Increasing contributions presentation

Increasing contributions in your retirement plan account

This material is not a recommendation to buy, sell, hold, or roll over any asset, adopt an investment strategy, retain a specific investment manager or use a particular account type. It does not take into account the specific investment objectives, tax and financial condition or particular needs of any specific person. Investors should work with their financial professional to discuss their specific situation.

Investing involves market risk, including possible loss of principal and possible fluctuations in value. Products may not be available in all states.

The Nationwide Group Retirement Series includes unregistered group fixed and variable annuities and trust programs. The unregistered group fixed and variable annuities are issued by Nationwide Life Insurance Company. Trust programs and trust services are offered by Nationwide Trust Company, a division of Nationwide Bank. Nationwide Investment Services Corporation, member FINRA. Nationwide Mutual Insurance Company and Affiliated Companies, Home Office: Columbus, OH 43215-2220.

Nationwide, My Interactive Retirement Planner, the Nationwide N and Eagle and Nationwide is on your side are service marks of Nationwide Mutual Insurance Company. © 2017 Nationwide.

PNM-2788AO.4 (11/17)

• Not a deposit • Not FDIC or NCUSIF insured • Not guaranteed by the institution• Not insured by any federal government agency • May lose value

Budgeting

Benefits of contributing

Increasing your contribution

Importance of retirement plans

Why should I contribute to my retirement plan?

4

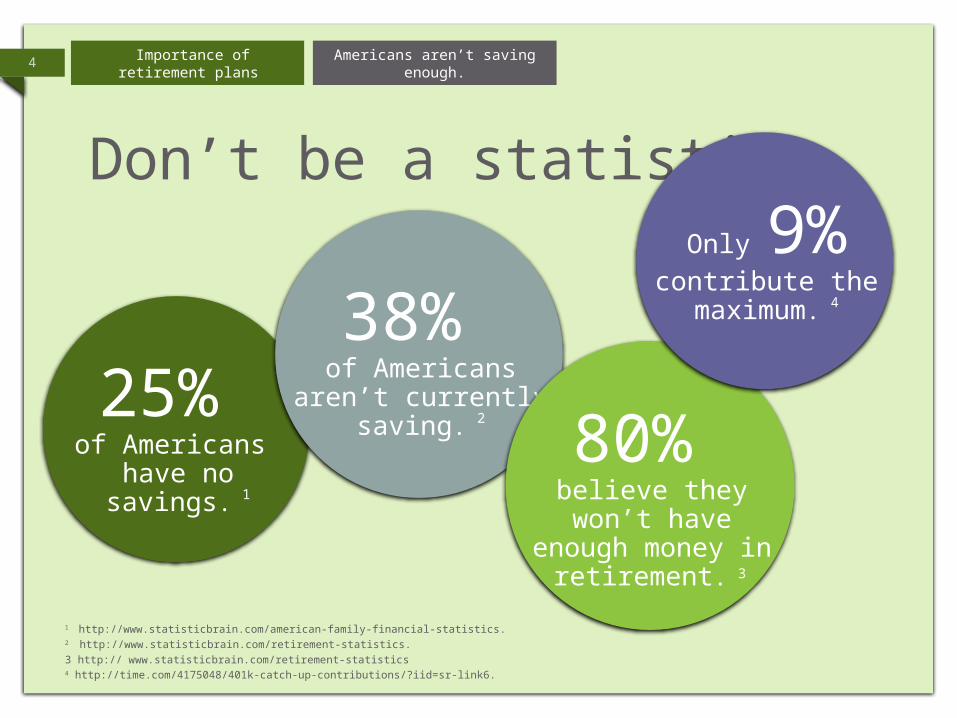

Don’t be a statistic.

Americans aren’t saving enough.

1 http://www.statisticbrain.com/american-family-financial-statistics.2 http://www.statisticbrain.com/retirement-statistics.3 http:// www.statisticbrain.com/retirement-statistics 4 http://time.com/4175048/401k-catch-up-contributions/?iid=sr-link6.

25% of Americans

have no savings. 1

38% of Americans aren’t currently saving. 2

80% believe they won’t

have enough money in retirement. 3

Only 9%contribute the maximum. 4

Importance of retirement plans

5

Less than half of Americans

have calculated how much they will

need for retirement.5

5 http://www.dol.gov/ebsa/publications/10_ways_to_prepare.html.

How much you’ll needImportance of retirement plans

6

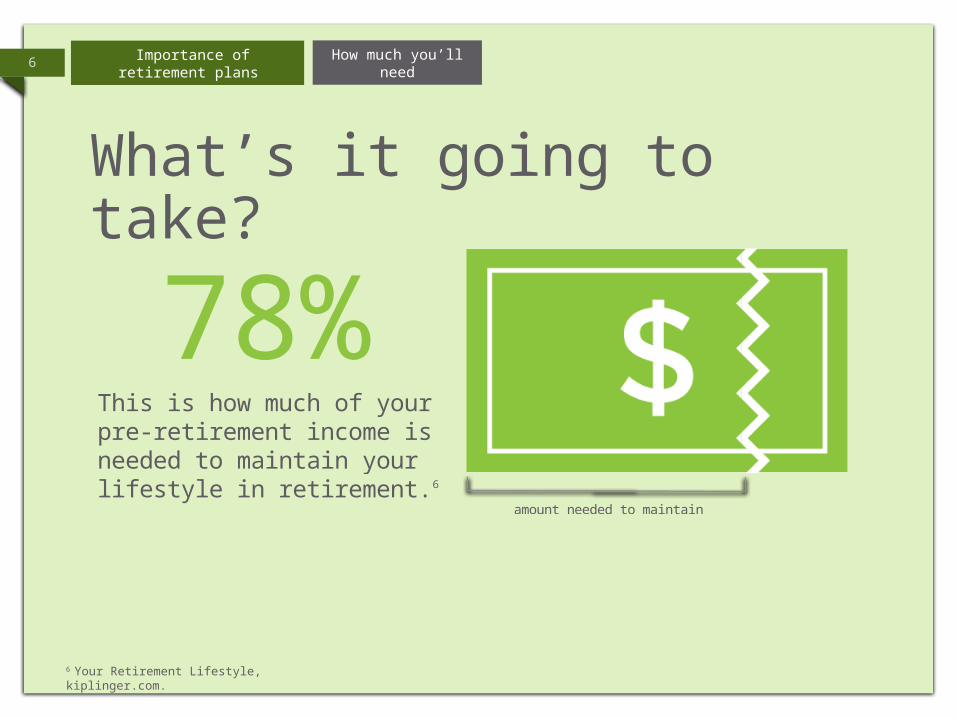

6 Your Retirement Lifestyle, kiplinger.com.

78%

How much you’ll need

What’s it going to take?

This is how much of your pre-retirement income is needed to maintain your lifestyle in retirement.6

amount needed to maintain

Importance of retirement plans

7

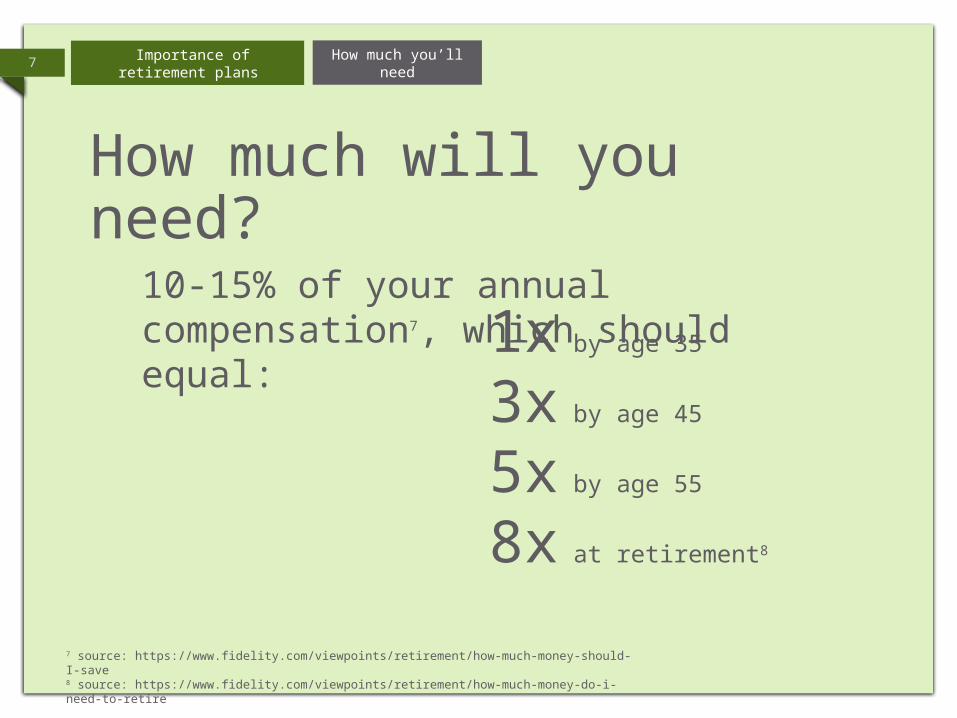

How much will you need?

10-15% of your annual compensation7, which should equal: 1x by age 35

3x by age 45

5x by age 55

8x at retirement8

7 source: https://www.fidelity.com/viewpoints/retirement/how-much-money-should-I-save8 source: https://www.fidelity.com/viewpoints/retirement/how-much-money-do-i-need-to-retire

How much you’ll needImportance of retirement plans

8

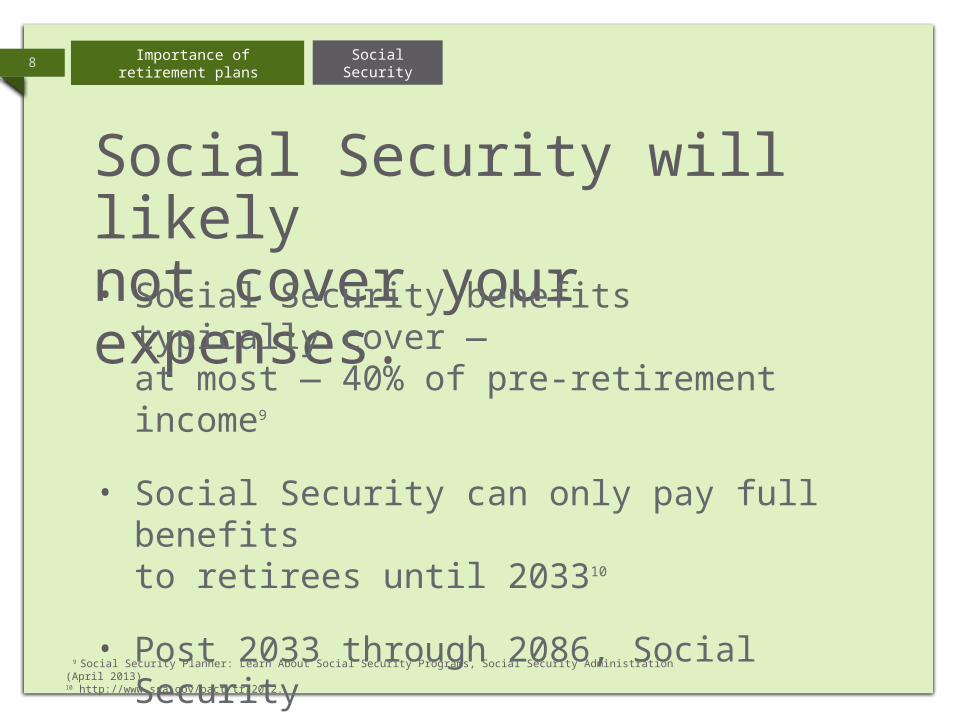

9 Social Security Planner: Learn About Social Security Programs, Social Security Administration (April 2013).10 http://www.ssa.gov/oact/tr/2012.

Social Security

Social Security will likely not cover your expenses.• Social Security benefits typically cover —

at most — 40% of pre-retirement income9

• Social Security can only pay full benefits to retirees until 203310

• Post 2033 through 2086, Social Security can cover 75% of benefits promised10

Importance of retirement plans

9

Full retirement

age

Early retirement

age

Deferredretirement

age

Social Security

Options for takingSocial Security benefits:

– permanently decreases payment

– permanently increases payment

Importance of retirement plans

Importance of retirement plans

Tax benefits

Increasing your contribution

Benefits of contributing

What are the benefits of contributing to a retirement plan?

11 Tax benefitsBenefits of contributing

Tax-deferred investing• Taxes are paid at

withdrawal, not when contributing

• Money has more potential to grow

12 Tax benefits

Other tax benefits:

Potential to be in lower tax bracket at retirement

Contributing to plan lowers taxable income

Benefits of contributing

13 Tax benefits

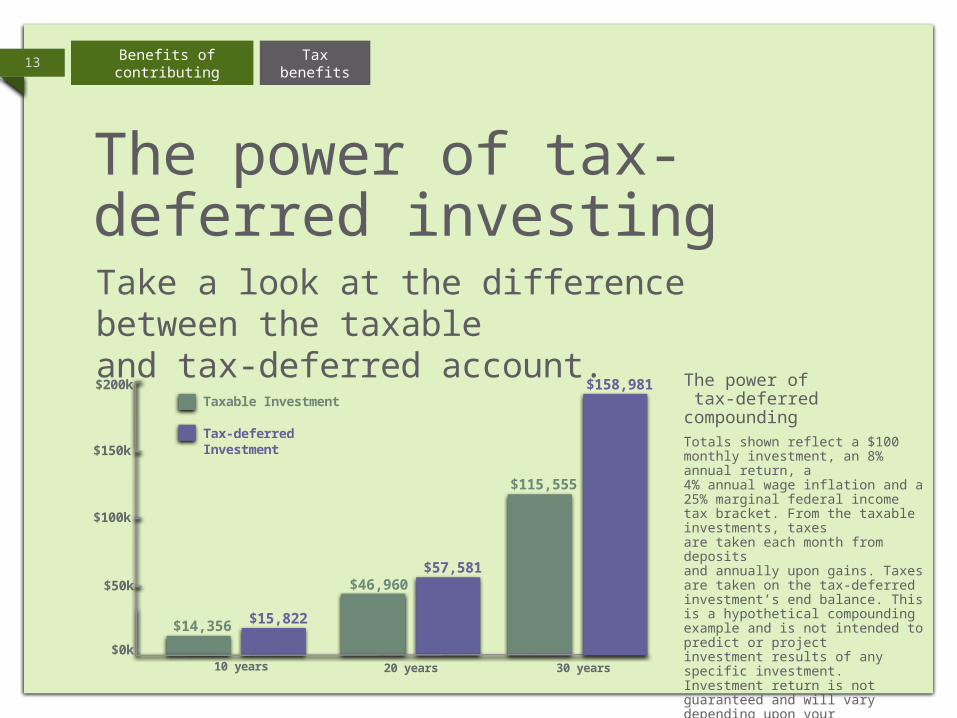

The power of tax-deferred investingTake a look at the difference between the taxable and tax-deferred account.

Taxable Investment

Tax-deferred Investment

$115,555

$57,581$46,960

$15,822$14,356

$200k

$150k

$100k

$50k

10 years 20 years 30 years$0k

The power of tax-deferred compoundingTotals shown reflect a $100 monthly investment, an 8% annual return, a4% annual wage inflation and a 25% marginal federal income tax bracket. From the taxable investments, taxes are taken each month from deposits and annually upon gains. Taxes are taken on the tax-deferred investment’s end balance. This is a hypothetical compounding example and is not intended to predict or project investment results of any specific investment. Investment return is not guaranteed and will vary depending upon your investments and market experience. If costs were reflected,the return would be less.

Benefits of contributing

$158,981

14 Tax benefits

• Incentive from IRS that gives credit to eligible participants for contributing to a retirement plan11

• Credits 50%, 20% or 10% up to $2,000 ($4,000 if joint filing)11

11 https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-savings-contributions-savers-credit

Tax Saver’s Credit

Benefits of contributing

15 Compounding interest

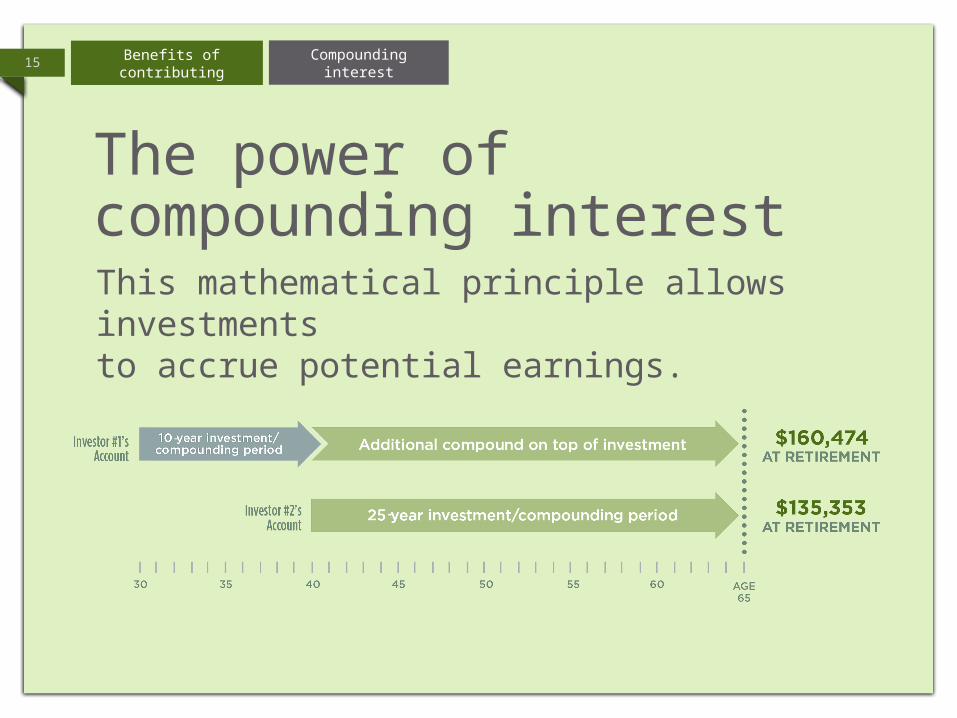

The power of compounding interestThis mathematical principle allows investments to accrue potential earnings.

Benefits of contributing

-

-

16

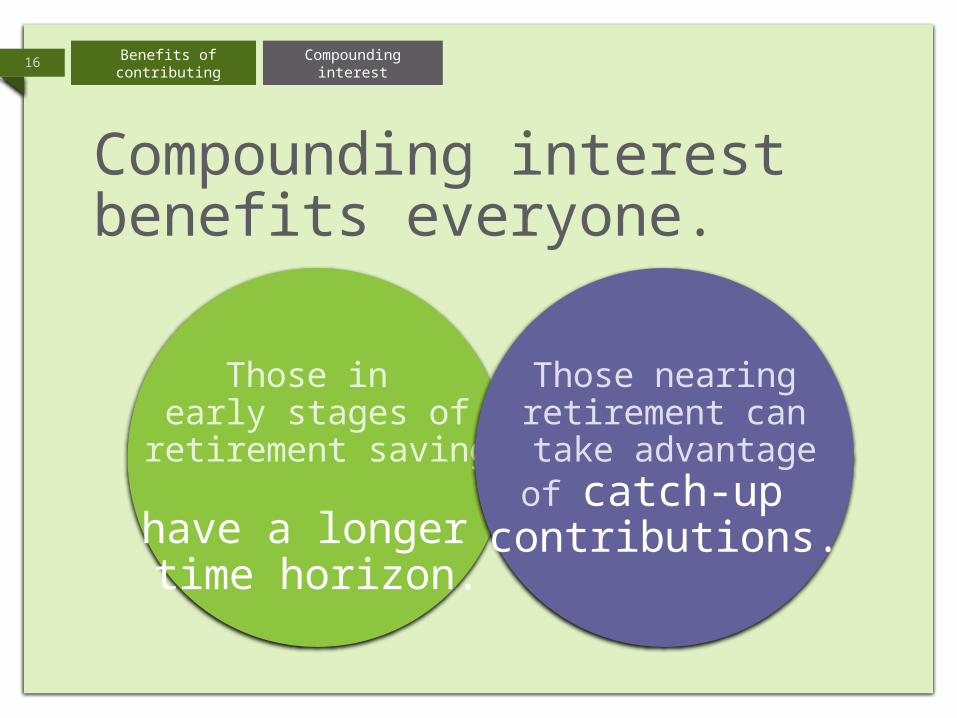

Compounding interest benefits everyone.

Compounding interest

Those in early stages of

retirement saving have a longer time horizon.

Those nearing retirement can

take advantage of catch-up

contributions.

Benefits of contributing

17

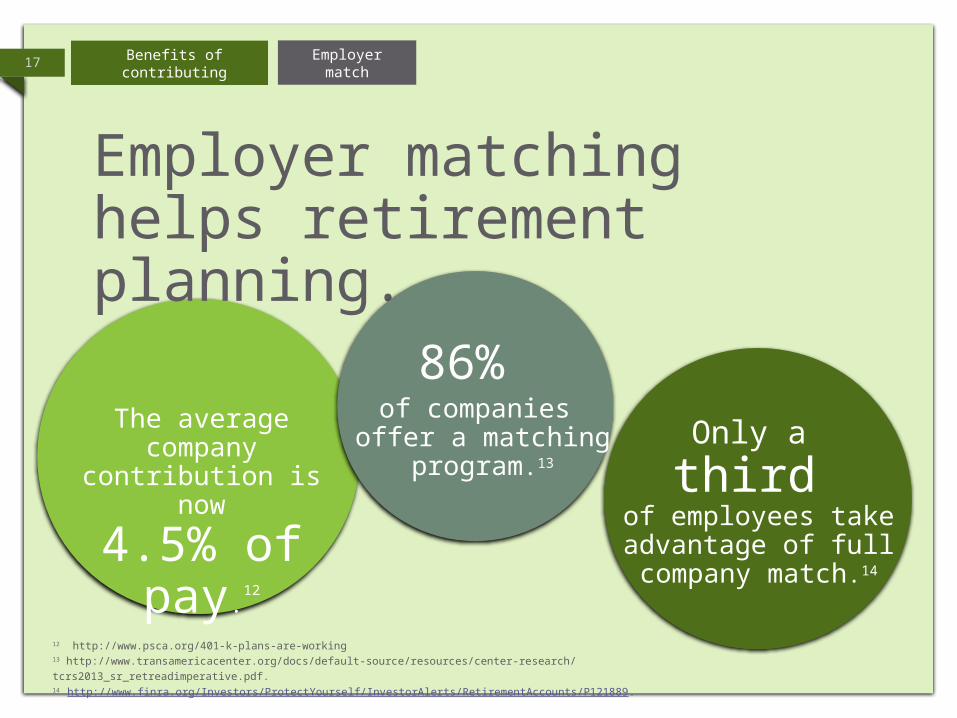

The average company contribution is now

4.5% of pay.12

Employer match

Employer matching helps retirement planning.

86% of companies

offer a matching program.13

Only a third

of employees take advantage of full company match.14

12 http://www.psca.org/401-k-plans-are-working13 http://www.transamericacenter.org/docs/default-source/resources/center-research/tcrs2013_sr_retreadimperative.pdf.14 http://www.finra.org/Investors/ProtectYourself/InvestorAlerts/RetirementAccounts/P121889.

Benefits of contributing

Importance of retirement plans

Benefits of contributing

The Learning CenterIncreasing your contribution

Why should I increase my contribution?

19 Save more.Increasing contribution

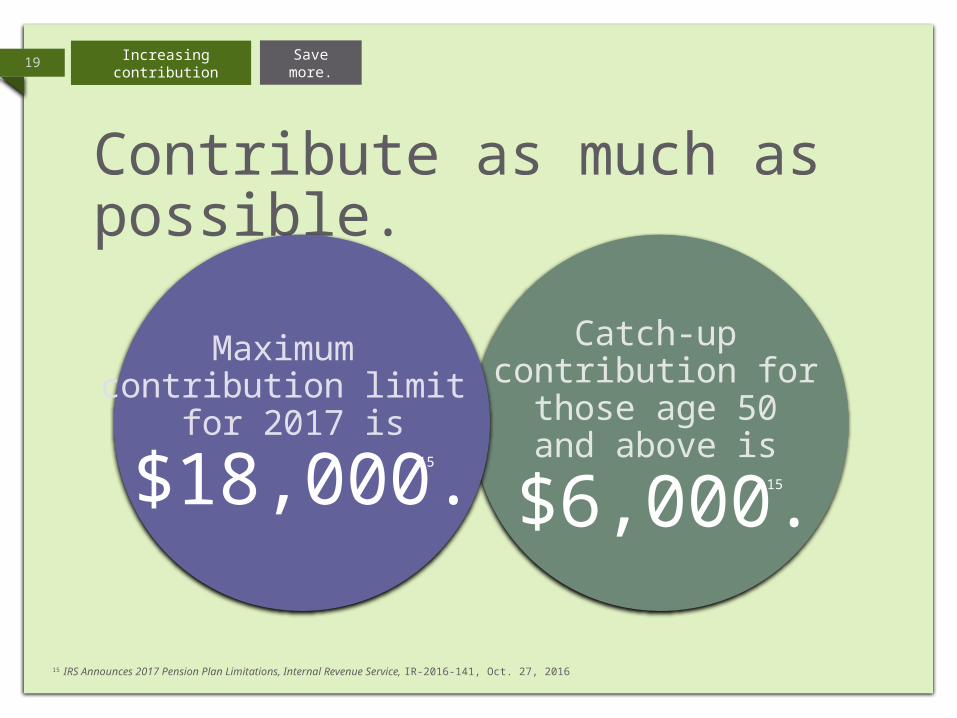

Contribute as much as possible.

Maximum contribution limit

for 2017 is

$18,000.

Catch-up contribution for those age 50 and above is

$6,000.15

15

15 IRS Announces 2017 Pension Plan Limitations, Internal Revenue Service, IR-2016-141, Oct. 27, 2016

20

• Set aside retirement savings before paying other expenses

• Automatic deductions from your paycheck make it easy

Pay yourself first.

Save more.Increasing contribution

21

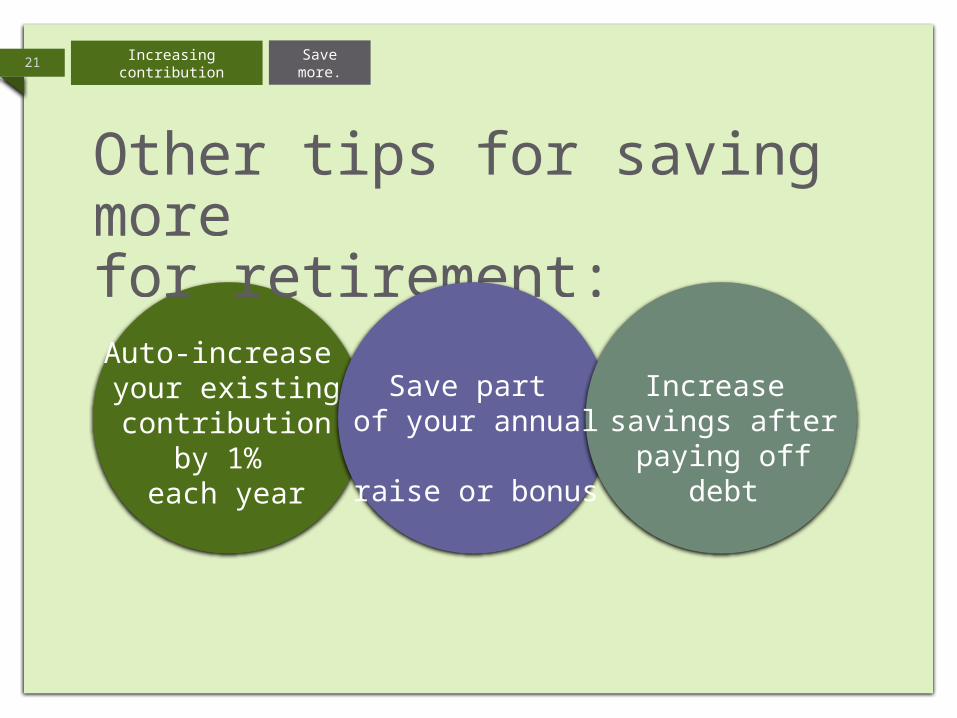

Auto-increase your existing contribution

by 1% each year

Save more.Increasing contribution

Other tips for saving more for retirement:

Save part of your annual raise or bonus

Increase savings after

paying off debt

22 Save more.Increasing contribution

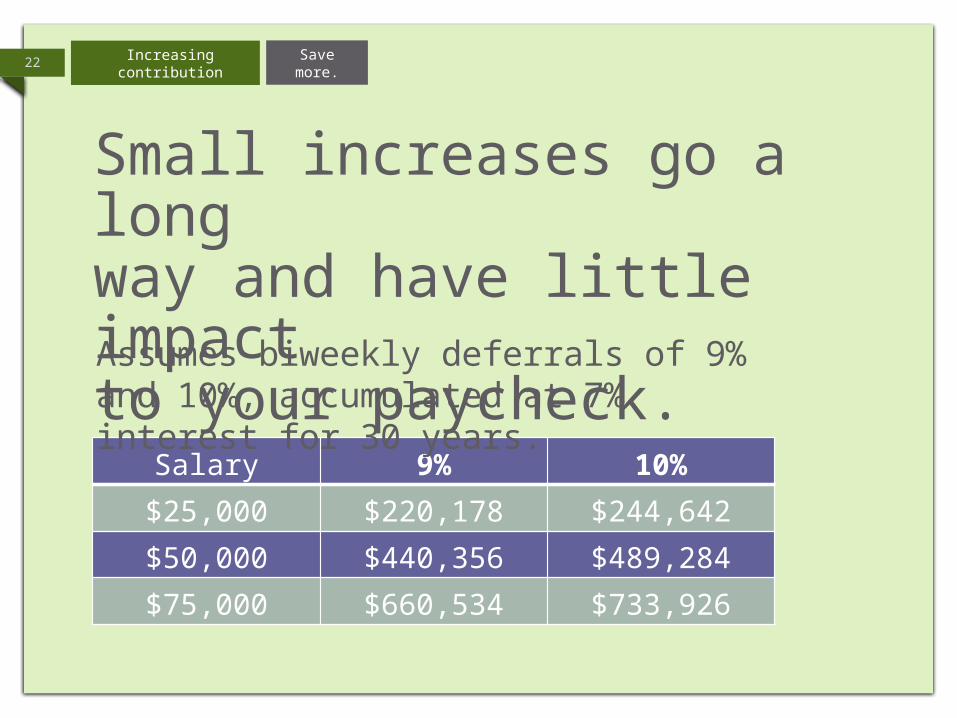

Small increases go a long way and have little impact to your paycheck.

Salary 9% 10%$25,000 $220,178 $244,642$50,000 $440,356 $489,284$75,000 $660,534 $733,926

Assumes biweekly deferrals of 9% and 10%, accumulated at 7% interest for 30 years.

23 The Learning CenterIncreasing contribution

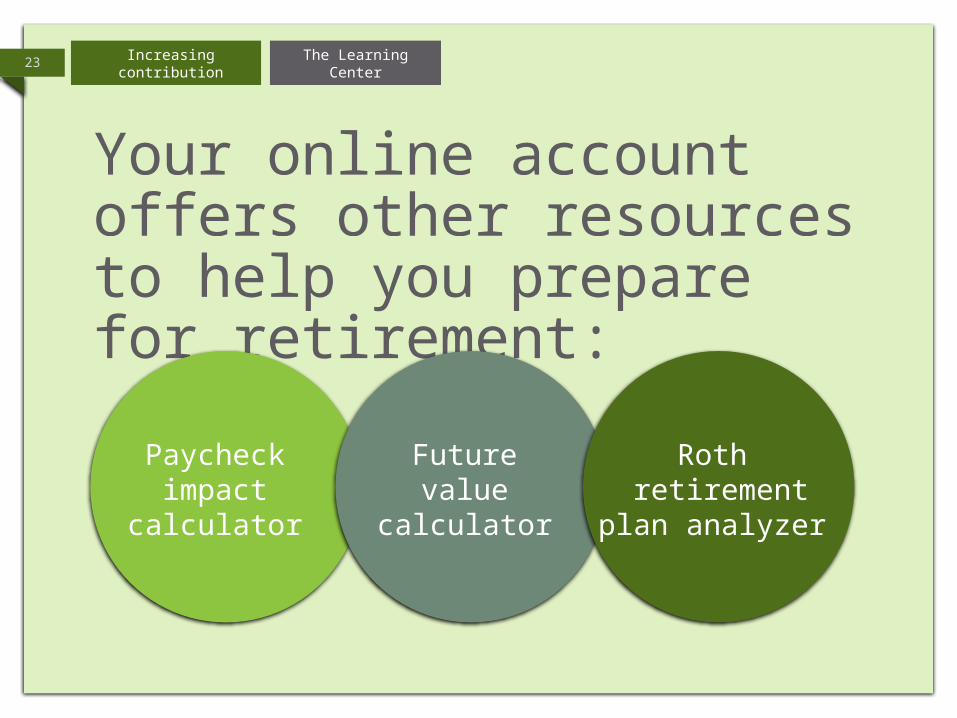

Your online account offers other resources to help you prepare for retirement:

Paycheck impact

calculator

Future value

calculator

Roth retirement plan

analyzer

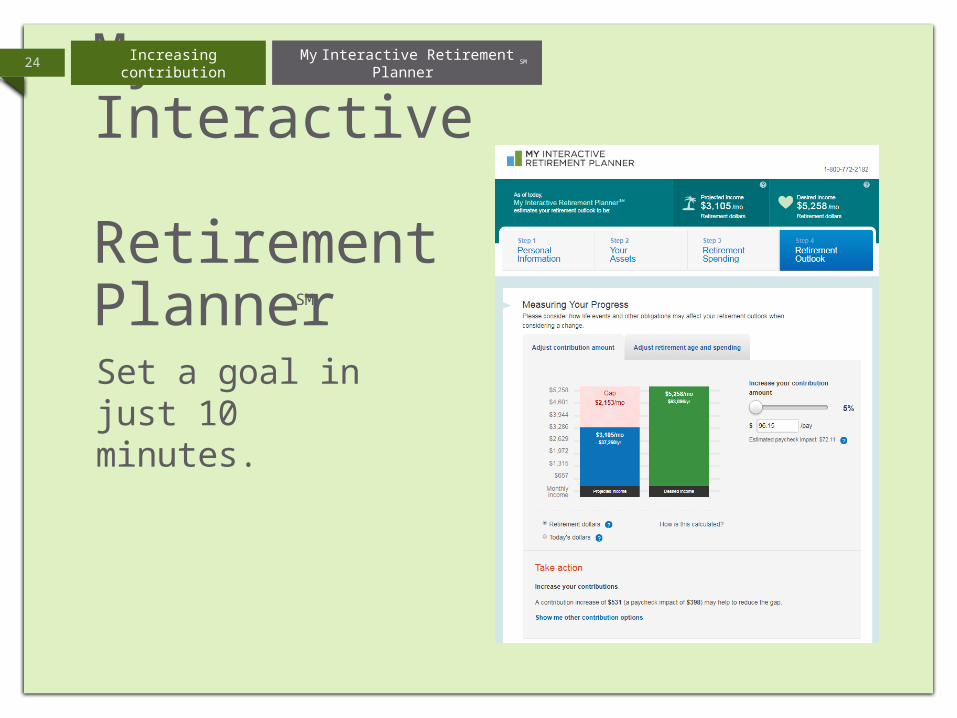

24

My Interactive Retirement PlannerSet a goal in just 10 minutes.

My Interactive Retirement Planner SMIncreasing contribution

SM

25

Points to remember

Talk to your Plan Sponsor

about making or increasing contributions to your plan.

Nationwide’s online tools and calculators

can help you see the impact of your contributions.

My Interactive Retirement Planner

can be a helpful tool in determining how much you will need in retirement.

Your company’s retirement plan

is important, and so is increasing contributions to it.

SummaryIncreasing contributions

Access your retirement account.

nationwide.com/myretirement

1-800-772-2182

Recommended