Embed Size (px)

Citation preview

4 March 2014 | Gokarna Forest Resort, Nepal

Workshop on Results-Based Project Reporting and Auditing: Special Focus on Donor Funded Projects

DAY 4 PROJECT FINANCIAL STATEMENTS

FORMAT AND CONTENT OF PROJECT FINANCIAL STATEMENTS Presenters: RAMU PRASAD DOTEL, OAG, Nepal, SHERAZADE SHAFIQ, FM Specialist, ADB TIMILA SHRESTHA, FM Consultant, WB Moderators: FCGO DAY 4

SESSION 9

2

Objective, Structure, & Output

Objective: To agree on improvements and refinements to the template for project financial statements.

Session Structure:

i. Audit Guidelines Template and Challenges faced (30 mins)

ii. Cash Basis IPSAS disclosure checklist (20 mins) iii. Accrual Basis Accounting Status iv. WB observation and experience in reviewing APFS v. Q & A (15 mins) vi. Group activity

Output: Agreed Changes to PFS template

SESSION 9

3

AUDIT GUIDELINES TEMPLATE Presenter: RAMU PRASAD DOTEL, OAG NEPAL

SESSION 9.a

4

CASH BASIS IPSAS DISCLOSURE CHECKLIST Presenter: SHERAZADE SHAFIQ

SESSION 9.b

5

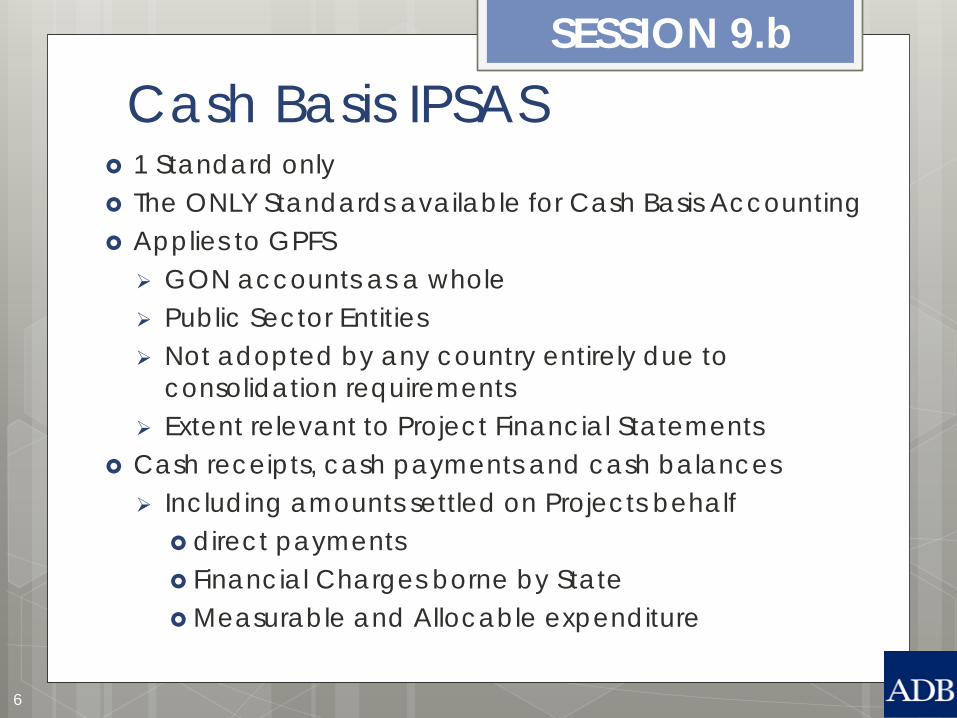

Cash Basis IPSAS 1 Standard only The ONLY Standards available for Cash Basis Accounting Applies to GPFS GON accounts as a whole Public Sector Entities Not adopted by any country entirely due to

consolidation requirements Extent relevant to Project Financial Statements

Cash receipts, cash payments and cash balances Including amounts settled on Projects behalf

direct payments Financial Charges borne by State Measurable and Allocable expenditure

SESSION 9.b

6

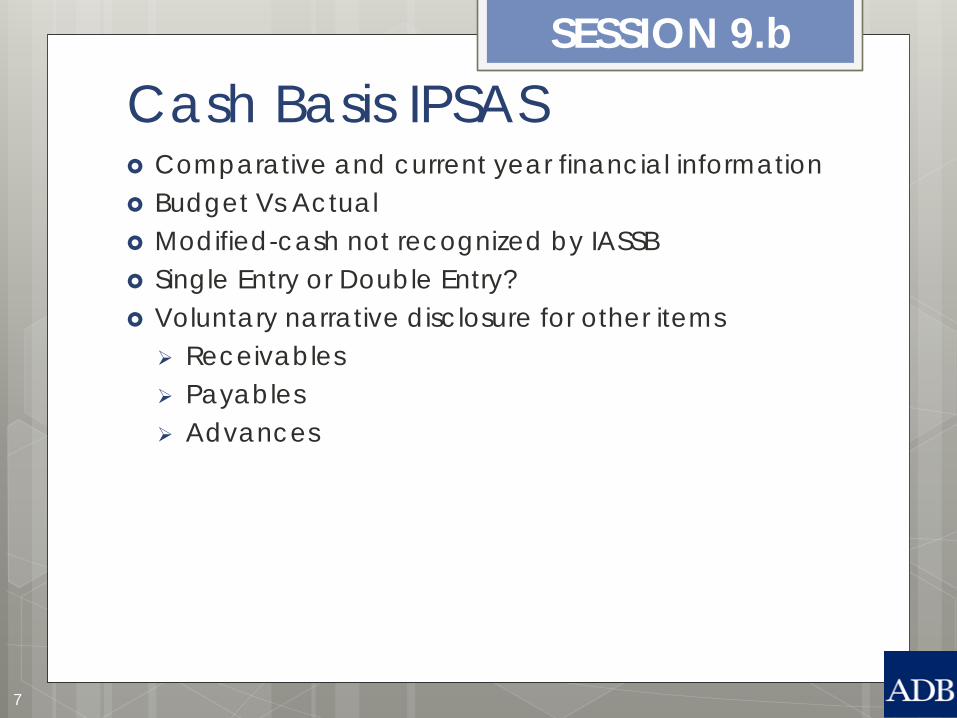

Cash Basis IPSAS Comparative and current year financial information Budget Vs Actual Modified-cash not recognized by IASSB Single Entry or Double Entry? Voluntary narrative disclosure for other items Receivables Payables Advances

SESSION 9.b

7

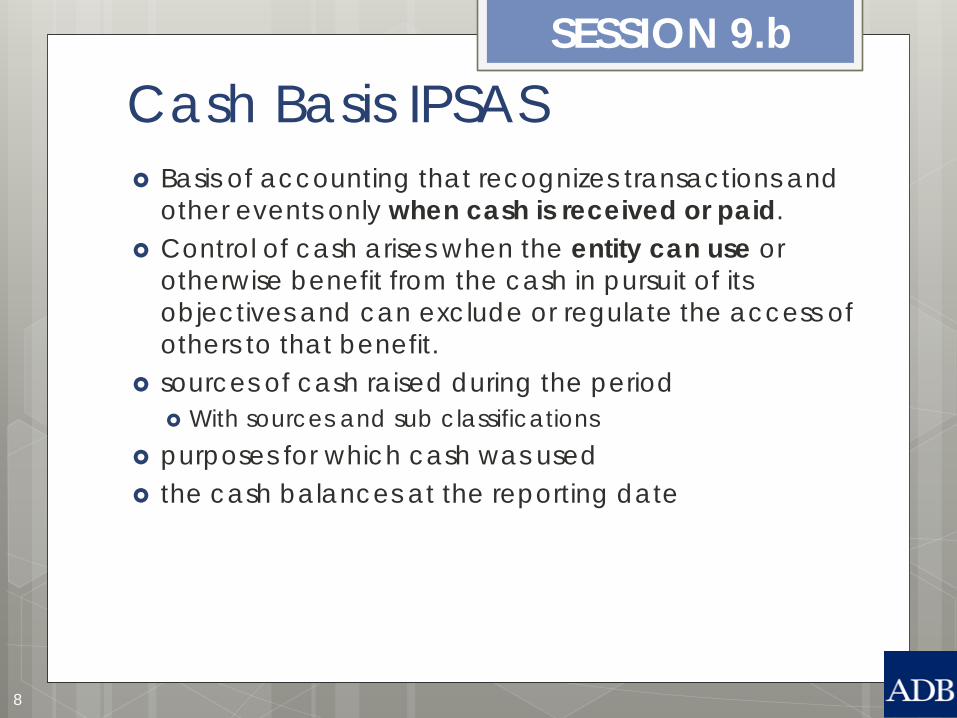

Cash Basis IPSAS Basis of accounting that recognizes transactions and

other events only when cash is received or paid. Control of cash arises when the entity can use or

otherwise benefit from the cash in pursuit of its objectives and can exclude or regulate the access of others to that benefit.

sources of cash raised during the period With sources and sub classifications

purposes for which cash was used the cash balances at the reporting date

SESSION 9.b

8

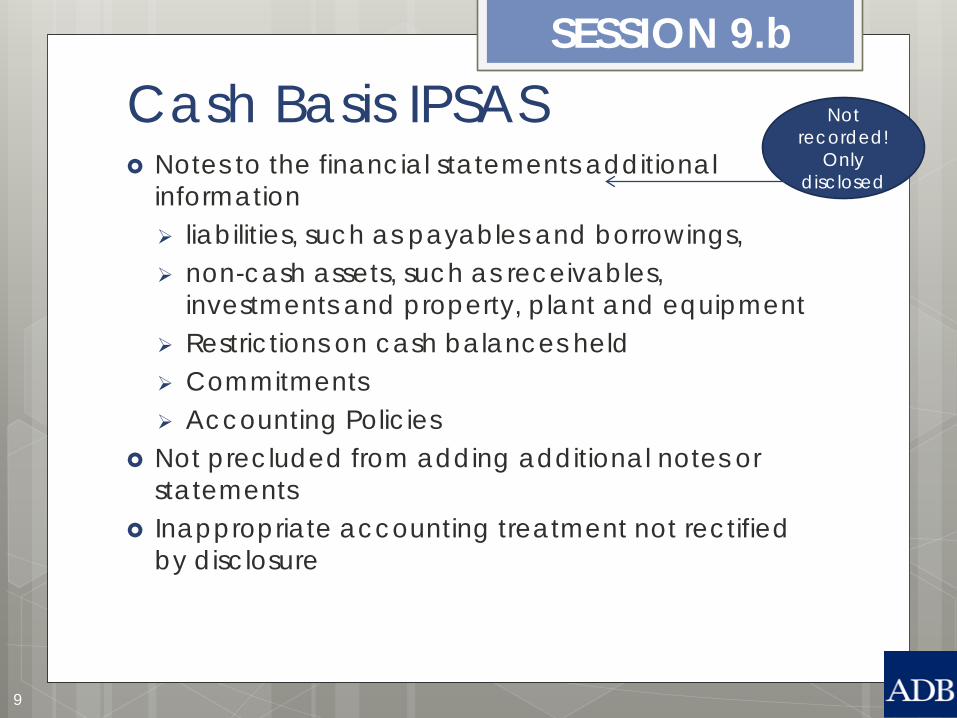

Cash Basis IPSAS Notes to the financial statements additional

information liabilities, such as payables and borrowings, non-cash assets, such as receivables,

investments and property, plant and equipment Restrictions on cash balances held Commitments Accounting Policies

Not precluded from adding additional notes or statements

Inappropriate accounting treatment not rectified by disclosure

SESSION 9.b

9

Not recorded!

Only disclosed

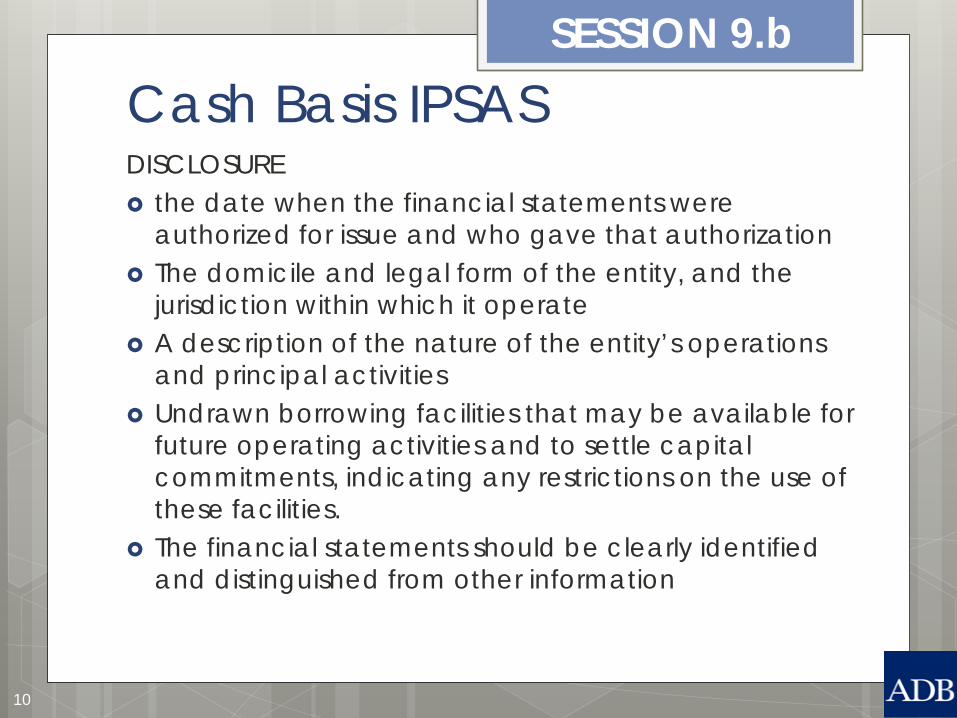

Cash Basis IPSAS DISCLOSURE the date when the financial statements were

authorized for issue and who gave that authorization The domicile and legal form of the entity, and the

jurisdiction within which it operate A description of the nature of the entity’s operations

and principal activities Undrawn borrowing facilities that may be available for

future operating activities and to settle capital commitments, indicating any restrictions on the use of these facilities.

The financial statements should be clearly identified and distinguished from other information

SESSION 9.b

10

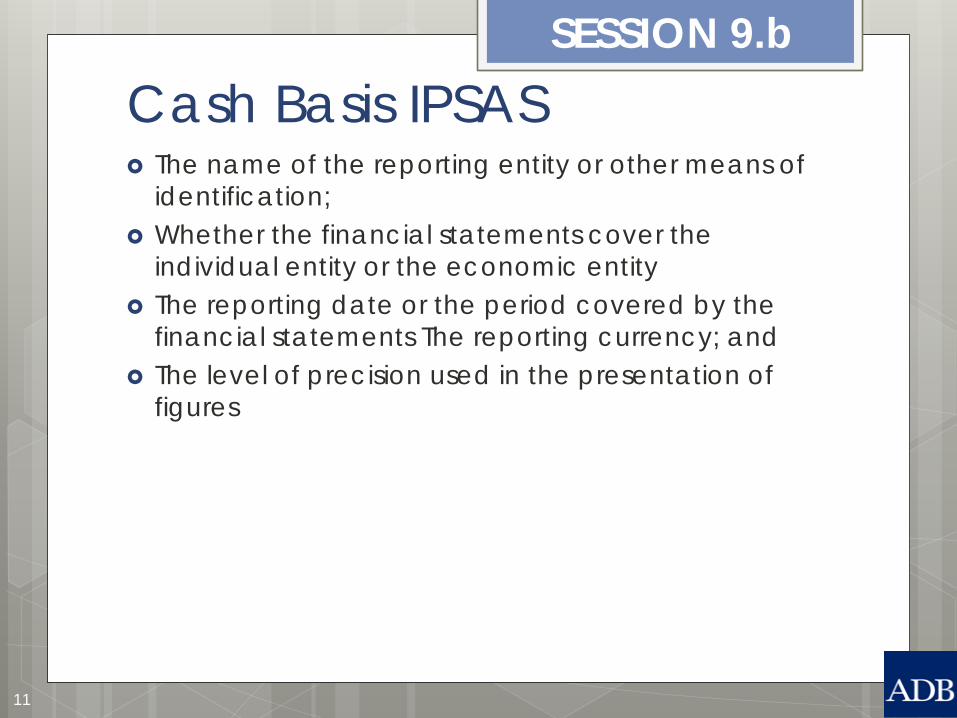

Cash Basis IPSAS The name of the reporting entity or other means of

identification; Whether the financial statements cover the

individual entity or the economic entity The reporting date or the period covered by the

financial statements The reporting currency; and The level of precision used in the presentation of

figures

SESSION 9.b

11

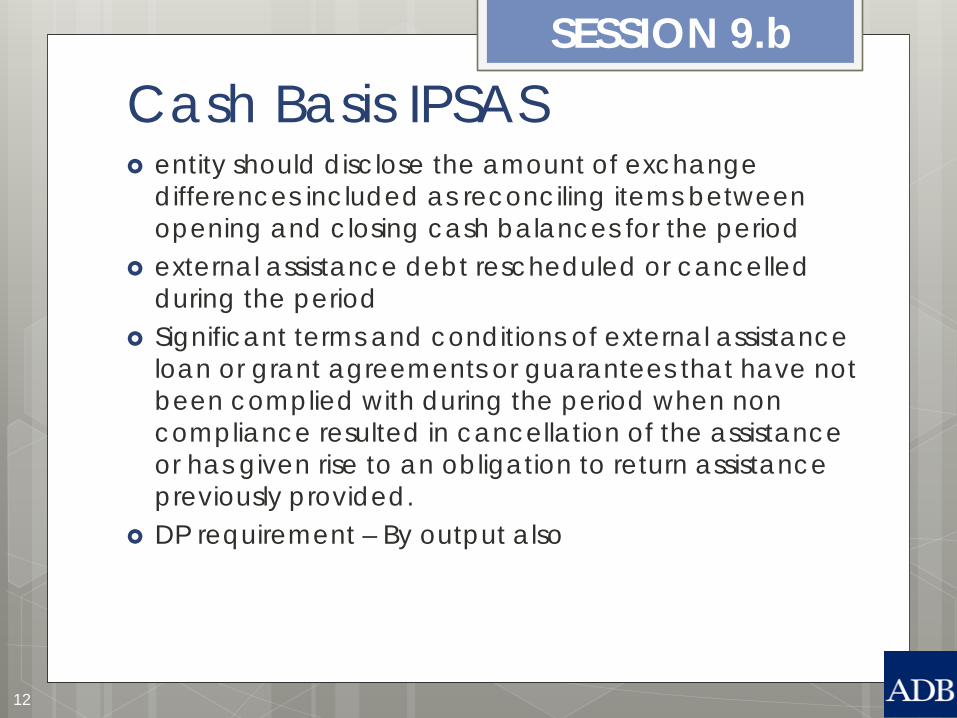

Cash Basis IPSAS entity should disclose the amount of exchange

differences included as reconciling items between opening and closing cash balances for the period

external assistance debt rescheduled or cancelled during the period

Significant terms and conditions of external assistance loan or grant agreements or guarantees that have not been complied with during the period when non compliance resulted in cancellation of the assistance or has given rise to an obligation to return assistance previously provided.

DP requirement – By output also

SESSION 9.b

12

13

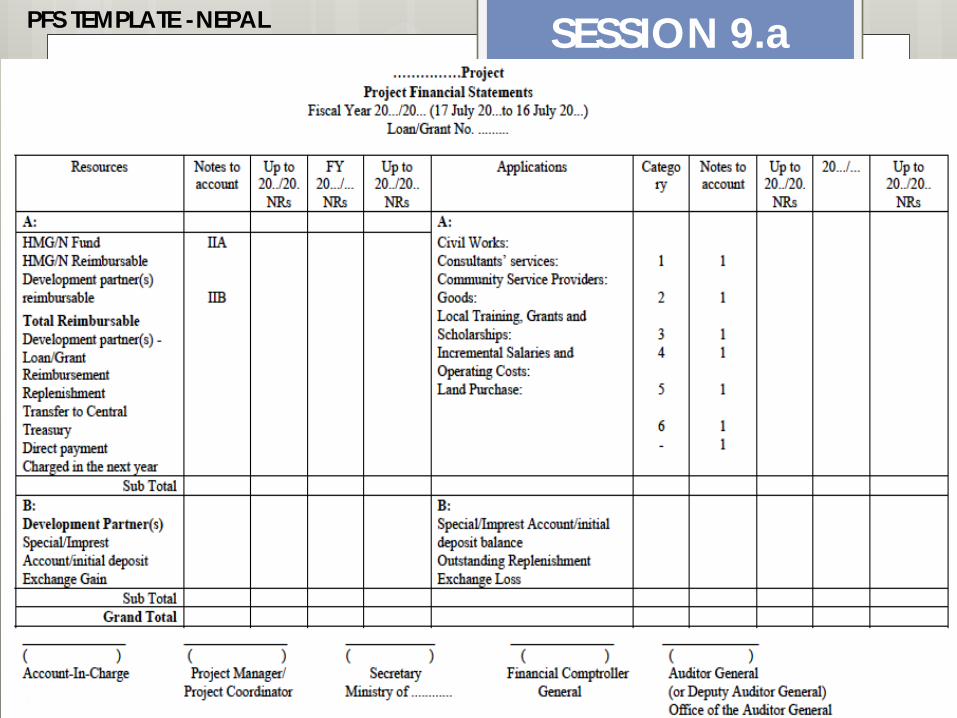

SESSION 9.a PFS TEMPLATE -NEPAL

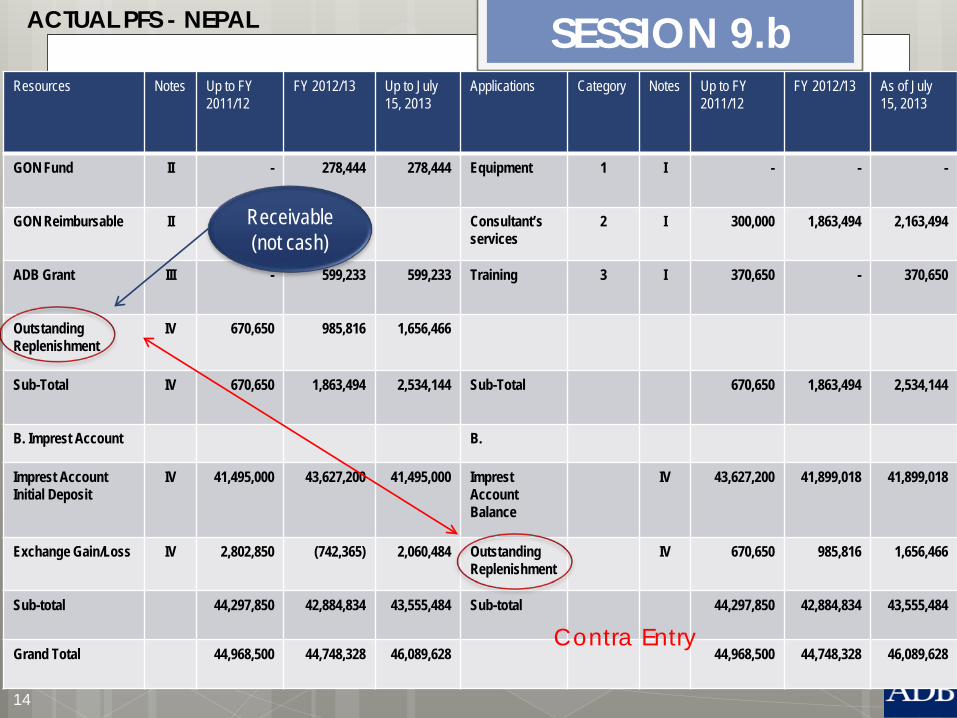

14

SESSION 9.b Resources Notes Up to FY

2011/12 FY 2012/13 Up to July

15, 2013 Applications Category Notes Up to FY

2011/12 FY 2012/13 As of July

15, 2013

GON Fund II - 278,444 278,444

Equipment 1 I - - -

GON Reimbursable II - - Consultant’s services

2 I 300,000 1,863,494 2,163,494

ADB Grant III - 599,233 599,233

Training 3 I 370,650 - 370,650

Outstanding Replenishment

IV 670,650 985,816 1,656,466

Sub-Total IV 670,650 1,863,494 2,534,144

Sub-Total 670,650 1,863,494 2,534,144

B. Imprest Account B.

Imprest Account Initial Deposit

IV 41,495,000 43,627,200 41,495,000

Imprest Account Balance

IV 43,627,200 41,899,018 41,899,018

Exchange Gain/Loss IV 2,802,850 (742,365) 2,060,484 Outstanding Replenishment

IV 670,650 985,816 1,656,466

Sub-total 44,297,850 42,884,834 43,555,484 Sub-total 44,297,850 42,884,834 43,555,484

Grand Total 44,968,500 44,748,328 46,089,628 44,968,500 44,748,328 46,089,628

ACTUAL PFS - NEPAL

Contra Entry

Receivable (not cash)

15

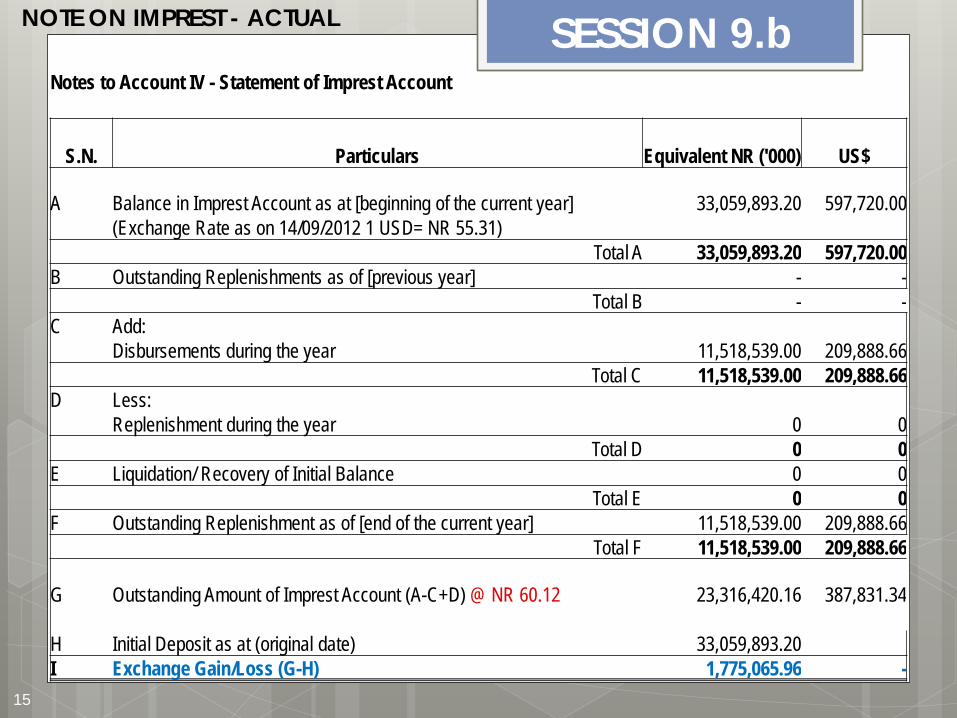

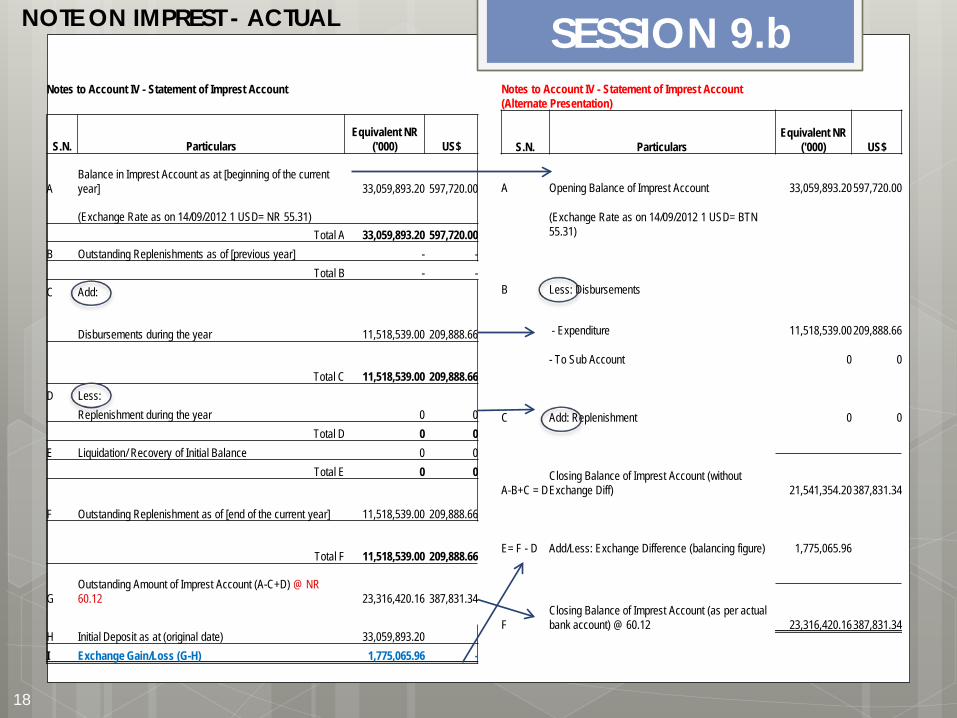

Notes to Account IV - Statement of Imprest Account

S.N. Particulars Equivalent NR ('000) US$

A Balance in Imprest Account as at [beginning of the current year] 33,059,893.20 597,720.00 (Exchange Rate as on 14/09/2012 1 USD= NR 55.31) Total A 33,059,893.20 597,720.00 B Outstanding Replenishments as of [previous year] - - Total B - - C Add: Disbursements during the year 11,518,539.00 209,888.66 Total C 11,518,539.00 209,888.66 D Less: Replenishment during the year 0 0 Total D 0 0 E Liquidation/ Recovery of Initial Balance 0 0 Total E 0 0 F Outstanding Replenishment as of [end of the current year] 11,518,539.00 209,888.66 Total F 11,518,539.00 209,888.66

G Outstanding Amount of Imprest Account (A-C+D) @ NR 60.12 23,316,420.16 387,831.34 H Initial Deposit as at (original date) 33,059,893.20 I Exchange Gain/Loss (G-H) 1,775,065.96 -

NOTE ON IMPREST - ACTUAL SESSION 9.b

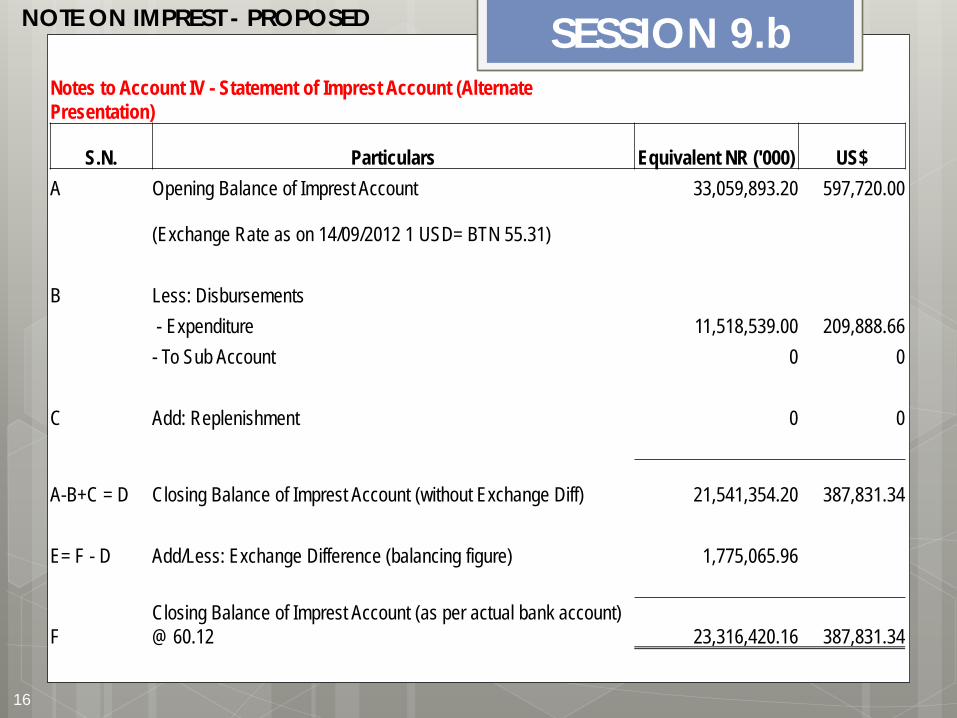

Notes to Account IV - Statement of Imprest Account (Alternate Presentation)

S.N. Particulars Equivalent NR ('000) US$ A Opening Balance of Imprest Account 33,059,893.20 597,720.00

(Exchange Rate as on 14/09/2012 1 USD= BTN 55.31) B Less: Disbursements - Expenditure 11,518,539.00 209,888.66 - To Sub Account 0 0 C Add: Replenishment 0 0

A-B+C = D Closing Balance of Imprest Account (without Exchange Diff) 21,541,354.20 387,831.34 E= F - D Add/Less: Exchange Difference (balancing figure) 1,775,065.96

F Closing Balance of Imprest Account (as per actual bank account) @ 60.12 23,316,420.16 387,831.34

16

SESSION 9.b NOTE ON IMPREST - PROPOSED

17

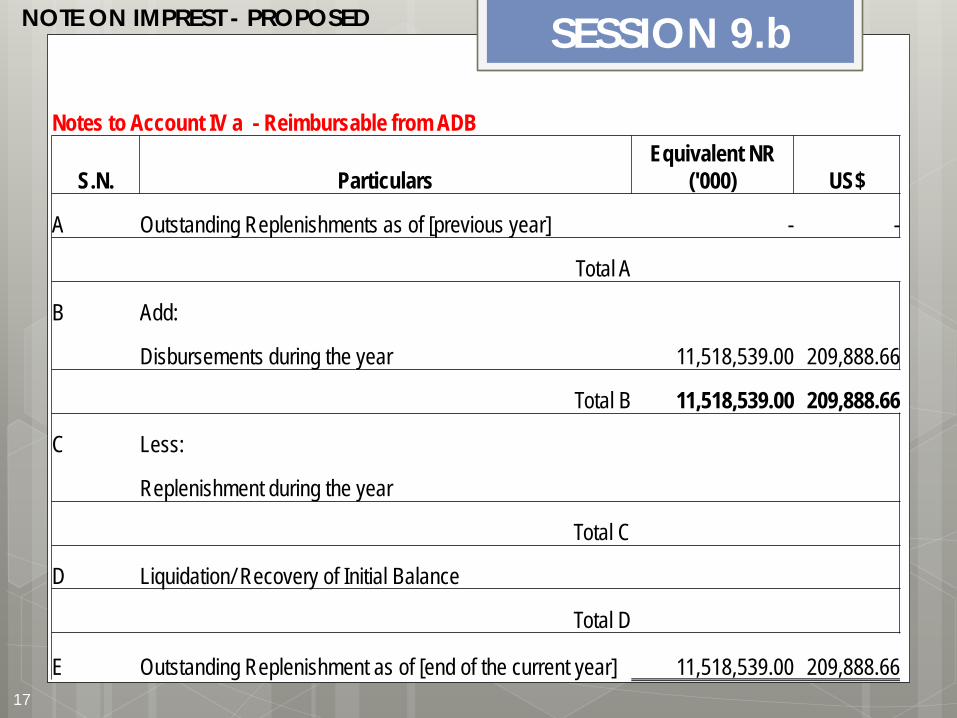

Notes to Account IV a - Reimbursable from ADB

S.N. Particulars Equivalent NR

('000) US$

A Outstanding Replenishments as of [previous year] - -

Total A

B Add:

Disbursements during the year 11,518,539.00 209,888.66

Total B 11,518,539.00 209,888.66

C Less:

Replenishment during the year

Total C

D Liquidation/ Recovery of Initial Balance

Total D

E Outstanding Replenishment as of [end of the current year] 11,518,539.00 209,888.66

SESSION 9.b NOTE ON IMPREST - PROPOSED

18

Notes to Account IV - Statement of Imprest Account

S.N. Particulars Equivalent NR

('000) US$

A Balance in Imprest Account as at [beginning of the current year] 33,059,893.20 597,720.00

(Exchange Rate as on 14/09/2012 1 USD= NR 55.31) Total A 33,059,893.20 597,720.00 B Outstanding Replenishments as of [previous year] - - Total B - - C Add:

Disbursements during the year 11,518,539.00 209,888.66

Total C 11,518,539.00 209,888.66 D Less: Replenishment during the year 0 0 Total D 0 0 E Liquidation/ Recovery of Initial Balance 0 0 Total E 0 0

F Outstanding Replenishment as of [end of the current year] 11,518,539.00 209,888.66

Total F 11,518,539.00 209,888.66

G Outstanding Amount of Imprest Account (A-C+D) @ NR 60.12 23,316,420.16 387,831.34

H Initial Deposit as at (original date) 33,059,893.20 I Exchange Gain/Loss (G-H) 1,775,065.96 -

NOTE ON IMPREST - ACTUAL SESSION 9.b Notes to Account IV - Statement of Imprest Account (Alternate Presentation)

S.N. Particulars Equivalent NR

('000) US$

A Opening Balance of Imprest Account 33,059,893.20

597,720.00

(Exchange Rate as on 14/09/2012 1 USD= BTN 55.31)

B Less: Disbursements

- Expenditure 11,518,539.00

209,888.66

- To Sub Account 0 0

C Add: Replenishment 0 0

A-B+C = D Closing Balance of Imprest Account (without Exchange Diff) 21,541,354.20

387,831.34

E= F - D Add/Less: Exchange Difference (balancing figure) 1,775,065.96

F Closing Balance of Imprest Account (as per actual bank account) @ 60.12 23,316,420.16

387,831.34

19

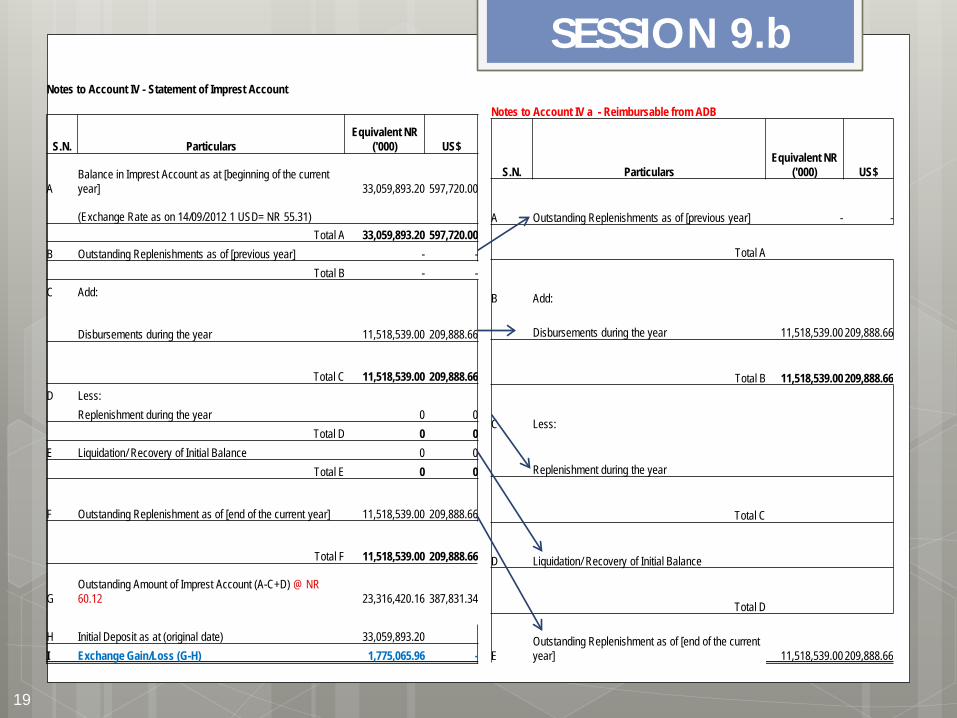

Notes to Account IV - Statement of Imprest Account

S.N. Particulars Equivalent NR

('000) US$

A Balance in Imprest Account as at [beginning of the current year] 33,059,893.20 597,720.00

(Exchange Rate as on 14/09/2012 1 USD= NR 55.31) Total A 33,059,893.20 597,720.00 B Outstanding Replenishments as of [previous year] - - Total B - - C Add:

Disbursements during the year 11,518,539.00 209,888.66

Total C 11,518,539.00 209,888.66 D Less: Replenishment during the year 0 0 Total D 0 0 E Liquidation/ Recovery of Initial Balance 0 0 Total E 0 0

F Outstanding Replenishment as of [end of the current year] 11,518,539.00 209,888.66

Total F 11,518,539.00 209,888.66

G Outstanding Amount of Imprest Account (A-C+D) @ NR 60.12 23,316,420.16 387,831.34

H Initial Deposit as at (original date) 33,059,893.20 I Exchange Gain/Loss (G-H) 1,775,065.96 -

Notes to Account IV a - Reimbursable from ADB

S.N. Particulars Equivalent NR

('000) US$

A Outstanding Replenishments as of [previous year] - -

Total A

B Add:

Disbursements during the year 11,518,539.00

209,888.66

Total B 11,518,539.00

209,888.66

C Less:

Replenishment during the year

Total C

D Liquidation/ Recovery of Initial Balance

Total D

E Outstanding Replenishment as of [end of the current year] 11,518,539.00

209,888.66

SESSION 9.b

Q & A Moderators: FCGO, RAMU DOTEL, OAG NEPAL, ADB & WB

SESSION 9.d

20

GROUP ACTIVITY Moderator: SHERAZADE SHAFIQ

SESSION 9.e-g

21

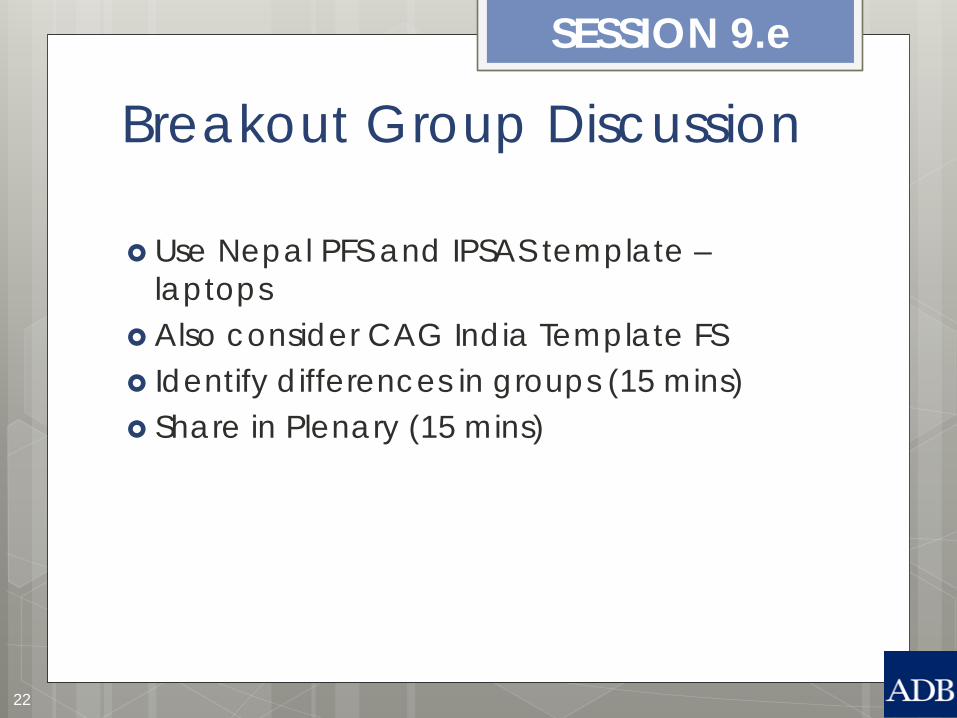

Breakout Group Discussion Use Nepal PFS and IPSAS template –

laptops Also consider CAG India Template FS Identify differences in groups (15 mins) Share in Plenary (15 mins)

SESSION 9.e

22

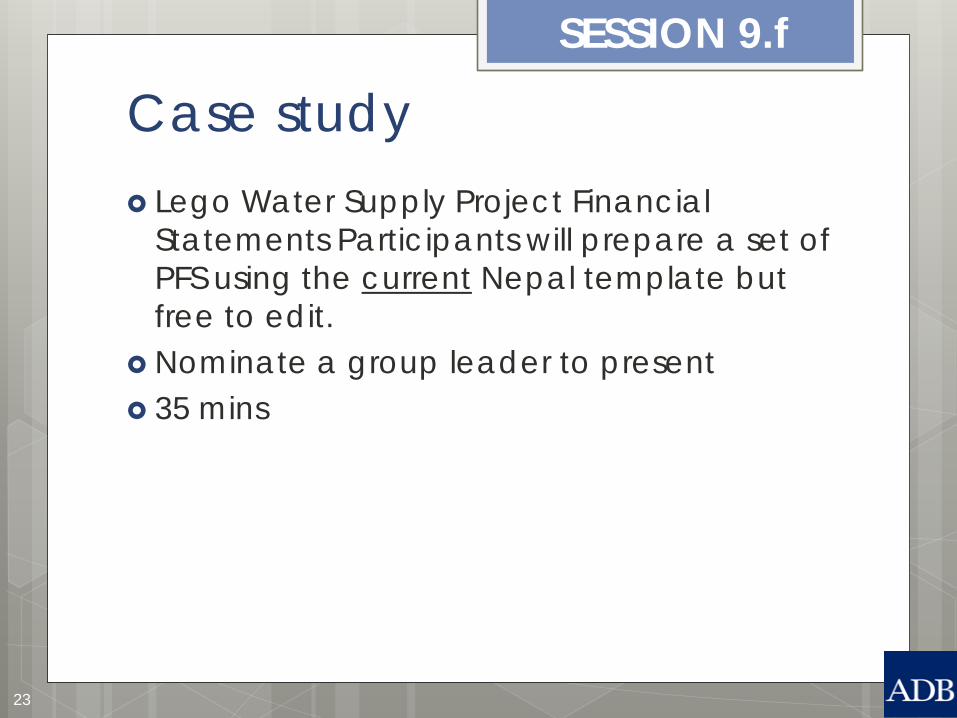

Case study Lego Water Supply Project Financial

Statements Participants will prepare a set of PFS using the current Nepal template but free to edit.

Nominate a group leader to present 35 mins

SESSION 9.f

23

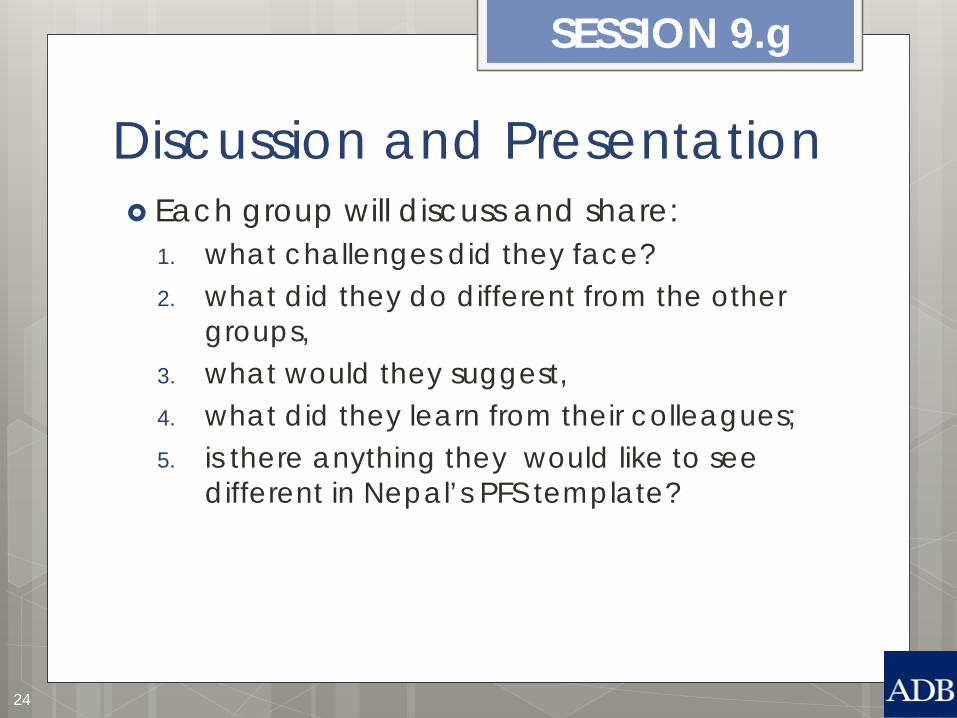

Discussion and Presentation Each group will discuss and share:

1. what challenges did they face? 2. what did they do different from the other

groups, 3. what would they suggest, 4. what did they learn from their colleagues; 5. is there anything they would like to see

different in Nepal’s PFS template?

SESSION 9.g

24

ACCRUAL BASIS IPSAS Presenter: Genevieve Buenaventura, FM Consultant, ADB

SESSION 9.c

25

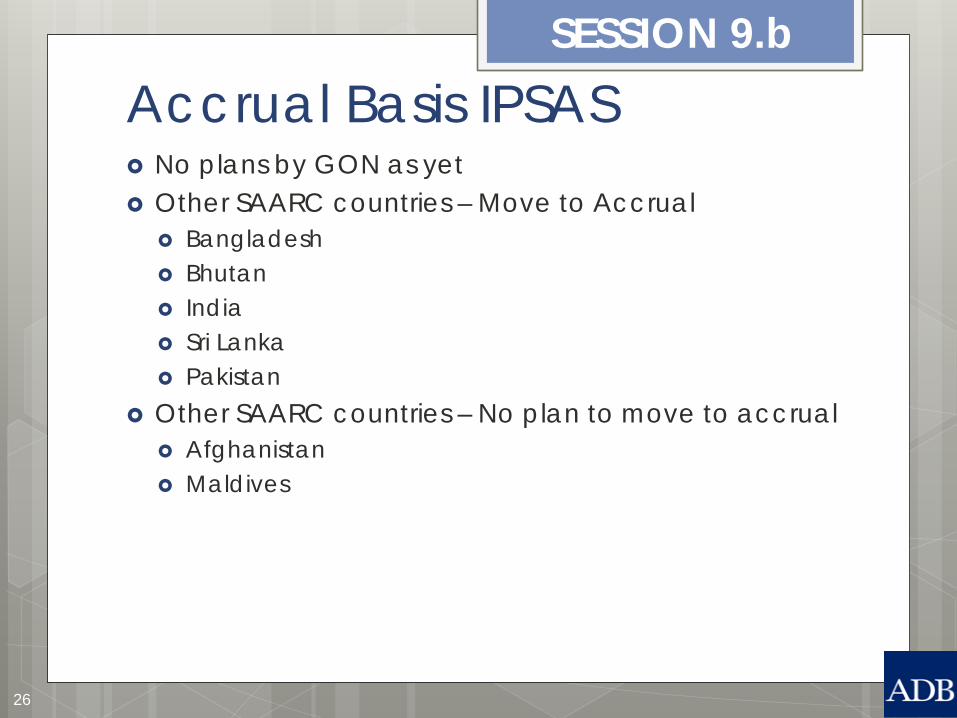

Accrual Basis IPSAS No plans by GON as yet Other SAARC countries – Move to Accrual

Bangladesh Bhutan India Sri Lanka Pakistan

Other SAARC countries – No plan to move to accrual Afghanistan Maldives

SESSION 9.b

26

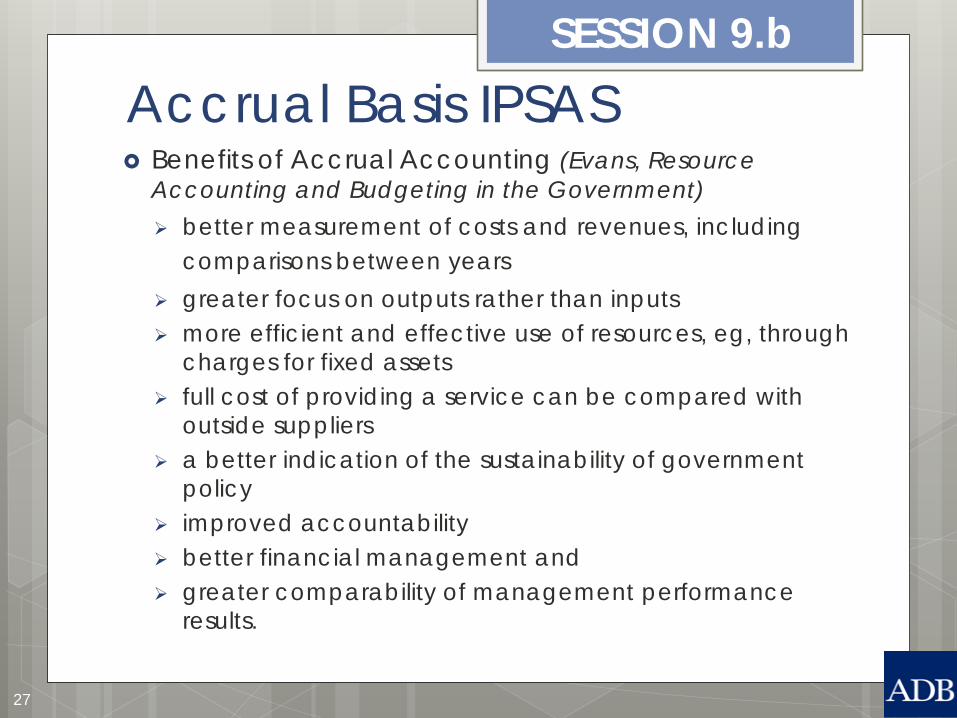

Accrual Basis IPSAS Benefits of Accrual Accounting (Evans, Resource

Accounting and Budgeting in the Government) better measurement of costs and revenues, including

comparisons between years greater focus on outputs rather than inputs more efficient and effective use of resources, eg, through

charges for fixed assets full cost of providing a service can be compared with

outside suppliers a better indication of the sustainability of government

policy improved accountability better financial management and greater comparability of management performance

results.

SESSION 9.b

27

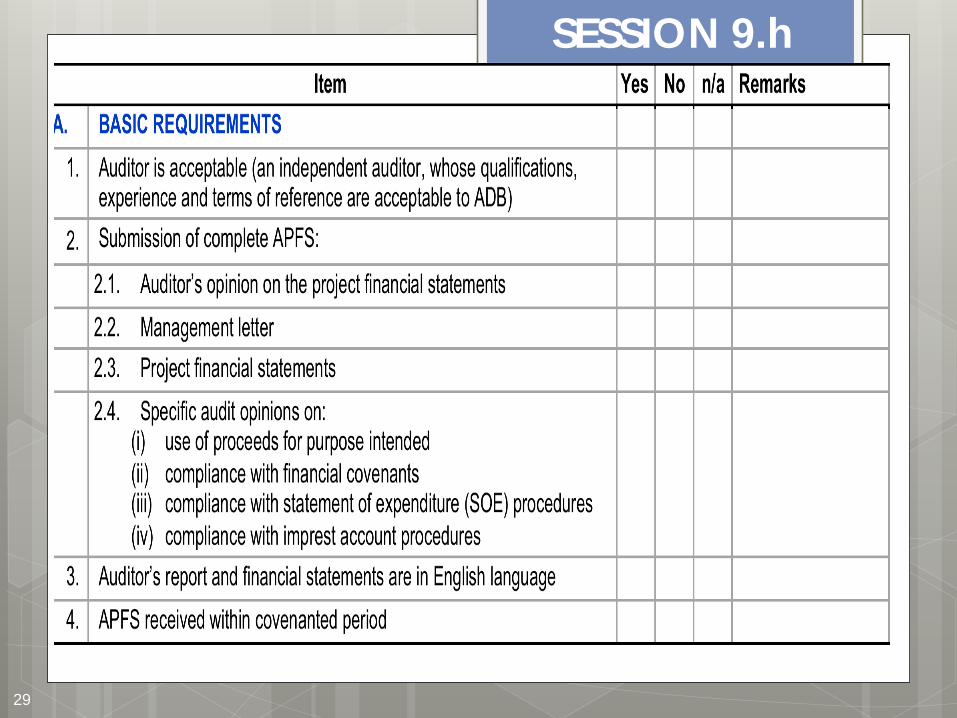

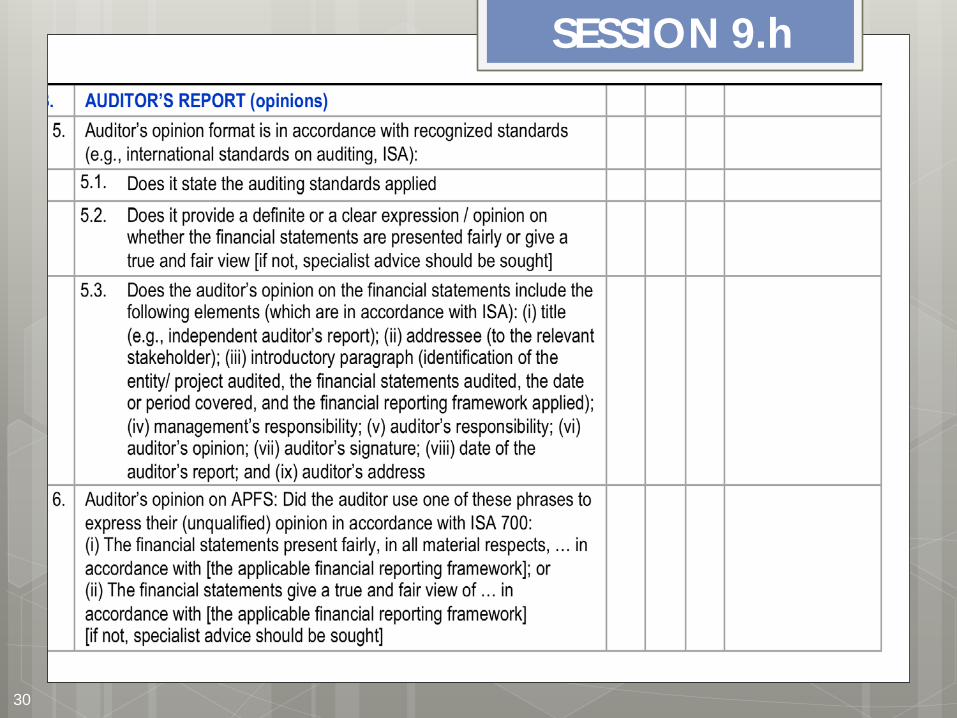

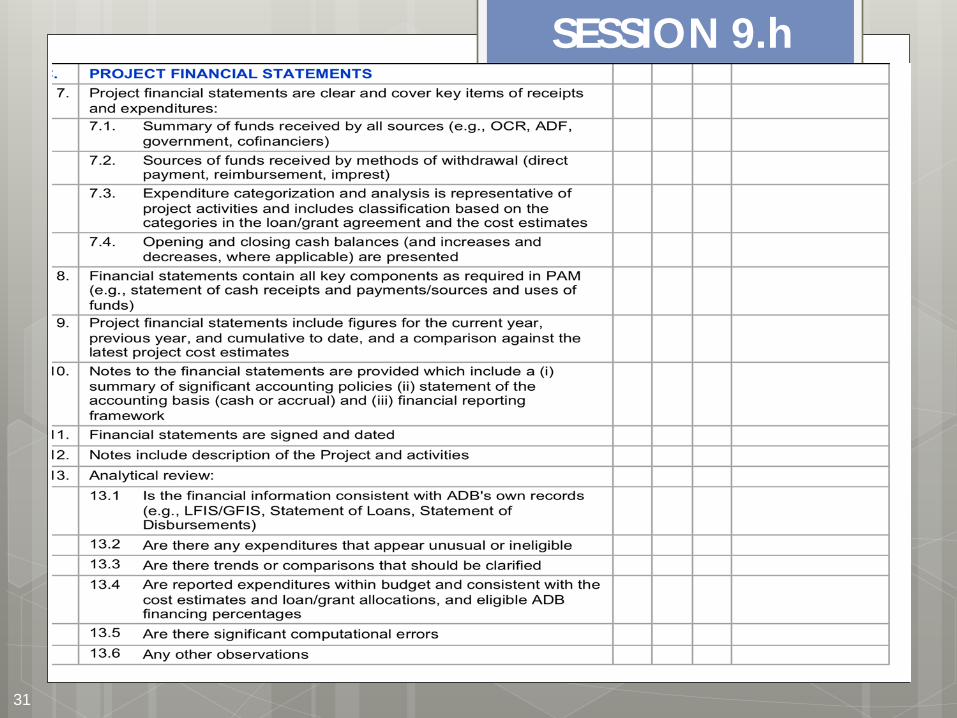

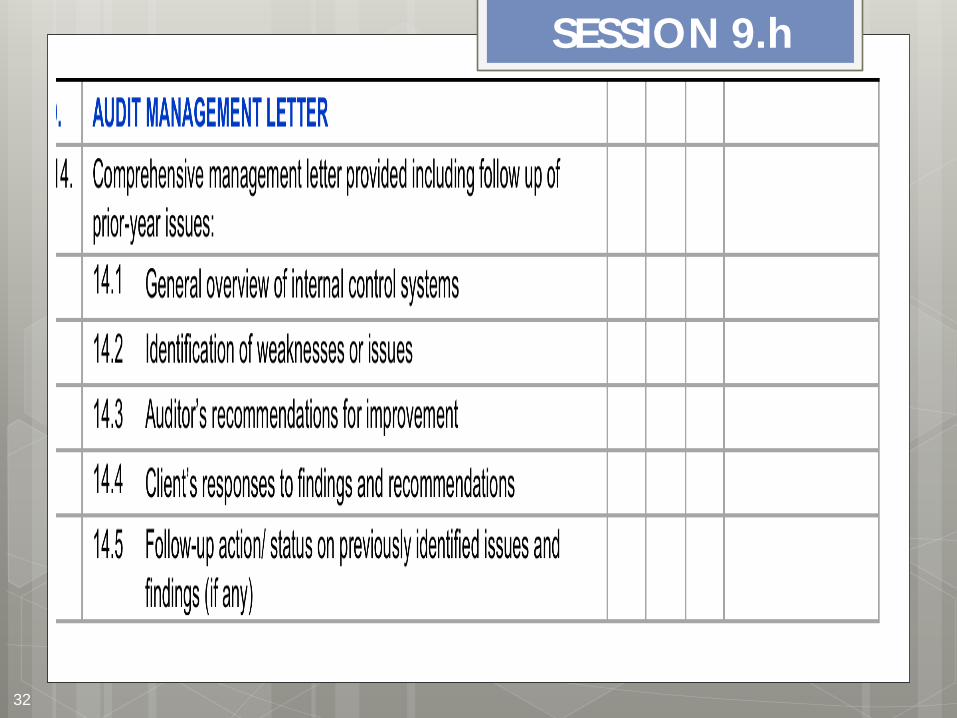

ADB’S APFS REVIEW CHECKLIST Presenter: SHERAZADE SHAFIQ

SESSION 9.h

28

SESSION 9.h

29

SESSION 9.h

30

SESSION 9.h

31

SESSION 9.h

32

Plenary Discussion Participants will discuss a possible action

plan for future consideration by GON Moderator: Timila, WB Discussants: Dr Asif, SAI Pakistan, Ibrahim

Fazeel, SAI Maldives, Ramu Prasad, OAG Nepal

SESSION 9.i

33

THANK YOU! END OF DAY 4 SESSIONS

SESSION 9

34