8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 1/67

1

CONTENTS

Serial No. Particulars Page No.

1. Introduction 2

2. History of Insurance 6

3. Industry Profile 13

4. Research Design 19

5. Company Profile 22

6. Research Methodology 34

7. Data analyses and interpretation 38

8. Hypothesis Testing 54

9. Observation and findings 57

10. Recommendation and Suggestion 59

11. Conclusion 61

Bibliography 63

Annexure 65

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 2/67

2

Chapter-1INTRODUCTION

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 3/67

3

Introduction of Insurance

Insurance is a tool which facilitates a small number is compensated out of funds

(premium payment) collected from plenteous. Insurance companies pay back for

financial losses arising out of occurrence of insured events, e.g. in personal accidentpolicy death due to accident policy death due to accident, in fire policy the insured events

are fire and other allied perils like riot and strike, explosion, etc. Hence, insurance is

safeguard against uncertainties. It provides financial recompose for losses suffered due to

incident of unanticipated events, insured within policy of insurance. Moreover, through a

number of acts of Parliament, specific types of insurances are legally enforced in our

country, e.g. third party insurance under Motor Vehicle Act, public liability insurance for

handlers of hazardous substances under Environment Protection Act, etc.

The insurance sector in India has come a full circle from being an open competitive

market to nationalization and back to a liberalized market again.

Tracing the developments in the Indian insurance sector reveals the 360-degree turn

witnessed over a period of almost 190 years.

The business of life insurance in India in its existing form started in India in the year

1818 with the establishment of the Oriental Life Insurance Company in Calcutta.

Some of the important milestones in the life insurance business in India are:

1912 - The Indian Life Assurance Companies Act enacted as the first statute to regulate

the life insurance business.

1928 - The Indian Insurance Companies Act enacted to enable the government to

collect statistical information about both life and non-life insurance businesses.

1938 - Earlier legislation consolidated and amended to by the Insurance Act with the

objective of protecting the interests of the insuring public.

1956 - 245 Indian and foreign insurers and provident societies taken over by the central

government and nationalized. LIC formed by an Act of Parliament, viz. LIC Act,1956, with a capital contribution of Rs. 5 crore from the Government of India.

The General insurance business in India, on the other hand, can trace its roots to the

Triton Insurance Company Ltd., the first general insurance company established in the

year 1850 in Calcutta by the British.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 4/67

4

Some of the important milestones in the general insurance business in India are:

1907 - The Indian Mercantile Insurance Ltd. set up, the first company to transact all

classes of general insurance business.

1957 - General Insurance Council, a wing of the Insurance Association of India, frames acode of conduct for ensuring fair conduct and sound business practices.

1968 - The Insurance Act amended to regulate investments and set minimum solvency

margins and the Tariff Advisory Committee set up.

1972 - The General Insurance Business (Nationalization) Act, 1972 nationalized the

general insurance business in India with effect from 1st January1973. 107 insurers

amalgamated and grouped into four companies viz. the National Insurance Company

Ltd., the New India Assurance Company Ltd., the Oriental Insurance Company Ltd.

and the United India Insurance Company Ltd. GIC incorporated as a company.

DEFINATION OF INSURANCE

Insurance may be defined as a contract wherein one party (the insurer) agrees to pay to

the other party (the insured) or his beneficiary, a certain sum upon a given contingency

(the risk) against which insurance is required.

Life insurance is a contract that pledges payment of an amount to the person assured (or

his nominee) on the happening of the event insured against.

Insurance that guarantees a specific sum of money to a designated beneficiary upon the

death of the insured or to the insured if he or she lives beyond a certain age.

The contract is valid for payment of the insured amount during:

The date of maturity, or Specified dates at periodic intervals, or Unfortunate death, if it occurs earlier.

Among other things, the contract also provides for the payment of premium periodically

to the Corporation by the policyholder. Life insurance is universally acknowledged to be

an institution, which eliminates 'risk', substituting certainty for uncertainty and comes to

the timely aid of the family in the unfortunate event of death of the breadwinner.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 5/67

5

By and large, life insurance is civilization‘s partial solution to the problems caused by

death. Life insurance, in short, is concerned with two hazards that stand across the life-

path of every person:

1. That of dying prematurely leaves a dependent family to fend for itself.

2. That of living till old age without visible means of support.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 6/67

6

Chapter-2

HISTORY

OF

INSURANCE

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 7/67

7

HISTORY OF INSURANCE

In some sense it can be said that insurance appears simultaneously with the appearance of human

society. There are two types of economies in human societies: money economies (with markets,

money, financial instruments and so on) and non-money or natural economies (without money,

markets, financial instruments and so on). The second type is a more ancient form than the first.

In such an economy and community, insurance can be seen in the form of people helping each

other. For example, if a house burns down, the members of the community help build a new one.

Should the same thing happen to one's neighbors, the other neighbors must help Otherwise;

neighbors will not receive help in the future. This type of insurance has survived to the present

day in some countries where modern money economy with its financial instruments is not

widespread (for example countries in the territory of the former Soviet Union).

Turning to insurance in the modern sense (i.e., insurance in a modern money economy, in which

insurance is part of the financial sphere), early methods of transferring or distributing risk were

practiced by Chinese and Babylonian traders as long ago as the 3rd and 2nd millennia BC,

respectively. Chinese merchants traveling treacherous river rapids would redistribute their wares

across many vessels to limit the loss due to any single vessel's capsizing. The Babylonians

developed a system which was recorded in the famous Code of Samurai, c. 1750 BC, and

practiced by early Mediterranean sailing merchants. If a merchant received a loan to fund his

shipment, he would pay the lender an additional sum in exchange for the lender's guarantee to

cancel the loan should the shipment be stolen.

Achaemenian monarchs were the first to insure their people and made it official by registering the

insuring process in governmental notary offices. The insurance tradition was performed each year

in Norouz (beginning of the Iranian New Year); the heads of different ethnic groups as well asothers willing to take part, presented gifts to the monarch. The most important gift was presented

during a special ceremony. When a gift was worth more than 10,000 Derrick (Achaemenian gold

coin weighing 8.35-8.42) the issue was registered in a special office. This was advantageous to

those who presented such special gifts. For others, the presents were fairly assessed by the

confidants of the court. Then the assessment was registered in special offices.

The purpose of registering was that whenever the person who presented the gift registered by the

court was in trouble, the monarch and the court would help him. Jahez, a historian and writer,

writes in one of his books on ancient Iran: "[W]henever the owner of the present is in trouble or

wants to construct a building, set up a feast, have his children married, etc. the one in charge of

this in the court would check the registration. If the registered amount exceeded 10,000 Derrik, heor she would receive an amount of twice as much."

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 8/67

8

A thousand years later, the inhabitants of Rhodes invented the concept of the 'general

average'. Merchants whose goods were being shipped together would pay a

proportionally divided premium which would be used to reimburse any merchant whose

goods were jettisoned during storm or sinkage.

The Greeks and Romans introduced the origins of health and life insurance c. 600 ADwhen they organized guilds called "benevolent societies" which cared for the families and

paid funeral expenses of members upon death. Guilds in the Middle Ages served a

similar purpose. The Talmud deals with several aspects of insuring goods. Before

insurance was established in the late 17th century, "friendly societies" existed in England,

in which people donated amounts of money to a general sum that could be used for

emergencies.

Separate insurance contracts (i.e., insurance policies not bundled with loans or other

kinds of contracts) were invented in Genoa in the 14th century, as were insurance pools

backed by pledges of landed estates. These new insurance contracts allowed insurance tobe separated from investment, a separation of roles that first proved useful in marine

insurance. Insurance became far more sophisticated in post-Renaissance Europe, and

specialized varieties developed.

Toward the end of the seventeenth century, London's growing importance as a center for

trade increased demand for marine insurance. In the late 1680s, Mr. Edward Lloyd

opened a coffee house that became a popular haunt of ship owners, merchants, and ships‘

captains, and thereby a reliable source of the latest shipping news. It became the meeting

place for parties wishing to insure cargoes and ships, and those willing to underwrite such

ventures. Today, Lloyd's of London remains the leading market (note that it is not aninsurance company) for marine and other specialist types of insurance, but it works rather

differently than the more familiar kinds of insurance.

Insurance today can be traced to the Great Fire of London, which in 1666 devoured

13,200 houses. In the aftermath of this disaster, Nicholas Barbon opened an office to

insure buildings. In 1680, he established England's first fire insurance company,

"The Fire Office," to insure brick and frame homes.

The first insurance company in the United States underwrote fire insurance and was

formed in Charles Town (modern-day Charleston), South Carolina, in 1732.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 9/67

9

Benjamin Franklin helped to popularize and make standard the practice of insurance,

particularly against fire in the form of perpetual insurance. In 1752, he founded the

Philadelphia Contributionship for the Insurance of Houses from Loss by Fire. Franklin's

company was the first to make contributions toward fire prevention. Not only did his

company warn against certain fire hazards, it refused to insure certain buildings where the

risk of fire was too great, such as all wooden houses.

In the United States, regulation of the insurance industry is highly Balkanized, with

primary responsibility assumed by individual state insurance departments. Whereas

insurance markets have become centralized nationally and internationally, state insurance

commissioners operate individually, though at times in concert through a national

insurance commissioners' organization. In recent years, some have called for a dual state

and federal regulatory system for insurance similar to that which oversees state banks and

national banks.

In the state of New York, which has unique laws in keeping with its stature as a globalbusiness center, former New York Attorney General Eliot Spitzer was in a unique

position to grapple with major national insurance brokerages. Spitzer alleged that Marsh

& McLennan steered business to insurance carriers based on the amount of contingent

commissions that could be extracted from carriers, rather than basing decisions on

whether carriers had the best deals for clients. Several of the largest commercial

insurance brokerages have since stopped accepting contingent commissions and have

adopted new business models.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 10/67

10

TYPES OF INSURANCE

The earliest traces of insurance in the ancient world are found in the form of marine trade loans or

carriers , contracts, which included an element of insurance. Evidence is on record that

arrangemts embodying the idea of insurance were in Babylonia and India at quite an early period

CLASSIFICATION ON THE BASIS OF NATURE OF INSURANCE

LIFE INSURANCE FIRE INSURANCE MARINE INSURANCE SOCIAL INSURANCE MISCELLANEOUS INSURANCE

CLASSIFICATION OF INSURANCE FROM BUSINESS POINT OF VIEW

LIFE INSURANCE GENERAL INSURANCE

CLASSIFICATION ON BASIS OF NATURE OF INSURANCE

1) LIFE INSURANCE

Life insurance may be defined as a contract in which the insurer, in consideration of a certain

premium, either in a lump sum or by other periodical payments, agrees to pay to the assured, or to

the other person for whose benefit the policy is taken, the assured sum of money, on to the person

for whose benefit the policy is taken, the assured sum of money, on the happening of a specified

event contigent on the human life or at the expiry of certain period. For life insurance, the risk ensured against is death. The life insurance company pays the sum assured to the insured in the

event of death. There are several types of insurance products / policies, which have been

discussed.

At present, life insurance enjoys maxium scope because the life is the most important

property of the society or an individual. Each and every person requires the insurance.

This insurance provides protection to the family at the premature death or gives adequate

amount at the old age when earnings capacities are reduced. The insurance is not only a

protection but is a sort of investment because a certain sum is returnable to the insured at

the death or at the expiry of a period

2) FIRE INSURANCE

A fire insurance is a contract whereby the insurer, in consideration of the premium paid,

undertakes to make good any loss or damage caused by fire during a specified period.

Normally, the fire insurance policy is for a period of one year after which it is to be

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 11/67

11

renewed from time to time. A claim for loss by fire must satisfy the following 2

conditions:

o Ther must be actual loss; and

o Fire must be accidental and non-intentional

The risk covered by a fire insurance contract is the loss resulting from fire or some cause,

which is the proximate cause of the loss. If damage is caused by overheating by

overheating without ignition, it will not be regarded as a fire loss within the meaning of

fire insurance and the loss will not be recoverable from the insurer

3) MARINE INSURANCE

A marine insurance contract is an agreement where by the insurer undertakes to

indemnify

The insured in the manner and to the extent there by agreed against marine losses .marine

insurance is an arrangement by which the insurer undertakes to compensate the owner of

a ship or cargo for complete or partial loss at sea.

Marine insurance provides protection against loss of marine perils. The marine perils are

collision with rock, or ship attacked by enemies, fire and capture by pirates, etc.

These perils cause damage, destruction or disappearance of the ship and cargo and non-

payment of freight. So, marine insurance insures ship (hull), cargo and freight.

4) SOCIAL INSURANCE

Social insurance has developed to provide economic security to weaker sections of the

society who are unable to pay the premium for adequate insurance. Pension plans,

disability benefits, unemployment benefits, sickness insurance, and industrial insurance

are the various forms of social insurance. With the increase of the socialistic ideas, the

social insurance is an obligatory duty of the nation.

5) MISCELLANEOUS INSURANCE

The process of fast development in the society gave rise to a number of risks or hazards.To provide security against such hazards, many other types of insurance also have been

developed

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 12/67

12

CLASSIFICATION FROM BUSINESS POINT OF VIEW

1) LIFE INSURANCE

2) GENERAL INSURANCE

1) LIFE INSURANCE- Life insurance may be defined as a contract in which the

insurer, in consideration of a certain premium, either in a lump sum or by other periodical

payments, agrees to pay to the assured, or to the person for whose benefit the policy is

taken, the assured sum of money, on the happenings of a specified event contingent on

the human life are at the expiry of certain period.

2) GENERAL INSURANCE-General insurance business refers to fire, marine and

miscellaneous insurance business whether carried on singly or in combination with one or

more of them.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 13/67

13

Chapter-3

INDUSTRY

PROFILE

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 14/67

14

INDUSTRY PROFILE

Insurance may be described as a social device to reduce or eliminate risk of life and

property. Under the plan of insurance, a large number of people associate themselves

by sharing risk, attached to individual.

The risk, which can be insured against include fire, the peril of sea, death, incident, &

burglary. Any risk contingent upon these may be insured against at a premium

commensurate with the risk involved.

Insurance is actually a contract between 2 parties whereby one party called insurer

undertakes in exchange for a fixed sum called premium to pay the other party happening

of a certain event. Insurance is a contract whereby, in return for the payment of premium

by the insured, the insurers pay the financial losses suffered by the insured as a result of

the occurrence of unforeseen events.

With the help of Insurance, large number of people exposed to a similar risk make

contributions to a common fund out of which the losses suffered by the unfortunate few,

due to accidental events, are made good.

MAX INIDA LTD.

Max India Limited is a multi-business corporate, driven by the spirit of enterprise and

focused on people and service oriented businesses. The Company‘s vision is to be one of

India‘s most admired corporates for Service Excellence.

It ‗Protects Life‘ through its Life Insurance subsidiary Max New York Life, a joint

venture between Max India and New York Life, a Fortune 100 company; ‗Cares for Life‘

through its Healthcare company, Max Healthcare, a subsidiary of Max India Limited;

‗Enhances Life‘ through its Health Insurance company, Max Bupa Health Insurance, a

joint venture between Max India and Bupa Finance Plc., UK which is set to launch after

statutory approvals; and ‗Improves Life‘ through its Clinical Research business, Max

Neeman, a fully owned subsidiary of Max India. From its past, Max India continues its

interest in manufacture of Speciality Products for the packaging industry.

Max India Group‘s consolidated turnover for half year ended Sept 09 was Rs. 4166 crore.

The consolidated operating revenue was Rs. 2543 Crore, a growth of 23% over the same

period last year. The Group is on a high growth path, with over 700 offices across around

400 locations in the Country and with people strength of 100,000+ persons as on 30 th

Sept 2009.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 15/67

15

NEW YORK LIFE LLC

New York Life Insurance Company, (www.newyorklife.com) a Fortune 100 company

founded in 1845, is the largest mutual life insurance company in the United States and

one of the largest life insurers in the world. Headquartered in New York City, New York

Life‘s family of companies offer life insurance, annuities and long-term care insurance.New York Life Investment Management LLC provides institutional asset management

and retirement plan services. Other New York Life affiliates provide an array of

securities products and services, as well as institutional and retail mutual funds.

The mission of New York Life is to maintain its superior 'financial strength', adhere to

the highest standards of 'integrity' and demonstrate 'humanity' by treating its customers,

agents and employees with compassion, consideration and respect.

New York Life is one of the largest and strongest life insurance companies in the world

with more than USD$215 billion assets under management and has received among thehighest ratings for financial strength from the life insurance industry's principal rating

agencies: A.M. Best (AA+), Standard & Poor's (AA+), Moody's (Aa1), Fitch (AAA).

According to Moody's,

"New York Life's rating reflects the company's good quality investment portfolio, ample

liquidity, and sound capitalization, as well as the good growth potential of its

international business.‖

As a leader in the insurance industry, New York Life continues to bring to its operations

new management concepts, advanced technologies, new distribution and training systems

and innovative insurance products

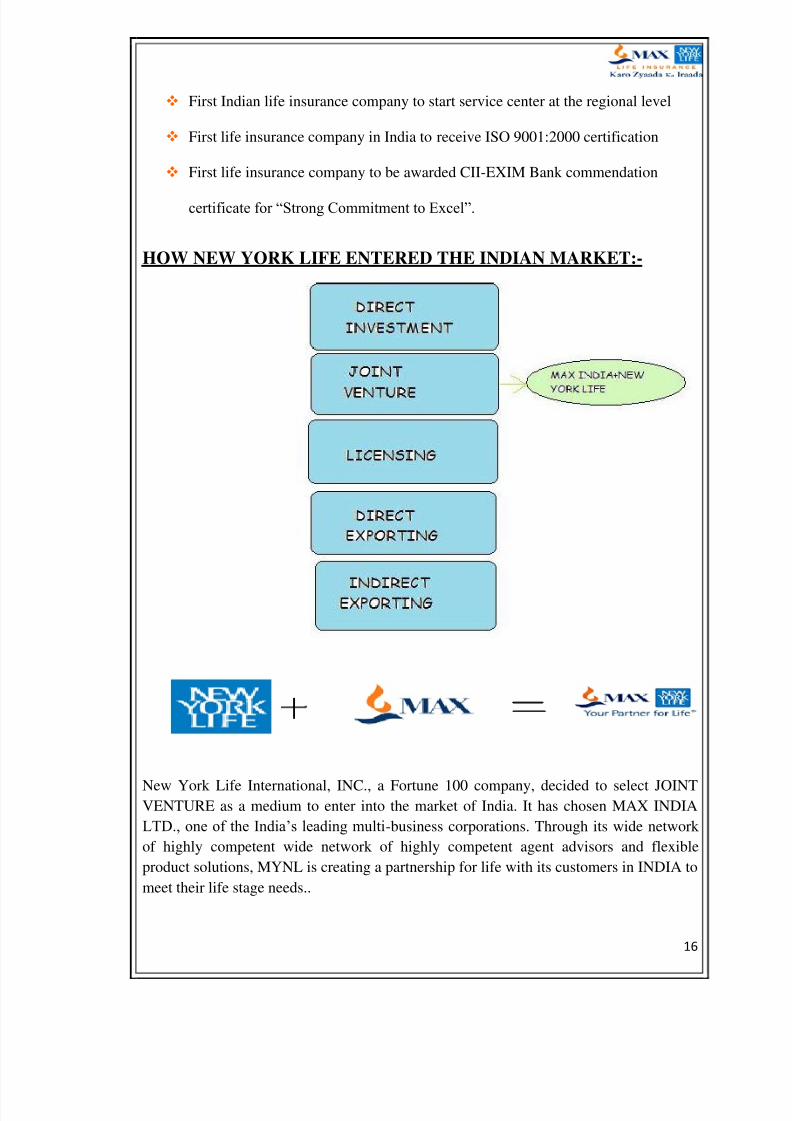

Some of the Industry Firsts

First company to provide Freelook period of 15 days to the customer. This was

later made mandatory by the regulator

First company to start toll free line for agent services

First and the only life insurance company in India to implement Lean

methodology of service excellence in service industry

First life insurance company in India to provide various services to the agents and

customers over phone

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 16/67

16

First Indian life insurance company to start service center at the regional level

First life insurance company in India to receive ISO 9001:2000 certification

First life insurance company to be awarded CII-EXIM Bank commendation

certificate for ―Strong Commitment to Excel‖.

HOW NEW YORK LIFE ENTERED THE INDIAN MARKET:-

New York Life International, INC., a Fortune 100 company, decided to select JOINTVENTURE as a medium to enter into the market of India. It has chosen MAX INDIA

LTD., one of the India‘s leading multi-business corporations. Through its wide network

of highly competent wide network of highly competent agent advisors and flexible

product solutions, MYNL is creating a partnership for life with its customers in INDIA to

meet their life stage needs..

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 17/67

17

Insurance companies:

IRDA has so far granted registration to 12 private life insurance companies and 9 general

insurance companies. If the existing public sector insurance companies are included,

there are currently 13 insurance companies in the life side and 13 companies operating in

general insurance business. General Insurance Corporation has been approved as the"Indian reinsurer" for underwriting only reinsurance business. Particulars of the life

insurance

companies and general insurance companies including their web address is given below:

LIFE INSURERS Websites

Public Sector

Life Insurance Corporation of India www.licindia.com

Private Sector

Allianz Bajaj Life Insurance Company Limited www.allianzbajaj.co.in

Birla Sun-Life Insurance Company Limited www.birlasunlife.com

HDFC Standard Life Insurance Co. Limited www.hdfcinsurance.com

ICICI Prudential Life Insurance Co. Limited www.iciciprulife.com

ING Vysya Life Insurance Company Limited www.ingvysayalife.com

Max New York Life Insurance Co. Limited www.maxnewyorklife.com

MetLife Insurance Company Limited www.metlife.com

SBI Life Insurance Company Limited www.sbilife.co.in

TATA AIG Life Insurance Company Limited www.tata-aig.com

AMP Sanmar Assurance Company Limited www.ampsanmar.com

Dabur CGU Life Insurance Co. Pvt. Limited www.avivaindia.com

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 18/67

18

GENERAL INSURERS

Public Sector

National Insurance Company Limited www.nationalinsuranceindia.com

New India Assurance Company Limited www.niacl.com

Oriental Insurance Company Limited www.orientalinsurance.nic.in

United India Insurance Company Limited www.uiic.co.in

Private Sector

Bajaj Allianz General Insurance Co. Limited www.bajajallianz.co.in

ICICI Lombard General Insurance Co. Ltd. www.icicilombard.com

IFFCO-Tokio General Insurance Co. Ltd. www.itgi.co.in

Reliance General Insurance Co. Limited www.ril.com Royal Sundaram Alliance Insurance Co. Ltd. www.royalsun.com

TATA AIG General Insurance Co. Limited www.tata-aig.com

Cholamandalam General Insurance Co. Ltd. www.cholainsurance.com

Export Credit Guarantee Corporation www.ecgcindia.com

REINSURER

General Insurance Corporation of India www.gicindia.com

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 19/67

19

Chapter-4

RESEARCH

DESIGN

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 20/67

20

Research Design

Research design tells us about which tools & techniques are used to find the results in a

better way. It is used to describe the market phenomena while trying to determine the

association among variables.

Title of the Study

“SALES PROCESS FOR MAX NEW YORK LIFE INSURANCE CO.

LTD.”

Problem Statement

A sales process, also known as a sales tunnel or a sales funnel, is a systematic approachto selling a product or service. the argument that ―no process‖ means ―no success‖ is

usually accurate — especially when you are dealing with the highly complex science of revenue generation. No other business process is more highly scrutinized than the salesprocess.We train around it. We strategize and plan around it. We project and allocatebudget around it.Frankly, the sales process is the most pivotal part of any business.

Most process problems are really people problems. People make mistakes.

People have personal issues that creep into their professional lives. They make bad,

scared decisions because of past times when they got hurt.Quite a lot of time our

projections for success are based on when we want to be successful — not when it islikely to occur. It takes time (sometimes lots and lots of time) for a dream and a great

process to turn out to be successful

OBJECTIVE

Main objective of the research is to have an analysis of Max New York life insurance

Company Ltd. Selling process. To accomplish this objective it has been divided into five.

To determine reasons behind opting for an insurance.

To know the most preferred policy.

To determine customers perception towards private insurance companies and their

expectation form private insurance companies.

To determine the feedback on services provided by an insurance agent.

To study the types of benefits provided by insurance services.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 21/67

21

SCOPE OF THE WORK

Project Report will cover the point of Selling process of Max New York LifeInsurance Company Ltd.

Project Report will play major role for investors in understanding the concept andrecent reforms in the field of life insurance policy of Max New York LifeInsurance Company Ltd.

Project report will be related to the investor‘s approach towards Life InsurancePolicy.

People of age between 18 to 60 and above will be covered in the survey. Area will be limited to Bilaspur [C.G.]. Project report will help the companies and other related entities to understand the

approach of the investors which will help them to formulate their target andmarketing strategies.

LIMITATIONS

The main limitation faced while conducting the research was the availability of the faculty

members at the training institute of MNYL . It was very difficult to be able to meet them

personally, since most of them were busy with the hectic training schedule.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 22/67

22

Chapter-5COMPANY

PROFILE

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 23/67

23

Company Profile

“Max New York Life wants people to view insurance as a financial protection

and wealth creation instrument and not just a tax-saving tool.”

Max New York Life Insurance Company Ltd. is a joint venture between New York Life,

a Fortune 100 company and Max India Limited, one of India's leading multi-business

corporations. The company has positioned itself on the quality platform. In line with its

vision to be the most admired life insurance company in India, it has developed a strong

corporate governance model based on the core values of excellence, honesty, knowledge,

caring, integrity and teamwork. The strategy is to establish itself as a trusted life

insurance specialist through a quality approach to business.

In line with its values of financial responsibility, Max New York Life has adopted

prudent financial practices to ensure safety of policyholder's funds. The Company's paid

up capital is Rs. 657 crore, which is more than the norm laid down by IRDA.

Max New York Life has identified individual agents as its primary channel of

distribution. The Company places a lot of emphasis on its selection process, which

comprises four stages - screening, psychometric test, career seminar and final interview.

The agent advisors are trained in-house to ensure optimal control on quality of training.

Max New York Life invests significantly in its training program and each agent is trained

for 152 hours as opposed to the mandatory 100 hours stipulated by the IRDA before

beginning to sell in the marketplace. Training is a continuous process for agents at

Max New York Life and ensures development of skills and knowledge through a

structured programme spread over 500 hours in two years. This focus on continuous

quality training has resulted in the company having amongst the highest agent pass rate in

IRDA examinations and the agents have the highest productivity among private life

insurers. 201 agent advisors have qualified for the Million Dollar Round Table (MDRT)

membership in 2005. MDRT is an exclusive congregation of the world‘s top selling

insurance agents and is internationally recognized as the standard of excellence in the life

insurance business.

Having set a best in class agency distribution model in place, the company is

spearheading a major thrust into additional distribution channels to further grow its

business. The company is using a five-pronged strategy to pursue alternative channels of

distribution. These include the franchisee model, rural business, direct sales force

involving group insurance and telemarketing opportunities, banc assurance and corporate

alliances.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 24/67

24

Max New York Life offers a suite of flexible products. It now has 26 life insurance

products and 8 riders that can be customised to over 400 combinations enabling

customers to choose the policy that best fits their need.

Max New York Life was among the top 25 companies to work with in India, according to

2003 Business World magazine, "Great Workplaces In India", Max New York Life wasranked at the 20th position. This survey is the local version of the "Great Places to Work"

survey carried out every year in 22 countries.

Max New York Life among top five most respected private life insurance companies in

India according to a 2004 and 2006 Business World survey.

Distribution

Max New York Life Insurance has multi-channel distribution spread across the country.Agency distribution is the primary channel complemented by partnership distribution,bancassurance, alliance marketing and dedicated distribution for emerging markets. TheCompany places a lot of emphasis on its selection process for agent advisors, whichcomprises four stages - screening, psychometric test, career seminar and final interview.The agent advisors are trained in-house to ensure optimal control on quality of training.The company currently has more than 71,000 agent advisors at 676 offices across 389cities. The company also has 50 tie-ups with banks, 30 partnership distributionrelationships Max New York Life has put in place a unique hub and spoke model of distribution to deepen our rural penetration. This is the first time such a model has beenput in place for rural marketing of insurance. The company has 139 offices dedicated torural areas.

Max New York Life Insurance Co. LTD. Bilaspur

Ghanshyam Chambers Vyapar Vihar Main Road Bilaspur – 495001 (C.G.)

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 25/67

25

Max New York Life Office Networks

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 26/67

26

ORGANIZATION CHART

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 27/67

27

VISION

To become one of the most admired life insurance company of India.

MISSION

Become one of the top quartile life insurance companies in India

Be a national player

Be the brand of first choice

Be the employer of choice

Become principal of choice for agents

VALUES

Knowledge:

Knowledge leads to expertise; and our expertise is in helping people protect themselves.Perfectly combining global expertise with local knowledge, we are India's life insurance

specialist. Max New York Life believes that for knowledge to be of value it must be

focused, current, tested and shared.

Caring:

Max New York Life is redefining the life insurance paradigm by focusing on customers

first. The service process is responsive, personalized, humane and empathetic. Every

individual who represents the company is for us our brand champion.

Honesty:

Honesty is the heart of the life insurance business. It is all about trust. Transparency,

integrity and dependability form the cornerstones of the Max New York Life experience.

The company ensures that everyone who represents the brand carries a promise : we care

— in word as well as deed.

Excellence:

Excellence at Max New York Life implies the ability to perform at a consistently high

level. Focused on the value of continuous improvement in people, processes and the

organization, the company strives for the highest standards of quality in every aspect of its business.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 28/67

28

ACHEIVEMENTS

Max New York Life is the first life insurance company in India to be awarded theIS0 9001:2000 certification.

Max New York Life was among the top 25 companies to work with in India,

according to 2003 Business World magazine, "Great Workplaces In India", MaxNew York Life was ranked at the 20th position. This survey is the local version of the "Great Places To Work" survey carried out every year in 22 countries.

Been among top five most respected private life insurance companies in Indiaaccording to a 2004 and 2006 Business World survey.

Have truly built an enviable sales force. With 345 agents becoming members of the MDRT in 2006, Max New York Life has moved up to 21st rank in MDRTglobal list.

Awards

BT Mercer – Ranked No7 in the ―Best companies to Work For‖

Awarded the Gallup Great Work Place Award 2009

CII – Exim Bank Commendation Certificate for Business Excellence – 2008

Recognized as a Superbrand

Recipient of 2008 CIO 100 Award for technology implementation

Golden Peacock Award for Innovation – 2008

Among the top 25 companies to work for in India, according to Business world

2003 ‗Great Workplaces of India‘

Among the top five most respected insurance companies in India as per Businessworld 2004 & 2006 survey

Won Indo-American Corporate Excellence Award for Best Indo-US company in

Financial Services Category in 2006

Received ‗Best Six Sigma Project‘ award at Sakal Six Sigma Excellence Awards

– 2006

Among top 3 in Asia Life Insurance Company of the Year Award 2007 instituted

by Asia Insurance Review

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 29/67

29

VARIOUS PRODUCTS OF MNYL INSURANCE

Max New York Life Insurance offers a suite of flexible products. It now has 25

individual life and health insurance products and 8 riders enabling customers to choose

the policy that best fits their need. Besides this, the company offers 6 products and 7

riders in group insurance business

Life is full of surprises. Unexpected events that strike without warning can disrupt the

smooth rhythm of life. You must be prepared at all times. As the primary earning

member, you need to make sure that your family is never lacking in anything even if you

are taken away from them forever. Do your best today to ensure that your family can

always enjoy a comfortable lifestyle. In double income families, both spouses should get

adequate life covers especially if there are dependent children involved. We have plans

that guarantee maximum protection at a low cost.

Your parenting is perfect but is your planning adequate? Are you thinking beyond the

immediate to the future, about higher education and professional courses, in India and

abroad? Many children are keen to pursue unconventional careers. Are you in tune with

their aspirations and passions? As parents you would never let money come in the way of

your children and the fulfillment of their true potential. Our plans will help build the

corpus that allows your children to dream big and soar high.

Building a nest egg is about aggregating surplus amounts regularly to allow them to grow

into a sizeable sum. Investments should be aligned to specific, long-term goals. Luxury

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 30/67

30

car, foreign holiday or dream house, create your own wish list and make it come true.

Your dreams are in your hands. Every move that you make today will bring you a step

closer to your goals. Our Investment Plans offer the dual benefit of protection and

market-linked returns with the flexibility to choose the premium and determine the

market exposure.

Let your golden years be the most precious of your life, full of freedom and choice. A

time to pursue your hobbies, travel and enjoy the good life. You will never miss your

salary cheque or be constrained by rising inflation. Even as you work hard to make a

better today, it is up to you to create a superior tomorrow. If you want to sustain yourcurrent lifestyle even after you stop working, make that money work for you. Our

Retirement Plans will keep you comfortable and content, and let you live the life you

deserve.

Do you know the cost of healthcare has climbed faster than inflation? Medical costs can

be a big drain on finances. A medical crisis can strike anyone, anytime and may even

force an individual to dip into savings to meet these sudden and steep costs. Such an

eventuality could delay or destroy a cherished financial goal. No wonder, health is

wealth. The health of every member of the family is precious and you need to safeguard

it as a priority. Use our Health Plans to make sure your family stays fit and fine

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 31/67

31

SALES PROCESS IN MAX NEW YORK LIFE

NA

NAME GATHERING

QUALIFYING NAMES

FIXING APPOINTMENT

NEED ANALYSIS

SOLUTION

CLOSURE

REFERENCES

PROBLEM FACTS

FINDING

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 32/67

32

COMPETITION INFORMATION

COMPETITORS:

1. ICICI LIFE INSURANCE

2. LIFE INSURANCE CORPORATION

3. AVIVA LIFE INSURANCE

4. MET LIFE

5. BAJAJ ALLIANZ

6. BIRLA LIFE INSURANCE

SWOT ANALYSIS OF MAX NEW YORK LIFE

STRENGTHS

Knowledge based

Being quality conscious rather than quantity oriented

Providing in-house training to advisors rather than online training

Cost effective organization

Persuasiveness of customer service representative to address the problems.

Effective customer Personal consulting for customized policy.

Perceived financial loyalty programmers.

Customized policies that cover the specific terminal disease.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 33/67

33

WEAKNESSES

Less Brand Awareness

Time consuming ( in picking advisors)

Process Oriented( process are too lengthy)

Fewer suggestions in terms of precautionary measures for avoiding perils.

Are pulled by the engine of powerful brands like TATA AIG and

Bajajallianz.

OPPORTUNITIES

It can enter in the General insurance sector.

Opportunity in the rural sector as there is an under-penetrated insurance market in

rural sector.

Relative market potential in not only the rural markets but also the semi-urban

markets.

Better customer services like utmost promptness in issuance of the policy,

giving cheque pick up facilities and not making customers waiting for months.

Making more loyal customers and attracting other customers with better

service.

THREATS

LIC being the major market share holder

Competitors in the private sector

With players like SBI Life and ICICI Prudential spending lot in

advertisements, it may take away the market. Focusing more on innovating new products takes the fruitfulness out of good

products.

Less number of agents compared to other companies leading to a bad

distribution network.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 34/67

34

Chapter-6

RESEARCH

METHODOLOGY

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 35/67

35

RESEARCH METHODOLOGY

TITLE:

To Study Sales process for Max New York Life Insurance Company Ltd..

TITLE JUSTIFICATION:

The above title is self explanatory. The study deals mainly with studying the Selling

pattern in the insurance industry with a special focus on Max New York life

Insurance. The various segments of the markets divided in terms of Insurance Needs,

Age groups, Satisfaction levels etc will also studied.

SCOPE OF THE STUDY

A big boom has been witnessed in Insurance Industry in recent times. A large number of

new players have entered the market and are trying to gain market share in this rapidly

improving market. The study deals with Max New York in focus and the various

segments that it caters to. The study then goes on to evaluate and analyze the findings so

as to present a clear picture of trends in the Insurance sector.

SIGNIFICANCE TO THE INDUSTRY:

This is a limited study which takes into consideration the responses of 100 people. This

data can be explorated to take in the trends across the industry. The significance for the

industry lies in studying these trends that emerge from the study. It is a rapidly changing

and evolving sector. People are only beginning to wake up to its vast possibilities. A

study like this can attempt to guide the future of the industry based on current trends.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 36/67

36

SIGNIFICANE FOR THE RESEARCHER:

To facilitate and provide useful information for the study of the company and the

insurance industry and also provide recommendations for Max New York Life.

RESEARCH DESIGN

NON-PROBABILITY

EXPLORATORY & DISCRIPTIVE EXPERIMENTAL RESEARCH

The research is primarily both exploratory as well as descriptive in nature. The sources of

information are both primary & secondary.

A well-structured questionnaire was prepared and personal interviews were conducted to

collect the customer‘s perception and buying behavior, through this questionnaire.

SAMPLING METHODOLOGY

Sampling Technique:

Initially, a rough draft was prepared keeping in mind the objective of the research. A pilot

study was done in order to know the accuracy of the Questionnaire. The final

Questionnaire was arrived only after certain important changes were done. Thus my

sampling came out to be judemental and convinent.

Sampling Unit:

The respondents who were asked to fill out questionnaires are the sampling units. These

comprise of employees of MNCs, Govt. Employees, Self Employed etc.

Sample size:

The sample size was restricted to only 100, which comprised of mainly peoples from

different regions of Bilaspur due to time constraints.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 37/67

37

Sampling Area:

The area of the research was Bilaspur, India.

LIMITATIONS OF THE RESEARCH

1. The research is confined to a certain parts of Bilaspur and does not necessarily

shows a pattern applicable to all of Country.

2. Some respondents were reluctant to divulge personal information which can affect

the validity of all responses.

3. In a rapidly changing industry, analysis on one day or in one segment can change

very quickly. The environmental changes are vital to be considered in order to

assimilate the findings.

1. Sample size 100

2. Sample unit MAX NEW YORK LIFE INSURANCE COMPANY

LTD.

3. Universe Bilaspur city

4. Research type Descriptive research

5. Statistical tools and

method

Chi- Square Test

6. Primary data Questionnaire

7 Secondary data Internet

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 38/67

38

CHAPTER 7DATA ANALYSIS

&

INTERPRETATION

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 39/67

39

DATA INTERPRETATION & ANALYSIS

Personal detail

Classes (Age) No of Respondents

18-25 2925-35 4035-45 2245-55 8

55 and above 1

ANALYSIS

Above diagram consists five classes of different age groups. Here 29 customers belong to18-25 age groups, 22 customers fall in the age group 35-45 years.

Other 8 customers comes in the class 45-55 years the age group of 25-35 consists 40

customer reaming customer is in age group 55 and above.

Here majority of customer belong to the group 25-35 years.

0

5

10

15

20

25

30

35

40

45

18-25 25-35 35-45 45-55 55 And Above

[Fig 1]

No of Respondents

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 40/67

40

1. Do you think is it essential to have Life Insurance?

YES NO

Yes No Total

No. of Respondents 90 10 100% of Respondents 90 10 100

ANALYSIS

To this question 90% consumers reported YES and 10% consumers reported NO.

90%

10%

010

20

30

40

50

60

70

80

90

100

yes no

[Fig 2]

No. of Respondentss

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 41/67

41

2. Types of insurance policy respondents have

Policy Type No. of Respondents Share (%)

Life Policy 75 75Non Life Policy 25 25Both 45 45

ANALYSIS

75% of the respondents have only Life Insurance Policy. 25% of the respondents have only Non-

life Policy, while 45% of the respondents have both.

75%

25%

45%

0

10

20

30

40

50

60

70

80

Life policy Non Life Policy Both

[Fig 3]

No. of Respondents

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 42/67

42

3. Which are the companies you invested your money for Life Insurance?

Companies No. of Respondents % of Respondents

Max New York LifeInsurance

37 37

LIC 22 22Bajaj Allianz - -Tata AIG 7 7Kotak Mahindra Life

Insurance

4 4

HDFC Life Insurance 7 7ICICI Prudential Life

Insurance

19 19

SBI 4 4

ANALYSIS

From the above figure we come to know that customer are also investing money in other

life insurance companies. The major player in insurance is the Max New York 37%

holding total sample. The second LIC holding 22% . The third major player ICICI is

holding 19%. HDFC and AIG are having equal share of 7%, Kotak Mahindra Life

Insurance & & SBI are having 4%.

Max New York

Life Insurance

37%

LIC

22%Tata AIG

7%

Kotak Mahindra

Life Insurance

4%

HDFC LifeInsurance

7%

ICICI Prudential

Life Insurance

19%

SBI

4% [Fig 4]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 43/67

43

4. Benefits of insurance received by respondents

Benefits No. Of

Respondents

Share (%)

Cover Future Uncertainty 55 55

Tax Deductions 20 20

Future Investment 25 25

TOTAL 100 100

ANALYSIS

55% of the respondents believe that covering future uncertainty is the biggest benefit of

an insurance policy. Whereas, 20% and 25% of them believe that the other benefits are

Tax deduction and future investments respectively.

cover future

Uncertainty

55%

Tax deducations

20%

Future Investment

25%

[Fig 5]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 44/67

44

5. Why did you choose Max New York Life Insurance?

No of Respondents % Of Respondents

ROI 31 31

Peer Pressure 15 15Tax Benefit 20 20Security /safety 24 24Low Premium 10 10TOTAL 100 100

ANALYSIS

The above diagram shows 31% of respondents choose because of good returns, 15%

because of peer pressure and 20% for tax benefit, 24% for security/safety, remaining 10%

for low premium.

ROI

31%

Peer Pressure

15%Tax Benefit

20%

Security / Safety

24%

LowPremium

10%

[Fig 6]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 45/67

45

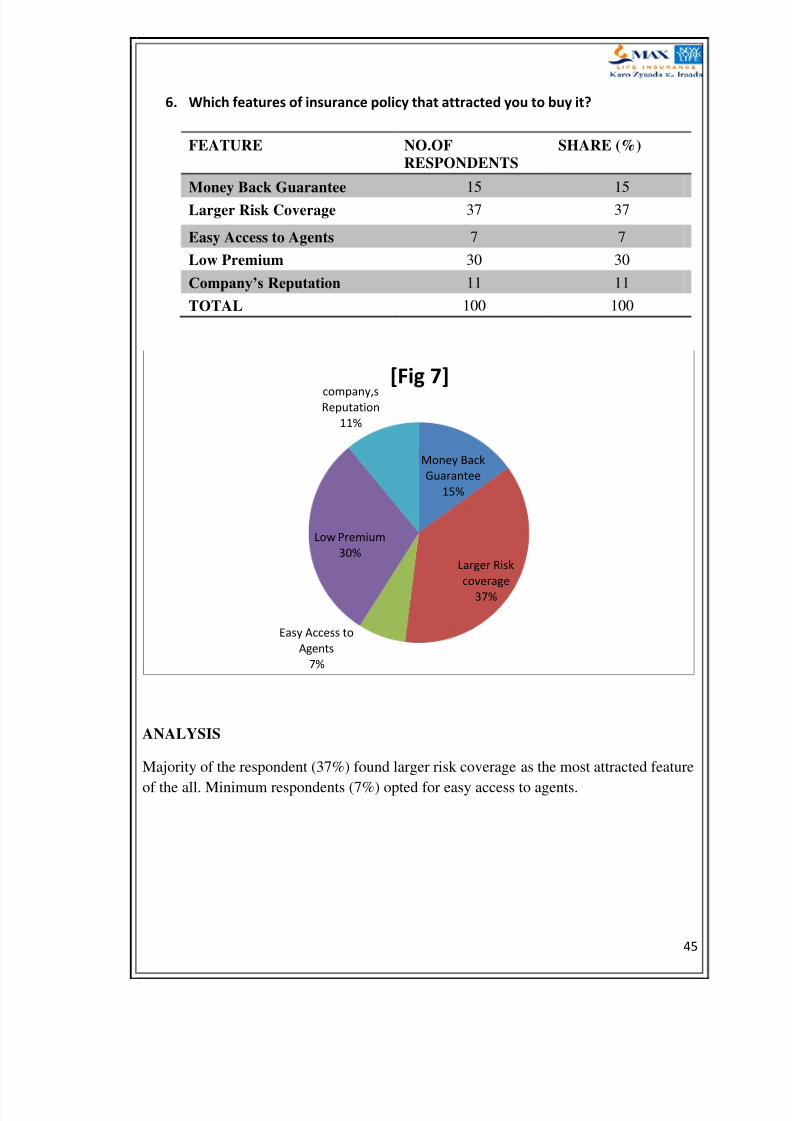

6. Which features of insurance policy that attracted you to buy it?

FEATURE NO.OF

RESPONDENTS

SHARE (%)

Money Back Guarantee 15 15

Larger Risk Coverage 37 37

Easy Access to Agents 7 7

Low Premium 30 30

Company’s Reputation 11 11

TOTAL 100 100

ANALYSIS

Majority of the respondent (37%) found larger risk coverage as the most attracted feature

of the all. Minimum respondents (7%) opted for easy access to agents.

Money Back

Guarantee

15%

Larger Risk

coverage

37%

Easy Access to

Agents

7%

Low Premium

30%

company,sReputation

11%

[Fig 7]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 46/67

46

7. People perception about insurance

Response No. Of Respondents Share (%)

A saving tool 81 81

A tax saving device 74 74

A tool to protect your family 100 100

ANALYSIS

81% of the respondents have perception of Insurance being a saving tool. And 74% of the

respondents have perception of Insurance being a tax saving device.

But 100% of the respondents are with the view that Insurance is a tool to protect your

family.

8174

100

0

20

40

60

80

100

120

A Saving Tool A Tax Saving Device A Tool to Protect Your

Family

[Fig 8]

[Fig 8]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 47/67

47

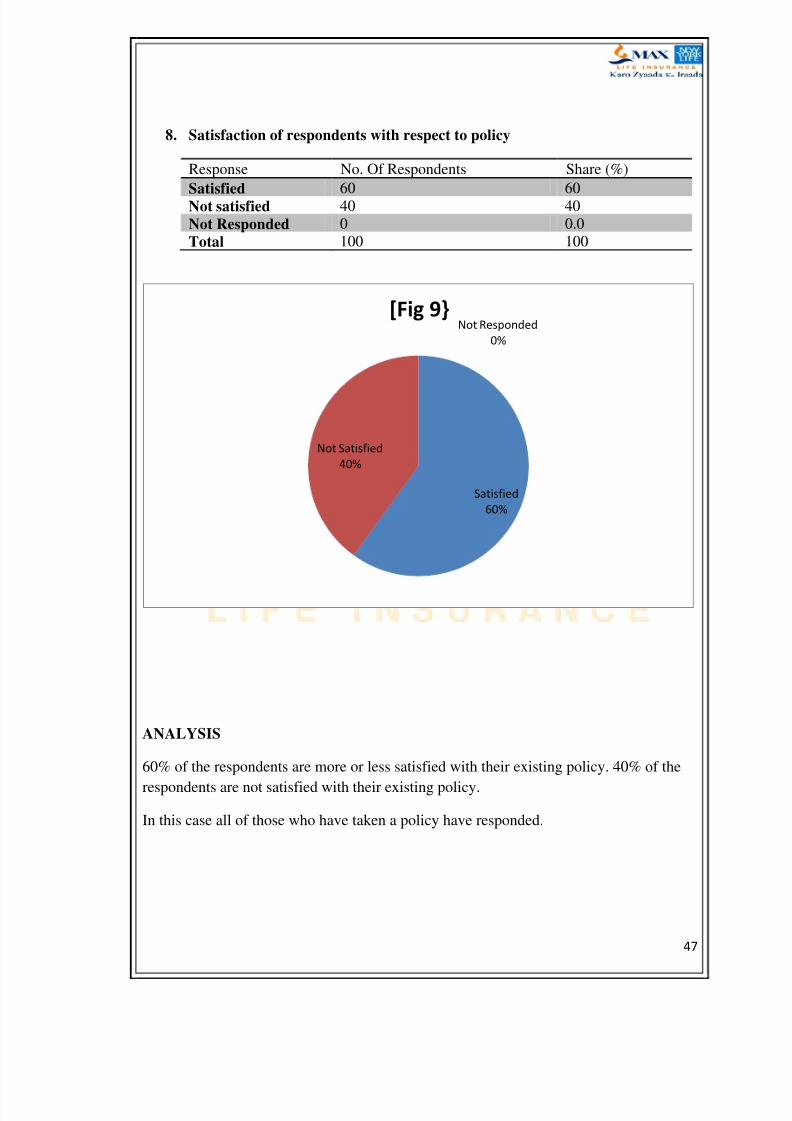

8. Satisfaction of respondents with respect to policy

Response No. Of Respondents Share (%)

Satisfied 60 60Not satisfied 40 40Not Responded 0 0.0Total 100 100

ANALYSIS

60% of the respondents are more or less satisfied with their existing policy. 40% of the

respondents are not satisfied with their existing policy.

In this case all of those who have taken a policy have responded.

Satisfied

60%

Not Satisfied

40%

Not Responded

0%

[Fig 9}

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 48/67

48

9. Satisfaction of +ve respondents with respect to service agent

Response No. Of Respondents Share (%)

Satisfied 44 44Not satisfied 54 54Not Responded 2 2Total 100 100

ANALYSIS

44% of the respondents are satisfied with their existing service agent. 54% of the

respondents are not satisfied with their existing insurance agent.

All of those who have taken a policy have responded only 2% have not responded.

Satisfied

44%

Not Satisfied

54%

Not Responded

2%

[Fig 10}

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 49/67

49

10. Number of respondents paying tax

Response No. Of Respondents Share (%)

Paying tax 100 100Not paying tax 0 0Total 100 100

ANALYSIS

Of the sample size of 100 respondents, all the respondents are paying tax.

Paying Tax

100%

Not Paying Tax

0%

[Fig 11]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 50/67

50

11. How will you rate the services given by Max New York Life Insurance?

No of Respondents % Of Respondents

Poor 3 3Average 30 30Good 47 47Excellent 12 12Outstanding 8 8TOTAL 100 100

ANALYSIS

Out of 100 respondents 47% have ratted Max New York Life Insurance services as

good and 30% have ratted as average. And remaining 12% have ratted as Excellent.

Poor

3%

Average

30%

Good

47%

Excellent

12%

Outstanding

8%

[Fig 12]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 51/67

51

12. What difference you find between Max new York & your previous

Insurance provider.

No of Respondents % Of Respondents

Good Returns 21 21Effective Service/liquidity 15 15Tax Planning 36 36Security/ Safety Benefit 28 28TOTAL 100 100

Note.

Some of customers are having more than one plan more Benefit are expected in one plan.

Total surveys of customers are100.

Good Returns

21%

effective

service/liquidity

15%

Tax planning

36%

security/ Safety

benefit

28%

[Fig 13]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 52/67

52

13. Do have any suggestion for Max New York Life Insurance?

YES NO

YES NO TOTAL

No of Respondents 78 22 100% Of Respondents 78 22 100

ANALYSIS

To this question 78 consumers reported YES and 22 consumers reported NO

Yes78%

No

22%

[Fig 14]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 53/67

53

14. In future, will you purchase policies from max New York Insurance?

YES NO

YES NO TOTAL

No of Respondents 64 36 50% Of Respondents 64 36 100

ANALYSIS

To this question 64 consumers reported YES and 36 consumers reported NO

Yes64%

No

36%

[Fig 15]

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 54/67

54

CHAPER 8

HYPOTHESIS

TESTING

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 55/67

55

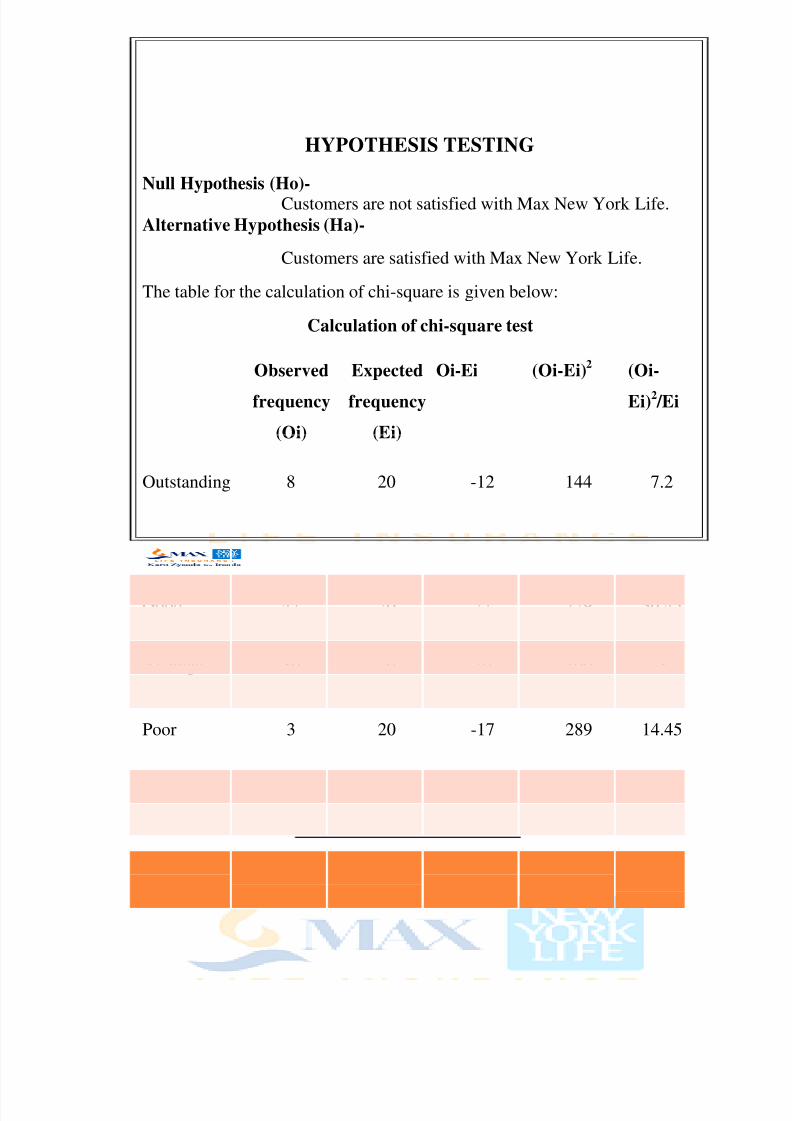

HYPOTHESIS TESTING

Null Hypothesis (Ho)-Customers are not satisfied with Max New York Life.

Alternative Hypothesis (Ha)-

Customers are satisfied with Max New York Life.

The table for the calculation of chi-square is given below:

Calculation of chi-square test

Observed

frequency

(Oi)

Expected

frequency

(Ei)

Oi-Ei (Oi-Ei)2 (Oi-

Ei)2 /Ei

Outstanding 8 20 -12 144 7.2

Excellent 12 20 -8 64 3.2

Good 47 20 27 729 36.45

Average 30 20 10 100 5

Poor 3 20 -17 289 14.45

Total 100 66.3

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 56/67

56

CALCULATION

•

X2

= ∑ (Oi-Ei)2

/Ei = 66.3

• Thus the value of chi square is 66.3

• Degree of freedom : n -1 = 5-1 = 4

• Level of significance = 5%

• The tabulated for degree of freedom 4 at 5% level of significance is

9.488

• So, Calculated Value = 66.3

• Tabulated value = 9.488

• Calculated Value > Tabulated value

• Interpretation: The calculated value is greater than the tabulated

value, so we reject the null hypothesis and accept the alternative

hypothesis.

• We can say that Customers are satisfied with Max New York Life

Insurance Company Ltd.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 57/67

57

CHAPER 9

OBSERVATION

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 58/67

58

OBSERVATIONS

Majority of the customer s belonged to age group of 25-35 years that is 40

consumers.

90 consumers think Life Insurance is essential for them.

Mostly respondents are investing in life insurance companies like Kotak Life

Insurance, LIC, Tata Allianz, Max New York, HDFC, ICICI and SBI.

37 percentages of the total respondents invest in Max New York Life

Insurance Company Ltd. for getting high ROI.

55 Percentages of the respondents believe that covering future uncertainty is the

biggest benefit of an insurance policy

31 Percentages of respondents choose because of good returns

60 percentage respondents satisfied with services given by Max New York

Life Insurance.

64% of respondents are willing to purchased policies from Max New York

Life Insurance in future.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 59/67

59

CHAPER 10

RECOMMENDATION

&

SUGGESTION

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 60/67

60

RECOMMENDATIONS

There is scope to sale insurance policy by concentrating on age group 18-

24 years here potential of customers are there.(Example. Software

professional, Engineers and professionals) Flexi plan can be sold by

concentrating on age group 35-45 years. (Example. Government

employees, executives and businessman)

As major respondents think to have life insurance policy is very

essential there is lot of scope for insurance company.

Max New York Life Insurance should try to build trust among the public

by making people aware of their investment is safe, high return on

investment, Tax Benefits.

As more respondents are investing in Max New York Life Insurance for

getting high return on investment the company should try to provide

attractive returns on investments in future.

Max New York Life Insurance should introduce attractive policies & also

attractive bonus on policies to attractive more potential customers.

Approx 36% of respondents differ with their previous insurance

provider, they field that Max New York Life Insurance providing good tax

benefit for their investment so Max New York Life Insurance if possible

try to provided more tax benefit customer.

64% respondents are willing to purchases Max New York Life

Insurance policies in future this benefit Max New York Life Insurance as

mort potential customer in future.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 61/67

61

CHAPER 11CONCLUSION

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 62/67

62

CONCLUSION

After conducting Sales Process research for Max New York Life Insurance

Company we came to know different needs of consumers, their valuable suggestions,

responses to the different questions. With this information we can conclude that there is

good market awareness about Max New York Life Insurance Company in the market.

Customer satisfaction level of most respondents is higher for Max New York Life

Insurance Company, which is provided by survey. Higher satisfaction level of Max New

York life insurance company was monthly due to Max provides good tax benefit for the

consumers also ROI, security etc.

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 63/67

63

BIBLIOGRAPHY

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 64/67

64

BIBLIOGRAPHY

REFERENCES

BOOKS

MAGAZINE

Business & Economy Magazine

COMPUTER WEBSITE

www.IRDA.com

www.licindia.com

www.hdfcinsurance.com

www.businessindiaonline.com

www.maxnewyorklife.com

www.brandonline.com

www.iciciprulife.com

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 65/67

65

ANNEXURE

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 66/67

66

QUESTIONNAIRE

Personal Detail

Name:

Age 18-25 25-35 35-45 45-55 55 and Above

Phone No.

1. Do you think is it essential to have Life Insurance

Yes No

2. Type of Insurance policy respondents have

Life Non-Life Both

3. Which are the companies you invested your money for Life Insurance?

Max New York Life Insurance LIC

Bajaj Allianz Tata AIG

Kotak Mahindra Life Insurance HDFC Life Insurance

ICICI Prudential Life Insurance SBI

4. Benefits of insurance perceived by Respondents

Cover Future Uncertainty Tax Deductions

Future Investment

5. Why do you Choose Max New York Life Insurance?

ROI Peer Pressure

Tax Benefit Security / Safety

Low Premium

6. Which Features of your policy attracted you buy it?

Low Premium Larger Risk Coverage

Money Back Guarantee Reputation of Company

Easy access to agents

7. What your Perception about insurance?

A Saving Tool A Tax Saving Device

A Tool to Protect Future

8/2/2019 Sales Process Max New

http://slidepdf.com/reader/full/sales-process-max-new 67/67

8. Satisfaction of Respondents with Respect to policy.

Satisfied Non Satisfied

Non Responded

9. Satisfaction of Positive Respondents with Respect to Service Agents.

Satisfied Non Satisfied

Non Responded

10. Number of Respondents Paying Tax.

Pay Tax Not Paying Tax

11. How will you rate the services given by Max New York Life Insurance?

Poor Average

Good Excellent

12. What difference you find between Max and Your Previous Insurance

Provider.

Good Returns (Highest)

Effective Service / Liquidity

Tax Planning

Security / Safety Benefit and Protection on Your Capital

13. Do have any Suggestion for Max New York Life Insurance?

Yes No

14. In future, will you Purchase Policies From Max New York Life Insurance?

Yes No

Recommended