DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

10 April 2017 Global

Equity Research Food Retail

Global online grocery The Credit Suisse Connections Series leverages our

exceptional breadth of macro and micro research to deliver

incisive cross-sector and cross-border thematic insights for

our clients.

Research Analysts

Stewart McGuire, CFA

44 20 7888 6531

Olga Bystrova, CFA

7 495 967 8871

A-Hyung Cho

82 2 3707 3735

Antonio Gonzalez, CFA

52 55 5283 8921

Stephen Ju

212 325 8662

Edward J. Kelly, CFA, CPA

212 325 3241

Andre Kukhnin, CFA

44 20 7888 0350

Victoria Petrova

49 69 75 38 2272

Grant Saligari

61 3 9280 1720

Tobias Stingelin, CFA

5511 3701 6301

Keiichi Yoneshima

81 3 4550 9740

Evan Zhou

852 2101 6745

CONNECTIONS SERIES

On the cusp of a seismic shift Online grocery adoption is increasing worldwide and threatens to upend the

economics of all food retailers, regardless of geography. We analyse the

options available to grocers and conclude that in developed countries, only

centralised, automated fulfilment can profitably meet the needs of customers.

The risks to incumbent food retailers are widespread and serious, particularly

for those companies with large supermarkets located too far from customers;

these risks increase with the size and duration of their store lease portfolios.

This report is published in conjunction with a report from our capital goods

team on Warehouse Automation and Robotics, specifically looking at the

companies with exposure to grocery supply chain automation.

■ Technology disruption is coming to grocery. The barriers to efficient

online grocery operations are falling as companies solve the main cost

problems of picking and delivery. We estimate that $37bn of online grocery

infrastructure will be spent in the US to achieve a 25% penetration rate.

■ Business model choice will separate winners from losers. We identify

~20 different permutations of picking and delivery methods within online

grocery. Very few meet the criteria of high service quality and reasonable

profitability due to the exceptionally difficult logistics and the low margins.

■ IGD projects double-digit CAGRs for online grocery in all key markets.

We expect developed regions to rapidly catch up to the UK in online

grocery. If the US had UK-levels of adoption, online grocery revenue would

be US$70bn vs. US$7bn currently.

■ Key companies to watch. We identify a number of companies that are

either leading, trialling or at risk from online grocery (often all three),

demonstrating the nascent and uncertain nature of the channel.

■ CORRECTION: In this version of the report we have corrected the RHS

axis of Figure 1, as the full values were truncated in the original publication.

Figure 1: Online grocery revenue – double-digit CAGRs to 2020

Source: IGD, Credit Suisse research

$0

$100

$200

$300

$400

$500

$600

$0bn

$10bn

$20bn

$30bn

China UK Japan US France S. Korea Germany Australia Belgium Netherlands

2015 (LHS)

2020 (LHS)

2015 Per capita (RHS)

2020 Per capita (RHS)

China; $41bn (2015)China; $178bn (2020)

10 April 2017

Global online grocery 2

Key tables and charts

Figure 2: Margin potential for centralised, automated fulfilment is materially higher than traditional grocery

Source: Credit Suisse research

Figure 3: Attitudes about buying groceries online Figure 4: Have shopped online for groceries (%)

Source: Nielsen Source: Nielsen

Figure 5: Ocado KPIs and LfLs Figure 6: Mixed palletising robot

Source: Company data, Credit Suisse research Source: Kuka

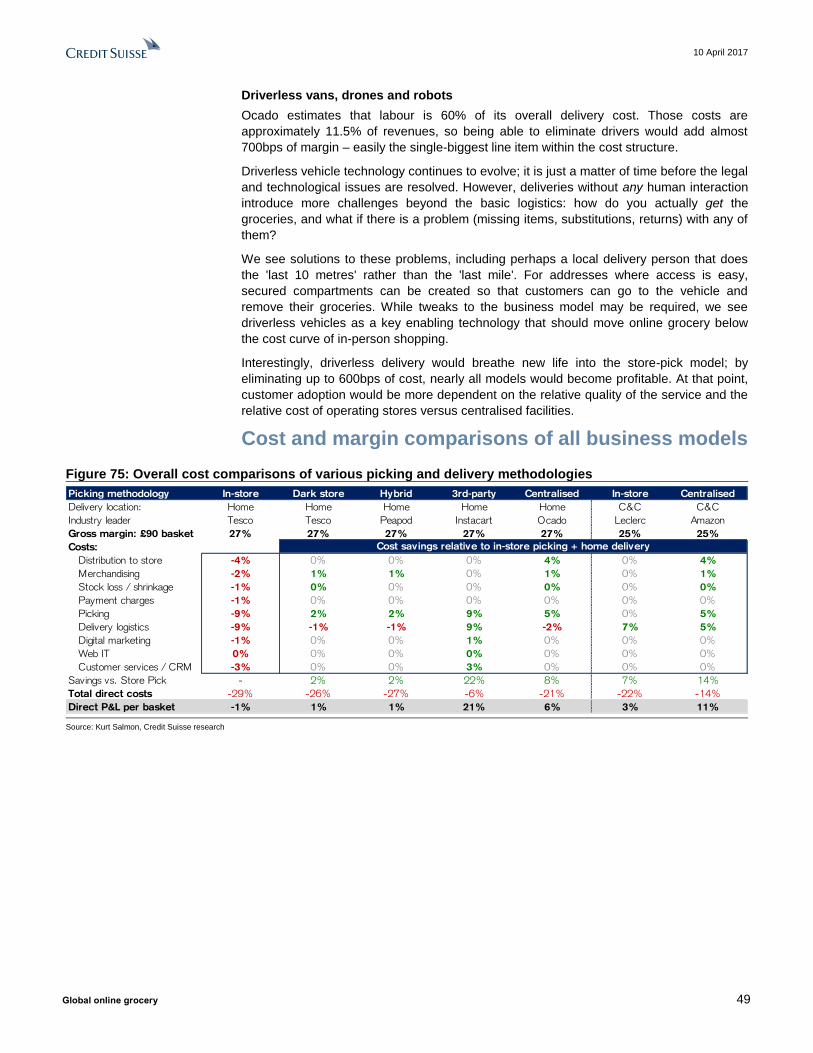

Picking location In-store Dark store Hybrid 3rd-party Centralised In-store Centralised Centralised Centralised

Picking technology Staff Staff Staff 3rd-party Staff Staff Staff Robotic Robotic

Delivery location Home Home Home Home Home C&C C&C Home Home

Delivery mechanism Driver Driver Driver 3rd-party Driver Customer Customer Driver Automated

Industry leader Tesco Tesco Peapod Instacart Ocado Leclerc n/a n/a n/a

Gross margin (avg. basket) 27% 27% 27% 27% 27% 25% 25% 27% 27%

Total direct costs -29% -26% -27% -6% -21% -22% -14% -19% -11%

Direct P&L per basket -1% 1% 1% 21% 6% 3% 11% 9% 17%

0% 20% 40% 60% 80% 100%

Global

Asia-Pacific

Europe

Africa / Middle East

Latin America

North America

Considerers Trialists Regulars Avoiders

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

China South

Korea

India Europe North

America

Africa /

Middle East

Latin

America

0%

5%

10%

15%

20%

80%

85%

90%

95%

100%

2011 2012 2013 2014 2015 2016

On time delivery or early

Order accuracy

LfLs (RHS)

10 April 2017

Global online grocery 3

Executive summary “The factory [or warehouse] of the future will have only two employees, a man and a dog.

The man will be there to feed the dog. The dog will be there to keep the man from

touching the equipment.” – Warren Bennis1. For further reading into warehouse and

logistics automation, we refer you to today's publication from our capital goods team

Warehouse Automation and Robotics.

Our eight key takeaways for the global online grocery market are:

■ Online grocery growth will accelerate in all key markets. Improved mobile phone

interfaces, easier to navigate web pages, tailored features, more valuable promotions,

automated 24-hour pick-up points, delivery passes, integration with home automation

systems and same day delivery all add tremendous value to the customer. The offline

model will likely be seen as static and passé, with a declining value proposition.

■ Centralisation is vital for scale, high service quality and margin. The abundance

of business models is a result of grocers trying to move online inexpensively. Third-

party solutions (i.e. Instacart) add material costs to the customer and are likely to be

short-term, niche solutions. Using an existing store estate as a quasi-distribution

network is also a stopgap measure.

■ Automation and scale will solve the delivery problem. The need for centralisation

runs counter to delivery economics, which improve when the picking operations move

closer to customers. Potential solutions exist to reduce delivery costs, including

shrinking fulfilment centres and locating them nearer customers, stand-alone click and

collect facilities, sophisticated routing algorithms, and driverless delivery technologies.

■ Low labour costs help, but high labour costs may help more. The paradox of

labour within online grocery is that low labour costs facilitate online grocery (as we see

in China – at least for now), but high labour costs are needed to provide the incentive

to switch to an automated, scaled solution. This ultimately leads to a point where a

lower variable cost model establishes a cost advantage over the traditional store.

■ Most developed markets are amenable to online grocery. The main factors that

provide the conditions for online grocery to flourish are improving in all jurisdictions.

The capital costs of the most efficient online business models continue to fall, which in

turn expands the addressable market. Even a modest shift in market share to online

(say, 20% to 30%), is likely to have far-reaching, negative ramifications for incumbents.

■ Technology changes cannot be overstated. The ability to substitute capital for

labour is reaching a level where automation is making inroads into the most

economically challenging parts of online grocery: picking a basket of goods and

delivering it to the customer. Where grocery was traditionally a local venture, we expect

the scale benefits of technology to spread rapidly across borders.

■ Amazon is a threat to incumbents. Despite AmazonFresh's slower-than-expected

rollout, the strategic and tactical implications remain positive because grocery is: (i) the

largest consumer spend vertical; (ii) drives greater engagement from higher shopping

frequency; (iii) leverages existing fulfilment infrastructure; (iv) accelerates share gain in

adjacent categories; and (v) decreases friction on handling returns.

■ Potential for the adoption of existing marketplace models. We are starting to see

the third-party marketplace model gain traction in grocery. Amazon's arrangement with

Morrisons in the UK offers customers access to multiple credible food sources. Marks

& Spencer does not have an online food strategy, and it would be groundbreaking to

see M&S and Morrisons products listed alongside branded goods on Amazon.com.

1 Mark Fisher (1991), The Millionaire's Book of Quotations

10 April 2017

Global online grocery 4

Key players within online grocery

This report is intended to show the opportunities and pitfalls of various business models

for online grocery. We are still at a very early stage in this channel shift with less than 1%

of global grocery revenues occurring online. The winners and losers from this shift are not

yet known, nor are they easy to predict because the outcome will be based largely on the

decisions that will be made by management teams over the next few years.

In this report, we have drawn together the perspectives of all our regional retail analysts.

We have identified a number of companies that are either market leaders in grocery (and

are therefore at risk), or are working on positioning for the shift to online, or both. These

include the companies listed in Figure 7. Out of all of the companies we cover, only one –

Ocado – stands out as a technological leader with no legacy assets, but this does not

necessarily make it the leader in a sector where access to capital and localised supply

chains remain significant barriers to entry.

We also refer readers to the report published from our capital goods team on Warehouse

Automation and Robotics, specifically looking at the companies with exposure to grocery

supply chain automation. The following players have the widest product offering, and

featured prominently in our discussions with industry experts: Dematic (KION), Swisslog

(KUKA), Daifuku, Bastian Solutions (private) and Intelligrated (Honeywell).

Figure 7: Country rankings2 and key companies

Source: Credit Suisse research

2 For an explanation of the 13 characteristics used in the ranking, please see Appendix A.

Country /

Region

Country

Score*

Companies to

WatchRating / TP Key companies within country / region for online grocery

US 66

Amazon

Walmart

Kroger

Ahold Delhaize

OUTPERFORM, TP $900

OUTPERFORM, TP $80

NEUTRAL, TP $30

OUTPERFORM, TP €24.50

Continues to expand grocery offerings in US and UK

Largest mass merchant globally with 19% share of the US grocery market

Rapid click and collect expansion; currently unwilling to invest in direct delivery

Multiple online operations in multiple jurisdictions

Canada 65Loblaws

Longo's

Not rated

Private

Offline leader; click and collect offered but no delivery

Toronto-based grocer with full-service online delivery

UK 63

Tesco

Ocado

Morrisons

UNDERPERFORM, TP 160p

OUTPERFORM, TP 410p

NEUTRAL, TP 230p

Sophisticated online operations, but levered to large stores and long leases

The leader in purpose-built automation for grocery

Strategic partnerships with Ocado and Amazon, plus upstream leverage

China 61

Alibaba

JD.com

Yihaodian

OUTPERFORM, TP $127

NEUTRAL, TP $32

Private

Parterning with top international supermarket brands, focus on fresh

Strong #2 to Alibaba, good strategic partnerships (Walmart, Yihaodian)

Strong procurement and fulfillment expertise

France 57 None

All major players have extensive click and collect or 'Drive' locations, which total

more than 4,000 throughout the country. France has a very high proportion of

hypermarkets, which is a strategic negative.

Germany 57 NoneHigh discounter penetration and lack of an anchor metropolitan area like London

or New York has placed German retailers relatively behind in online grocery.

Scandinavia 55 ICA Not rated Innovative 'delivery to fridge' model.

Australia 54Wesfamers

Metcash

NEUTRAL, TP A$41.92

OUTPERFORM, TP A$2.54

Heavy exposure to bricks and mortar retail but offering online grocery

Most likely wholesale distribution partner for Amazon in Australia

South Korea 54

E-MART

Homeplus

Lotte Mart

OUTPERFORM, TP W235,000

Private

NEUTRAL, TP W220,000

Two fulfillment centres and increasing penetration via same day delivery

Same-day delivery service

Growing SKU selection, planning to have 3 fulfillment centres by 2019

Russia 52 NoneMajor players are watching developments but are currently only in testing

phases.

Japan 49 None

Some private, B2B and niche players operate in key cities, but Japan is

currently lacking leadership from the large consolidated food players (such as

Ito-Yokado, Aeon and Seiyu) or well-capitalised internet-only disruptors.

Mexico 41 Walmex NEUTRAL, TP MXN39 Investing in online infrastructure, especially relative to competition

Brazil 37 GPA Food NEUTRAL, TP R$70 A pioneer of online grocery in Braz il with dedicated fulfilment capacity

* Country score is the sum of the 13 characterisics used to create the country spider charts in Part II

10 April 2017

Global online grocery 5

Table of contents

On the cusp of a seismic shift 1

Key tables and charts 2

Executive summary 3

Key players within online grocery ............................................................................. 4

Part I: The grocery sector 6

A very brief history of grocery ................................................................................... 6

Business models: Centralised or Distributed? ......................................................... 7

Other economic considerations for online grocery ................................................. 14

The growing role of Amazon .................................................................................. 15

The inflection point is coming ................................................................................. 17

Part II: Country analysis 18

Where does online grocery work best? .................................................................. 18

Geographic analysis ............................................................................................... 19

Part III: Online grocery economics 39

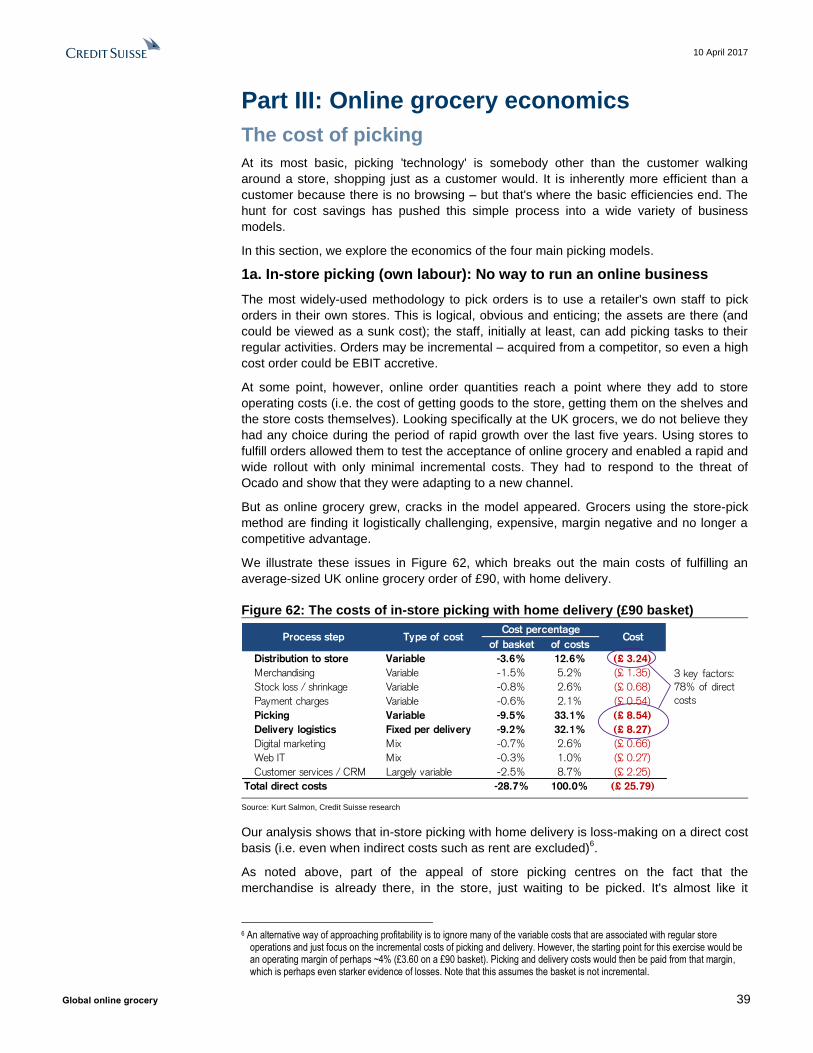

The cost of picking ................................................................................................. 39

The cost of delivery (or collection).......................................................................... 46

Cost and margin comparisons of all business models ........................................... 49

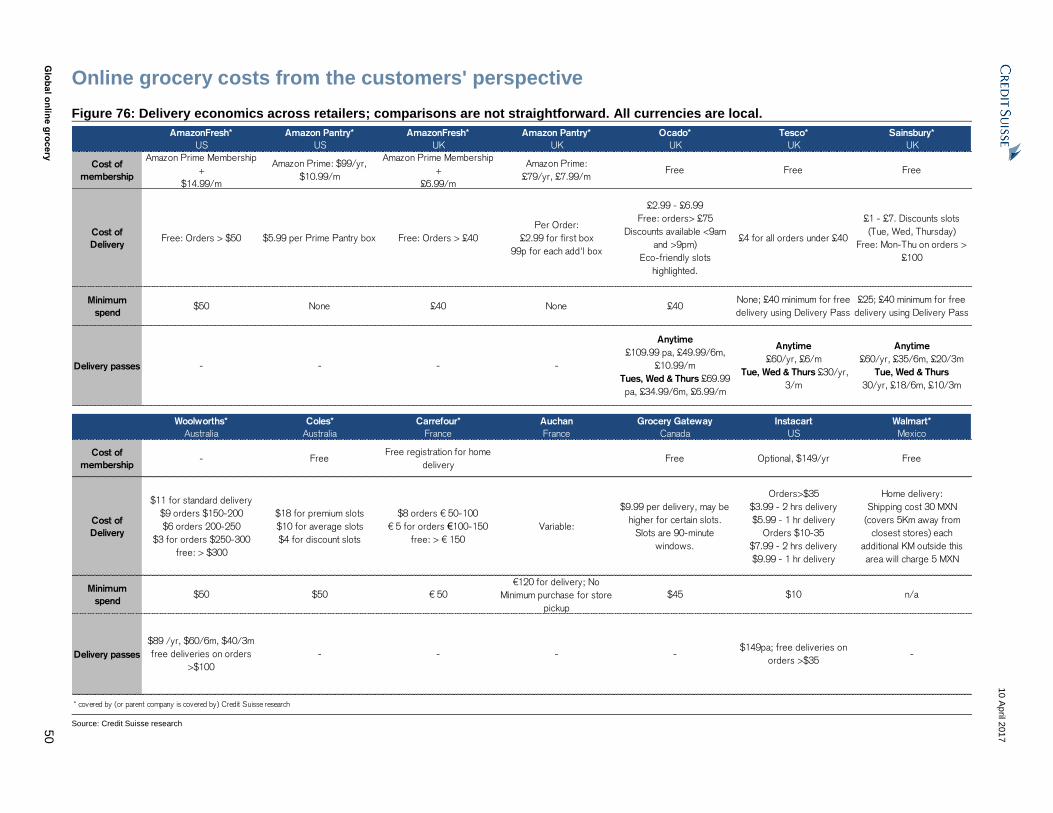

Online grocery costs from the customers' perspective .......................................... 50

Appendix A: Multi-factor country model 52

Appendix B: Further reading / viewing 54

10 April 2017

Global online grocery 6

Part I: The grocery sector

A very brief history of grocery

Step-changes in grocery distribution are not new. It wasn't until 1916 at a Piggly Wiggly in

the US that customers were able to browse groceries themselves rather than asking

someone behind a counter for them. It took another 20 years to incorporate produce,

baked goods and meat into what we now call a supermarket. The hypermarket, born in

Belgium 20 years later added general merchandise under the same roof. Format-wise,

things then remained reasonably static until the 1990s.

Webvan, the first online grocery delivery company of any size, was founded in 1996 and

went public at a valuation of $4.8bn. Five years later it was bankrupt, with the media

branding it one of the largest dot-com flops in history. The management of Ocado (a UK-

based, pure-play online grocer) cites the implosion of Webvan as a critical event that

provided the lead time to hone operations with few competitors. We also believe it soured

the appetite for online grocery within the US for a significant period of time.

As a result, consumable categories have been slower to gain traction amongst online

shoppers, with only certain categories (personal-care, beauty products online, packaged

grocery) growing well. Fresh groceries have much lower penetration. They are highest in

Asia, where 40% of Chinese, 39% of South Korean and just over 33% of Indian

respondents say they’ve purchased fresh groceries online (source: Nielsen). These

numbers drop materially in Europe (9%) and North America (9%), the traditional leaders in

online marketplaces. 64% of respondents were concerned about the freshness or quality

of products purchased online.

There are a large number of sceptics of

the online grocery model. Our research

shows that some believe online grocery

shopping is a niche service for time-

starved, cash-rich families, technology

buffs or foodies who are looking for

unusual or exotic ingredients. We also

read that consumers like going to the store

to buy groceries.

However, we believe the appeal is much

broader and the value proposition much

greater. From a customer's perspective,

there are good reasons to try online

grocery – but also, many more reasons

why, even after trying, customers switch

back to traditional stores (Figure 8).

This is particularly true when a lack of dedicated resources results in unmet expectations,

especially if there is a premium being charged for the service. So far, online grocery

underwhelms in most countries. We believe much of the blame lies in the choice of

business model of online grocery.

Done correctly, however, online grocery is of immense value to the consumer. According

to Kantar Worldpanel, households shop for the same 400 items on a weekly basis, if not

more often. If the outcome of an online shopping trip meets or exceeds an in-person shop

at similar price levels, we expect the shift to accelerate. We believe we are now

approaching that point.

Figure 8: Some pros, many cons

Source: Credit Suisse research

Positives Negatives

Shop at any time Sign-up hassle

Time savings Website navigation

Chore avoidance Selection issues

Wide range of items Substitutions

Hidden cost savings Returns

Delivery coordination

Slot availability

Premium cost

Fresh food anxiety

Lose out on "experience"

10 April 2017

Global online grocery 7

Business models: Centralised or Distributed?

Online grocery business models, fulfilment models, customer experiences and economic

sustainability are inextricably linked and vastly different. When looking at the logistics

value chain from a customer's perspective, there are four discrete elements to a shopping

trip: getting to the store, picking the basket, checking out (paying and packing) and

transporting the shopping home (Figure 9). We believe that many shoppers could consider

each of these tasks a chore – i.e. best avoided, if possible.

Within these four elements, the key component, in our view, is the picking function: For an

online grocer, this is the most time intensive part of the process (and so the highest labour

cost portion) and is also the target of customers' two main anxieties:

■ Are the fresh items the ones they would have picked?

■ If an item is unavailable, what is the best substitute?

Figure 9: The online logistics value chain; outsourcing chores

Source: Credit Suisse research

The business model (and its accompanying fulfilment model) has a material effect on

customer experience, so it ultimately drives overall adoption of online grocery. The most

straightforward model (and still the most common) is to pick from a store close to the

customer. In recent years, grocers have added 'dark stores (dedicated quasi-warehouses,

efficiently merchandised, not open to the public), hybrid stores (stores with some

dedicated non-public space for certain categories) and centralised fulfilment centres

(CFCs, large, warehouse-style operations that receive good from manufacturers), but

these still form a relatively small percentage of all online baskets.

If we take the fulfilment models and incorporate the two main options for getting a

completed basket to the customer's house (home delivery and 'Click and Collect' or C&C),

we can create the matrix in Figure 10. Each cell represents a unique economic model for

the grocer and a different value proposition for the customer, and each combination can

have either a subtle or significant impact on overall economics.

Figure 10: The way baskets are picked and delivered changes the economics

Source: Credit Suisse research

Create

shopping

list

Pick itemsCheckout

/ pay

Transport

to home

Pick itemsCheckout

/ pay

Transport

to home

Traditionalcustomer functions

Pick itemsCheckout

/ pay

Online grocer functions

Travel to

store

In-store Dark store Hybrid Centralised

Home Delivery

Store Pick Up ? ? Currently in use

Non-Store Pick Up Not currently used

Unattended Collection ? Most common

Picking Methodology

Delivery

Method

10 April 2017

Global online grocery 8

We worked with Kurt Salmon, an international consulting firm that specialises in retail and

consumer products, to analyse individual costs that are incurred within the UK during

online grocery fulfilment. Later in the report we explore detailed economics of the four

main picking models and the two main delivery options as well as the relative impact of the

cost of labour and capital between regions.

All online grocery is not created equal

Online grocery adoption has been slow. The negative issues highlighted in Figure 8 show

the main arguments against online grocery from a customer's perspective. The main

reason why these issues persist is cost. Online grocery is an order of magnitude more

difficult to execute than online general retail, which makes the economics for the grocers

extremely poor, and hence there are few incentives to solve the issues. Exacerbating this

issue is the fact that customers are exceptionally sensitive to substitutions and delivery

timing in grocery, which sets the bar very high.

There are four main reasons why this cost disadvantage exists:

■ Individual item values are low. Picking costs are very high as a percentage of value.

■ Orders have a large number of items. As number of items increases, achieving a

100% pick rate becomes challenging. Mistakes and substitutions introduce high-cost

return processes.

■ Temperature chain of custody. Food safety regulations require frozen and chilled

products to be handled independently, requiring much greater logistical effort.

■ Delivery timing is determined by the customer. Because delivery slots are chosen

by the customer (within a narrow window), delivery routing is inherently inefficient.

In addition to the high-cost nature of online fulfilment, cannibalisation of store-shopped

baskets is margin dilutive, reducing the incentive for grocers to move online. What we end

up with is a piecemeal approach, where tentative grocers link up with early adopters to

create a suboptimal system that grows slowly and creates a high degree of scepticism.

This partly explains why even in the UK, where the highest-quality offerings are available,

there are numerous impediments to a mass market shift to online grocery. Consumer

habits are hard to break, and the perception that online grocery is expensive, cumbersome

and delivers low-quality produce make it a challenge for marketers. Only 27% of the UK's

population shops online for groceries, and of that group, ~50% shop 5 or fewer times per

year. There is clearly work to be done to increase the frequency of those who already

shop online, and to increase the overall percentage of people who shop online.

Figure 11: UK frequency – mostly low Figure 12: UK penetration – modest

Source: Kantar Worldpanel, Credit Suisse research Source: Kantar Worldpanel, Credit Suisse research

0%

10%

20%

30%

40%

50%

60%

70%

1 to 12 13 to 20 21 to 30 31 to 40 41+

Frequency of Shop (per year)

?

0%

10%

20%

30%

40%

50%

60%

2012 2013 2014 2015 2016

?

10 April 2017

Global online grocery 9

We note penetration looks like it is actually slowing at a time it should be picking up. Why

do fewer than 30% of consumers shop online, and of those, perhaps only 20% could be

considered "high frequency" shoppers?

The data suggest that choice of business model has a material impact on acceptance and

growth of online grocery. Currently, the vast majority of online orders in the UK are still

picked in stores (Figure 14). The consumer does not differentiate between fulfilment

models, but relies on the same set of performance indicators to determine overall value:

assortment, product availability, freshness, substitutions and delivery performance.

Figure 13: UK online market share Figure 14: UK market share by model

Source: Kantar Worldpanel, Credit Suisse research Source: Kantar Worldpanel, Credit Suisse research

The arguments for centralisation

Assortment: Ocado has the broadest assortment among all UK grocers (online or offline)

with >50k grocery SKUs (2015: >47k, 2014: >43k, 2013: 34k). Inventory only needs to be

carried in a small number of locations (for Ocado: 2), and adding SKUs is inexpensive.

Availability: We compile the service and availability statistics that are published in a UK

trade publication and supplement the data with our own availability statistics on Ocado.

The consistency shown by the centralised model has been notable; out of the last 25

weeks of data, there were only two weeks where two items were out of stock and four

weeks where there one item was out of stock; the other 17 weeks had 100% in-stock

availability, materially better than in-store availability (Figure 15).

Figure 15: Product availability; the centralised model excels

Source: The Grocer, Credit Suisse research

Tesco

42%

Asda

16%Sainsbury

17%Morrisons

5%

Waitrose

3%

Ocado

17%

Amazon

0%

In-store

73%

Dark

store

5%

CFC

22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Nov-16 Dec-16 Jan-17 Mar-17

Asda Morrisons

Sainsbury's Tesco

Waitrose Ocado

10 April 2017

Global online grocery 10

Freshness: Centralised fulfilment centres receive goods directly from suppliers and orders

are shipped directly to customers. This shortens the supply chain and extends the lifespan

of fresh produce. A shorter supply chain coupled with FIFO inventory management also

minimises waste. A store-based fulfilment model must balance between high inventory

levels (to ensure availability), or low inventory levels (to maintain throughput and

freshness). Local demand fluctuations can have a material effect on this balance, and also

mean that customers in different regions will experience different service levels.

Substitutions: Substitutions are largely a function of inventory control, and are closely

related to availability. Centralised fulfilment has much greater availability, and so inherently

has fewer substitutions. More broadly, the customer is interested in order accuracy (which

is the metric that Ocado tracks). Accuracy is a combination of substitutions and errors.

Centralised operations have more automation and easier to maintain picking processes

that can reduce errors.

Delivery performance: We discuss the complexities of delivery in the next section, but we

believe that centralised order routing allows for more accurate delivery time estimates.

Ocado publishes KPIs with respect to delivery metrics and order accuracy. Figure 16

shows that both have been consistently high. We believe Ocado puts significant effort into

maintaining these metrics, but it is our view is that it is their business model that gives

them the opportunity to achieve these high scores. The corollary of this is an in-store

picking model, which is not inherently able to support high KPIs, even at great effort.

Figure 17 shows Ocado's revenue by year of customer acquisition. We would expect each

horizontal bar to trend downward over time; new customers cannot be added to a cohort

but existing customers leave (to competitors, moving away, or otherwise). However, each

of the bars in the diagram are quite flat, implying that any loss of customers is being

balanced by spending increases by the customers that remain.

Not only is each cohort's sales relatively flat, each subsequent cohort is adding an

increasing level of spend (i.e. the bars are getting wider). This is supported by Ocado's

organic growth, which has averaged 15% over the past five years. The high and consistent

KPIs give customers reasons to become repeat customers.

Figure 16: Ocado KPIs and LfLs Figure 17: Ocado sales by cohort

Source: Company data, Credit Suisse research Source: Ocado, Credit Suisse research

Our supposition is that the adoption of store-based fulfilment for online grocery is slowing

materially, either because companies are trying to slow down growth (due to low

profitability/cannibalisation), or customers are slowing adoption (due to poor value), or a

combination of both factors. The Kantar data in Figure 18 show that Tesco's contribution

to online growth was negative for much of 2016, while Ocado, Morrisons and Amazon – all

centralised fulfilment operations – continued growing strongly.

0%

5%

10%

15%

20%

80%

85%

90%

95%

100%

2011 2012 2013 2014 2015 2016

On time delivery or early

Order accuracy

LfLs (RHS)

2007 20142008 2009 2010 2011 2012 2013

£

10 April 2017

Global online grocery 11

Figure 18: Contribution to online growth by UK retailer

Source: Kantar Worldpanel

The arguments against centralisation

While there are many and varied benefits from centralisation, there are also two main

drawbacks that need to be considered. The first issue relates to drive times. By increasing

the distance between the central facility and customers, drive times increase, thereby

adding costs – both direct costs such as fuel and labour, but also indirect costs such as

depreciation on transportation infrastructure. The second issue relates to scale. A fully-

utilised facility would maximise profitability, but the ramp-up period of a large facility can

take a long time, thereby depressing IRRs.

Both of these issues raise the question of the optimal size of a CFC, and are the main

reasons why a grocer may decide to open a dark store close to customers rather than a

CFC. Currently the capacity crossover between a dark store and a CFC is in the £150m to

£350m/year range – anything larger than £350m would be a centralised operation, while

anything smaller than £150m would be a dark store. Ocado is currently aiming at reducing

the lower bound for CFCs to allow the construction of facilities that are closer to customers

(and to reduce capex requirements).

Ocado attempts to bridge the distance from its CFCs by 'trunking' – trucking consolidated

orders via tractor-trailer trucks to a 'spoke, where orders are broken out into delivery van

sizes. Currently, just one CFC fulfills orders for the entire London area, supplemented by

eight spokes, as shown in Figure 19. The commissioning of CFC4 in 2018 should alleviate

pressure on this CFC, and also reduce the trunking requirements into London.

The added step of trunking, and the potentially longer drive times from the nearest spoke

to the furthest away delivery are the main additional costs of centralised fulfilment when

compared to store picking. We estimate this to be ~2% of sales. To the extent that online

operators are able to position fulfilment centres closer to the ultimate catchment area, this

cost will decline, although we do not expect it to disappear.

-4%

0%

4%

8%

12%

16%

May 2015 2016 2017

Tesco Asda Sainsbury Morrisons

Waitrose Ocado Amazon Online

10 April 2017

Global online grocery 12

Figure 19: Ocado's current fulfilment infrastructure around London

Source: Company data, Map data ©2017 Google, Credit Suisse research

The data seem to bear out this headwind. As shown in Figure 21, trunking and delivery

costs as a percentage of sales have not fallen materially for Ocado, which is not surprising

given the lack of obvious leverage in the delivery model.

Figure 20: Ocado's London spokes Figure 21: Ocado delivery expenses

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

However, with drivers' labour representing ~60% of current trunking and delivery costs, it

could be argued that the other costs (capital, fuel) have fallen, implying higher efficiencies

overall. These efficiencies come from higher customer densities and improved routing –

both of which should continue to improve given that Ocado's market share is still low.

We can attempt to unpick these costs by looking at the increasing level of wage rates

using national statistics and backing into the total costs for trunking and delivery using

Ocado's published costs.

Centralised Fulfillment Centre (operational)

Centralised Fulfillment Centre (under construction)

Spoke

Shaded circles’ radius = 5km

Distance from

CFC (km)

Enfield 26 24

Park Royal 32 36

West Drayton 50 39

South Ruislip 31 45

Dagenham 63 48

Kent 69 51

Surrey 67 53

Wimbledon 51 76

SpokeDrive Time

(mins)

10%

11%

12%

13%

2010 2011 2012 2013 2014 2015 2016

10 April 2017

Global online grocery 13

Figure 22: UK labour rates Figure 23: Delivery cost breakdown

Source: ONS, Credit Suisse research Source: Company data, Credit Suisse research

But are these improvements any better than what we could expect from a store-pick

model? In our view, the answer is yes. We estimate that Tesco delivered £3.5bn of

groceries in 2016 using 5,500 vans, or £640k/year per van; Ocado delivered £1.2bn of

groceries per year using 1,350 vans, or £870k/year per van – a 30% delta after adjusting

for pricing differences3. The trunking costs that Ocado incur appear to be more than

compensated for by the efficiency gains it has been able to achieve from the 'last mile'. We

think this is due to three main issues:

■ The 'n+1' van problem. For each site, some number of redundant vans are required to

ensure continuity of service if there is a breakdown or a roadworthiness issue. The

more sites in operation (which are much greater in a store-based vs. centralised

model), the more redundant vans are required.

■ Routing efficiencies. In a store-based model, routes are optimised by individual van

(or potentially, by store). This reduces the ability to route efficiently, which requires

larger fleet sizes and larger catchment areas to provide optionality and flexibility.

Routing algorithms involve some of the most complex areas of study within

mathematics and computer science; for grocery, the added constraints of weight and

volume within a route plan further complicate the problem. The high level of complexity

offers myriad opportunities to squeeze out efficiencies if operations are centralised,

while a store-based model does not have these opportunities.

■ Coverage areas. Store picking allows for large coverage areas; both Tesco and

Sainsbury are able to reach the vast majority of the UK population with their online

offers, whereas Ocado reaches 70% of the population, but services only ~25% of the

area. The extended reach of store-based fulfilment creates locations where asset

utilisation is relatively low.

Taking all of these factors into consideration, it is difficult to come to a definitive conclusion

regarding the true costs of delivery for each business model. We believe that Ocado and

Tesco provide excellent case studies to analyse delivery issues, but neither should be

assumed to be a 'general case'; different implementations of their models could have

different outcomes. However, our analysis shows greater opportunities for cost savings

with wider catchment areas, and so we expect trunking and delivery costs to trend lower

for centralised operations, while store-based costs should remain relatively static. Longer-

term, step-changes in technology (for example, driverless vans, drone-bots) coupled with

tweaks to the business model have the potential to materially cut delivery costs.

3 The difference between £870k and £640k is 36%, but part of that difference is due to pricing rather than volume, which we argue

is not a function of delivery efficiency. Our analysis shows that Ocado prices at a 6% premium to Tesco. On a like-for-like volume basis, this would reduce the efficiency premium from 36% to 30%.

96%

98%

100%

102%

104%

106%

108%

110%

112%

114%

£420

£430

£440

£450

£460

£470

£480

£490

£500

£510

2010 2011 2012 2013 2014 2015 2016

Labour rates (£, LHS)

Labour rates (indexed, RHS)

35%

40%

45%

50%

55%

60%

2010 2011 2012 2013 2014 2015 2016

Driver labour

Residual (efficiency gains)

10 April 2017

Global online grocery 14

Other economic considerations for online grocery

The value of data

We see the increasing role of data analytics as a way for retailers to add value to their

suppliers (and in the process, monetise the data they accumulate). Ocado has shown it

can increase supplier revenue as a percentage of overall revenue (Figure 24), a trend that

we expect to continue. The majority of Ocado's orders are now placed via a mobile device,

where screen real estate is limited. The value of being able to place specific products on a

particular customer's screen is very powerful. Figure 25 shows offers on the home screen

of an Ocado customer who had made multiple purchases of each one of those items in

previous orders.

Figure 24: Supplier income (% revs.) Figure 25: Ocado app home page

Source: Company data, Credit Suisse research Source: Credit Suisse research

Differential product pricing

As an adjunct to the rising importance of data, an important benefit of online shopping is

that every 'storefront' can be customised for each consumer. Customisation is already

happening with promotions and delivery costs, but we should expect pricing to become

individualised (or at least categorised) as well.

National pricing is a 'taboo' subject in the UK – every grocer sells the same product in the

same format at the same price, no matter whether they are in Central London or in a

remote part of the country. These issues do not exist in larger countries (France, US,

Canada, for example), and we do not believe they should persist online either. Multi-

channel grocers are competing with their own stores, so price customisation may be more

challenging, but grocers with no store infrastructure would not be subject to the same

constraints.

Same day delivery: Not just a risk to convenience operations

We expect another step-change to occur when same day delivery (SDD) becomes

mainstream. SDD will enable grocers to move away from bad trading practices, drive

customer engagement and (potentially) boost margins.

When customers changed from daily shopping at a local market to a supermarket (and

subsequently to the hypermarket), they benefited from a wider assortment, higher quality

and lower prices. The trade-off was that customers then had specific, sometimes

inconvenient, shopping missions: e.g., a weekly shop, top-up shops, food for today, food

for now, special events. These benefits were driven by new stores and significant supply

chain efficiencies, but many consumer wants and needs remained unfulfilled. Their goal is

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2010 2011 2012 2013 2014 2015 2016

10 April 2017

Global online grocery 15

to have a complete inventory of fresh groceries at home, low costs, wide variety, and low

involvement.

These goals are extremely difficult to meet within the context of the existing large

supermarket infrastructure (and are challenging to meet with current online offerings,

although they come much closer). But once online can promise SDD, consumers will be

able to shop for groceries the way they always wanted to, with no planning, no stocking up

or bulk shopping. The size of the basket becomes reasonably consistent, which helps both

consumers and online operators; 'convenience' is redefined because proximity benefits

break down as delivery lag approaches zero. Waste is reduced and customers are happy.

The retailers (and ultimately, the suppliers) can then move away from their mass-

marketing, mass-promotion and mass-merchandising models. Promotional intensity would

fall as it would not be required to encourage customers to choose a particular store.

Consistent, at-home replenishment removes the focus on bulk shopping and a truly

personalised interface reduces price sensitivity and provides an easier path to trading up

and trading across.

The reward of this model will be loyalty. Traditional online fulfilment methods, such as in-

store picking or C&C, do not lend themselves to this model because of the built-in

inefficiencies and the fact that they have to follow the same pricing/promotion structure as

the mother stores. Only centrally-fulfilled (or large dark stores) offer the scale and

efficiencies to enable widespread SDD while maintaining a broad, in-stock assortment.

Home automation: Beyond music and the weather

Home automation has evolved into what is now a home assistant, with Amazon's Echo

perhaps the most recognisable example. And although Google Home was only released in

November 2016, we note that the underlying AI-based technology in the form of Assistant

is rapidly gaining distribution across the spectrum of Google's applications as well as

Android phones. While Amazon and Google are the frontrunners in commercialising this

technology, it is difficult to ignore Apple, as it was among the first to demonstrate its

expertise in natural language processing with the release of Siri.

In 2013, Google CEO Larry Page articulated the concept of a connected, multi-screen

home, a point worth raising once again as we are on the cusp of advancement of smart

home appliances/refrigerators that should be able to determine when replenishment is

required, in addition to performing the basic task of maintaining shopping lists. This

reduction of transactional friction should help the adoption of online grocery, in our view.

What may be a troubling development for grocers is that the number of companies who

have the technology/engineering resources to develop and maintain applications within a

connected home environment will be few and far between, with either Google and/or

Amazon (or Apple) serving as the primary consumer gateway for transactions.

The growing role of Amazon

The business that Amazon started in books has spread to all kinds of goods, but it wasn't

until 2010 that it started to test the feasibility of expanding into the single-largest sector

within retail: grocery. As noted earlier, there has been a spectacular failure (Webvan), and

some small successes (Peapod in the US, Tesco and Ocado in the UK), but online

grocery remains less than 1% of all grocery sales globally.

And just as Amazon has gained share over time in other product verticals, it would not

surprise us to learn that it has similar ambitions to be a Top 5 grocer over the longer term.

Amazon grocery model still in flux

That said, handling fresh produce is vastly different from other categories. And it should be

no surprise that Amazon's full offer grocery service (AmazonFresh) has seen a slower-

than-anticipated rollout. Our expectation in 2H13 when the company started to expand out

10 April 2017

Global online grocery 16

of its home base of Seattle and into Los Angeles and San Francisco, was for Fresh to be

offered in 25 additional markets by the end of 2014. (Please see our report, The Key

Product in Amazon Fresh is Not Just Produce but Rather Same Day Delivery from 17

December 2013) .

The complexity that food adds to the fulfilment process is extremely high, a summary of

which is in Figure 26.

Figure 26: Difference between food and non-food fulfilment

Source: Credit Suisse research

According to an academic paper that analysed Amazon's fulfilment processes4, Amazon

undertakes numerous other steps within fresh produce that have no parallels in non-food.

These include more advanced receiving functions, transforming cases to individual SKUs,

preparation (individual wrapping, for example), replenishment (from non-pickable locations

to pickable locations), produce-specific storage and packing, trimming, inspection, ongoing

rating and cleaning. Overall complexity is much higher than in non-food, and so training

requirements are necessarily higher, as are costs.

And just as it has already done across many other product verticals, Amazon has entered

into a number of deals that continue to demonstrate its ambivalence to source inventory as

well as first-party or third-party ownership – as long as the consumer gains access to the

best selection at the best price.

The delivery process is also not yet optimised. Amazon trucks (not third-party) transport

orders directly from the fulfilment centre in Seattle, whereas orders for customers in Los

Angeles and San Francisco are transported in bulk from fulfilment centres to local delivery

stations and then separated onto different delivery routes (similar to Ocado's trunking

operations).

Lack of current market share should be no comfort

Even after seven years, AmazonFresh remains relatively underpenetrated. It is not

available in most US cities, and overall market share is immaterial.

As we have noted previously, AmazonFresh as an offering should not be viewed just as an

encroachment into grocery, but rather a broader rollout of same day delivery. Amazon's

existing product selection within Prime Now has seen a faster rollout than grocery and

continues to expand vis-à-vis its third-party offering along with shipping discounts across a

greater array of products facilitated by Fulfilment By Amazon. Grocery is one of the last big

steps, which should aid consumer engagement and frequency.

4 V. Modi, Application of Flexible Labor and Standard Work in Fulfilment Center Produce Operations, MIT, 2015

Order fulfillment step Food Non-food

Temperature checksPotential disagreements with driver when

product arrives outside of specificationsNone

Prioritisation Required, due to freshness concerns None

Quality check In-depth, multi-faceted Cursory

Depalletising Complex; similar products look alike Straightforward

Storage Location findingHighly regulated, due to temperature

requirementsStored anywhere within FC

Expiration dates Closest date picked first No expiration dates

Order Fragile items segregated Based on routing efficiency

Quality controlMulti-faceted quality checks during

pickingCursory damage inspection

Item combinations Multiple exceptions (i.e. garlic + flowers) None

Temperature combinations Grouped, where possible None

Receiving

Picking

10 April 2017

Global online grocery 17

The inflection point is coming

After 20 years since the first pure-play online grocery operation started, we are seeing a

business model emerge that provides excellent service, but at a high cost. We expect this

business model to develop into one that companies can use to drive costs materially

lower, while maintaining, or even increasing KPIs.

The technological advances in customer interfaces, data analytics, robotics, and delivery

channels will make centralised online grocery a far superior value proposition to both

customers and grocers. In many ways, it is a mindset shift – away from costs added

(picking labour, delivery costs, IT infrastructure) to costs removed (store expenses, rent,

labour, utilities, maintenance).

Revisiting the pros and cons from Figure 8, we show the remedies for each of the

customer issues we raised. We expect that over the medium term, customers will receive

a significant increase in value without a commensurate rise in prices.

Figure 27: Technology, over time, will address all of the negatives

Source: Credit Suisse research

The end game

The complexities of grocery means that the sector is still at the very early stages of a shift

to online – perhaps five years behind general merchandise. In non-food, not only did

technology and software need to improve materially but so did the systems integration

processes, which are materially easier than those needed for food.

Figure 28 shows the gross profit contribution per basket for each of the main business

models using an average basket size for an online order (£90).

Figure 28: Centralised operations provide a clear path to materially higher margins

Source: Company data, Credit Suisse research

The reward for centralising and automating grocery fulfilment is significant: operating profit

margins are expected to be ~2x of those in traditional store-based models, and over 3x

once the next round of technology advances is implemented.

Positives Negatives Remedies

Shop at any time Sign-up hassle Use single sign on / 1-time event

Time savings Website navigation Website improvements

Chore avoidance Selection issues Website improvements / learning

Wide range of items Substitutions Operational improvements / scale

Hidden cost savings Returns Operational improvements

Delivery coordination Delivery alternatives / technology improvements

Slot availability Operational improvements / scale

Premium cost Scale / technology advancements

Fresh food anxiety Operational improvements / scale

Lose out on "experience" Virtual reality

Picking location In-store Dark store Hybrid 3rd-party Centralised In-store Centralised Centralised Centralised

Picking technology Staff Staff Staff 3rd-party Staff Staff Staff Robotic Robotic

Delivery location Home Home Home Home Home C&C C&C Home Home

Delivery mechanism Driver Driver Driver 3rd-party Driver Customer Customer Driver Automated

Industry leader Tesco Tesco Peapod Instacart Ocado Leclerc n/a n/a n/a

Gross margin (avg. basket) 27% 27% 27% 27% 27% 25% 25% 27% 27%

Total direct costs -29% -26% -27% -6% -21% -22% -14% -19% -11%

Direct P&L per basket -1% 1% 1% 21% 6% 3% 11% 9% 17%

10 April 2017

Global online grocery 18

Part II: Country analysis

Where does online grocery work best?

Global socioeconomic and demographic trends will contribute to rising demand for

convenience amongst an increasingly urban and ageing populace: According to the UN

60% of the world population is expected to live in urban areas by 2030; by 2050, the

number of persons over the age of 60 will triple, from 606m today to nearly 2bn. Both

trends will contribute to rising consumer demand for convenience offerings by retailers.

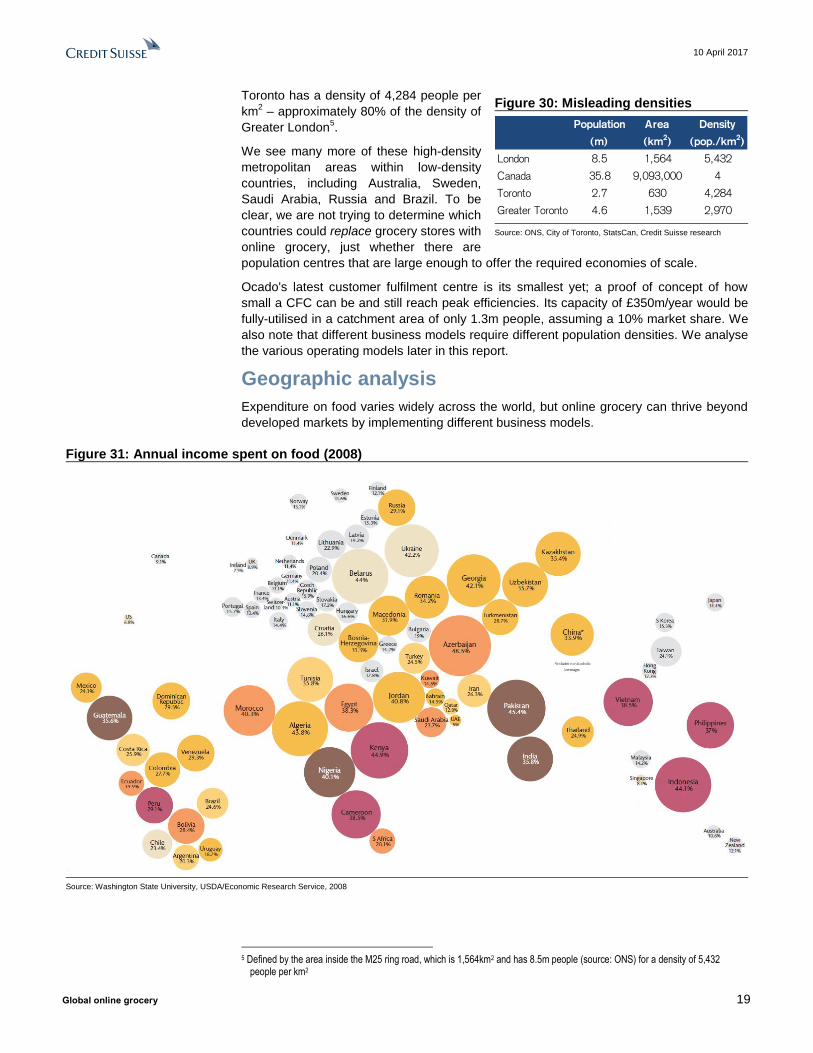

Dispelling the population density myth

One of the most common pushbacks we hear regarding online grocery is that it requires

very high population densities to work. London has become the epicenter of that argument

– it has a big, rich population that seems well-suited to online grocery.

Figure 29: Population densities and wealth of selected countries

Source: UN, World Bank, Credit Suisse research

But there are more cities similar to London than one might think. Canada is a good

example of just how misleading country statistics can be. With the world's second-largest

land mass and a modest population of 36m, Canada seems like a poor candidate for a

service that needs high population densities.

However, the region around Toronto encompasses 630km2 (a mere 0.007% of the

country) but it has a population of 2.7m (7.5% of the country).

Country Area (km2) Population (m) Pop. per km

2GDP per capita

South Korea 97,000 50.6 522 27.2

Netherlands 34,000 16.9 497 44.4

Belgium 30,000 11.3 377 40.3

Japan 365,000 127.0 348 34.5

United Kingdom 242,000 64.9 268 44.0

Germany 349,000 81.5 234 41.3

Switzerland 40,000 8.3 208 80.8

Italy 294,000 60.8 207 30.0

China 9,388,000 1371.0 146 8.0

Denmark 42,000 5.7 136 51.8

Thailand 511,000 68.1 133 5.8

Poland 306,000 38.0 124 12.6

France 548,000 64.4 118 37.6

Austria 83,000 8.6 104 43.8

Turkey 769,000 77.7 101 9.2

Spain 500,000 46.4 93 25.8

Republic of Ireland 69,000 4.6 67 61.7

Mexico 1,944,000 121.0 62 9.5

South Africa 1,213,000 54.0 45 5.8

Colombia 1,109,000 48.0 43 6.1

United States 9,147,000 321.0 35 56.2

Braz il 8,358,000 204.0 24 8.7

Sweden 407,000 9.7 24 51.1

Finland 304,000 5.5 18 42.2

Norway 365,000 5.2 14 74.4

Saudi Arabia 2,150,000 31.0 14 20.8

Russia 16,377,000 143.4 9 9.3

Canada 9,093,000 35.8 4 43.3

Australia 7,682,000 23.8 3 56.3

Total 71,816,000 3,108.2 43

10 April 2017

Global online grocery 19

Toronto has a density of 4,284 people per

km2 – approximately 80% of the density of

Greater London5.

We see many more of these high-density

metropolitan areas within low-density

countries, including Australia, Sweden,

Saudi Arabia, Russia and Brazil. To be

clear, we are not trying to determine which

countries could replace grocery stores with

online grocery, just whether there are

population centres that are large enough to offer the required economies of scale.

Ocado's latest customer fulfilment centre is its smallest yet; a proof of concept of how

small a CFC can be and still reach peak efficiencies. Its capacity of £350m/year would be

fully-utilised in a catchment area of only 1.3m people, assuming a 10% market share. We

also note that different business models require different population densities. We analyse

the various operating models later in this report.

Geographic analysis

Expenditure on food varies widely across the world, but online grocery can thrive beyond

developed markets by implementing different business models.

Figure 31: Annual income spent on food (2008)

Source: Washington State University, USDA/Economic Research Service, 2008

5 Defined by the area inside the M25 ring road, which is 1,564km2 and has 8.5m people (source: ONS) for a density of 5,432

people per km2

Figure 30: Misleading densities

Source: ONS, City of Toronto, StatsCan, Credit Suisse research

Population Area Density

(m) (km2) (pop./km

2)

London 8.5 1,564 5,432

Canada 35.8 9,093,000 4

Toronto 2.7 630 4,284

Greater Toronto 4.6 1,539 2,970

10 April 2017

Global online grocery 20

In order to assess the viability of online grocery within a given market, we created a multi-

dimensional model loosely-based on work first published by McKinsey & Co. to analyse

the European online grocery market. Our model measures characteristics that correlate to

the overall viability for high efficiency, centralised online grocery operations. These

characteristics can be grouped into three categories: infrastructure (such as broadband

penetration), economic viability (such as population and GDP), and latent demand (such

as prevalence of double-income households). For a complete description of our

methodology, please see Appendix A: Multi-factor country model.

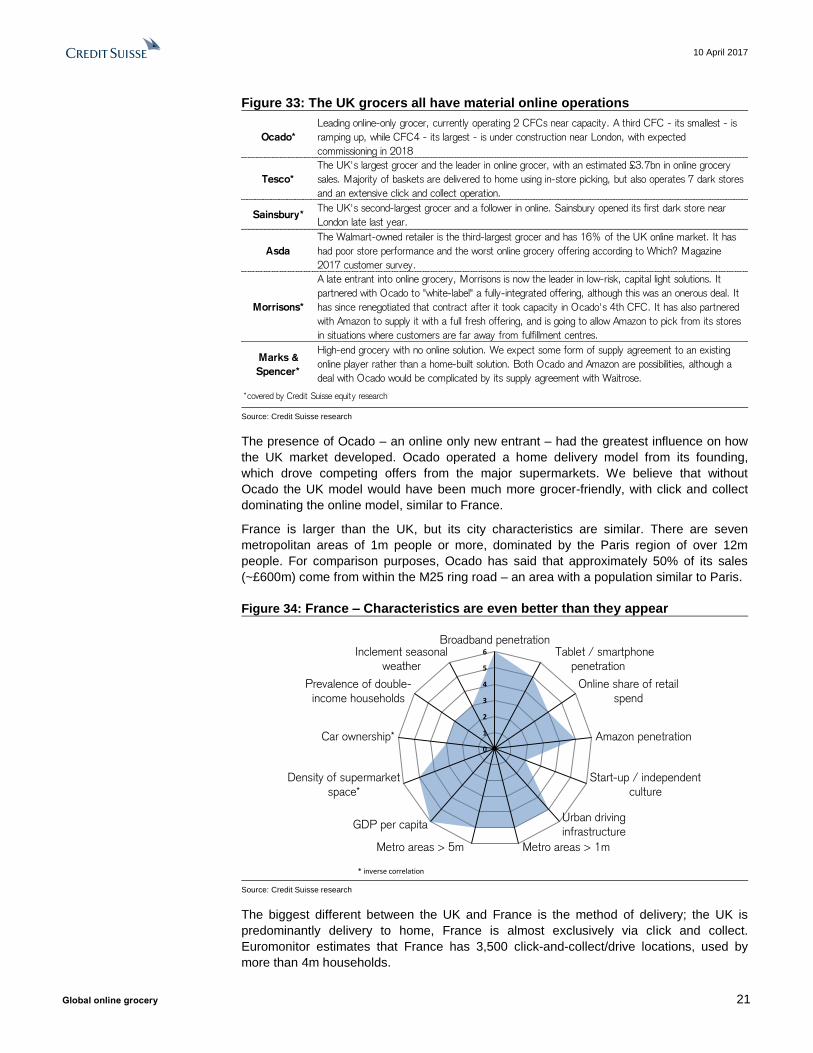

Europe: Leading characteristics

Within Europe, only the UK and France can lay claim to having a meaningful share for

online within grocery, at ~6-7%. Figure 32 shows the UK's characteristics which,

unsurprisingly, are mostly favourable.

Figure 32: UK grocery characteristics; only latent demand is weak

Source: Credit Suisse research

The UK has five highly-developed online grocery operators.

0

1

2

3

4

5

6

Broadband penetration Tablet / smartphone

penetration

Online share of retailspend

Amazon penetration

Start-up / independentculture

Urban drivinginfrastructure

Metro areas > 1mMetro areas > 5m

GDP per capita

Density of supermarketspace*

Car ownership*

Prevalence of double-income households

Inclement seasonalweather

* inverse correlation

10 April 2017

Global online grocery 21

Figure 33: The UK grocers all have material online operations

Source: Credit Suisse research

The presence of Ocado – an online only new entrant – had the greatest influence on how

the UK market developed. Ocado operated a home delivery model from its founding,

which drove competing offers from the major supermarkets. We believe that without

Ocado the UK model would have been much more grocer-friendly, with click and collect

dominating the online model, similar to France.

France is larger than the UK, but its city characteristics are similar. There are seven

metropolitan areas of 1m people or more, dominated by the Paris region of over 12m

people. For comparison purposes, Ocado has said that approximately 50% of its sales

(~£600m) come from within the M25 ring road – an area with a population similar to Paris.

Figure 34: France – Characteristics are even better than they appear

Source: Credit Suisse research

The biggest different between the UK and France is the method of delivery; the UK is

predominantly delivery to home, France is almost exclusively via click and collect.

Euromonitor estimates that France has 3,500 click-and-collect/drive locations, used by

more than 4m households.

Ocado*

Leading online-only grocer, currently operating 2 CFCs near capacity. A third CFC - its smallest - is

ramping up, while CFC4 - its largest - is under construction near London, with expected

commissioning in 2018

Tesco*

The UK's largest grocer and the leader in online grocer, with an estimated £3.7bn in online grocery

sales. Majority of baskets are delivered to home using in-store picking, but also operates 7 dark stores

and an extensive click and collect operation.

Sainsbury*The UK's second-largest grocer and a follower in online. Sainsbury opened its first dark store near

London late last year.

Asda

The Walmart-owned retailer is the third-largest grocer and has 16% of the UK online market. It has

had poor store performance and the worst online grocery offering according to Which? Magazine

2017 customer survey.

Morrisons*

A late entrant into online grocery, Morrisons is now the leader in low-risk, capital light solutions. It

partnered with Ocado to "white-label" a fully-integrated offering, although this was an onerous deal. It

has since renegotiated that contract after it took capacity in Ocado's 4th CFC. It has also partnered

with Amazon to supply it with a full fresh offering, and is going to allow Amazon to pick from its stores

in situations where customers are far away from fulfillment centres.

Marks &

Spencer*

High-end grocery with no online solution. We expect some form of supply agreement to an existing

online player rather than a home-built solution. Both Ocado and Amazon are possibilities, although a

deal with Ocado would be complicated by its supply agreement with Waitrose.

*covered by Credit Suisse equity research

0

1

2

3

4

5

6

Broadband penetration Tablet / smartphone

penetration

Online share of retailspend

Amazon penetration

Start-up / independentculture

Urban drivinginfrastructure

Metro areas > 1mMetro areas > 5m

GDP per capita

Density of supermarketspace*

Car ownership*

Prevalence of double-income households

Inclement seasonalweather

* inverse correlation

10 April 2017

Global online grocery 22

Germany is more decentralised, which reduces the economic appeal for online grocery.

Figure 35: Germany – Technology infrastructure and latent demand issues

Source: Credit Suisse research

Also, as the home market for the two dominant discount operators, Aldi and Lidl, there is

an inherent bias towards low-cost staples that would be an impediment in any rollout of

online grocery. However, the potential for a disruptor such as AmazonFresh to launch may

change this significantly, and force some of the more traditional grocers to increase their

online focus.

We also see potential for growth within northern Europe given the high internet

penetration. Key population centres around Stockholm (2.3m), Copenhagen (2.0m) and

Oslo (1.5m) could each support dedicated online facilities, even though overall population

figures are modest.

Figure 36: Scandinavia's lack of density is a barrier to adoption

Source: Credit Suisse research

Asia: Vast differences between countries

China is the world leader by total sales

China's retail e-commerce market grew by 36% in 2016 and accounted for ~15% of total

retail sales (source: National Bureau of Statistics of China) – a higher proportion of than

0

1

2

3

4

5

6

Broadband penetration Tablet / smartphone

penetration

Online share of retailspend

Amazon penetration

Start-up / independentculture

Urban driving

infrastructure

Metro areas > 1mMetro areas > 5m

GDP per capita

Density of supermarketspace*

Car ownership*

Prevalence of double-income households

Inclement seasonalweather

* inverse correlation

0

1

2

3

4

5

6

Broadband penetration Tablet / smartphone

penetration

Online share of retailspend

Amazon penetration

Start-up / independent

culture

Urban driving

infrastructure

Metro areas > 1mMetro areas > 5m

GDP per capita

Density of supermarket

space*

Car ownership*

Prevalence of double-income households

Inclement seasonalweather

* inverse correlation

10 April 2017

Global online grocery 23

that of the US, Japan and many other developed countries. Apparel and consumer

electronics products have been well-penetrated, and online shopper growth is maturing in

top tier cities.

Chinese consumers spend ~30% on food and beverage – much greater than developed

markets (US: 7%, Germany: 11%). Spending patterns are also very different: according to

Nielsen, Chinese consumers like to shop frequently for food, with a focus on fresh.

Online grocery has already reached high levels within China due to lower supermarket

density than developed markets, a relatively fragmented food retail market, low car

ownership, fast moving lifestyles and poor offline retail infrastructure. These characteristics

create latent demand for e-commerce grocery shopping.

According to CNNIC, China's internet penetration reached 53% (64% of whom shop

online), with top tier cities near developed countries' level. Smartphone/smart device

ownership continues to grow strongly. In China, the main online players are Alibaba and

JD (rather than Amazon).

Euromonitor estimates China's offline grocery retailing sales to reach Rmb4.9 trillion by

2020, representing ~3% five-year CAGR. In our view, online sales of groceries is likely to

take an increasing share of the total market, from Rmb245 billion (US$39bn) in 2015,

5.4% of grocery sales in total, to ~Rmb 1.3 trillion (US$178 bn) in 2020, or ~20% of the

market – a 40% CAGR over 2015-2020.

China's large population and high density in metropolitan area provides opportunities to

develop online delivery of food retail in urban areas (13 cities with greater than 10m

people). Nielsen's white paper on Fresh E-Commerce Development (October 2015)

reported that out of 1,600 interviewees living in seven megacities (>10m people), >63%

shopped for milk and dairy products online, >50% had purchased fruit, and 38% had

purchased meat, vegetables or seafood with higher basket sizes than offline shopping.

China's e-commerce giants Alibaba and JD.com are highly interested in online grocery

given China's population and customers' shopping habits. Both companies are

experiencing growth slowdown in their core categories, and see grocery as their next

opportunity. In addition, it is a very fragmented market, with various food specialty e-

retailers emerging rapidly.

Figure 37: China, unsurprisingly, leads in terms of population density

Source: Credit Suisse research

0

1

2

3

4

5

6

Broadband penetration Tablet / smartphone

penetration

Online share of retailspend

Alibaba penetration

Start-up / independentculture

Urban drivinginfrastructure

Metro areas > 1mMetro areas > 5m

GDP per capita

Density of supermarketspace*

Car ownership*

Prevalence of double-income households

Inclement seasonalweather

* inverse correlation

10 April 2017

Global online grocery 24

The main online grocery retailers are Alibaba's Tmall Supermarket and JD Supermarket.

Both offer a similar range of products and compete head-to-head in terms of price

(including promotion and user subsidies), product variety, quality and delivery service.

In July 2015, Alibaba announced the launch of an Rmb 1bn online grocery promotional

campaign, and teamed up with Cainiao (Not Covered) to offer the same-day delivery

services to Beijing residents. The service has now been expanded into more cities. On 14

July 2016, Tmall Supermarket announced the 'Double two billion plan' to provide Rmb 2

billion subsidies for consumers and will invest Rmb 2 billion into supply chain infrastructure

for service improvement.

The sheer scale of operations in China has led Alibaba to seek out multiple partners to

assist in sourcing, supply chain management, logistics and delivery. Tmall works closely

with western players such as Germany's Metro Group and Spain's DIA to bring more

premium and imported goods to Chinese consumers. Alibaba invested in and partnered

with Yiguo.com (Not Covered) to operate Tmall's fresh food section because of its strong

cold-chain logistics capability and focus on premier brands and quality fresh produce. In

addition, Alibaba invests actively in supply chain and logistics partners like warehouse

operation service provider ALOG and last-mile delivery service provider Ewinshine,

helping to strengthen the overall supply chain efficiency and ensure delivery quality. These

partnerships allow Alibaba to execute its strategy of offering same-day or next-day delivery

services while continuing to expand within China.

Figure 38: China online grocery led by Tmall and JD Supermarket

Source: Company data, Credit Suisse research

We think JD is the best-positioned online grocer in China. It is the strongest competitor to

Alibaba, and moved aggressively last year by forming a strategic alliance with offline

leader Yonghui supermarket (and acquiring a 10% stake). Yonghui is the country's fifth-

largest supermarket chain and has an excellent reputation for its fresh food business (45%

of total sales). JD also acquired the top online supermarket platform Yihaodian and signed

Tmall

Supermarket*

Partnering with top international supermarket brands for high-quality imported products and cooperate

with Yiguo.com to operate fresh produce. Leverage Cainiao (and partners) to manage warehousing

and fulfill orders. Avg. order size is >Rmb100 and free shipping from Rmb 88.

JD

Supermarket*

Allied with Walmart, Yihaodian for better product variety, and China's largest crowdsourcing logistics

platform Dada. Invested in Yonghui, China's top 5 local supermarket. Free delivery from Rmb99, and

offer "within 2 hour delivery" for Rmb 99.

Yihaodian

8-years of experience in online grocery now offering more than 8 million SKUs, well-equipped with in-

house fulfillment and strong procurement capability. Free delivery from Rmb68 for all major cities.

China's leading e-commerce company focusing on grocery. Strong in Eastern China (in particular

Greater Shanghai) due to its convenient logistics and high-quality groceries. However, due to the

ownership acquisition by Ping'An and later Wal-Mart, as well as the departure of founders, the

company has experienced slower for expansion in recent years. In late 2016, Wal-Mart sold YHD to

JD.com for Rmb40 billion.

Feiniu.com

(Sun Art*)

Launched in 2014. Large offer size. Average order is Rmb160-170 with monthly GMV at

Rmb250m. Delivery across China through its offline stores and 3rd-party couriers.

Benlai LifeSmall, specialty online retailer that offers ~5k SKUs of fresh produce. Has built out full cold-chain and

large warehouses and tier 1 cities and provides speedy delivery in selected regions.

Womai.comBacked by the state-owned grain group COFCO, Womai focused offer on premium imported food,

wine, oil and grain, etc. Geographically focused on tier 1 cities and nearby regions.

Others

Womai.com (a wholly-owned subsidiary of China National Cereals, Oils and Foodstuffs Corporation –

China's state-owned food processing holding company); SF Express' SFBest (a leading express

couriers' online marketplace selling food products); Fruitday (fruit specialty retailer), TooToo Organic

Farm (organic and high quality food retailer); Benlai Life (fresh produce e-commerce start-up), Fields

(Shanghai's premium online grocery store), Missfresh.cn.

Vanguard

(e-Wanjia)

Officially launched in June 2015, focusing on fresh food of more than 800 kinds. Vanguard aims to

develop the online platform by leveraging its robust offline resources and advantages in procurement

and logistics, and then broaden the geographic coverage and customer base.

*covered by Credit Suisse equity research

10 April 2017

Global online grocery 25

a cooperation agreement with Wal-Mart to improve procurement and warehousing

management. JD can leverage JD Daojia and the crowdsourcing platform Dada for more

efficient last-mile delivery in the country.

Japan has significant potential, but no integrated offerings yet

Japanese consumers tend to shop at small, local stores and convenience stores – a 'little

and often' strategy that is typically more difficult to supplant with online grocery, where

delivery costs are high (unlike China). One of the main themes in Japanese grocery

recently has been the consolidation of convenience chains and pressure on supermarket

operators to close unprofitable stores – a situation that is a tailwind to moving online.

Against that backdrop, it may be somewhat surprising to see that online grocery is well-

developed and large – the Yano Research Institute forecasts the domestic online food

market was ¥3,377bn in FY15 (US$30bn), and should continue to expand in the mid-

single digits.

The service is dominated by a paid membership co-operative called the Japanese

Consumers’ Co-operative Union (JCCU), which takes mail, internet and catalog orders.

JCCU has both legacy and internet order system. As of 2015, the JCCU had a dominant

41% market share in online grocery, compared to shopping websites at 35% and food

makers’ direct sales at 17%. We expect sales to increasingly migrate to online

supermarkets and shopping websites.

Figure 39: Online grocery by channel Figure 40: Online grocery trends

Source: Yano Research Institute, Credit Suisse research Source: Yano Research Institute (estimates), Credit Suisse research

Rakuten, the top domestic e-commerce player, and Yahoo Japan’s subsidiary ASKUL are

revamping their distribution networks in a bid to boost sales of daily sundries, and

ultimately fresh food. Amazon Japan has yet to enter the field, but it has a very good

logistics network already in place. Seven & I offers click-and-collect at all of its 15,000 7-

Eleven convenience stores, although the lack of in-store space makes high-volume, full

shopping baskets challenging.

We see the characteristics of the Japanese market generally favourable to online, with the

notable exception of smartphone penetration, which is very low for such a developed

economy.

Shopping

websites

JCCU

Bio food

retailers

Supermarkets

Convenience

stores Food

manufacturers

direct

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2012 2013 2014 2015 2016 2017e2018e2019e2020e

JPY

(bill

ions)

10 April 2017

Global online grocery 26

Figure 41: Latent demand drivers are weak but economic viability is strong

Source: Credit Suisse research

Overall, Japan is still searching for the best model, which is made incrementally more

difficult without the large consolidated food players (such as Ito-Yokado, Aeon and Seiyu)

to drive the market forward. The entry of AmazonFresh would be a material event, and

would hasten the shift from third-party services to the supermarkets/manufacturers .

Figure 42: Japanese online grocery evolving rapidly

Source: Company data, Credit Suisse research

Korea: High online growth; Grocery penetration material

Korea already has high e-commerce penetration with 22% share of retail spend in 2016,

one of the highest globally. However, we still expect this channel to register a 16% 2-year

CAGR (2016-18e) and remain the fastest growing, boosted by the intense competition and

changing consumer behavior.

0

1

2

3

4

5

6

Broadband penetration Tablet / smartphone

penetration

Online share of retailspend

Amazon penetration

Start-up / independent

culture

Urban drivinginfrastructure

Metro areas > 1mMetro areas > 5m