The Global Financial Services Industry in transition

July 27, 2009

By: A V Vedpuriswar

Views of an expert

Interview with Lord Turner, Chairman UK Financial Services Authority.

Source: Financial Times

Day in September

The Global meltdown : The events of September 2008

Event

7 Fannie Mae, Freddie Mac nationalised

14

16

15

22

Bank of America acquires Merrill

Collapse of Reserve Primary, AIG bailout

Collapse of Lehman Brothers

Goldman, Morgan become bank holding companies

25 Washington Mutual placed in receivership

Where are we headed? The worst recessions in the US

Great Depression : 1929 – 1933

Severe recession : 1973 - 1975

Severe recession : 1981 - 1982

Long deflation : 1873 –1879

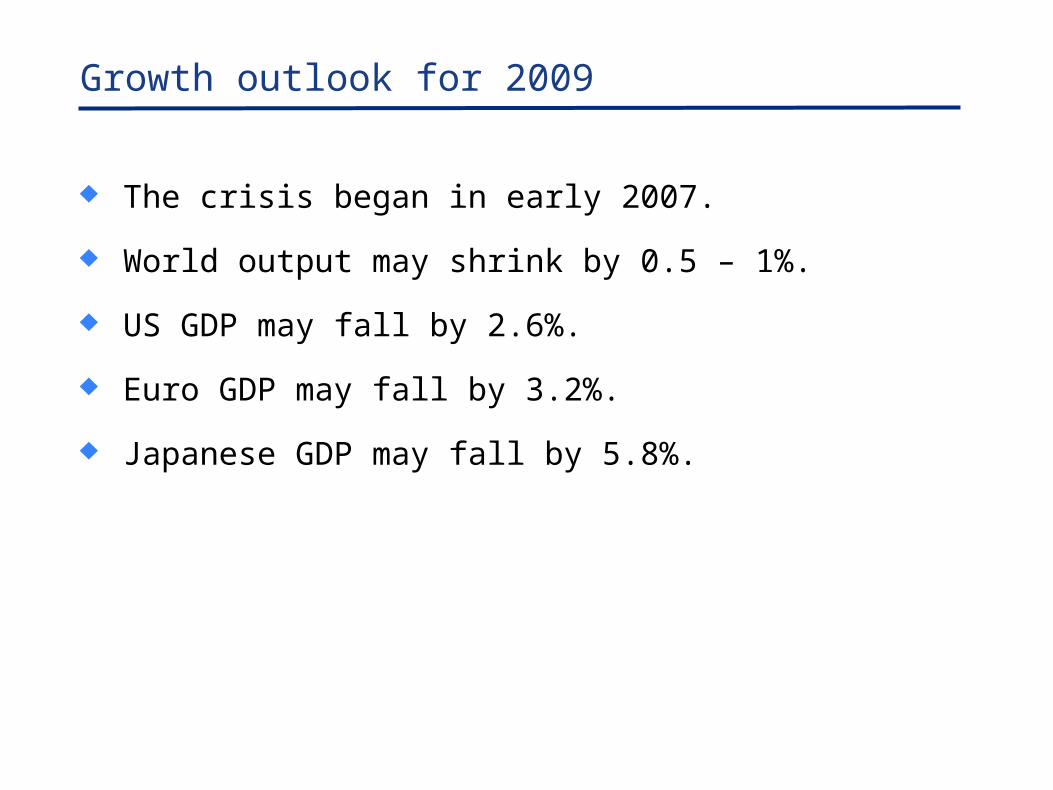

Growth outlook for 2009

The crisis began in early 2007.

World output may shrink by 0.5 – 1%.

US GDP may fall by 2.6%.

Euro GDP may fall by 3.2%.

Japanese GDP may fall by 5.8%.

Medium Term Unemployment Outlook

Philosophical views of the crisis(1) “The more risk we take because we believe the

environment is low risk in character, the less the environment continues to be low risk in character.”

- Peter Bernstein

“You cannot measure something and observe its movements at the same time because the act of measurement changes the character of motion.”

-Wener HeisenbergInterest rates remained too low for too long.

Between 2000 and mid 2008, the worldwide notional value of derivatives went up from $ 95 trillion to $ 684 trillion.

Philosophical views of the crisis(2)

“Every state nurtures forces that lead to its own destruction.”

- Hyman Minsky

“Stability inevitably leads to instability.”

- Hyman Minsky

“Instability leads inevitably to stability.”

- Peter Bernstein

10

Understanding Banking

What is special about banking?

Why is it such a regulated industry?

Channelise savings into productive investments.

Transform short term debt into long term loans.

Manage the risks involved.

Fragility

Government support

Regulation

The Strategic importance of Banking

The Economist July 11, 2009

12

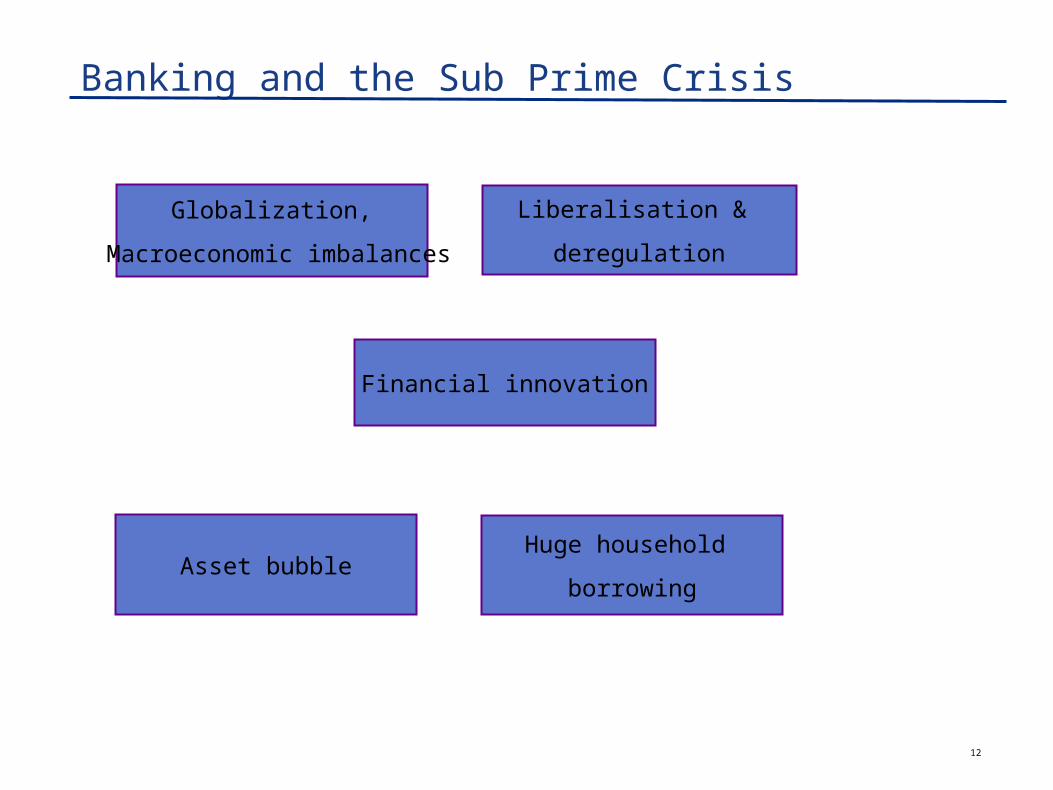

Banking and the Sub Prime Crisis

Globalization,

Macroeconomic imbalances

Liberalisation &

deregulation

Asset bubbleHuge household

borrowing

Financial innovation

13

The sub prime crisis at a glance

Rise in home prices Buyers priced out

Home sales rise Buyers can now afford

New affordable products

The housing bubble

15

The importance of US residential real estate (2007)

Real estate market $ 23 trillion

Mortgage debt $ 10.7 trillion

Homeowner equity $ 12.3 trillion

Securitised mortgage $ 6.3 trillion

Central Banking and Sub Prime :Federal Funds Rate movement (2000-2008)

17

Low inflation and interest rates- Explaining the Conundrum

In 2005 more than 800 million people of the world’s labour force were engaged in export oriented activities.

An increase of 500 million since the fall of the Berlin wall in 1989.

What were the implications?

This reduced world wages, inflation, inflation expectations and interest rates.

Emerging markets also ran big trade surpluses.

What were the implications?

Excess potential savings flooded global financial markets driving real interest rates lower.

The importance of emerging markets

Globalization of capital

Source: The Economist dt Oct 9, 2008

20

Rise of the Sovereign Wealth Funds

Value $m

Date

Target

Target Nationality

Acquirer

11,519 10/12/07 UBS (9%) Switzerland Government of Singapore Investment;

Undisclosed acquirer

7,500 27/11/07 Citigroup (4.9%)

US

Abu Dhabi Investment Authority, UAE

6,200 24/12/07 Merrill Lynch (Stake%) US Temasek Holdings; Domestic investors, Singapore

5,000 19/12/07 Morgan Stanley (9.9%)

US China Investment Corp, China

2,683 07/11/07 China Everbright Bank (70.92%)

China China Investment, Corp, China

2,005 13/07/07 Barclays (1.77%)

UK Temasek Holdings, Singapore

1,416 07/08/07 Standard Chartered (3.74%)

UK Temasek Holdings, Singapore

741 18/05/07 ICICI Bank Ltd (2.87%)

India Dubai International Capital, UAE

339 14/05/07 Pakistan Industrial Credit & Investment (63.38%)

Pakistan Temasek Holdings, Singapore

Top ten stake acquisitions in financial institutions, 2007

Financial innovation and the World of Derivatives

Type of Derivative

H1 2008 End 2007 H1 2001

Interest rate$464.7 trillion

$382.3 trillion

$ 57.305 trillion

Credit $54.6 trillion $62.2 trillion$ 631.497

billion

Equity $11.9 trillion $10 trillion

The Intoxicating world of Credit default swaps

23

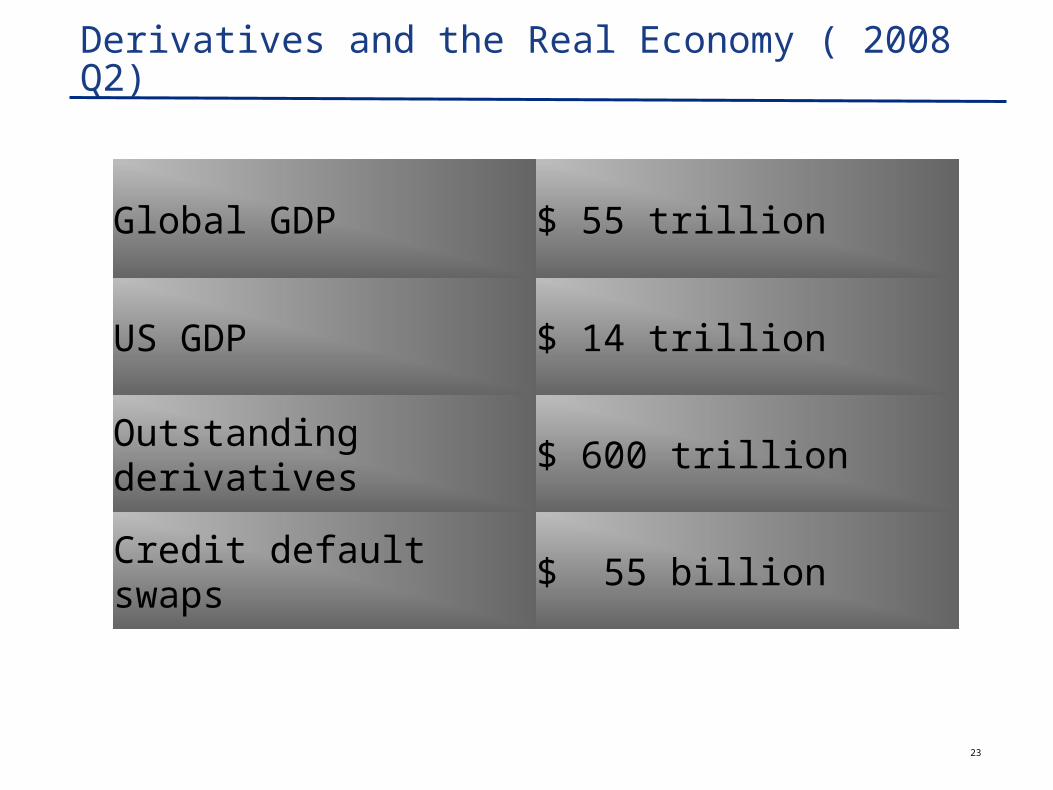

Derivatives and the Real Economy ( 2008 Q2)

Global GDP $ 55 trillion

US GDP $ 14 trillion

Outstanding derivatives

$ 600 trillion

Credit default swaps $ 55 billion

Long Term Outlook for US Government Finances

The looming debt crisis in developed countries

Government debt, % GDP across Western nations

*Forecast; † Difference between forecast primary budget balance in 2014 and primary balance needed for debt sustainability as calculated by the IMF.

Gross debt 2007

Net debt 2007

Gross debt

2014*

Fiscal adjustment required†

Australia

15.4 -6.0 16.6 1.2

Britain 46.9 30.2 87.8 5.7Canada 64.1 23.4 66.2 1.0France 70.1 34.4 89.7 4.5

Germany

65.5 44.5 91.0 1.8

Italy 113.2 87.6 129.4 4.8Japan 170.6 85.9 234.2 14.3Korea 28.9 -37.7 51.8 -0.7Spain 42.7 19.1 69.2 3.1

USA 62.9 43.0 106.7 3.5

The future of the Dollar

Long Term Inflation outlook

What does the rise in implied volatility in recent months mean ?

Ten-year Treasury bond yields have fluctuated between just over 2% and almost 4% since December.

Many countries are experiencing mild deflation.

But investors are worried about fiscal deficits and quantitative easing

Fortune Global 500 Banks - Shrinking Revenues (1)

RANK CORPORATIONS REVENUES

2008

2007

$ Millions

% change from 2007

21 20 HSBC HOLDINGS142,049.

0(3.0)

24 21 BNP PARIBAS136,096.

4(3.3)

35 58 BANCO SANTANDER117,803.

031.9

37 28 BANK OF AMERICA CORP.113,106.

0(5.1)

38 36 ROYAL BANK OF SCOTLAND113,087.

44.3

39 17 CITIGROUP112,372.

0(29.4)

43 43 SOCIETE GENERALE104,378.

30.9

49 32 J.P. MORGAN CHASE & CO.101,491.

0(12.8)

70 26 DEUTSCHE BANK 81,360.4 (33.7)

Fortune Global 500 Banks - Shrinking Revenues(2)

RANK CORPORATIONS REVENUES

2008

2007

$ Millions

% change from 2007

83 70 BARCLAYS75,135.

5(6.5)

92 133INDUSTRIAL AND COMMERCIAL BANK OF CHINA

108 62 MORGAN STANLEY62,262.

0(29.2)

113 134 BANCO BILBAO VIZCAYA ARGENTARIA61,183.

518.9

119 31 UBS59,881.

8(48.9)

125 171 CHINA CONSTRUCTION BANK57,976.

940.4

136 61 GOLDMAN SACHS GROUP53,579.

0(39.1)

141 126 WELLS FARGO51,652.

0(3.6)

164 74 CREDIT SUISSE45,296.

0(42.1)

Fortune Global 500 Banks - Shrinking Revenues(3)

RANK CORPORATIONS REVENUES

2008

2007

$ Millions

% change from 2007

171 175 ROCHE GROUP44,267.

59.8

174 282 BANCO BRASIL43,984.

253.8

211 194 ROYAL BANK OF CANADA36,615.

5(2.4

260 234 AMERICAN EXPRESS31,877.

0(1.4)

354 367 TORONTO-DOMINION BANK25,070.

29.5

363 380 STATE BANK OF INDIA24,577.

79.7

389 390 STANDARD CHARTERED GROUP23,738.

09.0

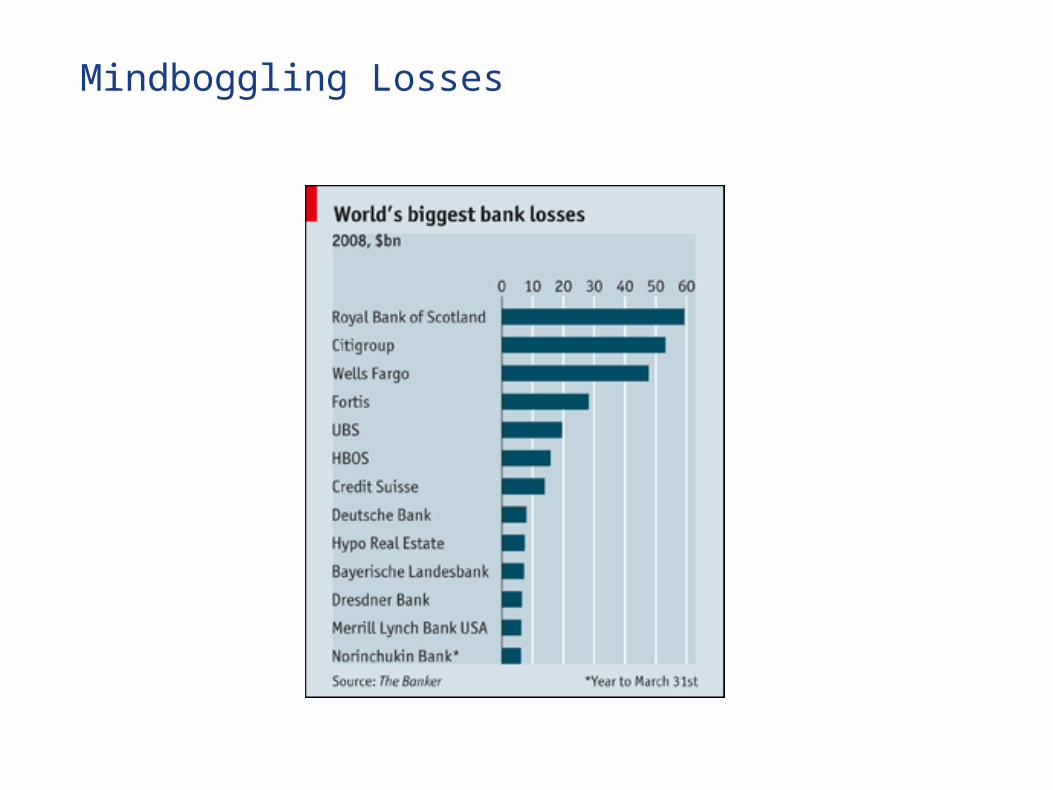

Mindboggling Losses

33

Banking industry market cap

USA

Global Banking : Average leverage ratios in 2008

12:1

Britain

France

Denmark

Switzerland

Germany

24:1

28:1

28:1

29:1

52:1

Source: Niall Ferguson, “The decent of finance,” HBR, Jul-Aug 2009.

100 years back, the leverage ratio was 4:1. In the 1970s, it was 10 – 12 : 1.

In 2006 it was Morgan- 33, Goldman-26, Merrill-32, Bear -34

35

Regulatory implications

Basle I

Basle II

Leverage ratio (Total assets / capital)

Regulation of liquidity

Macro prudential approach

New restrictions on derivatives / OTC trades

Controlling the shadow banking system

Revival of Glass Steagal Act?

36

From asset management to liability management

Quantity of capital

Duration & sources of funding

Lengthen the maturity of deposits

Dependence on more stable deposits

Tier 1 capital

Tier 1 only includes best-quality capital.

Absorbs losses, firm can continue as a going concern.

Is the core measure of a bank's financial strength.

Tier 2 capital

Includes mainly subordinated bonds.

Serves as capital buffer only in a case of bankruptcy.

39

Total assets of leading banks – 1Q09

Source: As reported by companies. Converted into USD, CHF at 1.14 and EUR at 1.32 at the end of Mar 09

1 UBS adjusted reflects PRVs based on Swiss GAAP netting (USD 153bn on 31 Mar 2009). DB adjusted represents US GAAP estimates as reported by company.

0

500

1'000

1'500

2'000

2'500

BoA JPM Citi DBadj.¹

UBSadj.¹

CS GS MS

(USD

bn)

Trading portfolio assets & PRVs Collateral trading Net loans All other assets

40

Source: As reported by companies. Converted into USD, CHF at 1.14 and EUR at 1.32 at the end of Mar 09

Net loans and allowances for loan losses – 1Q09

948

681 626

360 302209

70 31

29

2832

34

2

0

200

400

600

800

1'000

1'200

BoA JPM Citi DB UBS CS GS MS

(US

D b

n)

Net loans Allowance for loan losses

41

Risk weighted assets – end of 2008

Source: As reported by companies. Converted into USD, CHF at 1.07, EUR at 1.39 and GBP at 1.46 at the end of Dec 08

BoA, JPM and C did not disclose RWA by category (not a requirement under Basel I). At the end of 2008, MS and GS were regulated by the SEC as Consolidated Supervised Entities and disclosed capital ratios accordingly. Beginning in 1Q09, they report capital ratios in accordance with the capital adequacy standards for bank holding companies (Basel I)

Credit risk Market risk Operational risk Total RWA (Basel I)

USD bn

957 893

493346

216 152 176

7068

95

33

17726

80 37

184

1'3211'259

996

241279

400430

1'148

1'015

632

283

BoA JPM HSBC RBS Citi Barc DB GS UBS MS CS

42

Capital baseTier 1 ratios – 1Q09

14.1%

10.2% 10.1%

11.4%11.9%

13.7%2

16.7%2

10.5%

11.0%1

CS UBS DB MS GS Citi J PM BoA

Basel II Basel I

Source: Companies reporting. Updated on 15 May 2009

1 11.0% represents pro-forma Tier 1 ratio, taking into account the effects of the announced sale of UBS Pactual2 Beginning in 1Q09, MS and GS report Tier 1 ratio in accordance with the capital adequacy standards for bank holding companies

43

The emerging paradigm in Investment banking

Shift to less risky but profitable businesses.

And which need less capital

– Advisory services

– Providing trading platform

– Custody business

– Less proprietary trading

Global Merger Trends

The value of global mergers and acquisitions (M&A) fell by 35% in the first half of 2009 to $1,140 billion.

The number of deals collapsed by more than 15% in the three months to June.

Buy-outs by private-equity firms have fallen sharply by 82% to $24 billion in the six months to June.

Finance remains the centre of action , accounting for almost a fifth of deals by value, followed by health care and mining.

47

Towards Risk adjusted compensation

48

Emerging trends in Global Wealth Management

HNI lost $10 trillion (quarter of their wealth) during the crisis.

Global number of billionaires fell to 793 from 1125.

Clients highly dissatisfied with service.

Heightened client concerns because of Bernard Madoff.

Clients’ sense of financial security undermined by crisis.

49

Diminishing Trust

Move into “alternative” assets backfired for many clients.

Correlation increased, few diversification benefits.

Performance criteria for wealth managers vague.

Trust is critically important.

But trust is low today.

50

Future Outlook (Offshore banking)

There are doubts about the long term future of bank secrecy laws.

Off shore wealth is estimated at $5 - $7 trillion.

OECD has identified 40 tax havens.

49 agreements have been signed to exchange tax information since 2000.

UBS had to pay a fine of $780 million and disclose the names of 250 customers.

Germans have targeted bank accounts in Liechtenstein.

Swiss competitive advantage is under threat.

51

Future Outlook (Banking Business Models)

Standalone investment banks?

Pure retail banks?

Universal banks?

52

Future Outlook (Returns for shareholders)

Less leverage

More capital

Lower fees due to distrust of customers and government intervention

Higher barriers to entry

Overall lower return on equity

53

Conclusion : Revisiting Adam Smith

Markets as a self correcting mechanism

Smith did not advocate sufficiency of market economy

Values & institutions play a key role– Prudence

– Humanity

– Justice

– Generosity

– Public spirit

Reach & limits of market economy need to be understood carefully

54

Conclusion : Back to Keynesianism?

Human behavior is not completely rational.

Capitalism produces not only what people want but also what they think they want .

This can lead to bubbles.

Without government intervention, capitalist economies are inherently unstable.

Role of animal spirits must not be underestimated.

Recommended