Embed Size (px)

Citation preview

ZIONSOLUTIONSLLCAn EnargySD/utona Company

10 CFR 50.74

September 27, 2012 ZS-2012-0417

U.S. Nuclear Regulatory CommissionATTN: Document Control DeskWashington, DC 20555-0001

Zion Nuclear Power Station, Units 1 and 2Facility Operating License Nos. DPR-39 and DPR-48NRC Docket Nos. 50-295 and 50-304

Reference: NRC Letter, Hickman (NRC) to Christian (ZionSolutions, LLC), "Zion NuclearPower Station, Units 1 and 2 - 2012 Decommissioning Funding Status Report -

Request for Additional Information," provided August 13, 2012

Subject: ZionSolutions' Response to 2012 Decommissioning Funding Status ReportRequest for Information (RAIs/RFIs)

Dear Mr. Hickman,

This letter responds to your request of August 13, 2012 referenced above.

All information provided by ZionSolutions in response to the above referenced NRC requestscovers the time period from September 1, 2010 forward, which represents the period for whichZS has been responsible for the fiduciary duties. ZionSolutions does not possess the informationfor the period(s) prior to September 1, 2010 that is held by Exelon Generation Company, LLC(EGC).

This letter does not contain any regulatory commitments. Should you have any questions orrequire further information, please contact Mr. Patrick Thurman at (224) 789-4041.

Respectfully,

Patrick DalySenior VP & General Ma gerZionSolutions, LLC

cc: John Hickman, U.S. NRC Senior Project ManagerService List

101 Shiloh Boulevard, Zion - IL 60099(224) 789-4016 - Fax: (224) 789-4008 • www.zionsolutionscompany.com

ZionSolutions, LLCZS-2012-0417Page 2 of 14

ZionSolutions Draft Response to NRC RAI 2012 Decommissioning Funding Status Report

RAI#1: Decommissioning Cost

Provide the amount of decommissioning funds estimated to be required based on theformula from 10 CFR 50.75(b) and (c) for Zion Nuclear Power Station (ZNPS) Unit 1 and 2.

On March 26, 2012, ZS provided the following radiological decommissioning costsassociated with license termination for ZNPS:

Required Minimum at December 31, 2011 (A) $641,286,000

The required minimum funding assurance amount is based on the decommissioningscenario from the site-specific decommissioning cost estimate provided in Reference3. The cost estimate reflects actual experience to date, as well as, refinements madethrough the date of this filing.

Part 10 CFR 50.75(f)(1)The information in this report must include, at a minimum the amount ofdecommissioning funds estimated to be required under 10 CFR 50.75(b) and (c).

ZionSolutions Response

We understand the underlying purpose of 10 CFR 50.75(b) and (c) is to assure that operatingfacilities provide adequate decommissioning funding during the facility's operating life. Prior toZionSolutions' acquisition of the Zion Nuclear Power Station (ZNPS), its NDT and the 10 CFR50 facility licenses, EGC had placed the plant in SAFSTOR and was expending the NDT tosupport SAFSTOR and plan final decommissioning. Since then, active decommissioning byZionSolutions has further expended NDT funds for the past two years. Consequently, thefinancial assurance tests of 10 CFR 50.82 appear to provide a more appropriate basis forreporting on funding assurance for a permanently shutdown facility than 10 CFR 50.75.

Previous ZionSolutions financial estimates were submitted to the NRC in the License TransferApplication (LTA)' and Post-Shutdown Decommissioning Activities Report (PSDAR)2 thatestablished the initial decommissioning funding status, spent fuel management costs and site-specific estimated decommissioning cost at the inception of the ZionSolutions project. 10 CFR50.82 requires, in addition to the submittal of the PSDAR, that the licensee submit an annualreport3 to the NRC disclosing the facility's current condition including the remaining balance ofthe decommissioning funds, costs and available funds associated with fuel management, and asite-specific cost estimate needed to complete decommissioning. Previously submitted site-

'Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transfer and ConformingAdministrative License Amendments," dated January 25, 20082 ZionSolutions, LLC Letter, Daly to NRC, "Notification of Amended Post-Shutdown Decommissioning Activities

Report" (PSDAR) for Zion Nuclear Power Station, Units I and 2 in accordance with 10 CFR 50.82(a)(7)," datedMarch 18, 2008' ZionSolutions, LLC Letter, Daly to NRC, "Report on Status of Decommissioning Funding for ShutdownReactors," dated March 26, 2012

ZionSolutions, LLCZS-2012-0417Page 3 of 14

specific cost estimates more accurately reflect an estimate of the actual contracted costs for theproject in contrast to the 10 CFR 50.75 formula relative to funding assurance and regulatorycompliance for the ZNPS decommissioning project. Additional information in this regard isprovided below in the response to RAI #2.

RAI#2: Citation for Site-Specific Study

Provide the most recent site specific cost estimate for ZNPS, unless it was previouslysubmitted to NRC. If the cost estimate was previously submitted to NRC, then provide areference to its submittal. The site specific cost estimate should include a summaryschedule of annual expenses, projected earnings, and end-of-year fund balances, expressedin 2011 dollars.

Pursuant to 10 CFR 50.75(b), the cost estimate shall be in an amount that may be more, butnot less, than the amount estimated to be required under 10 CFR 50.75(b) and (c).

On March 26, 2012, ZS indicated the following:

The required minimum funding assurance amount is based on the decommissioningscenario from the site-specific decommissioning cost estimate provide in Reference3. The cost estimate reflects actual experience to date, as well as, refinements madethrough the date of this filing.

Per 10 CFR 50.75(f)(1)The information in this report must include, at a minimum the amount ofdecommissioning funds estimated to be required under 10 CFR 50.75(b) and (c).

ZionSolutions Response

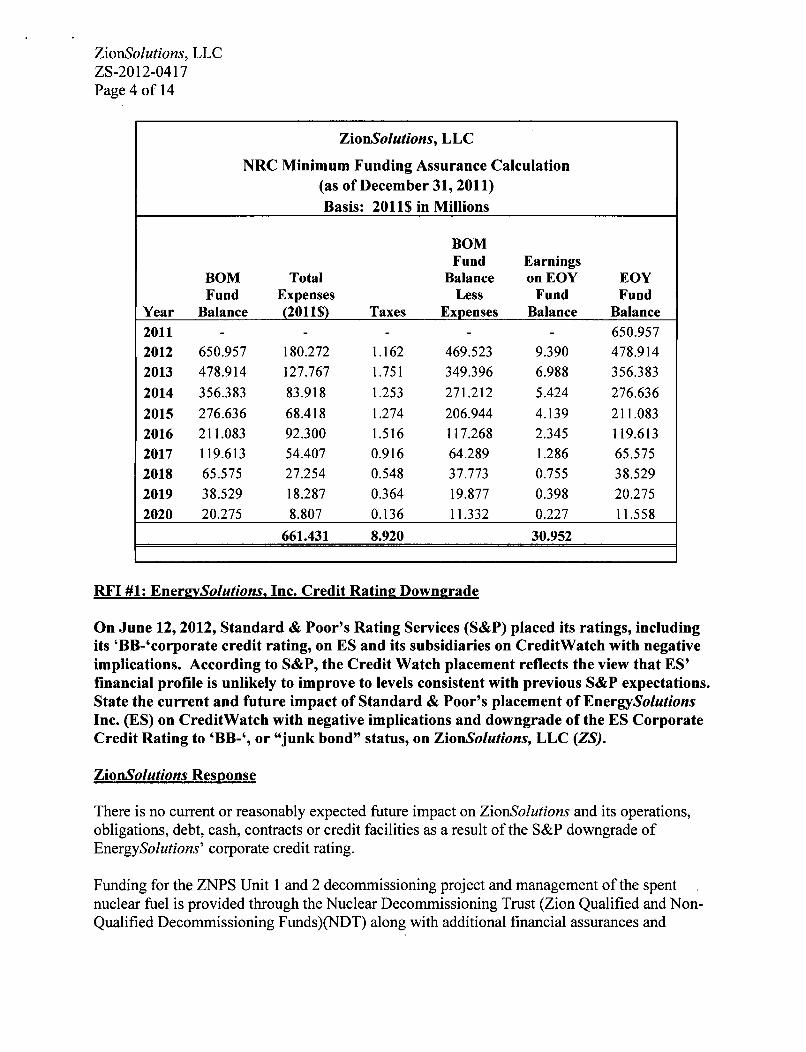

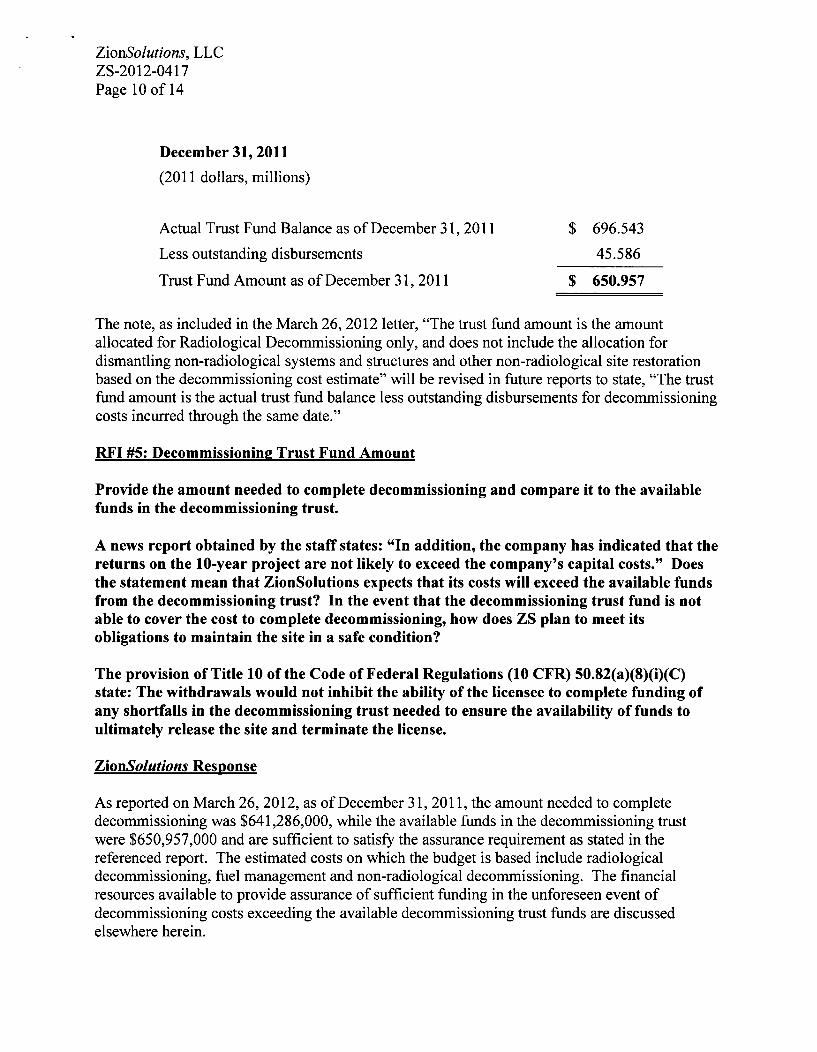

As indicated in RAI # 1 and 2 of this request and ZionSolutions' March 26, 2012 letter to theNRC, the required minimum funding assurance is based on the decommissioning scenario fromthe site-specific decommissioning cost estimate provided to the NRC in an earlier filing.4 Thecost estimate reflects actual experience to date, as well as, refinements made through the March26, 2012 filing. The table below represents a summary schedule of annual expenses based uponthe most recent site specific cost estimate, expressed in 2011 dollars, projected earnings, andend-of-year balances.

4 ZionSolutions, LLC Letter, Daly to NRC, "Notification of Amended Post-Shutdown Decommissioning ActivitiesReport (PSDAR) for Zion Nuclear Power Station, Unit I and 2," dated March 18, 2008.

ZionSolutions, LLCZS-2012-0417Page 4 of 14

ZionSolutions, LLC

NRC Minimum Funding Assurance Calculation(as of December 31, 2011)

Basis: 2011$ in Millions

BOMFund Earnings

BOM Total Balance on EOY EOYFund Expenses Less Fund Fund

Year Balance (2011$) Taxes Expenses Balance Balance2011 - - - - - 650.9572012 650.957 180.272 1.162 469.523 9.390 478.9142013 478.914 127.767 1.751 349.396 6.988 356.3832014 356.383 83.918 1.253 271.212 5.424 276.636

2015 276.636 68.418 1.274 206.944 4.139 211.0832016 211.083 92.300 1.516 117.268 2.345 119.6132017 119.613 54.407 0.916 64.289 1.286 65.5752018 65.575 27.254 0.548 37.773 0.755 38.5292019 38.529 18.287 0.364 19.877 0.398 20.2752020 20.275 8.807 0.136 11.332 0.227 11.558

661.431 8.920 30.952

RFI #1: EnergySolutions, Inc. Credit Rating Downgrade

On June 12, 2012, Standard & Poor's Rating Services (S&P) placed its ratings, includingits 'BB-'corporate credit rating, on ES and its subsidiaries on CreditWatch with negativeimplications. According to S&P, the Credit Watch placement reflects the view that ES'financial profile is unlikely to improve to levels consistent with previous S&P expectations.State the current and future impact of Standard & Poor's placement of EnergySolutionsInc. (ES) on CreditWatch with negative implications and downgrade of the ES CorporateCredit Rating to 'BB-', or "junk bond" status, on ZionSolutions, LLC (ZS).

ZionSolutions Response

There is no current or reasonably expected future impact on ZionSolutions and its operations,obligations, debt, cash, contracts or credit facilities as a result of the S&P downgrade ofEnergySolutions' corporate credit rating.

Funding for the ZNPS Unit 1 and 2 decommissioning project and management of the spentnuclear fuel is provided through the Nuclear Decommissioning Trust (Zion Qualified and Non-Qualified Decommissioning Funds)(NDT) along with additional financial assurances and

ZionSolutions, LLCZS-2012-0417Page 5 of 14

protections5 .6 To ensure NDT funds are used solely for their intended purpose ofdecommissioning ZNPS Unit 1 and 2, ZionSolutions is required to submit a DisbursementRequest to the NDT Trustee prior to the disbursement of funds. A requirement for theDisbursement Request is that an Authorized Officer of ZionSolutions must include a certificationand sworn statement that:

* (a) the project work, materials and services for which the disbursement is requested havebeen performed or delivered in connection with the decommissioning and other workrequired to achieve End State Condition and

* (b) ZionSolutions has comllied with the project budget and schedule as required underthe Asset Sale Agreement.

All interested parties are explicitly and legally bound to comply with the requirements associatedwith disbursements from the NDT as part of their fiduciary responsibilities.

RFI #2: EnerpsSolutions. Inc. Credit Rating Downgrade

State the current and future impact of Standard & Poor's placement of EnergySolutionsInc. (ES) on CreditWatch with negative implications and downgrade of the ES CorporateCredit Rating to '1B-', or "junk bond" status, on the following:

o The Irrevocable Letter of Credit (LOC) in the amount of $200 million established byEnergySolutions, LLC for the decommissioning of ZNPS, Units 1 and 2;

ZionSolutions Response

There is no current or reasonably expected future impact on the ZNPS Unit I and 2decommissioning project as a result of S&P's placement of EnergySolutions on CreditWatch orthe downgrade of EnergySolutions' Corporate Credit Rating.

The Irrevocable Letter of Credit (LOC) 8 is a fully cash collateralized instrument, secured by arestricted fund account, and is independent of EnergySolutions' performance or unilateralcontrol. The primary source of funding for the ZNPS Unit 1 and 2 decommissioning project isthe NDT. The LOC and the Asset Sale Agreement explicitly state that all amounts drawn fromthe LOC are to be deposited directly into the Backup NDT which is segregated from the ZionQualified and Non-Qualified Decommissioning Funds, and may only be used to the extent thedecommissioning costs cannot be reimbursed by the Qualified and Non-Qualified

5 Other financial assurances and protection include the Irrevocable Letter of Credit, Performance Guaranty and theIrrevocable Easement for Disposal Capacity at Clive, Utah.6 Exelon Generation Corporation (ECG) Letter RS-08-009, "Application for License Transfer and Conforming

Administrative License Amendments," dated January 25, 2008 (p. 10-11)7 Enclosure I to the Exelon Generation Corporation (ECG) Letter RS-08-009, "Application for License Transfer andConforming Administrative License Amendments," dated January 25, 2008 (ASA Exhibit L)8 See Generally Enclosure I to the Exelon Generation Corporation (EGC) Letter RS-08-009, "Application forLicense Transfer and Conforming Administrative License Amendments," dated January 25, 2008 (ASA Exhibit F,Credit Support Agreement)

ZionSolutions, LLCZS-2012-0417Page 6 of 14

Decommissioning Funds (collectively, the NDT).9 The LOC is guaranteed by JP Morgan andcannot be revoked except by the parties' prior agreement or with the consent of all interestedparties and notice to the Directors of FSME and NRR. In addition, the amount of the LOC willnot be reduced without prior notification to the NRC and agreement by the parties. 10

If EnergySolutions exhausts its resources and its ability to complete the D&D activities and amaterial default occurs (as defined within the Credit Support Agreement), EGC may exercise itsright to take possession of ZionSolutions. At that point, through their ownership ofZionSolutions, EGC is entitled to cause the funds associated with the LOC to be deposited in thebackup trust."1

The ability of EnergySolutions to obtain renewals and continue to pay the fees for the$200 million LOC; and

ZionSolutions Response

There are no current or reasonably expected future impacts on EnergySolutions' ability to obtainrenewal and continue to pay the LOC fees as a result of S&P's placement of EnergySolutions onCreditWatch or the downgrade of EnergySolutions' corporate credit rating.

As indicated above, the LOC is a fully collateralized instrument, secured by funds in a restrictedfunds account, with the purpose of providing financial assurance that the project will continue tobe funded in the event the NDT is exhausted. We understand the concern behind this RFI to be arisk that the LOC assurance may expire before the decommissioning is complete. This concernis addressed by the fact that, if ZionSolutions fails to confirm replacement or renewal of the LOCbefore it expires, such failure would itself allow EGC to cause the LOC proceeds to be depositedin the backup trust before the LOC expires. Therefore EnergySolutions cannot cause the LOCproceeds to become unavailable by failing to renew or replace the LOC.

* The Irrevocable Easement for Disposal Capacity of 7.5 million cubic feet at the Clive,Utah facility, established by EnergySolutions, LLC for the decommissioning of ZNPS,Units 1 and 2.

ZionSolutions Response

There is no current or reasonably expected future impact on the Irrevocable Easement forDisposal Capacity (Easement) at the Clive, Utah facility as a result of S&P's placement ofEnergySolutions on CreditWatch or the downgrade of EnergySolutions' corporate credit rating.

9Enclosure 1 to the Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transfer andConforming Administrative License Amendments," dated January 25, 2008 (ASA Exhibit F, Credit SupportAgreement (Section 4.2); p. 11)10 Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transfer and ConformingAdministrative License Amendments," dated January 25, 2008 (p. 11)"•Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transfer and ConformingAdministrative License Amendments," dated January 25, 2008 (p. 11); Enclosure I to the Exelon GenerationCorporation (EGC) Letter RS-08-009, "Application for License Transfer and Conforming Administrative LicenseAmendments," dated January 25, 2008 (ASA Exhibit F, Credit Support Agreement (Section 3.1)).

ZionSolutions, LLCZS-2012-0417Page 7 of 14

The Easement, as established in Exhibit G of the Asset Sale Agreement, provides ZionSolutionsrights to dispose of and deposit up to 7,500,000 cubic feet of Permitted Material in, on or over aportion of the Clive Disposal Facility. Permitted Materials include "all Class A Low LevelWaste situated at the Zion Station Site.. .or created during the course of Decommissioning theZion Station Site."'' 2 The Easement has been recorded against and attaches to the Clive Facilityitself (covenant runs with the land) thus providing ZionSolutions will access to the facilityregardless of the facility's ownership. 13 Section 5 of the Easement provides explicitly that "[t]heEasement continues until all of the Permitted Materials have been disposed of either at the CliveFacility or some other properly permitted Low Level Waste disposal facility."',4 As set forth inthe License Transfer documents, the Easement cannot be terminated without prior writtennotification to the Director of the FSME and the Director of NRR.

The Irrevocable Easement for Disposal Capacity is set forth in its entirety in Exhibit G of theZion Nuclear Power Station Unit 1 and 2 Asset Sale Agreement, dated December 11, 2007.15

The NRC staff is concerned that a negative credit rating for ES could adversely affect ES'ability to fulfill its financial obligations related to the decommissioning of ZNPS. Amongthese concerns is a S&P statement, found in a Reuters press release dated June 12, 2012,that, "Although the former management [of ES] expressed optimism that a plan of actionregarding the release of a $200 million cash-collateralized letter of credit related to thecompany's Zion decommissioning project was likely to be realized in 2012, it now appearsthat such resolution could be delayed." The additional financial assurance arrangements,and the financial viability of ES, were directly related to the approval of the transfer oflicenses for ZNPS, Units 1 and 2.

ZionSolutions Response

There was never a plan to release [emphasis added] the current LOC, but a search for areplacement instrument with equivalent assurances at a lower cost was being considered as aprudent action and always being subject to necessary approval of the parties. The currentfinancial assurance instruments were put in place in August of 2010, and these or otherequivalent instruments acceptable to all involved parties will continue through the end of theproject. In addition, ZionSolutions still intends to seek ways to reduce the cost associated withthe financial assurance instruments. Any changes to the current financial assurancearrangements will include their acceptability to the interested parties.

'2Enclosure 1 to the Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transfer andConforming Administrative License Amendments," dated January 25, 2008 (ASA Exhibit G, Irrevocable Easementfor Disposal Capacity (Section 1.d))'3 The Irrevocable Easement for Disposal Capacity was recorded in the Tooele County Recorder's Office, State ofUtah.14 Enclosure I to the Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transferand Conforming Administrative License Amendments," dated January 25, 2008 (ASA Exhibit G, IrrevocableEasement for Disposal Capacity (Section 4))15 Enclosure I to the Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transferand Conforming Administrative License Amendments," dated January 25, 2008 (ASA Exhibit G, IrrevocableEasement for Disposal Capacity)

ZionSolutions, LLCZS-2012-0417Page 8 of 14

RFI #3: EnergySolutions, Inc. Credit Rating Downgrade

On January 25, 2008, Exelon Generation Company, LLC (EGC) and ZS submitted anapplication requesting that the NRC consent to the transfer of Exelon GenerationCompany, (EGC) LLC's Facility Operating Licenses for ZNPS, Units 1 and 2(ML080310521). The application stated that EnergySolutions and its parent, ES, eachprovided a Performance Guaranty to EGC of the payment and performance, when due, ofall obligations of ZS.

State the impact of Standard & Poor's placement of EnergySolutions Inc. (ES) onCreditWatch with negative implications and downgrade of the ES Corporate Credit Ratingto 'BB-', or "junk bond" status, on the Performance Guaranty provided to EGC for allobligation of ZS.

ZionSolutions Response

There is no current or reasonably expected future impact on the Performance Guaranty for ZNPSdecommissioning project.

The NDT represents the primary funding instrument for the ZNPS Unit 1 and 2decommissioning project, and is expected to cover all costs over the life of the project. Thecontract between EnergySolutions and EGC is uniquely structured to mitigate concerns regardingthe adequacy of the NDT funding and the financial capacities of EnergySolutions andZionSolutions by providing multiple levels of financial assurances and protections. In the eventthe NDT funds prove insufficient, EnergySolutions has guaranteed EGC the full and promptpayment and performance, when due, of all obligations agreed to be performed by ZionSolutionsin connection with the ZNPS Unit 1 and 2 decommissioning project. Under this PerformanceGuaranty, as set forth in the License Transfer Application, EnergySolutions is required toexhaust all company resources to ensure the necessary funds exist for completion of thedecommissioning project. In addition, the License Transfer Application specifically states that"EnergySolutions has pledged its equity interest in ZionSolutions as collateral for its obligationsunder the Performance Guaranty. If any event constituting a specified default under the AssetSale Agreement (ASA) or other transaction agreement occurs, EGC will have the right to takepossession of and exercise voting control over ZionSolutions subject to NRC's prior approvalpursuant to 10 CFR 50.80.''17

If circumstances occur where the NDT funds are depleted and EnergySolutions' assets cannotfund the remainder, the Backup NDT consisting of the $200M Irrevocable Letter of Credit andDisposal Easement is in place to ensure the work will be completed and waste disposed of safely.

16 Enclosure 7 to the Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transfer

and Conforming Administrative License Amendments," dated January 25, 2008. (Performance Guaranty (Section2))17 Exelon Generation Corporation (EGC) Letter RS-08-009, "Application for License Transfer and ConformingAdministrative License Amendments," dated January 25, 2008 (See page 11)

ZionSolutions, LLCZS-2012-0417Page 9 of 14

It is important to note that the NDT is presently stronger financially then when the licensetransfer occurred. The NDT is producing higher returns than originally estimated while beingfunded by more stable investment instruments; the costs and risks for the project are now largelyknown and accounted for with a closely managed budget and schedule, and the financialassurance instruments are and will remain secure. The increased budget certainty, the strengthand stability of the NDT, and confidence provided by the availability of the financial assuranceinstruments reduce the financial risks associated with the performance guaranty and the projectas a whole are minimized.

Further, the EnergySolutions financial conditions are consistent with the conditions prior to theS&P actions with respect to liquidity, availability of long term credit arrangements and debt.There is no substantial change in EnergySolutions' ability to meet its Performance Guaranty asprovided to EGC.

The Performance Guaranty offered by EnergySolutions to EGC is set forth in Enclosure 7 to theApplication for License Transfer and Conforming Administrative License Amendments, datedJanuary 25, 2008.18

RFI #4: Decommissioning Trust Fund Amount

Provide the total amount of funds accumulated in the decommissioning trust fund forZNPS, Unit 1 and 2, including all the funds allocated for non-NRC dedicated activities.

On March 26, 2012, ZS reported the following in relation to the Decommissioning TrustFund (DTF) balance for ZNPS, Unit 1 and 2:

"The trust fund amount is the amount allocated for Radiological Decommissioningonly, and does not include the allocation for dismantling nonradiological systemsand structures and other non-radiological site restoration based on thedecommissioning cost estimate."

The provisions of 10 CFR 50.75(f)(1) and (2) require the licensee to report the amount offunds accumulated to the end of calendar year preceding the report.

ZionSolutions Response

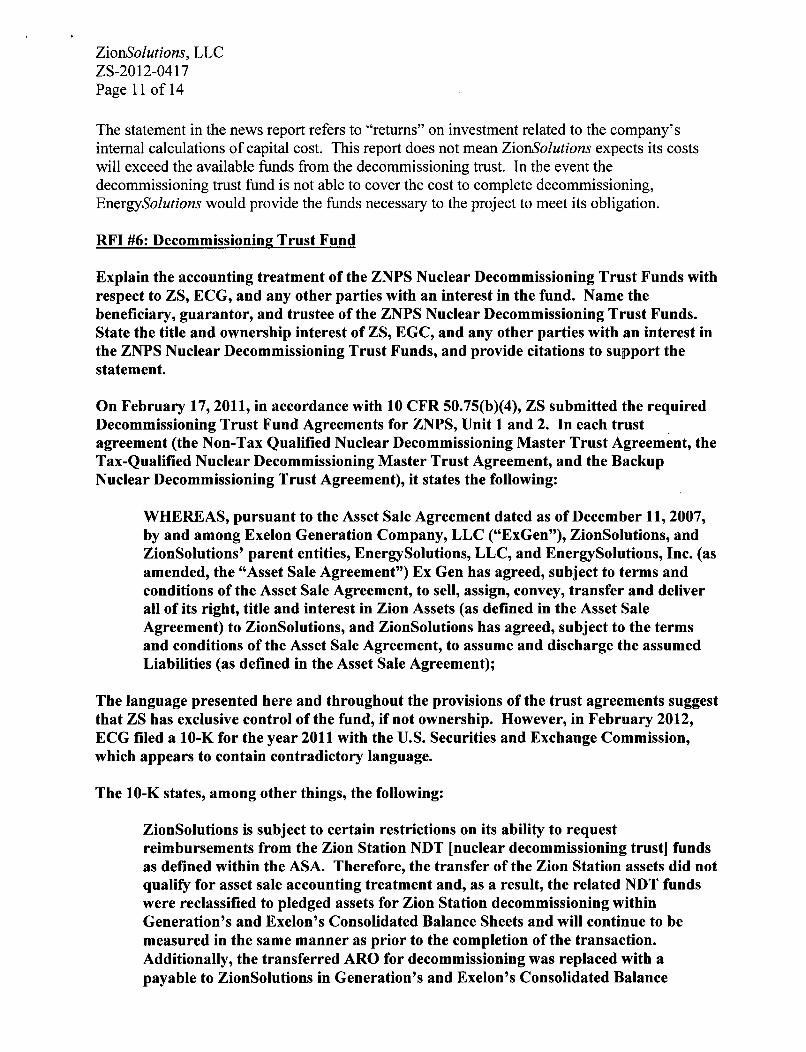

As reported on March 26, 2012, the total amount of funds accumulated in the decommissioningtrust fund, as of December 31, 2011, is $650,957,000. To clarify, the trust fund amount is theactual trust fund balance less outstanding disbursements for decommissioning costs incurredthrough the same date.

18 Enclosure 7 to the Exelon Generation Corporation (ECG) Letter RS-08-009, "Application for License Transfer

and Conforming Administrative License Amendments," dated January 25, 2008. (Performance Guaranty)

ZionSolutions, LLCZS-2012-0417Page 10 of 14

December 31, 2011

(2011 dollars, millions)

Actual Trust Fund Balance as of December 31, 2011 $ 696.543

Less outstanding disbursements 45.586

Trust Fund Amount as of December 31, 2011 $ 650.957

The note, as included in the March 26, 2012 letter, "The trust fund amount is the amountallocated for Radiological Decommissioning only, and does not include the allocation fordismantling non-radiological systems and structures and other non-radiological site restorationbased on the decommissioning cost estimate" will be revised in future reports to state, "The trustfund amount is the actual trust fund balance less outstanding disbursements for decommissioningcosts incurred through the same date."

RFI #5: Decommissioning Trust Fund Amount

Provide the amount needed to complete decommissioning and compare it to the availablefunds in the decommissioning trust.

A news report obtained by the staff states: "In addition, the company has indicated that thereturns on the 10-year project are not likely to exceed the company's capital costs." Doesthe statement mean that ZionSolutions expects that its costs will exceed the available fundsfrom the decommissioning trust? In the event that the decommissioning trust fund is notable to cover the cost to complete decommissioning, how does ZS plan to meet itsobligations to maintain the site in a safe condition?

The provision of Title 10 of the Code of Federal Regulations (10 CFR) 50.82(a)(8)(i)(C)state: The withdrawals would not inhibit the ability of the licensee to complete funding ofany shortfalls in the decommissioning trust needed to ensure the availability of funds toultimately release the site and terminate the license.

ZionSolutions Response

As reported on March 26, 2012, as of December 31, 2011, the amount needed to completedecommissioning was $641,286,000, while the available funds in the decommissioning trustwere $650,957,000 and are sufficient to satisfy the assurance requirement as stated in thereferenced report. The estimated costs on which the budget is based include radiologicaldecommissioning, fuel management and non-radiological decommissioning. The financialresources available to provide assurance of sufficient funding in the unforeseen event ofdecommissioning costs exceeding the available decommissioning trust funds are discussedelsewhere herein.

ZionSolutions, LLCZS-2012-0417Page 11 of 14

The statement in the news report refers to "returns" on investment related to the company'sinternal calculations of capital cost. This report does not mean ZionSolutions expects its costswill exceed the available funds from the decommissioning trust. In the event thedecommissioning trust fund is not able to cover the cost to complete decommissioning,EnergySolutions would provide the funds necessary to the project to meet its obligation.

RFI #6: Decommissioning Trust Fund

Explain the accounting treatment of the ZNPS Nuclear Decommissioning Trust Funds withrespect to ZS, ECG, and any other parties with an interest in the fund. Name thebeneficiary, guarantor, and trustee of the ZNPS Nuclear Decommissioning Trust Funds.State the title and ownership interest of ZS, EGC, and any other parties with an interest inthe ZNPS Nuclear Decommissioning Trust Funds, and provide citations to support thestatement.

On February 17, 2011, in accordance with 10 CFR 50.75(b)(4), ZS submitted the requiredDecommissioning Trust Fund Agreements for ZNPS, Unit I and 2. In each trustagreement (the Non-Tax Qualified Nuclear Decommissioning Master Trust Agreement, theTax-Qualified Nuclear Decommissioning Master Trust Agreement, and the BackupNuclear Decommissioning Trust Agreement), it states the following:

WHEREAS, pursuant to the Asset Sale Agreement dated as of December 11, 2007,by and among Exelon Generation Company, LLC ("ExGen"), ZionSolutions, andZionSolutions' parent entities, EnergySolutions, LLC, and EnergySolutions, Inc. (asamended, the "Asset Sale Agreement") Ex Gen has agreed, subject to terms andconditions of the Asset Sale Agreement, to sell, assign, convey, transfer and deliverall of its right, title and interest in Zion Assets (as defined in the Asset SaleAgreement) to ZionSolutions, and ZionSolutions has agreed, subject to the termsand conditions of the Asset Sale Agreement, to assume and discharge the assumedLiabilities (as defined in the Asset Sale Agreement);

The language presented here and throughout the provisions of the trust agreements suggestthat ZS has exclusive control of the fund, if not ownership. However, in February 2012,ECG filed a 10-K for the year 2011 with the U.S. Securities and Exchange Commission,which appears to contain contradictory language.

The 10-K states, among other things, the following:

ZionSolutions is subject to certain restrictions on its ability to requestreimbursements from the Zion Station NDT [nuclear decommissioning trust] fundsas defined within the ASA. Therefore, the transfer of the Zion Station assets did notqualify for asset sale accounting treatment and, as a result, the related NDT fundswere reclassified to pledged assets for Zion Station decommissioning withinGeneration's and Exelon's Consolidated Balance Sheets and will continue to bemeasured in the same manner as prior to the completion of the transaction.Additionally, the transferred ARO for decommissioning was replaced with apayable to ZionSolutions in Generation's and Exelon's Consolidated Balance

ZionSolutions, LLCZS-2012-0417Page 12 of 14

Sheets. Changes in the value of the Zion Station NDT assets, net of applicable taxes,will be recorded as a change in the payable to ZionSolutions. At no point will thepayable to ZionSolutions exceed the project budget of the costs remaining todecommission Zion Station. Any Zion Station NDT funds remaining after thecompletion of all decommissioning activities will be returned to ComEd customers.

The language suggests that Exelon retains some amount of title and ownership interest inthe decommissioning trust fund.

Per 10 CFR 50.75(a)This section establishes requirements for indicating to NRC how a licensee willprovide reasonable assurance that funds will be available for the decommissioningprocess. For power reactor licensees, reasonable assurance consists of a series ofsteps as provided in paragraphs (b), (c), (e), and (f) of this section.

ZionSolutions Response

ZionSolutions currently possesses the same level of access, ownership and control in thedecommissioning trust fund that EGC possessed, as set forth in each trust agreement (noted inRFI #6). The accounting treatments of the ZNPS Nuclear Decommissioning Trust Funds(NDTF), related liabilities, cost and revenue, are prescribed under the Generally AcceptedAccounting Principles (GAAP). On the date of the closing of the Asset Sale Agreement, thetrust fund investments previously held by Exelon for the purpose of decommissioning the ZionStation were transferred from Exelon's Tax- Qualified Decommissioning Trust to theZionSolutions Tax-Qualified Trust.

The language contained in EGC's 2011 10-K report, as noted in RFI #6, is required under theaccounting rules governing the sale or transfer of an asset. Accounting Standards Codification(ASC) 860-10 provides requirements for reporting, the transfer of legal title or ownership of anasset and whether the asset has been sold or transferred. ASC 860-10 requires, in part, asfollows:

Accounting for transfers in which the transferor has no continuing involvement with thetransferred financial assets or with the transferee is treated as a sale and is predicated onthe notion of surrender of control. However, transfers of financial assets often occur inwhich the transferor has some continuing involvement either with the assets transferredor with the transferee, and the accounting for these transfers can be complex.

ASC 860-10 requires companies to consider any continuing involvement and free or unrestricteduse of the assets in determining if a sale has occurred. While ZionSolutions has the same access,ownership and control in the decommissioning trust fund that EGC possessed, restrictions areincluded on the payments from the decommissioning trust fund to ensure the decommissioningtrust fund assets are used only for decommissioning activities. In addition, EGC maintains acontinuing involvement in the project through financial assurance instruments and theirmonitoring of decommissioning activities ($200 million letter of credit, establishment of projecttimelines, regular reporting of trust fund sufficiency and progress of the project, etc). Because ofthese restrictions on the use of the decommissioning trust fund assets and the continuing

ZionSolutions, LLCZS-2012-0417Page 13 of 14

involvement of EGC, the transfer of ownership of the NDT is not considered a sale under ASC860-10. This determination does not affect ZionSolutions' legal ownership, obligations orresponsibilities in the NDT, as provided in the ASA or trust agreements. However, thisdetermination does affect how EGC and ZionSolutions are required to account for and describethis transaction in their financial statements.

Additionally, there is a second set of accounting rules (ASC 810-10) that requires adetermination be made as to the primary beneficiary of a Variable Interest Entity (VIE), asdistinguished from the stated beneficiary of the trust fund. The primary beneficiary of the VIE isdefined being the entity that benefits from the earnings or gains or absorbing the losses of theVIE, and is required to consolidate the financial results of the VIE and disclose them on thebalance sheet. ZionSolutions is treated as the primary beneficiary for accounting purposes underASC 810-10. As such, ZionSolutions is required to disclose the consolidated financial results ofthe decommissioning trust fund.

As shown above, the accounting rules produce accounting disclosures and descriptions that seemto indicate that both ZionSolutions and EGC have ownership of and access to the NDTF.However, as to the legal title and ownership interest in the NDT, "Ex Gen has agreed, subject toterms and conditions of the Asset Sale Agreement, to sell, assign, convey, transfer and deliver allof its right, title and interest in Zion Assets (as defined in the Asset Sale Agreement) toZionSolutions, and ZionSolutions has agreed, subject to the terms and conditions of the AssetSale Agreement, to assume and discharge the assumed Liabilities."

Please direct any specific questions regarding EGC's accounting treatment of the ZNPS NDTFdirectly to EGC.

There is no stated beneficiary of the trust funds; however, the trust funds are established for theexclusive purpose of providing funds for the decommissioning of Zion Station.

The Bank of New York Mellon is the trustee of the funds.

RFI #7: Decommissioning Trust Fund Amount

Has ECG denied disbursement of decommissioning trust funds to ZS?

Per 10 CFR 50.75(a)This section establishes requirements for indicating to NRC how a licensee willprovide reasonable assurance that funds will be available for the decommissioningprocess. For power reactor licensees, reasonable assurance consists of a series ofsteps as provided in paragraphs (b), (c), (e), and (f) of this section.

ZionSolutions Response

No, EGC has not denied disbursement of decommissioning trust funds to ZionSolutions.

ZionSolutions, LLCZS-2012-0417Page 14 of 14

RFI #8: Spent Fuel Management

How does ZionSolutions plan to meet its obligation to manage spent fuel safely until thefuel is transferred to the Secretary of Energy for its ultimate disposal in a repository?

ZionSolutions Response

ZionSolutions has funds sufficient to meet its obligations to manage spent fuel safely as requisiteto the current cost estimates for the project. The current cost estimate includes both the cost totransfer the spent fuel from the current fuel pool to the to-be-constructed Interim Spent FuelStorage Installation (ISFSI) and the cost to safely manage it through completion of theZionSolutions project and its turn-back to EGC. All the related Security, Radiation Protection,Maintenance, etc. costs are also included in the cost estimate. The Funding Assurance Reportfiled with NRC in March 201219 for the December 31, 2011 reporting date shows that there aresufficient funds in the trust to cover all the remaining decommissioning cost including managingspent fuel safely.

Upon completion of the decommissioning project in approximately 2020, ZionSolutions willtransfer the ISFSI to EGC in accordance with the ASA. EGC will assume responsibility tomanage the spent fuel safely from that date until title to and possession of the irradiated fuel istransferred to the Secretary of Energy for its ultimate disposition. On September 1, 2010, inaccordance with the Asset Sale Agreement, EGC retained $25 million of the DecommissioningTrust Fund for this purpose.

Inquiries regarding the management of spent nuclear fuel beyond completion of thedecommissioning project from approximately 2020 onward should be directed to EGC.

RFI#9: Profit Margin

What profit margin (as a percentage and in dollars) was built into the decommissioningcost estimate from ZNPS submitted by ZS in the license transfer application, assupplemented, dated January 25, 2008.

ZionSolutions Response

There is no ZionSolutions' profit margin or fee currently included in ZionSolutions'decommissioning cost estimate or costs charged to the project. No ZionSolutions markups forprofit have been added to either gross costs or individual costs incurred to date. Any future feeor profit would only be available from projected surplus project funds at the time of projectcompletion.

ZionSolutions reserves the right to attached fees in excess of actual costs (consistent with theASA and other project agreements) should funds become available.

19 ZionSolutions, LLC Letter, Daly to NRC, "Report on Status of Decommissioning Funding for ShutdownReactors," dated March 26, 2012.

Zion Nuclear Power Station, Unit 1 and 2 License Transfer Service List

cc:

Patrick T. Daly

Senior VP and General Manager

ZionSolutions, LLC101 Shiloh Boulevard

Zion, IL 60099

Patrick Thurman, Esq.VP Regulatory Affairs, Licensing &Document Control

ZionSolutions, LLC

101 Shiloh BoulevardZion, IL 60099

Gary BouchardVP Engineering, Ops & Nuclear Securityand Decommissioning Plant ManagerZionSolutions, LLC101 Shiloh Boulevard

Zion, IL 60099

Alan ParkerPresident Projects GroupEnergySolutions

1009 Commerce Park Drive, Ste. 100Oak Ridge, TN 37830

John ChristianPresident of Logistics, Processing andDisposal (LP& D) GroupEnergySolutions

1750 Tysons Boulevard, Suite 1500

Mclean, VA 22102

Thomas Magette

Senior VP Nuclear Regulatory StrategyEnergySolutions

6350 Stevens Forest Road, Ste. 2000Columbia, MD 21046

Russ WorkmanGeneral Counsel

EnergySolutions423 West 300 South, Ste. 200

Salt Lake City, UT 84101

Illinois Department of Nuclear SafetyOffice of Nuclear Facility Safety1035 Outer Park Drive

Springfield, IL 62704

Kent McKenzieEmergency Management Coordinator

Lake County Emergency Management Agency

1303 N. Milwaukee AvenueLibertyville, IL 60048-1308

Regional Administrator

U.S. NRC, Region III2443 Warrenville RoadLisle, IL 60532-4352

John E. MatthewsMorgan, Lewis & Bockius LLP

1111 Pennsylvania Avenue, NWWashington, DC 20004