REPORT FOR ACTIVITIES OF

OHRIDSKA BANKA AD SKOPJE

FOR 2019

February 2020

Annual report for bank activites for 2019 2

1. ENVIROMENT IN 2019 AND PROJECTIONS FOR 2020

MACROECONOMIC MOVEMENTS

The global economy continued to grow in 2019, but at a slower pace, reflecting trends in both developed and

emerging economies. In line with weaker performances and expectations, the latest IMF projections (Oct 2019) on

world economic growth are revised from 3,6 % in 2018 to 3 % in 2019 (the lowest rate since the global economic

downturn) and then moderately accelerating to 3,4 % in 2020. Short to medium term, there are significant downward

risks to global economic growth, with some more favorable movements by the end of 2019, primarily due to a partial

agreement related to the US - China trade conflict, which remains a risk to global economic growth, and reduced

uncertainty over Brexit after the UK election, though the focus is now shifting to how to regulate future trade relations

with the EU within the agreed deadline. On the other hand, geopolitical risks are more emphasized, especially given

the developments in Iran. Other risks to the global economy include the possible slowdown in the growth of

systemically significant economies, the risks associated with the financial vulnerability of certain emerging economies,

and global disinflationary tendencies.

When it comes to N.Macedonia, as a small and open economy that is significantly related to the EU, given that 80 %

of exports are in the EU, 11 % in Western Balkan (countries which are also significantly related to the EU, and

together they account for about 91 % of the value of exports which is directly or indirectly related to the EU), the

perceptions of institutions on the EU economic movements, are more relevant and these perceptions are somewhat

more optimistic. The ECB in December performed a minimal upward revision of the euro area growth projections for

2019 (from 1,1 % in September to 1,2 %), mainly as a result of expectations for higher growth in gross investment than

previously estimated. In conditions of downward correction of foreign demand, growth in 2020 is minimally revised

down from 1,2% in September to 1,1 %, while there is no change in the projection for 2021 compared to September

(1,4 %,) and the same rate is expected for 2022.

In terms of the domestic economy, it is expected that real growth of 3,5 % in 2019, supported mainly by exports, will

be expected, with further growth in the activity of the new export-oriented capacities as well as in some of the

traditional export sectors , also growth in domestic demand, supported by higher investment activity, estimates related

to public infrastructure projects and higher private consumption estimates, supported by growth in all components of

disposable income.

Within the October macroeconomic scenario by the NBRNM for the current and following years, 2010-2022, the assessments for moderate acceleration of the economic growth include solid credit growth, absence of significant price pressures and balance of payments position providing growth of the Central Bank reserves. It is expected that economic growth will accelerate to 3,8 % in 2020 and 4 % in 2021, and the key factors for the growth, as in the previous projections cycle, are the estimates for further solid inflow of new FDI in the tradable sector, public investment in road infrastructure, export-oriented capacity activities, as well as growth in disposable income and stable household expectations.

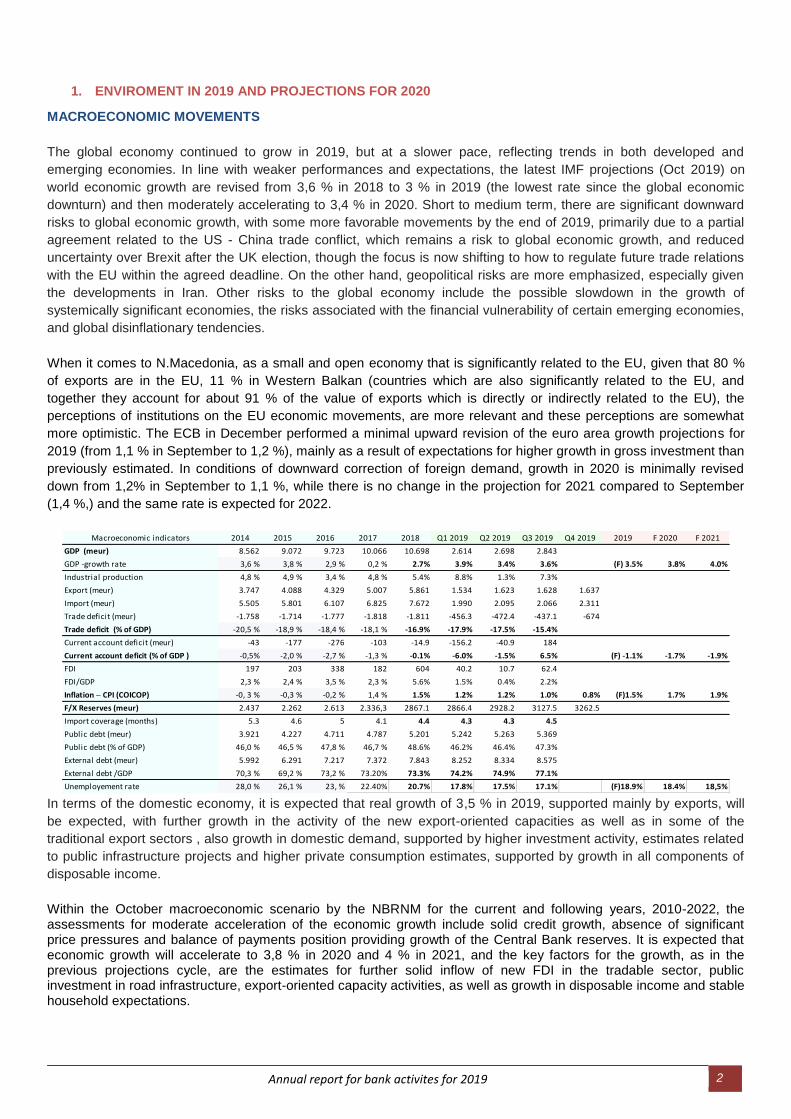

Macroeconomic indicators 2014 2015 2016 2017 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 2019 F 2020 F 2021

GDP (meur) 8.562 9.072 9.723 10.066 10.698 2.614 2.698 2.843

GDP -growth rate 3,6 % 3,8 % 2,9 % 0,2 % 2.7% 3.9% 3.4% 3.6% (F) 3.5% 3.8% 4.0%

Industrial production 4,8 % 4,9 % 3,4 % 4,8 % 5.4% 8.8% 1.3% 7.3%

Export (meur) 3.747 4.088 4.329 5.007 5.861 1.534 1.623 1.628 1.637

Import (meur) 5.505 5.801 6.107 6.825 7.672 1.990 2.095 2.066 2.311

Trade deficit (meur) -1.758 -1.714 -1.777 -1.818 -1.811 -456.3 -472.4 -437.1 -674

Trade deficit (% of GDP) -20,5 % -18,9 % -18,4 % -18,1 % -16.9% -17.9% -17.5% -15.4%

Current account deficit (meur) -43 -177 -276 -103 -14.9 -156.2 -40.9 184

Current account deficit (% of GDP ) -0,5% -2,0 % -2,7 % -1,3 % -0.1% -6.0% -1.5% 6.5% (F) -1.1% -1.7% -1.9%

FDI 197 203 338 182 604 40.2 10.7 62.4

FDI/GDP 2,3 % 2,4 % 3,5 % 2,3 % 5.6% 1.5% 0.4% 2.2%

Inflation – CPI (COICOP) -0, 3 % -0,3 % -0,2 % 1,4 % 1.5% 1.2% 1.2% 1.0% 0.8% (F)1.5% 1.7% 1.9%

F/X Reserves (meur) 2.437 2.262 2.613 2.336,3 2867.1 2866.4 2928.2 3127.5 3262.5

Import coverage (months) 5.3 4.6 5 4.1 4.4 4.3 4.3 4.5

Public debt (meur) 3.921 4.227 4.711 4.787 5.201 5.242 5.263 5.369

Public debt (% of GDP) 46,0 % 46,5 % 47,8 % 46,7 % 48.6% 46.2% 46.4% 47.3%

External debt (meur) 5.992 6.291 7.217 7.372 7.843 8.252 8.334 8.575

External debt /GDP 70,3 % 69,2 % 73,2 % 73.20% 73.3% 74.2% 74.9% 77.1%

Unemployement rate 28,0 % 26,1 % 23, % 22.40% 20.7% 17.8% 17.5% 17.1% (F)18.9% 18.4% 18,5%

Annual report for bank activites for 2019 3

In terms of the individual component contributions, within the October projection, it is expected that the growth will

result from investments and exports. It is expected that the favorable economic environment will stimulate further

growth of private consumption, wages and employment increase in the private sector. In addition to this the credit

activity of the banks is expected to have an additional positive impact. The growth of the components of the domestic

demand and exports will also lead to higher imports, but it is estimated that the increase in imports will be moderate

and will not disturb the external balance. In the longer term, by 2022, it is expected that the Macedonian economy will

continue to grow at a rate of about 4 %.

The banking sector is considered to be an important factor and support for the realization of economic growth. The

credit market has noticed increased lending activity in 2019 with growth of about 7 % (with isolated effect from

regulatory changes) and is expected to maintain solid growth rates in the following three years (2020 -2022) of about

8%. The estimations for the credit growth dynamics are based on the assumptions for stable growth of the deposit

base and favorable capital and liquidity position of the banks. When it comes to 2020 and the following two years 2021

and 2022, given the growth rates of the economy and further retention of the relatively high propensity to save in

banks, annual deposits growth is expected on average of 8,5 %.

In summary, the current macroeconomic trends and projections point to stable, safe and solid foundations of the

domestic economy, with potential for solid growth, supported by the lending activity of the banks, in absence of

inflationary pressures and maintaining favorable external position, providing a stable domestic environment, for foreign

investment, strengthening of the public infrastructure cycle, as well as growth of the foreign demand. The contingent

risks are also taken into account, the assumptions and projections are being monitored accordingly. Moreover the

monetary and credit policy instruments are also available in case of necessity.

GDP and Inflation

GDP ‒ In the third quarter of 2019, the domestic economy

registered a solid rate of real economic growth of 3,6 % on

annual basis, which is higher compared to the growth of 3,1%

in the second quarter. Positive growth rates were registered in

all sectors, with industry having the highest individual

contribution as a result of favorable performance in the energy

sector. Structural analysis of the components of GDP in terms

of demand shows that, as in the previous quarter, domestic

demand has had its greatest impact on growth, mainly driven

by gross investment and private consumption, while public

consumption had a less positive contribution. In terms of

developements in the fourth quarter, expectations are

positive. Further growth in personal and investment

consumption is indicated. This growth is expected to be

supported by the banks' lending activity, which continues to

grow during 2019. According to the NBRNM projection, by

2020 the economy is expected to grow by 3,8 %, while by

2021 it is expected to grow by 4 %. The relevant international

institutions issued similar projections: International Monetary

Fund (IMF) +3,1 % for 2020, World Bank with +3,1 % for

2020.

Inflation – In 2019, the annual inflation rate is 0,8 %, mainly

driven by the growth of the food component, and to a lesser

extent by the positive contribution of core inflation. The absence of significant price pressures had a positive impact on

the macroeconomic environment, which in 2019 is assessed as favorable and stable.

Annual report for bank activites for 2019 4

In terms of expectations for the inflation rate in the upcoming period, according to the National Bank Survey, economic

analysts expect that the inflation rate in 2020 and 2021 will be 1,7 % and 1,9 %, respectively. Such expectations are

similar to the projection of the National Bank as well as the expectations of relevant international institutions.

Gross f/x reserves – As of the fourth quarter of 2019, the f/x

reserves amounted to EUR 3.262 million and increased by EUR 396

million or 12,1 % on annual basis. Analyzed by the types of financial

instruments, most of the f/x reserves are placed in securities (77,2

%) followed by currencies and deposits (13,25 %) and monetary

gold (9,25 %). Foreign exchange reserves are maintained at the

appropriate level to cope with unpredictable outflows and to maintain

monetary and price stability by maintaining a stable exchange rate of

61,5 - the basic pillar of the monetary stability.

External Trade – the total value of foreign trade in 2019

amounted to EUR 14,887 million and it increased by EUR 1,354

million or 10% growth compared to 2018. Total value of the

export of goods from the Republic of Northern Macedonia in the

period January - December 2019 was 6.424 million euros,

increasing by 9.6% compared to the same period last year. Value

of imported goods in the period January - December 2019

amounted to EUR 8,463 million, which is 10.3% more than the

same period last year.

Trade deficit in the period January - December 201, amounted to

EUR 2,039 million, while Import – export ratio in the period

January - December 2019, amounted to 75.9%. In the period

January - December 2019, according to the total volume of

foreign trade, the Republic of Northern Macedonia traded mostly

with Germany, Great Britain, Greece, Serbia and Italy..

FINANCIAL SECTOR

Banking sector

Total assets in the banking sector at the end of the third

quarter of 2019 reached a level of EUR 8.595 million

compared to last year which is increase of EUR 725

million or 10,1 %. Ohridska Banka AD Skopje is the fifth

largest bank in the banking sector of the Republic of North

Macedonia, with a market share of 7,8 % and, in

accordance with the NBRNM internal segregation, is in the

group of large banks.

Annual report for bank activites for 2019 5

Total loans

In the third quarter of the year, lending activity continued to

grow, with total loans at the banking sector up 5,7 % anual

basis. The growth of lending activity was followed by the

households sector with 9,7 % growth as well as the support

to the corporate sector, which increased by 2,1 % compared

to the third quarter of 2018.

National Bank Credit Survey indicates further net loose of

total loan conditions with similar dynamics as in the previous

survey.

In the Households sector, oposed to the previous survey,

there is a net decrease in total demand due to the greater decrease in demand for all types of loans. Ohridska banka

grew by 4,1 % in the same period, with market share in total loans in banking sector of 9,2 %.

Total deposits

Total deposits at the banking sector in the third quarter of

2019 increased by 9,5 % compared to the same period of the

previous year.

The growth of deposits derives from the deposits of both

segments with a more pronounced increase in corporate

deposits.

Compared to segments, corporate deposits increased by

10,1%, while deposits of individuals increased by 9,1 %.

Deposits of Ohridska Banka AD Skopje in the same period

grew by 10,2 %, which is slightly higher than the growth of

the banking sector, retaining its market share of 6,9 %.

2. FINANCIAL PERFORMANCE OF THE BANK

The balance sheet of the Bank at the end of 2019 amounts 42.334 million denars, and compared to the end of 2018,

has increased for 2.775 million denars or 7.0 %, as a result of the increase in the total deposits, credit lines and

undistributed profit.

Table: Comparative Balance Sheet

balance sheet

in mmkd diff %

Cash and cash eqivalents 8.789 11.328 2.539 28,9%

Securities 1.266 1.189 -78 -6,2%

Loans and receivables from banks 0 0 0 -44,9%

Loans and receivables from clients 28.556 28.875 319 1,1%

gross loans 30.456 30.93 474 1,6%

impairment of value 1.899 2.054 155 8,2%

Fixed assets and other 946 942 -4 -0,5%

Total assets 39.558 42.334 2.775 7,0%

Bank deposits 682 1.332 650 95,3%

Deposits from clients 29.149 29.936 787 2,7%

short term 19.445 20.143 698 3,6%

long term 9.704 9.793 89 0,9%

Borrow ings 3.238 4.027 789 24,4%

Subordinated debt 1.803 1.799 -4 -0,2%

Other liabilities 395 710 315 79,9%

Capital and reserves 4.291 4.53 239 5,6%

Total liabilities, capital and reserves 39.559 42.334 2.775 7,0%

Dec-18 Dec-19Dec 19 / Dec 18

Annual report for bank activites for 2019 6

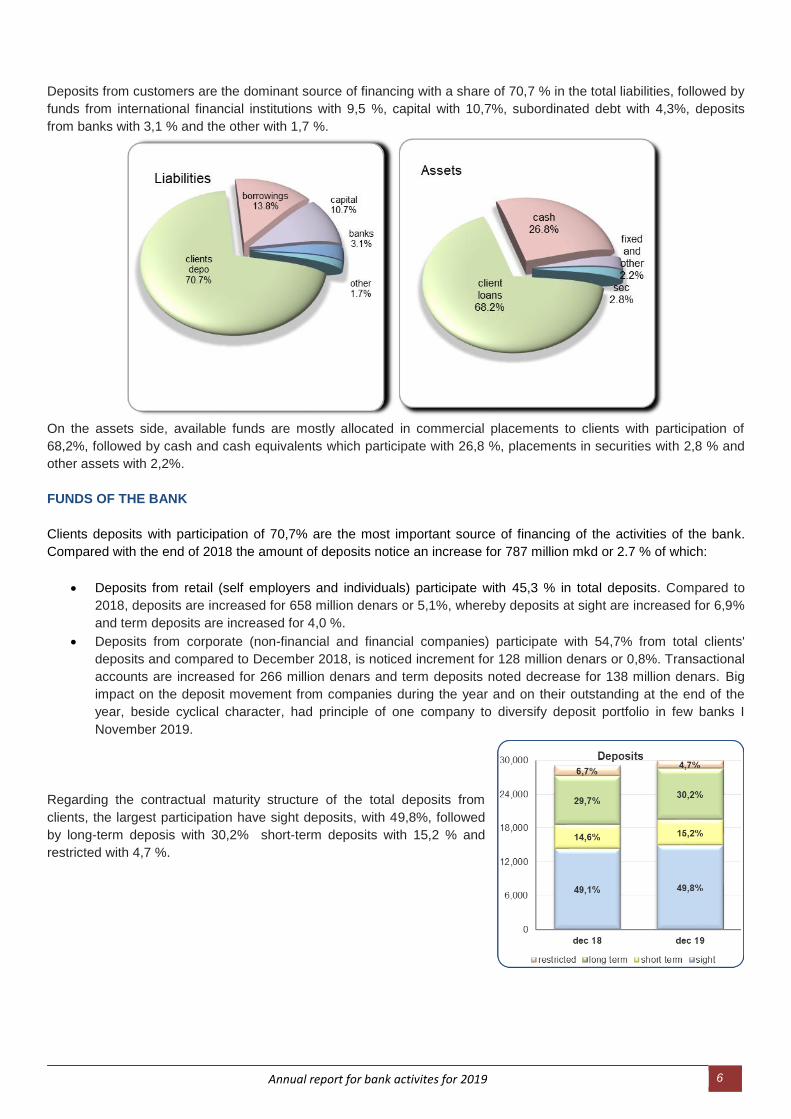

Deposits from customers are the dominant source of financing with a share of 70,7 % in the total liabilities, followed by

funds from international financial institutions with 9,5 %, capital with 10,7%, subordinated debt with 4,3%, deposits

from banks with 3,1 % and the other with 1,7 %.

On the assets side, available funds are mostly allocated in commercial placements to clients with participation of

68,2%, followed by cash and cash equivalents which participate with 26,8 %, placements in securities with 2,8 % and

other assets with 2,2%.

FUNDS OF THE BANK

Clients deposits with participation of 70,7% are the most important source of financing of the activities of the bank.

Compared with the end of 2018 the amount of deposits notice an increase for 787 million mkd or 2.7 % of which:

Deposits from retail (self employers and individuals) participate with 45,3 % in total deposits. Compared to

2018, deposits are increased for 658 million denars or 5,1%, whereby deposits at sight are increased for 6,9%

and term deposits are increased for 4,0 %.

Deposits from corporate (non-financial and financial companies) participate with 54,7% from total clients'

deposits and compared to December 2018, is noticed increment for 128 million denars or 0,8%. Transactional

accounts are increased for 266 million denars and term deposits noted decrease for 138 million denars. Big

impact on the deposit movement from companies during the year and on their outstanding at the end of the

year, beside cyclical character, had principle of one company to diversify deposit portfolio in few banks I

November 2019.

Regarding the contractual maturity structure of the total deposits from

clients, the largest participation have sight deposits, with 49,8%, followed

by long-term deposis with 30,2% short-term deposits with 15,2 % and

restricted with 4,7 %.

Annual report for bank activites for 2019 7

38,5 % 37,2 %

53,2 % 54,5 %

8,3 % 8,3 %

0

6.000

12.000

18.000

24.000

30.000

2018 2019

f/x EUR clause MKD

Regarding the currency structure, denar deposits at the end of 2019

participated with 58,5%, followed by deposits in eur with 33,7%, deposits

in USD with 4,8%, deposits in other currencies with 2,7% and denar

deposits with euro-clause with 0,3%.

Borrowings from International Financial Institutions account for 9,5% of

total liabilities, which include credit lines from EIB, EBRD, Bank for

development of N.Macedonia, GGF, EFSE, compared to December 2018

are increased for 24,4%. The increase is due to newly withdrawn funds

from EFSE and EBRD Credit Lines.

Deposits from banks are increased by 650 million denars or 95,3 %

compared to December 2018 as a result to the short-term deposits from Steiermärkische Bank und Sparkassen AG.

Shareholders equity and reserves of the bank are in amount of 4.530 mmkd and notice increase for 5,6 % compared

with previous year, mainly due to profit allocation from previous year in undistributed profit and reserves, which is in

line with the Bank’s plan for strengthening the capital base and increase of the commercial activities of the Bank.

ASSETS

Total gross loans to customers at the end of 2019 amounts 30.930 mmkd, of which 53,6 % are loans to companies,

and 46,4% loans to individuals. Annually, total loans are increased for 474 mmkd or 1,6 % where:

The loans to companies noted decrease by 1.136 million denars compared to December 2018, beside higher

production, The realized decrease of outstanding is result of several reasons: premature reimbursments due

to higher liquidity of good companies, exit strategies from some companies and refinancing by other banks

under more favourable terms even for higher risk profile companies.

Loans to individuals noted continuously stable growth trend and in 2019 noted increment by 1.610 million

denars, with the most significant contribution of two types of loans: consumer and housing loans.

In relation to maturity structure, 71,8% from total loans are long

term, short term loans participate with 22,1 %, and doubtful are

6,1%.

In relation to currency structure, the denar loans with fx clause

participate with 54,5 %, loans in denars participate with 37,2 %,

while loans in EUR participate with 8,3 %.

53,3 %58,5 %

34,7 %33,7 %

7,8 %4,8 %1,5 % 0,3 %

2,6 % 2,7 %

0

6.000

12.000

18.000

24.000

30.000

Dec 18 Dec 19

Deposits

MKD EUR USD EUR clause Other

Annual report for bank activites for 2019 8

The level and structure of the liquid assets is maintained in accordance with the liquidity needs of the Bank and the

clients with respect to the regulation regarding the currency compliance of the assets and liabilities, the needs for

fullfilling the average level of obligatory reserve and maintaining the profitable aspect.

Cash and cash equivalents on 31 December 2019 amount 11.328 million denars, compared to 2018 are increased by

28,9 % as a result of the overnight deposit at NBRSM. Treasury bills at the end of 2019 amount 1.595 million denars.

Investments in securities are 1.189 million denars, from which the Bank placed 991.6 million denars in treasury bills,

168.9 million denars in state bonds and 28 million denars in equity investments.

INCOME STATEMENT

Operating profit of the Bank for 2019 before taxes is 263,3 mmkd. This result is highly impacted by increased

impairment of financial assets and decrease of net interest margin, while net fees and net fx income evidenced

increase compared to previous year.

Net interest income for the current year is 1.109 mmkd and compared to previous year is decreased by 61,8

mmkd or 5,3%, on which impact had the increased volume of the deposits and credit lines and faster decrease

of active interest rate on securities and loans. The decrease on active interest rate was not followed with the

same dynamic on the local deposit market and its interest rates.

The net fees and commissions income in amount of 334,2 mmkd is increased for 18 mmkd or 5,7% compared

to the previous year. Fees and commissions income recorded a stronger growth by 39,2 mmkd with positive

impact from the payment operations fees, fees from credit products, issued guarantees, card operations,

newly introduced products such as packages and electronic and mobile banking, while the increase in the

expenses for commissions and fees is 21,2 mmkd, with influence of the activities related to the card

operations and cash management.

Net f/x income is 151,4 mmkd and compared to previous year is increased by 15,3 mmkd or 11,3%, due to the

effects of the increased volume of activities and transactions on the foreign exchange market, as well as the

positive impact of several transactions with big clients and intercurrency transactions for optimal utilization of

the currency structure for the current liquidity.

Other operational income is 130,3 mmkd and compared to 2018 is decreased by 17,4 million denars, or 11,8%

as a result of reduced revenues from previously written off principal and interest receivables. Also, an

additional effect on the amount of other incomes from last year had the realized capital gain from sale of

foreclosed property.

Operational expenses are 776,3 mmkd and compared to 2018 are increased for 14,4 mmkd or 1,9 %.

The impairment of the financial assets on a net basis at the end of 2019 is 685.3 mmkd and compared to 2018

is increased for 303,9 million denars.

Diff %

NBI 1.770,8 1,724,9 -45,9 -2,6%

NII 1.170,9 1.109,0 -61,8 -5,3%

- income 1.531,2 1.522,3 -8,9 -0,6%

- expenses 360,3 413,3 52,9 14,7%

Net fee and commission 316,2 334,2 18,0 5,7%

- Income 494,2 533,4 39,2 7,9%

- expenses 178,0 199,2 21,2 11,9%

Net FX 136,0 151,4 15,3 11,3%

Other 147,7 130,3 -17,4 -11,8%

OPEX 761,9 776,3 14,4 1,9%

- staff 333,6 360,6 27,0 8,1%

- other 428,4 415,7 -12,7 -3,0%

GOI 1.008,8 948,6 -60,2 -6,0%

provisions 381,5 685,3 303,9 79,7%

Gross income before taxation 627,4 263,3 -364,1 -58,0%

in mmkd 2018 20192019 / 2018

Annual report for bank activites for 2019 9

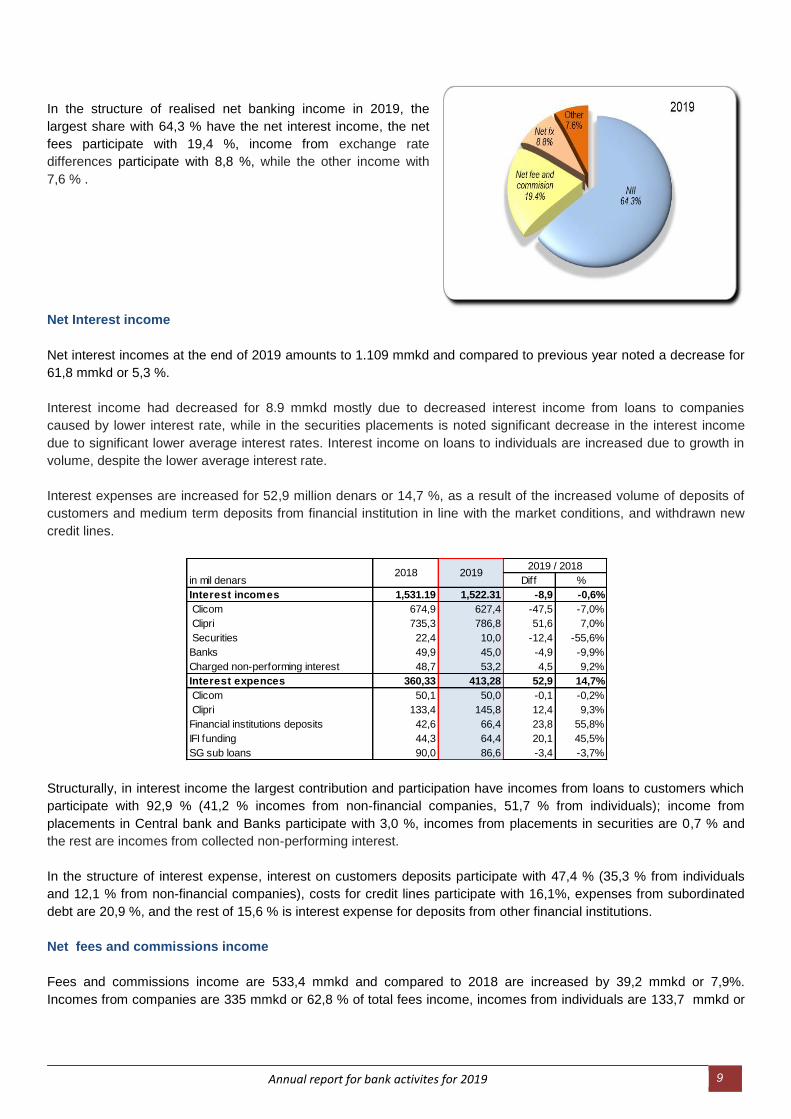

In the structure of realised net banking income in 2019, the

largest share with 64,3 % have the net interest income, the net

fees participate with 19,4 %, income from exchange rate

differences participate with 8,8 %, while the other income with

7,6 % .

Net Interest income

Net interest incomes at the end of 2019 amounts to 1.109 mmkd and compared to previous year noted a decrease for

61,8 mmkd or 5,3 %.

Interest income had decreased for 8.9 mmkd mostly due to decreased interest income from loans to companies

caused by lower interest rate, while in the securities placements is noted significant decrease in the interest income

due to significant lower average interest rates. Interest income on loans to individuals are increased due to growth in

volume, despite the lower average interest rate.

Interest expenses are increased for 52,9 million denars or 14,7 %, as a result of the increased volume of deposits of

customers and medium term deposits from financial institution in line with the market conditions, and withdrawn new

credit lines.

Structurally, in interest income the largest contribution and participation have incomes from loans to customers which

participate with 92,9 % (41,2 % incomes from non-financial companies, 51,7 % from individuals); income from

placements in Central bank and Banks participate with 3,0 %, incomes from placements in securities are 0,7 % and

the rest are incomes from collected non-performing interest.

In the structure of interest expense, interest on customers deposits participate with 47,4 % (35,3 % from individuals

and 12,1 % from non-financial companies), costs for credit lines participate with 16,1%, expenses from subordinated

debt are 20,9 %, and the rest of 15,6 % is interest expense for deposits from other financial institutions.

Net fees and commissions income

Fees and commissions income are 533,4 mmkd and compared to 2018 are increased by 39,2 mmkd or 7,9%.

Incomes from companies are 335 mmkd or 62,8 % of total fees income, incomes from individuals are 133,7 mmkd or

in mil denars Diff %

Interest incomes 1,531.19 1,522.31 -8,9 -0,6%

Clicom 674,9 627,4 -47,5 -7,0%

Clipri 735,3 786,8 51,6 7,0%

Securities 22,4 10,0 -12,4 -55,6%

Banks 49,9 45,0 -4,9 -9,9%

Charged non-performing interest 48,7 53,2 4,5 9,2%

Interest expences 360,33 413,28 52,9 14,7%

Clicom 50,1 50,0 -0,1 -0,2%

Clipri 133,4 145,8 12,4 9,3%

Financial institutions deposits 42,6 66,4 23,8 55,8%

IFI funding 44,3 64,4 20,1 45,5%

SG sub loans 90,0 86,6 -3,4 -3,7%

2018 20192019 / 2018

Annual report for bank activites for 2019 10

25,1 % from total incomes, while the fees from financial institutions are 64,7 mmkd or 12,1 % from total fees and

commission incomes.

Fees and commissions income recorded a strong growth due to increased incomes from fees in payment operations,

from credit products, issued guarantees, card operations, newly introduced products such as packages and electronic

and mobile banking.

Fees and commissions expenses are 199,2 mmkd and compared to 2018 are higher for 21,2 mmkd or 11,9 %, due to

the increased volume of activities of the Bank for cards, increased number of users of mass mailing services,

increased cash fee management activities due to change in NBRSM for cash transfer, increased fees for new credit

lines from international financial institutions and prepayment of one credit line due to change of ownership.

Operational expenses

Operational expenses in 2019 are 776,3 mmkd and compared to previous year, are increased by 14,4 mmkd or 1,9 %,

in terms of an increased volume of activity of the Bank.

Higher operational costs are noted in staff costs, expenses related to increased bank activities: card operation, cash

transport costs, hardware costs, deposit insurance premium, postal costs, litigation costs, while all other costs noted a

decrease.

in mmkd diff %

Fees income 494,2 533,4 39,2 7,9%

Clicom 308,7 335,0 26,3 8,5%

Clipri 116,4 133,7 17,3 14,9%

Financial institutions 69,2 64,7 -4,5 -6,4%

Fees expenses 178,0 199,2 21,2 11,9%

Cards and POS 97,8 118,4 20,6 21,1%

Domestic payment 30,3 31,5 1,2 4,0%

Payments abroad 41,2 40,6 -0,6 -1,4%

Fin. Inst. Services 5,9 6,3 0,4 6,9%

Other 2,8 2,4 -0,4 -15,7%

Net fees and commission 316,2 334,2 18,0 5,7%

2018 20192019 / 2018

OPEX in mmkd

2018 2019 diff %

Staff 333,6 360,6 27,0 8,1%

Depreciation 94,8 89,0 -5,8 -6,1%

softver 34,4 25,1 -9,4 -27,2%

fix assets and equipment 60,4 63,9 3,5 5,9%

Depo insurance 30,2 32,9 2,7 8,9%

Property insurance and employees 8,7 7,3 -1,4 -15,9%

Materials and services 208,4 205,6 -2,7 -1,3%

Administrative and marketing costs 26,3 24,7 -1,6 -6,0%

Other tax and contributions 8,2 9,8 1,6 19,3%

Rentals 33,6 33,9 0,4 1,1%

Litigation 4,2 8,4 4,1 96,8%

Net provisions 9,4 0,0 -9,4 -100,0%

Other 4,5 4,0 -0,5 -11,4%

Total OPEX 761,9 776,3 14,4 1,9%

2019/2018

Annual report for bank activites for 2019 11

3. BANK ACTIVITIES BY BUSINESS SEGMENTS

CORPORATE CLIENTS DIVISIONS

Department for Corporate clients and SME/s

Focusing on high quality corporate core of the domestic market, with continuous investment in development and

adjustment of the services and elevating the quality at its highest level, during 2019 we remain with the process of

continuous interactions with this client base through additional offers with tailor made solutions for these customers.

This year as well, we were allowed to gain the primate of a Bank of first choice for foreign investors, domestic big

corporate and domestic small businesses.

In the past year, it was felt significant pressure on the market by the competition, where at certain times and certain

competing banks were offering significantly lower prices of products and services, but also the year was characterized

by bigger risk appetite by some of other Banks. Although in some categories Bank achieved significant rise, there were

a fields on which because of these movements, Bank achieved fall in dealing with its activities.

Thanks to the quality service and building long-term stable relationships with customers, the Bank managed to achieve

growth in all segments of working with corporate customers and thereby increased its market share.

Corporate lending decreased by 6,3 % over the past year, and the deposit base decreased by 0,3 %. In the area of

foreign exchange market, the Bank continued to realize strong results, thereby these activities provided a significant

contribution to a successful working, and it is expected the growth of activities to be maintained in the upcoming years.

Client portfolio

The corporate department of the Bank even it achieved lower level of loan outstanding portfolio, the total real credit

production for 2019 was almost on similar level in 2018, which means that reduction of the outstanding loans was due

of bigger number of refinancing/s of existing credit products with loans funds provided by some of the other Banks due

of the increased risk appetite. Nevertheless, Bank managed to significantly increase the size of domestic and foreign

through the accounts in the Bank and to secure significant increase in all other parts.

Improvement of the services by using knowledge and innovation for development of new products, marginal levels and

challenge to develop franchise, improvement of the marketing and distribution channels on regional and global level,

suitable capitalization, are some of the areas in which the Bank is investing in order to accomplish the prescribed

goals.

The cooperation that the Bank has with more of 70 % of the big international companies successfully continues to be

maintained in order to increase the scope of activities and to generate greater profits. Regarding the cooperation with

international companies, the aim is to strengthen the position as Bank of first choice providing premium services and

palette of products that are not sufficiently developed or known on the Northern Macedonian financial market. Besides

the role of a trustworthy partner that supports regular business of well-known profitable companies, the Bank also

insisted in acting as a strategic partner willing to provide financial support of the expansion plans and significant

investment projects of these companies. The focus on corporate lending in the future will also remain to maintain

stable and efficient portfolio that realizes maximum profit with minimum risk.

Activities, directions and policies for meeting client’s needs and offer of new products

The driving force of the work of the Corporate Department is increase of the quality of the services and products that

are offered to the clients, adequate response to their needs as well as strengthening of the business relations

Annual report for bank activites for 2019 12

established with the large profitable companies in order to create solid grounds for cross sales between different

segments of group of products.

An attention is given on building long-term and stable relationships with the existing clients as well gaining over new

clients, corporate and individuals from specific target groups. Main goal and focus of the Bank is to offer quality

service. Along with it, the accent is stressed on ‘’cross selling”, i.e. increase of the number of products that are used by

single client. According to this, exists successful synergy between the corporate department and Individual clients

department and will continue to intensify, whereby the client’s satisfaction will increase and the Bank shall have

benefit.

In the previous year the Corporate continued with strengthening of the basis of its business operations and processes

through implementation of new products and services. As a result of the monitoring of the market changes, in 2019

new loan products were launched and the range of current loan products were upgraded and diversified with new

features and functionalities that responds to the client’s requests.

BIC and International Companies

The credit portfolio

The credit portfolio of the big and international companies in 2019 amounts 5.867 million denars and has decreased

21 % compared to 2018 as a result of 2 main factors: exit scenario in case of several domestic companies and sale of

receivables for loans in case of several other companies.

The high level of quality of the credit portfolio was maintained by building long-term and stable relations with clients,

prudent management of the credit risk by frequent estimations as well as by efficiently organized payment function.

The appropriate approach towards every client and adjusted offer followed by detailed financial analysis and efficient

approval procedure enabled placements of new loans and taking over new prestige companies.

Besides the role of a partner of trust that supports the regular business of well-known profitable companies, The

Department for large and international clients pursue to act as strategic partner willing to provide financial support of

the expansion plans and significant investment projects of these companies. For realization of business ideas, the

investment and long-term ventures in profitable project of the clients, the Bank offered broad and diversified range of

corporate loans covered by own sources, as well as from different credit lines.

The deposit portfolio

Total deposit base marks a fall of 0,3% in comparison with 2018. The attraction of deposits is as result of the

established image of the Bank of trust and the commitment to building long-term relations with the clients. These

deposits participate with 51%, in the base of deposits, which leads to conclusion that the deposit of the Big and

International companies remains a significant driving force of the bank’s deposit portfolio.

Trading with foreign currency

The Trading and Capital Markets Department (CMT Department) covers all activities on the domestic and international

financial markets that the Bank provides for its’ clients or undertakes for purpose of operational liquidity and balance

sheet management. The Capital Markets and Trading Department is eligible for conducting these activities based on

the obtained licenses issued by the National Bank of Republic of North Macedonia in line with the Banking Law.

The uncollateralized money market turnover shows significant decrease compared to 2018 for 82 %, the repo market

data show that there has not been a single transaction transacted in this market compared to the previous year where

the turnover stands at 4 billion Macedonian denars. The OTC market for fixed income securities has decreased for 52

% in 2019 compared to 2018. Therefore the Capital markets and Trading Department over the 2019 has been

functioning in very illiquid market with decreasing turnover.

Annual report for bank activites for 2019 13

The Bank is a market-maker based on the Agreement for FX market support of the National Bank of Republic of North

Macedonia and is one of the five banks that undertake such privilege and responsibility to actively participate with the

National Bank in the implementation of the monetary policy in the country. This systemic importance has been

confirmed with the significant FX clients’ market share of the Bank that has been confirmed with having the second

place in the banking sector measured by the FX profit. The FX profit for 2019 amounts to 151,4 million Macedonian

denars, showing an increase of 11.28 % compared to the previous year. The FX profit increase is based on the

increased efficiency of the Capital Markets and Trading Department processes and efficient and effective asset and

liability management of the bank.

SMALL AND MEDIUM ENTERPRISES

Bank’s activities focused towards financial support of small and medium enterprises (SME) in 2019 year, contributed

with 64,5 % participation in total portfolio. The Bank offers qualitative financial products which are specialy designed

and adjusted for this market segment such as loans for financing quick assets, investment loans, and loans for

companies for improving energy efficiency, loans for financing projects in domain of renewable sources of energy and

other suitable loans. According to increase of volume and assortment of supply, also price aspekts are noted in our

credit products, which are competitive on sector level.

For all suitable and supported creditworthyy clients, the Bank has qualitative and appropriate products, and also

continues to make efforts for supplying assets from foreign credit lines.

The main goal of SME lending policy was constant presence of the sales force on the field by intensifying the number

of visits of clients and presenting the possibilities for financing quality projects. The targets were larger SME clients

with manufacturing and trade activities, market leaders with good reputation in the business community. As a result of

these activities, the Bank gained several dozens of new SME clients with lending potentials and potential for further

growth in the payment operations and the total cooperation with the Bank.

Slower but increasing tempo of credit placement also continued in 2019. SME credit placement were increased for

0,8%, reaching 10.686,19 mmkd on gross basis.

OBSG will continue to be committed to supporting the needs of the companies for capital investment, modernization

and working capital through quality and competitive Offer of credit and service products.

Detailed and quality monitoring of the repayment of loans and intensive effort by the Bank, promotion of detailed credit

analysis in cooperation with the department for credit analysis, helped to preserve the quality of the loan portfolio.

Foreign currency loans from foreign credit lines

Ohridska Banka continuously strengthens the position on the market and the offer of products intended for lending to

the economy, supported by products from foreign credit lines.

During June the Bank has withdrawn second loan in amount of 15 mil eur, according agreement concluded with EBRD

(GEFF). The funds are used for approval of loans for highly profitable "green" technologies for the household sector.

In accordance with signed agreement with EBRD for participation in the regional program for competitiveness support

of SME, the Bank at the end of 2019 withdraw the second tranche of 5 mil eur, with repayment period of 7 years.

In December the Bank withdrew second tranche of 2 mil eur from EBRD Green for Growth Fund (GEFF) and the funds

will be further invested to support household investments in green technologies, materials and measures such as

water heaters, windows and lighting. The funds will support the improvement of energy efficiency of residential

buildings, help reduce gas collecting the “green house” effect and improve the quality of life for householders.

Annual report for bank activites for 2019 14

During the year, in order to optimize the current liquidity taking into account the cyclical movements of the major

depositors, the Bank until 4.11.2019 used short-term loans from Societe Generale.

According the agreement between Societe Generale SA Paris and Steiermarkische Bank und Sparkassen AG,

Societe Generale SA Paris (seller) transferred receivables on subordinated loans in total of 29 mil eur, and

Steiermarkische Bank und Sparkassen AG (buyer) purchased receivables on 4.11.2019, i.e. date of the change of the

ownership of Ohridska Banka AD Skopje,

RETAIL BANKING DIVISION

During 2019, Ohridska Banka continued with the growth and development in the segment of the retail clients. The

retail sector continues to focus on customer needs, attending to increase the number of its customers by improving

relationships and developing long-term customer relationships.

Credit portfolio

During 2019, it was achieved total production of loans for individuals of 8.503 credits, in total amount of 5.288 million denars, which is for 737 million denars higher production from 2018, continuing the upward trend in production in this segment.

During 2019 the following production of credit product for retail was achieved:

The growth of production in 2019 compared to previous year was achieved primarily due to large commercial activities

of the whole Department, focusing on the selling capacity of the bank to the client and the service quality.

Annual plans for increased production of credit products for retail were achieved during 2019 despite the changing and

unstable political environment that had influenced on banking activities throughout 2019.

Movements in loans to individuals are shown in the following graph:

Annual report for bank activites for 2019 15

The total number of issued and active cards also is increased compared to the previous year. The graph represents

the growth in the total number of active cards in 2019 compared to 2018.

Deposits of individuals grew for 5,19 % compared with deposits in 2019, or in absolute amounts deposits to individuals

noticed an increase to 13.545 mmkd on 31.12.2019, from 12.877 mmkd at the end of 2018. The graph shows the

growth of deposits for 2018 and year 2019. The growth is mainly due to the confidence that the clients have for the

Bank. The graph below represents the movement of deposits in the recent years in terms of maturity.

The number of active clients of the Bank has small increase during 2019. The following graph represents the total amounts and movement of the client base of individuals for the period from December 2018 to December 2019.

Annual report for bank activites for 2019 16

PRODUCT DEVELOPMENT

Enriching the product range, as well as improving and enhancement of the quality and functionalities

of existing products, is one of the major factors influencing the increase of the client satisfaction by

meeting their needs. OB constantly strives to improve its offer, and based on that new products were

introduced this year, but the existing ones were also improved, among which the most important are:

- Introduce the possibility of payment on credit card and loans liabilities through the ATM

network of the OB;

- Introducing ATM cash in functionality of two ATMs, one in Skopje and one in Ohrid;

- Expanding the contactless functionality of all Visa & Master brand cards;

- The new modernized design of My Bank mobile application, as well as additional

functionalities: push notifications, online management of debit and credit card daily limits, and

branch offices, ATMs and merchants where customers can pay on installments with the OB

credit cards introduced in 2018 for Android users, in 2019 it was also applied to iOS users.

- In 2019 was introduced also the possibility of online application for My Bank mobile

application without visiting branch office, thus giving clients the opportunity to view their

accounts and use the functionalities of the application without the possibility of making

payments. At the same time, the possibility of redistributing application codes has also been

introduced without the need to visit a bank branch office;

- Bearing in mind the interest of the clients and the excellent success of the "A ++" loan

introduced in 2018 in cooperation with the European Bank for Reconstruction and

Development, in 2019 a new Agreement has been concluded for the continuance of the

cooperation and obtaining additional funds to offer consumer loans support of energy efficient

household projects with a grant component.

During 2019, as in previous years, the focus is put on innovation, simplification and digitization of

the processes with the main aim of improving all aspects of products, services and processes that will

ultimately contribute to quality and fast service delivery to clients and meet their needs. At the same

time, market research and current changes have resulted in constant adjustments to the conditions,

as well as the organization of promotions with more competitive terms of loan products primarily with

the aim of increasing sales and acquisition of new clients.

Continued cooperation with the Ministry of Finance on the Buy a House, Buy an Apartment

project, with the Employment Agency on the self-employment project, with Western Union

International Payment Service, and with the EBRD to finance energy-efficient household projects

continues in order to maintain a wide range of products and services.

With the innovations introduced during 2019, OB realizes its commitment to set and mmaintain high

standards of the offer quality, consolidating its market position as a clients-selective bank,

recognizable for its quality and comprehensive service.

65.126

66.490

66000

66200

66400

66600

66800

67000

67200

2018 2019

Active clients

Annual report for bank activites for 2019 17

PAYMENT OPERATIONS

International payment

In the reported period, the Bank continued to perform its activities in the payment operations while

engaging in timely and effectively meeting the customer needs in order to improve the quality of the

services and the satisfaction of the customers in realizing their international payments.

In 2019 payment operations in both directions are realized at the amount of over EUR 7,80 million, i.e.

it is noticed an increment of EUR 1,57 million, compared with 2018. An increment was recorded in the

FX inflows for 776 million EUR and in the FX outflows for 794 million EUR compared to last year.

Structure and changes in fx payments in 000 eur:

In the period from January to 31 December 2019 are processed 37.423 MT 940 - Customer statement

message - Swift messages are processed at the request of the customers and depending on the

number of transactions performed on their accounts, which is decreased for 3.094 than the same

period in 2018, when that number was 40.517 MT940.

At the foregn payment instruments it is noticed:

The increase is a result of the significant continuous growth in 2019 for nostro and loro foreign

payments from legal entities, in value, as well as letter of credit, nostro, while the guarantees are

reduced in number and in amount.

12/31/2018 12/31/2019 19/18 12/31/2018 12/31/2019 19/18

Corporate 2.888.322 3.615.611 125,2 2.945.725 3.803.746 129,13

through foreign banks, remittances and

letters of credit 2.852.595 3.570.536 125,2 2.890.045 3.777.840 130,7

through domestic banks 35.727 45.075 126,2 55.680 25.906 46,5

Retail 61.299 51.786 84,5 24.984 23.938 95,8

Through foreign Banks 29.201 26.608 91,1 4.725 5.938 125,7

Through domestic Banks 3.729 3.744 100,4 0 0 0,0

Cash payments in the country 28.369 21.434 75,6 20.259 18.000 88,8

Nonresidents 34.908 47.831 137,0 49.871 23.229 46,6

Corporate 32.429 45.641 140,7 48.863 22.554 46,2

Retail 2.479 2.190 88,3 1.008 675 67,0

Exchange 141.479 142.672 100,8 13.867 13.266 95,7

Through authorized operators 108.571 116.520 107,3 0 0 0,0

Cash sales 32.908 26.152 79,5 13.867 13.266 95,7

Interbank 19.600 63.850 325,8 54.209 32.101 59,2

Total 3.145.608 3.921.750 124,7 3.088.656 3.896.280 126,1

INFLOWS OUTFLOWS

Structure and changes in fx payments in 000 euro

In 000 In 000 In 000

eur eur eur

Foreign payments 88.217 5.840.971 85.356 7.359.281 96,8 126,0

Nostro 37.544 2.894.825 34.843 3.712.586 92,8 128,2

Loro 50.673 2.946.146 50.513 3.646.695 99,7 123,8

Letter of credit 92 21.415 65 24.471 70,7 114,3

Nostro 84 20.803 54 24.189 64,3 116,3

Loro 8 612 11 282 137,5 46,1

Guaranties 182 24.103 118 14.576 64,8 60,5

Nostro 166 22.083 96 10.870 57,8 49,2

Loro 16 2.020 22 3.706 137,5 183,5

No. No. No.

2018 2019 Индекс

Annual report for bank activites for 2019 18

Domestic Payment

The scope and dynamics in internal payment and Interbank clearing for the period from January to 31

December 2019:

According to data, in 2019 are noted positive movements in domain of denar payments, in number of

transactions and in amount of transactions. The number of realized transactions increased for 1,2 %

compared to 2018, and the amount of realized transactions increased for 55,1%

From total amount of executed transactions, 45,0% are made through internal clearing, while 55,0 %

are realized through inter banking clearing. Orders relating to corporate clients participate with 86,0

%, while orders from individuals 14,0 %.

As of 31.12.2019 there are 115.775 accounts, from which 9.326 are accounts of legal entities,

106.449 are accounts of individuals.

The Market share of the Bank in denar payment in R.North Macedonia* is as it follows:

Share of OBSG in payment operations

2019 2018

Total payment transactions

Interbank payment transactions

5,33%

7,01%

Internal payment operations

22,64%

21,64%

Nr.of transactions

Interbank payment transactions

8,30%

8,57%

Internal payment operations

10,16%

9,82%

Nr. of accounts

Legal entities

5,33%

6,06%

Iindividuals

2,77%

2,88%

* The data refer to September, on the basis of the available data updated by the NBRSM

domestic payment Change Index

2018 2019 19/18 2018 2019 19/18

Internal 2.069.367 2.133.563 103,1 269.925 345.722 128,1

Interbank 2.617.662 2.609.338 99,7 440.747 756.176 171,6

sent 1.610.011 1.589.687 98,7 220.721 379.000 171,7

received 1.007.651 1.019.651 101,2 220.026 377.176 171,4

No. of transactions

amount of transactions in mil

mkd

Domestic payment change change

2018 2019 19/18 2018 2019 19/18

Corporate 4.081.025 4.078.050 99,9 694.265 1.083.410 156,1

Individuals 606.004 665.045 109,7 16.407 18.488 112,7

Number of transactionsamount of transactions in

mmkd

Annual report for bank activites for 2019 19

4. RISK MANAGEMENT

Credit risk

The total credit risk exposure of the Bank

as of 31.12.2019 is 47.148 mmkd and is

increased by 11% compared with

31.12.2018 when the total exposure of the

Bank was 42.323 mmkd.

The total provisions for credit risk as of

31.12.2019 amounts 2.209 mmkd and are

increased by 10.5% compared to the

provisions in 2018 which amounted 2.000

mmkd.

The Bank’s total exposure to the financial

sector is 8.861 mmkd. Compared to last

year, when the exposure was 4.686

mmkd there is an increase of 89 %.

The Bank’s total credit exposure to the nonfinancial sector as of 31.12.2019 is 38.287 mmkd and

compared to the end of 2018 when the exposure to the nonfinancial sector was 37.673 mmkd there is

an increase of 1,7 %. The exposure to corporate clients in 2019 is 23.293 mmkd and it is decreased

by 4 % compared to the exposure of 24.274 mmkd to corporate client in 2018. The exposure to

individual clients on 31.12.2019 is 14.993 mmkd and it is increased by 12,2 % compared to last year

when the exposure was 13.362 mmkd.

From the aspect of the participation of separate risk categories, in 2019, in the total credit risk

exposure to nonfinancial sector, A and B participate with 92,6 % compared to 2018 when their

participation was 93,1 %. The participation of risk categories V, G and D at the end of 2019 is 7,4 %

compared to last year when the participation is 6,9%.

From the total exposure to individual clients, 3% of the clients are classified in V, G and D risk

categories. The participation of the categories with lower risk A and B is 97%. At the corporate clients

10,2 % are classified in V, G and D risk categories. The participation of the categories with lower risk

A and B is 89.8 %. The top 10 largest exposures to corporate clients represent 26,8 % from the total

exposure to corporate clients.

The indicator provision opposed to the exposure to the nonfinancial sector as of 31.12.2019 is 5,8%

compared to 31.12.2018 when the participation of the provisions in the total credit risk exposure was

5,3%.

23% 24% 26% 20% 13% 11% 19%

50% 49%53%

54%57% 57% 49%

26% 27% 21% 25% 30% 32% 32%

0%

20%

40%

60%

80%

100%

Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Dec-19

Exposures per sectorsBanks

Corporate clients

Individual clients

Annual report for bank activites for 2019 20

As of 31.12.2019 the total credit risk exposure of the Bank is 47.148 mmkd. The participation of the V,

G and D risk groups in the total credit risk exposure is 6,0%, and the participation of D risk group in

the total credit risk exposure alone is 2,9%. The amount for provisions for credit risk participates with

4,7% in the total credit risk exposure. The indicator for participation of the non functional loans in the

total loans for nonfinancial sector is 6,1% as of 31.12.2019. The indicator for coverage of the total

non-functional loans with the provisions for non-functional loans (nonfinancial subjects) of the Bank on

31.12.2019 is 70 %.

Assets and Liabilities Management (АLМ)

The management with liquidity risk, currency risk and interest rate risk is a part of the whole risk

management system. The Bank has established particular policies and procedures for managing with

every structural risk, in accordance with the bank’s strategy for risk management, the local regulative

and the group guidelines. The internal documents integrate all the important components of the

management system with particular risk: organizational structure, measurement, follow-up and

reporting, information system, permanent control and stress test.

During 2019 structural risks were regularly followed through regular monthly information that informed

the bank’s bodies and this monthly information represents integrated report of liquidity risk, currency

risk and interest rates risk in the portfolio of banking activities.

Liquidity risk

In 2019, the liquidity position was maintained on optimal level which enabled performing of

operational work. During the year, the Bank serviced several big transactions from companies for

dividend payment and other commercial transactions maintaining complete compliance to regulatory

limits.

Throughout the year the amount of liquid assets enabled maintaining a level of liquidity indicators in

line with the limits defined in the Policy for liquidity risk management. The deposit concentration rate,

measured as a ratio between average deposits of the 20 largest depositors was around 33 %. The

concentration of transactional accounts was at higher level of around 37 % as a result of higher

outstanding on the clients current accounts. The Bank used efficiently the higher amount of

transactional accounts and their stable character for financing of the activities, optimizing the use of

new credit lines.

The gaps in the contractual maturity confirmed tendency of clients for holding of short tem deposits

(till 1Y) and high level of sight deposits in the first maturity block. Beside such short- term contractual

character of deposits, the expected stability of the deposit base is the main element of the positive

expected maturity structure.

The regulatory liquidity ratios up to 30 and 180 days were 1,57 and 1,33 respectively at the end of the

year. The rates are maintained above the minimum rate 1 throughout the whole year.

Banking sector Large banks Middle banks Small banks

Total credit exposure (in M MKD) 47.148 543.470 412.028 114.198 17.245

C, D, E / Total credit exposure 6,0% 4,1% 4,0% 4,6% 4,3%

E / Total credit exposure 2,9% 1,7% 1,8% 1,0% 1,9%

Provisions / total credit exposure 4,7% 3,5% 3,6% 3,0% 3,1%

Non-functional credit/ total credit

of non-financial sector6,1% 5,0% 4,7% 5,7% 4,8%

Coverage of default loans with

total provisions for default loans,

of non-financial sector

70,5% 66,9% 73,5% 49,2% 67,2%

IndicatorsOB

31.12.2019 30.9.2019

Annual report for bank activites for 2019 21

Currency Risk

Management Policy for currency risk and other internal regulations and rules governing the currency

risk relating to all activities and transactions in the balance sheet and off-balance sheet are recorded

in foreign currency and denars with FX clause and which according to the accounting rules are

evaluated/exchanged on a daily basis. Measuring and monitoring of the currency risk exposure is on

a daily basis.

The share of the foreign currency components

(including positions in denars with foreign

currency clause) in the total Balance Sheet is

49 % at the end of the year; however, the

exposure to the currency risk is at low level.

This stems from the regulation, i.e. the limit of

the open foreign currency position in relation

to own funds. The applied strategy of fixed

foreign exchange rate of the denar in relation

to the euro, is very important for very low

probability of realization of the currency risk.

Remaining currencies have relatively low shares in the balance sheet and does not represent risk.

At the end of December 2019, the Bank’s open currency position in accordance with the Decision on

the methodology on currency risk management was long and represented 21,6 % of the Own funds.

On daily basis, the Bank follows the open currency position and the limit compliance. During 2019,

Open currency position was in line with regular limits. Daily variations of position are as part of regular

transactions performed on initiative of client such as purchase of their fx inflow or deposit or

placement in loans with fx quality.

Risk of changes in interest rate in the portfolio of the banking activities

Management of the risk from the change of interest rates in the banking book is included in the overall

risk management system of the bank. The Bank has established Policy for management risk from

change of interest rates in portfolio of banking activities.

The Bank follows the ratio between the total weighted value of the portfolio of banking activities and

the amount of Bank's Own funds on monthly level. The Bank compiles a set of separate reports for

the positions in EUR, EUR clause, MKD and other currencies and separately for fixed, variable and

adjustable interest rates. The ratio is in line with regulation during whole 2019. At the end of the year

the ratio is 5,3 %. The Bank’s exposure to risk due to changes of interest rates in the portfolio of

banking activities is at acceptable level compared to the limit and lower in comparison to exposure to

other risks. This is a result of general principle of alignment of the placements to the sources

according to the interest rates.

The trend of increase of fixed rate positions and abandonment of adjustable rates will contribute to the

decrease of reputational and legal risk, but will increase the need of strengthening banks’ capacities for

management of interest rate risk.

Annual report for bank activites for 2019 22

Operational Risk and Reputation Risk

The Bank has established adequate framework for management and monitoring of the operational

risk exposure according to the nature, scope and complexity of the performed activities based on

Operational risk management policy and corresponding procedures for operational risk management

in compliance to the effective local regulation and methodology of the Group. That allows, within the

various processes in the Bank to identify risks arising from processes, their measurement, monitoring

and implementation of corrective actions in order to avoid or minimize the potential negative impact

on the financial results and capital position of the Bank.

The operational risk management structure is composed of different elements for recording,

measuring, controlling and decreasing the operational risk impact: gathering of internal loses, risk

control self assessment exercise (RCSA), key risk indicators (KRI),scenario analysis (SA),first level of

permanent control, business continuity (BCP). Operational risk management structure needs to

provide: identification of existing gaps, implementation of corrective action plans as response to the

existing gaps; corrective action plan fulfilment follow-up.

- Operational losses

The Bank declares on regular basis the events that led to operational risk losses as well booking of operational losses on accounts that are determined for that purpose (Group level and sub-group level). Collecting losses from operational risk is in compliance with the Procedure on collecting data for operational risk events and losses. In order to strengthen controls on the declared operational losses the Bank has defined thresholds (local) for reporting losses, appropriate to the size of the Bank. For declared events during the reporting period appropriate corrective measures and action plans have been taken.

- Key risk indicators

The Bank monitors on regular basis and gathers the information on the mandatory Key Risk

Indicators (KRI). KRI indicators enable monitoring on regular basis of the operational risk exposure.

Regular monitoring of trends enables to receive early warning signals for the future operational

losses. Besides the mandatory KRI, the Bank introduced local key risk indicators that are monitored

on regular basis. The local KRI monitor operational risk exposure that is typical for the banks business

environment.

- Scenario analysis

The Bank participated in implementation of scenarios characteristic for the basic activities, determined

by SG Group. Within the reporting period, the scenario analysis was conducted for one risk scenario.

For the scenario were selected participants that were experts in their area, analyzing the frequency of

appearance, potential losses, taking into account also the existing operational loses in the Bank. The

results from the scenario were validated by SG correspondent. By realization of the analysis, the

Bank’s risk profile was determined regarding the defined area from the scenario.

First level of Permenent control as operational risk management function

The first level of Permanent control is integral part of operational risk management system in

Ohridska Banka AD Skopje.

The first level of Permanent control is defined as the whole measures taken on permanent basis to

ensure legitimacy, authenticity and security of transactions carried out at operational level. Through its

dimension and quality implementation we contribute to decrease the risk that the Bank is facing and

easier detection of potential risks before they become too serious and generate losses.

In the reporting period the function of the first level of Permanent control is carried out through its two

pillars: operational controls and managerial supervision.

Annual report for bank activites for 2019 23

Operational controls concerns for proper application of rules and procedures by all employees and

controls of the accounts for which they are responsible.

The managerial supervision consists in series of checks carried out by the head of the departments in

order to ensure that the employees comply with the rules and procedures for processing the

transactions and for ensuring effective day to day security. The managerial supervision also includes

accounting controls of all accounts deemed as sensitive. The performed controls are formalized in

control files and their results are content of synthetic quarterly reports sent to the Risk management

committee and the Audit committee on quarterly basis.

Reputation Risk

The Bank overtakes all measures and actions to monitor, minimize and eliminate the reputation risk.

Managing reputational risk is a concern and task of all employees, organizational units and bodies of

the Bank. It is immeasurable risk which influence is based on evaluation, or qualitative estimation.

The key for good management of the reputation risk is transparent management system through open

communication for the events that the Bank is facing.

During 2019 there weren’t reports for events as an identified opportunity for reputational risk.

Regarding the reputational risk, a big challenge in 2019 was the buying of over 90% of the banks

shares from the new shareholder Steiermärkische Bank und Sparkassen AG from Austria. The whole

process was performed according the regulative and all needed consents and licenses were timely

provided.

At the same time the Bank has introduced an internal procedure for handling client’s complaints and

provides its proper implementation. The Bank has adopted a Procedure for handling client’s

complaints which sets the process for dealing of the received complaints in Ohridska Banka AD

Skopje, arising from individual or corporate clients and the manner of its submission, treatment and

response. Having in mind the above-mentioned, the process for dealing of the complaints has

methodological structure and enables satisfaction of client’s expectations. The report on received

complaints and their treatment is submitted quarterly to the Supervisory Board, Risk management

committee, and Management board of Ohridska Banka, as to the responsible of the commercial

sector/department and to the responsible/permanent supervision unit of the Bank.

Within the period January-December 2019, the Bank has no significant reputation risk exposure.

Compliance control of the Bank’s activities

Within the reporting period, the Bank continued to provide legitimacy and protection activities from

potential incompliance of the procedures. In order to provide compliance control of the Bank’s

activities the following activities were undertaken:

o Monitoring of the newly adopted regulation and estimation of its influence on the Bank’s

activities,

o Inform all organizational units and departments within the Bank regarding the

amendments in the legal and subordinate legislation and its impact on the organizational units

activities,

o Active participation in preparing and revising Bank’s internal procedures from its

compliance legislation point of view,

o Providing opinions, assistance and cooperation in the ongoing activities in order to provide

respect and implementation of the procedures,

o Report on regular basis to the Supervisory and Executive Board for the achievements of

the control compliance of the Bank’s activities on monthly and semiannual basis.

Annual report for bank activites for 2019 24

o Providing opinion for the newly introduced products in the Bank from the legal and

subordinate legislation compliance point of view.

o Project management for compliance with the Normative bank of Societe Generale Paris

regarding implementation of monitoring tools for compliance between the bank and legislation.

Training of employees on compliance topics (compliance controls, fight against corruption, protected

internal and external reporting, conflict of interest, reputational risk, FATCA regulation and protection

of personal data).

Anti-money laundering and Financing terrorism

The Bank has adopted and constantly applying a Procedure to prevent money laundering and several

internal acts that regulate this area and completely has implemented the instruments prescribed in the

regulative concerning detection and effective prevention of money laundering. In order to prevent anti

money laundering and financing terrorism, and in order to protect the reputation of the Bank in the

reporting period on a regular basis has been submitted the prescribed reports to the Financial

Intelligence office, reports on regular basis has been submitted to the Supervisory and Management

board; continuous training for implementation of the procedures for the new comers and other

employees has been performed. Also in the reporting period has been performed on site training for

implementation of the principle “Know your client” for the employees in the branches.

In the area of implementation and improvement of measures and activities to prevent money

laundering and terrorist financing, during the reporting period, Department for anti money laundering

and financing terrorismrun several projects in order to comply with the Group's standards.

The Department for Anti money laundering and financing terrorism will continue to perform their

regular activities in order to maintain and strengthen the culture of compliance of bank with rules to

prevent money laundering and financing of terrorism in order to achieve full compliance of the Bank

with the relevant regulations.

5. REPORT ON CORPORATE GOVERNANCE

During 2019, the Bank has accomplished its activities through the bodies of the Bank: Assembly of

the Bank, Supervisory Board, Management board, Risk Management Committee and Audit

Committee.

Corporate governance in Ohridska Banka is regulated by the Code of Corporate Governance (Code),

adopted by the Assembly of Shareholders in December 2008 and revised on annual basis in 2009,

2010, 2011, 2012, 2013, 2014, 2015, 2016, 2017, 2018 and 2019.

The Code defines in details the standards of governance and management of the authorities of

Ohridska Banka AD Skopje. In accordance with the principles of good corporate governance, the

Bank establishes the structure of relationships and processes in order to be able to successfully face

the changes in the environment, to build transparent and comprehensive management system which

increases the confidence of domestic and foreign investors, employees, customers, suppliers, the

competent institutions and community. Efficient corporate governance means that the roles and

relationships established in the company structure of the Bank are based on ethical behaviour and

minimize the conflicts of interests.

In accordance with the Code, the authorities of the Bank and all employees are guided by the

provisions contained therein, by acting honestly, fairly and ethically its obligations towards the Bank

and shareholders and in accordance with prescribed regulations.

Annual report for bank activites for 2019 25

MANAGEMENT STRUCTURE

SHAREHOLDERS ASSEMBLY

The shareholders assembly within its competencies performs all activities determinate by legislation

as well the Statute of the Bank. The assembly of the Bank consists of all shareholders, personally or

through their proxy representatives. During 2019, 3 sessions of the Assembly of shareholders took

place.

On the 41 Session of the Assembly held at 31st of January 2019 a Decision on amending and

consolidating the Statute of Ohridska Banka AD Skopje with Revised text of the Statute of Ohridska

banka AD Skopje have been adopted. Related to the amndmnets of the Satute that bank has

provided approval by the Central bank. At the same meeting of the Shareholders Assembly, a

Decision for appointing Goran Petrevski as an independent member of the Supervisory Board of

Ohridska banka was adopted. For his appointment as a member of the bank's Supervisory Board the

Governor of the National Bank issued prior consent.

On the 42 Session of the Assembly held on 28th of May 2019 the following materials have been

adopted: the annual account of the Bank and financial reports for 2018, all reports and proposed

materials related to the operations of the Bank in 2018, Decision on adopting of the Decision for

usage and allocation of the realized profit of Ohridska banka AD Skopje with the annual account for

2018 as well asDecision for appointment of an Audit house of the Ohridska Banka AD Skopje, for

calendar 2019 year.

SUPERVISORY BOARD

The supervisory board performs supervision over the operation of the Management Board, approves

the policies for performing finance activities, and supervises their implementation. This Board

provides good operation, management and stability of the Bank.

In 2019, the supervisory Board of the Bank was composed of five members appointed by the

Assembly of Shareholders for a term of four years, after prior consent by the Governor of the National

bank of North Macedonia.

During 2019, the Supervisory Board of Ohrid Bank operated in the following composition:

- Jean-Philippe Guillaume, member and president of the Supervisory Board starting

- Alan Conus, member of the Supervisory Board

- Maria Rousseva, a member of the Supervisory Board

- Cvetanka Simonovska, an independent member of the Supervisory Board

- Goran Petrevski, an independent member of the Supervisory Board from 27th of February

2019.

Jean-Philippe Guillaume – President and member of the Supervisory Board

Jean-Philippe Guillaume, acting as regional director for the “Balkans” (Montenegro, Serbia, North

Macedonia, Moldavia, Slovenia), & supervisor of Montenegro, Serbia & Slovenia, has been appointed

for a member of the Supervisory Board of Ohridska Banka by Decision of the Shareholders assembly

from 22/12/2016. Mr. Guillaume cared for the proper functioning of the Board in 2019. In the reporting

period, the sessions were scheduled by the President duly and timely according to the Rules of

procedure of the Supervisory Board. The President of the Supervisory Board adopted draft agenda for

the sessions, provided timely distribution of necessary materials, provided complete and accurate

information for the members of the Supervisory Board and sufficient time for the members to prepare.

During the sessions the President of the Supervisory Board initiated active and open discussion

Annual report for bank activites for 2019 26

giving enough space for additional questions and explanation for the submitted materials on the

session. Mr. Guillaume had active participation in the discussions and decisions and signed the

adopted decisions in the name of the Supervisory board. As President of the supervisory board gave

important contribution for efficient and successful operation of the Bank’s Supervisory Board till the

end of the year.

Alan Conus – member of Supervisory Board

Alain Conus – supervisor of N.Macedonia, Moldavia, KB & BRD, as member of the Supervisory

Board, appointed on 15.12.2011 by the Bank’s Assembly and reappointed on 29.10.2015 provided

sound operations of the board in 2019. M. Conus regularly participated in the discussions and gave

important contribution with its thirty yeras of experience in Societe Generale Group in the international

banking related issues, management of the control management, Societe General branch supervision

abroad, credit files management and corporate operations support.

Marija Rousseva – member of the Supervisory Board

Ms. Marija Rousseva – Executive Director of Societe generale in Serbia, as member of the

Supervisory Board appointed on 15.12.2011 by th Bank’s Assembly and reappointed on 29.10.2015

with its wide knowledge and practical experience in the banking contributed for successful

implementation of Supervisory Board’s activities in 2019 especially in the domain of risk operation

analysis and estimation. Ms. Rousseva actively participated in the work and decisions adoption the

Supervisory Board.

Cvetanka Simonovska – independent member

As independent member of Bank’s Supervisory board, Ms. Cvetanka Simonovska appointed on

17.04.2013 by th Bank’s Assembly and reappointed on 11.05.2017, has long experience of the

financial institutions in Republic of N.Macedonia and contributed for successful operations of the

Board Cvetanka Simonovska had active and objective attitude with its remarks and opinions,

participated in discussions related to Supervisory Board’s competency, reviewing and adopting of