Petrochemical Outlook for 2018: Final Conclusions

APLA Consultant’s Panel

Rio de Janeiro November 13, 2017

Polymer Consulting

International, Inc.

• Hurricane Harvey (and other events)

• Oil and Gas Prices

• Shale Gas Crackers: The Arrival

– Polyethylene exports

• Divergence of Polyethylene and Polypropylene

• China’s New Policies

• President Trump

There are some key issues for 2018

PCI

PCI

Hurricane Harvey

• Essentially every coastal and off-shore production facility in

the area of landfall was shut down

• More than 60 percent of US ethylene, polyethylene and

polypropylene capacity was shut down due to the hurricane

• While some plants have sustained only minimum damage,

some have been hit harder than others

• The damage to infrastructure (roads, rail, power, etc.) will

lengthen the impact/problem

• As a result, production was reduced and prices increased

• As of the end of October most plants are operating with some

operating at reduced rates

• By mid-to-late December, all plants are expected to be

operating at capacity; some logistics issues may still exist

• Some plants still under construction will be delayed

PCI

Harvey – the worst hurricane to hit Houston

and surroundings in history

• The recovery from Harvey, the other hurricanes and the

California fires will result in an increased demand for

polymers (homes, businesses, furnishings, cars, etc.) for the

next six to twelve months (possibly longer)

• This applies to the other countries/islands as well which will

need to import finished products and food

PCI

Harvey – the worst hurricane to hit Houston

and surroundings in history (continued)

A report from the Dallas Federal Reserve Bank (10/17)

estimated damage to Texas at 75-100 billion dollars.

Other estimates exceed $150 billion

PCI

Oil and Gas

• Oil price forecasts range from $45 to $75 for 2018. PCI believes

$50-$60 is more reasonable for 2018 unless OPEC makes a

more drastic production cut

• Recent prices above $60 would likely come down due to

increased US shale oil production

• Production of shale oil and gas has increased in 2017 with

further increases expected for 2018

• Natural gas prices (consensus) are expected to be between

$2.50-$3.50/MM BTU for 2018

• Gas production is increasing faster than demand promoting

increased exports

Oil and gas prices

Low oil (naphtha) prices reduce the competitive advantage

of shale gas ethane – but it is still therePCI

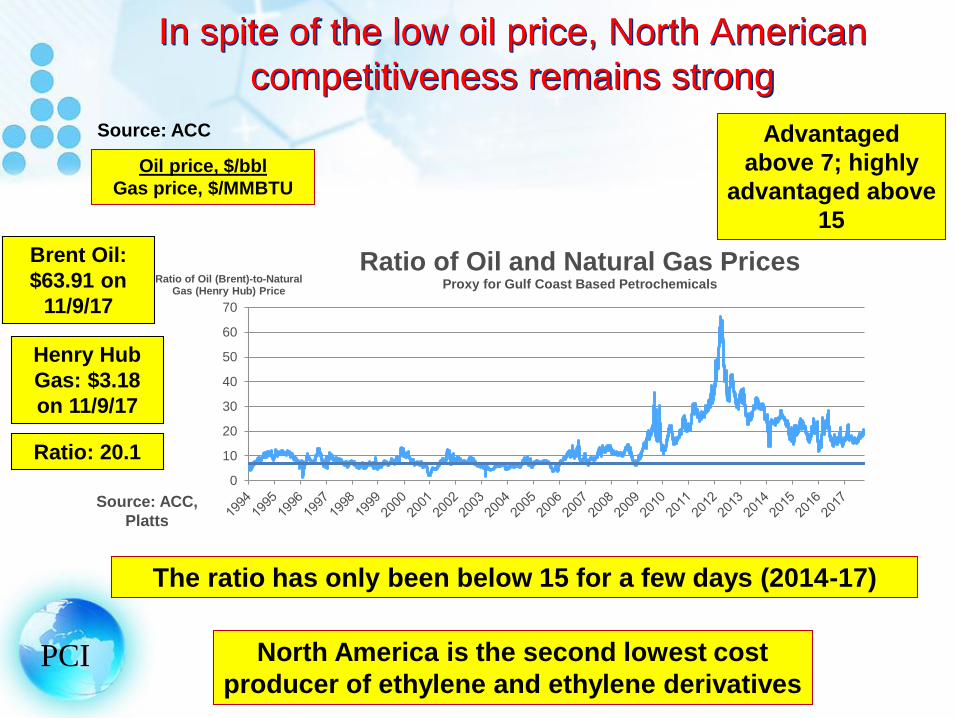

In spite of the low oil price, North American

competitiveness remains strong

Oil price, $/bbl

Gas price, $/MMBTU

North America is the second lowest cost

producer of ethylene and ethylene derivatives

Brent Oil:

$63.91 on

11/9/17

Henry Hub

Gas: $3.18

on 11/9/17

Ratio: 20.1

Source: ACC

The ratio has only been below 15 for a few days (2014-17)

Advantaged

above 7; highly

advantaged above

15

PCI

0

10

20

30

40

50

60

70

Ratio of Oil (Brent)-to-Natural Gas (Henry Hub) Price

Ratio of Oil and Natural Gas PricesProxy for Gulf Coast Based Petrochemicals

Source: ACC,

Platts

PCI

Shale Gas Investments:The Arrival

Gestation periods (from inception to birth)

PCI

Humans: 9 months

Elephants: 23 months

Ethylene crackers: 65 months

For some companies, their 65th month is in

the fourth quarter, 2017

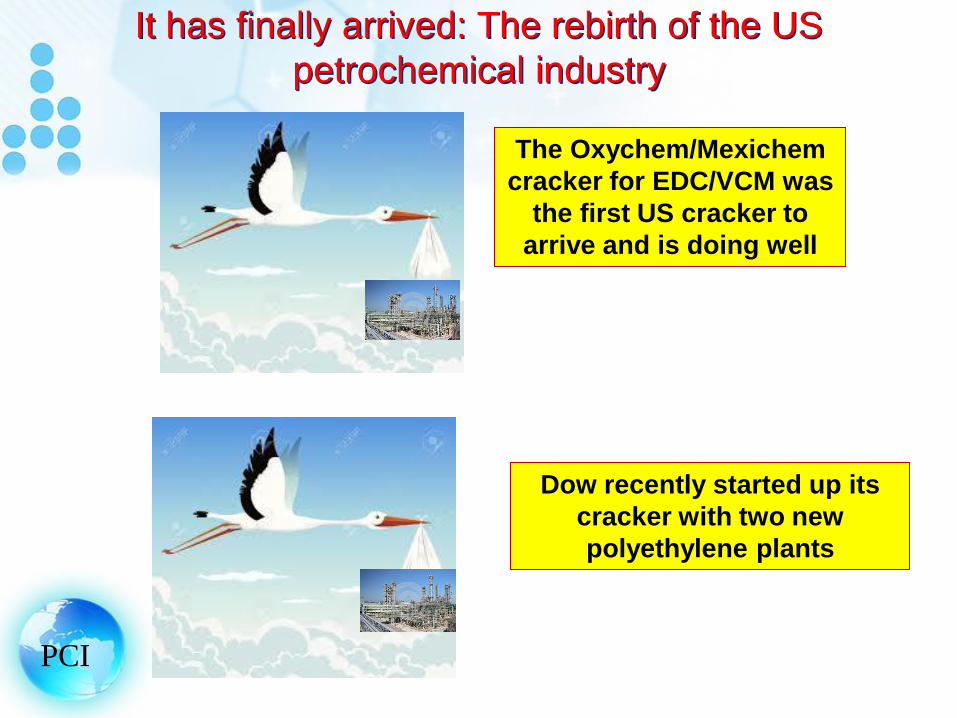

It has finally arrived: The rebirth of the US

petrochemical industry

PCI

The Oxychem/Mexichem

cracker for EDC/VCM was

the first US cracker to

arrive and is doing well

Dow recently started up its

cracker with two new

polyethylene plants

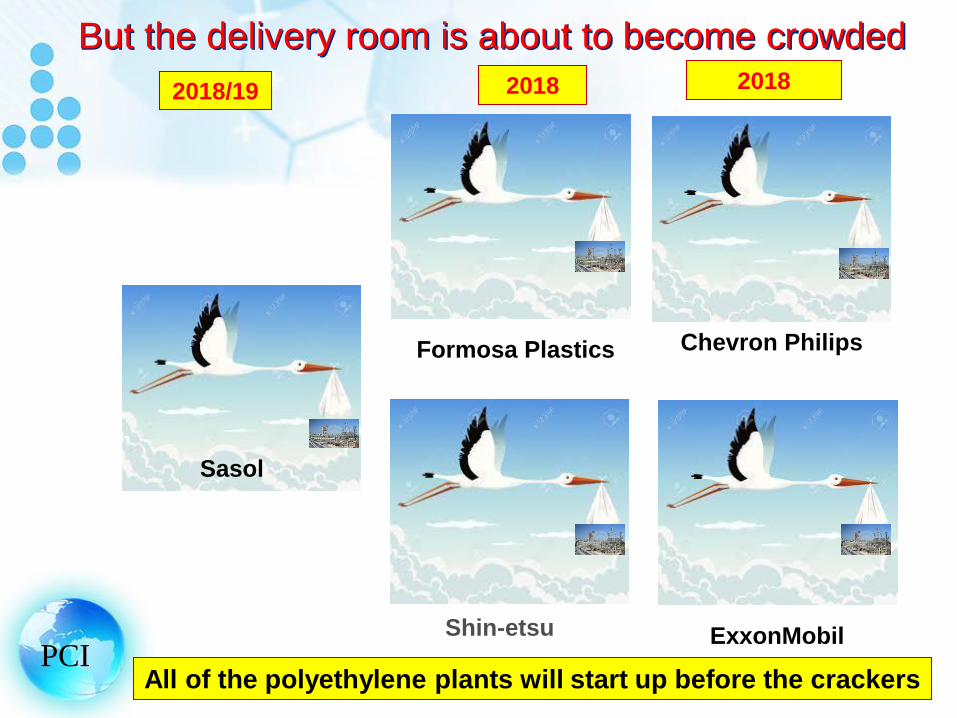

But the delivery room is about to become crowded

PCI

Chevron Philips

ExxonMobil

Formosa Plastics

Sasol

Shin-etsu

201820182018/19

All of the polyethylene plants will start up before the crackers

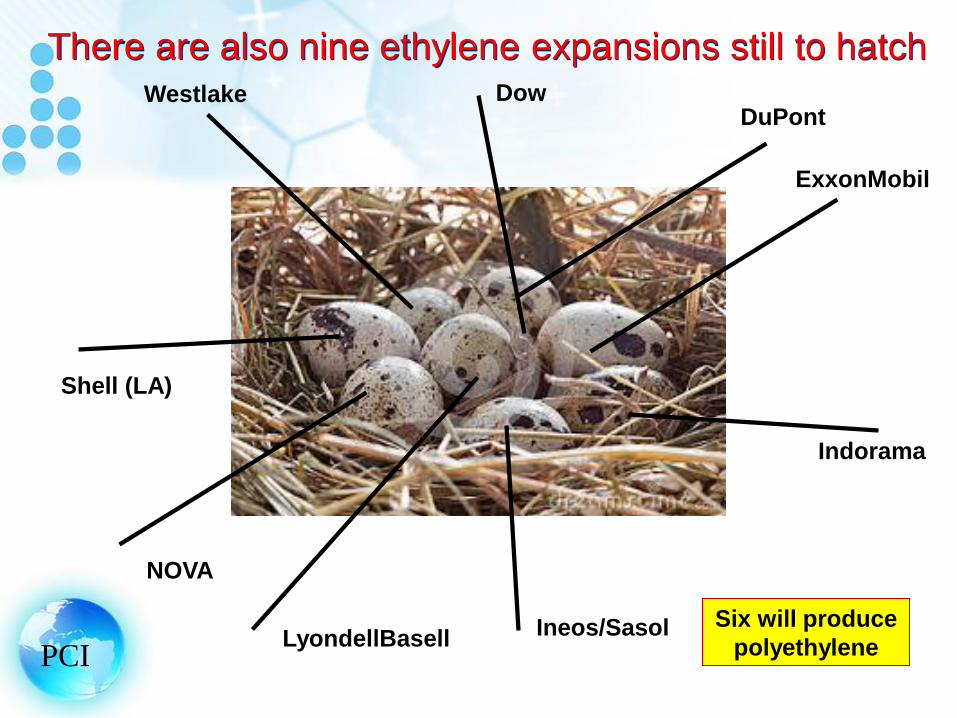

There are also nine ethylene expansions still to hatch

PCI

DowDuPont

ExxonMobil

Indorama

Ineos/SasolLyondellBasell

NOVA

Shell (LA)

Westlake

Six will produce

polyethylene

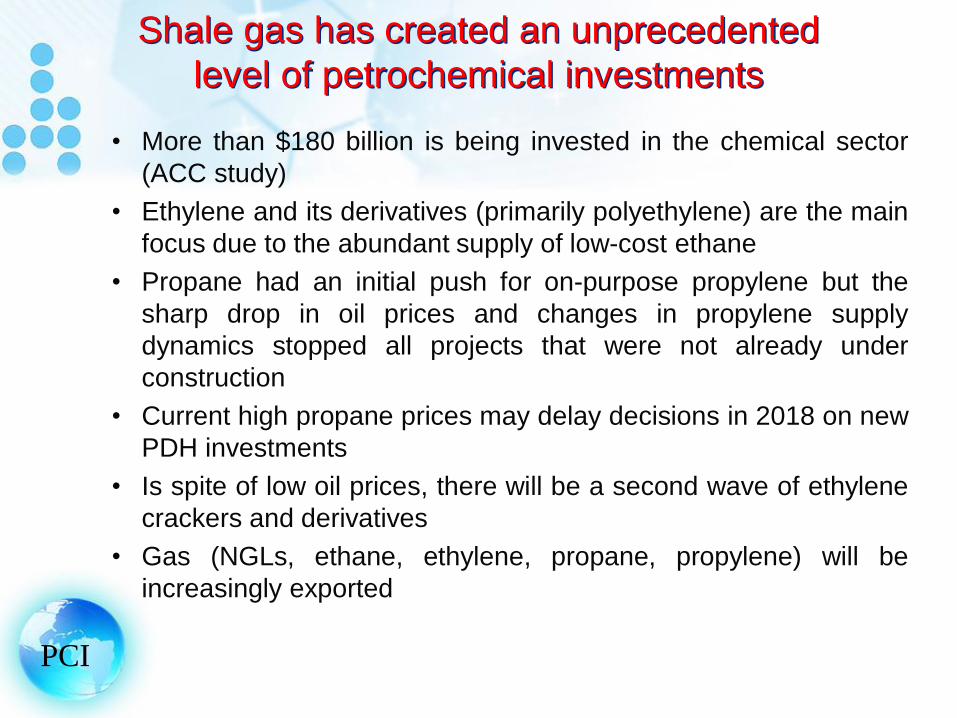

• More than $180 billion is being invested in the chemical sector

(ACC study)

• Ethylene and its derivatives (primarily polyethylene) are the main

focus due to the abundant supply of low-cost ethane

• Propane had an initial push for on-purpose propylene but the

sharp drop in oil prices and changes in propylene supply

dynamics stopped all projects that were not already under

construction

• Current high propane prices may delay decisions in 2018 on new

PDH investments

• Is spite of low oil prices, there will be a second wave of ethylene

crackers and derivatives

• Gas (NGLs, ethane, ethylene, propane, propylene) will be

increasingly exported

Shale gas has created an unprecedented

level of petrochemical investments

PCI

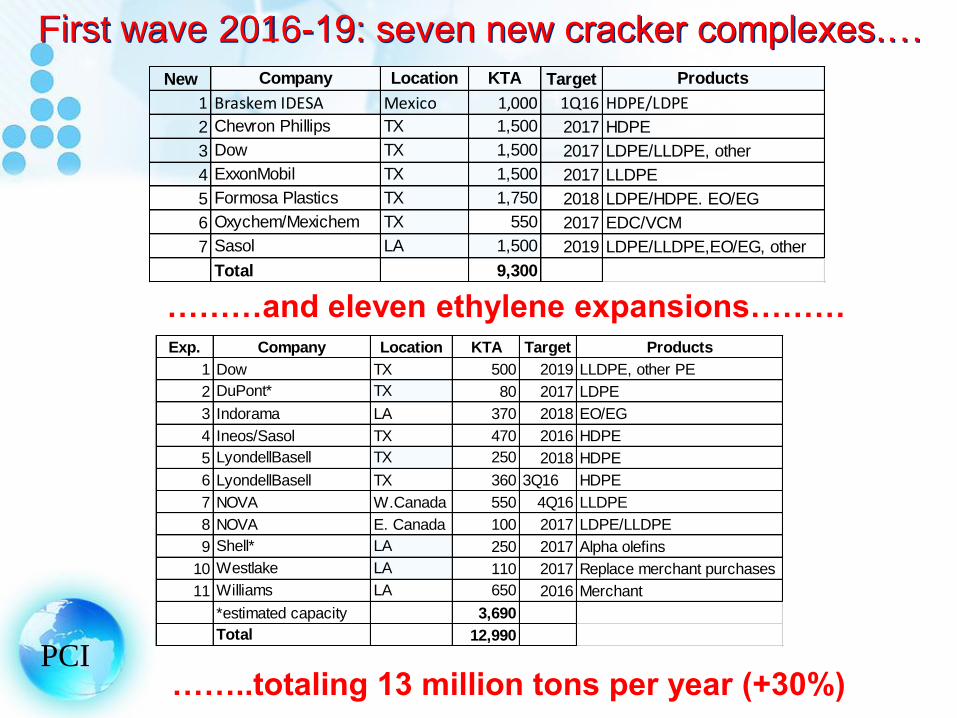

First wave 2016-19: seven new cracker complexes.…

………and eleven ethylene expansions………

……..totaling 13 million tons per year (+30%)

New Company Location KTA Target Products

1 Braskem IDESA Mexico 1,000 1Q16 HDPE/LDPE

2 Chevron Phillips TX 1,500 2017 HDPE

3 Dow TX 1,500 2017 LDPE/LLDPE, other

4 ExxonMobil TX 1,500 2017 LLDPE

5 Formosa Plastics TX 1,750 2018 LDPE/HDPE. EO/EG

6 Oxychem/Mexichem TX 550 2017 EDC/VCM

7 Sasol LA 1,500 2019 LDPE/LLDPE,EO/EG, other

Total 9,300

PCI

Exp. Company Location KTA Target Products

1 Dow TX 500 2019 LLDPE, other PE

2 DuPont* TX 80 2017 LDPE

3 Indorama LA 370 2018 EO/EG

4 Ineos/Sasol TX 470 2016 HDPE

5 LyondellBasell TX 250 2018 HDPE

6 LyondellBasell TX 360 3Q16 HDPE

7 NOVA W.Canada 550 4Q16 LLDPE

8 NOVA E. Canada 100 2017 LDPE/LLDPE

9 Shell* LA 250 2017 Alpha olefins

10 Westlake LA 110 2017 Replace merchant purchases

11 Williams LA 650 2016 Merchant

*estimated capacity 3,690

Total 12,990

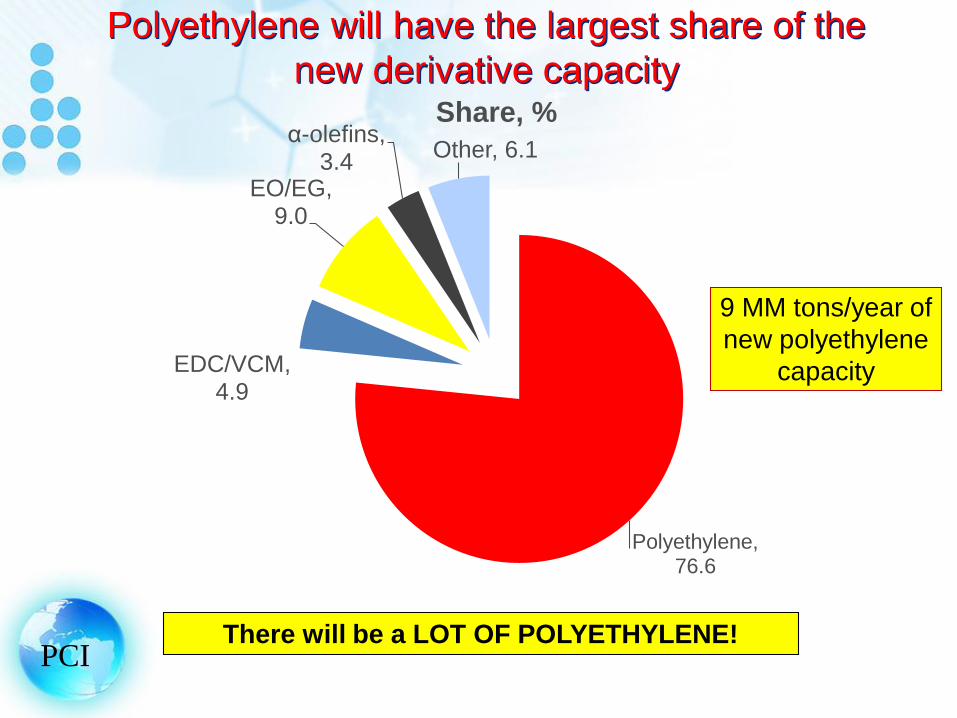

Polyethylene will have the largest share of the

new derivative capacity

Polyethylene, 76.6

EDC/VCM, 4.9

EO/EG, 9.0

α-olefins, 3.4

Other, 6.1

Share, %

There will be a LOT OF POLYETHYLENE!

9 MM tons/year of

new polyethylene

capacity

PCI

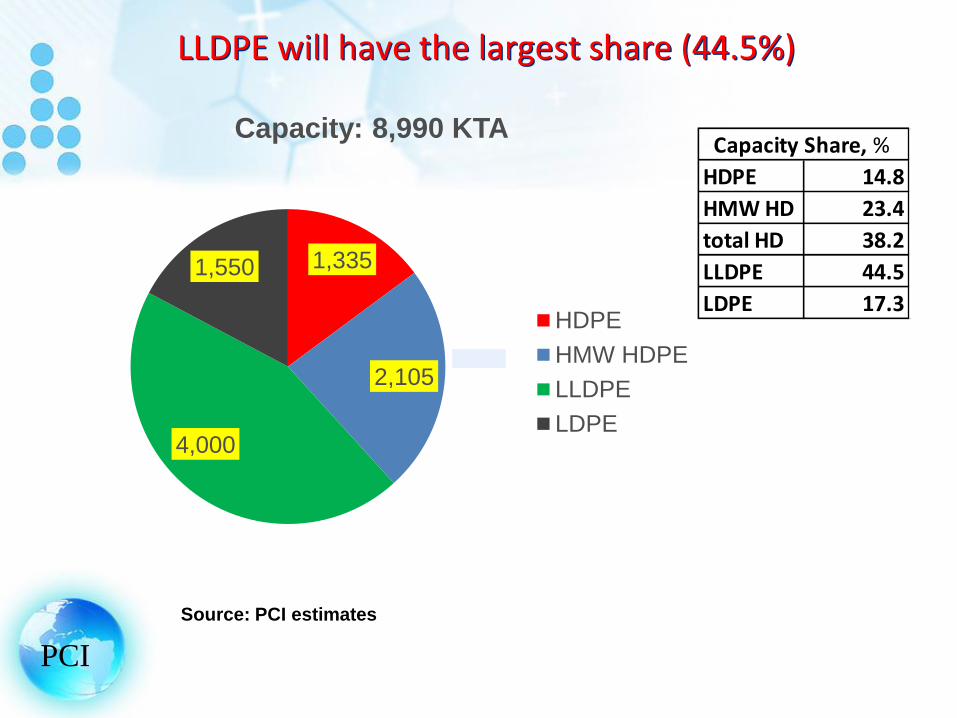

LLDPE will have the largest share (44.5%)

1,335

2,105

4,000

1,550

Capacity: 8,990 KTA

HDPE

HMW HDPE

LLDPE

LDPE

Source: PCI estimates

Capacity Share, %

HDPE 14.8

HMW HD 23.4

total HD 38.2

LLDPE 44.5

LDPE 17.3

PCI

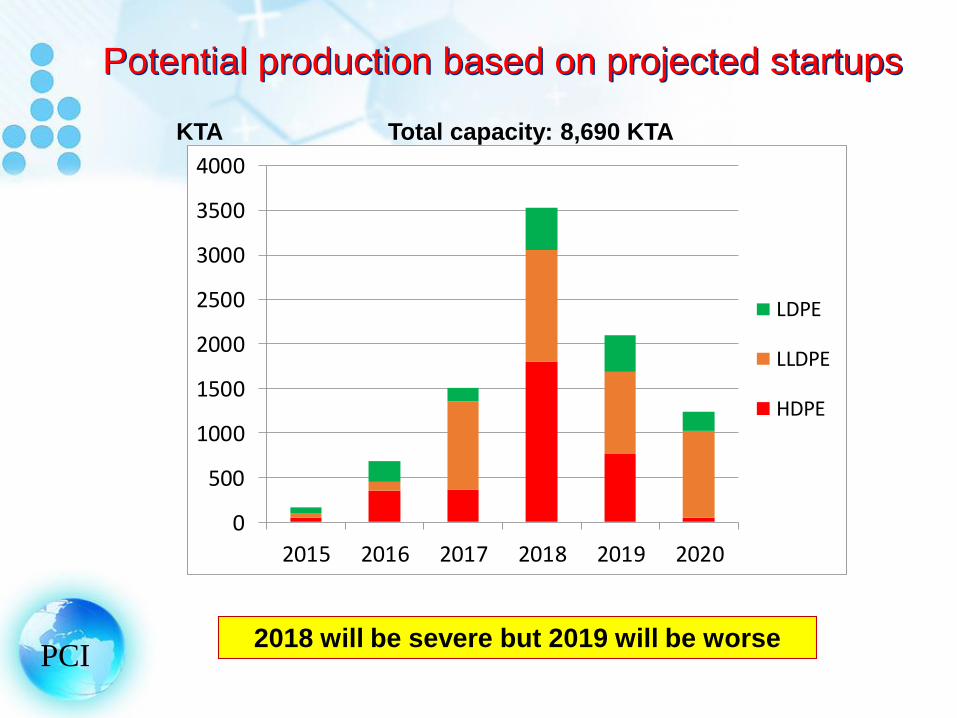

Potential production based on projected startups

0

500

1000

1500

2000

2500

3000

3500

4000

2015 2016 2017 2018 2019 2020

LDPE

LLDPE

HDPE

2018 will be severe but 2019 will be worse

KTA Total capacity: 8,690 KTA

PCI

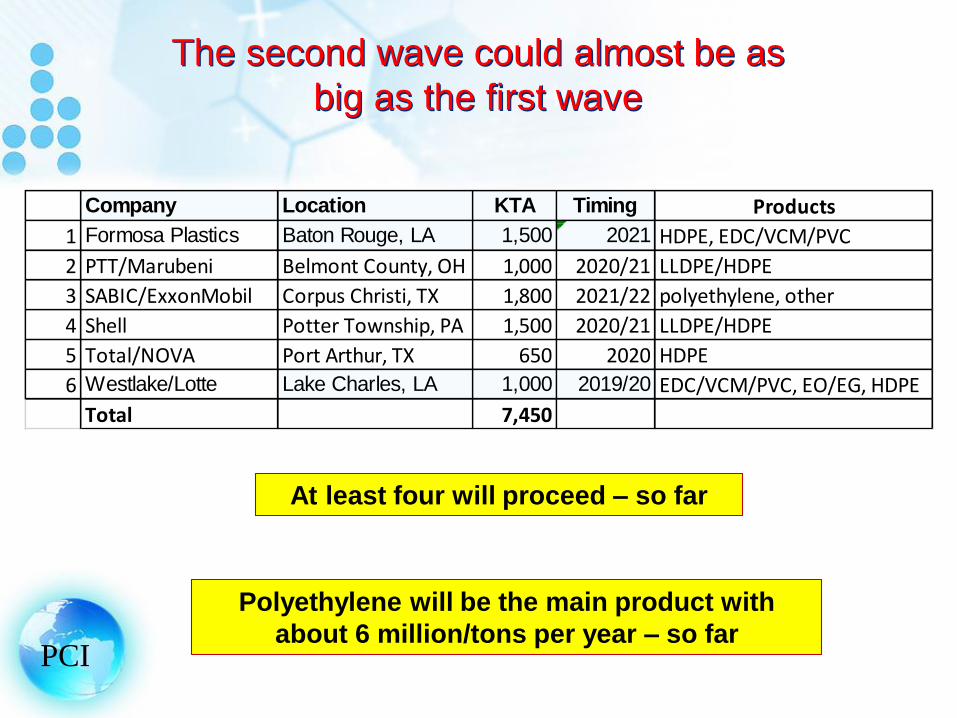

The second wave could almost be as

big as the first wave

PCI

At least four will proceed – so far

Polyethylene will be the main product with

about 6 million/tons per year – so far

Company Location KTA Timing Products

1 Formosa Plastics Baton Rouge, LA 1,500 2021 HDPE, EDC/VCM/PVC

2 PTT/Marubeni Belmont County, OH 1,000 2020/21 LLDPE/HDPE

3 SABIC/ExxonMobil Corpus Christi, TX 1,800 2021/22 polyethylene, other

4 Shell Potter Township, PA 1,500 2020/21 LLDPE/HDPE

5 Total/NOVA Port Arthur, TX 650 2020 HDPE

6 Westlake/Lotte Lake Charles, LA 1,000 2019/20 EDC/VCM/PVC, EO/EG, HDPE

Total 7,450

Mexico, Central and South America will be targets

• Mexico will be a battlefield due to favorable logistics (rail and

truck), market size and proximity. Prices could be the lowest in

North America

• US suppliers will likely have 95% of the market in Central

America due to logistics. All ports are on the Caribbean side

• South America has been the identified target of every US

producer – but PCI believes that hey are grossly overestimating

their success

• Demand growth for the past few years has been poor

• US producers already dominate the market and some Middle

East producers, such as SABIC, are strategically committed to

the region and are likely to try to increase their market share

• Brazil could impose anti-dumping duties which would wipe out

any net gain in the rest of the region

• High cost Asian suppliers will lose share but other geographies

will be neededPCI

Asia will be the main target – and it will not be easy

Of course, things could be worse

PCI You could be a small, high-cost polyethylene producer

Short-term outlook: Polyethylene

• By the first quarter of 2018, all of the polyethylene capacity

affected by Hurricane Harvey should be fully operational but

full rail service may take longer

• More than 3 million tons/year of polyethylene starting up in the

fourth quarter with an additional 1.6 million tons/year starting

up in 2018

• HDPE and LLDPE will be substantially over supplied

• Domestic and export prices could drop substantially

depending upon the actions of the individual producers (e.g.,

reduce other capacity/production/maintenance or fight for

market share)

• Export logistics will be an issue

PCI

More than 90 percent of the new polyethylene

production will have to be exported

PCI

Divergence of polyethylene and polypropylene

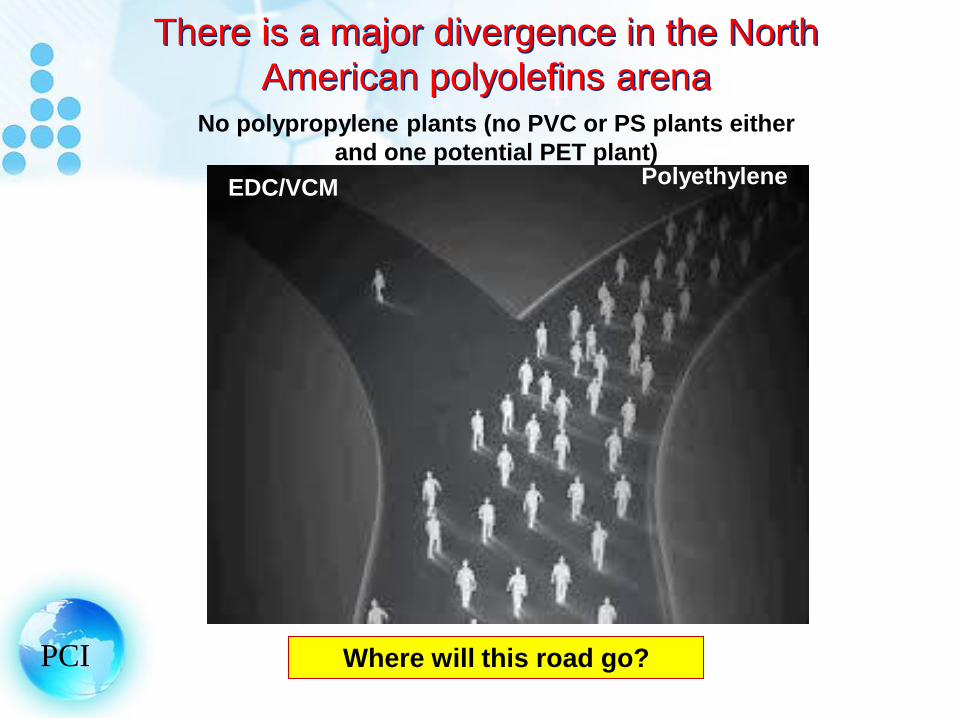

There is a major divergence in the North

American polyolefins arena

PCI

EDC/VCM

No polypropylene plants (no PVC or PS plants either

and one potential PET plant)Polyethylene

Where will this road go?

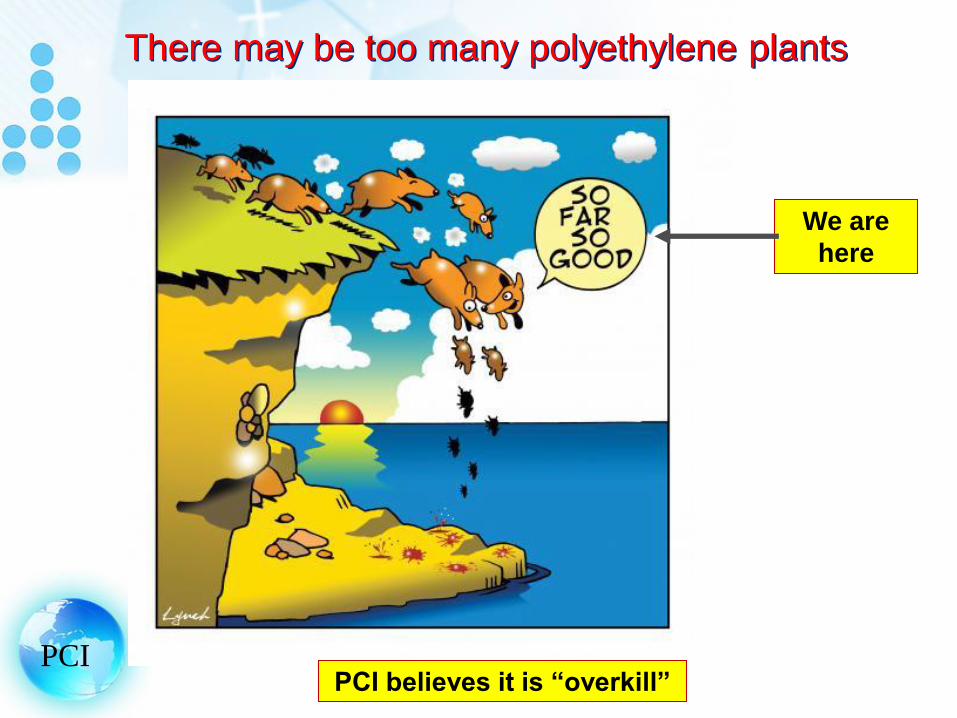

There may be too many polyethylene plants

PCIPCI believes it is “overkill”

We are

here

• While there will be too much polyethylene, there will not be

enough polypropylene

• Polypropylene producers are operating at high rates and there

are no new polypropylene plants under construction

• Polypropylene demand could surge in 2018 due to effects of the

hurricanes and fires (cars, furnishings, etc.)

• This will result in a tight supply and put upward pressure on

prices

• At best, it will be late-2019 before a new plant will startup

• So, in 2018

– US exports of polypropylene will decrease as prices increase

– US imports of polypropylene will increase

Divergence of polyethylene and polypropylene

PCI

• Propylene will be oversupplied when the Enterprise 750 KTA

PDH plant starts up (currently commissioning)

• This will put downward pressure on propylene prices and

similarly impact polypropylene prices – for a while

• Once polypropylene prices adjust for the low propylene price,

polypropylene prices are likely to increase (by mid-2018?)

In spite of the tight market, US polypropylene

prices could decrease in the short term

PCI

PCI

China

• Reduce bad/risky debt

• Improve the quality of life (health and safety)

• Emphasize consumerism and services

• Improve its import value chain (import feedstocks rather than

products)

• Increase exports of higher value products (e.g., cars)

• Invest globally through organic investments and acquisitions

China is making dramatic changes

PCI

Environmental action is a major focus. It is estimated that 1.6

million people die each year from poor environmental controls

Consumerism: The new family (status)

Removal of the one child rule in 2016: highest birthrate

in 2017 since 2000 (45% estimated to be a second child) PCI

Cars lined up in Lianyungang Port, Jiangsu

province to be shipped to Brazil

Photo: China Daily, January 2016PCI

• Small petrochemical plants with poor environmental controls are

being permanently shutdown

• Fines and forced shut-downs are occurring throughout the

production chain (including transformers) until environmental

controls are implemented

• There is a moratorium on new coal-based petrochemical

investments with greater accountability and controls for existing

ones

• A ban will take effect effective January 1, 2018 eliminating the

imports of post-consumer plastics due to repeated contamination

problems

China is taking drastic measures to improve

its environment

PCI

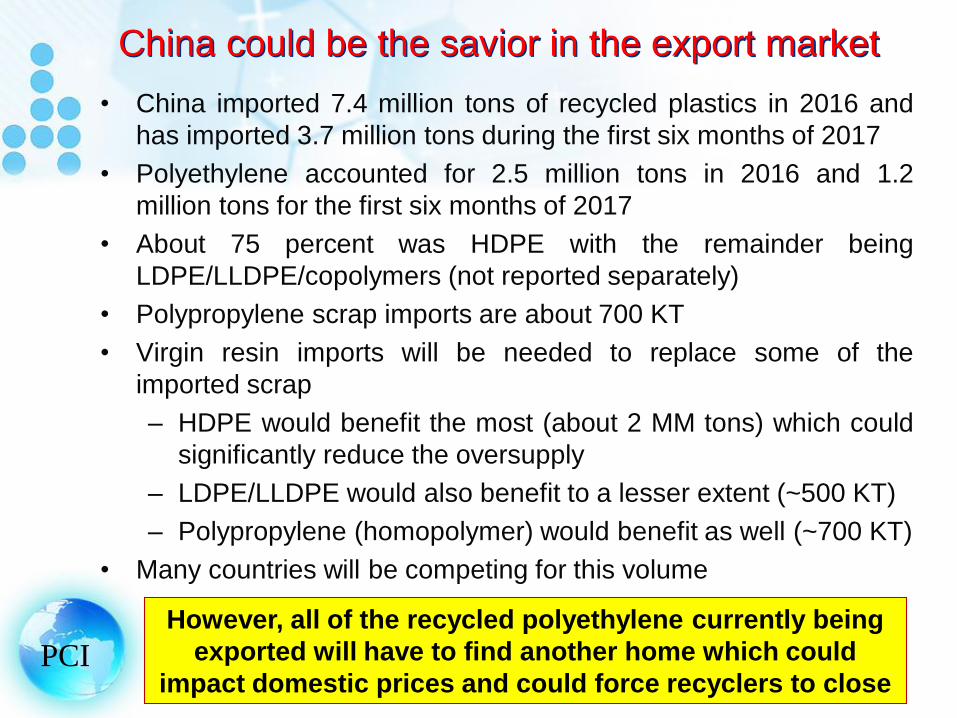

China could be the savior in the export market

• China imported 7.4 million tons of recycled plastics in 2016 and

has imported 3.7 million tons during the first six months of 2017

• Polyethylene accounted for 2.5 million tons in 2016 and 1.2

million tons for the first six months of 2017

• About 75 percent was HDPE with the remainder being

LDPE/LLDPE/copolymers (not reported separately)

• Polypropylene scrap imports are about 700 KT

• Virgin resin imports will be needed to replace some of the

imported scrap

– HDPE would benefit the most (about 2 MM tons) which could

significantly reduce the oversupply

– LDPE/LLDPE would also benefit to a lesser extent (~500 KT)

– Polypropylene (homopolymer) would benefit as well (~700 KT)

• Many countries will be competing for this volume

PCI

However, all of the recycled polyethylene currently being

exported will have to find another home which could

impact domestic prices and could force recyclers to close

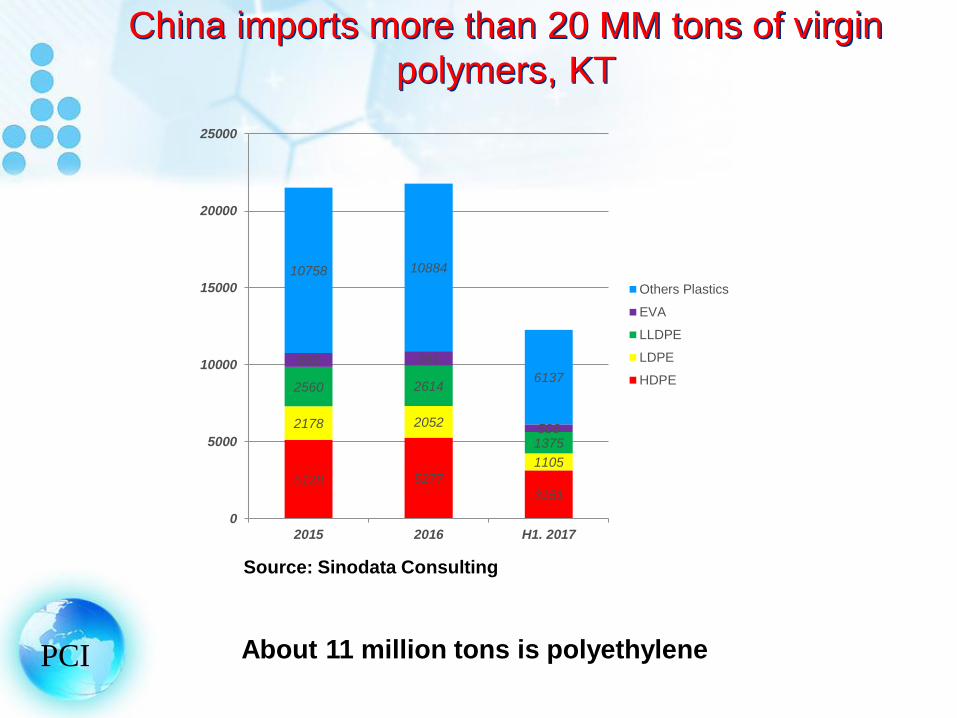

China imports more than 20 MM tons of virgin

polymers, KT

PCI

5128 5277

3151

2178 2052

1105

2560 2614

1375

892 941

506

10758 10884

6137

0

5000

10000

15000

20000

25000

2015 2016 H1. 2017

Others Plastics

EVA

LLDPE

LDPE

HDPE

Source: Sinodata Consulting

About 11 million tons is polyethylene

China imports more than 7 MM tons of

recycle/scrap plastics (2.5 MM tons polyethylene)

PCI

3568

2532

1218

91

92

59

236

446

176

2046

2533

1391

14131744

865

0

1000

2000

3000

4000

5000

6000

7000

8000

2015 2016 H1. 2017

Others

PET

PVC

Styrenics

PE

Source: Sinodata Consulting

Post-industrial scrap imports may not be affected

so virgin resin import requirements may be lower

25% of total imports

is scrap/recycled

polymer

PCI

President Trump

PCI

What will he do?

Frankly, nobody really knows

He has made many campaign

promises but as we all know,

promising and fulfilling them are

quite a different story

However, the economy and stock

market continues to strengthen

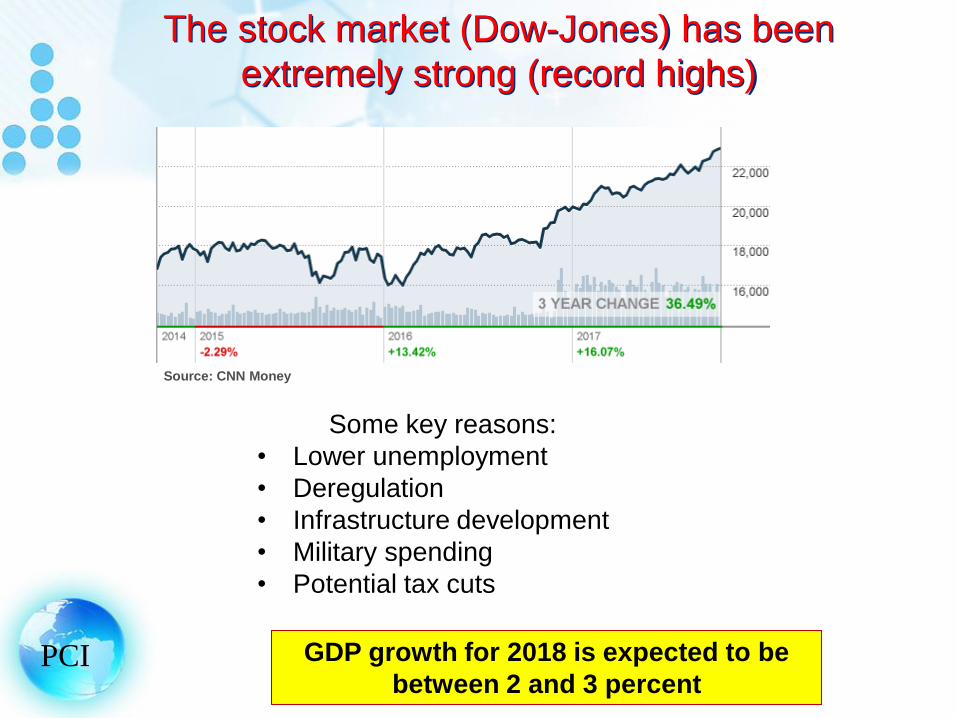

The stock market (Dow-Jones) has been

extremely strong (record highs)

PCI

Some key reasons:

• Lower unemployment

• Deregulation

• Infrastructure development

• Military spending

• Potential tax cuts

Source: CNN Money

GDP growth for 2018 is expected to be

between 2 and 3 percent

President Trump is pro-energy

Strong moves for increasing domestic energy

supply: infrastructure/pipelines, reduce legal

restrictions, deregulation, open federal lands

Revitalizing the coal industry could be problematic

but could be accomplished with subsidies for using

coal and for improving its environmental footprint –

but, so far, nothing has been done

However, higher domestic oil production will keep oil

prices low which is good for consumers (voters) but not

for oil and petrochemical companies

PCI

There are some serious problems going forward

• Most divisive administration with multiple resignations and firings

• Still battling the “Russian Election Involvement”

• Ad lib comments during speeches viewed as highly negative

• Confidence level below 40%

• In spite of the Republican majority in Congress, some

Republicans may no longer support him which will make it harder

to fulfill his campaign promises

• There are some key international conflict issues

– North Korea (escalating)

– ISIS (apparently losing ground)

– Afghanistan (committing more US troops)

– Syria civil war (conflict with Russia)

PCI

He often uses Twitter to announce his next

moves/policies before letting his staff know about them

PCI

Final Conclusions and Recommendations*

*not already covered

Survival of the fittest

PCI

Unfortunately, all the training in the world will not make a

difference – there is only one critical factor for success

COST!

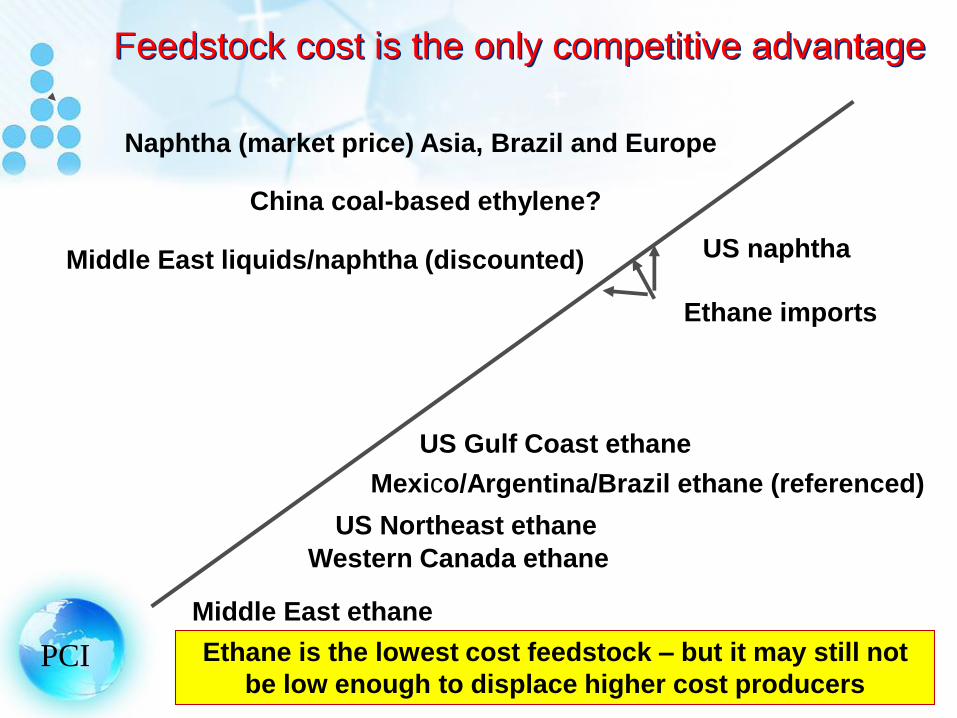

Feedstock cost is the only competitive advantage

Naphtha (market price) Asia, Brazil and Europe

Middle East ethane

Mexico/Argentina/Brazil ethane (referenced)

US Northeast ethane

Middle East liquids/naphtha (discounted)

Ethane is the lowest cost feedstock – but it may still not

be low enough to displace higher cost producers

China coal-based ethylene?

Western Canada ethane

US Gulf Coast ethane

US naphtha

Ethane imports

PCI

Conclusions and recommendations

• 2018 could be the start of one of the worst financial performance

periods in history for polyethylene

• However, if producers can keep ethylene operating rates high

enough to maintain a good margin, there can be some chain

profitability – but this may be wishful thinking

• Polyethylene financial performance in 2018 could affect the

decisions to actually going forward with second wave

investments and the timing

• US polypropylene and PVC demand growth will be stronger due

to the rebuilding and replacement of homes, businesses,

infrastructure and vehicles destroyed by the hurricane and fires

• US PVC prices will increase and exports will decrease but

domestic capacity can easily meet the increased demand

PCI

President Trump in 2018

• Subscribe to Trump’s twitter and you will find out his next move

before his staff and congress know it (or at least at the same time)

• The “Wall” – construction is likely to start using US taxpayer’s

money

• Tax reform will pass reducing taxes and significantly increasing

the deficit

• NAFTA is not likely to change – too many US companies benefit

from it (business decision)

• If relations with Venezuela deteriorate further, he could ban oil

imports

• Expect more white house staff problems

• Congressional cooperation will be an issue

PCI

www.poweredtemplates.com

Polymer Consulting

International, Inc.

Recommended