Company Profile · Product Information

Established in 1969, Seoul Guarantee Insurance has supplied a diverse range of guarantee and credit services that have paved the way for the development of Korea’s economy and the lives of individuals for more than 52 years.

In 2020, SGI established itself as the leading guarantee institution in Korea by delivering USD 1.8 billion in premium revenues and USD 302 million in net profit.

SGI was rated AA- by Fitch Ratings and A+ by Standard & Poor’s. With solid credit ratings, SGI expanded its business networks further by utilizing its global business presence: Hanoi Branch and representative offices in Beijing, Dubai and New York.

SGI’s vision, “Your Best Credit Partner: World’s Top-Tier Solutions to Realize Social Values” with a strategy slogan “Build the Future”, encompasses four key pillars of SGI such as Customers, Digitalization, Partnership Management and Pride in SGI. Under this framework, SGI will continue its journey to become the world’s leading company.

SGI, as a global guarantee insurer promoting the prosperity of both individuals and corporations, will exert its best efforts to bring its business to the next level and accommodate the needs of the fast changing financial market.

CONTENTS

02 2020 At a Glance

04 Financial Highlights

06 Contract Bonds

08 Counter Guarantee Bond

10 Reinsurance Business

12 Fronting Service

13 Global Business Division

14 Overview of SGI’s Business

16 Global Presence

COMPANY PROFILE · PRODUCT INFORMATION 0302 SEOUL GUARANTEE INSURANCE

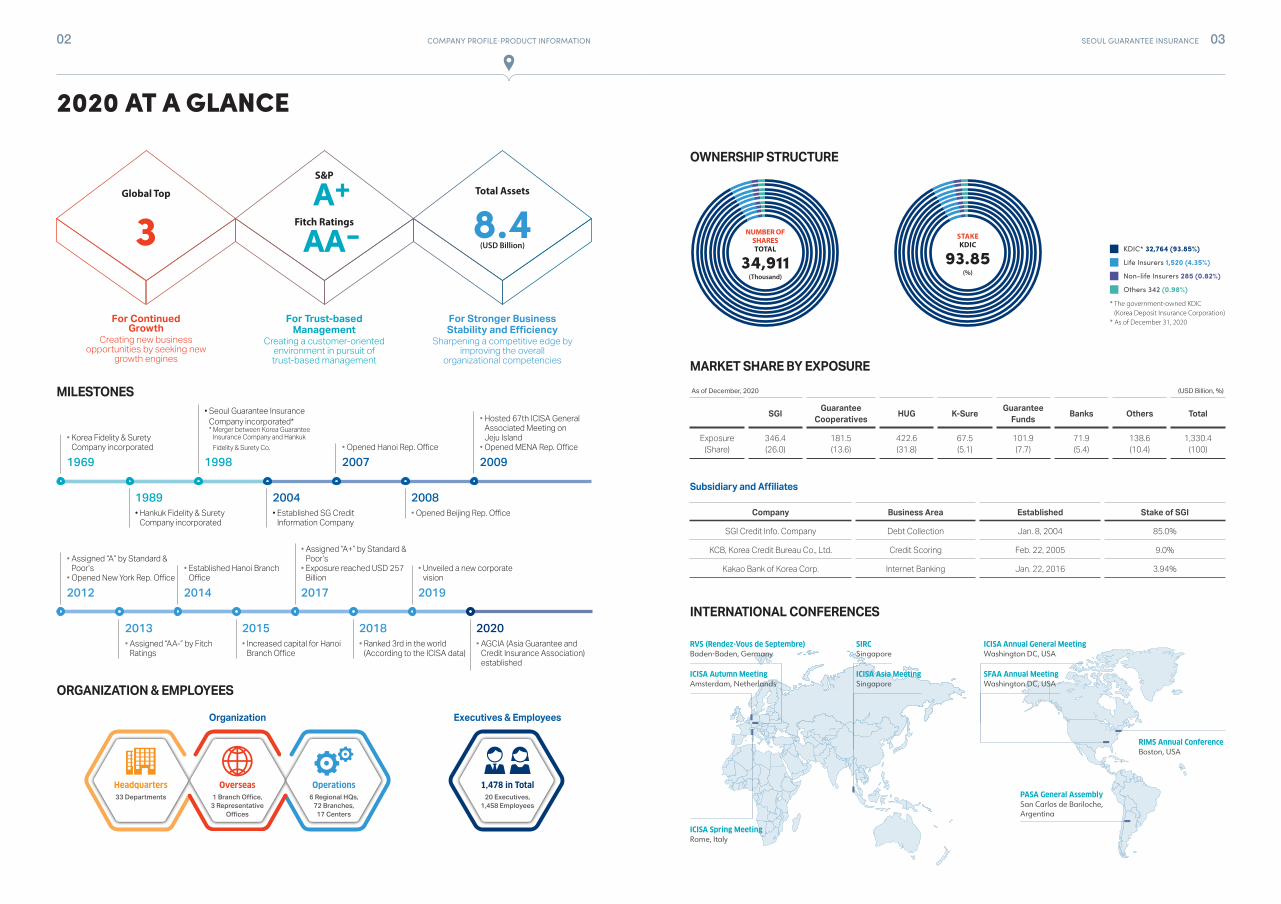

2020 AT A GLANCE

OWNERSHIP STRUCTURE

MARKET SHARE BY EXPOSURE

As of December, 2020 (USD Billion, %)

SGIGuarantee

CooperativesHUG K-Sure

Guarantee Funds

Banks Others Total

Exposure(Share)

346.4(26.0)

181.5(13.6)

422.6(31.8)

67.5(5.1)

101.9(7.7)

71.9(5.4)

138.6(10.4)

1,330.4(100)

Subsidiary and Affiliates

Company Business Area Established Stake of SGI

SGI Credit Info. Company Debt Collection Jan. 8, 2004 85.0%

KCB, Korea Credit Bureau Co., Ltd. Credit Scoring Feb. 22, 2005 9.0%

Kakao Bank of Korea Corp. Internet Banking Jan. 22, 2016 3.94%

INTERNATIONAL CONFERENCES

NUMBER OF SHARESTOTAL

34,911(Thousand)

STAKEKDIC

93.85(%)

For Continued Growth

Creating new business opportunities by seeking new

growth engines

Global Top

3

For Trust-basedManagement

Creating a customer-oriented environment in pursuit of trust-based management

S&P

A+Fitch Ratings

AA-

For Stronger BusinessStability and Efficiency

Sharpening a competitive edge by improving the overall

organizational competencies

Total Assets

8.4(USD Billion)

ORGANIZATION & EMPLOYEES

Executives & Employees

1,478 in Total 20 Executives,

1,458 Employees

Organization

Overseas1 Branch Office,

3 Representative Offices

Operations6 Regional HQs,

72 Branches, 17 Centers

Headquarters33 Departments

MILESTONES

• Korea Fidelity & Surety Company incorporated

1969

1989• Hankuk Fidelity & Surety

Company incorporated

2004• Established SG Credit

Information Company

2008• Opened Beijing Rep. Office

• Seoul Guarantee Insurance Company incorporated* * Merger between Korea Guarantee

Insurance Company and Hankuk

Fidelity & Surety Co.

1998• Opened Hanoi Rep. Office

2007

• Hosted 67th ICISA General Associated Meeting on Jeju Island

• Opened MENA Rep. Office

2009

• Assigned “A” by Standard & Poor’s

• Opened New York Rep. Office

2012

2013• Assigned “AA-” by Fitch

Ratings

2015• Increased capital for Hanoi

Branch Office

2018• Ranked 3rd in the world

(According to the ICISA data)

2020• AGCIA (Asia Guarantee and

Credit Insurance Association) established

• Established Hanoi Branch Office

2014

• Assigned “A+” by Standard & Poor’s

• Exposure reached USD 257 Billion

2017

• Unveiled a new corporate vision

2019

RVS (Rendez-Vous de Septembre)Baden-Baden, Germany

ICISA Autumn MeetingAmsterdam, Netherlands

ICISA Spring MeetingRome, Italy

SIRC Singapore

ICISA Asia MeetingSingapore

RIMS Annual Conference Boston, USA

PASA General Assembly San Carlos de Bariloche, Argentina

ICISA Annual General MeetingWashington DC, USA

SFAA Annual Meeting Washington DC, USA

* The government-owned KDIC (Korea Deposit Insurance Corporation)

* As of December 31, 2020

KDIC* 32,764 (93.85%)

Life Insurers 1,520 (4.35%)

Non-life Insurers 285 (0.82%)

Others 342 (0.98%)

COMPANY PROFILE · PRODUCT INFORMATION 0504 SEOUL GUARANTEE INSURANCE

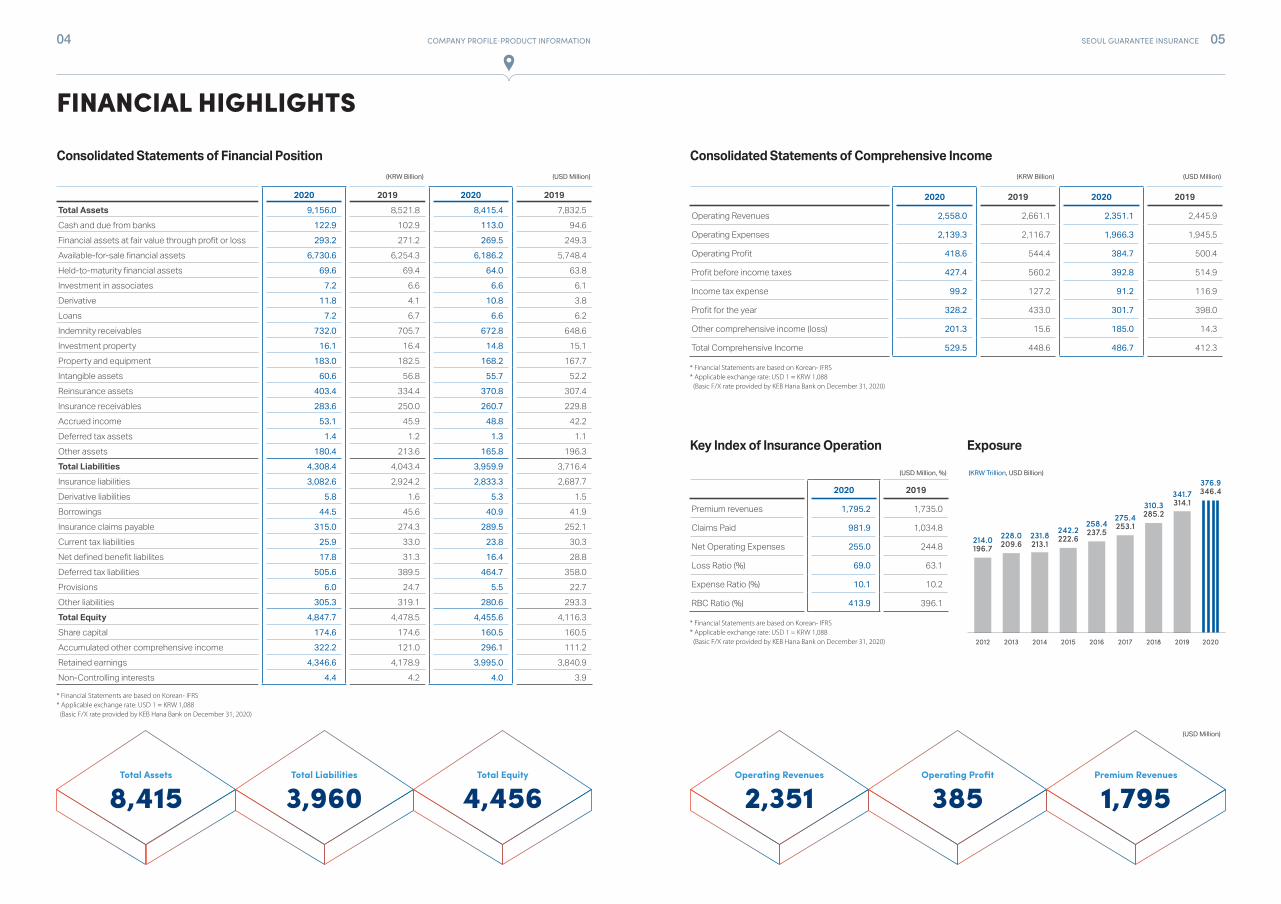

FINANCIAL HIGHLIGHTS

Consolidated Statements of Financial Position Consolidated Statements of Comprehensive Income(KRW Billion) (USD Million)

2020 2019 2020 2019

Total Assets 9,156.0 8,521.8 8,415.4 7,832.5

Cash and due from banks 122.9 102.9 113.0 94.6

Financial assets at fair value through profit or loss 293.2 271.2 269.5 249.3

Available-for-sale financial assets 6,730.6 6,254.3 6,186.2 5,748.4

Held-to-maturity financial assets 69.6 69.4 64.0 63.8

Investment in associates 7.2 6.6 6.6 6.1

Derivative 11.8 4.1 10.8 3.8

Loans 7.2 6.7 6.6 6.2

Indemnity receivables 732.0 705.7 672.8 648.6

Investment property 16.1 16.4 14.8 15.1

Property and equipment 183.0 182.5 168.2 167.7

Intangible assets 60.6 56.8 55.7 52.2

Reinsurance assets 403.4 334.4 370.8 307.4

Insurance receivables 283.6 250.0 260.7 229.8

Accrued income 53.1 45.9 48.8 42.2

Deferred tax assets 1.4 1.2 1.3 1.1

Other assets 180.4 213.6 165.8 196.3

Total Liabilities 4,308.4 4,043.4 3,959.9 3,716.4

Insurance liabilities 3,082.6 2,924.2 2,833.3 2,687.7

Derivative liabilities 5.8 1.6 5.3 1.5

Borrowings 44.5 45.6 40.9 41.9

Insurance claims payable 315.0 274.3 289.5 252.1

Current tax liabilities 25.9 33.0 23.8 30.3

Net defined benefit liabilites 17.8 31.3 16.4 28.8

Deferred tax liabilities 505.6 389.5 464.7 358.0

Provisions 6.0 24.7 5.5 22.7

Other liabilities 305.3 319.1 280.6 293.3

Total Equity 4,847.7 4,478.5 4,455.6 4,116.3

Share capital 174.6 174.6 160.5 160.5

Accumulated other comprehensive income 322.2 121.0 296.1 111.2

Retained earnings 4,346.6 4,178.9 3,995.0 3,840.9

Non-Controlling interests 4.4 4.2 4.0 3.9

* Financial Statements are based on Korean- IFRS * Applicable exchange rate: USD 1 = KRW 1,088 (Basic F/X rate provided by KEB Hana Bank on December 31, 2020)

(KRW Billion) (USD Million)

2020 2019 2020 2019

Operating Revenues 2,558.0 2,661.1 2,351.1 2,445.9

Operating Expenses 2,139.3 2,116.7 1,966.3 1,945.5

Operating Profit 418.6 544.4 384.7 500.4

Profit before income taxes 427.4 560.2 392.8 514.9

Income tax expense 99.2 127.2 91.2 116.9

Profit for the year 328.2 433.0 301.7 398.0

Other comprehensive income (loss) 201.3 15.6 185.0 14.3

Total Comprehensive Income 529.5 448.6 486.7 412.3

* Financial Statements are based on Korean- IFRS * Applicable exchange rate: USD 1 = KRW 1,088 (Basic F/X rate provided by KEB Hana Bank on December 31, 2020)

Key Index of Insurance Operation

(USD Million, %)

2020 2019

Premium revenues 1,795.2 1,735.0

Claims Paid 981.9 1,034.8

Net Operating Expenses 255.0 244.8

Loss Ratio (%) 69.0 63.1

Expense Ratio (%) 10.1 10.2

RBC Ratio (%) 413.9 396.1

* Financial Statements are based on Korean- IFRS * Applicable exchange rate: USD 1 = KRW 1,088 (Basic F/X rate provided by KEB Hana Bank on December 31, 2020)

Exposure

(KRW Trillion, USD Billion)

341.7 314.1

376.9 346.4

310.3 285.2 275.4

253.1 258.4 237.5 242.2

222.6 231.8 213.1

228.0 209.6 214.0

196.7

2012 2013 2014 2015 2016 2017 2018 2019 2020

(USD Million)

Total Assets

8,415 Total Liabilities

3,960 Total Equity

4,456 Operating Revenues

2,351 Operating Profit

385 Premium Revenues

1,795

COMPANY PROFILE · PRODUCT INFORMATION 0706 SEOUL GUARANTEE INSURANCE

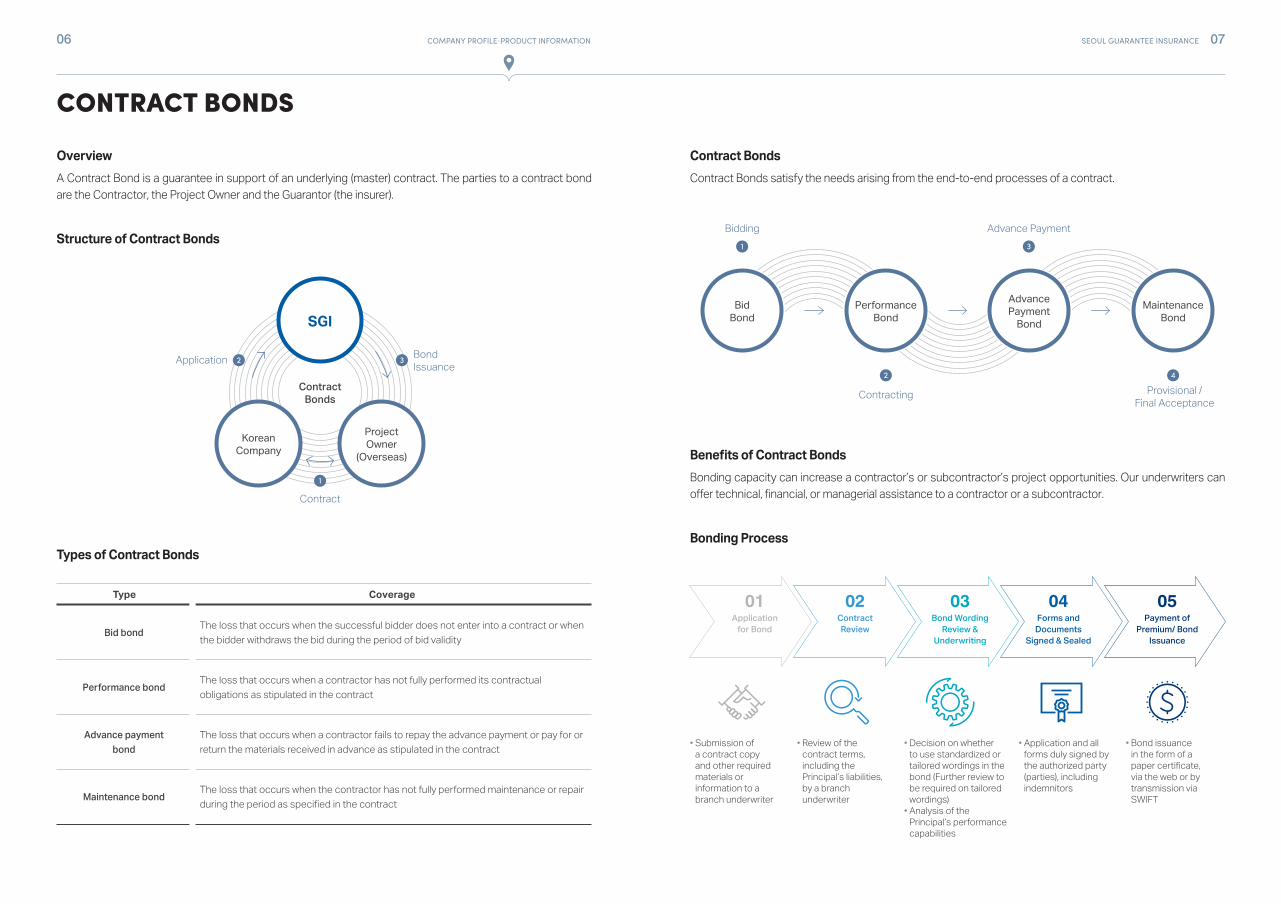

Overview

A Contract Bond is a guarantee in support of an underlying (master) contract. The parties to a contract bond are the Contractor, the Project Owner and the Guarantor (the insurer).

Structure of Contract Bonds

Types of Contract Bonds

Contract Bonds

Contract Bonds satisfy the needs arising from the end-to-end processes of a contract.

Benefits of Contract Bonds

Bonding capacity can increase a contractor’s or subcontractor’s project opportunities. Our underwriters can offer technical, financial, or managerial assistance to a contractor or a subcontractor.

Bonding Process

Bidding

Contracting

Advance Payment

Provisional / Final Acceptance

BidBond

PerformanceBond

AdvancePayment

Bond

MaintenanceBond

• Submission of a contract copy and other required materials or information to a branch underwriter

• Review of the contract terms, including the Principal’s liabilities, by a branch underwriter

• Decision on whether to use standardized or tailored wordings in the bond (Further review to be required on tailored wordings)

• Analysis of the Principal’s performance capabilities

• Application and all forms duly signed by the authorized party (parties), including indemnitors

• Bond issuance in the form of a paper certificate, via the web or by transmission via SWIFT

Application for Bond

ContractReview

Bond Wording Review &

Underwriting

Forms and Documents

Signed & Sealed

Payment of Premium/ Bond

Issuance

01 02 03 04 05

1

2

3

4Contract

Bonds

SGI

KoreanCompany

ProjectOwner

(Overseas)

Contract

1

Application 2 3 Bond Issuance

CONTRACT BONDS

Type Coverage

Bid bondThe loss that occurs when the successful bidder does not enter into a contract or when

the bidder withdraws the bid during the period of bid validity

Performance bondThe loss that occurs when a contractor has not fully performed its contractual

obligations as stipulated in the contract

Advance paymentbond

The loss that occurs when a contractor fails to repay the advance payment or pay for or

return the materials received in advance as stipulated in the contract

Maintenance bondThe loss that occurs when the contractor has not fully performed maintenance or repair

during the period as specified in the contract

COMPANY PROFILE · PRODUCT INFORMATION 0908 SEOUL GUARANTEE INSURANCE

COUNTER GUARANTEE BOND

SGI offers Counter Guarantee Bond to the companies that are in need of local bank guarantees for concluding an overseas project.

What is Counter Guarantee Bond?

In many cases, project owners request contractors to provide a guarantee issued by a financial institution. SGI’s Counter Guarantee Bond can be used as collateral for the issuance of such guarantee, in case the con-tractor needs to furnish a guarantee issued by a financial institution operating in the project owner’s country, or the contractor does not have enough credit limits to apply for a guarantee. In case the project owner de-mands payment to the financial institution that issued the guarantee on behalf of the contractor, SGI will pay the amount demanded by the project owner and the relevant expenses and costs to the financial institution. Counter Guarantee Bond, as a product that co-exists with guarantees, enhances the contractor’s creditworthi-ness. SGI has gained substantial trust from numerous financial institutions due to its high credit ratings.

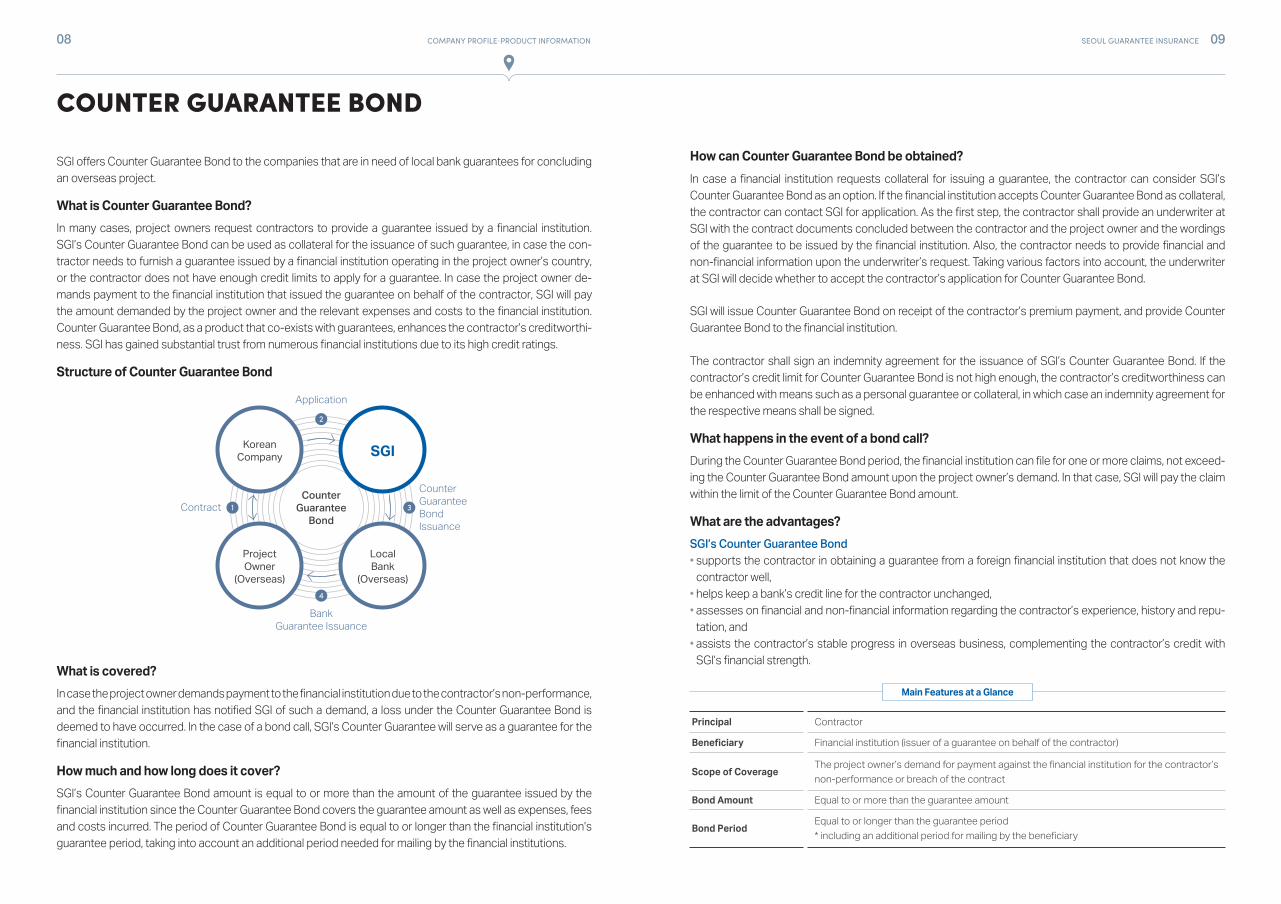

Structure of Counter Guarantee Bond

How can Counter Guarantee Bond be obtained?

In case a financial institution requests collateral for issuing a guarantee, the contractor can consider SGI’s Counter Guarantee Bond as an option. If the financial institution accepts Counter Guarantee Bond as collateral, the contractor can contact SGI for application. As the first step, the contractor shall provide an underwriter at SGI with the contract documents concluded between the contractor and the project owner and the wordings of the guarantee to be issued by the financial institution. Also, the contractor needs to provide financial and non-financial information upon the underwriter’s request. Taking various factors into account, the underwriter at SGI will decide whether to accept the contractor’s application for Counter Guarantee Bond.

SGI will issue Counter Guarantee Bond on receipt of the contractor’s premium payment, and provide Counter Guarantee Bond to the financial institution.

The contractor shall sign an indemnity agreement for the issuance of SGI’s Counter Guarantee Bond. If the contractor’s credit limit for Counter Guarantee Bond is not high enough, the contractor’s creditworthiness can be enhanced with means such as a personal guarantee or collateral, in which case an indemnity agreement for the respective means shall be signed.

What happens in the event of a bond call?

During the Counter Guarantee Bond period, the financial institution can file for one or more claims, not exceed-ing the Counter Guarantee Bond amount upon the project owner’s demand. In that case, SGI will pay the claim within the limit of the Counter Guarantee Bond amount.

What are the advantages?

SGI’s Counter Guarantee Bond• supports the contractor in obtaining a guarantee from a foreign financial institution that does not know the

contractor well,• helps keep a bank’s credit line for the contractor unchanged,• assesses on financial and non-financial information regarding the contractor’s experience, history and repu-

tation, and • assists the contractor’s stable progress in overseas business, complementing the contractor’s credit with

SGI’s financial strength.What is covered?

In case the project owner demands payment to the financial institution due to the contractor’s non-performance, and the financial institution has notified SGI of such a demand, a loss under the Counter Guarantee Bond is deemed to have occurred. In the case of a bond call, SGI’s Counter Guarantee will serve as a guarantee for the financial institution.

How much and how long does it cover?

SGI’s Counter Guarantee Bond amount is equal to or more than the amount of the guarantee issued by the financial institution since the Counter Guarantee Bond covers the guarantee amount as well as expenses, fees and costs incurred. The period of Counter Guarantee Bond is equal to or longer than the financial institution’s guarantee period, taking into account an additional period needed for mailing by the financial institutions.

Counter Guarantee

Bond

ProjectOwner

(Overseas)

LocalBank

(Overseas)

KoreanCompany SGI

Bank Guarantee Issuance

4

Contract 1

Counter Guarantee Bond Issuance

3

Application

2

Principal Contractor

Beneficiary Financial institution (issuer of a guarantee on behalf of the contractor)

Scope of CoverageThe project owner’s demand for payment against the financial institution for the contractor’s

non-performance or breach of the contract

Bond Amount Equal to or more than the guarantee amount

Bond PeriodEqual to or longer than the guarantee period

* including an additional period for mailing by the beneficiary

Main Features at a Glance

COMPANY PROFILE · PRODUCT INFORMATION 1110 SEOUL GUARANTEE INSURANCE

REINSURANCE BUSINESS

SGI has been running the reinsurance business for the last 52 years of corporate history. The Reinsurance Department is specialized in the reinsurance business, hedging against the risks of guarantee and credit in-surance underwritten through outward reinsurance. In parallel, the Department is generating a revenue stream from the inward reinsurance business based on sound financials and solid business networks.

Outward Reinsurance

In order to manage insurance risks and maintain business stability, SGI utilizes multiple ceding programs taking into account marketing strategies, capital allocation plans, and the market landscape. SGI has maintained long-term business relationships with more than twenty world-renowned reinsurers.

Inward Reinsurance

SGI’s inward reinsurance contributes to business diversification and corporate value enhancement. SGI’s wide global business network and enhanced portfolio mix are propping up inward reinsurance.

Through strict underwriting policies based on multifaceted risk analysis and well-established relationships with customers, SGI has earned recognition as a reliable reinsurer in the market. In addition, SGI expanded its rein-surance business territory further to include the US, China, Southeast Asia, and the Middle East.

SGI writes inward reinsurance primarily on property/engineering, motor and liability, but it also covers other non-life lines such as marine, bond/credit, and casualties. To achieve both sustainable growth and profitability, SGI keeps its business portfolio optimized for earnings.

Development of Reinsurance Business Network

SGI has held the Asia Surety and Credit Insurance Seminar since 2018 and has attended international rein-surance events regularly, such as the RVS and the SIRC, to broaden the global network and presence fur-ther. However, SGI’s business practice has been changed significantly since COVID-19 spread throughout the world. Particularly, the global business has been disrupted by the pandemic.

In order to deal with this unfavorable situation, SGI revised its business plan for 2020 reflecting contingency measures. In addition, SGI converted most of its face-to-face marketing activities into the ones that did not involve physical interactions but proved to be effective for engaging with global business partners. Despite the challenges posed by the pandemic, SGI will make efforts to maintain strong ties with its valued business partners across the world.

100(%)

TOTAL

48.8%

14.1%

2.8%2.5%

9.7%

2.6%

19.5%

DomesticChinaAfrica & Middle EastAsia(other than China)

North America Latin AmericaOthers

* Based on covered territory for each contract / Others include Southeast Asia, Europe and the contracts with worldwide coverage.

166,316

243,469

266,205

231,861 234,503

2016 2017 2018 2019 2020

Inward Reinsurance Portfolio by Type of Products in 2020

(in USD thousand, %)

Property/Engineering

Motor Liability Personal Accident

Bond/ CreditInsurance

Marine Others Total

90,292 31,192 25,531 13,353 1,722 16,960 55,451 234,503

38.5% 13.3% 10.9% 5.7% 0.7% 7.2% 23.6% 100.0%

* Applicable Exchange Rate: USD 1 = KRW 1,088 (Basic F/X rate provided by Hana Bank on December 31, 2020)

Inward Reinsurance Portfolio by Region in 2020(in USD thousand)

Inward Reinsurance Premium

COMPANY PROFILE · PRODUCT INFORMATION 1312 SEOUL GUARANTEE INSURANCE

FRONTING SERVICE GLOBAL BUSINESS DIVISION

What is the background?

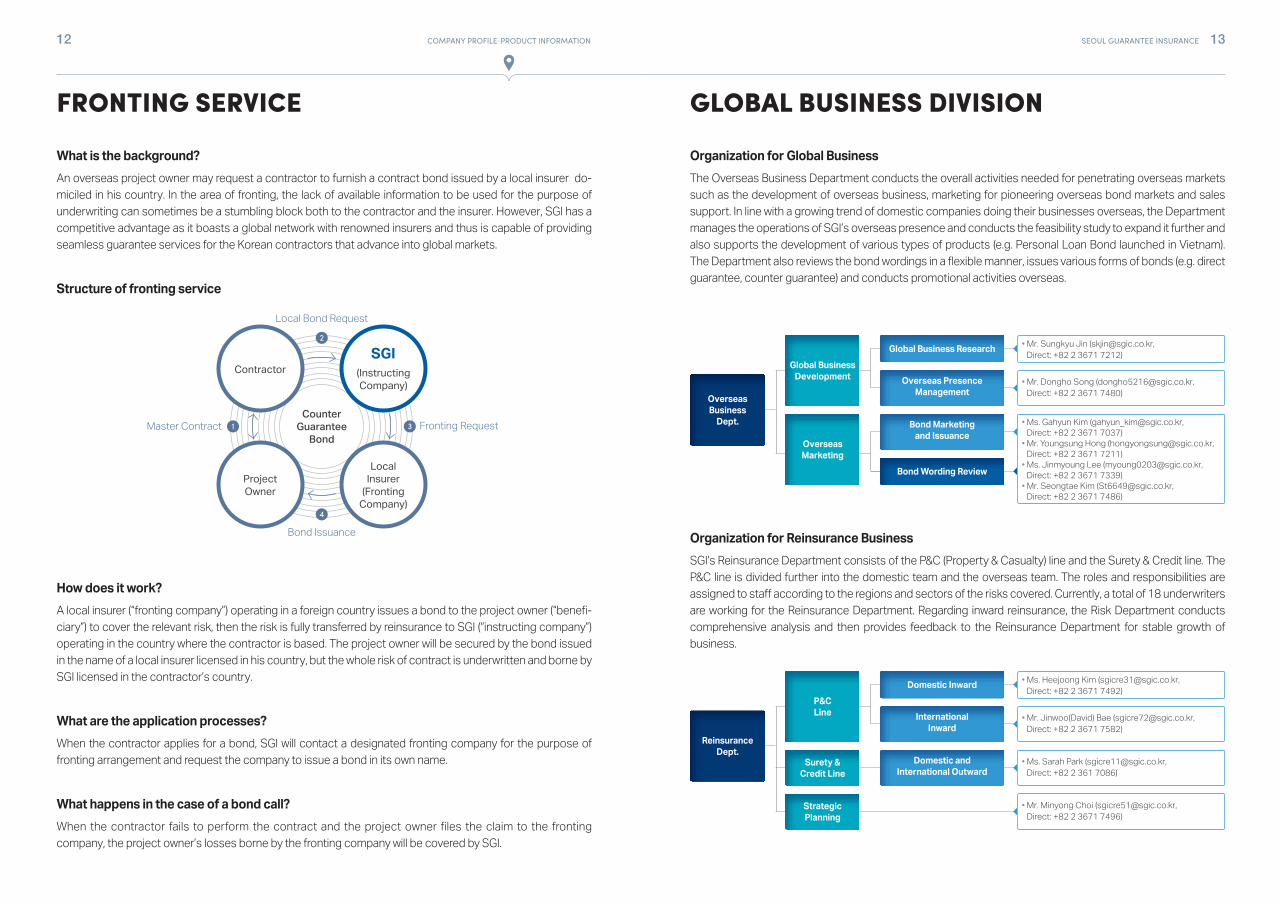

An overseas project owner may request a contractor to furnish a contract bond issued by a local insurer do-miciled in his country. In the area of fronting, the lack of available information to be used for the purpose of underwriting can sometimes be a stumbling block both to the contractor and the insurer. However, SGI has a competitive advantage as it boasts a global network with renowned insurers and thus is capable of providing seamless guarantee services for the Korean contractors that advance into global markets.

Structure of fronting service

Organization for Global Business

The Overseas Business Department conducts the overall activities needed for penetrating overseas markets such as the development of overseas business, marketing for pioneering overseas bond markets and sales support. In line with a growing trend of domestic companies doing their businesses overseas, the Department manages the operations of SGI’s overseas presence and conducts the feasibility study to expand it further and also supports the development of various types of products (e.g. Personal Loan Bond launched in Vietnam). The Department also reviews the bond wordings in a flexible manner, issues various forms of bonds (e.g. direct guarantee, counter guarantee) and conducts promotional activities overseas.

Organization for Reinsurance Business

SGI’s Reinsurance Department consists of the P&C (Property & Casualty) line and the Surety & Credit line. The P&C line is divided further into the domestic team and the overseas team. The roles and responsibilities are assigned to staff according to the regions and sectors of the risks covered. Currently, a total of 18 underwriters are working for the Reinsurance Department. Regarding inward reinsurance, the Risk Department conducts comprehensive analysis and then provides feedback to the Reinsurance Department for stable growth of business.

How does it work?

A local insurer (“fronting company”) operating in a foreign country issues a bond to the project owner (“benefi-ciary”) to cover the relevant risk, then the risk is fully transferred by reinsurance to SGI (“instructing company”) operating in the country where the contractor is based. The project owner will be secured by the bond issued in the name of a local insurer licensed in his country, but the whole risk of contract is underwritten and borne by SGI licensed in the contractor’s country.

What are the application processes?

When the contractor applies for a bond, SGI will contact a designated fronting company for the purpose of fronting arrangement and request the company to issue a bond in its own name.

What happens in the case of a bond call?

When the contractor fails to perform the contract and the project owner files the claim to the fronting company, the project owner’s losses borne by the fronting company will be covered by SGI.

Reinsurance Dept.

P&CLine

• Ms. Heejoong Kim ([email protected], Direct: +82 2 3671 7492)

• Mr. Jinwoo(David) Bae ([email protected], Direct: +82 2 3671 7582)

• Ms. Sarah Park ([email protected], Direct: +82 2 361 7086)

Domestic Inward

InternationalInward

Domestic andInternational Outward

Surety &Credit Line

• Mr. Minyong Choi ([email protected], Direct: +82 2 3671 7496)

Strategic Planning

Overseas Business

Dept.

Global BusinessDevelopment

• Mr. Sungkyu Jin ([email protected], Direct: +82 2 3671 7212)

• Mr. Dongho Song ([email protected], Direct: +82 2 3671 7480)

• Ms. Gahyun Kim ([email protected], Direct: +82 2 3671 7037)

• Mr. Youngsung Hong ([email protected], Direct: +82 2 3671 7211)

• Ms. Jinmyoung Lee ([email protected], Direct: +82 2 3671 7339)

• Mr. Seongtae Kim ([email protected], Direct: +82 2 3671 7486)

Global Business Research

Bond Wording Review

Overseas PresenceManagement

Overseas Marketing

Bond Marketing and Issuance

Counter Guarantee

Bond

ProjectOwner

LocalInsurer

(FrontingCompany)

Contractor SGI

Bond Issuance

4

Master Contract 1 Fronting Request3

Local Bond Request

2

(InstructingCompany)

COMPANY PROFILE · PRODUCT INFORMATION 1514 SEOUL GUARANTEE INSURANCE

OVERVIEW OF SGI’S BUSINESS

Global Business

Overseas Business Department1) Global Business Development

2) International Marketing and Issuance of CGB (Counter Guarantee Bond)

Reinsurance Department1) Reinsurance Strategy and Analysis

2) Reinsurance Structuring and Underwriting

3) Reinsurance Business Network Development

Strategic Business

Corporate Credit Insurance Department1) Underwriting of Installment Credit Insurance and Commercial Credit Insurance

2) Establishment of Marketing and Sales Plans

3) Customer and Market Management

Consumer Credit Insurance Department1) Underwriting of Mortgage and PFCI (Personal Financial Credit Insurance)

2) Customer and Market Management

3) Establishment of Marketing Plans

Commercial Credit Insurance Department1) Underwriting of Account Receivable Credit Insurance, Factoring Credit

Insurance and Foreign Investment Insurance

2) Conclusion and Management of Agreements

Marketing and Product Management

Marketing Service Department1) Operation of Customer Relationship Management (CRM)

2) Management and Evaluation of Sales Performance

3) Support and Management of Marketing and Agency Channels

Product Development Department1) Product Development and Research

2) Operation of Product Management Policies

3) Improvement and Management of Products

Product Actuarial Department1) Adjustment and Operation of Premium Rates

2) Accumulation and Management of Reserve for Indemnity Proceeds Payout

3) Review of Policy Conditions and Insurance Documents

Underwriting and Risk Management

Credit Evaluation Department1) Establishment of Underwriting Policies

2) Credit Evaluation and Analysis

3) Management of Credit Information and Evaluation Systems

Underwriting Department1) Review by Skilled Underwriters

2) Review of Reinsurance Underwriting

Risk Management Department1) Establishment of Risk Management Policies

2) Analysis and Examination of Risks

3) Management of Enterprise Data and Statistical Analysis

SGI has a robust marketing system that is supported by smooth cooperations among key departments and ample business know-how accumulated so far.

Its product portfolio encompassing guarantee insurance, credit insurance and reinsurance is solid enough to deliver a stable level of growth in sales.

In addition, SGI has an excellent credit rating methodology based on strong risk management policies. SGI prevents exposure to major risks by detecting various risk factors (e.g. bankruptcy of customers) early on.

SGI is promoting sales by developing new products and improving its existing products. It is also pioneering a new market by taking advantage of its strategic alliance with global partners.

Below are SGI’s strengths in its key business areas and its marketing competencies.

COMPANY PROFILE · PRODUCT INFORMATION16

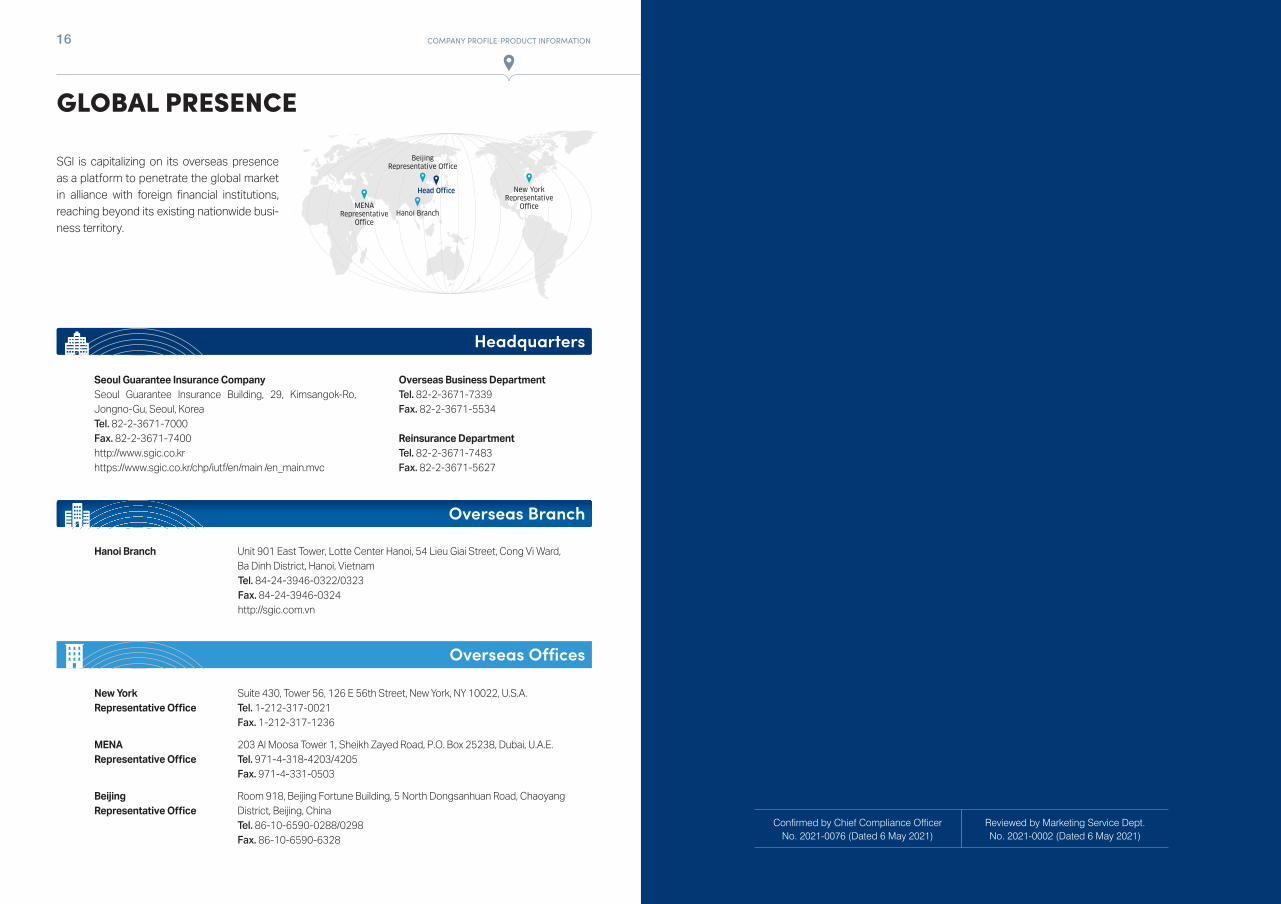

GLOBAL PRESENCE

Hanoi Branch

Head Office

MENARepresentative

Office

New YorkRepresentative

Office

Beijing Representative Office

Seoul Guarantee Insurance CompanySeoul Guarantee Insurance Building, 29, Kimsangok-Ro, Jongno-Gu, Seoul, KoreaTel. 82-2-3671-7000Fax. 82-2-3671-7400http://www.sgic.co.krhttps://www.sgic.co.kr/chp/iutf/en/main /en_main.mvc

Hanoi Branch Unit 901 East Tower, Lotte Center Hanoi, 54 Lieu Giai Street, Cong Vi Ward, Ba Dinh District, Hanoi, Vietnam

Tel. 84-24-3946-0322/0323 Fax. 84-24-3946-0324 http://sgic.com.vn

Overseas Business DepartmentTel. 82-2-3671-7339Fax. 82-2-3671-5534

Reinsurance DepartmentTel. 82-2-3671-7483Fax. 82-2-3671-5627

New York Suite 430, Tower 56, 126 E 56th Street, New York, NY 10022, U.S.A.Representative Office Tel. 1-212-317-0021 Fax. 1-212-317-1236

MENA 203 Al Moosa Tower 1, Sheikh Zayed Road, P.O. Box 25238, Dubai, U.A.E.Representative Office Tel. 971-4-318-4203/4205 Fax. 971-4-331-0503

Beijing Room 918, Beijing Fortune Building, 5 North Dongsanhuan Road, Chaoyang Representative Office District, Beijing, China Tel. 86-10-6590-0288/0298 Fax. 86-10-6590-6328

Overseas Branch

Overseas Offices

Headquarters

SGI is capitalizing on its overseas presence as a platform to penetrate the global market in alliance with foreign financial institutions, reaching beyond its existing nationwide busi-ness territory.

Confirmed by Chief Compliance OfficerNo. 2021-0076 (Dated 6 May 2021)

Reviewed by Marketing Service Dept.No. 2021-0002 (Dated 6 May 2021)

Recommended