Embed Size (px)

Citation preview

Women and WealthInvest in yourself. You deserve it. A step-by-step guide to help you achieve your financial goals.

Principal Funds

1 Principal Funds | Women and Wealth

Take Time for You

As a woman, you probably have a lot of responsibilities. So your days can get

pretty busy. But in the process of getting everything done, your own needs can get

lost in the shuffle. Your financial plan is a good example.

If you’ve never sat down and created a plan, now is the time to do it. That’s because women have some

unique challenges that make financial planning especially important.

Consider that:

• The “cost” of being a woman (due to time

off work for having children, caring for elderly

parents, etc.) is estimated at $430,480 over

a lifetime. Fewer earnings often translates

to lower Social Security benefits and fewer

dollars in retirement savings.1

• Women generally live longer than men.2

• Eighty-five percent of women aren’t saving

enough for retirement.3

• Our lives are busier than ever. More than

70 percent of moms are in the workforce

today4—compared to just 47 percent in 1975.5

And yet today’s moms spend 50 percent more

time with their kids than their mothers did.

• Many (but not all) women tend to be

less confident than men when it comes

to financial decisions. (Ironically, though,

women generally make better financial

decisions than men.)6

Combine all that with the high divorce rate—

and the fact that almost half the women

over 65 years of age in the United States are

widows7—and you can see why it’s so critical

for women to take charge of their finances.

It isn’t hard, and it doesn’t have to take a lot

of time. We’ll walk you through the basics.

Here’s the Process

This workbook will take you through the

process of setting financial goals, creating

a plan, and putting the plan in place.

Step 1: Get Organized

Step 2: Set Goals

Step 3: Prioritize

Step 4: Create Your Plan

Step 5: Educate Yourself

Step 6: Put Your Plan into Action

Step 7: Review Your Plan

1 National Women’s Law Center, April 2016.2 Social Security Administration. 3 Transamerica Center for Retirement Studies, 2015. 4 Employment Characteristics of Families, Bureau of Labor

Statistics, April 2016.5 Working Mothers in the U.S., Bureau of Labor Statistics.6 Male Investors vs. Female Investors, The Wall Street Journal,

May 2015.7 Serving Widowed Clients Whatever Their Age, Financial Advisor

Magazine, 2011 US Census Bureau July 2013.

2Principal Funds | Women and Wealth

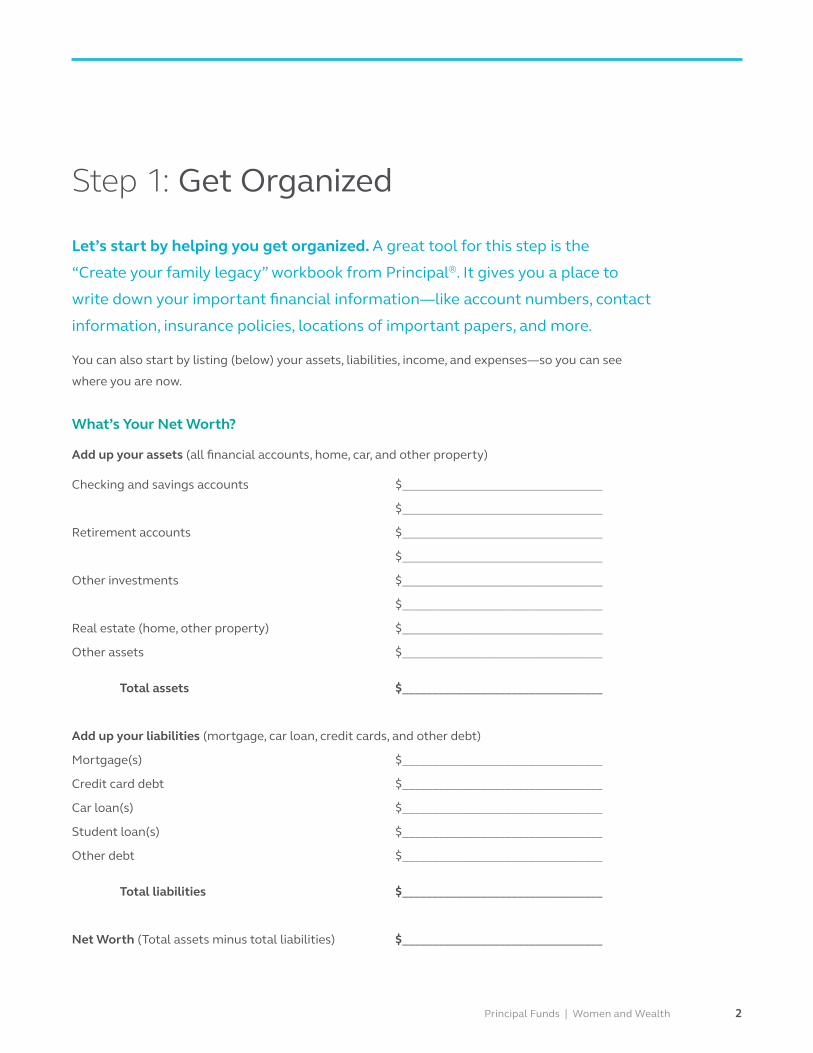

Let’s start by helping you get organized. A great tool for this step is the

“Create your family legacy” workbook from Principal®. It gives you a place to

write down your important financial information—like account numbers, contact

information, insurance policies, locations of important papers, and more.

You can also start by listing (below) your assets, liabilities, income, and expenses—so you can see

where you are now.

Step 1: Get Organized

What’s Your Net Worth?

Add up your assets (all financial accounts, home, car, and other property)

Checking and savings accounts $_________________________________

$_________________________________

Retirement accounts $_________________________________

$_________________________________

Other investments $_________________________________

$_________________________________

Real estate (home, other property) $_________________________________

Other assets $_________________________________

Total assets $_________________________________

Add up your liabilities (mortgage, car loan, credit cards, and other debt)

Mortgage(s) $_________________________________

Credit card debt $_________________________________

Car loan(s) $_________________________________

Student loan(s) $_________________________________

Other debt $_________________________________

Total liabilities $_________________________________

Net Worth (Total assets minus total liabilities) $_________________________________

3 Principal Funds | Women and Wealth

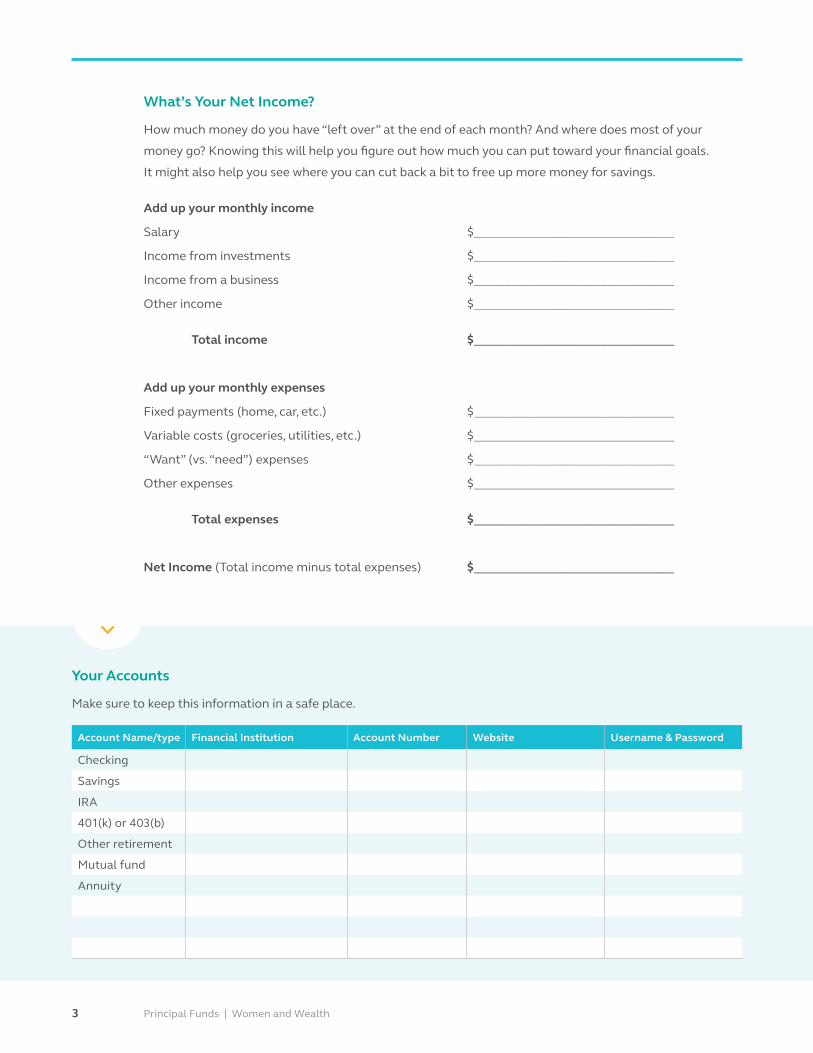

Account Name/type Financial Institution Account Number Website Username & Password

Checking

Savings

IRA

401(k) or 403(b)

Other retirement

Mutual fund

Annuity

What’s Your Net Income?

How much money do you have “left over” at the end of each month? And where does most of your

money go? Knowing this will help you figure out how much you can put toward your financial goals.

It might also help you see where you can cut back a bit to free up more money for savings.

Add up your monthly income

Salary $_________________________________

Income from investments $_________________________________

Income from a business $_________________________________

Other income $_________________________________

Total income $_________________________________

Add up your monthly expenses

Fixed payments (home, car, etc.) $_________________________________

Variable costs (groceries, utilities, etc.) $_________________________________

“Want” (vs. “need”) expenses $_________________________________

Other expenses $_________________________________

Total expenses $_________________________________

Net Income (Total income minus total expenses) $_________________________________

Your Accounts

Make sure to keep this information in a safe place.

4Principal Funds | Women and Wealth

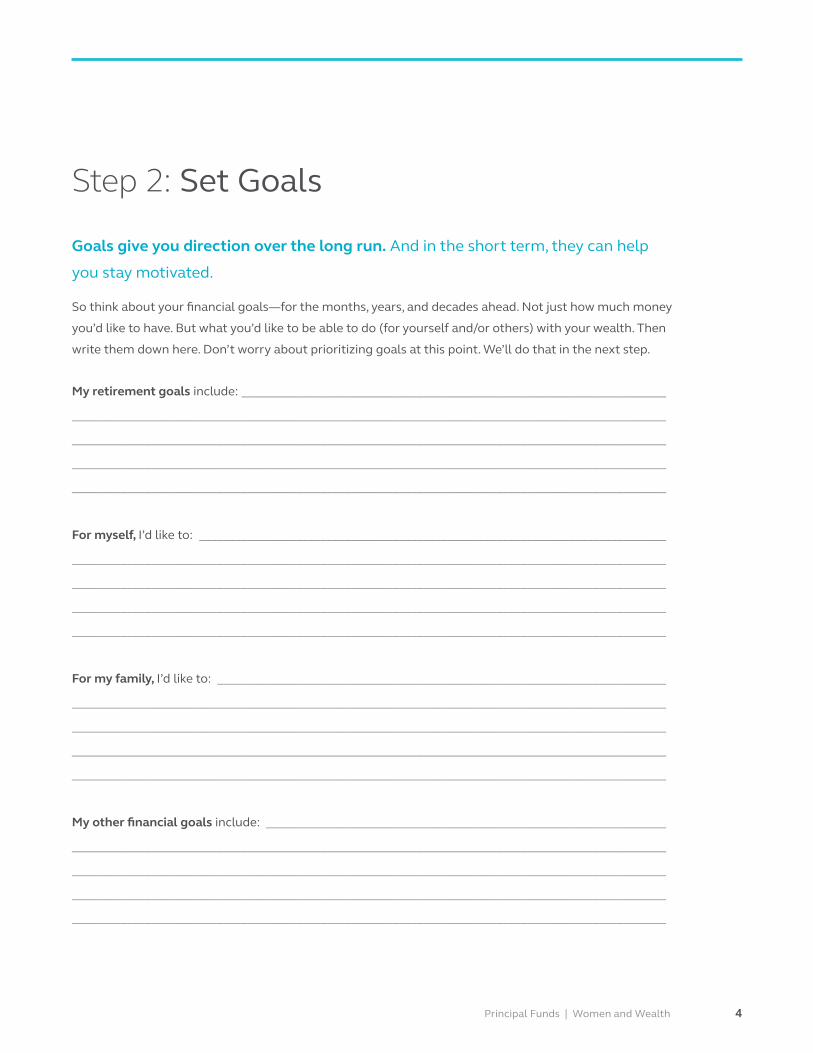

Goals give you direction over the long run. And in the short term, they can help

you stay motivated.

So think about your financial goals—for the months, years, and decades ahead. Not just how much money

you’d like to have. But what you’d like to be able to do (for yourself and/or others) with your wealth. Then

write them down here. Don’t worry about prioritizing goals at this point. We’ll do that in the next step.

My retirement goals include: ______________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

For myself, I’d like to: _____________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

For my family, I’d like to: __________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

My other financial goals include: __________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

Step 2: Set Goals

5 Principal Funds | Women and Wealth

Step 3: Prioritize

“Have to” Goals__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

“Need to” Goals__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

“Want to” Goals__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

__________________________________________________________________________________________________

Now that you’ve listed your goals, let’s figure out which ones are most important

to you.

Think about which goals you have to do (such as paying taxes and your mortgage or rent). Then consider

things you need to do (saving for retirement, for instance). Finally, decide which goals you want to do

(traveling, buying a second home, etc.).

6Principal Funds | Women and Wealth

We’re making progress! You know how much money you have left over each

month. You’ve listed your goals. And you’ve prioritized them.

Step 4: Create a Plan

Now you can work on a plan to make these

goals a reality. A financial advisor can help you

through the process.

Your Plan for Retirement

Consider these questions as you work with your

advisor on a plan for your retirement.

If you were to retire today, what percent of

your current household income would you

need to pay the bills and do the things you

want to do? ________ %

At what age would you like to retire? _______

When you retire, about how long do you

think your retirement will last? (Consider

your current health as well as your family’s

health history.) ________ years

How comfortable (or uncomfortable) are

you with risk? ____________________________

Keep Insurance in Mind

Insurance… yawn, right? It’s a pretty dry subject.

But when the chips are down, insurance can

quickly become one of the most important

things in your life.

As you work with your advisor, make sure

to chat about life insurance and disability

insurance. After all, even if you have life and

disability policies already, it doesn’t mean you

have enough—or the right kind.

How About Your Estate Plan?

You have the right to decide what should

happen with your home, your savings, and

your treasured belongings when you pass away.

An estate plan can help you put those wishes

in writing.

A good estate plan should also include a power

of attorney and a living will. And if you choose,

an estate plan can also include trusts for your

heirs or a favorite charity.

7 Principal Funds | Women and Wealth

One of the best things you can do for yourself is to learn more about saving and

investing. You don’t have to be the next Warren Buffett. But you should understand

some basic concepts.

Step 5: Educate Yourself

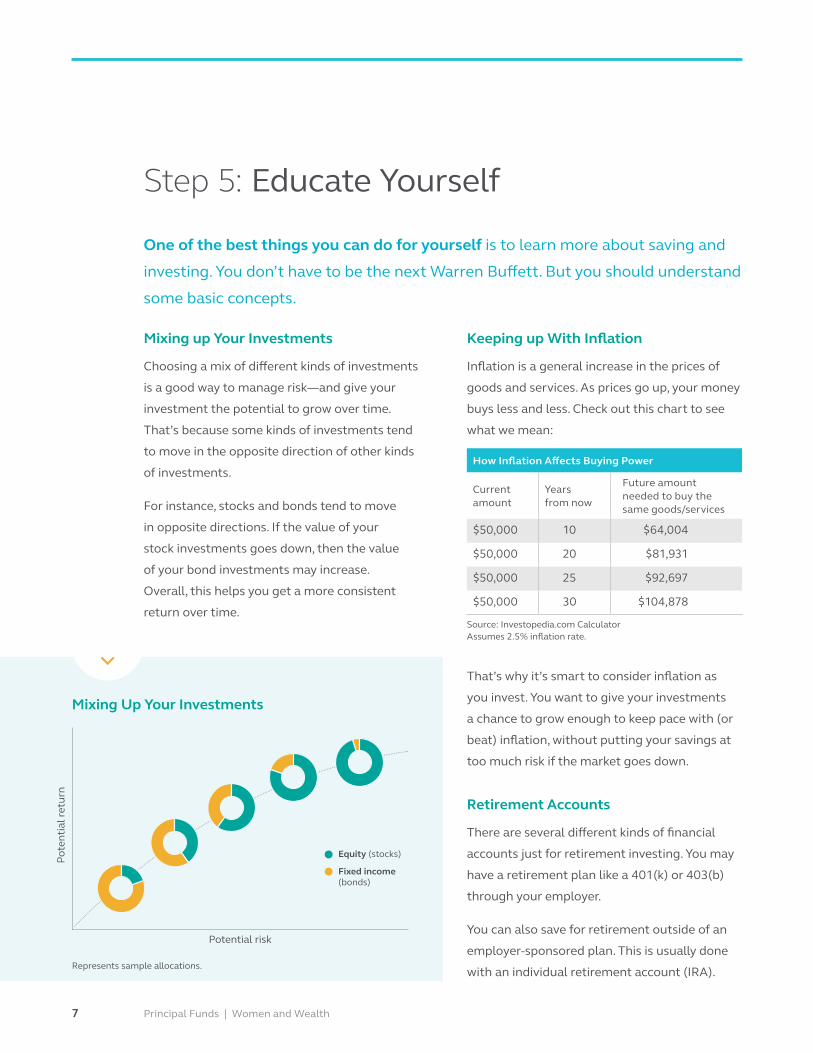

How Inflation Affects Buying Power

Current amount

Years from now

Future amount needed to buy the same goods/services

$50,000 10 $64,004

$50,000 20 $81,931

$50,000 25 $92,697

$50,000 30 $104,878

Source: Investopedia.com Calculator Assumes 2.5% inflation rate.

Mixing up Your Investments

Choosing a mix of different kinds of investments

is a good way to manage risk—and give your

investment the potential to grow over time.

That’s because some kinds of investments tend

to move in the opposite direction of other kinds

of investments.

For instance, stocks and bonds tend to move

in opposite directions. If the value of your

stock investments goes down, then the value

of your bond investments may increase.

Overall, this helps you get a more consistent

return over time.

Keeping up With Inflation

Inflation is a general increase in the prices of

goods and services. As prices go up, your money

buys less and less. Check out this chart to see

what we mean:

That’s why it’s smart to consider inflation as

you invest. You want to give your investments

a chance to grow enough to keep pace with (or

beat) inflation, without putting your savings at

too much risk if the market goes down.

Retirement Accounts

There are several different kinds of financial

accounts just for retirement investing. You may

have a retirement plan like a 401(k) or 403(b)

through your employer.

You can also save for retirement outside of an

employer-sponsored plan. This is usually done

with an individual retirement account (IRA).

Mixing Up Your Investments

Pote

ntia

l ret

urn

Potential risk

Represents sample allocations.

Equity (stocks)

Fixed income (bonds)

8Principal Funds | Women and Wealth

Like a 401(k) or 403(b) plan, contributions to

traditional IRAs are made on a pre-tax basis.

That means you don’t pay taxes on the money

you invest until you withdraw it.

An exception is the Roth IRA. Contributions to

a Roth IRA are made on an after-tax basis.

If you think you’ll be in a lower tax bracket

in retirement, then a traditional IRA might

make more sense. If you’re in a lower bracket

now, then a Roth IRA may be better. Your tax

professional can help you decide what works

best for your needs.

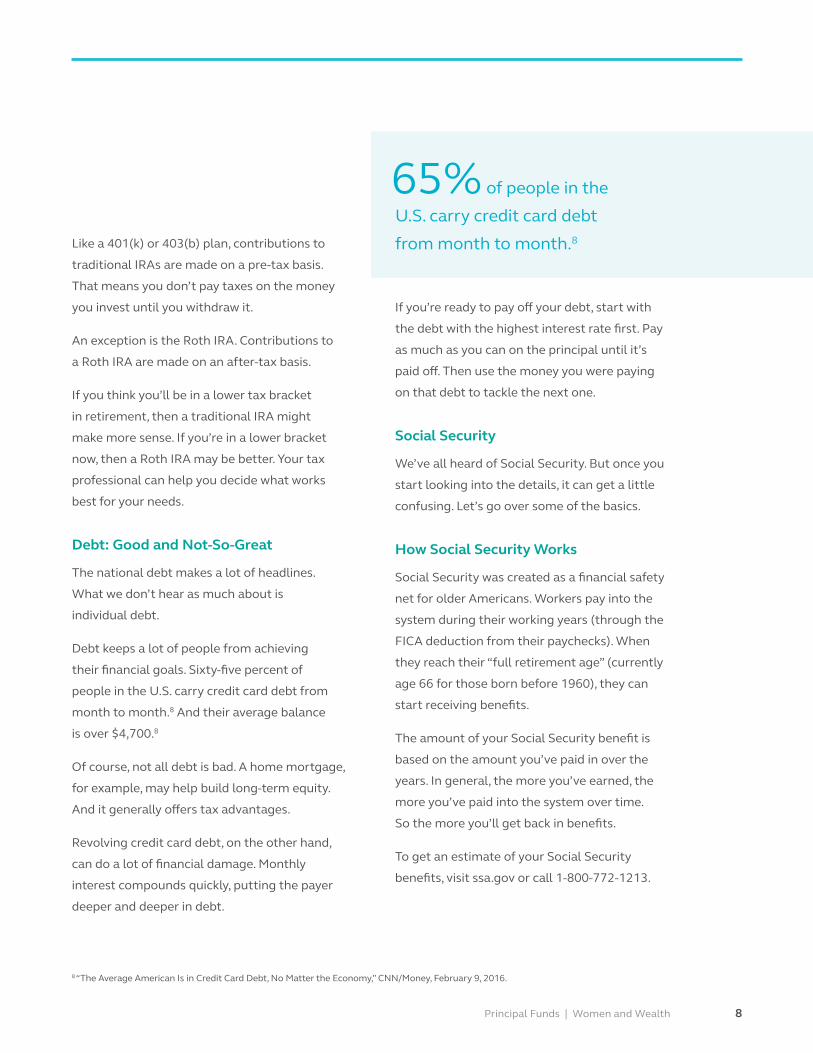

Debt: Good and Not-So-Great

The national debt makes a lot of headlines.

What we don’t hear as much about is

individual debt.

Debt keeps a lot of people from achieving

their financial goals. Sixty-five percent of

people in the U.S. carry credit card debt from

month to month.8 And their average balance

is over $4,700.8

Of course, not all debt is bad. A home mortgage,

for example, may help build long-term equity.

And it generally offers tax advantages.

Revolving credit card debt, on the other hand,

can do a lot of financial damage. Monthly

interest compounds quickly, putting the payer

deeper and deeper in debt.

If you’re ready to pay off your debt, start with

the debt with the highest interest rate first. Pay

as much as you can on the principal until it’s

paid off. Then use the money you were paying

on that debt to tackle the next one.

Social Security

We’ve all heard of Social Security. But once you

start looking into the details, it can get a little

confusing. Let’s go over some of the basics.

How Social Security Works

Social Security was created as a financial safety

net for older Americans. Workers pay into the

system during their working years (through the

FICA deduction from their paychecks). When

they reach their “full retirement age” (currently

age 66 for those born before 1960), they can

start receiving benefits.

The amount of your Social Security benefit is

based on the amount you’ve paid in over the

years. In general, the more you’ve earned, the

more you’ve paid into the system over time.

So the more you’ll get back in benefits.

To get an estimate of your Social Security

benefits, visit ssa.gov or call 1-800-772-1213.

8 “The Average American Is in Credit Card Debt, No Matter the Economy,” CNN/Money, February 9, 2016.

65% of people in the

U.S. carry credit card debt

from month to month.8

9 Principal Funds | Women and Wealth

Feeling a little overwhelmed? That’s OK. Just remember that you don’t have to do

this on your own. A financial advisor can help you through the whole process.

A good financial advisor can help you:

After you’ve interviewed each financial advisor, eliminate any who don’t meet your minimum

requirements. Then just trust your instincts. Go with the one you feel most comfortable with and who

you think will best help you reach your goals.

Step 6: Put Your Plan Into Action

Finding a Financial Advisor

If you don’t know any financial

advisors, ask for recommendations

from people you know and trust.

Collect the names of several. Then

choose several to interview. Ask

questions like these:

1. How long have you been

working as a financial advisor?

In general, the longer someone

has been in the business, the

more insights they may have on

what works and what doesn’t.

On the other hand, someone

with less experience but more

recent education and training

may be more open to new

products and strategies.

2. What are your credentials?

A financial advisor should have

the appropriate insurance licenses

and securities registrations.

Beyond that, there are several

professional designations they

could have. Examples include:

Certified Financial PlannerTM

(CFP®) or Chartered Financial

Consultant (ChFC®).

3. What kinds of financial

solutions do you offer?

It’s important to have access to a

broad range of solutions, because

you’ll likely have different

financial needs during your life—

saving for retirement, saving

for college, life and disability

insurance, and so on.

4. What’s your process?

Financial advisors who have a

very brief, narrow process for

creating a financial strategy

may just be trying to sell you

a product. You need someone

who will take the time to look

at your whole financial picture

and create a comprehensive

strategy for the future.

5. What are your fees?

As your financial advisor

works with you to help meet

your financial goals, be sure

to understand how he or she

is compensated for the value

brought to the process.

Assess your current financial situation

Set realistic— and achievable —goals

Create a financial strategy

Help you put your plan into action

Help you keep your plan on track

10Principal Funds | Women and Wealth

Changes like these can have big impacts on

your life. So your plan needs to change, too.

Keep your plan on track by reviewing it at

least once a year. If you work with an advisor,

go over the plan with him or her.

By creating a financial plan—and making sure

it keeps up with your life—you can achieve

your goals. And most important, live the life

you want to live.

Keep Track of Recent Life Events

Important milestones: __________________________________________________________________________________

_________________________________________________________________________________________________________

Changes in family circumstances: _______________________________________________________________________

_________________________________________________________________________________________________________

Changes in professional circumstances: _________________________________________________________________

_________________________________________________________________________________________________________

Events or other changes you’d like to discuss: ___________________________________________________________

_________________________________________________________________________________________________________

Progress made on goals: ________________________________________________________________________________

_________________________________________________________________________________________________________

Long-term vision for yourself and your family: __________________________________________________________

_________________________________________________________________________________________________________

_________________________________________________________________________________________________________

_________________________________________________________________________________________________________

Things change. Kids grow up. People get married. Or divorced. Jobs come and go.

Step 7: Review Your Plan

By creating a financial plan—and

making sure it keeps up with your

life—you can achieve your goals.

Principal Funds are distributed by Principal Funds Distributor, Inc.

© 2017 Principal Financial Group, Inc. | MM8866-02 | 05/2017 | t16122807qy

Investing involves risk, including possible loss of principal.

The subject matter in this communication is provided with the understanding that Principal® is not rendering legal, accounting, or tax advice. You should consult with appropriate counsel or other advisors on all matters pertaining to legal, tax, or accounting obligations and requireme

![Chapter 2. Women on Boards - SciTech Connectscitechconnect.elsevier.com/.../2016/03/Chapter-2-women-on-boards… · about 70% [12] of household purchasing decisions. Women are becom-ing](https://img.pdfslide.net/doc/110x75/5eb6dfd81ae2ed3f11096a68/chapter-2-women-on-boards-scitech-c-about-70-12-of-household-purchasing-decisions.jpg)