Embed Size (px)

Citation preview

37- JJ> 4 .:'., CIRCUATING CoPy RESTRICTED

TO BE RETURNED TO REPORTS DESK Report No. P1085

FtILE CcYThis report is for official use only by the Bank Group and specifically authorized organizationsor persons. It may not be published, quoted or cited without Bank Group authorization. TheBank Group does not accept responsibility for the accuracy or completeness of the report.

INTERNATIONAL DEVELOPMENT ASSOCIATION

REPORT AND RECOMMENDATION

OF THE

PRESIDENT

TO THE

EXECUTIVE DIRECTORS

ON A

PROPOSED CREDIT

TO

THE ISLAMIC REPUBLIC OF PAKISTAN

FOR AN

INDUSTRIAL IMPORTS PROGRAM

May 31, 1972

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Exchange Rate - Rps. 11.0 = US $1.00 *

Fiscal year ends June 30

* Country Data (Annex II)reflect, where applicable, pre-devaluationrupees as noted.

REPORT AND RECOMEDATION OF THE PRESIDENT TO THEEXECUTIVE DIRETORS ON A PROPOSED CREDIT TO THEISLAIC REPUBLIC OF PAKISTAN FOR AN IDUSTRIAL

IPORTS PROGRAM

1. I submit the foUoving report and recommendation on a proposeddevelopment credit to the Islamic Republic of Pakistan for the equivalentof US $50 million on standard IDA terms, to help finance the foreignexchange cost of industrial imports and fertilizer required during theperiod July 1, 1972 to June 30, 1973.

PART I - THE ECOONMY

Introduction

2. An economic report entitled "Economic Poaition and Prospectsof Pakistan" (R70-150, dated June 18, 1970) was distributed to the ExecutiveDirectors on July 28, 1970. A,summary of the Country Basic Data isattached as Annex II. An economic mission is scheduled to visit Pakistanin September to review the economic situation and prospects of the countryand progress in redefining development priorities. A Bank staff meterwif join an IMF review mission which wlll visit Pakistan in July 1972to review progress in the implementation of the recently announcedprogram of economic and financial reforms and to set credit ceilingsfor the standby arrangement after June 30, 1972. A mission iscurrently in Pakistan to review the power sector.

3. The application by the Goverrnment of Pakistan to the InternationalDevelopment Association for an industrial inports credit of $50 millioneqaivalent has been made against the background of the very difficultproblems of economic adjustment which the country is facing at the presenttine. The case for such a credit should be considered in the context ofthe Government's efforts to overcome these problems and to rebuild thebasis for development in Pakistan.

4. To these ends, the Government has already taken action, andintends to introduce further measures to improve substantially thegeneration and efficient use of resources for development. Thesemeasures will, however, take time to make themselves felt. In themeantime, the Government 'a imediate concern is to prevent any fartherslow-down in economic activity which, with its attendant social andpolitical problems, would seriously hamper the process of adjustment. Forthis reason the Government is seeking external assistance on a substantialscale. This assistance, to be effective, has to be quick-diabursing insupport of current economic activity. Apart from its application to IDA,the Govermnent has already obtained a standby of SDR 100 million from the

- 2 -

IMF and 1i endeavoring to restore ita aid arrangements with the membersof the Pakistan Consortium to a normal basis.

Recent Developments

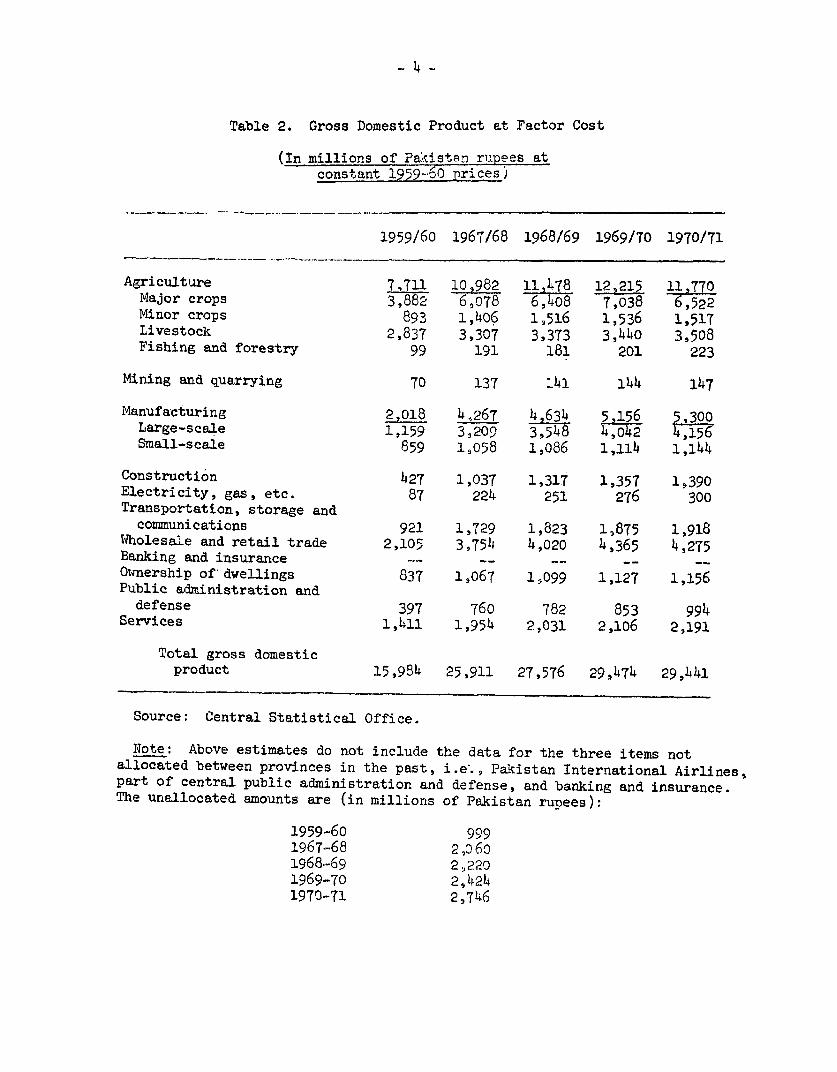

5. The severity of Pakistan'a current economic difficulties may beillustrated by recent trends in a number of key indicators . GDP atconstant prices stagnated during the past two years, following a periodof sustained growth in the 1960'e at an annual rate exceeding 6 percent.Thib deterioration reflects in part bad weather which particularlyaffected the wheat crop. However, ite underlying cause has been theprotracted decline in the growth of large-scale manufacturing output,from nearly 14 percent a year through 1967/68 to 2-3 percent in the pasttwo years.

6. Public development expenditures had by 1968/69 recovered fromthe effects of the 1965 war with India and two years of poor harveststo a level roughly equivalent to 10 percent of GDP. Since then, they havefallen to less than 6 percent of GDP, reflecting, mainly, the deteriorationin public savings, from nearly 3 percent of GDP to a current deficit of 1percent of GDP, which were squeezed between stagnating revenues and fastrising non-development outlays. At current prices, public developmentexpenditures declined from Rs. 3,200 million in 1968/69 to an estimatedlevel of RB. 2,400 million in the current fiscal year ending June 30,1972, which is being financed by bank credit on.a scale which cannot besustained, and by external assistance. In real terms the decline hasbeen even greater. As outlays on Indus/Tarbela have absorbed about Rs. 800million a year (excluding external grants), it has been very difficult toprovide adequate financing for other on-going development schemes, letalone for new ones.

7. Meaningful comparable data for private investment are notavailable, but there iB ample evidence that, because of lack of confidence,investment in the private sector has fallen considerably over the lastfew years. Rougb estimates suggest that total gross investment in 1971/72is down by about one fourth from the previous year and, at 12-13 percentof GDP, substantially below the level of about 18 percent prevailing throughthe late 1960's.

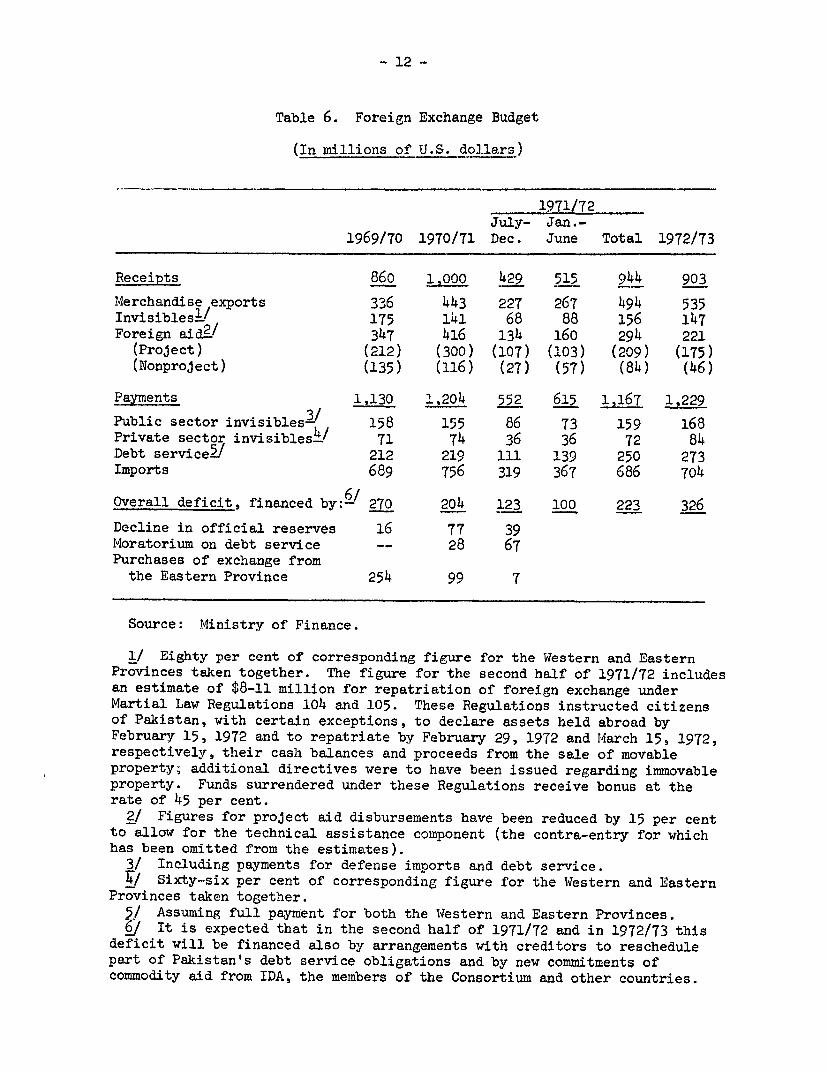

8. The imediate economic problems confronting Pakistan are alsoclearly shown in the balance of payuwnts. Late in 1969/70 and continuinginto 1970/71, in an attempt to revitalize industrial growth, which had for sometime suffered from inadequate supplies of imported materials, the authoritieseased restrictions on imports. Total imports in 1970/71 rose by about 10percent and imports other than food and capital equipment by 7 percent. Atthe same time, purchases of foreign exchange from East Pakistan fell sharplybecause of political disturbancea. The adverse effects of these two factorsfar exceeded the additions to receipts from exports and external assistance,forcing Pakistan to draw on its reserves, including SDR's, at a monthly rateof $16 million during the first nine months of the fiscal year. Since

reserves at the beginning of the year plus the 1971 allocation of SR?awere only $317 million, they fast approached a dangerously low level. Toavert an acute payments crisis, the authorities tightened import restrictionBfrcm January 1971 onwards, and in June of that year substantially raisedthe effective rupee cost of most imports through ad hoc adjustments in themultiple rate system. They also imposed a moratorium on payment of alarge part of Pakistan's debt service obligations to bilateral creditors.These measures, together with a further subatantial increase in exchangeearnings, succeeded recently in halting the steady decline in reserves.Gross reserves have since fluctuated around $200 million.

- 4 -

WEST PAKISTAN - FOREIGN EXCHANGE BUDGEr(US $ Million)

1969/70 1970/71 1971/72(Provisional)

Receipts 828 932 1,053

Merchandis 1 Exports2/ 338 420 570Invisibles_ 175 141 168Foreign Aid 315 371 315

(Project)3/ (180) (255) (210)(Non-Project)4/ (135) (116) (105)

Payments 1,130 1,203 1,247

Public Sector Invisibles5/ 158 155 202Private Sector InvisiblesZ/ 71 74 84Debt Se <i.ce7/ 212 219 251Imports_ 689 755 710

Overall Deficit 302 271 194

Financed by:Moratorium on Debt Service - 28 118Imputed Exchange Receipts fromForeign Earnings of theEastern Province 251 133 7

Use of Reserves°/ 51 110 69

Source: Government of Pakistan, Finance Division, Economic Affairs Division,Central Statistical Office and IBRD staff estimates.

1/ On shipment basis as recorded by CSO.2/ For 69/70 and 70/71, estimated at eighty percent of corresponding figure

for the Western and Eastern Provinces taken together. The figure for1971/72 includes an estimated $10 million for repatriation of foreign ex-change under Martial Law Regulations 104 and 105 which required citizensof Pakistan, with certain exceptions, to declare their assets held abroadand to repatriate within a specific time their cash balances and proceedsfrom the sale of movable property; special directives were given alsoregarding immovable property. Funds surrendered under these Regulationsreceived bonus at the rate of 45 percent.

3/ Project aid disbursements as shown are reduced by 15 percent to allow forthe usually associated technical assistance component (the contra-entryfor which normally is not reflected in the foreign exchange budget).

4/ Including food aid.Including payments for defense imports.

6 For 1969/70 and 70/71, estimated at sixty-six percent of correspondingfigure for the Western and Eastern Provinces taken together.

7/ Assuming full service on all debt outstanding as of December 1971.9/ Including use of SDR's plus IMF credit facility, and residual balances.

9. However, the stabilization was achieved at very considerablecost to the economy because imports, other than food to meet shortagesof foodgrains, edible oils and sugar, had to be reduced significantly 1/while the introduction of the moratorium further complicated Pakistan'srelations with the Consortium which has made no new commitments of aidsince early 1971. Thus, projections for 1972/73, prepared a few monthsago, suggested that Pakistan faced the prospect of having to cut totalimports by a further 30 percent and imports for current production evenmore.

10. The difficult economic situation that has been describedabove can be traced principally to two causes: first, the failure ofprevious Administrations in Pakistan over a period of several years totake action appropriate to deal with a deteriorating economic situation;secondly, the economic consequences for Pakistan of political eventssince early 1971, culminating in the separation of the former Provinceof East Pakistan, which declared its independence and became Bangladesh.The situation has been aggravated further by rapidly rising debt serviceobligations -- from $212 million in 1969/70 to $251 million in 1971/72and $281 million in 1972/73 2/ __ and the decline in disbursements ofnon-project assistance (excluding food aid) -- from $135 million in1969/70 to $78 million in 1971/72, reflecting the absence of new commit-ments since early 1971, other than for food. Non-project aid disburse-ments (excluding food) from the existing pipeline in 1972/73 areexpected to be only $57 million.

11. Among the inadequacies of past economic policies, those rela-ting to the exchange and fiscal systems have had the most pervasiveadverse effects. Both systems as they had developed through numerousad hoc adjustments, had come to embody very severe distortions thatproved increasingly inimical to efficient use of resources for develop-ment; and both systems were ill suited, in Pakistan's changingeconomic circumstances, for the generation of resources for developmentat a pace commensurate with the country's needs.

12. The multiple exchange rate system was initially introduced asa simple two rate regime intended to promote industrialization whileprotecting the balance of payments, and to give special incentives toexports of manufactures. In the course of the 1960's, the exchange ratesystem underwent many ad hoc adaptations to changing circumstances --partly, in response to a tightening exchange situation, to raise theeffective price of exchange with a view to atrengthening export incen-tives and relieving pressures on the import control system; partly, in

1/ The figures shown in the foregoing table understate the extent ofthe reduction because they do not take account of imports under inter-wing trade which in 1969/70 amounted to about $l10 million at inter-national prices and which have since ceased.

2/ Based on all external debt contracted by Pakistan up to December 1971.

-6-

response to the emergence of agriculture in the latter 1960's as apotential growth sector, to extend to the development of that sector(but with notable exceptions) the incentives previously given exclu--sively to industry.

13. By the end of the l960's, these adaptations had produced arange of effective prices of exchange so wide -- from Rs.3.10 to thedollar to Rs.20, including duties, other taxes and subsidies -- thatthe system could no longer function as a guide to the efficient alloca-tion of resources. In particular:

(a) On the export side, it discriminated greatly againstprimary products -- the rate being Rs.4.76 to thedollar as against about Rs. 8.50 for manufactures --at a time, when all indications were that strongprice incentives were necessary to promote increasedproduction of primary products for export.

(b) On the import side, the effective cost of exchange.for finished capital goods was about 60 percent lessthan for industrial raw material imports, clearlyfavoring the creation bf assets over their utiliza-tion, discouraging the development of the domesticcapital goods producing industry, and distortingfactor relations in favor of capital as againstlabor. These distortions were further reinforcedby the operation of the system of allocating importlicenses for industry, fiscal incentives for invest-ment, and the credit system. Further adaptation ofthe system in 1971 did not bring about essentialimprovements, except in the case of primary exports,the effective price of exchange for which.was raisedby Rs.0.90 per dollar, or nearly 20 percent. Thislargely accounted for the increase in the cotton cropin 1971/72 by about one third.

14. At the same time, the system required increasingly heavyreliance on quantitative restrictions to maintain the equilibriumbetween receipts and payments. The way in which these restrictionswere applied in controlling imports of industrial materials tended toreinforce the bias in the price system in favor of further additions ofproductive capacity, rather than increases in current production byfuller utilization of the existing capacity.

15. The fiscal system has suffered from the following weaknesses:

(a) The tax system has been highly inelastic with respect toincome so that, at any given set of tax rates, the shareof tax revenue in GDP has tended to fall over time,largely because income generated at the main sources ofgrowth -- manufacturing and, in the latter 196 0's,agriculture -- has either been excmpted altogether from

-7-

taxation or subjected to more or less fixed payments.Furthermore, tax revenues have remained heavilydependent on importa -- customs duties and relatedlevies account roughly for 40 percent of total taxrevenues -- while imports have tended to decline inrelation to GDP. As a result, substantial tax measureswhich the Government has taken over the years merelysucceeded in maintaining the tax rate at about 10-12percent of ODP. This is low by cotparison with otherdeveloping countries, and certainly ±nadequate inrelation to Pakistan's needs. Present estimatesindicate that in the current fiscal year, tax revenuesdeclined by about 5 percent.

(b) The revenue syatem has been inequitable betweenincome groups and between sectors, particularlybetween agriculture and the rest of the economy.As a remedy for the first inequity, the share ofdirect taxation -- only about 17 percent of totaltax revenue and Just over 2 percent of GDP --needs to be raised considerably. The latterraises the whole question of agricultural taxation(as well as subsidy and price policies) on which agood deal of staff work was done in the Govermentin 1969/70, only to be shelved beeause the Govern-ment at the time was reluctant to move.

(c) Over time, a wide array of Interventions has beenbuilt into the fiscal system, on both the revenueand expenditure sides (exemptions or deductions intaxes, subsidies) which, apart fram being incertain instances mutually contradictory or inconflict with incentives and disincentives builtinto the exchange system, have on the whole provedto be no longer useful or to have become positivelyharmful.

16. As regards the second principal cause of Pakistan's presenteconomic difficulties -- its truncation by the separation of its formerEast wing -- it needs to be remembered that what used to be West andEast Pakistan never constituted a thoroughly integrated economic unit.The high cost of transport between the two wings and the absence ofappropriate policies limited integration. Nevertheless, the independenceof Bangladesh has affected Pakistan in two vital areas, the balance ofpayments and public financee, sggranating difficulties of economic adjust-ment which Pakistan was already experiencing. Whether there was, in theperiod immediately preceding separation, a net flow of resources to whatis now Pakistan or to Bangladesh is impossible to determine definitively,in view of the lack of comprehensive data, the distortions introduced by

- 8 -

differential pricing, and the lack of a basis for judging what proportionof the cost of Central Government services should have been borne by theEast and how much of the external assistance obtained should have accruedto it.

17. First, in respect of the balance of payments, Pakistan, separatedfrom Bangladesh, has lost access to substantial amounts of foreign exchangewhich it used to purchase from the East tingg These purchases reflectedthe much greater degree of industrialization and the higher levels ofincome and expenditures in the West wing, and the fact that CentralGovernment expenditures were largely made in the West wing. As shown inthe table in paragraph 8, and on the assumptions set out in the footnotes,rough estimates place the amount of exchange so acquired by Pakistan atabout $250 million in 1969/70. At the same time, however, West Pakistanhad a sizeable surplus in inter-wing trade of Rs. 750 million, exportsbeing Rs. 1,665 million and imports Rs. 915 million. Because of wide dif-ferences in domestic prices it is difficult to translate these rupee figuresinto dollars at international prices. However, in rough orders of magnitude,exports might be put at $200 mlllion equivalent, imports at $110 million,and the trade surplus at $90 million.

18. Thus, even if it were possible immediately to convert inter-wingtrade into international trade, Pakistan's exchange gap would be about $130million larger than in 1969/70 (see table in paragraph 20). However, itshould be borne in mind that an important factor in this large increase inthe gap is the inclusion of the service of all the external debt contractedby Pakistan up to December 1971.

19. In fact, it would be unrealistic to expect that goods previouslyexported under inter-wing trade can immediately be converted into exportsto international markets. For some goods, notably cotton and cotton manu-factures, which have constituted about 30 percent of the total, diversionshould be fairly easy. For another 25 percent, comprising essentially riceand tobacco, it may be very difficult to find alternative markets. Theremainder consists very largely of a wide range of manufactures, many ofwhich Pakistan did not in the past export in sizeable quantities. The needto find new markets for them underscores the need noted above for adequateincentives for exports; inevitably, however, diversion of exp6rts will taketime. In contrast to these problems of adjustment on the export side, thereshould be no difficulty in switching to alternative sources of supply forgoods previously obtained under inter-wing trade. Moreover,, with the excep-tion of tea (27 percent of the total) and small quantities of essentialconsumer goods, these imports consisted of materials for production, andtherefore formed part of the supply of goods necessary to sustain production.

20. The pressures on the balance of payments or the level of economicactivity, by these problems of trade and other adjustments associated withthe separation of Bangladesh, are illustrated in the table below. It isimpossible to quantify all the balance of payments effects of separationand the table must be regarded purely as illustrative of orders of magni-tude. The figures for 1972/73 assume full diversion of inter-wing importsat the 1969/70 level.

- 9 -

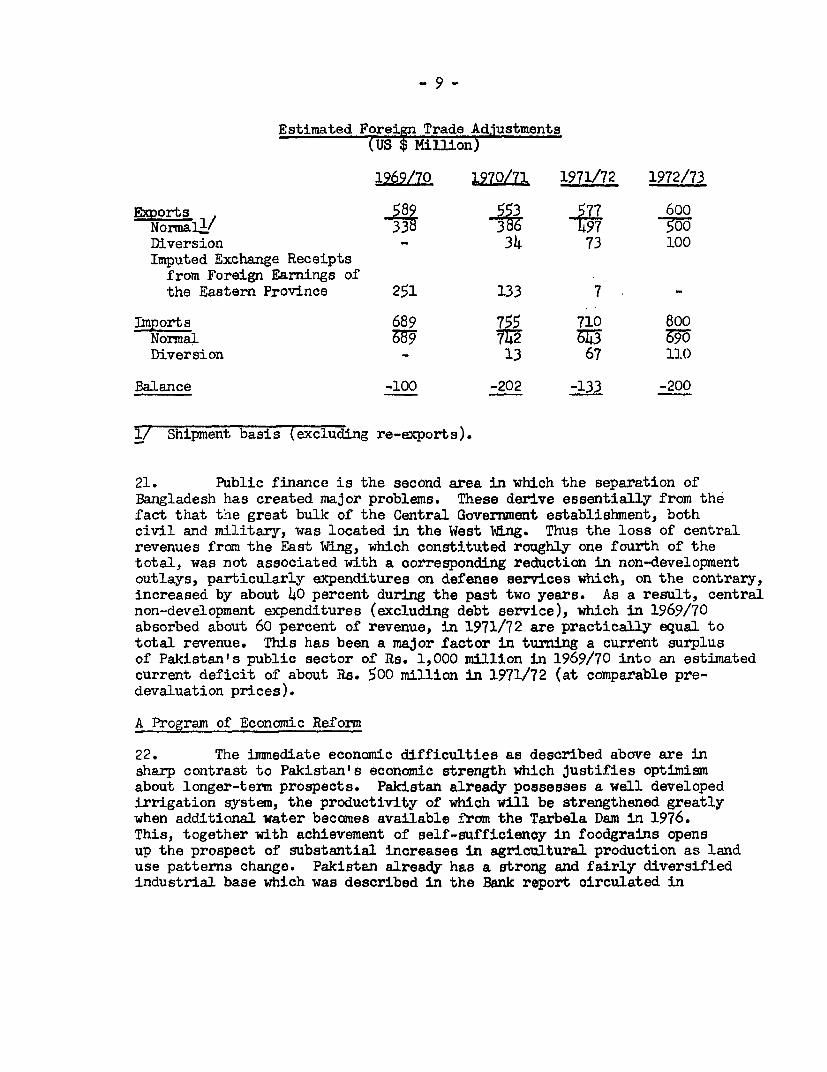

Estimated Foreign Trade Adjustments(US $ Million)

1969/70 1970/71 1971/72 1972/73

g&orts 589 553 577 600Normal_1/ 3d =3 497 7500Diversion - 34 73 100Imputed Exchange Receipts

from Foreign Earnings ofthe Eastern Province 251 133 7 .

Imports 689 755 710 800Normal W9 72E 69 0Diversion - 13 67 110

Balance -100 -202 -133 -200

1/ Shipment basis (excluding re-exports).

21. Public finance is the second area in which the separation ofBangladesh has created major problems. These derive essentially from thefact that the great bulk of the Central Government establishment, bothcivil and military, was located in the West Wlng. Thus the loss of centralrevenues from the East Wing, which constituted roughly one fourth of thetotal, was not associated with a corresponding reduction in non-developmentoutlays, particularly expenditures on defense services which, on the contrary,increased by about 40 percent during the past two years. As a result, centralnon-development expenditures (excluding debt service), which in 1969/70absorbed about 60 percent of revenue, in 1971/72 are practically equal tototal revenue. This has been a major factor in turning a current surplusof Pakistan's public sector of Rs. 1,000 million in 1969/70 into an estimatedcurrent deficit of about Ra. 500 million in 1971/72 (at comparable pre-devaluation prices).

A Program of Economic Reform

22. The immediate economic difficulties as described above are insharp contrast to Pakistan's economic strength which justifies optimismabout longer-term prospects. Pakistan already possesses a well developedirrigation system, the productivity of which will be strengthened greatlywhen additional water becomes available from the Tarbela Dam in 1976.This, together with achievement of self-sufficiency in foodgrains opensup the prospect of substantial increases in agricultural production as landuse patterns change. Pakistan already has a strong and fairly diversifiedindustrial base which was described in the Bank report circulated in

- 10 -

19701{ Its entrepreneurs have proved themselves capable of rapidly expandingproduction, not only for the damestic market but also for export, and the laborforce is easily trainable and hard working.

23. Having, during its initial months in office, been preoccupiedwith the political aspects of its task, President 3hutto's Administrationthen turned its attention to the difficult economic problems facing Pakistan.Recognizing that Pakistan can overcome its current difficulties and realizeits potential for development in the longer run only by thorough improvementof the economi-c policy framework, it has embarked on a comprehensive economicand financial program. Its purpose is to restore conditions conducive todevelopment by effecting substantial improvements in the mobilization ofresources, both foreign and domestic, and in the efficiency of their use.

24. The crucial importance of a suitable exchange rate system to itsefforts of rebuilding a basis for development was recognized and on May 12,1972 the Government announced a fundamental reform which raised the parvalue of the Pakistani rupee from Rs. 4.76 to Rs. 11.00 to the US dollar,abolished the previously existing system of multiple exchange rates, andintroduced measures designed to move towards a more liberal import policy.The contents of the reform and an analysis of its effects are presentedin detail in the recent IMF documents in Annexes IV and V.

25. For the reasons explained above, a thorough-going reform of theexchange system has long been regarded as essential to the resumptionof adequate growth of exports and of production and investment.. TheGovernment, with the reforms recently announced, has acted effectivelyto remedy a crucial weakness in Pakistan's economic policy framework, whichhas had pervasive effect on the economy, both on the mobilization and onthe use of resources for development. In particular, the reform:

(a) on the export side, raised the average rupee proceeds perdollar by about 20 percent; and by 30 percent for primaryproducts, after allowing for export duties;

(b) on the payments side, increased the effective rate forimports, on the average, by 40 percent and for invisiblepayments, including debt service, by 117 percent, the averagefor all payments being 66 percent;

1/ Industrialization of Pakistan, The Record, The Problems and TheProspects (R70-53; April 2, 1970)..

(c) through the new import policy provides for the elimination of allquotas, categories and entitlements as existed under the old scheme.Two basic "lists" replace the former regime of various categoriesof imports: the free list and the tied list. The latter is confinedto some 25 items financed under aid and barter, while most importsare on the free list comprising about 320 items. In addition, afew specified commodities, such as coal, fertilizer, rail andtrack material, electricity generating and transmission equipment,etc., are reserved for public sector import only, and certain luxurygoods continue to be banned.

26. As Pakistan's exchange system has for so long been marked by quanti-tative restrictions and numerous complexities, it is difficult to quantify theeffects of the reform on the balance of payments. It is reasonable to expectthat exchange receipts will, over time, increase substantially; exports ofcommodities have, in the past, proved highly elastic with respect to price.Most of Pakistan's exports represent only a small fraction of world trade and theprice elasticity of demand for them is high, so that Pakistan should be ableto increase its export volume considerably without a significant effect onprices; diversion to foreign markets of goods previously shipped under inter-wing trade should be easier.

27. The reforms will probably have only a very limited effect on thelevel of payments as import liberalization is accompanied by a substantialincrease in effective rates for imports. However, the structure of importsshould be significantly affected because, by eliminating the artificiallylow effective rate for imports of capital goods and the system of allocatinglicenses to individual users in the manufacturing sector, the use of existingcapacity and development of the domestic capital goods producing industryshould be encouraged.

28. While certain adjustments of the fiscal system have been made con-currently with the introduction of the exchange reform and import liberalization,the Government recognizes that the next steps must be directed towards a fun-damental reform of the fiscal system and containment of non-development expen-ditures. As the Government foresees a considerably enlarged role for the publicsector, the ultimate objective of such a reform must be to raise the sharesof public savings and public development expenditures above the levels of 3and 10 percent of GDP, respectively, achieved in 1968/69. In view of the deter-ioration that has since occurred and the low levels to which public savings anddevelopment outlays have fallen, it will undoubtedly take time to achieve thenecessary improvements, in part because measures to raise public savings willhave to be designed so as to be compatible with other important objectives offiscal reform, in particular, achievement of greater equity and the eliminationof the distorting effects on resource allocation contained in the presentfiscal system.

- 12 -

290 The Government intends to introduce measures in the next budget,due to be announced before the end of June, that will improve the working ofthe fiscal system in the financial year beginning July 1, 1972. To help preparerevenue measures, the Taxation Commission has been reconstituted and instructedto make proposals for the 1972/73 budget. An important objective of that budgetwill be-to raise significantly the contribution of donestically generated re-sources to public development, while reducing reliance on bank credit, andthereby to make possible a substantial increase in public development expenditures.

30. Meanwhile, the Government has introduced measures to bring about reformsin agriculture, industry, and financial institutions. A land reform programwas announced on March 1, and action is being taken to regulate relations betweenlandlords and tenants. With the objective of improving efficiency and combat-ting tax evasion in the manufacturing sector, the Government replaced the managersof all private companies in ten basic industries!/ by Government appointeesand the system of managing agencies was abolished. In the financial sphere,the State Bank's control over private commercial banks and their credit policieshas been greatly expanded with the objective of ensuring a more effective andequitable distribution of funds among the various sectors of the economy withspecial regard also to smaller and less priviledged borrowers, particularlyin agriculture and industry; in this connection a National Credit ConsultatiteCouncil wvith public and private representation is being formed. To deal withpressing social problems, a public works program and new programs in educationand health were anhounced.

31. For most of these policies, particularly those in the social field,detailed and staged plans remain to be worked out. At the same time, theGovernment is engaged in a, review of priorities for public development whichhas become necessary because the Fourth Five-Year Plan, adopted in mid-1970, is nolonger relevant in the light of the change in circumstances resulting from theseparation of the East wing. The Government is also considering how best to:reorganize public development planning to give effect to the increased respon-sibility allocated to the Provincial Governments. Work on an interim develop-ment program is planned to be completed and the results announced, in conjunctionwith the budget for 1972/73.

Aid Requirements

32. Comprehensive reforms along the lines described in the preceding sectionshould provide the basis for the restoration of an adequate rate of development.However, the measures already taken, in particular the exchange reform and imp ortliberalization, and those to be taken in connection with the budget for 1972/73,will take time to make themselves felt. In the meantime, to facilitate adjustmentand to avoid a sharp decline in imports which would further complicate an alreadydifficult economic situation, Pakistan will require external assistance ona scale substantially larger than it would normally need.

1/ Iron and steel; basic metals, heavy engineering, heavy electrical, motorvehicle assembly and manufacture tractor assembly and manufacture, heavyand basic chemicals, petrochemicals, cement and public utilities.

- U -

33. Present projections of the balance of payments for 1972/73, asshown below, indicat that Pakistan will require a net transfer of resourcesfrom abroad in the order of $285 million.

Balance of Payments(US $ Million)

1969/70 1972/73

Receipts Lco51t6j3Merchandise Exports- 3 XInvisibles 175 168

Payments 918 102Merchandise Iiports 9 80Public Sector nvsibles 158 168Private Sector Invisibles 71 84

Deficit on Goods and Services 405 284Imputed Exchange Receipts from

Foreign Eamings of theEastern Province 251 ---

Net Foreign Transfers, inoludinguse of reserves 154 264

I/ Shiipment basis

34. As shown in the table, exchange earnings are projected to be about75 percent higher in 1972/73 than they were three years ago. A relatively moderateincrease in foreign imports is expectedj assuming essentially a restoration of thelevel in 1969/70 plus substitution of additional requirements of about $110 millionpreviously met fron interwing trade, bringing the total to about $800 million.This projection, however, contains a considerable element of uncertainty as theultimate impact of the recent import liberalization measures in connection withthe exchange reform is, as yet, difficult to gauge. Moreover, while there werevery small imports of foodgrains in 1969/70, such imports are estimated to besubstantial (possibly as high as $50 million) in 1972/73 to overcome shortagesdue to poor wheat crops in the past two years because of drought and to safeguardagainst price pressures following devaluation. Thus, the above import projectionsactually imply a considerable constraint on total non-food imports and, therefore,are to be considered a minimum requirement to sustain economic activity at a levelcompatible with the objective of rebuilding the base for development. In regardto exports it must be observed that the very favorable performance in 1971/72,reflecting largely a bumper cotton crop supported by high international prices,cannot be expected to be repeated. The cotton crop may well remain below thisyear's level and cotton prices already show a declining trend. Thus, exportprojections too have to be viewed with ame caution.

35. To determine gross aid requirements to make possible the net transferestimated above, Pakistan's debt service obligations have to be taken intoaccount. As shown in the table below, debt service obligations, estimatedon this basis,. amount to $281 million in 1972/73, as compared to $212 millionin 1969/70.

Total Deficit and Financing(US $ Million)

1969/70 1972/73

Requirements

Deficit on Goods and Services 437 284Debt Service 212 281

Total 649 565

Financing

Imputed Exchange Receipts from Foreign Earningsof the Eastern Province 251 -

External Financing (including use of reserves) 398 -

Total 649

The 1972/73 requirement could be met as follows:Existing credits for projects 150Existing credits for commodities and food 118Additional financing requirements 297

Total 565

36. The Government has approached the IMF, the members of the PakistanConsortium and IDA to help cover the residual deficit of about $300 million.On May 17, 1972, the IMF Board approved Pakistan's request for a stand-bycredit of SDR 100 million, to provide net credit, after taking account ofrepurchases due during the period, of SDR 74 million. Recourse to theFund is essential to cover the time until longer-term financing becomesavailable and generally to supplement Pakistan's reserves in supportingthe exchange reform.

37. The Government's immediate objective must be -- and is -- therestoration of conditions conducive to adequate development and, in thatcontext, the maintenance of a reasonable level of economic activity tofacilitate the structural adjustments which are necessary. For externalassistance to be effective in supporting this objective it must be in aform suitable for financing imports for productive use of existing capa-city and be disbursed quickly.

38. To meet part of the financing requirements on the basis of theprojected deficit, the bilateral members of the Consortium in a meetingon May 26 agreed -- subject to concomitant bilateral arrangementsexpected to be completed shortly -- to extend debt relief to Pakistanequivalent to approximately US$234 million over the period from May 1,1971 to June 30, 1973; of this amount about US$90 million will provide

- 15 -

additional relief during fiscal year 1972/73. The Government of Pakistanhas also asked the Consortium (and non-Consortium) countries to make newcommitments of cammodity assistance. It is hoped that such commitmentswill be made shortly and in an amount sufficient to provide disbursementsof up to $130 million in 1972/73.

39. Commitments of such assistance to Pakistan, before the separa-tion of Bangladesh, have not in recent years exceeded $150 million, sothat the amount requested from the Consortium is very large. Even ifit is fully met, the remaining gap would be much too large for Pakistanto finance from its reserres and by drawings on the IMF. The proposedprogram credit, by helping to bridge this gap, would be Important inmaking more effective other external assistance, and in improving theprospect that the far-reaching measures of exchange reform and importliberalization recently introduced will be effective in restoring therate of economic and social development.

40. Thus, the IDA credit would be part of a financing plan forthe projected deficit as follows:

(US$ million)

Projected Deficit 300

Financing:

Bilateral Assistance 220Disbursement from New Commitmentsof Commodity Aid (130)

Debt Relief (90)

IDA Imports Program Credit 50

Sub-total 270

Use of Reserves and/or INF Stand-by Credit 30

Total 30Q0.

The above $30 million to be provided out of reserves and the IMF standbycredit would correspondingly increase if disbursements from new bilateralcommodity aid commitments fell short of the estimated $130 million.

- 16 -

PARr-Il - BANK GROUP OPERATIONS

41. The Bank and IDA have made thirty-one loans and thirty-eightdevelopment credits to Pakistan since 1952, in the following sectors:agriculture, transport, power, education, water supply and sewerage,communication and industry. The Bank Group has participated in thejoint financing of the projects financed through the Indus Basin andTarbela Development Funds and is the Administrator of these funds.Bank/IDA comitments as at April 30, 1972 totalled $1,173W,3 million,representing about 23 percent of Pakistan's total outstanding external debt.Of this total, fourteen projects accounting for $383.1 million were in theWest wing, including five projects which were administered by agenciesoperating in both wings, and twelve projects accounting 'for $137.6 millionwere in the East Wing. Annex I contains a summary statement of Bank loans,IDA credits and IFC investments as of April 30, 1972, and notes on progressin the execution of projects.

42. As the Executive Directors are aware, in December 1971 disburse-ments on all outstanding loans and credits for beneficiaries in EastPakistan were suspended. I expect to make-recommendations to the Execu-tive Directors with regard to the undisbursed balances on these loans andcredits as soon as current discussions with the governments have beencompleted. In the meantime, the Government of Pakistan, for the timebeing, is continuing to carry the liability for servicing the debt withrespect to commitments attributable to projects In what was East Pakistan.Action as reported in my memorandum to Executive Directors of April 4,1972 (R72-74) is being taken, with the support of Sweden and in consulta-tion with the Government of Bangladesh, with a view to resuming work onthese projects.

43. IFC has made eleven investments in Pakistan totalling aboutUS $26 million, including one in Bangladesh, Karnaphuli Paper Mills Ltd.(US $6.23 million), of which IFC currently holds US $15.4 million net ofcancellations, repayments and participations. IFS has some preliminaryapplications under consideration for investments in Pakistan.

44. This is the only lending operation in Pakistan which will bepresented for consideration this fiscal year.

45. The Bank Group's strategy in the next few months will be toassist, as Chairman of the Pakistan Consortium, the Government and theConsortium countries in reaching agreement on longer term debt reliefproposals, and to prepare, towards the end of this calendar year, anassessment of the economic situation and of the progress being made indevelopment planning in order to help establish the priorities for futuredevelopment assistance.

- 17 -

PART III - THE PROJECT

46. In support of recent economic reforms, the Government has requestedassistance in the form of an imports program credit from the Association.The proposed credit of US $50 million would complement the assistance by themember countries of the Pakistan Consortium and the IMF referred to inparagraph 36.

47. A mission to formulate the credit proposal visited Pakistan inMarch 1972. It had discussions with the Government and with industryrepresentatives and visited 24 large manufacturing enterprises, mainly inthe engineering sector, to assess the present situation and import needsof industry. Negotiations were held in Washington on May 19 through 25,1972. Pakistan was represented by a team headed by Mr. Zafar Iqbal,Joint Secretary, Economic Affairs Division, Government of Pakistan.

48. The Bank report "Industrialization of Pakistan"'/ dated March 10,1970, describes in full the past record, the problems and prospects ofindustry in Pakistan. The problems outlined in the report are low capacityutilization, unsteady and insufficient supply of imported raw materials,components and spare parts and widespread and increasing differences, atthe official exchange rate, between the domestic and foreign prices ofindustrial goods. The recent internal disturbances and hostilities withIndia have further aggravated these problems. Due to the lack of foreignexchange, low public and private investment expenditure and to some extentthe loss of the market in East Pakistan, average"'oapacity utilization inindustry is lower than ever. For example, in the engineering industry,which is heavily dependent on imported materials, it has fallen even lowerthan the 40-50 percent of 1969 to 30-40 percent.

49. The reforms now initiated by the Government offer the possibilityof overcoming these problems and of returning to reasonable levels ofcapacity utilization. The change in the parity of the rupee brings thedomestic price level of industrial goods back on to a comparable basiswith international prices. Equally important, the Government has substantiallychanged and simplified its import licensing system. As mentioned above,Pakistan has operated a complicated system of multiple exchange rates,import licenses and import entitlements, which has now been abolished.

50. The basic strategy of the new import policy is to minimize theadministrative controls and complications. Import licenses remain, butsolely as a means of registering imports. Apart from a limited range ofcommodities exclusively reserved for procurement against tied aid or barter,

1/ Industrialization of Pakistan, The Record, The Problems and TheProspects (R70-53; April 2, 1970),

- 18 -

imports will be permitted from world-wide sources. Import of machineryand equipment of up to Rs. 200,000 against cash and up to Rs. 500,000against barter or credits, will be allowed freely. Imports of machineryon a bigger scale will continue to be sanctioned subject to review bythe Ministry of Industries.

51. As explained in Part I above, public development expenditureshave fallen drastically during the current fiscal year. Private invest-ment, because of lack of confidence, has fallen considerably over alonger period. With the Government's actions to improve mobilizationof resources and its plans to increase public development expenditures,confidence appears to have returned and industrialists generally seemoptimistic about the prospects of industry. The loss of the market inEast Pakistan had comparatively little effect on industry as a whole.The cotton industry which sold the highest share of its output to theEast Wing, is also the industry with the best prospects to shift toother export markets. Other manufacturing industries (including theengineering industry), sold on an average only 6 percent of outputto the East Wing, and the loss of that market had comparatively littleeffect. Prospects for a return of industry to its pre-war level ofactivity are good, provided sufficient imported materials can be madeavailable. Ample capacity to manufacture a wide variety of goods domes-tically is available, and businesses are liquid. Industrial relations,after considerable disruptions and upheavals, now appear to be improving.

52. The proposed credit would be used to finance part of the importsrequired in 1972/73 by a wide range of manufacturing industries, includingtextiles, chemicals,paper making, leather goods, plastics and engineering.In addition, for the purpose of securing sufficient compound and phosphaticfertilizer for the crop to be planted in October, 1972, the credit wouldalso finance that part of the Government's program for the import of suchfertilizer which cannot be procured and financed from bilateral sources intime. Not more than $3-5 million of the credit will be disbursed on thesefertilizer imports. Items which will not be financed from the Credit areconsumer goods, military equipment,iteme custemarily imported for the publicsector under project aid and items reserved for procurement from designatedcountries. The list of'categories of goods to be financed out of the pro-ceeds of the Credit is included in Annex III.

53. In 1970/71 imports of the eligible goods, excluding fertilizer,amounted to $237 million. It is expected that imports in 1972/73 may reachthe 1970/71 level so that the proposed credit would finance about 20-25percent of industry's requirements of these goods. Some bilateral aid willalso be used to finance industrial and fertilizer imports. On the basis ofpast usage, if bilateral commodity aid amounts to $130 million, approximately$20 million will be used to import fertilizers and pesticides, $20 million willbe allocated for other public sector users, and about $90 million will be usedto finance private sector industrial imports. As the proposed credit andbilateral aid taken together will probably be substantially lower than therequirements of eligible goods, no difficulty is foreseen in disbursing the

- 19 -

credit as well as bilateral aid. Furthermore, as much of the bilateral aidmay become available somewhat later than the proposed credit, disbursementsare likely to be rapid.

54. Most of the imports to be financed by the credit would be directimports by the private firms through normal commercial channels. TheTrading Corporation of Pakistan (TGP), a state corporation, is the designatedimporter of a limited number of items where economies can be secured byimporting in bulk. Of these items, pig iron, steel strip, non-ferrousmetals, newsprint, pharmaceutical raw materials, wood pulp and manmadefibers may be financed by the IDA credit. Total annual requirements ofthese items amount to about $25 million. Part of the imports of theseitems may be financed by bilateral aid and it is, therefore, impossibleto make an estimate as to what share of the IDA credit would be used forimports through TCP. The Ministry of Agriculture is the designated govern-ment agency for the procurement of fertilizer. The Government has agreedthat goods and services to be procured through TCP or the Ministry ofAgriculture and to be financed out of the credit will be procured on thebasis of international competition. In passing on imports to industrialusers, TOP charges its actual cost plus a service fee ranging from 2-4percent, depending of the scale of the purchases.

55. For the time being, Pakistan is continuing to allow Commonwealthpreferences on a limited number of items. However, in the case of purchasesby TCP and the Ministry of Agriculture, tenders will be evaluated on thebasis of c.i.f. prices, so that tariff preferences will not be taken intoaccount.

56. All disbursements, covering the c.i.f. cost of qualifying imports,would be on a reimbursement basis. For administrative convenience,qualifying imports costing less than $5,000 would be ineligible for reimburse-ment. Wh-le no retrospective financing would be allowed, it is intendedto permit disbursement in respect of goods imported under licenses issuedbefore the date of the credit and paid for after June 30, 1972. The StateBank of Pakistan will be responsible for collecting, through nominatedbanks, invoices, evidence of shipment and evidence that the supplier hadreceived payment. Such evidence will be forwarded to the Bank in supportof withdrawal applications. The State Bank will also provide a certifica-tion in each case that the goods have been supplied from member countriesof the Bank or Switzerland and that they had not been financed already byany bilateral source or by another international development finance insti-tution. The credit should be disbursed over a period of nine to twelvemonths.

- 20 -

PART IV - LEGAL INSTRUMENTSAND AUTHORITY

57. The draft Credit Agreement between the Association and the IslamicRepublic of Pakistan and the Recommendation of the Committee provided forin Article V, Section l(d) of the Articles of Agreement, are being distri-buted to the Executive Directors separately.

58. Under Section 7.02 of the draft Development Credit Agreement, the

Association would be entitled to suspend further disbursement if, after

reviewing with the Government the progress made in implementing the variouseconomic and financial measures taken, it determines that the purpose ofthe Credit, i.e., the support of the successful implementation of the Govern-ment's economic and financial program, is not likely to be achieved.

59. I am satisfied that the proposed development credit w'ould complywith the Articles-of Agreement of the Association.

PART V - RECOMMENDATION

60. I recommend that the Executive Directors approve the proposed credit.

Attachments Robert S. McNamaraPresident

May 31, 1972

ANNEX IPage 1 of 5

THE STATUS OF BANK GROUP OPERATIONS IN PAKISTAN

STATEMENT OF BANK LOANS AND IDA CREDITS(as at April 30, 1972)

Amount (US $ Million)Loan or Less Cancellations

Credit Undis-Number Year Borrower Purpose Bank IDA bursed

Loans and credits fully disbursed 352.8 222.9Loans and credits being disbursed

266 1960 Pakistan Indus (multipurpose) 90.0 - 18.550 196)4 Pakistan Education - 8.5 3.3

376 196)4 Karachi Port Port Development 17.0 - 4.354 1964 Pakistan Highways - 17.0 1.4

106 1967 Pakistan Lahore Water Supply - 1.8 0.01548 1968 Pakistan Tarbela (multipurpose) 25.0 - 25.0549 1968 Dawood Hercules Fertilizer 32.0 - 0.002578 1968 Pakistan W.P. Highways II 1.1 - 0.1145 1969 Pakistan Telecommunications - 16.0 6.8590 1969 PICIC Industrial Development 40.0 - 3.8597 1969 SNGPL Sui Northern Gas II 8.0 - 0.2621 1969 Pakistan Western Railway 14.5 - 9.7157 1969 Pakistan Agricultural Bank III - 30.0 13.3177 1970 Pakistan Ind. Development (IDBP) - 20.0 11.6696 1970 SNGPL Sui Northern Gas III 19.2 - 6.7S-9 1970 Pakistan Port Engineering - 1.0 0.6186 1970 Pakistan Telecommunications II - 15.0 15.0206 1970 Pakistan Engineering Education - 4.0 4.0213 1970 Pakistan W.P. Power Distribution - 23.0 23.0

Sub-Total 2 7.31

Credits on which disbursements are suspended41 1963 Pakistan Dacca Water Supply - 13.2 7.242 1963 Pakistan Chittagong Water Supply - 7.0 3.749 1964 Pakistan Education 4.5 0.853 1964 Pakistan Highways 22.5 18.983 1966 Pakistan Foodgrain Storage - 19.2 0.887 1966 Pakistan Education II - 13.0 9.0

S-8 1969 Pakistan Dacca SW Irrigation (Eng.) - 0.8 0.06S-10 1970 Pakistan Irrigation Engineering - 2.4 1.1184 1970 Pakistan Chandpur II Irrigation - 13.0 12.4192 1970 Palcistan Small Industries - 3.0 2.8208 1970 Pakistan Tubewells - 14.0 13.9228 1971 Pakistan Reconstruction - 25.0 25.0

Sub-Total - 93 95. 6Total 599.6 496.8Of W[hich Has Been Repaid 171.1 0.45Total Now Outstanding 2 79-6Amount Sold 22.3O" Which Has Been Repaid 20.8 1.5Total Now Held by Bank & IDA 427.0 496.35

Total Undisbursed 68.3 174.67 242.97

ANNEX IPage 2 of 5

STATEMENT OF IFC INVESTMENTS(as at April 30, 1972)

Amount in US$ MillionYear Investment Type of Business Loan Equity Total

1958 Steel Corp. of Pakistan Rolled Steel Products 0.63 - o.63Ltd.

1959 Adanjee Industries Ltd. Textiles 0.75 - 0.75

1962- Ismail Cement Industries Cement 5.25 0.42 5.671965 Ltd.

1963- PICIC Development Financing - o.49 0.491969

1965 Crescent Jute Products Textiles 1.95 - 1.95Ltd.

1965 Packages Ltd. Paper Products 2.31 o.84 3.15

1967 Pakistan Paper Corp. Ltd. Paper 3.20 2.02 5.22

1969 Dawood Hercules Chemicals Fertilizers 1.00 2.92 3.92Ltd.

1969 Karnaphuli Paper Mills Pulp and Paper 5.60 0.63 6.23Ltd.

Total Gross Commitments 20.69 7.32 28.01

Less Cancellations, Terminations,Repaymients and Sales 11.74 0.91 12.65

Total Cmnmitments Now Held by IFC 8.95 6.41 15.36

Total Undisbursed 1.00 - 1.00

ANNEX IPage 3 of 5

C. PROJECTS IN EXECUTION

US$90.0 million (Indus Basin) loan of September 19, 1960 (Ln. 266)

All major project items (except Tarbela Dam) completed. Settlementof a number of claims and some remedial works outstanding. No fur-ther disbursement of Bank Loan is expected during remainder of thiscalendar year.

US$17.0 million (Karachi Port) loan of May 14, 1964 (Ln. 376)

Postponement of the Closing Date will be necessary. A supervisionmission is scheduled for June. The present Closing Date is June 30, 1972.

US$25.0 million (Tarbela Dam) loan of July 10, 1968 (Ln. 548)

Loan was limited to residual financing, therefore no disbursementsare expected until FY 1976. Good progress is being maintained on theworks.

US$32.0 million (Fertilizer) loan of July 10, 1968 (Ln. 549)

Construction work was completed in July 1971 and commercial productionwas started in February 1972. Only $1,900 is undisbursed.

US$1.1 million (Highways) loan of December 20, 1968 (Ln. 578)

A mission is tentatively scheduled for June to discuss therecommendations of the consultants' transportation study with theGovernment.

US$40.0 million (Development Finance Company) loan of March 21, 1969(Ln. 590)

Disbursement in full is expected by the Closing Date. A supervisionmission is tentatively scheduled for September 1972.

US$8.0 million (Gas Transmission) loan of May 13, 1969 (Ln. 597)

Project is virtually completed. A supervision mission visited theproject in early May.

US$19.2 million (Gas Transmission) loan of June 29, 1970 (Ln. 696)

The recent hostilities have delayed execution of this project and alsocaused cost increases. The nature and amount of these are beingascertained by the supervision mission which visited the project inearly May.

ANNEX IPage 4 of 5

US$14.5 million (Railways) loan of June 26, 1969 (Ln. 621)

No problems expected. Most recently, the Association has approvedthe Borrower's request to extend MIS Sofrerail's contract to includeimplementation of their recommendations and a study of some aspectsof the management of Pakistan Western Railways.

US$8.5 million (Education) credit of March 25., 1964 (Cr. 50)

Procurement for polytechnics in Sind and Punjab can,be completedbefore the Closing Date. At Agricultural University Lyallpur', con-struction cannot be completed by the Closing Date, but teachingbuildings should be substantially completed and equipped. The Govern-ment of Pakistan has requested postponement of the Closing Datefor an unspecified period, reallocation of the proceeds of the Creditto purchase additional instructional equipment for the AgriculturalUniversity amounting to $250,000, and increase in the reimbursementpercentage for local expenditures on construction to 25% (from 10%).This request is under consideration.

US$17.0 million (Highways) 'credit of June 11, 1964 (Cr. 54)

Construction is completed. The Association has approved a thirdpostponement of the Closing Date (to December 31, 1972) to permitthe settlement of contractors' outstanding claims.

US$1.75 million (Lahore-Water Supply, Sewerage and Drainage) credit ofMay 12, 1967 (Cr.,106)

SIDA participation is $1.75 million equivalent. The project is vir-tually completed. Lahore Improvement Trust (LIT) requested a changein withdrawal ratio between IDA and SIDA credits. The'Associationhas agreed to LIT's request in order to allow full utilization of bothcredits.

US$16.0 million (Telecommunications) credit of March 6, 1969 (Cr. 145)

Procurement problems are now largely resolved. A supervision missionwhich visited Pakistan in May discussed a revision of theproject in light of the suspension of those parts of it which arein East Pakistan. Postponement of the-Closing Date by about one yearis expected. The present Closing'Date is December 31, 1972.

US$15.0 million (Telecommunications) credit of May 22, 1970 (Cr. 186)

See Credit 145-PAK.

US$30.0 million. (Agricultural Development Bank) credit of June 26, 1969(Cr. 157)

Disbursements continue to be far behind schedule. Tractor supplieshave been disrupted because the Government has not issued licensessince September 1971. Lending for tubewells is continuing slowly asa result of difficulties in WAPDA providing electrical connections,due to power shortages. Postponement of the Closing Date by twelveto eighteen months is likely. The present Closing Date is June 30, 1972.

ANNEX IPage 5 of 5

US$20.0 million (Development Finance Company) credit of February 11,1970 (Cr. 177)

IDBP'a immediate future has been uncertain for some time as a resultof thela*c of a clear.industriaal policy and a change in ManagingDirector. A supervision mission is tentatively scheduled for lateJune.

US$4.0 million (Engineering Education) credit of June 29, 1970 (Cr. 206)

Construction scheduled to start in January 1973. Procurement isnot yet started. No major disbursements are expected during thecalendar year except for payments to consultants.

US$23.0 million (Electric Power Transmission and Distribution) creditof August 14, 1970 (Cr. 213)

After initial delays, the project has started to make some progress.Contracts have been awarded for power transformers ($4.7 millionequivalent), and for the Dharki-Rohri 132 KV transmission line ($h22,000equivalent). Bids for substations phase I (estimated foreign exchangecost $5.6 million) and power transformers phase II (estimated foreignexchange cost $2.4 million) have been opened but evaluation reportsare not yet received. Bids for 11 KV switch gear (estimated foreignexchange cost $1.6 million) and substations phase II (estimated foreignexchange cost $2.8 million) should have been opened but no informationhas been received about them. WAPDA has requested financing fromthe Credit for additional special transmission work in Lahore (totalcost about $1.0 million equivalent, of which $0.6 million equivalentis in foreign exchange), which will need a revision of the projectdescription in the Credit Agreement. This request is under.consider-ation.

US$1.0 million (Port Ehgineering) credit of June 10, 1970 (Cr. S-9)

Final report of engineering feasibility study was completed in mid-May. A preappraisal mission is scheduled for early June.

ANNEX 1I

Forma No. 81.02 WRDBN RU(5-72) WRDBN RU

COUNTRY DATA

COUJNTRY: Pakistan (West)

~~~ 794,613 ~~~~~~~~~~~~~~~~~~POPULATION: 60.07 mlllian 1970/71 DENSITY: 76 per ko

Nate of Growt 2.7 8 (fram 1969/70 to 1970/71) Thu= 316 Per km of to) tivatod l1nd

POP0trATCON CRARACTERISRTICU: HEALTH,:

CUde. mrtA Rate (per, 1,021) 0 1968 -Paoplstloa per physician 1970 4,361.

Crdteth Nate (Per 1,000)1 2C 1968Polt.np hsialbd 17 196Infant Mortality (per 1,000 lve births) (year.oaalmprheptlhl 170,9

jN,COMr DISTRI.BUTION: DIS~~~~~~~~~~~~~R1TRIBUTION OP LAND OWNERNSHIP

hjgheeotqaltina ) Nat available .of I-od oc-d by tap 107. o-areq ~~~~~~~~~~~ %~~~~7 of load owood by ..melest 10% macar) Rat availble

ACCrftI '10 P0TAB11 W4hrER (7 of pop.lotio-) ACCESSO'I0 ELECTRICITY' (7. of popalarlo-l

Rorol )Not -milahle nro)Rt av,abla .

0fTiOtN: GoOP.,ect. yar PERCAPITA: 814.6 1970/71 EDUCATICON:Caori clkNIA frrorvet yer At au~et factar _Tiktersay rate 11% 1961

Per capita Protein Rotate Cgraoone) (yswr) )c/A ost and at offiolal Primay schoil anrolmert (8) 4.6% 1970

parity rate of Ro.11R0S0 00G10T1C PROD100T (1970/71 (siae)4.76 per UI 8) AMML (COMP¶OUND) DATE, Opl Gop GROWTH (%, oonstanxt factor o..st)

GKP -t ... k.t prices 9,181 lui-.O ~~~~~~~~~~~~~1960 161-1964/6t 1965/66-1969/70 1970/71

Gro.. lI-.tstOat 1,575 17.0Grosa Cutlooci Soviage i,195 13.0 Agiouitur 3.7 5.6 -2.2

Corroat A-mocot Balanme 380 4.2 Induotry 2/ 13.1 7.5 2.9

Osporta of Goode, ((PU 8480 9.2 lervicee 6.8 .u42.8Teporte of Cod.NES 1,228 13.4. COPto _

OUTPUT. 0B0R PUORCE AllDPRODU0C'T0ITY IN -1970/71: (GDP estimates at ourret fc,otor coot)

faita Oddod .r,r r ~~~~~~~~~~~~~Voice idleS Par dorker

Agriculture 3.262 37.5 02 88 11.9 43Tud.aotry 2.123 24.3 . 2l8g12

Totl/Roerogo NM 100.0 25. 109 9 -. 100

PUBLIC PINA) CIT INl 1970/71

Co....lidated Csatr.1 and Pravimakl Govr,amea domamtst, e F l Ca. rmeIdRAouont %of Orp (R.. Milli..) 0--- of7 GDP-aoara.

Current R-1p- m~~~(s. illion) % of COP last tao years 5/1 drvot % of GOP last tam years 5/Correot Rrorlpcs r~~~~ ~ ~~~~~,182 16.4. 16.5 5,551 12.7 10.7

Ro:1-D-veopoe..t Empemdittree (tool. tranafers) 6,768 15.4. 14.8 6,158 14.1 13.8Correot Scro1os/Defi.tot 411. 0.9 1.6 - 607 - 1.1. 1.2

D-ovoim..eot.lopeeditare 2,810 6.4. 6.8 2,629 6.0 6.7bt-isrol .ioltar~.c (gross) 1,249 2.8 2.8 2,249 2.8 2.8

PRICES 01I0 CREITO?amd of year: (R,oleoalo Prima Iodeo 2m-b Crotll to Pobio leotor Both Cre1It to lrlvcto Ivotor

~~ 1P68/69 108am~~~~~~Id. 1959/60.100 % Chuwg (oct) % mh-mCe (-.n'ct) achaogo

PY 1969/70 132 15PG 197.1/71 137 + 3.8 (Na separt'e figure for West Paknistano)

Pebroamy 1970 138 Pab O.. ' 1971 148 +7.2

R3ALANCE Op PAYMENTS1 fIn last tom years) US OERCRANDIIE EXPORTS (Aveare af the last three X.ear)1968/69.1970/71 2/

R ... __ Hoo Rw Cotton 50 16

RMeoteh d. .P,t. 3 30 205 Cotton Mooc"tantr 113 30

T-ivlibles 3/ 175 1LI Rime 30 6Leather and Leather looads 30 8

Pezoonte Irot Flak 14. 4

Imisiblo. oi ~~~~~~~~~~~~~~~~Ohes12713bnvialilas ~~~~~~~229 229

Publio ISotor (58 (155) Total 372 100

Private Smctor (71) (74)bit lervAcs ~~~~~~212 219

Pntrestp. . 83N EXTERNAL. DEW ON JUnE 30. 1970

____________ __ ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~($Inv.)Overall flefimit -617 ~~~~ ~ ~~~~~~~~-612 Melian and Long-tern Credits, Poblim 2928

Edocomed by Roo~~~~~~~~~~~~~~N.-Gouraoteed Priv.at M0.TForeign Aid 9 315 371Moratoriumo or. Debt Osroime 28 Total Outstanding and Diebuorsad

Purhase of Foreign Excanege fromthe Eastern Provinos21 3

Use 0, Offi..1 Re.--- 5151 110 DENT 0 ER0ICERNATIO 197o/n7 1.0%

XRO/TIh L0911N1. APRIL 30. 1972 9/(8 mL.)IBRD lIDA

Outstanding and Disbursed 406 32-Uadiiabrsed 68 79

Outatanding incl. Undlebursed 4.74 10'

Nate of EunhanIge,, RS $1.01 R A. 1.76 Dots: lMaY 31, 1972Rupee 1.00 US0 8_0.21

Dooartmnet: South Asia

.1 M-aotuaturing, miniog, qoar.rying, monstruction, electricity, gas, eater mad aOootaryeroa.2/ E.mluding re-poorts.

Incloluding Workers' remittances.WProeiot aid disbu,rsaents 00ncoluded are reduced by 15 Perceot to adjust for tamally ontainmd serio.s

ooonal.v oot remarrdoas a0 moatr-entry in the forsige esohange budget.51 lomludlng 'toe of SD"0s PIus DI credit, and residual balances.

AlTotal debt burds (iooloeive of East Pakcistan,) related to West Pakistan,'sa foreign soohooge earnings only.13 Eamiuding inter-wing emports.

JThose loans and credits &lolh wer intended for disbursemnt in both wings are treated as for West Pakistan osly.2/1969/70 mad 1970/71 aoveas..

ANNEX IIIPage 1 of 2

PAKISTAN - INDUSTRIAL IMPORTS PROJECT

CREDIT AND PROJECT SUMMARY

Borrower: Islamic Republic of Pakistan

Amount: Equivalent in various currencies of US $50million.

Terms: Standard

Project Description: Provision of foreign exchange to pay forimports of industrial raw and semi-finishedmaterials, components, spare parts andmiscellaneous items of manufacturing equip-ment and fertilizers to oupport Pakistan'sprogram of economic development.

Procurement Arrangements: Mainly by private importers through commercialchannels. Some items to be bulked for importby Trading Corporation of Pakistan afterinternational competition. Compound andphosphate fertilizer, up to $5 millionafter international competition to beprocured by the Ministry of Agriculture.The categories of goods eligible fordisbursement are the following:

Raw vegetable materialsTanning and dyeing extractsVegetable oilsSalt sulphur chemicals and compoundsPhosphatic fertilizerPlastic materialsRubberRaw hides and skinsIndustrial woodPaper and paper boardSilk and textile materialsFire brick and graphiteIndustrial glassIron and steelNon-ferrous metalsManufactures of metalBoilersElectrical machinery and equipmentMechanical machinery and equipmentCommercial and industrial vechiles, partsthereof other than passenger cars

ANNEX IIIPage 2 of 2

Estinaated Disbursements: September 72 Quarter $ 5 million

December 72 Quarter $10 million

March 73 Quarter $20 million

June 73 Quarter $J5 million

ANNEX IVCONFIDEATIAL

INTERNATIONAL MONETARY FUND

Pakistan: Change of Par Value and Wider Margins

Prepared by the Middle Eastern Department andthe Exchange and Trade Relations Department

(In consultation with the Legal and Treasurer's Departments)

Approved by Ernest Sture and John W. Gunter

May 8, 1972

I. Introduction

In a letter dated May 4, 1972 (Appendix III) Pakistan has proposeda change in the par value of the Pakistan rupee from 0.186621 gram of finegold to 0.0744103 gram of fine gold per Pakistan rupee in accordance wit}Article IV, Section 5, that is to correct a fundamental disequilibrium. 1It is proposed that the change would be effective on May 11, 1972 at 10 p.m.Washington time. The Government of Pakistan has also stated that it availsitself of the wider margins under Executive Board Decision No. 3463-(71/126),adopted December 18, 1971, and that it will use the United States-dollar asits intervention currency.

The new par value now proposed represents a decrease in the gold valueof the Pakistan rupee of 60.13 per cent and corresponds to 11.9428 Pakistanrupees per special drawing right or, 0.0837321 special drawing right perPakistan rupee. At the new par values, the United States dollar is equalto 11 Pakistan rupees per U.S. dollar.

The proposed change is to be supported by a financial program submittedto the Fund in2/onnection with a stand-by arrangement which is the subjectof EBS/72/150.- Details of recent economic developments are described inthat paper.

II. Background to the Proposed Change

For many years Pakistan has operated a complex exchange and trade systeminvolving multiple e change rates and substantial reliance on exchange andtrade restrictions.3" The system utilized an Zxport Bonus Scheme introducedin 1959 as a stimulus to exporters. Exporters of specified commodities wereissued "bonus vouchers" up to specified percentages of their export proceeds.

1/ The initial par value of the Pakistan rupee agreed with the Fund onMarch 19, 1951, was 0.268601 gram of fine gold per rupee. This was changedto the present par value on July 30, 1955.2/ A Fund mission consisting of M4essrs. John W. Gunter, A. S. Gerakis,

J. Rose, S. Cnossen and H. Baas discussed the exchange reform and financialprogram with the Pakistan authorities in Islamabad, February 17-24, 1972.3/ The system is described in detail in SM/70/198 and SM/70/210. Changes

in the system since January 1, 1971 are set out in Appendix II.

- 2 -

These vouchers could be sold to importers as a form of entitlement to theimport of a range of specified goods or could be used. by the exportersthemselves for imports additional to licensed entitlements. While allpurchase and sale transactions of exchange itself were based on the exist-ing par value rate (PRs 4.7619 per US$1), effective exchange rates wreredetermined by: whether or not transactions were subject to the receiptor surrender of bonus vouchers: the percentage of the value of an exporttransaction for which vouchers were given or of an import transaction forwhich they were required; and the current market rate for vouchers. Overtime the scheme was subject to continual modifications reflecting thestate of the balance of payments and the use of multiple currency practicesin an effort to promote various economic and social objectives. Suchmodifications were achieved by: changes in the lists of export and importitems and, later, invisible payments and receipts covered by the scheme;in the rates of bonus epplied to transactions covered by the scheme; andin the period of validity of bonus vouchers and the timing of theirsurrender.

While the scheme doubtless contributed to the good experience Pakistanenjoyed for some years in the expansion of manufactured exports, it failedto produce an exchange rate system serving an appropriate pricing function.Despite the fact that the par value became increasingly unrealistic overtime, a large volume of transactions, including public sector paymentsand receipts and imports under aid and bilateral trade, continued to beeffected at that rate (although some such imports were subject to "equali-zation" taxes). On the other hand, the other rates for transactions coveredby the scheme were progressively depreciated so that the spread betweeneffective rates widened. Demand for imports remained excessive and thecontrol systemi was under continuous pressure in trying to rationalize thedistribution of available exchange resources for imports; in addition, therewas a stringent control over invisible payments. Complemented by the effectsof other policies, exchange policy resulted in serious distortions inresource allocation.

The existing exchange rate structure is set out in Table 1. Thestructure of the import licensing system is given in Appendix I and detailedchanges in the exchange and trade system since January 1971 in Appendix II.

- 3 -

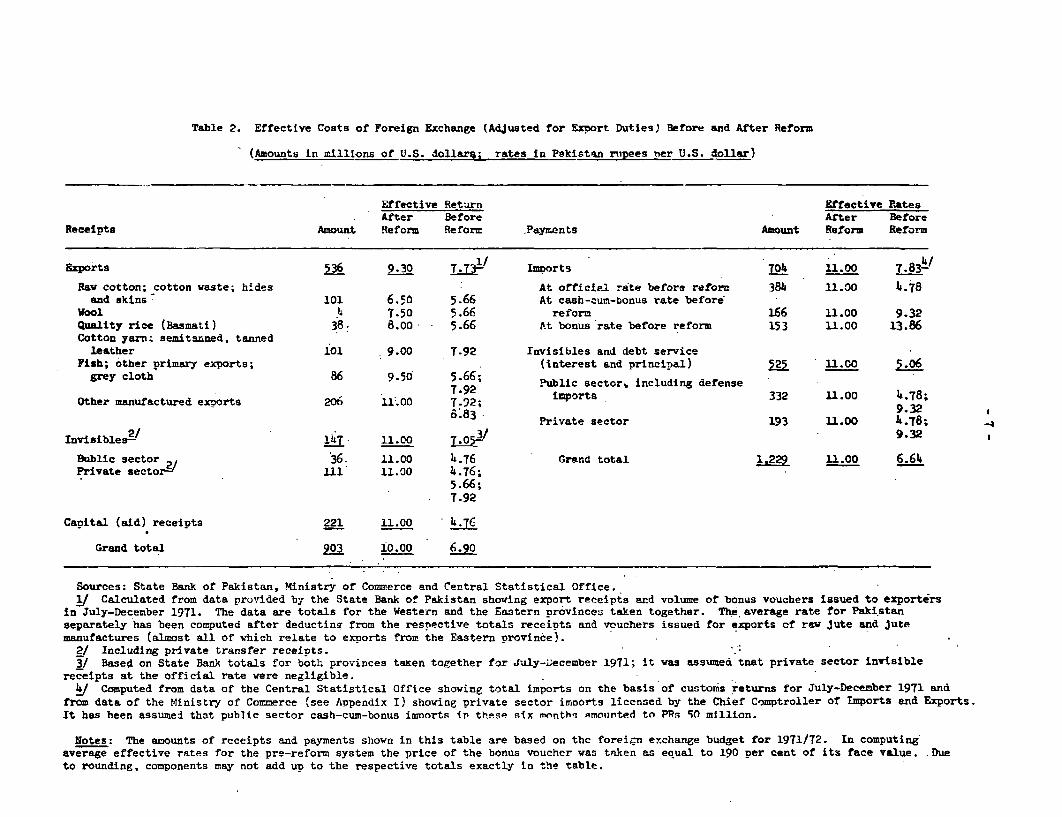

Table 1. Exchange Rate Structure-/

(Pakistan rupees per U.S. dollar)

Buying Selling

Official 4.76 Public sector Official 4.78 Public sector pay-invisibles and ments, imports underprivate sector aid/barter andinvisibles not invisibles notreceiving bonus subject to bonus

10% bonus 5.66 Primary goods; someprivate sectorinvisibles

35% bonus 7.92 Jute and cottonmanufactures

45% bonus 8.83 All other manu- 45% bonus 8.86 Certain invisiblesfactures and trans-actions 50% bonus 9.32 More essential non-

aid imports andcertain invisibles(so-called 'cash-cum bonus" rate)

100% bonus 13.86 INonessential imports,all imports in excessof licensed allocationand all other permittedtransactions

1/ Calculated on basis of market rate for bonus vouchers of PRs 190 perPRs 100 vouchers; actual market rates have been close to this rate in recentweeks.

During 1971, external policies reflected an extreme tightness in theforeign exchange position. Foreign exchange reserves fell from $343 millionin March 1970 to $174 million in iarch 1971 (equivalent to about five weeks9payments on current and capital account). In April 1971, the Governmentunilaterally declared a moratorium on a large part of its debt serviceobligations. Moreover, the half-yearly import program (January.-June), whichitself had been more restrictive in terms of new import prohibitions, under-went a severely restrictive revision at that time. More items were prohibited

- 4 -

and imports were made more costly by movements of items to import listssubject to more depreciated exchange rates. The import program for July-December 1971 remained essentially unchanged, but as nonproject aidavailabilities dwindled because the aid pipeline was not being replenished,many raw materials which had been available to industry from aid at theofficial rate (PRs 4.78 per US$1) could only be procured with free exchangeat the most depreciated selling rate (PRs 13.86 per US$1). Announcementof the import program for January-June 1972 was delayed until mid-Februaryand while structurally it remained virtually unchanged as compared to theprevious program, there was a continuing severe constraint on exchangeresources for its financing.

During 1971, exports from (West) Pakistan showed a strong growth,manufactured exports being assured of necessary imported inputs on aprivileged basis. There was also a continuing extension of the mostdepreciated buying rate (45 per cent bonus) to a widening range of invisiblereceipts. Exchange reserves, which, after the belt-tightening of April1971 as well as the impact of some temporary factors, had risen from $174million at end-March to $221 million at end°August and were at $217 millionat end-November, came under heavy pressure thereafter and fell to $190million at end-January 1972, despite the allocation of SDR 25 million inthat month.

In September 1971 the exchange rate for the Palcistan rupee, previouslypegged to sterling, was pegged to the U.S. dollar. In late December 1971,in response to the Managing Director's enquiry, the State Bank of Pakistaninformed the Fund that Pakistan would maintain unchanged its official ratefor rupees in terms of dollars.

III. The Proposed Exchange Reform

As a key element in a reformulation of economic policy, the Pakistanauthorities have decided to unify the exchange rate system at a fixed rateof US$1 = PRs 11. They believe that it is essential to adopt a fixed ratherthan transitionally floating rate in order to ensure public confidence inthe change. They feel confident that the proposed new par value is realisticand will support their intention to eliminate progressively nontariff traderestrictions and payments restrictions. The reform and the supportingstabilization program should, in their view, enable Pakistan to eliminateany further decline in net external reserves by not later than June 1974(see letter of intent for reouested stand-by arrangement).

As regards the import regime, it is proposed to establish a singlelicensable list including a large number of commodities for which allexisting restrictions will be eliminated and licenses issued freely.This list will conk-ain the bulk of raw materials, spare partsand componenits needed for industry. All imports not on the list will beprohibited. Given the balance of payments situation, the liberalizationpolicy cannot be pressed further immediately, but extensions in its coveragewill be feasible in due course, when foreign exchange receipts respond to

- 5 -

the devaluation. Mloreover, the existing structure of industry has developedbehind highly protective barriers and a rapid move to comprehensive liberali-zation might be quite disruptive. Therefore, the policy will be to reduceprogressively nontariff restrictions on imports as the pattern of domesticindustry is rationalized and its competitive ability is improved. Further-more, the authorities are undertaking a comprehensive review of the tariffschedule. While a primary objective of this review will be to raiserevenues,I' it is also intended to increase the use of the tariff as aninstrument of protection.

Some exceptions to the complete freedom of imports of items on thelicensable list will be made due to difficulties in the absorption of tiedaid and bilateral payments balances. Hitherto, this has been ensuredthrough the exchange system by giving tied aid and bilateral imports thepreferential official (par value) rate. To replace this loss of incentivefor the use of nonconvertible exchange resources by importers, it may benecessary to use fiscal measures and/or quantitative restrictions. It isexpected, however, that such measures will be applied on a limited scale;imports affected will probably be considerably less than one fifth of totalimports. Concurrent with import liberalization, there is to be a movementtoward liberalization of payments for current invisible transactions.

On the side of receipts, the Government will apply the followingduties on exports as temporary measures designed to siphon away windfallprofits which would otherwise accrue to exporters, and to raise revenuefor the budget:

Approximate export duty-/Commodities (In Pakistan rupees per US$1)

1. Raw cotton, cotton waste, hidesand skins 4.50

2. Wool 3.503. Quality (Basmati) rice 3.004. Cotton yarn, tanned and semi-

tanned leather 2.005. Fish, other primary commodities,

grey cloth 1.50

As indicated below, despite these duties, incentives for export productionwill be improved significantly during the initial period after the devalu-ation, and it is intended to encourage exports further with a gradualreduction of taxation.

1/ Tariff rates will be reduced on average less than in proportion tothe devaluation, so that the landed cost of imports will rise somewhat morethan the increase in effective exchange rates.2/ Some of the duties will be specific so that the indicated effective

taxes are approximate.

- 6 -

IV. Balance of Payments and Related Effects of the Reform