Embed Size (px)

Citation preview

WORKING PAPER MAY 2009

ISLAMIC FINANCE AND SRI:

ANY CROSSOVER?

© Novethic 2009. Islamic finance and SRI: any crossover? 2

Contents

Overview ........................................................................ 3

I. From Christian finance to SRI ......................................... 4

Sector-based exclusion........................................................................................ 4

Active ownership ................................................................................................ 5

Other SRI approaches ......................................................................................... 5

II. Islamic finance in practice ............................................. 7

Facts and figures ................................................................................................ 7

Markets ............................................................................................................. 7

Regulatory evolutions.......................................................................................... 9

Other initiatives.................................................................................................. 9

III. Principles of Islamic finance.........................................11

Motivations behind Islamic finance.......................................................................11

Islamic finance: ethical.......................................................................................11

… moral…..........................................................................................................12

… and financial! .................................................................................................12

IV. Crossover with SRI.....................................................14

Purpose and moral principles...............................................................................14

Sector-based exclusion.......................................................................................15

Norm-based exclusion and Global Compact ...........................................................15

Profit-sharing approach ......................................................................................17

In practice ........................................................................................................17

Conclusion: Compatibility and complementarity ...................19

Appendix: Main financial mechanisms ................................21

© Novethic 2009

Total or partial reproduction is prohibited without the prior consent of Novethic.

Using or citing information is allowed, provided that the source is indicated.

© Novethic 2009. Islamic finance and SRI: any crossover? 3

Overview

Since the onset of the financial crisis, a small number of investment strategies have

emerged, boasting growth amidst the current financial storm and resilience to the near-

collapse of other investment categories. Two of these strategies include Socially

Responsible Investment (SRI) and Islamic finance. These two investment approaches

remain relatively unexplored but have at least two similarities: they both apply extra-

financial criteria and have sparked interest as development opportunities on the London

and Paris financial markets. Although SRI as it is applied in France today has grown into

a strategy in its own right, it stems from a desire to transcribe the religious beliefs of

both individual and institutional investors into financial practices, like Islamic finance.

Novethic’s SRI research centre examined the crossover between these two investment

universes and assessed the following issues:

■ How do these investment strategies play off each other?

■ Can the religious precepts of Islamic finance compare with those that founded

ethical finance in predominantly Protestant and/or Catholic countries?

■ If so, could the extension of Islamic finance throughout the Muslim world suggest

any potential for the subsequent development of SRI as we know it in France

today?

This working paper points towards possible answers by first outlining the basic religious

beliefs of SRI and Islamic finance and then analysing any potential compatibility between

their processes and reviewing the new financial products on the market, the first to

combine the two strategies.

Islamic finance stems from the principles of the Sharia – Islamic law – which provides

guidelines for Muslims in terms of their relationship with money. It applies ethical and

extra-financial criteria that represent potential crossover with SRI. We must first examine

the foundations of Islamic finance and how it works, without succumbing to the

stereotypes and prejudices that often prevail in non-Islamic countries. In terms of the

extra-financial aspects of Islamic finance, it bears similarity to SRI in its socially

responsible purpose and the exclusion of businesses deemed unethical. Islamic finance

is, however, an entire financial system in its own right. The very recent emergence of a

special offer from Swiss SRI specialists brings some insight as to how these two

approaches can be combined. However, it is much too early to determine whether

Environment, Social and Governance (ESG) criteria can be extended to Islamic investors.

I. FROM CHRISTIAN FINANCE TO SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 4

I. From Christian finance to SRI

It is widely accepted that the current SRI movement derives from investment approaches

based on Christian beliefs, be they Catholic or Protestant1. Religious groups naturally

wanted to make investments that were consistent with their principles. Sector-

based exclusions and active ownership predominated early on in SRI strategy.

Christian groups also founded other SRI approaches, even if other larger institutional

investors, in terms of assets under management, have since taken over.

Sector-based exclusions

In 1760, John Wesley, founder of the Methodist Church, was a firm believer in the ties

between ethics and the use of money. He argued that investors should not act as owners

but as stewards or custodians of property and should not create wealth while harming

one’s neighbour. He was therefore one of the first opponents to slavery, following the

example of the Quakers, the members of the Religious Society of Friends. As early as

the late 19th century, the Quakers aligned extra-financial considerations with their

investment choices by applying a sector-based exclusion strategy in line with their

religious convictions.

In the United States

The Pioneer Fund, the first socially responsible fund, was launched in 1928 by the U.S.

Federal Council of Churches. Its investment policy excluded businesses involved in

alcohol, tobacco and pornography, sectors still on the blacklist of so-called ethical SRI

funds.

Investment in the fund was, however, restricted. It was not until 1971 that the first

ethical mutual fund, the Pax World Fund, was publicly available to individual investors. In

addition to the exclusion of traditional sin stocks such as tobacco and gambling, the basis

for this fund was to protest investments in companies that could profit from the Vietnam

War, hence the name, pax, meaning peace in Latin.

In Europe

The first ethical investment vehicle in Europe was launched by the Swedish Temperance

Society, as a fund called Ansvar. Like the Pioneer Fund, investment in the fund was

restricted to advocates of the movement.

In the United Kingdom, the Anglican Church began practicing ethical exclusions as part of

its investment rules in 1948, when the Church Commissioners were formed. A similar

body was initiated by the Methodist Church in 1960.

1 Sources for this section: Presentation by Russel Sparkes at the TBLI Conference (2000); “Extra-financial

analysis and ratings agencies: Which services for which investors?” by Émilie Alberola and Stéphanie Giamporcaro-Saunière; “Sustainable and Responsible Investing in the United States” by Steven J. Schueth.

I. FROM CHRISTIAN FINANCE TO SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 5

In France, the first two ethical funds were aimed at Christian investors. In 1983, the

investment firm Meeschaert and the not-for-profit organisation Éthique et Investissement

(Ethics and Investment), founded by a group of nuns who were the general treasurers of

their congregation, launched the fund Nouvelle Stratégie 50, which excluded the tobacco,

weapons, alcohol, pornography and gambling sectors. Geared towards a Christian client

base, the investment firm applies these exclusion criteria to its other SRI funds. The

second historic fund is Hymnos, launched by Crédit Lyonnais in 1989 to meet the specific

requirements of religious congregations. An ethical committee comprising of twenty

religious and non-religious figures meet on a quarterly basis to review the ethical criteria

to be applied in the sector-based assessment of companies and to ensure that securities

are screened against these criteria. Selected companies must be involved in businesses

that comply with Christian and humanist ethics.

Active ownership

The first SRI resolutions were filed in the late 1960s in the United States by church

groups and student organisations opposed to the war in Vietnam. Another notorious topic

was apartheid in South Africa. The US Episcopal Church filed a resolution at General

Motors’ annual general assembly in 1971. All of these initiatives led to the creation, two

years later, of the Interfaith Center on Corporate Responsibility (ICCR), now comprised of

275 Protestant, Catholic and Jewish institutions holding over USD 120 billion. The ICCR

has since spearheaded shareholder activism on social issues in the United States.

Religious activists in the United Kingdom also participated in the campaign against

apartheid from 1970 to 1984, notably challenging Barclays bank and oil giant Royal

Dutch/Shell. Their endeavours to convince institutional investors to divest from these

companies led to Barclays’ partial withdrawal from South Africa in 1985. Furthermore,

the development of this campaign on both sides of the Atlantic resulted in the departure

of over two-thirds of US companies active in South Africa.

Other SRI approaches

The role played by religious investors in the advancement of ethical investment, including

sector-based exclusions and shareholder activism, is clear, but their contribution to the

emergence of other SRI approaches is sometimes overlooked. EIRIS, the leading

provider of extra-financial research on issuers in the UK, was initiated on the impetus of

the Quakers and the Methodist Church in 1983. At the time, few funds were inclined to

use its reviews, but the religious sponsors of EIRIS successfully gambled on the principle

that demand would follow supply.

These Christian investors were pioneers in socially responsible investment, adopting new

practices to lay the foundations for the SRI movement: divestment from companies

involved in sectors or practices deemed irresponsible, initiation of dialogue with

companies and the exercise of voting rights and, more recently, investments in

companies with sound social and environmental practices.

Today, the SRI assets owned by churches and religious groups are marginal compared

with institutional investors such as insurance companies, welfare organisations or

pension funds, which do not particularly share the same convictions regarding extra-

I. FROM CHRISTIAN FINANCE TO SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 6

financial criteria, especially in France. Ironically, the development of SRI in the past ten

years by most asset management firms in France has led to a degree of aversion to

ethical investment approaches. This is due to two factors: the financial management

problems arising from the exclusion of certain securities or sectors and the difficulty in

identifying ethical standards shared by investors who are not united by a single religious

conviction. Much stronger significant emphasis has been placed on sustainable

development focused on Environmental, Social and Governance issues.

Nevertheless, some investors, particularly in Northern Europe, and NGOs such as

Amnesty have managed to establish the standardised exclusion of at least one ethical

issue: the opposition to controversial weapons (anti-personal mines and cluster bombs).

The Christian origins of SRI help understand how religious beliefs were incorporated into

finance. Islamic finance is a more formal, defined system, but before looking into how it

compares with SRI, we must first understand it.

II. ISLAMIC FINANCE IN PRACTICE

© Novethic 2009. Islamic finance and SRI: any crossover? 7

II. Islamic finance in practice

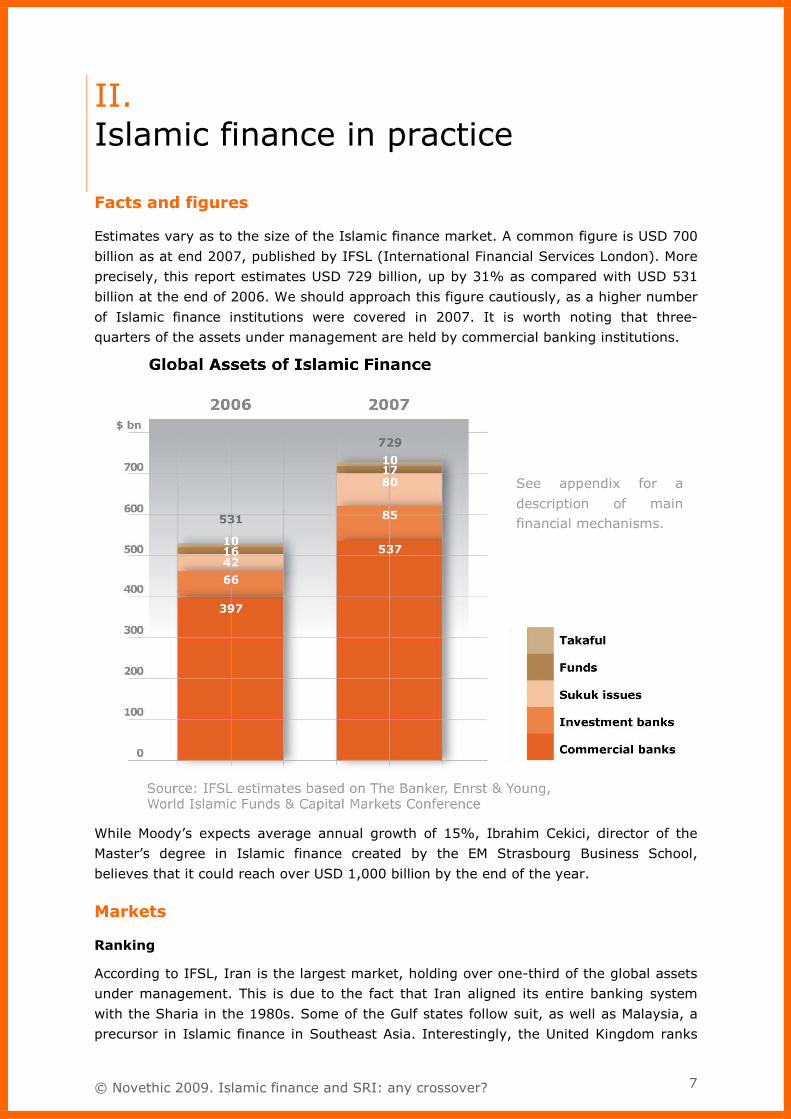

Facts and figures

Estimates vary as to the size of the Islamic finance market. A common figure is USD 700

billion as at end 2007, published by IFSL (International Financial Services London). More

precisely, this report estimates USD 729 billion, up by 31% as compared with USD 531

billion at the end of 2006. We should approach this figure cautiously, as a higher number

of Islamic finance institutions were covered in 2007. It is worth noting that three-

quarters of the assets under management are held by commercial banking institutions.

While Moody’s expects average annual growth of 15%, Ibrahim Cekici, director of the

Master’s degree in Islamic finance created by the EM Strasbourg Business School,

believes that it could reach over USD 1,000 billion by the end of the year.

Markets

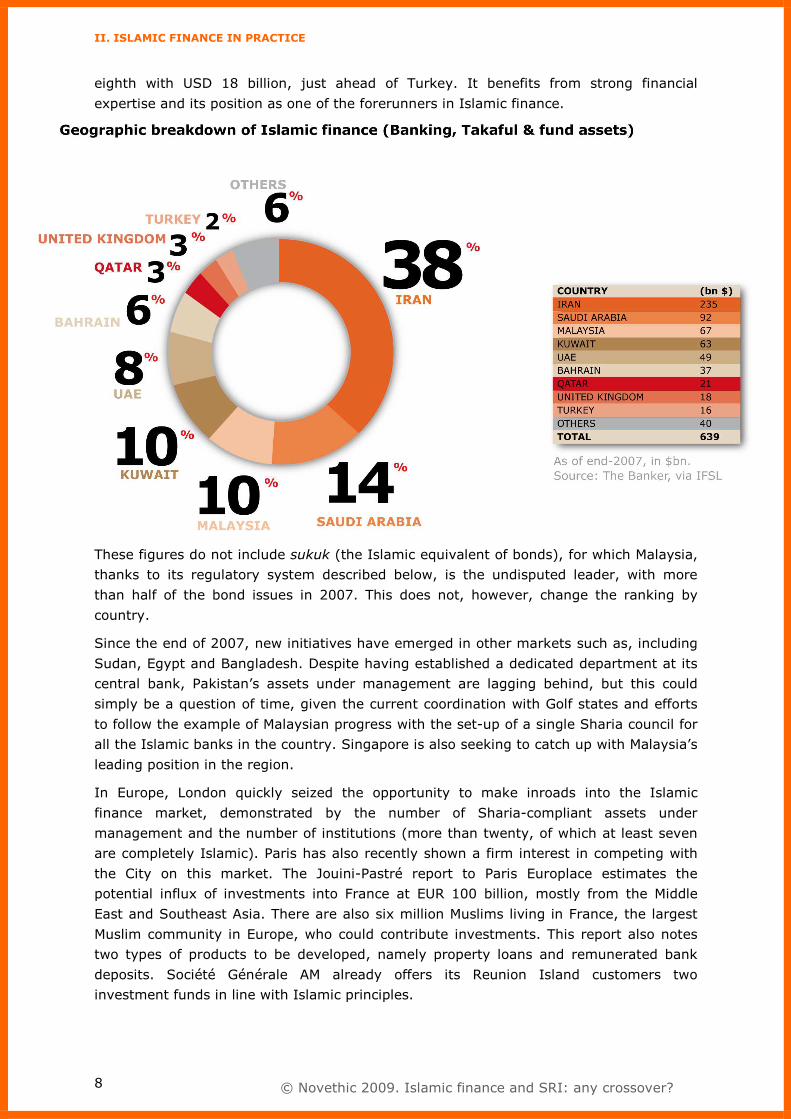

Ranking

According to IFSL, Iran is the largest market, holding over one-third of the global assets

under management. This is due to the fact that Iran aligned its entire banking system

with the Sharia in the 1980s. Some of the Gulf states follow suit, as well as Malaysia, a

precursor in Islamic finance in Southeast Asia. Interestingly, the United Kingdom ranks

See appendix for a

description of main financial mechanisms.

II. ISLAMIC FINANCE IN PRACTICE

© Novethic 2009. Islamic finance and SRI: any crossover? 8

eighth with USD 18 billion, just ahead of Turkey. It benefits from strong financial

expertise and its position as one of the forerunners in Islamic finance.

These figures do not include sukuk (the Islamic equivalent of bonds), for which Malaysia,

thanks to its regulatory system described below, is the undisputed leader, with more

than half of the bond issues in 2007. This does not, however, change the ranking by

country.

Since the end of 2007, new initiatives have emerged in other markets such as, including

Sudan, Egypt and Bangladesh. Despite having established a dedicated department at its

central bank, Pakistan’s assets under management are lagging behind, but this could

simply be a question of time, given the current coordination with Golf states and efforts

to follow the example of Malaysian progress with the set-up of a single Sharia council for

all the Islamic banks in the country. Singapore is also seeking to catch up with Malaysia’s

leading position in the region.

In Europe, London quickly seized the opportunity to make inroads into the Islamic

finance market, demonstrated by the number of Sharia-compliant assets under

management and the number of institutions (more than twenty, of which at least seven

are completely Islamic). Paris has also recently shown a firm interest in competing with

the City on this market. The Jouini-Pastré report to Paris Europlace estimates the

potential influx of investments into France at EUR 100 billion, mostly from the Middle

East and Southeast Asia. There are also six million Muslims living in France, the largest

Muslim community in Europe, who could contribute investments. This report also notes

two types of products to be developed, namely property loans and remunerated bank

deposits. Société Générale AM already offers its Reunion Island customers two

investment funds in line with Islamic principles.

II. ISLAMIC FINANCE IN PRACTICE

© Novethic 2009. Islamic finance and SRI: any crossover? 9

Regulatory evolutions

Necessary adjustments…

Due to its special and sometimes complex financial mechanisms (see appendix), Islamic

finance is less tax-friendly than traditional finance for similar types of investment

strategies under existing tax legislation. We will look at the example of purchasing a

residence: traditionally, the buyer takes out a loan at the bank, buys a residence from

the seller and then repays the loan. There is only one transaction, which is taxed only

once. However, to avoid the interest generated by the loan, an Islamic bank offers the

murabaha system, whereby the bank buys the residence and sells it piece by piece to the

buyer. This involves several transactions which are therefore taxed several times.

Another example is the tax benefits on interest earned on investments, which do not

apply to Islamic financial products since they do not generate fixed interest.

The expansion of Islamic finance has undergone and is undergoing regulatory

adjustments to allow for fair competition between traditional and Islamic financial

products and services.

… often made with some degree of opportunism

In 2003, the United Kingdom launched a series of legislative amendments introduced by

Gordon Brown, then Chancellor of the Exchequer. His current office at 10 Downing Street

offers reassurance to advocates of Islamic finance in London. However, France boasts a

number of strong arguments to challenge London as European leader in Islamic finance,

notably access to the Euro zone. This point was made in the Jouini-Pastré report

published in December 2008 by Paris-Europlace, which offers “ten proposals for collecting

EUR 100 billion”. Some of these proposals are of a legal nature, in particular concerning

double taxation on the non-speculative buy-sell transactions as mentioned above. On 18

December 2008, tax laws were adopted on the initiative of Europlace and Christine

Lagarde, Minister of Economic Affairs who clearly announced her intention to lighten the

regulatory and tax frameworks of Islamic finance, as is the case in London and other

markets.

Malaysia went a step further, positioning itself as the Islamic finance hub in Southeast

Asia. In 2006, tax incentives were put in place, such as tax exemptions through to 2016

for Islamic banks and funds. The result is clear: nearly 20% of bank assets are Sharia-

compliant, and the country is by far the largest issuer of sukuk.

Other initiatives

Due to the development of Islamic finance in Muslim countries as well as in the United

Kingdom and the United States Islamic banks have been created as independent entities

or as subsidiaries of major bank groups. Namely, HSBC Amanah, holding 87% of Sharia-

compliant bank assets in the United Kingdom, in addition to Deutsche Bank, UBS and

Citigroup. Regional and international institutions, such as the Islamic Development Bank,

established to act as a world bank for Muslim countries, and organisations such as the

International Association of Islamic Banks, attest to the globalisation of this approach. In

France, the financial authorities have expressed their decision to embrace Islamic

finance, resulting in a number of new Islamic banking prospects: Qatar Islamic Bank has

already announced its plans to open a French branch by 2010. BNP Paribas is already

II. ISLAMIC FINANCE IN PRACTICE

© Novethic 2009. Islamic finance and SRI: any crossover? 10

experimenting with a Sharia-compliant ETF, and Société Générale AM with Islamic

investment services on Reunion Island.

This development has given rise to a number of educational programmes on the subject.

A number of Master’s degrees are now available in France, notably at the EM Strasbourg

Business School. The United Kingdom has excelled in this area, even well ahead of

countries such as Malaysia or the United Arab Emirates, with programmes in 55 schools

out of a total of 205 in the world, according to the Research Intelligence Unit.

Furthermore, Islamic finance conferences and seminars are springing up throughout

France, due to the high media coverage of the subject and the current regulatory

changes.

III. PRINCIPLES OF ISLAMIC FINANCE

© Novethic 2009. Islamic finance and SRI: any crossover? 11

III. Principles of Islamic finance

Motivations behind Islamic finance

The Sharia, or Islamic law, is based on the writings of the Qur’an and sayings of the

Prophet, and acts as a framework for different aspects of day-to-day life for Muslims. In

particular, it lays down five major principles for dealing with money:

■ Prohibition of usury (riba)

■ Profit and loss sharing between the lender and the borrower

■ Prohibition of hazard or uncertainty (gharar), notably speculation

■ The existence of an underlying asset, i.e. the obligation to back all investments

with real assets

■ Prohibition of forbidden assets (haraam), determined as such by business sector

and the company’s financial position.

Another principle is one of the five pillars of Islam, almsgiving (zakat), which consists in

giving one-fortieth (2.5%) of one’s yearly income to charity.

The prohibition of usury, the fundamental and most widely known principle of Islamic

finance, is not specific to Islam as it is also commended in Christianity and Judaism.

However, the traditional financial system clearly contradicts this as well as several other

principles.

This is why a system consistent with the teachings of Islam is necessary to provide

access to everyday financial services. To do so, rather complex banking mechanisms

have been set up (see appendix), but with some differences in interpretation about what

is acceptable (halal) and what is forbidden in investments (haraam).

As such, each Islamic financial institution has a Sharia Board comprised of independent

experts (academics, jurists, specialised economists) that issues opinions on products

available on the market. Moreover, internal and external audits are performed on a

regular basis to confirm compliance with Islamic principles. Lastly, if the generation of

interest is suspected, “purification” systems have been put in place, mainly as donations

to the poor.

Islamic finance: ethical...

One of the Sharia-compliant investment principles relates to the prohibition of certain

assets. One of the criteria used to define these forbidden assets is the business involved,

which may be considered reprehensible from an ethical or religious standpoint. The list of

forbidden businesses varies but may include:

■ Alcohol

■ Tobacco (less systematic)

■ Weapons (less systematic)

III. PRINCIPLES OF ISLAMIC FINANCE

© Novethic 2009. Islamic finance and SRI: any crossover? 12

■ Gambling

■ Pornography

■ Leisure industries (music, cinema, etc.)

■ Finance industry

■ Pork products

There is some leeway, however. For example, to allow the financing of a major luxury

hotel, the construction of a casino was forbidden, but the sale of alcohol within the

establishment was tolerated, as it was deemed necessary for its economic viability.

However, the transaction then required purification by contributing to the fight against

alcoholism. The purification process thus applies when the forbidden activity is

unavoidable or considered difficult to ascertain due to the complexity of the businesses

and structures financed.

… moral…

Islamic finance is a system intended to be fair, with the aim of improving quality of life.

The prohibition of usury is based on two moral principles:

■ The application of a fixed interest rate is considered unfair and discriminatory.

First, it prevents the lowest-income groups from having access to credit. For

investments, it leads to an uneven distribution of risk and profits: the investor

receives fixed income without any correlation to the success or failure of the

business, while the entrepreneur bears all the risk. Conversely, in the event of

significant profits, the investor receives an insignificant share of the profits while

the entrepreneur takes the lion’s share. In other words, the profit attributed to

the capital is fixed, while that attributed to the labour is variable and tinged with

uncertainty.

■ Earning interest is by definition not correlated with the business itself. This

transgresses the principle that the creation of wealth is based on a real asset and

that the money itself cannot be a source of added value.

Another moral principle linking finance to the real economy is that of not selling what one

does not own. This particularly applies to speculation and partly explains why Islamic

banks have not been severely impacted by the crisis: they were not exposed to subprime

mortgages.

Lastly, the principle of zakat also upholds the idea of social equality. By recommending

that believers give a portion of their income (2.5%) to the poor, zakat allows for the

redistribution of wealth and helps correct inequality.

… and financial!

Islamic finance has developed a number of often complex mechanisms (explained in the

appendix to this document) to remain in line with the five principles listed above, among

which the prohibition of usury. This system has not only set moral rules and extra-

financial principles but has actually designed the tools necessary to apply them. Investing

only in real underlying assets and setting specific financial guidelines on Sharia-compliant

investments therefore require a particular type of financial analysis. The following ratios

III. PRINCIPLES OF ISLAMIC FINANCE

© Novethic 2009. Islamic finance and SRI: any crossover? 13

are those used by the Dow Jones Islamic Market indices, even if the thresholds may vary

from one institution to the next:

■ Total debt divided by trailing 12-month average market capitalization must not

exceed 33%.

■ The sum of a company's cash and interest-bearing securities divided by trailing

12-month average market capitalization must not exceed 33%

■ Accounts receivables divided by trailing 12-month average market capitalization

must not exceed 33%.

These ratios are in line with the principle that income is in relation to an existing

underlying activity and in line with the prohibition of usury: although it is, in practice,

inevitable that a company will be in debt, will earn interest and cash, most of its added-

value must be based on a genuine activity.

IV. CROSSOVER WITH SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 14

IV. Crossover with SRI

Islamic finance, as presented thus far, points to several commonalities with ethical

finance and SRI. However, major differences may arise between theory and practice.

Although some rules on financial practices are clearly defined, other moral principles of

the Sharia are barely applied in Islamic finance as it operates today.

Purpose and moral principles

Islam may be considered a system of standards based on moral and ethical values. The

purpose of Islamic finance is to improve living conditions and well-being, establish social

equity and prevent injustice in trade relations. This is precisely the reasoning behind the

prohibition of usury and its replacement with a system whereby profits and risk are

shared more equally.

This purpose resembles that of SRI as it has developed in recent years, with its focus on

sustainable development in its economic and social principles: creation of wealth for

society and improvement in the quality of life. The environment is also considered in

Islamic finance: one of the tenets of Islam is that man plays the role of steward over

divine creation. God’s creation, which encompasses not only nature and the environment

but also humans and society, belongs to God and is entrusted to man, who is vested with

the duty of maintaining and managing the earth on God’s behalf. The application of this

principle is often that wasting and useless, superfluous consumption are unacceptable.

The tie between religion and business ethics has been extensively studied by a cross-

religious group of representatives from the three major monotheistic religions

(Christianity, Islam and Judaism), an initiative of the British and Jordanian royal families

with the sponsorship of Prince Philip, Duke of Edinburgh, Prince Hassan of Jordan and Sir

Evelyn de Rothschild. The study concluded that there were four main crossovers between

the three religions: justice, mutual respect, the notion of stewardship entrusted by God

and honesty. The statement2 issued by this working group, which aims to establish a

code of business ethics shared by the three religions, lays down best practices to be

adopted in each of these areas, particularly in relation to stakeholders.

Although many of these best practices and, more generally, the principles based on the

writings of Islam, are criteria shared with SRI, especially relating to ESG Best-in-Class

screening which rewards the best behaviour, Islamic finance has not adopted these

principles as analysis or restrictive selection criteria.

2 "An Interfaith Declaration: A Code Of Ethics On International Business For Christians, Muslims And Jews"

IV. CROSSOVER WITH SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 15

Sector-based exclusions

Although Islamic finance differs somewhat from Best-in-Class, it is tantamount to ethical

finance. Sector-based exclusions, the basis of SRI as it is applied today, stems from

Protestant and Catholic religious convictions. It is therefore not surprising that the list of

forbidden sectors is essentially the same as for Islamic finance: alcohol, pornography,

gambling, tobacco and weapons are businesses that are generally condemned, deemed

harmful for man and society.

However, some sectors are specific to Islamic finance, namely the financial and leisure

(music, cinema, etc.) industries, but they are not systematically excluded from the

investment universe. Pork products are banned as their consumption is forbidden by the

Islamic religion.

Norm-based exclusions and the Global Compact

Unlike what may be the case for SRI, Islamic finance does not explicitly exclude issuers

guilty of the worst social and environmental practices. Nevertheless, a report by OWW

Consulting3, a CSR and SRI consulting firm in Southeast Asia, highlights the compatibility

between the tenets of Islam and those of the UN Global Compact.

The United Nations Global Compact4 is a strategic policy initiative for businesses that are

committed to aligning their operations and strategies with ten universally accepted

principles in the areas of human rights, labour, environment and anti-corruption.

These principles draw on the standard references in these areas, including the Universal

Declaration of Human Rights, the International Labour Organization Declaration on

Fundamental Principles and Rights at Work, the Rio Declaration on Environment and

Development and the United Nations Convention against Corruption. It should be noted

that the Global Compact does not enforce any regulation nor does it measure or review

the practices of signatories.

OWW Consulting’s report describes how the tenets of Islam comply with each of these

principles, despite being based on different sources and motivations and often stricter

ethical standards. It does not examine the application of these principles in Islamic

finance, which is significantly less effective.

3 Islam and CSR: The compatibility between the tenets of Islam and the UN Global Compact, available at

http://www.oww-consulting.com/downloads/research/islam-and-csr/download.html

4 Details of the 10 principles at http://www.unglobalcompact.org/

IV. CROSSOVER WITH SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 16

OWW Consulting’s analysis of the compatibility between Sharia and the UN

Global Compact

Human rights

The Sharia is based on the writings of the Qur’an and sayings of the Prophet,

advocating principles such as democracy (rule by consultation), the equality of races,

religions and sexes and the respect of non-Muslims and freedom of religion. The fact

that these principles are not always applied, such as gender equality, can be explained

by cultural and regional traditions rather than by religious precepts, or rather a

simplified and erroneous interpretation of religious writings. The concept of justice also

runs deep in Islam. Freedom of expression is encouraged to promote ethical and fair

behaviour, but is limited otherwise. As for the protection of privacy, it goes beyond the

practices of western societies as it also applies to people deemed potentially

dangerous. Finally, Islam believes that the role of the State, aside from acting in

consultation with the people, is to ensure the independence of the legal system and to

provide basic services, especially to the elderly, the orphans, and the sick.

Labour

This pillar of the Global Compact is based on the ILO’s fundamental conventions.

Although freedom of association is not clearly defined in the Sharia, forced labour is

clearly forbidden. The labour that is expected must be clearly defined, and the worker

must be compensated fairly once the work requested has been completed. The worker

must not be required to furnish more than he is capable of doing. Regarding child

labour, it is stipulated that a work contract must be established between individuals

considered adults, that is, those having reached puberty (this definition is disputable).

Discrimination is decried in the Prophet’s last sermon, in which he states that, in God’s

eyes, superiority and honour do not lie in race or colour but in righteousness and

honest living.

Environment

In view of the role of steward entrusted to man by God, it is rather clear that the

protection of the environment falls within the duty of man. This principle seems to be

explicit in the Sharia. Islam praises moderation and condemns waste, which includes

the excessive consumption of natural resources.

Anti-corruption

Corruption is viewed to be contrary to ethics since it involves unequal treatment with

regard to the law and transgresses the fundamental principle of justice. Based on the

sayings of the Prophet, the Sharia condemns the corrupter as well as the corrupted

and intermediary. Islam is extremely strict in terms of transparency, as it requires a

clear contract in writing for each transaction, containing all the information on the item

traded, and condemns any efforts to conceal any defects.

IV. CROSSOVER WITH SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 17

However, OWW Consulting has observed differences between the theory and practices

with regard to all of these principles. The most telling examples involve the

questionable practices in Muslim countries in terms of equality between men and

women or in corruption perception indices. OWW attributes these factors more to

socio-cultural aspects than religious principles, and therefore supports the emergence

of a more liberal and “European” form of Islam, with a view to highlighting these CSR

principles and tempering the cultural influences that are specific to Africa and the

Middle East.

A norm-based exclusion system for Islamic finance seems so close but yet so far. The

above-mentioned principles do not apply directly to finance, and nothing currently

suggests that Islamic finance is on its way to integrating them systematically, or even

informally, into investment strategies. Aside from the OWW Consulting report, little

research has been carried out on acceptable business practices for companies, apart from

prohibited sectors and financial ratios. In the same way, based on the information

available on some Sharia boards, nothing suggests that this will change.

Profit-sharing approach

For some, profit-sharing is a form of SRI practice, as it consists in donating a portion of

profits to NGOs or humanitarian organisations.

Islamic finance practices two forms of profit-sharing:

■ Zakat, one of the five pillars of Islam, is comparable to almsgiving or tithing. It is

a required donation of one-fortieth (2.5%) of one’s income to the poor. It is used

to purify the believer from any unholy thoughts (greed, etc.) and to provide for

the needs of the society. Islamic bank customers can arrange for the donation to

be deducted directly from their account; they can also choose which charity to

support.

■ Purification systems, also sometimes referred to as zakat relate to financial

transactions suspected of generating interest or forbidden activities considered to

be unavoidable. For example, the case of a luxury hotel authorised to sell alcohol

to ensure its economic viability in exchange for regular contributions to the fight

against alcoholism.

In practice

Novethic called on a number of experts specialised in both SRI and Islamic finance in

order to assess how this theoretical compatibility is reflected in management practices.

On the supply side, three asset management companies involved in both investment

strategies were consulted: Pictet and SAM – Sustainable Asset Management, (Swiss)

and F&C Investments (British). On the potential demand side, the sovereign fund

ADIA (Abu Dhabi Investment Authority) was contacted. The latter fund does not feel

concerned as it does not practice SRI or Sharia-compliant investments.

IV. CROSSOVER WITH SRI

© Novethic 2009. Islamic finance and SRI: any crossover? 18

Lastly, the viewpoints of ASrIA, an association dedicated to promoting SRI and CSR in

Asia, and OWW Consulting, an SRI and CSR consulting firm, were also taken into

account. These two organisations are located in Southeast Asia, the only geographical

region (outside the United Kingdom) where Islamic finance and SRI are developing side

by side.

CONCLUSION: COMPATIBILITY AND COMPLEMENTARITY

© Novethic 2009. Islamic finance and SRI: any crossover? 19

Conclusion: Compatibility and complementarity

Many in the financial community believe that Islamic finance and SRI are

compatible, but that there is no natural link between the two, first because they do

not employ the same expertise, and second because they do not target the same

clientele. Pictet is the perfect example: its SRI fund and Sharia-compliant fund were

launched separately, and its management teams are based in two different countries,

Switzerland for the former and the United Kingdom for the latter. OWW and ASrIA have

observed similar phenomena: in Southeast Asia, both markets are growing, but in

different countries. Islamic finance is strong in Malaysia, Indonesia and Singapore, while

SRI has a firmer foothold in Japan and South Korea.

For ASrIA, SRI and Islamic finance both enjoy a role as alternatives to traditional finance,

but issues are not treated in the same way. Along the same lines, Geoffrey Williams of

OWW Consulting asserts that two major differences exist:

■ In terms of extra-financial criteria, SRI takes a more comprehensive approach

than Islamic finance, going beyond the business sector. In addition, not all SRI

players screen companies by sector: for instance, the Dow Jones Sustainability

Indexes do not all exclude sectors such as tobacco.

■ The ban on interest and the relationship with risk and uncertainty have put

Islamic finance at a far stretch from classic western financing. As such, the

selection criteria used in traditional finance often have no place in Islamic finance.

In any case, OWW highlights the lack of dialogue between these two areas of finance.

Although SRI has its roots in Christian finance, it has become an approach in its own

right. Traditional investors show less enthusiasm with regard to religious finance,

expressing limited interest for what they consider to be a niche market, which, more

importantly, does not outperform indices (although Islamic finance may provide less

risk). They clearly lean towards the more buoyant environmental fund market.

Perhaps the only exception is SAM. The Swiss asset management firm is an expert in the

application of ESG criteria to sustainable investment themes and issuer practices. In

collaboration with the UK Islamic bank, Gatehouse, it recently launched a Sharia-

compliant fund focused on water. According to Daniel Wild, SRI and Islamic finance share

two fundamental principles.

■ In Islam, man acts as a steward on earth with the role of protecting natural

resources. This concept is consistent with sustainable development as defined in

the Brundtland report: “meeting the needs of the present without compromising

the ability of future generations to meet their own needs”.

■ The purpose of Islamic finance - to improve living conditions and social well-being

- is in full harmony with sustainability issues such as water preservation. This is a

particularly poignant issue in regions like the Middle East, where water is

increasingly scarce.

CONCLUSION: COMPATIBILITY AND COMPLEMENTARITY

© Novethic 2009. Islamic finance and SRI: any crossover? 20

The initiative of SAM and Gatehouse Bank therefore seemed perfectly coherent. SAM’s

"Sustainability" team had extensive discussions with Gatehouse’s Sharia Board, whose

members were very interested in theme-based and ESG analyses of issuers.

However, this compatibility is not seamless. SAM, an SRI-focused firm, launched a

Sharia-compliant fund that seized a market opportunity before taking into consideration

any crossovers in the philosophy. Despite the dialogue between the two institutions,

coherence is relative, considering that expertise is kept separate, the teams are in

different geographical locations, and their roles in the design of the fund are clearly

defined: Gatehouse provides SAM with a list of Sharia-compliant companies in the initial

universe, and SAM applies its extra-financial and financial criteria to the selection.

That said, the project initiated by SAM and Gatehouse Bank remains a unique example of

how SRI strategy can be combined with Islamic finance. Other initiatives may follow suit.

This is currently being analysed by the UK firm F&C Investments.

Like SRI, Islamic finance is a fragmented domain, but less so than SRI, as it is in

accordance with a law, the Sharia. Admittedly, this law is subject to interpretation, but a

consensus exists for the majority of the principles that apply to finance. SRI on the other

hand may take several shapes that do not necessarily overlap: ethical finance and its

sector-based exclusion, ESG Best-in-class screening or the exclusion of the worst

practices, shareholder activism, and on a wider scope community development and

sharing.

Notwithstanding the basic purpose of these types of finance which encourages social

well-being and environmental protection, Islamic finance remains a more formal system

that provides both financial and extra-financial guidelines. These guidelines, when

compared with responsible investment, are consistent with ethical finance and sharing,

both in their approach and objective, but do not preclude compatibility with other SRI

approaches.

Still, despite the fact that Islamic finance does not subject company practices to ESG

screening, it is in line with UN Global Compact principles, which are used by a number of

SRI managers in defining norm-based exclusions.

As long as these approaches do not have any conflicting purposes, they could, in fact, be

not only compatible but complementary, with the integration of ESG criteria offering both

ethical and financial added value, notably by limiting risk. The success of Islamic finance

and SRI does not seem correlated today, but it will be up to financial experts, research

centres, ratings agencies, NGOs and even regulators to consolidate the two approaches.

As they both focus on encouraging more ethical, responsible and transparent practices,

they could be developed jointly, as could their potential client bases, thus springboarding

SRI into new markets.

APPENDIX: MAIN FINANCIAL MECHANISMS

© Novethic 2009. Islamic finance and SRI: any crossover? 21

Appendix: Main financial mechanisms

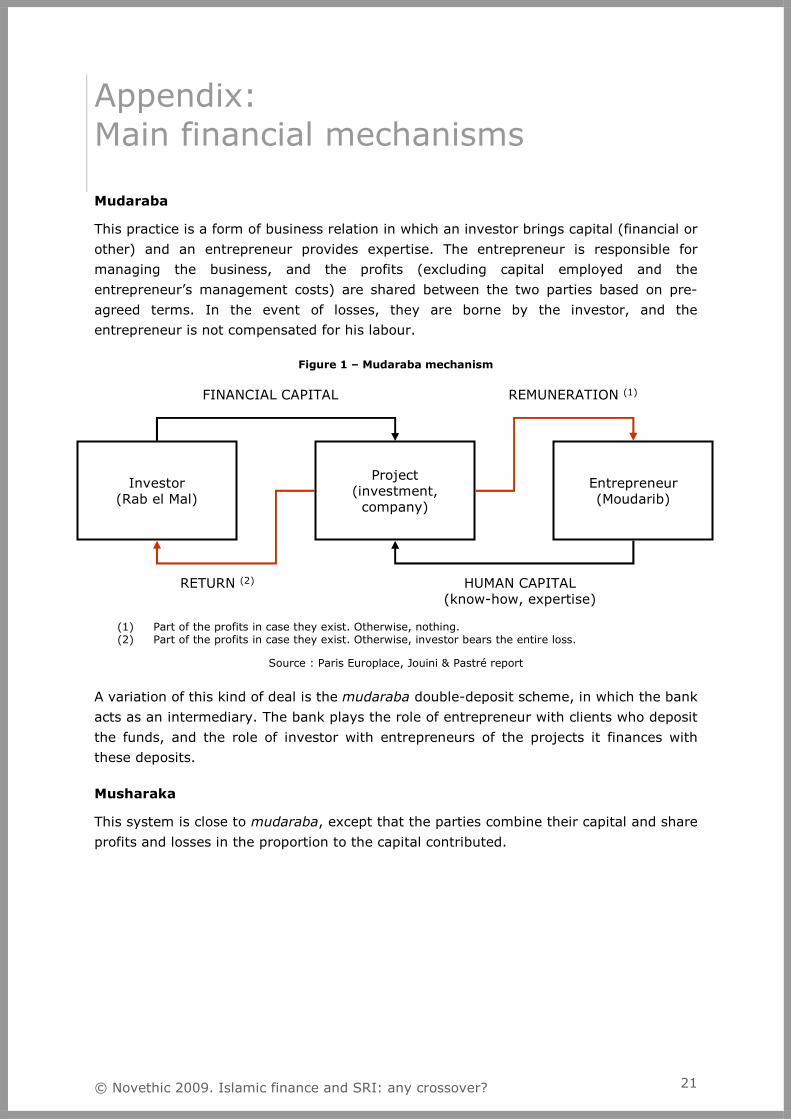

Mudaraba

This practice is a form of business relation in which an investor brings capital (financial or

other) and an entrepreneur provides expertise. The entrepreneur is responsible for

managing the business, and the profits (excluding capital employed and the

entrepreneur’s management costs) are shared between the two parties based on pre-

agreed terms. In the event of losses, they are borne by the investor, and the

entrepreneur is not compensated for his labour.

Figure 1 – Mudaraba mechanism

Investor(Rab el Mal)

Project (investment, company)

Entrepreneur (Moudarib)

FINANCIAL CAPITAL

RETURN (2)

REMUNERATION (1)

HUMAN CAPITAL(know-how, expertise)

(1) Part of the profits in case they exist. Otherwise, nothing.(2) Part of the profits in case they exist. Otherwise, investor bears the entire loss.

Source : Paris Europlace, Jouini & Pastré report

A variation of this kind of deal is the mudaraba double-deposit scheme, in which the bank

acts as an intermediary. The bank plays the role of entrepreneur with clients who deposit

the funds, and the role of investor with entrepreneurs of the projects it finances with

these deposits.

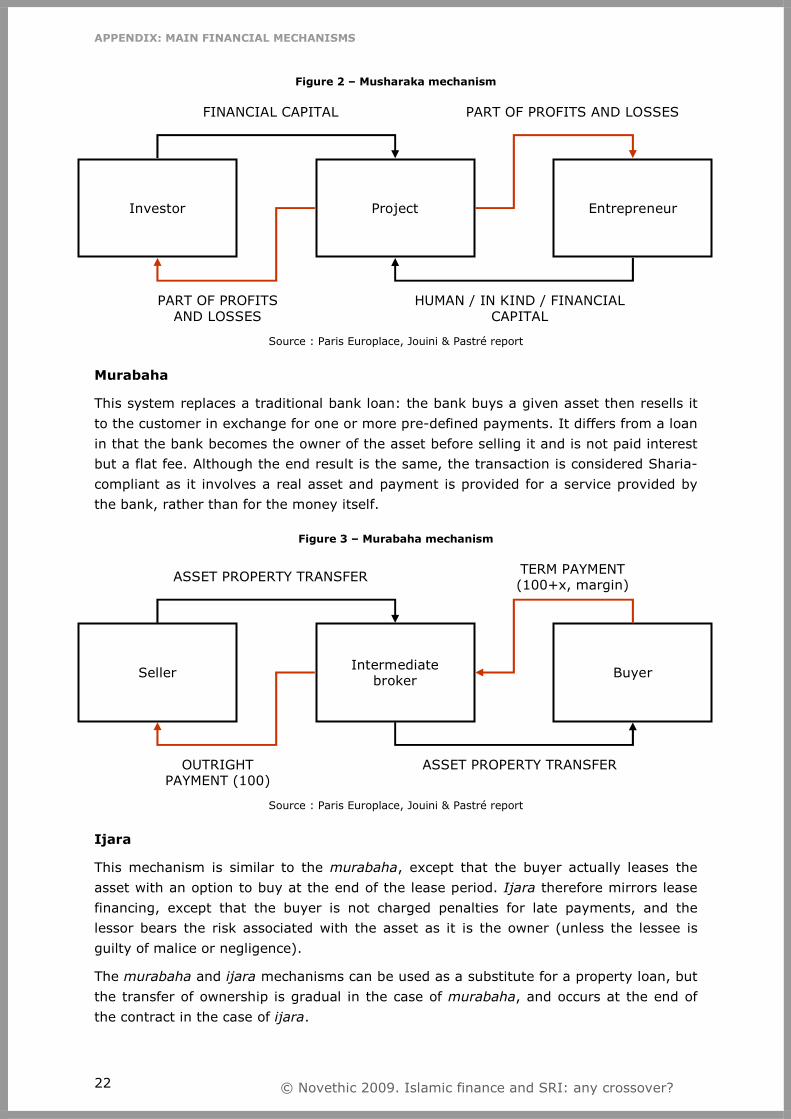

Musharaka

This system is close to mudaraba, except that the parties combine their capital and share

profits and losses in the proportion to the capital contributed.

APPENDIX: MAIN FINANCIAL MECHANISMS

© Novethic 2009. Islamic finance and SRI: any crossover? 22

Figure 2 – Musharaka mechanism

Investor Project Entrepreneur

FINANCIAL CAPITAL

PART OF PROFITS AND LOSSES

PART OF PROFITS AND LOSSES

HUMAN / IN KIND / FINANCIAL CAPITAL

Source : Paris Europlace, Jouini & Pastré report

Murabaha

This system replaces a traditional bank loan: the bank buys a given asset then resells it

to the customer in exchange for one or more pre-defined payments. It differs from a loan

in that the bank becomes the owner of the asset before selling it and is not paid interest

but a flat fee. Although the end result is the same, the transaction is considered Sharia-

compliant as it involves a real asset and payment is provided for a service provided by

the bank, rather than for the money itself.

Figure 3 – Murabaha mechanism

Seller Intermediatebroker

Buyer

ASSET PROPERTY TRANSFER

OUTRIGHT PAYMENT (100)

TERM PAYMENT(100+x, margin)

ASSET PROPERTY TRANSFER

Source : Paris Europlace, Jouini & Pastré report

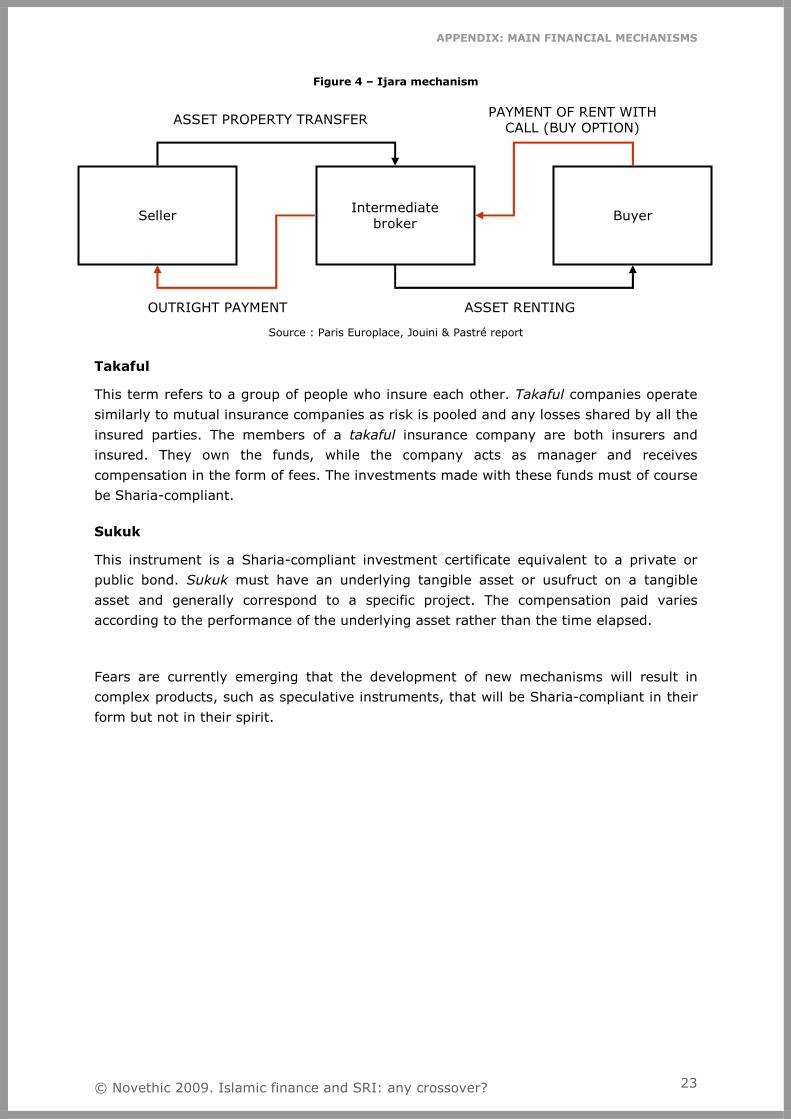

Ijara

This mechanism is similar to the murabaha, except that the buyer actually leases the

asset with an option to buy at the end of the lease period. Ijara therefore mirrors lease

financing, except that the buyer is not charged penalties for late payments, and the

lessor bears the risk associated with the asset as it is the owner (unless the lessee is

guilty of malice or negligence).

The murabaha and ijara mechanisms can be used as a substitute for a property loan, but

the transfer of ownership is gradual in the case of murabaha, and occurs at the end of

the contract in the case of ijara.

APPENDIX: MAIN FINANCIAL MECHANISMS

© Novethic 2009. Islamic finance and SRI: any crossover? 23

Figure 4 – Ijara mechanism

SellerIntermediate

brokerBuyer

ASSET PROPERTY TRANSFER

OUTRIGHT PAYMENT

PAYMENT OF RENT WITH CALL (BUY OPTION)

ASSET RENTING

Source : Paris Europlace, Jouini & Pastré report

Takaful

This term refers to a group of people who insure each other. Takaful companies operate

similarly to mutual insurance companies as risk is pooled and any losses shared by all the

insured parties. The members of a takaful insurance company are both insurers and

insured. They own the funds, while the company acts as manager and receives

compensation in the form of fees. The investments made with these funds must of course

be Sharia-compliant.

Sukuk

This instrument is a Sharia-compliant investment certificate equivalent to a private or

public bond. Sukuk must have an underlying tangible asset or usufruct on a tangible

asset and generally correspond to a specific project. The compensation paid varies

according to the performance of the underlying asset rather than the time elapsed.

Fears are currently emerging that the development of new mechanisms will result in

complex products, such as speculative instruments, that will be Sharia-compliant in their

form but not in their spirit.

Since 2001, Novethic provides expert resources and mobilises business leaders, investors, NGOs

and other stakeholders on key topics related to CSR and SRI. Novethic is the only source of

analytical and statistical information on the French SRI market. The SRI research team conducts

thematic studies, analyses product trends and assesses the SRI processes of asset management

firms.

ISLAMIC FINANCE AND SRI: ANY CROSSOVER?

Study conducted by Samer Hobeika from Novethic’s SRI research centre

and supervised by Anne-Catherine Husson-Traore, Novethic’s Chief Executive.

Novethic

56, rue de Lille – 75007 PARIS Tel : +33 (0)1 58 50 98 14 – Fax : +33 (0)1 58 50 00 30

E-mail: [email protected] www.novethic.com