Seventh Multi-year Expert Meeting on Commodities and Development

15-16 April 2015 Geneva

The current situation and outlook for grains, rice and oilseeds

By

Amy Reynolds Senior Economist, International Grains Council

The views expressed are those of the author and do not necessarily reflect the views of UNCTAD.

IGC 2011

www.igc.int

IGC 2015 igc.int

International Grains Council

UNCTAD Multi-Year Expert Meeting on

Commodities and Development

Geneva

15-16 April 2015

Amy Reynolds

International Grains Council

IGC 2011

www.igc.int

IGC 2015 igc.intTotal grains in 2014/15: Record supplies, falling

prices and currency movements

0

500

1000

1500

2000

2500

3000

Barley

Wheat

Maize

Other

Supplies up 3% y/y to 2.4bn t

m t

125.00

175.00

225.00

275.00

325.00

375.00Jan 2000 = 100

Grains* GOI at lowest since mid 2010

* Excluding oilseeds and rice

65

75

85

95

105Index

US$ index at 12-year high

IGC 2011

www.igc.int

IGC 2015 igc.intWheat: world supply and demand summary

m t 5-year

Ave. *

14/15

f’cast

15/16

proj.

Production 687 719 709

Supply 875 906 907

Trade 144 153 150

Consumption 687 708 711

Stocks 188 198 196

of which:

Major exporters **

62 66 65

* Refers to 2010/11-2014/15

** Argentina, Australia, Canada, EU, Kazakhstan, Russia, Ukraine, US.

POINTS TO NOTE

• 2015/16 areas up slightly, but lower

average yields to cut production by

1% y/y.

• Small increase in total consumption in

15/16: higher food use expected, but

lower feeding.

• World stocks seen falling at end

2015/16, but still comfortable.

• Trade to stay high in 15/16, albeit

slightly lower y/y. Growth in milling

wheat demand in Far East Asia and

Africa, but some retreat from high

2014/15 levels expected in Near East

Asia.

IGC 2011

www.igc.int

IGC 2015 igc.intWheat: 2015/16 consumption to be up marginally

0

100

200

300

400

500

600

700

800

900Other

Feed

Food

Food up 1.3%, feed down 4%

-20

-10

0

10

20

30

40

Feed

Food

m t m t

Annual volume changes

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0y/y % change

Long term changes in food demand

Some

upturn in

growth

recently

IGC 2011

www.igc.int

IGC 2015 igc.intWheat: Another year of strong export competition

in 2015/16?

0

5

10

15

20

25

30

35

40

45

50m t

Ukraine

Kazakhstan

Russia

0%

5%

10%

15%

20%

25%

30%

35%

US

EU

14/15 Black Sea exports high, despite

recent measures. But a fall in 15/16?

The EU overtakes the US to become

the largest wheat exporter

% of world exports

IGC 2011

www.igc.int

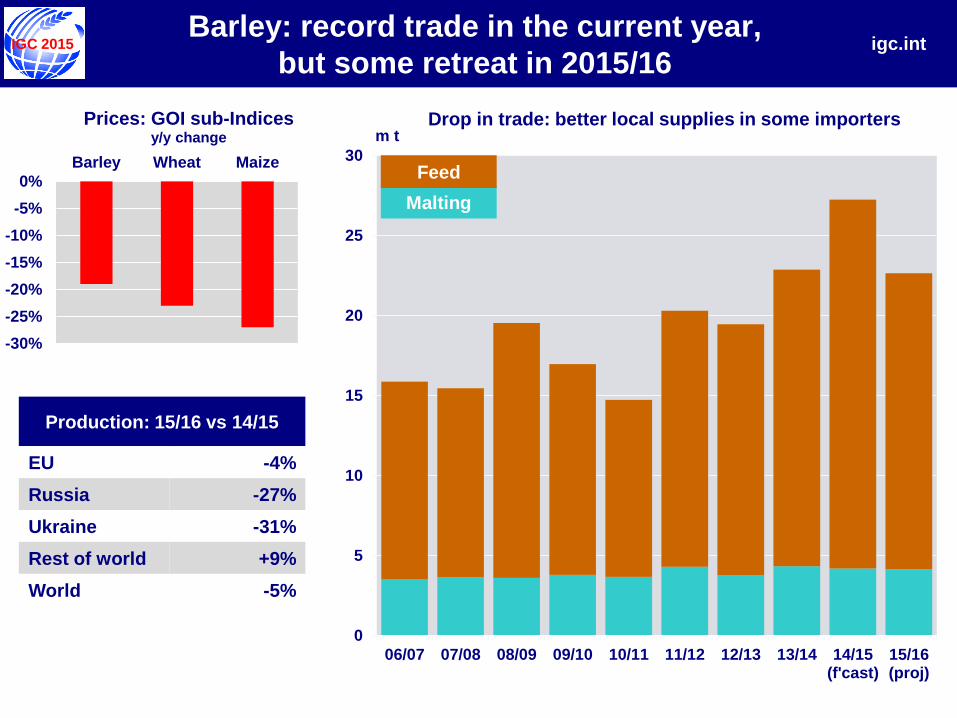

IGC 2015 igc.intBarley: record trade in the current year,

but some retreat in 2015/16

-30%

-25%

-20%

-15%

-10%

-5%

0%

Barley Wheat Maize

Prices: GOI sub-Indicesy/y change

Production: 15/16 vs 14/15

EU -4%

Russia -27%

Ukraine -31%

Rest of world +9%

World -5%

0

5

10

15

20

25

30

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15(f'cast)

15/16(proj)

Malting

Feed

m tDrop in trade: better local supplies in some importers

IGC 2011

www.igc.int

IGC 2015 igc.intMaize: world supply and demand summary

m t 5-year

Ave. *

14/15

f’cast

15/16

proj.

Production 910 990 941

Supply 1,051 1,164 1,131

Trade 105 116 118

Consumption 901 974 961

Stocks 150 191 171

of which:

Major exporters **

44 66 50

* Refers to 2010/11-2014/15

** Argentina, Brazil, Ukraine, US.

POINTS TO NOTE

• World harvested area in 2015/16 to

fall and, assuming some drop in

average yields, production seen down

by 5% y/y.

• Strong demand anticipated, but

slightly lower y/y, reflecting smaller

feed use.

• A 10% contraction in end-2015/16

stocks is projected, led by the major

exporters.

• Global trade placed 1% higher y/y, as

reduced local harvests will trigger

buying in some countries, incl. the EU

and Mexico.

IGC 2011

www.igc.int

IGC 2015 igc.intMaize: Global use at a record in 2014/15, with only a

small decline projected in 2015/16.

0

25

50

75

100

125

0

100

200

300

400

500

600

700

800

900

1,000

90/91 95/96 00/01 05/06 10/11 13/14 14/15f'cast

15/16proj

Industrial

Feed

m t

Food

Other Trade (Jul/Jun) >

-25 yrs -5 yrs-10 yrs-15 yrs-20 yrs

m t

IGC 2011

www.igc.int

IGC 2015 igc.int

150

165

180

195

210

225

240

255

270

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

No

v-1

4

De

c-1

4

Jan

-15

Feb

-15

Ma

r-1

5

Maize: Export prices are falling and spreads

between origins are unusually narrow

US$/t fob

Fob price range (main exporters)

150

175

200

225

250

275

300

325

350

Ma

r-1

0

Se

p-1

0

Ma

r-1

1

Se

p-1

1

Ma

r-1

2

Se

p-1

2

Ma

r-1

3

Se

p-1

3

Ma

r-1

4

Se

p-1

4

Ma

r-1

5

GOI maize sub Index

Jan 2000 = 100

IGC 2011

www.igc.int

IGC 2015 igc.intSorghum: Trade could reach a 30-year high in 2015/16

on surging demand from China

0

2

4

6

8

10

12

07/08 09/10 11/12 13/14 15/16 proj

m t

Japan

Mexico

Others

China

150

175

200

225

250

275

300

325

350

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15

US$/t fob

US maize, fob Gulf

US sorghum, fob Gulf

IGC 2011

www.igc.int

IGC 2015 igc.intRice: world supply and demand summary

m t (milled basis) 5-year

Ave. *

14/15

f’cast

15/16

proj.

Production 468 475 480

Supply 573 585 581

Trade 40 42 43

Consumption 467 483 487

Stocks 107 101 94

of which:

Major exporters **

35 31 26

* Refers to 2010/11-2014/15

** India, Pakistan, Thailand, US, Vietnam.

POINTS TO NOTE

• Total use of rice projected to exceed

production in 2015/16, resulting in a

7m t drop in world carryovers.

• Much of the decline concentrated in

the five major exporters, chiefly

Thailand and India, seen falling to an

eight-year low of 26m t.

• World trade to edge up in 2015/16, to

42.5m t, second highest total on

record, underpinned by demand from

African and Asian buyers.

• Thailand to remain the dominant

exporter, its shipments seen at more

than 11m t in calendar 2016.

IGC 2011

www.igc.int

IGC 2015 igc.intRice: major exporters stocks to

contract again in 2015/16, to an eight-year low

0

5

10

15

20

25

30

35

40

05/06 07/08 09/10 11/12 13/14 15/16proj.

Thailand

India

m t (milled basis)

Others *

* Pakistan, US, Vietnam

Declines due to India and Thailand

0

2

4

6

8

10

12

14

05/06 07/08 09/10 11/12 13/14 15/16proj.

Stocks

Exports

m t (milled basis)

Thailand’s stocks to fall as exports remain high

IGC 2011

www.igc.int

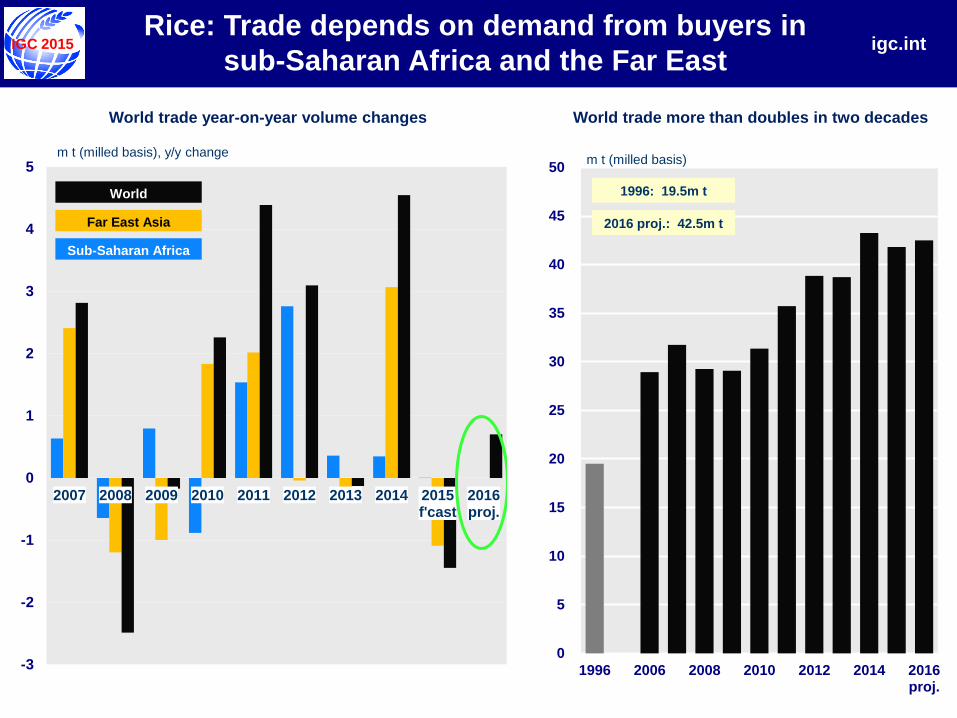

IGC 2015 igc.intRice: Trade depends on demand from buyers in

sub-Saharan Africa and the Far East

-3

-2

-1

0

1

2

3

4

5

2007 2008 2009 2010 2011 2012 2013 2014 2015f'cast

2016proj.

m t (milled basis), y/y change

Far East Asia

World

Sub-Saharan Africa

0

5

10

15

20

25

30

35

40

45

50

1996 2006 2008 2010 2012 2014 2016proj.

m t (milled basis)

1996: 19.5m t

2016 proj.: 42.5m t

World trade more than doubles in two decadesWorld trade year-on-year volume changes

IGC 2011

www.igc.int

IGC 2015 igc.intSoyabeans: world supply and demand summary

m t 5-year

Ave. *

14/15

f’cast

15/16

proj.

Production 276 314 311

Supply 305 344 355

Trade 102 116 122

Consumption 272 300 313

Stocks 32 44 42

of which:

Major exporters **

13 26 25

* Refers to 2010/11-2014/15

** Argentina, Brazil, US.

POINTS TO NOTE

• Production tentatively seen posting a

fractional y/y fall, but remaining high

and the second largest outturn on

record.

• World trade expected to rise to a fresh

peak, but growth still less than in

earlier years.

• China’s imports projected at close to

80m t in 2015/16 – equivalent to 65%

of global traded volumes.

• Aggregate end-season carryovers

likely to remain ample, with stocks

especially high in the major exporters.

IGC 2011

www.igc.int

IGC 2015 igc.int

0

4

8

12

16

05/06 07/08 09/10 11/12 13/14 15/16proj.

Soyabeans: Inventories to remain high

in the major exporters in 2015/16

0

4

8

12

16

05/06 07/08 09/10 11/12 13/14 15/16proj.

Brazilm t

0

4

8

12

16

05/06 07/08 09/10 11/12 13/14 15/16proj.

Argentinam tUS

m t

IGC 2011

www.igc.int

IGC 2015 igc.intSoyabeans: World trade up by 80% in 10 years,

shaped near-entirely by Asian needs

0

25

50

75

100

125

05/06 07/08 09/10 11/12 13/14 15/16proj.

m t

Other Asia

China

World

0

10

20

30

40

50

60

05/06 07/08 09/10 11/12 13/14 15/16proj.

m t

US

Brazil

Brazil and the US compete for top exporter spotImport demand dominated by China

IGC 2011

www.igc.int

IGC 2015 igc.int

For more information, please visit: www.igc.int

or email: [email protected]

Recommended

![Portfolio Manager, Author, Researcher, and Options Expert A … · 2020-06-12 · Zone Approach” , Technical Analysis of StockS & commoditieS, Volume 38: January. [2019]. “Stock](https://img.pdfslide.net/doc/110x75/5f0a7e7c7e708231d42be901/portfolio-manager-author-researcher-and-options-expert-a-2020-06-12-zone-approacha.jpg)