Presented to

Presented by

Overcoming InertiaA Better Way to Connect with Consumers

Key observation #1 – Consumer inertia

Problem: Consumer inertia is the single biggest marketing problem

1. “Cost” of hearing aids is the primary source of inertia and reason first‐time buyers delay purchase of hearing aids

Solution: Reduce or eliminate consumer inertia

1. Remove the cost and risk barrier, possibilities include

• 36‐months free financing (no interest)• Buy one get one 50% off• 90‐day money‐back guarantee• Free 3‐year extended warranty• No payment for 90‐days• $500 off purchase

2Source: The Hearing Review, Online survey among 179 US hearing care professionals, Dec. 2013

Key observation #1 – Consumer Inertia, cont’d

Problem: Consumer inertia is the single biggest marketing problem, cont’d

2. “Not ready yet” (vanity) is the second source of consumer inertia

• Vanity includes perceptions of being old, weak and frail. For Boomers, who believe “sixty is the new forty,” this is about ego. Admitting you’re aging and your hearing is declining is a huge life event, and not one they embrace

Solution: Reduce or eliminate consumer inertia, cont’d

2. “Not ready yet” (Vanity), possibilities include

• Reduce the stigma – promote star power, famous people who wear hearing aids

• Increase solution magnetism – promote how well the product solves their problems

• Increase the push away – show how bad their existing situation really is

• Decrease the fear and uncertainty of change –assure consumers that switching is quick and easy

• Decrease their attachment to the status quo –remove consumers’ irrational attachment to their current situation

3

Key observation #2 – Marketing to the right demo with the right messages will improve success

4Source: Scarborough, 2012, Release 1;forbes.com, “Gen X is from Mars, Gen Y is from Venus”, Jan. 2014

#1 Baby Boomers Profile (primary target)• 81MM or 26% of the U.S. population• Born between 1946 – 1964; in their 50s and 60s • 10,000 are turning 65 everyday for the next 15 years

• Internet savvy, health conscious• TV viewing

– Movies (57%)– Local evening news (53%)– Comedies (47%)– Local morning news (44%)

• Radio– Adult contemporary (30%)– News and talk (28%)– Classic hits (25%)

• Newspaper– National news (28%)

• Online– Travel reservations (23%)– Medical information (14%)

#1

#2 Silent Generation Profile• 20MM or 6% of U.S. population• Born between 1928 – 1945; in their 70s and 80s

• Second smallest generation born in the U.S. due to the depression

• In 2010, for the first time, the median net worth of households age 75+ ($228,400) was higher than that of any younger age bracket

• Many routinely pay for extended‐family vacations or subsidize their grown Boomer or Xer kids

#2

#3 Generation X Profile• 88.5MM or 28% of U.S population• Born between 1965 – 1980; in their 30s and 40’s

• Value freedom and autonomy to achieve desired goals and often prefer to work alone rather than in teams

• Dislike “meetings about meetings” and don’t want or need face time

#3

Key observation #2, cont’d – BoomersBoomers are the primary target audience

• 33% of the 195 million Internet users in the U.S. are over 50 years old

• 82% of the 82 million U.S. Boomers use the Internet to research health and wellness information

• Two‐thirds of Boomers shop online• 36% of Boomers own a smartphone• Almost half access the Internet with their smart phone daily

• 62% have broadband at home• 43% have wireless home network• Almost 30 million Boomers engage in social networking sites

• 50% of Boomers expect to live until they’re 90

Sources: Pew Internet & American Life Project5

Key observation #3 – Top 10 boomer DMAs vs MHC

6

Top 10 Affluent Boomer DMAs:

Top 10 Boomer DMAs

DMANumber of Baby

Boomers% of DMAAdults

Index(US = 100)

Washington 1,758,300 36.0% 104Boston 1,800,100 36.0% 104Philadelphia 2,179,100 35.4% 102S.F.‐Oakland‐San Jose 1,916,700 35.4% 102New York 5,676,000 35.1% 102Chicago 2,504,600 34.4% 99Atlanta 1,670,600 34.4% 99Houston 1,571,100 34.0% 98Dallas‐Fort Worth 1,760,800 33.4% 97Los Angeles 4,409,900 32.7% 95

DMANumber of Baby

Boomers% of DMAAdults

Index(US = 100)

Washington 866,900 17.7% 214S.F.‐Oakland‐San Jose 861,600 15.9% 192Boston 705,200 14.1% 170New York 2,140,000 13.2% 159Philadelphia 708,700 11.5% 139Houston 484,800 10.5% 126Los Angeles 1,365,200 10.1% 122Atlanta 482,600 9.9% 119Chicago 719,400 9.9% 119Dallas‐Fort Worth 509,300 9.7% 116

Affluent Boomer DMAs ($100,000+)

Source: Scarborough, 2012, Release 1

Chicago

AtlantaLos Angeles

Houston

PhiladelphiaNew York

Boston

Washington

Dallas‐Fort Worth

My HearingCenters (MHC):

S.F.‐Oakland‐San Jose

Key observation #4 – MHC locations compared to states with high concentrations of hearing loss consumers

With the exception of California, My Hearing Centers are not located in any Top 10 “hearing loss states”

7

Illinois1.1MM

Florida2.2MM

Texas2.5MM

California 3.8MM

Georgia945K

North Carolina1.0MMArizona

(5)

Arkansas(1)

SoCal(5)

Idaho( 3)

Nevada(4)

Oregon(5)

Utah(11)

Washington(1)

Wyoming(2)

Ohio1.4MM

Michigan1.2MM

Pennsylvania1.6MM

New York1.8MM

StateSize of Hearing Loss

PopulationEst. State

Population (000)Hearing LossIncidence (%)

California 3,868 36,757 10.5

Texas 2,525 24,327 10.4%

Florida 2,273 18,328 12.4

New York 1,849 19,490 9.5

Pennsylvania 1,601 12,448 12.9

Ohio 1,450 11,486 12.6

Michigan 1,249 10,003 12.5

Illinois 1,173 12,902 9.1

North Carolina 1,051 9,222 11.4

Georgia 945 9,686 9.8

Top 10 hearing loss states:Source: My Hearing Centers website;Better Hearing Institute, “MarkeTrak VIII: 25‐Year Trends in the Hearing Health Market”, Oct. 2009

My HearingCenters (MHC):

Key observation #5 – The consumer’s journey

8

Emotional

Phases Lack of Awareness

Shock & Denial

Pain & Depression

Anger & Bargaining

Reflection & Loneliness

Ready to TrySomething

Upward Turn

Reconstruction &Working Through Things

Acceptance & Hope

Hearing Loss

Step

s Don’t Notice /Ignore Signs

Start PayingAttention

Use CopingMechanisms

Talk withProfessional

Try Hearing Aid

Become RegularHearing Aid User

…………………………………………………………………………………………………………………..Frustrating Experiences Trigger Experiences Identity Crisis

Behavior

Stages Maintenance

Reflection

Adoption

Relapse/Inaction

ActionPreparationContemplationPre‐contemplation

Source: Hearing Industries Association survey, “Exploring the Consumer’s Journey”, 2012

Key observation #5, cont’d: Consumer’s journey –here’re the basic steps and MHC activities

9

Awareness Counseling Treatment Rehabilitation

MHC

Con

sumer

Activ

ities

Education• Promote vanity andfinancial appeals

• Print, online and mobile advertising, direct mail

• Offer: Simple, free, convenient in‐person or online assessment. (e.g., Online: 10‐word test video)

Education/Evaluation• Promote vanity and financial appeals

• Develop “lifestyle” campaign• Free lunch/dinner seminars• Complimentary electroacoustic

hearing aid analysis• Complimentary video otoscope• Other valued offers/services

Promote• Vanity and financial Appeals• Develop “Lifestyle” campaign that overcomes vanity and the stigma of hearing aids

• 36‐months free financing• Buy one get one 50% off• $500 off any purchase• No payment for 90‐days

Promote• Reinforce vanity appeals• Free adjustments for life• 50% off repairs• 30% off upgrades

Key observation #6 – Competitive creative

Creative approach• No brand reviewed has established a signature look

• No brand reviewed is using a celebrity spokesperson as the “face” of the brand

Opportunity• Establish a signature design style and look

• Consider expanding usage of current, part‐time spokesperson Merrill Osmond

• The My Hearing Centers brand needs a face and Merrill is a good candidate

10

Key observation #6, cont’d – Competitive creative . . . none leverage “vanity” as the creative hook, all are product/price centric

111‐Pg. Ad 2‐Pg. FSI, Front 2‐Pg. FSI, Back

Key observation #6, cont’d – Competitive creative . . . none leverage “vanity” as the creative hook, all are product/price centric

121‐Pg. Ad 1/2‐Pg. Ad 2‐Pg. FSI, Front

Key observation #7 – U.S. hearing aid CAGR

Hearing aid sales• Total hearing aid unit sales increased almost 5% to 2,990,104 units in 2013

– 90% of all hearing aids dispensed are digital– 75% of all aids featured wireless technology– 35% to 40% of population aged 65+ are

hearing‐impaired– 20% of hearing‐impaired use a hearing aid– Average age of first‐time user: 69 (USA)– Average age of all users: 72 (USA)

• Key drivers– Maturity of market – 2 billion mature

consumers in 2047– Third‐party payment– Penetration rate – access to distribution

2.8%

3.0%

2.9%

4.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2010 2011 2012 2013

Category Ann

ual G

rowth Rate

Hearing Aid CAGR by Year

Hearing Aid Unit Sales Growth

13Sources: Hearing Review, “Hearing Aid Sales Rise 5% in 2013; Industry Closes in on 3M Unit Mark.” Karl Strom, Editor‐in‐Chief, Feb. 26, 2014

“Trends and directions in the hearing healthcare market”, William Demant, 2012

Key observation #7 cont’d – Global hearing aid market

Sonova, 24% or 2.5MM units

William Demant, 24%, or 2.5MM units

Siemens, 17%, or 1.8MM units

GN Store Nord/Resound

Technologies, 16%, or 1.7MM units

Starkey Technologies, 9%, or 953K

units

Widex, 9%, or 953K units

2012 Global Market Share by Manufacturer

14

10.8 million hearing aids were sold worldwide in 2012 for a total wholesale value of $5.4 billion

• Europe: 45%• North America: 29%• Rest‐of‐World: 26%

The Big Six account for 98% of the world marketSonova and Demant have gained the greatest market share, increasing from 17% to 24% and 18% to 24% respectively over the past 8 yearsSiemens lost the greatest market share dropping from 23% to 17% in past 8 years

Source: Hearing News, “Research firm analyzes market share, retail activity and prospect of major hearing aid manufacturers”, July 3, 2013

Key observation #7, cont’d – 2013 hearing aid market by device type

Key market drivers• Open‐fit and RIC/RITE‐type aids• Feedback and speech‐in‐noise algorithms

• Wireless technology• Emergence of retail giants (most notably Costco)

• Binaural usage ratesRIC/RITEs, 52% or1.5MM units

Traditional BTEs, 22% or 657.8K units

Full‐Shell ITEs, 8% or239.2K units

ITCs, 8% or239.2K units

CICs, 6% or179.4K units

Half‐Shell ITEs, 4% or119.6K units

2013 Hearing Aid Unit Sales by Type

15Source: HearingReview.com, “Hearing Aid Sales Rise 5% in 2013;

Industry Closes in on 3M Unit Mark”, February 26, 2014

Key observation #7, cont’d – hearing aid market by distribution channelSituation

• In 2008 . . . – Audiologists fitted 31.2% of all devices, an

improvement of 6.3% from 2004– Hearing aid specialists saw a decline of

9.5% to 27.5%– Veterans Administration saw slight decline

of 0.4% to 14.5%– Ear doctor offices saw 0.6% gain to 9.2%

• In 2012 . . . – Independent dispenser channel was still the

most popular– Retail chain segment becoming global– Costco becomes one of the largest hearing

aid retailers with over 500 in‐store hearing booths and audiologists

– Walmart and Sam’s Club are following Costco’s lead

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

2000 2004 2008

Hearing Aid Source of Distribution

Audiologist's office #1 Hearing aid specialist office #2

Veterans administration #3 Ear doctor's office #4

Mail order #5 Wholsale club #6

Department store #7 Clinic #8

Military installation #9 Hospital #10

Family doctor's office #11 Drugstore #12

16

Key observation #8 – Brand differentiation & positioning

17

MHC’s logo “symbol” and blue color scheme are confusingly similar to “HearingPlanet.” Plus, all brands reviewed use the color blue, further reducing brand differentiation.

MHC’s logo “symbol” (sphere) is impersonal and a disconnect with “My” Hearing Centers. The symbol should key off of “My” not “Hearing” to help humanize the brand.

Key observation #8, cont’d – Brand differentiation & positioning

18

MHC’s logo “symbol” and blue color scheme are confusingly similar to “HearingPlanet.” Plus, all brands reviewed use the color blue, further reducing brand differentiation.

The color “blue” symbolizes trust, loyalty, wisdom, confidence, intelligence and truth – all positive attributes. And, “blue” is considered beneficial to the mind and body. It’s easy to understand why category brands use blue. Unfortunately, blue is a masculine color – potentially notconnecting with half the target market.

MHC’s tagline, “We Change Lives Through Better Hearing,” is a nice promise. And, one the Company delivers on. Unfortunately, it is confusingly similar to, “Welcome to a world of better hearing,” from HearingPlanet and does not sufficiently differentiate the brand.

MHC’s logo “symbol” (sphere) is impersonal and a disconnect with “My” Hearing Centers. The symbol should key off of “My” not “Hearing” to help humanize the brand.

Key observation #8, cont’d – Brand differentiation & positioning

19

MHC’s logo “symbol” and blue color scheme are confusingly similar to “HearingPlanet.” Plus, all brands reviewed use the color blue, further reducing brand differentiation.

The color “blue” symbolizes trust, loyalty, wisdom, confidence, intelligence and truth – all positive attributes. And, “blue” is considered beneficial to the mind and body. It’s easy to understand why category brands use blue. Unfortunately, blue is a masculine color – potentially notconnecting with half the target market.

The tagline, “We Change Lives Through Better Hearing,” is a nice promise. And, one the Company delivers on. Unfortunately, it is confusingly similar to, “Welcome to a world of better hearing,” from HearingPlanet and does not sufficiently differentiate the brand.

The logo “symbol” (sphere) is impersonal and a disconnect with “My” Hearing Centers. The symbol should key off of “My” not “Hearing” to help humanize the brand.

MY HEARING CENTERSWe Change Lives Through Better Hearing.When you’re ready to hear what you’re missing.

This tagline is emotional. It acknowledges each consumer deals with hearing loss in their own way and timeframe – further humanizing the brand. The combination of color and tagline reduces anxiety and promotes a more caring and relaxed atmosphere. It’s appropriate for a vanity appeal.

Green symbolizes harmony and freshness. It has a strong association with safety and the power of healing. It is the most restful color to the human eye. Green is appropriate for promoting drugs and medical products and will help differentiate the brand from the competitive set. It is not gender specific.

Key observation #8, cont’d – Brand differentiation & positioning

20

MHC’s logo “symbol” and blue color scheme are confusingly similar to “HearingPlanet.” Plus, all brands reviewed use the color blue, further reducing brand differentiation.

The color “blue” symbolizes trust, loyalty, wisdom, confidence, intelligence and truth – all positive attributes. And, “blue” is considered beneficial to the mind and body. It’s easy to understand why category brands use blue. Unfortunately, blue is a masculine color – potentially notconnecting with half the target market.

The tagline, “We Change Lives Through Better Hearing,” is a nice promise. And, one the Company delivers on. Unfortunately, it is confusingly similar to, “Welcome to a world of better hearing,” from HearingPlanet and does not sufficiently differentiate the brand.

The logo “symbol” (sphere) is impersonal and a disconnect with “My” Hearing Centers. The symbol should key off of “My” not “Hearing” to help humanize the brand.

MY HEARING CENTERSWe Change Lives Through Better Hearing.

This tagline is emotional. It acknowledges each consumer deals with hearing loss in their own way and timeframe – further humanizing the brand. The combination of color and tagline reduces anxiety and promotes a more caring and relaxed atmosphere. It’s appropriate for a vanity appeal.

When you’re ready to hear what you’re missing.The More Affordable Hearing Centers.

Green symbolizes harmony and freshness. It has a strong association with safety and the power of healing. It is the most restful color to the human eye. Green is appropriate for promoting drugs and medical products and will help differentiate the brand from the competitive set. It is not gender specific.

This logo “symbol” quickly and easily humanizes the “My” in the Company name. It is gender, race and generation neutral and can be interpreted to include everyone.

This tagline is rational. It directly addresses the #1 consumer barrier to purchase: “Cost”. It clearly differentiates the brand from the competitive set and positions it as “cost sensitive.”

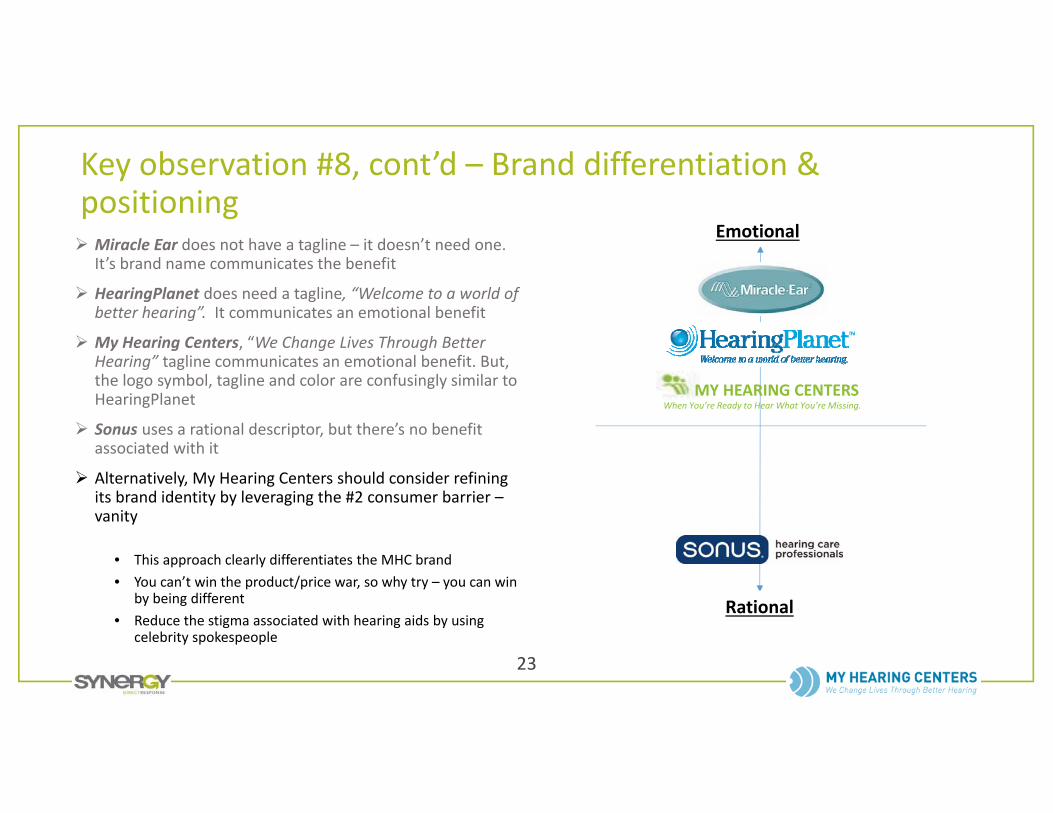

Key observation #8, cont’d – Brand differentiation & positioning Miracle Ear does not have a tagline – it doesn’t need one.

It’s brand name communicates the benefit

HearingPlanet does need a tagline, “Welcome to a world of better hearing”. It communicates an emotional benefit

My Hearing Centers, “We Change Lives Through Better Hearing” tagline communicates an emotional benefit. But, the logo symbol, tagline and color are confusingly similar to HearingPlanet

Sonus uses a rational descriptor, but there’s no benefit associated with it

My Hearing Centers should consider refining its brand identity

• Create more distinction from the sea of “blue”• Acknowledge the #1 consumer barrier is “cost” and position

the brand as, “Cost Sensitive”• Deliver on this promise with a variety of consumer financing

and discount offers

Emotional

Rational

21

Key observation #8, cont’d – Brand differentiation & positioning Miracle Ear does not have a tagline – it doesn’t need one.

It’s brand name communicates the benefit

HearingPlanet does need a tagline, “Welcome to a world of better hearing”. It communicates an emotional benefit

My Hearing Centers, “We Change Lives Through Better Hearing” tagline communicates an emotional benefit. But, the logo symbol, tagline and color are confusingly similar to HearingPlanet

Sonus uses a rational descriptor, but there’s no benefit associated with it

My Hearing Centers should consider refining its brand identity

• Create more distinction from the sea of “blue”• Acknowledge the #1 consumer barrier is “cost” and position

the brand as, “Cost Sensitive”• Deliver on this promise with a variety of consumer financing

and discount offers

Emotional

Rational

22

MY HEARING CENTERSThe More Affordable Hearing Centers.

Key observation #8, cont’d – Brand differentiation & positioning Miracle Ear does not have a tagline – it doesn’t need one.

It’s brand name communicates the benefit

HearingPlanet does need a tagline, “Welcome to a world of better hearing”. It communicates an emotional benefit

My Hearing Centers, “We Change Lives Through Better Hearing” tagline communicates an emotional benefit. But, the logo symbol, tagline and color are confusingly similar to HearingPlanet

Sonus uses a rational descriptor, but there’s no benefit associated with it

Alternatively, My Hearing Centers should consider refining its brand identity by leveraging the #2 consumer barrier –vanity

• This approach clearly differentiates the MHC brand• You can’t win the product/price war, so why try – you can win

by being different• Reduce the stigma associated with hearing aids by using

celebrity spokespeople

Emotional

Rational

23

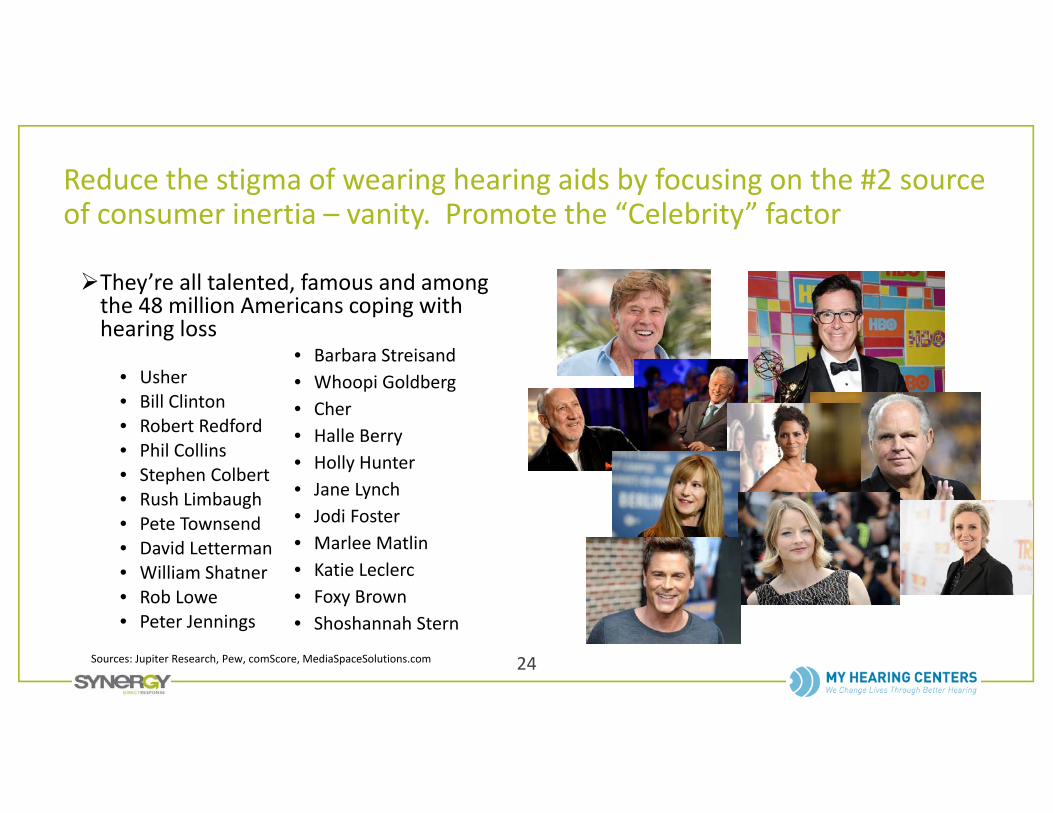

When You’re Ready to Hear What You’re Missing.MY HEARING CENTERS

Reduce the stigma of wearing hearing aids by focusing on the #2 source of consumer inertia – vanity. Promote the “Celebrity” factor

They’re all talented, famous and among the 48 million Americans coping with hearing loss

• Usher • Bill Clinton• Robert Redford• Phil Collins• Stephen Colbert• Rush Limbaugh• Pete Townsend• David Letterman• William Shatner• Rob Lowe• Peter Jennings

24Sources: Jupiter Research, Pew, comScore, MediaSpaceSolutions.com

• Barbara Streisand• Whoopi Goldberg• Cher• Halle Berry• Holly Hunter• Jane Lynch• Jodi Foster• Marlee Matlin• Katie Leclerc• Foxy Brown• Shoshannah Stern

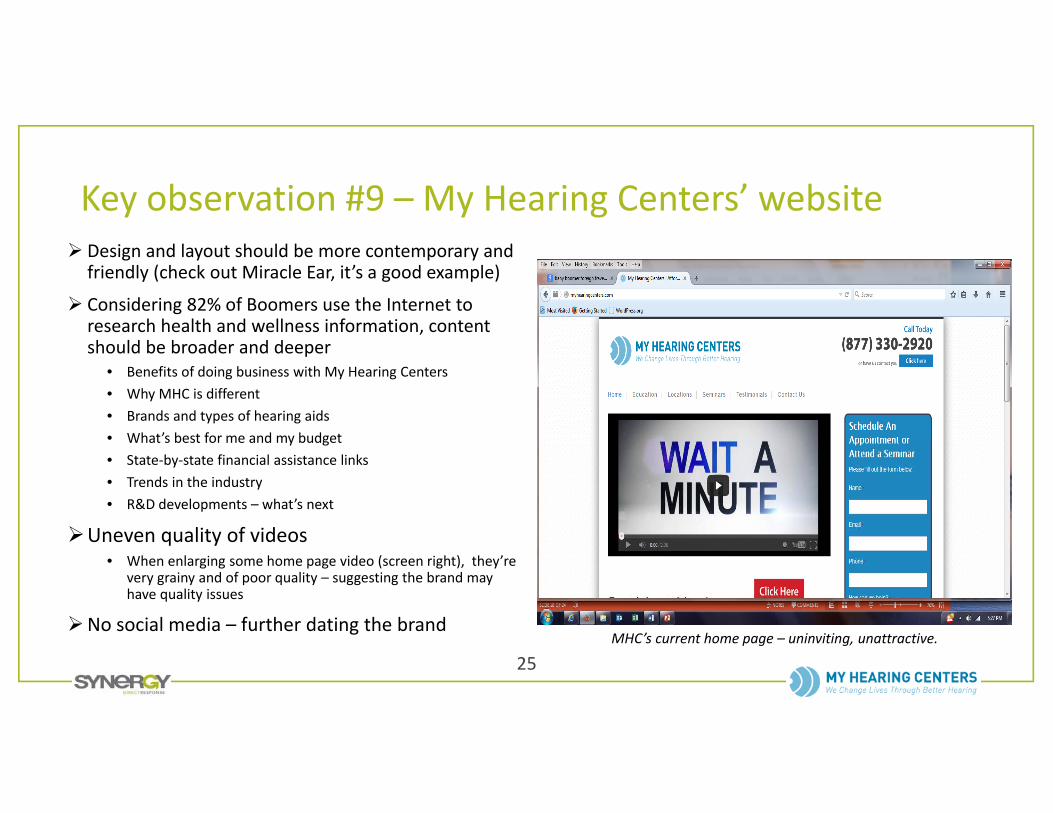

Key observation #9 – My Hearing Centers’ website Design and layout should be more contemporary and friendly (check out Miracle Ear, it’s a good example)

Considering 82% of Boomers use the Internet to research health and wellness information, content should be broader and deeper

• Benefits of doing business with My Hearing Centers• Why MHC is different• Brands and types of hearing aids• What’s best for me and my budget• State‐by‐state financial assistance links• Trends in the industry• R&D developments – what’s next

Uneven quality of videos• When enlarging some home page video (screen right), they’re

very grainy and of poor quality – suggesting the brand may have quality issues

No social media – further dating the brand

25MHC’s current home page – uninviting, unattractive.

Summary & recommendations

Summary of key observations

1. Consumer inertia is the number one marketing problem

2. Baby Boomers are the core target3. My Hearing Centers are located mostly in

2nd and 3rd tier markets 4. Most popular devices are RIC/RITE,

outpacing traditional BTEs by 2:15. Brand image and identity need help6. Website design, layout and content need

help

• Video quality is uneven• Lack of social media significantly dates site and brand

• Site should also be mobile friendly

Recommendations

1. Boomers are age sensitive. Consider developing a “lifestyle” campaign that overcomes vanity and the stigma of hearing aids associated with old, frail, weak people

2. Expand the brand into DMAs with high concentrations of hearing impaired consumers

3. Heavy‐up on RIC/RITE products by providing multiple brands (3‐4+) of devices

4. Refresh brand image and identity as suggested earlier. Consider using Merrill Osmond as official spokesperson and face of the brand

5. Website needs a complete refresh. Consider developing mobile app for consumers to test hearing on the go

26

Next steps

1. Agree to most pressing needs2. Conduct market research to fill information

gaps, e.g.,a. Why do consumers choose My Hearing

Centers rather than competitorsb. What differentiates My Hearing Centers

from competitive setc. BDI/CDI analysis

3. Appoint Synergy Agency of Record4. Go to work

27

+

A Winning Combination

Thank you.

28

Thank you.

Recommended