Embed Size (px)

Citation preview

What do we know, what have we learned? Michigan, US, and

Obamanomics

Jared Bernstein

Economic Policy Institute

MLHS Annual Meeting

Real Economy, macro

• It’s official—recession, that is…but you knew that.

• Consumer: retrenching, big time.• Investment: squeezed on credit and profit

sides• Exports/Imports: Maybe, maybe not…• Government: most reliable source of short

term growth?

-600

-500

-400

-300

-200

-100

0

100

200Ja

n-0

7

Fe

b-0

7

Ma

r-0

7

Ap

r-0

7

Ma

y-0

7

Jun

-07

Jul-

07

Au

g-0

7

Se

p-0

7

Oct

-07

No

v-0

7

De

c-0

7

Jan

-08

Fe

b-0

8

Ma

r-0

8

Ap

r-0

8

Ma

y-0

8

Jun

-08

Jul-

08

Au

g-0

8

Se

p-0

8

Oct

-08

No

v-0

8

Mo

nth

ly c

ha

ng

e in

em

plo

ym

en

t (t

ho

us

an

ds

)

Total

Private

Total and Private Payroll Employment, Jan. 07 - Nov. 08

Source: Bureau of Labor Statistics, EPI Employment Projections

Employment Declines Across Sectors

Source: Bureau of Labor Statistics

Housing Employment, Jan. 07 - Nov. 08

6600

6800

7000

7200

7400

7600

7800

8000

Mo

nth

ly e

mp

loym

ent

(th

ou

san

ds)

Source: EPI calculated housing index, including residential building, real estate, and credit intermediation

774,000 Jobs Lost (9.6%)

Manufacturing Employment, Jan. 07 - Nov. 08

12600

12800

13000

13200

13400

13600

13800

14000

14200

Mo

nth

ly e

mp

loym

ent

(th

ou

san

ds)

847,000 Jobs Lost (6.0%)

Retail Employment, Jan. 07 - Nov. 08

14800

14900

15000

15100

15200

15300

15400

15500

15600

Mo

nth

ly e

mp

loym

ent

(th

ou

san

ds)

402,000 Jobs Lost (2.6%)

Automotive Manufacturing Employment, Jan. 07 - Nov. 08

800

850

900

950

1000

1050

Mo

nth

ly e

mp

loym

ent

(th

ou

san

ds)

194,000 Jobs Lost (19.0%)

Source: Bureau of Labor Statistics

0%

2%

4%

6%

8%

10%

12%

Jan

-07

Fe

b-0

7

Ma

r-0

7

Ap

r-0

7

Ma

y-0

7

Jun

-07

Jul-

07

Au

g-0

7

Se

p-0

7

Oct

-07

No

v-0

7

De

c-0

7

Jan

-08

Fe

b-0

8

Ma

r-0

8

Ap

r-0

8

Ma

y-0

8

Jun

-08

Jul-

08

Au

g-0

8

Se

p-0

8

Oct

-08

No

v-0

8

Unemployment

Underemployment

Feb. 08: 4.8%

Feb. 08: 8.9%

Oct. 08: 6.7%

Nov. 08: 12.5%

Unemployment and Underemployment, Jan. 07 - Nov. 08

$50,000

$52,000

$54,000

$56,000

$58,000

$60,000

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Me

dia

n I

nc

om

e,

20

07

Do

lla

rsReal Median Income, Working-Age Households,

1989-2007

2000: $58,555

1993: $50,806

2007: $56,545

Source: Bureau of Labor Statistics

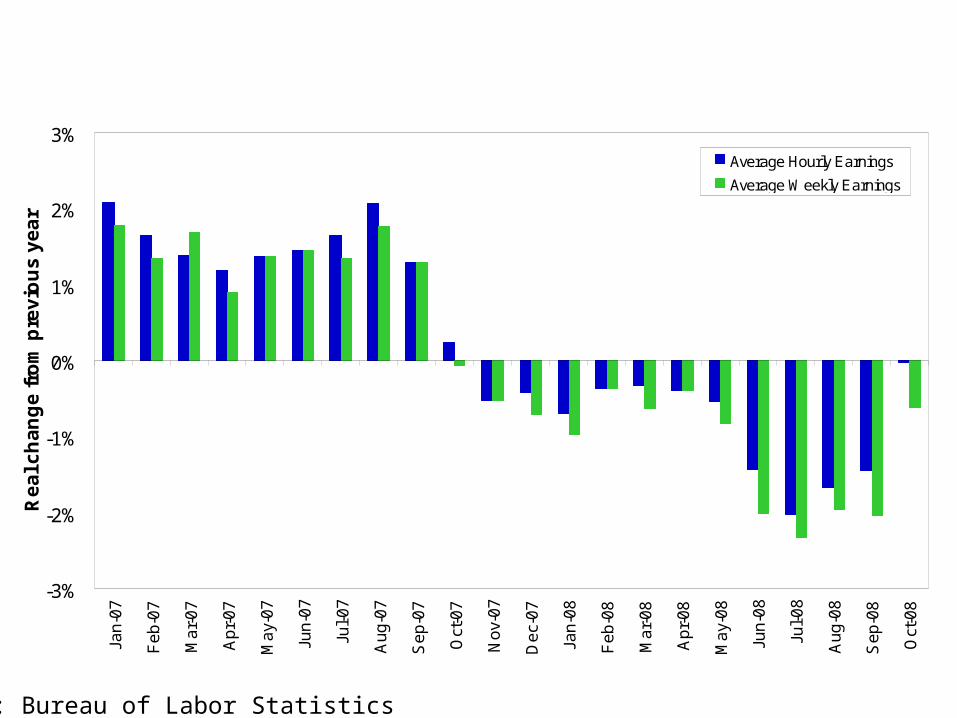

-3%

-2%

-1%

0%

1%

2%

3%Ja

n-0

7

Fe

b-0

7

Ma

r-0

7

Ap

r-0

7

Ma

y-0

7

Jun

-07

Jul-

07

Au

g-0

7

Se

p-0

7

Oct

-07

No

v-0

7

De

c-0

7

Jan

-08

Fe

b-0

8

Ma

r-0

8

Ap

r-0

8

Ma

y-0

8

Jun

-08

Jul-

08

Au

g-0

8

Se

p-0

8

Oct

-08

Re

al c

ha

ng

e f

rom

pre

vio

us

ye

ar

Average Hourly Earnings

Average Weekly Earnings

Yearly Changes in Average Weekly and Hourly Earnings, Jan. 07 - Oct. 08

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

Job Seekers Per Opening, Jan. 07 - Oct. 08

1.0

1.5

2.0

2.5

3.0

3.5

Jan-

07

Feb

-07

Mar

-07

Apr

-07

May

-07

Jun-

07

Jul-0

7

Aug

-07

Sep

-07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb

-08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Job

See

kers

Per

Op

enin

g

October 2008:3.3 job seekers per opening

January 2007:1.6 job seekers per opening

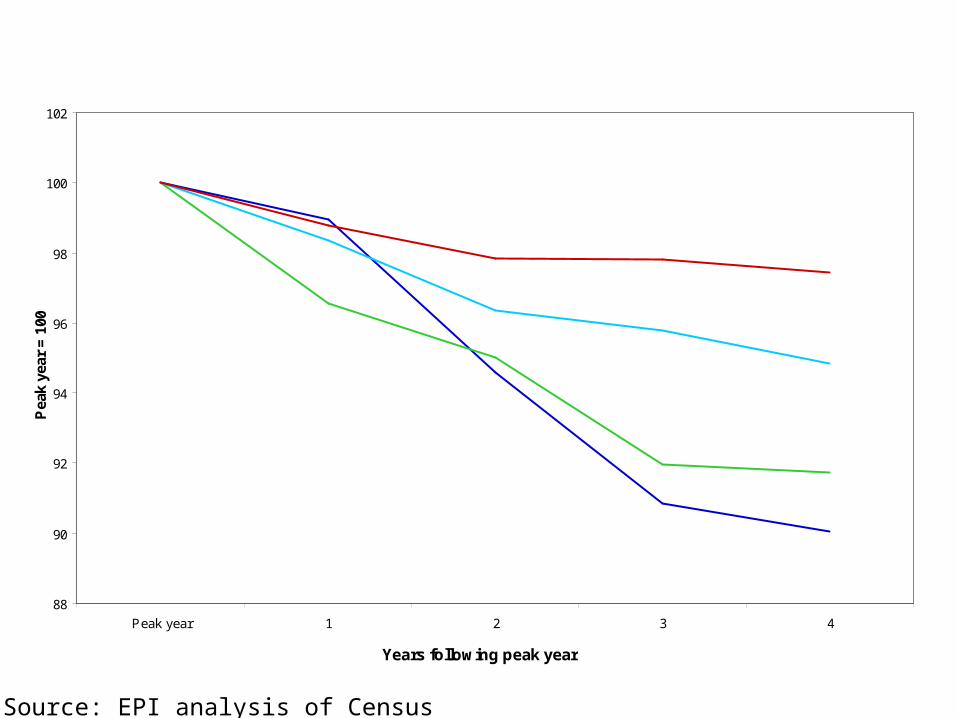

88

90

92

94

96

98

100

102

Peak year 1 2 3 4

Years following peak year

Pea

k ye

ar =

100

1989 Lowest fifth

2000 Lowest fifth

1989 Middle fifth

2000 Middle fifth

-3%

-5%

-8%

-10%

Change in Average Real Family Income Following Peak Years,by Selected Income Quintiles

Source: EPI analysis of Census Bureau data

$13,500

$14,000

$14,500

$15,000

$15,500

$16,000

$16,500

$17,000

$17,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Ave

rag

e In

com

e o

f B

ott

om

Fif

th (

2007

Do

llars

)

$56,000

$57,000

$58,000

$59,000

$60,000

$61,000

$62,000

Ave

rag

e In

com

e o

f M

idd

le F

ifth

(20

07 D

olla

rs)

Bottom Fifth

Bottom Fifth (Forecast)

Middle Fifth

Middle Fifth (Forecast)

Source: EPI Analysis of BLS data and Goldman-Sachs unemployment rate forecasts

2007 - 2009:Middle Fifth: $3,355 lost (-5.5%)Bottom Fifth: $1,128 lost (-7.0%)

Average Income of Bottom and Middle Fifths, 2000-2009 (Forecast)

Poverty Rate, 2000-2009 (Forecast)

0%

2%

4%

6%

8%

10%

12%

14%

16%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Po

ve

rty

Ra

te

Historical

Forecast

Source: EPI Analysis of BLS data and Goldman-Sachs unemployment rate forecasts

125

130

135

140

145

2005 2006 2007 2008 2009 2010 2011 2012

Pa

yro

ll E

mp

loy

me

nt

(Mill

ion

s)

With Stimulus

No Stimulus

Employment Projections, With and Without Stimulus Package

2012 Q4: 144 million

2012 Q4: 140 million

Stimulus creates 4 million jobs by Q4 2012

Source: Mark Zandi, Moody’s economy.com

0

2

4

6

8

10

12

2005 2006 2007 2008 2009 2010 2011 2012

Un

em

plo

ym

en

t R

ate

With Stimulus

No Stimulus

Unemployment Projections, With and Without Stimulus Package

2012 Q4: 7.6%

2012 Q4: 5.5%

Stimulus lowers unemployment by 2.1% in Q4 2012

Source: Mark Zandi, Moody’s economy.com

Un-Real Economy

• Financial Markets: Dow, Nasdaq, S&P 500, Russell 2000…all down about 40% ytd.

• But: good news…”Ted Spread” responding• Housing: some signs bottom in sight, but no

signs re uptick…prices still falling…inventory overhang;

• TARP: Certainly not a confidence builder yet.• Fed: pushing on string but not giving up.

Pres/VP Elect• Fiscal constraints?

• Deficit could go as high as 6% of GDP, but debt around 40% (avg 46% in 1990s).

• Must he alter his long-term plans--hth care/energy?

• There is a time for budget austerity; this ain’t it.

• Middle-class, poor, labor agenda (EFCA, min wg, UI reform, OSHA, etc…)

Their Agenda• Morph his recovery package with House

D’s (Making Work Pay tax cuts; new jobs tax credit; mortgage relief; small biz, UI)

• Manage TARP

• Tax agenda

• Energy/Health Care

• Infrastructure (who gets the jobs?)

• Regulation (Cooper Union speech)

What Have We Learned?

• Markets• Ineq• Public investment• No more TBTF• Financial markets

Learned…cont.

• Budget priorities• Supply-side• Amply funded gov’t• Shampoo economy• Better economists