Embed Size (px)

Citation preview

You can’t …See it.Feel it.Experience it.

Advocacy

BUT, you can’t do without it …

Issues affecting the profession and Indiana CPAs

Legislative and Regulatory Update

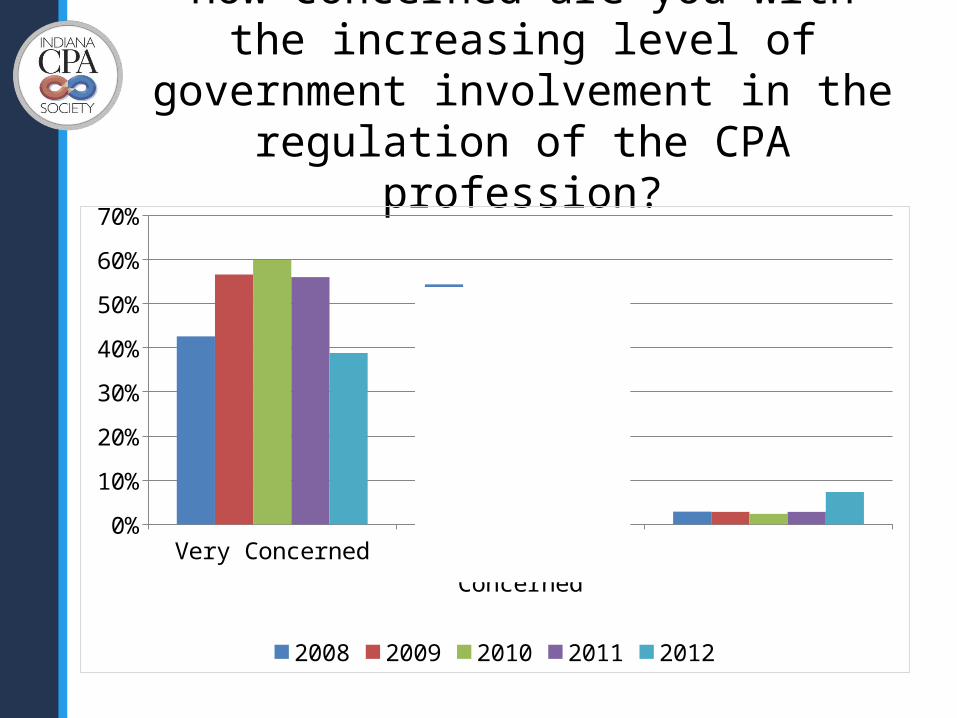

How concerned are you with the increasing level of government involvement in the

regulation of the CPA profession?

Very Concerned Somewhat Concerned Not Concerned0%

10%

20%

30%

40%

50%

60%

70%

2008 2009 2010 2011 2012

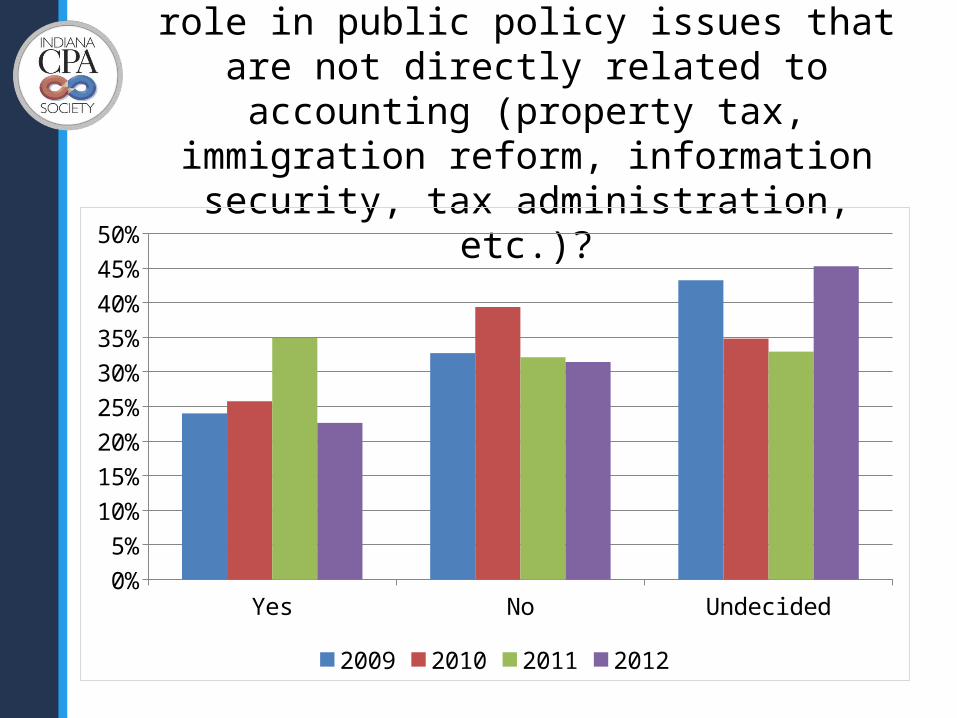

Should INCPAS take a more active role in public policy issues that are not directly related to

accounting (property tax, immigration reform, information security, tax administration, etc.)?

Yes No Undecided0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2009 2010 2011 2012

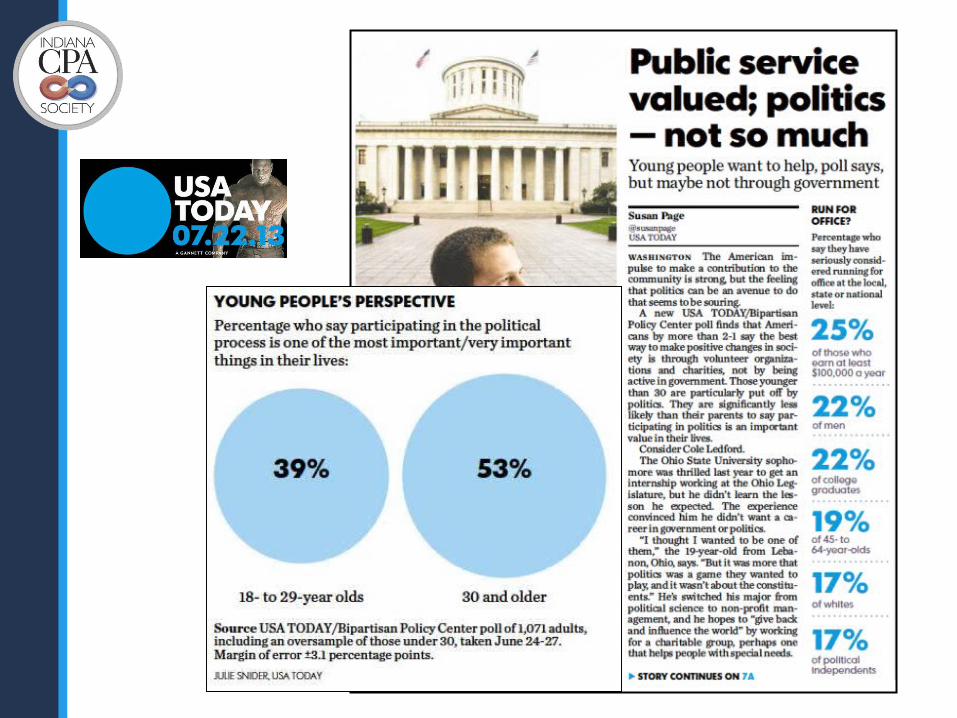

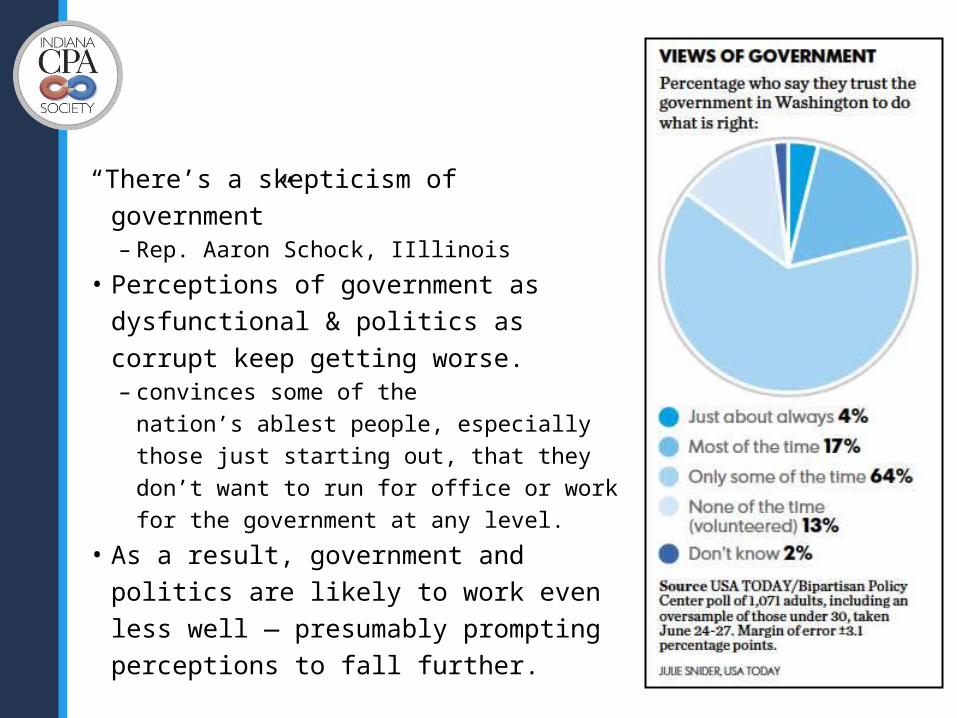

“There’s a skepticism of government”– Rep. Aaron Schock, IIllinois

• Perceptions of government as dysfunctional & politics as corrupt keep getting worse. – convinces some of the nation’s ablest

people, especially those just starting out, that they don’t want to run for office or work for the government at any level.

• As a result, government and politics are likely to work even less well — presumably prompting perceptions to fall further.

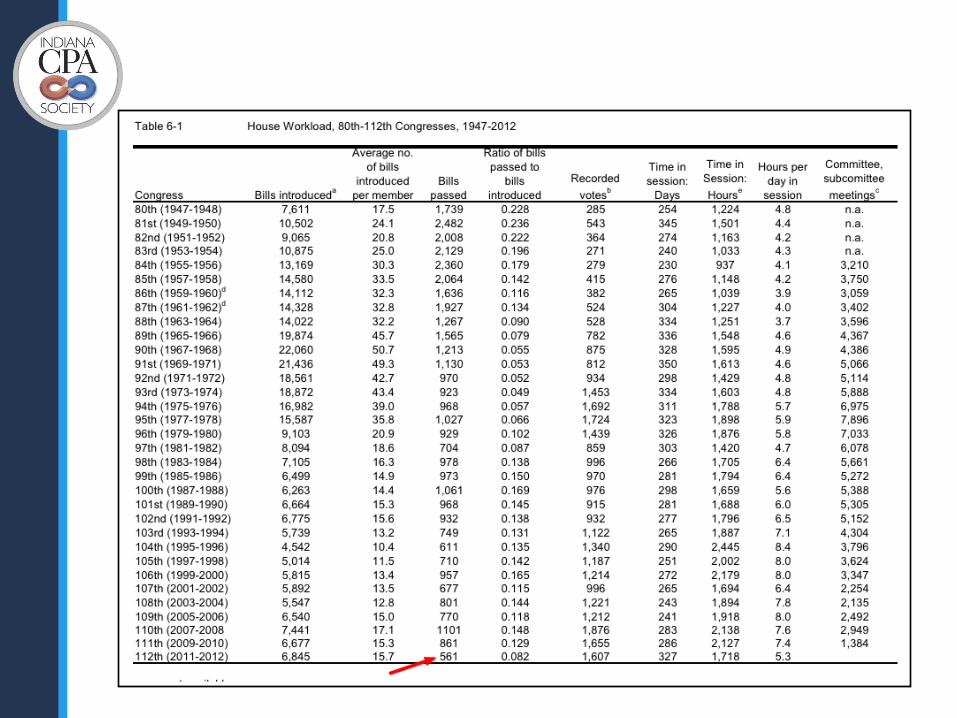

The least productive Congress ever

• 112th Congress – 1,607 recorded votes• 5th highest since Vital Stats began collecting data

– 561 bills passed• lowest number since 1947 (when data first collected)

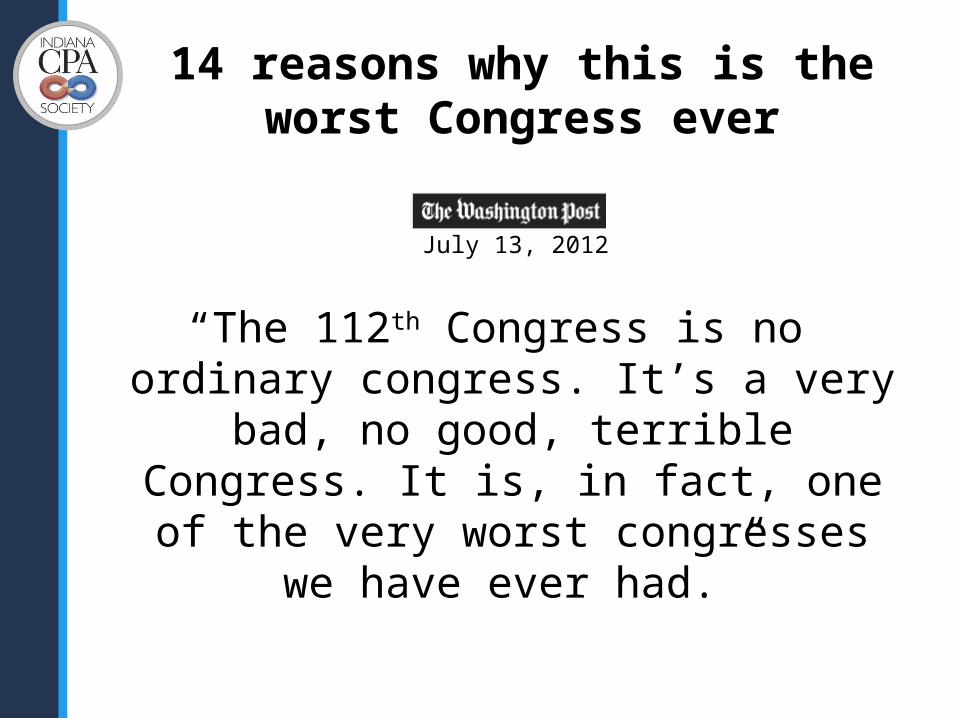

14 reasons why this is the worst Congress ever

“The 112th Congress is no ordinary congress. It’s a very bad, no good, terrible Congress. It is, in fact, one of the very worst congresses

we have ever had.”

July 13, 2012

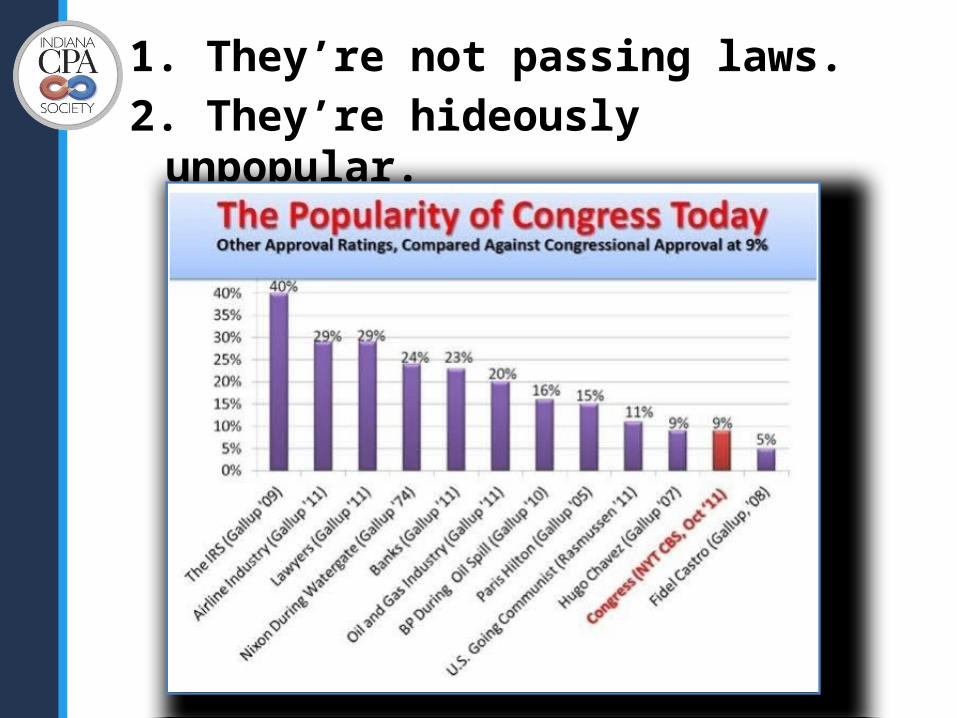

1. They’re not passing laws.2. They’re hideously unpopular.

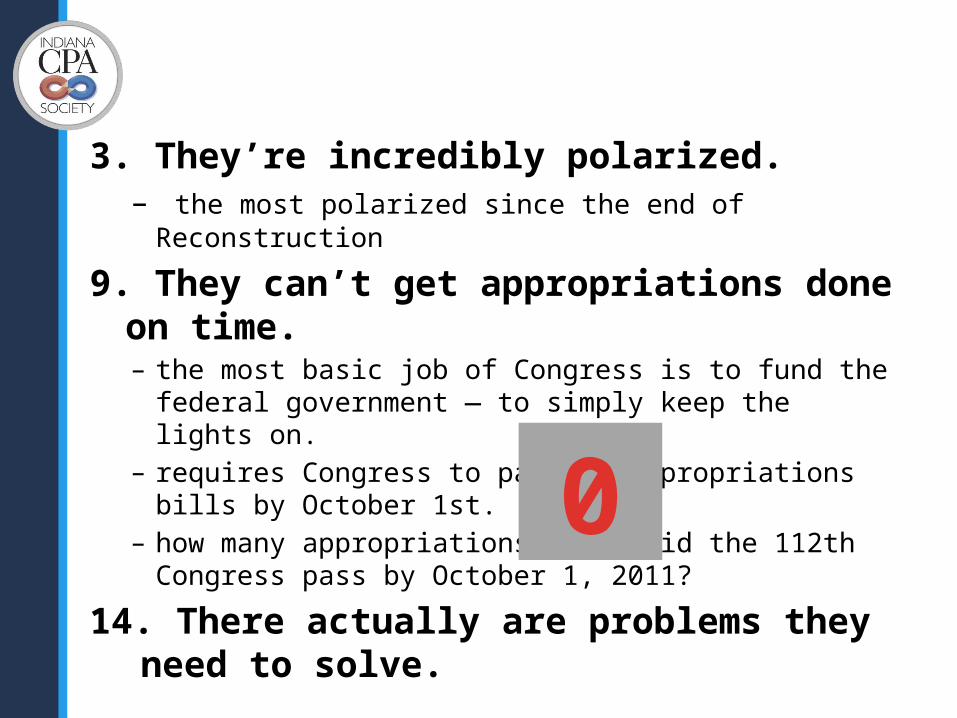

3. They’re incredibly polarized.– the most polarized since the end of Reconstruction

9. They can’t get appropriations done on time.– the most basic job of Congress is to fund the federal

government — to simply keep the lights on.– requires Congress to pass 13 appropriations bills by

October 1st. – how many appropriations bills did the 112th Congress

pass by October 1, 2011?

14. There actually are problems they need to solve.

0

Behind the Closed Doors of Washington lobbyists

October 7, 2012

"The most important function a lobbyist provides is to provide

facts and information" .

The Issues

Tax Due Date Simplification

Mobile Work Force (H.R. 1129)

Tax Reform

PCAOB & Audit Firm Rotation

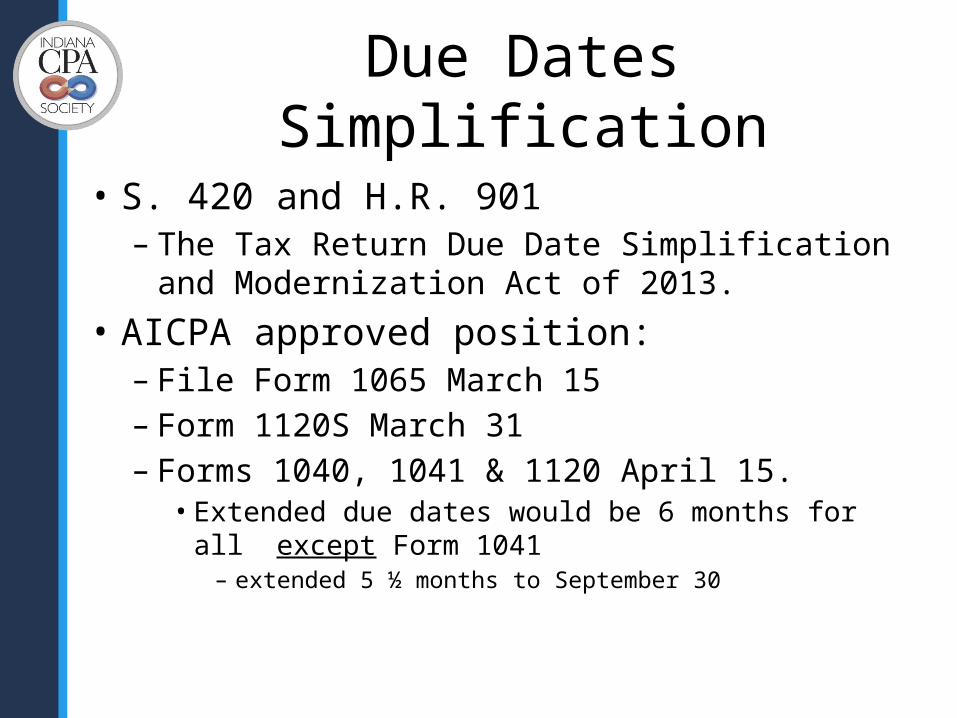

Due Dates Simplification

• S. 420 and H.R. 901– The Tax Return Due Date Simplification and

Modernization Act of 2013. • AICPA approved position:– File Form 1065 March 15– Form 1120S March 31– Forms 1040, 1041 & 1120 April 15.

• Extended due dates would be 6 months for all except Form 1041– extended 5 ½ months to September 30

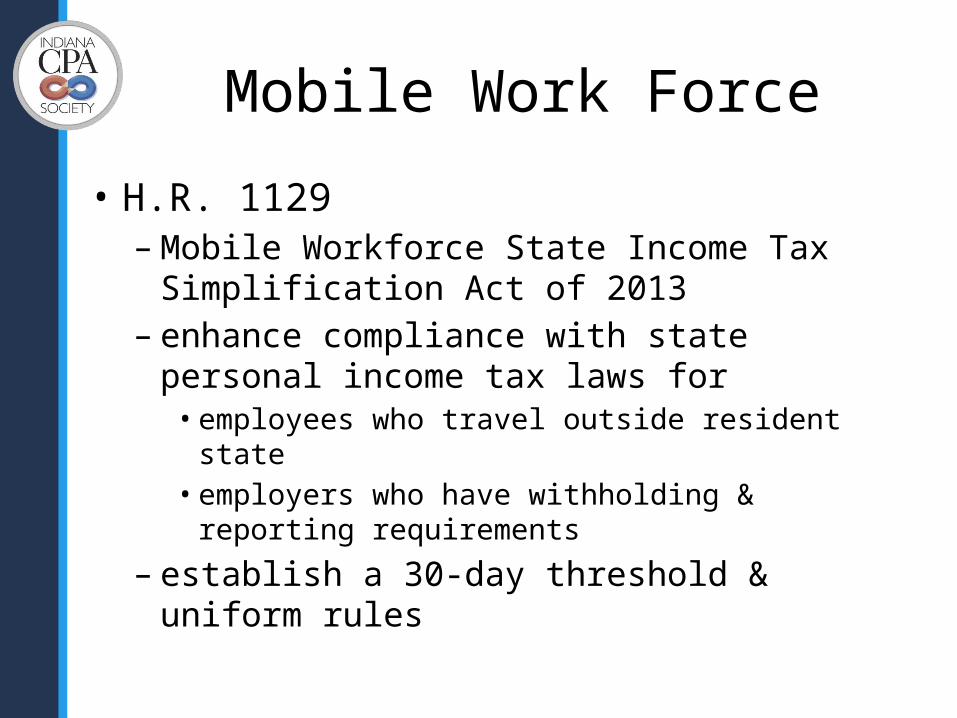

Mobile Work Force

• H.R. 1129– Mobile Workforce State Income Tax Simplification

Act of 2013– enhance compliance with state personal income

tax laws for• employees who travel outside resident state• employers who have withholding & reporting

requirements

– establish a 30-day threshold & uniform rules

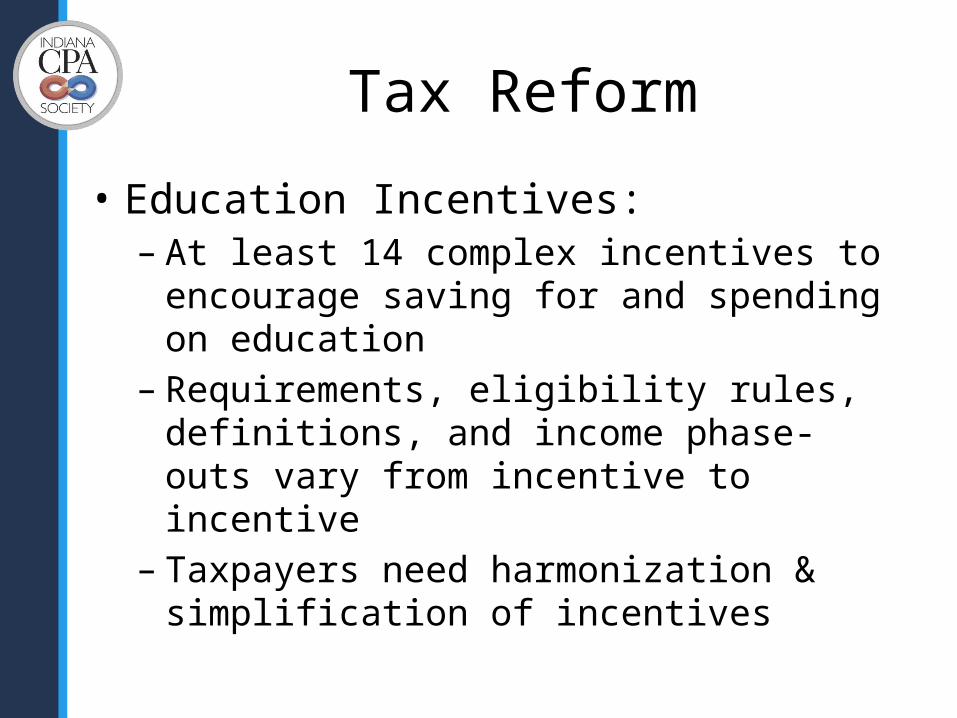

Tax Reform

• Education Incentives:– At least 14 complex incentives to encourage

saving for and spending on education– Requirements, eligibility rules, definitions, and

income phase-outs vary from incentive to incentive

– Taxpayers need harmonization & simplification of incentives

Tax Reform

• Retirement Plans:– More than a dozen tax-favored employer-sponsored

retirement planning vehicles• each subject to different rules pertaining to plan

documents, eligibility, contribution limits, tax treatment of contributions and distributions, the availability of loans, portability, nondiscrimination, reporting and disclosure.

– Provisions should be revised:• simpler• more readily understood• easier to comply with and administer• more effective in enabling taxpayers to accumulate

retirement assets

Tax Reform

• Kiddie Tax:– The Code taxes a portion of the unearned

income of children under the age of 18 (full-time students under the age of 24) at parents’ marginal tax rate, rather than at the child’s lower rate

– The rules should be simplified

Tax Reform

• Penalty Reform:– Civil tax penalties should be drafted to deter bad

conduct without deterring good conduct or punishing the innocent (i.e. unintentional errors)

• Corrected Form 1099:– permit taxpayers to report de minimis changes in

income from a corrected Form 1099 or amended Schedule K-1 in the year of receipt of the amended form

– streamline reporting process for government & taxpayer

Audit Firm Rotation

to solicit public comment on ways that auditor independence, objectivity and professional skepticism

could be enhanced. One possible approach on which the board is seeking comment is mandatory audit firm rotation

Audit Firm Rotation

• Already require auditor rotation:– Italy– South Korea– Brazil

• In discussion– Netherlands– U.K. (Competition Commission)– European Union

• European Parliament – April 25, 2013• 14 or 25 years

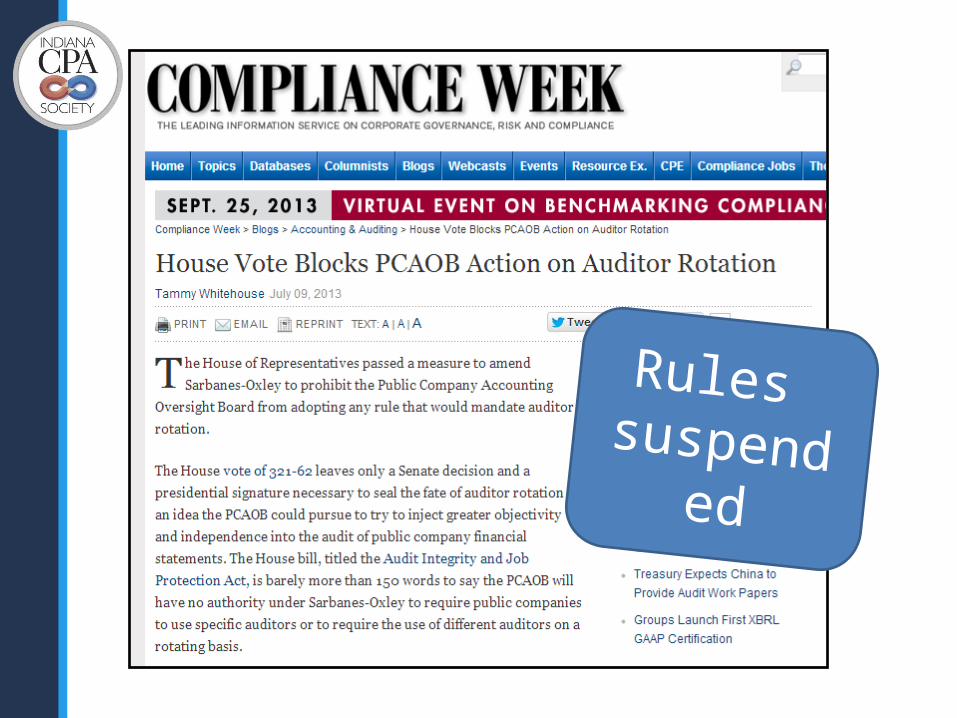

To amend the Sarbanes-Oxley Act of 2002 to prohibit the Public Company Accounting Oversight Board from

requiring public companies to use specific auditors or require the use of different auditors on a rotating basis.

Audit Integrity and Job Protection Act

Barely more than 150 words.

Audit Integrity and Job Protection Act

Audit Integrity and Job Protection Act

SEC. 2. LIMITATION ON AUTHORITY RELATING TO AUDITORS.

Section 103 of the Sarbanes-Oxley Act of 2002 (15 U.S.C. 7213) is amended by adding at the end the following:‘(e) Limitation on Authority- The Board shall have no

authority under this title to require that audits conducted for a particular issuer in accordance with the standards set forth under this section be conducted by specific registered public accounting firms, or that such audits be conducted for an issuer by different registered public accounting firms on a rotating basis.’

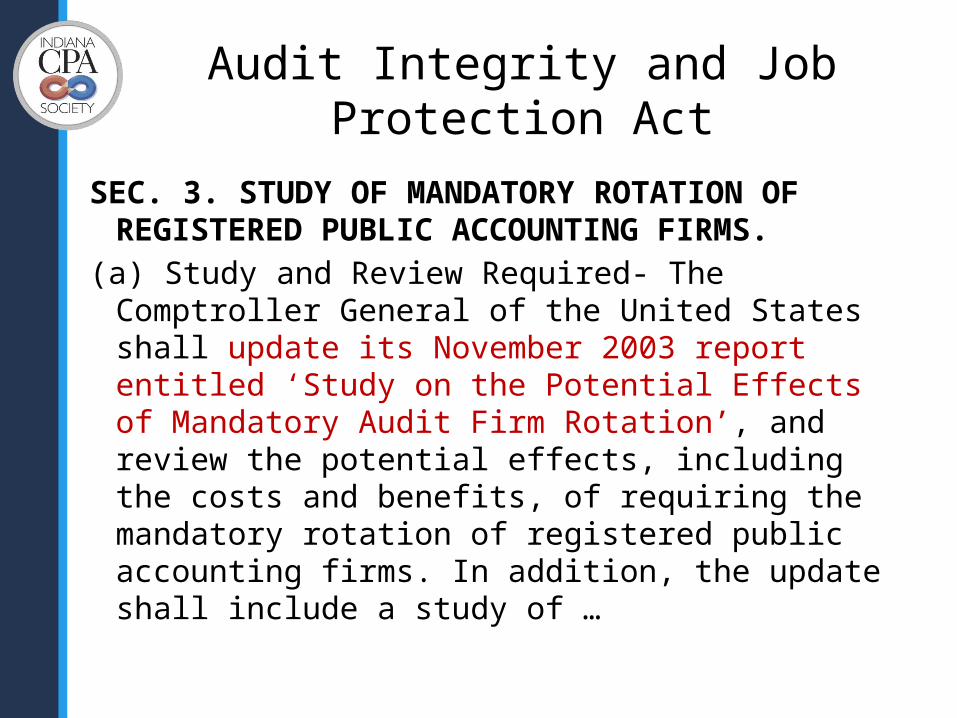

Audit Integrity and Job Protection Act

SEC. 3. STUDY OF MANDATORY ROTATION OF REGISTERED PUBLIC ACCOUNTING FIRMS.

(a) Study and Review Required- The Comptroller General of the United States shall update its November 2003 report entitled ‘Study on the Potential Effects of Mandatory Audit Firm Rotation’, and review the potential effects, including the costs and benefits, of requiring the mandatory rotation of registered public accounting firms. In addition, the update shall include a study of …

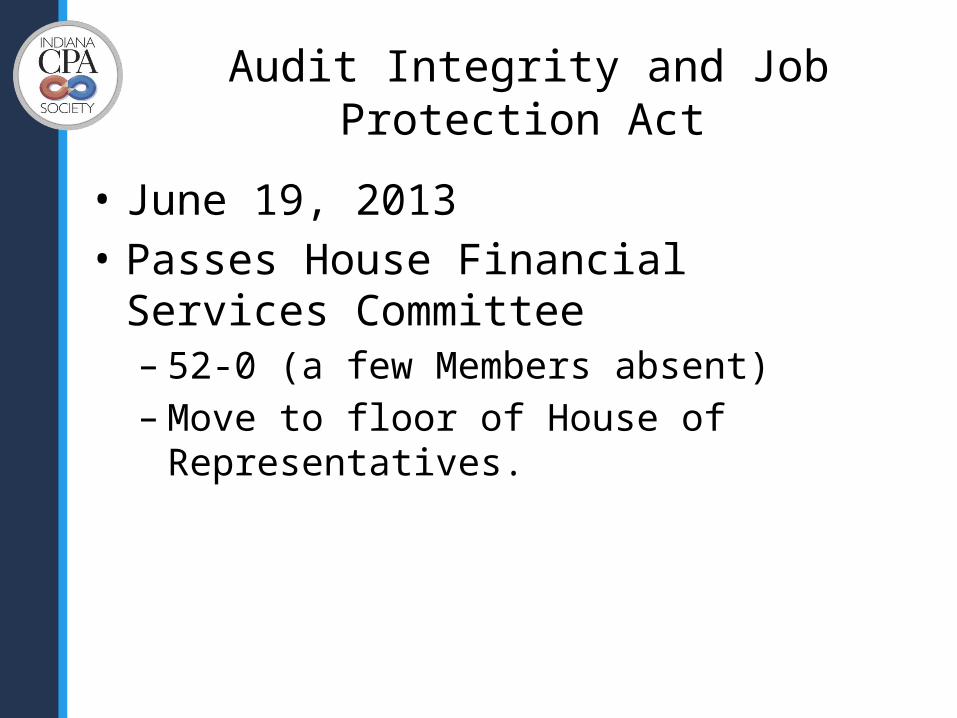

Audit Integrity and Job Protection Act

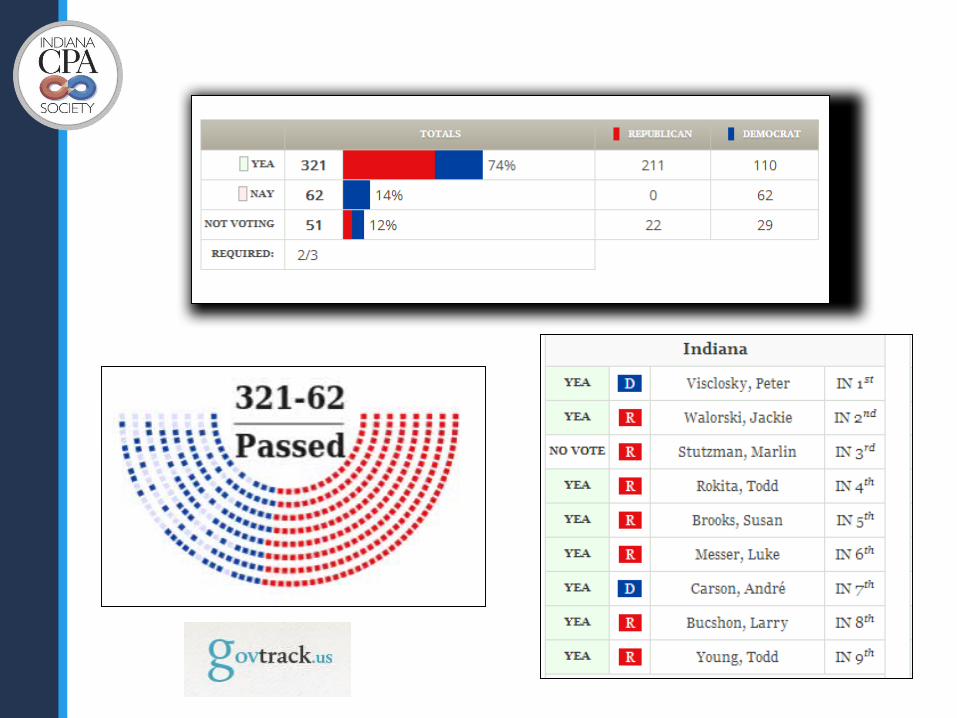

• June 19, 2013• Passes House Financial Services Committee– 52-0 (a few Members absent)– Move to floor of House of Representatives.

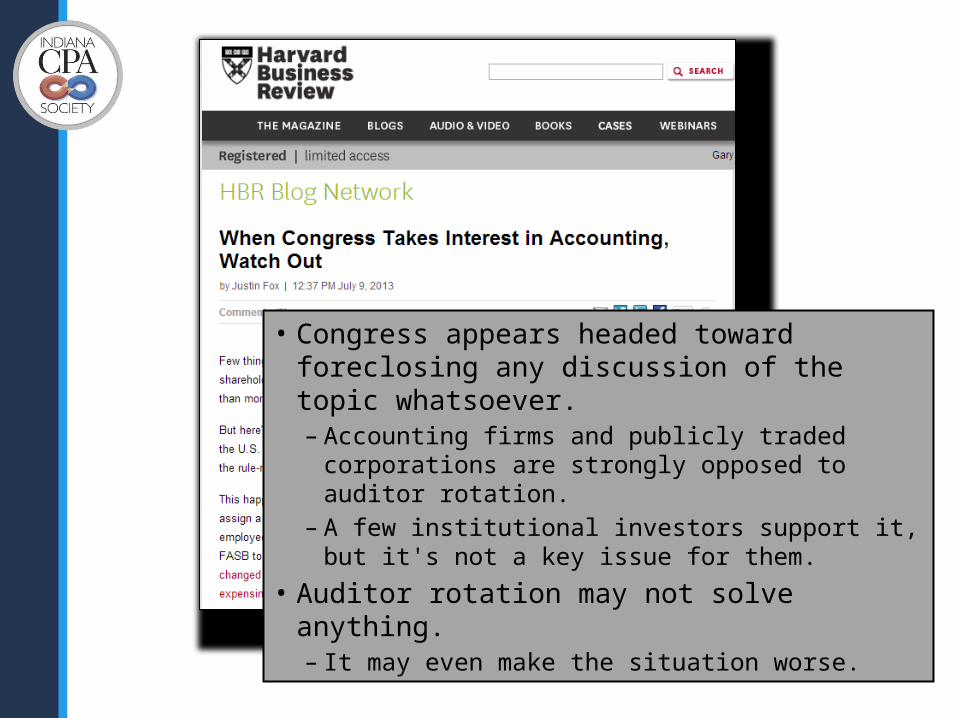

Rules suspended

• Congress appears headed toward foreclosing any discussion of the topic whatsoever. – Accounting firms and publicly traded

corporations are strongly opposed to auditor rotation.

– A few institutional investors support it, but it's not a key issue for them.

• Auditor rotation may not solve anything. – It may even make the situation worse.

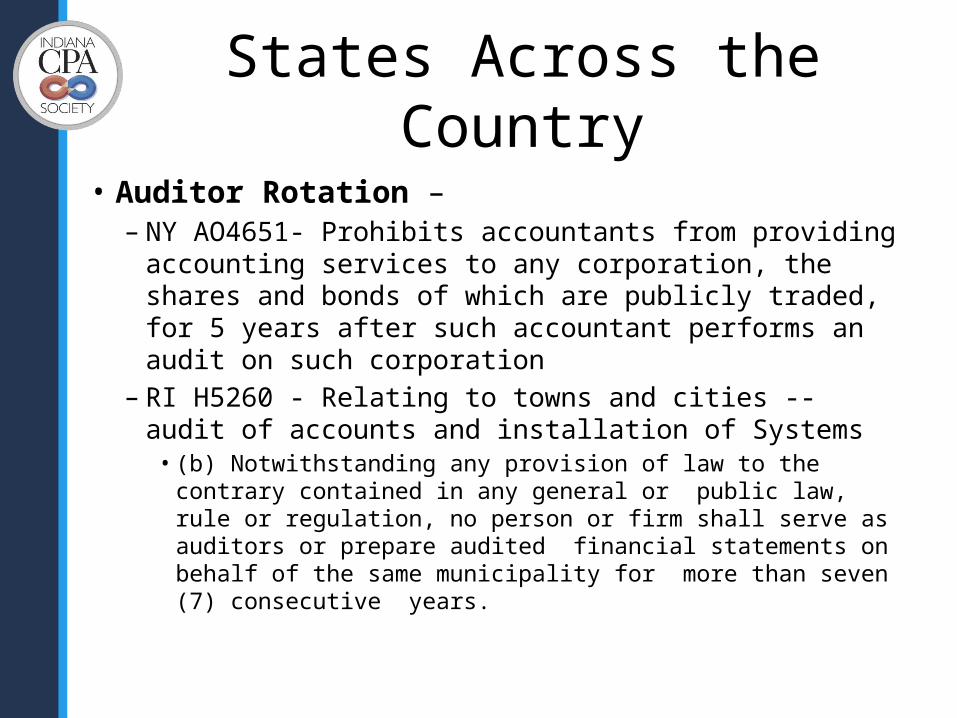

States Across the Country

States Across the Country

• Auditor Rotation – – NY AO4651- Prohibits accountants from providing

accounting services to any corporation, the shares and bonds of which are publicly traded, for 5 years after such accountant performs an audit on such corporation

– RI H5260 - Relating to towns and cities -- audit of accounts and installation of Systems • (b) Notwithstanding any provision of law to the contrary

contained in any general or public law, rule or regulation, no person or firm shall serve as auditors or prepare audited financial statements on behalf of the same municipality for more than seven (7) consecutive years.

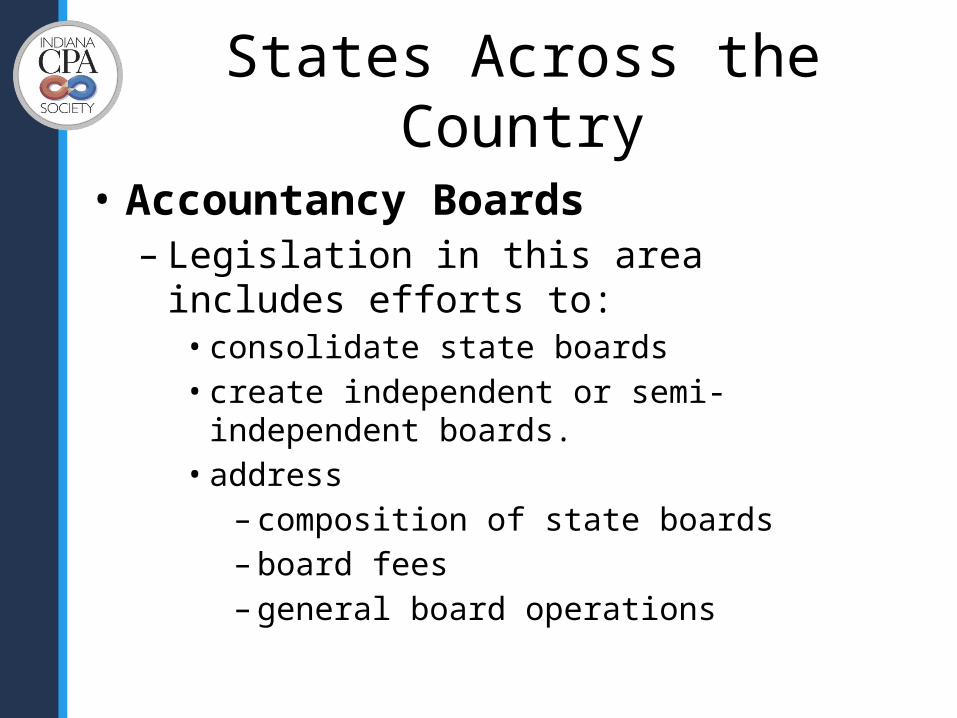

States Across the Country

• Accountancy Boards– Legislation in this area includes efforts to:• consolidate state boards• create independent or semi-independent boards.• address– composition of state boards– board fees – general board operations

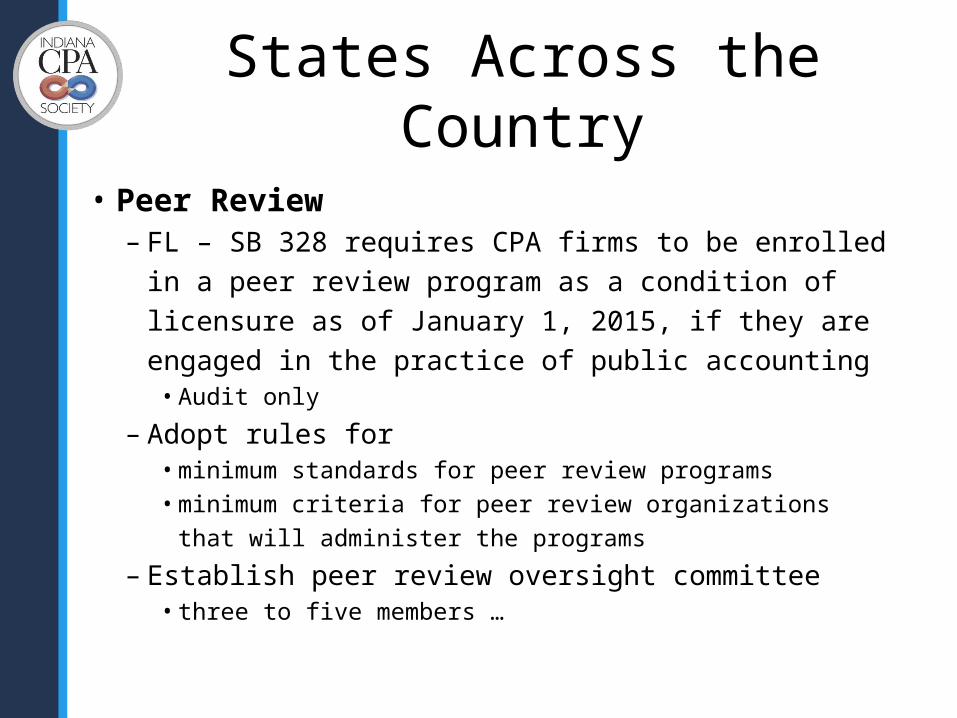

States Across the Country

• Peer Review– FL – SB 328 requires CPA firms to be enrolled in a peer

review program as a condition of licensure as of January 1, 2015, if they are engaged in the practice of public accounting• Audit only

– Adopt rules for• minimum standards for peer review programs• minimum criteria for peer review organizations that will

administer the programs

– Establish peer review oversight committee • three to five members …

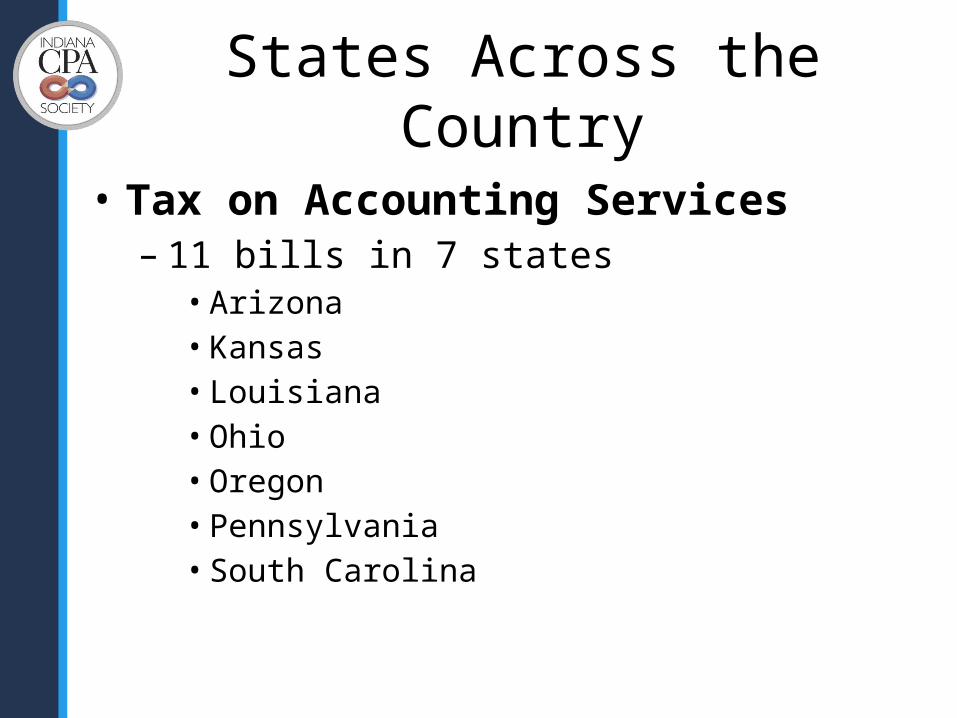

States Across the Country

• Tax on Accounting Services– 11 bills in 7 states • Arizona• Kansas• Louisiana• Ohio• Oregon• Pennsylvania• South Carolina

2013 General Assembly

• Volume– House bills introduced: 613• passed: 148

– Senate bills introduced: 619• passed: 147

Low Volume

2013 General Assembly

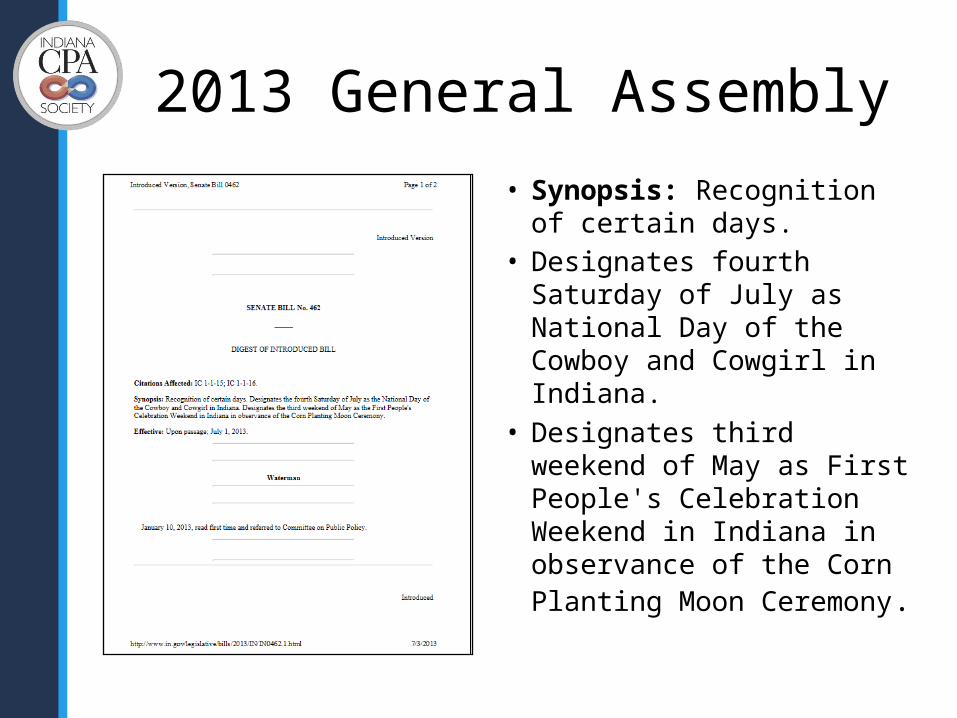

• Synopsis: Recognition of certain days.

• Designates fourth Saturday of July as National Day of the Cowboy and Cowgirl in Indiana.

• Designates third weekend of May as First People's Celebration Weekend in Indiana in observance of the Corn Planting Moon Ceremony.

2013 General Assembly

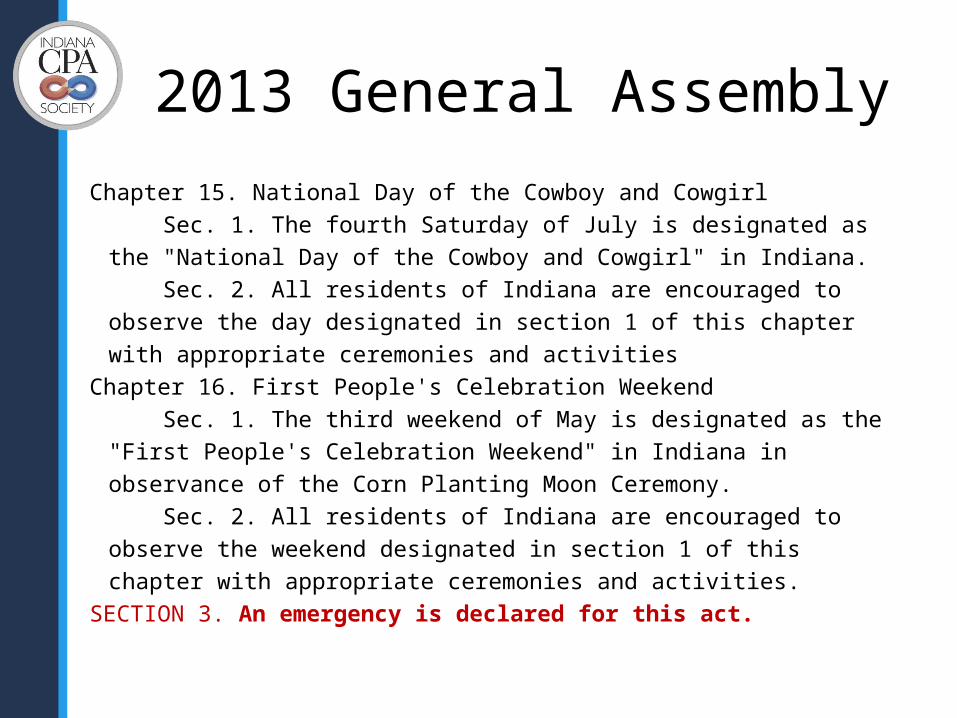

Chapter 15. National Day of the Cowboy and Cowgirl Sec. 1. The fourth Saturday of July is designated as the "National Day of the Cowboy and Cowgirl" in Indiana. Sec. 2. All residents of Indiana are encouraged to observe the day designated in section 1 of this chapter with appropriate ceremonies and activities

Chapter 16. First People's Celebration Weekend Sec. 1. The third weekend of May is designated as the "First People's Celebration Weekend" in Indiana in observance of the Corn Planting Moon Ceremony. Sec. 2. All residents of Indiana are encouraged to observe the weekend designated in section 1 of this chapter with appropriate ceremonies and activities.

SECTION 3. An emergency is declared for this act.

2013 General Assembly

• HB 1179 – Securities Matters– Audits under GAAP /GAAS

• SB 293 – Government Accounting Study Committee– GASB implementation issues– Statements 67 and 68 • would require state and local governments to report

significant pension-related liabilities far more prominently on their balance sheets

2013 General Assembly

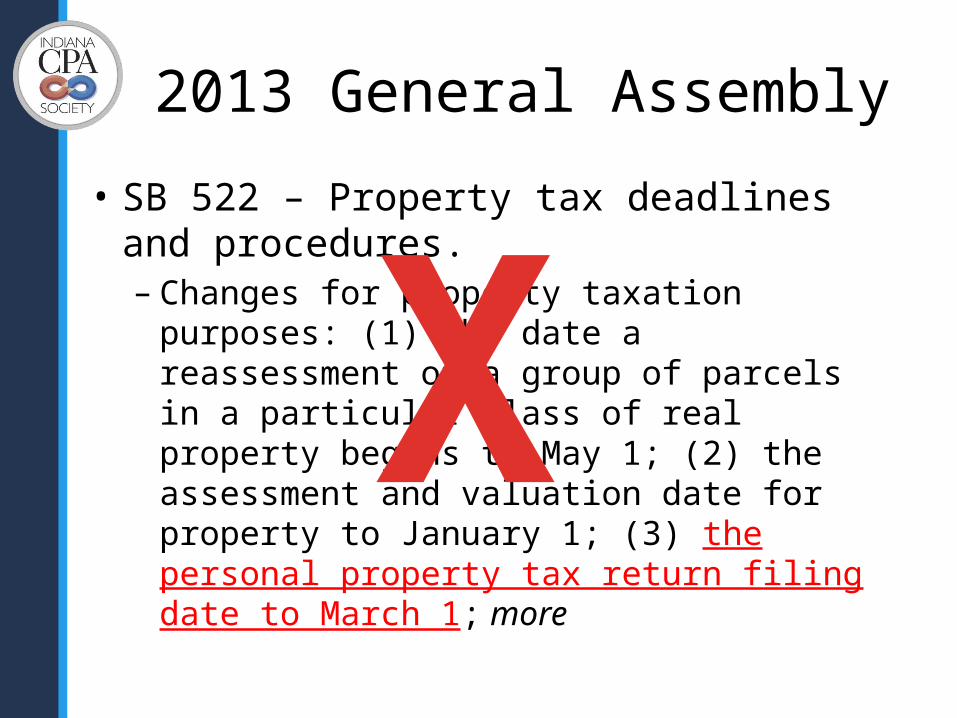

• SB 522 – Property tax deadlines and procedures.– Changes for property taxation purposes: (1) the

date a reassessment of a group of parcels in a particular class of real property begins to May 1; (2) the assessment and valuation date for property to January 1; (3) the personal property tax return filing date to March 1; more

X

2013 General Assembly

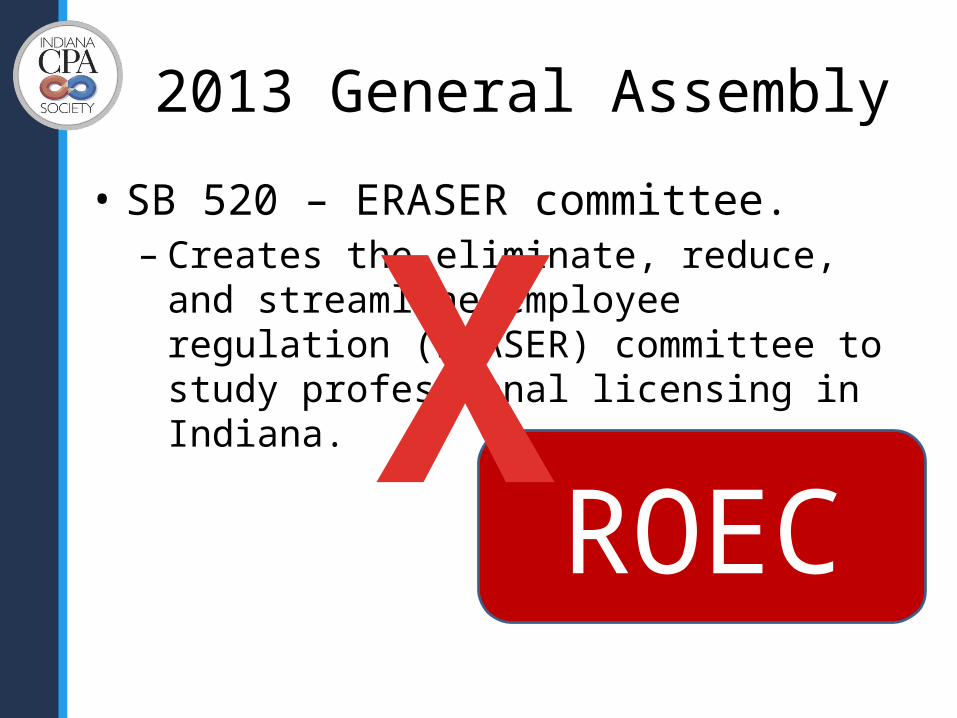

• SB 520 – ERASER committee. – Creates the eliminate, reduce, and streamline

employee regulation (ERASER) committee to study professional licensing in Indiana.

ROECX

2013 General Assembly

• SB 190 – Accrual Accounting– Requires

• after December 31, 2013, that state agencies, state educational institutions, and political subdivisions maintain accounts on an accrual basis and, after December 31, 2014, include information prepared on an accrual basis in budgets and financial reports.

• that the state board of accounts prescribe a plan for state agencies, state educational institutions, and political subdivisions to follow to convert to an accrual basis of accounting in budgets and financial reports.

• Plan must be prescribed before October 1, 2013.

X

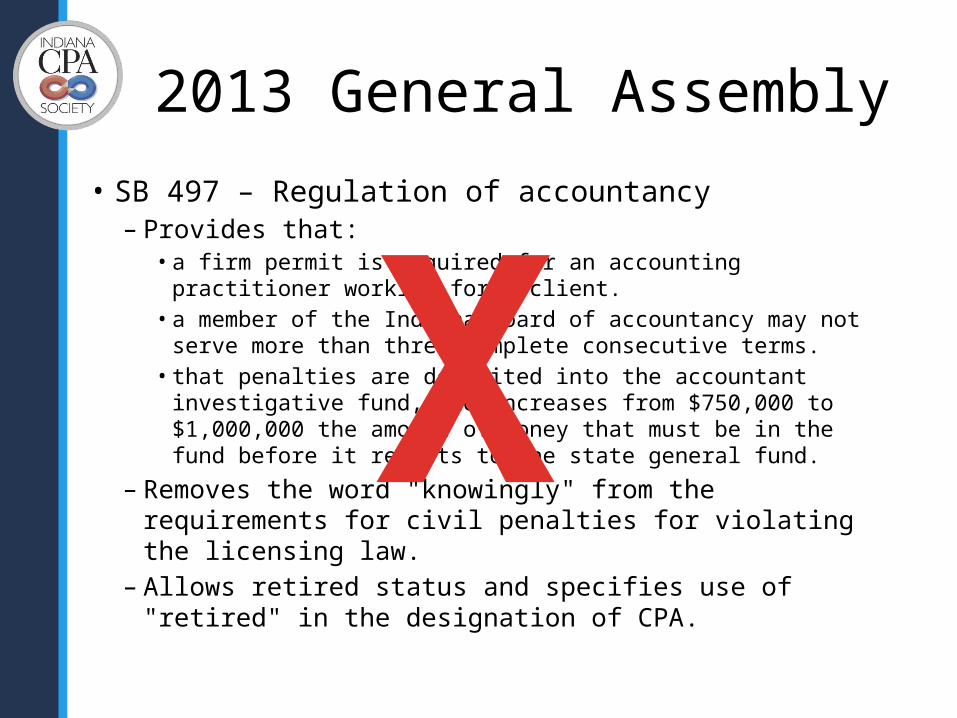

2013 General Assembly

• SB 497 – Regulation of accountancy– Provides that:

• a firm permit is required for an accounting practitioner working for a client.

• a member of the Indiana board of accountancy may not serve more than three complete consecutive terms.

• that penalties are deposited into the accountant investigative fund, and increases from $750,000 to $1,000,000 the amount of money that must be in the fund before it reverts to the state general fund.

– Removes the word "knowingly" from the requirements for civil penalties for violating the licensing law.

– Allows retired status and specifies use of "retired" in the designation of CPA.

X

Board of Accountancy

Board of Accountancy

• CPE Make Up Rule• 2012 License renewal• Failed Peer Review Reports– Peer Review Oversight Committee

• Regulated Occupations Evaluation Committee• CPE Standards

Board of Accountancy

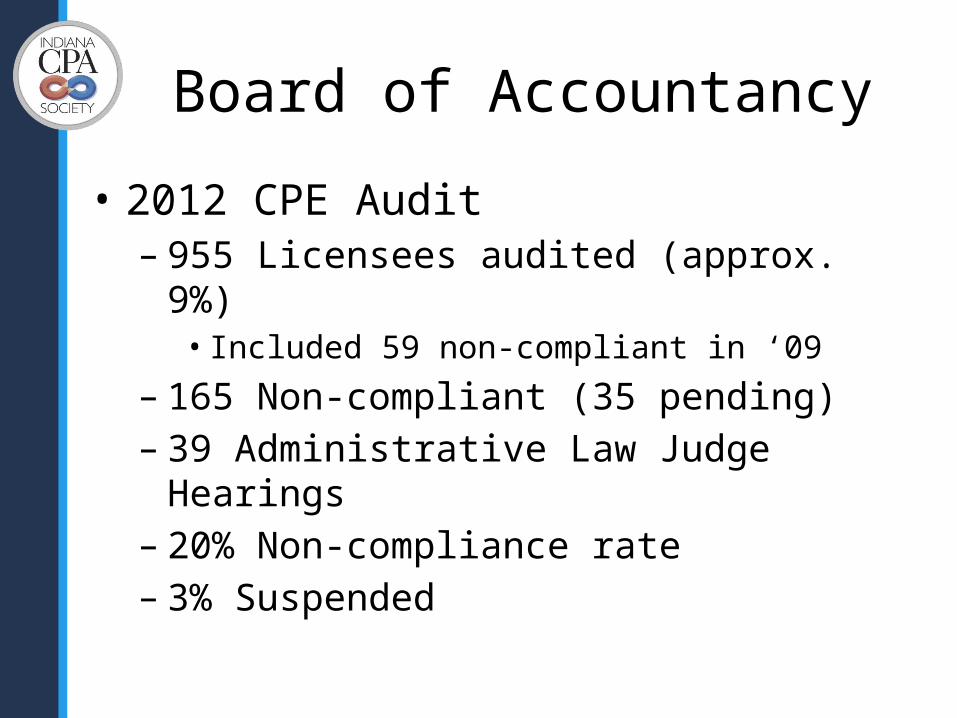

• 2012 CPE Audit– 955 Licensees audited (approx. 9%)• Included 59 non-compliant in ‘09

– 165 Non-compliant (35 pending)– 39 Administrative Law Judge Hearings– 20% Non-compliance rate – 3% Suspended

Board of Accountancy

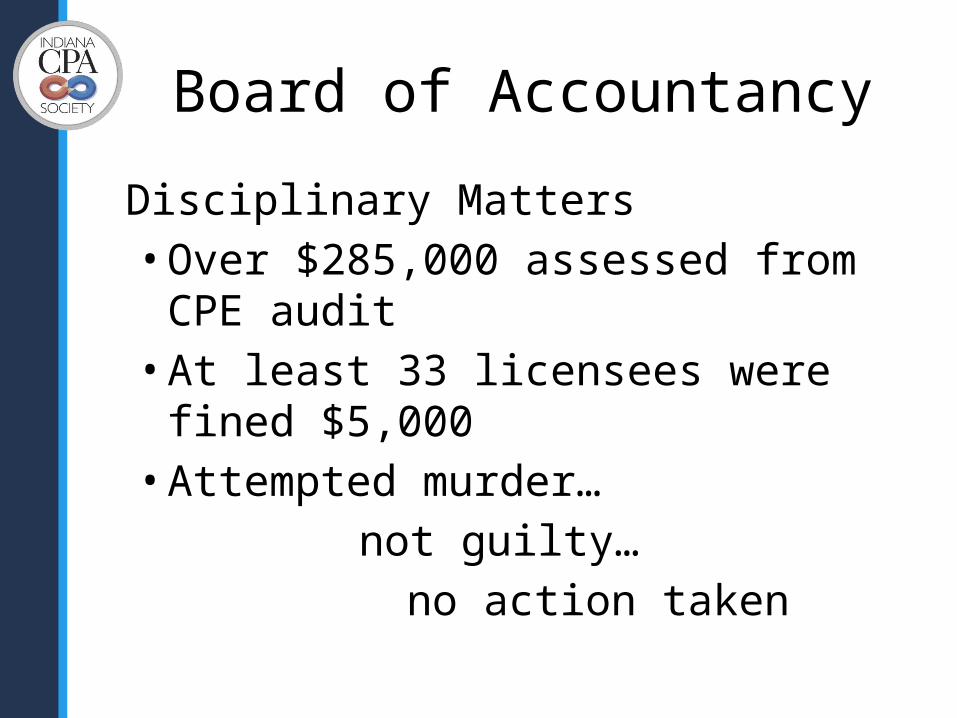

Disciplinary Matters• Over $285,000 assessed from CPE audit• At least 33 licensees were fined $5,000• Attempted murder…

not guilty…no action

taken

Board of Accountancy

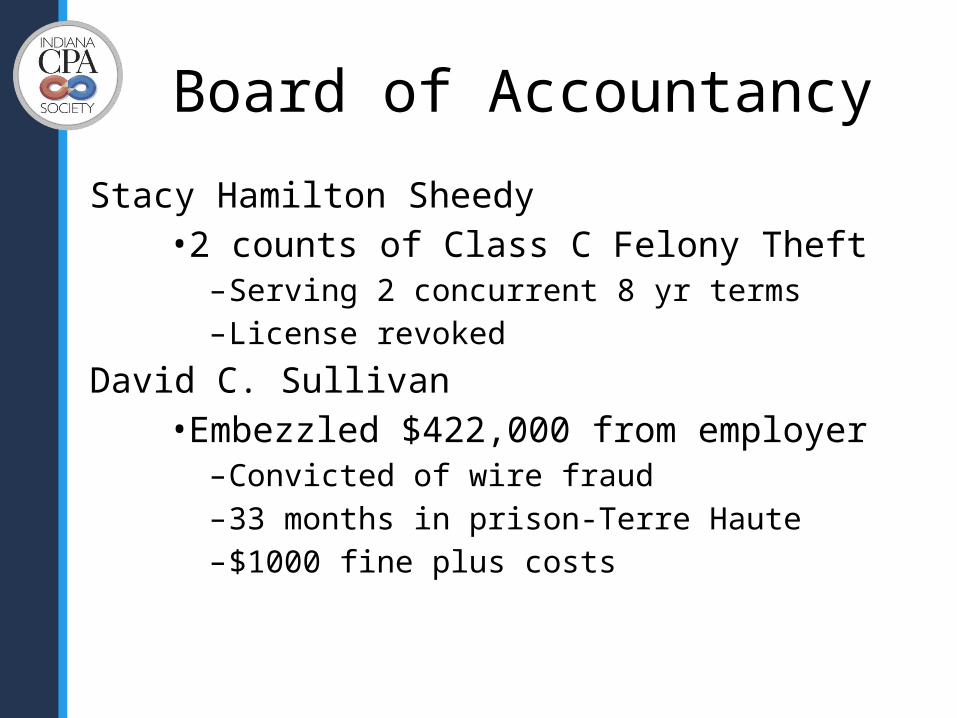

Stacy Hamilton Sheedy• 2 counts of Class C Felony Theft– Serving 2 concurrent 8 yr terms– License revoked

David C. Sullivan• Embezzled $422,000 from employer–Convicted of wire fraud–33 months in prison-Terre Haute–$1000 fine plus costs

Board of Accountancy

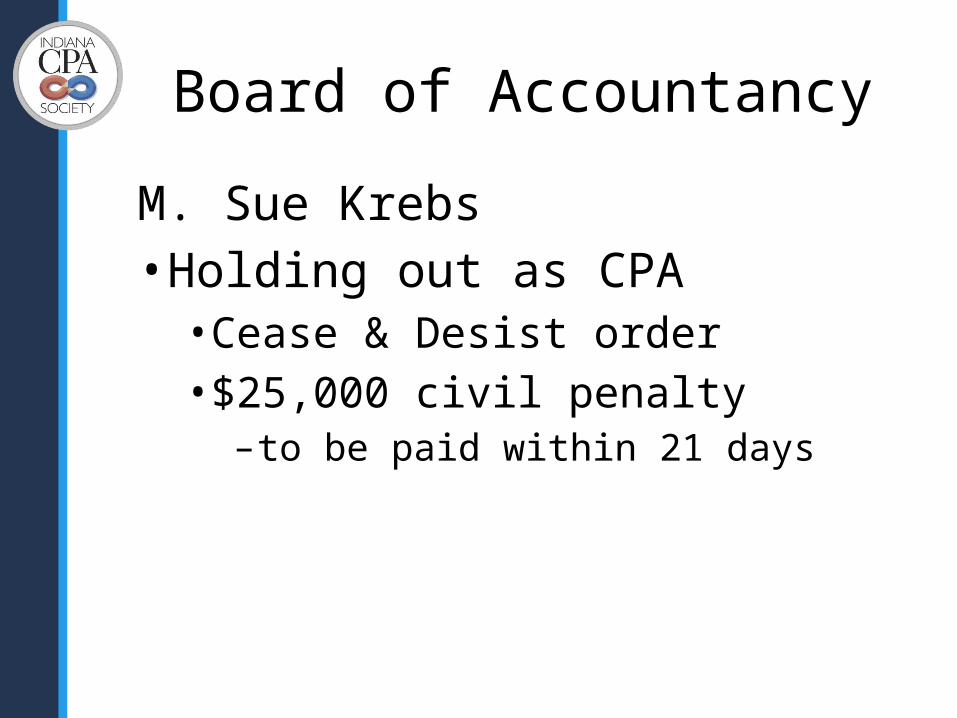

M. Sue Krebs• Holding out as CPA• Cease & Desist order • $25,000 civil penalty–to be paid within 21 days

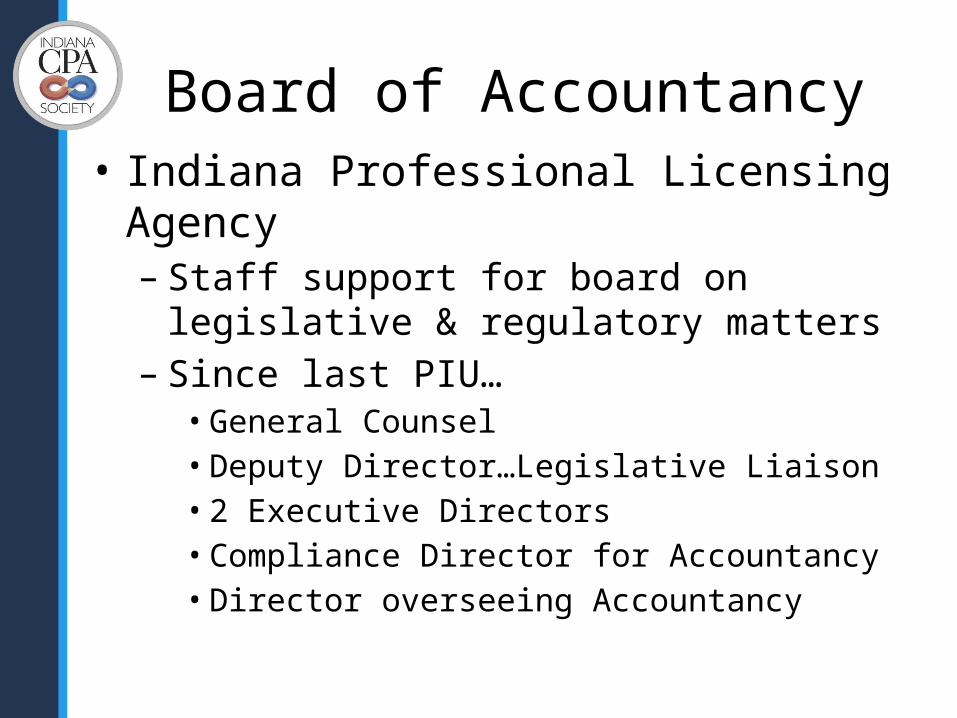

Board of Accountancy• Indiana Professional Licensing Agency – Staff support for board on legislative &

regulatory matters– Since last PIU…• General Counsel• Deputy Director…Legislative Liaison• 2 Executive Directors• Compliance Director for Accountancy• Director overseeing Accountancy

Peer Review

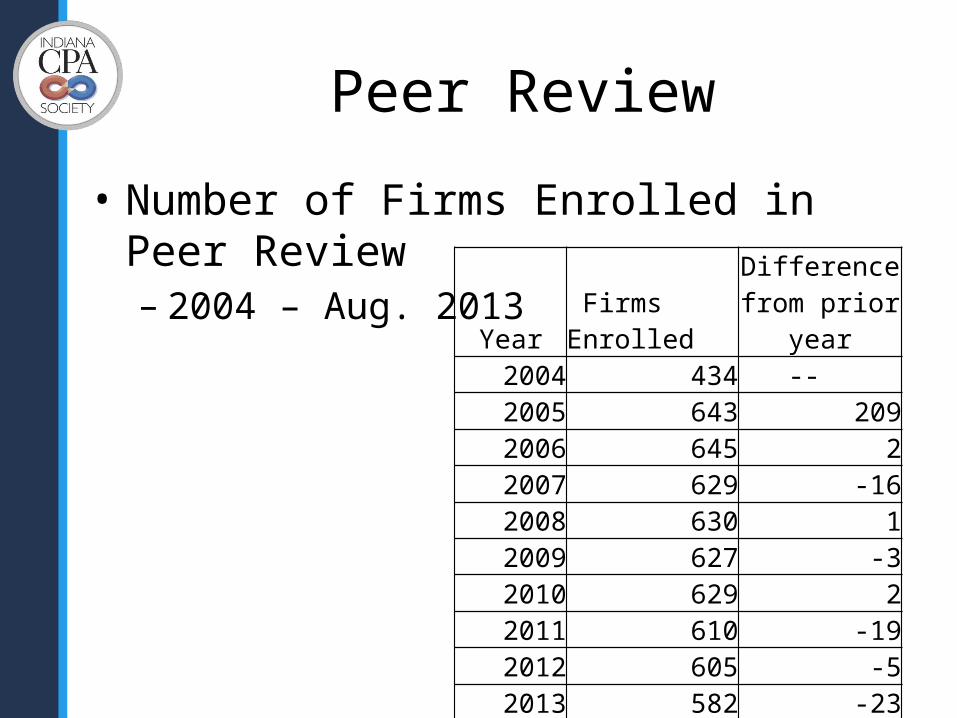

• Number of Firms Enrolled in Peer Review – 2004 – Aug. 2013

Year Firms Enrolled

Difference from prior

year2004 434 -- 2005 643 2092006 645 22007 629 -162008 630 12009 627 -32010 629 22011 610 -192012 605 -52013 582 -23

Peer Review

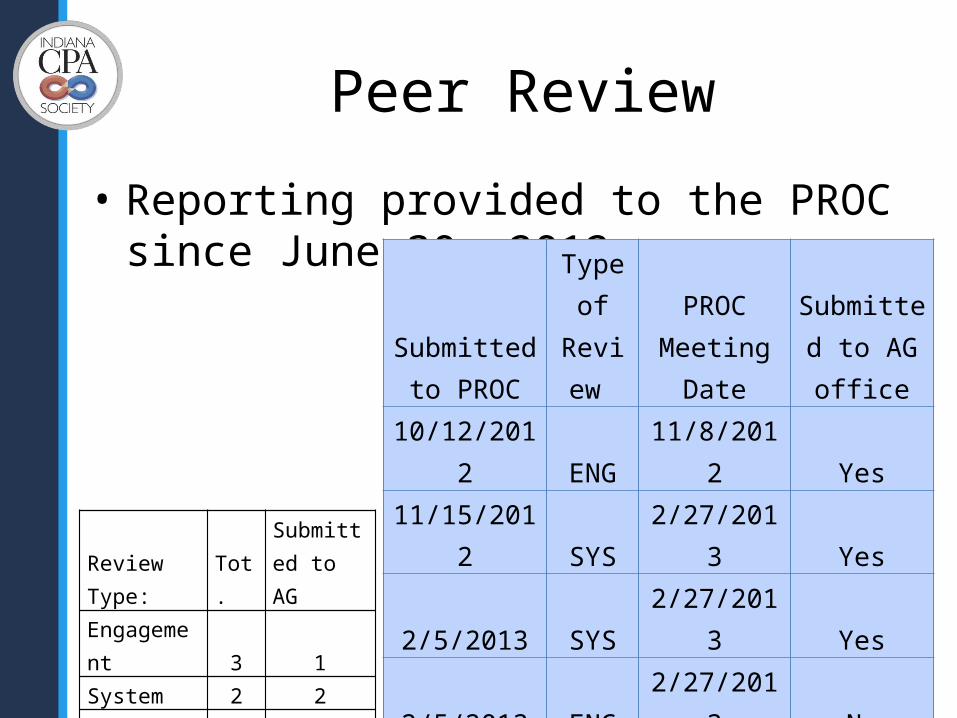

• Reporting provided to the PROC since June 30, 2012.

Submitted to PROC

Type of

Review

PROC Meeting

DateSubmitted

to AG office

10/12/2012 ENG 11/8/2012 Yes

11/15/2012 SYS 2/27/2013 Yes

2/5/2013 SYS 2/27/2013 Yes

2/5/2013 ENG 2/27/2013 No

2/8/2013 ENG 2/27/2013 No

5/21/2013 ENG 8/7/2013 TBD

7/25/2013 SYS 8/7/2013 TBD

Review Type: Tot.Submitted to AG

Engagement 3 1System 2 2YTD Total 5 3

Department of Revenue

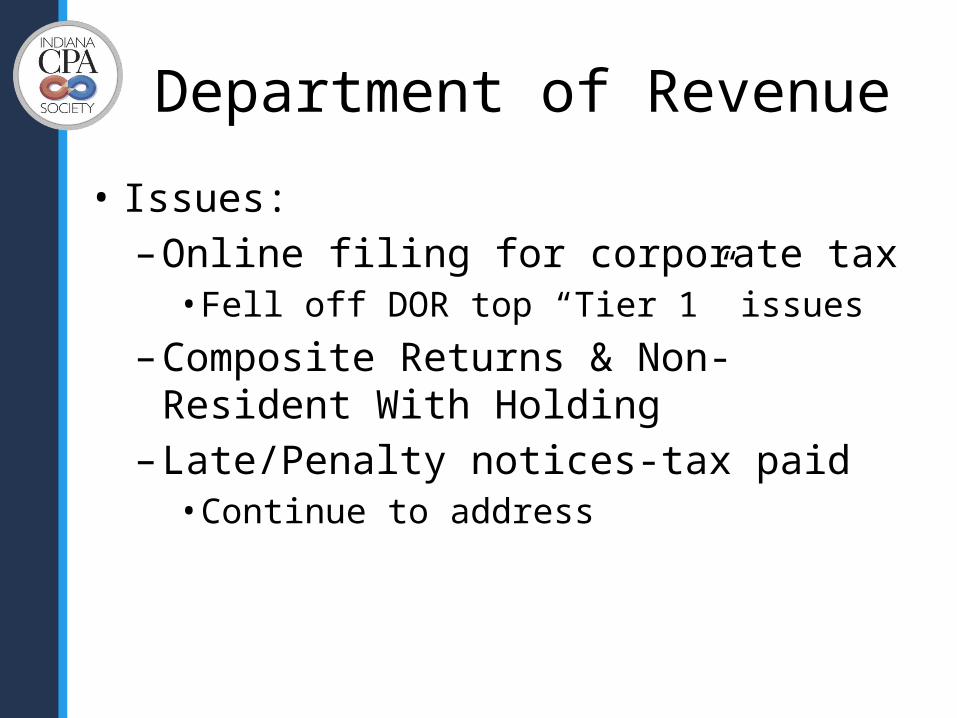

Department of Revenue

• Issues:–Online filing for corporate tax• Fell off DOR top “Tier 1” issues

–Composite Returns & Non-Resident With Holding– Late/Penalty notices-tax paid• Continue to address

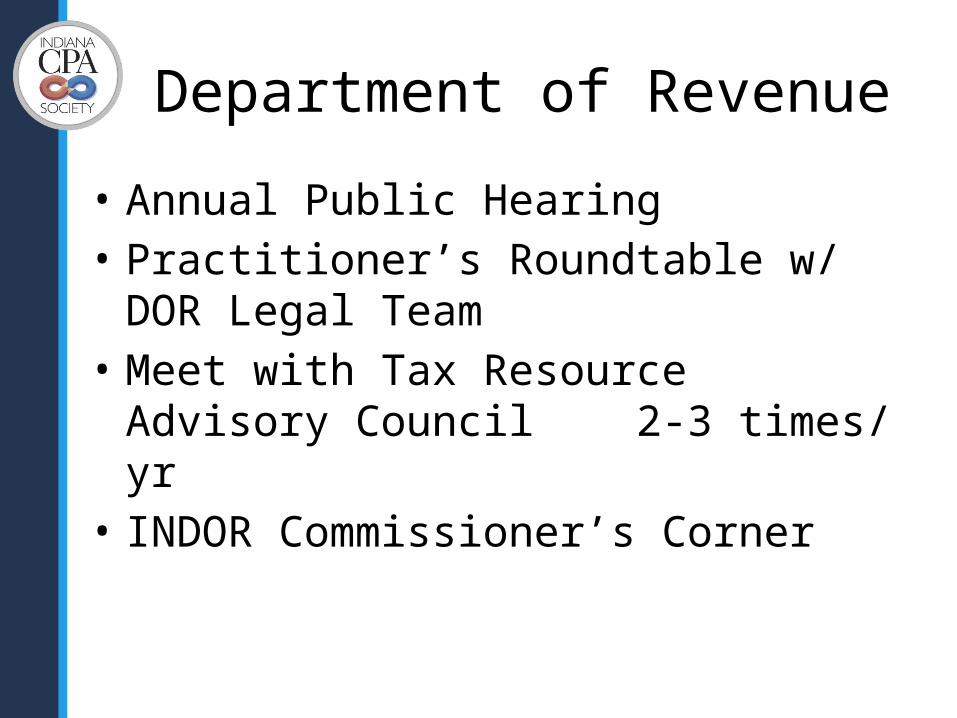

Department of Revenue

• Annual Public Hearing• Practitioner’s Roundtable w/ DOR Legal

Team• Meet with Tax Resource Advisory Council

2-3 times/ yr• INDOR Commissioner’s Corner

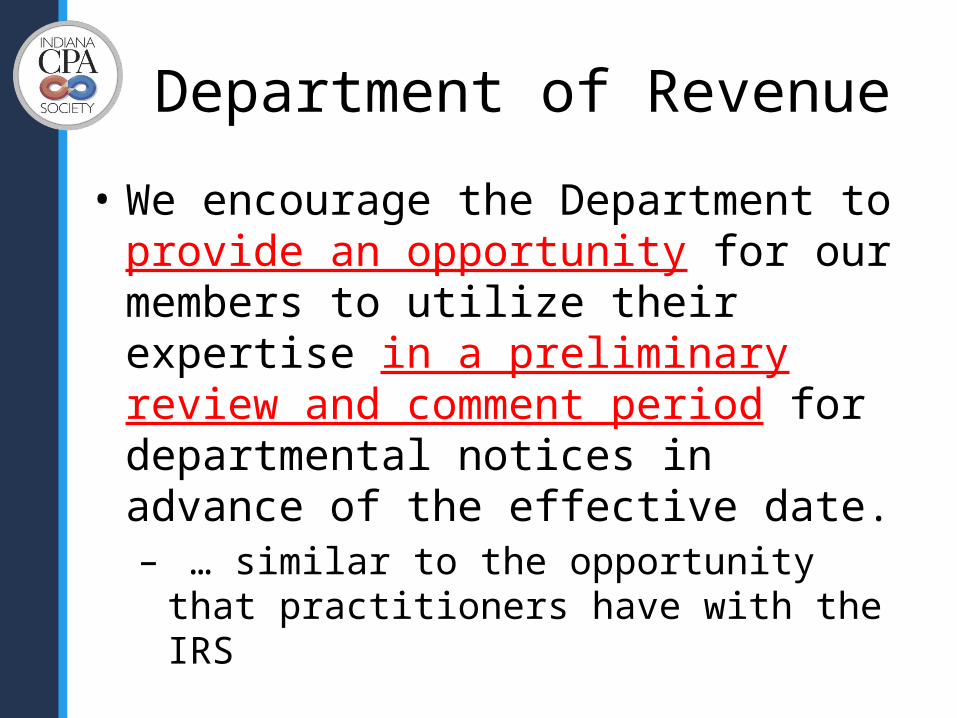

Department of Revenue

• We encourage the Department to provide an opportunity for our members to utilize their expertise in a preliminary review and comment period for departmental notices in advance of the effective date. – … similar to the opportunity that practitioners

have with the IRS

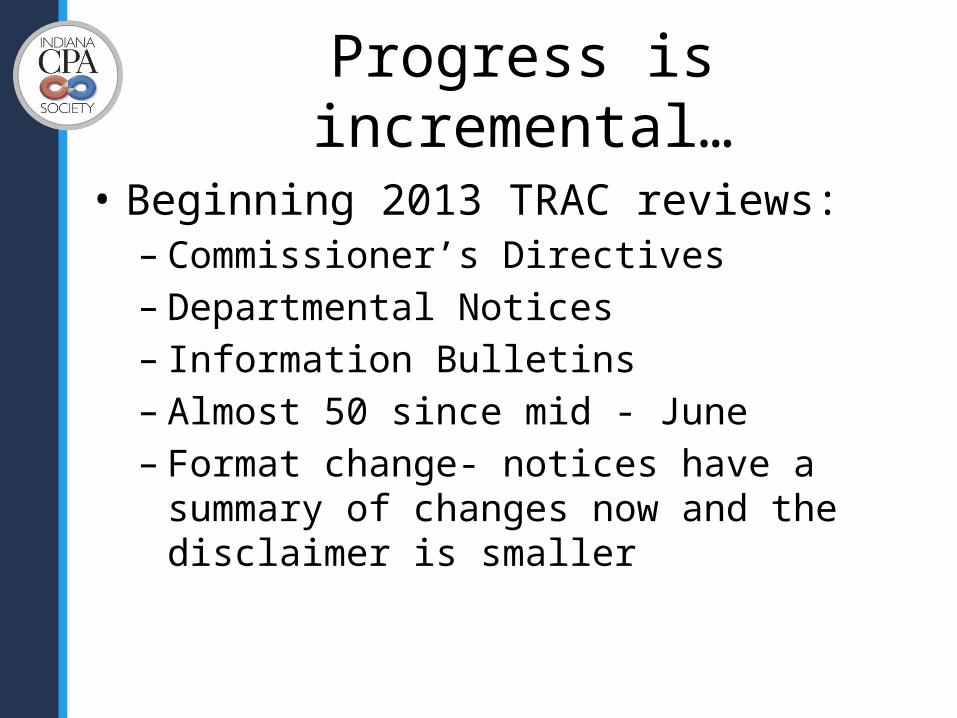

Progress is incremental…

• Beginning 2013 TRAC reviews:– Commissioner’s Directives– Departmental Notices– Information Bulletins– Almost 50 since mid - June– Format change- notices have a summary of

changes now and the disclaimer is smaller

Society’s Tax Resource Advisory Council is committed to helping address systemic issues and to improving communications between the Department and taxpayer representatives.

DOR Annual Meeting

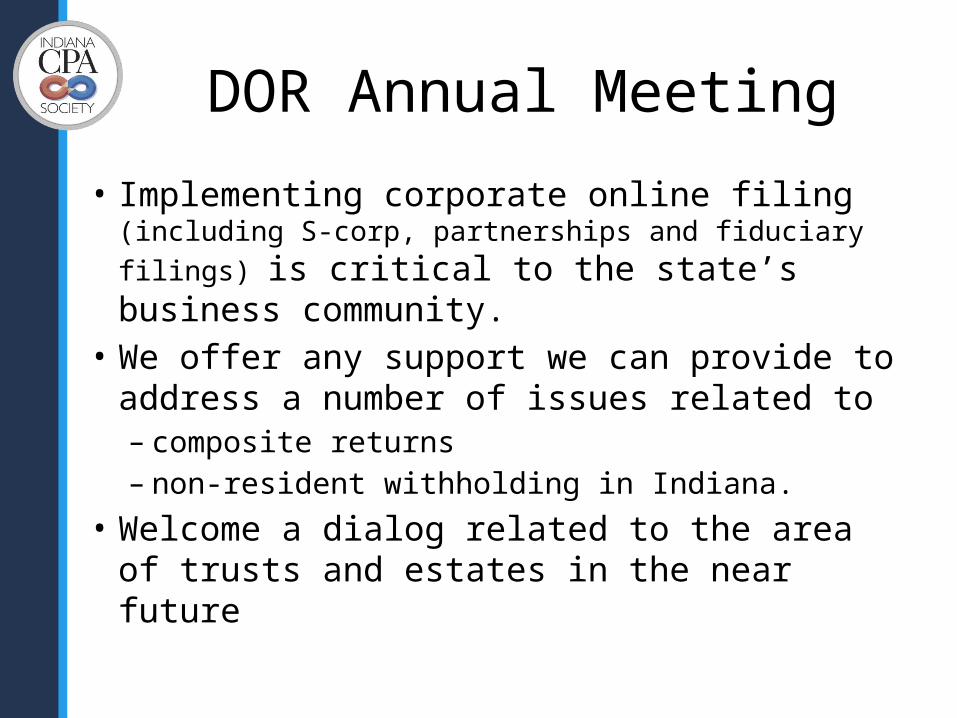

• Implementing corporate online filing (including S-corp, partnerships and fiduciary filings) is critical to the state’s business community.

• We offer any support we can provide to address a number of issues related to– composite returns– non-resident withholding in Indiana.

• Welcome a dialog related to the area of trusts and estates in the near future

DOR Annual Meeting

• We see several opportunities that would represent meaningful assistance for individual taxpayers and businesses in Indiana. We welcome the opportunity to lend our member’s expertise and support to any of these projects as appropriate. – The review of all returns for which the automatic taxpayer refund

credit was denied during the time period where the 90% requirement was inadvertently applied.

– The development of the Business One-Stop portal with the Secretary of State’s office integrating tax administration for businesses.

– Reducing the FUTA credit rate paid by Indiana businesses

Patent TrollsPatent Holding Companies (PHC)

Patent Assertion Entities (PAE)

Patent Issues

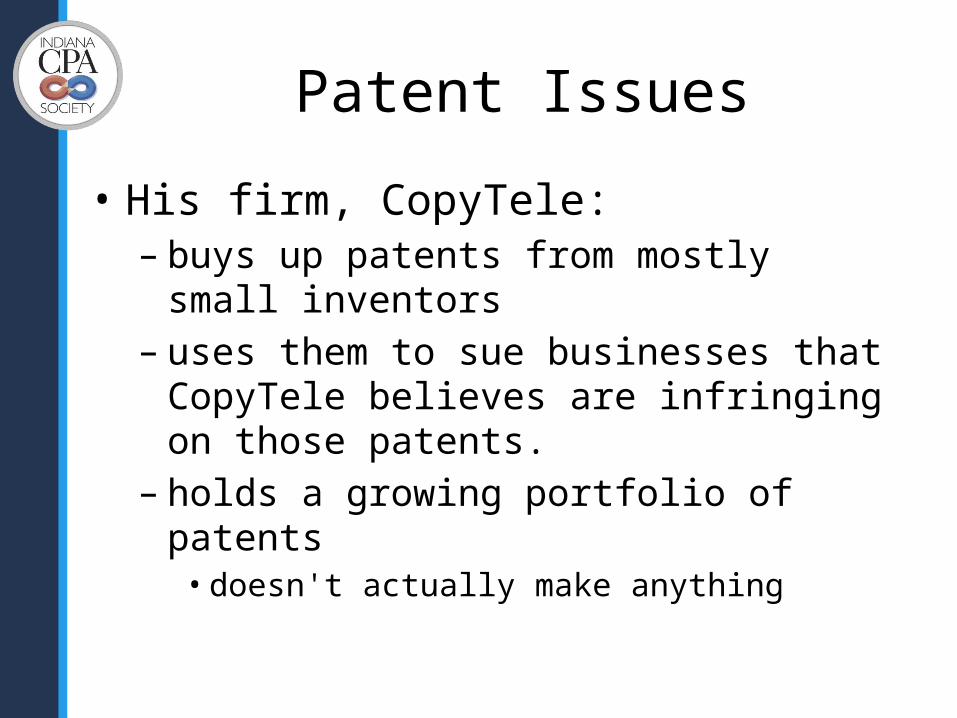

Patent Issues

• His firm, CopyTele:– buys up patents from mostly small inventors – uses them to sue businesses that CopyTele

believes are infringing on those patents. – holds a growing portfolio of patents• doesn't actually make anything

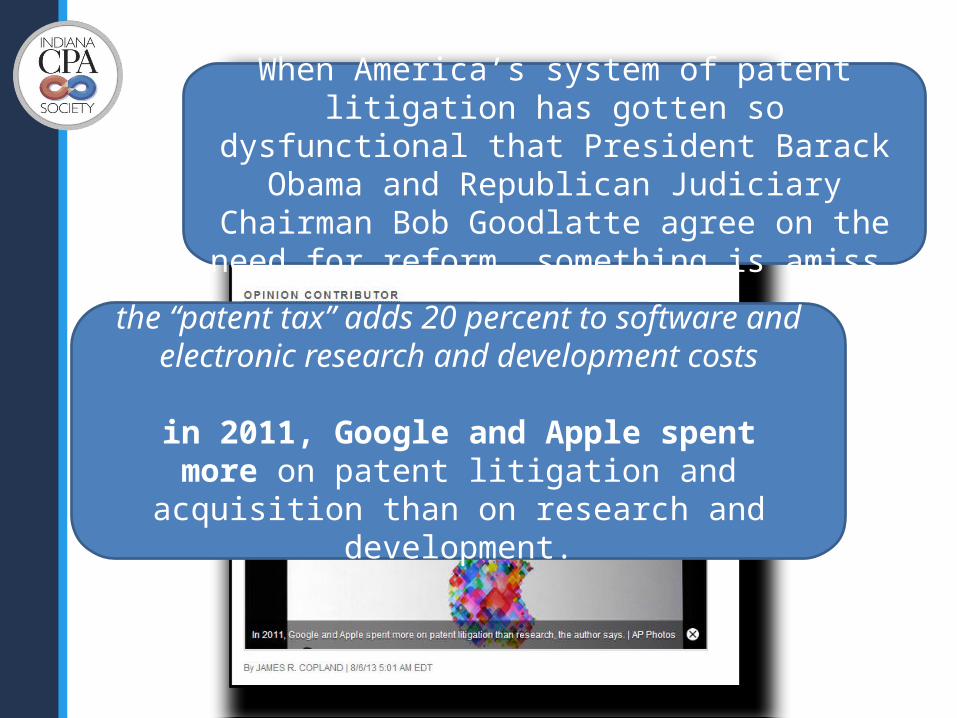

the “patent tax” adds 20 percent to software and electronic research and development costs

in 2011, Google and Apple spent more on patent litigation and acquisition than on research and

development.

When America’s system of patent litigation has gotten so dysfunctional that President Barack Obama and

Republican Judiciary Chairman Bob Goodlatte agree on the need for reform, something is amiss.

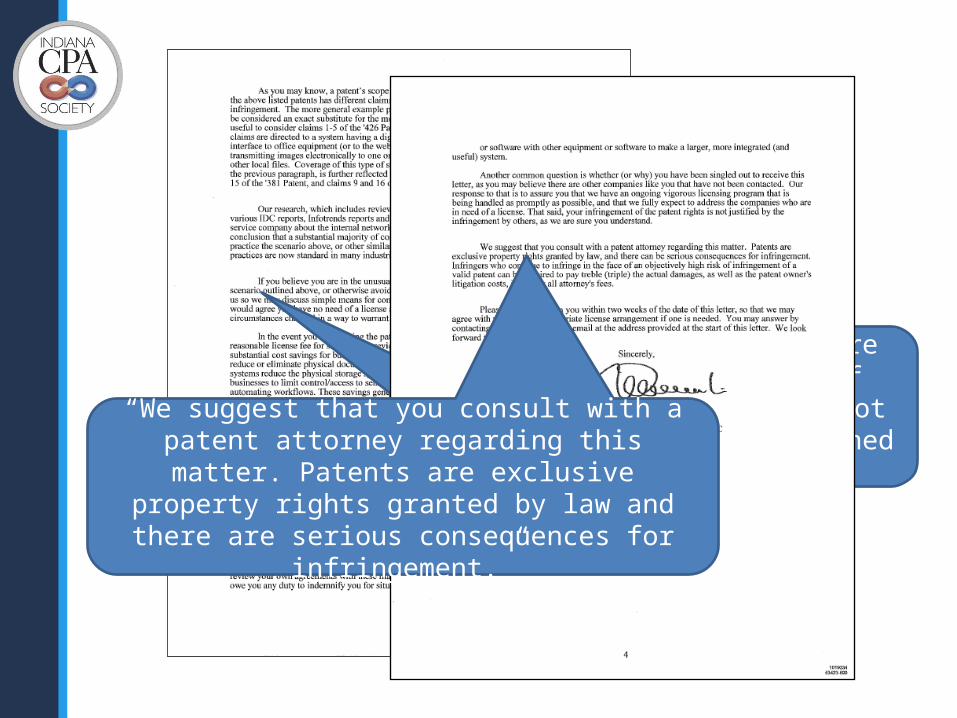

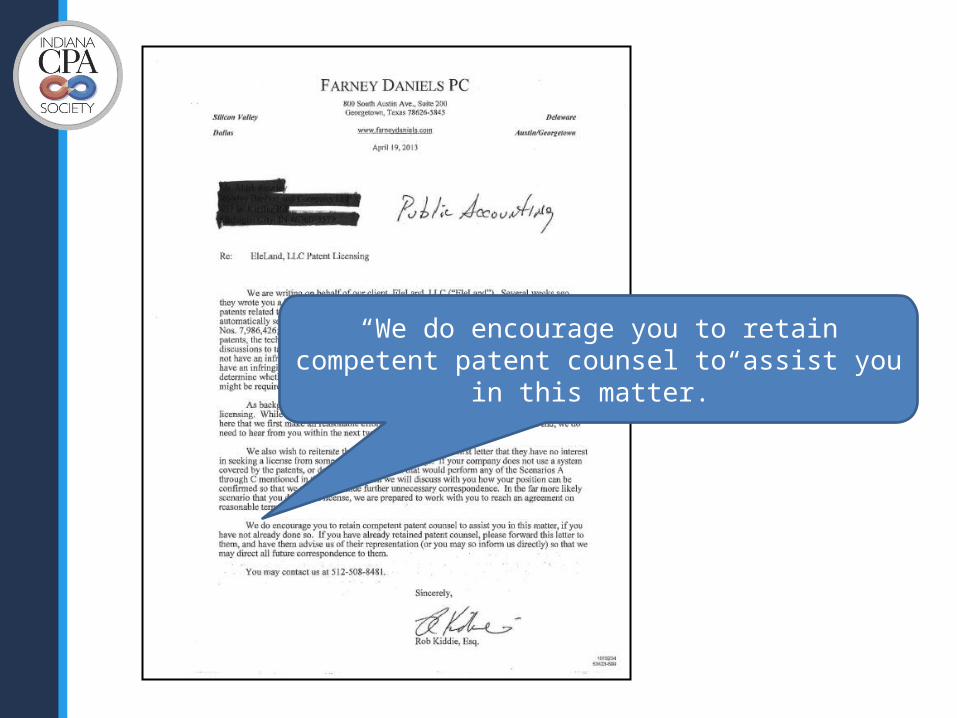

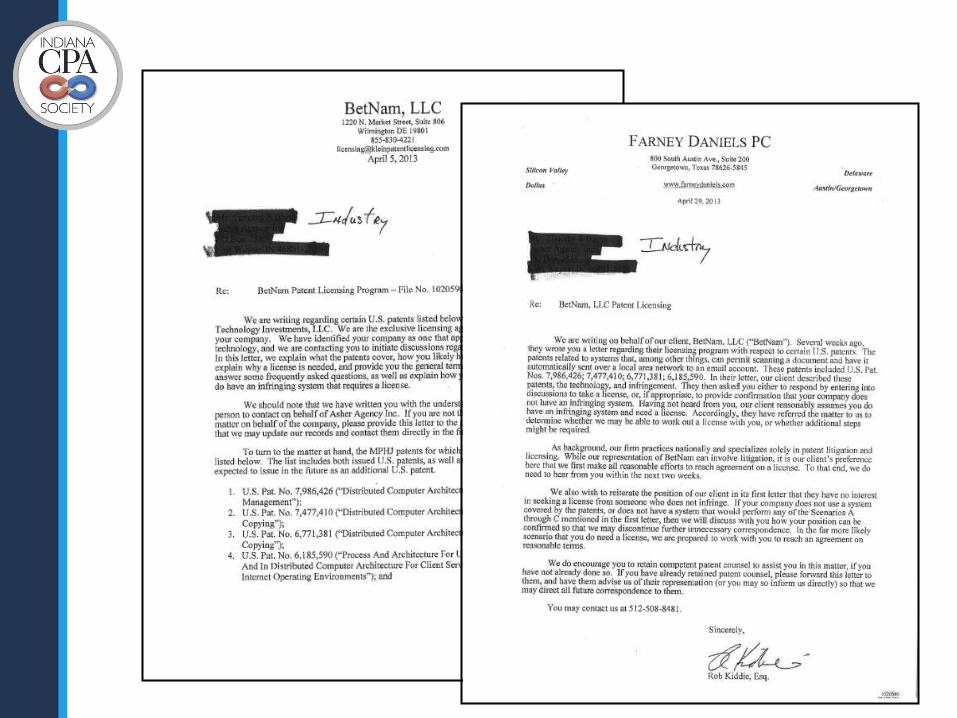

“we are contacting you to initiate discussions regarding your need for a license.”

“If you believe that you are in the unusual position of having a system that does not practice the scenario outlined above …”“We suggest that you consult with a patent attorney

regarding this matter. Patents are exclusive property rights granted by law and there are serious

consequences for infringement.”

“We do encourage you to retain competent patent counsel to assist you in this matter.”

Leahy-Smith America Invents Act (AIA)

• September 2011 (went into full effect in 2012)

• Key provisions of the AIA– fast-track option for patent processing– steps to reduce current patent backlog– increased ability of Americans to protect

intellectual property abroad. • Impact of aggressive litigation tactics by

PAEs and others not widely known during the seven years AIA under negotiation

The White House

• Task Force on High-Tech Patent Issues– June 4, 2013

• Protect innovators from frivolous litigation • Ensure the highest-quality patents – five executive actions – seven legislative recommendations designed to

Prepared by the President’s Council of Economic Advisers, the National Economic Council, and the Office of Science

& Technology Policy.

PAE Business Model

• Generally seen as combining characteristics such as the following:1. Do not “practice” their patents;

• they do not do research or develop any technology or products related to their patents

2. Do not help with “technology transfer”• the process of translating the patent language into a

usable product or process

3. Often wait until after industry participants have made irreversible investments before asserting their claims

PAE Business Model5. Acquire patents solely for the purpose of extracting

payments from alleged infringers; 6. Strategies for litigation take advantage of their non-practicing

status– makes them invulnerable to counter-claims of patent

infringement.

7. Acquire patents whose claim boundaries are unclear, and then (with little specific evidence of infringement) – ask many companies at once for moderate license fees, assuming

that some will settle instead of risking costly & uncertain trial.

8. May hide identity by creating numerous shell companies– require those who settle to sign non-disclosure agreements– difficult for defendants to form common defensive strategies

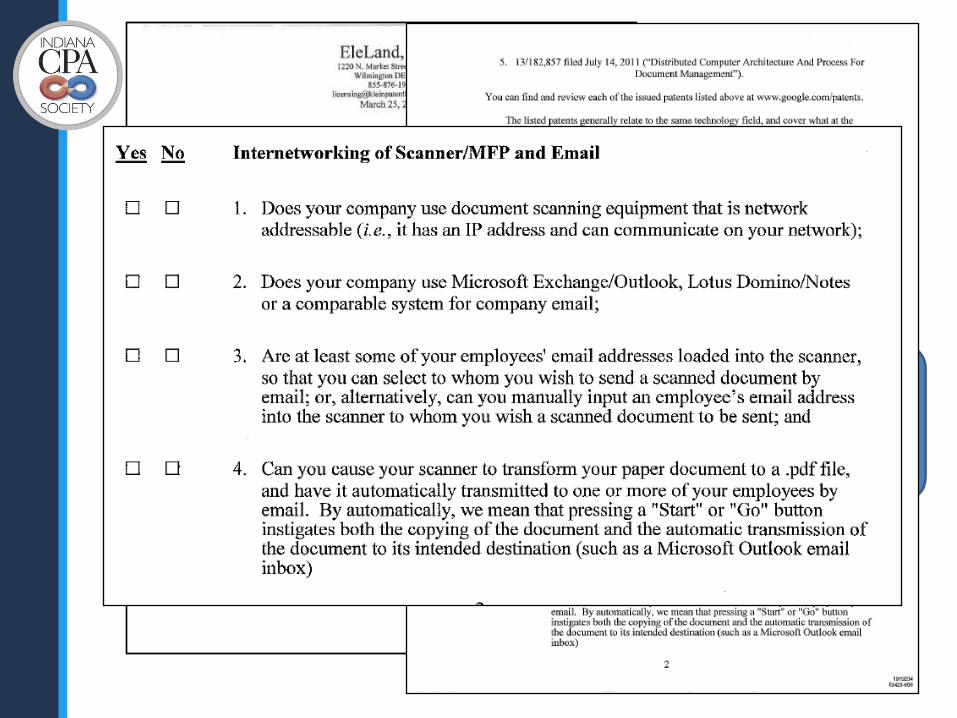

Small Company Example

• A PAE sent letters to hundreds of small businesses alleging infringements of patents if the businesses have document scanners integrated into their computer networks– demands “good faith payment” of $900-1,200 per

employee for a license– no specific evidence against the recipient– argues that general research “has led us to the conclusion

that an overwhelming majority of companies like yours utilize systems that are set up to practice at least one of the scenarios A through C” that are covered by the patents.

Small Company Example

• Vermont sued the PAE for unfair and deceptive practices (May 2013)– alleging that • the letters were targeted to businesses and non-

profits unlikely to be familiar with patent law• that they “shifted the entire burden of the pre-suit

investigation onto the small business that received the letters”, • despite repeated threats to sue if the payment is not

made, no such suits had been filed

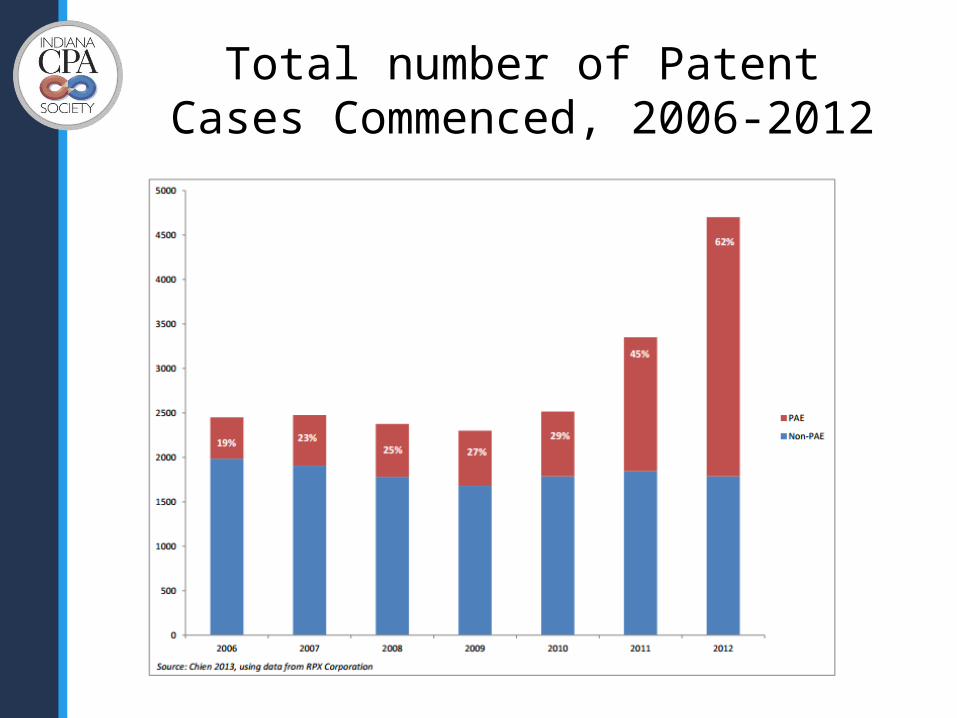

Total number of Patent Cases Commenced, 2006-2012

Costs

• Defendants & licensees paid PAE’s $29 billion in 2011 – 400% increase from 2005

• Harassing litigation tactics of some PAEs with substantial litigation costs – median of $650,000 for smaller cases– median of over $5 million per case where the

amount in controversy exceeds $25 million• Legal cost of defense exceeds settlement or

judgment amount in most PAE cases

The Voice of Indiana CPAs

PAC Facts

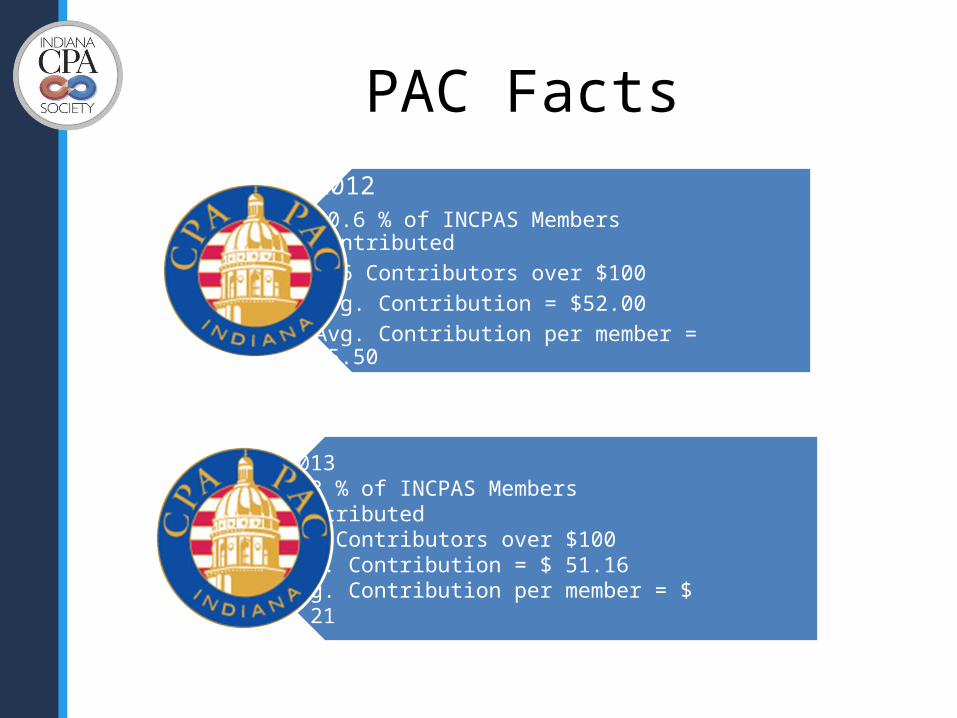

201210.6 % of INCPAS Members Contributed106 Contributors over $100Avg. Contribution = $52.00Avg. Contribution per member = $5.50

20136.3 % of INCPAS Members Contributed 77 Contributors over $100Avg. Contribution = $ 51.16Avg. Contribution per member = $ 3.21

12/31/05 12/31/07 12/31/09 12/31/10 12/31/11 12/31/12

Receipts ($) 18,608 21,477 27,712 34,810 29,512 40,868

Total # Contributors 399 425 574 756 675 788

New Contributors 242 160 15 226 125 179

Non-renewing contributors 118 153 30 105 121 98

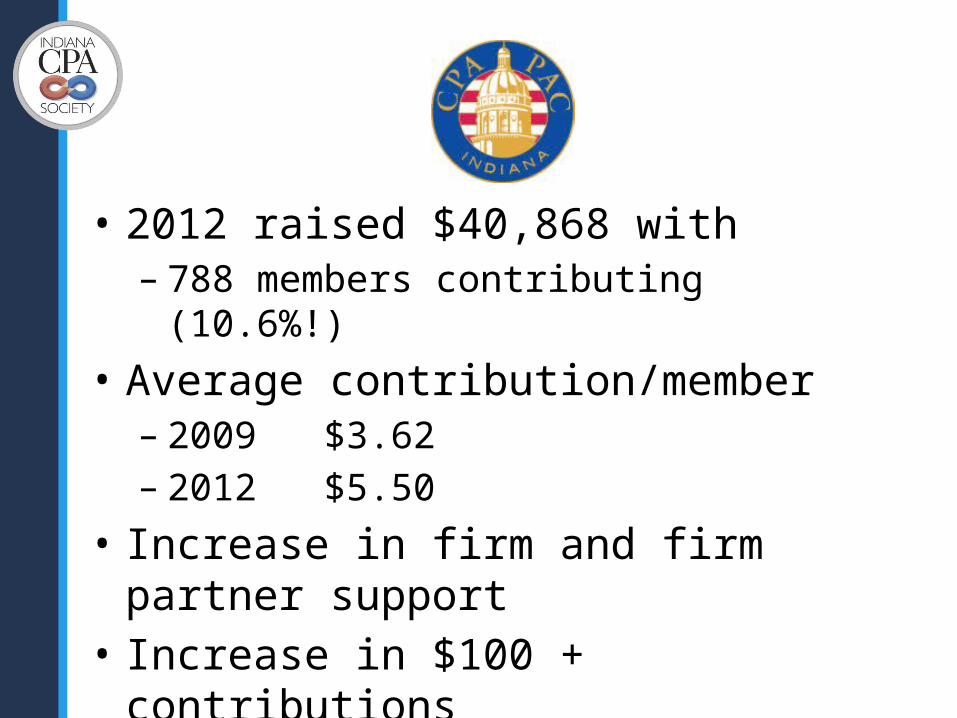

• 2012 raised $40,868 with – 788 members contributing (10.6%!)

• Average contribution/member– 2009 $3.62– 2012 $5.50

• Increase in firm and firm partner support• Increase in $100 + contributions

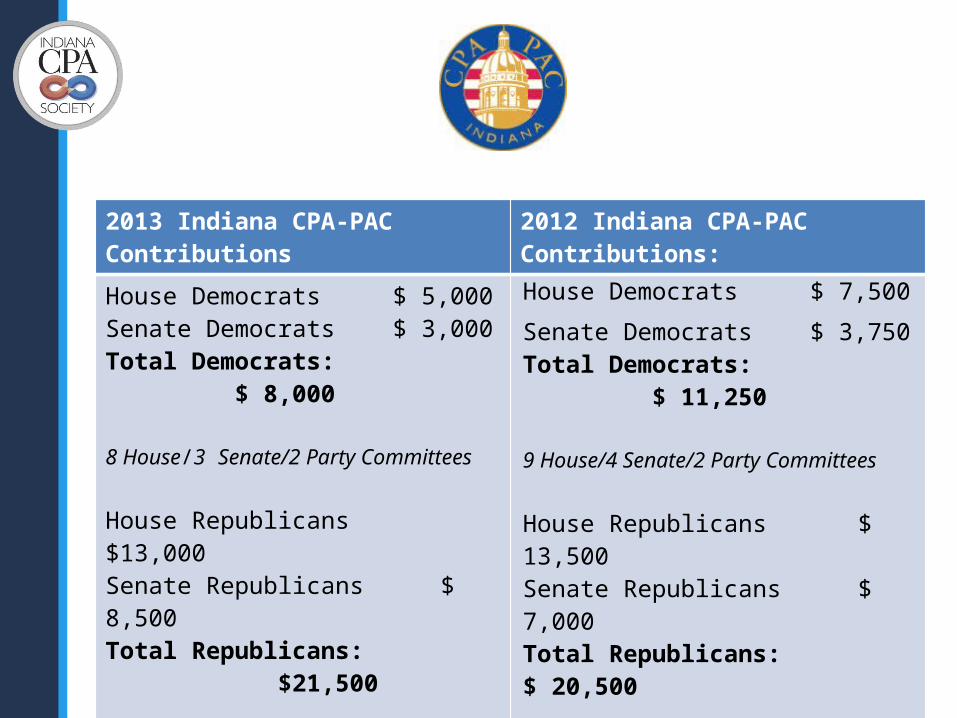

2013 Indiana CPA-PAC Contributions 2012 Indiana CPA-PAC Contributions:

House Democrats $ 5,000Senate Democrats $ 3,000Total Democrats: $ 8,000

8 House/3 Senate/2 Party Committees

House Republicans $13,000Senate Republicans $ 8,500Total Republicans: $21,500

20 House/9 Senate/2 Party Committees

Total Contributions $29,500

House Democrats $ 7,500Senate Democrats $ 3,750Total Democrats: $ 11,250

9 House/4 Senate/2 Party Committees

House Republicans $ 13,500Senate Republicans $ 7,000Total Republicans: $ 20,500

13 House /7 Senate/2 Party Committees

Total Contributions $ 32,750

Only PAC that represents YOU and

YOUR profession in Indiana!

Time for a break!

![“You can’t argue with a river, it is going to flow. You can dam it [or] deflect it, but you can’t argue with it.”— Dean Acheson So it is with Modigliani-](https://img.pdfslide.net/doc/110x75/56649e865503460f94b88c16/you-cant-argue-with-a-river-it-is-going-to-flow-you-can-dam-it-or.jpg)