Embed Size (px)

Citation preview

www.tutor2u.net

AQA AS Business

UNIT 1REVISION WORKSHOP

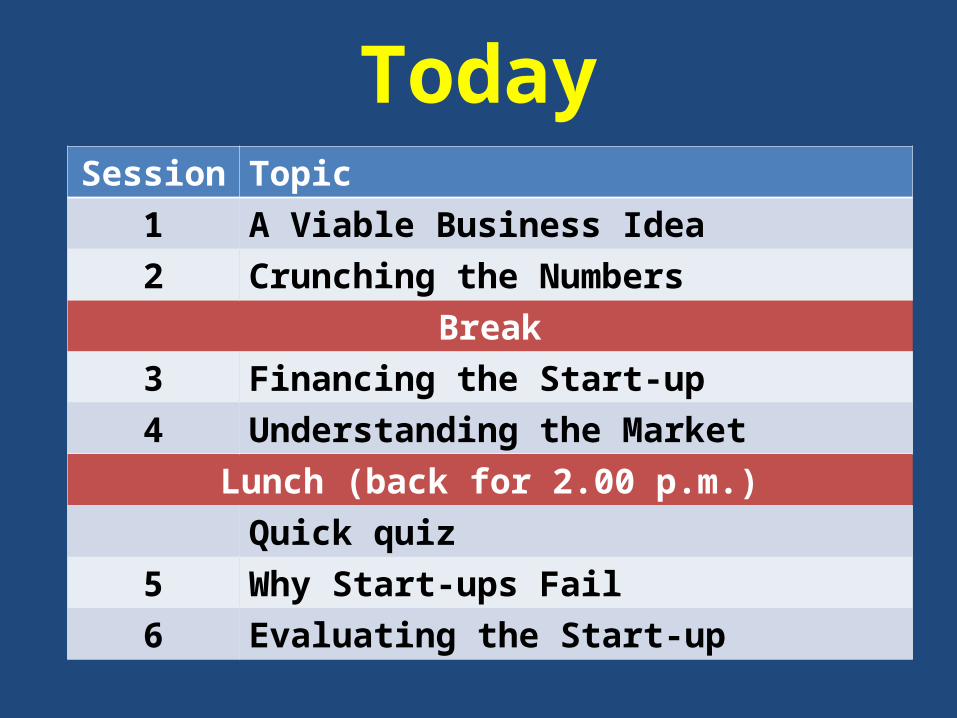

TodaySession Topic

1 A Viable Business Idea2 Crunching the Numbers

Break3 Financing the Start-up4 Understanding the Market

Lunch (back for 2.00 p.m.)Quick quiz

5 Why Start-ups Fail6 Evaluating the Start-up

www.tutor2u.net

Session 1

A Viable Business Idea

Some Important Concepts

ENTERPRISE RISK

RETURN OPPORTUNITYCOST

Can you define them?

Have a Go!

One sentence for each

More on Risk

Imagine you decide to invest your life savings

of £30,000 in setting up a new Subway franchise outlet

List 3 risks you are taking

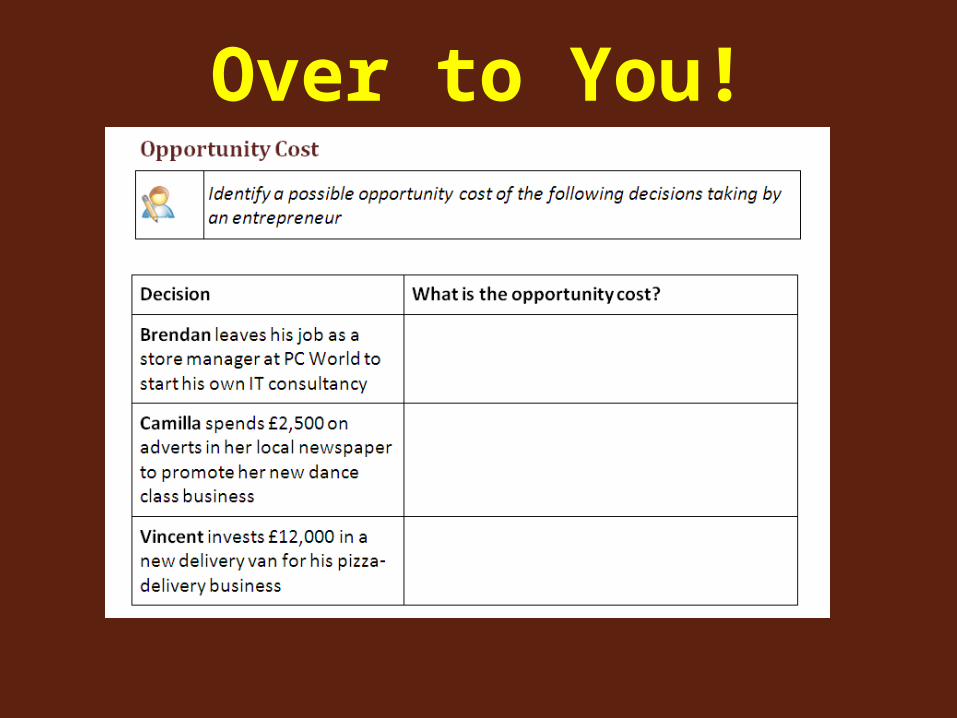

Over to You!

More on Opportunity Cost

Whenever a decision is made in business , there is always an alternative that was not chosenThis alternative is called the opportunity cost

Why this is important

Over to You!

Great businesses usually start with a good idea

No point creating a product or service unless people want it

Found a gap in the Market?

But is there a

market in the Gap?

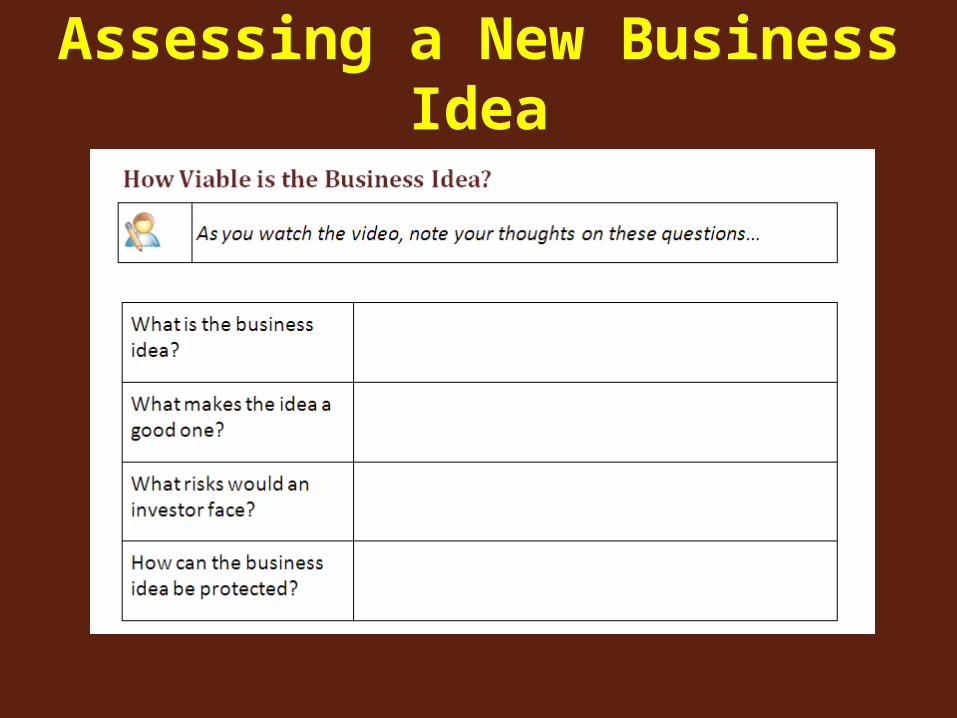

Assessing a New Business Idea

Rapstrap Now

www.tutor2u.net

Session 2

Crunching theNumbers

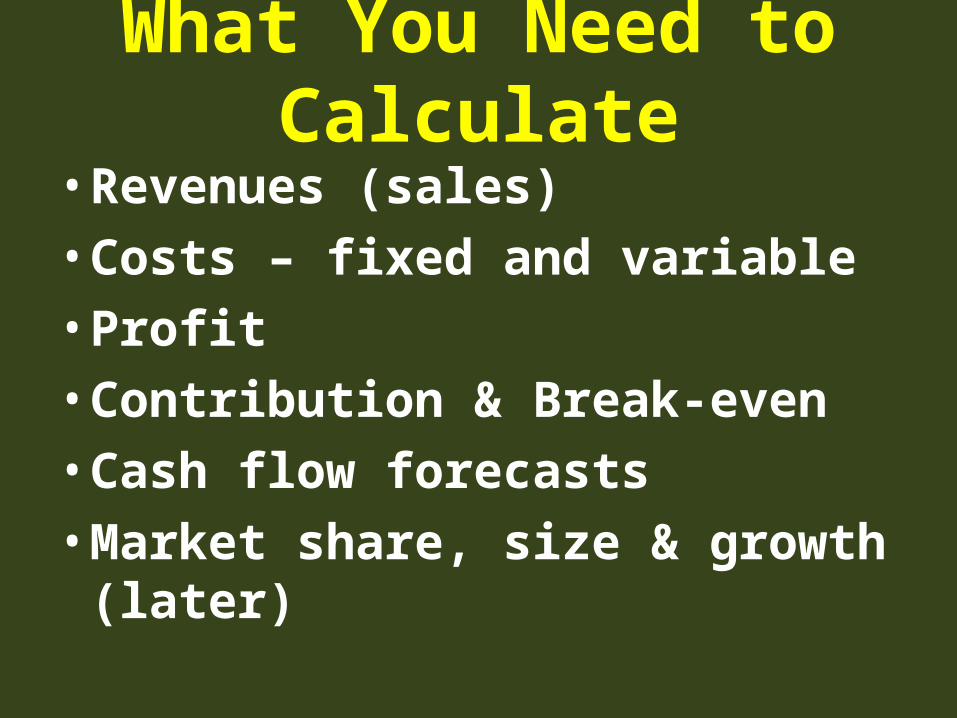

What You Need to Calculate• Revenues (sales)• Costs – fixed and variable• Profit• Contribution & Break-even• Cash flow forecasts• Market share, size & growth (later)

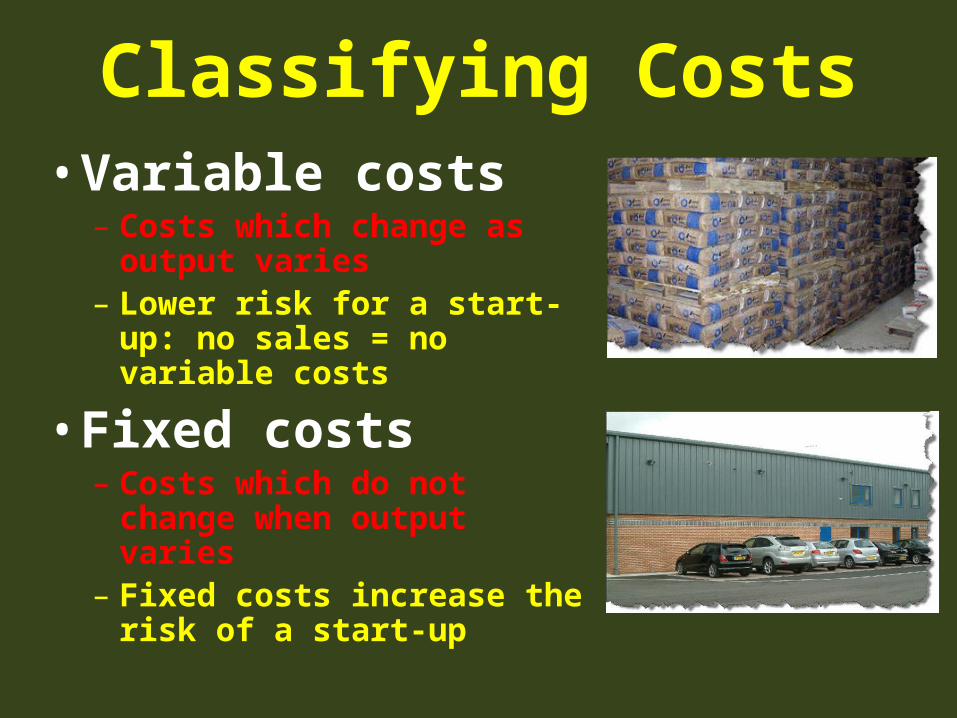

Classifying Costs• Variable costs

– Costs which change as output varies

– Lower risk for a start-up: no sales = no variable costs

• Fixed costs– Costs which do not change when

output varies– Fixed costs increase the risk of a

start-up

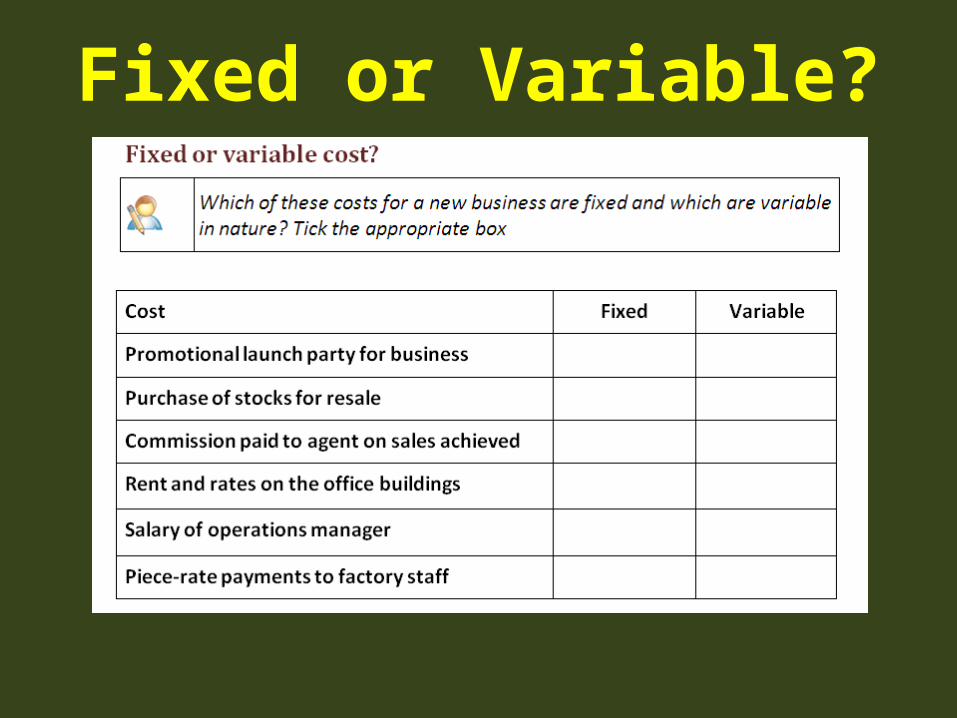

Fixed or Variable?

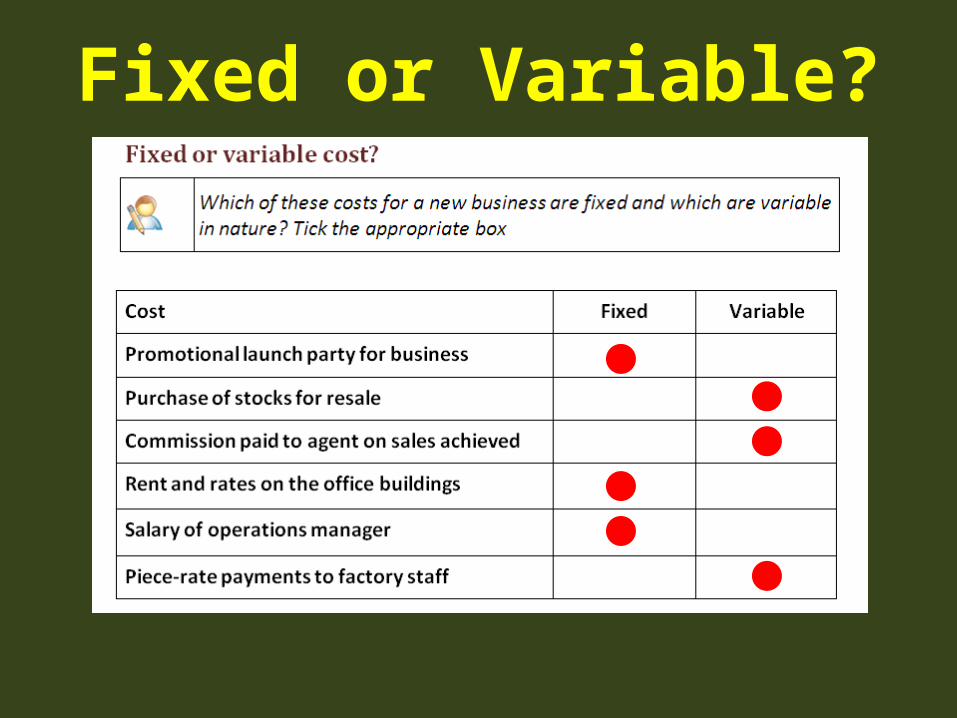

Fixed or Variable?

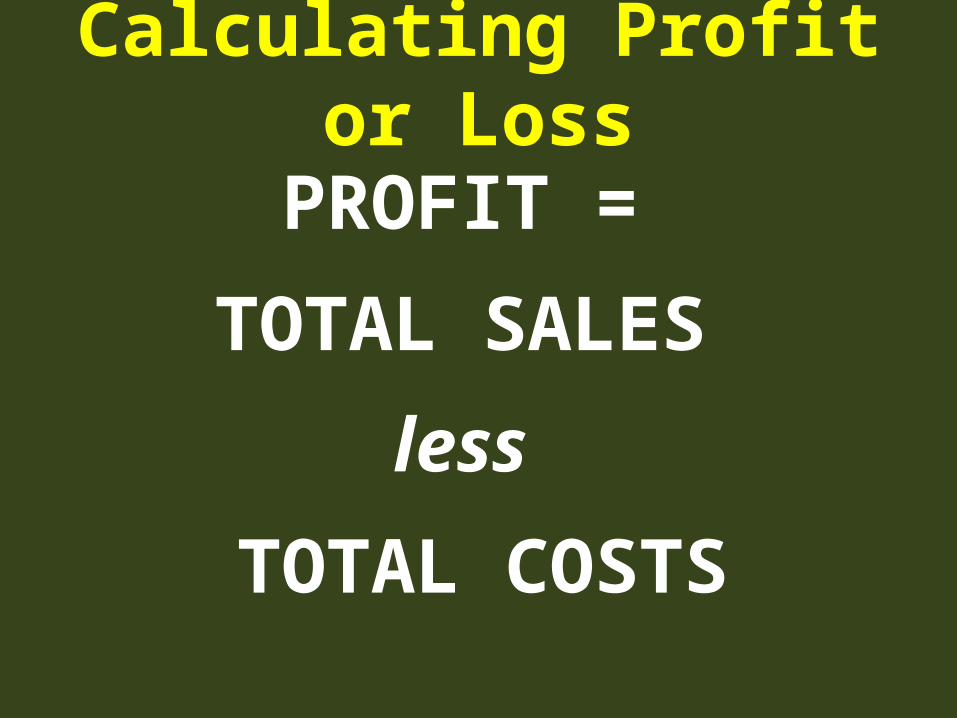

Calculating Profit or Loss

PROFIT =

TOTAL SALES

less

TOTAL COSTS

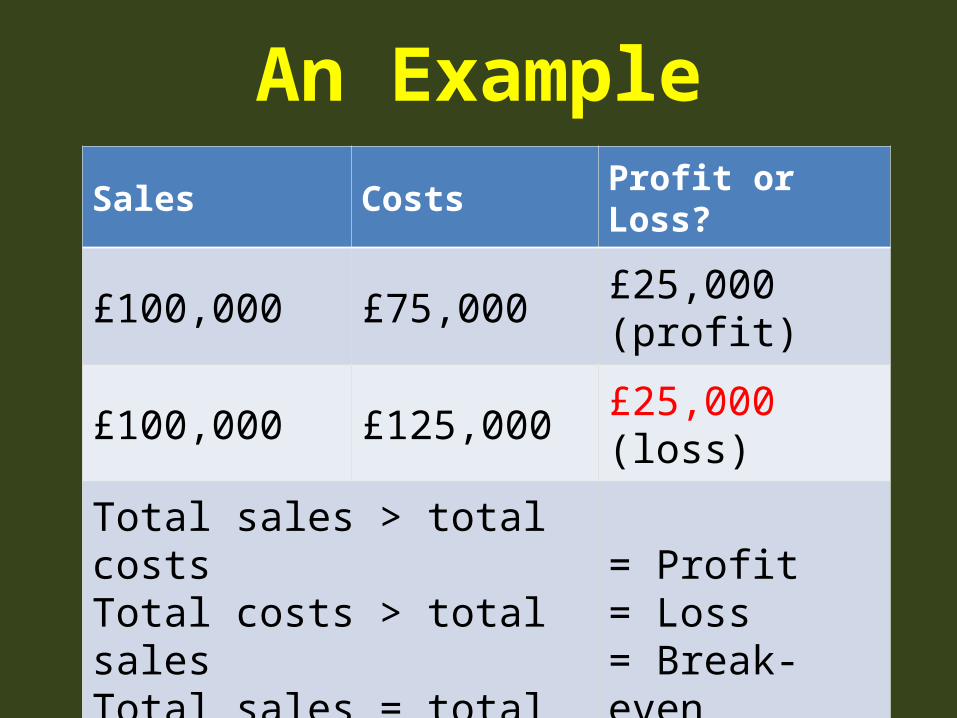

An ExampleSales Costs Profit or Loss?

£100,000 £75,000 £25,000 (profit)

£100,000 £125,000 £25,000 (loss)

Total sales > total costsTotal costs > total salesTotal sales = total costs

= Profit= Loss= Break-even

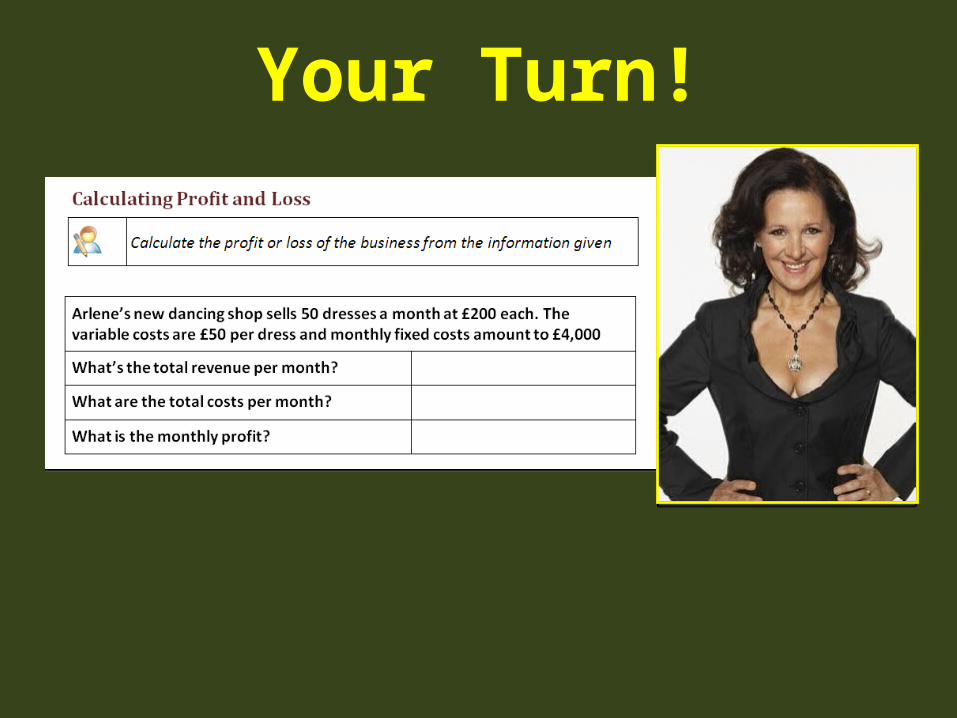

Your Turn!

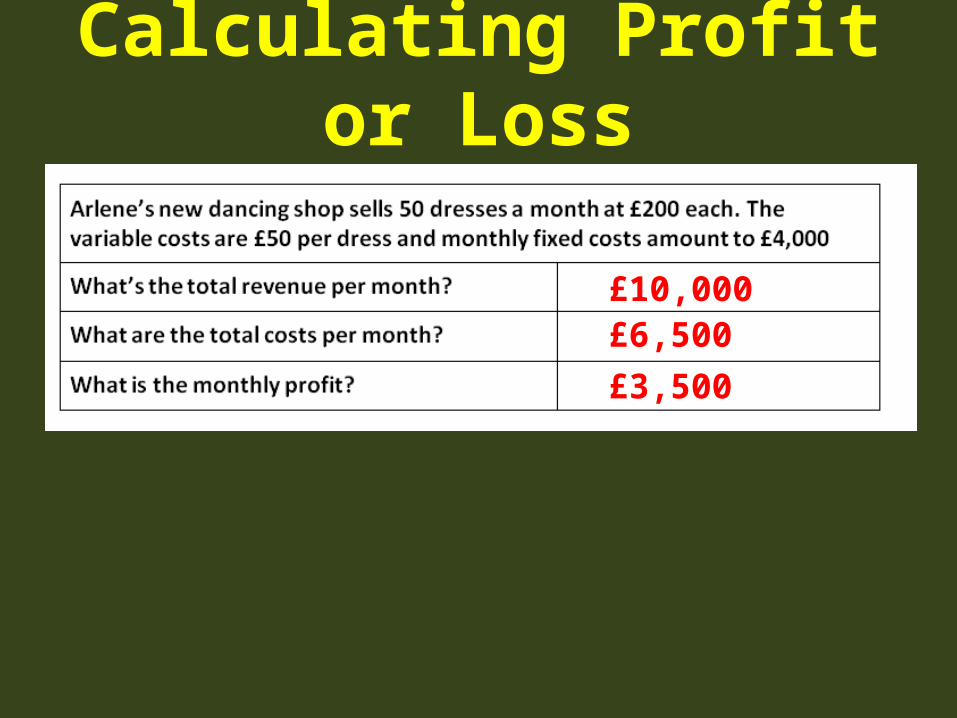

Calculating Profit or Loss

£10,000£6,500£3,500

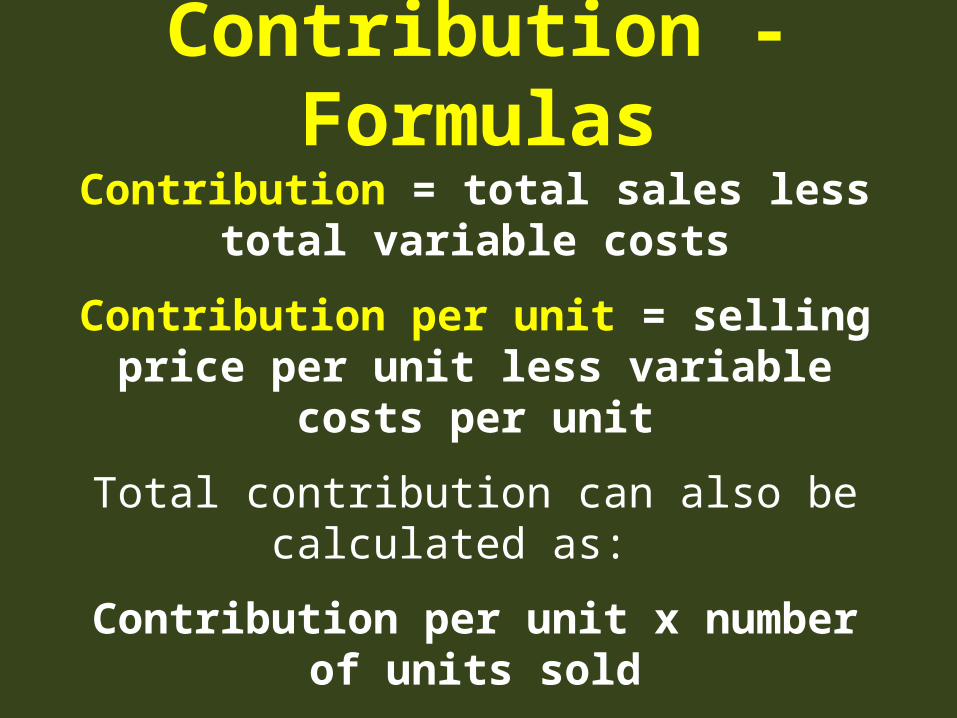

Contribution• Contribution looks at the profit made on

individual products• It is used in calculating how many items need to

be sold to cover all the business' total costs (variable + fixed)

• Contribution is the difference between sales and variable costs

Contribution - FormulasContribution = total sales less total variable

costs

Contribution per unit = selling price per unit less variable costs per unit

Total contribution can also be calculated as:

Contribution per unit x number of units sold

Profit = Contribution less Fixed Costs

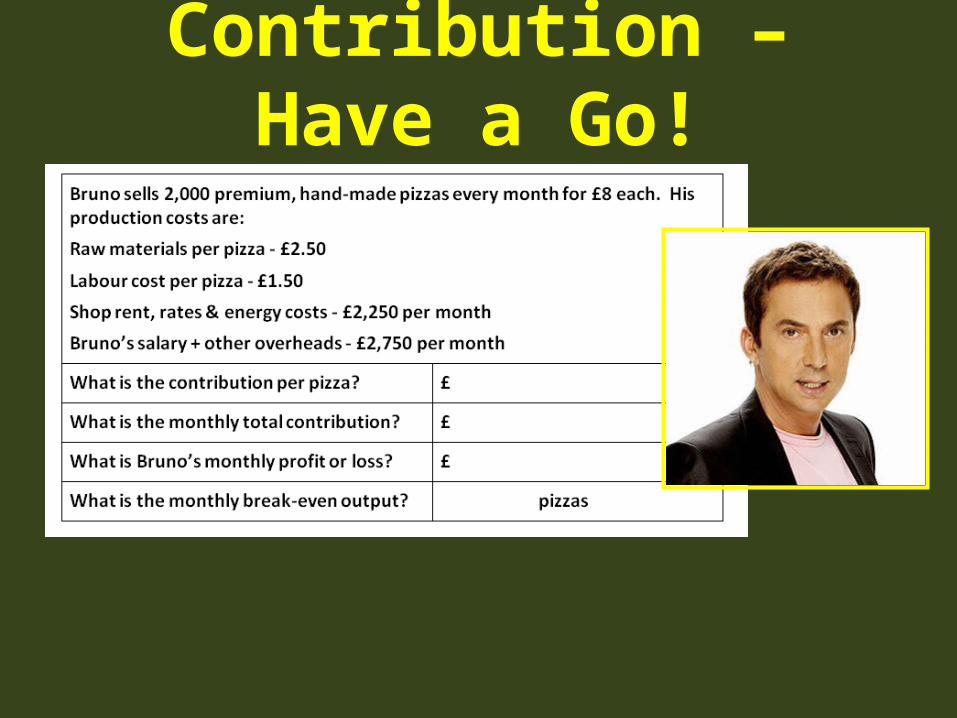

Contribution – Have a Go!

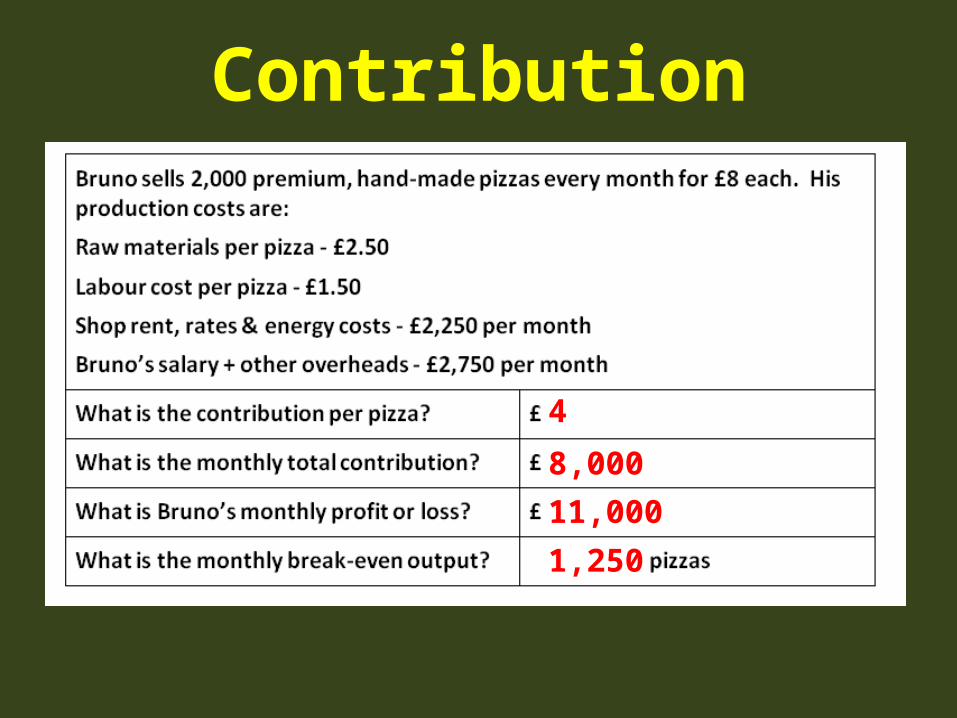

Contribution

4

8,00011,000

1,250

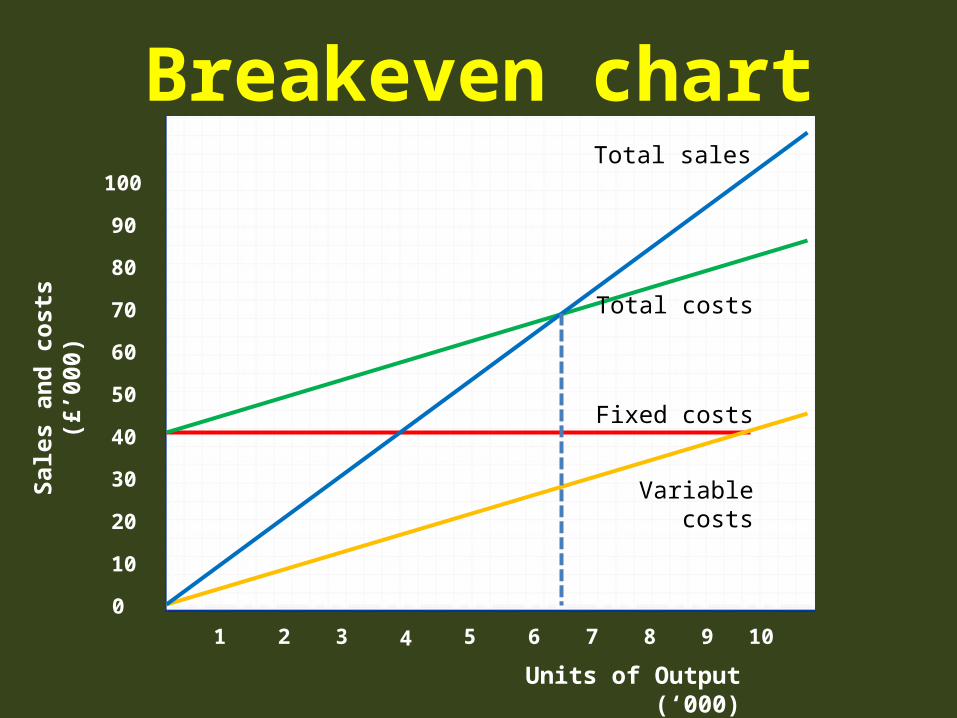

Breakeven chartSa

les

and

cost

s (£

’000

)

Units of Output (‘000)

10

0

30

20

50

40

70

60

90

80

100

1 2 3 4 5 6 7 8 9 10

Fixed costs

Variable costs

Total costs

Total sales

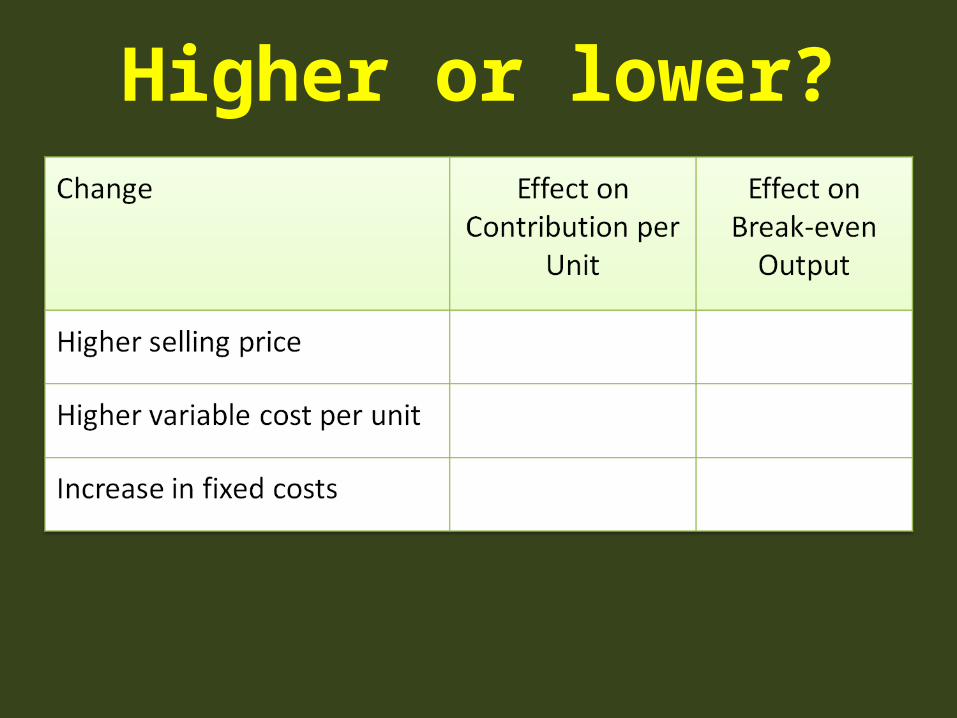

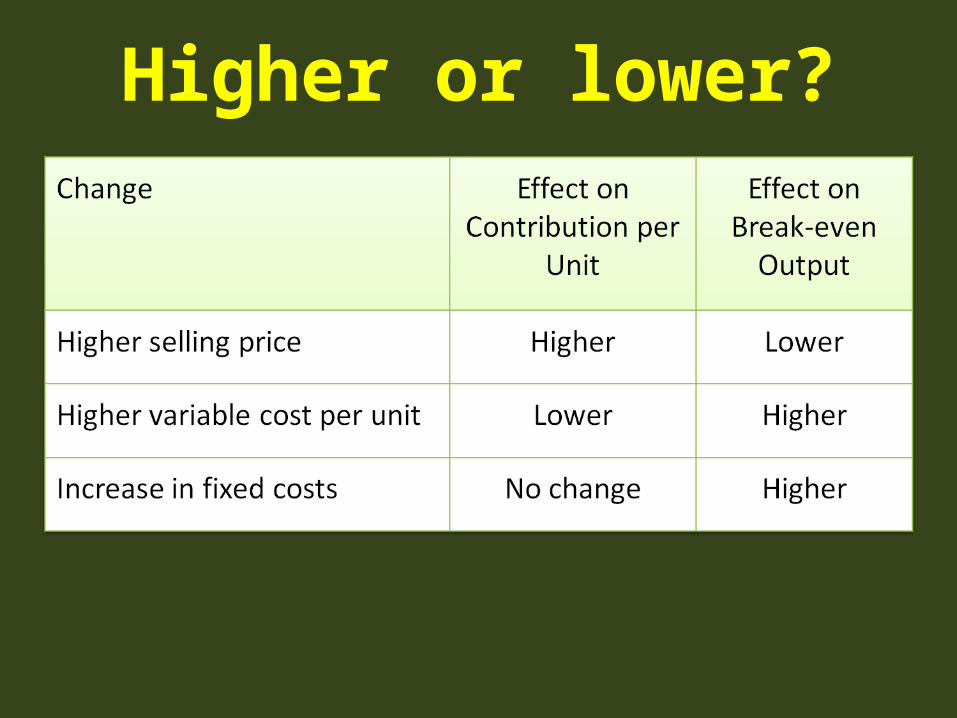

Higher or lower?

Higher or lower?

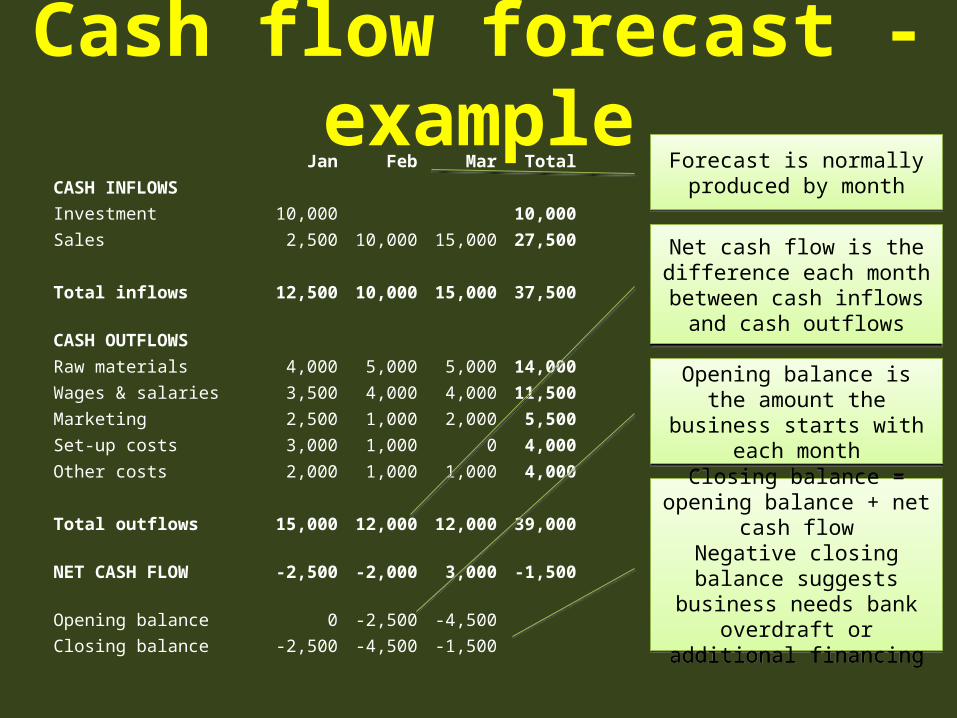

Cash flow forecast - exampleJan Feb Mar Total

CASH INFLOWS

Investment 10,000 10,000

Sales 2,500 10,000 15,000 27,500

Total inflows 12,500 10,000 15,000 37,500

CASH OUTFLOWS

Raw materials 4,000 5,000 5,000 14,000

Wages & salaries 3,500 4,000 4,000 11,500

Marketing 2,500 1,000 2,000 5,500

Set-up costs 3,000 1,000 0 4,000

Other costs 2,000 1,000 1,000 4,000

Total outflows 15,000 12,000 12,000 39,000

NET CASH FLOW -2,500 -2,000 3,000 -1,500

Opening balance 0 -2,500 -4,500

Closing balance -2,500 -4,500 -1,500

Forecast is normally produced by monthForecast is normally produced by month

Net cash flow is the difference each month

between cash inflows and cash outflows

Net cash flow is the difference each month

between cash inflows and cash outflows

Opening balance is the amount the business starts

with each month

Opening balance is the amount the business starts

with each month

Closing balance = opening balance + net cash flow

Negative closing balance suggests business needs

bank overdraft or additional financing

Closing balance = opening balance + net cash flow

Negative closing balance suggests business needs

bank overdraft or additional financing

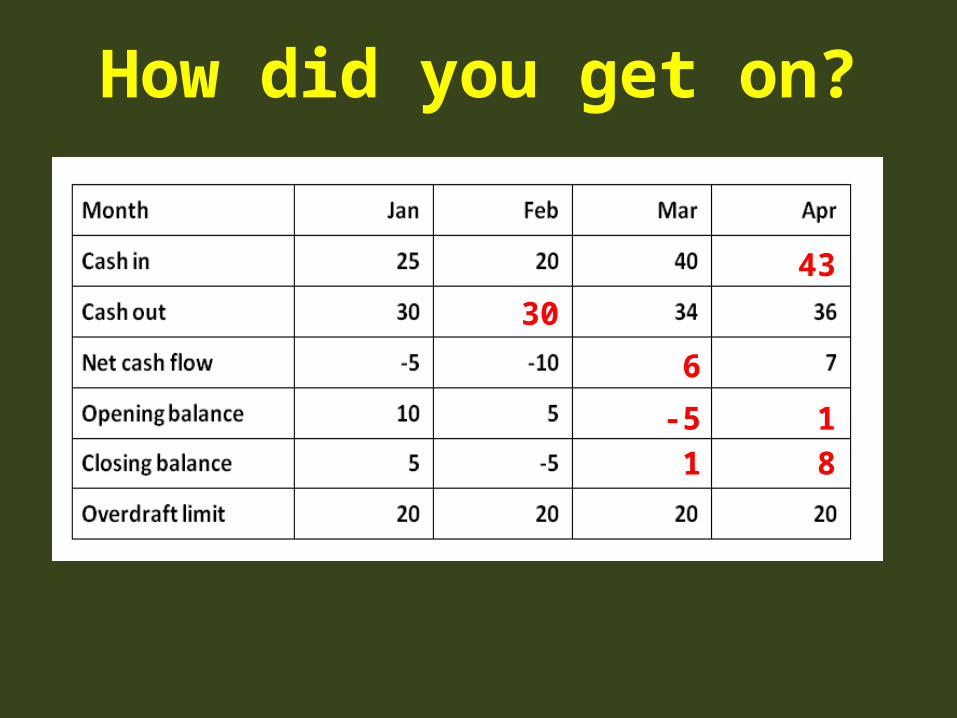

Complete the missing numbers

How did you get on?

30

6

-51

18

43

www.tutor2u.net

Session 3

Financing theStart-up

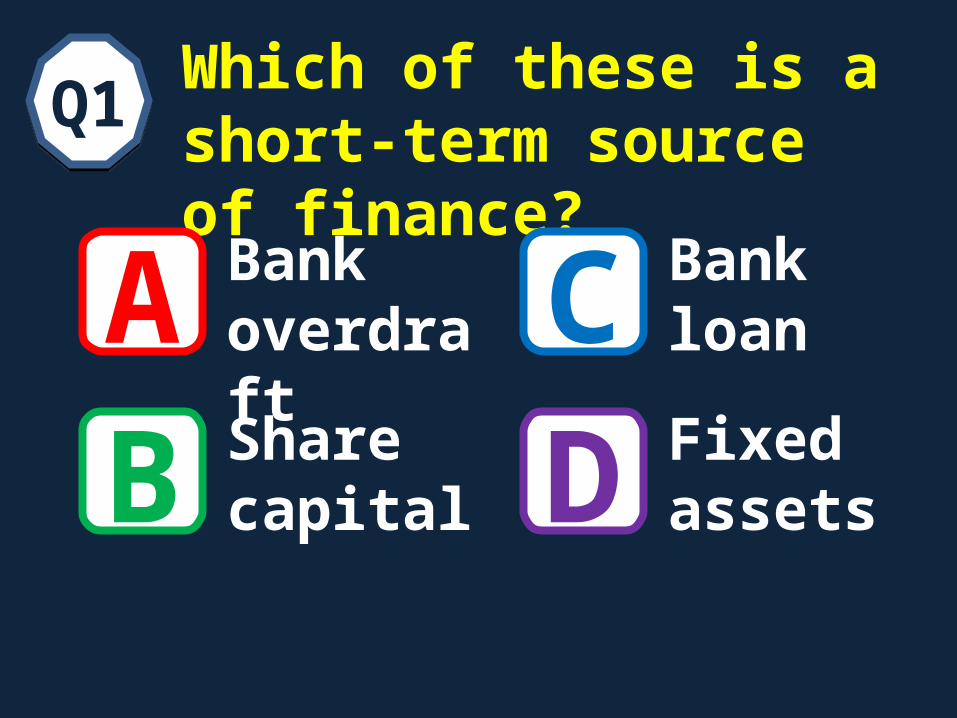

Which of these is a short-term source of finance?

A

Q1Q1

BCD

Bank overdraft

Bank loan

Share capital

Fixed assets

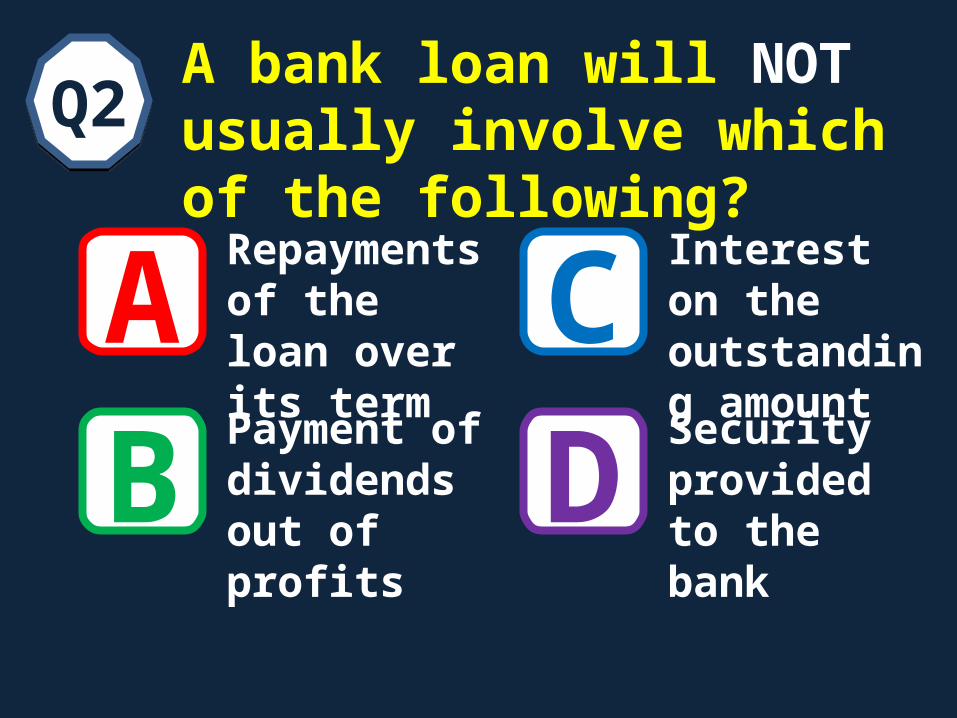

A bank loan will NOT usually involve which of the following?

A

Q2Q2

BCD

Repayments of the loan over its term

Interest on the outstanding amount

Payment of dividends out of profits

Security provided to the bank

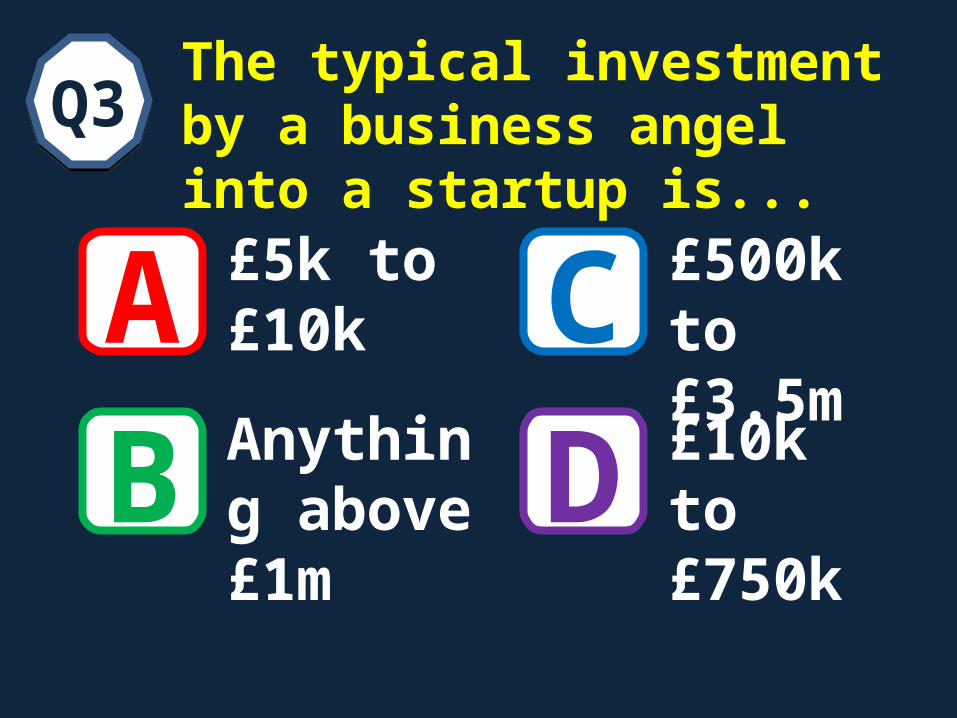

The typical investment by a business angel into a startup is...

A

Q3Q3

BCD

£5k to £10k

£500k to £3.5m

Anything above £1m

£10k to £750k

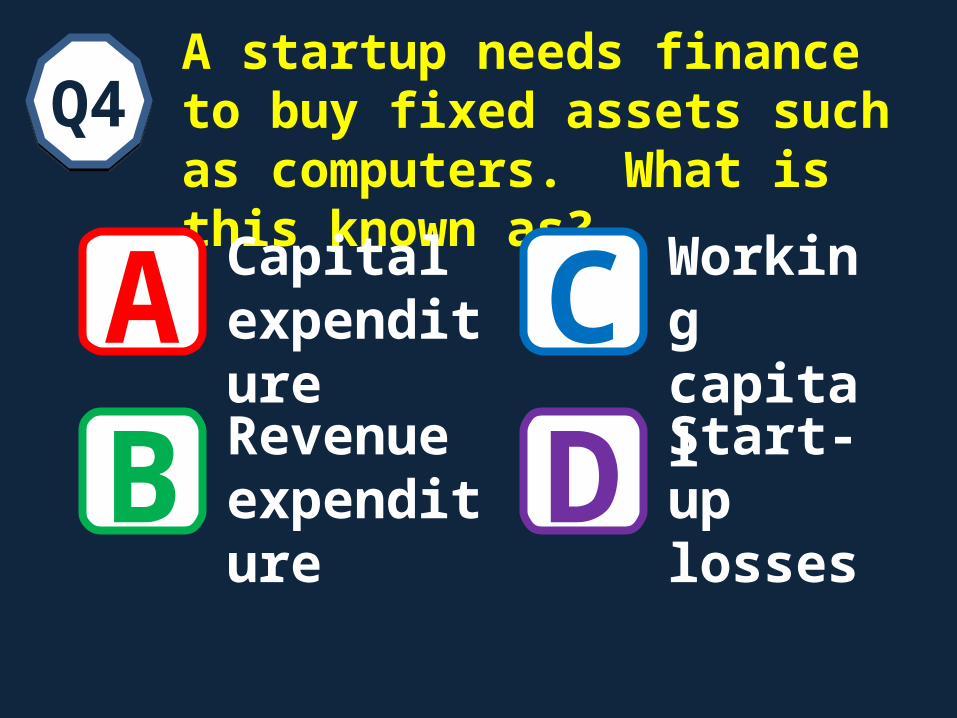

A startup needs finance to buy fixed assets such as computers. What is this known as?

A

Q4Q4

BCD

Capital expenditure

Working capital

Revenue expenditure

Start-up losses

A startup will need to finance...

A

Q5Q5

BCD

Cash sales to customers

Dividends paid to the bank

Interest on cash held at the bank

Pre-trading losses

Key Issues for Start-up Finance

• How much?– Enough v not too much– Safety buffer

• When?– All at once– Drip feed / as needed

• Challenges– Keeping control– Staying afloat

Finance needed for…

Business Set-up

Day-to-day trading

Growth

Main sources of start-up financeInternal Sources External Sources

Founder finance (personal sources of the entrepreneur)

Retained profits

Credit cards

Bank loan

Bank overdraft

Friends & family

Business angels

Loans & grants

+ Don’t forget “Sweat”Start-up entrepreneurs usually save cash and costs by working long hours for nothing

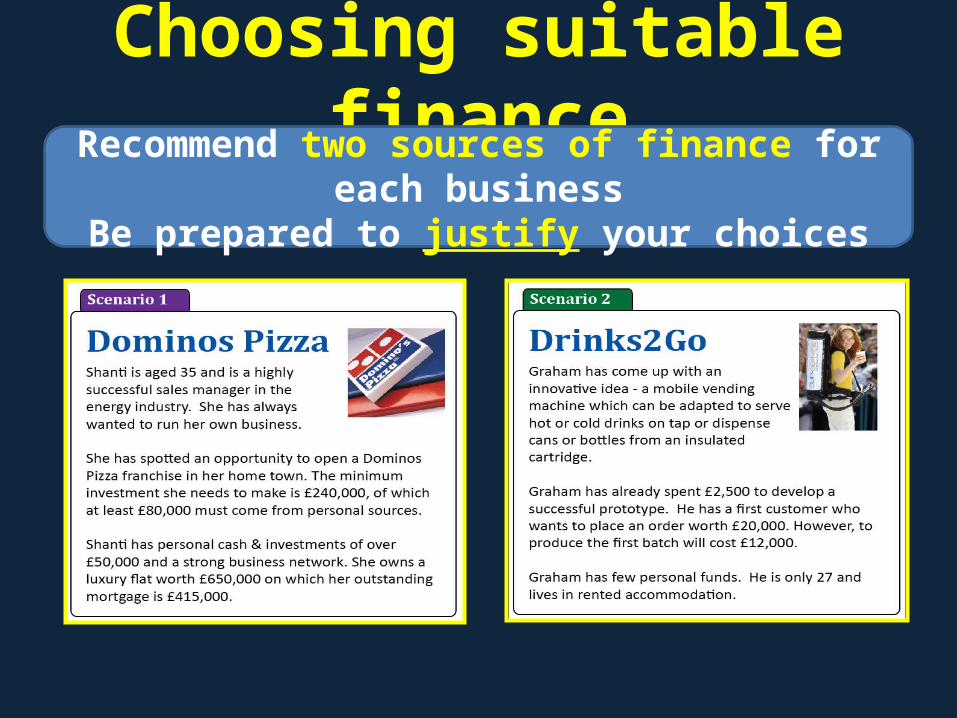

Choosing suitable financeRecommend two sources of finance for each business

Be prepared to justify your choices

www.tutor2u.net

Session 4

Understanding the Market

Some key terms

Demand Market share

Elasticity of demand Niche segment

Write a short definition for each

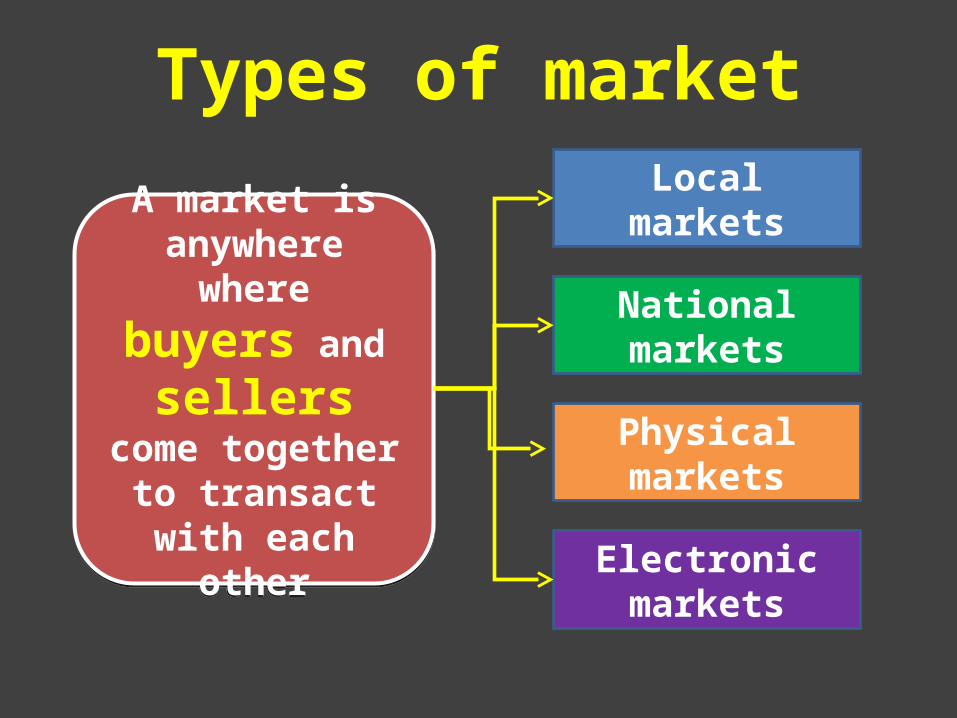

Types of market

A market is anywhere where

buyers and

sellers come together to

transact with each other

A market is anywhere where

buyers and

sellers come together to

transact with each other

Localmarkets

Nationalmarkets

Physicalmarkets

Electronicmarkets

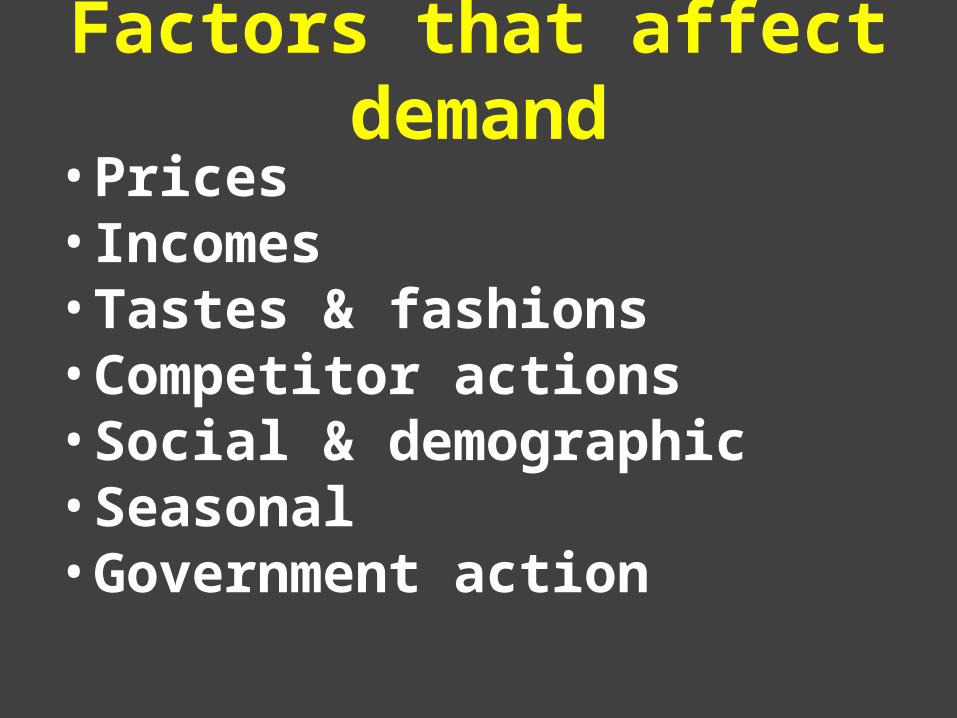

Factors that affect demand

Factors that affect demand• Prices• Incomes• Tastes & fashions• Competitor actions• Social & demographic• Seasonal• Government action

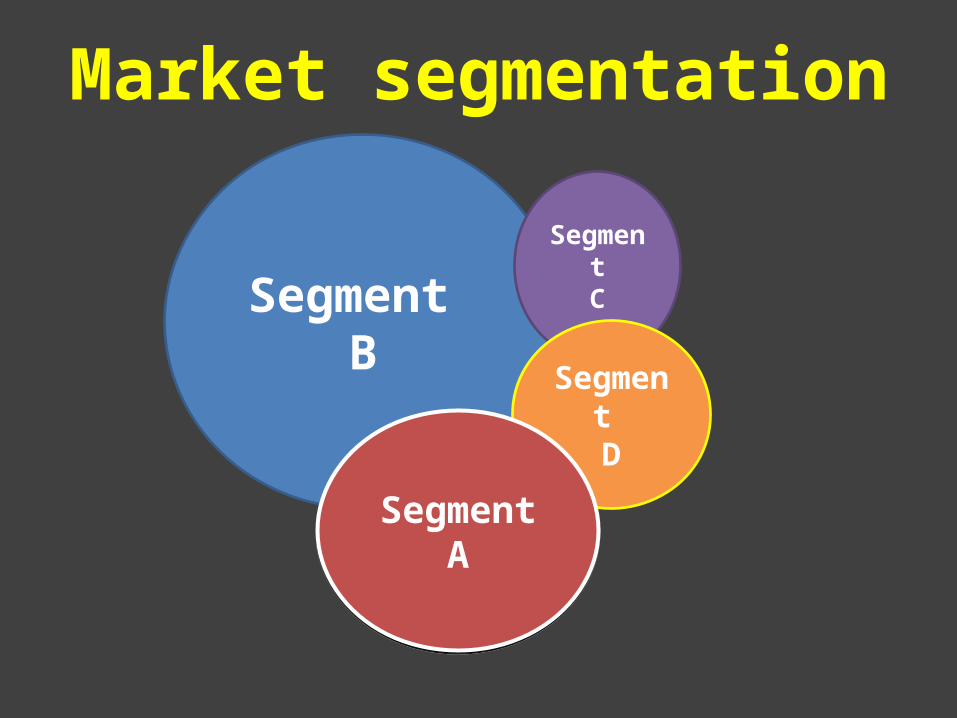

Market segmentation

Segment B

SegmentC

Segment D

SegmentA

SegmentA

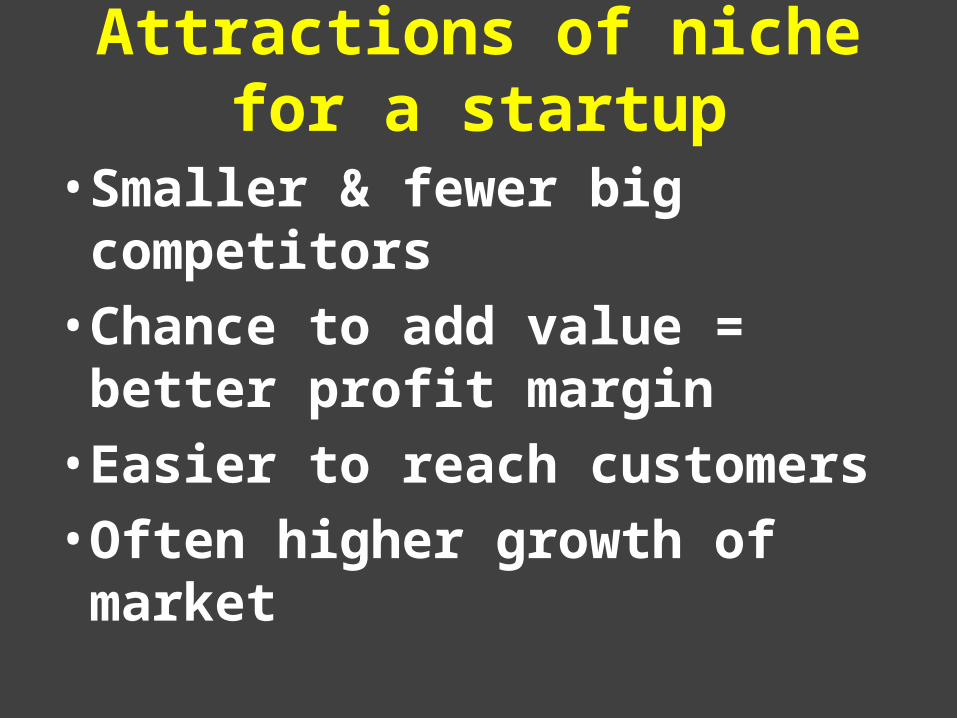

Attractions of niche for a startup

• Smaller & fewer big competitors• Chance to add value = better

profit margin• Easier to reach customers• Often higher growth of market

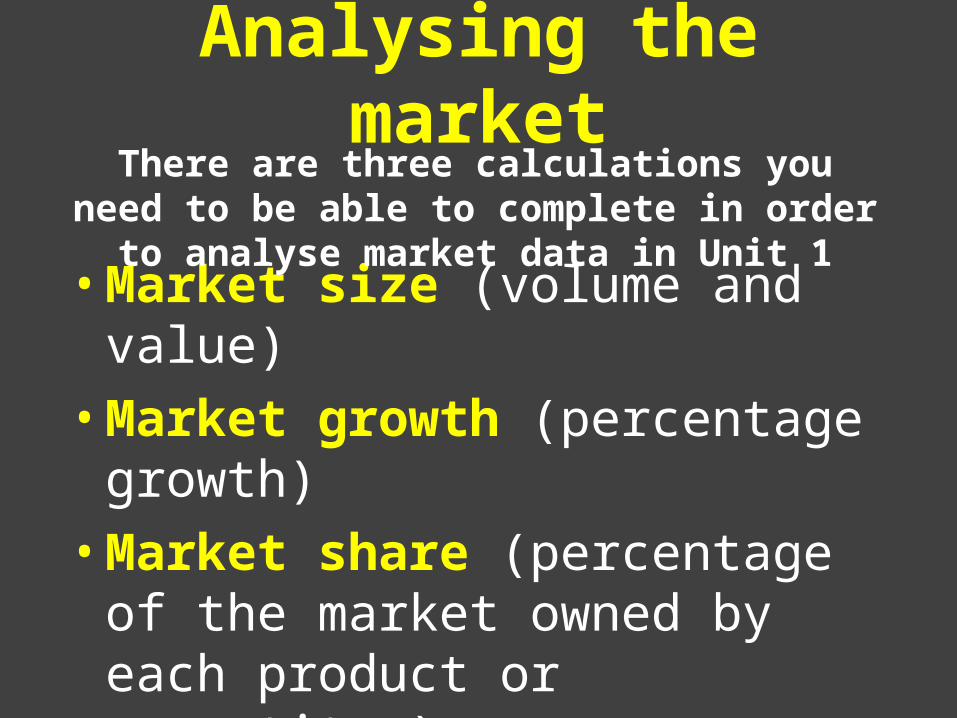

Analysing the market

• Market size (volume and value)• Market growth (percentage growth)• Market share (percentage of the

market owned by each product or competitor)

There are three calculations you need to be able to complete in order to analyse market data in Unit 1

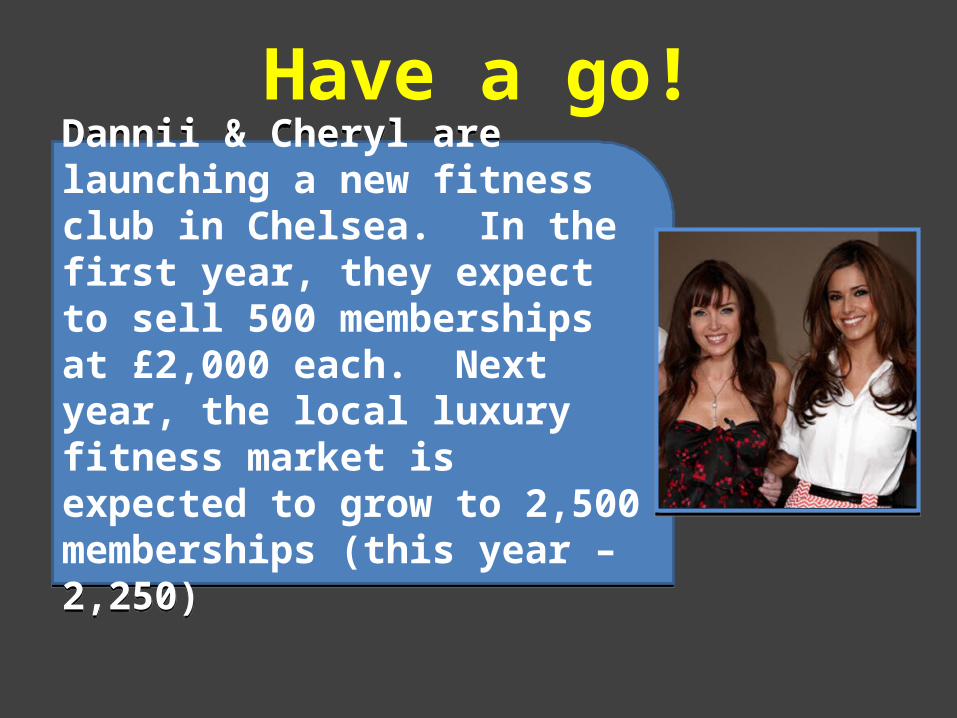

Have a go!

Dannii & Cheryl are launching a new fitness club in Chelsea. In the first year, they expect to sell 500 memberships at £2,000 each. Next year, the local luxury fitness market is expected to grow to 2,500 memberships (this year – 2,250)

Dannii & Cheryl are launching a new fitness club in Chelsea. In the first year, they expect to sell 500 memberships at £2,000 each. Next year, the local luxury fitness market is expected to grow to 2,500 memberships (this year – 2,250)

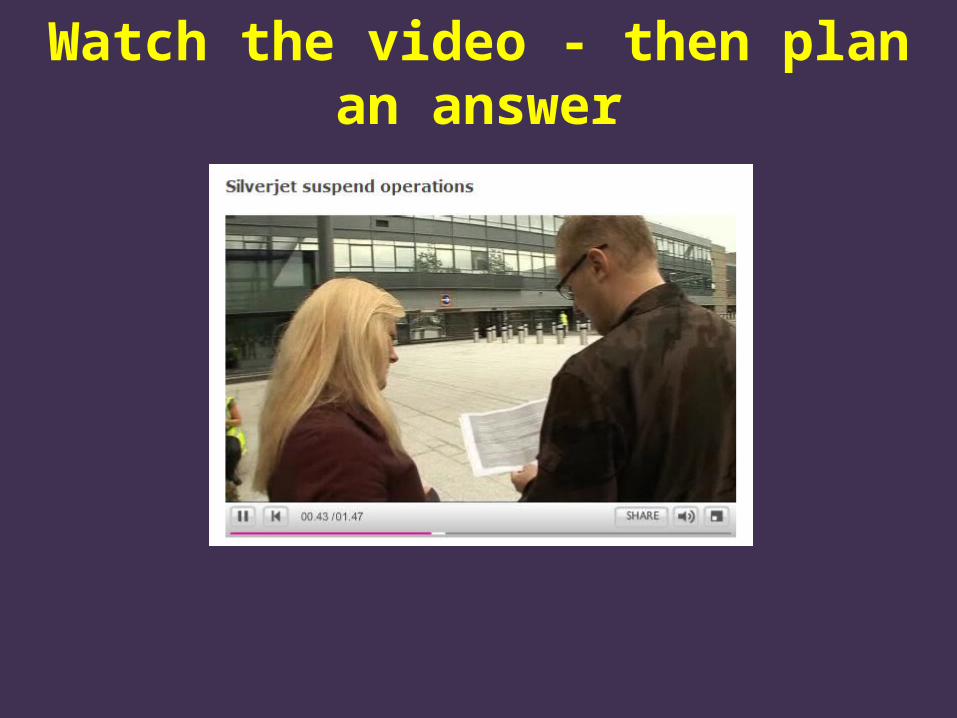

Evaluating the market opportunity

Watch the video and then plan your answer to the two questions

www.tutor2u.net

Session 5

Why Start-upsFail

What we’ll cover• Motives for starting a business• Aims and objectives of start-ups• Business planning• What can go wrong

Over to you!

Motives for being an entrepreneur

• Financial– Capital gains– Making a living

• Personal– Proving people wrong– Gaining control– Building something

• Social– Giving something back

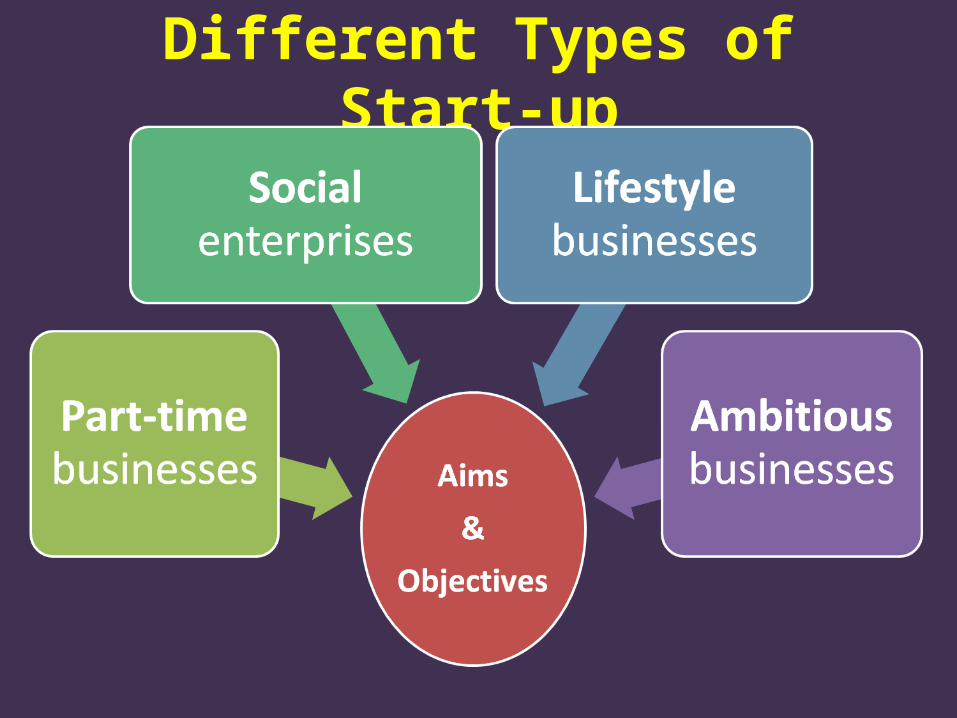

Different Types of Start-up

Business planning

• Two main purposes:• A detailed plan for success• A tool to raise finance

So what can go wrong with a business plan?

Over to you!

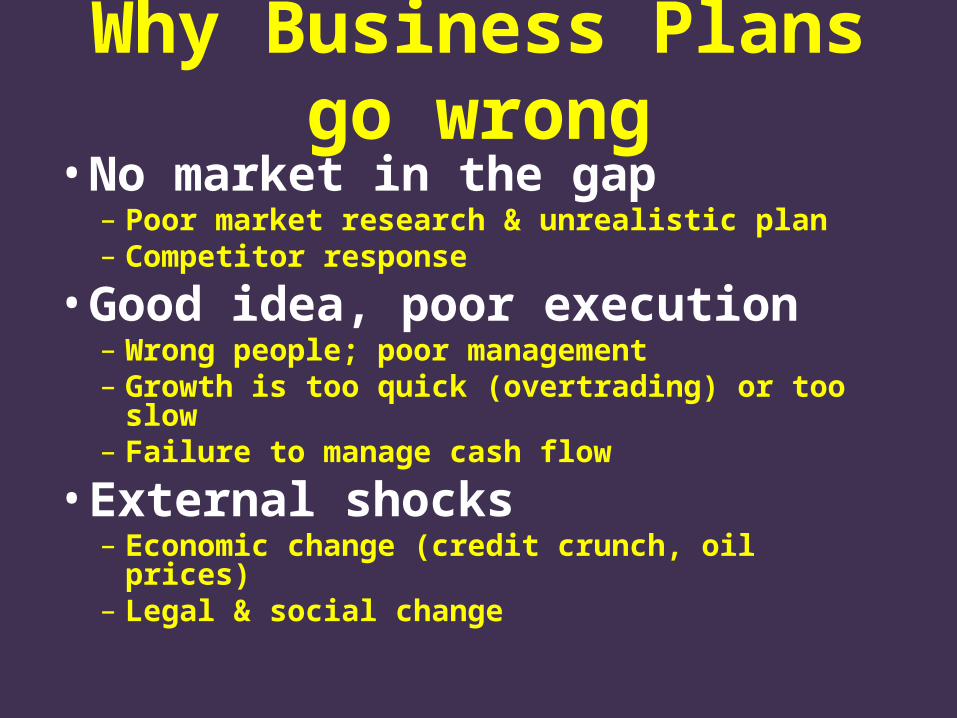

Why Business Plans go wrong• No market in the gap

– Poor market research & unrealistic plan– Competitor response

• Good idea, poor execution– Wrong people; poor management– Growth is too quick (overtrading) or too slow– Failure to manage cash flow

• External shocks– Economic change (credit crunch, oil prices)– Legal & social change

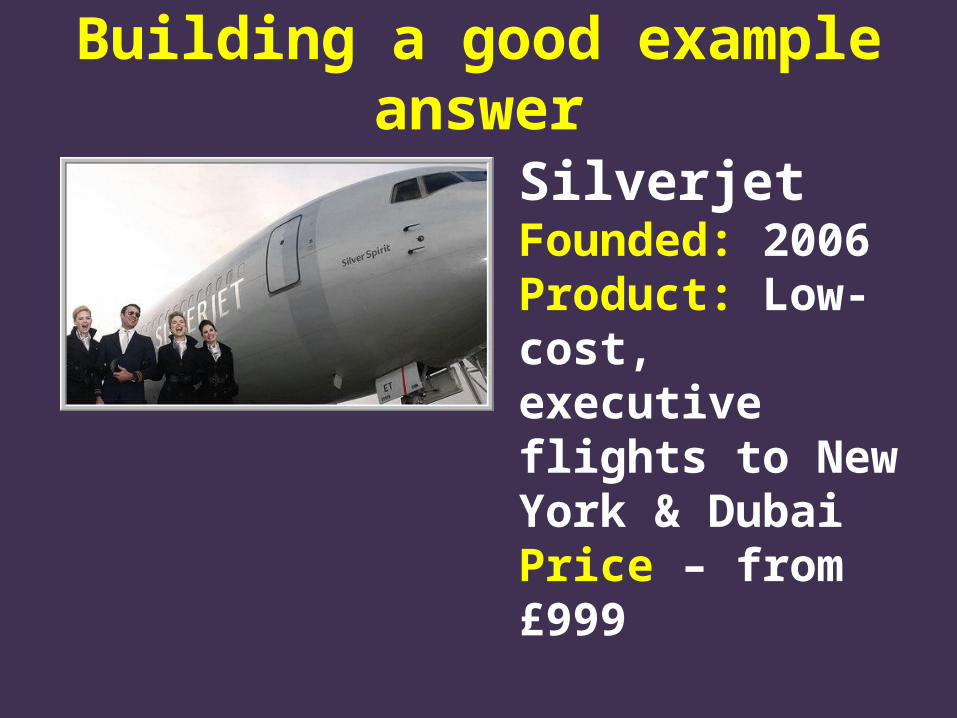

Building a good example answer

SilverjetFounded: 2006Product: Low-cost, executive flights to New York & DubaiPrice – from £999

www.tutor2u.net

Session 6

Evaluating the Start-up

Putting it all together• A tale of two start-ups• Which would you invest in?• Which one succeeded?• Which one failed?• Top tips for Unit 1 evaluation

A Tale of Two Start-ups• Here are two reali-life start-up

stories• Imagine you are a potential

investor• What would you want to know?

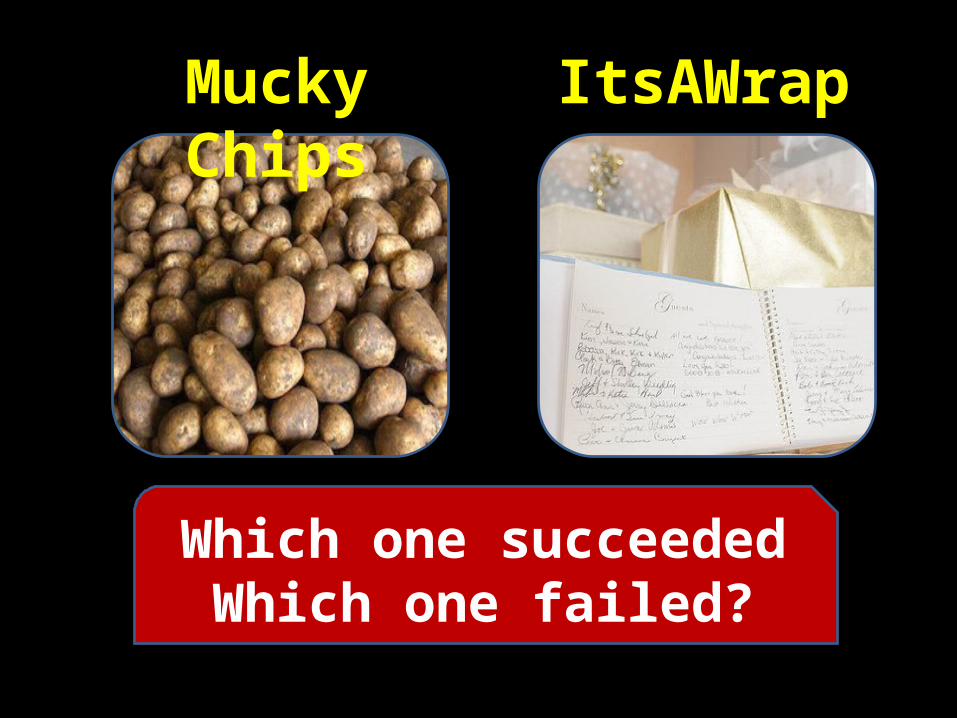

Mucky Chips ItsAWrap

What information would be useful to help you decide whether to invest?

Mucky Chips - IntroductionA new business for potato farmer Bob Mucky

His previous business went bankrupt and his existing business is performing poorly - supplying potatoes to supermarkets

The plan - use their own potatoes to make hand-fried potato chips

Mucky Chips – The MarketMarket size - £4bn; 10 billion packets per year

Dominated by Pepsico (Walkers) who have a 50% market share

Many other small hand-fried chip makers

Investment needed - £1m

Mucky Chips – The planSmall batch production using a own secret, refined traditional recipe

Sell direct to independent retailers (e.g. local delis)

Packaging - transparent packets so customers can see what is inside

Will start small and test samples with customers before investing in full-scale production facilities

Existing farm staff to be trained in all aspects of chip production

ItsaWrap - IntroductionThe ultimate wedding service

Idea of fashion expert Suzi Bianchi who has obtained backing from a variety of business angels

Product - manage wedding gift lists on behalf of couples

Focus on high standards of customer service

ItsaWrap – The MarketMarket size £200m and growing fast

But number of weddings in decline

Main competitors are mass market department stores – e.g. John Lewis, M&S

ItsaWrap – The PlanStrong cash flows – wedding guests pay in advance for their gifts

Personal selling via high street showrooms full of stock so customers can browse potential gifts

Target customers – 30+ professionals looking for special wedding gifts

Expect to manage 2,000 wedding lists p.a - £3,000 each

Mucky Chips ItsAWrap

Which one do you want to invest in?

Mucky Chips ItsAWrap

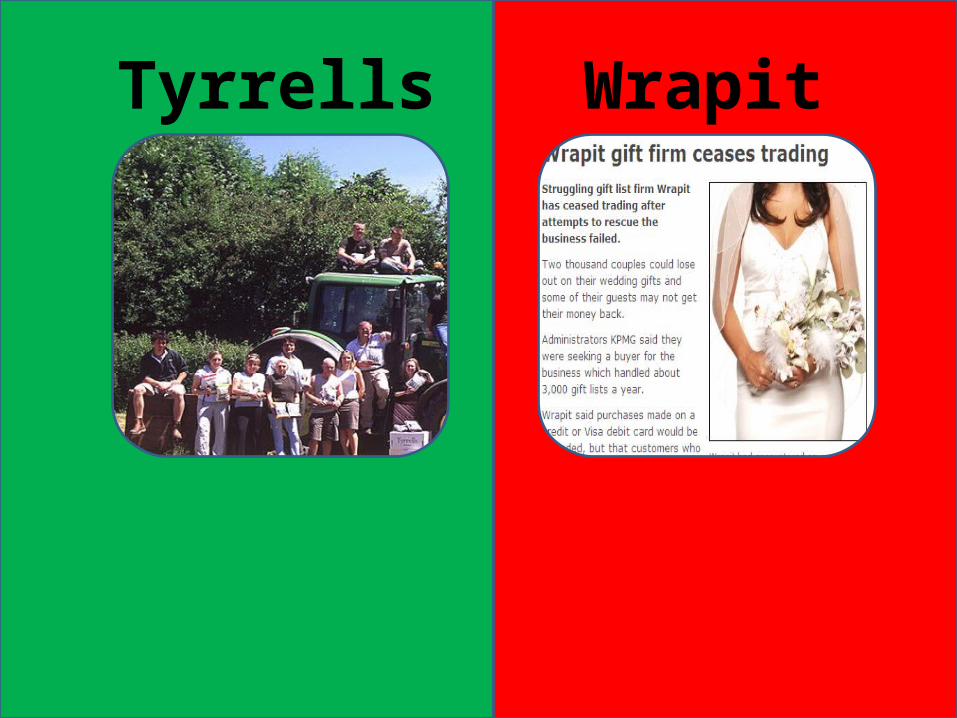

Which one succeededWhich one failed?

Tyrrells Wrapit

www.tutor2u.net

AQA AS Business

UNIT 1REVISION WORKSHOP