7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 1/12

Top stories

• Regulators move to enhance the system

• NAIC principals weigh in on systemic risk

• Credit scoring debate takes center stage

• NAIC ponders natural catastrophe solutions

• Next steps for climate change d isclosure

• Reinsurance modernization efforts advance

Also in this issue

• NAIC accounting update

What’s next

• July 9-12, 2009: NCOIL 2009 Summer National Meeting,Philadelphia, PA

• September 21-24: NAIC 2009 Fall National Meeting,Washington, D.C.

Minneapolis, MN – With the question of a federal

regulatory mechanism for insurance actively being

discussed in Washington, D.C., regulators and industry

representatives attending the National Association

of Insurance Commissioner’s Summer 2009 National

Meeting focused on measures meant to improve

and strengthen the state-based system for insurance

regulation that’s been in place for more than 150 years.

From considering enhancements to the supervision of

insurance groups to adopting a complete revision to the

NAIC’s approach to derivative investments, regulatorscontinued the work of dusting off and revising existing

models and creating new ones – all in the name of

meeting the challenges of today’s marketplace.

Another focus has been to maintain consumer

protection and the strength and solvency of the

insurance industry in the face of a significant natural

catastrophe, or “mega cat.” To this end – and after

several years of deliberation – regulators passed out

of a parent committee a catastrophe white paper that

represents divergent views on addressing this important

area of industry risk. In this arena, too, the NAIC is

considering the construction of a catastrophe model

for varied natural disasters. The tool would be of similar

caliber to those used by professional modeling firms

and would allow regulators a window on learning

the risks so that they might better know what are the

appropriate rates and policy pricing for insurers who

cover these risks.

The topic of climate change continued to take the floor

as well. After adopting its climate change disclosure

survey at the spring meeting in March, the NAIC and

industry continued discussion on next steps, includinga regulator proposal to have companies file their

disclosure forms on the NAIC web site, rather than with

the regulator of their state domicile, as had previously

been discussed.

While the answer to the question of a federal regulator

has yet to be revealed, items serving to keep up the

momentum at future meetings include credit-based

insurance scoring; the advancement of the Standard

Valuation Law and changes to the group insurance

model law.

Summer 2009

NAIC Update

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 2/12

2

With globalization ever at hand,regulators at the summer meetingdrove forward several model lawsmeant to modernize insuranceregulation.

Top stories

Regulators move to enhance the system

With globalization of the insurance industry ever at hand

and proposals both great and small in Washington, D.C.

to do everything from tweak to overhaul the current

state-based system of insurance regulation, regulators

at the summer meeting drove forward several important

model laws and revisions meant to modernize insurance

regulation. Some top items included: The passage of

a complete revision of the derivatives model law; the

advancement of principles-based reserving; and new

attention given to the supervision of insurance groups.

Derivatives

Regulators at the joint Executive Committee/Plenary

adopted amendments to the Derivatives Instrument Model

Regulation as part of a broader effort to modernize the

NAIC regulatory framework for these nancial instruments.

Since the 1990s, derivatives, including credit default swaps,

have become a signicant nancial instrument for insurers,

and therefore require more uniform and stringent oversight,

according to the NAIC.

One of the chief changes to the law is to require of insurers

a derivative use plan that has been reviewed and approved

by the state insurance regulator before a company would

be authorized to engage in derivatives transactions. The

plan must also be approved by a company’s board of

directors. The board would also be required to take action

to correct any deciencies in internal controls relative toderivative transactions.

Standard valuation law

Regulators took a signicant step towards making

principles-based reserving approach to the valuation of life

and annuity products a reality.

Passed out of the Life and Health Actuarial Task Force

following years of discussion, the revised Standard

Valuation Law was met with caution by the parent Life

Insurance and Annuities (A) Committee. Rather than pass

the item out to the Executive Committee, the A Committee

opted to open the item for a 30-day comment period to

be followed by a teleconference by the Principles-Based

Reserving Working Group and the Solvency Modernization

Initiative Task Force.

Insurance groups

The NAIC’s Group Solvency Issues working group is movingahead with its investigation into the feasibility of changes

to the NAIC Holding Company Model Act to better reect

challenges being seen in the marketplace.

At its meeting during the summer conference, the group

set its sights on scheduling an interim meeting that would

position regulators and industry to discuss divergent points

of view with hopes of coming to a consensus.

Comments received so far include those from regulators in

Illinois, Kansas, Missouri, Nebraska, North Carolina, South

Carolina, Virginia, Washington, and Wisconsin. Meanwhile,

interested parties weighing in include the Property Casualty

Insurers Association of America, the American Insurance

Association and the American Council of Life Insurers.

Emboldening oversight of insurer groups has been one

of the major goals of the NAIC’s Solvency Modernization

Initiative since it was formed amid notable changes in

the marketplace in the fall of 2008. The 2009 charge

of the working group regarding insurance groups is to

study the need to modify the model act to the extent it

addresses issues identied in the current environment. At

the conclusion of the study, the working group is to decide

whether a model law development/revision is in order.

As used in this document, “Deloitte” means Deloitte LLP and its subsidiaries.

Please review www.deloitte.com/us/about for a detailed description of the legal

structure of Deloitte LLP and its subsidiaries.

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 3/12

3

State regulators weigh in on systemic risk

The future of the state-based insurance regulation and

how that ts into what is being contemplated by the

Obama administration and the 111th Congress in regards

to changes in the oversight of the nancial sector are very

much top of mind for ofcials at the NAIC.

As the current environment has sparked considerable

interest to repair what are seen as gaps in the broader

nancial system, NAIC principals have found themselves

facing federal lawmakers a number of times in recent

months in an effort to both educate and to state the case

for state-based insurance regulation.

And while attendees at the Minneapolis meeting seemed to

fall on both sides of the issue – some in favor of a federal

regulator, others wanting to stick with the current regulatoryregime – NAIC President and New Hampshire Insurance

Regulator Roger Sevigny and NAIC CEO Terri Vaughan made

their thoughts very clear at the summer meeting.

“The rhetoric being tossed back and forth on Capitol Hill

questions the oversight offered by a state-based system,”

Sevigny said during the summer meeting opening session.

“As a whole, the insurance industry continues to be strong

in this erratic economy – in part because of the strengths of

our system. So the question is, why reinvent the wheel?”

For her part, Vaughan asked state regulators in attendance

to offer their input on how states might t into the council

approach being discussed on the federal level.

In response, NCOIL past President and Rhode Island Rep.

Brian Kennedy said that his group continues to “be against

insurance regulation at a national level but we’re warming

to the idea of a council, sharing thoughts on a state and

federal level.”

The inter-agency council approach has been advocated by

Sen. Susan Collins (R-Maine) as part of a broader package

to reform U.S. nancial regulation. More recently, President

Obama has released a white paper via the U.S. Treasury

which suggests a “council of regulators.”

NCOIL ofcials cautioned, however, that while it was

good to have a “seat at the table” on the federal front; it

should be kept very clear that the overall system of state-

based insurance supervision should continue to be the key

overseer of insurance regulation.

Credit scoring debate takes center stage

The heated topic of credit-based insurance was vetted at

no less than six sessions of the summer meeting as industry

representatives, consumers and regulators clashed on thefairness of the long-time underwriting tool.

While the debate is not new, recent attention to the issue

stems in part from the current challenges in the marketplace

and fears that the newly jobless might unduly be penalized

as their bills go unpaid and their credit scores begin to drop

– thus, putting them in line to pay higher policy premiums.

At the main event – a two-hour hearing – the NAIC’s

Property and Casualty Insurance Committee and Market

Regulation and Consumer Affairs Committee took

comments from an array of interested parties. However, the

joint group failed to take action on the matter as testimony

ran long. A continuation of the debate is scheduled for a

conference call in the near future.

As it stands, consumer representatives, believing that the

practice unfairly discriminates against low income and

minority populations, are urging regulators to ban the use

of credit-based insurance scoring or at the minimum, issue a

temporary moratorium on the tool until a consensus can be

reached by competing interests.

Proponents of the underwriting tool, such as the National

Association of Mutual Insurance Companies, cite the success

of a credit-based insurance scoring model issued by the

National Conference of Insurance Legislators, which balancesthe interests of both consumer and industry. Since adopted

by NCOIL in 2003, 22 states have passed some version of the

NCOIL law. Speaking at the meeting, Candace Thorson of

NCOIL noted that an amendment to the model that targets

consumers whose fallen credit is traceable to the nancial cri-

sis is expected to be considered by legislators at the group’s

summer meeting in July.

Top stories, cont.

NAIC principals leading effort to maintain state-based regulation

Therese M. (Terri) Vaughan

NAIC Chief Executive Ofcer

Roger Sevigny, NAIC President,

New Hampshire Insurance

Commissioner

Photos courtesy of the NAIC

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 4/12

4

NAIC ponders natural catastrophe solutions

Fifteen is a charm. At least it is for the NAIC’s Property and

Casualty Insurance (C) Committee, which, after 14 tries over

four years, has adopted a white paper that opines on what

consumers, insurers, and elected ofcials might do to curb

the impact of a so-called, "mega catastrophe."

While on the radar screen of the NAIC for years, the effort

toward the current white paper draft, “Natural Catastrophe

Risk: Creating a Comprehensive National Plan,” began in

2005, shortly following Hurricane Katrina. Since that time,

the document has been vetted by industry, state regulators,

consumer representatives, and other state governing

groups, such as the National Conference of Insurance

Legislators. Over time, controversial provisions, as with the

suggestion that insurers provide an “all perils” for properties

in high-risk zones, drew much disagreement, making

consensus difcult to achieve.

The nal framework outlines steps that regulators believe

must be taken to accomplish the dual purpose of providing

a comprehensive plan that protects the public, while

simultaneously providing assurances (such as a federal

backstop) to the insurance industry in the event of a

catastrophic natural event such as a major hurricane or

earthquake. The multilayered plan includes provisions

such as incentives to hurricane-proof properties (such with

the installation of wind-resistant garage doors), providing

tax-deferred catastrophe reserves for insurers, and making

mandatory offers of all-perils homeowner’s insurance,creating state and regional catastrophe backstops, and

installing a national catastrophe backstop.

The nal draft passed out of C Committee on June 15,

ofcially cited as version 15a, contains a good portion of

the original framework, plus an assortment of opinions and

11th-hour edits made by a collection of states. The white

paper now includes a disclaimer on the cover which notes

that the document represents various opinions and a number

of approaches to addressing natural catastrophe risk.

Next steps for climate change disclosure

With mandatory disclosure of large insurers’ climate

change-related business practices slated to begin in the

2009 reporting year, the NAIC Climate Change and Global

Warming Task Force is contemplating reporting options.

At the task force’s session during the summer confer-

ence, regulators gathered information on which insurance

companies would volunteer to do a test run of the survey

submissions. So far, a collection of life and health insurers

have stepped up to the plate to volunteer and are expected to

submit anonymous results to be released by the fall meeting.

NAIC staff at the session presented regulators with options

by which survey results might be submitted, compiled, and

distributed to the public. These include use of the NAIC’s

Consumer Information Source website, which is availableto regulators and the public, and/or use of the System for

Electronic Rate Form Filing.

As the program was originally slated to operate though

each insurers’ state domiciliary regulator, industry groups

such as the Property Casualty Insurers Association (PCI) have

expressed concern that the test run lays the groundwork for

the NAIC to eventually become the repository of company-

sensitive information.

“(This) opens the much larger question of (the NAIC’s)

authority as a trade association to collate and make

available industry data,” PCI d irector of policy analysis David

Kodama said in a statement issued by the trade.

As to questions on the uniformity of responses, task force

Chairman and Pennsylvania Insurance Commissioner Joel

Ario indicated that the NAIC would not be issuing guidance

as to how to ll out the survey questions.

Adopted at the spring national meeting, the Climate Risk

Disclosure Proposal includes eight questions that require

companies to disclose everything from the actions they

are taking to manage climate change risks to how they are

building climate change awareness into their investment

management strategies.

The proposal requires mandatory disclosure by insures with

premiums over $500 million in the 2009 reporting year

and insurers with premiums over $300 million in the 2010

reporting year.

NAIC Minneapolis meeting by the numbers

Average annual temperature in Minneapolis: 45ºAttendees: 1,500

Sessions: 72

Number of drafts to catastrophe white paper: 15

Changes to 2009 winter meeting location: 1

(Honolulu to San Francisco)

Top stories, cont.

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 5/12

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 6/12

6

NAIC accounting update

The National Association of Insurance Commissioners

(NAIC) held their 2009 Summer National Meeting in

Minneapolis, Minnesota from June 12 to June 16, 2009.

This section of the newsletter contains a summary of

the signicant matters impacting statutory accounting

discussed at the NAIC Summer 2009 National Meeting.

Summary

• The Statutory Accounting Principles Working Group

(SAPWG) conducted hearings and meetings to address

comments on certain substantive and nonsubstantive

issues (refer to pages 7 through 9 for details). The

comment deadline for the issues newly exposed at the

meeting is August 7, 2009. Refer to page 9 for details of

certain specic hot topics facing the industry including

– Re-REMIC transactions

– Changes to deferred tax asset admissibility

– Deferred premium asset and unearned premium reserve

• The Emerging Accounting Issues Working Group

(EAIWG) held a meeting to take action on certain

tentative positions and to address certain outstanding

issues (refer to page 10 for details). The comment

deadline for the issues newly exposed at the meeting is

August 7, 2009.

• The NAIC/AICPA Working Group updated the previously

provided results of a survey sent out to the states

regarding how the states plan on incorporating the

NAIC Model Audit Rule (MAR) in their state. Surveys are

being sent quarterly and the results of the May 2009

survey were as follows (includes District of Columbia in

the survey):

– Statute/Law – 13 states

– Regulation/Rule – 32 states

– Combination – 6 states

The survey also addresses when states plan to present the

MAR amendments to their legislature or when they plan to

change the related regulation. As of the May 2009 survey,

twenty-three (23) states have adopted changes to address

the MAR and the remaining twenty-eight (28) states

(includes District of Columbia in the survey) are expected to

present amendments or adopt changes to address the MAR

in 2009.

For those states that have presented the adopted changes

to the MAR to their respective legislature, none of the states

indicated any signicant problems with the proposed rule.

NAIC staff will continue to revise the implementation

guide and, specically, will address the questions related

to certain exposed wording which appeared to contradict

the disclaimer within Section 14 indicating that the section

shall not apply to SOX Compliant Entities or wholly owned

subsidiaries of SOX Compliant Entities. Regulators also

commented that it is their interpretation and expectation

that management’s report on internal control would

consider materiality at the regulated entity level and not on

a group basis.

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 7/12

7

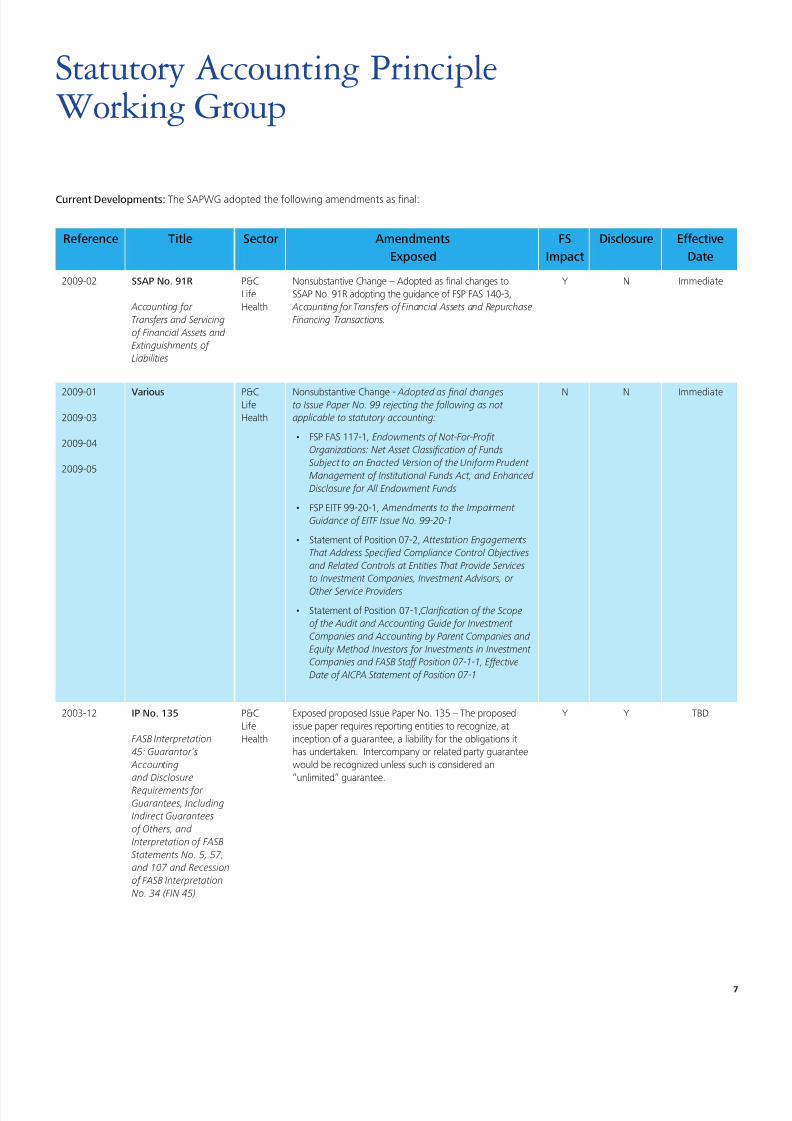

Statutory Accounting PrincipleWorking Group

Reference Title Sector Amendments

Exposed

FS

Impact

Disclosure Effective

Date

2009-02 SSAP No. 91R

Accounting or

Transers and Servicing

o Financial Assets and

Extinguishments o

Liabilities

P&CLifeHealth

Nonsubstantive Change – Adopted as nal changes toSSAP No. 91R adopting the guidance of FSP FAS 140-3,

Accounting or Transers o Financial Assets and Repurchase

Financing Transactions.

Y N Immediate

2009-01

2009-03

2009-04

2009-05

Various P&CLifeHealth

Nonsubstantive Change - Adopted as fnal changesto Issue Paper No. 99 rejecting the ollowing as not

applicable to statutory accounting:

FSP FAS 117-1,• Endowments o Not-For-Proft

Organizations: Net Asset Classifcation o Funds

Subject to an Enacted Version o the Uniorm Prudent

Management o Institutional Funds Act, and Enhanced

Disclosure or All Endowment Funds

FSP EITF 99-20-1,• Amendments to the Impairment

Guidance o EITF Issue No. 99-20-1

Statement of Position 07-2,• Attestation Engagements

That Address Specifed Compliance Control Objectives

and Related Controls at Entities That Provide Services

to Investment Companies, Investment Advisors, or

Other Service Providers

Statement of Position 07-1,• Clarifcation o the Scope

o the Audit and Accounting Guide or Investment

Companies and Accounting by Parent Companies and

Equity Method Investors or Investments in Investment

Companies and FASB Sta Position 07-1-1, Eective

Date o AICPA Statement o Position 07-1

N N Immediate

2003-12 IP No. 135

FASB Interpretation

45: Guarantor’s

Accounting

and Disclosure

Requirements or

Guarantees, Including

Indirect Guarantees

o Others, and

Interpretation o FASB

Statements No. 5, 57,

and 107 and Recession

o FASB Interpretation

No. 34 (FIN 45)

P&CLifeHealth

Exposed proposed Issue Paper No. 135 – The proposedissue paper requires reporting entities to recognize, atinception of a guarantee, a liability for the obligations ithas undertaken. Intercompany or related party guaranteewould be recognized unless such is considered an“unlimited” guarantee.

Y Y TBD

Current Developments: The SAPWG adopted the following amendments as nal:

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 8/12

8

Reference Title Sector AmendmentsExposed

FSImpact

Disclosure EffectiveDate

2008-28 IP No. 137

Transer o Property and

Casualty Reinsurance

Agreements in Run-o

P&C Substantive Change - This issue paper proposes amendingSSAP No. 62, Property and Casualty Reinsurance, allowingrun-off reinsurance contracts, meeting specied criteria, toreceive prospective accounting treatment.

Y Y 2010

2007-24 IP No. 138

Fair Value

Measurements

P&CLifeHealth

Substantive Change – This issue paper proposes adoptingwith modication FASB Statement No. 157, Fair Value

Measurements, and FSP FAS 157-4, Determining Fair

Value When the Volume and Level o Activity or the Asset

or Liability Have Signifcantly Decreased and Identiying

Transactions That Are Not Orderly . The denition of fair

value and the three-level fair value hierarchy are acceptedfor statutory accounting. This issue paper rejects theconsideration of an entities own credit risk in determiningthe fair value of a liability.

Y Y TBD

2009-09 SAAP No. 60

Financial Guaranty

Insurance

P&CLife

Nonsubstantive Change – Exposed revisions proposingthe disclosures similar to the intent of disclosures requiredby FASB No. 163, Accounting or Financial Guarantee

Contracts, but modied to be applicable under currentstatutory accounting guidance for nancial guaranteeinsurance contracts. This change impacts disclosures only,with review of possible accounting changes occurring at alater date.

N Y 2009

2009-08 FSP SOP 94-3-1 andAAG HCO-1

Omnibus Changes

to Consolidation

and Equity Method

Guidance or Not-For-

Proft Organizations

P&CLifeHealth

Nonsubstantive Change - Exposed changes to IssuePaper No. 99 rejecting as not applicable to statutoryaccounting.

N N TBD

Current Developments: The SAPWG adopted the following amendments as nal:

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 9/12

9

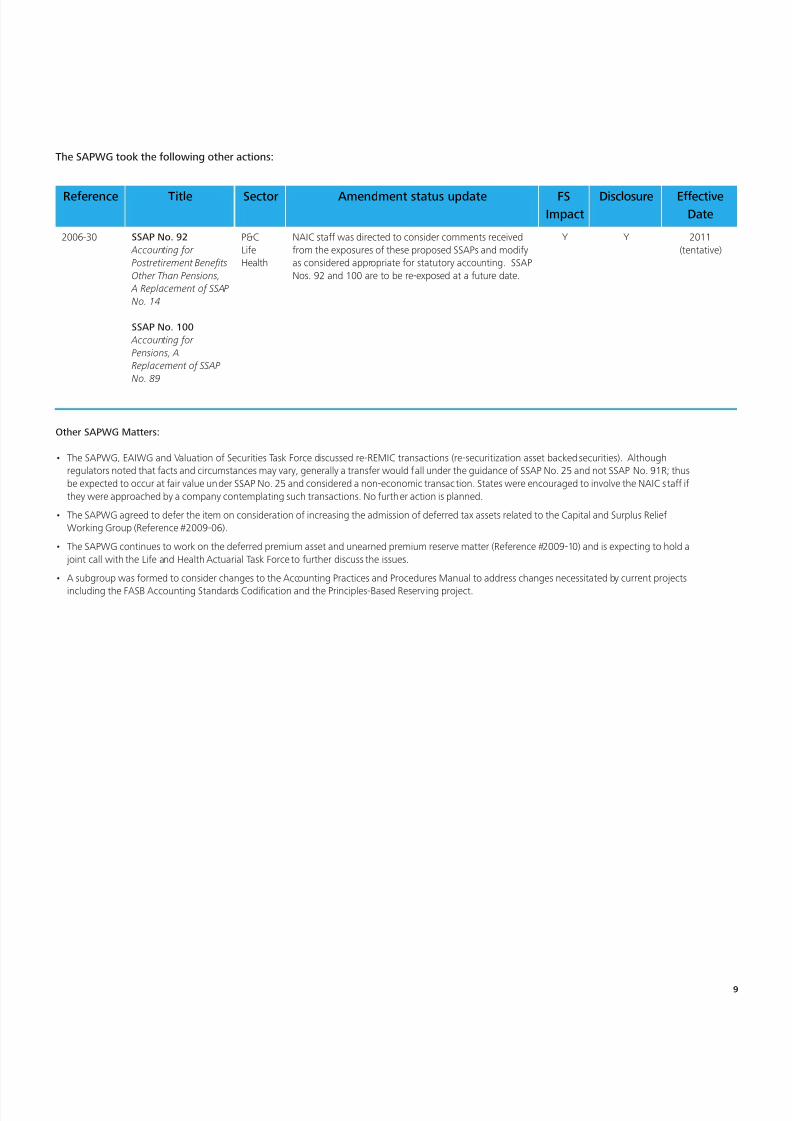

Reference Title Sector Amendment status update FSImpact

Disclosure EffectiveDate

2006-30 SSAP No. 92

Accounting or

Postretirement Benefts

Other Than Pensions,

A Replacement o SSAP

No. 14

SSAP No. 100

Accounting or

Pensions, A

Replacement o SSAP

No. 89

P&CLifeHealth

NAIC staff was directed to consider comments receivedfrom the exposures of these proposed SSAPs and modifyas considered appropriate for statutory accounting. SSAPNos. 92 and 100 are to be re-exposed at a future date.

Y Y 2011(tentative)

The SAPWG took the following other actions:

Other SAPWG Matters:

• The SAPWG, EAIWG and Valuation of Securities Task Force discussed re-REMIC transactions (re-securitization asset backed securities). Althoughregulators noted that facts and circumstances may vary, generally a transfer would fall under the guidance of SSAP No. 25 and not SSAP No. 91R; thusbe expected to occur at fair value under SSAP No. 25 and considered a non-economic transaction. States were encouraged to involve the NAIC staff ifthey were approached by a company contemplating such transactions. No further action is planned.

• The SAPWG agreed to defer the item on consideration of increasing the admission of deferred tax assets related to the Capital and Surplus ReliefWorking Group (Reference #2009-06).

• The SAPWG continues to work on the deferred premium asset and unearned premium reserve matter (Reference #2009-10) and is expecting to hold a joint call with the Life and Health Actuarial Task Force to further discuss the issues.

• A subgroup was formed to consider changes to the Accounting Practices and Procedures Manual to address changes necessitated by current projects

including the FASB Accounting Standards Codication and the Principles-Based Reserv ing project.

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 10/12

10

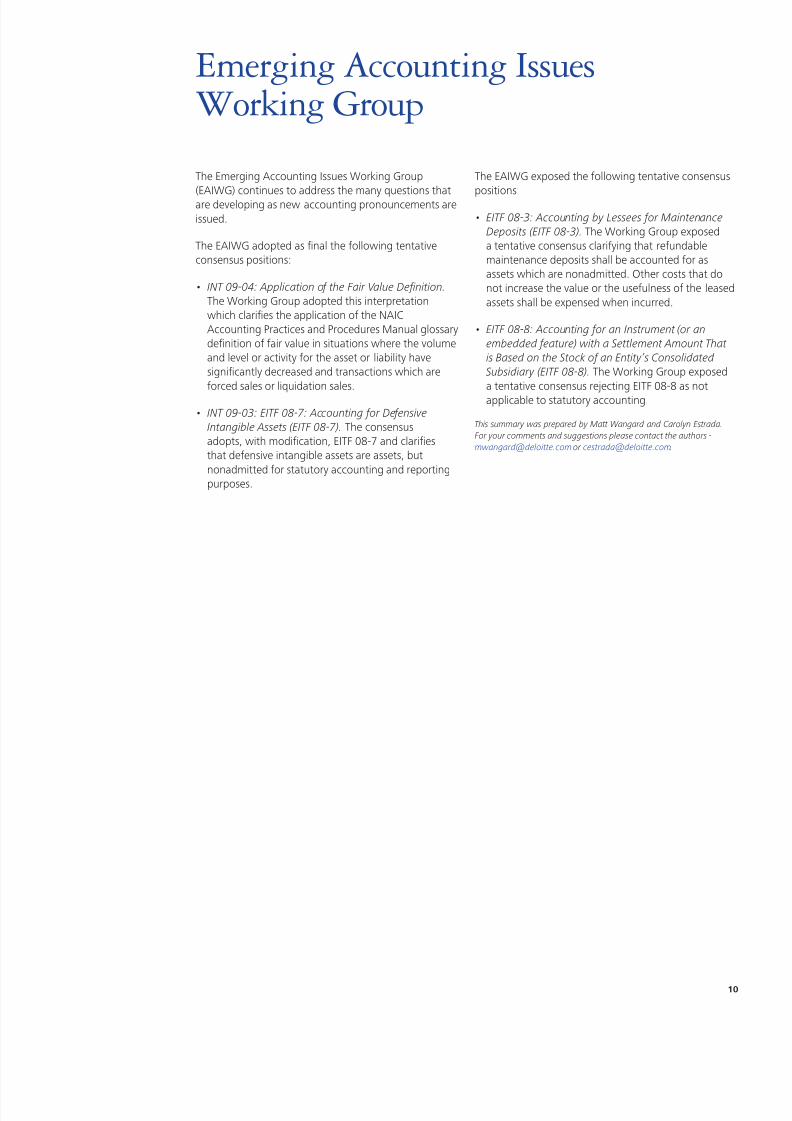

Emerging Accounting IssuesWorking Group

The Emerging Accounting Issues Working Group

(EAIWG) continues to address the many questions thatare developing as new accounting pronouncements areissued.

The EAIWG adopted as nal the following tentativeconsensus positions:

• INT09-04:ApplicationoftheFairValueDenition.

The Working Group adopted this interpretationwhich claries the application of the NAICAccounting Practices and Procedures Manual glossarydenition of fair value in situations where the volumeand level or activity for the asset or liability havesignicantly decreased and transactions which areforced sales or liquidation sales.

• INT09-03:EITF08-7:AccountingforDefensive

Intangible Assets (EITF 08-7). The consensusadopts, with modication, EITF 08-7 and clariesthat defensive intangible assets are assets, butnonadmitted for statutory accounting and reportingpurposes.

The EAIWG exposed the following tentative consensus

positions:

• EITF08-3:AccountingbyLesseesforMaintenance

Deposits (EITF 08-3). The Working Group exposeda tentative consensus clarifying that refundablemaintenance deposits shall be accounted for asassets which are nonadmitted. Other costs that donot increase the value or the usefulness of the leasedassets shall be expensed when incurred.

• EITF08-8:AccountingforanInstrument(oran

embedded eature) with a Settlement Amount That

is Based on the Stock o an Entity’s Consolidated

Subsidiary (EITF 08-8). The Working Group exposeda tentative consensus rejecting EITF 08-8 as notapplicable to statutory accounting.

This summary was prepared by Matt Wangard and Carolyn Estrada.

For your comments and suggestions please contact the authors -

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 11/12

11

Contributors

Eleanor Barrett

Senior ManagerDeloitte LLP

+1 (212) 436 2954

Carolyn Estrada

Senior ManagerDeloitte & Touche LLP

+1 (212) 436 2954

Matt Wangard

PartnerDeloitte & Touche LLP

+1 (312) 486 3224

For further information, visit our website at www.deloitte.com/us/insurance

ContactsFor more information, please contact:

Rebecca C. Amoroso

Vice Chairman

U.S. Insurance Leader

Deloitte LLP

+1 (973) 602 5385

Steve Foster

Director

Deloitte & Touche LLP

+1 (804) 697 1811

Howard Mills

Director & Chief Advisor

Insurance Industry Group

Deloitte LLP

+1 (212) 436 6752

Naru Navele

Partner

Deloitte & Touche LLP

+1 (973) 602 16801

Mark Parkin

Partner

Deloitte & Touche LLP+1 (212) 436 4761

Donald Schwegman

Partner

Deloitte & Touche LLP+1 (513) 784 7307

Ed Wilkins

Partner

Deloitte & Touche LLP+1 (402) 444 1810

7/30/2019 Us Fsi in NAIC UpdateSummer2009

http://slidepdf.com/reader/full/us-fsi-in-naic-updatesummer2009 12/12

About this newsletter

This newsletter is distributed for promotional purposes and is not intended to represent investment,

accounting, tax or legal advice. Any opinions and analyses presented or expressed herein are those of the

authors and are not intended to represent the position of Deloitte & Touche LLP or other individual members

of the rm. Data presented herein has been obtained from sources believed to be reliable.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member rms,

each of which isa legally separate and independent entity. Please see www.deloitte.com/aboutfor a detailed

description of the legal structureof Deloitte Touche Tohmatsu and its member rms. Please see www.deloitte.

com/us/aboutfor a detailed description of thelegal structure of Deloitte LLP and its subsidiaries.

Copyright ©2009 Deloitte Development LLC. All rights reserved.

Member of Deloitte Touche Tohmatsu

Recommended