Embed Size (px)

Citation preview

Why the Economy?

Raymond DuchUniversity of HoustonRandy StevensonRice University

Cross-national Studies of Economic Voting

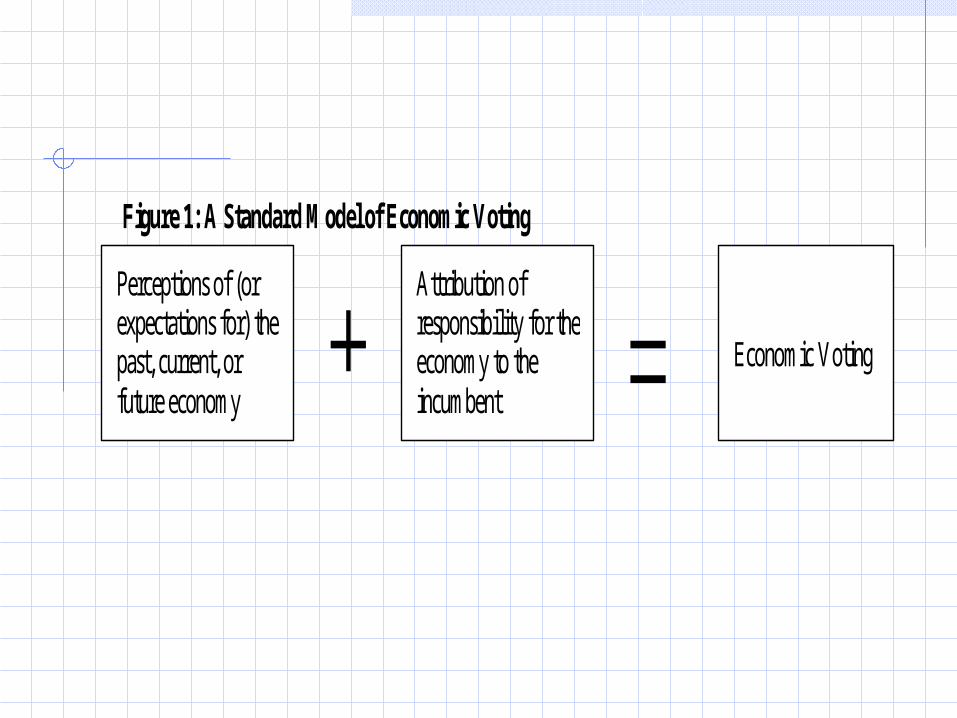

Figure 1: A Standard Model of Economic Voting

Perceptions of (or expectations for) the past, current, or future economy

Attribution of responsibility for the economy to the incumbent

Economic Voting

At the individual level, limited efforts to understand cross-national variation. Lewis-Beck 1988 Paldam 1991

Nonetheless some interesting differences in model results cross-nationally

At the aggregate level, considerable cross-national variation in economic voting results.

“Clarity of responsibility” is one effort to help understand – but limited.

Research Puzzle

We suspect individual-level economic voting models vary significantly cross-nationally.

But current published modeling efforts are not rich enough to draw meaningful conclusions.

Our Insights

Economic evaluations are attitudes – information processing, cueing and cognitive psychology literature.

Measure extent to which economic information is “mediated”.

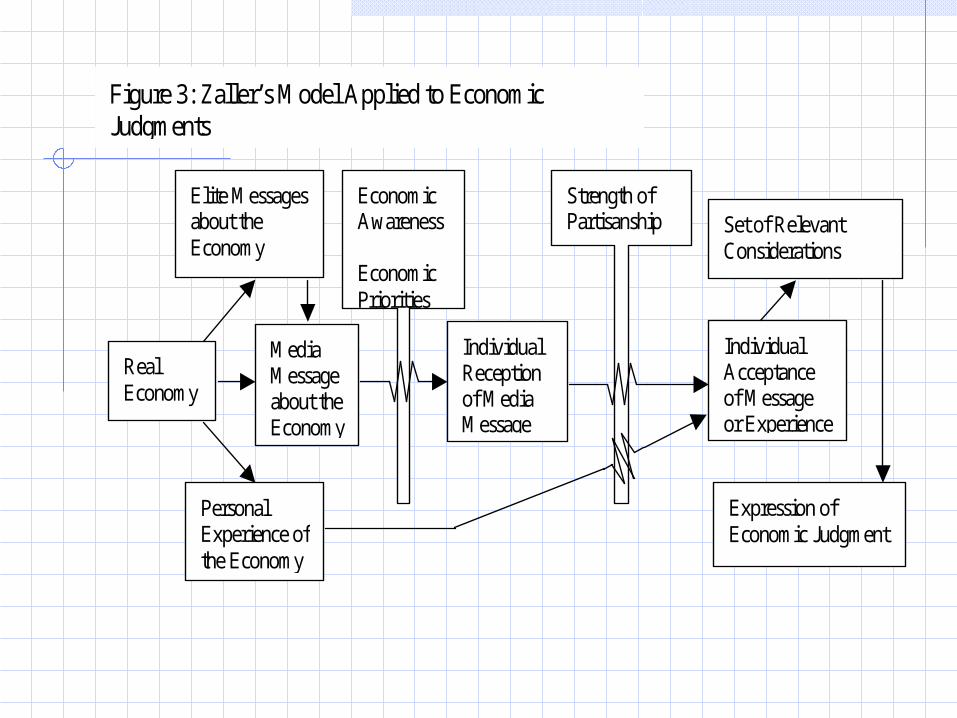

Media Message about the Economy

Real Economy

Personal Experience of the Economy

Elite Messages about the Economy

Individual Reception of Media Message

Individual Acceptance of Message or Experience

Expression of Economic Judgment

Set of Relevant Considerations

Economic Awareness Economic Priorities

Strength of Partisanship

Figure 3: Zaller’s Model Applied to Economic Judgments

The Research Project

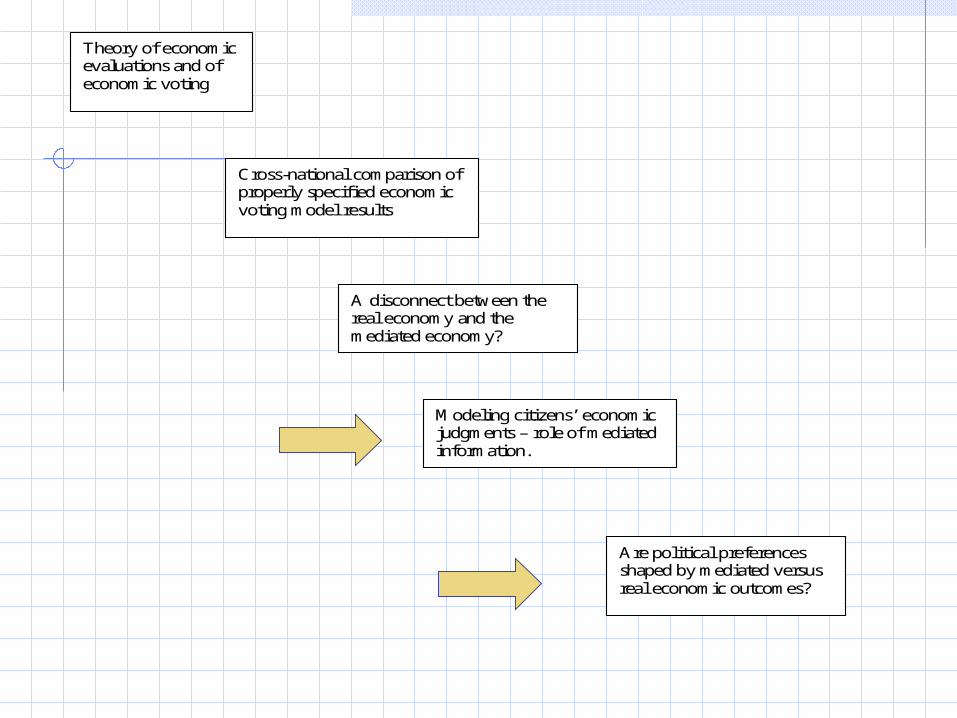

Theory of economic evaluations and of economic voting

Cross-national comparison of properly specified economic voting model results

A disconnect between the real economy and the mediated economy?

Modeling citizens’ economic judgments – role of mediated information.

Are political preferences shaped by mediated versus real economic outcomes?

Mediated Economic Cues

Citizens employ cues/information short-cuts in forming economic assessments

Luppia & McCubbins argument

Nevertheless information gathering costs matter

Political actors, elites, media attempt to shape these cues or “packaging” of messages

Zaller on the strategic manipulation of media by political actors

Iyengar on framing

Distorted messages regarding economy?

Some evidence from analyses of different media

Negativity bias Human interest bias

Distortions depend on:

Information gathering costs

Cross-national diversity of media

Institutional contexts

Implications for EV Models?

Economic evaluations are based on distorted information

Seriously questions the “democratic accountability” theory of EV

Null hypothesis

Economic perceptions and actual economic outcomes track each other in a regular fashion

The series are co-integrated and can be modeled as an ECM

Mediated cues argument

There is distortion in mass assessments of economic outcomes.

This distortion is a function of mediated messages regarding the economy (media, politicians, etc.)

Hypothesis

Distortion evidenced by poor ECM fit.

Mediation implies degree of distortion correlated with cost of information High for unemployment Low for inflation

Mediation implies asymmetric effects

Mediation also implies considerable cross-national variation in degrees of distortion

Mediation implies distortions in both mass and elite economic assessments

Data

Mass public’s economic assessments: Monthly consumer confidence surveys

conducted by the European Commission in all member countries 1986-2000

Elite’s economic assessments Monthly business confidence surveys

from European Commission 1967-2000

Economic indicators Quarterly GDP growth from OECD

(Palmer and Whitten) CPI and unemployment figures from The Economist

All variables are transformed into standardized z scores

Modeling Economic Attitudes

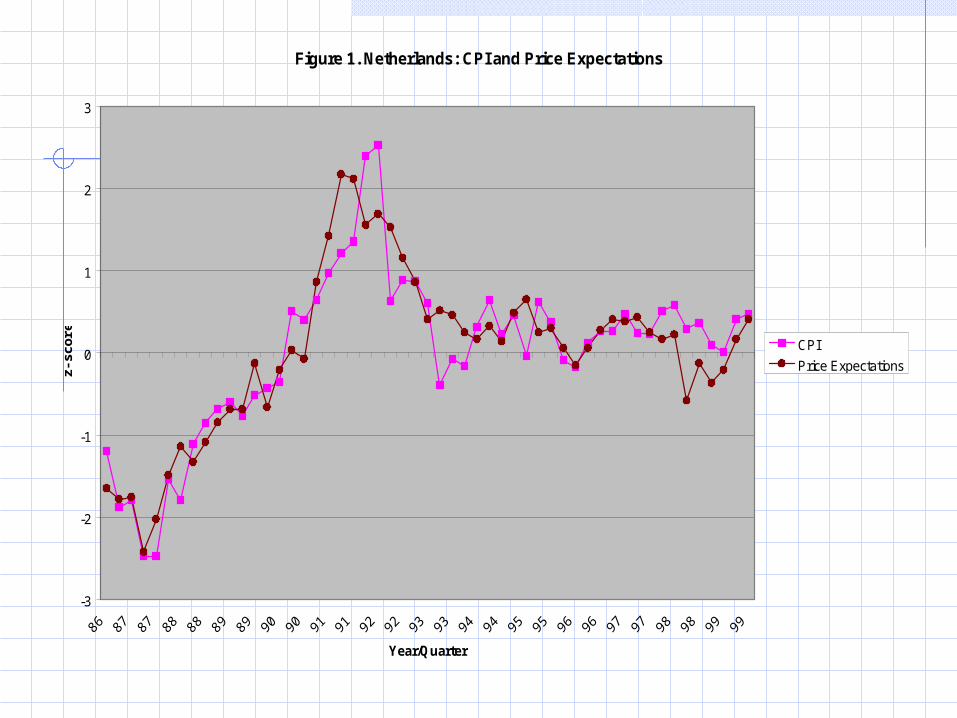

Figure 1. Netherlands: CPI and Price Expectations

-3

-2

-1

0

1

2

3

Year/Quarter

z-sc

ore

CPI

Price Expectations

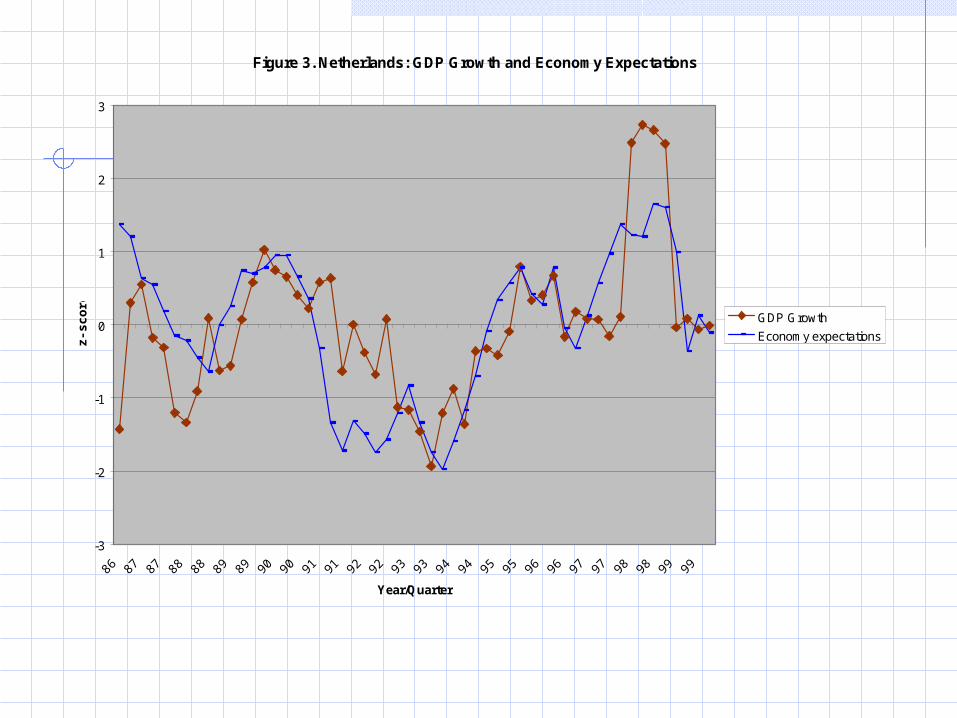

Figure 3. Netherlands: GDP Growth and Economy Expectations

-3

-2

-1

0

1

2

3

Year/Quarter

z-sc

ore GDP Growth

Economy expectations

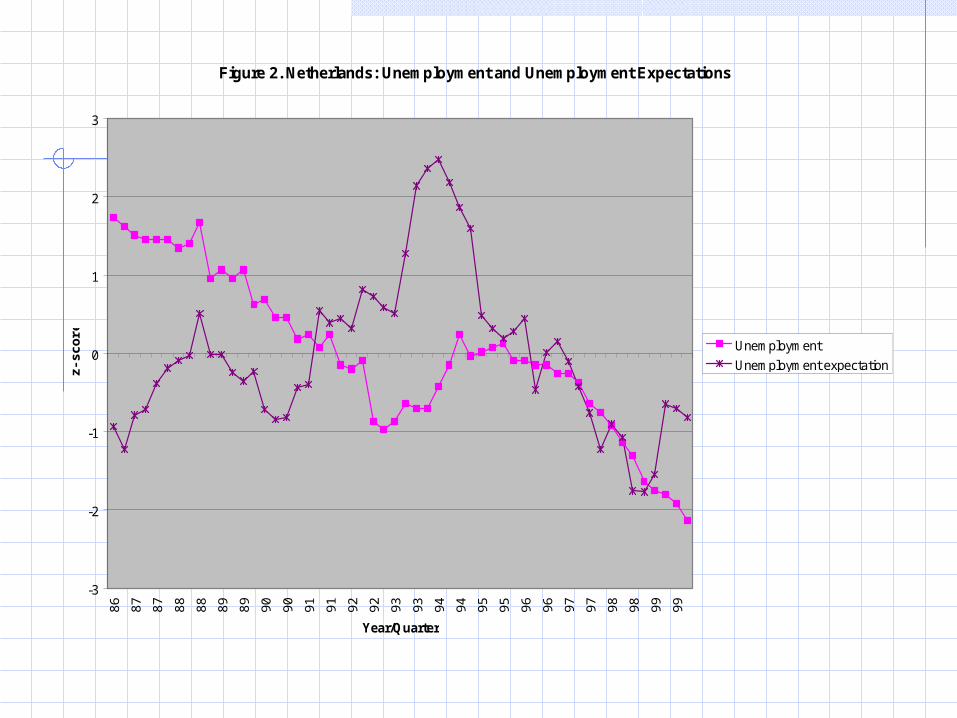

Figure 2. Netherlands: Unemployment and Unemployment Expectations

-3

-2

-1

0

1

2

386 87 87 88 88 89 89 90 90 91 91 92 92 93 93 94 94 95 95 96 96 97 97 98 98 99 99

Year/Quarter

z-sc

ore Unemployment

Unemployment expectation

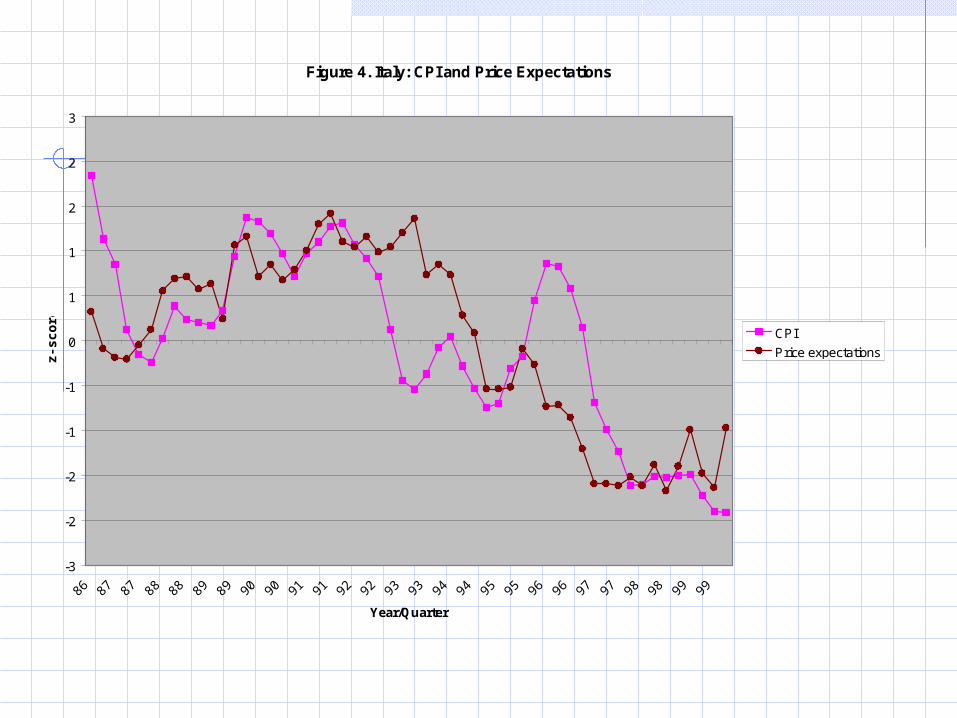

Figure 4. Italy: CPI and Price Expectations

-3

-2

-2

-1

-1

0

1

1

2

2

3

Year/Quarter

z-sc

ore CPI

Price expectations

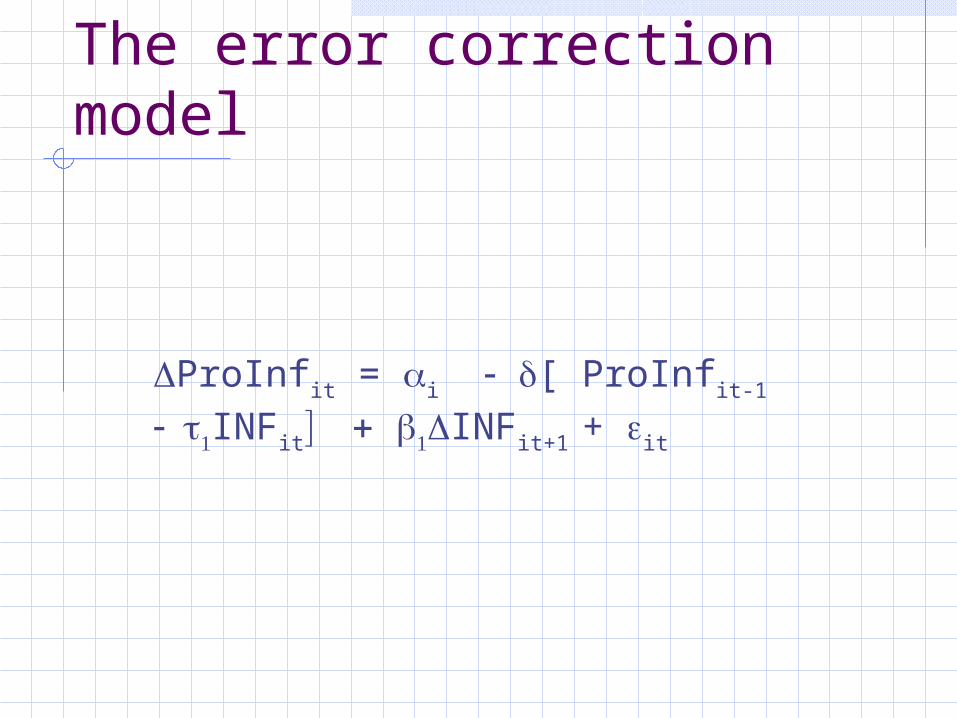

The error correction model

ProInfit = i [ ProInfit-1 INFit INFit+1 + it

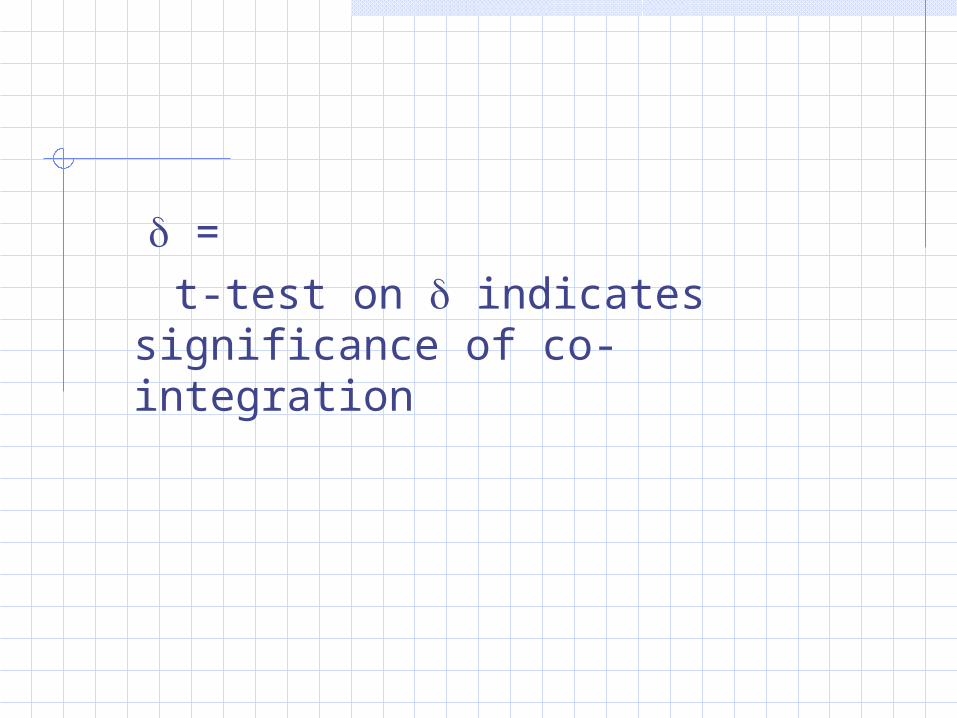

= t-test on indicates significance of

co-integration

=

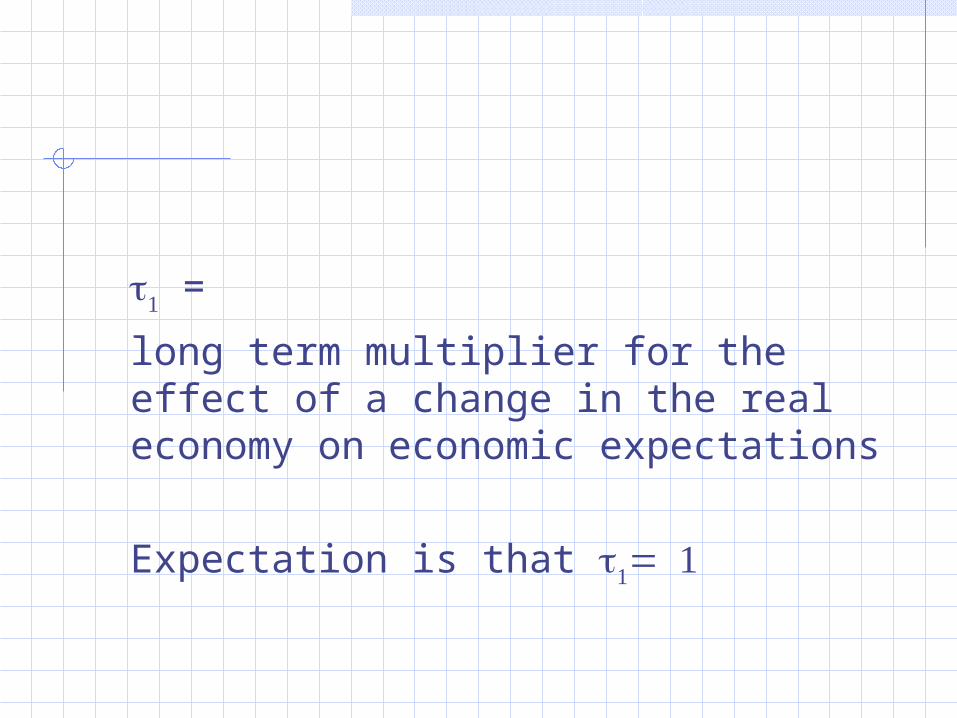

long term multiplier for the effect of a change in the real economy on economic expectations

Expectation is that

Results

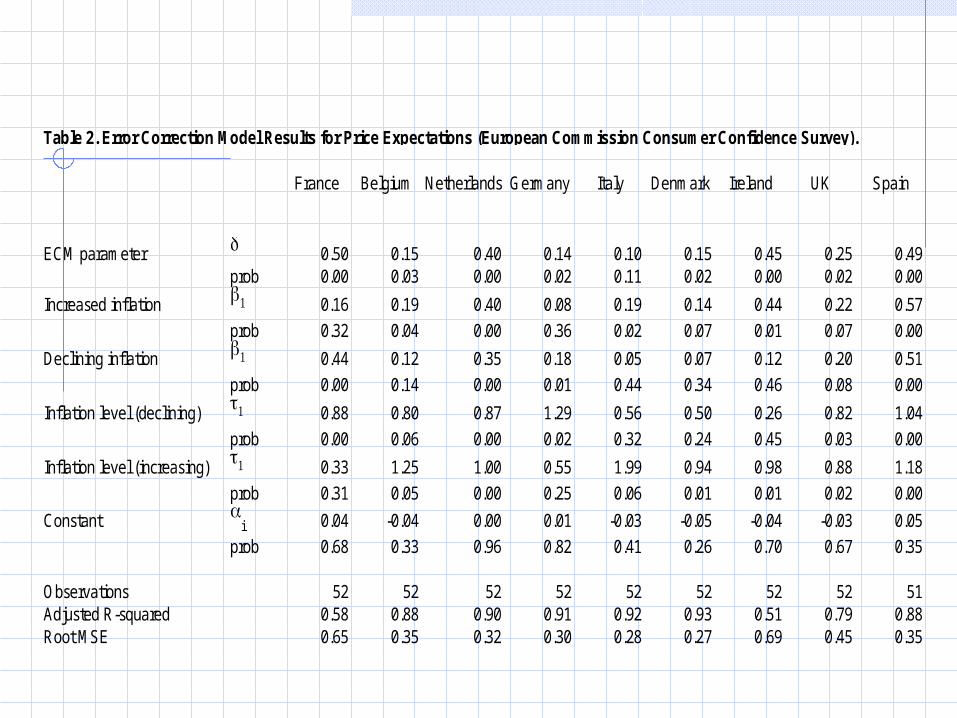

Table 2. Error Correction Model Results for Price Expectations (European Commission Consumer Confidence Survey).

France Belgium Netherlands Germany Italy Denmark Ireland UK Spain

ECM parameter 0.50 0.15 0.40 0.14 0.10 0.15 0.45 0.25 0.49prob 0.00 0.03 0.00 0.02 0.11 0.02 0.00 0.02 0.00

Increased inflation 0.16 0.19 0.40 0.08 0.19 0.14 0.44 0.22 0.57

prob 0.32 0.04 0.00 0.36 0.02 0.07 0.01 0.07 0.00

Declining inflation 0.44 0.12 0.35 0.18 0.05 0.07 0.12 0.20 0.51

prob 0.00 0.14 0.00 0.01 0.44 0.34 0.46 0.08 0.00

Inflation level (declining) 0.88 0.80 0.87 1.29 0.56 0.50 0.26 0.82 1.04

prob 0.00 0.06 0.00 0.02 0.32 0.24 0.45 0.03 0.00

Inflation level (increasing) 0.33 1.25 1.00 0.55 1.99 0.94 0.98 0.88 1.18

prob 0.31 0.05 0.00 0.25 0.06 0.01 0.01 0.02 0.00

Constant i 0.04 -0.04 0.00 0.01 -0.03 -0.05 -0.04 -0.03 0.05

prob 0.68 0.33 0.96 0.82 0.41 0.26 0.70 0.67 0.35

Observations 52 52 52 52 52 52 52 52 51Adjusted R-squared 0.58 0.88 0.90 0.91 0.92 0.93 0.51 0.79 0.88Root MSE 0.65 0.35 0.32 0.30 0.28 0.27 0.69 0.45 0.35

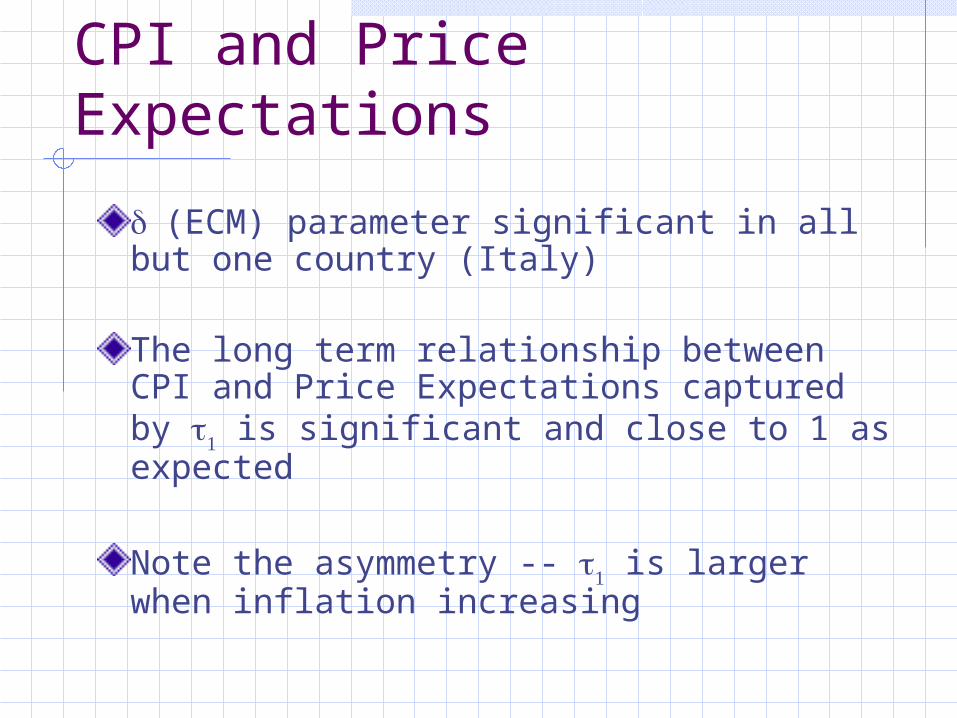

CPI and Price Expectations

(ECM) parameter significant in all but one country (Italy)

The long term relationship between CPI and Price Expectations captured by is significant and close to 1 as expected

Note the asymmetry -- is larger when inflation increasing

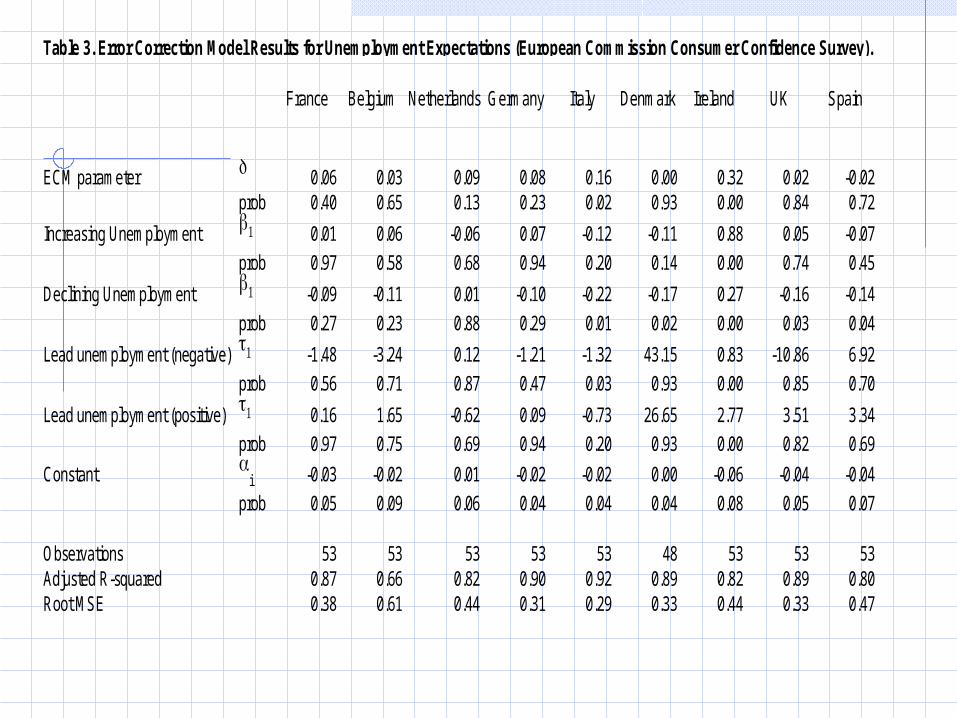

Table 3. Error Correction Model Results for Unemployment Expectations (European Commission Consumer Confidence Survey).

France Belgium Netherlands Germany Italy Denmark Ireland UK Spain

ECM parameter 0.06 0.03 0.09 0.08 0.16 0.00 0.32 0.02 -0.02prob 0.40 0.65 0.13 0.23 0.02 0.93 0.00 0.84 0.72

Increasing Unemployment 0.01 0.06 -0.06 0.07 -0.12 -0.11 0.88 0.05 -0.07

prob 0.97 0.58 0.68 0.94 0.20 0.14 0.00 0.74 0.45

Declining Unemployment -0.09 -0.11 0.01 -0.10 -0.22 -0.17 0.27 -0.16 -0.14

prob 0.27 0.23 0.88 0.29 0.01 0.02 0.00 0.03 0.04

Lead unemployment (negative) -1.48 -3.24 0.12 -1.21 -1.32 43.15 0.83 -10.86 6.92

prob 0.56 0.71 0.87 0.47 0.03 0.93 0.00 0.85 0.70

Lead unemployment (positive) 0.16 1.65 -0.62 0.09 -0.73 26.65 2.77 3.51 3.34

prob 0.97 0.75 0.69 0.94 0.20 0.93 0.00 0.82 0.69

Constant i -0.03 -0.02 0.01 -0.02 -0.02 0.00 -0.06 -0.04 -0.04

prob 0.05 0.09 0.06 0.04 0.04 0.04 0.08 0.05 0.07

Observations 53 53 53 53 53 48 53 53 53Adjusted R-squared 0.87 0.66 0.82 0.90 0.92 0.89 0.82 0.89 0.80Root MSE 0.38 0.61 0.44 0.31 0.29 0.33 0.44 0.33 0.47

Unemployment and Unemployment Expectations

(ECM) parameter significant is not significant

Suggesting the two series are not co-integrated.

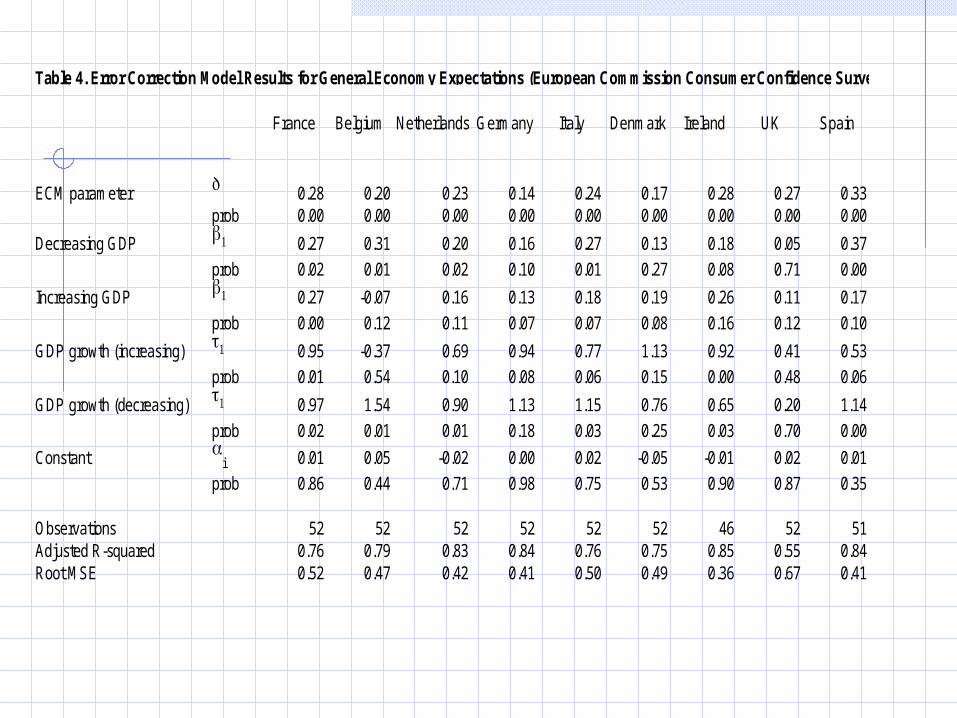

Table 4. Error Correction Model Results for General Economy Expectations (European Commission Consumer Confidence Survey).

France Belgium Netherlands Germany Italy Denmark Ireland UK Spain

ECM parameter 0.28 0.20 0.23 0.14 0.24 0.17 0.28 0.27 0.33prob 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Decreasing GDP 0.27 0.31 0.20 0.16 0.27 0.13 0.18 0.05 0.37

prob 0.02 0.01 0.02 0.10 0.01 0.27 0.08 0.71 0.00

Increasing GDP 0.27 -0.07 0.16 0.13 0.18 0.19 0.26 0.11 0.17

prob 0.00 0.12 0.11 0.07 0.07 0.08 0.16 0.12 0.10

GDP growth (increasing) 0.95 -0.37 0.69 0.94 0.77 1.13 0.92 0.41 0.53

prob 0.01 0.54 0.10 0.08 0.06 0.15 0.00 0.48 0.06

GDP growth (decreasing) 0.97 1.54 0.90 1.13 1.15 0.76 0.65 0.20 1.14

prob 0.02 0.01 0.01 0.18 0.03 0.25 0.03 0.70 0.00

Constant i 0.01 0.05 -0.02 0.00 0.02 -0.05 -0.01 0.02 0.01

prob 0.86 0.44 0.71 0.98 0.75 0.53 0.90 0.87 0.35

Observations 52 52 52 52 52 52 46 52 51Adjusted R-squared 0.76 0.79 0.83 0.84 0.76 0.75 0.85 0.55 0.84Root MSE 0.52 0.47 0.42 0.41 0.50 0.49 0.36 0.67 0.41

General Economy & GDP

(ECM) parameter significant in all countries

The long term relationship between general economy and GDP captured by is significant and close to 1 in vast majority of case

Asymmetry in is less consistent but evident

Cross national variation

Note there is cross-national variation in

The magnitude of t1

The incidence of asymmetry

Conclusions

Perceptions of the economy and the real economy are in many cases co-integrated and seem to fit an error correction process

There is evidence of distortion

There is also evidence that distortion results from mediated cues

Economic outcomes that are costly to monitor (unemployment) are perceived less well by the mass public than easily monitored outcomes (CPI)

Asymmetry in reactions to positive and negative economic news

Cross-national variation

Long-term equilibrium relationship between series

Asymmetry varies by nation

Suggests role of mediated economic information

The economy, economic attitudes and political preferences

What Drives Popularity Series?

Subjective assessments of the economy – which we think are shaped from mediated representations of the economy?

Or, the real economy?

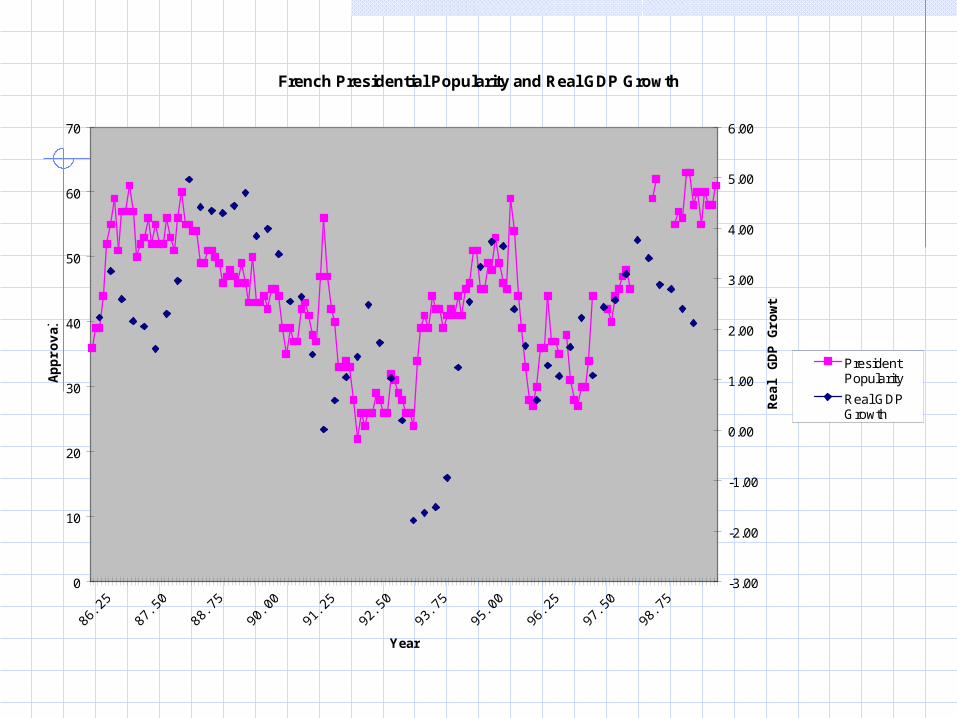

French Presidential Popularity and Real GDP Growth

0

10

20

30

40

50

60

70

86.2

587

.50

88.7

590

.00

91.2

592

.50

93.7

595

.00

96.2

597

.50

98.7

5

Year

Ap

pro

val

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Rea

l GD

P G

row

th

PresidentPopularity

Real GDPGrowth

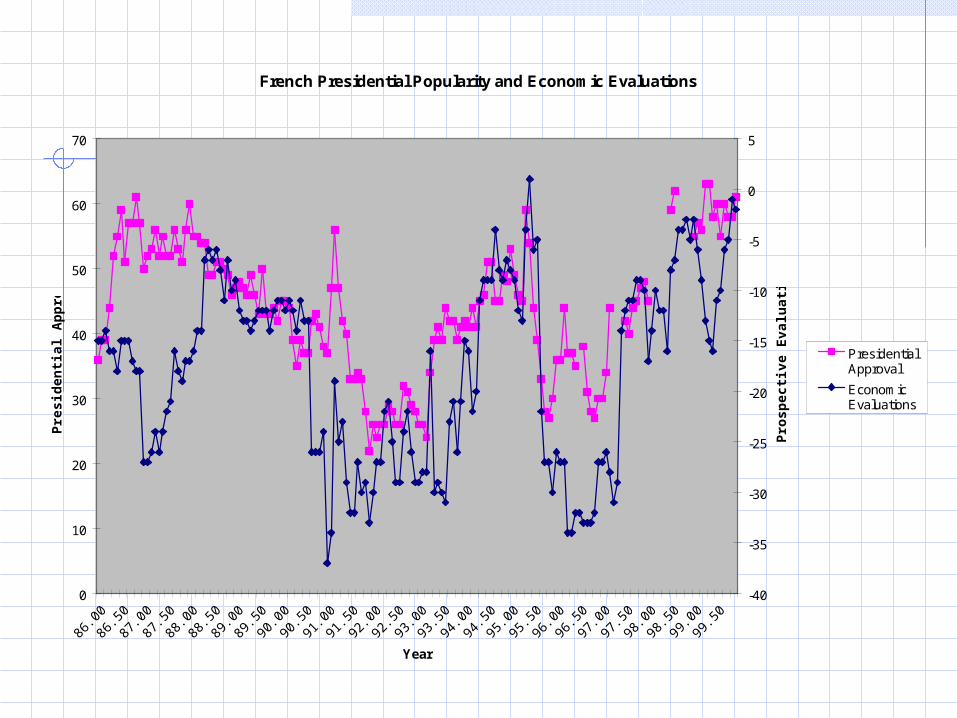

French Presidential Popularity and Economic Evaluations

0

10

20

30

40

50

60

70

86.0

086

.5087

.0087

.5088

.0088

.5089

.0089

.5090

.0090

.5091

.0091

.5092

.0092

.5093

.0093

.5094

.0094

.5095

.0095

.5096

.0096

.5097

.0097

.5098

.0098

.5099

.0099

.50

Year

Pre

sid

enti

al A

pp

rova

l

-40

-35

-30

-25

-20

-15

-10

-5

0

5

Pro

spec

tive

Eva

luat

ion

s

PresidentialApproval

EconomicEvaluations

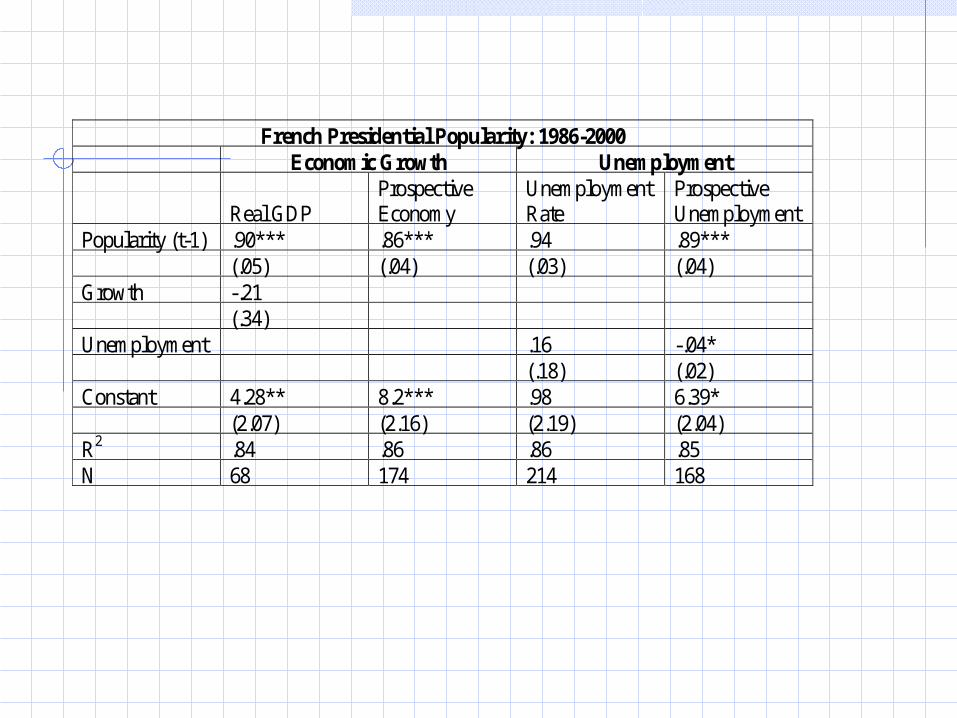

French Presidential Popularity: 1986-2000 Economic Growth Unemployment

Real GDP Prospective Economy

Unemployment Rate

Prospective Unemployment

Popularity (t-1) .90*** .86*** .94 .89*** (.05) (.04) (.03) (.04) Growth -.21 (.34) Unemployment .16 -.04* (.18) (.02) Constant 4.28** 8.2*** .98 6.39* (2.07) (2.16) (2.19) (2.04) R2 .84 .86 .86 .85 N 68 174 214 168