1

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Presented by:Robert S. Keebler, CPA, MST, AEP (Distinguished)920 739 [email protected]

Planning Opportunities Created by Roth IRA Conversions

2

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Roth IRAsGeneral Concepts

> 100% of growth is tax-exempt

> No required minimum distributions at age 70½> NOTE: Distributions from Roth IRAs cannot be used to fulfill the RMD

from a traditional IRA

> $100,000 Modified Adjusted Gross Income (MAGI) limitation

> RMDs on Inherited Roth IRAs

> Roth 401(k) plans

3

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> Starting in 2010, the $100,000 Modified Adjusted Gross Income (MAGI) limitation no longer applies> The taxable income recognized on a Roth IRA conversion in

2010 may be spread over the following two tax years (i.e. 2011 and 2012)

> Watch Out for the “Two Year Trap!”

> Married Filing Separately taxpayers can convert to a Roth IRA

Roth IRAsGeneral Concepts

4

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Computation of MAGI - New Rule (Conversions After 12/31/2004)Adjusted Gross Income $XX,XXXLess:

Income from Roth Conversion ($XX,XXX)Required Minimum Distribution (IRAs Only) (XX,XXX) (XX,XXX)

Add-in:Traditional IRA Deduction $X,XXXStudent Loan Interest X,XXXTuition & Fee Deduction X,XXXForeign Income/Housing Exclusion X,XXXForeign Housing Deduction X,XXXExclusion of Interest on U.S. Series EE Savings Bonds X,XXX XX,XXX

Modified Adjusted Gross Income (Must be less than $100,000) $XX,XXX

Roth IRAsGeneral Concepts

5

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Convertible accounts> Traditional IRAs

> 401(k) plans

> Profit sharing plans

> 403(b) annuity plans

> 457 plans

> “Inherited” 401(k) plans (see Notice 2008-30)

Roth IRAsGeneral Concepts

6

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Non-convertible accounts> “Inherited” IRAs

> Education IRAs

Roth IRAsGeneral Concepts

May be rolled into an IRA, Roth IRA, or other qualified plan

(unless, possibly, it is a distribution that (1) is part of a series of equal payments and (2) did not include any 2009

RMD)

Was the distribution a RMD for 2009?

Was the RMD a single or multiple distribution?

IRA or Qualified Plan Distribution

Any distribution may be rolled into a Roth IRA or

other qualified plan, however, only one

distribution may be rolled into a traditional IRA.

Rollovers Under Notice2009-82

Yes

No

Multiple distribution(s)Single distribution

Qualified Plan

IRA

2, 3

1. A distribution that would have been an RMD for the year 2009, but for the suspension of RMDs under 401(a)(9(h)2. Rollovers to Roth IRAs will be taxable3. Roth conversions will be subject to the $100,000 AGI limitation, IRC §408A(c)(3)(B)(i)4. One-rollover-per-year rule, IRC §408(d)(3)5. One or more payments in a series of substantially equal distributions (that include the 2009 RMDs) made at least annually and

expected to last for the life (or life expectancy) of the participant, the joint lives (or joint life expectancy) of the participant and the participant’s designated beneficiary or for a period of at least 100 years.

© 2009 Robert S. Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLPAll Rights [email protected]

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.

For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors.

4

Educational Information

E-mail [email protected] to be added to our newsletter, for

previous write-ups about the new IRA regulations, for a licensing agreement,

or for information about seminars, CDs or books.

Rollover Relief: The 60-day rollover period is extended so that it ends no earlier than November 30, 2009, for 2009 RMDs or payments that are part of a series of equal payments. Taxpayers have the later of Nov. 30, 2009, or 60 days after the date the distribution was received, to roll over the distribution.

5

1 Stop No Special Relief

8

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

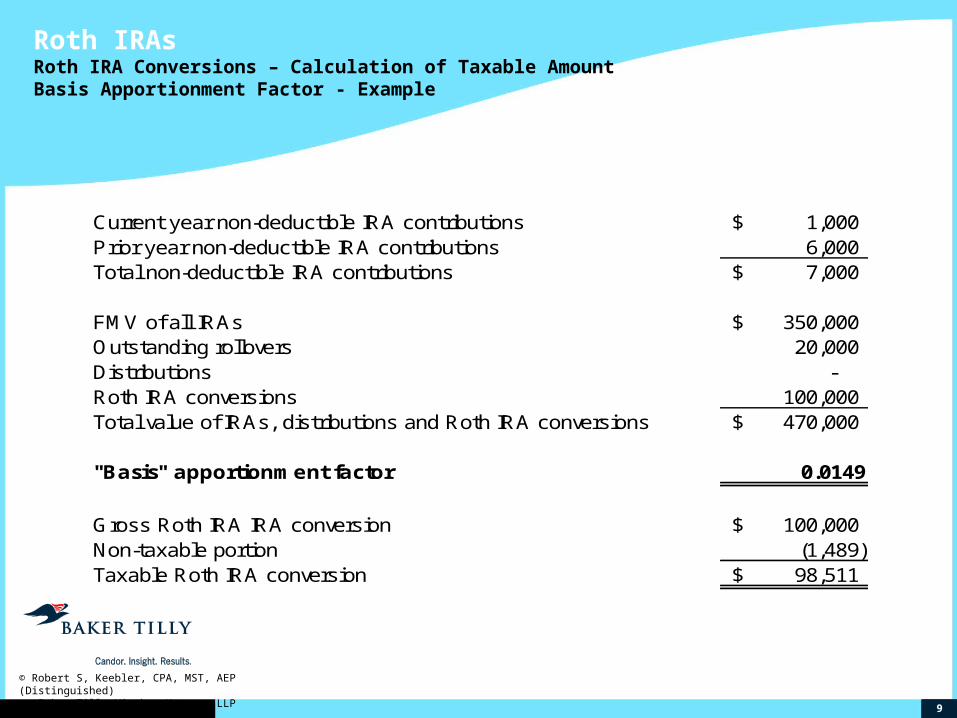

> When a traditional IRA has non-deductible contributions, a portion of the conversion to a Roth IRA will be non-taxable “basis” to the IRA owner

> In determining the non-taxable portion of a Roth IRA conversion, all traditional IRAs and IRA distributions during the year (including outstanding rollovers) must be combined for apportioning “basis”> See IRS Form 8606

Roth IRAsRoth IRA Conversions – Calculation of Taxable Amount

9

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Current year non-deductible IRA contributions 1,000$ Prior year non-deductible IRA contributions 6,000 Total non-deductible IRA contributions 7,000$

FMV of all IRAs 350,000$ Outstanding rollovers 20,000 Distributions - Roth IRA conversions 100,000 Total value of IRAs, distributions and Roth IRA conversions 470,000$

"Basis" apportionment factor 0.0149

Gross Roth IRA IRA conversion 100,000$ Non-taxable portion (1,489) Taxable Roth IRA conversion 98,511$

Roth IRAsRoth IRA Conversions – Calculation of Taxable AmountBasis Apportionment Factor - Example

10

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

The 5-year period for all of a participant’s Roth IRAs begins on January 1 of the first year for which a contribution was made to any Roth IRA owned by that participant.

> Except a surviving spouse gets to treat an inherited Roth IRA as one of her own for purposes of the 5-year rule.

> The 5-year period continues to run with the participant dies.

NOTE: If a participant dies within the 5-year period, distributions to a beneficiary are taxable until the 5-year period ends.

Roth IRAsGeneral Concepts

11

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> Qualified distributions are not subject to income tax

> Non- qualified distributions will be subject to income tax

Roth IRAsTaxation of Distributions

12

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> Basis Can be Withdrawn Tax-Free (FIFO Method)> Distributions are not subject to income tax if they do

not exceed aggregate contributions and/or conversions to the Roth IRA

Roth IRAsTaxation of Distributions

13

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Roth IRA Distribution Rules

Contributions> Regular contributions> Rollover contributions> Rollover from Roth 401(k)s

Earnings

Conversions (First in, first out basis)> Taxable portion of prior conversion> Non-taxable portion of prior conversion

Step 1: (Non-taxable/not subject to 10% penalty)

Step 2: (Non-taxable/potentially subject to 10% penalty)

Step 3: (Taxable/potentially subject to 10% penalty)

Does the taxpayer meet

any of the other statutory

exceptions?

Roth IRA Distribution

Is the taxpayer over age 59½?

Entire distribution is tax-free

No

Yes

© 2009 Prepared by Robert S. Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLPAll Rights [email protected]

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.

For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors.

Yes

No

3

1. IRC Sec. 408A(d)(2)(A)(i)2. IRC Sec 408A(d)(2)(B)3. IRC Sec. 408A(d)(2)(A)(ii)(iii)(iv)

• Death• Disability• First-time homebuyer expenses (up to $10K)

1 Has the taxpayer met the five-year holding

period test?2

Educational Information

E-mail [email protected] to be added to our newsletter, for

previous write-ups about the new IRA regulations, for a licensing agreement,

or for information about seminars, CDs or books.

No Yes

Roth IRA-Taxability of Distributions STOP

Distribution subject to income tax (only to the extent of amounts not

previously taxed)

STOP Distribution subject to

income tax (only to the extent of amounts not

previously taxed)

15

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> Withdrawals made within five years of conversion if owner under age 59½ and no other exception applies

> Five-year period independent of five-year period for qualified distribution

Roth IRAsTaxation of Distributions Early Withdrawal Tax

16

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> If attributable to a regular contribution: applicable to amounts includible in gross income

> If attributable to a rollover contribution: applicable to amounts that were included in gross income at rollover

Roth IRAsTaxation of Distributions Early Withdrawal Tax for Non-Qualified Distributions

17

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> The calculation of the amount of a non-qualified Roth IRA distribution subject to the 10% early withdrawal tax is determined as follows:

Gross non-qualified Roth IRA distribution

- First-time homebuyer expenses

- Prior year Roth IRA contributions

Gross non-qualified Roth IRA distribution subject to 10% tax

- Taxable portion of prior year Roth IRA conversions > 5 years

- Non-taxable portion of prior year Roth IRA conversions

Net non-qualified Roth IRA distribution subject to 10% tax

Roth IRAsRoth IRA Distributions – 10% Early Withdrawal TaxOrdering Rule - General

Is the taxpayer over age 59½?

Does the taxpayer have only contributory or

conversion IRAs?

Follow the “ordering rules” (as outlined in Form

8606 instructions)

Roth IRA -Application of 10% Early

Withdrawal PenaltyYes

No

No

Comingled Roth IRA

Yes

© 2009 Prepared by Robert S. Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLPAll Rights [email protected]

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.

For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors.

STOP No 10% Penalty

(“Qualified distribution”)

Did the distribution occur within five years

of conversion?

Is the distribution greater than prior contributions (i.e.

“basis”)?

Penalty only applies to earnings

No

Educational Information

E-mail [email protected] to be added to our newsletter, for

previous write-ups about the new IRA regulations, for a licensing agreement,

or for information about seminars, CDs or books.

100% conversion Roth IRA

100% contributory Roth IRA

STOPNo 10% Penalty

(return of non-deductible contributions)

Penalty applies to prior conversion

amounts and earnings1

Penalty applies unless excluded under one of the following exceptions of IRC Sec. 72(t)1.Death2.Disability3.Series of substantially equal periodic payments4.Medical expenses greater than 7.5% AGI5.Health insurance premiums for unemployed individuals6.Higher education expenses7.First-time homebuyer expenses (up to $10K)

1

Yes1 Penalty only applies to

earnings 1

19

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

(1) Taxpayers have special favorable tax attributes including charitable deduction carry-forwards, investment tax credits, high basis non-deductible traditional IRAs, etc.

(2) Suspension of the minimum distribution rules at age 70½ provides a considerable advantage to the Roth IRA holder.

(3) Taxpayers benefit from paying income tax before estate tax (when a Roth IRA election is made) compared to the income tax deduction obtained when a traditional IRA is subject to estate tax.

Roth IRAsNine Reasons Why to Convert to a Roth IRA

20

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

(4) Taxpayers who can pay the income tax on the IRA from non IRA funds benefit greatly from the Roth

IRA because of the ability to enjoy greater tax-free yields.

(5) Taxpayers who need to use IRA assets to fund their Unified Credit bypass trust are well advised to

consider making a Roth IRA election for that portion of their overall IRA funds.

(6) Future distributions to beneficiaries are generally tax-free.

Roth IRAsNine Reasons Why to Convert to a Roth IRA

21

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

(7) Because federal tax brackets are more favorable for married couples filing joint returns than for single individuals, Roth IRA distributions won’t cause an increase in tax rates for the surviving spouse when one spouse is deceased because the distributions are tax-free.> Important pre-mortem planning opportunity

(8) Suspension of required minimum distributions (RMDs) provides for additional tax-free compounded growth

(9) Ability to recharacterize a Roth IRA conversion is a significant tactical advantage because if provides the taxpayer the benefit of 20/20 hindsight (by allowing the taxpayer to specifically choose which conversions to keep)

Roth IRAsNine Reasons Why to Convert to a Roth IRA

22

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

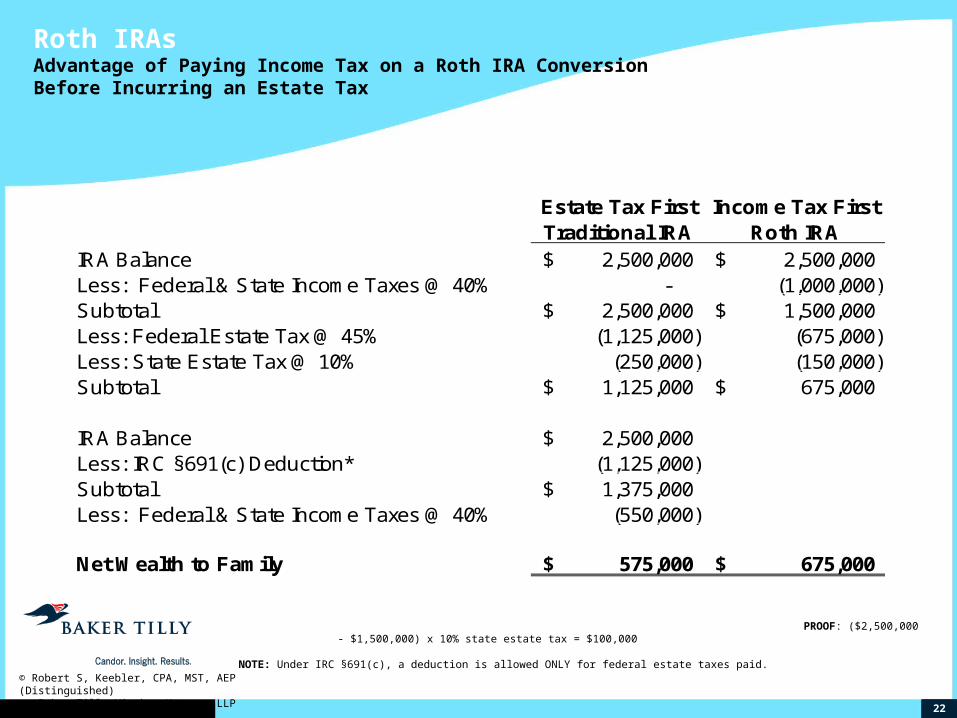

Estate Tax First Income Tax FirstTraditional IRA Roth IRA

IRA Balance 2,500,000$ 2,500,000$ Less: Federal & State Income Taxes @ 40% - (1,000,000) Subtotal 2,500,000$ 1,500,000$ Less: Federal Estate Tax @ 45% (1,125,000) (675,000) Less: State Estate Tax @ 10% (250,000) (150,000) Subtotal 1,125,000$ 675,000$

IRA Balance 2,500,000$ Less: IRC §691(c) Deduction* (1,125,000) Subtotal 1,375,000$ Less: Federal & State Income Taxes @ 40% (550,000)

Net Wealth to Family 575,000$ 675,000$

Roth IRAsAdvantage of Paying Income Tax on a Roth IRA Conversion Before Incurring an Estate Tax

PROOF: ($2,500,000 - $1,500,000) x 10% state estate tax = $100,000 NOTE: Under IRC §691(c), a deduction is allowed ONLY for federal estate taxes paid.

23

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

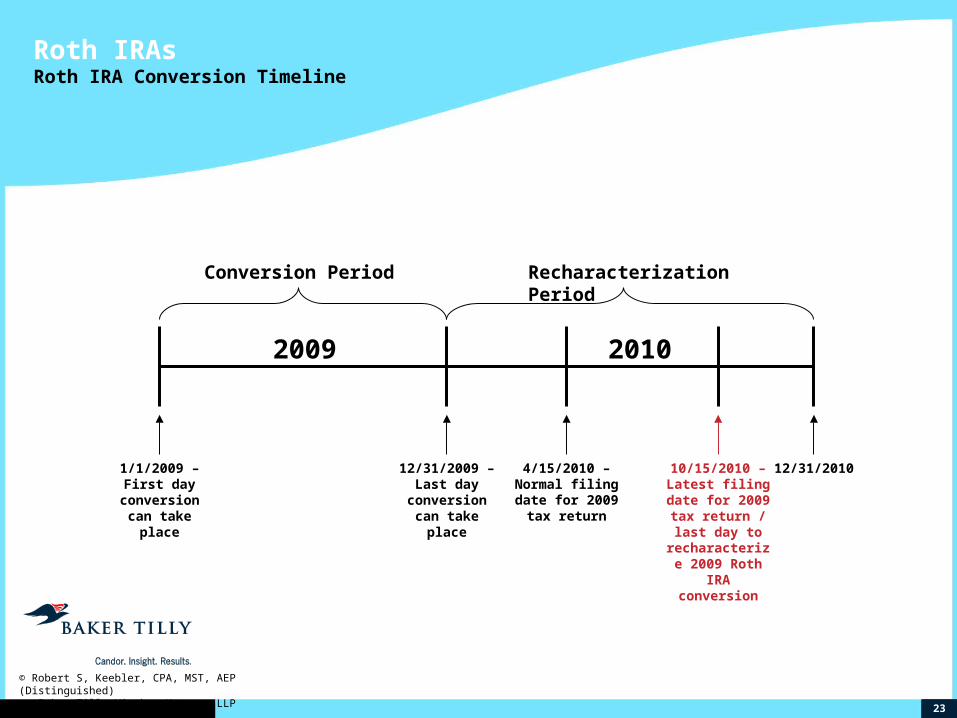

Conversion Period Recharacterization Period

1/1/2009 – First day conversion can take place

2009

12/31/2009 – Last day conversion can take place

4/15/2010 – Normal filing

date for 2009 tax return

10/15/2010 – Latest filing date

for 2009 tax return / last day to recharacterize

2009 Roth IRA conversion

12/31/2010

2010

Roth IRAsRoth IRA Conversion Timeline

24

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> In 2009, the $100,000 AGI limitation is still in effect

> For taxpayers who are below the $100,000 AGI threshold, serious consideration should be given to converting in 2009 because income tax rates are expected to increase as early as 2010

> For those taxpayers above the $100,000 AGI threshold, consideration should be given to harvesting losses (whether ordinary or capital) so as to lower income> Oil & gas investments

> Defined Benefit Plans

> Capital Loss Planning

Roth IRAsSpecial Conversion Opportunity in 2009

25

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> In 2010, there will be a “tsunami” of income tax planning as a result of the repeal of the $100,000 AGI limitation on Roth IRA conversions

> Consequently, planners need to begin now in gathering the necessary resources to handle the additional workload of analyzing Roth IRA conversions> Income tax and cash flow studies

> Comprehensive Roth IRA conversion software

> Comprehensive written materials explaining Roth IRA conversions and how a conversion will affect the client

Roth IRAsReadying for the Conversion Planning “Tsunami” in 2010

26

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA Planning

27

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningUnderstanding the Mechanics

In simplest terms, a traditional IRA will produce the same after-tax result as a Roth IRA provided that:> The annual growth rates are the same

> The tax rate in the conversion year is the same as the tax rate during the

withdrawal years (i.e. A x B x C = D; A x C x B = D)

28

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Traditional IRA Roth IRA2009 Account Balance 100,000$ 100,000$ Less: Income Taxes @ 40% - (40,000) Net Balance 100,000$ 60,000$

Growth Until Death 300.00% 300.00%

Account Balance @ Death 300,000$ 180,000$ Less: Income Taxes @ 40% (120,000) - Net Account Balance to Family 180,000$ 180,000$

Advanced Roth IRA PlanningUnderstanding the Mechanics

29

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Critical decision factors> Tax rate differential (year of conversion vs. withdrawal years)

> Use of “outside funds” to pay the income tax liability

> Need for IRA funds to meet annual living expenses

> Time horizon

Advanced Roth IRA PlanningUnderstanding the Mechanics

30

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

The key to successful Roth IRA conversions is to keep as much of the conversion income as possible in the current marginal tax bracket

> However, there are times when it may make sense to convert more and go into higher tax brackets

Advanced Roth IRA PlanningUnderstanding the Mechanics

Tax Rate Differential

31

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Single Married

Filing Jointly Head of Household

10% $8,350 $16,700 $11,950

15% $33,950 $67,900 $45,500

25% $82,250 $137,050 $117,450

28% $171,550 $208,850 $190,200

33% $372,950 $372,950 $372,950

35% > $372,950 > $372,950 > $372,950

2009 Tax Brackets

Advanced Roth IRA PlanningUnderstanding the Mechanics

Tax Rate Differential

32

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

10% tax bracket

15% tax bracket

25% tax bracket

28% tax bracket

33% tax bracket

35% tax bracket

Current taxable income

Target Roth IRA conversion amount

Optimum Roth IRA conversion amount

Advanced Roth IRA PlanningUnderstanding the Mechanics

Tax Rate Differential

33

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningUnderstanding the Mathematical MechanicsTax Rate Differential – Example #1 (50 Year Old)

ASSUMPTIONSIRA Owner's Age 50

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 40.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

34

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningUnderstanding the Mathematical MechanicsTax Rate Differential – Example #2 (50 Year Old)

ASSUMPTIONSIRA Owner's Age 50

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 40.00%Tax Rate - Future Years 30.00%

* Assumes 50% annual turnover on growth

35

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningUnderstanding the Mathematical MechanicsTax Rate Differential – Example #3 (50 Year Old)

ASSUMPTIONSIRA Owner's Age 50

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 30.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

36

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningUnderstanding the Mathematical MechanicsTax Rate Differential – Example #4 (70 Year Old)

ASSUMPTIONSIRA Owner's Age 70

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 40.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

37

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningUnderstanding the Mathematical MechanicsTax Rate Differential – Example #5 (70 Year Old)

ASSUMPTIONSIRA Owner's Age 70

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 40.00%Tax Rate - Future Years 30.00%

* Assumes 50% annual turnover on growth

38

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

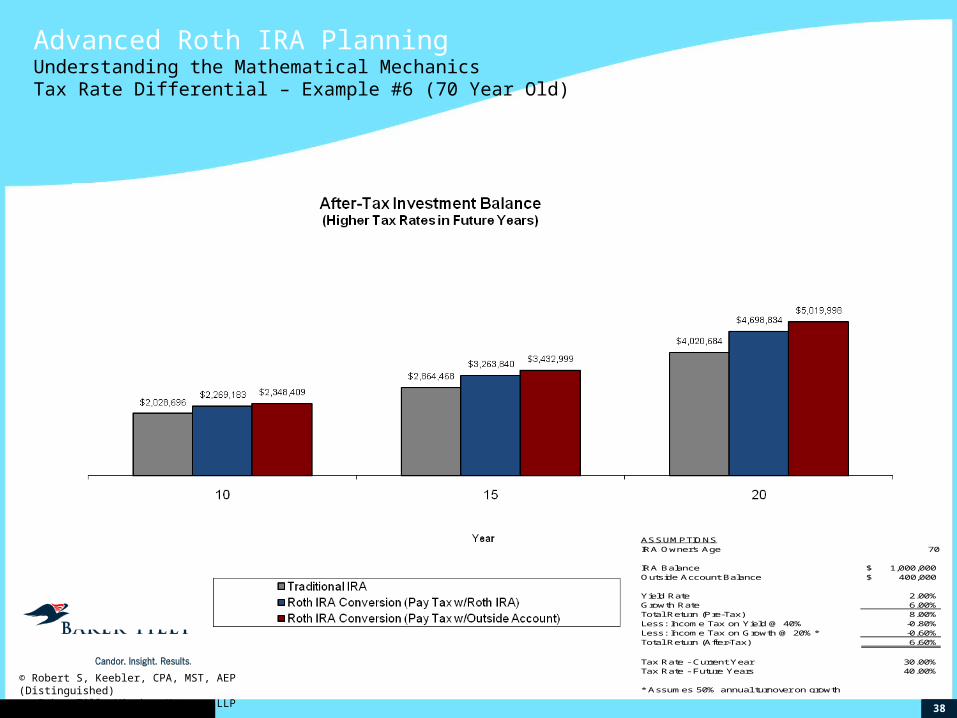

Advanced Roth IRA PlanningUnderstanding the Mathematical MechanicsTax Rate Differential – Example #6 (70 Year Old)

ASSUMPTIONSIRA Owner's Age 70

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 30.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

39

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningUnderstanding the Mathematical MechanicsTax Rate Differential – Example #7 (70 Year Old)

$-

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89

AgeOption 1 - Traditional IRAOption 2 - Roth IRA Conversion (Pay Tax w/Roth IRA)Option 3 - Roth IRA Conversion (Pay Tax w/Outside Account)

ASSUMPTIONSIRA Owner's Age 70

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 30.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

40

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Advanced Roth IRA PlanningTactical Considerations

> Unused charitable contribution carryovers

> Current year ordinary losses

> Net Operating Loss (NOL) carryovers from prior years

> Alternative Minimum Tax (AMT)

> Credit carryovers

41

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Taxpayers may “recharacterize” (i.e. undo) the Roth IRA conversion in current year or by the filing date of the current year’s tax return> Recharacterization can take place as late as 10/15 in the year

following the year of conversion

Taxpayers may choose to “reconvert” their recharacterization> Reconversion may only take place at the later of the following two dates:

(1) The tax year following the original conversion OR

(2) 30 days after the recharacterization

Advanced Roth IRA PlanningTactical Considerations

Interest Income

- Taxable

Capital Gain Income

-Preferential Rate

-Deferral until sale

Roth IRA and

Insurance

- Tax Free Growth/ Benefits

Real Estate, Oil & Gas and Tax Exempt Bonds

- Tax Preferences

Pension and

IRA Income

- Tax Deferred

Money market

Corporate bonds

US Treasury bonds

AttributesAnnual

income tax on interest

Taxed at highest marginal rates

Equity Securities

AttributesDeferral

until saleReduced

capital gains rate

Step-up basis at death

Real EstateDepreciation

tax shield1031

exchangesDeferral on

growth until sale

Oil & GasLarge up

front IDC deductions

Depletion allowances

Pension plansProfit sharing

plansAnnuities

AttributesGrowth during

lifetimeRMD for IRA

and qualified plans

No step-up

Roth IRATax-free growth during lifetimeNo 70½ RMDTax-free distributions out to beneficiaries life expectancy

Life InsuranceTax-deferred growthTax-exempt payout at death

TAX ASSET CLASSES

Dividend Income

Tax Exempt Interest

Equity securities

AttributesQualified

dividends at LTCG rate

Return of capital dividend

Capital gain dividends

Bonds issued by State and local Governmental entities

AttributesFederal tax

exemptState tax exempt

© 2009 Prepared by Robert S. Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLPAll Rights [email protected]

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.

For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors.

43

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

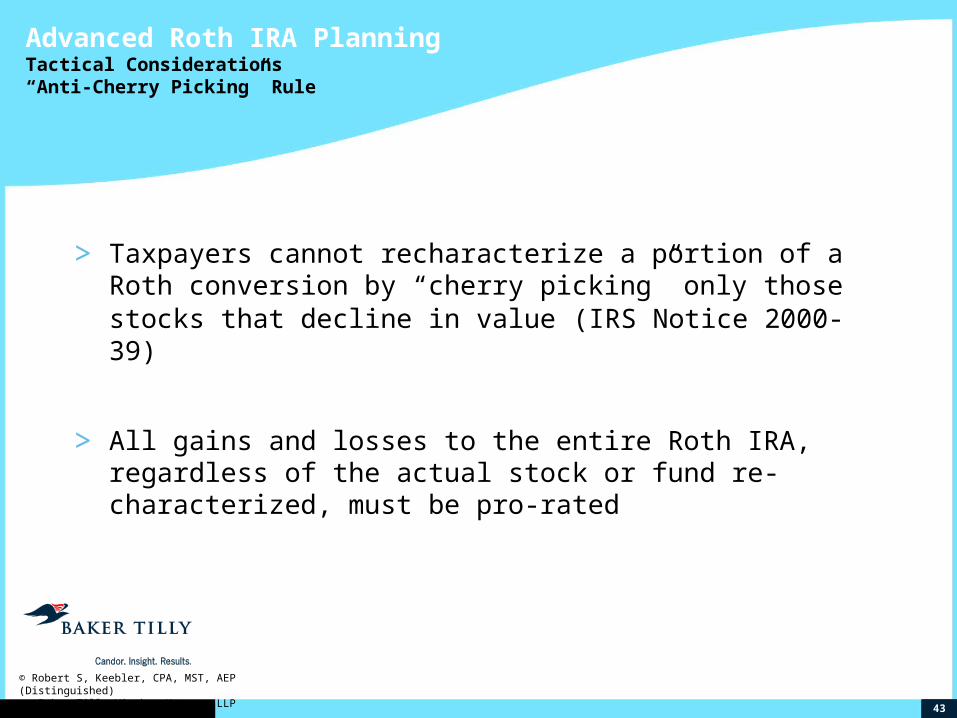

> Taxpayers cannot recharacterize a portion of a Roth conversion by “cherry picking” only those stocks that decline in value (IRS Notice 2000-39)

> All gains and losses to the entire Roth IRA, regardless of the actual stock or fund re-characterized, must be pro-rated

Advanced Roth IRA PlanningTactical Considerations“Anti-Cherry Picking” Rule

44

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

On January 2, 2009, when John Smith’s IRA was worth $500,000, he converted the entire amount to a Roth IRA. John will owe ordinary income tax on the entire $500,000. The IRA consisted of ABC Fund ($250,000) and XYZ Fund ($250,000). As of April 15, 2010, ABC Fund had declined in value to $100,000, while XYZ Fund had increased in value to $300,000. Thus, the total value of the IRA account declined in value to $400,000.

Even though John would like to re-characterize all of ABC Fund and leave XYZ fund in his Roth IRA, he must allocate the total loss to each fund pro-ratably. Therefore, John may only recharacterize $125,000 (25% x $500,000) of the original conversion amount instead of $250,000, resulting in taxable income of $375,000 ($500,000 - $125,000).

Advanced Roth IRA PlanningTactical Considerations“Anti-Cherry Picking” Rule - Example

Value @ Conversion

Current Value

Relative Percentages

(Current)ABC Fund 250,000$ 100,000$ 25%YYZ Fund 250,000$ 300,000$ 75%Total 500,000$ 400,000$ 100%

45

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Traditional IRAABC Fund: $250,000XYZ Fund: $250,000

Traditional IRA #1ABC Fund: $250,000

Traditional IRA #2XYZ Fund: $250,000

Advanced Roth IRA PlanningTactical ConsiderationsRoth IRA Conversion Segregation Strategy

STEP 1: Create separate IRAs for each asset, asset class or investment sector

46

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Traditional IRA #1ABC Fund: $250,000

Roth IRA #2XYZ Fund: $250,000

Advanced Roth IRA PlanningTactical ConsiderationsRoth IRA Conversion Segregation Strategy

STEP 2: Convert IRAs to separate Roth IRAs

Roth IRA #1ABC Fund: $250,000

Traditional IRA #2XYZ Fund: $250,000

47

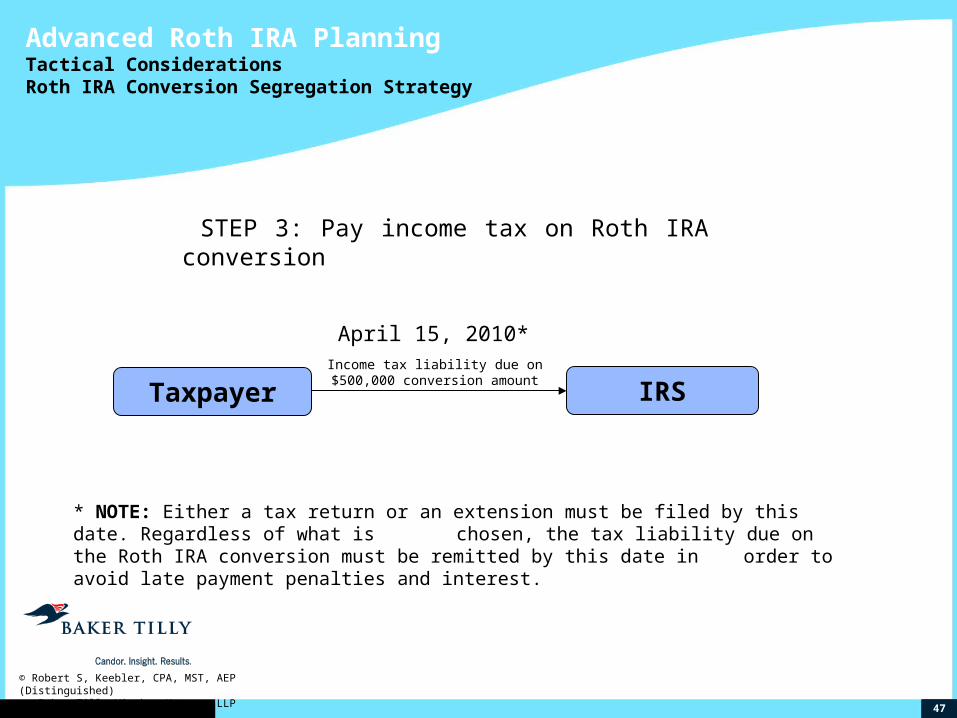

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

IRSTaxpayerIncome tax liability due on $500,000

conversion amount

April 15, 2010*

* NOTE: Either a tax return or an extension must be filed by this date. Regardless of what is chosen, the tax liability due on the Roth IRA conversion must be remitted by this date in order to avoid late payment penalties and interest.

Advanced Roth IRA PlanningTactical ConsiderationsRoth IRA Conversion Segregation Strategy

STEP 3: Pay income tax on Roth IRA conversion

48

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Roth IRA #1ABC Fund: $100,000

(Current Value)

Roth IRA #2XYZ Fund: $300,000

(Current Value)

Traditional IRA #1ABC Fund: $100,000

(Current Value)

Recharacterization of IRA using the value at the date of conversion

(e.g. $250,000)

October 15, 2010*

* NOTE: October 15, 2010 is the latest date for which a 2009 recharacterization can take place (either by filing extensions or by filing an amended return).

Advanced Roth IRA PlanningTactical ConsiderationsRoth IRA Conversion Segregation Strategy

STEP 4: Recharacterize Roth IRA conversion

49

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

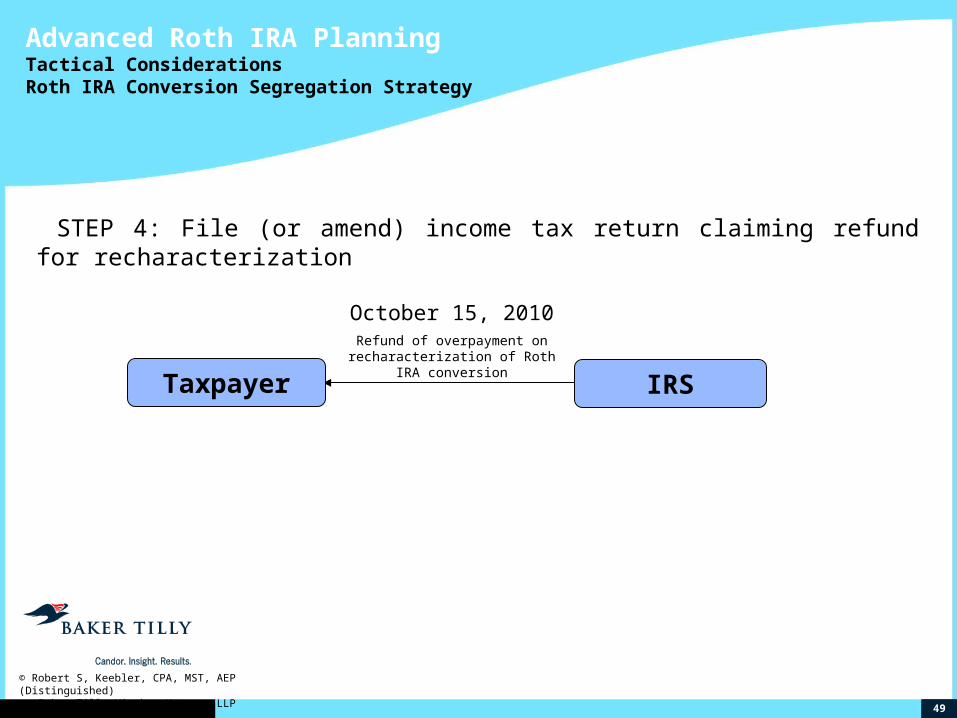

October 15, 2010Refund of overpayment on

recharacterization of Roth IRA conversion

Advanced Roth IRA PlanningTactical ConsiderationsRoth IRA Conversion Segregation Strategy

STEP 4: File (or amend) income tax return claiming refund for recharacterization

Taxpayer IRS

50

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

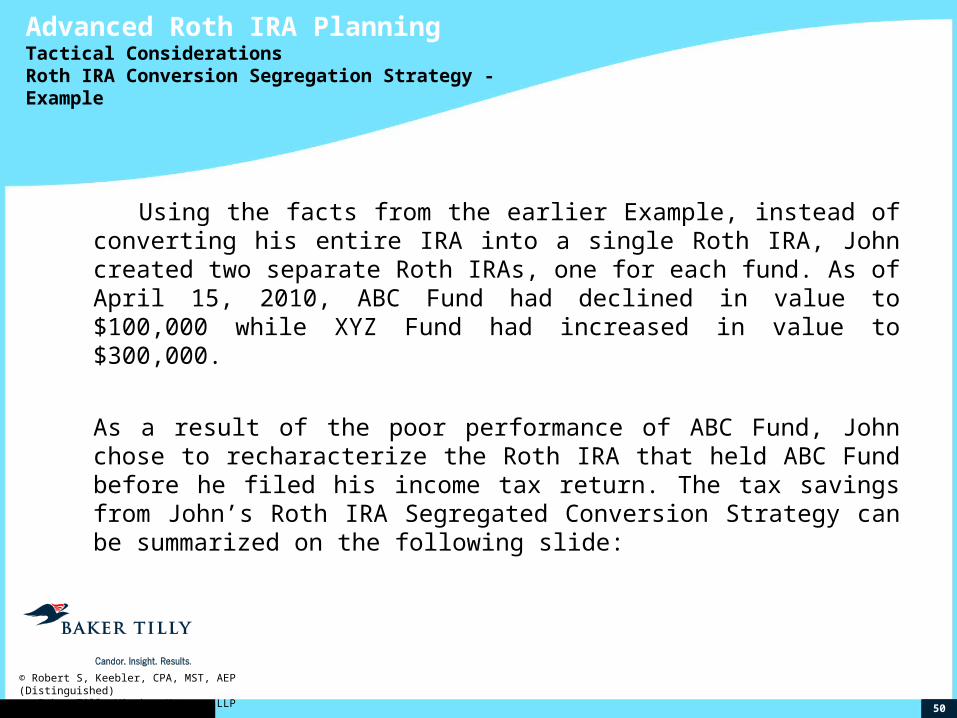

Using the facts from the earlier Example, instead of converting his entire IRA into a single Roth IRA, John created two separate Roth IRAs, one for each fund. As of April 15, 2010, ABC Fund had declined in value to $100,000 while XYZ Fund had increased in value to $300,000.

As a result of the poor performance of ABC Fund, John chose to recharacterize the Roth IRA that held ABC Fund before he filed his income tax return. The tax savings from John’s Roth IRA Segregated Conversion Strategy can be summarized on the following slide:

Advanced Roth IRA PlanningTactical ConsiderationsRoth IRA Conversion Segregation Strategy - Example

51

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Without Roth IRA

Segregation

With Roth IRA

Segregation DifferenceValue on Date of Conversion 500,000$ 500,000$ -$ Value of Roth IRA after recharacterization 300,000$ 300,000$ -$ Value of Traditional IRA after recharacterization 100,000$ 100,000$ -$ Ordinary Income Recognized 375,000$ 250,000$ (125,000)$ Ordinary Income Tax @ 28% 105,000$ 70,000$ (35,000)$

Advanced Roth IRA PlanningTactical ConsiderationsRoth IRA Conversion Segregation Strategy - Example

52

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Recharacterization – Comprehensive Example

1/1/10 Action 11/30/10 Action 1/1/11 Action 4/15/11 Action 10/15/11 Action 11/30/11 Action 1/1/12 Action

A $100,000 OriginalConversion

1/1/10

$125,000 Hold $130,000 Hold $130,000 Hold $135,000 Hold $130,000 N/A $130,000 N/A

B $100,000 OriginalConversion

1/1/10

$120,000 Hold $120,000 Hold $120,000 Hold $120,000 Hold $125,000 N/A $130,000 N/A

C $100,000 OriginalConversion

1/1/10

$100,000 Hold $100,000 Hold $95,000 Recharacterize4/15/11

$80,000 Reconvert5/16/11

$85,000 Hold $90,000 Hold

D $100,000 OriginalConversion

1/1/10

$ 75,000 Recharacterize11/30/10

$80,000 Reconvert1/1/11

$85,000 Hold $85,000 Hold $90,000 Hold $95,000 Hold

E $100,000 OriginalConversion

1/1/10

$ 75,000 Recharacterize11/30/10

$90,000 Reconvert1/1/11

$85,000 Hold $90,000 Hold $75,000 Recharacterize11/30/11

$80,000 Reconvert1/1/12

53

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Other Roth IRA Planning Issues

54

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

CONVERSION OF INHERITED QUALIFIED PLAN

> Notice 2008-30 – Section II, Q&A 7, allows non-spouse beneficiaries to convert inherited qualified plans to inherited Roth IRAs.

> Plan must allow for such transfers.

Other Roth IRA Planning IssuesRecognizing Losses on Roth IRAs

55

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> Taxpayers are generally allowed to deduct a loss on a Roth IRA in the year that the Roth IRA is fully liquidated> Loss is a miscellaneous itemized deduction subject to the 2% AGI

floor

> Deduction is an add-back for AMT purposes

> In order to recognize the loss, the taxpayer must liquidate all Roth IRAs within the same tax year

Other Roth IRA Planning IssuesRecognizing Losses on Roth IRAs

56

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> 11 U.S.C. §522 > Retirement asset protection

> IRA and Roth IRA limitations

> $1 Million

> Rollover IRA protection> Separate Accounts

> Protection for Business Owners

Other Roth IRA Planning IssuesBankruptcy/Creditor Protection2005 Bankruptcy Act

57

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

> Several states have “opt out” provisions that replace the U.S.C. with state law protection> It is important to assess the level of protection each state law provides

IRA owners to determine which set of laws (federal vs. state) to apply in a particular case

Other Roth IRA Planning IssuesBankruptcy/Creditor Protection

58

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Qualified Plan

Traditional IRA

Roth IRA

Bankruptcy and creditor protection may be lost as a result of the following series of transactions

Other Roth IRA Planning IssuesBankruptcy/Creditor Protection

59

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

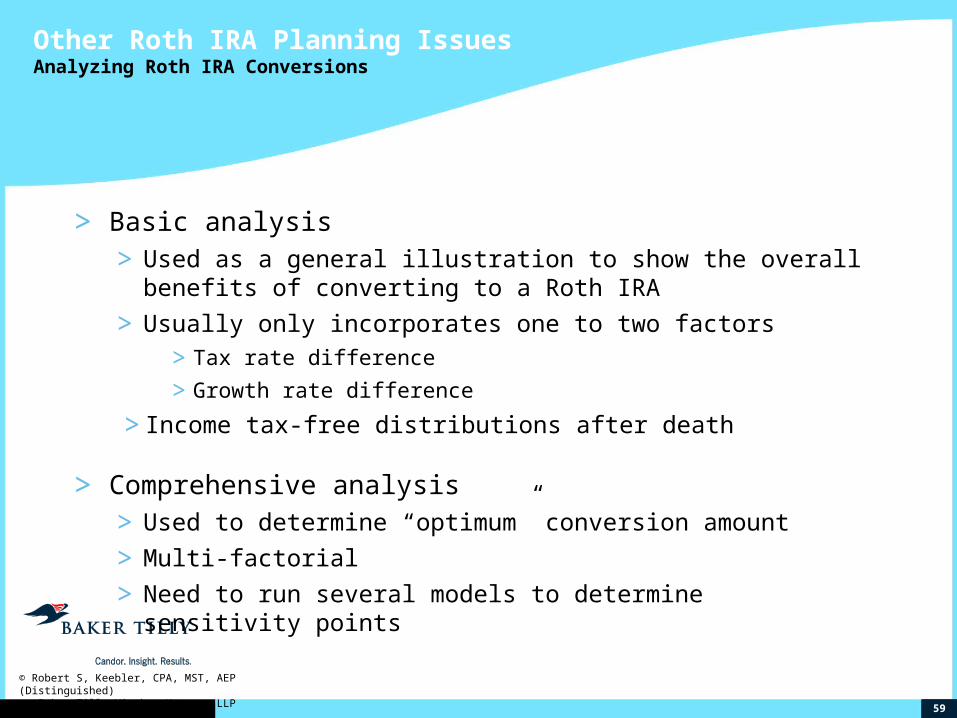

> Basic analysis> Used as a general illustration to show the overall benefits of

converting to a Roth IRA

> Usually only incorporates one to two factors

> Tax rate difference

> Growth rate difference

> Income tax-free distributions after death

> Comprehensive analysis> Used to determine “optimum” conversion amount

> Multi-factorial

> Need to run several models to determine sensitivity points

Other Roth IRA Planning IssuesAnalyzing Roth IRA Conversions

60

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Conclusion

61

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.

Although effort was taken to ensure the accuracy of these materials, Robert S. Keebler and Baker Tilly Virchow Krause, LLP assume no responsibility or liability for an individual’s reliance on these materials. These materials are being provided for educational and informational purposes only and are in no way to be construed as accounting, financial, tax, legal or other advice. Individual readers must consult their own professional tax and legal advisors.

62

© Robert S, Keebler, CPA, MST, AEP (Distinguished) Baker Tilly Virchow Krause, LLP

To be added to our IRA update newsletter, please [email protected]

Recommended