Embed Size (px)

Citation preview

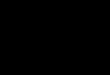

Yen

-4

-3

-2

-1

0

1

2

3

4

5

6

1 2 3 4 5 6 7 8 9 101112 1 2 3 4 5 6 7 8 9 101112

2005 2006

Swiss franc

-4

-3

-2

-1

0

1

2

3

4

5

6

1 2 3 4 5 6 7 8 9 101112 1 2 3 4 5 6 7 8 9 101112

2005 2006

Per c

ent

UNITED NATIONS

New York and Geneva, December 2007

GLOBAL AND REGIONALAPPROACHES TO TRADE

AND FINANCE

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENTGENEVA

Symbols of United Nations documents are composedof capital letters combined with figures. Mention ofsuch a symbol indicates a reference to a United Nationsdocument.

The designations employed and the presentation ofthe material in this publication do not imply theexpression of any opinion whatsoever on the part ofthe Secretariat of the United Nations concerning thelegal status of any country, territory, city or area, orof its authorities, or concerning the delimitation ofits frontiers or boundaries.

Material in this publication may be freely quoted;acknowledgement, however, is requested (includingreference to the document number). It would beappreciated if a copy of the publication containingthe quotation were sent to the Publications Assistant,Division on Globalization and Development Strategies,UNCTAD, Palais des Nations, CH-1211 Geneva 10.

UNITED NATIONS PUBLICATION

UNCTAD/GDS/2007/1

Copyright © United Nations, 2007

All rights reserved

Note

iii

Explanatory notes .................................................................................... viiAbbreviations ............................................................................................ ixList of regional blocs and membership ..................................................... x

I. INTRODUCTION ............................................................................... 1

II. FOSTERING COHERENCE BETWEENTHE INTERNATIONAL TRADING, MONETARYAND FINANCIAL SYSTEMS ............................................................ 5

A. Building the international competitivenessof developing-country exporters ............................................... 5

1. Conditions for competitiveness at the microeconomic level .... 82. Competitiveness of firms at the level of

the national economy ............................................................ 113. Transmission mechanisms between the national and

the international economy .................................................... 16

B. Impacts of monetary and financial factors on developingcountries’ export performance ............................................... 18

1. Impacts of exchange-rate changes on enterpriseinvestment and competitiveness ........................................... 21

2. Sharp exchange-rate changes and developing countries’export performance ............................................................... 23

C. Policy adjustment with open capital accounts ...................... 27

1. Speculative flows induced by carry trade ............................ 272. Changing opportunities for speculation in emerging

market economies ................................................................. 373. Speculative capital flows and real effects ............................ 394. The potential of un-coordinated national exchange-rate

policies to control external accounts .................................... 455. A multilateral solution .......................................................... 47

Contents

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE

iv

III. REGIONAL COOPERATION .......................................................... 51

A. The limitations of conventional thinking ............................... 54

1. Theoretical approaches to regional integration .................... 542. The role of geography, history and politics .......................... 57

B. Regionalization and policy cooperation ................................. 60

1. Industrialization and the integration challenge .................... 602. Bridging gaps and battling constraints ................................. 64

C. Regional cooperation and trade integrationamong developing countries .................................................... 66

1. Forms of regional cooperation and effectivetrade integration .................................................................... 67

2. Measures of regional trade integration ................................. 753. Composition of intraregional trade ....................................... 794. The potential role of South-South regional trade agreements .. 82

D. Regional financial and monetary cooperation ...................... 88

1. Regional cooperation for payment facilities andshort-term financing .............................................................. 92

2. Regional cooperation for development financing ................ 973. Exchange-rate mechanisms and monetary unions.............. 1054. Lessons from European monetary integration.................... 1075. Conclusion .......................................................................... 111

Notes ................................................................................................ 115

References ......................................................................................... 121

v

2.1 Innovative investment, exchange-rate changes, andinternational competitiveness: a numerical example ..................... 14

2.2 Impact of changes in exchange rates and income onexternal performance: estimation results for differentsizes of exchange-rate change, 1971–2002 ................................... 25

2.3 Impact of changes in exchange rates and income onthe merchandise trade balance: time path of adjustment,1971–2002 ...................................................................................... 26

3.1 Manufacturing value added, total trade and trade inmanufactures, EU-15, NAFTA and East Asia, 1991–2005 ........... 61

3.2 Main characteristics of different types of trade integrationarrangements .................................................................................. 68

3.3 Intraregional trade balance in selected regional blocs,2000–2006 ...................................................................................... 83

3.4 Bilateral Swap Arrangements under the Chiang Mai Initiative ...... 95

3.5 Regional development banks outstanding loans:total amount, distribution and debt ratings, 2005–2006 .............. 100

3.6 Portfolio investment assets, ASEAN and ASEAN+3,2001–2005 .................................................................................... 104

List of tables

vi

2.1 Carry trade opportunities of the yen and Swiss francvis-à-vis the dollar, 2005–2006...................................................... 31

2.2 Uncovered interest returns, exchange-rate changes, inflationand interest rate differentials, selected regions, 1995–2006 ......... 34

2.3 Average uncovered interest return and currency volatility,selected countries and periods ....................................................... 38

2.4 Real exchange-rate changes and uncovered interest returnsin selected regions, 1995–2006 ...................................................... 40

3.1 Trade-weighted tariffs in selected regional agreements ................ 71

3.2 Intraregional trade indicators for selected developingregions, 1970–2006 ........................................................................ 76

3.3 Share of intraregional trade in total trade:selected regional blocs ................................................................... 78

List of boxes

2.1 Uncovered interest parity ............................................................... 42

3.1 The MERCOSUR structural convergence fund ............................ 86

List of figures

vii

Explanatory notes

Classification by country or commodity group

The classification of countries has been adopted solely for the purposes ofstatistical or analytical convenience and does not necessarily imply anyjudgement concerning the stage of development of a particular country orarea.

The major country groupings follow the classification by the United NationsStatistical Office (UNSO). They are distinguished as:

» Developed or industrial(ized) countries: the countries members of theOECD (other than Mexico, the Republic of Korea and Turkey) plusthe new EU member countries and Israel.

» The category South-East Europe and Commonwealth of IndependentStates (CIS) replaces what was formerly referred to as “transitioneconomies”.

» Developing countries: all countries, territories or areas not specifiedabove.

The terms “country” / “economy” refer, as appropriate, also to territoriesor areas.

References to “Latin America” in the text or tables include the Caribbeancountries unless otherwise indicated.

References to “sub-Saharan Africa” in the text or tables include South Africaunless otherwise indicated.

For statistical purposes, regional groupings and classifications by commoditygroup follow generally those employed in the UNCTAD Handbook ofStatistics 2006–07 (United Nations publication, sales no. E/F.07.II.D.2) unlessotherwise stated.

viii

Other notes

References in the text to TDR are to the Trade and Development Report (ofa particular year). For example, TDR 2007 refers to Trade and DevelopmentReport, 2007 (United Nations publication, sales no. E.07.II.D.11).

The term “dollar” ($) refers to United States dollars, unless otherwisestated.

The term “billion” signifies 1,000 million.

Annual rates of growth and change refer to compound rates.

Exports are valued FOB and imports CIF, unless otherwise specified.

Use of a dash (–) between dates representing years, e.g. 1988–1990,signifies the full period involved, including the initial and final years.

Two dots (..) indicate that the data are not available, or are notseparately reported.

A dash (-) or a zero (0) indicates that the amount is nil or negligible.

Details and percentages do not necessarily add up to totals because ofrounding.

ix

ADB Asian Development BankAfDB African Development BankCIS Commonwealth of Independent StatesECLAC Economic Commission for Latin America and the

CaribbeanEMU European Economic and Monetary UnionEU European UnionFDI foreign direct investmentFTA free trade agreementGATT General Agreement on Tariffs and TradeGDP gross domestic productGNP gross national productIDB Inter-American Development BankIMF International Monetary FundIT information technologyLIBOR London interbank offered rateMFN most-favoured nationNIE newly industrializing economyODA official development assistanceOECD Organisation for Economic Co-operation and

DevelopmentPPP purchasing power parityPTA preferential trade agreementR&D research and developmentRTA regional trade agreementTDR Trade and Development ReportTNC transnational corporationUN/DESA United Nations Department of Economic and Social

AffairsUNCTAD United Nations Conference on Trade and DevelopmentWTO World Trade Organization

Abbreviations

x

List of regional blocs and membership

ANCOM Andean Community of Nations (Comunidad Andinade Naciones)Bolivia, Colombia, Ecuador, Peru, Venezuela(Bolivarian Republic of) (until 2006)

ASEAN Association of Southeast Asian NationsBrunei Darussalam, Cambodia, Indonesia, Lao People’sDemocratic Republic, Malaysia, Myanmar, Philippines,Singapore, Thailand, Viet Nam

ASEAN+3 Association of Southeast Asian Nations +3ASEAN plus China, Japan and the Republic of Korea

CACM Central American Common Market (MercadoComún Centroamericano)Costa Rica, El Salvador, Guatemala, Honduras,Nicaragua

CARICOM Caribbean CommunityAntigua and Barbuda, Bahamas, Barbados, Belize,Dominica, Grenada, Guyana, Haiti, Jamaica, Montserrat,Saint Kitts and Nevis, Saint Lucia, Saint Vincent and theGrenadines, Suriname, Trinidad and Tobago

CEMAC Economic and Monetary Community of CentralAfrica (Communauté Economique et Monétaire del’Afrique Centrale)Cameroon, Central African Republic, Chad, Congo,Equatorial Guinea, Gabon

CFA franc zone Coopération Financière en Afrique Centrale/Communauté Financière AfricaineCEMAC and UEMOA member States

CIS Commonwealth of Independent StatesArmenia, Azerbaijan, Belarus, Georgia, Kazakhstan,Kyrgyzstan, Republic of Moldova, Russian Federation,Tajikistan, Turkmenistan, Ukraine, Uzbekistan

CMA Common Monetary AreaLesotho, Namibia, South Africa, Swaziland

xi

COMESA Common Market for Eastern and Southern AfricaAngola, Burundi, Comoros, the Democratic Republic ofthe Congo, Djibouti, Egypt, Eritrea, Ethiopia, Kenya,the Libyan Arab Jamahiriya, Madagascar, Malawi,Mauritius, Rwanda, Seychelles, Sudan, Swaziland,Uganda, Zambia, Zimbabwe

ECOWAS Economic Community of West African StatesBenin, Burkina Faso, Cape Verde, Côte d’Ivoire,Gambia, Ghana, Guinea, Guinea-Bissau, Liberia, Mali,Niger, Nigeria, Senegal, Sierra Leone, Togo

EU-15 European Union-15Austria, Belgium, Denmark, Germany, Greece, France,Finland, Ireland, Italy, Luxembourg, the Netherlands,Portugal, Spain, Sweden, the United Kingdom

EU European UnionEU-15 plus Bulgaria, Cyprus, the Czech Republic,Estonia, Hungary, Latvia, Lithuania, Malta, Poland,Romania, Slovakia, Slovenia

GCC Gulf Cooperation CouncilBahrain, Kuwait, Oman, Qatar, Saudi Arabia, UnitedArab Emirates

LAIA Latin American Integration Association (AsociaciónLatinoamericana de Integración)Argentina, Bolivia, Brazil, Cuba, Chile, Colombia,Ecuador, Mexico, Paraguay, Peru, Uruguay, Venezuela(Bolivarian Republic of)

MERCOSUR Southern Common Market (Mercado Común del Sur)Argentina, Brazil, Paraguay, Uruguay

NAFTA North American Free Trade AgreementCanada, Mexico, United States

SAARC South Asian Association for Regional CooperationBangladesh, Bhutan, India, Maldives, Nepal, Pakistan,Sri Lanka

xii

SACU Southern African Customs UnionBotswana, Lesotho, Namibia, South Africa, Swaziland

SADC Southern African Development CommunityAngola, Botswana, the Democratic Republic of theCongo, Lesotho, Madagascar, Malawi, Mauritius,Mozambique, Namibia, South Africa, Swaziland, theUnited Republic of Tanzania, Zambia, Zimbabwe

UEMOA West African Economic and Monetary Union(Union Economique et Monétaire Ouest Africaine)Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau,Mali, Niger, Senegal, Togo

WAMZ West African Monetary ZoneGambia, Ghana, Guinea, Nigeria, Sierra Leone

I. INTRODUCTION

A coherent treatment of the interdependence between trade, macro-economic and financial issues was an important element in the debateleading to the post-War international economic system. The set-up of thepost-War international trade regime was predicated on the belief that, inconditions of strictly limited private international capital flows, aninternational monetary system with convertible currencies at fixed, butadjustable, exchange rates would provide a stable environment conduciveto trade and investment. Under the aegis of the General Agreement onTariffs and Trade (GATT), this regime considered tariffs as the only legitimatetrade policy measure. The adopted exchange rate regime supported the GATTapproach, as participants in international trade negotiations could predictthe full extent to which the competitive position of domestic industrieswould be affected by tariff cuts without having to be unduly concernedabout other exogenous factors.

The specific problems of developing countries participating in thepost-War international trading system were largely absent from the mandatesof the intergovernmental institutions created immediately after the SecondWorld War. This was despite the fact that, with international private capitalflows constrained and official development assistance still limited (andoften tied), the role of international trade was attracting increasing attentionas a dependable means of removing the resource constraints on economicgrowth in developing countries. Multilateral efforts at designing a tradingsystem that would take account of the policy options of developing countries,for which slow growth and adverse terms-of-trade movements weredistinctive features, culminated in the First United Nations Conference onTrade and Development in 1964. The Report to the Conference spelt out a

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE2

strategy designed to help poorer countries develop outwardly through strongcapital formation and continuing and accelerated expansion of exports –both traditional and non-traditional. Central to that agenda was the ideathat developing countries can base economic development on their ownefforts only if they have sufficient policy space to accelerate capitalformation, diversify their economic structure and give development greater“social depth”. This agenda also emphasized the interdependence betweentrade and finance, given that, particularly in the early stages of industrialization,imports would almost certainly grow faster than exports, and financing thegap would be key to accelerating growth.

The need for coherence between the international trading system andthe international monetary and financial system has gained in importancewith the abandoning of the system of fixed, but adjustable, exchange ratesand the adoption of widespread floating, combined with a return of privateinternational capital flows to levels similar to those that had caused mucheconomic and social instability in the inter-war period. In particular, theliberalization of capital movements has, on balance, had little impact onlevels of development finance, and the balance-of-payments constraint ofdeveloping countries has not been removed. Rather, there has been a de-linking of financial flows from international trade. This is most clearly thecase with short-term flows, where over 80 per cent of transactions relate toround-trip operations, motivated by hedging, arbitrage and speculativeconsiderations. Moreover, the increased level and volatility of short-termprivate international capital flows, associated with the often sharp swingsin exchange-rate expectations of international investors, have an adversebearing on the principle of non-discrimination in trade and on developing-country trade performance.

Thus, an evaluation of the trade performance of developing countriesshould take account not only of the functioning of the international tradingregime itself, but also of the way international monetary and financialrelationships impact on trade. This is the subject of this book.

The first part examines the problem of insufficient coherence betweenthe international trading, monetary and financial systems, and how it affectsthe formulation and successful implementation of national development

INTRODUCTION 3

strategies. It is argued that rapid financial liberalization, inasmuch as itmakes developing countries vulnerable to sharp and abrupt shifts in thedirection of largely autonomous short-term private international capitalflows, can have negative effects on their trade performance. Managedcurrency depreciations, proceeding on a smooth, long-term basis, canstrengthen the international cost competitiveness of domestic exporters andgenerally improve developing countries’ trade performance. However, thisis not the case for the sharp and abrupt exchange-rate depreciations thathave occurred in many financially open developing countries over the pastthree decades; they did not result in proportionally larger improvements intrade performance. This is because they were often accompanied by sharpdeclines in imports and reduced access to trade finance and working capital,which compromised the ability of domestic exporters to benefit from theirincreased international cost competitiveness stemming from the depreciation.The final section outlines a multilateral solution designed to avoid inter-national monetary and financial upheaval and thereby support developingcountries’ trade performance and foster their domestic supply capacities.

The second part of the publication starts from the recognition that aslong as such a multilateral solution is absent, regional cooperation amongdeveloping countries can be a way of fostering the creation of domesticsupply capacity, developing countries’ trade performance and their resilienceto international monetary and financial shocks. It is argued that regionalcooperation among developing countries does not only have the potentialto support national development strategies, but also to some extent fill thegaps in the global economic governance system. But in order to do so ithas to extend beyond regional trade liberalization to include policy areasthat strengthen the potential for growth and structural change in developingcountries, particularly macroeconomic and financial management. In thisrespect, regional monetary and financial cooperation can provide decisivesupport for the management of exchange rates by the members of a regionalbloc, without which further progress in trade integration would be verydifficult. It may also expand the supply of long-term financing through thecreation or reinforcement of regional financial institutions such asdevelopment banks and financial markets. Finally, it may reduce thevulnerability of the regional partners to the vagaries of the internationalfinancial markets by developing regional systems of payments and mutual

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE4

financing, enforcing the use of national currencies and establishing regionalmechanisms for policy coordination and macro-economic surveillance.However, regional efforts to strengthen financial cooperation do not pre-empt multilateral efforts aimed at improving the international financialsystem and promoting its greater coherence with the international tradingsystem. On the contrary, successful regional financial cooperation amongdeveloping countries may be one of the building blocks of an improvedinternational monetary order. The European experience of regional cooperationsuggests that such cooperation is unlikely to follow some established blueprint,that it takes considerable time to evolve and that the steady build-up ofinstitutional capacity is a critical dimension of success.

II. FOSTERING COHERENCE BETWEEN THEINTERNATIONAL TRADING, MONETARY

AND FINANCIAL SYSTEMS

A. Building the international competitivenessof developing-country exporters

Developing countries depend on a favourable international tradingenvironment to reap the full benefits of their integration into the worldeconomy. Equally important for their successful integration is the creationof strong supply capacities. An essential lesson from the experiences ofcountries that combined successful integration into the world economy withsustained growth is the critical role of active and well sequenced policiesto augment the existing stock of physical and human capital, enable theuse of more efficient technologies, and shift resources from traditional,low-productivity activities towards activities that offer a high potential forproductivity growth.

Transformation of the production structure requires entrepreneurs whoare capable and willing to invest in activities that are new to the domesticeconomy. Indeed, Schumpeter (1911) pointed to the importance of innovativeinvestment for economic development, and Baumol (2002) argues thatinnovation, and the consequent rise in productivity, account for much ofthe extraordinary growth record that has occurred in various parts of theworld since the Industrial Revolution. He suggests that market pressuresarising from oligopolistic competition force firms to integrate innovative

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE6

investment into their routine decision processes and activities – thus, theinnovation process is neither largely autonomous nor largely fortuitous.Market forces achieve much of this through financial incentives, byproviding higher pay-offs to those firms that are more efficient and whoseproducts are most closely adapted to the wishes of consumers.

However, the occurrence of innovative investment is not automatic;it could encounter structural and institutional impediments. Moreover, themacroeconomic environment could be inappropriate for encouraging andsupporting investors seeking to create or expand productive capacity and,in particular, to increase productivity and international competitiveness.The main incentive for investors to discover a more efficient way ofproducing an existing good or to produce a new good arises when they canappropriate at least part of the rent generated by the creation of newknowledge. Within this framework, for an innovative entrepreneur to enjoysuch benefits, a number of conditions must apply at different levels. Theseconditions relate to a wide range of linkages between investment, productivitygrowth, successful integration into the international trading and financialsystems, and economic development, which in recent years have often beenseen through the lens of international competitiveness.

The concept of competitiveness can contribute to an understanding ofthe distribution of wealth, both nationally and internationally, if it isrecognized that: (i) it can be applied at both the enterprise and the countrylevel, (ii) when applied at the enterprise level, it relates to profits or marketshares, (iii) when applied at the country level, it relates to both nationalincome and international trade performance, particularly in relation tospecific industrial sectors that are important in terms of, for example,employment or productivity and growth potential, (iv) it is based on aSchumpeterian logic that sees the nature of capitalist development as asequence of innovative investments associated with dynamic imperfectcompetition and productivity gains, and that sees a major role for publicpolicy in facilitating productivity-increasing investment,1 and (v) not allcountries can simultaneously improve the competitiveness of their firmsor sectors relative to other countries, but all countries can simultaneouslyraise productivity and wages to improve their overall economic welfarewithout altering their relative competitive positions.

FOSTERING COHERENCE 7

If new technology in the form of added capital per worker (or embodiedtechnological change) is at the heart of the development process throughwhich nations become rich, and if embodied technological change is drivenby investment based on either innovation of domestic entrepreneurs orputting imported capital equipment to efficient use, then approaching theconcept of competitiveness in the context of economic development needsto take account of the interdependence of investment, trade, finance andtechnology.

Looking at competitiveness from the perspective of interdependence,two key questions relate to how different price, wage, exchange rate andtrade arrangements (i) influence the determinants of innovative investment,and (ii) determine whether productivity gains of individual firms translateinto benefits for the overall economy, as reflected in rising living standards,while maintaining external balance.

Emphasizing interdependence also implies that competitiveness ininternational markets is determined by both real and monetary factors.Competitiveness may increase as a result of the relatively strong productivityperformance of companies or the national economy as a whole. But greatercompetitiveness can result also from a depreciation of a country’s realeffective exchange rate following either a depreciation of its nominaleffective exchange rate or a smaller rise in the ratio between wages andproductivity (i.e. unit labour costs) than in other countries.

There have been strong objections to the use of the concept ofcompetitiveness at the level of countries rather than at the level of individualfirms. Some of these objections raise valid concerns. Indeed, caution isneeded in presenting the concept as one of the economic challenges facingdeveloping countries.

Nonetheless, developing countries have valid concerns about theirexternal economic performance. First, countries in the early stages ofindustrialization require foreign-exchange earnings from exports to financemachinery and equipment imports that enable innovative investors to obtainproductivity gains. Second, countries further advanced in industrialization,and strongly integrated into international trading and financial markets,

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE8

may find it difficult to maintain a sufficient degree of flexibility in theirmonetary, wage and trade policies. Flexibility is needed to accommodateprice adjustments that arise from productivity-enhancing investment andto prevent profits earned through innovative investments from being spenton luxury imports rather than being reinvested. Third, and most importantly,changes in the relative importance of different economic sectors are a keyfactor for rapid and sustained productivity growth and higher livingstandards. This implies that the concept of competitiveness is of immediatepolicy relevance. It can be used to analyse under which conditionsproductivity gains at the microeconomic level translate into structural changeat the level of the national economy and enable upgrading of the technologycontent of a country’s export basket. It is also useful for identifying policymeasures that reduce the vulnerability of national economies to disturbancesemanating from the international economy and which may have adverseeffects on national economic development.2

Given the complexity of the issue of competitiveness, it is notsurprising that there is a multitude of competitiveness indicators. Someanalysts use competitiveness indices that combine several dozens ofindividual measures spanning across a wide range of economic and non-economic factors.3 However, the indicator that is most widely used in appliedeconomic analysis is the real exchange rate, based on either relativeconsumer price or relative unit labour cost indices expressed in a commoncurrency.

1. Conditions for competitiveness at the microeconomic level

Linkages between capital accumulation, technological progress andstructural change constitute the basis for rapid and sustained productivitygrowth, rising living standards and successful integration into the internationaleconomy. Investment holds a central place in this interplay, because it cansimultaneously generate income, expand productive capacity, and carrystrong complementarities with other elements in the growth process, suchas technological progress, skills acquisition and institutional deepening.

FOSTERING COHERENCE 9

However, a given rate of investment can generate different growthrates, depending on its nature and composition as well as the efficiencywith which production capacity is utilized. Particularly important forproductivity growth and structural change is investment in new techniquesand/or new products. This is because new procedures generally reduceproduction costs of established products, while new products are often moreattractive to consumers than any of the previously available alternatives.Assuming constant wages, successful innovative investment will be reflectedin growing market shares, if the investor chooses to pass on innovationrents in the form of lower prices; or it will lead to (temporary) monopolyprofits, if the investor chooses to leave sales prices unchanged and enjoyinnovation rents from the rising revenue-cost ratio until competitors succeedin imitating the innovator. Which mix of these two polar strategies theinvestor chooses will depend on the intensity of competition. This meansthat in the microeconomic sphere, changes in competitiveness relate tochanges in relative labour productivity across different firms, and thattechnological progress and the ensuing growth in labour productivity (i.e.the drivers of sustainably rising competitiveness) are associated witholigopolistic, rather than perfect, competition.

Innovative investment in developed countries extends the technologicalfrontier. By contrast, in developing countries it generally relates to theadoption, imitation and adaptation of technology invented elsewhere. Whilethis does not affect the key importance of productivity-enhancing investmentfor competitiveness at the firm level, or significantly alter the determinantsof investment decisions, there are three issues that specifically concernproductivity-enhancing investment in developing countries. First, in buildingtheir industrial capacity and competitive strength, newly industrializingcountries must typically import a large volume of capital goods and intermediateinputs. However, an inability to obtain additional export earnings (i.e. ifthe country’s products are not competitive on international markets or faceprohibitive market access or entry barriers), and thus to finance theseimports, may be a serious constraint on the industrialization process. Theextent of this balance-of-payments constraint and dependence of developingcountries on foreign technologies embodied in imported capital goods areperhaps greatest during the initial stages of industrialization. However, theneed for large-scale imports of machinery and equipment persists throughout

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE10

much of the industrialization process, especially when catching up is basedon imitating technological leaders.

Second, in addition to directly facilitating a rise in the level of technologyused by domestic firms, developing-country imports of goods that embodyforeign technology positively affect domestic imitation and innovation.4 Forexample, a notable feature of the process of technological improvement inthe East Asian economies in the early stages of their industrialization wastheir emphasis on research and development (R&D) spending, not only forbackward engineering but also to match or surpass the product quality offoreign manufacturers by adapting and improving imported technology.The former enabled firms, for example, to fully assess the merits of a newforeign technology and thus to determine whether to secure a licence ornot, and to unbundle foreign technology, thereby enhancing their bargainingpower in negotiating with suppliers. As the industrialization processunfolded and firms came to master imitation, an increasing share of R&Dspending was channelled into own innovation (TDR 1994, Part Two, chapterone). Taking a wider geographical perspective, and looking at a large numberof countries from all developing regions, a recent empirical study (Connolly,2003) also reveals the positive impact of technology imports from developedcountries on domestic imitation and innovation in developing countries.

Third, the realization of technological improvements in developingcountries is closely related both to the skill level of their labour force –which determines the amount and degree of sophistication of technologythat can be adopted and efficiently used – and to managerial capabilities,which must meet the requirements to function effectively in new sectorsand new markets. As such, technological upgrading in developing countriesis usually associated with a painstaking and cumulative process of technologicallearning. Human capital formation, including through learning, is instrumentalin preventing a decline in the marginal product of capital, despite the rapidgrowth in the capital-labour ratio generated by rapid accumulation ofphysical capital. It also helps prevent a decline in the marginal product oflabour, despite the rise in wages that results in a higher standard of living.

The competitiveness of affiliates of foreign transnational corporations(TNCs) is likely to be significantly higher than that of domestic firms.

FOSTERING COHERENCE 11

Labour productivity in TNC affiliates tends to be higher than in their domesticcounterparts, because they can combine the comparatively lower generallevel of labour costs in the host country5 with the advanced productiontechnology and management techniques used in their home countries, andwith supplies of raw materials and intermediate production inputs from thecheapest sources.6 Indeed, in the context of the concept of competitiveness,the decision of a foreign company to invest in production abroad is generallybased on the objective to reduce unit labour costs in production. Settingaside other host country characteristics (such as income or corporate taxtreatment or provision of infrastructure), this implies that for foreign directinvestment (FDI) to occur, the investor must expect the ratio between labourproductivity and wages in the affiliate to exceed that in the parent company.In other words, if expected unit labour costs in the host country are lowerthan in the TNC’s home country, the TNC will consider moving part of itsproduction activities abroad.

2. Competitiveness of firms at the level of the national economy

At the level of the national economy, the decisive factor for realizingtechnological upgrading and productivity-driven structural change is theability of investors to sell the products resulting from their product or processinnovations without a significant change in cost conditions (i.e. to enjoy a(temporary) monopoly profit). In other words, if an economy is characterizedby high domestic labour mobility and by a similar level of wages for workerswith similar qualifications across the economy, its dynamic developmentwill be driven by profit differentials, rather than wage differentials. Indeed,as noted by Keynes (1930: 141), “the departure of profits from zero is themainspring of change in the ... modern world. ... It is by altering the rate ofprofits in particular directions that entrepreneurs can be induced to producethis rather than that, and it is by altering the rate of profits in general thatthey can be induced to modify the average of their offers of remunerationto the factors of production.”

Hence, the closer actual conditions on the labour markets get to thelaw of one price, the stronger will be the effects of profit differentials on

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE12

the evolution of economic systems.7 The observed asymmetry betweenuneven productivity growth and the more even growth in wage rates acrossenterprises or industrial sectors is frequently emphasized as providing animportant source of both structural change in the domestic economy andchanges in the comparative cost advantages of different countries in specificindustrial sectors (see, e.g., Landesmann and Stehrer, 2004). Unevenproductivity growth across firms, combined with more even growth in wagerates, implies that workers in industries with relatively high productivitygrowth are not fully compensated.

Under this scenario, innovative investors may decide to leave salesprices unchanged and obtain a sizeable extra profit equal to the differencebetween their productivity gain and the economy-wide average growth inproductivity. Alternatively, they may prefer to reduce sales prices by theamount to which their cost per unit of output falls, and thus, assumingnormal price elasticities of demand, increase their market share. This willlead to a rise in their absolute level of profits in line with the rise in soldoutput. This potential for extra profits is the major incentive for startingthe process of “creative construction” or “destruction” along Schumpeterianlines, and hence for making innovative investments. By contrast, if wagesin each firm rise more in line with firm-specific productivity gains,innovative investors will obtain a much lower extra profit, which will bemuch less of an incentive for innovative investment.

Enterprises whose productivity gains fall short of the national averagewill experience shrinking profits if labour costs rise at equal rates acrossfirms. These enterprises will therefore attempt to raise the sales prices fortheir goods so as not to risk a complete erosion of profits.8 This implies thatsectorally uneven productivity gains, combined with even labour costincreases across the entire economy, generate price pressures in non-innovative sectors. However, the net impact of this supply-side effect onprice pressure depends on effects originating from the demand side. Risinglabour productivity induces increases in income, and hence consumption.If demand for innovated and non-innovated goods were to grow at the samerate, demand effects would not skew price pressure towards one or the othergroup of goods, thus the supply-side effect would dominate. By contrast, ifdemand for the innovated good were to grow faster than for the other goods,

FOSTERING COHERENCE 13

the supply-side effect would be offset, partly or completely. And if demandwere biased towards goods for which productivity gains were low (such asservices), the demand effect would reinforce the supply effect. This will bethe case particularly when productivity gains are high in the traded sector,while domestic consumption demand is biased towards non-traded goods.

A second important condition for innovative investment to governthe evolution of the economic system is that firms should have access toreliable, adequate and cost-effective sources for financing their investments.This condition is best met when profits themselves are the main source ofinvestment financing. Indeed, if an investment-profit nexus can be ignited,profits from innovative investments simultaneously increase the incentivefor firms to invest and their capacity to finance new investments.9 Whenenterprises are heavily dependent on borrowing to meet their needs forfixed investment and working capital, as is the case of new enterprises, thestance of domestic monetary policy is of crucial importance, because highlevels of nominal and real interest rates tend to increase production costs.In addition to its adverse impact on the cost of capital, a restrictive monetarypolicy may bias investment decisions in favour of financial assets, or fixedinvestment in production activities with known cost and demand schedulesover innovative production activities for which investors face uncertaintyas to the volume of sales and the true costs of production.

To understand how the mechanisms discussed here work in practice,it is useful to consider a two-country world comprising a developing country,with a low average level of both labour costs and labour productivity, anda developed country, with a high average level of labour costs and labourproductivity. Expressed in a common currency, these levels are assumed as5 and 10 in the developing country and 50 and 100 in the developed country(case 1 in table 2.1). Further, assuming that in both countries the average levelof labour costs reflects the average level of labour productivity, firms in bothcountries face the same average level of unit labour costs (i.e. 0.5 currencyunits). If labour is the only internationally immobile production factor,these assumptions imply that firms from both countries are, on average,internationally competitive. Moreover, if firms set sales prices on the basisof a mark-up of 100 per cent over labour costs, the absolute level of profits inthe developed country will be 10 times higher than in the developing country.10

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE14Ta

ble

2.1

INN

OV

AT

IVE

INV

ES

TM

EN

T, E

XC

HA

NG

E-R

AT

E C

HA

NG

ES

,A

ND

INT

ER

NA

TIO

NA

L C

OM

PE

TIT

IVE

NE

SS

: A N

UM

ER

ICA

L E

XA

MP

LE

Cas

e 1

Cas

e 2

Cas

e 3

No

inno

vativ

eIn

nova

tive

Non

-inno

vativ

eTN

C a

ffilia

tein

vest

men

tfir

m a

vera

gea

firm

ave

rage

inve

stin

g in

deve

lopi

ng-c

ount

ryD

evel

opin

gD

evel

oped

Dev

elop

ing

Dev

elop

edD

evel

opin

gD

evel

oped

expo

rt-or

ient

edco

untry

coun

tryco

untry

coun

tryco

untry

coun

trypr

oduc

tion

Pro

duct

ivity

1010

012

120

1010

012

0 >

prod

uctiv

ity >

10

Nom

inal

labo

ur c

osts

550

550

550

5U

nit l

abou

r cos

ts0.

50.

50.

40.

40.

50.

50.

5 >

ULC

> 0

.04

Pro

fits

per u

nit o

f out

put

550

550

550

115

> pr

ofits

> 5

Pric

e1

11-

x1-

y1+

x1+

y1-

z

1.U

ncha

nged

nom

inal

exc

hang

e ra

teE

xpor

t mar

ket s

hare

unch

ange

dun

chan

ged

upup

dow

ndo

wn

up

2.N

omin

al e

xcha

nge-

rate

b ap

prec

iatio

n by

mor

e th

an 2

0 pe

r cen

tE

xpor

t mar

ket s

hare

dow

nup

dow

nc

upc

dow

ncup

cup

3.N

omin

al e

xcha

nge-

rate

b de

prec

iatio

n by

mor

e th

an 2

0 pe

r cen

tE

xpor

t mar

ket s

hare

updo

wn

upc

dow

ncup

cdo

wnc

up

So

urc

e:U

NC

TA

D s

ecre

tari

at c

alcu

latio

ns.

No

te:

x an

d y

are

the

shar

es o

f the

inno

vativ

e in

vest

ors’

pro

duct

s in

the

tota

l con

sum

ptio

n of

thei

r re

spec

tive

econ

omie

s; z

is th

e sh

are

of th

e m

ultin

atio

nal

firm

’s r

eim

port

ed p

rodu

ct in

the

tota

l con

sum

ptio

n of

the

econ

omy

of th

e pa

rent

com

pany

.a

The

sce

nari

o in

the

tabl

e is

bas

ed o

n th

e as

sum

ptio

n th

at in

nova

tive

inve

stor

s fu

lly tr

ansm

it ga

ins

in p

rofit

s pe

r un

it of

out

put i

nto

pric

e re

duct

ions

.b

Dev

elop

ing-

coun

try

curr

ency

/dev

elop

ed-c

ount

ry c

urre

ncy.

cT

he n

et e

ffec

t dep

ends

on

the

rela

tion

betw

een

the

gain

in p

rodu

ctiv

ity a

nd th

e ex

chan

ge-r

ate

mis

alig

nmen

t. T

he a

ssum

ptio

n fo

r th

e ef

fect

s no

ted

inth

e ta

ble

is th

at th

e m

isal

ignm

ent i

s gr

eate

r th

an th

e ga

in in

pro

duct

ivity

.

FOSTERING COHERENCE 15

Case 2 in the table introduces the effects of innovative investment byassuming that productivity increases by 20 per cent in innovative firms ofboth countries. If the weight of these firms in their domestic economies istoo small for these productivity gains to have a marked impact on theeconomy-wide average level of productivity, nominal labour costs willremain unchanged, and unit labour costs in the innovative firms will declineby 20 per cent. Profits per unit of output will also remain unchanged if theinnovative firms reduce their sales prices in line with the decline of theirunit labour costs. This implies that the innovative firms from both countrieswill experience an increase in both their export-market shares and theirabsolute level of profits. By contrast, non-innovative firms will suffer adecline in export-market shares and in profit levels due to the increase intheir sales prices relative to those of the innovative firms.

Case 3 in the table shows that affiliates of TNCs can gain considerableadvantages in international competitiveness by combining developed-country technology with developing-country labour costs. The level of theaffiliate’s unit labour costs will be substantially lower than that of either itsparent company in the developed country or of domestic firms in thedeveloping country. While it is unlikely that the relatively less educatedworkers in the developing country can match the productivity level ofworkers in the developed country, it is probable that the TNC will experiencea strong reduction of its unit labour costs by moving its labour-intensiveproduction activities to a low-wage country.

Changes in the nominal exchange rate that are caused by “autonomous”capital flows (i.e. that are unrelated to the flow of goods) can offset theeffects discussed above. In case 1, export-market shares will move fromfirms of the country whose currency appreciates towards firms of the countrywhose currency depreciates, even though none of the firms has undertakenproductivity-enhancing investments and unit labour costs, measured indomestic currency units, have not changed in any of the firms. Moreimportantly, the innovative firms in case 2 will lose, rather than gain, export-market shares if the appreciation of the exchange rate exceeds productivitygains. For example, assuming the currency of the developing country toappreciate by more than the productivity gains achieved by innovative firms,these firms will lose export-market shares to both the innovative and non-

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE16

innovative firms of developed countries. This example shows that adverseexternal monetary shocks can wipe out the gains resulting from animprovement in the international competitiveness of developing-countryexporters based on innovative investments and a decline in unit labour costs.

3. Transmission mechanisms between the national and theinternational economy

Entrepreneurs invest in the industrial sector of that country in whichthey expect to realize the highest return on their investment. Cross-countrydifferences in the expected return on investment, expressed in a commoncurrency, are determined by a number of factors, including relative rates ofincome growth; relative wages and labour productivity; macroeconomicand institutional factors that influence the average level of nominal labourcosts in an economy as a whole; relative costs of intermediate productioninputs; relative transaction costs associated with information, communications,transportation and distribution; and the use of different currencies. Moreover,market access and entry conditions and the availability of trade finance alsodetermine whether improved cost competitiveness translates into improvedexport performance. This shows that a wide range of conditions mustcombine for firms that are competitive on the domestic market to becomesuccessful exporters.

First, the availability of adequate transport and communicationsinfrastructure and information systems has a crucial influence on the abilityof developing-country firms to conduct trade and to successfully competein foreign markets.11 Innovative investors in economies with comparativelyhigh communication, transport and information costs may need to offsetthis disadvantage by paying lower wages or reducing costs elsewhere inthe production process in order to be able to compete in world markets.Firms in countries that are landlocked or geographically distant from majorinternational shipping routes are particularly disadvantaged in this respect.While this is a well-known problem, the impact on trade flows of otherforms of trade facilitation, such as the availability of networked informationtechnology and compliance with product standards, has gained in importanceover the past few years.

FOSTERING COHERENCE 17

Second, trade finance provides the liquidity for firms to bring theirproducts to the market. Exporters with limited access to working capitaloften require credit to buy imported raw materials and intermediateproduction inputs, as well as financing to manufacture products beforereceiving payments. Trade finance may be provided directly through loansfrom commercial banks, pre-payments by buyers, and delayed paymentsby sellers, or indirectly from either export-credit agencies (in the form ofguarantees, insurance and government-backed loans), private insurancecompanies, or multilateral development banks.

Third, assuming constant nominal exchange rates, preserving theinternational cost competitiveness of domestic firms requires that the ratioof average nominal labour cost growth to average domestic productivitygrowth in the domestic economy does not rise faster than in the rest of theworld. Macroeconomic and institutional factors play an important role infulfilling this condition. For example, the pressure for sharp general wageincreases in an economy approaching full employment is likely to be higherthan in an economy with substantial unemployment. Moreover, indexationof wage rises based on factors other than productivity growth is likely tocause substantial and lasting divergence between wage and productivitydevelopments.12

Fourth, stable nominal exchange rates are perhaps the single mostimportant condition for the transmission of domestic productivity improve-ments to gains in international competitiveness. Exchange-rate movementsalter the relative competitive position of firms in different countries. Onthe one hand, this implies that a currency appreciation will wipe outimprovements in international competitiveness achieved by innovative firmson the basis of improved labour productivity if the change in the exchangerate exceeds the gain in productivity. If technological progress relies oncumulative and incremental innovations that individually lead to comparativelysmall productivity gains, it does not take exchange-rate changes of aspectacular size for this to occur.13 On the other hand, this implies that currencydepreciation can give a further boost to the international competitiveness ofan innovative firm and maintain the relative competitive position of non-innovative enterprises in the short run. However, there can be little doubtthat long-term economic success and maintaining international competitiveness

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE18

depend on sustained improvements in productivity. Moreover, resorting tocurrency depreciation may allow for some breathing space to adjust tochanges in the relative competitive position of foreign competitors, but italso entails the risk of igniting a process of competitive devaluations.

B. Impacts of monetary and financial factors ondeveloping countries’ export performance

Only productivity growth and technological upgrading can ensuresustained improvement in the external balance of developing countries.This can be achieved by a national development strategy that is successfulin augmenting the existing stock of physical and human capital, enablingthe use of more efficient technologies, and shifting resources away fromtraditional, low-productivity activities towards activities that offer a highpotential for productivity growth. Under some circumstances, andparticularly when a period of real currency appreciation has hampered exportperformance, real currency depreciations can improve international costcompetitiveness and boost exports.

The exchange rate has long been recognized as an important policyinstrument to make domestic entrepreneurs internationally competitive andprovide profit incentives for them to invest in non-traditional export sectors.For example, according to Agosin and Tussie (1993: 22) “The historicalrecord … shows that … [a]ll countries that have succeeded in generating asustained growth of their exports, leading to high rates of growth of outputover the long term, have also been able to maintain exchange rates that areattractive to exporters over long periods of time. The exchange rate in suchcountries has also tended to be fairly stable, enabling producers of tradeablesto make long-term investment plans.” In a similar vein, Rodrik (2003) arguesthat countries grow rich by increasing the range of products that theyproduce, and not by concentrating on what they already do well. Productdiversification requires entrepreneurs who are willing to invest in activitiesthat are new to the local economy, and that process may require positive

FOSTERING COHERENCE 19

inducements. Rodrik (2003: 21) concludes that “a credible, sustained realexchange-rate depreciation may constitute the most effective industrialpolicy there is.”

For successful trade performance, developing countries need to beable to manage their exchange rates in a way that allows them not only tosustain competitive rates over the longer term, but also to retain enoughpolicy space to be able to make orderly adjustments when faced withexogenous shocks. On some theoretical accounts, a regime of freely floatingexchange rates and free capital mobility would enable nominal exchange-rate movements to stabilize real exchange rates. This argument is based onthe premise that movements of the nominal rates eliminate temporarydisequilibrium in the pricing of goods in different currencies, and thatarbitraging currency speculators speed up the adjustment, thus helping tomaintain a correct set of real prices on which international traders andspeculators can base their decisions (see, for example, Friedman, 1953).

Floating exchange rates between the main reserve currencies wereintroduced into the international system of trade and finance in the early1970s. However, orderly balance-of-payments adjustments, increased realexchange-rate stability, greater macroeconomic policy autonomy andremoval of persistent currency misalignments and gyrations have not beenachieved. This is partly due to the liberalization of capital flows in the last30 years and to the sizeable increase in the scale and variety of cross-border financial transactions, whose direction can change rapidly in responseto shifts in expectations of international portfolio investors. As a result, thecurrencies of the major developed countries, as well as those of financiallyopen emerging-market economies, have been subject to strong volatilityand gyrations, which often represent endogenous responses to large andsharp changes in the direction of international financial flows. Thesedevelopments are reminiscent of the failure of financial markets to preventcurrency disorders and contagion in the 1930s (an insight that was widelyaccepted as the basis for the attempt to put in place multilateral financialarrangements after the Second World War).

For developing countries, capital inflows, both private and public,can be a source of development finance. However, volatility in international

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE20

financial markets, and particularly sharp and abrupt shifts in the directionof largely autonomous short-term private capital flows, have frequentlycontributed to problems in managing interest rates and exchange rates, andto financial crises including in countries with track records of macro-economic discipline. Since the early 1990s, a number of developingcountries, particularly those that had begun liberalizing their financialmarkets, have experienced substantial movements in their exchange rates.These movements have frequently been characterized by prolonged periodsof exchange-rate appreciation followed by abrupt and sharp devaluations,often associated with a sizeable slowdown in economic activity. Theseepisodes of sharp and abrupt currency depreciations include the well-knowncurrency crises when countries abandoned pegged exchange rates, startingwith Mexico in 1994, followed by East Asia (1997–1998), the RussianFederation (1998), Brazil (1999), Turkey (2001) and Argentina (2002). Therewere also instances of unusually sharp depreciations in countries with moreflexible exchange rates, such as Mexico and South Africa in 1998.

The scale of nominal exchange-rate depreciations in many developingcountries – even those with a record of macroeconomic discipline – overthe past few years has often caused large real exchange-rate depreciations.Given that real currency depreciations can generally be expected to improvea country’s trade balance, it could be assumed that sharp depreciations ofthe real exchange rate will provide an even greater impetus to the internationalcost competitiveness of domestic exporters and a boost to a country’s exports.

The main argument of this section is that the sharpness of recent realcurrency depreciations brings an additional dimension to the debate on theeffect of exchange-rate changes on trade flows. This is because, in the shortterm, large depreciations of the real exchange rate can seriously compromisethe ability of domestic exporters to benefit from their increased internationalcost competitiveness stemming from the depreciation. Adverse effects occurat two levels. At the level of individual enterprises, it can take the form ofa sharp decline in the availability, and/or a strong rise in the cost, of tradefinance and working capital. At the macroeconomic level, close tradingrelationships can provide a channel for the transmission of financial crisesand raise the risk of competitive devaluations, which can offset the rise indemand for exports created by the depreciation. Moreover, the steep decline

FOSTERING COHERENCE 21

in economic activity, often associated with sharp and abrupt real currencydepreciations, can have an adverse effect on the supply of exports. Suchdepreciations tend to violate two of the conditions necessary for domesticproductivity growth to translate into sustained international competitiveness:access of firms to reliable, adequate and cost-effective sources for financingtheir investments and stable nominal exchange rates at a level that does notimpair the international cost competitiveness of domestic exporters. Thissection examines more closely the impact that the absence of these twoconditions is likely to have on developing-country trade performance.

1. Impacts of exchange-rate changes on enterprise investmentand competitiveness

Uncertainty in currency markets adversely affects many types ofeconomic activities, particularly those that require forward planning andinvolve decisions that are only reversible, if at all, at high cost. Long-terminvestment by enterprises in export production capacity is a noteworthyexample of such activities, particularly when their production processutilizes imports from third countries. Consider a production unit whoseoutput would be sold in, for example, the United States for dollars, andwhich would utilize machinery and equipment purchased from Germany,partly on credit denominated in euros, with intermediate production inputsfrom Japan denominated in yen, and domestic labour remunerated indomestic currency. In such cases, the estimated rate of return on theinvestment project would be sensitive to the relative exchange rates betweenthe currencies in which the output is to be sold, the currencies in whichimported machinery, equipment and intermediate inputs are invoiced, andthe domestic currency. The greater the range of exchange-rate variation,the greater is the risk of the project. The project may be profitable onlyunder a given configuration of exchange rates. As a consequence, theinvestor will realize an extra profit if the exchange-rate configuration evolvesfavourably, but risk bankruptcy in the opposite case. Firm size and financialstrength, diversification of operations across products and markets,managing assets and liabilities in different currencies, as well as the use ofother risk management techniques, can limit exchange-rate risk. But thesemeasures entail additional costs and do not provide complete protection.

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE22

Monetary factors in the form of nominal exchange-rate changes canthus have a major impact on enterprise investment and internationalcompetitiveness. The form and strength of this impact depends on a varietyof factors operating through two channels: (i) marginal cost, where theimpact partly depends on the firm’s ratio of imported to domestically sourcedproduction inputs, the share of financing denominated in foreign currency,and the impact of exchange-rate changes on domestic monetary conditions;and (ii) a possible mark-up of price over marginal cost. These factors canpull in opposite directions, and their relative strength can change withthe length of time that elapses after the exchange-rate change. Moreover,they affect the instruments that firms can use to foster international costcompetitiveness in a sustainable way (i.e. making productivity-enhancinginvestment) and to fend off temporarily adverse influences on their competi-tiveness (i.e. accepting a profit squeeze or resorting to wage suppression orlabour shedding).

For example, firms can limit the adverse effects of currency appreciationson their international cost competitiveness temporarily, if they are able tofollow a pricing-to-market strategy and absorb at least part of the exchange-rate change by a squeeze in profit margins. But trying to do so over alonger period of time risks compromising profit-related incentives forinvestment. On the other hand, firms may not be able to benefit from sharpreal currency depreciations if the goods that they export, have a large importcontent, so that the net effect of the currency depreciation on the firms’international cost competitiveness is very small. More importantly, recentexperience shows that adverse impacts of sharp real currency depreciationscan compromise the ability of firms to expand production capacity or evenmaintain production at pre-depreciation levels. Indeed, the easing of capitalcontrols, combined with the movement away from detailed documentationrequirements for trade financing transactions, have seriously compromisedthe availability of trade finance from international sources in the aftermathof sharp currency depreciations. In addition, the tightening of domesticmonetary conditions associated with the depreciation has made it difficultfor domestic lenders to maintain their provision of short-term lending.

FOSTERING COHERENCE 23

2. Sharp exchange-rate changes and developing countries’export performance

At the macroeconomic level, maintaining a stable exchange rate at anappropriate level is crucial for successful exporting and structural changetowards high-productivity sectors. Discussions on the impact of exchange-rate changes on trade flows have frequently emphasized the effect ofexchange-rate volatility on trade, or the contribution of currency depreciationsto the removal of temporary imbalances in a country’s current account.Typically, the focus has been on the impact of exchange-rate changes thatare relatively small compared to the large gyrations in developing countries’real exchange rates that have frequently occurred since the early 1990s.This section, by contrast, focuses on the effects of large changes in realexchange rates, which are often associated with sharp and abrupt changesin the direction of short-term private international capital flows.

The large size of recent real exchange-rate changes brings an additionaldimension to the just mentioned elasticity debate for at least two reasons.First, sharp exchange-rate changes in one economy can adversely affectthe external trade position of other economies where the exchange rateremains relatively stable. For example, evidence from the Asian crisis pointsto competitive depreciations as an important form of contagion throughtrade linkages, as countries whose exporters compete directly with those inthe crisis-affected country also face pressure to depreciate their currenciesin order to avoid a loss in international competitiveness. This also meansthat exporters in the crisis-affected country do not experience the rise indemand for their products hoped for.

Second, the domestic impact of a sharp and abrupt exchange-ratedepreciation is more complex than the adjustments resulting from smallexchange-rate fluctuations, because sharp currency depreciations aretypically associated with a drop in domestic economic activity and a needto cut imports of intermediate and capital goods. Combined with the sharpdecline in the availability of trade finance, this tends to hamper the domesticsupply response and undermines the ability of exporters to take advantageof their improved international cost competitiveness.

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE24

A detailed econometric estimation by the UNCTAD secretariat (TDR2004: 113–124) highlighted the differences in the impact on developingcountry trade performance after “normal” and those following “major” realexchange-rate changes14 over the period 1970– 2002, i.e. the period thatincludes all major financial crises.

Table 2.2 shows that major currency depreciations boosted countries’export performance only slightly more than more normal depreciations.Most importantly, contrary to depreciations of relatively small size, majordepreciations did not lead to a statistically significant improvement in thetrade balance. By contrast, changes in domestic income and world incomehad a sizeable and strongly significant impact on the ability of exporters totake advantage of increased international price competitiveness. Indeed,the results show that following major currency movements, a rise in theincome share of exports was strongly and adversely affected by changes indomestic demand, while changes in domestic demand had no statisticallysignificant impact on the income share of imports.15 Thus currency depreciationsand changes in domestic income and world income had a markedly differentshort-term impact on countries’ trade performance when they were associatedwith major exchange-rate changes rather than with comparatively smaller ones.

This finding is supported by the results in table 2.3, which show thatcomparatively small exchange-rate changes improved the trade balance inthe short run, while there was no similar statistically significant effect ofmajor exchange-rate changes. The results in table 2.2 also show that, contraryto their impact on the trade balance, major currency depreciations led to astatistically significant improvement of the current-account balance. Thisis likely to be related to the decline in the commissions and fees such as forletters of credit or lines of credit that accompanied the sharp decline in theaccess of firms to trade finance and working capital provided by foreignbanks in the aftermath of financial crises. It may also reflect changes in theprovision of services with a relatively high elasticity with respect to changesin exchange-rates and income.

The finding that, compared to depreciations of a more normal size,major exchange-rate depreciations neither give a sizeable additional boostto export performance nor result in proportionally larger improvements in

FOSTERING COHERENCE 25

Table 2.2

IMPACT OF CHANGES IN EXCHANGE RATES AND INCOME ON EXTERNALPERFORMANCE: ESTIMATION RESULTS FOR DIFFERENT SIZES OF

EXCHANGE-RATE CHANGE, 1971–2002

Share inMerchandise Current Income Income world manu-

trade account share of share of facturedbalance balance exports imports exports

Major appreciations and depreciations

Real effective exchange rate -0.30 -0.08 -0.56* -0.26 -0.18Real domestic income -2.27* -1.79* -1.77* 0.65 0.51Real world income 3.91* 2.47** 5.75* 1.15 0.38

Other appreciations and depreciations

Real effective exchange rate -0.31* -0.23* -0.49* -0.11 0.07***Real domestic income -0.88* -0.83* -0.05 0.86* 1.00*Real world income 2.57* 1.09* 2.34* -0.58** 1.80*

R-square 0.22 0.24 0.31 0.10 0.27

Total panel observations 677 585 679 684 679

Major appreciations

Real effective exchange rate -0.13 0.13 -0.44 -0.29 -0.27Real domestic income -1.54 -1.26 -0.72 0.86 1.01Real world income 2.57 2.41 5.51** 2.69 1.22

Major depreciations

Real effective exchange rate -0.45 -0.41* -0.86* -0.46 -0.19Real domestic income -2.85* -2.13* -2.24* 0.78 0.41Real world income 3.70** 0.57 4.23** -0.37 0.16

Other appreciations and depreciations

Real effective exchange rate -0.31* -0.22* -0.49* -0.10 0.07Real domestic income -0.89* -0.84* -0.06 0.86* 1.01*Real world income 2.62* 1.16* 2.41* -0.56*** 1.79*

R-square 0.23 0.26 0.31 0.10 0.27

Total panel observations 677 585 679 684 679

Source: UNCTAD secretariat calculations, based on JP Morgan (2003) for exchange-rate data; IMF,International Financial Statistics database for current account data; and the UNCTAD databasefor trade and income data.

Note: * Denotes significant at the 1 per cent level.** Denotes significant at the 5 per cent level.

*** Denotes significant at the 10 per cent level.

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE26

the trade balance is likely to reflect also the impact of at least one otherfactor discussed earlier. The observed worsening of firms’ access to tradefinance from both international and domestic sources in the aftermath ofmajor currency depreciations makes it difficult for those firms to expandor even merely maintain activity levels. This seriously inhibits their supplyresponse to benefit from lower dollar-denominated export prices.

Table 2.3

IMPACT OF CHANGES IN EXCHANGE RATES ANDINCOME ON THE MERCHANDISE TRADE BALANCE:

TIME PATH OF ADJUSTMENT, 1971–2002

Merchandise trade balance

Major appreciations and depreciations

Real effective exchange rate -0.10

One year lagged -0.51Two years lagged 0.32Three years lagged 0.23Four years lagged 0.20Five years lagged -0.89**

Real domestic income -2.65*

Real world income 5.20*

Other appreciations and depreciations

Real effective exchange rate -0.26*

One year lagged -0.26*Two years lagged 0.22*Three years lagged 0.13**Four years lagged 0.11**Five years lagged -0.01

Real domestic income -0.79*

Real world income 1.19*

R-square 0.31

Total panel observations 547

Source: See table 2.2.Note: * Denotes significant at the 1 per cent level.

** Denotes significant at the 5 per cent level.*** Denotes significant at the 10 per cent level.

FOSTERING COHERENCE 27

C. Policy adjustment with open capital accounts

For policy makers in developing countries, the fact that exchange-ratechanges can influence the overall competitiveness of a country and havethe potential to directly improve the overall trade performance of themajority of their firms and the balance of payments is a promising prospect.On the other hand, the effectiveness of the exchange rate as an economicpolicy tool is constrained by the policy of other countries (the exchangerate of any country is, by definition, a multilateral phenomenon), as well asby the influence of the global capital market. The following section examineshow speculative short-term capital flows and resulting exchange-ratemisalignments are induced by short-term interest rate differentials andfloating currencies in open capital markets.

1. Speculative flows induced by carry trade

In the past couple of years a widespread and persistent speculativephenomenon involving currencies of developed and developing countrieswith large short-term interest rate differentials has drawn considerableattention from the media and financial analysts as well as concerns bycentral bankers. “Carry trade” has become a catchphrase to define thespecific financial operation of borrowing and selling a low-yielding currencyto buy and lend in a high-yielding currency. For example, an establishedspeculator such as a hedge fund might borrow 12,000 yen in Japan and buy$100 in the United States, invest this amount in United States bonds andobtain an interest revenue equal to the difference between the borrowingrate in Japan, say 0.25 per cent, and the higher lending rate in the UnitedStates, say 5 per cent. Exchange-rate changes between the time of borrowingand paying back the funding currency can add to the gains, or induce smallergains or even losses. But with stable exchange rates, the interest rate gainamounts to 4.75 per cent. However, both gains and losses are largely

GLOBAL AND REGIONAL APPROACHES TO TRADE AND FINANCE28

magnified by high leverage ratios, since traders typically use huge amountsof borrowed funds and very little equity. For instance, owning a capital of$10 and borrowing 10 times the equivalent of that value in yen, the leveragefactor of 10 leads to a net interest return on equity of 47.5 per cent.

This simple and hardly new form of speculation may appear toostraightforward to be possible in highly developed and integrated capitalmarkets, yet it has represented a substantial source of profits, inducing hugeamounts of capital flows and pressure on exchange rates since the collapseof the Bretton Woods system in the early 1970s. It has gained a new quantitativedimension, since more or less unregulated funds have virtually unlimitedaccess to massive pools of capital from pension funds or wealthy citizens.