Embed Size (px)

Citation preview

DNV GL © 2013 SAFER, SMARTER, GREENER

Mitch Rosenberg, Gomathi Sadhasivan, & Rachel Schiff

Whole House Retrofit Market Effects Study

1

CPUC EM&V WO54 – Market Assessment & Market

Effects

DNV GL © 2013

Table of Contents

Background

– Project Objectives & Methods

– Development of Whole House Retrofit/Home Performance Programs & Industry

– CA Program Activity

Customer View

– Prevalence of Energy Efficiency Measures in the Flow of Home Improvements

– Prevalence of Home Performance and Whole House Features

– Awareness, Knowledge, and Perceptions of Value for WH/HP Features

The Supply Chain

– Current Service Offerings v. the WH/HP Model

– Interest in offering WH/HP Services

– Case Studies of High Volume Contractors: Business Models and Practices

Conclusions and Implications for Program Strategies and Future Research

2

DNV GL © 2013

BACKGROUND

3

DNV GL © 2013

Project Objectives and Basic Approach

Objectives: Characterize and, to the extent possible, quantify the effect of CA IOU

programs that support whole house retrofit (WH) and home performance (HP) services

on the markets for and sales of those services in California.

Methods

– Prospective Study: Assess program effects on a targeted market in two phases

– First (Current) Phase: Develop baseline characterization of the WH/HP services

market in California and in Comparison Areas without major utility-funded programs

– Identify and quantify Market Transformation Indicators pertaining to customer

adoption and development of supply chain delivery capacity

– Characterize CA and Comparison Areas in terms of those indicators

– Supplement quantitative indicators with research to characterize the drivers &

barriers to customer and contractor adoption of WH/HP services

– Second Phase (in 2 - 3 years):

– Quantify the Market Transformation Indicators in CA and the Comparison Areas

– Use these data to assess differences in the pace of market development

– Combine cross-sectional comparisons of rates of market change with other data to

quantify program market effects of CA programs

4

DNV GL © 2013

Selection of Comparison Areas

Objective – construct an area that, in aggregate, represented the

major climate/economic zones of CA: coastal & interior

Out-of-State Comparison Areas: MSAs in NC, TX, TN

– No large active WH/HP programs funded by public goods charges

– Similarity in climate: coastal = low number of total degree days; interior =

relatively high number of CDD

– Similarity in housing and demographic variables: income, education, pop.

density, housing price/income ratio

Inside CA Comparison Area

– Added at recommendation of IOU evaluation staff

– Consists of selected areas within 14 counties in the PG&E service territory in

which the program was not heavily marketed as of May 2013

5

DNV GL © 2013

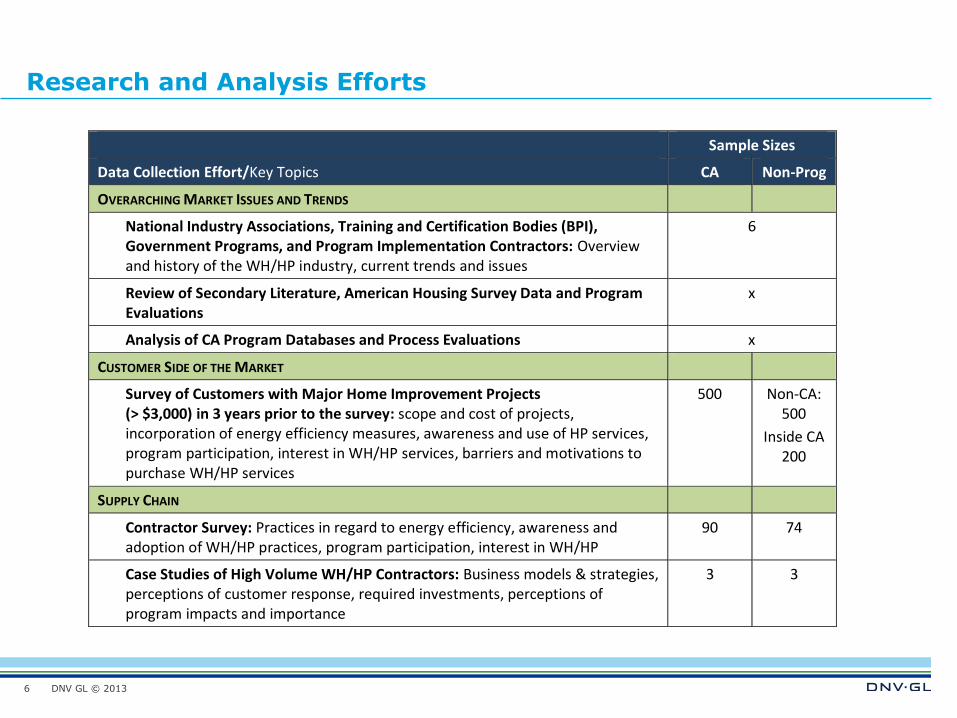

Research and Analysis Efforts

6

Sample Sizes

Data Collection Effort/Key Topics CA Non-Prog

OVERARCHING MARKET ISSUES AND TRENDS

National Industry Associations, Training and Certification Bodies (BPI), Government Programs, and Program Implementation Contractors: Overview and history of the WH/HP industry, current trends and issues

6

Review of Secondary Literature, American Housing Survey Data and Program Evaluations

x

Analysis of CA Program Databases and Process Evaluations x

CUSTOMER SIDE OF THE MARKET

Survey of Customers with Major Home Improvement Projects (> $3,000) in 3 years prior to the survey: scope and cost of projects, incorporation of energy efficiency measures, awareness and use of HP services, program participation, interest in WH/HP services, barriers and motivations to purchase WH/HP services

500 Non-CA: 500

Inside CA 200

SUPPLY CHAIN

Contractor Survey: Practices in regard to energy efficiency, awareness and adoption of WH/HP practices, program participation, interest in WH/HP

90 74

Case Studies of High Volume WH/HP Contractors: Business models & strategies, perceptions of customer response, required investments, perceptions of program impacts and importance

3 3

DNV GL © 2013

Selected Methodological Issues

Comparability of homeowner survey samples in the 3 study areas:

differences relatively small but some are statistically significant;

differences between areas not consistent across variables

– Age distribution: very little difference, skewed slightly older in CA

– Educational attainment: higher % of college grads in OOS (76%) v.

CA Program Area (67%)

– Income distribution more heavily weighted to middle in OOS than in

CA – which has more concentration in higher & lower ends

Over-representation of participants in program: 19% of CA sample v.

2% estimated from program records. Downweighted self-reported

participants in all study areas

Surveys conducted 2 years after program implementation

– Observed differences in between study areas in market indicators

likely reflect market effects, as well as other factors: code

differences, market effects of earlier programs.

7

DNV GL © 2013

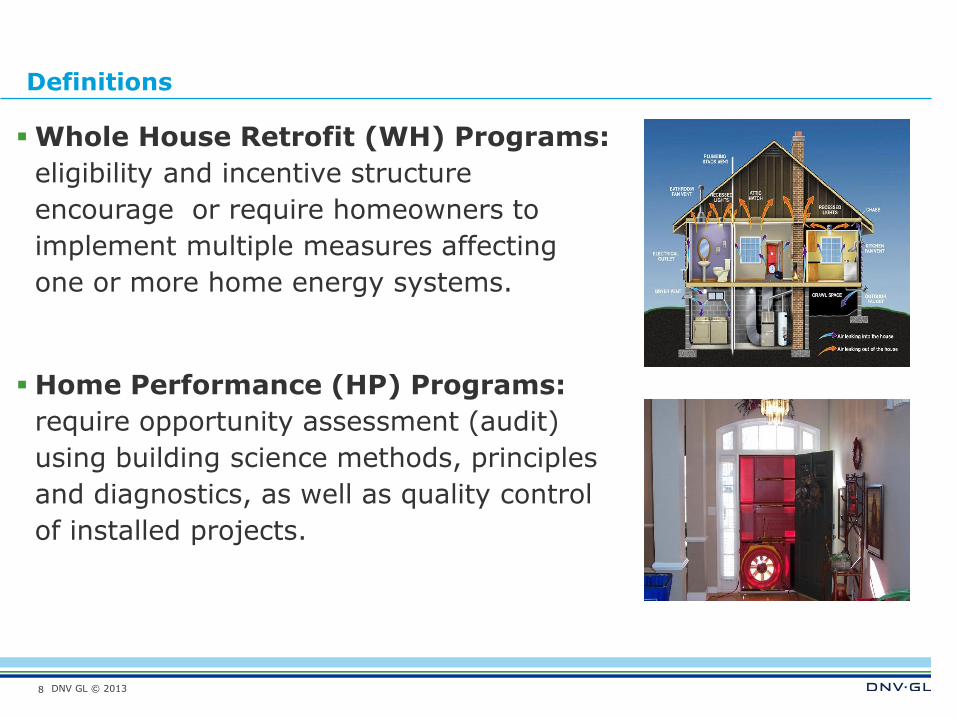

Definitions

Whole House Retrofit (WH) Programs:

eligibility and incentive structure

encourage or require homeowners to

implement multiple measures affecting

one or more home energy systems.

Home Performance (HP) Programs:

require opportunity assessment (audit)

using building science methods, principles

and diagnostics, as well as quality control

of installed projects.

8

DNV GL © 2013

Chronology of Key Events in Home Performance Industry Development

9

Year Key WH/HP Industry Events

1993 Building Performance Institute started as a program of New York State to improve standards of performance for weatherization programs

1996 BPI incorporated and issues first auditor certifications 1999 NYSERDA hires BPI and CSG to develop certification and delivery

protocols for private sector contractors 2001 EPA develops standards for Home Performance with Energy Star

programs. Hires CEE/NATE to develop standards and certification for HVAC installation; BPI to develop standards and certification for whole house contractors NYSERDA launches first Home Performance with Energy Star program

2004 EPA, DOE, and HUD hire CSG and BPI to promote national expansion of Home Performance programs

2008 Terms of stimulus funding for energy efficiency discussed 2009 ARRA funding released for home performance programs under

three programs ~$700 million 2010 ARRA programs in the field:

Programs listed in DSIRE - 126 2011 ARRA programs in the field 2012 ARRA programs wind down 2013 ARRA programs closed out except for some loan funds

Programs listed in DSIRE – 97

0

5

10

15

20

25

30

35

40

45

50

2008 2009 2010 2011 2012 2013

BP

I A

cti

ve C

erti

ficati

on

s

‘00

0s

The ARRA Era: The number of

WH/HP programs and BPI

certified technicians increased

significantly with ARRA funding

but have since declined sharply.

DNV GL © 2013

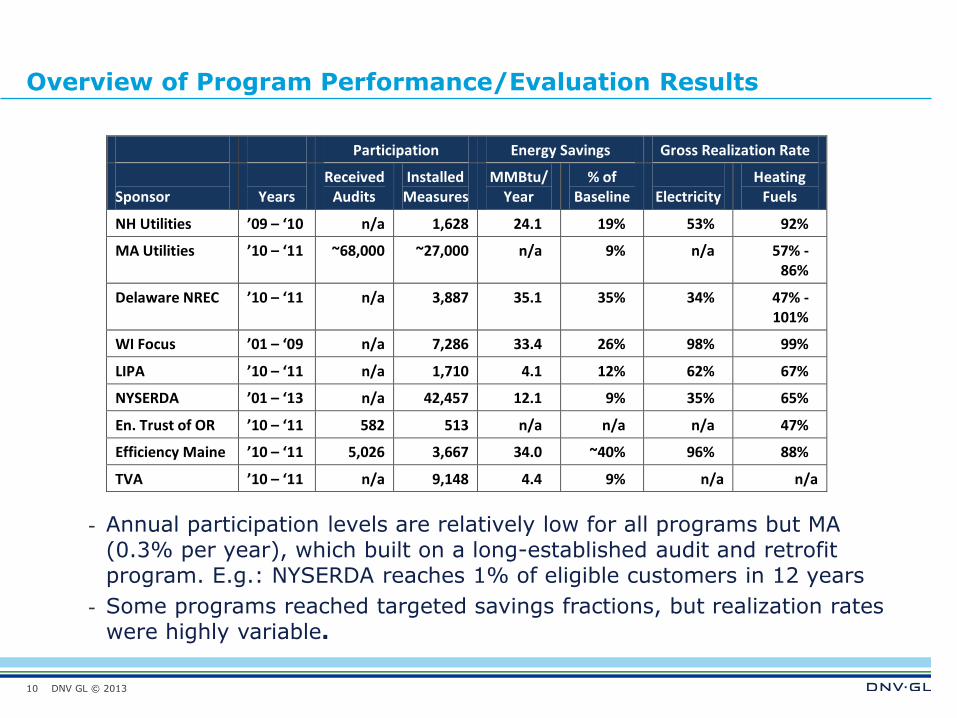

Overview of Program Performance/Evaluation Results

- Annual participation levels are relatively low for all programs but MA (0.3% per year), which built on a long-established audit and retrofit program. E.g.: NYSERDA reaches 1% of eligible customers in 12 years

- Some programs reached targeted savings fractions, but realization rates were highly variable.

Participation Energy Savings Gross Realization Rate

Sponsor

Years

Received Audits

Installed Measures

MMBtu/ Year

% of Baseline

Electricity

Heating Fuels

NH Utilities ’09 – ‘10 n/a 1,628 24.1 19% 53% 92%

MA Utilities ’10 – ‘11 ~68,000 ~27,000 n/a 9% n/a 57% - 86%

Delaware NREC ’10 – ‘11 n/a 3,887 35.1 35% 34% 47% - 101%

WI Focus ’01 – ‘09 n/a 7,286 33.4 26% 98% 99%

LIPA ’10 – ‘11 n/a 1,710 4.1 12% 62% 67%

NYSERDA ’01 – ‘13 n/a 42,457 12.1 9% 35% 65%

En. Trust of OR ’10 – ‘11 582 513 n/a n/a n/a 47%

Efficiency Maine ’10 – ‘11 5,026 3,667 34.0 ~40% 96% 88%

TVA ’10 – ‘11 n/a 9,148 4.4 9% n/a n/a

10

DNV GL © 2013

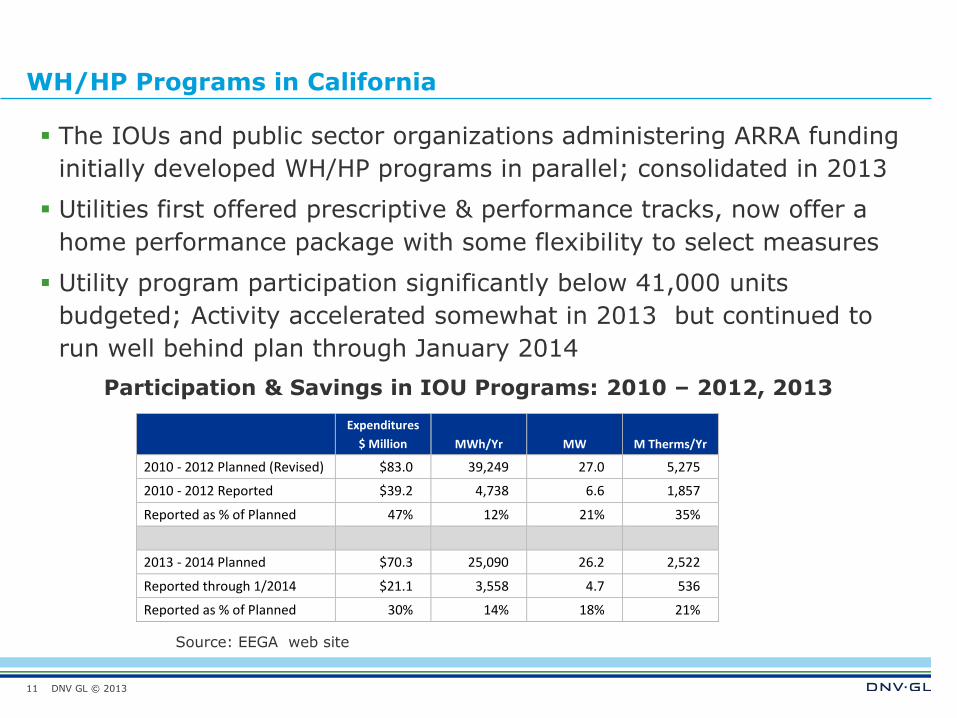

WH/HP Programs in California

The IOUs and public sector organizations administering ARRA funding

initially developed WH/HP programs in parallel; consolidated in 2013

Utilities first offered prescriptive & performance tracks, now offer a

home performance package with some flexibility to select measures

Utility program participation significantly below 41,000 units

budgeted; Activity accelerated somewhat in 2013 but continued to

run well behind plan through January 2014

Participation & Savings in IOU Programs: 2010 – 2012, 2013

11

Expenditures

$ Million MWh/Yr MW M Therms/Yr

2010 - 2012 Planned (Revised) $83.0 39,249 27.0 5,275

2010 - 2012 Reported $39.2 4,738 6.6 1,857

Reported as % of Planned 47% 12% 21% 35%

2013 - 2014 Planned $70.3 25,090 26.2 2,522

Reported through 1/2014 $21.1 3,558 4.7 536

Reported as % of Planned 30% 14% 18% 21%

Source: EEGA web site

DNV GL © 2013

THE CONSUMER MARKET

12

DNV GL © 2013

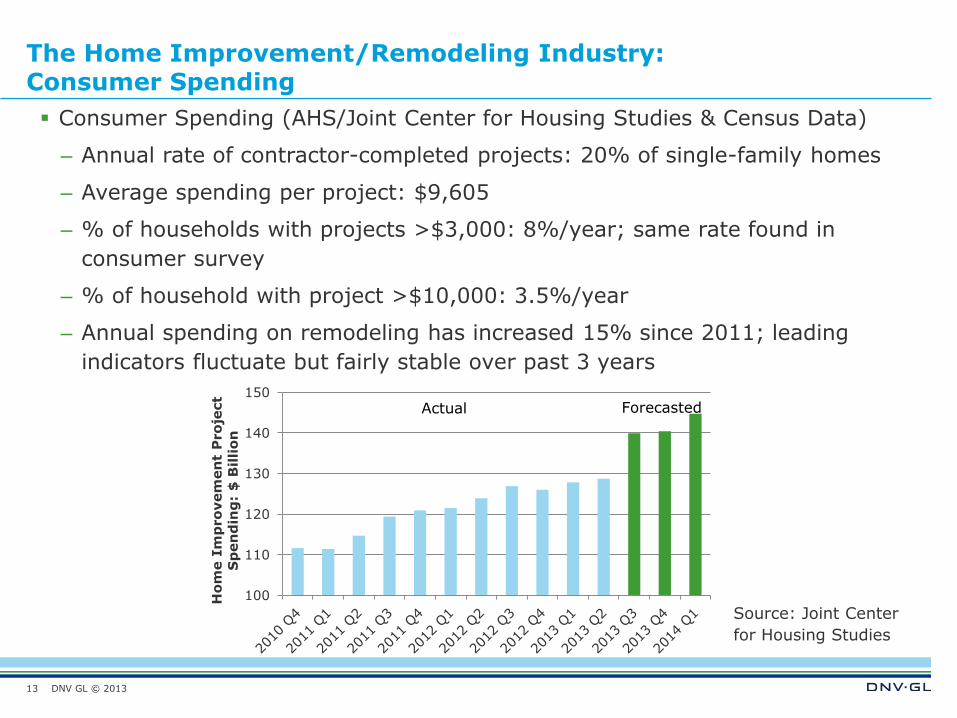

The Home Improvement/Remodeling Industry: Consumer Spending

Consumer Spending (AHS/Joint Center for Housing Studies & Census Data)

– Annual rate of contractor-completed projects: 20% of single-family homes

– Average spending per project: $9,605

– % of households with projects >$3,000: 8%/year; same rate found in

consumer survey

– % of household with project >$10,000: 3.5%/year

– Annual spending on remodeling has increased 15% since 2011; leading

indicators fluctuate but fairly stable over past 3 years

13

100

110

120

130

140

150

Ho

me I

mp

ro

vem

en

t P

ro

ject

Sp

en

din

g:

$ B

illio

n

Actual Forecasted

Source: Joint Center

for Housing Studies

DNV GL © 2013

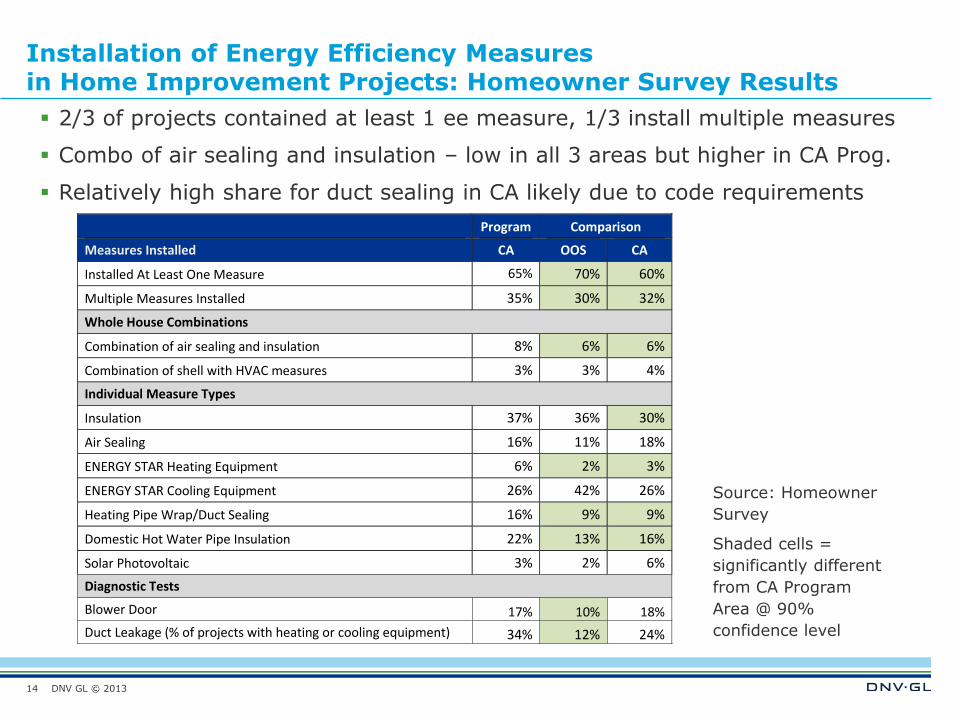

Installation of Energy Efficiency Measures in Home Improvement Projects: Homeowner Survey Results

2/3 of projects contained at least 1 ee measure, 1/3 install multiple measures

Combo of air sealing and insulation – low in all 3 areas but higher in CA Prog.

Relatively high share for duct sealing in CA likely due to code requirements

14

Program Comparison

Measures Installed CA OOS CA

Installed At Least One Measure 65% 70% 60%

Multiple Measures Installed 35% 30% 32%

Whole House Combinations

Combination of air sealing and insulation 8% 6% 6%

Combination of shell with HVAC measures 3% 3% 4%

Individual Measure Types

Insulation 37% 36% 30%

Air Sealing 16% 11% 18%

ENERGY STAR Heating Equipment 6% 2% 3%

ENERGY STAR Cooling Equipment 26% 42% 26%

Heating Pipe Wrap/Duct Sealing 16% 9% 9%

Domestic Hot Water Pipe Insulation 22% 13% 16%

Solar Photovoltaic 3% 2% 6%

Diagnostic Tests

Blower Door 17% 10% 18%

Duct Leakage (% of projects with heating or cooling equipment) 34% 12% 24%

Source: Homeowner

Survey

Shaded cells =

significantly different

from CA Program

Area @ 90%

confidence level

DNV GL © 2013

Installation of Energy Efficiency Measures in Home Improvement Projects by Program Participation Status

In CA program area, participation associated with higher rates of implementing

“Whole House Combinations”, air sealing, and duct sealing. This pattern not

present in non-program areas.

15

PROGRAM PARTICIPANTS NON-PARTICIPANTS

Program Comparison Program Comparison

CA OOS CA CA OOS CA

Received assistance from an ee program in completing project

19% 14% 13%

Multiple Measures Installed 52% 41% 31% 35% 30% 32%

Whole House Combinations

Combination of air sealing and insulation 19% 8% 4% 7% 6% 6%

Combination of shell with HVAC measures 13% 6% 4% 3% 3% 4%

Individual Measure Types

Insulation 44% 49% 28% 37% 36% 30%

Air Sealing 27% 14% 24% 16% 11% 18%

ENERGY STAR Heating Equipment 11% 3% 0% 6% 2% 3%

ENERGY STAR Cooling Equipment 36% 63% 42% 26% 41% 26%

Heating Pipe Wrap/Duct Sealing 32% 18% 9% 15% 9% 9%

Domestic Hot Water Pipe Insulation 24% 17% 8% 22% 13% 16%

Solar Photovoltaic 13% 4% 4% 3% 2% 6%

Diagnostic Tests

Blower Door 27% 14% 24% 14% 10% 16%

Duct Leakage (% of projects with heating or cooling equipment) 41% 22% 35% 29% 15% 26%

Source: Homeowner

Survey

Shaded cells =

significantly different

from CA Program

Area @ 90%

confidence level

DNV GL © 2013

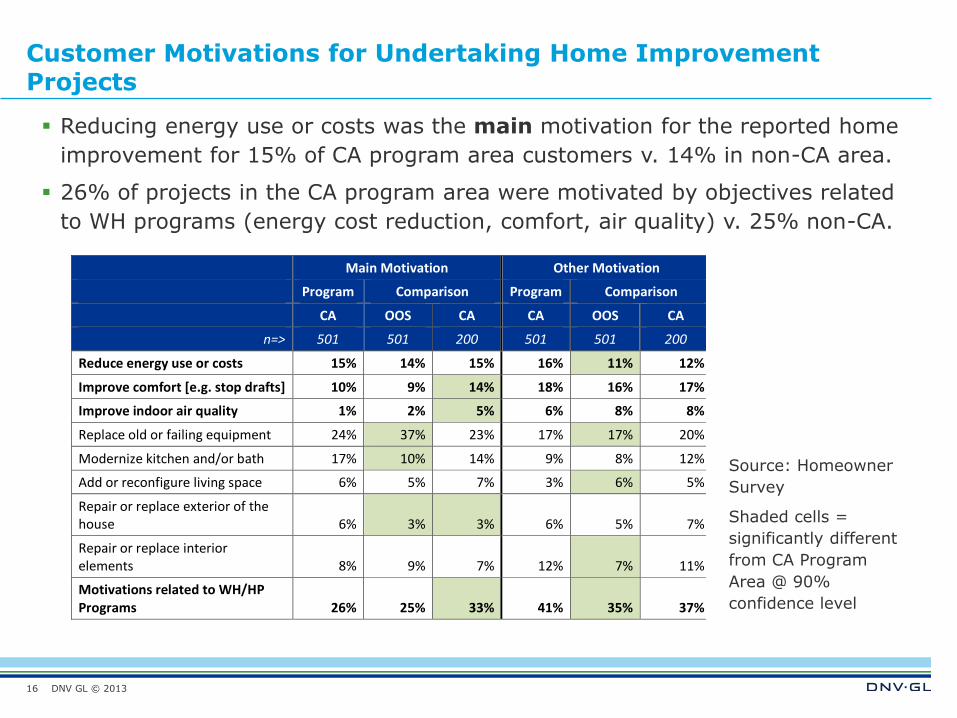

Customer Motivations for Undertaking Home Improvement Projects

Reducing energy use or costs was the main motivation for the reported home

improvement for 15% of CA program area customers v. 14% in non-CA area.

26% of projects in the CA program area were motivated by objectives related

to WH programs (energy cost reduction, comfort, air quality) v. 25% non-CA.

16

Main Motivation Other Motivation

Program Comparison Program Comparison

CA OOS CA CA OOS CA

n=> 501 501 200 501 501 200

Reduce energy use or costs 15% 14% 15% 16% 11% 12%

Improve comfort [e.g. stop drafts] 10% 9% 14% 18% 16% 17%

Improve indoor air quality 1% 2% 5% 6% 8% 8%

Replace old or failing equipment 24% 37% 23% 17% 17% 20%

Modernize kitchen and/or bath 17% 10% 14% 9% 8% 12%

Add or reconfigure living space 6% 5% 7% 3% 6% 5%

Repair or replace exterior of the house 6% 3% 3% 6% 5% 7%

Repair or replace interior elements 8% 9% 7% 12% 7% 11%

Motivations related to WH/HP Programs 26% 25% 33% 41% 35% 37%

Source: Homeowner

Survey

Shaded cells =

significantly different

from CA Program

Area @ 90%

confidence level

DNV GL © 2013

Cost of Home Improvement Projects

Roughly 50% of all reported projects in CA had reported costs above

$10,000.

Within areas, participation had little effect on the distribution of

program costs

17

0%

5%

10%

15%

20%

25%

30%

35%

Less than

$5000

Between

$5,000

and

$10,000

Between

$10,000

and

$25,000

$25,000 or

more

P: CA Prog

NP: CA Prog

0%

5%

10%

15%

20%

25%

30%

35%

Less than

$5000

Between

$5,000

and

$10,000

Between

$10,000

and

$25,000

$25,000

or more

P: Non-CA

NP: Non-CA

Distribution of Project Costs:

California Program Area

Distribution of Project Costs:

Outside California

Source: Homeowner Survey

DNV GL © 2013

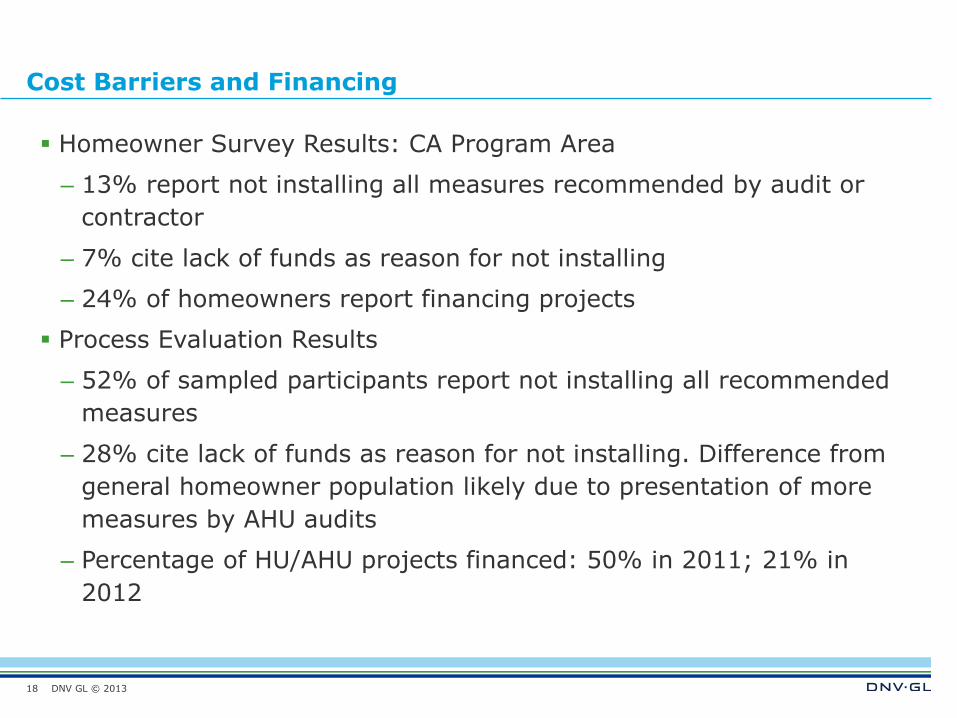

Cost Barriers and Financing

Homeowner Survey Results: CA Program Area

– 13% report not installing all measures recommended by audit or

contractor

– 7% cite lack of funds as reason for not installing

– 24% of homeowners report financing projects

Process Evaluation Results

– 52% of sampled participants report not installing all recommended

measures

– 28% cite lack of funds as reason for not installing. Difference from

general homeowner population likely due to presentation of more

measures by AHU audits

– Percentage of HU/AHU projects financed: 50% in 2011; 21% in

2012

18

DNV GL © 2013

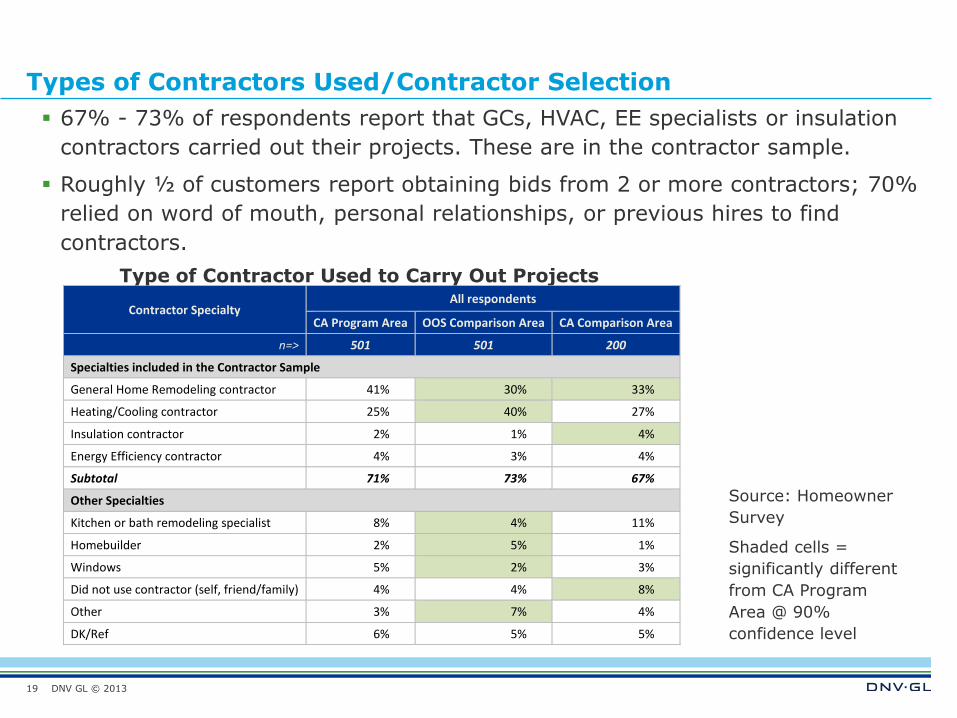

Types of Contractors Used/Contractor Selection

67% - 73% of respondents report that GCs, HVAC, EE specialists or insulation

contractors carried out their projects. These are in the contractor sample.

Roughly ½ of customers report obtaining bids from 2 or more contractors; 70%

relied on word of mouth, personal relationships, or previous hires to find

contractors.

19

Type of Contractor Used to Carry Out Projects

Contractor Specialty All respondents

CA Program Area OOS Comparison Area CA Comparison Area

n=> 501 501 200

Specialties included in the Contractor Sample

General Home Remodeling contractor 41% 30% 33%

Heating/Cooling contractor 25% 40% 27%

Insulation contractor 2% 1% 4%

Energy Efficiency contractor 4% 3% 4%

Subtotal 71% 73% 67%

Other Specialties

Kitchen or bath remodeling specialist 8% 4% 11%

Homebuilder 2% 5% 1%

Windows 5% 2% 3%

Did not use contractor (self, friend/family) 4% 4% 8%

Other 3% 7% 4%

DK/Ref 6% 5% 5%

Source: Homeowner

Survey

Shaded cells =

significantly different

from CA Program

Area @ 90%

confidence level

DNV GL © 2013

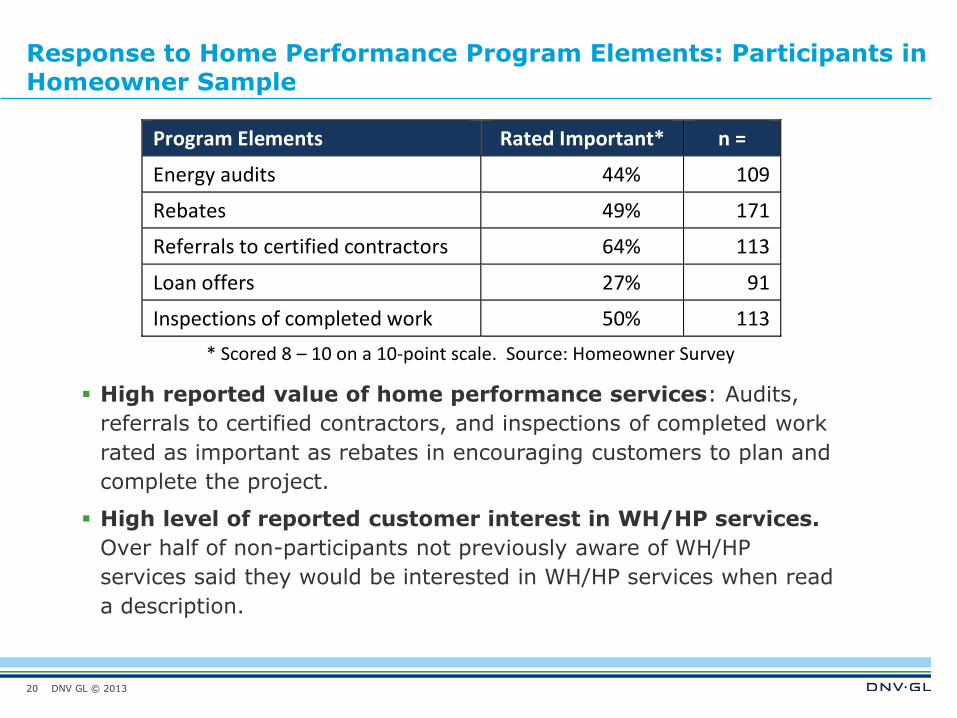

Response to Home Performance Program Elements: Participants in Homeowner Sample

High reported value of home performance services: Audits,

referrals to certified contractors, and inspections of completed work

rated as important as rebates in encouraging customers to plan and

complete the project.

High level of reported customer interest in WH/HP services.

Over half of non-participants not previously aware of WH/HP

services said they would be interested in WH/HP services when read

a description.

Program Elements Rated Important* n =

Energy audits 44% 109

Rebates 49% 171

Referrals to certified contractors 64% 113

Loan offers 27% 91

Inspections of completed work 50% 113

* Scored 8 – 10 on a 10-point scale. Source: Homeowner Survey

20

DNV GL © 2013

Nonparticipant Awareness of and Interest Whole House Programs

29% of non-participants in CA Program area were aware of program.

Similar results to Process Evaluation; significantly higher compared to OOS

and CA Program Areas

High level of reported customer interest in WH/HP services. Half of

non-participants not previously aware of WH/HP services said they would be

interested in WH/HP services

Willingness to Pay. Roughly ½ of nonparticipants report being willing to add

$5000 to project costs for energy efficiency measures with 5-year peayback

21

Perceptions of and Interest in Program Non – Participants

CA Program

OOS Comparison

CA Comparison

n=> 408 429 172

Aware of WH/HP program/program concepts 29% 13% 17%

Aware of WH/HP program prior to undertaking project 17% 8% 9%

Would have sought an assessment of energy savings opportunities if they had been aware of program prior to project.

49% 38% 53%

Would have incorporated energy saving measures that cost an additional $5000 and with a payback period of under 5 years (as a % of those willing to seek assessment of energy savings opportunities)

49% 57% 52%

Source: Homeowner Survey

DNV GL © 2013

THE CONTRACTOR MARKET

22

DNV GL © 2013

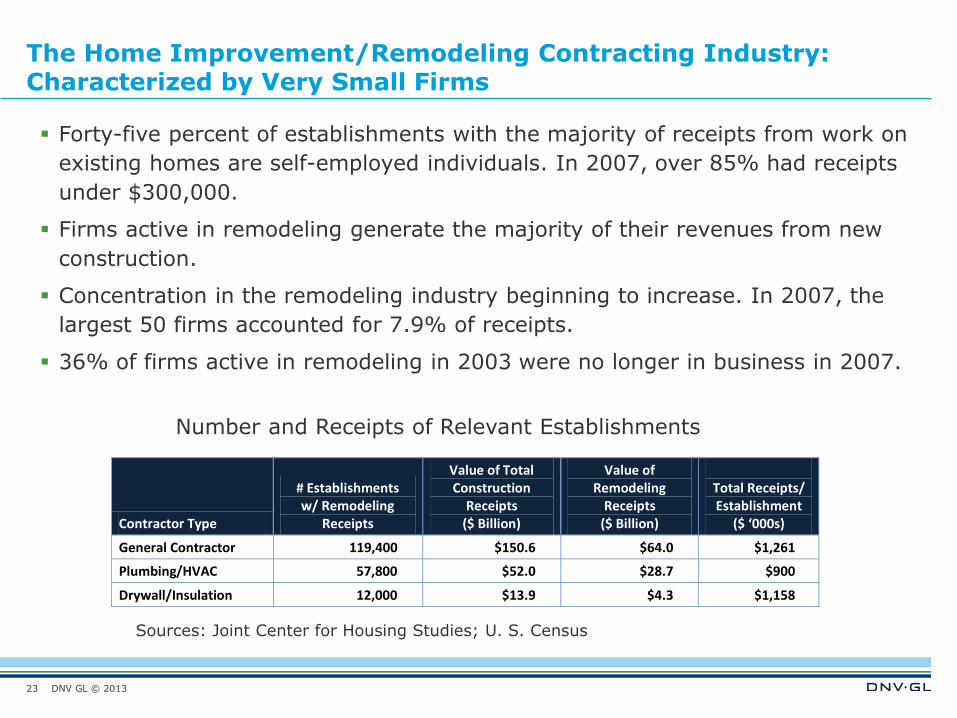

The Home Improvement/Remodeling Contracting Industry: Characterized by Very Small Firms

Forty-five percent of establishments with the majority of receipts from work on

existing homes are self-employed individuals. In 2007, over 85% had receipts

under $300,000.

Firms active in remodeling generate the majority of their revenues from new

construction.

Concentration in the remodeling industry beginning to increase. In 2007, the

largest 50 firms accounted for 7.9% of receipts.

36% of firms active in remodeling in 2003 were no longer in business in 2007.

Contractor Type

# Establishments w/ Remodeling

Receipts

Value of Total Construction

Receipts ($ Billion)

Value of Remodeling

Receipts ($ Billion)

Total Receipts/ Establishment

($ ‘000s)

General Contractor 119,400 $150.6 $64.0 $1,261

Plumbing/HVAC 57,800 $52.0 $28.7 $900

Drywall/Insulation 12,000 $13.9 $4.3 $1,158

Number and Receipts of Relevant Establishments

23

Sources: Joint Center for Housing Studies; U. S. Census

DNV GL © 2013

Case Studies of High Volume Contractors

24

All profiled contractors but one have 20 or more employees; firm with 7 employees subcontracts all installation

Only 5% of firms in the contractor population have more than 20 employees; 11% employ 10 or more workers

Areas

Served

Years Founded/ Started HP

Primary Business

# of

Employees

# of HP Projects

2012

Average Project

Cost

Range of Services

Offered

1 Arizona/So. California

2009/ 2009

Residential Energy Eff.

50 1,200 $14,000 HP, HVAC, Solar PV, DHW Meas.

2 Bay Area, California

2006/ 2006

Residential Energy Eff.

36 >200 $10,000 - $15,000

HP, HVAC, Solar PV, DHW Meas.

3 Maryland 2006/ 2006

Residential Energy Eff.

7 ~100 $8,000 HP, HVAC, Solar PV, DHW Meas.*

4 Southern California

2009/ 2009

Residential Energy Eff.

20 ~50 $17,000 HP, HVAC, Solar PV, DHW Meas.

5 New Jersey, NY, DE

1948/ 2007

Res & Sm. Com. HVAC

250 500 $16,000 - $18,000

HVAC sales & maintenance, HP

6 Upstate New York

1984/ 2007

Res & Sm. Com. HVAC

~100 400 $9,000 HVAC sales & maintenance, HP

DNV GL © 2013

Value Propositions and Business Models

HVAC Contractors: Add services to boost revenues and retain

customers

Today, it doesn't take a very savvy homeowner to …go on the Internet

and buy [a] furnace for the exact same cost you can go to your

wholesaler and buy it for. So there's no real margins on equipment and

you are trying to sell your quality of installation and service, which is

fine, but it becomes more and more difficult when you limit service to

just HVAC.

One Stop Shop for all benefits of energy-related home improvement

If we had bigger weather extremes, I think we'd be much busier. When

we talk to homeowners that are only focused on return on investment, I

say this program probably isn't for you. We live in paradise for a

reason. … The main motivating factors for clients are comfort and

safety. I can make every room in their house no more than two degrees

temperature difference no matter what floor it is. And that's a pretty

big selling point to people.

25

DNV GL © 2013

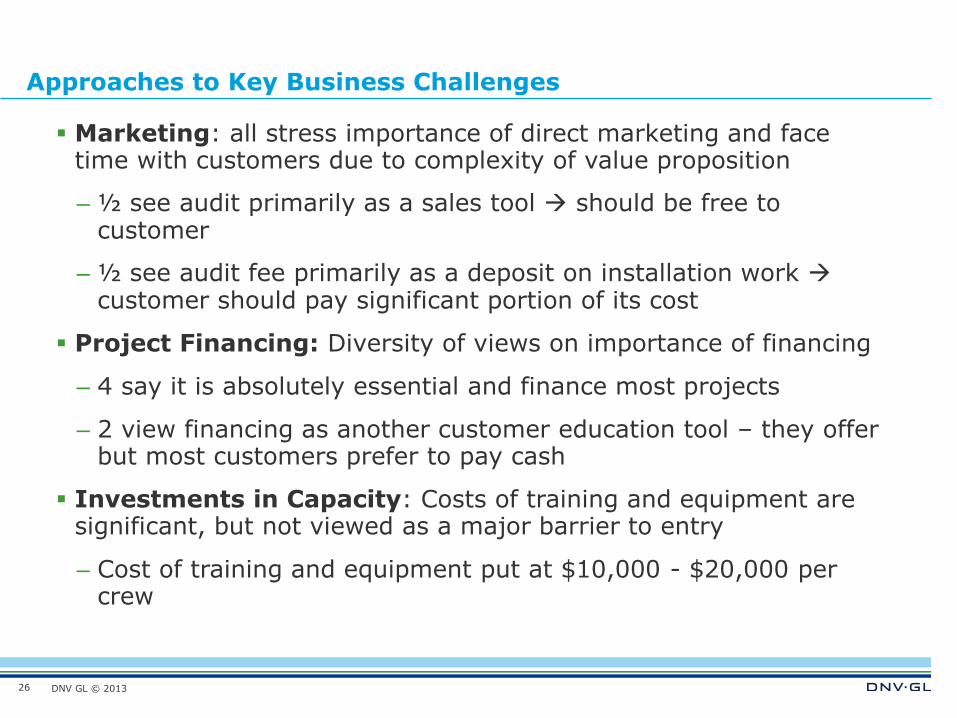

Approaches to Key Business Challenges

26

Marketing: all stress importance of direct marketing and face time with customers due to complexity of value proposition

– ½ see audit primarily as a sales tool should be free to customer

– ½ see audit fee primarily as a deposit on installation work customer should pay significant portion of its cost

Project Financing: Diversity of views on importance of financing

– 4 say it is absolutely essential and finance most projects

– 2 view financing as another customer education tool – they offer but most customers prefer to pay cash

Investments in Capacity: Costs of training and equipment are significant, but not viewed as a major barrier to entry

– Cost of training and equipment put at $10,000 - $20,000 per crew

DNV GL © 2013

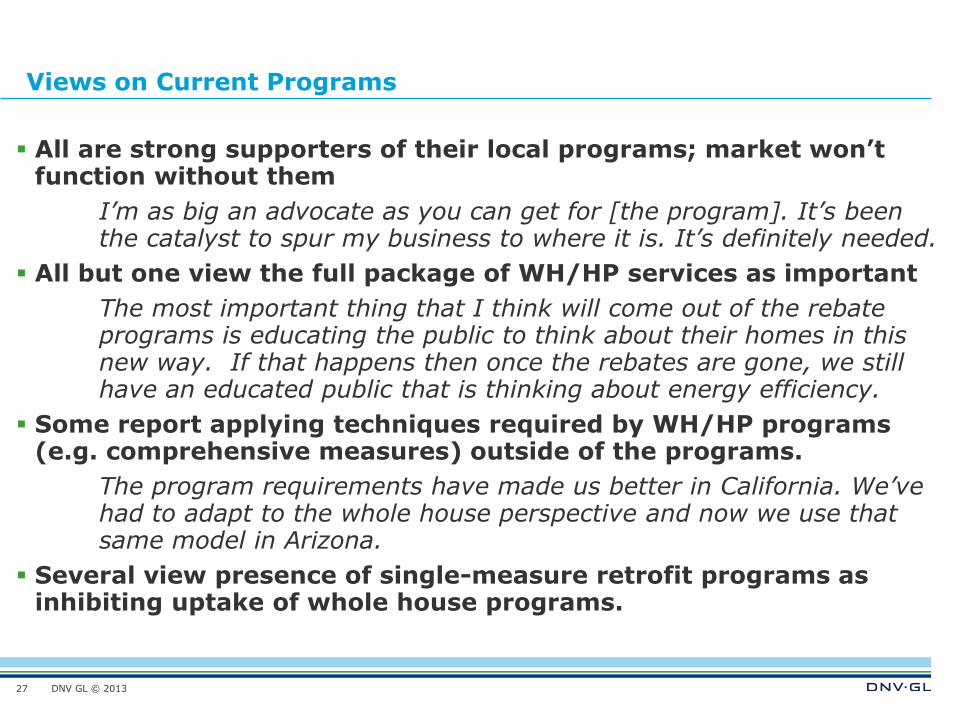

Views on Current Programs

All are strong supporters of their local programs; market won’t function without them

I’m as big an advocate as you can get for [the program]. It’s been the catalyst to spur my business to where it is. It’s definitely needed.

All but one view the full package of WH/HP services as important

The most important thing that I think will come out of the rebate programs is educating the public to think about their homes in this new way. If that happens then once the rebates are gone, we still have an educated public that is thinking about energy efficiency.

Some report applying techniques required by WH/HP programs (e.g. comprehensive measures) outside of the programs.

The program requirements have made us better in California. We’ve had to adapt to the whole house perspective and now we use that same model in Arizona.

Several view presence of single-measure retrofit programs as inhibiting uptake of whole house programs.

27

DNV GL © 2013

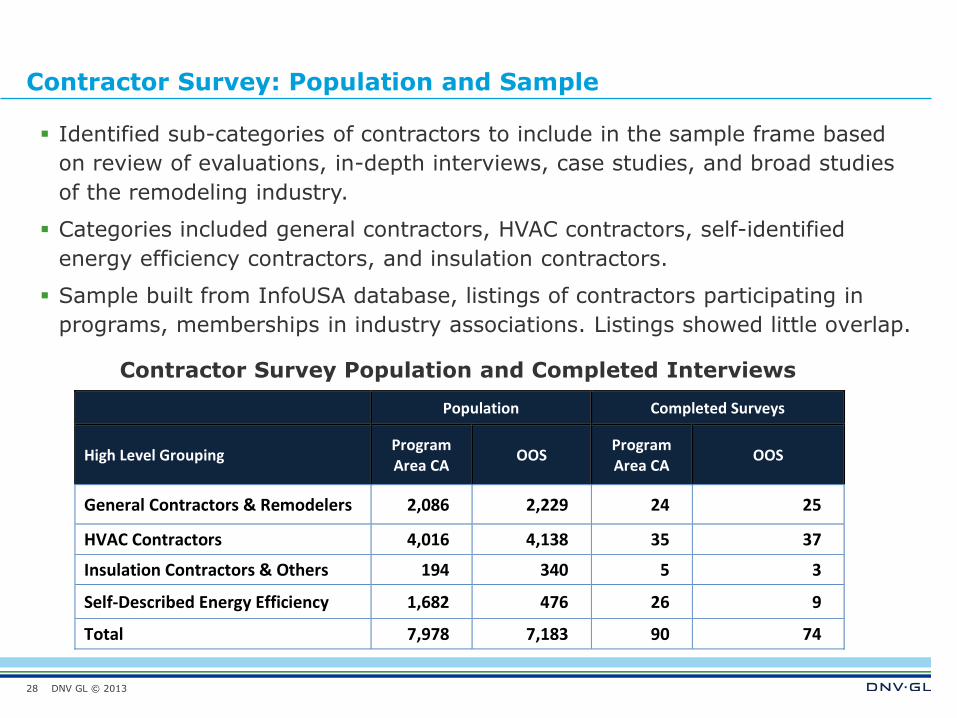

Contractor Survey: Population and Sample

Identified sub-categories of contractors to include in the sample frame based

on review of evaluations, in-depth interviews, case studies, and broad studies

of the remodeling industry.

Categories included general contractors, HVAC contractors, self-identified

energy efficiency contractors, and insulation contractors.

Sample built from InfoUSA database, listings of contractors participating in

programs, memberships in industry associations. Listings showed little overlap.

Contractor Survey Population and Completed Interviews

Population Completed Surveys

High Level Grouping Program Area CA

OOS Program Area CA

OOS

General Contractors & Remodelers 2,086 2,229 24 25

HVAC Contractors 4,016 4,138 35 37

Insulation Contractors & Others 194 340 5 3

Self-Described Energy Efficiency 1,682 476 26 9

Total 7,978 7,183 90 74

28

DNV GL © 2013

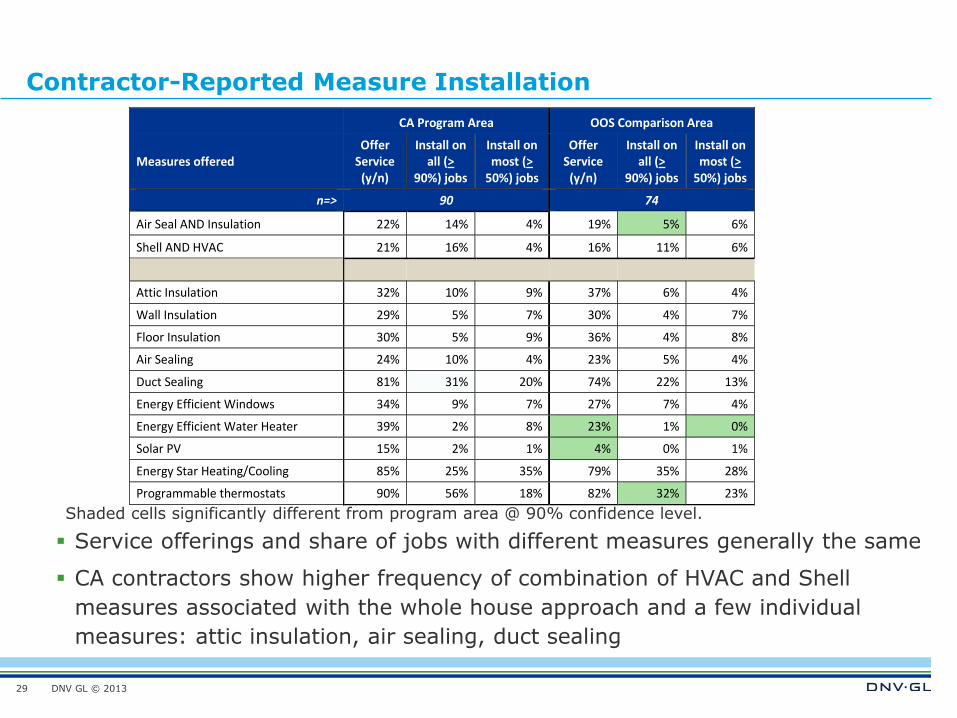

Contractor-Reported Measure Installation

29

Shaded cells significantly different from program area @ 90% confidence level.

Service offerings and share of jobs with different measures generally the same

CA contractors show higher frequency of combination of HVAC and Shell

measures associated with the whole house approach and a few individual

measures: attic insulation, air sealing, duct sealing

CA Program Area OOS Comparison Area

Measures offered Offer

Service (y/n)

Install on all (>

90%) jobs

Install on most (>

50%) jobs

Offer Service

(y/n)

Install on all (>

90%) jobs

Install on most (>

50%) jobs

n=> 90 74

Air Seal AND Insulation 22% 14% 4% 19% 5% 6%

Shell AND HVAC 21% 16% 4% 16% 11% 6%

Attic Insulation 32% 10% 9% 37% 6% 4%

Wall Insulation 29% 5% 7% 30% 4% 7%

Floor Insulation 30% 5% 9% 36% 4% 8%

Air Sealing 24% 10% 4% 23% 5% 4%

Duct Sealing 81% 31% 20% 74% 22% 13%

Energy Efficient Windows 34% 9% 7% 27% 7% 4%

Energy Efficient Water Heater 39% 2% 8% 23% 1% 0%

Solar PV 15% 2% 1% 4% 0% 1%

Energy Star Heating/Cooling 85% 25% 35% 79% 35% 28%

Programmable thermostats 90% 56% 18% 82% 32% 23%

DNV GL © 2013

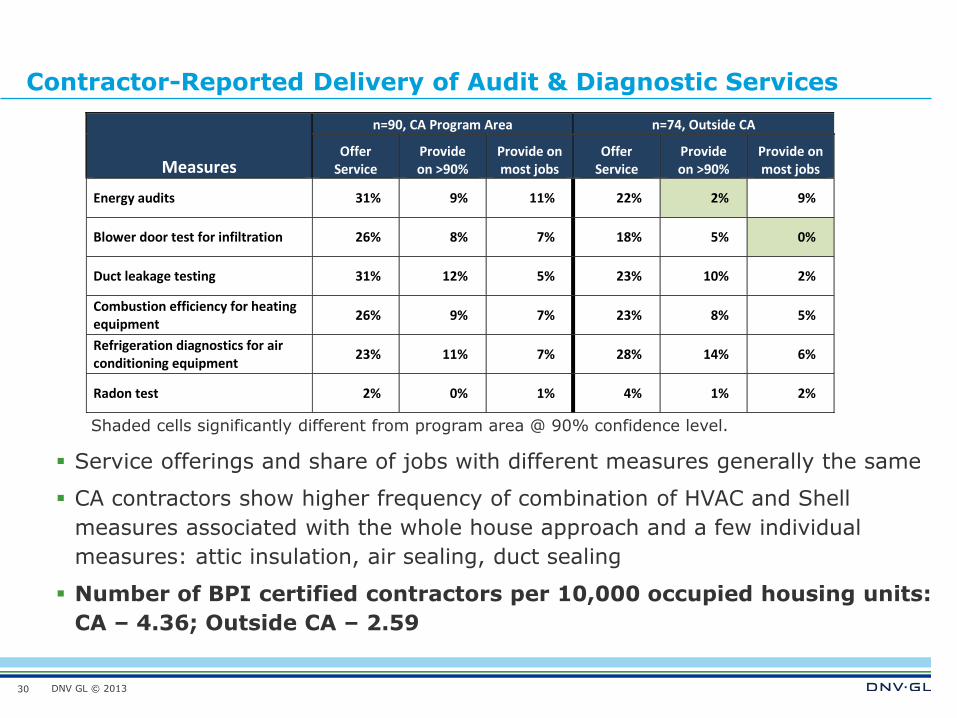

Contractor-Reported Delivery of Audit & Diagnostic Services

30

Shaded cells significantly different from program area @ 90% confidence level.

Service offerings and share of jobs with different measures generally the same

CA contractors show higher frequency of combination of HVAC and Shell

measures associated with the whole house approach and a few individual

measures: attic insulation, air sealing, duct sealing

Number of BPI certified contractors per 10,000 occupied housing units:

CA – 4.36; Outside CA – 2.59

Measures

n=90, CA Program Area n=74, Outside CA

Offer Service

Provide on >90%

Provide on most jobs

Offer Service

Provide on >90%

Provide on most jobs

Energy audits 31% 9% 11% 22% 2% 9%

Blower door test for infiltration 26% 8% 7% 18% 5% 0%

Duct leakage testing 31% 12% 5% 23% 10% 2%

Combustion efficiency for heating equipment

26% 9% 7% 23% 8% 5%

Refrigeration diagnostics for air conditioning equipment

23% 11% 7% 28% 14% 6%

Radon test 2% 0% 1% 4% 1% 2%

DNV GL © 2013

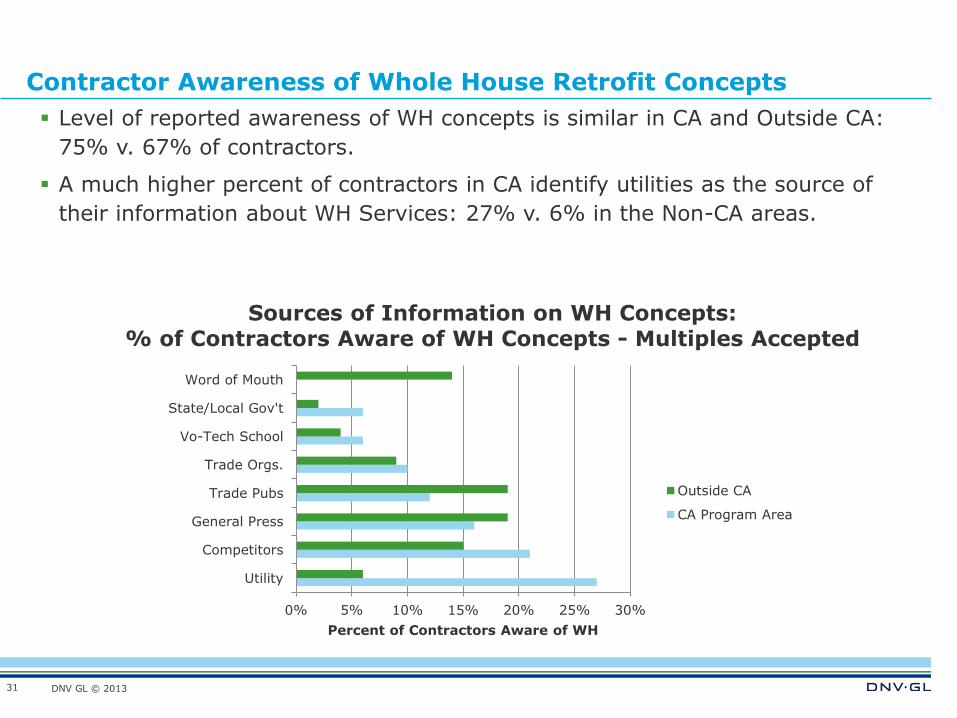

Contractor Awareness of Whole House Retrofit Concepts

31

Sources of Information on WH Concepts: % of Contractors Aware of WH Concepts - Multiples Accepted

Level of reported awareness of WH concepts is similar in CA and Outside CA:

75% v. 67% of contractors.

A much higher percent of contractors in CA identify utilities as the source of

their information about WH Services: 27% v. 6% in the Non-CA areas.

0% 5% 10% 15% 20% 25% 30%

Utility

Competitors

General Press

Trade Pubs

Trade Orgs.

Vo-Tech School

State/Local Gov't

Word of Mouth

Percent of Contractors Aware of WH

Outside CA

CA Program Area

DNV GL © 2013

Contractor Interest in Investing in WH/HP Services and Self-Assessed Capability to Deliver

32

A significantly higher portion of CA v. non-CA contractors believe that they

deliver WH/HP services now.

Prospective interest in delivering WH/HP services is equivalent in CA and the

comparison areas.

Most sample contractors believe they can deliver WH/HP services with their

current staff, with a slightly higher portion so believing outside of CA.

CA Program Area Outside CA

n=90 n=74

Would it be worthwhile for your company to invest in developing WH/HP delivery capability

Already provide 12% 4%

Yes 46% 47%

Maybe 14% 15%

No 25% 32%

Do you think you could market and deliver this kind of service with current employees? (Among those who believe WH is or may be a worthwhile investment.)

Market and deliver w current employees –yes 68% 81%

Market and deliver w current employees –no 22% 10%

Market and deliver w current employees -maybe 6% 0%

DNV GL © 2013

CONCLUSIONS AND IMPLICATIONS FOR PROGRAM STRATEGY AND

FURTHER RESEARCH

33

DNV GL © 2013

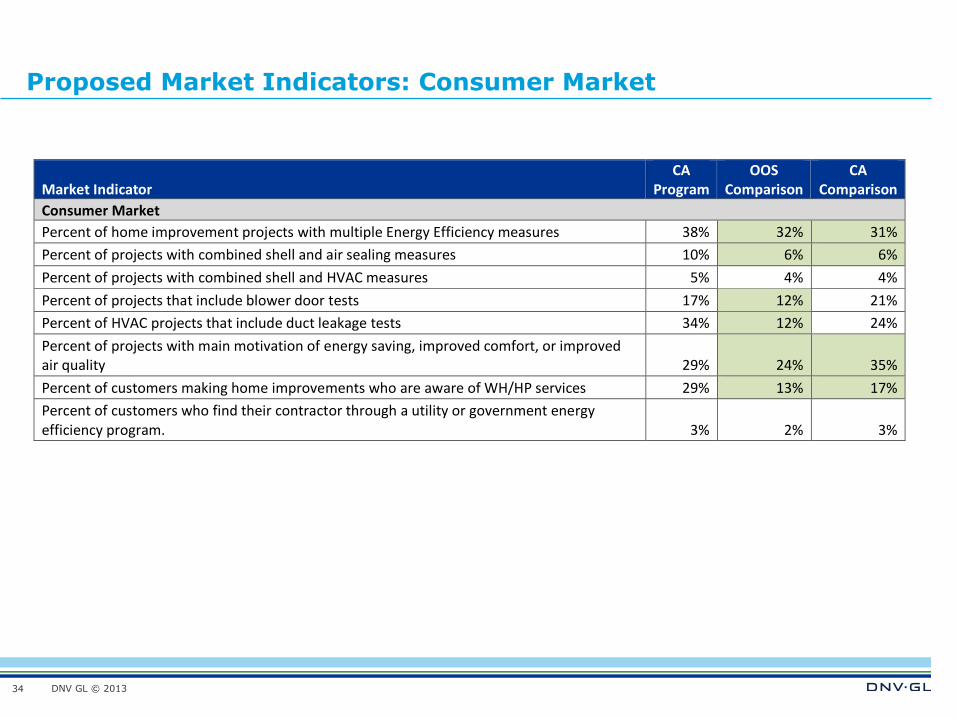

Proposed Market Indicators: Consumer Market

34

Market Indicator CA

Program OOS

Comparison CA

Comparison

Consumer Market

Percent of home improvement projects with multiple Energy Efficiency measures 38% 32% 31%

Percent of projects with combined shell and air sealing measures 10% 6% 6%

Percent of projects with combined shell and HVAC measures 5% 4% 4%

Percent of projects that include blower door tests 17% 12% 21%

Percent of HVAC projects that include duct leakage tests 34% 12% 24%

Percent of projects with main motivation of energy saving, improved comfort, or improved air quality 29% 24% 35%

Percent of customers making home improvements who are aware of WH/HP services 29% 13% 17%

Percent of customers who find their contractor through a utility or government energy efficiency program. 3% 2% 3%

DNV GL © 2013

Proposed Market Indicators: Supply Chain

35

Market Indicator CA

Program OOS

Comparison CA

Comparison

Supply Chain

Number of BPI-certified contractors per 10,000 occupied housing units 4.36 2.59

Share of market represented by contractors who deliver combined shell and air sealing measures in all or most projects 18% 11%

Share of market represented by contractors who deliver combined shell and HVAC measures in all or most projects 20% 17%

Share of market represented by contractors who deliver energy audits in all or most projects 20% 11%

Share of market represented by contractors who use blower door tests in all or most projects 15% 5%

Share of market represented by contractors who use duct leakage tests in all or most projects 17% 12%

Share of market represented by contractors aware of whole house retrofit concepts 75% 67%

Share of market represented by contractors who can accurately describe WH/HP practices 33% 30%

Share of market represented by contractors who are aware of WH/HP programs in their local markets 59% 44%

Share of market represented by contractors who report that they currently deliver WH/HP services 12 4%

DNV GL © 2013

Summary of Findings Related to Program Strategy - 1

Participation in HU/AHU programs is low

– Annual participation now captures about 2% of home improvement projects

over $10,000

– Savings installed and in pipeline running at 14% of current plan for

electricity; 21% for gas through first ½ of cycle.

Rate of unsubsidized adoption of Whole House/Home Performance

approaches is low

– Among non-participants, only 8%in the California Program Area and 6% in

the Comparison Areas reported installing combinations of shell and air

sealing measures. 3 – 4 percent reported installing combinations of shell and

HVAC measures.

– 14% of non-participants in the CA Program area reported having a blower

door test done as part of their project, as did 10% of non-participants in the

Comparison Areas.

– None of the high-volume contractors interviewed for the case studies

attempted to market their services without subsidies. None believed that the

services could be marketed profitably without program support.

36

DNV GL © 2013

Summary of Findings Related to Program Strategy - 2

Low levels of awareness of the WH/HP value proposition and restricted

contractor search practices are the major barriers to increased

adoption of WH/HP practices among consumers.

– 29% of sample homeowners who undertook home improvement projects

reported being aware of home performance programs

– 70 percent of homeowners used contractors found via word of mouth,

personal relationships, or previous projects

– Only 1 percent (OOS) to 2 percent (CA) of respondents reported using

contractors found through energy efficiency programs.

Costs of WH projects are a barrier for a large market segment, but not

decisive for overall program participation or market development.

– Only 7% of customers in any of the study areas reported that they were

unable to complete all recommended ee measures due to financial

constraints.

– Process evaluation interviews of participants find 28% deterred by costs from

completing all recommended measures.

– Relatively low percentage (20% – 25%) of customers took for projects.

37

DNV GL © 2013

Summary Findings Related to Program Strategy - 3

Effective delivery of WH/HP services and participation in WH/HP

programs requires a scale of contractor operations beyond the

capability of the large majority home improvement industry firms.

– Case studies demonstrate that success requires investment in marketing the

services, maintaining consistency and quality of delivery, and managing flow

of technical and administrative work required by programs.

– All but one of the six high-volume contractors employed 20 or more workers.

Only 5 percent of the California contractors employed 20 or more workers.

Lack of understanding of WH/HP services and their potential business

value is the major barrier to adoption of WH/HP practices and program

participation among contractors.

– 75 percent of the home improvement market in the CA Program area

reported being aware of WH/HP service concepts, but only roughly half of

those could accurately describe the WH/HP approach.

– About ½ of all contractors in the California Program Area sample reported

being interested in the WH/HP approach. However, the population of capable

firms is limited.

38

DNV GL © 2013

Summary Findings Related to Program Strategy - 4

Progress in developing the California market: consumer market. Despite

the challenges described above to the growth of WH/HP services market

indicators do show evidence of some program effects.

– Higher level of use of multiple measures, combination of air sealing and

insulation measures and blower door tests in CA Program Area v. OOS.

– Significantly higher percentage of homeowners in CA Program area aware of

WH/HP concepts and programs (29 percent v. 13 percent in OOS)

Progress in developing the California market: supply chain. Although

contractors in the CA Program Area report offering and installing WH/HP

components in a larger share of projects than their counterparts in the OOS

Comparison Area, these differences are small. Two clear-cut differences

– The number of BPI-certified contractors, normalized for market size, is 70%

higher in the CA Program Area than in the comparison area.

– Contractor awareness of WH/HP programs higher in CA: 59% v. 44%

– Reported rate of participation is higher in CA: 28% v. 14%

– Reported adoption of WH/HP practices is higher in CA: 12% v. 4%

39

DNV GL © 2013

Implications for Program Strategy

Building Customer Demand

– Structure messaging to emphasize the full range of consumer benefits:

energy savings, comfort, preservation of home value, green values;

convenience; quality product, reduced risk due to certification/quality control

– Target direct marketing to homebuyers – many undertake large remodeling

projects upon moving in.

Build contractor motivation and capacity to deliver WH/HP services

– Focus outreach to larger contracting firms

– Equip and motivate participating contractors to do personal selling.

– Materials, case studies, scripts, organizational tools, incentives and

recognition for high volume

– Competitions among contractors on volume, innovation in marketing and

delivery

– Stable incentive system

– Stable technical rules and procedures with consistency across sponsors

40

DNV GL © 2013

Future Research

Research methods generally worked as anticipated, with some issues

– Identification of non-program areas: relatively few areas with

climate/housing stock resembling parts of CA. Program sponsors may start

up Whole House programs at any point, but the popularity of the approach

seems to be stable or declining.

– The population of contractors in the CA non-program area is very small. We

would need to offer significant incentives from the start to attract

participation in the survey.

– Generally, completing interviews with contractors was difficult. We

recommend offering significant incentives ($100 or more) to ensure timely

completion and mitigate bias.

We believe the study design can be repeated with minor modifications

to provide a meaningful comparison of market status to the baseline

conditions documented here.

Given relatively slow market progress, suggest delaying follow up

study until 2016 at the earliest.

41

DNV GL © 2013

SAFER, SMARTER, GREENER

www.dnvgl.com

42