A Contribution to the A Contribution to the Global Measurement Global Measurement

of the ICT Sector: of the ICT Sector: ALETI CensusALETI Census

November 13th, 2013GPATS 2013

São Paulo – SP - Brazil

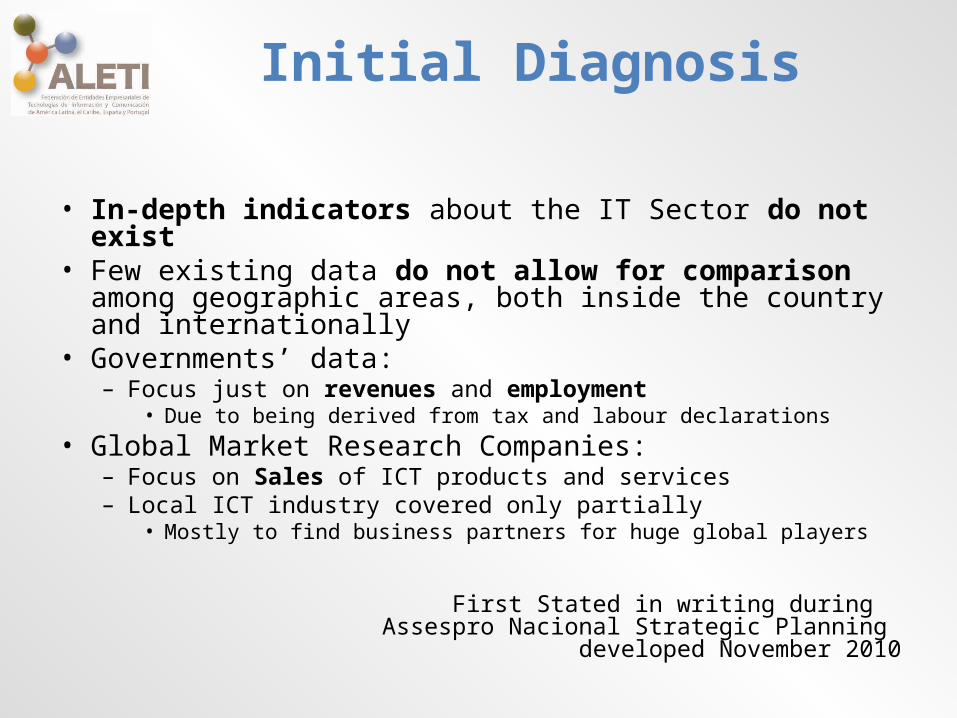

Initial Diagnosis

• In-depth indicators about the IT Sector do not exist• Few existing data do not allow for comparison among

geographic areas, both inside the country and internationally• Governments’ data:

– Focus just on revenues and employment• Due to being derived from tax and labour declarations

• Global Market Research Companies:– Focus on Sales of ICT products and services– Local ICT industry covered only partially

• Mostly to find business partners for huge global players

First Stated in writing during Assespro Nacional Strategic Planning

developed November 2010

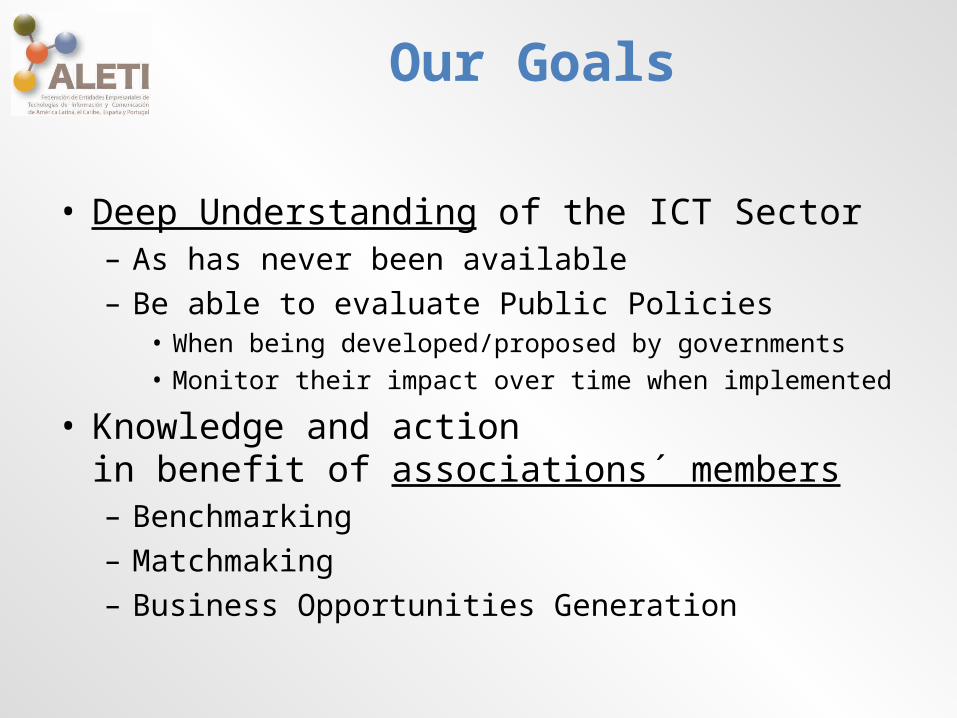

Our Goals

• Deep Understanding of the ICT Sector– As has never been available– Be able to evaluate Public Policies

• When being developed/proposed by governments• Monitor their impact over time when implemented

• Knowledge and action in benefit of associations´ members– Benchmarking– Matchmaking– Business Opportunities Generation

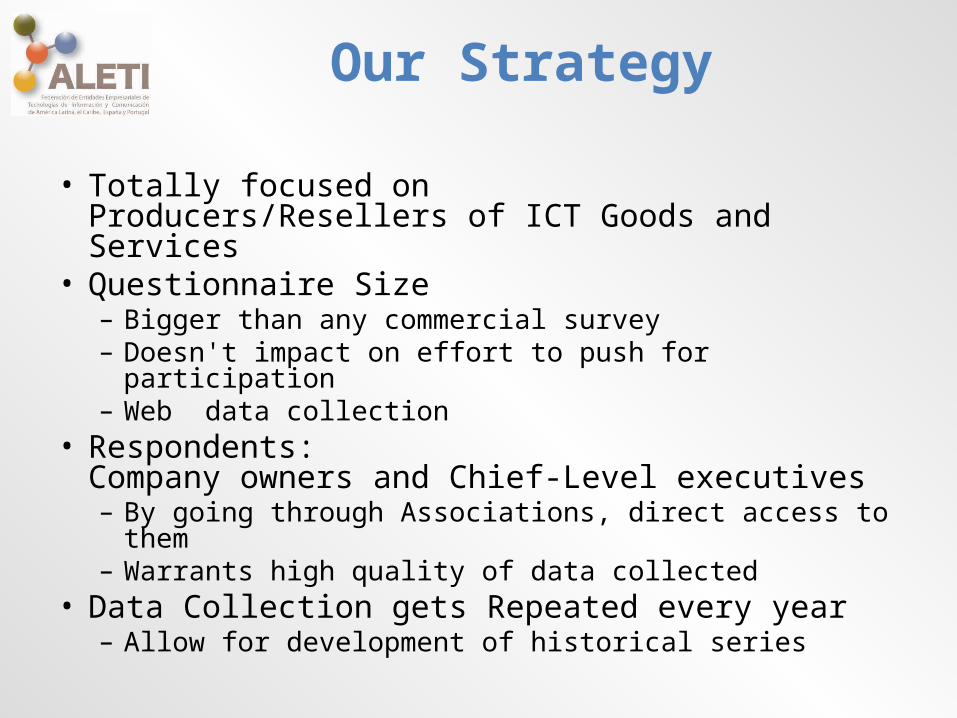

Our Strategy

• Totally focused on Producers/Resellers of ICT Goods and Services

• Questionnaire Size– Bigger than any commercial survey– Doesn't impact on effort to push for participation – Web data collection

• Respondents: Company owners and Chief-Level executives– By going through Associations, direct access to them– Warrants high quality of data collected

• Data Collection gets Repeated every year– Allow for development of historical series

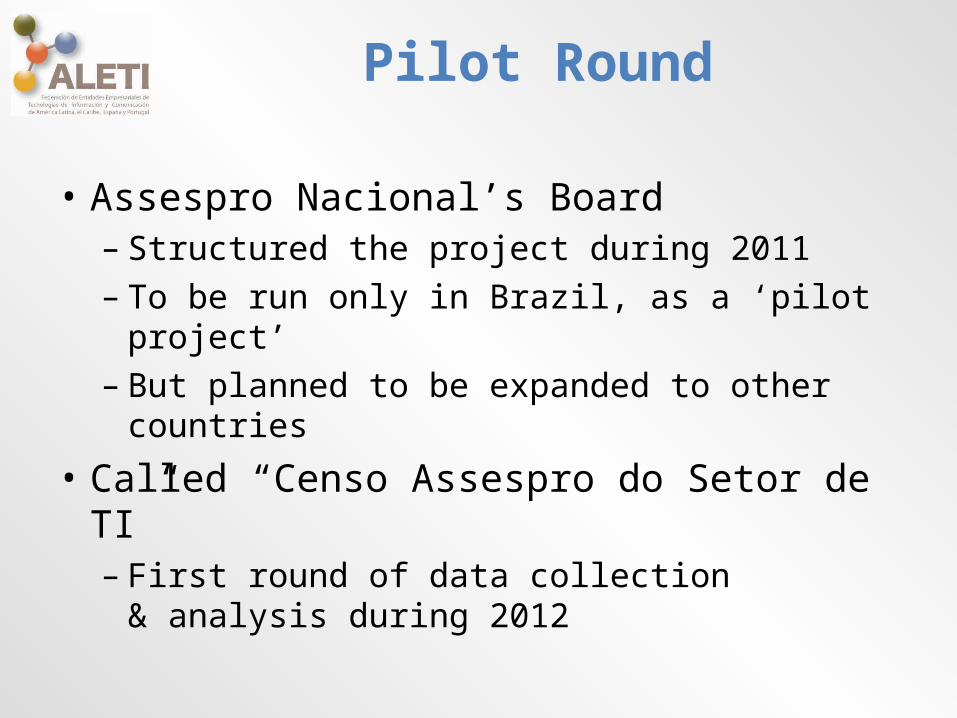

Pilot Round

• Assespro Nacional’s Board – Structured the project during 2011– To be run only in Brazil, as a ‘pilot project’– But planned to be expanded to other countries

• Called “Censo Assespro do Setor de TI”– First round of data collection

& analysis during 2012

Public Policy: A practical case

• Brazilian Science and Technology Ministry launched “TI Maior” (‘Bigger IT’) program Aug/2012– One of proposed measures:

• Develop a new national certification process (“CerTICs”) – Aimed at certifying

“local development of innovative products”– Certified products would receive 25% of margin of preference for

procurement by the Brazilian Federal Government

– Details not known during Census preparation, but able to evaluate:• Which companies would benefit• Real size of market impact

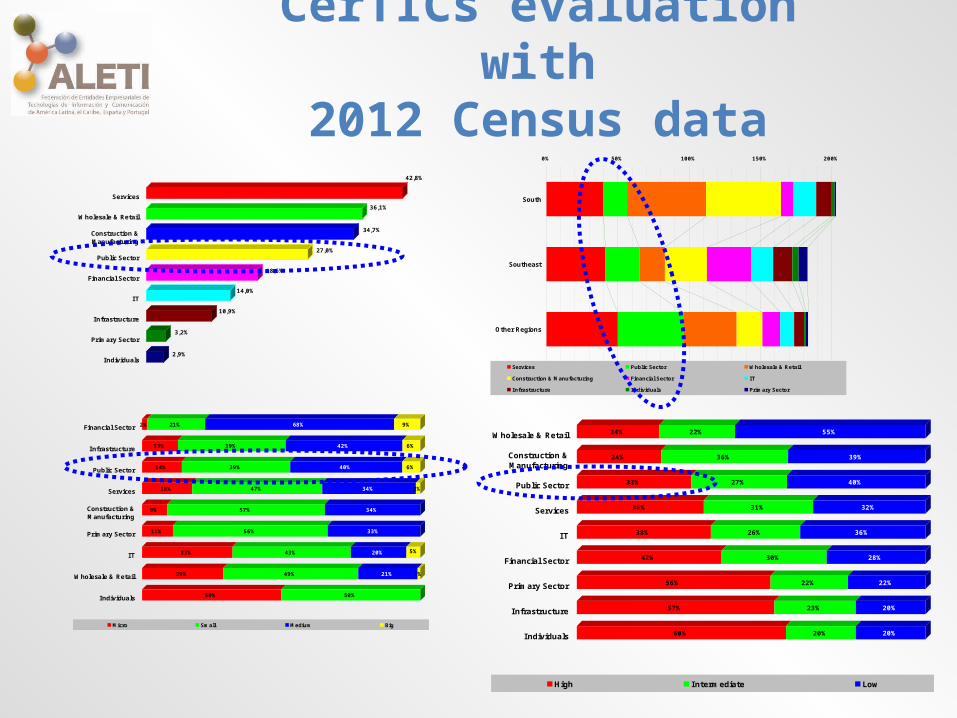

CerTICs evaluation with2012 Census data

2,9%

3,2%

10,9%

14,0%

18,6%

27,0%

34,7%

36,1%

42,8%

Services

Wholesale & Retail

Construction &Manufacturing

Public Sector

Financial Sector

IT

Infrastructure

Primary Sector

Individuals

0% 50% 100% 150% 200%

Other Regions

Southeast

South

Services Public Sector Wholesale & Retail

Construction & Manufacturing Financial Sector IT

Infrastructure Individuals Primary Sector

50% 50%

29% 49% 21% 1%

33% 43% 20% 5%

11% 56% 33%

9% 57% 34%

18% 47% 34% 2%

14% 39% 40% 6%

13% 39% 42% 6%

2% 21% 68% 9%

Individuals

Wholesale & Retail

IT

Primary Sector

Construction &Manufacturing

Services

Public Sector

Infrastructure

Financial Sector

Micro Small Medium Big

60% 20% 20%

57% 23% 20%

56% 22% 22%

42% 30% 28%

38% 26% 36%

36% 31% 32%

33% 27% 40%

24% 36% 39%

24% 22% 55%

Individuals

Infrastructure

Primary Sector

Financial Sector

IT

Services

Public Sector

Construction &Manufacturing

Wholesale & Retail

High Intermediate Low

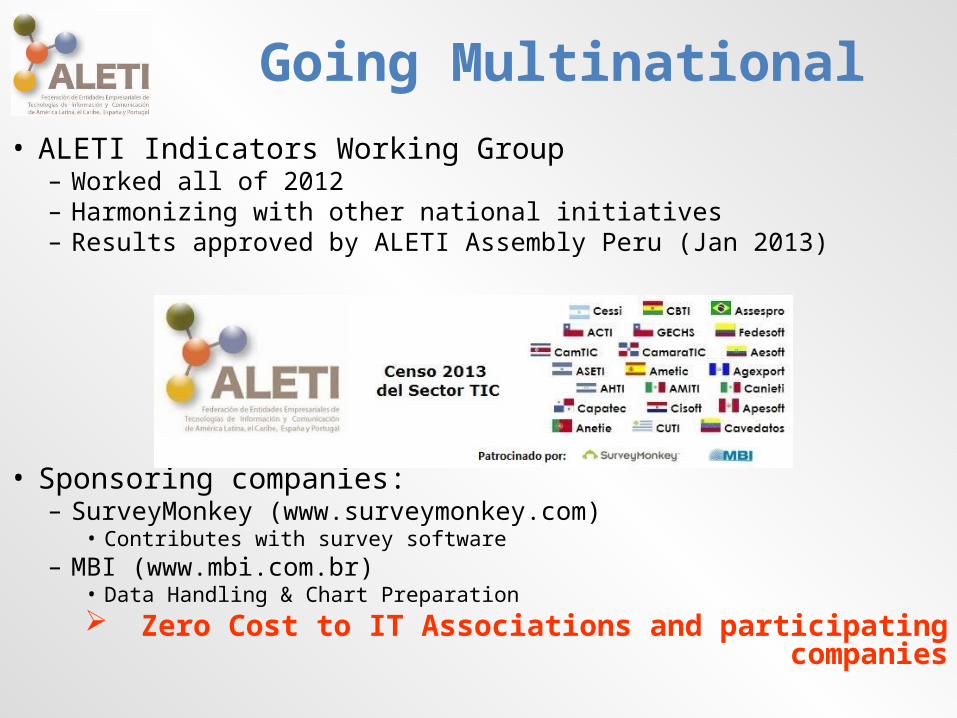

• ALETI Indicators Working Group– Worked all of 2012– Harmonizing with other national initiatives– Results approved by ALETI Assembly Peru (Jan 2013)

• Sponsoring companies:– SurveyMonkey (www.surveymonkey.com)

• Contributes with survey software– MBI (www.mbi.com.br)

• Data Handling & Chart Preparation Zero Cost to IT Associations and participating companies

Going Multinational

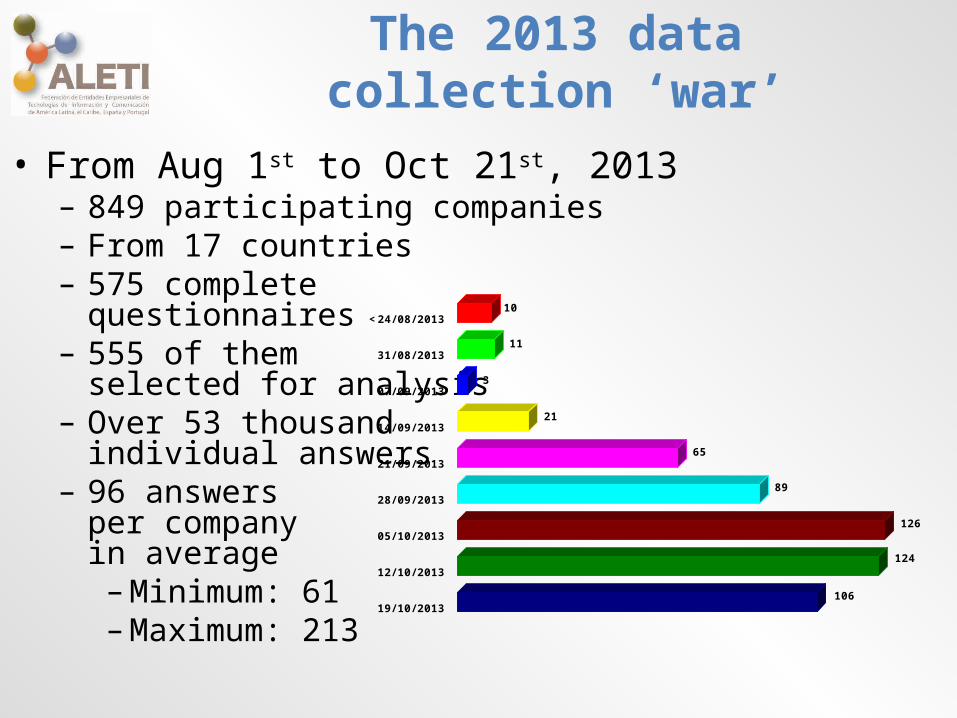

The 2013 data collection ‘war’

• From Aug 1st to Oct 21st, 2013– 849 participating companies– From 17 countries– 575 complete

questionnaires– 555 of them

selected for analysis– Over 53 thousand

individual answers– 96 answers

per company in average–Minimum: 61–Maximum: 213

106

124

126

89

65

21

3

11

10<24/ 08/ 2013

31/ 08/ 2013

07/ 09/ 2013

14/ 09/ 2013

21/ 09/ 2013

28/ 09/ 2013

05/ 10/ 2013

12/ 10/ 2013

19/ 10/ 2013

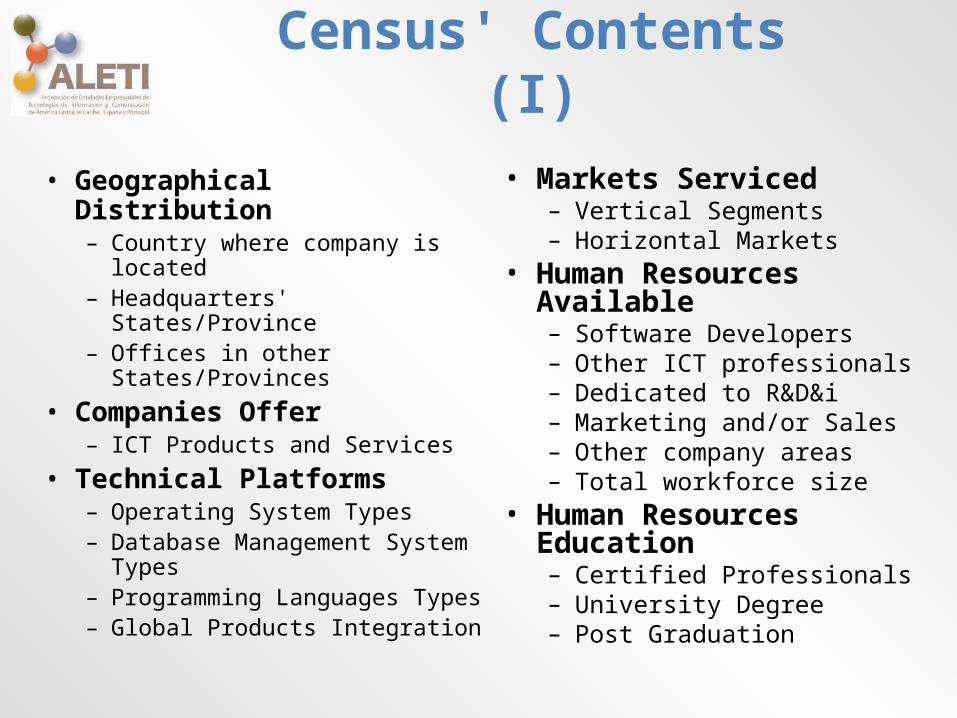

Census' Contents (I)

• Geographical Distribution– Country where company is

located– Headquarters' States/Province– Offices in other States/Provinces

• Companies Offer– ICT Products and Services

• Technical Platforms– Operating System Types– Database Management System

Types– Programming Languages Types– Global Products Integration

• Markets Serviced– Vertical Segments– Horizontal Markets

• Human Resources Available– Software Developers– Other ICT professionals– Dedicated to R&D&i– Marketing and/or Sales– Other company areas– Total workforce size

• Human Resources Education– Certified Professionals– University Degree– Post Graduation

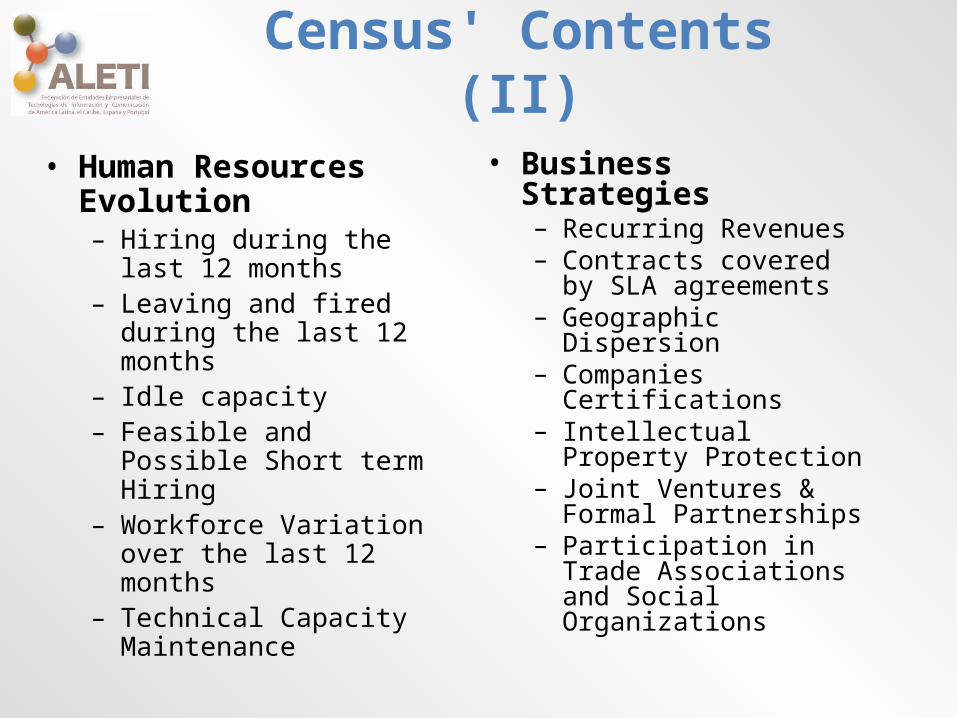

Census' Contents (II)

• Human Resources Evolution– Hiring during the last 12

months– Leaving and fired during the

last 12 months– Idle capacity– Feasible and Possible Short

term Hiring– Workforce Variation over the

last 12 months– Technical Capacity

Maintenance

• Business Strategies– Recurring Revenues– Contracts covered by SLA

agreements– Geographic Dispersion– Companies Certifications– Intellectual Property

Protection– Joint Ventures & Formal

Partnerships– Participation in Trade

Associations and Social Organizations

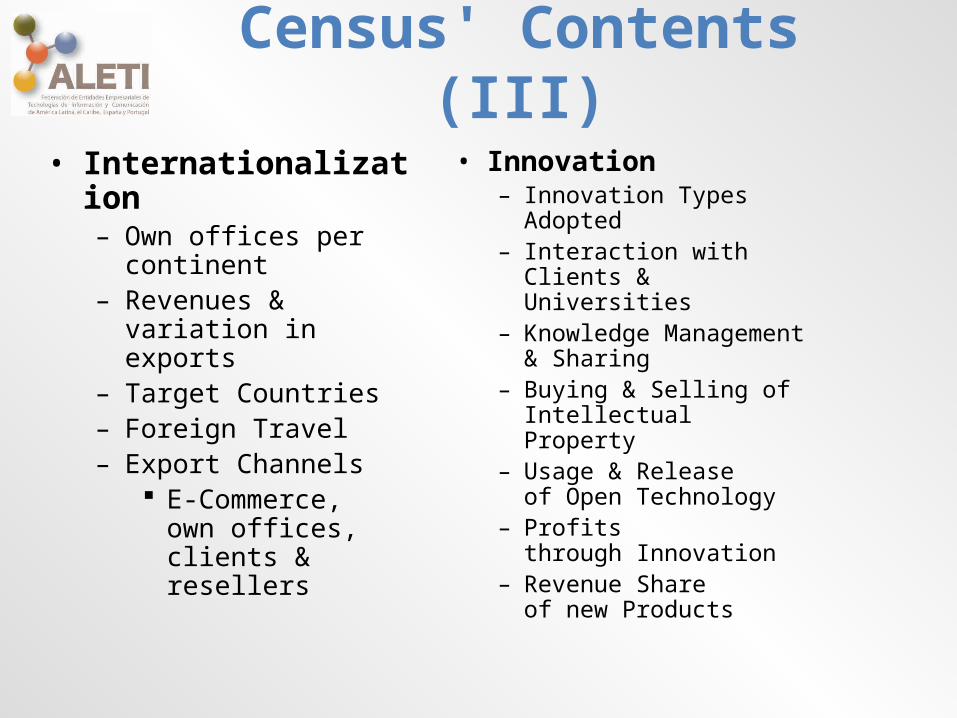

Census' Contents (III)

• Internationalization– Own offices per continent– Revenues & variation in

exports– Target Countries– Foreign Travel– Export Channels

E-Commerce, own offices, clients & resellers

• Innovation– Innovation Types

Adopted– Interaction with

Clients & Universities– Knowledge Management

& Sharing– Buying & Selling of

Intellectual Property– Usage & Release

of Open Technology– Profits

through Innovation– Revenue Share

of new Products

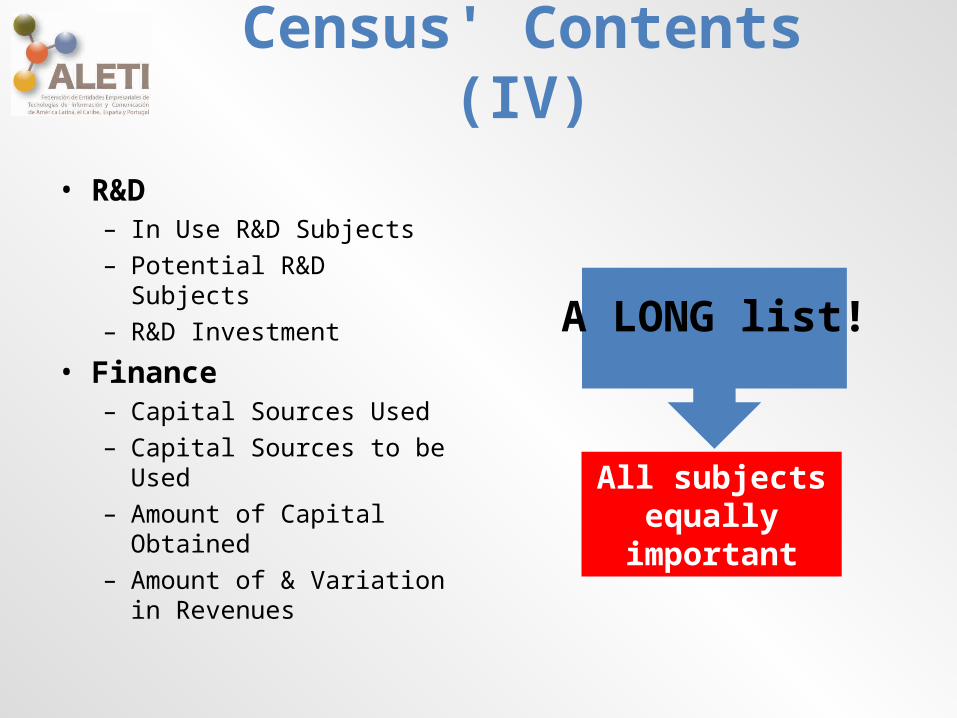

Census' Contents (IV)

• R&D– In Use R&D Subjects– Potential R&D Subjects– R&D Investment

• Finance– Capital Sources Used– Capital Sources to be Used– Amount of Capital Obtained– Amount of & Variation in

Revenues

All subjects equally important

A LONG list!

Designing Answers

• Usage of ranges instead of values– Easier to get answers– Range averages are more precise

• Based on standard classification systems– E.g. vertical markets, R&D subjects

• Need to be simultaneously:– Sufficiently detailed to allow for matchmaking– Structured to be grouped during analysis– In case specific answers are not selected

frequently enough to be statistically significant

Cross Analysis

• Understanding relations between apparently unrelated aspects

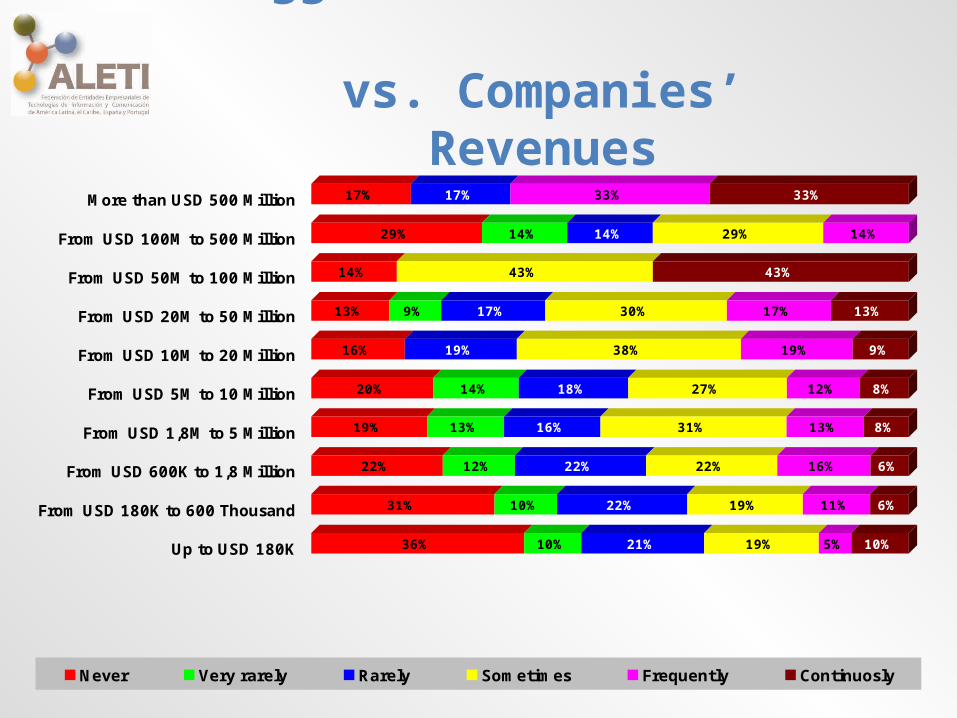

• Frequently reveals ‘pearls’ of wisdom• Let’s see TWO examples:– Which size of companies are the most aggressive

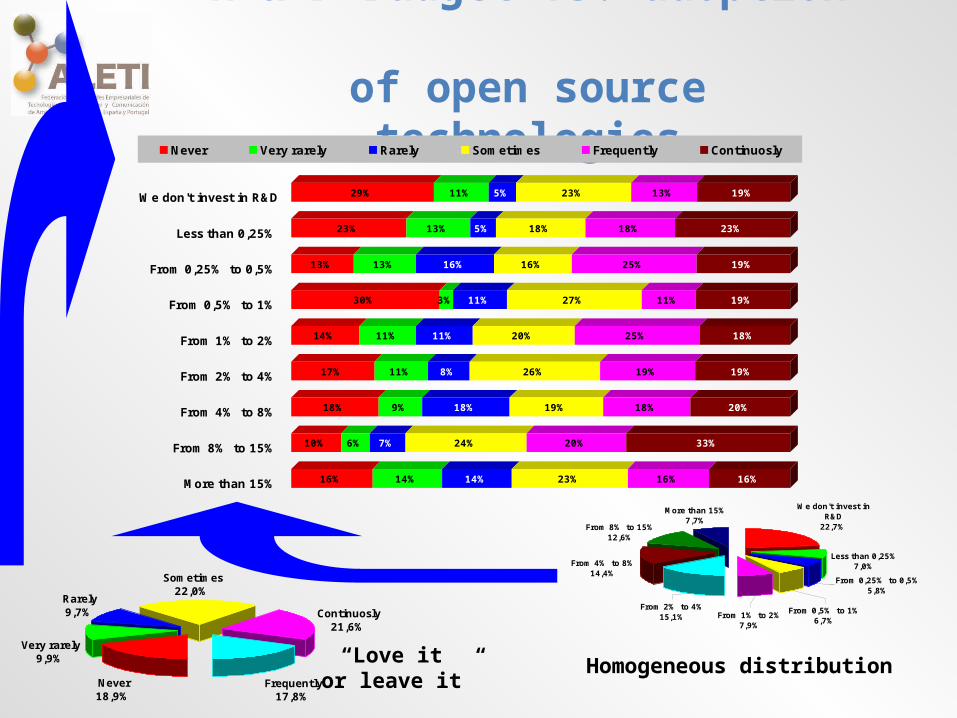

innovators?– How does R & D budget relate to the adoption of

open source technologies?

Aggressive Innovation vs. Companies’ Revenues

36% 10% 21% 19% 5% 10%

31% 10% 22% 19% 11% 6%

22% 12% 22% 22% 16% 6%

19% 13% 16% 31% 13% 8%

20% 14% 18% 27% 12% 8%

16% 19% 38% 19% 9%

13% 9% 17% 30% 17% 13%

14% 43% 43%

29% 14% 14% 29% 14%

17% 17% 33% 33%

Up to USD 180K

From USD 180K to 600 Thousand

From USD 600K to 1,8 Million

From USD 1,8M to 5 Million

From USD 5M to 10 Million

From USD 10M to 20 Million

From USD 20M to 50 Million

From USD 50M to 100 Million

From USD 100M to 500 Million

More than USD 500 Million

Never Very rarely Rarely Sometimes Frequently Continuosly

R & D Budget vs. adoption of open source technologies

16% 14% 14% 23% 16% 16%

10% 6% 7% 24% 20% 33%

18% 9% 18% 19% 18% 20%

17% 11% 8% 26% 19% 19%

14% 11% 11% 20% 25% 18%

30% 3% 11% 27% 11% 19%

13% 13% 16% 16% 25% 19%

23% 13% 5% 18% 18% 23%

29% 11% 5% 23% 13% 19%We don't invest in R&D

Less than 0,25%

From 0,25% to 0,5%

From 0,5% to 1%

From 1% to 2%

From 2% to 4%

From 4% to 8%

From 8% to 15%

More than 15%

Never Very rarely Rarely Sometimes Frequently Continuosly

We don't invest in R&D

22,7%

More than 15%7,7%

From 8% to 15%12,6%

From 4% to 8%14,4%

From 2% to 4%15,1%

From 0,25% to 0,5%5,8%

Less than 0,25%7,0%

From 0,5% to 1%6,7%

From 1% to 2%7,9%

Never18,9%

Very rarely9,9%

Rarely9,7%

Sometimes22,0%

Continuosly21,6%

Frequently17,8%

“Love it or leave it”

Homogeneous distribution

Subset Analysis

• Based on considering subset of companies with a specific answer to a specific question

• Examples:– Are revenues of companies betting on mobile

platforms higher or lower than the sector’s average?

– Do companies offering Software as a Service export more or less than average?

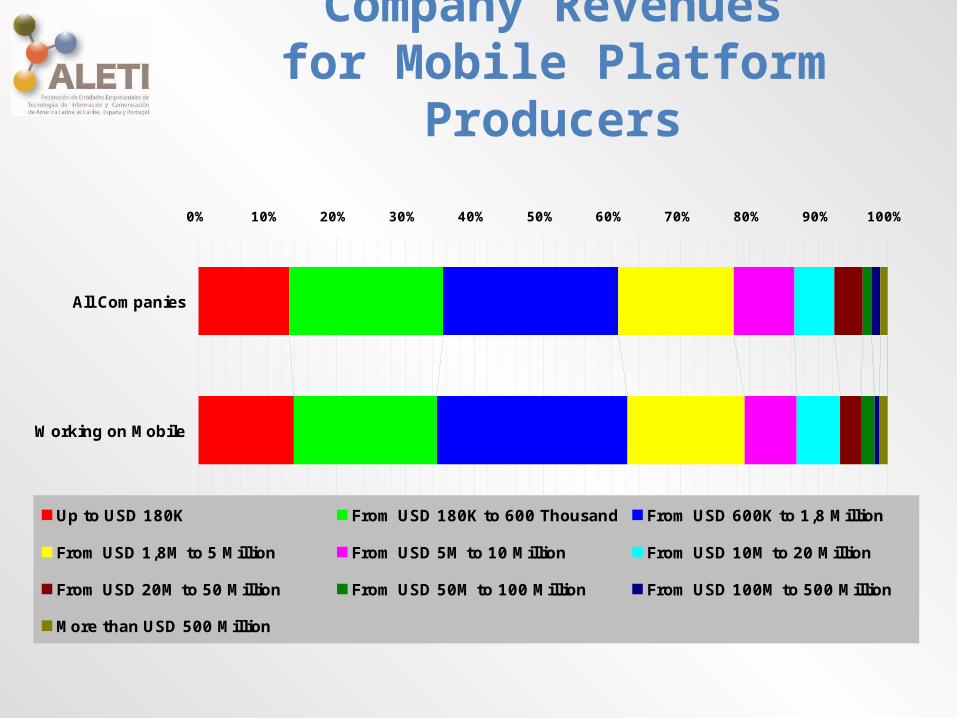

Company Revenuesfor Mobile Platform Producers

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Working on Mobile

All Companies

Up to USD 180K From USD 180K to 600 Thousand From USD 600K to 1,8 Million

From USD 1,8M to 5 Million From USD 5M to 10 Million From USD 10M to 20 Million

From USD 20M to 50 Million From USD 50M to 100 Million From USD 100M to 500 Million

More than USD 500 Million

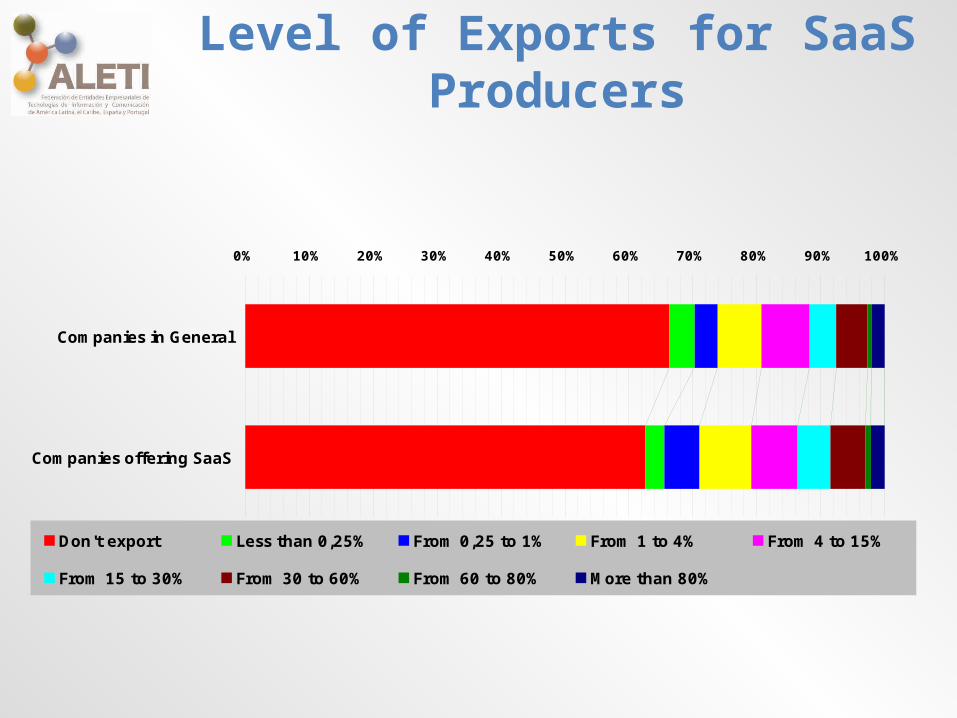

Level of Exports for SaaS Producers

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Companies offering SaaS

Companies in General

Don't export Less than 0,25% From 0,25 to 1% From 1 to 4% From 4 to 15%

From 15 to 30% From 30 to 60% From 60 to 80% More than 80%

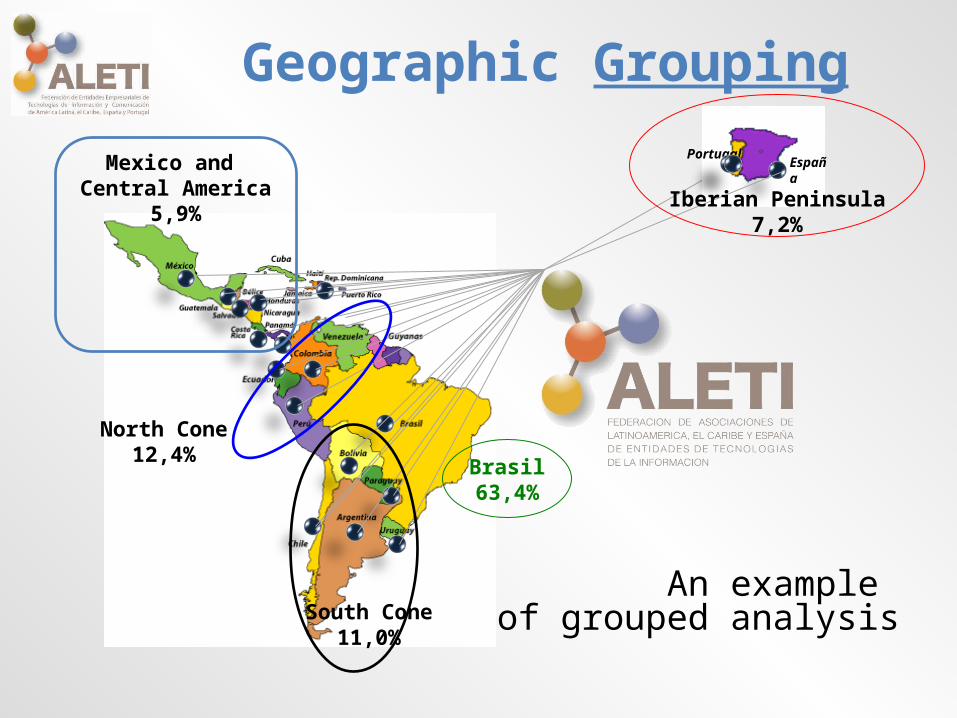

Geographic GroupingPortugal

España

Iberian Peninsula7,2%

Brasil63,4%

South Cone11,0%

North Cone12,4%

Mexico and Central America

5,9%

An example of grouped analysis

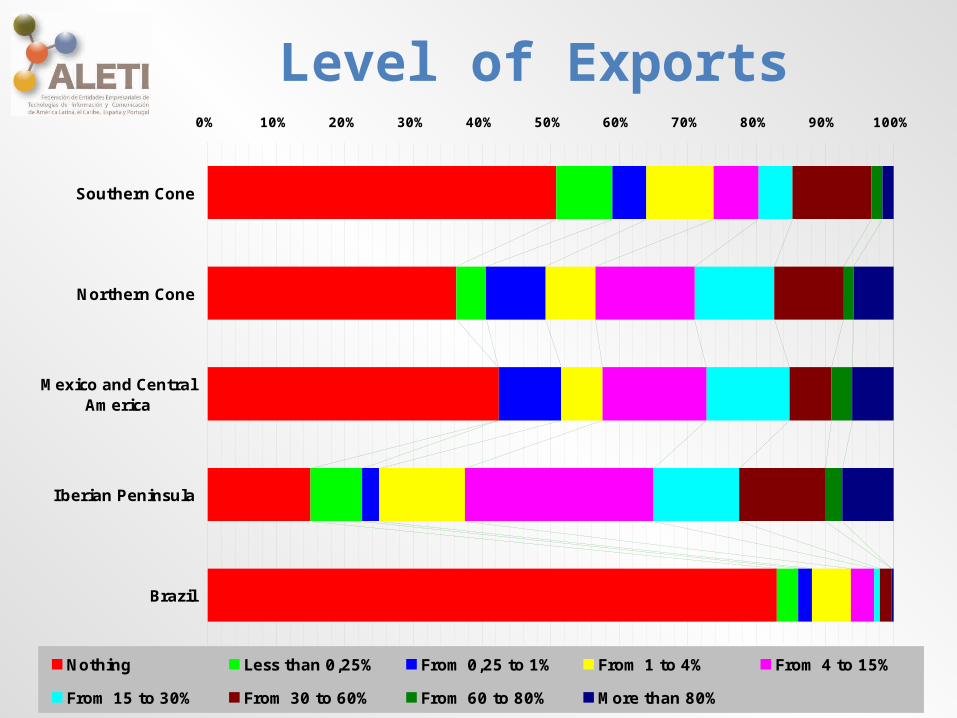

Level of Exports0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Brazil

Iberian Peninsula

Mexico and CentralAmerica

Northern Cone

Southern Cone

Nothing Less than 0,25% From 0,25 to 1% From 1 to 4% From 4 to 15%

From 15 to 30% From 30 to 60% From 60 to 80% More than 80%

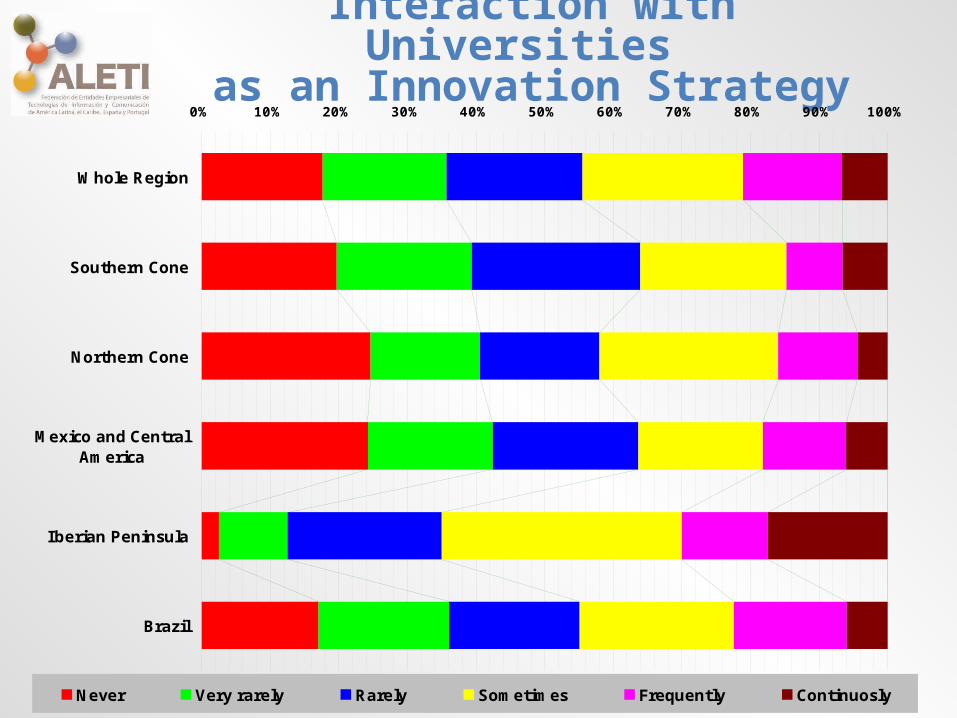

Interaction with Universities as an Innovation Strategy

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Brazil

Iberian Peninsula

Mexico and CentralAmerica

Northern Cone

Southern Cone

Whole Region

Never Very rarely Rarely Sometimes Frequently Continuosly

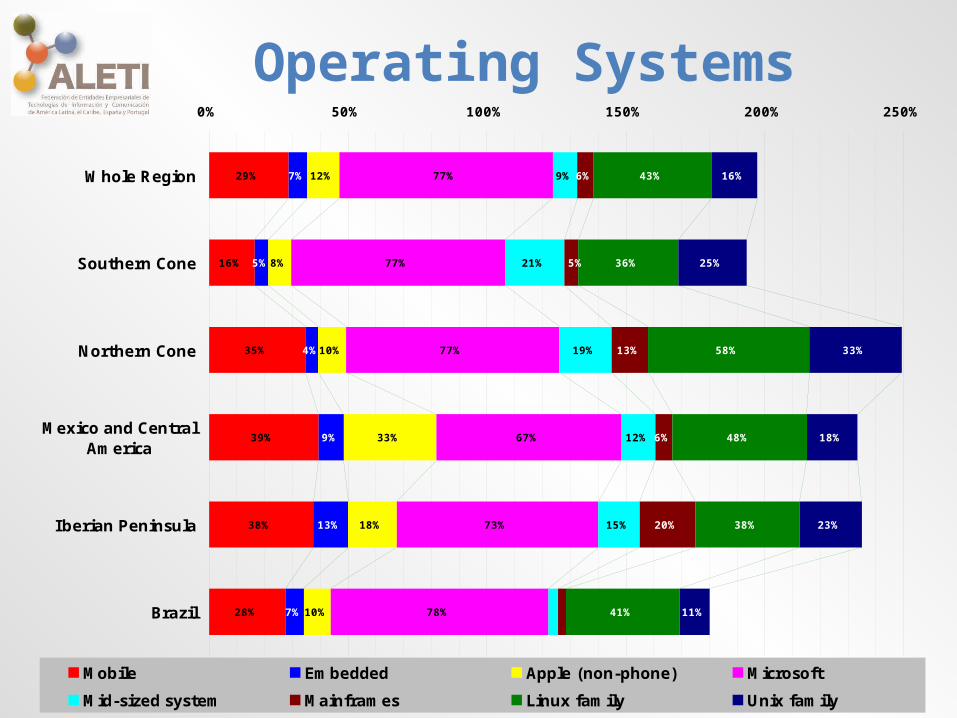

Operating Systems

28%

38%

39%

35%

16%

29%

7%

13%

9%

4%

5%

7%

10%

18%

33%

10%

8%

12%

78%

73%

67%

77%

77%

77%

15%

12%

19%

21%

9%

20%

6%

13%

6%

41%

38%

48%

58%

36%

43%

11%

23%

18%

33%

25%

16%

5%

0% 50% 100% 150% 200% 250%

Brazil

Iberian Peninsula

Mexico and CentralAmerica

Northern Cone

Southern Cone

Whole Region

Mobile Embedded Apple (non-phone) Microsoft

Mid-sized system Mainframes Linux family Unix family

Census’ Data Sharing Policy

• Because of:– Huge number of possible analysis

• Much bigger than IT associations resources– Wider usage of data brings wider recognition

• Census database is shared with interested:– Governments– Universities– Research Centers– International and Multilateral Organizations– Plus other non-profit organizations

• Free of Charge– We just ask for the signature of a simple MOU

Next Goals

• Grow number of participating companies – During each annual rollout

• Grow number of participating countries– Including new geographic areas

WITSA is our natural ‘network hub’

Thank you!

• WITSA Board Member (2012-2014)ALETI President (2011-2013)Assespro Nacional Vice-President (2011-2014)Assespro São Paulo President (2007-2010)Assespro São Paulo Director (2003-2006)Columnist at Information Week Brasil (since 1999)M.Sc. In Computer Science at São Paulo University (USP) - 1992Founder & CEO at MBI – since 1990Former University Professor in Computer Science (USP) - 1988-1998Working in IT since 1979

Roberto C. [email protected]

Recommended

![[GPATS 2013] Makoto (Mac) Yokozawa - Cyber Immune Systems That Helps Trust and Reliability, Helped By Cross Boarder Corporation](https://img.pdfslide.net/doc/110x75/545ca436b1af9f280a8b480f/gpats-2013-makoto-mac-yokozawa-cyber-immune-systems-that-helps-trust-and-reliability-helped-by-cross-boarder-corporation.jpg)

![[GPATS 2013 ] Bernd FRIEDRICH and Milena SEIBOLD - Measuring the IT Industry Globally the itib approach v0.4](https://img.pdfslide.net/doc/110x75/54532c19b1af9f7f248b57a3/gpats-2013-bernd-friedrich-and-milena-seibold-measuring-the-it-industry-globally-the-itib-approach-v04.jpg)

![[GPATS 2013] Luís Stein - Free Trade Policies in ICT Goods and Services](https://img.pdfslide.net/doc/110x75/545ca3e7af7959be0e8b48ae/gpats-2013-luis-stein-free-trade-policies-in-ict-goods-and-services.jpg)