Embed Size (px)

Citation preview

R&D offshoring and home industry productivity

Working Paper 2/16

Gaétan de Rassenfosse and Russell Thomson

2016

1

R&Doffshoringandhomeindustryproductivity

GaétandeRassenfosse‡andRussellThomson†

Abstract

Offshoringresearchanddevelopment(R&D)commonlyinvokesconcernsregardingthelossof

highvaluejobsandahollowingoutoftechnologicalcapabilities,butitcanalsobenefitdomestic

firmsbyenablingthemtotapintotheglobaltechnologicalfrontier.WestudytheeffectofR&D

offshoringonindustrialproductivityinthehomecountryusingindustry-leveldatafor18OECD

countries over a 26-year period. Simultaneity is addressed by using foreign tax policy as an

instrumentforoffshoredR&D.OurresultsshowthatR&Doffshoringcontributespositivelyto

productivityinthehomecountry,irrespectiveofthehostcountrydestination.

JELclassifications:O25,O33,O47,L6

Keywords:R&Doffshoring,globalization,productivity,foreignR&D

‡ÉcolepolytechniquefédéraledeLausanne,CollegeofManagementofTechnology,ODY201.1,Station5,1015Lausanne,Switzerland.+41216930096,[email protected]†CenterforTransformativeInnovation,SwinburneUniversityofTechnology,Melbourne,Australia.+61392145873,[email protected]

2

Introduction

Thisarticleinvestigatestheimpactofresearchanddevelopment(R&D)offshoringonindustrial

productivity in the home country and considers factors which may condition the effect.

Globalisedtechnologysourcingisadefiningfeatureofinnovationsystemsinthe21stcentury.

By2008,US-ownedmanufacturingcompaniesperformednearly20percentoftheirtotalR&D

outside the United States (NSF 2010). The extent of R&D offshoring by several European

countries includingSwitzerland,SwedenandGermanyappearstobeevengreater(European

Commission 2012). The growth in R&D offshoring has long been regarded as a worrisome

developmentfortechnologicallyadvancednationsinlightofthecentralroleofR&Dindriving

productivity and economic growth (Mansfield et al. 1979; Lall 1979; Dunning 1994).

Governmentsareincreasingly inclinedtooffer inducementsinordertoensurethat ‘national’

firmsmaintainR&Dactivitiesintheirhistoricalhomecountry.

RecentevidencehasshownthatfirmscangenerateprivatebenefitsfromoffshoringR&D.

Bytappingintothegloballydisparatetechnologicalfrontierfirmscanenhancetheirproductivity

andmarketposition(Cantwell1995).Forinstance,Samsung’sR&DoutpostinSiliconValleyis

creditedwithplayingavitalroleinthecompany’seventualdominanceinSDRAMtechnologies

(Kim1997).Analysisoffirm-leveldataforfirmsbasedintheUKandGermanyhaveshownthat

offshoringR&DtotheUnitedStatesprovidesameanstotapintotechnologicalspilloversand

enhanceperformance(Griffithetal.2006;Harhoffetal.2012).

Notwithstandingtheevidenceregardingbenefitstotheoffshoringfirmsthemselves,the

overallimpactonthehomecountryisnotyetclear.TheimportantroleofSamsunginKorean

economicdevelopmentsuggeststhatimpactscanpotentiallybesubstantial,buttowhatextent

isthisexampleanexceptionratherthanarule?Ofconcernisthelossof‘scientist-to-scientist’

spillovers, which are thought to occur at the location in which R&D is performed. Equally

3

importantly,benefitsassociatedwithoffshoredR&Dareexpected tobedispersedacross the

company’sglobaloperations;thereisnoguaranteethatasubstantivesharewillbecapturedby

operations in the home country. Additionally, benefits may be muted in the case of home

countriesatthetechnologicalfrontierbecausetherelativetechnologicalcapacityofthehome

countrydeterminesscope for learning(SongandShin2008;Songetal.2011).Theextent to

whichbenefitsmayhingeonoffshoring toa frontiereconomyhasnotbeensubject todirect

empiricalscrutinythoughGriffithetal.(2006)noteinpassingthattheyareunabletoconfirma

positiveimpactfromoffshoringtocountriesotherthantotheUnitedStates.Thisiscausefor

concerntopolicymakersintheUnitedStates,whichisthehomecountrytofirmsengagedthe

mostinR&Doffshoring.

Westudy theeffectofR&Doffshoringon industrialproductivity in thehomecountry

usingnewpatent-basedindicatorsofR&Doffshoringlinkedto2-digitmanufacturingproduction

datafrom18OECDcountriesbetween1981and2007.Ourindustry-levelapproachprovidesa

globalandlong-termviewandavoidsmanyofthesamplingandselectionissuesinherentinfirm

level studies. It captures thenet effect on local industry taking into account spillover effects

which are an important component of the policy puzzle. After all,we expect firms to derive

privatebenefitfromtheirownoffshoringdecisions,atleastonaverage.

We also extend the literature by tackling the difficult issue of simultaneity between

productivityandoffshoring.Simultaneityarisesbecausehomecountrytechnologicalcapacity

determinestheexistenceofleadingmultinationalenterprises(MNEs)aswellastheircapacity

tomanageandbenefitfromgloballydispersedR&Dassets(Vernon1966;PatelandPavitt1988,

1991;LeBasandSierra2002;SongandShin2008;Songetal.2011).Toaddresstheissueof

simultaneityweusecountry-industryspecificmeasuresofR&Dtaxpolicyasaninstrumentfor

R&Doffshoringactivity.R&Dtaxpolicyprovidesapromisinginstrumentsinceforeigntaxpolicy

isexogenoustodomesticproductivity;itisdifficulttoimagineamechanismthroughwhichR&D

4

specific tax incentives intheUKwillaffect industrialproductivity intheUSAexceptviatheir

influenceonthedistributionofcompanyR&Dbetweenthetwocountries.R&Dtaxincentives

havebeenshowntohaveasignificantinfluenceonR&Dlocationdecisions(BloomandGriffith

2001;Wilson2009).TheresultsarerobusttoWealsoconsideraconventionalapplicationof

systemsGMM(BlundellandBond1998).

OurresultsshowthatR&Doffshoringcontributespositivelytoproductivityinthehome

country,irrespectiveofthehostcountrydestination.However,wereportevidencesuggesting

thatthebenefitshingeonthenatureofoffshoringactivities,withtechnology-seekingoffshored

R&D bringing the most benefits and market-seeking offshored R&D potentially reducing

productivity.

Theoreticalframework

InlightoftheongoinggrowthinR&Doffshoringitwouldbedifficulttoarguethatfirmsarenot

generatingprivatebenefits. Scholarshave long recognized that offshoringprovides a critical

mechanismtotap intothegloballydisparatetechnological frontier(Ronstadt1978;Cantwell

1995).Offshoringprovidesameansforfirmstoprocuretechnologiesnotnecessarilyavailable

inthehomemarket.Allthe25mostpatentintensiveUScompaniesengageperformsomeR&D

abroad–andeveryoneoftheacquirepatentsfromabroadintechnologyareasthattheydonot

acquirefromlocalR&D(derivedfromUSPTO).

OurresearchquestiondealswithnotjustthemagnitudeofbenefitsofR&Doffshoringbutalso

thedistributionofthosebenefits.BenefitsfromR&Dactivityaccruetotheinvestingfirmandcan

alsospillovertoneighboringfirms.Inthissectionwebeginbyconsideringeachoftheseinturn,

withaviewtoarticulatingthemechanismthroughwhichR&Doffshoringimpactsproductivity

inthehomecountry.Factorsthatmaymitigateorconditiontheeffectarethendiscussed.

5

Someofthevaluegeneratedbynewtechnologywillbecapturedbytheplantwherethe

technologyisimplemented;thismaybethecountryinwhichtheresearchwasconducted,inthe

firm’shome-base,or inathirdcountry inwhichthefirmhasproductionassets.Valueisalso

captured at other points along the firm’s value chain. The share of value captured by

manufacturingactivitiesperseinglobalvaluechainsistypicallylowandappearstobefalling

(BartlettandGhoshal2000;Ali-YrkköandRouvinen2015).Valuealsopermeatesupstreamand

downstreamglobalvaluechains,withalargeshareofvalueaddedcapturedbyoperationsinthe

homecountry, includingheadquarteroperationsaswellasnichehighvaluecontributions to

productionactivities(Ali-YrkköandRouvinen2015).

ItiswellunderstoodthatfirmsgenerallydonotcaptureallbenefitsassociatedwithR&D

investment.Benefitsalsospillovertoneighboringfirmsandthesespilloversalsocontributeto

thegeographicdistributionofbenefitsofoffshoredR&D.Spilloverscanariseatthreelociofthe

innovationprocess:invention,productionandownership.Thoseattheinventionstagearewell

understoodand involve the formaland informalexchangeof informationbetweenscientists.

Althoughthe literatureemphasises thatknowledgespilloversarehighly localised(Jaffeetal.

1993), spillovers from offshored R&D to other firms in the home country have also been

documented (Criscuolo 2009). Spillovers associated with the production processes where

technologiesareimplementedaresimilarlywellunderstood.Likeinternalisedbenefits,theyare

diffused along the production chain and work through interactions with suppliers,

demonstrationeffectsandengineeringandmanagementconsultancy.Firmsinthehomecountry

can benefit from the offshoring activities of their compatriots via demonstration effects or

through supply-chain-mediated technology upgrading (Porter 1990). Trade in intermediate

goods is alsoan important transmissionmechanism forproductivitygainsat theproduction

stage (Griliches1979). Finally, technologyowners in thehome countryholdmanagerial and

strategicinsightsthatcanbenefitlocalupstreamanddownstreamactors.

6

Not all R&D offshoring is expected to bring equal benefits to the home country. For

instance,R&Doffshoringthatisintendedprimarilytoadaptproductsforspecificlocalmarkets

(knownas‘market-seeking’R&D)isunlikelytogenerateextensivespilloverstothefirm’shome

country(cf.ArvanitisandHollenstein2011). Scope for learningcanalso influence firmlevel

benefits(SongandShin2008;Songetal.2011).Recentresearchhasemphasisedtheimportance

ofoffshoringR&DtotechnologicalleadersandtheUnitedStatesinparticular(Griffithetal.2006;

Harhoff et al. 2014). Although the United States is certainly a leader by many aggregate

measures, the existence of centers of excellence around specific technology areas and niche

technical and scientific skills in other parts of theworld scarcely requires argument. Global

technologystrategyprovidesamechanismforsourcingthebesttechnologyfromanincreasingly

globallydisparatefrontier.Ifinformedfirmsactrationallyinchoosingthelocationofoffshored

R&DweshouldexpectalloffshoredR&Dinvestmentstogeneratereturnscommensuratewith

theriskandcoststheyinvolve.

The distribution of firms’ ability to benefit from R&D offshoring gives rise to the

importantconsiderationofsimultaneitybetweenoffshoringandperformancewhichhas,todate,

largelyescapedthemodelingeffortofempiricaleconomists(Griffithetal.2006:1873).Leading

MNEs havemost to gain fromR&D offshoring because of their superior absorptive capacity

(SongandShin2008).Leadingfirmsalsopossessorganizationcapabilitiesthatallowthemto

managethecomplexprocessofR&Doffshoring,sothattheyarethemostlikelytoengageinthat

activity.InsightsfrommanagementstudiessimilarlysuggestthatR&Doffshoringistheprivilege

of the fittest (Patel and Vega 1999; Le Bas and Sierra 2002). We tackle the problem of

simultaneityusinginstrumentalvariableswhichisexplainedfurtherinthenextsection.

7

MeasuringhomeandoffshoredR&D

Ideallywewould observe industry levelR&Dexpenditures by country of funding (the firms

homebase)andcountryofperformance(thehostcountry).Unfortunately,statisticalagencies

donotcollectsuchdatasystematically.Weresorttopatentdata,whichprovideanindicatorof

bothhomeandoffshoredR&D(GuellecandvanPottlesberghe2001;OECD2009;Picci2010;

Thomson2013).HomeR&Discapturedwithpatentsthathavebothdomesticapplicantsand

inventors.ApatentthatderivesfromoffshoredR&Disapatentwithadomesticapplicantanda

foreigninventor.Theapplicant’saddressprovidesanindicatoroftheMNEshomecountryand

inventor’scountryofresidenceindicatestheMNEsoffshoringlocation.

Inmostcases,ownersofvaluabletechnologywantprotectionfromwould-beimitators

inmanycountries.Toachievethis,theymustfilepatentapplicationstotheintellectualproperty

officeineachcountrytheywantprotection.Patentsaregenerallyfiledinproductioncenters,

majormarkets,andthelocationofcompetitorfirms.Thefirstfilingprotectinganinventionis

calledaprioritypatentapplication.Subsequentapplicationsprotectingthesameinventionin

otherjurisdictionsarecalledsecondfilings.Onlyprioritypatentapplicationsareincludedinour

measuresincesecondfilingsarenotindicativeofadditionalR&Dactivity.

Themeasureofoffshoring is calculatedusing theuniverseof inventor-applicantpairs

(including ‘inventor countries’ that are not in the OECD). Multi-inventor or multi-applicant

patents that spanmore than one country are fractionally counted. The data come from the

EuropeanPatentOffice(EPO)WorldwidePatentStatisticalDatabase(PATSTAT).Thealgorithm

usedtoidentifypriorityfilingsandtofillinmissingdataonapplicantandinventorcountryof

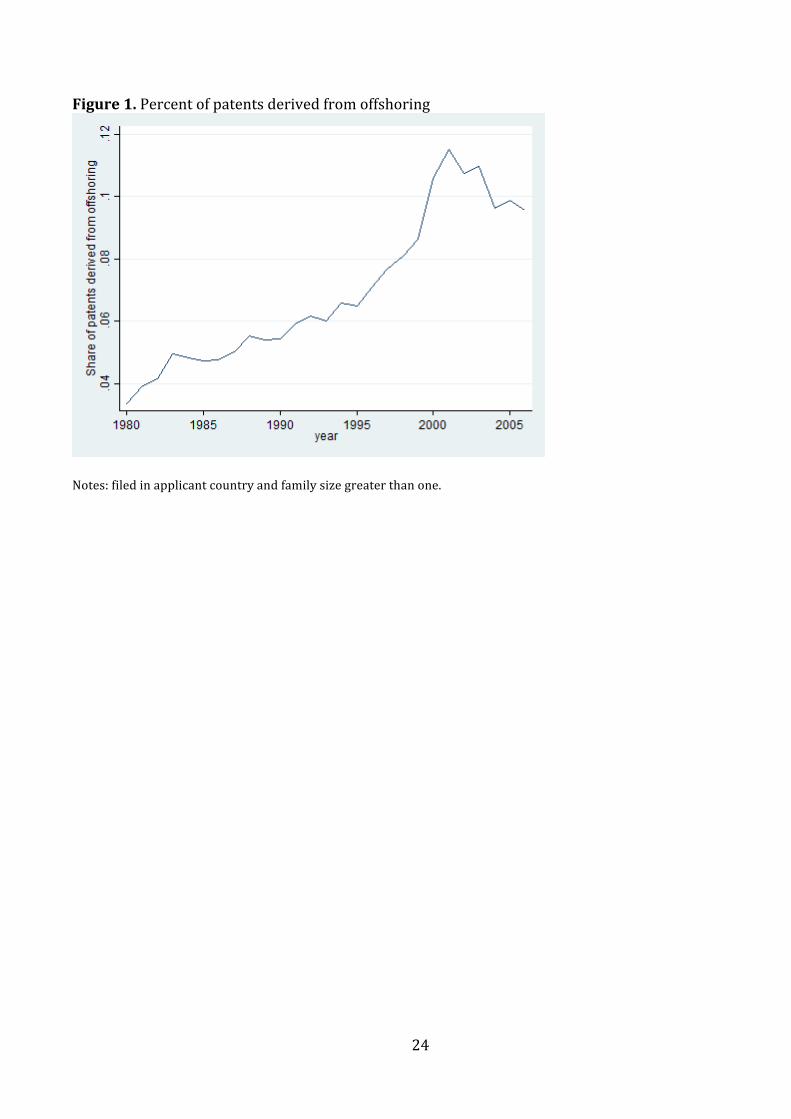

residence is discussed in de Rassenfosse et al. (2013). Figure 1 shows that the worldwide

8

proportionof‘offshoredpatents’hasgrown,from3percentintheearly1980stomorethan10

percentinthelate2000s.

[Figure1abouthere]

We allocate patents across industrial sectors using the International Patent

Classification (IPC)–industry concordance table developed by Schmoch et al. (2003).1 The

concordance table is derived from a complete enumeration of the patenting activity in

technology-based fieldsofmore than3,000 firmsthatareclassifiedby ISIC industrialsector.

Somemeasurementerrorisinevitableinsuchconcordanceprocedure,thoughweexpectthis

measurement error to be largely stable over time meaning it can be accommodated in the

econometricmodelinthesamemannerasothertimeinvariantheterogeneity.

Our patent data are unique because they provide a systematic, comprehensive and

globalview, thoughnaturally, theycapture thephenomenonof interestwithsomenoise.We

take a number of steps to increase confidence that our patent-based indicators are

representativeofR&Dactivities.Wediscusskeyaspectsnext.

Market-seekingR&Doffshoringisanticipatedtogeneratefewerbenefitstothefirms’

homecountry.Ouranalysis focuseson technology-seekingR&D,which is identifiedby those

patentswhicharefiledinthehomecountry.Wearguethatonecanusefilingbehaviortoidentify

technology- versus market-seeking R&D offshoring. Technology-seeking R&D is targeted at

developingnovel technologiesthatwillbeusedinthecompany’sglobaloperationssuchthat

therearestrongincentivestoseekprotectioninthehomecountry.Market-seekingoffshored

R&Disdirectedtowardsproducingatechnologyfor,oradaptingitto,thelocalmarket.Since

1TheIPCisahierarchicalpatentclassificationsystemusedinover100countriestoclassifythecontentofpatentsinthetechnologyareatowhichtheypertain.

9

technology generated via market-seeking R&D offshoring has relatively market-specific

usefulnessthereislimitedimpetusfortheinventingfirmtofileforpatentprotectioninthehome

country.2

By focusingonpatents thatare filed in thehome(applicant)countrywealso largely

avoidmeasurementerrorassociatedwith‘IPmigration’,whichiswheretheapplicantaddress

ischosenpurelyfortaxminimizationpurposes.Thereisnoincentiveforfirmstofileforpatent

protection in the Cayman Islands even if they allocates ownership to their Cayman Island

subsidiary for the purpose of taxminimization.3 Our sample avoidsmany of policies which

generatehighpoweredincentivestoundertakeIPmigration.Well-knowntaxhavenssuchasthe

CaymanIslandsarenotincludedinoursampleandtheperiodofanalysispre-datesthe‘patent

box’policiesimplementedintheNetherlands,Belgium,Luxembourg,andSpainafter2007.For

thecountries inoursample,aggregatepatternsofpatentassignmentarenotconsistentwith

whatwouldbepredictedbytaxminimization.Forexample,inlow-taxingIrelandmorepatents

inventedbyresidentsofIrelandareassignedtoforeignfirmsthanforeigninventedpatentsare

assigned to Irish affiliates—precisely the opposite of what tax minimizing behavior would

predict.Whileweseenostrongapriorireasontosuspectthatanymeasurementerrorarising

outofIPmigration,shoulditexist,shouldbesystematicallyrelatedtochangesinproductivityat

theindustrylevelweconsideraugmentedempiricalspecificationsinanefforttodirectlycontrol

forcorporateincometaxrateinthehomecountryaspartofourrobustnesschecking.

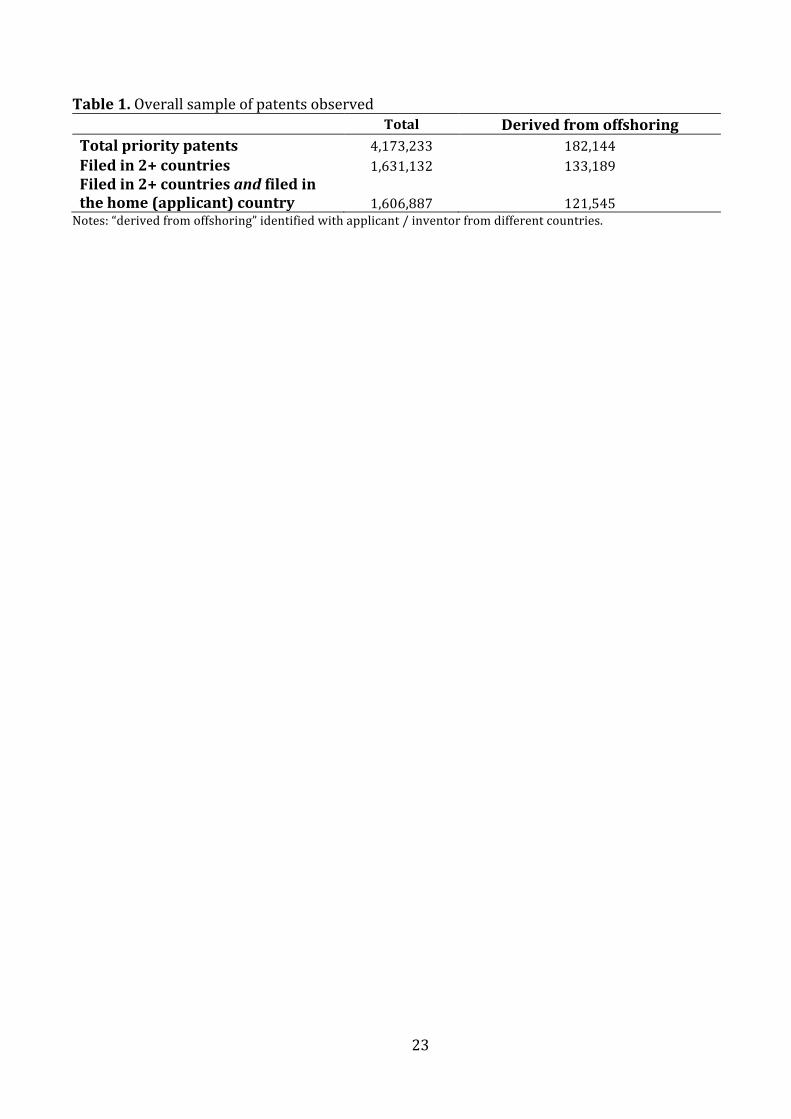

[Table1–abouthere]

2NotethatbyconstructionwefilteroutR&Dactivitiesthatareboth inventedbyandalsoassignedtoa foreignaffiliate.3Indeed,allocation/transferofownershipfortaxpurposesmainlytakestheformofintra-companytransferthatneedsnotbereportedtothepatentofficeinordertobeeffective.

10

Table1showsthattherewerefourmillionprioritypatentapplicationsfiledworldwide

intheperiodbetween1980to2007,amongwhich182thousand(4percent)aretheresultof

R&Doffshoring.Restrictingthecount topatentapplications filed inat least two jurisdictions

(thusfilteringoutalargenumberoflow-valuepatents)leadstoaworldwidecountof1.6million

patentapplications,ofwhichapproximately8percentresultfromR&Doffshoring.

We validate our measure of offshored R&D by considering the relationship between

patentsassignedtoforeignentitiesandtheinternationalflowsof financeforthepurposesof

R&D. Data on bilateral R&D flows do not exist, however total R&D financed from abroad

aggregatedacrosspartnercountriesarecollectedbynationalstatisticsagenciesbywayoffirm

level survey (effectively aggregate R&D ‘onshoring’). The measure is expected to comprise

primarilytechnologyseekingR&Dactivities.ThecriteriaforrecordingR&Dbysourceoffunds

in theFrascatimanualstipulates that “theremustbeadirect transferof resources [and] the

transfermustbebothintendedandusedfortheperformanceofR&D”(OECD2002:114).Itdoes

notincludeforeignsourcedloansorothergeneralcapitalraisingorgeneraltransfersfromthe

parent firm. It alsodoesnot includeR&DperformedbyMNEaffiliatesand financed through

retainedearnings.

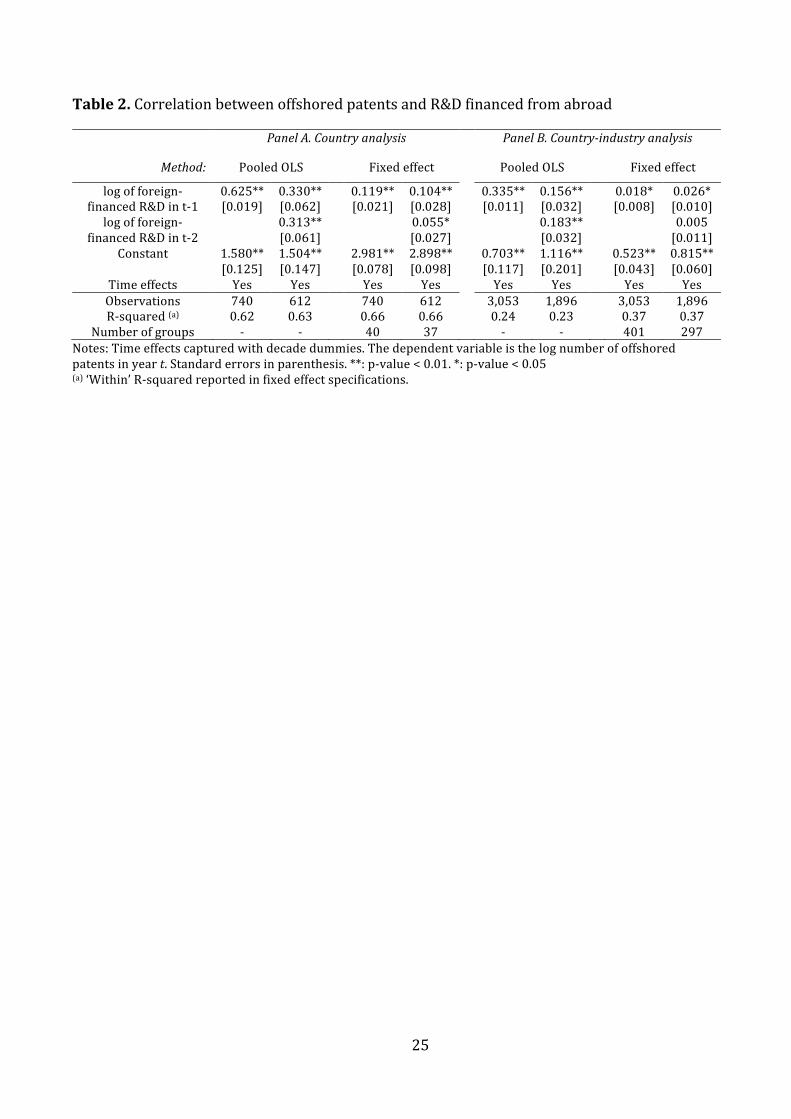

Table 2 reports a series of regression results aimed at testing this relationship. The

dependentvariableisthelaggedamountofR&Dfinancedfromabroad(inmillion2005USPPPs)

atthecountrylevelinpanelAandatthecountry-industrylevelinpanelB.Pooledcross-section

andfixedeffectestimatessuggestastrongrelationshipbetweenthepatent indicatorandthe

relevantR&Dflows,evenwhenaddingadditionallagstothespecification.Theresultsshowthat

theproductionofpatentswithforeignapplicantisstronglydeterminedbyforeignfinancedR&D.

TheyprovidefurtherconfidenceinthevalidityofourpatentbasedmeasureofoffshoredR&D.

[Table2–abouthere]

11

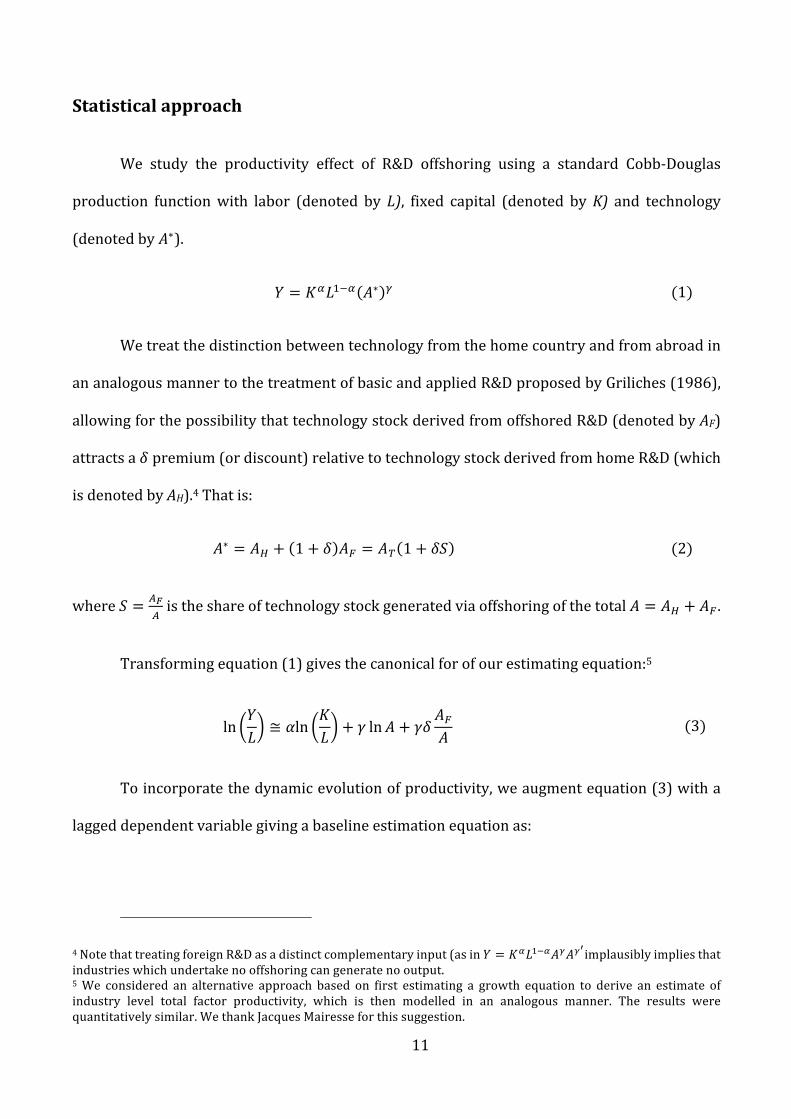

Statisticalapproach

We study the productivity effect of R&D offshoring using a standard Cobb-Douglas

production functionwith labor (denoted by L), fixed capital (denoted byK) and technology

(denotedbyD∗).

F = HIJKLI D∗ M (1)

Wetreatthedistinctionbetweentechnologyfromthehomecountryandfromabroadin

ananalogousmannertothetreatmentofbasicandappliedR&DproposedbyGriliches(1986),

allowingforthepossibilitythattechnologystockderivedfromoffshoredR&D(denotedbyAF)

attractsaPpremium(ordiscount)relativetotechnologystockderivedfromhomeR&D(which

isdenotedbyAH).4Thatis:

D∗ = DQ + 1 + P DS = DT 1 + PU (2)

whereU = VWV istheshareoftechnologystockgeneratedviaoffshoringofthetotalD = DQ + DS .

Transformingequation(1)givesthecanonicalforofourestimatingequation:5

ln FJ ≅ Yln H

J + Z lnD + ZP DSD (3)

Toincorporatethedynamicevolutionofproductivity,weaugmentequation(3)witha

laggeddependentvariablegivingabaselineestimationequationas:

4NotethattreatingforeignR&Dasadistinctcomplementaryinput(asinF = HIJKLIDMDM[implausiblyimpliesthatindustrieswhichundertakenooffshoringcangeneratenooutput.5We considered an alternative approach based on first estimating a growth equation to derive an estimate ofindustry level total factor productivity, which is then modelled in an analogous manner. The results werequantitativelysimilar.WethankJacquesMairesseforthissuggestion.

12

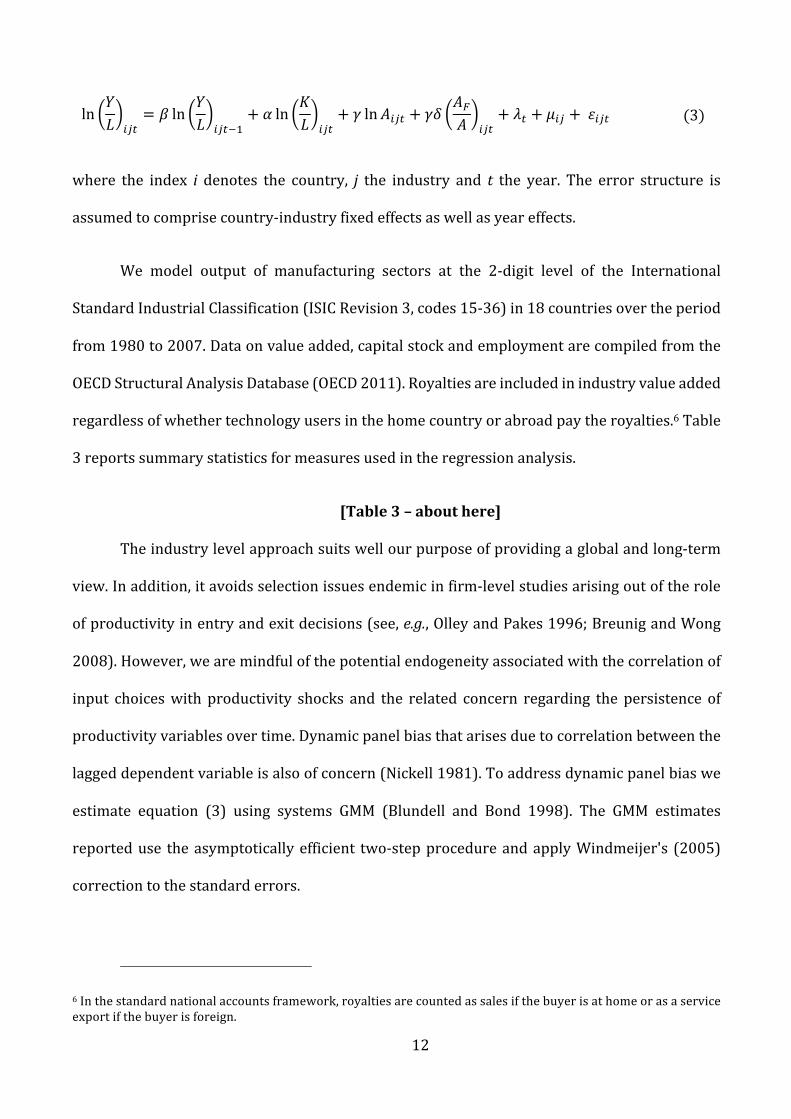

ln FJ \]^

= _ ln FJ \]^LK

+ Y ln HJ \]^

+ Z lnD\]^ + ZPDSD \]^

+ `^ + a\] +b\]^ (3)

where the index i denotes the country, j the industry and t the year. The error structure is

assumedtocomprisecountry-industryfixedeffectsaswellasyeareffects.

We model output of manufacturing sectors at the 2-digit level of the International

StandardIndustrialClassification(ISICRevision3,codes15-36)in18countriesovertheperiod

from1980to2007.Dataonvalueadded,capitalstockandemploymentarecompiledfromthe

OECDStructuralAnalysisDatabase(OECD2011).Royaltiesareincludedinindustryvalueadded

regardlessofwhethertechnologyusersinthehomecountryorabroadpaytheroyalties.6Table

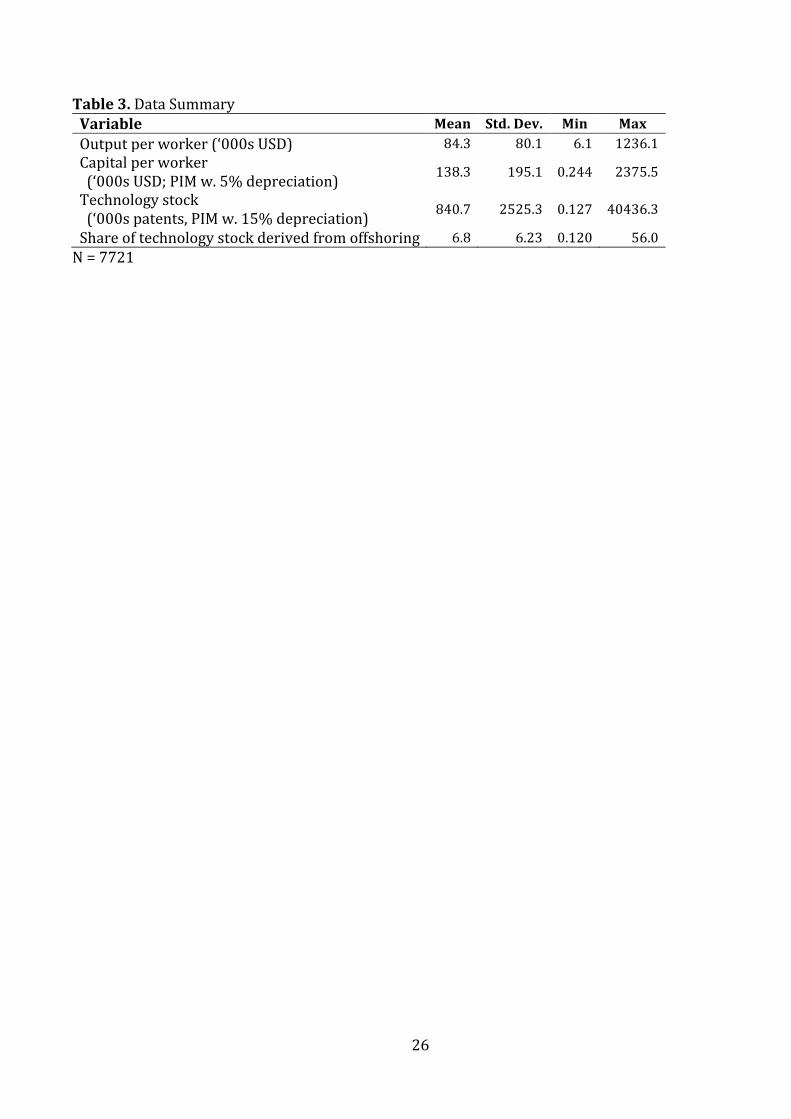

3reportssummarystatisticsformeasuresusedintheregressionanalysis.

[Table3–abouthere]

Theindustrylevelapproachsuitswellourpurposeofprovidingaglobalandlong-term

view.Inaddition,itavoidsselectionissuesendemicinfirm-levelstudiesarisingoutoftherole

ofproductivityinentryandexitdecisions(see,e.g.,OlleyandPakes1996;BreunigandWong

2008).However,wearemindfulofthepotentialendogeneityassociatedwiththecorrelationof

input choiceswith productivity shocks and the related concern regarding the persistence of

productivityvariablesovertime.Dynamicpanelbiasthatarisesduetocorrelationbetweenthe

laggeddependentvariableisalsoofconcern(Nickell1981).Toaddressdynamicpanelbiaswe

estimate equation (3) using systems GMM (Blundell and Bond 1998). The GMM estimates

reporteduse theasymptoticallyefficient two-stepprocedureandapplyWindmeijer's (2005)

correctiontothestandarderrors.

6Inthestandardnationalaccountsframework,royaltiesarecountedassalesifthebuyerisathomeorasaserviceexportifthebuyerisforeign.

13

As already discussed, accounting for potential simultaneity between productivity and

R&D offshoring is fundamental to any attribution of causality. We consider a number of

approachestoaccommodatingthisissue.First,weconsideraninstrumentalvariableapproach

usingameasureofthetaxtreatmentofR&DinthehomecountryandinpotentialoffshoreR&D

hostcountries.Wealsoconsideramoreconventionalroutetodisentanglethecausalimpacts

usingsystemsGMMbyinstrumentingoffshoredshareoftechnologystockinamanneranalogous

totheautoregressiveterm.Weelaboratetheinstrumentalvariableapproachbelow.

Theappropriatenessandvalidityoftaxpolicyasaninstrumentiswellsupported.Thea

prioricasethatforeigntaxpolicyisexogenoustodomesticproductivityissound.Itisdifficultto

imagineamechanismthroughwhichR&DspecifictaxincentivesintheUKwillaffectindustrial

productivityintheUSAexceptviatheirinfluenceonthedistributionofcompanyR&Dbetween

thetwocountries.EvidencesuggestsR&Dtaxpolicyinfluencesfirms’R&Dlocationdecisions

(Hines1993;BloomandGriffith2001;Wilson2009).Weexpecttaxpolicytoprimarilyinfluence

the intensivemargin(ratherthanextensive) fortechnology-seekingtypeR&Doffshoring;we

arguethatthemarginthatisamenabletotheinfluenceoffiscalincentivesisofgreatestinterest

to policy. Validity of the instrument also requires independencewith the outcome variable,

namelyproductivity.

Data used tomeasure R&D tax policy are adapted from Thomson (forthcoming). The

measure isbasedonthestandardadaptationof Jorgenson’s(1963) ‘usercostofcapital’ first

proposedbyMcFetridgeandWarda(1983)andsubsequentlydevelopedbyBloometal.(2002),

Wilson (2009) and others. The measure, referred to as the ‘tax-price of R&D’, reflects the

breakeven benefit-cost ratio for a representative firms’ marginal R&D investment to be

profitableaftertaxtakingintoaccountanyreductionstocorporatetaxliabilitiesassociatedwith

eachdollarinvestedinR&D.Ourcountry-industryspecificpolicymeasureincorporatescross-

14

countryvariationintaxtreatmentofdifferentR&Dexpendituretypes(e.g.,laborandcapital)as

wellasinter-industryvariationinmixofexpendituresbytype.Tomeasuretheeffectivetaxprice

of offshored R&D for each countrywe use the average tax price across potential offshoring

locations (i.e., allothercountries in thesample).Taxpolicydataareonlyavailable forOECD

memberstatessonon-OECDcountriesarenotincludedinthiscalculation.Thislimitationhas

negligibleimpactonthemeasuredweightedaverageoffshoredtaxpriceasonlyasmallfraction

ofpatentsareattributedtoinventorswhoareresidentsofcountriesforwhichwedonothave

taxpriceinformation(seealsoKumar2001;Thomson2013).

Doesoffshoringaffecthomecountryproductivity?

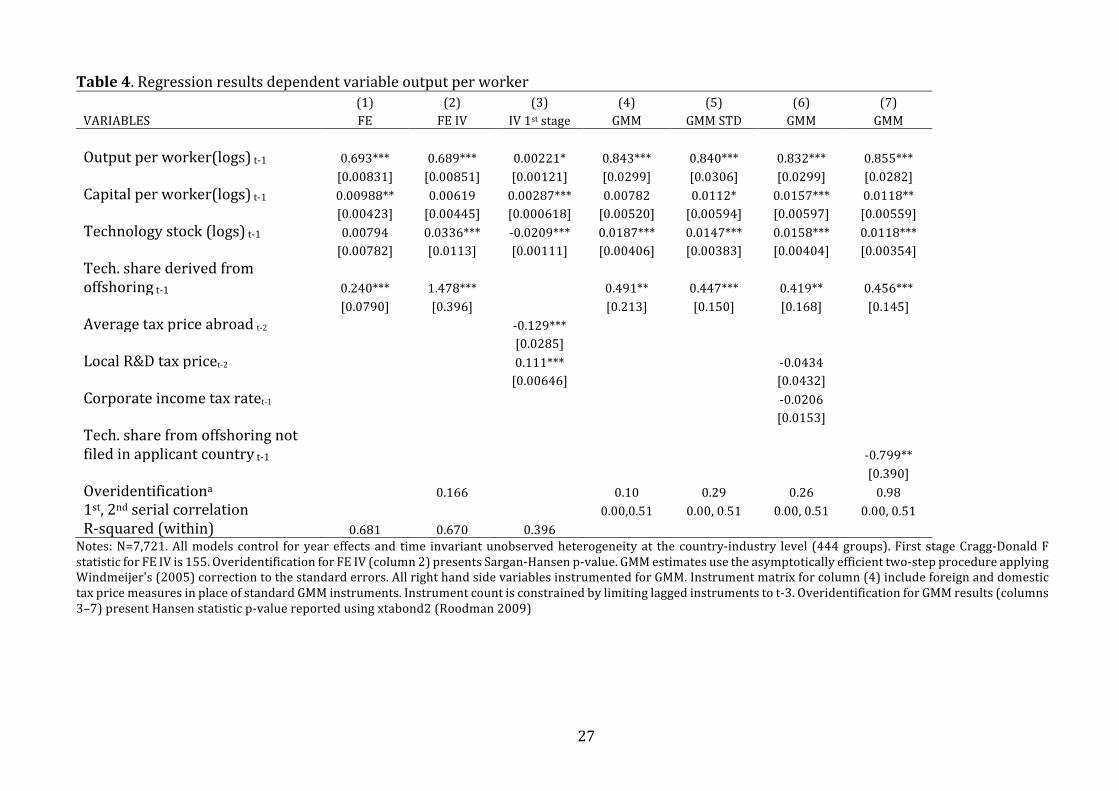

Table 4 depicts the main regression results. Column (1) presents a baseline fixed effects

estimate.Columns(2)and(3)showtheinstrumentalvariablemodel.Resultsofthefirststage

regression, which models the determinants of the share of technology stock derived from

offshoring,arepresentedincolumn(3)andareofconsiderableinterestintheirownright.These

resultsareconsistentwiththeviewthatthelocationofR&Disamenabletotheinfluenceoftax

subsidiesat themargin.The coefficientassociatedwith theaverageR&D taxpriceabroad is

negativeandsignificant,showingthatalowertaxpriceabroadiscorrelatedwithagreatershare

ofalltechnologystockbeingsourcedfromabroad.Correspondingly,domestic(homecountry)

taxpriceisfoundtobepositivelyrelatedtotheshareoftechnologysourcedfromabroad,which

impliesthatthehigherthelocaltaxpricethemoretechnologyissourcedfromoffshorelocations.

Thesecondstageresultsarepresentedincolumn(2).ADurbin-Wu-Hausmantestsupportsthe

theoretical prediction that offshoring is likely to be endogenous (p=0.001). The coefficient

associated with the offshoring share variable in the second stage equation is 1.478. These

15

estimatesmaybe affectedby the issuesofdynamicpanelbias and thepossibility that input

choice(physicalcapitalandtechnologystock)areendogenoustooutput.

Column(4)and(5)ofTable4presentGMMestimates.Bothcapitalstockperworkerand

technologystockperworkerareidentifiedviastandardsystemsGMMinstruments(differences

inthelevelequation,andlevelsinthedifferenceequation).Incolumn(5)theshareofpatent

stockgeneratedthroughoffshoringisalsoidentifiedusingthestandardsystemsGMMapproach.

Instrumentmatrixforcolumn(4)includesforeignanddomestictaxpricemeasuresinplaceof

standardGMMinstruments.Ascanbeseen, theresultsdonotvarygreatlybetween the two

identification approaches. The results suggest that as an industry increases the share of

technology generated via offshoring from the mean of around 10 percent to 20 percent,

productivitywillincreaseby4percent.TheimpliedpremiumassociatedwithoffshoredR&Dis

large,thoughreasonablycommensuratewithanticipatedadditionalcostsassociatedwithR&D

offshoringversusdomesticR&D.Ourfundamentalcontributionisfurnishingnewevidencethat

thehomecountry–notjustthefirm–canbenefitfromR&Doffshoring.

Column(6)reportsthefirstofourrobustnesscheckswherebyweaugmentthemodel

withbothcorporateincometaxrateandthelocalR&Dtaxprice.Thecoefficientsofinterestare

effectively unchanged which, we argue, provides further confidence that tax minimizing

intellectualpropertymigrationisnotundulyinfluencingourestimates.

[Table4abouthere]

WehavearguedpreviouslythatpatentsgeneratedviaoffshoredR&Dbutnotfiledinthe

homecountryarelikelytorepresentadaptive,market-seekingR&Dandarelesslikelytobenefit

thehomecountry.Empiricallytestingthispropositionismadecomplicatedbythefactthatthe

subsetofpatentsderivedfromoffshoringthatarefiledinthehomecountryarehighlycorrelated

withtotaloffshoring(correlationcoefficient0.94).Incolumn(7)wereportestimatesofamodel

that includes both the share of technology stock from technology-seeking type offshoring

16

(patents inventedabroadandalsofiled inthehomecountry)andthesharetechnologystock

from market-seeking type offshoring (patents invented abroad but not filed in the home

country). The coefficient associated with market-seeking R&D offshoring is negative and

significant.The estimate suggests thatmarket-seeking typeR&Doffshoring,which results in

patents that are not filed at home, may detract from home-base productivity. This finding

supports our conjecture that filing behavior provides a valuable indicator of whether the

technologybenefitshomecountryoperations.

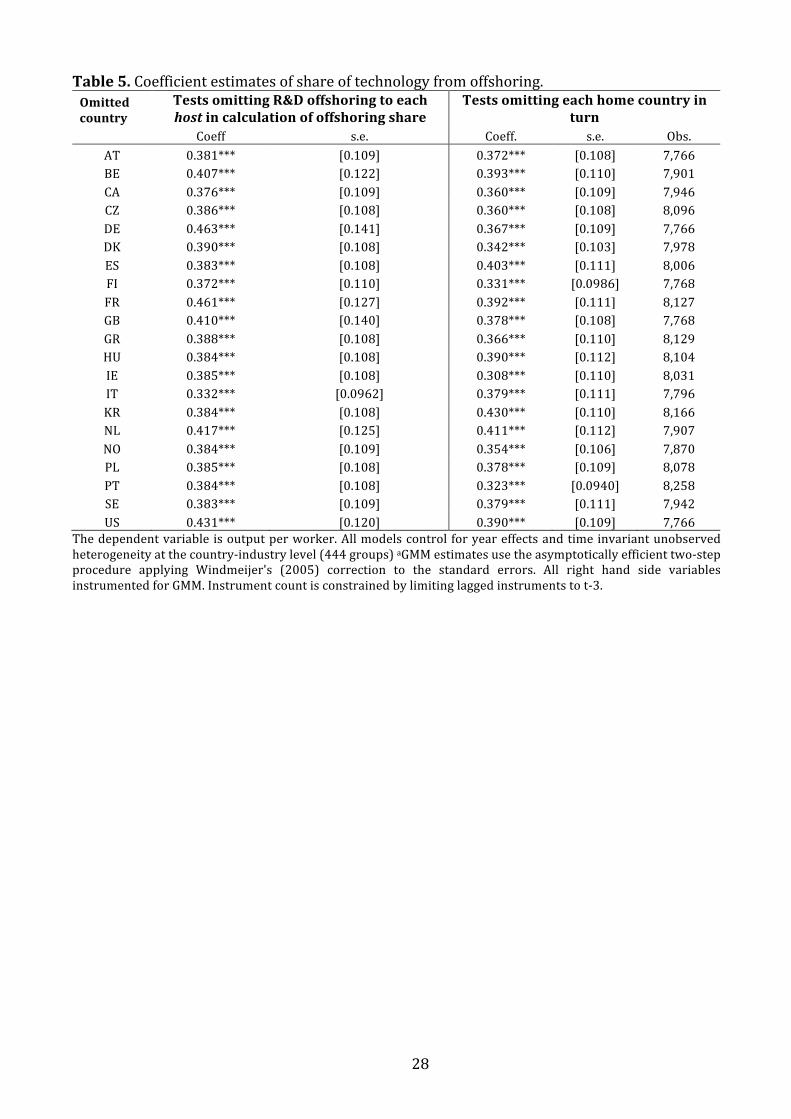

Animportantadvantageofourindustryleveldataistheexhaustiveandglobalnatureof

thesample.Itiswidelyconsideredthatfirms’benefitsfromoffshoringmaydependontheR&D

occurring ina frontiercountryorperhapsevenintheUnitedStatesspecifically.Thismaybe

cause for concern topolicymakers in theUnitedStates,which is thehomecountry to firms

engagedinthemostinR&Doffshoring.Usingourdata,weareabletotesttheextenttowhich

therelationshipbetweenoffshoringR&Dandhome-baseindustrialproductivitymaybedriven

byoffshoringtoanyspecificcountry.Toflushoutanyaboveaverageimpactofanyparticular

host country we re-estimate themodel 21 times, each time calculating a modified share of

technologystocksourcedfromoffshoringwithadifferenthostcountryomitted.Table5reports

estimatesofthecoefficientonshareoftechnologystockfromoffshoring,eachrowreflectinga

differentcountryomitted.Theseresultsshowthatnoonesinglecountryisdrivingtheestimated

parameter of interest. Put anotherway, in contrast toGriffith et al. (2006),we find nothing

‘special’aboutoffshoringtotheUnitedStates,conditionalontheoutputsoftheoffshoredR&D

beingfiledintheapplicantcountry(ourmeasureoftechnology-seekingR&Doffshoring).

[Table5abouthere]

WealsoconsideredthepossibilitythatatypicallylargebenefitsfromR&Doffshoringby

firms based in a specific home country may be driving the result. This may be the case if

17

absorptivecapacitythatiscrucialforestablishingoverallbenefitisdistributedunevenly.The

secondpanelofTable5presentsestimatesofthesamemodel,thistimesequentiallydroppinga

differenthomecountryforeachrow.Theestimatedcoefficientappearsquitestablegivingno

indicationthattheresulthingesonanyparticularcountry.Wealsoperformedsimilaranalysis

usingthefullsampleofcountriesbutdroppingoneindustryatatimeandfoundnoindication

thattheresultisovertlyinfluencedbytheoffshoringactivitiesofanysingleindustry.

Beforeofferingconcludingcommentsweconsidertheremaininglimitations.First,while

we provide a representative view of the average benefits reflecting the net impact on local

industry,includingbothprivateandspilloverbenefitsandlosses,theindustrylevelapproach

provides no new evidence on themechanism through which offshored R&D translates into

productivity improvements at home. These have been studied elsewhere and are

complementarytoourfinding(e.g.,Harhoffetal.2014).Directanalysisoftheextentofspillovers

wouldbeworthwhileandbestundertakenusingfirmleveldata.Second,weexpectthat,inpart,

ourresultreflectsahighercostofoffshoredR&D(thoughlowvaluepatentsarefilteredout).

Irrespective,ourresultsnewlyconfirmthatthehomecountry–notjustthefirm–benefitfrom

offshoringandindicatethatbenefitsarenotcontingentonthespecifichostlocations.Finally,we

arekeenlyawarethatanyinstrumentalvariableestimationisopentofundamentallyuntestable

criticismregardingtheveracityoftheassumptionofexogeneity.Wehavearguedthattheapriori

case that foreignR&D taxsubsidies isexogenous todomesticproductivity is soundand, this

appears tobeborneoutby standardoveridentification tests, notwithstanding their inherent

limitations.Weareperhapsmostreassuredbythefactthatresultappearsrobustacrosstwo

differentidentificationstrategies(IVandGMM).

18

Conclusion

ThepotentialforR&Doffshoringtoweakenthehomecountrytechnologicalcapabilitiesandthe

lossofproductivityspilloverscompromisinglong-termgrowthhasconcernedpolicymakersfor

alongtime.Wehaveinvestigatedthisconcernusingnewindustry-leveldataweemployedan

identification strategy which accommodates the potential simultaneity between industrial

performance and globalization Our results show that R&D offshoring can induce long-term

productivitybenefitsforhome-countryindustrialactorsatlarge.

WefindnoevidencethatbenefitsarerestrictedtofirmsoffshoringtotheUnitedStates—

oranyotherhostcountryinoursample.Thissupportstheviewthatfirmsthemselvesarebest

placedtochoosethelocationofR&Dwhichwillgeneratetechnologicaladvantageandequally

thatthegloballydispersedtechnologyfrontier isdifficulttocaptureusingaggregatenational

indicators.However,wefindthathomecountrybenefitshingeonthenatureofoffshoring.Our

resultsareconsistentwiththeargumentsmadebypreviousscholarsthatthebenefitsofmarket-

seekingR&Doffshoringwillprimarilyberestrictedtohostcountrymarkets.

OurresultshelptoreconciletraditionalfearsconcerningtheimpactofR&Doffshoringon

home economieswith the enduringly strong economic performance of those countriesmost

heavilyengaged in theactivity—theUnitedStatesandSwitzerlandareamong thehandfulof

OECDcountriesthatoffshoremoreR&Dthantheyhostwhichareallamongthemostproductive,

technologicallyadvancedeconomies (Thomson2013).Wehope that in this light, our results

might give pause for thought to policy makers who may otherwise be tempted to offer

inducementstocurboffshoring.

Naturally,moreresearchisneededinordertounderstandmoredetailedpatternsofthe

geographicaldistributionofbenefits,theextentofspilloverstootherfirmsinthehomecountry,

and the conditions underwhich benefitsmaybe enhanced. In this regard,wehope that the

19

methodologicalcontributionadvancedinthispapermaycontributetofutureworks.Specifically,

wehaveprovidedfirst-of-its-kindvalidationtestoftheuseofpatentdataasameasureofR&D

offshoring,makinguseoftheorigincountryofapplicantsandinventors.Moreover,theresults

suggestthatfilingpatternsprovideuseful informationaboutthegeographyofbenefitarising

frompatentedtechnologyand,morespeculatively,ameansofdistinguishingbetweenmarket-

seekingandtechnology-seekingR&Dactivities.Futurefirm-levelanalysisexploitinginformation

regardingfilingpatternscouldbeparticularlypromisinginelucidatingabetterunderstanding

aboutmultinationalenterprisetechnologystrategies.

20

References

Arvanitis,S.,&Hollenstein,H.(2011).HowdodifferentdriversofR&Dinvestmentinforeign

locationsaffectdomesticfirmperformance?AnanalysisbasedonSwisspanelmicrodata.

IndustrialandCorporateChange,20(2),605–640.

Bartlett,C.A.,&Ghoshal,S.(2000).Goingglobal:Lessonsfromlatemovers.HarvardBusiness

Review(March-April2000),132–142.

Ali-Yrkkö, J., & Rouvinen, P. (2015). Slicing up global value chains: amicro view. Journal of

Industry,CompetitionandTrade,15(1),69–85.

Bloom,N.,&Griffith,R.(2001).TheInternationalisationofUKR&D.FiscalStudies,22(3),337–

355.

Blundell,R.,&Bond,S.(1998).Initialconditionsandmomentrestrictionsindynamicpaneldata

models.JournalofEconometrics,87(1),115–143.

Breunig, R., & Wong, M. H. (2008). A richer understanding of Australia's productivity

performanceinthe1990s:Improvedestimatesbaseduponfirm-levelpaneldata.Economic

Record,84(265),157–176.

Criscuolo, P. (2009). Inter-firm reverse technology transfer: the home country effect ofR&D

internationalization.IndustrialandCorporateChange,18(5),869–899.

Cantwell,J.(1995).Theglobalisationoftechnology:whatremainsoftheproductcyclemodel?.

CambridgeJournalofEconomics,19(1),155–174.

deRassenfosse,G.,Dernis,H.,Guellec,D.,Picci,L.,&vanPottelsberghedelaPotterie,B.(2013).

Theworldwidecountofprioritypatents:Anew indicatorof inventiveactivity.Research

Policy,42(3),720–737.

Dunning, J.H. (1994).Multinational enterprisesand theglobalizationof innovatory capacity.

ResearchPolicy,23(1),67–88.

EuropeanCommission(2012).InternationalisationofbusinessinvestmentsinR&Dandanalysis

oftheireconomicimpact.EuropeanCommissiondocumentNo.EUR25195EN.

Griffith,R.,Harrison,R.,&VanReenen,J.(2006).Howspecialisthespecialrelationship?Using

the impactofUSR&DspilloversonUK firmsasa testof technologysourcing.American

EconomicReview,96(5),1859–1875.

Griliches, Z., 1979. Issues in assessing the contribution of research and development to

productivitygrowth.Thebelljournalofeconomics,pp.92-116.

21

Griliches, Z. (1986). Productivity, R&D, and basic research at the firm level in the 1970’s.

AmericanEconomicReview,76(1),141–154.

Guellec,D.,&vanPottelsberghedelaPotterie,B.(2001).Theinternationalisationoftechnology

analysedwithpatentdata.ResearchPolicy,30(8),1253–1266.

Harhoff,D.,Mueller,E.,&VanReenen,J.(2014).Whatarethechannelsfortechnologysourcing?

PaneldataevidencefromGermancompanies.JournalofEconomics&ManagementStrategy,

23(1),204–224.

Harhoff,D.,Scherer,F.M.,&Vopel,K.(2003).Citations,familysize,oppositionandthevalueof

patentrights.ResearchPolicy,32(8),1343–1363.

Hines, J. (1993). On the sensitivity of R&D to delicate tax changes: The behavior of U.S.

multinationals in the 1980s. In: A. Giovannini, R. Glenn Hubbard, and J Slemrod (eds),

StudiesinInternationalTaxation.Chicago:UniversityofChicagoPress.

Jaffe, A. B., Trajtenberg, M., & Henderson, R. (1993). Geographic localization of knowledge

spilloversasevidencedbypatentcitations.Quarterly JournalofEconomics,108(3),577–

598.

Kumar, N. (2001). Determinants of location of overseas R&D activity of multinational

enterprises:thecaseofUSandJapanesecorporations.ResearchPolicy,30(1),159–174.

Lall,S. (1979).The InternationalAllocationofResearchActivitybyUSMultinationals.Oxford

BulletinofEconomicsandStatistics,41(4),313–331.

LeBas,C.,&Sierra,C.(2002).‘Locationversushomecountryadvantages’inR&Dactivities:some

furtherresultsonmultinationals’locationalstrategies.Researchpolicy,31(4),589–609.

McFetridge,D.G.andJ.P.Warda(1983).CanadianR&DIncentives:TheirAdequacyandImpact,

CanadianTaxPaperNo.70.Toronto,CanadianTaxFoundation.

Mansfield,E.,Teece,D.,&Romeo,A.(1979).OverseasresearchanddevelopmentbyUS-based

firms.Economica,46(182),187–196.

Nickell,S.(1981).Biasesindynamicmodelswithfixedeffects.Econometrica,49(6),1417–1426.

NSF2010(http://www.nsf.gov/statistics/infbrief/nsf10322/)

OECD(2002).FrascatiManual2002–ProposedStandardPracticeforSurveysonResearchand

ExperimentalDevelopment.OECD:Paris,256pages.ISBN:9789264199033.

OECD(2009),Patentstatisticsmanual,Paris

OECD(2011),STANindicators,STAN:OECDStructuralAnalysisStatistics(database).

Olley, G. S., and A. Pakes. 1996. The dynamics of productivity in the telecommunicationsequipmentindustry.Econometrica64:1263–1297.

22

Patel, P., Pavitt, K., 1988. The international distribution and determinants of technological

activities.OxfordReviewofEconomicPolicy4,35–55.

Patel,P.,&Vega,M.(1999).Patternsofinternationalisationofcorporatetechnology:locationvs.

homecountryadvantages.ResearchPolicy,28(2),145–155.

Picci,L.(2010).Theinternationalizationofinventiveactivity:Agravitymodelusingpatentdata.

ResearchPolicy,39(8),1070–1081.

Porter,M.E.(1990),TheCompetitiveAdvantageofNations.NewYork,MacmillanInc.

Roodman,D. (2009).Howtodoxtabond2:An introduction todifferenceandsystemGMMin

Stata.StataJournal,9(1),86–136.

Schmoch,U.,Laville,F.,Patel,P.,&Frietsch,R.(2003).Linkingtechnologyareastoindustrial

sectors.FinalreporttotheEuropeanCommission-DGResearch.

Song, J., & Shin, J. (2008). The paradox of technological capabilities: a study of knowledge

sourcingfromhostcountriesofoverseasR&Doperations.JournalofInternationalBusiness

Studies,39(2),291–303.

Song,J.,Azakawa,K.,Chu,Y.,2011.Whatdeterminesknowledgesourcingfromhostlocationsof

overseas R&D operations? A study of global R&D activities of Japanese multinationals.

ResearchPolicy40,380–390.

Thomson,R.(2013).NationalscientificcapacityandR&Doffshoring.ResearchPolicy,42(2),517–

528.

Thomson, R., (forthcoming) The Effectiveness of R&D tax credits, Review of Economics and

Statistics,PostedOnlineNovember16,2015.

Vernon, R. (1966). International investment and international trade in the product cycle.

QuarterlyJournalofEconomics,80(2),190–207.

Wilson,D.J.(2009).Beggarthyneighbor?Thein-state,out-of-state,andaggregateeffectsofR&D

taxcredits.ReviewofEconomicsandStatistics,91(2),431–436.

Windmeijer,F.(2005).A finitesamplecorrectionforthevarianceof linearefficienttwo-stepGMMestimators.JournalofEconometrics,126(1),25–51.

23

Table1.Overallsampleofpatentsobserved Total DerivedfromoffshoringTotalprioritypatents 4,173,233 182,144Filedin2+countries 1,631,132 133,189Filedin2+countriesandfiledinthehome(applicant)country 1,606,887 121,545Notes:“derivedfromoffshoring”identifiedwithapplicant/inventorfromdifferentcountries.

24

Figure1.Percentofpatentsderivedfromoffshoring

Notes:filedinapplicantcountryandfamilysizegreaterthanone.

25

Table2.CorrelationbetweenoffshoredpatentsandR&Dfinancedfromabroad

PanelA.Countryanalysis PanelB.Country-industryanalysis

Method: PooledOLS Fixedeffect PooledOLS Fixedeffect

logofforeign-financedR&Dint-1

0.625**[0.019]

0.330**[0.062]

0.119**[0.021]

0.104**[0.028]

0.335**[0.011]

0.156**[0.032]

0.018*[0.008]

0.026*[0.010]

logofforeign-financedR&Dint-2

0.313**[0.061]

0.055*[0.027]

0.183**[0.032]

0.005[0.011]

Constant 1.580** 1.504** 2.981** 2.898** 0.703** 1.116** 0.523** 0.815** [0.125] [0.147] [0.078] [0.098] [0.117] [0.201] [0.043] [0.060]

Timeeffects Yes Yes Yes Yes Yes Yes Yes YesObservations 740 612 740 612 3,053 1,896 3,053 1,896R-squared(a) 0.62 0.63 0.66 0.66 0.24 0.23 0.37 0.37

Numberofgroups - - 40 37 - - 401 297Notes:Timeeffectscapturedwithdecadedummies.Thedependentvariableisthelognumberofoffshoredpatentsinyeart.Standarderrorsinparenthesis.**:p-value<0.01.*:p-value<0.05(a)‘Within’R-squaredreportedinfixedeffectspecifications.

26

Table3.DataSummaryVariable Mean Std.Dev. Min MaxOutputperworker(‘000sUSD) 84.3 80.1 6.1 1236.1Capitalperworker(‘000sUSD;PIMw.5%depreciation)

138.3 195.1 0.244 2375.5

Technologystock(‘000spatents,PIMw.15%depreciation)

840.7 2525.3 0.127 40436.3

Shareoftechnologystockderivedfromoffshoring 6.8 6.23 0.120 56.0

N=7721

27

Table4.Regressionresultsdependentvariableoutputperworker (1) (2) (3) (4) (5) (6) (7)VARIABLES FE FEIV IV1ststage GMM GMMSTD GMM GMM Outputperworker(logs)t-1 0.693*** 0.689*** 0.00221* 0.843*** 0.840*** 0.832*** 0.855*** [0.00831] [0.00851] [0.00121] [0.0299] [0.0306] [0.0299] [0.0282]Capitalperworker(logs)t-1 0.00988** 0.00619 0.00287*** 0.00782 0.0112* 0.0157*** 0.0118** [0.00423] [0.00445] [0.000618] [0.00520] [0.00594] [0.00597] [0.00559]Technologystock(logs)t-1 0.00794 0.0336*** -0.0209*** 0.0187*** 0.0147*** 0.0158*** 0.0118*** [0.00782] [0.0113] [0.00111] [0.00406] [0.00383] [0.00404] [0.00354]Tech.sharederivedfromoffshoringt-1 0.240*** 1.478*** 0.491** 0.447*** 0.419** 0.456*** [0.0790] [0.396] [0.213] [0.150] [0.168] [0.145]Averagetaxpriceabroadt-2 -0.129*** [0.0285] LocalR&Dtaxpricet-2 0.111*** -0.0434 [0.00646] [0.0432] Corporateincometaxratet-1 -0.0206 [0.0153] Tech.sharefromoffshoringnotfiledinapplicantcountryt-1 -0.799**

[0.390]Overidentificationa 0.166 0.10 0.29 0.26 0.981st,2ndserialcorrelation 0.00,0.51 0.00,0.51 0.00,0.51 0.00,0.51R-squared(within) 0.681 0.670 0.396 Notes:N=7,721.Allmodelscontrol foryeareffectsandtime invariantunobservedheterogeneityat thecountry-industry level (444groups).FirststageCragg-DonaldFstatisticforFEIVis155.OveridentificationforFEIV(column2)presentsSargan-Hansenp-value.GMMestimatesusetheasymptoticallyefficienttwo-stepprocedureapplyingWindmeijer's(2005)correctiontothestandarderrors.AllrighthandsidevariablesinstrumentedforGMM.Instrumentmatrixforcolumn(4)includeforeignanddomestictaxpricemeasuresinplaceofstandardGMMinstruments.Instrumentcountisconstrainedbylimitinglaggedinstrumentstot-3.OveridentificationforGMMresults(columns3–7)presentHansenstatisticp-valuereportedusingxtabond2(Roodman2009)

28

Table5.Coefficientestimatesofshareoftechnologyfromoffshoring.Omittedcountry

TestsomittingR&Doffshoringtoeachhostincalculationofoffshoringshare

Testsomittingeachhomecountryinturn

Coeff s.e. Coeff. s.e. Obs.AT 0.381*** [0.109] 0.372*** [0.108] 7,766BE 0.407*** [0.122] 0.393*** [0.110] 7,901CA 0.376*** [0.109] 0.360*** [0.109] 7,946CZ 0.386*** [0.108] 0.360*** [0.108] 8,096DE 0.463*** [0.141] 0.367*** [0.109] 7,766DK 0.390*** [0.108] 0.342*** [0.103] 7,978ES 0.383*** [0.108] 0.403*** [0.111] 8,006FI 0.372*** [0.110] 0.331*** [0.0986] 7,768FR 0.461*** [0.127] 0.392*** [0.111] 8,127GB 0.410*** [0.140] 0.378*** [0.108] 7,768GR 0.388*** [0.108] 0.366*** [0.110] 8,129HU 0.384*** [0.108] 0.390*** [0.112] 8,104IE 0.385*** [0.108] 0.308*** [0.110] 8,031IT 0.332*** [0.0962] 0.379*** [0.111] 7,796KR 0.384*** [0.108] 0.430*** [0.110] 8,166NL 0.417*** [0.125] 0.411*** [0.112] 7,907NO 0.384*** [0.109] 0.354*** [0.106] 7,870PL 0.385*** [0.108] 0.378*** [0.109] 8,078PT 0.384*** [0.108] 0.323*** [0.0940] 8,258SE 0.383*** [0.109] 0.379*** [0.111] 7,942US 0.431*** [0.120] 0.390*** [0.109] 7,766

Thedependentvariableisoutputperworker.Allmodelscontrol foryeareffectsandtimeinvariantunobservedheterogeneityatthecountry-industrylevel(444groups)aGMMestimatesusetheasymptoticallyefficienttwo-stepprocedure applying Windmeijer's (2005) correction to the standard errors. All right hand side variablesinstrumentedforGMM.Instrumentcountisconstrainedbylimitinglaggedinstrumentstot-3.