© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION• Presenter Title Goes Here

• Name of Presenter Goes Here

Repairing Warranty

ManagementIn Automotive Aftermarket

Maintenance Required

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

2

Rob ZomokSr. Director,Supply ChainPerformance Analytics

Dave MillerVice President ofMarketing,Automotive Aftermarket

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

AGENDA1. Review Impact of

Warranty on the Aftermarket

2. Current Industry Initiatives– AASA Warranty Task

Force– Channel Partner

Collaboration Success

3. A Look into Another Industry

4. Go Forward Strategy3

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

4

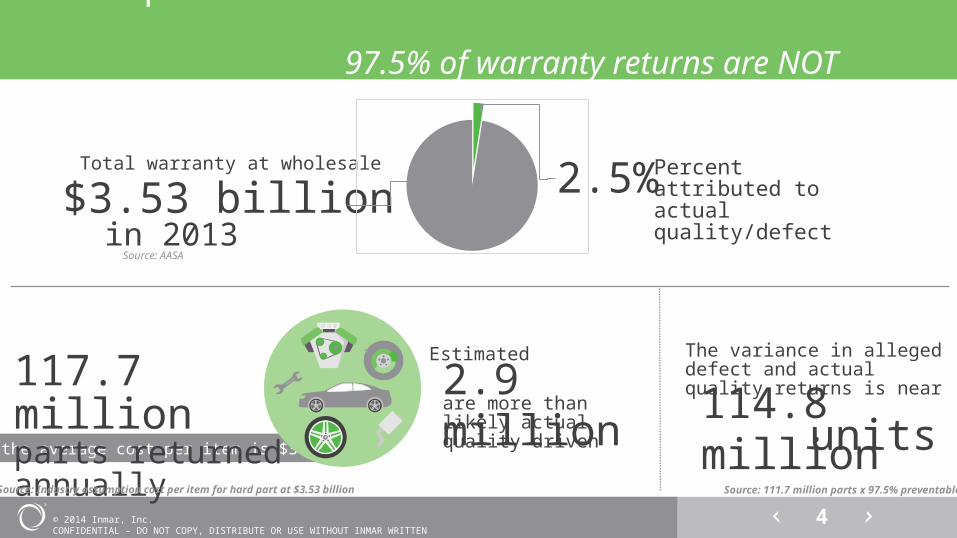

The Impact: 97.5% of warranty returns are NOT QUALITY RELATED

Total warranty at wholesale

$3.53 billionin 2013

2.5% Percent attributed to actual quality/defect

Source: AASA

*If the average cost per item is $30

117.7 millionparts returned annually

2.9 millionEstimated

are more than likely actual quality driven

The variance in alleged defect and actual quality returns is near

114.8 million units

Source: Industry assumption cost per item for hard part at $3.53 billion Source: 111.7 million parts x 97.5% preventable

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

5

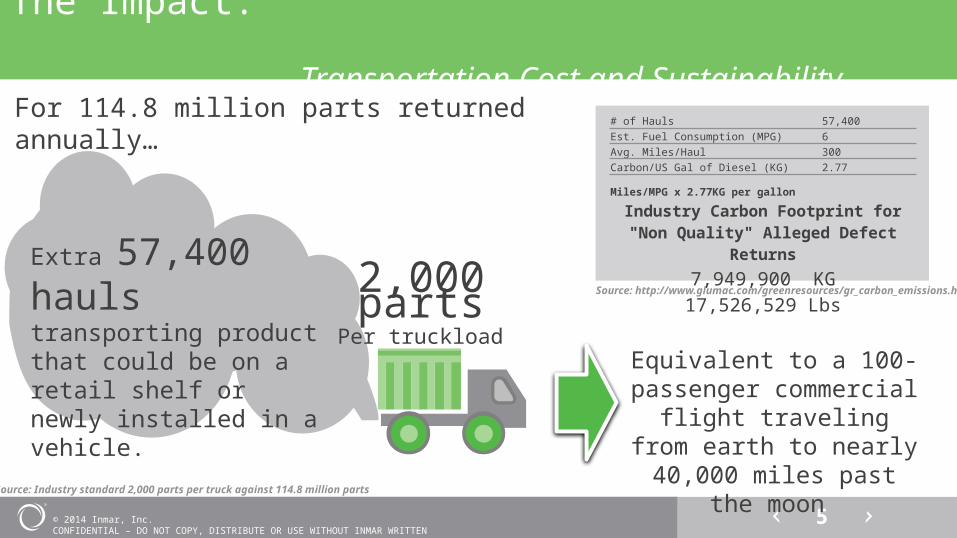

The Impact: Transportation Cost and Sustainability

# of Hauls 57,400 Est. Fuel Consumption (MPG) 6Avg. Miles/Haul 300Carbon/US Gal of Diesel (KG) 2.77

Miles/MPG x 2.77KG per gallonIndustry Carbon Footprint for "Non Quality"

Alleged Defect Returns7,949,900 KG

17,526,529 Lbs

2,000parts

Extra 57,400 hauls transporting product that could be on a retail shelf or newly installed in a vehicle.

Equivalent to a 100-passenger commercial

flight traveling from earth to nearly 40,000 miles past the moon

Source: http://www.glumac.com/greenresources/gr_carbon_emissions.html

For 114.8 million parts returned annually…

Per truckload

Source: Industry standard 2,000 parts per truck against 114.8 million parts

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

The Strain of Warranty Returns On Suppliers and Distribution Partners are identical

Source: AASA Special Summit on Warranty

DISTRIBUTOR/RETAILER

TransportationStorageHandling/Quality Review/LaborSales TimeCredit Issued/Warranty Not PaidCustomer ServiceDisputes Training/MarketingLost ProfitCost of Goods

SUPPLIER

6

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

7

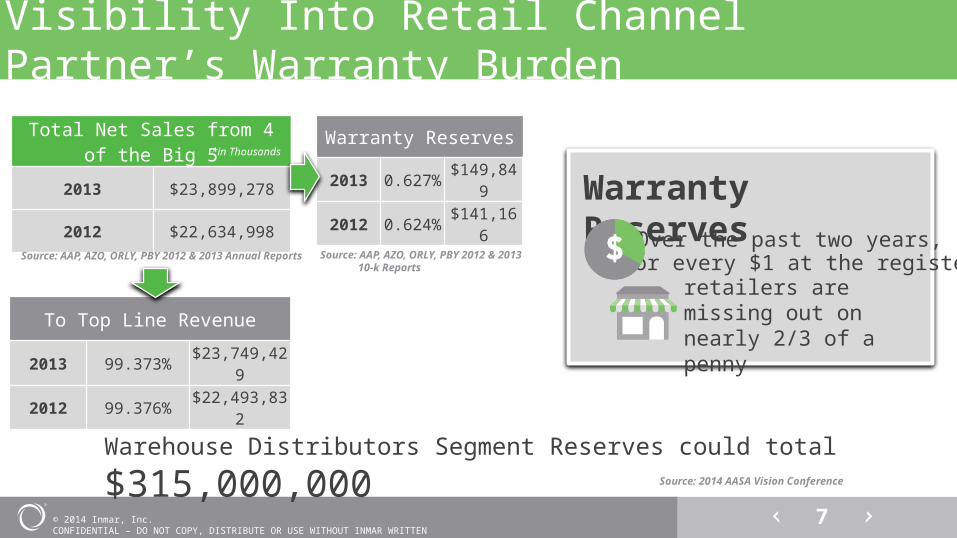

Total Net Sales from 4 of the Big 5

2013 $23,899,278

2012 $22,634,998

To Top Line Revenue

2013 99.373% $23,749,429

2012 99.376% $22,493,832

Warranty Reserves

2013 0.627% $149,849

2012 0.624% $141,166

Visibility Into Retail Channel Partner’s Warranty Burden

Warranty Reserves

Warehouse Distributors Segment Reserves could total $315,000,000

*in Thousands

Over the past two years,for every $1 at the registerretailers are missing out on nearly 2/3 of a penny

Source: AAP, AZO, ORLY, PBY 2012 & 2013 Annual Reports Source: AAP, AZO, ORLY, PBY 2012 & 2013 10-k Reports

Source: 2014 AASA Vision Conference

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

8

Visibility Into Retail Channel Partner’s Warranty Burden

* Excluding Costs associated with Destroy-in-Field policies

Assumed Retailer/WD Reverse Logistics Costs for Warranty Hard Parts Returns

$15MMDC Costs

$6.3MMTransportation

$3.2MMOther costs

Retail/WD Segment

$24.5MM

RETAIL/WD TOTAL WARRANTY COST $490 Million

Source: Inmar independent research

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

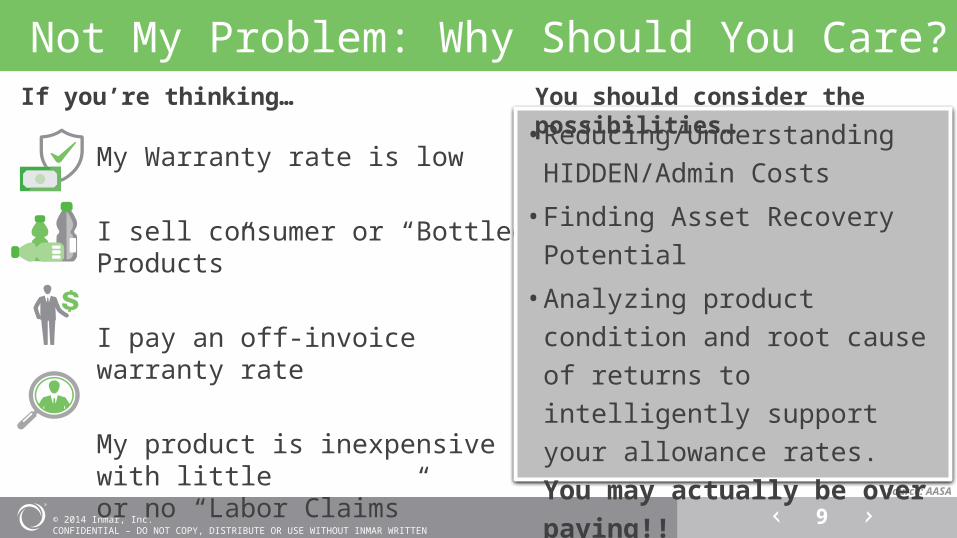

Not My Problem: Why Should You Care?

My Warranty rate is low

I sell consumer or “Bottled Products”

I pay an off-invoice warranty rate My product is inexpensive with little or no “Labor Claims”

Source: AASA

• Reducing/Understanding HIDDEN/Admin Costs

• Finding Asset Recovery Potential

• Analyzing product condition and root cause of returns to intelligently support your allowance rates. You may actually be over paying!!

• Improving Supply Chain handling practices

9

If you’re thinking… You should consider the possibilities…

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

10

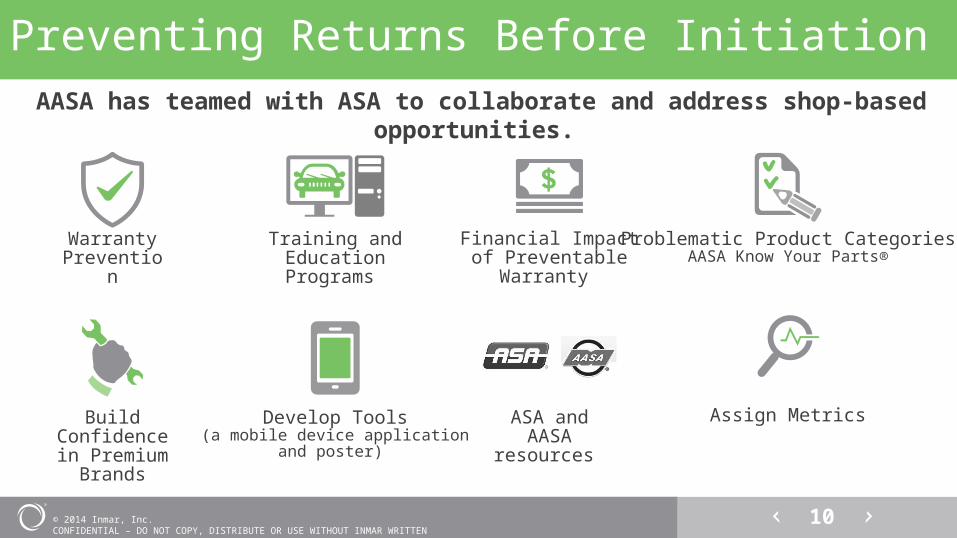

Preventing Returns Before InitiationAASA has teamed with ASA to collaborate and address shop-based opportunities.

Warranty Prevention

Training and Education Programs

Financial Impact of Preventable Warranty

Problematic Product CategoriesAASA Know Your Parts®

Build Confidence in

Premium Brands

Develop Tools(a mobile device application

and poster)

ASA and AASA

resources

Assign Metrics

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

11

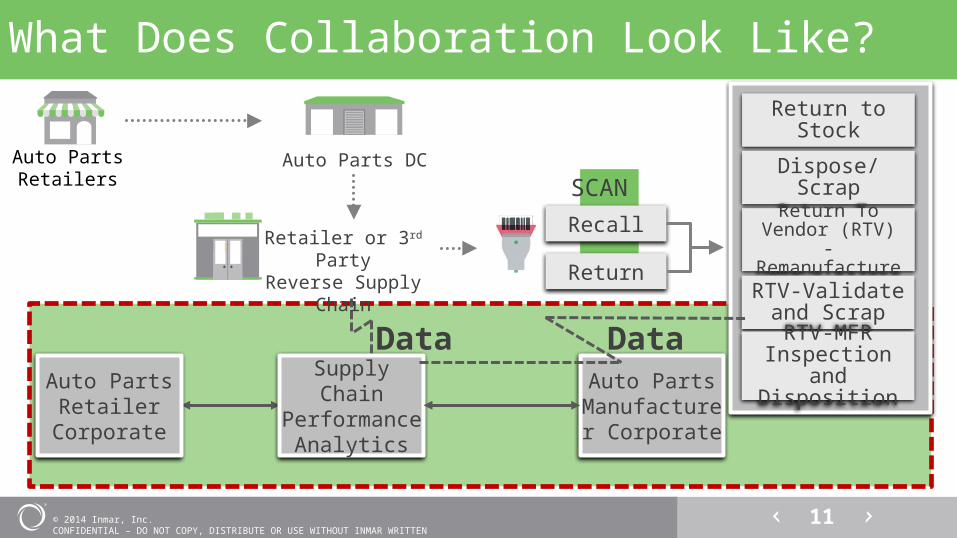

What Does Collaboration Look Like?

Recall

Return

Return to Stock

Dispose/Scrap

Return To Vendor (RTV) -

Remanufacture

RTV-Validate and Scrap

Supply Chain Performance

Analytics

Auto PartsRetailer

Corporate

Auto PartsManufacturer

Corporate

SCAN

Data RTV-MFR Inspection and

Disposition

Data

Auto PartsRetailers

Auto Parts DC

Retailer or 3rd PartyReverse Supply

Chain

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

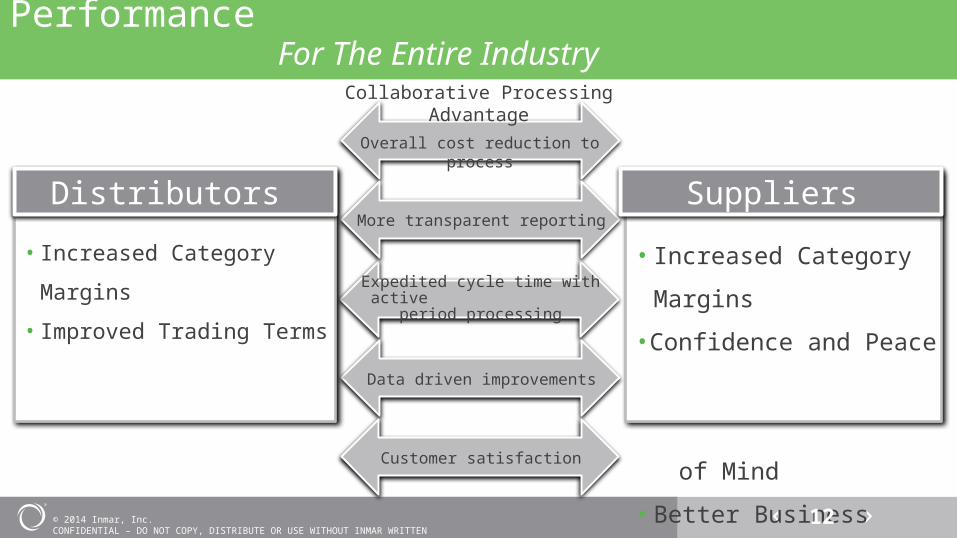

Collaboration Elevates Financial Performance For The Entire Industry

Expedited cycle time with active period

processing

Overall cost reduction to process

More transparent reporting

Data driven improvements

Collaborative Processing Advantage

• Increased Category Margins

• Improved Trading Terms

Distributors

• Increased Category Margins

•Confidence and Peace

of Mind

• Better Business Decisions

Suppliers

12

Customer satisfaction

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

13

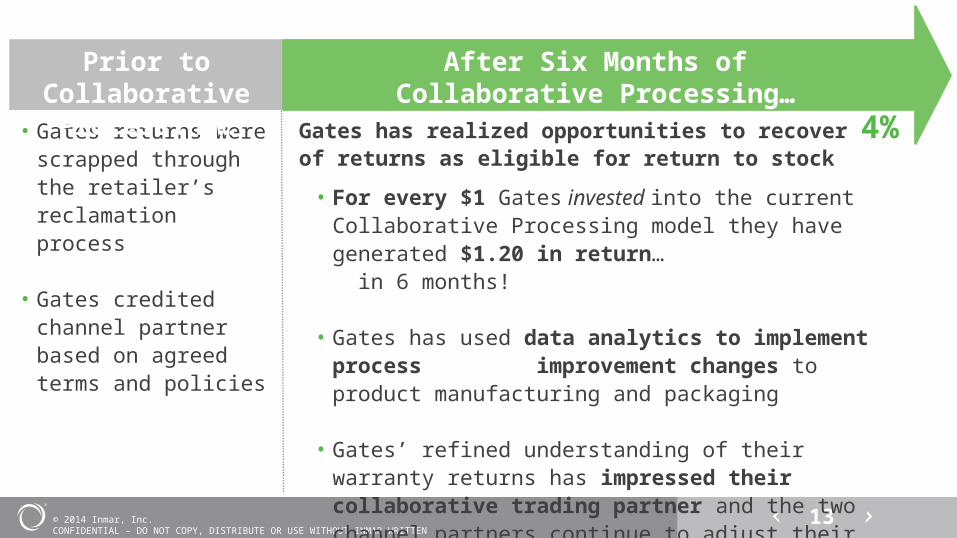

• Gates returns were scrapped through the retailer’s reclamation process

• Gates credited channel partner based on agreed terms and policies

Prior to Collaborative Processing…

After Six Months of Collaborative Processing…

Gates has realized opportunities to recover 4% of returns as eligible for return to stock

• For every $1 Gates invested into the current Collaborative Processing model they have generated $1.20 in return… in 6 months!

• Gates has used data analytics to implement process improvement changes to product manufacturing and packaging

• Gates’ refined understanding of their warranty returns has impressed their collaborative trading partner and the two channel partners continue to adjust their partnership policies for everyone’s best interest.

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

14

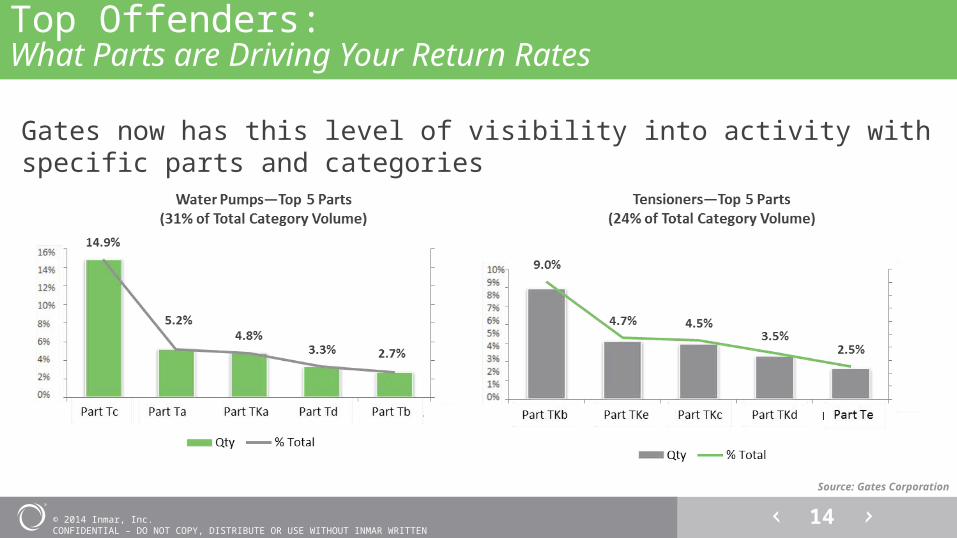

Top Offenders:What Parts are Driving Your Return Rates

Gates now has this level of visibility into activity with specific parts and categories

Source: Gates Corporation

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

15

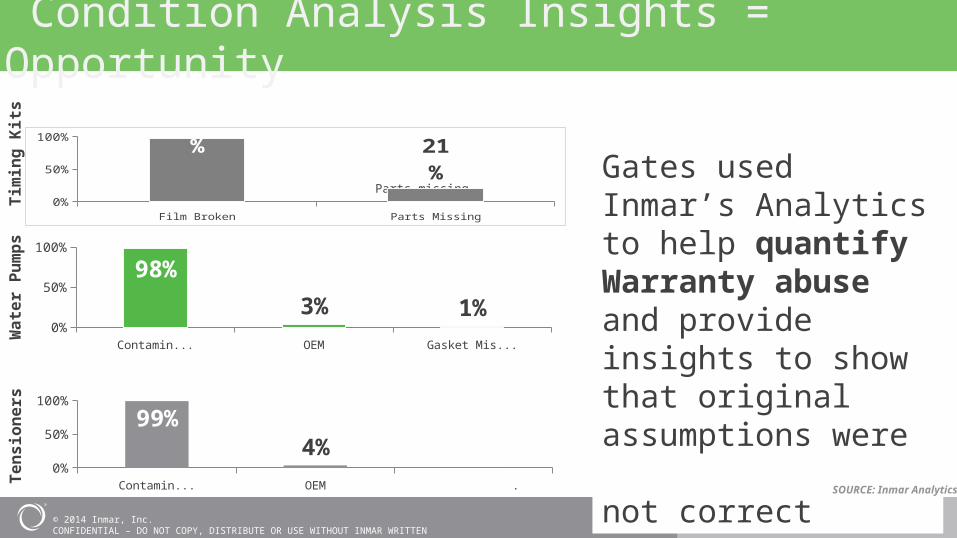

Condition Analysis Insights = Opportunity

Contaminated OEM Gasket Missing0%

20%40%60%80%

100%

98%

3% 1%

Contaminated OEM Gasket Missing0%

20%40%60%80%

100%

99%4%

0.2%

Gates used Inmar’s Analytics to help quantify Warranty abuse and provide insights to show that original assumptions were not correct

Parts missing

SOURCE: Inmar Analytics

Film Broken Parts Missing0%

20%40%60%80%

100% 97%

21%

Tim

ing

Kits

Wat

er P

umps

Tens

ione

rs

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

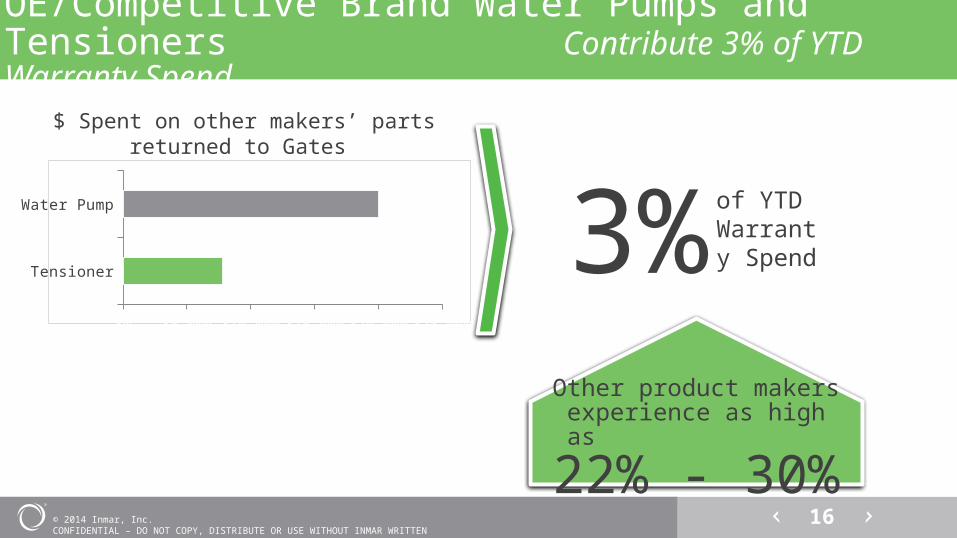

16

OE/Competitive Brand Water Pumps and Tensioners Contribute 3% of YTD Warranty Spend

Tensioner

Water Pump

$0 $5,000 $10,000 $15,000 $20,000 $25,000

3% of YTD Warranty Spend

Other product makers experience as high as

22% - 30%

$ Spent on other makers’ parts returned to Gates

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

17

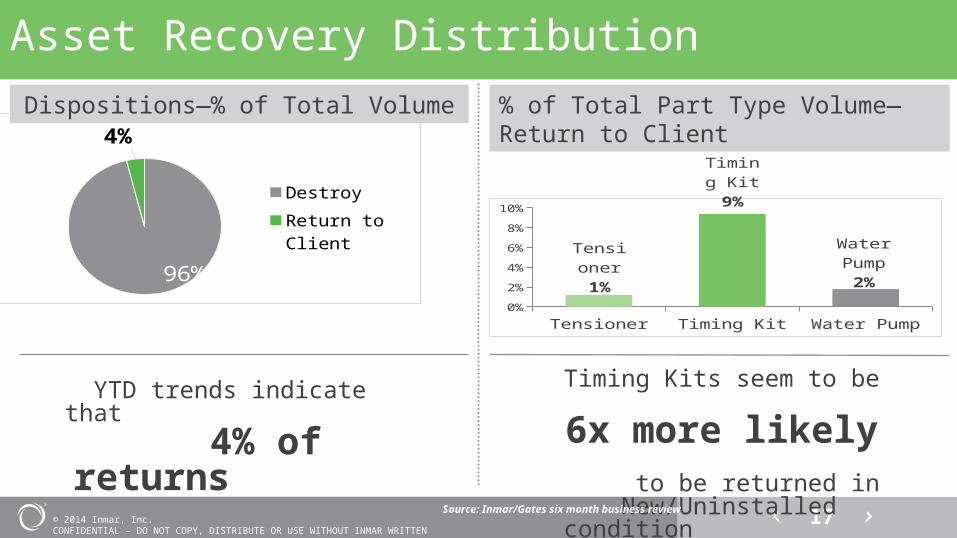

96%

4%

Destroy

Return to Client

Asset Recovery DistributionDispositions—% of Total Volume

YTD trends indicate that 4% of returns are

recovered as eligible for return to stock

Tensioner Timing Kit Water Pump0%

2%

4%

6%

8%

10%

Ten-sioner

1%

Timing Kit9%

Water Pump

2%

Timing Kits seem to be 6x more likely

to be returned in New/Uninstalled condition

than Tensioners and Water Pumps

% of Total Part Type Volume—Return to Client

Source: Inmar/Gates six month business review

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

18

Let’s Explore What’s Missing

We are not alone…other industries face these challenges

You are here

What they do:• Metrics in place to quantify results/losses• Industry benchmarks for competitive comparison• Agreement on policy related to costs of returns for

both sides• Collaboration between channel partners

Source: AASA

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

19

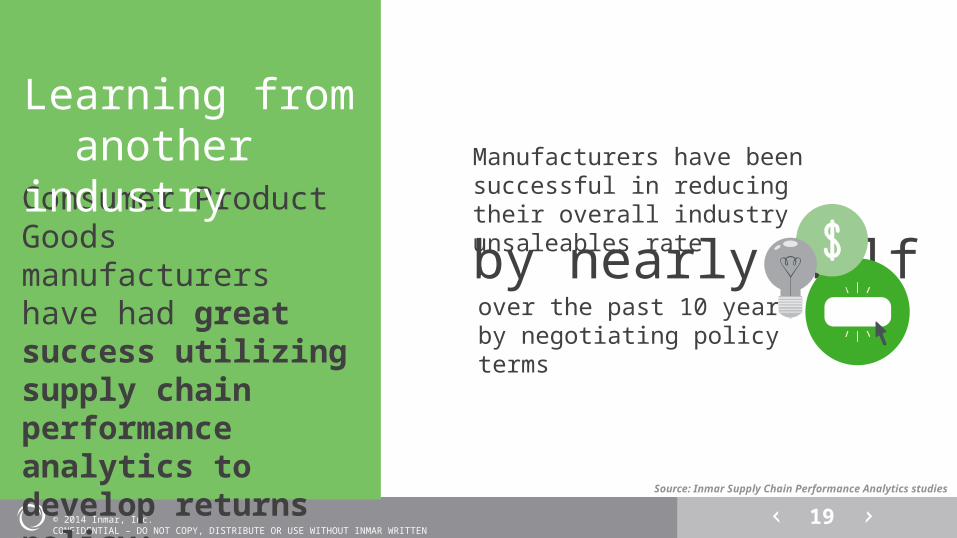

Consumer Product Goods manufacturers have had great success utilizing supply chain performance analytics to develop returns policy:

by nearly half

Learning from another industry Manufacturers have been

successful in reducing their overall industry unsaleables rate

over the past 10 years by negotiating policy terms

Source: Inmar Supply Chain Performance Analytics studies

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

20

The key to success is that both trading partners understand that there is shared responsibility when it comes to warranty

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

21

retail distribution center studies

consumer units included in benchmark

application

consumer units reviewed

retail store studies

unit loads analyzed

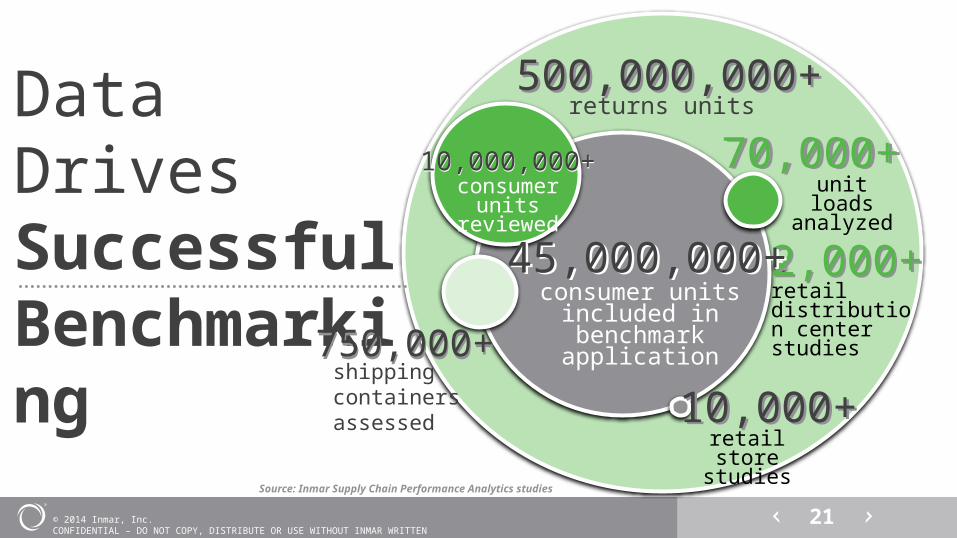

returns units Data Drives Successful Benchmarking

500,000,000+500,000,000+

10,000,000+10,000,000+ 70,000+70,000+

2,000+2,000+

10,000+

45,000,000+45,000,000+

10,000+

750,000+750,000+shipping containers assessed

Source: Inmar Supply Chain Performance Analytics studies

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

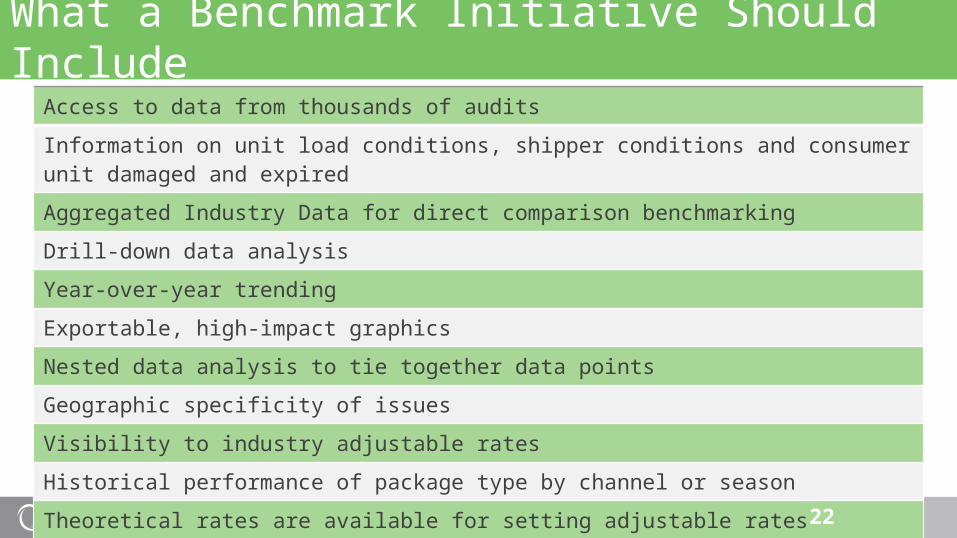

What a Benchmark Initiative Should Include Access to data from thousands of audits

Information on unit load conditions, shipper conditions and consumer unit damaged and expired

Aggregated Industry Data for direct comparison benchmarking

Drill-down data analysis

Year-over-year trending

Exportable, high-impact graphics

Nested data analysis to tie together data points

Geographic specificity of issues

Visibility to industry adjustable rates

Historical performance of package type by channel or season

Theoretical rates are available for setting adjustable rates

22

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

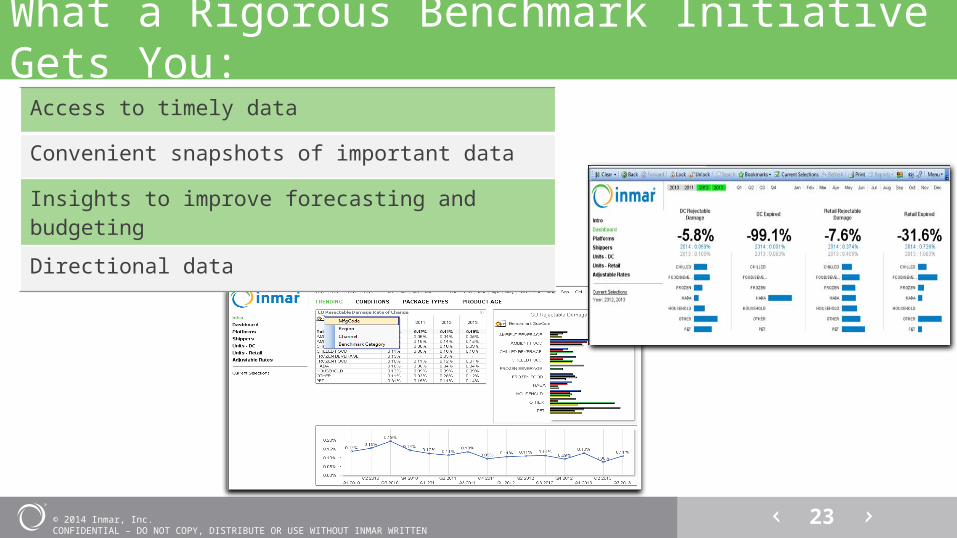

What a Rigorous Benchmark Initiative Gets You:Access to timely data

Convenient snapshots of important data

Insights to improve forecasting and budgeting

Directional data

23

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

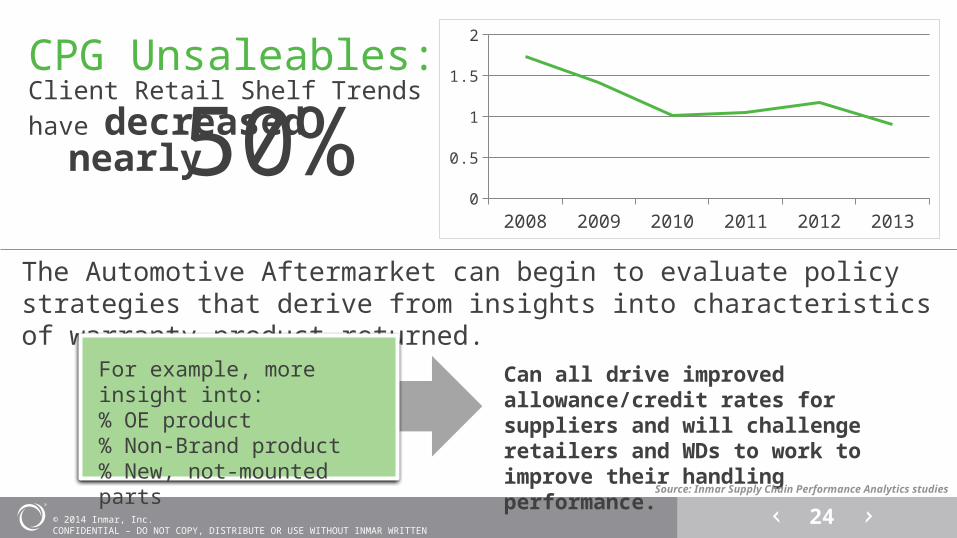

24Source: Inmar Supply Chain Data 2008--2013

2008 2009 2010 2011 2012 20130

0.20.40.60.8

11.21.41.61.8

2

CPG Unsaleables:Client Retail Shelf Trends have decreased

The Automotive Aftermarket can begin to evaluate policy strategies that derive from insights into characteristics of warranty product returned.

Can all drive improved allowance/credit rates for suppliers and will challenge retailers and WDs to work to improve their handling performance.

For example, more insight into:% OE product% Non-Brand product% New, not-mounted parts

nearly50%

Source: Inmar Supply Chain Performance Analytics studies

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

25

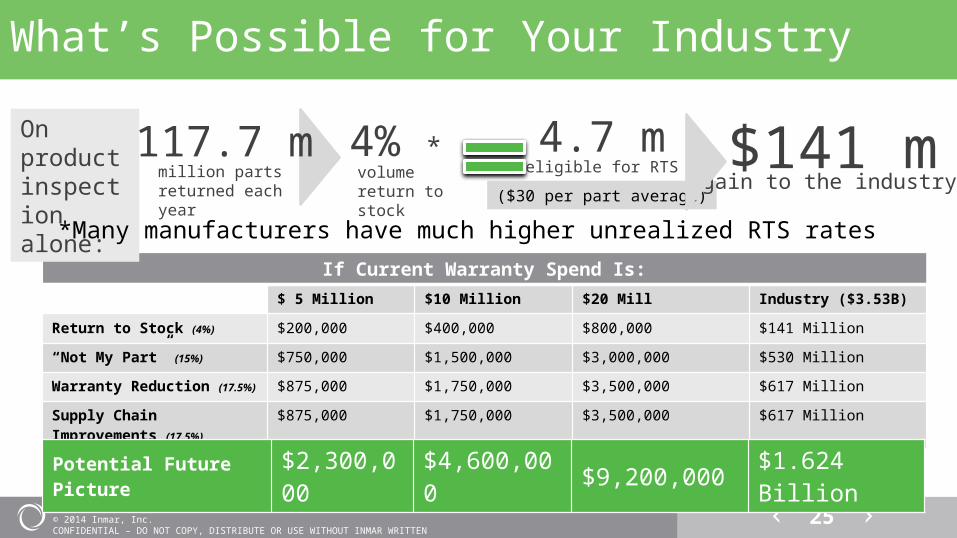

What’s Possible for Your Industry

If Current Warranty Spend Is:$ 5 Million $10 Million $20 Mill Industry ($3.53B)

Return to Stock (4%) $200,000 $400,000 $800,000 $141 Million

“Not My Part” (15%) $750,000 $1,500,000 $3,000,000 $530 Million

Warranty Reduction (17.5%) $875,000 $1,750,000 $3,500,000 $617 Million

Supply Chain Improvements (17.5%)

$875,000 $1,750,000 $3,500,000 $617 Million

Potential Future Picture $2,300,000 $4,600,000 $9,200,000 $1.624 Billion

On product inspection alone:

117.7 mmillion parts returned each year

4% *volume return to stock

4.7 meligible for RTS

($30 per part average)gain to the industry

$141 m*Many manufacturers have much higher unrealized RTS rates

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

26

The Key:Collaboration with Trading Partners for a Win-Win

Bring industry partnerstogether Data

visibility initiatives

Develop best

practicesWarranty reductio

n initiative

s

Returned product handling

Adapt process

flows: NAPA process flow

as a benchmark

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

27

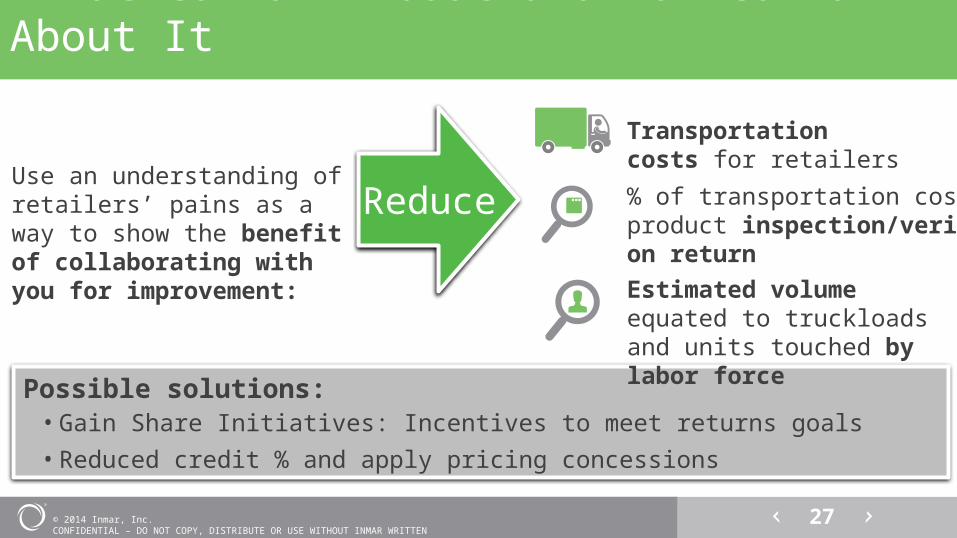

What to Talk About and How to Talk About It

Use an understanding of retailers’ pains as a way to show the benefit of collaborating with you for improvement:

Reduce

Possible solutions:• Gain Share Initiatives: Incentives to meet returns goals• Reduced credit % and apply pricing concessions

Transportation costs for retailers

% of transportation cost with product inspection/verification on returnEstimated volume equated to truckloads and units touched by labor force

© 2014 Inmar, Inc. CONFIDENTIAL – DO NOT COPY, DISTRIBUTE OR USE WITHOUT INMAR WRITTEN PERMISSION

28

To Talk in More Detail About Your Specific Goals and Objectives:

Set a meeting with us at Automotive Aftermarket Industry Week

Jeff Z. JohnsonSupply Chain Performance AnalyticsConsultant – Automotive Aftermarket

Con

tact

Info

:

Recommended