1

Business System Analysis & Decision Making- Lecture 14

Zhangxi Lin

ISQS 5340

Summer II 2006

2

Chapter 12: Improving Decision Making Outline of the chapter

Strategy 1: Acquiring Experience and Expertise

Strategy 2: Debiasing Judgment Strategy 3: Analogical Reasoning Strategy 4: Taking an Outsider’s View Strategy 5: Using Linear Models and Other

Statistical Techniques Strategy 6: Understanding Biases in Others

3

Decision Making in Sports

Statistics has outperformed experts in predicting the outcomes of sport games

The Future of NBA Statistics: Part 1, Part 2 Houston Rocket Performance in 2006

Yao Ming’s statistics Questions

Why did it take so long for rationality to enter into decision making in sports (baseball)?

To what extent are managers in other industries still replying on false expertise when better strategies exist?

4

Experience vs. Expertise

“Experience is a dear teacher” (Dawes 1988) “Learning from an experience of failure … is indeed

‘dear’, …” Need to realize the value of gaining a conceptual

understanding of how to make a rational decision, rather than simply depending on the relatively mindless, passive learning obtained via experience.

The final benefit of developing a strategic conceptualization of decision-making concerns transferability – the ability to pass on the knowledge to future generations.

Key element is to avoid the many biases in individual and group context.

5

Debiasing Judgment

Unfreezing Change Refreezing

6

Business Intelligence and Data Analysis

7

Adopting Business Intelligence Collecting data – database and data warehousing Using linear models - regression Using other statistical techniques – ANOVA, correlation analysis, time

series analysis, etc. Applying data mining techniques

Classification Clustering Association analysis Link analysis Text mining

Adopting new business intelligence ideas Web mining 6 sigmas Realtime advertising/marketing Accurate marketing Narrowcasting

8

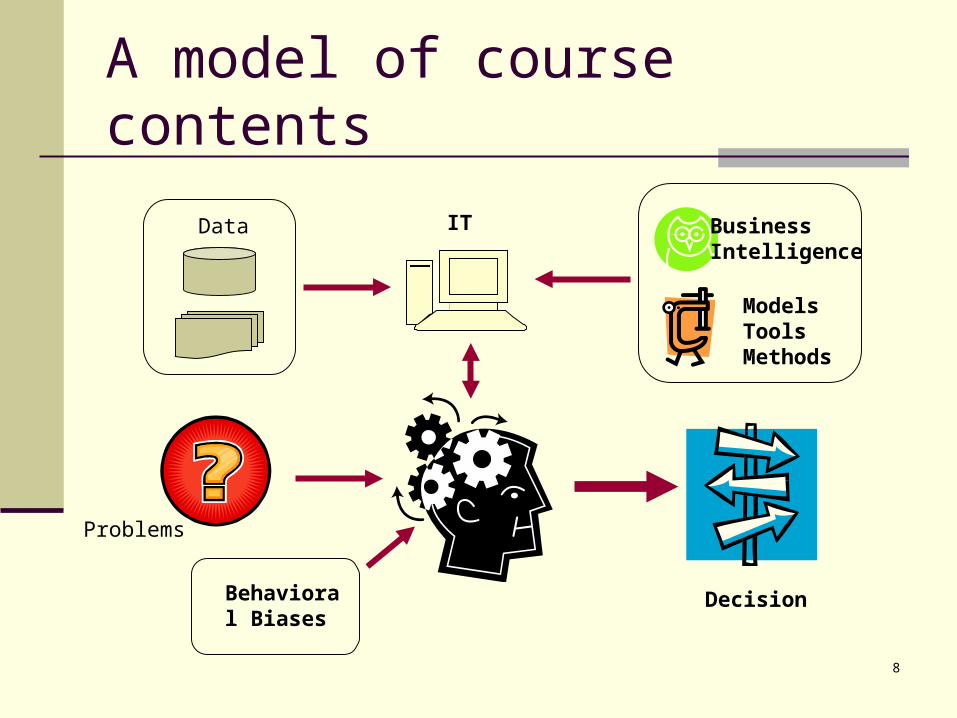

A model of course contents

IT BusinessIntelligence

Behavioral Biases

ModelsTools Methods

Data

Decision

Problems

9

Business Intelligence (restate)

Wikipedia.org’s definition: A broad category of applications and technologies for

gathering, providing access to, and analyzing data for the purpose of helping enterprise users make better business decisions.

The term implies having a comprehensive knowledge of all of the factors that affect your business. It is imperative that you have an in depth knowledge about factors such as your customers, competitors, business partners, economic environment, and internal operations to make effective and good quality business decisions.

Business intelligence enables you to make these kinds of decisions.

Reference: http://zlin.ba.ttu.edu/6347/ISQS6347.htm

10

Business Intelligence (restate)

The Data Warehousing Institute’s definition: The processes, technologies, and tools

needed to turn data into information, information into knowledge, and knowledge into plans that drive profitable business action. Business intelligence encompasses data warehousing, business analytic tools, and content/knowledge management.

11

Benefits for MBA Students in Business Intelligence Understand the growing trend of demand in data

mining from industry Know the general concepts and ideas in data

analysis Be able to manage data mining projects for

businesses Understand what technical people are doing Understand the outcomes from data mining projects Catch the advanced business concepts, business

processes and new working patterns

12

Sending Advertising Materials

100,000 customer Only 10% of them may be interested in life insurance Mailing an insurance advertising package costs $1

(material printing, stamp, processing, etc.) If someone purchases the insurance, the company

will make $4 net profit. So, if a letter results no purchase of the insurance package, the loss is $1.

Questions What is the total profit if sending the ad to all

customers? How to improve the efficiency of advertising and make

positive profits?

13

Data

What like of data we have now? Historical dataset. It shows previous life

insurance purchase history Customers’ profile dataset. It contains

customers’ properties and other information, except the information whether they will purchase the life insurance.

14

Case: Life Insurance Promotion

IncomeLife insurance

Credit card insurance Gender Age

40-50,000 No No Male 45

30-40,000 Yes Yes Female 40

40-50,000 No No Female 42

30-40,000 No Yes Male 43

50-60,000 Yes Yes Female 38

20-30,000 No No Female 55

30-40,000 Yes Yes Male 35

20-30,000 No No Male 27

30-40,000 No No Male 43

30-40,000 Yes No Female 41

15

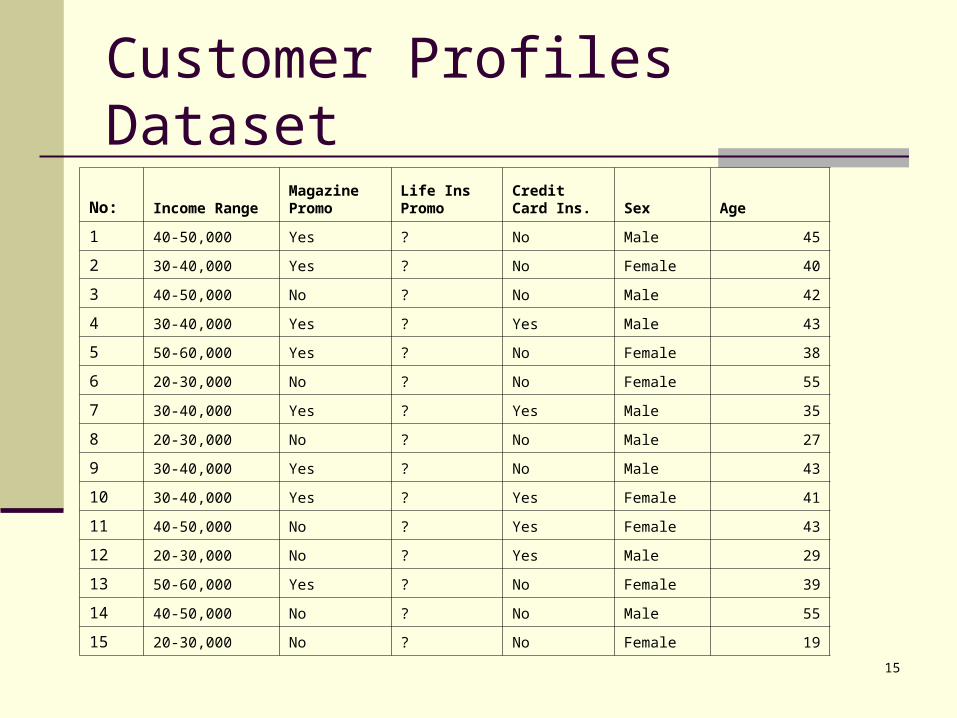

Customer Profiles Dataset

No: Income RangeMagazine Promo

Life Ins Promo

Credit Card Ins. Sex Age

1 40-50,000 Yes ? No Male 45

2 30-40,000 Yes ? No Female 40

3 40-50,000 No ? No Male 42

4 30-40,000 Yes ? Yes Male 43

5 50-60,000 Yes ? No Female 38

6 20-30,000 No ? No Female 55

7 30-40,000 Yes ? Yes Male 35

8 20-30,000 No ? No Male 27

9 30-40,000 Yes ? No Male 43

10 30-40,000 Yes ? Yes Female 41

11 40-50,000 No ? Yes Female 43

12 20-30,000 No ? Yes Male 29

13 50-60,000 Yes ? No Female 39

14 40-50,000 No ? No Male 55

15 20-30,000 No ? No Female 19

16

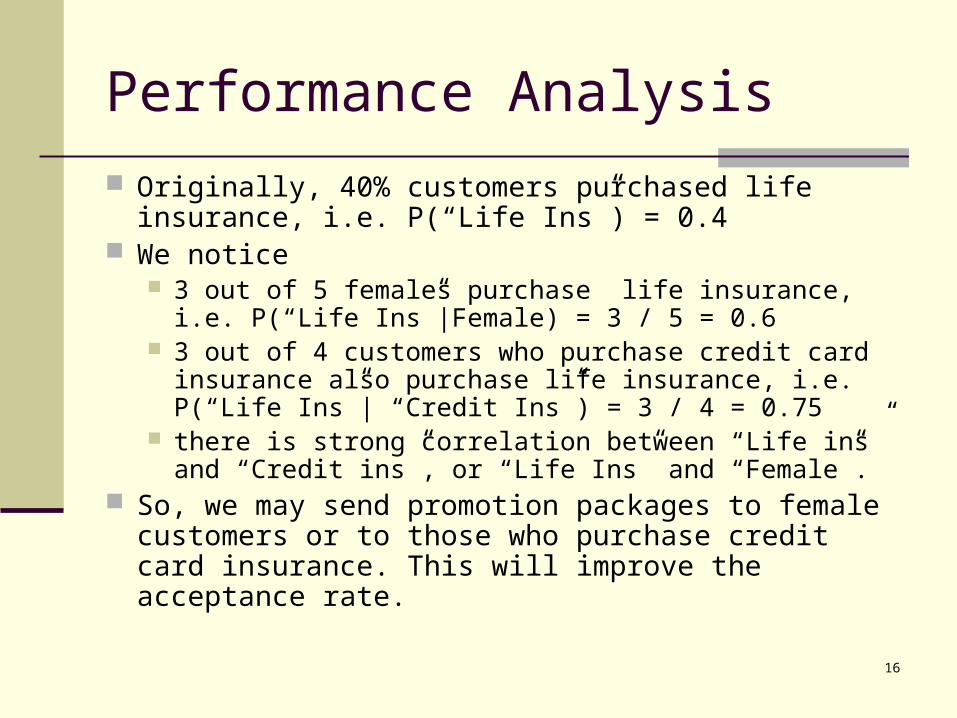

Performance Analysis

Originally, 40% customers purchased life insurance, i.e. P(“Life Ins”) = 0.4

We notice 3 out of 5 females purchase life insurance, i.e. P(“Life

Ins”|Female) = 3 / 5 = 0.6 3 out of 4 customers who purchase credit card

insurance also purchase life insurance, i.e. P(“Life Ins”| “Credit Ins”) = 3 / 4 = 0.75

there is strong correlation between “Life ins” and “Credit ins”, or “Life Ins” and “Female”.

So, we may send promotion packages to female customers or to those who purchase credit card insurance. This will improve the acceptance rate.

17

Definitions If we send the life insurance promotion package to female

customers, the acceptance rate is 0.6, which is called accuracy rate.

As the strategy will likely improve the acceptance rate from original 0.4 (based on all customers) to 0.6. The ratio of them, 0.6 / 0.4 = 1.5, is called Lift. A lift value greater than 1 indicates the improvement.

However, we can see that one of the customers who also purchases life insurance is a male. He will be excluded from the promotion mailing list. Therefore, using the rule “female” only covers 3 out of 4 customers who purchase life insurance. The ratio “# of included targets” / “# of all target”, i.e. 3 / 4 = 0.75 in this case, is called Coverage rate.

A coverage rate less than 1 implies some valuable customers are lost.

To improve the accuracy of decision-making, we may apply more than one criterion, e.g. “Female” plus “Credit Ins”.

18

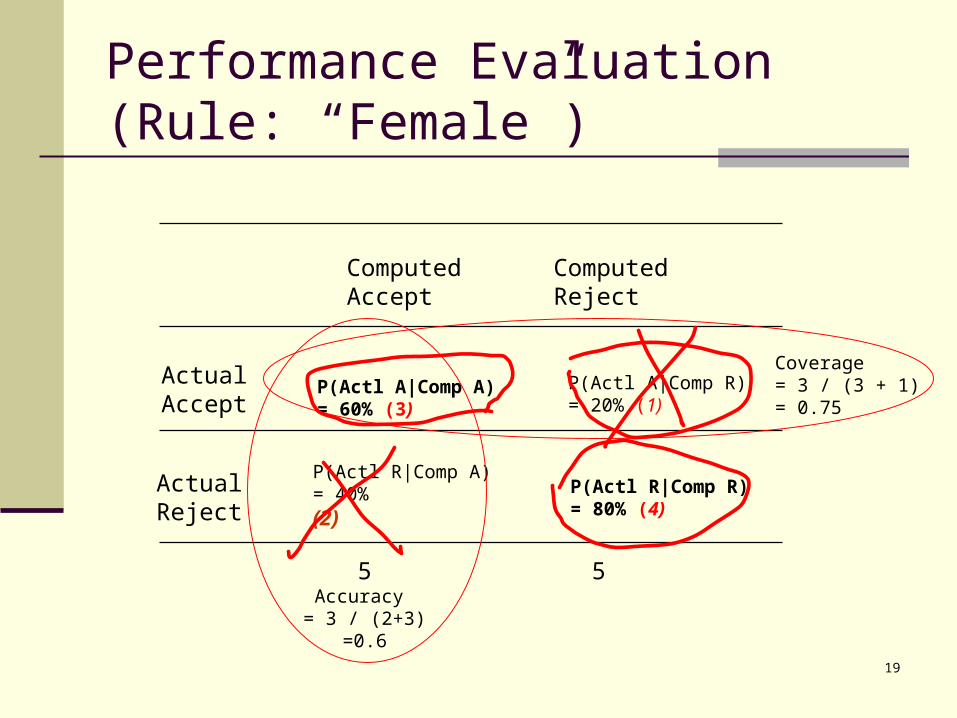

Performance Evaluation (Rule: “Female”) Using a Confusion Matrix

ActualAccept

ActualReject

Computed Accept

Computed Reject

True or 13

True or 14

False or 02

False or 01

5Accuracy = 3 / (2+3)

=0.6

5

Coverage= 3 / (3 + 1)= 0.75

19

Performance Evaluation (Rule: “Female”)

ActualAccept

ActualReject

Computed Accept

Computed Reject

P(Actl A|Comp A)= 60% (3)

P(Actl R|Comp R)= 80% (4)

P(Actl R|Comp A)= 40%(2)

P(Actl A|Comp R)= 20% (1)

5Accuracy = 3 / (2+3)

=0.6

5

Coverage= 3 / (3 + 1)= 0.75

20

Decision Tree (1)

Total: 10Accept: 4Reject: 6

Accuracy: 40%Coverage: 100%

Gender

Female

Male

Total: 5Accept: 3Reject: 2

Accuracy: 60%Coverage: 75%

Total: 5Accept: 1Reject: 4

Accuracy: 20%Coverage: 25%

Credit CardInsurance

Yes

No

Total: 2Accept: 2Reject: 0

Accuracy: 100%Coverage: 50%

Total: 3Accept: 1Reject: 2

Accuracy: 33.3%Coverage: 25%

21

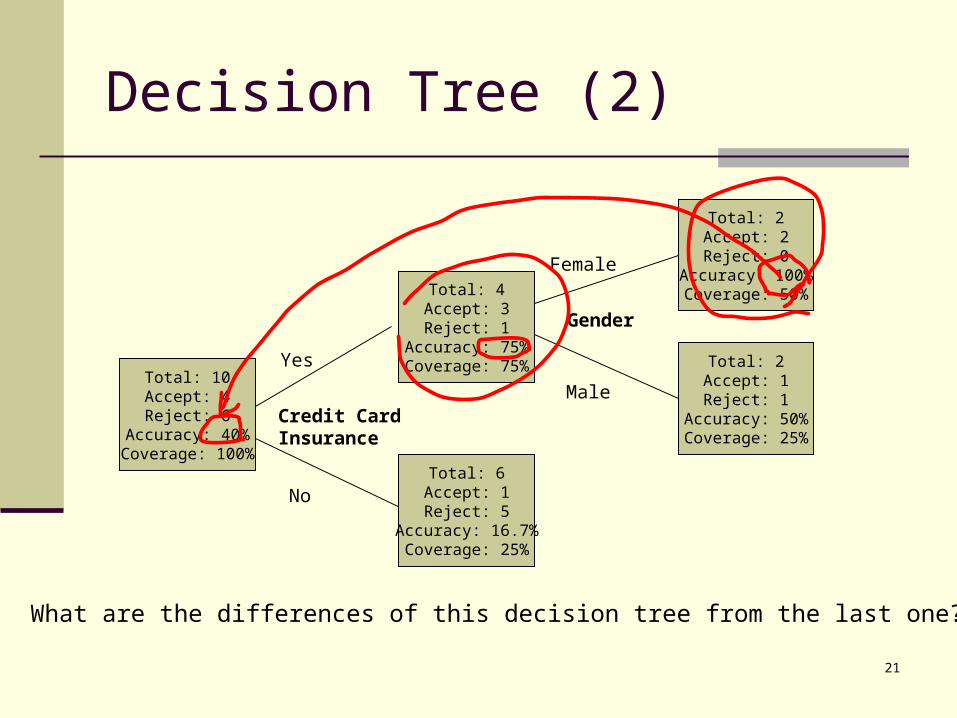

Decision Tree (2)

Total: 10Accept: 4Reject: 6

Accuracy: 40%Coverage: 100%

Gender

Female

Male

Total: 4Accept: 3Reject: 1

Accuracy: 75%Coverage: 75%

Total: 6Accept: 1Reject: 5

Accuracy: 16.7%Coverage: 25%

Credit CardInsurance

Yes

No

Total: 2Accept: 2Reject: 0

Accuracy: 100%Coverage: 50%

Total: 2Accept: 1Reject: 1

Accuracy: 50%Coverage: 25%

What are the differences of this decision tree from the last one?

22

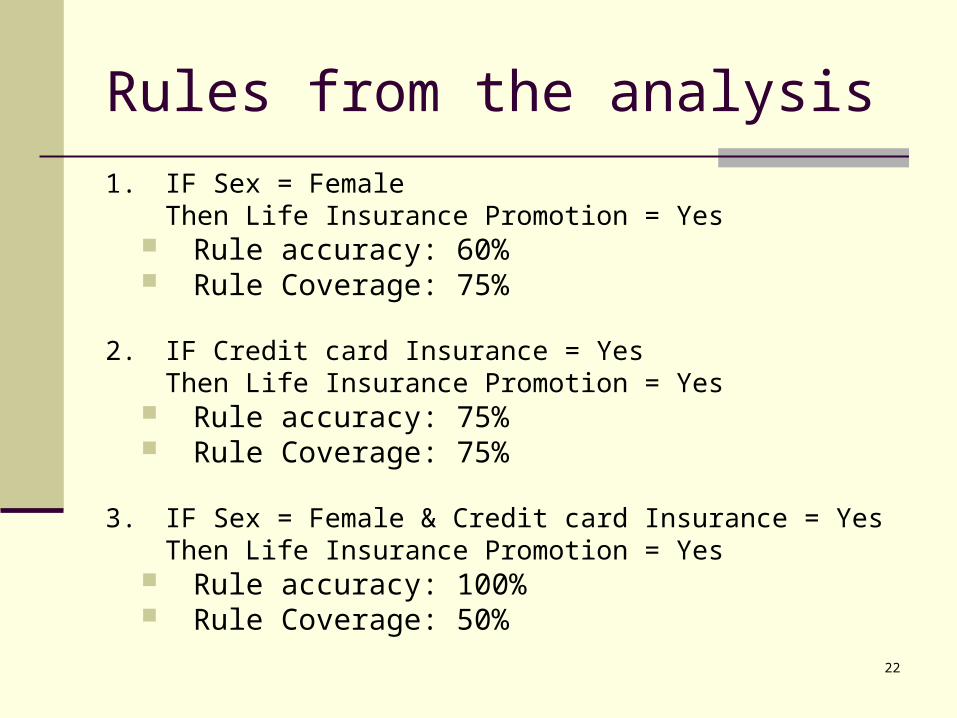

Rules from the analysis

1. IF Sex = FemaleThen Life Insurance Promotion = Yes

Rule accuracy: 60% Rule Coverage: 75%

2. IF Credit card Insurance = YesThen Life Insurance Promotion = Yes

Rule accuracy: 75% Rule Coverage: 75%

3. IF Sex = Female & Credit card Insurance = YesThen Life Insurance Promotion = Yes

Rule accuracy: 100% Rule Coverage: 50%

23

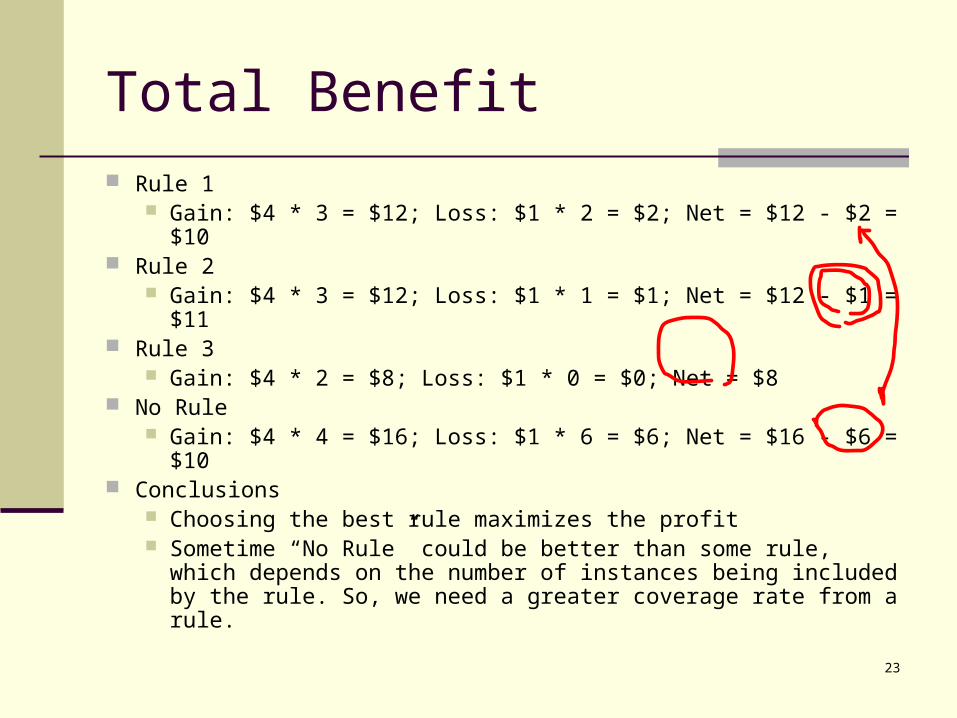

Total Benefit

Rule 1 Gain: $4 * 3 = $12; Loss: $1 * 2 = $2; Net = $12 - $2 = $10

Rule 2 Gain: $4 * 3 = $12; Loss: $1 * 1 = $1; Net = $12 - $1 = $11

Rule 3 Gain: $4 * 2 = $8; Loss: $1 * 0 = $0; Net = $8

No Rule Gain: $4 * 4 = $16; Loss: $1 * 6 = $6; Net = $16 - $6 = $10

Conclusions Choosing the best rule maximizes the profit Sometime “No Rule” could be better than some rule, which

depends on the number of instances being included by the rule. So, we need a greater coverage rate from a rule.

24

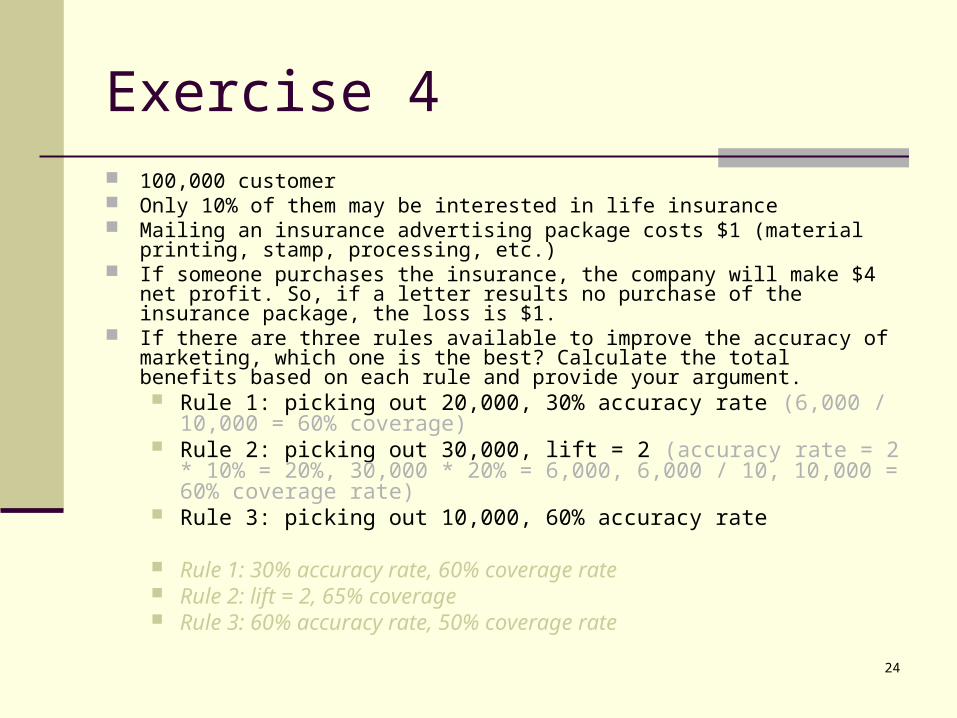

Exercise 4 100,000 customer Only 10% of them may be interested in life insurance Mailing an insurance advertising package costs $1 (material printing, stamp,

processing, etc.) If someone purchases the insurance, the company will make $4 net profit. So, if

a letter results no purchase of the insurance package, the loss is $1. If there are three rules available to improve the accuracy of marketing, which

one is the best? Calculate the total benefits based on each rule and provide your argument. Rule 1: picking out 20,000, 30% accuracy rate (6,000 / 10,000 = 60%

coverage) Rule 2: picking out 30,000, lift = 2 (accuracy rate = 2 * 10% = 20%,

30,000 * 20% = 6,000, 6,000 / 10, 10,000 = 60% coverage rate) Rule 3: picking out 10,000, 60% accuracy rate

Rule 1: 30% accuracy rate, 60% coverage rate Rule 2: lift = 2, 65% coverage Rule 3: 60% accuracy rate, 50% coverage rate

25

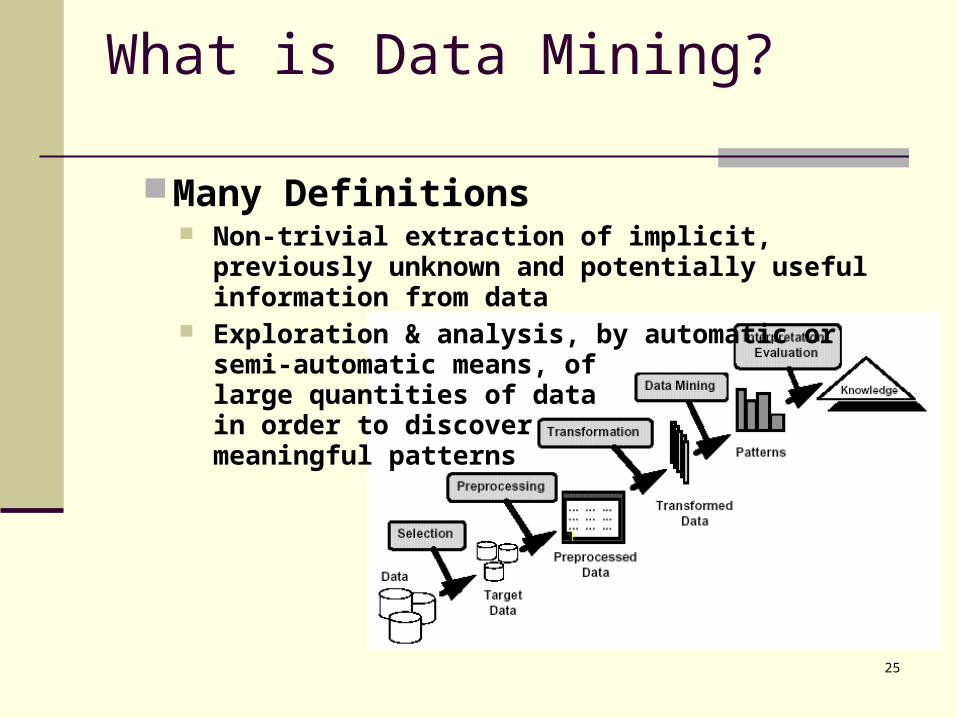

What is Data Mining?

Many Definitions Non-trivial extraction of implicit, previously unknown

and potentially useful information from data Exploration & analysis, by automatic or

semi-automatic means, of large quantities of data in order to discover meaningful patterns

26

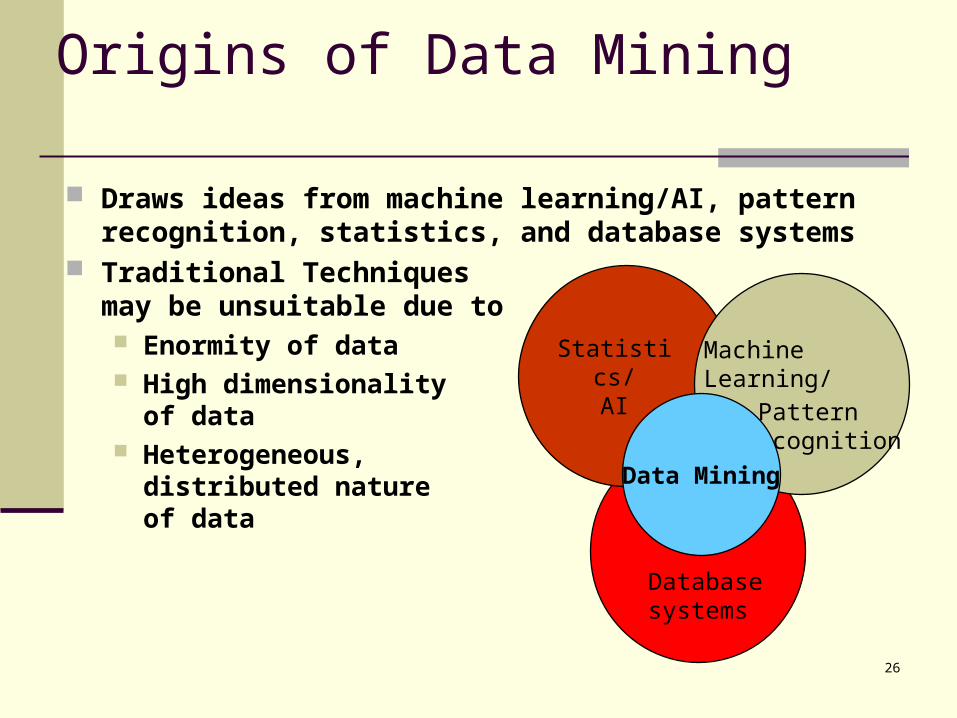

Draws ideas from machine learning/AI, pattern recognition, statistics, and database systems

Traditional Techniquesmay be unsuitable due to Enormity of data High dimensionality

of data Heterogeneous,

distributed nature of data

Origins of Data Mining

Machine Learning/Pattern

Recognition

Statistics/AI

Data Mining

Database systems

27

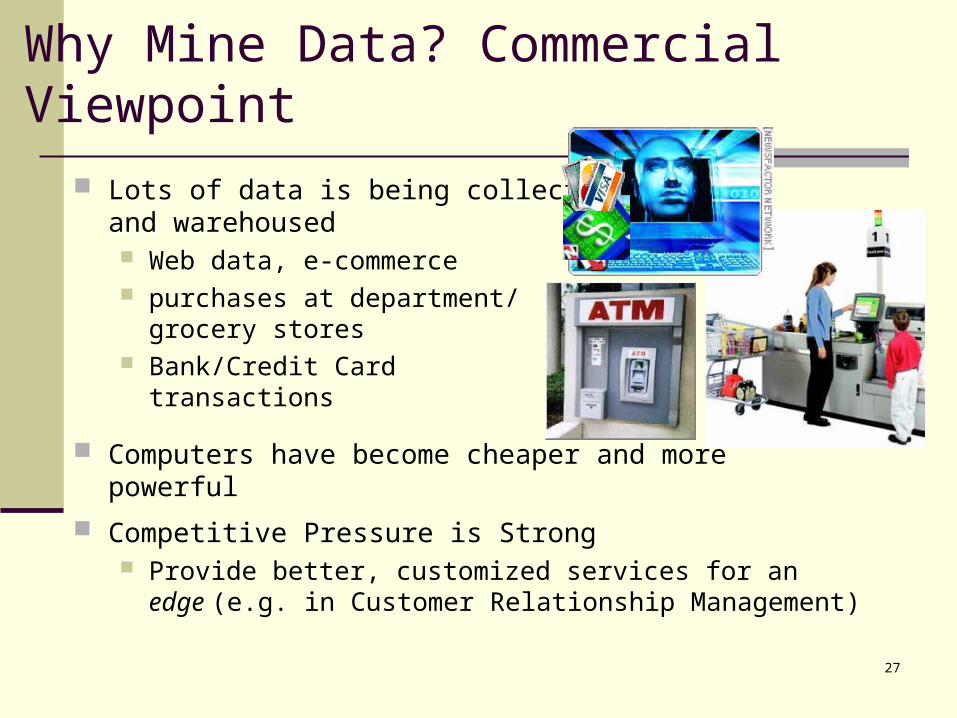

Lots of data is being collected and warehoused Web data, e-commerce purchases at department/

grocery stores Bank/Credit Card

transactions

Computers have become cheaper and more powerful

Competitive Pressure is Strong Provide better, customized services for an edge (e.g. in

Customer Relationship Management)

Why Mine Data? Commercial Viewpoint

28

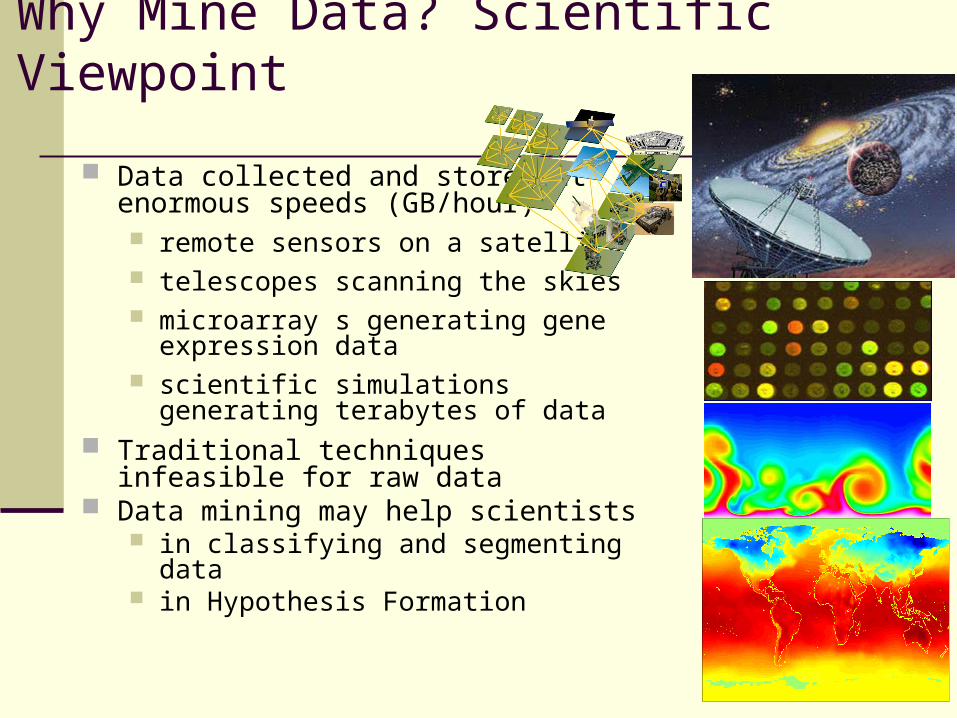

Why Mine Data? Scientific Viewpoint

Data collected and stored at enormous speeds (GB/hour) remote sensors on a satellite telescopes scanning the skies microarray s generating gene

expression data scientific simulations

generating terabytes of data Traditional techniques infeasible for raw

data Data mining may help scientists

in classifying and segmenting data in Hypothesis Formation

29

Data Mining Tasks

Prediction Methods Use some variables to predict unknown or

future values of other variables.

Description Methods Find human-interpretable patterns that

describe the data.

From [Fayyad, et.al.] Advances in Knowledge Discovery and Data Mining, 1996

30

Data Mining Tasks...

Classification [Predictive]

Clustering [Descriptive]

Association Rule Discovery [Descriptive]

Sequential Pattern Discovery [Descriptive]

Regression [Predictive]

Deviation Detection [Predictive]

31

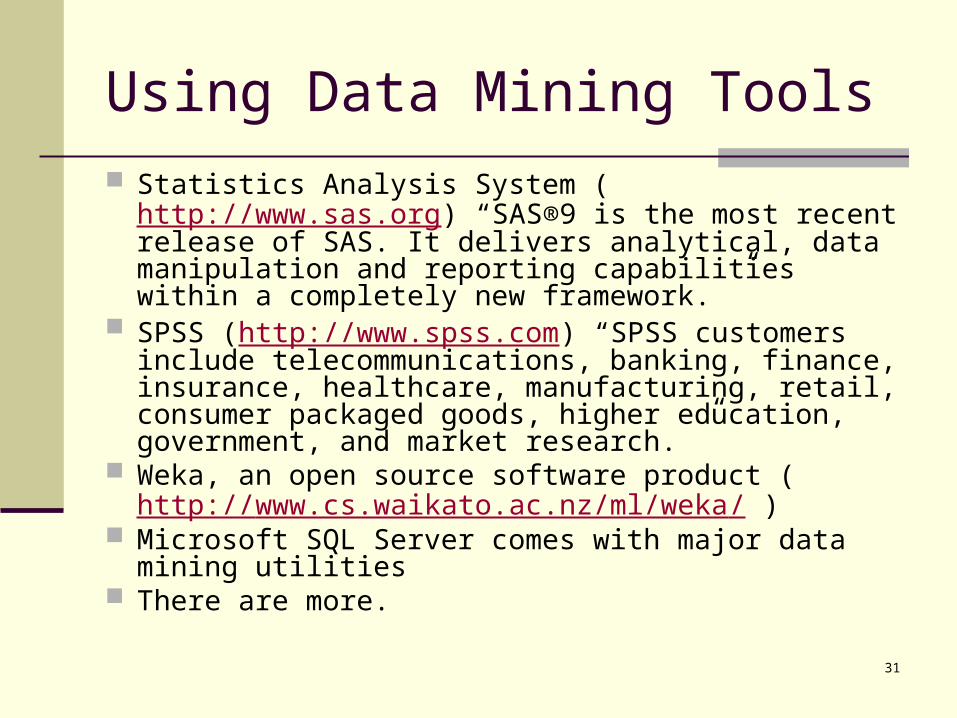

Using Data Mining Tools

Statistics Analysis System (http://www.sas.org) “SAS®9 is the most recent release of SAS. It delivers analytical, data manipulation and reporting capabilities within a completely new framework. ”

SPSS (http://www.spss.com) “SPSS customers include telecommunications, banking, finance, insurance, healthcare, manufacturing, retail, consumer packaged goods, higher education, government, and market research. ”

Weka, an open source software product (http://www.cs.waikato.ac.nz/ml/weka/ )

Microsoft SQL Server comes with major data mining utilities

There are more.

32

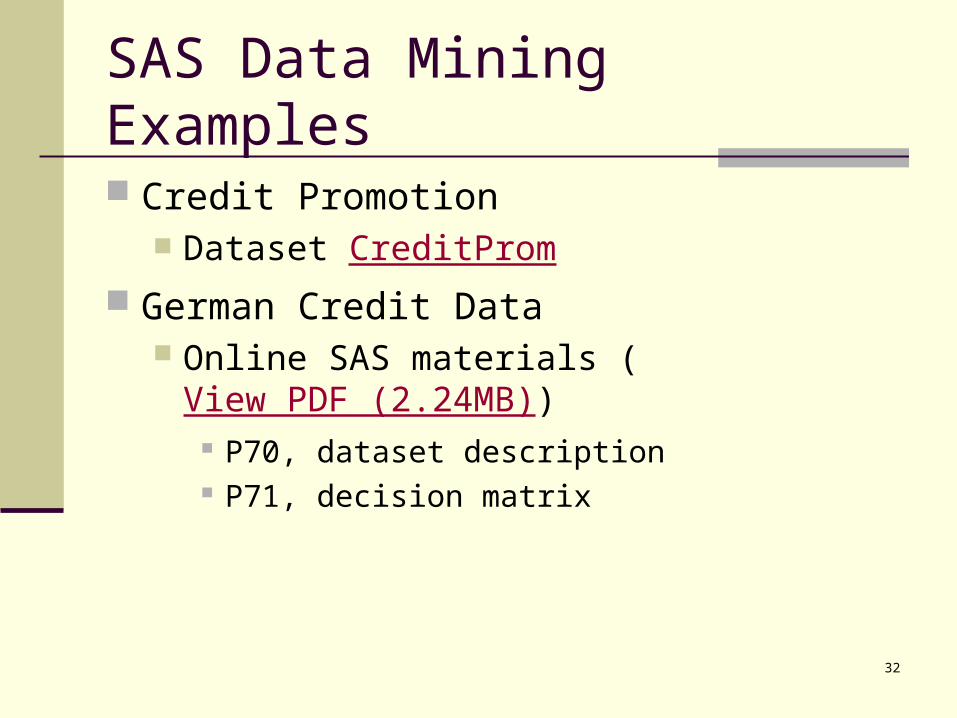

SAS Data Mining Examples

Credit Promotion Dataset CreditProm

German Credit Data Online SAS materials (View PDF (2.24MB))

P70, dataset description P71, decision matrix

33

Life Insurance Promotion Data (more detailed)

No: Income RangeMagazine Promo

Life Ins Promo

Credit Card Ins. Sex Age

1 40-50,000 Yes No No Male 45

2 30-40,000 Yes Yes No Female 40

3 40-50,000 No No No Male 42

4 30-40,000 Yes No Yes Male 43

5 50-60,000 Yes Yes No Female 38

6 20-30,000 No No No Female 55

7 30-40,000 Yes Yes Yes Male 35

8 20-30,000 No No No Male 27

9 30-40,000 Yes No No Male 43

10 30-40,000 Yes Yes Yes Female 41

11 40-50,000 No Yes Yes Female 43

12 20-30,000 No Yes Yes Male 29

13 50-60,000 Yes Yes No Female 39

14 40-50,000 No No No Male 55

15 20-30,000 No No No Female 19

Recommended