© 2013 Gartner, Inc. and/or its affiliates. All rights reserved. Gartner is a registered trademark of Gartner, Inc. or its affiliates. This publication may not be reproduced or distributed in any form without Gartner's prior written permission. If you are authorized to access this publication, your use of it is subject to the Usage Guidelines for Gartner Services posted on gartner.com. The information contained in this publication has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness or adequacy of such information and shall have no liability for errors, omissions or inadequacies in such information. This publication consists of the opinions of Gartner's research organization and should not be construed as statements of fact. The opinions expressed herein are subject to change without notice. Although Gartner research may include a discussion of related legal issues, Gartner does not provide legal advice or services and its research should not be construed or used as such. Gartner is a public company, and its shareholders may include firms and funds that have financial interests in entities covered in Gartner research. Gartner's Board of Directors may include senior managers of these firms or funds. Gartner research is produced independently by its research organization without input or influence from these firms, funds or their managers. For further information on the independence and integrity of Gartner research, see "Guiding Principles on Independence and Objectivity."

David Ackerman

March 18, 2014

Tweet: #GartnerLOC

Gartner Briefing: The Future of I & O

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved. © 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

I&O Perspective

1

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

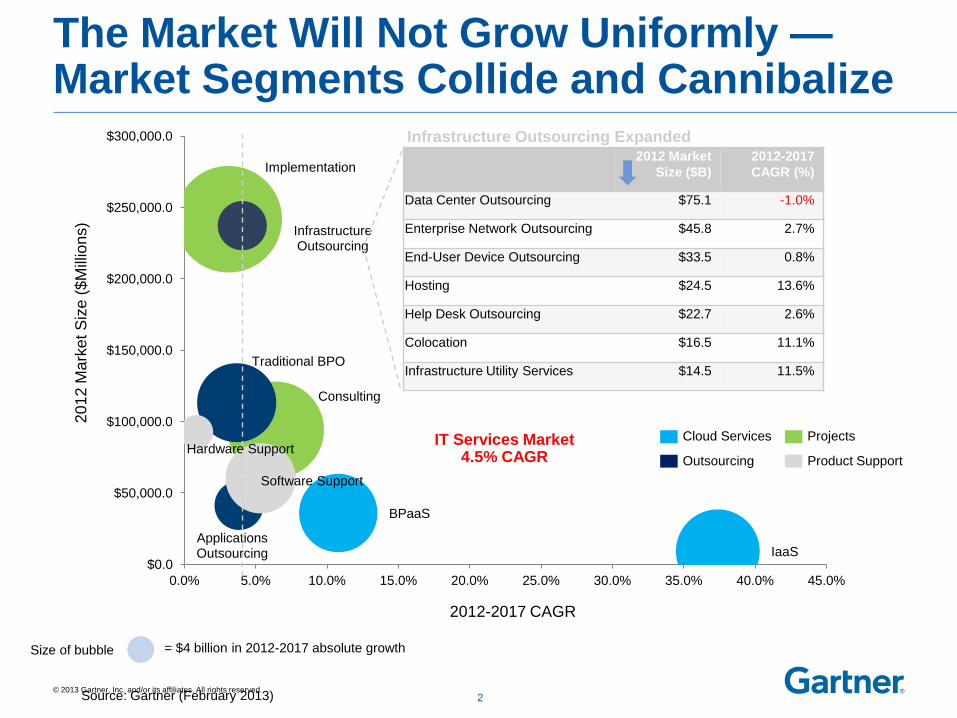

Consulting

Implementation

IaaS

Infrastructure Outsourcing

Applications Outsourcing

BPaaS

Traditional BPO

Software Support

Hardware Support

$0.0

$50,000.0

$100,000.0

$150,000.0

$200,000.0

$250,000.0

$300,000.0

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0%

2

The Market Will Not Grow Uniformly — Market Segments Collide and Cannibalize

20

12

Ma

rket S

ize

($M

illio

ns)

2012-2017 CAGR

= $4 billion in 2012-2017 absolute growth

Source: Gartner (February 2013)

IT Services Market 4.5% CAGR

Cloud Services

Outsourcing

Projects

Product Support

Size of bubble

2012 Market

Size ($B)

2012-2017

CAGR (%)

Data Center Outsourcing $75.1 -1.0%

Enterprise Network Outsourcing $45.8 2.7%

End-User Device Outsourcing $33.5 0.8%

Hosting $24.5 13.6%

Help Desk Outsourcing $22.7 2.6%

Colocation $16.5 11.1%

Infrastructure Utility Services $14.5 11.5%

Infrastructure Outsourcing Expanded

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

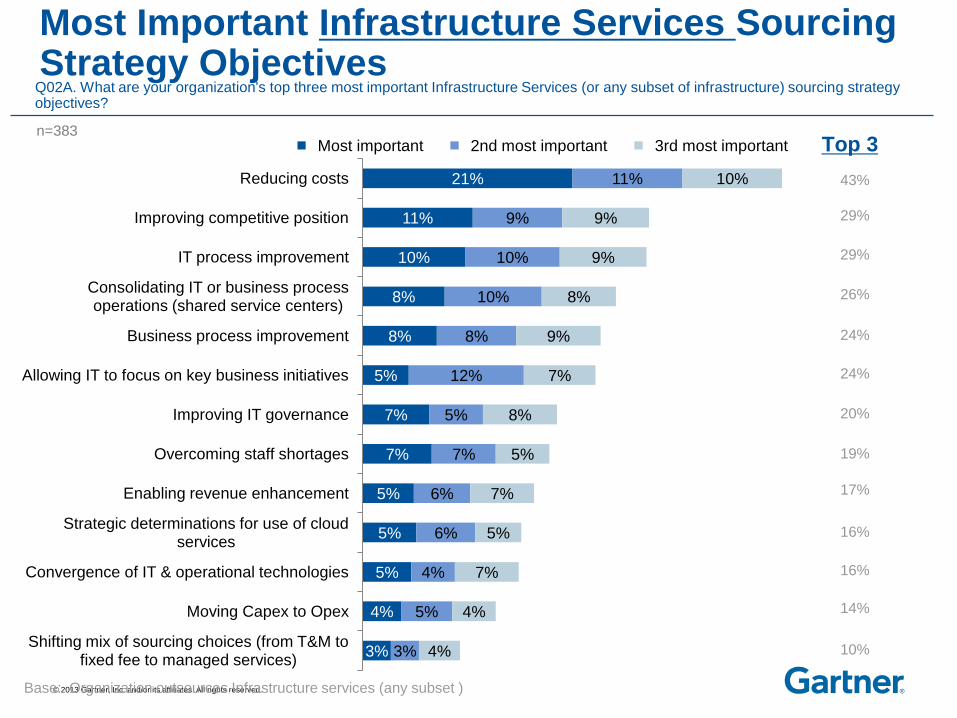

3%

4%

5%

5%

5%

7%

7%

5%

8%

8%

10%

11%

21%

3%

5%

4%

6%

6%

7%

5%

12%

8%

10%

10%

9%

11%

4%

4%

7%

5%

7%

5%

8%

7%

9%

8%

9%

9%

10%

Shifting mix of sourcing choices (from T&M to fixed fee to managed services)

Moving Capex to Opex

Convergence of IT & operational technologies

Strategic determinations for use of cloud services

Enabling revenue enhancement

Overcoming staff shortages

Improving IT governance

Allowing IT to focus on key business initiatives

Business process improvement

Consolidating IT or business process operations (shared service centers)

IT process improvement

Improving competitive position

Reducing costs

Most important 2nd most important 3rd most important

Q02A. What are your organization's top three most important Infrastructure Services (or any subset of infrastructure) sourcing strategy objectives?

Base: Organization outsources Infrastructure services (any subset )

Most Important Infrastructure Services Sourcing Strategy Objectives

43%

17%

29%

24%

20%

26%

10%

16%

29%

16%

24%

19%

14%

n=383 Top 3

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

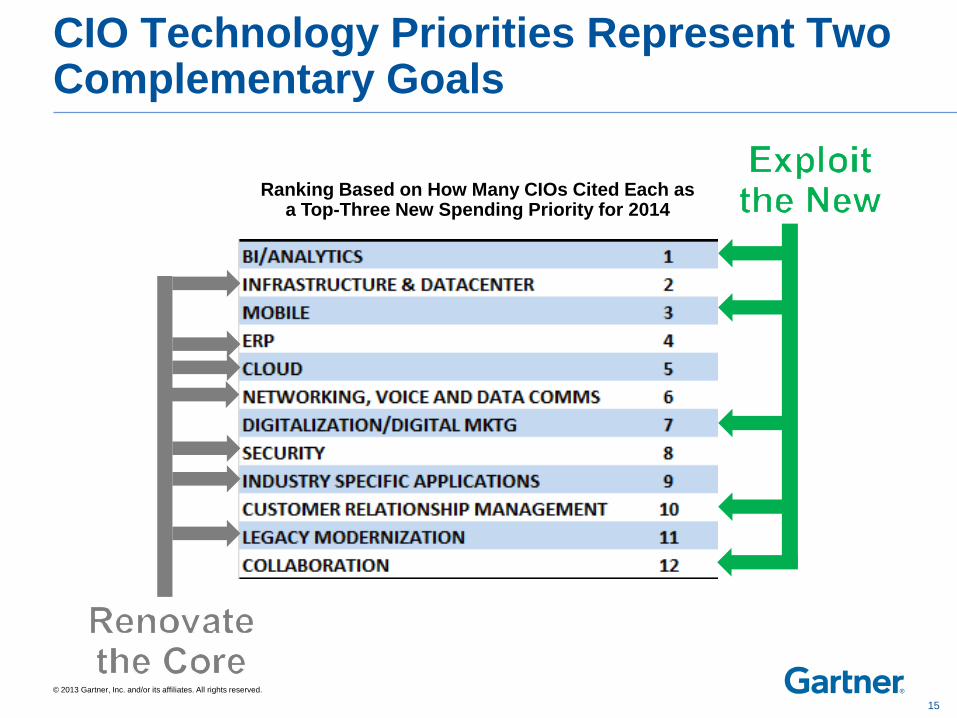

CIO Technology Priorities Represent Two Complementary Goals

Ranking Based on How Many CIOs Cited Each as a Top-Three New Spending Priority for 2014

15

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

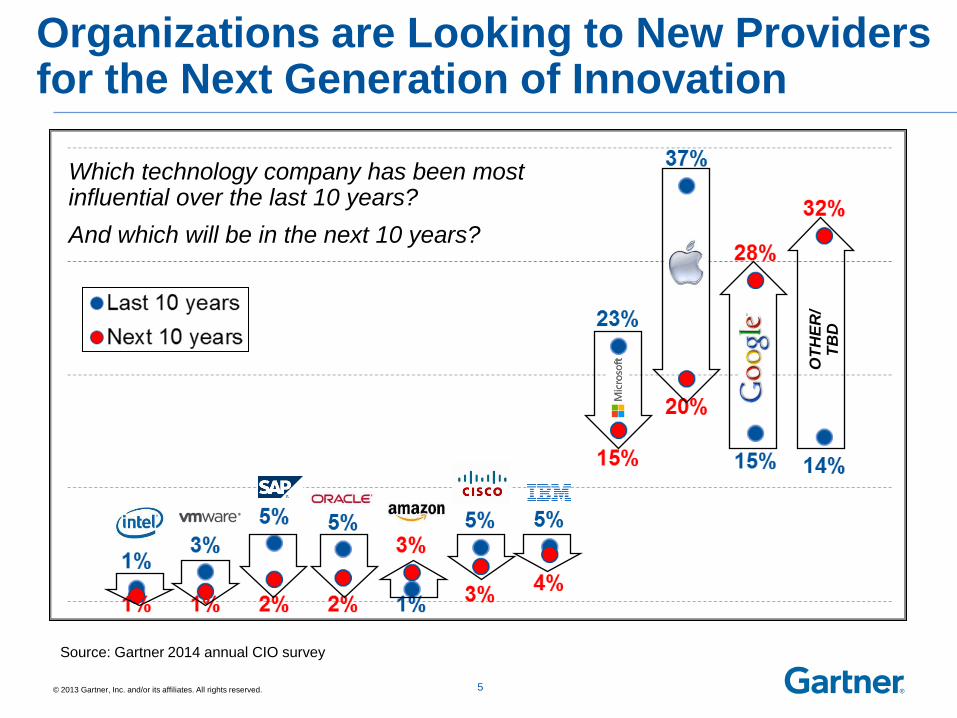

Organizations are Looking to New Providers for the Next Generation of Innovation

5

OT

HE

R/

TB

D

Which technology company has been most influential over the last 10 years?

And which will be in the next 10 years?

Source: Gartner 2014 annual CIO survey

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

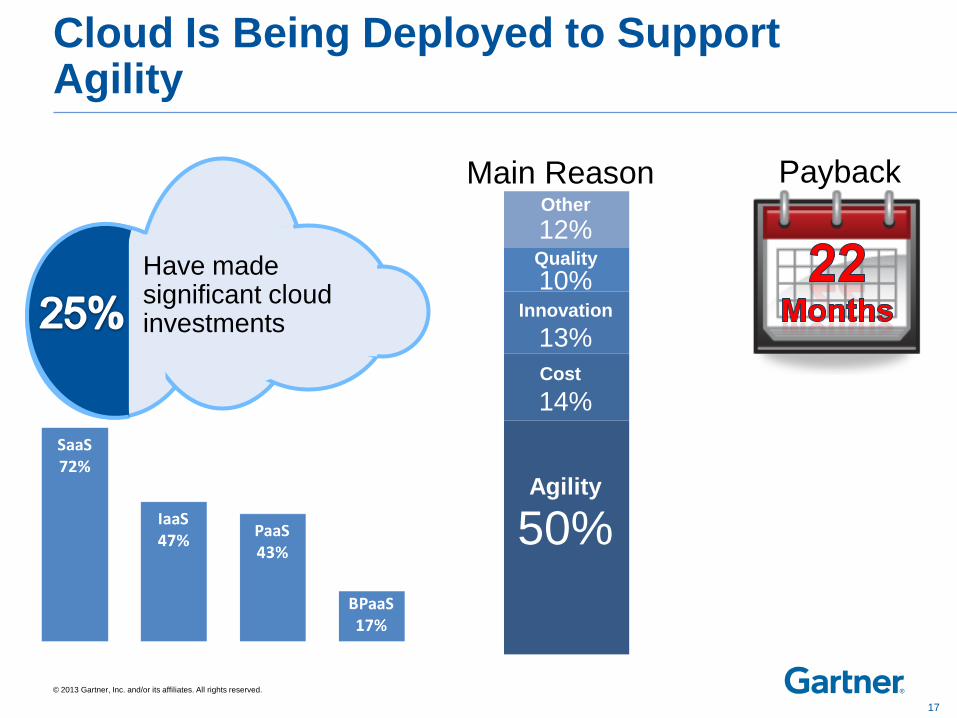

Cloud Is Being Deployed to Support Agility

Have made significant cloud investments

50%

14%

13%

10%

12%

Agility

Cost

Innovation

Quality

Other

Main Reason Payback

17

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

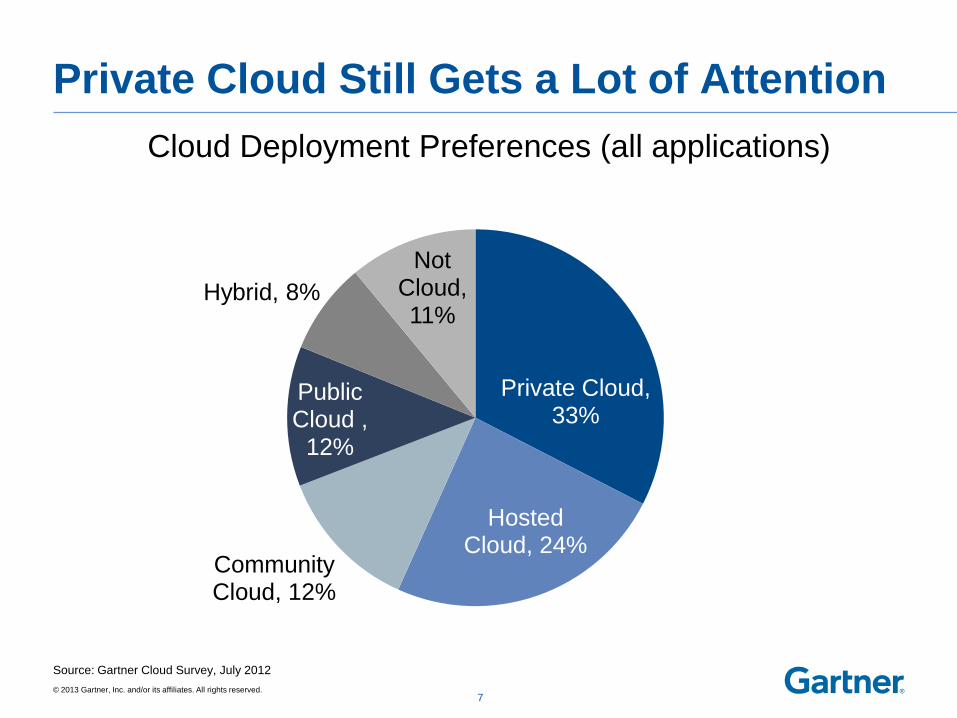

Private Cloud Still Gets a Lot of Attention

Source: Gartner Cloud Survey, July 2012

Cloud Deployment Preferences (all applications)

7

Private Cloud, 33%

Hosted Cloud, 24%

Community Cloud, 12%

Public Cloud ,

12%

Hybrid, 8%

Not Cloud, 11%

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

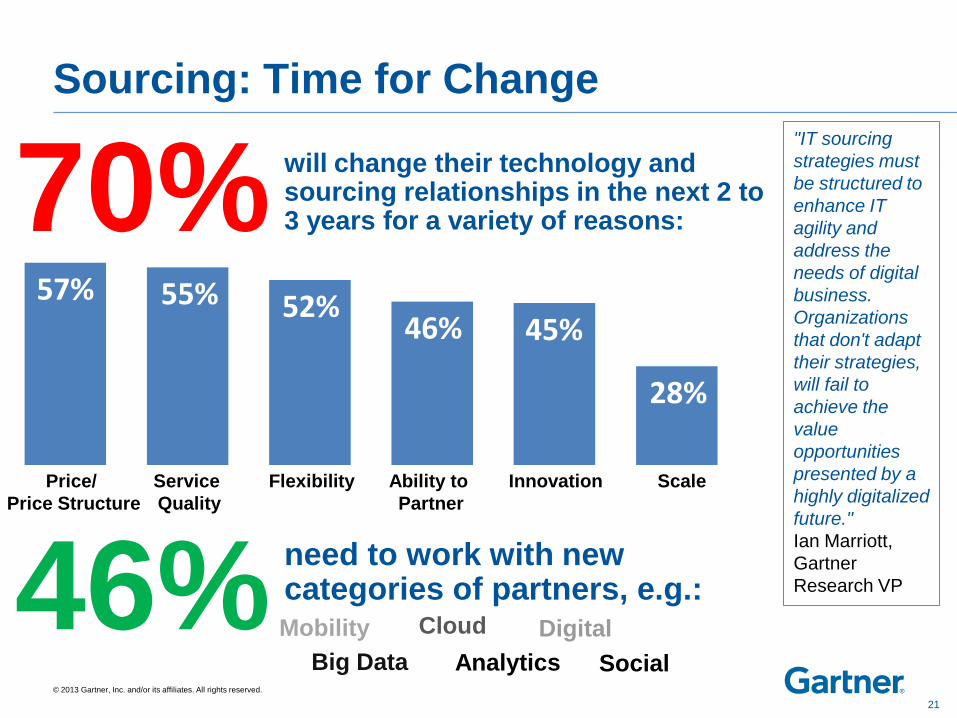

Sourcing: Time for Change

70% will change their technology and sourcing relationships in the next 2 to 3 years for a variety of reasons:

"IT sourcing

strategies must

be structured to

enhance IT

agility and

address the

needs of digital

business.

Organizations

that don't adapt

their strategies,

will fail to

achieve the

value

opportunities

presented by a

highly digitalized

future."

Ian Marriott,

Gartner

Research VP

57%

Price/

Price Structure

55%

Service

Quality

52%

Flexibility

46%

Ability to

Partner

45%

Innovation

28%

Scale

46% need to work with new categories of partners, e.g.: Mobility

Big Data

Cloud

Analytics

Digital

Social

21

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved. © 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

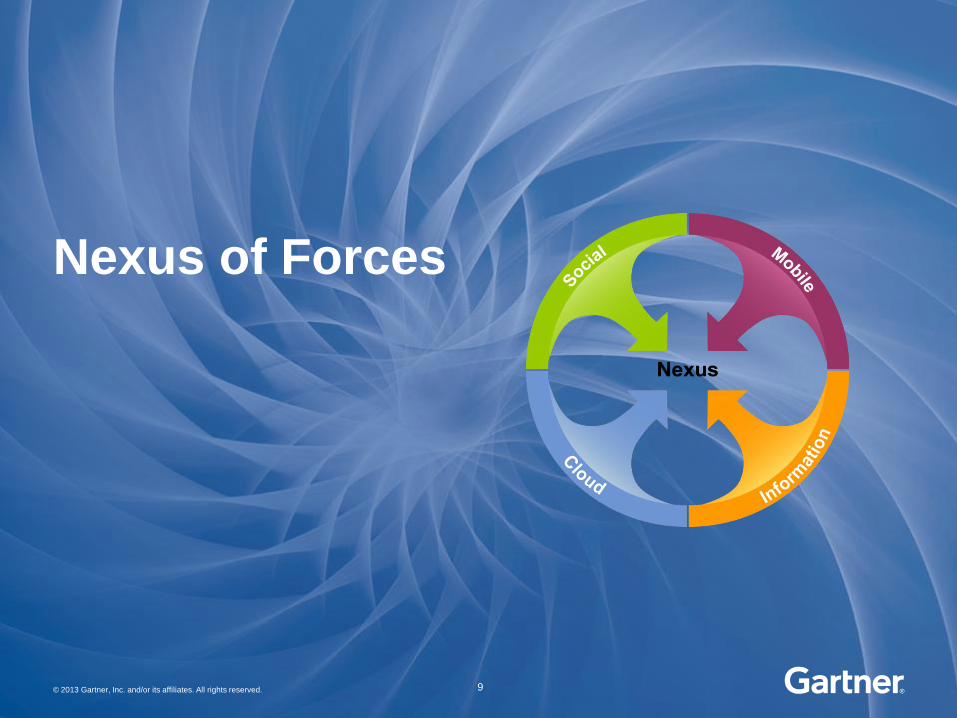

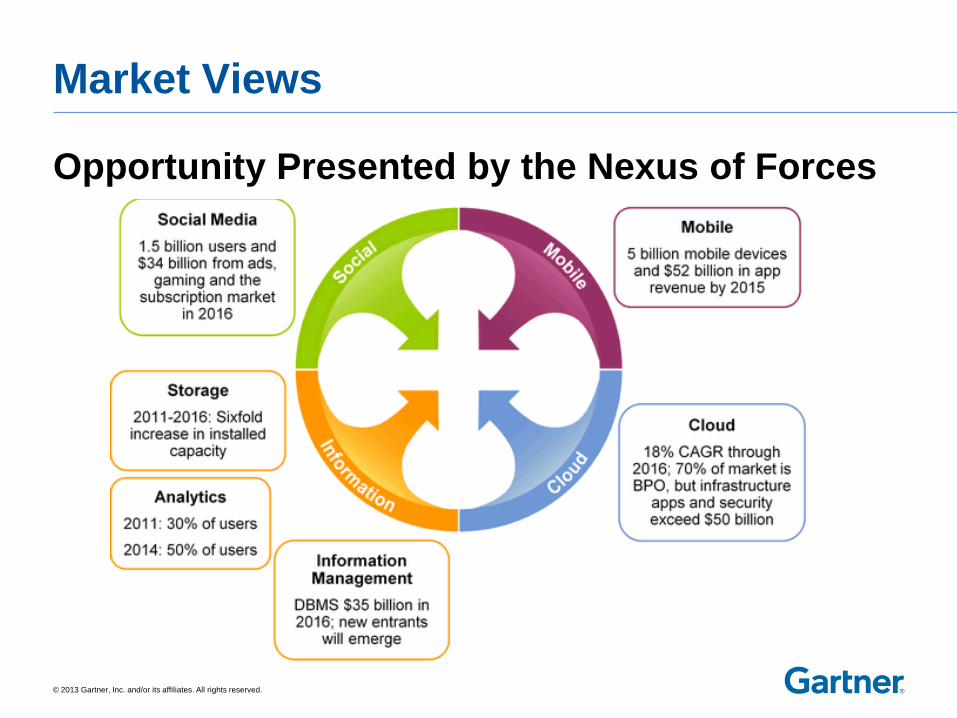

Nexus of Forces

9

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

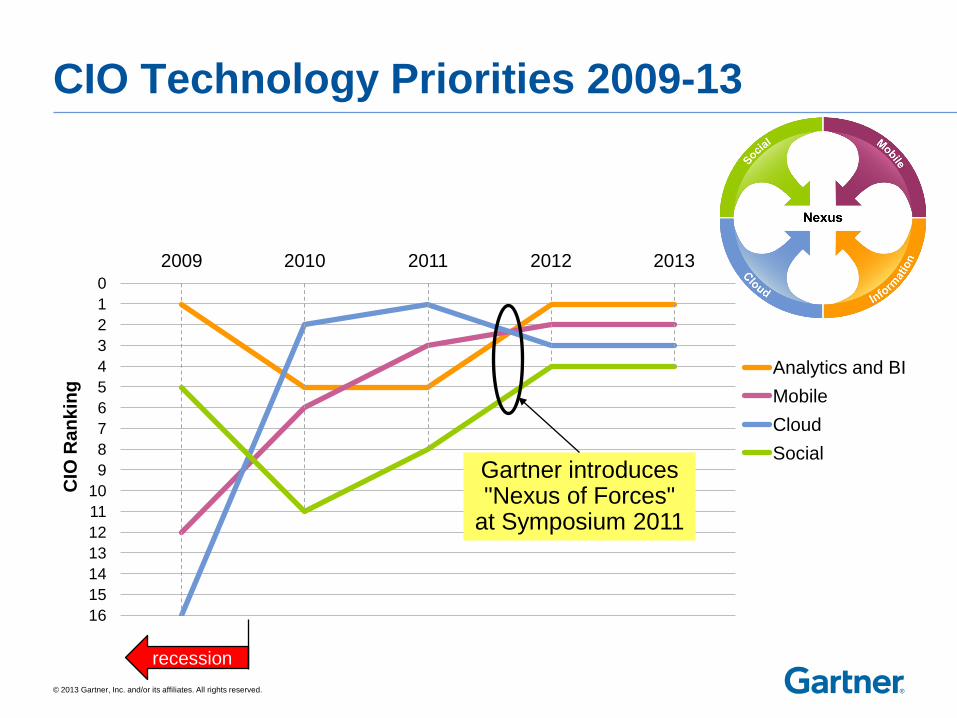

2009 2010 2011 2012 2013

CIO

Ra

nk

ing

Analytics and BI

Mobile

Cloud

Social

recession

Gartner introduces "Nexus of Forces"

at Symposium 2011

CIO Technology Priorities 2009-13

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

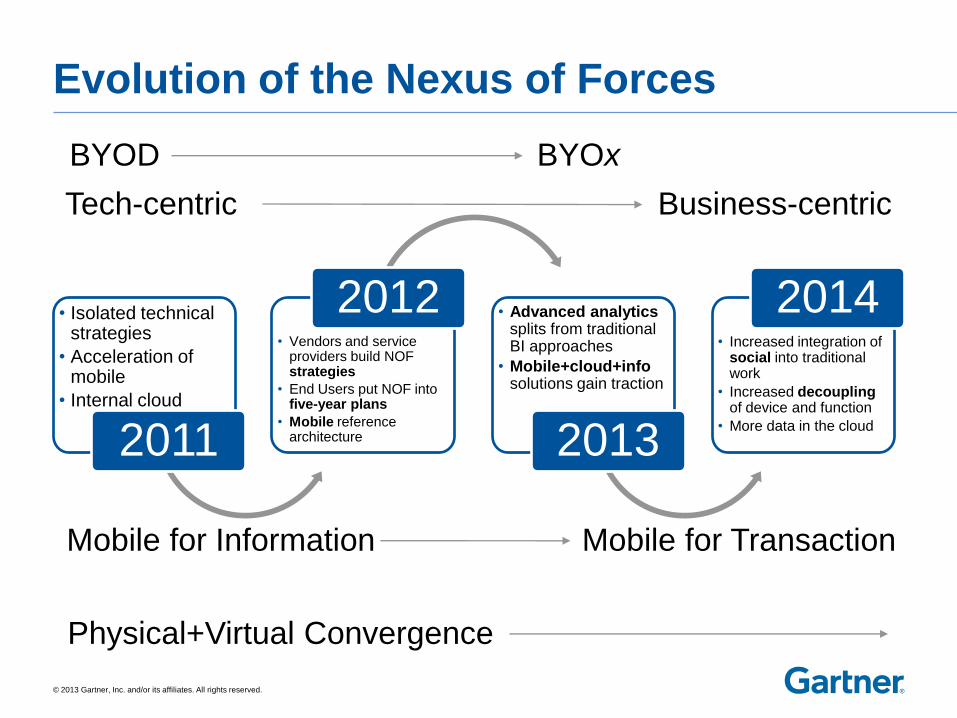

Evolution of the Nexus of Forces

• Isolated technical strategies

• Acceleration of mobile

• Internal cloud

2011

• Vendors and service providers build NOF strategies

• End Users put NOF into five-year plans

• Mobile reference architecture

2012 • Advanced analytics splits from traditional BI approaches

• Mobile+cloud+info solutions gain traction

2013

• Increased integration of social into traditional work

• Increased decoupling of device and function

• More data in the cloud

2014

BYOD BYOx

Tech-centric Business-centric

Mobile for Information Mobile for Transaction

Physical+Virtual Convergence

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Market Views

Opportunity Presented by the Nexus of Forces

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

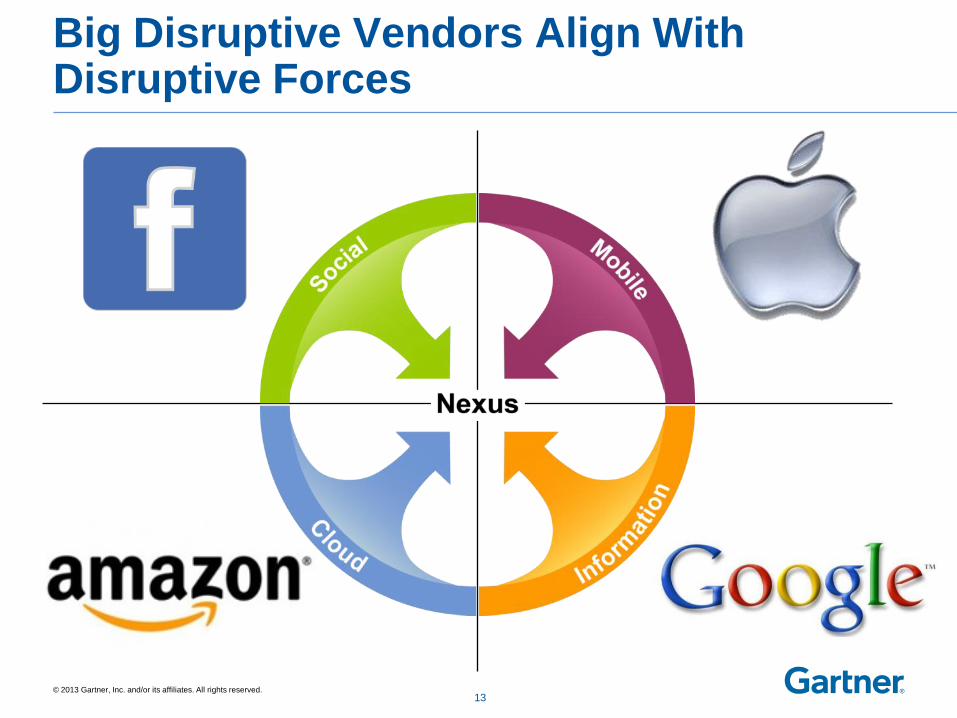

Big Disruptive Vendors Align With Disruptive Forces

13

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

"There is a growing disconnect between our increasingly nonlinear world and the linear mindsets, practices and

institutions that we deploy in our work."

John Hagel, co-chairman, Deloitte Center for the Edge

Digital Is Upon Us "My business and its IT organization are

being engulfed by a torrent of digital opportunities. We cannot respond in a timely fashion, and this threatens the

success of the business and the credibility of the IT organization."

"The IT organization has the right skills and capabilities in place to meet upcoming

challenges."

4

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

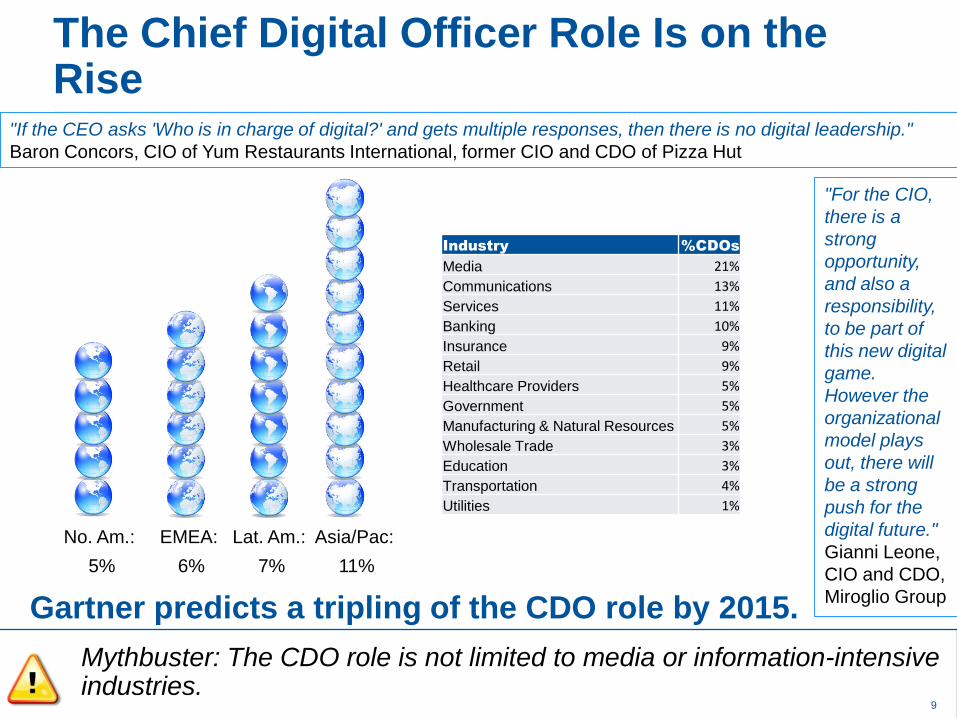

The Chief Digital Officer Role Is on the Rise

Asia/Pac:

11%

No. Am.:

5%

EMEA:

6%

Lat. Am.:

7%

Industry %CDOs

Media 21%

Communications 13%

Services 11%

Banking 10%

Insurance 9%

Retail 9%

Healthcare Providers 5%

Government 5%

Manufacturing & Natural Resources 5%

Wholesale Trade 3%

Education 3%

Transportation 4%

Utilities 1%

"If the CEO asks 'Who is in charge of digital?' and gets multiple responses, then there is no digital leadership."

Baron Concors, CIO of Yum Restaurants International, former CIO and CDO of Pizza Hut

Gartner predicts a tripling of the CDO role by 2015.

"For the CIO,

there is a

strong

opportunity,

and also a

responsibility,

to be part of

this new digital

game.

However the

organizational

model plays

out, there will

be a strong

push for the

digital future."

Gianni Leone,

CIO and CDO,

Miroglio Group

Mythbuster: The CDO role is not limited to media or information-intensive industries.

9

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

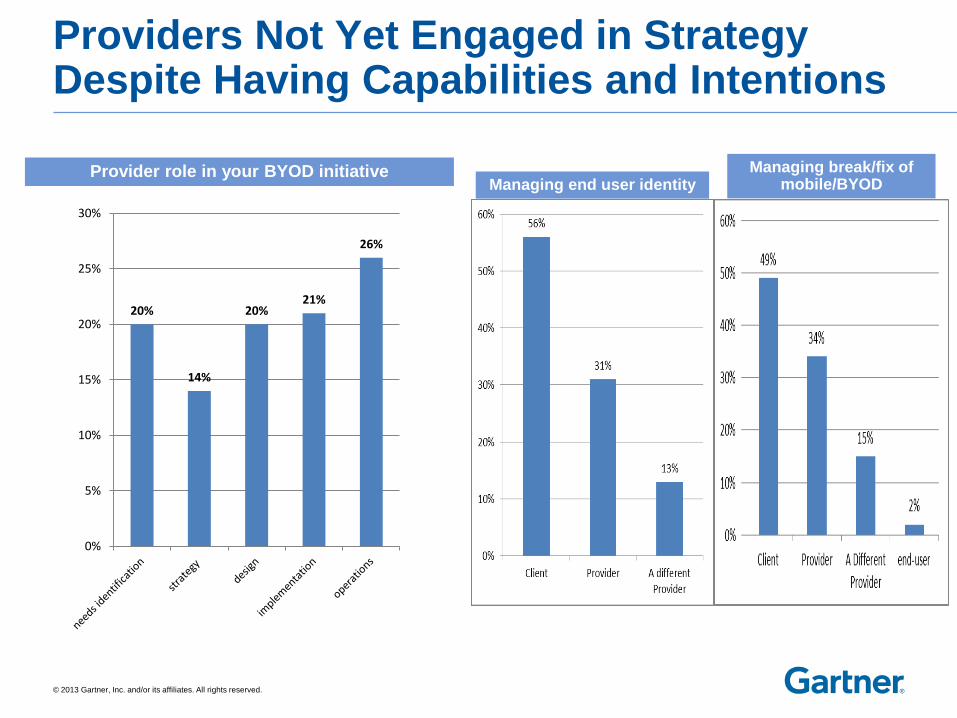

Providers Not Yet Engaged in Strategy Despite Having Capabilities and Intentions

Provider role in your BYOD initiative Managing end user identity

Managing break/fix of mobile/BYOD

20%

14%

20% 21%

26%

0%

5%

10%

15%

20%

25%

30%

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved. © 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Competitive Landscape A Cloud Journey

18

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

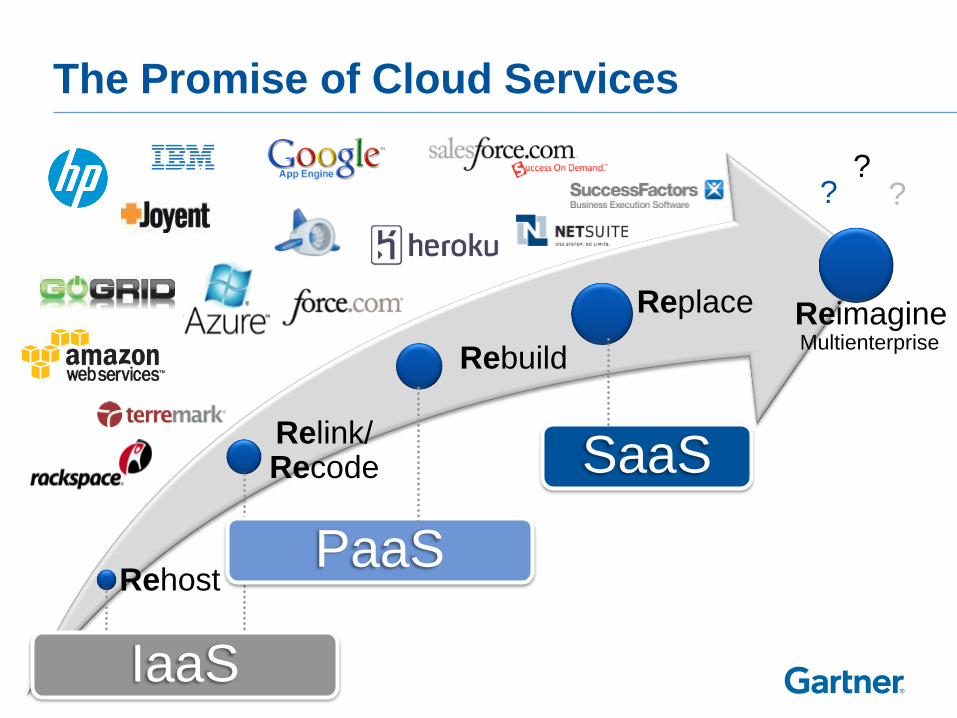

The Promise of Cloud Services

Rehost

Relink/ Recode

Rebuild

Replace

IaaS

PaaS

SaaS

Reimagine

? ? ?

Multienterprise

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

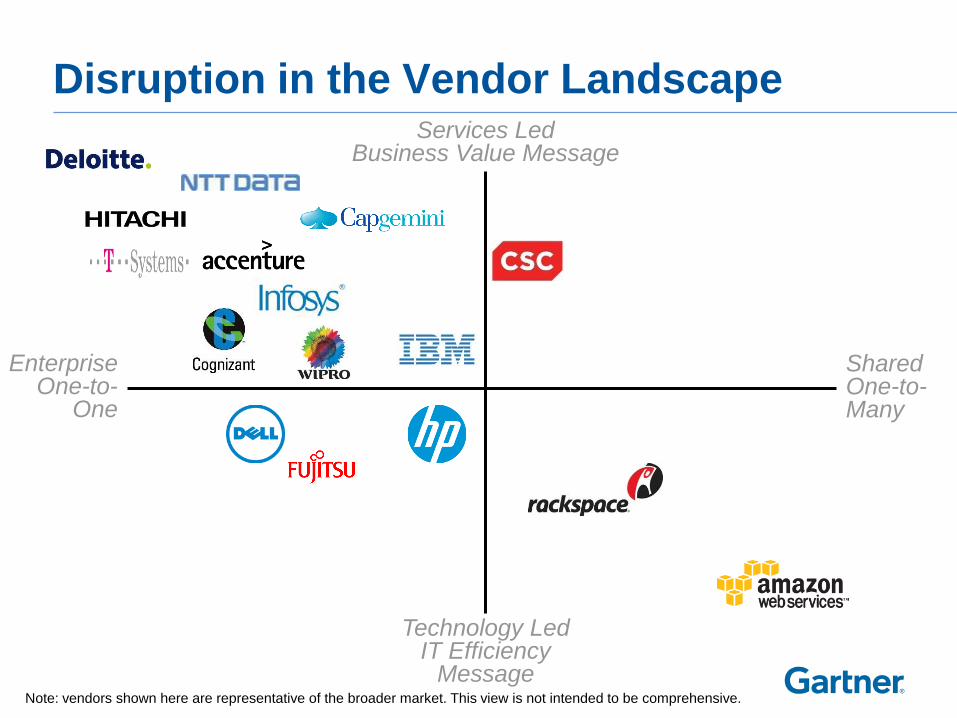

Disruption in the Vendor Landscape

Note: vendors shown here are representative of the broader market. This view is not intended to be comprehensive.

Shared One-to- Many

Services Led Business Value Message

Technology Led IT Efficiency

Message

Enterprise One-to-

One

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

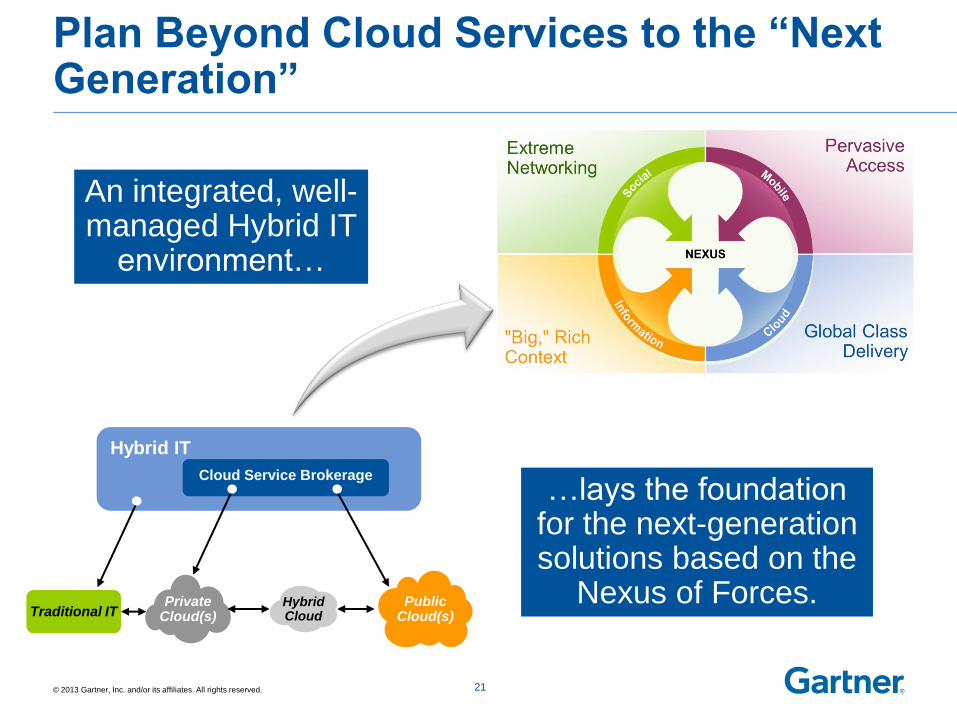

Plan Beyond Cloud Services to the ―Next Generation‖

Hybrid IT

Traditional IT

Cloud Service Brokerage

Private Cloud(s)

Public Cloud(s)

Hybrid Cloud

21

An integrated, well-managed Hybrid IT

environment…

…lays the foundation for the next-generation solutions based on the

Nexus of Forces.

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

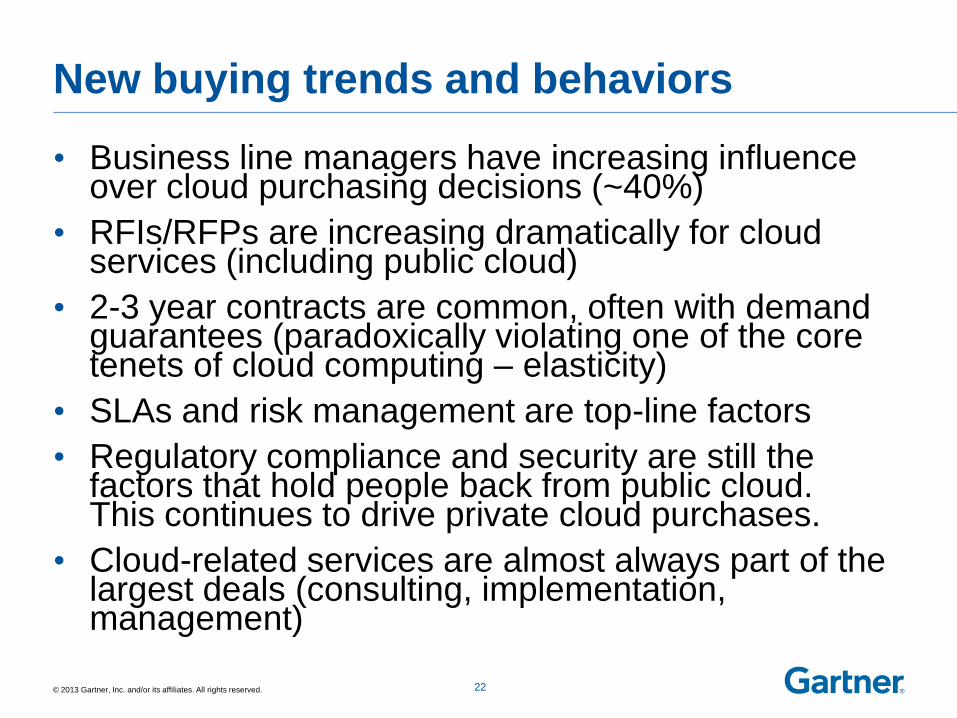

New buying trends and behaviors

• Business line managers have increasing influence over cloud purchasing decisions (~40%)

• RFIs/RFPs are increasing dramatically for cloud services (including public cloud)

• 2-3 year contracts are common, often with demand guarantees (paradoxically violating one of the core tenets of cloud computing – elasticity)

• SLAs and risk management are top-line factors

• Regulatory compliance and security are still the factors that hold people back from public cloud. This continues to drive private cloud purchases.

• Cloud-related services are almost always part of the largest deals (consulting, implementation, management)

22

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved. © 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Infrastructure Services

23

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

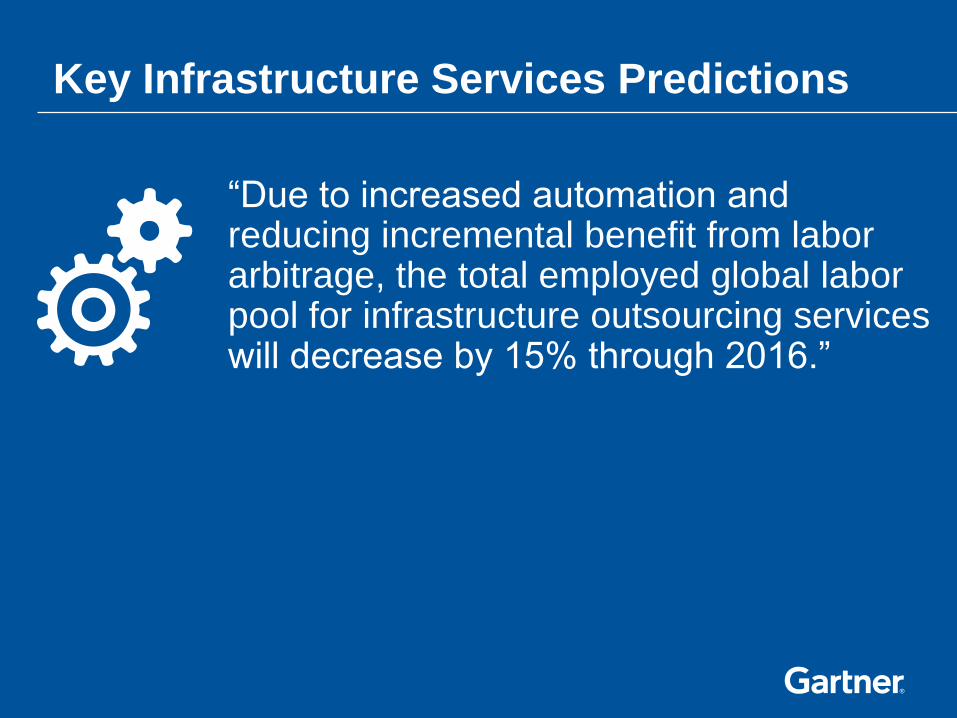

“Due to increased automation and reducing incremental benefit from labor arbitrage, the total employed global labor pool for infrastructure outsourcing services will decrease by 15% through 2016.”

Key Infrastructure Services Predictions

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

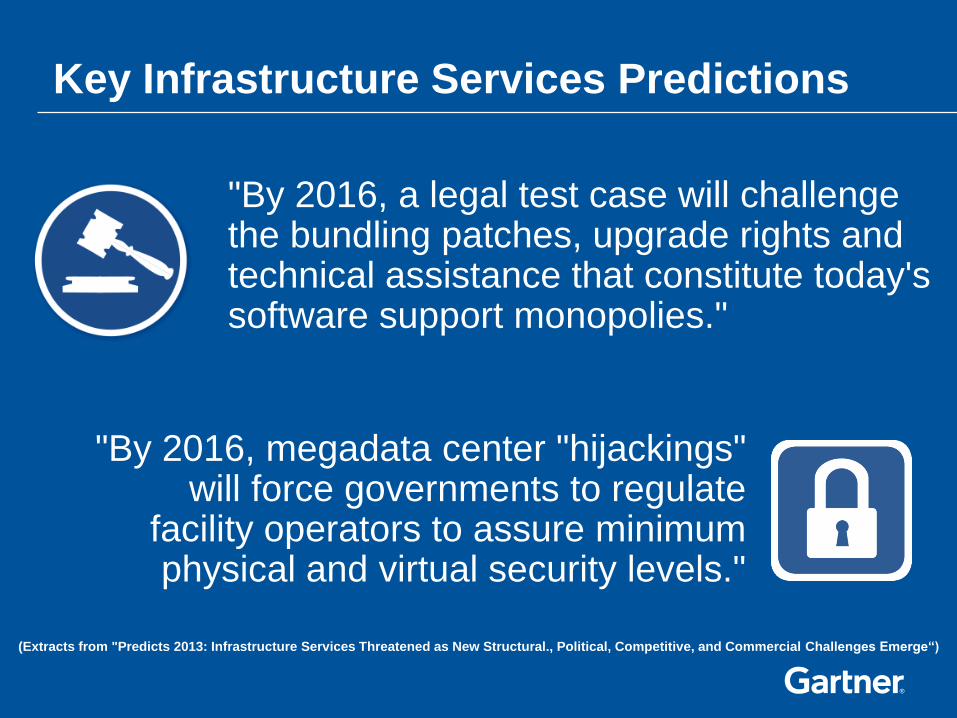

"By 2016, a legal test case will challenge the bundling patches, upgrade rights and technical assistance that constitute today's software support monopolies."

Key Infrastructure Services Predictions

"By 2016, megadata center "hijackings" will force governments to regulate

facility operators to assure minimum physical and virtual security levels."

(Extracts from "Predicts 2013: Infrastructure Services Threatened as New Structural., Political, Competitive, and Commercial Challenges Emerge―)

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

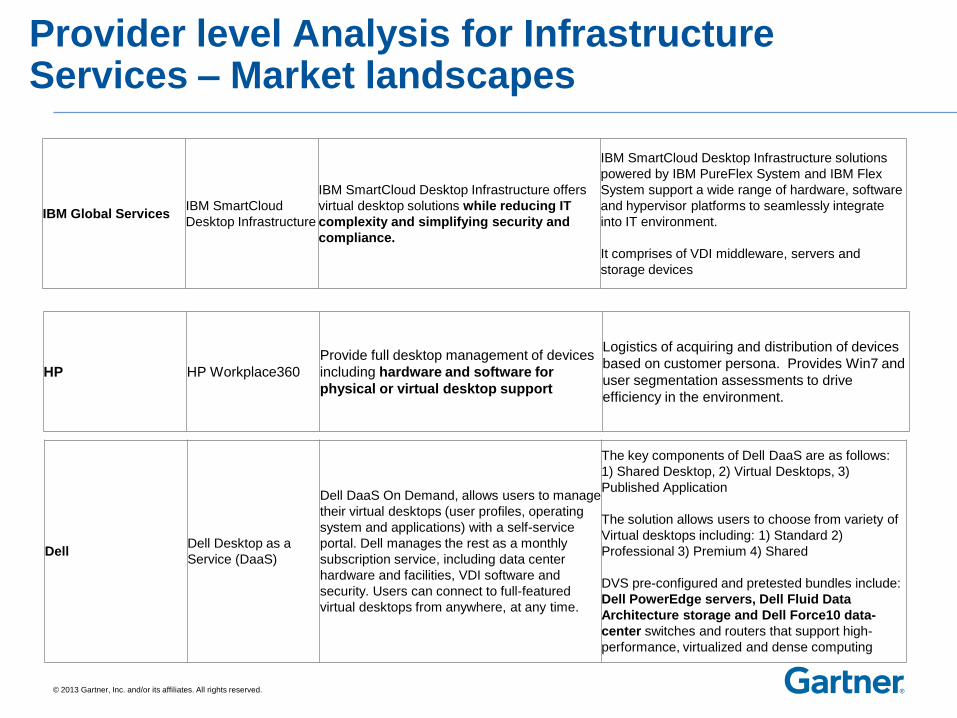

Provider level Analysis for Infrastructure Services – Market landscapes

IBM Global Services IBM SmartCloud

Desktop Infrastructure

IBM SmartCloud Desktop Infrastructure offers

virtual desktop solutions while reducing IT

complexity and simplifying security and

compliance.

IBM SmartCloud Desktop Infrastructure solutions

powered by IBM PureFlex System and IBM Flex

System support a wide range of hardware, software

and hypervisor platforms to seamlessly integrate

into IT environment.

It comprises of VDI middleware, servers and

storage devices

Dell Dell Desktop as a

Service (DaaS)

Dell DaaS On Demand, allows users to manage

their virtual desktops (user profiles, operating

system and applications) with a self-service

portal. Dell manages the rest as a monthly

subscription service, including data center

hardware and facilities, VDI software and

security. Users can connect to full-featured

virtual desktops from anywhere, at any time.

The key components of Dell DaaS are as follows:

1) Shared Desktop, 2) Virtual Desktops, 3)

Published Application

The solution allows users to choose from variety of

Virtual desktops including: 1) Standard 2)

Professional 3) Premium 4) Shared

DVS pre-configured and pretested bundles include:

Dell PowerEdge servers, Dell Fluid Data

Architecture storage and Dell Force10 data-

center switches and routers that support high-

performance, virtualized and dense computing

HP HP Workplace360

Provide full desktop management of devices

including hardware and software for

physical or virtual desktop support

Logistics of acquiring and distribution of devices

based on customer persona. Provides Win7 and

user segmentation assessments to drive

efficiency in the environment.

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Provider level Analysis for Infrastructure Services – Market landscapes

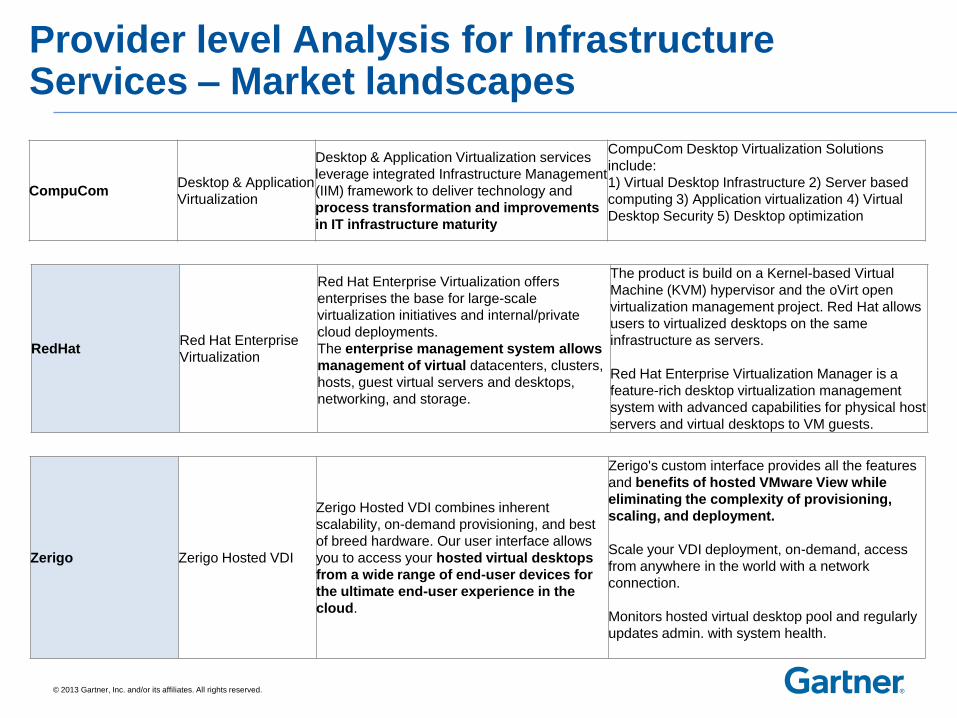

CompuCom Desktop & Application

Virtualization

Desktop & Application Virtualization services

leverage integrated Infrastructure Management

(IIM) framework to deliver technology and

process transformation and improvements

in IT infrastructure maturity

CompuCom Desktop Virtualization Solutions

include:

1) Virtual Desktop Infrastructure 2) Server based

computing 3) Application virtualization 4) Virtual

Desktop Security 5) Desktop optimization

RedHat Red Hat Enterprise

Virtualization

Red Hat Enterprise Virtualization offers

enterprises the base for large-scale

virtualization initiatives and internal/private

cloud deployments.

The enterprise management system allows

management of virtual datacenters, clusters,

hosts, guest virtual servers and desktops,

networking, and storage.

The product is build on a Kernel-based Virtual

Machine (KVM) hypervisor and the oVirt open

virtualization management project. Red Hat allows

users to virtualized desktops on the same

infrastructure as servers.

Red Hat Enterprise Virtualization Manager is a

feature-rich desktop virtualization management

system with advanced capabilities for physical host

servers and virtual desktops to VM guests.

Zerigo Zerigo Hosted VDI

Zerigo Hosted VDI combines inherent

scalability, on-demand provisioning, and best

of breed hardware. Our user interface allows

you to access your hosted virtual desktops

from a wide range of end-user devices for

the ultimate end-user experience in the

cloud.

Zerigo's custom interface provides all the features

and benefits of hosted VMware View while

eliminating the complexity of provisioning,

scaling, and deployment.

Scale your VDI deployment, on-demand, access

from anywhere in the world with a network

connection.

Monitors hosted virtual desktop pool and regularly

updates admin. with system health.

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Provider level Analysis for Infrastructure Services – Market landscapes

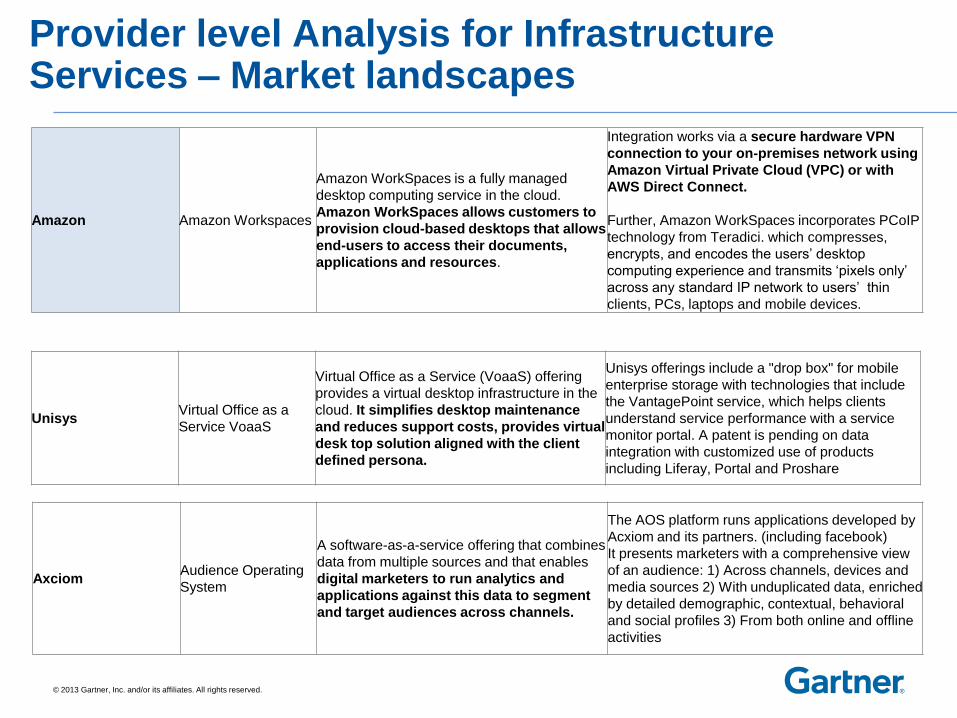

Amazon Amazon Workspaces

Amazon WorkSpaces is a fully managed

desktop computing service in the cloud.

Amazon WorkSpaces allows customers to

provision cloud-based desktops that allows

end-users to access their documents,

applications and resources.

Integration works via a secure hardware VPN

connection to your on-premises network using

Amazon Virtual Private Cloud (VPC) or with

AWS Direct Connect.

Further, Amazon WorkSpaces incorporates PCoIP

technology from Teradici. which compresses,

encrypts, and encodes the users‟ desktop

computing experience and transmits „pixels only‟

across any standard IP network to users‟ thin

clients, PCs, laptops and mobile devices.

Unisys Virtual Office as a

Service VoaaS

Virtual Office as a Service (VoaaS) offering

provides a virtual desktop infrastructure in the

cloud. It simplifies desktop maintenance

and reduces support costs, provides virtual

desk top solution aligned with the client

defined persona.

Unisys offerings include a "drop box" for mobile

enterprise storage with technologies that include

the VantagePoint service, which helps clients

understand service performance with a service

monitor portal. A patent is pending on data

integration with customized use of products

including Liferay, Portal and Proshare

Axciom Audience Operating

System

A software-as-a-service offering that combines

data from multiple sources and that enables

digital marketers to run analytics and

applications against this data to segment

and target audiences across channels.

The AOS platform runs applications developed by

Acxiom and its partners. (including facebook)

It presents marketers with a comprehensive view

of an audience: 1) Across channels, devices and

media sources 2) With unduplicated data, enriched

by detailed demographic, contextual, behavioral

and social profiles 3) From both online and offline

activities

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved. © 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Data Center Outsourcing

29

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

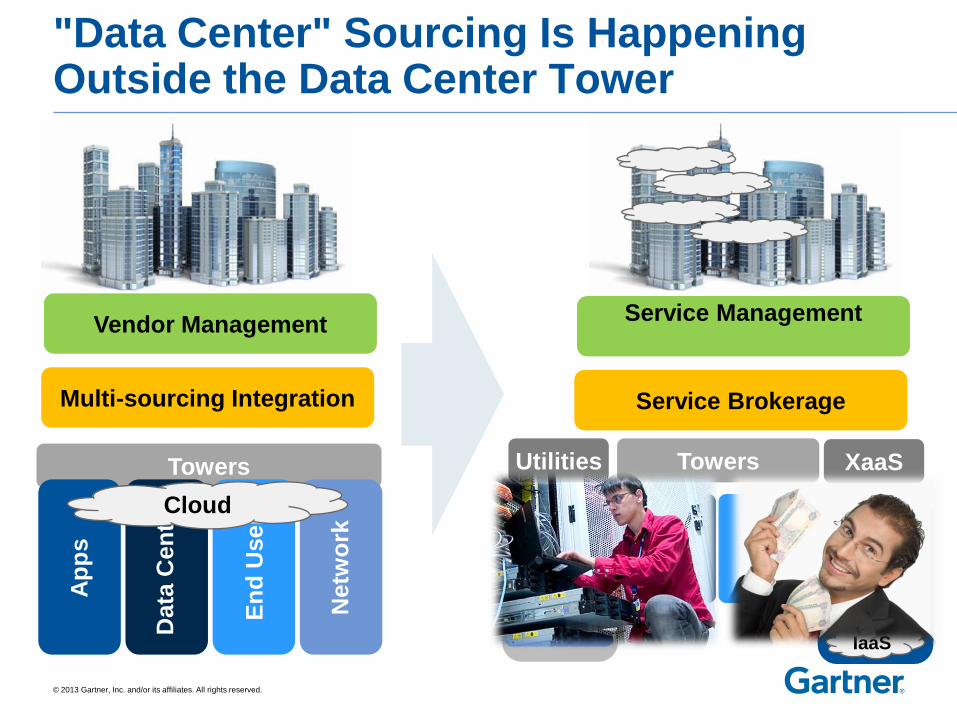

Towers

"Data Center" Sourcing Is Happening Outside the Data Center Tower

Multi-sourcing Integration

Data

Cen

ter

Ap

ps

Ne

two

rk

En

d U

ser

Vendor Management

Cloud

Service Brokerage

Service Management

SaaS

PaaS

IaaS

BPaaS

Data

Cen

ter

Ap

ps

Ne

two

rk

En

d U

ser

Data Center

Apps

Network

Towers XaaS Utilities

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

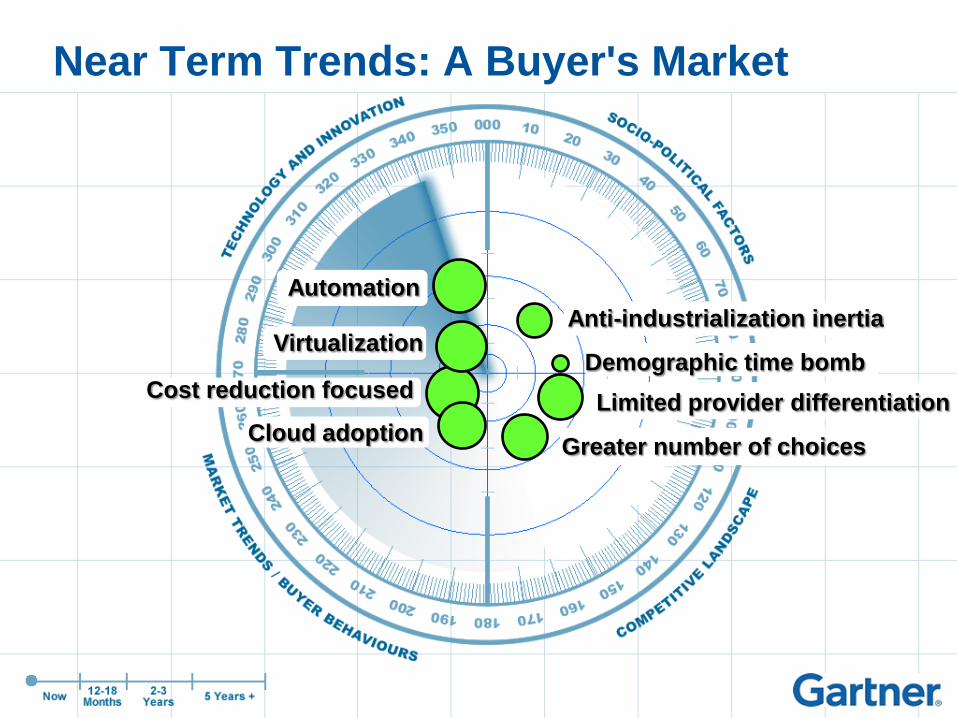

Near Term Trends: A Buyer's Market

Cost reduction focused

Cloud adoption

Virtualization

Automation

Demographic time bomb

Limited provider differentiation

Greater number of choices

Anti-industrialization inertia

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

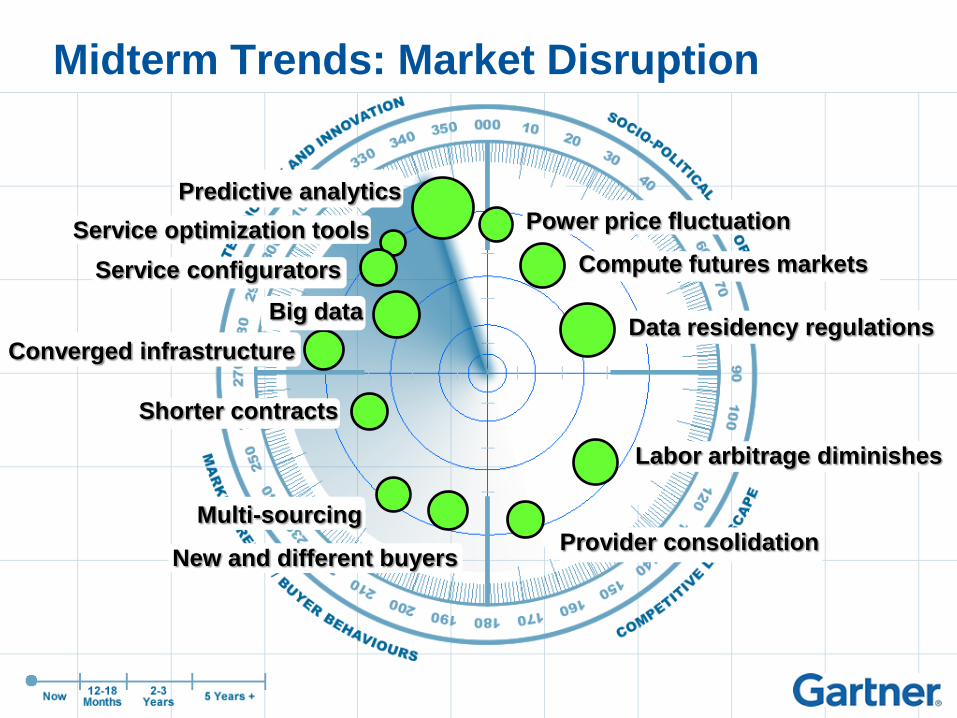

Midterm Trends: Market Disruption

Big data

Predictive analytics

Service optimization tools

Data residency regulations

Compute futures markets

Labor arbitrage diminishes

Provider consolidation

Converged infrastructure

Power price fluctuation

Service configurators

Shorter contracts

New and different buyers

Multi-sourcing

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

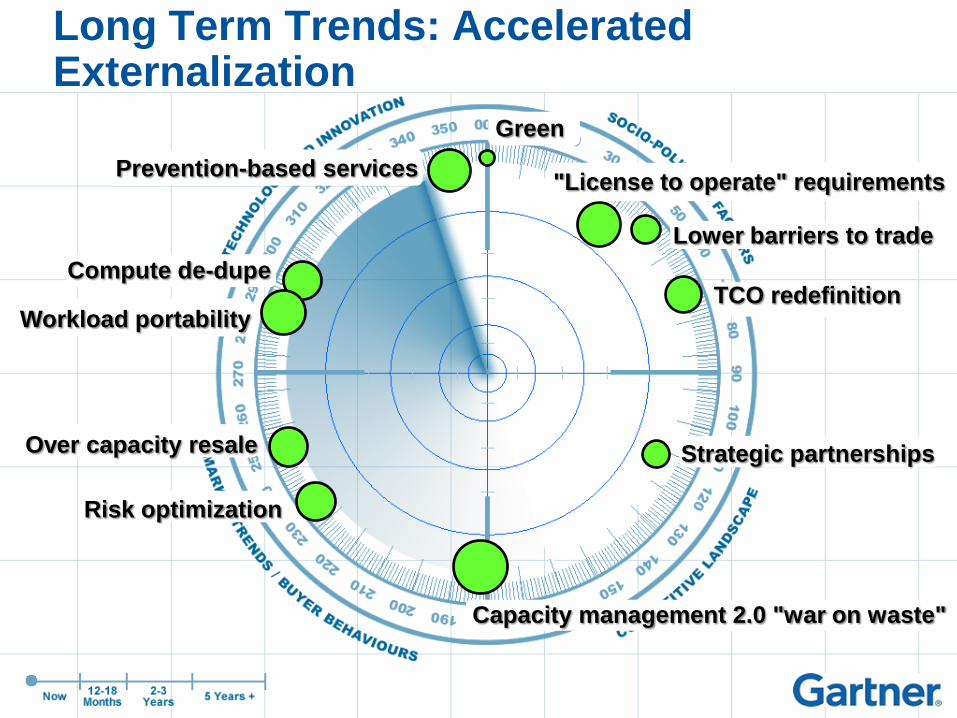

Long Term Trends: Accelerated Externalization

Green

Over capacity resale

Prevention-based services

Risk optimization

Compute de-dupe

Capacity management 2.0 "war on waste"

Workload portability

Lower barriers to trade

"License to operate" requirements

TCO redefinition

Strategic partnerships

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Top Buyer Insights from the MQ Research

• Buyers are reviewing multiple DC delivery offerings in a progression. (CoLo, Utility, managed services)

• Anticipate costs continue to go down year over year.

• Looking for innovation in the DC services with continued maturity and added solutions.

• Linkage to and bundling of DC services (thin client virtual desktops with DC support)

34

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved. © 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

End User Services (Desktop,

Service Desk and Mobility)

35

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

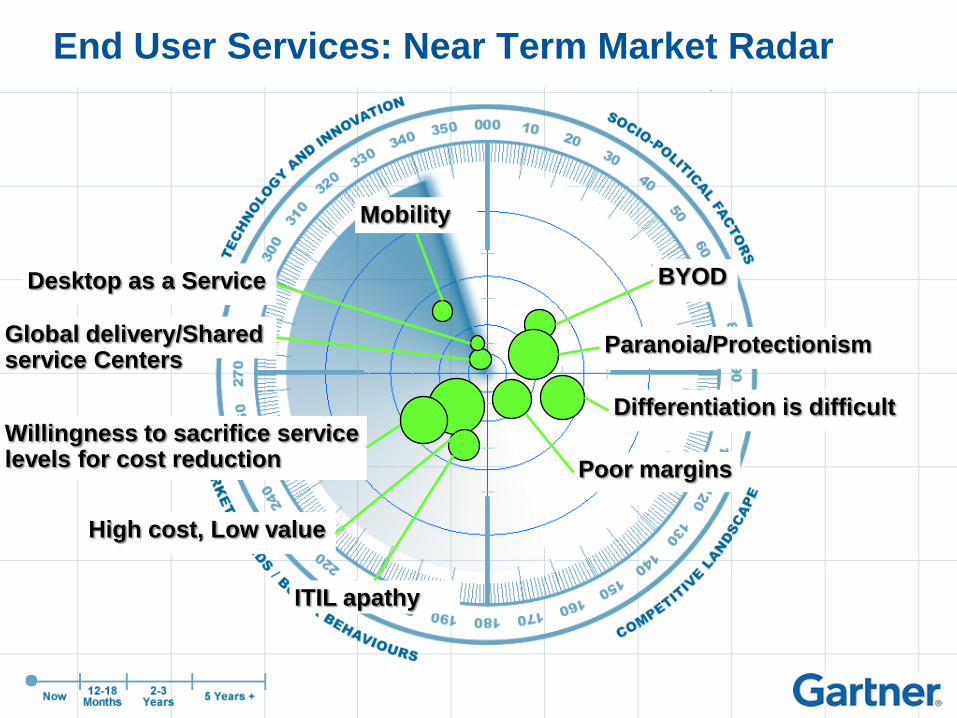

Differentiation is difficult

Poor margins

Global delivery/Shared service Centers

Willingness to sacrifice service levels for cost reduction

BYOD

Paranoia/Protectionism

ITIL apathy

High cost, Low value

Desktop as a Service

Mobility

End User Services: Near Term Market Radar

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

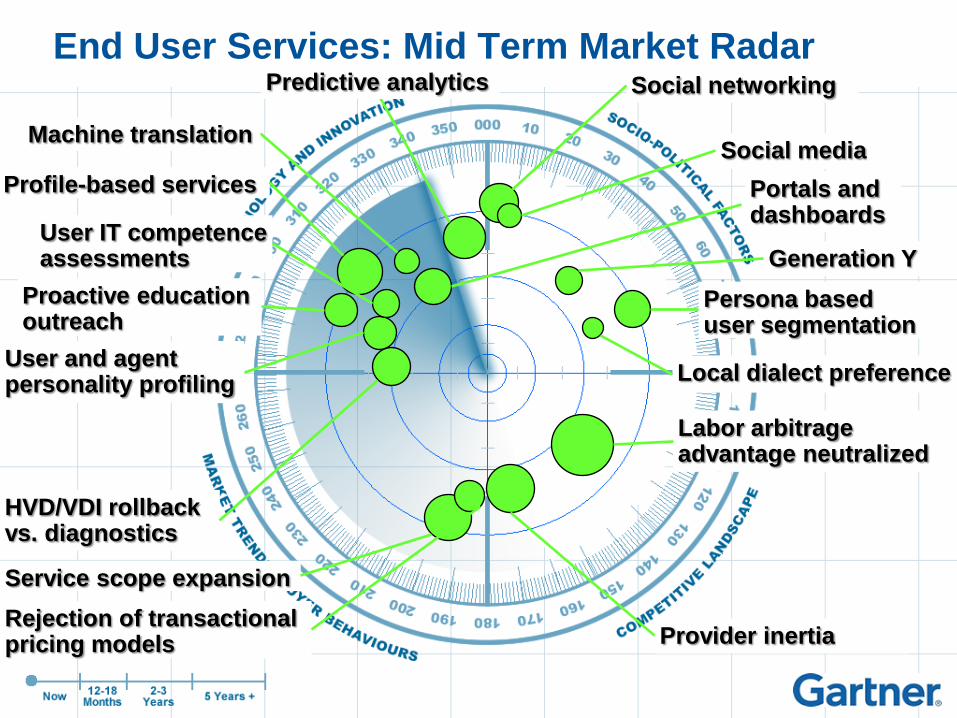

Generation Y

Persona based user segmentation

Social networking

Local dialect preference

Labor arbitrage advantage neutralized

HVD/VDI rollback vs. diagnostics

User and agent personality profiling

Social media

Profile-based services Portals and dashboards

Provider inertia Rejection of transactional pricing models

User IT competence assessments

Proactive education outreach

Service scope expansion

Predictive analytics

Machine translation

End User Services: Mid Term Market Radar

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

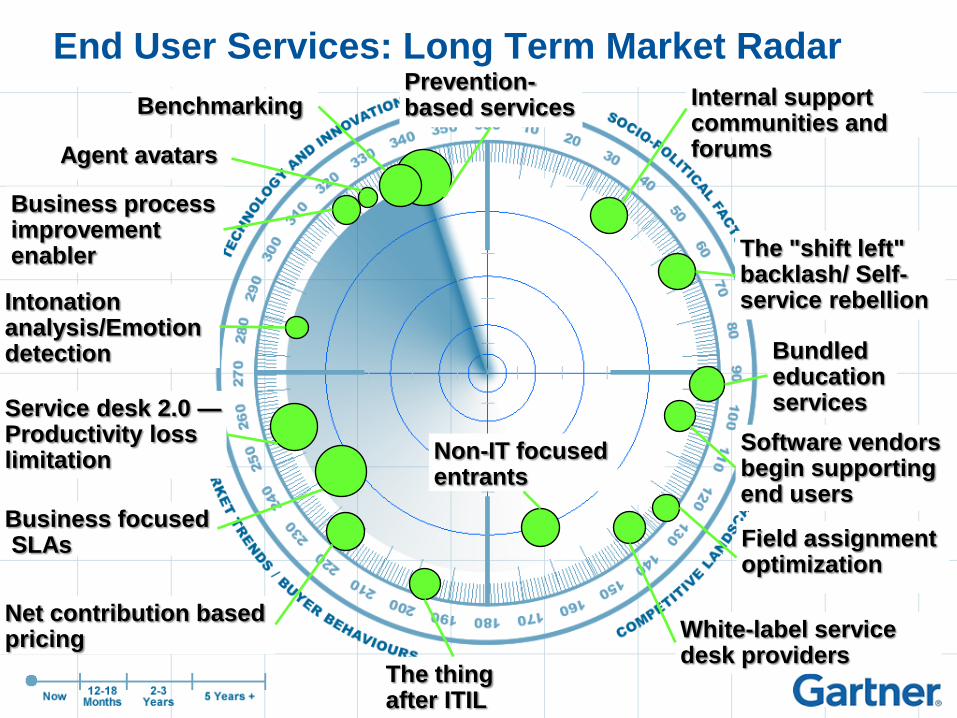

Net contribution based pricing

Intonation analysis/Emotion detection

White-label service desk providers

Non-IT focused entrants

Prevention-based services

Agent avatars

Service desk 2.0 —Productivity loss limitation

The "shift left" backlash/ Self-service rebellion

Bundled education services

Benchmarking

Software vendors begin supporting end users

Business focused SLAs

The thing after ITIL

Internal support communities and forums

Field assignment optimization

Business process improvement enabler

End User Services: Long Term Market Radar

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Top Buyer Insights from the MQ Research

• Organizations are looking for service in all three areas of EUS from a single vendor.

• Organizations demand is driving all vendors to work on developing mobility solutions.

• Looking for a simple, seamless, repeatable and integrated solution.

• Looking for pricing that will motivate the provider to work in the interest of the organization.

• See higher end technical resources retiring and need this capability via outsourcing.

39

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved.

Recommendations

Focus on business priorities:

Clearly defined purpose of Infrastructure and how it serves business.

Maintain governance to keep business and IT syncronized

Identify key initiatives and related time tables for:

Nexus of forces impact on business.

Plan for I&O changes:

To include technology and ability to access and retain skills.

Understand the current cost and level of services:

Benchmark to peers and anticipate budget needs to meet the goals of business.

Recommended