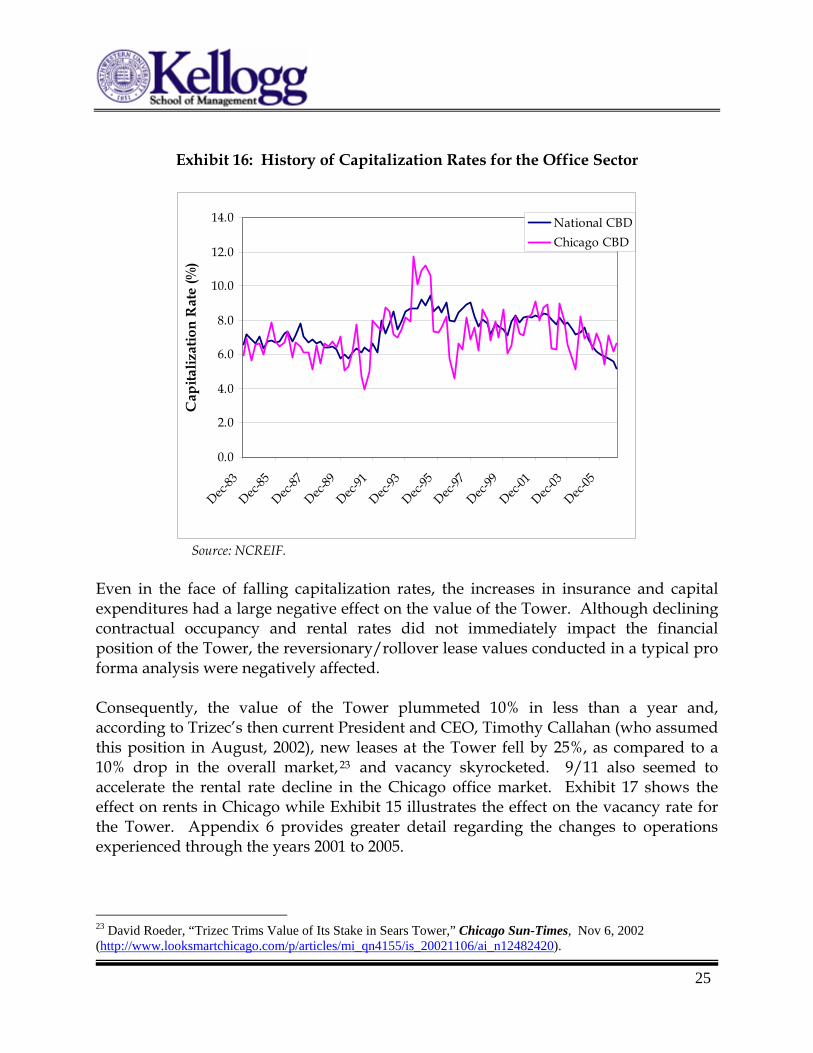

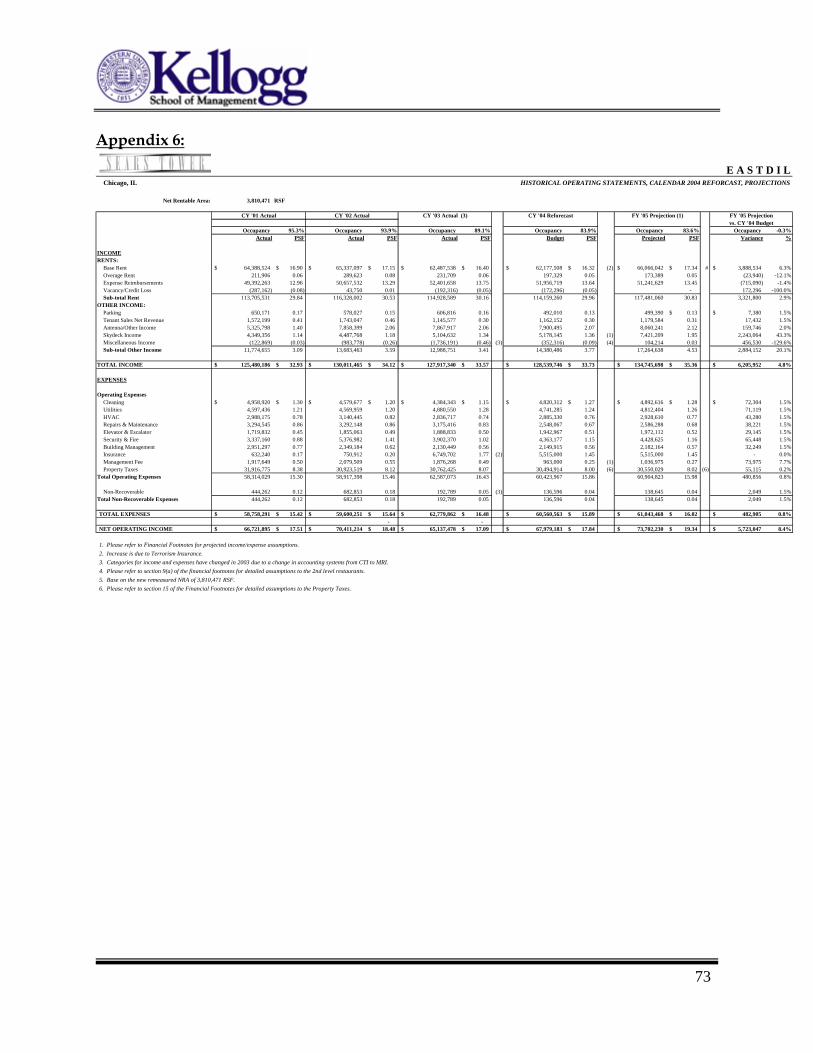

The Sears Tower January 1, 2007 building despite considerable remaining lease lengths reflected in contractual rent obligations – while other tenants felt similarly, not all acted upon such concerns. Despite significant tenant unease, the Tower had a very strong tenant roster both in terms of investment-grade financial strength and long lease maturities. The six largest tenants were all high-quality tenants with three rated by S&P with credit ratings of AA- or better and two others rated by Dun & Bradstreet with Composite Credit Appraisals of 2 (good). These six alone represented over 1,335,000 rentable square feet (or 35% of the Tower) with a weighted average lease commitment of over 8.3 years remaining. In fact, although physical occupancy plummeted from 95.3% in 2001 to 83.9% in 2004 and first-year net rent for new leases plunged from $26.32 in 2001 to $11.95 in 2003, the Tower’s NOI was actually forecasted to increase from $66,721,895 in 2001 to $67,979,183 in 2004 – see Appendix 6. This apparent discrepancy was largely attributable to contractual lease obligations providing rental income which was higher than then-current “spot” rates and to unoccupied space still paying rent (due to lease contracts with credit-worthy tenants); in addition, the number of new tenants leasing at historically low market rental rates was very small in comparison to the total space in the Tower. However, property insurance on the building jumped from approximately $751,000 in 2002 to $6.75 million in 2003 and held steady around $5.5 million during 2004 and 2005. 22 Further, capital expenditures of over $5 million for counter-terrorism improvements were made. With the exception of a sharp increase between 2000 at 6.89% to 7.98% in 2002, capitalization rates steadily fell to 6.40% in 2005. See Exhibit 16:

24

22 Eastdil Offering Memorandum.

25

Exhibit 16: History of Capitalization Rates for the Office Sector

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Dec-83

Dec-85

Dec-87

Dec-89

Dec-91

Dec-93

Dec-95

Dec-97

Dec-99

Dec-01

Dec-03

Dec-05

Cap

italiz

atio

n R

ate

(%)

National CBDChicago CBD

Source: NCREIF.

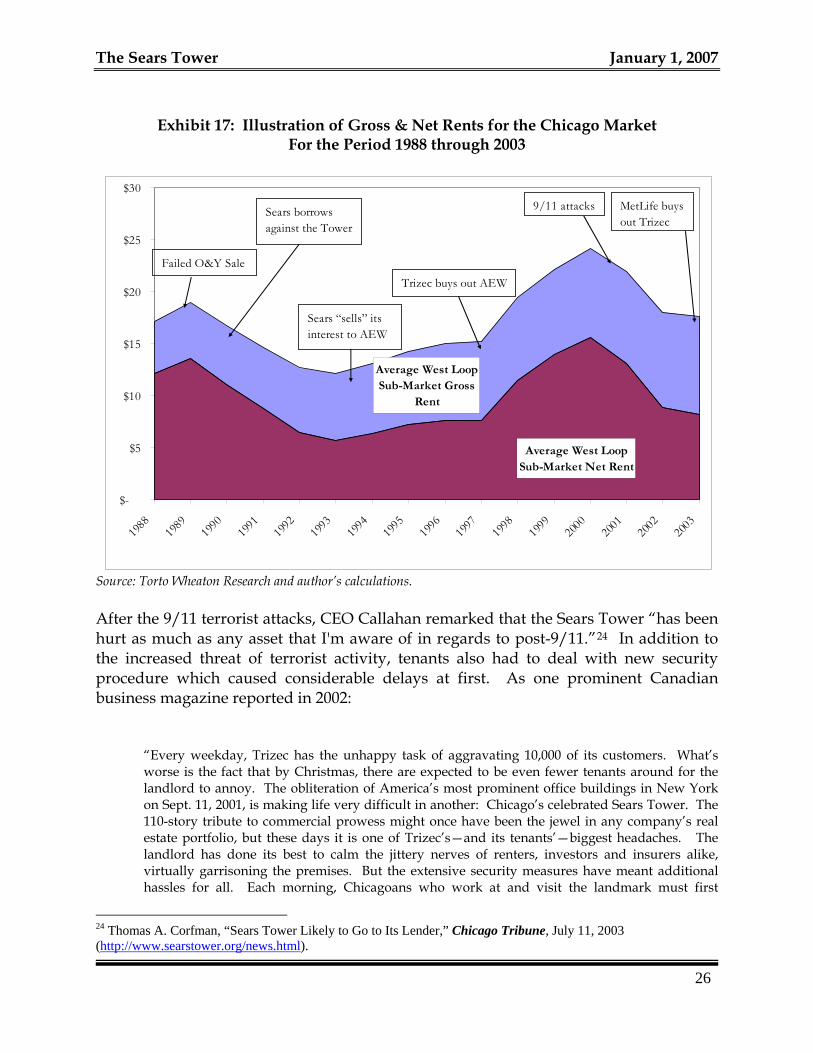

Even in the face of falling capitalization rates, the increases in insurance and capital expenditures had a large negative effect on the value of the Tower. Although declining contractual occupancy and rental rates did not immediately impact the financial position of the Tower, the reversionary/rollover lease values conducted in a typical pro forma analysis were negatively affected. Consequently, the value of the Tower plummeted 10% in less than a year and, according to Trizec’s then current President and CEO, Timothy Callahan (who assumed this position in August, 2002), new leases at the Tower fell by 25%, as compared to a 10% drop in the overall market,23 and vacancy skyrocketed. 9/11 also seemed to accelerate the rental rate decline in the Chicago office market. Exhibit 17 shows the effect on rents in Chicago while Exhibit 15 illustrates the effect on the vacancy rate for the Tower. Appendix 6 provides greater detail regarding the changes to operations experienced through the years 2001 to 2005.

23 David Roeder, “Trizec Trims Value of Its Stake in Sears Tower,” Chicago Sun-Times, Nov 6, 2002 (http://www.looksmartchicago.com/p/articles/mi_qn4155/is_20021106/ai_n12482420).

The Sears Tower January 1, 2007

Exhibit 17: Illustration of Gross & Net Rents for the Chicago Market For the Period 1988 through 2003

Average West Loop Sub-Market Net Rent

Average West Loop Sub-Market Gross

Rent

$-

$5

$10

$15

$20

$25

$30

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Sears borrows against the Tower

Sears “sells” its interest to AEW

Trizec buys out AEW

MetLife buys out Trizec

9/11 attacks

Failed O&Y Sale

Source: Torto Wheaton Research and author’s calculations. After the 9/11 terrorist attacks, CEO Callahan remarked that the Sears Tower “has been hurt as much as any asset that I'm aware of in regards to post-9/11.”24 In addition to the increased threat of terrorist activity, tenants also had to deal with new security procedure which caused considerable delays at first. As one prominent Canadian business magazine reported in 2002:

“Every weekday, Trizec has the unhappy task of aggravating 10,000 of its customers. What’s worse is the fact that by Christmas, there are expected to be even fewer tenants around for the landlord to annoy. The obliteration of America’s most prominent office buildings in New York on Sept. 11, 2001, is making life very difficult in another: Chicago’s celebrated Sears Tower. The 110-story tribute to commercial prowess might once have been the jewel in any company’s real estate portfolio, but these days it is one of Trizec’s—and its tenants’—biggest headaches. The landlord has done its best to calm the jittery nerves of renters, investors and insurers alike, virtually garrisoning the premises. But the extensive security measures have meant additional hassles for all. Each morning, Chicagoans who work at and visit the landmark must first

26

24 Thomas A. Corfman, “Sears Tower Likely to Go to Its Lender,” Chicago Tribune, July 11, 2003 (http://www.searstower.org/news.html).

27

negotiate the perimeter of concrete highway pillars that fortify its entrances against truck bombs. Then it’s a phalanx of security guards, examining each building pass, inspecting every bag. Guests must show photo identification and sign in at the front desk. Even deliveries are vetted by sniffer dogs trained to identify explosive material.”

Trizec Decides to Exit the Sears Tower

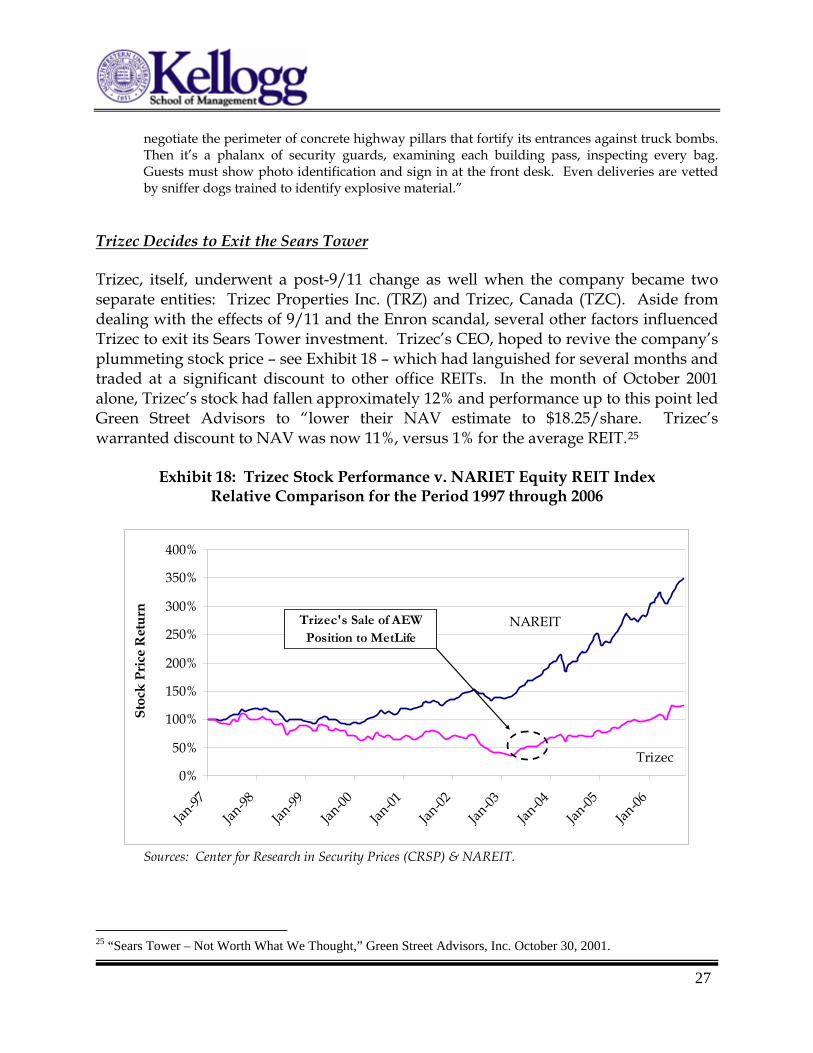

Trizec, itself, underwent a post-9/11 change as well when the company became two separate entities: Trizec Properties Inc. (TRZ) and Trizec, Canada (TZC). Aside from dealing with the effects of 9/11 and the Enron scandal, several other factors influenced Trizec to exit its Sears Tower investment. Trizec’s CEO, hoped to revive the company’s plummeting stock price – see Exhibit 18 – which had languished for several months and traded at a significant discount to other office REITs. In the month of October 2001 alone, Trizec’s stock had fallen approximately 12% and performance up to this point led Green Street Advisors to “lower their NAV estimate to $18.25/share. Trizec’s warranted discount to NAV was now 11%, versus 1% for the average REIT.25

Exhibit 18: Trizec Stock Performance v. NARIET Equity REIT Index

Relative Comparison for the Period 1997 through 2006

0%

50%

100%

150%

200%

250%

300%

350%

400%

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Stoc

k Pr

ice

Ret

urn

NAREIT

Trizec

Trizec's Sale of AEW Position to MetLife

Sources: Center for Research in Security Prices (CRSP) & NAREIT.

25 “Sears Tower – Not Worth What We Thought,” Green Street Advisors, Inc. October 30, 2001.

The Sears Tower January 1, 2007 One of the problems with Trizec’s stock was that its leverage ratio was around 65% as compared to its peer group average of around 50%. If Trizec became the owner of the Sears Tower, then the company would have added the $766 million first mortgage (including accrued interest) to its highly levered balance sheet, which would come due in 2005.26 Increasing its leverage, coupled with the soft office market, led investors and analysts to suggest selling the Sears Tower was Trizec’s best course of action. The Sears Tower only contributed about $0.02 per share to Trizec’s funds from operations (FFO). In mid-2002, the Sears Tower was 94% leased, but this was projected to drop to 91% by the fourth quarter of 2002.27

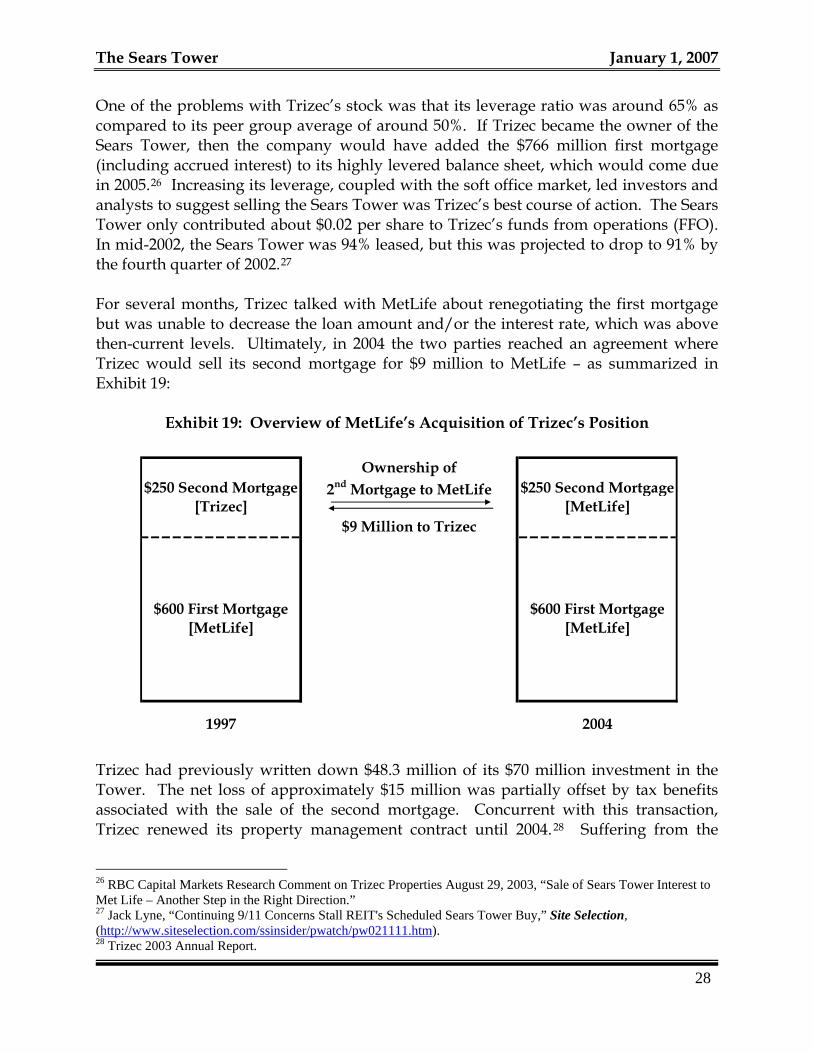

For several months, Trizec talked with MetLife about renegotiating the first mortgage but was unable to decrease the loan amount and/or the interest rate, which was above then-current levels. Ultimately, in 2004 the two parties reached an agreement where Trizec would sell its second mortgage for $9 million to MetLife – as summarized in Exhibit 19:

Exhibit 19: Overview of MetLife’s Acquisition of Trizec’s Position

Ownership of2nd Mortgage to MetLife

1997 2004

$600 First Mortgage [MetLife]

$600 First Mortgage [MetLife]

$250 Second Mortgage [Trizec]

$250 Second Mortgage [MetLife]

$9 Million to Trizec

Trizec had previously written down $48.3 million of its $70 million investment in the Tower. The net loss of approximately $15 million was partially offset by tax benefits associated with the sale of the second mortgage. Concurrent with this transaction, Trizec renewed its property management contract until 2004.28 Suffering from the

26 RBC Capital Markets Research Comment on Trizec Properties August 29, 2003, “Sale of Sears Tower Interest to Met Life – Another Step in the Right Direction.” 27 Jack Lyne, “Continuing 9/11 Concerns Stall REIT's Scheduled Sears Tower Buy,” Site Selection, (http://www.siteselection.com/ssinsider/pwatch/pw021111.htm).

28

28 Trizec 2003 Annual Report.

29

challenges posed by ownership of the Tower as well as poor stock performance overall, Trizec’s sale of its AEW position to MetLife had a minimal effect on the stock price. The Trizec entities were finally acquired in 2006 by Brookfield Properties Corporation and Blackstone Group in an $8.9 billion deal.29

The MetLife Years

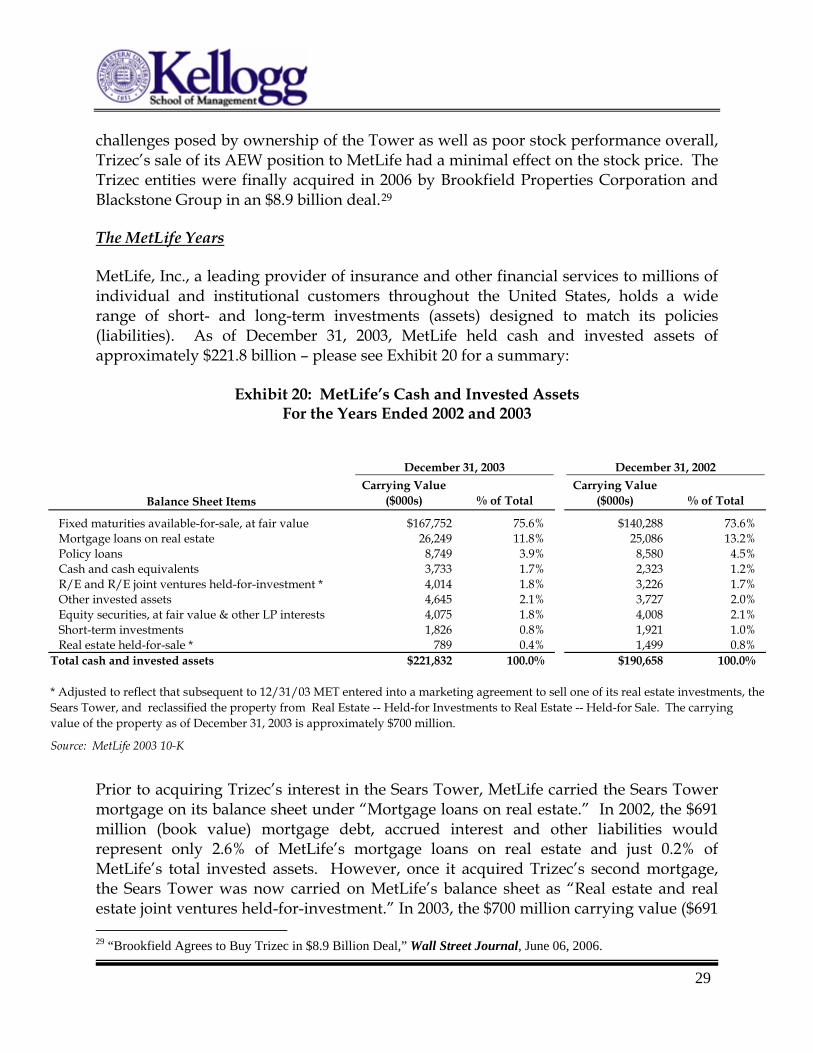

MetLife, Inc., a leading provider of insurance and other financial services to millions of individual and institutional customers throughout the United States, holds a wide range of short- and long-term investments (assets) designed to match its policies (liabilities). As of December 31, 2003, MetLife held cash and invested assets of approximately $221.8 billion – please see Exhibit 20 for a summary:

Exhibit 20: MetLife’s Cash and Invested Assets For the Years Ended 2002 and 2003

December 31, 2003 December 31, 2002

Balance Sheet ItemsCarrying Value

($000s) % of TotalCarrying Value

($000s) % of Total

Fixed maturities available-for-sale, at fair value $167,752 75.6% $140,288 73.6%Mortgage loans on real estate 26,249 11.8% 25,086 13.2%Policy loans 8,749 3.9% 8,580 4.5%Cash and cash equivalents 3,733 1.7% 2,323 1.2%R/E and R/E joint ventures held-for-investment * 4,014 1.8% 3,226 1.7%Other invested assets 4,645 2.1% 3,727 2.0%Equity securities, at fair value & other LP interests 4,075 1.8% 4,008 2.1%Short-term investments 1,826 0.8% 1,921 1.0%Real estate held-for-sale * 789 0.4% 1,499 0.8%

Total cash and invested assets $221,832 100.0% $190,658 100.0%

Source: MetLife 2003 10-K

* Adjusted to reflect that subsequent to 12/31/03 MET entered into a marketing agreement to sell one of its real estate investments, the Sears Tower, and reclassified the property from Real Estate -- Held-for Investments to Real Estate -- Held-for Sale. The carrying value of the property as of December 31, 2003 is approximately $700 million.

Prior to acquiring Trizec’s interest in the Sears Tower, MetLife carried the Sears Tower mortgage on its balance sheet under “Mortgage loans on real estate.” In 2002, the $691 million (book value) mortgage debt, accrued interest and other liabilities would represent only 2.6% of MetLife’s mortgage loans on real estate and just 0.2% of MetLife’s total invested assets. However, once it acquired Trizec’s second mortgage, the Sears Tower was now carried on MetLife’s balance sheet as “Real estate and real estate joint ventures held-for-investment.” In 2003, the $700 million carrying value ($691 29 “Brookfield Agrees to Buy Trizec in $8.9 Billion Deal,” Wall Street Journal, June 06, 2006.

The Sears Tower January 1, 2007 million mortgage plus $9 million cash purchase price from Trizec) of the Sears Tower would represent 17.4% of MetLife’s real estate and real estate joint ventures held-for-investment, but less than 0.32% of MetLife’s total invested assets.30 MetLife’s Decision to Purchase the Sears Tower According to a company press release, purchasing Trizec’s second mortgage on the Sears Tower allowed MetLife to “manage the long-term strategy of its investment”31 and “allows us more flexibility and operational control.”32 As mentioned previously, there were questions about whether Trizec would be able to repay the first mortgage on the Tower, especially during a time of declining building values. This transaction allowed – at least temporarily - MetLife to avoid any further asset impairment charges or write-downs. MetLife now carried the Sears Tower on its balance sheet at a value of $700 million. MetLife’s Decision to Sell the Sears Tower During 2003 and 2004, MetLife sold many of its commercial real estate holdings to take advantage of falling capitalization rates and rebounding asset prices. In November 2003, MetLife sold One Cal Plaza in Los Angeles to Maguire Properties for $225 million. In December 2003, MetLife agreed to sell 11 Madison Avenue (an art deco office building in Manhattan’s Midtown South District) to ZAR Realty for $675 million. After the sale of these two high-profile deals, MetLife estimated that there was an additional $3.6 billion of unrealized gains in its real estate portfolio. Shortly after purchasing the Sears Tower from Trizec, MetLife began discussions with brokers to explore its options, including an out-right sale as well as “selling a stake in the building to a joint venture partner or refinancing its debt, among other options.” Early in 2004, the Chicago office of Eastdil Realty won the assignment to sell the Sears Tower. They began marketing the Tower and expected bids in the range of $750 million, significantly higher than MetLife’s $700 million carrying value on its balance sheet. The sale of these assets increased MetLife’s statutory capital and allowed the company to repurchase more stock in efforts to boost its own share price. The sale would end MetLife’s relationship with the Sears Tower, which had begun in 1990, but take advantage of Chicago’s strengthening office market. Although economic uncertainty prevailed between 2002 and 2003, Chicago’s population had grown by 4% since 1990 and the city was ranked 5th best out of 31 markets in the

30 MetLife 2003 Annual Report. 31 “MetLife Acquires Sears Tower,” A/E/C Newswire, August 28, 2003 http://www.aecnewswire.com/industrynews/Detailed/470.shtml.

30

32 Kelly Quigley, “Trizec Sells Back Sears Tower Stake” Crain’s Chicago Business, 8/28/2003. (http://chicagobusiness.com/cgi-bin/news.pl?id=9912&rel=1).

31

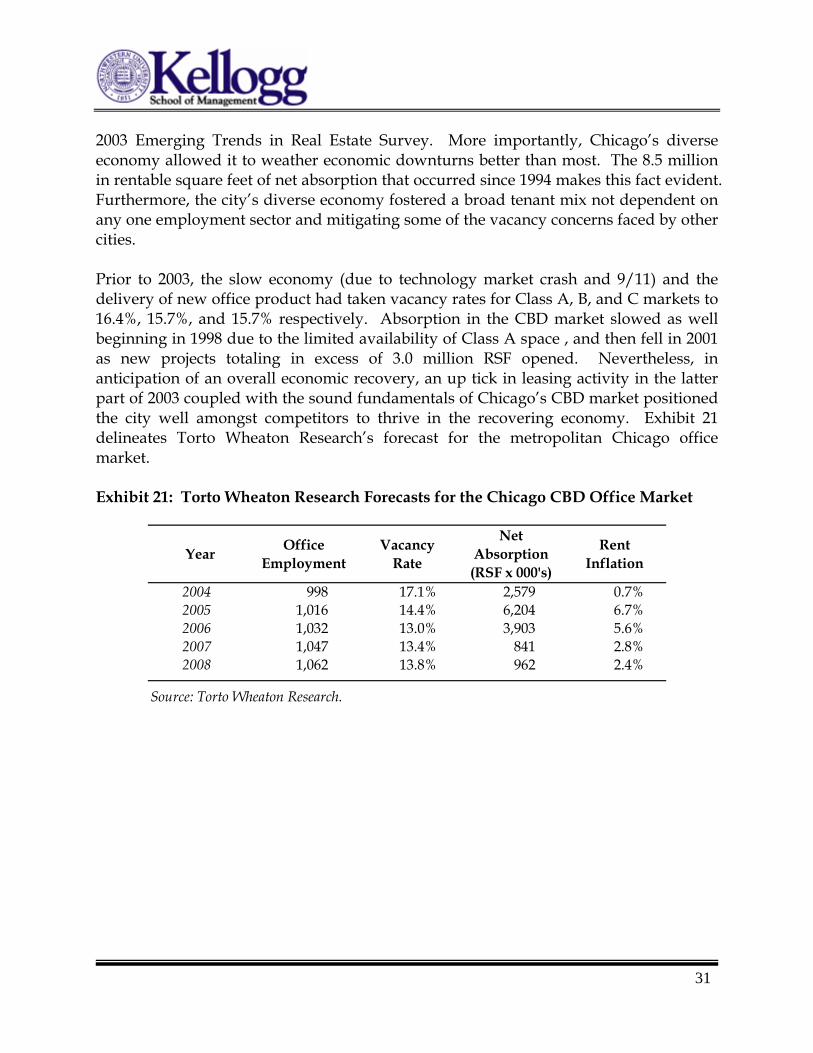

2003 Emerging Trends in Real Estate Survey. More importantly, Chicago’s diverse economy allowed it to weather economic downturns better than most. The 8.5 million in rentable square feet of net absorption that occurred since 1994 makes this fact evident. Furthermore, the city’s diverse economy fostered a broad tenant mix not dependent on any one employment sector and mitigating some of the vacancy concerns faced by other cities. Prior to 2003, the slow economy (due to technology market crash and 9/11) and the delivery of new office product had taken vacancy rates for Class A, B, and C markets to 16.4%, 15.7%, and 15.7% respectively. Absorption in the CBD market slowed as well beginning in 1998 due to the limited availability of Class A space , and then fell in 2001 as new projects totaling in excess of 3.0 million RSF opened. Nevertheless, in anticipation of an overall economic recovery, an up tick in leasing activity in the latter part of 2003 coupled with the sound fundamentals of Chicago’s CBD market positioned the city well amongst competitors to thrive in the recovering economy. Exhibit 21 delineates Torto Wheaton Research’s forecast for the metropolitan Chicago office market. Exhibit 21: Torto Wheaton Research Forecasts for the Chicago CBD Office Market

Year Office Employment

Vacancy Rate

Net Absorption (RSF x 000's)

Rent Inflation

2004 998 17.1% 2,579 0.7%2005 1,016 14.4% 6,204 6.7%2006 1,032 13.0% 3,903 5.6%2007 1,047 13.4% 841 2.8%2008 1,062 13.8% 962 2.4%

Source: Torto Wheaton Research.

The Sears Tower January 1, 2007

IV. Joseph Chetrit and Company Acquire the Sears Tower

Valuation of the Tower in 2004

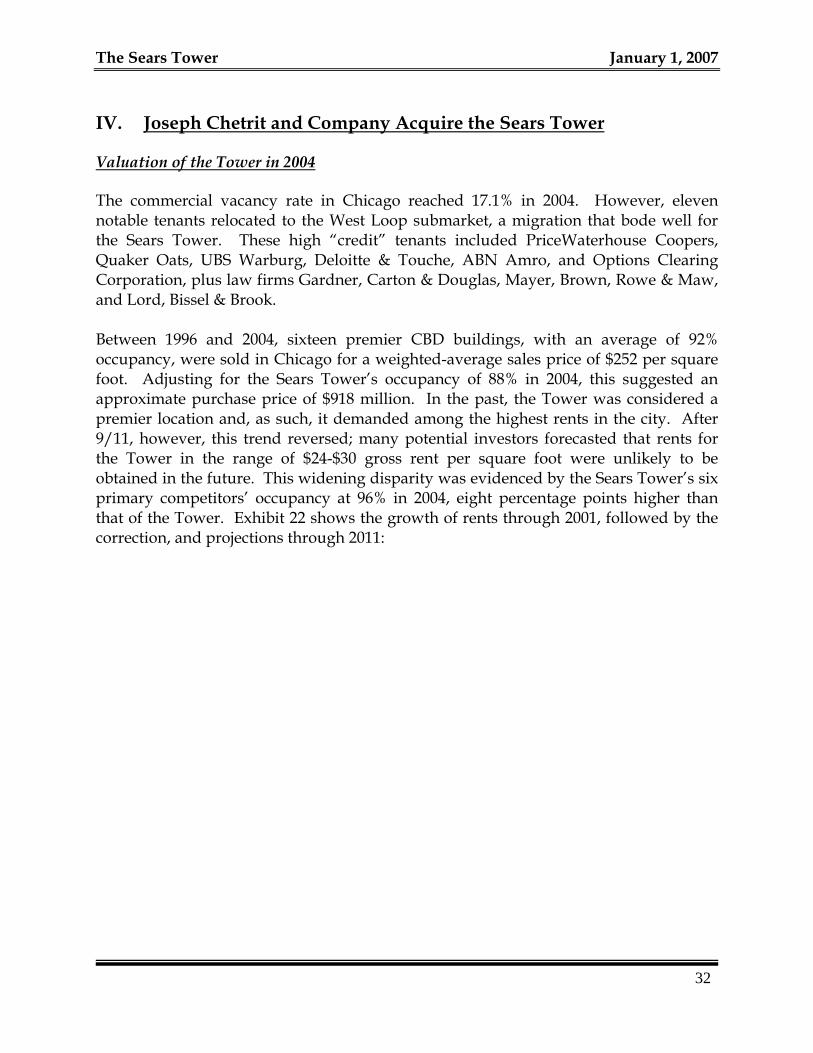

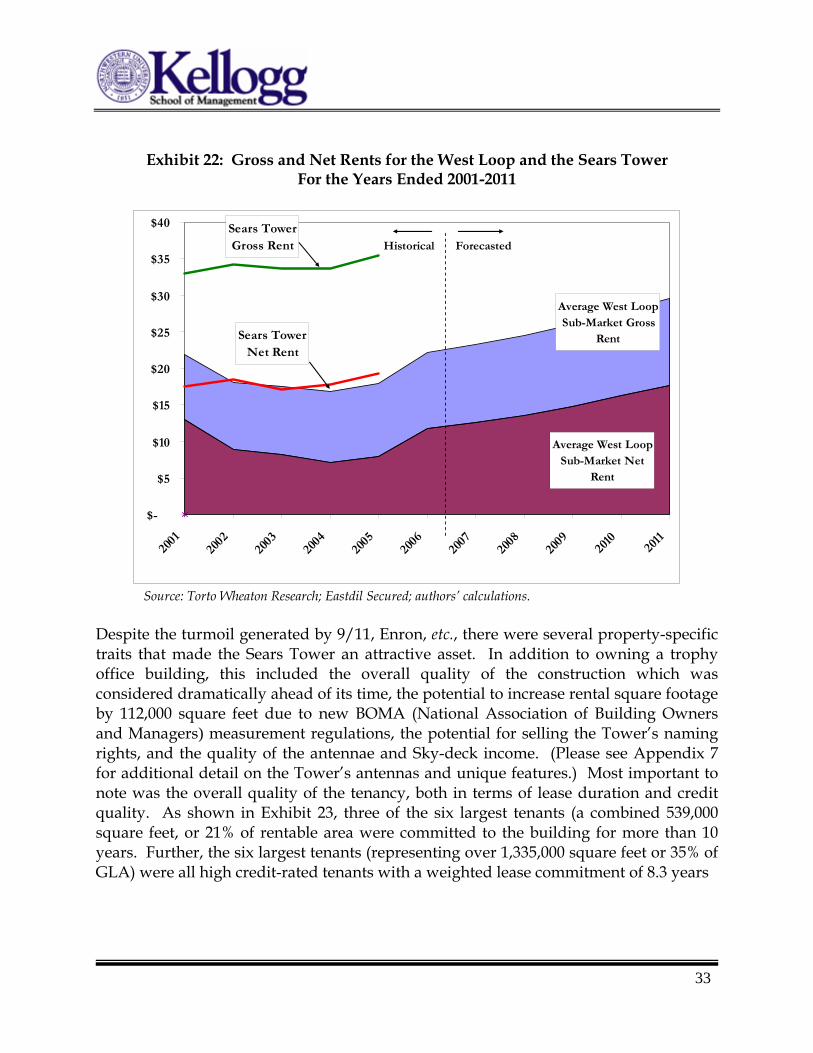

The commercial vacancy rate in Chicago reached 17.1% in 2004. However, eleven notable tenants relocated to the West Loop submarket, a migration that bode well for the Sears Tower. These high “credit” tenants included PriceWaterhouse Coopers, Quaker Oats, UBS Warburg, Deloitte & Touche, ABN Amro, and Options Clearing Corporation, plus law firms Gardner, Carton & Douglas, Mayer, Brown, Rowe & Maw, and Lord, Bissel & Brook. Between 1996 and 2004, sixteen premier CBD buildings, with an average of 92% occupancy, were sold in Chicago for a weighted-average sales price of $252 per square foot. Adjusting for the Sears Tower’s occupancy of 88% in 2004, this suggested an approximate purchase price of $918 million. In the past, the Tower was considered a premier location and, as such, it demanded among the highest rents in the city. After 9/11, however, this trend reversed; many potential investors forecasted that rents for the Tower in the range of $24-$30 gross rent per square foot were unlikely to be obtained in the future. This widening disparity was evidenced by the Sears Tower’s six primary competitors’ occupancy at 96% in 2004, eight percentage points higher than that of the Tower. Exhibit 22 shows the growth of rents through 2001, followed by the correction, and projections through 2011:

32

33

Exhibit 22: Gross and Net Rents for the West Loop and the Sears Tower

For the Years Ended 2001-2011

Average West Loop Sub-Market Net

Rent

Average West Loop Sub-Market Gross

Rent

Sears Tower Gross Rent

Sears Tower Net Rent

$-

$5

$10

$15

$20

$25

$30

$35

$40

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Historical Forecasted

Source: Torto Wheaton Research; Eastdil Secured; authors’ calculations.

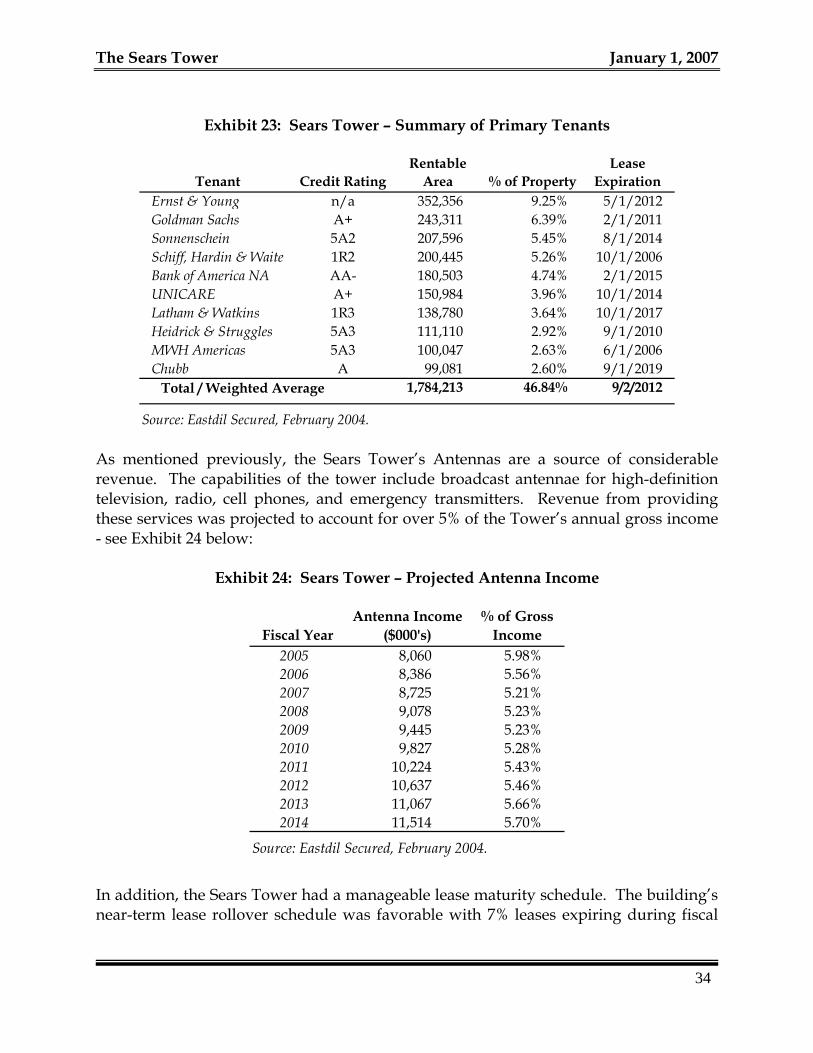

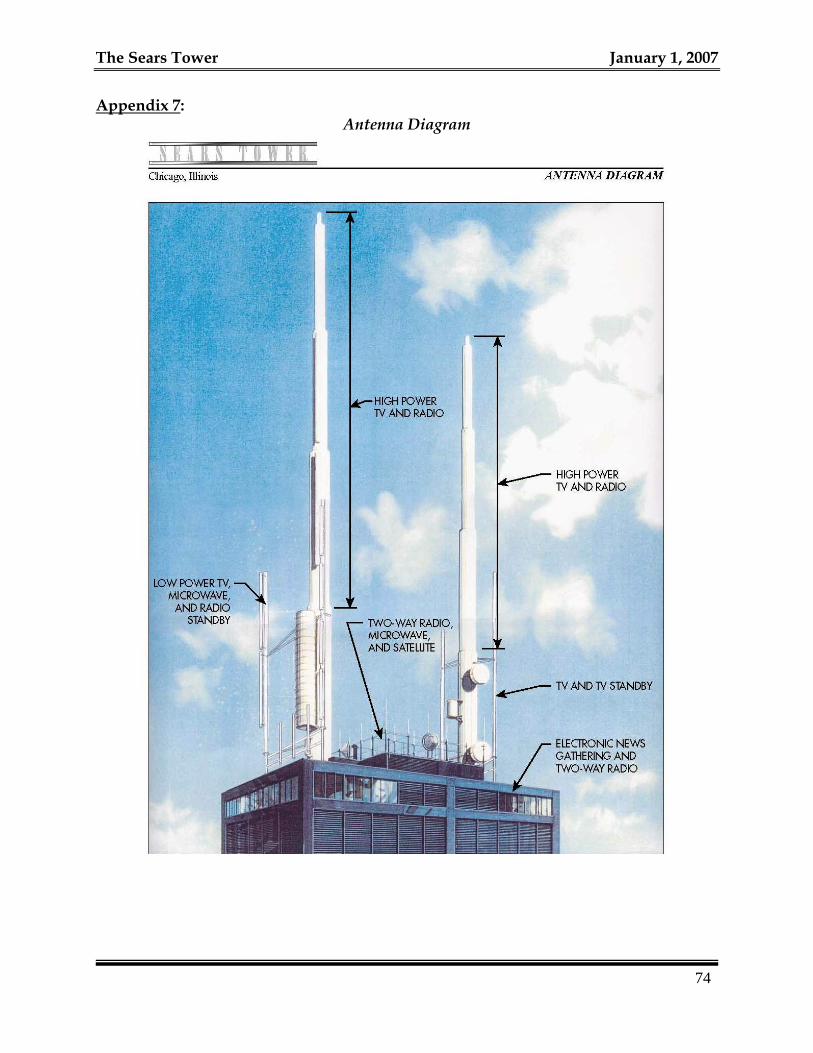

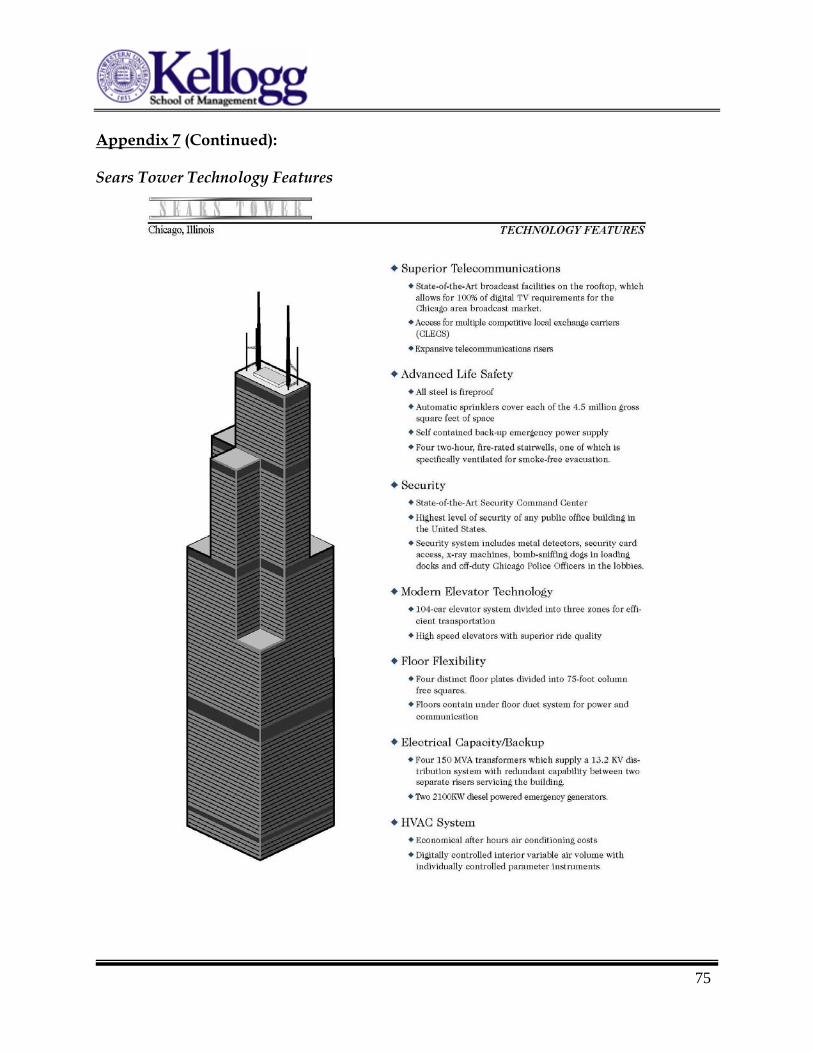

Despite the turmoil generated by 9/11, Enron, etc., there were several property-specific traits that made the Sears Tower an attractive asset. In addition to owning a trophy office building, this included the overall quality of the construction which was considered dramatically ahead of its time, the potential to increase rental square footage by 112,000 square feet due to new BOMA (National Association of Building Owners and Managers) measurement regulations, the potential for selling the Tower’s naming rights, and the quality of the antennae and Sky-deck income. (Please see Appendix 7 for additional detail on the Tower’s antennas and unique features.) Most important to note was the overall quality of the tenancy, both in terms of lease duration and credit quality. As shown in Exhibit 23, three of the six largest tenants (a combined 539,000 square feet, or 21% of rentable area were committed to the building for more than 10 years. Further, the six largest tenants (representing over 1,335,000 square feet or 35% of GLA) were all high credit-rated tenants with a weighted lease commitment of 8.3 years

The Sears Tower January 1, 2007

Exhibit 23: Sears Tower – Summary of Primary Tenants

Tenant Credit RatingRentable

Area % of PropertyLease

ExpirationErnst & Young n/a 352,356 9.25% 5/1/2012Goldman Sachs A+ 243,311 6.39% 2/1/2011Sonnenschein 5A2 207,596 5.45% 8/1/2014Schiff, Hardin & Waite 1R2 200,445 5.26% 10/1/2006Bank of America NA AA- 180,503 4.74% 2/1/2015UNICARE A+ 150,984 3.96% 10/1/2014Latham & Watkins 1R3 138,780 3.64% 10/1/2017Heidrick & Struggles 5A3 111,110 2.92% 9/1/2010MWH Americas 5A3 100,047 2.63% 6/1/2006Chubb A 99,081 2.60% 9/1/2019

Total / Weighted Average 1,784,213 46.84% 9/2/2012

Source: Eastdil Secured, February 2004. As mentioned previously, the Sears Tower’s Antennas are a source of considerable revenue. The capabilities of the tower include broadcast antennae for high-definition television, radio, cell phones, and emergency transmitters. Revenue from providing these services was projected to account for over 5% of the Tower’s annual gross income - see Exhibit 24 below:

Exhibit 24: Sears Tower – Projected Antenna Income

Fiscal YearAntenna Income

($000's)% of Gross

Income2005 8,060 5.98%2006 8,386 5.56%2007 8,725 5.21%2008 9,078 5.23%2009 9,445 5.23%2010 9,827 5.28%2011 10,224 5.43%2012 10,637 5.46%2013 11,067 5.66%2014 11,514 5.70%

Source: Eastdil Secured, February 2004.

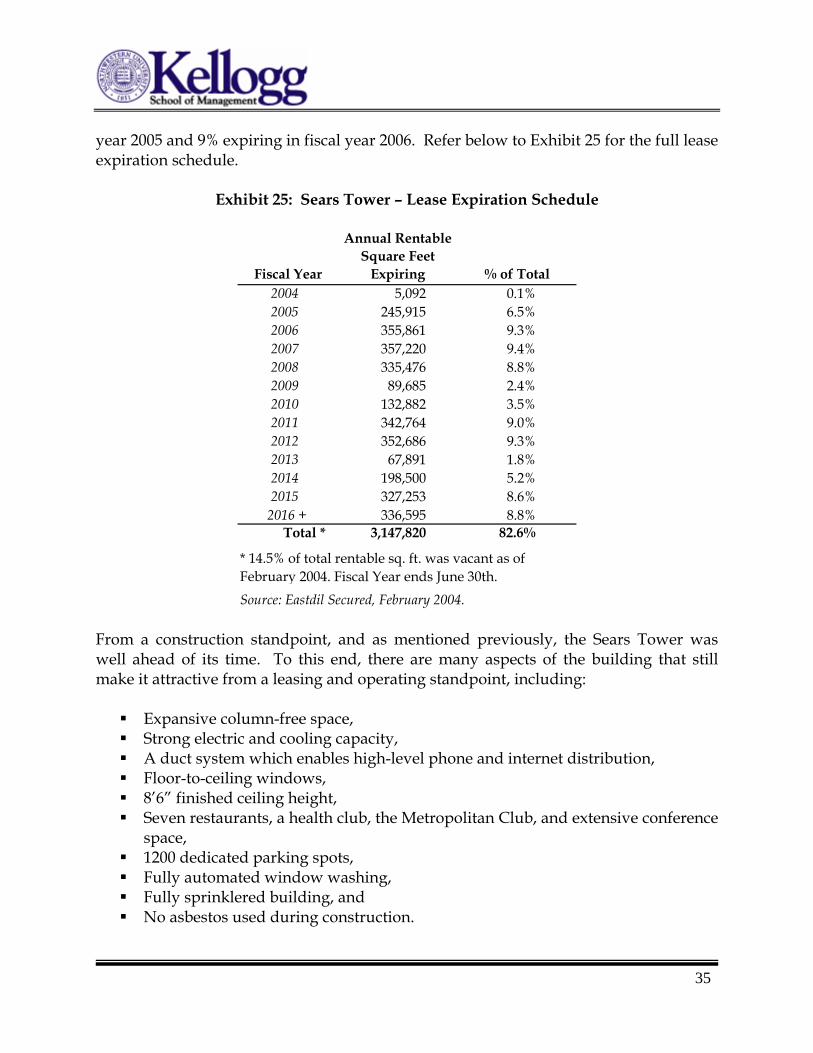

In addition, the Sears Tower had a manageable lease maturity schedule. The building’s near-term lease rollover schedule was favorable with 7% leases expiring during fiscal

34

35

year 2005 and 9% expiring in fiscal year 2006. Refer below to Exhibit 25 for the full lease expiration schedule.

Exhibit 25: Sears Tower – Lease Expiration Schedule

Fiscal Year

Annual Rentable Square Feet

Expiring % of Total2004 5,092 0.1%2005 245,915 6.5%2006 355,861 9.3%2007 357,220 9.4%2008 335,476 8.8%2009 89,685 2.4%2010 132,882 3.5%2011 342,764 9.0%2012 352,686 9.3%2013 67,891 1.8%2014 198,500 5.2%2015 327,253 8.6%

2016 + 336,595 8.8%Total * 3,147,820 82.6%

Source: Eastdil Secured, February 2004.

* 14.5% of total rentable sq. ft. was vacant as of February 2004. Fiscal Year ends June 30th.

From a construction standpoint, and as mentioned previously, the Sears Tower was well ahead of its time. To this end, there are many aspects of the building that still make it attractive from a leasing and operating standpoint, including:

Expansive column-free space, Strong electric and cooling capacity, A duct system which enables high-level phone and internet distribution, Floor-to-ceiling windows, 8’6” finished ceiling height, Seven restaurants, a health club, the Metropolitan Club, and extensive conference

space, 1200 dedicated parking spots, Fully automated window washing, Fully sprinklered building, and No asbestos used during construction.

The Sears Tower January 1, 2007 Based on NCREIF data, commercial capitalization rates in the Chicago area were approximately 7.27% for the quarter ending March 31, 2004. Using this estimate and the Sears Tower’s 2003 NOI of $65.1 million, the likely purchase price could be estimated at $896 million. As mentioned previously, however, many of the rents in the buildings were considered well-above market. Further, it was generally known that Goldman Sachs was planning on vacating the building in 6-7 years. Not only did Goldman Sachs represent the second largest tenant at 243,000 square feet, it also paid net rent of $25 per square foot, which most thought would be nearly impossible to replace.

Aggressive Financing Leads to Sky High Prices & Emergence of Private Buyers

Fueled by the “dot.com” implosion, low interest rates, investors “flocking to quality” and banks wanting to finance large deals, a glut of capital flooded the real estate market after 2001. Further, buyers with a healthy borrowing history were finding the opportunities to leverage close to 100 percent of the purchase price of an asset. Such financing often included a first mortgage for approximately 75% of the property’s value with the balance supplied by aggressive mezzanine financing. The looming Sears Tower transaction also highlighted a more general trend in which private individuals, as opposed to large institutions, were increasingly engineering mammoth deals to acquire trophy properties. Many wealthy investors were acquiring prized properties. For example:

• A group of investors, led by New York investor David Werner, paid $675 million at the end of 2003 to acquire 11 Madison Ave in New York City.

• Another group of investors along with David Werner invested $400 million for 50 percent stake in the Bank of America building in San Francisco in 2004.

• In 2004, New York investor Harry Macklowe stunned the real estate world with a record-setting $1.4 billion bid for the General Motors building, in New York.33

The rush of private capital into these properties resulted in driving down cap rates to well below historical levels for CBD office properties, which typically ranged between 7% and 8%. In 2004, it was not uncommon to see cap rates as low as 5%. Generally speaking, these low cap rates were attributable to the high prices paid by private buyers who were more comfortable (than their institutional counterparts) taking on substantially higher leverage ratios (and implicitly incurring substantially more risk).

36

33 Alison Gregor, “Will Building Buyers Bust?,” The Real Deal, March 2005 (http://www.therealdeal.net/deals/sales.php?deals_sales_sort_order=DESC&deals_sales_sort_field=price).

37

Referring to these bidding wars, Richard Baxter, an Executive Director at Cushman & Wakefield stated:

“The prices for the assets are considered high -- even bubbly. This is the market of the individual investor. They're dominating right now.”34

In addition, James Hanson, a Managing Director for Jones Lang LaSalle, stated at this time:

"Anybody who is going to use a high degree of leverage in an acquisition is going to have an advantage, given how low interest rates are, and also how aggressive lenders are just to put money out."

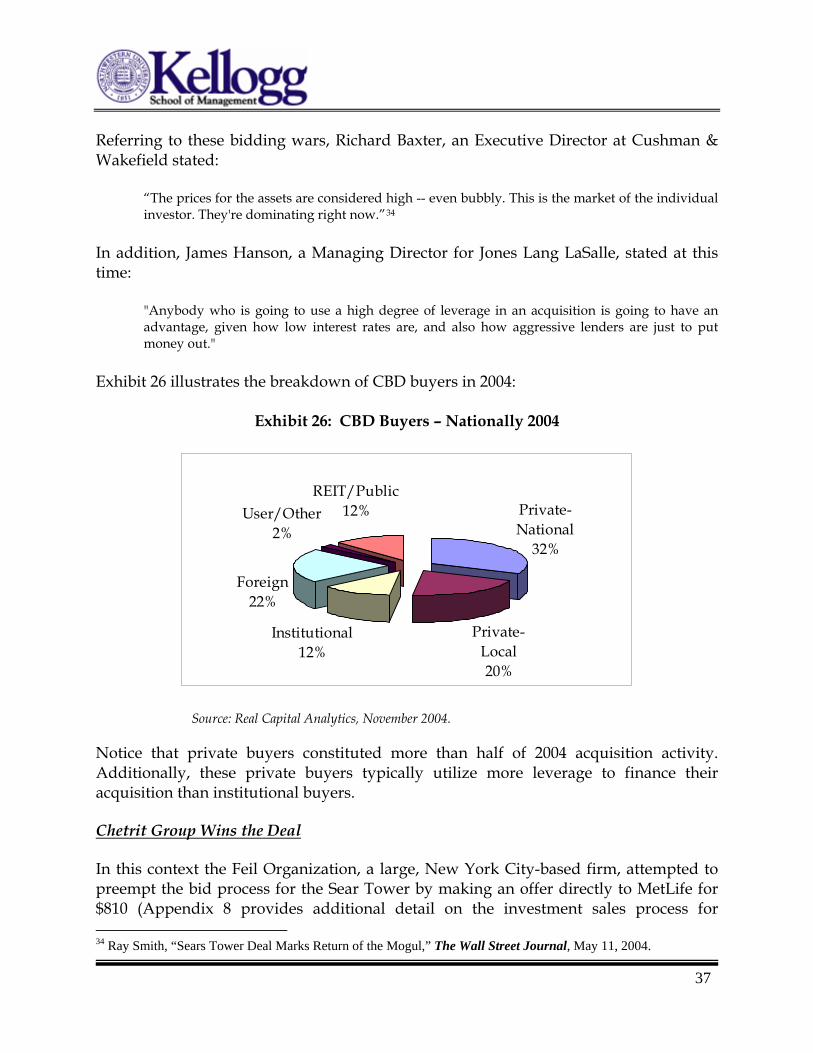

Exhibit 26 illustrates the breakdown of CBD buyers in 2004:

Exhibit 26: CBD Buyers – Nationally 2004

Private-National

32%

Private-Local20%

Institutional12%

Foreign22%

User/Other2%

REIT/Public12%

Source: Real Capital Analytics, November 2004.

Notice that private buyers constituted more than half of 2004 acquisition activity. Additionally, these private buyers typically utilize more leverage to finance their acquisition than institutional buyers.

Chetrit Group Wins the Deal

In this context the Feil Organization, a large, New York City-based firm, attempted to preempt the bid process for the Sear Tower by making an offer directly to MetLife for $810 (Appendix 8 provides additional detail on the investment sales process for 34 Ray Smith, “Sears Tower Deal Marks Return of the Mogul,” The Wall Street Journal, May 11, 2004.

The Sears Tower January 1, 2007 commercial real estate.) The offer was very credible as Feil had a respectable and well-known track record of successfully developing and managing millions of square feet of office buildings across the country up through 2003 (it was also rumored that Wachovia was to be Feil’s mortgage lender). MetLife, anxious to exit the deal, had the Sears Tower on the books for a carrying value of $700 million. Feil’s offer would get them out at a sizeable profit. Moreover, few in the industry believed that the Sears Tower would sell for over $800 million. MetLife verbally accepted Feil’s offer before bidding concluded, but because of the approaching end-of-year holidays, decided to wait to enter into a formal purchase-and-sale agreement. Meanwhile, Eastdil advised MetLife against accepting the deal and to wait for the auction process deadline to be reached. Although the Feil deal was reportedly under contract, Joseph Chetrit, a French-speaking, Moroccan-born New Yorker, formed a group and partnered with Joseph Moinian and Israel Gluck from American Landmark Properties to aggressively pursue the purchase of the Sears Tower. Chetrit, who pleaded guilty in 1990 to a felony count of violating federal customs law when he was operating his business of importing and exporting fabric,35 had already been active on the high-profile real estate scene. Just prior to his purchase of the Tower, Chetrit crafted the acquisition deals of two large Manhattan office properties—530 Fifth Avenue, for $210 million36 and 450 West 33rd Street for $171.5 million37—and in Miami—Roney Palace, a beach resort for $149.8 million38 – among others. In addition, Chetrit had already purchased other properties in the Chicago area. Moinian, an immigrant who came to the U.S. from Iran in the late 1970s, was also prominent in large real estate deals. Moinian and his group purchased several high-priced properties in New York City: 180 Maiden Lane for $355 million; 530 Fifth Avenue for $213 million; 95 Wall Street for $184 million; 1450 Broadway for $124 million; and 17 Battery Place North for $70 million.39

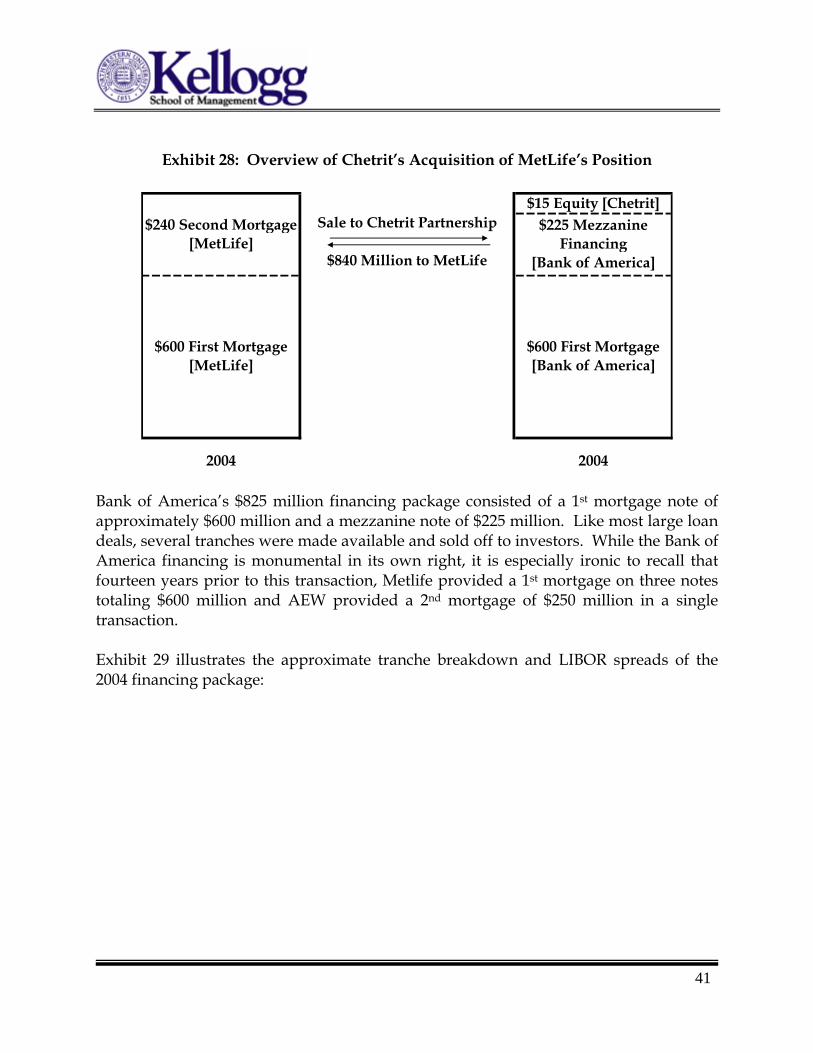

Chetrit’s group immediately made an offer of $840 million which MetLife accepted conditioned upon Chetrit forming a partnership with Feil to jointly acquire the Tower. Eastdil spoke with the other bidders, described as the “top five trophy landlords in the United States,” to see if any other offers were forthcoming at prices approaching this number. Eastdil received a unanimous response of “no” and Chetrit’s group won the deal.

35 Ray Smith, “Sears Tower Deal Marks Return of the Mogul,” The Wall Street Journal, May 11, 2004. 36 “$220 Million Fifth Ave. Sale - Joseph Chetrit,” Real Estate Weekly, February 25, 2004. 37 Real Estate Alert, January 14, 2004. 38 “Real Estate Developer Joseph Chetrit May or May Not Buy the Bankrupt Roney Palace Hotel and Condominiums for $153.5 million”, Knight Ridder/Tribune Business News, June 10, 2004.

38

39 Alison Gregor, “Will Building Buyers Bust?,” The Real Deal, March 2005.

39